London Property Management Association (LPMA) INTERROGATORY #1

|

|

|

- Amie Manning

- 5 years ago

- Views:

Transcription

1 Exhibit I Tab Schedule Page of London Property Management Association (LPMA) INTERROGATORY # Interrogatory Ref: Exhibit A, Tab 5, Schedule Please update Tables, and to reflect the most recent forecasts from Global Insight. Response Tables,, and below are updated with the most recent forecasts from Global Insight. Table Global Insight s Latest Forecast Released in May 04 (%) Historical Years Bridge Year Test Years Transmission Cost Escalation for Construction Transmission Cost Escalation for Operations & Maintenance Table Ontario CPI Forecast Released in June 04 (%) Historical Years Bridge Year Test Years CPI Ontario

2 Exhibit I Tab Schedule Page of 4 Description Exchange Rate Table Exchange Rate Forecast Released in June 04 (CDN$ per US$) Historical Years Bridge Year Test Years

3 Exhibit I Tab Schedule Page of London Property Management Association (LPMA) INTERROGATORY # Interrogatory Ref: Exhibit A, Tab 5, Schedule Had Hydro One incorporated any impact associated with the potential Ontario pension plan proposal? Response Hydro One did not incorporate any impact associated with the proposed Ontario pension plan (proposed by the Ontario Government in May 04).

4 Exhibit I Tab Schedule Page of London Property Management Association (LPMA) INTERROGATORY # Interrogatory Ref: Exhibit B, Tab, Schedule In the Report of the Board on Cost of Capital for Ontario's Regulated Utilities issued on December, 009, it was indicated that it was the OEB's intention to conduct its first regular review in 04 and any changes to the policy would apply to the setting of rates for the 05 rate year. Is Hydro One proposing that any changes that may result from the 04 review be reflected in the cost of capital for 05 and 06 or is the Hydro One proposal strictly based on the proposal shown at the bottom of page and top of page? Response Hydro One will implement any applicable outcomes from the 04 OEB review.

5 Exhibit I Tab Schedule 4 Page of London Property Management Association (LPMA) INTERROGATORY #4 Interrogatory Ref: Exhibit B, Tab, Schedule Please update the deemed short term debt rates of.9% for 05 and 4.45% for 06 using the most recent Global Insight forecast available. Response The deemed short-term rate is.7% for 05 and 4.00% for 06 using the June 04 Global Insight BA rate plus the average annual BA spread of 0.95% as per the OEB s Cost of Capital Parameters, dated November 5, 0, for Rates effective in 04. As stated on page of Exhibit B--, Hydro One assumes that the deemed short term debt rate for each test year will be updated in accordance with the Cost of Capital Report, upon the final decision in this case. Specifically, for 05, the Board would determine the deemed short term debt rate for Hydro One Transmission based on the September 04 Bank of Canada data which would be available in October 04 plus the average spread obtained by Board Staff in 04. Similarly, for 06, the Board would determine the deemed short term debt rate for Hydro One Transmission based on the September 05 Bank of Canada data which would be available in October 05 plus the average spread obtained by Board Staff in 05.

6 Exhibit I Tab Schedule 5 Page of London Property Management Association (LPMA) INTERROGATORY #5 Interrogatory Ref: Exhibit B, Tab, Schedule a) Has Hydro One issued any of the debt for 04 as shown in Table? If yes, please provide complete details of the issuances. b) Is the forecast of debt issuances shown in Table for 05 and 06 still based on the most recent information and projected requirements? If not, please update Table to reflect the most recent forecast. c) Please update Table 4 to reflect the most recent forecasts for the sources of the information listed. Response a) Hydro One has issued the following fixed rate MTN s as shown in Table during 04: During January 04, Hydro One Inc. issued $50 million of 50-year notes with a 4.9% coupon rate, of which $0 million was mapped to Hydro One Transmission. During June 04, Hydro One Inc. issued $50 million of 0-year notes with a 4.7% coupon rate, of which $98 million was mapped to Hydro One Transmission. b) Table is updated below to reflect the most recent forecast. Please see the response to part c) of this question for an explanation of how the coupon rates were derived. Principal Amount ($Millions) Table Forecast Debt Issues for 05 and Term (Years) Coupon Principal Amount ($Millions) Term (Years) Coupon % % % % % %

7 Exhibit I Tab Schedule 5 Page of c) Table 4 is updated below to reflect the most recent forecast. Table 4 Forecast Yield for Issuance Terms 04 5-year 0-year 0- year Government of Canada.98%.70%.% Hydro One Spread 0.7%.0%.5% Forecast Hydro One Yield.69%.7% 4.59% 05 5-year 0-year 0- year Government of Canada.48%.0%.7% Hydro One Spread 0.7%.0%.5% Forecast Hydro One Yield.9% 4.% 5.09% 06 5-year 0-year 0- year Government of Canada.8% 4.0% 4.6% Hydro One Spread 0.7%.0%.5% Forecast Hydro One Yield 4.09% 5.% 5.99% Each rate is comprised of the forecast Canada bond yield plus the Hydro One Inc. credit spread applicable to that term. The ten-year Government of Canada bond yield forecast for 04 is based on the month forecast and for 05 is based on the month forecast from the June 04 Consensus Forecast. The ten-year Government of Canada bond yield forecast for 06 is based on the April 04 Long Term Consensus Forecast. The fiveand 0-year Government of Canada bond yield forecasts are derived by adding the June, 04 average spreads (five-year to ten-year for the five-year forecast and 0-year to tenyear for the 0-year forecast) to the ten-year Government of Canada bond yield forecast. Hydro One s credit spreads over the Government of Canada bonds are based on the average of indicative new issue spreads for June, 04 obtained from the Company's MTN dealer group for each planned issuance term. Hydro One assumes that forecast debt issuance interest rates for each test year will be updated consistent with the ROE methodology, upon the final decision in this case. For rates effective January, 05, the forecast interest rate for Hydro One Transmission debt issues will based on the September 04 Consensus Forecasts and the average of indicative new issue spreads for September 04 which will be obtained from the Company's MTN dealer group for each planned issuance term. For rates effective January, 06, the forecast interest rate for Hydro One Transmission debt issues will be based on the September 05 Consensus Forecasts and the average of indicative new issue spreads for September 05 which will be obtained from the Company's MTN dealer group for each planned issuance term. In addition Hydro One assumes that long

8 Exhibit I Tab Schedule 5 Page of 4 term debt rate will be updated to reflect and take into account the actual issuances of debt since the time of original application consistent with the OEB s Decision on Hydro One Transmission s 0 and 04 rate application in EB-0-00 and changes in the interest rate forecast.

9 Exhibit I Tab Schedule 6 Page of London Property Management Association (LPMA) INTERROGATORY #6 Interrogatory Ref: Exhibit E, Tab, Schedule a) How many months of actual expenditures are included in Table in the 04 Bridge column? b) Please update the 04 Bridge column in Table to reflect the most recent year-todate figures available and the forecast for the remainder of 04. c) Please provide the most recent year-to-date actual expenditures in the same level of detail as shown in Table along with the figures for the corresponding period in 0. Response a) months of actual expenditures are included in Table in the 04 Bridge column. b) External Revenues ($ Millions) $M Remaining YTD Updated Bridge Forecast Actuals YE Original (July - Dec Q Forecast 04) Secondary Land Use Station Maintenance Engineering & Project Delivery Other External Revenues Totals

10 Exhibit I Tab Schedule 6 Page of c) $M 04 0 YTD Actuals (Q 04) YTD Actuals (Q 0) 4 5 Secondary Land Use Station Maintenance Engineering & Project Delivery Other External Revenues Totals

11 Exhibit I Tab Schedule 7 Page of London Property Management Association (LPMA) INTERROGATORY #7 Interrogatory Ref: Exhibit C, Tab 7, Schedule a) Please provide a copy of the new depreciation study that can be found at Exhibit C, Tab 7, Schedule, Attachment. b) What is the impact on the depreciation expense in each of 05 and 06 of the new depreciation study relative to the existing rates? c) Please provide the detailed depreciation schedules that are found at Exhibit C, Tab 4, Schedule. Response a) Please refer to response to CME s interrogatory 0 at Exhibit I, Tab, Schedule 0, part a. b) Please refer to response to CME s interrogatory 0 at Exhibit I, Tab, Schedule 0, part b. c) Please refer to response to SEC s interrogatory 9 at Exhibit I, Tab 0, Schedule 0.

12 Exhibit I Tab Schedule 8 Page of London Property Management Association (LPMA) INTERROGATORY #8 Interrogatory Ref: Exhibit C, Tab 8, Schedule a) Please provide the tax credits (federal job creation, Ontario apprenticeship, Ontario co-op education, etc.) claimed in each of 0 through 0 and the forecast for 04 through 06. b) Please provide the calculation of the income tax schedules equivalent to Exhibit C, Tab 5, Schedule, Attachments through 7 in EB for the transmission PILs. Response Please see the tax schedules filed as Attachment to 8 to this interrogatory response for part a) and b).

13 Exhibit I--8 Attachment Page of C CALCULATION OF UTILITY INCOME TAXES HYDRO ONE NETWORKS INC. TRANSMISSION Calculation of Utility Income Taxes Test Years (05 and 06) Year Ending December ($ Millions) Line No. Particulars (a) (b) Determination of Taxable Income Regulatory Net Income (before tax) $ $ 50.5 Book to Tax Adjustments: Other Post Employment Benefits expense Other Post Employment Benefits payments (5.5) (6.) 5 Inergi pension payments Depreciation and amortization Capital Cost Allowance (509.) (5.5) 8 Removal costs (.5) (.5) 9 Environmental costs (6.) (6.0) 0 Hedge loss - amortization Non-deductible meals & entertainment.7.7 Capital amounts expensed under $K.8.8 Research & Development ITC Federal Apprenticeship Tax Credits Capitalized overhead costs (.) (0.6) 6 Capitalized pension costs (4.4) (9.9) 7 Debt Issuance costs - amortization Debt Issuance costs (e) deduction (.6) (.9) 9 Premium/Discount - amortization (0.7) (0.9) 0 Bond discount deduction (0.6) (.) $ (9.9) $ (87.8) Regulatory Taxable Income $ 74. $ 5.7 Corporate Income Tax Rate 6.50 % 6.50 % 4 Subtotal $ 7.6 $ Less: R&D ITC / Federal Apprenticeship Tax Credits (0.9) (0.8) 6 Regulatory Income Tax $ 7.8 $ 8.8 Tax Rates 7 Federal Tax 5.00 % 5.00 % 8 Provincial Tax.50 %.50 % 9 Total Tax Rate 6.50 % 6.50 %

14 Exhibit I--8 Attachment Page of C CALCULATION OF CAPITAL COST ALLOWANCE TEST YEAR (05, 06) HYDRO ONE NETWORKS INC. TRANSMISSION Calculation of Capital Cost allowance (CCA) 05 Networks Allocation to Tx Year Ending December ($ Millions) 05 Opening Net UCC pre- 50% net UCC for CCA Closing CCA Class UCC Additions / yr additions CCA Rate CCA UCC, ,88.5.8,64.7 4% 86.6, % % % % % % % % % % % % % % , , ,5.7 8% 68., % , , ,607. CEC % , , , ,70.4 First Nations (0.) CCA not in rates (.) Total CCA for RR 509.

