EXECUTIVE COMPENSATION IN ESOP TRANSACTIONS AND ESOP COMPANIES

|

|

|

- Arline Wheeler

- 5 years ago

- Views:

Transcription

1 EXECUTIVE COMPENSATION IN ESOP TRANSACTIONS AND ESOP COMPANIES ESOP ASSOCIATION MID-ATLANTIC & CAROLINAS CHAPTERS OCTOBER 28, 2016

624-3171 clmclean@kaufcan.")

2 Matt Keene Chartwell (919) Christopher L. McLean Kaufman & Canoles (757) Andy Smith The McLean Group (703)

3 DESIGNING A COMPENSATION PROGRAM

4 Seattle CEO to cut his pay so every worker earns $70,000 SEATTLE Dan Price, chief executive of Gravity Payments, a credit card payment processing firm, stunned his 100-plus workers on Monday when he told them he was cutting his roughly $1 million salary to $70,000 and using company profits to ensure that everyone there would earn at least that much within three years. He's already gained new customers, too. For some workers, the increase will more than double their pay. One 21-year-old mother said she'll buy a house.

5 Compensation Philosophy Statement Expresses company s intent regarding executive compensation Helps to evidence a reasoned process o Document, document, document! Often discusses: o Positioning on total pay o Aligning pay with corporate objectives o Process for setting pay Should discuss tie to company culture

6 Targeted vs. Observed Results Base Pay Source Revenue Below 25th 26th 50th 51st 75th Above 75th 2011 PFG Survey: Targeted Result $356 0% 43% 48% 9% Chartwell Actual Observations $124 32% 40% 20% 9% Source: Principal Financial Group 2011 Survey of Compensation Practices of Selected S Corporations with Majority ESOP Shareholder

7 Targeted vs. Observed Results Total Cash Compensation Source Revenue Below 25th 26th 50th 51st 75th Above 75th 2011 PFG Survey: Targeted Result $356 5% 23% 54% 18% Chartwell Actual Observations $124 13% 36% 36% 15% Source: Principal Financial Group 2011 Survey of Compensation Practices of Selected S Corporations with Majority ESOP Shareholder

8 Incentive Pay Short- and Long-Term Incentive Prevalence 120% 97% 95% 100% 80% 56% 61% 60% 40% 20% Short - term Long-term 0% Source: WorldatWork and Vivient Consulting: Incentive Pay Practices Survey: Privately Held Companies 2014

9 Benefits of Long-Term Incentives Retention Recruitment Alignment of management interest with the shareholders (the ESOP) Motivates performance to achieve targeted financial objectives Wealth accumulation based on financial performance Targeted to key employees

10 Overview of Equity Incentive Plans for ESOP Companies Management incentive plans are not unique to ESOP companies These incentive plans can meet a variety of goals o Retention of key employees and contributors o Alignment of interests between management and shareholders o Provides performance incentives Can and should be used in 100% ESOP-owned companies Management incentive plans can take numerous forms o Profit sharing plans o Discretionary bonuses o Equity based compensation Equity based compensation will be our focus

11 Equity Based Deferred Compensation Vehicles Equity Based Awards o Phantom Stock (synthetic) o Stock Appreciation Rights (SARs) (synthetic) o Warrants o Restricted Stock Units (RSUs) (synthetic) Pure Equity Awards o Stock Options (can be either qualified or non-qualified) o Restricted Stock o Employee Stock Purchase Plan Cash Awards o Bonus Plan (short term or long term) o Incentive Payments o Nonqualified Deferred Compensation

12 Use of Phantom Equity Programs Phantom equity programs such as phantom stock and SARs are chosen for specific reasons o Company may not want employees to own shares or may have no shares available to offer to employees o Broader stock ownership may create control issues - and may raise securities law compliance issues There are also arguments against phantom equity programs o Phantom Equity is generally not tax-efficient o Awards may not be viewed by employees as valuable

13 Stock Appreciation Rights Participant receives a promise to pay the appreciation in value of a defined number of shares in the future o Deferred award is based on appreciation in the equity of the company over the term of the award o Participants can generally exercise SARs at any time after vesting o Participant generally receives excess of value over exercise price in cash o No risk of loss to participants o Can be paid in cash or stock-settled o SARs are taxable at exercise o Can be designed to be 409A exempt

14 Value of Common Equity Awards Value of One Share or Unit Grant Vest 2020 Payout Value Share Price $10 $11 $12 $13 $14 $15 Restricted Stock or Phantom Stock $10 $11 $12 $13 $14 $15 $15 Stock Option or SAR $0 $1 $2 $3 $4 $5 $5 Restricted stock or phantom stock are full value awards Stock options or stock appreciation rights are appreciation only awards

15 Internal Revenue Code Section 409A

16 Section 409A Overview A deferred compensation plan must provide that deferred compensation can be paid only upon the occurrence of one or more of the following events: - Separation from Service - Disability - Death - Specified time or pursuant to a fixed schedule - Change in Ownership - Unforeseen Emergency The plan must not permit acceleration of the time or schedule of payments under the plan ( hair cuts are no longer permitted) certain exceptions to rule Acceleration of vesting of deferred benefits is permitted

17 Section 409A (cont d) The plan must irrevocably specify the amount, time of payment and form of payment of deferred compensation Violations of 409A will result in a 20% penalty, income inclusion, and additional interest rate on the tax on the income for an earlier year SARs do not constitute deferred compensation under 409A if structured properly Consult your lawyer and ask whether your company s plan is Section 409A compliant or subject to an exemption

18 Valuation Impact

19 Valuation Methodology Valuation issue at the time of an ESOP transaction and annual valuation Intrinsic Value Method o Based on the difference between the FMV of the underlying stock and the exercise or strike price on the derivative security o Affects the valuation for the cash impact to the company upon exercise (treasury stock method) Option Pricing Method o Values the derivative security inclusive of speculative value o Typically based on the use of the Black-Scholes Option Pricing Formula

20 Analysis of Economic Dilution Comparison of economic dilution vs. projected increase in value Dilutive impact should not be unfair to ESOP Analysis performed with assistance/input from financial advisor, attorney, and compensation consultant Dilutive Impact Projected Increase in Value

21 Examining Impact of Economic Dilution No established test to confirm unfair economic dilution Trustee s examination of economic dilution should be a comprehensive, interactive process: o Financial Advisor o Compensation Consultant o Attorney o Accountant Show your process discuss and document

22 Implementation

23 Implementing Executive Compensation Arrangements How is the ESOP Involved? Corporate Governance Issues: o Approval of executive compensation arrangements may come from the Board of Directors, an appointed Compensation Committee, or the Company s Shareholders o Board has duty to act in best interests of company shareholders (shareholders elect the board) o Interested/conflicted Directors may desire outside review o Compelling reason for independent Board member(s) o Compensation consultant reports to independent Board member(s) Trustee represents ESOP s interest as a shareholder o Heightened scrutiny where there are no independent Board members Trustee s duty as an ERISA fiduciary is to act solely in the interests of ESOP participants and beneficiaries Fiduciary prudence review/monitor the impact of executive compensation arrangements

24 Prudent Reviewing/Monitoring Executive Compensation Arrangements Questions for prudent review and monitoring of executive compensation arrangements: o What process is required for formal approval of the plan/arrangement? Board approval? Committee approval? Shareholder approval? Trustee Consent? o Examine independence of decision are there any direct or indirect conflicts of interest? Involve independent consultants and outside Directors o Have the appropriate processes and procedures been observed in making the decision? o Were alternative plans/arrangements considered? o How was the key group of management personnel determined?

25 Reviewing/Monitoring Executive Compensation Arrangements (Cont.) How was the amount of compensation determined (e.g. use of an independent compensation consultant)? How were the performance incentive goals determined (e.g. input from compensation consultant, accountants, attorney, financial advisor to ESOP)? Are the performance incentive goals consistent with: o Company s business plan for long-term growth (discrepancy between goals and business plan are problematic) o Cash flow projections applied in an annual valuation? Have any non-competition/non-solicitation provisions been negotiated? Are there any 2 nd Class of Stock concerns? (S-Corp) What happens in the event of a change-in-control? Does the arrangement comply with 409A? (Attorney) How is the plan modified/amended?

