Unlocking the Power of Prefunding to Lower Liabilities, Reduce Costs, and Maximize Assets

|

|

|

- Thomas Davis

- 6 years ago

- Views:

Transcription

1 Unlocking the Power of Prefunding to Lower Liabilities, Reduce Costs, and Maximize Assets September 14, 2017

2 Former Finance Director, Sausalito

3

4

5 An actuarial assumption is an estimate of an uncertain variable input into a financial model, normally for the purposes of calculating premiums or benefits. For example, a common actuarial assumption relates to predicting a person's lifespan, given their age, gender, health conditions and other factors. Present Value of Benefits Future NC Contributions Current NC Contributions Actuarial Accrued Liability Unfunded Actuarial Accrued Liability (UAAL) Market Value Market of Value Assets of Assets An accountant monitors and records the actual flow of money through a business or organization. It is the responsibility of the accountant to verify the accuracy of all money transactions and to make sure that all these transactions are legal and follow current guidelines.

6 CalPERS UAL is amortized over 30 years (i.e., there is a 30 year plan to pay off the unfunded liability) $ 30 years

7 CalPERS UAL is amortized over 30 years (i.e., there is a 30 year plan to pay off the unfunded liability) $ 30 years

8 CalPERS UAL is amortized over 30 years (i.e., there is a 30 year plan to pay off the unfunded liability) $ 30 years

9 CalPERS UAL is amortized over 30 years (i.e., there is a 30 year plan to pay off the unfunded liability) $ 30 years

10 CalPERS UAL is amortized over 30 years (i.e., there is a 30 year plan to pay off the unfunded liability) $ 30 years

11 CalPERS UAL is amortized over 30 years (i.e., there is a 30 year plan to pay off the unfunded liability) $ 30 years

12

13

14 Is Prefunding a lower cost for the City than Pay-Go in a sense that a given pension benefit can be provided with a lower contribution rate under funding? Is Prefunding more fair from the standpoint of intergenerational redistribution than Pay-Go? Is Prefunding better than Pay-Go in signaling future pension costs, and therefore impose greater discipline on pension policy formation? Is Prefunding more capable of handling demographic and economic risk than Pay-Go? Is Prefunding associated with higher savings (increased capital stock) than Pay-Go?

15 Where do I find the money? How do I account for the money? When can I withdraw the money? How do I balance the budget?

16 CalPERS UAL is amortized over 30 years (i.e., there is a 30 year plan to pay off the unfunded liability) $ 30 years

17

18

19

20

21 OPEB 1. Close OPEB benefits for all new entrants! 2. Offer to transition current employees from defined benefit OPEB to defined contributions 3. Set up an irrevocable OPEB trust 4. Move income producing capital assets into the irrevocable OPEB trust fund 5. Pay all retiree health care costs out of the irrevocable OPEB trust fund 6. When there are no more PAY-Go annuitants, close the irrevocable OPEB trust fund and return all income producing assets back to the original fund of origin PENSION 1. Set up an irrevocable Pension Trust Fund with Reserves and annual surpluses 2. Annually appropriate deposits to Pension Trust Fund at 100% or higher of annual amortization 3. Advance pay all pension amortization payments out of Pension Trust Funds to take advantage of CalPERS 3.5% prepayment discount. 4. Accumulate balances for Pension Rate Stabilization Pension Investment Return Hedge

22 Senior Consultant Public Agency Retirement Services Senior Vice President Public Agency Retirement Services

23 Approximately 80% of Cities offer some type of retiree health care benefits* Approximately 50% fund on a pay-as-you-go basis, and 50% prefund in some way (reserves/trust) Data shows that the total retiree health care liability of $16 billion Only $4 billion has been set aside (reserves/trust) Only 25% of OPEB liabilities are funded Many agencies fund their obligations on a pay-as-you-go basis, often unconcerned or unaware about the future costs they will face. *Data obtained from League of Cities Study (2015)

24 GASB 75 will replace GASB 45, which had initially changed the way that public agencies recognize their retiree health care liabilities Effective FY , public agencies will be required to account for and report their net OPEB liabilities on the balance sheet Agencies that do not have an irrevocable trust or are not making sufficient contributions towards their OPEB obligations will face a higher liability Change in frequency regardless of size, an actuarial valuation is required at least every 2 years

25 Investing assets results in a greater rate of return which in turn lowers liabilities Contributions into an irrevocable trust are assets which offset liabilities on financial statements Credit rating companies look more favorably on agencies who adopt an Irrevocable Trust and pre-fund A higher credit rating equates to lower borrowing costs Lower liabilities gives an agency a chance to keep some form of retiree health benefit; higher liabilities might cause agency to eliminate post-employment benefits

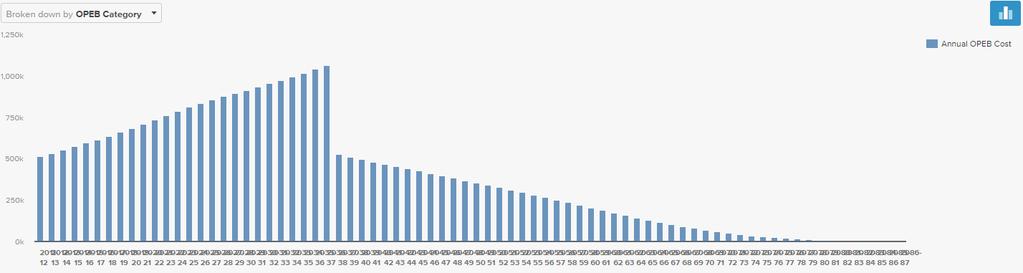

26 Retiree Health Care Costs as a Percentage of the Budget SAMPLE AGENCY $1,200,000 $1,000,000 Pay-as-you-Go Pre-Funding $800,000 $600,000 $400,000 $200,000 $0

27 Most California pension plans are underfunded (typically between 60-80% funded), resulting in increasing pension contribution rates New GASB 68 requirements to disclose Net Pension Liability on financial statements effective 14/15 FY In December 2016, CalPERS lowered the discount rate from 7.5% to 7.0% (with a 3 year phase in) Drop in the discount rate puts further pressure on participating member agencies budgets with increasing contribution rates and lower funding ratios

28 As of June 30, 2015, a Sample City s CalPERS pension plan is funded as: Actuarial Liability Assets Unfunded Liability $699.8 M $453.6 M $246.2 M Funded Ratio 64.8% Employer Contribution Amount ( ) $23.3 M * Data from Agency s CalPERS Actuarial Valuation

29 Projected misc. contributions increase from $7.9 M to $14.0 M in 6 years 59.00% 54.00% 49.00% 44.00% 39.00% 34.00% Projected CalPERS Rate (7.0%) Original CalPERS Rate (7.5%)

30 Projected safety contributions increase from $15.4 M to $27.4 M in 6 years % 95.00% 90.00% 85.00% 80.00% 75.00% 70.00% 65.00% 60.00% Projected CalPERS Rate (7.0%) Original CalPERS Rate (7.5%)

31 Previously, the only way to reduce retirement system unfunded liability was to send additional contributions in excess of annual required contribution to pension system As an alternative to sending more money directly to the retirement system, public agencies have setup their own locally controlled Section 115 retirement trust, separate and apart from the retirement system An IRS Private Letter Ruling has affirmed the tax-exempt status of the program More than one hundred (100) CA agencies (including nearly 50 cities) have adopted this program as of August 31, 2017, with many more entities considering adoption

32 Section 115 Trust can be used by local governments to fund essential governmental functions (i.e., retiree healthcare, pension) Trust is irrevocable and designed to pre-fund retirement plan obligations Assets are considered Fiduciary Funds that are legally set-aside assets that are available for use to reduce a city s Net Pension Liability Once contributions are placed into trust, assets from the trust can only be used for retirement plan purposes: reimburse agency for Retirement System contributions transferred directly to the Retirement System Pay retirement related expenditures (e.g., actuarial, audit, etc.)