15 Exhibit I--8 Attachment Page of HYDRO ONE NETWORKS INC. TRANSMISSION Calculation of Capital Cost allowance (CCA) 06 Networks Allocation to Tx Year Ending December ($ Millions) 06 Opening Net UCC pre- 50% net UCC for CCA Closing CCA Class UCC Additions / yr additions CCA Rate CCA UCC, , ,. 4% 84.9, % % % % % % % % % % % % % % , , ,580. 8% 86.4, % , , , ,668.7 CEC % , , , ,777.4 First Nations (0.) CCA not in rates (.9) Total CCA for RR 5.5

16 Exhibit I--8 Attachment Page of C CALCULATION OF UTILITY INCOME TAXES HISTORIC YEARS HYDRO ONE NETWORKS INC. Transmission Calculation of Utility Income Taxes Historic Years Calculation of Utility Income Taxes Historical Years (0, 0, 0) Year Ending December ($ Millions) Line No. Particulars 0 0 0* Calculation of Federal and ON Taxable Income Net Income Before Tax (NIBT) $ $ 56.4 $ 598. Required Adjustments to accounting NIBT Recurring items included in Revenue Requirement (RR): 4 Other Post Employment Benefit expense greater than payments 8. (0.5). 5 Depreciation and amortization Capital Cost Allowance (89.) (448.) (487.8) 7 Cumulative Eligible Capital (4.) (9.8) (9.) 8 Removal costs (.0) (.9) (.7) 9 Environmental costs paid (6.9) (5.9) (6.) 0 Non-deductible items (50% Meals & entertainment / interest) R & D Fed ITC/ Apprenticeship (prior yr addback) Capitalized overhead costs deducted (6.0) (0.6) (9.8) Capital additions deducted for accounting Capitalized Pension cost deductions (.) (4.4) (50.) 5 $ (6.) $ (09.4) $ (9.8) 6 Deferral accounts not part of RR: 7 RSVA/RRRP Restricted Depreciation Smart meter costs deferred Tx Export credit/deferred export Rev Deferred Pension (.) (.9) (5.9) Deferral a/c's etc Tax Changes deferral a/c s 0.0 (0.8) 0 4 Riders /6/ Station Revenue and Secondary Use $ 9.0 $ 8. $ Reversal of accounting adjustments not part of RR: 8 Contingent liability movement (5.6) Capitalized interest deductible for tax (45.9) (9.6) (.) 0 Capitalized SRED deducted for tax 0.0 (6.8) 0.0 $ (5.5) $ (45.6) $ (0.4)

17 Exhibit I--8 Attachment Page of HYDRO ONE NETWORKS INC. Transmission Calculation of Utility Income Taxes Historic Years Calculation of Utility Income Taxes Historical Years (0, 0, 0) Year Ending December ($ Millions) Line No. Particulars 0 0 0* Recurring items not part of RR: 4 Capital Contribution (CCRA True up) First Nations (CCA) (0.) (0.) (0.) 6 CCA on Capital Contributions and OPA directed projects (.9) 7 $ (0.) $ 8. $ (.) 8 Immaterial items not in business plan detail: 9 40 Reverse Insurance proceeds included in NIBT (.0) (4.) Net Underwriting/Finance costs (.5) (.6) (0.) 4 WSIB (0.8) Tenant Inducement 0.7 (0.9) (0.9) 44 Capital tax paid vs. accrued Other. 0. (.4) 46 $ 0.0 $ (7.) $ (4.6) NET Adjustments to Accounting NIBT $ (58.8) $ (5.9) $ (6.4) Taxable Income $ 99.0 $ 0.5 $ NOTE: 5 Transmission includes Five Nations data Taxable Income $ 99.0 $ Corporate Income Tax Rate 8.5 % 6.5 % Subtotal $ 84.5 $ Less: Tax credits (5.5) (4.7) (4.) 6 Income Tax $ 79.0 $ Tax Rates 67 Federal Tax 7.0 % 5.0 % Provincial Tax.5 %.5 %.5 69 Total Tax Rate 8.5 % 6.5 % 6.5 * 0 Numbers based on estimates as tax returns have not been finalized.

18 Exhibit I--8 Attachment 4 Page of C CALCULATION OF CAPITAL COST ALLOWANCE - HISTORIC (0, 0, 0) HYDRO ONE NETWORKS INC. TRANSMISSION Calculation of Capital Cost allowance (CCA) 0 Networks Allocation to Transmission Year Ending December ($ Millions) 0 Net UCC pre- 50% net Closing CCA Class Opening UCC Additions / yr additions UCC for CCA CCA Rate CCA UCC, ,49. -,49. 4% 99.7, % % % % % (0.). -. 5% % N/A % % % % %.4. 47, , ,80.9 8% 44., % % 0. - Total CCA 5, , , ,577.5 Less First Nations (0.) Total CCA for RR 89. CEC %

19 Exhibit I--8 Attachment 4 Page of HYDRO ONE NETWORKS INC. TRANSMISSION Calculation of Capital Cost allowance (CCA) 0 Networks Allocation to Transmission Year Ending December ($ Millions) 0 Net UCC pre- 50% net CCA Class Opening UCC Additions / yr additions UCC for CCA CCA Rate CCA Closing UCC, ,9.0 0.,9.90 4% 95.7, % % % % % % % % % % % % % %..9 47, , ,6.40 8% 86., % Total CCA 5, , , ,085. First Nations (0.0) Total CCA for RR 448. CEC %

20 Exhibit I--8 Attachment 4 Page of HYDRO ONE NETWORKS INC. TRANSMISSION Calculation of Capital Cost allowance (CCA) 0 Networks Allocation to Transmission Year Ending December ($ Millions) 0 Net UCC pre- 50% net Closing CCA Class Opening UCC Additions / yr additions UCC for CCA CCA Rate CCA UCC,96.5 (6.)*,80.4.6,77.7 4% 9., % % % % % % % % % % (0.) % % % % , , ,755. 8% 0.4, % Total CCA 6, , , ,7. First Nation (0.) Less CCA not in rates (.9) Total CCA for RR CEC % 9..6 *Due to audit adjustments which resulted in reclassification of CCA Class

21 Exhibit I--8 Attachment 5 Page of C CALCULATION OF CAPITAL COST ALLOWANCE BRIDGE YEAR 04 HYDRO ONE NETWORKS INC. TRANSMISSION Calculation of Capital Cost Allowance (CCA) 04 Networks Allocation to Transmission Year Ending December ($ Millions) 04 Opening Net UCC pre- 50% net UCC for CCA Closing CCA Class UCC Additions / yr additions CCA Rate CCA UCC, , ,09. 4% 88.4, % % % % % % % % % % % % % % , , ,06. 8% 4.9, % , , , ,408.0 CEC % , , , ,55.5 First Nations (0.0) CCA not in rates (.4) Total CCA for RR 506.5

22 Exhibit I--8 Attachment 6 Page of C CALCULATION OF APPRENTICESHIP AND EDUCATION TAX CREDIT TEST YEARS HYDRO ONE NETWORKS INC. Transmission Calculation of Apprenticeship and Education Tax Credit Tax Credit Test Years (05, 06) Year Ending December ($ Thousands) Line No Particulars ON Coop Education Credit $ 560 $ 560 Eligible Positions ON Apprenticeship Credit $,448 $,448 5 Eligible Positions Ontario Business Research 8 Institute Credit $ 6 $ Federal Apprenticeship Credit $ 00 $ 00 Eligible positions 7 7 SR&ED TOTAL TAX CREDIT $,970 $, Tax Credit included in tax expense () $ 900 $ Tax Credit included in OM&A () $,070 $,070 0 Total $,970 $,870 () In accordance with US GAAP, refundable tax credits included are recorded in OM&A and non refundable tax credits are recorded as a reduction to tax expense. Consequently, the tax credits relating Ontario Co-op, Ontario, Apprenticeship, and Ontario Business Research are recorded in OM&A

23 Exhibit I--8 Attachment 7 Page of C CALCULATION OF APPRENTICESHIP AND EDUCATION TAX CREDIT - HISTORIC YEARS HYDRO ONE NETWORKS INC. TRANSMISSION Calculation of Apprenticeship and Education Tax Historic Years 0, 0 Year Ending December ($ Thousands) Line No Particulars 0 0 ON Coop Education Credit $ 690 $ 55 Eligible Positions ON Apprenticeship Credit $,7 $,0 5 Eligible Positions Federal Apprenticeship Credit $ 4 $ 69 8 Eligible positions SR&ED $,7 $,78 TOTAL TAX CREDIT $ 5,486 $ 4,75

24 HYDRO ONE NETWORKS INC. Transmission Calculation of Utility Income Taxes Tax Credit Test Years (04, 05) Year Ending December ($ Thousands) Filed: Exhibit I--8 Attachment 8 Page of Line No Particulars 0* 04 ON Coop Education Credit $ 655 $ 560 Eligible Positions ON Apprenticeship Credit $,44 $,448 5 Eligible Positions Ontario Business Research 8 Institute Credit $ 5 $ Federal Apprenticeship Credit $ 0 $ 00 Eligible positions 6 7 SR&ED, TOTAL TAX CREDIT $ 4,56 $, Tax Credit included in tax expense $,75 $ 900 () 9 Tax Credit included in OM&A $,5 $,070 () 0 Total $ 4,56 $,970 * 0 numbers based on the 0 Tax returns filed for Hydro One Networks () In accordance with US GAAP, refundable tax credits included are recorded in OM&A and non refundable tax credits are recorded as a reduction to tax expense. Consequently, the tax credits relating Ontario Co-op, Ontario, Apprenticeship, and Ontario Business Research are recorded in OM&A.

25 Exhibit I Tab Schedule 9 Page of London Property Management Association (LPMA) INTERROGATORY #9 Interrogatory Ref: Exhibit A, Tab 5, Schedule a) Please provide the percentage salary increases that are "consistent with ratified collective agreement over the length of the agreement" for Society Staff and PWU Staff. b) What is the impact on the revenue requirement if the assumed net annual increase for both 05 and 06 is reduced by one percentage point in both years for the Society Staff and PWU Staff? c) What is the impact on the revenue requirement if the assumed annual increase for MCP staff is reduced in each of 05 and 06 by one percentage point? d) Please provide Exhibit C, Tab 4, Schedule that is referred to on page 6. Response a) In the most recent PWU settlement, the negotiated salary increases are.5% and.5% for 0 and 04. In the most recent Society settlement, negotiated salary increases are %,.5% and.5% for 0, 04 and 05 respectively. Note The deadline for response to this IR does not allow enough time to do the analysis for parts b and c. On a best efforts basis, answers have been prepared based on the previous Transmission filing. b) During Hydro One s EB-0-00 Transmission rate filing, the Consumers Council of Canada asked what the revenue requirement impact would be if wage escalations were reduced by % for Society, PWU, and MCP. Hydro One estimates that the impact on 05 and 06 revenue requirement would be in the same range as the previously filed responses. The EB-0-00 responses can be found in I CCC, I CCC 4, and I CCC 5, and are summarized in the table below.