26 Important Features For Consideration In Reviewing/Monitoring Executive Performance vesting of awards o o Compensation Time vesting not enough in many instances Trend is to also have performance hurdles for at least a portion of vesting of awards (ROI, EBITDA growth, etc.) Forfeiture for cause provisions o o Prevents payment to bad actors May be in plan, award or employment agreements Clawbacks o o Requires repayment for issues arising after awards vest Restatements of earnings, other material irregularities Specific provisions for change of control payments o o Escrows Earn-outs

27 POTENTIAL PITFALLS

28 Do Incentives Work? They may not motivate employees over the long run (motivation is intrinsic) They could produce burnout They may lead to myopia if improperly structured If properly structured, they can: o Solidify link between employees efforts and successful company outcomes o Make employees feel like valued partners o Encourage creativity in spurring results

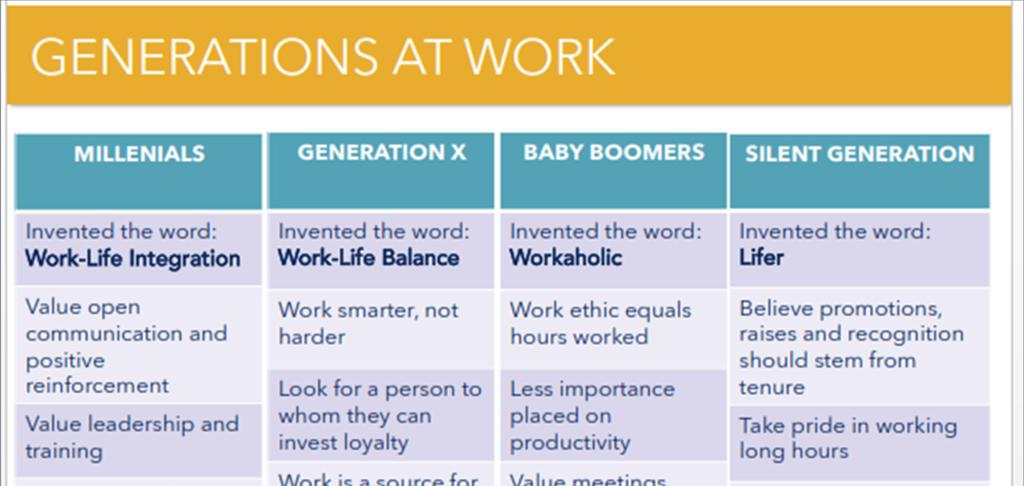

29 Understand Generational Differences

30 FINAL POINTS

31 Conclusions Equity incentive compensation plans are important to help align the economic interests of management and the ESOP If performance based, equity incentive compensation plans are not immediately dilutive to the ESOP and are only related to future appreciation Best performance-based measures: o Achievement of certain financial benchmarks (i.e. revenue and profitability) o Debt repayment o Impact vesting The value of the equity holders interest is diluted by the value allocable to the derivative security

32 Communicate Assumptions: o Employees understand our bonus drivers o Executives understand LTIP awards Reality: o Program details are often misunderstood o Companies miss a chance to reinforce the link between employee efforts, key company goals and successful outcomes

624-3171 clmclean@kaufcan.")

33 QUESTIONS? Matt Keene Chartwell (919) Christopher L. McLean Kaufman & Canoles (757) Andy Smith The McLean Group (703)

34 APPENDIX

35 Why Mid-term Incentives We see strong interest in mid-term incentives (3-6 years) o Key employee retention o Fosters annual grants tied to performance (no coasting as sometimes seen with high-value, one-time grants) Repurchase liability for pay-at-separation LTIP can be pronounced and punctuated for both company and participant

36 Mid-term Incentive Example Annual Grants; $100,000 Vested Value at Payout Grant Year ,000 1,000 1, ,000 1,000 1, ,000 1,000 1, ,000 1,000 1,000 Total Units Outstanding 1,000 2,000 3,000 3,000 3,000* 3,000* Cash Payouts 2014 Grant $ 100, Grant $ 100, Grant $ 100,000 Total Dollars to Exec $ $ $ $ 100,000 $ 100,000 $ 100,000 *Post 2017 grants not shown to save space, but 3,000 total units are outstanding

37 Warrants Long-term certificate giving holder right to purchase securities at designated price Similar to stock options with some significant differences o Warrants are generally freely tradable o Taxation of warrants is subject to section 83 Warrants issued in connection with the performance of services and without a substantial risk of forfeiture are subject to immediate income taxation Warrants are rarely used by private companies as a form of equity compensation used more in connection with transactions.

38 Restricted Stock Units Restricted stock units are similar to phantom stock except that awards are paid in shares of the underlying stock o Participant has right to receive shares at a future date or upon lapse of a risk of forfeiture o Differs from restricted stock as there is not opportunity for a 83(b) election as there is no transfer of property on grant o RSUs may or may not have a dividend equivalent o RSUs carry no voting rights

39 SARs & Section 409A A Stock Appreciation Rights Plan ( SAR ) does not constitute deferred compensation for 409A purposes if (i) compensation under the SAR cannot be greater than the excess of the fair market value of the stock on the date of grant of the SAR with respect to a number of shares fixed on or before the date of grant of the right, (ii) the SAR exercise price may never be less than the fair market value of the underlying stock, when (iii) the SAR does not include any feature for the deferral of compensation other than the deferral of recognition of income until the exercise of the SAR.

40 Internal Revenue Code Section 409(p)

41 Equity Based Compensation and S Corporation ESOPs Code 409(p) Non-allocation year o Non-allocation year occurs when 50% of ownership of S corporation stock is owned by disqualified persons o Ownership includes deemed owned shares and synthetic equity Disqualified person o An individual who owns at least 10% of deemed-owned shares o An individual, who with his family (family is broadly defined), owns at least 20% of the deemed owned shares o Synthetic equity included in calculation

42 Equity Based Compensation and S Corporation ESOPs -- The Impact of 409(p) 409(p) imposes a 50% excise tax on a prohibited allocation of stock in ESOP to disqualified person and value of synthetic equity owned by disqualified persons o Tax is imposed on fair market value of deemed-owned shares held by ESOP for a disqualified person Prohibited allocations are treated as distributions and included in income of disqualified person ESOP status will be lost if prohibited allocation occurs 409(p) applies only to S corporation ESOPs. Does not apply to C corporations

43 What constitutes synthetic equity for 409(p)? Equity-based deferred compensation programs o Stock appreciation rights, phantom stock, restricted stock units and other programs based on future value of underlying stock o Stock options, warrants, and restricted stock o Deferred compensation arrangements

44 Valuation Overview Potential Impact on Annual Administrative Valuations The terms of the plan are key to analyzing the dilution, including the related benchmarks o If performance based benchmarks, the dilution is generally related to future appreciation o If benchmarks are strictly driven by the passage of time, the dilution may be more immediate o The relevant exercise or strike prices for the plans are typically based upon the post-transaction ESOP values (which incorporates the effect of any transaction debt) Valuation approaches for the equity based compensation include an Intrinsic Value Method and an Option Pricing Method

45 Cash Flow and Valuation Impacts The dilution from the management incentive plans is incorporated into the annual ESOP valuations (i.e., management s claim to value) Consideration also needs to be given to the cash impacts of management exercising the units that they own o Cash is typically required to fund the obligation unless stock is issued (100% S-Corp considerations) Important because it impacts the amount of cash available to the company to fund operations, pay debt, expand and grow business, and fund repurchase obligations Operations $ Incentive Plans Debt Amortization Company Capital Expenditures $ $ $ $ ESOP Repurchases

46 Additional Concerns Understand the impact of arrangement on annual valuation o short-term vs. long-term Implementation in transaction o o Negotiations can impact the final terms of the plan/arrangement May see less sharing of analysis from fiduciary Non-transaction implementation o o Focus on conflicts of interest Successor trustee issues reviewing previously established plan Obsolescence of plan/arrangement o o Unforeseen circumstances (e.g. significant downturn in economy) Amendment and redesign concerns 409A issues Impact on repurchase liability, corporate acquisitions Communicating to ESOP participants

47 Trustee Focus in Reviewing Executive Compensation Arrangements Properly designed arrangement creates a win-win for both key management personnel and ESOP participants An effective design will achieve the following: o Entitlement to benefits comes from achieving real, measureable performance goals o Benefits should be EARNED o Satisfaction of performance goals(s) drives growth in Company stock value and offset any economic dilution of ESOP shares o Aggregate compensation paid to key management personnel is reasonable, yet competitive (analytical support from compensation consultant) o Long-term retention of key management personnel

48 Best Practices Review and understand existing corporate governance requirements Focus on independence of decisions (conflicts of interest) Use your teammates (financial advisor, attorney, compensation consultant, etc.) to assist you in examining the reasonableness of performance goals and compensation levels Understand impact on valuation Ask questions and document your process Remember your fiduciary duty act solely in the interests of participants and beneficiaries (trustee) act solely in the interests of shareholders (board of directors)

Current Trends in Compensation for ESOP Companies Midwest Regional ESOP Conference September 11, 2015

