Terminations. Presented by ROSS GIBSON

|

|

|

- Melvyn Parsons

- 5 years ago

- Views:

Transcription

1 Terminations Presented by ROSS GIBSON

2 Here are the facts!

3 Average Pay $6,250 per month + $5,000 Unused leave and Claiming Tax-free Threshold MARGINAL RATES CALCULATION Average Pay: $ 6,250 Gross amount to be taxed: $ 5,000 Plus 5% Lump Sum B: + $ 0 Taxable Termination Pay: = $ 5,000 Average Termination Pay: $ 416 Average Pay + Average Term Pay: $ 6,666 Tax: $ 1,599 Average Pay: $ 6,250 Tax: $ 1,456 Difference in Tax: $ 143 TOTAL TAX PAYABLE: $ 1,716 34% 3

4 TAPS Helpline Car Allowance Should an employee s payment of unused annual leave on termination be calculated using the rate for: Salary only, or Salary + Car Allowance? To answer this you will need to refer to the employee s contract and more importantly, how you apply it to the real world. 4

5 TAPS Helpline Car Allowance Fair Work Act states: Section 90 Payment for annual leave: (1) an employee takes a period of paid annual leave, the employer must pay the employee at the employee s base rate of pay (2) when the employment of an employee ends, the employee has a period of untaken paid annual leave, the employer must pay the employee the amount that would have been payable to the employee had the employee taken that period of leave. 5

6 TAPS Helpline Car Allowance Salary $52,000 p.a. plus Car allowance of $15,600 p.a. Method Amount per week Car Allowance Pay on working weeks only $325 x 48 $15,600 Pay on taking annual leave $300 x 52 $15,600 Both methods are correct!! 6

")

")

7 ETP Excluded ETP (Type R) Non-Excluded ETP (Type O) 7

Annual Leave and Leave Loading Long Service Leave It s an")

8 Employment Termination Payments If its not a payment for Ordinary Pay (incl Bonus & Commissions) Annual Leave and Leave Loading Long Service Leave It s an ETP 8

9 An ETP may include: Payments in lieu of notice Gratuity or golden handshake The excess amount of the lump sum D tax free amount Compensation for wrongful dismissal Unused personal carers leave Unused RDOs Payments made on death of an employee 9

10 Excluded ETP Code R Indexed figure: $205,000 Excess over Lump Sum D Settlement payments Unfair dismissal Discrimination Harassment Personal injury Invalidity Non-excluded ETP Code O Whole of Income cap: $180,000 Everything else! 10

11 Excluded ETP Code R Indexed figure: $205,000 Non-excluded ETP Code O Whole of Income cap: $180,000 47% $ ETP payment Less year-to-date income $ $180,000 17% or 32% $205,000 Less value of AL, LL & LSL $ Threshold Amount $ 11

12 GENUINE REDUNDANCY CRITERIA (JOB HAS BEEN ABOLISHED) The dismissal occurs before the employee turns 65, and before the employee would have had to retire anyway The payment is greater than the amount which would have been payable had the employee voluntarily resigned at the same time. ITAA Section No agreement for later employment 12

13 GENUINE REDUNDANCY AND EARLY RETIREMENT SCHEME PAYMENTS: (not applicable for Invalidity Payments) Limit: $10,399 + $5,200 per completed year of service COMPLETED YRS BASE RATE + SERVICE RATE TAX-FREE PORTION 1 $10,399 (1 x $5,200) $15,599 2 $10,399 (2 x $5,200) $20,799 3 $10,399 (3 x $5,200) $25,999 4 $10,399 (4 x $5,200) $31, months $10,399 - $10,399 13

14 TAPS Helpline What can be included in the Lump Sum D? Is this a payment due to redundancy? Resignation Redundancy Include in Lump Sum D? Sales Manager PILON PILON No Receptionist Work notice period PILON Yes 14

15 TAPS Helpline Taxing non-excluded items on redundancy One of our Sales Managers, William is being made redundant. He has been with the business for 5 years. William is being given $120,000 as payment in lieu of notice, regardless of his termination reason. Do I tax the payment in lieu of notice as: An ETP? or Include the payment in the tax-free portion? 15

16 TAPS Helpline Taxing non-excluded items on redundancy PAY ITEMS GENUINE REDUNDANCY 37yo Severance Pay: $ 80,000 Ex-gratia payment: $ 30,000 Unused Personal Leave: $ 15,000 Total payments due to redundancy: $125,000 Lump Sum D: [($5,200 x 5yrs) + $10,399] $ 36,399 Excess (Excluded ETP Type R): $ 88,601 Tax Withheld: $ 28,352 Age at End of Financial Year is 37 < Preservation Age is Payment in lieu of notice of $120,000 cannot be included in the Lump Sum D calculation. It will need to be taxed separately as a Non-excluded ETP! 16

17 Compare the two caps ITEMS INDEXED FIGURE WHOLE OF INCOME $205,000 $180,000 Less Year-to-date income: $ 60,000 Less Taxable value of any AL, LL or LSL: $ 10,000 Less Excluded ETP: $ 88,601 Threshold Amount: $116,399 $110,000 Taxing the Non-excluded ETP GROSS TAX RATE TAX 17% $110,000 32% $35,200 $ 10,000 47% $ 4,700 $120,000 TOTAL $39,900 17

18 TAPS Helpline Redundancy payments to employees over 65 years We are making a number of employees redundant. One of our employees, Charles, is 69 years old and has been with the business for 5 years. Is this a non-genuine redundancy? What is the difference between genuine and non-genuine redundancies when calculating the payment? 18

+ $10,399] $36,399 $ 0 Excess (Excluded ETP Type R): $ 88,601 $125,000 Tax Withheld: $ 28,352 $")

19 TAPS Helpline Redundancy payments to employees over 65 years PAY ITEMS NON-GENUINE REDUNDANCY NON-GENUINE REDUNDANCY Severance Pay: $80,000 $80,000 Ex-gratia payment: $30,000 $30,000 Unused Personal Leave: $15,000 $15,000 Total payments due to redundancy: $125,000 $125,000 Lump Sum D: [($5,200 x 5yrs) + $10,399] $36,399 $ 0 Excess (Excluded ETP Type R): $ 88,601 $125,000 Tax Withheld: $ 28, % Remember, annual Leave and long service leave will be taxed at marginal rates with a non-genuine redundancy! 19

20 TAPS Helpline Multiple Redundancy Payments Kate, one of our executives has been made redundant after 8 years of service. As part of their termination and due to cash flow issues, Kate has agreed to receive her ex-gratia payment by two instalments. Payment# 1 $140,000 to be paid on 20 th June 2018 Payment# 2 $140,000 to be paid on 20 th July

21 PAYMENT #1 - June 2018 $140,000 Lump Sum D : (8 x $5,078) + $10,155: $ 50,779 Excess (Excluded ETP Type R): $ 89,221 Total Tax on 32%: $ 28,551 Total Tax on 47%: PAYMENT #2 - July 2018 $140,000 Lump Sum D: Current Financial Year: (8 x $5,200) + $10,399: Less Previous Financial Year ATO limit: $ 51,999 $ 50,779 $ 1,220 Excess (Excluded ETP Type R): $138,780 ETP 32% on 1 st $205,000 ($205,000 - $89,221 = $115,779): $ 37,049 ETP 47% on $23,001: $ 10,810 Total Tax on ETP: $ 47,859 21

22 SUMMARY PAYMENT #1 PAYMENT #2 TOTAL Taxable Component: $ 89,221 $138,780 $228,001 Tax: $ 28,551 $ 47,859 $ 76,410 Net: $ 60,670 $90,921 $151,591 ETP Code: R S Use Code Use when you are currently paying and you have previously paid S: An Excluded ETP (Code R) a code R or O payment was paid in the previous financial year to the employee for the P: A Non-excluded ETP (Code O) same termination 22

23 TAPS Helpline Salary Sacrifice Arrangement Are staff allowed to salary sacrifice their termination pay into their superannuation fund? For example long service leave or an ex gratia payment? Possibly 23