26 Exhibit I Tab Schedule 9 Page of 4 5 Revenue Requirement impact of a % change in wage escalation rates, by Representation ($ millions) 0 04 Society PWU MCP c) See part b) d) Please see Attachment to this interrogatory.

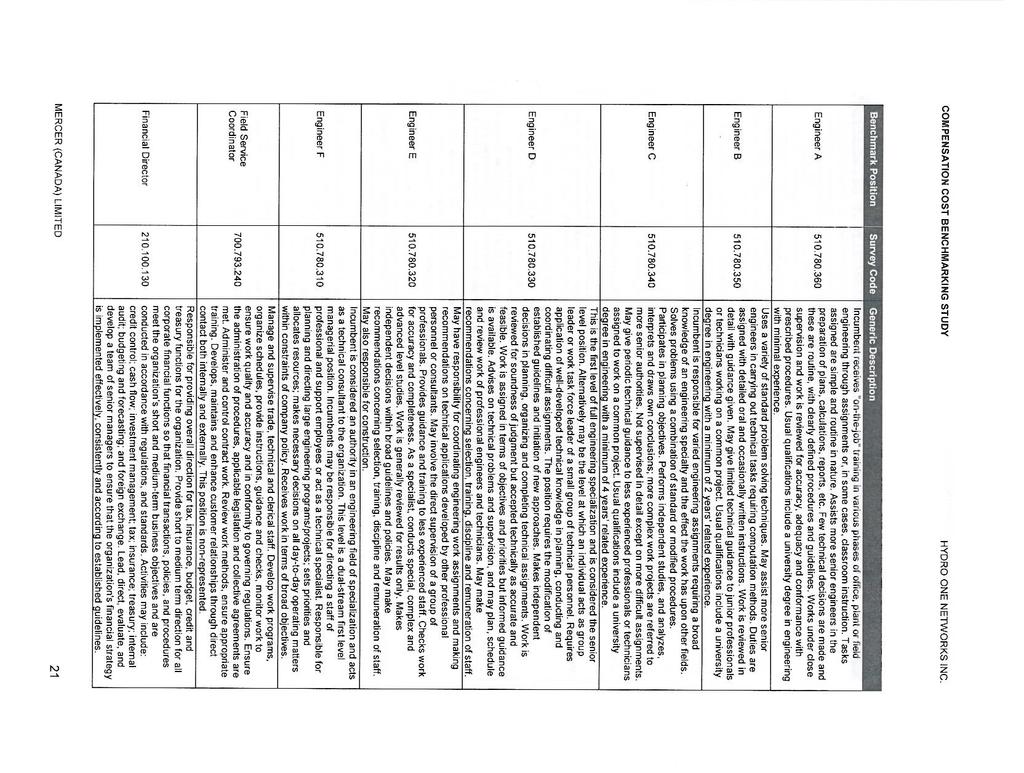

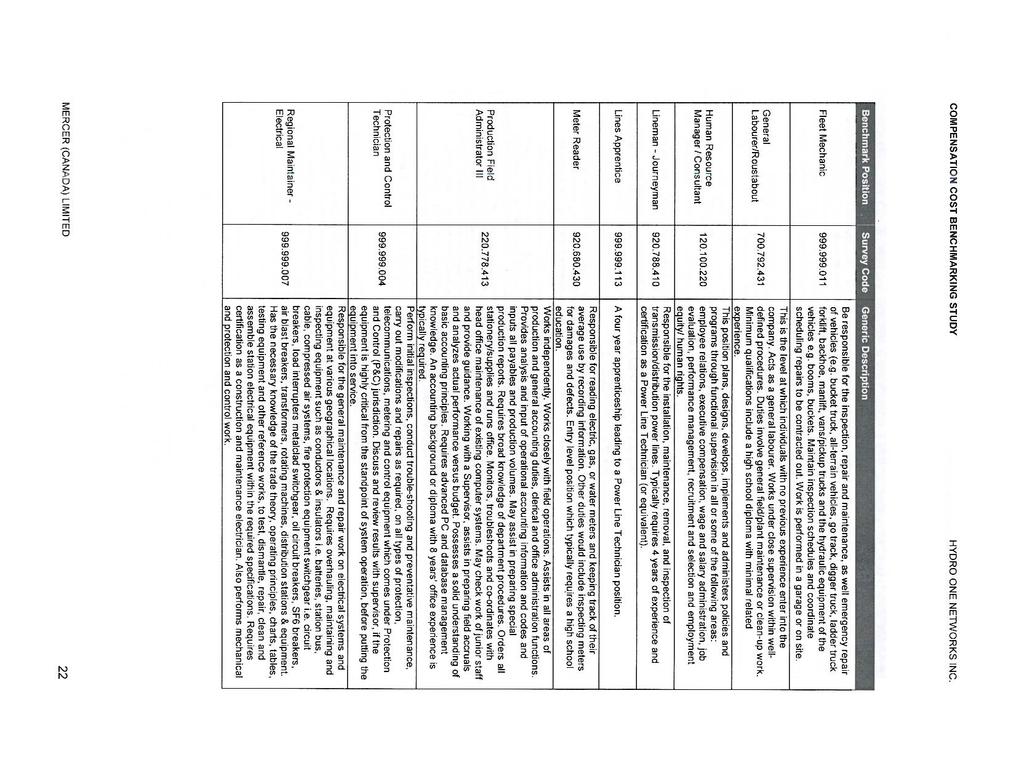

27 Exhibit I--9 Attachment Page of COMPENSATION, WAGES, BENEFITS Included in Attachment is as follows: Compensation, Wages, Benefits Attachment Compensation Cost Benchmarking Study Hydro One Networks Inc. Attachment Expert Evidence Statement from Mercer (Canada) Limited Attachment

28 Exhibit I--9 Attachment Page of 7 COMPENSATION, WAGES, BENEFITS.0 INTRODUCTION In previous Board decisions, the Board has expressed concerns with rising compensation levels at Hydro One. In a 006 Board Decision, Hydro One was directed to conduct a total compensation study and in a subsequent decision, the Board directed that the study be updated. At the first stakeholder session for EB a stakeholder enquired as to whether Hydro One would be updating the compensation study. In response to this request, Hydro One initiated another study to update the two previous studies. In total, three total compensation studies have been conducted and the results show that Hydro One has succeeded in lowering total employee compensation as compared to market median. The results of this Compensation Cost Benchmarking Study are detailed later in this exhibit as Attachment While lowering compensation cost relative to market median is desirable from a rate payer point of view, the fact remains, that Hydro One must attract, and engage a highly skilled workforce, in the face of an aging workforce and worldwide competition for similar skills. Coupled with the fact that Hydro One is heavily unionized and Hydro One was created with legacy collective agreements only adds to the challenge of further reducing compensation costs. For full details regarding the Hydro One corporate staffing strategy, see Exhibit C, Tab 4, Schedule Despite these challenges, Hydro One has been successful in balancing the competing pressures of reducing compensation costs relative to market median at the same time as attracting and maintaining an engaged workforce. Ultimately, the rate payers benefit from the quality, expertise and reliability of Hydro One employees.

29 Exhibit I Tab Schedule 9 Page of 7.0 TOTAL COMPENSATION STUDIES In EB , the Board directed Hydro One to file a total compensation study that will provide useful and reliable information concerning Hydro One s compensation costs, and how they compare to those of other regulated transmission and/or distribution utilities in North America. Following stakeholder sessions to obtain input on how this study would be conducted, Mercer undertook a Compensation Cost Benchmarking Study (the 008 Study ) and the results were filed in EB In EB , the Board directed Hydro One to revisit its compensation cost benchmarking study in an effort to more appropriately compare compensation costs to those of other regulated transmission and/or distribution utilities in North America. Further stakeholder sessions took place and Mercer once again conducted a total compensation study (the 0 Study ) that was filed in EB Responding to a stakeholder request for an updated study in the EB application, Hydro One requested Mercer to conduct another study (the 0 Study ). 8 9 Table compares the study results for all three studies.

30 Exhibit I--9 Attachment Page of 7 Table Mercer Compensation Benchmarking Study Results vs. Market Median Total Compensation Employee 0 0 Survey 008 Survey Total Group Survey Results Results Change from Results 008 to 0 Management -% -7% -% 0% Society 9% 5% 5% 4% PWU % 8% % -9% Overall 0% % 7% -7% The 0 study findings show that on an overall weighted average, Hydro One is positioned approximately 0% above market median. This is an improvement relative to the 008 Mercer study where Hydro One s overall weighted average was found to be 7% above market median. Mercer stated the shift towards market median was notable, especially given the peer group, like Hydro One, had worked to minimize labour costs through the substantial economic downturn which began in 008. In other words, Hydro One improved its standing against others in the peer group who were also attempting to reduce compensation costs For the individual groups, Hydro One management classifications surveyed were found to be % below market median. Compared to the 0 study, this shows that nonrepresented compensation has moved toward market median. The 0 study result was mainly due to the impact of a two year wage freeze on non-represented compensation. The 0 study results would indicate that non-represented classifications are closer to the desired non-represented compensation policy of being at the 50 th percentile. Professionals (Society of Energy Professionals the Society ) classifications were found to be 9% above market median. Power Workers Union (PWU) represented

31 Exhibit I Tab Schedule 9 Page 4 of 7 4 classifications were found to be % above market median, a significant improvement from the 008 result of % above market median reflecting the increased use of hiring hall staff and the increased pension contributions negotiated as part of the new collective agreement THE UNIONIZED ENVIRONMENT Approximately 90% of the Hydro One work force is unionized. Hydro One has collective agreements with the Power Workers Union (PWU), The Society of Energy Professionals (The Society), the Canadian Union of Skilled Workers (CUSW), and each of the 5 Building Trade Unions (BTUs) (via EPSCA) The collective agreements establish the terms and conditions of the employment relationship for a fixed period of time. It is critical to understand that Hydro One inherited collective agreements from Ontario Hydro which established terms of employment. These legacy collective agreements established a floor upon which future negotiations were based. While legacy collective agreements continue to strongly influence current Hydro One collective agreements, Hydro One has done much to change the status quo. Hydro One has been successful in incrementally reducing costs and/or increasing productivity through collective bargaining. Obtaining dramatic compensation reductions in the environment facing Hydro One is unrealistic Collective Agreements are legal contracts. In labour agreements, more so than commercial contracts, parties must also consider their longer term relationship. Hydro One s Human Resources strategy is to negotiate fair and reasonable collective agreements to foster and promote healthy union management relationships. 7

