Authorized for public release by the FOMC Secretariat on 08/12/2016. Indicators of Trends in Dealer-Intermediated Financing and Leverage

|

|

|

- Christine Carroll

- 5 years ago

- Views:

Transcription

1 October 28, 2010 Indicators of Trends in Dealer-Intermediated Financing and Leverage Matt Eichner, Michael Holscher, and Fabio Natalucci Summary This memorandum seeks to draw information from a variety of sources, including conversations with market participants, market surveillance data, and supervisory data, to present a composite picture of the leverage currently being provided through dealer-intermediated transactions. 1 Overall, these indicators suggest a broad but modest increase in the use of dealer-intermediated leverage by market participants since the beginning of September. The appetite for additional leverage on the part of most market participants appears to remain muted, however, as was the case during most of the summer, and indeed many investors are maintaining significant unutilized borrowing capacity under existing financing facilities. Placing these developments in a longer-term context, while the availability and use of leverage appears to have increased somewhat since reaching a nadir in mid- 2009, a variety of indicators suggest that leverage generally remains below the levels reached prior to the crisis. A modest upward trend in dealer-intermediate leverage visible during the early months of the year reversed rapidly in May and early June amid concerns about the possible implications of the European fiscal strains. Over the summer, the use of leverage by important classes of investors especially hedge funds changed little. Since September, as concerns about the European fiscal situation and possible risks to the European banking system abated, the willingness of levered investors to establish and maintain risk exposures has increased somewhat, reportedly reflecting in part expectations of additional monetary policy accommodation, pressures to boost returns 1 For a detailed discussion of the relevance of this issue for financial stability analysis, see the memorandum Indications of Trends in Financial System Leverage, by Matt Eichner, Michael Holscher, and Fabio Natalucci, which was sent to the Committee on August 6, That memorandum also discusses the importance of considering multiple indicators when seeking to develop a meaningful picture of aggregate dealer-supplied leverage. 1 of 13

2 prior to reporting results for the year, and somewhat more clarity with respect to certain regulatory changes. However, the most significant financial market flows during the period have reportedly been driven by the appetite of unlevered investors for fixedincome securities, including developed market corporate debt and syndicated loans as well as, more recently, emerging market bonds a phenomenon that market participants have referred to as search for yield. Our overall assessment is that leverage has risen moderately since the beginning of the year, but the potential for a rapid or disorderly deleveraging appears to remain limited at this point. Supporting this general view are developments in several areas over the intermeeting period: Prime brokerage debits have trended higher since late summer. 2 Hedge funds have displayed some renewed appetite for risk, and thus profited from market trends over the past month, notably from the strong returns on equities. Preliminary third-quarter performance appears comparatively strong by post-crisis standards, with the median hedge fund returning 3.6 percent for the period and only 14 percent of funds reporting losses. 3 However, most hedge funds reportedly remain cautious relative to pre-crisis norms, generally utilize only a fraction of the capacity provided by their lenders, and continue to maintain significant amounts of cash. Financing for higher-quality assets appears to be broadly available, with the maximum term of funding approaching six months. Market participants also report, as they did in September, increased willingness by dealers to lend against distressed assets and other less-liquid collateral, including bank loans and structured products. In particular, the availability of total return swaps (TRS) referencing bank loans reportedly increased, and several new transactions types are being explored that would similarly facilitate the funding of less liquid assets. But investor demand for such financing remains limited at present. 2 Prime brokerage debits are credit extensions by broker-dealers, typically to hedge funds, to finance the purchase of securities on margin. 3 These preliminary returns are computed with approximately 2400 of the almost 3600 hedge funds in the TASS database reporting. 2 of 13

3 Median haircuts applicable to several assets, including high-yield corporate bonds, Treasuries, and prime residential mortgage-backed securities (prime RMBS) declined modestly, on net, over the intermeeting period. These declines represent the first reported reductions in median haircut levels since the first quarter. By contrast, median haircuts for Alt-A mortgage-backed securities (MBS) increased in October. While this increase is coincident with concerns about the legal uncertainties regarding ownership and transfer of the mortgage loans underlying such securities, several market participants reported that they had seen no indication that the recent questions about servicing had affected securities financing markets. Activity in the triparty repo market continued to increase, with total average daily volume for September reaching a new post-crisis high despite a decline later in the month, as generally occurs at quarter end. The volume of securities lending reached a high for the year and the post-crisis period in October, continuing the rise seen through the summer. Unlevered investors including pension funds, mutual funds, and insurance companies, apparently remain the driver of demand in the corporate bond and loan markets. In their effort to meet nominal return targets, they are also reportedly increasing emerging-market exposure, notably by investing in localcurrency-denominated government bonds and, more recently, equities. New issue activity in the syndicated leveraged loan market, as well as the volume of transactions in the pipeline, has increased in September and October. In addition, market participants have begun to cite a renewal of pressure on terms over the past two months, noting higher leverage, spread compression, and an increased number of transactions motivated by considerations other than longerterm strategic goals such as dividend recap and sponsor-to-sponsor deals (also called secondary buyouts). But they seem to view the most important protection the ability of syndicators to adjust the pricing and structure of loans at the borrower s expense within specified limits to adapt to current market conditions as still firmly in place. 3 of 13

4 Although we view the potential for a disorderly deleveraging as limited at this point, several dynamics bear watching going forward: First, the pressure on terms in the syndicated leveraged loan market appears to have returned, and some market participants predict that this pressure will continue to intensify over the coming months. Banks leading syndications, which effectively function as dealers in this market, appear to still enjoy considerable contractual flexibility post-commitment to adjust the pricing and structure of loans at the expense of borrowers to market-clearing levels. But these institutions will possibly become more vulnerable to a change in market sentiment to the extent that competitive pressures lead to a reduction in these protections. Second, important classes of generally unlevered investors (e.g., pension funds) are finding it difficult in the present environment to meet nominal return targets using only their traditional strategies, and are reportedly considering adding riskier financial assets to their portfolios. These investors may also be developing an appetite for leveraged exposure to certain asset classes in which they are already active, and certain segments of the dealer community may be working to satisfy these demands by offering specialized products, such as asset-backed credit lines. Thus, there is potential for a gradual increase in the use of leverage by previously unlevered investors and through unfamiliar channels, which poses challenges to those in the dealer community and elsewhere seeking to monitor the overall degree of leverage in the financial system. Finally, there is apparently broad availability of funding to traditionally levered investors such as hedge funds. The operative constraint on risk taking at the moment appears to be uncertainties regarding the economic and financial market environment. To the extent that such uncertainties subside, the degree of leverage employed by such investors could increase quickly. In the remainder of the memorandum we discuss in greater detail our conversations with market participants and the indicators of dealer-supplied leverage that support our broad assessment of current conditions and the potential for a rapid or disorderly deleveraging. 4 of 13

5 Conversations with Market Participants 4 The most recent round of conversations with market participants again emphasized that robust demand by unlevered retail and institutional investors continues to support a high level of new issue activity in the investment-grade and high-yield bond markets. Perhaps motivated by a desire to boost returns in a low interest rate environment, investors appear to be taking increased risk. They have become active in markets for local-currency-denominated government bonds, particularly bonds issued in Asia. 5 More recently, their interest has begun to expand to the equity markets in these countries. These inflows into emerging market economies differ from those seen in the mid-2000s, which were driven by levered investors such as hedge funds. Some jurisdictions referencing a macroprudential approach to financial regulation have begun to implement capital controls to stem inflows, presumably to reduce the potential negative effects of a sudden reversal in flows and limit currency appreciation. However, these measures have been relatively modest to date, and market participants believed that their effectiveness would be limited. They noted that further monetary policy accommodation in the United States would likely move additional countries to consider similar steps. In discussing the activities of institutional investors, market participants note that the ability to generate strong returns without the use of leverage appears limited at this point given current asset valuations. For example, investors found opportunities to purchase syndicated loans and non-agency MBS at distressed levels during 2009 and profited handsomely as markets recovered. At this point, however, the supply of such legacy assets, and hence opportunities to generate significant returns without the use of leverage, is largely exhausted. Therefore, market participants suggested that there are some investors with sufficiently flexible mandates who are considering establishing levered positions in assets such as bank loans, structured products, and convertible bonds. A number of dealers are reportedly developing products tailored to such investors, including asset-backed 4 This section represents a distillation of discussions with senior business heads, risk management personnel, and economists at 10 firms, representing both the investor and dealer perspective. 5 Although their purchase of these instruments is commonly described as a carry trade, no leverage is actually employed. 5 of 13

