Disclosures. CD's are FDIC Insured and offer a fixed rate of return if held to maturity.

|

|

|

- Douglas Newton

- 5 years ago

- Views:

Transcription

1

2 Disclosures This statement has been prepared by Robert Young for informational purposes only and does not replace the statement(s) you should receive directly from your investment sponsor(s). The goal of this cash flow analysis is to assist in the development of your current and long-term financial strategy. These strategies are presented to assist you with important decisions regarding savings to meet intended retirement goals. Cash flow needs are based on the information you provided, which represents your situation at one point in time. As your situation changes, suggestions may change. The program is meant to provide representatives and their clients with a quick, yet detailed report of the client s current financial situation and hypothetical cash flow up until whatever age that is desired to be displayed. It is not meant to provide specific investment recommendations or advice. This report is not intended to provide legal or tax advice. For legal and tax matters, it is important that you consult with your legal and tax advisors regarding the affect on your personal situation. Hypothetical returns are for illustrative purposes only based on assumed growth rates for assets over the time period referenced. Assumed growth rates should not be considered indicative of future results. The assumed growth cannot be predicted nor is it guaranteed. This hypothetical illustration of mathematical principles is designed to model and evaluate alternative strategies for addressing your future cash flow needs. Note that the amounts are not intended to be exact. These are assumed figures and should only be used as guidelines and not as guaranteed projections. Projections throughout the report are intended to help you determine amounts you need to save to meet your various financial needs, but they are not a projection of the expected return of any specific assets that you own or purchase. Tax rates and rates of return are used for illustrative purposes only and do not represent a guarantee of actual federal tax rates or the performance of any specific investment. These calculations reflect federal and state income tax only and do not consider the effect of alternative minimum tax. This report has been prepared from data believed to be reliable but no representation is being made as to its accuracy or completeness. The figures presented should not be relied upon for tax purposes. International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. Selling bonds prior to maturity may make the actual yield differ from their advertised yield and may involve a loss or gain. Bond values will decline as interest rates rise and are subject to availability and change in price. Investing in real estate/reits involves special risks such as potential illiquidity and may not be suitable for all investors. There is no assurance that the investment objectives of this program will be attained. Past performance is no guarantee of future results. The market for all securities is subject to fluctuation such that upon sale an investor may lose principal. CD's are FDIC Insured and offer a fixed rate of return if held to maturity.

3 HOW TO READ THIS REPORT The goal of this report is to help you understand your current financial situation and assist in the development of your long term financial strategies. It is designed to quickly give you important information for making financial decisions and achieving your retirement goals. The report is based on the information you provided and represents your situation at one point in time. As your situation changes, the suggestions may also change or need to be updated. The reports use color to help you easily view the parts that make up your financial picture. Income, assets, and positive cash flows are shown in green. Investment items are shown in blue. Expenses, liabilities, and negative cash flow items are shown in red. Income & Expenses: This page of the report shows your income now and your estimated income at retirement. It also calculates your current expenses. It arrives at those expenses by taking your current income from all sources and subtracting the cost of taxes and the money you are regularly putting into savings. If money has not been saved, it must have been spent. It also divides the expenses into two types: 1. Expenses of limited duration such as mortgages and loans; 2. Expenses that continue for your lifetime such as food, utilities, gasoline, insurance, property taxes, travel, and entertainment, etc. This last category represents your current standard of living and, with adjustments for inflation, establishes the target amount you will need in retirement to maintain that standard of living. Assets & Liabilities: This page is simply a snapshot of your current financial situation at the point in time the report was prepared. It subtracts your debts and liabilities from your assets to arrive at your net worth. If you sold everything you own tomorrow and paid off all of your debts, this is approximately how much money you would have. It also shows any regular contributions you are making to particular accounts. Target Cash Flow Year-By-Year: These pages of the report project your expenses, adjusted for inflation over your lifetime. With five years shown on each page, this section of the report compares your income from all sources to your projected expenses in each of those years. The bottom line for each year shows if there is a cash flow surplus in green or a cash flow shortfall in red. The last page in this section displays the cash flow surplus or shortfall over your entire life expectancy. If there are shortfalls in any years, the program calculates the amount you would have to invest in a growth investment as a lump sum today, or each year, or each month going forward to meet the projected expenses in the year they are needed. The program does not assume that all surpluses are captured to offset expenses. That is not realistic. It simply calculates the size of the cash flow shortfall, if there is one, and you can then look at the years where there are surpluses and decide how much of it you can capture and invest to meet the shortfalls.

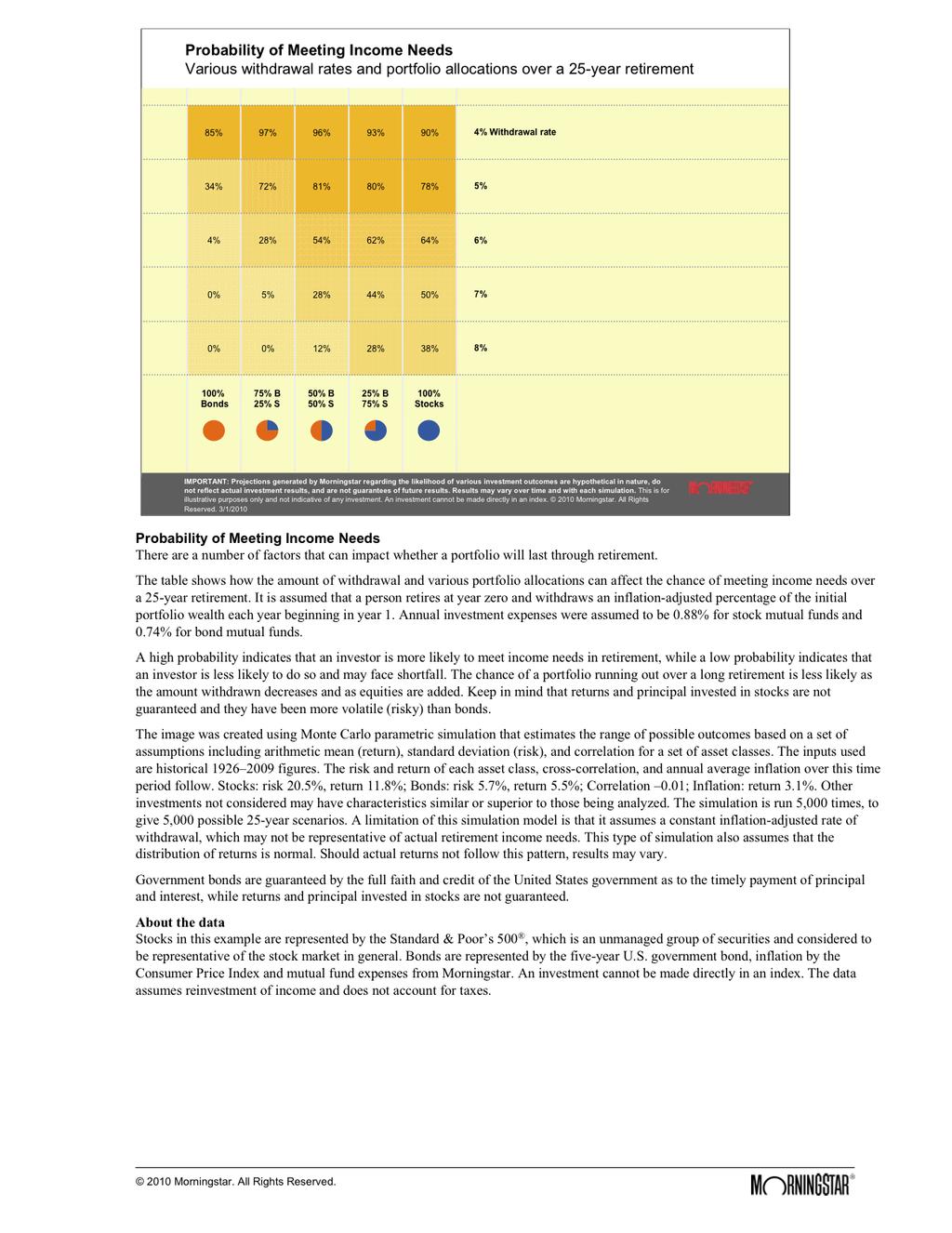

4 Strategies For Addressing Shortfalls: HOW TO READ THIS REPORT (cont.) If the report shows there are shortfalls in the current or future years, don t panic. There are many ways to address shortfalls and the earlier you identify them, the easier they are to address: 1. Increase Savings and Investments - Look at the surpluses for each year and any increases in income you may receive and decide how much you can realistically save or invest. 2. Increase the Returns on your Investments - If most of your investments are in conservative accounts or investments, consider diversifying them to potentially increase returns. 3. Increase Income - Evaluate your current employment. If you do not feel you are earning what you should based on your education and experience, a change of careers or employers may enable you to increase your income. Taking some classes and getting a more advanced degree or professional designation could increase your income. Starting your own business may be an option. 4. Decrease Expenses - Review your expenses and decide if there are any places you can cut back or reduce spending. 5. Work Longer or Part Time - People are living longer and healthier lives. The old concept of totally retiring at age 60 or 65 may not be the most desirable approach for most people. You could work part time for an employer you really like. The shortfall line will tell you how much you would need to work in any given year. You have accumulated valuable experience and knowledge that employers may need in order to train replacements for the baby boom retirees. 6. Sell or Reposition Assets Look at your assets and see if there are any that are generating low or no income that could be repositioned to create a larger income stream. 7. Any or All of the Above It is often difficult to address a shortfall using just one of the strategies listed above. A combination of the strategies listed above is usually the most realistic approach. Probability of Meeting Income Needs: In addition to the strategies for addressing cash flow shortfalls identified above, there is one additional strategy which is to withdraw both principal and income from your retirement accounts, as needed each year, to meet any shortfalls. To be conservative, Retirement in a Nutshell does not assume principal is used to address shortfalls. The buildup of principal in retirement accounts then becomes a back-up source of funds in later years if the other strategies fall short. Invading principal is a critical decision which should be discussed with your advisor before implementing this approach. If principal is invaded too early one could run out of both principal and income. The "Probability of Meeting Income Needs" chart uses probabilistic modeling (Monte Carlo) and statistical analysis of thousands of historical scenarios to determine the chances your assets will last through your retirement years if both principal and income are withdrawn as needed. It examines various withdrawal rates and portfolio allocations over a typical 25 year retirement period and displays the probability, as a percentage, that you will not run out of assets. It is intended to help you evaluate risk and the chances of success in meeting your retirement goals if you do decide to begin utilizing principal. Of course, there is no guarantee that actual future market returns will be consistent with this analysis.

