Chapter 20. Corporate Risk Management. Copyright 2011 Pearson Prentice Hall. All rights reserved.

|

|

|

- Hilda Copeland

- 6 years ago

- Views:

Transcription

1 Chapter 20 Corporate Risk Management 1

2 Chapter 14 Contents 1. Five-Step Corporate Risk Management Process 2. Managing Risk with Insurance Contracts 3. Managing Risk by Hedging with Forward Contracts 4. Managing Risk with Exchange-Traded Financial Derivatives 5. Valuing Options and Swaps

3 Learning Objectives 1. Define risk management in the context of the fivestep risk management process. 2. Understand how insurance contracts can be used to manage risk. 3. Use forward contracts to hedge commodity price risk. 4. Understand the advantages and disadvantages of using exchange traded futures and option contracts to hedge price risk. 5. Understand how to value option and how swaps work

4 Principles Used in This Chapter Principle 2: There is a Risk-Return Tradeoff. Business is inherently risky but a lot of risk that a firm is exposed to are at least partially controllable through the use of financial contracts. Corporations are devoting increasing amounts of time and resources to active management of their risk exposure

5 Five Step Corporate Risk Management Process 1. Identify and understand the firm s major risks. 2. Decide which type of risks to keep and which to transfer. 3. Decide how much risk to assume. 4. Incorporate risk into all the firm s decisions and processes. 5. Monitor and manage the risk that the firm assumes

6 Step1: Identify and Understand the Firm s Major Risks Identifying risks relates to understanding the factors that drive the firm s cash flow volatility. For example: Demand risk - fluctuations in demand Commodity risk fluctuations in prices of raw materials Country risk unfavorable government policies Operational risk cost overruns in firm s operations Exchange rate risk changes in exchange rates

7 Step1: Identify and Understand the Firm s Major Risks (cont.) All the listed sources of risk (except operational risk) are external to the firm. Risk management generally focuses on managing external factors that cause volatility in firm s cash flows

8 Step 2: Decide Which Type of Risk to Keep and Which to Transfer This is perhaps the most critical step. For example, oil and gas exploration and production firms have historically chosen to assume the risk of fluctuations in the price of oil and gas. However, some firms have chosen to actively manage the risk

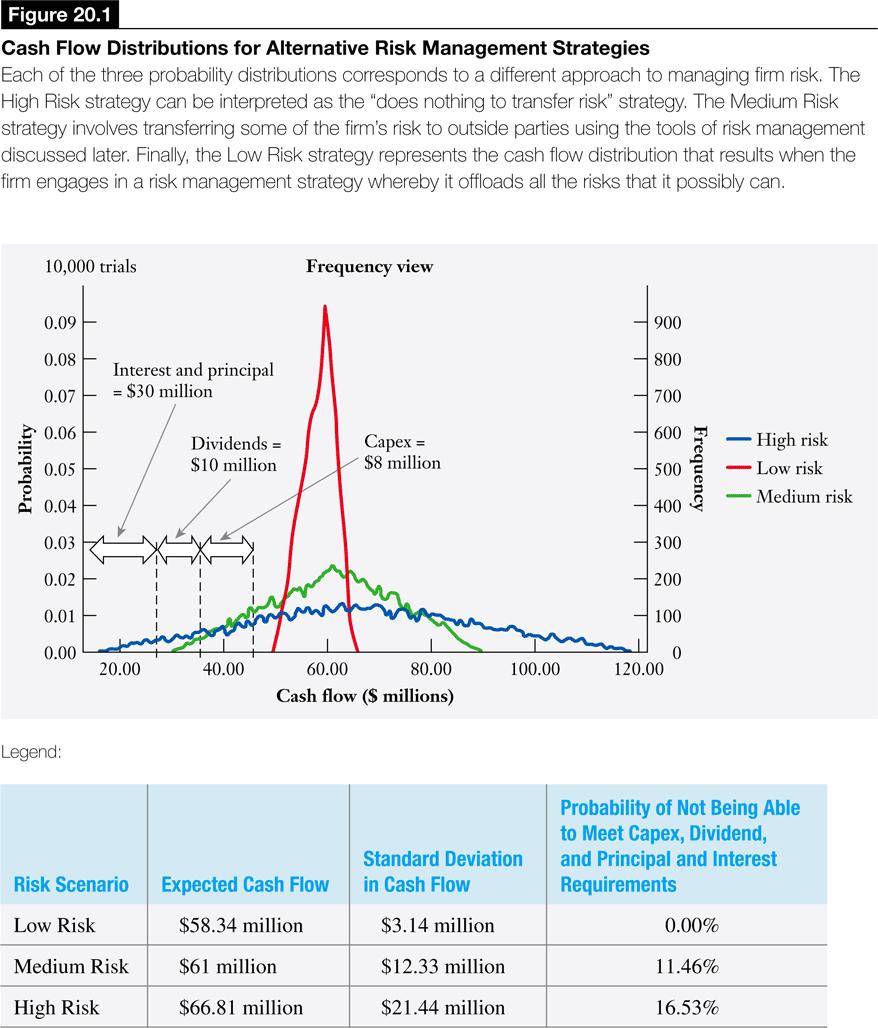

9 Step 3: Decide How Much Risk to Assume Figure 20-1 illustrates the cash flow distributions for three risk management strategies. The specific strategy chosen will depend upon the firm s attitude to risk and the cost/benefit analysis of risk management strategies

10

11 Step 4: Incorporate Risk into All the Firm s Decisions and Processes In this step, the firm must implement a system for controlling the firm s risk exposure. For example, for those risks that will be transferred, the firm must determine an appropriate means of transferring risk such as buying an insurance policy

12 Step 5: Monitor and Manage the Risk the Firm Assumes An effective monitoring system ensures that the firm s day-to-day decisions are consistent with its chosen risk profile. This may involve centralizing the firm s risk exposure with a chief risk officer who assumes responsibility for monitoring and regularly reporting to the CEO and to the firm s board

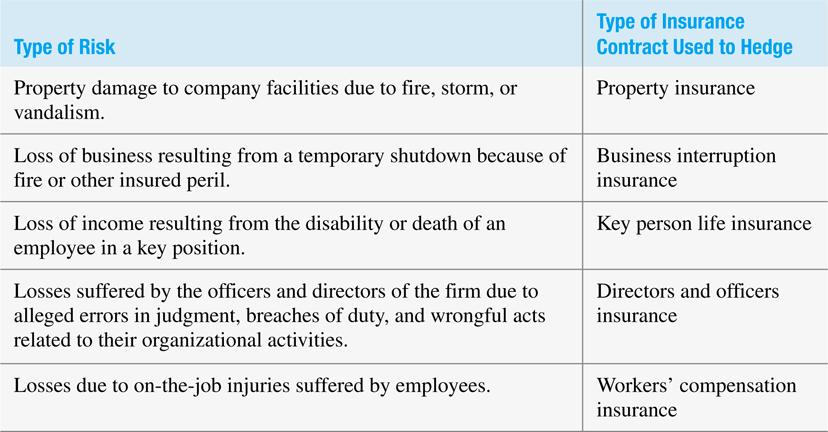

13 Managing Risk with Insurance Contracts Insurance is a method of transferring risk from the firm to an outside party, in exchange for a premium. There are many types of insurance contracts that provide protection against various events

14

15 Managing Risk by Hedging with Forward Contracts Hedging refers to a strategy designed to offset the exposure to price risk. Example 20.1 If you are planning to purchase 1 million Euros in 6 months, you may be concerned that if Euro strengthens it will cost you more in U.S. dollars. Such risk can be mitigated with forward contracts

