Pricing Guaranteed Annuity Option with Surrender Rates Consideration

|

|

|

- Susanna Lawson

- 5 years ago

- Views:

Transcription

1 Pricing Guaraneed Annuiy Opion wih Surrender Raes Consideraion Shing-Her Juang Deparmen of Financial Engineering & Acuarial Mahemaics, Soochow Universiy, Taiwan Shu-Chuan Chen Acuarial Deparmen, Bank Taiwan Life Insurance Chih-Hua Chiao Deparmen of Financial Engineering & Acuarial Mahemaics, Soochow Universiy, Taiwan Po-Kai Shen Produc Developmen & Managemen Deparmen, Nan Shan Life Insurance

2 Agenda Moivaion Inroducion Models Numerical Illusraions Summary

3 Moivaion Aging sociey Low birh rae, improving medical echnology, longer life expecancy Taiwan becomes an aged sociey in 2017 Economical safey is a major concern for older generaion Economic burden for younger generaion

4 Moivaion (con.) Life annuiy Guaraneed annuiy opion Dynamic surrender model Fair pricing

5 Life annuiy due Life annuiy due y a 1 p 1i y y 0 Age(y) Annuiy purchase rae (APR) annuian insurer 1 a y ay

6 Single premium deferred life annuiy Risk facors - Life able - Ineres rae Accumulaion period 1 ay T 0 Age (y) Age (y)+t T T+1 T+2

7 Guaranee annuiy opion Guaranee annuiy opion (GAO) APR ay T10 1 GAR ay T GAR Accumulaion period Guaranee Annuiy Rae (GAR) 0 T T+1 T+2

8 Level premium Accumulaion period Benefi period c h a r g e Accoun Value c h a r g e c h a r g e c h a r g e F T E Cash inflow - Cash ouflow =0 Max F APR a, F GAR a T 65 T 65 1 F F GARMax a T T 65,0 GAR Liabiliy from GAO Time T T+1 T+2 Age y y+1 y

9 Surrender 1 ax T Surrender? GAR 0 T T+1 T+2

10 Model Building Yang and Tang (2006) - Risk neural measure S: r: Asse price a ime ineres rae a ime 65 a 1 p P(65,65 ) ds S rd QS, S dr ˆ ˆ r d r dw Qr, r QS, Qr, dw dw dw d ˆ 2 2 e A65,65 ˆ e P(65,65 ) A 65,65 exp B 65,65 r B65,65 = ˆ r 2e 1 e ˆ ˆ ˆ 2 r Time T T+1 T+2 Age y y+1 y

11 Surrender model AAA and Min 1, Max 0.5,11.25 ITM 1.1 Guaraneed value a ime : adjus coefficien, ITM = Accoun value a ime ITM Surrender rae l l base q Surrender rae a ime q Experience rae x x

12 Surrender model (con.) Sandard Scenarios of AG 43

13 Proposed surrender model During Surrender charge period w 0.05 if ITM 1 q 0.03 if ITM 1 Beyond surrender charge period w q Min 0.1, Max 0.02, ITM -1 H Holding value a ime where, ITM F Accoun value a ime H?

14 Surrender ime If q w 3 3 Hold ile ime 4 H F 3 3 w 3 q vs.. 3 If q w 3 3 Surrender before ime 4 r r r r ime age Conrac value Holding value Max F APR a, F GAR a r3 e p J q DB H 3 J 4

15 Surrender ime (con.) If q w 2 2 Hold ile ime 3 H F 2 2 w 2 q vs.. 2 If q w 2 2 Surrender before ime 3 r r r r ime age Conrac value Holding value J3 F3 r2 H2 e p63 J3 q63 DB3

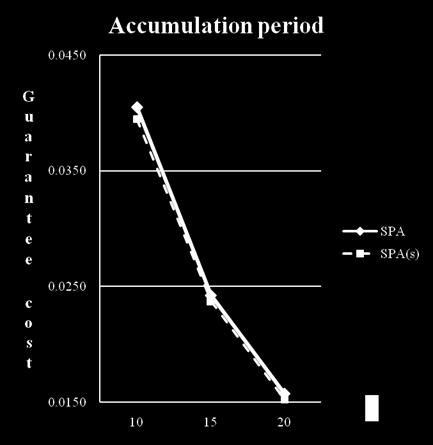

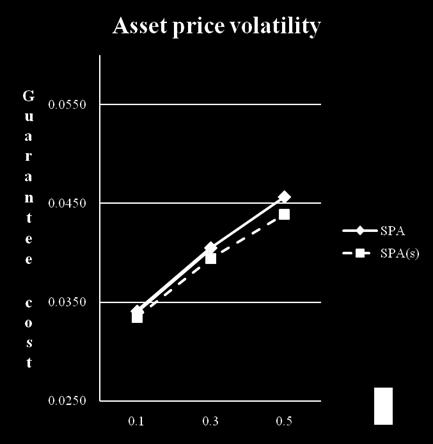

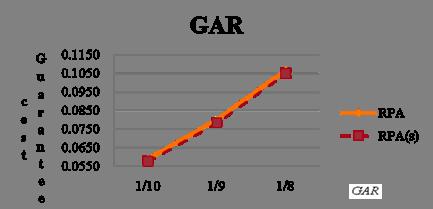

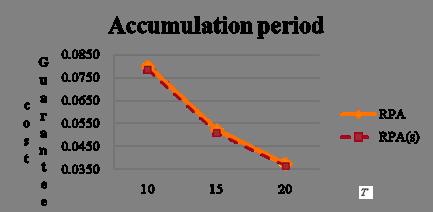

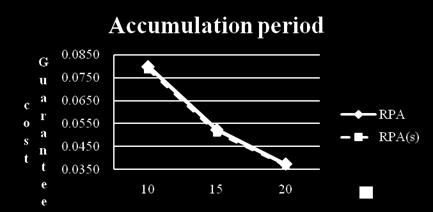

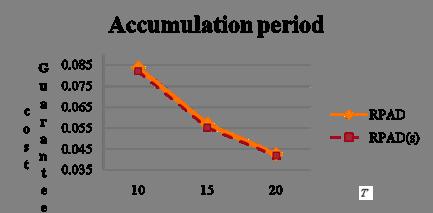

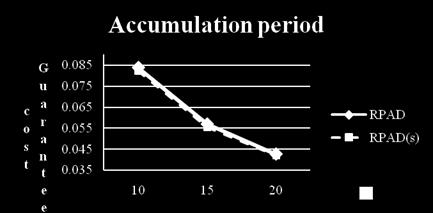

16 Assumpions - Gender:Male Numerical Illusraions - Premium pay:single premium, monhly premium - Accumulaion period:10, 15, 20 years - Premium Single premium:120,000 Monhly premium: - Annuiy dae:he 65 h BD Accumulaion period Premium amoun 1, Benefi: Surrender during accumulaion period, reurn he accoun value. Wih GMDB during accumulaion period, deah benefi = max(accoun value, oal premium) No GMDB during he accumulaion period, deah benefi = accoun value. Choice of APR or GAR a he annuiy dae.

