Commodities and Forex. By Dr. SHASHANK DESAI

|

|

|

- Eleanor Short

- 6 years ago

- Views:

Transcription

1 Commodities and Forex By Dr. SHASHANK DESAI

2 DERIVATIVES The more I read, more confused I get.

3 ACCOUNTING FOR DERIVATIVE MADE EASY

4 To have understanding of AS 30, AS 31, AS 32 in the context of foreign currency derivatives and commodities derivatives Importance of recognition of FA and FL Classification of FA and FL Meaning and types of derivatives Hedging and measurement of hedge effectiveness Disclosure in financial statements Application of theory to real life cases

5 Particulars AS 10 AS 30 Recognition Classification Initial & Subsequent measurement Derecognition Capital or revenue expenditure Land,Building,Plant & Machinery At Historical cost On sale/discarding fixed asset Derivative or non derivative Financial assets & Financial liability At fair value/ Amortised cost Contract terms are completed

6 Accounting Standards -AS Institute of Chartered Accountants of India- ICAI Converged Indian Accounting Standard -Ind AS The Companies Act, 1956-The Act. Ministry of Corporate Affairs-MCA Held for trading -HFT Fair value through Profit and Loss -FVTPL Available for sale -AFS Held to maturity -HTM Loans and Receivables- L&R

7

8 AS 30 AS 31 AS 32 Recognition and Derecognition Measurement Derivatives including embedded derivatives Presentation Disclosure Hedge accounting

9 Deferment of applicability of Ind AS In view of above deferment, AS 30, AS 31 and AS 32 to be applied in present form Mandatory from accounting period commencing from 1st April 2011

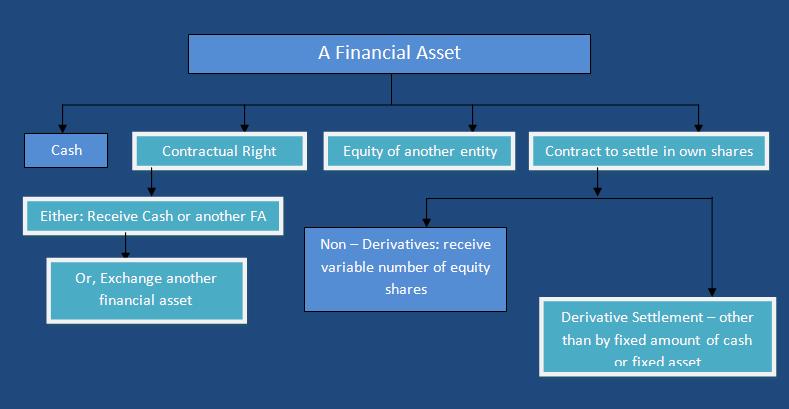

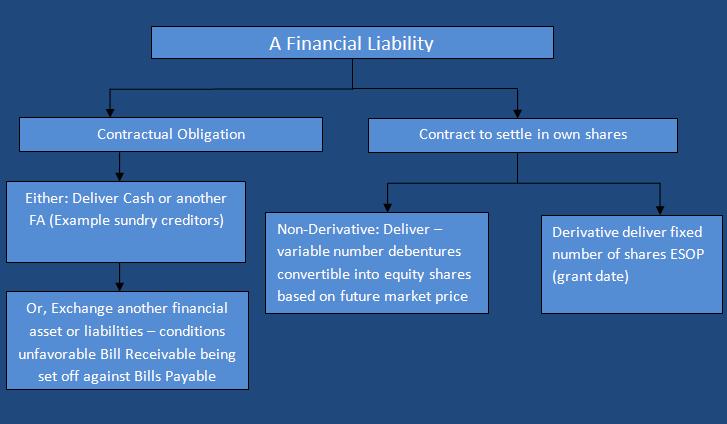

10 A financial instrument is any contract that gives rise to a financial asset of one entity and a financial liability or equity instrument of another entity. A financial instrument is a contract that gives rise to Financial Asset A Financial Liability or Equity In one Entity: Say Entity ABC Balance sheet of ABC (Asset side) Investment in Shares Investment in Debentures Sundry Debtors In another Entity: Say Entity XYZ Balance sheet of XYZ (Liabilities side) Equity capital of XYZ Debentures issued Sundry Creditors

11

12 Derivatives i. Futures ii. Options iii. Swaps iv. Forward Non Derivatives i. Cash ii. Deposits with other entities iii. Receivable (e.g. trade receivable) iv. Loan to other entities v. Investments in Bonds and other debt instruments issued by other entities. vi. Investments in shares and other equity instruments issued by other entities

13 Category Definition Financial assets at fair value through profit or loss Financial assets held for trading Derivatives, unless accounted for as hedges Financial asset designated to this category under the fair value option Loans and receivables Non-derivative financial assets with fixed or determinable payments that are not quoted in an active market Held-to-maturity Investments Non-derivative financial assets with fixed or determinable payments and fixed maturity that the entity has the positive intent and ability to hold to maturity Available-for-sale financial assets All non derivative financial assets that are not classified in another category are classified as available-for-sale Any financial asset designated to this category on initial recognition

14

15 Categories Definitions Financial liabilities at fair value through profit or loss Financial liabilities held for trading Financial liability designated as at fair value through profit or loss on initial recognition (fair value option) Other financial liabilities-at amortised cost All financial liabilities that are not classified at fair value through profit or loss

16 Fair value is the amount for which an asset could be exchanged, or a liability settled, between knowledgeable, willing parties in an arm s length transaction. Fair Value Underlying assumption Active Market No Active Market Active market: Quoted price Readily and regularly available from a reliable source.e.g.exchange,industy group, published price quotations. Non Active market: Recent arm s length market transaction between knowledgeable & willing parties; Reference to the current fair value of another instrument that is substantially same.

17 S Ltd, a manufacturer of earth moving equipments, has an equipment for which it is assessing fair value. To arrive at the fair value, it has obtained bids from various parties. Which of these bids would be considered appropriate for fair value measurement? Bids Received Bid of Rs. 3 Crores received from T Ltd, its parent company Bid of Rs. 2.8 Crores received from P Ltd, an unrelated company, whose primary business is securities trading, willing and able to transact Bid of Rs. 3.2 Crores received from Q Ltd, a fellow competitor, which has filed for bankruptcy Bid for Rs Crores from R Inc, a fellow competitor, willing and able to complete the transaction

18 Bids received Bid of Rs. 3 Crores received from T Ltd, its parent company Bid of Rs. 2.8 Crores received from P Ltd, an unrelated company, whose primary business is securities trading, willing and able to transact Bid of Rs. 3.2 Crores received from Q Ltd, a fellow competitor, which has filed for bankruptcy Bid for Rs Crores from R Inc, a fellow competitor, willing and able to complete the transaction Yes/No NO NO NO YES

19 I. Derivatives II. III. IV. Recognition, Measurement and Derecognition Embedded derivatives Hedging V. Disclosure as per AS 32 VI. Practical VII. Summary

20 Financial weapons of mass destruction -Warren Buffett

21 A derivative is a financial instrument or other contract within the scope of AS-30 with all three of the following characteristics: Derivative Value changes based on an underlying Initial investment is either low or nil Settlement at a future date

22 An underlying is a variable that, along with either a notional amount or payment provision, determines the settlement amount of a derivative. SN TypeofContract 1 Currency Swap (Foreign Exchange Swap)/ Currency Futures/ Currency Forward 2 Commodity Futures/ Commodity Swap/ Commodity forward. Main Pricing-Settlement Variable (Underlying Variable) Currency rates Commodity prices 3 Equity Forward/ Equity Swap Equity prices (equity of another entity)

23 UNDERLYING DERIVATIVE

24

25

26 An entity should recognise financial assets and financial liability on its balance sheet when, and only when, the entity becomes party to the contractual provisions of the instrument.

27 Trade date and settlement date: i.trade date: The trade date is the date that an entity itself to purchase or sell an asset. Trade date accounting refers to (a) the recognition of an asset to be received and the liability to pay for it on the trade date, and (b) derecognition of an asset that is sold, recognition of any gain or loss on disposal and the recognition of a receivable from the buyer for payment on the trade date. ii.settlement date: The settlement date is the date on which an asset is to or by an entity. Settlement date accounting refers to (a) the recognition of an asset on the day it is received by the entity, and (b) the derecognition of an asset and recognition of any gain or loss on disposal on the day that it is delivered by the entity.

28 A regular way purchase or sale of financial assets should be recognised and derecognised using trade date and settlement date accounting. A contract that requires or permits net settlement of the changes in the value of the contract is not a regular way contract. Instead, such contract is accounted for as a derivative in the period between the trade date and settlement date.

29 X Ltd purchases financial assets as on 29 th March 2010 for Rs. 100 lakhs. The fair value of the asset on 31 st March 2010(Year end) and 2 nd April 2010 (settlement date) are Rs. 105 lakhs and Rs. 103 lakhs respectively. Accounting treatment of the transaction based on classification of the financial asset as FVTPL is as follows.

30 Accounting entries: Date Particulars Dr Amt Cr Amt 29/03/2010 Financial Assets To Financial Liability 31/03/2010 Financial Assets To P&L 02/04/2010 P&L To Financial Asset 02/04/2010 Financial Liability To Cash

31 Financial Asset/liability Financial Assets at Fair Value through profit & loss Financial Liabilities at Fair Value through profit & loss Derivatives unless hedged Initial and Subsequent Measurement Fair value Fair value Fair value Value Changes P&L P&L P&L* * Other than effective cash flow hedge which is to be recognised in equity account.

32 Financial Asset: An entity should derecognise a financial asset when, and only when: (a) the contractual rights to the cash flows from the financial asset expire; or (b) it transfers the financial asset Financial Liability: An entity should remove a financial liability (or a part of a financial liability) from its balance sheet when, and only when, liability is extinguished i.e., when the obligation specified in the contract is discharged or cancelled or expires.