16 Managing Risk by Hedging with Forward Contracts (cont.) Forward contract is a contract wherein a price is agreed-upon today for asset to be sold or purchased in the future. Since the price is locked-in today, risk from future price fluctuation is reduced. These contracts are privately negotiated with an intermediary such as an investment bank

17 Managing Risk by Hedging with Forward Contracts (cont.) Thus in example 20.1, you could negotiate a rate today for Euros (say 1 Euro = $1.35) using a forward contract. In 6-months, regardless of whether Euro has appreciated or depreciated, your obligation will be to buy 1 million Euros at $1.35 each or $1.35 million

18 Managing Risk by Hedging with Forward Contracts (cont.) The following table shows potential future scenarios and the cash flows. It is seen that Forward contract helps to reduce risk if Euro appreciates. However, if Euro depreciates, Forward contract obligates the firm to pay a higher amount. Future Exchange Rate of Euro Cost with a Forward Contract Cost without a Forward contract Effect of Forward Contract $1.20 $1.35 million $1.20 million Unfavorable $1.30 $1.35 million $1.30 million Unfavorable $1.40 $1.35 million $1.40 million Favorable $1.50 $1.35 million $1.50 million Favorable

19 Checkpoint 20.1 Hedging Crude Oil Price Risk Using Forward Contracts Progressive Refining Inc. operates a specialty refining company that refines crude oil and sells the refined by-products to the cosmetic and plastic industries. The firm is currently planning for its refining needs for one year hence. The firm s analysts estimate that Progressive will need to purchase 1 million barrels of crude oil at the end of the current year to provide the feedstock for its refining needs for the coming year. The 1 million barrels of crude will be converted into by-products at an average cost of $30 per barrel. Progressive will then sell the by-products for $165 per barrel. The current spot price of oil is $125 per barrel, and Progressive has been offered a forward contract by its investment banker to purchase the needed oil for a delivery price in one year of $130 per barrel. a. Ignoring taxes, if oil prices in one year are as low as $110 or as high as $140, what will be Progressive s profits (assuming the firm does not enter into the forward contract)? b. If the firm were to enter into the forward contract to purchase oil for $130 per barrel, demonstrate how this would effectively lock in the firm s cost of fuel today, thus hedging the risk that fluctuating crude oil prices pose for the firm s profits for the next year

20 Checkpoint

21 Checkpoint

22 Checkpoint

23 Checkpoint

24 Checkpoint

25 Checkpoint 20.1: Check Yourself Consider the profits that Progressive might earn if it chooses to hedge only 80% of its anticipated 1 million barrels of crude oil under the conditions above

26 Step 1: Picture the Problem The figure shows that the future price of crude oil could have a dramatic impact on the total cost of 1 million barrels of crude oil. If the price is not managed, it will significantly affect the future profits of the firm

27 Step 2: Decide on a Solution Strategy The firm can hedge its risk by purchasing a forward contract. This will lock-in the future price of oil at the forward rate of $130 per barrel

28 Step 3: Solve The table on the next slide contains the calculation of firm profits for the case where the price of crude oil is not hedged (column E), the payoff to the forward contract (column F) and firm profits where the price of crude is 80% hedged (column G)

29 Step 3: Solve (cont.) Price of Oil/bbl Total Cost of Oil Total Revenues 80% Hedged Total Refining Costs Unhedged Annual Profits A B=Ax1m C D=$30x1m E=C+B+D Profit/Loss on Forward Contract =(A- $130)x1mx%Hedge 80% Hedged Annual Profits G=E+F $110 $(110,000,000) $165,000,000 $(30,000,000) $25,000,000 $(16,000,000) $9,000, (115,000,000) $165,000,000 (30,000,000) $20,000,000 $(12,000,000) 8,000, (120,000,000) $165,000,000 (30,000,000) $15,000,000 $(8,000,000) 7,000, (125,000,000) $165,000,000 (30,000,000) $10,000,000 $(4,000,000) 6,000, (130,000,000) $165,000,000 (30,000,000) $5,000,000 $ 5,000, (135,000,000) $165,000,000 (30,000,000) $0 $4,000,000 4,000, (140,000,000) $165,000,000 (30,000,000) $(5,000,000) $8,000,000 3,000,

30 Step 4: Analyze The total cost of crude oil increases as the price of crude oil increases. The unhedged annual profits range from a loss of $5 million to a gain of $25 million. With 80% hedging, losses are avoided and the firm ends with profits ranging from $3 million to $5million. The forward contract obviously benefits the firm when the price of oil is higher than $

31 Limitations of Forward Contract 1. Credit or default risk: Both parties are exposed to the risk that the other party may default on their obligation. 2. Sharing of strategic information: The parties know what specific risk is being hedged. 3. It is hard to determine the market values of negotiated contracts as these contracts are not traded

32 Limitations of Forward Contract These limitations of forward contracts can be addressed by using exchange-traded contracts such as exchange traded futures, options, and swap contracts

Agenda. Learning Objectives. Corporate Risk Management. Chapter 20. Learning Objectives Principles Used in This Chapter

Chapter 20 Corporate Risk Management Agenda Learning Objectives Principles Used in This Chapter 1. Five-Step Corporate Risk Management Process 2. Managing Risk with Insurance Contracts 3. Managing Risk

Chapter 20 Corporate Risk Management Agenda Learning Objectives Principles Used in This Chapter 1. Five-Step Corporate Risk Management Process 2. Managing Risk with Insurance Contracts 3. Managing Risk

BBK3273 International Finance

BBK3273 International Finance Prepared by Dr Khairul Anuar L6: Transaction Exposure www.notes638.wordpress.com Contents 1. Transaction Exposure 2. Policies for Hedging Transaction Exposure 3. Hedging Exposure

BBK3273 International Finance Prepared by Dr Khairul Anuar L6: Transaction Exposure www.notes638.wordpress.com Contents 1. Transaction Exposure 2. Policies for Hedging Transaction Exposure 3. Hedging Exposure

BBK3273 International Finance

BBK3273 International Finance Prepared by Dr Khairul Anuar L6: Transaction Exposure www.notes638.wordpress.com Contents 1. Transaction Exposure 2. Policies for Hedging Transaction Exposure 3. Hedging Exposure

BBK3273 International Finance Prepared by Dr Khairul Anuar L6: Transaction Exposure www.notes638.wordpress.com Contents 1. Transaction Exposure 2. Policies for Hedging Transaction Exposure 3. Hedging Exposure

The Cost of Capital. Principles Applied in This Chapter. The Cost of Capital: An Overview

The Cost of Capital Chapter 14 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of Value. Principle

The Cost of Capital Chapter 14 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of Value. Principle

The Cost of Capital. Chapter 14

The Cost of Capital Chapter 14 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of Value. Principle

The Cost of Capital Chapter 14 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of Value. Principle

Exercise Session #7 Suggested Solutions

JEM034 Corporate Finance Winter Semester 207/208 Instructor: Olga Bychkova Date: 2//207 Exercise Session #7 Suggested Solutions Problem. 22.9 Describe each of the following situations in the language of

JEM034 Corporate Finance Winter Semester 207/208 Instructor: Olga Bychkova Date: 2//207 Exercise Session #7 Suggested Solutions Problem. 22.9 Describe each of the following situations in the language of

AGENDA LEARNING OBJECTIVES THE COST OF CAPITAL. Chapter 14. Learning Objectives Principles Used in This Chapter. financing.

