Section I General Information The Core Benefits The Flexible Benefit Options... 4

|

|

|

- Marybeth Cobb

- 6 years ago

- Views:

Transcription

1

2 Table of Contents Introducing HEALTH3CHECK... 1 Section I General Information... 2 Section II How HEALTH3CHECK Works... 4 The Core Benefits... 4 The Flexible Benefit Options... 4 Coordination of Benefits (Applicable to Medical and Dental Plans)... 6 Your Dental Choices... 7 Your Vision Care Choices... 9 Your Life Insurance Choices Your Disability Coverage Choices Short-Term Disability (STD) Long-Term Disability (LTD) Coverage Choices Your Flexible Spending Account Choices Health Care Flexible Spending Account Dependent Care Flexible Spending Account Health Savings Account (HSA) Section III The Selection Process Additional Information/Notes Employee Cost Per Pay Period Estes reserves the right to amend or terminate benefit plans at any time. The requirements and entitlements contained in this booklet shall apply to all employees unless otherwise prescribed by any law to the contrary. This document/communication is approved and may be utilized by all Estes corporate operating entities, divisions and affiliates although they are separate legal entities.

insurance, and disability options new ways to lower your taxes personal control over")

3 Introducing HEALTH3CHECK Estes Express Lines is pleased to introduce HEALTH3CHECK, a program that allows you to tailor benefits to your needs. HEALTH3CHECK provides you with: medical, dental, vision, life insurance, accidental death and dismemberment (AD&D) insurance, and disability options new ways to lower your taxes personal control over how the Company s benefit dollars are spent With HEALTH3CHECK, you choose the benefits that are best for you from the options available. Each year you may choose different benefits if you like, so your coverage always fits your personal needs. This workbook gives you the information and materials you need to take advantage of HEALTH3CHECK, to bring you up-to-date on all revisions, updates or additions to existing plans and to introduce new benefits to you. It is divided into three main sections: the first two sections describe the HEALTH3CHECK plan, and the third section tells you how to complete your enrollment. I. General Information: This section gives a general definition of HEALTH3CHECK and answers many questions you may have regarding eligibility, length of coverage, changing your elections, etc. You will want to refer to this section frequently as you read the rest of the workbook. II. How HEALTH3CHECK Works: This section offers a broad overview of the different parts that make up the overall plan design. You will learn about what the Core Benefits are, what your Flexible Options are and how you pay for those options. This section also has a detailed description of each of the options available, with the exception of medical plan options, which are described in the back of the book. III. The Selection Process: This section includes instructions for completing your enrollment for HEALTH3CHECK and also illustrates the 2017 per-pay-period plan costs. Take some time to review these materials carefully, and share them with your family. If you have questions that aren t addressed here, your terminal manager/department supervisor will be happy to help, or you are welcome to call extensions 2211, 2264, 2362, 2390, 2592 or 2593 at the Corporate Office. If you are a new hire and do not enroll when first eligible, you will automatically be enrolled in Core Benefits. If for any reason your enrollment is not complete, or you have not designated a plan option, you will automatically be enrolled in Core Benefits. Core Benefits are not offered under the Medical Plan. Availability of Summary Health Information As an employee, the health benefits available to you represent a significant component of your compensation package. They also provide important protection for you and your family in the case of illness or injury. Your plan offers a series of health-coverage options. Choosing a health-coverage option is an important decision. To help you make an informed choice, your plan makes available a Summary of Benefits and Coverage (SBC), which summarizes important information about any health-coverage option in a standard format, to help you compare across options. The SBC is available on our website: then select Your Benefits > Open Enrollment. A paper copy is also available, free of charge, by calling (a toll-free number). All plan documents can also be found on 1

4 Section I: General Information What Kind of Plan Is HEALTH3CHECK? The HEALTH3CHECK plan is known as a flexible benefits plan because it gives you the flexibility to select the benefits that best meet your needs. HEALTH3CHECK allows you to choose among the following benefit options: Medical Dental Vision Supplemental Life Insurance Accidental Death & Dismemberment Short-term Disability Long-term Disability Flexible Spending Accounts Who Is Eligible? All regular, full-time (40 hours per week) employees of Estes Express Lines are eligible to participate in HEALTH3CHECK. If you are a regular, full-time employee and your hours are reduced from 40 hours per week to not less than 30 hours per week (as a result of schedule reductions initiated by the company), you will be eligible for coverage for up to 12 months from the date your schedule is first changed. Eligible dependents include: your lawful spouse, without access to coverage through their own employer.* (Any employee electing to cover a spouse will be required to complete an affidavit to attest that coverage is not available through the spouse s own employer.) each of your children** under the age of 26 years. You may also continue to cover dependent children over the age of 26 who are incapable of self-support due to a mental or physical incapacity that began prior to age 26. Your eligible dependent children are: your natural children your adopted children (from the moment the children are placed in your home) your stepchildren permanently residing in your household, 6 months of the year or longer, in a regular parent-child relationship (Proof of residency will be required.) children permanently residing in your household, for whom you are legal guardian through the courts and claim on your tax return as a dependent When Does Coverage Begin? You are eligible to participate in HEALTH3CHECK on the first day of the month following 60 days of continuous, full-time employment during which you are actively at work. Your eligibility waiting period will be explained to you during orientation. Your qualified dependents are eligible to participate in HEALTH3CHECK on the date your coverage begins, unless you or your dependent is hospitalized at the time coverage is to begin. Should that occur, coverage will begin for you or your eligible dependents on the date that you or your dependent are no longer hospitalized. When Will Coverage Cease? Coverage will cease for you and your covered dependents on the date of termination of employment or the date you are no longer a full-time employee. If medical, dental and/or vision coverage cease due to termination of employment (other than by reason of gross misconduct) or due to reduction in your regularly scheduled hours, you may elect to continue medical, dental and/or vision coverage for yourself and/or your eligible dependents. In order to do this, you must pay the required premium and make the appropriate election on a timely basis as required by applicable COBRA regulations. Employees enrolled in a Health Savings Account (HSA) will be required to pay any and all administration fees from the date active employment ends. Likewise, if coverage ceases for an eligible dependent due to any one of the following qualifying events, your dependent may elect to continue medical, dental and/or vision coverage provided they pay the required premium and make the appropriate election on a timely basis as required by applicable COBRA regulations: death of the covered employee divorce or legal separation the COBRA employee becoming entitled to Medicare benefits a dependent who no longer meets the dependent eligibility definition * Whenever HEALTH3CHECK uses the terms spouse, husband or wife, it is referring to a relationship between two individuals that is established pursuant to a ceremonial or formal marriage. The HEALTH3CHECK plan does not recognize common-law marriages. Accordingly, a party to a common-law is not eligible to be covered as a spouse, husband or wife for purposes of any benefit under the HEALTH3CHECK plan. (Please note: an informal marriage in the State of Texas evidenced only by a declaration and registration with the county clerk is treated as a common-law marriage.) ** In addition, a child who resides with you is not eligible as a dependent if he or she is the child of your common-law spouse. In order to cover a stepchild, you must be legally married to the child s mother/father and be able to produce a marriage certificate, if requested. 2

5 Are Retired Employees Eligible for Coverage? No. Retired employees are only covered under the following circumstances: Medical Retirement If an employee becomes disabled and has been employed with the company 15 years, the company will continue Medical coverage for the employee for 29 months or such sooner time as the employee is able to resume gainful employment or becomes eligible for Medicare. Any months applied toward this benefit will also be concurrently applied to any COBRA months. Early Retirement If an employee has 15 years of service with the company and is age 60 and decides to take an early retirement, the company will continue the employee Medical (CHP) coverage only to age 65 when he/she becomes eligible for Medicare, provided the employee does not accept employment elsewhere and become eligible for any group benefits there. In addition, retired employees are not eligible to receive HSA matching contributions. A minimum of 2 weeks notice is required to qualify as early retirement. All other coverage terminates upon retirement. When Do I Make My Benefit Selections Under the HEALTH3CHECK Plan? Once a year, the company will have an annual enrollment period. The annual enrollment period will generally be during the month of October or November. You choose among different benefit options during the annual enrollment period depending upon your individual needs at the time. The effective date of your plan elections will generally be January 1 unless this plan indicates a different coverage effective date. When Can I Change My Elections Under HEALTH3CHECK? The HEALTH3CHECK Plan Year runs from January 1 to December 31. You can change your elections once a year during the annual enrollment period for the following plan year. This means that once you elect coverage under HEALTH3CHECK, you may not add or drop coverage until the next annual enrollment period. Are There Any Exceptions to the Above Rule? Yes, you may change your benefit coverage during the year if you experience a qualified change in family status, including: marriage, divorce, legal separation, annulment or death of spouse birth, adoption, placement for adoption, death or change in custody of a child gain or loss of coverage by you, your spouse or your dependent change in work schedule (for example, from full-time to part-time, commencement of or return from an unpaid leave of absence) by you, your spouse or your dependent an event that causes your dependent to satisfy or cease to satisfy the requirements for coverage due to attainment of age or any similar circumstances as provided under the Plan a change of Plan availability or work site of you, your spouse or your dependent If you qualify for any of the above exceptions, you are required under the Plan to apply to your local terminal manager or department supervisor for coverage changes within 31 days of the effective date of the family status change. The plan administrator makes the final determination as to what constitutes a family status change. Any Plan change you make must be consistent with the change in family status (example: if you marry, changing from single to married coverage). It is very important that you remember to add your newborn children by completing an enrollment form and sending it to the Benefits Department within 31 days of birth. It is not necessary to wait for the child s social security number or birth certificate before completing and submitting the enrollment form. When Should I File My Claims? All claims should be submitted for payment within 90 days, if possible, after you receive services. Claims submitted more than one year after you have received the service will generally not be considered for payment. Is It Important to Change My Address If I Move? If you do not notify your terminal manager and have a Change of Address Notice sent to the Corporate Office, you will not receive your Identification Cards when they are issued and will not be able to access health care when you need it without the new card. 3

