Derivatives, Contingencies, Business Segments, and Interim Reports

|

|

|

- Cody Campbell

- 6 years ago

- Views:

Transcription

1 Ch.19 Derivatives, Contingencies, Business Segments, and Interim Reports 1. The concepts of derivatives and hedging activities 2. Different types of risk faced by a business 3. The characteristics of swaps, forwards, futures, and options 4. Define hedging and the difference between a fair value hedge and a cash flow hedge 5. Account for derivatives and for hedging 6. The contingent items to the areas of lawsuits and environmental liabilities 7. The supplemental disclosures of financial information by product line and by geographic area 8. The importance and difficulties of interim reports 19-1

2 1. Understand the business and accounting concepts connected with derivatives and hedging activities Simple Example of a Derivative On October 1, 2013, you purchase 100 shares of stock in Nauvoo Software Solutions (your employer) at the market price of $50 per share. On January 1, 2014, you need to make a college tuition payment of $5,000 on behalf of your daughter. Your employment contract states that any shares you purchase from the company must be held for at least three months before you can sell them. 19-2

3 Simple Example of a Derivative A downward movement in the stock price between now and January 1 would be disastrous for you. What is the solution to your dilemma? 19-3

4 Simple Example of a Derivative You can avoid downward movement if you make the following agreement: If the price of the stock is above $50 per share, you agree to pay cash equal to the excess to John Bennett, a local speculator. If the price goes below $50, Bennett will pay you a cash amount equal to the deficit. This agreement is called a derivative. 19-4

5 Simple Example of a Derivative A derivative is a financial instrument or contract that derives its value from the movement of the price, foreign exchange rate, or interest rate on some other underlying asset or financial instrument. No matter what happens to the price of Nauvoo stock between now and then, you will wind up with $5,000 on January 1. When the agreement is made, no journal entry is required, because it is merely an exchange of promises about some future action; that is, an executory contract. 19-5

6 2. Identify the different types of risk faced by a business Types of Risk Price risk is the uncertainty about the future price of an asset. Credit risk is the uncertainty that the party on the other side of the agreement will abide by the terms of the agreement. Interest rate risk is the uncertainty about future interest rates an their impact on future cash flows as well as on the fair value of existing assets and liabilities. Exchange rate risk is the uncertainty about the U.S. dollar cash flows arising when assets and liabilities are denominated in a foreign currency. 19-6

7 3. Describe the characteristics of the following types of derivatives: swaps, forwards, futures, and options Swap A swap is a contract in which two parties agree to exchange payments in the future based on the movement of some agreed-upon price or rate. A common type of swap is an interest rate swap where two parties agree to exchange future interest payments on a given loan amount (one set of interest payments is based on a fixed interest rate and the other is based on a variable interest rate). 19-7

8 Swap Pratt Company takes advantage of its good working relationship with a bank that issues only variable-rate loans. On January 1, 2013, Pratt receives a 2-year, $100,000 loan with interest payments occurring at the end of each year. The interest rate for the first year is 10%, and the rate in the second year will be equal to the market interest on January 1 of that year. 19-8

9 Swap Pratt enters into an interest rate swap agreement with another party whereby Pratt agrees to pay a fixed interest rate of 10% on the $100,000 loan to that party in exchange for receiving a variable amount based on the prevailing market rate. Pratt will receive an amount equal to [$100,000 (Jan. 1, 2014 interest rate 10%)] if the interest rate is above 10% and will pay the same amount if the rate is less than 10%. 19-9

10 Swap To see the impact of this interest rate swap, consider the following table: Pratt will pay $10,000 no matter what the prevailing interest rates in

11 Forwards A forward contract is an agreement between two parties to exchange a specified amount of a commodity, security or foreign currency at a specified date in the future with the price of the exchange rate being set now. On November 1, 2013, Clayton Company sold machine parts to Maruta Company for 30, to be received on January 1, The current exchange rate is 120 = $

12 Forwards Clayton enters into a forward contract with a large bank, agreeing that on January 1 Clayton will deliver 30,000,000 to the bank and the bank will give U.S. dollars in exchange at the rate of 120 = $1, or $250,000 ( 30,000,000/ 120 per $1). If on January 1, 2014, 30,000,000 is worth less than $250,000, the bank will pay Clayton the difference in cash (U.S. dollars). (continued) 19-12

13 Forwards If 30,000,000 is worth more than $250,000 Clayton pays the difference in cash. The impact of the forward exchange is shown in the following table: (continued) 19-13

14 Futures A futures contract is a contract, traded on an exchange, that allows a company to buy or sell a specified quantity of a commodity or a financial security at a specified price on a specified future date. It is very similar to a forward contract with the difference being that a forward contract is a private contract negotiated between two parties, whereas a futures contract is a standardized contract that is sponsored by a trading exchange

15 Futures Hyrum Bakery uses 1,000 bushels of wheat every month. On December 1, 2013, Hyrum decides to protect itself against price movements. Hyrum buys a futures contract to purchase 1,000 bushels of wheat on January 1, 2014, at $4 per bushel. This is a standardized exchange-traded futures contract, so Hyrum has no idea who is on the other side of the agreement. (continued) 19-15

16 Futures As with other derivatives, a wheat futures contract is usually settled by a cash payment at the end of the contract instead of the actual delivery of the wheat. The effect of the futures contract is illustrated in the following table: 19-16

17 Option An option is a contract giving the owner the right, but not the obligation, to buy or sell an asset at a specified price any time during a specified period in the future. A call option gives the owner the right to buy an asset at a specified price. A put option gives the owner the right to sell an asset at a specified price in exchange for the rights inherent in the option. The owner of the option pays an amount in advance to the party on the other side of the transaction, who is called the writer of the option

18 Option On October 1, 2013, Woodruff Company decides that it will need to purchase 1,000 ounces of gold for use in its computer chip manufacturing process in January, Gold is selling for $1,100 per ounce on October 1, For cash flow reasons, Woodruff plans to delay the purchase of gold until January 1, 2014, and is concerned about potential increases in the market price of gold between October 1, 2013, and January 1,

19 Option Woodruff enters into a call option contract on October 1. The contract gives Woodruff the right, but not the obligation, to purchase 1,000 ouches of gold at a price of $1,100 per ounce. The option period extends to January 1, Woodruff has to pay $20,000 to buy this option

20 Option The chart below shows the anticipated activity at three possible gold prices. The existence of the option contract means that Woodruff will pay no more than $1,100,000 for gold

21 4. Define hedging, and outline the difference between a fair value hedge and a cash flow hedge Types of Hedging Activities Broadly defined, hedging is the structuring of transactions to reduce risk. A fair value hedge is a derivative that offsets, at least partially, the change in the fair value of an asset or a liability. A cash flow hedge is a derivative that offsets, at least partially, the variability in cash flows from forecasted transactions that are probable

22 5. Account for a variety of different derivatives and for hedging relationships Overview of Accounting for Derivatives and Hedging Activities The accounting difficulty caused by derivatives is illustrated in this simple matrix: The historical cost focus of traditional accounting is misplaced with derivatives because derivatives often have little or no up-front historical cost

23 Overview of Accounting for Derivatives and Hedging Activities 1. Balance sheet. Derivatives should be reported in the balance sheet at their fair value as of the balance sheet date. No other measure of value is relevant for derivatives. 2. Income statement. When a derivative is used to hedge risks, the gains and losses on the derivative should be reported in the same income statement in which the income effects on the hedged items are reported

24 Overview of Accounting for Derivatives and Hedging Activities No hedge. All changes in the fair value of derivatives that are not designated as hedges are recognized as gains or losses in the income statement in the period in which the value changed. Fair value hedge. Changes in the fair value of derivatives designated as fair value hedges are recognized as gains or losses in the period of the value change

25 Overview of Accounting for Derivatives and Hedging Activities Cash flow hedge. Changes in the fair value of derivatives designated as cash flow hedges are recognized as part of the accumulated other comprehensive income account. To account for a derivative as a hedge, a company must define, in advance, how it will determine whether the derivative is functioning as an effective hedge

26 Disclosure Companies are required to provide a description of their risk management strategy and how derivatives fit into that strategy for both fair value and cash flow hedges. Companies must disclose the amount of derivative gains or losses that are included in income because of hedge ineffectiveness. For cash flow hedges, a company must describe the transactions that will cause deferred derivative gain and losses to be recognized in net income

27 Disclosure The notional amount is the total face amount of the asset or liability that underlies a derivative contract. The notional amount of derivative instruments is often reported and is frequently misleading. Notional amounts grossly overstate both the fair value and the potential cash flows of derivatives

28 Pratt Swap On January 1, 2013, Pratt Company received a two-year $100,000 variable-rate loan and also entered into an interest rate swap agreement. The journal entry to record this information follows: 2013 Jan. 1 Cash 100,000 Loan Payable 100,000 No entry is made to record the swap agreement because the swap has a fair value of $

29 Pratt Swap The actual market interest rate on December 31, 2013 is 11%. With this rate, Pratt will receive a $1,000 payment [$100,000 x ( )] at the end of On December 31, 2013, Pratt has a $1,000 receivable under the swap agreement, and the receivable has a present value of $901 (FV = $1,000, N =1, I = 11%)

30 Pratt Swap The impact of the change in interest rate on the interest rate swap and on reported interest expense is accounted for as follows: 19-30

