Financial Statements of

|

|

|

- Annis Martin

- 5 years ago

- Views:

Transcription

1 Financial Statements of For the year ended March 31, 2018

2 KPMG LLP Simon Avenue Abbotsford BC V2T 4W6 Canada Telephone (604) Fax (604) INDEPENDENT AUDITORS REPORT To the Board of Governors of the University of the Fraser Valley, and To the Minister of Advanced Education, Skills & Training, Province of British Columbia We have audited the accompanying financial statements of the University of the Fraser Valley, which comprise the statement of financial position as at March 31, 2018, the statements of operations and accumulated surplus, changes in net debt and cash flows for the year then ended, and notes, comprising a summary of significant accounting policies and other explanatory information. Management's Responsibility for the Financial Statements Management is responsible for the preparation of these financial statements in accordance with the financial reporting provisions of Section 23.1 of the Budget Transparency and Accountability Act of the Province of British Columbia, and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error. Auditors Responsibility Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with Canadian generally accepted auditing standards. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on our judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, we consider internal control relevant to the entity's preparation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained in our audit is sufficient and appropriate to provide a basis for our audit opinion. KPMG LLP is a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ( KPMG International ), a Swiss entity. KPMG Canada provides services to KPMG LLP.

3 Page 2 Opinion In our opinion, the financial statements of the University of the Fraser Valley as at March 31, 2018 and for the year then ended are prepared, in all material respects, in accordance with the financial reporting provisions of Section 23.1 of the Budget Transparency and Accountability Act of the Province of British Columbia. Emphasis of Matter Without modifying our opinion, we draw attention to Note 2(a) to the financial statements, which describes the basis of accounting and the significant differences between such basis of accounting and Canadian public sector accounting standards. Chartered Professional Accountants May 17, 2018 Abbotsford, Canada

4 March 31, 2018 CONTENTS Financial Statements Statement of Financial Position 1 Statement of Operations and Accumulated Surplus 2 Statement of Changes in Net Debt 3 Statement of Cash Flows 4 5 Page

5

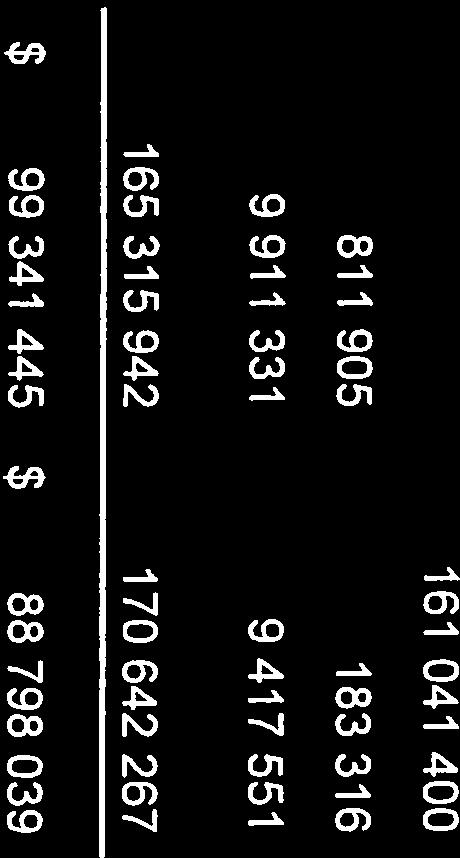

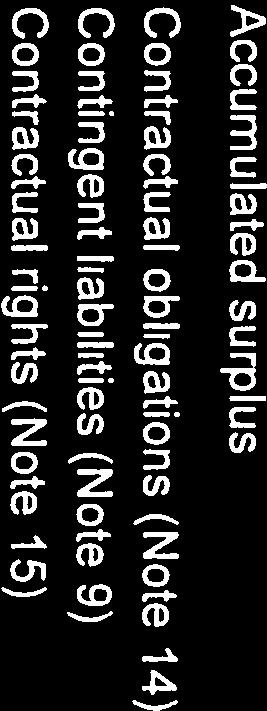

6 Statement of Operations and Accumulated Surplus For the year ended March 31, 2018,with comparative information for Budget (Note 2.k) (Recast - Note 3) Revenue Province of British Columbia $ 57,528,288 $ 55,998,964 $ 56,959,643 Tuition and student fees 51,070,545 56,236,895 50,518,582 Sales of goods and services 7,095,942 7,045,125 6,992,784 Amortization of deferred capital contributions 6,939,000 7,048,866 6,858,001 Other revenue 1,860,526 2,263,587 2,031,289 Donations, non-government grants and contracts 1,284,900 2,278,670 2,869,464 Government of Canada 825,225 1,052, ,778 Investment income 600,000 1,271, ,321 Income from government business enterprise (Note 5) - 429, ,224 Gains on disposal of assets (Note 16.a) - 3,053,241 3,351, ,204, ,678, ,872,936 Expenses Instruction and Support 121,386, ,094, ,269,341 Ancillary 5,817,734 5,535,060 5,880, ,204, ,629, ,149,863 Annual surplus from operations - 10,049,627 9,723,073 Other Income Endowment contributions - 493, ,206 Annual Surplus - 10,543,406 10,174,279 Accumulated surplus, beginning of year 88,798,039 88,798,039 78,623,760 Accumulated surplus, end of year $ 88,798,039 $ 99,341,445 $ 88,798,039 See accompanying notes to the financial statements. 2

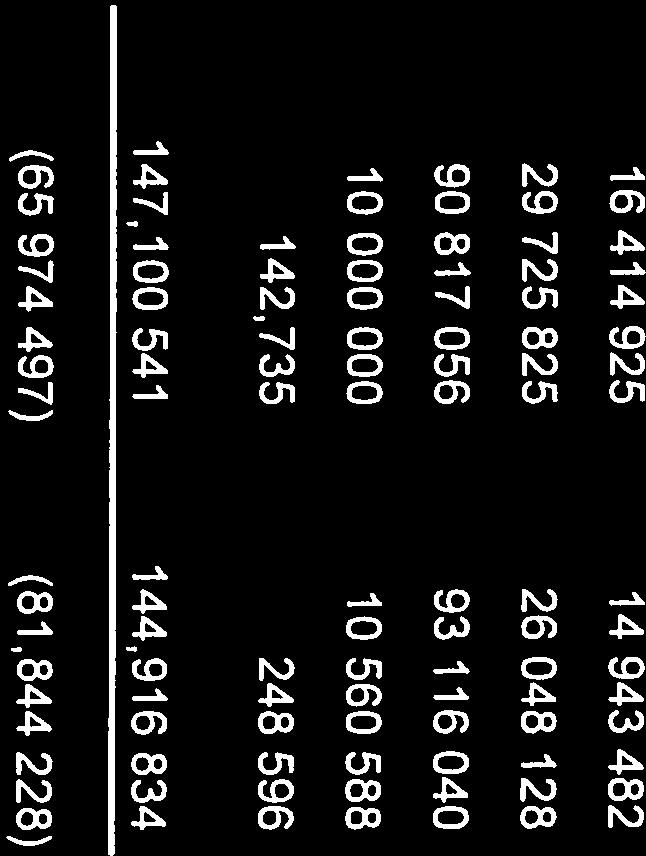

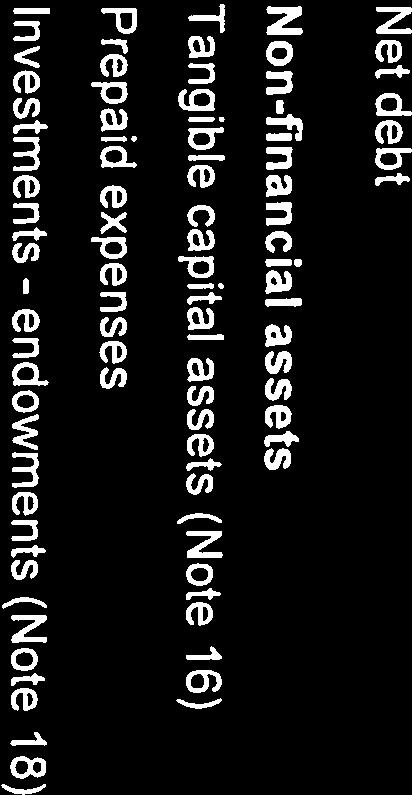

7 Statement of Changes in Net Debt 2018 Budget (Note 2.k) Annual surplus $ - $ 10,543,406 $ 10,174,279 Acquisition of tangible capital assets - (8,824,965) (4,774,037) Net transfer to (from) assets held for sale - 3,944,226 (1,273,916) Gain on sale of assets held for sale - (3,053,241) (3,351,850) Recognition of DCC on sale of assets held for sale - 1,192, ,802 Proceeds on sale of assets held for sale - 3,492,515 4,307,964 Amortization of tangible capital assets 9,500,000 9,697,806 9,555,515 9,500,000 6,448,693 4,781,478 Acquisition of prepaid expenses - (811,905) (183,316) Use of prepaid expenses - 183, ,945 - (628,589) 173,629 9,500,000 16,363,510 15,129,386 Endowment contributions - (493,779) (451,206) Decrease in net debt 9,500,000 15,869,731 14,678,180 Net debt, beginning of year (81,844,228) (81,844,228) (96,522,408) Net debt, end of year $ (72,344,228) $ (65,974,497) $ (81,844,228) See accompanying notes to the financial statements. 3

