A new approach for valuing a portfolio of illiquid assets

|

|

|

- Calvin Goodman

- 5 years ago

- Views:

Transcription

1 PRIN Conference Stochastic Methods in Finance Torino - July, 2008 A new approach for valuing a portfolio of illiquid assets Giacomo Scandolo - Università di Firenze Carlo Acerbi - AbaxBank Milano

2 Liquidity risk 1/23 What is liquidity risk? Treasurer s answer: the risk of running short of cash Trader s answer: the risk of trading in illiquid markets, i.e. markets where exchanging assets for cash may be difficult or uncertain Central Bank s answer: the risk of concentration of cash among few economic agents Setting a precise mathematical framework is not easy

3 Outline 2/23 The theoretical framework Portfolios and Marginal Supply-Demand Curves Liquidation value vs. usual mark-to-market value Liquidity policies and general mark-to-market values Coherent/convex risk measures and liquidity risk Some numerical examples

4 Portfolios 3/23 It is possible to trade in N 1 illiquid assets cash, which is by definition the only liquidity risk-free asset We define A portfolio is a vector p R N+1 p0 is the amount of cash p = (p1,..., p N ) is the assets position pn is the number of assets of type n

5 Liquid/Illiquid markets 4/23 Perfectly liquid market (S0(t) 1) Sn(t) is the unique price, at time t, for selling/buying a unit of asset n; this price does not depend on the size of the trade V (p, t) = p0 + N n=1 pnsn(t) is linear Illiquid markets (S0(t) 1) Sn(t) = Sn(t, x) will depend on the size x R (x > 0 is a sale) of the trade V (p, t) need not be linear anymore. A first idea is: V (p, t) = p0 + N n=1 pnsn(t, pn) But this is not the only sensible notion of value

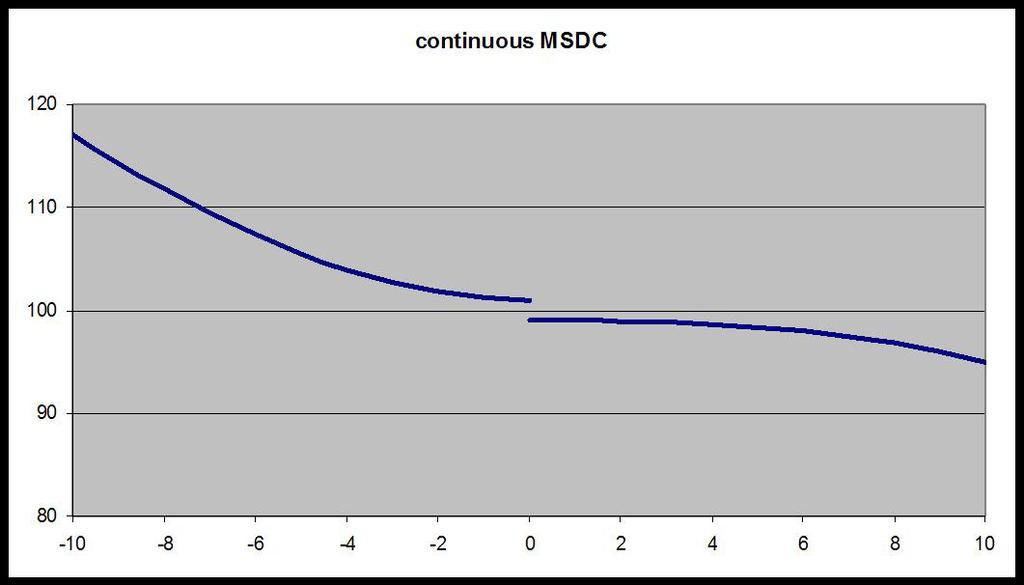

6 Marginal Supply-Demand Curves - 1 5/23 Some basic definitions A Marginal Supply-Demand Curve (msdc) is a decreasing function m : R (0, + ) m + = m(0+) and m = m(0 ) are the best bid (sell) and ask (buy) prices. Of course m + m. Let x be the size of the transaction (x > 0 sale, x < 0 purchase). The unit price is and the proceeds are S(x) = 1 x x 0 P (x) = xs(x) = m(y) dy > 0 x 0 m(y) dy 0 Same setting as in Cetin-Jarrow-Protter 2005, but our focus is on m.

7 a typical MSDC Bids Asks

8

9 Marginal Supply-Demand Curves - 2 6/23 We can also allow for (care is needed with the details): Assets which are not securities (e.g. swaps) and can display negative (marginal) prices: m : R R Securities with finite depth market: m(x) = + for x << 0 and/or m(x) = 0 for x >> 0 Swaps with finite depth market: m(x) = + for x << 0 and/or m(x) = for x >> 0

10 Two simple notions of value - 1 7/23 Given m = (m1,..., m N ) a vector of msdc. Let p R N+1 be a portfolio. The Liquidation Value of p is L(p) = p0 + N n=1 pnsn(pn) = p0 + N n=1 p n 0 m n(x) dx The Usual Mark-to-Market Value of p is U(p) = p0 + pnm + n + as if only the best bid and ask would matter. pn>0 pn<0 pnm n Note that U(p) L(p) for any p.

11 Two simple notions of value - 2 8/23 Some properties of L and U: concavity. both L and U are concave (but not linear) additivity. L is subadditive (L(p + q) L(p) + L(q)) whenever p and q are concordant (pnqn 0 for n 1); it is superadditive for discordant portfolios U is always superadditive, and it is additive for concordant portfolios scaling if λ 1 L(λp) λl(p) U(λp) = λu(p)

12 Two simple notions of value - 3 9/23 Liquidation Mark-to-Market Value (L): measure of the portfolio value as if we are forced to entirely liquidate it (so, liquidity risk is a big concern) Usual MtM Value (U): measure of the portfolio value as if we don t have to liquidate even a small part of it (so, liquidity risk is not a concern) Our aim is to introduce notions of value between the two extreme cases. Whether and what to liquidate is a need that may vary.

13 Acceptable portfolios /23 First we give a notion of acceptability for a portfolio: A liquidity policy is a convex and closed subset L R N+1 such that 1. p L implies p + a L for any a 0 (adding cash cannot worsen the liquidity properties of a portfolio) 2. (p0, p ) L implies (p0, 0 ) L (if a portfolio is acceptable, its cash component is acceptable as well) L collects the portfolios whose liquidity risk is not a concern and thus may be valued through U

14 Acceptable portfolios /23 Examples of liquidity policies: 1. L = R N+1 Every portfolio is acceptable: no need to liquidate (this will lead to U) 2. L = {p : p = 0 } Only pure-cash portfolios are acceptable: need to entirely liquidate p (this will lead to L) 3. L = {p : p0 a} (a 0 fixed) This is a typical requirement imposed by the ALM of an institution 4. other examples may be based on bounds on concentration...

15 Attainable portfolios 12/23 1. Start with a portfolio p, which need not be acceptable 2. Make it acceptable by liquidating the assets (sub)position q R N r = p q + L(0, q ) = (p0 + L(0, q ), p q ) L 3. Find the best way to do this, maximizing the Usual MtM value U(r) 4. Note that L is used in 2. and U in 3.: in 2. we care about liquidity risk, in 3. we don t as r L

16 A general definition of value 13/23 Having fixed a liquidity policy L we can define the associated MtM Value (sup = ) V L (p) = sup{u(r) : r = p q + L(0, q ) L, q R N } r R N+1 is optimal if V L (p) = U(r ). It is immediate to see that V L (r ) = U(r ) = V L (p) (there is no change in value passing from p to r ) The set over which U (concave) is maximized is convex. Thus The optimization program defining V L is always convex.