Current Trends in Compensation for ESOP Companies 2015 Midwest Regional ESOP Conference September 11, 2015 INTRODUCTION TO DAKOTA SUPPLY GROUP Presented by: Melissa Lunak Director of Human Resources Dakota

Current Trends in Compensation for ESOP Companies 2015 Midwest Regional ESOP Conference September 11, 2015 INTRODUCTION TO DAKOTA SUPPLY GROUP Presented by: Melissa Lunak Director of Human Resources Dakota

A Trustee s Perspective on Equity Compensation Plans for ESOP Companies

A Trustee s Perspective on Equity Compensation Plans for ESOP Companies Joni Andrioff, Partner Steptoe & Johnson LLP (202) 429-8064 jandrioff@steptoe.com Neil M. Brozen, CPA, Managing Director Bankers

A Trustee s Perspective on Equity Compensation Plans for ESOP Companies Joni Andrioff, Partner Steptoe & Johnson LLP (202) 429-8064 jandrioff@steptoe.com Neil M. Brozen, CPA, Managing Director Bankers

ASPPA s Quarterly Journal for Actuaries, Consultants, Administrators and Other Retirement Plan Professionals

SPRING 2009 :: VOL 39, NO 2 ASPPAJournal ASPPA s Quarterly Journal for Actuaries, Consultants, Administrators and Other Retirement Plan Professionals Taking Stock: An Introduction to Equity-based Compensation

SPRING 2009 :: VOL 39, NO 2 ASPPAJournal ASPPA s Quarterly Journal for Actuaries, Consultants, Administrators and Other Retirement Plan Professionals Taking Stock: An Introduction to Equity-based Compensation

Foley & Lardner LLP. May 13, :00 p.m. 2:00 p.m. EST

Attorney Advertising Prior results do not guarantee a similar outcome Models used are not clients but may be representative of clients 321 N. Clark Street, Suite 2800, Chicago, IL 60610 312.832.4500 Foley

Attorney Advertising Prior results do not guarantee a similar outcome Models used are not clients but may be representative of clients 321 N. Clark Street, Suite 2800, Chicago, IL 60610 312.832.4500 Foley

Nonqualified/Executive Compensation Plans. Kelsey H. Mayo, J.D. Partner Poyner Spruill LLP

Nonqualified/Executive Compensation Plans Kelsey H. Mayo, J.D. Partner Poyner Spruill LLP 1 What We ll Cover What are executive compensation plans? Why would a company have such a plan? What options are

Nonqualified/Executive Compensation Plans Kelsey H. Mayo, J.D. Partner Poyner Spruill LLP 1 What We ll Cover What are executive compensation plans? Why would a company have such a plan? What options are

ESOP CHECK-UP EVALUATING HOW AN ESOP IS WORKING

ESOP CHECK-UP EVALUATING HOW AN ESOP IS WORKING SPEAKERS CHRISTOPHER MCLEAN LINDSAY BAUBLITZ clmclean@kaufcan.com 703-770-9982 lbaublitz@schgroup.com 410-785-8012 AGENDA Plan sponsors and fiduciaries have

ESOP CHECK-UP EVALUATING HOW AN ESOP IS WORKING SPEAKERS CHRISTOPHER MCLEAN LINDSAY BAUBLITZ clmclean@kaufcan.com 703-770-9982 lbaublitz@schgroup.com 410-785-8012 AGENDA Plan sponsors and fiduciaries have

Emerging ESOP Structure and Corporate Governance Considerations

Emerging ESOP Structure and Corporate Governance Considerations Presented by: Allison T. Wilkerson McDermott, Will & Emery Dallas, TX 214.295.8010 Awilkerson@mwe.com Matthew Hricko Stout Risius Ross, LLC

Emerging ESOP Structure and Corporate Governance Considerations Presented by: Allison T. Wilkerson McDermott, Will & Emery Dallas, TX 214.295.8010 Awilkerson@mwe.com Matthew Hricko Stout Risius Ross, LLC

Process & Decision Making of the ESOP Administration Committee

Process & Decision Making of the ESOP Administration Committee The ESOP Association Mid-Atlantic Chapter, Spring Conference March 10, 2017 Nona K. Massengill Williams Mullen nmassengill@williamsmullen.com

Process & Decision Making of the ESOP Administration Committee The ESOP Association Mid-Atlantic Chapter, Spring Conference March 10, 2017 Nona K. Massengill Williams Mullen nmassengill@williamsmullen.com

Process & Decision Making of the ESOP Administration Committee

Process & Decision Making of the ESOP Administration Committee The ESOP Association Las Vegas Conference & Tradeshow November 10-11, 2016 Todd L. Denison Phelps Dunbar, LLP Todd.denison@phelps.com www.phelpsdunbar.com

Process & Decision Making of the ESOP Administration Committee The ESOP Association Las Vegas Conference & Tradeshow November 10-11, 2016 Todd L. Denison Phelps Dunbar, LLP Todd.denison@phelps.com www.phelpsdunbar.com

BROAD-BASED EMPLOYEE INCENTIVE ARRANGEMENTS

I. Equity-Based Compensation BROAD-BASED EMPLOYEE INCENTIVE ARRANGEMENTS A. Nonqualified Stock Option ( NSO ) Right to purchase stock from the issuer at a fixed price. Holder may exercise at any time (after

I. Equity-Based Compensation BROAD-BASED EMPLOYEE INCENTIVE ARRANGEMENTS A. Nonqualified Stock Option ( NSO ) Right to purchase stock from the issuer at a fixed price. Holder may exercise at any time (after

Executive Compensation, Employee Benefits and ERISA Alert

Executive Compensation, Employee Benefits and ERISA Alert November 8, 2017 Tax Cuts and Jobs Act On November 2, 2017, the Committee on Ways and Means of the U.S. House of Representatives released its tax

Executive Compensation, Employee Benefits and ERISA Alert November 8, 2017 Tax Cuts and Jobs Act On November 2, 2017, the Committee on Ways and Means of the U.S. House of Representatives released its tax

Using Benefits To Compensate Key Management & In Succession Planning

Using Benefits To Compensate Key Management & In Succession Planning Scott E. Galbreath, JD, LL.M. (Tax) The Burton Law Firm Sacramento and Roseville, CA What is Executive Compensation? A mix of salary

Using Benefits To Compensate Key Management & In Succession Planning Scott E. Galbreath, JD, LL.M. (Tax) The Burton Law Firm Sacramento and Roseville, CA What is Executive Compensation? A mix of salary

Issues Associated with Second-Stage ESOP Transactions

The ESOP Association California Western States 2017 Annual Conference October 11 13, 2017 Paradise Point, San Diego Issues Associated with Second-Stage ESOP Transactions Michael Harden Senior Managing

The ESOP Association California Western States 2017 Annual Conference October 11 13, 2017 Paradise Point, San Diego Issues Associated with Second-Stage ESOP Transactions Michael Harden Senior Managing

Protecting your ESOP Company from legal problems can be broken down into two main areas:

Presented by: Christopher McLean Kaufman & Canoles, P.C. McLean, VA Todd Denison Phelps Dunbar, Mobile, AL Protecting your ESOP Company from legal problems can be broken down into two main areas: Plan

Presented by: Christopher McLean Kaufman & Canoles, P.C. McLean, VA Todd Denison Phelps Dunbar, Mobile, AL Protecting your ESOP Company from legal problems can be broken down into two main areas: Plan

Back to Basics: Taxation

The 10th Annual New England NASPP Regional Conference co-hosted by the Boston and Connecticut NASPP Chapters July 11 th, 2018 Agenda 1. General Introduction to Concepts Related to Equity Compensation 2.

The 10th Annual New England NASPP Regional Conference co-hosted by the Boston and Connecticut NASPP Chapters July 11 th, 2018 Agenda 1. General Introduction to Concepts Related to Equity Compensation 2.

