Math Computational Finance Barrier option pricing using Finite Difference Methods (FDM)

|

|

|

- Morgan Peters

- 6 years ago

- Views:

Transcription

1 . Math Computational Finance Barrier option pricing using Finite Difference Methods (FDM) Pratik Mehta pbmehta@eden.rutgers.edu Masters of Science in Mathematical Finance Department of Mathematics, Rutgers University This paper describes the implementation of a C++ program to calculate the value of a european style call option and a discretely sampled up-and-out barrier option on an underlying asset, given input parameters for stock price (s=100), strike price (k=110),volatility (v=30%), interest rate (r=5%), maturity (T=1 year), U = 120 knock out usingclosed form solution, and Finite difference method. We compare the results of all these methods. The underlying stock price is assumed to follow geometric brownian motion. [2]. I. INTRODUCTION In this assignment we are pricing a European style vanilla call option and discretely monitored barrier option (t = 252) using closed form solution, and Finite difference method. ds(t) = (rs(t)dt + σs(t)dw (t) (1) the solution to the above Stochastic Differential Equation is, S(T ) = S(0)e (r 1 2 σ2 )T +σw (T ) the payoff for the call option is, (2) (S(T ) k) + (3) We also price an up-and-out barrier option. This can be represented by, II. (S(T ) k) + 1 maxs(t)<u (4) VANILLA CALL : CLOSED FORM BLACK-SCHOLES-MERTON Here, K is the strike price and S(T ) is the terminal stock price at the payoff date. The price of the underlying at terminal time,t, is given by [3] S(T ) = S(0)e (r a 1 2 σ2 )T +σw (T ) (5) A closed form solution for the price of a European Call and Put is given by [3] and c(t, x) = xe at N(d + (T, x)) e rt KN(d (τ, x)) (6) p(t, x) = e rt KN( d (T, x)) xe at N( d + (τ, x)). (7) Here, N is the Normal Cumulative Distribution density and the parameters, d + and d are given by d + = d + σ T = 1 [log σ xk (r T ) ] σ2 T.(8) The closed form solution to the option is implemented in the file BlackScholesFormulas.cpp and the formula is given below The output is as follows, Closed form option price = (9) III. BARRIER OPTIONS Barrier options are path-dependent options, with payoffs that depend on the price of the underlying asset at expiration and whether or not the asset price crosses a barrier during the life of the option. There are two categories or types of Barrier options: knock-in and knock-out. Knock-in or in options are paid for up front, but you do not receive the option until the asset price crosses the barrier. This Knock-in can be represented by, (S(T ) k) + 1 max(s(t)) U (10) Knock-out or out options come into existence on the issue date but becomes worthless if the asset price hits the barrier before the expiration date. If the option is a knock-in (knock-out), a predetermined cash rebate may be paid at expiration if the option has not been knocked in (knocked-out) during its lifetime. The barrier monitoring frequency specifies how often the price is checked for a breach of the barrier. All of the analytical models have a flag to change the monitoring frequency where the default frequency is continuous. Up-and-out options are represented as (S(T ) k) + 1 S(t)<U (11)

2 2 The closed form solution to the up and out barrier option is implemented in the file ClosedFormUpOutCall.cpp and the formula is given below C up = C(t, S(t)) S(t)e d(t t) N(x 1 ) + (12) ke r(t t) N(x 1 σ T t) + (13) S(t)e d(t t) N(x 1 )( H S(t) )2λ (N(y) N( y)) (14) ke r(t t) N(x 1 ( H S(t) )2λ 2 (N( y) σ T t) (15) The output is as follows, IV. N( y 1 σ T t) (16) Closed f orm option price = (17) NUMERICAL SOLUTION TO PDE USING FINITE DIFFERENCE METHOD There are many cases where the PDE cannot be analytically solved or the solution is very tedious. In these cases we can easily approximate the solution using numerical methods like Finite difference. Finite Difference Method generally seeks to approximate the solution to some PDE. Generally, the statement of a problem has two parts. Conditions: a Partial Differential Equation (PDE), boundary conditions, constraints, and so on. Data: initial values, final values (e.g. a payout function), boundary values, and so on. The Black and Scholes formula to calculate the value of an option is derived by solving the Black-Scholes partial differential equation: f f + rs t S σ2 S 2 2 f = rf, (18) S2 We can approximate the above PDE using Forward/Backward/Central difference. and u t u(x, t + t) u(x, t) t, (19) 2 u u(x + x, t) 2u(x, t) + u(x x, t) x2 x 2, (20) We can write the Black Scholes PDE using Finite difference as V k+1 i = A k i Vi 1 k + (1 + Bi k )Vi k + Ci k Vi+1 k (21) A = 1 2 (σ2 i 2 (r d)i)δt (22) B = (σ 2 i 2 + r)δt (23) C = 1 2 (σ2 i 2 + (r d)i)δt (24) The algorithm to compute the finite difference solution is given below[6] Divide the solution space into 2D mesh (25) F or i = 0 to asstetsteps (26) S(i) = i assetsteps (27) V (i, 0) = CallP ayoff(s(i)) (28) Define A B and C (29) next i (30) F or k = 0 to timesteps (31) F or i = 0 to asstetsteps (32) V k+1 i = A k i Vi 1 k + (1 + Bi k )Vi k + Ci k Vi+1 k (33) next i (34) V (0, k + 1) = 0 (35) VI k = IδS Strike e ( rkδt) (36) next k (37) We use the above algorithm to price a call option, F inite Difference call option price = (38) To price the up-and-out barrier option, we have to do a couple of changes, The first change is that we have to reduce the number of asset steps so that the value becomes 0 for any price above U. And the second is the boundary condition, the upper boundary at S=120, the value of the option is forced to be 0. F inite Difference barrier option price = (39) V. ANSWER TO THE QUESTIONS Q1 We have used explicit finite difference and we found that when the time steps T=252 and Space intervals N=50, the value of the vanilla and barrier options are in agreement to the closed form solutions. But explicit FD method has some disadvantages. First of all, the method does not converge and is stable all the time. The convergence and stability depends on the value of T (Time intervals) and N (Space intervals). Also there is a dependence of δt and δs on each other. They cannot be independently varied.paul WIlmott shows that for convergence and stablity the following conditions should me met, and δs 2a b (40) δt 1 σ 2 I 2 (41)