33 Complete Local Control over Assets City has complete control over contributions and disbursements; timing, amount, and risk tolerance level Pension Rate Stabilization Assets can be transferred to retirement system plan at the City s direction, which can reduce or eliminate large fluctuations in Employer contributions to retirement system Rainy Day Fund Emergency source of funds when Employer revenues are impaired based on economic or other conditions Lower Costs 115 Trust might have lower overall administrative and investment management costs compared to the retirement system

34 Addresses Pension Liabilities for GASB 68 Contributions placed in an exclusive benefit trust addresses City s unfunded pension liability Improved Credit Ratings Rating agencies may look favorably upon actions to reduce liabilities Actuarially Sound Retirement System Provide integrity and security for the source of funding for retirement benefits Diversified Investing/ Potential for Greater Return than General Fund Can choose risk tolerance level for City s unique needs

35 Contribute 50% of a given year s realized year-end surplus to address pension liability Contribute amount equal to annual PERS employer contribution ($6 million) in order to allow full access to trust assets at all times Contribute $4 million to stabilize PERS employer misc. Rates to 28% and safety rates to 44% through FY One equals five plan - Contribute $1 million per year for 5 years based on premise that every contribution will save taxpayers $5 million over 25 years

36 Using one-time revenue source plus on-going savings from CalPERS unfunded liability prepayment Maintains a 15% general fund reserve and is targeting to make contributions over and above that threshold into the Trust Earmarked a portion of a recently approved local sales tax measure to be set aside for unfunded pension liabilities

37 City maintains oversight of the investment manager and the portfolio s risk tolerance level Investment restrictions that apply to the general fund (CA Government Code 53601) are not applicable to assets held in an Irrevocable Section 115 Trust Assets held in an irrevocable trust can be invested per Government Code Section and Investments can be diversified and invested in a prudent fashion Investments can be tailored to the City s unique demographics and circumstances Increased Risk Diversification

38 Expected Model Return PARS ASSET ALLOCATION STRATEGIES Efficient Frontier: Equity Fixed Income Cash Capital Appreciation Moderate Balanced Moderately Conservative Investment Objectives Conservative Equity Fixed Income Cash Conservative 5-20% 60-95% 0-20% Moderately Conservative 20-40% 50-80% 0-20% Moderate 40-60% 40-60% 0-20% Balanced 50-70% 30-50% 0-20% Capital Appreciation 65-85% 10-30% 0-20% Expected Model Risk (standard deviation)

39 Strategy Equity (%) % of Agencies Money Market % Conservative 5-20% 10.00% Moderately Conservative 20-40% 34.00% Moderate 40-60% 27.00% Balanced 50-70% 17.00% Capital Appreciation 65-85% 5.00% Custom Account %

40 Agency adopts resolution to establish trust to address pension liabilities Agency establishes an irrevocable trust and seeks guidance from IRS that proceeds are tax exempt (IRS Private Letter Ruling) Legal Documents (including Plan and Trust Document) are executed Develop investment policy and guidelines for Investment Manager Develop policies and procedures for future annual contributions and/or disbursements Annual Review of Investment Performance

41 Assistant City Manager, Administrative Services City of Morgan Hill

42 In June 2015, Morgan Hill had approximately $35 million in pension liability (now $51 million) and $2.4 million in unfunded OPEB liability (now $3.3 million) Council directed staff to analyze ways to reduce unfunded liabilities

43 Morgan Hill did not have OPEB plan Funded through pay-as-you-go For pension, the other option was to commit additional funds to CalPERS

44 Pay-as-you-Go Earmark Funds Irrevocable Trust Fund

45 GFOA best practices Local control Improved credit rating Reduction of net liabilities

46 Assets are restricted and cannot be used for other purposes Used only for contributions/payment Transfer to CalPERS to eliminate fluctuations Investments options less restricted

47 Existing relationship with PARS through alternate retirement plans Only player in town with IRS private ruling at that time Greater local control and efficiency Diversify and mitigate CalPERS investment volatility

48 Trustee US Bank $300K/year goal and pay-as-you-go amount Balance as of 7/31/17: $1.1 million Investment objective Moderate Strategy 1-year annualized return of 10.3%

49 Trustee US Bank $300K/year goal and Annual Required Contribution (ARC) Balance as of 7/31/17: $0.8 million Investment objective Moderately Conservative Strategy 1-year annualized return of 6.12%

50

City of El Segundo PARS Pension Rate Stabilization Program (PRSP) August 31, 2017

August 31, 2017") City of El Segundo PARS Pension Rate Stabilization Program (PRSP) August 31, 2017 Pension Funding Status As of June 30, 2015, City of El Segundo s CalPERS pension plan is funded as follows: Actuarial Liability

City of El Segundo PARS Pension Rate Stabilization Program (PRSP) August 31, 2017 Pension Funding Status As of June 30, 2015, City of El Segundo s CalPERS pension plan is funded as follows: Actuarial Liability

RESOLUTION AUTHORIZES THE ADOPTION OF AN OPEB FUNDING POLICY FOR THE OTHER POST EMPLOYMENT BENEFITS ( OPEB ) TRUST

TRUST") 10940. RESOLUTION 15-08 - AUTHORIZES THE ADOPTION OF AN OPEB FUNDING POLICY FOR THE OTHER POST EMPLOYMENT BENEFITS ( OPEB ) TRUST WHEREAS, The Delaware River and Bay Authority (the Authority ) is a bi-state

10940. RESOLUTION 15-08 - AUTHORIZES THE ADOPTION OF AN OPEB FUNDING POLICY FOR THE OTHER POST EMPLOYMENT BENEFITS ( OPEB ) TRUST WHEREAS, The Delaware River and Bay Authority (the Authority ) is a bi-state

OPEB (Other Post Employment Benefits) Funding and Investing. Massachusetts Association of Regional Schools (MARS) October 14, 2014

Funding and Investing. Massachusetts Association of Regional Schools (MARS) October 14, 2014") OPEB (Other Post Employment Benefits) Funding and Investing Massachusetts Association of Regional Schools (MARS) October 14, 2014 INTRODUCTIONS MAUREEN TOAL, MPA PARS (Public Agency Retirement Services)

OPEB (Other Post Employment Benefits) Funding and Investing Massachusetts Association of Regional Schools (MARS) October 14, 2014 INTRODUCTIONS MAUREEN TOAL, MPA PARS (Public Agency Retirement Services)

Meeting Date: September 28, From: Amy Cunningham, Administrative Services Director

Town of Moraga Ordinances, Resolutions, Requests for Action Agenda Item. E. 0 0 0 0 Meeting Date: September, 0 TOWN OF MORAGA STAFF REPORT_ To: Honorable Mayor and Councilmembers From: Amy Cunningham,

Town of Moraga Ordinances, Resolutions, Requests for Action Agenda Item. E. 0 0 0 0 Meeting Date: September, 0 TOWN OF MORAGA STAFF REPORT_ To: Honorable Mayor and Councilmembers From: Amy Cunningham,

PROPOSED ALTERNATIVES TO STRATEGICALLY PLAN FOR THE CITY S UNFUNDED ACCRUED PENSION LIABILITIES

STAFF REPORT DATE: March 13, 2018 TO: FROM: City Council Tony Clark, Finance Manager Michael L. Antwine II, Assistant City Manager PRESENTER: Tony Clark, Finance Manager 922 Machin Avenue Novato, CA 94945

STAFF REPORT DATE: March 13, 2018 TO: FROM: City Council Tony Clark, Finance Manager Michael L. Antwine II, Assistant City Manager PRESENTER: Tony Clark, Finance Manager 922 Machin Avenue Novato, CA 94945

Authorization to Establish IRS Section 115 Trust Fund and Appoint the City Manager as the Plan Administrator

Page 1 of 10 Office of the City Manager June 26, 2018 To: From: Honorable Mayor and Members of the City Council Dee Williams-Ridley, City Manager Submitted by: Henry Oyekanmi, Director, Finance Department

Page 1 of 10 Office of the City Manager June 26, 2018 To: From: Honorable Mayor and Members of the City Council Dee Williams-Ridley, City Manager Submitted by: Henry Oyekanmi, Director, Finance Department

Pension Funding Stabilization State Association of County Auditors 2016 Annual Conference. April 20, 2016

Pension Funding Stabilization State Association of County Auditors 2016 Annual Conference April 20, 2016 PANEL PARTICIPANTS Rob Larkins, Managing Director and Western Region Manager, Public Finance, Raymond

Pension Funding Stabilization State Association of County Auditors 2016 Annual Conference April 20, 2016 PANEL PARTICIPANTS Rob Larkins, Managing Director and Western Region Manager, Public Finance, Raymond

MEETING DATE: 03/23/2017 ITEM NO: 2 TOWN OF LOS GATOS FINANCE COMMITTEE REPORT DATE: MARCH 17, 2017 COUNCIL FINANCE COMMITTEE

TOWN OF LOS GATOS FINANCE COMMITTEE REPORT MEETING DATE: 03/23/2017 ITEM NO: 2 DATE: MARCH 17, 2017 TO: FROM: SUBJECT: COUNCIL FINANCE COMMITTEE LAUREL PREVETTI, TOWN MANAGER REVIEW, DISCUSS, AND RECOMMEND

TOWN OF LOS GATOS FINANCE COMMITTEE REPORT MEETING DATE: 03/23/2017 ITEM NO: 2 DATE: MARCH 17, 2017 TO: FROM: SUBJECT: COUNCIL FINANCE COMMITTEE LAUREL PREVETTI, TOWN MANAGER REVIEW, DISCUSS, AND RECOMMEND

City Pension Program UPDATED PROJECTIONS AND COST SAVINGS ALTERNATIVES

City Pension Program UPDATED PROJECTIONS AND COST SAVINGS ALTERNATIVES Table of Contents Overview of City Liabilities Pension Cost Trends and Budget Impact Recent CalPERS Developments and Cost Projections

City Pension Program UPDATED PROJECTIONS AND COST SAVINGS ALTERNATIVES Table of Contents Overview of City Liabilities Pension Cost Trends and Budget Impact Recent CalPERS Developments and Cost Projections

CITY OF CONCORD JUNE 30, 2015 REQUIRED SUPPLEMENTARY INFORMATION

91 SCHEDULE OF FUNDING PROGRESS The tables below shows a three-year analysis of the actuarial value of assets as a percentage of the actuarial accrued liability and the unfunded actuarial liability as

91 SCHEDULE OF FUNDING PROGRESS The tables below shows a three-year analysis of the actuarial value of assets as a percentage of the actuarial accrued liability and the unfunded actuarial liability as

