Session 174 PD, Nested Stochastic Modeling Research. Moderator: Anthony Dardis, FSA, CERA, FIA, MAAA. Presenters: Runhuan Feng, FSA, CERA

|

|

|

- Gregory Hines

- 5 years ago

- Views:

Transcription

1 Session 174 PD, Nested Stochastic Modeling Research Moderator: Anthony Dardis, FSA, CERA, FIA, MAAA Presenters: Anthony Dardis, FSA, CERA, FIA, MAAA Runhuan Feng, FSA, CERA SOA Antitrust Disclaimer SOA Presentation Disclaimer

2 Nested Stochastic Modeling Research Tony Dardis 2016 SOA Annual Meeting & Exhibit October 26, 2016, 12pm 1.15pm

3 2

4 Nature of the Beast Taken from presentation by Tony Dardis (at the time with Moody s Analytics) at 2014 SOA Annual Meeting & Exhibit Session 88 PD ERM s Quantitative Components: Stress Testing and Economic Capital 3

5 Candidates to Tame the Beast (per the AAA Model Efficiency Work Group) Actuarial and Modeling Techniques Technology Solutions Scenario Design & Selection Hardware Design Mathematical and/or Model Design Software Design Model Data Building Techniques Hybrid Techniques 4

6 Thank you

7 2016 SOA study on nested stochastic modeling Jointly sponsored by SOA financial reporting section and modeling section

8 Background Nested stochastic modeling Do we really need it? More regulatory requirements move towards dependence on stochastic modeling Computational burden grows exponentially with nested modeling Run time can be too long to get results and take actions in a timely manner Stronger desire for efficient techniques

9 Purpose To create a resource to help financial reporting actuaries answer the following questions: Q1: In what situations is nested stochastic modeling commonly used? Q2: What other approaches can be used instead of nested stochastic modeling? Q3: What techniques can be used to accelerate the run time for nested stochastic modeling?

10 2016 SOA survey on nested stochastics Survey conducted in December 2015-January 2016 Sent to members of financial reporting section and modeling section Requested one response from each company Excluded consulting firms and software vendors 18 insurance companies participated in the survey and the majority of them focus on life and annuities

11 Survey content Part I: Context of survey participants Part II: Infrastructure and practice on general stochastic modeling Part III: Circumstances for nested stochastic modeling Part IV: Implementation Part V: Methodologies Part VI: Parting comments

12 Context of survey participants Total statutory assets at 12/31/2014 including separate accounts

13 Context of survey participants Approximate breakdown of assets backing each major product line (including separate accounts)

14 Context of survey participants Approximate breakdown of assets backing each major product line (including separate accounts)

15 Q1: In what circumstances is nested stochastics commonly used?

16 Q1: In what circumstances is nested stochastics commonly used? In what situations do you plan to use nested stochastic modeling in the future?

17 Q1: In what circumstances is nested stochastics commonly used? For which products do you plan to use nested stochastic modeling?

18 There are often possible competing factors that affect your decision to adopt a new stochastic modeling technique (e.g. a trade-off between efficiency and accuracy). Please identify the relevant factors on a scale of 1 to 5, where 1= least important at all, 5= most important Average of all respondents Average of those who plan to use nested stochastics Average of those with clear priorities

19 Important factor for adopting new technology in nested stochastics The three most important factors that affect an insurance company s decision to adopt a new stochastic modeling technique are: (in the order of importance by average rating) Timeliness of result delivery Accuracy Ability to interpret results

20 Nested stochastic modeling Nested stochastic modeling is theoretically required in a stochastic calculation where certain financial components are themselves stochastically determined.

Sequential allocation (ideal use of resources; can be slow due to dynamic")

21 Monte Carlo methods Crude Monte Carlo (easy to implement; can be extremely time-consuming) Optimal Budget Allocation (easy to implement; existing allocation strategies depend on specific risk measures) Sequential allocation (ideal use of resources; can be slow due to dynamic allocation)

22 Sequential budget allocation

23 Three categories of methods to improve efficiency Optimal allocation of resources between inner loops and outer loops Optimal budget allocation Sequential allocation Replace inner loops by approximations Analytical methods Partial differential equation methods Reduce inner loops by curve fitting techniques Preprocessed inner loops Least squared Monte Carlo Least squared Monte Carlo with basis selection

24 Preprocessed inner loops Pros Easy to understand and implement Accurate in low dimension Cons May be difficult to determine boundary points for interpolation Requires large grid in high dimensions Path-dependence (can be addressed by adding dimensions)

25 Least squared Monte Carlo Pros Accurate in low dimension Can be used for extrapolation Cons Little guidance for basis functions (can be addressed by basis selection techniques)

26 Least squared Monte Carlo Ordinary LSMC Response variable: risk metric (y) Predictor variable: time, risk factors (t, x) y=f(t,x) where f(t,x)=t+t^2+x+x^2+tx Can be more sophisticated with stepwise regression LSMC with basis selection More intelligent selection of bases from exponential functions

27 LSMC with basis selection

28 Partial differential equation methods Pros High efficiency by simultaneous computation of risk neutral values Cons Require expertise for stochastic analysis May require special algorithms for high dimensions

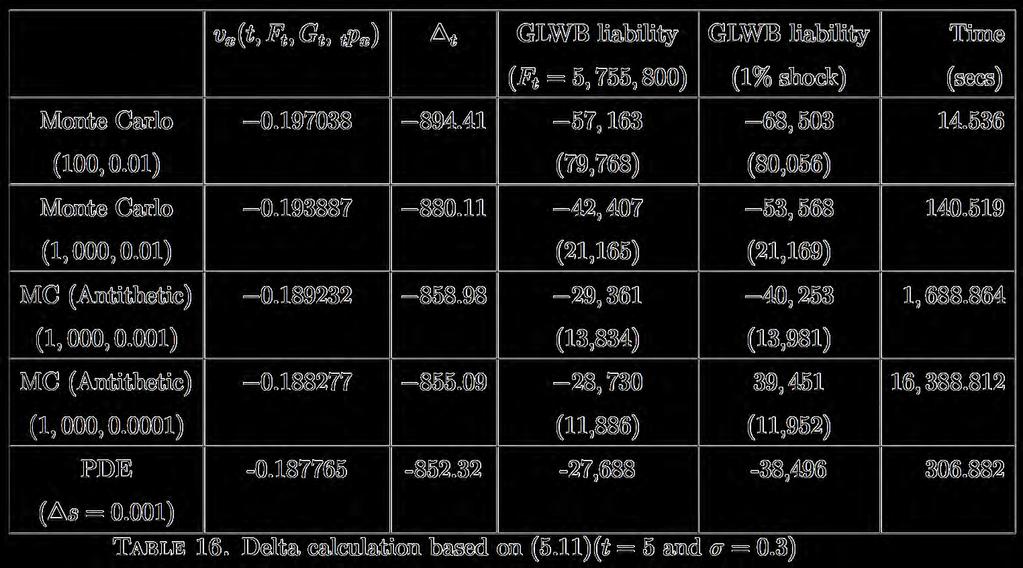

29 Test case II: AG-43 CTE calculation for guaranteed minimum withdrawal benefits Outer loop (AG-43 reserving CTE best efforts) Under each scenario of equity returns, we determine cash flows from separate accounts (withdrawal payments, step-up payments, interest on surplus, rider charges, management fees) and the cash flows from the hedging portfolio (buy and sell of index futures and bonds). The change in surplus is determined by the following recursive relation over each period. Change in surplus = Fee income + Surrender charge GLWB withdrawals Expenses +Investment income on cash flows Change in asset values +Investment income on surplus. An inner loop calculation is invoked every time a dynamic hedging portfolio is rebalanced.

30 Test case II: AG-43 CTE calculation for guaranteed minimum withdrawal benefits Inner loop (hedging program) The delta,, of the GLWB rider, which determines how many units of index futures to hold in the hedging portfolio, is calculated as follows. (1) Evaluate the risk-neutral value of the GLWB rider with the then-current account value and the then-current guarantee base. (2) Shock the then-current account value by 1% and evaluate the risk-neutral value of the GLWB rider. (3) Determine the delta by the difference quotient of riskneutral values.