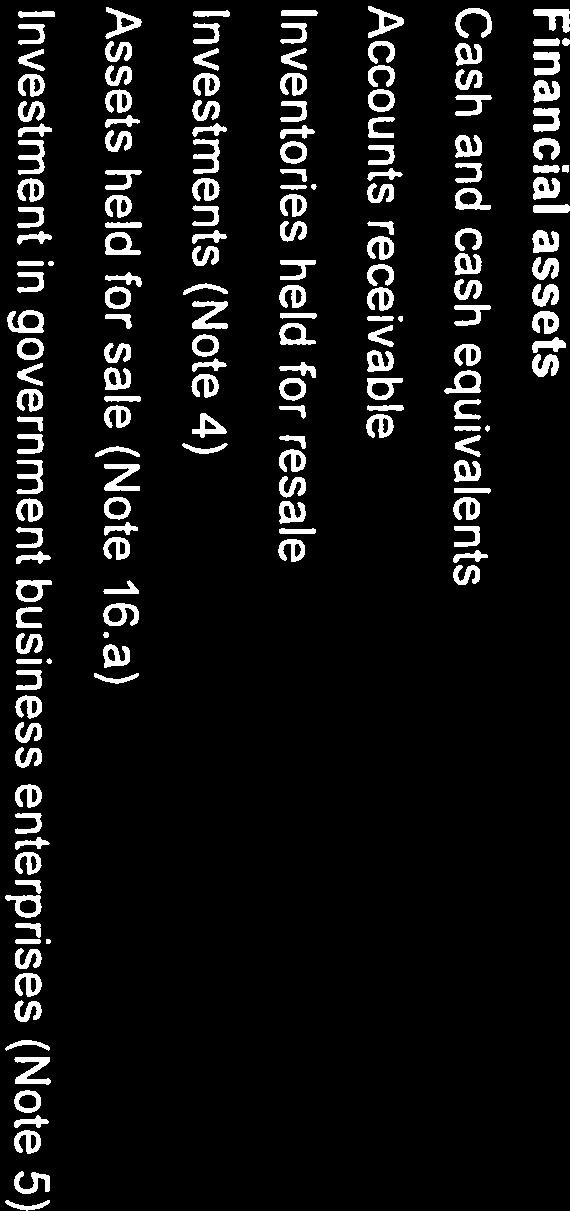

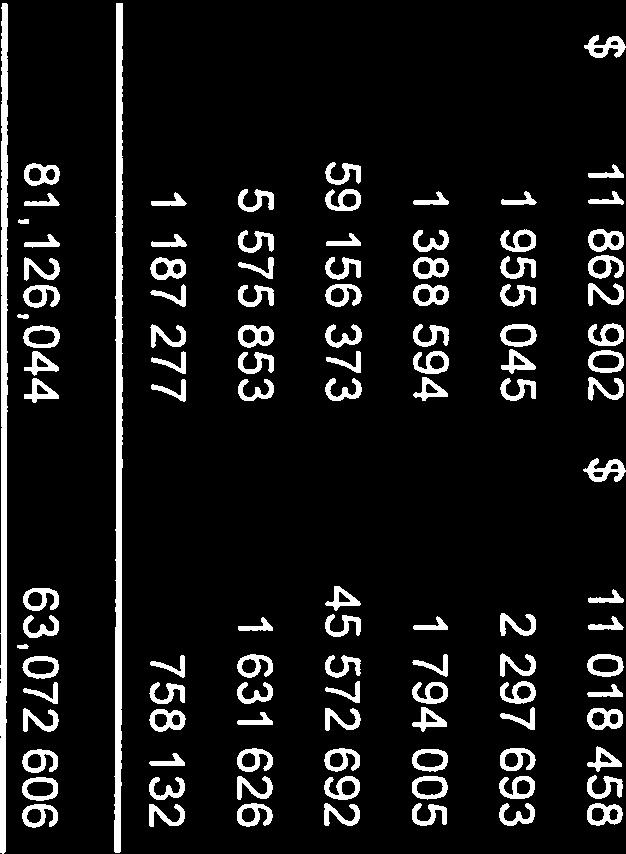

8 Statement of Cash Flows March 31, 2018 March 31, 2017 Cash provided by (used in): Operating activities Annual surplus $ 10,543,406 $ 10,174,279 Items not involving cash Amortization of tangible capital assets 9,697,806 9,555,515 Amortization of deferred capital contributions (7,048,866) (6,858,001) Income from government business enterprises (429,145) (702,224) Gain on sale of assets held for sale (3,053,241) (3,351,850) Change in non-cash operating working capital (Note 12) 4,268,610 4,837,585 Net change in cash from operating activities 13,978,570 13,655,304 Investing activities Increase in investments - non endowment (13,583,681) (14,168,657) Increase in investments - endowment (493,779) (451,206) Net change in cash from investing activities (14,077,460) (14,619,863) Capital activities Acquisition of tangible capital assets (8,824,965) (4,774,037) Proceeds on sale of tangible capital assets 3,492,515 4,307,964 Net change in cash from capital activities (5,332,450) (466,073) Financing activities Principal payment on tangible capital lease obligations (105,862) (98,974) Repayment of long term debt (560,588) (435,247) Deferred contributions received 6,942,234 3,428,071 Net change in cash from financing activities 6,275,784 2,893,850 Net change in cash and cash equivalents 844,444 1,463,218 Cash and cash equivalents, beginning of year 11,018,458 9,555,240 Cash and cash equivalents, end of year $ 11,862,902 $ 11,018,458 See accompanying notes to the financial statements. 4

9 1. Authority and purpose The University of the Fraser Valley (the "University" or "UFV") is a special purpose teaching university, partially funded by the Province of British Columbia, which operates under the authority of the University Act of British Columbia. The University is governed by a Board of Governors, the majority of which are appointed by the Province of British Columbia. The University is also a registered charity and is exempt from income taxes under section 149 of the Income Tax Act. 2. Significant accounting policies (a) Basis of accounting The financial statements have been prepared in accordance with Section 23.1 of the Budget Transparency and Accountability Act of the Province of British Columbia supplemented by Regulations 257/2010 and 198/2011 issued by the Province of British Columbia Treasury Board. The Budget Transparency and Accountability Act requires that the financial statements be prepared in accordance with the set of standards and guidelines that comprise generally accepted accounting principles for senior governments in Canada, or if the Treasury Board makes a regulation, the set of standards and guidelines that comprise generally accepted accounting principles for senior governments in Canada as modified by the alternate standard or guideline or part thereof adopted in the regulation. Regulation 257/2010 requires all tax-payer supported organizations in the Schools, Universities, Colleges and Hospitals sectors to adopt Canadian public sector accounting standards without any PS4200 elections effective their first fiscal year commencing after January 1, Regulation 198/2011 requires that restricted contributions received or receivable are to be reported as revenue depending on the nature of the restrictions on the use of the funds by the contributors as follows: i) Contributions for the purpose of acquiring or developing a depreciable tangible capital asset or contributions in the form of a depreciable tangible capital asset are recorded as deferred capital contributions and recognized in revenue at the same rate that amortization of the related tangible capital asset is recorded. The reduction of deferred capital contributions and recognition of revenue are accounted for in the fiscal period during which the tangible capital asset is used to provide services. ii) Contributions restricted for specific purposes other than those for the acquisition or development of a depreciable tangible capital asset are recorded in deferred contributions and recognized as revenue in the year in which the stipulation or restriction on the contributions have been met. For British Columbia tax payer supported organizations, these contributions include government transfers and externally restricted contributions. The accounting policy requirements under 198/2011 are significantly different from the requirements of Canadian public sector standards which requires that government transfers, which do not contain a stipulation that creates a liability, be recognized as revenue by the recipient when approved by the transferor and the eligibility criteria have been met in accordance with public sector standard PS3410. As a result, revenue recognized in the Statement of Operations and Accumulated Surplus and certain deferred capital contributions would be recorded differently under Canadian Public Sector Accounting Standards. 5

10 2. Significant accounting policies (continued) (b) Cash and cash equivalents Cash and cash equivalents include highly liquid investments with a term to maturity of three months or less at the date of purchase. (c) Financial instruments Financial instruments are classified into two categories: fair value or cost. (i) (ii) Fair value category: Includes portfolio investments that are quoted in an active market and derivative instruments reflected at fair value as at the reporting date. Sales and purchases of investments are recorded on the trade date. Transaction costs related to the acquisition of investments is recorded as an expense. Unrealized gains and losses on financial assets would be recognized in the Statement of Remeasurement Gains and Losses until such time that the financial asset is de-recognized due to disposal or impairment. At the time of de-recognition, the related realized gains and losses are recognized in the Statement of Operations and Accumulated Surplus. Unrealized gains and losses on endowment investments where earnings are restricted as to use are recorded as deferred revenue and recognized in revenue when disposed and when the related expenses are incurred. Cost category: Gains and losses are recognized in the Statement of Operations and Accumulated Surplus when the financial asset is derecognized due to disposal or impairment. Sales and purchases of investments are recorded on the trade date. Transaction costs related to the acquisition of investments is included in the cost of the related investments. (d) Investments Investments, non-endowment, are comprised of money market securities and other investments with terms that are capable of liquidation. Investments are recorded at cost plus any accrued interest to date. All interest income and realized gains and losses are recognized in the period in which they arise. (e) Inventories held for resale Inventories held for resale are recorded at the lower of cost or net realizable value. Cost includes the original purchase cost, plus shipping and applicable duties. Net realizable value is the estimated proceeds from sale less any costs incurred to sell. Inventories are written down to net realizable value when the cost of inventories is estimated not to be recoverable. When circumstances that previously caused inventories to be written down below cost no longer exist, the amount of write down previously recorded is reversed. 6

11 2. Significant accounting policies (continued) (f) Non-financial assets Non-financial assets are not available to discharge existing liabilities and are held for use in the provision of services. They have useful lives extending beyond the current year and are not intended for sale in the ordinary course of operations. (i) Tangible capital assets Tangible capital assets are recorded at cost, which includes amounts that are directly attributable to acquisition, construction, development or betterment of the asset. Interest is not capitalized whenever external debt is issued to finance the construction of tangible capital assets. The cost of the tangible capital assets are amortized on a straight-line basis over their estimated useful lives shown below. Land is not amortized as it is deemed to have a permanent value. Asset Basis Rate Buildings Straight-line years Furniture and equipment Straight-line 2-5 years Computer hardware and software Straight-line 2-4 years Leasehold improvements Straight-line Life of the lease Site improvements Straight-line 10 years Library books Straight-line 10 years Assets under construction are not amortized until the asset is put into productive use. Tangible capital assets are written down when conditions indicate that they no longer contribute to the University's ability to provide goods and services, or when the value of future economic benefits associated with the tangible capital assets are less than their net book value. The net write-downs are accounted for as expenses in the Statement of Operations. Contributed tangible capital assets are recorded into revenue at their fair market value on the date of donation, except in circumstances where fair value cannot be reasonably determined, in which case they are recognized at nominal value. (ii) Leased tangible capital assets Leases which transfer substantially all of the benefits and risks incidental to ownership of property are accounted for as obligations under capital lease. All other leases are accounted for as operating leases and the related payments are charged to expenses as incurred. (iii) Endowment investments Endowment investments quoted in an active market are reported at fair value. Investment income and unrealized gains and losses relating to the investments are reported as deferred revenue on the Statement of Financial Position. 7

