Introduction to the QIS spreadsheets using imaginary IORP

|

|

|

- Buck Lyons

- 5 years ago

- Views:

Transcription

1 Disclaimer Please note that these slides are not part of the formal QIS on IORPs documentation as issued by the European Commission. They are not intended to, and do not, replace the QIS on IORPs technical specifications. The European Commission technical specifications take precedence. 1

2 Introduction to the QIS spreadsheets using imaginary IORP Frankfurt QIS for pensions # Launch event Barthold Kuipers & Pierre#Jean Vouette, 19 October 2012

3 Content of the published package 3

4 Published package reference material Update expected for the matching adjustment 4

5 The Holistic Balance Sheet concept 5

6 The capital requirement 6

7 The supporting material 7

8 Presentation General organisation of the spreadsheet and questionnaire Explanation of the options tested by the scenarios Use of MyIORP to complete a full scenario 8

9 The main scenarios 9 9

10 The specific scenarios tested 10 10

11 Scenario basic data Scheme opened 20 years ago A 2% yearly increase of contributions per member since So far, the yield on assets was 5% So far, observed mortality is in line with the mortality table used Current average age is 45 Retirement date is 65 Scheduled yearly increase on annuities for pensioners is 4.2% / year A 30% quota share agreement with a (re)#insurer 24 October October

12 What can be done? Estimating the current balance sheet o Current asset level o Expected cash flow pattern # Assumption: the contributions level will stay on the +2% / year trend. o Current pension liability level # Assumption: constant one year forward rate at 5% o QISP liabilities # According to the nominal yield curve and sensitivity analysis 12

13 Contributions and benefits 13

14 Expected future cash flows 14

15 Evolution of asset level 15

16 The QIS value of liabilities Note: CCP is using the shifted upward yield curve. Part of the reduction in liability may be transferred to the asset side (e.g. 30%) 16

17 Origin of the funding gap Expected investment return was set at 5% o For the HBS: assumption that the assets will earn the risk free rate, significantly lower at end Tested in SET5: the CCP, temporary measure triggered by supervisors in specific conditions Predicted investment income around 1% in the short term. Consistency with predictability return on existing fixed interest portfolio with higher yield? Will be tested with the Matching adjustment. 17

18 Comparison of discounting assumptions 18

19 Options tested in the holistic balance sheet Long#term nature adjustment Conditional benefits # Ex#post # Ex#ante Sponsor support and PPS 19

20 Conditional benefits Example: the expected starting annuity of 705, growing then by 4.2% / year is made of o An unconditional commitment of 500 (not indexed) o The difference being pending some conditions Total Best estimate (8951) o =Best estimate of unconditional benefits (2040) o +Best estimate of mixed benefits (6911) SET 11 test the assumption of not considering them as liabilities. 20

21 Conditional benefits 21

22 Expected inflation Assumption: Contributions follows inflation, Benefits: inflation+2.2% 22

23 Expected inflation result Column1 Contributions Benefits Total Previous Inflation Inflation Inflation

24 Overview of scenarios 24

25 My IOPR Characteristics CURRENT SITUATION Assets 275,0 Liabilities 287,7 Funding ratio 96% #required 100% Cash#flows sponsor 50 Shareholders funds 125 Sponsor liability towards IORP 15 Discount rate 5,0% Duration 12 Average death rate 1,67% Contribitions ,5 Contribitions ,5 Sponsor support unlimited Sponsor rating BB PPS cover rate 90% 19 October

26 My IORP Asset allocation ASSET ALLOCATION 19 October 2012 % million EUR BREAKDOWN BY CREDIT million RATING % EUR Real assets 40,0% 110 Government bonds EEA 25,0% 68,8 Property 10,0% 28 # AAA 10% 27,5 Global equity 20,0% 55 # AA and lower 15% 41,3 Other equity 10,0% 28 Government bonds non#eea 15,0% 41,3 Fixed income 60,0% 165 # AAA 5,0% 13,8 Government bonds EEA 25,0% 69 # AA 5,0% 13,8 Government bonds non# EEA 15,0% 41 # A 2,5% 6,9 Corporate bonds 20% 55 # BBB 2,5% 6,9 # non#financials 13,3% 37 Corporate bonds 20% 55,0 # financials 6,7% 18 # AAA 0% 0,0 TOTAL 100% 275 # AA 5% 13,8 # A 5% 13,8 Foreign exchange exposure 20% 55 # BBB 2% 5,5 # BB 2% 5,5 Duration fixed income 7 # B 2% 5,5 # government bonds 8 # CCC or lower 2% 5,5 # corporate bonds 5 # unrated 2% 5,5 26

27 Participant information Participant information Q1 Intitution name Institution abbreviation (to be used in excel columns headers) MyIORP MyIORP Q2 Legal form of the institution - Q3 Type of institution IORP Q4 Ring-fenced occupational retirement provision (% total business) - Q5 Institution completing the QIS Q6 Type of data used Date of submission Supervisor Aggregate / Representative data - Reporting reference year 2011 Year end used Reporting currency used EUR Reporting unit used Million Country - National supervisor - Local registration number - 19 October

28 Current regime 1. Technical provisions and assets for pension liabilities Total of which: Pure DC of which: Health benefits of which: Others Technical provision for pensions liabilities (Gross) Are you using (re)-insurance instruments? - If yes, how are the recoverables currently recognized? - (Re)-insurance and SPV recoverables - Technical provision for pensions (net) 288 Other liabilities - Total liabilities 288 Investment assets 275 Sponsor support - Pension protection schemes - Other assets - Total assets 275 of which: assets held for pure defined contributions schemes - 2. Current funding requirements value of items eligible to cover current funding requirements 275 fundi ng requi rement (higher or uni que) 288 Surplus (higher) -13 funding requirement (minimum if more than one exists) - Surplus (minimum) October

29 Common Breakdown of bonds 19 October Indicative mapping of credit quality steps Government bonds and equivalents from non-eea Covered bonds Other bonds and loans (incl. bank deposits) Tradable securities based on repackaged loans (incl. mortgages) Total # Credit quality step 0 AAA # Credit quality step 1 AA # Credit quality step 2 A # Credit quality step 3 BBB # Credit quality step 4 BB # Credit quality step 5 B # Credit quality step 6 CCC or lower # Credit quality step unknown Unrated #

30 Common sheet - Investments Assets Sponsor support and PPS Investments (other than assets held for pure DC) 275 Property (including for own use) 28 Equities 83 global equities 55 other equities (incl. participations, private equ 28 Bonds and loans (excluding mortgages) 165 Government Bonds and equivalents 110 EEA States and equivalent 69 Others 41 Covered bonds 0 Other bonds and loans (incl. bank deposits) 55 Tradable securities based on repackaged loans ( 0 Mortgages - Derivatives - Residual Investment funds - Other investments - 19 October

31 Common sheet Level B returns Portfolio shares (EUR) Value # Expected return Fixed income 165 # - - AAA government bonds 41 # 2,98% - AA government bonds or lower 69 # 4,51% - Corporate bonds 37 # 3,88% - Banks bonds 18 # 3,96% - Other - # 3,93% Non-fixed income 110 # 5,98% Calculation of the "Level B" discount rate Shares # Expected return Fixed income asset 60,0% # 3,93% Non-fixed income asset 40,0% # 5,98% Discount rate used for the "Level B" # 4,75% 19 October

32 Common sheet Foreign currency exposure & contributions Net Assets Liabilities Currency name # exposure exposure exposures Euro EUR # British pound GBP # Norwegian krone NOK # Swedish krona SEK # Other currencies # Of which Pure Total Contributions and expenses defined amount contributio # n Gross contributions received (12 months prior to the previous 12# 18 - Total gross contributions received in the previous 12 months # 18 - Annual expenses in respect of pure DC obligations # - 19 October

33 Helper tab interest rate risk cash flows liabilities and assets Total Total In year Cash flow Spot curve ,065% ,962% ,006% ,190% ,385% ,576% ,743% ,874% ,985% ,083% ,175% ,258% ,319% ,363% ,393% ,410% ,416% ,415% ,410% ,402% ,420% ,459% ,509% ,563% ,618% ,672% ,724% ,774% ,821% ,866% ,908% ,948% ,985% ,021% ,054% ,086% ,116% ,144% ,171% ,196% ,221% ,244% ,266% ,287% ,308% ,327% ,345% ,363% ,380% ,396% ,412% ,427% ,442% ,456% ,469% ,482% ,495% ,507% ,519% ,530% In year Cash flow Spot curve ,065% ,962% ,006% ,190% ,385% ,576% ,743% ,874% ,985% ,083% ,175% ,258% ,319% 14 2,363% 15 2,393% 33