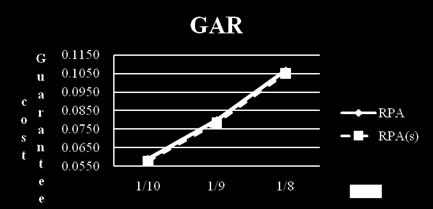

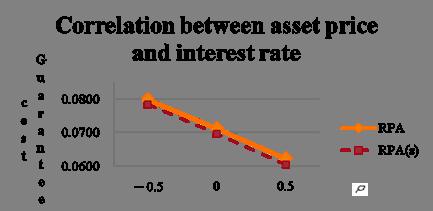

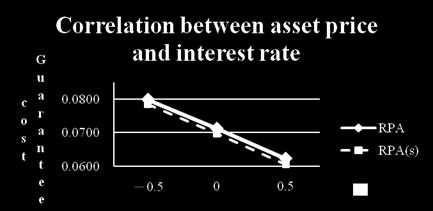

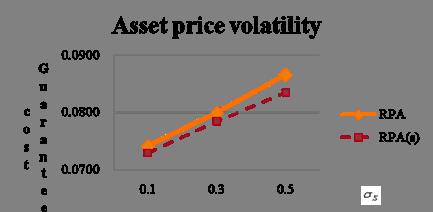

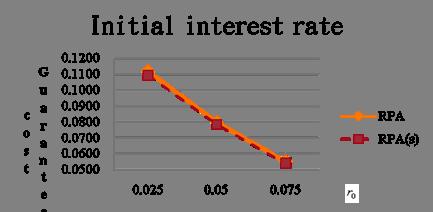

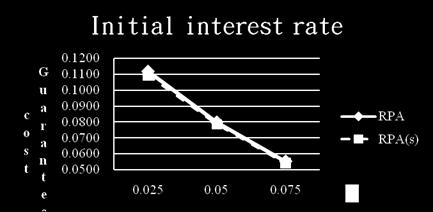

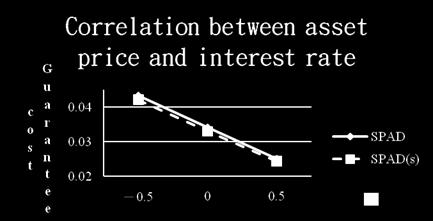

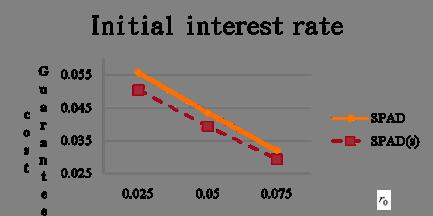

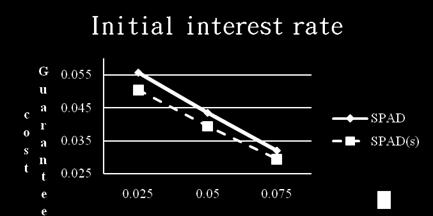

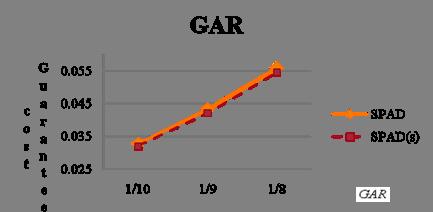

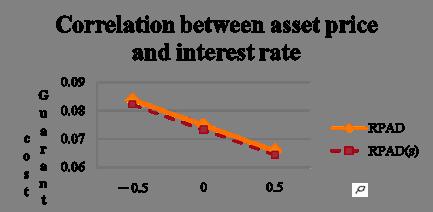

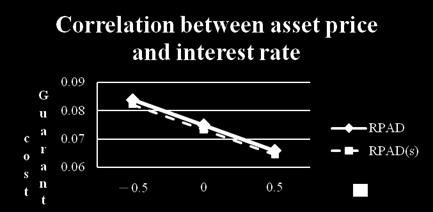

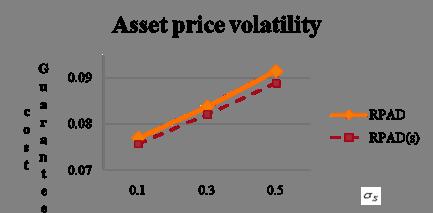

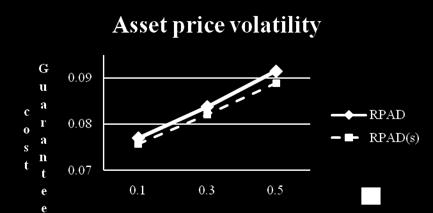

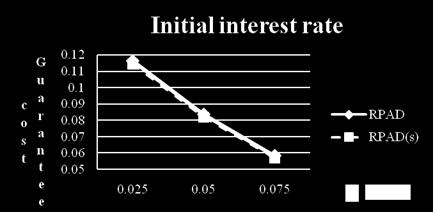

17 Numerical Illusraions (con.) Assumpions - Life able:1997 Taiwan Insurer Annuiy Life Table - Fracion age assumpion:udd assumpion - Sandard scenario: - Ineres rae model:chang(2010) Scenarios: - GAR: 0.1, 0.111, Accumulaion period (T): Correlaion coefficien :-0.5, 0, Asse price volailiy : 0.1, 0.3, Iniial ineres rae :0.025, 0.05, Moraliy:Life able 100%, Life able 90%, Life able 80% 1 GAR, T 10, 0.3, r , q 100% s x life able 9 ˆ 0.014, 0.026, r 0.06 r 0 S

18 Single premium GAO Charge: 7% Scenarios SPA SPA(s) Raio 1/ % GAR 1/ % 1/ % % T % % % % % % S % % % r % % % 死亡率 % % SPA() s SPA Raio SPA Raio 1.86% ~ 3.87%

")

19 Single Premium GAO (con. 1)

")

20 Single Premium GAO (con. 2)

")

21 Single Premium GAO (con. 3)

22 Monhly Premium GAO Charge 12% Scenarios RPA RPA(s) Raio 1/ % GAR 1/ % 1/ % % T % % % % % % S % % % r % % % 死亡率 % % Raio 1.61% ~ 3.58%

")

23 Monhly Premium GAO (con.)

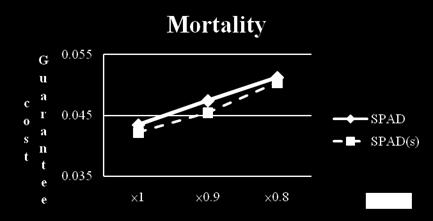

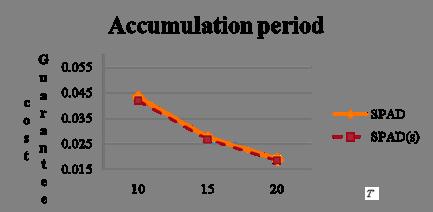

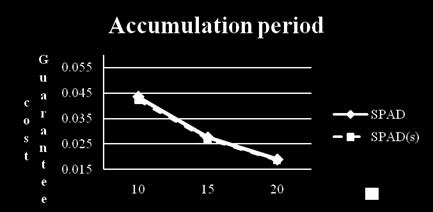

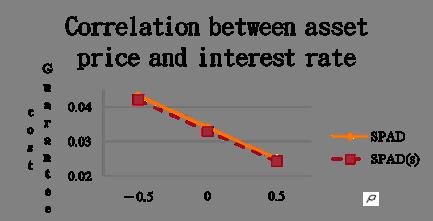

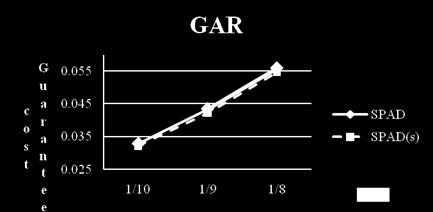

24 Single Premium GAO+GMDB Charge: 7% Scenarios SPAD SPAD(s) Raio 1/ % GAR 1/ % 1/ % % T % % % % % % S % % % r % % % 死亡率 % % Raio 1.42% ~ 4.23%

25 Single Premium GAO

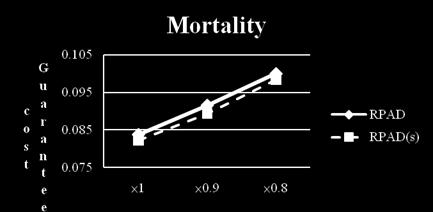

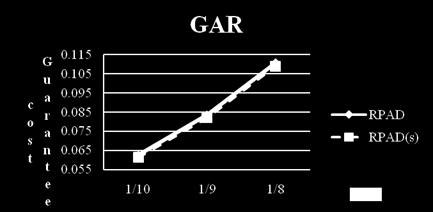

26 Monhly premium GAO+GMDB Charge: 12% Scenarios RPAD RPAD(s) Raio 1/ % GAR 1/ % 1/ % % T % % % % % % S % % % r % % % 死亡率 % % Raio 1.60% ~ 2.83%

27 Monhly premium GAO+GMDB(Con.)

28 Summary Single premium or monhly premium, GAO or GAO+GMDB - Guaranee cos m C GAR T S r 0 Moraliy - Guaranee cos reduced wih our surrender model

29 Thank you for your lisening!

Analyzing Surplus Appropriation Schemes in Participating Life Insurance from the Insurer s and the Policyholder s Perspective

Analyzing Surplus Appropriaion Schemes in Paricipaing Life Insurance from he Insurer s and he Policyholder s Perspecive AFIR Colloquium Madrid, Spain June 22, 2 Alexander Bohner and Nadine Gazer Universiy

Analyzing Surplus Appropriaion Schemes in Paricipaing Life Insurance from he Insurer s and he Policyholder s Perspecive AFIR Colloquium Madrid, Spain June 22, 2 Alexander Bohner and Nadine Gazer Universiy

Policyholder Exercise Behavior for Variable Annuities including Guaranteed Minimum Withdrawal Benefits 1

Policyholder Exercise Behavior for Variable Annuiies including Guaraneed Minimum Wihdrawal Benefis 1 2 Deparmen of Risk Managemen and Insurance, Georgia Sae Universiy 35 Broad Sree, 11h Floor; Alana, GA

Policyholder Exercise Behavior for Variable Annuiies including Guaraneed Minimum Wihdrawal Benefis 1 2 Deparmen of Risk Managemen and Insurance, Georgia Sae Universiy 35 Broad Sree, 11h Floor; Alana, GA

A pricing model for the Guaranteed Lifelong Withdrawal Benefit Option

A pricing model for he Guaraneed Lifelong Wihdrawal Benefi Opion Gabriella Piscopo Universià degli sudi di Napoli Federico II Diparimeno di Maemaica e Saisica Index Main References Survey of he Variable

A pricing model for he Guaraneed Lifelong Wihdrawal Benefi Opion Gabriella Piscopo Universià degli sudi di Napoli Federico II Diparimeno di Maemaica e Saisica Index Main References Survey of he Variable

Risk Management of a DB Underpin Pension Plan

Risk Managemen of a DB Underpin Pension Plan Kai Chen upervisor: Mary Hardy Acknowledge he UW Insiue for Quaniaive Finance and Insurance CKER ARC Travel Gran for heir uppor Ouline Inroducion and Background

Risk Managemen of a DB Underpin Pension Plan Kai Chen upervisor: Mary Hardy Acknowledge he UW Insiue for Quaniaive Finance and Insurance CKER ARC Travel Gran for heir uppor Ouline Inroducion and Background

HEDGING SYSTEMATIC MORTALITY RISK WITH MORTALITY DERIVATIVES

HEDGING SYSTEMATIC MORTALITY RISK WITH MORTALITY DERIVATIVES Workshop on moraliy and longeviy, Hannover, April 20, 2012 Thomas Møller, Chief Analys, Acuarial Innovaion OUTLINE Inroducion Moraliy risk managemen