12 2. Significant accounting policies (continued) (g) Revenue recognition Tuition and student fees and sales of goods and services are reported as revenue at the time the services are provided or the products are delivered, and collection is reasonably assured. Unrestricted donations and grants are recorded as revenue when received or receivable if the amounts can be estimated and collection is reasonably assured. Pledges from donors are recorded as revenue when payment is received by the University or the transfer of property is completed. Restricted donations and grants are reported as revenue depending on the nature of the restrictions on the use of the funds by the contributors as follows: (i) (ii) (iii) Contributions for the purpose of acquiring or developing a depreciable tangible capital asset or in the form of a depreciable tangible capital asset, in each case for use in providing services, are recorded and referred to as deferred capital contributions and recognized in revenue at the same rate that amortization of the tangible capital asset is recorded. The reduction of the deferred capital contributions and the recognition of the revenue are accounted for in the fiscal period during which the tangible capital asset is used to provide services. Contributions restricted for specific purposes other than for those to be held in perpetuity or the acquisition or development of a depreciable tangible capital asset are recorded as deferred revenue and recognized in revenue in the year in which the stipulation or restriction on the contribution have been met. Contributions restricted to be retained in perpetuity, allowing only the investment income earned thereon to be spent are recorded as endowment donations on the Statement of Operations for the portion to be held in perpetuity and as deferred revenue for any restricted investment income earned thereon. Investment income includes interest recorded on an accrual basis and dividends recorded as declared, realized gains and losses on the sale of investments, and write-downs on investments where the loss in value is determined to be other than temporary. Investment income excludes income from endowed investments. (h) Use of estimates Preparation of financial statements in accordance with the basis of accounting described in note 2(a) requires management to make estimates and assumptions that impact reported amounts of assets and liabilities at the date of the financial statements and revenues and expenses during the reporting periods. Significant areas requiring the use of management estimates relate to the potential impairment of assets, estimated useful lives of tangible capital assets, contingent liabilities and estimated employee future benefits. Actual results could differ from those estimates. 8

13 2. Significant accounting policies (continued) (i) Assets held for sale Long-lived assets are classified by the University as an asset held for sale at the point in time when the asset is in a condition to be sold and is publicly seen to be for sale, management has committed to selling the asset and has a plan in place, there is an active market, and it is reasonably anticipated that the sale will be completed within a one-year period. Assets held for sale are separately presented in the Statement of Financial Position as a financial asset, are reported at the lower of the carrying amount or fair value less costs to sell, and are no longer depreciated. (j) Foreign currency translation The University s functional currency is the Canadian dollar. Transactions in foreign currencies are translated into Canadian dollars at the exchange rate in effect on the transaction date. Monetary assets and liabilities denominated in foreign currencies and non-monetary assets and liabilities which were designated in the fair value category under the financial instrument standard are reflected in the financial statements in equivalent Canadian dollars at the exchange rate in effect on the Statement of Financial Position date. Any gain or loss resulting from a change in rates between the transaction date and the settlement date or Statement of Financial Position date would be recognized in the Statement of Re-measurement Gains and Losses. In the period of settlement, the related cumulative re-measurement gain/loss would be reversed in the Statement of Re-measurement Gains and Losses and the exchange gain or loss in relation to the exchange rate at the date of the item s initial recognition is recognized in the Statement of Operations. (k) Budget figures Budget figures have been provided for comparative purposes and have been derived from the 2017/2018 Budget approved by the Board of Governors of the University on April 6, The budget is reflected in the Statement of Operations and Accumulated Surplus and the Statement of Changes in Net Debt. (l) Expense functions Expense functions have been identified based upon the functional lines of service provided by the University. The University s services are provided by departments and their activities are reported by functional area in the Statement of Operations and Accumulated Surplus. The functional lines, along with the services they provide, are as follows: i) Instruction and support: This function includes activities related to delivering education. This includes instruction, education administration, student support, general administration, and the cost of space, safety, and equipment. ii) Ancillary: This function includes the activities of the ancillary operations. An ancillary operation is one that is generally outside of the normal functions of instruction and research, provides goods and services to students, staff or others, and that charges a fee directly related to the cost of providing the goods or services. Ancillary operations include parking, food services, and bookstores. Costs associated with this function include function-related contracts and general and financial administration and support costs. 9

14 2. Significant accounting policies (continued) (m) Investment in government business enterprises Government business enterprises are accounted for by the modified equity method. Under this method, the University's investment in the business enterprise and its net income and other changes in equity are recorded. No adjustment is made to conform the accounting policies of the government business enterprise to those of the University other than, if other comprehensive income exists, it is accounted for as an adjustment to accumulated surplus of the University. Inter-organizational transactions and balances have not been eliminated, except for any profit or loss on transactions between entities of assets that remain within the entities controlled by the University. The following organizations are controlled government business enterprises and are accounted for by the modified equity method: i) Indo Canadian Education Society, Chandigarh, India, a separate legal entity, administers and delivers business education to students in India using the University's Bachelor of Business curriculum. ii) UFV India Global Education, Chandigarh, India, a separate legal entity, administers and delivers UFV education programs to students in India using the University's curriculum. (n) Contaminated sites A liability for contaminated sites is recognized when a site is not in productive use and the following criteria are met: i) An environmental standard exists; ii) iii) iv) Contamination exceeds the environmental standard; The University is directly responsible or accepts responsibility; It is expected that future economic benefits will be given up; and v) A reasonable estimate of the amount can be made. The liability is recognized as management's estimate of the cost of post-remediation including operation, maintenance and monitoring that are an integral part of the remediation strategy for a contaminated site. 3. Recast of comparative figures During the year the University determined that an adjustment was required in its comparative figures to correct the presentation of the gain on disposal of assets in the Statement of Operations and Accumulated Surplus. This change in presentation resulted in an increase in revenue of $3,351,850 and an offsetting decrease to other income on the Statement of Operations and Accumulated Surplus. This presentation adjustment resulted in a net nil impact to the annual surplus. 10

15 4. Investments (a) Investments recorded at fair value Philips Hager North - UFV Endowment Fund $ 9,472,436 $ 8,517,215 Philips Hager North - CCIBED* Endowment Fund 3,371,623 3,265,986 12,844,059 11,783,201 Investments recorded at cost or amortized cost 56,223,645 43,207,042 69,067,704 54,990,243 Principal portion of endowments (9,911,331) (9,417,551) $ 59,156,373 $ 45,572,692 Investments held with Philips Hager North are recorded at fair value and are comprised of equity instruments quoted in an active market. Investments recorded at cost or amortized cost are comprised of cashable securities with terms ranging from one to five years. *CCIBED - Chair Canada India Business & Economic Development (b) Public Sector Accounting Standards define the fair value of a financial instrument as the amount at which the instrument could be exchanged in a current transaction between willing parties. The University uses the following methods and assumptions to estimate the fair value of each class of financial instruments for which the carrying amounts are included in the Statement of Financial Position under the following captions: (i) Cash and cash equivalents, accounts receivable, investments - non endowment and accounts payables and accrued liabilities - the carrying amounts approximate fair value because of the short maturity or ability to liquidate these instruments. The financial instruments measured at fair value held within each investment are classified according to a hierarchy which includes three levels, reflecting the reliability of the inputs involved in the fair value determination. The different levels are defined as follows: (i) (ii) (iii) Level 1: quoted prices (unadjusted) in active markets for identical assets or liabilities Level 2: inputs other than quoted prices included within Level 1 that are observable for the asset or liability, either directly (i.e. as prices) or indirectly (i.e. derived from prices) Level 3: inputs for the asset or liability that are not based on observable market data (unobservable inputs). The University s instruments are all considered to be level 1 financial instruments for which the fair value is determined based on quoted prices in active markets. Changes in financial instruments valuation methods or in the availability of market observable inputs may result in a transfer between levels. During the year there were no significant transfers of securities between the different levels. 11

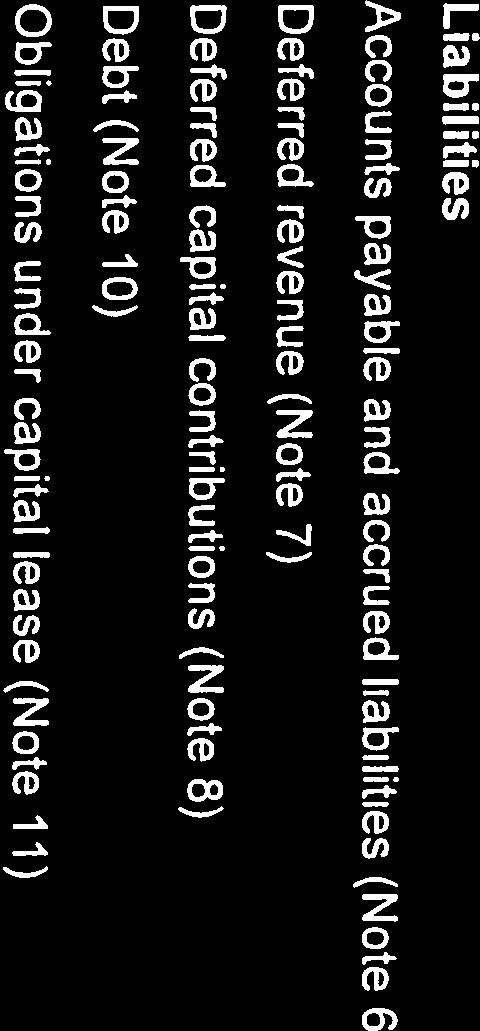

16 5. Investment in government business enterprises The University has controlling interest in the operations of UFV India Global Education and Indo Canadian Education Society located in Chandigarh, India. The operations of Indo Canadian Education Society were transferred to UFV India Global Education and the combined financial information is detailed below. The change in equity is as follows: Equity, beginning of year $ 758,132 $ 55,908 Net earnings 429, ,224 Equity, end of year $ 1,187,277 $ 758,132 Condensed financial information is as follows: Statement of Financial Position Assets $ 1,297,422 $ 952,216 Liabilities (110,145) (194,084) Accumulated surplus $ 1,187,277 $ 758,132 Statement of Operations Revenue $ 2,446,250 $ 3,070,509 Expenses 2,017,105 2,368,285 Annual surplus 429, ,224 Accumulated surplus, beginning of year 758,132 55,908 Accumulated surplus, end of year $ 1,187,277 $ 758, Accounts payable and accrued liabilities Accounts payable and accrued liabilities are comprised of the following: Trades payable $ 9,974,363 $ 8,019,156 Wages payable 270, ,622 Accrued vacation and overtime payable 6,170,275 5,992,704 $ 16,414,925 $ 14,943,482 12

17 7. Deferred revenue Deferred revenue is comprised of the following: 2017 Amounts Received Revenue Recognized 2018 Student tuition fees $ 9,266,946 $ 11,210,491 $ 9,251,195 $ 11,226,242 Student award funding 3,691, , ,738 3,830,356 Special purpose and research funding 3,438,776 4,882,354 4,024,182 4,296,948 Prepaid lease revenue (Note 8) 9,651,260 1,000, ,981 10,372,279 Total $ 26,048,128 $ 18,012,793 $ 14,335,096 $ 29,725, Deferred capital contributions Changes in the deferred capital contributions ("DCC") balance are as follows: Balance, beginning of year $ 93,116,040 $ 96,863,772 Contributions from the Province of British Columbia 6,942,234 3,351,751 Contributions from the Government of Canada - 41,132 Contribution from other restricted resources - 35,188 Transfer to prepaid lease revenue (Note 7) (1,000,000) - DCC recognized on sale of asset held for sale (1,192,352) (317,802) Amortization of deferred capital contributions (7,048,866) (6,858,001) Balance, end of year $ 90,817,056 $ 93,116, Contingent liabilities The University may, from time to time, be involved in legal proceedings, claims, and litigation that arise in the normal course of operations. In the event that any such claims or litigation are resolved against the University, such outcomes or resolutions could have a material effect on the business, financial condition, or results of operations of the University. The University has accrued for claims for which the amounts are known or can reasonably be estimated. The outcome of other claims is undeterminable at this time and accordingly no provision has been made for these claims. 13

