EARNINGS PER SHARE AS 20

|

|

|

- Griselda Bishop

- 5 years ago

- Views:

Transcription

1 EARNINGS PER SHARE AS 20 OBJECTIVE To prescribe principles for the determination and presentation of EPS which will improve comparison of performance among different enterprises for the same period and among different accounting periods for the same enterprise SCOPE 1. Mandatory for all enterprises except for SMCs and SMEs (Level II & III) who may not disclose diluted EPS. 2. In CFS information should be presented on basis of consolidated information. DEFINITIONS EQUITY SHARE is a share other than a preference share. PREFERENCE SHARE is a share carrying preferential rights to dividends and repayment of capital. FINANCIAL INSTRUMENT is any contract that gives rise to both a financial asset of one enterprise and a financial liability or equity shares of another enterprise. POTENTIAL EQUITY SHARE is a financial instrument or other contract that entitles, or may entitle, its holder to equity shares. SHARE WARRANTS or options are financial instruments that give the holder the right to acquire equity shares. EXAMPLES OF FINANCIAL ASSETS a) cash ; b) a contractual right to receive cash or another financial asset from another enterprise; c) a contractual right to exchange financial instruments with another enterprise under conditions that are potentially favourable; or d) an equity share of another enterprise. A financial liability is any liability that is a contractual obligation to deliver cash or another financial asset to another enterprise or to exchange financial instruments with another enterprise under conditions that are potentially unfavourable. EXAMPLES OF POTENTIAL EQUITY SHARES a) debt instruments or preference shares, that are convertible into equity shares; b) share warrants;

2 c) options including employee stock option plans under which employees of an enterprise are entitled to receive equity shares as part of their remuneration and other similar plans; and d) shares which would be issued upon the satisfaction of certain conditions resulting from contractual arrangements (contingently issuable shares), such as the acquisition of a business or other assets, or shares issuable under a loan contract upon default of payment of principal or Interest, if the contract so provides. PRESENTATION Basic and diluted earnings per share in p&l (even if amount is negative) for each class of equity shares for all periods presented. MEASUREMENT Basic EPS = Net profit or loss after tax less preference dividend weighted avg no. of equity shares during the period Net profit after tax is after deducting prior period item and extraordinary item. Preference dividend = + Weighted Avg no of = equity shares: Dividend on non-cumulative preference shares provided for the period Dividend on cumulative preference shares for the period whether provided/ not. Prior period dividends not to be included. (Equity shares as on xx + issued during year buy back during year) X Time weighting factor As summarized: Calculation of Profits/Loss attributable to Equity shareholder Net Profit/Loss for the period (after adjusting all prior period & extraordinary items) Less: Tax Liability (Current & Deferred Tax) Net Profit attributable to Shareholder's Less: Preference share dividend & any attributable tax on Pref. Dividend Net Profit/loss attributable to Equity shareholder's

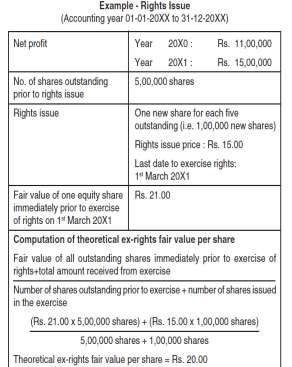

3 Shares are included in the weighted average number of shares from the date consideration for shares are receivable. 1. Equity shares for cash: when cash is receivable 2. Conversion of debt to equity: date of conversion 3. Equity shares in lieu of interest/ principal: date interest ceases to accrue 4. Equity shares in exchange of liability: date liability is settled 5. Equity shares for asset: date of acquisition 6. Equity shares for rendering services: when services are rendered 7. Amalgamation in nature of purchase: date of acquisition 8. Amalgamation in nature of merger: beginning of period 9. Partly paid equity shares: treated as a fraction of an equity share relative to a fully paid equity share 10. Shares with different nominal value: converting all shares to equivalent shares of same nominal value. EVENTS WHICH CHANGE THE NUMBER OF SHARES WITHOUT CHANGE IN RESOURCES a) Bonus issue b) Bonus element in rights issue c) Share split d) Consolidation of shares (reverse share split) BONUS ISSUE: Eg: bonus issue of 2 shares for every 1 share held Shares before issue X 3 = total no. of shares Shares before issue X 2 = additional shares In bonus issue Adjusted EPS is calculated for prior periods as if the issue had occurred in the beginning of those periods. RIGHTS ISSUE: Exercise price < FV of shares (hence a bonus element present) Step 1: Theoretical ex right FV per share = Adjustment Factor = = (A + B)/ (C+D) A= FV of all shares o/s before exercise of rights B= Amount received from exercise of rights C= no. of shares o/s before rights offer D= no of shares issued in exercise of rights FV per share before Rights Theoretical ex right FV per share EPS for current reporting period = Net profit for equity shareholders (shares o/s before rights x adjustment factor x time weight factor) + (shares after rights issue x time weight factor)

4 Restate EPS for previous period = Net profit of previous period (No. of shares o/s before rights offer x adjustment factor) DILUTED EPS In calculating diluted EPS effect is given to all dilutive potential equity shares o/s during that period. Adjustments to Net Profit Net Profit For The Period Add: Dividend recognized in the period for dilutive potential equity shares Add: Interest less tax recognized in the period for dilutive potential equity shares Add: after tax amount of any other change in expenses/ income due to conversion of dilutive potential equity shares Share application money pending allotment or advance share application money is treated as dilutive potential equity shares. WEIGHTED AVERAGE NO. OF EQUITY SHARES For Diluted EPS weighted average no. of equity shares o/s during the period is increased by weighted average no. of additional equity shares which would have been o/s assuming conversion of all dilutive potential equity shares. DILUTED EPS = Net profit for equity shareholders (After adjustment of diluted earnings) Weighted avg equity shares o/s during the period (assuming all dilutive potential equity shares are converted) DILUTED EARNINGS Net profit after tax for equity shareholders Add: dividend on convertible equity shares Add: Interest net of tax on convertible debentures Net profit available for diluted EPS

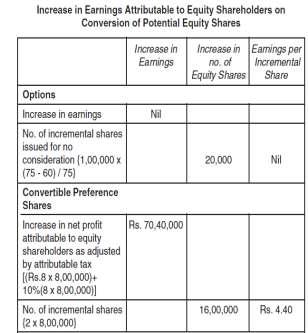

5 As summarized Diluted Earnings Net Profit/loss attributable to Equity shareholder's (as calculated in slide no. 8) Add: Payments that are not required to be made because of such conversion (eg. dividend on convertible pref. share or interest on convertible debt) Less: Payments that are required to be made because of such conversion (e.g expenses on conversion) Diluted Earnings SHARE OPTIONS It is assumed that all dilutive Options and dilutive Potential Equity Shares have been exercised. Fair Value= Avg price of the equity shares during the period. Options are dilutive if Issue price < Fair Value Hence Options contract consists of a) Certain no. of shares issued at FV b) Remaining no. of shares issued for NIL consideration Issue of shares at NIL consideration =No. of shares issuable under the Option less Equivalent no of shares that would have been issued at FV.