5 INCOME & EXPENSES 8/12/2012 CURRENT ANNUAL INCOME INCOME EXPENSES Ben - Gross Income (less employee pension/ss contributions) $84,420 Betty - Gross Income (less employee pension/ss contributions) $47,000 Real Estate & Other Income $2,020 Total Gross Income $133,440 CALCULATION OF CURRENT ANNUAL LIVING EXPENSES Gross Income $133,440 Less Income Tax (23.64 % of gross income excluding retirement contributions) $25,300 Less Retirement and Savings Contributions $26,400 Less Living Expenses/Payments of Limited Duration House Payment (Excl. Insurance and Property Tax) $25,200 Equity Loan Payments $7,200 Net Annual Living Expenses that Continue for Life $49,340 Net Monthly Living Expenses $4,112 RETIREMENT/SOCIAL SECURITY INCOME Age Ben Betty Retirement Plan/Pension (monthly) 65 $0 Social Security (monthly) 65 $1,500 x COLA (2.00 %) $1,760 Retirement Plan/Pension (monthly) 65 $3,333 Social Security (monthly) 65 $0 x COLA (0.00 %) $0

6 CURRENT ASSETS & LIABILITIES 8/12/2012 CURRENT MARKET MONTHLY ASSETS ASSET TYPE VALUE ADDITIONS Checking Bank Checking $4,000 Savings Emergency Funds $22,000 Residence Residence $350,000 Cabin Vacation Home $150,000 INVESTMENTS INVESTMENT TYPE Ben Betty Elm Street Rental Real Estate $400,000 Ben's 401k Tax Deferred - Qualified - 1 $100,000 $1,700 Betty 457 Tax Deferred - Qualified - 2 $60,000 $500 Betty IRA Tax Deferred - Qualified - 3 $33,000 LIABILITIES LIABILITY TYPE Residence Loan Residence Loan $170,000 Equity Loan Equity Loan $26,000 Rental Real Estate Elm Street Rental $150,000 Total Monthly Additions $2,200 NET WORTH $773,000

7 CASH FLOW ASSUMPTIONS 8/12/2012 * Assumed Assumed Asset Asset Annual Growth Withdrawal Category Owner Value Additions Rate %/Amt Tax Deferred - Qualified - 1 Client $100,000 $20,400 7% 5.00 % Tax Deferred - Qualified - 2 Spouse $60,000 $6,000 7% 5.00 % Tax Deferred - Qualified - 3 Spouse $33,000 $0 7% 5.00 % Elm Street Rental Joint $400,000 3% 0.51 % Income Taxes as a % of Net Income % Inflation Rate 3.00 % Years Until Retirement Client: 8 Spouse: 6 * Hypothetical growth is for illustration purposes only. There is no assurance that these results will be achieved. Actual results will vary.

8 HYPOTHETICAL CASH FLOW 8/12/ Age - Ben / Betty 57 / / / / / 63 Ben Salary - Ben $84,420 $86,108 $87,831 $89,587 $91,379 Betty Salary - Betty $47,000 $47,940 $48,899 $49,877 $50,874 Betty Pension - Betty Social Security - Ben Total Non-Investment Income $131,420 $134,048 $136,729 $139,464 $142,253 Elm Street Rental $400,000 $412,000 $424,360 $437,091 $450,204 Income $2,020 $2,536 $3,067 $3,615 $4,179 Client Retirement Assets Tax Deferred - Qualified - 1 $100,000 $127,400 $156,718 $188,088 $221,654 Income Spouse Retirement Assets Tax Deferred - Qualified - 2 $60,000 $70,200 $81,114 $92,792 $105,287 Income Tax Deferred - Qualified - 3 $33,000 $35,310 $37,782 $40,426 $43,256 Income Target Account Values $193,000 $232,910 $275,614 $321,307 $370,198 Target Investment Income $2,020 $2,536 $3,067 $3,615 $4,179 TOTAL INCOME $133,440 $136,584 $139,797 $143,079 $146,432 Invest/Retire Contributions - Client $20,400 $20,400 $20,400 $20,400 $20,400 Invest/Retire Contributions - Spouse $6,000 $6,000 $6,000 $6,000 $6,000 Income Taxes $25,300 $26,043 $26,803 $27,578 $28,371 NET INCOME $81,740 $84,141 $86,594 $89,101 $91,661 Annual Living Expenses $49,340 $50,820 $52,345 $53,915 $55,533 Residence Loan $25,200 $25,200 $25,200 $25,200 $25,200 Equity Loan $7,200 $7,200 $7,200 $7,200 $7,200 Total Annual Expenses $81,740 $83,220 $84,745 $86,315 $87,933 NET CASH FLOW $0 $921 $1,850 $2,785 $3,729 * Hypothetical growth is for illustration purposes only. There is no assurance that these results will be achieved. Actual results will vary.

9 HYPOTHETICAL CASH FLOW 8/12/ Age - Ben / Betty 62 / / / / / 68 Ben Salary - Ben $93,207 $95,071 $96,972 Betty Salary - Betty $51,892 Betty Pension - Betty $40,000 $40,800 $41,616 $42,448 Social Security - Ben $21,120 $21,543 Total Non-Investment Income $145,098 $135,071 $137,772 $62,736 $63,991 Elm Street Rental $463,710 $477,621 $491,950 $506,708 $521,909 Income $4,760 $5,358 $5,974 $6,608 $7,262 Client Retirement Assets Tax Deferred - Qualified - 1 $257,570 $296,000 $337,120 $381,119 $387,407 Income $19,056 $19,370 Spouse Retirement Assets Tax Deferred - Qualified - 2 $118,658 $132,964 $135,157 $137,388 $139,654 Income $6,648 $6,758 $6,869 $6,983 Tax Deferred - Qualified - 3 $46,284 $49,524 $50,341 $51,172 $52,016 Income $2,476 $2,517 $2,559 $2,601 Target Account Values $422,512 $478,488 $522,619 $569,678 $579,078 Target Investment Income $4,760 $14,482 $15,249 $35,092 $36,216 TOTAL INCOME $149,858 $149,553 $153,021 $97,829 $100,207 Invest/Retire Contributions - Client $20,400 $20,400 $20,400 Invest/Retire Contributions - Spouse $6,000 Income Taxes $29,181 $30,527 $31,346 $23,123 $23,685 NET INCOME $94,277 $98,626 $101,275 $74,706 $76,522 Annual Living Expenses $57,199 $58,915 $60,682 $62,502 $64,378 Residence Loan $25,200 $25,200 $25,200 $25,200 $25,200 Equity Loan $7,200 Total Annual Expenses $89,599 $84,115 $85,882 $87,702 $89,578 NET CASH FLOW $4,679 $14,512 $15,393 ($12,997) ($13,055) * Hypothetical growth is for illustration purposes only. There is no assurance that these results will be achieved. Actual results will vary.

10 HYPOTHETICAL CASH FLOW 8/12/ Age - Ben / Betty 67 / / / / / 73 Ben Salary - Ben Betty Salary - Betty Betty Pension - Betty $43,297 $44,163 $45,046 $45,947 $46,866 Social Security - Ben $21,974 $22,413 $22,861 $23,319 $23,785 Total Non-Investment Income $65,271 $66,576 $67,908 $69,266 $70,651 Elm Street Rental $537,567 $553,694 $570,304 $587,413 $605,036 Income $7,935 $8,629 $9,343 $10,079 $10,837 Client Retirement Assets Tax Deferred - Qualified - 1 $393,799 $400,297 $406,902 $413,616 $420,440 Income $19,690 $20,015 $20,345 $20,681 $21,022 Spouse Retirement Assets Tax Deferred - Qualified - 2 $141,959 $144,301 $146,682 $149,102 $151,562 Income $7,098 $7,215 $7,334 $7,455 $7,578 Tax Deferred - Qualified - 3 $52,874 $53,747 $54,634 $55,535 $56,452 Income $2,644 $2,687 $2,732 $2,777 $2,823 Target Account Values $588,633 $598,345 $608,218 $618,253 $628,454 Target Investment Income $37,367 $38,546 $39,754 $40,991 $42,259 TOTAL INCOME $102,638 $105,122 $107,662 $110,257 $112,911 Invest/Retire Contributions - Client Invest/Retire Contributions - Spouse Income Taxes $24,260 $24,847 $25,447 $26,060 $26,688 NET INCOME $78,378 $80,276 $82,215 $84,197 $86,223 Annual Living Expenses $66,309 $68,298 $70,347 $72,457 $74,631 Residence Loan $25,200 $25,200 $25,200 $25,200 $25,200 Equity Loan Total Annual Expenses $91,509 $93,498 $95,547 $97,657 $99,831 NET CASH FLOW ($13,130) ($13,222) ($13,332) ($13,460) ($13,608) * Hypothetical growth is for illustration purposes only. There is no assurance that these results will be achieved. Actual results will vary.