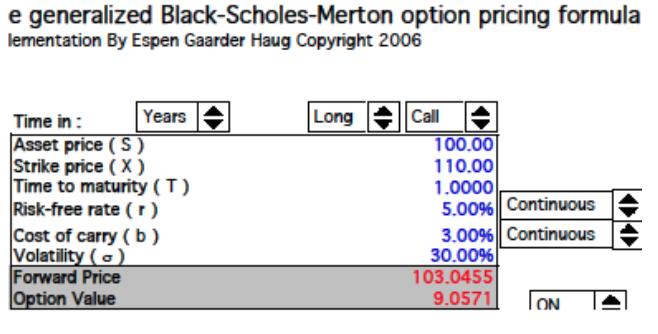

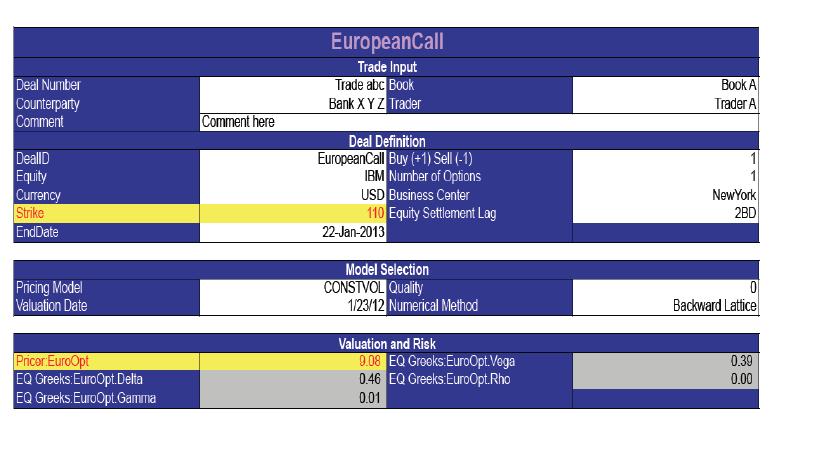

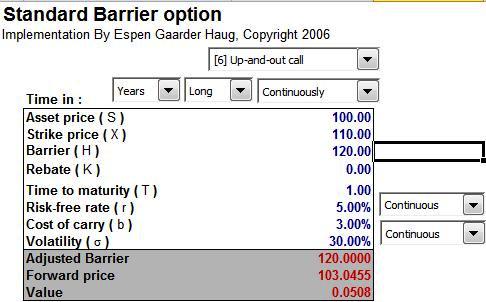

3 3 Using the above conditions we find that, δt 230 (42) We have tried a combination of step sizes to test robustness of the stability and convergence criteria. We calculated the option prices for various δt and δs. We varied δt from 100 to 500 and δs from 2 to 30. We find that the results blow up when δt is less than 200 (approx) and when δs is greater than 50. We have tabulated the results (below). Q2 If we vary S max, we also inadvertently change δs, if we increase S max without adjusting δs, we get inaccurate answers. Both of them will have to vary accordingly. In out C++ code, we varied S max and kept δs constant. We find that for δs = 4, S max 240 blows the answer. We have tabulated the results. VI. BENCHMARKING We have used many spreadsheet based models to benchmark our results. The summary go the benchmarking is given below and is also tabularised below. We have used Excel spreadsheets by Haug and Black and Numerix to price. The benchmarked results are in agreement with the results obtained from C++. The results are, N umerix option price vanilla = 9.08 (43) Numerix up in andout = 0.05 (44) Haug vanilla call = 9.05 (45) Haug up and out call = 0.05 (46)

4 4 TABLE I: Vanilla and Asian Call pricing using Methods for S(0)=100 and K=110 Option Closed Form Finite Difference Haug Numerix European Vanilla Call Barrier (Up-and-out) Call TABLE II: Effect of varying δs Strata size Vanilla Call Barrier call TABLE III: Effect of varying δt Strata size Vanilla Call Barrier call e TABLE IV: Effect of varying S max S max Vanilla Call Barrier call e

5 5

6 FIG. 2: Barrier 6

7 [1] wwwthep.physik.uni-mainz.de/ stefanw/download/lecture [2] M.S. Joshi, C++ design Patterns and Derivative Pricing, (Wiley 2008). [3] S.E. Shreve, Stochastic Calculus for Finance II Continuous Time Models, (Springer, 2004). [4] Wikipedia page for low discrepancy sequence [5] I M Sobol, USSR comp. Math [6] Jonathan Goodman,Courant Institute of Mathematical Science, NYU [7] ebert/teaching/lectures/552/ [8] rss.acs.unt.edu/rdoc/library/fexoticoptions [9] rss.acs.unt.edu/rdoc/library/fexoticoptions/latex/barrieroptions 7

Math Computational Finance Double barrier option pricing using Quasi Monte Carlo and Brownian Bridge methods

. Math 623 - Computational Finance Double barrier option pricing using Quasi Monte Carlo and Brownian Bridge methods Pratik Mehta pbmehta@eden.rutgers.edu Masters of Science in Mathematical Finance Department

. Math 623 - Computational Finance Double barrier option pricing using Quasi Monte Carlo and Brownian Bridge methods Pratik Mehta pbmehta@eden.rutgers.edu Masters of Science in Mathematical Finance Department

Math Computational Finance Option pricing using Brownian bridge and Stratified samlping

. Math 623 - Computational Finance Option pricing using Brownian bridge and Stratified samlping Pratik Mehta pbmehta@eden.rutgers.edu Masters of Science in Mathematical Finance Department of Mathematics,

. Math 623 - Computational Finance Option pricing using Brownian bridge and Stratified samlping Pratik Mehta pbmehta@eden.rutgers.edu Masters of Science in Mathematical Finance Department of Mathematics,

Math Option pricing using Quasi Monte Carlo simulation

. Math 623 - Option pricing using Quasi Monte Carlo simulation Pratik Mehta pbmehta@eden.rutgers.edu Masters of Science in Mathematical Finance Department of Mathematics, Rutgers University This paper

. Math 623 - Option pricing using Quasi Monte Carlo simulation Pratik Mehta pbmehta@eden.rutgers.edu Masters of Science in Mathematical Finance Department of Mathematics, Rutgers University This paper

Definition Pricing Risk management Second generation barrier options. Barrier Options. Arfima Financial Solutions

Arfima Financial Solutions Contents Definition 1 Definition 2 3 4 Contenido Definition 1 Definition 2 3 4 Definition Definition: A barrier option is an option on the underlying asset that is activated

Arfima Financial Solutions Contents Definition 1 Definition 2 3 4 Contenido Definition 1 Definition 2 3 4 Definition Definition: A barrier option is an option on the underlying asset that is activated

EFFICIENT MONTE CARLO ALGORITHM FOR PRICING BARRIER OPTIONS

Commun. Korean Math. Soc. 23 (2008), No. 2, pp. 285 294 EFFICIENT MONTE CARLO ALGORITHM FOR PRICING BARRIER OPTIONS Kyoung-Sook Moon Reprinted from the Communications of the Korean Mathematical Society

Commun. Korean Math. Soc. 23 (2008), No. 2, pp. 285 294 EFFICIENT MONTE CARLO ALGORITHM FOR PRICING BARRIER OPTIONS Kyoung-Sook Moon Reprinted from the Communications of the Korean Mathematical Society

MASM006 UNIVERSITY OF EXETER SCHOOL OF ENGINEERING, COMPUTER SCIENCE AND MATHEMATICS MATHEMATICAL SCIENCES FINANCIAL MATHEMATICS.

MASM006 UNIVERSITY OF EXETER SCHOOL OF ENGINEERING, COMPUTER SCIENCE AND MATHEMATICS MATHEMATICAL SCIENCES FINANCIAL MATHEMATICS May/June 2006 Time allowed: 2 HOURS. Examiner: Dr N.P. Byott This is a CLOSED

MASM006 UNIVERSITY OF EXETER SCHOOL OF ENGINEERING, COMPUTER SCIENCE AND MATHEMATICS MATHEMATICAL SCIENCES FINANCIAL MATHEMATICS May/June 2006 Time allowed: 2 HOURS. Examiner: Dr N.P. Byott This is a CLOSED

FE610 Stochastic Calculus for Financial Engineers. Stevens Institute of Technology

FE610 Stochastic Calculus for Financial Engineers Lecture 13. The Black-Scholes PDE Steve Yang Stevens Institute of Technology 04/25/2013 Outline 1 The Black-Scholes PDE 2 PDEs in Asset Pricing 3 Exotic

FE610 Stochastic Calculus for Financial Engineers Lecture 13. The Black-Scholes PDE Steve Yang Stevens Institute of Technology 04/25/2013 Outline 1 The Black-Scholes PDE 2 PDEs in Asset Pricing 3 Exotic

Assignment - Exotic options

Computational Finance, Fall 2014 1 (6) Institutionen för informationsteknologi Besöksadress: MIC, Polacksbacken Lägerhyddvägen 2 Postadress: Box 337 751 05 Uppsala Telefon: 018 471 0000 (växel) Telefax:

Computational Finance, Fall 2014 1 (6) Institutionen för informationsteknologi Besöksadress: MIC, Polacksbacken Lägerhyddvägen 2 Postadress: Box 337 751 05 Uppsala Telefon: 018 471 0000 (växel) Telefax:

