Lecture 3 Asset liquidity

|

|

|

- Wesley Baldwin

- 5 years ago

- Views:

Transcription

1 Lecture 3 Asset liquidity Shengxing Zhang LSE October 14, 2015

2 Liquidity, Business Cycles, and Monetary Policy Nobuhiro Kiyotaki and John Moore

3 Overview Amodelofamonetaryeconomywhereassetsaredifferentin there liquidity two frictions: pledgeability resellability links to Tobin s Q-theory, IS-LM curve of Keynes

4 Environment Infinite-horizon, discrete-time two types of agents entrepreneur worker P Preference: E 1 t s=t four objects traded capital nondurable output labor equity fiat money illiquid decrepiates with rate 2 (0, 1) s t u(c s ), u(c) =log c

5 Entrepreneurs technology to produce nondurable output y t = A t k t l 1 t technology to produce capital transforms output to capital, one-to-one the replacement cost of one capital is one output good accessible with probability new capital is available one period later k t+1 = k t + i t two key frictions moral hazard (pledgeability of output as collateral) asset liquidity (liquidity of the financial market)

6 Entrepreneurs: two frictions pledgeability a fraction 2 (0, 1) of new capital is pledgeable a borrowing constraint resaleability of equity equity: a claim of capital the book value of an equity is one output good the market value of an equity: q t Tobin s Q a fraction market value of installed capital/replacement cost of capital 2 (0, 1) of a firm s equity holding can be resold discussion: two parts of return from capital production committed return plegeable as collateral can be thought of as collateralized borrowing uncommitted return issue equity, subject to liquidity friction

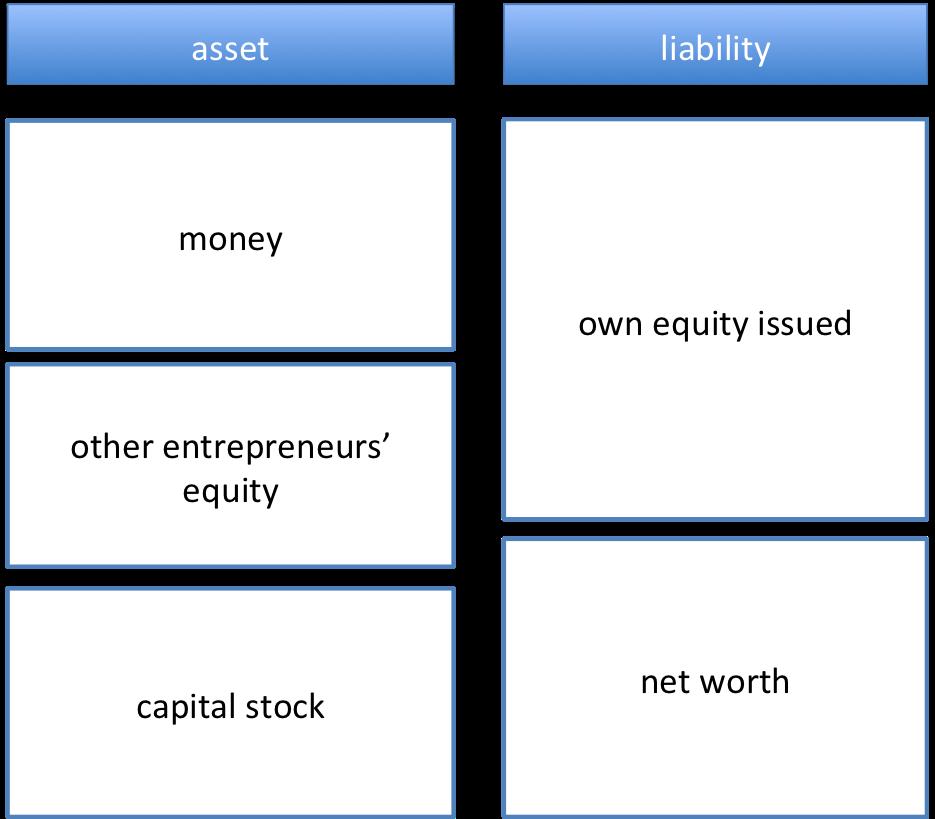

7 Entrepreneurs: balance sheet

8 Entrepreneurs: asset portfolio money other entrepreneurs equity unmortgaged capital stock Simplification: an entrepreneur can issue new equity against a fraction t of any uncommitted returns from old capital cash flow of unmortgaged capital and other entrepreneurs equity is the same resaleability of the equity is the same perfect substitutes: no distinction between inside equity and outside equity balance sheet after simplification asset: m t and n t+1 = k t+1 liability: n t, net worth (value of asset - the market value of a firm)

9 Entrepreneurs: constraints flow of funds constraint c t + i t + q t n t+1 + p t m t+1 = r t n t + q t ( n t + i t )+p t m t two liquidity constraints n {z} t+1 + t n {z } t + t i {z} t equity next period equity resale "mortgage" m t+1 0 i t + n t

10 Workers endowment: labor preference: E t P 1 s=t flow of funds constraint: s t U h c 0 s i! 1+ (l s) 0 1+ c 0 t + q t n 0 t+1 + p t m 0 t+1 = w t l 0 t + r t n 0 t + q t n 0 t + p t m 0 t liquidity constraints: n 0 t+1 0, m 0 t+1 0

11 Entrepreneur s problem max {c s,i s,k s+1,n s+1,m s+1 } 8s t E t s.t.k s+1 = i s + k s 1X s=t s t u(c s ) c s + i s + q s n s+1 + p s m s+1 = r s n s + q s ( n s + i s )+p s m s n s+1 (1 )i s +(1 s) n s m s+1, c s, i s 0

12 Worker s problem max {c 0 s,l 0 s,n0 s+1,m0 s+1} 8s t E t 1X s=t s t U apple c 0 s! 1 + (l 0 s) 1+ s.t.c 0 s + q s n 0 s+1 + p s m 0 s+1 = w s l 0 s + r s n 0 s + q s n 0 s+1, m 0 s+1, c 0 s 0 n 0 s + p s m 0 s

13 Definition of equilibrium An equilibrium, given k t,isasequenceofprices{p s, q s, w s } 8s t, {c s, i s, k s+1, n s+1, m s+1 } 8s t and c 0 s, l 0 s, n 0 s+1, m0 s+1 8s t such that: given prices, {c s, i s, k s+1, n s+1, m s+1 } 8s t solves entrepreneurs problem, and cs, 0 ls, 0 ns+1 0, m0 s+1 8s t solves workers problem markets for general output, labor, equity and money clear for all s t

14 When liquidity constraints are not binding If (1 ) + (1 )(1 ), thenintheneighbourhoodof the steady state: the allocation of resources is first best Tobin s q is equal to unity: q t = 1 money has no value: p t = 0 the gross dividend r t w 1

15 When liquidity constraints are binding If (1 ) + < (1 )(1 ), amongsomeadditional conditions, in the neighbourhood of the steady state: the price of money, p t,isstrictlypositive the price of capital, q t,isstrictlygreaterthan1 an entrepreneur with an investment opportunity faces binding liquidity constraints: mt+1 i = 0 nt+1 i =(1 )i t +(1 t) nt i From the flow of funds constraint ct i + (1 q t )i {z } t = r t nt i + tq t nt i + p {z } t mt i down payment revenue from resale

16 When liquidity constraints are binding From the flow of funds constraint ct i + (1 q t )i {z } t = r t nt i + tq t nt i + p {z } t mt i down payment revenue from resale h ct i + qt R nt+1 i = r t nt i + tq t +(1 t)q R t q R t 1 q t 1 < 1, as q t > 1 i n i t + p t m i t qt R (replacement cost): for every unit of investment, an entrepreneur needs a downpayment 1 q t,ofwhichhe retains 1 inside equity. two components for old equity a fraction t is resaleable and is priced at market value q t a fraction 1 t is not resaleable and is priced at effect replacement cost qt R