24 TAPS Helpline Salary Sacrifice Arrangement Effective SSA involves the employee agreeing to receive part of their total amount of remuneration as benefits before the employee has earned the entitlement to receive that amount as salary or wages. Taxation Ruling: 2001/10 Starting 01 November 2017, I would like to sacrifice 100% of all future annual leave accruals that will be paid out to me on termination of employment. 24

25 TAPS Helpline Child Support Is Child Support deducted from the employee s termination pay? Or just from their ordinary hours in their regular pay? 25

26 TAPS Helpline Child Support Contact Dept. Human Services when Employee intends to leave Resigns / Terminates Change in Pay Cycle Change in Employment Status Change in Business (e.g. merger, etc.) Deductions vary Child Support can be deduction from Salary or Wages Commissions Bonuses & Allowances Retirement or Termination Contract labour Other remuneration 26

27 TAPS Helpline Child Support Deduction notice Schedule of Child Support Deductions (subject to Protected Earning Amount) Notice Pursuant to Section 72A: This is a fixed percentage or dollar amount from any payments due to the employee. The Protected Earnings Amount does not apply in this case. 27

28 TAPS Helpline Child Support Alex is on a salary of $1,250 per week. 5 weeks on unused annual leave. A Section 72A is received for a lump sum amount of $2,000. Unused Annual Leave $6,250 marginal rates $2,132 Less Child Support $2,000 Net payment to employee $2,118 28

29 TAPS Helpline PAYG Variation One of our employees has a PAYG Variation for the current financial year for 15% PAYG on Salary & Wages. Can I apply the 15% to the employee s termination pay? Possibly 29

30 30

31 31

32 TAPS Helpline Superannuation on Leave Loading We pay annual leave loading when an employee takes annual leave. We also pay super on the leave loading. Is the leave loading superable if the employee terminates? No, the annual leave loading forms part of the unused annual leave on termination and is not part of the OTE definition. Therefore, no super is applicable to the annual leave or to the leave loading. 32

33 TAPS Helpline Service Casual to Permanent One of our redundant employees has the following history: Hired as a Casual: 01/08/11 Permanent status: 09/09/16 Termination date: 01/11/18 Are they entitled to a redundancy as they were casual for most of his employment? 33

34 TAPS Helpline Service Casual to Permanent There is no precise legal definition of a casual worker. It is accepted that a casual is hired on an informal, uncertain and irregular basis: - Irregular patterns of work - No expectation of ongoing employment - Series of separate contractual engagements 34

35 TAPS Helpline Service Casual to Permanent AMWU v Donau Pty Ltd Background: A number of permanent shipyard employees that were being retrenched had prior periods of service as casuals, working on a regular and systematic basis, with no break between the casual and permanent periods of service. - Casuals are not entitled to severance pay under the FWA s123(c) - During their casual employment these employees received a 25% casual loading. Decision: A period of continuous service as defined by the FWA s384(2)(a) includes a period of regular and systematic casual employment.

36 TAPS Helpline Payment in Lieu of Notice How do I calculate the payment in lieu of notice? Is unpaid leave included when calculating the service period? Does the payment accrue annual leave and long service leave? Do I calculate superannuation on the payment? What is the termination date? 36

37 TAPS Helpline Payment in Lieu of Notice Same value, if worked What about the extra week if the employee is over 45 and worked 2 years continuous service? Super is applicable Payment in Lieu of Notice No Accruals Term date is last day at work Clerks Private Sector Award states: 13.2 The notice of termination required to be given by an employee is the same as that required of an employer except that there is no requirement on the employee to give additional notice based on the age of the employee concerned. 37

38 TAPS Helpline Overpayments How do I process an overpayment for an employee that is terminating? Can I just deduct it from their termination pay or do I need their permission first? This is all about Permitted deductions FWA s324(1)(a) states: An employer may deduct an amount from an amount payable to an employee if the deduction is authorised in writing by the employee. 38

39 TAPS Helpline Overpayments Is there a requirement for the employee to repay the debt? Current Financial Year Immediately reverse Gross/Tax/Net The employer benefits from a reduction in the amount of PAYG in the next payment to the ATO The employee repays Net debt from Net Pay Previous Financial Year Immediately reverse Gross $ only Unable to reverse PAYG since the financial year is closed Issue an amended payment summary to the employee The employee has received the benefit of higher PAYG amount The employee repays Gross debt from Net Pay 39

40 TAPS Helpline Overpayments PREVIOUS FINANCIAL YEAR CURRENT FINANCIAL YEAR Item Paid Should Pay Overpayment Item Paid Should Pay Overpayment Gross $4,000 $2,000 $2,000 Gross $5,000 $3,000 $2,000 Tax $1,500 $1,000 $ 500 Tax $2,000 $1,500 $ 500 Net $2,500 $1,000 $1,500 Net $3,000 $1,500 $1,500 Employee repays the Gross amount from their Net pay. Employee repays the Net amount from their Net pay. 40

41 TAPS Helpline Overpayments Pay all outstanding entitlements Apply the appropriate tax Fair Work Ombudsman states: An employer can be liable to a penalty of up to $63,000 per contravention - Ending Employment Fact sheet. Deduct the overpayment (Gross or Net as required) from the Net pay 41

42 TAPS Helpline Bonuses William was made redundant earlier in the year. He qualified for a Short Term Incentive payment which is related to completing a project during employment. Is the bonus to be taxed as: Marginal rates? or An ETP? or Tax-free (Lump Sum D)? 42

43 TAPS Helpline Bonuses MARGINAL RATES Bonus for work-related performance Short Term Incentive Bonus Sign-on Bonus Referral Bonus BONUS LUMP SUM D (Redundancy) or ETP (Termination) Retention Bonus Non-qualifying Bonuses but given as an Ex-gratia payment 43

44 TAPS Helpline Unpaid leave effect on Service Harry is being made redundant. Commenced: 15/04/2014 Redundant: 14/10/2018 Harry had previously taken 12 months of unpaid leave to travel overseas. Is the period of unpaid leave included in the length of service for calculating notice and severance entitlements? 44

45 HARRY Employment period: Less Unpaid leave Service period: 4.5 years 1.0 year 3.5 years NOTICE REDUNDANCY Period of continuous service Minimum notice period Period of continuous service Redundancy pay 1 year or less 1 week At least 1 year <2 years 4 weeks More than 1 year 3 years 2 weeks At least 2 years <3 years 6 weeks More than 3 years 5 years 3 weeks At least 3 years <4 years 7 weeks More than 5 years 4 weeks At least 4 years <5 years 8 weeks 45

46 TAPS Helpline Notice Period: Contact Vs NES An employee s contract states that on termination the employee is entitled to a payment to the equivalent of 3 months salary. Under the Fair Work, the NES states that we owe the employee a minimum of 4 weeks notice. What is the employer obligated to pay? The NES amount for 4 weeks or the Contract amount for 3 months? 46

47 TAPS Helpline Notice Period: Contact Vs NES The contract is far more generous to the employee than the NES in regards to the notice period. Is the employee better off overall? The employee would be receiving a far greater value for the 3 months at their base salary rather than the 4 weeks as a payment in lieu of notice. The employee would have no recourse as they are receiving more at the base salary than the value of the payment in lieu of working the minimum period. 47

48 TAPS Helpline Q & A QUESTION Does HELP get applied to an employee s termination? Can an employee s final day be a public holiday? Can I withhold monies due on termination if the company property has not been returned? ANSWER No. HELP is applied to a marginal rates calculation for a bonus, but not on a termination. Yes. The physical last day at work will be the prior day. The official termination date is the public holiday. Leave will accrue up to and including the public holiday. No. Most awards allow for unworked notice to be deducted from termination pay, but there is no mention of a deduction for not returning company property. 48

49

Terminations. Presented by Ross Gibson C.P.S. The Association for Payroll Specialists