31 How does a PDE method work?

32 Model validation: accuracy test Valuation basis for closed-form solution

33 Model validation: accuracy test

34 Model validation: accuracy test

35 Comparative analysis: efficiency test

36 Comparative analysis: efficiency test

37 Comparative analysis: efficiency test

38 Comparative analysis: efficiency test

39 Accuracy versus complexity Why bother with 5% improvement of accuracy at the expense of introducing more complex machinery? The above-described calculation is required for every node of outer loop scenario. All computations are done on an imac with 2.7 GHz Intel Core i5 and 8 GB 1600 MHz DDR3.

40 Advantage of PDE methods PDE algorithm marches through all time-space grid points, thereby producing risk-neutral values all at once.

41 AG-43 CTE(best efforts) Sigma=0.3 Terminal surplus before and after hedging Four dimensional models for LSMC & Preprocessed (time, AV, GB, lapse rate)

42 AG-43 CTE(best efforts) Sigma=0.1 Terminal surplus before and after hedging Four dimensional models for LSMC & Preprocessed (time, AV, GB, lapse rate)

43 AG-43 CTE(best efforts) Sigma=0.1 Terminal surplus before and after hedging Two dimensional models for LSMC & Preprocessed (time, AV/GB)

44 Thank you! Special thanks to the POG and Ronora Stryker for their suggestions. Final reports for this research study as well as the industrial survey will be published by the SOA. Draft available upon request. Suggestions and comments are greatly appreciated!

In physics and engineering education, Fermi problems

A THOUGHT ON FERMI PROBLEMS FOR ACTUARIES By Runhuan Feng In physics and engineering education, Fermi problems are named after the physicist Enrico Fermi who was known for his ability to make good approximate

A THOUGHT ON FERMI PROBLEMS FOR ACTUARIES By Runhuan Feng In physics and engineering education, Fermi problems are named after the physicist Enrico Fermi who was known for his ability to make good approximate

Session 70 PD, Model Efficiency - Part II. Moderator: Anthony Dardis, FSA, CERA, FIA, MAAA

Session 70 PD, Model Efficiency - Part II Moderator: Anthony Dardis, FSA, CERA, FIA, MAAA Presenters: Anthony Dardis, FSA, CERA, FIA, MAAA Ronald J. Harasym, FSA, CERA, FCIA, MAAA Andrew Ching Ng, FSA,

Session 70 PD, Model Efficiency - Part II Moderator: Anthony Dardis, FSA, CERA, FIA, MAAA Presenters: Anthony Dardis, FSA, CERA, FIA, MAAA Ronald J. Harasym, FSA, CERA, FCIA, MAAA Andrew Ching Ng, FSA,

Least Squares Monte Carlo (LSMC) life and annuity application Prepared for Institute of Actuaries of Japan

life and annuity application Prepared for Institute of Actuaries of Japan") Least Squares Monte Carlo (LSMC) life and annuity application Prepared for Institute of Actuaries of Japan February 3, 2015 Agenda A bit of theory Overview of application Case studies Final remarks 2 Least

Least Squares Monte Carlo (LSMC) life and annuity application Prepared for Institute of Actuaries of Japan February 3, 2015 Agenda A bit of theory Overview of application Case studies Final remarks 2 Least

Session 83 PD, Modeling Managing and Pricing Living Benefits Risk. Moderator: Sean Michael Hayward, FSA, MAAA

Session 83 PD, Modeling Managing and Pricing Living Benefits Risk Moderator: Sean Michael Hayward, FSA, MAAA Presenters: Guillaume Briere-Giroux, FSA, MAAA Sean Michael Hayward, FSA, MAAA Eric L. Henderson,

Session 83 PD, Modeling Managing and Pricing Living Benefits Risk Moderator: Sean Michael Hayward, FSA, MAAA Presenters: Guillaume Briere-Giroux, FSA, MAAA Sean Michael Hayward, FSA, MAAA Eric L. Henderson,

Nested Stochastic Modeling for Insurance Companies

Nested Stochastic Modeling for Insurance Companies November 216 2 Nested Stochastic Modeling for Insurance Companies SPONSOR Financial Reporting Section Modeling Section Committee on Life Insurance Research

Nested Stochastic Modeling for Insurance Companies November 216 2 Nested Stochastic Modeling for Insurance Companies SPONSOR Financial Reporting Section Modeling Section Committee on Life Insurance Research

Proxy Techniques for Estimating Variable Annuity Greeks. Presenter(s): Aubrey Clayton, Aaron Guimaraes

: Aubrey Clayton, Aaron Guimaraes") Sponsored by and Proxy Techniques for Estimating Variable Annuity Greeks Presenter(s): Aubrey Clayton, Aaron Guimaraes Proxy Techniques for Estimating Variable Annuity Greeks Aubrey Clayton, Moody s Analytics

Sponsored by and Proxy Techniques for Estimating Variable Annuity Greeks Presenter(s): Aubrey Clayton, Aaron Guimaraes Proxy Techniques for Estimating Variable Annuity Greeks Aubrey Clayton, Moody s Analytics

Efficient Nested Simulation for CTE of Variable Annuities

Ou (Jessica) Dang jessica.dang@uwaterloo.ca Dept. Statistics and Actuarial Science University of Waterloo Efficient Nested Simulation for CTE of Variable Annuities Joint work with Dr. Mingbin (Ben) Feng

Ou (Jessica) Dang jessica.dang@uwaterloo.ca Dept. Statistics and Actuarial Science University of Waterloo Efficient Nested Simulation for CTE of Variable Annuities Joint work with Dr. Mingbin (Ben) Feng

American Academy of Actuaries Modeling Efficiency Work Group

American Academy of Actuaries Modeling Efficiency Work Group Tony Dardis, CERA, FIA, FSA, MAAA Chairperson, Modeling Efficiency Work Group Copyright 2013 by the American Academy of Actuaries All Rights

American Academy of Actuaries Modeling Efficiency Work Group Tony Dardis, CERA, FIA, FSA, MAAA Chairperson, Modeling Efficiency Work Group Copyright 2013 by the American Academy of Actuaries All Rights

Session 3B: Stress Testing from Macro-environment, to Scenario to Impacts and Decision. Moderator: Dariush A. Akhtari, FSA, MAAA, FCIA

Session 3B: Stress Testing from Macro-environment, to Scenario to Impacts and Decision Moderator: Dariush A. Akhtari, FSA, MAAA, FCIA Presenters: Ricky Power David Wicklund, FSA SOA Antitrust Disclaimer

Session 3B: Stress Testing from Macro-environment, to Scenario to Impacts and Decision Moderator: Dariush A. Akhtari, FSA, MAAA, FCIA Presenters: Ricky Power David Wicklund, FSA SOA Antitrust Disclaimer

Session 3B, Stochastic Investment Planning. Presenters: Paul Manson, CFA. SOA Antitrust Disclaimer SOA Presentation Disclaimer

Session 3B, Stochastic Investment Planning Presenters: Paul Manson, CFA SOA Antitrust Disclaimer SOA Presentation Disclaimer The 8 th SOA Asia Pacific Annual Symposium 24 May 2018 Stochastic Investment

Session 3B, Stochastic Investment Planning Presenters: Paul Manson, CFA SOA Antitrust Disclaimer SOA Presentation Disclaimer The 8 th SOA Asia Pacific Annual Symposium 24 May 2018 Stochastic Investment

Making Proxy Functions Work in Practice

whitepaper FEBRUARY 2016 Author Martin Elliot martin.elliot@moodys.com Contact Us Americas +1.212.553.165 clientservices@moodys.com Europe +44.20.7772.5454 clientservices.emea@moodys.com Making Proxy Functions

whitepaper FEBRUARY 2016 Author Martin Elliot martin.elliot@moodys.com Contact Us Americas +1.212.553.165 clientservices@moodys.com Europe +44.20.7772.5454 clientservices.emea@moodys.com Making Proxy Functions

Session 20 PD, Senior Management's Wander Through the Model Efficiency Countryside. Moderator: Anthony Dardis, FSA, CERA, FIA, MAAA

Session 20 PD, Senior Management's Wander Through the Model Efficiency Countryside Moderator: Anthony Dardis, FSA, CERA, FIA, MAAA Presenters: Mark A. Davis, FSA, MAAA Nazir Valani, FSA, FCIA, MAAA SOA

Session 20 PD, Senior Management's Wander Through the Model Efficiency Countryside Moderator: Anthony Dardis, FSA, CERA, FIA, MAAA Presenters: Mark A. Davis, FSA, MAAA Nazir Valani, FSA, FCIA, MAAA SOA