Chapter 14 THE COST OF CAPITAL AGENDA Learning Objectives Principles Used in This Chapter 1. The Cost of Capital: An Overview 2. Determining the Firm s Capital Structure Weights 3. Estimating the Costs

Chapter 14 THE COST OF CAPITAL AGENDA Learning Objectives Principles Used in This Chapter 1. The Cost of Capital: An Overview 2. Determining the Firm s Capital Structure Weights 3. Estimating the Costs

Derivatives and Hedging

Derivatives and Hedging Corporate Finance Ernst Maug University of Mannheim http://cf.bwl.uni-mannheim.de maug@cf.bwl.uni-mannheim.de Tel: +49 (621) 181-1952 Overview Introduction - The use of hedge instruments

Derivatives and Hedging Corporate Finance Ernst Maug University of Mannheim http://cf.bwl.uni-mannheim.de maug@cf.bwl.uni-mannheim.de Tel: +49 (621) 181-1952 Overview Introduction - The use of hedge instruments

DESCRIPTION OF FINANCIAL INSTRUMENTS AND INVESTMENT RISKS

DESCRIPTION OF FINANCIAL INSTRUMENTS AND INVESTMENT RISKS General provisions This brief description contains information about financial instruments and their inherent risks. It doesn t mean that this

DESCRIPTION OF FINANCIAL INSTRUMENTS AND INVESTMENT RISKS General provisions This brief description contains information about financial instruments and their inherent risks. It doesn t mean that this

Chapter 8. Swaps. Copyright 2009 Pearson Prentice Hall. All rights reserved.

Chapter 8 Swaps Introduction to Swaps A swap is a contract calling for an exchange of payments, on one or more dates, determined by the difference in two prices A swap provides a means to hedge a stream

Chapter 8 Swaps Introduction to Swaps A swap is a contract calling for an exchange of payments, on one or more dates, determined by the difference in two prices A swap provides a means to hedge a stream

In the previous session we learned about the various categories of Risk in agriculture. Of course the whole point of talking about risk in this

In the previous session we learned about the various categories of Risk in agriculture. Of course the whole point of talking about risk in this educational series is so that we can talk about managing

In the previous session we learned about the various categories of Risk in agriculture. Of course the whole point of talking about risk in this educational series is so that we can talk about managing

Derivative Instruments And Hedging Activities

Activities Activities Activities [Abstract] Activities 3 Months Ended Mar. 31, 2012 NOTE 12. DERIVATIVE FINANCIAL INSTRUMENTS AND HEDGING ACTIVITIES People's United Financial uses derivative financial

Activities Activities Activities [Abstract] Activities 3 Months Ended Mar. 31, 2012 NOTE 12. DERIVATIVE FINANCIAL INSTRUMENTS AND HEDGING ACTIVITIES People's United Financial uses derivative financial

Foreign Exchange Risk. Foreign Exchange Risk. Risks from International Investments. Foreign Exchange Transactions. Topics

Foreign Exchange Risk Topics Foreign Exchange Risk Foreign Exchange Exposure Financial Derivatives Forwards Futures Options Risks from International Investments Additional Risks Political Risk: Uncertainty

Foreign Exchange Risk Topics Foreign Exchange Risk Foreign Exchange Exposure Financial Derivatives Forwards Futures Options Risks from International Investments Additional Risks Political Risk: Uncertainty

CHAPTER 16: MANAGING BOND PORTFOLIOS

CHAPTER 16: MANAGING BOND PORTFOLIOS 1. The percentage change in the bond s price is: Duration 7.194 y = 0.005 = 0.0327 = 3.27% or a 3.27% decline. 1+ y 1.10 2. a. YTM = 6% (1) (2) (3) (4) (5) PV of CF

CHAPTER 16: MANAGING BOND PORTFOLIOS 1. The percentage change in the bond s price is: Duration 7.194 y = 0.005 = 0.0327 = 3.27% or a 3.27% decline. 1+ y 1.10 2. a. YTM = 6% (1) (2) (3) (4) (5) PV of CF

Financial Derivatives

Derivatives in ALM Financial Derivatives Swaps Hedge Contracts Forward Rate Agreements Futures Options Caps, Floors and Collars Swaps Agreement between two counterparties to exchange the cash flows. Cash

Derivatives in ALM Financial Derivatives Swaps Hedge Contracts Forward Rate Agreements Futures Options Caps, Floors and Collars Swaps Agreement between two counterparties to exchange the cash flows. Cash

Chapter 28 17/09/2016. Accounting for foreign currency transactions. Introduction to accounting for foreign currency transactions

Chapter 28 Accounting for foreign currency transactions 28-1 Introduction to accounting for foreign currency transactions Two general issues to be considered in foreign currency translations 1. Where debts,

Chapter 28 Accounting for foreign currency transactions 28-1 Introduction to accounting for foreign currency transactions Two general issues to be considered in foreign currency translations 1. Where debts,

Copyright 2009 Pearson Education Canada

CHAPTER NINE Qualitative Questions 1. What is the difference between a call option and a put option? For an option buyer, a call option is the right to buy, while a put option is the right to sell. For

CHAPTER NINE Qualitative Questions 1. What is the difference between a call option and a put option? For an option buyer, a call option is the right to buy, while a put option is the right to sell. For

Answers to Selected Problems

Answers to Selected Problems Problem 1.11. he farmer can short 3 contracts that have 3 months to maturity. If the price of cattle falls, the gain on the futures contract will offset the loss on the sale

Answers to Selected Problems Problem 1.11. he farmer can short 3 contracts that have 3 months to maturity. If the price of cattle falls, the gain on the futures contract will offset the loss on the sale

Chapter 11: Financial Markets Section 1

Chapter 11: Financial Markets Section 1 Objectives 1. Describe how investing contributes to the free enterprise system. 2. Explain how the financial system brings together savers and borrowers. 3. Explain

Chapter 11: Financial Markets Section 1 Objectives 1. Describe how investing contributes to the free enterprise system. 2. Explain how the financial system brings together savers and borrowers. 3. Explain

Deutsche Bank Foreign Exchange Management at Deutsche Bank

Deutsche Bank www.deutschebank.nl Foreign Exchange Management at Deutsche Bank Foreign Exchange Management at Deutsche Bank 1. Why is this prospectus important? In this prospectus we will provide general

Deutsche Bank www.deutschebank.nl Foreign Exchange Management at Deutsche Bank Foreign Exchange Management at Deutsche Bank 1. Why is this prospectus important? In this prospectus we will provide general

Investing over the life-cycle building wealth. Introduction:

Investing over the life-cycle building wealth Introduction: Many investors are currently confused as to how best to approach the construction of an appropriate portfolio of investments, in order to build

Investing over the life-cycle building wealth Introduction: Many investors are currently confused as to how best to approach the construction of an appropriate portfolio of investments, in order to build

Currency Option Combinations

APPENDIX5B Currency Option Combinations 160 In addition to the basic call and put options just discussed, a variety of currency option combinations are available to the currency speculator and hedger.

APPENDIX5B Currency Option Combinations 160 In addition to the basic call and put options just discussed, a variety of currency option combinations are available to the currency speculator and hedger.

