ISSUES SUPPLY SEEMS TO HAVE SLOWED BUT PEAK OIL IS PSEUDOSCIENCE EASY OIL IS GONE CHEAP OIL IS GONE $100 IS NEW FLOOR, DUE TO HIGH COSTS RESOURCE NATI

|

|

|

- Robert Nicholson

- 6 years ago

- Views:

Transcription

1 GLOBAL OIL SUPPLY OUTLOOK IEEJ TOKYO JULY 2013 Michael C. Lynch 1

2 ISSUES SUPPLY SEEMS TO HAVE SLOWED BUT PEAK OIL IS PSEUDOSCIENCE EASY OIL IS GONE CHEAP OIL IS GONE $100 IS NEW FLOOR, DUE TO HIGH COSTS RESOURCE NATIONALISM HUGE OBSTACLE 2

3 LESSONS FROM PAST FORECASTING MANY BAD MODELS USED HUBBERT, CREAMING CURVES PESSIMISTIC AFTER 1979 EVERYONE BUT MIDDLE EAST AT A PEAK PEAK KEEPS MOVING OUT OPTIMISM APPEARS LATE 1990S JUST AS PRICES COLLAPSE MAJOR CHANGES/TURNING POINTS NOT EXPECTED 3

4")

4 US DOE FORECASTS LDC SUPPLY ( ) 4 EARLY FORECASTS TOO LOW, LATER TOO HIGH.

5 IEA FORECAST OIL SUPPLY CHANGE IN MB/D 5 SHOWS PROJECTED CHANGE IN NON-OPEC OIL SUPPLY FROM

6 AND COMPARISON WITH 2010 WEO 6 SHOWS PROJECTED CHANGE IN NON-OPEC OIL SUPPLY FROM

7 SUPPLY WEAKNESS NON-OPEC LDCS 7

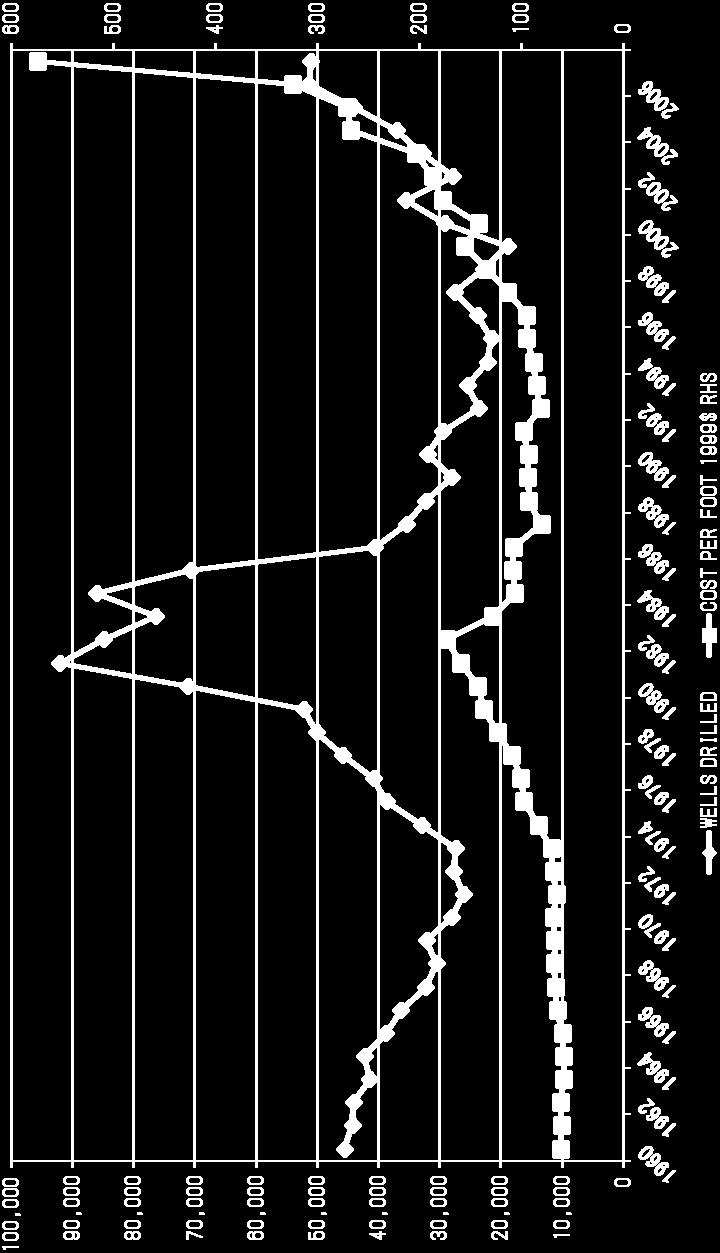

8 OIL RIG COUNT NON-OPEC, NON-OECD, NON-FSU 8

9 WHY ARE PRICES HIGH? DISRUPTED OIL SUPPLY 9

10 POLITICS MASSIVELY IMPORTANT MEXICO: BUDGET PROCESS LEADS TO DELAYS RUSSIA: GOVERNMENT CREATES UNCERTAINTY, DELAYS ARGENTINA, COLOMBIA, INDIA, ETC. GOVERNMENT POLICIES FLUCTUATE US, CANADA: PIPELINES, OFFSHORE DRILLING, GHG POLICY UNCERTAINTY 10

11 OPEC S CONTRIBUTION IRAQ MODERATE GROWTH IRAN/VENEZUELA/NIGERIA COULD RETURN WITH POLITICAL REFORM (DATE UNCERTAIN) ANGOLA/UAE SOME GROWTH POTENTIAL FOR POLITICAL DIFFICULTIES STILL SIGNIFICANT WILL SAUDI MAKE ROOM FOR IRAQ? 11

12 THE COST ISSUE DEFINITELY HIGHER, BUT WHY? ESTIMATES OFTEN IMPRECISE, INCORRECT INCLUDING TAXES OVERSTATES COSTS HIGHEST COST NOT NECESSARILY REPRESENTATIVE COST INFLATION: THREE FACTORS DEPLETION (EASY OIL IS GONE) GENERAL INFLATION: 1970S CYCLICAL INFLATION: 1970S, LATE 1990S, NOW? 12

13 FINDING COSTS

14 UPSTREAM COSTS 14

15 Global Oil Supply Costs Indonesia Eastern Canada US Stripper Wells US Gulf of Mexico 2000 Dollars per Barrel of Oil Equivalent Brazil Kazakhstan Algeria Oman Nigeria Alaska Venezuela Angola CMO North Sea 4.00 Kuwait 2.00 Iraq Saudi Arabi a Iran Source: Fagan, 2001 Liquid Productive Capacity (Mbd, Cumulative)

16 US WELLS AND COSTS 16

17 17 DO COSTS DRIVE PRICES? IN THEORY, ONLY OVER THE LONG-TERM MARGINAL COSTS VERY LOW IN SHORT- TERM PRICES DEFINITELY DRIVE COSTS 1998 PRICE DROP DRILLING CUTBACK NON-OPEC WEAKNESS HIGHER PRICES BUT THIS IS MORE LIKE 1986 PRICES AT ELEVATED LEVELS COSTS LIKELY TO DROP