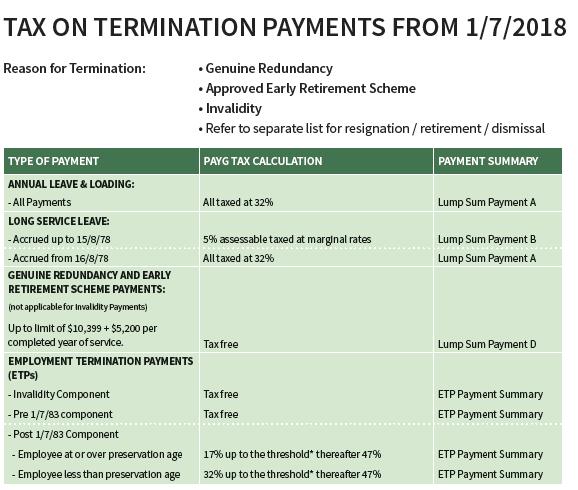

Terminations Presented by Ross Gibson C.P.S. The Association for Payroll Specialists TAPS Helpline How to Tax Annual Leave & LSL ITEM DATES RESIGNATION, RETIREMENT, DISMISSAL REDUNDANCY, APPROVED EARLY

Terminations Presented by Ross Gibson C.P.S. The Association for Payroll Specialists TAPS Helpline How to Tax Annual Leave & LSL ITEM DATES RESIGNATION, RETIREMENT, DISMISSAL REDUNDANCY, APPROVED EARLY

Termination Pays. Terminations... 2

Termination Pays Table of Contents Terminations... 2 Types of Terminations... 2 Notice Period of Termination... 2 Redundancy Weeks to pay... 3 What s included in a Termination?... 3 Employment Termination

Termination Pays Table of Contents Terminations... 2 Types of Terminations... 2 Notice Period of Termination... 2 Redundancy Weeks to pay... 3 What s included in a Termination?... 3 Employment Termination

TAPS HELPLINE - LIVE ON STAGE. Presented by Simone Dixon C.P.S and Tanya Geremia C.P.S. The Association for Payroll Specialists

TAPS HELPLINE - LIVE ON STAGE Presented by Simone Dixon C.P.S and Tanya Geremia C.P.S. The Association for Payroll Specialists TAPS Helpline - Backpackers Question: An employee has advised the employer

TAPS HELPLINE - LIVE ON STAGE Presented by Simone Dixon C.P.S and Tanya Geremia C.P.S. The Association for Payroll Specialists TAPS Helpline - Backpackers Question: An employee has advised the employer

Schedule 11 Tax table for employment termination payments

Schedule 11 Tax table for employment termination payments QC: 34733 Content revised: Yes Abstract revised: No Abstract: Use this table if you pay an individual an amount that is either an employment termination

Schedule 11 Tax table for employment termination payments QC: 34733 Content revised: Yes Abstract revised: No Abstract: Use this table if you pay an individual an amount that is either an employment termination

GOVERNING LEGISLATION APRA ASIC ATO

Introduction GOVERNING LEGISLATION APRA ASIC ATO TRUST DEED Establishes fund and defines rules ROLL-OVERS/ TRANSFERS To or from other funds SUPERANNUATION FUND Assets invested by trustee for benefit of

Introduction GOVERNING LEGISLATION APRA ASIC ATO TRUST DEED Establishes fund and defines rules ROLL-OVERS/ TRANSFERS To or from other funds SUPERANNUATION FUND Assets invested by trustee for benefit of

2013 End of Year Seminar Course Booklet

Course Booklet P: 02 9818 1931 E: eoy@austpayroll.com.au Table of Contents Table of Contents Key rates and thresholds for 2013/14 3 Changes to Superannuation 7 Reviews by Fair Work and the 2013 Budget

Course Booklet P: 02 9818 1931 E: eoy@austpayroll.com.au Table of Contents Table of Contents Key rates and thresholds for 2013/14 3 Changes to Superannuation 7 Reviews by Fair Work and the 2013 Budget

Attaché Sprint Refresh Payroll Termination Types and Payments (Australia)

") Attaché Sprint Refresh 2015 Payroll Termination Types and Payments (Australia) October 2015 Publication Number Publication Date Product A001434C.00 October 2015 Attaché Training Attaché Software Australia

Attaché Sprint Refresh 2015 Payroll Termination Types and Payments (Australia) October 2015 Publication Number Publication Date Product A001434C.00 October 2015 Attaché Training Attaché Software Australia

EOY Support Note # 5 Payment Summary Guide

EOY Support Note # 5 Payment Summary Guide The end of financial year deadline is fast approaching. This guide covers using MYOB to complete your PAYG payment summaries and other end of year payroll issues.

EOY Support Note # 5 Payment Summary Guide The end of financial year deadline is fast approaching. This guide covers using MYOB to complete your PAYG payment summaries and other end of year payroll issues.

Terminating an Employee in Accounts Business

Terminating an Employee in Accounts Business When workers leave the employ of the business, whether it is voluntary or involuntary, they will often be entitled to a number of additional payments above

Terminating an Employee in Accounts Business When workers leave the employ of the business, whether it is voluntary or involuntary, they will often be entitled to a number of additional payments above

Tax table for employment termination payments

Schedule 32 Pay as you go (PAYG) withholding NAT 70980 Tax table for employment termination payments Including delayed termination payments FOR PAYMENTS MADE ON OR AFTER 1 JULY 2012 From 1 July 2012, the

Schedule 32 Pay as you go (PAYG) withholding NAT 70980 Tax table for employment termination payments Including delayed termination payments FOR PAYMENTS MADE ON OR AFTER 1 JULY 2012 From 1 July 2012, the

Tax Rates Tables REVISED VERSION. September 2017

Tax Rates Tables 2017-18 REVISED VERSION September 2017 Individual income tax rates Residents 2016-17 Taxable income Marginal rate Tax on this income $0 $18,200 Nil Nil $18,201 $37,000 19% 19c for each

Tax Rates Tables 2017-18 REVISED VERSION September 2017 Individual income tax rates Residents 2016-17 Taxable income Marginal rate Tax on this income $0 $18,200 Nil Nil $18,201 $37,000 19% 19c for each

How to complete the PAYG payment summary employment termination payment

Instructions for subject PAYG withholding payers How to complete the PAYG payment summary employment termination payment Instructions to help you complete PAYG payment summary employment termination payment

Instructions for subject PAYG withholding payers How to complete the PAYG payment summary employment termination payment Instructions to help you complete PAYG payment summary employment termination payment

Paid Parental Leave scheme Employer Toolkit

Paid Parental Leave scheme Employer Toolkit humanservices.gov.au Contents 1. What we mean by table of terms and definitions 3 2. The Paid Parental Leave scheme in summary 4 2.1 What it is 4 2.2 Why we

Paid Parental Leave scheme Employer Toolkit humanservices.gov.au Contents 1. What we mean by table of terms and definitions 3 2. The Paid Parental Leave scheme in summary 4 2.1 What it is 4 2.2 Why we

Employment Termination Payments BEN SYMONS BARRISTER STATE CHAMBERS

Employment Termination Payments BEN SYMONS BARRISTER STATE CHAMBERS Employment termination payment Section 82-130 of the ITAA 1997 defined employment termination payment: (i) (ii) (iii) (iv) (v) (vi) Payment

Employment Termination Payments BEN SYMONS BARRISTER STATE CHAMBERS Employment termination payment Section 82-130 of the ITAA 1997 defined employment termination payment: (i) (ii) (iii) (iv) (v) (vi) Payment

Financial Considerations for Redundancy

Financial Considerations for Redundancy 16 September, 2013 The information contained within this presentation is intended to provide general advice only. It has been prepared without taking into account

Financial Considerations for Redundancy 16 September, 2013 The information contained within this presentation is intended to provide general advice only. It has been prepared without taking into account

Paid Parental Leave scheme Employer Toolkit

Paid Parental Leave scheme Employer Toolkit humanservices.gov.au Contents 1. What we mean by table of terms and definitions 3 2. The Paid Parental Leave scheme in summary 4 2.1 What it is 4 2.2 Why we

Paid Parental Leave scheme Employer Toolkit humanservices.gov.au Contents 1. What we mean by table of terms and definitions 3 2. The Paid Parental Leave scheme in summary 4 2.1 What it is 4 2.2 Why we

Dealing with redundancy

Dealing with redundancy What you need to know about your super Martin Kennedy Investor Education Manager What we ll cover today Your redundancy payment how it will be taxed and your ability to contribute

Dealing with redundancy What you need to know about your super Martin Kennedy Investor Education Manager What we ll cover today Your redundancy payment how it will be taxed and your ability to contribute

