Pension Session. California Society of Municipal Analysts Presenters: David A. Vaudt, GASB Chair Chuck Reed, Retirement Security Initiative

|

|

|

- Christina Thompson

- 5 years ago

- Views:

Transcription

1 Pension Session California Society of Municipal Analysts Presenters: David A. Vaudt, GASB Chair Chuck Reed, Retirement Security Initiative Moderator: Les Richmond, VP & Actuary, BAM November 3, 2016!

2 Agenda Today s public-sector pension funding landscape Current and Upcoming GASB Statements Pension Reform 2

3 Today s Public-Sector Pension Funding Landscape U.S. public pensions face historically large unfunded liabilities Current underfunding has been driven by multiple intersecting trends, including: Poor investment performance Insufficient contributions Demographic trends Benefit enhancements High expenses Estimates for the total unfunded liability vary widely, from $1 trillion to more than $4 trillion, with updated views ranging up to $6 trillion Wide range of outcomes is primarily due to the choice of investment return assumptions With unfunded liabilities historically large, actuarially determined contribution requirements far exceed those of the past and are causing unprecedented budget strains 3

4 Fiscal 2014: The Eye of the Storm Funding Ratios Benefitted From Market Gains California Pensions Follow Similar Pattern Source: Public Fund Survey March

5 Today s Public-Sector Pension Funding Landscape Asset allocations are shifting to boost returns, and in doing so are increasing risk California state pension systems taking steps to reduce risk 5

6 Today s Public-Sector Pension Funding Landscape Plan demographics are becoming less favorable for change California pension plan demographics follow similar pattern 6

7 Retirement Systems in California CalPERS CalSTRS University of California Retirement Plan (UCRP) 57 local retirement funds, including large cities like Los Angeles, San Francisco, and San Diego Nearly all the California credits we consider at BAM participate in CalPERS and/or CalSTRS, so the remainder of this discussion will focus on them 7

8 CalPERS: Funding Employers are required to fund 100% of the actuarially determined contribution Cost-sharing vs. agent multiple employer plans Local employer can terminate its contract with CalPERS by paying CalPERS difference between MVA and termination liability. For example, Citrus Pest Control District No. 2 of Riverside County Miscellaneous at 6/30/13: Plan funding 7.5%: $1.418 million Market value of assets: $1.993 million Hypothetical termination 3.72%: $2.191 million Cost of termination: $0.198 million (note: at 6/30/12, when interest rate was 2.98%, the bill would have been $0.541 million) 3.72% is yield on 30-year Treasury STRIPs at 6/30/13 8

9 CalPERS: Funding PERF only (excludes legislators and judges): Recent unfunded actuarial accrued liabilities and funded ratios ($ millions) 140, % 120, % 100,000 80, % 60, % UAAL (MVA) Funded RaIo (MVA) 40,000 20, % - (20,000) % 0.0% 9

10 CalPERS: Funding PERF only (excludes legislators and judges): Recent employer and member contribution history 16,000.0 Contribu.on History 14, , ,000.0 $ millions 8, ,000.0 Employer ContribuIons Member ContribuIons 4, ,

11 CalPERS: A Whole Lot of Attitude and Risk CalPERS is a fiduciary charged with protecting the interests of its members and upholding the laws of the State of California In that capacity, it strenuously defends benefit levels for members, and contribution requirements Deep pockets to carry out its mission No sympathy for participating employers struggling to pay their bills Risk that pension bills may become too burdensome: No flexibility around paying 100% of the ARC Events, such as another financial downturn, could increase already high contributions Fixed amortization periods, while preferable actuarially, may lead to sharply increasing contributions More San Bernardinos? 11

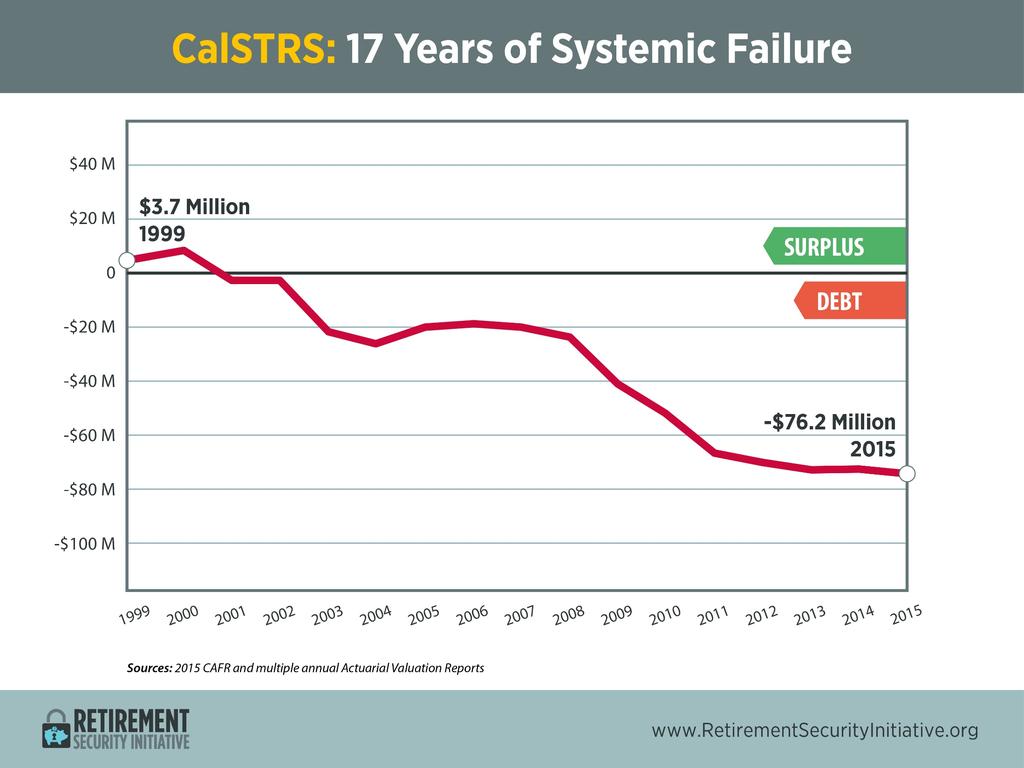

12 CalSTRS: Funding Cost-sharing multiple employer plan Responsibility for contributing to CalSTRS is shared by the State, the employers and the members In FYE 6/30/13, contributions expressed as a percentage of employer payroll were State (about 5.2%), employer (8.25%) and members (8.0%) Contributions as a percentage of payroll are legislated and are not actuarially determined In its 6/30/13 CAFR, CalSTRS stated that if funding continued on its current path, the fund would be depleted in about 30 years AB 1469: beginning 7/1/14, gradually raises employer contributions to 19.1% of payroll in FY 2021, and State contribution rate rises to 8.828% by FY 2017,with limited authority for CalSTRS Board to raise rates further if necessary to keep funding plan on track to eliminate 7/1/14 unfunded liability by

13 CalSTRS: Funding Recent unfunded actuarial accrued liabilities and funded ratios ($ millions) Funded History 80, % 70, % 60,000 50, % 40,000 30,000 20, % 40.0% UAAL (MVA) Funded RaIo (MVA) 10, % % 13

14 CalSTRS: Funding Recent employer and State contribution history Contribu.on History 9,000 70% 8,000 60% 7,000 50% 6,000 $ millions 5,000 4,000 40% 30% ShorQall State ContribuIons Employer ContribuIons Percentage of ARC Contributed 3,000 20% 2,000 1,000 10% % 14

15 CalSTRS: Risks Further revisions to funding schedule may be needed in light of subpar asset performance in FY 15 and 16 Shift of contribution costs to districts BAM analysis of California school districts assumes that the state continues at its current share of overall contributions Based on this assumption, typical metrics based on BAM adjustments are typically manageable Reducing state share could significantly increase pension metrics into the unacceptable range, though some might argue that state aid would increase as well 15

16 New GASB Pension Standards Statement 67: Financial Reporting for Pension Plans, effective for Plan fiscal years beginning after June 15, 2013 Statement 68: Accounting and Reporting for (Employer) Pensions, effective for Employer fiscal years beginning after June 15, 2014 Intended to enhance comparability and transparency of financial statements New rules standardize many calculations and balance sheet treatment of pension plans However, issuers will retain flexibility in setting investment return assumptions, so financial statements will still lack comparability Similar OPEB standards are on the way (Statements 74 and 75, effective for fiscal years beginning after 6/15/16 and 6/15/17, respectively) Impact on BAM pension analysis: increase to both accuracy and comparability 16

17 2016 Fall Conference California Society of Municipal Analysts Pension Panel David A. Vaudt GASB Chair The views expressed in this presentation are those of Mr. Vaudt. Official positions of the GASB on accounting and financial reporting matters are determined only after extensive due process and deliberation. Copyright 2016 by Financial Accounting Foundation, Norwalk, CT Copyright 2016 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