6 revolving credit lines and actively-managed investment structures similar to CLOs. Since the assets involved cannot, like more liquid fixed income and equity instruments, be funded on a secured basis with external counterparties, dealers must allocate a portion of their balance sheet to support these activities, and some appear willing to do so. Market participants described hedge funds as having been more willing to take on risk over the past two months due to a number of factors. These include an abatement of concerns about sovereign defaults and European banks, expectations of additional longer-term asset purchases by the Federal Reserve, and pressures to achieve return targets by year-end, including those upon which manager compensation are based. In particular, market participants cited increased willingness on the part of hedge funds to add long equity and short dollar positions, which have produced gains over the past month. Nonetheless, funds pursuing relative value equity strategies have reportedly found that the environment remains challenging, with high correlations in returns across equities limiting their ability to exploit their prowess at identifying differential performance of particular issuers or sectors. More generally, despite the fact that prime brokerage debits have risen since Labor Day, reflecting an increase in activity, most hedge funds reportedly remain cautious and are maintaining significant cash positions. Some market participants predicted that many of the equity and macro funds that have profited from recent foreign exchange and equity trades will seek to lock in those gains and adopt a more passive posture by Thanksgiving. Others, however, viewed the pressure to generate a respectable annual return as likely to manifest itself through the remainder of the year, with managers seeking to maintain risk positions. Longer term, market participants note that the hedge fund business model, which focuses on relative returns, faces significant challenges in an environment in which many investors are very focused on meeting their absolute return goals. A significant number of hedge funds, particularly those pursuing mandates consistent with exposure to macroeconomic events, have reportedly positioned themselves for additional monetary policy accommodation in the United States. Such a view has been expressed, inter alia, through short positions in the U.S. dollar, by extending the duration of fixed income portfolios, and by gaining exposure to equities. To the extent that Federal Reserve actions or communications were interpreted as 6 of 13

7 prevalent. 6 While these trends point to investors assuming greater risk, protections for the Authorized for public release by the FOMC Secretariat on 08/12/2016 differing significantly from current market expectations, market participants we spoke with saw a possibility of a repricing of some assets and deleveraging by hedge funds. Market participants broadly reported that the pressures on terms evident in the syndicated leveraged loan market earlier in the year, which had abated following the events in Europe during May and early June, have now returned. Investor appetite for the loan asset class is said to remain strong, among both retail and institutional investors, and a number of deals, including some LBOs, have been recently brought to market successfully. Market participants note that the leverage in these deals has risen, and also that certain transactions involving the financing of dividend payments to a financial sponsor or the sale of assets from one financial sponsor to another have become more lead banks in syndications, which facilitate initial distribution, have remained relatively robust in the leveraged loan market. Market participants noted that commitment periods, beyond which arrangers are no longer exposed should the transaction not come to fruition, remain limited to six months. In addition, syndicated loans continue to incorporate provisions that allow the arrangers flexibility within specified limits to adjust pricing and structure at the expense of the borrower to successfully place the deal with investors. Such flex represents a key protection against significant unwanted inventory and losses should investor appetite for leveraged loans diminish unexpectedly. A large inventory of hung deals was a hallmark of the crisis at many firms that operated as dealers in the syndicated loan market, and was a significant driver of losses in several cases. Several market participants indicated that their level of concern about conditions in the leveraged loan market would rise appreciably if commitment periods extended, their flexibility to adjust pricing and terms began to erode, or both. 6 In general, a financial sponsor, as distinct from a strategic purchaser, acquires a firm or a corporate asset with the intent to close its investment after a finite period, either through sale to a strategic buyer or through capital markets transactions, for example involving the issuance of debt or equity securities. 7 of 13

8 Indicator of Hedge Fund Leverage 7 As shown by the line in the upper-left panel of Exhibit 1, a broad indicator of hedge fund leverage moved back toward its longer run average level in August, probably reflecting the stabilization of industry performance during July. The indicator had declined dramatically in May and June, approaching its 2008 nadir. 8 These rapid changes in the indicator reflect in part the fact that the indicator is computed using data on longshort equity funds. Funds pursuing this strategy appear to have been particularly affected by events in May and June, and are generally able to adjust positions more quickly than funds pursuing strategies in less liquid markets. FINRA Portfolio Margining Debits The exhibit provides an overview of trends in the funding of securities, primarily equities, by prime brokers on behalf of sophisticated levered investors, notably in the hedge fund community, eligible for portfolio margining. Data for the third quarter indicates that the volume of such financing has risen, approaching its post-crisis high reached at the end of the first quarter. Currently, twenty-two U.S. broker-dealers offer portfolio margining programs to institutional clients who meet certain standards for financial and operational capacity. 9 Total portfolio margining debits at the close of the third quarter stood at $173 billion, compared to first quarter and second quarter levels of $181 billion and $157 billion, respectively. Taking a somewhat longer view, debits at the 7 This indicator does not capture the exact amount of leverage used by hedge funds, but rather focuses on trends in the use of leverage over time. This measure the median ratio of the standard deviation of returns for levered funds relative to that for unlevered funds compares return volatility for funds that reported having used leverage with return volatility for funds that reported not having used leverage. Unfortunately, information about the use of leverage is broadly available only for hedge funds that report using a long/short equity strategy (more than 600 funds out of about 3600 funds in the TASS database). It is unclear whether leveraging and deleveraging behavior among long/short equity strategy funds is representative of the industry as a whole. 8 One possible explanation for the seemingly large magnitude of the June drop may be an unusually wide distribution of returns reported by unlevered funds. 9 Since mid-2008, FINRA rules have permitted broker-dealers to utilize approved models, including those developed by firms for internal risk management purposes and by the Options Clearing Corporation, to compute margin requirements for customer portfolios containing a variety of equity-linked products. Interest on the part of prime brokers and their hedge fund clients in this portfolio margining program, which is implemented under Regulation T, grew considerably following the Lehman bankruptcy, which demonstrated the operational and financial risks of prime brokerage relationships with non-u.s. entities. 8 of 13