A A fresh guide start to managing redundancies

A fresh guide start to managing redundancies A A fresh guide start to managing 2014 2015redundancies 2013/14 Preparation date 03 March 2014 Issued by The Trustee, MLC Nominees Pty Ltd (MLC) ABN 93 002

A fresh guide start to managing redundancies A A fresh guide start to managing 2014 2015redundancies 2013/14 Preparation date 03 March 2014 Issued by The Trustee, MLC Nominees Pty Ltd (MLC) ABN 93 002

Salary sacrificing into superannuation

Salary sacrificing into superannuation TB 10 TECHNICAL SERVICES ISSUED ON 1 JULY 2018 ADVISER USE ONLY VERSION 1.5 1 Summary Salary sacrificing part of an employee s wage or salary into superannuation

Salary sacrificing into superannuation TB 10 TECHNICAL SERVICES ISSUED ON 1 JULY 2018 ADVISER USE ONLY VERSION 1.5 1 Summary Salary sacrificing part of an employee s wage or salary into superannuation

A A fresh guide start to managing redundancies

A fresh guide start to managing redundancies A A fresh guide start to managing 2015 2016redundancies 2013/14 Preparation date 03 March 2014 Issued by The Trustee, MLC Nominees Pty Ltd (MLC) ABN 93 002

A fresh guide start to managing redundancies A A fresh guide start to managing 2015 2016redundancies 2013/14 Preparation date 03 March 2014 Issued by The Trustee, MLC Nominees Pty Ltd (MLC) ABN 93 002

What this Ruling is about. Previous Rulings

Australian Taxation Office Superannuation Guarantee Ruling FOI status: may be released page 1 of 12 Superannuation Guarantee Ruling Ordinary time earnings contents para What this Ruling is about 1 Superannuation

Australian Taxation Office Superannuation Guarantee Ruling FOI status: may be released page 1 of 12 Superannuation Guarantee Ruling Ordinary time earnings contents para What this Ruling is about 1 Superannuation

A fresh start A guide to managing redundancies

A fresh start A guide to managing redundancies 2 012/13 Preparation date: 1 April 2013 Contents Make the most of Her s your what you ll fresh find within start. this document If you are leaving your employer

A fresh start A guide to managing redundancies 2 012/13 Preparation date: 1 April 2013 Contents Make the most of Her s your what you ll fresh find within start. this document If you are leaving your employer

A guide to managing redundancies

A guide to managing redundancies A fresh start 2016 2017 Regardless of what your next steps might be this guide may help you effectively manage your new financial position better. Contents A fresh start

A guide to managing redundancies A fresh start 2016 2017 Regardless of what your next steps might be this guide may help you effectively manage your new financial position better. Contents A fresh start

PAYG withholding. Guide for employers and businesses. What employers and businesses need to know to meet their PAYG withholding obligations

Guide for employers and businesses PAYG withholding What employers and businesses need to know to meet their PAYG withholding obligations For more information visit www.ato.gov.au NAT 8075-02.2009 Our

Guide for employers and businesses PAYG withholding What employers and businesses need to know to meet their PAYG withholding obligations For more information visit www.ato.gov.au NAT 8075-02.2009 Our

Single Touch Payroll. Site preparation guide

Single Touch Payroll Site preparation guide Copyright 2018 Pronto Software Limited. All rights reserved. Single Touch Payroll Preparation Guide Trademarks PRONTO, PRONTO ENTERPRISE MANAGEMENT SYSTEM, PRONTO

Single Touch Payroll Site preparation guide Copyright 2018 Pronto Software Limited. All rights reserved. Single Touch Payroll Preparation Guide Trademarks PRONTO, PRONTO ENTERPRISE MANAGEMENT SYSTEM, PRONTO

RELEVANT TO ACCA QUALIFICATION PAPER F6 (IRL) Studying Paper F6? Performance objectives 19 and 20 are relevant to this exam

Studying Paper F6? Performance objectives 19 and 20 are relevant to this exam") RELEVANT TO ACCA QUALIFICATION PAPER F6 (IRL) Studying Paper F6? Performance objectives 19 and 20 are relevant to this exam Taxation of termination payments From 2011, termination payments will be examinable

RELEVANT TO ACCA QUALIFICATION PAPER F6 (IRL) Studying Paper F6? Performance objectives 19 and 20 are relevant to this exam Taxation of termination payments From 2011, termination payments will be examinable

Casual Employees. Three Most Common Methods of Calculating Casual Loading... 5 Examples Using All Methods... 5

Casual Employees Table of Contents Employing Casual Employee (Worker)... 2 Overtime for Casuals... 2 How is Overtime for Casuals Calculated?... 4 Casual Loading Penalty... 5 Three Most Common Methods of

Casual Employees Table of Contents Employing Casual Employee (Worker)... 2 Overtime for Casuals... 2 How is Overtime for Casuals Calculated?... 4 Casual Loading Penalty... 5 Three Most Common Methods of

Superannuation guarantee

Guide for employers Superannuation guarantee How to meet your super obligations The super guarantee system affects most employers in Australia so it is important you understand your obligations. Your tax

Guide for employers Superannuation guarantee How to meet your super obligations The super guarantee system affects most employers in Australia so it is important you understand your obligations. Your tax

Payroll issues that keep you awake at night. Presented by JASON LOW

Payroll issues that keep you awake at night Presented by JASON LOW Super on Leave Loading What has the ATO website said since 2009? Super on Leave Loading What does the legislation say? SGR 2009/2 What

Payroll issues that keep you awake at night Presented by JASON LOW Super on Leave Loading What has the ATO website said since 2009? Super on Leave Loading What does the legislation say? SGR 2009/2 What

YOUR GUIDE TO THE FORTESCUE STAFF INCENTIVE PLAN (SIP)

") YOUR GUIDE TO THE FORTESCUE STAFF INCENTIVE PLAN (SIP) Financial year 2013 1 July 2012 to 30 June 2013 Contents 1. Intention 03 2. Summary detail 03 3. Incentive objectives and weightings 04 4. Remuneration

YOUR GUIDE TO THE FORTESCUE STAFF INCENTIVE PLAN (SIP) Financial year 2013 1 July 2012 to 30 June 2013 Contents 1. Intention 03 2. Summary detail 03 3. Incentive objectives and weightings 04 4. Remuneration

EMPLOYEE LEAVE ENTITLEMENTS

EMPLOYEE LEAVE ENTITLEMENTS Presenters: Danica Leys, Gracia Kusuma, Grant Smith OVERVIEW It is important to be aware of the various kinds of leave available to employees The types of leave an employee

EMPLOYEE LEAVE ENTITLEMENTS Presenters: Danica Leys, Gracia Kusuma, Grant Smith OVERVIEW It is important to be aware of the various kinds of leave available to employees The types of leave an employee

A guide to the right choices

Redundancy A guide to the right choices July 2005 A ASGARD Capital Management Limited ABN 92 009 279 592 Level 38, Central Park, 152 St.George s Terrace, Perth WA 6000 Telephone 08 9415 5688 Facsimile

Redundancy A guide to the right choices July 2005 A ASGARD Capital Management Limited ABN 92 009 279 592 Level 38, Central Park, 152 St.George s Terrace, Perth WA 6000 Telephone 08 9415 5688 Facsimile

Technical bulletin: Winter 2014

IOOF TechConnect Technical bulletin: Winter 2014 Employment termination payments: taking the complexity out of the equation 1 Deeming and account based pensions 5 Self-managed superannuation fund exit

IOOF TechConnect Technical bulletin: Winter 2014 Employment termination payments: taking the complexity out of the equation 1 Deeming and account based pensions 5 Self-managed superannuation fund exit

SA Metropolitan Fire Service Superannuation Scheme

SA Metropolitan Fire Service Superannuation Scheme Your Member Benefit Guide Permanent Employees Deferred Members Parked Members Prepared 17 October 2014 Trustee: SA Metropolitan Fire Service Superannuation

SA Metropolitan Fire Service Superannuation Scheme Your Member Benefit Guide Permanent Employees Deferred Members Parked Members Prepared 17 October 2014 Trustee: SA Metropolitan Fire Service Superannuation

NSW Catholic Independent Schools (Teachers Model C) Multi- Enterprise Agreement [2017]