18 GASB Postemployment Benefit Standards What: significantly revises postretirement accounting & financial reporting standards. Why: review of effectiveness found significant room for improvement When: Pensions issued in Plans fiscal years ending June 30, 2014 & later - Employers fiscal years ending June 30, 2015 & later OPEB issued in Plans fiscal years ending June 30, 2017 & later - Employers fiscal years ending June 30, 2018 & later 2 Copyright 2016 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

19 Fundamentals of the New Postemployment Benefit Standards Views the cost within the context of an ongoing, career-long employment relationship Uses an accounting-based versus funding-based approach to measure/report any net pension or OPEB liability on the statement of net position Means policy makers must work with their actuaries to determine the proper level of funding accounting standards do not provide funding answers Allows an evaluation of the extent to which promises have been funded 3 Copyright 2016 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

20 Postemployment Benefit Standards - The Big Changes Portion of the total liability not covered by plan assets will be recognized as a liability on the face of the financial statements the net pension or OPEB liability. Cost-sharing plans participating employers/nonemployer contributing entities report proportional share of the collective net pension or OPEB liability Discounting at the long-term expected rate of return is limited to the extent that assets are expected to be available to cover future benefit payments remainder discounted at the municipal bond rate Now only one actuarial valuation approach permitted (entry age, as a level percentage of payroll) 4 Copyright 2016 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

21 Postemployment Benefit Standards - The Big Changes Asset smoothing is eliminated from the measurement of the liability Amortization is eliminated for most changes in the liability and greatly shortened for others More robust note disclosures Much more extensive required supplementary information (RSI) schedules 5 Copyright 2016 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

22 Key Information in the Financial Statements Liabilities to the pension plan (payables) Liabilities to employees for pensions - Net pension liability (NPL) = total pension liability (TPL), net of pension plan s fiduciary net position - Cost-sharing employers recognize proportionate shares of collective NPL Changes in NPL - Recognized as expense immediately: service cost, interest on the TPL, changes in benefit terms, projected investment earnings - Recognized as expense over time: changes in assumptions, difference between assumed and actual demographic and economic factors, and difference between projected and actual investment earnings 6 Copyright 2016 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

23 Key Note Disclosures Discount rate information, including: - Long-term expected rate of return and how it was determined - Assumed asset allocation of the pension plan s portfolio and the long-term expected real rate of return for each major asset class - NPL measured at a discount rate 1 percentage point higher and 1 percentage point lower: 1% Decrease (6.75%) Discount Rate (7.75%) 1% Increase (8.75%) County's net pension liability $826,928 $751,753 $661,543 7 Copyright 2016 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

24 New RSI: NPL Components and Ratios Note: Only 5 years are presented here; 10 years of information will be required 8 Copyright 2016 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

25 New RSI: Contributions Note: Only 5 years are presented here; 10 years of information will be required 9 Copyright 2016 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

26 Fundamentals of the New Postemployment Benefit Standards The actuarially required contribution (ARC) has not disappeared, it is the actuarially determined contribution (ADC) it will continue to be the basis for determining funding policy for many governments It is no longer the basis for calculating expense for accounting and financial reporting purposes Be cautious regarding the ARC/ADC Consider the relevance of the ARC/ADC for a cost-sharing employer 10 Copyright 2016 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

27 GASB Resources for Analysts Variety of resources at Technical inquiry hotline New edition of the User Guide for Analysts coming soon Specially tailored sessions designed specifically for municipal analysts led by the GASB Research Manager 11 Copyright 2016 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

28 Overview of Sessions for Analysts Basic pension terminology How a pension obligation is measured Examples of how the pension liability and other pension information are being reported 12 Copyright 2016 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

29

30 RSI Reform Principles Retirement should be safe and secure Benefits and costs should be fair, sustainable and predictable Benefits should be funded as they are earned; incentives to underfund commitments should be eliminated Unfunded liabilities should be paid down Management should be open, transparent and non-political No single solution will work everywhere

31

32

33

34

35 States: Current and Required Pension, OPEB and Interest Payments as a Percentage of Own-Source Revenue, 2014 An Overview of the Pension/OPEB Landscape, Alicia H. Munnell & Jean-Pierre Aubry. July Data based on various FY 2014 plan and government financial reports and actuarial valuapons; U.S. Census Bureau (2014).

36 Large Coun/es: Current and Required Pension; OPEB and Interest Payments as a Percentage of Own-Source Revenue, 2014 An Overview of the Pension/OPEB Landscape, Alicia H. Munnell & Jean-Pierre Aubry. July Data based on various FY 2014 plan and government financial reports and actuarial valuapons; U.S. Census Bureau (2014).

37 Large Ci/es: Current and Required Pension; OPEB and Interest Payments as a Percentage of Own-Source Revenue, 2014 An Overview of the Pension/OPEB Landscape, Alicia H. Munnell & Jean-Pierre Aubry. July Data based on various FY 2014 plan and government financial reports and actuarial valuapons; U.S. Census Bureau (2014).

38 Learn more at: RePrementSecurityIniPaPve.org

Council of State Governments Alan Conroy GASB Overview & Update

Council of State Governments Alan Conroy GASB Overview & Update The views expressed in this presentation are those of Mr. Conroy. Official positions of the GASB on accounting matters are determined only

Council of State Governments Alan Conroy GASB Overview & Update The views expressed in this presentation are those of Mr. Conroy. Official positions of the GASB on accounting matters are determined only

May 16, 2016 National Conference on Public Employee Retirement Systems

May 16, 2016 National Conference on Public Employee Retirement Systems GASB Update: What NCPERS Members Need to Know David A. Vaudt GASB Chair The views expressed in this presentation are those of Mr.

May 16, 2016 National Conference on Public Employee Retirement Systems GASB Update: What NCPERS Members Need to Know David A. Vaudt GASB Chair The views expressed in this presentation are those of Mr.

Overview: GASB Statement 68 on Pensions

Overview: GASB Statement 68 on Pensions Michelle Czerkawski, GASB Project Manager The views expressed in this presentation are those of Ms. Czerkawski. Official positions of the Governmental Accounting

Overview: GASB Statement 68 on Pensions Michelle Czerkawski, GASB Project Manager The views expressed in this presentation are those of Ms. Czerkawski. Official positions of the Governmental Accounting

Accounting for the OPEB Obligation

Accounting for the OPEB Obligation Tom Swain, F.S.A. August 18, 2016 Agenda Overview and effective dates Significant changes Sample balance sheet pre/post changes Plan sponsor implications Planning steps

Accounting for the OPEB Obligation Tom Swain, F.S.A. August 18, 2016 Agenda Overview and effective dates Significant changes Sample balance sheet pre/post changes Plan sponsor implications Planning steps

INFORMATION SESSION Cd, 5/15/E

INFORMATION SESSION 1 50-923Cd, 5/15/E Background What is GASB 68? Governmental Accounting Standards Board (GASB) approved new rules that will affect employers Employers must include the following in their

INFORMATION SESSION 1 50-923Cd, 5/15/E Background What is GASB 68? Governmental Accounting Standards Board (GASB) approved new rules that will affect employers Employers must include the following in their

CITY OF CONCORD JUNE 30, 2016 REQUIRED SUPPLEMENTARY INFORMATION

90 SCHEDULE OF FUNDING PROGRESS The tables below shows a three-year analysis of the actuarial value of assets as a percentage of the actuarial accrued liability and the unfunded actuarial liability as

90 SCHEDULE OF FUNDING PROGRESS The tables below shows a three-year analysis of the actuarial value of assets as a percentage of the actuarial accrued liability and the unfunded actuarial liability as

REQUIRED SUPPLEMENTARY INFORMATION

REQUIRED SUPPLEMENTARY INFORMATION DW SCHEDULE OF CHANGES IN NET PENSION LIABILITY AND RELATED RATIOS DURING THE MEASUREMENT PERIOD County Miscellaneous, Agent Multiple Employer Plan Measurement Period

REQUIRED SUPPLEMENTARY INFORMATION DW SCHEDULE OF CHANGES IN NET PENSION LIABILITY AND RELATED RATIOS DURING THE MEASUREMENT PERIOD County Miscellaneous, Agent Multiple Employer Plan Measurement Period

GASB Pension Accounting Standards

GASB Pension Accounting Standards Michelle Czerkawski, Senior Project Manager Governmental Accounting Standards Board The views expressed in this presentation are those of Ms. Czerkawski. Official positions

GASB Pension Accounting Standards Michelle Czerkawski, Senior Project Manager Governmental Accounting Standards Board The views expressed in this presentation are those of Ms. Czerkawski. Official positions

CITY OF CONCORD JUNE 30, 2015 REQUIRED SUPPLEMENTARY INFORMATION

91 SCHEDULE OF FUNDING PROGRESS The tables below shows a three-year analysis of the actuarial value of assets as a percentage of the actuarial accrued liability and the unfunded actuarial liability as

91 SCHEDULE OF FUNDING PROGRESS The tables below shows a three-year analysis of the actuarial value of assets as a percentage of the actuarial accrued liability and the unfunded actuarial liability as

MEMORANDUM. CAFR Changes

MEMORANDUM DATE: February 2, 2015 TO: Members of the Board of Retirement FROM: Brenda Shott, Assistant CEO, Finance and Internal Operations SUBJECT: GASB 67/68 Update Recommendation: Receive and file.

