Chapter 18. Equity Valuation Models

|

|

|

- Hubert Dixon

- 6 years ago

- Views:

Transcription

1 Chapter 18 Equity Valuation Models

2 Models of Equity Valuation Balance Sheet Models Book Value Dividend Discount Models Price/Earning Ratios 2

3 Intrinsic Value and Market Price Intrinsic Value Self assigned Value Variety of models are used for estimation Market Price (MP) Consensus value of all potential traders Trading Signal IV > MP Buy IV < MP Sell or Short Sell IV = MP Hold or Fairly Priced 3

4 Dividend Discount Models: General Model V 0 = t=1 D t 1 + k t V 0 = Value of Stock D t = Dividend k = required return 4

5 No Growth Model V 0 = D 1 k The no growth model would work for common stocks that have earnings and dividends that are expected to remain constant (this assumption is probably not too realistic). A good example of a claim that has constant dividends is Preferred Stock 5

6 No Growth Model: Example D 1 = $5.00 k = 0.15 V 0 = D 1 k V 0 = $5.00 / 0.15 = $

7 The constant growth model V 0 = t=1 D g t (1 + k) t Where D 1 = D 0 (1+g) D 2 = D 1 (1+g) = D 0 (1+g) 2 and so on.. As long as k > g, the sum will converge to: V 0 = D 0(1 + g) k g = D 1 k g 7

8 Constant Growth Model: Example V 0 = D 0(1 + g) k g = D 1 k g k = 15% D 1 = $3.00 g = 8% (therefore: D 0 = 3/1.08) V 0 = 3.00 / ( ) = $

9 Constant growth continued On the previous slide we computed the intrinsic value as V 0 = 3/( )=$ Based on the constant growth model, what is the intrinsic value at t=1, V 1? V 1 = D 2 k g Because D 2 = D 1 (1+g), we can substitute this value for D 2 into the expression for V 1 as follows: V 1 = D g k g = D 1 k g 1 + g = V 0(1 + g) In words, the intrinsic value grows at the same rate, g, as dividends. 9

10 Constant growth continued V 0 = 3/( )=$42.86 and V 1 = 42.86(1.08) = What is the Holding Period Return from t = 0 to t = 1 if prices follow the DDM? HPR = V 1 V 0 + D 1 V 0 HPR = V 1 V 0 + D 1 V 0 V 0 HPR = 8% + 7% = 15% = k 10

11 Specified Holding Period Model V 0 = D k + D k D N + P N 1 + k N P N = the expected price for the stock at time N N = the specified number of years the stock is expected to be held P N = t=n+1 D t 1 + k t P N = D N+1 k g 2 Where the growth rate during the stage from N+1 to, g 2, may differ from the growth rate used from periods 1 to N. 11

12 Example of 2-stage model Assume that the current dividend is D 0 = 1.00 and dividends are expected to grow at 10% for the next 3 years (i.e., from t=0 to t=1, t=1 to t=2, and t=2 to t=3). Starting in year 3, dividends will grow at 4% indefinitely (i.e., from t=3 to infinity). Calculate the current intrinsic value based on these assumptions, given k = 8%. Step 1: Trace out all the dividends Growth in the first stage, g 1 = 10% D 1 = 1.00 x 1.10 = $1.10 D 2 = 1.00 x = $1.21 D 3 = 1.00 x = $1.33 D 4 = D 3 x 1.04 = $1.33 x 1.04 = $1.38 growing at 4% forever. 12

13 2-stage model continued Step 2: Compute the horizon value at t = 3 The second stage is infinite and dividends grow at g 2 = 4% Because dividends grow at 4% forever (and 4% < k=8%), we can use the constant growth dividend discount model to value the dividends from t=4 onward. With D 4 = $1.38, we can calculate P 3 as follows: P 3 = D 4 k g P 3 = $1.38/( ) = $34.5 Step 3: Compute overall intrinsic value at t=0 We can now use the holding period version of the dividend discount model to calculate the intrinsic value, V 0. V 0 = D k + D k 2 + D 3 + P k 3 V 0 = = $

14 2-stage model continued If the current market price is P 0 = $30.50, and we buy the stock, then we should expect to earn a holding period return of 8% from t=0 to t =1 (as long as actual prices follow the DDM). Let s see why. Under this model, the expected selling price at t = 1, P 1, is the present value of the dividends, D 2 and D 3, and the expected price at t=3, P 3. Let s calculate P 1 as follows: P 1 = = $31.84 Note the price does not grow by the initial 10% growth rate, since the initial calculation for the price does not depend on a single growth rate. The growth in price = 31.84/30.50 = or growth rate in price = 4.4% We can now compute the holding period return from t=0 to t=1 HPR = P 1 P 0 + D 1 P 0 = = 8% 14

15 Estimating Dividend Growth Rates g = ROE b g = growth rate in dividends ROE = Return on Equity for the firm b = plowback or retention percentage rate (1- dividend payout percentage rate) 15

16 Partitioning Value: Example ROE = 20%, b = 40% and (1-b) = 60% E 1 = $5.00 D 1 = $3.00 k = 15% g = 0.20 x 0.40 = 0.08 or 8% 16

17 Partitioning Value: Example V 0 = = $42.86 NGV 0 = = $33.33 PVGO = = $9.52 V 0 = value with growth NGV 0 = no growth component value PVGO = Present Value of Growth Opportunities 17

18 Price Earnings Ratios P/E Ratios are a function of two factors Required Rates of Return (k) Expected growth in Dividends Uses Relative valuation Extensive Use in industry 18

19 P/E Ratio: No Expected Growth P 0 = E 1 k P 0 E 1 = 1 k E 1 : expected earnings for next year E 1 is equal to D 1 under no growth k: required rate of return 19

20 P/E Ratio with Constant Growth P o = D 1 k g = P 0 E 1 = E 1 1 b k (b ROE) 1 b k b ROE b = retention ratio ROE = Return on Equity 20

21 Numerical Example: No Growth E 0 = $2.50 g = 0 k = 12.5% P 0 = D/k = $2.50/0.125 = $20.00 PE = 1/k = 1/0.125 = 8 21

22 Numerical Example with Growth b = 60% ROE = 15% (1-b) = 40% E 1 = $2.50 (1 + (0.6)(0.15)) = $2.73 D 1 = $2.73 (1-0.6) = $1.09 k = 12.5% g = 9% P 0 = 1.09/( ) = $31.14 PE = 31.14/2.73 = 11.4 PE = (1-0.60) / ( ) =

23 Table 18.3 Effect of ROE and Plowback on Growth and the P/E Ratio 23

24 Free Cash Flow Approach Discount the free cash flow for the firm Discount rate is the firm s cost of capital Components of free cash flow After tax EBIT Depreciation Capital expenditures Increase in net working capital 24