32 Exhibit I--9 Attachment Page 5 of COLLECTIVE BARGAINING 4. PWU The PWU represents over 70% of Hydro One employees. The PWU is an industrial union that represents the trades, controllers, technicians and clerical workers. Its members perform line work, forestry, electrical, mechanical, protection and control, meter reading, stock keeping, system operation, technical and clerical/administrative work An attempt by Hydro One to achieve significant cost reductions in wages, benefits and pension would likely result in a strike. The last PWU strike was in 985 and lasted days. It was handled by placing management and Society-represented staff in key functions to maintain operations/service to the extent possible. However, as a result of numerous downsizing programs, and reorganization of work, there is fewer management staff available today with the requisite skills and experience to occupy key PWU positions during a strike. Furthermore, unlike other industries, Hydro One does not have a product that can be stockpiled. As a result, the Company would be unable to continue operations for a sustained period of time during a PWU strike. 0 Rather than risk jeopardizing the supply of reliable electricity, the company has sought to achieve overall cost reductions by negotiating increased management flexibility to run the operations, as opposed to wide scale reductions in wages, benefits and pensions The Society of Energy Professionals The Society represents approximately 0% of Hydro One employees. Society-represented staff performs engineering, high level technical and administrative work as well as supervisory functions. The majority of the Society-represented employees in Hydro One

33 Exhibit I Tab Schedule 9 Page 6 of 7 have either post-secondary education (university degrees) and/or post-graduate education. These include graduate engineers, finance and telecommunication specialists In 005, the Society initiated a fifteen week strike in response to Hydro One s desire to reduce wages and benefits and increase hours of work for new employees. Hydro One was requested by the Shareholders to enter into mediation arbitration to end the strike. The arbitration award resulted in some cost savings for future hires, highlighted with less costly pension provisions for new Society employees COLLECTIVE BARGAINING The collective bargaining relationships at Hydro One are very complex and sophisticated. Hydro One and the bargaining agents with whom the Company negotiate are professionals and very seasoned in the area of collective bargaining. Hydro One has been able to achieve reasonable settlements with incremental cost reductions and increased flexibility in a variety of areas in every round of collective bargaining since 00. Examples include: elimination of costly incentive pay plans reasonable economic increases; reductions and cost containment in benefit improvements; introduction of new salary schedules with lower starting rates and lower maximum rates; introduction of a less costly pension plan; increased employee pension contributions; increased flexibility to contract out work; reduction in the hourly rate for a variety of jobs; increased flexibility to move staff;

34 Exhibit I--9 Attachment Page 7 of 7 4 increased utilization of contingent workers; introduction of less costly classifications; greater shift scheduling flexibility; and reduction in temporary work headquarter costs Recent Negotiation Highlights PWU Negotiations In 0, a new year collective agreement was successfully negotiated by the bargaining committees of Hydro One and the PWU and ratified by the PWU-represented staff. The term of this collective agreement ends on March st, 05. Modest economic increases were negotiated (.5% in each year). To lessen the cost impact of these increases, they were phased in on April st and October st in 0 and Employee pension contributions were also increased. In the last Transmission Decision, the Board commented that it expects to see demonstrated measurable progress towards increasing employee pension contributions. The Board stated that Hydro One must demonstrate measurable progress towards having its pension contributions reflect those prevailing in the public sector generally. The evidence suggests that an employee contribution level of 50% is the norm. In 0, Hydro One negotiated a 0.5% increase to the PWU employee pension contributions and in the most recent negotiations, employee contributions have increased by a further 0.75% in 0 and.0% in To address rising benefit costs, the parties agreed to the requirement to use mandatory generic prescribed drugs and to establish a joint committee to make recommendations to reduce costs in the area of biological and other expensive drugs.

35 Exhibit I Tab Schedule 9 Page 8 of 7 Increased resourcing flexibility was achieved by negotiating enhancements to use more temporary staff and to contract out more work Society Negotiations In 0, a new three year collective agreement was successfully negotiated by the bargaining committees of Hydro One and the Society and ratified by the Society- represented staff. The term of this collective agreement ends on March st, Modest economic increases were negotiated (%, % and.5%). Employee pension contributions were increased by 0.75%, % and 0.75% in each year of the term of the collective agreement Increased flexibility was achieved by increasing the length of new hire probationary periods and formalizing the deletion of the Purchase Service Agreement so that contracting out can be fully utilized when appropriate MANAGEMENT (MCP) COMPENSATION 9 0 Changes to management compensation are wholly at the discretion of senior management. The management compensation structure is comprised of two key programs, merit pay and short term incentive pay Merit Pay Merit pay is designed to reflect and reward increasing competency and performance in an employee s current role while also taking into account the extent to which Hydro One wishes to recognize and retain the employee. On this basis, merit pay is not an across-the-

36 Exhibit I--9 Attachment Page 9 of 7 board base pay program but rather it is recognition of performance/ potential based on managerial judgment The Broader Public Sector Accountability Act (BPSAA) 00 froze all management compensation from 00 to 0. The 0 Ontario Budget amended this Act so that compensation for Vice President s and above are frozen until such time that there is no deficit in the Budget Since the wage freeze legislation expired for management positions below the Vice President level, Hydro One has had a limited base merit pay program in 0. A rigorous process was used to align pay for performance by considering a number of factors such as overall performance, engagement scores, pay relative to performance of peers and potential flight risk. In 0, all MCP employees increased their pension contributions by 0.75% In 04, MCP employees were eligible for a merit pay program. A.5% merit pay adjustment fund was established for MCP employees Band 5 level and below. The merit program once again aligned pay and performance and was allocated in a manner that differentiates between levels of performance. For a second consecutive year, all MCP employees had their pension contributions increased by another 0.75%. 4 5 Short Term Incentive Pay A short term incentive (STI) program is a discretionary program and is based on the Hydro One Board and Senior Management s assessment of achievement of the corporate scorecard and achievement of individual performance agreements The STI program is a compensation strategy that drives performance and is separate and distinct from the merit pay program. The STI program is designed to establish a strong correlation between corporate performance, individual performance and at-risk pay. The

37 Exhibit I Tab Schedule 9 Page 0 of STI program provides an opportunity for MCP employees to earn an annual cash incentive based on two elements. The first is the achievement of corporate performance targets set by the Board of Directors. Corporate performance measures and targets are set annually through the use of a balanced scorecard. A balanced scorecard is designed to measure corporate performance broadly, covering key aspects of corporate performance. Measures included in the scorecard are designed to ensure the corporate strategy is achieved. The second element of the STI program is individual contributions to these targets. MCP employees have annual performance contracts that specify key goals and targets that individual performance is measured against. 0 4 The maximum percentage of funding for the STI program is at the discretion of the Hydro One Board of Directors, based on a recommendation by the Human Resources Committee of the Board. The maximum allowable individual short term incentive is established for each MCP salary band COMPENSATION STRATEGY Hydro One has experienced rapidly increasing transmission and distribution work programs since 004. Resourcing of these work programs must occur on the most cost effective basis possible within a highly competitive labour market Attachment provides year end compensation costs for Hydro One Networks (Transmission and Distribution) from 00 to 0 and forecasted year end compensation cost for the bridge year (04) and test years (05-06). The Company believes that the upward trend in these costs is reasonable in light of the steadily increasing transmission and distribution work programs since 004, as well as the negotiated increases in labour rates.

38 Exhibit I--9 Attachment Page of 7 Note this data represents year end payroll costs for Hydro One Networks in total (i.e. Distribution and Transmission). The purpose of this table is to illustrate the trend in compensation costs For the period 05-06, the total Networks (Transmission and Distribution) work program is expected to increase by approximately 0.4% while the regular headcount is expected to decrease by. % by year end Table Work Program and Head Count Forecast (007 to 06) Total Regular Staff Total Spend $M Actual 008 Actual 009 Actual 00 Actual 0 Actual 0 Actual 0 Actual 04 BP 05 BP 06 BP 0 Total Work Program $ Total Regular Staff Hydro One believes that the goal of reducing overall wages, pension and benefits for future new hires reflects a reasonable balance between the need to attract and retain new staff while pursuing a more favourable cost structure. This is a difficult balance to achieve. Too much of a reduction in compensation and benefits will impact the ability to

39 Exhibit I Tab Schedule 9 Page of attract the new skills necessary to replenish the workforce. However, as outlined in Exhibit C, Tab, Schedule, as the proportion of Hydro One staff qualifying for and taking early retirement is growing substantially, the goal of reducing compensation for future new hires will reduce overall compensation costs for Hydro One and its ratepayers. Hydro One s best performers are highly marketable, and a number of management staff have left the company in recent years. The Hydro One succession plan has facilitated internal promotion and a smooth transition in most cases, but our internal replacement capacity is now significantly diminished in key areas. External recruitment has proven challenging as our compensation levels and structures have fallen below the market for top people. 8.0 COMPARISON OF COLLECTIVE AGREEMENTS When assessing the prudency of Hydro One s collective agreements, a useful comparison is the compensation wage scales for similar PWU (table ) and Society (table 4) classifications in the Ontario Hydro successor companies as Hydro One competes for staff with these companies and is vulnerable to losing staff to these organizations. Such a comparison is instructive since all these wage scales have the same starting point, which is the establishment of the successor companies in 999. It is important to compare compensation escalation based on total dollar base rates of similar classifications. Simply comparing accumulated base rate percentage increases does not capture the true difference between total base compensation paid at the successor companies. 4 5 In the two wage scale comparison tables for each of PWU and Society staff which follow the wage scale rates shown are for the top end of the wage scale band As shown in Table for PWU staff, Hydro One has negotiated substantially lower wage scales than OPG and Bruce Power for all seven positions with the exception of one.

