- development of Customer. and beyond. NCSI Anniversary Presentation Seoul, Korea January 29 th, 2008 Jan Eklöf, EPSI Rating and SSE

|

|

|

- Hilary Tucker

- 5 years ago

- Views:

Transcription

1 - development of Customer satisfaction studies in Europe and beyond NCSI Anniversary Presentation Seoul, Korea January 29 th, 2008 Jan Eklöf, EPSI Rating and SSE

2 NCSI 10 Year Anniversary Presentation Congratulations to the first decade of national customer satisfaction assessment. Have a successful future! EPSI Rating, Pan-European counterpart 11/10/

3 Plan European Performance Satisfaction Index Why?

4 Why listen to the customers? The customer base, the only reason for existence of the company/venture The external customers generate all long-term revenues for the operation It is profitable to adopt to their expectations Customer perception is much more than just supplying good goods and services Any provider can work on customer expectations and perceived satisfaction to enhance sustainable profitability. Revive the dormant potentials. Prioritization crucial for financial strength Why? 11/10/

5 The customer is King But certainly not always right How to react to their wishes Should we always try to fulfil or even exceed their expectations How is the image and expectations handled by a supplier 11/10/

6 Deming said One has to focus on the customers Current customers satisfaction Future (potential) customers needs and demands Because there are no more any truly supply driven economies or markets, but demand sets the rule of the game 11/10/

7 Who are the customers? Internal Current employees Potential affiliates External Current clients Potential clients Those you want to do business with 11/10/

8 The EFQM Excellence Model - the basis for EPSI - The EPSI analysis Framework Why? 11/10/

9 (external) Customer Loyalty Satisfied customers might not be enough Loyal customer are key LOYAL CUSTOMERS Cost less to maintain Buy more products Buy more efficiently Act as ambassadors 11/10/

10 What is EPSI? Why? Economic Indicator Financial Indicator EPSI, European Performance Satisfaction Index, is an economic indicator based on modeling of customer assessment of the quality of goods and services purchased in European countries. It reflects causes and consequences of customer satisfaction and their mutual relationships. EPSI is an important indicator of economic performance, both for individual firms and on the industry and society levels. It is related to leading indicators that are able to predict consumer spending and stock -market growth. Integrated Indicator EPSI started as a voice of the customers and later proved to be most useful also as a reflection tool of Employees Satisfaction and Loyalty/trust. Further development allowed applying EPSI approach for other stakeholders Satisfaction and its drivers, for example, citizens in general and CSR (corporate Social Responsibility) assessment. 11/10/

11

12 Customer Satisfaction Index by Country 85 Customer Satis sfaction Index (EPSI) Denmark Finland Greece Portugal Sweden Ireland Iceland Russia Estonia Latvia Lithuania Norway Czech Republic Pan European Average Ukraine 11/10/

13 Customer Satisfaction Index by Sector Customer Satisf faction Index (EPSI) Banking Mobile Supermarket Insurance Pan European Average Datacom 11/10/

Estonia Latvia Lithuania Russia Czech Republic Greece France")

14 Main countries and sectors coverage Why? - Nations covered at present Denmark Finland Iceland Norway Sweden (initiator) Estonia Latvia Lithuania Russia Czech Republic Greece France (emerging) Germany (emerging) Ukraine United Kingdom (emerging) Portugal (affiliated) 11/10/

15 Main countries and sectors coverage - Industries/sectors covered at present Why? Banking (consumer and corporate segment) General Insurance (consumer and corporate segment) Life/pension insurance Retail Trade Mobile Telecoms and Broadband (consumer and corporate segment) Utilities (electricity etc.) Health services Education Police and public safety Public transport Public administration Logistics (corporate segment) Postal Services Business Services (IT, auditing, legal) 11/10/

16 History Why? The EPSI-initiative (started 1999 with 11 countries; 8 countries year 2001, about 15 in 2004 and almost 20 in 2008 ) under the Umbrella of EPSI Rating EPSI aim at cooperating with similar initiatives in USA (ACSI), Far East countries (like NCSI) and Middle East/Africa (SAS etc.) 11/10/

17 Comparability with other initiatives EPSI is in its core approach very similar to ACSI (the USA-counterpart) Model sructure and estimation techniques are harmonized Comparisons of results may be possible on both aggregate index and latent (driver) level For impacts-comparisons specific calibration (on industry level) should be done. 11/10/

18 Value of A model where the market value of a firm is related to the level of customer satisfaction previous year has been established Studies have been done for a number of industries (incl. banking and insurance) on the relationship between satisfaction and financial performance/market value showing positive correlation (with a time-lag) - Similar studies have been documented based on USAdata (Fornell et al) 11/10/

19 Pan-European CSI studies for Why? Ranking and promotion (beauty contest) Finding areas calling for improvements (SWOT-aspect) Identifying where more analysis is needed General benchmarking Analyzing effects of modifications Evaluating effects of strategic improvements Guiding customers All this is part of the EPSI agenda 11/10/

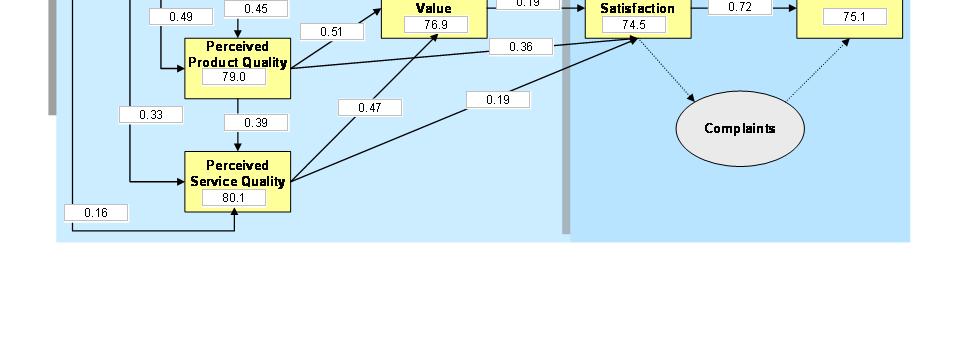

(SCSI) Loyalty (retention) Perceived Quality ------------ service quality Complaints (not part of the master model) 11/10/2009 www.epsi-rating.")

20 EPSI RATING Master Model Structure Image Customer Expectations Perceived Quality product quality Perceived Value Customer Satisfaction Index (CSI) (SCSI) Loyalty (retention) Perceived Quality service quality Complaints (not part of the master model) 11/10/

21 Design aspects (the Pan European approach) Survey design properties Questionnaire design Sample selection Field operation 11/10/

22 Questionnaire Design A set of master questionnaires is developed and tested; A common scale is used (1-10); The wording is calibrated on the Pan-European level (with adoption to national peculiarities ); Each latent variable is covered by at least 3 manifest questions. 11/10/

23 Level of Detail About 35 questions are included in the master questionnaire; Possible to add a limited number of specific questions by a company (similar to the entire market); Flexible results presentation possible, based on the full range of collected items, with extensive analysis on the driver side. 11/10/

24 Blocks of Questions Three standard questions are used for measuring the EPSI construct itself. These are: Overall satisfaction with the product/provider; Satisfaction compared to expectations; and The product/provider compared to an ideal (not always relevant, may be substituted; see below). 11/10/

25 Blocks of Questions (cont.) For loyalty, we use: Intention to buy again (or remain as a customer to the said company/product); Intention of cross-buying (buy another product from the same brand/company); Intention to switch to another brand/company/supplier; and Intention to recommend the brand/company to other consumers (word of mouth). 11/10/

26 Latents on Driver side Image Expectations Perceived Quality Product domain Service domain Perceived value 11/10/

27 Blocks of Questions (cont.) On the driver side we use about 20 questions relating to the image, expectations, product and service quality as well as to the perceived value. The definition of aspects differ slightly from sector to sector, depending of the characteristics of the industry: The exact wording of questions is standardized to allow comparative studies. 11/10/

28 Sample Selection Representative sample of current customers is key; Experience of the provider product is crucial; The reference period is industry-specific (banking 12 months, retail trade 3 months, car purchase 36, etc.); Consumers vs. corporate customers (B2C vs. B2B); Extensive non-response monitoring is conducted. About 250 observations for each study domain is required for comprehensive model analysis 11/10/

29 Field Operation Data collection is done by telephone as default; Only qualified field interviewers from recognized survey organizations - and specially trained - are used; A full-fledge CATI-system should be in operation by each considered data collection agency; A process quality control system developed; Validation in relation to population characteristics. Also other alternatives tested and introduced step-by-step (like. Web-based surveys) 11/10/