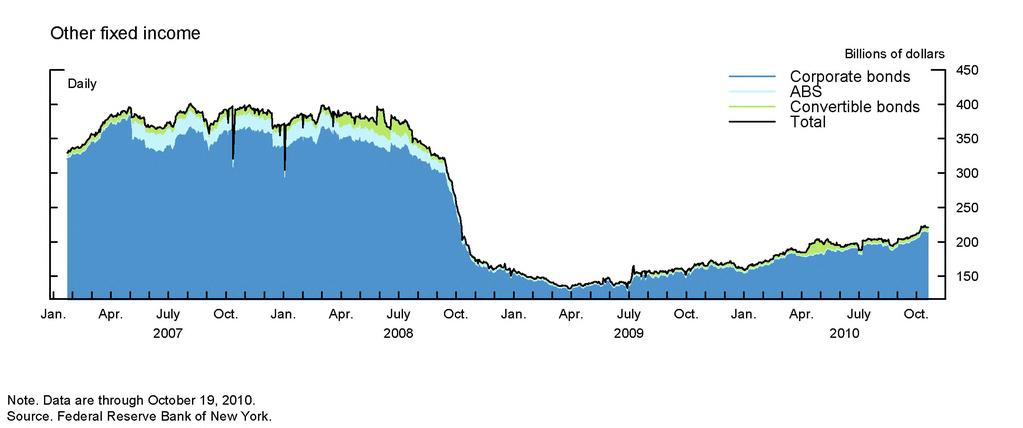

9 depth of the crisis after the first quarter 2009 stood at $92 billion, and by the end of that year had risen to $150 billion. 10 Weekly Report of Dealer Financing and Fails Additional information regarding the volume of financing of fixed-income securities obtained from the Weekly Report of Dealer Financing and Fails (also known as the FR2004C) is shown in the upper-right panel. 11 These data point to a modest upward trend in the volume of financing both utilized and provided by dealers over the intermeeting period. After remaining steady for much of 2010, haircuts applied to some collateral types shown in the panels on the bottom declined during the past month. 12 In particular, median haircuts applicable to high-yield corporate bonds, Treasuries, and prime RMBS fell, on net. Interestingly, haircuts applicable to Alt-A MBS actually increased over the same period. FRBNY Buyside Haircut Survey 13 Survey responses from buyside market participants pointed to further marginal easing in funding market conditions. Anecdotally, term financing was broadly available and contacts continued to note a modest increase in dealer willingness to extend funding beyond three months, particularly for less-liquid collateral. Contacts indicated that there continued to be some differentiation among counterparties by size, with smaller funds having less access to funding, reflected in both smaller trade size and shorter tenor, than the largest and most established funds. To date, according to buyside respondents, issues related to the ownership and transfer of mortgages have not significantly affected 10 While 22 broker-dealers are currently permitted by FINRA to provide portfolio margining to clients, one was granted permission after the fourth quarter 2009, and two more were granted permission in the third quarter While these three new additions were comparatively small firms, no adjustment has been made to the figures cited prior to their inclusion. 11 Depicted is the total volume of financing utilized by dealers (the red line) and the volume of financing provided by dealers to clients (the black line). The difference between these two series (the dotted blue line) can be interpreted as broadly reflecting the net financing used by dealers to support inventory and proprietary positions. 12 Data are obtained from the Federal Reserve Bank of New York s Weekly Survey of Primary Dealers. 13 Buyside in this context refers to the fact that the survey solicits the responses of investors, notably hedge funds, who are the secured borrowers in this market rather than dealers who are the secured lenders. 9 of 13

10 haircuts for mortgage-backed assets, although some contacts noted the potential in the near term for dealers to demand additional protection in the form of higher haircuts. Triparty Repo Market and Securities Lending Activity The last two exhibits provide an overview of trends in the triparty repo and securities lending markets. 14 The average daily volume of triparty activity shown in the upper-left panel of Exhibit 2 grew in July, August, and September, after declining in June. The total average daily volume for September reached a new post-crisis high of $1.8 trillion before declining at the end of the third quarter. The proportion of higherquality, Fed-eligible collateral remained stable, after increasing from 81 percent to 83 percent in June. 15 Securities lending activity shown in the last exhibit rebounded in October to $1.9 trillion, approaching the post-crisis high reached in May. 14 Triparty repo and securities lending data are collected by the Federal Reserve Bank of New York from the clearing banks and custodians, respectively. 15 Fed- or Fedwire-eligible collateral includes securities issued or guaranteed by the U.S. Treasury, other federal agencies, government sponsored enterprises, and certain international organizations, such as the World Bank. 10 of 13

11 Authorized for public release by the FOMC Secretariat on 08/12/2016 Exhibit 1 Indicators of Leverage in U.S. Financial Markets 11 of 13

12 Exhibit 2 Tri-Party Repo Market Activity 12 of 13

13 Exhibit 3 Securities Lending Activity 13 of 13

Senior Credit Officer Opinion Survey on Dealer Financing Terms

BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM DIVISION OF MONETARY AFFAIRS DIVISION OF RESEARCH AND STATISTICS For release at 2:00 p.m. EDT March 29, 2012 Senior Credit Officer Opinion Survey on Dealer

BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM DIVISION OF MONETARY AFFAIRS DIVISION OF RESEARCH AND STATISTICS For release at 2:00 p.m. EDT March 29, 2012 Senior Credit Officer Opinion Survey on Dealer

Senior Credit Officer Opinion Survey on Dealer Financing Terms September 2016

Page 1 of 93 Senior Credit Officer Opinion Survey on Dealer Financing Terms September 2016 Print Summary Results of the September 2016 Survey Summary The September 2016 Senior Credit Officer Opinion Survey

Page 1 of 93 Senior Credit Officer Opinion Survey on Dealer Financing Terms September 2016 Print Summary Results of the September 2016 Survey Summary The September 2016 Senior Credit Officer Opinion Survey

Indonesia: Changing patterns of financial intermediation and their implications for central bank policy

Indonesia: Changing patterns of financial intermediation and their implications for central bank policy Perry Warjiyo 1 Abstract As a bank-based economy, global factors affect financial intermediation

Indonesia: Changing patterns of financial intermediation and their implications for central bank policy Perry Warjiyo 1 Abstract As a bank-based economy, global factors affect financial intermediation

Brian P Sack: Implementing the Federal Reserve s asset purchase program

Brian P Sack: Implementing the Federal Reserve s asset purchase program Remarks by Mr Brian P Sack, Executive Vice President of the Federal Reserve Bank of New York, at the Global Interdependence Center

Brian P Sack: Implementing the Federal Reserve s asset purchase program Remarks by Mr Brian P Sack, Executive Vice President of the Federal Reserve Bank of New York, at the Global Interdependence Center

Survey Results on the Canadian Repo Market. bank-banque-canada.ca

Survey Results on the Canadian Market 25 April 2017 Disclaimer and Copyright Notice The results of the 2016 Committee on the Global Financial System (CGFS) survey on Market functioning in Canadian markets

Survey Results on the Canadian Market 25 April 2017 Disclaimer and Copyright Notice The results of the 2016 Committee on the Global Financial System (CGFS) survey on Market functioning in Canadian markets

Information, Liquidity, and the (Ongoing) Panic of 2007*

Panic of 2007*") Information, Liquidity, and the (Ongoing) Panic of 2007* Gary Gorton Yale School of Management and NBER Prepared for AER Papers & Proceedings, 2009. This version: December 31, 2008 Abstract The credit

Information, Liquidity, and the (Ongoing) Panic of 2007* Gary Gorton Yale School of Management and NBER Prepared for AER Papers & Proceedings, 2009. This version: December 31, 2008 Abstract The credit

Brian P Sack: The SOMA portfolio at $2.654 trillion

Brian P Sack: The SOMA portfolio at $2.654 trillion Remarks by Mr Brian P Sack, Executive Vice President of the Federal Reserve Bank of New York, before the Money Marketeers of New York University, New

Brian P Sack: The SOMA portfolio at $2.654 trillion Remarks by Mr Brian P Sack, Executive Vice President of the Federal Reserve Bank of New York, before the Money Marketeers of New York University, New

Shadow Banking and Financial Stability

Shadow Banking and Financial Stability Tobias Adrian, November 8, 2013 The views expressed here are those of the author exclusively and do not necessarily represent those of the Federal Reserve Bank of

Shadow Banking and Financial Stability Tobias Adrian, November 8, 2013 The views expressed here are those of the author exclusively and do not necessarily represent those of the Federal Reserve Bank of

Observation. January 18, credit availability, credit

January 18, 11 HIGHLIGHTS Underlying the improvement in economic indicators over the last several months has been growing signs that the economy is also seeing a recovery in credit conditions. The mortgage

January 18, 11 HIGHLIGHTS Underlying the improvement in economic indicators over the last several months has been growing signs that the economy is also seeing a recovery in credit conditions. The mortgage

Brian P Sack: Managing the Federal Reserve s balance sheet

Brian P Sack: Managing the Federal Reserve s balance sheet Remarks by Mr Brian P Sack, Executive Vice President of the Markets Group of the Federal Reserve Bank of New York, at the 2010 Chartered Financial

Brian P Sack: Managing the Federal Reserve s balance sheet Remarks by Mr Brian P Sack, Executive Vice President of the Markets Group of the Federal Reserve Bank of New York, at the 2010 Chartered Financial

January minutes: key signaling language

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: FOMC Minutes Wednesday, February 20, 2019 January minutes:

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: FOMC Minutes Wednesday, February 20, 2019 January minutes:

RETURN ENHANCEMENT WITH EUROPEAN ABS AND BANK LOANS IN SWISS INSTITUTIONAL PORTFOLIOS

H E A L T H W E A L T H C A R E E R RETURN ENHANCEMENT WITH EUROPEAN ABS AND BANK LOANS IN SWISS INSTITUTIONAL PORTFOLIOS JUNE 2017 INTRODUCTION In the aftermath of the global financial crisis, conventional

H E A L T H W E A L T H C A R E E R RETURN ENHANCEMENT WITH EUROPEAN ABS AND BANK LOANS IN SWISS INSTITUTIONAL PORTFOLIOS JUNE 2017 INTRODUCTION In the aftermath of the global financial crisis, conventional

APPENDIX SUMMARIZING NARRATIVE EVIDENCE ON FEDERAL RESERVE INTENTIONS FOR THE FEDERAL FUNDS RATE. Christina D. Romer David H.