MEMORANDUM DATE: February 2, 2015 TO: Members of the Board of Retirement FROM: Brenda Shott, Assistant CEO, Finance and Internal Operations SUBJECT: GASB 67/68 Update Recommendation: Receive and file.

Impacts of GASB 74/75 on CalSTRS and Employers. Presented on July 13, 2017

Impacts of GASB 74/75 on CalSTRS and Employers Presented on July 13, 2017 GASB Implementation Effective for CalSTRS FY 2016-17 Statement 74, Financial Reporting for Postemployment Benefit Plans Other Than

Impacts of GASB 74/75 on CalSTRS and Employers Presented on July 13, 2017 GASB Implementation Effective for CalSTRS FY 2016-17 Statement 74, Financial Reporting for Postemployment Benefit Plans Other Than

GASB 67 and 68 The New World of Public Pension Plan Accounting

GASB 67 and 68 The New World of Public Pension Plan Accounting Presented by Mark Olleman, FSA, EA, MAAA Daniel Wade, FSA, EA, MAAA TERS Retirement Board Meeting October 10, 2013 Agenda Timing Notable Issues

GASB 67 and 68 The New World of Public Pension Plan Accounting Presented by Mark Olleman, FSA, EA, MAAA Daniel Wade, FSA, EA, MAAA TERS Retirement Board Meeting October 10, 2013 Agenda Timing Notable Issues

OPEB Reporting Overview: Implications of the Choice to Fund or Not Fund

OPEB Reporting Overview: Implications of the Choice to Fund or Not Fund Dean Michael Mead Research Manager, Governmental Accounting Standards Board March 12, 2008 Disclaimer: The opinions expressed in

OPEB Reporting Overview: Implications of the Choice to Fund or Not Fund Dean Michael Mead Research Manager, Governmental Accounting Standards Board March 12, 2008 Disclaimer: The opinions expressed in

GASB 75 Overview. Presented by Josh Harner, WVDE School of Finance. GASB Statement No. 75

GASB 75 Overview Presented by Josh Harner, WVDE School of Finance GASB Statement No. 75 Accounting and Financial Reporting for Postemployment Benefits Other Than Pensions 2 1 General Information Objective

GASB 75 Overview Presented by Josh Harner, WVDE School of Finance GASB Statement No. 75 Accounting and Financial Reporting for Postemployment Benefits Other Than Pensions 2 1 General Information Objective

Upcoming Changes to Pension Reporting Under GASB 67 & 68 and the Impact to Municipalities Participating in PERA Retirement Plans

Upcoming Changes to Pension Reporting Under GASB 67 & 68 and the Impact to Municipalities Participating in PERA Retirement Plans Patricia (Patty) French, Board Chair, PERA Wayne Propst, Executive Director,

Upcoming Changes to Pension Reporting Under GASB 67 & 68 and the Impact to Municipalities Participating in PERA Retirement Plans Patricia (Patty) French, Board Chair, PERA Wayne Propst, Executive Director,

Other Postemployment Benefits (OPEB)

") Other Postemployment Benefits (OPEB) A Webinar for Users of State & Local Government Financial Information Scott Reeser, Project Manager Emily Clark, Project Research Associate Dean Mead, Research Manager

Other Postemployment Benefits (OPEB) A Webinar for Users of State & Local Government Financial Information Scott Reeser, Project Manager Emily Clark, Project Research Associate Dean Mead, Research Manager

REQUIRED SUPPLEMENTARY INFORMATION

REQUIRED SUPPLEMENTARY INFORMATION DC SCHEDULE OF CHANGES IN NET PENSION LIABILITY AND RELATED RATIOS DURING THE MEASUREMENT PERIOD Agent Multiple Employer Plan Measurement Period 2014-15 (1) 2013-14

REQUIRED SUPPLEMENTARY INFORMATION DC SCHEDULE OF CHANGES IN NET PENSION LIABILITY AND RELATED RATIOS DURING THE MEASUREMENT PERIOD Agent Multiple Employer Plan Measurement Period 2014-15 (1) 2013-14

Understanding GASB 74 and 75. Graham A. Schmidt, ASA, EA, FCA, MAAA Cheiron Anne Harper, FSA, EA, MAAA Cheiron

Understanding GASB 74 and 75 Graham A. Schmidt, ASA, EA, FCA, MAAA Cheiron Anne Harper, FSA, EA, MAAA Cheiron Background GASB Statements 67 and 68 issued in June 2012 Most retirement systems have reported

Understanding GASB 74 and 75 Graham A. Schmidt, ASA, EA, FCA, MAAA Cheiron Anne Harper, FSA, EA, MAAA Cheiron Background GASB Statements 67 and 68 issued in June 2012 Most retirement systems have reported

Minnesota Legislative Commission on Pensions and Retirement

Minnesota Legislative Commission on Pensions and Retirement January 31, 2017 Michael de Leon, FCA, ASA, EA, MAAA Judy Stromback, FSA, FCA, EA, MAAA Agenda Role of LCPR s Consulting Actuary Actuarial Valuation

Minnesota Legislative Commission on Pensions and Retirement January 31, 2017 Michael de Leon, FCA, ASA, EA, MAAA Judy Stromback, FSA, FCA, EA, MAAA Agenda Role of LCPR s Consulting Actuary Actuarial Valuation

WESTERN MUNICIPAL WATER DISTRICT RETIREMENT MEDICAL BENEFITS PLAN (OTHER POST EMPLOYMENT BENEFIT PLAN) FINANCIAL STATEMENTS

FINANCIAL STATEMENTS") WESTERN MUNICIPAL WATER DISTRICT RETIREMENT MEDICAL BENEFITS PLAN (OTHER POST EMPLOYMENT BENEFIT PLAN) FINANCIAL STATEMENTS WITH REPORT ON AUDIT BY INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS FOR THE FISCAL

WESTERN MUNICIPAL WATER DISTRICT RETIREMENT MEDICAL BENEFITS PLAN (OTHER POST EMPLOYMENT BENEFIT PLAN) FINANCIAL STATEMENTS WITH REPORT ON AUDIT BY INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS FOR THE FISCAL

Georgia Municipal Association Pre-Convention Workshop: Big Changes Coming to Retirement Plans

Georgia Municipal Association Pre-Convention Workshop: Big Changes Coming to Retirement Plans June 21, 2013 Leon F. (Rocky) Joyner, Jr. GMEBS Actuary Copyright 2013 by The Segal Group, Inc., parent of

Georgia Municipal Association Pre-Convention Workshop: Big Changes Coming to Retirement Plans June 21, 2013 Leon F. (Rocky) Joyner, Jr. GMEBS Actuary Copyright 2013 by The Segal Group, Inc., parent of

OPEB FUNDING POLICY DISCUSSION RON BAKER, CHIEF ADMINISTRATIVE OFFICER KOREN HOLDEN, SENIOR PROJECT MANAGER NOVEMBER 17, 2017

OPEB FUNDING POLICY DISCUSSION RON BAKER, CHIEF ADMINISTRATIVE OFFICER KOREN HOLDEN, SENIOR PROJECT MANAGER NOVEMBER 17, 2017 Agenda» Why now? Reasons for PERA Other Postemployment Benefits (OPEB) Funding

OPEB FUNDING POLICY DISCUSSION RON BAKER, CHIEF ADMINISTRATIVE OFFICER KOREN HOLDEN, SENIOR PROJECT MANAGER NOVEMBER 17, 2017 Agenda» Why now? Reasons for PERA Other Postemployment Benefits (OPEB) Funding

2015 MASBO Fall Conference GASB 73, 74 and 75 Postemployment Benefits Other Than Pensions An Actuarial Perspective.

2015 MASBO Fall Conference GASB 73, 74 and 75 Postemployment Benefits Other Than Pensions An Actuarial Perspective November 13, 2015 2015 MASBO Fall Conference This presentation was prepared for the 2015

2015 MASBO Fall Conference GASB 73, 74 and 75 Postemployment Benefits Other Than Pensions An Actuarial Perspective November 13, 2015 2015 MASBO Fall Conference This presentation was prepared for the 2015

1.02 TRINITY COUNTY. County Contract No. Board Item Request Form Department Personnel. Contact Carol Martin

County Contract No. Department Personnel TRINITY COUNTY 1.02 Board Item Request Form 2016-09-20 Contact Carol Martin Phone 530-623-1325 Requested Agenda Location Presentations Requested Board Action: Receive

County Contract No. Department Personnel TRINITY COUNTY 1.02 Board Item Request Form 2016-09-20 Contact Carol Martin Phone 530-623-1325 Requested Agenda Location Presentations Requested Board Action: Receive

Staff Report for the Regular Meeting of the Board of Directors March 8, 2017

Nevada Irrigation District Staff Report for the Regular Meeting of the Board of Directors March 8, 2017 TO: FROM: Board of Directors Marvin Davis, MBA, CPA, Finance Manager/Treasurer DATE: March 1, 2017

Nevada Irrigation District Staff Report for the Regular Meeting of the Board of Directors March 8, 2017 TO: FROM: Board of Directors Marvin Davis, MBA, CPA, Finance Manager/Treasurer DATE: March 1, 2017

How Big A Burden Are State and Local OPEB Benefits?