17 Euler equation u 0 (c t )=E t pt+1 p t (1 )u 0 (c s t+1)+ u 0 (c i t+1) =(1 )E t rt+1 + q t+1 q t u 0 (c s t+1) + E t ( rt+1 + t+1 q t+1 + (1 t+1)q R t+1 q t u 0 (c i t+1) ) u 0 (c i t+1 ) > u0 (c s t+1 ), qr t+1 < 1 < q t+1: equitycarriesan idiosyncratic risk. its effective return is negatively correlated with the idiosyncratic variations in marginal utility that stem from the stochastic investment opportunities. money is free from such a risk

18 Equilibrium return When liquidity constraints are binding equilibrium capital stock is les than first-best the expected rate of return on equity: E t a t+1 K 1 t+1 + q t+1 q t < 1 the expected rate of return on money is yet lower: p t+1 a t+1 K 1 t+1 E t < E + q t+1 t p t the expected return on equity contingent on having an investment opportunity is lower still: E t a t+1 K 1 t+1 + t q t+1 +(1 t+1) q R t+1 q t < E t p t+1 p t q t

19 Equilibrium return Discussion: 1 > Et a t+1 K 1 t+1 + q t+1 q t > E t p t+1 p t > E t a t+1 K 1 t+1 + t q t+1 +(1 t+1) q R t+1 q t Aspectrumofinterestrates!Theyreflecttheliquidity premium of different assets to finance investment. Workers do not need the liquidity for investment: they always sell.

20 Over-the-Counter Markets Duffie, Darrell, Nicolae Gârleanu, and Lasse Heje Pedersen

21 Overview Amodeloftheover-the-countermarkets Amicro-foundedmodelofmarketliquidity(resaleability) Determinent of liquidity search friction bargaining market structure future extension: asymmetric information

22 Environment continuous time, infinite horizon acontinuumofinvestors,withmeasure1 acontinuumofmarketmakerswithmeasure1 asset durable, indivisible fixed supply: s < 1 constant dividend flow numeraire good deep pockets can be stored with return r

23 Environment 1 Preference of investors: E t t e rs (u ij,t + c) dt valuation: i 2{h, l} asset holding j 2{o, n} u ho = 1, u lo = 1, u hn = u ln = 0. preference shock u: Poisson rate to switch from type l to type h d: Poisson rate to switch from type h to type l c: consumption of the numeraire good 1 Preference of dealers: E t t e rs cdt

24 Market structure

25 Market structure Interdealer market competitive, with price M t random matching between investors and dealers Poisson rate for an investor to meet a dealer: Nash bargaining: dealers bargaining power, z B t : bid price, the price when dealers bid from investors A t : ask price,the price dealers ask for to sell the asset to investors Illiquidity: Bid-ask spread: B t < A t delay in trade:

26 Value functions of investors rv lo = 1 + u (V h0 V lo )+ (B + V ln V lo )+ V lo rv ho = 1 + d (V lo V ho )+ V ho rv ln = u (V hn V ln )+ V ln rv hn = d (V ln V hn )+ (V ho V hn A)+ V hn

27 Bargaining and BA spread max A (V ho A V hn ) 1 z (A M) z max B (B + V ln V ln ) 1 z (M B) z A =(V ho V hn )z + M(1 z) B =(V lo V ln )z + M(1 z) A B = z [(V ho V lo ) (V hn V ln )] The spread depends on the difference in value between h type and l type the bargaining power of dealers

28 Law of motions µ lo = uµ lo + d µ ho µ lo µ ho = u µ lo d µ ho + µ hn µ ln = uµ ln + d µ hn + µ lo µ hn = u µ ln d µ hn µ hn

29 Equilibrium definition Asymmetricequilibriumisapathofprices{B t, A t, M t } t 0,apath of distributions µ and a path of value functions V and initial condition µ(0) such that, given the initial condition, given V (t) and µ(t), {B t, A t } t problem at t, 8t given {, equations 0 solves the bargaining }, V satisfies the Hamilton-Jacobi-Bellman µ is follows the laws of motion M t clears the interdealer market at t, 8t

30 Search-Based Endogenous Illiquidity and the Macroeconomy Wei Cui, Sören Radde

31 Overview Introduce endogenous resaleability to Kiyotaki Moore (2012) See Wei Cui s slides

32 References Kiyotaki, N. and Moore, J. (2012). Liquidity, Business Cycles, and Monetary Policy Duffie, D., Gârleanu, N. and Pedersen, L. H. (2005). Over-the-Counter Markets. Econometrica, 73(6), Cui, W. and Radde S. (2014). Search-Based Endogenous Liquidity and the Macroeconomy

Liquidity, Business Cycles, and Monetary Policy. Nobuhiro Kiyotaki and John Moore

Liquidity, Business Cycles, and Monetary Policy Nobuhiro Kiyotaki and John Moore 1 Question How does economy uctuate with shocks to productivity and liquidity?! Want to develop a canonical model of monetary

Liquidity, Business Cycles, and Monetary Policy Nobuhiro Kiyotaki and John Moore 1 Question How does economy uctuate with shocks to productivity and liquidity?! Want to develop a canonical model of monetary

Liquidity and Risk Management

Liquidity and Risk Management By Nicolae Gârleanu and Lasse Heje Pedersen Risk management plays a central role in institutional investors allocation of capital to trading. For instance, a risk manager

Liquidity and Risk Management By Nicolae Gârleanu and Lasse Heje Pedersen Risk management plays a central role in institutional investors allocation of capital to trading. For instance, a risk manager

NBER WORKING PAPER SERIES LIQUIDITY AND RISK MANAGEMENT. Nicolae B. Garleanu Lasse H. Pedersen. Working Paper

NBER WORKING PAPER SERIES LIQUIDITY AND RISK MANAGEMENT Nicolae B. Garleanu Lasse H. Pedersen Working Paper 12887 http://www.nber.org/papers/w12887 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts

NBER WORKING PAPER SERIES LIQUIDITY AND RISK MANAGEMENT Nicolae B. Garleanu Lasse H. Pedersen Working Paper 12887 http://www.nber.org/papers/w12887 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts

A Model with Costly Enforcement

A Model with Costly Enforcement Jesús Fernández-Villaverde University of Pennsylvania December 25, 2012 Jesús Fernández-Villaverde (PENN) Costly-Enforcement December 25, 2012 1 / 43 A Model with Costly

A Model with Costly Enforcement Jesús Fernández-Villaverde University of Pennsylvania December 25, 2012 Jesús Fernández-Villaverde (PENN) Costly-Enforcement December 25, 2012 1 / 43 A Model with Costly

Intro Model Equilibrium Results Fed Model Liquidity crises Conclusion Appx. A Model of Monetary Exchange in Over-the-Counter Markets

A Model of Monetary Exchange in Over-the-Counter Markets Ricardo Lagos New York University Shengxing Zhang London School of Economics Money in financial over-the-counter markets Broad question: Quantity

A Model of Monetary Exchange in Over-the-Counter Markets Ricardo Lagos New York University Shengxing Zhang London School of Economics Money in financial over-the-counter markets Broad question: Quantity

Money and Search - The Kiyotaki-Wright Model

Money and Search - The Kiyotaki-Wright Model Econ 208 Lecture 14 March 20, 2007 Econ 208 (Lecture 14) Kiyotaki-Wright March 20, 2007 1 / 9 Introduction Problem with the OLG model - can account for alternative