Dependent Life Insurance Spouse: $2,000 Child(ren): $2,000 Basic Accidental Death and Dismemberment")

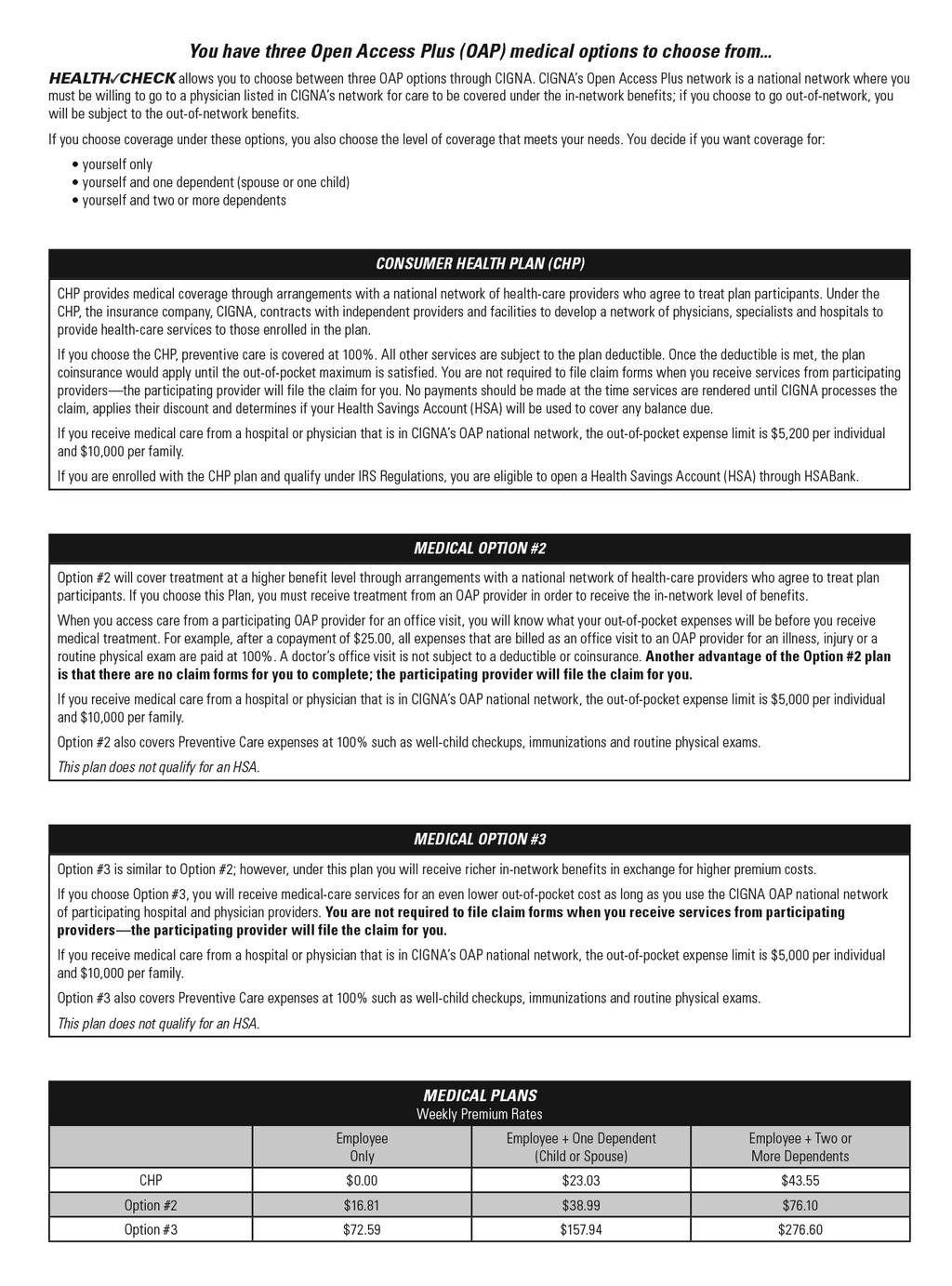

6 Section II: How HEALTH3CHECK Works The HEALTH3CHECK Plan is made up of three separate parts: The Core Benefits The Flexible Benefit Options The Cost of the Flexible Benefit Options Each part is explained below. The Core Benefits Estes Express Lines believes that all eligible employees should have certain benefits provided by the Company, which are called the Core Benefits. All employees who are eligible to participate in HEALTH3CHECK will have the same Core Benefits. Core Benefits are provided to you by Estes Express Lines. The Core Benefits are: Basic Life Insurance One-half of your base annual earnings (minimum $10,000) Dependent Life Insurance Spouse: $2,000 Child(ren): $2,000 Basic Accidental Death and Dismemberment Flat $10,000 Weekly Income Benefits Basic Long-term Disability 50% of base weekly earnings, up to a $200 maximum weekly benefit 50% of base monthly earnings, up to a $1,000 maximum monthly benefit The Flexible Benefit Options Estes Express Lines recognizes that your needs are unique; therefore, HEALTH3CHECK allows you to design your own benefits over and above the Core Benefits provided by the Company. You design your own benefit package by choosing from the Flexible Benefit Options listed on the following pages. The Flexible Benefit Options are: MEDICAL PLAN OPTIONS Are Indicated on the Fold-out in the Back of This Book. DENTAL PLAN CHOICES Dental Option #1 - Preferred (PPO) Dental Option #2 - Premier Dental Option #3 - No Coverage This plan option is available where a PPO network is available. You must receive treatment from a dentist who participates in the PPO network or pay out-of-network rates. Participating dentists are listed in the Delta Preferred PPO Dental Directory. This plan option is available to all employees without regard to networks. Under this option you may receive eligible dental treatment from the dentist of your choice; however, if you remain in the network, you will receive treatment at a discounted rate, which will result in cost savings for you. Refer to the Premier directory of participating dentists. You may choose no dental coverage. 4

7 VISION CARE CHOICES Vision Option #1: Vision Option #2: LIFE INSURANCE CHOICES You may choose coverage for yourself and your eligible dependents and pay for it on a pre-tax basis. You should select your vision care provider from the provided Davis Vision directory to receive the highest level of coverage. You may choose no vision coverage. Supplemental Life Insurance: You may choose additional life insurance in the following amounts: $20,000, $40,000, $60,000, $80,000, $100,000, $120,000, $140,000, $160,000, $180,000, $200,000, $220,000, $240,000, $260,000, $280,000 or $300,000. Maximum additional life cannot exceed 10 times annual earnings. DISABILITY CHOICES Voluntary Buyup Short-term Disability Insurance: Voluntary Buyup Long-term Disability Insurance: FLEXIBLE SPENDING ACCOUNT CHOICES Dependent Care Flexible Spending Account: Health Care Flexible Spending Account: Options 2 & 3 Participants Only ADDITIONAL CHOICES Health Savings Account (HSA): CHP Participants Only You may purchase additional coverage to bring your disability coverage up to 60% of your base annual earnings to a combined weekly benefit maximum of $2,000. You may purchase additional coverage to bring your disability coverage up to 60% of your base annual earnings to a combined monthly benefit maximum of $10,000. You may choose to make a before-tax contribution to an account from which you can be reimbursed for eligible dependent-care expenses (e.g., child or elder care). You may choose to make a before-tax contribution (annual maximum of $2,550) to an account from which you can be reimbursed for eligible health-care expenses (e.g., unreimbursed medical and dental expenses, copayments and deductibles). Employees enrolled in the CHP are NOT eligible for the Health Care Flexible Spending Account. Employees enrolled in the CHP medical plan and who qualify for an HSA account can contribute beforetax dollars (annual maximum contributions of $3,400 for single coverage and $6,750 for family coverage) to a bank account through HSABank. The account belongs to you and can be used towards out-of-pocket qualified medical expenses. Balances in the HSA account roll over from year to year and are not lost at year-end if not used. There is one option available to you on an after-tax basis. The After-Tax Benefit Option is described below: ACCIDENTAL DEATH AND DISMEMBERMENT CHOICES Supplemental AD&D You may choose additional accidental death and dismemberment insurance in the following amounts: $20,000, $40,000, $60,000, $80,000, $100,000, $120,000, $140,000, $160,000, $180,000, $200,000, $220,000, $240,000, $260,000, $280,000 or $300,000. The maximum combined AD&D cannot exceed 10 times annual earnings. How You Pay for Your Flexible Benefit Options Now that you know what your Core Benefits and Flexible Benefit Options are, we ll explain how you can buy the additional coverage under the Flexible Benefit Options. Most of your contributions will be made through salary reduction on a before-tax basis. By paying for your flexible benefit options with before-tax dollars, you reduce the amount of Federal, State (except in New Jersey) and FICA taxes you pay. Compared to purchasing the same benefits with after-tax dollars, you get more spending power by increasing your take-home pay. Detailed Descriptions of the Medical Plans Can Be Found in the Back of This Book! Your Medical Plan Fold-out will provide you with detailed information regarding the benefits offered to you based on your terminal location. Please refer to your fold-out when making your Medical Plan selection. Summary of Benefits and Coverage (SBC) can be found in the Employee Self-Service section on along with all Summary Plan Descriptions (SPD). However, other important information regarding medical benefits follows: 5

. Changing Your Medical Coverage You will have the opportunity to change your medical coverage during each annual enrollment period for the following calendar year.")

