Death benefits to children post 1 July

|

|

|

- Merryl Simpson

- 6 years ago

- Views:

Transcription

1 Death benefits to children post 1 July 14 March 2017 This article summarises the modified rules and implications of the super reforms when death benefits are paid to a child from 1 July Note: This article only examines the impact of the reforms on child death benefits and the modified application of the transfer balance cap rules for child beneficiaries. It assumes knowledge of the core related reforms. For an in-depth explanation of related reforms, including the $1.6m transfer balance cap and calculation of associated excess transfer balance tax, refer to our articles in the 'Super reforms' tab in the Overview page of the Technical Section of Adviser Online. Background The super reforms impact the rules and options available to child super death benefit beneficiaries from 1 July This may prompt a need to review and adjust estate planning strategies, should super death benefit pensions no longer be a viable or single solution. Existing child death benefit pensions will also be impacted, and action may need to be taken prior to 1 July 2017 to avoid an existing child pension beneficiary having an excess transfer balance amount. Of all the super reforms, the $1.6m transfer balance cap 1 arguably has the most significant impact on super death benefits and estate planning strategies. Children of a deceased superannuant are subject to a modified form of the transfer balance cap. Contents Who the modifications apply to... 1 Rules for child death benefits payable from 1 July Parent without transfer balance account... 2 Parent with transfer balance account... 3 Cap increment where both parents die... 5 Child commences member pension... 6 Existing child death benefit pensions... 6 The modified rules mean that regardless of whether the value of the death benefit is relatively small or large, children who receive death benefits may be impacted and the total benefit they can use to commence a death benefit pension will be constrained. It will be important to consider the merits of child death benefit pensions in relation to the appropriateness of other structures and estate planning investment vehicles going forward. Who the modifications apply to The modified rules operate to effectively ensure that a child beneficiary does not have their own $1.6m cap eroded by the payment of a death benefit pension from their parent. The modifications apply where a child beneficiary is both a child and a death benefit dependant of the deceased, 2 for super and tax purposes. This includes: minor children under 18 children who are financially dependent, and disabled children of any age. 3 1 In this article, we often refer to the concept of the general transfer balance cap as the $1.6m cap for simplicity. In 2017/18, this cap is set at $1.6m but may be indexed in future years. The cap which will therefore apply to a specific client scenario will be adjusted to reflect the prevailing cap in the relevant year. 2 ITAA97, s SIS Reg 6.21(2A) provides that the child must be disabled within the definition provided in s8(1) of the Disability Services Act

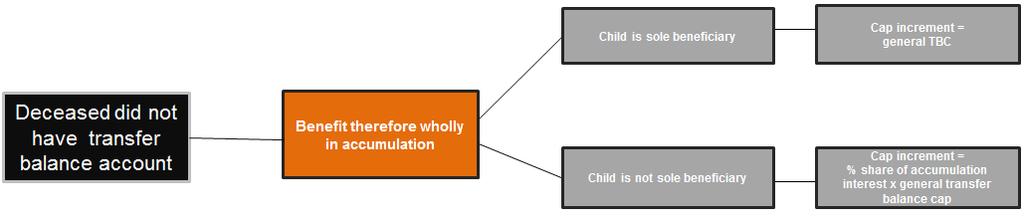

2 The modifications do not apply to a child beneficiary who is not a child of the deceased. These may be eligible to receive a death benefit pension as a financial dependant or interdependant, but they will be subject to the general $1.6m cap rules rather than the modified rules applicable to children of the deceased. The most common examples of when this may apply include where: a member makes a valid nomination to their grandchild as a financial dependant in the case of a step child, the relationship between the natural parent and step parent had ceased prior to the time the death benefit becomes payable, 4 or a child was otherwise financially dependent on a deceased individual who was not (for SIS purposes) their parent. Rules for child death benefits payable from 1 July 2017 The available transfer balance cap in respect of a death benefit interest payable to a child will be determined by what is known as the cap increment. Any amount used to commence a death benefit pension reduces the remaining cap increment. 5 The cap increment will be calculated based on whether the: deceased parent had a transfer balance account deceased parent had an excess transfer balance at the time of death child is the sole beneficiary of the interest, and if they are not, what proportionate share (%) the child has in the interest, and death benefit is from an accumulation and/or pension interest. A child may have multiple cap increments which are added to determine the maximum amount a child may transfer to pension phase. A child s total cap will include the sum of cap increments in respect of: the death of one parent the death of both parents, and/or their own member pension (eg where a disabled child commences a pension with structured settlement contributions). Children are required to fully commute any remaining death benefit pension interest once they turn 25 (unless disabled). It is at this point the modified transfer balance cap will be extinguished. If the death benefit pension balance is exhausted prior to 25, the modified transfer balance cap ceases at this earlier time. If the child is disabled, the modified transfer balance cap will continue beyond 25 until the balance of the pension is extinguished. This ensures that the child s own personal transfer balance cap is preserved and not eroded by the receipt of a death benefit pension. Below we outline the way in which a child beneficiary s cap increment is calculated, based on a range of possible scenarios. Appendix A provides a flowchart to illustrate the options available. Parent without transfer balance account The child s cap increment will be equal to their interest in the deceased s super accumulation benefit (as a percentage of the total interest) multiplied by the general transfer balance cap that prevails in the financial year that a death benefit is paid ($1.6m in 2017/18). 6 Therefore, in the case where a child of the deceased is the only beneficiary, their cap increment is equal to the general transfer balance cap and they may commence a death benefit pension with any amount up to that figure. Where the deceased had multiple accumulation interests this formula applies on a cumulative basis. Cap increment = % share of accumulation interest x general balance transfer cap 4 Includes where the natural parent has previously died, or where the natural parent and step parent have divorced. In the case where the step parent has legally adopted the step child, the child will be considered a child of the step parent for this purpose. 5 That is, the available cap increment may be more than or less than what is actually used to commence a death benefit pension. Any unused cap increment may be used at a later point, should the child subsequently commence a death benefit pension from the death of another parent, or in the unusual case where the child is eligible to commence their own member pension. 6 s

3 If the deceased client is survived by both a child and a spouse, for example, and the appropriate death benefit nominations are made, the spouse may choose to fully utilise their own transfer balance cap to commence a death benefit pension. In addition, the child may commence a child death benefit pension up to their available proportion of the transfer balance cap. This would maximise the amount of any death benefit interest from accumulation that could effectively be retained in the super environment. In this case, the spouse would have fully exhausted their transfer balance cap and would not be able to transfer additional amounts to pension phase 7, or benefit from any future indexation of the general cap. Note: The actual death benefit to which the child may be entitled may be greater than or less than the cap increment that arises in cases where the parent did not have a transfer balance account and the benefit is wholly from accumulation phase. In the case where a child becomes entitled to another death benefit from the death of the other parent, it may be possible to commence additional child death benefit pensions (see page 6). Example 1: No transfer balance account, benefit wholly from accumulation Sole beneficiary In December 2017, Mary passes away leaving her super accumulation interest of $1.9m to her daughter Rita as the sole beneficiary. Rita s cap increment is calculated as her interest in the $1.9m (100%) multiplied by the prevailing general transfer balance cap ($1.6m). Rita could therefore commence a death benefit pension with up to $1.6m. She would need to take the additional $300,000 as a lump sum death benefit as it exceeds her cap increment. Multiple beneficiaries If Rita was to instead be entitled to 50% of Mary s accumulation interest, with the other 50% payable to her father Tom, her cap increment would be calculated as follows: 50% x general balance transfer cap = $800,000. Rita could therefore commence a pension with $800,000 of her $950,000 entitlement and would need to take the remaining $150,000 as a lump sum death benefit. 7 Assuming that eligible debits to the transfer balance account do not occur, creating a future ability to make additional transfers. Parent with transfer balance account If a deceased parent had a transfer balance account, a death benefit to a child beneficiary may either be paid: wholly from a pension interest wholly from an accumulation interest, or partially from accumulation and pension. It is important to recall that the general $1.6m cap rules stipulate that when a person commences a pension, they will always have a transfer balance account, regardless of whether they continue to have a pension interest. 8 This means that if the parent had at some time in the past commenced a retirement pension, regardless of whether they continue to have a pension balance, or whether they have commuted the pension in part or in full, the way in which the cap increment is calculated is explained below. Transfer balance account and benefit paid wholly from pension Child is sole beneficiary If there is a single child beneficiary and the death benefit is wholly in pension phase at the time of the parent s death, the child beneficiary s cap increment is equal to the full balance of the pension interest at death, 9 regardless of whether the pension balance exceeds the prevailing general transfer balance cap at that point. 10 This means that it is possible for a child beneficiary to effectively commence a pension with an amount greater than the transfer balance cap. 11 Multiple beneficiaries In the case where there is more than one beneficiary, the child s cap increment will be calculated based on their interest in the deceased s pension interest (as a percentage) multiplied by the value of the deceased s pension interest. Cap increment = % share of pension interest x pension balance 12 8 For example, a person who commences a pension and either exhausts the account, or otherwise commutes the interest, will always have a transfer balance account. A person s transfer balance account only ceases upon their death. 9 s (2) 10 If parent died with an excess transfer balance amount that they had not rectified, see page 5 for modifications to child s available cap increment. 11 Account earnings that accrue from the time of the parent s death up until the time the death benefit pension commences to be paid are also treated as if they were part of the pension interest at the time of death and are accommodated under the cap increment. The proceeds of life policies are specifically excluded. 12 Pension balance less excess transfer balance amounts the parent had at the time of their death. 3