34 Best estimate technical provisions and duration Results Discounted cash flows for the best estimate: 398 Discounted cash flows under the upward interest rate scenario: 349 Discounted cash flows under the downward interest rate scenario: 460 Durations 14,14 13,14 15, Best estimate - Total (without pure DC) - health benefit obligations 398 total other benefits 14 Average duration of pension liabilities 398 Unconditional other obligations - (-) benefit reductions in case of sponsor default "Level B" value of pension liabilities - (-) BE of ex-post reduction - Total pure conditional benefits ====> of which - Ex-ante mechanism reduction - pure discretionary benefits - mixed benefits Sensitivity analysis 0 Pure defined contributions liabilities "Level A" value of pension liabilities - Deferred tax liabilities Under an upward stress (+100 bp) 0 Other liabilities Under a downward stress (-100 bp) 19 October

35 Level B and sensitivity analysis Level B Results Discounted cash flows for the best estimate: bps bps Results Discounted cash flows for the best estimate: 349 Results Discounted cash flows for the best estimate: Risk margin 398 Best estimate - Total (without pure DC) - health benefit obligations 398 total other benefits 14 Average duration of pension liabilities 398 Unconditional other obligations - (-) benefit reductions in case of sponsor default 296 "Level B" value of pension liabilities - (-) BE of ex-post reduction - Total pure conditional benefits ====> of which - Ex-ante mechanism reduction - pure discretionary benefits - mixed benefits Sensitivity analysis 0 Pure defined contributions liabilities "Level A" value of pension liabilities - Deferred tax liabilities 349 Under an upward stress (+100 bp) 0 Other liabilities 460 Under a downward stress (-100 bp) 19 October

36 Maximum sponsor support INPUT INPUT Duration of settlement sponsor support 14 EC t Sponsor default risk (annual probability) 1,2% Year Total Recovery plan Cash flows Shareholder funds of sponsor 125 contributions 100% Liabilities sponsor towards IORP Limit to maximum sponsor support OUTPUT Maximum sponsor support without credit risk Maximum sponsor support with credit risk

37 Value sponsor support INPUT Value financial assets 275 Value technical provisions 430 Duration of settlement sponsor support 14 Sponsor default risk (annual probability) 1,2% Value maximum sponsor support 304 Recovery rate sponsor support on default 30% OUTPUT Value sponsor support (limited to maximum) 145,7 Difference calculated and maximum value sponsor support (if > 0) 0 19 October

38 Value pension protection scheme INPUT Value financial assets 275 Value technical provisions 430 Duration of settlement sponsor support 14 Sponsor default risk (annual probability) 1,2% Recovery rate sponsor support on default 30% Coverage rate pension protection scheme (% technical provisions) 90% Difference calculated and maximum value sponsor support (if > 0) 0 OUTPUT Value pension protection scheme as an asset (incl. calculated minus maximum sponsor support) 3,6 Value pension protection scheme (incl. calculated minus maximum sponsor support) (100% coverage rate) 9 Value reduction benefits in case of sponsor support (with pension protection scheme) -5,7 19 October

39 Holistic balance sheet - completed Assets # Liabilities Sponsor support and PPS 149 # 425 Total balance sheet value Sponsor support 146 # Contingent assets - # Other 146 # 1 Excess of assets over liabilities Credit risk reduction due to PPS - # Pension protection scheme 4 # Investments (excluding pure DC) 275 # 31 Risk margin (Re)insurance / SPV recoverables 0 # 392 Best estimate - Total (without pure DC) health benefit obligations - # - health benefit obligations total other benefits 0 # 392 total other benefits Unconditional other obligations - # 398 Unconditional other obligations (-) benefit reductions in case of spons - # -6 (-) benefit reductions in case of sponsor default (-) BE of ex-post reduction - # - (-) BE of ex-post reduction Total pure conditional benefits - # - Total pure conditional benefits ====> pure discretionary benefits - # - pure discretionary benefits mixed benefits - # - mixed benefits Assets held for pure DC 0 # 0 Pure defined contributions liabilities Deferred tax assets - # - Deferred tax liabilities Other assets (excluding pure DC) 0 # 0 Other liabilities 19 October

40 Maximum loss-absorbency and qualitative questions Ancillary own funds Sponsor support as ancillary own fund - Max value of ex-post benefit reduction 392 Maximum sponsor support value 304 Maximum PPS value 387 Q32: Valuation method used to establish the unconditional benefits Deterministic valuation Q33: Valuation method used to establish the non-unconditional benefits Not applicable Q34: Methodology used for ex-post and maximum ex-post reduction assessment Not applicable Q48: Valuation method used to establish the market value of sponsor support Simplification 2 Q49: Valuation method used to establish the market value of PPS as an asset Value of pension protection scheme Q52: Method used to establish the maximum amount of sponsor support Standard method provided Q63: Method used to calculate the adjustment for default of the (re)insurer Not applicable 19 October

41 Operational & counterparty default risk Capital requirement for Operational risk Risk-Module level value 2 Contributions based risk component 1 Gross contributions received 18 of which pure DC - Contributions of previous 12 months 18 of which pure DC - TP based risk component 2 Tech. Prov. for pension obligations 392 of which pure DC 0 Annual expenses for pure DC (12 month - Gros s ri s k Adj. Net ri s k Capital requirement for Counterparty default risk Risk-Module level values SCR for counterparty default risk of type SCR for counterparty default risk of type 2 Methodology used 2 - standard method 19 October

42 Interest rate risk Initial position Assets Liabilities Net Asset Value Value Interest rate shock Assets Liabilities Net Asset Value Up Down October 2012 Net asset values pre-s tres s # Wi thout LAC Scenario based stressed values Stress scenario va lue # As s ets Lia bil ities Gros s ris k Adj. Net ris k Interest rates risk values # Scenario kept for interest rates stress # Interest rates altered upward # Interest rates altered downward # Nominal term structure altered upward -234 # Nominal term structure altered downwar -234 # Inflation term structure altered upward 1 # Inflation term structure altered downwar 1 # Down 42

43 Helper tab spread risk Mkt sp bonds loss absorbing capacity of technical provisions nmkt sp bonds Bonds ΣMV i average weighted duration sum per rating of 9,7 10 capital charge per rating MV i *dur i , , , , , , ,06 unrated ,83 Non-EEA sovereign bonds, issued in domestic currency ΣMV i weighted average duration sum per rating of MV i *m(dur i ) capital charge per rating , unrated October

44 Other market risk Equity risk values # Approach retained for equity risk # Duration Stress on the global equity portfolio 1 # Stress on the other equity portfolio 1 # Equity stress (Duration approach) 83 # Property stress and risk values 28 # Spread risk values # Spread on bonds and loans 96 # Spread on repackaged loans 1 # Spread on credit derivatives # Scenario kept for credit derivatives # Down Upward shock on credit derivatives 1 # Downward shock on credit derivatives 1 # Currency risk values # Currency stress upward 1 # Currency stress downward 55 # Concentration risk values # CCP risk 1 # October

45 Helper tab longevity risk 2 Longevity Result of the longevity risk (simplification) Best estimate contract subject to longevity risk Expected average death rate for the following year 1,67% Modified duration October

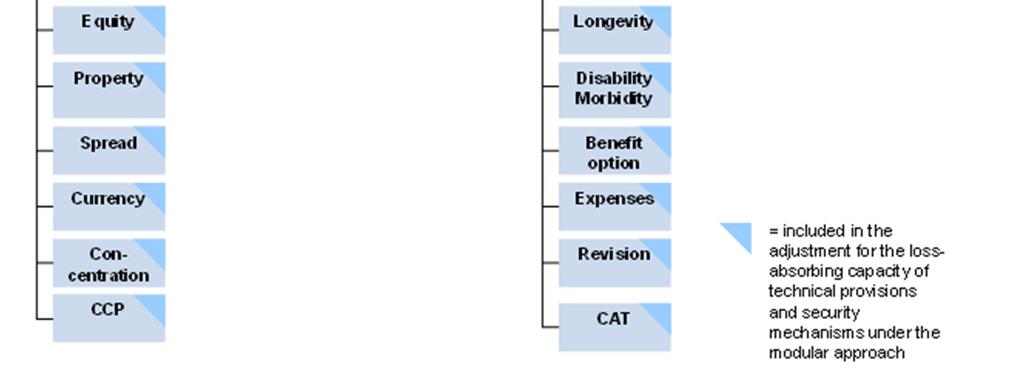

46 Pension liability risk Net asset values pre-s tres s # Wi thout LAC Scenario based stressed values Stress scenario value # Assets Liabilities Gross risk Adj. Net risk Stress on Mortality 1 # Stress on Longevity 1 # Stress on Disability 1 # Benefit option # Scenario retained for benefit option # Down Benefit option - lapse up 1 # Benefit option - lapse down 1 # Benefit option - mass 1 # Expenses 1 # Revision 1 # CAT 1 # October

47 Loss-absorbency of technical provisions and security mechanisms Gross stress Lossabsorbency A L SS PPS L Interest rate #up #11 #49 #35,7 #1,4 0,9 Interest rate # down ,0 2,0 #1,0 Equity #18 # 16,9 1,0 #0,1 Property #7 # 6,6 0,4 0,0 Currency #14 # 13,2 0,7 #0,1 Spread #10 # 9,4 0,5 0,0 Counterparty #75 # 0,0 39,6 #35,3 Longevity # 34 32,0 1,4 #0,6 19 October