18 FUTURE SUPPLIES RETURN OF OLD WINE IRAQ IRAN, VENEZUELA SOMEDAY? NEW WINE IN OLD BOTTLES ENHANCED RECOVERY SMALL PRODUCERS NEW WINE IN NEW BOTTLES BRAZIL, EAST AFRICA NEW WINE FROM BOXES SHALE OIL 18

19 SMALL PLAYERS 19

20 BRAZIL PRE-SALT HAS BBOE POTENTIAL GREATER THAN NORTH SEA TUPI ALONE IS 6-8 BLN BBLS. SERIOUS TECHNICAL CHALLENGES FIRST DEVELOPMENT PROBABLY LATE, OVER BUDGET THEN IT GETS EASIER, CHEAPER 20

21 OTHER DEEPWATER US, MEXICO, WEST AFRICA NOT AS GOOD AS BRAZIL PRE-SALT FIELDS ABOUT 1 BLN BBLS EACH ULTIMATE 1-2 MB/D INDONESIA, CENTRAL AMERICA, OTHER AREAS EARLY DAYS YET COULD CONTRIBUTE AFTE 2020 PROBABLY MODEST AMOUNTS 21

22 HEAVY OIL TO BOOM? OIL SANDS SHOULD SLOW OVERLOADED INFRASTRUCTURE RISING OPPOSITION (NATIVE, NIMBY) ECONOMICS IMPROVED QUALITY DIFFERENTIAL NOT AS IMPORTANT AT $100 NEW METHODS LIKE THAI MANY NEGLECTED DEPOSITS COLOMBIA, BRAZIL, KUWAIT, RUSSIA 22

23 SHALE LIQUIDS HUGE RESOURCE STILL LARGELY UNIDENTIFIED/ESTIMATED VERY LOW RECOVERY RATE BUT RISING 1% FIVE YEARS AGO, NOW 4-6% (BAKKEN) DELIVERY COMPLEX MEDIUM COST WELL PRODUCTIVITY LOWER THAN MIDDLE EAST, DEEPWATER: 1 TB/D QUICK DROP: 50% IN FIRST YEAR 23

24 Latest shale evaluation 24

25 OOPS, WE DID IT AGAIN NEW ARI/DOE REPORT 25

26 LATEST ESTIMATES BY REGION BILLION BARRELS 26 TRR IS TECHNICALLY RECOVERABLE RESERVES. ABOUT 3% RECOVERY FACTOR

27 IS US UNIQUE? PRIVATE OWNERSHIP OF MINERALS INFRASTRUCTURE MANY INDEPENDENT COMPANIES HUGE SERVICE INDUSTRY BUT: SOVIET UNION HAD NONE OF THOSE, STILL WAS LARGEST OIL PRODUCER IN THE WORLD NONE ARE INSURMOUNTABLE 27

28 SCENARIO FOR SHALE US BOOMING: AT LEAST 500 TB/D INCREASE EACH YEAR CANADA LESS SUPPLY BUT STARTING NOW COLOMBIA, ARGENTINA IN 2-3 YEARS RUSSIA, BRAZIL, MAYBE CHINA AND AUSTRALIA AFTER 5-6 YEARS LATER: NORTH AFRICA, CASPIAN, ETC. FRANCE??? BY 2018, SHOULD BE AT LEAST 1 MB/D OF NEW SUPPLY EACH YEAR 28

29 NEW MODEL OF SUPPLY FORECASTING FOR SMALL PRODUCERS GOVERNMENT ATTRACTS INVESTMENT SUPPLY RISES GOVERNMENT BECOMES COMPLACENT INVESTMENT TAPERS OFF SUPPLY PLATEAUS OR DECLINES GOVERNMENT ATTRACTS NEW INVESTMENT MEXICO AS CASE STUDY 29

30 MISINTERPRETATION OF SUPPLY CURVES NOT TIME FUNCTION SHOULD BE DYNAMIC DIFFERENT REGIONS/TYPES OF OIL WITH DIFFERENT DRIVERS DEPLETION INFRASTRUCTURE TECHNOLOGY 30

31 SUPPLY CURVE: STANDARD 31

32 WRONG INTERPRETATION TN T1 32

33 Contact: IEEJ: July 2013 All Right Reserved SUGGESTED MODEL ONLY PRIVATE SECTOR PRICE DRIVES REVENUE NON-LINEAR REVENUE DRIVES INVESTMENT NON-LINEAR TO LEFT INVESTMENT DRIVES ACTIVITY NON-LINEAR TO LEFT REGIONAL RESULTS 33

John Gerdes Head of Research. The Dynamic and Global Oil & Gas Industry Next Steps for 2016 & 2017

John Gerdes Head of Research The Dynamic and Global Oil & Gas Industry Next Steps for 2016 & 2017 Differentiated Energy Research Mission: Consistent, objective analysis of full-cycle economic returns derived

John Gerdes Head of Research The Dynamic and Global Oil & Gas Industry Next Steps for 2016 & 2017 Differentiated Energy Research Mission: Consistent, objective analysis of full-cycle economic returns derived

The Oil Supply Outlook in the New Oil Price Environment: The Long and Short Term Investment Cycles

The Oil Supply Outlook in the New Oil Price Environment: The Long and Short Term Investment Cycles Bassam Fattouh Oxford Institute for Energy Studies OIES OIL DAY, ST CATHERINE'S, OXFORD, NOVEMBER 17 215

The Oil Supply Outlook in the New Oil Price Environment: The Long and Short Term Investment Cycles Bassam Fattouh Oxford Institute for Energy Studies OIES OIL DAY, ST CATHERINE'S, OXFORD, NOVEMBER 17 215

The construction or provision of oil rigs, drilling. equipment, including seismic data collection.

The construction or provision of oil rigs, drilling equipment and other energy related service and equipment, including seismic data collection. Engaged in the exploration, production, marketing, refining

The construction or provision of oil rigs, drilling equipment and other energy related service and equipment, including seismic data collection. Engaged in the exploration, production, marketing, refining

Oil Value Chain & Markets. Global Oil Markets

Oil Value Chain & Markets Global Oil Markets World Oil Reserves WORLD OPEC Middle East Former Soviet Union Africa End 2006 End 2000 End 1990 End 1980 North America USA South & Central America Asia Pacific

Oil Value Chain & Markets Global Oil Markets World Oil Reserves WORLD OPEC Middle East Former Soviet Union Africa End 2006 End 2000 End 1990 End 1980 North America USA South & Central America Asia Pacific

Supply Trends ÖGEW / DGMK

Special Presentation Supply Trends ÖGEW / DGMK GROUP JBC, Johannes Benigni 17 October 2014 Disclaimer GROUP All statements other than statements of historical fact are, or may be deemed to be, forwardlooking

Special Presentation Supply Trends ÖGEW / DGMK GROUP JBC, Johannes Benigni 17 October 2014 Disclaimer GROUP All statements other than statements of historical fact are, or may be deemed to be, forwardlooking

Oil Markets: Where next?