4 Example 2: Parent had transfer balance cap, benefit wholly from pension Sole beneficiary Alex passes away in October At the time of his death he has an account based pension valued at $4m. He does not have an excess transfer balance amount. His minor daughter Paula is the sole beneficiary of the pension. Assuming the value of the pension at the time of payment is $4m, her cap increment is therefore equal to $4m and she can commence a pension with the full amount. Multiple beneficiaries Consider instead a case where Paula and her brother Liam are both beneficiaries of Alex s pension interest in equal proportions. Each would have a cap increment calculated as follows: 50% x $4m = $2m. Note that if Alex had instead passed away without a transfer balance account and the interest was instead paid wholly from accumulation, each child would only have a cap increment of $800,000. This means the maximum amount that they could hold in death benefit pensions would be $1.6m. The remaining $2.4m would be paid as $1.2m lump sum death benefits to each of the children. Transfer balance account and benefit paid wholly from accumulation When a parent commences a pension, the ATO creates a transfer balance account. This account can have a positive, zero or negative value but is only extinguished upon their death. This is regardless of whether the parent fully utilised their transfer balance cap, whether they fully commute back into accumulation or outside super, or otherwise exhaust their pension funds. If a parent who has a transfer balance account does not have a pension interest at the time of their death, regardless of what their accumulation balance is, or whether these funds were at any point held in pension phase and subsequently commuted to super, the child s cap increment will be nil. They will generally be unable to commence a death benefit pension with any of the proceeds. 13 The exception to this would be if the child had an unused cap increment which had previously arisen from the death of another parent or if the child beneficiary had commenced their own member pension and therefore had their own personal transfer balance cap. See pages 5 and 6 for further discussion on this. 13 s (3) Example 3: Transfer balance account, benefit wholly paid from accumulation Robert dies in March At the time of his death, he had an accumulation account with a balance of $250,000. Previously, Robert had commenced an account based pension but at the time of his death he had fully exhausted the pension. Eliza is the sole beneficiary of his accumulation interest. Because the entire benefit will be paid from accumulation, Eliza will have a cap increment of nil and will need to take the entire benefit as a death benefit lump sum. If Robert did not have a transfer balance account (ie he had never commenced an account based pension at any time in the past), Eliza would have been able to commence a death benefit pension with Robert s accumulation interest. Benefit paid from accumulation and pension If a deceased parent has an accumulation and pension interest, each child beneficiary will receive a cap increment equal to their share of the pension interest only and would only be able to commence a death benefit pension up to this limit. 14 This means that the child will be unable to start a death benefit pension with any of the deceased parent s accumulation interests 15. Cap increment = % share of pension interest x pension balance 16 Example 4: Pension and accumulation interests Junior dies on 9 June At the time of his death he has both an accumulation account with an account balance of $350,000 and an income stream with an account balance of $750,000. Junior has two dependants his wife Sybil and son Tony (5). If Tony was to receive all of Junior s accumulation and pension interests, he would be unable to commence a death benefit pension with the full amount. This is because Tony s cap increment would be equal to his share of the value of the pension interest at the time of Junior s death (100% x $750,000) and so the accumulation interest would have to be taken as a lump sum. 14 s (4) 15 An exception to this would be if a child had available cap increments from the death of a parent previously, or if the child had commenced their own member pension (for example where a disabled child has received a structured settlement). 16 Pension balance less excess transfer balance amounts the parent had at the time of their death. 4

5 Similarly, if Tony was to be the sole beneficiary of the accumulation interest and Sybil was to be the sole beneficiary of the pension, Tony s cap increment would be nil, given that Junior had a transfer balance account, and Tony s only entitlement was to the accumulation interest. Instead, if Junior s pension was paid to Tony, and a nomination was made in favour of Sybil for Junior s accumulation account, Tony could commence a death benefit pension with the $750,000 17, and Sybil could commence a death benefit pension with the $350,000 from Junior s accumulation account. This would enable all of Junior s super interests to initially be held in pension phase. Adjustments if parent had excess transfer balance account If a parent dies with an excess transfer amount, the amount of the excess will reduce the child s available cap increment. 18 That is: Cap increment = % share of pension interest x pension balance where: Pension balance is the value of the pension interest at death 19, less excess transfer balance amounts In the case where a child is the reversionary beneficiary and the parent had an excess transfer balance immediately prior to their death, the child will need to at least partially commute the pension to avoid an excess transfer balance. As the value of the pension at the date of the parent s death will be credited to the child s transfer balance account 12 months from the date of death 20, the child will have 12 months to make the commutation before an excess transfer balance occurs. Cap increment where both parents die In the unfortunate event that a child finds themselves in a situation where both parents are deceased, their total available cap will be determined by: calculating their available cap increment for each parent as outlined above adding the available cap increments together, and adding to that any personal transfer balance cap the child has in respect of their own member pension. This means that in a case where both parents pass away with accumulation balances (assuming neither parent has a transfer balance account) it may be possible for a child to commence death benefit pensions with a total of $3.2m. 21 It may also be possible for a child beneficiary who has an unused cap increment from the death of another parent, to use this amount to commence a larger pension upon the death of a second parent, than what the second cap increment would otherwise allow. Example 5: Cap increment where both parents die Thomas passes away in December 2017 with $500,000 in an accumulation account. He has never commenced a pension. His son Mark (13) is the sole beneficiary of the interest. Mark s cap increment is calculated as: 100% x general transfer balance cap In 2017/18, the general transfer balance cap is $1.6m. Therefore Mark s cap increment is $1.6m. He commences a death benefit pension with the full $500,000 balance. In March 2019, Mark s mother passes away. She had $1.95m in an accumulation interest and has never commenced a pension. Mark is the sole beneficiary of his mother s super interest and his cap increment in respect of his mother s death is therefore equal to the general transfer balance cap of $1.6m. Mark s total transfer balance cap is calculated by adding the cap increment generated from his father s death to that received in respect of his mother s death. That is, his total cap is $3.2m. 17 Assumes that she does not have a transfer balance account and has not previously commenced a pension herself. 18 s (5) 19 Includes growth on death benefit amounts that have accrued from death up until the benefit is paid. 20 In line with the general transfer balance cap rules, where an automatic reversionary death benefit pension is paid, the beneficiary will have 12 months from the date of death to address their affairs and to commute an amount that exceeds their available transfer balance cap to avoid an excess transfer balance amount. 21 Based on $1.6m general transfer balance cap in 2016/17. Cap is subject to indexation. Assumes child doesn t have their own personal transfer balance account. 5