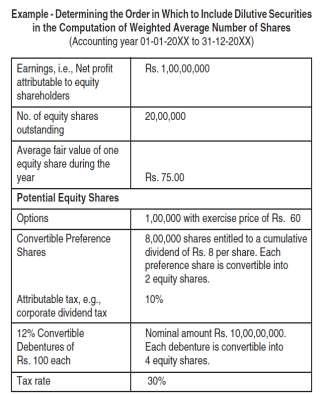

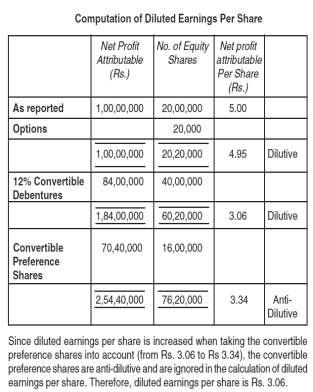

6 Potential equity shares should be treated as dilutive when, and only when, their conversion to equity shares would decrease net profit per share from continuing ordinary operations. The effect of anti-dilutive potential equity shares is ignored in calculating diluted EPS. Order in which potential equity shares are considered They are ranked in order of dilutive effect from the most dilutive to least dilutive. Dilutive effect = Increase in equity shares earnings due to conversion/increase in shares

7

8 Potential equity shares are weighted for the period they were outstanding. Potential equity shares that were cancelled or allowed to lapse during the reporting period are included in the computation of diluted earnings per share only for the portion of the period during which they were outstanding. Potential equity shares that have been converted into equity shares during the reporting period are included in the calculation of diluted earnings per share from the beginning of the period to the date of conversion. From the date of conversion, the resulting equity shares are included in computing both basic and diluted earnings per share. RE-STATEMENT If the number of equity shares or potential equity shares outstanding is increased as a result of bonus issue, share split, consolidation of shares, the calculation of basic and diluted equity per share should be adjusted for current period and previous periods. DISCLOSURE a) the amounts used as the numerators in calculating basic and diluted earnings per share, and a reconciliation of those amounts to the net profit or loss for the period; b) the weighted average number of equity shares used as the denominator in calculating basic and diluted earnings per share, and a reconciliation of these denominators to each other; and c) the nominal value of shares along with the earnings per share figures. EXAMPLES: from ICAI compendium on Accounting Standards (see below)

9

10 Courtesy: ICAI Study Materials and Compendium of Accounting Standards. A compilation by CA, CWA, B Com (Hons) piyali.sinha1@gmail.com

HKAS 33 Earnings per Share 1 November 2005

HKAS 33 Earnings per Share 1 November 2005 1. Objective of HKAS 33 The objective of HKAS 33 Earnings per Share is to prescribe principles for the determination and presentation of earnings per share, so

HKAS 33 Earnings per Share 1 November 2005 1. Objective of HKAS 33 The objective of HKAS 33 Earnings per Share is to prescribe principles for the determination and presentation of earnings per share, so

Indian Accounting Standard (Ind AS) 33. Earnings per Share

33. Earnings per Share") Indian Accounting Standard (Ind AS) 33 Earnings per Share 2 Indian Accounting Standard (Ind AS) 33 Earnings per Share CONTENTS Paragraphs OBJECTIVE 1 SCOPE 2 4A DEFINITIONS 5 8 MEASUREMENT 9 63 Basic earnings

Indian Accounting Standard (Ind AS) 33 Earnings per Share 2 Indian Accounting Standard (Ind AS) 33 Earnings per Share CONTENTS Paragraphs OBJECTIVE 1 SCOPE 2 4A DEFINITIONS 5 8 MEASUREMENT 9 63 Basic earnings

Page 2 of 34. When cash is receivable The dividend payment date. Date interest ceases accruing. Date interest ceases accruing. The settlement date

Chapter 17 EARNINGS PER SHARE (IAS 33) OBJECTIVE The objective of this IAS is to prescribe principles for the determination and presentation of earning per share. SCOPE This IAS shall apply to the entities

Chapter 17 EARNINGS PER SHARE (IAS 33) OBJECTIVE The objective of this IAS is to prescribe principles for the determination and presentation of earning per share. SCOPE This IAS shall apply to the entities

Earnings per share. Introduction

Earnings per share Topic list Syllabus reference 1 IAS 33 Earnings per share C11 2 Basic EPS C11 3 Effect on EPS of changes in capital structure C11 4 Diluted EPS C11 5 Presentation, disclosure and other

Earnings per share Topic list Syllabus reference 1 IAS 33 Earnings per share C11 2 Basic EPS C11 3 Effect on EPS of changes in capital structure C11 4 Diluted EPS C11 5 Presentation, disclosure and other

Sri Lanka Accounting Standard-LKAS 33. Earnings per Share -776-

Sri Lanka Accounting Standard-LKAS 33 Earnings per Share -776- APPENDIX -777- Sri Lanka Accounting Standard-LKAS 33 Earnings per Share Sri Lanka Accounting Standard LKAS 33 Earnings per Share is set out

Sri Lanka Accounting Standard-LKAS 33 Earnings per Share -776- APPENDIX -777- Sri Lanka Accounting Standard-LKAS 33 Earnings per Share Sri Lanka Accounting Standard LKAS 33 Earnings per Share is set out

IND AS 33 Earnings Per Share

33.1 IND AS 33 Earnings Per Share Example 1 (Question from Ind AS Lab) Ind AS 33 states that This Indian Accounting Standard shall apply to companies that have issued ordinary shares to which Indian Accounting

33.1 IND AS 33 Earnings Per Share Example 1 (Question from Ind AS Lab) Ind AS 33 states that This Indian Accounting Standard shall apply to companies that have issued ordinary shares to which Indian Accounting

International Accounting Standard 33 Earnings per Share

EC staff consolidated version as of 21 June 2012, EN IAS 33 FOR INFORMATION PURPOSES ONLY International Accounting Standard 33 Earnings per Share Objective 1 The objective of this Standard is to prescribe

EC staff consolidated version as of 21 June 2012, EN IAS 33 FOR INFORMATION PURPOSES ONLY International Accounting Standard 33 Earnings per Share Objective 1 The objective of this Standard is to prescribe

Sri Lanka Accounting Standard LKAS 33. Earnings per Share

Sri Lanka Accounting Standard LKAS 33 Earnings per Share CONTENTS paragraphs SRI LANKA ACCOUNTING STANDARD LKAS 33 EARNINGS PER SHARE OBJECTIVE 1 SCOPE 2 DEFINITIONS 5 MEASUREMENT 9 Basic earnings per

Sri Lanka Accounting Standard LKAS 33 Earnings per Share CONTENTS paragraphs SRI LANKA ACCOUNTING STANDARD LKAS 33 EARNINGS PER SHARE OBJECTIVE 1 SCOPE 2 DEFINITIONS 5 MEASUREMENT 9 Basic earnings per

Michael Farrell Online

EARNINGS PER SHARE QUESTION On 1 January 20X6 the issued share capital of Dose, a public limited company, was 12 million preference shares of $1 each and 10 million ordinary shares of $1 each. Assume where

EARNINGS PER SHARE QUESTION On 1 January 20X6 the issued share capital of Dose, a public limited company, was 12 million preference shares of $1 each and 10 million ordinary shares of $1 each. Assume where

New Zealand Equivalent to International Accounting Standard 33 Earnings per Share (NZ IAS 33)

") New Zealand Equivalent to International Accounting Standard 33 Earnings per Share (NZ IAS 33) Issued November 2004 and incorporates amendments up to and including 30 June 2011 other than consequential

New Zealand Equivalent to International Accounting Standard 33 Earnings per Share (NZ IAS 33) Issued November 2004 and incorporates amendments up to and including 30 June 2011 other than consequential

New Zealand Equivalent to International Accounting Standard 33 Earnings per Share (NZ IAS 33)

") New Zealand Equivalent to International Accounting Standard 33 Earnings per Share (NZ IAS 33) Issued November 2004 and incorporates amendments up to and including 30 November 2012 This Standard was issued

New Zealand Equivalent to International Accounting Standard 33 Earnings per Share (NZ IAS 33) Issued November 2004 and incorporates amendments up to and including 30 November 2012 This Standard was issued

HKAS 33 Revised May 2014September Hong Kong Accounting Standard 33. Earnings per Share

HKAS 33 Revised May 2014September 2018 Hong Kong Accounting Standard 33 Earnings per Share HKAS 33 COPYRIGHT Copyright 2018 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial

HKAS 33 Revised May 2014September 2018 Hong Kong Accounting Standard 33 Earnings per Share HKAS 33 COPYRIGHT Copyright 2018 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial

IAS Earnings Per Share. By:

IAS - 33 Earnings Per Share International Accounting Standard No. 33 (IAS 33) Earnings per share Objective 1. The objective of this Standard is to establish principles for determining and presenting the

