Math Computational Finance Option pricing using Brownian bridge and Stratified samlping

|

|

|

- Peter Bond

- 6 years ago

- Views:

Transcription

1 . Math Computational Finance Option pricing using Brownian bridge and Stratified samlping Pratik Mehta pbmehta@eden.rutgers.edu Masters of Science in Mathematical Finance Department of Mathematics, Rutgers University This paper describes the implementation of a C++ program to calculate the value of a european style call option, a discretely sampled arithmetic and geometric Asian option on an underlying asset, given input parameters for stock price (s=100), strike price (k=110),volatility (v=30%), interest rate (r=5%), maturity (T=1 year) usingbrownian bridge with terminal stratification, Quasi Monte Carlo simulation with low discrepancy Sobol sequences and Monte Carlo with antithetic sampling. We compare the results of all these methods. The underlying stock price is assumed to follow geometric brownian motion. The program calculates the option prices using the Monte Carlo/Quasi MC method with 10,000 simulations, 1000 strata for stratified sampling and uses the solution to the Stochastic differential equation of the stock process [3]. I. INTRODUCTION In this assignment we are pricing a European style vanilla call option and Asian option using Brownian Bridge with terminal stratification, low discrepancy Sobol sequences and comparing results with closed form solution and Monte Carlo using antithetic sampling. ds(t) = (rs(t)dt + σs(t)dw (t) (1) the solution to the above Stochastic Differential Equation is, S(T ) = S(0)e (r 1 2 σ2 )T +σw (T ) the payoff for the call option is, (2) (S(T ) k) + (3) and Asian option continuously averaged, ( + 1 T S u du K) (4) T 0 We have modified Joshi s code from chapter 7 (EquityFXMain.cpp), as was required for this assignment. II. VANILLA CALL : CLOSED FORM BLACK-SCHOLES-MERTON Here, K is the strike price and S(T ) is the terminal stock price at the payoff date. The price of the underlying at terminal time,t, is given by [4] A closed form solution for the price of a European Call and Put is given by [4] and c(t, x) = xe at N(d + (T, x)) e rt KN(d (τ, x)) (6) p(t, x) = e rt KN( d (T, x)) xe at N( d + (τ, x)). (7) Here, N is the Normal Cumulative Distribution density and the parameters, d + and d are given by d + = d + σ T = 1 [log σ xk (r T ) ] σ2 T.(8) The function bsm in the file Equity- MainFX.cpp describes the implementation of the above closed form Black Scholes Merton model. The output is as follows, Closed form option price = (9) III. VANILLA CALL : MONTE CARLO WITH PARK-MILLER AND ANTITHETIC SAMPLING Park-Miller is one of the many random number generators thats are used to produce random samples for Monte Carlo simulation. It is on of the Linear Congruential Generators (LCG). It has a period of, (10) The general form of a LCG generator is, x i+1 = (ax i + c) mod m 1 (11) u i+1 = x i+1 /m 1 (12) S(T ) = S(0)e (r a 1 2 σ2 )T +σw (T ) (5) x = initial seed

2 2 a = multiplier m = modulus c = shift The following are the values for the variables m = , a = (13) Park Miller s uniform random number generator is implemented by Mark Joshi. We then pass these uniform values to inverse cumulative distribution to get normally distributed variables. We use antithetic sampling which is described below. The files ParkMiller.h, Park- Miller.cpp, Antithetic.h and Antithetic.cpp implements the function for the above formula as a class. In Antithetic sampling we take one sample using Park Miller and the use the negative of the same value as second sample. In this was we get the following equation S(t i+1 ) = S(t i )(1 + rτ + σ T Z i+1 ) (14) S(t i+1 ) = S(t i )(1 + rτ σ T Z i+1 ) (15) Using the above formula, we can reduce the variance of the samples.the result of Monte Carlo simulation on using the above variance reduction technique. Ŷ AV = 1 + Y i n (Σni=1(Ỹi )) (16) 2 The output for out call option is, MC vanilla call with P ark Miller = 9.20 (17) IV. QUASI MONTE CARLO WITH SOBOL SEQUENCE A major drawback of Monte Carlo integration with pseudo-random numbers is given by the fact that the error term scales only as 1/ N.This is inherent to methods based on random numbers.this leads to the idea to choose the points deterministically such that to minimize the integration error.low-discrepancy sequence is a sequence with the property that for all values of N, its subsequence x1,..., xn has a low discrepancy. Roughly speaking, the discrepancy of a sequence is low if the number of points in the sequence falling into an arbitrary set B is close to proportional to the measure of B, as would happen on average (but not for particular samples) in the case of a uniform distribution[5]. We now have the main theorem of quasi-monte Carlo integration: If f has bounded variation on [0, 1] d then for any x 1,..., x N [0, 1] d we have 1 N N n=1 f(x n ) dxf(x) V (f)d (x 1,..., x N ). (18) Sobol sequences [6] are obtained by first choosing a primitive polynomial over Z of degree g: P = x g + a 1 x g a g 1 x + 1, (19) where each a i is either 0 or 1. The coefficients a i are used in the recurrence relation v i = a 1 v i 1 a 2 v i 2... a g 1 v i g+1 v i g [v i g /2 (20) g ], where denotes the bitwise exclusive-or operation and each v i is a number which can be written as v i = m i /(2 i ) with 0 < m i < 2 i. Consequetive quasi-random numbers are then obtained from the relation x n+1 = x n v c, (21) where the index c is equal to the place of the rightmost zero-bit in the binary representation of n. For example n = 11 has the binary representation 1011 and the rightmost zero-bit is the third one. Therefore c = 3 in this case. For a primitive polynomial of degree g we also have to choose the first g values for the m i. The only restriction is that the m i are all odd and m i < 2 i. There is an alternative way of computing x n : x n = g 1 v 1 g 2 v 2... (22) where...g 3 g 2 g 1 is the Gray code representation of n. The basic property of the Gray code is that the representations for n and n + 1 differ in only one position. The Gray code representation can be obtained from the binary representation according to...g 3 g 2 g 1 =...b 3 b 2 b 1...b 4 b 3 b 2. (23) The above description of the sobol sequence generation was taken from [2].We have used Sobol sequence generator by S.Joe and R.Y.Kuo. We pass a file with the primitive polynomial and values of all the coefficient. This Sobol generator is capable of producing vary high dimensional sequences from 0 to 1. In our application we need only 1 dimensional sequence since we are evaluating a vanilla call option at expiry. We have implemented a function MCSobol in Sobol.cpp which uses sobol sequences to implement Quasi Monte Carlo simulation. The function sobolpoints returns an array with sobol sequences which are used for option price calculation. The price with this method is, QM C vanilla call with Sobol sequences = (24) As we can see that the option price using sobol sequences and quasi monti carlo method is the closest to the closed formed solution. V. ASIAN CALL OPTIONS Asian options are path-dependent options, with payoffs that depend on the average price of the underlying

3 3 asset or the average exercise price. There are two categories or types of Asian options: average rate options (also known as average price options) and average strike options. The payoffs depend on the average price of the underlying asset over a predetermined time period. An average is less volatile than the underlying asset, therefore making Asian options less expensive than standard European options. Asian options are commonly used in currency and commodity markets. The payoff of asian option continuously averaged is, ( + 1 T S u du K) (25) T 0 The payoff of asian option using Arithmetic averaging is, ( 1 T + N S(t i ) K) (26) n=1 The Geometric average is the nth root of the product of the n sample points. The Arithmetic average is the sum of the stock values divided by the number of sampling points. Although Geometric Asian options are not commonly used in practice, they are often used as a good initial guess for the price of arithmetic Asian options. This technique is used to improve the convergence rate of the Monte Carlo model when pricing arithmetic Asian options.the above description of asian option was taken from [9] and the payoff of asian option using Geometric averaging is, ( exp( 1 T + N ln(s(t)) K) (27) n=1 The closed form C++ code for geometric averaged asian option is given in asianclosed().we have also implemented C++ pricing using Monte Carlo simulation with Park-Miller uniforms with antithetics for Arithmetic, Geometric Asian call and using Quasi Monte Carlo technique with Sobol sequences. The results are below For Geometric Asian call options Closed form geometric Asiancall = 3.80 (33) MC geometric, P ark Miller, antithetics = 3.03 (34) QMC geometric, Sobol sequence = 3.92 (35) For Geometric Asian call options MC arithmetic, P ark Miller, antithetics = 4.09(36) QM C arithmetic, Sobol sequence = 4.22(37) VI. BROWNIAN BRIDGE WITH TERMINAL STRATIFICATION The brownian bridge path generation is usually used in conjunction with variance reduction techniques like stratified sampling. Suppose W (t) is a R-valued Brownian motion and suppose we know the some values of Brownian motion, W (s 1 ) = x 1,..., W (s k ) = x k (38) we can find the value of W (s) where s in (s i, s i+1 ) conditional on the k values. This conditional distribution of W (s) is on W (s i ) = x i (39) W (s i+1 ) = x i+1 (40) Asian option with Geometric averaging also has a closed form solution which we have implemented in the C++ code. The closed form formula is given below, V = V (0)N(d 1 ) e rt KN(d 2 ) (28) (s s i )) + where ( ) 1 1 V (0) = D(t)exp (N + 1)v t N (N + 1)(2N + 1)σ2 twhere Z is Normally distributed random variable. (29) Stratified (Regional) sampling. σ avg = D(t) = e rt S(0) (30) σ 1 N(N + 1)(2N + 1) (31) N 3/2 6 v = r d σ2 2 (32) and is given by, W (s) = W (s i ) + (s s i )W (s i+1 ) (41) (42) Stratified sampling is a divide-and-conquer strategy which partitions the state space into regions, and then a sampling plan is devised for each region. Moreover, common sense suggests that the smaller the region, the less variance that should exist in that region, and so a variance reduction may be achievable in each of the smaller regions that partition the entire space.