Oil Markets: Where next? Christof Rühl, Global Head of Research Singapore September 2016 1 Content Oil and the economy: Recap Why did lower oil prices not support economic growth? OPEC vs. US two sides

Oil Markets: Where next? Christof Rühl, Global Head of Research Singapore September 2016 1 Content Oil and the economy: Recap Why did lower oil prices not support economic growth? OPEC vs. US two sides

Oil price. Laura Lungarini

Oil price Laura Lungarini Agenda Crude oil market What is behind oil price Fundamentals Main Players Geopolitics Financial market The price determinant Benchmark crude oils Brent Physical and paper market

Oil price Laura Lungarini Agenda Crude oil market What is behind oil price Fundamentals Main Players Geopolitics Financial market The price determinant Benchmark crude oils Brent Physical and paper market

Global Construction 2030 Expo EDIFICA 2017 Santiago Chile. 4-6 October 2017

Global Construction 2030 Expo EDIFICA 2017 Santiago Chile 4-6 October 2017 Graham Robinson Global Construction Perspectives Global Construction 2030 is the fourth in a series of global studies of the construction

Global Construction 2030 Expo EDIFICA 2017 Santiago Chile 4-6 October 2017 Graham Robinson Global Construction Perspectives Global Construction 2030 is the fourth in a series of global studies of the construction

Another Technological Revolution in the O&G Industry: A new Future for Onshore E&P. Ivan Sandrea Advisor to Petra Energia

Another Technological Revolution in the O&G Industry: A new Future for Onshore E&P Ivan Sandrea Advisor to Petra Energia Contents Another technological revolution in the O&G industry Key onshore stats

Another Technological Revolution in the O&G Industry: A new Future for Onshore E&P Ivan Sandrea Advisor to Petra Energia Contents Another technological revolution in the O&G industry Key onshore stats

4Q13 Earnings Presentation

4Q13 Earnings Presentation February 19, 2014 Presenter: Anthony G. Petrello Chairman, President & Chief Executive Officer Forward-Looking Statements We often discuss expectations regarding our markets,

4Q13 Earnings Presentation February 19, 2014 Presenter: Anthony G. Petrello Chairman, President & Chief Executive Officer Forward-Looking Statements We often discuss expectations regarding our markets,

MacroVoices Oil Discussion: OPEC Can t Fix The Problem of Low Oil Prices

MacroVoices Oil Discussion: OPEC Can t Fix The Problem of Low Oil Prices Art Berman November 30, 2016 Slide 1 Overview: OPEC Can t Fix The Problem of Low Oil Prices OPEC may reach some agreement today

MacroVoices Oil Discussion: OPEC Can t Fix The Problem of Low Oil Prices Art Berman November 30, 2016 Slide 1 Overview: OPEC Can t Fix The Problem of Low Oil Prices OPEC may reach some agreement today

Jeffrey Currie Goldman, Sachs & Co

The New Oil Order September 217 Jeffrey Currie Goldman, Sachs & Co. +1 212-357-681 jeffrey.currie@gs.com Goldman Sachs does and seeks to do business with companies covered in its research reports. As a

The New Oil Order September 217 Jeffrey Currie Goldman, Sachs & Co. +1 212-357-681 jeffrey.currie@gs.com Goldman Sachs does and seeks to do business with companies covered in its research reports. As a

Market Watch Presentation

Special Presentation Market Watch Presentation Petrotech Johannes Benigni December 2016 Disclaimer All statements other than statements of historical fact are, or may be deemed to be, forward-looking statements.

Special Presentation Market Watch Presentation Petrotech Johannes Benigni December 2016 Disclaimer All statements other than statements of historical fact are, or may be deemed to be, forward-looking statements.

BAKER HUGHES INC FORM 10-Q. (Quarterly Report) Filed 05/01/12 for the Period Ending 03/31/12

Filed 05/01/12 for the Period Ending 03/31/12") BAKER HUGHES INC FORM 10-Q (Quarterly Report) Filed 05/01/12 for the Period Ending 03/31/12 Address 2929 ALLEN PARKWAY SUITE 2100 HOUSTON, TX 77019-2118 Telephone 7134398600 CIK 0000808362 Symbol BHI SIC

BAKER HUGHES INC FORM 10-Q (Quarterly Report) Filed 05/01/12 for the Period Ending 03/31/12 Address 2929 ALLEN PARKWAY SUITE 2100 HOUSTON, TX 77019-2118 Telephone 7134398600 CIK 0000808362 Symbol BHI SIC

Looking Ahead on Oil & Gas

Looking Ahead on Oil & Gas Art Berman NACE Investor Speaker Luncheon Palm Beach Gardens, Florida March 16, 217 Slide 1 Oil Prices Fell Below $5 Floor Last Week: Deflation of the OPEC Expectation Premium

Looking Ahead on Oil & Gas Art Berman NACE Investor Speaker Luncheon Palm Beach Gardens, Florida March 16, 217 Slide 1 Oil Prices Fell Below $5 Floor Last Week: Deflation of the OPEC Expectation Premium

BAKER HUGHES INC FORM 10-Q. (Quarterly Report) Filed 10/24/12 for the Period Ending 09/30/12

Filed 10/24/12 for the Period Ending 09/30/12") BAKER HUGHES INC FORM 10-Q (Quarterly Report) Filed 10/24/12 for the Period Ending 09/30/12 Address 2929 ALLEN PARKWAY SUITE 2100 HOUSTON, TX 77019-2118 Telephone 7134398600 CIK 0000808362 Symbol BHI SIC

BAKER HUGHES INC FORM 10-Q (Quarterly Report) Filed 10/24/12 for the Period Ending 09/30/12 Address 2929 ALLEN PARKWAY SUITE 2100 HOUSTON, TX 77019-2118 Telephone 7134398600 CIK 0000808362 Symbol BHI SIC

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET AN INTERNATIONAL ENERGY FORUM PUBLICATION NOVEMBER 2018 RIYADH, SAUDI ARABIA NOVEMBER 2018 SUMMARY FINDINGS FROM A COMPARISON OF DATA AND FORECASTS

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET AN INTERNATIONAL ENERGY FORUM PUBLICATION NOVEMBER 2018 RIYADH, SAUDI ARABIA NOVEMBER 2018 SUMMARY FINDINGS FROM A COMPARISON OF DATA AND FORECASTS

The light tight oil revolution -- the rollover and the recovery Production in major US shale plays, millions of barrels/day

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Oil Monday, August 1, 1 The light tight oil revolution --

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Oil Monday, August 1, 1 The light tight oil revolution --

State of the Chemical and Petrochemical Industry Is India the next driver?

