NEW ISSUE BOOK-ENTRY ONLY. Dated: July 28, 2016 Interest Due: April 15 and October 15

|

|

|

- Emily Robinson

- 5 years ago

- Views:

Transcription

1 NEW ISSUE BOOK-ENTRY ONLY $14,765,000 WASHINGTON COUNTY INDUSTRIAL DEVELOPMENT AUTHORITY School Revenue Bonds, Series of 2016 (A. W. Beattie Career Center Project) (Allegheny County, Pennsylvania) Dated: July 28, 2016 Interest Due: April 15 and October 15 RATING: S&P: AA (Stable Outlook) (Insured) Moody s: A1 (Underlying) See Rating herein In the opinion of Bond Counsel, based upon an analysis of existing laws, regulations, rulings and court decisions, interest on the Bonds (including, in the case of Bonds sold at an original issue discount, the difference between the initial offering price and par) is excluded from gross income for Federal income tax purposes. Bond Counsel is also of the opinion that interest on the Bonds is not a specific item of tax preference under 57 of the Internal Revenue Code of 1986, as amended (the Code ) for purposes of Federal individual or corporate alternative minimum taxes. The Bonds, and the interest income therefrom, are free from taxation for purposes of personal income, corporate net income and personal property taxes within the Commonwealth of Pennsylvania. (See TAX MATTERS herein.). Principal Due: October 15, as shown on inside cover First Interest Payment: October 15, 2016 The School Revenue Bonds (A. W. Beattie Career Center Project), Series of 2016, in the aggregate principal amount of $14,765,000 (the Bonds ), will be issued in fully registered form, without coupons, in denominations of $5,000 or any integral multiple thereof. The Bonds will be registered in the name of Cede & Co., as the registered owner and nominee of The Depository Trust Company ( DTC ), New York, New York. Beneficial ownership of the Bonds may be acquired in denominations of $5,000 or any integral multiple thereof only under the book-entry only system maintained by DTC through its brokers and dealers who are, or act through, DTC Participants. The purchasers of the Bonds will not receive physical delivery of the Bonds. For so long as any purchaser is the beneficial owner of a Bond, that purchaser must maintain an account with a broker or a dealer who is, or acts through, a DTC Participant to receive payment of principal of and interest on the Bonds. See BOOK-ENTRY ONLY SYSTEM herein. If, under the circumstances described herein, Bonds are ever issued in certificated form, the Bonds will be subject to registration of transfer, exchange and payment as described herein. The principal of the Bonds will be paid to the registered owners or assigns, when due, upon presentation and surrender of the Bonds to ZB, National Association, (the Trustee ), acting as trustee and sinking fund depository, at its designated office in Pittsburgh, Pennsylvania. Interest on the Bonds is payable initially on October 15, 2016 and thereafter semiannually on April 15 and October 15 of each year, until the principal sum thereof is paid. Payment of interest on the Bonds will be made by check drawn on the Trustee mailed to the registered owners of the Bonds as of the Record Date (see The Bonds infra). THE BONDS ARE LIMITED OBLIGATIONS OF THE WASHINGTON COUNTY INDUSTRIAL DEVELOPMENT AUTHORITY (THE AUTHORITY ). NEITHER THE PRINCIPAL OR REDEMPTION PRICE OF THE BONDS, NOR THE INTEREST ACCRUING THEREON, SHALL CONSTITUTE A GENERAL INDEBTEDNESS OF THE AUTHORITY OR AN INDEBTEDNESS OF THE COMMONWEALTH OR ANY POLITICAL SUBDIVISION THEREOF (OTHER THAN AVONWORTH SCHOOL DISTRICT, DEER LAKES SCHOOL DISTRICT, FOX CHAPEL AREA SCHOOL DISTRICT, HAMPTON TOWNSHIP SCHOOL DISTRICT, NORTH ALLEGHENY SCHOOL DISTRICT, NORTH HILLS SCHOOL DISTRICT, NORTHGATE SCHOOL DISTRICT,PINE- RICHLAND SCHOOL DISTRICT AND SHALER AREA SCHOOL DISTRICT (THE SCHOOL DISTRICTS )) WITHIN THE MEANING OF ANY CONSTITUTIONAL OR STATUTORY PROVISION WHATSOEVER; CONSTITUTE A CHARGE AGAINST THE GENERAL CREDIT OF THE AUTHORITY OR THE GENERAL CREDIT OR TAXING POWER OF THE COMMONWEALTH OR ANY POLITICAL SUBDIVISION THEREOF (EXCEPT THE SCHOOL DISTRICTS); OR BE DEEMED TO BE A GENERAL OBLIGATION OF THE AUTHORITY OR AN OBLIGATION OF THE COMMONWEALTH OR ANY POLITICAL SUBDIVISION THEREOF (OTHER THAN THE SCHOOL DISTRICTS). THE AUTHORITY HAS NO TAXING POWER. The Bonds are subject to redemption prior to maturity as further described herein. Proceeds of the Bonds will be loaned to the Joint Operating Committee of the A.W. Beattie Career Center (the Joint Operating Committee of JOC ) and will be used to currently refund all of the outstanding State Public School Building Authority s, School Revenue Bonds, Series of 2008 (A.W. Beattie Career Center Project) and to pay the costs and expenses of issuing and insuring the Bonds. The Bonds are an authorized investment for fiduciaries in the Commonwealth pursuant to the Pennsylvania Probate, Estate and Fiduciaries Code, Act of June 30, 1972, No. 164, P.L. 508, as amended and supplemented. The scheduled payment of principal of and interest on the Bonds when due will be guaranteed under an insurance policy to be issued concurrently with the delivery of the Bonds by Build America Mutual Assurance Company ( BAM ). MATURITIES, AMOUNTS, RATES AND PRICES/YIELDS See Inside Front Cover The Bonds are offered when, as and if issued, subject to withdrawal or modification of the offer without notice, and subject to the approving legal opinion of Dinsmore & Shohl LLP, of Pittsburgh, Pennsylvania, Bond Counsel, to be furnished upon delivery of the Bonds. Certain other legal matters will be passed upon for the Authority by its Counsel, Houston Harbaugh, P.C., Pittsburgh, Pennsylvania, for the JOC by its Solicitor, Weiss Burkardt Kramer LLC, Pittsburgh, Pennsylvania. Public Financial Management, Inc., Harrisburg, Pennsylvania, is acting as Financial Advisor to the JOC in connection with the issuance of the Bonds. It is expected that the Bonds will be available for delivery in New York, New York, on or about July 28, Official Statement Dated: June 23, 2016

2 $14,765,000 WASHINGTON COUNTY INDUSTRIAL DEVELOPMENT AUTHORITY School Revenue Bonds, Series of 2016 (A.W. Beattie Career Center Project) (Allegheny County, Pennsylvania) Bonds Dated: July 28, 2016 Principal Due: October 15, as shown below Interest Due: April 15 and October 15 First Interest Payment: October 15, 2016 MATURITIES, AMOUNTS, INTEREST RATES, INITIAL OFFERING YIELDS AND CUSIPS Maturity Date (October 15) Principal Interest Initial Offering CUSIP Year Amounts Rates Yields Numbers (1) 2016 $1,025, % 0.500% 93859SAA , SAB , SAC , SAD ,020, SAE ,070, SAF ,125, SAG ,180, SAH ,240, SAJ ,290, SAK ,315, SAL ,340, SAM ,370, SAN5 (1) The above CUSIP (Committee on Uniform Securities Identification Procedures) numbers have been assigned by an organization not affiliated with the Authority or the Underwriter, and such parties are not responsible for the selection or use of the CUSIP numbers. The CUSIP numbers are included solely for the convenience of bondholders and no representation is made as to the correctness of such CUSIP numbers. CUSIP numbers assigned to securities may be changed during the term of such securities based on a number of factors including, but not limited to, the refunding or defeasance of such issue or the use of secondary market financial products. Neither the Authority nor the Underwriter has agreed to, and there is no duty or obligation to, update this Official Statement to reflect any change or correction in the CUSIP numbers set forth above.

3 Washington County Industrial Development Authority MEMBERS OF THE AUTHORITY John E. Artuso, Chairman Todd Ashmore, Vice Chairman Joseph M. Trifaro, Secretary William Stein, Treasurer Steve Johnson, Assistant Secretary/Treasurer COUNSEL TO THE AUTHORITY HOUSTON HARBAUGH, P.C. Pittsburgh, Pennsylvania BOND COUNSEL DINSMORE & SHOHL LLP Pittsburgh, Pennsylvania TRUSTEE ZB, National Association Pittsburgh, Pennsylvania AUTHORITY ADDRESS WASHINGTON COUNTY INDUSTRIAL DEVELOPMENT AUTHORITY 375 Southpointe Blvd, Suite 240 Canonsburg, Pennsylvania 15317