Session 76 PD, Modeling Indexed Products. Moderator: Leonid Shteyman, FSA. Presenters: Trevor D. Huseman, FSA, MAAA Leonid Shteyman, FSA

Session 76 PD, Modeling Indexed Products Moderator: Leonid Shteyman, FSA Presenters: Trevor D. Huseman, FSA, MAAA Leonid Shteyman, FSA Modeling Indexed Products Trevor Huseman, FSA, MAAA Managing Director

Session 76 PD, Modeling Indexed Products Moderator: Leonid Shteyman, FSA Presenters: Trevor D. Huseman, FSA, MAAA Leonid Shteyman, FSA Modeling Indexed Products Trevor Huseman, FSA, MAAA Managing Director

Session 118 PD - VM-20 Impact on Product Development: Research Study Phase 2. Moderator: Kelly J. Rabin, FSA, MAAA

Session 118 PD - VM-20 Impact on Product Development: Research Study Phase 2 Moderator: Kelly J. Rabin, FSA, MAAA Presenters: Paul Fedchak, FSA, MAAA Jacqueline M. Keating, FSA, MAAA Michael W. Santore,

Session 118 PD - VM-20 Impact on Product Development: Research Study Phase 2 Moderator: Kelly J. Rabin, FSA, MAAA Presenters: Paul Fedchak, FSA, MAAA Jacqueline M. Keating, FSA, MAAA Michael W. Santore,

Session 2. Predictive Analytics in Policyholder Behavior

SOA Predictive Analytics Seminar Malaysia 27 Aug. 2018 Kuala Lumpur, Malaysia Session 2 Predictive Analytics in Policyholder Behavior Eileen Burns, FSA, MAAA David Wang, FSA, FIA, MAAA Predictive Analytics

SOA Predictive Analytics Seminar Malaysia 27 Aug. 2018 Kuala Lumpur, Malaysia Session 2 Predictive Analytics in Policyholder Behavior Eileen Burns, FSA, MAAA David Wang, FSA, FIA, MAAA Predictive Analytics

Accelerated Option Pricing Multiple Scenarios

Accelerated Option Pricing in Multiple Scenarios 04.07.2008 Stefan Dirnstorfer (stefan@thetaris.com) Andreas J. Grau (grau@thetaris.com) 1 Abstract This paper covers a massive acceleration of Monte-Carlo

Accelerated Option Pricing in Multiple Scenarios 04.07.2008 Stefan Dirnstorfer (stefan@thetaris.com) Andreas J. Grau (grau@thetaris.com) 1 Abstract This paper covers a massive acceleration of Monte-Carlo

US Life Insurer Stress Testing

US Life Insurer Stress Testing Presentation to the Office of Financial Research June 12, 2015 Nancy Bennett, MAAA, FSA, CERA John MacBain, MAAA, FSA Tom Campbell, MAAA, FSA, CERA May not be reproduced

US Life Insurer Stress Testing Presentation to the Office of Financial Research June 12, 2015 Nancy Bennett, MAAA, FSA, CERA John MacBain, MAAA, FSA Tom Campbell, MAAA, FSA, CERA May not be reproduced

Session 88 PD, PBR: Practical Implementation and Governance Issues. Moderator: Helen Colterman, FSA, CERA, ACIA

Session 88 PD, PBR: Practical Implementation and Governance Issues Moderator: Helen Colterman, FSA, CERA, ACIA Presenters: Paul M. Fischer, FSA, MAAA Carrie Lee Kelley, FSA, MAAA Christopher Almer Whitney,

Session 88 PD, PBR: Practical Implementation and Governance Issues Moderator: Helen Colterman, FSA, CERA, ACIA Presenters: Paul M. Fischer, FSA, MAAA Carrie Lee Kelley, FSA, MAAA Christopher Almer Whitney,

Session 030 PD - PBR Stochastic Reserve - Challenges and Possible Solutions. Moderator: Sebastien Cimon Gagnon, FSA, CERA, MAAA

Session 030 PD - PBR Stochastic Reserve - Challenges and Possible Solutions Moderator: Sebastien Cimon Gagnon, FSA, CERA, MAAA Presenters: Timothy C. Cardinal, FSA, CERA, MAAA Andrew G. Steenman, FSA,

Session 030 PD - PBR Stochastic Reserve - Challenges and Possible Solutions Moderator: Sebastien Cimon Gagnon, FSA, CERA, MAAA Presenters: Timothy C. Cardinal, FSA, CERA, MAAA Andrew G. Steenman, FSA,

ORSA: Prospective Solvency Assessment and Capital Projection Modelling

FEBRUARY 2013 ENTERPRISE RISK SOLUTIONS B&H RESEARCH ESG FEBRUARY 2013 DOCUMENTATION PACK Craig Turnbull FIA Andy Frepp FFA Moody's Analytics Research Contact Us Americas +1.212.553.1658 clientservices@moodys.com

FEBRUARY 2013 ENTERPRISE RISK SOLUTIONS B&H RESEARCH ESG FEBRUARY 2013 DOCUMENTATION PACK Craig Turnbull FIA Andy Frepp FFA Moody's Analytics Research Contact Us Americas +1.212.553.1658 clientservices@moodys.com

The Actuarial Society of Hong Kong Modelling market risk in extremely low interest rate environment

The Actuarial Society of Hong Kong Modelling market risk in extremely low interest rate environment Eric Yau Consultant, Barrie & Hibbert Asia Eric.Yau@barrhibb.com 12 th Appointed Actuaries Symposium,

The Actuarial Society of Hong Kong Modelling market risk in extremely low interest rate environment Eric Yau Consultant, Barrie & Hibbert Asia Eric.Yau@barrhibb.com 12 th Appointed Actuaries Symposium,

Trends in Annuities. Products, Riders, and Reinsurance. Tiffany Wills, FSA, CERA, MAAA Assistant Vice President and Actuary

Trends in Annuities Products, Riders, and Reinsurance Tiffany Wills, FSA, CERA, MAAA Assistant Vice President and Actuary SEAC Conference June 2016 Topics of Discussion The Annuity Market Living Benefit

Trends in Annuities Products, Riders, and Reinsurance Tiffany Wills, FSA, CERA, MAAA Assistant Vice President and Actuary SEAC Conference June 2016 Topics of Discussion The Annuity Market Living Benefit

Article from: Risks & Rewards. August 2014 Issue 64

Article from: Risks & Rewards August 2014 Issue 64 MEASURING THE COST OF DURATION MISMATCH USING LEAST SQUARES MONTE CARLO (LSMC) By Casey Malone and David Wang Duration matching is perhaps the best-known

Article from: Risks & Rewards August 2014 Issue 64 MEASURING THE COST OF DURATION MISMATCH USING LEAST SQUARES MONTE CARLO (LSMC) By Casey Malone and David Wang Duration matching is perhaps the best-known

Optimized Least-squares Monte Carlo (OLSM) for Measuring Counterparty Credit Exposure of American-style Options

for Measuring Counterparty Credit Exposure of American-style Options") Optimized Least-squares Monte Carlo (OLSM) for Measuring Counterparty Credit Exposure of American-style Options Kin Hung (Felix) Kan 1 Greg Frank 3 Victor Mozgin 3 Mark Reesor 2 1 Department of Applied

Optimized Least-squares Monte Carlo (OLSM) for Measuring Counterparty Credit Exposure of American-style Options Kin Hung (Felix) Kan 1 Greg Frank 3 Victor Mozgin 3 Mark Reesor 2 1 Department of Applied

VA Guarantee Reinsurance Market Status. Ari Lindner

Equity-Based Insurance Guarantees Conference Nov. 5-6, 2018 Chicago, IL VA Guarantee Reinsurance Market Status Ari Lindner SOA Antitrust Compliance Guidelines SOA Presentation Disclaimer Sponsored by Image:

Equity-Based Insurance Guarantees Conference Nov. 5-6, 2018 Chicago, IL VA Guarantee Reinsurance Market Status Ari Lindner SOA Antitrust Compliance Guidelines SOA Presentation Disclaimer Sponsored by Image:

Session 60PD: US GAAP Income Statement Analysis. Moderator: Paul R Vogel, FSA, MAAA

Session 60PD: US GAAP Income Statement Analysis Moderator: Paul R Vogel, FSA, MAAA Presenters: Joshua Liu, FSA, MAAA Paul R Vogel, FSA, MAAA John R Washburn, FSA, MAAA SOA Antitrust Disclaimer SOA Presentation