State of the Chemical and Petrochemical Industry Is India the next driver? Presentation to IOC Conclave 29 July 217 Dave Witte Senior Vice President, IHS Markit GM - Oil Markets, Midstream, Downstream

State of the Chemical and Petrochemical Industry Is India the next driver? Presentation to IOC Conclave 29 July 217 Dave Witte Senior Vice President, IHS Markit GM - Oil Markets, Midstream, Downstream

The Lies We ve Been Told

The Lies We ve Been Told October 29, 2008 Role of Oil in US Energy Policy University of Southern Maine Conversations at Muskie Lucian Pugliaresi Energy Policy Research Foundation, Inc. Washington, DC www.eprinc.org

The Lies We ve Been Told October 29, 2008 Role of Oil in US Energy Policy University of Southern Maine Conversations at Muskie Lucian Pugliaresi Energy Policy Research Foundation, Inc. Washington, DC www.eprinc.org

In for the Long Haul Why Lower Oil Prices will be Good for You!

In for the Long Haul Why Lower Oil Prices will be Good for You! CO2-EOR Institute, 16 July 2015 BEG/CEE-UT, 1 Lower oil prices will Build demand Reduce competition to oil from non-oil alternatives (high

In for the Long Haul Why Lower Oil Prices will be Good for You! CO2-EOR Institute, 16 July 2015 BEG/CEE-UT, 1 Lower oil prices will Build demand Reduce competition to oil from non-oil alternatives (high

2Q14 Earnings Presentation

2Q14 Earnings Presentation July 23, 2014 Presenters: Anthony G. Petrello Chairman, President & Chief Executive Officer William Restrepo Chief Financial Officer Forward-Looking Statements We often discuss

2Q14 Earnings Presentation July 23, 2014 Presenters: Anthony G. Petrello Chairman, President & Chief Executive Officer William Restrepo Chief Financial Officer Forward-Looking Statements We often discuss

2015 Oil Outlook. january 21, 2015

Epoch Investment Partners, Inc. january 21, 2015 2015 Oil Outlook john p. reddan, cfa, managing director & senior research analyst After trading in a range from $90-$110 per barrel from late 2010 through

Epoch Investment Partners, Inc. january 21, 2015 2015 Oil Outlook john p. reddan, cfa, managing director & senior research analyst After trading in a range from $90-$110 per barrel from late 2010 through

WORLD ENERGY INVESTMENT OUTLOOK. Dr. Fatih Birol Chief Economist Head, Economic Analysis Division International Energy Agency / OECD

WORLD ENERGY INVESTMENT OUTLOOK Dr. Fatih Birol Chief Economist Head, Economic Analysis Division International Energy Agency / OECD Global Strategic Challenges Security of energy supplies Threat of environmental

WORLD ENERGY INVESTMENT OUTLOOK Dr. Fatih Birol Chief Economist Head, Economic Analysis Division International Energy Agency / OECD Global Strategic Challenges Security of energy supplies Threat of environmental

Oilfield Services and Equipment Sector Market Opportunity Update

May 2010 Oilfield Services and Equipment Sector Market Opportunity Update C O N F I D E N T I A L www.oliverwyman.com Contents Introduction and executive summary Global energy industry and oilfield services

May 2010 Oilfield Services and Equipment Sector Market Opportunity Update C O N F I D E N T I A L www.oliverwyman.com Contents Introduction and executive summary Global energy industry and oilfield services

M&G Emerging Markets Bond Fund Claudia Calich, Fund Manager. November 2015

M&G Emerging Markets Bond Fund Claudia Calich, Fund Manager November 2015 Agenda Macro update & government bonds Emerging market corporate bonds Fund positioning Emerging markets risks today Risks Slowing

M&G Emerging Markets Bond Fund Claudia Calich, Fund Manager November 2015 Agenda Macro update & government bonds Emerging market corporate bonds Fund positioning Emerging markets risks today Risks Slowing

Oil: An Ongoing Story of Supply and Demand

Oil: An Ongoing Story of Supply and Demand The new normal of oil prices The crude oil market has experienced a sea change since 214. Oil prices dropped sharply from above $1 in early 214, bottomed at $26

Oil: An Ongoing Story of Supply and Demand The new normal of oil prices The crude oil market has experienced a sea change since 214. Oil prices dropped sharply from above $1 in early 214, bottomed at $26

Francisco Monaldi, Ph.D.

Francisco Monaldi, Ph.D. Visiting Professor and Roy Family Senior Fellow, Harvard Kennedy School Non-Resident Fellow, Baker Institute, Rice University Faculty Associate, School of Government, Tecnologico

Francisco Monaldi, Ph.D. Visiting Professor and Roy Family Senior Fellow, Harvard Kennedy School Non-Resident Fellow, Baker Institute, Rice University Faculty Associate, School of Government, Tecnologico

LIGHT SWEET CRUDE OIL. Short term Update

24 th March 2008 Karvy Comtrade s LIGHT SWEET CRUDE OIL Short term Update Crude prices surpassed the psychological level of $100 and tested a high of $111.80 with funds interest supported by falling dollar

24 th March 2008 Karvy Comtrade s LIGHT SWEET CRUDE OIL Short term Update Crude prices surpassed the psychological level of $100 and tested a high of $111.80 with funds interest supported by falling dollar

Permian Reserves May Be Much Smaller Than You Think: Tight Oil and Long-Term Debt Cycle

Permian Reserves May Be Much Smaller Than You Think: Tight Oil and Long-Term Debt Cycle Arthur E. Berman September 11, 217 Slide 1 New Age of American Energy Dominance The U.S. is the 1th Largest Oil Reserve

Permian Reserves May Be Much Smaller Than You Think: Tight Oil and Long-Term Debt Cycle Arthur E. Berman September 11, 217 Slide 1 New Age of American Energy Dominance The U.S. is the 1th Largest Oil Reserve

Emerging Trends in the Energy Industry. Paul Horak Partner, Audit and Enterprise Risk Services Deloitte & Touche LLP

Emerging Trends in the Energy Industry Paul Horak Partner, Audit and Enterprise Risk Services Deloitte & Touche LLP August 2016 Agenda Introduction Drilling and Production Trends Crude Oil and Refined

Emerging Trends in the Energy Industry Paul Horak Partner, Audit and Enterprise Risk Services Deloitte & Touche LLP August 2016 Agenda Introduction Drilling and Production Trends Crude Oil and Refined

Global economic overview and the new oil price environment

IHS AUTOMOTIVE Presentation Global economic overview and the new oil price environment IHS Automotive Conference Tokyo 5 March 215 ihs.com Sara Johnson, Senior Research Director, Global Economics +1 781

IHS AUTOMOTIVE Presentation Global economic overview and the new oil price environment IHS Automotive Conference Tokyo 5 March 215 ihs.com Sara Johnson, Senior Research Director, Global Economics +1 781

Patrick Schorn Executive Vice President, Wells Cowen 8th Annual Energy & Natural Resources Conference

Patrick Schorn Executive Vice President, Wells 2018 Cowen 8th Annual Energy & Natural Resources Conference New York, December 4, 2018 Safe Harbor This presentation contains forward-looking statements within

Patrick Schorn Executive Vice President, Wells 2018 Cowen 8th Annual Energy & Natural Resources Conference New York, December 4, 2018 Safe Harbor This presentation contains forward-looking statements within

