A new approach to multiple curve Market Models of Interest Rates. Rodney Hoskinson

|

|

|

- Jayson Shields

- 5 years ago

- Views:

Transcription

1 A new approach to multiple curve Market Models of Interest Rates Rodney Hoskinson Rodney Hoskinson This presentation has been prepared for the Actuaries Institute 2014 Financial Services Forum. The Institute Council wishes it to be understood that opinions put forward herein are not necessarily those of the Institute and the Council is not responsible for those opinions.

2 Agenda Motivation/Context current challenges in term structure modelling Volatility modelling New model with multiple regimes Model statics implied volatility surface Market calibration example

3 Motivation/Context

4 New spread dynamics

5 Long expiry smile

6 Option-implied volatility regimes

7 Modelling requirements Non-zero and non-constant spread multiple curves Smile and smile evolution Arbitrage-free Tractable - rapid pricing and calibration formulas Capable of allowing for: Counterparty credit risk Collateral and re-hypothecation Funding liquidity risk Central clearing

8 Multiple curve term structure models with stochastic volatility Stochastic evolution of 2 curves: Discount rates and forward rates; or Discount rates and spreads Price contracts linked to Libor, Euribor or equivalent Instantaneous or discrete forwards Separate stochastic evolution of rate volatility

9 Model Definition

10 Stochastic Volatility modelling in term structure models - current methods 1. Heston (mean-reverting process): dddd(tt) = κκ zz 0 zz tt dddd + ηη(tt) zz tt dddd(tt) κκ mean reversion speed zz 0 mean reversion level ηη(tt) or ηη volatility of variance 2. SABR: (non mean reverting): dddd(tt) = ααzz tt dddd(tt) αα volatility of variance

11 Regime Switching + Mean Reversion Heston: dddd(tt) = κκ zz 0 zz tt dddd + ηη(tt) zz tt dddd(tt) Markov-switching Heston: dddd tt = κκ ff αα tt, tt zz tt dddd + ηη tt zz tt dddd tt ff(, ) deterministic function of αα tt and tt αα tt - continuous time Markov chain with discrete state space

12 Volatility Simulation Sample Path Two Heston Volatilities with Markov-Switching Mean Reversion Function of Markov Chain, Stochastic variance Trading Days

13 Interest Rate Definitions Discrete Forward Rate Model Times TT 0, TT 1, TT 2 to TT NN Discrete tenor xx spacing (e.g. xx = 3mm, 6mm) At time tt < TT nn, for period TT nn to TT nn+1 : LL nn xx tt = FF nn xx tt + SS nn xx tt - FRA rate - par swap rate against Libor over (TT nn, TT nn+1 ) exchanged at TT nn+1 FF nn xx tt - forward rate on OIS (overnight indexed swap) curve (for discounting) SS nn xx tt - forward rate of FRA-OIS spread

14 Example Full Model Dynamics Full Collateralisation OIS equation (n=1...n): ddff nn xx tt = zz 1 tt λλ nn FF tt φφ nn FF tt, FF nn xx tt ddyy FF nn tt Spread equation (n=1 N): ddss nn xx tt = zz 2 tt λλ nn SS tt TT φφ nn SS tt, SS nn xx tt ddyy SS nn tt OIS volatility: ddzz 1 tt = κκ 1 ff αα tt, tt zz 1 tt dddd + ηη 1 tt zz 1 tt ddzz 1 nn tt Spread vol.: ddzz 2 tt = κκ 2 gg αα tt, tt zz 2 tt dddd + ηη 2 tt zz 2 tt ddzz 2 nn (tt) λλ nn FF tt, λλ nn SS tt - deterministic volatility vectors defining vol term structure φφ nn FF tt, xx(tt) = bb nn tt xx(tt) + 1 bb nn tt xx(0) - displaced lognormal skew YY FF nn tt, YY SS nn tt, ZZ 1 nn tt, ZZ 2 nn (tt) Independent standard Brownian motions (YY FF nn tt, YY SS nn tt vectors) under OIS TT nn -forward martingale measure

15 Model Statics

16 Model-Generated Volatility Surface One SV, mean reversion rate = 0.25, volatility of variance = 1.5, 16 state Markov chain

