Modeling Capital Market with Financial Signal Processing

|

|

|

- Louisa Williams

- 5 years ago

- Views:

Transcription

1 Modeling Capital Market with Financial Signal Processing Jenher Jeng Ph.D., Statistics, U.C. Berkeley Founder & CTO of Harmonic Financial Engineering,

2 Outline Theory and Techniques Theoretic Framework of Modeling Capital Markets: Index-Based Composition Methodology Statistical Procedure of Model Construction and Extension: Wavelets-Based Financial Signal Processing Technique Implications and Applications (ex. S&P 5) Measuring Market Uncertainty and Volatility Formatting Dynamic Strategies into Strategic Curves: Adaptive Futures Leveraging & Efficient Options Pricing Monitoring Impacts of Smart-Money Timing Strategies Gauging Cyclic Structure & Forecasting Market Crises Converging Patterns towards Market Crashes and Bubbles

3 Theoretic Framework of Modeling Capital Markets Index-Based Composition Methodology R i+1 = r i + Ψ(S i ) + Σ(S i ) ε i+1, ε i s i.i.d. ~ N(,1). Strategic Index S i = Γ(R i-l+1,, R i ) static regression dynamic auto-regression Non-stationary Correlation Noise barrier R i+1 = r i + µ(r i-l+1,, R i ) + σ(r i-l+1,, R i ) ε i+1, µ = Ψ Γ ; σ = Σ Γ Dimension Curse R i+1 : (i+1)-th periodical short-term market return rate - say, S&P 5 monthly; r i : i-th periodical average short-term interest rate - say, FFR monthly average; S i : i-th periodically updated strategic index value say, STTB Index, shown next

4 Mission Impossible to De-noise through Dimension Curse Piecewise (Monthly) Constant Geometric Brownian Motion dx t /X t = r i + µ i + σ i dw t, for t i-1 t <t i Key of Long-Term Consistent Profitability: Low-Frequency Component of Market Fluctuation Patterns about Interactions between µ i s and σ i s on Time-Domain Non-Stationarity & High-Frequency Noise-Barrier Knowledge in Ψ and Σ on S-Domain

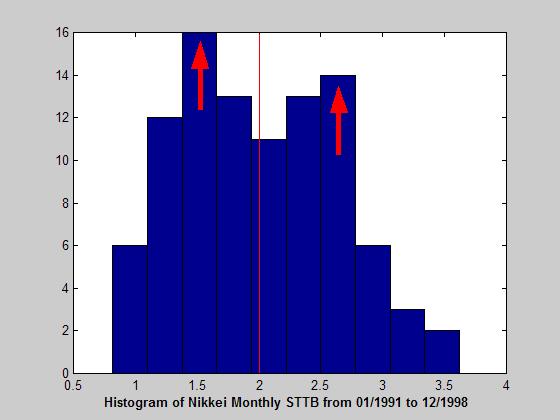

5 Month.2 9/ / / / / / / Strategic Index Short-Term Trend Bias (STTB) Γ (non-parametric statistic) A Typical Series of Patterns for Illustrating the Point of STTB Bar Chart of 12-M RR Line-Joined Chart of 12-M RR STTB

6 Distribution of STTB

7 Gauging the Structure of a Market Cycle Monthly S TTB 12-Month S TTB Moving Average 12-Month S &P 5 Return Rate M. A. (% ) /1951 2/23 higher Red up, steeper Blue down; longer Red stays up, deeper Blue sinks down; vice versa

8 Consistently Leading the Cyclic Trend Monthly S TTB 12-Month S TTB Moving Average 12-Month S &P 5 Return Rate M. A. (% ) /1981 6/1985 Red Series (MA_STTB) is leading Blue Series in turnaround in a smooth conclusive way

9 The Fundamental Model Quantitative Psychological Model Parametric Model: Linear Heteroscedastic Parabolic Model R i+1 -r i = Ψ(S i ) + Σ(S i ) ε i+1, Ψ(S) = k (S-a) 2 +b; Σ(S) = c S+d, for 1 S<3. a Maximum Uncertainty Level: MLE = 2.92 b Uncertainty Aversion Rate: MLE = -.14 k Rational Confidence Coefficient: MLE =.17 c Stability Coefficient: MLE =.96 d Efficient Market Volatility: MLE =.23 *** MLE results are based on S&P 5 monthly data from 1/1951 to 2/23 *** Market Volatility = Dynamic (Low-Freq.: Uncertainty) + Stochastic (High-Freq.: Stability) Certainty Ψ Unstability Σ a STTB STTB

10 Basic Structure of Shaping Dynamic Investment Strategies over Domain of Strategic Index Strategic Curve Action Parameter (for Investment Decision-Making) Θ(S) shape of strategic curve goal of the strategy knowledge about the market Elementary Examples Strategic Index S (e.g. STTB) Future Leveraging Strategy maximizing cumulative return of a simple portfolio combining S&P 5 Stock Index Future and Cash (leverage-multiple of the total invested capital) Θ(S) =Ψ(S) / Σ 2 (S) Option Pricing Strategy fairly pricing the value of a One-Month At-The-Money Call contract (as a fraction of the current value of the underlying asset) Θ(S) = Φ[(r/Σ 2 +Ψ/Σ 2 +1/2) Σ] e -(r+ψ) Φ[(r/Σ 2 +Ψ/Σ 2-1/2) Σ]

11 Efficient Options Pricing Black-Scholes Model R i+1 = r i + µ + σ ε i+1 L.H.P. Composite Model R i+1 = r i + Ψ(S i ) + Σ(S i ) ε i+1 Expected Return = r + µ?; Volatility = σ? Predict Expected Return & Volatility by Interest Rate and STTB

12 Adaptive Leveraging Strategy for S&P 5 Future in comparison with one via model-free simulation maximizing cumulative return without risk control H i Empirical Raw Optimal Strategy Theoretical Raw Optimal Strategy Ψ/Σ 2 6 4? S i The Mystery of The Missing Bump?

13 The Complex extending knowledge beyond the psychological factor Complex Additive Model R i+1 = [Ψ(S i ) + (S i ) + Ω(S i )] + Σ(S i ) ε i+1, ε i s i.i.d. ~ N(,1). Psychological Factor Strategical Factor Rationality-Oriented, such as Uncertainty, Momentum Ψ, Smooth Curve Discipline-Oriented, such as Contrarian, Hedge Fund Arbitrage = + 1,, Concentrated Missing Bump Economical Factor Policy-Oriented, such as Short-Term Interest Rate (Feds Fund Rate) Ω(S i ) = r i + δ(s i ), δ, asymmetrically distributed

14 Nonparametric Decomposition to realize Model-Free Simulation distinguishing and recognizing factors moving the market Advanced Financial Signal Processing via Wavelet Technique Raw Financial Signal: R i+1 -r i = [Ψ(S i ) + (S i ) + δ(s i )] + Σ(S i ) ε i+1, i=1,, n R (%).1 W a ve le t M ulti-r e solutio n C om p one nts o f the F ina n c ia l S igna l Ψ,, δ, N Σ S, δ, N ,, δ, N on Daubechies 5 Basis on Haar Basis decomposition levels (log 2 n) with higher resolution are ignored almost nothing living there except for the components of the heteroscedastic white noise LHP C

15 Two-Peak Phenomenon

16 A Clue to the Remarkable Story of the Great Crash value of parameter a Month S TTB Moving Average 12-Month S &P 5 Return M.A. (% ) Max 2 Unc e rta inty Line 1-1 Feb 1986 Oct Nov 1981 Jul 1993

17 Similar Sign before Another Crash in Another Market

18 Striking Coincidence

19 Principle of Cyclic Hazard from the above two pre-crash patterns, it is intuitive to perceive the following principle: When the market s behavior eventually evolves into a rapid oscillation around the maximum uncertainty level rather than taking a typical cyclic course, the chance for the market to crash and the crash extent will increase day-by-day until that happens.