6 Because he only commenced the initial death benefit pension from the death of his father with $500,000, this means he could elect to receive the entire interest of $1.95m as a death benefit pension. This is because both the $500,000 pension and the $1.95m pension would not exceed his available cap increment. Child commences member pension In the unusual case where a child beneficiary commences their own pension (and therefore has their own transfer balance account) either before or after becoming entitled to a child death benefit pension, their total transfer balance cap is: the general transfer balance cap in the year in which they commence their own member pension, plus cap increments (calculated as above) in relation to the death of one or both parents. For the purpose of determining any future uplift in the child s personal transfer balance cap as a result of indexation, cap increments that relate to the commencement of child death benefit pensions are ignored, and the calculation is as per the ordinary rules. This means that if a child has their own personal transfer balance account, they can make use of any unused cap they have to commence child death benefit pensions with amounts greater than the applicable death benefit cap increment would otherwise allow. This is most likely to occur in the case of a disabled child, where they have received a structured settlement and made a contribution to super. Example 6: Child beneficiary has personal transfer balance account On 1 August 2017, Barbara received a structured settlement of $5m as a result of an injury she suffered. On 1 September, she contributes the full amount to super and commences an account based pension with this amount, as well as $400,000 she has in her accumulation account. As per the general transfer balance cap rules, her cap is $1.6m in 2017/18. She receives a credit to her transfer balance account of $5.4m, and immediately also receives a debit of $5m to recognise the structured settlement contribution. She therefore has a transfer balance account of $400,000. Barbara is able to commence a death benefit pension with the full amount of Bob s death benefit (see page 4). Her total cap is calculated by adding her own personal transfer balance cap ($1.6m) to the cap increment received in respect of Bob s death ($1.8m), totalling $3.4m. Because Barbara has a transfer balance account of $400,000 (remember, $5m was debited as it was a structured settlement payment), she still has $1.2m of cap space remaining. For the purpose of future proportional indexation, the death benefit pension is ignored. Barbara s highest transfer balance is $400,000. Assuming no additional transfers to pensions are made, she will therefore receive 75% of any future indexation to the general transfer balance cap. 22 Existing child death benefit pensions Child death benefit pensions running prior to 1 July 2017 will have a transfer balance cap increment equal to the $1.6m general transfer balance cap on that day. 23. This reflects the maximum cap the deceased parent could have had at that time, should they have still been alive. For example, if Grant had an existing child death benefit pension with an account balance of $1m on 30 June 2017, he would have a cap increment available in respect of this pension of $1.6m on 1 July This means Grant would have a remaining unused cap increment of $600,000. If the account balance of an existing child death benefit pension exceeds their cap increment of $1.6m from 1 July, an excess transfer balance will occur and excess transfer balance tax will be incurred. An exception to this would be where a death benefit pension to a child was a reversionary pension. In this case, the credit to the child s modified cap would occur on the later of 12 months from the date of death of the parent or 1 July Existing child pensions should therefore be reviewed prior to 1 July On 1 January 2018, Barbara s father Bob passes away, leaving his entire $1.8m pension interest to Barbara as the sole beneficiary. Bob did not have an excess transfer balance. 22 As Barbara has used 25% of her transfer balance cap ($400,000/$1.6m) she will receive 75% of any future uplift. 23 s

7 Conclusion While child superannuation death benefit pensions may still be an attractive, practical and cost effective option, advice will need to be carefully formulated going forward, due to the limitations imposed by the transfer balance cap, and the modified rules applicable to children. Super alternatives will in some cases need to be considered. Clients should seek specialist advice from a legal practitioner where appropriate, to ensure that any financial advice provided and implemented is well supported by appropriate and executed estate planning arrangements. Contact details For further information, please contact MLC Technical Services on Important information and disclaimer This publication has been prepared by Technical & Development, a division of GWM Adviser Services Limited (ABN , AFSL ) ( GWMAS ), a member of the National Australia Bank group of companies ( NAB Group ), Miller Street, North Sydney Any advice and information in this publication is of a general nature only. It has been prepared without taking account of individual objectives, financial situation or needs and because of that you should consider the appropriateness of the advice before acting. It is solely for use by financial advisers and any distribution to customers is prohibited. GWMAS and the NAB Group do not accept any liability which arises as a result of dissemination of this publication to customers by financial advisers or a customer s reliance on this publication. Information in this publication is accurate as at March 2017 and subject to change without notice. In some cases the information has been provided to us by third parties. While it is believed the information is accurate and reliable, the accuracy of that information is not guaranteed in any way. Opinions constitute our judgement at the time of issue and are subject to change. Neither GWMAS nor any member of the NAB Group, nor their employees or directors give any warranty of accuracy, nor accept any responsibility for errors or omissions in this document. Any investment returns shown in any case studies in this publication are hypothetical examples only. They do not reflect the historical or future returns of any specific financial products. Any general tax information provided in this publication is intended as a guide only and is based on our general understanding of taxation laws. 7

8 Appendix A 8

9 9

Understanding the $1.6 million transfer balance cap Version 1.2

Understanding the $1.6 million transfer balance cap Version 1.2 This document provides some additional information about the $1.6 million transfer balance cap discussed in the SOA so that you can understand

Understanding the $1.6 million transfer balance cap Version 1.2 This document provides some additional information about the $1.6 million transfer balance cap discussed in the SOA so that you can understand

A A fresh guide start to managing redundancies

A fresh guide start to managing redundancies A A fresh guide start to managing 2015 2016redundancies 2013/14 Preparation date 03 March 2014 Issued by The Trustee, MLC Nominees Pty Ltd (MLC) ABN 93 002

A fresh guide start to managing redundancies A A fresh guide start to managing 2015 2016redundancies 2013/14 Preparation date 03 March 2014 Issued by The Trustee, MLC Nominees Pty Ltd (MLC) ABN 93 002

A A fresh guide start to managing redundancies

A fresh guide start to managing redundancies A A fresh guide start to managing 2014 2015redundancies 2013/14 Preparation date 03 March 2014 Issued by The Trustee, MLC Nominees Pty Ltd (MLC) ABN 93 002

A fresh guide start to managing redundancies A A fresh guide start to managing 2014 2015redundancies 2013/14 Preparation date 03 March 2014 Issued by The Trustee, MLC Nominees Pty Ltd (MLC) ABN 93 002

Understanding retirement income Version 5.2

Understanding retirement income Version 5.2 This document provides some additional information to help you understand the financial planning concepts discussed in the SOA in relation to understanding retirement.

Understanding retirement income Version 5.2 This document provides some additional information to help you understand the financial planning concepts discussed in the SOA in relation to understanding retirement.

Superannuation Caps and changes- update. Presented by Jenneke Mills Senior Technical Consultant MLC Technical Services MLC Advice and Professionalism

Superannuation Caps and changes- update Presented by Jenneke Mills Senior Technical Consultant MLC Technical Services MLC Advice and Professionalism Superannuation Caps & changes- update SUPERANNUATION:

Superannuation Caps and changes- update Presented by Jenneke Mills Senior Technical Consultant MLC Technical Services MLC Advice and Professionalism Superannuation Caps & changes- update SUPERANNUATION:

Super Changes Webinar 28 February 2017

Super Changes Webinar 28 February 2017 First, a little more about you 2 Welcome Super Changes Most changes start 1 July so it is important that you and your clients are prepared. Outline key aspects of

Super Changes Webinar 28 February 2017 First, a little more about you 2 Welcome Super Changes Most changes start 1 July so it is important that you and your clients are prepared. Outline key aspects of

Reversionary Pensions

SuperGuardian Information Reversionary Pensions A member s estate planning objectives should be taken into account when commencing any new pension. When a super fund member passes away, if they have a

SuperGuardian Information Reversionary Pensions A member s estate planning objectives should be taken into account when commencing any new pension. When a super fund member passes away, if they have a

Recontributions and other super interest(ing) pension strategies. Craig Day Executive Manager, FirstTech Colonial First State 97618: _4

pension strategies. Craig Day Executive Manager, FirstTech Colonial First State 97618: _4") Recontributions Craig Day Executive Manager, FirstTech Colonial First State 97618:4413748_4 CONTENTS Introduction... 3 Superannuation interests, proportioning and tax components... 3 Meaning of a superannuation

Recontributions Craig Day Executive Manager, FirstTech Colonial First State 97618:4413748_4 CONTENTS Introduction... 3 Superannuation interests, proportioning and tax components... 3 Meaning of a superannuation

RULE D4 Child s accrued allowance

Rule D4 sets out the terms of eligibility for the child of a former firefighter or optant-out who was entitled to a deferred pension. Part III of Schedule 4 explains how the award should be calculated.

Rule D4 sets out the terms of eligibility for the child of a former firefighter or optant-out who was entitled to a deferred pension. Part III of Schedule 4 explains how the award should be calculated.