17 Volatility surface Markov Chain Impact

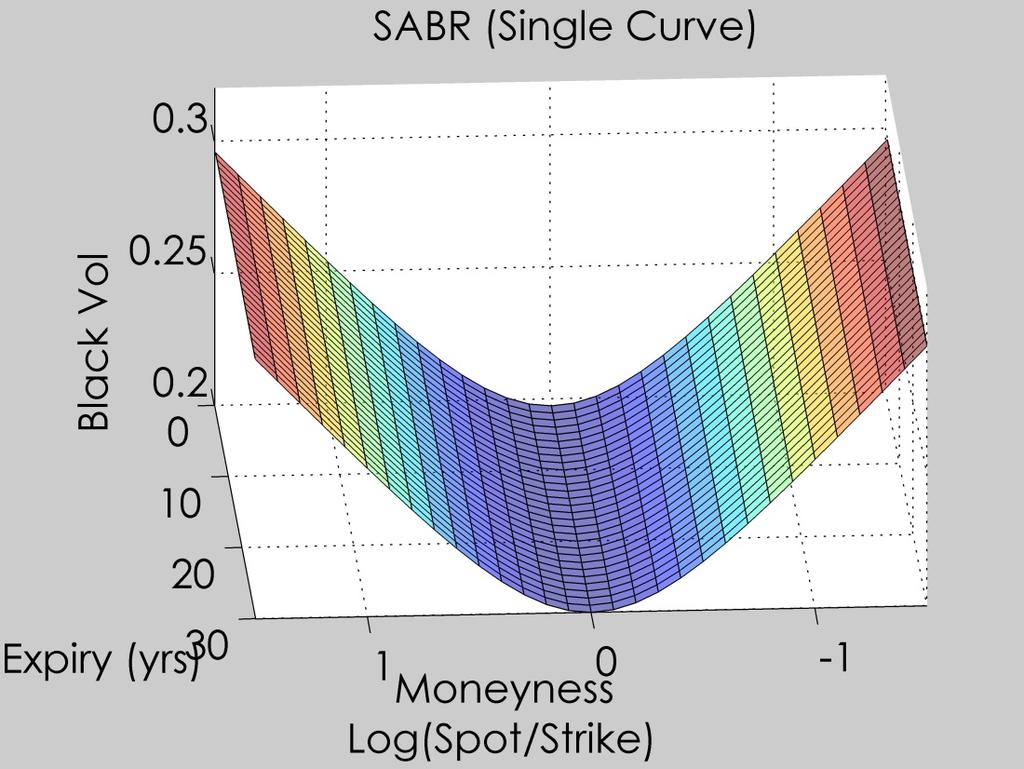

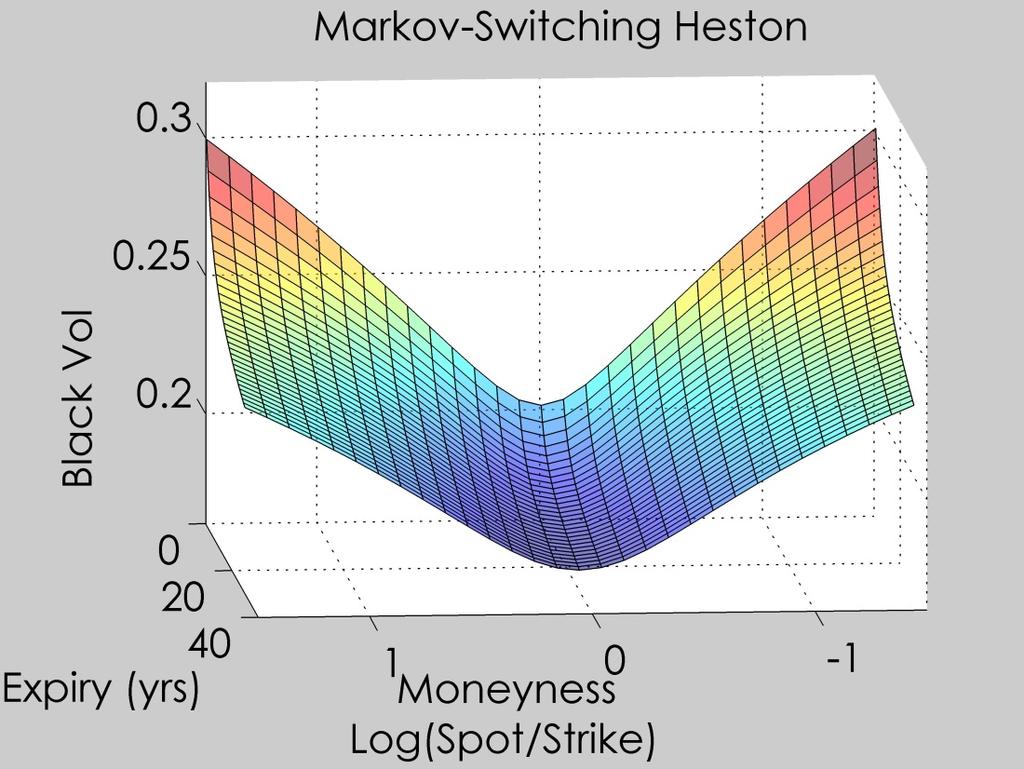

18 SABR vs Markov-Switching Heston

19 Traditionally Mean Reversion Kills the Smile Displaced lognormal Heston, volatility of variance = 1.5, OIS and Spread Skew 0.6

20 Kappa can now increase short end smile Markov-switching Heston, Volatility of variance = 0.5, OIS and Spread Skew 0.6

21 Smiles Without SV Sum of 2 Displaced Lognormal Processes

22 Empirics Term Parameter Calibration to Swaption Cube

23 Swaption cube Swaption option to enter interest rate swap at a fixed rate (strike) instead of the prevailing future par forward swap rate Swaption Cube Implied volatility (price) by 3 factors option expiry, underlying swap maturity, strike Bloomberg swaption cube implied volatilities available for Option expiries 3M, 1Y, 5Y, 10Y, 20Y and 30Y Swap maturities for each expiry 2Y, 5Y, 10Y, 20Y, 30Y 9 Strikes for each expiry/maturity pair At The Money and +/- 25,50,100,200 basis points 30 smiles each with 9 strikes Euro area money market : 6 month tenor

24 Swaption Cube 2yr/5yr Euro 1/9/11

25 Swaption Cube 10yr/20yr Euro 1/9/11

26 Swaption Cube 30yr Euro 1/9/11

27 Term Parameter Calibration Cube data as parameters of a set of models One model per smile Constant parameters Per smile parameters Global parameters Example for each swaption (expiry nn, maturity mm) : OIS : xx Spread: ddss nn,mm xx FF ddff nn,mm tt = zz nn,mm FF tt λλ nn,mm tt = λλ SS bb SS xx SS nn,mm bb FF xx FF nn,mm FF nn,mm tt + 1 bb nn,mm tt + 1 bb SS xx SS nn,mm tt ddyy nn,mm SS tt xx FF nn,mm tt ddyy nn,mm FF tt OIS volatility: FF ddzz nn,mm tt = κκ FF FF FF ff αα tt zz nn,mm tt dddd + ηη nn,mm FF zz nn,mm tt ddzz FF nn,mm tt

28 Fitted Term Parameters: Euro 1/9/2011 OIS Per Smile Parameters FF Volatility λλ nn,mm FF Skew bb nn,mm Maturity (yrs) Expiry 3 Months year Year Year Year Year FF Volatility of Variance ηη nn,mm Maturity (yrs) Expiry 3 Months year Year Year Year Year

29 Fitted Term Parameters: Euro 1/9/2011 Global Parameters OIS stochastic volatility mean reversion rate κκ FF 0.66 Spread deterministic volatility λλ SS 0.47 Spread Skew bb SS 1.00 Markov Chain Summary ff αα tt Occupation Time % % % % %

30 Pricing error short end IV basis points

31 Pricing error long end IV basis points Average absolute error 22bp of IV

32 Summary New SV TS model from new volatility dynamics First additive OIS+Spread Heston-based TS model First 2 curve TS with Markov switching Heston Smile persistence between Heston and SABR Heston-level mathematical rigour and tractability Solve Heston moment explosion Excellent fit to swaption cube FRA dynamics not conditionally lognormal

33 Further research Collateralisation, default and funding liquidity adjustments Impact on exotics prices Same volatility different TS models Jumps in Spread connected with volatility regime switches Times series of calibrations Greeks

Paper Review Hawkes Process: Fast Calibration, Application to Trade Clustering, and Diffusive Limit by Jose da Fonseca and Riadh Zaatour

Paper Review Hawkes Process: Fast Calibration, Application to Trade Clustering, and Diffusive Limit by Jose da Fonseca and Riadh Zaatour Xin Yu Zhang June 13, 2018 Mathematical and Computational Finance

Paper Review Hawkes Process: Fast Calibration, Application to Trade Clustering, and Diffusive Limit by Jose da Fonseca and Riadh Zaatour Xin Yu Zhang June 13, 2018 Mathematical and Computational Finance

Institute of Actuaries of India. Subject. ST6 Finance and Investment B. For 2018 Examinationspecialist Technical B. Syllabus

Institute of Actuaries of India Subject ST6 Finance and Investment B For 2018 Examinationspecialist Technical B Syllabus Aim The aim of the second finance and investment technical subject is to instil

Institute of Actuaries of India Subject ST6 Finance and Investment B For 2018 Examinationspecialist Technical B Syllabus Aim The aim of the second finance and investment technical subject is to instil

Advanced Topics in Derivative Pricing Models. Topic 4 - Variance products and volatility derivatives

Advanced Topics in Derivative Pricing Models Topic 4 - Variance products and volatility derivatives 4.1 Volatility trading and replication of variance swaps 4.2 Volatility swaps 4.3 Pricing of discrete

Advanced Topics in Derivative Pricing Models Topic 4 - Variance products and volatility derivatives 4.1 Volatility trading and replication of variance swaps 4.2 Volatility swaps 4.3 Pricing of discrete

Journal of Economics and Financial Analysis, Vol:2, No:2 (2018)

") Journal of Economics and Financial Analysis, Vol:2, No:2 (2018) 87-103 Journal of Economics and Financial Analysis Type: Double Blind Peer Reviewed Scientific Journal Printed ISSN: 2521-6627 Online ISSN:

Journal of Economics and Financial Analysis, Vol:2, No:2 (2018) 87-103 Journal of Economics and Financial Analysis Type: Double Blind Peer Reviewed Scientific Journal Printed ISSN: 2521-6627 Online ISSN:

Handbook of Financial Risk Management

Handbook of Financial Risk Management Simulations and Case Studies N.H. Chan H.Y. Wong The Chinese University of Hong Kong WILEY Contents Preface xi 1 An Introduction to Excel VBA 1 1.1 How to Start Excel

Handbook of Financial Risk Management Simulations and Case Studies N.H. Chan H.Y. Wong The Chinese University of Hong Kong WILEY Contents Preface xi 1 An Introduction to Excel VBA 1 1.1 How to Start Excel

ESGs: Spoilt for choice or no alternatives?