4 4 Divide U into k subdivisions, or strata, U i, where k is the total number of possible combinations described above. We have U = U 1 U 2... U k such that U i U j =, for all i j and 1i, j k. if we let N i = U i, then N = k N i. i=1 Draw a sample S i from each stratum U i. The above description of asian option was taken from [8] The algorithm for implementing Brownian bridge with Stratification is given below (43) for i = 1,..., k, (44) generate U nif[0, 1]; (45) V = (i 1 + U)/K; (46) W (t m ) = t m φ 1 (47) a = W (s i ) + (s s i )W (s i+1 ) (48) b = (s s i )) (49) W i = a + bz (50) return(w (t 1 )...W (t m )) (51) We have implemented this algorithm in the file GeometricBrownianPath.h and cpp. It is implemented as a class and uses different member function to calculate prices of Vanilla and Asian options. We have used the above algorithm in conjunction with Park-Miller uniforms. For vanilla Asian call options (52) MC V anilla, P ark Miller, stratified = 9.05 (53) For Geometric Asian call options (54) MC geometric, P ark Miller, stratified = 3.53 (55) For Arithmetic Asian call options (56) MC arithmetic, P ark Miller, stratified = 3.82 (57) VII. ANSWER TO THE QUESTIONS Brownian Bridge Suppose W (t) is a R-valued Brownian motion and suppose we know the some values of Brownian motion, W (s 1 ) = x 1,..., W (s k ) = x k (58) we can find the value of W (s) where s in (s i, s i+1 ) conditional on the k values. This conditional distribution of W (s) is on and is given by, W (s i ) = x i (59) W (s i+1 ) = x i+1 (60) W (s) = W (s i ) + (s s i )W (s i+1 ) (s s i )) + (61) (62) The brownian motions here are conditionally dependent. We begin by W (t 0 ) = 0 and we use inverse CDF to calculate W (t m ) and we use the above conditional distribution to calculate the intermediate Brownian motion. In this way we can calculate the brownian motions at all the required points. We use the algorithm described in the above section to pre-generate brownian motions at all the required intermediate points and the use them to calculate the spot process in the following way, logs(t i ) = logs(t i 1 ) + (r σ2 2 ) (t i t i 1 ) (63) +σ (W (t i) W (t i 1 )) (64) As we can see we use the regenerated pairs of brownian motions to calculate the spot process. Joshi s Method Mark Joshi uses the function GetGaussian to get a Independent gaussian variables and stores it in the array MJArray names Variates. This is in contradiction to the Brownian motions generated by Brownian Bridge where they are conditionally dependent on two neighboring brownian motion. Mark Joshi uses random numbers and implements the following equation to replace W(T), W (T ) = tn(0, 1) (65) And his code uses the above substitution of multiplying standard deviation with Normally distributed random variable. ) logs(t i ) = logs(t i 1 ) + (r σ2 (t i t i 1 ) (66) 2 ( ) +σ tn(0, 1) (67) Effect of varying strata size We have varied the number of strata, and hence the strata size and calculated the option price. We used the following number of strata, 1,50,100,500 and The results of varying the number of strata are presented in the second table below. We find that varying the size changes the answers marginally. The change is not significant. Besides the most optimal answers are found around the strata size of 100.

5 5 VIII. BENCHMARKING We have used many spreadsheet based model to benchmark our results. The summary go the benchmarking is given below and is also tabularised below. Numerix and the Excel spreadsheets by Haug does not provide the user the ability to produce Sobol sequences and also they use Arithmetic averaging. Hence we have benchmarked our results using the closed form and monte carlo simulations in Numerix and Haug VBA sheets.we have also used Kerry Back s spreadsheet for closed form solution to geometric averaging Asian option as well as Curran approximation for Arithmetic averaging.[7] N umerix option price vanilla = 9.08 (68) Haug Excel option price, vanilla = 9.05 (69) N umerix option price Asian = 4.66 (70) Haug Excel option price, Asian = 4.11 (71) Kerry Back s closed form = 3.81 (72) Curran approximation, arithmetic = 4.12 (73)

6 6 TABLE I: Vanilla and Asian Call pricing using Methods for S(0)=100 and K=110 Option Closed Form Park-Miller,Antithetic Park-Miller with Stratified Sobol sequence Numerix Haug European Vanilla Call Asian Geometric Call Asian Arithmetic Call TABLE II: Effect of varying Strata size S(0)=100 and K=110 Strata size Vanilla call Asian option, Geometric Asian option, Arithmetic

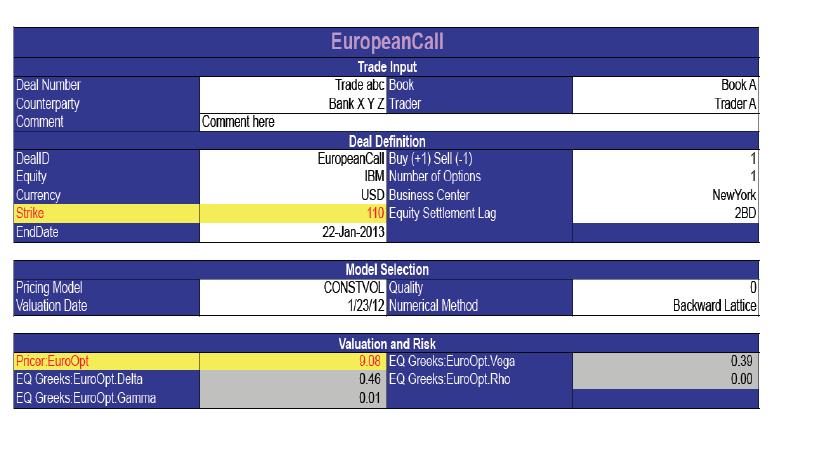

7 FIG. 1: Vanilla call 7

8 8 FIG. 2: Curran Approximation. FIG. 3: Closed form Asian, Back s model.