48 Post-stress balance sheet values Nominal term structure altered upward Nominal term structure altered downwar Inflation term structure altered upward Inflation term structure altered downwar Equity risk values Approach retained for equity risk Stress on the global equity portfolio 0 Duration Stress on the other equity portfolio Equity stress (Duration approach) Property stress and risk values Spread risk values Spread on bonds and loans Spread on repackaged loans Spread on credit derivatives Scenario kept for credit derivatives Upward shock on credit derivatives 0 Down Downward shock on credit derivatives Currency risk values Currency stress upward Currency stress downward

49 Capital requirements Own funds SCR OF - SCR MCR OF - MCR Own funds compared to capital requirements Excess of assets over liabilities at the 99.5% confidence level Ancillary own funds at the 97.5% confidence level Total own funds at the 95% confidence level Main results of the capital requirements according to formula defined in the QIS technical specifications Adjustments for loss absorbency # Exposure Diversif. Gross risk Adj. Net risk Risk module Part of the max. sponsor support availab 158 # Market risk Part of the maximum PPS available 383 # Counterparty default risk Discretionary / Conditional Liabilities 386 # Pension liability Adjustment for loss absorbency (AdjTS) -135 # Health risk Net deferred taxes in the HBS 0 # Intangible asset risk Magnitude of the DT shock -136 # Operational risk Post stress net deferred taxes - # Basic SCR (BSCR) before intangible risk Deferred taxes adjustment (AdjDT) - # Basic Solvency Capital Requirement (BSCR) Maximum value for Adj2 793 # Solvency capital requirement (SCR) [99.5%] Adjustment for loss absorbency (Adj2) -2 # Solvency capital requirement (SCR) [97.5%] Total adjustment for loss absorbency -137 # 88 0 Solvency capital requirement (SCR) [95%] 49

50 Overview Overall impact (= surplus (SCR) minus current surplus) at the 99.5% level 14 Overall impact (= surplus (SCR) minus current surplus) at the 97.5% level 14 Overall impact (= surplus (SCR) minus current surplus) at the 95% level 14 - change in value investments 0 - change in value sponsor support change in value pension protection schemes 4 - change in value (re-)insurance recoverables 0 - change in value other assets 0 - change in value best estimate technical provisions change in value risk margin change in value other liabilities 0 Change in excess of assets over liabilities (= HBS minus current) 14 - change in solvency capital requirement at the 99.5% level 0 - change in solvency capital requirement at the 97.5% level 0 - change in solvency capital requirement at the 95% level 0 - change in sponsor support as ancillary own funds - 50

51 Thank you Barthold Kuipers & Pierre#jean Vouette

User Guide for Input Spreadsheet QIS on IORPs

Updated 15 November 2012 User Guide for Input Spreadsheet QIS on IORPs Contents 1. Introduction... 2 2. Overview of spreadsheet... 2 3. Participant information... 4 4. Current regime... 5 5. Holistic balance

Updated 15 November 2012 User Guide for Input Spreadsheet QIS on IORPs Contents 1. Introduction... 2 2. Overview of spreadsheet... 2 3. Participant information... 4 4. Current regime... 5 5. Holistic balance

User Guide for Input Spreadsheet Long-Term Guarantees Assessment

12 February 2013 User Guide for Input Spreadsheet Long-Term Guarantees Assessment This user guide is not part of the formal LTGA documentation as issued. It is not intended to, and does not, replace the

12 February 2013 User Guide for Input Spreadsheet Long-Term Guarantees Assessment This user guide is not part of the formal LTGA documentation as issued. It is not intended to, and does not, replace the

Report on QIS on IORPs. Barthold Kuipers, Chair OPC Subgroup QIS QIS for Pensions closing event Frankfurt, 10 July 2013

Report on QIS on IORPs Barthold Kuipers, Chair OPC Subgroup QIS QIS for Pensions closing event Frankfurt, Outline Holistic balance sheet Participation in QIS Benchmark scenario Upper and lower bound scenario

Report on QIS on IORPs Barthold Kuipers, Chair OPC Subgroup QIS QIS for Pensions closing event Frankfurt, Outline Holistic balance sheet Participation in QIS Benchmark scenario Upper and lower bound scenario

Technical Specifications part II on the Long-Term Guarantee Assessment Final version

EIOPA/12/307 25 January 2013 Technical Specifications part II on the Long-Term Guarantee Assessment Final version Purpose of this document This document contains part II of the technical specifications

EIOPA/12/307 25 January 2013 Technical Specifications part II on the Long-Term Guarantee Assessment Final version Purpose of this document This document contains part II of the technical specifications

Introduction to Solvency II SCR Standard Formula for Market Risk. Erik Thoren 11 June 2015

Introduction to Solvency II SCR Standard Formula for Market Risk Erik Thoren 11 June 2015 Agenda Introduction to Solvency II Market risk module Asset allocation considerations Page 2 Introduction to Solvency

Introduction to Solvency II SCR Standard Formula for Market Risk Erik Thoren 11 June 2015 Agenda Introduction to Solvency II Market risk module Asset allocation considerations Page 2 Introduction to Solvency

Best Estimate Technical Provisions

Solvency II - QIS5 Non-Life Technical Provisions 15 September 2010 Dimitris Dimitriou 1 Best Estimate Technical Provisions 1 Agenda 1. Segmentation 2. Future Premiums 3. Valuation Techniques 4. Simplifications

Solvency II - QIS5 Non-Life Technical Provisions 15 September 2010 Dimitris Dimitriou 1 Best Estimate Technical Provisions 1 Agenda 1. Segmentation 2. Future Premiums 3. Valuation Techniques 4. Simplifications

Christos Patsalides President Cyprus Association of Actuaries

Christos Patsalides President Cyprus Association of Actuaries 1 Counter Party (Default) Risk Reinsurance Intermediaries Banks (cash at bank current ac/s only) Other Operational Risk Systems Risks Processes

Christos Patsalides President Cyprus Association of Actuaries 1 Counter Party (Default) Risk Reinsurance Intermediaries Banks (cash at bank current ac/s only) Other Operational Risk Systems Risks Processes

Solvency II and Mandatum Life. Sampo Group, Capital Markets Day 11 September 2015

Solvency II and Mandatum Life Sampo Group, Capital Markets Day 11 September 2015 Solvency II in a Nutshell New EU-level solvency framework In force 1 January 2016 Risks are measured in a market consistent

Solvency II and Mandatum Life Sampo Group, Capital Markets Day 11 September 2015 Solvency II in a Nutshell New EU-level solvency framework In force 1 January 2016 Risks are measured in a market consistent

EIOPA Stress Test 2014 Supporting material Frankfurt, May 2014

EIOPA Stress Test 2014 Supporting material https://eiopa.europa.eu/activities/financial-stability/insurance-stress-test-2014 Frankfurt, May 2014 PROGRAMME Introduction Description of stress test general

EIOPA Stress Test 2014 Supporting material https://eiopa.europa.eu/activities/financial-stability/insurance-stress-test-2014 Frankfurt, May 2014 PROGRAMME Introduction Description of stress test general

4 Dec SCR.9.2. NLpr Non-life premium & reserve risk. geographical diversification proportional reinsurance. Standard_SCR

4 Dec 2014 Related topic Subtopic No. Para. Keywords Your question Answer The template aims to inform supervisors of the split by country of the TP but it is not linked to the calculation of geographical

4 Dec 2014 Related topic Subtopic No. Para. Keywords Your question Answer The template aims to inform supervisors of the split by country of the TP but it is not linked to the calculation of geographical

S Solvency Capital Requirement for groups using the standard formula and partial internal model

S.25.02 Requirement for groups using the standard formula and partial internal model This section relates to opening and annual submission of information for groups, ring fenced funds, matching adjustment

S.25.02 Requirement for groups using the standard formula and partial internal model This section relates to opening and annual submission of information for groups, ring fenced funds, matching adjustment

An Introduction to Solvency II

An Introduction to Solvency II Peter Withey KPMG Agenda 1. Background to Solvency II 2. Pillar 1: Quantitative Pillar Basic building blocks Assets Technical Reserves Solvency Capital Requirement Internal

An Introduction to Solvency II Peter Withey KPMG Agenda 1. Background to Solvency II 2. Pillar 1: Quantitative Pillar Basic building blocks Assets Technical Reserves Solvency Capital Requirement Internal

April 2014 Summary of technical specifications for QIS 1. Singapore RBC 2 Review

April 2014 Summary of technical specifications for QIS 1 Singapore RBC 2 Review 1 Introduction The Monetary Authority of Singapore (MAS) recently issued a second consultation paper on the review of the

April 2014 Summary of technical specifications for QIS 1 Singapore RBC 2 Review 1 Introduction The Monetary Authority of Singapore (MAS) recently issued a second consultation paper on the review of the