30 The analysis tool The model is estimated by means of structural equation techniques (basically Partial Least Squares approaches); Results are obtained for: customer perceived index levels impact strength/importance of all aspects (manifests) Relative weights for manifest questions Model quality (accuracy, explanation power, robustness) 11/10/

31 Model Quality assessment Why? Quality requirements for: - Precision The 95 percent confidence interval for the CSI shall have a width of not more than 4 units (referring to an index scale of 0 100). - Explanatory power The econometric model must be able to explain approximately 65% of what drives customer satisfaction. 11/10/

32 Comparability In any comparison two aspects are at stake. The two main dimensions of comparability of course are: Over time Between similar phenomena (individuals, companies, industries, etc.) These two dimensions are often combined into a composite cross-section time-series approach. It would be fair to say that such analyses constitute the standard case in all economics and business studies. 11/10/

33 Benchmark Country specific differences are expected in the measurement process. EPSI Rating has developed a modelbases approach to measure this kind of effects. -This gives calibration factors by country and industry - Further, in-country differences occur due to the fact that consumers react differently to measurements (by i.a. age, gender and socio-demography etc.) 11/10/

5. Customer based differences 11/10/2009 www.epsi-rating.")

34 Benchmark studies Using data from major industries and several countries we have obtained measures of: 1. Country effects 2. Industry effecs 3. Segment effects 4. (B2B vs. B2C and customer profile) 5. Customer based differences 11/10/

35 Corporate Usage of EPSI (benchmark) Results The EPSI approach and empirical resultas are used internally for more than merely promotion in numerous major companies and organisations. More than 50 multi-national companies currently have EPSI as one performance dimension. Companies like: Nordea, Danske Bank, Handelsbanken, SEB, Swedbank, SBAB, SPP, Stadshypotek, Den Norske bank, Gjensidige Nor, If, Codan -Trygg Hansa, Folksam, TeliaSonea, Ax-food, ICA, Erste Bank, Athens Metro. EXAMPLES

36 De-regulation in Telecoms An Example relating to Business - to - business Fixed Telecommunications The old monopoly and the competitors In Sweden 11/10/

37 Trends in Telecoms S C S I fo r th e C o m p a n y - T im e D e v e lo p m e n t Index 5 6 The C o m pa ny /9 9 y e a r 11/10/

38 Trends in Telecoms W a tc h T h e C om p e tito r Index The C o mpa ny The C o mpe tito /9 9 Y ear 11/10/

39 Corporate Telecoms 1999 C u s to m e r V a lu a tio n In d e x T h e c o m p a n y T h e C o m p e tito 5 0 Image Expectations Product Quality Service Quality In d ic a t o r Perceived Value SCSI Loyalty 11/10/

40 Corporate Telecoms 1999 P e rc e iv e d v a lu e Procent V alu TE LI V alu A N N A In d e x 11/10/

41 Telia and its competitor(s) Telia och konkurrensen 70 Telia 65 Konkurrenten competitor N?d dhet / 흏 11/10/

42 Competition in the fixed phone sector: Sweden Fast telekom F? etagsmarknad i SKI Kundn? dhe et 60 Telia andra / 흏 11/10/

43 The third wave of market adoption Why? Fixed lines B2B market in Sweden EPSI Customer satisf faction Telia Tele2 Phonera Ventelo Annan / Year 11/10/

44 Insurance company usage - Finland B2B segment Priority setting The improvement candidates - Today and compared with the situation Last year 11/10/

45 Svenskt EPSI Kvalitetsindex Finland General Bank Privatmarknad Insurance B2B Company X Föreningssparbanken If Drivande Driving Factors Faktorer Image ,1 Resultat Results 0, ,20 Kund Expectations Förväntningar , , ,52 Perceived Upplevd Product Produktkvalitet Quality , ,50 0,24 0, , Perceived Prisvärde Value ,1 Customer ,16 Kundnöjdhet Satisfaction 0, , , , Complaints Klagomål Lojalitet Loyalty 73, , Perveived Upplevd Servicekvalitet Quality ,2 11/10/

46 Company X Why?

47 Total Effect from Divers to Customer Satisfaction EPSI Finland 2007 Driver is increased by one unit Total Effec ct Image Expectations Product Quality Service Quality Value Fennia If Pohjola A-Vakuutus Tapiola Other 11/10/

48 Total Impact from Drivers to Customer Satisfaction Driver is increased by one unit Fennia If Pohjola Tapiola Other Total Impa act Image Expectations ProdQ ServQ Value

49 Priority Map If Company X EPSI Finland Score Importanc e Image E xpect P rodq S ervq Value 11/10/

50 Prioritization Image is still the most important aspect for improvemnet (has the highest effect on satisfaction). However it has decreased slightly from Product Quality is this year almost as important as image (their relative impact has increased) Expectations come as third in importance. That will be achieved by increased image. 11/10/

51 Improving IMAGE By..

52 Score and Weight Image EPSI Finland Score Weight 0.23 Score Weight the image of being a reliable and transparent insurance company? the image of providing excellent overall customer service? the image of offeringthe image of being athe overall image of good value for money to the customers in terms of fees and claim settling? professional, stateof the-art insurance company? your insurance company? 0.15 *No big differences in relative weight, so concentrate on the ones that are cheapest to improve! 11/10/

53 Effect Calculation - Image A: Improve the image of providing excellent customer service with one unit on 1-10 scale 2007 yields (result 2006 in parenthesis). An increase in overall Image by 2.60 units (2.92 units last year). An increase in customer satisfaction by 1.63 units (1.93 units) B: Improve the image of providing value for money with one unit on 1-10 scale 2007 yields... An increase in overall Image by 2.10 units. An increase in customer satisfaction by 1.30 units 11/10/

54 Improving Product Quality By..

55 Score and Weight Product Quality EPSI Finland Score Weight Score Weight 6.5 the quality of the insurance functions offered (fees, coverage, etc.)? the quality of the the technical quality of the overall insurance reliability and accuracythe products (functions) quality of the functions (standing orders processed in accordance with offered (data transfer, Internet connection, that matter for you offered by your insurance company? instructions, accuracy of statements, etc.)? overall security system, etc.)? Relative importance of technical quality has increased from /10/

56 Effect Calculation - ProductQ A: Improving the quality of the reliability and accuracy with one unit on 1-10 scale 2007 yields (result 2006 in parenthesis). An increase in overall Product Quality by 2.94 units (3.14 units last year). An increase in customer satisfaction by 1.81 units (1.78 units) B: Improving the quality of product functions with one unit on 1-10 scale 2007 yields... An increase in overall Product Quality by 2.70 units. An increase in customer satisfaction by 1.66 units 11/10/

it is possible others have succeeded with improvements of 1 unit or more during 1 2 years time The customer satisfaction may (theoretically) improve with (up to) 6.4 units.")

57 Thus provided these above aspects can be improved in the eyes of the customers Why? With 1 unit each (from 7.9; 7.6; 7.9 and 8.1 respectively) it is possible others have succeeded with improvements of 1 unit or more during 1 2 years time The customer satisfaction may (theoretically) improve with (up to) 6.4 units. Highly significant indeed! 11/10/

58 But, maybe the strategies should be more select Focussing of special categories of customers..

59 Because, Customers are different Spread in customer satisfaction and other latents Complaints Claims and their handling

60 Spread Customer Satisfaction General Insurance B2B EPSI Finland % 50% Proport tion (%) 40% 30% 20% 10% 0% Index level If Pohjola A-Vakuutus Tapiola Other 11/10/

61

62 The integrated approach EPSI Customers and Employees integrated

63 The EFQM Excellence Model - The EPSI analysis Framework 11/10/

64 EPSI Employees There is a strong relationship?? Satisfied employees Satisfied customers 11/10/

65 Top Management Image EPSI Employees ---- Structural Model Framework My boss Cooperation Satisfaction (R 2 = ) Loyalty (R 2 = ) The daily work 80,4 Motivation Salary and other working regulations Personal development

66 Approach for integrated analysis From the integrated model we calculate:... Index for each latent Priority areas and possible conflicts (between consumer and employee perspective) Improvement possibilities 11/10/

