Marketmaking Middlemen

|

|

|

- Cory Tyler

- 5 years ago

- Views:

Transcription

1 Marketmaking Middlemen Pieter Gautier Bo Hu Makoto Watanabe VU University Amsterdam, Tinbergen Institute November, 2016

2 Objective Intermediation modes: Middlemen/Merchants: (buying/selling, inventory holdings) Market makers: (transaction/participation fees, platform) Explore a (simple) framework to study the determinant of intermediated market structure.

3

4

5 Examples Amazon: originally a pure middleman, but started platform business. NYSE/ NASDAQ: specialists The Trump Organization/ Trump International Realty

6 Key ingredients (1): search markets Decentralized market: random search, bilateral trade Intermediated (Centralized) market: directed search Market-maker: provide a market place with publicly announced fees Middleman: advanced inventory management technology for supply guarantee/proximity

7 Key ingredients (2): search technologies Single-market search: traditional retail markets (supermarkets, brick and mortar shops) High search costs, High transportation costs, One-trip shopping Multi-market search: online shopping, durable goods Advanced information/search technologies, Long search period

8 Buyers Decentralized Market Intermediated Market Market-maker: Trading slots for sellers Middleman: mass k inventory Sellers Wholesale Market

9 Setup Consider a one-period economy (no trade generates zero value). - Agents: B buyers and S sellers; a monopolistic intermediary; all risk neutral - Homogeneous goods: unit demand/ constant marginal production cost; common consumption value

10 Single-market search

11 Timing of events: 1. The intermediary announces whether to open platform S {S, 0}, a set of fees F = {f i }, i = b, s, and a stock K [0, B]; 2. Buyers and sellers decide simultaneously which market to participate in, C market or D market; 3. Trade occurs in each active market (yet to be specified shortly below).

12 D market: Meeting probability λ i, i = b, s (with λ b B = λ s S). Surplus share: Buyers s share β; Sellers share 1 β.

13 C market: (directed search market) 1. Each seller, or a middleman, announces a price, p s, p m ; 2. Observing those prices and capacities 1 or K, buyers decide which supplier to trade with, subject to coordination frictions; 3. Trade occurs at the announced price.

14 C market K ௦ ௦ S B

15 - Meeting process: A random number of buyers arrive at individual sellers/middleman. Sellers: η s = 1 e xs x s Middleman: η m = min{ K x m, 1} where Sx s + x m = B

16 - Determination of allocation, x m, x s : x m = where B if V m (B) V s (0) (0, B) if V m (x m ) = V s (x s ) 0 if V m (0) V s ( B S ), V s (x s ) = η s (x s )(1 p s f b ) V m (x m ) = η m (x m )(1 p m ).

17 Definition Pure middleman mode: x m = B and x s = 0 Pure market-maker mode: x m = 0 and x s = B S Market-making middleman mode: 0 < x m < B and 0 < x s < B S

18 - The participation constraint of buyers in the C market: V m (x m ) = η m (1 p m ) λ b β. Proposition 1 (Pure Middleman) Given single-market search technologies, the intermediary will act as a pure middleman with x m = K = B; p m = 1 λ b β; Π = B(1 λ b β).

19 Single market search: Pure Middleman mode xm =B=K* xs=0 S B

20 Two-sidedness Participation decision of one side depends on their beliefs on what the other side do Pessimistic belief: sellers believe zero buyers in C unless V B λ b β Divide and Conquer strategy (if K is not observable). subsidize buyers g b λ b β, tax sellers V s g s subsidize sellers g s λ s (1 β), tax buyers V b g b

21 Multi-market search

22 Buyers Decentralized Market Intermediated Market Market-maker: Trading slots for sellers Middleman: mass k inventory Sellers Wholesale Market

23 Outside option 1. Active platform x s > 0: 1 p s f b λ b (1 x s η s )β (1) p s f s λ s ξ(x m, K)(1 β) (2) 2. Active middleman x m > 0: 1 p m λ b (1 x s η s )β. (3)

24 Pure middleman: Given x m = B and x s = 0 (by announcing S = 0), the intermediary stocks K = B; sets p m = 1 λ b β (with the binding IC (3)); makes the profits Π(B) = B(1 λ b β).

25 Active platform (standard procedure to pin down an equilibrium price) - Suppose a seller sets her price to p p s and it attracts x buyers. - Buyers directed search: and V s (x) = η s (x)(1 p f b ) + (1 η s (x))λ b e xs β. give x = x(p V s ). V s (x) = V s,

26 - Profit maximization: p s (V s ) = argmax p {(1 e x(p V s) )(p f s ) + e x(p V s) λ s ξ(x m, K)(1 β)} - Equilibrium price: p s f s = ϕ s (x s )(v(x m, K) f) + λ s ξ(x m, K)(1 β), where ϕ s (x s ) = ηs / x s η s /x s.

27 Remark 1 Whenever a platform is active, conditions (1) - (3) are reduced to: where f v (x m, K), (4) v (x m, K) 1 λ b e xs β λ s ξ (x m, K) (1 β) Lemma 1 With multiple-market search, an active platform can enlarge the intermediation surplus v(x m, K).

28 Pure market-maker: Given the equilibrium price p s, and x m = 0 and x s = B S (by annoucing K = 0), the intermediary sets f = f b + f s = v(0, 0); makes the profits Π (0) = S ( 1 e B S ) v(0, 0).

29 Market-making middleman: Given p m satisfying V m (x m ) = V s (x s ), the intermediary s problem is: Π(x m ) = max x m,f,k Π (xm, f, K) = S(1 e xs )f + min {K, x m } p m subject to (4), f v(x m, K), and x m (0, B). Lemma 2 The market-making middleman sets: f = v(x m, K). K = x m and

30 Remark 2 Benefits of using an active platform: a larger intermediation surplus v(x m, K); a higher middleman price, p m = 1 λ b e xs β.

31 Proposition 2 (Market-making middleman/pure Market-maker) Given multi-market search technologies, the intermediary will open an active platform and act as: a market-making middleman if λ b β 1 2 or if λb β > 1 2 and B S x, some x (0, B); a pure market-maker if λ b β > 1 2 and B S < x.

32 Multi market search: Market-making Middleman mode 0<xm =K*<B 0<xs<B/S S B

33 Multi market search: x m =K*=0 Pure Market-maker mode x s =B/S S B

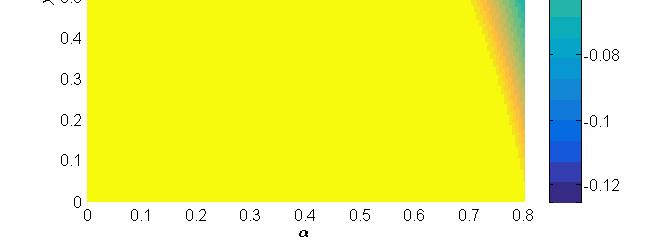

34 1.0 B λ b β 0.5

35 Buyers option value: e xs λ b β Corollary 1 (Comparative statics) Consider a parameter space in which the market-making middleman mode is profit-maximizing. Then, an increase in buyer s bargaining power β or buyer s meeting rate λ b in the D market, or a decrease in the buyer-seller population ratio, B S, leads to a smaller middleman sector xm and a larger platform x s.

36 Extension (1): Non-linear matching function Suppose that: λ b = λ b (x D ) is strictly concave and decreasing in x D. Suppose also that agents exit after successful trades in the C market: B D = max { B min{x m, K} S(1 e xs ), 0 } and S D = Se xs.