Money and Search - The Kiyotaki-Wright Model Econ 208 Lecture 14 March 20, 2007 Econ 208 (Lecture 14) Kiyotaki-Wright March 20, 2007 1 / 9 Introduction Problem with the OLG model - can account for alternative

Liquidity, Business Cycles, and Monetary Policy

Liquidity, Business Cycles, and Monetary Policy Nobuhiro Kiyotaki and John Moore y First version, June 2 This version, March 28 Abstract The paper presents a model of a monetary economy where there are

Liquidity, Business Cycles, and Monetary Policy Nobuhiro Kiyotaki and John Moore y First version, June 2 This version, March 28 Abstract The paper presents a model of a monetary economy where there are

Liquidity, Business Cycles, and Monetary Policy

Liquidity, Business Cycles, and Monetary Policy Nobuhiro Kiyotaki and John Moore First version, June 2 This version, November 2 Abstract This paper presents a model of monetary economy with di erences

Liquidity, Business Cycles, and Monetary Policy Nobuhiro Kiyotaki and John Moore First version, June 2 This version, November 2 Abstract This paper presents a model of monetary economy with di erences

Slides III - Complete Markets

Slides III - Complete Markets Julio Garín University of Georgia Macroeconomic Theory II (Ph.D.) Spring 2017 Macroeconomic Theory II Slides III - Complete Markets Spring 2017 1 / 33 Outline 1. Risk, Uncertainty,

Slides III - Complete Markets Julio Garín University of Georgia Macroeconomic Theory II (Ph.D.) Spring 2017 Macroeconomic Theory II Slides III - Complete Markets Spring 2017 1 / 33 Outline 1. Risk, Uncertainty,

1 Dynamic programming

1 Dynamic programming A country has just discovered a natural resource which yields an income per period R measured in terms of traded goods. The cost of exploitation is negligible. The government wants

1 Dynamic programming A country has just discovered a natural resource which yields an income per period R measured in terms of traded goods. The cost of exploitation is negligible. The government wants

Macroeconomics 2. Lecture 5 - Money February. Sciences Po

Macroeconomics 2 Lecture 5 - Money Zsófia L. Bárány Sciences Po 2014 February A brief history of money in macro 1. 1. Hume: money has a wealth effect more money increase in aggregate demand Y 2. Friedman

Macroeconomics 2 Lecture 5 - Money Zsófia L. Bárány Sciences Po 2014 February A brief history of money in macro 1. 1. Hume: money has a wealth effect more money increase in aggregate demand Y 2. Friedman

Sudden Stops and Output Drops

Federal Reserve Bank of Minneapolis Research Department Staff Report 353 January 2005 Sudden Stops and Output Drops V. V. Chari University of Minnesota and Federal Reserve Bank of Minneapolis Patrick J.

Federal Reserve Bank of Minneapolis Research Department Staff Report 353 January 2005 Sudden Stops and Output Drops V. V. Chari University of Minnesota and Federal Reserve Bank of Minneapolis Patrick J.

An Information-Based Theory of Time-Varying Liquidity

An Information-Based Theory of Time-Varying Liquidity Brett Green UC Berkeley, Haas School of Business joint with Brendan Daley Duke University, Fuqua School of Business Csef-Igier Symposium on Economics

An Information-Based Theory of Time-Varying Liquidity Brett Green UC Berkeley, Haas School of Business joint with Brendan Daley Duke University, Fuqua School of Business Csef-Igier Symposium on Economics

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics. Ph. D. Comprehensive Examination: Macroeconomics Fall, 2016

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Comprehensive Examination: Macroeconomics Fall, 2016 Section 1. (Suggested Time: 45 Minutes) For 3 of the following 6 statements, state

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Comprehensive Examination: Macroeconomics Fall, 2016 Section 1. (Suggested Time: 45 Minutes) For 3 of the following 6 statements, state

Sudden Stops and Output Drops

NEW PERSPECTIVES ON REPUTATION AND DEBT Sudden Stops and Output Drops By V. V. CHARI, PATRICK J. KEHOE, AND ELLEN R. MCGRATTAN* Discussants: Andrew Atkeson, University of California; Olivier Jeanne, International

NEW PERSPECTIVES ON REPUTATION AND DEBT Sudden Stops and Output Drops By V. V. CHARI, PATRICK J. KEHOE, AND ELLEN R. MCGRATTAN* Discussants: Andrew Atkeson, University of California; Olivier Jeanne, International

Imperfect Information and Market Segmentation Walsh Chapter 5

Imperfect Information and Market Segmentation Walsh Chapter 5 1 Why Does Money Have Real Effects? Add market imperfections to eliminate short-run neutrality of money Imperfect information keeps price from

Imperfect Information and Market Segmentation Walsh Chapter 5 1 Why Does Money Have Real Effects? Add market imperfections to eliminate short-run neutrality of money Imperfect information keeps price from

Transaction Cost Politics in Over the Counter Markets

Applied Mathematical Sciences, Vol. 12, 2018, no. 23, 1137-1156 HIKARI Ltd, www.m-hikari.com https://doi.org/10.12988/ams.2018.87103 Transaction Cost Politics in Over the Counter Markets Federico Flore

Applied Mathematical Sciences, Vol. 12, 2018, no. 23, 1137-1156 HIKARI Ltd, www.m-hikari.com https://doi.org/10.12988/ams.2018.87103 Transaction Cost Politics in Over the Counter Markets Federico Flore

B r i e f T a b l e o f C o n t e n t s

B r i e f T a b l e o f C o n t e n t s Chapter 1. Introduction Part I. CAPITAL ACCUMULATION AND ECONOMIC GROWTH Chapter 2. Neoclassical Growth Models Chapter 3. Endogenous Growth Models Chapter 4. Some

B r i e f T a b l e o f C o n t e n t s Chapter 1. Introduction Part I. CAPITAL ACCUMULATION AND ECONOMIC GROWTH Chapter 2. Neoclassical Growth Models Chapter 3. Endogenous Growth Models Chapter 4. Some

2. Preceded (followed) by expansions (contractions) in domestic. 3. Capital, labor account for small fraction of output drop,

by expansions (contractions) in domestic. 3. Capital, labor account for small fraction of output drop,") Mendoza (AER) Sudden Stop facts 1. Large, abrupt reversals in capital flows 2. Preceded (followed) by expansions (contractions) in domestic production, absorption, asset prices, credit & leverage 3. Capital,

Mendoza (AER) Sudden Stop facts 1. Large, abrupt reversals in capital flows 2. Preceded (followed) by expansions (contractions) in domestic production, absorption, asset prices, credit & leverage 3. Capital,

Lecture Notes on. Liquidity and Asset Pricing. by Lasse Heje Pedersen

Lecture Notes on Liquidity and Asset Pricing by Lasse Heje Pedersen Current Version: January 17, 2005 Copyright Lasse Heje Pedersen c Not for Distribution Stern School of Business, New York University,

Lecture Notes on Liquidity and Asset Pricing by Lasse Heje Pedersen Current Version: January 17, 2005 Copyright Lasse Heje Pedersen c Not for Distribution Stern School of Business, New York University,

Kiyotaki and Moore [1997]

![Kiyotaki and Moore [1997]](/thumbs/77/76435924.jpg "Kiyotaki and Moore [1997]") Kiyotaki and Moore [997] Econ 235, Spring 203 Heterogeneity: why else would you need markets! When assets serve as collateral, prices affect allocations Importance of who is pricing an asset Best users

Kiyotaki and Moore [997] Econ 235, Spring 203 Heterogeneity: why else would you need markets! When assets serve as collateral, prices affect allocations Importance of who is pricing an asset Best users