17 Some examples 14/23 1. If L = R N+1, then V L (p) = U(p) 2. If L = {p : p = 0 }, then V L (p) = L(p) 3. If L = {p : p0 a}, then V L (p) = sup{u(p q ) + L(0, q ) : L(0, q ) a p0, q R N+1 } which is not trivial (and non-linear)

18 Some properties 15/23 If L L, then V L V L. Thus, V L (p) U(p) L For any L, V L is concave and translational supervariant V L (p + a) V L (p) + a a 0

19 Computation of the value 16/23 As the problem defining V L is convex, many fast algorithms are available An analytical solution is sometime easy. Assume: {p : p0 a} mi continuous and strictly decreasing i Then if p0 a (p L) then r = p and V L (p) = U(p) if p0 < 0 then r i = m 1 i where λ is determined by L(r ) = p0 a. ( m i(0) 1 + λ )

20 Coherent risk measures /23 Coherent risk measures (CRM) ρ : L R (L space of r.v.) are characterized by (Artzner-Delbaen-Eber-Heath-98) 1. Translation invariance: ρ(x + c) = ρ(x) c c R; 2. Monotonicity: ρ(x) ρ(y ) whenever X Y 3. Positive homogeneity: ρ(λx) = λρ(x) λ 0 4. Subadditivity: ρ(x + Y ) ρ(x) + ρ(y ). Axioms 3 and 4 do not seem to take into account liquidity risk: if I double my portfolio, its risk should more than double in many cases. They were replaced (Follmer-Schied02, Frittelli-Rosazza02) by the weaker axiom of convexity.

21 Coherent risk measures /23 In our opinion, CRM are appropriate to deal with liquidity risk. The key point is that: If I double my portfolio... means p 2p, not X 2X The relation between p and its value X is not linear. We define risk measures defined directly on portfolios R = R(p) that are not necessarily positively homogeneous or subadditive.

22 Risk measures for portfolios 19/23 Given a liquidity policy L a probability space (Ω, F, P ) describing randomness up to T > 0 a coherent risk measure defined on some L L 0 (Ω, F, P ) the random future msdc: (mi(x, T )) for any i, where for any x, mi(x, T ) is a r.v. for any ω, x mi(x, T )(ω) is decreasing We compute V L (p) = V L (p, T )(ω) for any ω (it is a r.v.) and set R L (p) = ρ(v L (p))

23 Properties 20/23 Some properties (for general L and ρ) 1. R L is convex 2. R L is translational subvariant: R L (p + c) R L (p) c 3. R L is in general not homogeneous, nor subadditive 4. specific properties for R L may be derived from properties of V L (and coherency of ρ) 5. no monotonicity property can be introduced for R

24 A numerical example /23 Consider (T is fixed) mi(x) = αi exp{ βix}, where, Ai > 0 and βi 0 are r.v. There can be Market risk only: αi jointly lognormal, βi = 0 Market and non-random liquidity risk: αi jointly lognormal, βi > 0 non-random Market and independent random liquidity risk: (αi, βi)i jointly lognormal, with αi βi Market and correlated random liquidity risk: (αi, βi)i jointly lognormal, with αi and βi negatively correlated Market and correlated random liquidity risk with shocks: (αi, βi)i jointly lognormal, with αi and βi negatively correlated, βi = βi + εi

25 A numerical example /23 For a given portfolio p and L = {q : q0 a}, in any of the 5 previous situations we: set I = 10, αi and βi id. distr. for different i we perform 100k simulations of (mi(x))i for any outcome of the simulation we compute V L (p) we repeat for different inputs (p, a, mean, variances and correlations of αi and βi) A typical outcome is:

26

27 Conclusion 23/23 Messages: Liquidity risk arises when msdc are ignored Liquidity risk can be captured by a redefinition of the concept of value, which depends on a liquidity policy Coherent risk measures are perfectly adequate to deal with liquidity risk To do: study possible realistic (yet analytically tractable) stochastic models for a msdc (many studies of the bid-ask spread in the literature) portfolio optimization with liquidity risk

Portfolio Theory and Risk Management in the presence of Illiquidity

Portfolio Theory and Risk Management in the presence of Illiquidity A new formalism Carlo Acerbi Giacomo Scandolo, Università di Firenze Risk Europe - Frankfurt, Jun 5, 2009 1. Introduction 2. Assets and

Portfolio Theory and Risk Management in the presence of Illiquidity A new formalism Carlo Acerbi Giacomo Scandolo, Università di Firenze Risk Europe - Frankfurt, Jun 5, 2009 1. Introduction 2. Assets and

A generalized coherent risk measure: The firm s perspective

Finance Research Letters 2 (2005) 23 29 www.elsevier.com/locate/frl A generalized coherent risk measure: The firm s perspective Robert A. Jarrow a,b,, Amiyatosh K. Purnanandam c a Johnson Graduate School

Finance Research Letters 2 (2005) 23 29 www.elsevier.com/locate/frl A generalized coherent risk measure: The firm s perspective Robert A. Jarrow a,b,, Amiyatosh K. Purnanandam c a Johnson Graduate School

A class of coherent risk measures based on one-sided moments

A class of coherent risk measures based on one-sided moments T. Fischer Darmstadt University of Technology November 11, 2003 Abstract This brief paper explains how to obtain upper boundaries of shortfall

A class of coherent risk measures based on one-sided moments T. Fischer Darmstadt University of Technology November 11, 2003 Abstract This brief paper explains how to obtain upper boundaries of shortfall

SOLVENCY AND CAPITAL ALLOCATION

SOLVENCY AND CAPITAL ALLOCATION HARRY PANJER University of Waterloo JIA JING Tianjin University of Economics and Finance Abstract This paper discusses a new criterion for allocation of required capital.

SOLVENCY AND CAPITAL ALLOCATION HARRY PANJER University of Waterloo JIA JING Tianjin University of Economics and Finance Abstract This paper discusses a new criterion for allocation of required capital.

Dynamic Risk Management in Electricity Portfolio Optimization via Polyhedral Risk Functionals

Dynamic Risk Management in Electricity Portfolio Optimization via Polyhedral Risk Functionals A. Eichhorn and W. Römisch Humboldt-University Berlin, Department of Mathematics, Germany http://www.math.hu-berlin.de/~romisch

Dynamic Risk Management in Electricity Portfolio Optimization via Polyhedral Risk Functionals A. Eichhorn and W. Römisch Humboldt-University Berlin, Department of Mathematics, Germany http://www.math.hu-berlin.de/~romisch

Allocation of Risk Capital via Intra-Firm Trading

Allocation of Risk Capital via Intra-Firm Trading Sean Hilden Department of Mathematical Sciences Carnegie Mellon University December 5, 2005 References 1. Artzner, Delbaen, Eber, Heath: Coherent Measures

Allocation of Risk Capital via Intra-Firm Trading Sean Hilden Department of Mathematical Sciences Carnegie Mellon University December 5, 2005 References 1. Artzner, Delbaen, Eber, Heath: Coherent Measures

Optimal Portfolio Liquidation with Dynamic Coherent Risk

Optimal Portfolio Liquidation with Dynamic Coherent Risk Andrey Selivanov 1 Mikhail Urusov 2 1 Moscow State University and Gazprom Export 2 Ulm University Analysis, Stochastics, and Applications. A Conference

Optimal Portfolio Liquidation with Dynamic Coherent Risk Andrey Selivanov 1 Mikhail Urusov 2 1 Moscow State University and Gazprom Export 2 Ulm University Analysis, Stochastics, and Applications. A Conference

Capital Allocation Principles

Capital Allocation Principles Maochao Xu Department of Mathematics Illinois State University mxu2@ilstu.edu Capital Dhaene, et al., 2011, Journal of Risk and Insurance The level of the capital held by

Capital Allocation Principles Maochao Xu Department of Mathematics Illinois State University mxu2@ilstu.edu Capital Dhaene, et al., 2011, Journal of Risk and Insurance The level of the capital held by

Risk Measures and Optimal Risk Transfers

Risk Measures and Optimal Risk Transfers Université de Lyon 1, ISFA April 23 2014 Tlemcen - CIMPA Research School Motivations Study of optimal risk transfer structures, Natural question in Reinsurance.