How Big A Burden Are State and Local OPEB Benefits? By Alicia H. Munnell, Jean-Pierre Aubry, and Caroline V. Crawford Reprinted with permission from the Center for State & Local Government Excellence INTRODUCTION

How Big A Burden Are State and Local OPEB Benefits? By Alicia H. Munnell, Jean-Pierre Aubry, and Caroline V. Crawford Reprinted with permission from the Center for State & Local Government Excellence INTRODUCTION

WESTERN MUNICIPAL WATER DISTRICT RETIREMENT MEDICAL BENEFITS PLAN (OTHER POST EMPLOYMENT BENEFIT PLAN) FINANCIAL STATEMENTS

FINANCIAL STATEMENTS") WESTERN MUNICIPAL WATER DISTRICT RETIREMENT MEDICAL BENEFITS PLAN (OTHER POST EMPLOYMENT BENEFIT PLAN) FINANCIAL STATEMENTS WITH REPORT ON AUDIT BY INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS FOR THE FISCAL

WESTERN MUNICIPAL WATER DISTRICT RETIREMENT MEDICAL BENEFITS PLAN (OTHER POST EMPLOYMENT BENEFIT PLAN) FINANCIAL STATEMENTS WITH REPORT ON AUDIT BY INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS FOR THE FISCAL

OTHER POST EMPLOYMENT BENEFITS. GASB STATEMENTS NO. 43 and 45 REPORTING GUIDELINES FOR GOVERNMENT FINANCIAL STATEMENTS. A Civic Federation Issue Brief

OTHER POST EMPLOYMENT BENEFITS GASB STATEMENTS NO. 43 and 45 REPORTING GUIDELINES FOR GOVERNMENT FINANCIAL STATEMENTS A Civic Federation Issue Brief Prepared By The Civic Federation February 9, 2006 TABLE

OTHER POST EMPLOYMENT BENEFITS GASB STATEMENTS NO. 43 and 45 REPORTING GUIDELINES FOR GOVERNMENT FINANCIAL STATEMENTS A Civic Federation Issue Brief Prepared By The Civic Federation February 9, 2006 TABLE

GASB 67 & 68 Frequently Asked Questions (FAQs)

") GASB 67 & 68 Frequently Asked Questions (FAQs) 1. When do these new standards go into effect? Statement No. 67 replaces the requirements of the existing Statement No. 25, Financial Reporting for Defined

GASB 67 & 68 Frequently Asked Questions (FAQs) 1. When do these new standards go into effect? Statement No. 67 replaces the requirements of the existing Statement No. 25, Financial Reporting for Defined

Agenda. Pension and OPEB News GASB 67, 68, 71, 73, 74, and 75. July 23, 2015

Pension and OPEB News GASB 67, 68, 71, 73, 74, and 75 July 23, 2015 Mary Beth Redding mbredding@bartel-associates.com www.bartel-associates.com Agenda GASB 68 Overview 1 GASB68C CalPERS lpersreports 12

Pension and OPEB News GASB 67, 68, 71, 73, 74, and 75 July 23, 2015 Mary Beth Redding mbredding@bartel-associates.com www.bartel-associates.com Agenda GASB 68 Overview 1 GASB68C CalPERS lpersreports 12

City of Los Angeles Fire and Police Pension Plan

City of Los Angeles Fire and Police Pension Plan Actuarial Valuation and Review Of Retirement and Other Postemployment Benefits (OPEB) as of June 30, 2017 This report has been prepared at the request of

City of Los Angeles Fire and Police Pension Plan Actuarial Valuation and Review Of Retirement and Other Postemployment Benefits (OPEB) as of June 30, 2017 This report has been prepared at the request of

MISCELLANEOUS PLAN OF THE CITRUS PEST CONTROL DISTRICT #2 OF RIVERSIDE COUNTY (CalPERS ID: ) Annual Valuation Report as of June 30, 2013

Annual Valuation Report as of June 30, 2013") California Public Employees Retirement System Actuarial Office P.O. Box 942709 Sacramento, CA 94229-2709 TTY: (916) 795-3240 (888) 225-7377 phone (916) 795-2744 fax www.calpers.ca.gov October 2014 MISCELLANEOUS

California Public Employees Retirement System Actuarial Office P.O. Box 942709 Sacramento, CA 94229-2709 TTY: (916) 795-3240 (888) 225-7377 phone (916) 795-2744 fax www.calpers.ca.gov October 2014 MISCELLANEOUS

City of Oakland Postretirement Health Insurance Plan GASB 43/45 Actuarial Valuation Report as of July 1, 2015

City of Oakland Postretirement Health Insurance Plan GASB 43/45 Actuarial Valuation Report as of July 1, 2015 Produced by Cheiron May 2016 TABLE OF CONTENTS Section Page Letter of Transmittal... i Total

City of Oakland Postretirement Health Insurance Plan GASB 43/45 Actuarial Valuation Report as of July 1, 2015 Produced by Cheiron May 2016 TABLE OF CONTENTS Section Page Letter of Transmittal... i Total

RE: Preliminary Views on Economic Condition Reporting: Financial Projections

April 2, 2012 Mr. David Bean Director of Research and Technical Activities, Project No. 13-3 Governmental Accounting Standards Board 401 Merritt 7 P.O. Box 5116 Norwalk, CT 06856-5116 RE: Preliminary Views

April 2, 2012 Mr. David Bean Director of Research and Technical Activities, Project No. 13-3 Governmental Accounting Standards Board 401 Merritt 7 P.O. Box 5116 Norwalk, CT 06856-5116 RE: Preliminary Views

More of the same Are you ready for GASB 74 & 75?

Gulf Coast FGFOA Chapter Fall Conference October 7, 2016 More of the same Are you ready for GASB 74 & 75? Piotr Krekora, ASA, MAAA Pete N. Strong, FSA, EA, MAAA Copyright 2016 GRS All rights reserved.

Gulf Coast FGFOA Chapter Fall Conference October 7, 2016 More of the same Are you ready for GASB 74 & 75? Piotr Krekora, ASA, MAAA Pete N. Strong, FSA, EA, MAAA Copyright 2016 GRS All rights reserved.

Recent Significant GASB Pronouncements. William Feng, Chief Accountant October 2018

1d. GASB Review 1d. Recent Significant GASB Pronouncements William Feng, Chief Accountant October 2018 0 What is GASB? Governmental Accounting Standards Board (GASB) is the independent organization that

1d. GASB Review 1d. Recent Significant GASB Pronouncements William Feng, Chief Accountant October 2018 0 What is GASB? Governmental Accounting Standards Board (GASB) is the independent organization that

GASB 74/75 Frequently Asked Questions

Page 1 of 15 GASB 74/75 Frequently Asked Questions General Information What is GASB? Governmental Accounting Standards Board is an independent, non-profit, nongovernmental regulatory body charged with

Page 1 of 15 GASB 74/75 Frequently Asked Questions General Information What is GASB? Governmental Accounting Standards Board is an independent, non-profit, nongovernmental regulatory body charged with

Today s agenda. Overview of GASB 74/75. VGFOA Conference Spring, Presented by: William Dowd, MAAA, EA, FCA Daniel Homan, MAAA, EA

Today s agenda Overview of GASB 74/75 VGFOA Conference Spring, 2018 Presented by: William Dowd, MAAA, EA, FCA Daniel Homan, MAAA, EA Agenda» Why this? Why now?» Understanding the new reporting standards»