INTERTEMPORAL ASSET ALLOCATION: THEORY

INTERTEMPORAL ASSET ALLOCATION: THEORY Multi-Period Model The agent acts as a price-taker in asset markets and then chooses today s consumption and asset shares to maximise lifetime utility. This multi-period

INTERTEMPORAL ASSET ALLOCATION: THEORY Multi-Period Model The agent acts as a price-taker in asset markets and then chooses today s consumption and asset shares to maximise lifetime utility. This multi-period

Liquidity Policies and Systemic Risk Tobias Adrian and Nina Boyarchenko

Policies and Systemic Risk Tobias Adrian and Nina Boyarchenko The views presented here are the authors and are not representative of the views of the Federal Reserve Bank of New York or of the Federal

Policies and Systemic Risk Tobias Adrian and Nina Boyarchenko The views presented here are the authors and are not representative of the views of the Federal Reserve Bank of New York or of the Federal

Trade and Labor Market: Felbermayr, Prat, Schmerer (2011)

") Trade and Labor Market: Felbermayr, Prat, Schmerer (2011) Davide Suverato 1 1 LMU University of Munich Topics in International Trade, 16 June 2015 Davide Suverato, LMU Trade and Labor Market: Felbermayr,

Trade and Labor Market: Felbermayr, Prat, Schmerer (2011) Davide Suverato 1 1 LMU University of Munich Topics in International Trade, 16 June 2015 Davide Suverato, LMU Trade and Labor Market: Felbermayr,

AMH4 - ADVANCED OPTION PRICING. Contents

AMH4 - ADVANCED OPTION PRICING ANDREW TULLOCH Contents 1. Theory of Option Pricing 2 2. Black-Scholes PDE Method 4 3. Martingale method 4 4. Monte Carlo methods 5 4.1. Method of antithetic variances 5

AMH4 - ADVANCED OPTION PRICING ANDREW TULLOCH Contents 1. Theory of Option Pricing 2 2. Black-Scholes PDE Method 4 3. Martingale method 4 4. Monte Carlo methods 5 4.1. Method of antithetic variances 5

1 A tax on capital income in a neoclassical growth model

1 A tax on capital income in a neoclassical growth model We look at a standard neoclassical growth model. The representative consumer maximizes U = β t u(c t ) (1) t=0 where c t is consumption in period

1 A tax on capital income in a neoclassical growth model We look at a standard neoclassical growth model. The representative consumer maximizes U = β t u(c t ) (1) t=0 where c t is consumption in period

Credit Booms, Financial Crises and Macroprudential Policy

Credit Booms, Financial Crises and Macroprudential Policy Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 March 219 1 The views expressed in this paper are those

Credit Booms, Financial Crises and Macroprudential Policy Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 March 219 1 The views expressed in this paper are those

Household Debt, Financial Intermediation, and Monetary Policy

Household Debt, Financial Intermediation, and Monetary Policy Shutao Cao 1 Yahong Zhang 2 1 Bank of Canada 2 Western University October 21, 2014 Motivation The US experience suggests that the collapse

Household Debt, Financial Intermediation, and Monetary Policy Shutao Cao 1 Yahong Zhang 2 1 Bank of Canada 2 Western University October 21, 2014 Motivation The US experience suggests that the collapse

QI SHANG: General Equilibrium Analysis of Portfolio Benchmarking

General Equilibrium Analysis of Portfolio Benchmarking QI SHANG 23/10/2008 Introduction The Model Equilibrium Discussion of Results Conclusion Introduction This paper studies the equilibrium effect of

General Equilibrium Analysis of Portfolio Benchmarking QI SHANG 23/10/2008 Introduction The Model Equilibrium Discussion of Results Conclusion Introduction This paper studies the equilibrium effect of

Monetary Economics. Lecture 23a: inside and outside liquidity, part one. Chris Edmond. 2nd Semester 2014 (not examinable)

") Monetary Economics Lecture 23a: inside and outside liquidity, part one Chris Edmond 2nd Semester 2014 (not examinable) 1 This lecture Main reading: Holmström and Tirole, Inside and outside liquidity, MIT

Monetary Economics Lecture 23a: inside and outside liquidity, part one Chris Edmond 2nd Semester 2014 (not examinable) 1 This lecture Main reading: Holmström and Tirole, Inside and outside liquidity, MIT

Corporate Finance and Monetary Policy

Corporate Finance and Monetary Policy Guillaume Rocheteau Randall Wright Cathy Zhang U. of California, Irvine U. of Wisconsin, Madison Purdue University CIGS Conference on Macroeconomic Theory and Policy,

Corporate Finance and Monetary Policy Guillaume Rocheteau Randall Wright Cathy Zhang U. of California, Irvine U. of Wisconsin, Madison Purdue University CIGS Conference on Macroeconomic Theory and Policy,

Chapter 9 Dynamic Models of Investment

George Alogoskoufis, Dynamic Macroeconomic Theory, 2015 Chapter 9 Dynamic Models of Investment In this chapter we present the main neoclassical model of investment, under convex adjustment costs. This

George Alogoskoufis, Dynamic Macroeconomic Theory, 2015 Chapter 9 Dynamic Models of Investment In this chapter we present the main neoclassical model of investment, under convex adjustment costs. This

1 Answers to the Sept 08 macro prelim - Long Questions

Answers to the Sept 08 macro prelim - Long Questions. Suppose that a representative consumer receives an endowment of a non-storable consumption good. The endowment evolves exogenously according to ln

Answers to the Sept 08 macro prelim - Long Questions. Suppose that a representative consumer receives an endowment of a non-storable consumption good. The endowment evolves exogenously according to ln

General Examination in Macroeconomic Theory. Fall 2010

HARVARD UNIVERSITY DEPARTMENT OF ECONOMICS General Examination in Macroeconomic Theory Fall 2010 ----------------------------------------------------------------------------------------------------------------

HARVARD UNIVERSITY DEPARTMENT OF ECONOMICS General Examination in Macroeconomic Theory Fall 2010 ----------------------------------------------------------------------------------------------------------------

Liquidity. Why do people choose to hold fiat money despite its lower rate of return?

Liquidity Why do people choose to hold fiat money despite its lower rate of return? Maybe because fiat money is less risky than most of the other assets. Maybe because fiat money is more liquid than alternative

Liquidity Why do people choose to hold fiat money despite its lower rate of return? Maybe because fiat money is less risky than most of the other assets. Maybe because fiat money is more liquid than alternative

Transactions and Money Demand Walsh Chapter 3

Transactions and Money Demand Walsh Chapter 3 1 Shopping time models 1.1 Assumptions Purchases require transactions services ψ = ψ (m, n s ) = c where ψ n s 0, ψ m 0, ψ n s n s 0, ψ mm 0 positive but diminishing

Transactions and Money Demand Walsh Chapter 3 1 Shopping time models 1.1 Assumptions Purchases require transactions services ψ = ψ (m, n s ) = c where ψ n s 0, ψ m 0, ψ n s n s 0, ψ mm 0 positive but diminishing

Unemployment (fears), Precautionary Savings, and Aggregate Demand

, Precautionary Savings, and Aggregate Demand") Unemployment (fears), Precautionary Savings, and Aggregate Demand Wouter den Haan (LSE), Pontus Rendahl (Cambridge), Markus Riegler (LSE) ESSIM 2014 Introduction A FT-esque story: Uncertainty (or fear)

Unemployment (fears), Precautionary Savings, and Aggregate Demand Wouter den Haan (LSE), Pontus Rendahl (Cambridge), Markus Riegler (LSE) ESSIM 2014 Introduction A FT-esque story: Uncertainty (or fear)