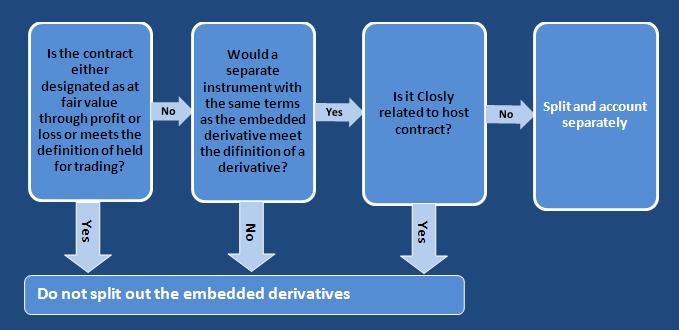

33

34 What is an embedded derivative? An embedded derivative is a component of a hybrid (combined) instrument that also includes a nonderivative host contract with the effect that some of the cash flows of the combined instrument vary in a way similar to a stand-alone derivative.

35 Company X holds a bond which is convertible into the equity shares of Company Y. Hybrid contract Host contract Embedded derivative - convertible bond; - bond and - conversion option

36 A lease contract contains a provision that rentals increase each year by 10%. Is there an embedded derivative in this contract?

37 No, there is no embedded derivative since the lease rental increase does not depend on some underlying. There is no underlying in this case; hence there is no embedded derivative

38 X Co. sells furniture to Y CO. in USD, both companies are in India and make purchase and sales of furniture in rupees. The entire sale contract which will be settled in USD is hybrid contract in which is included the embedded derivative of foreign exchange rupees/usd forward as the cash flow will also be dependent not only on the price of furniture but rupees/usd exchange rate.

39

40 Company X issues ten-year notes with no stated coupon. Embedded in the notes is a provision that adjusts the interest paid by reference in changes in the price of corn. The embedded derivative would be accounted for separately because the adjustment to interest payments based on changes in corn prices is not closely related to the host debt instrument.

41 Company X issues bonds with BBB rating. The bonds have a provision that if Company X violates a certain debt-to-equity ratio covenant, or Company X s credit rating is downgraded, the interest rate will reset to the then current market rate for Company X. The interest rate reset is considered to be closely related to the host contract and since it relates to default in a credit risk related covenant and Company X s credit rating, the embedded derivative would not be accounted for separately.

42

43

44 Business risk and uncertain economic environment Steps to mitigate exposures to risk

45 Hedged item: An asset, liability firm commitment, highly probable forecast transaction or net investment in a foreign operation that a) exposes the entity to risk of changes in fair value or future cash flows and b) is designed as being hedged.

46 Firm commitment: A firm commitment is a for the exchange of a specified quantity of resources at a specified price on a specified future date or dates. Forecast transaction: A forecast transaction is an but future transaction.

47 A hedging instrument is (a) a designated derivative or (b) for a hedge of the risk of changes in foreign currency exchange rates only, a designated nonderivative financial asset or non-derivative financial liability whose fair value or cash flows are expected to offset changes in the fair value or cash flows of a designated hedged item.

48 To qualify for designation the hedged item should create an exposure to risk that affects profit or loss. The followings can be designated as hedged item: i. A recognised single or group of assets/liabilities 1. ii. Unrecognised firm commitments or highly probable forecast transactions 2. iii. Net investments in foreign operations with similar risk characteristic.

49 Hedging instrument. Hedged item specifically designated. There should be a relationship between the hedged item and the hedging instrument with formal documentation. The relationship should be effective so as to offset the effects on profit or loss of changes in fair value of the hedging instrument and hedged item. The effectiveness of the hedge should be reliably measured. Hedge relationship must be expected to be highly effective at inception and subsequent periods.

50 Prospective Hedging Policy Hedged item and hedgeable risks Hedging Instrument Assessing effectiveness and measuring ineffectiveness

51 Types of Hedging Fair value hedge Cash flow hedge Hedge of net investment in a foreign operation

52 Fair value hedge: A hedge of exposure to of -a recognised asset or a liability or an or an identified portion of such portion of such asset, liability or a firm commitment, that is attributable to a particular risk and - Could affect profit and loss. Cash flow Hedge: - A hedge of exposure to that the is attributable to a particular risk associated with a recognised asset or a liability or a and - Could affect profit and loss.

53 Hedge of net investments in foreign operations (NIFO): Hedges of NIFO, including hedge of a monetary items that is accounted for as a part of net investment, should be accounted for similarly to cash flow hedges

54 Fair Value Hedged Cash Flow Hedged Fixed rate liabilities like loans; Fixed rate assets like investments in bonds; Investments in equity securities; Firm commitments to buy/sell non financial items at a fixed price. Variable rates liabilities like loans; Variable rate assets like investments in bonds; Forecast reinvestment of interest & principal received on fixed rate assets; Highly probable forecast sales & purchases; Highly probable future issuance of fixed rate debt

55 The standard do not specify a single method for assessing hedge effectiveness. Appropriateness depends upon type of risk being hedged and hedging instrument. At the inception of the hedge and in subsequent periods, the hedge is expected to be highly effective in achieving offsetting changes. A hedge is effective if actual results are within a range of 80% and 125%.

56 Mathematical techniques : i. ratio analysis i.e. comparison of hedging gains and losses with corresponding gains and losses on the hedged item at a point of time ii)statistical measurement technique such as Regression Analysis.

57 Accounting for fair value hedge: Derivative Instruments & Hedged item Initial and subsequent measurement At fair value, in the statement of profit and loss

58 Accounting for cash flow hedge & Net Investment in Operations: Derivative Instruments & Hedged item Initial and subsequent measurement If hedge is not effective In the statement of profit and loss account If hedge is effective In appropriate equity account

59 Fair Value Hedge Accounting: On 1 St January 2010, Company C issued Rs. 100 lakhs of 5 year 8% fixed rate debt. Company C has a BBB credit rating at the issuance date. The fixed interest rate on the debt is 150 basis points higher than the 5 year swap rate. Interest on the debt is payable annually. Company C s interest rate risk policy requires that all debt is at variable rates which is achieved either through issuing variable rate debt or by issuing fixed rate debt and swapping it into variable. In order to maintain compliance with this policy, Company C entered into an interest rate swap on 1 st January 2010 to convert the debt from fixed rate to variable and designated the swap (identifying and documenting all critical terms) as a fair value hedge of interest rate risk on the fixed rate debt (credits spreads are purposely not hedged). The swap is a 5 year pay MIBOR, receive 6.5% fixed interest rate swap.

60 The fair value of the swap and the carrying amount of the debt following the adjustment for changes in fair value attributable to be hedged risk are as follows: The required entries are as follows (Rs.): 1 January 2010 Dr Cash 100, 00,000 Cr Debt 100,00,000 To record the issuance of debt 1/1/ /06/ /12/2010 Issued Debt Rs. (100L) Rs. (105L) Rs. (102L) Swap Rs. Nil Rs. 5L Rs. 2L No entries are required in respect of the swap as it was entered into at the money when fair value was zero.

61 30 June 2010 Dr Profit and Loss 5,00,000 Cr Debt 5,00,000 Dr Swap 5,00,000 Cr Profit and Loss 5,00,000 The Net impact on Profit or Loss of Rs. Nil reflects that the changes in fair value of the swap offset fully the changes in fair value of the debt for the designated risk.

62 31 December 2010 Dr Debt 3,00,000 Cr Profit and Loss 3,00,000 Dr Profit and Loss 3,00,000 Cr Swap 3,00,000 The Net impact on Profit or Loss of Rs. Nil reflects that the changes in fair value of the swap offset fully the changes in fair value of the debt for the designated risk.

63 Cash Flow Hedge Accounting: On 4 January 2010 Company B has a forecast sale of 500 tonnes of rice expected to occur on or about 31 December On 4 January 2010 Company B designates the cash flows of the forecasted sale as a hedged item and enters into rice futures contract to sell 500 tonnes at Rs. 11,00,000 on 31 December At inception of the hedge, the derivative is at-the-money (fair value is zero). The terms of the forecast sale and the derivative match. On 31 December 2010, the rice futures contract has a fair value of Rs.25,000 and is closed out. Company B sells the inventory for Rs.10,75,000. Cost of inventory is Rs. 10,00,000.

64 The required entries are as follows: 31 December 2010 Dr Rice futures contract 25,000 Cr Equity 25,000 To record the rice futures contract at fair value (note that the changes in fair value of the derivative are recorded in equity until the hedged forecast sale occurs). 31 December 2010 Dr Cash 25,000 Cr Rice futures contact 25,000

65 To record the settlement of the rice futures contract Dr Cash 10,75,000 Dr Cost of goods sold 10,00,000 Cr Revenue 10,75,000 Cr Inventory 10,00,000 To record the inventory sale Dr Equity 25,000 Cr Revenue 25,000 Revenue of Rs. 11,00,000 is recognized. This represents Rs. 10,75,000 from the sale of rice at spot prices, plus the gain on the derivative.

66

67 To provide disclosure on: a. significance of financial instruments for entity s financial position and performance b. Nature, extent of risk arising from the financial instruments and management of these risks

68 Balance Sheet: Carrying amount of four categories of financial assets and two types of financial liabilities. In particular financial assets and financial liabilities at FVTPL showing separately i. Those designated as such upon initial recognition and ii. held for trading

69 Profit & loss account: Net gains or losses on financial asset or financial liability classified as : i. FVTPL showing separately designated upon initial recognition and those held for trading, ii. AFS showing separately amount directly recognised in equity account and in the statement of profit and loss iii. Held to Maturity (HTM) Iv. Loans and Receivable (L&R) v. Total interest income and expenses Interest income and expenses for financial Assets and financial liabilities through FVTPL using effective interest method Impairment income and impairment loss for each class of financial asset.

70 1. Accounting policies In accordance with AS 1, Presentation of Financial statements 1, Disclosure of accounting policies regarding recognition and measurement of financial assets and financial liabilities 1 Revised As 1 is under preparation

71 2. Hedge accounting An entity should disclose the following separately for each type of hedge described in AS 30. a. a description of each type of hedge; b. a description of the financial instruments designated as hedging instruments and their fair values at the reporting date; and c. the nature of the risks being hedged.

72 In respect of cash flow hedge: a. periods when the cash flows are expected to occur and when they are expected to affect profit or loss; b. a description of any forecast transaction for which hedge accounting had previously been used, but which is no longer expected to occur; c. the amount that was recognised in the appropriate equity account during the period; removed from the appropriate equity account and included in the statement of profit and loss and such removed amount included in the initial cost or other carrying amount of a non-financial asset or non-financial liability.