IAS - 33 Earnings Per Share International Accounting Standard No. 33 (IAS 33) Earnings per share Objective 1. The objective of this Standard is to establish principles for determining and presenting the

New Zealand Equivalent to International Accounting Standard 33 Earnings per Share (NZ IAS 33)

") New Zealand Equivalent to International Accounting Standard 33 Earnings per Share (NZ IAS 33) Issued November 2004 and incorporates amendments to 31 December 2016 This Standard was issued by the New Zealand

New Zealand Equivalent to International Accounting Standard 33 Earnings per Share (NZ IAS 33) Issued November 2004 and incorporates amendments to 31 December 2016 This Standard was issued by the New Zealand

Ind AS 33 Earnings per Share EIRC, Kolkata Mohit Jain 16 February For discussion purposes only

Ind AS 33 Earnings per Share EIRC, Kolkata Mohit Jain 16 February 2018 For discussion purposes only 0 Scope Ind AS 33 is applicable to companies that have issued ordinary shares to which Ind ASs notified

Ind AS 33 Earnings per Share EIRC, Kolkata Mohit Jain 16 February 2018 For discussion purposes only 0 Scope Ind AS 33 is applicable to companies that have issued ordinary shares to which Ind ASs notified

INTERMEDIATE ACCOUNTING

Chapter 16 Retained Earnings and Earnings Per Share INTERMEDIATE ACCOUNTING whole or in part. Objectives 1. Explain the accounting and reporting for different types of dividends. 2. Discuss the accounting

Chapter 16 Retained Earnings and Earnings Per Share INTERMEDIATE ACCOUNTING whole or in part. Objectives 1. Explain the accounting and reporting for different types of dividends. 2. Discuss the accounting

IAS 33, IAS 34 and IFRS 8 November 2008

IAS 33, IAS 34 and IFRS 8 November 2008 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2006-08 Nelson 1 Today s Agenda IAS 33 Earnings per Share IAS 34 Interim Financial

IAS 33, IAS 34 and IFRS 8 November 2008 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2006-08 Nelson 1 Today s Agenda IAS 33 Earnings per Share IAS 34 Interim Financial

Comparative statement on Indian GAAP and IFRS

Comparative statement on Indian GAAP and IFRS (As on 1 January 2010) 2010 edition Contents i ii 6 Basic standards 7 First-time adoption 7 Small and medium sized entities (SMEs)/Small and medium sized companies

Comparative statement on Indian GAAP and IFRS (As on 1 January 2010) 2010 edition Contents i ii 6 Basic standards 7 First-time adoption 7 Small and medium sized entities (SMEs)/Small and medium sized companies

Paper-12 : COMPANY ACCOUNTS & AUDIT

Paper-12 : COMPANY ACCOUNTS & AUDIT Study Note 1: Conceptual Framework for Preparation and Presentation of Financial Statements Question No. 1 Discuss the use of the General Purpose Financial Statement

Paper-12 : COMPANY ACCOUNTS & AUDIT Study Note 1: Conceptual Framework for Preparation and Presentation of Financial Statements Question No. 1 Discuss the use of the General Purpose Financial Statement

Accounting Standard (AS) 24 Discontinuing Operations. CA Manish C. Iyer

24 Discontinuing Operations. CA Manish C. Iyer") Accounting Standard (AS) 24 Discontinuing Operations 74 Objective and Scope To establish principles for reporting information about discontinuing operations, thereby enhancing the ability of users of financial

Accounting Standard (AS) 24 Discontinuing Operations 74 Objective and Scope To establish principles for reporting information about discontinuing operations, thereby enhancing the ability of users of financial

CPA P1 Corporate Reporting. TOPIC 39 - IAS 33 Earnings Per Share

TOPIC 39 - IAS 33 Earnings Per Share 1 2 3 4 5 6 Basic EPS Example On 1 April 20x1, a company issued $1,250,000 8% Convertible unsecured bonds for cash at par. Each $100 nominal of the loan stock will

TOPIC 39 - IAS 33 Earnings Per Share 1 2 3 4 5 6 Basic EPS Example On 1 April 20x1, a company issued $1,250,000 8% Convertible unsecured bonds for cash at par. Each $100 nominal of the loan stock will

Revisionary Test Paper_Final_Syllabus 2008_Dec2013

Question No.1(a) Paper 16 Advanced Financial Accounting & Reporting What is 'discontinuing operations' as per AS-24? Answer: As per Para 3 of the standard, a discontinuing operation is a component of an

Question No.1(a) Paper 16 Advanced Financial Accounting & Reporting What is 'discontinuing operations' as per AS-24? Answer: As per Para 3 of the standard, a discontinuing operation is a component of an

Weighted Shares Beginning balance Issued shares Reacquired shares. Shares Outstanding

EXERCISE 17-2 (15-20 minutes) (a) Event Dates Outstanding Shares Outstanding Fraction of Year Weighted Shares Beginning balance Issued shares Reacquired shares Jan. 1 May 1 May 1 Oct. 31 Oct. 31 Dec. 31

EXERCISE 17-2 (15-20 minutes) (a) Event Dates Outstanding Shares Outstanding Fraction of Year Weighted Shares Beginning balance Issued shares Reacquired shares Jan. 1 May 1 May 1 Oct. 31 Oct. 31 Dec. 31

SUGGESTED SOLUTION. Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022)

, Mumbai 69. Tel : (022)") SUGGESTED SOLUTION Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666 1 P a g e Ans. 1 (a) Computation of Weighted Average Number of Shares Outstanding

SUGGESTED SOLUTION Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666 1 P a g e Ans. 1 (a) Computation of Weighted Average Number of Shares Outstanding

C H A P T E R 16 DILUTIVE SECURITIES AND EARNINGS PER SHARE

16-1 C H A P T E R 16 DILUTIVE SECURITIES AND EARNINGS PER SHARE Intermediate Accounting 13th Edition Kieso, Weygandt, and Warfield 16-2 Dilutive Securities and Earnings Per Share Dilutive Securities and

16-1 C H A P T E R 16 DILUTIVE SECURITIES AND EARNINGS PER SHARE Intermediate Accounting 13th Edition Kieso, Weygandt, and Warfield 16-2 Dilutive Securities and Earnings Per Share Dilutive Securities and

DISCLOSURES BY BOARD OF DIRECTORS AS PER REGULATION 14 OF SECURITIES AND EXCHANGE BOARD OF INDIA (SHARE BASED EMPLOYEE BENEFITS) REGULATIONS, 2014

REGULATIONS, 2014") DISCLOSURES BY BOARD OF DIRECTORS AS PER REGULATION 14 OF SECURITIES AND EXCHANGE BOARD OF INDIA (SHARE BASED EMPLOYEE BENEFITS) REGULATIONS, 2014 A. Disclosures in terms of the 'Guidance note on accounting

DISCLOSURES BY BOARD OF DIRECTORS AS PER REGULATION 14 OF SECURITIES AND EXCHANGE BOARD OF INDIA (SHARE BASED EMPLOYEE BENEFITS) REGULATIONS, 2014 A. Disclosures in terms of the 'Guidance note on accounting

26 th Regional Conference of WIRC. Revised Schedule VI. CA N. Venkatram 16th December, 2011

26 th Regional Conference of WIRC Revised Schedule VI CA N. Venkatram 16th December, 2011 Agenda Background and Applicability Structure of Revised Schedule VI Points and Issues Comparison with the Existing

26 th Regional Conference of WIRC Revised Schedule VI CA N. Venkatram 16th December, 2011 Agenda Background and Applicability Structure of Revised Schedule VI Points and Issues Comparison with the Existing

Independent Auditors Report

Independent Auditors Report TO THE MEMBERS OF, INDIABULLS VENTURE CAPITAL TRUSTEE COMPANY LIMITED Reports on the Financial Statements We have audited the accompanying financial statements of Indiabulls

Independent Auditors Report TO THE MEMBERS OF, INDIABULLS VENTURE CAPITAL TRUSTEE COMPANY LIMITED Reports on the Financial Statements We have audited the accompanying financial statements of Indiabulls