NONQUALIFIED DEFERRED COMPENSATION LEGISLATIVE PROPOSALS * FEATURE LEGISLATIVE PROPOSALS COMMENTS

NONQUALIFIED DEFERRED COMPENSATION LEGISLATIVE PROPOSALS * FEATURE LEGISLATIVE PROPOSALS COMMENTS Types of Arrangements Affected The proposals apply broadly to deferred compensation arrangements, including

NONQUALIFIED DEFERRED COMPENSATION LEGISLATIVE PROPOSALS * FEATURE LEGISLATIVE PROPOSALS COMMENTS Types of Arrangements Affected The proposals apply broadly to deferred compensation arrangements, including

Executive Benefits for Nonprofit & Tax-Exempt Organizations

Executive Benefits for Nonprofit & Tax-Exempt Organizations Recruit, retain, and reward your top talent with nonqualified retirement or estate planning benefits As a nonprofit or tax-exempt organization,

Executive Benefits for Nonprofit & Tax-Exempt Organizations Recruit, retain, and reward your top talent with nonqualified retirement or estate planning benefits As a nonprofit or tax-exempt organization,

New Stock Option Rules for Early Stage Companies

New Stock Option Rules for Early Stage Companies Dr. Stanley Jay Feldman, Axiom Valuation Solutions Ken Appleby, Foley & Lardner Jack Malley, First Jensen Group 2 Agenda I. Overview of Fair Value Changes

New Stock Option Rules for Early Stage Companies Dr. Stanley Jay Feldman, Axiom Valuation Solutions Ken Appleby, Foley & Lardner Jack Malley, First Jensen Group 2 Agenda I. Overview of Fair Value Changes

Denny s Corporation. Shares of Common Stock offered under the Denny s Corporation 2012 Omnibus Incentive Plan

PROSPECTUS Denny s Corporation Shares of Common Stock offered under the Denny s Corporation 2012 Omnibus Incentive Plan This prospectus relates to shares of common stock of Denny s Corporation (the Company

PROSPECTUS Denny s Corporation Shares of Common Stock offered under the Denny s Corporation 2012 Omnibus Incentive Plan This prospectus relates to shares of common stock of Denny s Corporation (the Company

Complexities in ESOP Administration

Complexities in ESOP Administration Barbara M. Clough, QPA, QKA, Director, Plan Administration, Blue Ridge ESOP Associates Barbara Clough, QPA, QKA Director, Plan Administration, Blue Ridge ESOP Associates

Complexities in ESOP Administration Barbara M. Clough, QPA, QKA, Director, Plan Administration, Blue Ridge ESOP Associates Barbara Clough, QPA, QKA Director, Plan Administration, Blue Ridge ESOP Associates

Know What You Don t Know: Tips, Traps in Representing Executives - Before, During and After Employment

Know What You Don t Know: Tips, Traps in Representing Executives - Before, During and After Employment Joseph Y. Ahmad Ahmad, Zavitsanos, Anaipakos, Alavi & Mensing P.C. 1221 McKinney Street, Suite 2500

Know What You Don t Know: Tips, Traps in Representing Executives - Before, During and After Employment Joseph Y. Ahmad Ahmad, Zavitsanos, Anaipakos, Alavi & Mensing P.C. 1221 McKinney Street, Suite 2500

Advanced Markets Because You Asked

Advanced Markets Because You Asked June 2007 Answers to Questions Frequently Asked of the Advanced Markets Group The Impact of Section 409A on Nonqualified Deferred Compensation Plans Advanced Markets

Advanced Markets Because You Asked June 2007 Answers to Questions Frequently Asked of the Advanced Markets Group The Impact of Section 409A on Nonqualified Deferred Compensation Plans Advanced Markets

How to Design Equity Compensation Plans. December 2, Ted D. Rosen Herrick, Feinstein LLP New York, New York

How to Design Equity Compensation Plans December 2, 2008 Ted D. Rosen Herrick, Feinstein LLP New York, New York Agenda Introduction to Types of Equity Compensation Plans- Ted D. Rosen, Counsel, Herrick,

How to Design Equity Compensation Plans December 2, 2008 Ted D. Rosen Herrick, Feinstein LLP New York, New York Agenda Introduction to Types of Equity Compensation Plans- Ted D. Rosen, Counsel, Herrick,

Ownership Structures and Incentive Programs for Design Professional Firms

Ownership Structures and Incentive Programs for Design Professional Firms May 10, 2018 Authors: Michael Strogoff, FAIA, Strogoff Consulting, Inc. Karen Kauh, Strogoff Consulting, Inc. With contributions

Ownership Structures and Incentive Programs for Design Professional Firms May 10, 2018 Authors: Michael Strogoff, FAIA, Strogoff Consulting, Inc. Karen Kauh, Strogoff Consulting, Inc. With contributions

Ronald J. Kruszewski Chairman of the Board and Chief Executive Officer. St. Louis, Missouri August 21, 2018

STIFEL FINANCIAL CORP. One Financial Plaza 501 North Broadway St. Louis, Missouri 63102 NOTICE OF SPECIAL MEETING OF SHAREHOLDERS TO BE HELD ON SEPTEMBER 25, 2018 Fellow Shareholders: We cordially invite

STIFEL FINANCIAL CORP. One Financial Plaza 501 North Broadway St. Louis, Missouri 63102 NOTICE OF SPECIAL MEETING OF SHAREHOLDERS TO BE HELD ON SEPTEMBER 25, 2018 Fellow Shareholders: We cordially invite

Non-Qualified Deferred Compensation (NQDC) & Compensatory Stock Options

& Compensatory Stock Options") Non-Qualified Deferred Compensation (NQDC) & Compensatory Stock Options Robert S. Keebler, CPA, MST, AEP Keebler & Associates, LLP 420 South Washington Street Green Bay, WI 54301 Robert.keebler@keeblerandassociates.com

Non-Qualified Deferred Compensation (NQDC) & Compensatory Stock Options Robert S. Keebler, CPA, MST, AEP Keebler & Associates, LLP 420 South Washington Street Green Bay, WI 54301 Robert.keebler@keeblerandassociates.com

Executive Compensation in Privately Owned Businesses: How It s the Same and How It s Very Different

Executive Compensation in Privately Owned Businesses: How It s the Same and How It s Very Different Don Delves, Director, Willis Towers Watson June 6, 2017 2017 Willis Towers Watson. All rights reserved.

Executive Compensation in Privately Owned Businesses: How It s the Same and How It s Very Different Don Delves, Director, Willis Towers Watson June 6, 2017 2017 Willis Towers Watson. All rights reserved.

Code Section 409A: Revisiting the Basics

409A Basics A Webinar Series Code Section 409A: Revisiting the Basics Presenters: Althea R. Day Daniel L. Hogans Leslie E. DuPuy www.morganlewis.com March 29, 2012 Section 409A Background The American

409A Basics A Webinar Series Code Section 409A: Revisiting the Basics Presenters: Althea R. Day Daniel L. Hogans Leslie E. DuPuy www.morganlewis.com March 29, 2012 Section 409A Background The American

Compensation Planning for Tax-Exempt Entities: Navigating IRC Section 457(f) Presented by Mary E. Powell, Marc Fosse and Eric Schillinger

Presented by Mary E. Powell, Marc Fosse and Eric Schillinger") Compensation Planning for Tax-Exempt Entities: Navigating IRC Section 457(f) Presented by Mary E. Powell, Marc Fosse and Eric Schillinger June 8, 2016 Agenda Internal Revenue Code ( Code ) Section 457(f)

Compensation Planning for Tax-Exempt Entities: Navigating IRC Section 457(f) Presented by Mary E. Powell, Marc Fosse and Eric Schillinger June 8, 2016 Agenda Internal Revenue Code ( Code ) Section 457(f)

Equity Compensation Strategies for Technology Companies to Consider in Merger and Presenters

Employee Benefit Issues and Equity Compensation Strategies for Technology Companies to Consider in Merger and Presenters Acquisition Transactions y y Amy Pocino Kelly Jeffrey P. Bodle May 15, 2013 This

Employee Benefit Issues and Equity Compensation Strategies for Technology Companies to Consider in Merger and Presenters Acquisition Transactions y y Amy Pocino Kelly Jeffrey P. Bodle May 15, 2013 This

NONQUALIFIED DEFERRED COMPENSATION & CODE 409A

NONQUALIFIED DEFERRED COMPENSATION & CODE 409A I. REVIEW OF NQDC PRIOR TO CODE 409A A. Nonqualified Deferred Compensation ( NQDC ) Plan - a plan, agreement, or arrangement between an employer and an employee

NONQUALIFIED DEFERRED COMPENSATION & CODE 409A I. REVIEW OF NQDC PRIOR TO CODE 409A A. Nonqualified Deferred Compensation ( NQDC ) Plan - a plan, agreement, or arrangement between an employer and an employee

Back to Basics: Taxation

The 10th Annual New England NASPP Regional Conference co-hosted by the Boston and Connecticut NASPP Chapters July 11 th, 2018 Agenda 1. General Introduction to Tax Law Related to Equity Compensation 2.

The 10th Annual New England NASPP Regional Conference co-hosted by the Boston and Connecticut NASPP Chapters July 11 th, 2018 Agenda 1. General Introduction to Tax Law Related to Equity Compensation 2.