8 Coordination of Benefits (Applicable to Medical and Dental) If you or a covered dependent have expenses that can be considered under HEALTH3CHECK and another group benefit plan, HEALTH3CHECK will consider those expenses that are not duplicated by the other coverage. HEALTH3CHECK and the other plan will coordinate benefits. For example, if your child has group medical insurance through his/her employer that pays 80% after a $300 deductible, which is similar to HEALTH3CHECK, and you enroll your child under HEALTH3CHECK too, HEALTH3CHECK will not duplicate payments or benefits paid by your child's plan and will pay nothing. HEALTH3CHECK will not pay again on benefits paid elsewhere. However, if your child s plan paid 70% after a $300 deductible, and HEALTH3CHECK paid 90%, HEALTH3CHECK would pay the additional 20% (the difference between your child s coverage and what is offered under HEALTH3CHECK). Changing Your Medical Coverage You will have the opportunity to change your medical coverage during each annual enrollment period for the following calendar year. You can also change your coverage during the year if you have a qualified change in family status, as described on page 3. Waiving Medical Coverage Option #4 You may not need or want medical coverage if you are covered under another plan. For example, your spouse may already have family medical coverage through another employer. Remember: If you waive medical coverage for yourself and/or your eligible dependents, you will not be able to elect to be covered under a medical coverage option until the next annual enrollment period, unless you have a qualified change in family status, as described on page 3. 6

9 Your Dental Choices With HEALTH3CHECK, you can choose dental coverage that helps pay for many types of dental services for you and your family. Each annual enrollment period, you will have the opportunity to enroll in or cancel your coverage for the following year. You have three different dental plan options from which to choose under HEALTH3CHECK: (1) Delta Dental Preferred Plan (2) Delta Dental Premier Plan and (3) No Dental Coverage. Under dental plan Option #1 - Preferred, you must receive treatment from a participating dentist as listed in the Preferred dental directory, or you will have to pay outof-network rates for your treatments (and you will not receive the discounts provided by participating dentists). When choosing dental Option #1, please check to make sure that there is a dentist available to you under this plan. If you choose an out-of-network dentist, you will receive the reduced out-of-network benefit. You will receive a Directory of Participating Dentists during the annual enrollment meetings. Under dental plan Option #2 - Premier, you can receive treatment from a participating dentist as listed in the Premier dental directory, or you can elect to go to the dentist of your choice. However, if you go to a dentist listed in the directory, you will pay a discounted rate for your treatments. This means that you save on the cost of the treatment. If the dentist is not a participating dentist, you will pay retail rates for your dental care. How Do the Preferred (Option #1) and Premier (Option #2) Work? If you choose the Preferred option, you must go to a dentist listed in your directory, or you will pay for your treatments at out-of-network rates. If you choose the Premier option, you may receive treatment from any dentist you wish. Both options offer a discount as long as you stay in the network. If you go out-of-network, you will have higher out-of-pocket costs. For more information regarding participating dentists, you can call or visit The chart below illustrates the major provisions of each dental plan option: DENTAL PLANS Benefits OPTION #1 - Preferred (PPO) OPTION #2 - Premier In-network Out-of-network In-network Out-of-network Calendar Year Maximum $1,000 $750 $1,000 $1,000 Calendar Year Deductible Individual $50 Family $150 Class I Expenses Diagnostic and Preventive (Oral Exams, X-rays and Cleanings)* Class II Expenses Basic Restorative (Fillings, Root Canals and Extractions) Class III Expenses Major Restorative (Crowns, Inlays, Dentures and Bridges) Individual $75 Family $225 Individual $75 Family $225 Individual $75 Family $ % 80% 80% 80% 80% 60% 50% 50% 50% 40% 50% 50% Class IV (Ortho) (Braces) 50% Not covered 50% 50% Lifetime Ortho Max $1,500 Not applicable $1,500 $1,500 *These services are exempt from the deductible and annual benefit maximum. No Coverage (Option #3) You may elect not to participate in any dental coverage option. Remember: If you do not choose dental coverage, you will not be able to choose dental coverage until the next annual enrollment period, unless you have a qualified change in family status, as described on page 3. 7

yourself and two or more dependents Which Dental Plan Option Should I Choose?")

10 Your Flexible Dental Plan Cost As with your medical choices, the cost of the Dental Plan will depend on the plan option and number of family members you choose to cover: yourself only yourself and one dependent (spouse or one child) yourself and two or more dependents Which Dental Plan Option Should I Choose? If you re not sure whether or not you want dental coverage, you may be interested in comparing your situation with these sample employees. Example 1: Betty s husband doesn t have dental coverage where he works. Each of the four people in her family have routine check-ups, and Betty is expecting that one of her children will need braces. Betty works at a terminal location where a Preferred network is available, so Betty chooses to be covered under Option #1. Example 2: Pete and his wife both visit the dentist routinely, and they both need regular repairs. Pete works at a terminal location where a Preferred network is not available. Pete elects to participate in the Premier Option #2 plan, but there are no network dentists in his area. Pete and his wife will pay more for their dental care because they will not be able to access a network dentist. However, they will not pay a penalty for going out-of-network. They may pay a combined deductible of $150, but each can receive up to $1,000 in benefits from the plan for the year, so Pete chooses to be covered under the Option #2 plan. Dental Decision Maker Your answers to the following questions may also help guide you to a decision about dental coverage. Do you and your family receive regular semi-annual exams? How much do these exams cost you each year? How does this cost compare to your monthly contributions for coverage under the Dental Plan? How much have you spent on dental care in the past few years? Were these preventive or major expenses? Does your spouse s employer offer a family Dental Plan? How much does the Plan pay? How much does it cost to participate? Your premium costs for the Dental Plan can be found on page 21. Do you plan to use the Health Care Flexible Spending Account? 8

11 Your Davis Vision Care Choices With HEALTH3CHECK, you can choose vision care that will help pay for a routine eye examination and eyeglasses (or contact lenses in lieu of eyeglasses) on an annual basis, from the date of service. Any questions you may have regarding your vision care benefits can be answered by calling If you choose this option, you will select a doctor for yourself and your covered dependents from the directory provided. You will need to call the doctor to schedule an appointment, identify yourself as an Estes Express Lines employee, provide the doctor with your member ID number and the year of birth of the person receiving the service. How Does the Vision Care Plan Work? When you visit a participating provider, you will receive a routine eye examination, including dilation as professionally indicated, and a complete pair of eyeglasses or contact lenses. You will pay: a $10.00 copay toward your eye examination a $20.00 copay toward spectacle lenses a $0.00 copay toward your frames from the Tower Collection or a $20.00 copay toward Davis Vision s contact lens collection (including disposables, toric, multi-focal or planned replacement contacts)in lieu of eyeglasses What Will Happen If I Go to an Out-Of-Network Provider? If you elect to receive services from an out-of-network provider, you must pay the provider directly for all charges, submit a claim for reimbursement to Vision Care Processing Unit, P.O. Box 1525, Latham, NY 12110, and you will be reimbursed based on a schedule of maximums as follows: Eye examination $30.00 Single vision lenses $25.00 (per pair) Bifocal lenses $35.00 (per pair) Trifocal lenses $45.00 (per pair) A frame $30.00 Contact lenses $75.00 You will receive the greatest value and maximize your benefit dollars if you select a doctor who participates in the network. Your Vision Care Plan Cost As with your medical and dental plan choices, the cost of the Vision Care Plan will depend on the number of family members you choose to cover: yourself only yourself and one dependent (spouse or one child) yourself and two or more dependents Vision Care Decision Maker Your answers to the following questions may also help guide you to a decision about vision care coverage. Do you and your family receive regular eye exams? How much do these cost you each year? How does this cost compare to what the monthly contributions for coverage under the Vision Plan would cost? How much have you spent on vision care in the past few years? Does your spouse s employer offer a family Vision Care Plan? How much does it cost to participate? How much does it pay? Do you plan to use the Health Care Flexible Spending Account for eye-care expenses? Your premium costs for the Vision Care Plan can be found on page 21. 9

.")