20 Bubble Phenomena: a dynamic picture for the principle of cyclic hazard Nikkei 225 S&P /85 12/9 4/96 4/1 as the cycles keep converging to, thus oscillating around, the maximum uncertainty level, accumulating fear of uncertainty builds up to end up with a market crisis

21 Underlying Mechanism for Principle of Cyclic Hazard Ping-Pong Hazard - a physical illustration with a pendulum

ARCH Models and Financial Applications

Christian Gourieroux ARCH Models and Financial Applications With 26 Figures Springer Contents 1 Introduction 1 1.1 The Development of ARCH Models 1 1.2 Book Content 4 2 Linear and Nonlinear Processes 5

Christian Gourieroux ARCH Models and Financial Applications With 26 Figures Springer Contents 1 Introduction 1 1.1 The Development of ARCH Models 1 1.2 Book Content 4 2 Linear and Nonlinear Processes 5

The Black-Scholes Model

IEOR E4706: Foundations of Financial Engineering c 2016 by Martin Haugh The Black-Scholes Model In these notes we will use Itô s Lemma and a replicating argument to derive the famous Black-Scholes formula

IEOR E4706: Foundations of Financial Engineering c 2016 by Martin Haugh The Black-Scholes Model In these notes we will use Itô s Lemma and a replicating argument to derive the famous Black-Scholes formula

Financial Risk Management

Financial Risk Management Professor: Thierry Roncalli Evry University Assistant: Enareta Kurtbegu Evry University Tutorial exercices #3 1 Maximum likelihood of the exponential distribution 1. We assume

Financial Risk Management Professor: Thierry Roncalli Evry University Assistant: Enareta Kurtbegu Evry University Tutorial exercices #3 1 Maximum likelihood of the exponential distribution 1. We assume

Dynamic Portfolio Choice II

Dynamic Portfolio Choice II Dynamic Programming Leonid Kogan MIT, Sloan 15.450, Fall 2010 c Leonid Kogan ( MIT, Sloan ) Dynamic Portfolio Choice II 15.450, Fall 2010 1 / 35 Outline 1 Introduction to Dynamic

Dynamic Portfolio Choice II Dynamic Programming Leonid Kogan MIT, Sloan 15.450, Fall 2010 c Leonid Kogan ( MIT, Sloan ) Dynamic Portfolio Choice II 15.450, Fall 2010 1 / 35 Outline 1 Introduction to Dynamic

Modelling the Term Structure of Hong Kong Inter-Bank Offered Rates (HIBOR)

") Economics World, Jan.-Feb. 2016, Vol. 4, No. 1, 7-16 doi: 10.17265/2328-7144/2016.01.002 D DAVID PUBLISHING Modelling the Term Structure of Hong Kong Inter-Bank Offered Rates (HIBOR) Sandy Chau, Andy Tai,

Economics World, Jan.-Feb. 2016, Vol. 4, No. 1, 7-16 doi: 10.17265/2328-7144/2016.01.002 D DAVID PUBLISHING Modelling the Term Structure of Hong Kong Inter-Bank Offered Rates (HIBOR) Sandy Chau, Andy Tai,

MODELLING OPTIMAL HEDGE RATIO IN THE PRESENCE OF FUNDING RISK

MODELLING OPTIMAL HEDGE RATIO IN THE PRESENCE O UNDING RISK Barbara Dömötör Department of inance Corvinus University of Budapest 193, Budapest, Hungary E-mail: barbara.domotor@uni-corvinus.hu KEYWORDS

MODELLING OPTIMAL HEDGE RATIO IN THE PRESENCE O UNDING RISK Barbara Dömötör Department of inance Corvinus University of Budapest 193, Budapest, Hungary E-mail: barbara.domotor@uni-corvinus.hu KEYWORDS

Risk Control of Mean-Reversion Time in Statistical Arbitrage,

Risk Control of Mean-Reversion Time in Statistical Arbitrage George Papanicolaou Stanford University CDAR Seminar, UC Berkeley April 6, 8 with Joongyeub Yeo Risk Control of Mean-Reversion Time in Statistical

Risk Control of Mean-Reversion Time in Statistical Arbitrage George Papanicolaou Stanford University CDAR Seminar, UC Berkeley April 6, 8 with Joongyeub Yeo Risk Control of Mean-Reversion Time in Statistical

FE501 Stochastic Calculus for Finance 1.5:0:1.5

Descriptions of Courses FE501 Stochastic Calculus for Finance 1.5:0:1.5 This course introduces martingales or Markov properties of stochastic processes. The most popular example of stochastic process is

Descriptions of Courses FE501 Stochastic Calculus for Finance 1.5:0:1.5 This course introduces martingales or Markov properties of stochastic processes. The most popular example of stochastic process is

OULU BUSINESS SCHOOL. Ilkka Rahikainen DIRECT METHODOLOGY FOR ESTIMATING THE RISK NEUTRAL PROBABILITY DENSITY FUNCTION

OULU BUSINESS SCHOOL Ilkka Rahikainen DIRECT METHODOLOGY FOR ESTIMATING THE RISK NEUTRAL PROBABILITY DENSITY FUNCTION Master s Thesis Finance March 2014 UNIVERSITY OF OULU Oulu Business School ABSTRACT

OULU BUSINESS SCHOOL Ilkka Rahikainen DIRECT METHODOLOGY FOR ESTIMATING THE RISK NEUTRAL PROBABILITY DENSITY FUNCTION Master s Thesis Finance March 2014 UNIVERSITY OF OULU Oulu Business School ABSTRACT

Statistical Models and Methods for Financial Markets

Tze Leung Lai/ Haipeng Xing Statistical Models and Methods for Financial Markets B 374756 4Q Springer Preface \ vii Part I Basic Statistical Methods and Financial Applications 1 Linear Regression Models

Tze Leung Lai/ Haipeng Xing Statistical Models and Methods for Financial Markets B 374756 4Q Springer Preface \ vii Part I Basic Statistical Methods and Financial Applications 1 Linear Regression Models

Beyond the Black-Scholes-Merton model

Econophysics Lecture Leiden, November 5, 2009 Overview 1 Limitations of the Black-Scholes model 2 3 4 Limitations of the Black-Scholes model Black-Scholes model Good news: it is a nice, well-behaved model

Econophysics Lecture Leiden, November 5, 2009 Overview 1 Limitations of the Black-Scholes model 2 3 4 Limitations of the Black-Scholes model Black-Scholes model Good news: it is a nice, well-behaved model

INVESTMENTS Class 2: Securities, Random Walk on Wall Street

15.433 INVESTMENTS Class 2: Securities, Random Walk on Wall Street Reto R. Gallati MIT Sloan School of Management Spring 2003 February 5th 2003 Outline Probability Theory A brief review of probability