ESGs: Spoilt for choice or no alternatives? FA L K T S C H I R S C H N I T Z ( F I N M A ) 1 0 3. M i t g l i e d e r v e r s a m m l u n g S AV A F I R, 3 1. A u g u s t 2 0 1 2 Agenda 1. Why do we need

ESGs: Spoilt for choice or no alternatives? FA L K T S C H I R S C H N I T Z ( F I N M A ) 1 0 3. M i t g l i e d e r v e r s a m m l u n g S AV A F I R, 3 1. A u g u s t 2 0 1 2 Agenda 1. Why do we need

Multi-Curve Pricing of Non-Standard Tenor Vanilla Options in QuantLib. Sebastian Schlenkrich QuantLib User Meeting, Düsseldorf, December 1, 2015

Multi-Curve Pricing of Non-Standard Tenor Vanilla Options in QuantLib Sebastian Schlenkrich QuantLib User Meeting, Düsseldorf, December 1, 2015 d-fine d-fine All rights All rights reserved reserved 0 Swaption

Multi-Curve Pricing of Non-Standard Tenor Vanilla Options in QuantLib Sebastian Schlenkrich QuantLib User Meeting, Düsseldorf, December 1, 2015 d-fine d-fine All rights All rights reserved reserved 0 Swaption

Riccardo Rebonato Global Head of Quantitative Research, FM, RBS Global Head of Market Risk, CBFM, RBS

Why Neither Time Homogeneity nor Time Dependence Will Do: Evidence from the US$ Swaption Market Cambridge, May 2005 Riccardo Rebonato Global Head of Quantitative Research, FM, RBS Global Head of Market

Why Neither Time Homogeneity nor Time Dependence Will Do: Evidence from the US$ Swaption Market Cambridge, May 2005 Riccardo Rebonato Global Head of Quantitative Research, FM, RBS Global Head of Market

Introduction to Financial Mathematics

Department of Mathematics University of Michigan November 7, 2008 My Information E-mail address: marymorj (at) umich.edu Financial work experience includes 2 years in public finance investment banking

Department of Mathematics University of Michigan November 7, 2008 My Information E-mail address: marymorj (at) umich.edu Financial work experience includes 2 years in public finance investment banking

Crashcourse Interest Rate Models

Crashcourse Interest Rate Models Stefan Gerhold August 30, 2006 Interest Rate Models Model the evolution of the yield curve Can be used for forecasting the future yield curve or for pricing interest rate

Crashcourse Interest Rate Models Stefan Gerhold August 30, 2006 Interest Rate Models Model the evolution of the yield curve Can be used for forecasting the future yield curve or for pricing interest rate

Pricing of a European Call Option Under a Local Volatility Interbank Offered Rate Model

American Journal of Theoretical and Applied Statistics 2018; 7(2): 80-84 http://www.sciencepublishinggroup.com/j/ajtas doi: 10.11648/j.ajtas.20180702.14 ISSN: 2326-8999 (Print); ISSN: 2326-9006 (Online)

American Journal of Theoretical and Applied Statistics 2018; 7(2): 80-84 http://www.sciencepublishinggroup.com/j/ajtas doi: 10.11648/j.ajtas.20180702.14 ISSN: 2326-8999 (Print); ISSN: 2326-9006 (Online)

Callability Features

2 Callability Features 2.1 Introduction and Objectives In this chapter, we introduce callability which gives one party in a transaction the right (but not the obligation) to terminate the transaction early.

2 Callability Features 2.1 Introduction and Objectives In this chapter, we introduce callability which gives one party in a transaction the right (but not the obligation) to terminate the transaction early.

AN ANALYTICALLY TRACTABLE UNCERTAIN VOLATILITY MODEL

AN ANALYTICALLY TRACTABLE UNCERTAIN VOLATILITY MODEL FABIO MERCURIO BANCA IMI, MILAN http://www.fabiomercurio.it 1 Stylized facts Traders use the Black-Scholes formula to price plain-vanilla options. An

AN ANALYTICALLY TRACTABLE UNCERTAIN VOLATILITY MODEL FABIO MERCURIO BANCA IMI, MILAN http://www.fabiomercurio.it 1 Stylized facts Traders use the Black-Scholes formula to price plain-vanilla options. An

Martingale Methods in Financial Modelling

Marek Musiela Marek Rutkowski Martingale Methods in Financial Modelling Second Edition \ 42 Springer - . Preface to the First Edition... V Preface to the Second Edition... VII I Part I. Spot and Futures

Marek Musiela Marek Rutkowski Martingale Methods in Financial Modelling Second Edition \ 42 Springer - . Preface to the First Edition... V Preface to the Second Edition... VII I Part I. Spot and Futures

Risk managing long-dated smile risk with SABR formula

Risk managing long-dated smile risk with SABR formula Claudio Moni QuaRC, RBS November 7, 2011 Abstract In this paper 1, we show that the sensitivities to the SABR parameters can be materially wrong when

Risk managing long-dated smile risk with SABR formula Claudio Moni QuaRC, RBS November 7, 2011 Abstract In this paper 1, we show that the sensitivities to the SABR parameters can be materially wrong when

Negative Rates: The Challenges from a Quant Perspective

Negative Rates: The Challenges from a Quant Perspective 1 Introduction Fabio Mercurio Global head of Quantitative Analytics Bloomberg There are many instances in the past and recent history where Treasury

Negative Rates: The Challenges from a Quant Perspective 1 Introduction Fabio Mercurio Global head of Quantitative Analytics Bloomberg There are many instances in the past and recent history where Treasury

Martingale Methods in Financial Modelling

Marek Musiela Marek Rutkowski Martingale Methods in Financial Modelling Second Edition Springer Table of Contents Preface to the First Edition Preface to the Second Edition V VII Part I. Spot and Futures

Marek Musiela Marek Rutkowski Martingale Methods in Financial Modelling Second Edition Springer Table of Contents Preface to the First Edition Preface to the Second Edition V VII Part I. Spot and Futures

Economic Scenario Generators

Economic Scenario Generators A regulator s perspective Falk Tschirschnitz, FINMA Bahnhofskolloquium Motivation FINMA has observed: Calibrating the interest rate model of choice has become increasingly

Economic Scenario Generators A regulator s perspective Falk Tschirschnitz, FINMA Bahnhofskolloquium Motivation FINMA has observed: Calibrating the interest rate model of choice has become increasingly

Interest Rate Volatility

Interest Rate Volatility III. Working with SABR Andrew Lesniewski Baruch College and Posnania Inc First Baruch Volatility Workshop New York June 16-18, 2015 Outline Arbitrage free SABR 1 Arbitrage free

Interest Rate Volatility III. Working with SABR Andrew Lesniewski Baruch College and Posnania Inc First Baruch Volatility Workshop New York June 16-18, 2015 Outline Arbitrage free SABR 1 Arbitrage free

Things You Have To Have Heard About (In Double-Quick Time) The LIBOR market model: Björk 27. Swaption pricing too.

The LIBOR market model: Björk 27. Swaption pricing too.") Things You Have To Have Heard About (In Double-Quick Time) LIBORs, floating rate bonds, swaps.: Björk 22.3 Caps: Björk 26.8. Fun with caps. The LIBOR market model: Björk 27. Swaption pricing too. 1 Simple

Things You Have To Have Heard About (In Double-Quick Time) LIBORs, floating rate bonds, swaps.: Björk 22.3 Caps: Björk 26.8. Fun with caps. The LIBOR market model: Björk 27. Swaption pricing too. 1 Simple

ABSA Technical Valuations Session JSE Trading Division

ABSA Technical Valuations Session JSE Trading Division July 2010 Presented by: Dr Antonie Kotzé 1 Some members are lost.. ABSA Technical Valuation Session Introduction 2 some think Safex talks in tongues.

ABSA Technical Valuations Session JSE Trading Division July 2010 Presented by: Dr Antonie Kotzé 1 Some members are lost.. ABSA Technical Valuation Session Introduction 2 some think Safex talks in tongues.