Today s agenda Overview of GASB 74/75 VGFOA Conference Spring, 2018 Presented by: William Dowd, MAAA, EA, FCA Daniel Homan, MAAA, EA Agenda» Why this? Why now?» Understanding the new reporting standards»

An Analysis of Connecticut s State Employees Retirement System (SERS): Final Report

: Final Report") An Analysis of Connecticut s State Employees Retirement System (SERS): Final Report Jean-Pierre Aubry Center for Retirement Research at Boston College Connecticut Pension Analysis Nov 10th, 2015 Hartford,

An Analysis of Connecticut s State Employees Retirement System (SERS): Final Report Jean-Pierre Aubry Center for Retirement Research at Boston College Connecticut Pension Analysis Nov 10th, 2015 Hartford,

Meeting Date: September 28, From: Amy Cunningham, Administrative Services Director

Town of Moraga Ordinances, Resolutions, Requests for Action Agenda Item. E. 0 0 0 0 Meeting Date: September, 0 TOWN OF MORAGA STAFF REPORT_ To: Honorable Mayor and Councilmembers From: Amy Cunningham,

Town of Moraga Ordinances, Resolutions, Requests for Action Agenda Item. E. 0 0 0 0 Meeting Date: September, 0 TOWN OF MORAGA STAFF REPORT_ To: Honorable Mayor and Councilmembers From: Amy Cunningham,

AGENDA BOARD OF FIRE AND POLICE PENSION COMMISSIONERS. December 1, :30 a.m.

AGENDA BOARD OF FIRE AND POLICE PENSION COMMISSIONERS December 1, 2016 8:30 a.m. Sam Diannitto Boardroom Los Angeles Fire and Police Pensions Building 701 East Third Street, Suite 400 Los Angeles, CA 90013

AGENDA BOARD OF FIRE AND POLICE PENSION COMMISSIONERS December 1, 2016 8:30 a.m. Sam Diannitto Boardroom Los Angeles Fire and Police Pensions Building 701 East Third Street, Suite 400 Los Angeles, CA 90013

Implementing GASB 68

W a s h i n g t o n S t a t e A u d i t o r s O f f i c e Implementing GASB 68 GASB pension statements GASB number Title 78 Non-governmental plans 2016 73 Plans not within the scope of GASB 68 2017 71

W a s h i n g t o n S t a t e A u d i t o r s O f f i c e Implementing GASB 68 GASB pension statements GASB number Title 78 Non-governmental plans 2016 73 Plans not within the scope of GASB 68 2017 71

Title: Understanding Pension Actuarial Reports

TUESDAY MAY 23, 2017 3:35-4:50PM Title: Understanding Pension Actuarial Reports MODERATOR SPEAKERS Mark Nannini Chief Financial Officer, Illinois Municipal Retirement Fund Paul Angelo Senior Vice President

TUESDAY MAY 23, 2017 3:35-4:50PM Title: Understanding Pension Actuarial Reports MODERATOR SPEAKERS Mark Nannini Chief Financial Officer, Illinois Municipal Retirement Fund Paul Angelo Senior Vice President

GASB 67/68 The New Pension Standards. The Reasoning Behind the Pronouncements

GASB 67/68 The New Pension Standards The Reasoning Behind the Pronouncements Presented by: Stephen W. Blann, CPA, CGFM, CGMA Director of Government Audit Quality Rehmann, Grand Rapids, MI Larry Langer,

GASB 67/68 The New Pension Standards The Reasoning Behind the Pronouncements Presented by: Stephen W. Blann, CPA, CGFM, CGMA Director of Government Audit Quality Rehmann, Grand Rapids, MI Larry Langer,

City of Los Angeles Department of Water and Power

City of Los Angeles Department of Water and Power Actuarial Valuation and Review of Other Postemployment Benefits (OPEB) as of June 30, 2017 In accordance with GASB Statement No. 45 This report has been

City of Los Angeles Department of Water and Power Actuarial Valuation and Review of Other Postemployment Benefits (OPEB) as of June 30, 2017 In accordance with GASB Statement No. 45 This report has been

Proposed Statement of the Governmental Accounting Standards Board: Plain-Language Supplement

June 27, 2011 EXPOSURE DRAFT SUPPLEMENT Proposed Statement of the Governmental Accounting Standards Board: Plain-Language Supplement Pension Accounting and Financial Reporting This plain-language supplement

June 27, 2011 EXPOSURE DRAFT SUPPLEMENT Proposed Statement of the Governmental Accounting Standards Board: Plain-Language Supplement Pension Accounting and Financial Reporting This plain-language supplement

GASB Issues Final Rules Governing Reporting for Postemployment Benefits Other Than Pensions

GASB Issues Final Rules Governing Reporting for Postemployment Benefits Other Than Pensions Table of Contents EXECUTIVE SUMMARY... 3 GASB 75 EMPLOYER STANDARD... 5 BACKGROUND & IMPACT OF CHANGE... 5 SCOPE...

GASB Issues Final Rules Governing Reporting for Postemployment Benefits Other Than Pensions Table of Contents EXECUTIVE SUMMARY... 3 GASB 75 EMPLOYER STANDARD... 5 BACKGROUND & IMPACT OF CHANGE... 5 SCOPE...

GOVERNMENTAL DEFINED BENEFIT PENSION PLANS

GOVERNMENTAL DEFINED BENEFIT PENSION PLANS UNDERSTANDING GASB 67 / 68 GGFOA 2014 ANNUAL CONFERENCE Presented By: Donald L. McGrath Jr., CPA, Partner Crace Galvis McGrath, LLC Sponsored By: Georgia Government

GOVERNMENTAL DEFINED BENEFIT PENSION PLANS UNDERSTANDING GASB 67 / 68 GGFOA 2014 ANNUAL CONFERENCE Presented By: Donald L. McGrath Jr., CPA, Partner Crace Galvis McGrath, LLC Sponsored By: Georgia Government

2014 Survey of GASB Accounting Measures for Public Pension Plans

2014 Survey of GASB Accounting Measures for Public Pension Plans By Paul Zorn 1 In June 2012, the Governmental Accounting Standards Board (GASB) made significant changes to the accounting and financial

2014 Survey of GASB Accounting Measures for Public Pension Plans By Paul Zorn 1 In June 2012, the Governmental Accounting Standards Board (GASB) made significant changes to the accounting and financial

CENTER FOR MUNICIPAL FINANCE. From High to Low: Understanding How the Pennsylvania Public School Employees Retirement System Became Underfunded

CENTER FOR MUNICIPAL FINANCE From High to Low: Understanding How the Pennsylvania Public School Employees Retirement System Became Underfunded From High to Low: Understanding How the Pennsylvania Public

CENTER FOR MUNICIPAL FINANCE From High to Low: Understanding How the Pennsylvania Public School Employees Retirement System Became Underfunded From High to Low: Understanding How the Pennsylvania Public

County of Sonoma. Distributed to JLMBC on December 7, 2011

County of Sonoma Actuarial Valuation and Review of Other Postemployment Benefits (OPEB) as of June 30, 2011 In accordance with GASB Statements No. 43 and No. 45 Copyright 2011 by The Segal Group, Inc.,

County of Sonoma Actuarial Valuation and Review of Other Postemployment Benefits (OPEB) as of June 30, 2011 In accordance with GASB Statements No. 43 and No. 45 Copyright 2011 by The Segal Group, Inc.,

San Diego City Employees Retirement System San Diego County Regional Airport Authority

San Diego City Employees Retirement System San Diego County Regional Airport Authority GASB 67/68 Report as of June 30, 2016 Produced by Cheiron November 2016 TABLE OF CONTENTS Section Page Letter of Transmittal...

San Diego City Employees Retirement System San Diego County Regional Airport Authority GASB 67/68 Report as of June 30, 2016 Produced by Cheiron November 2016 TABLE OF CONTENTS Section Page Letter of Transmittal...

GASB 74 & 75 The new GASB OPEB standards & an overview of upcoming pronouncements. Jeff Straus, CPA Principal

GASB 74 & 75 The new GASB OPEB standards & an overview of upcoming pronouncements Jeff Straus, CPA Principal jstraus@manercpa.com Session Overview 1. What are Other Post Employment Benefits (OPEB)? 2.

GASB 74 & 75 The new GASB OPEB standards & an overview of upcoming pronouncements Jeff Straus, CPA Principal jstraus@manercpa.com Session Overview 1. What are Other Post Employment Benefits (OPEB)? 2.