Risk Measures and Optimal Risk Transfers Université de Lyon 1, ISFA April 23 2014 Tlemcen - CIMPA Research School Motivations Study of optimal risk transfer structures, Natural question in Reinsurance.

IEOR E4602: Quantitative Risk Management

IEOR E4602: Quantitative Risk Management Risk Measures Martin Haugh Department of Industrial Engineering and Operations Research Columbia University Email: martin.b.haugh@gmail.com Reference: Chapter 8

IEOR E4602: Quantitative Risk Management Risk Measures Martin Haugh Department of Industrial Engineering and Operations Research Columbia University Email: martin.b.haugh@gmail.com Reference: Chapter 8

Pricing and risk of financial products

and risk of financial products Prof. Dr. Christian Weiß Riga, 27.02.2018 Observations AAA bonds are typically regarded as risk-free investment. Only examples: Government bonds of Australia, Canada, Denmark,

and risk of financial products Prof. Dr. Christian Weiß Riga, 27.02.2018 Observations AAA bonds are typically regarded as risk-free investment. Only examples: Government bonds of Australia, Canada, Denmark,

Mathematics in Finance

Mathematics in Finance Steven E. Shreve Department of Mathematical Sciences Carnegie Mellon University Pittsburgh, PA 15213 USA shreve@andrew.cmu.edu A Talk in the Series Probability in Science and Industry

Mathematics in Finance Steven E. Shreve Department of Mathematical Sciences Carnegie Mellon University Pittsburgh, PA 15213 USA shreve@andrew.cmu.edu A Talk in the Series Probability in Science and Industry

MESURES DE RISQUE DYNAMIQUES DYNAMIC RISK MEASURES

from BMO martingales MESURES DE RISQUE DYNAMIQUES DYNAMIC RISK MEASURES CNRS - CMAP Ecole Polytechnique March 1, 2007 1/ 45 OUTLINE from BMO martingales 1 INTRODUCTION 2 DYNAMIC RISK MEASURES Time Consistency

from BMO martingales MESURES DE RISQUE DYNAMIQUES DYNAMIC RISK MEASURES CNRS - CMAP Ecole Polytechnique March 1, 2007 1/ 45 OUTLINE from BMO martingales 1 INTRODUCTION 2 DYNAMIC RISK MEASURES Time Consistency

Risk, Coherency and Cooperative Game

Risk, Coherency and Cooperative Game Haijun Li lih@math.wsu.edu Department of Mathematics Washington State University Tokyo, June 2015 Haijun Li Risk, Coherency and Cooperative Game Tokyo, June 2015 1

Risk, Coherency and Cooperative Game Haijun Li lih@math.wsu.edu Department of Mathematics Washington State University Tokyo, June 2015 Haijun Li Risk, Coherency and Cooperative Game Tokyo, June 2015 1

Optimizing S-shaped utility and risk management

Optimizing S-shaped utility and risk management Ineffectiveness of VaR and ES constraints John Armstrong (KCL), Damiano Brigo (Imperial) Quant Summit March 2018 Are ES constraints effective against rogue

Optimizing S-shaped utility and risk management Ineffectiveness of VaR and ES constraints John Armstrong (KCL), Damiano Brigo (Imperial) Quant Summit March 2018 Are ES constraints effective against rogue

Measures of Contribution for Portfolio Risk

X Workshop on Quantitative Finance Milan, January 29-30, 2009 Agenda Coherent Measures of Risk Spectral Measures of Risk Capital Allocation Euler Principle Application Risk Measurement Risk Attribution

X Workshop on Quantitative Finance Milan, January 29-30, 2009 Agenda Coherent Measures of Risk Spectral Measures of Risk Capital Allocation Euler Principle Application Risk Measurement Risk Attribution

Value at Risk. january used when assessing capital and solvency requirements and pricing risk transfer opportunities.

january 2014 AIRCURRENTS: Modeling Fundamentals: Evaluating Edited by Sara Gambrill Editor s Note: Senior Vice President David Lalonde and Risk Consultant Alissa Legenza describe various risk measures

january 2014 AIRCURRENTS: Modeling Fundamentals: Evaluating Edited by Sara Gambrill Editor s Note: Senior Vice President David Lalonde and Risk Consultant Alissa Legenza describe various risk measures

References. H. Föllmer, A. Schied, Stochastic Finance (3rd Ed.) de Gruyter 2011 (chapters 4 and 11)

de Gruyter 2011 (chapters 4 and 11)") General references on risk measures P. Embrechts, R. Frey, A. McNeil, Quantitative Risk Management, (2nd Ed.) Princeton University Press, 2015 H. Föllmer, A. Schied, Stochastic Finance (3rd Ed.) de Gruyter

General references on risk measures P. Embrechts, R. Frey, A. McNeil, Quantitative Risk Management, (2nd Ed.) Princeton University Press, 2015 H. Föllmer, A. Schied, Stochastic Finance (3rd Ed.) de Gruyter

Liquidity-Adjusted Risk Measures

Liquidity-Adjusted Risk Measures S. Weber, W. Anderson, A.-M. Hamm, T. Knispel, M. Liese, T. Salfeld January 18, 213 Abstract Liquidity risk is an important type of risk, especially during times of crises.

Liquidity-Adjusted Risk Measures S. Weber, W. Anderson, A.-M. Hamm, T. Knispel, M. Liese, T. Salfeld January 18, 213 Abstract Liquidity risk is an important type of risk, especially during times of crises.

Maturity as a factor for credit risk capital

Maturity as a factor for credit risk capital Michael Kalkbrener Λ, Ludger Overbeck y Deutsche Bank AG, Corporate & Investment Bank, Credit Risk Management 1 Introduction 1.1 Quantification of maturity

Maturity as a factor for credit risk capital Michael Kalkbrener Λ, Ludger Overbeck y Deutsche Bank AG, Corporate & Investment Bank, Credit Risk Management 1 Introduction 1.1 Quantification of maturity

Risk measures: Yet another search of a holy grail

Risk measures: Yet another search of a holy grail Dirk Tasche Financial Services Authority 1 dirk.tasche@gmx.net Mathematics of Financial Risk Management Isaac Newton Institute for Mathematical Sciences

Risk measures: Yet another search of a holy grail Dirk Tasche Financial Services Authority 1 dirk.tasche@gmx.net Mathematics of Financial Risk Management Isaac Newton Institute for Mathematical Sciences

Efficient Portfolio Valuation Incorporating Liquidity Risk

Efficient Portfolio Valuation Incorporating Liquidity Risk Yu Tian School of Mathematical Sciences, Monash University, VIC 3800, Melbourne E-mail: oscar.tian@monash.edu Ron Rood RBS - The Royal Bank of

Efficient Portfolio Valuation Incorporating Liquidity Risk Yu Tian School of Mathematical Sciences, Monash University, VIC 3800, Melbourne E-mail: oscar.tian@monash.edu Ron Rood RBS - The Royal Bank of

The Statistical Mechanics of Financial Markets

The Statistical Mechanics of Financial Markets Johannes Voit 2011 johannes.voit (at) ekit.com Overview 1. Why statistical physicists care about financial markets 2. The standard model - its achievements

The Statistical Mechanics of Financial Markets Johannes Voit 2011 johannes.voit (at) ekit.com Overview 1. Why statistical physicists care about financial markets 2. The standard model - its achievements

RISKMETRICS. Dr Philip Symes

1 RISKMETRICS Dr Philip Symes 1. Introduction 2 RiskMetrics is JP Morgan's risk management methodology. It was released in 1994 This was to standardise risk analysis in the industry. Scenarios are generated