2. Value of Machine to be recognized in the Books of Lessee(1 ½ marks) OR Whichever is lower. = ` 1, 50,000

OR Whichever is lower. = ` 1, 50,000") INTER CA MAY 2018 PAPER 5 :ADVANCED ACCOUNTS Branch: Multiple Date: Q 1 (A) 1. Provisions of AS 9: (2 marks) (a) When the Claim made is in the course of ordinary activities of the Company, it can be recognized

INTER CA MAY 2018 PAPER 5 :ADVANCED ACCOUNTS Branch: Multiple Date: Q 1 (A) 1. Provisions of AS 9: (2 marks) (a) When the Claim made is in the course of ordinary activities of the Company, it can be recognized

Revised Schedule VI. By: Purushottam Nyati Mukul Rathi. July 27, Page 1

Revised Schedule VI July 27, 2012 By: Purushottam Nyati Mukul Rathi Page 1 Contents of the Session Introduction Why Revised Schedule VI? Journey so far Key Features Format of Balance Sheet Format of Statement

Revised Schedule VI July 27, 2012 By: Purushottam Nyati Mukul Rathi Page 1 Contents of the Session Introduction Why Revised Schedule VI? Journey so far Key Features Format of Balance Sheet Format of Statement

FINANCIAL STATEMENTS UNDER IND AS: OVER ALL CONSIDERATIONS

FINANCIAL STATEMENTS UNDER IND AS: OVER ALL CONSIDERATIONS October 2016 1 Titre de la présentation CONSTITUENTS OF FINANCIAL STATEMENTS Balance sheet Statement of profit and loss (title not entirely representative

FINANCIAL STATEMENTS UNDER IND AS: OVER ALL CONSIDERATIONS October 2016 1 Titre de la présentation CONSTITUENTS OF FINANCIAL STATEMENTS Balance sheet Statement of profit and loss (title not entirely representative

Shareholder's funds Share capital 3 1,777,885,036 1,777,885,036 Reserves and surplus 4 (7,552,905,671) (309,099,121) (5,775,020,635) 1,468,785,915

(309,099,121) (5,775,020,635) 1,468,785,915") WIPRO SOLUTIONS CANADA LIMITED (Formerly WIPRO TECHNOLOGIES CANADA LTD) Balance sheet (Amount in, except share and per share data, unless otherwise stated) EQUITY AND LIABILITIES As at As at Sch No. 31

WIPRO SOLUTIONS CANADA LIMITED (Formerly WIPRO TECHNOLOGIES CANADA LTD) Balance sheet (Amount in, except share and per share data, unless otherwise stated) EQUITY AND LIABILITIES As at As at Sch No. 31

MINDTREE CONSULTING LIMITED Schedule 15 Significant accounting policies and notes to the accounts For the half year ended September 30, 2007

Schedule 15 Significant accounting policies and notes to the accounts 1. Background MindTree Consulting Limited ( MindTree Consulting or the Company ) [formerly MindTree Consulting Private Limited ] is

Schedule 15 Significant accounting policies and notes to the accounts 1. Background MindTree Consulting Limited ( MindTree Consulting or the Company ) [formerly MindTree Consulting Private Limited ] is

WIPRO TECHNOLOGIES SDN BHD (formerly known as PLANET PSG SDN BHD), MALAYSIA FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015

, MALAYSIA FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015") WIPRO TECHNOLOGIES SDN BHD (formerly known as PLANET PSG SDN BHD), MALAYSIA FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015 WIPRO TECHNOLOGIES SDN BHD (formerly known as PLANET PSG SDN

WIPRO TECHNOLOGIES SDN BHD (formerly known as PLANET PSG SDN BHD), MALAYSIA FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015 WIPRO TECHNOLOGIES SDN BHD (formerly known as PLANET PSG SDN

REVISED SCHEDULE VI. By : CA Kusai Goawala

REVISED SCHEDULE VI By : CA Kusai Goawala Old Schedule VI was operative from 1956. Outdated format for Balance Sheet replaced Revised Schedule VI is a step towards convergence with IFRS Based on IAS1 or

REVISED SCHEDULE VI By : CA Kusai Goawala Old Schedule VI was operative from 1956. Outdated format for Balance Sheet replaced Revised Schedule VI is a step towards convergence with IFRS Based on IAS1 or

Company Accounts. iii. Need to reduce risks for non-corporate forms of organisations (sole proprietor, partnership or HUF),

,") Company Accounts With i. Increasing scale of operations ii. Increasing capital requirements iii. Need to reduce risks for non-corporate forms of organisations (sole proprietor, partnership or HUF), A relatively

Company Accounts With i. Increasing scale of operations ii. Increasing capital requirements iii. Need to reduce risks for non-corporate forms of organisations (sole proprietor, partnership or HUF), A relatively

1. Consolidated Financial Statement Means

1 1. Consolidated Financial Statement Means Consolidated Balance Sheet Consolidated Profit & Loss Consolidated Cash Flow Statement Consolidated Statement of Change in Equity Additional Information in Consolidated

1 1. Consolidated Financial Statement Means Consolidated Balance Sheet Consolidated Profit & Loss Consolidated Cash Flow Statement Consolidated Statement of Change in Equity Additional Information in Consolidated

b) Goodwill reserve from the acquisition of Swanney Plc for the year ended 31 December 2014.

Goodwill reserve from the acquisition of Swanney Plc for the year ended 31 December 2014.") MIA QE March 2015 Suggested Solution and Marking Scheme ANSWER 1 a) When Swift Bhd acquired 70% of the ordinary shares of Gagah Bhd on 2 January 2014, Gagah Bhd became a subsidiary of Swift Bhd. Swift

MIA QE March 2015 Suggested Solution and Marking Scheme ANSWER 1 a) When Swift Bhd acquired 70% of the ordinary shares of Gagah Bhd on 2 January 2014, Gagah Bhd became a subsidiary of Swift Bhd. Swift

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS International Qualifying Scheme Examination HONG KONG FINANCIAL ACCOUNTING JUNE 2011 Suggested

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS International Qualifying Scheme Examination HONG KONG FINANCIAL ACCOUNTING JUNE 2011 Suggested

No. of ordinary shares

Monthly Return of Equity Issuer on Movements in Securities For the ended : 31/12/2018 To : Hong Kong Exchanges and Clearing Limited Name of Issuer MMG Limited Date Submitted 7 January 2019 I. Movements

Monthly Return of Equity Issuer on Movements in Securities For the ended : 31/12/2018 To : Hong Kong Exchanges and Clearing Limited Name of Issuer MMG Limited Date Submitted 7 January 2019 I. Movements

RELIANCE COMTRADE PRIVATE LIMITED 1. Reliance Comtrade Private Limited

RELIANCE COMTRADE PRIVATE LIMITED 1 Reliance Comtrade Private Limited 2 RELIANCE COMTRADE PRIVATE LIMITED Independent Auditor s Report To the Members of Reliance Comtrade Private Limited Report on the

RELIANCE COMTRADE PRIVATE LIMITED 1 Reliance Comtrade Private Limited 2 RELIANCE COMTRADE PRIVATE LIMITED Independent Auditor s Report To the Members of Reliance Comtrade Private Limited Report on the

APPROVAL BY THE BOARD OF IAS 33 ISSUED IN DECEMBER 2003 BASIS FOR CONCLUSIONS ILLUSTRATIVE EXAMPLES

IAS 33 IASB documents published to accompany International Accounting Standard 33 Earnings per Share The text of the unaccompanied IAS 33 is contained in Part A of this edition. Its effective date when

IAS 33 IASB documents published to accompany International Accounting Standard 33 Earnings per Share The text of the unaccompanied IAS 33 is contained in Part A of this edition. Its effective date when

WIPRO TECHNOLOGIES NORWAY AS FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015

WIPRO TECHNOLOGIES NORWAY AS FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015 WIPRO TECHNOLOGIES NORWAY AS BALANCE SHEET (Amount in ` except share and per share data, unless otherwise stated)