Session 60PD: US GAAP Income Statement Analysis Moderator: Paul R Vogel, FSA, MAAA Presenters: Joshua Liu, FSA, MAAA Paul R Vogel, FSA, MAAA John R Washburn, FSA, MAAA SOA Antitrust Disclaimer SOA Presentation

Optimizing Modular Expansions in an Industrial Setting Using Real Options

Optimizing Modular Expansions in an Industrial Setting Using Real Options Abstract Matt Davison Yuri Lawryshyn Biyun Zhang The optimization of a modular expansion strategy, while extremely relevant in

Optimizing Modular Expansions in an Industrial Setting Using Real Options Abstract Matt Davison Yuri Lawryshyn Biyun Zhang The optimization of a modular expansion strategy, while extremely relevant in

Proxy Methods for Hedge Projection: Two Variable Annuity Case Studies

MAY 2016 RESEARCH INSURANCE Proxy Methods for Hedge Projection: Two Variable Annuity Case Studies Authors Aubrey Clayton PhD Steven Morrison PhD Moody's Analytics Research Contact Us Americas +1.212.553.1658

MAY 2016 RESEARCH INSURANCE Proxy Methods for Hedge Projection: Two Variable Annuity Case Studies Authors Aubrey Clayton PhD Steven Morrison PhD Moody's Analytics Research Contact Us Americas +1.212.553.1658

Financial Modeling of Variable Annuities

0 Financial Modeling of Variable Annuities Robert Chen 18 26 June, 2007 1 Agenda Building blocks of a variable annuity model A Stochastic within Stochastic Model Rational policyholder behaviour Discussion

0 Financial Modeling of Variable Annuities Robert Chen 18 26 June, 2007 1 Agenda Building blocks of a variable annuity model A Stochastic within Stochastic Model Rational policyholder behaviour Discussion

Proxy Function Fitting: Some Implementation Topics

OCTOBER 2013 ENTERPRISE RISK SOLUTIONS RESEARCH OCTOBER 2013 Proxy Function Fitting: Some Implementation Topics Gavin Conn FFA Moody's Analytics Research Contact Us Americas +1.212.553.1658 clientservices@moodys.com

OCTOBER 2013 ENTERPRISE RISK SOLUTIONS RESEARCH OCTOBER 2013 Proxy Function Fitting: Some Implementation Topics Gavin Conn FFA Moody's Analytics Research Contact Us Americas +1.212.553.1658 clientservices@moodys.com

Guidance paper on the use of internal models for risk and capital management purposes by insurers

Guidance paper on the use of internal models for risk and capital management purposes by insurers October 1, 2008 Stuart Wason Chair, IAA Solvency Sub-Committee Agenda Introduction Global need for guidance

Guidance paper on the use of internal models for risk and capital management purposes by insurers October 1, 2008 Stuart Wason Chair, IAA Solvency Sub-Committee Agenda Introduction Global need for guidance

Session 48PD: PBR - Real Life Applications. Moderator: Alberto A Abalo FSA,MAAA,CERA

Session 48PD: PBR - Real Life Applications Moderator: Alberto A Abalo FSA,MAAA,CERA Presenters: Alberto A Abalo FSA,MAAA,CERA Lauren M Cross FSA,MAAA Martin Snow FSA,MAAA Erzhe Zhang FSA,MAAA SOA Antitrust

Session 48PD: PBR - Real Life Applications Moderator: Alberto A Abalo FSA,MAAA,CERA Presenters: Alberto A Abalo FSA,MAAA,CERA Lauren M Cross FSA,MAAA Martin Snow FSA,MAAA Erzhe Zhang FSA,MAAA SOA Antitrust

Multi-year Projection of Run-off Conditional Tail Expectation (CTE) Reserves

Reserves") JUNE 2013 ENTERPRISE RISK SOLUTIONS B&H RESEARCH ESG JUNE 2013 DOCUMENTATION PACK Steven Morrison PhD Craig Turnbull FIA Naglis Vysniauskas Moody's Analytics Research Contact Us Craig.Turnbull@moodys.com

JUNE 2013 ENTERPRISE RISK SOLUTIONS B&H RESEARCH ESG JUNE 2013 DOCUMENTATION PACK Steven Morrison PhD Craig Turnbull FIA Naglis Vysniauskas Moody's Analytics Research Contact Us Craig.Turnbull@moodys.com

WHITE PAPER THINKING FORWARD ABOUT PRICING AND HEDGING VARIABLE ANNUITIES

WHITE PAPER THINKING FORWARD ABOUT PRICING AND HEDGING VARIABLE ANNUITIES We can t solve problems by using the same kind of thinking we used when we created them. Albert Einstein As difficult as the recent

WHITE PAPER THINKING FORWARD ABOUT PRICING AND HEDGING VARIABLE ANNUITIES We can t solve problems by using the same kind of thinking we used when we created them. Albert Einstein As difficult as the recent

GN47: Stochastic Modelling of Economic Risks in Life Insurance

GN47: Stochastic Modelling of Economic Risks in Life Insurance Classification Recommended Practice MEMBERS ARE REMINDED THAT THEY MUST ALWAYS COMPLY WITH THE PROFESSIONAL CONDUCT STANDARDS (PCS) AND THAT

GN47: Stochastic Modelling of Economic Risks in Life Insurance Classification Recommended Practice MEMBERS ARE REMINDED THAT THEY MUST ALWAYS COMPLY WITH THE PROFESSIONAL CONDUCT STANDARDS (PCS) AND THAT

Session 55 PD, Pricing in a MCEV Environment. Moderator: Kendrick D. Lombardo, FSA, MAAA

Session 55 PD, Pricing in a MCEV Environment Moderator: Kendrick D. Lombardo, FSA, MAAA Presenters: Christopher Kirk Brown, FSA, MAAA Seng Siang Goh, FSA, MAAA Kendrick D. Lombardo, FSA, MAAA PRICING IN

Session 55 PD, Pricing in a MCEV Environment Moderator: Kendrick D. Lombardo, FSA, MAAA Presenters: Christopher Kirk Brown, FSA, MAAA Seng Siang Goh, FSA, MAAA Kendrick D. Lombardo, FSA, MAAA PRICING IN

NAIC s Center for Insurance Policy and Research Summit: Exploring Insurers Liabilities

NAIC s Center for Insurance Policy and Research Summit: Exploring Insurers Liabilities Session 3: Life Panel Issues with Internal Modeling Dave Neve, FSA, MAAA, CERA Chairperson, American Academy of Actuaries

NAIC s Center for Insurance Policy and Research Summit: Exploring Insurers Liabilities Session 3: Life Panel Issues with Internal Modeling Dave Neve, FSA, MAAA, CERA Chairperson, American Academy of Actuaries

Hedging Strategy Simulation and Backtesting with DSLs, GPUs and the Cloud

Hedging Strategy Simulation and Backtesting with DSLs, GPUs and the Cloud GPU Technology Conference 2013 Aon Benfield Securities, Inc. Annuity Solutions Group (ASG) This document is the confidential property

Hedging Strategy Simulation and Backtesting with DSLs, GPUs and the Cloud GPU Technology Conference 2013 Aon Benfield Securities, Inc. Annuity Solutions Group (ASG) This document is the confidential property

SOA Risk Management Task Force

SOA Risk Management Task Force Update - Session 25 May, 2002 Dave Ingram Hubert Mueller Jim Reiskytl Darrin Zimmerman Risk Management Task Force Update Agenda Risk Management Section Formation CAS/SOA

SOA Risk Management Task Force Update - Session 25 May, 2002 Dave Ingram Hubert Mueller Jim Reiskytl Darrin Zimmerman Risk Management Task Force Update Agenda Risk Management Section Formation CAS/SOA

Fast Convergence of Regress-later Series Estimators

Fast Convergence of Regress-later Series Estimators New Thinking in Finance, London Eric Beutner, Antoon Pelsser, Janina Schweizer Maastricht University & Kleynen Consultants 12 February 2014 Beutner Pelsser

Fast Convergence of Regress-later Series Estimators New Thinking in Finance, London Eric Beutner, Antoon Pelsser, Janina Schweizer Maastricht University & Kleynen Consultants 12 February 2014 Beutner Pelsser

Session 176 PD - Emerging Trends in Model Risk Management for Small Companies. Moderator: Vikas Sharan, FSA, FIA, MAAA