Stock Awards Keeping Pace with Equity Alternatives

Stock Awards Keeping Pace with Equity Alternatives Thursday, April 27, 2006 4:00pm 5:00pm Virginia L. Gibson White & Case LLP vgibson@whitecase.com Goals of Equity Compensation Recruit Motivate Retain

Stock Awards Keeping Pace with Equity Alternatives Thursday, April 27, 2006 4:00pm 5:00pm Virginia L. Gibson White & Case LLP vgibson@whitecase.com Goals of Equity Compensation Recruit Motivate Retain

INITIAL GUIDANCE ON NEW DEFERRED COMPENSATION RULES

CLIENT MEMORANDUM INITIAL GUIDANCE ON NEW DEFERRED COMPENSATION RULES The Treasury has issued initial guidance under Section 409A of the Internal Revenue Code. Section 409A, added to the Code as part of

CLIENT MEMORANDUM INITIAL GUIDANCE ON NEW DEFERRED COMPENSATION RULES The Treasury has issued initial guidance under Section 409A of the Internal Revenue Code. Section 409A, added to the Code as part of

Long Term Incentive Plans

Long Term Incentive Plans September 26, 2017 OFFICES: CHICAGO, ILLINOIS CEDAR RAPIDS, IOWA Copyright 2017 - The Overture Group Presented by Mark Reilly Mark is Managing Director of Compensation. He has

Long Term Incentive Plans September 26, 2017 OFFICES: CHICAGO, ILLINOIS CEDAR RAPIDS, IOWA Copyright 2017 - The Overture Group Presented by Mark Reilly Mark is Managing Director of Compensation. He has

The Impact of Code Section 409A on Global Compensation Plans

The Impact of Code Section 409A on Global Compensation Plans April 27, 2006 11:30 am 12:30 pm Fredric S. Singerman, fsingerman@seyfarth.com David M. Weiner, dweiner@seyfarth.com Partners, Seyfarth Shaw

The Impact of Code Section 409A on Global Compensation Plans April 27, 2006 11:30 am 12:30 pm Fredric S. Singerman, fsingerman@seyfarth.com David M. Weiner, dweiner@seyfarth.com Partners, Seyfarth Shaw

Executives Beware: States May Look To Equity Compensation for Revenue

Executives Beware: States May Look To Equity Compensation for Revenue by Cara Griffith Cara Griffith is a legal editor of State Tax Notes. Many public corporations and even some closely held businesses

Executives Beware: States May Look To Equity Compensation for Revenue by Cara Griffith Cara Griffith is a legal editor of State Tax Notes. Many public corporations and even some closely held businesses

Subject: Comments regarding Incentive-based Compensation Arrangements Section 956(e) of the Dodd-Frank Act 12 CFR Part 236

of the Dodd-Frank Act 12 CFR Part 236") July 22, 2016 Board of Governors of the Federal Reserve System Subject: Comments regarding Incentive-based Compensation Arrangements Section 956(e) of the Dodd-Frank Act 12 CFR Part 236 Compensation Advisory

July 22, 2016 Board of Governors of the Federal Reserve System Subject: Comments regarding Incentive-based Compensation Arrangements Section 956(e) of the Dodd-Frank Act 12 CFR Part 236 Compensation Advisory

White Paper: Nonqualified Deferred Compensation Plans

White Paper: Nonqualified Deferred Compensation Plans www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC,

White Paper: Nonqualified Deferred Compensation Plans www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC,

The Autopsy. of an ESOP

The Autopsy of an ESOP 1 A home is often viewed as one of the largest assets you will own. However, when it comes to the small business owner, often times the value of their business will over shadow the

The Autopsy of an ESOP 1 A home is often viewed as one of the largest assets you will own. However, when it comes to the small business owner, often times the value of their business will over shadow the

The value of equity-based compensation

The value of equity-based compensation VALUATION AND ACCOUNTING FOR TOTAL SHAREHOLDER RETURN (TSR) PLANS By David Howell and David Grubb Overview Performance-based equity compensation plans continue to

The value of equity-based compensation VALUATION AND ACCOUNTING FOR TOTAL SHAREHOLDER RETURN (TSR) PLANS By David Howell and David Grubb Overview Performance-based equity compensation plans continue to

Presenting a live 90-minute webinar with interactive Q&A. Today s faculty features: Elizabeth A. Gartland, Esq., Fenwick & West, San Francisco

Presenting a live 90-minute webinar with interactive Q&A Structuring Management Carve-Out Plans for Privately Held Corporations: Mechanics, Tax Obstacles and Optimization Guidance for Employee Benefits

Presenting a live 90-minute webinar with interactive Q&A Structuring Management Carve-Out Plans for Privately Held Corporations: Mechanics, Tax Obstacles and Optimization Guidance for Employee Benefits

Compensation of Founders and Key Employees of Emerging Companies After The Enactment of Section 409A * Kenneth R. Hoffman Venable LLP Washington, D.C.

Compensation of Founders and Key Employees of Emerging Companies After The Enactment of Section 409A * Kenneth R. Hoffman Venable LLP Washington, D.C. October 21, 2005 The American Jobs Creation Act of

Compensation of Founders and Key Employees of Emerging Companies After The Enactment of Section 409A * Kenneth R. Hoffman Venable LLP Washington, D.C. October 21, 2005 The American Jobs Creation Act of

PROSPECTUS 626,600,000 SHARES COMMON STOCK 2003 KEY ASSOCIATE STOCK PLAN, AS AMENDED AND RESTATED EFFECTIVE APRIL 28, 2010

PROSPECTUS 626,600,000 SHARES BANK OF AMERICA CORPORATION COMMON STOCK 2003 KEY ASSOCIATE STOCK PLAN, AS AMENDED AND RESTATED EFFECTIVE APRIL 28, 2010 This Prospectus relates to the offer and sale of up

PROSPECTUS 626,600,000 SHARES BANK OF AMERICA CORPORATION COMMON STOCK 2003 KEY ASSOCIATE STOCK PLAN, AS AMENDED AND RESTATED EFFECTIVE APRIL 28, 2010 This Prospectus relates to the offer and sale of up

Executives: What to know about your compensation if your company is sold

Executives: What to know about your compensation if your company is sold Please disable popup blocking software before viewing this webcast Original Publication Date: July 20, 2017 CPE Credit is not available

Executives: What to know about your compensation if your company is sold Please disable popup blocking software before viewing this webcast Original Publication Date: July 20, 2017 CPE Credit is not available

Executive Compensation & Employee Benefits July 30, 2004

Planning Should Begin Now To Prepare For Changes To Nonqualified Deferred Compensation Arrangements Under Legislative Proposals Executive Compensation & Employee Benefits Both the Senate and the House

Planning Should Begin Now To Prepare For Changes To Nonqualified Deferred Compensation Arrangements Under Legislative Proposals Executive Compensation & Employee Benefits Both the Senate and the House

Executive Compensation:

Executive Compensation: Are your nonqualified deferred compensation plans up-to-date and being administered properly? PRESENTED BY: BILL ENCK, CPA, CPC, APA ROGER PRINCE, JD, APA Reviewed: JANUARY 7, 2017

Executive Compensation: Are your nonqualified deferred compensation plans up-to-date and being administered properly? PRESENTED BY: BILL ENCK, CPA, CPC, APA ROGER PRINCE, JD, APA Reviewed: JANUARY 7, 2017

Dealing with ERISA Fiduciary Responsibility & Liability

Qualified and Non Qualified Retirement Plans Pitfalls for the Practitioner Representing the Small Business Owner Dealing with ERISA Fiduciary Responsibility & Liability Irwin N. Rubin, Esq. 19 th Annual

Qualified and Non Qualified Retirement Plans Pitfalls for the Practitioner Representing the Small Business Owner Dealing with ERISA Fiduciary Responsibility & Liability Irwin N. Rubin, Esq. 19 th Annual

Deferred Compensation for Dummies: The Section 409A Compliance Clock is Ticking

Deferred Compensation for Dummies: The Section 409A Compliance Clock is Ticking OCTOBER 17, 2008 PUBLICATIONS Most of us involved in the practice of law are familiar with the benefits of tax deferral.

Deferred Compensation for Dummies: The Section 409A Compliance Clock is Ticking OCTOBER 17, 2008 PUBLICATIONS Most of us involved in the practice of law are familiar with the benefits of tax deferral.