WIPRO TECHNOLOGIES NORWAY AS FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015 WIPRO TECHNOLOGIES NORWAY AS BALANCE SHEET (Amount in ` except share and per share data, unless otherwise stated)

Paper-18 : CORPORATE FINANCIAL REPORTING

Paper-18 : CORPORATE FINANCIAL REPORTING 1. (a) Write a note on IFRS. (b) Accounts of R Ltd. show a net profit of `7,20,000 for the third quarter of 2014 after incorporating the following: (i) Bad debts

Paper-18 : CORPORATE FINANCIAL REPORTING 1. (a) Write a note on IFRS. (b) Accounts of R Ltd. show a net profit of `7,20,000 for the third quarter of 2014 after incorporating the following: (i) Bad debts

INTERNAL RECONSTRUCTION

CHAPTER-4 Q. 1. Green Limited had decided to reconstruct the Balance Sheet since it has accumulated huge losses. The following is the summarized Balance Sheet of the Company on 31.3.2012 before reconstruction

CHAPTER-4 Q. 1. Green Limited had decided to reconstruct the Balance Sheet since it has accumulated huge losses. The following is the summarized Balance Sheet of the Company on 31.3.2012 before reconstruction

RELIANCE VANTAGE RETAIL LIMITED. Reliance Vantage Retail Limited

RELIANCE VANTAGE RETAIL LIMITED 1 Reliance Vantage Retail Limited 2 RELIANCE VANTAGE RETAIL LIMITED Independent Auditor s Report To the Members of Reliance Vantage Retail Limited Report on the Financial

RELIANCE VANTAGE RETAIL LIMITED 1 Reliance Vantage Retail Limited 2 RELIANCE VANTAGE RETAIL LIMITED Independent Auditor s Report To the Members of Reliance Vantage Retail Limited Report on the Financial

CHAPTER 17 EARNINGS PER SHARE AND RETAINED EARNINGS. E17-1 Weighted Average Shares. (Moderate) Stock dividend, stock split, reacquisition.

Stock dividend, stock split, reacquisition.") CHAPTER 17 EARNINGS PER SHARE AND RETAINED EARNINGS CONTENT ANALYSIS OF EXERCISES AND PROBLEMS Number Content Time Range (minutes) E17-1 Weighted Average Shares. (Moderate) Stock dividend, stock split,

CHAPTER 17 EARNINGS PER SHARE AND RETAINED EARNINGS CONTENT ANALYSIS OF EXERCISES AND PROBLEMS Number Content Time Range (minutes) E17-1 Weighted Average Shares. (Moderate) Stock dividend, stock split,

Capsule on Accounting Standards

Capsule on Accounting Standards Conducted by Young Members Empowerment Committee jointly with Accounting Standards Board Presented by CA Manish C. Iyer, Deputy Director, Technical Directorate, ICAI 1 Standards

Capsule on Accounting Standards Conducted by Young Members Empowerment Committee jointly with Accounting Standards Board Presented by CA Manish C. Iyer, Deputy Director, Technical Directorate, ICAI 1 Standards

RELIANCE COMTRADE PRIVATE LIMITED FINANCIAL STATEMENTS

RELIANCE COMTRADE PRIVATE LIMITED 1 RELIANCE COMTRADE PRIVATE LIMITED FINANCIAL STATEMENTS 2016-17 2 RELIANCE COMTRADE PRIVATE LIMITED Independent Auditor s Report TO THE MEMBERS OF RELIANCE COMTRADE PRIVATE

RELIANCE COMTRADE PRIVATE LIMITED 1 RELIANCE COMTRADE PRIVATE LIMITED FINANCIAL STATEMENTS 2016-17 2 RELIANCE COMTRADE PRIVATE LIMITED Independent Auditor s Report TO THE MEMBERS OF RELIANCE COMTRADE PRIVATE

RRB MEDIASOFT PRIVATE LIMITED ANNUAL ACCOUNTS - FY :

RRB MEDIASOFT PRIVATE LIMITED 1 RRB MEDIASOFT PRIVATE LIMITED ANNUAL ACCOUNTS - FY : 2016-17 2 RRB MEDIASOFT PRIVATE LIMITED Independent Auditor s Report TO THE MEMBERS OF RRB MEDIASOFT PRIVATE LIMITED

RRB MEDIASOFT PRIVATE LIMITED 1 RRB MEDIASOFT PRIVATE LIMITED ANNUAL ACCOUNTS - FY : 2016-17 2 RRB MEDIASOFT PRIVATE LIMITED Independent Auditor s Report TO THE MEMBERS OF RRB MEDIASOFT PRIVATE LIMITED

Annexure to Directors Report for Financial Year Disclosure pursuant to SEBI (Share Based Employee Benefits) Regulations, 2014

Regulations, 2014") Annexure to Directors Report for Financial Year 2017-18 Disclosure pursuant to SEBI (Share Based Employee Benefits) Regulations, 2014 The Securities and Exchange Board of India (SEBI), vide its notification

Annexure to Directors Report for Financial Year 2017-18 Disclosure pursuant to SEBI (Share Based Employee Benefits) Regulations, 2014 The Securities and Exchange Board of India (SEBI), vide its notification

WATERMARK INFRATECH PRIVATE LIMITED ANNUAL ACCOUNTS - FY :

WATERMARK INFRATECH PRIVATE LIMITED 1 WATERMARK INFRATECH PRIVATE LIMITED ANNUAL ACCOUNTS - FY : 2016-17 2 WATERMARK INFRATECH PRIVATE LIMITED Independent Auditor s Report TO THE MEMBERS OF WATERMARK INFRATECH

WATERMARK INFRATECH PRIVATE LIMITED 1 WATERMARK INFRATECH PRIVATE LIMITED ANNUAL ACCOUNTS - FY : 2016-17 2 WATERMARK INFRATECH PRIVATE LIMITED Independent Auditor s Report TO THE MEMBERS OF WATERMARK INFRATECH

Suggested Answer_Syl2012_Dec2015_Paper 12 FINAL EXAMINATION

FINAL EXAMINATION GROUP II (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2015 Paper-12 : COMPANY ACCOUNTS AND AUDIT Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on the right

FINAL EXAMINATION GROUP II (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2015 Paper-12 : COMPANY ACCOUNTS AND AUDIT Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on the right

KOTAK MAHINDRA BANK LIMITED. ESOPs / SARs Disclosure (For FY )

") KOTAK MAHINDRA BANK LIMITED ESOPs / SARs Disclosure (For FY 2016-17) [Pursuant to Regulation 14 of the SEBI (Share Based Employee Benefits) Regulations, 2014] The shareholders of the Bank at its Annual

KOTAK MAHINDRA BANK LIMITED ESOPs / SARs Disclosure (For FY 2016-17) [Pursuant to Regulation 14 of the SEBI (Share Based Employee Benefits) Regulations, 2014] The shareholders of the Bank at its Annual

WIPRO HOLDINGS HUNGARY KORLATOLT FELEL.SSEG TARSASAG STANDALONE FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015

WIPRO HOLDINGS HUNGARY KORLATOLT FELEL.SSEG TARSASAG STANDALONE FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015 1 WIPRO HOLDINGS HUNGARY KORLATOLT FELEL.SSEG TARSASAG BALANCE SHEET AS

WIPRO HOLDINGS HUNGARY KORLATOLT FELEL.SSEG TARSASAG STANDALONE FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015 1 WIPRO HOLDINGS HUNGARY KORLATOLT FELEL.SSEG TARSASAG BALANCE SHEET AS

KDF1D Advanced Corporate Accounting and. Accounting Standards Unit : 1-5

KDF1D Advanced Corporate Accounting and Accounting Standards Unit : 1-5 UNIT-1 (SYLLABUS) Advanced problems in share capital Debenture transactions including underwriting Valuation of goodwill and shares

KDF1D Advanced Corporate Accounting and Accounting Standards Unit : 1-5 UNIT-1 (SYLLABUS) Advanced problems in share capital Debenture transactions including underwriting Valuation of goodwill and shares

PAPER 5 : ADVANCED ACCOUNTING

PAPER 5 : ADVANCED ACCOUNTING Question No.1 is compulsory. Candidates are also required to answer any five questions from the remaining six questions. Working notes should form part of the respective answers.