Lecture 1: Traditional Open Macro Models and Monetary Policy

Lecture 1: Traditional Open Macro Models and Monetary Policy Isabelle Méjean isabelle.mejean@polytechnique.edu http://mejean.isabelle.googlepages.com/ Master Economics and Public Policy, International

Lecture 1: Traditional Open Macro Models and Monetary Policy Isabelle Méjean isabelle.mejean@polytechnique.edu http://mejean.isabelle.googlepages.com/ Master Economics and Public Policy, International

Monetary Economics. Financial Markets and the Business Cycle: The Bernanke and Gertler Model. Nicola Viegi. September 2010

Monetary Economics Financial Markets and the Business Cycle: The Bernanke and Gertler Model Nicola Viegi September 2010 Monetary Economics () Lecture 7 September 2010 1 / 35 Introduction Conventional Model

Monetary Economics Financial Markets and the Business Cycle: The Bernanke and Gertler Model Nicola Viegi September 2010 Monetary Economics () Lecture 7 September 2010 1 / 35 Introduction Conventional Model

Part A: Answer Question A1 (required) and Question A2 or A3 (choice).

and Question A2 or A3 (choice).") Ph.D. Core Exam -- Macroeconomics 7 January 2019 -- 8:00 am to 3:00 pm Part A: Answer Question A1 (required) and Question A2 or A3 (choice). A1 (required): Short-Run Stabilization Policy and Economic Shocks

Ph.D. Core Exam -- Macroeconomics 7 January 2019 -- 8:00 am to 3:00 pm Part A: Answer Question A1 (required) and Question A2 or A3 (choice). A1 (required): Short-Run Stabilization Policy and Economic Shocks

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics. Ph. D. Comprehensive Examination: Macroeconomics Spring, 2009

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Comprehensive Examination: Macroeconomics Spring, 2009 Section 1. (Suggested Time: 45 Minutes) For 3 of the following 6 statements,

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Comprehensive Examination: Macroeconomics Spring, 2009 Section 1. (Suggested Time: 45 Minutes) For 3 of the following 6 statements,

Lecture 12. Asset pricing model. Randall Romero Aguilar, PhD I Semestre 2017 Last updated: June 15, 2017

Lecture 12 Asset pricing model Randall Romero Aguilar, PhD I Semestre 2017 Last updated: June 15, 2017 Universidad de Costa Rica EC3201 - Teoría Macroeconómica 2 Table of contents 1. Introduction 2. The

Lecture 12 Asset pricing model Randall Romero Aguilar, PhD I Semestre 2017 Last updated: June 15, 2017 Universidad de Costa Rica EC3201 - Teoría Macroeconómica 2 Table of contents 1. Introduction 2. The

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics. Ph. D. Preliminary Examination: Macroeconomics Fall, 2009

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Preliminary Examination: Macroeconomics Fall, 2009 Instructions: Read the questions carefully and make sure to show your work. You

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Preliminary Examination: Macroeconomics Fall, 2009 Instructions: Read the questions carefully and make sure to show your work. You

Incentives and economic growth

Econ 307 Lecture 8 Incentives and economic growth Up to now we have abstracted away from most of the incentives that agents face in determining economic growth (expect for the determination of technology

Econ 307 Lecture 8 Incentives and economic growth Up to now we have abstracted away from most of the incentives that agents face in determining economic growth (expect for the determination of technology

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics. Ph. D. Comprehensive Examination: Macroeconomics Fall, 2010

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Comprehensive Examination: Macroeconomics Fall, 2010 Section 1. (Suggested Time: 45 Minutes) For 3 of the following 6 statements, state

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Comprehensive Examination: Macroeconomics Fall, 2010 Section 1. (Suggested Time: 45 Minutes) For 3 of the following 6 statements, state

Lecture 1: Lucas Model and Asset Pricing

Lecture 1: Lucas Model and Asset Pricing Economics 714, Spring 2018 1 Asset Pricing 1.1 Lucas (1978) Asset Pricing Model We assume that there are a large number of identical agents, modeled as a representative

Lecture 1: Lucas Model and Asset Pricing Economics 714, Spring 2018 1 Asset Pricing 1.1 Lucas (1978) Asset Pricing Model We assume that there are a large number of identical agents, modeled as a representative

The I Theory of Money

The I Theory of Money Markus K. Brunnermeier & Yuliy Sannikov Princeton University CSEF-IGIER Symposium Capri, June 24 th, 2015 Motivation Framework to study monetary and financial stability Interaction

The I Theory of Money Markus K. Brunnermeier & Yuliy Sannikov Princeton University CSEF-IGIER Symposium Capri, June 24 th, 2015 Motivation Framework to study monetary and financial stability Interaction

David Skeie Federal Reserve Bank of New York Bank of Canada Annual Economic Conference on New Developments in Payments and Settlement

Discussion i of Emergence and Fragility of Repo Markets by Hajime Tomura David Skeie Federal Reserve Bank of New York 2011 Bank of Canada Annual Economic Conference on New Developments in Payments and

Discussion i of Emergence and Fragility of Repo Markets by Hajime Tomura David Skeie Federal Reserve Bank of New York 2011 Bank of Canada Annual Economic Conference on New Developments in Payments and

Dynamic Macroeconomics

Chapter 1 Introduction Dynamic Macroeconomics Prof. George Alogoskoufis Fletcher School, Tufts University and Athens University of Economics and Business 1.1 The Nature and Evolution of Macroeconomics

Chapter 1 Introduction Dynamic Macroeconomics Prof. George Alogoskoufis Fletcher School, Tufts University and Athens University of Economics and Business 1.1 The Nature and Evolution of Macroeconomics

Lecture 2: Stochastic Discount Factor

Lecture 2: Stochastic Discount Factor Simon Gilchrist Boston Univerity and NBER EC 745 Fall, 2013 Stochastic Discount Factor (SDF) A stochastic discount factor is a stochastic process {M t,t+s } such that

Lecture 2: Stochastic Discount Factor Simon Gilchrist Boston Univerity and NBER EC 745 Fall, 2013 Stochastic Discount Factor (SDF) A stochastic discount factor is a stochastic process {M t,t+s } such that

A Macroeconomic Model with Financial Panics

A Macroeconomic Model with Financial Panics Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 March 218 1 The views expressed in this paper are those of the authors

A Macroeconomic Model with Financial Panics Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 March 218 1 The views expressed in this paper are those of the authors

Exchange Rate Adjustment in Financial Crises

Exchange Rate Adjustment in Financial Crises Michael B. Devereux 1 Changhua Yu 2 1 University of British Columbia 2 Peking University Swiss National Bank June 2016 Motivation: Two-fold Crises in Emerging

Exchange Rate Adjustment in Financial Crises Michael B. Devereux 1 Changhua Yu 2 1 University of British Columbia 2 Peking University Swiss National Bank June 2016 Motivation: Two-fold Crises in Emerging

TOBB-ETU, Economics Department Macroeconomics II (ECON 532) Practice Problems III

Practice Problems III") TOBB-ETU, Economics Department Macroeconomics II ECON 532) Practice Problems III Q: Consumption Theory CARA utility) Consider an individual living for two periods, with preferences Uc 1 ; c 2 ) = uc 1

TOBB-ETU, Economics Department Macroeconomics II ECON 532) Practice Problems III Q: Consumption Theory CARA utility) Consider an individual living for two periods, with preferences Uc 1 ; c 2 ) = uc 1

Payments, Credit & Asset Prices

Payments, Credit & Asset Prices Monika Piazzesi Stanford & NBER Martin Schneider Stanford & NBER CITE August 13, 2015 Piazzesi & Schneider Payments, Credit & Asset Prices CITE August 13, 2015 1 / 31 Dollar