37 Proposition 3 With a non-linear matching function in the D market outlined above, a pure middleman mode can be profitable even with multi-market search technologies only if the middleman s price is inelastic at the full capacity x m = K = B. Otherwise, the intermediary should be a marketmaking middleman or a pure market maker.

38

39

40 Extension (2): Endowment economy (Assume β = 1) - Each seller is endowed with a unit of good. - A middleman can assess αs sellers in the wholesales market. Resource constraint: K αs Wholesales price: p w W (x s ), where x s = B xm S K

41 Proposition 4 Consider the endowment economy outlined above with single-market search technology, and the zero trade share of sellers in the D market. The intermediation chooses to be: a pure middleman if B αs; a market-making middleman with K = αs x m if B > αs. Proposition 5 Consider the endowment economy outlined above with multi-market search technology, and the zero trade share of sellers in the D market. The intermediation chooses to be a market-making middleman or a pure market-maker with x m K = αs.

42

43

44 - Comparison: For αs B, essentially the same as in the benchmark setup. For αs < B, the size of middleman sector, x m, is smaller with multi-market search.

45 Applications Amazon: Moved towards a market-making middleman at the time of high entry of web-based retailers. Market behaviors: re-launch business in Amazon platform/ use Amazon as primary site NYSE/ NASDAQ: Changing competitive environment faced by securities exchanges/ NYSE Arca

46 Less active assets: small cap securities / designated dealers in auction The Trump Organization/Trump International Realty: Added a brokering business at the time of high entry of web-based platforms. Supply security: co-development business

47 Literature Rubinstein and Wolinsky (1987), Duffie, Garleanu, and Pedersen (2006), Lagos and Rocheteau (2009), Lagos, Rocheteau, and Weill (2010), Weill (2007), Shevichenko (2004), Johri and Leach (2002), Masters (2007), Watanabe (2010, 2013), Wong and Wright (2014), Holzner and Watanabe (2015), Nosal, Wong and Wright (2015) Baye and Morgan (2001), Rochet and Tirole (2003, 2006), Caillaud and Jullien (2003), Rysman (2004), Armstrong (2006), Hagiu (2006), Nocke et al. (2007), Galeotti and Moraga- Gonzalez (2009), Weyl (2010), Loertscher and Niedermayer (2012), Edelman and Wright (2015)

48 Rust and Hall (2003) Rust and Hall (JPE, 2003) An important function of intermediaries is to hold inventory to provide a buffer stock that offers their customers liquidity at times when there is an imbalance between supply and demand. In the securities business, liquidity means being able to buy or sell a reasonable quantity of shares on short notice. In the steel market, liquidity is also associated with a demand for immediacy so that a customer can be guaranteed of receiving shipment of an order within a few days of placement. Lacking inventories and stockouts, this model cannot be used to analyze the important role of intermediaries in providing liquidity. (page 401).

49 Conclusion A simple framework to study the determination of intermediated market structure Emergence of market-making middleman

Marketmaking Middlemen

Marketmaking Middlemen Pieter Gautier Bo Hu Makoto Watanabe VU Amsterdam, Tinbergen Institute February 15, 2016 Abstract This paper develops a model in which market structure is determined endogenously

Marketmaking Middlemen Pieter Gautier Bo Hu Makoto Watanabe VU Amsterdam, Tinbergen Institute February 15, 2016 Abstract This paper develops a model in which market structure is determined endogenously

Marketmaking Middlemen

Marketmaking Middlemen Pieter Gautier Bo Hu Makoto Watanabe VU Amsterdam, Tinbergen Institute August 26, 2017 Abstract This paper develops a model in which market structure is determined endogenously by

Marketmaking Middlemen Pieter Gautier Bo Hu Makoto Watanabe VU Amsterdam, Tinbergen Institute August 26, 2017 Abstract This paper develops a model in which market structure is determined endogenously by

Marketmaking Middlemen

Marketmaking Middlemen Pieter Gautier Bo Hu Makoto Watanabe VU Amsterdam, Tinbergen Institute October 10, 2018 Abstract This paper develops a model in which market structure is determined endogenously

Marketmaking Middlemen Pieter Gautier Bo Hu Makoto Watanabe VU Amsterdam, Tinbergen Institute October 10, 2018 Abstract This paper develops a model in which market structure is determined endogenously

Marketmaking Middlemen

Marketmaking Middlemen Pieter Gautier y Bo Hu z Makoto Watanabe x March 15, 2015 Preliminary Version Abstract This paper develops a model in which market structure is determined endogenously by the choice

Marketmaking Middlemen Pieter Gautier y Bo Hu z Makoto Watanabe x March 15, 2015 Preliminary Version Abstract This paper develops a model in which market structure is determined endogenously by the choice

Middlemen: the bid-ask spread

Middlemen: the bid-ask spread Makoto Watanabe Universidad Carlos III de Madrid January 30, 2006 This version: March 3, 2008 Abstract This paper studies the bid-ask spread set in an intermediated market

Middlemen: the bid-ask spread Makoto Watanabe Universidad Carlos III de Madrid January 30, 2006 This version: March 3, 2008 Abstract This paper studies the bid-ask spread set in an intermediated market

Liquidity and the Threat of Fraudulent Assets

Liquidity and the Threat of Fraudulent Assets Yiting Li, Guillaume Rocheteau, Pierre-Olivier Weill May 2015 Liquidity and the Threat of Fraudulent Assets Yiting Li, Guillaume Rocheteau, Pierre-Olivier

Liquidity and the Threat of Fraudulent Assets Yiting Li, Guillaume Rocheteau, Pierre-Olivier Weill May 2015 Liquidity and the Threat of Fraudulent Assets Yiting Li, Guillaume Rocheteau, Pierre-Olivier

Price Theory of Two-Sided Markets

The E. Glen Weyl Department of Economics Princeton University Fundação Getulio Vargas August 3, 2007 Definition of a two-sided market 1 Two groups of consumers 2 Value from connecting (proportional to

The E. Glen Weyl Department of Economics Princeton University Fundação Getulio Vargas August 3, 2007 Definition of a two-sided market 1 Two groups of consumers 2 Value from connecting (proportional to

Flea Market and Bazaar: Profit-Maximizing Platform Mechanisms for Matching and Search

Flea Market and Bazaar: Profit-Maximizing Platform Mechanisms for Matching and Search Andras Niedermayer Artyom Shneyerov December 2, 211 Abstract We consider optimal pricing mechanisms of a profit maximizing

Flea Market and Bazaar: Profit-Maximizing Platform Mechanisms for Matching and Search Andras Niedermayer Artyom Shneyerov December 2, 211 Abstract We consider optimal pricing mechanisms of a profit maximizing

Counterparty Risk in the Over-the-Counter Derivatives Market: Heterogeneous Insurers with Non-commitment

Counterparty Risk in the Over-the-Counter Derivatives Market: Heterogeneous Insurers with Non-commitment Hao Sun November 26, 2017 Abstract I study risk-taking and optimal contracting in the over-the-counter

Counterparty Risk in the Over-the-Counter Derivatives Market: Heterogeneous Insurers with Non-commitment Hao Sun November 26, 2017 Abstract I study risk-taking and optimal contracting in the over-the-counter

Intermediation as Rent Extraction

Intermediation as Rent Extraction MARYAM FARBOODI Princeton University GREGOR JAROSCH Princeton University and NBER GUIDO MENZIO University of Pennsylvania and NBER December 22, 2017 Abstract We propose