18 10. Debt Debt is comprised of the following: BC Immigrant Investment Fund Ltd. (a) $ - $ 10,560,588 Ministry of Finance of British Columbia (b) 10,000,000 - $ 10,000,000 $ 10,560,588 (a) Discharge of long-term loan The University held long-term debt, recorded at amortized cost, with BC Immigrant Investment Fund Ltd. (BCIIF). This debt was secured by a general security agreement payable in quarterly installments of $248,304, including interest at 5.15%, and was fully repaid on August 1, Interest on this debt in the amount of $180,353 ( $554,255) is included in the Statement of Operations and Accumulated Surplus. (b) New financing The University assumed new short-term debt, recorded at amortized cost, with the Ministry of Finance of British Columbia. This debt is payable in full in the amount of $10,125,044, including interest at 1.25% on August 1, Interest on this debt in the amount of $83,363 is included in the Statement of Operations and Accumulated Surplus. 11. Obligations under capital lease Repayments of obligations under capital leases are due as follows: 2018 $ - $ 120, , , ,027 30,027 Total minimum lease payments 150, ,247 Less amounts representing interest at 6.8% (7,402) (21,651) Present value of net minimum capital lease payments $ 142,735 $ 248,596 Total interest expensed on leases for the year was $14,305 ( $21,191) and is included in the statement of operations and accumulated surplus. 14

19 12. Supplemental cash flow information The change in non-cash operating working capital is comprised of the following: Accounts receivable $ 342,648 $ 777,077 Prepaid expenses (628,589) 173,629 Inventories held for resale 405,411 (214,355) Accounts payable and accrued liabilities 1,471,443 2,620,097 Deferred revenue 2,677,697 1,481,137 $ 4,268,610 $ 4,837, Related party transactions The University is related through common ownership to all Province of British Columbia ministries, agencies, school districts, health authorities, colleges, universities, and crown corporations. Transactions with these entities, unless disclosed separately, are considered to be in the normal course of operations and are recorded at the exchange amount. 14. Contractual obligations The nature of the University's activities can result in multi-year contracts and obligations whereby the University will be committed to make future payments. Significant contractual obligations related to operations that can be reasonably estimated are as follows: Long-term lease commitments $ 610,955 $ 516,409 $ 412,649 $ 310,885 $ 59, Contractual rights The University has entered into multi-year contracts with third parties that entitles the University to receive the following amounts: $ 302,740 $ 267,223 $ 192,080 $ 162,464 $ 100,000 15

20 16. Tangible capital assets 2018 Cost Land Buildings Furniture and equipment Computer hardware and software Leasehold improvements Site improvements Library books Assets under construction Balance, beginning of year $ 8,339,408 $ 204,822,720 $ 45,581,183 $ 15,001,342 $ 1,619,974 $ 9,223,312 $ 10,227,249 $ 339,524 $ 295,154,712 Additions - 4,375,178 3,315, , ,695-8,824,965 Transfer to assets held for sale (496,466) (11,926,543) (12,423,009) Transfer of assets under construction - 339, (339,524) - Balance, end of year 7,842, ,610,879 48,896,690 15,997,927 1,619,974 9,223,312 10,364, ,556, Accumulated Amortization Balance, beginning of year - 68,095,303 35,898,446 13,793,724 1,001,720 6,301,451 9,022, ,113,312 Amortization - 4,915,732 2,833, , , , ,521-9,697,806 Transfer to assets held for sale - (6,847,156) (6,847,156) Balance, end of year - 66,163,879 38,732,230 14,579,732 1,131,878 7,082,054 9,274, ,963, Net Book Value 7,842, ,447,000 10,164,460 1,418, ,096 2,141,258 1,090, ,592, Total 2017 Net Book Value $ 8,339,408 $ 136,727,417 $ 9,682,737 $ 1,207,618 $ 618,254 $ 2,921,861 $ 1,204,581 $ 339,524 $ 161,041,400 (a) Assets classified as held for sale The University sold the Chilliwack North property that was held for sale at March 31, 2017 for proceeds of $3,492,515. The University has entered into a purchase and sale agreement for the remainder of the campus in North Chilliwack and the sale is expected to complete within one year. 16

21 17. Financial risk management The University has exposure to the following risks from its use of financial instruments: credit risk, market risk and liquidity risk. The Board of Governors ensures that the University has identified its major risks and ensures that management monitors and controls them. (a) Credit risk Credit risk is the risk of financial loss to the University if a party to a financial instrument fails to meet its contractual obligations. Such risk arises principally from certain financial assets held by the University consisting of cash and cash equivalents, accounts receivable and investments. Accounts receivable: Management believes risk with respect to accounts receivable is limited. Student accounts receivable is a large population of limited amounts where the University has the ability to stop further enrolments and granting of transcripts until payment is made. Other receivables and tax recoveries are generally with governments and other credit-worthy institutions. Investments: The University has an Investment Policy to ensure funds are managed appropriately in order to balance preservation of capital, liquidity requirements and returns. The University retains an external investment firm to manage endowed funds in accordance with its investment policy utilizing diverse agreed upon investment strategies primarily in active trading markets. (b) Market risk Market risk is the risk that changes in market prices, such as interest rates, will affect the University s income. The University cash and cash equivalents and investments include amounts on deposit with financial institutions that earn interest at market rates. The University manages its cash by maximizing the interest income earned on excess funds while maintaining the liquidity necessary to conduct operations on a day to day basis. Fluctuation in market rates of interest does not have a significant effect on the University`s cash and cash equivalents and investments. The primary objective of the University with respect to its investment of endowed funds is to ensure the security of principal amounts while achieving a satisfactory investment return. (c) Liquidity risk Liquidity risk is the risk that the University will not be able to meet its financial obligations as they become due. The University meets its liquidity risk requirements by continually monitoring actual and forecasted cash flows and anticipating investment and financing activities to ensure, as far as possible, that it will always have sufficient liquidity to meet its liabilities when due. 17

22 18. Investments - endowments Changes to the endowment balances are as follows: Balance, beginning of year $ 9,417,551 $ 8,966,345 Contributions received during the year 435, ,121 Capitalization of endowment surplus 58,226 46,085 Balance, end of year $ 9,911,331 $ 9,417, Expenses by object The following is a summary of expenses by object: Salaries and wages $ 71,385,007 $ 68,149,902 Employee benefits 16,862,695 16,867,473 Amortization of tangible capital assets 9,697,806 9,555,515 Contracted services 5,654,081 5,884,514 Other operating expenses 5,619,563 5,258,942 Supplies and books 4,654,743 4,169,370 Cost of goods sold 3,142,445 2,790,951 Travel and conferences 2,727,373 2,461,341 Utilities 2,063,043 1,952,002 Scholarships and bursaries 1,667,491 1,999,355 Minor renovations and repairs 1,424,185 1,186,827 Rentals and leases 829, ,168 Printing and advertising 627, ,058 Interest 274, ,445 $ 126,629,232 $ 122,149,863 18

23 20. Pension plans The University and its employees contribute to the College Pension Plan and Municipal Pension Plan (jointly trusteed pension plans). The boards of trustees for these plans, representing plan members and employers, are responsible for administering the pension plans, including investing assets and administering benefits. The plans are multi-employer defined benefit pension plans. Basic pension benefits are based on a formula. As at August 31, 2017, the College Pension Plan has about 14,000 active members, and approximately 7,500 retired members. As at December 31, 2016, the Municipal Pension Plan has about 193,000 active members, including approximately 5,800 from colleges. Every three years, an actuarial valuation is performed to assess the financial position of the plans and adequacy of plan funding. The actuary determines an appropriate combined employer and member contribution rate to fund the plans. The actuary s calculated contribution rate is based on the entry- age normal cost method, which produces the long-term rate of member and employer contributions sufficient to provide benefits for average future entrants to the plans. This rate may be adjusted for the amortization of any actuarial funding surplus and will be adjusted for the amortization of any unfunded actuarial liability. The most recent actuarial valuation for the College Pension Plan as at August 31, 2015, indicated a $67 million surplus for basic pension benefits on a going concern basis. The most recent valuation for the Municipal Pension Plan as at December 31, 2015, indicated a $2,224 million funding surplus for basic pension benefits on a going concern basis. As a result of the 2015 basic account actuarial valuation surplus and pursuant to the joint trustee agreement, $1,927 million was transferred to the rate stabilization account and $297 million of the surplus ensured the required contribution rates remained unchanged. The University paid $6,465,497 ( $6,185,256) for employer contributions to the plans in fiscal The next valuation for the College Pension Plan will be as at August 31, 2018, with results available in The next valuation for the Municipal Pension Plan will be December 31, 2018, with results available in Employers participating in the plans record their pension expense as the amount of employer contributions made during the fiscal year (defined contribution pension plan accounting). This is because the plans record accrued liabilities and accrued assets for each plan in aggregate, resulting in no consistent and reliable basis for allocating the obligation, assets and cost to individual employers participating in the plans. 21. Comparative information Certain comparative information has been reclassified to conform with the financial statement presentation adopted in the current period. 19

This Page Intentionally Left Blank

ANNUAL FINANCIAL REPORT 2016-2017 This Page Intentionally Left Blank Financial Discussion & Analysis FINANCIAL DISCUSSION AND ANALYSIS The attached financial statements present the financial results of

ANNUAL FINANCIAL REPORT 2016-2017 This Page Intentionally Left Blank Financial Discussion & Analysis FINANCIAL DISCUSSION AND ANALYSIS The attached financial statements present the financial results of

KWANTLEN POLYTECHNIC UNIVERSITY

Financial Statements of KWANTLEN POLYTECHNIC UNIVERSITY KPMG LLP 3 rd Floor 8506 200 th Street Langley BC V2Y 0M1 Canada Telephone (604) 455-4000 Fax (604) 881-4988 INDEPENDENT AUDITORS REPORT To the

Financial Statements of KWANTLEN POLYTECHNIC UNIVERSITY KPMG LLP 3 rd Floor 8506 200 th Street Langley BC V2Y 0M1 Canada Telephone (604) 455-4000 Fax (604) 881-4988 INDEPENDENT AUDITORS REPORT To the