11 HYPOTHETICAL CASH FLOW 8/12/ Age - Ben / Betty 72 / / / / / 78 Ben Salary - Ben Betty Salary - Betty Betty Pension - Betty $47,804 $48,760 $49,735 $50,730 $51,744 Social Security - Ben $24,261 $24,746 $25,241 $25,746 $26,261 Total Non-Investment Income $72,064 $73,506 $74,976 $76,475 $78,005 Elm Street Rental $623,187 $641,883 $661,139 $680,973 $701,402 Income $11,617 $12,421 $13,249 $14,102 $14,980 Client Retirement Assets Tax Deferred - Qualified - 1 $427,378 $434,429 $441,597 $448,884 $456,290 Income $21,369 $21,721 $22,080 $22,444 $22,815 Spouse Retirement Assets Tax Deferred - Qualified - 2 $154,063 $156,605 $159,189 $161,816 $164,486 Income $7,703 $7,830 $7,959 $8,091 $8,224 Tax Deferred - Qualified - 3 $57,383 $58,330 $59,292 $60,271 $61,265 Income $2,869 $2,916 $2,965 $3,014 $3,063 Target Account Values $638,824 $649,364 $660,079 $670,970 $682,041 Target Investment Income $43,558 $44,889 $46,253 $47,650 $49,082 TOTAL INCOME $115,623 $118,395 $121,229 $124,126 $127,087 Invest/Retire Contributions - Client Invest/Retire Contributions - Spouse Income Taxes $27,329 $27,984 $28,654 $29,338 $30,038 NET INCOME $88,294 $90,411 $92,575 $94,787 $97,049 Annual Living Expenses $76,870 $79,176 $81,552 $83,998 $86,518 Residence Loan $25,200 $25,200 $25,200 $25,200 $25,200 Equity Loan Total Annual Expenses $102,070 $104,376 $106,752 $109,198 $111,718 NET CASH FLOW ($13,776) ($13,965) ($14,176) ($14,411) ($14,669) * Hypothetical growth is for illustration purposes only. There is no assurance that these results will be achieved. Actual results will vary.

12 HYPOTHETICAL CASH FLOW 8/12/ Age - Ben / Betty 77 / / / / / 83 Ben Salary - Ben Betty Salary - Betty Betty Pension - Betty $52,779 $53,835 $54,911 $56,010 $57,130 Social Security - Ben $26,786 $27,321 $27,868 $28,425 $28,994 Total Non-Investment Income $79,565 $81,156 $82,779 $84,435 $86,124 Elm Street Rental $722,444 $744,118 $766,441 $789,435 $813,118 Income $31,065 $31,997 $32,957 $33,946 $34,964 Client Retirement Assets Tax Deferred - Qualified - 1 $463,819 $471,472 $479,252 $487,159 $495,197 Income $23,191 $23,574 $23,963 $24,358 $24,760 Spouse Retirement Assets Tax Deferred - Qualified - 2 $167,200 $169,959 $172,763 $175,614 $178,511 Income $8,360 $8,498 $8,638 $8,781 $8,926 Tax Deferred - Qualified - 3 $62,276 $63,303 $64,348 $65,410 $66,489 Income $3,114 $3,165 $3,217 $3,270 $3,324 Target Account Values $693,295 $704,734 $716,362 $728,182 $740,197 Target Investment Income $65,730 $67,234 $68,775 $70,355 $71,974 TOTAL INCOME $145,295 $148,390 $151,554 $154,790 $158,098 Invest/Retire Contributions - Client Invest/Retire Contributions - Spouse Income Taxes $34,342 $35,073 $35,821 $36,586 $37,368 NET INCOME $110,953 $113,316 $115,733 $118,204 $120,730 Annual Living Expenses $89,114 $91,787 $94,541 $97,377 $100,298 Residence Loan $25,200 Equity Loan Total Annual Expenses $114,314 $91,787 $94,541 $97,377 $100,298 NET CASH FLOW ($3,361) $21,530 $21,192 $20,827 $20,432 * Hypothetical growth is for illustration purposes only. There is no assurance that these results will be achieved. Actual results will vary.

13 HYPOTHETICAL CASH FLOW 8/12/ Age - Ben / Betty 82 / / / / / 88 Ben Salary - Ben Betty Salary - Betty Betty Pension - Betty $58,272 $59,438 $60,627 $61,839 $63,076 Social Security - Ben $29,574 $30,165 $30,768 $31,384 $32,011 Total Non-Investment Income $87,846 $89,603 $91,395 $93,223 $95,087 Elm Street Rental $837,511 $862,637 $888,516 $915,171 $942,626 Income $36,013 $37,093 $38,206 $39,352 $40,533 Client Retirement Assets Tax Deferred - Qualified - 1 $503,368 $511,674 $520,116 $528,698 $537,422 Income $25,168 $25,584 $26,006 $26,435 $26,871 Spouse Retirement Assets Tax Deferred - Qualified - 2 $181,457 $184,451 $187,494 $190,588 $193,732 Income $9,073 $9,223 $9,375 $9,529 $9,687 Tax Deferred - Qualified - 3 $67,586 $68,701 $69,835 $70,987 $72,158 Income $3,379 $3,435 $3,492 $3,549 $3,608 Target Account Values $752,411 $764,826 $777,445 $790,273 $803,312 Target Investment Income $73,634 $75,335 $77,078 $78,866 $80,699 TOTAL INCOME $161,480 $164,938 $168,473 $172,089 $175,786 Invest/Retire Contributions - Client Invest/Retire Contributions - Spouse Income Taxes $38,167 $38,985 $39,820 $40,675 $41,549 NET INCOME $123,312 $125,953 $128,653 $131,414 $134,237 Annual Living Expenses $103,307 $106,406 $109,598 $112,886 $116,273 Residence Loan Equity Loan Total Annual Expenses $103,307 $106,406 $109,598 $112,886 $116,273 NET CASH FLOW $20,005 $19,547 $19,055 $18,528 $17,964 * Hypothetical growth is for illustration purposes only. There is no assurance that these results will be achieved. Actual results will vary.

14 HYPOTHETICAL CASH FLOW 8/12/ Age - Ben / Betty 87 / / / / 92 Ben Salary - Ben Betty Salary - Betty Betty Pension - Betty $64,337 $65,624 $66,937 $68,275 Social Security - Ben $32,652 $33,305 $33,971 $34,650 Total Non-Investment Income $96,989 $98,929 $100,908 $102,926 Elm Street Rental $970,905 $1,000,032 $1,030,033 $1,060,934 Income $41,749 $43,001 $44,291 $45,620 Client Retirement Assets Tax Deferred - Qualified - 1 $546,289 $555,303 $564,465 $573,779 Income $27,314 $27,765 $28,223 $28,689 Spouse Retirement Assets Tax Deferred - Qualified - 2 $196,929 $200,178 $203,481 $206,839 Income $9,846 $10,009 $10,174 $10,342 Tax Deferred - Qualified - 3 $73,349 $74,559 $75,789 $77,040 Income $3,667 $3,728 $3,789 $3,852 Target Account Values $816,567 $830,040 $843,736 $857,658 Target Investment Income $82,577 $84,503 $86,478 $88,503 TOTAL INCOME $179,566 $183,432 $187,386 $191,429 Invest/Retire Contributions - Client Invest/Retire Contributions - Spouse Income Taxes $42,442 $43,356 $44,291 $45,246 NET INCOME $137,124 $140,076 $143,095 $146,183 Annual Living Expenses $119,761 $123,354 $127,055 $130,866 Residence Loan Equity Loan Total Annual Expenses $119,761 $123,354 $127,055 $130,866 NET CASH FLOW $17,363 $16,722 $16,041 $15,316 * Hypothetical growth is for illustration purposes only. There is no assurance that these results will be achieved. Actual results will vary.

15 CASH FLOW AT A GLANCE Hypothetical Year Client/Spouse Age Surplus/Shortfall Amount /59 $ /60 $ /61 $1, /62 $2, /63 $3, /64 $4, /65 $14, /66 $15, /67 ($12,997) /68 ($13,055) /69 ($13,130) /70 ($13,222) /71 ($13,332) /72 ($13,460) /73 ($13,608) /74 ($13,776) /75 ($13,965) /76 ($14,176) /77 ($14,411) /78 ($14,669) /79 ($3,361) /80 $21, /81 $21, /82 $20, /83 $20, /84 $20, /85 $19, /86 $19, /87 $18, /88 $17, /89 $17, /90 $16, /91 $16, /92 $15,316 * Hypothetical growth is for illustration purposes only. There is no assurance that these results will be achieved. Actual results will vary.

16 HYPOTHETICAL SHORTFALL ANALYSIS 8/12/2012 Cash Flow Surplus Before Retirement * Lump Sum - One Time: or Annual Available: or Monthly Available: Surplus Surplus Surplus Contributions Needed to Meet Cash Flow (Shortfall) After Retirement * Lump Sum - One Time: $53,490 or Annual Contributions: $8,866 or Monthly Contributions: $756 * Using a 7% hypothetical growth rate ** Hypothetical growth is for illustration purposes only. There is no assurance that these results will be achieved. Actual results will vary.