![NSW Catholic Independent Schools (Teachers Model C) Multi- Enterprise Agreement [2017]](/thumbs/75/71984957.jpg "NSW Catholic Independent Schools (Teachers Model C) Multi- Enterprise Agreement [2017]") NSW Catholic Independent Schools (Teachers Model C) Multi- Enterprise Agreement [2017] 1 ARRANGEMENT PART A APPLICATION AND OPERATION 1. Title of the Agreement 2. Coverage of the Agreement 3. Term and

NSW Catholic Independent Schools (Teachers Model C) Multi- Enterprise Agreement [2017] 1 ARRANGEMENT PART A APPLICATION AND OPERATION 1. Title of the Agreement 2. Coverage of the Agreement 3. Term and

How super is taxed guide (AP.4)

") How super is taxed guide (AP.4) Issued 25 January 2018 The information in this document forms part of the ESSSuper Accumulation Plan Product Disclosure Statement dated 25 January 2018. Contents Providing

How super is taxed guide (AP.4) Issued 25 January 2018 The information in this document forms part of the ESSSuper Accumulation Plan Product Disclosure Statement dated 25 January 2018. Contents Providing

NEW SOUTH WALES WAGE RATE BULLETIN NO. 6

THIS APPLIES TO MEMBERS IN NEW SOUTH WALES WAGE RATE BULLETIN NO. 6 CLERKS PRIVATE SECTOR AWARD 2010 Issued: 27 June, 2014. Wages are effective from the first full pay period commencing on or after 1 July,

THIS APPLIES TO MEMBERS IN NEW SOUTH WALES WAGE RATE BULLETIN NO. 6 CLERKS PRIVATE SECTOR AWARD 2010 Issued: 27 June, 2014. Wages are effective from the first full pay period commencing on or after 1 July,

n Print clearly, using a BLACK pen only. n Place X in ALL applicable boxes.

Self-managed superannuation fund annual return 2013 WHO SHOULD COMPLETE THIS ANNUAL RETURN? Only self-managed superannuation funds (SMSFs) can complete this annual return All other funds must complete

Self-managed superannuation fund annual return 2013 WHO SHOULD COMPLETE THIS ANNUAL RETURN? Only self-managed superannuation funds (SMSFs) can complete this annual return All other funds must complete

VICTORIAN WAGE RATE BULLETIN No. 25 ELECTRICAL, ELECTRONIC AND COMMUNICATIONS CONTRACTING AWARD 2010

VICTORIAN WAGE RATE BULLETIN No. 25 ELECTRICAL, ELECTRONIC AND COMMUNICATIONS CONTRACTING AWARD 2010 Wage rates and allowances applying from the first pay period on or after 1 July 2015 (Note: these rates

VICTORIAN WAGE RATE BULLETIN No. 25 ELECTRICAL, ELECTRONIC AND COMMUNICATIONS CONTRACTING AWARD 2010 Wage rates and allowances applying from the first pay period on or after 1 July 2015 (Note: these rates

Adviser AT YOUR FINANCIAL SERVICE. Life Solutions Wealth Solutions. Super Fast Facts 2006/07

Adviser AT YOUR FINANCIAL SERVICE Life Solutions Wealth Solutions Super Fast Facts 2006/07 Issued July 2006 Important note The information contained in this booklet is of a general nature only and does

Adviser AT YOUR FINANCIAL SERVICE Life Solutions Wealth Solutions Super Fast Facts 2006/07 Issued July 2006 Important note The information contained in this booklet is of a general nature only and does

Chartered Accountants. The taxation of employment termination payments. Also in this issue: Client Newsletter - Tax, Super & Business Ideas

Chartered Accountants Client Newsletter - Tax, Super & Business Ideas May 2015 The taxation of employment termination payments An employment termination payment (ETP) is generally a lump sum amount paid

Chartered Accountants Client Newsletter - Tax, Super & Business Ideas May 2015 The taxation of employment termination payments An employment termination payment (ETP) is generally a lump sum amount paid

MLC Facts and Figures

For adviser use only MLC Facts and Figures 2017/18 Contents Tax 1 12 Super accumulation phase 13 30 Super access and taxation of benefits 31 44 Super pension phase 45 56 Social security 57 66 Aged care

For adviser use only MLC Facts and Figures 2017/18 Contents Tax 1 12 Super accumulation phase 13 30 Super access and taxation of benefits 31 44 Super pension phase 45 56 Social security 57 66 Aged care

Super Living Strategies for superannuation 2006/2007

Super Living Strategies for superannuation 2006/2007 This brochure is published by MLC Limited (ABN 90 000 000 402), 105 153 Miller Street, North Sydney, NSW 2060. It is intended to provide general information

Super Living Strategies for superannuation 2006/2007 This brochure is published by MLC Limited (ABN 90 000 000 402), 105 153 Miller Street, North Sydney, NSW 2060. It is intended to provide general information

Federal budget 2012/13

Federal budget 2012/13 9 May 2012 It was a budget that had one goal a surplus or bust. To do it, the Government has put a stop to the drop in the company tax ($4.8 billion over four years), sliced $2.4

Federal budget 2012/13 9 May 2012 It was a budget that had one goal a surplus or bust. To do it, the Government has put a stop to the drop in the company tax ($4.8 billion over four years), sliced $2.4

SA-HELP. Information for

SA-HELP Information for 2012 www.goingtouni.gov.au You must read this booklet before signing the commonwealth assistance form below SA-HELP form USING THIS BOOKLET As you read through, you will notice

SA-HELP Information for 2012 www.goingtouni.gov.au You must read this booklet before signing the commonwealth assistance form below SA-HELP form USING THIS BOOKLET As you read through, you will notice

This form is to be used by a party to a financial case, such as property settlement, maintenance, child support or financial enforcement.

Financial Statement 1 FORM 13 Federal Magistrates Court Rules ~ RULE 24.02 Please type or print clearly and mark [X] all boxes that apply. Attach extra pages if you need more space to answer any questions.

Financial Statement 1 FORM 13 Federal Magistrates Court Rules ~ RULE 24.02 Please type or print clearly and mark [X] all boxes that apply. Attach extra pages if you need more space to answer any questions.

How super is taxed. Inside. UniSuper Accumulation 1 and Personal Account members. Edith Cowan University

How super is taxed UniSuper Accumulation 1 and Personal Account members The information in this document forms part of the UniSuper Accumulation 1 Product Disclosure Statement and UniSuper Personal Account

How super is taxed UniSuper Accumulation 1 and Personal Account members The information in this document forms part of the UniSuper Accumulation 1 Product Disclosure Statement and UniSuper Personal Account

Lesson 7 - Tax Offsets

Tax Training School Contents Tax Offsets 2 Refundable Tax Offsets 2 Tax Offsets on the return 2 T1 - Senior and Pensioners (including self-funded retirees) 4 T2 - Australian Superannuation Income Stream

Tax Training School Contents Tax Offsets 2 Refundable Tax Offsets 2 Tax Offsets on the return 2 T1 - Senior and Pensioners (including self-funded retirees) 4 T2 - Australian Superannuation Income Stream

FirstTech Super guide. FirstTech was ranked 1st by advisers for Technical Support in the 2011 Wealth Insights Fund Manager Service Survey.