9 FIG. 4: Haug s model 9

10 [1] wwwthep.physik.uni-mainz.de/ stefanw/download/lecture [2] M.S. Joshi, C++ design Patterns and Derivative Pricing, (Wiley 2008). [3] S.E. Shreve, Stochastic Calculus for Finance II Continuous Time Models, (Springer, 2004). [4] Wikipedia page for low discrepancy sequence [5] I M Sobol, USSR comp. Math [6] used Daksh Aggrawal s computer for some of the benchmarking [7] ebert/teaching/lectures/552/ [8] rss.acs.unt.edu/rdoc/library/fexoticoptions 10

Math Computational Finance Double barrier option pricing using Quasi Monte Carlo and Brownian Bridge methods

. Math 623 - Computational Finance Double barrier option pricing using Quasi Monte Carlo and Brownian Bridge methods Pratik Mehta pbmehta@eden.rutgers.edu Masters of Science in Mathematical Finance Department

. Math 623 - Computational Finance Double barrier option pricing using Quasi Monte Carlo and Brownian Bridge methods Pratik Mehta pbmehta@eden.rutgers.edu Masters of Science in Mathematical Finance Department

Math Option pricing using Quasi Monte Carlo simulation

. Math 623 - Option pricing using Quasi Monte Carlo simulation Pratik Mehta pbmehta@eden.rutgers.edu Masters of Science in Mathematical Finance Department of Mathematics, Rutgers University This paper

. Math 623 - Option pricing using Quasi Monte Carlo simulation Pratik Mehta pbmehta@eden.rutgers.edu Masters of Science in Mathematical Finance Department of Mathematics, Rutgers University This paper

Math Computational Finance Barrier option pricing using Finite Difference Methods (FDM)

") . Math 623 - Computational Finance Barrier option pricing using Finite Difference Methods (FDM) Pratik Mehta pbmehta@eden.rutgers.edu Masters of Science in Mathematical Finance Department of Mathematics,

. Math 623 - Computational Finance Barrier option pricing using Finite Difference Methods (FDM) Pratik Mehta pbmehta@eden.rutgers.edu Masters of Science in Mathematical Finance Department of Mathematics,

2.1 Mathematical Basis: Risk-Neutral Pricing

Chapter Monte-Carlo Simulation.1 Mathematical Basis: Risk-Neutral Pricing Suppose that F T is the payoff at T for a European-type derivative f. Then the price at times t before T is given by f t = e r(t

Chapter Monte-Carlo Simulation.1 Mathematical Basis: Risk-Neutral Pricing Suppose that F T is the payoff at T for a European-type derivative f. Then the price at times t before T is given by f t = e r(t

Computational Finance Improving Monte Carlo

Computational Finance Improving Monte Carlo School of Mathematics 2018 Monte Carlo so far... Simple to program and to understand Convergence is slow, extrapolation impossible. Forward looking method ideal

Computational Finance Improving Monte Carlo School of Mathematics 2018 Monte Carlo so far... Simple to program and to understand Convergence is slow, extrapolation impossible. Forward looking method ideal

ELEMENTS OF MONTE CARLO SIMULATION

APPENDIX B ELEMENTS OF MONTE CARLO SIMULATION B. GENERAL CONCEPT The basic idea of Monte Carlo simulation is to create a series of experimental samples using a random number sequence. According to the

APPENDIX B ELEMENTS OF MONTE CARLO SIMULATION B. GENERAL CONCEPT The basic idea of Monte Carlo simulation is to create a series of experimental samples using a random number sequence. According to the

Chapter 2 Uncertainty Analysis and Sampling Techniques

Chapter 2 Uncertainty Analysis and Sampling Techniques The probabilistic or stochastic modeling (Fig. 2.) iterative loop in the stochastic optimization procedure (Fig..4 in Chap. ) involves:. Specifying

Chapter 2 Uncertainty Analysis and Sampling Techniques The probabilistic or stochastic modeling (Fig. 2.) iterative loop in the stochastic optimization procedure (Fig..4 in Chap. ) involves:. Specifying

Monte Carlo Methods in Financial Engineering

Paul Glassennan Monte Carlo Methods in Financial Engineering With 99 Figures

Paul Glassennan Monte Carlo Methods in Financial Engineering With 99 Figures

MONTE CARLO EXTENSIONS

MONTE CARLO EXTENSIONS School of Mathematics 2013 OUTLINE 1 REVIEW OUTLINE 1 REVIEW 2 EXTENSION TO MONTE CARLO OUTLINE 1 REVIEW 2 EXTENSION TO MONTE CARLO 3 SUMMARY MONTE CARLO SO FAR... Simple to program

MONTE CARLO EXTENSIONS School of Mathematics 2013 OUTLINE 1 REVIEW OUTLINE 1 REVIEW 2 EXTENSION TO MONTE CARLO OUTLINE 1 REVIEW 2 EXTENSION TO MONTE CARLO 3 SUMMARY MONTE CARLO SO FAR... Simple to program

EFFICIENT MONTE CARLO ALGORITHM FOR PRICING BARRIER OPTIONS

Commun. Korean Math. Soc. 23 (2008), No. 2, pp. 285 294 EFFICIENT MONTE CARLO ALGORITHM FOR PRICING BARRIER OPTIONS Kyoung-Sook Moon Reprinted from the Communications of the Korean Mathematical Society

Commun. Korean Math. Soc. 23 (2008), No. 2, pp. 285 294 EFFICIENT MONTE CARLO ALGORITHM FOR PRICING BARRIER OPTIONS Kyoung-Sook Moon Reprinted from the Communications of the Korean Mathematical Society

Definition Pricing Risk management Second generation barrier options. Barrier Options. Arfima Financial Solutions

Arfima Financial Solutions Contents Definition 1 Definition 2 3 4 Contenido Definition 1 Definition 2 3 4 Definition Definition: A barrier option is an option on the underlying asset that is activated

Arfima Financial Solutions Contents Definition 1 Definition 2 3 4 Contenido Definition 1 Definition 2 3 4 Definition Definition: A barrier option is an option on the underlying asset that is activated

Monte Carlo Methods for Uncertainty Quantification

Monte Carlo Methods for Uncertainty Quantification Abdul-Lateef Haji-Ali Based on slides by: Mike Giles Mathematical Institute, University of Oxford Contemporary Numerical Techniques Haji-Ali (Oxford)

Monte Carlo Methods for Uncertainty Quantification Abdul-Lateef Haji-Ali Based on slides by: Mike Giles Mathematical Institute, University of Oxford Contemporary Numerical Techniques Haji-Ali (Oxford)

NEWCASTLE UNIVERSITY SCHOOL OF MATHEMATICS, STATISTICS & PHYSICS SEMESTER 1 SPECIMEN 2 MAS3904. Stochastic Financial Modelling. Time allowed: 2 hours

NEWCASTLE UNIVERSITY SCHOOL OF MATHEMATICS, STATISTICS & PHYSICS SEMESTER 1 SPECIMEN 2 Stochastic Financial Modelling Time allowed: 2 hours Candidates should attempt all questions. Marks for each question

NEWCASTLE UNIVERSITY SCHOOL OF MATHEMATICS, STATISTICS & PHYSICS SEMESTER 1 SPECIMEN 2 Stochastic Financial Modelling Time allowed: 2 hours Candidates should attempt all questions. Marks for each question

Stochastic Differential Equations in Finance and Monte Carlo Simulations

Stochastic Differential Equations in Finance and Department of Statistics and Modelling Science University of Strathclyde Glasgow, G1 1XH China 2009 Outline Stochastic Modelling in Asset Prices 1 Stochastic

Stochastic Differential Equations in Finance and Department of Statistics and Modelling Science University of Strathclyde Glasgow, G1 1XH China 2009 Outline Stochastic Modelling in Asset Prices 1 Stochastic

1.1 Basic Financial Derivatives: Forward Contracts and Options

Chapter 1 Preliminaries 1.1 Basic Financial Derivatives: Forward Contracts and Options A derivative is a financial instrument whose value depends on the values of other, more basic underlying variables

Chapter 1 Preliminaries 1.1 Basic Financial Derivatives: Forward Contracts and Options A derivative is a financial instrument whose value depends on the values of other, more basic underlying variables

Computational Finance

Path Dependent Options Computational Finance School of Mathematics 2018 The Random Walk One of the main assumption of the Black-Scholes framework is that the underlying stock price follows a random walk

Path Dependent Options Computational Finance School of Mathematics 2018 The Random Walk One of the main assumption of the Black-Scholes framework is that the underlying stock price follows a random walk

Optimal Search for Parameters in Monte Carlo Simulation for Derivative Pricing

Optimal Search for Parameters in Monte Carlo Simulation for Derivative Pricing Prof. Chuan-Ju Wang Department of Computer Science University of Taipei Joint work with Prof. Ming-Yang Kao March 28, 2014

Optimal Search for Parameters in Monte Carlo Simulation for Derivative Pricing Prof. Chuan-Ju Wang Department of Computer Science University of Taipei Joint work with Prof. Ming-Yang Kao March 28, 2014

Computer Exercise 2 Simulation

Lund University with Lund Institute of Technology Valuation of Derivative Assets Centre for Mathematical Sciences, Mathematical Statistics Fall 2017 Computer Exercise 2 Simulation This lab deals with pricing

Lund University with Lund Institute of Technology Valuation of Derivative Assets Centre for Mathematical Sciences, Mathematical Statistics Fall 2017 Computer Exercise 2 Simulation This lab deals with pricing