67 Challenges for the future Opportunities and Threats In the European EPSI environment

68 Opportunities Why? It is becoming increasingly important for the corporate image to have good customer satisfaction; More and more multi-national companies are using non-financial performance indicators for assessment (like in BSC-systems); EPSI is becoming increasingly using in such applications (both strategic and more operational); Priority setting and evaluation of improvement schemes is more and more critical for costefficiency in the industry; and Society-activities (public sector) call for more and more of prioritization based on user-responsiveness. 11/10/

69 Threats Short-term financial monitoring dominates, and longer-term investing in customers get too little priority; Data collection is becoming increasingly difficult and costly generating nonrepresentative samples; and Reaction patterns by customers are changing calling for adaptive modelling 11/10/

70 EPSI Challenges Develop and Run national as well as corporate customer satisfaction studies in Europe Have EPSI accepted as a standard performance indicator in corporate society Cooperate with similar initiatives on other continents Offer benchmark opportunities using interaction between performance areas 11/10/

71 For more information European Performance Satisfaction Index Webb-plats: /10/

How to use public resources in such a way that government agencies can provide better service at lower cost to a growing number of citizens

How to use public resources in such a way that government agencies can provide better service at lower cost to a growing number of citizens Professor Claes Fornell University of Michigan Improving Public

How to use public resources in such a way that government agencies can provide better service at lower cost to a growing number of citizens Professor Claes Fornell University of Michigan Improving Public

FöreningsSparbanken. Nils-Fredrik Nyblæus. Deputy President and CFO

FöreningsSparbanken Nils-Fredrik Nyblæus Deputy President and CFO 2 Group objectives Market position Customers Employees Financial position 3 Basics of sustainable profitability Customer satisfaction Human

FöreningsSparbanken Nils-Fredrik Nyblæus Deputy President and CFO 2 Group objectives Market position Customers Employees Financial position 3 Basics of sustainable profitability Customer satisfaction Human

Update on crowdfunding user s awareness

Update on crowdfunding user s awareness Nikos Daskalakis 4 th ECSF Meeting 17 February 2016 Overview Final results of the Oxera study "Crowdfunding from the user s perspective" - FSUG Preliminary results

Update on crowdfunding user s awareness Nikos Daskalakis 4 th ECSF Meeting 17 February 2016 Overview Final results of the Oxera study "Crowdfunding from the user s perspective" - FSUG Preliminary results

Nordea Market s Insurance Seminar January 10, 2011 Group CFO Peter Johansson

Nordea Market s Insurance Seminar 2011 January 10, 2011 Group CFO Peter Johansson Disclaimer This presentation may contain forward-looking statements that reflect management s current views with respect

Nordea Market s Insurance Seminar 2011 January 10, 2011 Group CFO Peter Johansson Disclaimer This presentation may contain forward-looking statements that reflect management s current views with respect

Electricity & Gas Prices in Ireland. Annex Business Electricity Prices per kwh 2 nd Semester (July December) 2016

2016") Electricity & Gas Prices in Ireland Annex Business Electricity Prices per kwh 2 nd Semester (July December) 2016 ENERGY POLICY STATISTICAL SUPPORT UNIT 1 Electricity & Gas Prices in Ireland Annex Business

Electricity & Gas Prices in Ireland Annex Business Electricity Prices per kwh 2 nd Semester (July December) 2016 ENERGY POLICY STATISTICAL SUPPORT UNIT 1 Electricity & Gas Prices in Ireland Annex Business

CERP report on the application of EN regarding national needs and peculiarities

CERP PL 2009 / 1 Doc 9c E CERP report on the application of EN 13850 regarding national needs and peculiarities Table of contents 1 Introduction...2 2 Executive summary...3 3 The scope of the measurement...4

CERP PL 2009 / 1 Doc 9c E CERP report on the application of EN 13850 regarding national needs and peculiarities Table of contents 1 Introduction...2 2 Executive summary...3 3 The scope of the measurement...4

Pan-European opinion poll on occupational safety and health

REPORT Pan-European opinion poll on occupational safety and health Results across 36 European countries Final report Conducted by Ipsos MORI Social Research Institute at the request of the European Agency

REPORT Pan-European opinion poll on occupational safety and health Results across 36 European countries Final report Conducted by Ipsos MORI Social Research Institute at the request of the European Agency

November 5, Very preliminary work in progress

November 5, 2007 Very preliminary work in progress The forecasting horizon of inflationary expectations and perceptions in the EU Is it really 2 months? Lars Jonung and Staffan Lindén, DG ECFIN, Brussels.

November 5, 2007 Very preliminary work in progress The forecasting horizon of inflationary expectations and perceptions in the EU Is it really 2 months? Lars Jonung and Staffan Lindén, DG ECFIN, Brussels.

Global Consumer Confidence

Global Consumer Confidence The Conference Board Global Consumer Confidence Survey is conducted in collaboration with Nielsen 4TH QUARTER 2017 RESULTS CONTENTS Global Highlights Asia-Pacific Africa and

Global Consumer Confidence The Conference Board Global Consumer Confidence Survey is conducted in collaboration with Nielsen 4TH QUARTER 2017 RESULTS CONTENTS Global Highlights Asia-Pacific Africa and

A GER AMWAY GLOBAL ENTREPRENEURSHIP REPORT WHAT DRIVES THE ENTREPRENEURIAL SPIRIT

A GER 2018 AMWAY GLOBAL ENTREPRENEURSHIP REPORT WHAT DRIVES THE ENTREPRENEURIAL SPIRIT S U R V E Y D E S I G N KEY FACTS OF THIS YEAR S SURVEY EDITION PARTNER RESEARCH INSTITUTE 8 th edition FIELDWORK

A GER 2018 AMWAY GLOBAL ENTREPRENEURSHIP REPORT WHAT DRIVES THE ENTREPRENEURIAL SPIRIT S U R V E Y D E S I G N KEY FACTS OF THIS YEAR S SURVEY EDITION PARTNER RESEARCH INSTITUTE 8 th edition FIELDWORK

EUROPEAN UNION SOUTH KOREA TRADE AND INVESTMENT 5 TH ANNIVERSARY OF THE FTA. Delegation of the European Union to the Republic of Korea

EUROPEAN UNION SOUTH KOREA TRADE AND INVESTMENT 5 TH ANNIVERSARY OF THE FTA 2016 Delegation of the European Union to the Republic of Korea 16 th Floor, S-tower, 82 Saemunan-ro, Jongno-gu, Seoul, Korea

EUROPEAN UNION SOUTH KOREA TRADE AND INVESTMENT 5 TH ANNIVERSARY OF THE FTA 2016 Delegation of the European Union to the Republic of Korea 16 th Floor, S-tower, 82 Saemunan-ro, Jongno-gu, Seoul, Korea

ABOLISHING CASH IN EUROPE: THE BENEFITS AND DRAWBACKS OF ELECTRONIC TRANSACTIONS

Financial Market Central European Review of Economics & Finance GIKAS 1, Alina HYZ 2, Periklis TAGKAS 3 ABOLISHING CASH IN EUROPE: THE BENEFITS AND DRAWBACKS OF ELECTRONIC TRANSACTIONS payment during the

Financial Market Central European Review of Economics & Finance GIKAS 1, Alina HYZ 2, Periklis TAGKAS 3 ABOLISHING CASH IN EUROPE: THE BENEFITS AND DRAWBACKS OF ELECTRONIC TRANSACTIONS payment during the

Low employment among the 50+ population in Hungary

Low employment among the + population in Hungary The role of incentives, health and cognitive capacities Janos Divenyi (Central European University) and Gabor Kezdi (Central European University and IE-CRSHAS)

Low employment among the + population in Hungary The role of incentives, health and cognitive capacities Janos Divenyi (Central European University) and Gabor Kezdi (Central European University and IE-CRSHAS)

Pohjola Group. Interim Report Q4/2010 Financial Statements for 2010

1 Pohjola Group Interim Report Q4/21 Financial Statements for 21 2 Pohjola Group Interim Report Q4/21 Financial Statements for 21 3 Contents Interim Report Q4/21 Financial Statements for 21 4 2 Dividend

1 Pohjola Group Interim Report Q4/21 Financial Statements for 21 2 Pohjola Group Interim Report Q4/21 Financial Statements for 21 3 Contents Interim Report Q4/21 Financial Statements for 21 4 2 Dividend

Chart pack to council for cooperation on macroprudential policy

Chart pack to council for cooperation on macroprudential policy Contents List of charts... 3 Macro and macro-financial setting... 5 Swedish macroeconomic setting... 5 Foreign macroeconomic setting... Macro-financial