4 WASHINGTON COUNTY INDUSTRIAL DEVELOPMENT AUTHORITY School Revenue Bonds, Series of 2016 A.W. Beattie Career Center Project) (Allegheny County, Pennsylvania) MEMBER SCHOOL DISTRICTS AVONWORTH SCHOOL DISTRICT Dr. Thomas Ralston, Superintendent DEER LAKES SCHOOL DISTRICT Dr. Janell Logue-Belden, Superintendent FOX CHAPEL AREA SCHOOL DISTRICT Dr. Gene Freeman, Superintendent HAMPTON TOWNSHIP SCHOOL DISTRICT Dr. John C. Hoover, Superintendent NORTH HILLS SCHOOL DISTRICT Dr. Patrick J. Mannarino, Superintendent NORTHGATE SCHOOL DISTRICT Ms. Caroline Johns, Superintendent PINE-RICHLAND SCHOOL DISTRICT Dr. Brian Miller, Superintendent SHALER AREA SCHOOL DISTRICT Mr. Sean Aiken, Superintendent NORTH ALLEGHENY SCHOOL DISTRICT Dr. Robert J. Scherrer, Superintendent SUPERINTENDENT OF RECORD Dr. Patrick J. Mannarino North Hills School District EXECUTIVE DIRECTOR Eric C. Heasley DIRECTOR OF FINANCE Cathy Hill SOLICITOR TO THE CAREER CENTER Ira Weiss, Esquire Weiss Burkardt Kramer, LLC BOND COUNSEL DINSMORE & SHOHL LLP Pittsburgh, Pennsylvania FINANCIAL ADVISOR PUBLIC FINANCIAL MANAGEMENT, INC. Harrisburg, Pennsylvania UNDERWRITER JANNEY MONTGOMERY SCOTT LLC Pittsburgh, Pennsylvania CAREER CENTER ADDRESS 9600 Babcock Boulevard Allison Park, Pennsylvania 15101

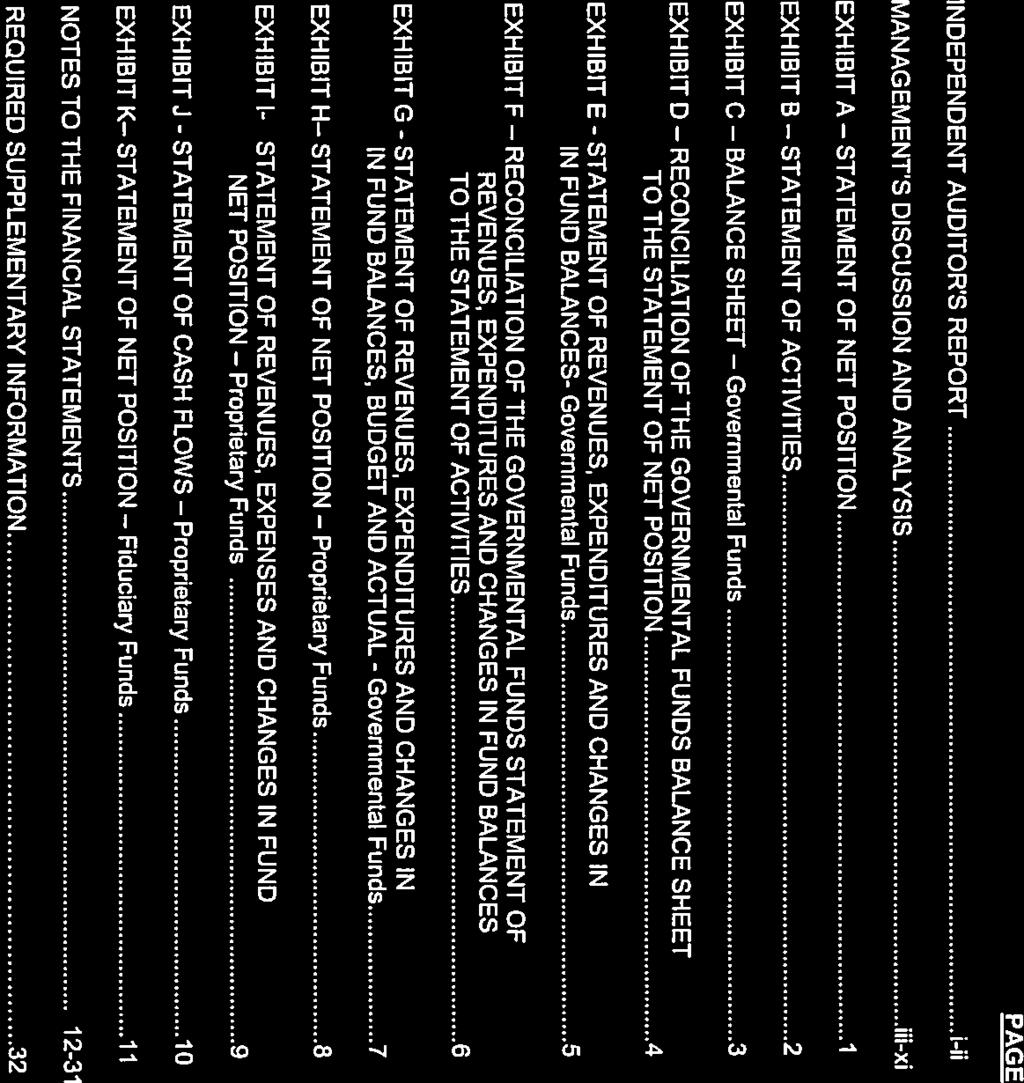

5 No dealer, broker, salesman or other person has been authorized by the Authority, the JOC or the School Districts to give information or to make any representations, other than those contained in this Official Statement, and if given or made, such other information or representations must not be relied upon. This Official Statement does not constitute an offer to sell or the solicitation of an offer to buy, nor shall there be any sale of the Bonds in any jurisdiction in which it is unlawful to make such offer, solicitation or sale. The information set forth herein has been obtained from the Authority, the JOC and the School Districts and from other sources which are believed to be reliable, but the Authority, the JOC, and the School Districts do not guarantee the accuracy or completeness of information from sources other than the Authority, the JOC and the School Districts. The information and expressions of opinion herein are subject to change without notice and neither the delivery of this Official Statement nor any sale made hereunder shall, under any circumstances, create any implication that there has been no change in any of the information set forth herein since the date hereof. The Authority, the JOC and the School Districts have deemed this Official Statement to be final for the purposes of Rule 15c2-12(b)(3) of the Securities and Exchange Commission. Build America Mutual Assurance Company ( BAM ) makes no representation regarding the Bonds or the advisability of investing in the Bonds. In addition, BAM has not independently verified, makes no representation regarding, and does not accept any responsibility for the accuracy or completeness of this Official Statement or any information or disclosure contained herein, or omitted herefrom, other than with respect to the accuracy of the information regarding BAM, supplied by BAM and presented under the heading Bond Insurance and Appendix M - Specimen Municipal Bond Insurance Policy. TABLE OF CONTENTS Page INTRODUCTION... 1 PURPOSE OF THE ISSUE... 1 THE AUTHORITY... 2 THE BONDS... 3 Description... 3 Payment of Principal and Interest... 3 Transfer, Exchange and Registration of Bonds... 3 REDEMPTION OF BONDS... 4 Optional Redemption... 4 Notice of Redemption... 4 Security and Source of Payment State Aid... 4 Additional Bonds... 5 BOOK-ENTRY ONLY SYSTEM... 6 SUMMARIES OF CERTAIN PROVISIONS... 8 OF THE LOAN AGREEMENT AND THE INDENTURE... 8 The Loan Agreement... 8 The Indenture MUNICIPAL BOND INSURANCE A.W. BEATTIE CAREER CENTER CAREER CENTER FINANCES LABOR RELATIONS Pension Program INFORMATION REGARDING THE SCHOOL DISTRICTS TAXING POWERS OF THE SCHOOL DISTRICTS COMMONWEALTH AID TO THE SCHOOL DISTRICTS ABSENCE OF LITIGATION CONTINUING DISCLOSURE UNDERTAKING RATING Page UNDERWRITING LEGAL OPINION FINANCIAL ADVISOR MISCELLANEOUS JOINT OPERATING COMMITTEE CERTIFICATION APPENDIX A - AVONWORTH SCHOOL DISTRICT APPENDIX B - DEER LAKES SCHOOL DISTRICT APPENDIX C - FOX CHAPEL AREA SCHOOL DISTRICT APPENDIX D - HAMPTON TOWNSHIP SCHOOL DISTRICT APPENDIX E - NORTH ALLEGHENY SCHOOL DISTRICT APPENDIX F - NORTH HILLS SCHOOL DISTRICT APPENDIX G - NORTHGATE SCHOOL DISTRICT APPENDIX H - PINE-RICHLAND SCHOOL DISTRICT APPENDIX I - SHALER AREA SCHOOL DISTRICT APPENDIX J - BOND COUNSEL OPINION SCHOOL REVENUE BONDS, SERIES OF 2016 APPENDIX K - FORM OF CONTINUING DISCLOSURE CERTIFICATE APPENDIX L - AUDITED FIANCIAL STATEMENTS FOR THE CAREER CENTER APPENDIX M - SPECIMEN MUNICIPAL BOND INSURANCE POLICY i

6 [ THIS PAGE INTENTIONALLY LEFT BLANK ]