APPENDIX SUMMARIZING NARRATIVE EVIDENCE ON FEDERAL RESERVE INTENTIONS FOR THE FEDERAL FUNDS RATE Christina D. Romer David H. Romer To accompany A New Measure of Monetary Shocks: Derivation and Implications,

APPENDIX SUMMARIZING NARRATIVE EVIDENCE ON FEDERAL RESERVE INTENTIONS FOR THE FEDERAL FUNDS RATE Christina D. Romer David H. Romer To accompany A New Measure of Monetary Shocks: Derivation and Implications,

DEBT CAPITAL MARKETS EXECUTIVE SUMMARY MIDDLE MARKET

MARKET INSIGHTS 2Q 2018 DEBT CAPITAL MARKETS EXECUTIVE SUMMARY Middle market clients have a unique borrowing opportunity, with banks competing to originate new loans for clients. In the leveraged loan

MARKET INSIGHTS 2Q 2018 DEBT CAPITAL MARKETS EXECUTIVE SUMMARY Middle market clients have a unique borrowing opportunity, with banks competing to originate new loans for clients. In the leveraged loan

Written Testimony of Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston

Written Testimony of Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston Field hearing of the Committee on Financial Services of the U.S. House of Representatives: Seeking

Written Testimony of Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston Field hearing of the Committee on Financial Services of the U.S. House of Representatives: Seeking

file:///c:/users/cathy/appdata/local/microsoft/windows/temporary Int...

1 of 5 9/25/17, 8:57 AM A Publication of the National Association of Manufacturers September 25, 2017 As expected, the Federal Reserve opted to not raise short-term interest rates at its September 19 20

1 of 5 9/25/17, 8:57 AM A Publication of the National Association of Manufacturers September 25, 2017 As expected, the Federal Reserve opted to not raise short-term interest rates at its September 19 20

Part 3: Private Equity Strategies

Private Equity Education Series Part 3: Private Equity Strategies Reports in this series Report Highlights Page Part 1: What is Private Equity (PE)? Part 2: Investing in Private Equity Part 3: Private

Private Equity Education Series Part 3: Private Equity Strategies Reports in this series Report Highlights Page Part 1: What is Private Equity (PE)? Part 2: Investing in Private Equity Part 3: Private

RICS Economic Research

RICS Economic Research / February 7 th 2014 Michael Hanley Economist www.rics.org/economics The Outlook for the Construction Sector Growth of 4% expected over 2014 Private housing and infrastructure to

RICS Economic Research / February 7 th 2014 Michael Hanley Economist www.rics.org/economics The Outlook for the Construction Sector Growth of 4% expected over 2014 Private housing and infrastructure to

2014 Annual Review & Outlook

2014 Annual Review & Outlook As we enter 2014, the current economic expansion is 4.5 years in duration, roughly the average life of U.S. economic expansions. There is every reason to believe it will continue,

2014 Annual Review & Outlook As we enter 2014, the current economic expansion is 4.5 years in duration, roughly the average life of U.S. economic expansions. There is every reason to believe it will continue,

Survey of Credit Underwriting Practices 2005 Office of the Comptroller of the Currency National Credit Committee

Survey of Credit Underwriting Practices 25 Office of the Comptroller of the Currency National Credit Committee June 25 1 Table of Contents Introduction 3 Part I: Overall Results Primary Findings 4 Commentary...6

Survey of Credit Underwriting Practices 25 Office of the Comptroller of the Currency National Credit Committee June 25 1 Table of Contents Introduction 3 Part I: Overall Results Primary Findings 4 Commentary...6

Swap Markets CHAPTER OBJECTIVES. The specific objectives of this chapter are to: describe the types of interest rate swaps that are available,

15 Swap Markets CHAPTER OBJECTIVES The specific objectives of this chapter are to: describe the types of interest rate swaps that are available, explain the risks of interest rate swaps, identify other

15 Swap Markets CHAPTER OBJECTIVES The specific objectives of this chapter are to: describe the types of interest rate swaps that are available, explain the risks of interest rate swaps, identify other

September Market Overview: Private Distressed Debt. Eric J. Petroff, CFA Director of Research WURTS & ASSOCIATES

September 2008 Market Overview: Private Distressed Debt Eric J. Petroff, CFA Director of Research epetroff@wurts.com WURTS & ASSOCIATES SEATTLE 999 Third Avenue Suite 3650 Seattle, Washington 98104 206.622.3700

September 2008 Market Overview: Private Distressed Debt Eric J. Petroff, CFA Director of Research epetroff@wurts.com WURTS & ASSOCIATES SEATTLE 999 Third Avenue Suite 3650 Seattle, Washington 98104 206.622.3700

Financial System Stabilized, but Exit, Reform, and Fiscal Challenges Lie Ahead

January 21 Financial System Stabilized, but Exit, Reform, and Fiscal Challenges Lie Ahead Systemic risks have continued to subside as economic fundamentals have improved and substantial public support

January 21 Financial System Stabilized, but Exit, Reform, and Fiscal Challenges Lie Ahead Systemic risks have continued to subside as economic fundamentals have improved and substantial public support

RISK DISCLOSURE STATEMENT FOR SECURITY FUTURES CONTRACTS

RISK DISCLOSURE STATEMENT FOR SECURITY FUTURES CONTRACTS This disclosure statement discusses the characteristics and risks of standardized security futures contracts traded on regulated U.S. exchanges.

RISK DISCLOSURE STATEMENT FOR SECURITY FUTURES CONTRACTS This disclosure statement discusses the characteristics and risks of standardized security futures contracts traded on regulated U.S. exchanges.

Risk Taking and Interest Rates: Evidence from Decades in the Global Syndicated Loan Market

Risk Taking and Interest Rates: Evidence from Decades in the Global Syndicated Loan Market Seung Jung Lee FRB Lucy Qian Liu IMF Viktors Stebunovs FRB BIS CCA Research Conference on "Low interest rates,

Risk Taking and Interest Rates: Evidence from Decades in the Global Syndicated Loan Market Seung Jung Lee FRB Lucy Qian Liu IMF Viktors Stebunovs FRB BIS CCA Research Conference on "Low interest rates,

Survey on credit terms and conditions in euro-denominated securities financing and OTC derivatives markets (SESFOD)

") Survey on credit terms and conditions in euro-denominated securities financing and OTC derivatives markets (SESFOD) As a follow-up to the recommendation in the Committee on the Global Financial System

Survey on credit terms and conditions in euro-denominated securities financing and OTC derivatives markets (SESFOD) As a follow-up to the recommendation in the Committee on the Global Financial System

Since the April 2007 Global Financial Stability

Since the April 2007 Global Financial Stability Report (GFSR), global financial stability has endured an important test. Credit and market risks have risen and markets have become more volatile. Markets

Since the April 2007 Global Financial Stability Report (GFSR), global financial stability has endured an important test. Credit and market risks have risen and markets have become more volatile. Markets

May 1, THE MERGER FUND Investor Class Shares (MERFX) Institutional Class Shares (MERIX)

Institutional Class Shares (MERIX)") May 1, 2018 Summary Prospectus THE MERGER FUND Investor Class Shares (MERFX) Institutional Class Shares (MERIX) Before you invest, you may want to review the Fund s prospectus, which contains more information

May 1, 2018 Summary Prospectus THE MERGER FUND Investor Class Shares (MERFX) Institutional Class Shares (MERIX) Before you invest, you may want to review the Fund s prospectus, which contains more information

Lecture notes on risk management, public policy, and the financial system Forms of leverage

Lecture notes on risk management, public policy, and the financial system Allan M. Malz Columbia University 2018 Allan M. Malz Last updated: March 12, 2018 2 / 18 Outline 3/18 Key postwar developments

Lecture notes on risk management, public policy, and the financial system Allan M. Malz Columbia University 2018 Allan M. Malz Last updated: March 12, 2018 2 / 18 Outline 3/18 Key postwar developments

THE EURO AREA BANK LENDING SURVEY 2ND QUARTER OF 2013

THE EURO AREA BANK LENDING SURVEY 2ND QUARTER OF 213 JULY 213 European Central Bank, 213 Address Kaiserstrasse 29, 6311 Frankfurt am Main, Germany Postal address Postfach 16 3 19, 666 Frankfurt am Main,

THE EURO AREA BANK LENDING SURVEY 2ND QUARTER OF 213 JULY 213 European Central Bank, 213 Address Kaiserstrasse 29, 6311 Frankfurt am Main, Germany Postal address Postfach 16 3 19, 666 Frankfurt am Main,

Unless otherwise noted, tabular amounts are in thousands of Canadian dollars.