Intermediation as Rent Extraction MARYAM FARBOODI Princeton University GREGOR JAROSCH Princeton University and NBER GUIDO MENZIO University of Pennsylvania and NBER December 22, 2017 Abstract We propose

Liquidity and the Threat of Fraudulent Assets

Liquidity and the Threat of Fraudulent Assets Yiting Li, Guillaume Rocheteau, Pierre-Olivier Weill NTU, UCI, UCLA, NBER, CEPR 1 / 21 fraudulent behavior in asset markets in this paper: with sufficient

Liquidity and the Threat of Fraudulent Assets Yiting Li, Guillaume Rocheteau, Pierre-Olivier Weill NTU, UCI, UCLA, NBER, CEPR 1 / 21 fraudulent behavior in asset markets in this paper: with sufficient

Corporate Finance and Monetary Policy

Corporate Finance and Monetary Policy Guillaume Rocheteau Randall Wright Cathy Zhang U. of California, Irvine U. of Wisconsin, Madison Purdue University CIGS Conference on Macroeconomic Theory and Policy,

Corporate Finance and Monetary Policy Guillaume Rocheteau Randall Wright Cathy Zhang U. of California, Irvine U. of Wisconsin, Madison Purdue University CIGS Conference on Macroeconomic Theory and Policy,

A Comparison of the Wholesale Structure and the Agency Structure in Differentiated Markets. Liang Lu

A Comparison of the Wholesale Structure and the Agency Structure in Differentiated Markets Liang Lu 1 Vertically-Related Markets Suppliers and consumers do not deal directly An economic agent who o Purchases

A Comparison of the Wholesale Structure and the Agency Structure in Differentiated Markets Liang Lu 1 Vertically-Related Markets Suppliers and consumers do not deal directly An economic agent who o Purchases

Intermediation as Rent Extraction

Intermediation as Rent Extraction MARYAM FARBOODI Princeton University GREGOR JAROSCH Princeton University and NBER GUIDO MENZIO University of Pennsylvania and NBER November 7, 2017 Abstract This paper

Intermediation as Rent Extraction MARYAM FARBOODI Princeton University GREGOR JAROSCH Princeton University and NBER GUIDO MENZIO University of Pennsylvania and NBER November 7, 2017 Abstract This paper

Essential interest-bearing money

Essential interest-bearing money David Andolfatto Federal Reserve Bank of St. Louis The Lagos-Wright Model Leading framework in contemporary monetary theory Models individuals exposed to idiosyncratic

Essential interest-bearing money David Andolfatto Federal Reserve Bank of St. Louis The Lagos-Wright Model Leading framework in contemporary monetary theory Models individuals exposed to idiosyncratic

Counterparty Risk in the Over-the-Counter Derivatives Market: Heterogeneous Insurers with Non-commitment

Counterparty Risk in the Over-the-Counter Derivatives Market: Heterogeneous Insurers with Non-commitment Hao Sun November 16, 2017 Abstract I study risk-taking and optimal contracting in the over-the-counter

Counterparty Risk in the Over-the-Counter Derivatives Market: Heterogeneous Insurers with Non-commitment Hao Sun November 16, 2017 Abstract I study risk-taking and optimal contracting in the over-the-counter

Liquidity and Risk Management

Liquidity and Risk Management By Nicolae Gârleanu and Lasse Heje Pedersen Risk management plays a central role in institutional investors allocation of capital to trading. For instance, a risk manager

Liquidity and Risk Management By Nicolae Gârleanu and Lasse Heje Pedersen Risk management plays a central role in institutional investors allocation of capital to trading. For instance, a risk manager

The Coordination of Intermediation

The Coordination of Intermediation Ming Yang Duke University Yao Zeng University of Washington February, 209 Abstract We study decentralized trading among financial intermediaries (i.e., dealers), the

The Coordination of Intermediation Ming Yang Duke University Yao Zeng University of Washington February, 209 Abstract We study decentralized trading among financial intermediaries (i.e., dealers), the

Notes on Dixit-Stiglitz Size Distribution Model Econ 8601

Notes on Dixit-Stiglitz Size Distribution Model Econ 86. Model Consider the following partial equilibrium model of an industry. The final good in the industry is a composite of differentiated products.

Notes on Dixit-Stiglitz Size Distribution Model Econ 86. Model Consider the following partial equilibrium model of an industry. The final good in the industry is a composite of differentiated products.

Two-Sided Markets Monopoly: Joint Production and Externalities

University of Pisa Sant Anna School of Advanced Studies Department of Economics and Management Master of Science in Economics Master s Thesis Two-Sided Markets Monopoly: Joint Production and Externalities

University of Pisa Sant Anna School of Advanced Studies Department of Economics and Management Master of Science in Economics Master s Thesis Two-Sided Markets Monopoly: Joint Production and Externalities

Search Intermediaries

Search Intermediaries Xianwen Shi & Aloysius Siow // March 2011 University of Toronto Javier Fernández-Blanco (My) Motivation Frictionless world, room for intermediation activity. With frictions, intermediaries

Search Intermediaries Xianwen Shi & Aloysius Siow // March 2011 University of Toronto Javier Fernández-Blanco (My) Motivation Frictionless world, room for intermediation activity. With frictions, intermediaries

Bid-Ask Spreads and Volume: The Role of Trade Timing

Bid-Ask Spreads and Volume: The Role of Trade Timing Toronto, Northern Finance 2007 Andreas Park University of Toronto October 3, 2007 Andreas Park (UofT) The Timing of Trades October 3, 2007 1 / 25 Patterns

Bid-Ask Spreads and Volume: The Role of Trade Timing Toronto, Northern Finance 2007 Andreas Park University of Toronto October 3, 2007 Andreas Park (UofT) The Timing of Trades October 3, 2007 1 / 25 Patterns

Liquidity and Payments Fraud

Liquidity and Payments Fraud Yiting Li and Jia Jing Lin NTU, TIER November 2013 Deposit-based payments About 61% of organizations experienced attempted or actual payments fraud in 2012, and 87% of respondents

Liquidity and Payments Fraud Yiting Li and Jia Jing Lin NTU, TIER November 2013 Deposit-based payments About 61% of organizations experienced attempted or actual payments fraud in 2012, and 87% of respondents

Sequential Credit Markets

Sequential Credit Markets Ulf Axelson and Igor Makarov December 7, 2016 ABSTRACT Entrepreneurs who seek financing for projects typically do so in decentralized markets where they need to approach investors

Sequential Credit Markets Ulf Axelson and Igor Makarov December 7, 2016 ABSTRACT Entrepreneurs who seek financing for projects typically do so in decentralized markets where they need to approach investors

Money Inventories in Search Equilibrium

MPRA Munich Personal RePEc Archive Money Inventories in Search Equilibrium Aleksander Berentsen University of Basel 1. January 1998 Online at https://mpra.ub.uni-muenchen.de/68579/ MPRA Paper No. 68579,

MPRA Munich Personal RePEc Archive Money Inventories in Search Equilibrium Aleksander Berentsen University of Basel 1. January 1998 Online at https://mpra.ub.uni-muenchen.de/68579/ MPRA Paper No. 68579,

Efficient Insurance in a Market Theory of Payroll and Self-Employment

Efficient Insurance in a Market Theory of Payroll and Self-Employment Piotr Denderski, Florian Sniekers June 19, 2016 Work in Progress, Comments Welcome Abstract We propose a theory of self-employment

Efficient Insurance in a Market Theory of Payroll and Self-Employment Piotr Denderski, Florian Sniekers June 19, 2016 Work in Progress, Comments Welcome Abstract We propose a theory of self-employment