7 OFFICIAL STATEMENT $14,765,000 WASHINGTON COUNTY INDUSTRIAL DEVELOPMENT AUTHORITY School Revenue Bonds, Series of 2016 (A. W. Beattie Career Center Project) (Allegheny County, Pennsylvania) INTRODUCTION This Official Statement, including the cover page and inside cover page hereof and Appendices hereto, is furnished by the Washington County Industrial Development Authority (the Authority or WCIDA ) and the Joint Operating Committee of the A. W. Beattie Career Center Board (the Joint Operating Committee or JOC ), Allegheny County, Pennsylvania, in connection with the offering of the Authority s $14,765,000 aggregate principal amount School Revenue Bonds (A. W. Beattie Career Center Project), Series of 2016, dated as of July 28, 2016 (the Bonds ). The Bonds are authorized to be issued pursuant to the Economic Development Financing Law of the Commonwealth of Pennsylvania, Act of August 23, 1967, P.L. 251, as amended (the Act ), and are secured by a Trust Indenture dated as of July 28, 2016, (the Indenture ), entered into between the Authority and ZB, National Association, Pittsburgh, Pennsylvania, as Trustee (the Trustee ). The Bonds are secured by the terms of the Indenture between the Authority and the Trustee, and are payable solely from the specified payments by each of the School Districts under the terms of the Loan Agreement, dated as of July 28, 2016 (the Loan Agreement ), between the Authority, the Joint Operating Committee of the Career Center and each of the School Districts. Each School District has been duly organized and is validly existing under the laws of the Commonwealth, particularly the Section 633 of the Pennsylvania Public School Code of 1949, as amended by Act 154 of 1998 (the School Code ), and is authorized by law to enter into a loan agreement with the Authority and to make loan payments under the loan agreement and to include in its annual budget amounts sufficient to meet such payments. The Bonds will be payable from, and secured by an assignment of the amounts payable to the Authority by Avonworth School District, Deer Lakes School District, Fox Chapel Area School District, Hampton Township School District, North Allegheny School District, North Hills School District, Northgate School District, Pine-Richland School District and Shaler Area School District (collectively, the School Districts ), as borrowers under the Loan Agreement and the respective General Obligation Notes, Series of 2016 (the Notes ) issued by each one of the School Districts. PURPOSE OF THE ISSUE Proceeds of the Bonds will be used for and towards the current refunding of the State Public School Building Authority s, School Revenue Bonds, Series of 2008 (A.W. Beattie Career Center Project), currently outstanding in the aggregate principal amount of $15,345,000 (the 2008 Bonds ), and paying all costs of issuance of the Bonds. The 2008 Bonds will be called for optional redemption, at a redemption price of 100% of principal amount plus accrued interest, pursuant to the optional redemption provisions applicable to the 2008 Bonds on October 15, The following is a summary of the sources and uses of the proceeds from the issuance of the Bonds. SOURCES: Bond Proceeds... $14,765, Net Original Issue Premium... 1,234, Total... $15,999, USES: Amount to Call the 2008 Bonds... $15,674, Cost of Issuance (1) , Total... $15,999, (1) Includes legal, financial advisor, printing, rating, bond discount, municipal bond insurance premium, CUSIP, trustee and miscellaneous costs. 1

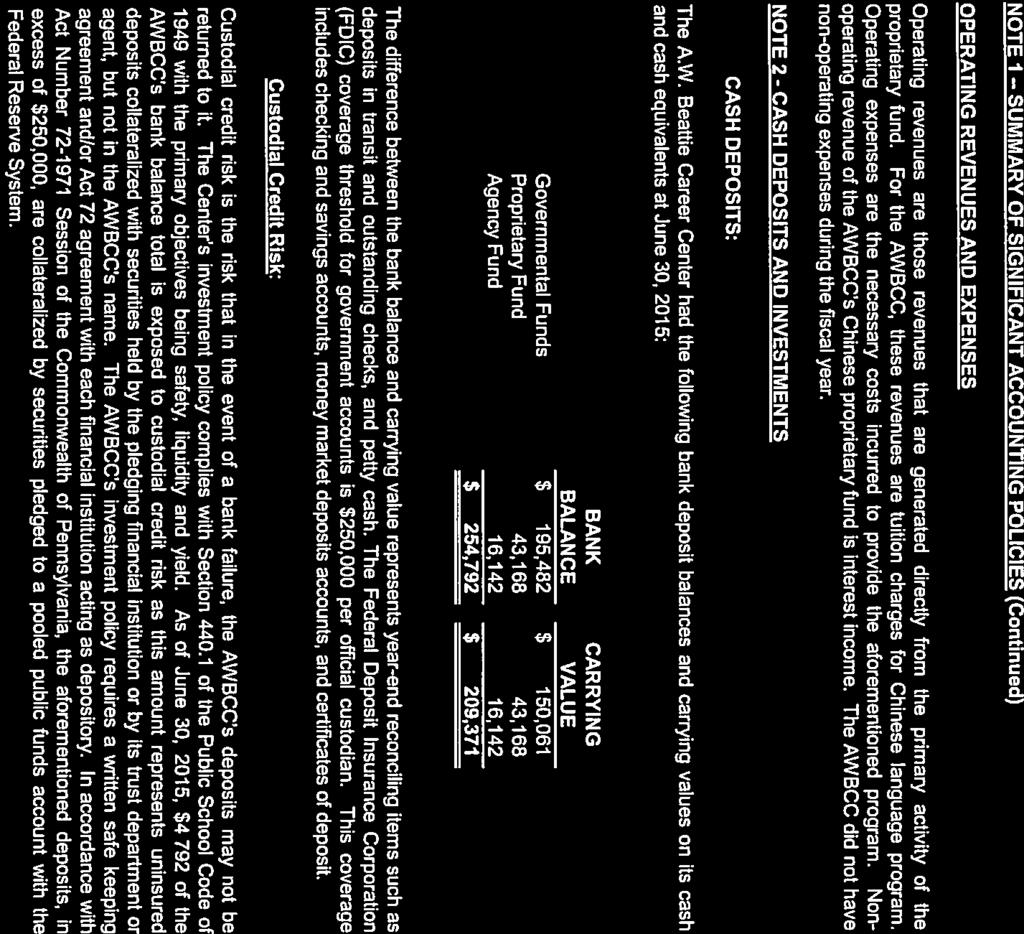

8 THE AUTHORITY The Washington County Industrial Development Authority (the Authority ) is a public instrumentality and a body corporate and politic, duly organized, existing and in good standing under the laws of the Commonwealth of Pennsylvania (the Commonwealth ) and is authorized under the Act, which declares it to be the policy of the Commonwealth to promote the health, safety, morals, employment, business opportunities and general welfare of the people of the Commonwealth by providing for the creation of industrial and commercial development authorities which shall exist and operate as public instrumentalities of the Commonwealth for the public purpose of alleviating unemployment, maintaining employment at a high level, eliminating and preventing blight, and creating and developing new business opportunities by the construction, improvement, rehabilitation, revitalization and financing of industrial, specialized, commercial, manufacturing and research and development enterprises and to promote and establish educational facilities. Resolutions authorizing the issuance of the Bonds have been adopted by the Board of the Authority. The Authority has no taxing power and no source of funds for payment of the Bonds, other than the underlying contractual obligations made by the Career Center. The Authority does not and will not in the future monitor the financial condition of the Career Center or otherwise monitor payment of the Bonds or compliance with the documents relating thereto. The Authority will rely entirely upon the Trustee to carry out its respective responsibilities under the Indenture and the Loan Agreement. The Authority has other assets and may obtain additional assets in the future. However, such assets are not pledged to secure payment of the Bonds, and the Authority has no obligation or expectation of making such assets subject to the lien of the Bond Indenture. None of the Authority or its attorneys, agents or independent contractors have furnished, reviewed, investigated or verified the information contained in this Official Statement other than the information contained in this section. The Authority has determined that no financial or operating data concerning the Authority is material to any decision to purchase, hold or sell the Bonds, and the Authority will not provide any such information. The Authority has not, and will not, undertake any responsibilities to provide continuing disclosure with respect to the Bonds or the security therefor, and the Authority will have no liability to holders of the Bonds with respect to any such disclosures. There is not now pending or, to the knowledge of the Authority, threatened any litigation restraining or enjoining the issuance or delivery of the Bonds or questioning or affecting the validity of the Bonds or the proceedings or authority under which the Bonds are to be issued. None of the creation, organization or existence of the Authority or the title of any of the present members or other officials of the Board of the Authority to their respective offices is being contested. There is no litigation pending or, to its knowledge, threatened, which in any manner questions the right of the Authority to enter into the Indenture or the Loan Agreement or secure the Bonds in the manner provided in the Indenture and the Act. As described above, the Authority has the power to and has issued bonds and notes for the purpose of financing projects for other facilities which are payable from the revenues of the particular project. Revenue bonds and notes issued by the Authority for other projects may have been or may be in default as to principal and interest. The source of payment, however, for any such defaulted bonds is separate and distinct from the source of payment for the Bonds and, therefore, any default on such bonds is not considered a material fact with respect to the payment of the Bonds offered hereby. The Authority has not prepared or assisted in the preparation of this Official Statement except for the statements under this section in respect of the Authority, and except as aforesaid. The Authority is not responsible for any statements made herein, and will not participate in, nor otherwise be responsible for, the offer, sale or distribution of the Bonds. Accordingly, except as aforesaid, the Authority disclaims responsibility for the disclosure set forth herein made in connection with the offer, sale and distribution of the Bonds. THE BONDS AND THE INTEREST THEREON SHALL NOT BE DEEMED TO CONSTITUTE A DEBT OR A PLEDGE OF THE FAITH AND CREDIT OF THE COMMONWEALTH OF PENNSYLVANIA, OR ANY POLITICAL SUBDIVISION THEREOF, INCLUDING THE AUTHORITY AND THE COUNTY OF WASHINGTON, PENNSYLVANIA. NEITHER THE COMMONWEALTH OF PENNSYLVANIA, NOR ANY POLITICAL SUBDIVISION THEREOF, INCLUDING THE AUTHORITY AND THE COUNTY OF WASHINGTON, PENNSYLVANIA SHALL BE OBLIGATED TO PAY PRINCIPAL OF OR PREMIUM, IF ANY, OR INTEREST ON THE BONDS OR OTHER COSTS INCIDENT THERETO EXCEPT FROM THE REVENUES AND RECEIPTS PLEDGED THEREFOR, AND NEITHER THE FAITH AND CREDIT NOR THE TAXING POWER OF THE COMMONWEALTH OF PENNSYLVANIA OR ANY POLITICAL SUBDIVISION THEREOF (EXCEPT THE SCHOOL DISTRICTS), INCLUDING THE AUTHORITY AND THE COUNTY OF WASHINGTON, PENNSYLVANIA, IS PLEDGED TO THE PAYMENT OF PRINCIPAL OF THE BONDS OR INTEREST THEREON OR OTHER COSTS INCIDENT THERETO. THE AUTHORITY HAS NO TAXING POWER. 2