73 In respect of fair value hedge: An entity should disclose separately: (a) in fair value hedges, gains or losses: (i) on the hedging instrument; and (ii) on the hedged item attributable to the hedged risk. b) the ineffectiveness recognised in the statement of profit and loss that arises from cash flow hedges; and from hedges of net investments in foreign operations. C ) the ineffectiveness recognised in the statement of profit and loss that arises from hedges of net investments in foreign operations.

74 Except certain circumstances, for each class of financial assets and financial Liabilities, an entity should disclose the fair value of that class of assets and liabilities in a way that permits it to be compared with its carrying amount. (a) the methods and, when a valuation technique is used, the assumptions applied in determining fair values of each class of financial assets or financial liabilities. e.g. if applicable, an entity discloses information about the assumptions relating to prepayment rates, rates of estimated credit losses, and interest rates or discount rates.

75 In disclosing fair values, an entity should group financial assets and financial liabilities into classes, but should offset them only to the extent that their carrying amounts are offset in the balance sheet. Disclosure of fair value is not required in case of carrying amounts is a reasonable approximation of fair value, for example, for financial instruments such as short-term trade receivables and payables and or an investment in equity instruments that do not have a quoted market price in an active market, or derivatives linked to such equity instruments.

76 Qualitative Disclosures: For each type of risk arising from financial instruments, an entity should disclose: (a) the exposures to risk and how they arise; (b) its objectives, policies and processes for managing the risk and the methods used to measure the risk; and (c) any changes in (a) or (b) from the previous period.

77 Quantitative Disclosures: i. For each type of risk arising from financial instruments Summary quantitative data about its exposure to that risk at the reporting date. the disclosures in respect of credit risk, liquidity risk and market risk as referred in above paragraph, has not been provided, reason for non disclosure of the said data, unless the risk is not material. ii) If the quantitative data disclosed as at the reporting date are unrepresentative of an entity s exposure to risk during the period, an entity should provide further information that is representative.

78 In respect of each class of financial instrument: (a)the amount that best represents its maximum exposure to credit risk at the reporting date without taking account of any collateral held or other credit enhancements; (b) a description of collateral held as security and other credit enhancement; (c) the credit quality of financial assets that are neither past due nor impaired; and (d) the carrying amount of financial assets that would otherwise be past due or impaired whose terms have been renegotiated.

79 (a) a maturity analysis for financial liabilities that shows the remaining contractual maturities; and (b) a description of how it manages the liquidity risk inherent as mentioned in above paragraph.

80 Sensitivity analysis: A sensitivity analysis for each type of market risk, showing how profit or loss and equity would have been affected by changes in the relevant risk variable the methods and assumptions used in preparing the sensitivity analysis; and changes from the previous period in the methods and assumptions used and the reasons for such changes.

81 If an entity prepares a sensitivity analysis, such as value-at-risk, that reflects interdependencies between risk variables (e.g. interest rates and exchange rates) and uses it to manage financial risks, it may use that sensitivity analysis, The entity should also disclose: (a) an explanation of the method used in preparing such a sensitivity analysis, and of the main parameters and assumptions underlying the data provided; and (b) an explanation of the objective of the method used and of limitations that may result in the information not fully reflecting the fair value of the assets and liabilities involved.

82

83 Type of Contract Sale of sugar futures Margin Money Rs. 25,00,000 Quantity, Rate and Date of transaction 100MT quantity at the rate of Rs.2,965/- on 04/01/2011 Expiry Date 20/04/2011 FV as at 31/03/2011 Discharge of contract FV as at 20/04/2011 Rs. 2,990 per quintal Net settlement opted to be in cash Rs. 2,895 per quintal There being no initial investment, there is underlying of sugar prices and the contract settles at future date, the contract is a derivative contract.

84 Date Particulars Debit Credit 04/01/2011 Margin Money A/c 2,500,000 To Bank A/c 2,500,000 04/01/2011 Financial Assets A/c 2,965,000 To Financial Liability A/c 2,965,000 (Being booking of sugar commodity future of 100 expires on 20/4/11) 31/03/2011 Financial Assets A/c 25,000 To Profit & Loss A/c 25,000 (Being reinstatement of future contract on market rate of Rs.2990/-)

85 20/04/2011 Financial Liability A/c 2,965,000 To Financial Asset A/c 2,895,000 To Cash/Bank A/c 70,000 (Being sugar commodity future settled through buy Qtl. On expiry date) 20/04/2011 Profit & Loss A/c 95,000 To Financial Assets A/c 95,000 (Being profit on sugar commodity future accounted)

86 Number, value and period of convertible bonds Proceeds received 4000 bonds, issued at beginning of year 1, face value of Rs per bond (3 year validity) Rs. 40 lacs Interest rate on the bond Conversion Prevailing market rate 6% p.a. payable annually At the bond holders discretion, at 250 ordinary shares for each bond of Rs % p.a., for bonds issued without conversion option Present value factors for 9% 1, 0.917, 0.841, 0.772

87 Steps to find the equity and the liability component Step 1: Ascertaining Fair value of liability component Step 2: Ascertaining equity component Step 3: Initial recognition at the inception of bond Step 4: Debenture liability at the end of the year Step 5: Finance charges for each year

88 Step 1: Ascertaining Fair value of liability component PV of Rs. 40lacs repayable 3 rd year 3088,000 PV of interest payable at the end of each year: Year ,080 Year ,840 Year ,280 Liability component (B) 36,95,200 Step 2: Ascertaining equity component Fair value of Instrument (A) 40,00,000 Less: Liability component (B) 36,95,200 Equity Component (A-B) 304,800

89 Step 3: Initial recognition at the inception of bond Particulars Debit Credit Cash/Bank 40,00,000 To Convertible Bond liability 36,95,200 To Equity reserve 304,800

90 Step 4: Debenture liability at the end of the year Step 5: Finance charges for each year Particulars Finance charges (9%) Year 1 Year 2 Year 3 Beginning 36,95,200 37,87,768 38,88,668 + Interest 9% 332, , ,982 Subtotal 40,27,768 41,28,668 42,38,650 Rounding off - - 1,350 - Interest 6% (240,000) (240,000) (240,000) Carrying amount 37,87,768 38,88,668 40,00,000 Year 1 Year 2 Year 3 Debit Credit Debit Credit Debit Credit 332, , ,332 Debenture 92, , ,332 Cash/Bank (6%) 240, , ,000

91 Importer A Ltd hedge the forecasted import purchase cash flow through forward contract as per detail given below : Date Particulars Amount(FC) Rate Remarks Purchase Contract Forward Contract 100,000 Delivery March,2008 &Due June, , Cash flow hedged for June,2008 Date Spot Rate Forward Rate Change in Fair Value of Derivative (400) (2,000) (2,400)

92 Date Particulars Debit Credit Narration No Change in Fair value Appropriate Equity A/c Forward Liability A/c Appropriate Equity A/c Forward Liability A/c Purchase A/c Payable A/c Purchase A/c Appropriate Equity A/c 400 1, ,400 2, , ,400 2,000 Being Loss on forward contract parked in appropriate equity account. Being Loss on forward contract parked in appropriate equity account. Being purchase recorded at spot rate on Being cumulative loss on forward contract recognised in P & L A/c Payable A/c Bank A/c P & L A/c 107, , Being settlement of payable at spot rate P & L A/c Forward Liability A/c Being loss accounted on forward contract Forward Liability A/c Bank A/c 2,400 2,400 Being forward contract settled.

93 Hedge Effectiveness Evaluate whether the below hedging relationship is highly effective at the end of each period Assuming actual purchase take place on 20 th June, 2008 Particulars Spot Rate Forward rate as on 30 th June of respective year Forward rate as on 20 th June of respective year Fair value of forward contract Fair value of cash flows (purchase) (400) (2,000) (2,400) ,150 2,350 Effectiveness 80% 93% 102%

94

95 Derivative (Including Embedded derivative) Financial Instrument Non Derivative FVTPL AFS Hedge Non Hedge P&L CFH FVH Effective Appropriate Equity A/C Non effective P&L P&L AFS Available for Sale FVTPL Fair Value Through P&L CFH Cash Flow Hedge FVH Fair Value Hedge

96

Exposure Draft. Accounting Standard (AS) 109. Financial Instruments. Last date for the comments: June 30, 2018

109. Financial Instruments. Last date for the comments: June 30, 2018") Exposure Draft Accounting Standard (AS) 109 Financial Instruments Last date for the comments: June 30, 2018 Issued by Accounting Standards Board The Institute of Chartered Accountants of India 1 Exposure

Exposure Draft Accounting Standard (AS) 109 Financial Instruments Last date for the comments: June 30, 2018 Issued by Accounting Standards Board The Institute of Chartered Accountants of India 1 Exposure

Financial Instruments Standards 11 November Nelson Lam 林智遠 CFA FCCA FCPA(Practising) MBA MSc BBA CPA(US) ACA Nelson 1

MBA MSc BBA CPA(US) ACA Nelson 1") Instruments Standards 11 November 2006 Nelson Lam 林智遠 CFA FCCA FCPA(Practising) MBA MSc BBA CPA(US) ACA 2005-06 Nelson 1 Instruments HKAS 32 Disclosure and presentation HKAS 39 Recognition and measurement

Instruments Standards 11 November 2006 Nelson Lam 林智遠 CFA FCCA FCPA(Practising) MBA MSc BBA CPA(US) ACA 2005-06 Nelson 1 Instruments HKAS 32 Disclosure and presentation HKAS 39 Recognition and measurement

GN(A) 33 (Issued 2015) Guidance Note on Accounting for Derivative Contracts

33 (Issued 2015) Guidance Note on Accounting for Derivative Contracts") Introduction GN(A) 33 (Issued 2015) Guidance Note on Accounting for Derivative Contracts 1. In the year 2007, the Institute of Chartered Accountants of India (ICAI), issued Accounting Standard (AS) 30,

Introduction GN(A) 33 (Issued 2015) Guidance Note on Accounting for Derivative Contracts 1. In the year 2007, the Institute of Chartered Accountants of India (ICAI), issued Accounting Standard (AS) 30,

Accounting Standard (AS) 32 Financial Instruments: Disclosures. Issued by The Institute of Chartered Accountants of India New Delhi

32 Financial Instruments: Disclosures. Issued by The Institute of Chartered Accountants of India New Delhi") Accounting Standard (AS) 32 Financial Instruments: Disclosures Issued by The Institute of Chartered Accountants of India New Delhi 2 Accounting Standard (AS) 32 Financial Instruments: Disclosures Contents

Accounting Standard (AS) 32 Financial Instruments: Disclosures Issued by The Institute of Chartered Accountants of India New Delhi 2 Accounting Standard (AS) 32 Financial Instruments: Disclosures Contents

Accounting and Reporting of Financial Instruments

CHAPTER 6 Accounting and Reporting of Financial Instruments BASIC CONCEPTS Financial Instrument is contract that may give rise to financial asset of one entity and a financial liability of another entity.