Estate Planning Strategies

Estate Planning Strategies Overview of Our Services Services SuperIQ and Super Concepts provides a full range of SMSF services SMSF accounting and administration services End of Year service (closed to

Estate Planning Strategies Overview of Our Services Services SuperIQ and Super Concepts provides a full range of SMSF services SMSF accounting and administration services End of Year service (closed to

Superannuation Changes: Estate Planning

2017 Superannuation Series Superannuation Changes: Estate Planning In the third instalment of our Superannuation Changes series, we consider the impact these changes will have on your estate planning affairs.

2017 Superannuation Series Superannuation Changes: Estate Planning In the third instalment of our Superannuation Changes series, we consider the impact these changes will have on your estate planning affairs.

Superannuation reform: transfer balance cap

Law Companion Guideline LCG 2016/9 Page status: legally binding Superannuation reform: transfer balance cap Relying on this Guideline This Guideline is a public ruling for the purposes of the Taxation

Law Companion Guideline LCG 2016/9 Page status: legally binding Superannuation reform: transfer balance cap Relying on this Guideline This Guideline is a public ruling for the purposes of the Taxation

ANZ OneAnswer. Pension. Incorporated Material

ANZ OneAnswer Pension Incorporated Material 5 May 2008 i How do I read this Incorporated Material? This Incorporated Material provides further information and/or specific terms and conditions referred

ANZ OneAnswer Pension Incorporated Material 5 May 2008 i How do I read this Incorporated Material? This Incorporated Material provides further information and/or specific terms and conditions referred

Westpac Protection Plans Technical Guide.

Westpac Protection Plans Technical Guide. 19 October 2009 This document outlines important information about Taxation and Superannuation, relevant to your Westpac Protection Plans products. It should be

Westpac Protection Plans Technical Guide. 19 October 2009 This document outlines important information about Taxation and Superannuation, relevant to your Westpac Protection Plans products. It should be

Smart strategies for running your own super fund 2012/13

Smart strategies for running your own super fund 2012/13 Set your super free Self managed super is the largest and fastest growing super sector in Australia. Over 2,000 new funds are established every

Smart strategies for running your own super fund 2012/13 Set your super free Self managed super is the largest and fastest growing super sector in Australia. Over 2,000 new funds are established every

MLC Facts and Figures

For adviser use only MLC Facts and Figures 2017/18 Contents Tax 1 12 Super accumulation phase 13 30 Super access and taxation of benefits 31 44 Super pension phase 45 56 Social security 57 66 Aged care

For adviser use only MLC Facts and Figures 2017/18 Contents Tax 1 12 Super accumulation phase 13 30 Super access and taxation of benefits 31 44 Super pension phase 45 56 Social security 57 66 Aged care

Superannuation: Income streams

Technical Services TB 31 Superannuation: Income streams Issued by Technical Services on 1 November 2009. Summary There are a number of issues to consider when selecting the appropriate superannuation income

Technical Services TB 31 Superannuation: Income streams Issued by Technical Services on 1 November 2009. Summary There are a number of issues to consider when selecting the appropriate superannuation income

YOUR ULTIMATE DEADLINE What happens to my superannuation when I die? SEPL s death benefits guide

YOUR ULTIMATE DEADLINE What happens to my superannuation when I die? SEPL s death benefits guide KNOWLEDGE + INNOVATION + SKILL = SOLUTIONS DON T RISK MISSING YOUR ULTIMATE DEADLINE 0 Table of contents

YOUR ULTIMATE DEADLINE What happens to my superannuation when I die? SEPL s death benefits guide KNOWLEDGE + INNOVATION + SKILL = SOLUTIONS DON T RISK MISSING YOUR ULTIMATE DEADLINE 0 Table of contents

Upon the death of a member, a superannuation fund trustee must, where

The Australian Journal of Financial Planning 1 Death Benefit Nominations in Superannuation By Tim Sanderson Senior Technical Services Manager, Colonial First State Tim Sanderson joined FirstTech in 2010.

The Australian Journal of Financial Planning 1 Death Benefit Nominations in Superannuation By Tim Sanderson Senior Technical Services Manager, Colonial First State Tim Sanderson joined FirstTech in 2010.

Understanding superannuation

Understanding superannuation Version 5.2 This document has been published by GWM Adviser Services Limited AFSL 230692, registered address 105-153 Miller St North Sydney NSW 2060, ABN 96 002 071 749 for

Understanding superannuation Version 5.2 This document has been published by GWM Adviser Services Limited AFSL 230692, registered address 105-153 Miller St North Sydney NSW 2060, ABN 96 002 071 749 for

Estate Planning Seminar Creating Certainty - 18 th August 2014 Presented by:

Estate Planning Seminar Creating Certainty - 18 th August 2014 Presented by: Tony Gilham Founding Partner Certified Financial Planner SMSF Specialist Advisor www.gfmwealth.com.au Andrew Lord Director Lawyer

Estate Planning Seminar Creating Certainty - 18 th August 2014 Presented by: Tony Gilham Founding Partner Certified Financial Planner SMSF Specialist Advisor www.gfmwealth.com.au Andrew Lord Director Lawyer

BT Portfolio SuperWrap Essentials

BT Portfolio SuperWrap Essentials Information Brochure Personal Super Plan Pension Plan Term Allocated Pension Plan Product Disclosure Statement ( PDS ) The distributor of BT Portfolio SuperWrap Essentials

BT Portfolio SuperWrap Essentials Information Brochure Personal Super Plan Pension Plan Term Allocated Pension Plan Product Disclosure Statement ( PDS ) The distributor of BT Portfolio SuperWrap Essentials

Example: calculation of transfer balance cap and tax

$1.6m super transfer balance cap by Ben Miller, Senior Writer, Wolters Kluwer CCH Abstract: With the announcement of the federal Budget on 2 May 2016, superannuation laws regarding pensions were tipped

$1.6m super transfer balance cap by Ben Miller, Senior Writer, Wolters Kluwer CCH Abstract: With the announcement of the federal Budget on 2 May 2016, superannuation laws regarding pensions were tipped

9/02/2018. How Estate Planning has to change. Session overview. SMSFs by asset size 12% Peter Burgess

How Estate Planning has to change Peter Burgess General Manager, Technical Services and Education, SuperConcepts Session overview Rule changes Is TBA control in compression trusted hands? SMSFs by asset

How Estate Planning has to change Peter Burgess General Manager, Technical Services and Education, SuperConcepts Session overview Rule changes Is TBA control in compression trusted hands? SMSFs by asset

The Super Brief newsletter

Update on New Regulations and Legislation as at 1st July 2013 As a result of the midyear economic update in June there are a number of policy announcements and Legislation that was intended to be implemented

Update on New Regulations and Legislation as at 1st July 2013 As a result of the midyear economic update in June there are a number of policy announcements and Legislation that was intended to be implemented

Super Product Disclosure Statement

Local Government Super Product Disclosure Statement Retirement Scheme How to use this Product Disclosure Statement This Product Disclosure Statement (PDS) provides you with important details about the

Local Government Super Product Disclosure Statement Retirement Scheme How to use this Product Disclosure Statement This Product Disclosure Statement (PDS) provides you with important details about the

$1.6 Million transfer balance cap

$1.6 Million transfer balance cap 1 July 2017 super changes From 1 July 2017, a transfer balance cap applies to the value of pensions that can be transferred to retirement phase as well as those already

$1.6 Million transfer balance cap 1 July 2017 super changes From 1 July 2017, a transfer balance cap applies to the value of pensions that can be transferred to retirement phase as well as those already

Flexi Pension. Your guide to pensions. Product Disclosure Statement issued 1 July 2017 by UniSuper Limited ABN AFSL No.