MANAGEMENT S DISCUSSION AND ANALYSIS The following management s discussion and analysis ( MD&A ) of financial condition and results of operations is prepared as of February 27, 2018. This discussion should

MANAGEMENT S DISCUSSION AND ANALYSIS The following management s discussion and analysis ( MD&A ) of financial condition and results of operations is prepared as of February 27, 2018. This discussion should

14. What Use Can Be Made of the Specific FSIs?

14. What Use Can Be Made of the Specific FSIs? Introduction 14.1 The previous chapter explained the need for FSIs and how they fit into the wider concept of macroprudential analysis. This chapter considers

14. What Use Can Be Made of the Specific FSIs? Introduction 14.1 The previous chapter explained the need for FSIs and how they fit into the wider concept of macroprudential analysis. This chapter considers

Eaton Vance Global Macro Absolute Return Fund

Click here to view the Fund s Prospectus Click here to view the Fund s Statement of Additional Information Summary Prospectus dated March 1, 2018 Eaton Vance Global Macro Absolute Return Fund Class /Ticker

Click here to view the Fund s Prospectus Click here to view the Fund s Statement of Additional Information Summary Prospectus dated March 1, 2018 Eaton Vance Global Macro Absolute Return Fund Class /Ticker

Appendix 1: Materials used by Mr. Dudley

Presentation Materials (PDF) Pages 169 to 188 of the Transcript Appendix 1: Materials used by Mr. Dudley Class II FOMC - Restricted FR Page 1 (1) Title: Spread between Jumbo and Conforming Mortgage Rates

Presentation Materials (PDF) Pages 169 to 188 of the Transcript Appendix 1: Materials used by Mr. Dudley Class II FOMC - Restricted FR Page 1 (1) Title: Spread between Jumbo and Conforming Mortgage Rates

Survey on credit terms and conditions in euro-denominated securities financing and OTC derivatives markets (SESFOD)

") Survey on credit terms and conditions in euro-denominated securities financing and OTC derivatives markets (SESFOD) December 2016 As a follow-up to the recommendation in the Committee on the Global Financial

Survey on credit terms and conditions in euro-denominated securities financing and OTC derivatives markets (SESFOD) December 2016 As a follow-up to the recommendation in the Committee on the Global Financial

Survey of Credit Underwriting Practices Office of the Comptroller of the Currency National Credit Committee October 2004

Survey of Credit Underwriting Practices 2004 Office of the Comptroller of the Currency National Credit Committee October 2004 Table of Contents Introduction 3 Part I: Overall Results Primary Findings 4

Survey of Credit Underwriting Practices 2004 Office of the Comptroller of the Currency National Credit Committee October 2004 Table of Contents Introduction 3 Part I: Overall Results Primary Findings 4

William C Dudley: A bit better, but very far from best US economic outlook and the challenges facing the Federal Reserve

William C Dudley: A bit better, but very far from best US economic outlook and the challenges facing the Federal Reserve Remarks by Mr William C Dudley, President and Chief Executive Officer of the Federal

William C Dudley: A bit better, but very far from best US economic outlook and the challenges facing the Federal Reserve Remarks by Mr William C Dudley, President and Chief Executive Officer of the Federal

Monetary Policy on the Way out of the Crisis

Monetary Policy on the Way out of the Crisis Professor Juergen von Hagen - Bruegel and University of Bonn 1. THE END OF THE CRISIS IS AT HANDS More than two years after the beginning, in August 2007, of

Monetary Policy on the Way out of the Crisis Professor Juergen von Hagen - Bruegel and University of Bonn 1. THE END OF THE CRISIS IS AT HANDS More than two years after the beginning, in August 2007, of

November minutes: key signaling language

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: FOMC Minutes Thursday, November 29, 2018 November minutes:

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: FOMC Minutes Thursday, November 29, 2018 November minutes:

Current Economic Conditions and Selected Forecasts

Order Code RL30329 Current Economic Conditions and Selected Forecasts Updated May 20, 2008 Gail E. Makinen Economic Policy Consultant Government and Finance Division Current Economic Conditions and Selected

Order Code RL30329 Current Economic Conditions and Selected Forecasts Updated May 20, 2008 Gail E. Makinen Economic Policy Consultant Government and Finance Division Current Economic Conditions and Selected

A guide to the incremental borrowing rate Assessing the impact of IFRS 16 Leases. Audit & Assurance

A guide to the incremental borrowing rate Assessing the impact of IFRS 16 Leases Audit & Assurance Given a significant number of organisations are unlikely to have the necessary historical data to determine

A guide to the incremental borrowing rate Assessing the impact of IFRS 16 Leases Audit & Assurance Given a significant number of organisations are unlikely to have the necessary historical data to determine

FRBSF Economic Letter

FRBSF Economic Letter 217-34 November 2, 217 Research from Federal Reserve Bank of San Francisco A New Conundrum in the Bond Market? Michael D. Bauer When the Federal Reserve raises short-term interest

FRBSF Economic Letter 217-34 November 2, 217 Research from Federal Reserve Bank of San Francisco A New Conundrum in the Bond Market? Michael D. Bauer When the Federal Reserve raises short-term interest

Eaton Vance Diversified Currency Income Fund Class A Shares - EAIIX Class C Shares - ECIMX Class I Shares - EIIMX

To view a Funds Summary Prospectus click on the Fund name below Click here to view the Fund s Statement of Additional Information Eaton Vance Diversified Currency Income Fund Class A Shares - EAIIX Class

To view a Funds Summary Prospectus click on the Fund name below Click here to view the Fund s Statement of Additional Information Eaton Vance Diversified Currency Income Fund Class A Shares - EAIIX Class

Strategic Allocaiton to High Yield Corporate Bonds Why Now?

Strategic Allocaiton to High Yield Corporate Bonds Why Now? May 11, 2015 by Matthew Kennedy of Rainier Investment Management HIGH YIELD CORPORATE BONDS - WHY NOW? The demand for higher yielding fixed income

Strategic Allocaiton to High Yield Corporate Bonds Why Now? May 11, 2015 by Matthew Kennedy of Rainier Investment Management HIGH YIELD CORPORATE BONDS - WHY NOW? The demand for higher yielding fixed income

Shadow Banking & the Financial Crisis

& the Financial Crisis April 24, 2013 & the Financial Crisis Table of contents 1 Backdrop A bit of history 2 3 & the Financial Crisis Origins Backdrop A bit of history Banks perform several vital roles

& the Financial Crisis April 24, 2013 & the Financial Crisis Table of contents 1 Backdrop A bit of history 2 3 & the Financial Crisis Origins Backdrop A bit of history Banks perform several vital roles

Key Takeaways. What it may mean for investors WEEKLY GUIDANCE ON ECONOMIC AND GEOPOLITICAL EVENTS. Luis Alvarado Investment Strategy Analyst

Luis Alvarado Investment Strategy Analyst WEEKLY GUIDANCE ON ECONOMIC AND GEOPOLITICAL EVENTS December 12, 2017 The Mystery of Inflation and What Lies Ahead Key Takeaways» As most investors know, inflation

Luis Alvarado Investment Strategy Analyst WEEKLY GUIDANCE ON ECONOMIC AND GEOPOLITICAL EVENTS December 12, 2017 The Mystery of Inflation and What Lies Ahead Key Takeaways» As most investors know, inflation

Regulatory Notice 14-02

Regulatory Notice 14-02 Margin Requirements FINRA Requests Comment on Proposed Amendments to FINRA Rule 4210 for Transactions in the TBA Market Comment Period Expires: February 26, 2014 Executive Summary

Regulatory Notice 14-02 Margin Requirements FINRA Requests Comment on Proposed Amendments to FINRA Rule 4210 for Transactions in the TBA Market Comment Period Expires: February 26, 2014 Executive Summary

Liquidity levels and liquidity risk Yves Nosbusch

ECONOMIC RESEARCH DEPARTMENT Liquidity levels and liquidity risk Yves Nosbusch There have been a number of structural changes to market liquidity provision since the financial crisis. These include the

ECONOMIC RESEARCH DEPARTMENT Liquidity levels and liquidity risk Yves Nosbusch There have been a number of structural changes to market liquidity provision since the financial crisis. These include the

Second-Lien Loans: Increased Use in LBO Financing

DDJ CAPITAL MANAGEMENT, LLC SPECIALISTS IN HIGH YIELD AND LEVERAGED CREDIT INVESTMENTS NOVEMBER 2017 VOLUME 4 ISSUE 4 Second-Lien Loans: Increased Use in LBO Financing > Favorable call profile typical

DDJ CAPITAL MANAGEMENT, LLC SPECIALISTS IN HIGH YIELD AND LEVERAGED CREDIT INVESTMENTS NOVEMBER 2017 VOLUME 4 ISSUE 4 Second-Lien Loans: Increased Use in LBO Financing > Favorable call profile typical

Securities Lending Outlook

WORLDWIDE SECURITIES SERVICES Outlook Managing Value Generation and Risk Securities lending and its risk/reward profile have been in the headlines as the credit and liquidity crisis has continued to unfold.