PAPER 5 : ADVANCED ACCOUNTING Question No.1 is compulsory. Candidates are also required to answer any five questions from the remaining six questions. Working notes should form part of the respective answers.

RELIANCE UNIVERSAL COMMERCIAL LIMITED 1. Reliance Universal Commercial Limited

RELIANCE UNIVERSAL COMMERCIAL LIMITED 1 Reliance Universal Commercial Limited 2 RELIANCE UNIVERSAL COMMERCIAL LIMITED Independent Auditor s Report To the Members of Reliance Universal Commercial Limited

RELIANCE UNIVERSAL COMMERCIAL LIMITED 1 Reliance Universal Commercial Limited 2 RELIANCE UNIVERSAL COMMERCIAL LIMITED Independent Auditor s Report To the Members of Reliance Universal Commercial Limited

ADVENTURE MARKETING PRIVATE LIMITED ANNUAL ACCOUNTS - FY :

1 ANNUAL ACCOUNTS - FY : 2016-17 2 Independent Auditor s Report TO THE MEMBERS OF Report on the Financial Statements We have audited the accompanying financial statements of Adventure Marketing Private

1 ANNUAL ACCOUNTS - FY : 2016-17 2 Independent Auditor s Report TO THE MEMBERS OF Report on the Financial Statements We have audited the accompanying financial statements of Adventure Marketing Private

Punj Lloyd Pte Limited Consolidated Balance Sheet as at March 31, 2016 (All amounts in SGD Thousand, unless otherwise stated)

") Consolidated Balance Sheet as at Notes Equity and liabilities Shareholders funds Share capital 3 242,335 242,335 Reserves and surplus 4 (339,373) (382,065) (97,039) (139,730) Minority interest (39,597)

Consolidated Balance Sheet as at Notes Equity and liabilities Shareholders funds Share capital 3 242,335 242,335 Reserves and surplus 4 (339,373) (382,065) (97,039) (139,730) Minority interest (39,597)

Our responsibility is to express an opinion on these financial statements based on our audit.

INDEPENDENT AUDITOR S REPORT To the Members of Ashva Stud and Agricultural Farms Limited Report on the Financial Statements We have audited the accompanying financial statements of Ashva Stud and Agricultural

INDEPENDENT AUDITOR S REPORT To the Members of Ashva Stud and Agricultural Farms Limited Report on the Financial Statements We have audited the accompanying financial statements of Ashva Stud and Agricultural

\WIPRO TECHNOLOGIES SPAIN STANDALONE FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015

\WIPRO TECHNOLOGIES SPAIN STANDALONE FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 1 WIPRO TECHNOLOGIES SPAIN BALANCE SHEET AS AT MARCH 31, (Amount in INR, except share and per share data,

\WIPRO TECHNOLOGIES SPAIN STANDALONE FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 1 WIPRO TECHNOLOGIES SPAIN BALANCE SHEET AS AT MARCH 31, (Amount in INR, except share and per share data,

Suggested Answer_Syl12_Dec2014_Paper_18 FINAL EXAMINATION

FINAL EXAMINATION GROUP IV (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2014 Paper-18: CORPORATE FINANCIAL REPORTING Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on the

FINAL EXAMINATION GROUP IV (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2014 Paper-18: CORPORATE FINANCIAL REPORTING Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on the

Condensed Consolidated Financial Statements of CEQUENCE ENERGY LTD. September 30, 2018 and 2017

Condensed Consolidated Financial Statements of CEQUENCE ENERGY LTD. 2018 and 2017 Condensed Consolidated Balance Sheets (Unaudited)(Expressed in thousands of Canadian dollars) 2018 December 31, 2017 ASSETS

Condensed Consolidated Financial Statements of CEQUENCE ENERGY LTD. 2018 and 2017 Condensed Consolidated Balance Sheets (Unaudited)(Expressed in thousands of Canadian dollars) 2018 December 31, 2017 ASSETS

TERMS AND CONDITIONS OF THE BONDS

TERMS AND CONDITIONS OF THE BONDS The following, other than the paragraphs in italics, are the terms and conditions of the Bonds, substantially as they will appear on the reverse of the Bonds in definitive

TERMS AND CONDITIONS OF THE BONDS The following, other than the paragraphs in italics, are the terms and conditions of the Bonds, substantially as they will appear on the reverse of the Bonds in definitive

Financial reporting developments. A comprehensive guide. Earnings per share

Financial reporting developments A comprehensive guide Earnings per share September 2011 To our clients and other friends We are pleased to provide you with the latest edition of our Financial reporting

Financial reporting developments A comprehensive guide Earnings per share September 2011 To our clients and other friends We are pleased to provide you with the latest edition of our Financial reporting

IFRS 2 Share-based Payment

IFRS 2 Share-based Payment Scope Share-based Payment Transaction where the entity receives goods or services as consideration Examples Equity instruments of the entity (including share options) Incurring

IFRS 2 Share-based Payment Scope Share-based Payment Transaction where the entity receives goods or services as consideration Examples Equity instruments of the entity (including share options) Incurring

PROPOSED INCREASE IN THE AUTHORISED SHARE CAPITAL; AND

LAY HONG BERHAD ( LHB OR THE COMPANY ) PROPOSED BONUS ISSUE OF SHARES; PROPOSED SHARE SPLIT; PROPOSED FREE WARRANTS ISSUE; PROPOSED INCREASE IN THE AUTHORISED SHARE CAPITAL; AND PROPOSED AMENDMENT (COLLECTIVELY

LAY HONG BERHAD ( LHB OR THE COMPANY ) PROPOSED BONUS ISSUE OF SHARES; PROPOSED SHARE SPLIT; PROPOSED FREE WARRANTS ISSUE; PROPOSED INCREASE IN THE AUTHORISED SHARE CAPITAL; AND PROPOSED AMENDMENT (COLLECTIVELY

No. of ordinary shares

Monthly Return of Equity Issuer on Movements in Securities For the ended : 31/5/2018 To : Hong Kong Exchanges and Clearing Limited Name of Issuer Date Submitted 4/6/2018 Realord Group Holdings Limited

Monthly Return of Equity Issuer on Movements in Securities For the ended : 31/5/2018 To : Hong Kong Exchanges and Clearing Limited Name of Issuer Date Submitted 4/6/2018 Realord Group Holdings Limited

RELIANCE LNG LIMITED ANNUAL REPORT FY:

RELIANCE LNG LIMITED 1 RELIANCE LNG LIMITED ANNUAL REPORT FY: 2016-17 2 RELIANCE LNG LIMITED Independent Auditor s Report TO THE MEMBERS OF RELIANCE LNG LIMITED Report on the Financial Statements We have

RELIANCE LNG LIMITED 1 RELIANCE LNG LIMITED ANNUAL REPORT FY: 2016-17 2 RELIANCE LNG LIMITED Independent Auditor s Report TO THE MEMBERS OF RELIANCE LNG LIMITED Report on the Financial Statements We have

CYNAPSUS THERAPEUTICS INC.