40 Exhibit I--9 Attachment Page of 7 Table Power Workers Union Wage Comparisons, 999 and Percent Change Mechanical Maintainer/Regional Maintainer - Mechanical Hydro One $ 8. $ % OPG $ 9.08 $ % Bruce Power $ 9.08 $ % Shift Control Technician/Regional Maintainer Electrical Hydro One $ 8. $ % OPG $ 0. $ % Bruce Power $ 0. $ % Clerical Grade 56 (based on a 5-hour work week) Hydro One $.46 $.0 5 % OPG $.46 $ % Bruce Power $.46 $ % Clerical Grade 58 (based on a 5-hour work week) Hydro One $ 4.0 $ % OPG $ 4.0 $ % Bruce Power $ 4.0 $ % Regional Field Mechanic/Transport & Work Equipment Mechanic Hydro One $ 6.0 $ % OPG $ 6.0 $ % Bruce Power $ 6.0 $ % Stockkeeper

41 Exhibit I Tab Schedule 9 Page 4 of Percent Change Hydro One $.7 $ % OPG $.7 $ % Bruce Power * $.7 $ % Labourer Hydro One $ 9.0 $ % OPG $ 9.0 $ % Bruce Power * $ 9.0 $ % * Assumes that the position falls within the Civil Maintainer II classification and corresponding wage rate 4 5 Table 4 Society of Energy Professional Wage Comparisons 999 and Percent Change MP Hydro One $ 77, $ 00, % OPG $ 77, $ 0,.9 0 % Bruce Power $ 77, $ 0,.46 % IESO $ 77, $ 8, % MP4 Hydro One $ 88,65.9 $, % OPG $ 88,65.9 $ 5, % Bruce Power $ 88,65.9 $ 6,045.4 % IESO $ 88,65.9 $ 4,8.0 5 %

42 Exhibit I--9 Attachment Page 5 of Percent Change MP6 Hydro One $ 00, $ 9, % OPG $ 00, $ 0, % Bruce Power $ 00, $,907.4 % IESO $ 00, $ 5, % 4 5 For Society staff, Hydro One, OPG and Bruce Power have successfully negotiated lower end rates as compared to the PWU wages. However, for all three Society categories, Hydro One has lower wage scales than OPG and Bruce Power. The IESO has continued with the wage schedule structure that existed at demerger It is quite clear that compared to these four other companies, Hydro One has been quite successful in controlling costs in collective bargaining over the past ten years to the benefit of all ratepayers POWER LINE TECHNICIAN RATE COMPARISON Within Ontario, the largest LDCs are Hydro One Networks Inc., Toronto Hydro Electric System Limited, Hydro Ottawa Limited, Enersource Hydro Mississauga Inc., London Hydro Inc., Horizon Utilities Corp. and Powerstream Inc. Each of the LDCs employ Power Line Maintainers (PLMs). Table 5 compares the PLM rate at each of the LDCs to the PLM rate paid at Hydro One Networks. The PLM classification was chosen since it represents a highly skilled and highly populated classification that is core to the other LDCs.

43 Exhibit I Tab Schedule 9 Page 6 of 7 Table 5 POWER LINE MAINTAINER WAGE COMPARISON Company Classification Wage 0($hr) H % Difference Hydro One Power Line Maintainer Toronto Hydro Power Line or Cable % Person Enersource Power Line Technician % Powerstream Linesperson 8. +.% Horizon Power Line Maintainer % London Hydro Power Line Maintainer % Hydro Ottawa Power Line Maintainer % Hydro One uses a multi-skilled position called a Regional Maintainer Lines classification (RLM). The RLM uses the PLM as the base job with additional duties such as lead hand, contract monitor, establishment and holding of work protection as well as additional technical, trade and customer relations skills beyond the Power Line Maintainer classification Table 4 illustrates that the PLM rate at Hydro One ranges from being slightly below to slightly above the larger LDCs in Ontario. Despite the rates being very close, the type of work and skills required at Hydro One are often more complex. Hydro One employees often work in a more rural setting than their counterparts in other LDCs. As a consequence, Hydro One employees can work in conditions and with equipment not normally required at these LDCs. Trades employees working on lines maintenance often work on both Distribution and Transmission assets and are required to be knowledgeable and proficient with overhead, underground and submarine cable. Again, this is not typical of the PLM role in other Ontario LDCs.

44 Exhibit I--9 Attachment Page 7 of SUMMARY Compensation levels at Hydro One are reasonable and appropriate given the environment in which the Company operates. In recent years, despite significantly increased work volumes, overall costs have been minimized by the simplification of required job skills and pay levels where appropriate. Hydro One s demographic challenge requires the Company to be active in the labour market and with worldwide competition for these skills there is a need for competitive compensation The updated Mercer Total Compensation Benchmarking Study demonstrates that there has been a significant improvement in total compensation costs at Hydro One relative to market median. It is important to emphasize that in a time where other organizations are facing similar cost pressures, Hydro One has lowered its overall total compensation from 008 to 0 by 7% against the peer group A strong barometer of Hydro One s ability to restrict compensation increases is a direct comparison to companies such as OPG, Bruce Power, and IESO. Hydro One competes directly with these organizations for skilled workers. Hydro One is also at risk of losing experienced staff to these organizations if our compensation is not competitive. Despite these competitive pressures, Hydro One has negotiated compensation levels that are less costly than OPG, Bruce Power and the IESO In addition, in a heavily unionized environment, there are significant constraints on an employer s ability to reduce compensation costs per employee. However, despite these constraints, the Corporation has made gains with the reduction in the area of compensation and benefit reductions.

45 Tx 05-6 Rates Exhibit C-4- Attachment Page of 0

46

47

48

49

50

51

52

53

54

55

56

57

58

59

60

61

62

63

64

65

66

67

68

69

COMPENSATION, WAGES, BENEFITS

Filed: 0-- EB-0-0 Exhibit C Tab Page of COMPENSATION, WAGES, BENEFITS.0 INTRODUCTION 0 In previous Board decisions, the Board has expressed concerns with rising compensation levels at Hydro One. In a 00

Filed: 0-- EB-0-0 Exhibit C Tab Page of COMPENSATION, WAGES, BENEFITS.0 INTRODUCTION 0 In previous Board decisions, the Board has expressed concerns with rising compensation levels at Hydro One. In a 00

COMPENSATION, WAGES, BENEFITS

Filed: September, 00 EB-00-00 Exhibit C Tab Schedule Page of COMPENSATION, WAGES, BENEFITS.0 OVERVIEW Hydro One has experienced rapidly increasing transmission and distribution work programs since 00.

Filed: September, 00 EB-00-00 Exhibit C Tab Schedule Page of COMPENSATION, WAGES, BENEFITS.0 OVERVIEW Hydro One has experienced rapidly increasing transmission and distribution work programs since 00.

COMPENSATION, WAGES, BENEFITS

Exhibit C Tab Schedule Page of 0 COMPENSATION, WAGES, BENEFITS.0 INTRODUCTION In earlier Distribution and Transmission decisions, the Board has expressed concerns regarding the size and growth of compensation

Exhibit C Tab Schedule Page of 0 COMPENSATION, WAGES, BENEFITS.0 INTRODUCTION In earlier Distribution and Transmission decisions, the Board has expressed concerns regarding the size and growth of compensation

CALCULATION OF UTILITY INCOME TAXES

Exhibit C2 Tab 6 Schedule 1 Page 1 of 7 1 CALCULATION OF UTILITY INCOME TAXES 2 3 4 5 6 7 8 Attachment 1: Test Years (2009, 2010) Attachment 2: Calculation of Capital Cost Allowance Test Year (2009, 2010)

Exhibit C2 Tab 6 Schedule 1 Page 1 of 7 1 CALCULATION OF UTILITY INCOME TAXES 2 3 4 5 6 7 8 Attachment 1: Test Years (2009, 2010) Attachment 2: Calculation of Capital Cost Allowance Test Year (2009, 2010)

COMPENSATION AND BENEFITS

Exhibit F4 Tab 3 Schedule 1 Page 1 of 23 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 COMPENSATION AND BENEFITS 1.0 PURPOSE The purpose of this exhibit is to: Describe

Exhibit F4 Tab 3 Schedule 1 Page 1 of 23 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 COMPENSATION AND BENEFITS 1.0 PURPOSE The purpose of this exhibit is to: Describe

ECONOMIC INDICATORS. 2.1 Distribution Cost Escalation for Construction, Operations and Maintenance

EB-00-0 Tab Schedule Page of.0 INTRODUCTION ECONOMIC INDICATORS Appendix A of, Tab, Schedule provides the costing assumptions underlying the 00 Business Plans. This exhibit provides additional background

EB-00-0 Tab Schedule Page of.0 INTRODUCTION ECONOMIC INDICATORS Appendix A of, Tab, Schedule provides the costing assumptions underlying the 00 Business Plans. This exhibit provides additional background

PAYMENTS IN LIEU OF CORPORATE INCOME TAXES

Filed: September, 00 EB-00-00 Tab Page of PAYMENTS IN LIEU OF CORPORATE INCOME TAXES Under the Electricity Act,, Hydro One Networks Inc. ( Networks ) is required to make payments in lieu of corporate income

Filed: September, 00 EB-00-00 Tab Page of PAYMENTS IN LIEU OF CORPORATE INCOME TAXES Under the Electricity Act,, Hydro One Networks Inc. ( Networks ) is required to make payments in lieu of corporate income

PAYMENTS IN LIEU OF CORPORATE INCOME TAXES

Filed: May, 0 EB-0-00 Tab Page of PAYMENTS IN LIEU OF CORPORATE INCOME TAXES.0 INTRODUCTION Under the Electricity Act,, Hydro One Networks Inc. ( Networks ) is required to make payments in lieu of corporate

Filed: May, 0 EB-0-00 Tab Page of PAYMENTS IN LIEU OF CORPORATE INCOME TAXES.0 INTRODUCTION Under the Electricity Act,, Hydro One Networks Inc. ( Networks ) is required to make payments in lieu of corporate

COMPENSATION AND BENEFITS

Filed: 0-0- EB-0-0 Exhibit F Tab Schedule Page of 0.0 PURPOSE The purpose of this Exhibit is to: COMPENSATION AND BENEFITS Detail the total test period compensation and benefits costs included in the revenue

Filed: 0-0- EB-0-0 Exhibit F Tab Schedule Page of 0.0 PURPOSE The purpose of this Exhibit is to: COMPENSATION AND BENEFITS Detail the total test period compensation and benefits costs included in the revenue

PENSION. Filed: August 17, 2005 RP /EB Exhibit C1 Tab 4 Schedule 3 Page 1 of OVERVIEW

Filed: August, 00 RP 00-000/EB-00-0 Tab Schedule Page of PENSION.0 OVERVIEW 0 Hydro One Networks is a participant in the Hydro One Pension Plan ( the Plan ). The Plan is a contributory, defined-benefit

Filed: August, 00 RP 00-000/EB-00-0 Tab Schedule Page of PENSION.0 OVERVIEW 0 Hydro One Networks is a participant in the Hydro One Pension Plan ( the Plan ). The Plan is a contributory, defined-benefit

COMPENSATION AND BENEFITS

Filed: 00--0 EB-00-00 Exhibit F Schedule Page of 0 0 0 COMPENSATION AND BENEFITS.0 PURPOSE The purpose of this evidence is to present the compensation and benefits framework associated with OPG s regulated

Filed: 00--0 EB-00-00 Exhibit F Schedule Page of 0 0 0 COMPENSATION AND BENEFITS.0 PURPOSE The purpose of this evidence is to present the compensation and benefits framework associated with OPG s regulated

PAYMENTS IN LIEU OF CORPORATE INCOME TAXES

Filed: September 0, 00 EB-00-0 Tab Page of PAYMENTS IN LIEU OF CORPORATE INCOME TAXES.0 INTRODUCTION Under the Electricity Act,, Hydro One Networks Inc. ( Networks ) is required to make payments in lieu

Filed: September 0, 00 EB-00-0 Tab Page of PAYMENTS IN LIEU OF CORPORATE INCOME TAXES.0 INTRODUCTION Under the Electricity Act,, Hydro One Networks Inc. ( Networks ) is required to make payments in lieu