Pricing Variance Swaps under Stochastic Volatility Model with Regime Switching - Discrete Observations Case

Pricing Variance Swaps under Stochastic Volatility Model with Regime Switching - Discrete Observations Case Guang-Hua Lian Collaboration with Robert Elliott University of Adelaide Feb. 2, 2011 Robert Elliott,

Pricing Variance Swaps under Stochastic Volatility Model with Regime Switching - Discrete Observations Case Guang-Hua Lian Collaboration with Robert Elliott University of Adelaide Feb. 2, 2011 Robert Elliott,

A Two Factor Forward Curve Model with Stochastic Volatility for Commodity Prices arxiv: v2 [q-fin.pr] 8 Aug 2017

![A Two Factor Forward Curve Model with Stochastic Volatility for Commodity Prices arxiv: v2 [q-fin.pr] 8 Aug 2017](/thumbs/77/76675488.jpg "A Two Factor Forward Curve Model with Stochastic Volatility for Commodity Prices arxiv: v2 [q-fin.pr] 8 Aug 2017") A Two Factor Forward Curve Model with Stochastic Volatility for Commodity Prices arxiv:1708.01665v2 [q-fin.pr] 8 Aug 2017 Mark Higgins, PhD - Beacon Platform Incorporated August 10, 2017 Abstract We describe

A Two Factor Forward Curve Model with Stochastic Volatility for Commodity Prices arxiv:1708.01665v2 [q-fin.pr] 8 Aug 2017 Mark Higgins, PhD - Beacon Platform Incorporated August 10, 2017 Abstract We describe

Modelling Credit Spread Behaviour. FIRST Credit, Insurance and Risk. Angelo Arvanitis, Jon Gregory, Jean-Paul Laurent

Modelling Credit Spread Behaviour Insurance and Angelo Arvanitis, Jon Gregory, Jean-Paul Laurent ICBI Counterparty & Default Forum 29 September 1999, Paris Overview Part I Need for Credit Models Part II

Modelling Credit Spread Behaviour Insurance and Angelo Arvanitis, Jon Gregory, Jean-Paul Laurent ICBI Counterparty & Default Forum 29 September 1999, Paris Overview Part I Need for Credit Models Part II

FX Barrien Options. A Comprehensive Guide for Industry Quants. Zareer Dadachanji Director, Model Quant Solutions, Bremen, Germany

FX Barrien Options A Comprehensive Guide for Industry Quants Zareer Dadachanji Director, Model Quant Solutions, Bremen, Germany Contents List of Figures List of Tables Preface Acknowledgements Foreword

FX Barrien Options A Comprehensive Guide for Industry Quants Zareer Dadachanji Director, Model Quant Solutions, Bremen, Germany Contents List of Figures List of Tables Preface Acknowledgements Foreword

With Examples Implemented in Python

SABR and SABR LIBOR Market Models in Practice With Examples Implemented in Python Christian Crispoldi Gerald Wigger Peter Larkin palgrave macmillan Contents List of Figures ListofTables Acknowledgments

SABR and SABR LIBOR Market Models in Practice With Examples Implemented in Python Christian Crispoldi Gerald Wigger Peter Larkin palgrave macmillan Contents List of Figures ListofTables Acknowledgments

OIS and Its Impact on Modeling, Calibration and Funding of OTC Derivatives. May 31, 2012 Satyam Kancharla SVP, Client Solutions Group Numerix LLC

OIS and Its Impact on Modeling, Calibration and Funding of OTC Derivatives May 31, 2012 Satyam Kancharla SVP, Client Solutions Group Numerix LLC Agenda Changes in Interest Rate market dynamics after the

OIS and Its Impact on Modeling, Calibration and Funding of OTC Derivatives May 31, 2012 Satyam Kancharla SVP, Client Solutions Group Numerix LLC Agenda Changes in Interest Rate market dynamics after the

Economic Scenario Generation: Some practicalities. David Grundy October 2010

Economic Scenario Generation: Some practicalities David Grundy October 2010 my perspective as an empiricist rather than a theoretician as stochastic model owner and user All my comments today are my own

Economic Scenario Generation: Some practicalities David Grundy October 2010 my perspective as an empiricist rather than a theoretician as stochastic model owner and user All my comments today are my own

It Takes Two: Why Mortality Trend Modeling is more than modeling one Mortality Trend

It Takes Two: Why Mortality Trend Modeling is more than modeling one Mortality Trend Johannes Schupp Joint work with Matthias Börger and Jochen Russ IAA Life Section Colloquium, Barcelona, 23 th -24 th

It Takes Two: Why Mortality Trend Modeling is more than modeling one Mortality Trend Johannes Schupp Joint work with Matthias Börger and Jochen Russ IAA Life Section Colloquium, Barcelona, 23 th -24 th

DOWNLOAD PDF INTEREST RATE OPTION MODELS REBONATO

Chapter 1 : Riccardo Rebonato Revolvy Interest-Rate Option Models: Understanding, Analysing and Using Models for Exotic Interest-Rate Options (Wiley Series in Financial Engineering) Second Edition by Riccardo

Chapter 1 : Riccardo Rebonato Revolvy Interest-Rate Option Models: Understanding, Analysing and Using Models for Exotic Interest-Rate Options (Wiley Series in Financial Engineering) Second Edition by Riccardo

Latest Developments: Interest Rate Modelling & Interest Rate Exotic & Hybrid Products

Latest Developments: Interest Rate Modelling & Interest Rate Exotic & Hybrid Products London: 30th March 1st April 2009 This workshop provides THREE booking options Register to ANY ONE day TWO days or

Latest Developments: Interest Rate Modelling & Interest Rate Exotic & Hybrid Products London: 30th March 1st April 2009 This workshop provides THREE booking options Register to ANY ONE day TWO days or

Model Risk Assessment

Model Risk Assessment Case Study Based on Hedging Simulations Drona Kandhai (PhD) Head of Interest Rates, Inflation and Credit Quantitative Analytics Team CMRM Trading Risk - ING Bank Assistant Professor

Model Risk Assessment Case Study Based on Hedging Simulations Drona Kandhai (PhD) Head of Interest Rates, Inflation and Credit Quantitative Analytics Team CMRM Trading Risk - ING Bank Assistant Professor

Impact of negative rates on pricing models. Veronica Malafaia ING Bank - FI/FM Quants, Credit & Trading Risk Amsterdam, 18 th November 2015

Impact of negative rates on pricing models Veronica Malafaia ING Bank - FI/FM Quants, Credit & Trading Risk Amsterdam, 18 th November 2015 Disclaimer: The views and opinions expressed in this presentation

Impact of negative rates on pricing models Veronica Malafaia ING Bank - FI/FM Quants, Credit & Trading Risk Amsterdam, 18 th November 2015 Disclaimer: The views and opinions expressed in this presentation

INTEREST RATES AND FX MODELS

INTEREST RATES AND FX MODELS 7. Risk Management Andrew Lesniewski Courant Institute of Mathematical Sciences New York University New York March 8, 2012 2 Interest Rates & FX Models Contents 1 Introduction

INTEREST RATES AND FX MODELS 7. Risk Management Andrew Lesniewski Courant Institute of Mathematical Sciences New York University New York March 8, 2012 2 Interest Rates & FX Models Contents 1 Introduction

Dynamic Relative Valuation

Dynamic Relative Valuation Liuren Wu, Baruch College Joint work with Peter Carr from Morgan Stanley October 15, 2013 Liuren Wu (Baruch) Dynamic Relative Valuation 10/15/2013 1 / 20 The standard approach

Dynamic Relative Valuation Liuren Wu, Baruch College Joint work with Peter Carr from Morgan Stanley October 15, 2013 Liuren Wu (Baruch) Dynamic Relative Valuation 10/15/2013 1 / 20 The standard approach

Economic Scenario Generation: Some practicalities. David Grundy July 2011

Economic Scenario Generation: Some practicalities David Grundy July 2011 my perspective stochastic model owner and user practical rather than theoretical 8 economies, 100 sensitivity tests per economy

Economic Scenario Generation: Some practicalities David Grundy July 2011 my perspective stochastic model owner and user practical rather than theoretical 8 economies, 100 sensitivity tests per economy

Managing the Newest Derivatives Risks

Managing the Newest Derivatives Risks Michel Crouhy IXIS Corporate and Investment Bank / A subsidiary of NATIXIS Derivatives 2007: New Ideas, New Instruments, New markets NYU Stern School of Business,

Managing the Newest Derivatives Risks Michel Crouhy IXIS Corporate and Investment Bank / A subsidiary of NATIXIS Derivatives 2007: New Ideas, New Instruments, New markets NYU Stern School of Business,

Arbitrage-free construction of the swaption cube

Arbitrage-free construction of the swaption cube Simon Johnson Bereshad Nonas Financial Engineering Commerzbank Corporates and Markets 60 Gracechurch Street London EC3V 0HR 5th January 2009 Abstract In