City of Stockton. Retiree Healthcare Plan June 30, 2007 Actuarial Valuation Executive Summary

Retiree Healthcare Plan June 30, 2007 Actuarial Valuation Executive Summary June 2007 O:\Clients\\OPEB\2007\Reports\BA executive summary 07-06-22 OPEB valuation.doc On June 21, 2004, the Governmental Accounting

Retiree Healthcare Plan June 30, 2007 Actuarial Valuation Executive Summary June 2007 O:\Clients\\OPEB\2007\Reports\BA executive summary 07-06-22 OPEB valuation.doc On June 21, 2004, the Governmental Accounting

TCDRS Funding Policy. Effective as of the Dec. 31, 2014 Valuation

TCDRS Funding Policy Effective as of the Dec. 31, 2014 Valuation Approved by the TCDRS Board of Trustees on June 25, 2015 Table of Contents Introduction... 3 TCDRS funding overview... 3 Methodology for

TCDRS Funding Policy Effective as of the Dec. 31, 2014 Valuation Approved by the TCDRS Board of Trustees on June 25, 2015 Table of Contents Introduction... 3 TCDRS funding overview... 3 Methodology for

Investment Policy for OPEB

Investment Policy for OPEB Massachusetts Collectors & Treasurers Association 42 nd Annual School August 14, 2012 Presented by: Dan Sullivan of Sullivan, Rogers & Company and Joshua Paul of Bartholomew

Investment Policy for OPEB Massachusetts Collectors & Treasurers Association 42 nd Annual School August 14, 2012 Presented by: Dan Sullivan of Sullivan, Rogers & Company and Joshua Paul of Bartholomew

AGENDA REPORT. Meeting Date: December 19, 2017 Item Number: F-il To:

AGENDA REPORT Meeting Date: December 19, 2017 Item Number: F-il To: Honorable Mayor & City Council From: Don Rhoads, Director of Administrative Services/Chief Financial Officer Tatiana Szerwinski, Assistant

AGENDA REPORT Meeting Date: December 19, 2017 Item Number: F-il To: Honorable Mayor & City Council From: Don Rhoads, Director of Administrative Services/Chief Financial Officer Tatiana Szerwinski, Assistant

BOARD OF TRUSTEES Agenda Item Description

BOARD OF TRUSTEES Agenda Item Description BOARD MEETING DATE: 5/12/2016 SUBJECT: Acceptance of Napa Valley Community College District Governmental Accounting Standards Board (GASB) Actuarial Valuation

BOARD OF TRUSTEES Agenda Item Description BOARD MEETING DATE: 5/12/2016 SUBJECT: Acceptance of Napa Valley Community College District Governmental Accounting Standards Board (GASB) Actuarial Valuation

PRIVATE. August 7, Ms. Katie White Director of Fiscal Services MiraCosta Community College (MS #6) One Barnard Drive Oceanside, CA 92056

One Barnard Drive Oceanside, CA 92056") 530 B Street, Suite 900 San Diego, CA 92101-4404 (p) 619-239-0831 (f ) 619-239-0807 www.nyhart.com August 7, 2015 PRIVATE Ms. Katie White Director of Fiscal Services MiraCosta Community College (MS #6)

530 B Street, Suite 900 San Diego, CA 92101-4404 (p) 619-239-0831 (f ) 619-239-0807 www.nyhart.com August 7, 2015 PRIVATE Ms. Katie White Director of Fiscal Services MiraCosta Community College (MS #6)

GASB 43 AND 45, FUND 73, ACT 99

AN INTRODUCTION TO OPEB: GASB 43 AND 45, FUND 73, ACT 99 WASBO SPRING CONFERENCE 2015 Derek Sliter, School Finance Auditor Wisconsin Department of Public Instruction Gene Fornecker, School Finance Auditor

AN INTRODUCTION TO OPEB: GASB 43 AND 45, FUND 73, ACT 99 WASBO SPRING CONFERENCE 2015 Derek Sliter, School Finance Auditor Wisconsin Department of Public Instruction Gene Fornecker, School Finance Auditor

OPEB Trust Creation, Implementation, and Management and Hybrid DB-DC plans

OPEB Trust Creation, Implementation, and Management and Hybrid DB-DC plans Asset Management LLC San Francisco CA Los Angeles CA April 20, 2011 CMTA Presented By: Girard Miller, Senior Strategist Asset

OPEB Trust Creation, Implementation, and Management and Hybrid DB-DC plans Asset Management LLC San Francisco CA Los Angeles CA April 20, 2011 CMTA Presented By: Girard Miller, Senior Strategist Asset

CALPERS UPDATES, RATES AND ALTERNATIVES. Basic Pension Rule: Benefits + Expenses. Contributions* + Investment Earnings. Agenda

CALPERS UPDATES, RATES AND ALTERNATIVES Agenda Topic Definitions How We Got Here and CalPERS Changes Current and Historical Plan Information Contribution Projections PEPRA Cost Sharing Paying Down the

CALPERS UPDATES, RATES AND ALTERNATIVES Agenda Topic Definitions How We Got Here and CalPERS Changes Current and Historical Plan Information Contribution Projections PEPRA Cost Sharing Paying Down the

1.02 TRINITY COUNTY. County Contract No. Board Item Request Form Department Personnel. Contact Carol Martin

County Contract No. Department Personnel TRINITY COUNTY 1.02 Board Item Request Form 2016-09-20 Contact Carol Martin Phone 530-623-1325 Requested Agenda Location Presentations Requested Board Action: Receive

County Contract No. Department Personnel TRINITY COUNTY 1.02 Board Item Request Form 2016-09-20 Contact Carol Martin Phone 530-623-1325 Requested Agenda Location Presentations Requested Board Action: Receive

TOWN OF SUDBURY OTHER POSTEMPLOYMENT BENEFITS PROGRAM ACTUARIAL VALUATION

TOWN OF SUDBURY OTHER POSTEMPLOYMENT BENEFITS PROGRAM ACTUARIAL VALUATION July 1, 2015 Prepared by: Linda L. Bournival, FSA, EA, MAAA KMS Actuaries, LLC Fellow, Society of Actuaries Enrolled Actuary Member,

TOWN OF SUDBURY OTHER POSTEMPLOYMENT BENEFITS PROGRAM ACTUARIAL VALUATION July 1, 2015 Prepared by: Linda L. Bournival, FSA, EA, MAAA KMS Actuaries, LLC Fellow, Society of Actuaries Enrolled Actuary Member,

Other Post-Employment Benefits Irrevocable Trust. May 15, 2018

Other Post-Employment Benefits Irrevocable Trust May 15, 2018 What are Other Post-Employment Benefits (OPEB) Benefits offered by local government agencies to employees that are unrelated to pension benefits

Other Post-Employment Benefits Irrevocable Trust May 15, 2018 What are Other Post-Employment Benefits (OPEB) Benefits offered by local government agencies to employees that are unrelated to pension benefits

***ADDENDUM TWO*** REQUEST FOR PROPOSALS (RFP) Post Employment Benefits Other than Pensions Actuarial Valuation June 15, 2018

Post Employment Benefits Other than Pensions Actuarial Valuation June 15, 2018") ***ADDENDUM TWO*** REQUEST FOR PROPOSALS (RFP) Post Employment Benefits Other than Pensions Actuarial Valuation June 15, 2018 The following are answers to questions received by potential proposers. 1.

***ADDENDUM TWO*** REQUEST FOR PROPOSALS (RFP) Post Employment Benefits Other than Pensions Actuarial Valuation June 15, 2018 The following are answers to questions received by potential proposers. 1.

TOWN OF COHASSET, MASSACHUSETTS OTHER POSTEMPLOYMENT BENEFITS PROGRAM

TOWN OF COHASSET, MASSACHUSETTS OTHER POSTEMPLOYMENT BENEFITS PROGRAM ACTUARIAL VALUATION as of July 1, 2016 FINANCIAL REPORTING AND DISCLOSURES UNDER GASB 45 and GASB 74 as of June 30, 2017 KMS Actuaries,

TOWN OF COHASSET, MASSACHUSETTS OTHER POSTEMPLOYMENT BENEFITS PROGRAM ACTUARIAL VALUATION as of July 1, 2016 FINANCIAL REPORTING AND DISCLOSURES UNDER GASB 45 and GASB 74 as of June 30, 2017 KMS Actuaries,

To: Board of Directors Date: April 13, 2016

To: Board of Directors Date: April 13, 2016 From: Erick Cheung, Director of Finance Reviewed by: SUBJECT: OPEB Actuarial Valuation SUMMMARY OF ISSUES: The Government Accounting Standards Board (GASB) issued

To: Board of Directors Date: April 13, 2016 From: Erick Cheung, Director of Finance Reviewed by: SUBJECT: OPEB Actuarial Valuation SUMMMARY OF ISSUES: The Government Accounting Standards Board (GASB) issued

Other Postemployment Benefits OPEB

Other Postemployment Benefits OPEB Presented by James Powers ATFC October 19, 2013 October 19, 2013 Powers & Sullivan, LLC 1 Applicable GASB Statements - Pension GASB 25 - Financial Reporting for Defined