15.433 INVESTMENTS Class 2: Securities, Random Walk on Wall Street Reto R. Gallati MIT Sloan School of Management Spring 2003 February 5th 2003 Outline Probability Theory A brief review of probability

On modelling of electricity spot price

, Rüdiger Kiesel and Fred Espen Benth Institute of Energy Trading and Financial Services University of Duisburg-Essen Centre of Mathematics for Applications, University of Oslo 25. August 2010 Introduction

, Rüdiger Kiesel and Fred Espen Benth Institute of Energy Trading and Financial Services University of Duisburg-Essen Centre of Mathematics for Applications, University of Oslo 25. August 2010 Introduction

CLASS 4: ASSEt pricing. The Intertemporal Model. Theory and Experiment

CLASS 4: ASSEt pricing. The Intertemporal Model. Theory and Experiment Lessons from the 1- period model If markets are complete then the resulting equilibrium is Paretooptimal (no alternative allocation

CLASS 4: ASSEt pricing. The Intertemporal Model. Theory and Experiment Lessons from the 1- period model If markets are complete then the resulting equilibrium is Paretooptimal (no alternative allocation

Lecture 4. Finite difference and finite element methods

Finite difference and finite element methods Lecture 4 Outline Black-Scholes equation From expectation to PDE Goal: compute the value of European option with payoff g which is the conditional expectation

Finite difference and finite element methods Lecture 4 Outline Black-Scholes equation From expectation to PDE Goal: compute the value of European option with payoff g which is the conditional expectation

Weak Reflection Principle and Static Hedging of Barrier Options

Weak Reflection Principle and Static Hedging of Barrier Options Sergey Nadtochiy Department of Mathematics University of Michigan Apr 2013 Fields Quantitative Finance Seminar Fields Institute, Toronto

Weak Reflection Principle and Static Hedging of Barrier Options Sergey Nadtochiy Department of Mathematics University of Michigan Apr 2013 Fields Quantitative Finance Seminar Fields Institute, Toronto

Valuing Investments A Statistical Perspective. Bob Stine Department of Statistics Wharton, University of Pennsylvania

Valuing Investments A Statistical Perspective Bob Stine, University of Pennsylvania Overview Principles Focus on returns, not cumulative value Remove market performance (CAPM) Watch for unseen volatility

Valuing Investments A Statistical Perspective Bob Stine, University of Pennsylvania Overview Principles Focus on returns, not cumulative value Remove market performance (CAPM) Watch for unseen volatility

Vladimir Spokoiny (joint with J.Polzehl) Varying coefficient GARCH versus local constant volatility modeling.

Varying coefficient GARCH versus local constant volatility modeling.") W e ie rstra ß -In stitu t fü r A n g e w a n d te A n a ly sis u n d S to c h a stik STATDEP 2005 Vladimir Spokoiny (joint with J.Polzehl) Varying coefficient GARCH versus local constant volatility modeling.

W e ie rstra ß -In stitu t fü r A n g e w a n d te A n a ly sis u n d S to c h a stik STATDEP 2005 Vladimir Spokoiny (joint with J.Polzehl) Varying coefficient GARCH versus local constant volatility modeling.

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2011, Mr. Ruey S. Tsay. Solutions to Final Exam.

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2011, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (32 pts) Answer briefly the following questions. 1. Suppose

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2011, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (32 pts) Answer briefly the following questions. 1. Suppose

IEOR E4703: Monte-Carlo Simulation

IEOR E4703: Monte-Carlo Simulation Simulating Stochastic Differential Equations Martin Haugh Department of Industrial Engineering and Operations Research Columbia University Email: martin.b.haugh@gmail.com

IEOR E4703: Monte-Carlo Simulation Simulating Stochastic Differential Equations Martin Haugh Department of Industrial Engineering and Operations Research Columbia University Email: martin.b.haugh@gmail.com

Practical Hedging: From Theory to Practice. OSU Financial Mathematics Seminar May 5, 2008

Practical Hedging: From Theory to Practice OSU Financial Mathematics Seminar May 5, 008 Background Dynamic replication is a risk management technique used to mitigate market risk We hope to spend a certain

Practical Hedging: From Theory to Practice OSU Financial Mathematics Seminar May 5, 008 Background Dynamic replication is a risk management technique used to mitigate market risk We hope to spend a certain

Lecture One. Dynamics of Moving Averages. Tony He University of Technology, Sydney, Australia

Lecture One Dynamics of Moving Averages Tony He University of Technology, Sydney, Australia AI-ECON (NCCU) Lectures on Financial Market Behaviour with Heterogeneous Investors August 2007 Outline Related

Lecture One Dynamics of Moving Averages Tony He University of Technology, Sydney, Australia AI-ECON (NCCU) Lectures on Financial Market Behaviour with Heterogeneous Investors August 2007 Outline Related

The Effects of Monetary Policy on Asset Price Bubbles: Some Evidence

The Effects of Monetary Policy on Asset Price Bubbles: Some Evidence Jordi Galí Luca Gambetti September 2013 Jordi Galí, Luca Gambetti () Monetary Policy and Bubbles September 2013 1 / 17 Monetary Policy

The Effects of Monetary Policy on Asset Price Bubbles: Some Evidence Jordi Galí Luca Gambetti September 2013 Jordi Galí, Luca Gambetti () Monetary Policy and Bubbles September 2013 1 / 17 Monetary Policy

1. What is Implied Volatility?

Numerical Methods FEQA MSc Lectures, Spring Term 2 Data Modelling Module Lecture 2 Implied Volatility Professor Carol Alexander Spring Term 2 1 1. What is Implied Volatility? Implied volatility is: the

Numerical Methods FEQA MSc Lectures, Spring Term 2 Data Modelling Module Lecture 2 Implied Volatility Professor Carol Alexander Spring Term 2 1 1. What is Implied Volatility? Implied volatility is: the

Mathematics in Finance

Mathematics in Finance Steven E. Shreve Department of Mathematical Sciences Carnegie Mellon University Pittsburgh, PA 15213 USA shreve@andrew.cmu.edu A Talk in the Series Probability in Science and Industry

Mathematics in Finance Steven E. Shreve Department of Mathematical Sciences Carnegie Mellon University Pittsburgh, PA 15213 USA shreve@andrew.cmu.edu A Talk in the Series Probability in Science and Industry

Chapter 5 Univariate time-series analysis. () Chapter 5 Univariate time-series analysis 1 / 29

Chapter 5 Univariate time-series analysis 1 / 29") Chapter 5 Univariate time-series analysis () Chapter 5 Univariate time-series analysis 1 / 29 Time-Series Time-series is a sequence fx 1, x 2,..., x T g or fx t g, t = 1,..., T, where t is an index denoting

Chapter 5 Univariate time-series analysis () Chapter 5 Univariate time-series analysis 1 / 29 Time-Series Time-series is a sequence fx 1, x 2,..., x T g or fx t g, t = 1,..., T, where t is an index denoting

Microeconomic Foundations of Incomplete Price Adjustment

Chapter 6 Microeconomic Foundations of Incomplete Price Adjustment In Romer s IS/MP/IA model, we assume prices/inflation adjust imperfectly when output changes. Empirically, there is a negative relationship