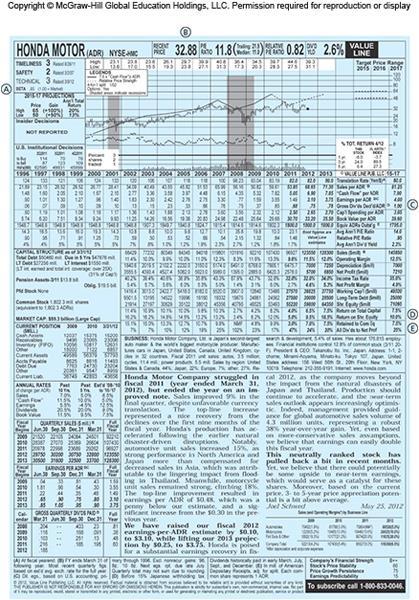

25 Value Line Investment Example for Honda (May 25, 2012) (see pages in the text ). Value Line report is the last slide in this. You can get Value Line reports from the UNL Library ( Log onto your My.UNL Account; Choose E-resources, Browse under the letter V. Relevant information for late 2009 (row is indicated by letters A E) Beta (row A) = 0.95 Recent Price (row B) = $32.88 Dividends (row C) = $1.00 (forecast for 2016) ROE (row D) = 10% Dividend payout ratio (row E) = 25% Growth = g = ROE x b = 10.0% x (1-0.25) = 7.50% We will use an investment horizon of 2016 and the intrinsic value will be computed as the PV of the dividends for 2013, 2014, 2015, 2016 and the horizon price for 2016 (i.e., P 2016 ) 25

26 Honda example, continued P 2016 = D 2017 / (k g) = $1.00 (1.075)/(k-0.075) Now we need an estimate of k and we will use the CAPM Inputs given are as follows: r(f) = 2.0% and suppose the market risk premium is 8.0% k = 2.0% ( ) = 9.6% P 2016 = ; D(2013) = 0.78, D(2014) = 0.85, D(2015) = 0.92, and D(2016) = 1.00, The intrinsic value for 2012, V(2012) is now the present value of the stream of dividends and the horizon value (all discounted at 9.6%%). V(2012) = $

27 27

Chapter 13. (Cont d)

") Chapter 13 Equity Valuation (Cont d) Expected Holding Period Return The return on a stock investment comprises cash dividends and capital gains or losses Assuming a one-year holding period Expected HPR=

Chapter 13 Equity Valuation (Cont d) Expected Holding Period Return The return on a stock investment comprises cash dividends and capital gains or losses Assuming a one-year holding period Expected HPR=

Valuation: Fundamental Analysis. Equity Valuation Models. Models of Equity Valuation. Valuation by Comparables

Valuation: Fundamental Analysis 22-2 Equity Valuation Models Fundamental analysis models a company s value by assessing its current and future profitability. The purpose of fundamental analysis is to identify

Valuation: Fundamental Analysis 22-2 Equity Valuation Models Fundamental analysis models a company s value by assessing its current and future profitability. The purpose of fundamental analysis is to identify

Chapter 18. Equity Valuation Models

Chapter 18 Equity Valuation Models Fundamental Stock Analysis: Models of Equity Valuation One approach to firm valuation is to focus on the firm's book value, either as it appears on the balance sheet

Chapter 18 Equity Valuation Models Fundamental Stock Analysis: Models of Equity Valuation One approach to firm valuation is to focus on the firm's book value, either as it appears on the balance sheet

Valuation: Fundamental Analysis

Valuation: Fundamental Analysis Equity Valuation Models Fundamental analysis models a company s value by assessing its current and future profitability. The purpose of fundamental analysis is to identify

Valuation: Fundamental Analysis Equity Valuation Models Fundamental analysis models a company s value by assessing its current and future profitability. The purpose of fundamental analysis is to identify

Investment Analysis (FIN 383) Fall Homework 7

Fall Homework 7") Investment Analysis (FIN 383) Fall 28 Homework 7 Instructions: please read carefully You should show your work how to get the answer for each calculation question to get full credit The due date is Tue

Investment Analysis (FIN 383) Fall 28 Homework 7 Instructions: please read carefully You should show your work how to get the answer for each calculation question to get full credit The due date is Tue

SECURITY VALUATION STOCK VALUATION

SECURITY VALUATION STOCK VALUATION Features: 1. Claim to residual value of the firm (after claims against firm are paid). 2. Voting rights 3. Investment value: Dividends and Capital gains. 4. Multiple

SECURITY VALUATION STOCK VALUATION Features: 1. Claim to residual value of the firm (after claims against firm are paid). 2. Voting rights 3. Investment value: Dividends and Capital gains. 4. Multiple

CHAPTER 18: EQUITY VALUATION MODELS

CHAPTER 18: EQUITY VALUATION MODELS PROBLEM SETS 1. Theoretically, dividend discount models can be used to value the stock of rapidly growing companies that do not currently pay dividends; in this scenario,

CHAPTER 18: EQUITY VALUATION MODELS PROBLEM SETS 1. Theoretically, dividend discount models can be used to value the stock of rapidly growing companies that do not currently pay dividends; in this scenario,

Key Concepts and Skills. Chapter 8 Stock Valuation. Topics Covered. Dividend Discount Model (DDM)

") Chapter 8 Stock Valuation Konan Chan Financial Management, Fall 8 Key Concepts and Skills Understand how stock prices depend on future dividends and dividend growth Be able to compute stock prices using

Chapter 8 Stock Valuation Konan Chan Financial Management, Fall 8 Key Concepts and Skills Understand how stock prices depend on future dividends and dividend growth Be able to compute stock prices using

CA - FINAL SECURITY VALUATION. FCA, CFA L3 Candidate

CA - FINAL SECURITY VALUATION FCA, CFA L3 Candidate 2.1 Security Valuation Study Session 2 LOS 1 : Introduction Note: Total Earnings mean Earnings available to equity share holders Income Statement

CA - FINAL SECURITY VALUATION FCA, CFA L3 Candidate 2.1 Security Valuation Study Session 2 LOS 1 : Introduction Note: Total Earnings mean Earnings available to equity share holders Income Statement

Security Analysis. macroeconomic factors and industry level analysis

Security Analysis (Text reference: Chapter 14) discounted cash flow techniques price-earnings ratios other multiples example #1: U.S. retail stores more on price to book value multiples more on price to

Security Analysis (Text reference: Chapter 14) discounted cash flow techniques price-earnings ratios other multiples example #1: U.S. retail stores more on price to book value multiples more on price to

FN428 : Investment Banking. Lecture 23 : Revision class

FN428 : Investment Banking Lecture 23 : Revision class Recap : Theory of Financial Intermediary An overview of Investment Banking Investment Bank vs. Commercial Bank Which are the various divisions of

FN428 : Investment Banking Lecture 23 : Revision class Recap : Theory of Financial Intermediary An overview of Investment Banking Investment Bank vs. Commercial Bank Which are the various divisions of

PowerPoint. to accompany. Chapter 9. Valuing Shares

PowerPoint to accompany Chapter 9 Valuing Shares 9.1 Share Basics Ordinary share: a share of ownership in the corporation, which gives its owner rights to vote on the election of directors, mergers or

PowerPoint to accompany Chapter 9 Valuing Shares 9.1 Share Basics Ordinary share: a share of ownership in the corporation, which gives its owner rights to vote on the election of directors, mergers or

Stock valuation. Chapter 10

Stock valuation Chapter 10 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk Reward Tradeoff. Principle 3: Cash Flows are the Source of Value. Principle