Your guide to pensions Flexi Pension Product Disclosure Statement issued 1 July 2017 by UniSuper Limited ABN 54 006 027 121 AFSL No. 492806 Tony and Virginia McKittrick 3 ABOUT THIS PRODUCT DISCLOSURE

Your guide to pensions Flexi Pension Product Disclosure Statement issued 1 July 2017 by UniSuper Limited ABN 54 006 027 121 AFSL No. 492806 Tony and Virginia McKittrick 3 ABOUT THIS PRODUCT DISCLOSURE

GUARANTEED ANNUITIES LIFESTREAM GUARANTEED INCOME. POLICY DOCUMENT Issue date: 12 June 2017 For new investors from: 12 June 2017

GUARANTEED ANNUITIES LIFESTREAM GUARANTEED INCOME POLICY DOCUMENT Issue date: 12 June 2017 For new investors from: 12 June 2017 Contents 1. Definitions and interpretation 3 1.1 Definitions 3 2. Your Policy

GUARANTEED ANNUITIES LIFESTREAM GUARANTEED INCOME POLICY DOCUMENT Issue date: 12 June 2017 For new investors from: 12 June 2017 Contents 1. Definitions and interpretation 3 1.1 Definitions 3 2. Your Policy

Estate Planning Superannuation death benefits

Estate Planning Superannuation death benefits Nominating a beneficiary to receive your superannuation benefits upon your death gives you peace of mind knowing that the funds will be paid according to your

Estate Planning Superannuation death benefits Nominating a beneficiary to receive your superannuation benefits upon your death gives you peace of mind knowing that the funds will be paid according to your

Understanding superannuation Version 5.2

Understanding superannuation Version 5.2 This document provides some additional information to help you understand the financial planning concepts discussed in the SOA in relation to superannuation. This

Understanding superannuation Version 5.2 This document provides some additional information to help you understand the financial planning concepts discussed in the SOA in relation to superannuation. This

Transfer balance account credits and debits

Guidance note for super 16 account credits and debits Towards a sustainable superannuation system In the 2016 17 Budget, the government announced a number of changes designed to improve the sustainability,

Guidance note for super 16 account credits and debits Towards a sustainable superannuation system In the 2016 17 Budget, the government announced a number of changes designed to improve the sustainability,

Tackling the retirement challenge

Tackling the retirement challenge Securitor Conference Nathalie Bouquet Head of Technical Services Disclaimer The information contained in this presentation is current as at 30 March 2012 unless otherwise

Tackling the retirement challenge Securitor Conference Nathalie Bouquet Head of Technical Services Disclaimer The information contained in this presentation is current as at 30 March 2012 unless otherwise

Matrix Superannuation Master Trust Superannuation, Rollovers and Allocated Pensions

Matrix Superannuation Master Trust Superannuation, Rollovers and Allocated Pensions Product Disclosure Statement Part 1 of 4 parts General Information Issued 3 March 2008 This document is a Product Disclosure

Matrix Superannuation Master Trust Superannuation, Rollovers and Allocated Pensions Product Disclosure Statement Part 1 of 4 parts General Information Issued 3 March 2008 This document is a Product Disclosure

About your insurance benefits

Product disclosure statement 1 July 2017 Guide 6 Your death and disablement benefits Equip Rio Tinto Fund Employee members 01 About your insurance benefits 02 Eligibility for insurance cover 03 Choosing

Product disclosure statement 1 July 2017 Guide 6 Your death and disablement benefits Equip Rio Tinto Fund Employee members 01 About your insurance benefits 02 Eligibility for insurance cover 03 Choosing

ADDITIONAL INFORMATION BOOKLET

ADDITIONAL INFORMATION BOOKLET Issued by Diversa Trustees Limited (ABN 49 006 421 638, AFSL 235153, RSE Licence No. L0000635) as Trustee of the HUB24 Super Fund (ABN 60 910 190 523, RSE R1074659, USI 60

ADDITIONAL INFORMATION BOOKLET Issued by Diversa Trustees Limited (ABN 49 006 421 638, AFSL 235153, RSE Licence No. L0000635) as Trustee of the HUB24 Super Fund (ABN 60 910 190 523, RSE R1074659, USI 60

Additional information guide (1 September 2017) Challenger Guaranteed Annuity (Liquid Lifetime)

Challenger Guaranteed Annuity (Liquid Lifetime)") Additional information guide (1 September 2017) Challenger Guaranteed Annuity Table of contents How the Annuity is taxed 1 Senior Australians and Pensioners Tax Offset 2 Social security 3 Maximum periods

Additional information guide (1 September 2017) Challenger Guaranteed Annuity Table of contents How the Annuity is taxed 1 Senior Australians and Pensioners Tax Offset 2 Social security 3 Maximum periods

THE 3 AARRRR S OF WEALTH PROTECTION AND ESTATE PLANNING. Matt Manning Technical Consultant

THE 3 AARRRR S OF WEALTH PROTECTION AND ESTATE PLANNING Matt Manning Technical Consultant Agenda 1. Super death benefits refresher 2. Super EP strategies 3. Non-super EP strategies Death benefits refresher

THE 3 AARRRR S OF WEALTH PROTECTION AND ESTATE PLANNING Matt Manning Technical Consultant Agenda 1. Super death benefits refresher 2. Super EP strategies 3. Non-super EP strategies Death benefits refresher

SMSF Legislative Changes Applicable from 1 July 2013

SMSF Legislative Changes Applicable from 1 July 2013 Essential SMSF Update (Current at 3 September 2013) www. accesssuperaudit.com.au TEL: 1300 371 186 GPO Box 2467 901, 50 Clarence St admin@accesssuperaudit.com.au

SMSF Legislative Changes Applicable from 1 July 2013 Essential SMSF Update (Current at 3 September 2013) www. accesssuperaudit.com.au TEL: 1300 371 186 GPO Box 2467 901, 50 Clarence St admin@accesssuperaudit.com.au

The Transfer Balance Cap & Death Benefits. Nicholas Ali Super Concepts

The Transfer Balance Cap & Death Benefits Nicholas Ali Super Concepts Estate Planning and the TBC March 2018 What you need to know This content of this presentation has been prepared to provide you with

The Transfer Balance Cap & Death Benefits Nicholas Ali Super Concepts Estate Planning and the TBC March 2018 What you need to know This content of this presentation has been prepared to provide you with

Dealing with step children in super

IOOF AdviserConnect IOOF TechConnect Quarterly technical bulletin: Summer 2012 1 Dealing with step children in super By Julie Steed, Technical Services Manager 3 Super grandparents: Are your clients missing

IOOF AdviserConnect IOOF TechConnect Quarterly technical bulletin: Summer 2012 1 Dealing with step children in super By Julie Steed, Technical Services Manager 3 Super grandparents: Are your clients missing

Your insurance provider

Product disclosure statement 1 July 2017 Guide 7 Your death and disablement benefits Equip Rio Tinto Fund Personal members 01 About your insurance benefits 02 Your insurance provider 03 Eligibility for

Product disclosure statement 1 July 2017 Guide 7 Your death and disablement benefits Equip Rio Tinto Fund Personal members 01 About your insurance benefits 02 Your insurance provider 03 Eligibility for

SuperWrap features and benefits. SuperWrap tax and administration benefits to clients

SuperWrap features and benefits SuperWrap tax and administration benefits to clients Contents Tax deductible expenses and excess deductions 3 Tax benefits and capital losses 6 Moving from Super to Pension

SuperWrap features and benefits SuperWrap tax and administration benefits to clients Contents Tax deductible expenses and excess deductions 3 Tax benefits and capital losses 6 Moving from Super to Pension

Commuting Defined Benefit Pensions in an SMSF

Commuting Defined Benefit Pensions in an SMSF The information in this presentation has been prepared by Accurium Pty Limited ABN 13 009 492 219 (Accurium). It is general information only and is not intended

Commuting Defined Benefit Pensions in an SMSF The information in this presentation has been prepared by Accurium Pty Limited ABN 13 009 492 219 (Accurium). It is general information only and is not intended

Smart strategies for running your own super fund

Smart strategies for running your own super fund 2011 Set your super free Self managed super is the largest and fastest growing super sector in Australia. Over 2,000 new funds are established every month,

Smart strategies for running your own super fund 2011 Set your super free Self managed super is the largest and fastest growing super sector in Australia. Over 2,000 new funds are established every month,

Types of contributions concessional, non-concessional, capital gains tax (CGT) cap contributions and personal injury contributions.

cap contributions and personal injury contributions.") TB 59 Contributions Issued on 1 July 2013. Summary A superannuation fund has strict rules set by law for the acceptance of. The client s age, the type of contribution and work status are some of the factors

TB 59 Contributions Issued on 1 July 2013. Summary A superannuation fund has strict rules set by law for the acceptance of. The client s age, the type of contribution and work status are some of the factors