CHAPTER 6 Accounting and Reporting of Financial Instruments BASIC CONCEPTS Financial Instrument is contract that may give rise to financial asset of one entity and a financial liability of another entity.

IFRS 9 Financial Instruments Thai Life Assurance Association

IFRS 9 Financial Instruments Thai Life Assurance Association 13 December 2016 What impact will IFRS 9 have on your business? More data required IFRS 9 More judgment involved Detailed guidance which may

IFRS 9 Financial Instruments Thai Life Assurance Association 13 December 2016 What impact will IFRS 9 have on your business? More data required IFRS 9 More judgment involved Detailed guidance which may

Topics to be discussed. HKAS 32 & 39 and HKFRS 7 Part II 8 November 2006

HKAS 32 & 39 and HKFRS 7 Part II 8 November 2006 Nelson Lam 林智遠 CFA FCCA FCPA(Practising) MBA MSc BBA CPA(US) ACA 2005-06 Nelson 1 Topics to be discussed Recap on recognition and measurement (HKAS 39)

HKAS 32 & 39 and HKFRS 7 Part II 8 November 2006 Nelson Lam 林智遠 CFA FCCA FCPA(Practising) MBA MSc BBA CPA(US) ACA 2005-06 Nelson 1 Topics to be discussed Recap on recognition and measurement (HKAS 39)

The IFRS for SMEs Topic 2.1 Section 11 Basic Financial Instruments Section 12 Other Fin. Inst. Issues Section 22 Liabilities and Equity

The IFRS for SMEs 1 Topic 2.1 Section 11 Basic Financial Instruments Section 12 Other Fin. Inst. Issues Section 22 Liabilities and Equity This PowerPoint presentation was prepared by IFRS Foundation education

The IFRS for SMEs 1 Topic 2.1 Section 11 Basic Financial Instruments Section 12 Other Fin. Inst. Issues Section 22 Liabilities and Equity This PowerPoint presentation was prepared by IFRS Foundation education

IAS 32 & 39 and IFRS 7 Part Two 10 September MBA MSc BBA ACA CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA Nelson 1

CPA(US) FCCA FCPA(Practising) MSCA Nelson 1") IAS 32 & 39 and IFRS 7 Part Two 10 September 2007 Nelson Lam 林智遠 MBA MSc BBA ACA CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2005-07 Nelson 1 Today s Agenda Anyone who says they understand IAS 39

IAS 32 & 39 and IFRS 7 Part Two 10 September 2007 Nelson Lam 林智遠 MBA MSc BBA ACA CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2005-07 Nelson 1 Today s Agenda Anyone who says they understand IAS 39

The IFRS for SMEs Topic 2.1 Section 11 Basic Financial Instruments Michael Wells

The IFRS for SMEs 1 Topic 2.1 Section 11 Basic Financial Instruments Michael Wells Sections 11-12 Introduction 2 Financial instruments split into two sections: Sec. 11 Basic Financial Instruments Sec.

The IFRS for SMEs 1 Topic 2.1 Section 11 Basic Financial Instruments Michael Wells Sections 11-12 Introduction 2 Financial instruments split into two sections: Sec. 11 Basic Financial Instruments Sec.

Financial Instruments Standards (Part 2) 18 June 2015

18 June 2015") Financial Instruments Standards (Part 2) 18 June 2015 LAM Chi Yuen Nelson 林智遠 MBA MSc BBA ACS ACIS CFA CGMA CPA(US) CTA FCA FCCA FCPA FCPA(Aust.) FHKIoD FTIHK MHKSI MSCA 2006-15 Nelson Consulting Limited

Financial Instruments Standards (Part 2) 18 June 2015 LAM Chi Yuen Nelson 林智遠 MBA MSc BBA ACS ACIS CFA CGMA CPA(US) CTA FCA FCCA FCPA FCPA(Aust.) FHKIoD FTIHK MHKSI MSCA 2006-15 Nelson Consulting Limited

IAS 32 & 39 and IFRS 7 Part II 18 August MBA MSc BBA ACA CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA Nelson 1

CPA(US) FCCA FCPA(Practising) MSCA Nelson 1") IAS 32 & 39 and IFRS 7 Part II 18 August 2007 Nelson Lam 林智遠 MBA MSc BBA ACA CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2005-07 Nelson 1 Today s Agenda Derivatives Derecognition Hedging Afternoon

IAS 32 & 39 and IFRS 7 Part II 18 August 2007 Nelson Lam 林智遠 MBA MSc BBA ACA CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2005-07 Nelson 1 Today s Agenda Derivatives Derecognition Hedging Afternoon

IFRS 9 Financial Instruments Thai General Assurance Association

IFRS 9 Financial Instruments Thai General Assurance Association 9 March 2017 What impact will IFRS 9 have on your business? More data required IFRS 9 More judgment involved Detailed guidance which may

IFRS 9 Financial Instruments Thai General Assurance Association 9 March 2017 What impact will IFRS 9 have on your business? More data required IFRS 9 More judgment involved Detailed guidance which may

IAS 32, IAS 39, IFRS 4 and IFRS 7 (Part 2) October MBA MSc BBA ACA ACIS CFA CPA(Aust.) CPA(US) FCCA FCPA(Practising) MSCA Nelson 1

October MBA MSc BBA ACA ACIS CFA CPA(Aust.) CPA(US) FCCA FCPA(Practising) MSCA Nelson 1") IAS 32, IAS 39, IFRS 4 and IFRS 7 (Part 2) October 2008 Nelson Lam 林智遠 MBA MSc BBA ACA ACIS CFA CPA(Aust.) CPA(US) FCCA FCPA(Practising) MSCA 2006-08 Nelson 1 Main Coverage IAS 32 IAS 39 Presentation Classification

IAS 32, IAS 39, IFRS 4 and IFRS 7 (Part 2) October 2008 Nelson Lam 林智遠 MBA MSc BBA ACA ACIS CFA CPA(Aust.) CPA(US) FCCA FCPA(Practising) MSCA 2006-08 Nelson 1 Main Coverage IAS 32 IAS 39 Presentation Classification

IFRS for SMEs IFRS Foundation-World Bank

!International Financial Reporting Standards 1 IFRS for SMEs IFRS Foundation-World Bank 11 13 January 2011 Astana, Kazakhstan Copyright 2010 IFRS Foundation. All rights reserved. The IFRS for SMEs 2 Topic

!International Financial Reporting Standards 1 IFRS for SMEs IFRS Foundation-World Bank 11 13 January 2011 Astana, Kazakhstan Copyright 2010 IFRS Foundation. All rights reserved. The IFRS for SMEs 2 Topic

IFRS 9 Financial Instruments

A C C O U N T I N G S U M M A R Y IFRS 9 Financial Instruments Objective The objective of this Standard is to establish principles for the financial reporting of financial assets and financial liabilities

A C C O U N T I N G S U M M A R Y IFRS 9 Financial Instruments Objective The objective of this Standard is to establish principles for the financial reporting of financial assets and financial liabilities

Topics to be discussed. HKAS 32 and 39 Part 2. Nelson Lam CFA FCCA FCPA(Practising) MBA MSc BBA CPA(US) ACA. Simple but Comprehensive

MBA MSc BBA CPA(US) ACA. Simple but Comprehensive") HKAS 32 and 39 Part 2 18 May 2006 Nelson Lam CFA FCCA FCPA(Practising) MBA MSc BBA CPA(US) ACA 2005-06 Nelson 1 Topics to be discussed A. Recap on recognition and measurement (HKAS 39) B. Definitions of

HKAS 32 and 39 Part 2 18 May 2006 Nelson Lam CFA FCCA FCPA(Practising) MBA MSc BBA CPA(US) ACA 2005-06 Nelson 1 Topics to be discussed A. Recap on recognition and measurement (HKAS 39) B. Definitions of

Measurement. Before 2005 / Financial Instruments: Recognition and Measurement (HKAS 39) 12 July 2006

12 July 2006") Instruments: Recognition and Measurement (HKAS 39) 12 July 2006 Nelson Lam CFA FCCA FCPA(Practising) MBA MSc BBA CPA(US) ACA 2005-06 Nelson 1 Measurement Before 2005 / 2006 SSAP 24 Held-to-maturity HTM

Instruments: Recognition and Measurement (HKAS 39) 12 July 2006 Nelson Lam CFA FCCA FCPA(Practising) MBA MSc BBA CPA(US) ACA 2005-06 Nelson 1 Measurement Before 2005 / 2006 SSAP 24 Held-to-maturity HTM

Indian Accounting Standard (Ind AS) 39. Financial Instruments: Recognition and Measurement

39. Financial Instruments: Recognition and Measurement") Indian Accounting Standard (Ind AS) 39 Financial Instruments: Recognition and Measurement 1 2 Indian Accounting Standard (Ind AS) 39 Financial Instruments: Recognition and Measurement Contents Paragraphs

Indian Accounting Standard (Ind AS) 39 Financial Instruments: Recognition and Measurement 1 2 Indian Accounting Standard (Ind AS) 39 Financial Instruments: Recognition and Measurement Contents Paragraphs

Accounting for Financial Instruments

International Financial Reporting Standards Accounting for Financial Instruments (IAS 39) Executive IFRS workshop for Regulators Diplomatic Academy of Vienna Darrel Scott, IASB member The views expressed

International Financial Reporting Standards Accounting for Financial Instruments (IAS 39) Executive IFRS workshop for Regulators Diplomatic Academy of Vienna Darrel Scott, IASB member The views expressed