Other Postemployment Benefits OPEB Presented by James Powers ATFC October 19, 2013 October 19, 2013 Powers & Sullivan, LLC 1 Applicable GASB Statements - Pension GASB 25 - Financial Reporting for Defined

TOWN OF KINGSTON, MASSACHUSETTS OTHER POSTEMPLOYMENT BENEFITS PROGRAM

TOWN OF KINGSTON, MASSACHUSETTS OTHER POSTEMPLOYMENT BENEFITS PROGRAM ACTUARIAL VALUATION as of July 1, 2016 FINANCIAL REPORTING AND DISCLOSURES UNDER GASB 45 and GASB 74 as of June 30, 2017 KMS Actuaries,

TOWN OF KINGSTON, MASSACHUSETTS OTHER POSTEMPLOYMENT BENEFITS PROGRAM ACTUARIAL VALUATION as of July 1, 2016 FINANCIAL REPORTING AND DISCLOSURES UNDER GASB 45 and GASB 74 as of June 30, 2017 KMS Actuaries,

DUKES COUNTY POOLED OPEB TRUST OTHER POSTEMPLOYMENT BENEFITS PROGRAM ACTUARIAL VALUATION

DUKES COUNTY POOLED OPEB TRUST OTHER POSTEMPLOYMENT BENEFITS PROGRAM ACTUARIAL VALUATION July 1, 2012 Prepared by: Linda L. Bournival, FSA, EA, MAAA KMS Actuaries, LLC Fellow, Society of Actuaries Enrolled

DUKES COUNTY POOLED OPEB TRUST OTHER POSTEMPLOYMENT BENEFITS PROGRAM ACTUARIAL VALUATION July 1, 2012 Prepared by: Linda L. Bournival, FSA, EA, MAAA KMS Actuaries, LLC Fellow, Society of Actuaries Enrolled

Mayors & Council Members Executive Forum GASB 74/75 and the Cadillac Tax

Mayors & Council Members Executive Forum GASB 74/75 and the Cadillac Tax Presented By: Anil Comelo - City of Oakland Steve Gedestad - Keenan Patrick Clark PC Consulting June 23, 2016a License No. 0451271

Mayors & Council Members Executive Forum GASB 74/75 and the Cadillac Tax Presented By: Anil Comelo - City of Oakland Steve Gedestad - Keenan Patrick Clark PC Consulting June 23, 2016a License No. 0451271

CITY OF ROHNERT PARK CITY COUNCIL AGENDA REPORT

Mission Statement We Care for Our Residents by Working Together to Build a Better Community for Today and Tomorrow. ITEM NO. CITY OF ROHNERT PARK CITY COUNCIL AGENDA REPORT Meeting Date: November 10, 2015

Mission Statement We Care for Our Residents by Working Together to Build a Better Community for Today and Tomorrow. ITEM NO. CITY OF ROHNERT PARK CITY COUNCIL AGENDA REPORT Meeting Date: November 10, 2015

Stabilization Program (PRSP) Hartnell College. February 16, 2016

Hartnell College. February 16, 2016") Pension Rate Stabilization Program (PRSP) Hartnell College February 16, 2016 BACKGROUND GASB 68 now requires multiple employer pension plans to report each employers net pension liability Employers are

Pension Rate Stabilization Program (PRSP) Hartnell College February 16, 2016 BACKGROUND GASB 68 now requires multiple employer pension plans to report each employers net pension liability Employers are

June 30, Ms. Cathy Orme Finance Director Central Marin Police Authority 400 Magnolia Ave Larkspur, CA 94939

June 30, 2017 Ms. Cathy Orme Finance Director Central Marin Police Authority 400 Magnolia Ave Larkspur, CA 94939 Re: July 1, 2015 Actuarial Report on GASB 45 Retiree Benefit Valuation Dear Ms. Orme: We

June 30, 2017 Ms. Cathy Orme Finance Director Central Marin Police Authority 400 Magnolia Ave Larkspur, CA 94939 Re: July 1, 2015 Actuarial Report on GASB 45 Retiree Benefit Valuation Dear Ms. Orme: We

THE AEROSPACE CORPORATION RETIREE MEDICAL PLAN

THE AEROSPACE CORPORATION RETIREE MEDICAL PLAN SEPTEMBER 30, 2016 VALUATION FUNDING AND COST ACCOUNTING FINANCIAL REPORT FOR THE FISCAL YEAR ENDING SEPTEMBER 30, 2017 APRIL 2017 CONTENTS Executive Summary...

THE AEROSPACE CORPORATION RETIREE MEDICAL PLAN SEPTEMBER 30, 2016 VALUATION FUNDING AND COST ACCOUNTING FINANCIAL REPORT FOR THE FISCAL YEAR ENDING SEPTEMBER 30, 2017 APRIL 2017 CONTENTS Executive Summary...

CONTRA COSTA COUNTY COMMUNITY COLLEGE DISTRICT FUTURIS TRUST RETIRMENT BOARD OF AUTHORITY BYLAWS PREAMBLE

CONTRA COSTA COUNTY COMMUNITY COLLEGE DISTRICT FUTURIS TRUST RETIRMENT BOARD OF AUTHORITY BYLAWS PREAMBLE The objectives of the Contra Costa County Community College District (Public Entity) in establishing

CONTRA COSTA COUNTY COMMUNITY COLLEGE DISTRICT FUTURIS TRUST RETIRMENT BOARD OF AUTHORITY BYLAWS PREAMBLE The objectives of the Contra Costa County Community College District (Public Entity) in establishing

RESOLUTION AUTHORIZES THE ADOPTION OF A PENSION FUNDING POLICY FOR THE DELAWARE RIVER AND BAY AUTHORITY EMPLOYEES RETIREMENT PLAN

10940. RESOLUTION 15-07 - AUTHORIZES THE ADOPTION OF A PENSION FUNDING POLICY FOR THE DELAWARE RIVER AND BAY AUTHORITY EMPLOYEES RETIREMENT PLAN WHEREAS, The Delaware River and Bay Authority ( the Authority

10940. RESOLUTION 15-07 - AUTHORIZES THE ADOPTION OF A PENSION FUNDING POLICY FOR THE DELAWARE RIVER AND BAY AUTHORITY EMPLOYEES RETIREMENT PLAN WHEREAS, The Delaware River and Bay Authority ( the Authority

City of Oakland Postretirement Health Insurance Plan GASB 43/45 Actuarial Valuation Report as of July 1, 2015

City of Oakland Postretirement Health Insurance Plan GASB 43/45 Actuarial Valuation Report as of July 1, 2015 Produced by Cheiron May 2016 TABLE OF CONTENTS Section Page Letter of Transmittal... i Total

City of Oakland Postretirement Health Insurance Plan GASB 43/45 Actuarial Valuation Report as of July 1, 2015 Produced by Cheiron May 2016 TABLE OF CONTENTS Section Page Letter of Transmittal... i Total

CALIFORNIA EMPLOYERS RETIREE BENEFIT TRUST PROGRAM ("CERBT") AGREEMENT AND ELECTION OF. Count of Siskiyou (NAME OF EMPLOYER)

AGREEMENT AND ELECTION OF. Count of Siskiyou (NAME OF EMPLOYER)") CALIFORNIA EMPLOYERS RETIREE BENEFIT TRUST PROGRAM ("CERBT") AGREEMENT AND ELECTION OF Count of Siskiyou (NAME OF EMPLOYER) TO PREFUND OTHER POST-EMPLOYMENT BENEFITS THROUGH CalPERS WHEREAS (1) Government

CALIFORNIA EMPLOYERS RETIREE BENEFIT TRUST PROGRAM ("CERBT") AGREEMENT AND ELECTION OF Count of Siskiyou (NAME OF EMPLOYER) TO PREFUND OTHER POST-EMPLOYMENT BENEFITS THROUGH CalPERS WHEREAS (1) Government

RIVERSIDE COMMUNITY COLLEGE DISTRICT POST EMPLOYMENT BENEFITS OTHER THAN PENSIONS GASB 45 ACTUARIAL VALUATION

RIVERSIDE COMMUNITY COLLEGE DISTRICT POST EMPLOYMENT BENEFITS OTHER THAN PENSIONS GASB 45 ACTUARIAL VALUATION AS OF JULY 1, 2009 TABLE OF CONTENTS EXECUTIVE SUMMARY... 1 ACTUARIAL CERTIFICATION... 4 ACCOUNTING

RIVERSIDE COMMUNITY COLLEGE DISTRICT POST EMPLOYMENT BENEFITS OTHER THAN PENSIONS GASB 45 ACTUARIAL VALUATION AS OF JULY 1, 2009 TABLE OF CONTENTS EXECUTIVE SUMMARY... 1 ACTUARIAL CERTIFICATION... 4 ACCOUNTING

CalPERS Update and Path Forward

CalPERS Update and Path Forward Kelly Fox, Chief, Stakeholder Relations December 13, 2017 League of California Cities Fire Chiefs Facts & Figures 2 CalPERS Retirement Benefits 3 3,000+ employers 4 Financial

CalPERS Update and Path Forward Kelly Fox, Chief, Stakeholder Relations December 13, 2017 League of California Cities Fire Chiefs Facts & Figures 2 CalPERS Retirement Benefits 3 3,000+ employers 4 Financial

Actuarial Basics. Presented by Mike Overley, Regional Manager Tony Radjenovich, Regional Manager