CYNAPSUS THERAPEUTICS INC. Condensed Interim Consolidated Financial Statements For the Three Months Ended (Expressed in Canadian Dollars) Unaudited NOTICE OF NO AUDITOR REVIEW OF CONDENSED INTERIM CONSOLIDATED

CYNAPSUS THERAPEUTICS INC. Condensed Interim Consolidated Financial Statements For the Three Months Ended (Expressed in Canadian Dollars) Unaudited NOTICE OF NO AUDITOR REVIEW OF CONDENSED INTERIM CONSOLIDATED

Monthly Return of Equity Issuer on Movements in Securities. For the month ended (dd/mm/yyyy) : 28/02/2018

: 28/02/2018") Monthly Return of Equity Issuer on Movements in Securities For the month ended : 28/02/2018 To : Hong Kong Exchanges and Clearing Limited Name of Issuer Date Submitted 01/03/2018 Branding China Group Limited

Monthly Return of Equity Issuer on Movements in Securities For the month ended : 28/02/2018 To : Hong Kong Exchanges and Clearing Limited Name of Issuer Date Submitted 01/03/2018 Branding China Group Limited

Consolidated Financial Statements of. DataWind Inc. For the year ended March 31, 2015 (in thousands of Canadian dollars)

") Consolidated Financial Statements of DataWind Inc. For the year ended March 31, 2015 (in thousands of Canadian dollars) Contents Independent Auditor s Report 2 Consolidated statement of financial position

Consolidated Financial Statements of DataWind Inc. For the year ended March 31, 2015 (in thousands of Canadian dollars) Contents Independent Auditor s Report 2 Consolidated statement of financial position

Financial Instruments: Presentation INTRODUCTION

IAS 32 Financial Instruments: Presentation INTRODUCTION Objective Scope Application The stated objective of IAS 32 is to establish principles for presenting financial instruments as liabilities or equity

IAS 32 Financial Instruments: Presentation INTRODUCTION Objective Scope Application The stated objective of IAS 32 is to establish principles for presenting financial instruments as liabilities or equity

Our responsibility is to express an opinion on these financial statements based on our audit.

INDEPENDENT AUDITOR S REPORT To the Members of Milky Way Buildcon Limited Report on the Financial Statements We have audited the accompanying financial statements of Milky Way Buildcon Limited ( the Company

INDEPENDENT AUDITOR S REPORT To the Members of Milky Way Buildcon Limited Report on the Financial Statements We have audited the accompanying financial statements of Milky Way Buildcon Limited ( the Company

STATEMENT OF STANDALONE/ CONSOLIDATED AUDITED RESULTS FOR THE QUARTER AND YEAR ENDED MARCH

PART I CIN: L15420UP1931PLC065243 Regd. Office: Golagokarannath, Lakhimpur-Kheri, District Kheri, Uttar Pradesh- 262802 Tel.:+91-5876-233754/5/7/8, 233403, Fax:+91-5876-233401, Website:www.bajajhindusthan.com

PART I CIN: L15420UP1931PLC065243 Regd. Office: Golagokarannath, Lakhimpur-Kheri, District Kheri, Uttar Pradesh- 262802 Tel.:+91-5876-233754/5/7/8, 233403, Fax:+91-5876-233401, Website:www.bajajhindusthan.com

WIPRO TRADEMARKS HOLDING LIMITED STANDALONE FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2016

WIPRO TRADEMARKS HOLDING LIMITED STANDALONE FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2016 1 2 3 4 1. Company overview WIPRO TRADEMARKS HOLDING LIMITED NOTES TO THE FINANCIAL STATEMENTS

WIPRO TRADEMARKS HOLDING LIMITED STANDALONE FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2016 1 2 3 4 1. Company overview WIPRO TRADEMARKS HOLDING LIMITED NOTES TO THE FINANCIAL STATEMENTS

HCL TECHNOLOGIES LIMITED

a HCL TECHNOLOGIES LIMITED CONSOLIDATED FINANCIAL STATEMENTS AS OF JUNE 30, 1999 AND 2000 AND FOR THE YEARS THEN ENDED TOGETHER WITH REPORT OF INDEPENDENT AUDITORS To the Board of Directors and Stockholders

a HCL TECHNOLOGIES LIMITED CONSOLIDATED FINANCIAL STATEMENTS AS OF JUNE 30, 1999 AND 2000 AND FOR THE YEARS THEN ENDED TOGETHER WITH REPORT OF INDEPENDENT AUDITORS To the Board of Directors and Stockholders

RELIANCE RETAIL FINANCE LIMITED 1. Reliance Retail Finance Limited

RELIANCE RETAIL FINANCE LIMITED 1 Reliance Retail Finance Limited 2 RELIANCE RETAIL FINANCE LIMITED Independent Auditor s Report To the Members of Reliance Retail Finance Limited Report on the Financial

RELIANCE RETAIL FINANCE LIMITED 1 Reliance Retail Finance Limited 2 RELIANCE RETAIL FINANCE LIMITED Independent Auditor s Report To the Members of Reliance Retail Finance Limited Report on the Financial

No. of ordinary shares

Monthly Return of Equity Issuer on Movements in Securities For the ended : 30/09/2018 To : Hong Kong Exchanges and Clearing Limited Name of Issuer Date Submitted 4 October 2018 China Public Procurement

Monthly Return of Equity Issuer on Movements in Securities For the ended : 30/09/2018 To : Hong Kong Exchanges and Clearing Limited Name of Issuer Date Submitted 4 October 2018 China Public Procurement

REGULATIONS FOR TRADING STOCK FUTURES CONTRACTS

REGULATIONS FOR TRADING STOCK FUTURES CONTRACTS INTERPRETATION 001 These Regulations may be cited as the Regulations for trading Stock Futures Contracts (hereinafter referred to as the "Regulations").

REGULATIONS FOR TRADING STOCK FUTURES CONTRACTS INTERPRETATION 001 These Regulations may be cited as the Regulations for trading Stock Futures Contracts (hereinafter referred to as the "Regulations").

Ind AS 105: Non-current Assets Held for Sale

Ind AS 105: Non-current Assets Held for Sale Contents 1. Navigating the standard 2. Definitions 3. Non-current asset & disposal group Classification 4. Initial measurement 5. Non-current asset held for

Ind AS 105: Non-current Assets Held for Sale Contents 1. Navigating the standard 2. Definitions 3. Non-current asset & disposal group Classification 4. Initial measurement 5. Non-current asset held for

PROPOSED AMENDMENTS TO THE MEMORANDUM AND ARTICLES OF ASSOCIATION OF TCB ( PROPOSED AMENDMENTS ); AND

; AND") TALIWORKS CORPORATION BERHAD ( TCB OR THE COMPANY ) (I) PROPOSED SHARE SPLIT INVOLVING THE SUBDIVISION OF EVERY TWO (2) EXISTING ORDINARY SHARES OF RM0.50 EACH IN TCB HELD BY THE ENTITLED SHAREHOLDERS

TALIWORKS CORPORATION BERHAD ( TCB OR THE COMPANY ) (I) PROPOSED SHARE SPLIT INVOLVING THE SUBDIVISION OF EVERY TWO (2) EXISTING ORDINARY SHARES OF RM0.50 EACH IN TCB HELD BY THE ENTITLED SHAREHOLDERS

Outline Guidance Notes regarding adoption of CLASS XII Revised Schedule VI to the Companies Act 1956 in the subject of Accountancy (Effective for Board Examination 2013) Shiksha Kendra, 2, Community Centre,

Outline Guidance Notes regarding adoption of CLASS XII Revised Schedule VI to the Companies Act 1956 in the subject of Accountancy (Effective for Board Examination 2013) Shiksha Kendra, 2, Community Centre,

Maricann Group Inc. For the three and nine months ended September 30, 2017 and 2016

Condensed interim consolidated financial statements [Unaudited, expressed in Canadian dollars] Maricann Group Inc. For the three and nine months ended September 30, 2017 and 2016 As at Condensed interim

Condensed interim consolidated financial statements [Unaudited, expressed in Canadian dollars] Maricann Group Inc. For the three and nine months ended September 30, 2017 and 2016 As at Condensed interim

RELIANCE ENERGY AND PROJECT DEVELOPMENT LIMITED 1. Reliance Energy and Project Development Limited

RELIANCE ENERGY AND PROJECT DEVELOPMENT LIMITED 1 Reliance Energy and Project Development Limited 2 RELIANCE ENERGY AND PROJECT DEVELOPMENT LIMITED Independent Auditor s Report To the Members of Reliance

RELIANCE ENERGY AND PROJECT DEVELOPMENT LIMITED 1 Reliance Energy and Project Development Limited 2 RELIANCE ENERGY AND PROJECT DEVELOPMENT LIMITED Independent Auditor s Report To the Members of Reliance