Balsam Lake Coalition Interrogatory # 8

Tab Schedule BLC- Page of 0 0 0 Balsam Lake Coalition Interrogatory # Issue : Are the proposed amounts, disposition and continuance of Hydro One s existing deferral and variance accounts appropriate? Ontario

Tab Schedule BLC- Page of 0 0 0 Balsam Lake Coalition Interrogatory # Issue : Are the proposed amounts, disposition and continuance of Hydro One s existing deferral and variance accounts appropriate? Ontario

CALCULATION OF INCREMENTAL CAPITAL MODULE REVENUE REQUIREMENT

Updated: August 9, 0 Page of 6 CALCULATION OF INCREMENTAL CAPITAL MODULE REVENUE REQUIREMENT.0 OVERVIEW 6 7 8 9 0 In calculating the revenue requirement for the proposed ICM introduced in,, Schedule, the

Updated: August 9, 0 Page of 6 CALCULATION OF INCREMENTAL CAPITAL MODULE REVENUE REQUIREMENT.0 OVERVIEW 6 7 8 9 0 In calculating the revenue requirement for the proposed ICM introduced in,, Schedule, the

CENTRALLY HELD COSTS

Filed: 00-0- EB-00-000 Exhibit F Tab Schedule Page of 0 0 0 CENTRALLY HELD COSTS.0 PURPOSE This evidence presents OPG s centrally held costs. Centrally held costs primarily consist of: Certain pension

Filed: 00-0- EB-00-000 Exhibit F Tab Schedule Page of 0 0 0 CENTRALLY HELD COSTS.0 PURPOSE This evidence presents OPG s centrally held costs. Centrally held costs primarily consist of: Certain pension

SUMMARY OF APPLICATION

Filed: September, 00 EB-00-00 Schedule Page of SUMMARY OF APPLICATION Hydro One Networks ( Hydro One or Hydro One Transmission ) is applying for an Order approving the revenue requirement, cost allocation

Filed: September, 00 EB-00-00 Schedule Page of SUMMARY OF APPLICATION Hydro One Networks ( Hydro One or Hydro One Transmission ) is applying for an Order approving the revenue requirement, cost allocation

Ontario Energy Board (Board Staff) INTERROGATORY #16 List 1

INTERROGATORY #16 List 1") Filed: October,, 0 Schedule.0 Staff Page of 0 0 Ontario Energy Board (Board Staff) INTERROGATORY # List Issue Is Hydro One's proposal with respect to the capital contribution Ref: Exhibit B/Tab/Sch/page

Filed: October,, 0 Schedule.0 Staff Page of 0 0 Ontario Energy Board (Board Staff) INTERROGATORY # List Issue Is Hydro One's proposal with respect to the capital contribution Ref: Exhibit B/Tab/Sch/page

EB Hydro One Networks Inc. s 2019 Transmission Revenue Requirement Application and Evidence Filing

Hydro One Networks Inc. th Floor, South Tower Bay Street Toronto, Ontario MG P www.hydroone.com Tel: () -0 Cell: () - Frank.Dandrea@HydroOne.com Frank D Andrea Vice President, Chief Regulatory Officer,

Hydro One Networks Inc. th Floor, South Tower Bay Street Toronto, Ontario MG P www.hydroone.com Tel: () -0 Cell: () - Frank.Dandrea@HydroOne.com Frank D Andrea Vice President, Chief Regulatory Officer,

HYDRO ONE NETWORKS INC. DISTRIBUTION Revenue Deficiency/(Sufficiency) Year Ending December 31, 2010 and 2011 ($ Millions)

Year Ending December 31, 2010 and 2011 ($ Millions)") HYDRO ONE NETWORKS INC. DISTRIBUTION Revenue Deficiency/(Sufficiency) Year Ending December, 0 and 0 ($ Millions) Updated: September, 00 Schedule Attachment Page of Line No. Particulars 0 0 Revenue requirement

HYDRO ONE NETWORKS INC. DISTRIBUTION Revenue Deficiency/(Sufficiency) Year Ending December, 0 and 0 ($ Millions) Updated: September, 00 Schedule Attachment Page of Line No. Particulars 0 0 Revenue requirement

PRUDENT MANAGEMENT OF PILS/TAXES

EB-0-0 Exhibit H Tab Schedule Page of TAXES AND PILS 0 INTRODUCTION The revenue requirement filed at Exhibit J, Tab, Schedule of this Application reflects amounts for Payments in Lieu of Taxes ( PILs )

EB-0-0 Exhibit H Tab Schedule Page of TAXES AND PILS 0 INTRODUCTION The revenue requirement filed at Exhibit J, Tab, Schedule of this Application reflects amounts for Payments in Lieu of Taxes ( PILs )

OVERVIEW OF DEFERRAL AND VARIANCE ACCOUNTS

Filed: 0-- EB-0-00 Exhibit H Tab Schedule Page of 0 0 OVERVIEW OF DEFERRAL AND VARIANCE ACCOUNTS.0 PURPOSE This evidence provides an overview of OPG s deferral and variance accounts and presents the amounts

Filed: 0-- EB-0-00 Exhibit H Tab Schedule Page of 0 0 OVERVIEW OF DEFERRAL AND VARIANCE ACCOUNTS.0 PURPOSE This evidence provides an overview of OPG s deferral and variance accounts and presents the amounts

DEFERRAL AND VARIANCE ACCOUNTS

Toronto Hydro-Electric System Limited EB-2014-0116 Tab 1 Schedule 1 ORIGINAL Page 1 of 30 1 DEFERRAL AND VARIANCE ACCOUNTS 2 3 4 5 This evidence provides a summary of Toronto Hydro s deferral and variance

Toronto Hydro-Electric System Limited EB-2014-0116 Tab 1 Schedule 1 ORIGINAL Page 1 of 30 1 DEFERRAL AND VARIANCE ACCOUNTS 2 3 4 5 This evidence provides a summary of Toronto Hydro s deferral and variance

DISPOSITION OF SMART METER DEFERRAL ACCOUNT AND STRANDED METER BALANCES

Toronto Hydro-Electric System Limited Filed Sep 30, 11 Page 1 of 15 1 2 DISPOSITION OF SMART METER DEFERRAL ACCOUNT AND STRANDED METER BALANCES 3 4 5 6 7 8 9 INTRODUCTION In accordance with OEB guidelines

Toronto Hydro-Electric System Limited Filed Sep 30, 11 Page 1 of 15 1 2 DISPOSITION OF SMART METER DEFERRAL ACCOUNT AND STRANDED METER BALANCES 3 4 5 6 7 8 9 INTRODUCTION In accordance with OEB guidelines

REGULATORY ASSETS, VARIANCE AND DEFERRAL ACCOUNTS

EB-0-0 Exhibit J Tab Page of REGULATORY ASSETS, VARIANCE AND DEFERRAL ACCOUNTS This evidence provides a summary of THESL s regulatory assets, variance and deferral accounts. The account balances, when

EB-0-0 Exhibit J Tab Page of REGULATORY ASSETS, VARIANCE AND DEFERRAL ACCOUNTS This evidence provides a summary of THESL s regulatory assets, variance and deferral accounts. The account balances, when

REGULATORY ASSETS. The purpose of this evidence is to provide a description of Hydro One Transmission s Regulatory Assets.

Filed: May, 0 EB-0-000 Page of REGULATORY ASSETS.0 INTRODUCTION The purpose of this evidence is to provide a description of Hydro One Transmission s Regulatory Assets. All of the Regulatory Assets reported

Filed: May, 0 EB-0-000 Page of REGULATORY ASSETS.0 INTRODUCTION The purpose of this evidence is to provide a description of Hydro One Transmission s Regulatory Assets. All of the Regulatory Assets reported

Canadian Manufacturers & Exporters (CME) INTERROGATORY #1 List 1

INTERROGATORY #1 List 1") Filed: December, 00 Schedule Page of 0 0 0 0 Canadian Manufacturers & Exporters (CME) INTERROGATORY # List General Issues. Ref: Exhibit A, Tab, Schedule, paragraph Exhibit A, Tab, Schedule, page Exhibit

Filed: December, 00 Schedule Page of 0 0 0 0 Canadian Manufacturers & Exporters (CME) INTERROGATORY # List General Issues. Ref: Exhibit A, Tab, Schedule, paragraph Exhibit A, Tab, Schedule, page Exhibit

Energy Probe (EP) INTERROGATORY #50 List 1

INTERROGATORY #50 List 1") Exhibit I Tab 8 Schedule 3.01 EP 50 Page 1 of 3 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 Energy Probe (EP) INTERROGATORY #50 List 1 Issue

Exhibit I Tab 8 Schedule 3.01 EP 50 Page 1 of 3 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 Energy Probe (EP) INTERROGATORY #50 List 1 Issue

IN THE MATTER OF AN INTEREST ARBITRATION INERGI L.P. and. THE SOCIETY OF ENERGY PROFESSIONALS IFPTE, Local 160

IN THE MATTER OF AN INTEREST ARBITRATION BETWEEN INERGI L.P. ( Inergi ) and THE SOCIETY OF ENERGY PROFESSIONALS IFPTE, Local 160 (the Society ) SOLE MEDIATOR-ARBITRATOR: John Stout APPEARANCES: For Inergi:

IN THE MATTER OF AN INTEREST ARBITRATION BETWEEN INERGI L.P. ( Inergi ) and THE SOCIETY OF ENERGY PROFESSIONALS IFPTE, Local 160 (the Society ) SOLE MEDIATOR-ARBITRATOR: John Stout APPEARANCES: For Inergi:

REGULATORY ACCOUNTS. The purpose of this evidence is to provide a description of Hydro One Transmission s Regulatory Accounts.

Exhibit F Schedule Page of REGULATORY ACCOUNTS. INTRODUCTION The purpose of this evidence is to provide a description of Hydro One Transmission s Regulatory Accounts. 0 All of the Regulatory Accounts reported

Exhibit F Schedule Page of REGULATORY ACCOUNTS. INTRODUCTION The purpose of this evidence is to provide a description of Hydro One Transmission s Regulatory Accounts. 0 All of the Regulatory Accounts reported

EXECUTIVE SUMMARY OF APPLICATION

Updated: 0-0-0 EB-0-00 Page of EXECUTIVE SUMMARY OF APPLICATION. SCOPE OF APPLICATION Hydro One Networks Inc. ( Hydro One ) is applying for an Order approving the revenue requirement, cost allocation and

Updated: 0-0-0 EB-0-00 Page of EXECUTIVE SUMMARY OF APPLICATION. SCOPE OF APPLICATION Hydro One Networks Inc. ( Hydro One ) is applying for an Order approving the revenue requirement, cost allocation and

London Property Management Association (LPMA) INTERROGATORY #29 List 1. Issue 18 Is the forecast of long term debt for appropriate?