Session 176 PD - Emerging Trends in Model Risk Management for Small Companies Moderator: Vikas Sharan, FSA, FIA, MAAA Presenters: Brody D. Lipperman, FSA, CERA, MAAA Stefanie J. Porta, ASA, MAAA Vikas

Session 176 PD - Emerging Trends in Model Risk Management for Small Companies Moderator: Vikas Sharan, FSA, FIA, MAAA Presenters: Brody D. Lipperman, FSA, CERA, MAAA Stefanie J. Porta, ASA, MAAA Vikas

Using Least Squares Monte Carlo techniques in insurance with R

Using Least Squares Monte Carlo techniques in insurance with R Sébastien de Valeriola sebastiendevaleriola@reacfincom Amsterdam, June 29 th 2015 Solvency II The major difference between Solvency I and

Using Least Squares Monte Carlo techniques in insurance with R Sébastien de Valeriola sebastiendevaleriola@reacfincom Amsterdam, June 29 th 2015 Solvency II The major difference between Solvency I and

Session 63 PD, Annuity Policyholder Behavior. Moderator: Kendrick D. Lombardo, FSA, MAAA

Session 63 PD, Annuity Policyholder Behavior Moderator: Kendrick D. Lombardo, FSA, MAAA Presenters: Eileen Sheila Burns, FSA, MAAA Kendrick D. Lombardo, FSA, MAAA Timothy S. Paris, FSA, MAAA Timothy Paris,

Session 63 PD, Annuity Policyholder Behavior Moderator: Kendrick D. Lombardo, FSA, MAAA Presenters: Eileen Sheila Burns, FSA, MAAA Kendrick D. Lombardo, FSA, MAAA Timothy S. Paris, FSA, MAAA Timothy Paris,

Educational Note. Reflection of Hedging in Segregated Fund Valuation

Educational Note Reflection of Hedging in Segregated Fund Valuation Committee on Life Insurance Financial Reporting May 2012 Document 212027 Ce document est disponible en français 2012 Canadian Institute

Educational Note Reflection of Hedging in Segregated Fund Valuation Committee on Life Insurance Financial Reporting May 2012 Document 212027 Ce document est disponible en français 2012 Canadian Institute

Model Governance: Is YOUR Company There Yet? Past, Present and Future of Model Governance. Moderator: Ronald J. Harasym, FSA, CERA, FCIA, MAAA

Model Governance: Is YOUR Company There Yet? Past, Present and Future of Model Governance Moderator: Ronald J. Harasym, FSA, CERA,, FCIA, MAAA Presenters: Dave Czernicki, FSA, MAAA Ronald J. Harasym, FSA,

Model Governance: Is YOUR Company There Yet? Past, Present and Future of Model Governance Moderator: Ronald J. Harasym, FSA, CERA,, FCIA, MAAA Presenters: Dave Czernicki, FSA, MAAA Ronald J. Harasym, FSA,

Pricing with a Smile. Bruno Dupire. Bloomberg

CP-Bruno Dupire.qxd 10/08/04 6:38 PM Page 1 11 Pricing with a Smile Bruno Dupire Bloomberg The Black Scholes model (see Black and Scholes, 1973) gives options prices as a function of volatility. If an

CP-Bruno Dupire.qxd 10/08/04 6:38 PM Page 1 11 Pricing with a Smile Bruno Dupire Bloomberg The Black Scholes model (see Black and Scholes, 1973) gives options prices as a function of volatility. If an

VOLATILITY EFFECTS AND VIRTUAL ASSETS: HOW TO PRICE AND HEDGE AN ENERGY PORTFOLIO

VOLATILITY EFFECTS AND VIRTUAL ASSETS: HOW TO PRICE AND HEDGE AN ENERGY PORTFOLIO GME Workshop on FINANCIAL MARKETS IMPACT ON ENERGY PRICES Responsabile Pricing and Structuring Edison Trading Rome, 4 December

VOLATILITY EFFECTS AND VIRTUAL ASSETS: HOW TO PRICE AND HEDGE AN ENERGY PORTFOLIO GME Workshop on FINANCIAL MARKETS IMPACT ON ENERGY PRICES Responsabile Pricing and Structuring Edison Trading Rome, 4 December

Basel II Quantitative Masterclass

Basel II Quantitative Masterclass 4-Day Professional Development Workshop East Asia Training & Consultancy Pte Ltd invites you to attend a four-day professional development workshop on Basel II Quantitative

Basel II Quantitative Masterclass 4-Day Professional Development Workshop East Asia Training & Consultancy Pte Ltd invites you to attend a four-day professional development workshop on Basel II Quantitative

Session 04PD: Statutory Life and Annuity Issues. Moderator: Thomas A Campbell FSA,MAAA,CERA

Session 04PD: Statutory Life and Annuity Issues Moderator: Thomas A Campbell FSA,MAAA,CERA Presenters: Donna R Claire FSA,MAAA,CERA David E Neve FSA,MAAA,CERA SOA Antitrust Disclaimer SOA Presentation

Session 04PD: Statutory Life and Annuity Issues Moderator: Thomas A Campbell FSA,MAAA,CERA Presenters: Donna R Claire FSA,MAAA,CERA David E Neve FSA,MAAA,CERA SOA Antitrust Disclaimer SOA Presentation

2018 Investment Symposium

2018 Investment Symposium Session 3B: Duration Matching Versus Cash Flow Matching for Pension Plans Moderator: Thomas J. Egan, Jr., FSA, EA, CFP Presenters: Kevin McLaughlin, Insight Investment Matthew

2018 Investment Symposium Session 3B: Duration Matching Versus Cash Flow Matching for Pension Plans Moderator: Thomas J. Egan, Jr., FSA, EA, CFP Presenters: Kevin McLaughlin, Insight Investment Matthew

How Can YOU Use it? Artificial Intelligence for Actuaries. SOA Annual Meeting, Gaurav Gupta. Session 058PD

Artificial Intelligence for Actuaries How Can YOU Use it? SOA Annual Meeting, 2018 Session 058PD Gaurav Gupta Founder & CEO ggupta@quaerainsights.com Audience Poll What is my level of AI understanding?

Artificial Intelligence for Actuaries How Can YOU Use it? SOA Annual Meeting, 2018 Session 058PD Gaurav Gupta Founder & CEO ggupta@quaerainsights.com Audience Poll What is my level of AI understanding?

Financial Risk Management for the Life Insurance / Wealth Management Industry. Wade Matterson

Financial Risk Management for the Life Insurance / Wealth Management Industry Wade Matterson Agenda 1. Introduction 2. Products with Guarantees 3. Understanding & Managing the Risks INTRODUCTION The Argument

Financial Risk Management for the Life Insurance / Wealth Management Industry Wade Matterson Agenda 1. Introduction 2. Products with Guarantees 3. Understanding & Managing the Risks INTRODUCTION The Argument

Moderator: Donna Christine Megregian, FSA, MAAA

Session 46 PD, Newly Proposed ASOPs: Pricing, Modeling and Setting Assumptions Moderator: Donna Christine Megregian, FSA, MAAA Presenters: Donna Christine Megregian, FSA, MAAA James A. Miles, FSA, MAAA

Session 46 PD, Newly Proposed ASOPs: Pricing, Modeling and Setting Assumptions Moderator: Donna Christine Megregian, FSA, MAAA Presenters: Donna Christine Megregian, FSA, MAAA James A. Miles, FSA, MAAA

Stochastic Pricing. Southeastern Actuaries Conference. Cheryl Angstadt. November 15, Towers Perrin

Stochastic Pricing Southeastern Actuaries Conference Cheryl Angstadt November 15, 2007 2007 Towers Perrin Agenda Background Drivers Case Study PBA and SOS Approaches 2007 Towers Perrin 2 Background What

Stochastic Pricing Southeastern Actuaries Conference Cheryl Angstadt November 15, 2007 2007 Towers Perrin Agenda Background Drivers Case Study PBA and SOS Approaches 2007 Towers Perrin 2 Background What

Risk-Neutral Valuation in Practice: Implementing a Hedging Strategy for Segregated Fund Guarantees

Risk-Neutral Valuation in Practice: Implementing a Hedging Strategy for Segregated Fund Guarantees Martin le Roux December 8, 2000 martin_le_roux@sunlife.com Hedging: Pros and Cons Pros: Protection against

Risk-Neutral Valuation in Practice: Implementing a Hedging Strategy for Segregated Fund Guarantees Martin le Roux December 8, 2000 martin_le_roux@sunlife.com Hedging: Pros and Cons Pros: Protection against