12 Your Life Insurance Choices Under HEALTH3CHECK, eligible employees are provided a Core Life Insurance and Accidental Death and Dismemberment insurance benefit at no cost to you. Following are the Core Benefits provided by Estes: LIFE INSURANCES Employee Life Insurance One-half base annual earnings, rounded up to the next higher $1,000 ($10,000 minimum). Dependent Life Insurance Spouse: $2,000 Child(ren): $2,000 Accidental Death and Dismemberment Flat $10,000 In addition to your Core Benefits, you may choose to purchase additional life and/or accidental death and dismemberment insurance. You decide how much life and accident insurance best suits your needs. SUPPLEMENTAL LIFE Supplemental Term Life Insurance Supplemental AD&D You may purchase additional life insurance in the following amounts: $20,000 $40,000 $60,000 $80,000 $100,000 $120,000 $140,000 $160,000 $180,000 $200,000 $220,000 $240,000 $260,000 $280,000 $300,000 Your maximum additional life insurance cannot exceed 10 times your base annual earnings. You may purchase additional AD&D insurance in the following amounts: $20,000 $40,000 $60,000 $80,000 $100,000 $120,000 $140,000 $160,000 $180,000 $200,000 $220,000 $240,000 $260,000 $280,000 $300,000 Your maximum combined core and supplementary AD&D cannot exceed 10 times your base annual earnings. Changing Your Life Insurance Coverage for the Following Year You may change your life insurance election each year during the HEALTH3CHECK annual enrollment period subject to the requirement for evidence of insurability shown below. Your Life Insurance Cost Your premium cost for the supplemental life insurance is based on your age. You may find the cost for optional life insurance attractive since it is offered at group rates. See Section III for an illustration of the weekly pay period costs. You will pay for your supplemental life insurance with before-tax dollars and the supplemental AD&D with after-tax dollars. Important Notes Regarding Evidence of Insurability New Hires Evidence of Insurability will be waived for new hires who enroll within 31 days of becoming eligible for supplemental life insurance coverage. Individuals who do not enroll within 31 days of becoming eligible for coverage will be required to submit Evidence of Insurability, regardless of whether application is made during an Open Enrollment period. Evidence of Insurability will be required for increases in coverage that exceed $40,000 in supplemental life coverage. Evidence of Insurability will be waived for a change in family status, limited to $40,000 increases of supplemental life insurance coverage. 10

13 How Much Insurance Should I Have? Here are examples of the insurance coverages that three different employees might decide to choose. Example 1: Ed is single and has no significant financial obligations or dependents to provide for. He chooses not to purchase supplemental life insurance. He feels the Core Benefit will be adequate to cover any expenses or obligations. Example 2: Steve is the sole support for his family. He s already purchased an additional amount of life insurance outside the company, but he chooses to take advantage of the supplemental life insurance coverage available to him. He purchases the maximum supplemental life insurance coverage. Example 3: Judy s family relies on her annual income. Judy chooses an additional $100,000 in supplemental life insurance and $100,000 of supplemental AD&D for her family. Life Insurance Decision Maker Answering the following questions may help guide you to a decision about how much life insurance you need. Are you the sole support of your family? Does your family rely on your income? Do you have insurance to pay off your home mortgage if you die? Do you have adequate life insurance coverage through other sources? Do you have major financial obligations that your family would be responsible for after your death? Your premium costs for Supplemental Term Life Insurance and AD&D Insurance can be found on pages

cover 50% of your base weekly earnings up to a weekly maximum of $200.")

14 Your Disability Coverage Choices HEALTH3CHECK provides four levels of coverage for income replacement for all eligible employees for any income lost due to an illness or injury. Weekly Income Benefits Weekly Income Benefits (WIB) cover 50% of your base weekly earnings up to a weekly maximum of $200. Benefits begin on the eighth day of your disability caused by an accident or illness, but begin on the first day of a hospital confinement or outpatient surgery. Weekly Income Benefits are payable for a maximum period of 26 weeks. Those injuries and illnesses filed under other disability plans, i.e., Workers Compensation or state temporary disability insurance, will not be covered under this plan. Weekly Income Benefits are a Core Benefit under HEALTH3CHECK and are fully paid for by Estes Express Lines. Voluntary Short-Term Disability (STD) Through HEALTH3CHECK, you have the opportunity to purchase additional voluntary Short-term Disability income protection. Benefits begin on the 31st day of a qualified disability. This coverage pays a benefit (when combined with the WIB benefits) of 60% of your base weekly earnings to the lesser of a total maximum weekly benefit of $2,000. If you choose voluntary STD coverage, you pay your share of the cost (which is based on your base earnings) with before-tax dollars through payroll deduction. Voluntary STD coverage is payable for a maximum period of 22 weeks. Voluntary Short-term Disability benefits are not payable for work-related injuries. Voluntary STD Benefit 60% of your base weekly earnings when combined with the WIB benefits to a weekly maximum benefit of $2,000. How Much Disability Insurance Should I Have? Here are examples of the insurance coverages that two different employees might decide to choose. Example 1: Paul is single, earns $25,000 and has no significant financial obligations or dependents to provide for. He chooses not to purchase Voluntary STD insurance. He feels the Core Benefit will be adequate to cover any expenses or obligations. Example 2: Becky s family relies on her $35,000 annual income. Becky chooses to purchase the Voluntary STD insurance. Voluntary STD Insurance Decision Maker Answering the following questions may help guide you to a decision about how much STD insurance you need. Are you the sole supporter of your family? Does your family rely on your income? Do you have adequate STD insurance coverage through other sources? Do you have major financial obligations that your family would be responsible for if you were disabled? Basic Long-Term Disability (LTD) For those illnesses and injuries that are expected to have a long duration, HEALTH3CHECK provides Long-term Disability income protection. Benefits begin on the 181st day of a covered disability. Basic LTD Benefit 50% of your base monthly earnings to a maximum monthly benefit of $1,000. Long-term Disability Benefits are a Core Benefit under HEALTH3CHECK and are fully paid for by Estes Express Lines and coordinate with any other benefit you may receive, e.g., Social Security, State Disability and Workers Compensation. 12

to a monthly maximum benefit of $10,000.")

15 Voluntary Long-Term Disability You can purchase Voluntary Long-term Disability coverage through HEALTH3CHECK. This coverage pays a benefit of 60% of your base monthly earnings combined with the Core LTD benefit to a total maximum monthly benefit of $10,000. If you choose Voluntary LTD coverage, you pay your share of the cost (which is based on your base earnings) with before-tax dollars through payroll deduction. Voluntary LTD Benefit Additional 10% of your base monthly earnings (60% of your base earnings when combined with the Basic LTD benefit) to a monthly maximum benefit of $10,000. Your Voluntary Long-Term Disability (LTD) Costs Your cost for the Voluntary LTD is based on your age and your base total compensation. You may find the cost for Voluntary LTD coverage attractive since it is offered at group rates. See Section III for an illustration of the weekly pay period costs. Important Notes Regarding Evidence of Insurability New Hires Evidence of Insurability will be waived for new hires who enroll within 31 days of becoming eligible for supplemental Short-term or Long-term Disability coverage. Individuals who do not enroll within 31 days of becoming eligible for coverage will be required to submit Evidence of Insurability, regardless of whether application is made during an Open Enrollment period. Evidence of Insurability will be waived for a change in family status. How Much LTD Insurance Should I Have? Here are examples of the insurance coverages that two different employees might decide to choose. Example 1: Ed is single, earns $25,000 and has no significant financial obligations or dependents to provide for. He chooses not to purchase Voluntary LTD insurance. He feels the Core Benefit will be adequate to cover any expenses or obligations. Example 2: Judy s family relies on her $35,000 annual income. Judy chooses to purchase the voluntary LTD insurance. LTD Insurance Decision Maker Answering the following questions may help guide you to a decision about how much LTD insurance you need. Are you the sole supporter of your family? Does your family rely on your income? Do you have adequate LTD insurance coverage through other sources? Do you have major financial obligations that your family would be responsible for if you were disabled? 13

provide a way to help pay for certain health-care and dependent-care expenses with before-tax dollars.")