9 THE BONDS Description The aggregate principal amount of the Bonds is $14,765,000. The Bonds will be issued in fully registered form in denominations of $5,000 and integral multiples thereof. The Bonds will be dated as of July 28, 2016, and will bear interest at the rates and mature in the amounts and on the dates set forth on the inside cover page of this Official Statement. Interest on the Bonds will be payable initially on October 15, 2016 and semiannually on April 15 and October 15 of each year thereafter until the principal sum thereof is paid. When issued, the Bonds will be registered in the name of Cede & Co., as nominee for The Depository Trust Company ( DTC ), New York, New York. Purchasers of the Bonds (the Beneficial Owners ) will not receive any physical delivery of Bonds certificates, and beneficial ownership of the Bonds will be evidenced only by book entries. See BOOK ENTRY ONLY SYSTEM herein. Payment of Principal and Interest So long as Cede & Co., as nominee of DTC, is the registered owner of the Bonds, payments of principal of, redemption premium, if any, and interest on the Bonds, when due, are to be made to DTC and all such payments shall be valid and effective to satisfy fully and to discharge the obligations of the Authority with respect to, and to the extent of, principal, redemption premium, if any, and interest so paid. If the use of the Book-Entry Only System for the Bonds is discontinued for any reason, Bonds certificates will be issued to the Beneficial Owners of the Bonds and payment of principal, redemption premium, if any, and interest on the Bonds shall be made as described in the following paragraphs. Principal of certificated Bonds will be paid to the registered owners thereof or assigns, when due, upon surrender of such Bonds at the designated corporate trust office of the Trustee. Interest is payable to the registered owner of a Bond from the interest payment date next preceding the date of registration and authentication of the Bond, unless: (a) such Bond is registered and authenticated as of an interest payment date, in which event such Bond shall bear interest from said interest payment date, or (b) such Bond is registered and authenticated after a Record Date (hereinafter defined) and before the next succeeding interest payment date, in which event such Bond shall bear interest from such interest payment date, or (c) such Bond is registered and authenticated on or prior to the Record Date preceding October 15, 2016, in which event such Bond shall bear interest from July 28, 2016, or (d) as shown by the records of the Trustee, interest on such Bond shall be in default, in which event such Bonds shall bear interest from the date to which interest was last paid on such Bond. Interest shall be paid initially on October 15, 2016 and thereafter, semiannually on April 15 and October 15 of each year, until the principal sum is paid. Interest on a certificated Bond is payable by check drawn on the Trustee, which shall be mailed to the registered owner whose name and address shall appear, at the close of business on the last calendar day (whether or not a day on which the Trustee is open for business) of the month immediately preceding each interest payment date (the "Record Date"), on the registration books maintained by the Trustee, irrespective of any transfer or exchange of the Bond subsequent to such Record Date and prior to such interest payment date, unless WCIDA shall be in default in payment of interest due on such interest payment date. In the event of any such default, such defaulted interest shall be payable to the person in whose name the Bond is registered at the close of business on a special record date for the payment of such defaulted interest established to be fixed by the Trustee, such special record date to be not more than fifteen (15) days nor less than ten (10) days prior to the date of payment of defaulted interest. If the date for payment of the principal of or interest on any Bonds shall be a Saturday, Sunday, legal holiday or a day on which banking institutions in the Commonwealth of Pennsylvania are authorized by law or executive order to close, then the date for payment of such principal or interest shall be the next succeeding day which is not a Saturday, Sunday, legal holiday or a day on which such banking institutions are authorized to close, and payment on such date shall have the same force and effect as if made on the nominal date established for such payment. Transfer, Exchange and Registration of Bonds Subject to the provisions described below under Book-Entry Only System, certificate Bonds are transferable by the registered owner thereof in person or by his attorney duly authorized in writing or legal representative at the office of the Trustee at its designated corporate trust office, but only in the manner, subject to the limitations and upon payment of charges provided by the Indenture, and upon surrender and cancellation of such Bond accompanied by a duly executed instrument of transfer in form and with guarantee of signature satisfactory to the Trustee. Upon such transfer, a new Bond or Bonds of the same maturity and of authorized denomination or denominations, for the same aggregate principal amount and bearing the same rate of interest, will be issued to the transferee in exchange therefor at the earliest practicable time. In like manner each Bond may be exchanged by the registered owner or by his duly authorized attorney or other legal representative for Bonds of the same maturity and of authorized denomination or denominations in the same aggregate principal amount and bearing the same rate of interest. Any such transfer or exchange as described herein shall be made without charge, except for the payment of any taxes or other governmental charges relating thereto. No exchange or transfer shall be required to be made (i) between the Record Date and the related Interest Payment Date, (ii) during a period beginning at the opening of business (15) days before the date of the mailing notice of redemption of Bonds selected for redemption and ending at the close of business on the day of such mailing, or (iii) for 3

10 any Bonds so selected for redemption in whole or in part. WCIDA and the Trustee may treat and consider the person in whose name a Bond is registered as the absolute owner thereof for the purpose for receiving payment of, or on account of, the principal or redemption price thereof and the interest due thereon and for all other purposes whatsoever. Optional Redemption REDEMPTION OF BONDS In the manner and upon the terms and conditions provided in the Indenture, the Bonds stated to mature on and after October 15, 2025, are subject to redemption prior to maturity at the option of the Authority, at the direction of the Joint Operating Committee, or the School Districts in any order of maturities either as a whole, or in part, at any time on or after October 15, 2024, and, if in part, by lot within a maturity, at a redemption price equal to 100% of the principal amount thereof, together with accrued interest to the date fixed for redemption. Notice of Redemption Notice of any redemption shall be given by depositing a copy of the redemption notice by first class mail not more than sixty (60) days and not less than thirty (30) days prior to the date fixed for redemption addressed to each of the registered owners of Bonds to be redeemed, in whole or in part at the addresses shown on the registration books; provided, however, that failure to give such notice by mailing, or any defect therein or in the mailing thereof shall not affect the validity of any proceeding for redemption of other Bonds called for redemption as to which proper notice has been given. On the date designated for redemption, notice having been provided as aforesaid, and money for payment of the principal and accrued interest being held by the Trustee, interest on the Bonds and portions thereof so called for redemption shall cease to accrue and such Bonds or portions thereof shall cease to be entitled to any benefit or security of the Indenture, and registered owners of such Bonds or portions thereof so called for redemption shall have no rights with respect to such Bonds, except to receive payment of the principal of and accrued interest on such Bonds to the date fixed for redemption. Manner of Redemption If a Bond is of a denomination larger than $5,000, a portion of such Bond may be redeemed. For the purposes of redemption, a Bond shall be treated as representing that number of Bonds which is obtained by dividing the principal amount thereof by $5,000, each $5,000 portion of such Bonds being subject to redemption. In the case of partial redemption of a Bond, payment of the redemption price shall be made only upon surrender of such Bond in exchange for Bonds of authorized denominations in aggregate principal amount equal to the unredeemed portion of the principal amount thereof. If the redemption date for any Bonds shall be a Saturday, Sunday, legal holiday or a day on which banking institutions in the Commonwealth of Pennsylvania are authorized by law or executive order to close, then the date for payment of the principal, premium, if any, and interest upon such redemption shall be the next succeeding day which is not a Saturday, Sunday, legal holiday or a day on which such banking institutions are authorized to close, and payment on such date shall have the same force and effect as if made on the nominal date of redemption. Security and Source of Payment State Aid The Authority will enter into a Loan Agreement dated as of July 28, 2016, (the Loan Agreement ) with the School Districts and the Joint Operating Committee pursuant to which the Authority will lend the proceeds of the Bonds to the School Districts for the purpose of financing the Project. Under the Loan Agreement, each School District will agree to repay its proportionate share of such loan in such amounts and at such times as will provide sufficient funds to meet their related share of the debt service requirements on the Bonds. Each School District will deliver its general obligation promissory note dated as of July 28, 2016 (the Notes ) to the Authority evidencing its obligations under the Loan Agreement. The Bonds will be secured under the Indenture by the assignment and pledge to the Trustee of the payments under the Notes and the Loan Agreement. The full faith, credit and taxing power of the School Districts have been pledged for the timely payment of all amounts due under the Notes. The payments due under the Notes are payable from the respective School Districts tax and other general revenues, from whatever source derived, which include ad valorem taxes (limited as to rate) and State reimbursement. See School Tax Data and Taxpayer Relief Act herein. The Authority, at the time of the settlement for Bonds, will assign all its right (except the right to indemnification, the right to payment of certain fees and expenses, if any, and the right to receive notices), title and interest in the Notes and Loan Agreement and the payments thereunder to the Trustee. The Bonds will be secured by and payable under the Indenture from the funds held by the Trustee and payments made pursuant to the Notes and Loan Agreement. The execution of the Notes by the School Districts constitutes the issuance of general obligation debt by such School Districts and must be approved by the Department of Community and Economic Development. This approval will be obtained prior to issuance and delivery of the Bonds. 4