31 Pratt Swap The journal entry to record Pratt s 2013 interest payment, along with the adjusting entry to recognize the change in the fair value, is as follows: 2013 Dec 31 Interest Expense 10,000 Cash ($100, ) 10, Interest Rate Swap (asset) 901 Other Comprehensive Income 901 The journal entries at the end of 2014 are on Slide

32 2014 Pratt Swap Dec. 31 Interest Expense 11,000 Cash ($100, ) 11, Cash (from swap agreement) 1,000 Interest Rate Swap (asset) 901 Other Comprehensive Income ($ ) Accumulated Other Comprehensive Income 1,000 Interest Expense 1, Loan Payable 100,000 Cash 100,

33 Clayton Forward On November 1, 2013, Clayton Company sold machine parts to Maruta Company for 30,000,000 to be received on January 1, On the same date, Clayton also entered into a yen forward contract. The required entry is as follows: 2013 Nov. 1 Yen Receivable 250,000 Sales 250,000 30,000,000/ 120 per $

34 Clayton Forward The actual exchange rate on December 31, 2013 is 119 = $1. Clayton will have a loss on the forward contract and will be required to make a $2,101 payment [( 30,000,000/ 119 per $1) $250,000]. The impact of the change in the yen exchange rate is as follows: 19-34

35 Clayton Forward The adjusting entries to recognize the change in the fair value of the forward contract and in the U. S. dollar value of the yen receivable are as follows: 2013 Dec. 31 Loss on Forward Contract 2,101 Forward Contract 2, Yen Receivable 2,101 Gain on Foreign Currency 2,

36 Clayton Forward The journal entries necessary in Clayton s books on January 1, 2014, to record receipt of the yen payment and settlement of the yen forward contract are as follows: 2014 Jan. 1 Cash ( 30,0000,000/ 119 per $1) 252,101 Yen Receivable 252,101 1 Forward Contract (liability) 2,101 Cash (forward contract settlement) 2,

37 Clayton Forward It should be noted that the Clayton forward contract does not qualify for hedge accounting under FASB ASC Topic 815. Derivatives that serve as economic hedges of foreign currency assets and liabilities are accounted for as speculations, with all gains and losses recognized as part of income immediately

38 Hyrum Future On December 1, 2013, Hyrum Company decided to hedge against potential fluctuations in the price of wheat for its forecasted January 2014 purchases. The firm bought a futures contract entitling and obligating Hyrum to purchase 1,000 bushels of wheat on January 1, 2014, for $4.00 per bushel

39 Hyrum Future No entry is made to record the futures contract because, as of December 31, 2013, the future has a fair value of $0. The actual price of wheat on December 31, 2013, is $4.40 per bushel. Hyrum will receive a $400 payment [1,000 bushels ($4.40 $4.00)] on January 1, 2014, to settle the futures contract

40 Hyrum Future The impact of the change on the anticipated cost of wheat when purchased in January 2014 is accounted for as follows: 19-40

400 Other Comprehensive Income 400 The gain from the increase in the value of Hyrum s futures contract is deferred as a part")

41 The adjusting entry to recognize the change in the fair value of the futures contract is as follows: 2013 Hyrum Future Dec. 31 Wheat Futures Contract (asset) 400 Other Comprehensive Income 400 The gain from the increase in the value of Hyrum s futures contract is deferred as a part of other comprehensive income

42 The journal entries necessary to record the purchase of 1,000 bushels of wheat in the open market and the cash settlement of the wheat futures contracts are as follows: 2014 Hyrum Future Jan. 1 Wheat Inventory 4,400 Cash 4,400 1,000 bushels x $ Cash (future contract settlement) 400 Wheat Futures Contract (asset) Accumulated Other Comprehensive Income 400 Gain on Futures Contract

43 Woodruff Option On October 1, 2013, Woodruff Company paid $20,000 to purchase a call option to buy 1,000 ounces of gold at a price of $1,100 per ounce some time before January 1, Because Woodruff paid cash for the gold option, the following journal entry is made on October 1: 2013 Oct. 1 Gold Call Option (asset) 20,000 Cash 20,

($1,100 x 1,000 ounces)] on January 1, 2014, to settle the call option.")

44 Woodruff Option The actual price of gold on December 31, 2013, is $1,128 per ounce. Woodruff will receive a $28,00 payment [($1,128 x 1,000 ounces) ($1,100 x 1,000 ounces)] on January 1, 2014, to settle the call option. The impact on the change in price of gold is accounted for as follows: 19-44

45 Woodruff Option The gold call option is reported at its fair value of $28,000 in the December 31, 2013, balance sheet. The adjusting entry to recognize the change in the fair value of the option is as follows: 2013 Dec. 31 Gold Call Option ($28,000 $20,000) 8,000 Other Comprehensive Income 8,

46 Woodruff Option The journal entry necessary in Woodruff s book on January 1, 2014, to record the purchase of 1,000 ounces of gold and the cash settlement of the option contract are as follows: 2014 Jan. 1 Gold Inventory 1,128,000 Cash 1,128,000 1 Cash 1,000 (gold ounces call option x $1,128 settlement) 28,000 Gold Call Option (asset) 28,000 1 Accumulated Other Comprehensive Income 8,000 Gain on Gold Call Option 8,