1 RISKMETRICS Dr Philip Symes 1. Introduction 2 RiskMetrics is JP Morgan's risk management methodology. It was released in 1994 This was to standardise risk analysis in the industry. Scenarios are generated

Financial Risk Management and Governance Beyond VaR. Prof. Hugues Pirotte

Financial Risk Management and Governance Beyond VaR Prof. Hugues Pirotte 2 VaR Attempt to provide a single number that summarizes the total risk in a portfolio. What loss level is such that we are X% confident

Financial Risk Management and Governance Beyond VaR Prof. Hugues Pirotte 2 VaR Attempt to provide a single number that summarizes the total risk in a portfolio. What loss level is such that we are X% confident

Markets with convex transaction costs

1 Markets with convex transaction costs Irina Penner Humboldt University of Berlin Email: penner@math.hu-berlin.de Joint work with Teemu Pennanen Helsinki University of Technology Special Semester on Stochastics

1 Markets with convex transaction costs Irina Penner Humboldt University of Berlin Email: penner@math.hu-berlin.de Joint work with Teemu Pennanen Helsinki University of Technology Special Semester on Stochastics

To split or not to split: Capital allocation with convex risk measures

To split or not to split: Capital allocation with convex risk measures Andreas Tsanakas October 31, 27 Abstract Convex risk measures were introduced by Deprez and Gerber (1985). Here the problem of allocating

To split or not to split: Capital allocation with convex risk measures Andreas Tsanakas October 31, 27 Abstract Convex risk measures were introduced by Deprez and Gerber (1985). Here the problem of allocating

Capital Conservation and Risk Management

Capital Conservation and Risk Management Peter Carr, Dilip Madan, Juan Jose Vincente Alvarez Discussion by Fabio Trojani University of Lugano and Swiss Finance Institute Swissquote Conference EPFL, October

Capital Conservation and Risk Management Peter Carr, Dilip Madan, Juan Jose Vincente Alvarez Discussion by Fabio Trojani University of Lugano and Swiss Finance Institute Swissquote Conference EPFL, October

Why Bankers Should Learn Convex Analysis

Jim Zhu Western Michigan University Kalamazoo, Michigan, USA March 3, 2011 A tale of two financial economists Edward O. Thorp and Myron Scholes Influential works: Beat the Dealer(1962) and Beat the Market(1967)

Jim Zhu Western Michigan University Kalamazoo, Michigan, USA March 3, 2011 A tale of two financial economists Edward O. Thorp and Myron Scholes Influential works: Beat the Dealer(1962) and Beat the Market(1967)

Conditional Value-at-Risk: Theory and Applications

The School of Mathematics Conditional Value-at-Risk: Theory and Applications by Jakob Kisiala s1301096 Dissertation Presented for the Degree of MSc in Operational Research August 2015 Supervised by Dr

The School of Mathematics Conditional Value-at-Risk: Theory and Applications by Jakob Kisiala s1301096 Dissertation Presented for the Degree of MSc in Operational Research August 2015 Supervised by Dr

Risk Measurement: History, Trends and Challenges

Risk Measurement: History, Trends and Challenges Ruodu Wang (wang@uwaterloo.ca) Department of Statistics and Actuarial Science University of Waterloo, Canada PKU-Math International Workshop on Financial

Risk Measurement: History, Trends and Challenges Ruodu Wang (wang@uwaterloo.ca) Department of Statistics and Actuarial Science University of Waterloo, Canada PKU-Math International Workshop on Financial

Order book resilience, price manipulations, and the positive portfolio problem

Order book resilience, price manipulations, and the positive portfolio problem Alexander Schied Mannheim University PRisMa Workshop Vienna, September 28, 2009 Joint work with Aurélien Alfonsi and Alla

Order book resilience, price manipulations, and the positive portfolio problem Alexander Schied Mannheim University PRisMa Workshop Vienna, September 28, 2009 Joint work with Aurélien Alfonsi and Alla

On Risk Measures, Market Making, and Exponential Families

On Risk Measures, Market Making, and Exponential Families JACOB D. ABERNETHY University of Michigan and RAFAEL M. FRONGILLO Harvard University and SINDHU KUTTY University of Michigan In this note we elaborate

On Risk Measures, Market Making, and Exponential Families JACOB D. ABERNETHY University of Michigan and RAFAEL M. FRONGILLO Harvard University and SINDHU KUTTY University of Michigan In this note we elaborate

Capital requirements, market, credit, and liquidity risk

Capital requirements, market, credit, and liquidity risk Ernst Eberlein Department of Mathematical Stochastics and Center for Data Analysis and (FDM) University of Freiburg Joint work with Dilip Madan

Capital requirements, market, credit, and liquidity risk Ernst Eberlein Department of Mathematical Stochastics and Center for Data Analysis and (FDM) University of Freiburg Joint work with Dilip Madan

Indices of Acceptability as Performance Measures. Dilip B. Madan Robert H. Smith School of Business

Indices of Acceptability as Performance Measures Dilip B. Madan Robert H. Smith School of Business An Introduction to Conic Finance A Mini Course at Eurandom January 13 2011 Outline Operationally defining

Indices of Acceptability as Performance Measures Dilip B. Madan Robert H. Smith School of Business An Introduction to Conic Finance A Mini Course at Eurandom January 13 2011 Outline Operationally defining

Performance Measurement with Nonnormal. the Generalized Sharpe Ratio and Other "Good-Deal" Measures

Performance Measurement with Nonnormal Distributions: the Generalized Sharpe Ratio and Other "Good-Deal" Measures Stewart D Hodges forcsh@wbs.warwick.uk.ac University of Warwick ISMA Centre Research Seminar

Performance Measurement with Nonnormal Distributions: the Generalized Sharpe Ratio and Other "Good-Deal" Measures Stewart D Hodges forcsh@wbs.warwick.uk.ac University of Warwick ISMA Centre Research Seminar

Prudence, risk measures and the Optimized Certainty Equivalent: a note

Working Paper Series Department of Economics University of Verona Prudence, risk measures and the Optimized Certainty Equivalent: a note Louis Raymond Eeckhoudt, Elisa Pagani, Emanuela Rosazza Gianin WP

Working Paper Series Department of Economics University of Verona Prudence, risk measures and the Optimized Certainty Equivalent: a note Louis Raymond Eeckhoudt, Elisa Pagani, Emanuela Rosazza Gianin WP

Statistical Methods in Financial Risk Management

Statistical Methods in Financial Risk Management Lecture 1: Mapping Risks to Risk Factors Alexander J. McNeil Maxwell Institute of Mathematical Sciences Heriot-Watt University Edinburgh 2nd Workshop on

Statistical Methods in Financial Risk Management Lecture 1: Mapping Risks to Risk Factors Alexander J. McNeil Maxwell Institute of Mathematical Sciences Heriot-Watt University Edinburgh 2nd Workshop on

Strategies and Nash Equilibrium. A Whirlwind Tour of Game Theory

Strategies and Nash Equilibrium A Whirlwind Tour of Game Theory (Mostly from Fudenberg & Tirole) Players choose actions, receive rewards based on their own actions and those of the other players. Example,

Strategies and Nash Equilibrium A Whirlwind Tour of Game Theory (Mostly from Fudenberg & Tirole) Players choose actions, receive rewards based on their own actions and those of the other players. Example,

LECTURE 4: BID AND ASK HEDGING

LECTURE 4: BID AND ASK HEDGING 1. Introduction One of the consequences of incompleteness is that the price of derivatives is no longer unique. Various strategies for dealing with this exist, but a useful

LECTURE 4: BID AND ASK HEDGING 1. Introduction One of the consequences of incompleteness is that the price of derivatives is no longer unique. Various strategies for dealing with this exist, but a useful