11 Provisions of the Public School Code of 1949, as amended (the Public School Code ) require that, should any school district fail to make its required debt service payments with respect to a general obligation note such as the Notes, the Secretary of Education of the Commonwealth is required to withhold from such school district out of any subsidy payment of any type due such school district, an amount equal to the debt service payments owed by such school district. Any amounts so withheld are assigned to the sinking fund depository for the general obligation bonds or notes issued to finance such school s project. These withholding provisions are not part of any contract with the holder of the bonds or notes, and may be amended by future legislation. The Public School Code also provides that in the event a school district is in default with respect to the general obligation debt or lease rental debt to a municipal authority or the Authority, there shall be a withholding from subsidy payments of amounts necessary to remedy such defaults, on an equal basis with default payments under such debt. In addition, the Local Government Unit Debt Act (the Act ) prescribes certain other remedies. In the event of failure of a school district to pay principal of or interest on general obligation notes such as the Notes for a period of 30 days from when it becomes due and payable, the holder of the note shall have the right to recover the amount due by bringing an action in assumpsit in the Court of Common Pleas in the county in which the school district is located. The Debt Act provides that any judgment shall have an appropriate priority upon moneys next coming into the treasury of the school district. The Debt Act further provides that upon a default in the payment of principal or interest, which continues at least 30 days, holders of at least 25% of such defaulted debt may appoint a trustee to represent them. The Debt Act provides certain other remedies and further qualified the above-described remedies. See DEBT AND DEBT LIMITS in each Appendix A through I for descriptions of the outstanding debt of each of the School Districts. All public school subsidies in the Commonwealth are subject to appropriation by the General Assembly. Although the Constitution of the Commonwealth provides that the General Assembly shall provide for the maintenance and support of a thorough and efficient system of public education to serve the needs of the Commonwealth, the General Assembly is not legally obligated to appropriate such subsidies and there can be no assurance that it will do so in the future. The allocation formula pursuant to which the Commonwealth distributes such subsidies to the various school districts throughout the Commonwealth may be amended at any time by the General Assembly. Moreover, the Commonwealth s ability to make such disbursements will be dependent upon its own financial condition. At various times in the past, the enactment of budget and appropriation laws by the Commonwealth has been delayed, resulting in interim borrowing by school districts pending the authorization and payment of state aid. Consequently, there can be no assurance that financial support from the Commonwealth for schools, either for capital projects or education programs in general will continue at present levels or that moneys will be payable to a school district if indebtedness of such school is not paid when due Pennsylvania Budget Impasse Pennsylvania was without a current budget until December 29, 2015, when the Governor signed a partial state budget for the fiscal year that commenced on July 1, The Governor line item vetoed approximately $6 billion of the $30 billion budget approved by both houses of the legislature. The partial state budget contained an amount of approximately six months of basic education funding for all school districts for the fiscal year. On February 9, 2016, the proposed state budget for fiscal year was introduced by the Governor and the budgetary process for the fiscal year commenced. On March 17, 2016 the General Assembly passed a state budget which provided basic education funding to Commonwealth school districts for the fiscal year, which is at least equal to the funding school districts received in the prior fiscal year. On March 27, 2016 that budget became law when the Governor failed to sign or veto the bill within the ten (10) day period prescribed under the laws of the Commonwealth. Future budget impasses may affect the timeliness or amount of payments by the Commonwealth under the withholding provisions of Section 633 of the Public School Code. The Authority has no taxing power. Neither the general credit of the Authority nor the credit or taxing power of the United States of America, the Commonwealth of Pennsylvania or any political subdivision (other than the School Districts) thereof is pledged for the payment of principal of, or the interest on, the Bonds; nor shall any of the Bonds be deemed obligations of the United States of America, the Commonwealth of Pennsylvania of any political subdivisions thereof (other than the School Districts). Additional Bonds The Authority may issue Additional Bonds on parity with the Bonds (other than with respect to certain funds under the Indenture). In connection with the issuance of Additional Bonds, additional funds may be established under the Indenture for the benefit of such additional series of bonds. In such event, the holders of the Bonds will have no claims or right to any such funds. For a further description of the conditions under which such Additional Bonds may be issued, see SUMMARIES OF CERTAIN PROVISIONS OF THE LOAN AGREEMENT AND THE INDENTURE- The Indenture herein. 5

12 BOOK-ENTRY ONLY SYSTEM Portions of the following information concerning The Depository Trust Company ( DTC ) and DTC's book-entry-only system have been obtained from DTC. The Authority (sometimes herein referred to as the Issuer ), CCTI, the Financial Advisor, and the Underwriter make no representation as to the accuracy of such information. The Depository Trust Company ( DTC ), New York, New York, will act as securities depository for the securities (the Securities ). The Securities will be issued as fully-registered securities registered in the name of Cede & Co. (DTC's partnership nominee) or such other name as may be requested by an authorized representative of DTC. One fully-registered Security certificate will be issued for the Securities, in the aggregate principal amount of such issue, and will be deposited with DTC. DTC the world's largest securities depository, is a limited-purpose trust company organized under the New York Banking Law, a banking organization within the meaning of the New York Banking Law, a member of the Federal Reserve System. a clearing corporation within the meaning of the New York Uniform Commercial Code, and a clearing agency registered pursuant to the provisions of Section 17A of the Securities Exchange Act of DTC holds and provides asset servicing for over 3.6 million issues of U.S. and non-u.s. equity issues, corporate and municipal debt issues, and money market instruments (from over 100 countries) that DTC's participants ( Direct Participants ) deposit with DTC. DTC also facilitates the post-trade settlement among Direct Participants of sales and other securities transactions in deposited securities, through electronic computerized book-entry transfers and pledges between Direct Participants' accounts. This eliminates the need for physical movement of securities certificates. Direct Participants include both U.S. and non-u.s. securities brokers and dealers, banks, trust companies, clearing corporations, and certain other organizations. DTC is a wholly-owned subsidiary of The Depository Trust & Clearing Corporation ( DTCC ). DTCC is the holding company for DTC, National Securities Clearing Corporation and Fixed Income Clearing Corporation, all of which are registered clearing agencies. DTCC is owned by the users of its regulated subsidiaries. Access to the DTC system is also available to others such as both U.S. and non-u.s. securities brokers and dealers, banks, trust companies, and clearing corporations that clear through or maintain a custodial relationship with a Direct Participant, either directly or indirectly ( Indirect Participants ). DTC has a Standard & Poor's rating of AA+. The DTC Rules applicable to its Participants are on file with the Securities and Exchange Commission. More information about DTC can be found at Purchases of Securities under the DTC system must be made by or through Direct Participants, which will receive a credit for the Securities on DTC's records. The ownership interest of each actual purchaser of each Security ( Beneficial Owner ) is in turn to be recorded on the Direct and Indirect Participants' records. Beneficial Owners will not receive written confirmation from DTC of their purchase. Beneficial Owners are, however, expected to receive written confirmations providing details of the transaction, as well as periodic statements of their holdings, from the Direct or Indirect Participant through which the Beneficial Owner entered into the transaction. Transfers of ownership interests in the Securities are to be accomplished by entries made on the books of Direct and Indirect Participants acting on behalf of Beneficial Owners. Beneficial Owners will not receive certificates representing their ownership interests in Securities, except in the event that use of the book-entry system for the Securities is discontinued. To facilitate subsequent transfers, all Securities deposited by Direct Participants with DTC are registered in the name of DTC's partnership nominee, Cede & Co., or such other name as may be requested by an authorized representative of DTC. The deposit of Securities with DTC and their registration in the name of Cede & Co. or such other DTC nominee do not affect any change in beneficial ownership. DTC has no knowledge of the actual Beneficial Owners of the Securities: DTC's records reflect only the identity of the Direct Participants to whose accounts such Securities are credited, which may or may not be the Beneficial Owners. The Direct and Indirect Participants will remain responsible for keeping account of their holdings on behalf of their customers. Conveyance of notices and other communications by DTC to Direct Participants, by Direct Participants to Indirect Participants, and by Direct Participants and Indirect Participants to Beneficial Owners will be governed by arrangements among them, subject to any statutory or regulatory requirements as may be in effect from time to time. Beneficial Owners of Securities may wish to take certain steps to augment the transmission to them of notices of significant events with respect to the Securities, such as redemptions, tenders, defaults, and proposed amendments to the Security documents. For example, Beneficial Owners of Securities may wish to ascertain that the nominee holding the Securities for their benefit bas agreed to obtain and transmit notices to Beneficial Owners. In the alternative, Beneficial Owners may wish to provide their names and addresses to the registrar and request that copies of notices be provided directly to them. Redemption notices shall be sent to DTC. If less than all of the Securities within an issue are being redeemed, DTC's practice is to determine by lot the amount of the interest of each Direct Participant in such issue to be redeemed. Neither DTC nor Cede & Co. (nor any other DTC nominee) will consent or vote with respect to Securities unless authorized by a Direct Participant in accordance with DTC's MMI Procedures. Under its usual procedures, DTC mails an Omnibus Proxy to Issuer as soon as possible after the record date. The Omnibus Proxy assigns Cede & Co.'s consenting or voting rights to those Direct Participants to whose accounts Securities are credited on the record date (identified in a listing attached to the Omnibus Proxy). 6