Preparing for Solvency II Theoretical and Practical issues in Building Internal Economic Capital Models Using Nested Stochastic Projections

Preparing for Solvency II Theoretical and Practical issues in Building Internal Economic Capital Models Using Nested Stochastic Projections Ed Morgan, Italy, Marc Slutzky, USA Milliman Abstract: This paper

Preparing for Solvency II Theoretical and Practical issues in Building Internal Economic Capital Models Using Nested Stochastic Projections Ed Morgan, Italy, Marc Slutzky, USA Milliman Abstract: This paper

Session 127 PD, Life and Annuity In-Force Management. Moderator: David J. Weinsier, FSA, MAAA

Session 127 PD, Life and Annuity In-Force Management Moderator: David J. Weinsier, FSA, MAAA Presenters: Jennifer L. McGinnis, FSA, CERA, MAAA Brock E. Robbins, FSA, FCIA, MAAA David J. Weinsier, FSA,

Session 127 PD, Life and Annuity In-Force Management Moderator: David J. Weinsier, FSA, MAAA Presenters: Jennifer L. McGinnis, FSA, CERA, MAAA Brock E. Robbins, FSA, FCIA, MAAA David J. Weinsier, FSA,

The American Academy of Actuaries Duration Blanks Work Group Response to the NAIC Blanks Working Group Proposal. May 2011

The American Academy of Actuaries Duration Blanks Work Group Response to the NAIC Blanks Working Group Proposal May 2011 The American Academy of Actuaries is a 17,000-member professional association whose

The American Academy of Actuaries Duration Blanks Work Group Response to the NAIC Blanks Working Group Proposal May 2011 The American Academy of Actuaries is a 17,000-member professional association whose

Session 14 PD, The Search for Model Efficiency Through Data Compression. Moderator: Trevor C. Howes, FSA, FCIA, MAAA

Session 14 PD, The Search for Model Efficiency Through Data Compression Moderator: Trevor C. Howes, FSA, FCIA, MAAA Presenters: Dan (Danielle) Li, FSA Andrey Marchenko SOA Antitrust Disclaimer SOA Presentation

Session 14 PD, The Search for Model Efficiency Through Data Compression Moderator: Trevor C. Howes, FSA, FCIA, MAAA Presenters: Dan (Danielle) Li, FSA Andrey Marchenko SOA Antitrust Disclaimer SOA Presentation

The Financial Reporter

Article from: The Financial Reporter March 2006 Issue No. 64 RBC C3 Phase II: Easier Said Than Done by Patricia Matson and Don Wilson The stochastic projection is performed using real world, as opposed

Article from: The Financial Reporter March 2006 Issue No. 64 RBC C3 Phase II: Easier Said Than Done by Patricia Matson and Don Wilson The stochastic projection is performed using real world, as opposed

Monte Carlo Methods in Structuring and Derivatives Pricing

Monte Carlo Methods in Structuring and Derivatives Pricing Prof. Manuela Pedio (guest) 20263 Advanced Tools for Risk Management and Pricing Spring 2017 Outline and objectives The basic Monte Carlo algorithm

Monte Carlo Methods in Structuring and Derivatives Pricing Prof. Manuela Pedio (guest) 20263 Advanced Tools for Risk Management and Pricing Spring 2017 Outline and objectives The basic Monte Carlo algorithm

New Actuarial Standards of Practice No. 46 Risk Evaluation in ERM No. 47 Risk Treatment in ERM

New Actuarial Standards of Practice No. 46 Risk Evaluation in ERM No. 47 Risk Treatment in ERM August 1, 2013 1 Professional Disclaimer Any opinions expressed within this presentation are the presenter

New Actuarial Standards of Practice No. 46 Risk Evaluation in ERM No. 47 Risk Treatment in ERM August 1, 2013 1 Professional Disclaimer Any opinions expressed within this presentation are the presenter

XSG. Economic Scenario Generator. Risk-neutral and real-world Monte Carlo modelling solutions for insurers

XSG Economic Scenario Generator Risk-neutral and real-world Monte Carlo modelling solutions for insurers 2 Introduction to XSG What is XSG? XSG is Deloitte s economic scenario generation software solution,

XSG Economic Scenario Generator Risk-neutral and real-world Monte Carlo modelling solutions for insurers 2 Introduction to XSG What is XSG? XSG is Deloitte s economic scenario generation software solution,

ESGs: Spoilt for choice or no alternatives?

ESGs: Spoilt for choice or no alternatives? FA L K T S C H I R S C H N I T Z ( F I N M A ) 1 0 3. M i t g l i e d e r v e r s a m m l u n g S AV A F I R, 3 1. A u g u s t 2 0 1 2 Agenda 1. Why do we need

ESGs: Spoilt for choice or no alternatives? FA L K T S C H I R S C H N I T Z ( F I N M A ) 1 0 3. M i t g l i e d e r v e r s a m m l u n g S AV A F I R, 3 1. A u g u s t 2 0 1 2 Agenda 1. Why do we need

2017 Predictive Analytics Symposium

2017 Predictive Analytics Symposium Session 29, Predictive Analytics for Inforce Management Moderator: Rohan Noel Alahakone, ASA, MAAA Presenters: Jenny Jin, FSA, MAAA Assaf Mizan Martin Snow, FSA, MAAA

2017 Predictive Analytics Symposium Session 29, Predictive Analytics for Inforce Management Moderator: Rohan Noel Alahakone, ASA, MAAA Presenters: Jenny Jin, FSA, MAAA Assaf Mizan Martin Snow, FSA, MAAA

Stochastic Modeling Concerns and RBC C3 Phase 2 Issues

Stochastic Modeling Concerns and RBC C3 Phase 2 Issues ACSW Fall Meeting San Antonio Jason Kehrberg, FSA, MAAA Friday, November 12, 2004 10:00-10:50 AM Outline Stochastic modeling concerns Background,

Stochastic Modeling Concerns and RBC C3 Phase 2 Issues ACSW Fall Meeting San Antonio Jason Kehrberg, FSA, MAAA Friday, November 12, 2004 10:00-10:50 AM Outline Stochastic modeling concerns Background,

SOCIETY OF ACTUARIES Individual Life & Annuities United States Design & Pricing Exam DP-IU MORNING SESSION

SOCIETY OF ACTUARIES Individual Life & Annuities United States Design & Pricing Exam DP-IU MORNING SESSION Date: Thursday, October 30, 2008 Time: 8:30 a.m. 11:45 a.m. INSTRUCTIONS TO CANDIDATES General

SOCIETY OF ACTUARIES Individual Life & Annuities United States Design & Pricing Exam DP-IU MORNING SESSION Date: Thursday, October 30, 2008 Time: 8:30 a.m. 11:45 a.m. INSTRUCTIONS TO CANDIDATES General

ALM processes and techniques in insurance

ALM processes and techniques in insurance David Campbell 18 th November. 2004 PwC Asset Liability Management Matching or management? The Asset-Liability Management framework Example One: Asset risk factors

ALM processes and techniques in insurance David Campbell 18 th November. 2004 PwC Asset Liability Management Matching or management? The Asset-Liability Management framework Example One: Asset risk factors

Vanguard Global Capital Markets Model

Vanguard Global Capital Markets Model Research brief March 1 Vanguard s Global Capital Markets Model TM (VCMM) is a proprietary financial simulation engine designed to help our clients make effective asset

Vanguard Global Capital Markets Model Research brief March 1 Vanguard s Global Capital Markets Model TM (VCMM) is a proprietary financial simulation engine designed to help our clients make effective asset

PBR Reserve Movement and Earnings Analysis

PBR Reserve Movement and Earnings Analysis Rich Harris, FSA, FCIA, MAAA VP & US Appointed Actuary John Hancock Session 25PD PBR Attribution Analysis August 27, 2018 SOCIETY OF ACTUARIES Antitrust Compliance

PBR Reserve Movement and Earnings Analysis Rich Harris, FSA, FCIA, MAAA VP & US Appointed Actuary John Hancock Session 25PD PBR Attribution Analysis August 27, 2018 SOCIETY OF ACTUARIES Antitrust Compliance

Session 97 PD, Variable Annuity Guaranteed Living Benefit Utilization Studies and Benefit Utilization in Fixed Indexed Annuities

Session 97 PD, Variable Annuity Guaranteed Living Benefit Utilization Studies and Benefit Utilization in Fixed Indexed Annuities Moderator: Patrick David Nolan, FSA, MAAA Presenters: Jafor Iqbal Joseph

Session 97 PD, Variable Annuity Guaranteed Living Benefit Utilization Studies and Benefit Utilization in Fixed Indexed Annuities Moderator: Patrick David Nolan, FSA, MAAA Presenters: Jafor Iqbal Joseph

SOA Life & Annuity Symposium May 16-17, Session 31 PD, Does Anyone Else Want to be Illustration Actuary this Year?