Chart pack to council for cooperation on macroprudential policy Contents List of charts... 3 Macro and macro-financial setting... 5 Swedish macroeconomic setting... 5 Foreign macroeconomic setting... Macro-financial

THE FUTURE OF CASH AND PAYMENTS

THE FUTURE OF CASH AND PAYMENTS Retail Banking Research January 2010 CONFIDENTIALITY AND COPYRIGHT This report is published by Retail Banking Research Ltd (RBR). The information and data within this report

THE FUTURE OF CASH AND PAYMENTS Retail Banking Research January 2010 CONFIDENTIALITY AND COPYRIGHT This report is published by Retail Banking Research Ltd (RBR). The information and data within this report

Investor meetings. March Visit for further information

Investor meetings March 2007 Visit www.trygvesta.com for further information 1 Contents Highlights 2006......3 Claims and run-off..8 Business areas...10 Outlook, capital and dividend..20 Outlook 2007.23

Investor meetings March 2007 Visit www.trygvesta.com for further information 1 Contents Highlights 2006......3 Claims and run-off..8 Business areas...10 Outlook, capital and dividend..20 Outlook 2007.23

Keefe, Bruyette & Woods. Financials Conference. Group CFO Peter Johansson 20 September 2011

Keefe, Bruyette & Woods 211 UK Day and European Financials Conference Group CFO Peter Johansson 2 September 211 Structure Sampo plc Parent company for the Group Market Cap ~ EUR 11 bn* 21.3% Over 2% Nordea

Keefe, Bruyette & Woods 211 UK Day and European Financials Conference Group CFO Peter Johansson 2 September 211 Structure Sampo plc Parent company for the Group Market Cap ~ EUR 11 bn* 21.3% Over 2% Nordea

Borderline cases for salary, social contribution and tax

Version Abstract 1 (5) 2015-04-21 Veronica Andersson Salary and labour cost statistics Borderline cases for salary, social contribution and tax (Workshop on Labour Cost Survey, Rome, Italy 5-6 May 2015)

Version Abstract 1 (5) 2015-04-21 Veronica Andersson Salary and labour cost statistics Borderline cases for salary, social contribution and tax (Workshop on Labour Cost Survey, Rome, Italy 5-6 May 2015)

Dow Jones Sustainability Indexes (DJSI) Annual Review 2005

Annual Review 2005") Dow Jones Sustainability Indexes (DJSI) Annual Review 2005 Zurich, Switzerland 7 September 2005 A cooperation of Dow Jones Indexes, STOXX Ltd. and SAM Group 1 Content I. Key Facts II. III. IV. Research

Dow Jones Sustainability Indexes (DJSI) Annual Review 2005 Zurich, Switzerland 7 September 2005 A cooperation of Dow Jones Indexes, STOXX Ltd. and SAM Group 1 Content I. Key Facts II. III. IV. Research

Consumer credit market in Europe 2013 overview

Consumer credit market in Europe 2013 overview Crédit Agricole Consumer Finance published its annual survey of the consumer credit market in 28 European Union countries for seven years running. 9 July

Consumer credit market in Europe 2013 overview Crédit Agricole Consumer Finance published its annual survey of the consumer credit market in 28 European Union countries for seven years running. 9 July

PUBLIC PROCUREMENT INDICATORS 2011, Brussels, 5 December 2012

PUBLIC PROCUREMENT INDICATORS 2011, Brussels, 5 December 2012 1. INTRODUCTION This document provides estimates of three indicators of performance in public procurement within the EU. The indicators are

PUBLIC PROCUREMENT INDICATORS 2011, Brussels, 5 December 2012 1. INTRODUCTION This document provides estimates of three indicators of performance in public procurement within the EU. The indicators are

Cross-border mergers and divisions

Cross-border mergers and divisions Cross-border mergers and divisions Consultation by the European Commission, DG MARKT INTRODUCTION Preliminary Remark The purpose of this questionnaire is to collect information,

Cross-border mergers and divisions Cross-border mergers and divisions Consultation by the European Commission, DG MARKT INTRODUCTION Preliminary Remark The purpose of this questionnaire is to collect information,

Flash Eurobarometer 408 EUROPEAN YOUTH REPORT

Flash Eurobarometer EUROPEAN YOUTH REPORT Fieldwork: December 2014 Publication: April 2015 This survey has been requested by the European Commission, Directorate-General for Education and Culture and co-ordinated

Flash Eurobarometer EUROPEAN YOUTH REPORT Fieldwork: December 2014 Publication: April 2015 This survey has been requested by the European Commission, Directorate-General for Education and Culture and co-ordinated

E-Communications Household Survey

Special Eurobarometer 293 European Commission E-Communications Household Survey Fieldwork November December 2007 Publication June 2008 Report Special Eurobarometer 293 / Wave 68.2 TNS opinion & social

Special Eurobarometer 293 European Commission E-Communications Household Survey Fieldwork November December 2007 Publication June 2008 Report Special Eurobarometer 293 / Wave 68.2 TNS opinion & social

The Rule of Law as a Factor for Competitiveness

The Rule of Law as a Factor for Competitiveness Lessons from the Global Competitiveness Index 2008-2009 Irene Mia Director, Senior Economist Global Competitiveness Network, World Economic Forum OECD Workshop

The Rule of Law as a Factor for Competitiveness Lessons from the Global Competitiveness Index 2008-2009 Irene Mia Director, Senior Economist Global Competitiveness Network, World Economic Forum OECD Workshop

The Economics of Public Health Care Reform in Advanced and Emerging Economies

The Economics of Public Health Care Reform in Advanced and Emerging Economies Benedict Clements Fiscal Affairs Department, IMF November 2012 This presentation represents the views of the author and should

The Economics of Public Health Care Reform in Advanced and Emerging Economies Benedict Clements Fiscal Affairs Department, IMF November 2012 This presentation represents the views of the author and should

Working Group on Public Health statistics

Working Group on Public Health statistics Agenda item 8.2 Main projects and data collection Health Expenditure Statistics (SHA) 26-27 October 2009 EUROSTAT: Working Group Public Health Meeting SHA Joint

Working Group on Public Health statistics Agenda item 8.2 Main projects and data collection Health Expenditure Statistics (SHA) 26-27 October 2009 EUROSTAT: Working Group Public Health Meeting SHA Joint

Data ENCJ Survey on the Independence of Judges. Co-funded by the Justice Programme of the European Union

Data ENCJ Survey on the Independence of Judges 2016-2017 Co-funded by the Justice Programme of the European Union Table of content 1. Introduction 3 2. Executive Summary of the outcomes of the survey 4

Data ENCJ Survey on the Independence of Judges 2016-2017 Co-funded by the Justice Programme of the European Union Table of content 1. Introduction 3 2. Executive Summary of the outcomes of the survey 4

International Seminar on Strengthening Public Investment and Managing Fiscal Risks from Public-Private Partnerships

International Seminar on Strengthening Public Investment and Managing Fiscal Risks from Public-Private Partnerships Budapest, Hungary March 7 8, 2007 The views expressed in this paper are those of the

International Seminar on Strengthening Public Investment and Managing Fiscal Risks from Public-Private Partnerships Budapest, Hungary March 7 8, 2007 The views expressed in this paper are those of the

Standard Eurobarometer

Standard Eurobarometer 67 / Spring 2007 Standard Eurobarometer European Commission SPECIAL EUROBAROMETER EUROPEANS KNOWELEDGE ON ECONOMICAL INDICATORS 1 1 This preliminary analysis is done by Antonis PAPACOSTAS

Standard Eurobarometer 67 / Spring 2007 Standard Eurobarometer European Commission SPECIAL EUROBAROMETER EUROPEANS KNOWELEDGE ON ECONOMICAL INDICATORS 1 1 This preliminary analysis is done by Antonis PAPACOSTAS

Leasing in Europe State of Play and Outlook. Bucharest, Romania 19 November

Leasing in Europe State of Play and Outlook Bucharest, Romania 19 November Agenda o About Leaseurope o Leasing in Europe o Leased Assets & Customers o State of the Industry o Industry Performance o Business

Leasing in Europe State of Play and Outlook Bucharest, Romania 19 November Agenda o About Leaseurope o Leasing in Europe o Leased Assets & Customers o State of the Industry o Industry Performance o Business

Defining Issues. EU Audit Reforms: The Countdown Begins. April 2016, No Key Facts for U.S. Companies

Defining Issues April 2016, No. 16-12 EU Audit Reforms: The Countdown Begins Only two months remain before the European Union (EU) audit reforms come into full effect. These reforms will affect many U.S.