The Future of the U.S. Energy Industry Presentation to: GIC-DABE Economic Forum Denver, CO

The Future of the U.S. Energy Industry Presentation to: GIC-DABE Economic Forum Denver, CO By: John Harpole July 18, 2016 What Happened? Thanks to hydraulic fracturing, horizontal drilling and private

The Future of the U.S. Energy Industry Presentation to: GIC-DABE Economic Forum Denver, CO By: John Harpole July 18, 2016 What Happened? Thanks to hydraulic fracturing, horizontal drilling and private

The Political Economy of Oil in Latin America:

The Political Economy of Oil in Latin America: Endowments, Institutions, and Incentives Francisco Monaldi Director, Center on Energy and the Environment, IESA, Caracas Robert F. Kennedy Visiting Profesor,

The Political Economy of Oil in Latin America: Endowments, Institutions, and Incentives Francisco Monaldi Director, Center on Energy and the Environment, IESA, Caracas Robert F. Kennedy Visiting Profesor,

Presentation to the Financial Community. First Half 2011 Results

Presentation to the Financial Community First Half 2011 Results July 2011 Forward-Looking Statements By their nature, forward-looking statements are subject to risk and uncertainty since they are dependent

Presentation to the Financial Community First Half 2011 Results July 2011 Forward-Looking Statements By their nature, forward-looking statements are subject to risk and uncertainty since they are dependent

Oil Report 4Q 2016 Earnings Summary for International Oil Companies (IOCs) & Outlook

& Outlook") March 15, 2017 4Q 2016 Earnings Summary for IOCs & Outlook Page 1 Quarterly & Annual Chart Summary (Aggregate of IOCs) Pages 2-4 Earnings Side Notes Page 5-7 Results by IOC Pages 8-13 Oil Report 4Q 2016

March 15, 2017 4Q 2016 Earnings Summary for IOCs & Outlook Page 1 Quarterly & Annual Chart Summary (Aggregate of IOCs) Pages 2-4 Earnings Side Notes Page 5-7 Results by IOC Pages 8-13 Oil Report 4Q 2016

5 Reasons to Expect Higher Oil Prices

5 Reasons to Expect Higher Oil Prices May 31, 2017 by Neil Dwane of Allianz Global Investors Why we're constructive on oil Not many investors have been bullish on the price of oil recently, but Allianz

5 Reasons to Expect Higher Oil Prices May 31, 2017 by Neil Dwane of Allianz Global Investors Why we're constructive on oil Not many investors have been bullish on the price of oil recently, but Allianz

Managing Volatility in Oil and Gas Revenues

Managing Volatility in Oil and Gas Revenues Presentation to the Revenue Stabilization and Tax Policy Committee September 12, 2008 Thomas Clifford, PhD Research Director New Mexico Tax Research Institute

Managing Volatility in Oil and Gas Revenues Presentation to the Revenue Stabilization and Tax Policy Committee September 12, 2008 Thomas Clifford, PhD Research Director New Mexico Tax Research Institute

OPEC extends oil output cut through March 2018

Economics Research Desk Market Highlights: Oil & Gas update 25 May 2017 OPEC extends oil output cut through March 2018 Oil prices swung between sharp gains and losses in volatile trade on Thursday, after

Economics Research Desk Market Highlights: Oil & Gas update 25 May 2017 OPEC extends oil output cut through March 2018 Oil prices swung between sharp gains and losses in volatile trade on Thursday, after

Investor Presentation

Investor Presentation Disclaimer This presentation contains forward-looking statements. Forward-looking statements are based on management s current views and assumptions and involve known and unknown

Investor Presentation Disclaimer This presentation contains forward-looking statements. Forward-looking statements are based on management s current views and assumptions and involve known and unknown

The Persian Gulf s predominance endangered? Amrita Sen, 13 November 2013

The Persian Gulf s predominance endangered? Amrita Sen, 13 November 2013 The sudden burst of shale was viewed as a key threat to OPEC US oil production North Dakota oil production 12.0 1.0 11.0 10.0 9.0

The Persian Gulf s predominance endangered? Amrita Sen, 13 November 2013 The sudden burst of shale was viewed as a key threat to OPEC US oil production North Dakota oil production 12.0 1.0 11.0 10.0 9.0

Oil Market Outlook. Oil Market Outlook. Executive Summary. Executive SummaryS. October Report Series

Report Series Oil Market Outlook Executive Summary Oil Market Outlook Lower oil prices were supposed to bring a supply response from non- OPEC producers, but this is happening more slowly than expected,

Report Series Oil Market Outlook Executive Summary Oil Market Outlook Lower oil prices were supposed to bring a supply response from non- OPEC producers, but this is happening more slowly than expected,

Investor Presentation

Investor Presentation Disclaimer This presentation contains forward-looking statements. Forward-looking statements are based on management s current views and assumptions and involve known and unknown

Investor Presentation Disclaimer This presentation contains forward-looking statements. Forward-looking statements are based on management s current views and assumptions and involve known and unknown

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET AN INTERNATIONAL ENERGY FORUM PUBLICATION AUGUST 2018 RIYADH, SAUDI ARABIA AUGUST 2018 SUMMARY FINDINGS FROM A COMPARISON OF DATA AND FORECASTS

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET AN INTERNATIONAL ENERGY FORUM PUBLICATION AUGUST 2018 RIYADH, SAUDI ARABIA AUGUST 2018 SUMMARY FINDINGS FROM A COMPARISON OF DATA AND FORECASTS

Investor Presentation

Investor Presentation Disclaimer This presentation contains forward-looking statements. Forward-looking statements are based on management s current views and assumptions and involve known and unknown

Investor Presentation Disclaimer This presentation contains forward-looking statements. Forward-looking statements are based on management s current views and assumptions and involve known and unknown

Domestic and Foreign Debt: Global Projections to 2050

Domestic and Foreign Debt: Global Projections to 2050 John L Perkins National Institute of Economics and Industry Research, Melbourne. Project LINK, 26 October 2011 Outline Long term model features Government

Domestic and Foreign Debt: Global Projections to 2050 John L Perkins National Institute of Economics and Industry Research, Melbourne. Project LINK, 26 October 2011 Outline Long term model features Government

Ben Brunnen, Vice President, Oil Sands January 19, Upstream Oil and Gas Industry Outlook Presentation to Alberta s Industrial Heartland

Ben Brunnen, Vice President, Oil Sands January 19, 2017 Upstream Oil and Gas Industry Outlook Presentation to Alberta s Industrial Heartland 2 About CAPP and Canada s Oil and Gas Industry Large and small

Ben Brunnen, Vice President, Oil Sands January 19, 2017 Upstream Oil and Gas Industry Outlook Presentation to Alberta s Industrial Heartland 2 About CAPP and Canada s Oil and Gas Industry Large and small

Supplementary Information: Definitions and reconciliation of non-gaap measures.