Arbitrage-free construction of the swaption cube Simon Johnson Bereshad Nonas Financial Engineering Commerzbank Corporates and Markets 60 Gracechurch Street London EC3V 0HR 5th January 2009 Abstract In

Counterparty Credit Risk Simulation

Counterparty Credit Risk Simulation Alex Yang FinPricing http://www.finpricing.com Summary Counterparty Credit Risk Definition Counterparty Credit Risk Measures Monte Carlo Simulation Interest Rate Curve

Counterparty Credit Risk Simulation Alex Yang FinPricing http://www.finpricing.com Summary Counterparty Credit Risk Definition Counterparty Credit Risk Measures Monte Carlo Simulation Interest Rate Curve

MODELLING VOLATILITY SURFACES WITH GARCH

MODELLING VOLATILITY SURFACES WITH GARCH Robert G. Trevor Centre for Applied Finance Macquarie University robt@mafc.mq.edu.au October 2000 MODELLING VOLATILITY SURFACES WITH GARCH WHY GARCH? stylised facts

MODELLING VOLATILITY SURFACES WITH GARCH Robert G. Trevor Centre for Applied Finance Macquarie University robt@mafc.mq.edu.au October 2000 MODELLING VOLATILITY SURFACES WITH GARCH WHY GARCH? stylised facts

Developments in Volatility Derivatives Pricing

Developments in Volatility Derivatives Pricing Jim Gatheral Global Derivatives 2007 Paris, May 23, 2007 Motivation We would like to be able to price consistently at least 1 options on SPX 2 options on

Developments in Volatility Derivatives Pricing Jim Gatheral Global Derivatives 2007 Paris, May 23, 2007 Motivation We would like to be able to price consistently at least 1 options on SPX 2 options on

MULTISCALE STOCHASTIC VOLATILITY FOR EQUITY, INTEREST RATE, AND CREDIT DERIVATIVES

MULTISCALE STOCHASTIC VOLATILITY FOR EQUITY, INTEREST RATE, AND CREDIT DERIVATIVES Building upon the ideas introduced in their previous book, Derivatives in Financial Markets with Stochastic Volatility,

MULTISCALE STOCHASTIC VOLATILITY FOR EQUITY, INTEREST RATE, AND CREDIT DERIVATIVES Building upon the ideas introduced in their previous book, Derivatives in Financial Markets with Stochastic Volatility,

No-Arbitrage Conditions for the Dynamics of Smiles

No-Arbitrage Conditions for the Dynamics of Smiles Presentation at King s College Riccardo Rebonato QUARC Royal Bank of Scotland Group Research in collaboration with Mark Joshi Thanks to David Samuel The

No-Arbitrage Conditions for the Dynamics of Smiles Presentation at King s College Riccardo Rebonato QUARC Royal Bank of Scotland Group Research in collaboration with Mark Joshi Thanks to David Samuel The

SYLLABUS. IEOR E4728 Topics in Quantitative Finance: Inflation Derivatives

SYLLABUS IEOR E4728 Topics in Quantitative Finance: Inflation Derivatives Term: Summer 2007 Department: Industrial Engineering and Operations Research (IEOR) Instructor: Iraj Kani TA: Wayne Lu References:

SYLLABUS IEOR E4728 Topics in Quantitative Finance: Inflation Derivatives Term: Summer 2007 Department: Industrial Engineering and Operations Research (IEOR) Instructor: Iraj Kani TA: Wayne Lu References:

LIBOR models, multi-curve extensions, and the pricing of callable structured derivatives

Weierstrass Institute for Applied Analysis and Stochastics LIBOR models, multi-curve extensions, and the pricing of callable structured derivatives John Schoenmakers 9th Summer School in Mathematical Finance

Weierstrass Institute for Applied Analysis and Stochastics LIBOR models, multi-curve extensions, and the pricing of callable structured derivatives John Schoenmakers 9th Summer School in Mathematical Finance

Lecture 9: Practicalities in Using Black-Scholes. Sunday, September 23, 12

Lecture 9: Practicalities in Using Black-Scholes Major Complaints Most stocks and FX products don t have log-normal distribution Typically fat-tailed distributions are observed Constant volatility assumed,

Lecture 9: Practicalities in Using Black-Scholes Major Complaints Most stocks and FX products don t have log-normal distribution Typically fat-tailed distributions are observed Constant volatility assumed,

Market interest-rate models

Market interest-rate models Marco Marchioro www.marchioro.org November 24 th, 2012 Market interest-rate models 1 Lecture Summary No-arbitrage models Detailed example: Hull-White Monte Carlo simulations

Market interest-rate models Marco Marchioro www.marchioro.org November 24 th, 2012 Market interest-rate models 1 Lecture Summary No-arbitrage models Detailed example: Hull-White Monte Carlo simulations

Modern Derivatives. Pricing and Credit. Exposure Anatysis. Theory and Practice of CSA and XVA Pricing, Exposure Simulation and Backtest!

Modern Derivatives Pricing and Credit Exposure Anatysis Theory and Practice of CSA and XVA Pricing, Exposure Simulation and Backtest!ng Roland Lichters, Roland Stamm, Donal Gallagher Contents List of Figures

Modern Derivatives Pricing and Credit Exposure Anatysis Theory and Practice of CSA and XVA Pricing, Exposure Simulation and Backtest!ng Roland Lichters, Roland Stamm, Donal Gallagher Contents List of Figures

Adjusting the Black-Scholes Framework in the Presence of a Volatility Skew

Adjusting the Black-Scholes Framework in the Presence of a Volatility Skew Mentor: Christopher Prouty Members: Ping An, Dawei Wang, Rui Yan Shiyi Chen, Fanda Yang, Che Wang Team Website: http://sites.google.com/site/mfmmodelingprogramteam2/

Adjusting the Black-Scholes Framework in the Presence of a Volatility Skew Mentor: Christopher Prouty Members: Ping An, Dawei Wang, Rui Yan Shiyi Chen, Fanda Yang, Che Wang Team Website: http://sites.google.com/site/mfmmodelingprogramteam2/

Session 76 PD, Modeling Indexed Products. Moderator: Leonid Shteyman, FSA. Presenters: Trevor D. Huseman, FSA, MAAA Leonid Shteyman, FSA

Session 76 PD, Modeling Indexed Products Moderator: Leonid Shteyman, FSA Presenters: Trevor D. Huseman, FSA, MAAA Leonid Shteyman, FSA Modeling Indexed Products Trevor Huseman, FSA, MAAA Managing Director

Session 76 PD, Modeling Indexed Products Moderator: Leonid Shteyman, FSA Presenters: Trevor D. Huseman, FSA, MAAA Leonid Shteyman, FSA Modeling Indexed Products Trevor Huseman, FSA, MAAA Managing Director

Point De Vue: Operational challenges faced by asset managers to price OTC derivatives Laurent Thuilier, SGSS. Avec le soutien de

Point De Vue: Operational challenges faced by asset managers to price OTC derivatives 2012 01 Laurent Thuilier, SGSS Avec le soutien de JJ Mois Année Operational challenges faced by asset managers to price

Point De Vue: Operational challenges faced by asset managers to price OTC derivatives 2012 01 Laurent Thuilier, SGSS Avec le soutien de JJ Mois Année Operational challenges faced by asset managers to price

Fuel Hedging. Management. Strategien for Airlines, Shippers, VISHNU N. GAJJALA

Fuel Hedging andrisk Management Strategien for Airlines, Shippers, and Other Consumers S. MOHAMED DAFIR VISHNU N. GAJJALA WlLEY Contents Preface Acknovuledgments Almut the Aiithors xiii xix xxi CHAPTER

Fuel Hedging andrisk Management Strategien for Airlines, Shippers, and Other Consumers S. MOHAMED DAFIR VISHNU N. GAJJALA WlLEY Contents Preface Acknovuledgments Almut the Aiithors xiii xix xxi CHAPTER