Structure of Revised Schedule VI Key Changes Key Points

Revised Scheduled VI Structure of Presentation Setting the Context Structure of Revised Schedule VI Key Changes Key Points Setting the Context Setting the Context Towards International Format: Harmonize

Revised Scheduled VI Structure of Presentation Setting the Context Structure of Revised Schedule VI Key Changes Key Points Setting the Context Setting the Context Towards International Format: Harmonize

15 Earnings Per Share

15 Earnings Per Share Earnings Per Share 15 LEARNING OUTCOME After studying this chapter students should be able to: interpret a full range of accounting ratios. This chapter completes the work begun in

15 Earnings Per Share Earnings Per Share 15 LEARNING OUTCOME After studying this chapter students should be able to: interpret a full range of accounting ratios. This chapter completes the work begun in

Corresponding. Year ended Preceding three months ended ended

Part I CHOLAMANDALAM INVESTMENT AND FINANCE COMPANY LIMITED CIN L65993TN1978PLC007576 Registered Office : DARE HOUSE, 2, NSC Bose Road, Chennai 600 001. Statement of and Financial Results for the and year

Part I CHOLAMANDALAM INVESTMENT AND FINANCE COMPANY LIMITED CIN L65993TN1978PLC007576 Registered Office : DARE HOUSE, 2, NSC Bose Road, Chennai 600 001. Statement of and Financial Results for the and year

No. of ordinary shares

Monthly Return of Equity Issuer on Movements in Securities For the ended : 31/03/2015 To : Hong Kong Exchanges and Clearing Limited Name of Issuer Date Submitted 1 April 2015 Courage Marine Group Limited

Monthly Return of Equity Issuer on Movements in Securities For the ended : 31/03/2015 To : Hong Kong Exchanges and Clearing Limited Name of Issuer Date Submitted 1 April 2015 Courage Marine Group Limited

RELIANCE AROMATICS AND PETROCHEMICALS LIMITED. Reliance Aromatics and Petrochemicals Limited Financial Statements FY :

923 Reliance Aromatics and Petrochemicals Limited Financial Statements FY : 2017-18 924 RELIANCE AROMATICS AND PETROCHEMICALS LIMITED Independent Auditor's Report TO THE MEMBERS OF RELIANCE AROMATICS AND

923 Reliance Aromatics and Petrochemicals Limited Financial Statements FY : 2017-18 924 RELIANCE AROMATICS AND PETROCHEMICALS LIMITED Independent Auditor's Report TO THE MEMBERS OF RELIANCE AROMATICS AND

RELIANCE INNOVATIVE BUILDING SOLUTIONS PRIVATE LIMITED. Reliance Innovative Building Solutions Private Limited

RELIANCE INNOVATIVE BUILDING SOLUTIONS PRIVATE LIMITED 1 Reliance Innovative Building Solutions Private Limited 2 RELIANCE INNOVATIVE BUILDING SOLUTIONS PRIVATE LIMITED Independent Auditor s Report To

RELIANCE INNOVATIVE BUILDING SOLUTIONS PRIVATE LIMITED 1 Reliance Innovative Building Solutions Private Limited 2 RELIANCE INNOVATIVE BUILDING SOLUTIONS PRIVATE LIMITED Independent Auditor s Report To

No. of ordinary shares. Balance at close of preceding month 20,000,000, ,000,000.00

Monthly Return of Equity Issuer on Movements in Securities For the ended : 30/11/2018 To : Hong Kong Exchanges and Clearing Limited Name of Issuer FIH Mobile Limited Date Submitted 03/12/2018 I. Movements

Monthly Return of Equity Issuer on Movements in Securities For the ended : 30/11/2018 To : Hong Kong Exchanges and Clearing Limited Name of Issuer FIH Mobile Limited Date Submitted 03/12/2018 I. Movements

CYNAPSUS THERAPEUTICS INC. (Formerly Cannasat Therapeutics Inc.)

") CYNAPSUS THERAPEUTICS INC. (Formerly Cannasat Therapeutics Inc.) Condensed Interim Financial Statements For the Three Months Ended (Expressed in Canadian Dollars) Unaudited NOTICE OF NO AUDITOR REVIEW

CYNAPSUS THERAPEUTICS INC. (Formerly Cannasat Therapeutics Inc.) Condensed Interim Financial Statements For the Three Months Ended (Expressed in Canadian Dollars) Unaudited NOTICE OF NO AUDITOR REVIEW

Financial statements. Financial strength

Financial statements Financial strength Consolidated Income Statement 66 Consolidated Statement of Comprehensive Income 67 Consolidated Statement of Financial Position 68 Consolidated Statement of Changes

Financial statements Financial strength Consolidated Income Statement 66 Consolidated Statement of Comprehensive Income 67 Consolidated Statement of Financial Position 68 Consolidated Statement of Changes

CLUSTER COMMERCIAL PRIVATE LIMITED. Cluster Commercial Private Limited

CLUSTER COMMERCIAL PRIVATE LIMITED 1 Cluster Commercial Private Limited 2 CLUSTER COMMERCIAL PRIVATE LIMITED Independent Auditor s Report TO BOARD OF DIRECTORS CLUSTER COMMERCIALS PRIVATE LIMITED Report

CLUSTER COMMERCIAL PRIVATE LIMITED 1 Cluster Commercial Private Limited 2 CLUSTER COMMERCIAL PRIVATE LIMITED Independent Auditor s Report TO BOARD OF DIRECTORS CLUSTER COMMERCIALS PRIVATE LIMITED Report

INTERNAL RECONSTRUCTION

5 INTERNAL RECONSTRUCTION Learning Objectives After studying this chapter, you will be able to: Understand the meaning of term reconstruction. Sub-divide and consolidate shares. Convert shares into stock

5 INTERNAL RECONSTRUCTION Learning Objectives After studying this chapter, you will be able to: Understand the meaning of term reconstruction. Sub-divide and consolidate shares. Convert shares into stock

Aepona Limited CONDENSED BALANCE SHEET AS AT MARCH 31, 2016

CONDENSED BALANCE SHEET AS AT MARCH 31, 2016 Notes EQUITY AND LIABILITIES Shareholders funds Share capital 1 1,230,620,264 Reserves and surplus 2 (1,137,001,443) (A) 93,618,821 Non- current liabilities

CONDENSED BALANCE SHEET AS AT MARCH 31, 2016 Notes EQUITY AND LIABILITIES Shareholders funds Share capital 1 1,230,620,264 Reserves and surplus 2 (1,137,001,443) (A) 93,618,821 Non- current liabilities

PREMIUM INCOME CORPORATION

ANNUAL INFORMATION FORM PREMIUM INCOME CORPORATION Preferred Shares and Class A Shares January 30, 2017 Table of Contents FORWARD-LOOKING STATEMENTS... 1 THE FUND... 2 Share Offerings... 2 INVESTMENT OBJECTIVES

ANNUAL INFORMATION FORM PREMIUM INCOME CORPORATION Preferred Shares and Class A Shares January 30, 2017 Table of Contents FORWARD-LOOKING STATEMENTS... 1 THE FUND... 2 Share Offerings... 2 INVESTMENT OBJECTIVES

CHAPTER 16. Retained Earnings and Earnings per Share CONTENT ANALYSIS OF END-OF-CHAPTER ASSIGNMENTS. 1 Easy 5 Analytic Measurement Comprehension

16-1 CONTENT ANALYSIS OF END-OF-CHAPTER ASSIGNMENTS CHAPTER 16 Retained Earnings and Earnings per Share NUMBER TOPIC CONTENT LO ADAPTED DIFFICULTY 16-1 Dividend Dates Four important dates for recording

16-1 CONTENT ANALYSIS OF END-OF-CHAPTER ASSIGNMENTS CHAPTER 16 Retained Earnings and Earnings per Share NUMBER TOPIC CONTENT LO ADAPTED DIFFICULTY 16-1 Dividend Dates Four important dates for recording