16 Your Flexible Spending Account Choices HEALTH3CHECK offers you two spending account options: Health Care Flexible Spending Account* Dependent Care Flexible Spending Account These Flexible Spending Accounts (FSAs) provide a way to help pay for certain health-care and dependent-care expenses with before-tax dollars. This means that contributions to the plan will be deducted from your pay before it is taxed, therefore, it is tax-free! This, in turn, will increase your take-home pay (compared to the same contributions made on an after-tax basis), since Federal, State and FICA taxes will be less. IRS rules require that if you do not use all of the money that you contribute to your account by the end of the plan year (bills must be incurred by December 31, and you have until March 31 to request a refund), any remaining balance is forfeited and will be used to offset future plan expenses. This is known as the "use it or lose it" rule. Also, should your employment terminate, you have 31 days in which to submit your bills for refund. The Flexible Spending Accounts are your accounts, containing your money. You can contribute dollars directly from your pay to either one or both flexible spending accounts. Health Care Flexible Spending Account You can save on taxes through the use of a Health Care Flexible Spending Account since you can contribute money to it on a before-tax basis. What Are Eligible Health-Care Expenses Under the Plan? Some of the eligible expenses for which you can use your Health Care Flexible Spending Account are: Deductibles for health insurance plans Copayments for health insurance plans Routine physicals or other health-care expenses not covered by health insurance plans Well baby care Routine vision care Routine hearing care Dental expenses not covered by dental insurance plans Long-term rehabilitation services (alcoholism and drug abuse) Payments for charges in excess of medical or dental reasonable and customary allowances Non-educational treatment of developmental disabilities Fitness programs prescribed by a physician How Can I Estimate Health-Care Expenses? The Health Care Flexible Spending Account can be advantageous to almost any eligible employee. In order to determine how much to contribute, you should first estimate what your expenses will be until the next plan anniversary date. Here s an example of what Joe s family situation might look like during a calendar year: INCLUDABLE EXPENSES AMOUNT Family medical deductible $ Family dental deductible $ Eyeglasses/contact lenses expenses for two people $ Patients portion of dental expenses for three people $ Total Out-of-Pocket Expenses $ 1, How Does the Health Care Flexible Spending Account Work? Joe estimated that he would have $1,250 in eligible, unreimbursed medical, dental and vision care expenses during the year for himself and his family. He would divide $1,250 by 52 pay periods to determine his contribution of $24.04 per pay period to the Health Care Flexible Spending Account. The following example illustrates Joe s estimated tax savings assuming Joe is in the 27.65% tax bracket (15% Federal, 5% State and 7.65% Social Security) compared to paying the same amount after-tax without the spending account. WITHOUT SPENDING ACCOUNT WITH SPENDING ACCOUNT Adjusted Pay (per week) $ Adjusted Pay (per week) $ Taxes (27.65%) - $ Spending Account for Health Care Expenses - $ Take-Home $ Taxable Pay $ Non-covered Health Care Expenses - $ Taxes (27.65%) - $ BALANCE $ BALANCE $ If your combined tax bracket is higher than 27.65%, savings will be even greater. Joe saves $6.65 per pay period; $ annually. *If you are enrolled in the CHP medical plan, you are not eligible to participate in the Health Care Flexible Spending Account. 14

.")

17 How Much Can I Contribute? You may contribute before-tax dollars to your Health Care Flexible Spending Account. You choose how much you contribute to your Health Care Flexible Spending Account. You can contribute any amount up to $2,550 in a plan year ($49.03 per week). If you do not use all of the money in your account by the end of the plan year (December 31), any remaining balance must be forfeited according to Internal Revenue Service regulations. Important Notes IRS regulations for participants in the Health Care Flexible Spending Account plan require the following: Once you make an election to the Health Care Flexible Spending Account, you cannot change that election until the beginning of the next plan year (January 1) unless you have a change in your family status (see page 3 for the definition of family status change). If you do not use all of the money in your account by the end of the plan year (bills must be incurred by December 31, and you have until March 31 to request a refund), any remaining balance is forfeited and will be used to offset future plan expenses. Because of this use it or lose it rule, you should carefully estimate what you expect your expenses to be before deciding upon the appropriate amount to contribute to the Flexible Spending Account. You may submit eligible expenses up to your annual contribution as they are incurred. Expenses reimbursed from your account cannot be claimed as deductions on your income tax. If you are enrolled in the medical CHP plan, you are not eligible to participate in the Health Care Flexible Spending Account. Dependent Care Flexible Spending Account HEALTH3CHECK will allow you to save taxes through the use of a Dependent Care Flexible Spending Account. This account allows you to pay for certain dependent care expenses (e.g., child or elder care) with before-tax dollars if you have dependents who require care in order for you to work. How Does the Dependent Care Flexible Spending Account Work? You may contribute your own before-tax dollars to this account. Estes Express Lines will deduct the amount you choose to contribute before Federal, State and FICA (Social Security) taxes are deducted. This money will be deposited into an account maintained especially for you. As expenses are incurred, you can file for reimbursement up to the full amount of your account balance. Who May Participate in the Dependent Care Flexible Spending Account Plan? If you are married, your spouse must work, be a full-time student, or be mentally or physically unable to care for him or herself in order for you to be eligible to participate in this plan. You may also participate in this plan if you are not married and incur eligible dependent care expenses. Expenses That Can Be Submitted Under This Plan You can claim dependent care expenses for qualifying individuals, such as your children under age 13 and other relatives, such as a parent, whom you can claim as an exemption on your tax return; or a spouse or other dependent who is physically or mentally incapable of caring for him or herself. These children and relatives must live with you. Eligible Dependent Care Expenses Care in your home or someone else s home Child care or dependent care facilities, including day care centers and nurseries Housekeeping services in your home which include day care You cannot, however, claim payments made to a dependent, or to one of your own children under age 19, who babysits for you. Also, kindergarten or other educational services are not eligible for reimbursement from the Dependent Care Spending Account. For example: your 5-year-old child goes to kindergarten in the morning and in the afternoon attends an after-school day care program at the same school. Your total cost for sending the child to school is $3,000, of which $1,800 is for the after-school program. Only $1,800 qualifies for reimbursement. How Much Can I Contribute? You choose how much you contribute to your dependent care account. Under current IRS regulations, you can contribute any amount up to $5,000 in a plan year if you are married and filing a joint return ($96.15 per week) or up to $2,550 in a plan year if you are single or married and filing a separate return ($49.03 per week). Your total contributions cannot exceed either your income or your spouse s income, whichever is less. NOTE: If your spouse is a full-time student at an educational institution or is physically or mentally incapable of caring for him or herself, the annual contribution maximum is $3,000 for one qualified dependent or $6,000 for two or more qualified dependents. 15

18 Dependent Care and the Federal Tax Credit If you have eligible dependents, you may choose to use either or both the Dependent Care Flexible Spending Account and the Federal dependent care tax credit when you file your annual return. Whatever you contribute to the Dependent Care Flexible Spending Account will reduce the amount of the available Federal tax credit. You are eligible for a Federal income tax credit for up to $3,000 of eligible dependent care expenses for one qualified dependent (up to $6,000 for two or more qualified dependents). The amount of your tax credit depends on your adjusted gross income reported on your Federal income tax return. If you choose to participate in the Dependent Care Flexible Spending Account, your contributions will be made through pay reduction and will be made on a before-tax basis. This means that contributions to this plan will be deducted from your pay before taxes and are, therefore, tax-free. This will increase your net take-home pay since Federal, State and FICA taxes will be less. You choose whether using the Dependent Care Flexible Spending Account or taking the Federal dependent care tax credit for your dependent care expenses will give you more tax savings. If you are uncertain as to which is best for you, we recommend that you check with a tax advisor before making your final decision. Your Costs You may contribute before-tax dollars to your Dependent Care Flexible Spending Account. The maximum contribution to this account is $96.15 per week (or $49.03 per week if you are single or married and filing a separate return). Important Notes IRS regulations for participants in the Dependent Care Flexible Spending Account plan require the following: Once you make an election to contribute to the Dependent Care Flexible Spending Account, you cannot change that election until the beginning of the following plan year (January 1) unless you have a change in your family status (see page 3). If you do not use all the money in your account by the end of the plan year (qualified expenses must be incurred by December 31, and you have until March 31 to request a refund), any remaining balance is forfeited and will be used to offset future plan expenses. Because of this use it or lose it rule, you should carefully estimate what you expect your expenses to be before deciding upon the appropriate amount to contribute to this spending account. Expenses reimbursed from your account cannot be claimed under the Federal Tax Credit. You may submit eligible expenses up to your credit balance. The IRS requires that you submit your day-care provider s name, address and Social Security number or tax identification number in order to receive reimbursement from a Dependent Day Care Flexible Spending Account. You can obtain this information by asking your dependent day-care provider to complete IRS Form W-10. Getting Payments from Your Spending Accounts As you pay qualified expenses for health care and dependent care throughout the year, you submit the receipt for reimbursement. You can be reimbursed from your account for any qualified claims you have submitted. To request reimbursement, you ll need to attach your receipts to a Reimbursement Request Form and submit it directly for processing. Money in your account is not taxable to you when it goes into your account or when you are reimbursed. After the end of each year, you will have until March 31 to submit expenses from the prior year and still be reimbursed. Spending Account Decision Maker Paying predictable expenses through a Flexible Spending Account can save you a lot of money, but you need to estimate your expenses carefully based on your other benefit decisions. Your answers to the following questions may also help guide you to a decision about Flexible Spending Accounts. How much did you pay out-of-pocket for health-care or dependent day-care expenses last year? Which Flex medical and dental options did you choose? How much is each Plan s deductible? Copayment? What expenses do you expect to incur in the coming year that are not covered by your Medical or Dental Plans? Do you or your dependents need glasses, contacts or eye exams? Does the Federal income tax credit or Dependent Care Flexible Spending Account provide more tax savings for you? 16