Understanding superannuation

Version 4.2 This document provides some additional information to help you understand the financial planning concepts discussed in the SOA in relation to. Important information This document has been published

Version 4.2 This document provides some additional information to help you understand the financial planning concepts discussed in the SOA in relation to. Important information This document has been published

Macquarie Life Super Protector. Macquarie Life

Macquarie Life Super Protector Macquarie Life Product Disclosure Statement issued by: Macquarie Life Limited ABN 56 003 963 773 AFSL 237 497 Dated 23 April 2010 Contents 01 The importance of insurance

Macquarie Life Super Protector Macquarie Life Product Disclosure Statement issued by: Macquarie Life Limited ABN 56 003 963 773 AFSL 237 497 Dated 23 April 2010 Contents 01 The importance of insurance

Understanding superannuation Version 5.0

Understanding superannuation Version 5.0 This document provides some additional information to help you understand the financial planning concepts discussed in the SOA in relation to superannuation. This

Understanding superannuation Version 5.0 This document provides some additional information to help you understand the financial planning concepts discussed in the SOA in relation to superannuation. This

Transition to retirement pensions

Transition to retirement pensions No matter how many hours you work, if you are over preservation age 1, you can access your super as a transition to retirement (TTR) pension, even if you are still working

Transition to retirement pensions No matter how many hours you work, if you are over preservation age 1, you can access your super as a transition to retirement (TTR) pension, even if you are still working

Transfer balance cap and transfer balance accounts

Transfer balance cap and transfer balance accounts Peter Burgess, SuperConcepts August 2017 What you need to know The content of this presentation has been prepared to provide you with general information

Transfer balance cap and transfer balance accounts Peter Burgess, SuperConcepts August 2017 What you need to know The content of this presentation has been prepared to provide you with general information

Welcome. Estate Planning. 25 May Speakers Dale Edwards, Advivo Emily O Brien, Redchip Gavin Barnes, Redchip

Welcome Estate Planning 25 May 2017 Speakers Dale Edwards, Advivo Emily O Brien, Redchip Gavin Barnes, Redchip - SPEAKERS - Dale Edwards Partner and Business Advisory Specialist Advivo Emily O Brien Associate

Welcome Estate Planning 25 May 2017 Speakers Dale Edwards, Advivo Emily O Brien, Redchip Gavin Barnes, Redchip - SPEAKERS - Dale Edwards Partner and Business Advisory Specialist Advivo Emily O Brien Associate

Managing aged care costs Smart strategies for

Managing aged care costs Smart strategies for 2014 2015 Aged care costs can be very high and could increase as our population ages. Contents Get the care you need at a lower cost 4 The five steps to entering

Managing aged care costs Smart strategies for 2014 2015 Aged care costs can be very high and could increase as our population ages. Contents Get the care you need at a lower cost 4 The five steps to entering

HOW S POST 30 JUNE WORKING OUT FOR YOU? A CHECKLIST OF WHAT S NEXT

HOW S POST 30 JUNE WORKING OUT FOR YOU? A CHECKLIST OF WHAT S NEXT Presented by Tim Miller Miller Super Solutions Disclaimer The material shown in this presentation has been prepared by Tim Miller from

HOW S POST 30 JUNE WORKING OUT FOR YOU? A CHECKLIST OF WHAT S NEXT Presented by Tim Miller Miller Super Solutions Disclaimer The material shown in this presentation has been prepared by Tim Miller from

How super is taxed. Inside. UniSuper Accumulation 1 and Personal Account members. Edith Cowan University

How super is taxed UniSuper Accumulation 1 and Personal Account members The information in this document forms part of the UniSuper Accumulation 1 Product Disclosure Statement and UniSuper Personal Account

How super is taxed UniSuper Accumulation 1 and Personal Account members The information in this document forms part of the UniSuper Accumulation 1 Product Disclosure Statement and UniSuper Personal Account

Understanding superannuation

Understanding superannuation Client Fact Sheet February 2012 Superannuation is an investment vehicle designed to assist Australians save for retirement. The Federal Government encourages saving through

Understanding superannuation Client Fact Sheet February 2012 Superannuation is an investment vehicle designed to assist Australians save for retirement. The Federal Government encourages saving through

QIEC Income Stream INSIDE: Product Disclosure Statement. How to start a. QIEC Income Stream

QIEC Income Stream Product Disclosure Statement Issued 29 September 2017 INSIDE: How to start a QIEC Income Stream Transition to Retirement Account and Retirement Income Account benefits How to invest

QIEC Income Stream Product Disclosure Statement Issued 29 September 2017 INSIDE: How to start a QIEC Income Stream Transition to Retirement Account and Retirement Income Account benefits How to invest

Retirement income getting started

Retirement getting started A regular stream from an account-based or an annuity can be an effective way to fund your retirement. Some retirees may also be eligible for social security benefits from the

Retirement getting started A regular stream from an account-based or an annuity can be an effective way to fund your retirement. Some retirees may also be eligible for social security benefits from the

SuperWrap Annual Report. For the year ended 30 June 2015

SuperWrap Annual Report For the year ended 30 June 2015 Contents Welcome page 1 Recent legislative change page 2 Investment information page 4 Other important information page 8 Financial information page

SuperWrap Annual Report For the year ended 30 June 2015 Contents Welcome page 1 Recent legislative change page 2 Investment information page 4 Other important information page 8 Financial information page

INSURANCE IN YOUR SUPER. Money when it matters most

INSURANCE IN YOUR SUPER Money when it matters most Effective 26 May 2018 Contents Page Why you need cover 5 Income Protection cover 8 Death and TPD cover 18 Terminal illness benefit 26 Nominate your beneficiaries

INSURANCE IN YOUR SUPER Money when it matters most Effective 26 May 2018 Contents Page Why you need cover 5 Income Protection cover 8 Death and TPD cover 18 Terminal illness benefit 26 Nominate your beneficiaries

AF1/J02 Part 4: Taxation of Trusts (3)

") AF1/J02 Part 4: Taxation of Trusts (3) This final part of taxation will cover the IHT treatment of trusts. The milestones are to understand: Which trusts are subject to the relevant property regime and

AF1/J02 Part 4: Taxation of Trusts (3) This final part of taxation will cover the IHT treatment of trusts. The milestones are to understand: Which trusts are subject to the relevant property regime and

Estate Planning & Superannuation

Estate Planning & Superannuation An Executive Summary Luke Atkins Manager, SMSF Consultants Pty Ltd Question What s your idea of superannuation? Answer Q) What s your idea of superannuation? Designed for

Estate Planning & Superannuation An Executive Summary Luke Atkins Manager, SMSF Consultants Pty Ltd Question What s your idea of superannuation? Answer Q) What s your idea of superannuation? Designed for

Challenger Guaranteed Annuity

Challenger Guaranteed Annuity Product Disclosure Statement (PDS) Dated 13 June 2014 Challenger Guaranteed Annuity (SPIN CHG0005AU) Issuer Challenger Life Company Limited (ABN 44 072 486 938) (AFSL 234670)

Challenger Guaranteed Annuity Product Disclosure Statement (PDS) Dated 13 June 2014 Challenger Guaranteed Annuity (SPIN CHG0005AU) Issuer Challenger Life Company Limited (ABN 44 072 486 938) (AFSL 234670)

A guide to managing redundancies

A guide to managing redundancies A fresh start 2016 2017 Regardless of what your next steps might be this guide may help you effectively manage your new financial position better. Contents A fresh start

A guide to managing redundancies A fresh start 2016 2017 Regardless of what your next steps might be this guide may help you effectively manage your new financial position better. Contents A fresh start

RULE C8 Limitation where spouses or civil partners living apart

Rule C8 explains a limitation on death benefits if husband and wife, or civil partners were living apart at the date of death. Part V of Schedule 3 shows how a minimum level of pension should be calculated.

Rule C8 explains a limitation on death benefits if husband and wife, or civil partners were living apart at the date of death. Part V of Schedule 3 shows how a minimum level of pension should be calculated.