INTERROGATORY #29 List 1. Issue 18 Is the forecast of long term debt for appropriate?") Exhibit I Tab 18 Schedule 2.01 LPMA 29 Page 1 of 2 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 London Property Management Association (LPMA) INTERROGATORY #29 List 1 Issue 18 Is the forecast

Exhibit I Tab 18 Schedule 2.01 LPMA 29 Page 1 of 2 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 London Property Management Association (LPMA) INTERROGATORY #29 List 1 Issue 18 Is the forecast

TAXES. Filed: EB Exhibit F4 Tab 2 Schedule 1 Page 1 of 16

Filed: 06-05-7 Page of 6 5 6 7 9 0 5 6 7 9 0 5 6 7 9 0 TAXES.0 PURPOSE This evidence presents taxes, including income tax, commodity tax, and property tax, for the regulated nuclear facilities for the

Filed: 06-05-7 Page of 6 5 6 7 9 0 5 6 7 9 0 5 6 7 9 0 TAXES.0 PURPOSE This evidence presents taxes, including income tax, commodity tax, and property tax, for the regulated nuclear facilities for the

DEFERRAL AND VARIANCE ACCOUNTS

Toronto Hydro-Electric System Limited EB-2014-0116 Tab 1 Schedule 1 ORIGINAL Page 1 of 30 1 DEFERRAL AND VARIANCE ACCOUNTS 2 3 4 5 This evidence provides a summary of Toronto Hydro s deferral and variance

Toronto Hydro-Electric System Limited EB-2014-0116 Tab 1 Schedule 1 ORIGINAL Page 1 of 30 1 DEFERRAL AND VARIANCE ACCOUNTS 2 3 4 5 This evidence provides a summary of Toronto Hydro s deferral and variance

REGULATORY ACCOUNTS. The purpose of this Exhibit is to provide a description of Hydro One Distribution s regulatory accounts.

Updated: 000 Tab Page of REGULATORY ACCOUNTS. INTRODUCTION The purpose of this Exhibit is to provide a description of Hydro One Distribution s regulatory accounts. 0 All of the regulatory accounts reported

Updated: 000 Tab Page of REGULATORY ACCOUNTS. INTRODUCTION The purpose of this Exhibit is to provide a description of Hydro One Distribution s regulatory accounts. 0 All of the regulatory accounts reported

TORONTO HYDRO CORPORATION MANAGEMENT S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS FOR THE YEAR ENDED DECEMBER 31, 2005

TORONTO HYDRO CORPORATION MANAGEMENT S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS FOR THE YEAR ENDED DECEMBER 31, 2005 The following discussion and analysis should be read

TORONTO HYDRO CORPORATION MANAGEMENT S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS FOR THE YEAR ENDED DECEMBER 31, 2005 The following discussion and analysis should be read

COMPENSATION COST AND PRODUCTIVITY BENCHMARKING STUDY

Filed: September 30, 2008 EB-2008-0272 Exhibit A Tab 16 Schedule 2 Page 1 of 3 1 2 3 4 5 6 7 8 9 10 11 12 COMPENSATION COST AND PRODUCTIVITY BENCHMARKING STUDY In its Decision on Hydro One s last Transmission

Filed: September 30, 2008 EB-2008-0272 Exhibit A Tab 16 Schedule 2 Page 1 of 3 1 2 3 4 5 6 7 8 9 10 11 12 COMPENSATION COST AND PRODUCTIVITY BENCHMARKING STUDY In its Decision on Hydro One s last Transmission

IN THE MATTER OF the Ontario Energy Board Act, 1998, S. O. 1998, c.15, Schedule B;

Ontario Energy Board Commission de l énergie de l Ontario IN THE MATTER OF the Ontario Energy Board Act, 1998, S. O. 1998, c.15, Schedule B; AND IN THE MATTER OF an application by Hydro One Networks Inc.

Ontario Energy Board Commission de l énergie de l Ontario IN THE MATTER OF the Ontario Energy Board Act, 1998, S. O. 1998, c.15, Schedule B; AND IN THE MATTER OF an application by Hydro One Networks Inc.

SECOND QUARTER REPORT JUNE 30, 2015

SECOND QUARTER REPORT JUNE 30, 2015 TORONTO HYDRO CORPORATION TABLE OF CONTENTS Glossary 3 Management s Discussion and Analysis 4 Executive Summary 5 Introduction 5 Business of Toronto Hydro Corporation

SECOND QUARTER REPORT JUNE 30, 2015 TORONTO HYDRO CORPORATION TABLE OF CONTENTS Glossary 3 Management s Discussion and Analysis 4 Executive Summary 5 Introduction 5 Business of Toronto Hydro Corporation

Horizon Holdings Inc. Auditors Report to the Shareholders and Consolidated Financial Statements Year Ended December 31, 2016 and December 31, 2015

Auditors Report to the Shareholders and Consolidated Financial Statements Year Ended December 31, 2016 and December 31, 2015 KPMG LLP Commerce Place 21 King Street West, Suite 700 Hamilton Ontario L8P

Auditors Report to the Shareholders and Consolidated Financial Statements Year Ended December 31, 2016 and December 31, 2015 KPMG LLP Commerce Place 21 King Street West, Suite 700 Hamilton Ontario L8P

Consolidated Financial Statements. Toronto Hydro Corporation DECEMBER 31, 2007

Consolidated Financial Statements DECEMBER 31, Consolidated Financial Statements DECEMBER 31, Contents Page Auditors' Report 1 Consolidated Balance Sheet 2 Consolidated Statement of Income 3 Consolidated

Consolidated Financial Statements DECEMBER 31, Consolidated Financial Statements DECEMBER 31, Contents Page Auditors' Report 1 Consolidated Balance Sheet 2 Consolidated Statement of Income 3 Consolidated

Enersource Hydro Mississauga Inc. Application for Distribution Rates Effective May 1, 2012 Board File No. EB Evidence Update

3240 Mavis Road Mississauga, Ontario L5C 3K1 Tel: (905) 273-4098 Fax (905) 566-2737 November 25, 2011 VIA RESS and Overnight Courier Ms. Kirsten Walli Board Secretary Ontario Energy Board P. O. Box 2319

3240 Mavis Road Mississauga, Ontario L5C 3K1 Tel: (905) 273-4098 Fax (905) 566-2737 November 25, 2011 VIA RESS and Overnight Courier Ms. Kirsten Walli Board Secretary Ontario Energy Board P. O. Box 2319

PENSION AND OPEB COST VARIANCE ACCOUNT

Corrected: 2013-02-08 Exhibit H2 Tab 1 Schedule 3 Page 1 of 12 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 PENSION AND OPEB COST VARIANCE ACCOUNT 1.0 OVERVIEW The

Corrected: 2013-02-08 Exhibit H2 Tab 1 Schedule 3 Page 1 of 12 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 PENSION AND OPEB COST VARIANCE ACCOUNT 1.0 OVERVIEW The

Ontario Energy Board Commission de l énergie de l Ontario DECISION AND RATE ORDER EB HYDRO ONE NETWORKS INC.

Ontario Energy Board Commission de l énergie de l Ontario DECISION AND RATE ORDER EB-2017-0050 HYDRO ONE NETWORKS INC. Application for rates and other charges to be effective May 1, 2018 for the former

Ontario Energy Board Commission de l énergie de l Ontario DECISION AND RATE ORDER EB-2017-0050 HYDRO ONE NETWORKS INC. Application for rates and other charges to be effective May 1, 2018 for the former

Power Workers' Union (PWU) INTERROGATORY #1. Ref (a): Participant Information Package: Exhibit C1-2-1, Page 5 of 6, Table 2 (OM&A Expenditures)

INTERROGATORY #1. Ref (a): Participant Information Package: Exhibit C1-2-1, Page 5 of 6, Table 2 (OM&A Expenditures)") Filed: 0-0- 0-0 Tx Rates Schedule Page of Power Workers' Union (PWU) INTERROGATORY # Ref (a): Participant Information Package: Exhibit C--, Page of, Table (OM&A Expenditures) Table : 0 Board Approved versus

Filed: 0-0- 0-0 Tx Rates Schedule Page of Power Workers' Union (PWU) INTERROGATORY # Ref (a): Participant Information Package: Exhibit C--, Page of, Table (OM&A Expenditures) Table : 0 Board Approved versus

Enersource Hydro Mississauga Inc. Application for Distribution Rates Effective January 1, 2017 Board File No.: EB

August 15, 2016 BY RESS & OVERNIGHT COURIER Ms. Kirsten Walli Board Secretary Ontario Energy Board P.O. Box 2319 2300 Yonge Street, Suite 2700 Toronto, Ontario M4P 1E4 Dear Ms. Walli: Re: Enersource Hydro

August 15, 2016 BY RESS & OVERNIGHT COURIER Ms. Kirsten Walli Board Secretary Ontario Energy Board P.O. Box 2319 2300 Yonge Street, Suite 2700 Toronto, Ontario M4P 1E4 Dear Ms. Walli: Re: Enersource Hydro

COST OF LONG-TERM DEBT

Filed: 00-0- EB-00-000 Exhibit C Tab Schedule Page of 0 0 0 COST OF LONG-TERM DEBT.0 PURPOSE This evidence describes how the methodology approved by the OEB in EB-00-00 was used to determine the long-term

Filed: 00-0- EB-00-000 Exhibit C Tab Schedule Page of 0 0 0 COST OF LONG-TERM DEBT.0 PURPOSE This evidence describes how the methodology approved by the OEB in EB-00-00 was used to determine the long-term

Notice to Readers of Enersource s Audited 2012 Financial Statements. Adoption of International Financial Reporting Standards

Notice to Readers of Enersource s Audited 2012 Financial Statements Adoption of International Financial Reporting Standards Effective January 1, 2012, Enersource Corporation and all of its subsidiary companies

Notice to Readers of Enersource s Audited 2012 Financial Statements Adoption of International Financial Reporting Standards Effective January 1, 2012, Enersource Corporation and all of its subsidiary companies

OTHER OPERATING COST ITEMS

Filed: 2007-11-30 EB-2007-0905 Exhibit F3 Tab 2 Schedule 1 Page 1 of 18 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 OTHER OPERATING COST ITEMS 1.0 PURPOSE The purpose

Filed: 2007-11-30 EB-2007-0905 Exhibit F3 Tab 2 Schedule 1 Page 1 of 18 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 OTHER OPERATING COST ITEMS 1.0 PURPOSE The purpose

Ontario Power Generation Inc. Application for payment amounts for the period from January 1, 2017 to December 31, 2021

Ontario Energy Board Commission de l énergie de l Ontario Application for payment amounts for the period from January 1, 2017 to December 31, 2021 DECISION ON DRAFT PAYMENT AMOUNTS ORDER AND PROCEDURAL

Ontario Energy Board Commission de l énergie de l Ontario Application for payment amounts for the period from January 1, 2017 to December 31, 2021 DECISION ON DRAFT PAYMENT AMOUNTS ORDER AND PROCEDURAL