Stock valuation Chapter 10 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk Reward Tradeoff. Principle 3: Cash Flows are the Source of Value. Principle

Introduction to Stock Valuation

Introduction to Stock Valuation (Text reference: Chapter 5 (Sections 5.4-5.9)) Topics background dividend discount models parameter estimation growth opportunities price-earnings ratios some final points

Introduction to Stock Valuation (Text reference: Chapter 5 (Sections 5.4-5.9)) Topics background dividend discount models parameter estimation growth opportunities price-earnings ratios some final points

Valuation and Tax Policy

Valuation and Tax Policy Lakehead University Winter 2005 Formula Approach for Valuing Companies Let EBIT t Earnings before interest and taxes at time t T Corporate tax rate I t Firm s investments at time

Valuation and Tax Policy Lakehead University Winter 2005 Formula Approach for Valuing Companies Let EBIT t Earnings before interest and taxes at time t T Corporate tax rate I t Firm s investments at time

Dividend Decisions. LOS 1 : Introduction 1.1

1.1 Dividend Decisions LOS 1 : Introduction Note: Total Earnings mean Earnings available to equity share holders Income Statement Sales Less: Variable cost Contribution Less: Fixed cost excluding Dep.

1.1 Dividend Decisions LOS 1 : Introduction Note: Total Earnings mean Earnings available to equity share holders Income Statement Sales Less: Variable cost Contribution Less: Fixed cost excluding Dep.

IMPORTANT INFORMATION: This study guide contains important information about your module.

217 University of South Africa All rights reserved Printed and published by the University of South Africa Muckleneuk, Pretoria INV371/1/218 758224 IMPORTANT INFORMATION: This study guide contains important

217 University of South Africa All rights reserved Printed and published by the University of South Africa Muckleneuk, Pretoria INV371/1/218 758224 IMPORTANT INFORMATION: This study guide contains important

Lecture 4 Valuation of Stocks (a)

") Lecture 4 Valuation of Stocks (a) After examining the characteristics of bonds and their valuation, we now turn our attention towards the more common financial asset we all know as share or stock Equity

Lecture 4 Valuation of Stocks (a) After examining the characteristics of bonds and their valuation, we now turn our attention towards the more common financial asset we all know as share or stock Equity

Firm valuation (1) Class 6 Financial Management,

Class 6 Financial Management,") Firm valuation (1) Class 6 Financial Management, 15.414 Today Firm valuation Dividend discount model Cashflows, profitability, and growth Reading Brealey and Myers, Chapter 4 Firm valuation The WSJ reports

Firm valuation (1) Class 6 Financial Management, 15.414 Today Firm valuation Dividend discount model Cashflows, profitability, and growth Reading Brealey and Myers, Chapter 4 Firm valuation The WSJ reports

Absolute and relative security valuation

Absolute and relative security valuation Bertrand Groslambert bertrand.groslambert@skema.edu Skema Business School Portfolio Management 1 Course Outline Introduction (lecture 1) Presentation of portfolio

Absolute and relative security valuation Bertrand Groslambert bertrand.groslambert@skema.edu Skema Business School Portfolio Management 1 Course Outline Introduction (lecture 1) Presentation of portfolio

Chapter 15: Stock Valuation

Chapter 15: Stock Valuation Investment Management Lakehead University Company Analysis vs Stock Valuation The common stock of a good company is not necessarily a good investment. A stock is a good investment

Chapter 15: Stock Valuation Investment Management Lakehead University Company Analysis vs Stock Valuation The common stock of a good company is not necessarily a good investment. A stock is a good investment

Practice Set #2 and Solutions.

Bo Sjö 2011-04-19 Practice Set #2 and Solutions. What to do with this practice set? Practice sets are handed out to help students master the material of the course and prepare for the final exam. These

Bo Sjö 2011-04-19 Practice Set #2 and Solutions. What to do with this practice set? Practice sets are handed out to help students master the material of the course and prepare for the final exam. These

Chapter 6. Valuing Stocks. Fundamentals of Corporate Finance. Fifth Edition. Slides by Matthew Will. McGraw-Hill/Irwin

Fundamentals of Corporate Finance Chapter 6 Valuing Stocks Fifth Edition Slides by Matthew Will 6-2 Topics Covered Stocks and the Stock Market Book Values, Liquidation Values and Market Values Valuing

Fundamentals of Corporate Finance Chapter 6 Valuing Stocks Fifth Edition Slides by Matthew Will 6-2 Topics Covered Stocks and the Stock Market Book Values, Liquidation Values and Market Values Valuing

FREDERICK OWUSU PREMPEH

EXCEL PROFESSIONAL INSTITUTE 3.3 ADVANCED FINANCIAL MANAGEMENT LECTURES SLIDES FREDERICK OWUSU PREMPEH EXCEL PROFESSIONAL INSTITUTE Lecture 9 Valuation and the use of free cash flows The free cash flow

EXCEL PROFESSIONAL INSTITUTE 3.3 ADVANCED FINANCIAL MANAGEMENT LECTURES SLIDES FREDERICK OWUSU PREMPEH EXCEL PROFESSIONAL INSTITUTE Lecture 9 Valuation and the use of free cash flows The free cash flow

Financial'Market'Analysis'(FMAx) Module'5

Module'5") Financial'Market'Analysis'(FMAx) Module'5 Equity Pricing This training material is the property of the International Monetary Fund (IMF) and is intended for use in IMF Institute for Capacity Development

Financial'Market'Analysis'(FMAx) Module'5 Equity Pricing This training material is the property of the International Monetary Fund (IMF) and is intended for use in IMF Institute for Capacity Development

JEM034 Corporate Finance Winter Semester 2017/2018

JEM034 Corporate Finance Winter Semester 2017/2018 Lecture #2 Olga Bychkova Topics Covered Today Review of key finance concepts Valuation of stocks (chapter 4 in BMA) NPV and other investment criteria

JEM034 Corporate Finance Winter Semester 2017/2018 Lecture #2 Olga Bychkova Topics Covered Today Review of key finance concepts Valuation of stocks (chapter 4 in BMA) NPV and other investment criteria

Corporate Finance, Module 3: Common Stock Valuation. Illustrative Test Questions and Practice Problems. (The attached PDF file has better formatting.