NEWCASTLE UNIVERSITY SCHOOL OF MATHEMATICS, STATISTICS & PHYSICS SEMESTER 1 SPECIMEN 2 MAS3904. Stochastic Financial Modelling. Time allowed: 2 hours

NEWCASTLE UNIVERSITY SCHOOL OF MATHEMATICS, STATISTICS & PHYSICS SEMESTER 1 SPECIMEN 2 Stochastic Financial Modelling Time allowed: 2 hours Candidates should attempt all questions. Marks for each question

NEWCASTLE UNIVERSITY SCHOOL OF MATHEMATICS, STATISTICS & PHYSICS SEMESTER 1 SPECIMEN 2 Stochastic Financial Modelling Time allowed: 2 hours Candidates should attempt all questions. Marks for each question

The Black-Scholes Model

The Black-Scholes Model Liuren Wu Options Markets (Hull chapter: 12, 13, 14) Liuren Wu ( c ) The Black-Scholes Model colorhmoptions Markets 1 / 17 The Black-Scholes-Merton (BSM) model Black and Scholes

The Black-Scholes Model Liuren Wu Options Markets (Hull chapter: 12, 13, 14) Liuren Wu ( c ) The Black-Scholes Model colorhmoptions Markets 1 / 17 The Black-Scholes-Merton (BSM) model Black and Scholes

The Black-Scholes Equation

The Black-Scholes Equation MATH 472 Financial Mathematics J. Robert Buchanan 2018 Objectives In this lesson we will: derive the Black-Scholes partial differential equation using Itô s Lemma and no-arbitrage

The Black-Scholes Equation MATH 472 Financial Mathematics J. Robert Buchanan 2018 Objectives In this lesson we will: derive the Black-Scholes partial differential equation using Itô s Lemma and no-arbitrage

Lecture 15: Exotic Options: Barriers

Lecture 15: Exotic Options: Barriers Dr. Hanqing Jin Mathematical Institute University of Oxford Lecture 15: Exotic Options: Barriers p. 1/10 Barrier features For any options with payoff ξ at exercise

Lecture 15: Exotic Options: Barriers Dr. Hanqing Jin Mathematical Institute University of Oxford Lecture 15: Exotic Options: Barriers p. 1/10 Barrier features For any options with payoff ξ at exercise

Option Valuation with Sinusoidal Heteroskedasticity

Option Valuation with Sinusoidal Heteroskedasticity Caleb Magruder June 26, 2009 1 Black-Scholes-Merton Option Pricing Ito drift-diffusion process (1) can be used to derive the Black Scholes formula (2).

Option Valuation with Sinusoidal Heteroskedasticity Caleb Magruder June 26, 2009 1 Black-Scholes-Merton Option Pricing Ito drift-diffusion process (1) can be used to derive the Black Scholes formula (2).

Queens College, CUNY, Department of Computer Science Computational Finance CSCI 365 / 765 Fall 2017 Instructor: Dr. Sateesh Mane.

Queens College, CUNY, Department of Computer Science Computational Finance CSCI 365 / 765 Fall 217 Instructor: Dr. Sateesh Mane c Sateesh R. Mane 217 13 Lecture 13 November 15, 217 Derivation of the Black-Scholes-Merton

Queens College, CUNY, Department of Computer Science Computational Finance CSCI 365 / 765 Fall 217 Instructor: Dr. Sateesh Mane c Sateesh R. Mane 217 13 Lecture 13 November 15, 217 Derivation of the Black-Scholes-Merton

Financial derivatives exam Winter term 2014/2015

Financial derivatives exam Winter term 2014/2015 Problem 1: [max. 13 points] Determine whether the following assertions are true or false. Write your answers, without explanations. Grading: correct answer

Financial derivatives exam Winter term 2014/2015 Problem 1: [max. 13 points] Determine whether the following assertions are true or false. Write your answers, without explanations. Grading: correct answer

The Black-Scholes Model

The Black-Scholes Model Liuren Wu Options Markets Liuren Wu ( c ) The Black-Merton-Scholes Model colorhmoptions Markets 1 / 18 The Black-Merton-Scholes-Merton (BMS) model Black and Scholes (1973) and Merton

The Black-Scholes Model Liuren Wu Options Markets Liuren Wu ( c ) The Black-Merton-Scholes Model colorhmoptions Markets 1 / 18 The Black-Merton-Scholes-Merton (BMS) model Black and Scholes (1973) and Merton

Stochastic Differential Equations in Finance and Monte Carlo Simulations

Stochastic Differential Equations in Finance and Department of Statistics and Modelling Science University of Strathclyde Glasgow, G1 1XH China 2009 Outline Stochastic Modelling in Asset Prices 1 Stochastic

Stochastic Differential Equations in Finance and Department of Statistics and Modelling Science University of Strathclyde Glasgow, G1 1XH China 2009 Outline Stochastic Modelling in Asset Prices 1 Stochastic

Pricing Barrier Options under Local Volatility

Abstract Pricing Barrier Options under Local Volatility Artur Sepp Mail: artursepp@hotmail.com, Web: www.hot.ee/seppar 16 November 2002 We study pricing under the local volatility. Our research is mainly

Abstract Pricing Barrier Options under Local Volatility Artur Sepp Mail: artursepp@hotmail.com, Web: www.hot.ee/seppar 16 November 2002 We study pricing under the local volatility. Our research is mainly

4. Black-Scholes Models and PDEs. Math6911 S08, HM Zhu

4. Black-Scholes Models and PDEs Math6911 S08, HM Zhu References 1. Chapter 13, J. Hull. Section.6, P. Brandimarte Outline Derivation of Black-Scholes equation Black-Scholes models for options Implied

4. Black-Scholes Models and PDEs Math6911 S08, HM Zhu References 1. Chapter 13, J. Hull. Section.6, P. Brandimarte Outline Derivation of Black-Scholes equation Black-Scholes models for options Implied

Math 623 (IOE 623), Winter 2008: Final exam

, Winter 2008: Final exam") Math 623 (IOE 623), Winter 2008: Final exam Name: Student ID: This is a closed book exam. You may bring up to ten one sided A4 pages of notes to the exam. You may also use a calculator but not its memory

Math 623 (IOE 623), Winter 2008: Final exam Name: Student ID: This is a closed book exam. You may bring up to ten one sided A4 pages of notes to the exam. You may also use a calculator but not its memory

Options. An Undergraduate Introduction to Financial Mathematics. J. Robert Buchanan. J. Robert Buchanan Options

Options An Undergraduate Introduction to Financial Mathematics J. Robert Buchanan 2014 Definitions and Terminology Definition An option is the right, but not the obligation, to buy or sell a security such

Options An Undergraduate Introduction to Financial Mathematics J. Robert Buchanan 2014 Definitions and Terminology Definition An option is the right, but not the obligation, to buy or sell a security such

MÄLARDALENS HÖGSKOLA

MÄLARDALENS HÖGSKOLA A Monte-Carlo calculation for Barrier options Using Python Mwangota Lutufyo and Omotesho Latifat oyinkansola 2016-10-19 MMA707 Analytical Finance I: Lecturer: Jan Roman Division of

MÄLARDALENS HÖGSKOLA A Monte-Carlo calculation for Barrier options Using Python Mwangota Lutufyo and Omotesho Latifat oyinkansola 2016-10-19 MMA707 Analytical Finance I: Lecturer: Jan Roman Division of

Financial Derivatives Section 5

Financial Derivatives Section 5 The Black and Scholes Model Michail Anthropelos anthropel@unipi.gr http://web.xrh.unipi.gr/faculty/anthropelos/ University of Piraeus Spring 2018 M. Anthropelos (Un. of

Financial Derivatives Section 5 The Black and Scholes Model Michail Anthropelos anthropel@unipi.gr http://web.xrh.unipi.gr/faculty/anthropelos/ University of Piraeus Spring 2018 M. Anthropelos (Un. of