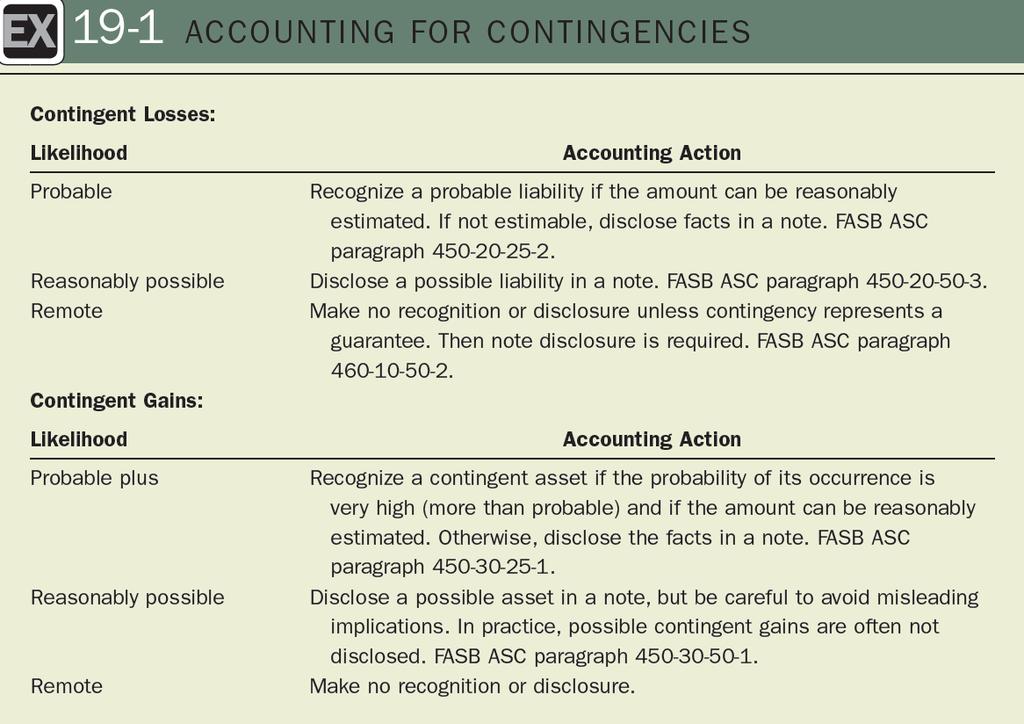

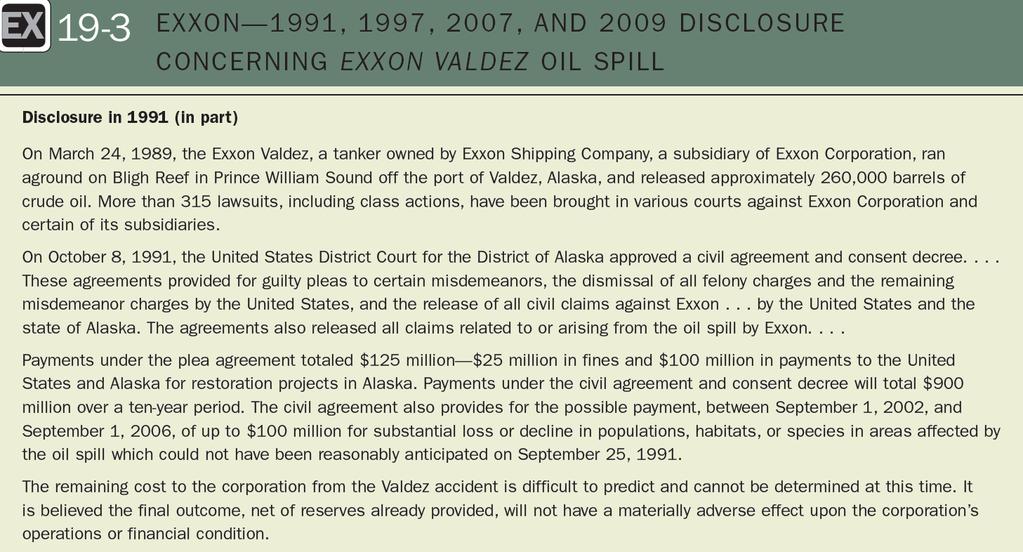

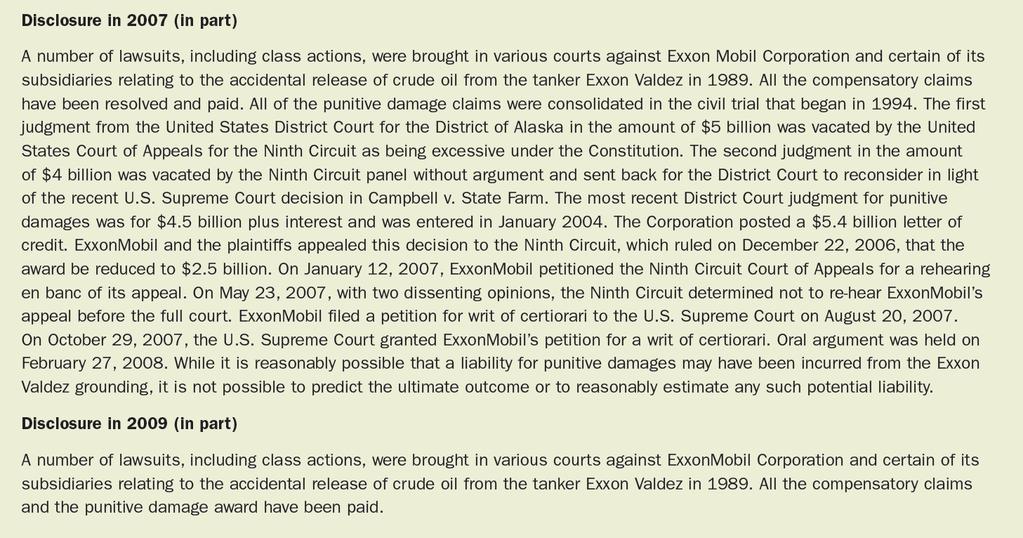

47 6. Apply the accounting rules for contingent items to the areas of lawsuits and environmental liabilities Accounting for Contingencies Contingent losses. Circumstances involving potential losses that will not be resolved until some future event occurs. Contingent gains. Circumstances involving potential gains that will not be resolved until some future event occurs

48 19-48

49 19-49

50 Accounting for Lawsuits In ASC Topic 450, the FASB identifies several key factors to consider in making the decision. These include the following: 1. The nature of the lawsuit 2. Progress of the case 3. Views of legal counsel as to the probability of loss 4. Prior experience with similar cases 5. Management s intended response to the lawsuit 19-50

51 19-51

52 19-52

53 19-53

54 Disclosure Some companies do not disclose any information regarding potential liabilities from lawsuits. Others provide a brief, general description of pending lawsuits. Sometimes companies provide fairly specific information about pending actions and claims. They generally do not disclose dollar amounts of potential losses

55 Accounting for Environmental Liabilities The SEC staff issued Staff Accounting Bulletin No. 92, which set forth the SEC s interpretation of GAAP regarding contingent liabilities, with particular applicability to companies with environmental liabilities. The AICPA issued SOP 96-1 outlining key events that can be used to determine whether an environmental liability is probable

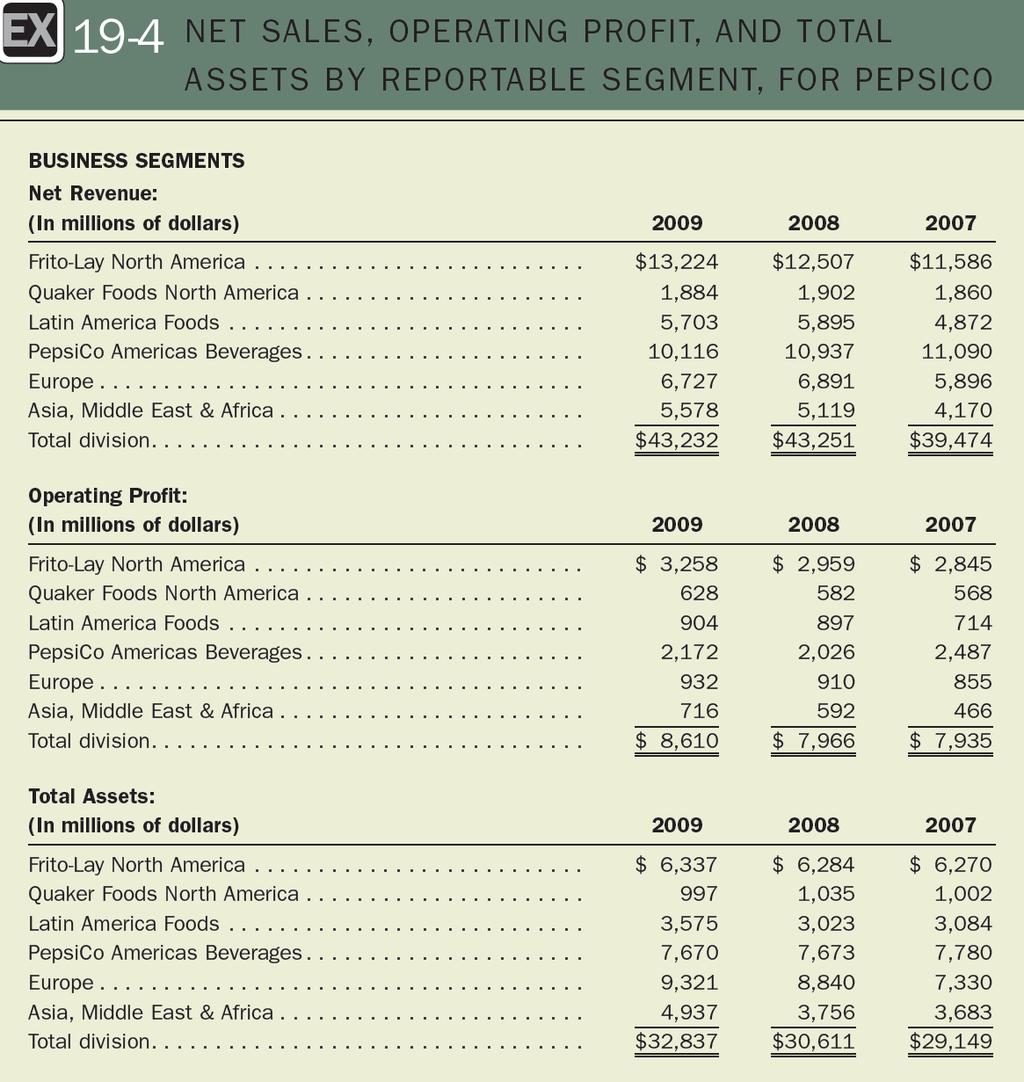

56 7. Prepare the necessary supplemental disclosures of financial information by product line and by geographic area Business Segments Information to be disclosed in the financial statement notes under the provisions of Pre- Codification FASB Statement No. 14 included revenues, operating profit, and identifiable assets for each significant industry segment of a company. Other provisions of the statement required disclosure of revenues from major customers and information about foreign operations and export sales

57 1. Total segment operating profit or loss 2. Amounts of certain income statement items such as operating revenues, depreciation, interest revenue, interest expense, tax expense, and significant noncash expenses 3. Total segment assets Business Segments According to the provisions of FASB ASC Topic 280, companies are required to disclose the following information concerning business segments: 19-57

58 Business Segments 4. Total capital expenditures 5. Reconciliation of the sum of segment totals to the company total for each of the following items: Revenues Operating profits Assets 19-58

59 Business Segments Separate segment disclosure is required if a segment meets any one of the following three criteria: Revenue test. A segment should be reported if its total revenue is 10% or more of the company s total revenue (external and internal)

60 Business Segments Profit test. A segment should be reported if the absolute value of its operating profit (or loss) is more than 10% of the total of the operating profit for all segments that report profits (or the total of the losses for all segments that reported losses). Asset test. A segment should be reported if it contains 10% or more of the combined assets of all operating segments

61 Business Segments The FASB also decided that segments can be combined for reporting purposes, even if they are treated as separate segments internally, if the segments have similar products or services, similar processes, similar customers, similar distribution methods, and are subject to similar regulations

62 19-62

63 8. Recognize the importance of interim reports, and outline the difficulties encountered when preparing those reports Interim Reports Statements showing financial position and operating results for intervals of less than a year are referred to as interim financial statements. Under the integral part of annual period concept, the same general accounting principles and reporting practices employed for annual reports are to be utilized for interim statements, but modifications may be required so the interim results will better relate to the total results of operations for the annual period

64 Interim Reports Example of a Modification Assume a company uses the LIFO method of inventory valuation and encounters a situation where liquidation of the base period inventory occurs at an interim date but the inventory is expected to be replaced by the end of the annual period. The inventory should not reflect the LIFO liquidation by including the cost of replacing the liquidated LIFO base

65 19-65

Derivatives, Contingencies, Business Segments, and Interim Reports

19 Derivatives, Contingencies, Business Segments, and Interim Reports Overview This chapter contains a potpourri of topics which are either combined here because they don t fit in well elsewhere or because

19 Derivatives, Contingencies, Business Segments, and Interim Reports Overview This chapter contains a potpourri of topics which are either combined here because they don t fit in well elsewhere or because

Financial Accounting Level 4 Module 7

Financial Accounting Level 4 Module 7 IMPORTANT Exchange rates can be stated in two different ways: 1. Canadian dollar equivalent method: This is when we are given how much it will cost in Canadian funds