QRT Appendix S.02.01.02 Balance sheet Solvency II Value Statutory accounts value Assets C0010 C0020 R0010 Goodwill - R0020 Deferred acquisition costs 208.073 R0030 Intangible assets - 1.349.412 R0040 Deferred

QRT Appendix S.02.01.02 Balance sheet Solvency II Value Statutory accounts value Assets C0010 C0020 R0010 Goodwill - R0020 Deferred acquisition costs 208.073 R0030 Intangible assets - 1.349.412 R0040 Deferred

2016 Public Quantitative Reporting Templates Solvency II Aegon Spaarkas N.V.

216 Public Quantitative Reporting Templates Solvency II N.V. This document contains the following quantitative reporting templates (QRTs) which relate to the position at 31 December 216: S.2.1.2 Balance

216 Public Quantitative Reporting Templates Solvency II N.V. This document contains the following quantitative reporting templates (QRTs) which relate to the position at 31 December 216: S.2.1.2 Balance

s Solvency Capital Requirement for undertakings on Standard Formula

s.25.01 Requirement for undertakings on Standard Formula This section relates to opening and annual submission of information for individual entities, ring fenced funds, matching adjustment portfolios

s.25.01 Requirement for undertakings on Standard Formula This section relates to opening and annual submission of information for individual entities, ring fenced funds, matching adjustment portfolios

NBB Insurance Stress Test Start event

- Start event NBB - July 6 th 2017 Nicolas COLPAERT - Geoffroy HERBERIGS Agenda Technical Specifications Framework NBB Low for Long IMF FSAP Insurance Stress Test Timeline Process Technical Information

- Start event NBB - July 6 th 2017 Nicolas COLPAERT - Geoffroy HERBERIGS Agenda Technical Specifications Framework NBB Low for Long IMF FSAP Insurance Stress Test Timeline Process Technical Information

Table of content Disclosure QRT's Proteq Levensverzekeringen NV

Table of content Disclosure QRT's Proteq Levensverzekeringen NV 1 Balance Sheet 2 Premiums, claims and expenses by line of business 3 Premiums, claims and expenses by country 4 Life and Health SLT Technical

Table of content Disclosure QRT's Proteq Levensverzekeringen NV 1 Balance Sheet 2 Premiums, claims and expenses by line of business 3 Premiums, claims and expenses by country 4 Life and Health SLT Technical

Page 1. LongTerm Guarantees Assessment EIOPA/13/067. Questions & Answers as of 13 Feb 2013

LongTerm Guarantees Assessment s & s as of 13 Feb 2013 EIOPA/13/067 New questions and answers are marked with blue font. 13 February 2013 TS part I TP Segmentation 1005a TS part I TP ( Segmentation TP

LongTerm Guarantees Assessment s & s as of 13 Feb 2013 EIOPA/13/067 New questions and answers are marked with blue font. 13 February 2013 TS part I TP Segmentation 1005a TS part I TP ( Segmentation TP

Compromise proposal on Omnibus II

Compromise proposal on Omnibus II On 25 November 2013 a compromise proposal on the Omnibus II Directive was published. This was based on a provisional agreement from the European Parliament, the European

Compromise proposal on Omnibus II On 25 November 2013 a compromise proposal on the Omnibus II Directive was published. This was based on a provisional agreement from the European Parliament, the European

Financial Assurance Company Limited

Financial Assurance Company Limited Solvency and Financial Condition Report Disclosures 31 December 2016 (Monetary amounts in GBP thousands) General information Undertaking name Financial Assurance Company

Financial Assurance Company Limited Solvency and Financial Condition Report Disclosures 31 December 2016 (Monetary amounts in GBP thousands) General information Undertaking name Financial Assurance Company

Cirencester Friendly Society Limited Solvency and Financial Condition Report Disclosures 31 December 2016 (Monetary amounts in GBP thousands) General information Undertaking name Cirencester Friendly Society

Cirencester Friendly Society Limited Solvency and Financial Condition Report Disclosures 31 December 2016 (Monetary amounts in GBP thousands) General information Undertaking name Cirencester Friendly Society

MARKET CONSISTENT VALUATION UNDER THE SOLVENCY II DIRECTIVE

MARKET CONSISTENT VALUATION UNDER THE SOLVENCY II DIRECTIVE BY ANNE STIGUM THESIS for the degree of MASTER OF SCIENCE (Modeling and Data Analysis) Faculty of Mathematics and Natural Sciences University

MARKET CONSISTENT VALUATION UNDER THE SOLVENCY II DIRECTIVE BY ANNE STIGUM THESIS for the degree of MASTER OF SCIENCE (Modeling and Data Analysis) Faculty of Mathematics and Natural Sciences University

12 April 2018 Kurt Svoboda, CFRO. UNIQA Insurance Group AG Economic Capital and Embedded Value 2017

12 April 2018 Kurt Svoboda, CFRO UNIQA Insurance Group AG Economic Capital and Embedded Value 2017 Executive Summary Economic Capital position remains extraordinary strong Economic Capital Ratio (ECR-ratio)

12 April 2018 Kurt Svoboda, CFRO UNIQA Insurance Group AG Economic Capital and Embedded Value 2017 Executive Summary Economic Capital position remains extraordinary strong Economic Capital Ratio (ECR-ratio)

RISK BASED CAPITAL AND SOLVENCY

RISK BASED CAPITAL AND SOLVENCY 1 1 N O V E M B E R 2 0 1 5 N E I L TAV E R N E R, S E N I O R A C T U A R Y AIMS OF RISK BASED CAPITAL AND SOLVENCY WORKSTREAM Establish a high level of observance of IAIS

RISK BASED CAPITAL AND SOLVENCY 1 1 N O V E M B E R 2 0 1 5 N E I L TAV E R N E R, S E N I O R A C T U A R Y AIMS OF RISK BASED CAPITAL AND SOLVENCY WORKSTREAM Establish a high level of observance of IAIS

Hong Kong RBC First Quantitative Impact Study

Milliman Asia e-alert 1 17 August 2017 Hong Kong RBC First Quantitative Impact Study Introduction On 28 July 2017, the Insurance Authority (IA) of Hong Kong released the technical specifications for the

Milliman Asia e-alert 1 17 August 2017 Hong Kong RBC First Quantitative Impact Study Introduction On 28 July 2017, the Insurance Authority (IA) of Hong Kong released the technical specifications for the

Solvency II, messages and findings from QIS 5. Carlos Montalvo Rebuelta Executive Director Brussels, 7 March 2011

Solvency II, messages and findings from QIS 5 Carlos Montalvo Rebuelta Executive Director Brussels, 7 March 2011 Index Preparedness of Insureres and Supervisors Impact of the proposed regime Feasibility

Solvency II, messages and findings from QIS 5 Carlos Montalvo Rebuelta Executive Director Brussels, 7 March 2011 Index Preparedness of Insureres and Supervisors Impact of the proposed regime Feasibility

OHRA Ziektekostenverzekeringen N.V.

OHRA Ziektekostenverzekeringen N.V. Solvency and Financial Condition Report 2017 disclosure templates (Amount x 1.000) Content of submission s.02.01 Balance Sheet s.05.01 Premiums, claims and expenses

OHRA Ziektekostenverzekeringen N.V. Solvency and Financial Condition Report 2017 disclosure templates (Amount x 1.000) Content of submission s.02.01 Balance Sheet s.05.01 Premiums, claims and expenses

2016 Public Quantitative Reporting Templates Solvency II Aegon Levensverzekering N.V.

216 Public Quantitative Reporting Templates Solvency II Aegon Levensverzekering N.V. This document contains the following quantitative reporting templates (QRTs) which relate to the position at 31 December

216 Public Quantitative Reporting Templates Solvency II Aegon Levensverzekering N.V. This document contains the following quantitative reporting templates (QRTs) which relate to the position at 31 December

Delta Lloyd Zorgverzekering N.V.