SOA Life & Annuity Symposium May 16-17, 2011 Session 31 PD, Does Anyone Else Want to be Illustration Actuary this Year? Moderator: Donna Christine Megregian, FSA, MAAA Presenters: Gayle L. Donato, FSA,

SOA Life & Annuity Symposium May 16-17, 2011 Session 31 PD, Does Anyone Else Want to be Illustration Actuary this Year? Moderator: Donna Christine Megregian, FSA, MAAA Presenters: Gayle L. Donato, FSA,

The Pennsylvania State University. The Graduate School. Department of Industrial Engineering AMERICAN-ASIAN OPTION PRICING BASED ON MONTE CARLO

The Pennsylvania State University The Graduate School Department of Industrial Engineering AMERICAN-ASIAN OPTION PRICING BASED ON MONTE CARLO SIMULATION METHOD A Thesis in Industrial Engineering and Operations

The Pennsylvania State University The Graduate School Department of Industrial Engineering AMERICAN-ASIAN OPTION PRICING BASED ON MONTE CARLO SIMULATION METHOD A Thesis in Industrial Engineering and Operations

Session 80 PD, Cash Balance Plan Update. Moderator: Emily Brantley Donavant, ASA

Session 80 PD, Cash Balance Plan Update Moderator: Emily Brantley Donavant, ASA Presenters: Alan R. Glickstein, ASA, EA Mary R. Hardy, FSA, CERA, ACIA, FIA SOA Antitrust Disclaimer SOA Presentation Disclaimer

Session 80 PD, Cash Balance Plan Update Moderator: Emily Brantley Donavant, ASA Presenters: Alan R. Glickstein, ASA, EA Mary R. Hardy, FSA, CERA, ACIA, FIA SOA Antitrust Disclaimer SOA Presentation Disclaimer

Field Tests of Economic Value-Based Solvency Regime. Summary of the Results

May 24 2011 Financial Services Agency Field Tests of Economic Value-Based Solvency Regime Summary of the Results In June through December 2010 the Financial Services Agency (FSA) conducted field tests

May 24 2011 Financial Services Agency Field Tests of Economic Value-Based Solvency Regime Summary of the Results In June through December 2010 the Financial Services Agency (FSA) conducted field tests

Inforce Management 2014 ACHS Fall Meeting

Inforce Management 2014 ACHS Fall Meeting November 11, 2014 Dave Wiland, FSA, CERA, MAAA, CFA IMPORTANT INFORMATION The information in this presentation is intended to be generic in nature to help foster

Inforce Management 2014 ACHS Fall Meeting November 11, 2014 Dave Wiland, FSA, CERA, MAAA, CFA IMPORTANT INFORMATION The information in this presentation is intended to be generic in nature to help foster

Session 102 PD - Impact of VM-20 on Life Insurance Pricing. Moderator: Trevor D. Huseman, FSA, MAAA

Session 102 PD - Impact of VM-20 on Life Insurance Pricing Moderator: Trevor D. Huseman, FSA, MAAA Presenters: Carrie Lee Kelley, FSA, MAAA William Gus Mehilos, FSA, MAAA SOA Antitrust Compliance Guidelines

Session 102 PD - Impact of VM-20 on Life Insurance Pricing Moderator: Trevor D. Huseman, FSA, MAAA Presenters: Carrie Lee Kelley, FSA, MAAA William Gus Mehilos, FSA, MAAA SOA Antitrust Compliance Guidelines

The Value of Storage Forecasting storage flows and gas prices

Amsterdam, 9 May 2017 FLAME conference The Value of Storage Forecasting storage flows and gas prices www.kyos.com, +31 (0)23 5510221 Cyriel de Jong, dejong@kyos.com KYOS Energy Analytics Analytical solutions

Amsterdam, 9 May 2017 FLAME conference The Value of Storage Forecasting storage flows and gas prices www.kyos.com, +31 (0)23 5510221 Cyriel de Jong, dejong@kyos.com KYOS Energy Analytics Analytical solutions

Quantitative Finance Investment Advanced Exam

Quantitative Finance Investment Advanced Exam Important Exam Information: Exam Registration Order Study Notes Introductory Study Note Case Study Past Exams Updates Formula Package Table Candidates may

Quantitative Finance Investment Advanced Exam Important Exam Information: Exam Registration Order Study Notes Introductory Study Note Case Study Past Exams Updates Formula Package Table Candidates may

Risks and Rewards Newsletter

Article from: Risks and Rewards Newsletter September 2000 Issue No. 35 RISKS and REWARDS The Newsletter of the Investment Section of the Society of Actuaries NUMBER 35 SEPTEMBER 2000 Chairperson s Corner

Article from: Risks and Rewards Newsletter September 2000 Issue No. 35 RISKS and REWARDS The Newsletter of the Investment Section of the Society of Actuaries NUMBER 35 SEPTEMBER 2000 Chairperson s Corner

Rethinking Fixed Deferred Annuities: Applying a Risk-Based Economic Value Approach

Rethinking Fixed Deferred Annuities: Applying a Risk-Based Economic Value Approach Noel Harewood, FSA, MAAA Dominique Lebel, FSA, FCIA, MAAA Mark Scanlon, FSA, CFA, CERA, FIA Presented at 2010 Enterprise

Rethinking Fixed Deferred Annuities: Applying a Risk-Based Economic Value Approach Noel Harewood, FSA, MAAA Dominique Lebel, FSA, FCIA, MAAA Mark Scanlon, FSA, CFA, CERA, FIA Presented at 2010 Enterprise

UPDATED IAA EDUCATION SYLLABUS

II. UPDATED IAA EDUCATION SYLLABUS A. Supporting Learning Areas 1. STATISTICS Aim: To enable students to apply core statistical techniques to actuarial applications in insurance, pensions and emerging

II. UPDATED IAA EDUCATION SYLLABUS A. Supporting Learning Areas 1. STATISTICS Aim: To enable students to apply core statistical techniques to actuarial applications in insurance, pensions and emerging

VALUATION OF VARIABLE ANNUITIES USING GRID COMPUTING AXA LIFE EUROPE HEDGING SERVICES (ALEHS) 05/06/2008

05/06/2008") VALUATION OF VARIABLE ANNUITIES USING GRID COMPUTING AXA LIFE EUROPE HEDGING SERVICES (ALEHS) 05/06/2008 Structure Variable annuities ALEHS liability valuation software (MoSes. Tower Perrin) The run time

VALUATION OF VARIABLE ANNUITIES USING GRID COMPUTING AXA LIFE EUROPE HEDGING SERVICES (ALEHS) 05/06/2008 Structure Variable annuities ALEHS liability valuation software (MoSes. Tower Perrin) The run time

The Impact of Stochastic Volatility and Policyholder Behaviour on Guaranteed Lifetime Withdrawal Benefits

and Policyholder Guaranteed Lifetime 8th Conference in Actuarial Science & Finance on Samos 2014 Frankfurt School of Finance and Management June 1, 2014 1. Lifetime withdrawal guarantees in PLIs 2. policyholder

and Policyholder Guaranteed Lifetime 8th Conference in Actuarial Science & Finance on Samos 2014 Frankfurt School of Finance and Management June 1, 2014 1. Lifetime withdrawal guarantees in PLIs 2. policyholder

Session 31 PD, Product Design & Policyholder Behavior. Moderator: Timothy S. Paris, FSA, MAAA

Session 31 PD, Product Design & Policyholder Behavior Moderator: Timothy S. Paris, FSA, MAAA Presenters: Michael Anthony Cusumano, FSA Timothy S. Paris, FSA, MAAA Product Design and Policyholder Behavior

Session 31 PD, Product Design & Policyholder Behavior Moderator: Timothy S. Paris, FSA, MAAA Presenters: Michael Anthony Cusumano, FSA Timothy S. Paris, FSA, MAAA Product Design and Policyholder Behavior