IAS 32, IAS 39, IFRS 4 and IFRS 7 (Morning Session) 6 October 2007

6 October 2007") IAS 32, IAS 39, IFRS 4 and IFRS 7 (Morning Session) 6 October 2007 Nelson Lam 林智遠 MBA MSc BBA ACA CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2005-07 Nelson 1 IAS 32, IAS 39, IFRS 4 and IFRS 7 Anyone

IAS 32, IAS 39, IFRS 4 and IFRS 7 (Morning Session) 6 October 2007 Nelson Lam 林智遠 MBA MSc BBA ACA CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2005-07 Nelson 1 IAS 32, IAS 39, IFRS 4 and IFRS 7 Anyone

IFRS AT A GLANCE IFRS 9 Financial Instruments

IFRS AT A GLANCE Page 1 of 5 INITIAL RECOGNITION IFRS 9 replaces the multiple classification and measurement models in IAS 39 for financial assets and liabilities with a single model that has only two

IFRS AT A GLANCE Page 1 of 5 INITIAL RECOGNITION IFRS 9 replaces the multiple classification and measurement models in IAS 39 for financial assets and liabilities with a single model that has only two

Financial Instruments Standards (Part 1) 18 August 2011

18 August 2011") Instruments Standards (Part 1) 18 August 2011 Lam Chi Yuen, Nelson 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) CTA FCCA FCPA FHKIoD FTIHK MHKSI MSCA 2006-11 Nelson Consulting Limited 1 HKAS 32, HKAS

Instruments Standards (Part 1) 18 August 2011 Lam Chi Yuen, Nelson 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) CTA FCCA FCPA FHKIoD FTIHK MHKSI MSCA 2006-11 Nelson Consulting Limited 1 HKAS 32, HKAS

Sri Lanka Accounting Standard-SLFRS 7. Financial Instruments: Disclosures

Sri Lanka Accounting Standard-SLFRS 7 Financial Instruments: Disclosures CONTENTS SRI LANKA ACCOUNTING STANDARD-SLFRS 7 FINANCIAL INSTRUMENTS: DISCLOSURES paragraphs OBJECTIVE 1 2 SCOPE 3 5 CLASSES OF

Sri Lanka Accounting Standard-SLFRS 7 Financial Instruments: Disclosures CONTENTS SRI LANKA ACCOUNTING STANDARD-SLFRS 7 FINANCIAL INSTRUMENTS: DISCLOSURES paragraphs OBJECTIVE 1 2 SCOPE 3 5 CLASSES OF

HKFRS 7 and Amendments to HKAS 1 & October 2006

HKFRS 7 and Amendments to HKAS 1 & 39 16 October 2006 Nelson Lam 林智遠 CFA FCCA FCPA(Practising) MBA MSc BBA CPA(US) ACA 2005-06 Nelson 1 Today s Agenda Financial Instruments: Disclosure (HKFRS 7) 7) Amendment

HKFRS 7 and Amendments to HKAS 1 & 39 16 October 2006 Nelson Lam 林智遠 CFA FCCA FCPA(Practising) MBA MSc BBA CPA(US) ACA 2005-06 Nelson 1 Today s Agenda Financial Instruments: Disclosure (HKFRS 7) 7) Amendment

As at March 31, Note No. INR INR INR A 1

Balance Sheet as at March 31, 2017 As at March 31, 2017 As at March 31, 2016 (Amounts in lakhs) As at April 01, 2015 A 1 ASSETS Non-current assets (a) Property, Plant and Equipment 4 42,192.53 44,452.57

Balance Sheet as at March 31, 2017 As at March 31, 2017 As at March 31, 2016 (Amounts in lakhs) As at April 01, 2015 A 1 ASSETS Non-current assets (a) Property, Plant and Equipment 4 42,192.53 44,452.57

Financial Instruments. October 2015 Slide 2

Presented by: Cost transaction price (in general) Amortised Cost (B/s) EIR - Effective interest method (I/s) OCI - Other Comprehensive Income FVTPL Fair value through profit or loss FVOCI Fair value through

Presented by: Cost transaction price (in general) Amortised Cost (B/s) EIR - Effective interest method (I/s) OCI - Other Comprehensive Income FVTPL Fair value through profit or loss FVOCI Fair value through

Financial Instruments Standards (Part 1) 13 April 2010

13 April 2010") Instruments Standards (Part 1) 13 April 2010 Nelson Lam 林智遠 MBA MSc BBA ACA ACIS CFA CPA(Aust.) CPA(US) FCCA FCPA FHKIoD MSCA 2006-10 Nelson Consulting Limited 1 HKAS 32, HKAS 39, HKFRS 7 and HKFRS 9 Anyone

Instruments Standards (Part 1) 13 April 2010 Nelson Lam 林智遠 MBA MSc BBA ACA ACIS CFA CPA(Aust.) CPA(US) FCCA FCPA FHKIoD MSCA 2006-10 Nelson Consulting Limited 1 HKAS 32, HKAS 39, HKFRS 7 and HKFRS 9 Anyone

Financial Instruments: Disclosures

IFRS 7 International Financial Reporting Standard 7 Financial Instruments: Disclosures This version includes amendments resulting from IFRSs issued up to 31 December 2008. IAS 30 Disclosures in the Financial

IFRS 7 International Financial Reporting Standard 7 Financial Instruments: Disclosures This version includes amendments resulting from IFRSs issued up to 31 December 2008. IAS 30 Disclosures in the Financial

HKAS 32, HKAS 39 and HKFRS 7

Assets & Liabilities (HKAS 39) 24 April 2008 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2005-08 Nelson 1 HKAS 32, HKAS 39 and HKFRS 7 Anyone who says they understand

Assets & Liabilities (HKAS 39) 24 April 2008 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2005-08 Nelson 1 HKAS 32, HKAS 39 and HKFRS 7 Anyone who says they understand

Hong Kong Accounting Standard 39 Financial Instruments: Recognition and Measurement

Hong Kong Accounting Standard 39 Financial Instruments: Recognition and Measurement 1 Contents Hong Kong Accounting Standard 39 Financial Instruments: Recognition and Measurement paragraphs OBJECTIVE 1

Hong Kong Accounting Standard 39 Financial Instruments: Recognition and Measurement 1 Contents Hong Kong Accounting Standard 39 Financial Instruments: Recognition and Measurement paragraphs OBJECTIVE 1

Exposure Draft. Indian Accounting Standard (Ind AS) 109, Financial Instruments

109, Financial Instruments") Exposure Draft Indian Accounting Standard (Ind AS) 109, Financial Instruments (Last date for Comments: October 25, 2014) Issued by Accounting Standards Board The Institute of Chartered Accountants of India

Exposure Draft Indian Accounting Standard (Ind AS) 109, Financial Instruments (Last date for Comments: October 25, 2014) Issued by Accounting Standards Board The Institute of Chartered Accountants of India

Financial Instruments Standards Ind AS 32, 109 and 107. For internal use only

Financial Instruments Standards Ind AS 32, 109 and 107 Acknowledgements To my institutions where I have worked and have encouraged to share the knowledge To ICAI on whose standard, my presentation is published

Financial Instruments Standards Ind AS 32, 109 and 107 Acknowledgements To my institutions where I have worked and have encouraged to share the knowledge To ICAI on whose standard, my presentation is published

EUROPEAN UNION ACCOUNTING RULE 11 FINANCIAL INSTRUMENTS

EUROPEAN UNION ACCOUNTING RULE 11 FINANCIAL INSTRUMENTS Page 2 of 35 I N D E X 1. Objective... 3 2. Scope... 3 3. Definitions... 3 4. Presentation... 7 5. Recognition... 9 6. Measurement... 10 6.1 Initial

EUROPEAN UNION ACCOUNTING RULE 11 FINANCIAL INSTRUMENTS Page 2 of 35 I N D E X 1. Objective... 3 2. Scope... 3 3. Definitions... 3 4. Presentation... 7 5. Recognition... 9 6. Measurement... 10 6.1 Initial

INFORMATION FOR OBSERVERS

30 Cannon Street, London EC4M 6XH, United Kingdom Tel: +44 (0)20 7246 6410 Fax: +44 (0)20 7246 6411 E-mail: iasb@iasb.org Website: www.iasb.org International Accounting Standards Board This document is

30 Cannon Street, London EC4M 6XH, United Kingdom Tel: +44 (0)20 7246 6410 Fax: +44 (0)20 7246 6411 E-mail: iasb@iasb.org Website: www.iasb.org International Accounting Standards Board This document is

Financial Instruments: Disclosures

International Financial Reporting Standard 7 Financial Instruments: Disclosures This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 30 Disclosures in the Financial

International Financial Reporting Standard 7 Financial Instruments: Disclosures This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 30 Disclosures in the Financial

Ind AS 39 Financial Instruments

Ind AS 39 Financial Instruments Contents 1. Definition 2. Classification 3. Measurement 4. Reclassification 5. Derivatives and Embedded derivatives 6. Impairment 7. Hedge Accounting 1 Definition Definition

Ind AS 39 Financial Instruments Contents 1. Definition 2. Classification 3. Measurement 4. Reclassification 5. Derivatives and Embedded derivatives 6. Impairment 7. Hedge Accounting 1 Definition Definition

26 BUSINESS ACCOUNTING STANDARD DERIVATIVE FINANCIAL INSTRUMENTS I. GENERAL PROVISIONS

APPROVED by Order No. VAS-6 of 17 September 2007 of the Director of the Public Establishment the Institute of Accounting of the Republic of Lithuania 26 BUSINESS ACCOUNTING STANDARD DERIVATIVE FINANCIAL

APPROVED by Order No. VAS-6 of 17 September 2007 of the Director of the Public Establishment the Institute of Accounting of the Republic of Lithuania 26 BUSINESS ACCOUNTING STANDARD DERIVATIVE FINANCIAL

What are the common difficulties in studying financial assets and liabilities?