Merton s Jump Diffusion Model. David Bonnemort, Yunhye Chu, Cory Steffen, Carl Tams

Merton s Jump Diffusion Model David Bonnemort, Yunhye Chu, Cory Steffen, Carl Tams Outline Background The Problem Research Summary & future direction Background Terms Option: (Call/Put) is a derivative

Merton s Jump Diffusion Model David Bonnemort, Yunhye Chu, Cory Steffen, Carl Tams Outline Background The Problem Research Summary & future direction Background Terms Option: (Call/Put) is a derivative

A Moment Matching Approach To The Valuation Of A Volume Weighted Average Price Option

A Moment Matching Approach To The Valuation Of A Volume Weighted Average Price Option Antony Stace Department of Mathematics and MASCOS University of Queensland 15th October 2004 AUSTRALIAN RESEARCH COUNCIL

A Moment Matching Approach To The Valuation Of A Volume Weighted Average Price Option Antony Stace Department of Mathematics and MASCOS University of Queensland 15th October 2004 AUSTRALIAN RESEARCH COUNCIL

CS 774 Project: Fall 2009 Version: November 27, 2009

CS 774 Project: Fall 2009 Version: November 27, 2009 Instructors: Peter Forsyth, paforsyt@uwaterloo.ca Office Hours: Tues: 4:00-5:00; Thurs: 11:00-12:00 Lectures:MWF 3:30-4:20 MC2036 Office: DC3631 CS

CS 774 Project: Fall 2009 Version: November 27, 2009 Instructors: Peter Forsyth, paforsyt@uwaterloo.ca Office Hours: Tues: 4:00-5:00; Thurs: 11:00-12:00 Lectures:MWF 3:30-4:20 MC2036 Office: DC3631 CS

CHAPTER 10 OPTION PRICING - II. Derivatives and Risk Management By Rajiv Srivastava. Copyright Oxford University Press

CHAPTER 10 OPTION PRICING - II Options Pricing II Intrinsic Value and Time Value Boundary Conditions for Option Pricing Arbitrage Based Relationship for Option Pricing Put Call Parity 2 Binomial Option

CHAPTER 10 OPTION PRICING - II Options Pricing II Intrinsic Value and Time Value Boundary Conditions for Option Pricing Arbitrage Based Relationship for Option Pricing Put Call Parity 2 Binomial Option

- 1 - **** d(lns) = (µ (1/2)σ 2 )dt + σdw t

= (µ (1/2)σ 2 )dt + σdw t") - 1 - **** These answers indicate the solutions to the 2014 exam questions. Obviously you should plot graphs where I have simply described the key features. It is important when plotting graphs to label

- 1 - **** These answers indicate the solutions to the 2014 exam questions. Obviously you should plot graphs where I have simply described the key features. It is important when plotting graphs to label

2 f. f t S 2. Delta measures the sensitivityof the portfolio value to changes in the price of the underlying

Sensitivity analysis Simulating the Greeks Meet the Greeks he value of a derivative on a single underlying asset depends upon the current asset price S and its volatility Σ, the risk-free interest rate

Sensitivity analysis Simulating the Greeks Meet the Greeks he value of a derivative on a single underlying asset depends upon the current asset price S and its volatility Σ, the risk-free interest rate

Queens College, CUNY, Department of Computer Science Computational Finance CSCI 365 / 765 Fall 2017 Instructor: Dr. Sateesh Mane.

Queens College, CUNY, Department of Computer Science Computational Finance CSCI 365 / 765 Fall 2017 Instructor: Dr. Sateesh Mane c Sateesh R. Mane 2017 14 Lecture 14 November 15, 2017 Derivation of the

Queens College, CUNY, Department of Computer Science Computational Finance CSCI 365 / 765 Fall 2017 Instructor: Dr. Sateesh Mane c Sateesh R. Mane 2017 14 Lecture 14 November 15, 2017 Derivation of the

AN IMPROVED BINOMIAL METHOD FOR PRICING ASIAN OPTIONS

Commun. Korean Math. Soc. 28 (2013), No. 2, pp. 397 406 http://dx.doi.org/10.4134/ckms.2013.28.2.397 AN IMPROVED BINOMIAL METHOD FOR PRICING ASIAN OPTIONS Kyoung-Sook Moon and Hongjoong Kim Abstract. We

Commun. Korean Math. Soc. 28 (2013), No. 2, pp. 397 406 http://dx.doi.org/10.4134/ckms.2013.28.2.397 AN IMPROVED BINOMIAL METHOD FOR PRICING ASIAN OPTIONS Kyoung-Sook Moon and Hongjoong Kim Abstract. We

King s College London

King s College London University Of London This paper is part of an examination of the College counting towards the award of a degree. Examinations are governed by the College Regulations under the authority

King s College London University Of London This paper is part of an examination of the College counting towards the award of a degree. Examinations are governed by the College Regulations under the authority

A Continuity Correction under Jump-Diffusion Models with Applications in Finance

A Continuity Correction under Jump-Diffusion Models with Applications in Finance Cheng-Der Fuh 1, Sheng-Feng Luo 2 and Ju-Fang Yen 3 1 Institute of Statistical Science, Academia Sinica, and Graduate Institute

A Continuity Correction under Jump-Diffusion Models with Applications in Finance Cheng-Der Fuh 1, Sheng-Feng Luo 2 and Ju-Fang Yen 3 1 Institute of Statistical Science, Academia Sinica, and Graduate Institute

No ANALYTIC AMERICAN OPTION PRICING AND APPLICATIONS. By A. Sbuelz. July 2003 ISSN

No. 23 64 ANALYTIC AMERICAN OPTION PRICING AND APPLICATIONS By A. Sbuelz July 23 ISSN 924-781 Analytic American Option Pricing and Applications Alessandro Sbuelz First Version: June 3, 23 This Version:

No. 23 64 ANALYTIC AMERICAN OPTION PRICING AND APPLICATIONS By A. Sbuelz July 23 ISSN 924-781 Analytic American Option Pricing and Applications Alessandro Sbuelz First Version: June 3, 23 This Version:

FIN FINANCIAL INSTRUMENTS SPRING 2008

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 The Greeks Introduction We have studied how to price an option using the Black-Scholes formula. Now we wish to consider how the option price changes, either

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 The Greeks Introduction We have studied how to price an option using the Black-Scholes formula. Now we wish to consider how the option price changes, either

Risk Neutral Pricing Black-Scholes Formula Lecture 19. Dr. Vasily Strela (Morgan Stanley and MIT)

") Risk Neutral Pricing Black-Scholes Formula Lecture 19 Dr. Vasily Strela (Morgan Stanley and MIT) Risk Neutral Valuation: Two-Horse Race Example One horse has 20% chance to win another has 80% chance $10000

Risk Neutral Pricing Black-Scholes Formula Lecture 19 Dr. Vasily Strela (Morgan Stanley and MIT) Risk Neutral Valuation: Two-Horse Race Example One horse has 20% chance to win another has 80% chance $10000

Homework Set 6 Solutions

MATH 667-010 Introduction to Mathematical Finance Prof. D. A. Edwards Due: Apr. 11, 018 P Homework Set 6 Solutions K z K + z S 1. The payoff diagram shown is for a strangle. Denote its option value by

MATH 667-010 Introduction to Mathematical Finance Prof. D. A. Edwards Due: Apr. 11, 018 P Homework Set 6 Solutions K z K + z S 1. The payoff diagram shown is for a strangle. Denote its option value by

MATH4143: Scientific Computations for Finance Applications Final exam Time: 9:00 am - 12:00 noon, April 18, Student Name (print):

:") MATH4143 Page 1 of 17 Winter 2007 MATH4143: Scientific Computations for Finance Applications Final exam Time: 9:00 am - 12:00 noon, April 18, 2007 Student Name (print): Student Signature: Student ID: Question

MATH4143 Page 1 of 17 Winter 2007 MATH4143: Scientific Computations for Finance Applications Final exam Time: 9:00 am - 12:00 noon, April 18, 2007 Student Name (print): Student Signature: Student ID: Question

MATH3075/3975 FINANCIAL MATHEMATICS TUTORIAL PROBLEMS

MATH307/37 FINANCIAL MATHEMATICS TUTORIAL PROBLEMS School of Mathematics and Statistics Semester, 04 Tutorial problems should be used to test your mathematical skills and understanding of the lecture material.