The Honorable Orrin Hatch November 11, 2017 Page 2

The Honorable Orrin Hatch Chairman Senate Committee on Finance United States Senate 219 Dirksen Senate Office Building Washington, DC 20510 RE: Center On Executive Compensation Comments on Nonqualified

The Honorable Orrin Hatch Chairman Senate Committee on Finance United States Senate 219 Dirksen Senate Office Building Washington, DC 20510 RE: Center On Executive Compensation Comments on Nonqualified

Nuts & Bolts of Section 409A: Practical Issues to Consider in Every Practice

Nuts & Bolts of Section 409A: Practical Issues to Consider in Every Practice June 9, 2016 Sponsored by the ABA Joint Committee on Employee Benefits and the American College of Employee Benefits Counsel

Nuts & Bolts of Section 409A: Practical Issues to Consider in Every Practice June 9, 2016 Sponsored by the ABA Joint Committee on Employee Benefits and the American College of Employee Benefits Counsel

Deferred Compensation

Deferred Compensation Concept A non-qualified deferred compensation plan is an agreement between an employer and an executive to defer the payment and receipt of compensation to the future for services

Deferred Compensation Concept A non-qualified deferred compensation plan is an agreement between an employer and an executive to defer the payment and receipt of compensation to the future for services

The Impact of Plan Design and Operations on Ownership Culture

The Impact of Plan Design and Operations on Ownership Culture Thomas Roback, Jr., CEP, QKA Blue Ridge ESOP Associates Christopher L. McLean, Esq. Kaufman & Canoles, P.C. Bios Christopher L. McLean, Esq.

The Impact of Plan Design and Operations on Ownership Culture Thomas Roback, Jr., CEP, QKA Blue Ridge ESOP Associates Christopher L. McLean, Esq. Kaufman & Canoles, P.C. Bios Christopher L. McLean, Esq.

Executive Bonus Plans and Restricted Endorsement Bonus Arrangements

Executive Bonus Plans and Restricted Endorsement Bonus Arrangements ADVISOR COMPANION BUSINESS PLANNING A simple and flexible plan to motivate and reward key employees It can be very challenging for business

Executive Bonus Plans and Restricted Endorsement Bonus Arrangements ADVISOR COMPANION BUSINESS PLANNING A simple and flexible plan to motivate and reward key employees It can be very challenging for business

It s All About the Business

It s All About the Business Planning Strategies Integrated with Life Insurance to Help a Business Owner Accomplish Goals for Retirement, Business Perpetuation, Successful Business Transition, and Estate

It s All About the Business Planning Strategies Integrated with Life Insurance to Help a Business Owner Accomplish Goals for Retirement, Business Perpetuation, Successful Business Transition, and Estate

Client Alert. New Tax Law Will Require Substantial Changes to Many Non-Qualified Deferred Compensation Arrangements.

October 19, 2004 Client Alert An informational newsletter from Goodwin Procter LLP New Tax Law Will Require Substantial Changes to Many Non-Qualified Deferred Compensation Arrangements Employers must take

October 19, 2004 Client Alert An informational newsletter from Goodwin Procter LLP New Tax Law Will Require Substantial Changes to Many Non-Qualified Deferred Compensation Arrangements Employers must take

Insights on Single Family Office Executive Compensation

Insights on Single Family Office Executive Compensation Research Provides Peer Group Comparisons of Compensation and Benefits Practices Appropriate and competitive compensation is a key component of recruiting

Insights on Single Family Office Executive Compensation Research Provides Peer Group Comparisons of Compensation and Benefits Practices Appropriate and competitive compensation is a key component of recruiting

In October 2004, the American Jobs Creation Act

Long-Awaited Final Regulations Under Code Sec. 409A Are Issued As Transition Relief Nears an End * By David G. Johnson and Elizabeth Buchbinder ** Dave Johnson and Elizabeth Buchbinder discuss the new

Long-Awaited Final Regulations Under Code Sec. 409A Are Issued As Transition Relief Nears an End * By David G. Johnson and Elizabeth Buchbinder ** Dave Johnson and Elizabeth Buchbinder discuss the new

Nonqualified Deferred Compensation Plans

Nonqualified Deferred Compensation Plans Presented by: Michael Roesler Managing RVP NQ Plans The Principal Financial Group 1 The #1 provider of nonqualified plans 1 NONQUALIFIED FOCUS LESS THAN 2% CLIENT

Nonqualified Deferred Compensation Plans Presented by: Michael Roesler Managing RVP NQ Plans The Principal Financial Group 1 The #1 provider of nonqualified plans 1 NONQUALIFIED FOCUS LESS THAN 2% CLIENT

SUMMARY PLAN DESCRIPTION FOR. DAYMON WORLDWIDE INC. 401(k) PROFIT SHARING PLAN AMENDMENT AND RESTATEMENT EFFECTIVE JANUARY 1, 2016

PROFIT SHARING PLAN AMENDMENT AND RESTATEMENT EFFECTIVE JANUARY 1, 2016") SUMMARY PLAN DESCRIPTION FOR DAYMON WORLDWIDE INC. 401(k) PROFIT SHARING PLAN AMENDMENT AND RESTATEMENT EFFECTIVE JANUARY 1, 2016 Table of Contents Article 1... Introduction Article 2... General Plan Information

SUMMARY PLAN DESCRIPTION FOR DAYMON WORLDWIDE INC. 401(k) PROFIT SHARING PLAN AMENDMENT AND RESTATEMENT EFFECTIVE JANUARY 1, 2016 Table of Contents Article 1... Introduction Article 2... General Plan Information

Executive Compensation: Selected Topics

Executive Compensation: Selected Topics Robin M. Solomon Washington, DC (202) 662-3474 Tax Executives Institute Los Angeles Chapter Benjamin L. Grosz Washington, DC (202) 662-3422 Executive Compensation

Executive Compensation: Selected Topics Robin M. Solomon Washington, DC (202) 662-3474 Tax Executives Institute Los Angeles Chapter Benjamin L. Grosz Washington, DC (202) 662-3422 Executive Compensation

Retirement Plan Services

OVERVIEW Helping your employees prepare for retirement is one of the most valued benefits you can offer. At CIBC, we understand the important role retirement planning plays in your overall benefits package.

OVERVIEW Helping your employees prepare for retirement is one of the most valued benefits you can offer. At CIBC, we understand the important role retirement planning plays in your overall benefits package.

Denny s Corporation. Shares of Common Stock offered under the Denny s Corporation 2008 Omnibus Incentive Plan

PROSPECTUS Denny s Corporation Shares of Common Stock offered under the Denny s Corporation 2008 Omnibus Incentive Plan This prospectus relates to shares of common stock of Denny s Corporation (the Company

PROSPECTUS Denny s Corporation Shares of Common Stock offered under the Denny s Corporation 2008 Omnibus Incentive Plan This prospectus relates to shares of common stock of Denny s Corporation (the Company

Executive Benefits for ESOP Owned S Corporations Post IRC Secs. 409A and 409(p)

") Journal of Financial Service Professionals May 2007 Executive Benefits for ESOP Owned S Corporations Post IRC Secs. 409A and 409(p) Daniel M. Zugell, CLU, ChFC, LUTCF Pete Shuler Fred H. Thomas Abstract:

Journal of Financial Service Professionals May 2007 Executive Benefits for ESOP Owned S Corporations Post IRC Secs. 409A and 409(p) Daniel M. Zugell, CLU, ChFC, LUTCF Pete Shuler Fred H. Thomas Abstract:

Practising Law Institute ERISA: The Evolving World 2014 An Introduction to Executive Compensation/ Nonqualified Deferred Compensation Plans/SERPs

Practising Law Institute ERISA: The Evolving World 2014 An Introduction to Executive Compensation/ Nonqualified Deferred Compensation Plans/SERPs August 4, 2014 Regina Olshan Charmaine L. Slack Introduction

Practising Law Institute ERISA: The Evolving World 2014 An Introduction to Executive Compensation/ Nonqualified Deferred Compensation Plans/SERPs August 4, 2014 Regina Olshan Charmaine L. Slack Introduction

TOP ADMINISTRATIVE MISTAKES AND HOW TO CORRECT THEM. September 12, Midwest Conference

TOP ADMINISTRATIVE MISTAKES AND HOW TO CORRECT THEM September 12, 2014 2014 Midwest Conference Vicki Graft ESOP Partners LLC vgraft@esoppartners.com Brian L. Anderson Dewitt Ross & Stevens S.C. bla@dewittross.com

TOP ADMINISTRATIVE MISTAKES AND HOW TO CORRECT THEM September 12, 2014 2014 Midwest Conference Vicki Graft ESOP Partners LLC vgraft@esoppartners.com Brian L. Anderson Dewitt Ross & Stevens S.C. bla@dewittross.com

ESOPS: CONTINUING A LEGACY

ESOPS: CONTINUING A LEGACY November 19, 2015 Cara Benningfield, CPA Director cbenningfield@bkd.com 1 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing

ESOPS: CONTINUING A LEGACY November 19, 2015 Cara Benningfield, CPA Director cbenningfield@bkd.com 1 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing

Tax matters: what should the board be thinking about?