Financial Accounting Level 4 Module 7 IMPORTANT Exchange rates can be stated in two different ways: 1. Canadian dollar equivalent method: This is when we are given how much it will cost in Canadian funds

Erikson Institute. Financial Report June 30, 2018

Financial Report June 30, 2018 Contents Independent auditor s report 1-2 Financial statements Statements of financial position 3 Statements of activities 4-5 Statements of functional expenses 6-7 Statements

Financial Report June 30, 2018 Contents Independent auditor s report 1-2 Financial statements Statements of financial position 3 Statements of activities 4-5 Statements of functional expenses 6-7 Statements

Foreign Currency. Handbook US GAAP. March kpmg.com/us/frv

Foreign Currency Handbook US GAAP March 2018 kpmg.com/us/frv Contents Preface 1. Overview of Accounting for Foreign Currency... 1 2. Functional Currency... 5 3. Foreign Currency Transactions... 18 4. Translation

Foreign Currency Handbook US GAAP March 2018 kpmg.com/us/frv Contents Preface 1. Overview of Accounting for Foreign Currency... 1 2. Functional Currency... 5 3. Foreign Currency Transactions... 18 4. Translation

C ONSOLIDATED F INANCIAL S TATEMENTS. Billing Services Group Limited Years Ended December 31, 2010 and 2009 With Report of Independent Auditors

C ONSOLIDATED F INANCIAL S TATEMENTS Billing Services Group Limited Years Ended December 31, 2010 and 2009 With Report of Independent Auditors Ernst & Young LLP Consolidated Financial Statements Years

C ONSOLIDATED F INANCIAL S TATEMENTS Billing Services Group Limited Years Ended December 31, 2010 and 2009 With Report of Independent Auditors Ernst & Young LLP Consolidated Financial Statements Years

NATIONAL BANK OF CANADA FINANCIAL INC.

Statement of Financial Condition As of (Unaudited) NATIONAL BANK OF CANADA FINANCIAL INC. (SEC I.D. No. 8-39947) Table of Contents Statement of Financial Condition... 1 Notes to Statement of Financial

Statement of Financial Condition As of (Unaudited) NATIONAL BANK OF CANADA FINANCIAL INC. (SEC I.D. No. 8-39947) Table of Contents Statement of Financial Condition... 1 Notes to Statement of Financial

JANNEY MONTGOMERY SCOTT LLC Consolidated Statement of Financial Condition Year ended December 31, 2016

JANNEY MONTGOMERY SCOTT LLC Consolidated Statement of Financial Condition Year ended December 31, 2016 Janney Montgomery Scott LLC Consolidated Statement of Financial Condition and Notes For the year

JANNEY MONTGOMERY SCOTT LLC Consolidated Statement of Financial Condition Year ended December 31, 2016 Janney Montgomery Scott LLC Consolidated Statement of Financial Condition and Notes For the year

Equity Financing 13-1

Ch.13 Equity Financing 1. Stock Rights (common and preferred stock) 2. Stock Issuance for cash, noncash assets or for services 3. Treasury stock 4. Stock rights and warrants 5. Compensation expense with

Ch.13 Equity Financing 1. Stock Rights (common and preferred stock) 2. Stock Issuance for cash, noncash assets or for services 3. Treasury stock 4. Stock rights and warrants 5. Compensation expense with

New Developments Summary

May 10, 2016 NDS 2016-07 New Developments Summary FASB Transition Resource Group for Revenue Recognition meeting highlights Summary of April 18 meeting Summary The U.S. based members of the Joint Transition

May 10, 2016 NDS 2016-07 New Developments Summary FASB Transition Resource Group for Revenue Recognition meeting highlights Summary of April 18 meeting Summary The U.S. based members of the Joint Transition

Makita Corporation. Additional Information for the year ended March 31, Consolidated Financial Statements

Makita Corporation Additional Information for the year ended March 31, 2013 Consolidated Financial Statements (Partial translation of "YUKASHOKEN HOKOKUSHO" originally issued in Japanese) CONTENTS Accounting-Consolidated

Makita Corporation Additional Information for the year ended March 31, 2013 Consolidated Financial Statements (Partial translation of "YUKASHOKEN HOKOKUSHO" originally issued in Japanese) CONTENTS Accounting-Consolidated

Williams College Consolidated Financial Statements June 30, 2017 and 2016

Consolidated Financial Statements Index Page(s) Report of Independent Auditors... 1 2 Consolidated Financial Statements Statements of Financial Position... 3 Statements of Activities... 4 5 Statements

Consolidated Financial Statements Index Page(s) Report of Independent Auditors... 1 2 Consolidated Financial Statements Statements of Financial Position... 3 Statements of Activities... 4 5 Statements

The new revenue recognition standard technology

No. 2014-16 26 August 2014 Technical Line FASB final guidance The new revenue recognition standard technology In this issue: Overview... 1 Scope, transition and effective date... 3 Summary of the new model...

No. 2014-16 26 August 2014 Technical Line FASB final guidance The new revenue recognition standard technology In this issue: Overview... 1 Scope, transition and effective date... 3 Summary of the new model...

Authoritative Accounting and Reporting Standards For Employee Benefit Plans:

Authoritative Accounting and Reporting Standards For Employee Benefit Plans: FASB Accounting Standards Codification TM The EBPAQC has prepared this document to provide a general understanding of the source

Authoritative Accounting and Reporting Standards For Employee Benefit Plans: FASB Accounting Standards Codification TM The EBPAQC has prepared this document to provide a general understanding of the source

REPORTS. Exhibit Management s Report on Internal Control over Financial Reporting

REPORTS Exhibit 99.2 Management s Report on Internal Control over Financial Reporting Management is responsible for establishing and maintaining adequate internal control over financial reporting. Under

REPORTS Exhibit 99.2 Management s Report on Internal Control over Financial Reporting Management is responsible for establishing and maintaining adequate internal control over financial reporting. Under

AUDITED FINANCIAL STATEMENTS. DaVinci Reinsurance Ltd. December 31, 2017 and 2016

AUDITED FINANCIAL STATEMENTS DaVinci Reinsurance Ltd. December 31, 2017 and 2016 Ernst & Young Ltd. 3 Bermudiana Road Hamilton HM 08, Bermuda P.O. Box 463 Hamilton HM BX, Bermuda Tel: +1 441 295 7000 Fax:

AUDITED FINANCIAL STATEMENTS DaVinci Reinsurance Ltd. December 31, 2017 and 2016 Ernst & Young Ltd. 3 Bermudiana Road Hamilton HM 08, Bermuda P.O. Box 463 Hamilton HM BX, Bermuda Tel: +1 441 295 7000 Fax:

ARKALON ETHANOL, LLC Liberal, Kansas

ARKALON ETHANOL, LLC Liberal, Kansas FINANCIAL STATEMENTS Years Ended December 31, 2013 and 2012 with Independent Auditors' Report ARKALON ETHANOL, LLC Liberal, Kansas CONTENTS Page INDEPENDENT AUDITORS'

ARKALON ETHANOL, LLC Liberal, Kansas FINANCIAL STATEMENTS Years Ended December 31, 2013 and 2012 with Independent Auditors' Report ARKALON ETHANOL, LLC Liberal, Kansas CONTENTS Page INDEPENDENT AUDITORS'

C ONSOLIDATED F INANCIAL S TATEMENTS. Billing Services Group Limited Years Ended December 31, 2011 and 2010 With Report of Independent Auditors

C ONSOLIDATED F INANCIAL S TATEMENTS Billing Services Group Limited Years Ended December 31, 2011 and 2010 With Report of Independent Auditors Ernst & Young LLP Consolidated Financial Statements Years

C ONSOLIDATED F INANCIAL S TATEMENTS Billing Services Group Limited Years Ended December 31, 2011 and 2010 With Report of Independent Auditors Ernst & Young LLP Consolidated Financial Statements Years

Consolidated Statement of Financial Condition Period ended June 30, 2017 (Unaudited)

") JANNEY MONTGOMERY SCOTT LLC Consolidated Statement of Financial Condition Period ended June 30, 2017 (Unaudited) Janney Montgomery Scott LLC Consolidated Statement of Financial Condition and Notes For

JANNEY MONTGOMERY SCOTT LLC Consolidated Statement of Financial Condition Period ended June 30, 2017 (Unaudited) Janney Montgomery Scott LLC Consolidated Statement of Financial Condition and Notes For

Harley-Davidson, Inc. (Exact name of registrant as specified in its charter)

") UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D. C. 20549 FORM 10-Q x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D. C. 20549 FORM 10-Q x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended

IAS 39, Financial Instruments: Recognition and Measurement. 3. IASB Exposure Draft, Hedge Accounting. 4

October 16, 2012 Volume 19, Issue 27 Heads Up In This Issue: Background Hedging Instruments Hedged Items Qualifying Criteria for Applying Hedge Accounting Accounting for Qualifying Hedges Modifying and

October 16, 2012 Volume 19, Issue 27 Heads Up In This Issue: Background Hedging Instruments Hedged Items Qualifying Criteria for Applying Hedge Accounting Accounting for Qualifying Hedges Modifying and

Dopaco Combined Financial Statements December 26, 2010, December 27, 2009 and December 28, 2008 (in thousands of US dollars)

") Combined Financial Statements December 26, 2010, December 27, 2009 and December 28, 2008 (in thousands of US dollars) Report of Independent Registered Public Accounting Firm To the Management of Cascades

Combined Financial Statements December 26, 2010, December 27, 2009 and December 28, 2008 (in thousands of US dollars) Report of Independent Registered Public Accounting Firm To the Management of Cascades

The IFRS for SMEs Topic 2.1 Section 11 Basic Financial Instruments Section 12 Other Fin. Inst. Issues Section 22 Liabilities and Equity

The IFRS for SMEs 1 Topic 2.1 Section 11 Basic Financial Instruments Section 12 Other Fin. Inst. Issues Section 22 Liabilities and Equity This PowerPoint presentation was prepared by IFRS Foundation education

The IFRS for SMEs 1 Topic 2.1 Section 11 Basic Financial Instruments Section 12 Other Fin. Inst. Issues Section 22 Liabilities and Equity This PowerPoint presentation was prepared by IFRS Foundation education

Harley-Davidson, Inc. (Exact name of registrant as specified in its charter)

") UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D. C. 20549 FORM 10-Q x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D. C. 20549 FORM 10-Q x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended

Technical Line FASB final guidance

No. 2017-30 Updated 15 March 2018 Technical Line FASB final guidance A closer look at the new guidance on recognizing and measuring financial instruments In this issue: Overview... 1 Equity investments...