Actuarial Basics Presented by Mike Overley, Regional Manager Tony Radjenovich, Regional Manager 1 Objectives Funding Concepts of Retirement Plans Actuarial Valuations Actuarial Terminology 2 Funding Concepts

Actuarial Basics Presented by Mike Overley, Regional Manager Tony Radjenovich, Regional Manager 1 Objectives Funding Concepts of Retirement Plans Actuarial Valuations Actuarial Terminology 2 Funding Concepts

Accounting for the OPEB Obligation

Accounting for the OPEB Obligation Tom Swain, F.S.A. August 18, 2016 Agenda Overview and effective dates Significant changes Sample balance sheet pre/post changes Plan sponsor implications Planning steps

Accounting for the OPEB Obligation Tom Swain, F.S.A. August 18, 2016 Agenda Overview and effective dates Significant changes Sample balance sheet pre/post changes Plan sponsor implications Planning steps

EXHIBIT A Page 1 of 26

Page 1 of 26 530 B Street, Suite 900 San Diego, CA 92101-4404 (p) 619-239-0831 (f ) 619-239-0807 www.nyhart.com January 23, 2017 Ms. Kim McCord Executive Director, Fiscal Services South Orange County CCD

Page 1 of 26 530 B Street, Suite 900 San Diego, CA 92101-4404 (p) 619-239-0831 (f ) 619-239-0807 www.nyhart.com January 23, 2017 Ms. Kim McCord Executive Director, Fiscal Services South Orange County CCD

October 13, 2016 Actuarial Valuation Report: The City of Newport, Rhode Island Post-Retirement Benefits Plan as of July 1, 2016

October 13, 2016 Actuarial Valuation Report: The City of Newport, Rhode Island Post-Retirement Benefits Plan as of July 1, 2016 Prepared by: Korn Ferry Hay Group, Inc. 12012 Sunset Hills Road, Suite 920

October 13, 2016 Actuarial Valuation Report: The City of Newport, Rhode Island Post-Retirement Benefits Plan as of July 1, 2016 Prepared by: Korn Ferry Hay Group, Inc. 12012 Sunset Hills Road, Suite 920

ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, City of Plantation General Employees Retirement System

ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2014 City of Plantation General Employees Retirement System ANNUAL EMPLOYER CONTRIBUTION IS DETERMINED BY THIS VALUATION FOR THE FISCAL YEAR ENDING SEPTEMBER

ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2014 City of Plantation General Employees Retirement System ANNUAL EMPLOYER CONTRIBUTION IS DETERMINED BY THIS VALUATION FOR THE FISCAL YEAR ENDING SEPTEMBER

TOWN OF TISBURY OTHER POSTEMPLOYMENT BENEFITS PROGRAM

TOWN OF TISBURY Participant in the Dukes County Pooled OPEB Trust OTHER POSTEMPLOYMENT BENEFITS PROGRAM ACTUARIAL VALUATION as of July 1, 2016 FINANCIAL REPORTING AND DISCLOSURES UNDER GASB 45 and GASB

TOWN OF TISBURY Participant in the Dukes County Pooled OPEB Trust OTHER POSTEMPLOYMENT BENEFITS PROGRAM ACTUARIAL VALUATION as of July 1, 2016 FINANCIAL REPORTING AND DISCLOSURES UNDER GASB 45 and GASB

Managing Your OPEB & Other Benefit Liabilities

Managing Your OPEB & Other Benefit Liabilities Eric O Leary, PARS Debbie Fry, School Services of California Teri Burns, CSBA October 18, 2016 Today s Presenters Eric O Leary Senior Vice President, PARS

Managing Your OPEB & Other Benefit Liabilities Eric O Leary, PARS Debbie Fry, School Services of California Teri Burns, CSBA October 18, 2016 Today s Presenters Eric O Leary Senior Vice President, PARS

CITY OF CONCORD JUNE 30, 2016 REQUIRED SUPPLEMENTARY INFORMATION

90 SCHEDULE OF FUNDING PROGRESS The tables below shows a three-year analysis of the actuarial value of assets as a percentage of the actuarial accrued liability and the unfunded actuarial liability as

90 SCHEDULE OF FUNDING PROGRESS The tables below shows a three-year analysis of the actuarial value of assets as a percentage of the actuarial accrued liability and the unfunded actuarial liability as

September 10, 2015 PRIVATE

530 B Street, Suite 900 San Diego, CA 92101-8002 (p) 619-239-0831 (f ) 619-239-0807 www.nyhart.com September 10, 2015 PRIVATE Mr. Doug Smith Vice Chancellor of Administrative Services San Jose/Evergreen

530 B Street, Suite 900 San Diego, CA 92101-8002 (p) 619-239-0831 (f ) 619-239-0807 www.nyhart.com September 10, 2015 PRIVATE Mr. Doug Smith Vice Chancellor of Administrative Services San Jose/Evergreen

CITY OF SAUSALITO MISCELLANEOUS AND SAFETY PLANS. CalPERS Actuarial Issues 6/30/14 Valuation Preliminary Results

CITY OF SAUSALITO MISCELLANEOUS AND SAFETY PLANS CalPERS Actuarial Issues 6/30/14 Valuation Preliminary Results Presented by John Bartel, President Prepared by Bianca Lin, Assistant Vice President Kevin

CITY OF SAUSALITO MISCELLANEOUS AND SAFETY PLANS CalPERS Actuarial Issues 6/30/14 Valuation Preliminary Results Presented by John Bartel, President Prepared by Bianca Lin, Assistant Vice President Kevin

History & Cost of the City of Concord s Retiree Healthcare Benefit Program

History & Cost of the City of Concord s Retiree Healthcare Benefit Program Executive Summary Substantially all full-time City of Concord employees and their qualified dependents are eligible for retiree

History & Cost of the City of Concord s Retiree Healthcare Benefit Program Executive Summary Substantially all full-time City of Concord employees and their qualified dependents are eligible for retiree

REQUIRED SUPPLEMENTARY INFORMATION

REQUIRED SUPPLEMENTARY INFORMATION DW SCHEDULE OF CHANGES IN NET PENSION LIABILITY AND RELATED RATIOS DURING THE MEASUREMENT PERIOD County Miscellaneous, Agent Multiple Employer Plan Measurement Period

REQUIRED SUPPLEMENTARY INFORMATION DW SCHEDULE OF CHANGES IN NET PENSION LIABILITY AND RELATED RATIOS DURING THE MEASUREMENT PERIOD County Miscellaneous, Agent Multiple Employer Plan Measurement Period

M E M O R A N D U M. Mayor Gavin Newsom Members of the Board of Supervisors. Report on Retiree (Postemployment) Medical Benefit Costs

Medical Benefit Costs") CITY AND COUNTY OF SAN FRANCISCO OFFICE OF THE CONTROLLER Ben Rosenfield Controller Monique Zmuda Deputy Controller M E M O R A N D U M TO: FROM: Mayor Gavin Newsom Members of the Board of Supervisors

CITY AND COUNTY OF SAN FRANCISCO OFFICE OF THE CONTROLLER Ben Rosenfield Controller Monique Zmuda Deputy Controller M E M O R A N D U M TO: FROM: Mayor Gavin Newsom Members of the Board of Supervisors

November 15, 2016 PRIVATE

530 B Street, Suite 900 San Diego, CA 92101-4404 (p) 619-239-0831 (f ) 619-239-0807 www.nyhart.com November 15, 2016 PRIVATE Mr. Steve Dickinson Assistant Superintendent of Administrative Services Oxnard

530 B Street, Suite 900 San Diego, CA 92101-4404 (p) 619-239-0831 (f ) 619-239-0807 www.nyhart.com November 15, 2016 PRIVATE Mr. Steve Dickinson Assistant Superintendent of Administrative Services Oxnard

MARTHA'S VINEYARD LAND BANK OTHER POSTEMPLOYMENT BENEFITS PROGRAM

MARTHA'S VINEYARD LAND BANK Participant in the Dukes County Pooled OPEB Trust OTHER POSTEMPLOYMENT BENEFITS PROGRAM ACTUARIAL VALUATION as of July 1, 2016 FINANCIAL REPORTING AND DISCLOSURES UNDER GASB

MARTHA'S VINEYARD LAND BANK Participant in the Dukes County Pooled OPEB Trust OTHER POSTEMPLOYMENT BENEFITS PROGRAM ACTUARIAL VALUATION as of July 1, 2016 FINANCIAL REPORTING AND DISCLOSURES UNDER GASB

City of Palo Alto (ID # 7553) City Council Staff Report

City Council Staff Report") City of Palo Alto (ID # 7553) City Council Staff Report Report Type: Consent Calendar Meeting Date: 1/23/2017 Summary Title: Pension Trust Supplemental Funds Title: Authorization to Establish a Supplemental

City of Palo Alto (ID # 7553) City Council Staff Report Report Type: Consent Calendar Meeting Date: 1/23/2017 Summary Title: Pension Trust Supplemental Funds Title: Authorization to Establish a Supplemental

UP-ISLAND REGIONAL SCHOOL DISTRICT OTHER POSTEMPLOYMENT BENEFITS PROGRAM

UP-ISLAND REGIONAL SCHOOL DISTRICT Participant in the Dukes County Pooled OPEB Trust OTHER POSTEMPLOYMENT BENEFITS PROGRAM ACTUARIAL VALUATION as of July 1, 2016 FINANCIAL REPORTING AND DISCLOSURES UNDER

UP-ISLAND REGIONAL SCHOOL DISTRICT Participant in the Dukes County Pooled OPEB Trust OTHER POSTEMPLOYMENT BENEFITS PROGRAM ACTUARIAL VALUATION as of July 1, 2016 FINANCIAL REPORTING AND DISCLOSURES UNDER

System Keynotes. Investment Strategy Actuarial Results, Funded Levels, Contributions, Demographics

City Council Working Session February 13, 2012 Agenda System Keynotes Trust Performance, Market Returns, Investment Strategy Actuarial Results, Funded Levels, Contributions, Demographics 1 City Ordinance

City Council Working Session February 13, 2012 Agenda System Keynotes Trust Performance, Market Returns, Investment Strategy Actuarial Results, Funded Levels, Contributions, Demographics 1 City Ordinance

THE PERFORMETER. A Financial Statement Analysis of Oklahoma County As of and for the year ended June 30, by Crawford & Associates, P.C.