17

18 OPTIONS FOR THE NEXT GENERATION 8/12/ Option 1: Lump Sum $857,658 Taxes 40% $343,063 Net Lump Sum Invested at 8% Taxable (6% After Taxes) * $514,595 $532,859 $571,357 $612,635 $656,896 Annual W/D of 5%/Yr. $25,730 $26,643 $28,568 $30,632 $32,845 Total Withdrawals $1,718,124 Option 2: Lump Sum $857,658 Withdrawal of 25% $214,414 Taxes 40% $85,766 Net after Tax $128,649 Balance Invested at 8% Tax Deferred * $643,243 $816,117 $1,211,331 $1,426,457 $513,269 Annual W/D using remaining Life Exp. $18,378 $25,504 $55,060 $118,871 $256,635 Total Withdrawals $3,507,407 Option 3: Withdrawals over Lifetime of 35 Years $857,658 Balance Invested at 8% Tax Deferred * $857,658 $1,088,156 $1,615,107 $1,901,943 $684,359 Annual W/D using remaining Life Exp. $24,505 $34,005 $73,414 $158,495 $342,179 Total Withdrawals $4,676,543 This report is only intended to illustrate the power of a beneficiary "stretching" the withdrawals from your tax deferred accounts over their life expectancy rather than taking a lump sum up front and paying a large portion to the government off the top. The difference in total withdrawals over a 35 year life expectancy of the beneficiary is dramatic. Multi-generational withdrawal strategy may not be appropriate for investors who will rely upon investments for retirement income. Furthermore, changes in tax rates may make the scenario portrayed less favorable. * Hypothetical growth is for illustration purposes only. There is no assurance that these results will be achieved. Actual results will vary.

Personal Financial Plan. John and Mary Sample

For October 21, 2013 Prepared by Public Retirement Planners, LLC 820 Davis Street Suite 434 Evanston IL 60714 224-567-1854 This presentation provides a general overview of some aspects of your personal

For October 21, 2013 Prepared by Public Retirement Planners, LLC 820 Davis Street Suite 434 Evanston IL 60714 224-567-1854 This presentation provides a general overview of some aspects of your personal

RETIREMENT STRATEGIES. Your IRA Planning for Tomorrow Today

RETIREMENT STRATEGIES Your IRA Planning for Tomorrow Today Achieving a comfortable future requires more from you more planning and more resources than in the past. Investment Products: ARE NOT INSURED

RETIREMENT STRATEGIES Your IRA Planning for Tomorrow Today Achieving a comfortable future requires more from you more planning and more resources than in the past. Investment Products: ARE NOT INSURED

Lifetime Retirement Planning with Wells Fargo Advisors Income guarantees for your retirement savings

Lifetime Retirement Planning with Wells Fargo Advisors Income guarantees for your retirement savings Get there. Your way. Lifetime Retirement Planning with Wells Fargo Advisors 1 Guaranteed income for

Lifetime Retirement Planning with Wells Fargo Advisors Income guarantees for your retirement savings Get there. Your way. Lifetime Retirement Planning with Wells Fargo Advisors 1 Guaranteed income for

Learn how to prepare for retirement. Investor education

Learn how to prepare for retirement Investor education Soon you ll embark on one of the biggest changes in your life...... the transition to retirement. When you retire, you ll be spending your nest egg

Learn how to prepare for retirement Investor education Soon you ll embark on one of the biggest changes in your life...... the transition to retirement. When you retire, you ll be spending your nest egg

Joe and Jane Coastal Member

Retirement Plan Joe and Jane Coastal Member Prepared by: Catherine Bryant Financial Advisor Coastal Wealth Management/CUSO FS January 31, 2018 Table Of Contents Personal Information and Summary of Financial

Retirement Plan Joe and Jane Coastal Member Prepared by: Catherine Bryant Financial Advisor Coastal Wealth Management/CUSO FS January 31, 2018 Table Of Contents Personal Information and Summary of Financial

John and Margaret Boomer

Retirement Lifestyle Plan Using Projected Returns John and Margaret Boomer Prepared by : Sample Advisor Financial Advisor September 17, 2008 Table Of Contents IMPORTANT DISCLOSURE INFORMATION 1-7 Presentation

Retirement Lifestyle Plan Using Projected Returns John and Margaret Boomer Prepared by : Sample Advisor Financial Advisor September 17, 2008 Table Of Contents IMPORTANT DISCLOSURE INFORMATION 1-7 Presentation

Getting Ready to Retire

How to Prepare for Your Retirement A GUIDE TO: Getting Ready to Retire EDUCATION GUIDE Create a plan now for a more comfortable retirement If you re five years or less from retirement, now is the time

How to Prepare for Your Retirement A GUIDE TO: Getting Ready to Retire EDUCATION GUIDE Create a plan now for a more comfortable retirement If you re five years or less from retirement, now is the time

Retirement Goal Analysis Self-Study Guide

NaviPlan Standard Online/Offline Retirement Goal Analysis Self-Study Guide USA version 11.2 EISI, Winnipeg Disclaimer This software is designed to allow a financial planner to demonstrate and evaluate

NaviPlan Standard Online/Offline Retirement Goal Analysis Self-Study Guide USA version 11.2 EISI, Winnipeg Disclaimer This software is designed to allow a financial planner to demonstrate and evaluate

Delaware Life Target Income 10 SM. Fixed Index Annuity. Plan for your retirement lifestyle. Issued by Delaware Life Insurance Company

Target Income 10 SM Fixed Index Annuity Plan for your retirement lifestyle Issued by Delaware Life Insurance Company What Is a Fixed Index Annuity? A fixed index annuity (FIA) is long-term contract with

Target Income 10 SM Fixed Index Annuity Plan for your retirement lifestyle Issued by Delaware Life Insurance Company What Is a Fixed Index Annuity? A fixed index annuity (FIA) is long-term contract with

Retirement. Mr. Sample and Mrs. Anna 401k Participant. Prepared for: November 19, (Main Scenario)

") Prepared for: Mr Sample and Mrs Anna 401k (Main Scenario) November 19, 2008 Mr Sample and Mrs Anna 401k Retirement Table of Contents Title Page 1 Table of Contents 2 Spending Goal 3 Current Funding 4 Additional

Prepared for: Mr Sample and Mrs Anna 401k (Main Scenario) November 19, 2008 Mr Sample and Mrs Anna 401k Retirement Table of Contents Title Page 1 Table of Contents 2 Spending Goal 3 Current Funding 4 Additional

GENERATE FUTURE RETIREMENT INCOME

GENERATE FUTURE RETIREMENT INCOME Using a Fixed Indexed Annuity with an Optional Benefit FAC0760-1117 WHAT MIGHT YOU FACE IN RETIREMENT? During your working years, you are likely focused on saving for

GENERATE FUTURE RETIREMENT INCOME Using a Fixed Indexed Annuity with an Optional Benefit FAC0760-1117 WHAT MIGHT YOU FACE IN RETIREMENT? During your working years, you are likely focused on saving for

Retirement Chapters 10 Fixed Index Annuity

Retirement Chapters 10 Fixed Index Annuity Plan for your retirement lifestyle Issued by Delaware Life Insurance Company Delaware Life Delaware Life is dedicated to supporting you with valuable, straightforward

Retirement Chapters 10 Fixed Index Annuity Plan for your retirement lifestyle Issued by Delaware Life Insurance Company Delaware Life Delaware Life is dedicated to supporting you with valuable, straightforward

Delaware Life. Retirement Stages 7 Fixed Index Annuity. Plan for your retirement lifestyle. Issued by Delaware Life Insurance Company

Retirement Stages 7 Fixed Index Annuity Plan for your retirement lifestyle Issued by Delaware Life Insurance Company 1 Delaware Life Delaware Life is dedicated to supporting you with valuable, straightforward

Retirement Stages 7 Fixed Index Annuity Plan for your retirement lifestyle Issued by Delaware Life Insurance Company 1 Delaware Life Delaware Life is dedicated to supporting you with valuable, straightforward

Annuities in Retirement Income Planning

For much of the recent past, individuals entering retirement could look to a number of potential sources for the steady income needed to maintain a decent standard of living: Defined benefit (DB) employer

For much of the recent past, individuals entering retirement could look to a number of potential sources for the steady income needed to maintain a decent standard of living: Defined benefit (DB) employer

What s Your Strategy? Design a Personal Income Strategy to help you navigate your way to a secure retirement

What s Your Strategy? Design a Personal Income Strategy to help you navigate your way to a secure retirement Is your Income Strategy designed to guide you through changing markets? One of the most important

What s Your Strategy? Design a Personal Income Strategy to help you navigate your way to a secure retirement Is your Income Strategy designed to guide you through changing markets? One of the most important

PREPARING FOR A MORE COMFORTABLE RETIREMENT

PREPARING FOR A MORE COMFORTABLE RETIREMENT As financial professionals who specialize in helping government employees transition from work to retirement, we understand that you may have questions about

PREPARING FOR A MORE COMFORTABLE RETIREMENT As financial professionals who specialize in helping government employees transition from work to retirement, we understand that you may have questions about

Make your money work as hard as you do.