FirstTech 2011 12 Super guide FirstTech was ranked 1st by advisers for Technical Support in the 2011 Wealth Insights Fund Manager Service Survey. This Super guide has been developed to provide you with

FirstTech 2011 12 Super guide FirstTech was ranked 1st by advisers for Technical Support in the 2011 Wealth Insights Fund Manager Service Survey. This Super guide has been developed to provide you with

CROWN EMPLOYEES (NSW POLICE FORCE (NURSES')) AWARD 2018

) AWARD 2018") CROWN EMPLOYEES (NSW POLICE FORCE (NURSES')) AWARD 2018 This Award includes: Matter No. Details of Variation Effective Date Gazettal Ref. IRC 2018/00193311 Chief Commissioner P Kite New Award Increase

CROWN EMPLOYEES (NSW POLICE FORCE (NURSES')) AWARD 2018 This Award includes: Matter No. Details of Variation Effective Date Gazettal Ref. IRC 2018/00193311 Chief Commissioner P Kite New Award Increase

CLERKS - PRIVATE SECTOR AWARD 2010

TIMBER TRADE INDUSTRIAL ASSOCIATION CLERKS - PRIVATE SECTOR AWARD 2010 This summary has been prepared as an easy reading guide for Members of the Timber Trade Industrial Association. It is not intended

TIMBER TRADE INDUSTRIAL ASSOCIATION CLERKS - PRIVATE SECTOR AWARD 2010 This summary has been prepared as an easy reading guide for Members of the Timber Trade Industrial Association. It is not intended

Employment Termination Payments (BP 16) Finance in Practice, Taxation Unit, General Tax

Finance in Practice, Taxation Unit, General Tax") Employment Termination Payments (BP 16) Finance in Practice, Taxation Unit, General Tax Custodian/Review Officer: Principal Finance Officer, General Tax Version no: 2 Applicable To: QH staff Approval Date:

Employment Termination Payments (BP 16) Finance in Practice, Taxation Unit, General Tax Custodian/Review Officer: Principal Finance Officer, General Tax Version no: 2 Applicable To: QH staff Approval Date:

2018 RATES OF PAY. Contact REEF today COPY WITH COMPLIMENTS OF REEF IN THE REAL ESTATE INDUSTRY OPERATIVE DATE

COPY WITH COMPLIMENTS OF REEF 2018 RATES OF PAY IN THE REAL ESTATE INDUSTRY OPERATIVE DATE The rates of pay in this booklet are operative from the first full pay period to commence on or after 1 July 2018.

COPY WITH COMPLIMENTS OF REEF 2018 RATES OF PAY IN THE REAL ESTATE INDUSTRY OPERATIVE DATE The rates of pay in this booklet are operative from the first full pay period to commence on or after 1 July 2018.

Budget Speech 2011, 2012 & 2013 Quick Reference Summary Table (TAX)

") Budget Speech 2011, 2012 & 2013 Quick Reference Summary Table (TA) 2011 2012 2013 TA YEAR SITE limit Only > 65 years : R540pa R45pm Only for > 65 years : R540pa R45pm Only for > 65 years : Tax Rebates

Budget Speech 2011, 2012 & 2013 Quick Reference Summary Table (TA) 2011 2012 2013 TA YEAR SITE limit Only > 65 years : R540pa R45pm Only for > 65 years : R540pa R45pm Only for > 65 years : Tax Rebates

Southend University Hospital NHS Foundation Trust NHSI Board Committee/ Panel

Appendix A - Scheme of Delegation Authorised Approvals Scheme of Financial Delegation Southend University Hospital NHS Foundation Trust NHSI Board / Financial of HR 3 Business Planning, Budgets, Budgetary

Appendix A - Scheme of Delegation Authorised Approvals Scheme of Financial Delegation Southend University Hospital NHS Foundation Trust NHSI Board / Financial of HR 3 Business Planning, Budgets, Budgetary

Fast Facts Facts and Figures 1 January 2018

Fast Facts Facts and Figures 1 January 2018 Tax Rates and thresholds Individual resident tax rates 1 (Excludes minors and working holiday makers) Taxable income Tax % tax on excess $18,200 Nil 19.0% $37,000

Fast Facts Facts and Figures 1 January 2018 Tax Rates and thresholds Individual resident tax rates 1 (Excludes minors and working holiday makers) Taxable income Tax % tax on excess $18,200 Nil 19.0% $37,000

Monthly tax table. Schedule 4 Pay as you go (PAYG) withholding NAT 1007

withholding NAT 1007") Schedule 4 Pay as you go (PAYG) withholding NAT 1007 tax table Incorporating Medicare levy and temporary flood and cyclone reconstruction levy (flood levy) FOR PAYMENTS MADE ON OR AFTER 1 JULY 2011 TO

Schedule 4 Pay as you go (PAYG) withholding NAT 1007 tax table Incorporating Medicare levy and temporary flood and cyclone reconstruction levy (flood levy) FOR PAYMENTS MADE ON OR AFTER 1 JULY 2011 TO

Superannuation Caps and changes- update. Presented by Jenneke Mills Senior Technical Consultant MLC Technical Services MLC Advice and Professionalism

Superannuation Caps and changes- update Presented by Jenneke Mills Senior Technical Consultant MLC Technical Services MLC Advice and Professionalism Superannuation Caps & changes- update SUPERANNUATION:

Superannuation Caps and changes- update Presented by Jenneke Mills Senior Technical Consultant MLC Technical Services MLC Advice and Professionalism Superannuation Caps & changes- update SUPERANNUATION:

FirstTech Pocket guide. Adviser use only

FirstTech 2011 12 Pocket guide FirstTech was ranked 1st by advisers for Technical Support in the 2011 Wealth Insights Fund Manager Service Survey. Contents Income tax rates 2 Capital gains tax (CGT) 8

FirstTech 2011 12 Pocket guide FirstTech was ranked 1st by advisers for Technical Support in the 2011 Wealth Insights Fund Manager Service Survey. Contents Income tax rates 2 Capital gains tax (CGT) 8

Section 3 Leave Entitlements

Section 3 Leave Entitlements Annual Leave Annual leave is provided to enable you to enjoy a break from work. You are entitled to Annual Leave in accordance with the terms of the Holidays Act 2003. All

Section 3 Leave Entitlements Annual Leave Annual leave is provided to enable you to enjoy a break from work. You are entitled to Annual Leave in accordance with the terms of the Holidays Act 2003. All

Pre Retirement Planning

Pre Retirement Planning 19 August, 2013 The information contained within this presentation is intended to provide general advice only. It has been prepared without taking into account your objectives,

Pre Retirement Planning 19 August, 2013 The information contained within this presentation is intended to provide general advice only. It has been prepared without taking into account your objectives,

MTA EMPLOYMENT RELATIONS FACT SHEET

FAIR WORK ACT 2009 ANNUAL LEAVE 14 November 2012 Update Operative: On and from 1 January 2010 MTA EMPLOYMENT RELATIONS FACT SHEET The Fair Work Act 2009 includes a Division 6 Annual Leave of Part 2-2 The

FAIR WORK ACT 2009 ANNUAL LEAVE 14 November 2012 Update Operative: On and from 1 January 2010 MTA EMPLOYMENT RELATIONS FACT SHEET The Fair Work Act 2009 includes a Division 6 Annual Leave of Part 2-2 The

Super 2013 The next 12 months

Super 2013 The next 12 months Content Super 2013... 4 1 July 2012 Confirmed changes... 4 Minimum pension payments... 4 Reduction to concessional contributions cap... 5 Low income superannuation contribution

Super 2013 The next 12 months Content Super 2013... 4 1 July 2012 Confirmed changes... 4 Minimum pension payments... 4 Reduction to concessional contributions cap... 5 Low income superannuation contribution

Tax file number declaration

Instructions and form for taxpayers Tax file number declaration Information you provide in this declaration will allow your payer to This is not a TFN application form. ato.gov.au/tfn Terms we use When

Instructions and form for taxpayers Tax file number declaration Information you provide in this declaration will allow your payer to This is not a TFN application form. ato.gov.au/tfn Terms we use When

Defined Benefit Scheme

Defined Benefit Scheme Product Disclosure Statement 1 October 2018 About the Product Disclosure Statement (PDS) This PDS is issued by Energy Industries Superannuation Scheme Pty Limited ABN 72 077 947

Defined Benefit Scheme Product Disclosure Statement 1 October 2018 About the Product Disclosure Statement (PDS) This PDS is issued by Energy Industries Superannuation Scheme Pty Limited ABN 72 077 947

DOING BUSINESS IN AUSTRALIA

COMPANY FORMATION IN Internationals are encouraged to visit Australia, meet with advisors and have the right conversations before establishing an Australian business footprint. MAIN FORMS OF COMPANY/BUSINESS

COMPANY FORMATION IN Internationals are encouraged to visit Australia, meet with advisors and have the right conversations before establishing an Australian business footprint. MAIN FORMS OF COMPANY/BUSINESS

Employer Guide. Data Dictionary and Rules. as at 30 May 2017

Employer Guide Data Dictionary and Rules as at 30 May 2017 1 Table of Contents Contact and support information 2 Dictionary 4 Rules 9 Contact and support information The below provides information on where