Chapter 6 Microeconomic Foundations of Incomplete Price Adjustment In Romer s IS/MP/IA model, we assume prices/inflation adjust imperfectly when output changes. Empirically, there is a negative relationship

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2012, Mr. Ruey S. Tsay. Solutions to Final Exam

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2012, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (40 points) Answer briefly the following questions. 1. Consider

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2012, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (40 points) Answer briefly the following questions. 1. Consider

Lecture 8: The Black-Scholes theory

Lecture 8: The Black-Scholes theory Dr. Roman V Belavkin MSO4112 Contents 1 Geometric Brownian motion 1 2 The Black-Scholes pricing 2 3 The Black-Scholes equation 3 References 5 1 Geometric Brownian motion

Lecture 8: The Black-Scholes theory Dr. Roman V Belavkin MSO4112 Contents 1 Geometric Brownian motion 1 2 The Black-Scholes pricing 2 3 The Black-Scholes equation 3 References 5 1 Geometric Brownian motion

Assicurazioni Generali: An Option Pricing Case with NAGARCH

Assicurazioni Generali: An Option Pricing Case with NAGARCH Assicurazioni Generali: Business Snapshot Find our latest analyses and trade ideas on bsic.it Assicurazioni Generali SpA is an Italy-based insurance

Assicurazioni Generali: An Option Pricing Case with NAGARCH Assicurazioni Generali: Business Snapshot Find our latest analyses and trade ideas on bsic.it Assicurazioni Generali SpA is an Italy-based insurance

FEAR &GREED VOLATILITY MARKETS. Emanuel Derman. Quantitative Strategies Group Goldman Sachs & Co. Quantitative Strategies. Page 1 of 24. Fear&Greed.

FEAR &GREED IN VOLATILITY MARKETS ~ Emanuel Derman Group Goldman Sachs & Co. Page 1 of 24 Fear&Greed.fm Are There Patterns to Volatility Changes? Since 1987, global index options markets are persistently

FEAR &GREED IN VOLATILITY MARKETS ~ Emanuel Derman Group Goldman Sachs & Co. Page 1 of 24 Fear&Greed.fm Are There Patterns to Volatility Changes? Since 1987, global index options markets are persistently

B35150 Winter 2014 Quiz Solutions

B35150 Winter 2014 Quiz Solutions Alexander Zentefis March 16, 2014 Quiz 1 0.9 x 2 = 1.8 0.9 x 1.8 = 1.62 Quiz 1 Quiz 1 Quiz 1 64/ 256 = 64/16 = 4%. Volatility scales with square root of horizon. Quiz

B35150 Winter 2014 Quiz Solutions Alexander Zentefis March 16, 2014 Quiz 1 0.9 x 2 = 1.8 0.9 x 1.8 = 1.62 Quiz 1 Quiz 1 Quiz 1 64/ 256 = 64/16 = 4%. Volatility scales with square root of horizon. Quiz

Financial Returns: Stylized Features and Statistical Models

Financial Returns: Stylized Features and Statistical Models Qiwei Yao Department of Statistics London School of Economics q.yao@lse.ac.uk p.1 Definitions of returns Empirical evidence: daily prices in

Financial Returns: Stylized Features and Statistical Models Qiwei Yao Department of Statistics London School of Economics q.yao@lse.ac.uk p.1 Definitions of returns Empirical evidence: daily prices in

ASC Topic 718 Accounting Valuation Report. Company ABC, Inc.

ASC Topic 718 Accounting Valuation Report Company ABC, Inc. Monte-Carlo Simulation Valuation of Several Proposed Relative Total Shareholder Return TSR Component Rank Grants And Index Outperform Grants

ASC Topic 718 Accounting Valuation Report Company ABC, Inc. Monte-Carlo Simulation Valuation of Several Proposed Relative Total Shareholder Return TSR Component Rank Grants And Index Outperform Grants

Principal Component Analysis of the Volatility Smiles and Skews. Motivation

Principal Component Analysis of the Volatility Smiles and Skews Professor Carol Alexander Chair of Risk Management ISMA Centre University of Reading www.ismacentre.rdg.ac.uk 1 Motivation Implied volatilities

Principal Component Analysis of the Volatility Smiles and Skews Professor Carol Alexander Chair of Risk Management ISMA Centre University of Reading www.ismacentre.rdg.ac.uk 1 Motivation Implied volatilities

Should Norway Change the 60% Equity portion of the GPFG fund?

Should Norway Change the 60% Equity portion of the GPFG fund? Pierre Collin-Dufresne EPFL & SFI, and CEPR April 2016 Outline Endowment Consumption Commitments Return Predictability and Trading Costs General

Should Norway Change the 60% Equity portion of the GPFG fund? Pierre Collin-Dufresne EPFL & SFI, and CEPR April 2016 Outline Endowment Consumption Commitments Return Predictability and Trading Costs General

Fractional Brownian Motion as a Model in Finance

Fractional Brownian Motion as a Model in Finance Tommi Sottinen, University of Helsinki Esko Valkeila, University of Turku and University of Helsinki 1 Black & Scholes pricing model In the classical Black

Fractional Brownian Motion as a Model in Finance Tommi Sottinen, University of Helsinki Esko Valkeila, University of Turku and University of Helsinki 1 Black & Scholes pricing model In the classical Black

Trinity College and Darwin College. University of Cambridge. Taking the Art out of Smart Beta. Ed Fishwick, Cherry Muijsson and Steve Satchell

Trinity College and Darwin College University of Cambridge 1 / 32 Problem Definition We revisit last year s smart beta work of Ed Fishwick. The CAPM predicts that higher risk portfolios earn a higher return

Trinity College and Darwin College University of Cambridge 1 / 32 Problem Definition We revisit last year s smart beta work of Ed Fishwick. The CAPM predicts that higher risk portfolios earn a higher return

Lecture 17. The model is parametrized by the time period, δt, and three fixed constant parameters, v, σ and the riskless rate r.

Lecture 7 Overture to continuous models Before rigorously deriving the acclaimed Black-Scholes pricing formula for the value of a European option, we developed a substantial body of material, in continuous

Lecture 7 Overture to continuous models Before rigorously deriving the acclaimed Black-Scholes pricing formula for the value of a European option, we developed a substantial body of material, in continuous

Energy Price Processes

Energy Processes Used for Derivatives Pricing & Risk Management In this first of three articles, we will describe the most commonly used process, Geometric Brownian Motion, and in the second and third

Energy Processes Used for Derivatives Pricing & Risk Management In this first of three articles, we will describe the most commonly used process, Geometric Brownian Motion, and in the second and third

Expected Inflation Regime in Japan

Expected Inflation Regime in Japan Tatsuyoshi Okimoto (Okki) Crawford School of Public Policy Australian National University June 26, 2017 IAAE 2017 Expected Inflation Regime in Japan Expected Inflation

Expected Inflation Regime in Japan Tatsuyoshi Okimoto (Okki) Crawford School of Public Policy Australian National University June 26, 2017 IAAE 2017 Expected Inflation Regime in Japan Expected Inflation

Rough volatility models: When population processes become a new tool for trading and risk management

Rough volatility models: When population processes become a new tool for trading and risk management Omar El Euch and Mathieu Rosenbaum École Polytechnique 4 October 2017 Omar El Euch and Mathieu Rosenbaum