On the Scrambled Sobol sequences Lecture Notes in Computer Science 3516, , Springer 2005

On the Scrambled Sobol sequences Lecture Notes in Computer Science 3516, 775-782, Springer 2005 On the Scrambled Soboĺ Sequence Hongmei Chi 1, Peter Beerli 2, Deidre W. Evans 1, and Micheal Mascagni 2

On the Scrambled Sobol sequences Lecture Notes in Computer Science 3516, 775-782, Springer 2005 On the Scrambled Soboĺ Sequence Hongmei Chi 1, Peter Beerli 2, Deidre W. Evans 1, and Micheal Mascagni 2

Valuation of performance-dependent options in a Black- Scholes framework

Valuation of performance-dependent options in a Black- Scholes framework Thomas Gerstner, Markus Holtz Institut für Numerische Simulation, Universität Bonn, Germany Ralf Korn Fachbereich Mathematik, TU

Valuation of performance-dependent options in a Black- Scholes framework Thomas Gerstner, Markus Holtz Institut für Numerische Simulation, Universität Bonn, Germany Ralf Korn Fachbereich Mathematik, TU

Asian Option Pricing: Monte Carlo Control Variate. A discrete arithmetic Asian call option has the payoff. S T i N N + 1

Asian Option Pricing: Monte Carlo Control Variate A discrete arithmetic Asian call option has the payoff ( 1 N N + 1 i=0 S T i N K ) + A discrete geometric Asian call option has the payoff [ N i=0 S T

Asian Option Pricing: Monte Carlo Control Variate A discrete arithmetic Asian call option has the payoff ( 1 N N + 1 i=0 S T i N K ) + A discrete geometric Asian call option has the payoff [ N i=0 S T

Computer Exercise 2 Simulation

Lund University with Lund Institute of Technology Valuation of Derivative Assets Centre for Mathematical Sciences, Mathematical Statistics Spring 2010 Computer Exercise 2 Simulation This lab deals with

Lund University with Lund Institute of Technology Valuation of Derivative Assets Centre for Mathematical Sciences, Mathematical Statistics Spring 2010 Computer Exercise 2 Simulation This lab deals with

King s College London

King s College London University Of London This paper is part of an examination of the College counting towards the award of a degree. Examinations are governed by the College Regulations under the authority

King s College London University Of London This paper is part of an examination of the College counting towards the award of a degree. Examinations are governed by the College Regulations under the authority

Monte Carlo Methods in Finance

Monte Carlo Methods in Finance Peter Jackel JOHN WILEY & SONS, LTD Preface Acknowledgements Mathematical Notation xi xiii xv 1 Introduction 1 2 The Mathematics Behind Monte Carlo Methods 5 2.1 A Few Basic

Monte Carlo Methods in Finance Peter Jackel JOHN WILEY & SONS, LTD Preface Acknowledgements Mathematical Notation xi xiii xv 1 Introduction 1 2 The Mathematics Behind Monte Carlo Methods 5 2.1 A Few Basic

Valuation of Asian Option. Qi An Jingjing Guo

Valuation of Asian Option Qi An Jingjing Guo CONTENT Asian option Pricing Monte Carlo simulation Conclusion ASIAN OPTION Definition of Asian option always emphasizes the gist that the payoff depends on

Valuation of Asian Option Qi An Jingjing Guo CONTENT Asian option Pricing Monte Carlo simulation Conclusion ASIAN OPTION Definition of Asian option always emphasizes the gist that the payoff depends on

Monte Carlo Methods for Uncertainty Quantification

Monte Carlo Methods for Uncertainty Quantification Abdul-Lateef Haji-Ali Based on slides by: Mike Giles Mathematical Institute, University of Oxford Contemporary Numerical Techniques Haji-Ali (Oxford)

Monte Carlo Methods for Uncertainty Quantification Abdul-Lateef Haji-Ali Based on slides by: Mike Giles Mathematical Institute, University of Oxford Contemporary Numerical Techniques Haji-Ali (Oxford)

Assignment - Exotic options

Computational Finance, Fall 2014 1 (6) Institutionen för informationsteknologi Besöksadress: MIC, Polacksbacken Lägerhyddvägen 2 Postadress: Box 337 751 05 Uppsala Telefon: 018 471 0000 (växel) Telefax:

Computational Finance, Fall 2014 1 (6) Institutionen för informationsteknologi Besöksadress: MIC, Polacksbacken Lägerhyddvägen 2 Postadress: Box 337 751 05 Uppsala Telefon: 018 471 0000 (växel) Telefax:

Numerical schemes for SDEs

Lecture 5 Numerical schemes for SDEs Lecture Notes by Jan Palczewski Computational Finance p. 1 A Stochastic Differential Equation (SDE) is an object of the following type dx t = a(t,x t )dt + b(t,x t

Lecture 5 Numerical schemes for SDEs Lecture Notes by Jan Palczewski Computational Finance p. 1 A Stochastic Differential Equation (SDE) is an object of the following type dx t = a(t,x t )dt + b(t,x t

Importance Sampling for Option Pricing. Steven R. Dunbar. Put Options. Monte Carlo Method. Importance. Sampling. Examples.

for for January 25, 2016 1 / 26 Outline for 1 2 3 4 2 / 26 Put Option for A put option is the right to sell an asset at an established price at a certain time. The established price is the strike price,

for for January 25, 2016 1 / 26 Outline for 1 2 3 4 2 / 26 Put Option for A put option is the right to sell an asset at an established price at a certain time. The established price is the strike price,

Market interest-rate models

Market interest-rate models Marco Marchioro www.marchioro.org November 24 th, 2012 Market interest-rate models 1 Lecture Summary No-arbitrage models Detailed example: Hull-White Monte Carlo simulations

Market interest-rate models Marco Marchioro www.marchioro.org November 24 th, 2012 Market interest-rate models 1 Lecture Summary No-arbitrage models Detailed example: Hull-White Monte Carlo simulations

The Black-Scholes Model

The Black-Scholes Model Liuren Wu Options Markets (Hull chapter: 12, 13, 14) Liuren Wu ( c ) The Black-Scholes Model colorhmoptions Markets 1 / 17 The Black-Scholes-Merton (BSM) model Black and Scholes

The Black-Scholes Model Liuren Wu Options Markets (Hull chapter: 12, 13, 14) Liuren Wu ( c ) The Black-Scholes Model colorhmoptions Markets 1 / 17 The Black-Scholes-Merton (BSM) model Black and Scholes

Math 623 (IOE 623), Winter 2008: Final exam

, Winter 2008: Final exam") Math 623 (IOE 623), Winter 2008: Final exam Name: Student ID: This is a closed book exam. You may bring up to ten one sided A4 pages of notes to the exam. You may also use a calculator but not its memory

Math 623 (IOE 623), Winter 2008: Final exam Name: Student ID: This is a closed book exam. You may bring up to ten one sided A4 pages of notes to the exam. You may also use a calculator but not its memory

Quasi-Monte Carlo for Finance

Quasi-Monte Carlo for Finance Peter Kritzer Johann Radon Institute for Computational and Applied Mathematics (RICAM) Austrian Academy of Sciences Linz, Austria NCTS, Taipei, November 2016 Peter Kritzer

Quasi-Monte Carlo for Finance Peter Kritzer Johann Radon Institute for Computational and Applied Mathematics (RICAM) Austrian Academy of Sciences Linz, Austria NCTS, Taipei, November 2016 Peter Kritzer

Gamma. The finite-difference formula for gamma is

Gamma The finite-difference formula for gamma is [ P (S + ɛ) 2 P (S) + P (S ɛ) e rτ E ɛ 2 ]. For a correlation option with multiple underlying assets, the finite-difference formula for the cross gammas

Gamma The finite-difference formula for gamma is [ P (S + ɛ) 2 P (S) + P (S ɛ) e rτ E ɛ 2 ]. For a correlation option with multiple underlying assets, the finite-difference formula for the cross gammas

Pricing of European and Asian options with Monte Carlo simulations

Pricing of European and Asian options with Monte Carlo simulations Variance reduction and low-discrepancy techniques Alexander Ramstro m Umea University Fall 2017 Bachelor Thesis, 15 ECTS Department of

Pricing of European and Asian options with Monte Carlo simulations Variance reduction and low-discrepancy techniques Alexander Ramstro m Umea University Fall 2017 Bachelor Thesis, 15 ECTS Department of