HKICPA Module A Financial Reporting Agenda Financial Assets and Liabilities What are the common difficulties in studying financial assets and liabilities? In today s seminar, we will discuss the following:

HKICPA Module A Financial Reporting Agenda Financial Assets and Liabilities What are the common difficulties in studying financial assets and liabilities? In today s seminar, we will discuss the following:

Financial Assets & Financial Liabilities (HKAS 39) 17 October 2008

17 October 2008") Assets & Liabilities (HKAS 39) 17 October 2008 Nelson Lam 林智遠 MBA MSc BBA ACA ACIS CFA CPA(Aust.) CPA(US) FCCA FCPA(Practising) MSCA 2006-08 Nelson 1 Assets & Liabilities Anyone who says they understand

Assets & Liabilities (HKAS 39) 17 October 2008 Nelson Lam 林智遠 MBA MSc BBA ACA ACIS CFA CPA(Aust.) CPA(US) FCCA FCPA(Practising) MSCA 2006-08 Nelson 1 Assets & Liabilities Anyone who says they understand

Financial Instruments Standards (Part 1) 21 May 2015

21 May 2015") Instruments Standards (Part 1) 21 May 2015 LAM Chi Yuen Nelson 林智遠 MBA MSc BBA ACS ACIS CFA CGMA CPA(US) CTA FCA FCCA FCPA FCPA(Aust.) FHKIoD FTIHK MHKSI MSCA 2006-15 Nelson Consulting Limited 1 Background

Instruments Standards (Part 1) 21 May 2015 LAM Chi Yuen Nelson 林智遠 MBA MSc BBA ACS ACIS CFA CGMA CPA(US) CTA FCA FCCA FCPA FCPA(Aust.) FHKIoD FTIHK MHKSI MSCA 2006-15 Nelson Consulting Limited 1 Background

Financial Instruments

IFRS 9 Financial Instruments In April 2001 the International Accounting Standards Board (the Board) adopted IAS 39 Financial Instruments: Recognition and Measurement, which had originally been issued by

IFRS 9 Financial Instruments In April 2001 the International Accounting Standards Board (the Board) adopted IAS 39 Financial Instruments: Recognition and Measurement, which had originally been issued by

11326/16 ADD 1 LM/CDP/vpl DGG 3 B

Council of the European Union Brussels, 19 July 2016 (OR. en) 11326/16 ADD 1 DRS 32 ECOFIN 719 EF 244 COVER NOTE From: European Commission date of receipt: 6 July 2016 To: No. Cion doc.: Subject: General

Council of the European Union Brussels, 19 July 2016 (OR. en) 11326/16 ADD 1 DRS 32 ECOFIN 719 EF 244 COVER NOTE From: European Commission date of receipt: 6 July 2016 To: No. Cion doc.: Subject: General

IAS 32, IAS 39, IFRS 4 and IFRS 7 (Morning Session) 21 July 2007

21 July 2007") IAS 32, IAS 39, IFRS 4 and IFRS 7 (Morning Session) 21 July 2007 Nelson Lam 林智遠 MBA MSc BBA ACA CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2005-07 Nelson 1 IAS 32, IAS 39, IFRS 4 and IFRS 7 Anyone

IAS 32, IAS 39, IFRS 4 and IFRS 7 (Morning Session) 21 July 2007 Nelson Lam 林智遠 MBA MSc BBA ACA CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2005-07 Nelson 1 IAS 32, IAS 39, IFRS 4 and IFRS 7 Anyone

CAISSE POPULAIRE GROUPE FINANCIER LTÉE. Consolidated Financial Statements For the year ended September 30, 2011

CAISSE POPULAIRE GROUPE FINANCIER LTÉE Consolidated Financial Statements For the year ended September 30, 2011 Consolidated Financial Statements For the year ended September 30, 2011 Contents Independent

CAISSE POPULAIRE GROUPE FINANCIER LTÉE Consolidated Financial Statements For the year ended September 30, 2011 Consolidated Financial Statements For the year ended September 30, 2011 Contents Independent

NALCOR ENERGY - OIL AND GAS INC. CONDENSED INTERIM FINANCIAL STATEMENTS June 30, 2018 (Unaudited)

") CONDENSED INTERIM FINANCIAL STATEMENTS June 30, 2018 (Unaudited) STATEMENT OF FINANCIAL POSITION (Unaudited) June 30 December 31 As at (thousands of Canadian dollars) Notes 2018 2017 ASSETS Current assets

CONDENSED INTERIM FINANCIAL STATEMENTS June 30, 2018 (Unaudited) STATEMENT OF FINANCIAL POSITION (Unaudited) June 30 December 31 As at (thousands of Canadian dollars) Notes 2018 2017 ASSETS Current assets

Regular way purchase or sale of financial assets

International Financial Reporting Standard 9 Financial Instruments Chapter 1 Objective 1.1 The objective of this IFRS is to establish principles for the financial reporting of financial assets and financial

International Financial Reporting Standard 9 Financial Instruments Chapter 1 Objective 1.1 The objective of this IFRS is to establish principles for the financial reporting of financial assets and financial

Accounting & Reporting of Financial Instruments 2016

Illustration 1 (Exchange of Financial Liability at Unfavorable terms) A company borrowed 50 lacs @ 12% p.a. Tenure of the loan is 10 years. Interest is payable every year and the principal is repayable

Illustration 1 (Exchange of Financial Liability at Unfavorable terms) A company borrowed 50 lacs @ 12% p.a. Tenure of the loan is 10 years. Interest is payable every year and the principal is repayable

BANK VTB (AZERBAIJAN) OPEN JOINT STOCK COMPANY

OPEN JOINT STOCK COMPANY") BANK VTB (AZERBAIJAN) OPEN JOINT STOCK COMPANY The International Financial Reporting Standards Financial Statements and Independent Auditors Report For the Year Ended 2010 TABLE OF CONTENTS Page STATEMENT

BANK VTB (AZERBAIJAN) OPEN JOINT STOCK COMPANY The International Financial Reporting Standards Financial Statements and Independent Auditors Report For the Year Ended 2010 TABLE OF CONTENTS Page STATEMENT

Financial Instruments: Disclosures

International Financial Reporting Standard 7 Financial Instruments: Disclosures In April 2001 the International Accounting Standards Board (IASB) adopted IAS 30 Disclosures in the Financial Statements

International Financial Reporting Standard 7 Financial Instruments: Disclosures In April 2001 the International Accounting Standards Board (IASB) adopted IAS 30 Disclosures in the Financial Statements

ZAO Bank Credit Suisse (Moscow) Financial Statements for the year ended 31 December 2010

Financial Statements for the year ended 31 December 2010") Financial Statements for the year ended 31 December 2010 Contents Independent Auditors Report... 3 Statement of Comprehensive Income... 4 Statement of Financial Position... 5 Statement of Cash Flows...

Financial Statements for the year ended 31 December 2010 Contents Independent Auditors Report... 3 Statement of Comprehensive Income... 4 Statement of Financial Position... 5 Statement of Cash Flows...

Financial instruments

International Financial Reporting Standards Financial instruments The views expressed in this presentation are those of the presenter, not necessarily those of the IASB or IFRS Foundation IASB s work on

International Financial Reporting Standards Financial instruments The views expressed in this presentation are those of the presenter, not necessarily those of the IASB or IFRS Foundation IASB s work on

Indian Accounting Standard (Ind AS) 109 Financial Instruments

109 Financial Instruments") Indian Accounting Standard (Ind AS) 109 Financial Instruments (The Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority. Paragraphs in bold type indicate

Indian Accounting Standard (Ind AS) 109 Financial Instruments (The Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority. Paragraphs in bold type indicate

NATURE AND EXTENT OF RISKS ARISING FROM FINANCIAL INSTRUMENTS Quantitative disclosures. Collateral and other credit enhancements pledged

Appendix D GUIDANCE ON IMPLEMENTING AS 32, FINANCIAL INSTRUMENTS: DISCLOSURES INTRODUCTION Materiality CLASSES OF FINANCIAL INSTRUMENTS AND LEVEL OF DISCLOSURE SIGNIFICANCE OF FINANCIAL INSTRUMENTS FOR

Appendix D GUIDANCE ON IMPLEMENTING AS 32, FINANCIAL INSTRUMENTS: DISCLOSURES INTRODUCTION Materiality CLASSES OF FINANCIAL INSTRUMENTS AND LEVEL OF DISCLOSURE SIGNIFICANCE OF FINANCIAL INSTRUMENTS FOR

Ind AS Transition Facilitation Group (ITFG) Clarification Bulletin 2

Clarification Bulletin 2") Ind AS Transition Facilitation Group (ITFG) Clarification Bulletin 2 The Accounting Standards Board (ASB) of the ICAI has constituted Ind AS Transition Facilitation Group (ITFG) 1 for providing clarifications

Ind AS Transition Facilitation Group (ITFG) Clarification Bulletin 2 The Accounting Standards Board (ASB) of the ICAI has constituted Ind AS Transition Facilitation Group (ITFG) 1 for providing clarifications

EMIRATES NBD BANK PJSC

GROUP CONSOLIDATED FINANCIAL STATEMENTS These Audited Preliminary Financial Statements are subject to Central Bank of UAE Approval and adoption by Shareholders at the Annual General Meeting GROUP CONSOLIDATED

GROUP CONSOLIDATED FINANCIAL STATEMENTS These Audited Preliminary Financial Statements are subject to Central Bank of UAE Approval and adoption by Shareholders at the Annual General Meeting GROUP CONSOLIDATED

TAX IMPLICATIONS RELATED TO THE IMPLEMENTATION OF FRS 139: FINANCIAL INSTRUMENTS: RECOGNITION & MEASUREMENT (FOR NON-FINANCIAL INSTITUTIONS)

") The Malaysian Institute of Certified Public Accountants DISCUSSION PAPER TAX IMPLICATIONS RELATED TO THE IMPLEMENTATION OF FRS 139: FINANCIAL INSTRUMENTS: RECOGNITION & MEASUREMENT (FOR NON-FINANCIAL INSTITUTIONS)

The Malaysian Institute of Certified Public Accountants DISCUSSION PAPER TAX IMPLICATIONS RELATED TO THE IMPLEMENTATION OF FRS 139: FINANCIAL INSTRUMENTS: RECOGNITION & MEASUREMENT (FOR NON-FINANCIAL INSTITUTIONS)

IAS 32, IAS 39 & IFRS 7 AA

GLOBAL AUDIT LEARNING AND DEVELOPMENT IAS 32, IAS 39 & IFRS 7 AA 2012-2013 Università degli Studi di Bergamo Anael Francillon Ivan Lucci Bergamo, 22 febbraio 2013. The information contained herein is of