Rough volatility models: When population processes become a new tool for trading and risk management Omar El Euch and Mathieu Rosenbaum École Polytechnique 4 October 2017 Omar El Euch and Mathieu Rosenbaum

Prospect Theory, Partial Liquidation and the Disposition Effect

Prospect Theory, Partial Liquidation and the Disposition Effect Vicky Henderson Oxford-Man Institute of Quantitative Finance University of Oxford vicky.henderson@oxford-man.ox.ac.uk 6th Bachelier Congress,

Prospect Theory, Partial Liquidation and the Disposition Effect Vicky Henderson Oxford-Man Institute of Quantitative Finance University of Oxford vicky.henderson@oxford-man.ox.ac.uk 6th Bachelier Congress,

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2009, Mr. Ruey S. Tsay. Solutions to Final Exam

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2009, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (42 pts) Answer briefly the following questions. 1. Questions

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2009, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (42 pts) Answer briefly the following questions. 1. Questions

BROWNIAN MOTION Antonella Basso, Martina Nardon

BROWNIAN MOTION Antonella Basso, Martina Nardon basso@unive.it, mnardon@unive.it Department of Applied Mathematics University Ca Foscari Venice Brownian motion p. 1 Brownian motion Brownian motion plays

BROWNIAN MOTION Antonella Basso, Martina Nardon basso@unive.it, mnardon@unive.it Department of Applied Mathematics University Ca Foscari Venice Brownian motion p. 1 Brownian motion Brownian motion plays

Ultra High Frequency Volatility Estimation with Market Microstructure Noise. Yacine Aït-Sahalia. Per A. Mykland. Lan Zhang

Ultra High Frequency Volatility Estimation with Market Microstructure Noise Yacine Aït-Sahalia Princeton University Per A. Mykland The University of Chicago Lan Zhang Carnegie-Mellon University 1. Introduction

Ultra High Frequency Volatility Estimation with Market Microstructure Noise Yacine Aït-Sahalia Princeton University Per A. Mykland The University of Chicago Lan Zhang Carnegie-Mellon University 1. Introduction

Corresponding author: Gregory C Chow,

Co-movements of Shanghai and New York stock prices by time-varying regressions Gregory C Chow a, Changjiang Liu b, Linlin Niu b,c a Department of Economics, Fisher Hall Princeton University, Princeton,

Co-movements of Shanghai and New York stock prices by time-varying regressions Gregory C Chow a, Changjiang Liu b, Linlin Niu b,c a Department of Economics, Fisher Hall Princeton University, Princeton,

Introduction to Financial Mathematics

Department of Mathematics University of Michigan November 7, 2008 My Information E-mail address: marymorj (at) umich.edu Financial work experience includes 2 years in public finance investment banking

Department of Mathematics University of Michigan November 7, 2008 My Information E-mail address: marymorj (at) umich.edu Financial work experience includes 2 years in public finance investment banking

Credit Spreads and the Macroeconomy

Credit Spreads and the Macroeconomy Simon Gilchrist Boston University and NBER Joint BIS-ECB Workshop on Monetary Policy & Financial Stability Bank for International Settlements Basel, Switzerland September

Credit Spreads and the Macroeconomy Simon Gilchrist Boston University and NBER Joint BIS-ECB Workshop on Monetary Policy & Financial Stability Bank for International Settlements Basel, Switzerland September

Definition Pricing Risk management Second generation barrier options. Barrier Options. Arfima Financial Solutions

Arfima Financial Solutions Contents Definition 1 Definition 2 3 4 Contenido Definition 1 Definition 2 3 4 Definition Definition: A barrier option is an option on the underlying asset that is activated

Arfima Financial Solutions Contents Definition 1 Definition 2 3 4 Contenido Definition 1 Definition 2 3 4 Definition Definition: A barrier option is an option on the underlying asset that is activated

Estimating Pricing Kernel via Series Methods

Estimating Pricing Kernel via Series Methods Maria Grith Wolfgang Karl Härdle Melanie Schienle Ladislaus von Bortkiewicz Chair of Statistics Chair of Econometrics C.A.S.E. Center for Applied Statistics

Estimating Pricing Kernel via Series Methods Maria Grith Wolfgang Karl Härdle Melanie Schienle Ladislaus von Bortkiewicz Chair of Statistics Chair of Econometrics C.A.S.E. Center for Applied Statistics

Factors in Implied Volatility Skew in Corn Futures Options

1 Factors in Implied Volatility Skew in Corn Futures Options Weiyu Guo* University of Nebraska Omaha 6001 Dodge Street, Omaha, NE 68182 Phone 402-554-2655 Email: wguo@unomaha.edu and Tie Su University

1 Factors in Implied Volatility Skew in Corn Futures Options Weiyu Guo* University of Nebraska Omaha 6001 Dodge Street, Omaha, NE 68182 Phone 402-554-2655 Email: wguo@unomaha.edu and Tie Su University

Math 416/516: Stochastic Simulation

Math 416/516: Stochastic Simulation Haijun Li lih@math.wsu.edu Department of Mathematics Washington State University Week 13 Haijun Li Math 416/516: Stochastic Simulation Week 13 1 / 28 Outline 1 Simulation

Math 416/516: Stochastic Simulation Haijun Li lih@math.wsu.edu Department of Mathematics Washington State University Week 13 Haijun Li Math 416/516: Stochastic Simulation Week 13 1 / 28 Outline 1 Simulation

Analyzing Oil Futures with a Dynamic Nelson-Siegel Model

Analyzing Oil Futures with a Dynamic Nelson-Siegel Model NIELS STRANGE HANSEN & ASGER LUNDE DEPARTMENT OF ECONOMICS AND BUSINESS, BUSINESS AND SOCIAL SCIENCES, AARHUS UNIVERSITY AND CENTER FOR RESEARCH

Analyzing Oil Futures with a Dynamic Nelson-Siegel Model NIELS STRANGE HANSEN & ASGER LUNDE DEPARTMENT OF ECONOMICS AND BUSINESS, BUSINESS AND SOCIAL SCIENCES, AARHUS UNIVERSITY AND CENTER FOR RESEARCH

Asset Pricing Models with Underlying Time-varying Lévy Processes

Asset Pricing Models with Underlying Time-varying Lévy Processes Stochastics & Computational Finance 2015 Xuecan CUI Jang SCHILTZ University of Luxembourg July 9, 2015 Xuecan CUI, Jang SCHILTZ University

Asset Pricing Models with Underlying Time-varying Lévy Processes Stochastics & Computational Finance 2015 Xuecan CUI Jang SCHILTZ University of Luxembourg July 9, 2015 Xuecan CUI, Jang SCHILTZ University

MSc Finance & Economics

MSc Finance & Economics Programme Structure Week Zero Induction Week TERM 1 Weeks 1-10 EC9760 EC9570 IB9EN0 IB9EM0 Econometrics Microeconomics Asset Pricing Corporate & Investments Financial Mgmt. Week

MSc Finance & Economics Programme Structure Week Zero Induction Week TERM 1 Weeks 1-10 EC9760 EC9570 IB9EN0 IB9EM0 Econometrics Microeconomics Asset Pricing Corporate & Investments Financial Mgmt. Week

Mean Reverting Asset Trading. Research Topic Presentation CSCI-5551 Grant Meyers

Mean Reverting Asset Trading Research Topic Presentation CSCI-5551 Grant Meyers Table of Contents 1. Introduction + Associated Information 2. Problem Definition 3. Possible Solution 1 4. Problems with