Employer Guide Data Dictionary and Rules as at 30 May 2017 1 Table of Contents Contact and support information 2 Dictionary 4 Rules 9 Contact and support information The below provides information on where

SUPER FUTURE MAKE YOUR SUPER ASSURED RETIREMENT SAVINGS ACCOUNT (RSA) defencebank.com.au/super

defencebank.com.au/super") defencebank.com.au/super RSA MAKE YOUR FUTURE SUPER SUPER ASSURED RETIREMENT SAVINGS ACCOUNT (RSA) General Information and Application Form Product Disclosure Statement (PDS) Effective 09 Oct 2017 GUARANTEE

defencebank.com.au/super RSA MAKE YOUR FUTURE SUPER SUPER ASSURED RETIREMENT SAVINGS ACCOUNT (RSA) General Information and Application Form Product Disclosure Statement (PDS) Effective 09 Oct 2017 GUARANTEE

Income Tax Return Checklist Year end 30 June 2018

Income Tax Return Checklist Year end 30 June 2018 Name: Date of Birth: ABN (if applicable): Please provide the following information in order for us to complete your tax return Personal details: Are you

Income Tax Return Checklist Year end 30 June 2018 Name: Date of Birth: ABN (if applicable): Please provide the following information in order for us to complete your tax return Personal details: Are you

Accumulation Basic Stevedores Division Membership Supplement

Accumulation Basic Stevedores Division Membership Supplement 1 November 2018 Membership Supplement Stevedores Division Accumulation Basic 1 November 2018 About this Supplement The information in this Supplement

Accumulation Basic Stevedores Division Membership Supplement 1 November 2018 Membership Supplement Stevedores Division Accumulation Basic 1 November 2018 About this Supplement The information in this Supplement

MLC Facts and Figures

For adviser use only MLC Facts and Figures 2015/16 Contents Tax 1 14 Super 15 38 Income streams 39 50 Social security 51 60 Aged care 61 66 Insurance 67 74 Important information and disclaimer This publication

For adviser use only MLC Facts and Figures 2015/16 Contents Tax 1 14 Super 15 38 Income streams 39 50 Social security 51 60 Aged care 61 66 Insurance 67 74 Important information and disclaimer This publication

Fast Facts Facts and Figures 1 July 2018

Fast Facts Facts and Figures 1 July 2018 Tax Rates and thresholds Individual resident tax rates 1 (Excludes minors and working holiday makers) Taxable income Tax % tax on excess $18,200 Nil 19.0% $37,000

Fast Facts Facts and Figures 1 July 2018 Tax Rates and thresholds Individual resident tax rates 1 (Excludes minors and working holiday makers) Taxable income Tax % tax on excess $18,200 Nil 19.0% $37,000

TIMBER INDUSTRY AWARD 2010

TIMBER INDUSTRY AWARD 2010 Note: This summary has been prepared as an easy reading guide for Members of the Timber Trade Industrial Association. It is not intended to replace the award but to be read in

TIMBER INDUSTRY AWARD 2010 Note: This summary has been prepared as an easy reading guide for Members of the Timber Trade Industrial Association. It is not intended to replace the award but to be read in

TAX TREATMENT OF PAYMENTS RECEIVED AT THE END OF THE WORKING RELATIONSHIP

TAX TREATMENT OF PAYMENTS RECEIVED AT THE END OF THE WORKING RELATIONSHIP Kevin Munro Munro Lawyers 12 June 2014 Harmers Workplace Lawyers 1. Termination Payments There are many different types of payments

TAX TREATMENT OF PAYMENTS RECEIVED AT THE END OF THE WORKING RELATIONSHIP Kevin Munro Munro Lawyers 12 June 2014 Harmers Workplace Lawyers 1. Termination Payments There are many different types of payments

Defined Benefit Scheme

Defined Benefit Scheme Product Disclosure Statement 29 September 2017 About the Product Disclosure Statement (PDS) This PDS is issued by Energy Industries Superannuation Scheme Pty Limited ABN 72 077 947

Defined Benefit Scheme Product Disclosure Statement 29 September 2017 About the Product Disclosure Statement (PDS) This PDS is issued by Energy Industries Superannuation Scheme Pty Limited ABN 72 077 947

C A V E N D I S H S U P E R A N N U A T I O N P T Y L T D

S U P E R A N N U A T I O N P T Y L T D S P E C I A L I S T S I N S E L F M A N A G E D S U P E R A N N U A T I O N ABN 30 007 778 341 T E C H N I C A L U P D A T E B U D GET S PECIAL I N T H I S I SSUE

S U P E R A N N U A T I O N P T Y L T D S P E C I A L I S T S I N S E L F M A N A G E D S U P E R A N N U A T I O N ABN 30 007 778 341 T E C H N I C A L U P D A T E B U D GET S PECIAL I N T H I S I SSUE

HOW MY SUPER IS TAXED GUIDE

HOW MY SUPER IS TAXED GUIDE Prepared and issued The information in this document forms part of the following Energy Super Product Disclosure Statements (PDSs), each issued by Electricity Supply Industry

HOW MY SUPER IS TAXED GUIDE Prepared and issued The information in this document forms part of the following Energy Super Product Disclosure Statements (PDSs), each issued by Electricity Supply Industry

Employer Manual Emergency Services Superannuation DB Fund. Proudly serving our members. As at 1 July 2017

Employer Manual Emergency Services Superannuation DB Fund Proudly serving our members As at 1 July 2017 Issued by: Emergency Services Superannuation Board ABN 28 161 296 741 as Trustee of the Emergency

Employer Manual Emergency Services Superannuation DB Fund Proudly serving our members As at 1 July 2017 Issued by: Emergency Services Superannuation Board ABN 28 161 296 741 as Trustee of the Emergency

[Work in Progress: Do Not Quote or Cite Without Author s Permission]

![[Work in Progress: Do Not Quote or Cite Without Author s Permission]](/thumbs/81/83971720.jpg "[Work in Progress: Do Not Quote or Cite Without Author s Permission]") Insolvency and Social Protection 1 Argentina Written notice of dismissal at least one month in advance Certain claims for amount owed for work performed have 1 ST priority over all creditors. Other employee

Insolvency and Social Protection 1 Argentina Written notice of dismissal at least one month in advance Certain claims for amount owed for work performed have 1 ST priority over all creditors. Other employee

Contents. Contact us.

This document is for permanent employees of BOC Limited. Retained and Spouse members should refer to their version of the Other information document. BOCSUPER Contents 3 How super works 7 Your benefits

This document is for permanent employees of BOC Limited. Retained and Spouse members should refer to their version of the Other information document. BOCSUPER Contents 3 How super works 7 Your benefits

Genuine redundancy payments conditions & tax treatment

batallion legal keepin it simple Genuine redundancy payments conditions & tax treatment By Wai Kien Ng, Lawyer & Luis Batalha, Director 24 April 2009 The ATO issued Taxation Ruling TR 2009/2 in final form

batallion legal keepin it simple Genuine redundancy payments conditions & tax treatment By Wai Kien Ng, Lawyer & Luis Batalha, Director 24 April 2009 The ATO issued Taxation Ruling TR 2009/2 in final form

A Clear Direction Financial Planning Level 19, 10 Eagle Street, Brisbane QLD 4000 (07) ABN:

ABN:") A Clear Direction Financial Planning Level 19, 10 Eagle Street, Brisbane QLD 4000 scottk@acleardirection.com.au (07) 3379 6068 ABN: 85 147 572 870 The budget has provided a number of significant changes

A Clear Direction Financial Planning Level 19, 10 Eagle Street, Brisbane QLD 4000 scottk@acleardirection.com.au (07) 3379 6068 ABN: 85 147 572 870 The budget has provided a number of significant changes

THE EXCEPTIONAL TOPDOCS SMSF DEED SMSF CHANGES OVER TIME

Superannuation in Australia has been undergoing a constantly evolving process. Some industry participants suggest that change needs to cease, as it tends to undermine confidence in Australia s Retirement

Superannuation in Australia has been undergoing a constantly evolving process. Some industry participants suggest that change needs to cease, as it tends to undermine confidence in Australia s Retirement