City of Richmond Heights Policemen s and Firemen s Retirement Fund GASB Statement No. 68 Employer Reporting Accounting Schedules July 1, 2017

City of Richmond Heights Policemen s and Firemen s Retirement Fund GASB Statement No. 68 Employer Reporting Accounting Schedules July 1, 2017 December 20, 2017 Board of Trustees City of Richmond Heights

City of Richmond Heights Policemen s and Firemen s Retirement Fund GASB Statement No. 68 Employer Reporting Accounting Schedules July 1, 2017 December 20, 2017 Board of Trustees City of Richmond Heights

Pensions for Pros: A Detailed Look at the GASB s New Pension. Standards

Pensions for Pros: A Detailed Look at the GASB s New Pension QR Code Presenters: Standards Moderator: Debra Roberts Maryland Supplemental Retirement Plans James J. Rizzo Gabriel Roeder Smith & Co. Sean

Pensions for Pros: A Detailed Look at the GASB s New Pension QR Code Presenters: Standards Moderator: Debra Roberts Maryland Supplemental Retirement Plans James J. Rizzo Gabriel Roeder Smith & Co. Sean

What you should know about the new Other Postemployment Benefits (OPEB) standard (GASB 75) WGFOA Spring Conference April 19, 2018

standard (GASB 75) WGFOA Spring Conference April 19, 2018") What you should know about the new Other Postemployment Benefits (OPEB) standard (GASB 75) WGFOA Spring Conference April 19, 2018 Baker Tilly refers to Baker Tilly Virchow Krause, LLP, an independently

What you should know about the new Other Postemployment Benefits (OPEB) standard (GASB 75) WGFOA Spring Conference April 19, 2018 Baker Tilly refers to Baker Tilly Virchow Krause, LLP, an independently

Pension De-Risking. 112 th Annual Conference May 6-9, 2018 St. Louis, Missouri

1:30 2:30 May 6, 2018 Room 100-102 112 th Annual Conference May 6-9, 2018 St. Louis, Missouri Moderator/Speakers: Mark Whelan Chief Financial Officer, Kentucky Teachers Retirement System Les Richmond,

1:30 2:30 May 6, 2018 Room 100-102 112 th Annual Conference May 6-9, 2018 St. Louis, Missouri Moderator/Speakers: Mark Whelan Chief Financial Officer, Kentucky Teachers Retirement System Les Richmond,

L A B O R E R S A N D R E T I R E M E N T B O A R D E M P L O Y E E S A N N U I T Y A N D B E N E F I T F U N D O F C H I C A G O ACTUARIAL VALUATION

L A B O R E R S A N D R E T I R E M E N T B O A R D E M P L O Y E E S A N N U I T Y A N D B E N E F I T F U N D O F C H I C A G O ACTUARIAL VALUATION R E P O R T FOR THE YEAR ENDING D E C E M B E R 3 1,

L A B O R E R S A N D R E T I R E M E N T B O A R D E M P L O Y E E S A N N U I T Y A N D B E N E F I T F U N D O F C H I C A G O ACTUARIAL VALUATION R E P O R T FOR THE YEAR ENDING D E C E M B E R 3 1,

GASB 75 Accounting and Financial Reporting For Postemployment Benefits Other Than Pensions

GASB 75 Accounting and Financial Reporting For Postemployment Benefits Other Than Pensions Presented By: Marianne Van Duyne, CPA Managing Partner R.S. Abrams & Co., LLP 1 New York State Government Finance

GASB 75 Accounting and Financial Reporting For Postemployment Benefits Other Than Pensions Presented By: Marianne Van Duyne, CPA Managing Partner R.S. Abrams & Co., LLP 1 New York State Government Finance

GASB 68 ACCOUNTING VALUATION REPORT

GASB 68 ACCOUNTING VALUATION REPORT () Rate Plan Identifier: 595 Prepared for the SAN FRANCISCO COMMUNITY COLLEGE DISTRICT BOOKSTORE AUXILIARY MISCELLANEOUS PLAN, a Cost-Sharing Multiple-Employer Defined

GASB 68 ACCOUNTING VALUATION REPORT () Rate Plan Identifier: 595 Prepared for the SAN FRANCISCO COMMUNITY COLLEGE DISTRICT BOOKSTORE AUXILIARY MISCELLANEOUS PLAN, a Cost-Sharing Multiple-Employer Defined

CONTENTS. I. Introduction II. Background III. Funding Goals IV. Annual Actuarial Metrics...2. V. Funding Valuation Elements...

COLORADO PERA DEFINED BENEFIT OPEB PLAN FUNDING POLICY ADOPTED JANUARY 19, 2018 CONTENTS I. Introduction... 1 II. Background... 1 III. Funding Goals... 1 IV. Annual Actuarial Metrics...2 V. Funding Valuation

COLORADO PERA DEFINED BENEFIT OPEB PLAN FUNDING POLICY ADOPTED JANUARY 19, 2018 CONTENTS I. Introduction... 1 II. Background... 1 III. Funding Goals... 1 IV. Annual Actuarial Metrics...2 V. Funding Valuation

CENTER FOR MUNICIPAL FINANCE. From High to Low: Understanding How the Education Retirement Board of New Mexico Became Underfunded

CENTER FOR MUNICIPAL FINANCE From High to Low: Understanding How the Education Retirement Board of New Mexico Became Underfunded From High to Low: Understanding How the Education Retirement Board of New

CENTER FOR MUNICIPAL FINANCE From High to Low: Understanding How the Education Retirement Board of New Mexico Became Underfunded From High to Low: Understanding How the Education Retirement Board of New

Action Item. Board of Trustees and Superintendent of Schools. Steve Dickinson, Assistant Superintendent Administrative Services

Action Item TO: PRESENTED BY: BOARD AGENDA ITEM: Board of Trustees and Superintendent of Schools Steve Dickinson, Assistant Superintendent Administrative Services Consideration of Acceptance of 2015 Oxnard

Action Item TO: PRESENTED BY: BOARD AGENDA ITEM: Board of Trustees and Superintendent of Schools Steve Dickinson, Assistant Superintendent Administrative Services Consideration of Acceptance of 2015 Oxnard

San Diego City Employees Retirement System. San Diego Unified Port District. GASB 67/68 Report as of June 30, Produced by Cheiron

San Diego City Employees Retirement System San Diego Unified Port District GASB 67/68 Report as of June 30, 2015 Produced by Cheiron November 2015 TABLE OF CONTENTS Section Page Letter of Transmittal...

San Diego City Employees Retirement System San Diego Unified Port District GASB 67/68 Report as of June 30, 2015 Produced by Cheiron November 2015 TABLE OF CONTENTS Section Page Letter of Transmittal...

Actuarial Basics. Presented by Mike Overley, Regional Manager Tony Radjenovich, Regional Manager

Actuarial Basics Presented by Mike Overley, Regional Manager Tony Radjenovich, Regional Manager 1 Objectives Funding Concepts of Retirement Plans Actuarial Valuations Actuarial Terminology 2 Funding Concepts

Actuarial Basics Presented by Mike Overley, Regional Manager Tony Radjenovich, Regional Manager 1 Objectives Funding Concepts of Retirement Plans Actuarial Valuations Actuarial Terminology 2 Funding Concepts

The Water and Power Employees' Retirement Plan of the City of Los Angeles Actuarial Valuation and Review as of July 1, 2014

The Water and Power Employees' Retirement Plan of the City of Los Angeles Actuarial Valuation and Review as of July 1, 2014 This report has been prepared at the request of the Board of Administration to

The Water and Power Employees' Retirement Plan of the City of Los Angeles Actuarial Valuation and Review as of July 1, 2014 This report has been prepared at the request of the Board of Administration to

YourPublicMoney.Com Memo 6/21/2010 v.1c. One Page Summary - Key Proposed Changes

Possible Changes in Pension Accounting and Financial Reporting Plain-Language Supplement to Preliminary Views Governmental Accounting Standards Board June 16, 2010 YourPublicMoney.Com Memo 6/21/2010 v.1c

Possible Changes in Pension Accounting and Financial Reporting Plain-Language Supplement to Preliminary Views Governmental Accounting Standards Board June 16, 2010 YourPublicMoney.Com Memo 6/21/2010 v.1c

Required Supplementary Information

Required Supplementary Information 159 SCHEDULE OF CHANGES IN THE NET PENSION LIABILITY AND RELATED RATIOS FOR THE CARROLL COUNTY EMPLOYEE PENSION PLAN RSI -1 Total pension liability Service cost $ 3,513

Required Supplementary Information 159 SCHEDULE OF CHANGES IN THE NET PENSION LIABILITY AND RELATED RATIOS FOR THE CARROLL COUNTY EMPLOYEE PENSION PLAN RSI -1 Total pension liability Service cost $ 3,513

Funding Basics of Retirement Programs

Funding Basics of Retirement Programs Monroe County Employees Retirement System Monroe County Retiree Health Care Plan Presented by: Mark Buis, F.S.A. September 11, 2012 Copyright 2012 GRS All rights reserved.