No. 2017-30 Updated 15 March 2018 Technical Line FASB final guidance A closer look at the new guidance on recognizing and measuring financial instruments In this issue: Overview... 1 Equity investments...

A shift in the top line

A shift in the top line A new global standard on accounting for revenue The FASB, along with the IASB, has finally issued ASU 2014-09, Revenue from Contracts with Customers, its new standard on revenue.

A shift in the top line A new global standard on accounting for revenue The FASB, along with the IASB, has finally issued ASU 2014-09, Revenue from Contracts with Customers, its new standard on revenue.

Statement of Financial Accounting Standards No. 80

Statement of Financial Accounting Standards No. 80 Note: This Statement has been completely superseded FAS80 Status Page FAS80 Summary Accounting for Futures Contracts August 1984 Financial Accounting

Statement of Financial Accounting Standards No. 80 Note: This Statement has been completely superseded FAS80 Status Page FAS80 Summary Accounting for Futures Contracts August 1984 Financial Accounting

Quarterly Report KOMATSU LTD. From October 1, 2017 to December 31, (Third Quarter of the 149 th Fiscal Year)

") (Translation) This document has been translated from the Japanese original for the convenience of overseas stakeholders. In the event of any discrepancy between this document and the Japanese original,

(Translation) This document has been translated from the Japanese original for the convenience of overseas stakeholders. In the event of any discrepancy between this document and the Japanese original,

New Revenue Recognition Framework: Will Your Entity Be Affected?

New Revenue Recognition Framework: Will Your Entity Be Affected? One of the most significant changes to financial accounting and reporting in recent history is soon to be effective. Reporting entities

New Revenue Recognition Framework: Will Your Entity Be Affected? One of the most significant changes to financial accounting and reporting in recent history is soon to be effective. Reporting entities

C ONSOLIDATED F INANCIAL S TATEMENTS. Billing Services Group Limited Years Ended December 31, 2012 and 2011 With Independent Auditor s Report

C ONSOLIDATED F INANCIAL S TATEMENTS Billing Services Group Limited Years Ended December 31, 2012 and 2011 With Independent Auditor s Report Consolidated Financial Statements Years Ended December 31, 2012

C ONSOLIDATED F INANCIAL S TATEMENTS Billing Services Group Limited Years Ended December 31, 2012 and 2011 With Independent Auditor s Report Consolidated Financial Statements Years Ended December 31, 2012

FASB Emerging Issues Task Force

EITF Issue No. 08-1 FASB Emerging Issues Task Force Issue No. 08-1 Title: Revenue Arrangements with Multiple Deliverables Document: Issue Summary No. 2 Date prepared: October 20, 2008 FASB Staff: Maples

EITF Issue No. 08-1 FASB Emerging Issues Task Force Issue No. 08-1 Title: Revenue Arrangements with Multiple Deliverables Document: Issue Summary No. 2 Date prepared: October 20, 2008 FASB Staff: Maples

HONDA MOTOR CO., LTD. AND SUBSIDIARIES. Consolidated Financial Statements. September 30, 2014

Consolidated Financial Statements Consolidated Balance Sheets March 31, and Assets March 31, unaudited unaudited Current assets: Cash and cash equivalents 1,168,914 1,162,705 Trade accounts and notes receivable,

Consolidated Financial Statements Consolidated Balance Sheets March 31, and Assets March 31, unaudited unaudited Current assets: Cash and cash equivalents 1,168,914 1,162,705 Trade accounts and notes receivable,

TENNANT COMPANY (Exact name of registrant as specified in its charter)

") UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q [ ü] QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 OR For the quarterly period

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q [ ü] QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 OR For the quarterly period

EITF ABSTRACTS. An enterprise issues debt instruments with both guaranteed and contingent payments. The

EITF ABSTRACTS Issue No. 86-28 Title: Accounting Implications of Indexed Debt Instruments Dates Discussed: October 16, 1986; December 4, 1986 References: ISSUE FASB Statement No. 5, Accounting for Contingencies

EITF ABSTRACTS Issue No. 86-28 Title: Accounting Implications of Indexed Debt Instruments Dates Discussed: October 16, 1986; December 4, 1986 References: ISSUE FASB Statement No. 5, Accounting for Contingencies

DAIWA. Daiwa Capital Markets America Inc. (A Wholly Owned Subsidiary of Daiwa Capital Markets America Holdings Inc.) S e p t e m b e r 3 0

S e p t e m b e r 3 0") DAIWA Daiwa Capital Markets America Inc. (A Wholly Owned Subsidiary of Daiwa Capital Markets America Holdings Inc.) S e p t e m b e r 3 0 2014 (Unaudited) DAIWA CAPITAL MARKETS AMERICA INC. (A Wholly Owned

DAIWA Daiwa Capital Markets America Inc. (A Wholly Owned Subsidiary of Daiwa Capital Markets America Holdings Inc.) S e p t e m b e r 3 0 2014 (Unaudited) DAIWA CAPITAL MARKETS AMERICA INC. (A Wholly Owned

Q Financial Information

Q3 2015 Financial Information Financial Information 3 Key Figures 8 Interim Consolidated Financial Information (unaudited) 8 Interim Consolidated Income Statements 9 Interim Condensed Consolidated Statements

Q3 2015 Financial Information Financial Information 3 Key Figures 8 Interim Consolidated Financial Information (unaudited) 8 Interim Consolidated Income Statements 9 Interim Condensed Consolidated Statements

Statement of Financial Condition Year ended December 31, 2015

JANNEY MONTGOMERY SCOTT LLC Statement of Financial Condition Year ended December 31, 2015 Janney Montgomery Scott LLC Statement of Financial Condition and Notes For the year ended December 31, 2015 Contents

JANNEY MONTGOMERY SCOTT LLC Statement of Financial Condition Year ended December 31, 2015 Janney Montgomery Scott LLC Statement of Financial Condition and Notes For the year ended December 31, 2015 Contents

Notes to Consolidated Financial Statements Hitachi Chemical Co., Ltd. and Consolidated Subsidiaries For the Years Ended March 31, 2005, 2004 and 2003

Notes to Consolidated Financial Statements Hitachi Chemical Co., Ltd. and Consolidated Subsidiaries For the Years Ended March 31, 2005, 2004 and 2003 1. BASIS OF PRESENTATION AND SUMMARY OF SIGNIFICANT

Notes to Consolidated Financial Statements Hitachi Chemical Co., Ltd. and Consolidated Subsidiaries For the Years Ended March 31, 2005, 2004 and 2003 1. BASIS OF PRESENTATION AND SUMMARY OF SIGNIFICANT

NARUC: REVENUE RECOGNITION JULIE PETIT AUDIT SENIOR MANAGER BRIAN JONES AUDIT SENIOR MANAGER MONDAY, SEPTEMBER 11 TH, 2017

NARUC: REVENUE RECOGNITION JULIE PETIT AUDIT SENIOR MANAGER BRIAN JONES AUDIT SENIOR MANAGER MONDAY, SEPTEMBER 11 TH, 2017 Mazars USA LLP is an independent member firm of Mazars Group. Mazars USA LLP is

NARUC: REVENUE RECOGNITION JULIE PETIT AUDIT SENIOR MANAGER BRIAN JONES AUDIT SENIOR MANAGER MONDAY, SEPTEMBER 11 TH, 2017 Mazars USA LLP is an independent member firm of Mazars Group. Mazars USA LLP is

COPYRIGHTED MATERIAL. Index

A AAERs (Accounting and Auditing Enforcement Releases), 191 Absences, compensated, 435 436 Accelerated depreciation methods, 327 330 Accounting, 841 868 accrual, 6 11 budgetary, 852 854 for cash, 240 242

A AAERs (Accounting and Auditing Enforcement Releases), 191 Absences, compensated, 435 436 Accelerated depreciation methods, 327 330 Accounting, 841 868 accrual, 6 11 budgetary, 852 854 for cash, 240 242

(SEC I.D. No )

") C ONSOLIDATED S TATEMENT OF F INANCIAL C ONDITION CIBC World Markets Corp. and Subsidiaries October 31, 2016 With Report of Independent Registered Public Accounting Firm (SEC I.D. No.8-18333) Consolidated