HEDGING SYSTEMATIC MORTALITY RISK WITH MORTALITY DERIVATIVES Workshop on moraliy and longeviy, Hannover, April 20, 2012 Thomas Møller, Chief Analys, Acuarial Innovaion OUTLINE Inroducion Moraliy risk managemen

FAIR VALUATION OF INSURANCE LIABILITIES. Pierre DEVOLDER Université Catholique de Louvain 03/ 09/2004

FAIR VALUATION OF INSURANCE LIABILITIES Pierre DEVOLDER Universié Caholique de Louvain 03/ 09/004 Fair value of insurance liabiliies. INTRODUCTION TO FAIR VALUE. RISK NEUTRAL PRICING AND DEFLATORS 3. EXAMPLES

FAIR VALUATION OF INSURANCE LIABILITIES Pierre DEVOLDER Universié Caholique de Louvain 03/ 09/004 Fair value of insurance liabiliies. INTRODUCTION TO FAIR VALUE. RISK NEUTRAL PRICING AND DEFLATORS 3. EXAMPLES

Optimal Funding of a Defined Benefit Pension Plan

Opimal Funding of a Defined Benefi Pension Plan G. Deelsra 1 D. Hainau 2 1 Deparmen of Mahemaics and ECARES Universié Libre de Bruxelles (U.L.B.), Belgium 2 Insiu des sciences acuarielles Universié Caholique

Opimal Funding of a Defined Benefi Pension Plan G. Deelsra 1 D. Hainau 2 1 Deparmen of Mahemaics and ECARES Universié Libre de Bruxelles (U.L.B.), Belgium 2 Insiu des sciences acuarielles Universié Caholique

INSTITUTE OF ACTUARIES OF INDIA

INSIUE OF ACUARIES OF INDIA EAMINAIONS 23 rd May 2011 Subjec S6 Finance and Invesmen B ime allowed: hree hours (9.45* 13.00 Hrs) oal Marks: 100 INSRUCIONS O HE CANDIDAES 1. Please read he insrucions on

INSIUE OF ACUARIES OF INDIA EAMINAIONS 23 rd May 2011 Subjec S6 Finance and Invesmen B ime allowed: hree hours (9.45* 13.00 Hrs) oal Marks: 100 INSRUCIONS O HE CANDIDAES 1. Please read he insrucions on

Pricing formula for power quanto options with each type of payoffs at maturity

Global Journal of Pure and Applied Mahemaics. ISSN 0973-1768 Volume 13, Number 9 (017, pp. 6695 670 Research India Publicaions hp://www.ripublicaion.com/gjpam.hm Pricing formula for power uano opions wih

Global Journal of Pure and Applied Mahemaics. ISSN 0973-1768 Volume 13, Number 9 (017, pp. 6695 670 Research India Publicaions hp://www.ripublicaion.com/gjpam.hm Pricing formula for power uano opions wih

Equivalent Martingale Measure in Asian Geometric Average Option Pricing

Journal of Mahemaical Finance, 4, 4, 34-38 ublished Online Augus 4 in SciRes hp://wwwscirporg/journal/jmf hp://dxdoiorg/436/jmf4447 Equivalen Maringale Measure in Asian Geomeric Average Opion ricing Yonggang

Journal of Mahemaical Finance, 4, 4, 34-38 ublished Online Augus 4 in SciRes hp://wwwscirporg/journal/jmf hp://dxdoiorg/436/jmf4447 Equivalen Maringale Measure in Asian Geomeric Average Opion ricing Yonggang

Supplement to Models for Quantifying Risk, 5 th Edition Cunningham, Herzog, and London

Supplemen o Models for Quanifying Risk, 5 h Ediion Cunningham, Herzog, and London We have received inpu ha our ex is no always clear abou he disincion beween a full gross premium and an expense augmened

Supplemen o Models for Quanifying Risk, 5 h Ediion Cunningham, Herzog, and London We have received inpu ha our ex is no always clear abou he disincion beween a full gross premium and an expense augmened

LIDSTONE IN THE CONTINUOUS CASE by. Ragnar Norberg

LIDSTONE IN THE CONTINUOUS CASE by Ragnar Norberg Absrac A generalized version of he classical Lidsone heorem, which deals wih he dependency of reserves on echnical basis and conrac erms, is proved in

LIDSTONE IN THE CONTINUOUS CASE by Ragnar Norberg Absrac A generalized version of he classical Lidsone heorem, which deals wih he dependency of reserves on echnical basis and conrac erms, is proved in

Acceleration Techniques for Life Cash Flow Projection Based on Many Interest Rates Scenarios Cash Flow Proxy Functions

Acceleraion Techniques for Life Cash Flow Projecion Based on Many Ineres Raes Scenarios Cash Flow Proxy Funcions Auhor: Marin Janeček, Tools4F, s.r.o. and Economic Universiy in Prague, 207 Acknowledgmen:

Acceleraion Techniques for Life Cash Flow Projecion Based on Many Ineres Raes Scenarios Cash Flow Proxy Funcions Auhor: Marin Janeček, Tools4F, s.r.o. and Economic Universiy in Prague, 207 Acknowledgmen:

Option Valuation of Oil & Gas E&P Projects by Futures Term Structure Approach. Hidetaka (Hugh) Nakaoka

Nakaoka") Opion Valuaion of Oil & Gas E&P Projecs by Fuures Term Srucure Approach March 9, 2007 Hideaka (Hugh) Nakaoka Former CIO & CCO of Iochu Oil Exploraion Co., Ld. Universiy of Tsukuba 1 Overview 1. Inroducion

Opion Valuaion of Oil & Gas E&P Projecs by Fuures Term Srucure Approach March 9, 2007 Hideaka (Hugh) Nakaoka Former CIO & CCO of Iochu Oil Exploraion Co., Ld. Universiy of Tsukuba 1 Overview 1. Inroducion

Hull-White one factor model Version

Hull-Whie one facor model Version 1.0.17 1 Inroducion This plug-in implemens Hull and Whie one facor models. reference on his model see [?]. For a general 2 How o use he plug-in In he Fairma user inerface

Hull-Whie one facor model Version 1.0.17 1 Inroducion This plug-in implemens Hull and Whie one facor models. reference on his model see [?]. For a general 2 How o use he plug-in In he Fairma user inerface

IJRSS Volume 2, Issue 2 ISSN:

A LOGITIC BROWNIAN MOTION WITH A PRICE OF DIVIDEND YIELDING AET D. B. ODUOR ilas N. Onyango _ Absrac: In his paper, we have used he idea of Onyango (2003) he used o develop a logisic equaion used in naural

A LOGITIC BROWNIAN MOTION WITH A PRICE OF DIVIDEND YIELDING AET D. B. ODUOR ilas N. Onyango _ Absrac: In his paper, we have used he idea of Onyango (2003) he used o develop a logisic equaion used in naural

Fair Valuation of Participating Policies in Stochastic Interest Rate Models: Two-dimensional Cox-Ross-Rubinstein Approaches

Fair Valuaion of aricipaing olicies in Sochasic Ineres Rae Models: Two-dimensional Cox-Ross-Rubinsein Approaches Liao, Szu-Lang Deparmen of Money and anking, Naional Chengchi Universiy, Taipei, Taiwan,

Fair Valuaion of aricipaing olicies in Sochasic Ineres Rae Models: Two-dimensional Cox-Ross-Rubinsein Approaches Liao, Szu-Lang Deparmen of Money and anking, Naional Chengchi Universiy, Taipei, Taiwan,

Li Gan Guan Gong Michael Hurd. April, 2006

Ne Inergeneraional Transfers from an Increase in Social Securiy Benefis Li Gan Guan Gong Michael Hurd April, 2006 ABSTRACT When he age of deah is uncerain, individuals will leave bequess even if hey have

Ne Inergeneraional Transfers from an Increase in Social Securiy Benefis Li Gan Guan Gong Michael Hurd April, 2006 ABSTRACT When he age of deah is uncerain, individuals will leave bequess even if hey have

Stochastic Interest Rate Approach of Pricing Participating Life Insurance Policies with Embedded Surrender Option

American Journal of Mahemaical and Compuer Modelling 28; 3(): -2 hp://www.sciencepublishinggroup.com/j/ajmcm doi:.648/j.ajmcm.283.2 Sochasic Ineres Rae Approach of ricing aricipaing Life Insurance olicies

American Journal of Mahemaical and Compuer Modelling 28; 3(): -2 hp://www.sciencepublishinggroup.com/j/ajmcm doi:.648/j.ajmcm.283.2 Sochasic Ineres Rae Approach of ricing aricipaing Life Insurance olicies

The Interaction of Guarantees, Surplus Distribution, and Asset Allocation in With Profit Life Insurance Policies

The Ineracion of Guaranees, Surplus Disribuion, and Asse Allocaion in Wih Profi Life Insurance Policies Alexander Kling Universiy of Ulm, Germany phone: +49 731 5031183, fax: +49 731 5031239 alkli@mahemaik.uni-ulm.de

The Ineracion of Guaranees, Surplus Disribuion, and Asse Allocaion in Wih Profi Life Insurance Policies Alexander Kling Universiy of Ulm, Germany phone: +49 731 5031183, fax: +49 731 5031239 alkli@mahemaik.uni-ulm.de

Matematisk statistik Tentamen: kl FMS170/MASM19 Prissättning av Derivattillgångar, 9 hp Lunds tekniska högskola. Solution.