Volatility Smiles and Yield Frowns

Volatility Smiles and Yield Frowns Peter Carr NYU CBOE Conference on Derivatives and Volatility, Chicago, Nov. 10, 2017 Peter Carr (NYU) Volatility Smiles and Yield Frowns 11/10/2017 1 / 33 Interest Rates

Volatility Smiles and Yield Frowns Peter Carr NYU CBOE Conference on Derivatives and Volatility, Chicago, Nov. 10, 2017 Peter Carr (NYU) Volatility Smiles and Yield Frowns 11/10/2017 1 / 33 Interest Rates

MATH FOR CREDIT. Purdue University, Feb 6 th, SHIKHAR RANJAN Credit Products Group, Morgan Stanley

MATH FOR CREDIT Purdue University, Feb 6 th, 2004 SHIKHAR RANJAN Credit Products Group, Morgan Stanley Outline The space of credit products Key drivers of value Mathematical models Pricing Trading strategies

MATH FOR CREDIT Purdue University, Feb 6 th, 2004 SHIKHAR RANJAN Credit Products Group, Morgan Stanley Outline The space of credit products Key drivers of value Mathematical models Pricing Trading strategies

1) Understanding Equity Options 2) Setting up Brokerage Systems

Understanding Equity Options 2) Setting up Brokerage Systems") 1) Understanding Equity Options 2) Setting up Brokerage Systems M. Aras Orhan, 12.10.2013 FE 500 Intro to Financial Engineering 12.10.2013, ARAS ORHAN, Intro to Fin Eng, Boğaziçi University 1 Today s agenda

1) Understanding Equity Options 2) Setting up Brokerage Systems M. Aras Orhan, 12.10.2013 FE 500 Intro to Financial Engineering 12.10.2013, ARAS ORHAN, Intro to Fin Eng, Boğaziçi University 1 Today s agenda

Oil Price Volatility and Asymmetric Leverage Effects

Oil Price Volatility and Asymmetric Leverage Effects Eunhee Lee and Doo Bong Han Institute of Life Science and Natural Resources, Department of Food and Resource Economics Korea University, Department

Oil Price Volatility and Asymmetric Leverage Effects Eunhee Lee and Doo Bong Han Institute of Life Science and Natural Resources, Department of Food and Resource Economics Korea University, Department

IEOR E4602: Quantitative Risk Management

IEOR E4602: Quantitative Risk Management Model Risk Martin Haugh Department of Industrial Engineering and Operations Research Columbia University Email: martin.b.haugh@gmail.com Outline Introduction to

IEOR E4602: Quantitative Risk Management Model Risk Martin Haugh Department of Industrial Engineering and Operations Research Columbia University Email: martin.b.haugh@gmail.com Outline Introduction to

A Consistent Pricing Model for Index Options and Volatility Derivatives

A Consistent Pricing Model for Index Options and Volatility Derivatives 6th World Congress of the Bachelier Society Thomas Kokholm Finance Research Group Department of Business Studies Aarhus School of

A Consistent Pricing Model for Index Options and Volatility Derivatives 6th World Congress of the Bachelier Society Thomas Kokholm Finance Research Group Department of Business Studies Aarhus School of

Local and Stochastic Volatility Models: An Investigation into the Pricing of Exotic Equity Options

Local and Stochastic Volatility Models: An Investigation into the Pricing of Exotic Equity Options A dissertation submitted to the Faculty of Science, University of the Witwatersrand, Johannesburg, South

Local and Stochastic Volatility Models: An Investigation into the Pricing of Exotic Equity Options A dissertation submitted to the Faculty of Science, University of the Witwatersrand, Johannesburg, South

MSc Financial Mathematics

MSc Financial Mathematics Programme Structure Week Zero Induction Week MA9010 Fundamental Tools TERM 1 Weeks 1-1 0 ST9080 MA9070 IB9110 ST9570 Probability & Numerical Asset Pricing Financial Stoch. Processes

MSc Financial Mathematics Programme Structure Week Zero Induction Week MA9010 Fundamental Tools TERM 1 Weeks 1-1 0 ST9080 MA9070 IB9110 ST9570 Probability & Numerical Asset Pricing Financial Stoch. Processes

Interest Rate Modeling

Chapman & Hall/CRC FINANCIAL MATHEMATICS SERIES Interest Rate Modeling Theory and Practice Lixin Wu CRC Press Taylor & Francis Group Boca Raton London New York CRC Press is an imprint of the Taylor & Francis

Chapman & Hall/CRC FINANCIAL MATHEMATICS SERIES Interest Rate Modeling Theory and Practice Lixin Wu CRC Press Taylor & Francis Group Boca Raton London New York CRC Press is an imprint of the Taylor & Francis

Best Practices for Maximizing Returns in Multi-Currency Rates Trading. Copyright FinancialCAD Corporation. All rights reserved.

Best Practices for Maximizing Returns in Multi-Currency Rates Trading Copyright FinancialCAD Corporation. All rights reserved. Introduction In the current market environment, it is particularly important

Best Practices for Maximizing Returns in Multi-Currency Rates Trading Copyright FinancialCAD Corporation. All rights reserved. Introduction In the current market environment, it is particularly important

Table of Contents. Part I. Deterministic Models... 1

Preface...xvii Part I. Deterministic Models... 1 Chapter 1. Introductory Elements to Financial Mathematics.... 3 1.1. The object of traditional financial mathematics... 3 1.2. Financial supplies. Preference

Preface...xvii Part I. Deterministic Models... 1 Chapter 1. Introductory Elements to Financial Mathematics.... 3 1.1. The object of traditional financial mathematics... 3 1.2. Financial supplies. Preference

Multi-level Stochastic Valuations

Multi-level Stochastic Valuations 14 March 2016 High Performance Computing in Finance Conference 2016 Grigorios Papamanousakis Quantitative Strategist, Investment Solutions Aberdeen Asset Management 0

Multi-level Stochastic Valuations 14 March 2016 High Performance Computing in Finance Conference 2016 Grigorios Papamanousakis Quantitative Strategist, Investment Solutions Aberdeen Asset Management 0

MSc Financial Mathematics

MSc Financial Mathematics The following information is applicable for academic year 2018-19 Programme Structure Week Zero Induction Week MA9010 Fundamental Tools TERM 1 Weeks 1-1 0 ST9080 MA9070 IB9110

MSc Financial Mathematics The following information is applicable for academic year 2018-19 Programme Structure Week Zero Induction Week MA9010 Fundamental Tools TERM 1 Weeks 1-1 0 ST9080 MA9070 IB9110

Valuation of Arithmetic Average of Fed Funds Rates and Construction of the US dollar Swap Yield Curve

Valuation of Arithmetic Average of Fed Funds Rates and Construction of the US dollar Swap Yield Curve Katsumi Takada September 3, 2 Abstract Arithmetic averages of Fed Funds (FF) rates are paid on the

Valuation of Arithmetic Average of Fed Funds Rates and Construction of the US dollar Swap Yield Curve Katsumi Takada September 3, 2 Abstract Arithmetic averages of Fed Funds (FF) rates are paid on the

The role of the Model Validation function to manage and mitigate model risk

arxiv:1211.0225v1 [q-fin.rm] 21 Oct 2012 The role of the Model Validation function to manage and mitigate model risk Alberto Elices November 2, 2012 Abstract This paper describes the current taxonomy of

arxiv:1211.0225v1 [q-fin.rm] 21 Oct 2012 The role of the Model Validation function to manage and mitigate model risk Alberto Elices November 2, 2012 Abstract This paper describes the current taxonomy of

AN INFORMATION-BASED APPROACH TO CREDIT-RISK MODELLING. by Matteo L. Bedini Universitè de Bretagne Occidentale

AN INFORMATION-BASED APPROACH TO CREDIT-RISK MODELLING by Matteo L. Bedini Universitè de Bretagne Occidentale Matteo.Bedini@univ-brest.fr Agenda Credit Risk The Information-based Approach Defaultable Discount

AN INFORMATION-BASED APPROACH TO CREDIT-RISK MODELLING by Matteo L. Bedini Universitè de Bretagne Occidentale Matteo.Bedini@univ-brest.fr Agenda Credit Risk The Information-based Approach Defaultable Discount