C ONSOLIDATED S TATEMENT OF F INANCIAL C ONDITION CIBC World Markets Corp. and Subsidiaries October 31, 2016 With Report of Independent Registered Public Accounting Firm (SEC I.D. No.8-18333) Consolidated

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C FORM 10-Q

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 10-Q QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 10-Q QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended

Consolidated Financial Statements Toho Zinc Co., Ltd. and Consolidated Subsidiaries

Consolidated Financial Statements Toho Zinc Co., Ltd. and Consolidated Subsidiaries For the year ended March 31, 2018 with Independent Auditor s Report Toho Zinc Co., Ltd. and Consolidated Subsidiaries

Consolidated Financial Statements Toho Zinc Co., Ltd. and Consolidated Subsidiaries For the year ended March 31, 2018 with Independent Auditor s Report Toho Zinc Co., Ltd. and Consolidated Subsidiaries

JUNIPER NETWORKS, INC. (Exactnameofregistrantasspecifiedinitscharter)

") UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q (Mark One) x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q (Mark One) x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly

LOM FINANCIAL LIMITED

Consolidated Financial Statements and Independent Auditors' Report For the years ended Deloitte Ltd. Corner House 20 Parliament Street P.O. Box HM 1556 Hamilton HM FX Bermuda Tel: + 1 (441) 292 1500 Fax:

Consolidated Financial Statements and Independent Auditors' Report For the years ended Deloitte Ltd. Corner House 20 Parliament Street P.O. Box HM 1556 Hamilton HM FX Bermuda Tel: + 1 (441) 292 1500 Fax:

by Joe DiLeo and Ermir Berberi, Deloitte & Touche LLP

Heads Up May 11, 2016 Volume 23, Issue 14 In This Issue Collectibility Presentation of Sales Taxes and Similar Taxes Collected From Customers Noncash Consideration Contract Modifications and Completed

Heads Up May 11, 2016 Volume 23, Issue 14 In This Issue Collectibility Presentation of Sales Taxes and Similar Taxes Collected From Customers Noncash Consideration Contract Modifications and Completed

Williams College Consolidated Financial Statements June 30, 2018 and 2017

Consolidated Financial Statements Index Page(s) Report of Independent Auditors... 1 2 Consolidated Financial Statements Consolidated Statements of Financial Position... 3 Consolidated Statements of Activities...

Consolidated Financial Statements Index Page(s) Report of Independent Auditors... 1 2 Consolidated Financial Statements Consolidated Statements of Financial Position... 3 Consolidated Statements of Activities...

TENNANT COMPANY (Exact name of registrant as specified in its charter)

") UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q [ ü] QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 OR For the quarterly period

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q [ ü] QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 OR For the quarterly period

Revenue for power and utilities companies

Revenue for power and utilities companies New standard. New challenges. US GAAP March 2018 kpmg.com/us/frv b Revenue for power and utilities companies Revenue viewed through a new lens Again and again,

Revenue for power and utilities companies New standard. New challenges. US GAAP March 2018 kpmg.com/us/frv b Revenue for power and utilities companies Revenue viewed through a new lens Again and again,

View Filing Data Energy 11, L.P. (Filer) CIK: Print Document

CIK: Print Document") Home Latest Filings Previous Page View Filing Data Search the Next-Generation EDGAR System SEC Home» Search the Next-Generation EDGAR System» Company Search» Current Page Energy 11, L.P. (Filer) CIK: 0001581552

Home Latest Filings Previous Page View Filing Data Search the Next-Generation EDGAR System SEC Home» Search the Next-Generation EDGAR System» Company Search» Current Page Energy 11, L.P. (Filer) CIK: 0001581552

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C FORM 10-Q

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 10-Q QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 10-Q QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended

Illustrative financial statements

Illustrative financial statements Hedge funds September 2017 kpmg.com The information contained in these illustrative financial statements is of a general nature related to private investment companies

Illustrative financial statements Hedge funds September 2017 kpmg.com The information contained in these illustrative financial statements is of a general nature related to private investment companies

MAXAM GOLD CORPORATION, INC QUARTERLY REDPORT MARCH 31, 2013

MAXAM GOLD CORPORATION, INC QUARTERLY REDPORT MARCH 31, 2013 MAXAM GOLD CORPORATION BALANCE SHEET AS OF MARCH 31, 2013 AND MARCH 31, 2012 2013 2012 ASSETS Current Assets: Cash And Cash Equivalents $ -

MAXAM GOLD CORPORATION, INC QUARTERLY REDPORT MARCH 31, 2013 MAXAM GOLD CORPORATION BALANCE SHEET AS OF MARCH 31, 2013 AND MARCH 31, 2012 2013 2012 ASSETS Current Assets: Cash And Cash Equivalents $ -

Applying IFRS. Joint Transition Resource Group discusses additional revenue implementation issues. July 2015

Applying IFRS Joint Transition Resource Group discusses additional revenue implementation issues July 2015 Contents Overview 2 1. Issues that may require further discussion 2 1.1 Application of the constraint

Applying IFRS Joint Transition Resource Group discusses additional revenue implementation issues July 2015 Contents Overview 2 1. Issues that may require further discussion 2 1.1 Application of the constraint

APPENDIX 4H. Disclosure Checklist for Income Tax Basis Financial Statements. Financial Statement Date:

4 51 APPENDIX 4H Disclosure Checklist for Income Tax Basis Financial Statements Entity: Prepared by: Financial Statement Date: Date: Explanatory Comments This checklist includes the more common disclosure

4 51 APPENDIX 4H Disclosure Checklist for Income Tax Basis Financial Statements Entity: Prepared by: Financial Statement Date: Date: Explanatory Comments This checklist includes the more common disclosure

Technical Line FASB final guidance

No. 2017-22 Updated 4 December 2017 Technical Line FASB final guidance How the new revenue standard affects life sciences entities In this issue: Overview... 1 Collaborative arrangements... 2 Effect of

No. 2017-22 Updated 4 December 2017 Technical Line FASB final guidance How the new revenue standard affects life sciences entities In this issue: Overview... 1 Collaborative arrangements... 2 Effect of

Survey Results of Merger & Acquisition Damage Claims

Survey Results of Merger & Acquisition Damage Claims One of the significant practice areas at is addressing damage claims related to merger and acquisition transactions. Generally, the damages being alleged

Survey Results of Merger & Acquisition Damage Claims One of the significant practice areas at is addressing damage claims related to merger and acquisition transactions. Generally, the damages being alleged

Q Financial information 1 Q FINANCIAL INFORMATION

April 17, 2019 Q1 2019 Financial information 1 Q1 2019 FINANCIAL INFORMATION Financial Information Contents 03 05 Key Figures 06 32 Consolidated Financial Information (unaudited) 33 41 Supplemental Reconciliations

April 17, 2019 Q1 2019 Financial information 1 Q1 2019 FINANCIAL INFORMATION Financial Information Contents 03 05 Key Figures 06 32 Consolidated Financial Information (unaudited) 33 41 Supplemental Reconciliations

Harley-Davidson, Inc. (Exact name of registrant as specified in its charter)

") UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D. C. 20549 FORM 10-Q x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D. C. 20549 FORM 10-Q x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended

Third Quarter Message from the Chairman of the Board and the President and Chief Executive Officer. Third quarter.

Third Quarter 2015 Message from the Chairman of the Board and the President and Chief Executive Officer Third quarter For the third quarter of 2015, Hydro-Québec posted a net result of $339 million, compared

Third Quarter 2015 Message from the Chairman of the Board and the President and Chief Executive Officer Third quarter For the third quarter of 2015, Hydro-Québec posted a net result of $339 million, compared

INTERNET DISCLOSURE ITEMS FOR NOTICE OF CONVOCATION OF THE 122ND ORDINARY GENERAL MEETING OF SHAREHOLDERS NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

June 8, 2018 To Shareholders INTERNET DISCLOSURE ITEMS FOR NOTICE OF CONVOCATION OF THE 122ND ORDINARY GENERAL MEETING OF SHAREHOLDERS NOTES TO CONSOLIDATED FINANCIAL STATEMENTS [122nd Fiscal Year (From

June 8, 2018 To Shareholders INTERNET DISCLOSURE ITEMS FOR NOTICE OF CONVOCATION OF THE 122ND ORDINARY GENERAL MEETING OF SHAREHOLDERS NOTES TO CONSOLIDATED FINANCIAL STATEMENTS [122nd Fiscal Year (From

Oil and Gas Year-End Accounting and Auditing Update

1 Oil and Gas Year-End Accounting and Auditing Update 2 Today s Agenda FAS 133 Frequent Problem Areas FAS 143 Implementation Accounting for Costs Associated with Exit or Disposal Activities FAS 146 Accounting

1 Oil and Gas Year-End Accounting and Auditing Update 2 Today s Agenda FAS 133 Frequent Problem Areas FAS 143 Implementation Accounting for Costs Associated with Exit or Disposal Activities FAS 146 Accounting

Harley-Davidson, Inc. (Exact name of registrant as specified in its charter)

") UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D. C. 20549 FORM 10-Q x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D. C. 20549 FORM 10-Q x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended

Rosenthal Collins Group, L.L.C.