ISC: UNRESTRICTED AC Attachment. Hedging Audit (Foreign Exchange and Fuel)

") Hedging Audit (Foreign Exchange and Fuel) July 8, 2016 THIS PAGE LEFT INTENTIONALLY BLANK ISC: UNRESTRICTED Table of Contents Executive Summary... 5 1.0 Background... 7 2.0 Audit Objectives, Scope and

Hedging Audit (Foreign Exchange and Fuel) July 8, 2016 THIS PAGE LEFT INTENTIONALLY BLANK ISC: UNRESTRICTED Table of Contents Executive Summary... 5 1.0 Background... 7 2.0 Audit Objectives, Scope and

Product Factsheet for Foreign Exchange contracts

Please note that this document is not a financial promotion, and is solely for use by customers of MUFG Bank (Europe) N.V. Product Factsheet for Foreign Exchange contracts This document is designed to

Please note that this document is not a financial promotion, and is solely for use by customers of MUFG Bank (Europe) N.V. Product Factsheet for Foreign Exchange contracts This document is designed to

Managing and Identifying Risk

Managing and Identifying Risk Fall 2013 Stephen Sapp All of life is the management of risk, not its elimination Risk is the volatility of unexpected outcomes. In the context of financial risk the volatility

Managing and Identifying Risk Fall 2013 Stephen Sapp All of life is the management of risk, not its elimination Risk is the volatility of unexpected outcomes. In the context of financial risk the volatility

Agenda. Learning Objectives. Chapter 19. International Business Finance. Learning Objectives Principles Used in This Chapter

Chapter 19 International Business Finance Agenda Learning Objectives Principles Used in This Chapter 1. Foreign Exchange Markets and Currency Exchange Rates 2. Interest Rate and Purchasing-Power Parity

Chapter 19 International Business Finance Agenda Learning Objectives Principles Used in This Chapter 1. Foreign Exchange Markets and Currency Exchange Rates 2. Interest Rate and Purchasing-Power Parity

Risk Management Solutions for Oil Refineries

Risk Management Solutions for Oil Refineries CompuHedge Ltd. provides various strategic Risk Management solutions for corporations in the areas of currency, interest rates, commodities and energy market

Risk Management Solutions for Oil Refineries CompuHedge Ltd. provides various strategic Risk Management solutions for corporations in the areas of currency, interest rates, commodities and energy market

NISM-Series-I: Currency Derivatives Certification Examination

SAMPLE QUESTIONS 1) The market where currencies are traded is known as the. (a) Equity Market (b) Bond Market (c) Fixed Income Market (d) Foreign Exchange Market 2) The USD/CAD (US Canadian Dollars) currency

SAMPLE QUESTIONS 1) The market where currencies are traded is known as the. (a) Equity Market (b) Bond Market (c) Fixed Income Market (d) Foreign Exchange Market 2) The USD/CAD (US Canadian Dollars) currency

Exchange Futures for Physical (EFPs) October 13, 2005

October 13, 2005") Exchange Futures for Physical (EFPs) October 13, 2005 Copyright Intercontinental Exchange, Inc. 2005. All Rights Reserved. IPE Brent Crude The ICE Futures offers the facility for participants in oil markets

Exchange Futures for Physical (EFPs) October 13, 2005 Copyright Intercontinental Exchange, Inc. 2005. All Rights Reserved. IPE Brent Crude The ICE Futures offers the facility for participants in oil markets

Functional Training & Basel II Reporting and Methodology Review: Derivatives

Functional Training & Basel II Reporting and Methodology Review: Copyright 2010 ebis. All rights reserved. Page i Table of Contents 1 EXPOSURE DEFINITIONS...2 1.1 DERIVATIVES...2 1.1.1 Introduction...2

Functional Training & Basel II Reporting and Methodology Review: Copyright 2010 ebis. All rights reserved. Page i Table of Contents 1 EXPOSURE DEFINITIONS...2 1.1 DERIVATIVES...2 1.1.1 Introduction...2

Donald L Kohn: Asset-pricing puzzles, credit risk, and credit derivatives

Donald L Kohn: Asset-pricing puzzles, credit risk, and credit derivatives Remarks by Mr Donald L Kohn, Vice Chairman of the Board of Governors of the US Federal Reserve System, at the Conference on Credit

Donald L Kohn: Asset-pricing puzzles, credit risk, and credit derivatives Remarks by Mr Donald L Kohn, Vice Chairman of the Board of Governors of the US Federal Reserve System, at the Conference on Credit

CAPITAL STRUCTURE POLICY. Principles Applied in This Chapter 15.1 A GLANCE AT CAPITAL STRUCTURE CHOICES IN PRACTICE

CAPITAL STRUCTURE POLICY Chapter 15 Principles Applied in This Chapter Principle 2: There is a Risk-Return Tradeoff Principle 3: Cash Flows Are the Source of Value Principle 5: Investors Respond to Incentives

CAPITAL STRUCTURE POLICY Chapter 15 Principles Applied in This Chapter Principle 2: There is a Risk-Return Tradeoff Principle 3: Cash Flows Are the Source of Value Principle 5: Investors Respond to Incentives

Chapter 11 Currency Risk Management

Chapter 11 Currency Risk Management Note: In these problems, the notation / is used to mean per. For example, 158/$ means 158 per $. 1. To lock in the rate at which yen can be converted into U.S. dollars,

Chapter 11 Currency Risk Management Note: In these problems, the notation / is used to mean per. For example, 158/$ means 158 per $. 1. To lock in the rate at which yen can be converted into U.S. dollars,

Lecture 11. SWAPs markets. I. Background of Interest Rate SWAP markets. Types of Interest Rate SWAPs

Lecture 11 SWAPs markets Agenda: I. Background of Interest Rate SWAP markets II. Types of Interest Rate SWAPs II.1 Plain vanilla swaps II.2 Forward swaps II.3 Callable swaps (Swaptions) II.4 Putable swaps

Lecture 11 SWAPs markets Agenda: I. Background of Interest Rate SWAP markets II. Types of Interest Rate SWAPs II.1 Plain vanilla swaps II.2 Forward swaps II.3 Callable swaps (Swaptions) II.4 Putable swaps

32. Management of financial risks

298 F CONSOLIDATED FINANCIAL STATEMENTS NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS 32. Management of financial risks General information on financial risks As a result of its businesses and the global

298 F CONSOLIDATED FINANCIAL STATEMENTS NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS 32. Management of financial risks General information on financial risks As a result of its businesses and the global

Long-Term Debt Financing

18 Long-Term Debt Financing CHAPTER OBJECTIVES The specific objectives of this chapter are to: explain how an MNC uses debt financing in a manner that minimizes its exposure to exchange rate risk, explain

18 Long-Term Debt Financing CHAPTER OBJECTIVES The specific objectives of this chapter are to: explain how an MNC uses debt financing in a manner that minimizes its exposure to exchange rate risk, explain

CAPITAL STRUCTURE POLICY. Chapter 15

CAPITAL STRUCTURE POLICY Chapter 15 Principles Applied in This Chapter Principle 2: There is a Risk-Return Tradeoff Principle 3: Cash Flows Are the Source of Value Principle 5: Investors Respond to Incentives

CAPITAL STRUCTURE POLICY Chapter 15 Principles Applied in This Chapter Principle 2: There is a Risk-Return Tradeoff Principle 3: Cash Flows Are the Source of Value Principle 5: Investors Respond to Incentives

Arbitrage is a trading strategy that exploits any profit opportunities arising from price differences.