Loss Aversion Leading to Advantageous Selection

Loss Aversion Leading to Advantageous Selection Christina Aperjis and Filippo Balestrieri HP Labs [This version April 211. Work in progress. Please do not circulate.] Abstract Even though classic economic

Loss Aversion Leading to Advantageous Selection Christina Aperjis and Filippo Balestrieri HP Labs [This version April 211. Work in progress. Please do not circulate.] Abstract Even though classic economic

Financial Intermediation Chains in an OTC Market

Financial Intermediation Chains in an OTC Market Ji Shen Peking University shenjitoq@gmail.com Bin Wei Federal Reserve Bank of Atlanta bin.wei@atl.frb.org Hongjun Yan Rutgers University hongjun.yan.2011@gmail.com

Financial Intermediation Chains in an OTC Market Ji Shen Peking University shenjitoq@gmail.com Bin Wei Federal Reserve Bank of Atlanta bin.wei@atl.frb.org Hongjun Yan Rutgers University hongjun.yan.2011@gmail.com

Macroeconomics and finance

Macroeconomics and finance 1 1. Temporary equilibrium and the price level [Lectures 11 and 12] 2. Overlapping generations and learning [Lectures 13 and 14] 2.1 The overlapping generations model 2.2 Expectations

Macroeconomics and finance 1 1. Temporary equilibrium and the price level [Lectures 11 and 12] 2. Overlapping generations and learning [Lectures 13 and 14] 2.1 The overlapping generations model 2.2 Expectations

EX-ANTE PRICE COMMITMENT WITH RENEGOTIATION IN A DYNAMIC MARKET

EX-ANTE PRICE COMMITMENT WITH RENEGOTIATION IN A DYNAMIC MARKET ADRIAN MASTERS AND ABHINAY MUTHOO Abstract. This paper studies the endogenous determination of the price formation procedure in markets characterized

EX-ANTE PRICE COMMITMENT WITH RENEGOTIATION IN A DYNAMIC MARKET ADRIAN MASTERS AND ABHINAY MUTHOO Abstract. This paper studies the endogenous determination of the price formation procedure in markets characterized

Market Liquidity and Performance Monitoring The main idea The sequence of events: Technology and information

Market Liquidity and Performance Monitoring Holmstrom and Tirole (JPE, 1993) The main idea A firm would like to issue shares in the capital market because once these shares are publicly traded, speculators

Market Liquidity and Performance Monitoring Holmstrom and Tirole (JPE, 1993) The main idea A firm would like to issue shares in the capital market because once these shares are publicly traded, speculators

Payment card interchange fees and price discrimination

Payment card interchange fees and price discrimination Rong Ding Julian Wright April 8, 2016 Abstract We consider the implications of platform price discrimination in the context of card platforms. Despite

Payment card interchange fees and price discrimination Rong Ding Julian Wright April 8, 2016 Abstract We consider the implications of platform price discrimination in the context of card platforms. Despite

Commitment in First-price Auctions

Commitment in First-price Auctions Yunjian Xu and Katrina Ligett November 12, 2014 Abstract We study a variation of the single-item sealed-bid first-price auction wherein one bidder (the leader) publicly

Commitment in First-price Auctions Yunjian Xu and Katrina Ligett November 12, 2014 Abstract We study a variation of the single-item sealed-bid first-price auction wherein one bidder (the leader) publicly

Efficient Insurance in a Market Theory of Payroll and Self-Employment

Efficient Insurance in a Market Theory of Payroll and Self-Employment Piotr Denderski, Florian Sniekers October 9, 2016 Work in Progress, Comments Welcome Abstract We propose a theory of self-employment

Efficient Insurance in a Market Theory of Payroll and Self-Employment Piotr Denderski, Florian Sniekers October 9, 2016 Work in Progress, Comments Welcome Abstract We propose a theory of self-employment

Financial Intermediation Chains in an OTC Market

MPRA Munich Personal RePEc Archive Financial Intermediation Chains in an OTC Market Ji Shen and Bin Wei and Hongjun Yan October 2016 Online at https://mpra.ub.uni-muenchen.de/74925/ MPRA Paper No. 74925,

MPRA Munich Personal RePEc Archive Financial Intermediation Chains in an OTC Market Ji Shen and Bin Wei and Hongjun Yan October 2016 Online at https://mpra.ub.uni-muenchen.de/74925/ MPRA Paper No. 74925,

Blind Portfolio Auctions via Intermediaries

Blind Portfolio Auctions via Intermediaries Michael Padilla Stanford University (joint work with Benjamin Van Roy) April 12, 2011 Computer Forum 2011 Michael Padilla (Stanford University) Blind Portfolio

Blind Portfolio Auctions via Intermediaries Michael Padilla Stanford University (joint work with Benjamin Van Roy) April 12, 2011 Computer Forum 2011 Michael Padilla (Stanford University) Blind Portfolio

PRICES AS OPTIMAL COMPETITIVE SALES MECHANISMS

PRICES AS OPTIMAL COMPETITIVE SALES MECHANISMS Jan Eeckhout 1 Philipp Kircher 2 1 University Pompeu Fabra 2 Oxford University 1,2 University of Pennsylvania Cowles Foundation and JET Symposium on Search

PRICES AS OPTIMAL COMPETITIVE SALES MECHANISMS Jan Eeckhout 1 Philipp Kircher 2 1 University Pompeu Fabra 2 Oxford University 1,2 University of Pennsylvania Cowles Foundation and JET Symposium on Search

Multiproduct Pricing Made Simple

Multiproduct Pricing Made Simple Mark Armstrong John Vickers Oxford University September 2016 Armstrong & Vickers () Multiproduct Pricing September 2016 1 / 21 Overview Multiproduct pricing important for:

Multiproduct Pricing Made Simple Mark Armstrong John Vickers Oxford University September 2016 Armstrong & Vickers () Multiproduct Pricing September 2016 1 / 21 Overview Multiproduct pricing important for:

Allocating and Funding Universal Service Obligations in a Competitive Network Market

Allocating and Funding Universal Service Obligations in a Competitive Network Market Philippe Choné, Laurent Flochel, Anne Perrot October 1999 Abstract We examine, in a network market open to competition,

Allocating and Funding Universal Service Obligations in a Competitive Network Market Philippe Choné, Laurent Flochel, Anne Perrot October 1999 Abstract We examine, in a network market open to competition,

UNR Joint Economics Working Paper Series Working Paper No Private Money as a Competing Medium of Exchange

UNR Joint Economics Working Paper Series Working Paper No 08-004 Private oney as a Competing edium of Exchange ark Pingle and Sankar ukhopadhyay Department of Economics /0030 University of Nevada, Reno

UNR Joint Economics Working Paper Series Working Paper No 08-004 Private oney as a Competing edium of Exchange ark Pingle and Sankar ukhopadhyay Department of Economics /0030 University of Nevada, Reno

Federal Reserve Bank of New York Staff Reports

Federal Reserve Bank of New York Staff Reports Liquidity and Congestion Gara M. Afonso Staff Report no. 349 October 2008 Revised November 2010 This paper presents preliminary findings and is being distributed

Federal Reserve Bank of New York Staff Reports Liquidity and Congestion Gara M. Afonso Staff Report no. 349 October 2008 Revised November 2010 This paper presents preliminary findings and is being distributed

Financial Intermediation Chains in an OTC Market

Financial Intermediation Chains in an OTC Market Ji Shen London School of Economics shenjitoq@gmail.com Bin Wei Federal Reserve Bank of Atlanta bin.wei@atl.frb.org Hongjun Yan Yale School of Management