Maemaisk saisik Tenamen: 8 5 8 kl 8 13 Maemaikcenrum FMS17/MASM19 Prissäning av Derivaillgångar, 9 hp Lunds ekniska högskola Soluion. 1. In he firs soluion we look a he dynamics of X using Iôs formula.

Maemaisk saisik Tenamen: 8 5 8 kl 8 13 Maemaikcenrum FMS17/MASM19 Prissäning av Derivaillgångar, 9 hp Lunds ekniska högskola Soluion. 1. In he firs soluion we look a he dynamics of X using Iôs formula.

Models of Default Risk

Models of Defaul Risk Models of Defaul Risk 1/29 Inroducion We consider wo general approaches o modelling defaul risk, a risk characerizing almos all xed-income securiies. The srucural approach was developed

Models of Defaul Risk Models of Defaul Risk 1/29 Inroducion We consider wo general approaches o modelling defaul risk, a risk characerizing almos all xed-income securiies. The srucural approach was developed

Constructing Out-of-the-Money Longevity Hedges Using Parametric Mortality Indexes. Johnny Li

1 / 43 Consrucing Ou-of-he-Money Longeviy Hedges Using Parameric Moraliy Indexes Johnny Li Join-work wih Jackie Li, Udiha Balasooriya, and Kenneh Zhou Deparmen of Economics, The Universiy of Melbourne

1 / 43 Consrucing Ou-of-he-Money Longeviy Hedges Using Parameric Moraliy Indexes Johnny Li Join-work wih Jackie Li, Udiha Balasooriya, and Kenneh Zhou Deparmen of Economics, The Universiy of Melbourne

Surrender Risk in the Context of the Quantitative Assessment of Participating Life Insurance Contracts under Solvency II

risks Aricle Surrender Risk in he Conex of he Quaniaive Assessmen of Paricipaing Life Insurance Conracs under Solvency II Tobias Burkhar ifa (Insiue for Finance and Acuarial Sciences), Lise-Meiner-Srasse

risks Aricle Surrender Risk in he Conex of he Quaniaive Assessmen of Paricipaing Life Insurance Conracs under Solvency II Tobias Burkhar ifa (Insiue for Finance and Acuarial Sciences), Lise-Meiner-Srasse

Single Premium of Equity-Linked with CRR and CIR Binomial Tree

The 7h SEAMS-UGM Conference 2015 Single Premium of Equiy-Linked wih CRR and CIR Binomial Tree Yunia Wulan Sari 1,a) and Gunardi 2,b) 1,2 Deparmen of Mahemaics, Faculy of Mahemaics and Naural Sciences,

The 7h SEAMS-UGM Conference 2015 Single Premium of Equiy-Linked wih CRR and CIR Binomial Tree Yunia Wulan Sari 1,a) and Gunardi 2,b) 1,2 Deparmen of Mahemaics, Faculy of Mahemaics and Naural Sciences,

MORNING SESSION. Date: Wednesday, April 26, 2017 Time: 8:30 a.m. 11:45 a.m. INSTRUCTIONS TO CANDIDATES

SOCIETY OF ACTUARIES Quaniaive Finance and Invesmen Core Exam QFICORE MORNING SESSION Dae: Wednesday, April 26, 2017 Time: 8:30 a.m. 11:45 a.m. INSTRUCTIONS TO CANDIDATES General Insrucions 1. This examinaion

SOCIETY OF ACTUARIES Quaniaive Finance and Invesmen Core Exam QFICORE MORNING SESSION Dae: Wednesday, April 26, 2017 Time: 8:30 a.m. 11:45 a.m. INSTRUCTIONS TO CANDIDATES General Insrucions 1. This examinaion

Pricing FX Target Redemption Forward under. Regime Switching Model

In. J. Conemp. Mah. Sciences, Vol. 8, 2013, no. 20, 987-991 HIKARI Ld, www.m-hikari.com hp://dx.doi.org/10.12988/ijcms.2013.311123 Pricing FX Targe Redempion Forward under Regime Swiching Model Ho-Seok

In. J. Conemp. Mah. Sciences, Vol. 8, 2013, no. 20, 987-991 HIKARI Ld, www.m-hikari.com hp://dx.doi.org/10.12988/ijcms.2013.311123 Pricing FX Targe Redempion Forward under Regime Swiching Model Ho-Seok

On the Edge of Completeness

On he Edge of Compleeness May 2000 Jean-Paul LAURENT Professor, ISFA Acuarial School, Universiy of Lyon, Scienific Advisor, BNP Paribas Correspondence lauren.jeanpaul@online.fr On he Edge of Compleeness:

On he Edge of Compleeness May 2000 Jean-Paul LAURENT Professor, ISFA Acuarial School, Universiy of Lyon, Scienific Advisor, BNP Paribas Correspondence lauren.jeanpaul@online.fr On he Edge of Compleeness:

Introduction to Black-Scholes Model

4 azuhisa Masuda All righs reserved. Inroducion o Black-choles Model Absrac azuhisa Masuda Deparmen of Economics he Graduae Cener, he Ciy Universiy of New York, 365 Fifh Avenue, New York, NY 6-439 Email:

4 azuhisa Masuda All righs reserved. Inroducion o Black-choles Model Absrac azuhisa Masuda Deparmen of Economics he Graduae Cener, he Ciy Universiy of New York, 365 Fifh Avenue, New York, NY 6-439 Email:

by Dr. Mizanur Rahman Professor of Accounting & Public Policy University of Dhaka

Fundamenal Valuaion and Financial Saemen Analysis by Dr. Mizanur ahman Professor of Accouning & Public Policy Universiy of Dhaka -mail: mizan@univdhaka.edu Training Program on Capial Marke esearch Organized

Fundamenal Valuaion and Financial Saemen Analysis by Dr. Mizanur ahman Professor of Accouning & Public Policy Universiy of Dhaka -mail: mizan@univdhaka.edu Training Program on Capial Marke esearch Organized

FINAL EXAM EC26102: MONEY, BANKING AND FINANCIAL MARKETS MAY 11, 2004

FINAL EXAM EC26102: MONEY, BANKING AND FINANCIAL MARKETS MAY 11, 2004 This exam has 50 quesions on 14 pages. Before you begin, please check o make sure ha your copy has all 50 quesions and all 14 pages.

FINAL EXAM EC26102: MONEY, BANKING AND FINANCIAL MARKETS MAY 11, 2004 This exam has 50 quesions on 14 pages. Before you begin, please check o make sure ha your copy has all 50 quesions and all 14 pages.

How Risky is Electricity Generation?

How Risky is Elecriciy Generaion? Tom Parkinson The NorhBridge Group Inernaional Associaion for Energy Economics New England Chaper 19 January 2005 19 January 2005 The NorhBridge Group Agenda Generaion

How Risky is Elecriciy Generaion? Tom Parkinson The NorhBridge Group Inernaional Associaion for Energy Economics New England Chaper 19 January 2005 19 January 2005 The NorhBridge Group Agenda Generaion

Financial Markets And Empirical Regularities An Introduction to Financial Econometrics

Financial Markes And Empirical Regulariies An Inroducion o Financial Economerics SAMSI Workshop 11/18/05 Mike Aguilar UNC a Chapel Hill www.unc.edu/~maguilar 1 Ouline I. Hisorical Perspecive on Asse Prices

Financial Markes And Empirical Regulariies An Inroducion o Financial Economerics SAMSI Workshop 11/18/05 Mike Aguilar UNC a Chapel Hill www.unc.edu/~maguilar 1 Ouline I. Hisorical Perspecive on Asse Prices

AN EASY METHOD TO PRICE QUANTO FORWARD CONTRACTS IN THE HJM MODEL WITH STOCHASTIC INTEREST RATES

Inernaional Journal of Pure and Applied Mahemaics Volume 76 No. 4 212, 549-557 ISSN: 1311-88 (prined version url: hp://www.ijpam.eu PA ijpam.eu AN EASY METHOD TO PRICE QUANTO FORWARD CONTRACTS IN THE HJM

Inernaional Journal of Pure and Applied Mahemaics Volume 76 No. 4 212, 549-557 ISSN: 1311-88 (prined version url: hp://www.ijpam.eu PA ijpam.eu AN EASY METHOD TO PRICE QUANTO FORWARD CONTRACTS IN THE HJM

Fee Structure and Surrender Incentives in Variable Annuities

Fee Srucure and Surrender Incenives in Variable Annuiies by Anne MacKay A hesis presened o he Universiy of Waerloo in fulfillmen of he hesis requiremen for he degree of Docor of Philosophy in Acuarial

Fee Srucure and Surrender Incenives in Variable Annuiies by Anne MacKay A hesis presened o he Universiy of Waerloo in fulfillmen of he hesis requiremen for he degree of Docor of Philosophy in Acuarial

ECONOMIC GROWTH. Student Assessment. Macroeconomics II. Class 1

Suden Assessmen You will be graded on he basis of In-class aciviies (quizzes worh 30 poins) which can be replaced wih he number of marks from he regular uorial IF i is >=30 (capped a 30, i.e. marks from

Suden Assessmen You will be graded on he basis of In-class aciviies (quizzes worh 30 poins) which can be replaced wih he number of marks from he regular uorial IF i is >=30 (capped a 30, i.e. marks from

APRA Research Methodology for Analysis of Superannuation Funds

Curren Research Quesions APRA Research Mehodology for Analysis of Superannuaion Funds Wha are he deerminans of he cross-secional variaion in superannuaion reurns? Asse allocaion, manager skill, expenses/axes