5. ARBITRAGE AND SPOT EXCHANGE RATES 5 Arbitrage and Spot Exchange Rates Arbitrage is a trading strategy that exploits any profit opportunities arising from price differences. Arbitrage is the most basic

5. ARBITRAGE AND SPOT EXCHANGE RATES 5 Arbitrage and Spot Exchange Rates Arbitrage is a trading strategy that exploits any profit opportunities arising from price differences. Arbitrage is the most basic

Foreign Exchange Hedging Strategies at General Motors: Transactional and Translational Exposures

Foreign Exchange Hedging Strategies at General Motors: Transactional and Translational Exposures Prepared By: Danial Wahaj Khan EXECUTIVE SUMMARY: This report is based on a practical scenario solution

Foreign Exchange Hedging Strategies at General Motors: Transactional and Translational Exposures Prepared By: Danial Wahaj Khan EXECUTIVE SUMMARY: This report is based on a practical scenario solution

Problems and Solutions Manual

Problems and Solutions Manual to accompany Derivatives: Principles & Practice Rangarajan K. Sundaram Sanjiv R. Das April 2, 2010 Sundaram & Das: Derivatives - Problems and Solutions..................................1

Problems and Solutions Manual to accompany Derivatives: Principles & Practice Rangarajan K. Sundaram Sanjiv R. Das April 2, 2010 Sundaram & Das: Derivatives - Problems and Solutions..................................1

Types of Exposure. Forward Market Hedge. Transaction Exposure. Forward Market Hedge. Forward Market Hedge: an Example INTERNATIONAL FINANCE.

Types of Exposure INTERNATIONAL FINANCE Chapter 8 Transaction exposure sensitivity of realized domestic currency values of the firm s contractual cash flows denominated in foreign currencies to unexpected

Types of Exposure INTERNATIONAL FINANCE Chapter 8 Transaction exposure sensitivity of realized domestic currency values of the firm s contractual cash flows denominated in foreign currencies to unexpected

Risk Management Using Derivatives Securities

Risk Management Using Derivatives Securities 1 Definition of Derivatives A derivative is a financial instrument whose value is derived from the price of a more basic asset called the underlying asset.

Risk Management Using Derivatives Securities 1 Definition of Derivatives A derivative is a financial instrument whose value is derived from the price of a more basic asset called the underlying asset.

MiFID II: Information on Financial instruments

MiFID II: Information on Financial instruments A. Introduction This information is provided to you being categorized as a Professional client to inform you on financial instruments offered by Rabobank

MiFID II: Information on Financial instruments A. Introduction This information is provided to you being categorized as a Professional client to inform you on financial instruments offered by Rabobank

Risk and Return - Capital Market Theory. Chapter 8

1 Risk and Return - Capital Market Theory Chapter 8 Learning Objectives 2 1. Calculate the expected rate of return and volatility for a portfolio of investments and describe how diversification affects

1 Risk and Return - Capital Market Theory Chapter 8 Learning Objectives 2 1. Calculate the expected rate of return and volatility for a portfolio of investments and describe how diversification affects

Analyzing Project Cash Flows. Principles Applied in This Chapter. Learning Objectives. Chapter 12. Principle 3: Cash Flows Are the Source of Value.

Analyzing Project Cash Flows Chapter 12 1 Principles Applied in This Chapter Principle 3: Cash Flows Are the Source of Value. Principle 5: Individuals Respond to Incentives. Learning Objectives 1. Identify

Analyzing Project Cash Flows Chapter 12 1 Principles Applied in This Chapter Principle 3: Cash Flows Are the Source of Value. Principle 5: Individuals Respond to Incentives. Learning Objectives 1. Identify

Ksenia Yudaeva: The policy of the Bank of Russia for ensuring financial stability in an environment of economic recovery

Ksenia Yudaeva: The policy of the Bank of Russia for ensuring financial stability in an environment of economic recovery Speech by Ms Ksenia Yudaeva, Deputy Governor of the Bank of Russia, at the Forum

Ksenia Yudaeva: The policy of the Bank of Russia for ensuring financial stability in an environment of economic recovery Speech by Ms Ksenia Yudaeva, Deputy Governor of the Bank of Russia, at the Forum

Risk and Return - Capital Market Theory. Chapter 8

Risk and Return - Capital Market Theory Chapter 8 Principles Applied in This Chapter Principle 2: There is a Risk-Return Tradeoff. Principle 4: Market Prices Reflect Information. Portfolio Returns and

Risk and Return - Capital Market Theory Chapter 8 Principles Applied in This Chapter Principle 2: There is a Risk-Return Tradeoff. Principle 4: Market Prices Reflect Information. Portfolio Returns and

Foreign Exchange Services

Foreign Exchange Services Economic Development Committee for the Prince William County Chamber of Commerce Hedging FX Risk M&T Bank Treasury Capital Markets Foreign Exchange Services Why most every company

Foreign Exchange Services Economic Development Committee for the Prince William County Chamber of Commerce Hedging FX Risk M&T Bank Treasury Capital Markets Foreign Exchange Services Why most every company

Slide 3: What are Policy Analysis and Policy Options Analysis?

1 Module on Policy Analysis and Policy Options Analysis Slide 3: What are Policy Analysis and Policy Options Analysis? Policy Analysis and Policy Options Analysis are related methodologies designed to

1 Module on Policy Analysis and Policy Options Analysis Slide 3: What are Policy Analysis and Policy Options Analysis? Policy Analysis and Policy Options Analysis are related methodologies designed to

BANK OF CHINA (CANADA) BASEL III DISCLOSURES AS AT DECEMBER 31, 2013

BASEL III DISCLOSURES AS AT DECEMBER 31, 2013") BANK OF CHINA (CANADA) BASEL III DISCLOSURES AS AT DECEMBER 31, 2013 Table of Contents 1. Scope of Application... 1 2. Capital Management... 2 (a) Capital structure... 2 (b) Capital adequacy ratio... 2

BANK OF CHINA (CANADA) BASEL III DISCLOSURES AS AT DECEMBER 31, 2013 Table of Contents 1. Scope of Application... 1 2. Capital Management... 2 (a) Capital structure... 2 (b) Capital adequacy ratio... 2

Chapter 5. Time Value of Money

Chapter 5 Time Value of Money Using Timelines to Visualize Cashflows A timeline identifies the timing and amount of a stream of payments both cash received and cash spent - along with the interest rate

Chapter 5 Time Value of Money Using Timelines to Visualize Cashflows A timeline identifies the timing and amount of a stream of payments both cash received and cash spent - along with the interest rate

Chapter 5. Learning Objectives. Principals Applied in this Chapter. Time Value of Money. Principle 1: Money Has a Time Value.

Chapter 5 Time Value of Money Learning Objectives 1. Construct cash flow timelines to organize your analysis of problems involving the time value of money. 2. Understand compounding and calculate the future

Chapter 5 Time Value of Money Learning Objectives 1. Construct cash flow timelines to organize your analysis of problems involving the time value of money. 2. Understand compounding and calculate the future

Currency Futures or FX Futures Introduction and Pricing Guide

s or FX Futures Introduction and Pricing Guide Michael Taylor FinPricing A currency future or an FX future is a future contract between two parties to exchange one currency for another at a fixed exchange

s or FX Futures Introduction and Pricing Guide Michael Taylor FinPricing A currency future or an FX future is a future contract between two parties to exchange one currency for another at a fixed exchange

11 06 Class 12 Forwards and Futures

11 06 Class 12 Forwards and Futures From banks to futures markets Financial i l markets as insurance markets Instruments and exchanges; The counterparty risk problem 1 From last time Banks face bank runs

11 06 Class 12 Forwards and Futures From banks to futures markets Financial i l markets as insurance markets Instruments and exchanges; The counterparty risk problem 1 From last time Banks face bank runs

Answers to Selected Problems

Answers to Selected Problems Problem 1.11. he farmer can short 3 contracts that have 3 months to maturity. If the price of cattle falls, the gain on the futures contract will offset the loss on the sale

Answers to Selected Problems Problem 1.11. he farmer can short 3 contracts that have 3 months to maturity. If the price of cattle falls, the gain on the futures contract will offset the loss on the sale