Statement of Financial Condition December 31, 2017 This report is deemed PUBLIC in accordance with Regulation 1.10(g) under the Commodity Exchange Act. Contents Report of Independent Registered Public

Statement of Financial Condition December 31, 2017 This report is deemed PUBLIC in accordance with Regulation 1.10(g) under the Commodity Exchange Act. Contents Report of Independent Registered Public

Revenue from contracts with customers (ASC 606)

") Financial reporting developments A comprehensive guide Revenue from contracts with customers (ASC 606) August 2015 To our clients and other friends In May 2014, the Financial Accounting Standards Board

Financial reporting developments A comprehensive guide Revenue from contracts with customers (ASC 606) August 2015 To our clients and other friends In May 2014, the Financial Accounting Standards Board

ORIGINAL PRONOUNCEMENTS

Financial Accounting Standards Board ORIGINAL PRONOUNCEMENTS AS AMENDED Statement of Financial Accounting Standards No. 133 Accounting for Derivative Instruments and Hedging Activities Copyright 2008 by

Financial Accounting Standards Board ORIGINAL PRONOUNCEMENTS AS AMENDED Statement of Financial Accounting Standards No. 133 Accounting for Derivative Instruments and Hedging Activities Copyright 2008 by

Cautionary Statement with Regard to Forward-Looking Statements

- Cautionary Statement with Regard to Forward-Looking Statements In this semi-annual report, all non-empirical information, including current plants, forecasts, strategies, assurances and other matters,

- Cautionary Statement with Regard to Forward-Looking Statements In this semi-annual report, all non-empirical information, including current plants, forecasts, strategies, assurances and other matters,

JANNEY MONTGOMERY SCOTT LLC Consolidated Statement of Financial Condition Period ended June 30, 2018 (Unaudited)

") JANNEY MONTGOMERY SCOTT LLC Consolidated Statement of Financial Condition Period ended June 30, 2018 (Unaudited) Janney Montgomery Scott LLC Consolidated Statement of Financial Condition and Notes For

JANNEY MONTGOMERY SCOTT LLC Consolidated Statement of Financial Condition Period ended June 30, 2018 (Unaudited) Janney Montgomery Scott LLC Consolidated Statement of Financial Condition and Notes For

STATEMENT OF FINANCIAL CONDITION AND SUPPLEMENTAL INFORMATION

STATEMENT OF FINANCIAL CONDITION AND SUPPLEMENTAL INFORMATION TD Ameritrade Futures & Forex LLC September 30, 2017 With Report of Independent Registered Public Accounting Firm Statement of Financial Condition

STATEMENT OF FINANCIAL CONDITION AND SUPPLEMENTAL INFORMATION TD Ameritrade Futures & Forex LLC September 30, 2017 With Report of Independent Registered Public Accounting Firm Statement of Financial Condition

Accounting and financial reporting developments for private companies

Accounting and financial reporting developments for private companies YEAR-END 2018 UPDATE In this update, we highlight some of the more important 2018 year-end accounting and financial reporting activities

Accounting and financial reporting developments for private companies YEAR-END 2018 UPDATE In this update, we highlight some of the more important 2018 year-end accounting and financial reporting activities

Simplified Accounting for a Perfect Fair Value Hedge

DEPT DEPARTMENTS I Accounting Interest Rate Swaps Simplified Accounting for a Perfect Fair Value Hedge By Josef Rashty T he U.S. economy has been improving steadily for the past seven years, and interest

DEPT DEPARTMENTS I Accounting Interest Rate Swaps Simplified Accounting for a Perfect Fair Value Hedge By Josef Rashty T he U.S. economy has been improving steadily for the past seven years, and interest

Guide to preparing carve-out financial statements

Guide to preparing carve-out financial statements Contents 1 Introduction... 1 1.1 Carve-out financial statements... 1 1.2 When carve-out financial statements may be required... 2 1.2.1 Financial statements

Guide to preparing carve-out financial statements Contents 1 Introduction... 1 1.1 Carve-out financial statements... 1 1.2 When carve-out financial statements may be required... 2 1.2.1 Financial statements

Revenue for Telecoms. Issues In-Depth. September IFRS and US GAAP. kpmg.com

Revenue for Telecoms Issues In-Depth September 2016 IFRS and US GAAP kpmg.com Contents Facing the challenges 1 Introduction 2 Putting the new standard into context 6 1 Scope 9 1.1 In scope 9 1.2 Out of

Revenue for Telecoms Issues In-Depth September 2016 IFRS and US GAAP kpmg.com Contents Facing the challenges 1 Introduction 2 Putting the new standard into context 6 1 Scope 9 1.1 In scope 9 1.2 Out of

Power & Utilities Spotlight Generating a Discussion About the FASB s New Revenue Standard

August 2014 Power & Utilities Spotlight Generating a Discussion About the FASB s New Revenue Standard In This Issue: Background Key Accounting Issues Effective Date and Transition Implementation Challenges

August 2014 Power & Utilities Spotlight Generating a Discussion About the FASB s New Revenue Standard In This Issue: Background Key Accounting Issues Effective Date and Transition Implementation Challenges

TOYOTA MOTOR CORPORATION Unaudited Consolidated Financial Statements For the period ended June 30, 2017

TOYOTA MOTOR CORPORATION Unaudited Consolidated Financial Statements For the period ended June 30, 2017 Analysis of Results of Operations For the first quarter ended June 30, 2017 Financial Results Consolidated

TOYOTA MOTOR CORPORATION Unaudited Consolidated Financial Statements For the period ended June 30, 2017 Analysis of Results of Operations For the first quarter ended June 30, 2017 Financial Results Consolidated

Statement No. 53 of the. Governmental Accounting Standards Board. Accounting and Financial Reporting for Derivative Instruments

NO. 279-B JUNE 2008 Governmental Accounting Standards Series Statement No. 53 of the Governmental Accounting Standards Board Accounting and Financial Reporting for Derivative Instruments Governmental Accounting

NO. 279-B JUNE 2008 Governmental Accounting Standards Series Statement No. 53 of the Governmental Accounting Standards Board Accounting and Financial Reporting for Derivative Instruments Governmental Accounting

Q Financial information

FEBRUARY 8, 2018 Q4 2017 Financial information Financial Information Contents 03 07 Key Figures 08 34 Interim Consolidated Financial Information (unaudited) 35 51 Supplemental Reconciliations and Definitions

FEBRUARY 8, 2018 Q4 2017 Financial information Financial Information Contents 03 07 Key Figures 08 34 Interim Consolidated Financial Information (unaudited) 35 51 Supplemental Reconciliations and Definitions

C ONSOLIDATED F INANCIAL S TATEMENTS. Billing Services Group Limited Years Ended December 31, 2016 and 2015 With Independent Auditor s Report

C ONSOLIDATED F INANCIAL S TATEMENTS Years Ended With Independent Auditor s Report Consolidated Financial Statements Years Ended Contents Independent Auditor s Report...1 Consolidated Financial Statements

C ONSOLIDATED F INANCIAL S TATEMENTS Years Ended With Independent Auditor s Report Consolidated Financial Statements Years Ended Contents Independent Auditor s Report...1 Consolidated Financial Statements

Q Financial information

July 19, 2018 Q2 2018 Financial information Financial Information Contents 03 07 Key Figures 08 35 Interim Consolidated Financial Information (unaudited) 36 48 Supplemental Reconciliations and Definitions

July 19, 2018 Q2 2018 Financial information Financial Information Contents 03 07 Key Figures 08 35 Interim Consolidated Financial Information (unaudited) 36 48 Supplemental Reconciliations and Definitions

DAIWA CAPITAL MARKETS AMERICA INC. (A Wholly Owned Subsidiary of Daiwa Capital Markets America Holdings Inc.) Statement of Financial Condition and

Statement of Financial Condition and") Statement of Financial Condition and Supplementary Schedules (With Report of Independent Registered Public Accounting Firm Thereon) KPMG LLP 345 Park Avenue New York, NY 10154-0102 Report of Independent

Statement of Financial Condition and Supplementary Schedules (With Report of Independent Registered Public Accounting Firm Thereon) KPMG LLP 345 Park Avenue New York, NY 10154-0102 Report of Independent

Speaker Bio Cline Comer

AICPA Revision Project Audit and Accounting Guide, Health Care Organizations FICPA Annual Health Care Conference April 28-29, 2011 C. Cline Comer, CPA 1 Speaker Bio Cline Comer Cline Comer is a Partner

AICPA Revision Project Audit and Accounting Guide, Health Care Organizations FICPA Annual Health Care Conference April 28-29, 2011 C. Cline Comer, CPA 1 Speaker Bio Cline Comer Cline Comer is a Partner

Mesirow Financial, Inc.