Market Volatility and Risk Proxies

Market Volatility and Risk Proxies... an introduction to the concepts 019 Gary R. Evans. This slide set by Gary R. Evans is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International

Market Volatility and Risk Proxies... an introduction to the concepts 019 Gary R. Evans. This slide set by Gary R. Evans is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International

Stochastic Modelling in Finance

in Finance Department of Mathematics and Statistics University of Strathclyde Glasgow, G1 1XH April 2010 Outline and Probability 1 and Probability 2 Linear modelling Nonlinear modelling 3 The Black Scholes

in Finance Department of Mathematics and Statistics University of Strathclyde Glasgow, G1 1XH April 2010 Outline and Probability 1 and Probability 2 Linear modelling Nonlinear modelling 3 The Black Scholes

Optimized Least-squares Monte Carlo (OLSM) for Measuring Counterparty Credit Exposure of American-style Options

for Measuring Counterparty Credit Exposure of American-style Options") Optimized Least-squares Monte Carlo (OLSM) for Measuring Counterparty Credit Exposure of American-style Options Kin Hung (Felix) Kan 1 Greg Frank 3 Victor Mozgin 3 Mark Reesor 2 1 Department of Applied

Optimized Least-squares Monte Carlo (OLSM) for Measuring Counterparty Credit Exposure of American-style Options Kin Hung (Felix) Kan 1 Greg Frank 3 Victor Mozgin 3 Mark Reesor 2 1 Department of Applied

10. Monte Carlo Methods

10. Monte Carlo Methods 1. Introduction. Monte Carlo simulation is an important tool in computational finance. It may be used to evaluate portfolio management rules, to price options, to simulate hedging

10. Monte Carlo Methods 1. Introduction. Monte Carlo simulation is an important tool in computational finance. It may be used to evaluate portfolio management rules, to price options, to simulate hedging

King s College London

King s College London University Of London This paper is part of an examination of the College counting towards the award of a degree. Examinations are governed by the College Regulations under the authority

King s College London University Of London This paper is part of an examination of the College counting towards the award of a degree. Examinations are governed by the College Regulations under the authority

1 The continuous time limit

Derivative Securities, Courant Institute, Fall 2008 http://www.math.nyu.edu/faculty/goodman/teaching/derivsec08/index.html Jonathan Goodman and Keith Lewis Supplementary notes and comments, Section 3 1

Derivative Securities, Courant Institute, Fall 2008 http://www.math.nyu.edu/faculty/goodman/teaching/derivsec08/index.html Jonathan Goodman and Keith Lewis Supplementary notes and comments, Section 3 1

Week 1 Quantitative Analysis of Financial Markets Distributions B

Week 1 Quantitative Analysis of Financial Markets Distributions B Christopher Ting http://www.mysmu.edu/faculty/christophert/ Christopher Ting : christopherting@smu.edu.sg : 6828 0364 : LKCSB 5036 October

Week 1 Quantitative Analysis of Financial Markets Distributions B Christopher Ting http://www.mysmu.edu/faculty/christophert/ Christopher Ting : christopherting@smu.edu.sg : 6828 0364 : LKCSB 5036 October

Financial Risk Forecasting Chapter 7 Simulation methods for VaR for options and bonds

Financial Risk Forecasting Chapter 7 Simulation methods for VaR for options and bonds Jon Danielsson 2017 London School of Economics To accompany Financial Risk Forecasting www.financialriskforecasting.com

Financial Risk Forecasting Chapter 7 Simulation methods for VaR for options and bonds Jon Danielsson 2017 London School of Economics To accompany Financial Risk Forecasting www.financialriskforecasting.com

Lecture outline. Monte Carlo Methods for Uncertainty Quantification. Importance Sampling. Importance Sampling

Lecture outline Monte Carlo Methods for Uncertainty Quantification Mike Giles Mathematical Institute, University of Oxford KU Leuven Summer School on Uncertainty Quantification Lecture 2: Variance reduction

Lecture outline Monte Carlo Methods for Uncertainty Quantification Mike Giles Mathematical Institute, University of Oxford KU Leuven Summer School on Uncertainty Quantification Lecture 2: Variance reduction

1 Geometric Brownian motion

Copyright c 05 by Karl Sigman Geometric Brownian motion Note that since BM can take on negative values, using it directly for modeling stock prices is questionable. There are other reasons too why BM is

Copyright c 05 by Karl Sigman Geometric Brownian motion Note that since BM can take on negative values, using it directly for modeling stock prices is questionable. There are other reasons too why BM is

MATH3075/3975 FINANCIAL MATHEMATICS TUTORIAL PROBLEMS

MATH307/37 FINANCIAL MATHEMATICS TUTORIAL PROBLEMS School of Mathematics and Statistics Semester, 04 Tutorial problems should be used to test your mathematical skills and understanding of the lecture material.

MATH307/37 FINANCIAL MATHEMATICS TUTORIAL PROBLEMS School of Mathematics and Statistics Semester, 04 Tutorial problems should be used to test your mathematical skills and understanding of the lecture material.

Results for option pricing

Results for option pricing [o,v,b]=optimal(rand(1,100000 Estimators = 0.4619 0.4617 0.4618 0.4613 0.4619 o = 0.46151 % best linear combination (true value=0.46150 v = 1.1183e-005 %variance per uniform

Results for option pricing [o,v,b]=optimal(rand(1,100000 Estimators = 0.4619 0.4617 0.4618 0.4613 0.4619 o = 0.46151 % best linear combination (true value=0.46150 v = 1.1183e-005 %variance per uniform

The Black-Scholes Model

The Black-Scholes Model Liuren Wu Options Markets Liuren Wu ( c ) The Black-Merton-Scholes Model colorhmoptions Markets 1 / 18 The Black-Merton-Scholes-Merton (BMS) model Black and Scholes (1973) and Merton

The Black-Scholes Model Liuren Wu Options Markets Liuren Wu ( c ) The Black-Merton-Scholes Model colorhmoptions Markets 1 / 18 The Black-Merton-Scholes-Merton (BMS) model Black and Scholes (1973) and Merton

Module 10:Application of stochastic processes in areas like finance Lecture 36:Black-Scholes Model. Stochastic Differential Equation.

Stochastic Differential Equation Consider. Moreover partition the interval into and define, where. Now by Rieman Integral we know that, where. Moreover. Using the fundamentals mentioned above we can easily

Stochastic Differential Equation Consider. Moreover partition the interval into and define, where. Now by Rieman Integral we know that, where. Moreover. Using the fundamentals mentioned above we can easily

Math 416/516: Stochastic Simulation

Math 416/516: Stochastic Simulation Haijun Li lih@math.wsu.edu Department of Mathematics Washington State University Week 13 Haijun Li Math 416/516: Stochastic Simulation Week 13 1 / 28 Outline 1 Simulation

Math 416/516: Stochastic Simulation Haijun Li lih@math.wsu.edu Department of Mathematics Washington State University Week 13 Haijun Li Math 416/516: Stochastic Simulation Week 13 1 / 28 Outline 1 Simulation

As we saw in Chapter 12, one of the many uses of Monte Carlo simulation by

Financial Modeling with Crystal Ball and Excel, Second Edition By John Charnes Copyright 2012 by John Charnes APPENDIX C Variance Reduction Techniques As we saw in Chapter 12, one of the many uses of Monte

Financial Modeling with Crystal Ball and Excel, Second Edition By John Charnes Copyright 2012 by John Charnes APPENDIX C Variance Reduction Techniques As we saw in Chapter 12, one of the many uses of Monte

Contents Critique 26. portfolio optimization 32

Contents Preface vii 1 Financial problems and numerical methods 3 1.1 MATLAB environment 4 1.1.1 Why MATLAB? 5 1.2 Fixed-income securities: analysis and portfolio immunization 6 1.2.1 Basic valuation of

Contents Preface vii 1 Financial problems and numerical methods 3 1.1 MATLAB environment 4 1.1.1 Why MATLAB? 5 1.2 Fixed-income securities: analysis and portfolio immunization 6 1.2.1 Basic valuation of

Brooks, Introductory Econometrics for Finance, 3rd Edition

P1.T2. Quantitative Analysis Brooks, Introductory Econometrics for Finance, 3rd Edition Bionic Turtle FRM Study Notes Sample By David Harper, CFA FRM CIPM and Deepa Raju www.bionicturtle.com Chris Brooks,