Funding Basics of Retirement Programs Monroe County Employees Retirement System Monroe County Retiree Health Care Plan Presented by: Mark Buis, F.S.A. September 11, 2012 Copyright 2012 GRS All rights reserved.

GASB Statement 68 Government Financial Reporting of Pension Finances Summary Explanation of Predictor Model 10/16/12

GASB Statement 68 Government Financial Reporting of Pension Finances Summary Explanation of Predictor Model 10/16/12 The Governmental Accounting Standards Board (GASB) voted to approve new standards that

GASB Statement 68 Government Financial Reporting of Pension Finances Summary Explanation of Predictor Model 10/16/12 The Governmental Accounting Standards Board (GASB) voted to approve new standards that

The Water and Power Employees' Retirement Plan of the City of Los Angeles Actuarial Valuation and Review as of July 1, 2012

The Water and Power Employees' Retirement Plan of the City of Los Angeles Actuarial Valuation and Review as of July 1, 2012 Copyright 2012 by The Segal Group, Inc., parent of The Segal Company. All rights

The Water and Power Employees' Retirement Plan of the City of Los Angeles Actuarial Valuation and Review as of July 1, 2012 Copyright 2012 by The Segal Group, Inc., parent of The Segal Company. All rights

City of Holyoke Retirement System Actuarial Valuation and Review as of January 1, 2016

City of Holyoke Retirement System Actuarial Valuation and Review as of January 1, 2016 Copyright 2016 by The Segal Group, Inc. All rights reserved. 116 Huntington Ave., 8th Floor Boston, MA 02116 T 617.424.7300

City of Holyoke Retirement System Actuarial Valuation and Review as of January 1, 2016 Copyright 2016 by The Segal Group, Inc. All rights reserved. 116 Huntington Ave., 8th Floor Boston, MA 02116 T 617.424.7300

New Pension Standard. August

GASB Statement No. 68 New Pension Standard August 2013 Mary Beth Redding www.bartel-associates.com GASB 27 What Was It? Recognize e Net Pension Obligation (NPO) if Plan Sponsor did not contribute Annual

GASB Statement No. 68 New Pension Standard August 2013 Mary Beth Redding www.bartel-associates.com GASB 27 What Was It? Recognize e Net Pension Obligation (NPO) if Plan Sponsor did not contribute Annual

National Association of State Comptrollers

National Association of State Comptrollers GASB Update The views expressed in this presentation are those of Chair Vaudt, Vice-Chair Sylvis, and Mr. Bean. Official positions of the GASB on accounting matters

National Association of State Comptrollers GASB Update The views expressed in this presentation are those of Chair Vaudt, Vice-Chair Sylvis, and Mr. Bean. Official positions of the GASB on accounting matters

Pension Risks Growing for US State and Local Governments

Pension Risks Growing for US State and Local Governments Southern Municipal Finance Society September 2016 Tom Aaron, Vice President - Senior Analyst Budgetary risk from size, volatility of pension plans»

Pension Risks Growing for US State and Local Governments Southern Municipal Finance Society September 2016 Tom Aaron, Vice President - Senior Analyst Budgetary risk from size, volatility of pension plans»

RIVERSIDE COMMUNITY COLLEGE DISTRICT POST EMPLOYMENT BENEFITS OTHER THAN PENSIONS GASB 45 ACTUARIAL VALUATION

RIVERSIDE COMMUNITY COLLEGE DISTRICT POST EMPLOYMENT BENEFITS OTHER THAN PENSIONS GASB 45 ACTUARIAL VALUATION AS OF JULY 1, 2009 TABLE OF CONTENTS EXECUTIVE SUMMARY... 1 ACTUARIAL CERTIFICATION... 4 ACCOUNTING

RIVERSIDE COMMUNITY COLLEGE DISTRICT POST EMPLOYMENT BENEFITS OTHER THAN PENSIONS GASB 45 ACTUARIAL VALUATION AS OF JULY 1, 2009 TABLE OF CONTENTS EXECUTIVE SUMMARY... 1 ACTUARIAL CERTIFICATION... 4 ACCOUNTING

REQUIRED SUPPLEMENTARY INFORMATION

REQUIRED SUPPLEMENTARY INFORMATION THIS PAGE LEFT BLANK INTENTIONALLY REQUIRED SUPPLEMENTARY INFORMATION LAW ENFORCEMENT OFFICERS AND FIREFIGHTERS (LEOFF1) SCHEDULE OF FUNDING PROGRESS Actuarial Accrued

REQUIRED SUPPLEMENTARY INFORMATION THIS PAGE LEFT BLANK INTENTIONALLY REQUIRED SUPPLEMENTARY INFORMATION LAW ENFORCEMENT OFFICERS AND FIREFIGHTERS (LEOFF1) SCHEDULE OF FUNDING PROGRESS Actuarial Accrued

4/25/ MASBO Annual Conference

2017 MASBO Annual Conference Mark Schulte, FSA, EA, MAAA May 11, 2017 1 Background 2 What s changing Report frequency Report timing Terminology Financial disclosures Discount rate 3 What to do now 1 Compliance

2017 MASBO Annual Conference Mark Schulte, FSA, EA, MAAA May 11, 2017 1 Background 2 What s changing Report frequency Report timing Terminology Financial disclosures Discount rate 3 What to do now 1 Compliance

Update NASACT. GASB Update Due Process Documents

Update NASACT GASB Update Due Process Documents The views expressed in this presentation are those of the presenters. Official positions of the GASB are reached only after extensive due process and deliberations.

Update NASACT GASB Update Due Process Documents The views expressed in this presentation are those of the presenters. Official positions of the GASB are reached only after extensive due process and deliberations.

August 13, Segal Consulting, a Member of The Segal Group, Inc. By: JB/hy

Alameda County Employees Retirement Association Governmental Accounting Standards Board (GASB) Statement 68 Actuarial Valuation Based on December 31, 2014 Measurement Date for Employer Reporting as of

Alameda County Employees Retirement Association Governmental Accounting Standards Board (GASB) Statement 68 Actuarial Valuation Based on December 31, 2014 Measurement Date for Employer Reporting as of

August 28, Dear Mr. Bean:

Deloitte & Touche LLP Ten Westport Road P.O. Box 820 Wilton, CT 06897-0820 Tel: +1 203 761 3000 Fax: +1 203 834 2200 www.deloitte.com Mr. David R. Bean Director of Research and Technical Activities Governmental

Deloitte & Touche LLP Ten Westport Road P.O. Box 820 Wilton, CT 06897-0820 Tel: +1 203 761 3000 Fax: +1 203 834 2200 www.deloitte.com Mr. David R. Bean Director of Research and Technical Activities Governmental

In addressing some possible viable options and recommendations, the Pension Subcommittee has prepared a presentation enumerates a number of basic fina

To: Honorable Mayor Sinnott and Council Member Corti Liaisons to the Finance Committee From: Jeffrey G. Sturgis Chair, Finance Committee Date: May 1, 2013 Subject: Finance Committee Recommendations regarding

To: Honorable Mayor Sinnott and Council Member Corti Liaisons to the Finance Committee From: Jeffrey G. Sturgis Chair, Finance Committee Date: May 1, 2013 Subject: Finance Committee Recommendations regarding

PRIVATE. August 7, Ms. Katie White Director of Fiscal Services MiraCosta Community College (MS #6) One Barnard Drive Oceanside, CA 92056

One Barnard Drive Oceanside, CA 92056") 530 B Street, Suite 900 San Diego, CA 92101-4404 (p) 619-239-0831 (f ) 619-239-0807 www.nyhart.com August 7, 2015 PRIVATE Ms. Katie White Director of Fiscal Services MiraCosta Community College (MS #6)

530 B Street, Suite 900 San Diego, CA 92101-4404 (p) 619-239-0831 (f ) 619-239-0807 www.nyhart.com August 7, 2015 PRIVATE Ms. Katie White Director of Fiscal Services MiraCosta Community College (MS #6)

Preliminary Views. Governmental Accounting Standards Series. Pension Accounting and Financial Reporting by Employers

NO. 34P JUNE 16, 2010 Governmental Accounting Standards Series Preliminary Views of the Governmental Accounting Standards Board on major issues related to Pension Accounting and Financial Reporting by

NO. 34P JUNE 16, 2010 Governmental Accounting Standards Series Preliminary Views of the Governmental Accounting Standards Board on major issues related to Pension Accounting and Financial Reporting by

Susan Combs, Texas Comptroller of Public Accounts. Path to Stability: ERS at the Crossroads

Susan Combs, Texas Comptroller of Public Accounts Path to Stability: ERS at the Crossroads EMPLOYEES RETIREMENT SYSTEM: THE BASICS The Employees Retirement System of Texas (ERS), established in 1947 by