Defining Issues April 2016, No. 16-12 EU Audit Reforms: The Countdown Begins Only two months remain before the European Union (EU) audit reforms come into full effect. These reforms will affect many U.S.

Sandra KAISER. Austrian Budget Reform

Sandra KAISER Austrian Budget Reform Paris/January 12th, 2015 Contents Overview of the Austrian budget reform - A. Design and Concept - B. Medium Term Fiscal Framework - C. Budget Structure - D. Accrual

Sandra KAISER Austrian Budget Reform Paris/January 12th, 2015 Contents Overview of the Austrian budget reform - A. Design and Concept - B. Medium Term Fiscal Framework - C. Budget Structure - D. Accrual

2017/SOM3/DIA/005. GATS Plus - Services. Submitted by: Australia

2017/SOM3/DIA/005 GATS Plus - Services Submitted by: Australia Dialogue on Regional Trade Agreements and Free Trade Agreements Ho Chi Minh City, Viet Nam 27 August 2017 GATS PLUS SERVICES Ambassador Simon

2017/SOM3/DIA/005 GATS Plus - Services Submitted by: Australia Dialogue on Regional Trade Agreements and Free Trade Agreements Ho Chi Minh City, Viet Nam 27 August 2017 GATS PLUS SERVICES Ambassador Simon

Recommendation of the Council on Tax Avoidance and Evasion

Recommendation of the Council on Tax Avoidance and Evasion OECD Legal Instruments This document is published under the responsibility of the Secretary-General of the OECD. It reproduces an OECD Legal Instrument

Recommendation of the Council on Tax Avoidance and Evasion OECD Legal Instruments This document is published under the responsibility of the Secretary-General of the OECD. It reproduces an OECD Legal Instrument

Special Eurobarometer 418 SOCIAL CLIMATE REPORT

Special Eurobarometer 418 SOCIAL CLIMATE REPORT Fieldwork: June 2014 Publication: November 2014 This survey has been requested by the European Commission, Directorate-General for Employment, Social Affairs

Special Eurobarometer 418 SOCIAL CLIMATE REPORT Fieldwork: June 2014 Publication: November 2014 This survey has been requested by the European Commission, Directorate-General for Employment, Social Affairs

Key Considerations for Expanding Your Subscription Business Internationally

Education Series Key Considerations for Expanding Your Subscription Business Internationally November 18, 2015 Presented by Ben Bowler - Director Product Management, Recurly Alexa Boyce - Senior Manager

Education Series Key Considerations for Expanding Your Subscription Business Internationally November 18, 2015 Presented by Ben Bowler - Director Product Management, Recurly Alexa Boyce - Senior Manager

Flash Eurobarometer 398 WORKING CONDITIONS REPORT

Flash Eurobarometer WORKING CONDITIONS REPORT Fieldwork: April 2014 Publication: April 2014 This survey has been requested by the European Commission, Directorate-General for Employment, Social Affairs

Flash Eurobarometer WORKING CONDITIONS REPORT Fieldwork: April 2014 Publication: April 2014 This survey has been requested by the European Commission, Directorate-General for Employment, Social Affairs

Executive summary. Interim results January - June

Executive summary Interim results January - June 2005 www.sebgroup.com 1 SEB Focus SEB traditional strengths - Corporates - Affluent individuals Growth Broadening platform New home markets /acquisitions

Executive summary Interim results January - June 2005 www.sebgroup.com 1 SEB Focus SEB traditional strengths - Corporates - Affluent individuals Growth Broadening platform New home markets /acquisitions

Pohjola Group. Interim Report for 1 January 30 September Pohjola/IR

Pohjola Group Interim Report for 1 January 3 September 29 2 Contents Pohjola in Brief 3 Strategy and Financial targets 7 Interim Report for Q1 3/9 14 Review by Business Segment Banking 26 Asset Management

Pohjola Group Interim Report for 1 January 3 September 29 2 Contents Pohjola in Brief 3 Strategy and Financial targets 7 Interim Report for Q1 3/9 14 Review by Business Segment Banking 26 Asset Management

InnovFin SME Guarantee

InnovFin SME Guarantee Implementation Update Reporting date: 30/09/2017 Disclaimer This presentation contains general information about the implementation results of InnovFin SME Guarantee, a facility

InnovFin SME Guarantee Implementation Update Reporting date: 30/09/2017 Disclaimer This presentation contains general information about the implementation results of InnovFin SME Guarantee, a facility

Special Eurobarometer 465. Gender Equality 2017

Summary Gender Equality 01 Gender Pay Gap Survey requested by the European Commission, Directorate-General for Justice and Consumers and co-ordinated by the Directorate-General for Communication This document

Summary Gender Equality 01 Gender Pay Gap Survey requested by the European Commission, Directorate-General for Justice and Consumers and co-ordinated by the Directorate-General for Communication This document

Sampo plc Annual General Meeting 24 April Kari Stadigh Group CEO and President

Sampo plc Annual General Meeting 24 April 2014 Kari Stadigh Group CEO and President Sampo Group had an excellent year 2013 EURm 1,800 1,600 1,400 1,200 1,000 800 600 400 200 0 200 864 929 Sampo Group s

Sampo plc Annual General Meeting 24 April 2014 Kari Stadigh Group CEO and President Sampo Group had an excellent year 2013 EURm 1,800 1,600 1,400 1,200 1,000 800 600 400 200 0 200 864 929 Sampo Group s

Approach to Employment Injury (EI) compensation benefits in the EU and OECD

compensation benefits in the EU and OECD") Approach to (EI) compensation benefits in the EU and OECD The benefits of protection can be divided in three main groups. The cash benefits include disability pensions, survivor's pensions and other short-

Approach to (EI) compensation benefits in the EU and OECD The benefits of protection can be divided in three main groups. The cash benefits include disability pensions, survivor's pensions and other short-

Unless otherwise stated, the figures apply to the DNB Group.

Unless otherwise stated, the figures apply to the DNB Group. The table shows relevant key figures for all topics identified in the materiality analysis. There is an overlap between some of the key figures

Unless otherwise stated, the figures apply to the DNB Group. The table shows relevant key figures for all topics identified in the materiality analysis. There is an overlap between some of the key figures

European Union Statistics on Income and Living Conditions (EU-SILC)

") European Union Statistics on Income and Living Conditions (EU-SILC) European Union Statistics on Income and Living Conditions (EU-SILC) is a household survey that was launched in 23 on the basis of a gentlemen's

European Union Statistics on Income and Living Conditions (EU-SILC) European Union Statistics on Income and Living Conditions (EU-SILC) is a household survey that was launched in 23 on the basis of a gentlemen's

Fiscal sustainability challenges in Romania

Preliminary Draft For discussion only Fiscal sustainability challenges in Romania Bucharest, May 10, 2011 Ionut Dumitru Anca Paliu Agenda 1. Main fiscal sustainability challenges 2. Tax collection issues

Preliminary Draft For discussion only Fiscal sustainability challenges in Romania Bucharest, May 10, 2011 Ionut Dumitru Anca Paliu Agenda 1. Main fiscal sustainability challenges 2. Tax collection issues

MedTech Europe Code of Ethical Business Practice. Disclosure Guidelines

MedTech Europe Code of Ethical Business Practice Disclosure Guidelines Final version: 13 September 2016 Table of Contents Preamble... 2 Chapter 1: Applicability of these Guidelines... 3 1. Scope... 3 2.

MedTech Europe Code of Ethical Business Practice Disclosure Guidelines Final version: 13 September 2016 Table of Contents Preamble... 2 Chapter 1: Applicability of these Guidelines... 3 1. Scope... 3 2.