Supplementary Information: Definitions and reconciliation of non-gaap measures. The information below has been provided to enhance understanding of the terminology and performance measures that have been

Supplementary Information: Definitions and reconciliation of non-gaap measures. The information below has been provided to enhance understanding of the terminology and performance measures that have been

Global investment event Winners and losers from the recent oil price rally

For client use only Global investment event Winners and losers from the recent oil price rally Since mid-2017, oil prices have been on an upward trend. Strong oil demand growth, OPECled production cuts,

For client use only Global investment event Winners and losers from the recent oil price rally Since mid-2017, oil prices have been on an upward trend. Strong oil demand growth, OPECled production cuts,

1. What will the global economic recovery be like? Anaemic growth, perhaps even a double-dip? Key questions 2. How will oil demand respond to renewed

IEA/IEEJ Forum on Global Oil Market Challenges Global oil market outlook Dr. Leo P. Drollas Deputy Director and Chief Economist Centre for Global Energy Studies Tokyo 26 th February 2010 1. What will the

IEA/IEEJ Forum on Global Oil Market Challenges Global oil market outlook Dr. Leo P. Drollas Deputy Director and Chief Economist Centre for Global Energy Studies Tokyo 26 th February 2010 1. What will the

Econ 366. Fall 2012 The International Oil Market: The Cartel Era

Econ 366 Fall 2012 The International Oil Market: The Cartel Era A brief history of oil markets 4 major phases preceded creation of OPEC 1. Oil Rush in US (1859 1870) rush to buy land (landowner owns underground

Econ 366 Fall 2012 The International Oil Market: The Cartel Era A brief history of oil markets 4 major phases preceded creation of OPEC 1. Oil Rush in US (1859 1870) rush to buy land (landowner owns underground

Update On Alberta Oil Sands Projects: Keeping Things In Perspective David Knapp Energy Intelligence Group Canada Think Day Center For Energy

Update On Alberta Oil Sands Projects: Keeping Things In Perspective David Knapp Energy Intelligence Group Canada Think Day Center For Energy Economics Houston, Texas - Mar. 9, 2006 OUTLINE The Global Role

Update On Alberta Oil Sands Projects: Keeping Things In Perspective David Knapp Energy Intelligence Group Canada Think Day Center For Energy Economics Houston, Texas - Mar. 9, 2006 OUTLINE The Global Role

Oil Report 1Q 2017 Earnings Summary for International Oil Companies (IOCs) & Outlook

& Outlook") May 17, 2017 1Q 2017 Earnings Summary for IOCs & Outlook Page 1 Quarterly Chart Summary (Aggregate of IOCs) Pages 2-3 Earnings Side Notes Page 4-6 Results by IOC Pages 7-10 Oil Report 1Q 2017 Earnings

May 17, 2017 1Q 2017 Earnings Summary for IOCs & Outlook Page 1 Quarterly Chart Summary (Aggregate of IOCs) Pages 2-3 Earnings Side Notes Page 4-6 Results by IOC Pages 7-10 Oil Report 1Q 2017 Earnings

Robert Haddad Ashley Hughes AmirAli Motamedi Masoudieh

Robert Haddad Ashley Hughes AmirAli Motamedi Masoudieh Size and Composition Business and Economic Analysis Financial Analysis Valuation Analysis Recommendation Composed of companies involved in the production

Robert Haddad Ashley Hughes AmirAli Motamedi Masoudieh Size and Composition Business and Economic Analysis Financial Analysis Valuation Analysis Recommendation Composed of companies involved in the production

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET AN INTERNATIONAL ENERGY FORUM PUBLICATION SEPTEMBER 2018 RIYADH, SAUDI ARABIA SEPTEMBER 2018 SUMMARY FINDINGS FROM A COMPARISON OF DATA AND FORECASTS

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET AN INTERNATIONAL ENERGY FORUM PUBLICATION SEPTEMBER 2018 RIYADH, SAUDI ARABIA SEPTEMBER 2018 SUMMARY FINDINGS FROM A COMPARISON OF DATA AND FORECASTS

April 2015 Fiscal Monitor

International Monetary Fund April 17, 2015 April 2015 Fiscal Monitor Now is the Time: Fiscal Policies for Sustainable Growth Xavier Debrun Deputy Chief, Fiscal Policy and Surveillance, Fiscal Affairs Department

International Monetary Fund April 17, 2015 April 2015 Fiscal Monitor Now is the Time: Fiscal Policies for Sustainable Growth Xavier Debrun Deputy Chief, Fiscal Policy and Surveillance, Fiscal Affairs Department

Seismic shifts in the oil and gas business

Seismic shifts in the oil and gas business Copenhagen Wednesday, 07 October 2015 Strategy with substance www.woodmac.com Jan-13 May-13 Sep-13 Jan-14 May-14 Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16

Seismic shifts in the oil and gas business Copenhagen Wednesday, 07 October 2015 Strategy with substance www.woodmac.com Jan-13 May-13 Sep-13 Jan-14 May-14 Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16

Recent oil market trends and future drivers

Multi-year Expert Meeting on COMMODITIES AND DEVELOPMENT 6-7 April, Geneva Recent oil market trends and future drivers by Mr. David Fyfe, Head of Industry and s Division, Editor, International Energy Agency,

Multi-year Expert Meeting on COMMODITIES AND DEVELOPMENT 6-7 April, Geneva Recent oil market trends and future drivers by Mr. David Fyfe, Head of Industry and s Division, Editor, International Energy Agency,

Overview of Canada s Oil Sands Industry

Overview of Canada s Oil Sands Industry CSSE Awards Banquet May 14, 2011 Calgary, Alberta Bob Dunbar Strategy West Inc. 12-1 Photo Source: Syncrude Canada Limited Presentation Outline Industry Overview

Overview of Canada s Oil Sands Industry CSSE Awards Banquet May 14, 2011 Calgary, Alberta Bob Dunbar Strategy West Inc. 12-1 Photo Source: Syncrude Canada Limited Presentation Outline Industry Overview

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET AN INTERNATIONAL ENERGY FORUM PUBLICATION JUNE 2018 RIYADH, SAUDI ARABIA JUNE 2018 SUMMARY FINDINGS FROM A COMPARISON OF DATA AND FORECASTS ON

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET AN INTERNATIONAL ENERGY FORUM PUBLICATION JUNE 2018 RIYADH, SAUDI ARABIA JUNE 2018 SUMMARY FINDINGS FROM A COMPARISON OF DATA AND FORECASTS ON

Bank of America / Merrill Lynch 2009 Energy Conference

Bank of America / Merrill Lynch 2009 Energy Conference Pat Yarrington Vice President and Chief Financial Officer Chevron Corporation New York City November 17, 2009 Cautionary Statement CAUTIONARY STATEMENT

Bank of America / Merrill Lynch 2009 Energy Conference Pat Yarrington Vice President and Chief Financial Officer Chevron Corporation New York City November 17, 2009 Cautionary Statement CAUTIONARY STATEMENT

26 MAY Boustead Singapore Limited / Boustead Projects Limited Joint FY2015 Financial Results Presentation

26 MAY 2015 Boustead Singapore Limited / Boustead Projects Limited Joint FY2015 Financial Results Presentation Disclaimer This presentation contains certain statements that are not statements of historical