Consolidated Financial Statements of CAPILANO UNIVERSITY. Year ended March 31, 2018

Consolidated Financial Statements of CAPILANO UNIVERSITY STATEMENT OF MANAGEMENT RESPONSIBILITY Management is responsible for the preparation of the annual financial statements, and has prepared the accompanying

Consolidated Financial Statements of CAPILANO UNIVERSITY STATEMENT OF MANAGEMENT RESPONSIBILITY Management is responsible for the preparation of the annual financial statements, and has prepared the accompanying

NORTH ISLAND COLLEGE FINANCIAL STATEMENTS For the year ended March 31, 2017

NORTH ISLAND COLLEGE FINANCIAL STATEMENTS For the year ended March 31, 2017 Index to the Financial Statements For the year ended March 31, 2017 Page INDEPENDENT AUDITORS' REPORT FINANCIAL STATEMENTS Statement

NORTH ISLAND COLLEGE FINANCIAL STATEMENTS For the year ended March 31, 2017 Index to the Financial Statements For the year ended March 31, 2017 Page INDEPENDENT AUDITORS' REPORT FINANCIAL STATEMENTS Statement

Consolidated Financial Statements of CAPILANO UNIVERSITY. Years ended March 31, 2013 and 2012

Consolidated Financial Statements of CAPILANO UNIVERSITY ABCD KPMG LLP Chartered Accountants Metrotower II Suite 2400-4720 Kingsway Burnaby BC V5H 4N2 Canada Telephone (604) 527-3600 Fax (604) 527-3636

Consolidated Financial Statements of CAPILANO UNIVERSITY ABCD KPMG LLP Chartered Accountants Metrotower II Suite 2400-4720 Kingsway Burnaby BC V5H 4N2 Canada Telephone (604) 527-3600 Fax (604) 527-3636

Consolidated Financial Statements of CAPILANO UNIVERSITY. Year ended March 31, 2017

Consolidated Financial Statements of STATEMENT OF MANAGEMENT RESPONSIBILITY Management is responsible for the preparation of the annual financial statements, and has prepared the accompanying consolidated

Consolidated Financial Statements of STATEMENT OF MANAGEMENT RESPONSIBILITY Management is responsible for the preparation of the annual financial statements, and has prepared the accompanying consolidated

Financial Statements of DOUGLAS COLLEGE. Year ended March 31, 2017

Financial Statements of DOUGLAS COLLEGE KPMG LLP Metro Tower I 4710 Kingsway, Suite 2400 Burnaby BC V5H 4M2 Canada Telephone (604) 527-3600 Fax (604) 527-3636 INDEPENDENT AUDITORS REPORT To the Board

Financial Statements of DOUGLAS COLLEGE KPMG LLP Metro Tower I 4710 Kingsway, Suite 2400 Burnaby BC V5H 4M2 Canada Telephone (604) 527-3600 Fax (604) 527-3636 INDEPENDENT AUDITORS REPORT To the Board

Consolidated Financial Statements

Consolidated Financial Statements Year Ended March 31, 2017 www.unbc.ca/finance/statements University of Northern British Columbia Consolidated Financial Statements Table of Contents Page STATEMENT OF

Consolidated Financial Statements Year Ended March 31, 2017 www.unbc.ca/finance/statements University of Northern British Columbia Consolidated Financial Statements Table of Contents Page STATEMENT OF

Independent auditors report

Independent auditors report To the Board of Governors of Okanagan College and the Ministry of Advanced Education Grant Thornton LLP 200-1633 Ellis Street Kelowna BC V1Y 2A8 T (250) 712-6800 (800) 661-4244

Independent auditors report To the Board of Governors of Okanagan College and the Ministry of Advanced Education Grant Thornton LLP 200-1633 Ellis Street Kelowna BC V1Y 2A8 T (250) 712-6800 (800) 661-4244

OKANAGAN COLLEGE FINANCIAL STATEMENTS MARCH 31, 2015

OKANAGAN COLLEGE FINANCIAL STATEMENTS MARCH 31, 2015 Independent auditors report To the Board of Governors of Okanagan College and the Ministry of Advanced Education Grant Thornton LLP 200-1633 Ellis Street

OKANAGAN COLLEGE FINANCIAL STATEMENTS MARCH 31, 2015 Independent auditors report To the Board of Governors of Okanagan College and the Ministry of Advanced Education Grant Thornton LLP 200-1633 Ellis Street

VANCOUVER ISLAND UNIVERSITY

CONSOLIDATED FINANCIAL STATEMENTS MARCH 31, 2016 Consolidated Financial Statements Table of Contents Statement of Administrative Responsibility for Financial Statements Independent Auditors' Report Consolidated

CONSOLIDATED FINANCIAL STATEMENTS MARCH 31, 2016 Consolidated Financial Statements Table of Contents Statement of Administrative Responsibility for Financial Statements Independent Auditors' Report Consolidated

CONSOLIDATED FINANCIAL STATEMENTS YEAR ENDED MARCH 31, 2017

CONSOLIDATED FINANCIAL STATEMENTS YEAR ENDED MARCH 31, 2017 Table of Contents Statement of Management Responsibility... 2 Consolidated Statement of Financial Position... 5 Consolidated Statement of Operations...

CONSOLIDATED FINANCIAL STATEMENTS YEAR ENDED MARCH 31, 2017 Table of Contents Statement of Management Responsibility... 2 Consolidated Statement of Financial Position... 5 Consolidated Statement of Operations...

THOMPSON RIVERS UNIVERSITY. Consolidated Financial Statements. For the year ended March 31, 2015

g ~ THOMPSON RIVERS UNIVERSITY Consolidated Financial Statements For the year ended March 31, 2015 Index to Consolidated Financial Statements Statement of Administrative Responsibility for Consolidated

g ~ THOMPSON RIVERS UNIVERSITY Consolidated Financial Statements For the year ended March 31, 2015 Index to Consolidated Financial Statements Statement of Administrative Responsibility for Consolidated

School District No. 75 (Mission)

") Audited Financial Statements of June 30, 2017 September 07, 2017 11:39 June 30, 2017 Table of Contents Management Report... 1 Independent Auditors' Report... 2-3 Statement of Financial Position - Statement

Audited Financial Statements of June 30, 2017 September 07, 2017 11:39 June 30, 2017 Table of Contents Management Report... 1 Independent Auditors' Report... 2-3 Statement of Financial Position - Statement

JUSTICE INSTITUTE OF BRITISH COLUMBIA

Financial Statements of KPMG LLP Chartered Accountants Metrotower II 4720 Kingsway, Suite 2400 Burnaby, BC V5H 4N2 Telephone (604) 527-3600 Fax (604) 527-3636 Internet www.kpmg.ca INDEPENDENT AUDITORS

Financial Statements of KPMG LLP Chartered Accountants Metrotower II 4720 Kingsway, Suite 2400 Burnaby, BC V5H 4N2 Telephone (604) 527-3600 Fax (604) 527-3636 Internet www.kpmg.ca INDEPENDENT AUDITORS

Financial Statements of CAMOSUN COLLEGE. Year ended March 31, 2018

Financial Statements of CAMOSUN COLLEGE MANAGEMENT S RESPONSIBILITY FOR THE FINANCIAL STATEMENTS The financial statements have been prepared by management in accordance with Section 23.1 of the Budget

Financial Statements of CAMOSUN COLLEGE MANAGEMENT S RESPONSIBILITY FOR THE FINANCIAL STATEMENTS The financial statements have been prepared by management in accordance with Section 23.1 of the Budget

School District No. 27 (Cariboo-Chilcotin)

") Audited Financial Statements of School District No. 27 (Cariboo-Chilcotin) June 30, 2018 September 25, 2018 15:30 School District No. 27 (Cariboo-Chilcotin) June 30, 2018 Table of Contents Management Report...

Audited Financial Statements of School District No. 27 (Cariboo-Chilcotin) June 30, 2018 September 25, 2018 15:30 School District No. 27 (Cariboo-Chilcotin) June 30, 2018 Table of Contents Management Report...

2013 Financial Statements March 31,

2013 Financial Statements March 31, 2013 www.okanagan. bc.ca STATEMENT 2 OKANAGAN COLLEGE STATEMENT OF OPERATIONS AND ACCUMULATED SURPLUS FOR THE YEAR ENDED MARCH 31, 2013 Budget 2013 2013 2012 Revenue

2013 Financial Statements March 31, 2013 www.okanagan. bc.ca STATEMENT 2 OKANAGAN COLLEGE STATEMENT OF OPERATIONS AND ACCUMULATED SURPLUS FOR THE YEAR ENDED MARCH 31, 2013 Budget 2013 2013 2012 Revenue

Financial Statements of CAMOSUN COLLEGE. Year ended March 31, 2016

Financial Statements of CAMOSUN COLLEGE Statement of Management Responsibility The financial statements have been prepared by management in accordance with Section 23.1 of the Budget Transparency and Accountability

Financial Statements of CAMOSUN COLLEGE Statement of Management Responsibility The financial statements have been prepared by management in accordance with Section 23.1 of the Budget Transparency and Accountability

Financial Statements of CAMOSUN COLLEGE. Year ended March 31, 2017

Financial Statements of CAMOSUN COLLEGE KPMG LLP St. Andrew s Square II 800-730 View Street Victoria BC V8W 3Y7 Canada Telephone 250-480-3500 Fax 250-480-3539 INDEPENDENT AUDITORS REPORT To the Board

Financial Statements of CAMOSUN COLLEGE KPMG LLP St. Andrew s Square II 800-730 View Street Victoria BC V8W 3Y7 Canada Telephone 250-480-3500 Fax 250-480-3539 INDEPENDENT AUDITORS REPORT To the Board

VANCOUVER COMMUNITY COLLEGE

Financial Statements of VANCOUVER COMMUNITY COLLEGE Statement of Management Responsibility The financial statements have been prepared by management in accordance with Section 23.1 of the Budget Transparency

Financial Statements of VANCOUVER COMMUNITY COLLEGE Statement of Management Responsibility The financial statements have been prepared by management in accordance with Section 23.1 of the Budget Transparency

VANCOUVER ISLAND UNIVERSITY

CONSOLIDATED FINANCIAL STATEMENTS MARCH 31, 2014 Consolidated Financial Statements Table of Contents Statement of Administrative Responsibility for Financial Statements Independent Auditors' Report Consolidated

CONSOLIDATED FINANCIAL STATEMENTS MARCH 31, 2014 Consolidated Financial Statements Table of Contents Statement of Administrative Responsibility for Financial Statements Independent Auditors' Report Consolidated