January 2014 Euro area international trade in goods surplus 0.9 bn euro 13.0 bn euro deficit for EU28

STAT/14/41 18 March 2014 January 2014 Euro area international trade in goods surplus 0.9 13.0 deficit for EU28 The first estimate for the euro area 1 (EA18) trade in goods balance with the rest of the

STAT/14/41 18 March 2014 January 2014 Euro area international trade in goods surplus 0.9 13.0 deficit for EU28 The first estimate for the euro area 1 (EA18) trade in goods balance with the rest of the

Effects of using International Financial Reporting Standards (IFRS) in the EU: public consultation

in the EU: public consultation") Effects of using International Financial Reporting Standards (IFRS) in the EU: public consultation Fields marked with are mandatory. Impact of International Financial Reporting Standards (IFRS) in the

Effects of using International Financial Reporting Standards (IFRS) in the EU: public consultation Fields marked with are mandatory. Impact of International Financial Reporting Standards (IFRS) in the

REGIONAL PROGRESS OF THE LISBON STRATEGY OBJECTIVES IN THE EUROPEAN REGION EGRI, ZOLTÁN TÁNCZOS, TAMÁS

REGIONAL PROGRESS OF THE LISBON STRATEGY OBJECTIVES IN THE EUROPEAN REGION EGRI, ZOLTÁN TÁNCZOS, TAMÁS Key words: Lisbon strategy, mobility factor, education-employment factor, human resourches. CONCLUSIONS

REGIONAL PROGRESS OF THE LISBON STRATEGY OBJECTIVES IN THE EUROPEAN REGION EGRI, ZOLTÁN TÁNCZOS, TAMÁS Key words: Lisbon strategy, mobility factor, education-employment factor, human resourches. CONCLUSIONS

May 2012 Euro area international trade in goods surplus of 6.9 bn euro 3.8 bn euro deficit for EU27

108/2012-16 July 2012 May 2012 Euro area international trade in goods surplus of 6.9 3.8 deficit for EU27 The first estimate for the euro area 1 (EA17) trade in goods balance with the rest of the world

108/2012-16 July 2012 May 2012 Euro area international trade in goods surplus of 6.9 3.8 deficit for EU27 The first estimate for the euro area 1 (EA17) trade in goods balance with the rest of the world

Banks in Sweden. Facts about the Swedish banking market. Contents

Facts about the Swedish banking market Contents The Swedish financial market 1 Structure of the banking industry 2 Deposits and lending 3 The major banking groups 4 Banks in Sweden 5 Mortgage credit institutions

Facts about the Swedish banking market Contents The Swedish financial market 1 Structure of the banking industry 2 Deposits and lending 3 The major banking groups 4 Banks in Sweden 5 Mortgage credit institutions

Retail banking. Section 4.2

Retail banking Section 4.2 Retail banking: CheBanca! profile CheBanca! KPIs Strong funding arm: 13.3bn direct deposits plus 1bn indirect deposits Best Italian online bank in 2012* Scalable and efficient

Retail banking Section 4.2 Retail banking: CheBanca! profile CheBanca! KPIs Strong funding arm: 13.3bn direct deposits plus 1bn indirect deposits Best Italian online bank in 2012* Scalable and efficient

DDFs Virksomhedsdag Finansanalytikerforeningens Virksomhedsdag 2008 CFO Morten Hübbe

1 Finansanalytikerforeningens Virksomhedsdag 2008 CFO Morten Hübbe Facts about TrygVesta 2 Shares outstanding 68m Market cap DKK 26bn (USD 5.4bn) Danish institutions 15% Non-Danish institutions 7% Smaller

1 Finansanalytikerforeningens Virksomhedsdag 2008 CFO Morten Hübbe Facts about TrygVesta 2 Shares outstanding 68m Market cap DKK 26bn (USD 5.4bn) Danish institutions 15% Non-Danish institutions 7% Smaller

Electricity & Gas Prices in Ireland. Annex Household Electricity Prices per kwh 2 nd Semester (July December) 2016

2016") Electricity & Gas Prices in Ireland Annex Household Electricity Prices per kwh 2 nd Semester (July December) 2016 ENERGY POLICY STATISTICAL SUPPORT UNIT 1 Electricity & Gas Prices in Ireland Annex Household

Electricity & Gas Prices in Ireland Annex Household Electricity Prices per kwh 2 nd Semester (July December) 2016 ENERGY POLICY STATISTICAL SUPPORT UNIT 1 Electricity & Gas Prices in Ireland Annex Household

June 2012 Euro area international trade in goods surplus of 14.9 bn euro 0.4 bn euro surplus for EU27

121/2012-17 August 2012 June 2012 Euro area international trade in goods surplus of 14.9 0.4 surplus for EU27 The first estimate for the euro area 1 (EA17) trade in goods balance with the rest of the world

121/2012-17 August 2012 June 2012 Euro area international trade in goods surplus of 14.9 0.4 surplus for EU27 The first estimate for the euro area 1 (EA17) trade in goods balance with the rest of the world

Gender pension gap economic perspective

Gender pension gap economic perspective Agnieszka Chłoń-Domińczak Institute of Statistics and Demography SGH Part of this research was supported by European Commission 7th Framework Programme project "Employment

Gender pension gap economic perspective Agnieszka Chłoń-Domińczak Institute of Statistics and Demography SGH Part of this research was supported by European Commission 7th Framework Programme project "Employment

Flash Eurobarometer 458. Report. The euro area

The euro area Survey requested by the European Commission, Directorate-General for Economic and Financial Affairs and co-ordinated by the Directorate-General for Communication This document does not represent

The euro area Survey requested by the European Commission, Directorate-General for Economic and Financial Affairs and co-ordinated by the Directorate-General for Communication This document does not represent

ENTREPRENEURSHIP IN THE EU AND BEYOND

Flash Eurobarometer 354 ENTREPRENEURSHIP IN THE EU AND BEYOND COUNTRY REPORT SPAIN Fieldwork: June 2012 This survey has been requested by the European Commission, Directorate-General Enterprise and Industry

Flash Eurobarometer 354 ENTREPRENEURSHIP IN THE EU AND BEYOND COUNTRY REPORT SPAIN Fieldwork: June 2012 This survey has been requested by the European Commission, Directorate-General Enterprise and Industry

August 2012 Euro area international trade in goods surplus of 6.6 bn euro 12.6 bn euro deficit for EU27

146/2012-16 October 2012 August 2012 Euro area international trade in goods surplus of 6.6 12.6 deficit for EU27 The first estimate for the euro area 1 (EA17) trade in goods balance with the rest of the

146/2012-16 October 2012 August 2012 Euro area international trade in goods surplus of 6.6 12.6 deficit for EU27 The first estimate for the euro area 1 (EA17) trade in goods balance with the rest of the

Traffic Safety Basic Facts Main Figures. Traffic Safety Basic Facts Traffic Safety. Motorways Basic Facts 2015.

Traffic Safety Basic Facts 2013 - Main Figures Traffic Safety Basic Facts 2015 Traffic Safety Motorways Basic Facts 2015 Motorways General Almost 30.000 people were killed in road accidents on motorways

Traffic Safety Basic Facts 2013 - Main Figures Traffic Safety Basic Facts 2015 Traffic Safety Motorways Basic Facts 2015 Motorways General Almost 30.000 people were killed in road accidents on motorways

Competition Policy in a Small Economy: the Case of Iceland

Competition Policy in a Small Economy: the Case of Iceland Friðrik M. Baldursson Department of Economics University of Iceland April 7, 2006 1 Goals of competition policy Competition is not an end in itself,

Competition Policy in a Small Economy: the Case of Iceland Friðrik M. Baldursson Department of Economics University of Iceland April 7, 2006 1 Goals of competition policy Competition is not an end in itself,

Financial Accounting Advisory Services

Financial Accounting Advisory Services May 2013 Agenda About EY 3 5 Appendix 13 Contacts 15 Page 2 About EY Page 3 EMEIA Sub-areas Africa Angola, Botswana, Republic of Congo, Equatorial Guinea, Ethiopia,

Financial Accounting Advisory Services May 2013 Agenda About EY 3 5 Appendix 13 Contacts 15 Page 2 About EY Page 3 EMEIA Sub-areas Africa Angola, Botswana, Republic of Congo, Equatorial Guinea, Ethiopia,

COMMISSION OF THE EUROPEAN COMMUNITIES REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL

EN EN EN COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, 25.06.2007 COM(2007) 207 final REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL on certain issues relating to Motor Insurance

EN EN EN COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, 25.06.2007 COM(2007) 207 final REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL on certain issues relating to Motor Insurance

Capital market day Stockholm, Sweden November 30, FöreningsSparbanken. Annika Wijkström Group EVP and Head of Business Area Alliances

Capital market day Stockholm, Sweden November 30, 2001 FöreningsSparbanken Annika Wijkström Group EVP and Head of Business Area Alliances International alliances 3 Rationale for alliances Potential for

Capital market day Stockholm, Sweden November 30, 2001 FöreningsSparbanken Annika Wijkström Group EVP and Head of Business Area Alliances International alliances 3 Rationale for alliances Potential for