Corporate Finance, Module 3: Common Stock Valuation Illustrative Test Questions and Practice Problems (The attached PDF file has better formatting.) These problems combine common stock valuation (module

Corporate Finance, Module 3: Common Stock Valuation Illustrative Test Questions and Practice Problems (The attached PDF file has better formatting.) These problems combine common stock valuation (module

Business 5039, Fall 2004

Business 5039, Fall 4 Assignment 3 Suggested Answers 1. Financial Planning Using the financial statements for Rosengarten, Inc., in Table 1, answer the following questions. a) 10 points) Construct Rosengarten

Business 5039, Fall 4 Assignment 3 Suggested Answers 1. Financial Planning Using the financial statements for Rosengarten, Inc., in Table 1, answer the following questions. a) 10 points) Construct Rosengarten

FINA Homework 2

FINA3313-005 Homework 2 Chapter 04 Measuring Corporate Performance True / False Questions 1. The higher the times interest earned ratio, the higher the interest expense. 2. The asset turnover ratio and

FINA3313-005 Homework 2 Chapter 04 Measuring Corporate Performance True / False Questions 1. The higher the times interest earned ratio, the higher the interest expense. 2. The asset turnover ratio and

Sample Final Exam Fall Some Useful Formulas

15.401 Sample Final Exam Fall 2008 Please make sure that your copy of the examination contains 25 pages (including this one). Write your name and MIT ID number on every page. You are allowed two 8 1 11

15.401 Sample Final Exam Fall 2008 Please make sure that your copy of the examination contains 25 pages (including this one). Write your name and MIT ID number on every page. You are allowed two 8 1 11

Strategic Financial Management By CA. Gaurav Jain

1 ISS RATHORE INSTITUTE ISS Strategic Financial Management By CA. Gaurav Jain 100% Coverage More than 300 Concepts covered in Just 25 Classes + 2 Theory Classes All Classes At: 1/50 iss Building, Lalita

1 ISS RATHORE INSTITUTE ISS Strategic Financial Management By CA. Gaurav Jain 100% Coverage More than 300 Concepts covered in Just 25 Classes + 2 Theory Classes All Classes At: 1/50 iss Building, Lalita

Earnings per Share Payout Ratio 10% 20% 30% 40% 45%

Money & Capital Markets Fall 2011 Homework #3 Due: Friday, Nov. 11 th 1. An analyst has made the following forecasts for a corporation s earnings and payout ratio. The analyst believes that after 2016,

Money & Capital Markets Fall 2011 Homework #3 Due: Friday, Nov. 11 th 1. An analyst has made the following forecasts for a corporation s earnings and payout ratio. The analyst believes that after 2016,

Homework #2 Suggested Solutions

JEM034 Corporate Finance Winter Semester 017/018 Instructor: Olga Bychkova Homework # Suggested Solutions Problem 1. (4.1) Consider the following three stocks: (a) Stock A is expected to provide a dividend

JEM034 Corporate Finance Winter Semester 017/018 Instructor: Olga Bychkova Homework # Suggested Solutions Problem 1. (4.1) Consider the following three stocks: (a) Stock A is expected to provide a dividend

Lecture 6 Cost of Capital

Lecture 6 Cost of Capital What Types of Long-term Capital do Firms Use? 2 Long-term debt Preferred stock Common equity What Types of Long-term Capital do Firms Use? Capital components are sources of funding

Lecture 6 Cost of Capital What Types of Long-term Capital do Firms Use? 2 Long-term debt Preferred stock Common equity What Types of Long-term Capital do Firms Use? Capital components are sources of funding

Chapter 10. Learning Objectives Principles Used in This Chapter 1.Common Stock 2.The Comparables Approach to Valuing Common

Chapter 10 Learning Objectives Principles Used in This Chapter 1.Common Stock 2.The Comparables Approach to Valuing Common Stock 3.Preferred Stock 4.The Stock Market 1. Identify the basic characteristics

Chapter 10 Learning Objectives Principles Used in This Chapter 1.Common Stock 2.The Comparables Approach to Valuing Common Stock 3.Preferred Stock 4.The Stock Market 1. Identify the basic characteristics

BUSI 370 Business Finance

Review Session 2 February 7 th, 2016 Road Map 1. BONDS 2. COMMON SHARES 3. PREFERRED SHARES 4. TREASURY BILLS (T Bills) ANSWER KEY WITH COMMENTS 1. BONDS // Calculate the price of a ten-year annual pay

Review Session 2 February 7 th, 2016 Road Map 1. BONDS 2. COMMON SHARES 3. PREFERRED SHARES 4. TREASURY BILLS (T Bills) ANSWER KEY WITH COMMENTS 1. BONDS // Calculate the price of a ten-year annual pay

FEEDBACK TUTORIAL LETTER

FEEDBACK TUTORIAL LETTER 2 nd SEMESTER 2017 ASSIGNMENT 1 MANAGERIAL FINANCE 4B MAF412S 1 Assignment 1 QUESTION 1 COMPANY A & B a) Co. A Co. B Net Operating Income 5,000,000 5,000,000 Less: interest -1,500,000

FEEDBACK TUTORIAL LETTER 2 nd SEMESTER 2017 ASSIGNMENT 1 MANAGERIAL FINANCE 4B MAF412S 1 Assignment 1 QUESTION 1 COMPANY A & B a) Co. A Co. B Net Operating Income 5,000,000 5,000,000 Less: interest -1,500,000

Review Class Handout Corporate Finance, Sections 001 and 002

. Problem Set, Q 3 Review Class Handout Corporate Finance, Sections 00 and 002 Suppose you are given a choice of the following two securities: (a) an annuity that pays $0,000 at the end of each of the

. Problem Set, Q 3 Review Class Handout Corporate Finance, Sections 00 and 002 Suppose you are given a choice of the following two securities: (a) an annuity that pays $0,000 at the end of each of the

Portfolio Management Philip Morris has issued bonds that pay coupons annually with the following characteristics:

Portfolio Management 010-011 1. a. Critically discuss the mean-variance approach of portfolio theory b. According to Markowitz portfolio theory, can we find a single risky optimal portfolio which is suitable

Portfolio Management 010-011 1. a. Critically discuss the mean-variance approach of portfolio theory b. According to Markowitz portfolio theory, can we find a single risky optimal portfolio which is suitable

Firm valuation (2) Class 7 Financial Management,

Class 7 Financial Management,") Firm valuation (2) Class 7 Financial Management, 15.414 Today Firm valuation x Free cashflows x Profitability, financial ratios, and terminal value Reading x Brealey and Myers, Chapter 12.4 12.6 x Wilson

Firm valuation (2) Class 7 Financial Management, 15.414 Today Firm valuation x Free cashflows x Profitability, financial ratios, and terminal value Reading x Brealey and Myers, Chapter 12.4 12.6 x Wilson

CHAPTER 9 STOCK VALUATION

CHAPTER 9 STOCK VALUATION Answers to Concept Questions 1. The value of any investment depends on the present value of its cash flows; i.e., what investors will actually receive. The cash flows from a share

CHAPTER 9 STOCK VALUATION Answers to Concept Questions 1. The value of any investment depends on the present value of its cash flows; i.e., what investors will actually receive. The cash flows from a share

Lecture 1: Security selection and securities analysis

Lecture 1: Security selection and securities analysis In this lecture we will focus on the main methods used to select individual securities for a portfolio. These may be summarized on the one hand as

Lecture 1: Security selection and securities analysis In this lecture we will focus on the main methods used to select individual securities for a portfolio. These may be summarized on the one hand as

FINAN303 Principles of Finance Spring Time Value of Money Part B

Time Value of Money Part B 1. Examples of multiple cash flows - PV Mult = a. Present value of a perpetuity b. Present value of an annuity c. Uneven cash flows T CF t t=0 (1+i) t 2. Annuity vs. Perpetuity

Time Value of Money Part B 1. Examples of multiple cash flows - PV Mult = a. Present value of a perpetuity b. Present value of an annuity c. Uneven cash flows T CF t t=0 (1+i) t 2. Annuity vs. Perpetuity