Curren Research Quesions APRA Research Mehodology for Analysis of Superannuaion Funds Wha are he deerminans of he cross-secional variaion in superannuaion reurns? Asse allocaion, manager skill, expenses/axes

MATURITY GUARANTEES EMBEDDED IN UNIT-LINKED CONTRACTS VALUATION & RISK MANAGEMENT *

ABSRAC MAURIY GUARANEES EMBEDDED IN UNI-LINKED CONRACS VALUAION & RISK MANAGEMEN * Floren PERNOUD hierry FAVRE-BONVIN A key feaure of mauriy guaranees aached o uni-linked life insurance conracs is he uncerainy

ABSRAC MAURIY GUARANEES EMBEDDED IN UNI-LINKED CONRACS VALUAION & RISK MANAGEMEN * Floren PERNOUD hierry FAVRE-BONVIN A key feaure of mauriy guaranees aached o uni-linked life insurance conracs is he uncerainy

Scale of Longevity Risks for Pension and Life Annuity Providers. Henry JIN, BEng, MCom Centre for Pension and Superannuation, UNSW

Scale of Longeviy Risks for Pension and Life Annuiy Providers Henry JIN BEng MCom Cenre for Pension and Superannuaion UNSW Ouline Norman Cohen s criique moivaion of he paper Mahemaical framework Force

Scale of Longeviy Risks for Pension and Life Annuiy Providers Henry JIN BEng MCom Cenre for Pension and Superannuaion UNSW Ouline Norman Cohen s criique moivaion of he paper Mahemaical framework Force

VaR and Low Interest Rates

VaR and Low Ineres Raes Presened a he Sevenh Monreal Indusrial Problem Solving Workshop By Louis Doray (U de M) Frédéric Edoukou (U de M) Rim Labdi (HEC Monréal) Zichun Ye (UBC) 20 May 2016 P r e s e n

VaR and Low Ineres Raes Presened a he Sevenh Monreal Indusrial Problem Solving Workshop By Louis Doray (U de M) Frédéric Edoukou (U de M) Rim Labdi (HEC Monréal) Zichun Ye (UBC) 20 May 2016 P r e s e n

An Indian Journal FULL PAPER. Trade Science Inc. The principal accumulation value of simple and compound interest ABSTRACT KEYWORDS

[Type ex] [Type ex] [Type ex] ISSN : 0974-7435 Volume 0 Issue 8 BioTechnology 04 An Indian Journal FULL PAPER BTAIJ, 08), 04 [0056-006] The principal accumulaion value of simple and compound ineres Xudong

[Type ex] [Type ex] [Type ex] ISSN : 0974-7435 Volume 0 Issue 8 BioTechnology 04 An Indian Journal FULL PAPER BTAIJ, 08), 04 [0056-006] The principal accumulaion value of simple and compound ineres Xudong

Agenda. What is an ESG? GIRO Convention September 2008 Hilton Sorrento Palace

GIRO Convenion 23-26 Sepember 2008 Hilon Sorreno Palace A Pracical Sudy of Economic Scenario Generaors For General Insurers Gareh Haslip Benfield Group Agenda Inroducion o economic scenario generaors Building

GIRO Convenion 23-26 Sepember 2008 Hilon Sorreno Palace A Pracical Sudy of Economic Scenario Generaors For General Insurers Gareh Haslip Benfield Group Agenda Inroducion o economic scenario generaors Building

Description of the CBOE S&P 500 2% OTM BuyWrite Index (BXY SM )

") Descripion of he CBOE S&P 500 2% OTM BuyWrie Index (BXY SM ) Inroducion. The CBOE S&P 500 2% OTM BuyWrie Index (BXY SM ) is a benchmark index designed o rack he performance of a hypoheical 2% ou-of-he-money

Descripion of he CBOE S&P 500 2% OTM BuyWrie Index (BXY SM ) Inroducion. The CBOE S&P 500 2% OTM BuyWrie Index (BXY SM ) is a benchmark index designed o rack he performance of a hypoheical 2% ou-of-he-money

Available online at ScienceDirect

Available online a www.sciencedirec.com ScienceDirec Procedia Economics and Finance 8 ( 04 658 663 s Inernaional Conference 'Economic Scienific Research - Theoreical, Empirical and Pracical Approaches',

Available online a www.sciencedirec.com ScienceDirec Procedia Economics and Finance 8 ( 04 658 663 s Inernaional Conference 'Economic Scienific Research - Theoreical, Empirical and Pracical Approaches',

EVA NOPAT Capital charges ( = WACC * Invested Capital) = EVA [1 P] each

![EVA NOPAT Capital charges ( = WACC * Invested Capital) = EVA [1 P] each](/thumbs/92/109302006.jpg "EVA NOPAT Capital charges ( = WACC * Invested Capital) = EVA [1 P] each") VBM Soluion skech SS 2012: Noe: This is a soluion skech, no a complee soluion. Disribuion of poins is no binding for he correcor. 1 EVA, free cash flow, and financial raios (45) 1.1 EVA wihou adjusmens

VBM Soluion skech SS 2012: Noe: This is a soluion skech, no a complee soluion. Disribuion of poins is no binding for he correcor. 1 EVA, free cash flow, and financial raios (45) 1.1 EVA wihou adjusmens

THIS study focuses on the valuation problem of an

IAENG Inernaional Journal of Applied Mahemaics, 46:4, IJAM_46_4_ The Valuaion of an Equiy-inked ife Insurance Using he Theory of Indifference ricing Jungmin Choi Absrac This sudy addresses he valuaion

IAENG Inernaional Journal of Applied Mahemaics, 46:4, IJAM_46_4_ The Valuaion of an Equiy-inked ife Insurance Using he Theory of Indifference ricing Jungmin Choi Absrac This sudy addresses he valuaion

Money-Back Guarantees in Individual Pension Accounts: Evidence from the German Pension Reform

Money-Back Guaranees in Individual Pension Accouns: Evidence from he German Pension Reform Raimond Maurer and Chrisian Schlag PRC WP 22-11 Pension Research Council Working Paper Pension Research Council

Money-Back Guaranees in Individual Pension Accouns: Evidence from he German Pension Reform Raimond Maurer and Chrisian Schlag PRC WP 22-11 Pension Research Council Working Paper Pension Research Council

Principles of Finance CONTENTS

Principles of Finance CONENS Value of Bonds and Equiy... 3 Feaures of bonds... 3 Characerisics... 3 Socks and he sock marke... 4 Definiions:... 4 Valuing equiies... 4 Ne reurn... 4 idend discoun model...

Principles of Finance CONENS Value of Bonds and Equiy... 3 Feaures of bonds... 3 Characerisics... 3 Socks and he sock marke... 4 Definiions:... 4 Valuing equiies... 4 Ne reurn... 4 idend discoun model...

BUDGET ECONOMIC AND FISCAL POSITION REPORT

BUDGET ECONOMIC AND FISCAL POSITION REPORT - 2004 Issued by he Hon. Miniser of Finance in Terms of Secion 7 of he Fiscal Managemen (Responsibiliy) Ac No. 3 of 1. Inroducion Secion 7 of he Fiscal Managemen

BUDGET ECONOMIC AND FISCAL POSITION REPORT - 2004 Issued by he Hon. Miniser of Finance in Terms of Secion 7 of he Fiscal Managemen (Responsibiliy) Ac No. 3 of 1. Inroducion Secion 7 of he Fiscal Managemen

(1 + Nominal Yield) = (1 + Real Yield) (1 + Expected Inflation Rate) (1 + Inflation Risk Premium)

= (1 + Real Yield) (1 + Expected Inflation Rate) (1 + Inflation Risk Premium)") 5. Inflaion-linked bonds Inflaion is an economic erm ha describes he general rise in prices of goods and services. As prices rise, a uni of money can buy less goods and services. Hence, inflaion is an

5. Inflaion-linked bonds Inflaion is an economic erm ha describes he general rise in prices of goods and services. As prices rise, a uni of money can buy less goods and services. Hence, inflaion is an

t=1 C t e δt, and the tc t v t i t=1 C t (1 + i) t = n tc t (1 + i) t C t (1 + i) t = C t vi

t = n tc t (1 + i) t C t (1 + i) t = C t vi") Exam 4 is Th. April 24. You are allowed 13 shees of noes and a calculaor. ch. 7: 137) Unless old oherwise, duraion refers o Macaulay duraion. The duraion of a single cashflow is he ime remaining unil mauriy,

Exam 4 is Th. April 24. You are allowed 13 shees of noes and a calculaor. ch. 7: 137) Unless old oherwise, duraion refers o Macaulay duraion. The duraion of a single cashflow is he ime remaining unil mauriy,

The Mathematics Of Stock Option Valuation - Part Four Deriving The Black-Scholes Model Via Partial Differential Equations

The Mahemaics Of Sock Opion Valuaion - Par Four Deriving The Black-Scholes Model Via Parial Differenial Equaions Gary Schurman, MBE, CFA Ocober 1 In Par One we explained why valuing a call opion as a sand-alone

The Mahemaics Of Sock Opion Valuaion - Par Four Deriving The Black-Scholes Model Via Parial Differenial Equaions Gary Schurman, MBE, CFA Ocober 1 In Par One we explained why valuing a call opion as a sand-alone

Market Models. Practitioner Course: Interest Rate Models. John Dodson. March 29, 2009

s Praciioner Course: Ineres Rae Models March 29, 2009 In order o value European-syle opions, we need o evaluae risk-neural expecaions of he form V (, T ) = E [D(, T ) H(T )] where T is he exercise dae,

s Praciioner Course: Ineres Rae Models March 29, 2009 In order o value European-syle opions, we need o evaluae risk-neural expecaions of he form V (, T ) = E [D(, T ) H(T )] where T is he exercise dae,