Stock valuation. Chapter 10

Stock valuation Chapter 10 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk Reward Tradeoff. Principle 3: Cash Flows are the Source of Value. Principle

Stock valuation Chapter 10 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk Reward Tradeoff. Principle 3: Cash Flows are the Source of Value. Principle

CVR REFINING REPORTS 2013 SECOND QUARTER RESULTS

CVR REFINING REPORTS 2013 SECOND QUARTER RESULTS 2013 second quarter cash distribution of $1.35 per common unit, bringing 2013 cumulative cash distributions to $2.93 SUGAR LAND, Texas (Aug. 1, 2013) CVR

CVR REFINING REPORTS 2013 SECOND QUARTER RESULTS 2013 second quarter cash distribution of $1.35 per common unit, bringing 2013 cumulative cash distributions to $2.93 SUGAR LAND, Texas (Aug. 1, 2013) CVR

Condensed Consolidated Interim Financial Statements as of September 30, 2017

Bazan Ltd. Condensed Consolidated Interim Financial Statements as of September 30, 2017 (Unaudited) A-1 Bazan Ltd. Contents Chapter A: Directors Report on the State of the Company s Affairs A-1 Page Description

Bazan Ltd. Condensed Consolidated Interim Financial Statements as of September 30, 2017 (Unaudited) A-1 Bazan Ltd. Contents Chapter A: Directors Report on the State of the Company s Affairs A-1 Page Description

JEM034 Corporate Finance Winter Semester 2017/2018

JEM034 Corporate Finance Winter Semester 2017/2018 Lecture #7 Olga Bychkova Topics Covered Today Risk Management (chapter 26 in BMA) Hedging with Forwards and Futures Futures and Spot Contracts Swaps Hedging

JEM034 Corporate Finance Winter Semester 2017/2018 Lecture #7 Olga Bychkova Topics Covered Today Risk Management (chapter 26 in BMA) Hedging with Forwards and Futures Futures and Spot Contracts Swaps Hedging

AFM 371 Winter 2008 Chapter 26 - Derivatives and Hedging Risk Part 2 - Interest Rate Risk Management ( )

") AFM 371 Winter 2008 Chapter 26 - Derivatives and Hedging Risk Part 2 - Interest Rate Risk Management (26.4-26.7) 1 / 30 Outline Term Structure Forward Contracts on Bonds Interest Rate Futures Contracts

AFM 371 Winter 2008 Chapter 26 - Derivatives and Hedging Risk Part 2 - Interest Rate Risk Management (26.4-26.7) 1 / 30 Outline Term Structure Forward Contracts on Bonds Interest Rate Futures Contracts

CALCULATING CAPITAL REQUIREMENTS FOR SETTLEMENT AND COUNTERPARTY CREDIT RISK

CALCULATING CAPITAL REQUIREMENTS FOR SETTLEMENT AND COUNTERPARTY CREDIT RISK Introduction 1. Settlement and counterparty risk arises in both the banking book and the trading book. A capital charge, as

CALCULATING CAPITAL REQUIREMENTS FOR SETTLEMENT AND COUNTERPARTY CREDIT RISK Introduction 1. Settlement and counterparty risk arises in both the banking book and the trading book. A capital charge, as

FOREX RISK MANAGEMENT STRATEGIES FOR INDIAN IT COMPANIES

FOREX RISK MANAGEMENT STRATEGIES FOR INDIAN IT COMPANIES Mihir Dash Alliance Business School mihir@alliancebschool.ac.in +91-994518465 ABSTRACT Foreign exchange risk is the effect that unanticipated exchange

FOREX RISK MANAGEMENT STRATEGIES FOR INDIAN IT COMPANIES Mihir Dash Alliance Business School mihir@alliancebschool.ac.in +91-994518465 ABSTRACT Foreign exchange risk is the effect that unanticipated exchange

Hedging Sales Revenue by Commodity Production

Hedging Sales Revenue by Commodity Production By: Andrew Volz, Solutions Consultant, Reval April 8, 2010 CONTENT Executive Summary Introduction Life Cycle of the Producer Evaluate the Ability to Hedge

Hedging Sales Revenue by Commodity Production By: Andrew Volz, Solutions Consultant, Reval April 8, 2010 CONTENT Executive Summary Introduction Life Cycle of the Producer Evaluate the Ability to Hedge

Subject SP5 Investment and Finance Specialist Principles Syllabus

Subject SP5 Investment and Finance Specialist Principles Syllabus for the 2019 exams 1 June 2018 Investment and Finance Specialist Principles Aim The aim of the Investment and Finance Principles subject

Subject SP5 Investment and Finance Specialist Principles Syllabus for the 2019 exams 1 June 2018 Investment and Finance Specialist Principles Aim The aim of the Investment and Finance Principles subject

Financial Derivatives Section 1

Financial Derivatives Section 1 Forwards & Futures Michail Anthropelos anthropel@unipi.gr http://web.xrh.unipi.gr/faculty/anthropelos/ University of Piraeus Spring 2018 M. Anthropelos (Un. of Piraeus)

Financial Derivatives Section 1 Forwards & Futures Michail Anthropelos anthropel@unipi.gr http://web.xrh.unipi.gr/faculty/anthropelos/ University of Piraeus Spring 2018 M. Anthropelos (Un. of Piraeus)

Part III: Swaps. Futures, Swaps & Other Derivatives. Swaps. Previous lecture set: This lecture set -- Parts II & III. Fundamentals

Futures, Swaps & Other Derivatives Previous lecture set: Interest-Rate Derivatives FRAs T-bills futures & Euro$ Futures This lecture set -- Parts II & III Swaps Part III: Swaps Swaps Fundamentals what,

Futures, Swaps & Other Derivatives Previous lecture set: Interest-Rate Derivatives FRAs T-bills futures & Euro$ Futures This lecture set -- Parts II & III Swaps Part III: Swaps Swaps Fundamentals what,

Financial Markets & Institutions. forwards.

Financial Markets & Institutions Introduction to derivatives. Futures and forwards. Slides by Emilia Garcia-Appendini The Nature of Derivatives A derivative is an instrument whose value depends on the

Financial Markets & Institutions Introduction to derivatives. Futures and forwards. Slides by Emilia Garcia-Appendini The Nature of Derivatives A derivative is an instrument whose value depends on the

October 10, To: The International Accounting Standards Board. Japanese Bankers Association

October 10, 2014 To: The International Accounting Standards Board Japanese Bankers Association Comment on the International Accounting Standards Board (IASB) s Discussion Paper Accounting for Dynamic Risk

October 10, 2014 To: The International Accounting Standards Board Japanese Bankers Association Comment on the International Accounting Standards Board (IASB) s Discussion Paper Accounting for Dynamic Risk

Special Considerations in Auditing Complex Financial Instruments Draft International Auditing Practice Statement 1000

Special Considerations in Auditing Complex Financial Instruments Draft International Auditing Practice Statement CONTENTS [REVISED FROM JUNE 2010 VERSION] Paragraph Scope of this IAPS... 1 3 Section I

Special Considerations in Auditing Complex Financial Instruments Draft International Auditing Practice Statement CONTENTS [REVISED FROM JUNE 2010 VERSION] Paragraph Scope of this IAPS... 1 3 Section I

FNCE4040 Derivatives Chapter 1

FNCE4040 Derivatives Chapter 1 Introduction The Landscape Forwards and Option Contracts What is a Derivative? A derivative is an instrument whose value depends on, or is derived from, the value of another

FNCE4040 Derivatives Chapter 1 Introduction The Landscape Forwards and Option Contracts What is a Derivative? A derivative is an instrument whose value depends on, or is derived from, the value of another