Lifetime Income Track Living benefit guide Make your money work as hard as you do. Your key to retirement income potential. A Nationwide Destination SM Series 2.0 variable annuity with the Nationwide Lifetime

Lifetime Income Track Living benefit guide Make your money work as hard as you do. Your key to retirement income potential. A Nationwide Destination SM Series 2.0 variable annuity with the Nationwide Lifetime

Delaware Life. Retirement Stages 7 Fixed Index Annuity. Plan for your retirement lifestyle. Issued by Delaware Life Insurance Company

Retirement Stages 7 Fixed Index Annuity Plan for your retirement lifestyle Issued by Delaware Life Insurance Company 1 Delaware Life Delaware Life is dedicated to supporting you with valuable, straightforward

Retirement Stages 7 Fixed Index Annuity Plan for your retirement lifestyle Issued by Delaware Life Insurance Company 1 Delaware Life Delaware Life is dedicated to supporting you with valuable, straightforward

RETIREMENT QUESTIONS GOVERNMENT EMPLOYEES SHOULD BE ASKING

RETIREMENT QUESTIONS GOVERNMENT EMPLOYEES SHOULD BE ASKING 8/25/16 Preparing For a More Comfortable Retirement As financial professionals who specialize in helping government employees transition from

RETIREMENT QUESTIONS GOVERNMENT EMPLOYEES SHOULD BE ASKING 8/25/16 Preparing For a More Comfortable Retirement As financial professionals who specialize in helping government employees transition from

Financial Goal Plan. Jane and John Doe. Prepared by: Alex Schmitz, CFP Director of Financial Planning

Financial Goal Plan Jane and John Doe Prepared by: Alex Schmitz, CFP Director of Financial Planning March 07, 2018 Table Of Contents Table of Contents Section Title IMPORTANT DISCLOSURE INFORMATION 1-5

Financial Goal Plan Jane and John Doe Prepared by: Alex Schmitz, CFP Director of Financial Planning March 07, 2018 Table Of Contents Table of Contents Section Title IMPORTANT DISCLOSURE INFORMATION 1-5

Especially Prepared For: John and Betty Doe (Hypothetical Client)

") Especially Prepared For: By: Heywood A. Turner, III, RICP General Information 1 Disclaimer - Important Note 2 Client Objectives 4 Analysis Summary 5 Need vs. Current Plan 11 Financial Statements 12 Cash

Especially Prepared For: By: Heywood A. Turner, III, RICP General Information 1 Disclaimer - Important Note 2 Client Objectives 4 Analysis Summary 5 Need vs. Current Plan 11 Financial Statements 12 Cash

Supplementing Retirement Income with Life Insurance

Supplementing Retirement Income with Life Insurance CLIENT SNAPSHOT INDIVIDUAL NEEDS Protection for today, income for tomorrow Protecting your family and planning for a long retirement are likely to top

Supplementing Retirement Income with Life Insurance CLIENT SNAPSHOT INDIVIDUAL NEEDS Protection for today, income for tomorrow Protecting your family and planning for a long retirement are likely to top

Accumulating Funds in an Annuity: A Deferred Fixed Interest and Indexed Annuity Review

Accumulating Funds in an Annuity: A Deferred Fixed Interest and Indexed Annuity Review Did you know that an annuity can be used to systematically accumulate money for retirement purposes, as well as to

Accumulating Funds in an Annuity: A Deferred Fixed Interest and Indexed Annuity Review Did you know that an annuity can be used to systematically accumulate money for retirement purposes, as well as to

INVESTMENT POLICY GUIDANCE REPORT. Living in Retirement. A Successful Foundation

INVESTMENT POLICY GUIDANCE REPORT Living in Retirement A Successful Foundation Developing Your The process for creating a strategy Plan for the Expected Your Retirement Journey It all starts with you.

INVESTMENT POLICY GUIDANCE REPORT Living in Retirement A Successful Foundation Developing Your The process for creating a strategy Plan for the Expected Your Retirement Journey It all starts with you.

Make your money work as hard as you do

Lifetime Income Track Living Benefit guide Make your money work as hard as you do Your key to retirement income potential The Nationwide Destination SM Architect 2.0 variable annuity with the Nationwide

Lifetime Income Track Living Benefit guide Make your money work as hard as you do Your key to retirement income potential The Nationwide Destination SM Architect 2.0 variable annuity with the Nationwide

PENTEGRA RETIREMENT SERVICES DISTRIBUTION PATHTM. The path to helping participants plan successfully

PENTEGRA RETIREMENT SERVICES DISTRIBUTION PATHTM The path to helping participants plan successfully Making a secure retirement a reality. What are your choices? What s the right amount? What s the best

PENTEGRA RETIREMENT SERVICES DISTRIBUTION PATHTM The path to helping participants plan successfully Making a secure retirement a reality. What are your choices? What s the right amount? What s the best

Six steps to help secure your retirement

Six steps to help secure your retirement The average age for retirement in America is 62.* If you retire at age 65, you can expect to spend 19 years in retirement.** *Source: Gallup **Source: The Wall

Six steps to help secure your retirement The average age for retirement in America is 62.* If you retire at age 65, you can expect to spend 19 years in retirement.** *Source: Gallup **Source: The Wall

Nationwide Quatro Select Annuity. Spend more time with the people who matter most and less time planning for retirement.

Spend more time with the people who matter most and less time planning for retirement. Nationwide Quatro Select Annuity Not a deposit Not FDIC or NCUSIF insured Not guaranteed by the institution Not insured

Spend more time with the people who matter most and less time planning for retirement. Nationwide Quatro Select Annuity Not a deposit Not FDIC or NCUSIF insured Not guaranteed by the institution Not insured

Facilitator Guide. Program Goal: To define and examine practices that maximizes money for retirees.

Facilitator Guide Maximizing Your Dollars in Retirement The trouble with retirement is that you never get a day off. Abe Lemons Rationale: Feeling financially secure is important at all stages of life.

Facilitator Guide Maximizing Your Dollars in Retirement The trouble with retirement is that you never get a day off. Abe Lemons Rationale: Feeling financially secure is important at all stages of life.

ANICO. Annuity PLUS. A Multi-Strategy Indexed Annuity Issued By American National Insurance Company

ANICO Strategy 10 Indexed Annuity PLUS A Multi-Strategy Indexed Annuity Issued By American National Insurance Company Your Life. Your Strategies. Whether you are already enjoying retirement or are still

ANICO Strategy 10 Indexed Annuity PLUS A Multi-Strategy Indexed Annuity Issued By American National Insurance Company Your Life. Your Strategies. Whether you are already enjoying retirement or are still

An Insider s Guide to Annuities. The Safe Money Guide. retirement security investment growth

The Safe Money Guide retirement security investment growth An Insider s Guide to Annuities 1 Presented by Joe Brown Brown Advisory Group, LLC http://joebrown.retirevillage.com An Insider s Guide to Annuities

The Safe Money Guide retirement security investment growth An Insider s Guide to Annuities 1 Presented by Joe Brown Brown Advisory Group, LLC http://joebrown.retirevillage.com An Insider s Guide to Annuities

Retirement Planning. Overview. Description and Operation

Retirement Planning Overview Retirement planning is the process of developing a realistic approach to adequately funding one s The process can be somewhat complex due to the numerous issues and variables

Retirement Planning Overview Retirement planning is the process of developing a realistic approach to adequately funding one s The process can be somewhat complex due to the numerous issues and variables

John and Margaret Boomer

Retirement Lifestyle Plan Everything but the kitchen sink John and Margaret Boomer Prepared by : Sample Advisor Financial Advisor September 17, 28 Table Of Contents IMPORTANT DISCLOSURE INFORMATION 1-7

Retirement Lifestyle Plan Everything but the kitchen sink John and Margaret Boomer Prepared by : Sample Advisor Financial Advisor September 17, 28 Table Of Contents IMPORTANT DISCLOSURE INFORMATION 1-7

for INCOME How to optimize your retirement income Client Guide INCOME SOLUTIONS Prime Income Optimizer TM fixed indexed annuity

Prime Income Optimizer TM fixed indexed annuity Preparing How to optimize your retirement income for INCOME Insurance products issued by: The Lincoln National Life Insurance Company Not a deposit Not FDIC-insured

Prime Income Optimizer TM fixed indexed annuity Preparing How to optimize your retirement income for INCOME Insurance products issued by: The Lincoln National Life Insurance Company Not a deposit Not FDIC-insured

Measuring Retirement Plan Effectiveness

T. Rowe Price Measuring Retirement Plan Effectiveness T. Rowe Price Plan Meter helps sponsors assess and improve plan performance Retirement Insights Once considered ancillary to defined benefit (DB) pension

T. Rowe Price Measuring Retirement Plan Effectiveness T. Rowe Price Plan Meter helps sponsors assess and improve plan performance Retirement Insights Once considered ancillary to defined benefit (DB) pension

Your Financial Legacy

Your Financial Legacy An Illustration to Help You Pass Your IRA Assets to Future Generations Prepared for John F. Sample and Susan G. Sample Prepared by Michael J. Prestwich ImagiSOFT, Inc. PO Box 1328

Your Financial Legacy An Illustration to Help You Pass Your IRA Assets to Future Generations Prepared for John F. Sample and Susan G. Sample Prepared by Michael J. Prestwich ImagiSOFT, Inc. PO Box 1328

WHETHER YOUR RETIREMENT IS 40 YEARS AWAY OR ON THE HORIZON, IT IS IMPORTANT TO TAKE STOCK OF YOUR SITUATION AND TAKE CHARGE.

WHETHER YOUR RETIREMENT IS 40 YEARS AWAY OR ON THE HORIZON, IT IS IMPORTANT TO TAKE STOCK OF YOUR SITUATION AND TAKE CHARGE. Industry professionals estimate that some Americans will spend nearly one third

WHETHER YOUR RETIREMENT IS 40 YEARS AWAY OR ON THE HORIZON, IT IS IMPORTANT TO TAKE STOCK OF YOUR SITUATION AND TAKE CHARGE. Industry professionals estimate that some Americans will spend nearly one third

YOU DESERVE BOTH. PROTECTION AND GROWTH OPPORTUNITY. PruSecure Select SM FIXED INDEXED ANNUITY. Prudential Annuities

Prudential Annuities PruSecure Select SM FIXED INDEXED ANNUITY PROTECTION AND GROWTH OPPORTUNITY. YOU DESERVE BOTH. Issued by Prudential Annuities Life Assurance Corporation. This material must be preceded

Prudential Annuities PruSecure Select SM FIXED INDEXED ANNUITY PROTECTION AND GROWTH OPPORTUNITY. YOU DESERVE BOTH. Issued by Prudential Annuities Life Assurance Corporation. This material must be preceded

Determining a Realistic Withdrawal Amount and Asset Allocation in Retirement

Determining a Realistic Withdrawal Amount and Asset Allocation in Retirement >> Many people look forward to retirement, but it can be one of the most complicated stages of life from a financial planning

Determining a Realistic Withdrawal Amount and Asset Allocation in Retirement >> Many people look forward to retirement, but it can be one of the most complicated stages of life from a financial planning