THE PERFORMETER A Financial Statement Analysis of Oklahoma County As of and for the year ended June 30, 2008 by Crawford & Associates, P.C. What is a Performeter? An analysis that takes governmental financial

THE PERFORMETER A Financial Statement Analysis of Oklahoma County As of and for the year ended June 30, 2008 by Crawford & Associates, P.C. What is a Performeter? An analysis that takes governmental financial

MEETING YOUR OPEB OBLIGATIONS PREPARING FOR GASB 75

MEETING YOUR OPEB OBLIGATIONS PREPARING FOR GASB 75 Presented by: Tanya Rocchio, Managing Director, Business Development Ronald J. Smith, FSA, Director, Actuarial Services This presentation is for general

MEETING YOUR OPEB OBLIGATIONS PREPARING FOR GASB 75 Presented by: Tanya Rocchio, Managing Director, Business Development Ronald J. Smith, FSA, Director, Actuarial Services This presentation is for general

CITY OF FREEPORT ACCOUNTING FOR POST-EMPLOYMENT BENEFIT PLANS UNDER GASB #45 FOR FISCAL YEAR ENDING APRIL 30, 2017

CITY OF FREEPORT ACCOUNTING FOR POST-EMPLOYMENT BENEFIT PLANS UNDER GASB #45 FOR FISCAL YEAR ENDING APRIL 30, 2017 JUNE 2017 TABLE OF CONTENTS BACKGROUND Retiree Medical Plan... 1 Funding Versus Accounting...

CITY OF FREEPORT ACCOUNTING FOR POST-EMPLOYMENT BENEFIT PLANS UNDER GASB #45 FOR FISCAL YEAR ENDING APRIL 30, 2017 JUNE 2017 TABLE OF CONTENTS BACKGROUND Retiree Medical Plan... 1 Funding Versus Accounting...

ACTUARIAL SURS2015. Letter of Certification. Actuarial Report. Analysis of Funding. Tests of Financial Soundness

ANALYZING ACTUARIAL Letter of Certification Actuarial Report Analysis of Funding Tests of Financial Soundness SURS2015 The Comprehensive Annual Financial Report for Fiscal Year Ended June 30, 2015 Letter

ANALYZING ACTUARIAL Letter of Certification Actuarial Report Analysis of Funding Tests of Financial Soundness SURS2015 The Comprehensive Annual Financial Report for Fiscal Year Ended June 30, 2015 Letter

SAN JOSÉ/EVERGREEN COMMUNITY COLLEGE DISTRICT San Jose, California

SAN JOSÉ/EVERGREEN COMMUNITY COLLEGE DISTRICT San Jose, California RETIREMENT FUTURIS PUBLIC ENTITY INVESTMENT TRUST FINANCIAL STATEMENTS June 30, 2014 San Jose, California FINANCIAL STATEMENTS June 30,

SAN JOSÉ/EVERGREEN COMMUNITY COLLEGE DISTRICT San Jose, California RETIREMENT FUTURIS PUBLIC ENTITY INVESTMENT TRUST FINANCIAL STATEMENTS June 30, 2014 San Jose, California FINANCIAL STATEMENTS June 30,

RESOLUTION ADOPTING A CITY COUNCIL POLICY FOR FUNDING OTHER POST RETIREMENT BENEFITS (OPEB) RELATED TO RETIREE HEALTHCARE

RELATED TO RETIREE HEALTHCARE") TO: FROM: Honorable Mayor and City Council Laura C. Kuhn, City Manager Agenda Item No. 9B November 10, 2015 SUBJECT: RESOLUTION ADOPTING A CITY COUNCIL POLICY FOR FUNDING OTHER POST RETIREMENT BENEFITS

TO: FROM: Honorable Mayor and City Council Laura C. Kuhn, City Manager Agenda Item No. 9B November 10, 2015 SUBJECT: RESOLUTION ADOPTING A CITY COUNCIL POLICY FOR FUNDING OTHER POST RETIREMENT BENEFITS

To: Administration and Finance Committee Date: March 26, 2014

To: Administration and Finance Committee Date: March 26, 2014 From: Kathy Casenave, Director of Finance Reviewed by: SUBJECT: OPEB ACTUARIAL VALUATION Summary of Issues: The Government Accounting Standards

To: Administration and Finance Committee Date: March 26, 2014 From: Kathy Casenave, Director of Finance Reviewed by: SUBJECT: OPEB ACTUARIAL VALUATION Summary of Issues: The Government Accounting Standards

Sample Funding Strategies

Sample Funding Strategies Below is a list of sample funding strategies. To jump to a specific strategy view bookmarks on the left and click on that strategy, or simply scroll down. Sample Funding Statement

Sample Funding Strategies Below is a list of sample funding strategies. To jump to a specific strategy view bookmarks on the left and click on that strategy, or simply scroll down. Sample Funding Statement

CITY OF YPSILANTI ACCOUNTING FOR POST EMPLOYMENT BENEFIT PLANS UNDER GASB #45 AS OF JUNE 30, 2017 FOR FISCAL YEAR ENDING JUNE 30, 2017

CITY OF YPSILANTI ACCOUNTING FOR POST EMPLOYMENT BENEFIT PLANS UNDER GASB #45 AS OF JUNE 30, 2017 FOR FISCAL YEAR ENDING JUNE 30, 2017 OCTOBER 2017 TABLE OF CONTENTS BACKGROUND Summary of Principal Results...

CITY OF YPSILANTI ACCOUNTING FOR POST EMPLOYMENT BENEFIT PLANS UNDER GASB #45 AS OF JUNE 30, 2017 FOR FISCAL YEAR ENDING JUNE 30, 2017 OCTOBER 2017 TABLE OF CONTENTS BACKGROUND Summary of Principal Results...

August 31, 2017 PRIVATE

August 31, 2017 PRIVATE Mr. Doug Smith Vice Chancellor of Administrative Services San Jose/Evergreen Community College District 40 S. Market Street, 6th Floor San Jose, CA 95113-2367 Re: OPEB Actuarial

August 31, 2017 PRIVATE Mr. Doug Smith Vice Chancellor of Administrative Services San Jose/Evergreen Community College District 40 S. Market Street, 6th Floor San Jose, CA 95113-2367 Re: OPEB Actuarial

Prepared by the Metropolitan Transit Authority Of Harris County, Texas Divisions of Accounting and Treasury Services

Metropolitan Transit Authority Transport Workers Union Pension Plan, Local 260, AFL-CIO Comprehensive Annual Financial Report December 31, 2013 and 2012 Prepared by the Metropolitan Transit Authority Of

Metropolitan Transit Authority Transport Workers Union Pension Plan, Local 260, AFL-CIO Comprehensive Annual Financial Report December 31, 2013 and 2012 Prepared by the Metropolitan Transit Authority Of

GOGEBIC COUNTY EMPLOYEES RETIREMENT SYSTEM ACTUARIAL FUNDING POLICY

GOGEBIC COUNTY EMPLOYEES RETIREMENT SYSTEM ACTUARIAL FUNDING POLICY WHEREAS, the Gogebic County Employees Retirement System ( Retirement System ) is established and administered pursuant to the County

GOGEBIC COUNTY EMPLOYEES RETIREMENT SYSTEM ACTUARIAL FUNDING POLICY WHEREAS, the Gogebic County Employees Retirement System ( Retirement System ) is established and administered pursuant to the County

March 11, Ms. Kim McCord Executive Director, Fiscal Services South Orange County CCD Marguerite Parkway Mission Viejo, CA 92692

Page 1 of 26 450 B Street, Suite 750 San Diego, CA 92101-8002 (p) 619-239-0831 (f ) 619-239-0807 www.nyhart.com March 11, 2015 Ms. Kim McCord Executive Director, Fiscal Services South Orange County CCD

Page 1 of 26 450 B Street, Suite 750 San Diego, CA 92101-8002 (p) 619-239-0831 (f ) 619-239-0807 www.nyhart.com March 11, 2015 Ms. Kim McCord Executive Director, Fiscal Services South Orange County CCD