P1.T2. Quantitative Analysis Brooks, Introductory Econometrics for Finance, 3rd Edition Bionic Turtle FRM Study Notes Sample By David Harper, CFA FRM CIPM and Deepa Raju www.bionicturtle.com Chris Brooks,

Practical example of an Economic Scenario Generator

Practical example of an Economic Scenario Generator Martin Schenk Actuarial & Insurance Solutions SAV 7 March 2014 Agenda Introduction Deterministic vs. stochastic approach Mathematical model Application

Practical example of an Economic Scenario Generator Martin Schenk Actuarial & Insurance Solutions SAV 7 March 2014 Agenda Introduction Deterministic vs. stochastic approach Mathematical model Application

AN IMPROVED BINOMIAL METHOD FOR PRICING ASIAN OPTIONS

Commun. Korean Math. Soc. 28 (2013), No. 2, pp. 397 406 http://dx.doi.org/10.4134/ckms.2013.28.2.397 AN IMPROVED BINOMIAL METHOD FOR PRICING ASIAN OPTIONS Kyoung-Sook Moon and Hongjoong Kim Abstract. We

Commun. Korean Math. Soc. 28 (2013), No. 2, pp. 397 406 http://dx.doi.org/10.4134/ckms.2013.28.2.397 AN IMPROVED BINOMIAL METHOD FOR PRICING ASIAN OPTIONS Kyoung-Sook Moon and Hongjoong Kim Abstract. We

Lecture 8: The Black-Scholes theory

Lecture 8: The Black-Scholes theory Dr. Roman V Belavkin MSO4112 Contents 1 Geometric Brownian motion 1 2 The Black-Scholes pricing 2 3 The Black-Scholes equation 3 References 5 1 Geometric Brownian motion

Lecture 8: The Black-Scholes theory Dr. Roman V Belavkin MSO4112 Contents 1 Geometric Brownian motion 1 2 The Black-Scholes pricing 2 3 The Black-Scholes equation 3 References 5 1 Geometric Brownian motion

Monte Carlo Simulations

Monte Carlo Simulations Lecture 1 December 7, 2014 Outline Monte Carlo Methods Monte Carlo methods simulate the random behavior underlying the financial models Remember: When pricing you must simulate

Monte Carlo Simulations Lecture 1 December 7, 2014 Outline Monte Carlo Methods Monte Carlo methods simulate the random behavior underlying the financial models Remember: When pricing you must simulate

About Black-Sholes formula, volatility, implied volatility and math. statistics.

About Black-Sholes formula, volatility, implied volatility and math. statistics. Mark Ioffe Abstract We analyze application Black-Sholes formula for calculation of implied volatility from point of view

About Black-Sholes formula, volatility, implied volatility and math. statistics. Mark Ioffe Abstract We analyze application Black-Sholes formula for calculation of implied volatility from point of view

Queens College, CUNY, Department of Computer Science Computational Finance CSCI 365 / 765 Fall 2017 Instructor: Dr. Sateesh Mane.

Queens College, CUNY, Department of Computer Science Computational Finance CSCI 365 / 765 Fall 217 Instructor: Dr. Sateesh Mane c Sateesh R. Mane 217 13 Lecture 13 November 15, 217 Derivation of the Black-Scholes-Merton

Queens College, CUNY, Department of Computer Science Computational Finance CSCI 365 / 765 Fall 217 Instructor: Dr. Sateesh Mane c Sateesh R. Mane 217 13 Lecture 13 November 15, 217 Derivation of the Black-Scholes-Merton

Monte Carlo Methods in Structuring and Derivatives Pricing

Monte Carlo Methods in Structuring and Derivatives Pricing Prof. Manuela Pedio (guest) 20263 Advanced Tools for Risk Management and Pricing Spring 2017 Outline and objectives The basic Monte Carlo algorithm

Monte Carlo Methods in Structuring and Derivatives Pricing Prof. Manuela Pedio (guest) 20263 Advanced Tools for Risk Management and Pricing Spring 2017 Outline and objectives The basic Monte Carlo algorithm

A Moment Matching Approach To The Valuation Of A Volume Weighted Average Price Option

A Moment Matching Approach To The Valuation Of A Volume Weighted Average Price Option Antony Stace Department of Mathematics and MASCOS University of Queensland 15th October 2004 AUSTRALIAN RESEARCH COUNCIL

A Moment Matching Approach To The Valuation Of A Volume Weighted Average Price Option Antony Stace Department of Mathematics and MASCOS University of Queensland 15th October 2004 AUSTRALIAN RESEARCH COUNCIL

Black-Scholes Option Pricing

Black-Scholes Option Pricing The pricing kernel furnishes an alternate derivation of the Black-Scholes formula for the price of a call option. Arbitrage is again the foundation for the theory. 1 Risk-Free

Black-Scholes Option Pricing The pricing kernel furnishes an alternate derivation of the Black-Scholes formula for the price of a call option. Arbitrage is again the foundation for the theory. 1 Risk-Free

Financial Risk Modeling on Low-power Accelerators: Experimental Performance Evaluation of TK1 with FPGA

Financial Risk Modeling on Low-power Accelerators: Experimental Performance Evaluation of TK1 with FPGA Rajesh Bordawekar and Daniel Beece IBM T. J. Watson Research Center 3/17/2015 2014 IBM Corporation

Financial Risk Modeling on Low-power Accelerators: Experimental Performance Evaluation of TK1 with FPGA Rajesh Bordawekar and Daniel Beece IBM T. J. Watson Research Center 3/17/2015 2014 IBM Corporation

Quasi-Monte Carlo Methods in Financial Engineering: An Equivalence Principle and Dimension Reduction

Quasi-Monte Carlo Methods in Financial Engineering: An Equivalence Principle and Dimension Reduction Xiaoqun Wang,2, and Ian H. Sloan 2,3 Department of Mathematical Sciences, Tsinghua University, Beijing

Quasi-Monte Carlo Methods in Financial Engineering: An Equivalence Principle and Dimension Reduction Xiaoqun Wang,2, and Ian H. Sloan 2,3 Department of Mathematical Sciences, Tsinghua University, Beijing

The Pennsylvania State University. The Graduate School. Department of Industrial Engineering AMERICAN-ASIAN OPTION PRICING BASED ON MONTE CARLO

The Pennsylvania State University The Graduate School Department of Industrial Engineering AMERICAN-ASIAN OPTION PRICING BASED ON MONTE CARLO SIMULATION METHOD A Thesis in Industrial Engineering and Operations

The Pennsylvania State University The Graduate School Department of Industrial Engineering AMERICAN-ASIAN OPTION PRICING BASED ON MONTE CARLO SIMULATION METHOD A Thesis in Industrial Engineering and Operations

A No-Arbitrage Theorem for Uncertain Stock Model

Fuzzy Optim Decis Making manuscript No (will be inserted by the editor) A No-Arbitrage Theorem for Uncertain Stock Model Kai Yao Received: date / Accepted: date Abstract Stock model is used to describe

Fuzzy Optim Decis Making manuscript No (will be inserted by the editor) A No-Arbitrage Theorem for Uncertain Stock Model Kai Yao Received: date / Accepted: date Abstract Stock model is used to describe

Multilevel quasi-monte Carlo path simulation

Multilevel quasi-monte Carlo path simulation Michael B. Giles and Ben J. Waterhouse Lluís Antoni Jiménez Rugama January 22, 2014 Index 1 Introduction to MLMC Stochastic model Multilevel Monte Carlo Milstein

Multilevel quasi-monte Carlo path simulation Michael B. Giles and Ben J. Waterhouse Lluís Antoni Jiménez Rugama January 22, 2014 Index 1 Introduction to MLMC Stochastic model Multilevel Monte Carlo Milstein

BROWNIAN MOTION Antonella Basso, Martina Nardon

BROWNIAN MOTION Antonella Basso, Martina Nardon basso@unive.it, mnardon@unive.it Department of Applied Mathematics University Ca Foscari Venice Brownian motion p. 1 Brownian motion Brownian motion plays

BROWNIAN MOTION Antonella Basso, Martina Nardon basso@unive.it, mnardon@unive.it Department of Applied Mathematics University Ca Foscari Venice Brownian motion p. 1 Brownian motion Brownian motion plays

Monte Carlo Methods for Uncertainty Quantification

Monte Carlo Methods for Uncertainty Quantification Mike Giles Mathematical Institute, University of Oxford Contemporary Numerical Techniques Mike Giles (Oxford) Monte Carlo methods 2 1 / 24 Lecture outline

Monte Carlo Methods for Uncertainty Quantification Mike Giles Mathematical Institute, University of Oxford Contemporary Numerical Techniques Mike Giles (Oxford) Monte Carlo methods 2 1 / 24 Lecture outline

The Use of Importance Sampling to Speed Up Stochastic Volatility Simulations

The Use of Importance Sampling to Speed Up Stochastic Volatility Simulations Stan Stilger June 6, 1 Fouque and Tullie use importance sampling for variance reduction in stochastic volatility simulations.