West Virginia Housing Development Fund. Debt Management Policy

West Virginia Housing Development Fund Debt Management Policy Approved December 21, 2017 Table of Contents Debt Management Policy... 1 Variable Rate Debt and Interest Rate Swap Management Plan... 5 Variable

West Virginia Housing Development Fund Debt Management Policy Approved December 21, 2017 Table of Contents Debt Management Policy... 1 Variable Rate Debt and Interest Rate Swap Management Plan... 5 Variable

3/15/2018 DUALITY AND GLOBALITY IN RISK MANAGEMENT STRATEGGY DUALITY

DUALITY AND GLOBALITY IN RISK MANAGEMENT STRATEGGY DUALITY The essence of duality is that in managing risks one can: Address the cause of the risk i.e. remove the risk Address the effect of the risk -

DUALITY AND GLOBALITY IN RISK MANAGEMENT STRATEGGY DUALITY The essence of duality is that in managing risks one can: Address the cause of the risk i.e. remove the risk Address the effect of the risk -

DUALITY AND GLOBALITY IN RISK MANAGEMENT STRATEGGY

DUALITY AND GLOBALITY IN RISK MANAGEMENT STRATEGGY DUALITY The essence of duality is that in managing risks one can: Address the cause of the risk i.e. remove the risk Address the effect of the risk -

DUALITY AND GLOBALITY IN RISK MANAGEMENT STRATEGGY DUALITY The essence of duality is that in managing risks one can: Address the cause of the risk i.e. remove the risk Address the effect of the risk -

Cash and cash equivalents 619,525 Trade accounts receivable and others 951,653 Total 1,571,178 Net $ 229,209

11. Derivative financial instruments The Entity has exposure to market risks, operating risks and financial risks arising from the use of financial instruments that involves interest rates, credit risks,

11. Derivative financial instruments The Entity has exposure to market risks, operating risks and financial risks arising from the use of financial instruments that involves interest rates, credit risks,

Finance for non-financials

Finance for non-financials Case-study workshop for Managers in Business Case studies from world known Business Schools Duration: Two modules, two days each Finance 1: Warsaw 18-19 April 2018 Finance 2:

Finance for non-financials Case-study workshop for Managers in Business Case studies from world known Business Schools Duration: Two modules, two days each Finance 1: Warsaw 18-19 April 2018 Finance 2:

International Financial and Foreign Exchange Markets. Derivatives and Hedging Techniques. Market Efficiency. Exercise Handbook.

Exercise Handbook March 30, 2018 Table of Contents Exercise XXIV Mr. Brown sold a put option on Canadian dollars for 0.03 USD, with strike price equal to 0.75 USD. At the same time, he sold short 50,000

Exercise Handbook March 30, 2018 Table of Contents Exercise XXIV Mr. Brown sold a put option on Canadian dollars for 0.03 USD, with strike price equal to 0.75 USD. At the same time, he sold short 50,000

Constellation Energy Analyst Meeting Derivative and Fair Value Accounting Summary August 27, 2008

Constellation Energy Analyst Meeting Page 2 Index Introduction... 3 Section I Understanding the Accounting Principles for Derivatives... 4 Accounting standards governing derivatives and fair value... 4

Constellation Energy Analyst Meeting Page 2 Index Introduction... 3 Section I Understanding the Accounting Principles for Derivatives... 4 Accounting standards governing derivatives and fair value... 4

INTRODUCTION TO EXCHANGE RATES AND THE FOREIGN EXCHANGE MARKET

INTRODUCTION TO EXCHANGE RATES AND THE FOREIGN EXCHANGE MARKET 13 1 Exchange Rate Essentials 2 Exchange Rates in Practice 3 The Market for Foreign Exchange 4 Arbitrage and Spot Exchange Rates 5 Arbitrage

INTRODUCTION TO EXCHANGE RATES AND THE FOREIGN EXCHANGE MARKET 13 1 Exchange Rate Essentials 2 Exchange Rates in Practice 3 The Market for Foreign Exchange 4 Arbitrage and Spot Exchange Rates 5 Arbitrage

Mr. Robert dev. Frierson April 16, 2014 Page 2

Mr. Robert dev. Frierson Secretary Board of Governors of the Federal Reserve System 20th Street and Constitution Avenue, NW Washington, DC 20551 Via Agency Website Re: Docket No. 1479 and RIN 7100 AE-10:

Mr. Robert dev. Frierson Secretary Board of Governors of the Federal Reserve System 20th Street and Constitution Avenue, NW Washington, DC 20551 Via Agency Website Re: Docket No. 1479 and RIN 7100 AE-10:

4 QUESTIONS YOU NEED TO ASK ABOUT INCOME INVESTING IN

4 QUESTIONS YOU NEED TO ASK ABOUT INCOME INVESTING IN 2014 Understanding risks // Evaluating your portfolio // Taking action INTRODUCTION The markets today present investors with challenges interest rate

4 QUESTIONS YOU NEED TO ASK ABOUT INCOME INVESTING IN 2014 Understanding risks // Evaluating your portfolio // Taking action INTRODUCTION The markets today present investors with challenges interest rate

2) Double-pronged approached to FX risk management consists of FX risk mitigation and FX risk transfer.

Double-pronged approached to FX risk management consists of FX risk mitigation and FX risk transfer.") Question 1 FX risk management is an issue of much concern for EADS. Due to cash flow mismatch between dollar denominated revenues and costs, which are largely incurred in euro, EADS has to conduct hedging

Question 1 FX risk management is an issue of much concern for EADS. Due to cash flow mismatch between dollar denominated revenues and costs, which are largely incurred in euro, EADS has to conduct hedging

7. The acs group s Risk management

7. The acs group s Risk management dual system of risk Control and supervision The acs group conducts its business activities in a variety of sectors, countries and socio-economic and legal environments

7. The acs group s Risk management dual system of risk Control and supervision The acs group conducts its business activities in a variety of sectors, countries and socio-economic and legal environments

Fabio Cannizzo Head, Quantitative Finance Centre BP, Integrated Supply & Trading

Real Options & Complex Energy Contracts Fabio Cannizzo Head, Quantitative Finance Centre BP, Integrated Supply & Trading cannf1@bp.com Quantitative Finance Centre Integrated Supply & Trading (IST) centralises

Real Options & Complex Energy Contracts Fabio Cannizzo Head, Quantitative Finance Centre BP, Integrated Supply & Trading cannf1@bp.com Quantitative Finance Centre Integrated Supply & Trading (IST) centralises

18. Forwards and Futures

18. Forwards and Futures This is the first of a series of three lectures intended to bring the money view into contact with the finance view of the world. We are going to talk first about interest rate

18. Forwards and Futures This is the first of a series of three lectures intended to bring the money view into contact with the finance view of the world. We are going to talk first about interest rate

Exchange rate and interest rates. Rodolfo Helg, February 2018 (adapted from Feenstra Taylor)

") Exchange rate and interest rates Rodolfo Helg, February 2018 (adapted from Feenstra Taylor) Defining the Exchange Rate Exchange rate (E domestic/foreign ) The price of a unit of foreign currency in terms

Exchange rate and interest rates Rodolfo Helg, February 2018 (adapted from Feenstra Taylor) Defining the Exchange Rate Exchange rate (E domestic/foreign ) The price of a unit of foreign currency in terms

CHAPTER 2 Futures Markets and Central Counterparties

Options Futures and Other Derivatives 10th Edition Hull SOLUTIONS MANUAL Full download at: https://testbankreal.com/download/options-futures-and-other-derivatives- 10th-edition-hull-solutions-manual-2/