Fixed Income Modelling

Fixed Income Modelling CLAUS MUNK OXPORD UNIVERSITY PRESS Contents List of Figures List of Tables xiii xv 1 Introduction and Overview 1 1.1 What is fixed income analysis? 1 1.2 Basic bond market terminology

Fixed Income Modelling CLAUS MUNK OXPORD UNIVERSITY PRESS Contents List of Figures List of Tables xiii xv 1 Introduction and Overview 1 1.1 What is fixed income analysis? 1 1.2 Basic bond market terminology

Derivative Securities Fall 2012 Final Exam Guidance Extended version includes full semester

Derivative Securities Fall 2012 Final Exam Guidance Extended version includes full semester Our exam is Wednesday, December 19, at the normal class place and time. You may bring two sheets of notes (8.5

Derivative Securities Fall 2012 Final Exam Guidance Extended version includes full semester Our exam is Wednesday, December 19, at the normal class place and time. You may bring two sheets of notes (8.5

Stochastic Volatility (Working Draft I)

") Stochastic Volatility (Working Draft I) Paul J. Atzberger General comments or corrections should be sent to: paulatz@cims.nyu.edu 1 Introduction When using the Black-Scholes-Merton model to price derivative

Stochastic Volatility (Working Draft I) Paul J. Atzberger General comments or corrections should be sent to: paulatz@cims.nyu.edu 1 Introduction When using the Black-Scholes-Merton model to price derivative

Building a Zero Coupon Yield Curve

Building a Zero Coupon Yield Curve Clive Bastow, CFA, CAIA ABSTRACT Create and use a zero- coupon yield curve from quoted LIBOR, Eurodollar Futures, PAR Swap and OIS rates. www.elpitcafinancial.com Risk-

Building a Zero Coupon Yield Curve Clive Bastow, CFA, CAIA ABSTRACT Create and use a zero- coupon yield curve from quoted LIBOR, Eurodollar Futures, PAR Swap and OIS rates. www.elpitcafinancial.com Risk-

Unlocking the secrets of the swaptions market Shalin Bhagwan and Mark Greenwood The Actuarial Profession

Unlocking the secrets of the swaptions market Shalin Bhagwan and Mark Greenwood Agenda Types of swaptions Case studies Market participants Practical consideratons Volatility smiles Real world and market

Unlocking the secrets of the swaptions market Shalin Bhagwan and Mark Greenwood Agenda Types of swaptions Case studies Market participants Practical consideratons Volatility smiles Real world and market

SMILE EXTRAPOLATION OPENGAMMA QUANTITATIVE RESEARCH

SMILE EXTRAPOLATION OPENGAMMA QUANTITATIVE RESEARCH Abstract. An implementation of smile extrapolation for high strikes is described. The main smile is described by an implied volatility function, e.g.

SMILE EXTRAPOLATION OPENGAMMA QUANTITATIVE RESEARCH Abstract. An implementation of smile extrapolation for high strikes is described. The main smile is described by an implied volatility function, e.g.

Volatility Smiles and Yield Frowns

Volatility Smiles and Yield Frowns Peter Carr NYU IFS, Chengdu, China, July 30, 2018 Peter Carr (NYU) Volatility Smiles and Yield Frowns 7/30/2018 1 / 35 Interest Rates and Volatility Practitioners and

Volatility Smiles and Yield Frowns Peter Carr NYU IFS, Chengdu, China, July 30, 2018 Peter Carr (NYU) Volatility Smiles and Yield Frowns 7/30/2018 1 / 35 Interest Rates and Volatility Practitioners and

Option Pricing under Delay Geometric Brownian Motion with Regime Switching

Science Journal of Applied Mathematics and Statistics 2016; 4(6): 263-268 http://www.sciencepublishinggroup.com/j/sjams doi: 10.11648/j.sjams.20160406.13 ISSN: 2376-9491 (Print); ISSN: 2376-9513 (Online)

Science Journal of Applied Mathematics and Statistics 2016; 4(6): 263-268 http://www.sciencepublishinggroup.com/j/sjams doi: 10.11648/j.sjams.20160406.13 ISSN: 2376-9491 (Print); ISSN: 2376-9513 (Online)

Discrete-time Asset Pricing Models in Applied Stochastic Finance

Discrete-time Asset Pricing Models in Applied Stochastic Finance P.C.G. Vassiliou ) WILEY Table of Contents Preface xi Chapter ^Probability and Random Variables 1 1.1. Introductory notes 1 1.2. Probability

Discrete-time Asset Pricing Models in Applied Stochastic Finance P.C.G. Vassiliou ) WILEY Table of Contents Preface xi Chapter ^Probability and Random Variables 1 1.1. Introductory notes 1 1.2. Probability

INTRODUCTION TO THE ECONOMICS AND MATHEMATICS OF FINANCIAL MARKETS. Jakša Cvitanić and Fernando Zapatero

INTRODUCTION TO THE ECONOMICS AND MATHEMATICS OF FINANCIAL MARKETS Jakša Cvitanić and Fernando Zapatero INTRODUCTION TO THE ECONOMICS AND MATHEMATICS OF FINANCIAL MARKETS Table of Contents PREFACE...1

INTRODUCTION TO THE ECONOMICS AND MATHEMATICS OF FINANCIAL MARKETS Jakša Cvitanić and Fernando Zapatero INTRODUCTION TO THE ECONOMICS AND MATHEMATICS OF FINANCIAL MARKETS Table of Contents PREFACE...1

IEOR E4602: Quantitative Risk Management Spring 2016 c 2016 by Martin Haugh. Model Risk

IEOR E4602: Quantitative Risk Management Spring 2016 c 2016 by Martin Haugh Model Risk We discuss model risk in these notes, mainly by way of example. We emphasize (i) the importance of understanding the

IEOR E4602: Quantitative Risk Management Spring 2016 c 2016 by Martin Haugh Model Risk We discuss model risk in these notes, mainly by way of example. We emphasize (i) the importance of understanding the

Volatility derivatives in the Heston framework

Volatility derivatives in the Heston framework Abstract A volatility derivative is a financial contract where the payoff depends on the realized variance of a specified asset s returns. As volatility is

Volatility derivatives in the Heston framework Abstract A volatility derivative is a financial contract where the payoff depends on the realized variance of a specified asset s returns. As volatility is

MBAX Credit Default Swaps (CDS)

") MBAX-6270 Credit Default Swaps Credit Default Swaps (CDS) CDS is a form of insurance against a firm defaulting on the bonds they issued CDS are used also as a way to express a bearish view on a company

MBAX-6270 Credit Default Swaps Credit Default Swaps (CDS) CDS is a form of insurance against a firm defaulting on the bonds they issued CDS are used also as a way to express a bearish view on a company

Cash Settled Swaption Pricing

Cash Settled Swaption Pricing Peter Caspers (with Jörg Kienitz) Quaternion Risk Management 30 November 2017 Agenda Cash Settled Swaption Arbitrage How to fix it Agenda Cash Settled Swaption Arbitrage How

Cash Settled Swaption Pricing Peter Caspers (with Jörg Kienitz) Quaternion Risk Management 30 November 2017 Agenda Cash Settled Swaption Arbitrage How to fix it Agenda Cash Settled Swaption Arbitrage How

Latest Developments: Interest Rate Modelling & Interest Rate Exotic & FX Hybrid Products

Latest Developments: Interest Rate Modelling & Interest Rate Exotic & FX Hybrid Products London: 24th 26th November 2008 This workshop provides THREE booking options Register to ANY ONE day TWO days or

Latest Developments: Interest Rate Modelling & Interest Rate Exotic & FX Hybrid Products London: 24th 26th November 2008 This workshop provides THREE booking options Register to ANY ONE day TWO days or

1 Mathematics in a Pill 1.1 PROBABILITY SPACE AND RANDOM VARIABLES. A probability triple P consists of the following components:

1 Mathematics in a Pill The purpose of this chapter is to give a brief outline of the probability theory underlying the mathematics inside the book, and to introduce necessary notation and conventions