MATH307/37 FINANCIAL MATHEMATICS TUTORIAL PROBLEMS School of Mathematics and Statistics Semester, 04 Tutorial problems should be used to test your mathematical skills and understanding of the lecture material.

The Black-Scholes Model

IEOR E4706: Foundations of Financial Engineering c 2016 by Martin Haugh The Black-Scholes Model In these notes we will use Itô s Lemma and a replicating argument to derive the famous Black-Scholes formula

IEOR E4706: Foundations of Financial Engineering c 2016 by Martin Haugh The Black-Scholes Model In these notes we will use Itô s Lemma and a replicating argument to derive the famous Black-Scholes formula

Lecture 11: Ito Calculus. Tuesday, October 23, 12

Lecture 11: Ito Calculus Continuous time models We start with the model from Chapter 3 log S j log S j 1 = µ t + p tz j Sum it over j: log S N log S 0 = NX µ t + NX p tzj j=1 j=1 Can we take the limit

Lecture 11: Ito Calculus Continuous time models We start with the model from Chapter 3 log S j log S j 1 = µ t + p tz j Sum it over j: log S N log S 0 = NX µ t + NX p tzj j=1 j=1 Can we take the limit

FINITE DIFFERENCE METHODS

FINITE DIFFERENCE METHODS School of Mathematics 2013 OUTLINE Review 1 REVIEW Last time Today s Lecture OUTLINE Review 1 REVIEW Last time Today s Lecture 2 DISCRETISING THE PROBLEM Finite-difference approximations

FINITE DIFFERENCE METHODS School of Mathematics 2013 OUTLINE Review 1 REVIEW Last time Today s Lecture OUTLINE Review 1 REVIEW Last time Today s Lecture 2 DISCRETISING THE PROBLEM Finite-difference approximations

Math489/889 Stochastic Processes and Advanced Mathematical Finance Solutions to Practice Problems

Math489/889 Stochastic Processes and Advanced Mathematical Finance Solutions to Practice Problems Steve Dunbar No Due Date: Practice Only. Find the mode (the value of the independent variable with the

Math489/889 Stochastic Processes and Advanced Mathematical Finance Solutions to Practice Problems Steve Dunbar No Due Date: Practice Only. Find the mode (the value of the independent variable with the

1.1 Basic Financial Derivatives: Forward Contracts and Options

Chapter 1 Preliminaries 1.1 Basic Financial Derivatives: Forward Contracts and Options A derivative is a financial instrument whose value depends on the values of other, more basic underlying variables

Chapter 1 Preliminaries 1.1 Basic Financial Derivatives: Forward Contracts and Options A derivative is a financial instrument whose value depends on the values of other, more basic underlying variables

Computational Finance

Path Dependent Options Computational Finance School of Mathematics 2018 The Random Walk One of the main assumption of the Black-Scholes framework is that the underlying stock price follows a random walk

Path Dependent Options Computational Finance School of Mathematics 2018 The Random Walk One of the main assumption of the Black-Scholes framework is that the underlying stock price follows a random walk

Numerical schemes for SDEs

Lecture 5 Numerical schemes for SDEs Lecture Notes by Jan Palczewski Computational Finance p. 1 A Stochastic Differential Equation (SDE) is an object of the following type dx t = a(t,x t )dt + b(t,x t

Lecture 5 Numerical schemes for SDEs Lecture Notes by Jan Palczewski Computational Finance p. 1 A Stochastic Differential Equation (SDE) is an object of the following type dx t = a(t,x t )dt + b(t,x t

Monte Carlo Methods for Uncertainty Quantification

Monte Carlo Methods for Uncertainty Quantification Mike Giles Mathematical Institute, University of Oxford Contemporary Numerical Techniques Mike Giles (Oxford) Monte Carlo methods 2 1 / 24 Lecture outline

Monte Carlo Methods for Uncertainty Quantification Mike Giles Mathematical Institute, University of Oxford Contemporary Numerical Techniques Mike Giles (Oxford) Monte Carlo methods 2 1 / 24 Lecture outline

Valuation of Asian Option. Qi An Jingjing Guo

Valuation of Asian Option Qi An Jingjing Guo CONTENT Asian option Pricing Monte Carlo simulation Conclusion ASIAN OPTION Definition of Asian option always emphasizes the gist that the payoff depends on

Valuation of Asian Option Qi An Jingjing Guo CONTENT Asian option Pricing Monte Carlo simulation Conclusion ASIAN OPTION Definition of Asian option always emphasizes the gist that the payoff depends on

Lecture 4. Finite difference and finite element methods

Finite difference and finite element methods Lecture 4 Outline Black-Scholes equation From expectation to PDE Goal: compute the value of European option with payoff g which is the conditional expectation

Finite difference and finite element methods Lecture 4 Outline Black-Scholes equation From expectation to PDE Goal: compute the value of European option with payoff g which is the conditional expectation

Analysis of the sensitivity to discrete dividends : A new approach for pricing vanillas

Analysis of the sensitivity to discrete dividends : A new approach for pricing vanillas Arnaud Gocsei, Fouad Sahel 5 May 2010 Abstract The incorporation of a dividend yield in the classical option pricing

Analysis of the sensitivity to discrete dividends : A new approach for pricing vanillas Arnaud Gocsei, Fouad Sahel 5 May 2010 Abstract The incorporation of a dividend yield in the classical option pricing

American Foreign Exchange Options and some Continuity Estimates of the Optimal Exercise Boundary with respect to Volatility

American Foreign Exchange Options and some Continuity Estimates of the Optimal Exercise Boundary with respect to Volatility Nasir Rehman Allam Iqbal Open University Islamabad, Pakistan. Outline Mathematical

American Foreign Exchange Options and some Continuity Estimates of the Optimal Exercise Boundary with respect to Volatility Nasir Rehman Allam Iqbal Open University Islamabad, Pakistan. Outline Mathematical

1 The continuous time limit

Derivative Securities, Courant Institute, Fall 2008 http://www.math.nyu.edu/faculty/goodman/teaching/derivsec08/index.html Jonathan Goodman and Keith Lewis Supplementary notes and comments, Section 3 1

Derivative Securities, Courant Institute, Fall 2008 http://www.math.nyu.edu/faculty/goodman/teaching/derivsec08/index.html Jonathan Goodman and Keith Lewis Supplementary notes and comments, Section 3 1

Lecture 8: The Black-Scholes theory

Lecture 8: The Black-Scholes theory Dr. Roman V Belavkin MSO4112 Contents 1 Geometric Brownian motion 1 2 The Black-Scholes pricing 2 3 The Black-Scholes equation 3 References 5 1 Geometric Brownian motion

Lecture 8: The Black-Scholes theory Dr. Roman V Belavkin MSO4112 Contents 1 Geometric Brownian motion 1 2 The Black-Scholes pricing 2 3 The Black-Scholes equation 3 References 5 1 Geometric Brownian motion

An Asymptotic Expansion Formula for Up-and-Out Barrier Option Price under Stochastic Volatility Model

CIRJE-F-873 An Asymptotic Expansion Formula for Up-and-Out Option Price under Stochastic Volatility Model Takashi Kato Osaka University Akihiko Takahashi University of Tokyo Toshihiro Yamada Graduate School