19 Understanding a Health Savings Account (HSA) What Is a Health Savings Account (HSA)? An HSA is a special tax-advantaged account that is used with a high-deductible health plan (HDHP). An HSA allows you to pay for qualified medical expenses for you and your family. You may contribute money to your HSA, and it earns interest tax-free. There are annual limits set by federal regulations on how much you can contribute, but your balances carry over year to year. If you change employers, your HSA dollars belong to you. You are no longer able to contribute to the HSA unless you enroll in another qualified high-deductible health plan; however, you can continue to use the funds in your account to pay for qualified medical expenses. What Are the Annual Maximum Contributions to an HSA for 2017? You may contribute any amount up to $3,400 for Single Coverage and $6,750 for Family Coverage in a plan year if you are under age 55. You may contribute an additional $1,000 (considered a catch-up contribution) if you are 55 or over. How Are Contributions Made to the HSA? Both you and your employer are permitted to contribute to your HSA. Your employer can choose to fund contributions to your account directly, and at your request, you can make pre-tax contributions through payroll deductions.* You, the account holder, can make post-tax deposits or transfers to your HSA account and you can transfer money from other HSA accounts. How Can You Access Funds from Your HSA? You have several options on accessing funds: You can use the MasterCard-branded debit card to pay for out-of-pocket qualified medical expenses. You can review claims on and select which ones you would like to pay directly from your HSA. You can purchase a checkbook and write checks to make payments. You may also elect to have qualified medical expenses paid directly from your HSA by choosing the Automatic Claim Forwarding feature on This would allow qualified expenses to be paid automatically from your account. What Is the Difference in a Consumer Health Plan (CHP) with an HSA and a Traditional Medical Plan? The CHP High Deductible Plan has a lower premium but a higher deductible. The CHP medical plan begins to pay after the deductible is met; however, funds in your HSA can be used to cover eligible health expenses, such as the deductible. Unused money remaining in your HSA rolls over to the next year. The CHP uses the same networks and offers the same choice of doctors and hospitals. The plan begins to pay after the deductible is met; however, Preventive Care Services and certain preventive generic prescriptions are covered at 100% and are not subject to the plan deductible. Who Is Eligible to Open an HSA? There are certain eligibility rules that apply to HSAs. You must be enrolled in a qualified high-deductible health plan (HDHP). The CHP is a qualified high-deductible health plan. You cannot have any other health coverage. This applies to the employee only. You cannot be covered through a spouse s medical or pharmacy plan. You cannot be covered through Medicare Part A, Part B, Part D, or through TRICARE. You cannot be covered through a general-purpose Flexible Spending Account (FSA). This includes a spouse s FSA. You cannot be claimed as a dependent on another person s tax return. How Do I Enroll in the HSA? First you must select medical option CHP during your enrollment period. Second, you must fully complete and submit the HSA Contribution Arrangement Form allowing Estes to make tax-free payroll contributions to your account. An account will be opened for you at HSABank. The HSABank account belongs to you. *Certain states do not permit pre-tax deductions to an HSA; you should consult your tax advisor if you have any questions regarding your state limitations. 17

20 Will Estes Contribute to My HSA? Estes will provide a dollar-for-dollar matching contribution of up to $1,000 to your HSABank account if you are enrolled with CHP employee-only or employee and one dependent coverage, or up to a $1,500 matching contribution to your HSA if you are enrolled with CHP employee and two or more dependents. Deposits from Estes will only be made to active employees. No company contributions or match will be paid once employment ends. When Must My HSA Account Through HSA Bank be Opened? A bank account at HSABank will automatically be opened when you enroll with the CHP plan. $0.01 will be deposited to open the account. Qualified medical expenses are only reimbursable through your HSA account as of the date the account is active. If you have medical expenses prior to the effective date of your HSA account, those expenses are not eligible for reimbursement. In addition, contributions to your account and/or match will not begin until the account is active and there will be no look-back/retroactive funding for missed contributions. Matching contributions will begin as of the date you begin making pre-tax contributions. 18

21 Flexible Spending Account and HSA Worksheet This worksheet is designed to help you estimate how much you should contribute to a Health Care Flexible Spending Account,* a Health Savings Account for those enrolled in the CHP medical plan or a Dependent Day Care Flexible Spending Account. Remember that the IRS limits your opportunities to stop, start, increase or decrease your contributions during the year unless you have a change in family status, and any money left in your Health Care Flexible Spending Account(s) that can t be used for the year s expenses will be forfeited. Money remaining in your HSA will roll over to the next year and will NOT be lost. HEALTH CARE FLEXIBLE SPENDING ACCOUNT OR HEALTH SAVINGS ACCOUNT LINE ANNUAL ESTIMATED COST Medical Dental Deductible(s) 1 + $ Your copayments 2 + $ Expenses for benefits not covered by the plan 3 + $ Subtotal (Add lines 1 3) 4 = $ Deductible(s) 5 + $ Your copayments for preventive, restorative or major expenses not paid by the plan 6 + $ Your copayments for orthodontia expenses 7 + $ Subtotal (Add lines 5 7) 8 = $ Other Eyeglasses or contacts 9 + $ Vision exams 10 + $ Hearing exams 11 + $ Other: 12 + $ Subtotal (Add lines 9 12) 13 = $ Total Expenses (Not to exceed plan maximum per year) (Add lines ) Per Pay Period (Weekly=52) (Divide the amount in line 14 by the number of pay periods (52) per year to see how much you should deposit each pay period to your Health Care Account for the calendar year.) You may refer to IRS Section 213 B for allowable reimbursable expenses. DEPENDENT CARE FLEXIBLE SPENDING ACCOUNT Dependent Care in Your Home 14 = $ Line 14 / 52 Weeks = $ ANNUAL ESTIMATED COST Wages or salary paid to care providers 15 + $ Social Security taxes (FICA) and other taxes that you pay on behalf of providers 16 + $ Expenses for household services related to the care of qualified dependent 17 + $ Dependent Care Outside Your Home Payments to qualified, licensed day-care facility 18 + $ Payments to other outside care providers 19 + $ Total Dependent Care Flexible Spending Account Expenses (Not to exceed plan maximum per year) (Add lines 15 19) Per Pay Period (Weekly=52) (Divide the amount in line 20 by the number of pay periods (52) per year to see how much you should deposit each pay period to your Dependent Care Spending Account for the calendar year.) * If you are enrolled in the medical CHP plan, you are not eligible to participate in the Health Care Flexible Spending Account = $ Line 20 / 52 Weeks = $ (Please refer to page 15 for maximum amount per year.)

22 Section III: The Selection Process Before you make your choices, you should figure out how HEALTH3CHECK adds up for you. Make your selections, write down the costs of your choices and add it all up. Remember: the big advantage of HEALTH3CHECK is that you choose the benefits that matter most to you. Additional Information Here s some additional information about participation in HEALTH3CHECK. In most cases, before-tax contributions to HEALTH3CHECK are not subject to state income taxes. However, these before-tax contributions are currently subject to state taxes in New Jersey and Puerto Rico. You will not pay Social Security taxes when you make before-tax contributions for Flex benefits and Flexible Spending Accounts. As a result, your participation in HEALTH3CHECK may have an impact on your future Social Security benefits. The amount of the reduction in your benefits will depend on how long and how much you contribute for benefits. In most cases, Social Security benefits are reduced by a minimal amount. The descriptions in this booklet present only the highlights of the benefits plans available to you and will also act as your Summary of Material Modifications. Summary Plan Descriptions (SPD) that provide more details about the plans can be found on the Employee Self-Service section of NOTES: 20

23 HEALTH3CHECK Estes Express Lines Flexible Benefits Plan 2017 Employee Cost Per Pay Period (Weekly) EMPLOYEE ONLY DENTAL PLANS EMPLOYEE + ONE DEPENDENT EMPLOYEE + TWO OR MORE DEPENDENTS Option #1 - Preferred $ 4.54 $ 8.59 $ Option #2 - Premier $ 4.56 $ 8.65 $ VISION CARE PLAN Vision Care $ 0.91 $ 1.91 $ 3.05 SUPPLEMENTAL TERM LIFE INSURANCE Per Pay Period Cost for Each $20,000 of Coverage Insurance Age Tobacco User Non-Tobacco User Age 01 through Age 29 $ 0.35 $ 0.17 Age 30 through Age 34 $ 0.38 $ 0.21 Age 35 through Age 39 $ 0.55 $ 0.35 Age 40 through Age 44 $ 0.87 $ 0.48 Age 45 through Age 49 $ 1.42 $ 0.69 Age 50 through Age 54 $ 2.28 $ 1.42 Age 55 through Age 59 $ 3.53 $ 2.21 Age 60 through Age 64 $ 5.57 $ 3.50 Age 65 through Age 69 $ 9.82 $ 6.16 Note: To figure your cost per pay period for Supplemental Term Life Insurance, find the cost based on your age. For example, if you are a nonsmoker and turn 30 years old, then your cost for $20,000 of life insurance coverage is $0.21. If you wish to choose $100,000 of supplemental life insurance coverage, multiply your cost per pay period by five. If during the coverage year your age puts you in a new bracket, your rates are subject to change. To help figure your cost per pay period for supplemental term life insurance, use the following method: ENTER YOUR AGE ENTER THE COST PER PAY PERIOD FOR YOUR AGE BELOW FOR $20,000 OF COVERAGE ENTER THE MULTIPLE OF $20,000 YOU WISH TO BUY MULTIPLY THE COST PER $20,000 OF COVERAGE TIMES THE MULTIPLE TO DETERMINE COST EXAMPLE 30 $ 0.21 X 5 = $ 1.05 YOUR COST X = $