January 2017 Tax matters: what should the board be thinking about? Tax issues how pay is taxed, when, and whether that tax can be deferred can be a key driver in designing executive pay packages. The potential

January 2017 Tax matters: what should the board be thinking about? Tax issues how pay is taxed, when, and whether that tax can be deferred can be a key driver in designing executive pay packages. The potential

Webinar Series ESOPS: CONTINUING A LEGACY 10/31/2017. October 31, Cara Benningfield Partner

Webinar Series ESOPS: CONTINUING A LEGACY October 31, 2017 Cara Benningfield Partner cbenningfield@bkd.com Angela Fisher Manager afisher@bkd.com 1 TO RECEIVE CPE CREDIT Participate in entire webinar Answer

Webinar Series ESOPS: CONTINUING A LEGACY October 31, 2017 Cara Benningfield Partner cbenningfield@bkd.com Angela Fisher Manager afisher@bkd.com 1 TO RECEIVE CPE CREDIT Participate in entire webinar Answer

A Survey of Current Trends. 2014/2015 edition

Executive Benefits: A Survey of Current Trends 2014/2015 edition Contents Introduction 1 Executive Summary 2 Methodology 4 Goals and Satisfaction 5 Non-Qualified Deferred Compensation Plans 11 Offering

Executive Benefits: A Survey of Current Trends 2014/2015 edition Contents Introduction 1 Executive Summary 2 Methodology 4 Goals and Satisfaction 5 Non-Qualified Deferred Compensation Plans 11 Offering

Nonqualified deferred compensation arrangements

Strategies for Competitive Business Nonqualified deferred compensation arrangements The art of recruiting, retaining and rewarding Business Needs-based Planning Strategies Contents 1 A primer on nonqualified

Strategies for Competitive Business Nonqualified deferred compensation arrangements The art of recruiting, retaining and rewarding Business Needs-based Planning Strategies Contents 1 A primer on nonqualified

FirstEnergy Corp Incentive Plan

FirstEnergy Corp. 2007 Incentive Plan Amendment and Restatement Effective May 15, 2007 {2007 INCENTIVE PLAN.DOC;1} Contents Article 1. Establishment, Purpose, and Duration... 1 Article 2. Definitions...

FirstEnergy Corp. 2007 Incentive Plan Amendment and Restatement Effective May 15, 2007 {2007 INCENTIVE PLAN.DOC;1} Contents Article 1. Establishment, Purpose, and Duration... 1 Article 2. Definitions...

Sustainability. Strategic Management of ESOP Operation. How to Keep the Hamster Running

Sustainability Strategic Management of ESOP Operation 1 How to Keep the Hamster Running 2016 Mid-Atlantic Chapter Spring Conference March 17 th 18 th 2016, Williamsburg, Virginia Cecilia Loftus Bob Bye

Sustainability Strategic Management of ESOP Operation 1 How to Keep the Hamster Running 2016 Mid-Atlantic Chapter Spring Conference March 17 th 18 th 2016, Williamsburg, Virginia Cecilia Loftus Bob Bye

Compensating Your Management Team

Compensating Your Management Team Presented by: Tim Woods, CPA, MBA, MSF Managing Director and Shareholder CBIZ & Mayer Hoffman McCann April 17, 2014 Today s Presenter Tim Woods, CPA, MBA, MSF Shareholder

Compensating Your Management Team Presented by: Tim Woods, CPA, MBA, MSF Managing Director and Shareholder CBIZ & Mayer Hoffman McCann April 17, 2014 Today s Presenter Tim Woods, CPA, MBA, MSF Shareholder

ESOPs: Continuing a Legacy 10/30/2018. THOUGHTWARE Manufacturing & Distribution THOUGHTWARE. Cara Benningfield Partner Bowling Green

THOUGHTWARE Manufacturing & Distribution THOUGHTWARE ESOPs: Continuing a Legacy Cara Benningfield Partner Bowling Green 270.781.0111 Angela Fisher Managing Consultant Bowling Green 270.781.0111 November

THOUGHTWARE Manufacturing & Distribution THOUGHTWARE ESOPs: Continuing a Legacy Cara Benningfield Partner Bowling Green 270.781.0111 Angela Fisher Managing Consultant Bowling Green 270.781.0111 November

April 5, To our fellow stockholders:

April 5, 2017 To our fellow stockholders: Fiscal 2016 was a year of significant accomplishment for Primerica. Our Board of Directors continues to work to create stockholder value and achieve success through

April 5, 2017 To our fellow stockholders: Fiscal 2016 was a year of significant accomplishment for Primerica. Our Board of Directors continues to work to create stockholder value and achieve success through

SILVER, FREEDMAN & TAFF, L.L.P. A LIMITED LIABILITY PARTNERSHIP INCLUDING PROFESSIONAL CORPORATIONS

LAW OFFICES SILVER, FREEDMAN & TAFF, L.L.P. A LIMITED LIABILITY PARTNERSHIP INCLUDING PROFESSIONAL CORPORATIONS 3299 K STREET, N.W., SUITE 100 WASHINGTON, D.C. 20007 PHONE: (202) 295-4500 FAX: (202) 337-5502

LAW OFFICES SILVER, FREEDMAN & TAFF, L.L.P. A LIMITED LIABILITY PARTNERSHIP INCLUDING PROFESSIONAL CORPORATIONS 3299 K STREET, N.W., SUITE 100 WASHINGTON, D.C. 20007 PHONE: (202) 295-4500 FAX: (202) 337-5502

A comprehensive guide to ESOPs

A comprehensive guide to ESOPs Audit / Tax / Advisory / Risk / Performance Smart decisions. Lasting value. Contents Introduction... 3 What is an ESOP?... 5 ESOPs as a corporate financing mechanism... 6

A comprehensive guide to ESOPs Audit / Tax / Advisory / Risk / Performance Smart decisions. Lasting value. Contents Introduction... 3 What is an ESOP?... 5 ESOPs as a corporate financing mechanism... 6

GRANTING EQUITY TO EMPLOYEES AND CONTRACTORS. Curt P. Creely, Esq. Foley & Lardner LLP October 2012

GRANTING EQUITY TO EMPLOYEES AND CONTRACTORS Curt P. Creely, Esq. Foley & Lardner LLP October 2012 Examples of Equity Grants: Grants of stock or membership units (generally granted in the form of restricted

GRANTING EQUITY TO EMPLOYEES AND CONTRACTORS Curt P. Creely, Esq. Foley & Lardner LLP October 2012 Examples of Equity Grants: Grants of stock or membership units (generally granted in the form of restricted

Amended and Restated Wachovia Corporation 2003 Stock Incentive Plan

THIS DOCUMENT CONSTITUTES PART OF A PROSPECTUS COVERING SECURITIES THAT HAVE BEEN REGISTERED UNDER THE U.S. SECURITIES ACT OF 1933. Amended and Restated Wachovia Corporation 2003 Stock Incentive Plan Prospectus

THIS DOCUMENT CONSTITUTES PART OF A PROSPECTUS COVERING SECURITIES THAT HAVE BEEN REGISTERED UNDER THE U.S. SECURITIES ACT OF 1933. Amended and Restated Wachovia Corporation 2003 Stock Incentive Plan Prospectus

Administrative Procedures for the Teachers Retirement Board s Compensation Policy Section 700

Administrative Procedures for the Teachers Retirement Board s Compensation Policy Section 700 PURPOSE The purpose of this document is to provide the terms, conditions, and plan mechanics related to CalSTRS

Administrative Procedures for the Teachers Retirement Board s Compensation Policy Section 700 PURPOSE The purpose of this document is to provide the terms, conditions, and plan mechanics related to CalSTRS

August 28, Incentive Compensation Strategies to Build Your Company, Win New Business & Develop a Strategic Exit Plan

August 28, 2014 Incentive Compensation Strategies to Build Your Company, Win New Business & Develop a Strategic Exit Plan 1 Determine Appropriate Starting Point Income taxes Who are you going reward? Valuation

August 28, 2014 Incentive Compensation Strategies to Build Your Company, Win New Business & Develop a Strategic Exit Plan 1 Determine Appropriate Starting Point Income taxes Who are you going reward? Valuation

Compensating the CEO of a Single Family Office

Compensating the CEO of a Single Family Office Henry C. Blackiston, Esq, Senior Counsel Seyfarth Shaw LLP As a family member responsible for a single family office, assume you have just hired the ideal

Compensating the CEO of a Single Family Office Henry C. Blackiston, Esq, Senior Counsel Seyfarth Shaw LLP As a family member responsible for a single family office, assume you have just hired the ideal

IRS Finalizes Regulations Under Section 409A, Finally

April 18, 2007 IRS Finalizes Regulations Under Section 409A, Finally On April 10 th, the IRS issued long-awaited final regulations under Code section 409A. The regulations primarily finalize rules contained