EU BUDGET AND NATIONAL BUDGETS

DIRECTORATE GENERAL FOR INTERNAL POLICIES POLICY DEPARTMENT ON BUDGETARY AFFAIRS EU BUDGET AND NATIONAL BUDGETS 1999-2009 October 2010 INDEX Foreward 3 Table 1. EU and National budgets 1999-2009; EU-27

DIRECTORATE GENERAL FOR INTERNAL POLICIES POLICY DEPARTMENT ON BUDGETARY AFFAIRS EU BUDGET AND NATIONAL BUDGETS 1999-2009 October 2010 INDEX Foreward 3 Table 1. EU and National budgets 1999-2009; EU-27

1 Pohjola April 2008

Pohjola April 2008 1 OP-Pohjola Group & Pohjola Bank in brief 2 The leading financial services company in Finland - with a strong diversified presence in Retail and corporate banking Insurance Mutual Funds

Pohjola April 2008 1 OP-Pohjola Group & Pohjola Bank in brief 2 The leading financial services company in Finland - with a strong diversified presence in Retail and corporate banking Insurance Mutual Funds

6 OF 7 MARKETS 5BN/YEAR INTERIM REPORT JANUARY MARCH 2018 GOOD START OF 2018 JOHAN DENNELIND PRESIDENT & CEO MOBILE GROWTH ACROSS FOOTPRINT

INTERIM REPORT JANUARY MARCH 2018 Q1 JOHAN DENNELIND PRESIDENT & CEO GOOD START OF 2018 MOBILE GROWTH ACROSS FOOTPRINT 6 OF 7 MARKETS REPORTED EBITDA GROWTH +7.4% STRONG OPERATIONAL FREE CASH FLOW 4.3BN

INTERIM REPORT JANUARY MARCH 2018 Q1 JOHAN DENNELIND PRESIDENT & CEO GOOD START OF 2018 MOBILE GROWTH ACROSS FOOTPRINT 6 OF 7 MARKETS REPORTED EBITDA GROWTH +7.4% STRONG OPERATIONAL FREE CASH FLOW 4.3BN

Flash Eurobarometer 470. Report. Work-life balance

Work-life balance Survey requested by the European Commission, Directorate-General for Justice and Consumers and co-ordinated by the Directorate-General for Communication This document does not represent

Work-life balance Survey requested by the European Commission, Directorate-General for Justice and Consumers and co-ordinated by the Directorate-General for Communication This document does not represent

Developments for age management by companies in the EU

Developments for age management by companies in the EU Erika Mezger, Deputy Director EUROFOUND, Dublin Workshop on Active Ageing and coping with demographic change Prague, 6 September 2012 12/09/2012 1

Developments for age management by companies in the EU Erika Mezger, Deputy Director EUROFOUND, Dublin Workshop on Active Ageing and coping with demographic change Prague, 6 September 2012 12/09/2012 1

UBS Global Financial Services conference New York, May 16, Jan Lidén CEO

UBS Global Financial Services conference New York, May 16, 27 Jan Lidén CEO The leading bank in four small countries Sweden Total population: 9.m Private customers: 4.1m Corp. customers: 262, Organisations:

UBS Global Financial Services conference New York, May 16, 27 Jan Lidén CEO The leading bank in four small countries Sweden Total population: 9.m Private customers: 4.1m Corp. customers: 262, Organisations:

Third Revised Decision of the Council concerning National Treatment

Third Revised Decision of the Council concerning National Treatment OECD Legal Instruments This document is published under the responsibility of the Secretary-General of the OECD. It reproduces an OECD

Third Revised Decision of the Council concerning National Treatment OECD Legal Instruments This document is published under the responsibility of the Secretary-General of the OECD. It reproduces an OECD

PROGRESS TOWARDS THE LISBON OBJECTIVES 2010 IN EDUCATION AND TRAINING

PROGRESS TOWARDS THE LISBON OBJECTIVES IN EDUCATION AND TRAINING In 7, reaching the benchmarks for continues to pose a serious challenge for education and training systems in Europe, except for the goal

PROGRESS TOWARDS THE LISBON OBJECTIVES IN EDUCATION AND TRAINING In 7, reaching the benchmarks for continues to pose a serious challenge for education and training systems in Europe, except for the goal

Eurostars. What s in it for you?

Eurostars. What s in it for you? Eurostars is a joint programme between national funding bodies gathered within EUREKA - and the EU. Eurostars focuses on R&D-performing SMEs that wish to lead transnational

Eurostars. What s in it for you? Eurostars is a joint programme between national funding bodies gathered within EUREKA - and the EU. Eurostars focuses on R&D-performing SMEs that wish to lead transnational

October 2017 degroofpetercam.com. Sustainability Ranking. Developed Countries

October 2017 degroofpetercam.com Sustainability Ranking Developed Countries Sustainability Ranking - DEVELOPED countries Half-yearly report October 2017 While sustainable and ESG research on corporates

October 2017 degroofpetercam.com Sustainability Ranking Developed Countries Sustainability Ranking - DEVELOPED countries Half-yearly report October 2017 While sustainable and ESG research on corporates

ANNUAL REVIEW BY THE COMMISSION. of Member States' Annual Activity Reports on Export Credits in the sense of Regulation (EU) No 1233/2011

No 1233/2011") EUROPEAN COMMISSION Brussels, 7.2.2017 COM(2017) 67 final ANNUAL REVIEW BY THE COMMISSION of Member States' Annual Activity Reports on Export Credits in the sense of Regulation (EU) No 1233/2011 EN EN

EUROPEAN COMMISSION Brussels, 7.2.2017 COM(2017) 67 final ANNUAL REVIEW BY THE COMMISSION of Member States' Annual Activity Reports on Export Credits in the sense of Regulation (EU) No 1233/2011 EN EN

Corporate Governance and

Corporate Governance and Third Edition Jill Solomon )WILEY A John Wiley and Sons, Ltd, Publication Preface Acknowledgements Introducton xv xvii xix Part I Corporate governance: frameworks and mechanisms

Corporate Governance and Third Edition Jill Solomon )WILEY A John Wiley and Sons, Ltd, Publication Preface Acknowledgements Introducton xv xvii xix Part I Corporate governance: frameworks and mechanisms

Fair taxation of the digital economy

Contribution ID: 13311b6b-0b4c-4bf0-a3d9-c6b94f5ab400 Date: 02/01/2018 21:27:35 Fair taxation of the digital economy Fields marked with * are mandatory. 1 Introduction The objective of the initiative is

Contribution ID: 13311b6b-0b4c-4bf0-a3d9-c6b94f5ab400 Date: 02/01/2018 21:27:35 Fair taxation of the digital economy Fields marked with * are mandatory. 1 Introduction The objective of the initiative is

Inequality and Poverty in EU- SILC countries, according to OECD methodology RESEARCH NOTE

Inequality and Poverty in EU- SILC countries, according to OECD methodology RESEARCH NOTE Budapest, October 2007 Authors: MÁRTON MEDGYESI AND PÉTER HEGEDÜS (TÁRKI) Expert Advisors: MICHAEL FÖRSTER AND

Inequality and Poverty in EU- SILC countries, according to OECD methodology RESEARCH NOTE Budapest, October 2007 Authors: MÁRTON MEDGYESI AND PÉTER HEGEDÜS (TÁRKI) Expert Advisors: MICHAEL FÖRSTER AND

EIOPA Statistics - Accompanying note

EIOPA Statistics - Accompanying note Publication references: and Published statistics: [Balance sheet], [Premiums, claims and expenses], [Own funds and SCR] Disclaimer: Data is drawn from the published

EIOPA Statistics - Accompanying note Publication references: and Published statistics: [Balance sheet], [Premiums, claims and expenses], [Own funds and SCR] Disclaimer: Data is drawn from the published

Swedbank New York and Boston roadshow, September 24 26, Mikael Inglander, Chief Financial Officer

Swedbank New York and Boston roadshow, September 24 26, 27 Mikael Inglander, Chief Financial Officer The leading bank in four small countries Sweden Total population: 9.m Private customers: 4.1m Corp.

Swedbank New York and Boston roadshow, September 24 26, 27 Mikael Inglander, Chief Financial Officer The leading bank in four small countries Sweden Total population: 9.m Private customers: 4.1m Corp.