26 MAY 2015 Boustead Singapore Limited / Boustead Projects Limited Joint FY2015 Financial Results Presentation Disclaimer This presentation contains certain statements that are not statements of historical

The Economic Transformation of the Caspian Region and the Falling Price of Oil

The Economic Transformation of the Caspian Region and the Falling Price of Oil Professor Yelena Kalyuzhnova Vice-Dean International, Henley Business School, Director of the Centre for Euro-Asian Studies

The Economic Transformation of the Caspian Region and the Falling Price of Oil Professor Yelena Kalyuzhnova Vice-Dean International, Henley Business School, Director of the Centre for Euro-Asian Studies

Key Priorities and Challenges for Canadian Oil

Key Priorities and Challenges for Canadian Oil Canadian Heavy Oil Association April 15, 2013 Greg Stringham 1 Photo: Cenovus Enabling Responsible Development 2 Global Primary Energy Demand 20,000 18,000

Key Priorities and Challenges for Canadian Oil Canadian Heavy Oil Association April 15, 2013 Greg Stringham 1 Photo: Cenovus Enabling Responsible Development 2 Global Primary Energy Demand 20,000 18,000

Why do Chevron s capex projects determine production growth?

Why do Chevron s capex projects determine production growth? By Keisha Bandz May 16, 2014. 02:00 PM Chevron Corporation: A must-know brief overview Chevron Corporation C hevron C orporation (C VX), headquartered

Why do Chevron s capex projects determine production growth? By Keisha Bandz May 16, 2014. 02:00 PM Chevron Corporation: A must-know brief overview Chevron Corporation C hevron C orporation (C VX), headquartered

The impact of plummeting crude oil prices on company finances

The impact of plummeting crude oil prices on company finances Crude awakening What has caused the sudden fall in oil price? What effect will this have on the industry? Who will be the winners and who will

The impact of plummeting crude oil prices on company finances Crude awakening What has caused the sudden fall in oil price? What effect will this have on the industry? Who will be the winners and who will

26 MAY Boustead Singapore Limited FY2010 Financial Results Presentation

26 MAY 2010 Boustead Singapore Limited FY2010 Financial Results Presentation Disclaimer This presentation contains certain statements that are not statements of historical fact such as forward-looking

26 MAY 2010 Boustead Singapore Limited FY2010 Financial Results Presentation Disclaimer This presentation contains certain statements that are not statements of historical fact such as forward-looking

COMCEC Trade OUTLOOK 2015

COMCEC Trade OUTLOOK 2015 Trade Working Group 6 th Meeting September 17, 2015 Ankara, Turkey OUTLINE Recent Trends in Trade Between the OIC Member States and the World Recent Trends in Intra-OIC Trade

COMCEC Trade OUTLOOK 2015 Trade Working Group 6 th Meeting September 17, 2015 Ankara, Turkey OUTLINE Recent Trends in Trade Between the OIC Member States and the World Recent Trends in Intra-OIC Trade

FOR OIL & GAS WORLD FISCAL SYSTEMS BAC.

BAC ACCREDITED WORLD FISCAL SYSTEMS FOR OIL & GAS DATE: LOCATION: 03-07 March 2014 Singapore 09-13 June 2014 Amsterdam, The Netherlands 16-20 November 2014 Dubai, UAE Receive the most comprehensive overview

BAC ACCREDITED WORLD FISCAL SYSTEMS FOR OIL & GAS DATE: LOCATION: 03-07 March 2014 Singapore 09-13 June 2014 Amsterdam, The Netherlands 16-20 November 2014 Dubai, UAE Receive the most comprehensive overview

Global Economic Outlook

Global Economic Outlook The Institute of Strategic and International Studies Kuala Lumpur, November 2012 Mangal Goswami Mangal Goswami Deputy Director IMF Singapore Regional Training Institute Action Needed

Global Economic Outlook The Institute of Strategic and International Studies Kuala Lumpur, November 2012 Mangal Goswami Mangal Goswami Deputy Director IMF Singapore Regional Training Institute Action Needed

Natural Resource Taxation: Challenges in Africa

Philip Daniel Fiscal Affairs Department International Monetary Fund Natural Resource Taxation: Challenges in Africa Management of Natural Resources in Sub-Saharan Africa Kinshasa Conference, March 22,

Philip Daniel Fiscal Affairs Department International Monetary Fund Natural Resource Taxation: Challenges in Africa Management of Natural Resources in Sub-Saharan Africa Kinshasa Conference, March 22,

December Nigeria's operating landscape

Nigeria's operating landscape Caveat This document has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information

Nigeria's operating landscape Caveat This document has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information

First quarter 2018 earnings conference call and webcast

First quarter 2018 earnings conference call and webcast Pat Yarrington Vice President and Chief Financial Officer Mark Nelson Vice President, Midstream, Strategy and Policy Frank Mount / Wayne Borduin

First quarter 2018 earnings conference call and webcast Pat Yarrington Vice President and Chief Financial Officer Mark Nelson Vice President, Midstream, Strategy and Policy Frank Mount / Wayne Borduin

The Challenges & Opportunities From Falling Energy Prices March 2015

The Challenges & Opportunities From Falling Energy Prices March 2015 page 1 Agenda Oil Market: Macro Overview Deep Dive: Houston Economy & CRE Markets Beneficiaries: Who Stands To Gain From Cheap Oil?

The Challenges & Opportunities From Falling Energy Prices March 2015 page 1 Agenda Oil Market: Macro Overview Deep Dive: Houston Economy & CRE Markets Beneficiaries: Who Stands To Gain From Cheap Oil?

CHEVRON REPORTS FOURTH QUARTER NET INCOME OF $5.3 BILLION, UP FROM $3.1 BILLION IN FOURTH QUARTER 2009

Policy, Government and Public Affairs Chevron Corporation P.O. Box 6078 San Ramon, CA 94583-0778 www.chevron.com FOR RELEASE AT 5:30 AM PST JANUARY 28, 2011 CHEVRON REPORTS FOURTH QUARTER NET INCOME OF

Policy, Government and Public Affairs Chevron Corporation P.O. Box 6078 San Ramon, CA 94583-0778 www.chevron.com FOR RELEASE AT 5:30 AM PST JANUARY 28, 2011 CHEVRON REPORTS FOURTH QUARTER NET INCOME OF

Economics Program Working Paper Series

Economics Program Working Paper Series Projecting Economic Growth with Growth Accounting Techniques: The Conference Board Global Economic Outlook 2012 Sources and Methods Vivian Chen Ben Cheng Gad Levanon

Economics Program Working Paper Series Projecting Economic Growth with Growth Accounting Techniques: The Conference Board Global Economic Outlook 2012 Sources and Methods Vivian Chen Ben Cheng Gad Levanon

IN HOUSE TRAINING COURSES:

World Training for Oil and Gas Course leader: Pedro van Meurs IN HOUSE TRAINING COURSES: 2015-2016 Computer interactive training course available in 3-day, 4-day and 5-day programs Run over 35 years now,