The Use of Importance Sampling to Speed Up Stochastic Volatility Simulations Stan Stilger June 6, 1 Fouque and Tullie use importance sampling for variance reduction in stochastic volatility simulations.

Quasi-Monte Carlo for finance applications

ANZIAM J. 50 (CTAC2008) pp.c308 C323, 2008 C308 Quasi-Monte Carlo for finance applications M. B. Giles 1 F. Y. Kuo 2 I. H. Sloan 3 B. J. Waterhouse 4 (Received 14 August 2008; revised 24 October 2008)

ANZIAM J. 50 (CTAC2008) pp.c308 C323, 2008 C308 Quasi-Monte Carlo for finance applications M. B. Giles 1 F. Y. Kuo 2 I. H. Sloan 3 B. J. Waterhouse 4 (Received 14 August 2008; revised 24 October 2008)

AMH4 - ADVANCED OPTION PRICING. Contents

AMH4 - ADVANCED OPTION PRICING ANDREW TULLOCH Contents 1. Theory of Option Pricing 2 2. Black-Scholes PDE Method 4 3. Martingale method 4 4. Monte Carlo methods 5 4.1. Method of antithetic variances 5

AMH4 - ADVANCED OPTION PRICING ANDREW TULLOCH Contents 1. Theory of Option Pricing 2 2. Black-Scholes PDE Method 4 3. Martingale method 4 4. Monte Carlo methods 5 4.1. Method of antithetic variances 5

Multilevel Monte Carlo for Basket Options

MLMC for basket options p. 1/26 Multilevel Monte Carlo for Basket Options Mike Giles mike.giles@maths.ox.ac.uk Oxford University Mathematical Institute Oxford-Man Institute of Quantitative Finance WSC09,

MLMC for basket options p. 1/26 Multilevel Monte Carlo for Basket Options Mike Giles mike.giles@maths.ox.ac.uk Oxford University Mathematical Institute Oxford-Man Institute of Quantitative Finance WSC09,

Sensitivity of American Option Prices with Different Strikes, Maturities and Volatilities

Applied Mathematical Sciences, Vol. 6, 2012, no. 112, 5597-5602 Sensitivity of American Option Prices with Different Strikes, Maturities and Volatilities Nasir Rehman Department of Mathematics and Statistics

Applied Mathematical Sciences, Vol. 6, 2012, no. 112, 5597-5602 Sensitivity of American Option Prices with Different Strikes, Maturities and Volatilities Nasir Rehman Department of Mathematics and Statistics

Quasi-Monte Carlo for Finance Applications

Quasi-Monte Carlo for Finance Applications M.B. Giles F.Y. Kuo I.H. Sloan B.J. Waterhouse October 2008 Abstract Monte Carlo methods are used extensively in computational finance to estimate the price of

Quasi-Monte Carlo for Finance Applications M.B. Giles F.Y. Kuo I.H. Sloan B.J. Waterhouse October 2008 Abstract Monte Carlo methods are used extensively in computational finance to estimate the price of

Rapid computation of prices and deltas of nth to default swaps in the Li Model

Rapid computation of prices and deltas of nth to default swaps in the Li Model Mark Joshi, Dherminder Kainth QUARC RBS Group Risk Management Summary Basic description of an nth to default swap Introduction

Rapid computation of prices and deltas of nth to default swaps in the Li Model Mark Joshi, Dherminder Kainth QUARC RBS Group Risk Management Summary Basic description of an nth to default swap Introduction

Monte Carlo Simulation of a Two-Factor Stochastic Volatility Model

Monte Carlo Simulation of a Two-Factor Stochastic Volatility Model asymptotic approximation formula for the vanilla European call option price. A class of multi-factor volatility models has been introduced

Monte Carlo Simulation of a Two-Factor Stochastic Volatility Model asymptotic approximation formula for the vanilla European call option price. A class of multi-factor volatility models has been introduced

Chapter 15: Jump Processes and Incomplete Markets. 1 Jumps as One Explanation of Incomplete Markets

Chapter 5: Jump Processes and Incomplete Markets Jumps as One Explanation of Incomplete Markets It is easy to argue that Brownian motion paths cannot model actual stock price movements properly in reality,

Chapter 5: Jump Processes and Incomplete Markets Jumps as One Explanation of Incomplete Markets It is easy to argue that Brownian motion paths cannot model actual stock price movements properly in reality,

Implementing Models in Quantitative Finance: Methods and Cases

Gianluca Fusai Andrea Roncoroni Implementing Models in Quantitative Finance: Methods and Cases vl Springer Contents Introduction xv Parti Methods 1 Static Monte Carlo 3 1.1 Motivation and Issues 3 1.1.1

Gianluca Fusai Andrea Roncoroni Implementing Models in Quantitative Finance: Methods and Cases vl Springer Contents Introduction xv Parti Methods 1 Static Monte Carlo 3 1.1 Motivation and Issues 3 1.1.1

Lecture 17. The model is parametrized by the time period, δt, and three fixed constant parameters, v, σ and the riskless rate r.

Lecture 7 Overture to continuous models Before rigorously deriving the acclaimed Black-Scholes pricing formula for the value of a European option, we developed a substantial body of material, in continuous

Lecture 7 Overture to continuous models Before rigorously deriving the acclaimed Black-Scholes pricing formula for the value of a European option, we developed a substantial body of material, in continuous

MATH6911: Numerical Methods in Finance. Final exam Time: 2:00pm - 5:00pm, April 11, Student Name (print): Student Signature: Student ID:

: Student Signature: Student ID:") MATH6911 Page 1 of 16 Winter 2007 MATH6911: Numerical Methods in Finance Final exam Time: 2:00pm - 5:00pm, April 11, 2007 Student Name (print): Student Signature: Student ID: Question Full Mark Mark 1

MATH6911 Page 1 of 16 Winter 2007 MATH6911: Numerical Methods in Finance Final exam Time: 2:00pm - 5:00pm, April 11, 2007 Student Name (print): Student Signature: Student ID: Question Full Mark Mark 1

Journal of Mathematical Analysis and Applications

J Math Anal Appl 389 (01 968 978 Contents lists available at SciVerse Scienceirect Journal of Mathematical Analysis and Applications wwwelseviercom/locate/jmaa Cross a barrier to reach barrier options

J Math Anal Appl 389 (01 968 978 Contents lists available at SciVerse Scienceirect Journal of Mathematical Analysis and Applications wwwelseviercom/locate/jmaa Cross a barrier to reach barrier options

Risk Neutral Valuation

copyright 2012 Christian Fries 1 / 51 Risk Neutral Valuation Christian Fries Version 2.2 http://www.christian-fries.de/finmath April 19-20, 2012 copyright 2012 Christian Fries 2 / 51 Outline Notation Differential

copyright 2012 Christian Fries 1 / 51 Risk Neutral Valuation Christian Fries Version 2.2 http://www.christian-fries.de/finmath April 19-20, 2012 copyright 2012 Christian Fries 2 / 51 Outline Notation Differential

Option Pricing Using Bayesian Neural Networks

Option Pricing Using Bayesian Neural Networks Michael Maio Pires, Tshilidzi Marwala School of Electrical and Information Engineering, University of the Witwatersrand, 2050, South Africa m.pires@ee.wits.ac.za,

Option Pricing Using Bayesian Neural Networks Michael Maio Pires, Tshilidzi Marwala School of Electrical and Information Engineering, University of the Witwatersrand, 2050, South Africa m.pires@ee.wits.ac.za,

Monte Carlo Methods in Option Pricing. UiO-STK4510 Autumn 2015

Monte Carlo Methods in Option Pricing UiO-STK4510 Autumn 015 The Basics of Monte Carlo Method Goal: Estimate the expectation θ = E[g(X)], where g is a measurable function and X is a random variable such