Mean Reverting Asset Trading Research Topic Presentation CSCI-5551 Grant Meyers Table of Contents 1. Introduction + Associated Information 2. Problem Definition 3. Possible Solution 1 4. Problems with

Volatility Trading Strategies: Dynamic Hedging via A Simulation

Volatility Trading Strategies: Dynamic Hedging via A Simulation Approach Antai Collage of Economics and Management Shanghai Jiao Tong University Advisor: Professor Hai Lan June 6, 2017 Outline 1 The volatility

Volatility Trading Strategies: Dynamic Hedging via A Simulation Approach Antai Collage of Economics and Management Shanghai Jiao Tong University Advisor: Professor Hai Lan June 6, 2017 Outline 1 The volatility

Evaluating Electricity Generation, Energy Options, and Complex Networks

Evaluating Electricity Generation, Energy Options, and Complex Networks John Birge The University of Chicago Graduate School of Business and Quantstar 1 Outline Derivatives Real options and electricity

Evaluating Electricity Generation, Energy Options, and Complex Networks John Birge The University of Chicago Graduate School of Business and Quantstar 1 Outline Derivatives Real options and electricity

ARCH and GARCH models

ARCH and GARCH models Fulvio Corsi SNS Pisa 5 Dic 2011 Fulvio Corsi ARCH and () GARCH models SNS Pisa 5 Dic 2011 1 / 21 Asset prices S&P 500 index from 1982 to 2009 1600 1400 1200 1000 800 600 400 200

ARCH and GARCH models Fulvio Corsi SNS Pisa 5 Dic 2011 Fulvio Corsi ARCH and () GARCH models SNS Pisa 5 Dic 2011 1 / 21 Asset prices S&P 500 index from 1982 to 2009 1600 1400 1200 1000 800 600 400 200

MSc Finance with Behavioural Science detailed module information

MSc Finance with Behavioural Science detailed module information Example timetable Please note that information regarding modules is subject to change. TERM 1 24 September 14 December 2012 TERM 2 7 January

MSc Finance with Behavioural Science detailed module information Example timetable Please note that information regarding modules is subject to change. TERM 1 24 September 14 December 2012 TERM 2 7 January

Results for option pricing

Results for option pricing [o,v,b]=optimal(rand(1,100000 Estimators = 0.4619 0.4617 0.4618 0.4613 0.4619 o = 0.46151 % best linear combination (true value=0.46150 v = 1.1183e-005 %variance per uniform

Results for option pricing [o,v,b]=optimal(rand(1,100000 Estimators = 0.4619 0.4617 0.4618 0.4613 0.4619 o = 0.46151 % best linear combination (true value=0.46150 v = 1.1183e-005 %variance per uniform

Continuous Processes. Brownian motion Stochastic calculus Ito calculus

Continuous Processes Brownian motion Stochastic calculus Ito calculus Continuous Processes The binomial models are the building block for our realistic models. Three small-scale principles in continuous

Continuous Processes Brownian motion Stochastic calculus Ito calculus Continuous Processes The binomial models are the building block for our realistic models. Three small-scale principles in continuous

Volatility. Roberto Renò. 2 March 2010 / Scuola Normale Superiore. Dipartimento di Economia Politica Università di Siena

Dipartimento di Economia Politica Università di Siena 2 March 2010 / Scuola Normale Superiore What is? The definition of volatility may vary wildly around the idea of the standard deviation of price movements

Dipartimento di Economia Politica Università di Siena 2 March 2010 / Scuola Normale Superiore What is? The definition of volatility may vary wildly around the idea of the standard deviation of price movements

When is supranational supervision optimal? Wolf Wagner (Tilburg University)

") When is supranational supervision optimal? Wolf Wagner (Tilburg University) 1 Motivation Following recent crisis, policy debate on regulation and supervision of international banks Triggered by experience

When is supranational supervision optimal? Wolf Wagner (Tilburg University) 1 Motivation Following recent crisis, policy debate on regulation and supervision of international banks Triggered by experience

M.I.T Fall Practice Problems

M.I.T. 15.450-Fall 2010 Sloan School of Management Professor Leonid Kogan Practice Problems 1. Consider a 3-period model with t = 0, 1, 2, 3. There are a stock and a risk-free asset. The initial stock

M.I.T. 15.450-Fall 2010 Sloan School of Management Professor Leonid Kogan Practice Problems 1. Consider a 3-period model with t = 0, 1, 2, 3. There are a stock and a risk-free asset. The initial stock

EMPIRICAL EVIDENCE ON ARBITRAGE BY CHANGING THE STOCK EXCHANGE

Advances and Applications in Statistics Volume, Number, This paper is available online at http://www.pphmj.com 9 Pushpa Publishing House EMPIRICAL EVIDENCE ON ARBITRAGE BY CHANGING THE STOCK EXCHANGE JOSÉ

Advances and Applications in Statistics Volume, Number, This paper is available online at http://www.pphmj.com 9 Pushpa Publishing House EMPIRICAL EVIDENCE ON ARBITRAGE BY CHANGING THE STOCK EXCHANGE JOSÉ

Smooth pasting as rate of return equalisation: A note

mooth pasting as rate of return equalisation: A note Mark hackleton & igbjørn ødal May 2004 Abstract In this short paper we further elucidate the smooth pasting condition that is behind the optimal early

mooth pasting as rate of return equalisation: A note Mark hackleton & igbjørn ødal May 2004 Abstract In this short paper we further elucidate the smooth pasting condition that is behind the optimal early

Factor Performance in Emerging Markets

Investment Research Factor Performance in Emerging Markets Taras Ivanenko, CFA, Director, Portfolio Manager/Analyst Alex Lai, CFA, Senior Vice President, Portfolio Manager/Analyst Factors can be defined

Investment Research Factor Performance in Emerging Markets Taras Ivanenko, CFA, Director, Portfolio Manager/Analyst Alex Lai, CFA, Senior Vice President, Portfolio Manager/Analyst Factors can be defined

Demographics and the behavior of interest rates

Demographics and the behavior of interest rates (C. Favero, A. Gozluklu and H. Yang) Discussion by Michele Lenza European Central Bank and ECARES-ULB Firenze 18-19 June 2015 Rubric Persistence in interest

Demographics and the behavior of interest rates (C. Favero, A. Gozluklu and H. Yang) Discussion by Michele Lenza European Central Bank and ECARES-ULB Firenze 18-19 June 2015 Rubric Persistence in interest

High-Frequency Data Analysis and Market Microstructure [Tsay (2005), chapter 5]

![High-Frequency Data Analysis and Market Microstructure [Tsay (2005), chapter 5]](/thumbs/79/79153367.jpg "High-Frequency Data Analysis and Market Microstructure [Tsay (2005), chapter 5]") 1 High-Frequency Data Analysis and Market Microstructure [Tsay (2005), chapter 5] High-frequency data have some unique characteristics that do not appear in lower frequencies. At this class we have: Nonsynchronous

1 High-Frequency Data Analysis and Market Microstructure [Tsay (2005), chapter 5] High-frequency data have some unique characteristics that do not appear in lower frequencies. At this class we have: Nonsynchronous