Mesirow Financial, Inc. (SEC I.D. No. 8-28816) Statement of Financial Condition as of March 31, 2015 and Report of Independent Registered Public Accounting Firm Filed pursuant to Rule 17a-5(e)(3) under

Mesirow Financial, Inc. (SEC I.D. No. 8-28816) Statement of Financial Condition as of March 31, 2015 and Report of Independent Registered Public Accounting Firm Filed pursuant to Rule 17a-5(e)(3) under

Accounting and financial reporting activities for private companies

Accounting and financial reporting activities for private companies SECOND-QUARTER 2018 In this update, we highlight some of the more important 2018 second-quarter accounting and financial reporting activities

Accounting and financial reporting activities for private companies SECOND-QUARTER 2018 In this update, we highlight some of the more important 2018 second-quarter accounting and financial reporting activities

MODEC, INC. and Subsidiaries. Consolidated Financial Statements As of December 31, 2003 and 2002

MODEC, INC. and Subsidiaries Consolidated Financial Statements As of December 31, 2003 and 2002 MODEC, INC. and Subsidiaries CONSOLIDATED BALANCE SHEETS December 31, 2003 and 2002 A S S E T S Japanese

MODEC, INC. and Subsidiaries Consolidated Financial Statements As of December 31, 2003 and 2002 MODEC, INC. and Subsidiaries CONSOLIDATED BALANCE SHEETS December 31, 2003 and 2002 A S S E T S Japanese

Rockwell Automation, Inc. (Exact name of registrant as specified in its charter)

") UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the Quarterly Period Ended

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the Quarterly Period Ended

OJSC NOVOLIPETSK STEEL INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

OJSC NOVOLIPETSK STEEL INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS PREPARED IN ACCORDANCE WITH ACCOUNTING PRINCIPLES GENERALLY ACCEPTED IN THE UNITED STATES OF AMERICA AS AT MARCH 31, 2014 AND

OJSC NOVOLIPETSK STEEL INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS PREPARED IN ACCORDANCE WITH ACCOUNTING PRINCIPLES GENERALLY ACCEPTED IN THE UNITED STATES OF AMERICA AS AT MARCH 31, 2014 AND

COPYRIGHTED MATERIAL INDEX 1087

INDEX 1087 A Accelerated depreciation, 233 Accounting basis of, 49, 140 Cash to accrual conversion, 51 Accounting changes, 106 Interim reporting, 789 Accounting information Qualitative characteristics

INDEX 1087 A Accelerated depreciation, 233 Accounting basis of, 49, 140 Cash to accrual conversion, 51 Accounting changes, 106 Interim reporting, 789 Accounting information Qualitative characteristics

Priority Ambulance, LLC

AMR 9B - 001 Consolidated Financial Statements As of and for the Year Ended December 31, 2014 and the short period from December 5, 2013 (inception) to December 31, 2013 (unaudited) and Independent Auditor

AMR 9B - 001 Consolidated Financial Statements As of and for the Year Ended December 31, 2014 and the short period from December 5, 2013 (inception) to December 31, 2013 (unaudited) and Independent Auditor

CONSOLIDATED FINANCIAL STATEMENTS

CONSOLIDATED FINANCIAL STATEMENTS LTD. and Consolidated Subsidiaries Consolidated Balance Sheet March 31, U.S. Dollars (Note 1) ASSETS 2016 CURRENT ASSETS: Cash and cash equivalents (Note 15) 77,051 67,133

CONSOLIDATED FINANCIAL STATEMENTS LTD. and Consolidated Subsidiaries Consolidated Balance Sheet March 31, U.S. Dollars (Note 1) ASSETS 2016 CURRENT ASSETS: Cash and cash equivalents (Note 15) 77,051 67,133

Condensed Financial Statements

UNITED WISCONSIN GRAIN PRODUCERS LLC Condensed Financial Statements FRIESLAND, WISCONSIN 3/31/2016 UNITED WISCONSIN GRAIN PRODUCERS LLC Contents Condensed Financial Statements Page Condensed Balance Sheets

UNITED WISCONSIN GRAIN PRODUCERS LLC Condensed Financial Statements FRIESLAND, WISCONSIN 3/31/2016 UNITED WISCONSIN GRAIN PRODUCERS LLC Contents Condensed Financial Statements Page Condensed Balance Sheets

New Developments Summary

October 9, 2017 NDS 2017-06 New Developments Summary Natural disasters and other loss events Accounting and financial reporting considerations Summary The financial implications of natural disasters and

October 9, 2017 NDS 2017-06 New Developments Summary Natural disasters and other loss events Accounting and financial reporting considerations Summary The financial implications of natural disasters and

Report to the Audit Committee of the Board of Governors 2017 Audit Results

Report to the Audit Committee of the Board of Governors 2017 Audit Results California Independent System Operator Corporation May 16, 2018 Table of Contents Executive Summary 3 Audit Results Audit Risks

Report to the Audit Committee of the Board of Governors 2017 Audit Results California Independent System Operator Corporation May 16, 2018 Table of Contents Executive Summary 3 Audit Results Audit Risks

Financial Instruments Accounting

IFRS REPORTING Financial Instruments Accounting AUDIT AUDIT TAX ADVISORY Preface IAS 39 Financial Instruments: Recognition and Measurement has been in effect for several years and most entities reporting

IFRS REPORTING Financial Instruments Accounting AUDIT AUDIT TAX ADVISORY Preface IAS 39 Financial Instruments: Recognition and Measurement has been in effect for several years and most entities reporting

CKD Corporation and Consolidated Subsidiaries. Consolidated Financial Statements for the Years Ended March 31, 2009 and 2008

CKD Corporation and Consolidated Subsidiaries Consolidated Financial Statements for the Years Ended March 31, 2009 and 2008 CKD Corporation and Consolidated Subsidiaries Consolidated Balance Sheets March

CKD Corporation and Consolidated Subsidiaries Consolidated Financial Statements for the Years Ended March 31, 2009 and 2008 CKD Corporation and Consolidated Subsidiaries Consolidated Balance Sheets March

AMERICAN HONDA FINANCE CORPORATION (Exact name of registrant as specified in its charter)

") od UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 10-Q (Mark One) QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 OR For the quarterly

od UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 10-Q (Mark One) QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 OR For the quarterly

CANNAMED 4PETS INC. (A DEVELOPMENT STAGE COMPANY) FINANCIAL STATEMENTS NOVEMBER 30, 2015

FINANCIAL STATEMENTS NOVEMBER 30, 2015") CANNAMED 4PETS INC. FINANCIAL STATEMENTS CANNAMED4PETS INC. BALANCE SHEETS (unaudited) AS OF AND FEBRUARY 28, 2015 November 30, 2015 (restated) February 28, 2015 (restated) ASSETS Current assets Cash and

CANNAMED 4PETS INC. FINANCIAL STATEMENTS CANNAMED4PETS INC. BALANCE SHEETS (unaudited) AS OF AND FEBRUARY 28, 2015 November 30, 2015 (restated) February 28, 2015 (restated) ASSETS Current assets Cash and

NATIONAL BANK OF CANADA FINANCIAL INC. AND SUBSIDIARIES

Consolidated Statement of Financial Condition as of NATIONAL BANK OF CANADA FINANCIAL INC. (SEC I.D. No. 8-39947) Table of Contents Report of Independent Registered Public Accountant Firm... 1 Consolidated

Consolidated Statement of Financial Condition as of NATIONAL BANK OF CANADA FINANCIAL INC. (SEC I.D. No. 8-39947) Table of Contents Report of Independent Registered Public Accountant Firm... 1 Consolidated

5,493,033 (Cost $5,492,519) (c) Net Other Assets and Liabilities 24.2%... 1,749,230 Net Assets 100.0%... $ 7,242,263

(c) Net Other Assets and Liabilities 24.2%... 1,749,230 Net Assets 100.0%... $ 7,242,263") Consolidated Portfolio of Investments Principal TREASURY BILLS 75.8% Description Stated Coupon Stated Maturity $ 1,000,000 U.S. Treasury Bill (a)... (b) 10/19/17 $ 999,569 2,500,000 U.S. Treasury Bill

Consolidated Portfolio of Investments Principal TREASURY BILLS 75.8% Description Stated Coupon Stated Maturity $ 1,000,000 U.S. Treasury Bill (a)... (b) 10/19/17 $ 999,569 2,500,000 U.S. Treasury Bill

SECURITIES & EXCHANGE COMMISSION EDGAR FILING. NaturalShrimp Inc. Form: 10-Q. Date Filed:

SECURITIES & EXCHANGE COMMISSION EDGAR FILING NaturalShrimp Inc Form: 10-Q Date Filed: 2019-02-14 Corporate Issuer CIK: 1465470 Copyright 2019, Issuer Direct Corporation. All Right Reserved. Distribution

SECURITIES & EXCHANGE COMMISSION EDGAR FILING NaturalShrimp Inc Form: 10-Q Date Filed: 2019-02-14 Corporate Issuer CIK: 1465470 Copyright 2019, Issuer Direct Corporation. All Right Reserved. Distribution

Application of US GAAP

Application of US GAAP Price The cost of the 8-day programme if paid upfront Option 1 6690 zł + 23% VAT Option 2 6790 zł + 23% VAT Option 3 7000 zł + 23% VAT Client Relations Officer Aleksandra Trych tel.

Application of US GAAP Price The cost of the 8-day programme if paid upfront Option 1 6690 zł + 23% VAT Option 2 6790 zł + 23% VAT Option 3 7000 zł + 23% VAT Client Relations Officer Aleksandra Trych tel.

DAIWA CAPITAL MARKETS AMERICA INC. (A Wholly Owned Subsidiary of Daiwa Capital Markets America Holdings Inc.) Statement of Financial Condition and

Statement of Financial Condition and") Statement of Financial Condition and Supplementary Schedules (With Report of Independent Registered Public Accounting Firm Thereon) KPMG LLP 345 Park Avenue New York, NY 10154-0102 Report of Independent

Statement of Financial Condition and Supplementary Schedules (With Report of Independent Registered Public Accounting Firm Thereon) KPMG LLP 345 Park Avenue New York, NY 10154-0102 Report of Independent