GLOBAL AUDIT LEARNING AND DEVELOPMENT IAS 32, IAS 39 & IFRS 7 AA 2012-2013 Università degli Studi di Bergamo Anael Francillon Ivan Lucci Bergamo, 22 febbraio 2013. The information contained herein is of

Sri Lanka Accounting Standard SLFRS 9. Financial Instruments

Sri Lanka Accounting Standard SLFRS 9 Financial Instruments CONTENTS from paragraph Sri Lanka Accounting Standard SLFRS 9 Financial Instruments CHAPTERS 1. OBJECTIVE 1.1 2. SCOPE 2.1 3. RECOGNITION AND

Sri Lanka Accounting Standard SLFRS 9 Financial Instruments CONTENTS from paragraph Sri Lanka Accounting Standard SLFRS 9 Financial Instruments CHAPTERS 1. OBJECTIVE 1.1 2. SCOPE 2.1 3. RECOGNITION AND

SUPPLEMENT. to the publication. Accounting for Financial Instruments - Standards, Interpretations, and Implementation Guidance

NOVEMBER 2001 SUPPLEMENT to the publication Accounting for Financial Instruments - Standards, Interpretations, and Implementation Guidance originally issued in July 2001 This document includes the final

NOVEMBER 2001 SUPPLEMENT to the publication Accounting for Financial Instruments - Standards, Interpretations, and Implementation Guidance originally issued in July 2001 This document includes the final

ASPE AT A GLANCE. Section Financial Instruments

ASPE AT A GLANCE Section 3856 - Financial Instruments December 2014 Section 3856 Financial Instruments Effective Date Fiscal years beginning on or after January 1, 2011 1 SCOPE Applies to all financial

ASPE AT A GLANCE Section 3856 - Financial Instruments December 2014 Section 3856 Financial Instruments Effective Date Fiscal years beginning on or after January 1, 2011 1 SCOPE Applies to all financial

Anesu Daka CA(SA) - CAA

- CAA") FAC4863 4 August 2015 Tut 105/106 1. IAS 21- The effects of changes in foreign exchange rates 2. IAS32/39/IFRS9&7-Financial instruments 3. IAS 39-Hedging 4. IAS 33-Earnings per share 5. IAS 17- Leases

FAC4863 4 August 2015 Tut 105/106 1. IAS 21- The effects of changes in foreign exchange rates 2. IAS32/39/IFRS9&7-Financial instruments 3. IAS 39-Hedging 4. IAS 33-Earnings per share 5. IAS 17- Leases

Notes to the Financial Statements

85 Notes to the Financial Statements for the year ended 31 December 2010 These Notes are integral to the financial statements. The consolidated financial statements for the year ended 31 December 2010

85 Notes to the Financial Statements for the year ended 31 December 2010 These Notes are integral to the financial statements. The consolidated financial statements for the year ended 31 December 2010

1 Summary of significant accounting policies (continued)

") (g) (g) Impairment of financial assets (continued) '()*+, Financial assets carried at amortised cost (continued) If there is objective evidence that an impairment loss on financial assets carried at amortised

(g) (g) Impairment of financial assets (continued) '()*+, Financial assets carried at amortised cost (continued) If there is objective evidence that an impairment loss on financial assets carried at amortised

FRS 102 FACTSHEET 4 FINANCIAL INSTRUMENTS

FRS 102 FACTSHEET 4 FINANCIAL INSTRUMENTS Financial instruments FRS 102 significantly changed the accounting for financial instruments in comparison to the requirements applicable to most UK and Ireland

FRS 102 FACTSHEET 4 FINANCIAL INSTRUMENTS Financial instruments FRS 102 significantly changed the accounting for financial instruments in comparison to the requirements applicable to most UK and Ireland

Before 2005 / Investments for NPO/NGO. Nelson Lam CFA FCCA FCPA(Practising) MBA MSc BBA CPA(US) ACA. Case

MBA MSc BBA CPA(US) ACA. Case") Investments for NPO/NGO 24 May 2006 Nelson Lam CFA FCCA FCPA(Practising) MBA MSc BBA CPA(US) ACA 2005-06 Nelson 1 Before 2005 / 2006 Case Accounting policy (2004/05) on long-term (partial): Unlisted guaranteed

Investments for NPO/NGO 24 May 2006 Nelson Lam CFA FCCA FCPA(Practising) MBA MSc BBA CPA(US) ACA 2005-06 Nelson 1 Before 2005 / 2006 Case Accounting policy (2004/05) on long-term (partial): Unlisted guaranteed

Revisionary Test Paper_Dec 2018

Final Group IV Paper 17 : CORPORATE FINANCIAL REPORTING (SYLLABUS 2016) 1. Multiple Choice Questions: Objectives (i) Mittal Ltd. has provided the following information: Depreciation as per accounting records

Final Group IV Paper 17 : CORPORATE FINANCIAL REPORTING (SYLLABUS 2016) 1. Multiple Choice Questions: Objectives (i) Mittal Ltd. has provided the following information: Depreciation as per accounting records

Nueclear Healthcare Limited

Standalone Balance sheet As at 31 March 2018 Note 31 March 2018 31 March 2017 1 April 2016 Assets Non-current assets Property, plant and equipment 4A. 871.81 621.53 591.91 Capital-work-in progress 4B.

Standalone Balance sheet As at 31 March 2018 Note 31 March 2018 31 March 2017 1 April 2016 Assets Non-current assets Property, plant and equipment 4A. 871.81 621.53 591.91 Capital-work-in progress 4B.

Financial Reporting, Topic Area 3 Financial Instruments

www.acasimplified.com Sample Q&A Financial Reporting, Topic Area 3 69 short questions and answers to drill the narrative and numerical aspects of the topic The Q&A will work best if you cover the answer

www.acasimplified.com Sample Q&A Financial Reporting, Topic Area 3 69 short questions and answers to drill the narrative and numerical aspects of the topic The Q&A will work best if you cover the answer

1 The Theoretical Framework

1 The Theoretical Framework IAS 39 Financial Instruments: Recognition and Measurement is a complex standard. It establishes accounting principles for recognising, measuring and disclosing information about

1 The Theoretical Framework IAS 39 Financial Instruments: Recognition and Measurement is a complex standard. It establishes accounting principles for recognising, measuring and disclosing information about

Notes to the Consolidated Financial Statements (Amount in millions of Renminbi, unless otherwise stated)

") (Amount in millions of Renminbi, unless otherwise stated) I GENERAL INFORMATION AND PRINCIPAL ACTIVITIES Bank of China Limited (the Bank ), formerly known as Bank of China, a State-owned joint stock commercial

(Amount in millions of Renminbi, unless otherwise stated) I GENERAL INFORMATION AND PRINCIPAL ACTIVITIES Bank of China Limited (the Bank ), formerly known as Bank of China, a State-owned joint stock commercial

SLFRS 7 Sri Lanka Accounting Standard SLFRS 7

Sri Lanka Accounting Standard SLFRS 7 Financial Instruments: Disclosures CONTENTS SRI LANKA ACCOUNTING STANDARD SLFRS 7 FINANCIAL INSTRUMENTS: DISCLOSURES paragraphs OBJECTIVE 1 SCOPE 3 CLASSES OF FINANCIAL

Sri Lanka Accounting Standard SLFRS 7 Financial Instruments: Disclosures CONTENTS SRI LANKA ACCOUNTING STANDARD SLFRS 7 FINANCIAL INSTRUMENTS: DISCLOSURES paragraphs OBJECTIVE 1 SCOPE 3 CLASSES OF FINANCIAL

Current Assets Financial Assets (i) Cash and Cash Equivalents 4 76,190. Total Current Assets 76,190 TOTAL ASSETS 76,190

Cash and Cash Equivalents 4 76,190. Total Current Assets 76,190 TOTAL ASSETS 76,190") Balance Sheet as at March 31, 2017 Notes As at March 31, 2017 ASSETS Current Assets Financial Assets (i) Cash and Cash Equivalents 4 76,190 Total Current Assets 76,190 TOTAL ASSETS 76,190 EQUITY AND LIABILITIES

Balance Sheet as at March 31, 2017 Notes As at March 31, 2017 ASSETS Current Assets Financial Assets (i) Cash and Cash Equivalents 4 76,190 Total Current Assets 76,190 TOTAL ASSETS 76,190 EQUITY AND LIABILITIES

Anesu Daka CA(SA)- CAA

- CAA") FAC4861 4 August 2015 Tut 105/106 1. IAS32/39/IFRS9&7-Financial instruments 2. IAS 33-Earnings per share 3. IAS 17- Leases Forex Transactions: IAS 21 Effects in foreign exchange rates transactions IAS

FAC4861 4 August 2015 Tut 105/106 1. IAS32/39/IFRS9&7-Financial instruments 2. IAS 33-Earnings per share 3. IAS 17- Leases Forex Transactions: IAS 21 Effects in foreign exchange rates transactions IAS

Notes to the Consolidated Financial Statements

251 Deutsche Bank Consolidated Statement of Income 245 Annual Report 2015 Consolidated Statement of Consolidated Financial Statements 251 Consolidated Statement of Consolidated Balance Sheet 289 Consolidated

251 Deutsche Bank Consolidated Statement of Income 245 Annual Report 2015 Consolidated Statement of Consolidated Financial Statements 251 Consolidated Statement of Consolidated Balance Sheet 289 Consolidated

Prospera Credit Union. Consolidated Financial Statements December 31, 2012 (expressed in thousands of dollars)

") Consolidated Financial Statements February 19, 2013 Independent Auditor s Report To the Members of Prospera Credit Union We have audited the accompanying consolidated financial statements of Prospera Credit

Consolidated Financial Statements February 19, 2013 Independent Auditor s Report To the Members of Prospera Credit Union We have audited the accompanying consolidated financial statements of Prospera Credit

Ahli Bank Q.S.C. CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2017

CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2017 CONTENTS CONSOLIDATED FINANCIAL STATEMENTS Page(s) Independent auditors report -- Consolidated statement of financial position 1 Consolidated statement

CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2017 CONTENTS CONSOLIDATED FINANCIAL STATEMENTS Page(s) Independent auditors report -- Consolidated statement of financial position 1 Consolidated statement

IFRS 7 Financial Instruments: Disclosures

IFRS 7 Financial Instruments: Disclosures Overview Standard looks at disclosures of: Significance of Financial Instruments for financial position and performance Statement of Financial Position Statement