Financial Intermediation Chains in an OTC Market Ji Shen London School of Economics shenjitoq@gmail.com Bin Wei Federal Reserve Bank of Atlanta bin.wei@atl.frb.org Hongjun Yan Yale School of Management

Counterfeiting, Screening and Government Policy

Counterfeiting, Screening and Government Policy Kee Youn Kang Washington University in St. Louis January 22, 2017 Abstract We construct a search theoretic model of money in which counterfeit money can

Counterfeiting, Screening and Government Policy Kee Youn Kang Washington University in St. Louis January 22, 2017 Abstract We construct a search theoretic model of money in which counterfeit money can

Monetary Economics. Chapter 5: Properties of Money. Prof. Aleksander Berentsen. University of Basel

Monetary Economics Chapter 5: Properties of Money Prof. Aleksander Berentsen University of Basel Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 5 1 / 40 Structure of this chapter

Monetary Economics Chapter 5: Properties of Money Prof. Aleksander Berentsen University of Basel Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 5 1 / 40 Structure of this chapter

Optimal Fees in Internet Auctions

Optimal Fees in Internet Auctions Alexander Matros a,, Andriy Zapechelnyuk b a Department of Economics, University of Pittsburgh, PA, USA b Kyiv School of Economics, Kyiv, Ukraine January 14, 2008 Abstract

Optimal Fees in Internet Auctions Alexander Matros a,, Andriy Zapechelnyuk b a Department of Economics, University of Pittsburgh, PA, USA b Kyiv School of Economics, Kyiv, Ukraine January 14, 2008 Abstract

Liquidity and Asset Prices: A New Monetarist Approach

Liquidity and Asset Prices: A New Monetarist Approach Ying-Syuan Li and Yiting Li May 2017 Motivation A monetary economy in which lenders cannot force borrowers to repay their debts, and financial assets

Liquidity and Asset Prices: A New Monetarist Approach Ying-Syuan Li and Yiting Li May 2017 Motivation A monetary economy in which lenders cannot force borrowers to repay their debts, and financial assets

Auction. Li Zhao, SJTU. Spring, Li Zhao Auction 1 / 35

Auction Li Zhao, SJTU Spring, 2017 Li Zhao Auction 1 / 35 Outline 1 A Simple Introduction to Auction Theory 2 Estimating English Auction 3 Estimating FPA Li Zhao Auction 2 / 35 Background Auctions have

Auction Li Zhao, SJTU Spring, 2017 Li Zhao Auction 1 / 35 Outline 1 A Simple Introduction to Auction Theory 2 Estimating English Auction 3 Estimating FPA Li Zhao Auction 2 / 35 Background Auctions have

A Market Theory of Self-Employment: Competitive Search Equilibrium and Policy Implications

A Market Theory of Self-Employment: Competitive Search Equilibrium and Policy Implications Piotr Denderski, Florian Sniekers August 21, 2015 Work in Progress, Comments Welcome Abstract We propose a novel

A Market Theory of Self-Employment: Competitive Search Equilibrium and Policy Implications Piotr Denderski, Florian Sniekers August 21, 2015 Work in Progress, Comments Welcome Abstract We propose a novel

Liquidity and Asset Prices: A New Monetarist Approach

Liquidity and Asset Prices: A New Monetarist Approach Ying-Syuan Li and Yiting Li November 2016 Motivation A monetary economy in which lenders cannot force borrowers to repay their debts, and financial

Liquidity and Asset Prices: A New Monetarist Approach Ying-Syuan Li and Yiting Li November 2016 Motivation A monetary economy in which lenders cannot force borrowers to repay their debts, and financial

University of Konstanz Department of Economics. Maria Breitwieser.

University of Konstanz Department of Economics Optimal Contracting with Reciprocal Agents in a Competitive Search Model Maria Breitwieser Working Paper Series 2015-16 http://www.wiwi.uni-konstanz.de/econdoc/working-paper-series/

University of Konstanz Department of Economics Optimal Contracting with Reciprocal Agents in a Competitive Search Model Maria Breitwieser Working Paper Series 2015-16 http://www.wiwi.uni-konstanz.de/econdoc/working-paper-series/

Online appendix for Price Pressures. Terrence Hendershott and Albert J. Menkveld

Online appendix for Price Pressures Terrence Hendershott and Albert J. Menkveld This document has the following supplemental material: 1. Section 1 presents the infinite horizon version of the Ho and Stoll

Online appendix for Price Pressures Terrence Hendershott and Albert J. Menkveld This document has the following supplemental material: 1. Section 1 presents the infinite horizon version of the Ho and Stoll

LI Reunión Anual. Noviembre de Managing Strategic Buyers: Should a Seller Ban Resale? Beccuti, Juan Coleff, Joaquin

ANALES ASOCIACION ARGENTINA DE ECONOMIA POLITICA LI Reunión Anual Noviembre de 016 ISSN 185-00 ISBN 978-987-8590-4-6 Managing Strategic Buyers: Should a Seller Ban Resale? Beccuti, Juan Coleff, Joaquin

ANALES ASOCIACION ARGENTINA DE ECONOMIA POLITICA LI Reunión Anual Noviembre de 016 ISSN 185-00 ISBN 978-987-8590-4-6 Managing Strategic Buyers: Should a Seller Ban Resale? Beccuti, Juan Coleff, Joaquin

WORKING PAPER NO COMMENT ON CAVALCANTI AND NOSAL S COUNTERFEITING AS PRIVATE MONEY IN MECHANISM DESIGN

WORKING PAPER NO. 10-29 COMMENT ON CAVALCANTI AND NOSAL S COUNTERFEITING AS PRIVATE MONEY IN MECHANISM DESIGN Cyril Monnet Federal Reserve Bank of Philadelphia September 2010 Comment on Cavalcanti and

WORKING PAPER NO. 10-29 COMMENT ON CAVALCANTI AND NOSAL S COUNTERFEITING AS PRIVATE MONEY IN MECHANISM DESIGN Cyril Monnet Federal Reserve Bank of Philadelphia September 2010 Comment on Cavalcanti and

Keynesian Inefficiency and Optimal Policy: A New Monetarist Approach

Keynesian Inefficiency and Optimal Policy: A New Monetarist Approach Stephen D. Williamson Washington University in St. Louis Federal Reserve Banks of Richmond and St. Louis May 29, 2013 Abstract A simple

Keynesian Inefficiency and Optimal Policy: A New Monetarist Approach Stephen D. Williamson Washington University in St. Louis Federal Reserve Banks of Richmond and St. Louis May 29, 2013 Abstract A simple

Search, Welfare and the Hot Potato E ect of In ation

Search, Welfare and the Hot Potato E ect of In ation Ed Nosal December 2008 Abstract An increase in in ation will cause people to hold less real balances and may cause them to speed up their spending.

Search, Welfare and the Hot Potato E ect of In ation Ed Nosal December 2008 Abstract An increase in in ation will cause people to hold less real balances and may cause them to speed up their spending.