Multi-Period Trading via Convex Optimization

Multi-Period Trading via Convex Optimization Stephen Boyd Enzo Busseti Steven Diamond Ronald Kahn Kwangmoo Koh Peter Nystrup Jan Speth Stanford University & Blackrock City University of Hong Kong September

Multi-Period Trading via Convex Optimization Stephen Boyd Enzo Busseti Steven Diamond Ronald Kahn Kwangmoo Koh Peter Nystrup Jan Speth Stanford University & Blackrock City University of Hong Kong September

No-arbitrage and the decay of market impact and rough volatility: a theory inspired by Jim

No-arbitrage and the decay of market impact and rough volatility: a theory inspired by Jim Mathieu Rosenbaum École Polytechnique 14 October 2017 Mathieu Rosenbaum Rough volatility and no-arbitrage 1 Table

No-arbitrage and the decay of market impact and rough volatility: a theory inspired by Jim Mathieu Rosenbaum École Polytechnique 14 October 2017 Mathieu Rosenbaum Rough volatility and no-arbitrage 1 Table

CFA Level I - LOS Changes

CFA Level I - LOS Changes 2018-2019 Topic LOS Level I - 2018 (529 LOS) LOS Level I - 2019 (525 LOS) Compared Ethics 1.1.a explain ethics 1.1.a explain ethics Ethics Ethics 1.1.b 1.1.c describe the role

CFA Level I - LOS Changes 2018-2019 Topic LOS Level I - 2018 (529 LOS) LOS Level I - 2019 (525 LOS) Compared Ethics 1.1.a explain ethics 1.1.a explain ethics Ethics Ethics 1.1.b 1.1.c describe the role

The Black-Scholes Model

The Black-Scholes Model Liuren Wu Options Markets Liuren Wu ( c ) The Black-Merton-Scholes Model colorhmoptions Markets 1 / 18 The Black-Merton-Scholes-Merton (BMS) model Black and Scholes (1973) and Merton

The Black-Scholes Model Liuren Wu Options Markets Liuren Wu ( c ) The Black-Merton-Scholes Model colorhmoptions Markets 1 / 18 The Black-Merton-Scholes-Merton (BMS) model Black and Scholes (1973) and Merton

What Can Rational Investors Do About Excessive Volatility and Sentiment Fluctuations?

What Can Rational Investors Do About Excessive Volatility and Sentiment Fluctuations? Bernard Dumas INSEAD, Wharton, CEPR, NBER Alexander Kurshev London Business School Raman Uppal London Business School,

What Can Rational Investors Do About Excessive Volatility and Sentiment Fluctuations? Bernard Dumas INSEAD, Wharton, CEPR, NBER Alexander Kurshev London Business School Raman Uppal London Business School,

King s College London

King s College London University Of London This paper is part of an examination of the College counting towards the award of a degree. Examinations are governed by the College Regulations under the authority

King s College London University Of London This paper is part of an examination of the College counting towards the award of a degree. Examinations are governed by the College Regulations under the authority

Growth Opportunities, Investment-Specific Technology Shocks and the Cross-Section of Stock Returns

Growth Opportunities, Investment-Specific Technology Shocks and the Cross-Section of Stock Returns Leonid Kogan 1 Dimitris Papanikolaou 2 1 MIT and NBER 2 Northwestern University Boston, June 5, 2009 Kogan,

Growth Opportunities, Investment-Specific Technology Shocks and the Cross-Section of Stock Returns Leonid Kogan 1 Dimitris Papanikolaou 2 1 MIT and NBER 2 Northwestern University Boston, June 5, 2009 Kogan,

Pricing Dynamic Solvency Insurance and Investment Fund Protection

Pricing Dynamic Solvency Insurance and Investment Fund Protection Hans U. Gerber and Gérard Pafumi Switzerland Abstract In the first part of the paper the surplus of a company is modelled by a Wiener process.

Pricing Dynamic Solvency Insurance and Investment Fund Protection Hans U. Gerber and Gérard Pafumi Switzerland Abstract In the first part of the paper the surplus of a company is modelled by a Wiener process.

What Can the Log-periodic Power Law Tell about Stock Market Crash in India?

Applied Economics Journal 17 (2): 45-54 Copyright 2010 Center for Applied Economics Research ISSN 0858-9291 What Can the Log-periodic Power Law Tell about Stock Market Crash in India? Varun Sarda* Acropolis,

Applied Economics Journal 17 (2): 45-54 Copyright 2010 Center for Applied Economics Research ISSN 0858-9291 What Can the Log-periodic Power Law Tell about Stock Market Crash in India? Varun Sarda* Acropolis,

Human - currency exchange rate prediction based on AR model

Volume 04 - Issue 07 July 2018 PP. 84-88 Human - currency exchange rate prediction based on AR model Jin-yuanWang 1, Ping Xiao 2* 1 (School of Hunan University of Humanities, Science and Technology, Hunan

Volume 04 - Issue 07 July 2018 PP. 84-88 Human - currency exchange rate prediction based on AR model Jin-yuanWang 1, Ping Xiao 2* 1 (School of Hunan University of Humanities, Science and Technology, Hunan

Resolution of a Financial Puzzle

Resolution of a Financial Puzzle M.J. Brennan and Y. Xia September, 1998 revised November, 1998 Abstract The apparent inconsistency between the Tobin Separation Theorem and the advice of popular investment

Resolution of a Financial Puzzle M.J. Brennan and Y. Xia September, 1998 revised November, 1998 Abstract The apparent inconsistency between the Tobin Separation Theorem and the advice of popular investment

Part III. Cycles and Growth:

Part III. Cycles and Growth: UMSL Max Gillman Max Gillman () AS-AD 1 / 56 AS-AD, Relative Prices & Business Cycles Facts: Nominal Prices are Not Real Prices Price of goods in nominal terms: eg. Consumer

Part III. Cycles and Growth: UMSL Max Gillman Max Gillman () AS-AD 1 / 56 AS-AD, Relative Prices & Business Cycles Facts: Nominal Prices are Not Real Prices Price of goods in nominal terms: eg. Consumer

Empirical Distribution Testing of Economic Scenario Generators

1/27 Empirical Distribution Testing of Economic Scenario Generators Gary Venter University of New South Wales 2/27 STATISTICAL CONCEPTUAL BACKGROUND "All models are wrong but some are useful"; George Box

1/27 Empirical Distribution Testing of Economic Scenario Generators Gary Venter University of New South Wales 2/27 STATISTICAL CONCEPTUAL BACKGROUND "All models are wrong but some are useful"; George Box

Financial Mathematics III Theory summary

Financial Mathematics III Theory summary Table of Contents Lecture 1... 7 1. State the objective of modern portfolio theory... 7 2. Define the return of an asset... 7 3. How is expected return defined?...

Financial Mathematics III Theory summary Table of Contents Lecture 1... 7 1. State the objective of modern portfolio theory... 7 2. Define the return of an asset... 7 3. How is expected return defined?...