Anders Ek Executive Vice President, Head of Strategic and International Banking. Tokyo March 14, 2007

Anders Ek Executive Vice President, Head of Strategic and International Banking Tokyo March 14, 2007 Swedbank - an introduction (2) A leading Nordic-Baltic bank Other markets, niche banking Denmark - Swedbank

Anders Ek Executive Vice President, Head of Strategic and International Banking Tokyo March 14, 2007 Swedbank - an introduction (2) A leading Nordic-Baltic bank Other markets, niche banking Denmark - Swedbank

Banking in a tough environment

Banking in a tough environment Carnegie Nordic Large Cap Seminar Stockholm Tonny Thierry Andersen CFO & Member of the Executive Board March 3, 2009 The real economy is now severely affected Index Industrial

Banking in a tough environment Carnegie Nordic Large Cap Seminar Stockholm Tonny Thierry Andersen CFO & Member of the Executive Board March 3, 2009 The real economy is now severely affected Index Industrial

THE IMPACT OF THE PUBLIC DEBT STRUCTURE IN THE EUROPEAN UNION MEMBER COUNTRIES ON THE POSSIBILITY OF DEBT OVERHANG

THE IMPACT OF THE PUBLIC DEBT STRUCTURE IN THE EUROPEAN UNION MEMBER COUNTRIES ON THE POSSIBILITY OF DEBT OVERHANG Robert Huterski, PhD Nicolaus Copernicus University in Toruń Faculty of Economic Sciences

THE IMPACT OF THE PUBLIC DEBT STRUCTURE IN THE EUROPEAN UNION MEMBER COUNTRIES ON THE POSSIBILITY OF DEBT OVERHANG Robert Huterski, PhD Nicolaus Copernicus University in Toruń Faculty of Economic Sciences

EFPIA Disclosure Code 2016 Disclosures Shire Pharmaceuticals (including Baxalta US Inc.)

") EFPIA Disclosure Code 2016 Disclosures Shire Pharmaceuticals (including Baxalta US Inc.) 1 Section 1: Reporting Approach for 2016 Data: On June 3rd, 2016, Shire acquired Baxalta. Due to the complexity

EFPIA Disclosure Code 2016 Disclosures Shire Pharmaceuticals (including Baxalta US Inc.) 1 Section 1: Reporting Approach for 2016 Data: On June 3rd, 2016, Shire acquired Baxalta. Due to the complexity

Preliminary Findings From CEER Report On Network Losses. Ognjen Radovic

1 Preliminary Findings From CEER Report On Network Losses Ognjen Radovic The Council of European Energy Regulators (CEER) CEER is the voice of Europe's national regulators of electricity and gas at EU

1 Preliminary Findings From CEER Report On Network Losses Ognjen Radovic The Council of European Energy Regulators (CEER) CEER is the voice of Europe's national regulators of electricity and gas at EU

Fiscal transparency in the European Union

Theoretical and Applied Economics FFet al Volume XXII (2015), No. 1(602), pp. 227-232 Fiscal transparency in the European Union Alexandra ADAM Bucharest University of Economic Studies, Romania alexandra.adam@economie.ase.ro

Theoretical and Applied Economics FFet al Volume XXII (2015), No. 1(602), pp. 227-232 Fiscal transparency in the European Union Alexandra ADAM Bucharest University of Economic Studies, Romania alexandra.adam@economie.ase.ro

PENSIONS IN OECD COUNTRIES: INDICATORS AND DEVELOPMENTS

PENSIONS IN OECD COUNTRIES: INDICATORS AND DEVELOPMENTS Marius Lüske Directorate for Employment, Labour and Social Affairs, OECD Lisbon, 28.09.2018 Marius.LUSKE@oecd.org www.oecd.org/els OUTLINE Talk based

PENSIONS IN OECD COUNTRIES: INDICATORS AND DEVELOPMENTS Marius Lüske Directorate for Employment, Labour and Social Affairs, OECD Lisbon, 28.09.2018 Marius.LUSKE@oecd.org www.oecd.org/els OUTLINE Talk based

Svenska Handelsbanken Third quarter 2002

Svenska Handelsbanken Third quarter 2002 22 October 2002 Profit and loss account, January - September Handelsbanken Group Change SEKm 2002 2001 % Net interest income 10 611 9 856 8 Commission, net 3 782

Svenska Handelsbanken Third quarter 2002 22 October 2002 Profit and loss account, January - September Handelsbanken Group Change SEKm 2002 2001 % Net interest income 10 611 9 856 8 Commission, net 3 782

EIOPA Statistics - Accompanying note

EIOPA Statistics - Accompanying note Publication references: Published statistics: [Balance sheet], [Premiums, claims and expenses], [Own funds and SCR] Disclaimer: Data is drawn from the published statistics

EIOPA Statistics - Accompanying note Publication references: Published statistics: [Balance sheet], [Premiums, claims and expenses], [Own funds and SCR] Disclaimer: Data is drawn from the published statistics

Consultation on the European Pillar of Social Rights

Contribution ID: 05384989-c4b4-45c1-af8b-3faefd6298df Date: 23/12/2016 11:12:47 Consultation on the European Pillar of Social Rights Fields marked with * are mandatory. Welcome to the European Commission's

Contribution ID: 05384989-c4b4-45c1-af8b-3faefd6298df Date: 23/12/2016 11:12:47 Consultation on the European Pillar of Social Rights Fields marked with * are mandatory. Welcome to the European Commission's

Composition of capital IT044 IT044 POWSZECHNAIT044 UNIONE DI BANCHE ITALIANE SCPA (UBI BANCA)

") Composition of capital POWSZECHNA (in million Euro) Capital position CRD3 rules A) Common equity before deductions (Original own funds without hybrid instruments and government support measures other than

Composition of capital POWSZECHNA (in million Euro) Capital position CRD3 rules A) Common equity before deductions (Original own funds without hybrid instruments and government support measures other than

Sources of Government Revenue in the OECD, 2018

FISCAL FACT No. 581 Mar. 2018 Sources of Government Revenue in the OECD, 2018 Amir El-Sibaie Analyst Key Findings In 2015, OECD countries relied heavily on consumption taxes, such as the value-added tax,

FISCAL FACT No. 581 Mar. 2018 Sources of Government Revenue in the OECD, 2018 Amir El-Sibaie Analyst Key Findings In 2015, OECD countries relied heavily on consumption taxes, such as the value-added tax,

Ralentissement dans les BRIC: faut-il s en inquiéter?

Ralentissement dans les BRIC: faut-il s en inquiéter? Présentation : Andrea Goldstein, Economiste à l OCDE Mercredi 18 décembre 213, 18 rue de Martignac - 757 Paris The BRICs in the International Investment

Ralentissement dans les BRIC: faut-il s en inquiéter? Présentation : Andrea Goldstein, Economiste à l OCDE Mercredi 18 décembre 213, 18 rue de Martignac - 757 Paris The BRICs in the International Investment

Financial wealth of private households worldwide

Economic Research Financial wealth of private households worldwide Munich, October 217 Recovery in turbulent times Assets and liabilities of private households worldwide in EUR trillion and annualrate

Economic Research Financial wealth of private households worldwide Munich, October 217 Recovery in turbulent times Assets and liabilities of private households worldwide in EUR trillion and annualrate

Annika Falkengren. The relationship bank of the Nordics. CEO & President. Copenhagen January 11, 2011

Annika Falkengren CEO & President The relationship bank of the Nordics Copenhagen January 11, 2011 SEB s anatomy 2010 in summary Outlook Conclusions 2 SEB a unique Nordic Bank Relationships Corporates

Annika Falkengren CEO & President The relationship bank of the Nordics Copenhagen January 11, 2011 SEB s anatomy 2010 in summary Outlook Conclusions 2 SEB a unique Nordic Bank Relationships Corporates

FSMA_2017_05-01 of 24/02/2017

FSMA_2017_05-01 of 24/02/2017 This Communication is addressed to Belgian alternative investment fund managers who intend to market, to professional investors, units or shares of European Economic Area

FSMA_2017_05-01 of 24/02/2017 This Communication is addressed to Belgian alternative investment fund managers who intend to market, to professional investors, units or shares of European Economic Area

BTSF FOOD HYGIENE AND FLEXIBILITY. Notification To NCPs

BTSF FOOD HYGIENE AND FLEXIBILITY Notification To NCPs Organisation and implementation of training activities on food hygiene and the flexibility provisions provided in the food hygiene package under the

BTSF FOOD HYGIENE AND FLEXIBILITY Notification To NCPs Organisation and implementation of training activities on food hygiene and the flexibility provisions provided in the food hygiene package under the