CalPERS Update & Additional Payment Discussion

CalPERS Update & Additional Payment Discussion CITY COUNCIL FEBRUARY 20, 2018 2/20/18 1 La Palma Pension Plan 3 Miscellaneous Plans Tier I 2.7% @ 55 Effective 2003 Tier II 2.0% @60 Effective 2011 Tier

CalPERS Update & Additional Payment Discussion CITY COUNCIL FEBRUARY 20, 2018 2/20/18 1 La Palma Pension Plan 3 Miscellaneous Plans Tier I 2.7% @ 55 Effective 2003 Tier II 2.0% @60 Effective 2011 Tier

TIBURON FIRE PROTECTION DISTRICT

TIBURON FIRE PROTECTION DISTRICT VALUATION OF RETIREE HEALTH BENEFITS REPORT OF GASB 45 VALUATION AS OF JANUARY 1, 2015 Prepared by: North Bay Pensions November 21, 2015 1 CONTENTS OF THIS REPORT Actuarial

TIBURON FIRE PROTECTION DISTRICT VALUATION OF RETIREE HEALTH BENEFITS REPORT OF GASB 45 VALUATION AS OF JANUARY 1, 2015 Prepared by: North Bay Pensions November 21, 2015 1 CONTENTS OF THIS REPORT Actuarial

AGENDA ITEM 1 I Consent Item. California Employer s Retiree Benefit Trust Program (CERBT) funding for Other Post-Employment Benefits Funding (OPEB)

funding for Other Post-Employment Benefits Funding (OPEB)") AGENDA ITEM 1 I Consent Item MEMORANDUM DATE: March 1, 2018 TO: FROM: SUBJECT: El Dorado County Transit Authority Julie Petersen, Finance Manager California Employer s Retiree Benefit Trust Program (CERBT)

AGENDA ITEM 1 I Consent Item MEMORANDUM DATE: March 1, 2018 TO: FROM: SUBJECT: El Dorado County Transit Authority Julie Petersen, Finance Manager California Employer s Retiree Benefit Trust Program (CERBT)

KALKASKA COUNTY ROAD COMMISSION OPEB BENEFITS Kalkaska County Road Commission

Kalkaska County Road Commission ACCOUNTING REPORT AND VALUATION AS PROVIDED FOR UNDER THE ALTERNATE CALCULATION PROVISIONS OF GASB STATEMENTS NO. 43 & 45 For the Period January 1, 2016 to December 31,

Kalkaska County Road Commission ACCOUNTING REPORT AND VALUATION AS PROVIDED FOR UNDER THE ALTERNATE CALCULATION PROVISIONS OF GASB STATEMENTS NO. 43 & 45 For the Period January 1, 2016 to December 31,

FOREST PRESERVE DISTRICT OF WILL COUNTY, ILLINOIS RETIREE HEALTH INSURANCE TRUST FUND ANNUAL FINANCIAL REPORT

FOREST PRESERVE DISTRICT OF WILL COUNTY, ILLINOIS ANNUAL FINANCIAL REPORT For the Years Ended December 31, 2014 and 2013 FOREST PRESERVE DISTRICT OF WILL COUNTY, ILLINOIS TABLE OF CONTENTS Page(s) INDEPENDENT

FOREST PRESERVE DISTRICT OF WILL COUNTY, ILLINOIS ANNUAL FINANCIAL REPORT For the Years Ended December 31, 2014 and 2013 FOREST PRESERVE DISTRICT OF WILL COUNTY, ILLINOIS TABLE OF CONTENTS Page(s) INDEPENDENT

General Employees Retirement Plan

Freiman Little Actuaries, LLC Phone 321 453 6542 4105 Savannahs Trail Fax 321 453 6998 Merritt Island, FL 32953 City of Rockledge General Employees Retirement Plan Actuarial Valuation as of October 1,

Freiman Little Actuaries, LLC Phone 321 453 6542 4105 Savannahs Trail Fax 321 453 6998 Merritt Island, FL 32953 City of Rockledge General Employees Retirement Plan Actuarial Valuation as of October 1,

CITY OF LARKSPUR Staff Report. November 19, 2014 Council Meeting. Honorable Mayor Morrison and Members of the City Council

AGENDA ITEM 7.2 CITY OF LARKSPUR Staff Report November 19, 2014 Council Meeting DATE: November 14, 2014 TO: FROM: SUBJECT: Honorable Mayor Morrison and Members of the City Council Dan Schwarz, City Manager

AGENDA ITEM 7.2 CITY OF LARKSPUR Staff Report November 19, 2014 Council Meeting DATE: November 14, 2014 TO: FROM: SUBJECT: Honorable Mayor Morrison and Members of the City Council Dan Schwarz, City Manager

Accounting for Retiree Health Care: An Overview of GASB OPEB

Accounting for Retiree Health Care: An Overview of GASB OPEB A Presentation to the 2004 Legislative Conference by Paul Zorn Gabriel, Roeder, Smith & Company (www.grsnet.com) Washington, DC February 10,

Accounting for Retiree Health Care: An Overview of GASB OPEB A Presentation to the 2004 Legislative Conference by Paul Zorn Gabriel, Roeder, Smith & Company (www.grsnet.com) Washington, DC February 10,

Multiple Employer Trusts and OPEB Prefunding by CERBT Employers. Rand Anderson CalPERS Constituent Relations Office

Multiple Employer Trusts and OPEB Prefunding by CERBT Employers Rand Anderson CalPERS Constituent Relations Office Discussion Overview Multiple Employer Trusts Well Known Providers Legal Basis Tax Form

Multiple Employer Trusts and OPEB Prefunding by CERBT Employers Rand Anderson CalPERS Constituent Relations Office Discussion Overview Multiple Employer Trusts Well Known Providers Legal Basis Tax Form

Postretirement Benefit Valuation Report Under GASB 45 for Fiscal Year Ending October 31, 2010

December 14, 2010 Postretirement Benefit Valuation Report Under GASB 45 for Fiscal Year Ending October 31, 2010 New York State Housing Finance Agency State of New York Mortgage Agency New York State Affordable

December 14, 2010 Postretirement Benefit Valuation Report Under GASB 45 for Fiscal Year Ending October 31, 2010 New York State Housing Finance Agency State of New York Mortgage Agency New York State Affordable

GASB 45: Reporting the True Cost of Other Post-Employment Benefits

A RESEARCH SERIES FROM THE OFFICE OF THE NEW YORK STATE COMPTROLLER Thomas P. DiNapoli State Comptroller DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY LOCAL GOVERNMENT ISSUES IN FOCUS GASB 45:

A RESEARCH SERIES FROM THE OFFICE OF THE NEW YORK STATE COMPTROLLER Thomas P. DiNapoli State Comptroller DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY LOCAL GOVERNMENT ISSUES IN FOCUS GASB 45:

Pension Funding & Plan Design

Pension Funding & Plan Design Part 1 The Fundamentals Presented by Sue Feinberg and Matt Taylor Agenda Overview of MERS How Defined Benefit Plans Work Fundamentals of Pension Funding Determining Annual

Pension Funding & Plan Design Part 1 The Fundamentals Presented by Sue Feinberg and Matt Taylor Agenda Overview of MERS How Defined Benefit Plans Work Fundamentals of Pension Funding Determining Annual

Other Post-Employment Benefits ( OPEB ) Pre-Funding

Pre-Funding") Other Post-Employment Benefits ( OPEB ) Pre-Funding John C. Robinson, CTP Senior Managing Consultant Multi-Asset Class Portfolio Strategist December 4, 2017 PFM Asset Management LLC. 221 West 6 th Street

Other Post-Employment Benefits ( OPEB ) Pre-Funding John C. Robinson, CTP Senior Managing Consultant Multi-Asset Class Portfolio Strategist December 4, 2017 PFM Asset Management LLC. 221 West 6 th Street

Agenda. Pension and OPEB News GASB 67, 68, 71, 73, 74, and 75. July 23, 2015

Pension and OPEB News GASB 67, 68, 71, 73, 74, and 75 July 23, 2015 Mary Beth Redding mbredding@bartel-associates.com www.bartel-associates.com Agenda GASB 68 Overview 1 GASB68C CalPERS lpersreports 12

Pension and OPEB News GASB 67, 68, 71, 73, 74, and 75 July 23, 2015 Mary Beth Redding mbredding@bartel-associates.com www.bartel-associates.com Agenda GASB 68 Overview 1 GASB68C CalPERS lpersreports 12

M U N I C I P A L E M P L O Y E E S A N N U I T Y A N D B E N E F I T F U N D O F C H I C A G O ACTUARIAL VALUATION R E P O R T F O R T H E Y E A R

M U N I C I P A L E M P L O Y E E S A N N U I T Y A N D B E N E F I T F U N D O F C H I C A G O ACTUARIAL VALUATION R E P O R T F O R T H E Y E A R ENDING DECEMBER 31, 2013 APRIL 2 0 1 4 April 10, 2014

M U N I C I P A L E M P L O Y E E S A N N U I T Y A N D B E N E F I T F U N D O F C H I C A G O ACTUARIAL VALUATION R E P O R T F O R T H E Y E A R ENDING DECEMBER 31, 2013 APRIL 2 0 1 4 April 10, 2014

Actuarial Section. Actuarial Section THE BOTTOM LINE. The average MSEP retirement benefit is $15,609 per year.