Payments, Credit & Asset Prices Monika Piazzesi Stanford & NBER Martin Schneider Stanford & NBER CITE August 13, 2015 Piazzesi & Schneider Payments, Credit & Asset Prices CITE August 13, 2015 1 / 31 Dollar

OVER-THE-COUNTER MARKETS

Econometrica, Vol. 73, No. 6 (November, 2005), 1815 1847 OVER-THE-COUNTER MARKETS BY DARRELL DUFFIE, NICOLAE GÂRLEANU, AND LASSE HEJE PEDERSEN 1 We study how intermediation and asset prices in over-the-counter

Econometrica, Vol. 73, No. 6 (November, 2005), 1815 1847 OVER-THE-COUNTER MARKETS BY DARRELL DUFFIE, NICOLAE GÂRLEANU, AND LASSE HEJE PEDERSEN 1 We study how intermediation and asset prices in over-the-counter

Household income risk, nominal frictions, and incomplete markets 1

Household income risk, nominal frictions, and incomplete markets 1 2013 North American Summer Meeting Ralph Lütticke 13.06.2013 1 Joint-work with Christian Bayer, Lien Pham, and Volker Tjaden 1 / 30 Research

Household income risk, nominal frictions, and incomplete markets 1 2013 North American Summer Meeting Ralph Lütticke 13.06.2013 1 Joint-work with Christian Bayer, Lien Pham, and Volker Tjaden 1 / 30 Research

DSGE Models with Financial Frictions

DSGE Models with Financial Frictions Simon Gilchrist 1 1 Boston University and NBER September 2014 Overview OLG Model New Keynesian Model with Capital New Keynesian Model with Financial Accelerator Introduction

DSGE Models with Financial Frictions Simon Gilchrist 1 1 Boston University and NBER September 2014 Overview OLG Model New Keynesian Model with Capital New Keynesian Model with Financial Accelerator Introduction

Intermediary Leverage Cycles and Financial Stability Tobias Adrian and Nina Boyarchenko

Intermediary Leverage Cycles and Financial Stability Tobias Adrian and Nina Boyarchenko The views presented here are the authors and are not representative of the views of the Federal Reserve Bank of New

Intermediary Leverage Cycles and Financial Stability Tobias Adrian and Nina Boyarchenko The views presented here are the authors and are not representative of the views of the Federal Reserve Bank of New

Problem Set 3. Thomas Philippon. April 19, Human Wealth, Financial Wealth and Consumption

Problem Set 3 Thomas Philippon April 19, 2002 1 Human Wealth, Financial Wealth and Consumption The goal of the question is to derive the formulas on p13 of Topic 2. This is a partial equilibrium analysis

Problem Set 3 Thomas Philippon April 19, 2002 1 Human Wealth, Financial Wealth and Consumption The goal of the question is to derive the formulas on p13 of Topic 2. This is a partial equilibrium analysis

Intertemporal choice: Consumption and Savings

Econ 20200 - Elements of Economics Analysis 3 (Honors Macroeconomics) Lecturer: Chanont (Big) Banternghansa TA: Jonathan J. Adams Spring 2013 Introduction Intertemporal choice: Consumption and Savings

Econ 20200 - Elements of Economics Analysis 3 (Honors Macroeconomics) Lecturer: Chanont (Big) Banternghansa TA: Jonathan J. Adams Spring 2013 Introduction Intertemporal choice: Consumption and Savings

Economics 2010c: Lecture 4 Precautionary Savings and Liquidity Constraints

Economics 2010c: Lecture 4 Precautionary Savings and Liquidity Constraints David Laibson 9/11/2014 Outline: 1. Precautionary savings motives 2. Liquidity constraints 3. Application: Numerical solution

Economics 2010c: Lecture 4 Precautionary Savings and Liquidity Constraints David Laibson 9/11/2014 Outline: 1. Precautionary savings motives 2. Liquidity constraints 3. Application: Numerical solution

Financial Intermediation and the Supply of Liquidity

Financial Intermediation and the Supply of Liquidity Jonathan Kreamer University of Maryland, College Park November 11, 2012 1 / 27 Question Growing recognition of the importance of the financial sector.

Financial Intermediation and the Supply of Liquidity Jonathan Kreamer University of Maryland, College Park November 11, 2012 1 / 27 Question Growing recognition of the importance of the financial sector.

Lecture note on moral hazard explanations of efficiency wages

Lecture note on moral hazard explanations of efficiency wages (Background for this lecture is the article by Shapiro and Stiglitz, in the reading list) The value function approach. This approach is used

Lecture note on moral hazard explanations of efficiency wages (Background for this lecture is the article by Shapiro and Stiglitz, in the reading list) The value function approach. This approach is used

MACROECONOMICS. Prelim Exam

MACROECONOMICS Prelim Exam Austin, June 1, 2012 Instructions This is a closed book exam. If you get stuck in one section move to the next one. Do not waste time on sections that you find hard to solve.

MACROECONOMICS Prelim Exam Austin, June 1, 2012 Instructions This is a closed book exam. If you get stuck in one section move to the next one. Do not waste time on sections that you find hard to solve.

Nobel Symposium Money and Banking

Nobel Symposium Money and Banking https://www.houseoffinance.se/nobel-symposium May -, 0 Clarion Hotel Sign, Stockholm Inside Money and Liquidity Nobuhiro Kiyotaki and John Moore Questions Under what environment

Nobel Symposium Money and Banking https://www.houseoffinance.se/nobel-symposium May -, 0 Clarion Hotel Sign, Stockholm Inside Money and Liquidity Nobuhiro Kiyotaki and John Moore Questions Under what environment

The Ramsey Model. Lectures 11 to 14. Topics in Macroeconomics. November 10, 11, 24 & 25, 2008

The Ramsey Model Lectures 11 to 14 Topics in Macroeconomics November 10, 11, 24 & 25, 2008 Lecture 11, 12, 13 & 14 1/50 Topics in Macroeconomics The Ramsey Model: Introduction 2 Main Ingredients Neoclassical

The Ramsey Model Lectures 11 to 14 Topics in Macroeconomics November 10, 11, 24 & 25, 2008 Lecture 11, 12, 13 & 14 1/50 Topics in Macroeconomics The Ramsey Model: Introduction 2 Main Ingredients Neoclassical

Macroeconomics and finance

Macroeconomics and finance 1 1. Temporary equilibrium and the price level [Lectures 11 and 12] 2. Overlapping generations and learning [Lectures 13 and 14] 2.1 The overlapping generations model 2.2 Expectations

Macroeconomics and finance 1 1. Temporary equilibrium and the price level [Lectures 11 and 12] 2. Overlapping generations and learning [Lectures 13 and 14] 2.1 The overlapping generations model 2.2 Expectations

Chapter 6 Money, Inflation and Economic Growth

George Alogoskoufis, Dynamic Macroeconomic Theory, 2015 Chapter 6 Money, Inflation and Economic Growth In the models we have presented so far there is no role for money. Yet money performs very important

George Alogoskoufis, Dynamic Macroeconomic Theory, 2015 Chapter 6 Money, Inflation and Economic Growth In the models we have presented so far there is no role for money. Yet money performs very important

ECOM 009 Macroeconomics B. Lecture 7

ECOM 009 Macroeconomics B Lecture 7 Giulio Fella c Giulio Fella, 2014 ECOM 009 Macroeconomics B - Lecture 7 187/231 Plan for the rest of this lecture Introducing the general asset pricing equation Consumption-based