SELKIRK COLLEGE CONSOLIDATED FINANCIAL STATEMENTS MARCH 31, 2017

CONSOLIDATED FINANCIAL STATEMENTS MARCH 31, 2017 INDEX TO THE CONSOLIDATED FINANCIAL STATEMENTS Management's Responsibility for Financial Reporting Independent Auditor's Report Financial Statements Consolidated

CONSOLIDATED FINANCIAL STATEMENTS MARCH 31, 2017 INDEX TO THE CONSOLIDATED FINANCIAL STATEMENTS Management's Responsibility for Financial Reporting Independent Auditor's Report Financial Statements Consolidated

Vancouver Community College. Statement of Financial Information. Schedules required by the Financial Information Act

Vancouver Community College Statement of Financial Information Schedules required by the Financial Information Act For the year ended March 31, 2018 Vancouver Community College Statement of Financial Information

Vancouver Community College Statement of Financial Information Schedules required by the Financial Information Act For the year ended March 31, 2018 Vancouver Community College Statement of Financial Information

SIR SANDFORD FLEMING COLLEGE OF APPLIED ARTS AND TECHNOLOGY

Financial Statements of SIR SANDFORD FLEMING COLLEGE OF APPLIED ARTS AND TECHNOLOGY KPMG LLP Vaughan Metropolitan Centre 100 New Park Place, Suite 1400 Vaughan ON L4K 0J3 Canada Tel 905-265-5900 Fax 905-265-6390

Financial Statements of SIR SANDFORD FLEMING COLLEGE OF APPLIED ARTS AND TECHNOLOGY KPMG LLP Vaughan Metropolitan Centre 100 New Park Place, Suite 1400 Vaughan ON L4K 0J3 Canada Tel 905-265-5900 Fax 905-265-6390

CONSOLIDATED FINANCIAL STATEMENTS

CONSOLIDATED FINANCIAL STATEMENTS For year ended March 31, 2016 Vancouver, B.C. Canada Consolidated Financial Statements Statement of Management Responsibility The consolidated financial statements of

CONSOLIDATED FINANCIAL STATEMENTS For year ended March 31, 2016 Vancouver, B.C. Canada Consolidated Financial Statements Statement of Management Responsibility The consolidated financial statements of

CONSOLIDATED FINANCIAL STATEMENTS

For year ended March 31, 2017 Vancouver, B.C. Canada KPMG LLP PO Box 10426 777 Dunsmuir Street Vancouver BC V7Y 1K3 Canada Telephone (604) 691-3000 Fax (604) 691-3031 INDEPENDENT AUDITORS REPORT To the

For year ended March 31, 2017 Vancouver, B.C. Canada KPMG LLP PO Box 10426 777 Dunsmuir Street Vancouver BC V7Y 1K3 Canada Telephone (604) 691-3000 Fax (604) 691-3031 INDEPENDENT AUDITORS REPORT To the

BOARD OF EDUCATION OF SCHOOL DISTRICT NO. 61 (GREATER VICTORIA) FINANCIAL STATEMENTS FOR THE YEAR ENDED JUNE 30, 2016

FINANCIAL STATEMENTS FOR THE YEAR ENDED JUNE 30, 2016") BOARD OF EDUCATION OF SCHOOL DISTRICT NO. 61 (GREATER VICTORIA) FINANCIAL STATEMENTS FOR THE YEAR ENDED JUNE 30, 2016 Audited Financial Statements of June 30, 2016 September 19, 2016 15:34 June 30, 2016

BOARD OF EDUCATION OF SCHOOL DISTRICT NO. 61 (GREATER VICTORIA) FINANCIAL STATEMENTS FOR THE YEAR ENDED JUNE 30, 2016 Audited Financial Statements of June 30, 2016 September 19, 2016 15:34 June 30, 2016

School District No. 22 (Vernon)

") Consolidated Audited Financial Statements of School District No. 22 (Vernon) June 30, 2014 September 24, 2014 9:14 School District No. 22 (Vernon) June 30, 2014 Table of Contents Management Report... 1

Consolidated Audited Financial Statements of School District No. 22 (Vernon) June 30, 2014 September 24, 2014 9:14 School District No. 22 (Vernon) June 30, 2014 Table of Contents Management Report... 1

School District No. 62 (Sooke)

") Audited Financial Statements of School District No. 62 (Sooke) June 30, 2018 September 20, 2018 12:07 School District No. 62 (Sooke) June 30, 2018 Table of Contents Management Report... 1 Independent Auditors'

Audited Financial Statements of School District No. 62 (Sooke) June 30, 2018 September 20, 2018 12:07 School District No. 62 (Sooke) June 30, 2018 Table of Contents Management Report... 1 Independent Auditors'

NOVA SCOTIA COMMUNITY COLLEGE

Consolidated Financial Statements of NOVA SCOTIA COMMUNITY COLLEGE March 31, 2017 KPMG LLP Telephone (902) 492-6000 Suite 1500 Purdy s Wharf Tower 1 Fax (902) 492-1307 1959 Upper Water Street Internet

Consolidated Financial Statements of NOVA SCOTIA COMMUNITY COLLEGE March 31, 2017 KPMG LLP Telephone (902) 492-6000 Suite 1500 Purdy s Wharf Tower 1 Fax (902) 492-1307 1959 Upper Water Street Internet

School District No. 45 (West Vancouver)

") Audited Financial Statements of June 30, 2017 September 20, 2017 11:27 June 30, 2017 Table of Contents Management Report... 1 Independent Auditors' Report... 2-3 Statement of Financial Position - Statement

Audited Financial Statements of June 30, 2017 September 20, 2017 11:27 June 30, 2017 Table of Contents Management Report... 1 Independent Auditors' Report... 2-3 Statement of Financial Position - Statement

School District No. 36 (Surrey) June 30, 2015

June 30, 2015") Financial Statements June 30, 2015 June 30, 2015 Table of Contents Management Report... 1 Independent Auditors' Report... 2-3 Statement of Financial Position - Statement 1... 4 Statement of Operations

Financial Statements June 30, 2015 June 30, 2015 Table of Contents Management Report... 1 Independent Auditors' Report... 2-3 Statement of Financial Position - Statement 1... 4 Statement of Operations

VANCOUVER ISLAND HEALTH AUTHORITY

Consolidated Financial Statements of VANCOUVER ISLAND HEALTH AUTHORITY ABCD KPMG LLP Chartered Accountants St. Andrew s Square II Telephone (250) 480-3500 800-730 View Street Telefax (250) 480-3539 Victoria

Consolidated Financial Statements of VANCOUVER ISLAND HEALTH AUTHORITY ABCD KPMG LLP Chartered Accountants St. Andrew s Square II Telephone (250) 480-3500 800-730 View Street Telefax (250) 480-3539 Victoria

JUSTICE INSTITUTE OF BRITISH COLUMBIA

Financial Statements of JUSTICE INSTITUTE OF BRITISH COLUMBIA ABCD KPMG LLP Chartered Accountants Box 10426, 777 Dunsmuir Street Vancouver BC V7Y 1K3 Telephone (604) 691-3000 Telefax (604) 691-3031 Internet

Financial Statements of JUSTICE INSTITUTE OF BRITISH COLUMBIA ABCD KPMG LLP Chartered Accountants Box 10426, 777 Dunsmuir Street Vancouver BC V7Y 1K3 Telephone (604) 691-3000 Telefax (604) 691-3031 Internet

Financial Statements of INNOVATE BC (FORMERLY BRITISH COLUMBIA INNOVATION COUNCIL ) Year ended March 31, 2018

Year ended March 31, 2018") Financial Statements of KPMG LLP Metro Tower I 4710 Kingsway, Suite 2400 Burnaby BC V5H 4M2 Canada Telephone (604) 527-3600 Fax (604) 527-3636 INDEPENDENT AUDITORS' REPORT To the Board of Directors and

Financial Statements of KPMG LLP Metro Tower I 4710 Kingsway, Suite 2400 Burnaby BC V5H 4M2 Canada Telephone (604) 527-3600 Fax (604) 527-3636 INDEPENDENT AUDITORS' REPORT To the Board of Directors and

Financial Statements of VANCOUVER ECONOMIC COMMISSION

Financial Statements of VANCOUVER ECONOMIC COMMISSION Year Ended December 31, 2017 1 KPMG LLP Metro Tower I 4710 Kingsway, Suite 2400 Burnaby BC V5H 4M2 Canada Telephone (604) 527-3600 Fax (604) 527-3636

Financial Statements of VANCOUVER ECONOMIC COMMISSION Year Ended December 31, 2017 1 KPMG LLP Metro Tower I 4710 Kingsway, Suite 2400 Burnaby BC V5H 4M2 Canada Telephone (604) 527-3600 Fax (604) 527-3636

School District No. 8 (Kootenay Lake)

") Audited Financial Statements of School District No. 8 (Kootenay Lake) June 30, 2018 September 28, 2018 12:52 School District No. 8 (Kootenay Lake) June 30, 2018 Table of Contents Management Report... 1

Audited Financial Statements of School District No. 8 (Kootenay Lake) June 30, 2018 September 28, 2018 12:52 School District No. 8 (Kootenay Lake) June 30, 2018 Table of Contents Management Report... 1

School District No. 22 (Vernon)

") Consolidated Audited Financial Statements of June 30, 2017 September 08, 2017 14:58 June 30, 2017 Table of Contents Management Report... 1 Independent Auditors' Report... 2-3 Consolidated Statement of

Consolidated Audited Financial Statements of June 30, 2017 September 08, 2017 14:58 June 30, 2017 Table of Contents Management Report... 1 Independent Auditors' Report... 2-3 Consolidated Statement of

VANCOUVER ISLAND HEALTH AUTHORITY

Consolidated Financial Statements of VANCOUVER ISLAND HEALTH AUTHORITY KPMG LLP St. Andrew s Square II 800-730 View Street Victoria BC V8W 3Y7 Canada Telephone 250-480-3500 Fax 250-480-3539 INDEPENDENT

Consolidated Financial Statements of VANCOUVER ISLAND HEALTH AUTHORITY KPMG LLP St. Andrew s Square II 800-730 View Street Victoria BC V8W 3Y7 Canada Telephone 250-480-3500 Fax 250-480-3539 INDEPENDENT

School District No. 8 (Kootenay Lake)

") Audited Financial Statements of School District No. 8 (Kootenay Lake) June 30, 2017 September 19, 2017 13:47 School District No. 8 (Kootenay Lake) June 30, 2017 Table of Contents Management Report... 1

Audited Financial Statements of School District No. 8 (Kootenay Lake) June 30, 2017 September 19, 2017 13:47 School District No. 8 (Kootenay Lake) June 30, 2017 Table of Contents Management Report... 1

School District No. 47 (Powell River)

") Audited Financial Statements of School District No. 47 (Powell River) June 30, 2014 October 01, 2014 10:30 School District No. 47 (Powell River) June 30, 2014 Table of Contents Management Report... 1 Independent

Audited Financial Statements of School District No. 47 (Powell River) June 30, 2014 October 01, 2014 10:30 School District No. 47 (Powell River) June 30, 2014 Table of Contents Management Report... 1 Independent

RIGHT nscc now.ca HERE.