IFRS 7 Financial Instruments: Disclosures Overview Standard looks at disclosures of: Significance of Financial Instruments for financial position and performance Statement of Financial Position Statement

Financial Instruments

Financial Instruments Madhu Sudan Kankani June 2017 KPMG.com/in 2017 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International

Financial Instruments Madhu Sudan Kankani June 2017 KPMG.com/in 2017 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International

Financial Instruments: Recognition and Classification

Risk and Accounting Financial Instruments: Recognition and Classification Marco Venuti 2018 Agenda Recognition Transaction costs Classification Classification financial assets Fair value option Embedded

Risk and Accounting Financial Instruments: Recognition and Classification Marco Venuti 2018 Agenda Recognition Transaction costs Classification Classification financial assets Fair value option Embedded

HKAS 32, HKAS 39 and HKFRS 7

HKAS 32 & 39 and HKFRS 7 Part One 10 March 2008 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2005-08 Nelson 1 HKAS 32, HKAS 39 and HKFRS 7 Anyone who says they understand

HKAS 32 & 39 and HKFRS 7 Part One 10 March 2008 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2005-08 Nelson 1 HKAS 32, HKAS 39 and HKFRS 7 Anyone who says they understand

2007 Financial Statements. Consolidated Financial Statements of the Nestlé Group Financial Statements of Nestlé S.A.

2007 Financial Statements Consolidated Financial Statements of the Nestlé Group Financial Statements of Nestlé S.A. Consolidated Financial Statements of the Nestlé Group Principal exchange rates...2 Consolidated

2007 Financial Statements Consolidated Financial Statements of the Nestlé Group Financial Statements of Nestlé S.A. Consolidated Financial Statements of the Nestlé Group Principal exchange rates...2 Consolidated

Summary of Key Changes on Singapore Financial Reporting Standards (FRS) as at September 2006

as at September 2006") Effective dates FRS Annual periods beginning 1 January 2006 to FRS 19 Employee Benefits to FRS 21 The Effects of Changes in Foreign Exchange Rates to FRS 32 Disclosure Presentation to FRS 39 Recognition

Effective dates FRS Annual periods beginning 1 January 2006 to FRS 19 Employee Benefits to FRS 21 The Effects of Changes in Foreign Exchange Rates to FRS 32 Disclosure Presentation to FRS 39 Recognition

Ras Al Khaimah National Insurance Company P.S.C.

Financial statements 31 December 2014 Financial statements 31 December 2014 Contents Page Independent auditors' report 1-2 Statement of financial position 3 Statement of profit or loss 4 Statement of comprehensive

Financial statements 31 December 2014 Financial statements 31 December 2014 Contents Page Independent auditors' report 1-2 Statement of financial position 3 Statement of profit or loss 4 Statement of comprehensive

ITNL OFFSHORE PTE. LTD.

Prepared on The attached draft financial statements, which have been prepared by management of the Company, are subject to changes that may arise from the resolution of outstanding audit matters which

Prepared on The attached draft financial statements, which have been prepared by management of the Company, are subject to changes that may arise from the resolution of outstanding audit matters which

BHARTI AIRTEL (JAPAN) Private LIMITED. Ind AS Financial Statements

Private LIMITED. Ind AS Financial Statements") BHARTI AIRTEL (JAPAN) Private LIMITED Ind AS Financial Statements March 2017 BHARTI AIRTEL (JAPAN) PRIVATE LIMITED Ind AS Financial Statements March 2017 Contents Page No. 1) Independent Auditor s Report

BHARTI AIRTEL (JAPAN) Private LIMITED Ind AS Financial Statements March 2017 BHARTI AIRTEL (JAPAN) PRIVATE LIMITED Ind AS Financial Statements March 2017 Contents Page No. 1) Independent Auditor s Report

New Zealand Equivalent to International Accounting Standard 39 Financial Instruments: Recognition and Measurement (NZ IAS 39)

") New Zealand Equivalent to International Accounting Standard 39 Financial Instruments: Recognition and Measurement (NZ IAS 39) Issued November 2004 and incorporates amendments up to and including 30 November

New Zealand Equivalent to International Accounting Standard 39 Financial Instruments: Recognition and Measurement (NZ IAS 39) Issued November 2004 and incorporates amendments up to and including 30 November

Notes to the consolidated financial statements

Notes to the consolidated financial statements Canadian Imperial Bank of Commerce (CIBC) is a diversified financial institution governed by the Bank Act (Canada). CIBC was formed through the amalgamation

Notes to the consolidated financial statements Canadian Imperial Bank of Commerce (CIBC) is a diversified financial institution governed by the Bank Act (Canada). CIBC was formed through the amalgamation

Voices on Reporting. 18 November KPMG.com/in

Voices on Reporting 18 November 2015 KPMG.com/in Welcome Series of knowledge sharing calls Covering current and emerging reporting issues Scheduled towards the end of each month Look out for our Accounting

Voices on Reporting 18 November 2015 KPMG.com/in Welcome Series of knowledge sharing calls Covering current and emerging reporting issues Scheduled towards the end of each month Look out for our Accounting

RELEVANT TO ACCA QUALIFICATION PAPERS F7 AND P2 What is a financial instrument? Let us start by looking at the definition of a financial instrument, which is that a financial instrument is a contract that

RELEVANT TO ACCA QUALIFICATION PAPERS F7 AND P2 What is a financial instrument? Let us start by looking at the definition of a financial instrument, which is that a financial instrument is a contract that

1 SIGNIFICANT ACCOUNTING POLICIES The principal accounting policies adopted in the preparation of these financial statements as set out below have

1 SIGNIFICANT ACCOUNTING POLICIES The principal accounting policies adopted in the preparation of these financial statements as set out below have been applied consistently to all periods presented in

1 SIGNIFICANT ACCOUNTING POLICIES The principal accounting policies adopted in the preparation of these financial statements as set out below have been applied consistently to all periods presented in

In $ millions Note

DBS BANK LTD AND ITS SUBSIDIARIES CONSOLIDATED INCOME STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2006 Group In $ millions Note 2006 2005 2006 2005 Income Interest income 7,809 5,542 5,324 3,774 Interest

DBS BANK LTD AND ITS SUBSIDIARIES CONSOLIDATED INCOME STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2006 Group In $ millions Note 2006 2005 2006 2005 Income Interest income 7,809 5,542 5,324 3,774 Interest

IIPL USA LLC FINANCIAL STATEMENTS

FINANCIAL STATEMENTS - - (1) 0 - Balance sheet as at March Notes As at As at As at March March 31, April 1, 2015 ASSETS Non-current Assets (a) Property, plant and equipment 4 21,848,458 - - (b) Intangible

FINANCIAL STATEMENTS - - (1) 0 - Balance sheet as at March Notes As at As at As at March March 31, April 1, 2015 ASSETS Non-current Assets (a) Property, plant and equipment 4 21,848,458 - - (b) Intangible

LKAS 39 Sri Lanka Accounting Standard LKAS 39

Sri Lanka Accounting Standard LKAS 39 Financial Instruments: Recognition and Measurement CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 39 FINANCIAL INSTRUMENTS: RECOGNITION AND MEASUREMENT paragraphs OBJECTIVE

Sri Lanka Accounting Standard LKAS 39 Financial Instruments: Recognition and Measurement CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 39 FINANCIAL INSTRUMENTS: RECOGNITION AND MEASUREMENT paragraphs OBJECTIVE

Total assets 214,589, ,246,479

CONSOLIDATED STATEMENT OF FINANCIAL POSITION As at December 31, and Notes ASSETS Cash and balances with SAMA 4 25,315,736 20,928,549 Due from banks and other financial institutions 5 3,914,504 4,438,656

CONSOLIDATED STATEMENT OF FINANCIAL POSITION As at December 31, and Notes ASSETS Cash and balances with SAMA 4 25,315,736 20,928,549 Due from banks and other financial institutions 5 3,914,504 4,438,656

Arab Banking Corporation (B.S.C.)

") INTERIM CONDENSED CONSOLIDATED FINANCIAL 30 SEPTEMBER 2018 (REVIEWED) INTERIM CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME Ninemonth period ended Reviewed Three months ended Nine months ended 30 September

INTERIM CONDENSED CONSOLIDATED FINANCIAL 30 SEPTEMBER 2018 (REVIEWED) INTERIM CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME Ninemonth period ended Reviewed Three months ended Nine months ended 30 September

Arab Banking Corporation (B.S.C.)

") INTERIM CONDENSED CONSOLIDATED FINANCIAL 31 MARCH 2018 (REVIEWED) INTERIM CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME Threemonth period ended All figures in US$ Million Reviewed Three months ended

INTERIM CONDENSED CONSOLIDATED FINANCIAL 31 MARCH 2018 (REVIEWED) INTERIM CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME Threemonth period ended All figures in US$ Million Reviewed Three months ended

Notes to the Consolidated Financial Statements (Amount in millions of Renminbi, unless otherwise stated)

") Notes to the Consolidated Financial Statements (Amount in millions of Renminbi, unless otherwise stated) I GENERAL INFORMATION AND PRINCIPAL ACTIVITIES Bank of China Limited (the Bank ), formerly known

Notes to the Consolidated Financial Statements (Amount in millions of Renminbi, unless otherwise stated) I GENERAL INFORMATION AND PRINCIPAL ACTIVITIES Bank of China Limited (the Bank ), formerly known

IFRS IN PRACTICE IFRS 9 Financial Instruments

IFRS IN PRACTICE 2018 IFRS 9 Financial Instruments 2 IFRS IN PRACTICE 2018 IFRS 9 FINANCIAL INSTRUMENTS IFRS IN PRACTICE 2018 IFRS 9 FINANCIAL INSTRUMENTS 3 TABLE OF CONTENTS 1. Introduction 5 2. Definitions

IFRS IN PRACTICE 2018 IFRS 9 Financial Instruments 2 IFRS IN PRACTICE 2018 IFRS 9 FINANCIAL INSTRUMENTS IFRS IN PRACTICE 2018 IFRS 9 FINANCIAL INSTRUMENTS 3 TABLE OF CONTENTS 1. Introduction 5 2. Definitions

Revised Standards on Financial Instruments