Actuarial Section THE BOTTOM LINE The average MSEP retirement benefit is $15,609 per year. Actuarial Section Actuarial Section 89 Actuary s Certification Letter 91 Summary of Actuarial Assumptions 97 Actuarial

Actuarial Section THE BOTTOM LINE The average MSEP retirement benefit is $15,609 per year. Actuarial Section Actuarial Section 89 Actuary s Certification Letter 91 Summary of Actuarial Assumptions 97 Actuarial

Retiree Health Insurance Subsidy Actuarial Assumption Estimating Conference

Retiree Health Insurance Subsidy Actuarial Assumption Estimating Conference Executive Summary for October 19, 2010 The Florida Retirement System Actuarial Assumption Conference met on October 19, 2010

Retiree Health Insurance Subsidy Actuarial Assumption Estimating Conference Executive Summary for October 19, 2010 The Florida Retirement System Actuarial Assumption Conference met on October 19, 2010

RESOLUTION ELECTING TO ESTABLISH A HEALTH BENEFIT VESTING REQUIREMENT FOR FUTURE RETIREES UNDER THE PUBLIC EMPLOYEES MEDICAL AND HOSPITAL CARE ACT

Agenda Item No. 9a November 11, 2008 TO: FROM: SUBJECT: Honorable Mayor and City Council Attention: David J. Van Kirk, City Manager Dawn M. Villarreal, Director of Human Resources RESOLUTION APPROVING

Agenda Item No. 9a November 11, 2008 TO: FROM: SUBJECT: Honorable Mayor and City Council Attention: David J. Van Kirk, City Manager Dawn M. Villarreal, Director of Human Resources RESOLUTION APPROVING

CSMFO CalPERS Actuarial Issues

CSMFO CalPERS Actuarial Issues Presented by Prepared by John E. Bartel Mary Elizabeth Redding, Partner Bianca Lin, Assistant Vice President Matthew Childs, Actuarial Analyst James Yuan, Actuarial Analyst

CSMFO CalPERS Actuarial Issues Presented by Prepared by John E. Bartel Mary Elizabeth Redding, Partner Bianca Lin, Assistant Vice President Matthew Childs, Actuarial Analyst James Yuan, Actuarial Analyst

City of Manchester Employees Contributory Retirement System GASB Statement No. 74, Financial Reporting for Postemployment Benefit Plans Other Than

City of Manchester Employees Contributory Retirement System GASB Statement No. 74, Financial Reporting for Postemployment Benefit Plans Other Than Pension Plans December 31, 2017 May 18, 2018 Board of

City of Manchester Employees Contributory Retirement System GASB Statement No. 74, Financial Reporting for Postemployment Benefit Plans Other Than Pension Plans December 31, 2017 May 18, 2018 Board of

RETIREMENT PLAN FOR POLICE OFFICERS AND FIREFIGHTERS

RETIREMENT PLAN FOR POLICE OFFICERS AND FIREFIGHTERS FINANCIAL STATEMENTS TABLE OF CONTENTS PAGE INDEPENDENT AUDITOR S REPORT 1-3 MANAGEMENT S DISCUSSION AND ANALYSIS 4-7 FINANCIAL STATEMENTS Statement

RETIREMENT PLAN FOR POLICE OFFICERS AND FIREFIGHTERS FINANCIAL STATEMENTS TABLE OF CONTENTS PAGE INDEPENDENT AUDITOR S REPORT 1-3 MANAGEMENT S DISCUSSION AND ANALYSIS 4-7 FINANCIAL STATEMENTS Statement

Subject: Actuarial Valuation Report for the Year Ending December 31, 2008

POLICEMEN S ANNUITY AND BENEFIT FUND OF CHICAGO ACTUARIAL VALUATION REPORT FOR THE YEAR ENDING DECEMBER 31, 2008 April 9, 2009 Board of Trustees Policemen's Annuity and Benefit Fund City of Chicago 221

POLICEMEN S ANNUITY AND BENEFIT FUND OF CHICAGO ACTUARIAL VALUATION REPORT FOR THE YEAR ENDING DECEMBER 31, 2008 April 9, 2009 Board of Trustees Policemen's Annuity and Benefit Fund City of Chicago 221

Actuary s Certification Letter (Pension Trust Fund)

") Actuarial Actuary s Certification Letter (Pension Trust Fund) April 30, 2009 Board of Trustees Texas Municipal System Austin, Texas Dear Trustees: In accordance with the Texas Municipal System ( TMRS )

Actuarial Actuary s Certification Letter (Pension Trust Fund) April 30, 2009 Board of Trustees Texas Municipal System Austin, Texas Dear Trustees: In accordance with the Texas Municipal System ( TMRS )

REQUIRED SUPPLEMENTARY INFORMATION

REQUIRED SUPPLEMENTARY INFORMATION DC SCHEDULE OF CHANGES IN NET PENSION LIABILITY AND RELATED RATIOS DURING THE MEASUREMENT PERIOD Agent Multiple Employer Plan Measurement Period 2014-15 (1) 2013-14

REQUIRED SUPPLEMENTARY INFORMATION DC SCHEDULE OF CHANGES IN NET PENSION LIABILITY AND RELATED RATIOS DURING THE MEASUREMENT PERIOD Agent Multiple Employer Plan Measurement Period 2014-15 (1) 2013-14

RIVERSIDE TRANSIT AGENCY 1825 Third Street Riverside, CA May 24, 2007

RIVERSIDE TRANSIT AGENCY 1825 Third Street Riverside, CA 92507 May 24, 2007 TO: THRU: FROM: BOARD OF DIRECTORS Larry Rubio, Chief Executive Officer Craig Fajnor, Chief Financial Officer SUBJECT: Pre-funding

RIVERSIDE TRANSIT AGENCY 1825 Third Street Riverside, CA 92507 May 24, 2007 TO: THRU: FROM: BOARD OF DIRECTORS Larry Rubio, Chief Executive Officer Craig Fajnor, Chief Financial Officer SUBJECT: Pre-funding

Impacts of GASB 74/75 on CalSTRS and Employers. Presented on July 13, 2017

Impacts of GASB 74/75 on CalSTRS and Employers Presented on July 13, 2017 GASB Implementation Effective for CalSTRS FY 2016-17 Statement 74, Financial Reporting for Postemployment Benefit Plans Other Than

Impacts of GASB 74/75 on CalSTRS and Employers Presented on July 13, 2017 GASB Implementation Effective for CalSTRS FY 2016-17 Statement 74, Financial Reporting for Postemployment Benefit Plans Other Than

P O L I C E M E N S A N N U I T Y A N D B E N E F I T F U N D O F C H I C A G O A C T U A R I A L V A L U A T I O N R E P O R T F O R T H E Y E A R E

P O L I C E M E N S A N N U I T Y A N D B E N E F I T F U N D O F C H I C A G O A C T U A R I A L V A L U A T I O N R E P O R T F O R T H E Y E A R E N D I N G D E C E M B E R 3 1, 2 0 1 5 June 10, 2016

P O L I C E M E N S A N N U I T Y A N D B E N E F I T F U N D O F C H I C A G O A C T U A R I A L V A L U A T I O N R E P O R T F O R T H E Y E A R E N D I N G D E C E M B E R 3 1, 2 0 1 5 June 10, 2016

CITY OF MORENO VALLEY RETIREE HEALTHCARE PLAN

CITY OF MORENO VALLEY RETIREE HEALTHCARE PLAN June 30, 2013 Actuarial Valuation Final Results Bartel Associates, LLC John E. Bartel, President Joseph R. D Onofrio, Assistant Vice President Katherine Moore,

CITY OF MORENO VALLEY RETIREE HEALTHCARE PLAN June 30, 2013 Actuarial Valuation Final Results Bartel Associates, LLC John E. Bartel, President Joseph R. D Onofrio, Assistant Vice President Katherine Moore,

Actuarial Valuation Report: The City of Newport, Rhode Island Post Retirement Benefits Plan as of July 1, 2013

Actuarial Valuation Report: The City of Newport, Rhode Island Post Retirement Benefits Plan as of July 1, 2013 Sanjit Puri, ASA, MAAA Principal Grady Catterall, FSA, MAAA Senior Consultant Hay Group, Inc.

Actuarial Valuation Report: The City of Newport, Rhode Island Post Retirement Benefits Plan as of July 1, 2013 Sanjit Puri, ASA, MAAA Principal Grady Catterall, FSA, MAAA Senior Consultant Hay Group, Inc.

CONTRA COSTA COMMUNITY COLLEGE DISTRICT RETIREMENT FUTURIS PUBLIC ENTITY INVESTMENT TRUST

CONTRA COSTA COMMUNITY COLLEGE DISTRICT RETIREMENT FUTURIS PUBLIC ENTITY INVESTMENT TRUST FINANCIAL STATEMENTS FOR THE FISCAL YEARS ENDED WITH INDEPENDENT AUDITOR S REPORT JAMES MARTA & COMPANY LLP 701

CONTRA COSTA COMMUNITY COLLEGE DISTRICT RETIREMENT FUTURIS PUBLIC ENTITY INVESTMENT TRUST FINANCIAL STATEMENTS FOR THE FISCAL YEARS ENDED WITH INDEPENDENT AUDITOR S REPORT JAMES MARTA & COMPANY LLP 701