Modeling dynamic diurnal patterns in high frequency financial data

Modeling dynamic diurnal patterns in high frequency financial data Ryoko Ito 1 Faculty of Economics, Cambridge University Email: ri239@cam.ac.uk Website: www.itoryoko.com This paper: Cambridge Working

Modeling dynamic diurnal patterns in high frequency financial data Ryoko Ito 1 Faculty of Economics, Cambridge University Email: ri239@cam.ac.uk Website: www.itoryoko.com This paper: Cambridge Working

The Information Content of Implied Volatility Skew: Evidence on Taiwan Stock Index Options

Data Science and Pattern Recognition c 2017 ISSN 2520-4165 Ubiquitous International Volume 1, Number 1, February 2017 The Information Content of Implied Volatility Skew: Evidence on Taiwan Stock Index

Data Science and Pattern Recognition c 2017 ISSN 2520-4165 Ubiquitous International Volume 1, Number 1, February 2017 The Information Content of Implied Volatility Skew: Evidence on Taiwan Stock Index

The Black-Scholes Model

The Black-Scholes Model Liuren Wu Options Markets (Hull chapter: 12, 13, 14) Liuren Wu ( c ) The Black-Scholes Model colorhmoptions Markets 1 / 17 The Black-Scholes-Merton (BSM) model Black and Scholes

The Black-Scholes Model Liuren Wu Options Markets (Hull chapter: 12, 13, 14) Liuren Wu ( c ) The Black-Scholes Model colorhmoptions Markets 1 / 17 The Black-Scholes-Merton (BSM) model Black and Scholes

Stock Prices and the Stock Market

Stock Prices and the Stock Market ECON 40364: Monetary Theory & Policy Eric Sims University of Notre Dame Fall 2017 1 / 47 Readings Text: Mishkin Ch. 7 2 / 47 Stock Market The stock market is the subject

Stock Prices and the Stock Market ECON 40364: Monetary Theory & Policy Eric Sims University of Notre Dame Fall 2017 1 / 47 Readings Text: Mishkin Ch. 7 2 / 47 Stock Market The stock market is the subject

On the evolution of probability-weighting function and its impact on gambling

Edith Cowan University Research Online ECU Publications Pre. 2011 2001 On the evolution of probability-weighting function and its impact on gambling Steven Li Yun Hsing Cheung Li, S., & Cheung, Y. (2001).

Edith Cowan University Research Online ECU Publications Pre. 2011 2001 On the evolution of probability-weighting function and its impact on gambling Steven Li Yun Hsing Cheung Li, S., & Cheung, Y. (2001).

Project Proposals for MS&E 444. Lisa Borland and Jeremy Evnine. Evnine and Associates, Inc. April 2008

Project Proposals for MS&E 444 Lisa Borland and Jeremy Evnine Evnine and Associates, Inc. April 2008 1 Portfolio Construction using Prospect Theory Single asset: -Maximize expected long run profit based

Project Proposals for MS&E 444 Lisa Borland and Jeremy Evnine Evnine and Associates, Inc. April 2008 1 Portfolio Construction using Prospect Theory Single asset: -Maximize expected long run profit based

Important Concepts LECTURE 3.2: OPTION PRICING MODELS: THE BLACK-SCHOLES-MERTON MODEL. Applications of Logarithms and Exponentials in Finance

Important Concepts The Black Scholes Merton (BSM) option pricing model LECTURE 3.2: OPTION PRICING MODELS: THE BLACK-SCHOLES-MERTON MODEL Black Scholes Merton Model as the Limit of the Binomial Model Origins

Important Concepts The Black Scholes Merton (BSM) option pricing model LECTURE 3.2: OPTION PRICING MODELS: THE BLACK-SCHOLES-MERTON MODEL Black Scholes Merton Model as the Limit of the Binomial Model Origins

Fractional Brownian Motion as a Model in Finance

Fractional Brownian Motion as a Model in Finance Tommi Sottinen, University of Helsinki Esko Valkeila, University of Turku and University of Helsinki 1 Black & Scholes pricing model In the classical Black

Fractional Brownian Motion as a Model in Finance Tommi Sottinen, University of Helsinki Esko Valkeila, University of Turku and University of Helsinki 1 Black & Scholes pricing model In the classical Black

An Introduction to Stochastic Calculus

An Introduction to Stochastic Calculus Haijun Li lih@math.wsu.edu Department of Mathematics Washington State University Week 2-3 Haijun Li An Introduction to Stochastic Calculus Week 2-3 1 / 24 Outline

An Introduction to Stochastic Calculus Haijun Li lih@math.wsu.edu Department of Mathematics Washington State University Week 2-3 Haijun Li An Introduction to Stochastic Calculus Week 2-3 1 / 24 Outline

1. Money in the utility function (continued)

") Monetary Economics: Macro Aspects, 19/2 2013 Henrik Jensen Department of Economics University of Copenhagen 1. Money in the utility function (continued) a. Welfare costs of in ation b. Potential non-superneutrality

Monetary Economics: Macro Aspects, 19/2 2013 Henrik Jensen Department of Economics University of Copenhagen 1. Money in the utility function (continued) a. Welfare costs of in ation b. Potential non-superneutrality

Motif Capital Horizon Models: A robust asset allocation framework

Motif Capital Horizon Models: A robust asset allocation framework Executive Summary By some estimates, over 93% of the variation in a portfolio s returns can be attributed to the allocation to broad asset

Motif Capital Horizon Models: A robust asset allocation framework Executive Summary By some estimates, over 93% of the variation in a portfolio s returns can be attributed to the allocation to broad asset

The Welfare Cost of Asymmetric Information: Evidence from the U.K. Annuity Market

The Welfare Cost of Asymmetric Information: Evidence from the U.K. Annuity Market Liran Einav 1 Amy Finkelstein 2 Paul Schrimpf 3 1 Stanford and NBER 2 MIT and NBER 3 MIT Cowles 75th Anniversary Conference

The Welfare Cost of Asymmetric Information: Evidence from the U.K. Annuity Market Liran Einav 1 Amy Finkelstein 2 Paul Schrimpf 3 1 Stanford and NBER 2 MIT and NBER 3 MIT Cowles 75th Anniversary Conference

Time Dependent Relative Risk Aversion

SFB 649 Discussion Paper 2006-020 Time Dependent Relative Risk Aversion Enzo Giacomini* Michael Handel** Wolfgang K. Härdle* * C.A.S.E. Center for Applied Statistics and Economics, Humboldt-Universität

SFB 649 Discussion Paper 2006-020 Time Dependent Relative Risk Aversion Enzo Giacomini* Michael Handel** Wolfgang K. Härdle* * C.A.S.E. Center for Applied Statistics and Economics, Humboldt-Universität

CFA Level I - LOS Changes

CFA Level I - LOS Changes 2017-2018 Topic LOS Level I - 2017 (534 LOS) LOS Level I - 2018 (529 LOS) Compared Ethics 1.1.a explain ethics 1.1.a explain ethics Ethics 1.1.b describe the role of a code of

CFA Level I - LOS Changes 2017-2018 Topic LOS Level I - 2017 (534 LOS) LOS Level I - 2018 (529 LOS) Compared Ethics 1.1.a explain ethics 1.1.a explain ethics Ethics 1.1.b describe the role of a code of

Market risk measurement in practice

Lecture notes on risk management, public policy, and the financial system Allan M. Malz Columbia University 2018 Allan M. Malz Last updated: October 23, 2018 2/32 Outline Nonlinearity in market risk Market

Lecture notes on risk management, public policy, and the financial system Allan M. Malz Columbia University 2018 Allan M. Malz Last updated: October 23, 2018 2/32 Outline Nonlinearity in market risk Market