Bringing cost transparency to the life annuity market

Bringing cos ransparency o he life annuiy marke Caherine Donnelly Monserra Guillén Jens Perch Nielsen January 24, 2014 Absrac The financial indusry has recenly seen a push away from srucured producs and

Bringing cos ransparency o he life annuiy marke Caherine Donnelly Monserra Guillén Jens Perch Nielsen January 24, 2014 Absrac The financial indusry has recenly seen a push away from srucured producs and

The Impact of Stochastic Volatility on Pricing, Hedging, and Hedge Efficiency of Variable Annuity Guarantees

The Impac of Sochasic Volailiy on Pricing, Hedging, and Hedge Efficiency of Variable Annuiy Guaranees Alexander Kling *, Frederik Ruez and Jochen Ruß This Version: Augus 14, 2009 Absrac We analyze differen

The Impac of Sochasic Volailiy on Pricing, Hedging, and Hedge Efficiency of Variable Annuiy Guaranees Alexander Kling *, Frederik Ruez and Jochen Ruß This Version: Augus 14, 2009 Absrac We analyze differen

Static versus dynamic longevity risk hedging

ISSN 2279-9362 Saic versus dynamic longeviy risk hedging Clemene De Rosa Elisa Luciano Luca Regis No. 403 March 2015 www.carloalbero.org/research/working-papers 2015 by Clemene De Rosa, Elisa Luciano and

ISSN 2279-9362 Saic versus dynamic longeviy risk hedging Clemene De Rosa Elisa Luciano Luca Regis No. 403 March 2015 www.carloalbero.org/research/working-papers 2015 by Clemene De Rosa, Elisa Luciano and

Forwards and Futures

Handou #6 for 90.2308 - Spring 2002 (lecure dae: 4/7/2002) orward Conrac orward and uure A ime (where 0 < ): ener a forward conrac, in which you agree o pay O (called "forward price") for one hare of he

Handou #6 for 90.2308 - Spring 2002 (lecure dae: 4/7/2002) orward Conrac orward and uure A ime (where 0 < ): ener a forward conrac, in which you agree o pay O (called "forward price") for one hare of he

Tentamen i 5B1575 Finansiella Derivat. Måndag 27 augusti 2007 kl Answers and suggestions for solutions.

Tenamen i 5B1575 Finansiella Deriva. Måndag 27 augusi 2007 kl. 14.00 19.00. Answers and suggesions for soluions. 1. (a) For he maringale probabiliies we have q 1 + r d u d 0.5 Using hem we obain he following

Tenamen i 5B1575 Finansiella Deriva. Måndag 27 augusi 2007 kl. 14.00 19.00. Answers and suggesions for soluions. 1. (a) For he maringale probabiliies we have q 1 + r d u d 0.5 Using hem we obain he following

(fylls i av ansvarig) Datum för tentamen Sal. Financial Markets and Financial Institutions, Risk Management Institution

Datum för tentamen Sal. Financial Markets and Financial Institutions, Risk Management Institution") AID-kod: Daum: -- Blad nr: Kurskod: 7G rovkod: EXA Försäsblad ill skriflig enamen vid Linköpings Universie (fylls i av ansvarig) Daum för enamen -- Sal ER id 8- Kurskod 7G rovkod EXA Kursnamn/benämning

AID-kod: Daum: -- Blad nr: Kurskod: 7G rovkod: EXA Försäsblad ill skriflig enamen vid Linköpings Universie (fylls i av ansvarig) Daum för enamen -- Sal ER id 8- Kurskod 7G rovkod EXA Kursnamn/benämning

Roger Mercken 1, Lisette Motmans 2, Ghislain Houben Call options in a nutshell

No more replicaing porfolios : a simple convex combinaion o undersand he ris-neural valuaion mehod for he muli-sep binomial valuaion of a call opion Roger Mercen, Lisee Momans, Ghislain Houben 3 Hassel

No more replicaing porfolios : a simple convex combinaion o undersand he ris-neural valuaion mehod for he muli-sep binomial valuaion of a call opion Roger Mercen, Lisee Momans, Ghislain Houben 3 Hassel

On the Interaction between Transfer Restrictions and Crediting Strategies in Guaranteed Funds

Georgia Sae Universiy ScholarWorks @ Georgia Sae Universiy Risk Managemen and Insurance Faculy Publicaions Deparmen of Risk Managemen and Insurance 2015 On he Ineracion beween Transfer Resricions and Crediing

Georgia Sae Universiy ScholarWorks @ Georgia Sae Universiy Risk Managemen and Insurance Faculy Publicaions Deparmen of Risk Managemen and Insurance 2015 On he Ineracion beween Transfer Resricions and Crediing

Longevity Risk and Annuities in Singapore

1 Longeviy Risk and Annuiies in Singapore Joelle H.Y. Fong, Olivia S. Michell, and Benedic S. K. Koh* Absrac This paper explores he curren annuiy marke in Singapore and discusses he pros and cons of a

1 Longeviy Risk and Annuiies in Singapore Joelle H.Y. Fong, Olivia S. Michell, and Benedic S. K. Koh* Absrac This paper explores he curren annuiy marke in Singapore and discusses he pros and cons of a

Session 4.2: Price and Volume Measures

Session 4.2: Price and Volume Measures Regional Course on Inegraed Economic Saisics o Suppor 28 SNA Implemenaion Leonidas Akriidis Office for Naional Saisics Unied Kingdom Conen 1. Inroducion 2. Price

Session 4.2: Price and Volume Measures Regional Course on Inegraed Economic Saisics o Suppor 28 SNA Implemenaion Leonidas Akriidis Office for Naional Saisics Unied Kingdom Conen 1. Inroducion 2. Price

Funded and unfunded systems: two ends of the same stick. Angrisani Massimo

unded and unfunded sysems: wo ends of he same sick Angrisani Massimo Universià degli sudi di Roma "a Sapienza" acolà di Economia Diparimeno di maemaica per le Decisioni Economiche, inanziarie ed Assicuraive

unded and unfunded sysems: wo ends of he same sick Angrisani Massimo Universià degli sudi di Roma "a Sapienza" acolà di Economia Diparimeno di maemaica per le Decisioni Economiche, inanziarie ed Assicuraive

Black-Scholes Model and Risk Neutral Pricing

Inroducion echniques Exercises in Financial Mahemaics Lis 3 UiO-SK45 Soluions Hins Auumn 5 eacher: S Oriz-Laorre Black-Scholes Model Risk Neural Pricing See Benh s book: Exercise 44, page 37 See Benh s

Inroducion echniques Exercises in Financial Mahemaics Lis 3 UiO-SK45 Soluions Hins Auumn 5 eacher: S Oriz-Laorre Black-Scholes Model Risk Neural Pricing See Benh s book: Exercise 44, page 37 See Benh s

MORNING SESSION. Date: Wednesday, October 30, 2013 Time: 8:30 a.m. 11:45 a.m. INSTRUCTIONS TO CANDIDATES

SOCIETY OF ACTUARIES Quaniaive Finance and Invesmens Core Exam QFI CORE MORNING SESSION Dae: Wednesday, Ocober 30, 013 Time: 8:30 a.m. 11:45 a.m. INSTRUCTIONS TO CANDIDATES General Insrucions 1. This examinaion

SOCIETY OF ACTUARIES Quaniaive Finance and Invesmens Core Exam QFI CORE MORNING SESSION Dae: Wednesday, Ocober 30, 013 Time: 8:30 a.m. 11:45 a.m. INSTRUCTIONS TO CANDIDATES General Insrucions 1. This examinaion

ARWG Report to LATF's VM-22 Subgroup Concerning Potential VM-22 Reserve Methodology

ARWG Repor o ATF's VM-22 Subgroup Concerning Poenial VM-22 Reserve Meodology Indianapolis, IN Augus 22, 2013 The Annuiy Reserve Work Group (ARWG) of e American Academy of Acuaries 1 is pleased o provide

ARWG Repor o ATF's VM-22 Subgroup Concerning Poenial VM-22 Reserve Meodology Indianapolis, IN Augus 22, 2013 The Annuiy Reserve Work Group (ARWG) of e American Academy of Acuaries 1 is pleased o provide

VALUATION OF THE AMERICAN-STYLE OF ASIAN OPTION BY A SOLUTION TO AN INTEGRAL EQUATION

Aca Universiais Mahiae Belii ser. Mahemaics, 16 21, 17 23. Received: 15 June 29, Acceped: 2 February 21. VALUATION OF THE AMERICAN-STYLE OF ASIAN OPTION BY A SOLUTION TO AN INTEGRAL EQUATION TOMÁŠ BOKES

Aca Universiais Mahiae Belii ser. Mahemaics, 16 21, 17 23. Received: 15 June 29, Acceped: 2 February 21. VALUATION OF THE AMERICAN-STYLE OF ASIAN OPTION BY A SOLUTION TO AN INTEGRAL EQUATION TOMÁŠ BOKES

CURRENCY TRANSLATED OPTIONS

CURRENCY RANSLAED OPIONS Dr. Rober ompkins, Ph.D. Universiy Dozen, Vienna Universiy of echnology * Deparmen of Finance, Insiue for Advanced Sudies Mag. José Carlos Wong Deparmen of Finance, Insiue for