CIRJE-F-873 An Asymptotic Expansion Formula for Up-and-Out Option Price under Stochastic Volatility Model Takashi Kato Osaka University Akihiko Takahashi University of Tokyo Toshihiro Yamada Graduate School

1 Dynamics, initial values, final values

Derivative Securities, Courant Institute, Fall 008 http://www.math.nyu.edu/faculty/goodman/teaching/derivsec08/index.html Jonathan Goodman and Keith Lewis Supplementary notes and comments, Section 8 1

Derivative Securities, Courant Institute, Fall 008 http://www.math.nyu.edu/faculty/goodman/teaching/derivsec08/index.html Jonathan Goodman and Keith Lewis Supplementary notes and comments, Section 8 1

MATH6911: Numerical Methods in Finance. Final exam Time: 2:00pm - 5:00pm, April 11, Student Name (print): Student Signature: Student ID:

: Student Signature: Student ID:") MATH6911 Page 1 of 16 Winter 2007 MATH6911: Numerical Methods in Finance Final exam Time: 2:00pm - 5:00pm, April 11, 2007 Student Name (print): Student Signature: Student ID: Question Full Mark Mark 1

MATH6911 Page 1 of 16 Winter 2007 MATH6911: Numerical Methods in Finance Final exam Time: 2:00pm - 5:00pm, April 11, 2007 Student Name (print): Student Signature: Student ID: Question Full Mark Mark 1

Stochastic Modelling in Finance

in Finance Department of Mathematics and Statistics University of Strathclyde Glasgow, G1 1XH April 2010 Outline and Probability 1 and Probability 2 Linear modelling Nonlinear modelling 3 The Black Scholes

in Finance Department of Mathematics and Statistics University of Strathclyde Glasgow, G1 1XH April 2010 Outline and Probability 1 and Probability 2 Linear modelling Nonlinear modelling 3 The Black Scholes

Computational Finance Finite Difference Methods

Explicit finite difference method Computational Finance Finite Difference Methods School of Mathematics 2018 Today s Lecture We now introduce the final numerical scheme which is related to the PDE solution.

Explicit finite difference method Computational Finance Finite Difference Methods School of Mathematics 2018 Today s Lecture We now introduce the final numerical scheme which is related to the PDE solution.

A Study on Numerical Solution of Black-Scholes Model

Journal of Mathematical Finance, 8, 8, 37-38 http://www.scirp.org/journal/jmf ISSN Online: 6-44 ISSN Print: 6-434 A Study on Numerical Solution of Black-Scholes Model Md. Nurul Anwar,*, Laek Sazzad Andallah

Journal of Mathematical Finance, 8, 8, 37-38 http://www.scirp.org/journal/jmf ISSN Online: 6-44 ISSN Print: 6-434 A Study on Numerical Solution of Black-Scholes Model Md. Nurul Anwar,*, Laek Sazzad Andallah

Evaluation of Asian option by using RBF approximation

Boundary Elements and Other Mesh Reduction Methods XXVIII 33 Evaluation of Asian option by using RBF approximation E. Kita, Y. Goto, F. Zhai & K. Shen Graduate School of Information Sciences, Nagoya University,

Boundary Elements and Other Mesh Reduction Methods XXVIII 33 Evaluation of Asian option by using RBF approximation E. Kita, Y. Goto, F. Zhai & K. Shen Graduate School of Information Sciences, Nagoya University,

Numerical Methods in Option Pricing (Part III)

") Numerical Methods in Option Pricing (Part III) E. Explicit Finite Differences. Use of the Forward, Central, and Symmetric Central a. In order to obtain an explicit solution for the price of the derivative,

Numerical Methods in Option Pricing (Part III) E. Explicit Finite Differences. Use of the Forward, Central, and Symmetric Central a. In order to obtain an explicit solution for the price of the derivative,

Module 10:Application of stochastic processes in areas like finance Lecture 36:Black-Scholes Model. Stochastic Differential Equation.

Stochastic Differential Equation Consider. Moreover partition the interval into and define, where. Now by Rieman Integral we know that, where. Moreover. Using the fundamentals mentioned above we can easily

Stochastic Differential Equation Consider. Moreover partition the interval into and define, where. Now by Rieman Integral we know that, where. Moreover. Using the fundamentals mentioned above we can easily

Journal of Mathematical Analysis and Applications

J Math Anal Appl 389 (01 968 978 Contents lists available at SciVerse Scienceirect Journal of Mathematical Analysis and Applications wwwelseviercom/locate/jmaa Cross a barrier to reach barrier options

J Math Anal Appl 389 (01 968 978 Contents lists available at SciVerse Scienceirect Journal of Mathematical Analysis and Applications wwwelseviercom/locate/jmaa Cross a barrier to reach barrier options

The Black-Scholes PDE from Scratch

The Black-Scholes PDE from Scratch chris bemis November 27, 2006 0-0 Goal: Derive the Black-Scholes PDE To do this, we will need to: Come up with some dynamics for the stock returns Discuss Brownian motion

The Black-Scholes PDE from Scratch chris bemis November 27, 2006 0-0 Goal: Derive the Black-Scholes PDE To do this, we will need to: Come up with some dynamics for the stock returns Discuss Brownian motion

Practical Hedging: From Theory to Practice. OSU Financial Mathematics Seminar May 5, 2008

Practical Hedging: From Theory to Practice OSU Financial Mathematics Seminar May 5, 008 Background Dynamic replication is a risk management technique used to mitigate market risk We hope to spend a certain

Practical Hedging: From Theory to Practice OSU Financial Mathematics Seminar May 5, 008 Background Dynamic replication is a risk management technique used to mitigate market risk We hope to spend a certain

King s College London

King s College London University Of London This paper is part of an examination of the College counting towards the award of a degree. Examinations are governed by the College Regulations under the authority

King s College London University Of London This paper is part of an examination of the College counting towards the award of a degree. Examinations are governed by the College Regulations under the authority

Economathematics. Problem Sheet 1. Zbigniew Palmowski. Ws 2 dw s = 1 t

Economathematics Problem Sheet 1 Zbigniew Palmowski 1. Calculate Ee X where X is a gaussian random variable with mean µ and volatility σ >.. Verify that where W is a Wiener process. Ws dw s = 1 3 W t 3

Economathematics Problem Sheet 1 Zbigniew Palmowski 1. Calculate Ee X where X is a gaussian random variable with mean µ and volatility σ >.. Verify that where W is a Wiener process. Ws dw s = 1 3 W t 3

Chapter 9 - Mechanics of Options Markets

Chapter 9 - Mechanics of Options Markets Types of options Option positions and profit/loss diagrams Underlying assets Specifications Trading options Margins Taxation Warrants, employee stock options, and

Chapter 9 - Mechanics of Options Markets Types of options Option positions and profit/loss diagrams Underlying assets Specifications Trading options Margins Taxation Warrants, employee stock options, and

2.1 Mathematical Basis: Risk-Neutral Pricing

Chapter Monte-Carlo Simulation.1 Mathematical Basis: Risk-Neutral Pricing Suppose that F T is the payoff at T for a European-type derivative f. Then the price at times t before T is given by f t = e r(t

Chapter Monte-Carlo Simulation.1 Mathematical Basis: Risk-Neutral Pricing Suppose that F T is the payoff at T for a European-type derivative f. Then the price at times t before T is given by f t = e r(t

Valuing Stock Options: The Black-Scholes-Merton Model. Chapter 13

Valuing Stock Options: The Black-Scholes-Merton Model Chapter 13 1 The Black-Scholes-Merton Random Walk Assumption l Consider a stock whose price is S l In a short period of time of length t the return

Valuing Stock Options: The Black-Scholes-Merton Model Chapter 13 1 The Black-Scholes-Merton Random Walk Assumption l Consider a stock whose price is S l In a short period of time of length t the return