WORLDWIDE SECURITIES SERVICES Outlook Managing Value Generation and Risk Securities lending and its risk/reward profile have been in the headlines as the credit and liquidity crisis has continued to unfold.

Trends in financial intermediation: Implications for central bank policy

Trends in financial intermediation: Implications for central bank policy Monetary Authority of Singapore Abstract Accommodative global liquidity conditions post-crisis have translated into low domestic

Trends in financial intermediation: Implications for central bank policy Monetary Authority of Singapore Abstract Accommodative global liquidity conditions post-crisis have translated into low domestic

Leveraged Finance Q Leveraged Finance Market Resurgence Continues. In This Report Issuer-friendly conditions continue

Q3 2016 Leveraged Finance Market Resurgence Continues In This Report Issuer-friendly conditions continue Institutional market surges Leveraged Finance Rise of the unitranche Active high-yield market amid

Q3 2016 Leveraged Finance Market Resurgence Continues In This Report Issuer-friendly conditions continue Institutional market surges Leveraged Finance Rise of the unitranche Active high-yield market amid

Lecture 5. Notes on the Current Crisis

Lecture 5 Notes on the Current Crisis Mark Gertler NYU June 29 .4 Real GDP growth.3.2.1.1.2.3 1975 198 1985 199 1995 2 25 18 16 core inflation federal funds rate 14 12 1 8 6 4 2 1975 198 1985 199 1995

Lecture 5 Notes on the Current Crisis Mark Gertler NYU June 29 .4 Real GDP growth.3.2.1.1.2.3 1975 198 1985 199 1995 2 25 18 16 core inflation federal funds rate 14 12 1 8 6 4 2 1975 198 1985 199 1995

Eaton Vance Management Two International Place Boston, MA 02110

Eaton Vance Management Two International Place Boston, MA 02110 www.eatonvance.com Form ADV Part 2A January 31, 2018 This brochure provides information about the qualifications and business practices of

Eaton Vance Management Two International Place Boston, MA 02110 www.eatonvance.com Form ADV Part 2A January 31, 2018 This brochure provides information about the qualifications and business practices of

SUPPLEMENT TO THE CURRENTLY EFFECTIVE SUMMARY PROSPECTUSES OF EACH OF THE LISTED FUNDS

SUPPLEMENT TO THE CURRENTLY EFFECTIVE SUMMARY PROSPECTUSES OF EACH OF THE LISTED FUNDS The following changes will take effect on or about July 2, 2018: Deutsche Investment Management Americas Inc., the

SUPPLEMENT TO THE CURRENTLY EFFECTIVE SUMMARY PROSPECTUSES OF EACH OF THE LISTED FUNDS The following changes will take effect on or about July 2, 2018: Deutsche Investment Management Americas Inc., the

Performance Trust Strategic Bond Fund (Symbol: PTIAX)

") Summary Prospectus December 29, 2017 Performance Trust Strategic Bond Fund (Symbol: PTIAX) Before you invest, you may want to review the Performance Trust Strategic Bond Fund s (the Strategic Bond Fund

Summary Prospectus December 29, 2017 Performance Trust Strategic Bond Fund (Symbol: PTIAX) Before you invest, you may want to review the Performance Trust Strategic Bond Fund s (the Strategic Bond Fund

Liquidity Coverage Ratio Disclosures Report. For the Quarterly Period Ended March 31, 2018

Liquidity Coverage Ratio Disclosures Report For the Quarterly Period Ended March 31, 2018 LCR DISCLOSURES REPORT For the quarterly period ended March 31, 2018 Table of Contents Page 1 Morgan Stanley 1

Liquidity Coverage Ratio Disclosures Report For the Quarterly Period Ended March 31, 2018 LCR DISCLOSURES REPORT For the quarterly period ended March 31, 2018 Table of Contents Page 1 Morgan Stanley 1

Multi-Strategy Total Return Fund A fund seeking attractive risk adjusted returns through a global portfolio of stocks, bonds, and other investments.

SUMMARY PROSPECTUS TMSRX TMSSX TMSAX Investor Class I Class Advisor Class March 1, 2018 T. Rowe Price Multi-Strategy Total Return Fund A fund seeking attractive risk adjusted returns through a global portfolio

SUMMARY PROSPECTUS TMSRX TMSSX TMSAX Investor Class I Class Advisor Class March 1, 2018 T. Rowe Price Multi-Strategy Total Return Fund A fund seeking attractive risk adjusted returns through a global portfolio

Government of Canada Debt Distribution Framework Consultations

Government of Canada Debt Distribution Framework Consultations 1. Overview The Department of Finance and the Bank of Canada (BoC) are seeking the views of Government Securities Distributors (GSD), institutional

Government of Canada Debt Distribution Framework Consultations 1. Overview The Department of Finance and the Bank of Canada (BoC) are seeking the views of Government Securities Distributors (GSD), institutional

Financial Stability: The Role of Real Estate Values

EMBARGOED UNTIL 9:45 P.M. on Tuesday, March 21, 2017 U.S. Eastern Time which is 9:45 A.M. on Wednesday, March 22, 2017 in Bali, Indonesia OR UPON DELIVERY Financial Stability: The Role of Real Estate Values

EMBARGOED UNTIL 9:45 P.M. on Tuesday, March 21, 2017 U.S. Eastern Time which is 9:45 A.M. on Wednesday, March 22, 2017 in Bali, Indonesia OR UPON DELIVERY Financial Stability: The Role of Real Estate Values

Why Now for European Senior Secured Loans?

Why Now for European Senior Secured Loans? Market Features, Relative Value & Portfolio Inclusion Benefits The syndicated senior secured loan market, which until 2009 was the dominant sub-investment grade

Why Now for European Senior Secured Loans? Market Features, Relative Value & Portfolio Inclusion Benefits The syndicated senior secured loan market, which until 2009 was the dominant sub-investment grade

Eaton Vance Short Duration Strategic Income Fund

Click here to view the Fund s Prospectus Click here to view the Fund s Statement of Additional Information Summary Prospectus dated March 1, 2018 Eaton Vance Short Duration Strategic Income Fund Class

Click here to view the Fund s Prospectus Click here to view the Fund s Statement of Additional Information Summary Prospectus dated March 1, 2018 Eaton Vance Short Duration Strategic Income Fund Class

What is the appropriate level of currency hedging?

For Investment Professionals DIVERSIFIED THINKING What is the appropriate level of currency hedging? Recent currency market volatility, particularly the fall in the value of the pound, has highlighted

For Investment Professionals DIVERSIFIED THINKING What is the appropriate level of currency hedging? Recent currency market volatility, particularly the fall in the value of the pound, has highlighted

SECURITIES LENDING DRAFT FOR DISCUSSION PURPOSES ONLY

I. Introduction Securities lending plays a significant role in today s capital markets. In general, securities lending is believed to improve overall market efficiency and liquidity. In addition, securities

I. Introduction Securities lending plays a significant role in today s capital markets. In general, securities lending is believed to improve overall market efficiency and liquidity. In addition, securities

1.2 Product nature of credit derivatives

1.2 Product nature of credit derivatives Payoff depends on the occurrence of a credit event: default: any non-compliance with the exact specification of a contract price or yield change of a bond credit

1.2 Product nature of credit derivatives Payoff depends on the occurrence of a credit event: default: any non-compliance with the exact specification of a contract price or yield change of a bond credit

Survey of Credit Underwriting Practices 2010

Survey of Credit Underwriting Practices 2010 Office of the Comptroller of the Currency August 2010 Contents Introduction...1 Part I: Overall Results...2 Primary Findings... 2 Commentary on Credit Risk...