GERMAN ECONOMIC ASSOCIATION OF BUSINESS ADMINISTRATION GEABA DISCUSSION PAPER SERIES IN ECONOMICS AND MANAGEMENT

DISCUSSION PAPER SERIES IN ECONOMICS AND MANAGEMENT Tax and Managerial Effects of Transfer Pricing on Capital and Physical Products Oliver Duerr, Thomas Rüffieux Discussion Paper No. 17-19 GERMAN ECONOMIC

DISCUSSION PAPER SERIES IN ECONOMICS AND MANAGEMENT Tax and Managerial Effects of Transfer Pricing on Capital and Physical Products Oliver Duerr, Thomas Rüffieux Discussion Paper No. 17-19 GERMAN ECONOMIC

Lectures on Externalities

Lectures on Externalities An externality is present whenever the well-being of a consumer or the production possibilities of a firm are directly affected by the actions of another agent in the economy.

Lectures on Externalities An externality is present whenever the well-being of a consumer or the production possibilities of a firm are directly affected by the actions of another agent in the economy.

Homework # 8 - [Due on Wednesday November 1st, 2017]

![Homework # 8 - [Due on Wednesday November 1st, 2017]](/thumbs/93/112043254.jpg "Homework # 8 - [Due on Wednesday November 1st, 2017]") Homework # 8 - [Due on Wednesday November 1st, 2017] 1. A tax is to be levied on a commodity bought and sold in a competitive market. Two possible forms of tax may be used: In one case, a per unit tax

Homework # 8 - [Due on Wednesday November 1st, 2017] 1. A tax is to be levied on a commodity bought and sold in a competitive market. Two possible forms of tax may be used: In one case, a per unit tax

Supplemental Online Appendix to Han and Hong, Understanding In-House Transactions in the Real Estate Brokerage Industry

Supplemental Online Appendix to Han and Hong, Understanding In-House Transactions in the Real Estate Brokerage Industry Appendix A: An Agent-Intermediated Search Model Our motivating theoretical framework

Supplemental Online Appendix to Han and Hong, Understanding In-House Transactions in the Real Estate Brokerage Industry Appendix A: An Agent-Intermediated Search Model Our motivating theoretical framework

The Emergence of Market Structure

The Emergence of Market Structure Maryam Farboodi Princeton University Gregor Jarosch Stanford University March 5, 17 Robert Shimer University of Chicago Abstract What market structure emerges when market

The Emergence of Market Structure Maryam Farboodi Princeton University Gregor Jarosch Stanford University March 5, 17 Robert Shimer University of Chicago Abstract What market structure emerges when market

Department of Economics The Ohio State University Midterm Questions and Answers Econ 8712

Prof. James Peck Fall 06 Department of Economics The Ohio State University Midterm Questions and Answers Econ 87. (30 points) A decision maker (DM) is a von Neumann-Morgenstern expected utility maximizer.

Prof. James Peck Fall 06 Department of Economics The Ohio State University Midterm Questions and Answers Econ 87. (30 points) A decision maker (DM) is a von Neumann-Morgenstern expected utility maximizer.

WORKING PAPER NO OPTIMAL MONETARY POLICY IN A MODEL OF MONEY AND CREDIT. Pedro Gomis-Porqueras Australian National University

WORKING PAPER NO. 11-4 OPTIMAL MONETARY POLICY IN A MODEL OF MONEY AND CREDIT Pedro Gomis-Porqueras Australian National University Daniel R. Sanches Federal Reserve Bank of Philadelphia December 2010 Optimal

WORKING PAPER NO. 11-4 OPTIMAL MONETARY POLICY IN A MODEL OF MONEY AND CREDIT Pedro Gomis-Porqueras Australian National University Daniel R. Sanches Federal Reserve Bank of Philadelphia December 2010 Optimal

A Model of (the Threat of) Counterfeiting

Counterfeiting") w o r k i n g p a p e r 04 01 A Model of (the Threat of) Counterfeiting by Ed Nosal and Neil Wallace FEDERAL RESERVE BANK OF CLEVELAND Working papers of the Federal Reserve Bank of Cleveland are preliminary

w o r k i n g p a p e r 04 01 A Model of (the Threat of) Counterfeiting by Ed Nosal and Neil Wallace FEDERAL RESERVE BANK OF CLEVELAND Working papers of the Federal Reserve Bank of Cleveland are preliminary

Reputation and Persistence of Adverse Selection in Secondary Loan Markets

Reputation and Persistence of Adverse Selection in Secondary Loan Markets V.V. Chari UMN, FRB Mpls Ali Shourideh Wharton Ariel Zetlin-Jones CMU - Tepper School October 29th, 2013 Introduction Trade volume

Reputation and Persistence of Adverse Selection in Secondary Loan Markets V.V. Chari UMN, FRB Mpls Ali Shourideh Wharton Ariel Zetlin-Jones CMU - Tepper School October 29th, 2013 Introduction Trade volume

QI SHANG: General Equilibrium Analysis of Portfolio Benchmarking

General Equilibrium Analysis of Portfolio Benchmarking QI SHANG 23/10/2008 Introduction The Model Equilibrium Discussion of Results Conclusion Introduction This paper studies the equilibrium effect of

General Equilibrium Analysis of Portfolio Benchmarking QI SHANG 23/10/2008 Introduction The Model Equilibrium Discussion of Results Conclusion Introduction This paper studies the equilibrium effect of

Markets, Banks and Shadow Banks

Markets, Banks and Shadow Banks David Martinez-Miera Rafael Repullo U. Carlos III, Madrid, Spain CEMFI, Madrid, Spain AEA Session Macroprudential Policy and Banking Panics Philadelphia, January 6, 2018

Markets, Banks and Shadow Banks David Martinez-Miera Rafael Repullo U. Carlos III, Madrid, Spain CEMFI, Madrid, Spain AEA Session Macroprudential Policy and Banking Panics Philadelphia, January 6, 2018

An Equilibrium Analysis of Competing Double Auction Marketplaces Using Fictitious Play

An Equilibrium Analysis of Competing Double Auction Marketplaces Using Fictitious Play Bing Shi and Enrico H. Gerding and Perukrishnen Vytelingum and Nicholas R. Jennings 1 Abstract. In this paper, we

An Equilibrium Analysis of Competing Double Auction Marketplaces Using Fictitious Play Bing Shi and Enrico H. Gerding and Perukrishnen Vytelingum and Nicholas R. Jennings 1 Abstract. In this paper, we

Loss-leader pricing and upgrades

Loss-leader pricing and upgrades Younghwan In and Julian Wright This version: August 2013 Abstract A new theory of loss-leader pricing is provided in which firms advertise low below cost) prices for certain

Loss-leader pricing and upgrades Younghwan In and Julian Wright This version: August 2013 Abstract A new theory of loss-leader pricing is provided in which firms advertise low below cost) prices for certain

Asset Pricing under Asymmetric Information Rational Expectations Equilibrium

Asset Pricing under Asymmetric s Equilibrium Markus K. Brunnermeier Princeton University November 16, 2015 A of Market Microstructure Models simultaneous submission of demand schedules competitive rational

Asset Pricing under Asymmetric s Equilibrium Markus K. Brunnermeier Princeton University November 16, 2015 A of Market Microstructure Models simultaneous submission of demand schedules competitive rational

Transaction Cost Politics in Over the Counter Markets

Applied Mathematical Sciences, Vol. 12, 2018, no. 23, 1137-1156 HIKARI Ltd, www.m-hikari.com https://doi.org/10.12988/ams.2018.87103 Transaction Cost Politics in Over the Counter Markets Federico Flore

Applied Mathematical Sciences, Vol. 12, 2018, no. 23, 1137-1156 HIKARI Ltd, www.m-hikari.com https://doi.org/10.12988/ams.2018.87103 Transaction Cost Politics in Over the Counter Markets Federico Flore