1 Mathematics in a Pill The purpose of this chapter is to give a brief outline of the probability theory underlying the mathematics inside the book, and to introduce necessary notation and conventions

A Multi-factor Statistical Model for Interest Rates

A Multi-factor Statistical Model for Interest Rates Mar Reimers and Michael Zerbs A term structure model that produces realistic scenarios of future interest rates is critical to the effective measurement

A Multi-factor Statistical Model for Interest Rates Mar Reimers and Michael Zerbs A term structure model that produces realistic scenarios of future interest rates is critical to the effective measurement

Collateral Management & CSA Discounting. Anna Barbashova Product Specialist CrossAsset Client Solutions Group, Numerix December 11, 2013

Collateral Management & CSA Discounting Anna Barbashova Product Specialist CrossAsset Client Solutions Group, Numerix December 11, 2013 About Our Presenters Contact Our Presenters: Follow Us: Anna Barbashova

Collateral Management & CSA Discounting Anna Barbashova Product Specialist CrossAsset Client Solutions Group, Numerix December 11, 2013 About Our Presenters Contact Our Presenters: Follow Us: Anna Barbashova

No arbitrage conditions in HJM multiple curve term structure models

No arbitrage conditions in HJM multiple curve term structure models Zorana Grbac LPMA, Université Paris Diderot Joint work with W. Runggaldier 7th General AMaMeF and Swissquote Conference Lausanne, 7-10

No arbitrage conditions in HJM multiple curve term structure models Zorana Grbac LPMA, Université Paris Diderot Joint work with W. Runggaldier 7th General AMaMeF and Swissquote Conference Lausanne, 7-10

Monte Carlo Methods in Structuring and Derivatives Pricing

Monte Carlo Methods in Structuring and Derivatives Pricing Prof. Manuela Pedio (guest) 20263 Advanced Tools for Risk Management and Pricing Spring 2017 Outline and objectives The basic Monte Carlo algorithm

Monte Carlo Methods in Structuring and Derivatives Pricing Prof. Manuela Pedio (guest) 20263 Advanced Tools for Risk Management and Pricing Spring 2017 Outline and objectives The basic Monte Carlo algorithm

TEST OF BOUNDED LOG-NORMAL PROCESS FOR OPTIONS PRICING

TEST OF BOUNDED LOG-NORMAL PROCESS FOR OPTIONS PRICING Semih Yön 1, Cafer Erhan Bozdağ 2 1,2 Department of Industrial Engineering, Istanbul Technical University, Macka Besiktas, 34367 Turkey Abstract.

TEST OF BOUNDED LOG-NORMAL PROCESS FOR OPTIONS PRICING Semih Yön 1, Cafer Erhan Bozdağ 2 1,2 Department of Industrial Engineering, Istanbul Technical University, Macka Besiktas, 34367 Turkey Abstract.

Advanced Quantitative Methods for Asset Pricing and Structuring

MSc. Finance/CLEFIN 2017/2018 Edition Advanced Quantitative Methods for Asset Pricing and Structuring May 2017 Exam for Non Attending Students Time Allowed: 95 minutes Family Name (Surname) First Name

MSc. Finance/CLEFIN 2017/2018 Edition Advanced Quantitative Methods for Asset Pricing and Structuring May 2017 Exam for Non Attending Students Time Allowed: 95 minutes Family Name (Surname) First Name

6. Pricing deterministic payoffs

Some of the content of these slides is based on material from the book Introduction to the Economics and Mathematics of Financial Markets by Jaksa Cvitanic and Fernando Zapatero. Pricing Options with Mathematical

Some of the content of these slides is based on material from the book Introduction to the Economics and Mathematics of Financial Markets by Jaksa Cvitanic and Fernando Zapatero. Pricing Options with Mathematical

Modeling via Stochastic Processes in Finance

Modeling via Stochastic Processes in Finance Dimbinirina Ramarimbahoaka Department of Mathematics and Statistics University of Calgary AMAT 621 - Fall 2012 October 15, 2012 Question: What are appropriate

Modeling via Stochastic Processes in Finance Dimbinirina Ramarimbahoaka Department of Mathematics and Statistics University of Calgary AMAT 621 - Fall 2012 October 15, 2012 Question: What are appropriate

IMES DISCUSSION PAPER SERIES

IMES DISCUSSION PAPER SERIES Variation of Wrong-Way Risk Management and Its Impact on Security Price Changes Tetsuya Adachi and Yoshihiko Uchida Discussion Paper No. 2015-E-11 INSTITUTE FOR MONETARY AND

IMES DISCUSSION PAPER SERIES Variation of Wrong-Way Risk Management and Its Impact on Security Price Changes Tetsuya Adachi and Yoshihiko Uchida Discussion Paper No. 2015-E-11 INSTITUTE FOR MONETARY AND

Pricing Options with Mathematical Models

Pricing Options with Mathematical Models 1. OVERVIEW Some of the content of these slides is based on material from the book Introduction to the Economics and Mathematics of Financial Markets by Jaksa Cvitanic

Pricing Options with Mathematical Models 1. OVERVIEW Some of the content of these slides is based on material from the book Introduction to the Economics and Mathematics of Financial Markets by Jaksa Cvitanic

Unified Credit-Equity Modeling

Unified Credit-Equity Modeling Rafael Mendoza-Arriaga Based on joint research with: Vadim Linetsky and Peter Carr The University of Texas at Austin McCombs School of Business (IROM) Recent Advancements

Unified Credit-Equity Modeling Rafael Mendoza-Arriaga Based on joint research with: Vadim Linetsky and Peter Carr The University of Texas at Austin McCombs School of Business (IROM) Recent Advancements

Challenges In Modelling Inflation For Counterparty Risk

Challenges In Modelling Inflation For Counterparty Risk Vinay Kotecha, Head of Rates/Commodities, Market and Counterparty Risk Analytics Vladimir Chorniy, Head of Market & Counterparty Risk Analytics Quant

Challenges In Modelling Inflation For Counterparty Risk Vinay Kotecha, Head of Rates/Commodities, Market and Counterparty Risk Analytics Vladimir Chorniy, Head of Market & Counterparty Risk Analytics Quant

From Discrete Time to Continuous Time Modeling

From Discrete Time to Continuous Time Modeling Prof. S. Jaimungal, Department of Statistics, University of Toronto 2004 Arrow-Debreu Securities 2004 Prof. S. Jaimungal 2 Consider a simple one-period economy

From Discrete Time to Continuous Time Modeling Prof. S. Jaimungal, Department of Statistics, University of Toronto 2004 Arrow-Debreu Securities 2004 Prof. S. Jaimungal 2 Consider a simple one-period economy

Financial Risk Management

r r Financial Risk Management A Practitioner's Guide to Managing Market and Credit Risk Second Edition STEVEN ALLEN WILEY John Wiley & Sons, Inc. Contents Foreword Preface Acknowledgments About the Author

r r Financial Risk Management A Practitioner's Guide to Managing Market and Credit Risk Second Edition STEVEN ALLEN WILEY John Wiley & Sons, Inc. Contents Foreword Preface Acknowledgments About the Author

Economic Scenario Generator: Applications in Enterprise Risk Management. Ping Sun Executive Director, Financial Engineering Numerix LLC

Economic Scenario Generator: Applications in Enterprise Risk Management Ping Sun Executive Director, Financial Engineering Numerix LLC Numerix makes no representation or warranties in relation to information

Economic Scenario Generator: Applications in Enterprise Risk Management Ping Sun Executive Director, Financial Engineering Numerix LLC Numerix makes no representation or warranties in relation to information

Smile-consistent CMS adjustments in closed form: introducing the Vanna-Volga approach

Smile-consistent CMS adjustments in closed form: introducing the Vanna-Volga approach Antonio Castagna, Fabio Mercurio and Marco Tarenghi Abstract In this article, we introduce the Vanna-Volga approach

Smile-consistent CMS adjustments in closed form: introducing the Vanna-Volga approach Antonio Castagna, Fabio Mercurio and Marco Tarenghi Abstract In this article, we introduce the Vanna-Volga approach