Chapter 5: How to Value Bonds and Stocks

Chapter 5: How to Value Bonds and Stocks 5.1 The present value of any pure discount bond is its face value discounted back to the present. a. PV = F / (1+r) 10 = $1,000 / (1.05) 10 = $613.91 b. PV = $1,000

Chapter 5: How to Value Bonds and Stocks 5.1 The present value of any pure discount bond is its face value discounted back to the present. a. PV = F / (1+r) 10 = $1,000 / (1.05) 10 = $613.91 b. PV = $1,000

CAPITAL STRUCTURE AND VALUE

UV3929 Rev. Jun. 30, 2011 CAPITAL STRUCTURE AND VALUE The underlying principle of valuation is that the discount rate must match the risk of the cash flows being valued. Furthermore, when we include the

UV3929 Rev. Jun. 30, 2011 CAPITAL STRUCTURE AND VALUE The underlying principle of valuation is that the discount rate must match the risk of the cash flows being valued. Furthermore, when we include the

The Valuation of Common Stock Where do Stock Prices Come From?

70391 - Finance The Valuation of Common Stock Where do Stock Prices Come From? 70391 Finance Fall 2016 Tepper School of Business Carnegie Mellon University c 2016 Chris Telmer. Some content from slides

70391 - Finance The Valuation of Common Stock Where do Stock Prices Come From? 70391 Finance Fall 2016 Tepper School of Business Carnegie Mellon University c 2016 Chris Telmer. Some content from slides

Advanced Corporate Finance Exercises Session 1 «Pre-requisites: a reminder»

Advanced Corporate Finance Exercises Session 1 «Pre-requisites: a reminder» Professor Kim Oosterlinck E-mail: koosterl@ulb.ac.be Teaching assistants: Nicolas Degive (ndegive@ulb.ac.be) Laurent Frisque

Advanced Corporate Finance Exercises Session 1 «Pre-requisites: a reminder» Professor Kim Oosterlinck E-mail: koosterl@ulb.ac.be Teaching assistants: Nicolas Degive (ndegive@ulb.ac.be) Laurent Frisque

Part B: The stock price is next year s dividend divided by the difference between the capitalization rate (r) and the dividend growth rate (g):

and the dividend growth rate (g):") Corporate Finance, Module 3: Value of Common Stocks, practice problems (The attached PDF file has better formatting.) Brealey and Myers, Chapter 4 ** Exercise 3.1: Present Value of Growth Opportunities

Corporate Finance, Module 3: Value of Common Stocks, practice problems (The attached PDF file has better formatting.) Brealey and Myers, Chapter 4 ** Exercise 3.1: Present Value of Growth Opportunities

Chapter 8: Prospective Analysis: Valuation Implementation

Chapter 8: Prospective Analysis: Valuation Implementation Key Concepts in Chapter 8 Two key issues must be addressed to implement valuation theory: 1. Determining the appropriate discount rate to use in

Chapter 8: Prospective Analysis: Valuation Implementation Key Concepts in Chapter 8 Two key issues must be addressed to implement valuation theory: 1. Determining the appropriate discount rate to use in

Valuation. August 2018

Valuation August 2018 Dr. G. Kevin Spellman, aka Coach David O. Nicholas Director of Investment Management and Senior Lecturer Investment Management Certificate Program, UW-Milwaukee www.lubar.uwm.edu/imcp

Valuation August 2018 Dr. G. Kevin Spellman, aka Coach David O. Nicholas Director of Investment Management and Senior Lecturer Investment Management Certificate Program, UW-Milwaukee www.lubar.uwm.edu/imcp

Midterm Review. P resent value = P V =

JEM034 Corporate Finance Winter Semester 2018/2019 Instructor: Olga Bychkova Midterm Review F uture value of $100 = $100 (1 + r) t Suppose that you will receive a cash flow of C t dollars at the end of

JEM034 Corporate Finance Winter Semester 2018/2019 Instructor: Olga Bychkova Midterm Review F uture value of $100 = $100 (1 + r) t Suppose that you will receive a cash flow of C t dollars at the end of

Chapter Organization. The future value (FV) is the cash value of. an investment at some time in the future.

is the cash value of. an investment at some time in the future.") Chapter 5 The Time Value of Money Chapter Organization 5.2. Present Value and Discounting The future value (FV) is the cash value of an investment at some time in the future Suppose you invest 100 in a

Chapter 5 The Time Value of Money Chapter Organization 5.2. Present Value and Discounting The future value (FV) is the cash value of an investment at some time in the future Suppose you invest 100 in a

Chapter 14: Company Analysis & Stock Valuation

Chapter 14: Company Analysis & Stock Valuation Analysis of Investments & Management of Portfolios 10 TH EDITION Reilly & Brown Growth Companies & Growth Stocks Growth Companies Historically, consistently

Chapter 14: Company Analysis & Stock Valuation Analysis of Investments & Management of Portfolios 10 TH EDITION Reilly & Brown Growth Companies & Growth Stocks Growth Companies Historically, consistently

QUESTION NO.2A (Exam Question) Compute: (a) (b) (c) QUESTION NO.4A (i) (ii) (iii) QUESTION NO.5A (Exam Question)(8 Marks) Years

Compute: (a) (b) (c) QUESTION NO.4A (i) (ii) (iii) QUESTION NO.5A (Exam Question)(8 Marks) Years") 1 QUESTION NO.2A(Exam Question)A share of T Ltd. is quoted at a price-earning ratio of 7.5 times. The retained earning per share being 37.5% is Rs. 3 per share. Compute: (a)the company's cost of equity

1 QUESTION NO.2A(Exam Question)A share of T Ltd. is quoted at a price-earning ratio of 7.5 times. The retained earning per share being 37.5% is Rs. 3 per share. Compute: (a)the company's cost of equity

Chapter 14 The Cost of Capital

Topics Covered Chapter 14 The Cost of Capital Konan Chan Financial Management, Fall 2018 Cost of capital Weighted average cost of capital (WACC) Capital structure Required rates of return Divisional costs

Topics Covered Chapter 14 The Cost of Capital Konan Chan Financial Management, Fall 2018 Cost of capital Weighted average cost of capital (WACC) Capital structure Required rates of return Divisional costs

Valuation! Cynic: A person who knows the price of everything but the value of nothing.. Oscar Wilde. Aswath Damodaran! 1!