April 18, 2007 IRS Finalizes Regulations Under Section 409A, Finally On April 10 th, the IRS issued long-awaited final regulations under Code section 409A. The regulations primarily finalize rules contained

STOCK OPTIONS AND EQUITY COMPENSATION

STOCK OPTIONS AND EQUITY COMPENSATION 47 th Annual Texas CPA Tax Institute Houston, Dallas, San Antonio November 14-16, 2000 William H. Hornberger James R. Griffin whornberger@jw.com jgriffin@jw.com 214

STOCK OPTIONS AND EQUITY COMPENSATION 47 th Annual Texas CPA Tax Institute Houston, Dallas, San Antonio November 14-16, 2000 William H. Hornberger James R. Griffin whornberger@jw.com jgriffin@jw.com 214

February 19, Alternatives to Sharing Stock How to Share Value with Diluting Equity

February 19, 2015 4 Alternatives to Sharing Stock How to Share Value with Diluting Equity Today s Presenter: Ken Gibson Senior Vice President (949) 265-5703 kgibson@vladvisors.com 7700 Irvine Center Drive,

February 19, 2015 4 Alternatives to Sharing Stock How to Share Value with Diluting Equity Today s Presenter: Ken Gibson Senior Vice President (949) 265-5703 kgibson@vladvisors.com 7700 Irvine Center Drive,

Equity-Based Compensation What Issues Do We Need to Consider?

BishopDulaneyJoyner&Abner Equity-Based Compensation What Issues Do We Need to Consider? by J. Dain Dulaney Jr., Attorney J. Dain Dulaney, Jr., Attorney ddulaney@bdjalaw.com v Dain s practice focuses on

BishopDulaneyJoyner&Abner Equity-Based Compensation What Issues Do We Need to Consider? by J. Dain Dulaney Jr., Attorney J. Dain Dulaney, Jr., Attorney ddulaney@bdjalaw.com v Dain s practice focuses on

NONQUALIFIED DEFERRED COMPENSATION: THE EFFECT OF THE NEW RULES NOW AND IN THE FUTURE

NONQUALIFIED DEFERRED COMPENSATION: THE EFFECT OF THE NEW RULES NOW AND IN THE FUTURE By Deloitte Tax LLP This special report was authored by Deborah Walker, partner (former deputy to the benefits tax

NONQUALIFIED DEFERRED COMPENSATION: THE EFFECT OF THE NEW RULES NOW AND IN THE FUTURE By Deloitte Tax LLP This special report was authored by Deborah Walker, partner (former deputy to the benefits tax

Creative Employee Incentive Plans Creating a Win-Win December 2016

Creative Employee Incentive Plans Creating a Win-Win December 2016 1 The Lanehaven Experience Key Components of a Plan Plan Structures Case Study Two Perspectives Sally Hollis Owner Kathleen Walton Principal/Growth

Creative Employee Incentive Plans Creating a Win-Win December 2016 1 The Lanehaven Experience Key Components of a Plan Plan Structures Case Study Two Perspectives Sally Hollis Owner Kathleen Walton Principal/Growth

RETIREMENT TAXATION UPDATE

RETIREMENT TAXATION UPDATE UNDERSTANDING EMPLOYEE STOCK OWNERSHIP PLANS Marc S. Schechter Butterfield Schechter LLP SCHECHTER LLP ATTORNEYS & COUNSELORS 10616 Scripps Summit Court, Suite 200 San Diego,

RETIREMENT TAXATION UPDATE UNDERSTANDING EMPLOYEE STOCK OWNERSHIP PLANS Marc S. Schechter Butterfield Schechter LLP SCHECHTER LLP ATTORNEYS & COUNSELORS 10616 Scripps Summit Court, Suite 200 San Diego,

EMPLOYEE INCENTIVE PLANNING

EMPLOYEE INCENTIVE PLANNING WHITE PAPER Chuck Baldwin Baldwin & Clarke Advisory Services, Inc. 116 A South River Road Coldstream Park Bedford, NH 03110 Phone: 603-668-4353 http://www.baldwinclarke.com

EMPLOYEE INCENTIVE PLANNING WHITE PAPER Chuck Baldwin Baldwin & Clarke Advisory Services, Inc. 116 A South River Road Coldstream Park Bedford, NH 03110 Phone: 603-668-4353 http://www.baldwinclarke.com

Medtronic Savings and Investment Plan

DB1/ 87571888.13 Medtronic Savings and Investment Plan (Also known as the Medtronic 401(k) Plan ) January 1, 2016 MEDTRONIC SAVINGS AND INVESTMENT PLAN This document is a summary of the Medtronic Savings

DB1/ 87571888.13 Medtronic Savings and Investment Plan (Also known as the Medtronic 401(k) Plan ) January 1, 2016 MEDTRONIC SAVINGS AND INVESTMENT PLAN This document is a summary of the Medtronic Savings

Alan Taylor. Partner Bowling Green, KY BKD, LLP.

ESOPs: Creating a Legacy June 28, 2012 Alan Taylor Partner Bowling Green, KY BKD, LLP ataylor@bkd.com To Receive CPE Credit Participate in entire webinar Answer polls when they are provided If you are

ESOPs: Creating a Legacy June 28, 2012 Alan Taylor Partner Bowling Green, KY BKD, LLP ataylor@bkd.com To Receive CPE Credit Participate in entire webinar Answer polls when they are provided If you are

ROCK N ROLL DUTIES: Fiduciary Duty Issues for Employee Stock Ownership Plans

ROCK N ROLL DUTIES: Fiduciary Duty Issues for Employee Stock Ownership Plans New South Chapter of the ESOP Association Fall Conference - September 19, 2013 Gordon Earle Nichols Eileen Wyatt babc.com ALABAMA

ROCK N ROLL DUTIES: Fiduciary Duty Issues for Employee Stock Ownership Plans New South Chapter of the ESOP Association Fall Conference - September 19, 2013 Gordon Earle Nichols Eileen Wyatt babc.com ALABAMA

Fund Appreciation Rights

Fund Appreciation Rights What They Are and How They Can Work for Institutional Investors and Hedge Fund Managers Panelists: Joel D. Almquist, K&L Gates Partner James E. Earle, K&L Gates Partner Rick Ehrhart,

Fund Appreciation Rights What They Are and How They Can Work for Institutional Investors and Hedge Fund Managers Panelists: Joel D. Almquist, K&L Gates Partner James E. Earle, K&L Gates Partner Rick Ehrhart,

Planning for Retirement Needs

Planning for Retirement Needs Equity Based Compensation Plans Chapter 16 Chapter 16: Equity Based Compensation Why equity based compensation Nonqualified stock options Incentive stock options (ISO) Employee

Planning for Retirement Needs Equity Based Compensation Plans Chapter 16 Chapter 16: Equity Based Compensation Why equity based compensation Nonqualified stock options Incentive stock options (ISO) Employee

Prospectus. Alcoa Corporation. Common Stock. Alcoa Corporation 2016 Stock Incentive Plan (As Amended and Restated)

") Prospectus Alcoa Corporation Common Stock Alcoa Corporation 2016 Stock Incentive Plan (As Amended and Restated) This prospectus relates to shares of common stock, par value $0.01 per share (the Common

Prospectus Alcoa Corporation Common Stock Alcoa Corporation 2016 Stock Incentive Plan (As Amended and Restated) This prospectus relates to shares of common stock, par value $0.01 per share (the Common

Directors Compensation Policy Approved by 91.71% of shareholders on 7 June 2017

Approved by 91.71% of shareholders on 7 June 2017 The Compensation Committee presents the proposed for 2017-2019. It is the intention of the committee that this policy will be maintained for three years

Approved by 91.71% of shareholders on 7 June 2017 The Compensation Committee presents the proposed for 2017-2019. It is the intention of the committee that this policy will be maintained for three years

June Private Foundation

June 2017 Private Foundation A private foundation is a legal entity created, funded and operated for the primary purpose of making grants to charities. Because of its charitable mission, a private foundation

June 2017 Private Foundation A private foundation is a legal entity created, funded and operated for the primary purpose of making grants to charities. Because of its charitable mission, a private foundation

Part III. Administrative, Procedural, and Miscellaneous

Part III. Administrative, Procedural, and Miscellaneous Guidance Under 409A of the Internal Revenue Code Notice 2005 1 I. Purpose and Overview Section 885 of the recently enacted American Jobs Creation

Part III. Administrative, Procedural, and Miscellaneous Guidance Under 409A of the Internal Revenue Code Notice 2005 1 I. Purpose and Overview Section 885 of the recently enacted American Jobs Creation