STRATEGIES TO HELP YOU KEEP MORE OF YOUR INVESTMENT EARNINGS

STRATEGIES TO HELP YOU KEEP MORE OF YOUR INVESTMENT EARNINGS VLC0774-0118 CONSIDER TAX-EFFICIENT STRATEGIES THAT HELP INCREASE YOUR INVESTMENT EARNINGS The income we keep after taxes are paid is referred

STRATEGIES TO HELP YOU KEEP MORE OF YOUR INVESTMENT EARNINGS VLC0774-0118 CONSIDER TAX-EFFICIENT STRATEGIES THAT HELP INCREASE YOUR INVESTMENT EARNINGS The income we keep after taxes are paid is referred

Managing Money in Retirement. A Guide to Retiree Financial Strategies

Managing Money in Retirement A Guide to Retiree Financial Strategies Managing Money in Retirement Managing Money in Retirement QUICK REFERENCE 2 A New Era of Retirement 3 Identifying Your Retirement Needs

Managing Money in Retirement A Guide to Retiree Financial Strategies Managing Money in Retirement Managing Money in Retirement QUICK REFERENCE 2 A New Era of Retirement 3 Identifying Your Retirement Needs

Allen & Betty Abbett. Personal Financial Analysis. Sample Financial Plan - TOTAL Goal-Based Planning

Mar 29, 2018 Personal Financial Analysis Allen & Betty Abbett John Smith Asset Advisors Example, LLC A Registered Investment Advisor 2430 NW Professional Drive Corvallis, OR 97330 877-421-9815 www.moneytree.com

Mar 29, 2018 Personal Financial Analysis Allen & Betty Abbett John Smith Asset Advisors Example, LLC A Registered Investment Advisor 2430 NW Professional Drive Corvallis, OR 97330 877-421-9815 www.moneytree.com

Retirement Guide: Saving and Planning

Retirement Guide: Saving and Planning It s Never Too Early to Start What You Need to Know About Saving for Retirement Many of us don t realize how much time we may spend in retirement. In fact, statistics

Retirement Guide: Saving and Planning It s Never Too Early to Start What You Need to Know About Saving for Retirement Many of us don t realize how much time we may spend in retirement. In fact, statistics

Financial Goal Plan. Jack and Diane Smith

Financial Goal Plan Jack and Diane Smith July 13, 2016 Table Of Contents Summary of Goals and Resources Personal Information and Summary of Financial Goals Net Worth Summary - All Resources Net Worth Detail

Financial Goal Plan Jack and Diane Smith July 13, 2016 Table Of Contents Summary of Goals and Resources Personal Information and Summary of Financial Goals Net Worth Summary - All Resources Net Worth Detail

Retirement Matters: Distributions from Retirement Plans. Slide 1

Slide 1 If you re like many Americans, you ve been setting aside money for your retirement. Now that you re nearing retirement age, it may soon be time to start drawing money from your qualified retirement

Slide 1 If you re like many Americans, you ve been setting aside money for your retirement. Now that you re nearing retirement age, it may soon be time to start drawing money from your qualified retirement

Invest now to help make your retirement dreams a reality

Invest now to help make your retirement dreams a reality What s inside The sooner you start, the better off you ll be... 1 Chart your path to a comfortable retirement.... 2 Why Vanguard?... 5 Choose the

Invest now to help make your retirement dreams a reality What s inside The sooner you start, the better off you ll be... 1 Chart your path to a comfortable retirement.... 2 Why Vanguard?... 5 Choose the

Financial Planning Analysis Bill and Judy Sample

Financial Planning Analysis Bill and Judy Sample August 1, 2017 Sample Report Pages William Patterson Senior Wealth Advisor ABC Wealth Advisors Table of Contents Statement of Net Worth... 2 Summary...

Financial Planning Analysis Bill and Judy Sample August 1, 2017 Sample Report Pages William Patterson Senior Wealth Advisor ABC Wealth Advisors Table of Contents Statement of Net Worth... 2 Summary...

John and Margaret Boomer

Retirement Lifestyle Plan Includes Insurance and Estate - Using Projected Returns John and Margaret Boomer Prepared by : Sample Report June 06, 2012 Table Of Contents IMPORTANT DISCLOSURE INFORMATION 1-9

Retirement Lifestyle Plan Includes Insurance and Estate - Using Projected Returns John and Margaret Boomer Prepared by : Sample Report June 06, 2012 Table Of Contents IMPORTANT DISCLOSURE INFORMATION 1-9

Complete your retirement picture with guaranteed income

Complete your retirement picture with guaranteed income ANNUITIES INCOME Brighthouse Income Annuity SM Add immediate income for more certainty. All guarantees are subject to the claims-paying ability and

Complete your retirement picture with guaranteed income ANNUITIES INCOME Brighthouse Income Annuity SM Add immediate income for more certainty. All guarantees are subject to the claims-paying ability and

Retire with. Confidence. A helpful guide to retirement planning. Growing, Managing and Protecting Your Assets

Retire with Confidence A helpful guide to retirement planning Growing, Managing and Protecting Your Assets No matter what stage you are in planning, nearing or already retired there are things you can

Retire with Confidence A helpful guide to retirement planning Growing, Managing and Protecting Your Assets No matter what stage you are in planning, nearing or already retired there are things you can

Wealthcare Financial Plan

Wealthcare Financial Plan PREPARED FOR: Mr. and Mrs. Client August 09, 2014 PREPARED BY: Martin A. Smith, CRPC, AIFA President, Retirement Planning Financial Advisor 4800 Hampden Lane, Suite 200 Bethesda,

Wealthcare Financial Plan PREPARED FOR: Mr. and Mrs. Client August 09, 2014 PREPARED BY: Martin A. Smith, CRPC, AIFA President, Retirement Planning Financial Advisor 4800 Hampden Lane, Suite 200 Bethesda,

Tax-Free Retirement Strategy

Tax-Free Retirement Strategy WITH PERMANENT LIFE INSURANCE Life Insurance BEYOND the Death Benefit Helping Achieve LIFETIME Income Needs Products issued by National Life Insurance Company Life Insurance

Tax-Free Retirement Strategy WITH PERMANENT LIFE INSURANCE Life Insurance BEYOND the Death Benefit Helping Achieve LIFETIME Income Needs Products issued by National Life Insurance Company Life Insurance

Nationwide Trio Select+

Spend more time with the people who matter most and less time planning for retirement. Nationwide Trio Select+ SM Fixed Annuity Not a deposit Not FDIC or NCUSIF insured Not guaranteed by the institution

Spend more time with the people who matter most and less time planning for retirement. Nationwide Trio Select+ SM Fixed Annuity Not a deposit Not FDIC or NCUSIF insured Not guaranteed by the institution

Roth Conversion Analysis

Roth Conversion Analysis Prepared For : Stretch Smith February 11, 2010 Prepared By : Financial Consultant This information is hypothetical and is provided for informational purposes only. It is not intended

Roth Conversion Analysis Prepared For : Stretch Smith February 11, 2010 Prepared By : Financial Consultant This information is hypothetical and is provided for informational purposes only. It is not intended

Plan Data. moneytree.com Toll free

Plan Data Assumptions (p. 5-17) - Basic scenario information such as the clients retirement age and life expectancy and important planning assumptions. A majority of the items in the assumption section

Plan Data Assumptions (p. 5-17) - Basic scenario information such as the clients retirement age and life expectancy and important planning assumptions. A majority of the items in the assumption section

Managing Retirement Security with an Income Advantage

Managing Retirement Security with an Income Advantage The VantageTrust Retirement IncomeAdvantage Fund 0185372-00001-00 As a plan sponsor, you want to make sure that your employees have the tools necessary

Managing Retirement Security with an Income Advantage The VantageTrust Retirement IncomeAdvantage Fund 0185372-00001-00 As a plan sponsor, you want to make sure that your employees have the tools necessary

The Safe Money Guide. An Insider s Guide to Annuities

The Safe Money Guide retirement security investment growth An Insider s Guide to Annuities pg. 1 Copyright Retire Village 2018 An Insider s Guide to Annuities Plus Secrets the Insurance Companies don t

The Safe Money Guide retirement security investment growth An Insider s Guide to Annuities pg. 1 Copyright Retire Village 2018 An Insider s Guide to Annuities Plus Secrets the Insurance Companies don t

Tom and Jane Lundquist

Financial Goal Plan Tom and Jane Lundquist Prepared by: Joe Advisor Financial Consultant December 2, 216 Table Of Contents Expectations and Concerns 1 Summary of Goals and Resources Personal Information

Financial Goal Plan Tom and Jane Lundquist Prepared by: Joe Advisor Financial Consultant December 2, 216 Table Of Contents Expectations and Concerns 1 Summary of Goals and Resources Personal Information

Retirement Strategies for Women RETIREMENT

Retirement Strategies for Women RETIREMENT Contents Retirement Facts for Women... 1 Planning for Retirement...3 Financial Net Worth...4 Cash Flow...5 What Is Important to You?...6 10 Ways to Put Your House

Retirement Strategies for Women RETIREMENT Contents Retirement Facts for Women... 1 Planning for Retirement...3 Financial Net Worth...4 Cash Flow...5 What Is Important to You?...6 10 Ways to Put Your House

Nationwide Clear Horizon Fixed & Indexed Annuity. Spend more time with the people who matter most, and less time planning for retirement.

Spend more time with the people who matter most, and less time planning for retirement. Nationwide Clear Horizon Fixed & Indexed Annuity Not a deposit Not FDIC or NCUSIF insured Not guaranteed by the institution

Spend more time with the people who matter most, and less time planning for retirement. Nationwide Clear Horizon Fixed & Indexed Annuity Not a deposit Not FDIC or NCUSIF insured Not guaranteed by the institution

RETIREMENT PLANNING. Created by Raymond James using Ibbotson Presentation Materials 2011 Morningstar, Inc. All rights reserved. Used with permission.