13 Redemption proceeds, distributions, and dividend payments on the Securities will be made to Cede & Co., or such other nominee as may be requested by an authorized representative of DTC. DTC's practice is to credit Direct Participants' accounts upon DTC's receipt of funds and corresponding detail information from Issuer or Agent, on payable date in accordance with their respective holdings shown on DTC's records. Payments by Participants to Beneficial Owners will be governed by standing instructions and customary practices, as is the case with securities held for the accounts of customers in bearer form or registered in street name, and will be the responsibility of such Participant and not of DTC, Agent, or Issuer, subject to any statutory or regulatory requirements as may be in effect from time to time. Payment of redemption proceeds, distributions, and dividend payments to Cede & Co. (or such other nominee as may be requested by an authorized representative of DTC) is the responsibility of Issuer or Agent, disbursement of such payments to Direct Participants will be the responsibility of DTC, and disbursement of such payments to the Beneficial Owners will be the responsibility of Direct and Indirect Participants. A Beneficial Owner shall give notice to elect to have its Securities purchased or tendered, through its Participant, to Tender Agent, and shall effect delivery of such Securities by causing the Direct Participant to transfer the Participant's interest in the Securities, on DTC's records, to Tender Agent. The requirement for physical delivery of Securities in connection with an optional tender or a mandatory purchase will be deemed satisfied when the ownership rights in the Securities are transferred by Direct Participants on DTC's records and followed by a book-entry credit of tendered Securities to Tender Agent's DTC account. DTC may discontinue providing its services as depository with respect to the Securities at any time by giving reasonable notice to Issuer or Agent. Under such circumstances, in the event that a successor depository is not obtained, Security certificates are required to be printed and delivered. Issuer may decide to discontinue use of the system of book-entry-only transfers through DTC (or a successor securities depository). In that event, Security certificates will be printed and delivered to DTC. The information in this section concerning DTC and DTC's book-entry system has been obtained from sources that Issuer believes to be reliable, but Issuer takes no responsibility for the accuracy thereof. NEITHER THE AUTHORITY NOR THE TRUSTEE SHALL HAVE ANY RESPONSIBILITY OR OBLIGATION TO ANY DTC PARTICIPANT OR ANY BENEFICIAL OWNER OR ANY OTHER PERSON NOT SHOWN ON THE REGISTRATION BOOKS OF THE TRUSTEE AS BEING A BONDHOLDER WITH RESPECT TO EITHER: (1) THE ACCURACY OF ANY RECORDS MAINTAINED BY DTC OR ANY DTC PARTICIPANT; (2) THE PAYMENT BY DTC OR ANY DTC PARTICIPANT OF ANY AMOUNT DUE TO ANY BENEFICIAL OWNER IN RESPECT OF THE PRINCIPAL OR REDEMPTION PRICE OF OR INTEREST ON THE BONDS; (3) THE DELIVERY OR THE TIMELINESS OF ANY NOTICE TO ANY BENEFICIAL OWNER WHICH IS REQUIRED OR PERMITTED UNDER THE TERMS OF THE INDENTURE TO BE GIVEN TO THE OWNER OF THE BONDS; OR (4) ANY CONSENT GIVEN OR OTHER ACTION TAKEN BY DTC AS BONDHOLDER. Neither the Authority nor the Trustee shall have any responsibility or obligation to any DTC Participant or Indirect Participant with respect to: (i) the accuracy of the records of DTC, its nominee or any DTC Participant or Indirect Participant with respect to any beneficial ownership interest in any Bonds; (ii) the delivery to any DTC Participant or Indirect Participant or any other Person, other than the registered owner of a Bond, as shown in the Bond Register, of any notice with respect to any Bond, including, without limitation, any notice of redemption; (iii) the selection by DTC or any DTC Participant or Indirect Participant of any person to receive payment in the event of a partial redemption of Bonds; (iv) the payment to any DTC Participant or Indirect Participant or any other Person other than the registered owner of a Bond, as shown in the Bond Register, of any amount with respect to the principal of, redemption price, or interest on, any Bond; or (v) any consent given by DTC as registered owner. 7

14 Prior to the discontinuation of the book-entry only system as described herein, the Authority and the Trustee may treat DTC and any successor securities depository to be the absolute owner of the Bonds for all purposes, including, without limitation: (i) (ii) the payment of principal of redemption price or interest on the Bonds; giving notices of redemption and other matters with respect to the Bonds; (iii) registering transfers with respect to the Bonds; and (iv) the selection of Bonds for redemption. The Beneficial Owners of the Bonds have no right to a securities depository for the Bonds. DTC or any successor securities depository may resign as depository for the Bonds by giving notice to the Trustee and discharging its responsibilities under applicable law. In addition, the Authority, or the Authority at the request of the CCTI, may remove DTC or a successor securities depository for any reason at any time. In such event, the Authority shall (i) appoint a securities depository qualified to act as such under Section 17(a) of the Securities Exchange Act of 1934, notify the prior securities depository of the appointment of such successor depository and transfer separate bond certificates to such successor securities depository or (ii) notify the securities depository of the availability through the securities depository of bond certificates and transfer one or more separate bond certificates to Depository Participants having Bonds credited to their accounts at the securities depository. In such event, such Bonds shall no longer be restricted to being registered in the registration books of the Authority in the name of the securities depository or its nominee, but may be registered in the name of the successor securities depository or its nominee, or in whatever name or names the Depository Participants receiving such Bonds shall designate, in accordance with the provisions of the Indenture. Discontinuance of Book-Entry Only System The book-entry only system for registration of the ownership of the Bonds may be discontinued at any time if: (i) DTC determines to resign as securities depository for the Bonds; or (ii) the Authority determines that continuation of the system of book-entry transfers through DTC (or through a successor securities depository) is not in the best interests of the Beneficial Owners. In either such event (unless the Authority appoints a successor securities depository), Bonds will then be delivered in registered certificate form to such persons, and in such maturities and principal amounts, as may be designated by DTC, but without any liability on the part of the Authority, or the Trustee for the accuracy of such designation. Whenever DTC requests the Authority or the Trustee to do so, the Authority or the Trustee shall cooperate with DTC in taking appropriate action after reasonable notice to arrange for another securities depository to maintain custody of certificates evidencing the Bonds. THE AUTHORITY, CCTI AND THE TRUSTEE CANNOT AND DO NOT GIVE ANY ASSURANCES THAT DTC, THE DIRECT PARTICIPANTS OR THE INDIRECT PARTICIPANTS WILL DISTRIBUTE TO THE BENEFICIAL OWNERS OF THE BONDS (I) PAYMENTS OF PRINCIPAL OR REDEMPTION PRICE OF OR INTEREST ON THE BONDS, (II) CERTIFICATES REPRESENTING AN OWNERSHIP INTEREST OR OTHER CONFIRMATION OF BENEFICIAL OWNERSHIP INTERESTS IN THE BONDS, OR (III) REDEMPTION OR OTHER NOTICES SENT TO DTC OR CEDE & CO., ITS NOMINEE, AS THE REGISTERED OWNER OF THE BONDS, OR THAT THEY WILL DO SO ON A TIMELY BASIS OR THAT DTC, DIRECT PARTICIPANTS OR INDIRECT PARTICIPANTS WILL SERVE AND ACT IN THE MANNER DESCRIBED IN THIS OFFICIAL STATEMENT. SUMMARIES OF CERTAIN PROVISIONS OF THE LOAN AGREEMENT AND THE INDENTURE The following pages contain descriptions of certain provisions of the Loan Agreement and the Indenture. The Bonds are secured by the Indenture and are payable from payments due under the Loan Agreement. These descriptions are brief summaries and do not purport to be and should not be regarded as complete statements of the terms of either the Loan Agreement or the Indenture or as complete synopses thereof. Reference is made to the documents in their entirety, copies of which may be obtained from the Trustee, for a complete statement of the terms and conditions therein. The Loan Agreement In connection with the issuance of Bonds, the Authority will enter into the Loan Agreement with the School Districts and the Joint Operating Committee pursuant to which the Authority will loan the proceeds of the Bonds to the JOC on behalf of the School Districts. The Loan Agreement requires the School Districts to make loan repayments to the Authority in the amounts sufficient to pay the debt service on the Bonds. The School Districts are obligated under the Loan Agreement to pay only their respective shares, as set forth below. The failure of one School District to pay its proportionate share will not increase the liabilities or obligations of any other School District, or require it to remedy such a payment default. Representations, Warranties and Covenants: The School Districts make certain representations, warranties and covenants under the Loan Agreement, including without limitation, with respect to the existence and authority of the School Districts, the enforceability of the Loan Agreement and Notes and the absence of material litigation. 8

15 Source of Debt Service Payments: The debt service payments are payable by the School Districts from their revenues from whatever source derived which include ad valorem taxes (limited as to rate) and State reimbursements. Each School District has covenanted to include payments due each fiscal year in its operating budget for such fiscal year during the term of the Loan Agreement and to make the loan payments required to be paid to the Authority with respect to such School District s Note and the Loan Agreement. The obligations of the each of the School Districts under the Loan Agreement and their proportionate share is shown on the following table: School District Proportionate Share Principal Amount Avonworth 3.71% $593,912 Deer Lakes 5.04% $807,111 Fox Chapel Area 15.56% $2,494,268 Hampton Township 8.62% $1,380,985 North Allegheny 24.28% $3,892,084 North Hills 14.64% $2,346,792 Northgate 3.20% $512,960 Pine-Richland 11.26% $1,804,978 Shaler Area 13.71% $2,196,912 Source: Preliminary debt service schedules. Assignment of Loan Agreement: The loan payments shall be paid directly to the Trustee under an assignment by the Authority to the Trustee of such payments for the benefit and security of the Bondholders under the Indenture. Unconditional Obligation: The obligations of the School Districts to pay the principal and interest due under the Notes and Loan Agreement and all other sums payable under the Loan Agreement are absolute and unconditional. The payments are required to be made in full directly to the Trustee, as assignee, when due without delay or diminution for any cause whatsoever, including without limitation thereto, destruction of any School facilities, and without right of set-off for default on the part of the Authority under the Loan Agreement. Events of Default: Any one or more of the following events shall constitute an Event of Default under the Loan Agreement: (a) a School District fails to make any payment required under its respective Note; (b) a School District or the Joint Operating Committee shall fail or refuse to comply with its tax covenants set forth in the Loan Agreement; (c) a School District or the Joint Operating Committee shall default in the due and punctual performance of any other of the covenants and agreements contained in the Loan Agreement and such default shall continue for 60 days after written notice specifying such default and requiring the same to be remedied shall have been given to the School District or the Joint Operating Committee by the Authority; (d) if an Event of Default shall have occurred and be continuing under the Indenture and as a result of such Event or Default the Bonds shall have been declared due and payable by acceleration in accordance with the Indenture; or (e) the School Districts and the Joint Operating Committee shall fail, discontinue or unreasonably delay in carrying out the Project and shall fail to remedy such failure, discontinuance or delay within 30 days of notice thereof by the Authority. Remedies: If an Event of Default has occurred and is continuing: (a) The Authority (or the Trustee as its assignee) may, in addition to its other rights and remedies as may be provided in the Loan Agreement or may exist at the time at law or in equity, exercise any one or more of the following remedies: (i) (ii) upon notice to the School Districts, declare all sums due or to become due under the Loan Agreement and under the Notes to be immediately due and payable; or by suit, action or proceeding at law or in equity, enforce all rights of the Authority, and require the School Districts and the Joint Operating Committee to carry out any 9