MLC Facts and Figures

For adviser use only MLC Facts and Figures 2016/17 Contents Tax 1 14 Super 15 38 Income streams 39 50 Social security 51 60 Aged care 61 68 Insurance 69 76 NOTE: Footnotes have been included where appropriate

For adviser use only MLC Facts and Figures 2016/17 Contents Tax 1 14 Super 15 38 Income streams 39 50 Social security 51 60 Aged care 61 68 Insurance 69 76 NOTE: Footnotes have been included where appropriate

Contents. Application INCOME TAX INTERPRETATION BULLETIN. INCOME TAX ACT Retiring Allowances

INCOME TAX INTERPRETATION BULLETIN NO.: IT-337R4 (Consolidated) DATE: February 1, 2006 SUBJECT: REFERENCE: INCOME TAX ACT Retiring Allowances Paragraph 60(j.1), subparagraph 56(1)(a)(ii) and the definition

INCOME TAX INTERPRETATION BULLETIN NO.: IT-337R4 (Consolidated) DATE: February 1, 2006 SUBJECT: REFERENCE: INCOME TAX ACT Retiring Allowances Paragraph 60(j.1), subparagraph 56(1)(a)(ii) and the definition

Medicare levy variation declaration

Instructions and form for taxpayers Medicare levy variation declaration WHO SHOULD COMPLETE THIS DECLARATION? You should complete this declaration if you want to: n increase the amount withheld from payments

Instructions and form for taxpayers Medicare levy variation declaration WHO SHOULD COMPLETE THIS DECLARATION? You should complete this declaration if you want to: n increase the amount withheld from payments

DISCLAIMERS. Given the above diversity issues and our time limitation today, I have not included any references to Agency Specific Agreements.

DISCLAIMERS Professional Disclaimer This presentation is of general information only, to provide guidance on what sorts of issues to consider in decision making about your retirement planning. Given the

DISCLAIMERS Professional Disclaimer This presentation is of general information only, to provide guidance on what sorts of issues to consider in decision making about your retirement planning. Given the

Member Booklet Product Disclosure Statement

mysuper.watsonwyatt.com/wwa Australia February 2008 Watson Wyatt Superannuation Fund Category A Member Booklet Product Disclosure Statement For defined benefit members who joined the Fund prior to 1 March

mysuper.watsonwyatt.com/wwa Australia February 2008 Watson Wyatt Superannuation Fund Category A Member Booklet Product Disclosure Statement For defined benefit members who joined the Fund prior to 1 March

Freelancers, the self-employed & super.

YOUR SUPER Freelancers, the self-employed & super. If you are self-employed or a freelance or contract worker Media Super can help you understand your super and tax options, and what you can do to maximise

YOUR SUPER Freelancers, the self-employed & super. If you are self-employed or a freelance or contract worker Media Super can help you understand your super and tax options, and what you can do to maximise

Weekly tax table. Schedule 2 Pay as you go (PAYG) withholding NAT Including instructions for calculating monthly and quarterly withholding

withholding NAT Including instructions for calculating monthly and quarterly withholding") Schedule 2 Pay as you go (PAYG) withholding NAT 1005 tax table Including instructions for calculating monthly and quarterly withholding FOR PAYMENTS MADE ON OR AFTER 1 JULY 2012 From 1 July 2012, the temporary

Schedule 2 Pay as you go (PAYG) withholding NAT 1005 tax table Including instructions for calculating monthly and quarterly withholding FOR PAYMENTS MADE ON OR AFTER 1 JULY 2012 From 1 July 2012, the temporary

Superannuation Guarantee

Australian Taxation Office Superannuation Guarantee Instruction Guide and Statement Valid for all years up to and including 2002/2003 For those employers who have NOT paid the required amount of superannuation

Australian Taxation Office Superannuation Guarantee Instruction Guide and Statement Valid for all years up to and including 2002/2003 For those employers who have NOT paid the required amount of superannuation

Legal Considerations when Employing an Employee in Hong Kong

Legal Considerations when Employing an Employee in Hong Kong Contents The Employment Ordinance and the Minimum Wage Ordinance 2 Who Do The EO and the MWO Apply To? 2 Statutory Minimum Wage under the MWO

Legal Considerations when Employing an Employee in Hong Kong Contents The Employment Ordinance and the Minimum Wage Ordinance 2 Who Do The EO and the MWO Apply To? 2 Statutory Minimum Wage under the MWO

What you need to report through Single Touch Payroll

Page 1 of 26 What you need to report through Single Touch Payroll Print entire document https://www.ato.gov.au/business/single-touch-payroll/in-detail/what-youneed-to-report-through-single-touch-payroll/

Page 1 of 26 What you need to report through Single Touch Payroll Print entire document https://www.ato.gov.au/business/single-touch-payroll/in-detail/what-youneed-to-report-through-single-touch-payroll/

For BT Panorama Investments (SMSF account holders)

") Panorama Tax Policy Guide For the year ended 30 June 2017 Tax Guide For BT Panorama Investments (SMSF account holders) Part 1 General Information and Panorama Tax Policy Guide Part 2 Completing the Fund

Panorama Tax Policy Guide For the year ended 30 June 2017 Tax Guide For BT Panorama Investments (SMSF account holders) Part 1 General Information and Panorama Tax Policy Guide Part 2 Completing the Fund

Your super. Paving the way to your financial future. Proudly serving our members

Your super A guide to understanding your super For MFB/CFA new operational paid employees Issued January 2014 Proudly serving our members Paving the way to your financial future. We re proud to be the

Your super A guide to understanding your super For MFB/CFA new operational paid employees Issued January 2014 Proudly serving our members Paving the way to your financial future. We re proud to be the

Accumulation Plus Stevedores Division Membership Supplement

Accumulation Plus Stevedores Division Membership Supplement 1 November 2018 Membership Supplement Stevedores Division Accumulation Plus 1 November 2018 About this Supplement The information in this Supplement

Accumulation Plus Stevedores Division Membership Supplement 1 November 2018 Membership Supplement Stevedores Division Accumulation Plus 1 November 2018 About this Supplement The information in this Supplement

Asgard Elements Super/Pension

Asgard Elements Super/Pension Supplementary Product Disclosure Statement (SPDS) This SPDS, dated 30 September 2017, supplements information contained in the Product Disclosure Statement (PDS) dated 1 July

Asgard Elements Super/Pension Supplementary Product Disclosure Statement (SPDS) This SPDS, dated 30 September 2017, supplements information contained in the Product Disclosure Statement (PDS) dated 1 July

CLIENT: DATE: ADVISER: Australian Financial Services Licence No FACT FIND. Version: BG1.00. The FinancialLink Group Pty Ltd

CLIENT: DATE: Australian Financial Services Licence No. 240938 ADVISER: FACT FIND Version: BG1.00 The FinancialLink Group Pty Ltd BG1.00 Retirement Age INCOME ASSETS Client 1 Client 2 Combined Retirement

CLIENT: DATE: Australian Financial Services Licence No. 240938 ADVISER: FACT FIND Version: BG1.00 The FinancialLink Group Pty Ltd BG1.00 Retirement Age INCOME ASSETS Client 1 Client 2 Combined Retirement

Lesson 6 - Temporary Budget Repair Levy, Medicare Levy and Tax Calculation

Tax Training School Lesson 6 - Temporary Budget Repair Levy, Medicare Levy and Tax Calculation Table of Contents Taxable income and rates of tax 2 Budget repair levy 2 The Medicare levy 2 Exemptions from

Tax Training School Lesson 6 - Temporary Budget Repair Levy, Medicare Levy and Tax Calculation Table of Contents Taxable income and rates of tax 2 Budget repair levy 2 The Medicare levy 2 Exemptions from

CLIENT FACT FIND COMPREHENSIVE

CLIENT FACT FIND COMPREHENSIVE This Client Fact Find is issued by: Rimbal Investment Services Pty Ltd ( Rimbal ) Australian Financial Services Licence No. 472548 Client Name/s.. Date Rimbal Authorised

CLIENT FACT FIND COMPREHENSIVE This Client Fact Find is issued by: Rimbal Investment Services Pty Ltd ( Rimbal ) Australian Financial Services Licence No. 472548 Client Name/s.. Date Rimbal Authorised