Options Futures and Other Derivatives 10th Edition Hull SOLUTIONS MANUAL Full download at: https://testbankreal.com/download/options-futures-and-other-derivatives- 10th-edition-hull-solutions-manual-2/

Condensed Interim Consolidated Financial Statements of. Canada Pension Plan Investment Board

Condensed Interim Consolidated Financial Statements of Canada Pension Plan Investment Board December 31, 2016 Condensed Interim Consolidated Balance Sheet December 31, 2016 December 31, 2016 March 31,

Condensed Interim Consolidated Financial Statements of Canada Pension Plan Investment Board December 31, 2016 Condensed Interim Consolidated Balance Sheet December 31, 2016 December 31, 2016 March 31,

ALFA FINANCIALS (PTY) LTD. RISK DISCLOSURE AND WARNINGS NOTICE FOR CLIENTS IN COMPLEX FINANCIAL PRODUCTS

LTD. RISK DISCLOSURE AND WARNINGS NOTICE FOR CLIENTS IN COMPLEX FINANCIAL PRODUCTS") ALFA FINANCIALS (PTY) LTD. RISK DISCLOSURE AND WARNINGS NOTICE FOR CLIENTS IN COMPLEX FINANCIAL PRODUCTS Version 1.0 May 2016 RISK DISCLOSURE AND WARNINGS NOTICE FOR CLIENTS IN COMPLEX FINANCIAL PRODUCTS

ALFA FINANCIALS (PTY) LTD. RISK DISCLOSURE AND WARNINGS NOTICE FOR CLIENTS IN COMPLEX FINANCIAL PRODUCTS Version 1.0 May 2016 RISK DISCLOSURE AND WARNINGS NOTICE FOR CLIENTS IN COMPLEX FINANCIAL PRODUCTS

1. Primary markets are markets in which users of funds raise cash by selling securities to funds' suppliers.

Test Bank Financial Markets and Institutions 6th Edition Saunders Complete download Financial Markets and Institutions 6th Edition TEST BANK by Saunders, Cornett: https://testbankarea.com/download/financial-markets-institutions-6th-editiontest-bank-saunders-cornett/

Test Bank Financial Markets and Institutions 6th Edition Saunders Complete download Financial Markets and Institutions 6th Edition TEST BANK by Saunders, Cornett: https://testbankarea.com/download/financial-markets-institutions-6th-editiontest-bank-saunders-cornett/

INVESTMENTS Assignment 3: Futures. Reto R. Gallati MIT Sloan School of Management

15.433 INVESTMENTS Assignment 3: Futures Reto R. Gallati MIT Sloan School of Management 1. A futures contract is available on a company that pays an annual dividend of $5 and whose stock is currently priced

15.433 INVESTMENTS Assignment 3: Futures Reto R. Gallati MIT Sloan School of Management 1. A futures contract is available on a company that pays an annual dividend of $5 and whose stock is currently priced

Paper 14 Strategic Financial Management

Paper 14 Strategic Financial Management DoS, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 14 Strategic Financial Management Full Marks: 100 Time allowed:

Paper 14 Strategic Financial Management DoS, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 14 Strategic Financial Management Full Marks: 100 Time allowed:

Standardized Approach for Calculating the Solvency Buffer for Market Risk. Joint Committee of OSFI, AMF, and Assuris.

Standardized Approach for Calculating the Solvency Buffer for Market Risk Joint Committee of OSFI, AMF, and Assuris November 2008 DRAFT FOR COMMENT TABLE OF CONTENTS Introduction...3 Approach to Market

Standardized Approach for Calculating the Solvency Buffer for Market Risk Joint Committee of OSFI, AMF, and Assuris November 2008 DRAFT FOR COMMENT TABLE OF CONTENTS Introduction...3 Approach to Market

Reporting Financial Information

Learning Objectives LO1 Prepare an income statement for a service business. LO2 Calculate and analyze financial ratios using income statement amounts. Lesson 7-1 Reporting Financial Information LO1 The

Learning Objectives LO1 Prepare an income statement for a service business. LO2 Calculate and analyze financial ratios using income statement amounts. Lesson 7-1 Reporting Financial Information LO1 The

CHAPTER 2 LITERATURE REVIEW

CHAPTER 2 LITERATURE REVIEW Capital budgeting is the process of analyzing investment opportunities and deciding which ones to accept. (Pearson Education, 2007, 178). 2.1. INTRODUCTION OF CAPITAL BUDGETING

CHAPTER 2 LITERATURE REVIEW Capital budgeting is the process of analyzing investment opportunities and deciding which ones to accept. (Pearson Education, 2007, 178). 2.1. INTRODUCTION OF CAPITAL BUDGETING

FRAMEWORK FOR SUPERVISORY INFORMATION

FRAMEWORK FOR SUPERVISORY INFORMATION ABOUT THE DERIVATIVES ACTIVITIES OF BANKS AND SECURITIES FIRMS (Joint report issued in conjunction with the Technical Committee of IOSCO) (May 1995) I. Introduction

FRAMEWORK FOR SUPERVISORY INFORMATION ABOUT THE DERIVATIVES ACTIVITIES OF BANKS AND SECURITIES FIRMS (Joint report issued in conjunction with the Technical Committee of IOSCO) (May 1995) I. Introduction

Description of Nature of Financial Instruments and Inherent Risk

Description of Nature of Financial Instruments and Inherent Risk Applicable from for Danske Bank A/S Estonia branch, Danske Bank A/S Latvia branch and Danske Bank A/S Lithuania branch 1. GENERAL INFORMATION

Description of Nature of Financial Instruments and Inherent Risk Applicable from for Danske Bank A/S Estonia branch, Danske Bank A/S Latvia branch and Danske Bank A/S Lithuania branch 1. GENERAL INFORMATION

KNPC Risk Approach for Projects Economic Evaluation

KNPC Risk Approach for Projects Economic Evaluation Implementation Approach March 2015 Presented by Eng. May Al-Ebrahim Introduction Investment decisions require special attention because they involve

KNPC Risk Approach for Projects Economic Evaluation Implementation Approach March 2015 Presented by Eng. May Al-Ebrahim Introduction Investment decisions require special attention because they involve

CIFFA: Managing FX Risks MAY 2016

CIFFA: Managing FX Risks MAY 2016 Today s Objectives 2 Discuss the recent volatility of currency, and what makes the future value of currency so difficult to predict Assess FX risk to freight forwarders

CIFFA: Managing FX Risks MAY 2016 Today s Objectives 2 Discuss the recent volatility of currency, and what makes the future value of currency so difficult to predict Assess FX risk to freight forwarders

Information Statement & Disclosure for Material Risks

Information Statement & Disclosure for Material Risks Material Risks CFTC Rule 23.431(a)(1) requires Wells Fargo Bank, N.A. ( WFBNA, we, us or our ) to disclose to you the material risks of a swap before

Information Statement & Disclosure for Material Risks Material Risks CFTC Rule 23.431(a)(1) requires Wells Fargo Bank, N.A. ( WFBNA, we, us or our ) to disclose to you the material risks of a swap before

University of Siegen

University of Siegen Faculty of Economic Disciplines, Department of economics Univ. Prof. Dr. Jan Franke-Viebach Seminar Risk and Finance Summer Semester 2008 Topic 4: Hedging with currency futures Name

University of Siegen Faculty of Economic Disciplines, Department of economics Univ. Prof. Dr. Jan Franke-Viebach Seminar Risk and Finance Summer Semester 2008 Topic 4: Hedging with currency futures Name