Valuation! Cynic: A person who knows the price of everything but the value of nothing.. Oscar Wilde Aswath Damodaran! 1! First Principles! Aswath Damodaran! 2! Three approaches to valuation! Intrinsic

Valuation! Cynic: A person who knows the price of everything but the value of nothing.. Oscar Wilde Aswath Damodaran! 1! First Principles! Aswath Damodaran! 2! Three approaches to valuation! Intrinsic

Study Unit Cost of Equity, Debt and the WACC 133. Cost of Equity, Debt and the WACC

www.charteredgrindschool.com 133 Study Unit 12 Contents Page A. The Opportunity Cost of Equity Capital 135 B. The Opportunity Cost of Debt Capital 137 C. The Weighted Average Cost of Capital 137 134 www.charteredgrindschool.com

www.charteredgrindschool.com 133 Study Unit 12 Contents Page A. The Opportunity Cost of Equity Capital 135 B. The Opportunity Cost of Debt Capital 137 C. The Weighted Average Cost of Capital 137 134 www.charteredgrindschool.com

Chapters 10&11 - Debt Securities

Chapters 10&11 - Debt Securities Bond characteristics Interest rate risk Bond rating Bond pricing Term structure theories Bond price behavior to interest rate changes Duration and immunization Bond investment

Chapters 10&11 - Debt Securities Bond characteristics Interest rate risk Bond rating Bond pricing Term structure theories Bond price behavior to interest rate changes Duration and immunization Bond investment

LECTURE 7 : CHAPTER 10 The Cost of Capital

LECTURE 7 : CHAPTER 10 The Cost of Capital Sources of capital Component costs WACC (Weighted Average Cost of Capital) Adjusting for flotation costs Adjusting for risk What sources of long-term capital

LECTURE 7 : CHAPTER 10 The Cost of Capital Sources of capital Component costs WACC (Weighted Average Cost of Capital) Adjusting for flotation costs Adjusting for risk What sources of long-term capital

Midterm Review. P resent value = P V =

JEM034 Corporate Finance Winter Semester 2017/2018 Instructor: Olga Bychkova Midterm Review F uture value of $100 = $100 (1 + r) t Suppose that you will receive a cash flow of C t dollars at the end of

JEM034 Corporate Finance Winter Semester 2017/2018 Instructor: Olga Bychkova Midterm Review F uture value of $100 = $100 (1 + r) t Suppose that you will receive a cash flow of C t dollars at the end of

Investment Assignment. Silvia Zia Islam

Investment Assignment Silvia Zia Islam silvia.islam@rmit.edu.au Company overview Executive Summary Historical performance reflects companies earnings How the nature of the company decide the level of the

Investment Assignment Silvia Zia Islam silvia.islam@rmit.edu.au Company overview Executive Summary Historical performance reflects companies earnings How the nature of the company decide the level of the

Stock Valuation. Lakehead University. Outline of the Lecture. Fall Common Stock Valuation. Common Stock Features. Preferred Stock Features

Stock Valuation Lakehead University Fall 2004 Outline of the Lecture Common Stock Valuation Common Stock Features Preferred Stock Features 2 Common Stock Valuation Consider a stock that promises to pay

Stock Valuation Lakehead University Fall 2004 Outline of the Lecture Common Stock Valuation Common Stock Features Preferred Stock Features 2 Common Stock Valuation Consider a stock that promises to pay

Stock Valuation. Lakehead University. Fall 2004

Stock Valuation Lakehead University Fall 2004 Outline of the Lecture Common Stock Valuation Common Stock Features Preferred Stock Features 2 Common Stock Valuation Consider a stock that promises to pay

Stock Valuation Lakehead University Fall 2004 Outline of the Lecture Common Stock Valuation Common Stock Features Preferred Stock Features 2 Common Stock Valuation Consider a stock that promises to pay

CHAPTER 17. Payout Policy

CHAPTER 17 1 Payout Policy 1. a. Distributes a relatively low proportion of current earnings to offset fluctuations in operational cash flow; lower P/E ratio. b. Distributes a relatively high proportion

CHAPTER 17 1 Payout Policy 1. a. Distributes a relatively low proportion of current earnings to offset fluctuations in operational cash flow; lower P/E ratio. b. Distributes a relatively high proportion

Financial Markets Management 183 Economics 173A. Equity Valuation. Updated 5/13/17

Financial Markets Management 183 Economics 173A Equity Valuation Updated 5/13/17 Perspective and Objective 1. Diversification: Risk reduction. 2. Speculation: I ve got a feeling. 3. Long term: Buy & Hold.

Financial Markets Management 183 Economics 173A Equity Valuation Updated 5/13/17 Perspective and Objective 1. Diversification: Risk reduction. 2. Speculation: I ve got a feeling. 3. Long term: Buy & Hold.

CHAPTER 19. Valuation and Financial Modeling: A Case Study. Chapter Synopsis

CHAPTER 19 Valuation and Financial Modeling: A Case Study Chapter Synopsis 19.1 Valuation Using Comparables A valuation using comparable publicly traded firm valuation multiples may be used as a preliminary

CHAPTER 19 Valuation and Financial Modeling: A Case Study Chapter Synopsis 19.1 Valuation Using Comparables A valuation using comparable publicly traded firm valuation multiples may be used as a preliminary

Chapter 6. Stock Valuation

Chapter 6 Stock Valuation Comprehend that stock prices depend on future dividends and dividend growth Compute stock prices using the dividend growth model Understand how growth opportunities affect stock

Chapter 6 Stock Valuation Comprehend that stock prices depend on future dividends and dividend growth Compute stock prices using the dividend growth model Understand how growth opportunities affect stock

Name:... ECO 4368 Summer 2016 Midterm 2. There are 4 problems and 8 True-False questions. TOTAL POINTS: 100

Name:... ECO 4368 Summer 2016 Midterm 2 There are 4 problems and 8 True-False questions. TOTAL POINTS: 100 Question 1 (20 points): A company with a stock price P 0 = $108 had a constant dividend growth

Name:... ECO 4368 Summer 2016 Midterm 2 There are 4 problems and 8 True-False questions. TOTAL POINTS: 100 Question 1 (20 points): A company with a stock price P 0 = $108 had a constant dividend growth

12. Cost of Capital. Outline

12. Cost of Capital 0 Outline The Cost of Capital: What is it? The Cost of Equity The Costs of Debt and Preferred Stock The Weighted Average Cost of Capital Economic Value Added 1 1 Required Return The

12. Cost of Capital 0 Outline The Cost of Capital: What is it? The Cost of Equity The Costs of Debt and Preferred Stock The Weighted Average Cost of Capital Economic Value Added 1 1 Required Return The

The Weighted-Average Cost of Capital and Company Valuation

The Weighted-Average Cost of Capital and Company Valuation Topics Covered Weighted Average Cost of Capital (WACC) Measuring Capital Structure Calculating Required Rates of Return Calculating WACC Interpreting

The Weighted-Average Cost of Capital and Company Valuation Topics Covered Weighted Average Cost of Capital (WACC) Measuring Capital Structure Calculating Required Rates of Return Calculating WACC Interpreting

Key Concepts. Some Features of Common Stock Common Stock Valuation How stock prices are quoted Preferred Stock

1 Key Concepts Some Features of Common Stock Common Stock Valuation How stock prices are quoted Preferred Stock 2 1 I. Common Stock 3 1. Basic Features of Common Stock Forms the major part of corporate

1 Key Concepts Some Features of Common Stock Common Stock Valuation How stock prices are quoted Preferred Stock 2 1 I. Common Stock 3 1. Basic Features of Common Stock Forms the major part of corporate

Stock valuation. A reading prepared by Pamela Peterson-Drake, Florida Atlantic University

Stock valuation A reading prepared by Pamela Peterson-Drake, Florida Atlantic University O U T L I N E. Valuation of common stock. Returns on stock. Summary. Valuation of common stock "[A] stock is worth