Survey of Credit Underwriting Practices 2010 Office of the Comptroller of the Currency August 2010 Contents Introduction...1 Part I: Overall Results...2 Primary Findings... 2 Commentary on Credit Risk...

The Hidden Risks of Fixed Income Indexing

The Hidden Risks of Fixed Income Indexing A White Paper by Manning & Napier www.manning-napier.com Unless otherwise noted, all figures are based in USD. 1 of 7 Introduction Conventional wisdom is to check

The Hidden Risks of Fixed Income Indexing A White Paper by Manning & Napier www.manning-napier.com Unless otherwise noted, all figures are based in USD. 1 of 7 Introduction Conventional wisdom is to check

The Relation between Government Bonds Liquidity and Yield

Capital Markets The Relation between Government Bonds Liquidity and Yield Pil-kyu Kim, Senior Research Fellow* In this article, I analyze the microstructure of government bonds liquidity using trading

Capital Markets The Relation between Government Bonds Liquidity and Yield Pil-kyu Kim, Senior Research Fellow* In this article, I analyze the microstructure of government bonds liquidity using trading

Christopher Kent: Financial conditions and the Australian dollar - recent developments

Christopher Kent: Financial conditions and the Australian dollar - recent developments Address by Mr Christopher Kent, Assistant Governor (Financial Markets) of the Reserve Bank of Australia, to the XE

Christopher Kent: Financial conditions and the Australian dollar - recent developments Address by Mr Christopher Kent, Assistant Governor (Financial Markets) of the Reserve Bank of Australia, to the XE

Alternative assets. An insight into the future of investing in alternatives

Alternative assets 2014 An insight into the future of investing in alternatives Contents 01 In this, the eleventh year of our Global Alternatives Survey, we pause to consider what may lie ahead for alternatives

Alternative assets 2014 An insight into the future of investing in alternatives Contents 01 In this, the eleventh year of our Global Alternatives Survey, we pause to consider what may lie ahead for alternatives

COPYRIGHTED MATERIAL. 1 The Credit Derivatives Market 1.1 INTRODUCTION

1 The Credit Derivatives Market 1.1 INTRODUCTION Without a doubt, credit derivatives have revolutionised the trading and management of credit risk. They have made it easier for banks, who have historically

1 The Credit Derivatives Market 1.1 INTRODUCTION Without a doubt, credit derivatives have revolutionised the trading and management of credit risk. They have made it easier for banks, who have historically

the U.S. balance of payments deficit showed substantial improvement after midyear.

DURING 1963 THE Federal Reserve continued to encourage monetary and credit expansion with a view to stimulating a further rise in economic activity. The availability of bank reserves was reduced somewhat

DURING 1963 THE Federal Reserve continued to encourage monetary and credit expansion with a view to stimulating a further rise in economic activity. The availability of bank reserves was reduced somewhat

SUMMARY PROSPECTUS. May 1, 2018

SUMMARY PROSPECTUS May 1, 2018 REMS INTERNATIONAL REAL ESTATE VALUE-OPPORTUNITY FUND INSTITUTIONAL SHARES (Ticker: REIFX) PLATFORM SHARES (Ticker: REIYX) Z SHARES (Ticker: REIZX).Before you invest, you

SUMMARY PROSPECTUS May 1, 2018 REMS INTERNATIONAL REAL ESTATE VALUE-OPPORTUNITY FUND INSTITUTIONAL SHARES (Ticker: REIFX) PLATFORM SHARES (Ticker: REIYX) Z SHARES (Ticker: REIZX).Before you invest, you

KDP ASSET MANAGEMENT, INC.

ASSET MANAGEMENT, INC. High Yield Bond and Senior Secured Bank Loan Outlook June 2017 Asset Management, Inc. 24 Elm Street Montpelier, Vermont 802.223.0440 HighYield@kdpam.com The Case for High Yield Bonds

ASSET MANAGEMENT, INC. High Yield Bond and Senior Secured Bank Loan Outlook June 2017 Asset Management, Inc. 24 Elm Street Montpelier, Vermont 802.223.0440 HighYield@kdpam.com The Case for High Yield Bonds

Finance Operations CHAPTER OBJECTIVES. The specific objectives of this chapter are to: identify the main sources and uses of finance company funds,

22 Finance Operations CHAPTER OBJECTIVES The specific objectives of this chapter are to: identify the main sources and uses of finance company funds, describe how finance companies are exposed to various

22 Finance Operations CHAPTER OBJECTIVES The specific objectives of this chapter are to: identify the main sources and uses of finance company funds, describe how finance companies are exposed to various

Not created equal: Surveying investments in non-investment grade

Winter 2018 Not created equal: Surveying investments in non-investment grade U.S. corporate debt Institutional investors searching for yield and current income opportunities have increased their allocations

Winter 2018 Not created equal: Surveying investments in non-investment grade U.S. corporate debt Institutional investors searching for yield and current income opportunities have increased their allocations

Capital Advisory Group Institutional Investor Survey

INSIGHTS Global Capital Advisory Group 2018 Institutional Investor Survey Capital Advisory Group This material is provided by J.P. Morgan s Capital Advisory Group for informational purposes only. It is

INSIGHTS Global Capital Advisory Group 2018 Institutional Investor Survey Capital Advisory Group This material is provided by J.P. Morgan s Capital Advisory Group for informational purposes only. It is

SUNAMERICA SERIES TRUST SA BLACKROCK VCP GLOBAL MULTI ASSET PORTFOLIO

SUMMARY PROSPECTUS MAY 1, 2017 SUNAMERICA SERIES TRUST SA BLACKROCK VCP GLOBAL MULTI ASSET PORTFOLIO (CLASS 1 AND CLASS 3 SHARES) s Statutory Prospectus and Statement of Additional Information dated May

SUMMARY PROSPECTUS MAY 1, 2017 SUNAMERICA SERIES TRUST SA BLACKROCK VCP GLOBAL MULTI ASSET PORTFOLIO (CLASS 1 AND CLASS 3 SHARES) s Statutory Prospectus and Statement of Additional Information dated May

Joseph S Tracy: A strategy for the 2011 economic recovery

Joseph S Tracy: A strategy for the 2011 economic recovery Remarks by Mr Joseph S Tracy, Executive Vice President of the Federal Reserve Bank of New York, at Dominican College, Orangeburg, New York, 28

Joseph S Tracy: A strategy for the 2011 economic recovery Remarks by Mr Joseph S Tracy, Executive Vice President of the Federal Reserve Bank of New York, at Dominican College, Orangeburg, New York, 28

The international environment

The international environment This article (1) discusses developments in the global economy since the August 1999 Quarterly Bulletin. Domestic demand growth remained strong in the United States, and with

The international environment This article (1) discusses developments in the global economy since the August 1999 Quarterly Bulletin. Domestic demand growth remained strong in the United States, and with

Appendix 1: Materials used by Mr. Kos

Presentation Materials (PDF) Pages 192 to 203 of the Transcript Appendix 1: Materials used by Mr. Kos Page 1 Top panel Title: Current U.S. 3-Month Deposit Rates and Rates Implied by Traded Forward Rate

Presentation Materials (PDF) Pages 192 to 203 of the Transcript Appendix 1: Materials used by Mr. Kos Page 1 Top panel Title: Current U.S. 3-Month Deposit Rates and Rates Implied by Traded Forward Rate

2. Investment Policies I. DEFINITIONS

2. Investment Policies I. DEFINITIONS PURPOSE The purpose of this Investment Policy Statement is to establish a clear understanding of the philosophy and the investment objectives for The University at

2. Investment Policies I. DEFINITIONS PURPOSE The purpose of this Investment Policy Statement is to establish a clear understanding of the philosophy and the investment objectives for The University at

Information Memorandum

03 July 2017 Information Memorandum Franklin Templeton s Australia Limited (ABN 87 006 972 247, AFS Licence number 225328) TABLE OF CONTENTS 1. FUND STRUCTURE 2 2. INVESTMENT PROFILE OF THE FUNDS 2 3.

03 July 2017 Information Memorandum Franklin Templeton s Australia Limited (ABN 87 006 972 247, AFS Licence number 225328) TABLE OF CONTENTS 1. FUND STRUCTURE 2 2. INVESTMENT PROFILE OF THE FUNDS 2 3.