Delta Lloyd Zorgverzekering N.V. Solvency and Financial Condition Report 2017 disclosure templates (Amount x 1.000) Content of submission s.02.01 Balance Sheet s.05.01 Premiums, claims and expenses by

Delta Lloyd Zorgverzekering N.V. Solvency and Financial Condition Report 2017 disclosure templates (Amount x 1.000) Content of submission s.02.01 Balance Sheet s.05.01 Premiums, claims and expenses by

Challenger Life Company Limited Comparability of capital requirements across different regulatory regimes

Challenger Life Company Limited Comparability of capital requirements across different regulatory regimes 26 August 2014 Challenger Life Company Limited Level 15 255 Pitt Street Sydney NSW 2000 26 August

Challenger Life Company Limited Comparability of capital requirements across different regulatory regimes 26 August 2014 Challenger Life Company Limited Level 15 255 Pitt Street Sydney NSW 2000 26 August

QIS5 planning. 26 August 2010 Page 2

Disclaimer Please note that those slides are not part of the formal QIS5 documentation as issued by the European Commission. They are not intended to, and do not, replace the QIS5 Technical Specifications

Disclaimer Please note that those slides are not part of the formal QIS5 documentation as issued by the European Commission. They are not intended to, and do not, replace the QIS5 Technical Specifications

DISCLOSURE QRT REPORT Proteq Levensverzekeringen 2017

DISCLOSURE QRT REPORT Proteq Levensverzekeringen 2017 S.02.01 - Balance Sheet S.02.01... 2 S.05.01 - Premiums, claims and expenses by line of business S.05.01... 3 S.05.02 - Premiums, claims and expenses

DISCLOSURE QRT REPORT Proteq Levensverzekeringen 2017 S.02.01 - Balance Sheet S.02.01... 2 S.05.01 - Premiums, claims and expenses by line of business S.05.01... 3 S.05.02 - Premiums, claims and expenses

EIOPA Stress Test 2014

EIOPA Questions & Answers 18 June 2014 Reporting template 1 eiopa-14-216-st14- BS+.Assets(CF) Could you please explain in more detail what is to be entered here, I found no advice in the Technical Specifications,

EIOPA Questions & Answers 18 June 2014 Reporting template 1 eiopa-14-216-st14- BS+.Assets(CF) Could you please explain in more detail what is to be entered here, I found no advice in the Technical Specifications,

Quantitative reporting templates Appendix Verslag over de solvabiliteit en de financiële toestand Loyalis Leven 2017

Quantitative reporting templates 2017 Appendix Verslag over de solvabiliteit en de financiële toestand Loyalis Leven 2017 2017 Inhoud Balance sheet....3 Premiums, claims and expenses by line of business....5

Quantitative reporting templates 2017 Appendix Verslag over de solvabiliteit en de financiële toestand Loyalis Leven 2017 2017 Inhoud Balance sheet....3 Premiums, claims and expenses by line of business....5

Quantitave reporting templates Appendix SFCR Leven. jij, je pensioen en

Quantitave reporting templates 2016 Appendix SFCR Leven jij, je pensioen en Inhoud Balance sheet.... 3 Life... 5 Home Country - life.... 6 Life and Health SLT Technical Provisions.... 7 Impact of long

Quantitave reporting templates 2016 Appendix SFCR Leven jij, je pensioen en Inhoud Balance sheet.... 3 Life... 5 Home Country - life.... 6 Life and Health SLT Technical Provisions.... 7 Impact of long

5 S Calculation of Solvency Capital Requirement

S.No Table Code Table Label 1 S.02.01.01.01 Balance sheet 2 S.23.01.01.01 Own funds 3 S.23.01.01.02 Reconciliation reserve 4 S.25.01.01.01 Basic Solvency Capital Requirement 5 S.25.01.01.02 Calculation

S.No Table Code Table Label 1 S.02.01.01.01 Balance sheet 2 S.23.01.01.01 Own funds 3 S.23.01.01.02 Reconciliation reserve 4 S.25.01.01.01 Basic Solvency Capital Requirement 5 S.25.01.01.02 Calculation

OWM CZ groep Aanvullende verzekering Zorgverzekeraar U.A.

OWM CZ groep Aanvullende verzekering Zorgverzekeraar U.A. Solvency and Financial Condition Report 2017 disclosure templates (Amount x 1.000) Content of submission s.02.01 Balance Sheet s.05.01 Premiums,

OWM CZ groep Aanvullende verzekering Zorgverzekeraar U.A. Solvency and Financial Condition Report 2017 disclosure templates (Amount x 1.000) Content of submission s.02.01 Balance Sheet s.05.01 Premiums,

Sparebank 1 Skadeforsikring AS

Sparebank 1 Skadeforsikring AS Solvency and Financial Condition Report Disclosures 31 December 2017 (Monetary amounts in NOK thousands) General information Undertaking name Sparebank 1 Skadeforsikring

Sparebank 1 Skadeforsikring AS Solvency and Financial Condition Report Disclosures 31 December 2017 (Monetary amounts in NOK thousands) General information Undertaking name Sparebank 1 Skadeforsikring

solvency and financial condition report - disclosure ASR Aanvullende Ziektekostenverzekeringen N.V. (Monetary amounts in thousands)

") 2016 solvency and financial condition report - disclosure ASR Aanvullende Ziektekostenverzekeringen N.V. (Monetary amounts in thousands) S.02.01.02 - Balance sheet 2 2016 Solvency II Value Assets Intangible

2016 solvency and financial condition report - disclosure ASR Aanvullende Ziektekostenverzekeringen N.V. (Monetary amounts in thousands) S.02.01.02 - Balance sheet 2 2016 Solvency II Value Assets Intangible

Results of the QIS5 Report

aktuariat-witzel Universität Basel Frühjahrssemester 2011 Dr. Ruprecht Witzel ruprecht.witzel@aktuariat-witzel.ch On 5 July 2010 the European Commission published the QIS5 Technical Specifications The

aktuariat-witzel Universität Basel Frühjahrssemester 2011 Dr. Ruprecht Witzel ruprecht.witzel@aktuariat-witzel.ch On 5 July 2010 the European Commission published the QIS5 Technical Specifications The

Valuing Sponsor Support Alternative Simplified Approach

Valuing Sponsor Support Alternative Simplified Approach Adain O Mahony The Pensions Regulator / EIOPA Sponsor Support Working Group Sponsor Support Event Frankfurt, Agenda 1. Sponsor Support in the HBS

Valuing Sponsor Support Alternative Simplified Approach Adain O Mahony The Pensions Regulator / EIOPA Sponsor Support Working Group Sponsor Support Event Frankfurt, Agenda 1. Sponsor Support in the HBS

RAPPORT SUR LA SOLVABILITE ET LA SITUATION FINANCIERE

RAPPORT SUR LA SOLVABILITE ET LA SITUATION FINANCIERE Cardif Assurances Risques Divers Annexes Quantitative Reporting Templates - QRT 31 décembre 2016 Balance sheet S.02.01.21 Solvency II value C0010 Assets

RAPPORT SUR LA SOLVABILITE ET LA SITUATION FINANCIERE Cardif Assurances Risques Divers Annexes Quantitative Reporting Templates - QRT 31 décembre 2016 Balance sheet S.02.01.21 Solvency II value C0010 Assets

Storebrand 1Q Apr Odd Arild Grefstad CEO Lars Aa. Løddesøl CFO. Storebrand celebrates 250 years in 2017

Storebrand Q 207 Storebrand celebrates 250 years in 207 27 Apr 207 Odd Arild Grefstad CEO Lars Aa. Løddesøl CFO Highlights Q 207 Group result 7% Unit Linked AuM growth 3 67 MNOK 208 463 32% Retail Bank

Storebrand Q 207 Storebrand celebrates 250 years in 207 27 Apr 207 Odd Arild Grefstad CEO Lars Aa. Løddesøl CFO Highlights Q 207 Group result 7% Unit Linked AuM growth 3 67 MNOK 208 463 32% Retail Bank

S Balance sheet. in thousand EUR. Solvency II value

Index S.02.01_Balance Sheet S.05.01_Premiums, claims and expenses by line of business S.05.02_Premiums, claims and expenses by country S.17.01_Non - life Technical Provisions S.19.01_Non-life Insurance

Index S.02.01_Balance Sheet S.05.01_Premiums, claims and expenses by line of business S.05.02_Premiums, claims and expenses by country S.17.01_Non - life Technical Provisions S.19.01_Non-life Insurance

Supervisory Statement SS7/17 Solvency II: Data collection of market risk sensitivities. October 2017

Supervisory Statement SS7/17 Solvency II: Data collection of market risk sensitivities October 2017 Prudential Regulation Authority 20 Moorgate London EC2R 6DA Supervisory Statement SS7/17 Solvency II:

Supervisory Statement SS7/17 Solvency II: Data collection of market risk sensitivities October 2017 Prudential Regulation Authority 20 Moorgate London EC2R 6DA Supervisory Statement SS7/17 Solvency II:

Aioi Nissay Dowa Insurance Company of Europe Limited

Aioi Nissay Dowa Insurance Company of Europe Limited Solvency and Financial Condition Report Disclosures 31 December 2016 (Monetary amounts in GBP thousands) General information Undertaking name Aioi Nissay

Aioi Nissay Dowa Insurance Company of Europe Limited Solvency and Financial Condition Report Disclosures 31 December 2016 (Monetary amounts in GBP thousands) General information Undertaking name Aioi Nissay

S Balance sheet. in EUR. Solvency II value

S.02.01.02 Balance sheet Solvency II value Assets C0010 Intangible assets R0030 - Deferred tax assets R0040 - Pension benefit surplus R0050 - Property, plant & equipment held for own use R0060 174.280.265

S.02.01.02 Balance sheet Solvency II value Assets C0010 Intangible assets R0030 - Deferred tax assets R0040 - Pension benefit surplus R0050 - Property, plant & equipment held for own use R0060 174.280.265

Western Captive Insurance Company DAC. Solvency and Financial Condition Report. For Financial Year Ending 31 st December 2016 (the reporting period )