RETIREMENT PLANNING Erik Melville 603 N Indian River Drive, Suite 300 Fort Pierce, FL 34950 772-460-2500 erik.melville@raymondjames.com www.melvillewealthmanagement.com Created by Raymond James using Ibbotson

RETIREMENT PLANNING Erik Melville 603 N Indian River Drive, Suite 300 Fort Pierce, FL 34950 772-460-2500 erik.melville@raymondjames.com www.melvillewealthmanagement.com Created by Raymond James using Ibbotson

Mindfulness. and investing. Tradeoffs quiz. Weather the year-end tax season. November 2016

Previous issues Are you finding the right balance between today s needs and tomorrow s goals? > Test your knowledge Mindfulness and Weather the year-end tax season These strategies could impact your income

Previous issues Are you finding the right balance between today s needs and tomorrow s goals? > Test your knowledge Mindfulness and Weather the year-end tax season These strategies could impact your income

Understanding Traditional and Roth IRAs Investor Guide

Retirement IRA Understanding Traditional and Roth IRAs Investor Guide Not FDIC Insured May Lose Value Not Bank Guaranteed Get Ready for Retirement... Your Way Forget rocking chairs and lingering sunsets.

Retirement IRA Understanding Traditional and Roth IRAs Investor Guide Not FDIC Insured May Lose Value Not Bank Guaranteed Get Ready for Retirement... Your Way Forget rocking chairs and lingering sunsets.

My retirement, March 18 April 15, Explore Compare Choose. Retirement Choice Decision Guide For Johns Hopkins University Support Staff

My retirement, Retirement Choice Decision Guide For Johns Hopkins University Support Staff March 18 April 15, 2011 Explore Compare Choose You need to make an important decision regarding your retirement

My retirement, Retirement Choice Decision Guide For Johns Hopkins University Support Staff March 18 April 15, 2011 Explore Compare Choose You need to make an important decision regarding your retirement

Annuity Customer Identification and Suitability Confirmation Worksheet

Annuity Customer Identification and Suitability Confirmation Worksheet Thank you for your interest in purchasing an annuity offered by Guggenheim Life and Annuity Company, doing business in California

Annuity Customer Identification and Suitability Confirmation Worksheet Thank you for your interest in purchasing an annuity offered by Guggenheim Life and Annuity Company, doing business in California

Case study #3. Robert establishes a plan to generate retirement income and realize a life goal. Solutions that click.

Making Retirement Case study Better #3 Solutions that click Case study #3 Robert establishes a plan to generate retirement income and realize a life goal For advisor use only. This document is not intended

Making Retirement Case study Better #3 Solutions that click Case study #3 Robert establishes a plan to generate retirement income and realize a life goal For advisor use only. This document is not intended

Build your bridge. MetLife Guaranteed Access Benefit. Transition from saving to spending with more confidence ANNUITIES PREMIUMI DEFERRED VARIABLE

GLE PREMIUMI DEFERRED ANNUITIES VARIABLE MetLife Guaranteed Access Benefit SM Build your bridge Transition from saving to spending with more confidence ISSUED BY METLIFE INSURANCE COMPANY USA AND IN NEW

GLE PREMIUMI DEFERRED ANNUITIES VARIABLE MetLife Guaranteed Access Benefit SM Build your bridge Transition from saving to spending with more confidence ISSUED BY METLIFE INSURANCE COMPANY USA AND IN NEW

Making Informed Rollover Decisions

Making Informed Rollover Decisions WHAT TO DO WITH YOUR EMPLOYER-SPONSORED RETIREMENT PLAN ASSETS DEFINED CONTRIBUTION PLANS: A defined contribution plan does not promise a specific amount of benefits

Making Informed Rollover Decisions WHAT TO DO WITH YOUR EMPLOYER-SPONSORED RETIREMENT PLAN ASSETS DEFINED CONTRIBUTION PLANS: A defined contribution plan does not promise a specific amount of benefits

Actively planning for your retirement can be one of the most important choices you'll ever make.

Retirement Planning Actively planning for your retirement can be one of the most important choices you'll ever make. Many people underestimate how much money they will need to maintain their lifestyle

Retirement Planning Actively planning for your retirement can be one of the most important choices you'll ever make. Many people underestimate how much money they will need to maintain their lifestyle

Retirement by Design. Participant Workbook. Your Name: Member SIPC

Retirement by Design Participant Workbook Your Name: www.edwardjones.com Member SIPC Welcome Retirement by Design Retirement can be a word filled with emotion excitement, fear, anticipation, uncertainty.

Retirement by Design Participant Workbook Your Name: www.edwardjones.com Member SIPC Welcome Retirement by Design Retirement can be a word filled with emotion excitement, fear, anticipation, uncertainty.

Susan & David Example

Cash Flow Analysis for Susan & David Example Asset Advisors Example, LLC A Registered Investment Advisor 2430 NW Professional Drive Corvallis, OR 97330 877-421-9815 www.moneytree.com IMPORTANT: The illustrations

Cash Flow Analysis for Susan & David Example Asset Advisors Example, LLC A Registered Investment Advisor 2430 NW Professional Drive Corvallis, OR 97330 877-421-9815 www.moneytree.com IMPORTANT: The illustrations

Financial Goal Plan. John and Jane Doe. Prepared by: William LaChance Financial Advisor

Financial Goal Plan John and Jane Doe Prepared by: William LaChance Financial Advisor December 15, 215 Table Of Contents Summary of Goals and Resources Personal Information and Summary of Financial Goals

Financial Goal Plan John and Jane Doe Prepared by: William LaChance Financial Advisor December 15, 215 Table Of Contents Summary of Goals and Resources Personal Information and Summary of Financial Goals

a roadmap for your retirement

retirement savings a roadmap for your retirement enrollment and review guide AXA Equitable Life Insurance Company (NY, NY) Enrollment and Review Guide This guide, in conjunction with other enrollment materials,

retirement savings a roadmap for your retirement enrollment and review guide AXA Equitable Life Insurance Company (NY, NY) Enrollment and Review Guide This guide, in conjunction with other enrollment materials,

Planning ahead. Understanding your 403(b) plan. Plan Participant Guide RETIREMENT PLAN SERVICES

plan. Plan Participant Guide RETIREMENT PLAN SERVICES") Planning ahead Understanding your 403(b) plan The Lincoln National Life Insurance Company Lincoln Life & Annuity Company of New York Plan Participant Guide RETIREMENT PLAN SERVICES 2073285 It all starts

Planning ahead Understanding your 403(b) plan The Lincoln National Life Insurance Company Lincoln Life & Annuity Company of New York Plan Participant Guide RETIREMENT PLAN SERVICES 2073285 It all starts

Finding the Perfect Match

Finding the Perfect Match A Financial Professional s Guide for Client Suitability This material is provided by Athene Annuity and Life Company headquartered in West Des Moines, Iowa, which issues annuities

Finding the Perfect Match A Financial Professional s Guide for Client Suitability This material is provided by Athene Annuity and Life Company headquartered in West Des Moines, Iowa, which issues annuities

SURVIVOR SUPPLEMENTAL RETIREMENT INCOME FUNDED WITH LIFE INSURANCE. Presented for Valued Client

Presented for Valued Client Presented by John M. Webster HMS Insurance Associates, Inc. johnwebster@financialguide.com 443-632-3436 Page 1 of 8 The Purpose Survivor supplemental retirement income funded

Presented for Valued Client Presented by John M. Webster HMS Insurance Associates, Inc. johnwebster@financialguide.com 443-632-3436 Page 1 of 8 The Purpose Survivor supplemental retirement income funded

INSIDE THIS ISSUE. When Is It a Good Time to Sell Investments (p. 1)

") INSIDE THIS ISSUE When Is It a Good Time to Sell Investments (p. 1) Required Minimum Distribution A Primer (p. 4) Equalize Inheritances with Life Insurance (p. 6) Municipals Under the Microscope (p. 7)

INSIDE THIS ISSUE When Is It a Good Time to Sell Investments (p. 1) Required Minimum Distribution A Primer (p. 4) Equalize Inheritances with Life Insurance (p. 6) Municipals Under the Microscope (p. 7)

Ameritas Accumulation 7 Index Annuity. Issued by Ameritas Life Insurance Corp. AN

Ameritas Accumulation 7 Index Annuity Issued by Ameritas Life Insurance Corp. AN 508-9 Helping grow your assets with protection 73% of retirees who own an annuity feel they are able to live the lifestyle

Ameritas Accumulation 7 Index Annuity Issued by Ameritas Life Insurance Corp. AN 508-9 Helping grow your assets with protection 73% of retirees who own an annuity feel they are able to live the lifestyle

Planning for Income to Last

Planning for Income to Last Retirement Income Planning Not FDIC Insured May Lose Value No Bank Guarantee This guide explains why you should consider developing a retirement income plan. It also discusses

Planning for Income to Last Retirement Income Planning Not FDIC Insured May Lose Value No Bank Guarantee This guide explains why you should consider developing a retirement income plan. It also discusses

Allen & Betty Abbett. Personal Investment Analysis. Sample Financial Plan - TOTAL Goal-Based Planning

Mar 29, 2018 Personal Investment Analysis Allen & Betty Abbett John Smith Asset Advisors Example, LLC A Registered Investment Advisor 2430 NW Professional Drive Corvallis, OR 97330 877-421-9815 www.moneytree.com

Mar 29, 2018 Personal Investment Analysis Allen & Betty Abbett John Smith Asset Advisors Example, LLC A Registered Investment Advisor 2430 NW Professional Drive Corvallis, OR 97330 877-421-9815 www.moneytree.com