Entry-Deterring Agency

Entry-Deterring Agency Simon Loertscher Andras Niedermayer December 12, 2018 Abstract We provide a model in which an intermediary can choose between wholesale or agency. The possibility that buyers and

Entry-Deterring Agency Simon Loertscher Andras Niedermayer December 12, 2018 Abstract We provide a model in which an intermediary can choose between wholesale or agency. The possibility that buyers and

Competition in the Presence of Individual Demand Uncertainty

Competition in the Presence of Individual Demand Uncertainty Marc Möller Makoto Watanabe Abstract This article offers a tractable model of (oligopolistic) competition in differentiated product markets

Competition in the Presence of Individual Demand Uncertainty Marc Möller Makoto Watanabe Abstract This article offers a tractable model of (oligopolistic) competition in differentiated product markets

Profit-sharing rules and taxation of multinational two-sided platforms

Profit-sharing rules and taxation of multinational two-sided platforms Francis Bloch Gabrielle Demange September 18, 2018 Abstract This paper analyzes taxation of a two-sided platform attracting users

Profit-sharing rules and taxation of multinational two-sided platforms Francis Bloch Gabrielle Demange September 18, 2018 Abstract This paper analyzes taxation of a two-sided platform attracting users

Price Coherence and Excessive Intermediation

Price Coherence and Excessive Intermediation Benjamin Edelman and Julian Wright March 215 Abstract Suppose an intermediary provides a benefit to buyers when they purchase from sellers using the intermediary

Price Coherence and Excessive Intermediation Benjamin Edelman and Julian Wright March 215 Abstract Suppose an intermediary provides a benefit to buyers when they purchase from sellers using the intermediary

Monetary union enlargement and international trade

Monetary union enlargement and international trade Alessandro Marchesiani and Pietro Senesi June 30, 2006 Abstract This paper studies the effects of monetary union enlargement on international trade in

Monetary union enlargement and international trade Alessandro Marchesiani and Pietro Senesi June 30, 2006 Abstract This paper studies the effects of monetary union enlargement on international trade in

TOWARD A SYNTHESIS OF MODELS OF REGULATORY POLICY DESIGN

TOWARD A SYNTHESIS OF MODELS OF REGULATORY POLICY DESIGN WITH LIMITED INFORMATION MARK ARMSTRONG University College London Gower Street London WC1E 6BT E-mail: mark.armstrong@ucl.ac.uk DAVID E. M. SAPPINGTON

TOWARD A SYNTHESIS OF MODELS OF REGULATORY POLICY DESIGN WITH LIMITED INFORMATION MARK ARMSTRONG University College London Gower Street London WC1E 6BT E-mail: mark.armstrong@ucl.ac.uk DAVID E. M. SAPPINGTON

Answers to Microeconomics Prelim of August 24, In practice, firms often price their products by marking up a fixed percentage over (average)

") Answers to Microeconomics Prelim of August 24, 2016 1. In practice, firms often price their products by marking up a fixed percentage over (average) cost. To investigate the consequences of markup pricing,

Answers to Microeconomics Prelim of August 24, 2016 1. In practice, firms often price their products by marking up a fixed percentage over (average) cost. To investigate the consequences of markup pricing,

Macroprudential Policies in a Low Interest-Rate Environment

Macroprudential Policies in a Low Interest-Rate Environment Margarita Rubio 1 Fang Yao 2 1 University of Nottingham 2 Reserve Bank of New Zealand. The views expressed in this paper do not necessarily reflect

Macroprudential Policies in a Low Interest-Rate Environment Margarita Rubio 1 Fang Yao 2 1 University of Nottingham 2 Reserve Bank of New Zealand. The views expressed in this paper do not necessarily reflect

Intermediation, Compensation and Collusion in Insurance Markets

Intermediation, Compensation and Collusion in Insurance Markets Uwe Focht, Andreas Richter, Jörg Schiller Discussion Paper 7- April 7 LMU LUDWIG-MAXIMILIANS-UNIVERSITÄT MÜNCHEN MUNICH SCHOOL OF MANAGEMENT

Intermediation, Compensation and Collusion in Insurance Markets Uwe Focht, Andreas Richter, Jörg Schiller Discussion Paper 7- April 7 LMU LUDWIG-MAXIMILIANS-UNIVERSITÄT MÜNCHEN MUNICH SCHOOL OF MANAGEMENT

Economics 121b: Intermediate Microeconomics Final Exam Suggested Solutions

Dirk Bergemann Department of Economics Yale University Economics 121b: Intermediate Microeconomics Final Exam Suggested Solutions 1. Both moral hazard and adverse selection are products of asymmetric information,

Dirk Bergemann Department of Economics Yale University Economics 121b: Intermediate Microeconomics Final Exam Suggested Solutions 1. Both moral hazard and adverse selection are products of asymmetric information,

Central Bank Purchases of Private Assets

Central Bank Purchases of Private Assets Stephen D. Williamson Washington University in St. Louis Federal Reserve Banks of Richmond and St. Louis September 29, 2013 Abstract A model is constructed in which

Central Bank Purchases of Private Assets Stephen D. Williamson Washington University in St. Louis Federal Reserve Banks of Richmond and St. Louis September 29, 2013 Abstract A model is constructed in which

The Market for OTC Credit Derivatives

The Market for OTC Credit Derivatives Andrew G. Atkeson Andrea L. Eisfeldt Pierre-Olivier Weill UCLA Economics UCLA Anderson UCLA Economics July 23, 213 over-the-counter (OTC) derivatives Credit default

The Market for OTC Credit Derivatives Andrew G. Atkeson Andrea L. Eisfeldt Pierre-Olivier Weill UCLA Economics UCLA Anderson UCLA Economics July 23, 213 over-the-counter (OTC) derivatives Credit default

LECTURE 12: FRICTIONAL FINANCE

Lecture 12 Frictional Finance (1) Markus K. Brunnermeier LECTURE 12: FRICTIONAL FINANCE Lecture 12 Frictional Finance (2) Frictionless Finance Endowment Economy Households 1 Households 2 income will decline

Lecture 12 Frictional Finance (1) Markus K. Brunnermeier LECTURE 12: FRICTIONAL FINANCE Lecture 12 Frictional Finance (2) Frictionless Finance Endowment Economy Households 1 Households 2 income will decline

FUNDAÇÃO GETULIO VARGAS ECONOMIA. Caio Augusto Colango Teles. Money distribution with intermediation

FUNDAÇÃO GETULIO VARGAS ESCOLA DE PÓS-GRADUAÇÃO EM ECONOMIA Caio Augusto Colango Teles Money distribution with intermediation Rio de Janeiro 213 Caio Augusto Colango Teles Money distribution with intermediation

FUNDAÇÃO GETULIO VARGAS ESCOLA DE PÓS-GRADUAÇÃO EM ECONOMIA Caio Augusto Colango Teles Money distribution with intermediation Rio de Janeiro 213 Caio Augusto Colango Teles Money distribution with intermediation

Auction is a commonly used way of allocating indivisible

Econ 221 Fall, 2018 Li, Hao UBC CHAPTER 16. BIDDING STRATEGY AND AUCTION DESIGN Auction is a commonly used way of allocating indivisible goods among interested buyers. Used cameras, Salvator Mundi, and

Econ 221 Fall, 2018 Li, Hao UBC CHAPTER 16. BIDDING STRATEGY AND AUCTION DESIGN Auction is a commonly used way of allocating indivisible goods among interested buyers. Used cameras, Salvator Mundi, and

Double Auction Markets vs. Matching & Bargaining Markets: Comparing the Rates at which They Converge to Efficiency