National Utility Survey Ontario Power Generation

National Utility Survey Ontario Power Generation Survey Findings September 6, 2013 Prepared by Aon Hewitt Talent & Rewards Consulting 225 King Street West, Suite 1600, Toronto, Ontario Presentation to

National Utility Survey Ontario Power Generation Survey Findings September 6, 2013 Prepared by Aon Hewitt Talent & Rewards Consulting 225 King Street West, Suite 1600, Toronto, Ontario Presentation to

EXHIBIT 9 DEFERRAL AND VARIANCE ACCOUNTS

acr EXHIBIT DEFERRAL AND VARIANCE ACCOUNTS 0 Cost of Service Chapleau Public Utilities Corporation Page of 0 0. TABLE OF CONTENTS.. TABLE OF CONTENTS. Table of Contents..... Table of Contents..... List

acr EXHIBIT DEFERRAL AND VARIANCE ACCOUNTS 0 Cost of Service Chapleau Public Utilities Corporation Page of 0 0. TABLE OF CONTENTS.. TABLE OF CONTENTS. Table of Contents..... Table of Contents..... List

Operation, maintenance and administration (Note 23) Depreciation and amortization (Note 5) ,140 1,122 2,358 2,477

Depreciation and amortization (Note 5) ,140 1,122 2,358 2,477") CONDENSED INTERIM CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE INCOME (unaudited) Three months ended June 30 Six months ended June 30 (millions of Canadian dollars, except per share amounts)

CONDENSED INTERIM CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE INCOME (unaudited) Three months ended June 30 Six months ended June 30 (millions of Canadian dollars, except per share amounts)

BRUCE GENERATING STATIONS - REVENUES AND COSTS

Filed: 0-0- EB-0-0 Exhibit G Tab Schedule Page of 0 0 0 0 BRUCE GENERATING STATIONS - REVENUES AND COSTS.0 PURPOSE This evidence presents the revenues earned by OPG under the Bruce Lease agreement and

Filed: 0-0- EB-0-0 Exhibit G Tab Schedule Page of 0 0 0 0 BRUCE GENERATING STATIONS - REVENUES AND COSTS.0 PURPOSE This evidence presents the revenues earned by OPG under the Bruce Lease agreement and

2009 PILS / CORPORATE TAX FILING

Page 1 of 44 29 PILS / CORPORATE TAX FILING Sheet Index: Title Page Input Information Summary Tax Rates & Exemptions 28 Adjusted Taxable Income 28 Taxable Income Additions 28 Taxable Income Deductions

Page 1 of 44 29 PILS / CORPORATE TAX FILING Sheet Index: Title Page Input Information Summary Tax Rates & Exemptions 28 Adjusted Taxable Income 28 Taxable Income Additions 28 Taxable Income Deductions

NIAGARA-ON-THE-LAKE HYDRO INC.

Financial Statements of NIAGARA-ON-THE-LAKE HYDRO INC. Years ended December 31, 2015 and 2014 KPMG LLP 80 King Street Suite 620 PO Box 1294 Stn Main St. Catharines ON L2R 7A7 Telephone (905) 685-4811 Telefax

Financial Statements of NIAGARA-ON-THE-LAKE HYDRO INC. Years ended December 31, 2015 and 2014 KPMG LLP 80 King Street Suite 620 PO Box 1294 Stn Main St. Catharines ON L2R 7A7 Telephone (905) 685-4811 Telefax

May 19 Topic Presenter. 10:55-11:30 Rate Base, Depreciation, Nuclear Liabilities, Pension/OPEB, Deferral and Variance Accounts

May 19 Topic Presenter 8:00 8:30 Arrival and Continental Breakfast 8:30-8:40 Welcome and Introductions 8:40-8:50 Facilitator s Opening Remarks and Session Protocol 8:50-9:40 Application Overview and Regulatory

May 19 Topic Presenter 8:00 8:30 Arrival and Continental Breakfast 8:30-8:40 Welcome and Introductions 8:40-8:50 Facilitator s Opening Remarks and Session Protocol 8:50-9:40 Application Overview and Regulatory

2008 HYDRO ONE NETWORKS INCOME TAX RETURN

Filed: May 19, 2010 EB-2010-0002 Exhibit C2 Tab 5 Schedule 2 Page 1 of 1 1 2008 HYDRO ONE NETWORKS INCOME TAX RETURN 2 3 4 5 6 7 Attachment A: Federal and Ontario Income Tax Return Attachment B: Calculation

Filed: May 19, 2010 EB-2010-0002 Exhibit C2 Tab 5 Schedule 2 Page 1 of 1 1 2008 HYDRO ONE NETWORKS INCOME TAX RETURN 2 3 4 5 6 7 Attachment A: Federal and Ontario Income Tax Return Attachment B: Calculation

IN THE MATTER OF the Ontario Energy Board Act, 1998, S.O. 1998, c. 15, (Schedule B);

;") Ontari o Energy Board Commission de l énergie de l Ontario IN THE MATTER OF the Ontario Energy Board Act, 1998, S.O. 1998, c. 15, (Schedule B); AND IN THE MATTER OF an application by Hydro One Remote Communities

Ontari o Energy Board Commission de l énergie de l Ontario IN THE MATTER OF the Ontario Energy Board Act, 1998, S.O. 1998, c. 15, (Schedule B); AND IN THE MATTER OF an application by Hydro One Remote Communities

SECOND IMPACT STATEMENT

Filed: 2017-02-22 Page 1 of 7 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 SECOND IMPACT STATEMENT 1.0 PURPOSE The purpose of this exhibit is to show the impact of certain

Filed: 2017-02-22 Page 1 of 7 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 SECOND IMPACT STATEMENT 1.0 PURPOSE The purpose of this exhibit is to show the impact of certain

TORONTO HYDRO CORPORATION

TORONTO HYDRO CORPORATION MANAGEMENT S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS FOR THE THREE MONTHS AND SIX MONTHS ENDED JUNE 30, 2010 The following discussion and analysis

TORONTO HYDRO CORPORATION MANAGEMENT S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS FOR THE THREE MONTHS AND SIX MONTHS ENDED JUNE 30, 2010 The following discussion and analysis

The Filing includes the Application; the Manager s Summary; and live versions of the following models:

August th, 206 Via RESS and Courier Ms. Kirsten Walli, Board Secretary Ontario Energy Board 2300 Yonge Street, 27th Floor Toronto, Ontario M4P E4 Dear Ms. Walli, Re: Electricity Distribution Licence ED-2006-003

August th, 206 Via RESS and Courier Ms. Kirsten Walli, Board Secretary Ontario Energy Board 2300 Yonge Street, 27th Floor Toronto, Ontario M4P E4 Dear Ms. Walli, Re: Electricity Distribution Licence ED-2006-003

Report on the Sustainability of Electricity Sector Pension Plans to the Minister of Finance. By the Special Advisor

Report on the Sustainability of Electricity Sector Pension Plans to the Minister of Finance By the Special Advisor March 18, 2014 March 18, 2014 Hon. Charles Sousa Minister of Finance for Ontario Dear

Report on the Sustainability of Electricity Sector Pension Plans to the Minister of Finance By the Special Advisor March 18, 2014 March 18, 2014 Hon. Charles Sousa Minister of Finance for Ontario Dear

IN THE MATTER OF the Ontario Energy Board Act, 1998, S.O. 1998, c. 15, (Schedule B);

;") Ontario Energy Board Commission de l énergie de l Ontario IN THE MATTER OF the Ontario Energy Board Act, 1998, S.O. 1998, c. 15, (Schedule B); AND IN THE MATTER OF an application by for an accounting order

Ontario Energy Board Commission de l énergie de l Ontario IN THE MATTER OF the Ontario Energy Board Act, 1998, S.O. 1998, c. 15, (Schedule B); AND IN THE MATTER OF an application by for an accounting order

TABLE OF CONTENTS. C. Business Planning and Budgeting Process and Economic Assumptions

TABLE OF CONTENTS Table of Contents Page of A. Rate Plan. Rate Plan. Specific Proposals B. Bill Impacts and Proposed Rates. Rate Impact Summary C. Business Planning and Budgeting Process and Economic Assumptions

TABLE OF CONTENTS Table of Contents Page of A. Rate Plan. Rate Plan. Specific Proposals B. Bill Impacts and Proposed Rates. Rate Impact Summary C. Business Planning and Budgeting Process and Economic Assumptions

NIAGARA-ON-THE-LAKE HYDRO INC.

Financial Statements of NIAGARA-ON-THE-LAKE HYDRO INC. KPMG LLP 80 King Street, Suite 620 St. Catharines ON L2R 7G1 Canada Tel 905-685-4811 Fax 905-682-2008 INDEPENDENT AUDITORS REPORT To the Shareholder

Financial Statements of NIAGARA-ON-THE-LAKE HYDRO INC. KPMG LLP 80 King Street, Suite 620 St. Catharines ON L2R 7G1 Canada Tel 905-685-4811 Fax 905-682-2008 INDEPENDENT AUDITORS REPORT To the Shareholder

EXHIBIT LIST. Administration. Summary of Board Directives and Undertakings from Previous Proceedings A 5 1 Corporate Organization Charts

Page 1 of 9 1 EXHIBIT LIST A Administration A 1 1 Exhibit List A 2 1 Application A 2 1 1 Certification of Evidence A 3 1 Executive Summary A 4 1 Compliance with OEB Filing Requirements for Electricity

Page 1 of 9 1 EXHIBIT LIST A Administration A 1 1 Exhibit List A 2 1 Application A 2 1 1 Certification of Evidence A 3 1 Executive Summary A 4 1 Compliance with OEB Filing Requirements for Electricity

2011 PILS / CORPORATE TAX FILING

Page 1 of 33 2011 PILS / CORPORATE TAX FILING Sheet Index: Title Page Input Information Summary Tax Rates & Exemptions Test Year Sch 8 and 10 UCC&CEC Test Year UCC and CEC Additions & Disposals Test Year

Page 1 of 33 2011 PILS / CORPORATE TAX FILING Sheet Index: Title Page Input Information Summary Tax Rates & Exemptions Test Year Sch 8 and 10 UCC&CEC Test Year UCC and CEC Additions & Disposals Test Year

ENERSOURCE HYDRO MISSISSAUGA INC. HORIZON UTILITIES CORPORATION & POWERSTREAM INC.

Commission de l énergie de l Ontario DECISION AND ORDER ENERSOURCE HYDRO MISSISSAUGA INC. HORIZON UTILITIES CORPORATION & POWERSTREAM INC. Application for approval to amalgamate to form LDC Co and for

Commission de l énergie de l Ontario DECISION AND ORDER ENERSOURCE HYDRO MISSISSAUGA INC. HORIZON UTILITIES CORPORATION & POWERSTREAM INC. Application for approval to amalgamate to form LDC Co and for

RP EB IN THE MATTER OF the Ontario Energy Board Act, 1998, S.O. 1998, c.15, Schedule B