MEMBERS Horizon Annuity: New Possibilities for Diversified Investing

MEMBERS Horizon Annuity: New Possibilities for Diversified Investing MHA-1724847(CM) FOR REGISTERED REPRESENTATIVE USE ONLY. NOT FOR USE BY THE GENERAL PUBLIC. 2-0618-0720 2018 CUNA Mutual Group MEMBERS

MEMBERS Horizon Annuity: New Possibilities for Diversified Investing MHA-1724847(CM) FOR REGISTERED REPRESENTATIVE USE ONLY. NOT FOR USE BY THE GENERAL PUBLIC. 2-0618-0720 2018 CUNA Mutual Group MEMBERS

FINE-TUNE YOUR RETIREMENT WITHDRAWAL STRATEGY

FINE-TUNE YOUR RETIREMENT WITHDRAWAL STRATEGY To increase the likelihood your retire- ment savings will last your lifetime, it s critical to prepare ment withdrawal a sustainable strategy. Take retiretime

FINE-TUNE YOUR RETIREMENT WITHDRAWAL STRATEGY To increase the likelihood your retire- ment savings will last your lifetime, it s critical to prepare ment withdrawal a sustainable strategy. Take retiretime

SecureLiving Income Provider

Single Premium Immediate Annuity I SecureLiving Series SecureLiving Income Provider Do what you love. Issued by Genworth Life Insurance Company & Genworth Life and Annuity Insurance Company 130800 08/22/13

Single Premium Immediate Annuity I SecureLiving Series SecureLiving Income Provider Do what you love. Issued by Genworth Life Insurance Company & Genworth Life and Annuity Insurance Company 130800 08/22/13

Lincoln InvestmentSolutions SM

Lincoln InvestmentSolutions SM RIA variable annuity With options for guaranteed growth and income LINCOLN ANNUITIES Not a deposit Not FDIC-insured May go down in value Not insured by any federal government

Lincoln InvestmentSolutions SM RIA variable annuity With options for guaranteed growth and income LINCOLN ANNUITIES Not a deposit Not FDIC-insured May go down in value Not insured by any federal government

Are You Paying Avoidable Taxes on Your Social Security Benefits?

Are You Paying Avoidable Taxes on Your Social Security Benefits? The information provided here has been taken from third party sources and is deemed to be reliable, but is not guaranteed. It is believed

Are You Paying Avoidable Taxes on Your Social Security Benefits? The information provided here has been taken from third party sources and is deemed to be reliable, but is not guaranteed. It is believed

RETIREMENT INCOME STRATEGY PROPOSAL

123 Main Street Phoenix, AZ 85021 Retirement Plan October-09 Presented By: Valued Producer PFG Marketing Group, Inc. 2240 W. Mission Lane, Suite 11 Phoenix, AZ 85021 Telephone: (602) 944-2220 E-Mail: pfginfo@pfg-inc.com

123 Main Street Phoenix, AZ 85021 Retirement Plan October-09 Presented By: Valued Producer PFG Marketing Group, Inc. 2240 W. Mission Lane, Suite 11 Phoenix, AZ 85021 Telephone: (602) 944-2220 E-Mail: pfginfo@pfg-inc.com

Future PREPARING FOR THE INTRODUCING YOUR UNIVERSITY OF MANITOBA PENSION PLAN (1993) What is inside. May 2012

What is inside. May 2012") May 2012 PREPARING FOR THE Future INTRODUCING YOUR UNIVERSITY OF MANITOBA PENSION PLAN (1993) What is inside Your Pension at a Glance...2 Welcome to Your Plan...3 Joining the Plan...4 Contributions...5

May 2012 PREPARING FOR THE Future INTRODUCING YOUR UNIVERSITY OF MANITOBA PENSION PLAN (1993) What is inside Your Pension at a Glance...2 Welcome to Your Plan...3 Joining the Plan...4 Contributions...5

HIGHLIGHTS OF THE ROTH 401(k) Provision

Provision") HIGHLIGHTS OF THE ROTH 401(k) Provision What Is It? The is a new feature available for 401(k) plans that has generated recent attention from the press. Newly effective in 2006, a 401(k) plan may now permit

HIGHLIGHTS OF THE ROTH 401(k) Provision What Is It? The is a new feature available for 401(k) plans that has generated recent attention from the press. Newly effective in 2006, a 401(k) plan may now permit

Put your retirement savings to work for your future.

Put your retirement savings to work for your future. P H O E N I X P E R S O N A L R E T I R E M E N T C H O I C E SM A single-premium fixed indexed annuity with an optional Guaranteed Lifetime Income

Put your retirement savings to work for your future. P H O E N I X P E R S O N A L R E T I R E M E N T C H O I C E SM A single-premium fixed indexed annuity with an optional Guaranteed Lifetime Income

MULTI-GENERATIONAL DISTRIBUTION OPTION CREATING A FINANCIAL FUTURE. 9061Z REV 07-12

MULTI-GENERATIONAL DISTRIBUTION OPTION CREATING A FINANCIAL FUTURE. 9061Z REV 07-12 Multi-Generational Distribution Option Many people spend much of their working life building their retirement savings

MULTI-GENERATIONAL DISTRIBUTION OPTION CREATING A FINANCIAL FUTURE. 9061Z REV 07-12 Multi-Generational Distribution Option Many people spend much of their working life building their retirement savings

A GUIDE TO PREPARING FOR RETIREMENT

A GUIDE TO PREPARING FOR RETIREMENT MaineSaves A Guide to Preparing for Retirement MaineSaves, the State of Maine s voluntary retirement savings plan, is designed to help you move forward on your journey

A GUIDE TO PREPARING FOR RETIREMENT MaineSaves A Guide to Preparing for Retirement MaineSaves, the State of Maine s voluntary retirement savings plan, is designed to help you move forward on your journey

Tax strategies for higher-income taxpayers

Tax strategies for higher-income taxpayers This overview summarizes some of the key areas that you and your tax advisor should assess. Your Financial Advisor can assist in evaluating investment decisions

Tax strategies for higher-income taxpayers This overview summarizes some of the key areas that you and your tax advisor should assess. Your Financial Advisor can assist in evaluating investment decisions

MENTOR PROGRAM. The Circle of Wealth System Client Process. (321)

") The Circle of Wealth System Client Process MENTOR PROGRAM SESSION 3 Workbook We are in a belief changing business. Two things will differentiate you from other advisors - what you know & what you can communicate.

The Circle of Wealth System Client Process MENTOR PROGRAM SESSION 3 Workbook We are in a belief changing business. Two things will differentiate you from other advisors - what you know & what you can communicate.

Lifetime Withdrawal GuaranteeSM

Lifetime Withdrawal GuaranteeSM ANNUITIES VARIABLE Brighthouse Prime Options SM Variable Annuity Annuities are issued by Brighthouse Life Insurance Company. Guarantees are subject to the financial strength

Lifetime Withdrawal GuaranteeSM ANNUITIES VARIABLE Brighthouse Prime Options SM Variable Annuity Annuities are issued by Brighthouse Life Insurance Company. Guarantees are subject to the financial strength

Individuals guide to a governmental 457(b) deferred compensation plan

deferred compensation plan") Individuals guide to a governmental 457(b) deferred compensation plan Making informed decisions today and acting on them may make all the difference to individuals future. With individuals employer s 457(b),

Individuals guide to a governmental 457(b) deferred compensation plan Making informed decisions today and acting on them may make all the difference to individuals future. With individuals employer s 457(b),

REPORT PREPARED FOR Client Sample & Co-client Sample

REPORT PREPARED FOR Client Sample & Co-client Sample by Steve Harvey Steve Harvey LLC Generated on 01/30/2019 Steve Harvey 119 Oronoco Street, Suite 102 Alexandria, Virginia 22314 steve@steveharveyllc.com

REPORT PREPARED FOR Client Sample & Co-client Sample by Steve Harvey Steve Harvey LLC Generated on 01/30/2019 Steve Harvey 119 Oronoco Street, Suite 102 Alexandria, Virginia 22314 steve@steveharveyllc.com

Receiving Required Minimum Distributions. Making it simple with TIAA

Receiving Required Minimum Distributions Making it simple with TIAA Required Minimum Distributions what you need to know What are Required Minimum Distributions? 1 How can you receive minimum distributions

Receiving Required Minimum Distributions Making it simple with TIAA Required Minimum Distributions what you need to know What are Required Minimum Distributions? 1 How can you receive minimum distributions

Plan today for tomorrow s destination.

VARIABLE ANNUITY GUIDE Plan today for tomorrow s destination. Waddell & Reed Advisors Select Preferred AnnuitySM 2.0 Waddell & Reed Advisors Select Preferred Annuity 2.0 & SM Waddell & Reed Advisors Select

VARIABLE ANNUITY GUIDE Plan today for tomorrow s destination. Waddell & Reed Advisors Select Preferred AnnuitySM 2.0 Waddell & Reed Advisors Select Preferred Annuity 2.0 & SM Waddell & Reed Advisors Select

Target Income 10. Fixed Index Annuity Plan for your retirement lifestyle. Issued by Delaware Life Insurance Company

Target Income 10 Fixed Index Annuity Plan for your retirement lifestyle Issued by Delaware Life Insurance Company The Retirement Planning Challenge: Creating Income That Lasts Retirement will likely be

Target Income 10 Fixed Index Annuity Plan for your retirement lifestyle Issued by Delaware Life Insurance Company The Retirement Planning Challenge: Creating Income That Lasts Retirement will likely be

a 457(b) plan can help me save enough to retire

plan can help me save enough to retire") retirement plan a 457(b) plan can help me save enough to retire EQUI-VEST Strategies sm series 900 and 901 group variable deferred annuity for 457(b) EDC plans Variable Annuities: Are Not a Deposit of

retirement plan a 457(b) plan can help me save enough to retire EQUI-VEST Strategies sm series 900 and 901 group variable deferred annuity for 457(b) EDC plans Variable Annuities: Are Not a Deposit of