COHERENT VAR-TYPE MEASURES. 1. VaR cannot be used for calculating diversification

COHERENT VAR-TYPE MEASURES GRAEME WEST 1. VaR cannot be used for calculating diversification If f is a risk measure, the diversification benefit of aggregating portfolio s A and B is defined to be (1)

COHERENT VAR-TYPE MEASURES GRAEME WEST 1. VaR cannot be used for calculating diversification If f is a risk measure, the diversification benefit of aggregating portfolio s A and B is defined to be (1)

University of California Berkeley

Working Paper # 2015-03 Diversification Preferences in the Theory of Choice Enrico G. De Giorgi, University of St. Gallen Ola Mahmoud, University of St. Gallen July 8, 2015 University of California Berkeley

Working Paper # 2015-03 Diversification Preferences in the Theory of Choice Enrico G. De Giorgi, University of St. Gallen Ola Mahmoud, University of St. Gallen July 8, 2015 University of California Berkeley

Optimal Hedge Ratio under a Subjective Re-weighting of the Original Measure

Optimal Hedge Ratio under a Subjective Re-weighting of the Original Measure MASSIMILIANO BARBI and SILVIA ROMAGNOLI THIS VERSION: February 8, 212 Abstract In this paper we propose a risk-minimizing optimal

Optimal Hedge Ratio under a Subjective Re-weighting of the Original Measure MASSIMILIANO BARBI and SILVIA ROMAGNOLI THIS VERSION: February 8, 212 Abstract In this paper we propose a risk-minimizing optimal

Characterization of the Optimum

ECO 317 Economics of Uncertainty Fall Term 2009 Notes for lectures 5. Portfolio Allocation with One Riskless, One Risky Asset Characterization of the Optimum Consider a risk-averse, expected-utility-maximizing

ECO 317 Economics of Uncertainty Fall Term 2009 Notes for lectures 5. Portfolio Allocation with One Riskless, One Risky Asset Characterization of the Optimum Consider a risk-averse, expected-utility-maximizing

Optimal investment and contingent claim valuation in illiquid markets

and contingent claim valuation in illiquid markets Teemu Pennanen King s College London Ari-Pekka Perkkiö Technische Universität Berlin 1 / 35 In most models of mathematical finance, there is at least

and contingent claim valuation in illiquid markets Teemu Pennanen King s College London Ari-Pekka Perkkiö Technische Universität Berlin 1 / 35 In most models of mathematical finance, there is at least

Conditional Value-at-Risk, Spectral Risk Measures and (Non-)Diversification in Portfolio Selection Problems A Comparison with Mean-Variance Analysis

Diversification in Portfolio Selection Problems A Comparison with Mean-Variance Analysis") Conditional Value-at-Risk, Spectral Risk Measures and (Non-)Diversification in Portfolio Selection Problems A Comparison with Mean-Variance Analysis Mario Brandtner Friedrich Schiller University of Jena,

Conditional Value-at-Risk, Spectral Risk Measures and (Non-)Diversification in Portfolio Selection Problems A Comparison with Mean-Variance Analysis Mario Brandtner Friedrich Schiller University of Jena,

Robustness issues on regulatory risk measures

Robustness issues on regulatory risk measures Ruodu Wang http://sas.uwaterloo.ca/~wang Department of Statistics and Actuarial Science University of Waterloo Robust Techniques in Quantitative Finance Oxford

Robustness issues on regulatory risk measures Ruodu Wang http://sas.uwaterloo.ca/~wang Department of Statistics and Actuarial Science University of Waterloo Robust Techniques in Quantitative Finance Oxford

Optimizing S-shaped utility and risk management: ineffectiveness of VaR and ES constraints

Optimizing S-shaped utility and risk management: ineffectiveness of VaR and ES constraints John Armstrong Dept. of Mathematics King s College London Joint work with Damiano Brigo Dept. of Mathematics,

Optimizing S-shaped utility and risk management: ineffectiveness of VaR and ES constraints John Armstrong Dept. of Mathematics King s College London Joint work with Damiano Brigo Dept. of Mathematics,

arxiv:math/ v1 [math.pr] 2 May 2006

![arxiv:math/ v1 [math.pr] 2 May 2006](/thumbs/87/96374460.jpg "arxiv:math/ v1 [math.pr] 2 May 2006") CAPM, REWARDS, AND EMPIRICAL ASSET PRICING WITH COHERENT RISK Alexander S. Cherny, Dilip B. Madan arxiv:math/0605065v [math.pr] 2 May 2006 Moscow State University Faculty of Mechanics and Mathematics Department

CAPM, REWARDS, AND EMPIRICAL ASSET PRICING WITH COHERENT RISK Alexander S. Cherny, Dilip B. Madan arxiv:math/0605065v [math.pr] 2 May 2006 Moscow State University Faculty of Mechanics and Mathematics Department

Risk aversion in multi-stage stochastic programming: a modeling and algorithmic perspective

Risk aversion in multi-stage stochastic programming: a modeling and algorithmic perspective Tito Homem-de-Mello School of Business Universidad Adolfo Ibañez, Santiago, Chile Joint work with Bernardo Pagnoncelli

Risk aversion in multi-stage stochastic programming: a modeling and algorithmic perspective Tito Homem-de-Mello School of Business Universidad Adolfo Ibañez, Santiago, Chile Joint work with Bernardo Pagnoncelli

Risk measure pricing and hedging in incomplete markets

Risk measure pricing and hedging in incomplete markets Mingxin Xu Department of Mathematics and Statistics, University of North Carolina, 9201 University City Boulevard, Charlotte, NC 28223, USA (e-mail:

Risk measure pricing and hedging in incomplete markets Mingxin Xu Department of Mathematics and Statistics, University of North Carolina, 9201 University City Boulevard, Charlotte, NC 28223, USA (e-mail:

KIER DISCUSSION PAPER SERIES

KIER DISCUSSION PAPER SERIES KYOTO INSTITUTE OF ECONOMIC RESEARCH Discussion Paper No.981 Optimal Initial Capital Induced by the Optimized Certainty Equivalent Takuji Arai, Takao Asano, and Katsumasa Nishide

KIER DISCUSSION PAPER SERIES KYOTO INSTITUTE OF ECONOMIC RESEARCH Discussion Paper No.981 Optimal Initial Capital Induced by the Optimized Certainty Equivalent Takuji Arai, Takao Asano, and Katsumasa Nishide

Risk-Averse Decision Making and Control

Marek Petrik University of New Hampshire Mohammad Ghavamzadeh Adobe Research February 4, 2017 Introduction to Risk Averse Modeling Outline Introduction to Risk Averse Modeling (Average) Value at Risk Coherent

Marek Petrik University of New Hampshire Mohammad Ghavamzadeh Adobe Research February 4, 2017 Introduction to Risk Averse Modeling Outline Introduction to Risk Averse Modeling (Average) Value at Risk Coherent

Pricing & Risk Management of Synthetic CDOs

Pricing & Risk Management of Synthetic CDOs Jaffar Hussain* j.hussain@alahli.com September 2006 Abstract The purpose of this paper is to analyze the risks of synthetic CDO structures and their sensitivity

Pricing & Risk Management of Synthetic CDOs Jaffar Hussain* j.hussain@alahli.com September 2006 Abstract The purpose of this paper is to analyze the risks of synthetic CDO structures and their sensitivity

Financial Risk Management

Financial Risk Management Professor: Thierry Roncalli Evry University Assistant: Enareta Kurtbegu Evry University Tutorial exercices #4 1 Correlation and copulas 1. The bivariate Gaussian copula is given

Financial Risk Management Professor: Thierry Roncalli Evry University Assistant: Enareta Kurtbegu Evry University Tutorial exercices #4 1 Correlation and copulas 1. The bivariate Gaussian copula is given