CURRENCY RANSLAED OPIONS Dr. Rober ompkins, Ph.D. Universiy Dozen, Vienna Universiy of echnology * Deparmen of Finance, Insiue for Advanced Sudies Mag. José Carlos Wong Deparmen of Finance, Insiue for

Proceedings of the 48th European Study Group Mathematics with Industry 1

Proceedings of he 48h European Sudy Group Mahemaics wih Indusry 1 ADR Opion Trading Jasper Anderluh and Hans van der Weide TU Delf, EWI (DIAM), Mekelweg 4, 2628 CD Delf jhmanderluh@ewiudelfnl, JAMvanderWeide@ewiudelfnl

Proceedings of he 48h European Sudy Group Mahemaics wih Indusry 1 ADR Opion Trading Jasper Anderluh and Hans van der Weide TU Delf, EWI (DIAM), Mekelweg 4, 2628 CD Delf jhmanderluh@ewiudelfnl, JAMvanderWeide@ewiudelfnl

Lu Xia Effectivity in Hedging Longevity Risk A Life Insurance Scheme of a Child Plan

Effeciviy in Hedging Longeviy Ris A Life Insurance Scheme of a Child Plan MSc Thesis 2012-039 Tilburg Universiy e EFFECTIVITY IN HEDGING LONGEVITY RISK: A LIFE INSURANCE SCHEME OF A CHILD PLAN MASTER THESIS

Effeciviy in Hedging Longeviy Ris A Life Insurance Scheme of a Child Plan MSc Thesis 2012-039 Tilburg Universiy e EFFECTIVITY IN HEDGING LONGEVITY RISK: A LIFE INSURANCE SCHEME OF A CHILD PLAN MASTER THESIS

DYNAMIC ECONOMETRIC MODELS Vol. 7 Nicolaus Copernicus University Toruń Krzysztof Jajuga Wrocław University of Economics

DYNAMIC ECONOMETRIC MODELS Vol. 7 Nicolaus Copernicus Universiy Toruń 2006 Krzyszof Jajuga Wrocław Universiy of Economics Ineres Rae Modeling and Tools of Financial Economerics 1. Financial Economerics

DYNAMIC ECONOMETRIC MODELS Vol. 7 Nicolaus Copernicus Universiy Toruń 2006 Krzyszof Jajuga Wrocław Universiy of Economics Ineres Rae Modeling and Tools of Financial Economerics 1. Financial Economerics

NBER WORKING PAPER SERIES THE EFFECT OF UNCERTAIN LABOR INCOME AND SOCIAL SECURITY ON LIFE-CYCLE PORTFOLIOS

NBER WORKING PAPER SERIES THE EFFECT OF UNCERTAIN LABOR INCOME AND SOCIAL SECURITY ON LIFE-CYCLE PORTFOLIOS Raimond Maurer Olivia S. Michell Ralph Rogalla Working Paper 15682 hp://www.nber.org/papers/w15682

NBER WORKING PAPER SERIES THE EFFECT OF UNCERTAIN LABOR INCOME AND SOCIAL SECURITY ON LIFE-CYCLE PORTFOLIOS Raimond Maurer Olivia S. Michell Ralph Rogalla Working Paper 15682 hp://www.nber.org/papers/w15682

The Fair Value of Insurance Contracts by Sam Gutterman, David Rogers, Larry Rubin, David Scheinerman

The Fair Value of Insurance Conracs by Sam Guerman, David Rogers, Larry Rubin, David Scheinerman Execuive summary Over he las decades, accouning sandard seers have given greaer emphasis o he use of fair

The Fair Value of Insurance Conracs by Sam Guerman, David Rogers, Larry Rubin, David Scheinerman Execuive summary Over he las decades, accouning sandard seers have given greaer emphasis o he use of fair

Assumptions: exogenous path of govenrment expenditure; financing by tax or public debt

.3 Neolassial heory of publi deb Analyse he effes of publi deb in he OLG model Assumpions: exogenous pah of govenrmen expendiure; finaning by ax or publi deb Exhange of finanial insrumens: In period governmen

.3 Neolassial heory of publi deb Analyse he effes of publi deb in he OLG model Assumpions: exogenous pah of govenrmen expendiure; finaning by ax or publi deb Exhange of finanial insrumens: In period governmen

Optimal Investment for a. Defined-Contribution Pension Scheme under. a Regime Switching Model

Opimal Invesmen for a Defined-Conribuion Pension Scheme under a Regime Swiching Model An Chen, Lukasz Delong Universiy of Ulm, Insiue of Insurance Science Helmholzsrasse 20, 89069 Ulm, Germany an.chen@uni-ulm.de

Opimal Invesmen for a Defined-Conribuion Pension Scheme under a Regime Swiching Model An Chen, Lukasz Delong Universiy of Ulm, Insiue of Insurance Science Helmholzsrasse 20, 89069 Ulm, Germany an.chen@uni-ulm.de

Some Remarks on Derivatives Markets (third edition, 2013)

") Some Remarks on Derivaives Markes (hird ediion, 03) Elias S. W. Shiu. The parameer δ in he Black-Scholes formula The Black-Scholes opion-pricing formula is given in Chaper of McDonald wihou proof. A raher

Some Remarks on Derivaives Markes (hird ediion, 03) Elias S. W. Shiu. The parameer δ in he Black-Scholes formula The Black-Scholes opion-pricing formula is given in Chaper of McDonald wihou proof. A raher

Jarrow-Lando-Turnbull model

Jarrow-Lando-urnbull model Characerisics Credi raing dynamics is represened by a Markov chain. Defaul is modelled as he firs ime a coninuous ime Markov chain wih K saes hiing he absorbing sae K defaul

Jarrow-Lando-urnbull model Characerisics Credi raing dynamics is represened by a Markov chain. Defaul is modelled as he firs ime a coninuous ime Markov chain wih K saes hiing he absorbing sae K defaul

A Method for Estimating the Change in Terminal Value Required to Increase IRR

A Mehod for Esimaing he Change in Terminal Value Required o Increase IRR Ausin M. Long, III, MPA, CPA, JD * Alignmen Capial Group 11940 Jollyville Road Suie 330-N Ausin, TX 78759 512-506-8299 (Phone) 512-996-0970

A Mehod for Esimaing he Change in Terminal Value Required o Increase IRR Ausin M. Long, III, MPA, CPA, JD * Alignmen Capial Group 11940 Jollyville Road Suie 330-N Ausin, TX 78759 512-506-8299 (Phone) 512-996-0970

The Impact of Interest Rate Liberalization Announcement in China on the Market Value of Hong Kong Listed Chinese Commercial Banks

Journal of Finance and Invesmen Analysis, vol. 2, no.3, 203, 35-39 ISSN: 224-0998 (prin version), 224-0996(online) Scienpress Ld, 203 The Impac of Ineres Rae Liberalizaion Announcemen in China on he Marke

Journal of Finance and Invesmen Analysis, vol. 2, no.3, 203, 35-39 ISSN: 224-0998 (prin version), 224-0996(online) Scienpress Ld, 203 The Impac of Ineres Rae Liberalizaion Announcemen in China on he Marke

Aid, Policies, and Growth

Aid, Policies, and Growh By Craig Burnside and David Dollar APPENDIX ON THE NEOCLASSICAL MODEL Here we use a simple neoclassical growh model o moivae he form of our empirical growh equaion. Our inenion

Aid, Policies, and Growh By Craig Burnside and David Dollar APPENDIX ON THE NEOCLASSICAL MODEL Here we use a simple neoclassical growh model o moivae he form of our empirical growh equaion. Our inenion

INSTITUTE OF ACTUARIES OF INDIA

INSTITUTE OF ACTUARIES OF INDIA EXAMINATIONS 05 h November 007 Subjec CT8 Financial Economics Time allowed: Three Hours (14.30 17.30 Hrs) Toal Marks: 100 INSTRUCTIONS TO THE CANDIDATES 1) Do no wrie your

INSTITUTE OF ACTUARIES OF INDIA EXAMINATIONS 05 h November 007 Subjec CT8 Financial Economics Time allowed: Three Hours (14.30 17.30 Hrs) Toal Marks: 100 INSTRUCTIONS TO THE CANDIDATES 1) Do no wrie your

Mathematical methods for finance (preparatory course) Simple numerical examples on bond basics

Simple numerical examples on bond basics") Mahemaical mehods for finance (preparaory course) Simple numerical examples on bond basics . Yield o mauriy for a zero coupon bond = 99.45 = 92 days (=0.252 yrs) Face value = 00 r 365 00 00 92 99.45 2.22%

Mahemaical mehods for finance (preparaory course) Simple numerical examples on bond basics . Yield o mauriy for a zero coupon bond = 99.45 = 92 days (=0.252 yrs) Face value = 00 r 365 00 00 92 99.45 2.22%

Assessing Manufacturing Capital Investments in the Global Market

Paper ID #7476 Assessing Manufacuring Capial Invesmens in he Global Marke Dr. Rex C Kanu, Ball Sae Universiy Dr. Rex Kanu is he coordinaor of he manufacuring engineering echnology program in he Deparmen

Paper ID #7476 Assessing Manufacuring Capial Invesmens in he Global Marke Dr. Rex C Kanu, Ball Sae Universiy Dr. Rex Kanu is he coordinaor of he manufacuring engineering echnology program in he Deparmen

Risk Management of Variable Annuities

Fakulä für Mahemaik und Wirschafswissenschafen Insiu für Versicherungswissenschafen Risk Managemen of Variable Annuiies Disseraion zur Erlangung des akademischen Grades eines Dokors der Wirschafswissenschafen