Computer Exercise 2 Simulation

Lund University with Lund Institute of Technology Valuation of Derivative Assets Centre for Mathematical Sciences, Mathematical Statistics Spring 2010 Computer Exercise 2 Simulation This lab deals with

Lund University with Lund Institute of Technology Valuation of Derivative Assets Centre for Mathematical Sciences, Mathematical Statistics Spring 2010 Computer Exercise 2 Simulation This lab deals with

Math 416/516: Stochastic Simulation

Math 416/516: Stochastic Simulation Haijun Li lih@math.wsu.edu Department of Mathematics Washington State University Week 13 Haijun Li Math 416/516: Stochastic Simulation Week 13 1 / 28 Outline 1 Simulation

Math 416/516: Stochastic Simulation Haijun Li lih@math.wsu.edu Department of Mathematics Washington State University Week 13 Haijun Li Math 416/516: Stochastic Simulation Week 13 1 / 28 Outline 1 Simulation

MASSACHUSETTS INSTITUTE OF TECHNOLOGY 6.265/15.070J Fall 2013 Lecture 19 11/20/2013. Applications of Ito calculus to finance

MASSACHUSETTS INSTITUTE OF TECHNOLOGY 6.265/15.7J Fall 213 Lecture 19 11/2/213 Applications of Ito calculus to finance Content. 1. Trading strategies 2. Black-Scholes option pricing formula 1 Security

MASSACHUSETTS INSTITUTE OF TECHNOLOGY 6.265/15.7J Fall 213 Lecture 19 11/2/213 Applications of Ito calculus to finance Content. 1. Trading strategies 2. Black-Scholes option pricing formula 1 Security

The Merton Model. A Structural Approach to Default Prediction. Agenda. Idea. Merton Model. The iterative approach. Example: Enron

The Merton Model A Structural Approach to Default Prediction Agenda Idea Merton Model The iterative approach Example: Enron A solution using equity values and equity volatility Example: Enron 2 1 Idea

The Merton Model A Structural Approach to Default Prediction Agenda Idea Merton Model The iterative approach Example: Enron A solution using equity values and equity volatility Example: Enron 2 1 Idea

Valuation of Equity / FX Instruments

Technical Paper: Valuation of Equity / FX Instruments MathConsult GmbH Altenberger Straße 69 A-4040 Linz, Austria 14 th October, 2009 1 Vanilla Equity Option 1.1 Introduction A vanilla equity option is

Technical Paper: Valuation of Equity / FX Instruments MathConsult GmbH Altenberger Straße 69 A-4040 Linz, Austria 14 th October, 2009 1 Vanilla Equity Option 1.1 Introduction A vanilla equity option is

Monte Carlo Simulations

Monte Carlo Simulations Lecture 1 December 7, 2014 Outline Monte Carlo Methods Monte Carlo methods simulate the random behavior underlying the financial models Remember: When pricing you must simulate

Monte Carlo Simulations Lecture 1 December 7, 2014 Outline Monte Carlo Methods Monte Carlo methods simulate the random behavior underlying the financial models Remember: When pricing you must simulate

PDE Methods for the Maximum Drawdown

PDE Methods for the Maximum Drawdown Libor Pospisil, Jan Vecer Columbia University, Department of Statistics, New York, NY 127, USA April 1, 28 Abstract Maximum drawdown is a risk measure that plays an

PDE Methods for the Maximum Drawdown Libor Pospisil, Jan Vecer Columbia University, Department of Statistics, New York, NY 127, USA April 1, 28 Abstract Maximum drawdown is a risk measure that plays an

Basic Concepts in Mathematical Finance

Chapter 1 Basic Concepts in Mathematical Finance In this chapter, we give an overview of basic concepts in mathematical finance theory, and then explain those concepts in very simple cases, namely in the

Chapter 1 Basic Concepts in Mathematical Finance In this chapter, we give an overview of basic concepts in mathematical finance theory, and then explain those concepts in very simple cases, namely in the

Aspects of Financial Mathematics:

Aspects of Financial Mathematics: Options, Derivatives, Arbitrage, and the Black-Scholes Pricing Formula J. Robert Buchanan Millersville University of Pennsylvania email: Bob.Buchanan@millersville.edu

Aspects of Financial Mathematics: Options, Derivatives, Arbitrage, and the Black-Scholes Pricing Formula J. Robert Buchanan Millersville University of Pennsylvania email: Bob.Buchanan@millersville.edu

Queens College, CUNY, Department of Computer Science Computational Finance CSCI 365 / 765 Spring 2018 Instructor: Dr. Sateesh Mane.

Queens College, CUNY, Department of Computer Science Computational Finance CSCI 365 / 765 Spring 218 Instructor: Dr. Sateesh Mane c Sateesh R. Mane 218 19 Lecture 19 May 12, 218 Exotic options The term

Queens College, CUNY, Department of Computer Science Computational Finance CSCI 365 / 765 Spring 218 Instructor: Dr. Sateesh Mane c Sateesh R. Mane 218 19 Lecture 19 May 12, 218 Exotic options The term

AN OPERATOR SPLITTING METHOD FOR PRICING THE ELS OPTION

J. KSIAM Vol.14, No.3, 175 187, 21 AN OPERATOR SPLITTING METHOD FOR PRICING THE ELS OPTION DARAE JEONG, IN-SUK WEE, AND JUNSEOK KIM DEPARTMENT OF MATHEMATICS, KOREA UNIVERSITY, SEOUL 136-71, KOREA E-mail

J. KSIAM Vol.14, No.3, 175 187, 21 AN OPERATOR SPLITTING METHOD FOR PRICING THE ELS OPTION DARAE JEONG, IN-SUK WEE, AND JUNSEOK KIM DEPARTMENT OF MATHEMATICS, KOREA UNIVERSITY, SEOUL 136-71, KOREA E-mail

Hedging Credit Derivatives in Intensity Based Models

Hedging Credit Derivatives in Intensity Based Models PETER CARR Head of Quantitative Financial Research, Bloomberg LP, New York Director of the Masters Program in Math Finance, Courant Institute, NYU Stanford

Hedging Credit Derivatives in Intensity Based Models PETER CARR Head of Quantitative Financial Research, Bloomberg LP, New York Director of the Masters Program in Math Finance, Courant Institute, NYU Stanford

Black-Scholes-Merton Model

Black-Scholes-Merton Model Weerachart Kilenthong University of the Thai Chamber of Commerce c Kilenthong 2017 Weerachart Kilenthong University of the Thai Chamber Black-Scholes-Merton of Commerce Model

Black-Scholes-Merton Model Weerachart Kilenthong University of the Thai Chamber of Commerce c Kilenthong 2017 Weerachart Kilenthong University of the Thai Chamber Black-Scholes-Merton of Commerce Model

Advanced Stochastic Processes.