3.4 Copula approach for modeling default dependency. Two aspects of modeling the default times of several obligors

3.4 Copula approach for modeling default dependency Two aspects of modeling the default times of several obligors 1. Default dynamics of a single obligor. 2. Model the dependence structure of defaults

3.4 Copula approach for modeling default dependency Two aspects of modeling the default times of several obligors 1. Default dynamics of a single obligor. 2. Model the dependence structure of defaults

Portfolio selection with multiple risk measures

Portfolio selection with multiple risk measures Garud Iyengar Columbia University Industrial Engineering and Operations Research Joint work with Carlos Abad Outline Portfolio selection and risk measures

Portfolio selection with multiple risk measures Garud Iyengar Columbia University Industrial Engineering and Operations Research Joint work with Carlos Abad Outline Portfolio selection and risk measures

Market Risk: FROM VALUE AT RISK TO STRESS TESTING. Agenda. Agenda (Cont.) Traditional Measures of Market Risk

Traditional Measures of Market Risk") Market Risk: FROM VALUE AT RISK TO STRESS TESTING Agenda The Notional Amount Approach Price Sensitivity Measure for Derivatives Weakness of the Greek Measure Define Value at Risk 1 Day to VaR to 10 Day

Market Risk: FROM VALUE AT RISK TO STRESS TESTING Agenda The Notional Amount Approach Price Sensitivity Measure for Derivatives Weakness of the Greek Measure Define Value at Risk 1 Day to VaR to 10 Day

Master s in Financial Engineering Foundations of Buy-Side Finance: Quantitative Risk and Portfolio Management. > Teaching > Courses

Master s in Financial Engineering Foundations of Buy-Side Finance: Quantitative Risk and Portfolio Management www.symmys.com > Teaching > Courses Spring 2008, Monday 7:10 pm 9:30 pm, Room 303 Attilio Meucci

Master s in Financial Engineering Foundations of Buy-Side Finance: Quantitative Risk and Portfolio Management www.symmys.com > Teaching > Courses Spring 2008, Monday 7:10 pm 9:30 pm, Room 303 Attilio Meucci

Model Risk: A Conceptual Framework for Risk Measurement and Hedging

Model Risk: A Conceptual Framework for Risk Measurement and Hedging Nicole Branger Christian Schlag This version: January 15, 24 Both authors are from the Faculty of Economics and Business Administration,

Model Risk: A Conceptual Framework for Risk Measurement and Hedging Nicole Branger Christian Schlag This version: January 15, 24 Both authors are from the Faculty of Economics and Business Administration,

Calculating VaR. There are several approaches for calculating the Value at Risk figure. The most popular are the

VaR Pro and Contra Pro: Easy to calculate and to understand. It is a common language of communication within the organizations as well as outside (e.g. regulators, auditors, shareholders). It is not really

VaR Pro and Contra Pro: Easy to calculate and to understand. It is a common language of communication within the organizations as well as outside (e.g. regulators, auditors, shareholders). It is not really

Financial Risk Measurement/Management

550.446 Financial Risk Measurement/Management Week of September 23, 2013 Interest Rate Risk & Value at Risk (VaR) 3.1 Where we are Last week: Introduction continued; Insurance company and Investment company

550.446 Financial Risk Measurement/Management Week of September 23, 2013 Interest Rate Risk & Value at Risk (VaR) 3.1 Where we are Last week: Introduction continued; Insurance company and Investment company

THE TEMPORAL DIMENSION OF RISK

THE TEMPORAL DIMENSION OF RISK OLA MAHMOUD 1 Abstract. Multi-period measures of risk account for the path that the value of an investment portfolio takes. In the context of probabilistic risk measures,

THE TEMPORAL DIMENSION OF RISK OLA MAHMOUD 1 Abstract. Multi-period measures of risk account for the path that the value of an investment portfolio takes. In the context of probabilistic risk measures,

Risk Measurement in Credit Portfolio Models

9 th DGVFM Scientific Day 30 April 2010 1 Risk Measurement in Credit Portfolio Models 9 th DGVFM Scientific Day 30 April 2010 9 th DGVFM Scientific Day 30 April 2010 2 Quantitative Risk Management Profit

9 th DGVFM Scientific Day 30 April 2010 1 Risk Measurement in Credit Portfolio Models 9 th DGVFM Scientific Day 30 April 2010 9 th DGVFM Scientific Day 30 April 2010 2 Quantitative Risk Management Profit

ERM (Part 1) Measurement and Modeling of Depedencies in Economic Capital. PAK Study Manual

Measurement and Modeling of Depedencies in Economic Capital. PAK Study Manual") ERM-101-12 (Part 1) Measurement and Modeling of Depedencies in Economic Capital Related Learning Objectives 2b) Evaluate how risks are correlated, and give examples of risks that are positively correlated

ERM-101-12 (Part 1) Measurement and Modeling of Depedencies in Economic Capital Related Learning Objectives 2b) Evaluate how risks are correlated, and give examples of risks that are positively correlated

Risk Measures for Derivative Securities: From a Yin-Yang Approach to Aerospace Space

Risk Measures for Derivative Securities: From a Yin-Yang Approach to Aerospace Space Tak Kuen Siu Department of Applied Finance and Actuarial Studies, Faculty of Business and Economics, Macquarie University,

Risk Measures for Derivative Securities: From a Yin-Yang Approach to Aerospace Space Tak Kuen Siu Department of Applied Finance and Actuarial Studies, Faculty of Business and Economics, Macquarie University,

Sensible and Efficient Capital Allocation for Credit Portfolios

Sensible and Efficient Capital Allocation for Credit Portfolios Michael Kalkbrener, Hans Lotter, Ludger Overbeck Deutsche Bank AG, Corporate & Investment Bank, Credit Risk Management Abstract The expected

Sensible and Efficient Capital Allocation for Credit Portfolios Michael Kalkbrener, Hans Lotter, Ludger Overbeck Deutsche Bank AG, Corporate & Investment Bank, Credit Risk Management Abstract The expected

based on two joint papers with Sara Biagini Scuola Normale Superiore di Pisa, Università degli Studi di Perugia

Marco Frittelli Università degli Studi di Firenze Winter School on Mathematical Finance January 24, 2005 Lunteren. On Utility Maximization in Incomplete Markets. based on two joint papers with Sara Biagini

Marco Frittelli Università degli Studi di Firenze Winter School on Mathematical Finance January 24, 2005 Lunteren. On Utility Maximization in Incomplete Markets. based on two joint papers with Sara Biagini

Model risk adjusted risk forecasting

Model risk adjusted risk forecasting Fernanda Maria Müller a,, Marcelo Brutti Righi a a Business School, Federal University of Rio Grande do Sul, Washington Luiz, 855, Porto Alegre, Brazil, zip 90010-460

Model risk adjusted risk forecasting Fernanda Maria Müller a,, Marcelo Brutti Righi a a Business School, Federal University of Rio Grande do Sul, Washington Luiz, 855, Porto Alegre, Brazil, zip 90010-460

MFM Practitioner Module: Quantitative Risk Management. John Dodson. September 6, 2017

MFM Practitioner Module: Quantitative September 6, 2017 Course Fall sequence modules quantitative risk management Gary Hatfield fixed income securities Jason Vinar mortgage securities introductions Chong

MFM Practitioner Module: Quantitative September 6, 2017 Course Fall sequence modules quantitative risk management Gary Hatfield fixed income securities Jason Vinar mortgage securities introductions Chong

Portfolio Management and Optimal Execution via Convex Optimization

Portfolio Management and Optimal Execution via Convex Optimization Enzo Busseti Stanford University April 9th, 2018 Problems portfolio management choose trades with optimization minimize risk, maximize

Portfolio Management and Optimal Execution via Convex Optimization Enzo Busseti Stanford University April 9th, 2018 Problems portfolio management choose trades with optimization minimize risk, maximize

Tangent Lévy Models. Sergey Nadtochiy (joint work with René Carmona) Oxford-Man Institute of Quantitative Finance University of Oxford.