16 agreements with or for the benefit of the owners of the Bonds and to perform their duties under the Act, the Loan Agreement and the Notes; or (b) Upon the occurrence of an Event of Default described in paragraph (a) under Events of Default above, the Authority shall, in addition to the exercise of any other remedy hereunder, notify the Secretary of the Department of Education of such Event of Default and request the Secretary, in accordance with the appropriate provisions of Pennsylvania law, to notify the defaulting School Districts of their obligations under the Loan Agreement and to withhold out of any appropriation due such School Districts under the Pennsylvania School Code an amount equal to the sum or sums owing by such School Districts to the Authority under the Loan Agreement and under the respective Notes, and shall pay over the amount so withheld to the Trustee, as sinking fund depository for the Notes, on behalf of the Authority. The Indenture Limited Obligations of the Authority: The Bonds are limited obligations of the Authority and are secured solely by a pledge and assignment to the Trustee of the loan payments and other revenues or income derived by or for the Authority from or with respect to the Loan Agreement and all moneys to be paid over to the Trustee under the provisions of the Indenture. The Authority has no taxing power. Neither the general credit of the Authority nor the credit or taxing power of the United States of America, the Commonwealth of Pennsylvania, the County of Washington or any political subdivision thereof (other than the School Districts) is pledged for the payment of the principal of, or the interest on the Bonds; nor shall the Bonds be deemed to be obligations of the Authority, the Commonwealth of Pennsylvania, the County of Washington or any political subdivision thereof (other than the School Districts). The School Districts are empowered to levy ad volorem taxes, in order to make the payments in the amounts required under the Notes and the Loan Agreement as described herein subject to certain limitations (see Limitations on the Taxing Powers of the School Districts-Act 1 Special Session of 2006 (Taxpayer Relief Act) herein. Pledge and Assignment of Certain Revenues: The Authority has pledged to the Trustee, in the Indenture, a security interest in all loan payments, and other sums payable under the Loan Agreement, for the benefit and security of the registered owners of the Bonds issued under such Indenture. Revenue Fund: All payments under the Loan Agreement are required to be deposited in the Revenue Fund established with the Trustee at the times set forth in the Indenture. All moneys in the Revenue Fund are required to be transferred by the Trustee at the times set forth in the Indenture to the various other Funds established under the Indenture. Debt Service Fund: There is established under the Indenture a Debt Service Fund from moneys in the Revenue Fund, on or before each April 15 and October 15, commencing October 15, 2016 moneys in an amount sufficient to make the interest payments due on the Bonds on each such date and to make principal payments (including mandatory sinking fund redemption) due on the Bonds on October 15 of each year commencing October 15, Rebate Fund: The Trustee shall establish a Rebate Fund. The Authority, upon the written request of the JOC, will periodically, and upon retirement of the last Bond, determine the sum required to be deposited in the Rebate Fund (if any) and direct the Trustee to transfer such sum from the other funds and accounts established under the Indenture. The Authority will direct the Trustee to pay to the United States Government the sums on deposit in the Rebate Fund at the times and in the amounts (if any) required by the Internal Revenue Code of 1986, as amended, and all extant regulations promulgated thereunder. Investment of Funds: Moneys held in the Revenue Fund and the Debt Service Fund thereunder will be invested in accordance with the Indenture. Additional Bonds: The Indenture permits under certain circumstances and conditions, the issuance of additional bonds for the purposes of refunding any series of outstanding bonds of the Authority issued on behalf of the School Districts or to finance any project of the School Districts authorized by the School Code for which the Authority is authorized to issue bonds under the Act. Default and Remedies: The Act provides remedies to the Bondholders in the event of default or failure on the part of the Authority to fulfill its covenants under the Indenture. Under the Indenture, in the event of any default therein, the Trustee may enforce, and upon written request of the holders of 25% in principal amount of the Bonds then outstanding accompanied by indemnity as provided in the Indenture, shall enforce, for the benefit of all Bondholders all their rights of entry, of bringing suit, action or proceeding at law or in equity and of having a receiver appointed. Neither the Trustee nor any receiver, however, may sell, assign, mortgage, or otherwise dispose of any assets of the Authority. For more complete statement of rights and remedies of the Bondholders and for limitations thereon, reference is made to the Indenture. 10

17 Modifications and Amendments: Amendments to the Indenture are permitted without consent of Bondholders for certain purposes, including the imposition of additional restrictions and conditions respecting the issuance of bonds, the addition of covenants and agreements by the Authority, the modification of the Indenture to conform the same with governmental regulations (so long as the rights of the Bondholders issued thereunder are not adversely affected thereby), the curing of any ambiguity, defect or inconsistency in the Indenture, and the making of provision for matters which are necessary or desirable and which do not adversely affect the interests of Bondholders. Certain other modifications may be made to the Indenture, but only with the consent of the Issuer and the owners of not less than 66 2/3% in principal amount of Outstanding Bonds (as defined in the Indenture) issued thereunder. Insurance Provisions: Certain rights are granted to BAM under the Indenture. These rights include, among others, the approval of amendments, consents in addition to bondholder consents, control and direction of remedies, receipt and copies of notices, and third-party beneficiary status. Bond Insurance Policy MUNICIPAL BOND INSURANCE Concurrently with the issuance of the Bonds, Build America Mutual Assurance Company ( BAM ) will issue its Municipal Bond Insurance Policy for the Bonds (the Policy ). The Policy guarantees the scheduled payment of principal of and interest on the Bonds when due as set forth in the form of the Policy included as an appendix to this Official Statement. The Policy is not covered by any insurance security or guaranty fund established under New York, California, Connecticut or Florida insurance law. Build America Mutual Assurance Company BAM is a New York domiciled mutual insurance corporation. BAM provides credit enhancement products solely to issuers in the U.S. public finance markets. BAM will only insure obligations of states, political subdivisions, integral parts of states or political subdivisions or entities otherwise eligible for the exclusion of income under section 115 of the U.S. Internal Revenue Code of 1986, as amended. No member of BAM is liable for the obligations of BAM. The address of the principal executive offices of BAM is: 200 Liberty Street, 27th Floor, New York, New York 10281, its telephone number is: , and its website is located at: BAM is licensed and subject to regulation as a financial guaranty insurance corporation under the laws of the State of New York and in particular Articles 41 and 69 of the New York Insurance Law. BAM s financial strength is rated AA/Stable by S&P Global Ratings, a Standard & Poor s Financial Services LLC business ( S&P ). An explanation of the significance of the rating and current reports may be obtained from S&P at The rating of BAM should be evaluated independently. The rating reflects the S&P s current assessment of the creditworthiness of BAM and its ability to pay claims on its policies of insurance. The above rating is not a recommendation to buy, sell or hold the Bonds, and such rating is subject to revision or withdrawal at any time by S&P, including withdrawal initiated at the request of BAM in its sole discretion. Any downward revision or withdrawal of the above rating may have an adverse effect on the market price of the Bonds. BAM only guarantees scheduled principal and scheduled interest payments payable by the issuer of the Bonds on the date(s) when such amounts were initially scheduled to become due and payable (subject to and in accordance with the terms of the Policy), and BAM does not guarantee the market price or liquidity of the Bonds, nor does it guarantee that the rating on the Bonds will not be revised or withdrawn. Capitalization of BAM BAM s total admitted assets, total liabilities, and total capital and surplus, as of March 31, 2016 and as prepared in accordance with statutory accounting practices prescribed or permitted by the New York State Department of Financial Services were $475.0 million, $41.6 million and $433.4 million, respectively. BAM is party to a first loss reinsurance treaty that provides first loss protection up to a maximum of 15% of the par amount outstanding for each policy issued by BAM, subject to certain limitations and restrictions. BAM s most recent Statutory Annual Statement, which has been filed with the New York State Insurance Department and posted on BAM s website at is incorporated herein by reference and may be obtained, without charge, upon request to BAM at its address provided above (Attention: Finance Department). Future financial statements will similarly be made available when published. BAM makes no representation regarding the Bonds or the advisability of investing in the Bonds. In addition, BAM has not independently verified, makes no representation regarding, and does not accept any responsibility for the accuracy or completeness of this Official Statement or any information or disclosure contained herein, or omitted herefrom, other than with respect to the accuracy of the information regarding BAM, supplied by BAM and presented under the heading BOND INSURANCE. 11