") Western Captive Insurance Company DAC Solvency and Financial Condition Report For Financial Year Ending 31 st December 2016 (the reporting period ) 1 Executive Summary Western Captive Insurance Company

Western Captive Insurance Company DAC Solvency and Financial Condition Report For Financial Year Ending 31 st December 2016 (the reporting period ) 1 Executive Summary Western Captive Insurance Company

(Text with EEA relevance)

") 31.12.2015 L 347/1285 COMMISSION IMPLEMTING REGULATION (EU) 2015/2452 of 2 December 2015 laying down implementing technical standards with regard to the procedures, formats and templates of the solvency

31.12.2015 L 347/1285 COMMISSION IMPLEMTING REGULATION (EU) 2015/2452 of 2 December 2015 laying down implementing technical standards with regard to the procedures, formats and templates of the solvency

2017 Public Quantitative Reporting Templates Solvency II Aegon Levensverzekering N.V.

2017 Public Quantitative Reporting Templates Solvency II Aegon Levensverzekering N.V. This document contains the following quantitative reporting templates (QRTs) which relate to the position at 31 December

2017 Public Quantitative Reporting Templates Solvency II Aegon Levensverzekering N.V. This document contains the following quantitative reporting templates (QRTs) which relate to the position at 31 December

QIS5 Workshop. Warsaw, 5 October 2010

QIS5 Workshop Warsaw, 5 October 2010 Agenda 10:00 10:15 Introduction and opening remarks 10:15 11:00 Speaker from the EC 11:00 12:30 Technical Specifications QIS5 (part 1) Valuation Own Funds 12:30 13:30

QIS5 Workshop Warsaw, 5 October 2010 Agenda 10:00 10:15 Introduction and opening remarks 10:15 11:00 Speaker from the EC 11:00 12:30 Technical Specifications QIS5 (part 1) Valuation Own Funds 12:30 13:30

De Friesland Zorgverzekeraar N.V. Openbaar te maken QRT's

De Friesland Zorgverzekeraar N.V. Openbaar te maken QRT's 2016 S.02.01.02 - Balance sheet 1.000 Assets Solvency II value Intangible assets 0 Deferred tax assets 0 Pension benefit surplus 0 Property, plant

De Friesland Zorgverzekeraar N.V. Openbaar te maken QRT's 2016 S.02.01.02 - Balance sheet 1.000 Assets Solvency II value Intangible assets 0 Deferred tax assets 0 Pension benefit surplus 0 Property, plant

Financial Insurance Company Limited

Financial Insurance Company Limited Solvency and Financial Condition Report Disclosures 31 December 2016 (Monetary amounts in GBP thousands) General information Undertaking name Financial Insurance Company

Financial Insurance Company Limited Solvency and Financial Condition Report Disclosures 31 December 2016 (Monetary amounts in GBP thousands) General information Undertaking name Financial Insurance Company

N.V. Hagelunie. Openbaar te maken QRT's

N.V. Hagelunie Openbaar te maken QRT's 216 S.2.1.2 - Balance sheet 1. Assets Solvency II value Intangible assets Deferred tax assets Pension benefit surplus Property, plant & equipment held for own use

N.V. Hagelunie Openbaar te maken QRT's 216 S.2.1.2 - Balance sheet 1. Assets Solvency II value Intangible assets Deferred tax assets Pension benefit surplus Property, plant & equipment held for own use

21 April 2017 Kurt Svoboda, CFRO. UNIQA Insurance Group AG Economic Capital and Embedded Value 2016

21 April 2017 Kurt Svoboda, CFRO UNIQA Insurance Group AG Economic Capital and Embedded Value 2016 Executive Summary Overall positive development for the Group s economic position based on strong operating

21 April 2017 Kurt Svoboda, CFRO UNIQA Insurance Group AG Economic Capital and Embedded Value 2016 Executive Summary Overall positive development for the Group s economic position based on strong operating

Technical Specification on the Long Term Guarantee Assessment (Part I)

") EIOPA-DOC-13/061 28 January 2013 Technical Specification on the Long Term Guarantee Assessment (Part I) This document contains part I of the technical specifications for the long-term guarantees assessment

EIOPA-DOC-13/061 28 January 2013 Technical Specification on the Long Term Guarantee Assessment (Part I) This document contains part I of the technical specifications for the long-term guarantees assessment

COVER NOTE TO ACCOMPANY THE DRAFT QIS5 TECHNICAL SPECIFICATIONS

EUROPEAN COMMISSION Internal Market and Services DG FINANCIAL INSTITUTIONS Insurance and Pensions 1. Introduction COVER NOTE TO ACCOMPANY THE DRAFT QIS5 TECHNICAL SPECIFICATIONS Brussels, 15 April 2010

EUROPEAN COMMISSION Internal Market and Services DG FINANCIAL INSTITUTIONS Insurance and Pensions 1. Introduction COVER NOTE TO ACCOMPANY THE DRAFT QIS5 TECHNICAL SPECIFICATIONS Brussels, 15 April 2010

De Friesland Particuliere Ziektekostenverzekeringen N.V. Openbaar te maken QRT's

De Friesland Particuliere Ziektekostenverzekeringen N.V. Openbaar te maken QRT's 2016 S.02.01.02 - Balance sheet 1.000 Assets Solvency II value Intangible assets 0 Deferred tax assets 0 Pension benefit

De Friesland Particuliere Ziektekostenverzekeringen N.V. Openbaar te maken QRT's 2016 S.02.01.02 - Balance sheet 1.000 Assets Solvency II value Intangible assets 0 Deferred tax assets 0 Pension benefit

AVÉRO ACHMEA ZORGVERZEKERINGEN N.V. Openbaar te maken QRT's

AVÉRO ACHMEA ZORGVERZEKERINGEN N.V. Openbaar te maken QRT's 2016 S.02.01.02 - Balance sheet 1.000 Assets Solvency II value Intangible assets 0 Deferred tax assets 0 Pension benefit surplus 0 Property,

AVÉRO ACHMEA ZORGVERZEKERINGEN N.V. Openbaar te maken QRT's 2016 S.02.01.02 - Balance sheet 1.000 Assets Solvency II value Intangible assets 0 Deferred tax assets 0 Pension benefit surplus 0 Property,

Appointed Actuary Symposium 2007 Solvency II Update

watsonwyatt.com Appointed Actuary Symposium 2007 Solvency II Update Naomi Burger 7 November 2007 Agenda Overview Pillar 1 - Capital requirements Pillar 2 - Supervisory review Pillar 3 - Disclosure Conclusions

watsonwyatt.com Appointed Actuary Symposium 2007 Solvency II Update Naomi Burger 7 November 2007 Agenda Overview Pillar 1 - Capital requirements Pillar 2 - Supervisory review Pillar 3 - Disclosure Conclusions

Annex I S Balance sheet Solvency II value Assets

S.02.01.02 Balance sheet Solvency II value Assets C0010 Intangible assets R0030 - Deferred tax assets R0040 80,694,193 Pension benefit surplus R0050 53,827,400 Property, plant & equipment held for own

S.02.01.02 Balance sheet Solvency II value Assets C0010 Intangible assets R0030 - Deferred tax assets R0040 80,694,193 Pension benefit surplus R0050 53,827,400 Property, plant & equipment held for own

Verslag inzake de Solvabiliteit en de Financiële Toestand bedragen in duizenden. DSW Ziektekostenverzekeringen N.V.

Verslag inzake de Solvabiliteit en de Financiële Toestand 217 bedragen in duizenden DSW Ziektekostenverzekeringen N.V. Inhoudsopgave: 2.1 Balance Sheet 5.1 Premiums, claims and expenses by line of business

Verslag inzake de Solvabiliteit en de Financiële Toestand 217 bedragen in duizenden DSW Ziektekostenverzekeringen N.V. Inhoudsopgave: 2.1 Balance Sheet 5.1 Premiums, claims and expenses by line of business

Technical Specification for the Preparatory Phase (Part I)

") EIOPA-14/209 30 April 2014 Technical Specification for the Preparatory Phase (Part I) This document contains part I of the technical specifications for the preparatory phase. It needs to be applied in

EIOPA-14/209 30 April 2014 Technical Specification for the Preparatory Phase (Part I) This document contains part I of the technical specifications for the preparatory phase. It needs to be applied in

July Solvency II benchmark A comparison of the Dutch Insurance Market FY2016

July 2017 Solvency II benchmark A comparison of the Dutch Insurance Market FY2016 SCR ( mrd) Solvency II market overview of 6 insurance groups Diverse position of major players 7 6 5 4 3 2 1 - Delta Lloyd

July 2017 Solvency II benchmark A comparison of the Dutch Insurance Market FY2016 SCR ( mrd) Solvency II market overview of 6 insurance groups Diverse position of major players 7 6 5 4 3 2 1 - Delta Lloyd

First EU Stress Test for Occupational Pensions. Frankfurt, 24 February 2016 Daniel Perez

First EU Stress Test for Occupational Pensions Frankfurt, 24 February 2016 Daniel Perez OBJECTIVES OF THE EXERCISE To produce a comprehensive picture of the heterogeneous European occupational pensions