24 ACCIDENTAL DEATH & DISMEMBERMENT INSURANCE (AD&D) Coverage Amount Cost Per Pay Period $ 20,000 $ 0.12 $ 40,000 $ 0.23 $ 60,000 $ 0.35 $ 80,000 $ 0.46 $ 100,000 $ 0.58 $ 120,000 $ 0.69 $ 140,000 $ 0.81 $ 160,000 $ 0.92 $ 180,000 $ 1.04 $ 200,000 $ 1.15 $ 220,000 $ 1.27 $ 240,000 $ 1.38 $ 260,000 $ 1.50 $ 280,000 $ 1.62 $ 300,000 $ 1.73 VOLUNTARY LONG-TERM DISABILITY (LTD) COVERAGE Insurance Age Cost Factor Per Pay Period Age 01 through Age Age 25 through Age Age 30 through Age Age 35 through Age Age 40 through Age Age 45 through Age Age 50 through Age Age 55 through Age Age 60 through Age Age 65 through Age Note: To figure your cost per pay period for Voluntary LTD Coverage, find the cost factor above based on your age. For example, if you turn 30, then your cost factor per pay period will be Next, determine your current base monthly compensation. Multiply your base monthly compensation by the cost factor per pay period to determine your LTD cost per pay period. So if your monthly compensation is $2,000 and you turn 30, your Voluntary LTD cost per pay period will be $0.60. If during the coverage year your age puts you in a new bracket or your salary changes, your rates are subject to change. To help figure your Voluntary LTD cost per pay period, use the following method: ENTER YOUR AGE ENTER THE COST FACTOR PER PAY PERIOD BELOW FOR YOUR AGE ENTER YOUR CURRENT BASE MONTHLY COMPENSATION MULTIPLY THE COST FACTOR PER PAY PERIOD BY YOUR MONTHLY COMPENSATION EXAMPLE X $ 2,000 = $ 0.60 YOUR COST X = $

25 NOTES: 23

26 NOTES: 24

27

28 Plan Design for Consumer Health Plan (CHP) BENEFITS IN-NETWORK OUT-OF-NETWORK Annual Maximum Unlimited Unlimited Calendar Year Deductible (CYD) Individual/Family Maximum $2,600 per individual/$5,200 per family $5,000/$10,000 Out-of-Pocket Maximum Individual/Family Maximum $5,200 per individual/$10,000 per family $10,000/$20,000 Health Savings Account (HSA) - Estes will match dollar-for-dollar up to $1,000 if enrolled with Single or Employee+One Dependent coverage or up to a $1,500 match if you are enrolled with Employee & Two or More Dependents. Refer to page 17 for all rules and details. Outpatient Doctor s Office Visits* For illness/injury Specialty physician 80% after CYD 50% after CYD Preventive Care* Routine preventive care for adults and children (including immunizations) Routine physicals Well woman care (including office visit and Pap Test for females) Routine Mammogram 100% Per the Preventive Care Guidelines of the American Medical Association (AMA) 50% after CYD Inpatient Hospital - Facility Services 80% after CYD 50% after CYD Inpatient Hospital Doctor s Visits/Consultations and Doctor s Surgical Expenses 80% after CYD 50% after CYD Outpatient Surgical Facility Services 80% after CYD 50% after CYD Outpatient Professional Services 80% after CYD 50% after CYD Emergency Care Doctor s office (participating/non-participating) Hospital Emergency Room or outpatient facility Urgent Care facility Independent Lab and X-ray Services (Facility and Professional Services) Hospital outpatient 80% after CYD True emergencies are covered at In-Network level. Lab and x-ray facility 80% after CYD 50% after CYD Doctor s office Maternity Initial visit to determine pregnancy All subsequent prenatal visits, postnatal visits and delivery Hospital confinement 80% after CYD 50% after CYD Birthing centers Mental Health, Alcohol/Substance Abuse Inpatient Outpatient Facility 80% after CYD 50% after CYD Chiropractic Care 80% after CYD 50% after CYD Prescription Drugs 30-day supply Mail Order drugs 90-day supply Pre-Existing Condition Limitation 80% after CYD/100% Preventive Generic** 80% after CYD There are no pre-existing limitations. 50% after CYD * Lab expenses are covered as described under Independent Lab and X-ray Services. **CIGNA s list of preventive generic drugs is available on

29 Plan Design for Medical Option 2 BENEFITS IN-NETWORK OUT-OF-NETWORK Annual Maximum Unlimited Unlimited Calendar Year Deductible (CYD) Individual/Family Maximum $500 per individual/$1,500 per family $1,000/$2,000 Out-of-Pocket Maximum Individual/Family Maximum $5,000 per individual/$10,000 per family $10,000/$20,000 Health Savings Account (HSA) Does Not Qualify Does Not Qualify Outpatient Doctor s Office Visits* For illness/injury Specialty physician Preventive Care* Routine preventive care for adults and children (including immunizations) Routine physicals Well woman care (including office visit and Pap Test for females) Routine Mammogram 100% after $25 per visit copay 100% after $50 per visit copay 100% Per the Preventive Care Guidelines of the American Medical Association (AMA) 50% after CYD 50% after CYD Inpatient Hospital - Facility Services 80% after $300 per confinement copay 50% after CYD Inpatient Hospital Doctor s Visits/Consultations and Doctor s Surgical Expenses 100% 50% after CYD Outpatient Surgical Facility Services 80% after CYD 50% after CYD Outpatient Professional Services 80% after CYD 50% after CYD Emergency Care Doctor s office (participating/non-participating) Hospital Emergency Room or outpatient facility Urgent Care facility Independent Lab and X-ray Services (Facility and Professional Services) 100% after $25 per visit copay ($50 for Specialist) 80% after CYD (waived if admitted) 100% after $25 per visit copay ($50 for Specialist) True emergencies are covered as In-Network. Hospital outpatient 100% 50% after CYD Lab and x-ray facility 100% 50% after CYD Doctor s office Maternity 100% (included in $25 per visit copay if performed and billed by treating physician) 50% after CYD Initial visit to determine pregnancy 100% after $25 copay or ($50 for Specialist) 50% after CYD All subsequent prenatal visits, postnatal visits and delivery 100% 50% after CYD Hospital confinement 80% after $300 per confinement copay 50% after CYD Birthing centers Mental Health, Alcohol/Substance Abuse (no cross accumulation) Covered if associated with participating hospital; 80% after $300 per confinement copay 50% after CYD Inpatient 80% after $300 per confinement copay 50% after CYD Outpatient Facility 80% after CYD 50% after CYD Chiropractic Care $50 copay per visit. 30 day CY maximum Prescription Drugs 30-day supply $10 copay generic (tier 1) or $35 copay brand (tier 2); $70 copay brand (tier 3) 50% to $500 CY combined max for manual medical manipulations 50% after CYD Mail Order drugs 90-day supply 2 times copays listed above 50% after CYD Pre-Existing Condition Limitation There are no pre-existing limitations. * Lab expenses are covered as described under Independent Lab and X-ray Services.

30 Plan Design for Medical Option 3 BENEFITS IN-NETWORK OUT-OF-NETWORK Annual Maximum Unlimited Unlimited Calendar Year Deductible (CYD) Individual/Family Maximum $500 per individual/$1,500 per family $1,000/$2,000 Out-of-Pocket Maximum Individual/Family Maximum $5,000 per individual/$10,000 per family $10,000/$20,000 Health Savings Account (HSA) Does Not Qualify Does Not Qualify Outpatient Doctor s Office Visits* For illness/injury Specialty physician Preventive Care* Routine preventive care for adults and children (including immunizations) Routine physicals Well woman care (including office visit and Pap Test for females) Routine Mammogram 100% after $20 per visit copay 100% after $40 per visit copay 100% Per the Preventive Care Guidelines of the American Medical Association (AMA) 50% after CYD 50% after CYD Inpatient Hospital - Facility Services 90% after $300 per confinement copay 50% after CYD Inpatient Hospital Doctor s Visits/Consultations and Doctor s Surgical Expenses 100% 50% after CYD Outpatient Surgical Facility Services 90% after CYD 50% after CYD Outpatient Professional Services 90% after CYD 50% after CYD Emergency Care Doctor s office (participating/non-participating) Hospital Emergency Room or outpatient facility Urgent Care facility Independent Lab and X-ray Services (Facility and Professional Services) 100% after $20 per visit copay ($40 for Specialist) 90% after CYD (waived if admitted) 100% after $20 per visit copay ($40 for Specialist) True emergencies are covered as In-Network. Hospital outpatient 100% 50% after CYD Lab and x-ray facility 100% 50% after CYD Doctor s office 100% 50% after CYD Maternity Initial visit to determine pregnancy 100% after $20 copay or ($40 for Specialist) 50% after CYD All subsequent prenatal visits, postnatal visits and delivery 100% 50% after CYD Hospital confinement 90% after $300 per confinement copay 50% after CYD Birthing centers Mental Health, Alcohol/Substance Abuse (no cross accumulation) Covered if associated with participating hospital; 90% after $300 per confinement copay 50% after CYD Inpatient 80% after $300 per confinement copay 50% after CYD Outpatient Facility 90% after CYD 50% after CYD Chiropractic Care $40 copay per visit. 30 day CY maximum Prescription Drugs 30-day supply $10 copay generic (tier 1) or $35 copay brand (tier 2); $70 copay brand (tier 3) 50% to $500 CY combined max for manual medical manipulations 50% after CYD Mail Order drugs 90-day supply 2 times copays listed above 50% after CYD Pre-Existing Condition Limitation There are no pre-existing limitations. * Lab expenses are covered as described under Independent Lab and X-ray Services.