Susan Combs, Texas Comptroller of Public Accounts Path to Stability: ERS at the Crossroads EMPLOYEES RETIREMENT SYSTEM: THE BASICS The Employees Retirement System of Texas (ERS), established in 1947 by

MSBO Annual Conference Implementing GASB 75. Presented by Chris Geck and Eric Formberg

MSBO Annual Conference Implementing GASB 75 Presented by Chris Geck and Eric Formberg Accounting and Auditing Update Topics GASB 75 implementation year is here! GASB 68 - connecting the dots MPSERS contribution

MSBO Annual Conference Implementing GASB 75 Presented by Chris Geck and Eric Formberg Accounting and Auditing Update Topics GASB 75 implementation year is here! GASB 68 - connecting the dots MPSERS contribution

Invitation to Comment: Plain-Language Supplement

March 31, 2009 Invitation to Comment: Plain-Language Supplement Pension Accounting and Financial Reporting This plain-language supplement to an Invitation to Comment is issued for public comment. Written

March 31, 2009 Invitation to Comment: Plain-Language Supplement Pension Accounting and Financial Reporting This plain-language supplement to an Invitation to Comment is issued for public comment. Written

MEETING DATE: 03/23/2017 ITEM NO: 2 TOWN OF LOS GATOS FINANCE COMMITTEE REPORT DATE: MARCH 17, 2017 COUNCIL FINANCE COMMITTEE

TOWN OF LOS GATOS FINANCE COMMITTEE REPORT MEETING DATE: 03/23/2017 ITEM NO: 2 DATE: MARCH 17, 2017 TO: FROM: SUBJECT: COUNCIL FINANCE COMMITTEE LAUREL PREVETTI, TOWN MANAGER REVIEW, DISCUSS, AND RECOMMEND

TOWN OF LOS GATOS FINANCE COMMITTEE REPORT MEETING DATE: 03/23/2017 ITEM NO: 2 DATE: MARCH 17, 2017 TO: FROM: SUBJECT: COUNCIL FINANCE COMMITTEE LAUREL PREVETTI, TOWN MANAGER REVIEW, DISCUSS, AND RECOMMEND

Healthcare Analytics Consulting. Actuarial Valuation of Postemployment Benefits as of Fiscal Year End June 30, Arthur J. Gallagher & Co.

Healthcare Analytics Consulting Village of Milford Actuarial Valuation of Postemployment Benefits as of Fiscal Year End June 30, 2017 July 31, 2017 Arthur J. Gallagher & Co. Healthcare Analytics Consulting

Healthcare Analytics Consulting Village of Milford Actuarial Valuation of Postemployment Benefits as of Fiscal Year End June 30, 2017 July 31, 2017 Arthur J. Gallagher & Co. Healthcare Analytics Consulting

Recent VRS Changes and the New Pension GASB Standard. VGFOA Fall Conference October 17 th, 2012

Recent VRS Changes and the New Pension GASB Standard VGFOA Fall Conference October 17 th, 2012 Panel: William H Leighty, DecideSmart, LLC Robert H Churchman, CPA William M Dowd, Sageview Consulting Barry

Recent VRS Changes and the New Pension GASB Standard VGFOA Fall Conference October 17 th, 2012 Panel: William H Leighty, DecideSmart, LLC Robert H Churchman, CPA William M Dowd, Sageview Consulting Barry

Kern County Employees Retirement Association

Kern County Employees Retirement Association Governmental Accounting Standard (GAS) 68 Actuarial Valuation Based on June 30, 2017 Measurement Date for Employer Reporting as of June 30, 2018 This report

Kern County Employees Retirement Association Governmental Accounting Standard (GAS) 68 Actuarial Valuation Based on June 30, 2017 Measurement Date for Employer Reporting as of June 30, 2018 This report

GASB 68: Bet You Can t Wait! Presenters. Agenda. Date: October 7, 2014

GASB 68: Bet You Can t Wait! Taking a closer look at GASB s new pension standards Barrie Wilkes, Mary Hill Central Michigan University Katie Thornton Plante Moran, PLLC Date: October 7, 2014 Presenters

GASB 68: Bet You Can t Wait! Taking a closer look at GASB s new pension standards Barrie Wilkes, Mary Hill Central Michigan University Katie Thornton Plante Moran, PLLC Date: October 7, 2014 Presenters

The Water and Power Employees' Retirement Plan of the City of Los Angeles Actuarial Valuation and Review as of July 1, 2017

The Water and Power Employees' Retirement Plan of the City of Los Angeles Actuarial Valuation and Review as of July 1, 2017 This report has been prepared at the request of the Board of Administration to

The Water and Power Employees' Retirement Plan of the City of Los Angeles Actuarial Valuation and Review as of July 1, 2017 This report has been prepared at the request of the Board of Administration to

Pension Plan for Bargaining Unit Employees of TriMet

Pension Plan for Bargaining Unit Employees of TriMet Actuarial Valuation Report as of July 1, 2018 Produced by Cheiron September 2018 TABLE OF CONTENTS Section Page Section I Board Summary...1 Section

Pension Plan for Bargaining Unit Employees of TriMet Actuarial Valuation Report as of July 1, 2018 Produced by Cheiron September 2018 TABLE OF CONTENTS Section Page Section I Board Summary...1 Section

Rating Agency Perspectives on Current Credit Issues. Friday, May 6, 2016

Rating Agency Perspectives on Current Credit Issues Friday, May 6, 2016 Panelists: Moderator: Ted Damutz, Moody s Investors Service Carol Spain, S&P Global Ratings Juliet Huang, Chapman and Cutler LLP

Rating Agency Perspectives on Current Credit Issues Friday, May 6, 2016 Panelists: Moderator: Ted Damutz, Moody s Investors Service Carol Spain, S&P Global Ratings Juliet Huang, Chapman and Cutler LLP

GASB: What Legislative Staff Need to Know

GASB: What Legislative Staff Need to Know Fiscal Analysts Seminar Dean Michael Mead October 22, 2014 The views expressed in this presentation are those of Mr. Mead. Official positions of the GASB on accounting

GASB: What Legislative Staff Need to Know Fiscal Analysts Seminar Dean Michael Mead October 22, 2014 The views expressed in this presentation are those of Mr. Mead. Official positions of the GASB on accounting

Sacramento County Employees Retirement System (SCERS)

") Sacramento County Employees Retirement System (SCERS) Governmental Accounting Standards Board Statement 68 (GASBS 68) Actuarial Valuation Based on June 30, 2017 Measurement Date for Employer Reporting

Sacramento County Employees Retirement System (SCERS) Governmental Accounting Standards Board Statement 68 (GASBS 68) Actuarial Valuation Based on June 30, 2017 Measurement Date for Employer Reporting

Office of the City Auditor. Agreed-Upon Procedures applied to the 2018 Actuarial Valuation of Other Post Employment Benefits (OPEB)

") Agreed-Upon Procedures applied to the 2018 Actuarial Valuation of Other Post Employment Benefits (OPEB) Report Date: July 3, 2018 Contact Information Office of the City Auditor Promoting Accountability

Agreed-Upon Procedures applied to the 2018 Actuarial Valuation of Other Post Employment Benefits (OPEB) Report Date: July 3, 2018 Contact Information Office of the City Auditor Promoting Accountability

GASB STATEMENT NO. 45 OTHER (THAN PENSIONS) POSTEMPLOYMENT BENEFITS. Plan Sponsor Reporting and Disclosure

POSTEMPLOYMENT BENEFITS. Plan Sponsor Reporting and Disclosure") GASB STATEMENT NO. 45 OTHER (THAN PENSIONS) POSTEMPLOYMENT BENEFITS November 2005 o:\technical\articles\gasb 45 summary article 05-11.doc 12/5/2005 1:37 PM GASB: OTHER (THAN PENSIONS) POSTEMPLOYMENT BENEFITS

GASB STATEMENT NO. 45 OTHER (THAN PENSIONS) POSTEMPLOYMENT BENEFITS November 2005 o:\technical\articles\gasb 45 summary article 05-11.doc 12/5/2005 1:37 PM GASB: OTHER (THAN PENSIONS) POSTEMPLOYMENT BENEFITS

IMPACT OF PUBLIC SECTOR ASSUMED RETURNS ON INVESTMENT CHOICES

RETIREMENT RESEARCH State and Local Pension Plans Number 63, January 2019 IMPACT OF PUBLIC SECTOR ASSUMED RETURNS ON INVESTMENT CHOICES By Jean-Pierre Aubry and Caroline V. Crawford* Introduction State

RETIREMENT RESEARCH State and Local Pension Plans Number 63, January 2019 IMPACT OF PUBLIC SECTOR ASSUMED RETURNS ON INVESTMENT CHOICES By Jean-Pierre Aubry and Caroline V. Crawford* Introduction State