ECOM 009 Macroeconomics B Lecture 7 Giulio Fella c Giulio Fella, 2014 ECOM 009 Macroeconomics B - Lecture 7 187/231 Plan for the rest of this lecture Introducing the general asset pricing equation Consumption-based

Asymmetric Information and Inventory Concerns in Over-the-Counter Markets

Asymmetric nformation and nventory Concerns in Over-the-Counter Markets Julien Cujean U of Maryland (Smith) jcujean@rhsmith.umd.edu Rémy Praz Copenhagen Business School rpr.fi@cbs.dk Thematic Semester

Asymmetric nformation and nventory Concerns in Over-the-Counter Markets Julien Cujean U of Maryland (Smith) jcujean@rhsmith.umd.edu Rémy Praz Copenhagen Business School rpr.fi@cbs.dk Thematic Semester

Exploding Bubbles In a Macroeconomic Model. Narayana Kocherlakota

Bubbles Exploding Bubbles In a Macroeconomic Model Narayana Kocherlakota presented by Kaiji Chen Macro Reading Group, Jan 16, 2009 1 Bubbles Question How do bubbles emerge in an economy when collateral

Bubbles Exploding Bubbles In a Macroeconomic Model Narayana Kocherlakota presented by Kaiji Chen Macro Reading Group, Jan 16, 2009 1 Bubbles Question How do bubbles emerge in an economy when collateral

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics. Ph. D. Comprehensive Examination: Macroeconomics Spring, 2016

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Comprehensive Examination: Macroeconomics Spring, 2016 Section 1. Suggested Time: 45 Minutes) For 3 of the following 6 statements,

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Comprehensive Examination: Macroeconomics Spring, 2016 Section 1. Suggested Time: 45 Minutes) For 3 of the following 6 statements,

Department of Economics The Ohio State University Midterm Questions and Answers Econ 8712

Prof. James Peck Fall 06 Department of Economics The Ohio State University Midterm Questions and Answers Econ 87. (30 points) A decision maker (DM) is a von Neumann-Morgenstern expected utility maximizer.

Prof. James Peck Fall 06 Department of Economics The Ohio State University Midterm Questions and Answers Econ 87. (30 points) A decision maker (DM) is a von Neumann-Morgenstern expected utility maximizer.

Monetary Exchange in Over-the-Counter Markets: A Theory of Speculative Bubbles, the Fed Model, and Self-fulfilling Liquidity Crises

Monetary Exchange in Over-the-Counter Markets: A Theory of Speculative Bubbles, the Fed Model, and Self-fulfilling Liquidity Crises Ricardo Lagos New York University Shengxing Zhang London School of Economics

Monetary Exchange in Over-the-Counter Markets: A Theory of Speculative Bubbles, the Fed Model, and Self-fulfilling Liquidity Crises Ricardo Lagos New York University Shengxing Zhang London School of Economics

Notes on Financial Frictions Under Asymmetric Information and Costly State Verification. Lawrence Christiano

Notes on Financial Frictions Under Asymmetric Information and Costly State Verification by Lawrence Christiano Incorporating Financial Frictions into a Business Cycle Model General idea: Standard model

Notes on Financial Frictions Under Asymmetric Information and Costly State Verification by Lawrence Christiano Incorporating Financial Frictions into a Business Cycle Model General idea: Standard model

We are now introducing a capital, an alternative asset besides fiat money, which enables individual to acquire consumption when old.

Capital We are now introducing a capital, an alternative asset besides fiat money, which enables individual to acquire consumption when old. Consider the following production technology: o If k t units

Capital We are now introducing a capital, an alternative asset besides fiat money, which enables individual to acquire consumption when old. Consider the following production technology: o If k t units

Collateral and Amplification

Collateral and Amplification Macroeconomics IV Ricardo J. Caballero MIT Spring 2011 R.J. Caballero (MIT) Collateral and Amplification Spring 2011 1 / 23 References 1 2 Bernanke B. and M.Gertler, Agency

Collateral and Amplification Macroeconomics IV Ricardo J. Caballero MIT Spring 2011 R.J. Caballero (MIT) Collateral and Amplification Spring 2011 1 / 23 References 1 2 Bernanke B. and M.Gertler, Agency

Liquidity and the Threat of Fraudulent Assets

Liquidity and the Threat of Fraudulent Assets Yiting Li, Guillaume Rocheteau, Pierre-Olivier Weill NTU, UCI, UCLA, NBER, CEPR 1 / 21 fraudulent behavior in asset markets in this paper: with sufficient

Liquidity and the Threat of Fraudulent Assets Yiting Li, Guillaume Rocheteau, Pierre-Olivier Weill NTU, UCI, UCLA, NBER, CEPR 1 / 21 fraudulent behavior in asset markets in this paper: with sufficient

13.3 A Stochastic Production Planning Model

13.3. A Stochastic Production Planning Model 347 From (13.9), we can formally write (dx t ) = f (dt) + G (dz t ) + fgdz t dt, (13.3) dx t dt = f(dt) + Gdz t dt. (13.33) The exact meaning of these expressions

13.3. A Stochastic Production Planning Model 347 From (13.9), we can formally write (dx t ) = f (dt) + G (dz t ) + fgdz t dt, (13.3) dx t dt = f(dt) + Gdz t dt. (13.33) The exact meaning of these expressions

Asset Pricing with Heterogeneous Consumers

, JPE 1996 Presented by: Rustom Irani, NYU Stern November 16, 2009 Outline Introduction 1 Introduction Motivation Contribution 2 Assumptions Equilibrium 3 Mechanism Empirical Implications of Idiosyncratic

, JPE 1996 Presented by: Rustom Irani, NYU Stern November 16, 2009 Outline Introduction 1 Introduction Motivation Contribution 2 Assumptions Equilibrium 3 Mechanism Empirical Implications of Idiosyncratic

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics. Ph. D. Comprehensive Examination: Macroeconomics Spring, 2013

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Comprehensive Examination: Macroeconomics Spring, 2013 Section 1. (Suggested Time: 45 Minutes) For 3 of the following 6 statements,

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Comprehensive Examination: Macroeconomics Spring, 2013 Section 1. (Suggested Time: 45 Minutes) For 3 of the following 6 statements,

(Incomplete) summary of the course so far

summary of the course so far") (Incomplete) summary of the course so far Lecture 9a, ECON 4310 Tord Krogh September 16, 2013 Tord Krogh () ECON 4310 September 16, 2013 1 / 31 Main topics This semester we will go through: Ramsey (check)

(Incomplete) summary of the course so far Lecture 9a, ECON 4310 Tord Krogh September 16, 2013 Tord Krogh () ECON 4310 September 16, 2013 1 / 31 Main topics This semester we will go through: Ramsey (check)

Money in an RBC framework

Money in an RBC framework Noah Williams University of Wisconsin-Madison Noah Williams (UW Madison) Macroeconomic Theory 1 / 36 Money Two basic questions: 1 Modern economies use money. Why? 2 How/why do

Money in an RBC framework Noah Williams University of Wisconsin-Madison Noah Williams (UW Madison) Macroeconomic Theory 1 / 36 Money Two basic questions: 1 Modern economies use money. Why? 2 How/why do

Limited Attention and News Arrival in Limit Order Markets

Limited Attention and News Arrival in Limit Order Markets Jérôme Dugast Banque de France Market Microstructure: Confronting many Viewpoints #3 December 10, 2014 This paper reflects the opinions of the

Limited Attention and News Arrival in Limit Order Markets Jérôme Dugast Banque de France Market Microstructure: Confronting many Viewpoints #3 December 10, 2014 This paper reflects the opinions of the