Retirement. Optimal Asset Allocation in Retirement: A Downside Risk Perspective. JUne W. Van Harlow, Ph.D., CFA Director of Research ABSTRACT

Putnam Institute JUne 2011 Optimal Asset Allocation in : A Downside Perspective W. Van Harlow, Ph.D., CFA Director of Research ABSTRACT Once an individual has retired, asset allocation becomes a critical

Putnam Institute JUne 2011 Optimal Asset Allocation in : A Downside Perspective W. Van Harlow, Ph.D., CFA Director of Research ABSTRACT Once an individual has retired, asset allocation becomes a critical

Liquidity Coverage Ratio Disclosures Report. For the Quarterly Period Ended September 30, 2017

Liquidity Coverage Ratio Disclosures Report For the Quarterly Period Ended September 30, 2017 U.S. LCR DISCLOSURES REPORT For the quarterly period ended September 30, 2017 Table of Contents Page 1 Morgan

Liquidity Coverage Ratio Disclosures Report For the Quarterly Period Ended September 30, 2017 U.S. LCR DISCLOSURES REPORT For the quarterly period ended September 30, 2017 Table of Contents Page 1 Morgan

August 2017 The information contained in this publication is not intended as investment advice or recommendation. Non contractual document.

Demystifying Chinese Bond Investing August 2017 The information contained in this publication is not intended as investment advice or recommendation. Non contractual document. Chinese bonds have been in

Demystifying Chinese Bond Investing August 2017 The information contained in this publication is not intended as investment advice or recommendation. Non contractual document. Chinese bonds have been in

HATTERAS ALPHA HEDGED STRATEGIES FUND

Summary Prospectus April 30, 2017 HATTERAS ALPHA HEDGED STRATEGIES FUND CLASS A CLASS C INSTITUTIONAL CLASS Ticker Symbol: APHAX APHCX ALPIX Before you invest, you may want to review the Hatteras Alpha

Summary Prospectus April 30, 2017 HATTERAS ALPHA HEDGED STRATEGIES FUND CLASS A CLASS C INSTITUTIONAL CLASS Ticker Symbol: APHAX APHCX ALPIX Before you invest, you may want to review the Hatteras Alpha

Responses to Survey of Market Participants

Responses to Survey of Market Participants Markets Group, Reserve Bank of New York December 2015 Page 1 of 15 Responses to Survey of Market Participants Distributed: 12/03/2015 Received by: 12/07/2015

Responses to Survey of Market Participants Markets Group, Reserve Bank of New York December 2015 Page 1 of 15 Responses to Survey of Market Participants Distributed: 12/03/2015 Received by: 12/07/2015

Global Investment Committee Themes

Global Investment Committee Themes The Global Investment Committee (GIC), which meets monthly to review the economic and political environment and asset allocation models for Morgan Stanley Wealth Management

Global Investment Committee Themes The Global Investment Committee (GIC), which meets monthly to review the economic and political environment and asset allocation models for Morgan Stanley Wealth Management

Why we re not getting too comfortable in our fixed income risk assessment

Lyle Sankar Why we re not getting too comfortable in our fixed income risk assessment Lyle joined the Fixed Income team at PSG Asset Management in 2014. He performs credit and fixed income analysis and

Lyle Sankar Why we re not getting too comfortable in our fixed income risk assessment Lyle joined the Fixed Income team at PSG Asset Management in 2014. He performs credit and fixed income analysis and

Russell Survey on Alternative Investing

RUSSELL RESEARCH THE 25-26 Russell Survey on Alternative Investing A SURVEY OF ORGANIZATIONS IN NORTH AMERICA, EUROPE, AUSTRALIA, AND JAPAN EXECUTIVE SUMMARY OF KEY FINDINGS Looking for Answers In 1992,

RUSSELL RESEARCH THE 25-26 Russell Survey on Alternative Investing A SURVEY OF ORGANIZATIONS IN NORTH AMERICA, EUROPE, AUSTRALIA, AND JAPAN EXECUTIVE SUMMARY OF KEY FINDINGS Looking for Answers In 1992,

Ben S Bernanke: Modern risk management and banking supervision

Ben S Bernanke: Modern risk management and banking supervision Remarks by Mr Ben S Bernanke, Chairman of the Board of Governors of the US Federal Reserve System, at the Stonier Graduate School of Banking,

Ben S Bernanke: Modern risk management and banking supervision Remarks by Mr Ben S Bernanke, Chairman of the Board of Governors of the US Federal Reserve System, at the Stonier Graduate School of Banking,

Survey on credit terms and conditions in euro-denominated securities financing and OTC derivatives markets (SESFOD)

") Survey on credit terms and conditions in euro-denominated securities financing and OTC derivatives markets (SESFOD) As a follow-up to the recommendation in the Committee on the Global Financial System

Survey on credit terms and conditions in euro-denominated securities financing and OTC derivatives markets (SESFOD) As a follow-up to the recommendation in the Committee on the Global Financial System

Goldman Sachs Presentation to Bernstein Strategic Decisions Conference

Goldman Sachs Presentation to Bernstein Strategic Decisions Conference Comments by Gary Cohn, President and Chief Operating Officer May 31, 2012 Slide 2 Thanks Brad, good morning to everyone. Slide 3 In

Goldman Sachs Presentation to Bernstein Strategic Decisions Conference Comments by Gary Cohn, President and Chief Operating Officer May 31, 2012 Slide 2 Thanks Brad, good morning to everyone. Slide 3 In

Franklin Australian Core Plus Bond Fund

03 July 2017 Franklin Australian Core Plus Bond Fund ARSN 617 966 042 Information Memorandum Franklin Templeton Investments Australia Limited (ABN 87 006 972 247, AFS Licence number 225328) TABLE OF CONTENTS

03 July 2017 Franklin Australian Core Plus Bond Fund ARSN 617 966 042 Information Memorandum Franklin Templeton Investments Australia Limited (ABN 87 006 972 247, AFS Licence number 225328) TABLE OF CONTENTS

KDP ASSET MANAGEMENT, INC.

ASSET MANAGEMENT, INC. High Yield Bond and Senior Secured Bank Loan Outlook January 2019 Asset Management, Inc. 24 Elm Street Montpelier, Vermont 802.223.0440 HighYield@kdpam.com High Yield Observations

ASSET MANAGEMENT, INC. High Yield Bond and Senior Secured Bank Loan Outlook January 2019 Asset Management, Inc. 24 Elm Street Montpelier, Vermont 802.223.0440 HighYield@kdpam.com High Yield Observations

HUSSMAN STRATEGIC GROWTH FUND

HUSSMAN STRATEGIC GROWTH FUND TICKER SYMBOL: HSGFX The Fund seeks to achieve long-term capital appreciation, with added emphasis on the protection of capital during unfavorable market conditions. It pursues

HUSSMAN STRATEGIC GROWTH FUND TICKER SYMBOL: HSGFX The Fund seeks to achieve long-term capital appreciation, with added emphasis on the protection of capital during unfavorable market conditions. It pursues

FINANCIAL INSTRUMENTS AND THEIR RISKS

FINANCIAL INSTRUMENTS AND THEIR RISKS This document presents an overview of the main financial instruments that Amundi uses in providing its investment services and the risks associated with these instruments.

FINANCIAL INSTRUMENTS AND THEIR RISKS This document presents an overview of the main financial instruments that Amundi uses in providing its investment services and the risks associated with these instruments.

Not created equal: Surveying investments in non-investment grade U.S. corporate debt

Winter 2016 Not created equal: Surveying investments in non-investment grade U.S. corporate debt Institutional investors seeking yield and current income opportunities have increased their allocations

Winter 2016 Not created equal: Surveying investments in non-investment grade U.S. corporate debt Institutional investors seeking yield and current income opportunities have increased their allocations

Goldman Sachs Presentation to Bernstein Strategic Decisions Conference

Goldman Sachs Presentation to Bernstein Strategic Decisions Conference Comments by Gary Cohn, President and Chief Operating Officer May 30, 2013 Slide 1 Thanks Brad, and good morning to everyone. The operating

Goldman Sachs Presentation to Bernstein Strategic Decisions Conference Comments by Gary Cohn, President and Chief Operating Officer May 30, 2013 Slide 1 Thanks Brad, and good morning to everyone. The operating