31

32

A Guide to Your Benefits 2019

A Guide to Your Benefits 2019 Lamers Bus Lines, Inc. offers a comprehensive suite of benefits to promote health and financial security for you and your family. This booklet provides you with a summary

A Guide to Your Benefits 2019 Lamers Bus Lines, Inc. offers a comprehensive suite of benefits to promote health and financial security for you and your family. This booklet provides you with a summary

Veritas Management Group EMPLOYEE BENEFITS

Veritas Management Group EMPLOYEE BENEFITS Benefit plans effective February 1, 2016 January 31, 2017 Table of Contents How Benefits Work Benefits Eligibility... 3 Enrollment... 3 Changing Your Benefits

Veritas Management Group EMPLOYEE BENEFITS Benefit plans effective February 1, 2016 January 31, 2017 Table of Contents How Benefits Work Benefits Eligibility... 3 Enrollment... 3 Changing Your Benefits

Employee Benefits Guide

Employee Benefits Guide Plans effective January 1, 2017 Full-Time Faculty Welcome to Montgomery County Community College! Montgomery County Community College (the College) strives to offer you and your

Employee Benefits Guide Plans effective January 1, 2017 Full-Time Faculty Welcome to Montgomery County Community College! Montgomery County Community College (the College) strives to offer you and your

Veritas Management Group EMPLOYEE BENEFITS

Veritas Management Group EMPLOYEE BENEFITS Benefit plans effective February 1, 2017 January 31, 2018 Table of Contents How Benefits Work Benefits Eligibility... 3 Enrollment... 3 Changing Your Benefits

Veritas Management Group EMPLOYEE BENEFITS Benefit plans effective February 1, 2017 January 31, 2018 Table of Contents How Benefits Work Benefits Eligibility... 3 Enrollment... 3 Changing Your Benefits

HEALTH & WELFARE BENEFITS PLAN

HEALTH & WELFARE BENEFITS PLAN for employees in OCEA-represented units 2018 OCEA-Administered Health & Welfare Benefits Plan These benefits are provided at no additional cost to employees in regular or

HEALTH & WELFARE BENEFITS PLAN for employees in OCEA-represented units 2018 OCEA-Administered Health & Welfare Benefits Plan These benefits are provided at no additional cost to employees in regular or

2016 Regions Benefits Enrollment FAQs

2016 Regions Benefits Enrollment FAQs Q: What happens if I don t enroll during the open enrollment period? A: If you don t enroll between November 2 nd and November 13th, you will NOT have coverage for

2016 Regions Benefits Enrollment FAQs Q: What happens if I don t enroll during the open enrollment period? A: If you don t enroll between November 2 nd and November 13th, you will NOT have coverage for

Vision Service Plan. $10 Copay every 12 months. $25 Copay every 12 months. $130 allowance every 24 months

Vision Service Plan Bonner County will pay the cost of employee coverage. You may choose to cover dependents through a payroll deduction. Monthly costs are listed below. VSP Services Exam Lenses Frames

Vision Service Plan Bonner County will pay the cost of employee coverage. You may choose to cover dependents through a payroll deduction. Monthly costs are listed below. VSP Services Exam Lenses Frames

Enrollment Procedure

2017 Benefit Guide Enrollment Procedure Due to Federal Regulations, all benefit eligible employees are REQUIRED to enroll online to confirm their choices. This includes employees who are not making any

2017 Benefit Guide Enrollment Procedure Due to Federal Regulations, all benefit eligible employees are REQUIRED to enroll online to confirm their choices. This includes employees who are not making any

USE BENEFITS THAT WORK TO ACHIEVE YOUR WELLNESS GOALS IN 2018

2018 BENEFITS GUIDE FOR NEW EMPLOYEES USE BENEFITS THAT WORK TO ACHIEVE YOUR WELLNESS GOALS IN 2018 What s Inside Your Enrollment Checklist... INSIDE FRONT COVER Benefits That Work... PAGES 2 11 Additional

2018 BENEFITS GUIDE FOR NEW EMPLOYEES USE BENEFITS THAT WORK TO ACHIEVE YOUR WELLNESS GOALS IN 2018 What s Inside Your Enrollment Checklist... INSIDE FRONT COVER Benefits That Work... PAGES 2 11 Additional

Your Flexible Benefit Plan -- Premium Conversion and the Flexible Spending Accounts

Your Flexible Benefit Plan -- Premium Conversion and the Flexible Spending Accounts Updated: April 2015 YOUR FLEXIBLE BENEFIT PLAN PREMIUM CONVERSION AND THE FLEXIBLE SPENDING ACCOUNTS Introduction The

Your Flexible Benefit Plan -- Premium Conversion and the Flexible Spending Accounts Updated: April 2015 YOUR FLEXIBLE BENEFIT PLAN PREMIUM CONVERSION AND THE FLEXIBLE SPENDING ACCOUNTS Introduction The

Benefits Highlights. Table of Contents

I. Benefits Highlights Table of Contents Inside This Document...1 Participating Employers...2 An Overview of the Benefits Program...3 Benefits-at-a-Glance...5 Eligibility...7 Eligible s...8 If You and

I. Benefits Highlights Table of Contents Inside This Document...1 Participating Employers...2 An Overview of the Benefits Program...3 Benefits-at-a-Glance...5 Eligibility...7 Eligible s...8 If You and

Flexible Benefits Guide

Flexible Benefits Guide Carroll County Public Schools 125 North Court Street Westminster, MD 21157 2016 Flexible Benefits Program This guide will provide information on all your available benefit options.

Flexible Benefits Guide Carroll County Public Schools 125 North Court Street Westminster, MD 21157 2016 Flexible Benefits Program This guide will provide information on all your available benefit options.

Blount Open Enrollment Guideline

Blount Open Enrollment Guideline Enrollment dates: November 7 11, 2016 Benefits effective 01/01/2017 1. Medical Plan Options United Healthcare Plan A United Healthcare Plan B with Health Savings Account

Blount Open Enrollment Guideline Enrollment dates: November 7 11, 2016 Benefits effective 01/01/2017 1. Medical Plan Options United Healthcare Plan A United Healthcare Plan B with Health Savings Account

Flexible Spending Account Benefit Programs

Flexible Spending Account Benefit Programs The Flexible Spending Accounts (FSAs) offered under the Bosch Choice Welfare Benefit Plan help you save money by letting you set aside money on a Pre-Tax basis

Flexible Spending Account Benefit Programs The Flexible Spending Accounts (FSAs) offered under the Bosch Choice Welfare Benefit Plan help you save money by letting you set aside money on a Pre-Tax basis

YOUR BENEFITS GUIDE. Benefit plans effective January 1, 2017, through December 31, 2017.

YOUR BENEFITS GUIDE Benefit plans effective January 1, 2017, through December 31, 2017. The Oakley Transport Benefits Package Benefits are an integral part of the overall compensation package provided

YOUR BENEFITS GUIDE Benefit plans effective January 1, 2017, through December 31, 2017. The Oakley Transport Benefits Package Benefits are an integral part of the overall compensation package provided

2018 Benefit Summary

2018 Benefit Summary Benefits Overview Knox College is proud to offer a comprehensive benefits package to eligible employees. Eligibility is based on employees scheduled to work 30 hours or more per week,

2018 Benefit Summary Benefits Overview Knox College is proud to offer a comprehensive benefits package to eligible employees. Eligibility is based on employees scheduled to work 30 hours or more per week,

Employee Benefits Guide

Employee Benefits Guide Plans effective January 1, 2017 Regular Part-Time Administrators Welcome to Montgomery County Community College! Montgomery County Community College (the College) strives to offer

Employee Benefits Guide Plans effective January 1, 2017 Regular Part-Time Administrators Welcome to Montgomery County Community College! Montgomery County Community College (the College) strives to offer

Savanna Energy Services. Your 2016 Guide to Benefits

S Savanna Energy Services Your 2016 Guide to Benefits Benefits at a Glance Copay: A fixed dollar amount you must pay for a specific service, such as an office visit or emergency room. Coinsurance: The

S Savanna Energy Services Your 2016 Guide to Benefits Benefits at a Glance Copay: A fixed dollar amount you must pay for a specific service, such as an office visit or emergency room. Coinsurance: The

Diocese of Monterey. July 2018-June 2019 Benefits Summary. Diocese of Monterey. 425 Church Street, Monterey, California 93940

Diocese of Monterey July 2018-June 2019 Benefits Summary Diocese of Monterey 425 Church Street, Monterey, California 93940 831.373.4345 www.dioceseofmonterey.org Benefits Overview The Diocese of Monterey