First EU Stress Test for Occupational Pensions Frankfurt, 24 February 2016 Daniel Perez OBJECTIVES OF THE EXERCISE To produce a comprehensive picture of the heterogeneous European occupational pensions

Lancashire Insurance Company (UK) Ltd

Ltd") Lancashire Insurance Company (UK) Ltd Solvency and Financial Condition Report Disclosures 31 December 2017 (Monetary amounts in USD thousands) General information Undertaking name Lancashire Insurance

Lancashire Insurance Company (UK) Ltd Solvency and Financial Condition Report Disclosures 31 December 2017 (Monetary amounts in USD thousands) General information Undertaking name Lancashire Insurance

Stress Test Exercise Questions & Answers

EIOPA-FS-11/17 Version 17 May 2011 Stress Test Exercise 2011 Questions & Answers Stress Test - List of Methodological Issues Raised by Participants and Supervisors General Disclaimer The answers given

EIOPA-FS-11/17 Version 17 May 2011 Stress Test Exercise 2011 Questions & Answers Stress Test - List of Methodological Issues Raised by Participants and Supervisors General Disclaimer The answers given

S Balance sheet Solvency II value

S.02.01.02(A,S) Balance sheet S.02.01.02.01 Balance sheet Solvency II value C0010 Assets Goodwill R0010 Deferred acquisition costs R0020 Intangible assets R0030 0 k Deferred tax assets R0040 870 k Pension

S.02.01.02(A,S) Balance sheet S.02.01.02.01 Balance sheet Solvency II value C0010 Assets Goodwill R0010 Deferred acquisition costs R0020 Intangible assets R0030 0 k Deferred tax assets R0040 870 k Pension

Life under Solvency II Be prepared!

Life under Solvency II Be prepared! Moderator: Hugh Rosenbaum, Towers Watson Speakers: Tomas Wittbjer, Global Head of Insurance, IKANO SA Lorraine Stack, Marsh Management Services Dublin Session Overview

Life under Solvency II Be prepared! Moderator: Hugh Rosenbaum, Towers Watson Speakers: Tomas Wittbjer, Global Head of Insurance, IKANO SA Lorraine Stack, Marsh Management Services Dublin Session Overview

Achmea Regular Supervisory Report. Achmea Summary Solvency and Financial Condition Report

Achmea Regular Supervisory Report Achmea Summary Solvency and Financial Condition Report Solvency and Financial Condition Report Achmea 2017 Summary Solvency and Financial Condition Report 2 Achmea Solvency

Achmea Regular Supervisory Report Achmea Summary Solvency and Financial Condition Report Solvency and Financial Condition Report Achmea 2017 Summary Solvency and Financial Condition Report 2 Achmea Solvency

Quantitave reporting templates Appendix SFCR Schade. jij, je pensioen en

Quantitave reporting templates 2016 Appendix SFCR Schade jij, je pensioen en Inhoud Balance sheet.... 3 Non-Life.... 5 Life... 6 Home Country - non-life obligations.... 7 Total Top 5 and home country -

Quantitave reporting templates 2016 Appendix SFCR Schade jij, je pensioen en Inhoud Balance sheet.... 3 Non-Life.... 5 Life... 6 Home Country - non-life obligations.... 7 Total Top 5 and home country -

Quarterly results

Quarterly results 31.03.2017 26.06.2017 Agenda 2 Key highlights Main events in Financial performance BGAAP ¹ Financial performance IFRS ² Solvency II of Ethias SA³ Investment portfolio ² Rating Appendix

Quarterly results 31.03.2017 26.06.2017 Agenda 2 Key highlights Main events in Financial performance BGAAP ¹ Financial performance IFRS ² Solvency II of Ethias SA³ Investment portfolio ² Rating Appendix

SOLVENCY II Level 2 Implementing Measures

SOLVENCY II Level 2 Implementing Measures Position after the 3 waves of Consultation Papers and the Quantitative Impact Study 5 Technical Specifications Dr. Thomas Guidon CASUALTY LOSS RESERVE SEMINAR

SOLVENCY II Level 2 Implementing Measures Position after the 3 waves of Consultation Papers and the Quantitative Impact Study 5 Technical Specifications Dr. Thomas Guidon CASUALTY LOSS RESERVE SEMINAR

Solvency II Year-End Standard Formula Exercise Guidance Notes September 2017

Solvency II 2017 Year-End Standard Formula Exercise Guidance Notes September 2017 Disclaimer No responsibility or liability is accepted by the Society of Lloyd s, the Council, or any Committee of Board

Solvency II 2017 Year-End Standard Formula Exercise Guidance Notes September 2017 Disclaimer No responsibility or liability is accepted by the Society of Lloyd s, the Council, or any Committee of Board

Hot Topic: Understanding the implications of QIS5

Hot Topic: Understanding the 17 March 2011 Summary On 14 March 2011 the European Insurance and Occupational Pensions Authority (EIOPA) published the results of the fifth Quantitative Impact Study (QIS5)

Hot Topic: Understanding the 17 March 2011 Summary On 14 March 2011 the European Insurance and Occupational Pensions Authority (EIOPA) published the results of the fifth Quantitative Impact Study (QIS5)

Battle of the Balance Sheets

Battle of the Balance Sheets Stuart Morris FIA, Deloitte Dr. Robin Thompson, RBS Andrew Kenyon FIA, RBS 07 November 2016 Agenda Risk-based capital requirements: Banks vs. Insurers Available capital Case

Battle of the Balance Sheets Stuart Morris FIA, Deloitte Dr. Robin Thompson, RBS Andrew Kenyon FIA, RBS 07 November 2016 Agenda Risk-based capital requirements: Banks vs. Insurers Available capital Case

AVIVA Solvency and Financial Condition Report ( SFCR )

") AVIVA 2016 Solvency and Financial Condition Report ( SFCR ) 2 Disclaimer Cautionary statements: This should be read in conjunction with the documents distributed by Aviva plc (the Company or Aviva ) through

AVIVA 2016 Solvency and Financial Condition Report ( SFCR ) 2 Disclaimer Cautionary statements: This should be read in conjunction with the documents distributed by Aviva plc (the Company or Aviva ) through

S Balance sheet. in thousand EUR. Solvency II value

Index S.02.01_Balance Sheet S.05.01_Premiums, claims and expenses by line of business S.05.02_Premiums, claims and expenses by country S.12.01_Life and Health SLT Technical Provisions S.22.01_Impact of

Index S.02.01_Balance Sheet S.05.01_Premiums, claims and expenses by line of business S.05.02_Premiums, claims and expenses by country S.12.01_Life and Health SLT Technical Provisions S.22.01_Impact of

10 April 2019 Kurt Svoboda, CFRO. UNIQA Insurance Group AG Economic Capital and Embedded Value 2018

10 April 2019 Kurt Svoboda, CFRO UNIQA Insurance Group AG Economic Capital and Embedded Value 2018 Executive summary Economic Capital Embedded Value Economic Capital Ratio 205% Unrestricted Tier 1 Capital

10 April 2019 Kurt Svoboda, CFRO UNIQA Insurance Group AG Economic Capital and Embedded Value 2018 Executive summary Economic Capital Embedded Value Economic Capital Ratio 205% Unrestricted Tier 1 Capital

Understanding the prudential balance sheet. Lars Dieckhoff Principal expert Solvency II

Understanding the prudential balance sheet Lars Dieckhoff Principal expert Solvency II Understanding the prudential balance sheet Content Overview of the prudential balance sheet Solvency Capital Requirement

Understanding the prudential balance sheet Lars Dieckhoff Principal expert Solvency II Understanding the prudential balance sheet Content Overview of the prudential balance sheet Solvency Capital Requirement

Solvency and Financial Condition Report (SFCR)

") A Introduction Solvency and Financial Condition Report (SFCR) DEVK Rückversicherungs- und Beteiligungs-AG is an active unlisted stock corporation. The registered office of the company is Cologne. The company

A Introduction Solvency and Financial Condition Report (SFCR) DEVK Rückversicherungs- und Beteiligungs-AG is an active unlisted stock corporation. The registered office of the company is Cologne. The company

Senior Insurance I Managers Regime (SIMR) The Chief Executive is responsible for allocating each of the SIMR prescribed responsibilities to one or more approved persons in accordance with the PRA Rulebook

Senior Insurance I Managers Regime (SIMR) The Chief Executive is responsible for allocating each of the SIMR prescribed responsibilities to one or more approved persons in accordance with the PRA Rulebook

UNIQA Insurance Group AG. Group Economic Capital Report 2017

UNIQA Insurance Group AG Group Economic Capital Report 2017 Table of Contents 1 Executive Summary... 3 2 Risk Strategy UNIQA Group... 4 3 Risk Management Framework... 5 4 Own Funds... 5 4.1 Own Funds Development...