World Training for Oil and Gas Course leader: Pedro van Meurs IN HOUSE TRAINING COURSES: 2015-2016 Computer interactive training course available in 3-day, 4-day and 5-day programs Run over 35 years now,

FOR RELEASE AT 5:30 AM PDT OCTOBER 31, 2008 CHEVRON REPORTS THIRD QUARTER NET INCOME OF $7.9 BILLION, UP FROM $3.7 BILLION IN THIRD QUARTER 2007

Policy, Government and Public Affairs Chevron Corporation P.O. Box 6078 San Ramon, CA 94583-0778 www.chevron.com FOR RELEASE AT 5:30 AM PDT OCTOBER 31, 2008 CHEVRON REPORTS THIRD QUARTER NET INCOME OF

Policy, Government and Public Affairs Chevron Corporation P.O. Box 6078 San Ramon, CA 94583-0778 www.chevron.com FOR RELEASE AT 5:30 AM PDT OCTOBER 31, 2008 CHEVRON REPORTS THIRD QUARTER NET INCOME OF

Investor Presentation. March 2019

Investor Presentation March 2019 Forward-Looking Statements and Other Disclaimers The foregoing contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended,

Investor Presentation March 2019 Forward-Looking Statements and Other Disclaimers The foregoing contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended,

STATISTICS Last update: 03/07/2017

STATISTICS 2012-2016 Last update: 03/07/2017 BU NEWS BUSINESS [USD, BILLIONS] New business by year, vs. total world exports 3,000 2,500 2,000 1,500 1,000 500 12,131 1,138 40 127 971 14,023 1,323 53 143

STATISTICS 2012-2016 Last update: 03/07/2017 BU NEWS BUSINESS [USD, BILLIONS] New business by year, vs. total world exports 3,000 2,500 2,000 1,500 1,000 500 12,131 1,138 40 127 971 14,023 1,323 53 143

The New Petrodollar Flows

1 The New Petrodollar Flows 20 June 2006 Brad Bourland, CFA Chief Economist Oil Price Trends 2 Oil Prices, 1986-2006 80 70 60 50 40 30 20 10 0 Jan-86 Jan-87 Jan-88 Jan-89 Jan-90 Jan-91 Jan-92 Jan-93 Jan-94

1 The New Petrodollar Flows 20 June 2006 Brad Bourland, CFA Chief Economist Oil Price Trends 2 Oil Prices, 1986-2006 80 70 60 50 40 30 20 10 0 Jan-86 Jan-87 Jan-88 Jan-89 Jan-90 Jan-91 Jan-92 Jan-93 Jan-94

Today's CPI data: what you need to know

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Friday, July 14,

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Friday, July 14,

July 2014 Kagiso Asset Management Quarterly

July 2014 Kagiso Asset Management Quarterly Global brewers: working harder for growth pg 1 Volkswagen s ambitious vision pg 5 The coal conundrum pg 13 www.kagisoam.com Hospital groups face tougher times

July 2014 Kagiso Asset Management Quarterly Global brewers: working harder for growth pg 1 Volkswagen s ambitious vision pg 5 The coal conundrum pg 13 www.kagisoam.com Hospital groups face tougher times

Fit for $50 oil in Africa

Fit for $50 oil in Africa Will the boom go bust? February 2015 www.pwc.co.za Africa has seen enormous successes in the exploration for hydrocarbons over the last decade, which has seen the entry of new

Fit for $50 oil in Africa Will the boom go bust? February 2015 www.pwc.co.za Africa has seen enormous successes in the exploration for hydrocarbons over the last decade, which has seen the entry of new

Today's CPI data: what you need to know

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Wednesday, December

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Wednesday, December

Today's CPI data: what you need to know

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Wednesday, February

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Wednesday, February

The yellow highlighted areas are bear markets with NO recession.

Part 3, Final Report: Major Market Reversal Model This is the third and final report on my major market reversal model. This portion of the model focuses on the domestic and international economy. I ve

Part 3, Final Report: Major Market Reversal Model This is the third and final report on my major market reversal model. This portion of the model focuses on the domestic and international economy. I ve

Today's CPI data: what you need to know

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Thursday, July

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Thursday, July

Today's CPI data: what you need to know

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Friday, January

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Friday, January

Today's CPI data: what you need to know

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Wednesday, April

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Wednesday, April

Today's CPI data: what you need to know

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Friday, October

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Friday, October

Today's CPI data: what you need to know

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Friday, August

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Friday, August

Today's CPI data: what you need to know

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Wednesday, November

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Wednesday, November

Investor Presentation. November 2018

Investor Presentation November 2018 Forward-Looking Statements and Other Disclaimers Forward-Looking Statements and Cautionary Statements The foregoing contains forward-looking statements within the meaning

Investor Presentation November 2018 Forward-Looking Statements and Other Disclaimers Forward-Looking Statements and Cautionary Statements The foregoing contains forward-looking statements within the meaning

OSU Energy Conference The Benefits of Demerging

OSU Energy Conference The Benefits of Demerging April 17, 2012 Howard J. Thill VP Investor Relations & Public Affairs Forward-Looking Statement Except for historical information, this presentation contains

OSU Energy Conference The Benefits of Demerging April 17, 2012 Howard J. Thill VP Investor Relations & Public Affairs Forward-Looking Statement Except for historical information, this presentation contains

Drill or Acquire? Both? Neither? IPAA Private Capital Conference January 24, 2012

Drill or Acquire? Both? Neither? IPAA Private Capital Conference January 24, 2012 Ursa Background The Ursa Bakken Story Denham Team Ursa Team Good Plan Great Result 2008: Ursa initiates study of the Bakken

Drill or Acquire? Both? Neither? IPAA Private Capital Conference January 24, 2012 Ursa Background The Ursa Bakken Story Denham Team Ursa Team Good Plan Great Result 2008: Ursa initiates study of the Bakken

Commodity Prices and Sovereign Default: A New Perspective on the Harberger-Laursen-Metzler Effect

Commodity Prices and Sovereign Default: A New Perspective on the Harberger-Laursen-Metzler Effect Franz Hamann 1 Enrique G. Mendoza 2 Paulina Restrepo-Echavarria 3 ASSA Meetings, Philadelphia 2018 Introduction

Commodity Prices and Sovereign Default: A New Perspective on the Harberger-Laursen-Metzler Effect Franz Hamann 1 Enrique G. Mendoza 2 Paulina Restrepo-Echavarria 3 ASSA Meetings, Philadelphia 2018 Introduction

Today's CPI data: what you need to know

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Thursday, October

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Thursday, October

Oil market rebalancing Journey s end?

Oil market rebalancing Journey s end? JOHN KEMP REUTERS 3 Aug 2017 Outline Prices in long-run perspective Current position in the cycle Next steps on the journey Sources of uncertainty What do we mean

Oil market rebalancing Journey s end? JOHN KEMP REUTERS 3 Aug 2017 Outline Prices in long-run perspective Current position in the cycle Next steps on the journey Sources of uncertainty What do we mean