ANNEXE 5 OPTIONS FOR DEPENDANTS BENEFITS BASED ON SERVICE BEFORE 1 APRIL 1972

OPTIONS FOR DEPENDANTS BENEFITS BASED ON SERVICE BEFORE 1 APRIL 1972 A firefighter s service before 1 April 1972 did not attract widow s half rate pension cover this was introduced with effect from 1 April

OPTIONS FOR DEPENDANTS BENEFITS BASED ON SERVICE BEFORE 1 APRIL 1972 A firefighter s service before 1 April 1972 did not attract widow s half rate pension cover this was introduced with effect from 1 April

MAXIMISING NON-CONCESSIONAL CONTRIBUTIONS TECH UPDATE

MAXIMISING NON-CONCESSIONAL CONTRIBUTIONS TECH UPDATE Release Date l February 2017 CHANGES TO NON-CONCESSIONAL CONTRIBUTIONS By: Peter Kelly, Superannuation, SMSF, and Retirement Specialist, Centrepoint

MAXIMISING NON-CONCESSIONAL CONTRIBUTIONS TECH UPDATE Release Date l February 2017 CHANGES TO NON-CONCESSIONAL CONTRIBUTIONS By: Peter Kelly, Superannuation, SMSF, and Retirement Specialist, Centrepoint

Insurance in Super versus Insurance outside Super - Buy-Sell Agreements

Insurance in Super versus Insurance outside Super - Buy-Sell Agreements Jeffrey Scott SSA Acting National Manager, Life Insurance Products, BT Financial Group JEFFREY SCOTT 1 1 Introduction Insurance in

Insurance in Super versus Insurance outside Super - Buy-Sell Agreements Jeffrey Scott SSA Acting National Manager, Life Insurance Products, BT Financial Group JEFFREY SCOTT 1 1 Introduction Insurance in

Tax on contributions. Non-concessional (after tax) contribution caps. Concessional (before tax) contributions

contribution caps. Concessional (before tax) contributions") This document summarises the main Federal Government taxes that apply to superannuation at the time of publication. For more information, contact Catholic Super on 1300 655 002 or the Australian Taxation

This document summarises the main Federal Government taxes that apply to superannuation at the time of publication. For more information, contact Catholic Super on 1300 655 002 or the Australian Taxation

KELLOGG RETIREMENT FUND

KELLOGG RETIREMENT FUND Disclaimer This Super Guide has been issued by Kellogg Superannuation Pty Limited (ABN 89 008 426 131), the Trustee of the Fund. It describes the main benefits and features of the

KELLOGG RETIREMENT FUND Disclaimer This Super Guide has been issued by Kellogg Superannuation Pty Limited (ABN 89 008 426 131), the Trustee of the Fund. It describes the main benefits and features of the

Super Reform in Practice

Super Reform in Practice Webinar 4: Pre and post 30 June SMSF administration March 2017 Web 4 Super Reform in Practice 1 Contents Slides... 4 Notes... 20 SMSF asset valuations... 20 General valuation principles...

Super Reform in Practice Webinar 4: Pre and post 30 June SMSF administration March 2017 Web 4 Super Reform in Practice 1 Contents Slides... 4 Notes... 20 SMSF asset valuations... 20 General valuation principles...

NATIONAL SUPERANNUATION CONFERENCE

NATIONAL SUPERANNUATION CONFERENCE Session 9B Written by: Lyn Formica Director McPhersons Stuart Forsyth Director McPhersons Presented by: Stuart Forsyth Director McPhersons National Division 25-26 August

NATIONAL SUPERANNUATION CONFERENCE Session 9B Written by: Lyn Formica Director McPhersons Stuart Forsyth Director McPhersons Presented by: Stuart Forsyth Director McPhersons National Division 25-26 August

Tax and super. Member Booklet Supplement. 1 March 2018

Member Booklet Supplement Tax and super March 208 The information in this document forms part of the First State Super Member Booklets (Product Disclosure Statements) for: Employer Sponsored members dated

Member Booklet Supplement Tax and super March 208 The information in this document forms part of the First State Super Member Booklets (Product Disclosure Statements) for: Employer Sponsored members dated

The information in this Guide forms part of the Product Disclosure Statement (PDS) for the Core Superannuation Service Division

for the Core Superannuation Service Division") Core Superannuation Service The information in this Guide forms part of the Product Disclosure Statement (PDS) for the Core Superannuation Service Division 15 June 2018 Issued by Diversa Trustees Limited

Core Superannuation Service The information in this Guide forms part of the Product Disclosure Statement (PDS) for the Core Superannuation Service Division 15 June 2018 Issued by Diversa Trustees Limited

AIA SUPERANNUATION FUND

AIA SUPERANNUATION FUND ANNUAL REPORT TO MEMBERS FOR THE YEAR ENDING 30 NOVEMBER 2013 This Annual Report forms Part 2 of your Annual Periodic Statement. It should be read with the Annual Member Statement

AIA SUPERANNUATION FUND ANNUAL REPORT TO MEMBERS FOR THE YEAR ENDING 30 NOVEMBER 2013 This Annual Report forms Part 2 of your Annual Periodic Statement. It should be read with the Annual Member Statement

RETIREMENT INCOME GETTING STARTED

RETIREMENT INCOME GETTING STARTED A regular income stream from an account-based or an annuity can be an effective way to fund your retirement. Some retirees may also be eligible for social security benefits

RETIREMENT INCOME GETTING STARTED A regular income stream from an account-based or an annuity can be an effective way to fund your retirement. Some retirees may also be eligible for social security benefits

SUPER FUTURE MAKE YOUR SUPER ASSURED RETIREMENT SAVINGS ACCOUNT (RSA) defencebank.com.au/super

defencebank.com.au/super") defencebank.com.au/super RSA MAKE YOUR FUTURE SUPER SUPER ASSURED RETIREMENT SAVINGS ACCOUNT (RSA) General Information and Application Form Product Disclosure Statement (PDS) Effective 09 Oct 2017 GUARANTEE

defencebank.com.au/super RSA MAKE YOUR FUTURE SUPER SUPER ASSURED RETIREMENT SAVINGS ACCOUNT (RSA) General Information and Application Form Product Disclosure Statement (PDS) Effective 09 Oct 2017 GUARANTEE

Product and investment changes. Zurich Master Superannuation Fund

Product and investment changes Zurich Master Superannuation Fund Date of preparation: 10 November 2015 This Significant Events Notice provides members of the Zurich Master Superannuation Fund ( Fund )

Product and investment changes Zurich Master Superannuation Fund Date of preparation: 10 November 2015 This Significant Events Notice provides members of the Zurich Master Superannuation Fund ( Fund )

ewrap Super/Pension Additional Information Booklet

ewrap Super/Pension Additional Information Booklet Issue date: 30 September 2017 This ewrap Super/Pension Additional Information Booklet (this Booklet) has been prepared by the trustee of ewrap Super/Pension:

ewrap Super/Pension Additional Information Booklet Issue date: 30 September 2017 This ewrap Super/Pension Additional Information Booklet (this Booklet) has been prepared by the trustee of ewrap Super/Pension:

Additional information about your superannuation

Elphinstone Group Superannuation Fund 19 March 2018 Additional information about your superannuation Contents Important information 1 How super works 2 Benefits of investing with the Elphinstone Group

Elphinstone Group Superannuation Fund 19 March 2018 Additional information about your superannuation Contents Important information 1 How super works 2 Benefits of investing with the Elphinstone Group

ENERGY SUPER DEFINED BENEFIT HANDBOOK. Prepared and issued 1 July 2018

ENERGY SUPER DEFINED BENEFIT HANDBOOK Prepared and issued 1 July 2018 CONTENTS About Energy Super 1 Member services 2 Growing your super 3 How your super is invested 5 Your benefits 7 Nominating your beneficiaries

ENERGY SUPER DEFINED BENEFIT HANDBOOK Prepared and issued 1 July 2018 CONTENTS About Energy Super 1 Member services 2 Growing your super 3 How your super is invested 5 Your benefits 7 Nominating your beneficiaries

Member Booklet Product Disclosure Statement

mysuper.watsonwyatt.com/wwa Australia February 2008 Watson Wyatt Superannuation Fund Category A Member Booklet Product Disclosure Statement For defined benefit members who joined the Fund prior to 1 March

mysuper.watsonwyatt.com/wwa Australia February 2008 Watson Wyatt Superannuation Fund Category A Member Booklet Product Disclosure Statement For defined benefit members who joined the Fund prior to 1 March

IOOF LifeTrack employer super general reference guide (LT.13)