1 Multiple Choice (30 points)

") 1 Multiple Choice (30 points) Answer the following questions. You DO NOT need to justify your answer. 1. (6 Points) Consider an economy with two goods and two periods. Data are Good 1 p 1 t = 1 p 1 t+1

1 Multiple Choice (30 points) Answer the following questions. You DO NOT need to justify your answer. 1. (6 Points) Consider an economy with two goods and two periods. Data are Good 1 p 1 t = 1 p 1 t+1

Final Exam II ECON 4310, Fall 2014

Final Exam II ECON 4310, Fall 2014 1. Do not write with pencil, please use a ball-pen instead. 2. Please answer in English. Solutions without traceable outlines, as well as those with unreadable outlines

Final Exam II ECON 4310, Fall 2014 1. Do not write with pencil, please use a ball-pen instead. 2. Please answer in English. Solutions without traceable outlines, as well as those with unreadable outlines

Edinburgh Research Explorer

Edinburgh Research Explorer From shells and gold to plastic and silicon: a theory of the evolution of money, in the spirit of Keynes Citation for published version: Hardman-Moore, J 2007, 'From shells

Edinburgh Research Explorer From shells and gold to plastic and silicon: a theory of the evolution of money, in the spirit of Keynes Citation for published version: Hardman-Moore, J 2007, 'From shells

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics. Ph. D. Preliminary Examination: Macroeconomics Spring, 2007

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Preliminary Examination: Macroeconomics Spring, 2007 Instructions: Read the questions carefully and make sure to show your work. You

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Preliminary Examination: Macroeconomics Spring, 2007 Instructions: Read the questions carefully and make sure to show your work. You

Financial Market Imperfections Uribe, Ch 7

Financial Market Imperfections Uribe, Ch 7 1 Imperfect Credibility of Policy: Trade Reform 1.1 Model Assumptions Output is exogenous constant endowment (y), not useful for consumption, but can be exported

Financial Market Imperfections Uribe, Ch 7 1 Imperfect Credibility of Policy: Trade Reform 1.1 Model Assumptions Output is exogenous constant endowment (y), not useful for consumption, but can be exported

A dynamic model with nominal rigidities.

A dynamic model with nominal rigidities. Olivier Blanchard May 2005 In topic 7, we introduced nominal rigidities in a simple static model. It is time to reintroduce dynamics. These notes reintroduce the

A dynamic model with nominal rigidities. Olivier Blanchard May 2005 In topic 7, we introduced nominal rigidities in a simple static model. It is time to reintroduce dynamics. These notes reintroduce the

Optimal Credit Market Policy. CEF 2018, Milan

Optimal Credit Market Policy Matteo Iacoviello 1 Ricardo Nunes 2 Andrea Prestipino 1 1 Federal Reserve Board 2 University of Surrey CEF 218, Milan June 2, 218 Disclaimer: The views expressed are solely

Optimal Credit Market Policy Matteo Iacoviello 1 Ricardo Nunes 2 Andrea Prestipino 1 1 Federal Reserve Board 2 University of Surrey CEF 218, Milan June 2, 218 Disclaimer: The views expressed are solely

Asymmetric Labor Market Fluctuations in an Estimated Model of Equilibrium Unemployment

Asymmetric Labor Market Fluctuations in an Estimated Model of Equilibrium Unemployment Nicolas Petrosky-Nadeau FRB San Francisco Benjamin Tengelsen CMU - Tepper Tsinghua - St.-Louis Fed Conference May

Asymmetric Labor Market Fluctuations in an Estimated Model of Equilibrium Unemployment Nicolas Petrosky-Nadeau FRB San Francisco Benjamin Tengelsen CMU - Tepper Tsinghua - St.-Louis Fed Conference May

Financial Intermediation and Credit Policy in Business Cycle Analysis. Gertler and Kiotaki Professor PengFei Wang Fatemeh KazempourLong

Financial Intermediation and Credit Policy in Business Cycle Analysis Gertler and Kiotaki 2009 Professor PengFei Wang Fatemeh KazempourLong 1 Motivation Bernanke, Gilchrist and Gertler (1999) studied great

Financial Intermediation and Credit Policy in Business Cycle Analysis Gertler and Kiotaki 2009 Professor PengFei Wang Fatemeh KazempourLong 1 Motivation Bernanke, Gilchrist and Gertler (1999) studied great

WORKING PAPER NO THE ELASTICITY OF THE UNEMPLOYMENT RATE WITH RESPECT TO BENEFITS. Kai Christoffel European Central Bank Frankfurt

WORKING PAPER NO. 08-15 THE ELASTICITY OF THE UNEMPLOYMENT RATE WITH RESPECT TO BENEFITS Kai Christoffel European Central Bank Frankfurt Keith Kuester Federal Reserve Bank of Philadelphia Final version

WORKING PAPER NO. 08-15 THE ELASTICITY OF THE UNEMPLOYMENT RATE WITH RESPECT TO BENEFITS Kai Christoffel European Central Bank Frankfurt Keith Kuester Federal Reserve Bank of Philadelphia Final version

Bernanke and Gertler [1989]

![Bernanke and Gertler [1989]](/thumbs/90/103712154.jpg "Bernanke and Gertler [1989]") Bernanke and Gertler [1989] Econ 235, Spring 2013 1 Background: Townsend [1979] An entrepreneur requires x to produce output y f with Ey > x but does not have money, so he needs a lender Once y is realized,

Bernanke and Gertler [1989] Econ 235, Spring 2013 1 Background: Townsend [1979] An entrepreneur requires x to produce output y f with Ey > x but does not have money, so he needs a lender Once y is realized,

The Fisher Equation and Output Growth

The Fisher Equation and Output Growth A B S T R A C T Although the Fisher equation applies for the case of no output growth, I show that it requires an adjustment to account for non-zero output growth.

The Fisher Equation and Output Growth A B S T R A C T Although the Fisher equation applies for the case of no output growth, I show that it requires an adjustment to account for non-zero output growth.

Financing Durable Assets

Duke University, NBER, and CEPR Finance Seminar MIT Sloan School of Management February 10, 2016 Effect of Durability on Financing Durability essential feature of capital Fixed assets comprise as much

Duke University, NBER, and CEPR Finance Seminar MIT Sloan School of Management February 10, 2016 Effect of Durability on Financing Durability essential feature of capital Fixed assets comprise as much

The Representative Household Model

Chapter 3 The Representative Household Model The representative household class of models is a family of dynamic general equilibrium models, based on the assumption that the dynamic path of aggregate consumption

Chapter 3 The Representative Household Model The representative household class of models is a family of dynamic general equilibrium models, based on the assumption that the dynamic path of aggregate consumption

1. Money in the utility function (start)

") Monetary Policy, 8/2 206 Henrik Jensen Department of Economics University of Copenhagen. Money in the utility function (start) a. The basic money-in-the-utility function model b. Optimal behavior and steady-state

Monetary Policy, 8/2 206 Henrik Jensen Department of Economics University of Copenhagen. Money in the utility function (start) a. The basic money-in-the-utility function model b. Optimal behavior and steady-state

Aggregation with a double non-convex labor supply decision: indivisible private- and public-sector hours

Ekonomia nr 47/2016 123 Ekonomia. Rynek, gospodarka, społeczeństwo 47(2016), s. 123 133 DOI: 10.17451/eko/47/2016/233 ISSN: 0137-3056 www.ekonomia.wne.uw.edu.pl Aggregation with a double non-convex labor

Ekonomia nr 47/2016 123 Ekonomia. Rynek, gospodarka, społeczeństwo 47(2016), s. 123 133 DOI: 10.17451/eko/47/2016/233 ISSN: 0137-3056 www.ekonomia.wne.uw.edu.pl Aggregation with a double non-convex labor