Fakulä für Mahemaik und Wirschafswissenschafen Insiu für Versicherungswissenschafen Risk Managemen of Variable Annuiies Disseraion zur Erlangung des akademischen Grades eines Dokors der Wirschafswissenschafen

Description of the CBOE Russell 2000 BuyWrite Index (BXR SM )

") Descripion of he CBOE Russell 2000 BuyWrie Index (BXR SM ) Inroducion. The CBOE Russell 2000 BuyWrie Index (BXR SM ) is a benchmark index designed o rack he performance of a hypoheical a-he-money buy-wrie

Descripion of he CBOE Russell 2000 BuyWrie Index (BXR SM ) Inroducion. The CBOE Russell 2000 BuyWrie Index (BXR SM ) is a benchmark index designed o rack he performance of a hypoheical a-he-money buy-wrie

Valuing Real Options on Oil & Gas Exploration & Production Projects

Valuing Real Opions on Oil & Gas Exploraion & Producion Projecs March 2, 2006 Hideaka (Hugh) Nakaoka Former CIO & CCO of Iochu Oil Exploraion Co., Ld. Universiy of Tsukuba 1 Overview 1. Inroducion 2. Wha

Valuing Real Opions on Oil & Gas Exploraion & Producion Projecs March 2, 2006 Hideaka (Hugh) Nakaoka Former CIO & CCO of Iochu Oil Exploraion Co., Ld. Universiy of Tsukuba 1 Overview 1. Inroducion 2. Wha

STOCHASTIC METHODS IN CREDIT RISK MODELLING, VALUATION AND HEDGING

STOCHASTIC METHODS IN CREDIT RISK MODELLING, VALUATION AND HEDGING Tomasz R. Bielecki Deparmen of Mahemaics Norheasern Illinois Universiy, Chicago, USA T-Bielecki@neiu.edu (In collaboraion wih Marek Rukowski)

STOCHASTIC METHODS IN CREDIT RISK MODELLING, VALUATION AND HEDGING Tomasz R. Bielecki Deparmen of Mahemaics Norheasern Illinois Universiy, Chicago, USA T-Bielecki@neiu.edu (In collaboraion wih Marek Rukowski)

Annuities in NDC by Juha Alho 1, Jorge Bravo 2, and Edward Palmer 3

Draf (Unfinished) November 30, 2009 Annuiies in NDC by Juha Alho 1, Jorge Bravo 2, and Edward Palmer 3 1 Inroducion In a defined conribuion sysem he pension akes he form of a life annuiy, regardless of

Draf (Unfinished) November 30, 2009 Annuiies in NDC by Juha Alho 1, Jorge Bravo 2, and Edward Palmer 3 1 Inroducion In a defined conribuion sysem he pension akes he form of a life annuiy, regardless of

Securitized Senior Life Settlements Macauley Duration and Longevity Risk

1 Securiized Senior Life Selemens Macauley Duraion and Longeviy Risk Carlos E. Oriz Arcadia Universiy Deparmen of Mahemaics and Compuer Science oriz@arcadia.edu Charles A. Sone Brooklyn College, Ciy Universiy

1 Securiized Senior Life Selemens Macauley Duraion and Longeviy Risk Carlos E. Oriz Arcadia Universiy Deparmen of Mahemaics and Compuer Science oriz@arcadia.edu Charles A. Sone Brooklyn College, Ciy Universiy

EFFICIENT POST-RETIREMENT ASSET ALLOCATION

EFFICIENT POST-RETIREMENT ASSET ALLOCATION Barry Freedman* ABSTRACT To examine pos-reiremen asse allocaion, an exension o he classic Markowiz risk-reurn framework is suggesed. Assuming ha reirees make

EFFICIENT POST-RETIREMENT ASSET ALLOCATION Barry Freedman* ABSTRACT To examine pos-reiremen asse allocaion, an exension o he classic Markowiz risk-reurn framework is suggesed. Assuming ha reirees make

Multi-Period Optimization Model for ånancial planning

Muli-Period Opimizaion Model for ånancial planning Norio Hibiki É July 2, 28 1 Inroducion We discuss an opimizaion model o obain an opimal invesmen and insurance sraegy for a household. A household is

Muli-Period Opimizaion Model for ånancial planning Norio Hibiki É July 2, 28 1 Inroducion We discuss an opimizaion model o obain an opimal invesmen and insurance sraegy for a household. A household is

Comments on Defying Gravity: How Long Will Japanese Government Bond Prices Remain High? by Takeo Hoshi and Takatoshi Ito

Commens on Defying Graviy: How Long Will Japanese Governmen Bond Prices Remain High? by Takeo Hoshi and Takaoshi Io Bob Hodrick Nomura Professor of Inernaional Finance Columbia Business School April il4,

Commens on Defying Graviy: How Long Will Japanese Governmen Bond Prices Remain High? by Takeo Hoshi and Takaoshi Io Bob Hodrick Nomura Professor of Inernaional Finance Columbia Business School April il4,

Asymmetry and Leverage in Stochastic Volatility Models: An Exposition

Asymmery and Leverage in Sochasic Volailiy Models: An xposiion Asai, M. a and M. McAleer b a Faculy of conomics, Soka Universiy, Japan b School of conomics and Commerce, Universiy of Wesern Ausralia Keywords:

Asymmery and Leverage in Sochasic Volailiy Models: An xposiion Asai, M. a and M. McAleer b a Faculy of conomics, Soka Universiy, Japan b School of conomics and Commerce, Universiy of Wesern Ausralia Keywords:

Macroeconomics II THE AD-AS MODEL. A Road Map

Macroeconomics II Class 4 THE AD-AS MODEL Class 8 A Road Map THE AD-AS MODEL: MICROFOUNDATIONS 1. Aggregae Supply 1.1 The Long-Run AS Curve 1.2 rice and Wage Sickiness 2.1 Aggregae Demand 2.2 Equilibrium

Macroeconomics II Class 4 THE AD-AS MODEL Class 8 A Road Map THE AD-AS MODEL: MICROFOUNDATIONS 1. Aggregae Supply 1.1 The Long-Run AS Curve 1.2 rice and Wage Sickiness 2.1 Aggregae Demand 2.2 Equilibrium

REPUBLIC OF KENYA MINISTRY OF FINANCE MONTHLY DEBT BULLETIN

REPUBLIC OF KENYA MINISTRY OF FINANCE MONTHLY DEBT BULLETIN MARCH 2012 1.0 PUBLIC DEBT 1.1 Inroducion As a end March 2012, public and publicly guaraneed deb sood a Kshs 1,564.20 billion or 46.9 percen

REPUBLIC OF KENYA MINISTRY OF FINANCE MONTHLY DEBT BULLETIN MARCH 2012 1.0 PUBLIC DEBT 1.1 Inroducion As a end March 2012, public and publicly guaraneed deb sood a Kshs 1,564.20 billion or 46.9 percen

How Much Do Means-Tested Benefits Reduce the Demand for Annuities?

How Much Do Means-Tesed Benefis Reduce he Demand for Annuiies? by Monika BÜTLER Kim PEIJNENBURG Sefan STAUBLI Working Paper No. 1311 December 2013 Suppored by he Ausrian Science Funds The Ausrian Cener

How Much Do Means-Tesed Benefis Reduce he Demand for Annuiies? by Monika BÜTLER Kim PEIJNENBURG Sefan STAUBLI Working Paper No. 1311 December 2013 Suppored by he Ausrian Science Funds The Ausrian Cener

Spring 2011 Social Sciences 7418 University of Wisconsin-Madison

Economics 32, Sec. 1 Menzie D. Chinn Spring 211 Social Sciences 7418 Universiy of Wisconsin-Madison Noes for Econ 32-1 FALL 21 Miderm 1 Exam The Fall 21 Econ 32-1 course used Hall and Papell, Macroeconomics

Economics 32, Sec. 1 Menzie D. Chinn Spring 211 Social Sciences 7418 Universiy of Wisconsin-Madison Noes for Econ 32-1 FALL 21 Miderm 1 Exam The Fall 21 Econ 32-1 course used Hall and Papell, Macroeconomics

An Extended Model of Asset Price Dynamics

Iranian In. J. Sci. 6(), 005, p.15-5 An Exended Model of Asse Price Dynamics M. H. Nojumi Deparmen of Maemaical Sciences, Sarif Universiy of Tecnology P.O. Box 11365-9415, Teran, Iran. e-mail: nojumi@sina.sarif.edu

Iranian In. J. Sci. 6(), 005, p.15-5 An Exended Model of Asse Price Dynamics M. H. Nojumi Deparmen of Maemaical Sciences, Sarif Universiy of Tecnology P.O. Box 11365-9415, Teran, Iran. e-mail: nojumi@sina.sarif.edu

No. 2004/01. Betting on Death and Capital Markets in Retirement: A Shortfall Risk Analysis of Life Annuities versus Phased Withdrawal Plans

No. 2004/01 Being on Deah and Capial Markes in Reiremen: A Shorfall Risk Analysis of Life Annuiies versus Phased Wihdrawal Plans Ivica Dus, Raimond Maurer, Olivia S. Michell Cener for Financial Sudies

No. 2004/01 Being on Deah and Capial Markes in Reiremen: A Shorfall Risk Analysis of Life Annuiies versus Phased Wihdrawal Plans Ivica Dus, Raimond Maurer, Olivia S. Michell Cener for Financial Sudies