RIGHT HERE. Consolidated Financial Statements 2015 I have a big heart and I want to use it. READ MORE: bit.ly/tyradenny CONSOLIDATED FINANCIAL STATEMENTS 2015 INDEPENDENT AUDITORS REPORT To the Board of

RIGHT HERE. Consolidated Financial Statements 2015 I have a big heart and I want to use it. READ MORE: bit.ly/tyradenny CONSOLIDATED FINANCIAL STATEMENTS 2015 INDEPENDENT AUDITORS REPORT To the Board of

Independent auditor s report

Independent auditor s report Grant Thornton LLP 200-1633 Ellis Street Kelowna, BC V1Y 2A8 T +1 250 712 6800 F +1 250 712 6850 www.grantthornton.ca To the Board of Education of School District No. 23 (Central

Independent auditor s report Grant Thornton LLP 200-1633 Ellis Street Kelowna, BC V1Y 2A8 T +1 250 712 6800 F +1 250 712 6850 www.grantthornton.ca To the Board of Education of School District No. 23 (Central

BRITISH COLUMBIA CANCER AGENCY BRANCH

Consolidated Financial Statements of BRITISH COLUMBIA CANCER AGENCY BRANCH May 28, 2018 Independent Auditor s Report To the Board of British Columbia Cancer Agency Branch We have audited the accompanying

Consolidated Financial Statements of BRITISH COLUMBIA CANCER AGENCY BRANCH May 28, 2018 Independent Auditor s Report To the Board of British Columbia Cancer Agency Branch We have audited the accompanying

UNIVERSITY OF VICTORIA STATEMENT OF FINANCIAL INFORMATION MARCH 31, 2015

STATEMENT OF FINANCIAL INFORMATION MARCH 31, 2015 Published in accordance with the requirements of the Financial Information Act TABLE OF CONTENTS Financial Information Approval Statement of Administrative

STATEMENT OF FINANCIAL INFORMATION MARCH 31, 2015 Published in accordance with the requirements of the Financial Information Act TABLE OF CONTENTS Financial Information Approval Statement of Administrative

Consolidated Financial Statements 2016

Consolidated Financial Statements 2016 CONSOLIDATED FINANCIAL STATEMENTS INDEPENDENT AUDITORS REPORT To the Board of Governors of the Nova Scotia Community College We have audited the accompanying consolidated

Consolidated Financial Statements 2016 CONSOLIDATED FINANCIAL STATEMENTS INDEPENDENT AUDITORS REPORT To the Board of Governors of the Nova Scotia Community College We have audited the accompanying consolidated

School District No. 58 (Nicola-Similkameen)

") Audited Financial Statements of June 30, 2017 September 08, 2017 9:00 June 30, 2017 Table of Contents Management Report... 1 Independent Auditors' Report... 2 Statement of Financial Position - Statement

Audited Financial Statements of June 30, 2017 September 08, 2017 9:00 June 30, 2017 Table of Contents Management Report... 1 Independent Auditors' Report... 2 Statement of Financial Position - Statement

Table of Contents. Athabasca University. Year ended March 31, 2017

Financial Statements March 31, 2017 Table of Contents Statement of Management Responsibility.......................... 1 Independent Auditor's Report................................... 2 Financial Statements

Financial Statements March 31, 2017 Table of Contents Statement of Management Responsibility.......................... 1 Independent Auditor's Report................................... 2 Financial Statements

CONSOLIDATED FINANCIAL STATEMENTS 2017

CONSOLIDATED FINANCIAL STATEMENTS 2017 CONSOLIDATED FINANCIAL STATEMENTS INDEPENDENT AUDITORS REPORT To the Board of Governors of the Nova Scotia Community College We have audited the accompanying consolidated

CONSOLIDATED FINANCIAL STATEMENTS 2017 CONSOLIDATED FINANCIAL STATEMENTS INDEPENDENT AUDITORS REPORT To the Board of Governors of the Nova Scotia Community College We have audited the accompanying consolidated

INTERIOR HEALTH AUTHORITY

Financial Statements of INTERIOR HEALTH AUTHORITY KPMG LLP Telephone (250) 979-7150 200-3200 Richter Street Fax (250) 763-0044 Kelowna BC www.kpmg.ca V1W 5K9 INDEPENDENT AUDITORS' REPORT To the Board

Financial Statements of INTERIOR HEALTH AUTHORITY KPMG LLP Telephone (250) 979-7150 200-3200 Richter Street Fax (250) 763-0044 Kelowna BC www.kpmg.ca V1W 5K9 INDEPENDENT AUDITORS' REPORT To the Board

PROVINCIAL HEALTH SERVICES AUTHORITY

Consolidated Financial Statements of PROVINCIAL HEALTH SERVICES AUTHORITY June 29, 2016 Independent Auditor s Report To the Board of Provincial Health Services Authority and Minister of Health, Province

Consolidated Financial Statements of PROVINCIAL HEALTH SERVICES AUTHORITY June 29, 2016 Independent Auditor s Report To the Board of Provincial Health Services Authority and Minister of Health, Province

To the Board of Education of School District No. 53 (Okanagan Similkameen), and To the Minister of Education, Province of British Columbia

, and To the Minister of Education, Province of British Columbia") INDEPENDENT AUDITOR'S REPORT To the Board of Education of School District No. 53 (Okanagan Similkameen), and To the Minister of Education, Province of British Columbia I have audited the accompanying consolidated

INDEPENDENT AUDITOR'S REPORT To the Board of Education of School District No. 53 (Okanagan Similkameen), and To the Minister of Education, Province of British Columbia I have audited the accompanying consolidated

ST. JOSEPH S GENERAL HOSPITAL

Financial Statements of ST. JOSEPH S GENERAL HOSPITAL Management s Responsibility for the Financial Statements Management is responsible for the preparation and presentation of the accompanying financial

Financial Statements of ST. JOSEPH S GENERAL HOSPITAL Management s Responsibility for the Financial Statements Management is responsible for the preparation and presentation of the accompanying financial

FINANCIAL STATEMENTS APRIL 30, 2018

FINANCIAL STATEMENTS APRIL 30, 2018 UNIVERSITY OF WATERLOO FINANCIAL STATEMENTS APRIL 30, 2018 I N D E X Statement of Management Responsibility 1 Independent Auditors' Report 2 Financial Statements Balance

FINANCIAL STATEMENTS APRIL 30, 2018 UNIVERSITY OF WATERLOO FINANCIAL STATEMENTS APRIL 30, 2018 I N D E X Statement of Management Responsibility 1 Independent Auditors' Report 2 Financial Statements Balance

School District No. 85 (Vancouver Island North)

") Audited Financial Statements of School District No. 85 (Vancouver Island North) June 30, 2017 September 01, 2017 15:49 School District No. 85 (Vancouver Island North) June 30, 2017 Table of Contents Management

Audited Financial Statements of School District No. 85 (Vancouver Island North) June 30, 2017 September 01, 2017 15:49 School District No. 85 (Vancouver Island North) June 30, 2017 Table of Contents Management

COMMUNITY SOCIAL SERVICES EMPLOYERS ASSOCIATION OF BRITISH COLUMBIA

Financial Statements of COMMUNITY SOCIAL SERVICES EMPLOYERS ASSOCIATION OF BRITISH COLUMBIA KPMG LLP Metro Tower I 4710 Kingsway, Suite 2400 Burnaby BC V5H 4M2 Canada Telephone (604) 527-3600 Fax (604)

Financial Statements of COMMUNITY SOCIAL SERVICES EMPLOYERS ASSOCIATION OF BRITISH COLUMBIA KPMG LLP Metro Tower I 4710 Kingsway, Suite 2400 Burnaby BC V5H 4M2 Canada Telephone (604) 527-3600 Fax (604)

THE CAMBRIAN COLLEGE OF APPLIED ARTS AND TECHNOLOGY

Consolidated Financial Statements of THE CAMBRIAN COLLEGE OF APPLIED ARTS Index to Consolidated Financial Statements and Schedules Page Independent Auditors Report Consolidated Statement of Financial Position

Consolidated Financial Statements of THE CAMBRIAN COLLEGE OF APPLIED ARTS Index to Consolidated Financial Statements and Schedules Page Independent Auditors Report Consolidated Statement of Financial Position

CONSOLIDATED FINANCIAL STATEMENTS

For year ended March 31, 2018 Vancouver, B.C. Canada Consolidated Financial Statements Year ended March 31, 2018 Statement of Management Responsiblllty The consolidated financial statements of the University

For year ended March 31, 2018 Vancouver, B.C. Canada Consolidated Financial Statements Year ended March 31, 2018 Statement of Management Responsiblllty The consolidated financial statements of the University

School District No. 37 (Delta)

") Audited Financial Statements of School District No. 37 (Delta) June 30, 2015 September 10, 2015 16:15 School District No. 37 (Delta) June 30, 2015 Table of Contents Management Report... 1 Independent Auditors'

Audited Financial Statements of School District No. 37 (Delta) June 30, 2015 September 10, 2015 16:15 School District No. 37 (Delta) June 30, 2015 Table of Contents Management Report... 1 Independent Auditors'

SIR SANDFORD FLEMING COLLEGE OF APPLIED ARTS AND TECHNOLOGY

Financial Statements of SIR SANDFORD FLEMING COLLEGE OF APPLIED ARTS AND TECHNOLOGY KPMG LLP Telephone (416) 228-7000 Yonge Corporate Centre Fax (416) 228-7123 4100 Yonge Street Suite 200 Internet www.kpmg.ca

Financial Statements of SIR SANDFORD FLEMING COLLEGE OF APPLIED ARTS AND TECHNOLOGY KPMG LLP Telephone (416) 228-7000 Yonge Corporate Centre Fax (416) 228-7123 4100 Yonge Street Suite 200 Internet www.kpmg.ca

UNIVERSITY OF WATERLOO FINANCIAL STATEMENTS

UNIVERSITY OF WATERLOO FINANCIAL STATEMENTS APRIL 30, 2015 I N D E X Statement of Management Responsibility 1 Independent Auditors' Report 2 Financial Statements Balance Sheet 3 Statement of Operations

UNIVERSITY OF WATERLOO FINANCIAL STATEMENTS APRIL 30, 2015 I N D E X Statement of Management Responsibility 1 Independent Auditors' Report 2 Financial Statements Balance Sheet 3 Statement of Operations

The Conestoga College Institute of Technology and Advanced Learning FINANCIAL STATEMENTS