UNIQA Insurance Group AG Group Economic Capital Report 2017 Table of Contents 1 Executive Summary... 3 2 Risk Strategy UNIQA Group... 4 3 Risk Management Framework... 5 4 Own Funds... 5 4.1 Own Funds Development...

Life 2008 Spring Meeting June 16-18, Session 14, Key Issues Arising from Solvency II. Moderator Marc Slutzky, FSA, MAAA

Life 2008 Spring Meeting June 16-18, 2008 Session 14, Key Issues Arising from Moderator Marc Slutzky, FSA, MAAA Authors Mark Chaplin, FIA Matthew P. Clark, FSA, MAAA Henk van Broekhoven, AAG watsonwyatt.com

Life 2008 Spring Meeting June 16-18, 2008 Session 14, Key Issues Arising from Moderator Marc Slutzky, FSA, MAAA Authors Mark Chaplin, FIA Matthew P. Clark, FSA, MAAA Henk van Broekhoven, AAG watsonwyatt.com

Solvency II Update Tokyo, 16 October Dr. Winfried Heinen

Solvency II Update Tokyo, 16 October 2008 Dr. Winfried Heinen Agenda The Solvency II Project: Reminder & Current State A Look at the Framework Directive Pillar 1 Central Idea SCR QIS4 Technical Specifications

Solvency II Update Tokyo, 16 October 2008 Dr. Winfried Heinen Agenda The Solvency II Project: Reminder & Current State A Look at the Framework Directive Pillar 1 Central Idea SCR QIS4 Technical Specifications

S Balance sheet. in thousand EUR. Solvency II value Assets

Index S.02.01_Balance Sheet S.05.01_Premiums, claims and expenses by line of business S.05.02_Premiums, claims and expenses by country S.12.01_Life and Health SLT Technical Provisions S.17.01_Non - life

Index S.02.01_Balance Sheet S.05.01_Premiums, claims and expenses by line of business S.05.02_Premiums, claims and expenses by country S.12.01_Life and Health SLT Technical Provisions S.17.01_Non - life

Annex I S Balance sheet Solvency II value Assets

S.02.01.02 Balance sheet Solvency II value Assets C0010 Intangible assets R0030 0 Deferred tax assets R0040 2 062 111 Pension benefit surplus R0050 0 Property, plant & equipment held for own use R0060

S.02.01.02 Balance sheet Solvency II value Assets C0010 Intangible assets R0030 0 Deferred tax assets R0040 2 062 111 Pension benefit surplus R0050 0 Property, plant & equipment held for own use R0060

2017 Solvency II Public Quantitative Reporting Templates Blue Square Re N.V.

2017 Solvency II Public Quantitative Reporting Templates Blue Square Re N.V. Blue Square Re N.V. Aegonplein 50 2591 TV The Hague Template Template title code S.02.01 Balance sheet S.05.01 Premiums, claims

2017 Solvency II Public Quantitative Reporting Templates Blue Square Re N.V. Blue Square Re N.V. Aegonplein 50 2591 TV The Hague Template Template title code S.02.01 Balance sheet S.05.01 Premiums, claims

Lancashire Holdings Limited

Lancashire Holdings Limited Solvency and Financial Condition Report Disclosures 31 December 2017 (Monetary amounts in USD thousands) General information Participating undertaking name Lancashire Holdings

Lancashire Holdings Limited Solvency and Financial Condition Report Disclosures 31 December 2017 (Monetary amounts in USD thousands) General information Participating undertaking name Lancashire Holdings

Index-linked and unit-linked insurance Other life insurance Annuities stemming from non-life insurance. Contracts with options or guarantees

S.12.1.2 Life and Health SLT Technical Provisions Insurance with profit participation Indexlinked and unitlinked Other life Annuities stemming from nonlife Contracts without options and guarantees Contracts

S.12.1.2 Life and Health SLT Technical Provisions Insurance with profit participation Indexlinked and unitlinked Other life Annuities stemming from nonlife Contracts without options and guarantees Contracts

12 June Errata to the Technical Specifications for the Preparatory Phase

12 June 2014 Errata to the Technical Specifications for the Preparatory Phase Version of 30 April 2014 Reference Wording in Technical Specifications Corrected Wording 1 TS (II) - 1.2.2.1 The adjustment

12 June 2014 Errata to the Technical Specifications for the Preparatory Phase Version of 30 April 2014 Reference Wording in Technical Specifications Corrected Wording 1 TS (II) - 1.2.2.1 The adjustment

LONGEVITY SWAPS. Impact of Solvency II AN EFFECTIVE, INNOVATIVE WAY TO MANAGE THE LONGEVITY RISK. Presenter: Tom O Sullivan, F.S.A, F.C.I.A, M.A.A.A.

LONGEVITY SWAPS AN EFFECTIVE, INNOVATIVE WAY TO MANAGE THE LONGEVITY RISK Impact of Solvency II Presenter: Tom O Sullivan, F.S.A, F.C.I.A, M.A.A.A. Date: December 3, 2010 AGENDA 1. Solvency II - Background

LONGEVITY SWAPS AN EFFECTIVE, INNOVATIVE WAY TO MANAGE THE LONGEVITY RISK Impact of Solvency II Presenter: Tom O Sullivan, F.S.A, F.C.I.A, M.A.A.A. Date: December 3, 2010 AGENDA 1. Solvency II - Background

European insurers in the starting blocks

Solvency Consulting Knowledge Series European insurers in the starting blocks Contacts: Martin Brosemer Tel.: +49 89 38 91-43 81 mbrosemer@munichre.com Dr. Kathleen Ehrlich Tel.: +49 89 38 91-27 77 kehrlich@munichre.com

Solvency Consulting Knowledge Series European insurers in the starting blocks Contacts: Martin Brosemer Tel.: +49 89 38 91-43 81 mbrosemer@munichre.com Dr. Kathleen Ehrlich Tel.: +49 89 38 91-27 77 kehrlich@munichre.com

S Balance sheet. in thousand EUR. Solvency II value

Index S.02.01_Balance Sheet S.05.01_Premiums, claims and expenses by line of business S.05.02_Premiums, claims and expenses by country S.12.01_Life and Health SLT Technical Provisions S.22.01_Impact of

Index S.02.01_Balance Sheet S.05.01_Premiums, claims and expenses by line of business S.05.02_Premiums, claims and expenses by country S.12.01_Life and Health SLT Technical Provisions S.22.01_Impact of

Solvency Assessment and Management: Steering Committee Position Paper 44 1 (v 4) Concentration Risk

Concentration Risk") Solvency Assessment and Management: Steering Committee Position Paper 44 1 (v 4) Concentration Risk EXECUTIVE SUMMARY This document discusses the structure and calibration of the concentration risk sub-module

Solvency Assessment and Management: Steering Committee Position Paper 44 1 (v 4) Concentration Risk EXECUTIVE SUMMARY This document discusses the structure and calibration of the concentration risk sub-module

Solvency II Year-End Standard Formula Exercise Guidance Notes September 2018

Solvency II 2018 Year-End Standard Formula Exercise Guidance Notes September 2018 Disclaimer No responsibility or liability is accepted by the Society of Lloyd s, the Council, or any Committee of Board

Solvency II 2018 Year-End Standard Formula Exercise Guidance Notes September 2018 Disclaimer No responsibility or liability is accepted by the Society of Lloyd s, the Council, or any Committee of Board

Report on long-term guarantees measures and measures on equity risk

EIOPA REGULAR USE EIOPA-BoS-17/334 20 December 2017 Report on long-term guarantees measures and measures on equity risk 2017 1/171 Table of Contents Executive summary... 3 I. Introduction... 6 I.1 Review

EIOPA REGULAR USE EIOPA-BoS-17/334 20 December 2017 Report on long-term guarantees measures and measures on equity risk 2017 1/171 Table of Contents Executive summary... 3 I. Introduction... 6 I.1 Review

Quantitative Reporting Templates (QRTs) Europæiske Rejseforsikring A/S

Europæiske Rejseforsikring A/S") Quantitative Reporting Templates (QRTs) 2017 Europæiske Rejseforsikring A/S Template Code S.01.02 S.02.01 S.05.01 S.05.02 S.12.01 S.17.01 S.19.01 S.23.01 S.25.01 S.28.01 S.32.01 Template name Basic Information

Quantitative Reporting Templates (QRTs) 2017 Europæiske Rejseforsikring A/S Template Code S.01.02 S.02.01 S.05.01 S.05.02 S.12.01 S.17.01 S.19.01 S.23.01 S.25.01 S.28.01 S.32.01 Template name Basic Information

Opinion on the solvency position of insurance and reinsurance undertakings in light of the withdrawal of the United Kingdom from the European Union

EIOPA-BoS-18/201 18 May 2018 Opinion on the solvency position of insurance and reinsurance undertakings in light of the withdrawal of the United Kingdom from the European Union 1. Legal basis 1.1. The

EIOPA-BoS-18/201 18 May 2018 Opinion on the solvency position of insurance and reinsurance undertakings in light of the withdrawal of the United Kingdom from the European Union 1. Legal basis 1.1. The