Oxford-Man Institute of Quantitative Finance University of Oxford.") Tangent Lévy Models Sergey Nadtochiy (joint work with René Carmona) Oxford-Man Institute of Quantitative Finance University of Oxford June 24, 2010 6th World Congress of the Bachelier Finance Society Sergey

Tangent Lévy Models Sergey Nadtochiy (joint work with René Carmona) Oxford-Man Institute of Quantitative Finance University of Oxford June 24, 2010 6th World Congress of the Bachelier Finance Society Sergey

Introduction to Financial Mathematics

Department of Mathematics University of Michigan November 7, 2008 My Information E-mail address: marymorj (at) umich.edu Financial work experience includes 2 years in public finance investment banking

Department of Mathematics University of Michigan November 7, 2008 My Information E-mail address: marymorj (at) umich.edu Financial work experience includes 2 years in public finance investment banking

A Robust Option Pricing Problem

IMA 2003 Workshop, March 12-19, 2003 A Robust Option Pricing Problem Laurent El Ghaoui Department of EECS, UC Berkeley 3 Robust optimization standard form: min x sup u U f 0 (x, u) : u U, f i (x, u) 0,

IMA 2003 Workshop, March 12-19, 2003 A Robust Option Pricing Problem Laurent El Ghaoui Department of EECS, UC Berkeley 3 Robust optimization standard form: min x sup u U f 0 (x, u) : u U, f i (x, u) 0,

ON A CONVEX MEASURE OF DRAWDOWN RISK

ON A CONVEX MEASURE OF DRAWDOWN RISK LISA R. GOLDBERG 1 AND OLA MAHMOUD 2 Abstract. Maximum drawdown, the largest cumulative loss from peak to trough, is one of the most widely used indicators of risk

ON A CONVEX MEASURE OF DRAWDOWN RISK LISA R. GOLDBERG 1 AND OLA MAHMOUD 2 Abstract. Maximum drawdown, the largest cumulative loss from peak to trough, is one of the most widely used indicators of risk

University of California Berkeley

Working Paper # 2015-04 The Temporal Dimension of Drawdown Ola Mahmoud, University of St. Gallen July 13, 2015 University of California Berkeley THE TEMPORA DIMENSION OF DRAWDOWN OA MAHMOUD 1 Abstract.

Working Paper # 2015-04 The Temporal Dimension of Drawdown Ola Mahmoud, University of St. Gallen July 13, 2015 University of California Berkeley THE TEMPORA DIMENSION OF DRAWDOWN OA MAHMOUD 1 Abstract.

Can a coherent risk measure be too subadditive?

Can a coherent risk measure be too subadditive? J. Dhaene,,, R.J.A. Laeven,, S. Vanduffel, G. Darkiewicz, M.J. Goovaerts, Catholic University of Leuven, Dept. of Applied Economics, Naamsestraat 69, B-3000

Can a coherent risk measure be too subadditive? J. Dhaene,,, R.J.A. Laeven,, S. Vanduffel, G. Darkiewicz, M.J. Goovaerts, Catholic University of Leuven, Dept. of Applied Economics, Naamsestraat 69, B-3000

2 Control variates. λe λti λe e λt i where R(t) = t Y 1 Y N(t) is the time from the last event to t. L t = e λr(t) e e λt(t) Exercises

= t Y 1 Y N(t) is the time from the last event to t. L t = e λr(t) e e λt(t) Exercises") 96 ChapterVI. Variance Reduction Methods stochastic volatility ISExSoren5.9 Example.5 (compound poisson processes) Let X(t) = Y + + Y N(t) where {N(t)},Y, Y,... are independent, {N(t)} is Poisson(λ) with

96 ChapterVI. Variance Reduction Methods stochastic volatility ISExSoren5.9 Example.5 (compound poisson processes) Let X(t) = Y + + Y N(t) where {N(t)},Y, Y,... are independent, {N(t)} is Poisson(λ) with

Lecture 6: Risk and uncertainty

Lecture 6: Risk and uncertainty Prof. Dr. Svetlozar Rachev Institute for Statistics and Mathematical Economics University of Karlsruhe Portfolio and Asset Liability Management Summer Semester 2008 Prof.

Lecture 6: Risk and uncertainty Prof. Dr. Svetlozar Rachev Institute for Statistics and Mathematical Economics University of Karlsruhe Portfolio and Asset Liability Management Summer Semester 2008 Prof.

Short Course Theory and Practice of Risk Measurement

Short Course Theory and Practice of Risk Measurement Part 4 Selected Topics and Recent Developments on Risk Measures Ruodu Wang Department of Statistics and Actuarial Science University of Waterloo, Canada

Short Course Theory and Practice of Risk Measurement Part 4 Selected Topics and Recent Developments on Risk Measures Ruodu Wang Department of Statistics and Actuarial Science University of Waterloo, Canada

Problem 1: Random variables, common distributions and the monopoly price

Problem 1: Random variables, common distributions and the monopoly price In this problem, we will revise some basic concepts in probability, and use these to better understand the monopoly price (alternatively

Problem 1: Random variables, common distributions and the monopoly price In this problem, we will revise some basic concepts in probability, and use these to better understand the monopoly price (alternatively

Alternative Risk Measures for Alternative Investments

Alternative Risk Measures for Alternative Investments A. Chabaane BNP Paribas ACA Consulting Y. Malevergne ISFA Actuarial School Lyon JP. Laurent ISFA Actuarial School Lyon BNP Paribas F. Turpin BNP Paribas

Alternative Risk Measures for Alternative Investments A. Chabaane BNP Paribas ACA Consulting Y. Malevergne ISFA Actuarial School Lyon JP. Laurent ISFA Actuarial School Lyon BNP Paribas F. Turpin BNP Paribas

arxiv:cond-mat/ v1 [cond-mat.stat-mech] 16 Feb 2001

![arxiv:cond-mat/ v1 [cond-mat.stat-mech] 16 Feb 2001](/thumbs/79/80109428.jpg "arxiv:cond-mat/ v1 [cond-mat.stat-mech] 16 Feb 2001") arxiv:cond-mat/0102304v1 [cond-mat.stat-mech] 16 Feb 2001 Expected Shortfall as a Tool for Financial Risk Management Carlo Acerbi, Claudio Nordio and Carlo Sirtori Abaxbank, Corso Monforte 34, 20122 Milano

arxiv:cond-mat/0102304v1 [cond-mat.stat-mech] 16 Feb 2001 Expected Shortfall as a Tool for Financial Risk Management Carlo Acerbi, Claudio Nordio and Carlo Sirtori Abaxbank, Corso Monforte 34, 20122 Milano

CHOICE THEORY, UTILITY FUNCTIONS AND RISK AVERSION

CHOICE THEORY, UTILITY FUNCTIONS AND RISK AVERSION Szabolcs Sebestyén szabolcs.sebestyen@iscte.pt Master in Finance INVESTMENTS Sebestyén (ISCTE-IUL) Choice Theory Investments 1 / 65 Outline 1 An Introduction

CHOICE THEORY, UTILITY FUNCTIONS AND RISK AVERSION Szabolcs Sebestyén szabolcs.sebestyen@iscte.pt Master in Finance INVESTMENTS Sebestyén (ISCTE-IUL) Choice Theory Investments 1 / 65 Outline 1 An Introduction

Value at Risk, Expected Shortfall, and Marginal Risk Contribution, in: Szego, G. (ed.): Risk Measures for the 21st Century, p , Wiley 2004.