Stock valuation A reading prepared by Pamela Peterson-Drake, Florida Atlantic University O U T L I N E. Valuation of common stock. Returns on stock. Summary. Valuation of common stock "[A] stock is worth

CHAPTER 19: FINANCIAL STATEMENT ANALYSIS

CHAPTER 19: FINANCIAL STATEMENT ANALYSIS 1. ROE Net profits/equity Net profits/sales Sales/Assets Assets/Equity Net profit margin Asset turnover Leverage ratio 5.5% 2.0 2.2 24.2% 2. ROA ROS ATO The only

CHAPTER 19: FINANCIAL STATEMENT ANALYSIS 1. ROE Net profits/equity Net profits/sales Sales/Assets Assets/Equity Net profit margin Asset turnover Leverage ratio 5.5% 2.0 2.2 24.2% 2. ROA ROS ATO The only

Chapter 13 Equity Valuation

Chapter 3 Equity Valuation. = $9.9 2. (a) and (b) 3. a. = 2% b. $8.8 The price falls in response to the more pessimistic forecast of dividend growth. The forecast for current earnings, however, is unchanged.

Chapter 3 Equity Valuation. = $9.9 2. (a) and (b) 3. a. = 2% b. $8.8 The price falls in response to the more pessimistic forecast of dividend growth. The forecast for current earnings, however, is unchanged.

Concepts of Value. Book Value Market value Liquidation Value

Book Value Market value Liquidation Value Concepts of Value Fair Market Value ( FMV ) & Intrinsic Value a thorough appreciation of the Company, its Value Proposition, and its future prospects in a competitive

Book Value Market value Liquidation Value Concepts of Value Fair Market Value ( FMV ) & Intrinsic Value a thorough appreciation of the Company, its Value Proposition, and its future prospects in a competitive

Introduction to Corporate Finance, Fourth Edition. Chapter 7: Equity Valuation

Chater 7: Equity Valuation Multile Choice Questions 6. Section: 7.3 Common Share Valuation: The Dividend Discount Model (DDM) A D 0 $2.00. D 1 $2.00 (1 + 0.065) $2.13 RF + Ris Premium 4% + 7.5% 11.5% P

Chater 7: Equity Valuation Multile Choice Questions 6. Section: 7.3 Common Share Valuation: The Dividend Discount Model (DDM) A D 0 $2.00. D 1 $2.00 (1 + 0.065) $2.13 RF + Ris Premium 4% + 7.5% 11.5% P

CVX Chevron Corporation Sector: Energy SELL

Analysts: Zachary Haller, Andrew Paley Brown and Sean Miller Washburn University Applied Portfolio Management CVX Sector: Energy SELL Report Date: 4/18/2016 Market Cap (mm) $157,566 Annual Dividend $4.28

Analysts: Zachary Haller, Andrew Paley Brown and Sean Miller Washburn University Applied Portfolio Management CVX Sector: Energy SELL Report Date: 4/18/2016 Market Cap (mm) $157,566 Annual Dividend $4.28

CHARTERED INSTITUTE OF STOCKBROKERS. September 2018 Specialised Certification Examination. Paper 2.5 Equities Dealing

CHARTERED INSTITUTE OF STOCKBROKERS September 2018 Specialised Certification Examination Paper 2.5 Equities Dealing 2 Question 2 - Equity Valuation and Analysis 2a) An analyst gathered the following data:

CHARTERED INSTITUTE OF STOCKBROKERS September 2018 Specialised Certification Examination Paper 2.5 Equities Dealing 2 Question 2 - Equity Valuation and Analysis 2a) An analyst gathered the following data:

Midterm Review Package Tutor: Chanwoo Yim

COMMERCE 298 Intro to Finance Midterm Review Package Tutor: Chanwoo Yim BCom 2016, Finance 1. Time Value 2. DCF (Discounted Cash Flow) 2.1 Constant Annuity 2.2 Constant Perpetuity 2.3 Growing Annuity 2.4

COMMERCE 298 Intro to Finance Midterm Review Package Tutor: Chanwoo Yim BCom 2016, Finance 1. Time Value 2. DCF (Discounted Cash Flow) 2.1 Constant Annuity 2.2 Constant Perpetuity 2.3 Growing Annuity 2.4

Suggested Answer_Syl2008_Jun2014_Paper_18 FINAL EXAMINATION

FINAL EXAMINATION GROUP IV (SYLLABUS 2008) SUGGESTED ANSWERS TO QUESTIONS JUNE 2014 Paper- 18 : BUSINESS VALUATION MANAGEMENT Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on the right

FINAL EXAMINATION GROUP IV (SYLLABUS 2008) SUGGESTED ANSWERS TO QUESTIONS JUNE 2014 Paper- 18 : BUSINESS VALUATION MANAGEMENT Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on the right

Week 6 Equity Valuation 1

Week 6 Equity Valuation 1 Overview of Valuation The basic assumption of all these valuation models is that the future value of all returns can be discounted back to today s present value. Where t = time

Week 6 Equity Valuation 1 Overview of Valuation The basic assumption of all these valuation models is that the future value of all returns can be discounted back to today s present value. Where t = time

Use the following information to answer Questions 25 through 30. Exhibit 1: Selected Financial Information for BMC. Income Statement $600.

Morning Session Use the following information to answer Questions 25 through 30. Jared Rojas, CFA, is an analyst at Van Westmoreland Investments, an international equities investment firm. Rojas has been

Morning Session Use the following information to answer Questions 25 through 30. Jared Rojas, CFA, is an analyst at Van Westmoreland Investments, an international equities investment firm. Rojas has been

BOND & STOCK VALUATION

Chapter 7 BOND & STOCK VALUATION Bond & Stock Valuation 7-2 1. OBJECTIVE # Use PV to calculate what prices of stocks and bonds should be! Basic bond terminology and valuation! Stock and preferred stock

Chapter 7 BOND & STOCK VALUATION Bond & Stock Valuation 7-2 1. OBJECTIVE # Use PV to calculate what prices of stocks and bonds should be! Basic bond terminology and valuation! Stock and preferred stock

FIN Chapter 10. Stock Valuation. Liuren Wu

FIN 3000 Chapter 10 Stock Valuation Liuren Wu Overview 1. Common Stock Identify the basic characteristics and features of common stock and use the discounted cash flow model to value common shares. 2.

FIN 3000 Chapter 10 Stock Valuation Liuren Wu Overview 1. Common Stock Identify the basic characteristics and features of common stock and use the discounted cash flow model to value common shares. 2.