PBA Reserve Workshop What Will PBA Mean to You and Your Software? Trevor Howes, FCIA, FSA, MAAA. Agenda. Overview to PBA project

Southeastern Actuaries Conference 2010 Spring Meeting June 16, 2010 PBA Reserve Workshop What Will PBA Mean to You and Your Software? Trevor Howes, FCIA, FSA, MAAA Michael LeBoeuf, FSA, MAAA Agenda Overview

Southeastern Actuaries Conference 2010 Spring Meeting June 16, 2010 PBA Reserve Workshop What Will PBA Mean to You and Your Software? Trevor Howes, FCIA, FSA, MAAA Michael LeBoeuf, FSA, MAAA Agenda Overview

GETTING THE MOST OUT OF AXIS

Consulting Actuaries Volume 9 FALL 2018 GETTING THE MOST OUT OF AXIS ADAPTING TO AN EVER-CHANGING LANDSCAPE Editor s words: Welcome to the Fall 2018 edition of our AXIS newsletter. This issue outlines

Consulting Actuaries Volume 9 FALL 2018 GETTING THE MOST OUT OF AXIS ADAPTING TO AN EVER-CHANGING LANDSCAPE Editor s words: Welcome to the Fall 2018 edition of our AXIS newsletter. This issue outlines

Moderator: Sean Michael Hayward FSA,MAAA. Presenters: Joshua S Y Chee FSA Sean Michael Hayward FSA,MAAA Michael Porcelli FSA,MAAA

SOA Antitrust Disclaimer SOA Presentation Disclaimer Session 63PD: Modeling Function: To Centralize or Not To Centralize? Moderator: Sean Michael Hayward FSA,MAAA Presenters: Joshua S Y Chee FSA Sean Michael

SOA Antitrust Disclaimer SOA Presentation Disclaimer Session 63PD: Modeling Function: To Centralize or Not To Centralize? Moderator: Sean Michael Hayward FSA,MAAA Presenters: Joshua S Y Chee FSA Sean Michael

Modelling optimal decisions for financial planning in retirement using stochastic control theory

Modelling optimal decisions for financial planning in retirement using stochastic control theory Johan G. Andréasson School of Mathematical and Physical Sciences University of Technology, Sydney Thesis

Modelling optimal decisions for financial planning in retirement using stochastic control theory Johan G. Andréasson School of Mathematical and Physical Sciences University of Technology, Sydney Thesis

A hybrid approach to valuing American barrier and Parisian options

A hybrid approach to valuing American barrier and Parisian options M. Gustafson & G. Jetley Analysis Group, USA Abstract Simulation is a powerful tool for pricing path-dependent options. However, the possibility

A hybrid approach to valuing American barrier and Parisian options M. Gustafson & G. Jetley Analysis Group, USA Abstract Simulation is a powerful tool for pricing path-dependent options. However, the possibility

Moderator: Eric L Clapprood FSA,CERA. Presenters: Dwayne Allen Husbands FSA,MAAA Youyou Tao FSA,CERA

Session 3: How to Effectively Embed Stress Testing into a Risk Management Framework to Support Management Action SOA Antitrust Disclaimer SOA Presentation Disclaimer Moderator: Eric L Clapprood FSA,CERA

Session 3: How to Effectively Embed Stress Testing into a Risk Management Framework to Support Management Action SOA Antitrust Disclaimer SOA Presentation Disclaimer Moderator: Eric L Clapprood FSA,CERA

Investment Symposium March F7: Investment Implications of a Principal-Based Approach to Capital. Moderator Ross Bowen

Investment Symposium March 2010 F7: Investment Implications of a Principal-Based Approach to Capital David Wicklund Arnold Dicke Moderator Ross Bowen Investment Implications of a Principle Based Approach

Investment Symposium March 2010 F7: Investment Implications of a Principal-Based Approach to Capital David Wicklund Arnold Dicke Moderator Ross Bowen Investment Implications of a Principle Based Approach

Market Risk Analysis Volume I

Market Risk Analysis Volume I Quantitative Methods in Finance Carol Alexander John Wiley & Sons, Ltd List of Figures List of Tables List of Examples Foreword Preface to Volume I xiii xvi xvii xix xxiii

Market Risk Analysis Volume I Quantitative Methods in Finance Carol Alexander John Wiley & Sons, Ltd List of Figures List of Tables List of Examples Foreword Preface to Volume I xiii xvi xvii xix xxiii

Numerix Economic Scenario Generator

Numerix Economic Scenario Generator Transparency and Flexibility in an Easy-to-Use Application Risk neutral and real world scenarios Built on the world s largest capital market model library Easy to use

Numerix Economic Scenario Generator Transparency and Flexibility in an Easy-to-Use Application Risk neutral and real world scenarios Built on the world s largest capital market model library Easy to use

GETTING THE MOST OUT OF AXIS

Consulting Actuaries Volume 3 FALL 2015 GETTING THE MOST OUT OF AXIS IN THIS ISSUE EXECUTIVE CORNER Upcoming AXIS structural changes IN THE SPOTLIGHT Using the AXIS Flexible Scenario Format TIPS & TRICKS

Consulting Actuaries Volume 3 FALL 2015 GETTING THE MOST OUT OF AXIS IN THIS ISSUE EXECUTIVE CORNER Upcoming AXIS structural changes IN THE SPOTLIGHT Using the AXIS Flexible Scenario Format TIPS & TRICKS

An Impact Analysis of Proposed Targeted Improvements

Proposed Changes to US GAAP An Impact Analysis of Proposed Targeted Improvements June 2017 Karthik Yadatore, FSA, MAAA Craig Reynolds, FSA, MAAA William Hines, FSA, MAAA Shamit Gupta, BSC, FIA, FIAI, CERA

Proposed Changes to US GAAP An Impact Analysis of Proposed Targeted Improvements June 2017 Karthik Yadatore, FSA, MAAA Craig Reynolds, FSA, MAAA William Hines, FSA, MAAA Shamit Gupta, BSC, FIA, FIAI, CERA

Session 024 PD - Life Reinsurance in Bermuda. Moderator: Gokul Sudarsana, FSA, CERA, FCIA

Session 024 PD - Life Reinsurance in Bermuda Moderator: Gokul Sudarsana, FSA, CERA, FCIA Presenters: Manfred Maske Sylvia Martin Oliveira, FSA, MAAA Scott D. Selkirk, FSA, MAAA SOA Antitrust Compliance

Session 024 PD - Life Reinsurance in Bermuda Moderator: Gokul Sudarsana, FSA, CERA, FCIA Presenters: Manfred Maske Sylvia Martin Oliveira, FSA, MAAA Scott D. Selkirk, FSA, MAAA SOA Antitrust Compliance

Computational Finance Least Squares Monte Carlo

Computational Finance Least Squares Monte Carlo School of Mathematics 2019 Monte Carlo and Binomial Methods In the last two lectures we discussed the binomial tree method and convergence problems. One

Computational Finance Least Squares Monte Carlo School of Mathematics 2019 Monte Carlo and Binomial Methods In the last two lectures we discussed the binomial tree method and convergence problems. One

François Morin, FCAS, CFA, is a Principal with Tillinghast-Towers Perrin, 175 Powder Forest Drive, Weatogue, CT 06089,

RISK POSITION REPORTING Stephen Britt 1, Anthony Dardis 2, Mary Gilkison 3, François Morin 4, Mary M. Wilson 5 ABSTRACT Risk management is central to running a successful insurance operation. This means

RISK POSITION REPORTING Stephen Britt 1, Anthony Dardis 2, Mary Gilkison 3, François Morin 4, Mary M. Wilson 5 ABSTRACT Risk management is central to running a successful insurance operation. This means

RED 2.1 & 4.2: Quantifying Risk Exposure for ORSA. Moderator: Presenters: Lesley R. Bosniack, CERA, FCAS, MAAA

RED 2.1 & 4.2: Quantifying Risk Exposure for ORSA Moderator: Lesley R. Bosniack, CERA, FCAS, MAAA Presenters: Lesley R. Bosniack, CERA, FCAS, MAAA William Robert Wilkins, ASA, CERA, FCAS, MAAA SOA Antitrust

RED 2.1 & 4.2: Quantifying Risk Exposure for ORSA Moderator: Lesley R. Bosniack, CERA, FCAS, MAAA Presenters: Lesley R. Bosniack, CERA, FCAS, MAAA William Robert Wilkins, ASA, CERA, FCAS, MAAA SOA Antitrust