Advanced Stochastic Processes. David Gamarnik LECTURE 16 Applications of Ito calculus to finance Lecture outline Trading strategies Black Scholes option pricing formula 16.1. Security price processes,

Advanced Stochastic Processes. David Gamarnik LECTURE 16 Applications of Ito calculus to finance Lecture outline Trading strategies Black Scholes option pricing formula 16.1. Security price processes,

MATH 476/567 ACTUARIAL RISK THEORY FALL 2016 PROFESSOR WANG

MATH 476/567 ACTUARIAL RISK THEORY FALL 206 PROFESSOR WANG Homework 5 (max. points = 00) Due at the beginning of class on Tuesday, November 8, 206 You are encouraged to work on these problems in groups

MATH 476/567 ACTUARIAL RISK THEORY FALL 206 PROFESSOR WANG Homework 5 (max. points = 00) Due at the beginning of class on Tuesday, November 8, 206 You are encouraged to work on these problems in groups

In this lecture we will solve the final-value problem derived in the previous lecture 4, V (1) + rs = rv (t < T )

+ rs = rv (t < T )") MSC FINANCIAL ENGINEERING PRICING I, AUTUMN 2010-2011 LECTURE 5: THE BLACK AND SCHOLES FORMULA AND ITS GREEKS RAYMOND BRUMMELHUIS DEPARTMENT EMS BIRKBECK In this lecture we will solve the final-value problem

MSC FINANCIAL ENGINEERING PRICING I, AUTUMN 2010-2011 LECTURE 5: THE BLACK AND SCHOLES FORMULA AND ITS GREEKS RAYMOND BRUMMELHUIS DEPARTMENT EMS BIRKBECK In this lecture we will solve the final-value problem

STOCHASTIC CALCULUS AND BLACK-SCHOLES MODEL

STOCHASTIC CALCULUS AND BLACK-SCHOLES MODEL YOUNGGEUN YOO Abstract. Ito s lemma is often used in Ito calculus to find the differentials of a stochastic process that depends on time. This paper will introduce

STOCHASTIC CALCULUS AND BLACK-SCHOLES MODEL YOUNGGEUN YOO Abstract. Ito s lemma is often used in Ito calculus to find the differentials of a stochastic process that depends on time. This paper will introduce

A Classical Approach to the Black-and-Scholes Formula and its Critiques, Discretization of the model - Ingmar Glauche

A Classical Approach to the Black-and-Scholes Formula and its Critiques, Discretization of the model - Ingmar Glauche Physics Department Duke University Durham, North Carolina 30th April 2001 3 1 Introduction

A Classical Approach to the Black-and-Scholes Formula and its Critiques, Discretization of the model - Ingmar Glauche Physics Department Duke University Durham, North Carolina 30th April 2001 3 1 Introduction

Solutions of Exercises on Black Scholes model and pricing financial derivatives MQF: ACTU. 468 S you can also use d 2 = d 1 σ T

1 KING SAUD UNIVERSITY Academic year 2016/2017 College of Sciences, Mathematics Department Module: QMF Actu. 468 Bachelor AFM, Riyadh Mhamed Eddahbi Solutions of Exercises on Black Scholes model and pricing

1 KING SAUD UNIVERSITY Academic year 2016/2017 College of Sciences, Mathematics Department Module: QMF Actu. 468 Bachelor AFM, Riyadh Mhamed Eddahbi Solutions of Exercises on Black Scholes model and pricing

Project 1: Double Pendulum

Final Projects Introduction to Numerical Analysis II http://www.math.ucsb.edu/ atzberg/winter2009numericalanalysis/index.html Professor: Paul J. Atzberger Due: Friday, March 20th Turn in to TA s Mailbox:

Final Projects Introduction to Numerical Analysis II http://www.math.ucsb.edu/ atzberg/winter2009numericalanalysis/index.html Professor: Paul J. Atzberger Due: Friday, March 20th Turn in to TA s Mailbox:

Utility Indifference Pricing and Dynamic Programming Algorithm

Chapter 8 Utility Indifference ricing and Dynamic rogramming Algorithm In the Black-Scholes framework, we can perfectly replicate an option s payoff. However, it may not be true beyond the Black-Scholes

Chapter 8 Utility Indifference ricing and Dynamic rogramming Algorithm In the Black-Scholes framework, we can perfectly replicate an option s payoff. However, it may not be true beyond the Black-Scholes

Short-time-to-expiry expansion for a digital European put option under the CEV model. November 1, 2017

Short-time-to-expiry expansion for a digital European put option under the CEV model November 1, 2017 Abstract In this paper I present a short-time-to-expiry asymptotic series expansion for a digital European

Short-time-to-expiry expansion for a digital European put option under the CEV model November 1, 2017 Abstract In this paper I present a short-time-to-expiry asymptotic series expansion for a digital European

Extensions to the Black Scholes Model

Lecture 16 Extensions to the Black Scholes Model 16.1 Dividends Dividend is a sum of money paid regularly (typically annually) by a company to its shareholders out of its profits (or reserves). In this

Lecture 16 Extensions to the Black Scholes Model 16.1 Dividends Dividend is a sum of money paid regularly (typically annually) by a company to its shareholders out of its profits (or reserves). In this

Option Pricing Model with Stepped Payoff

Applied Mathematical Sciences, Vol., 08, no., - 8 HIARI Ltd, www.m-hikari.com https://doi.org/0.988/ams.08.7346 Option Pricing Model with Stepped Payoff Hernán Garzón G. Department of Mathematics Universidad

Applied Mathematical Sciences, Vol., 08, no., - 8 HIARI Ltd, www.m-hikari.com https://doi.org/0.988/ams.08.7346 Option Pricing Model with Stepped Payoff Hernán Garzón G. Department of Mathematics Universidad

Chapter 5 Finite Difference Methods. Math6911 W07, HM Zhu

Chapter 5 Finite Difference Methods Math69 W07, HM Zhu References. Chapters 5 and 9, Brandimarte. Section 7.8, Hull 3. Chapter 7, Numerical analysis, Burden and Faires Outline Finite difference (FD) approximation

Chapter 5 Finite Difference Methods Math69 W07, HM Zhu References. Chapters 5 and 9, Brandimarte. Section 7.8, Hull 3. Chapter 7, Numerical analysis, Burden and Faires Outline Finite difference (FD) approximation

The Black-Scholes Equation using Heat Equation

The Black-Scholes Equation using Heat Equation Peter Cassar May 0, 05 Assumptions of the Black-Scholes Model We have a risk free asset given by the price process, dbt = rbt The asset price follows a geometric

The Black-Scholes Equation using Heat Equation Peter Cassar May 0, 05 Assumptions of the Black-Scholes Model We have a risk free asset given by the price process, dbt = rbt The asset price follows a geometric

Risk Neutral Valuation

copyright 2012 Christian Fries 1 / 51 Risk Neutral Valuation Christian Fries Version 2.2 http://www.christian-fries.de/finmath April 19-20, 2012 copyright 2012 Christian Fries 2 / 51 Outline Notation Differential

copyright 2012 Christian Fries 1 / 51 Risk Neutral Valuation Christian Fries Version 2.2 http://www.christian-fries.de/finmath April 19-20, 2012 copyright 2012 Christian Fries 2 / 51 Outline Notation Differential

Review Direct Integration Discretely observed options Summary QUADRATURE. Dr P. V. Johnson. School of Mathematics

QUADRATURE Dr P.V.Johnson School of Mathematics 2011 OUTLINE Review 1 REVIEW Story so far... Today s lecture OUTLINE Review 1 REVIEW Story so far... Today s lecture 2 DIRECT INTEGRATION OUTLINE Review

QUADRATURE Dr P.V.Johnson School of Mathematics 2011 OUTLINE Review 1 REVIEW Story so far... Today s lecture OUTLINE Review 1 REVIEW Story so far... Today s lecture 2 DIRECT INTEGRATION OUTLINE Review

Approximation Methods in Derivatives Pricing

Approximation Methods in Derivatives Pricing Minqiang Li Bloomberg LP September 24, 2013 1 / 27 Outline of the talk A brief overview of approximation methods Timer option price approximation Perpetual

Approximation Methods in Derivatives Pricing Minqiang Li Bloomberg LP September 24, 2013 1 / 27 Outline of the talk A brief overview of approximation methods Timer option price approximation Perpetual

Introduction to Game-Theoretic Probability

Introduction to Game-Theoretic Probability Glenn Shafer Rutgers Business School January 28, 2002 The project: Replace measure theory with game theory. The game-theoretic strong law. Game-theoretic price

Introduction to Game-Theoretic Probability Glenn Shafer Rutgers Business School January 28, 2002 The project: Replace measure theory with game theory. The game-theoretic strong law. Game-theoretic price