Double Auction Markets vs. Matching & Bargaining Markets: Comparing the Rates at which They Converge to Efficiency Mark Satterthwaite Northwestern University October 25, 2007 1 Overview Bargaining, private

Double Auction Markets vs. Matching & Bargaining Markets: Comparing the Rates at which They Converge to Efficiency Mark Satterthwaite Northwestern University October 25, 2007 1 Overview Bargaining, private

MPhil F510 Topics in International Finance Petra M. Geraats Lent Course Overview

Course Overview MPhil F510 Topics in International Finance Petra M. Geraats Lent 2016 1. New micro approach to exchange rates 2. Currency crises References: Lyons (2001) Masson (2007) Asset Market versus

Course Overview MPhil F510 Topics in International Finance Petra M. Geraats Lent 2016 1. New micro approach to exchange rates 2. Currency crises References: Lyons (2001) Masson (2007) Asset Market versus

Monetary Exchange in Over-the-Counter Markets: A Theory of Speculative Bubbles, the Fed Model, and Self-fulfilling Liquidity Crises

Monetary Exchange in Over-the-Counter Markets: A Theory of Speculative Bubbles, the Fed Model, and Self-fulfilling Liquidity Crises Ricardo Lagos New York University Shengxing Zhang London School of Economics

Monetary Exchange in Over-the-Counter Markets: A Theory of Speculative Bubbles, the Fed Model, and Self-fulfilling Liquidity Crises Ricardo Lagos New York University Shengxing Zhang London School of Economics

A Search Model of the Aggregate Demand for Safe and Liquid Assets

A Search Model of the Aggregate Demand for Safe and Liquid Assets Ji Shen London School of Economics Hongjun Yan Yale School of Management January 7, 24 We thank Nicolae Garleanu, Arvind Krishnamurthy,

A Search Model of the Aggregate Demand for Safe and Liquid Assets Ji Shen London School of Economics Hongjun Yan Yale School of Management January 7, 24 We thank Nicolae Garleanu, Arvind Krishnamurthy,

Secret Contracting and Interlocking Relationships. Bergen Competition Policy Conference - April 24, 2015

Secret Contracting and Interlocking Relationships Patrick Rey (TSE) Thibaud Vergé (ENSAE and BECCLE) Bergen Competition Policy Conference - April 24, 2015 Vertical restraints : theory vs practice Literature

Secret Contracting and Interlocking Relationships Patrick Rey (TSE) Thibaud Vergé (ENSAE and BECCLE) Bergen Competition Policy Conference - April 24, 2015 Vertical restraints : theory vs practice Literature

Deposits and Bank Capital Structure

Deposits and Bank Capital Structure Franklin Allen 1 Elena Carletti 2 Robert Marquez 3 1 University of Pennsylvania 2 Bocconi University 3 UC Davis June 2014 Franklin Allen, Elena Carletti, Robert Marquez

Deposits and Bank Capital Structure Franklin Allen 1 Elena Carletti 2 Robert Marquez 3 1 University of Pennsylvania 2 Bocconi University 3 UC Davis June 2014 Franklin Allen, Elena Carletti, Robert Marquez

UCLA Department of Economics Ph.D. Preliminary Exam Industrial Organization Field Exam (Spring 2010) Use SEPARATE booklets to answer each question

Use SEPARATE booklets to answer each question") Wednesday, June 23 2010 Instructions: UCLA Department of Economics Ph.D. Preliminary Exam Industrial Organization Field Exam (Spring 2010) You have 4 hours for the exam. Answer any 5 out 6 questions. All

Wednesday, June 23 2010 Instructions: UCLA Department of Economics Ph.D. Preliminary Exam Industrial Organization Field Exam (Spring 2010) You have 4 hours for the exam. Answer any 5 out 6 questions. All

Monetary Policy and Asset Prices: A Mechanism Design Approach

Monetary Policy and Asset Prices: A Mechanism Design Approach Tai-Wei Hu Northwestern University Guillaume Rocheteau University of California, Irvine LEMMA, University of Pantheon-Assas, Paris 2 Second

Monetary Policy and Asset Prices: A Mechanism Design Approach Tai-Wei Hu Northwestern University Guillaume Rocheteau University of California, Irvine LEMMA, University of Pantheon-Assas, Paris 2 Second

Game Theory with Applications to Finance and Marketing, I

Game Theory with Applications to Finance and Marketing, I Homework 1, due in recitation on 10/18/2018. 1. Consider the following strategic game: player 1/player 2 L R U 1,1 0,0 D 0,0 3,2 Any NE can be

Game Theory with Applications to Finance and Marketing, I Homework 1, due in recitation on 10/18/2018. 1. Consider the following strategic game: player 1/player 2 L R U 1,1 0,0 D 0,0 3,2 Any NE can be

Ph.D. Preliminary Examination MICROECONOMIC THEORY Applied Economics Graduate Program August 2017

Ph.D. Preliminary Examination MICROECONOMIC THEORY Applied Economics Graduate Program August 2017 The time limit for this exam is four hours. The exam has four sections. Each section includes two questions.

Ph.D. Preliminary Examination MICROECONOMIC THEORY Applied Economics Graduate Program August 2017 The time limit for this exam is four hours. The exam has four sections. Each section includes two questions.

Over-the-Counter Trade and the Value of Assets as Collateral

Over-the-Counter Trade and the Value of Assets as Collateral Athanasios Geromichalos, Jiwon Lee, Seungduck Lee, and Keita Oikawa University of California - Davis This Version: April 2015 ABSTRACT We study

Over-the-Counter Trade and the Value of Assets as Collateral Athanasios Geromichalos, Jiwon Lee, Seungduck Lee, and Keita Oikawa University of California - Davis This Version: April 2015 ABSTRACT We study

Competitive Outcomes, Endogenous Firm Formation and the Aspiration Core

Competitive Outcomes, Endogenous Firm Formation and the Aspiration Core Camelia Bejan and Juan Camilo Gómez September 2011 Abstract The paper shows that the aspiration core of any TU-game coincides with

Competitive Outcomes, Endogenous Firm Formation and the Aspiration Core Camelia Bejan and Juan Camilo Gómez September 2011 Abstract The paper shows that the aspiration core of any TU-game coincides with

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics. Ph. D. Comprehensive Examination: Macroeconomics Fall, 2010

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Comprehensive Examination: Macroeconomics Fall, 2010 Section 1. (Suggested Time: 45 Minutes) For 3 of the following 6 statements, state

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Comprehensive Examination: Macroeconomics Fall, 2010 Section 1. (Suggested Time: 45 Minutes) For 3 of the following 6 statements, state

Financial Economics Field Exam August 2011

Financial Economics Field Exam August 2011 There are two questions on the exam, representing Macroeconomic Finance (234A) and Corporate Finance (234C). Please answer both questions to the best of your

Financial Economics Field Exam August 2011 There are two questions on the exam, representing Macroeconomic Finance (234A) and Corporate Finance (234C). Please answer both questions to the best of your

Ramsey Asset Taxation Under Asymmetric Information

Ramsey Asset Taxation Under Asymmetric Information Piero Gottardi EUI Nicola Pavoni Bocconi, IFS & CEPR Anacapri, June 2014 Asset Taxation and the Financial System Structure of the financial system differs

Ramsey Asset Taxation Under Asymmetric Information Piero Gottardi EUI Nicola Pavoni Bocconi, IFS & CEPR Anacapri, June 2014 Asset Taxation and the Financial System Structure of the financial system differs