Chapter 9 Valuing Stocks

Chapter 9 Valuing Stocks Copyright 2011 Pearson Prentice Hall. All rights reserved. Chapter Outline 9.1 The Dividend Discount Model 9.2 Applying the Dividend Discount Model 9.3 Total Payout and Free Cash

Chapter 9 Valuing Stocks Copyright 2011 Pearson Prentice Hall. All rights reserved. Chapter Outline 9.1 The Dividend Discount Model 9.2 Applying the Dividend Discount Model 9.3 Total Payout and Free Cash

Study Session 10. Equity Valuation: Valuation Concepts

Study Session 10 : Valuation Concepts Quantitative Methods Study Session 10 Valuation Concepts 30. : Applications and Processes 31. Valuation Concepts LOS 30.a Define/Explain CFAI V4 p. 6, Schweser B3

Study Session 10 : Valuation Concepts Quantitative Methods Study Session 10 Valuation Concepts 30. : Applications and Processes 31. Valuation Concepts LOS 30.a Define/Explain CFAI V4 p. 6, Schweser B3

Chapter 6. Stock Valuation

Chapter 6 Stock Valuation Comprehend that stock prices depend on future dividends and dividend growth Compute stock prices using the dividend growth model Understand how growth opportunities affect stock

Chapter 6 Stock Valuation Comprehend that stock prices depend on future dividends and dividend growth Compute stock prices using the dividend growth model Understand how growth opportunities affect stock

Financing decisions (2) Class 16 Financial Management,

Class 16 Financial Management,") Financing decisions (2) Class 16 Financial Management, 15.414 Today Capital structure M&M theorem Leverage, risk, and WACC Reading Brealey and Myers, Chapter 17 Key goal Financing decisions Ensure that

Financing decisions (2) Class 16 Financial Management, 15.414 Today Capital structure M&M theorem Leverage, risk, and WACC Reading Brealey and Myers, Chapter 17 Key goal Financing decisions Ensure that

Reading #33 DCF-Discounted Dividend Model (DDM)

") Reading #33 DCF-Discounted Dividend Model (DDM) Rd.33 Discounted Dividend Model General Discounted Dividend Model (DDM) Idea of John Burr Williams DDM (1938) V = D 1+g 1+r =D 1+r = D +V 1+r +D 1+r Where

Reading #33 DCF-Discounted Dividend Model (DDM) Rd.33 Discounted Dividend Model General Discounted Dividend Model (DDM) Idea of John Burr Williams DDM (1938) V = D 1+g 1+r =D 1+r = D +V 1+r +D 1+r Where

CHAPTER 2. How to Calculate Present Values

Chapter 02 - How to Calculate Present Values CHAPTER 2 How to Calculate Present Values The values shown in the solutions may be rounded for display purposes. However, the answers were derived using a spreadsheet

Chapter 02 - How to Calculate Present Values CHAPTER 2 How to Calculate Present Values The values shown in the solutions may be rounded for display purposes. However, the answers were derived using a spreadsheet

Chapter 7. Analyzing Common Stocks. Security Analysis. Top-Down Approach Kaplan Financial

Chapter 7 Analyzing Common Stocks Security Analysis Process of gathering, organizing, and using information to determine the intrinsic value of a common stock. Intrinsic value is the underlying or inherent

Chapter 7 Analyzing Common Stocks Security Analysis Process of gathering, organizing, and using information to determine the intrinsic value of a common stock. Intrinsic value is the underlying or inherent

CHAPTER 8. Personal Finance. Copyright 2015, 2011, 2007 Pearson Education, Inc. Section 8.4, Slide 1

CHAPTER 8 Personal Finance Copyright 2015, 2011, 2007 Pearson Education, Inc. Section 8.4, Slide 1 8.4 Compound Interest Copyright 2015, 2011, 2007 Pearson Education, Inc. Section 8.4, Slide 2 Objectives

CHAPTER 8 Personal Finance Copyright 2015, 2011, 2007 Pearson Education, Inc. Section 8.4, Slide 1 8.4 Compound Interest Copyright 2015, 2011, 2007 Pearson Education, Inc. Section 8.4, Slide 2 Objectives

CHAPTER 4 SHOW ME THE MONEY: THE BASICS OF VALUATION

1 CHAPTER 4 SHOW ME THE MOEY: THE BASICS OF VALUATIO To invest wisely, you need to understand the principles of valuation. In this chapter, we examine those fundamental principles. In general, you can

1 CHAPTER 4 SHOW ME THE MOEY: THE BASICS OF VALUATIO To invest wisely, you need to understand the principles of valuation. In this chapter, we examine those fundamental principles. In general, you can

A. Huang Date of Exam December 20, 2011 Duration of Exam. Instructor. 2.5 hours Exam Type. Special Materials Additional Materials Allowed

Instructor A. Huang Date of Exam December 20, 2011 Duration of Exam 2.5 hours Exam Type Special Materials Additional Materials Allowed Calculator Marking Scheme: Question Score Question Score 1 /20 5 /9

Instructor A. Huang Date of Exam December 20, 2011 Duration of Exam 2.5 hours Exam Type Special Materials Additional Materials Allowed Calculator Marking Scheme: Question Score Question Score 1 /20 5 /9

(S1) Soluções da Primeira Avaliação

Soluções da Primeira Avaliação") Professor: Victor Filipe Monitor: Christiam Miguel EPGE-FGV Graduação em Ciências Econômicas Finanças Corporativas Setembro 2000 (S) Soluções da Primeira Avaliação Question (2.5 points). Casper has $200,000

Professor: Victor Filipe Monitor: Christiam Miguel EPGE-FGV Graduação em Ciências Econômicas Finanças Corporativas Setembro 2000 (S) Soluções da Primeira Avaliação Question (2.5 points). Casper has $200,000

4. E , = + (0.08)(20, 000) 5. D. Course 2 Solutions 51 May a

(20, 000) 5. D. Course 2 Solutions 51 May a") . D According to the semi-strong version of the efficient market theory, prices accurately reflect all publicly available information about a security. Thus, by this theory, actively managed portfolios

. D According to the semi-strong version of the efficient market theory, prices accurately reflect all publicly available information about a security. Thus, by this theory, actively managed portfolios

Mid Term Papers. Spring 2009 (Session 02) MGT201. (Group is not responsible for any solved content)

MGT201. (Group is not responsible for any solved content)") Spring 2009 (Session 02) MGT201 (Group is not responsible for any solved content) Subscribe to VU SMS Alert Service To Join Simply send following detail to bilal.zaheem@gmail.com Full Name Master Program

Spring 2009 (Session 02) MGT201 (Group is not responsible for any solved content) Subscribe to VU SMS Alert Service To Join Simply send following detail to bilal.zaheem@gmail.com Full Name Master Program

SECTION HANDOUT #1 : Review of Topics

SETION HANDOUT # : Review of Topics MBA 0 October, 008 This handout contains some of the topics we have covered so far. You are not required to read it, but you may find some parts of it helpful when you

SETION HANDOUT # : Review of Topics MBA 0 October, 008 This handout contains some of the topics we have covered so far. You are not required to read it, but you may find some parts of it helpful when you

A model predicts that the adult population of the town will increase by 3% each year, forming a geometric sequence.

1. The adult population of a town is 25 000 at the end of Year 1. A model predicts that the adult population of the town will increase by 3% each year, forming a geometric sequence. (a) Show that the predicted

1. The adult population of a town is 25 000 at the end of Year 1. A model predicts that the adult population of the town will increase by 3% each year, forming a geometric sequence. (a) Show that the predicted

Valuation. Aswath Damodaran. Aswath Damodaran 186

Valuation Aswath Damodaran Aswath Damodaran 186 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle rate should be higher for riskier projects

Valuation Aswath Damodaran Aswath Damodaran 186 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle rate should be higher for riskier projects