: Risk Measures for the 21st Century, p , Wiley 2004.") Rau-Bredow, Hans: Value at Risk, Expected Shortfall, and Marginal Risk Contribution, in: Szego, G. (ed.): Risk Measures for the 21st Century, p. 61-68, Wiley 2004. Copyright geschützt 5 Value-at-Risk,

Rau-Bredow, Hans: Value at Risk, Expected Shortfall, and Marginal Risk Contribution, in: Szego, G. (ed.): Risk Measures for the 21st Century, p. 61-68, Wiley 2004. Copyright geschützt 5 Value-at-Risk,

Minimization of the Total Required Capital by Reinsurance

Minimization of the Total Required Capital by Reinsurance Yingjie Zhang CNA Insurance Companies 333 S. Wabash Ave., 30S, Chicago, IL 60604, USA Email: yingjie.zhang@cna.com Abstract Reinsurance reduces

Minimization of the Total Required Capital by Reinsurance Yingjie Zhang CNA Insurance Companies 333 S. Wabash Ave., 30S, Chicago, IL 60604, USA Email: yingjie.zhang@cna.com Abstract Reinsurance reduces

Illiquidity Spirals in Coupled Over-the-Counter Markets 1

Illiquidity Spirals in Coupled Over-the-Counter Markets 1 Christoph Aymanns University of St. Gallen Co-Pierre Georg Bundesbank and University of Cape Town Benjamin Golub Harvard May 30, 2018 1 The views

Illiquidity Spirals in Coupled Over-the-Counter Markets 1 Christoph Aymanns University of St. Gallen Co-Pierre Georg Bundesbank and University of Cape Town Benjamin Golub Harvard May 30, 2018 1 The views

Coherent allocation of risk capital

Coherent allocation of risk capital Michel Denault École des HEC (Montréal) January 21 Original version:september 1999 Abstract The allocation problem stems from the diversification effect observed in

Coherent allocation of risk capital Michel Denault École des HEC (Montréal) January 21 Original version:september 1999 Abstract The allocation problem stems from the diversification effect observed in

Liquidity-Sensitive Automated Market Makers via Homogeneous Risk Measures

Liquidity-Sensitive Automated Market Makers via Homogeneous Risk Measures Abraham Othman and Tuomas Sandholm Computer Science Department, Carnegie Mellon University {aothman,sandholm}@cs.cmu.edu Abstract.

Liquidity-Sensitive Automated Market Makers via Homogeneous Risk Measures Abraham Othman and Tuomas Sandholm Computer Science Department, Carnegie Mellon University {aothman,sandholm}@cs.cmu.edu Abstract.

Put Call Parity and Market Frictions

Put Call Parity and Market Frictions S. Cerreia-Vioglio, F. Maccheroni, M. Marinacci Università Bocconi and IGIER August 2014 Abstract We extend the Fundamental Theorem of Finance and the Pricing Rule

Put Call Parity and Market Frictions S. Cerreia-Vioglio, F. Maccheroni, M. Marinacci Università Bocconi and IGIER August 2014 Abstract We extend the Fundamental Theorem of Finance and the Pricing Rule

Risk based capital allocation

Proceedings of FIKUSZ 10 Symposium for Young Researchers, 2010, 17-26 The Author(s). Conference Proceedings compilation Obuda University Keleti Faculty of Business and Management 2010. Published by Óbuda

Proceedings of FIKUSZ 10 Symposium for Young Researchers, 2010, 17-26 The Author(s). Conference Proceedings compilation Obuda University Keleti Faculty of Business and Management 2010. Published by Óbuda

Chapter 2 Uncertainty Analysis and Sampling Techniques

Chapter 2 Uncertainty Analysis and Sampling Techniques The probabilistic or stochastic modeling (Fig. 2.) iterative loop in the stochastic optimization procedure (Fig..4 in Chap. ) involves:. Specifying

Chapter 2 Uncertainty Analysis and Sampling Techniques The probabilistic or stochastic modeling (Fig. 2.) iterative loop in the stochastic optimization procedure (Fig..4 in Chap. ) involves:. Specifying

Lecture 1 of 4-part series. Spring School on Risk Management, Insurance and Finance European University at St. Petersburg, Russia.

Principles and Lecture 1 of 4-part series Spring School on Risk, Insurance and Finance European University at St. Petersburg, Russia 2-4 April 2012 s University of Connecticut, USA page 1 s Outline 1 2

Principles and Lecture 1 of 4-part series Spring School on Risk, Insurance and Finance European University at St. Petersburg, Russia 2-4 April 2012 s University of Connecticut, USA page 1 s Outline 1 2

Building Consistent Risk Measures into Stochastic Optimization Models

Building Consistent Risk Measures into Stochastic Optimization Models John R. Birge The University of Chicago Graduate School of Business www.chicagogsb.edu/fac/john.birge JRBirge Fuqua School, Duke University

Building Consistent Risk Measures into Stochastic Optimization Models John R. Birge The University of Chicago Graduate School of Business www.chicagogsb.edu/fac/john.birge JRBirge Fuqua School, Duke University

Expected utility theory; Expected Utility Theory; risk aversion and utility functions

; Expected Utility Theory; risk aversion and utility functions Prof. Massimo Guidolin Portfolio Management Spring 2016 Outline and objectives Utility functions The expected utility theorem and the axioms

; Expected Utility Theory; risk aversion and utility functions Prof. Massimo Guidolin Portfolio Management Spring 2016 Outline and objectives Utility functions The expected utility theorem and the axioms

Arbitrage Theory without a Reference Probability: challenges of the model independent approach

Arbitrage Theory without a Reference Probability: challenges of the model independent approach Matteo Burzoni Marco Frittelli Marco Maggis June 30, 2015 Abstract In a model independent discrete time financial

Arbitrage Theory without a Reference Probability: challenges of the model independent approach Matteo Burzoni Marco Frittelli Marco Maggis June 30, 2015 Abstract In a model independent discrete time financial

Financial Mathematics III Theory summary

Financial Mathematics III Theory summary Table of Contents Lecture 1... 7 1. State the objective of modern portfolio theory... 7 2. Define the return of an asset... 7 3. How is expected return defined?...

Financial Mathematics III Theory summary Table of Contents Lecture 1... 7 1. State the objective of modern portfolio theory... 7 2. Define the return of an asset... 7 3. How is expected return defined?...

This version: December 3, 2009

Rethinking risk capital allocation in a RORAC framework Arne Buch a, Gregor Dorfleitner b,*, Maximilian Wimmer b a d-fine GmbH, Opernplatz 2, 60313 Frankfurt, Germany b Department of Finance, University

Rethinking risk capital allocation in a RORAC framework Arne Buch a, Gregor Dorfleitner b,*, Maximilian Wimmer b a d-fine GmbH, Opernplatz 2, 60313 Frankfurt, Germany b Department of Finance, University

Coherent liquidity risk measures

Coherent liquidity risk measures Erwan KOCH ISFA, Université Lyon 1 and CREST-ENSAE, Paris 6th Financial Risks INTERNATIONAL FORUM Erwan KOCH (ISFA and CREST) Coherent liquidity risk measures March 25,

Coherent liquidity risk measures Erwan KOCH ISFA, Université Lyon 1 and CREST-ENSAE, Paris 6th Financial Risks INTERNATIONAL FORUM Erwan KOCH (ISFA and CREST) Coherent liquidity risk measures March 25,

Lecture 10: Performance measures

Lecture 10: Performance measures Prof. Dr. Svetlozar Rachev Institute for Statistics and Mathematical Economics University of Karlsruhe Portfolio and Asset Liability Management Summer Semester 2008 Prof.

Lecture 10: Performance measures Prof. Dr. Svetlozar Rachev Institute for Statistics and Mathematical Economics University of Karlsruhe Portfolio and Asset Liability Management Summer Semester 2008 Prof.