Monte Carlo Methods in Option Pricing UiO-STK4510 Autumn 015 The Basics of Monte Carlo Method Goal: Estimate the expectation θ = E[g(X)], where g is a measurable function and X is a random variable such

A Continuity Correction under Jump-Diffusion Models with Applications in Finance

A Continuity Correction under Jump-Diffusion Models with Applications in Finance Cheng-Der Fuh 1, Sheng-Feng Luo 2 and Ju-Fang Yen 3 1 Institute of Statistical Science, Academia Sinica, and Graduate Institute

A Continuity Correction under Jump-Diffusion Models with Applications in Finance Cheng-Der Fuh 1, Sheng-Feng Luo 2 and Ju-Fang Yen 3 1 Institute of Statistical Science, Academia Sinica, and Graduate Institute

An Efficient Quasi-Monte Carlo Simulation for Pricing Asian Options under Heston's Model

An Efficient Quasi-Monte Carlo Simulation for Pricing Asian Options under Heston's Model by Kewei Yu A thesis presented to the University of Waterloo in fulfillment of the thesis requirement for the degree

An Efficient Quasi-Monte Carlo Simulation for Pricing Asian Options under Heston's Model by Kewei Yu A thesis presented to the University of Waterloo in fulfillment of the thesis requirement for the degree

Stratified Sampling in Monte Carlo Simulation: Motivation, Design, and Sampling Error

South Texas Project Risk- Informed GSI- 191 Evaluation Stratified Sampling in Monte Carlo Simulation: Motivation, Design, and Sampling Error Document: STP- RIGSI191- ARAI.03 Revision: 1 Date: September

South Texas Project Risk- Informed GSI- 191 Evaluation Stratified Sampling in Monte Carlo Simulation: Motivation, Design, and Sampling Error Document: STP- RIGSI191- ARAI.03 Revision: 1 Date: September

Introduction to Game-Theoretic Probability

Introduction to Game-Theoretic Probability Glenn Shafer Rutgers Business School January 28, 2002 The project: Replace measure theory with game theory. The game-theoretic strong law. Game-theoretic price

Introduction to Game-Theoretic Probability Glenn Shafer Rutgers Business School January 28, 2002 The project: Replace measure theory with game theory. The game-theoretic strong law. Game-theoretic price

GRAPHICAL ASIAN OPTIONS

GRAPHICAL ASIAN OPTIONS MARK S. JOSHI Abstract. We discuss the problem of pricing Asian options in Black Scholes model using CUDA on a graphics processing unit. We survey some of the issues with GPU programming

GRAPHICAL ASIAN OPTIONS MARK S. JOSHI Abstract. We discuss the problem of pricing Asian options in Black Scholes model using CUDA on a graphics processing unit. We survey some of the issues with GPU programming

Lecture 7: Computation of Greeks

Lecture 7: Computation of Greeks Ahmed Kebaier kebaier@math.univ-paris13.fr HEC, Paris Outline 1 The log-likelihood approach Motivation The pathwise method requires some restrictive regularity assumptions

Lecture 7: Computation of Greeks Ahmed Kebaier kebaier@math.univ-paris13.fr HEC, Paris Outline 1 The log-likelihood approach Motivation The pathwise method requires some restrictive regularity assumptions

Introduction Dickey-Fuller Test Option Pricing Bootstrapping. Simulation Methods. Chapter 13 of Chris Brook s Book.

Simulation Methods Chapter 13 of Chris Brook s Book Christopher Ting http://www.mysmu.edu/faculty/christophert/ Christopher Ting : christopherting@smu.edu.sg : 6828 0364 : LKCSB 5036 April 26, 2017 Christopher

Simulation Methods Chapter 13 of Chris Brook s Book Christopher Ting http://www.mysmu.edu/faculty/christophert/ Christopher Ting : christopherting@smu.edu.sg : 6828 0364 : LKCSB 5036 April 26, 2017 Christopher

Reading: You should read Hull chapter 12 and perhaps the very first part of chapter 13.

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 Asset Price Dynamics Introduction These notes give assumptions of asset price returns that are derived from the efficient markets hypothesis. Although a hypothesis,

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 Asset Price Dynamics Introduction These notes give assumptions of asset price returns that are derived from the efficient markets hypothesis. Although a hypothesis,

MÄLARDALENS HÖGSKOLA

MÄLARDALENS HÖGSKOLA A Monte-Carlo calculation for Barrier options Using Python Mwangota Lutufyo and Omotesho Latifat oyinkansola 2016-10-19 MMA707 Analytical Finance I: Lecturer: Jan Roman Division of

MÄLARDALENS HÖGSKOLA A Monte-Carlo calculation for Barrier options Using Python Mwangota Lutufyo and Omotesho Latifat oyinkansola 2016-10-19 MMA707 Analytical Finance I: Lecturer: Jan Roman Division of

AMSTERDAM BOSTON HEIDELBERG LONDON NEW YORK OXFORD PARIS SAN DIEGO SAN FRANCISCO SINGAPORE SYDNEY TOKYO Academic Press is an Imprint of Elsevier

Computational Finance Using C and C# Derivatives and Valuation SECOND EDITION George Levy ELSEVIER AMSTERDAM BOSTON HEIDELBERG LONDON NEW YORK OXFORD PARIS SAN DIEGO SAN FRANCISCO SINGAPORE SYDNEY TOKYO

Computational Finance Using C and C# Derivatives and Valuation SECOND EDITION George Levy ELSEVIER AMSTERDAM BOSTON HEIDELBERG LONDON NEW YORK OXFORD PARIS SAN DIEGO SAN FRANCISCO SINGAPORE SYDNEY TOKYO

STOCHASTIC CALCULUS AND BLACK-SCHOLES MODEL

STOCHASTIC CALCULUS AND BLACK-SCHOLES MODEL YOUNGGEUN YOO Abstract. Ito s lemma is often used in Ito calculus to find the differentials of a stochastic process that depends on time. This paper will introduce

STOCHASTIC CALCULUS AND BLACK-SCHOLES MODEL YOUNGGEUN YOO Abstract. Ito s lemma is often used in Ito calculus to find the differentials of a stochastic process that depends on time. This paper will introduce

Handbook of Financial Risk Management

Handbook of Financial Risk Management Simulations and Case Studies N.H. Chan H.Y. Wong The Chinese University of Hong Kong WILEY Contents Preface xi 1 An Introduction to Excel VBA 1 1.1 How to Start Excel

Handbook of Financial Risk Management Simulations and Case Studies N.H. Chan H.Y. Wong The Chinese University of Hong Kong WILEY Contents Preface xi 1 An Introduction to Excel VBA 1 1.1 How to Start Excel

STOCHASTIC VOLATILITY AND OPTION PRICING

STOCHASTIC VOLATILITY AND OPTION PRICING Daniel Dufresne Centre for Actuarial Studies University of Melbourne November 29 (To appear in Risks and Rewards, the Society of Actuaries Investment Section Newsletter)

STOCHASTIC VOLATILITY AND OPTION PRICING Daniel Dufresne Centre for Actuarial Studies University of Melbourne November 29 (To appear in Risks and Rewards, the Society of Actuaries Investment Section Newsletter)

Accelerated Option Pricing Multiple Scenarios

Accelerated Option Pricing in Multiple Scenarios 04.07.2008 Stefan Dirnstorfer (stefan@thetaris.com) Andreas J. Grau (grau@thetaris.com) 1 Abstract This paper covers a massive acceleration of Monte-Carlo

Accelerated Option Pricing in Multiple Scenarios 04.07.2008 Stefan Dirnstorfer (stefan@thetaris.com) Andreas J. Grau (grau@thetaris.com) 1 Abstract This paper covers a massive acceleration of Monte-Carlo

A NEW EFFICIENT SIMULATION STRATEGY FOR PRICING PATH-DEPENDENT OPTIONS

Proceedings of the 2006 Winter Simulation Conference L. F. Perrone, F. P. Wieland, J. Liu, B. G. Lawson, D. M. Nicol, and R. M. Fujimoto, eds. A NEW EFFICIENT SIMULATION STRATEGY FOR PRICING PATH-DEPENDENT

Proceedings of the 2006 Winter Simulation Conference L. F. Perrone, F. P. Wieland, J. Liu, B. G. Lawson, D. M. Nicol, and R. M. Fujimoto, eds. A NEW EFFICIENT SIMULATION STRATEGY FOR PRICING PATH-DEPENDENT