") Employer and Corporate Super Issued: 1 October 2012 IOOF LifeTrack employer super general reference guide (LT.13) LifeTrack Employer Superannuation LifeTrack Corporate Superannuation Contents Everything

Employer and Corporate Super Issued: 1 October 2012 IOOF LifeTrack employer super general reference guide (LT.13) LifeTrack Employer Superannuation LifeTrack Corporate Superannuation Contents Everything

A Guide to Segregation

A Guide to Segregation 1 / Introduction In theory the tax rules surrounding superannuation balances that support pensions are very simple : no tax is paid on the investment income they generate. This income

A Guide to Segregation 1 / Introduction In theory the tax rules surrounding superannuation balances that support pensions are very simple : no tax is paid on the investment income they generate. This income

A fresh start A guide to managing redundancies

A fresh start A guide to managing redundancies 2 012/13 Preparation date: 1 April 2013 Contents Make the most of Her s your what you ll fresh find within start. this document If you are leaving your employer

A fresh start A guide to managing redundancies 2 012/13 Preparation date: 1 April 2013 Contents Make the most of Her s your what you ll fresh find within start. this document If you are leaving your employer

SELF MANAGED SUPERANNUATION FUNDS

SELF MANAGED SUPERANNUATION FUNDS What are Self Managed Superannuation Funds? Self Managed Superannuation Funds (SMSF) are becoming increasingly popular these days to assist with the growth of family wealth.

SELF MANAGED SUPERANNUATION FUNDS What are Self Managed Superannuation Funds? Self Managed Superannuation Funds (SMSF) are becoming increasingly popular these days to assist with the growth of family wealth.

Toyota Australia Superannuation Plan. Your Pension Guide. Product Disclosure Statement ISSUED: 1 OCTOBER 2015

Toyota Australia Superannuation Plan Your Pension Guide Product Disclosure Statement ISSUED: 1 OCTOBER 2015 Contents Introducing your pension 1 How your pension works 3 Investing your pension 8 Tax and

Toyota Australia Superannuation Plan Your Pension Guide Product Disclosure Statement ISSUED: 1 OCTOBER 2015 Contents Introducing your pension 1 How your pension works 3 Investing your pension 8 Tax and

Death and Incapacity cover brochure

Death and Incapacity cover brochure For members of the Contributory Scheme. Information in this brochure is current as at 1 July 2017. Contents Eligibility for cover 1 Interim Invalidity Pension 2 Total

Death and Incapacity cover brochure For members of the Contributory Scheme. Information in this brochure is current as at 1 July 2017. Contents Eligibility for cover 1 Interim Invalidity Pension 2 Total

A Guide to your Account-Based Pension

CITIBANK AUSTRALIA STAFF SUPERANNUATION FUND A Guide to your Account-Based Pension This Guide explains: Page no. Who can take out an Account-Based Pension in the Fund?... 1 How the Fund s Account-Based

CITIBANK AUSTRALIA STAFF SUPERANNUATION FUND A Guide to your Account-Based Pension This Guide explains: Page no. Who can take out an Account-Based Pension in the Fund?... 1 How the Fund s Account-Based

Qantas Super Gateway Member Guide Supplement

Issued 1 October 2018 Qantas Super Gateway Member Guide Supplement Contents About this document 2 How super works 3 Building your benefits 3 Accessing your benefits 4 Choice of fund and portability 6 Benefits

Issued 1 October 2018 Qantas Super Gateway Member Guide Supplement Contents About this document 2 How super works 3 Building your benefits 3 Accessing your benefits 4 Choice of fund and portability 6 Benefits

The type of assets into which investments are made will depend on the investment strategy of your fund.

Super funds 1 July 2018 (updated annually) Creating your investment portfolio by making contributions to a superannuation fund can be one of the most effective ways to save for your retirement. What is

Super funds 1 July 2018 (updated annually) Creating your investment portfolio by making contributions to a superannuation fund can be one of the most effective ways to save for your retirement. What is

POLICY NUMBER: POL 12

Chapter: CLAIMS Subject: SURVIVOR BENEFITS Effective Date: November 8, 1994 Last Update: January 10, 2019 PURPOSE STATEMENT: The purpose of the policy is to describe the benefits payable to a worker s

Chapter: CLAIMS Subject: SURVIVOR BENEFITS Effective Date: November 8, 1994 Last Update: January 10, 2019 PURPOSE STATEMENT: The purpose of the policy is to describe the benefits payable to a worker s

EXPLANATORY STATEMENT. Issued by authority of the Minister for Revenue and Financial Services

EXPLANATORY STATEMENT Issued by authority of the Minister for Revenue and Financial Services Income Tax Assessment Act 1997 Retirement Savings Accounts Act 1997 Superannuation Industry (Supervision) Act

EXPLANATORY STATEMENT Issued by authority of the Minister for Revenue and Financial Services Income Tax Assessment Act 1997 Retirement Savings Accounts Act 1997 Superannuation Industry (Supervision) Act

ESSSuper Transport Scheme Handbook. Proudly serving our members. Issued 1 November 2016

ESSSuper Transport Scheme Handbook Proudly serving our members Issued 1 November 2016 Issued by: Emergency Services Superannuation Board ABN 28 161 296 741 as Trustee of the Emergency Services Superannuation

ESSSuper Transport Scheme Handbook Proudly serving our members Issued 1 November 2016 Issued by: Emergency Services Superannuation Board ABN 28 161 296 741 as Trustee of the Emergency Services Superannuation

Table of Contents. Page 1

Page 0 Table of Contents Table of Contents... 1 Key Advice Issues... 2 Outline... 2 Transfer Balance Cap... 2 Why events-based reporting?... 3 Transfer Balance Account... 3 What to report... 3 When to

Page 0 Table of Contents Table of Contents... 1 Key Advice Issues... 2 Outline... 2 Transfer Balance Cap... 2 Why events-based reporting?... 3 Transfer Balance Account... 3 What to report... 3 When to

MEMBER GUIDE TIDSWELL MASTER SUPERANNUATION PLAN. 29 September 2017

TIDSWELL MASTER SUPERANNUATION PLAN MEMBER GUIDE 29 September 2017 The information in this document forms part of the Tidswell Master Superannuation Plan Product Disclosure Statement (PDS) dated 29 September

TIDSWELL MASTER SUPERANNUATION PLAN MEMBER GUIDE 29 September 2017 The information in this document forms part of the Tidswell Master Superannuation Plan Product Disclosure Statement (PDS) dated 29 September

Market Linked Pensions

Market Linked Pensions 6 October 2016 Market linked pensions are a type of complying income stream available for retirees in a Self-managed superannuation fund (SMSF). The terms of a market linked pension

Market Linked Pensions 6 October 2016 Market linked pensions are a type of complying income stream available for retirees in a Self-managed superannuation fund (SMSF). The terms of a market linked pension

Integrating Superannuation into Estate Planning. Michelle Meyer Consulting Principal

Integrating Superannuation into Estate Michelle Meyer Consulting Principal Super Disasters Gov t has made it clear superannuation cannot be used to facilitate estate. Sole purpose test with prescribed

Integrating Superannuation into Estate Michelle Meyer Consulting Principal Super Disasters Gov t has made it clear superannuation cannot be used to facilitate estate. Sole purpose test with prescribed

ABOUT YOUR SUPER PLAN Issued: 1 March 2018

Deseret Benefit Plan for Australia ABOUT YOUR SUPER PLAN Issued: 1 March 2018 CONTENTS Introduction 2 Plan overview 2 How super works 3 Benefits of investing with the Plan 7 Risks of super 17 How we invest

Deseret Benefit Plan for Australia ABOUT YOUR SUPER PLAN Issued: 1 March 2018 CONTENTS Introduction 2 Plan overview 2 How super works 3 Benefits of investing with the Plan 7 Risks of super 17 How we invest

Greyson Legal Publications

Greyson Legal Publications Superannuation, Life Insurance and Estate Planning Address: PO Box 61, Sandgate Qld 4017 Tel: 1300 667 362 Fax: 07 3910 1102 Email: info@greysonlegal.com.au Web: www.greysonlegal.com.au

Greyson Legal Publications Superannuation, Life Insurance and Estate Planning Address: PO Box 61, Sandgate Qld 4017 Tel: 1300 667 362 Fax: 07 3910 1102 Email: info@greysonlegal.com.au Web: www.greysonlegal.com.au