The Conestoga College Institute of Technology and Advanced Learning FINANCIAL STATEMENTS March 31, 2018 May 28, 2018 Independent Auditor s Report To the Board of Governors of The Conestoga College Institute

The Conestoga College Institute of Technology and Advanced Learning FINANCIAL STATEMENTS March 31, 2018 May 28, 2018 Independent Auditor s Report To the Board of Governors of The Conestoga College Institute

Financial Statements March 31, 2014

Financial Statements March 31, 2014 Financial Statements Table of Contents Auditor s Report...3 Financial Statements Statement of Financial Position...4 Statement of Operations...5 Statement of Cash Flows...6

Financial Statements March 31, 2014 Financial Statements Table of Contents Auditor s Report...3 Financial Statements Statement of Financial Position...4 Statement of Operations...5 Statement of Cash Flows...6

UNIVERSITY OF WATERLOO FINANCIAL STATEMENTS

UNIVERSITY OF WATERLOO FINANCIAL STATEMENTS APRIL 30, 2017 I N D E X Statement of Management Responsibility 1 Independent Auditors' Report 2 Financial Statements Balance Sheet 3 Statement of Operations

UNIVERSITY OF WATERLOO FINANCIAL STATEMENTS APRIL 30, 2017 I N D E X Statement of Management Responsibility 1 Independent Auditors' Report 2 Financial Statements Balance Sheet 3 Statement of Operations

Financial Statements M A R C H 3 1, Future Ready. Learning for Life. M O H A W K C O L L E G E. C A

Financial Statements M A R C H 3 1, 2 0 1 6 Future Ready. Learning for Life. M O H A W K C O L L E G E. C A FINANCIAL STATEMENTS AND SUPPLEMENTARY SCHEDULES I N D E X FINANCIAL STATEMENTS: Independent

Financial Statements M A R C H 3 1, 2 0 1 6 Future Ready. Learning for Life. M O H A W K C O L L E G E. C A FINANCIAL STATEMENTS AND SUPPLEMENTARY SCHEDULES I N D E X FINANCIAL STATEMENTS: Independent

CONSOLIDATED FINANCIAL STATEMENTS

CONSOLIDATED FINANCIAL STATEMENTS Independent Auditors' Report 2 Consolidated Financial Statements Consolidated Balance Sheet 4 Consolidated Statement of Operations 5 Consolidated Statement of Changes

CONSOLIDATED FINANCIAL STATEMENTS Independent Auditors' Report 2 Consolidated Financial Statements Consolidated Balance Sheet 4 Consolidated Statement of Operations 5 Consolidated Statement of Changes

PROVINCIAL HEALTH SERVICES AUTHORITY

Consolidated Financial Statements of PROVINCIAL HEALTH SERVICES AUTHORITY Provincial Health Services Authority Management Report The consolidated financial statements of the Provincial Health Services

Consolidated Financial Statements of PROVINCIAL HEALTH SERVICES AUTHORITY Provincial Health Services Authority Management Report The consolidated financial statements of the Provincial Health Services

UNIVERSITY OF VICTORIA FOUNDATION FINANCIAL STATEMENTS MARCH 31, Statement of Administrative Responsibility for Financial Statements 2

UNIVERSITY OF VICTORIA FOUNDATION FINANCIAL STATEMENTS MARCH 31, 2018 Page Statement of Administrative Responsibility for Financial Statements 2 Independent Auditors' Report 3 Statement of Financial Position

UNIVERSITY OF VICTORIA FOUNDATION FINANCIAL STATEMENTS MARCH 31, 2018 Page Statement of Administrative Responsibility for Financial Statements 2 Independent Auditors' Report 3 Statement of Financial Position

BRITISH COLUMBIA TRANSIT

Consolidated Financial Statements of BRITISH COLUMBIA TRANSIT Year ended March 31, 2018 INDEPENDENT AUDITOR S REPORT To the Board of Directors of British Columbia Transit, and To the Minister of Transportation

Consolidated Financial Statements of BRITISH COLUMBIA TRANSIT Year ended March 31, 2018 INDEPENDENT AUDITOR S REPORT To the Board of Directors of British Columbia Transit, and To the Minister of Transportation

UNIVERSITY OF WATERLOO FINANCIAL STATEMENTS

UNIVERSITY OF WATERLOO FINANCIAL STATEMENTS APRIL 30, 2016 I N D E X Statement of Management Responsibility 1 Independent Auditors' Report 2 Financial Statements Balance Sheet 3 Statement of Operations

UNIVERSITY OF WATERLOO FINANCIAL STATEMENTS APRIL 30, 2016 I N D E X Statement of Management Responsibility 1 Independent Auditors' Report 2 Financial Statements Balance Sheet 3 Statement of Operations

CONSOLIDATED FINANCIAL STATEMENTS

CONSOLIDATED FINANCIAL STATEMENTS Independent Auditors' Report 2 Consolidated Financial Statements Consolidated Balance Sheet 4 Consolidated Statement of Operations 5 Consolidated Statement of Changes

CONSOLIDATED FINANCIAL STATEMENTS Independent Auditors' Report 2 Consolidated Financial Statements Consolidated Balance Sheet 4 Consolidated Statement of Operations 5 Consolidated Statement of Changes

Financial Statements of BRITISH COLUMBIA EMERGENCY HEALTH SERVICES

Financial Statements of BRITISH COLUMBIA EMERGENCY HEALTH May 28, 2018 Independent Auditor s Report To the Board of British Columbia Emergency Health Services We have audited the accompanying financial

Financial Statements of BRITISH COLUMBIA EMERGENCY HEALTH May 28, 2018 Independent Auditor s Report To the Board of British Columbia Emergency Health Services We have audited the accompanying financial

PROVINCIAL HEALTH SERVICES AUTHORITY

Consolidated Financial Statements (Expressed in thousands of dollars) PROVINCIAL HEALTH SERVICES AUTHORITY August 28, 2013 Independent Auditor s Report To the Board of Provincial Health Services Authority

Consolidated Financial Statements (Expressed in thousands of dollars) PROVINCIAL HEALTH SERVICES AUTHORITY August 28, 2013 Independent Auditor s Report To the Board of Provincial Health Services Authority

PACIFIC NATIONAL EXHIBITION

Financial Statements of PACIFIC NATIONAL EXHIBITION KPMG LLP Chartered Accountants Metrotower II Suite 2400-4720 Kingsway Burnaby BC V5H 4N2 Canada Telephone (604) 527-3600 Fax (604) 527-3636 Internet

Financial Statements of PACIFIC NATIONAL EXHIBITION KPMG LLP Chartered Accountants Metrotower II Suite 2400-4720 Kingsway Burnaby BC V5H 4N2 Canada Telephone (604) 527-3600 Fax (604) 527-3636 Internet

ST. PAUL S HOSPITAL FOUNDATION OF VANCOUVER

Financial Statements of ST. PAUL S HOSPITAL FOUNDATION OF VANCOUVER KPMG LLP PO Box 10426 777 Dunsmuir Street Vancouver BC V7Y 1K3 Canada Telephone (604) 691-3000 Fax (604) 691-3031 INDEPENDENT AUDITORS'

Financial Statements of ST. PAUL S HOSPITAL FOUNDATION OF VANCOUVER KPMG LLP PO Box 10426 777 Dunsmuir Street Vancouver BC V7Y 1K3 Canada Telephone (604) 691-3000 Fax (604) 691-3031 INDEPENDENT AUDITORS'

VANCOUVER ISLAND UNIVERSITY

CONSOLIDATED FINANCIAL STATEMENTS MARCH 31, 2010 Consolidated Financial Statements Table of Contents Statement of Administrative Responsibility Auditors' Report Consolidated Statement of Financial Position

CONSOLIDATED FINANCIAL STATEMENTS MARCH 31, 2010 Consolidated Financial Statements Table of Contents Statement of Administrative Responsibility Auditors' Report Consolidated Statement of Financial Position

School District No. 6 (Rocky Mountain)

") Audited Financial Statements of June 30, 2018 September 11, 2018 17:12 June 30, 2018 Table of Contents Management Report... 1 Independent Auditors' Report... 2 Statement of Financial Position - Statement

Audited Financial Statements of June 30, 2018 September 11, 2018 17:12 June 30, 2018 Table of Contents Management Report... 1 Independent Auditors' Report... 2 Statement of Financial Position - Statement

HOLLAND BLOORVIEW KIDS REHABILITATION HOSPITAL

Financial Statements of HOLLAND BLOORVIEW KIDS REHABILITATION KPMG LLP Vaughan Metropolitan Centre 100 New Park Place, Suite 1400 Vaughan ON L4K 0J3 Canada Tel 905-265-5900 Fax 905-265-6390 INDEPENDENT

Financial Statements of HOLLAND BLOORVIEW KIDS REHABILITATION KPMG LLP Vaughan Metropolitan Centre 100 New Park Place, Suite 1400 Vaughan ON L4K 0J3 Canada Tel 905-265-5900 Fax 905-265-6390 INDEPENDENT

School District Statement of Financial Information (SOFI) School District No. 85 (Vancouver Island North) Fiscal Year Ended June 30, 2017

School District No. 85 (Vancouver Island North) Fiscal Year Ended June 30, 2017") School District Statement of Financial Information (SOFI) School District No. 85 (Vancouver Island North) Fiscal Year Ended June 30, 2017 Table of Contents. Documents are arranged in the following order:

School District Statement of Financial Information (SOFI) School District No. 85 (Vancouver Island North) Fiscal Year Ended June 30, 2017 Table of Contents. Documents are arranged in the following order:

BOARD OF EDUCATION OF SCHOOL DISTRICT NO. 36 (SURREY) STATEMENT OF FINANCIAL INFORMATION

STATEMENT OF FINANCIAL INFORMATION") BOARD OF EDUCATION OF SCHOOL DISTRICT NO. 36 (SURREY) STATEMENT OF FINANCIAL INFORMATION FOR THE YEAR ENDED JUNE 30, 2017 1 School District Statement of Financial Information (SOFI) Board of Education

BOARD OF EDUCATION OF SCHOOL DISTRICT NO. 36 (SURREY) STATEMENT OF FINANCIAL INFORMATION FOR THE YEAR ENDED JUNE 30, 2017 1 School District Statement of Financial Information (SOFI) Board of Education

School District No. 6 (Rocky Mountain)

") Audited Financial Statements of June 30, 2017 September 12, 2017 15:11 June 30, 2017 Table of Contents Management Report... 1 Independent Auditors' Report... 2 Statement of Financial Position - Statement

Audited Financial Statements of June 30, 2017 September 12, 2017 15:11 June 30, 2017 Table of Contents Management Report... 1 Independent Auditors' Report... 2 Statement of Financial Position - Statement

UNIVERSITY OF VICTORIA