18 Additional Information Available from BAM Credit Insights Videos. For certain BAM-insured issues, BAM produces and posts a brief Credit Insights video that provides a discussion of the obligor and some of the key factors BAM s analysts and credit committee considered when approving the credit for insurance. The Credit Insights videos are easily accessible on BAM's website at buildamerica.com/creditinsights/. (The preceding website address is provided for convenience of reference only. Information available at such address is not incorporated herein by reference.) Credit Profiles. Prior to the pricing of bonds that BAM has been selected to insure, BAM may prepare a pre-sale Credit Profile for those bonds. These pre-sale Credit Profiles provide information about the sector designation (e.g. general obligation, sales tax); a preliminary summary of financial information and key ratios; and demographic and economic data relevant to the obligor, if available. Subsequent to closing, for any offering that includes bonds insured by BAM, any pre-sale Credit Profile will be updated and superseded by a final Credit Profile to include information about the gross par insured by CUSIP, maturity and coupon. BAM pre-sale and final Credit Profiles are easily accessible on BAM's website at buildamerica.com/obligor/. BAM will produce a Credit Profile for all bonds insured by BAM, whether or not a pre-sale Credit Profile has been prepared for such bonds. (The preceding website address is provided for convenience of reference only. Information available at such address is not incorporated herein by reference.) Disclaimers. The Credit Profiles and the Credit Insights videos and the information contained therein are not recommendations to purchase, hold or sell securities or to make any investment decisions. Credit-related and other analyses and statements in the Credit Profiles and the Credit Insights videos are statements of opinion as of the date expressed, and BAM assumes no responsibility to update the content of such material. The Credit Profiles and Credit Insight videos are prepared by BAM; they have not been reviewed or approved by the issuer of or the underwriter for the Bonds, and the issuer and underwriter assume no responsibility for their content. BAM receives compensation (an insurance premium) for the insurance that it is providing with respect to the Bonds. Neither BAM nor any affiliate of BAM has purchased, or committed to purchase, any of the Bonds, whether at the initial offering or otherwise. A. W. BEATTIE CAREER CENTER The governing body of the Career Center is the Joint Operating Committee (the JOC or the Board ) consisting of 18 members (2 from each School District) appointed annually. Each of the participating School Districts appoints members of the JOC. Officers of the JOC are appointed by the members. The JOC officers, their offices, and the School District they represent are set forth below: Officers of the Joint Operating Committee NAME APPOINTING SCHOOL DISTRICT OFFICE Larry Vasko Hampton Township School District President Daniel O Keefe Northgate School District Vice-President Beau Blaser Avonworth School District Board Secretary James Fisher Shaler Area School District Treasurer 12

19 The preliminary allocation of capital expenditures and debt service of the nine School Districts is as follows: Member School District Total Cost State Share* Local Share Avonworth School District $593,912 $125,256 $468,656 Deer Lakes School District $807,111 $177,675 $629,435 Fox Chapel Area School District $2,494,268 $526,041 $1,968,227 Hampton Township School District $1,380,985 $315,365 $1,065,619 North Allegheny School District $3,892,084 $820,841 $3,071,243 North Hills School District $2,346,792 $494,938 $1,851,854 Northgate School District $512,960 $150,505 $362,455 Pine -Richland School District $1,804,978 $419,955 $1,385,023 Shaler Area School District $2,196,912 $606,590 $1,590,322 TOTALS $16,030,000 $3,637,166 $12,392,834 *State Share to be received as reimbursement on bond issue semi-annual payments and differs for each District. Estimated, subject to change. A.W. Beattie Career Center Course/Programs for the school year Advanced Computer Programming Advertising Design Agile Robotics/Advanced Manufacturing Automotive Collision Technology Automotive Technology Carpentry/Building Construction Computer Systems Technology Cosmetology Culinary Arts Dental Careers Early Childhood Education Emergency Response Technology Health and Nursing Sciences Heating, Ventilating and Air-Conditioning (HVAC) Network Engineering Technology Pastry Arts Pharmacy Mandarin Chinese Source: Career Center Adult Education A year-round non-credit adult education program that provides employment-related training classes, professional certifications, vocational and personal enrichment courses. 13

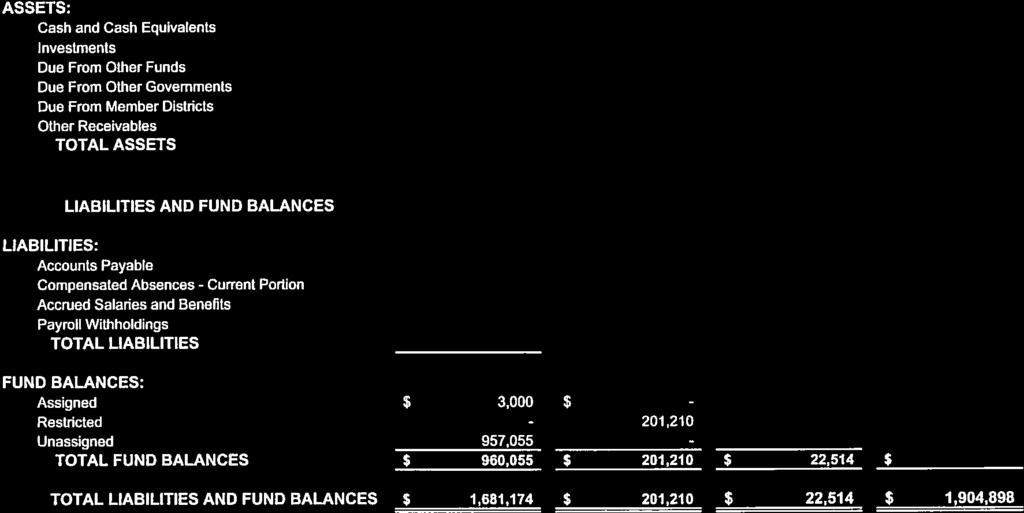

20 CAREER CENTER FINANCES Introduction The Career Center budgets and expends funds according to procedures mandated by the Pennsylvania Department of Education. An annual operating budget is prepared by the Director and Business Manager and submitted to the School Districts of the Career Center for approval prior to the beginning of each fiscal year on July 1. Financial Reporting The Career Center s financial statements are audited annually by an independent certified public accountant, as required by Commonwealth law. Summary and Discussion of Financial Results A summary of Comparative General Fund balance sheet and changes in fund balances for the Career Center is presented in the following Tables. A summary of Comparative General Fund balance sheet and changes in fund balances for the Career Center is presented in Table 1 and revenues and expenditures as shown on Table 2 which follow. TABLE 1 A. W. BEATTIE CAREER CENTER GENERAL FUND BALANCE SHEET (Fiscal Years Ending June 30) ASSETS Cash and Cash Equivalents... $67,723 $1,252,572 $176,003 $131,806 $126,632 Investments... 1,486, , , ,966 1,120,430 Due from Other Governments... 48, , , , ,880 Due from Other Member Districts ,598 15,068 Due from Other Funds ,188 Prepaid Expenses... 21, Other Receivables... 88,106 32,022 96,113 6,131 6,436 TOTAL ASSETS... $1,711,267 $1,581,178 $1,281,841 $960,756 $1,680,634 LIABILITIES Due to Other Funds... $0 $0 $16,277 $0 $0 Current Portion of Long-Term Debt , Accounts Payable... 17,290 19,049 46,951 24, ,269 Accrued Salaries and Benefits , , , , ,241 Payroll Deductions and Withholdings , , , ,568 Other Current Liabilities ,960 52,041 TOTAL LIABILITIES , , , , ,119 Fund Balances Nonspendable... $21,061 $0 $0 $3,000 $3,000 Unassigned... 1,383,298 1,220, , , ,055 Total Fund Balances... $1,404,359 $1,220,422 $824,826 $397,188 $960,055 TOTAL LIABILITIES AND FUND BALANCES... $1,711,267 $1,581,178 $1,281,841 $960,756 $1,681,174 Source: Annual Financial Reports. 14

21 TABLE 2 A. W. BEATTIE CAREER CENTER GENERAL FUND STATEMENT OF REVENUES, EXPENDITURES AND CHANGES IN FUND BALANCE* (Fiscal Years Ending June 30) REVENUE: (1) Total Local Sources... $6,403,995 $4,611,958 $5,934,489 $6,409,142 $7,494,413 $7,588,147 Total State Sources , , , , ,567 1,051,292 Total Federal Sources , , , , , ,000 Total Other Sources TOTAL REVENUE... $7,483,135 $5,675,993 $7,047,143 $7,589,418 $8,777,901 $8,914,439 Actual Budget EXPENDITURES: Instruction... $3,891,290 $3,355,228 $3,338,932 $3,897,528 $3,982,333 4,236,296 Support Services , ,279 2,348,794 2,191,842 2,370,655 2,653,737 Administrative and Financial Support Services , , Operation and Maintenance of Plant Services , , Operation of Noninstructional Services , , , , , ,400 Debt Service... 1,577,820 1,579,550 1,575,319 1,579,319 1,579,175 1,583,006 Capital Outlays... 63, Refund of prior year revenues Budgetary Reserve ,000 TOTAL EXPENDITURES... $7,621,250 $7,410,900 $7,491,624 $7,930,660 $8,235,838 $9,039,439 SURPLUS (DEFICIT) OF REVENUES OVER EXPENDITURES... (138,115) (1,734,907) (444,481) (341,242) 542,063 (125,000) OTHER FINANCING SOURCES (USES) Operating Transfers In... $0 $1,550,970 $109,627 $0 $0 Operating Transfers Out (60,742) (18,000) 0 TOTAL OTHER FINANCING SOURCES... $0 $1,550,970 $48,885 (18,000) $0 Net Changes in Fund Balance... (138,115) (183,937) (395,596) (359,242) 542,063 Beginning Fund Balance... $1,542,474 $1,404,359 $1,220,422 $824,826 $397,188 Ending Fund Balance... $1,404,359 $1,220,422 $824,826 $397,188 $960,055 *Totals may not add due to rounding. (1) Budget, as adopted by the Career Center on June 25, Source: Annual Financial Reports and Budget. 15