Business Combinations IND AS 103

|

|

|

- Toby Lawrence

- 6 years ago

- Views:

Transcription

1 Business Combinations IND AS 103 For many men, the acquisition of wealth does not end their troubles, it only changes them. - Lucius Annaeus Seneca

2 Scope of Business Combination Identification of Business Combination Acquirer and Acquisition Date Consideration transferred as part of BC Identification of Assets and Liabilities Assumed Goodwill / Bargain Purchase Measurement after Initial Recognition Disclosures

3 You have been working in the Accounts Department of Cook India Ltd (CIL). Your boss calls you up and says we are in the process of finalising an acquisition of Linda Foods (LF).

4 Here are some of the options considered for acquisition. You need to advise which one leads to BC CIL purchases 100% equity of LF CIL directly purchases Net Assets of LF CIL purchases one of the three units of LF CIL forms new company Singapore Inc. and transfers the business of LF to this new company. CIL does not have shares but all decision making powers for Singapore Inc. CIL enters into a Joint Venture with LF to combine their businesses Q On the Screen

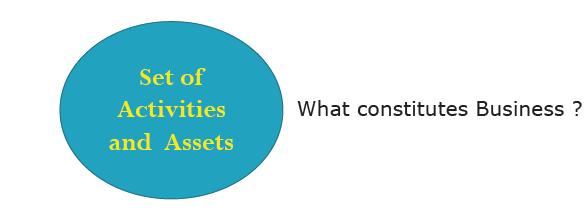

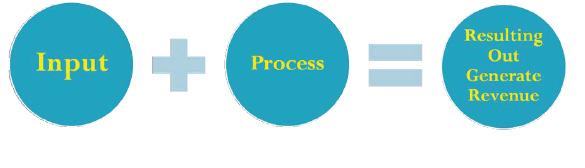

5 Key Definitions:- Business Combination - A transaction or other event in which an acquirer obtains control of one or more businesses. Business - an integrated set of activities and assets conducted and managed for providing.return to investor or economic benefit to stakeholders.generally consists of inputs and processes applied to those inputs, and resulting in outputs that are, or will be used to generate revenues. If goodwill is present in a transferred set of activities and assets, the transferred set shall be presumed to be a business.

6

7 Which of these is a BC? Q Company P acquires operations of Company S. Q - Company P acquires operations of Company S, except for a vital Patent which is very important part of S s business Q - Company P acquires operations of Company S, except for a vital Patent which is very important part of S s business, but it enters into an agreement with S use its Patents on a long term basis - On the Screen

8 Business Combination? Acquisition Merger Need for consolidated information New formation Joint Venture Hostile take-over 8

9 Issues that arise are? What constitutes control? What is control? Factors influencing control! Control or no control? That is the question! Control is defined as:- Power to govern the operating and financial policies of an entity so as to gain benefits from its activities.

10 When is control said to be established:- Equity Shareholding Ability to appoint directors to the board Potential Voting Rights Special Purpose Entities Control Agreement Defacto Control

11 De facto Control Under this model, the power to govern through majority of voting rights, or other legal means does not exist, But ability in practise to control i.e. by majority of votes actually cast Thus it can lead to consolidation by minority shareholder 11

12 How does business combination differ in case of entities Under common Control? - On the Screen

13 Looking to this Chart, Can I have A subsidiary with 0% stake? 13

14 Minutes of Board Meeting. We're interested in diversifying our business and we've decided to enter the drinking chocolate market. Negotiations have been entered into to buy a company in France called LF. LF manufactures hot chocolate and supplies its products throughout Europe. We have narrowed down our options to two, but no decision has been made as to how we will acquire control over the company. The options are: 1. Purchasing a percentage of the company and having the power to govern the financial and operating policies of the business. 2. Purchasing one of the trademarks of LF Inc - the brand name for its 'Famous Hot Chocolate' drink.

15 Under each of the proposed plans for LF, would the acquisition constitute a business? - Q 1 / Q2 of Paperbook

16 Who is the acquirer? IND AS says that all Business Combinations should be accounted for by applying the acquisition method. Thus acquirer should recognise acquiree s:- Identifiable assets and Liabilities At the fair value at the acquisition date.

17 Although there was a merger between Arcelor and Mittal Sahara & Jet Kingfisher and Air Deccan but ultimately who controlled the company

18 Do you still believe in mergers. 18

19 Acquisition Date Some issues Agreement entered into on 23 rd May but it may provide that date of control effective from 1 st April Agreement provides that effective date of transfer is 1 st April but it is subject to shareholder approval on 1 st May Shares are acquired on April 1 but the same need to be registered with regulators. They are registered on June 1 Public offer for purchase of 75% shares made, 51% shares received on 23 rd May and offer closes on 31 st May

20 Date of Exchange V/S Acquisition Date Date of exchange is date of each exchange transaction whereas acquisition date is date of obtaining control of acquiree. Valuation is based on date of exchange but all the components that existed at the date of acquisition are recognised.

21 What is the cost of a business combination? Fair values, at the date of exchange, of assets given (including Fair Value of Contingent Consideration), liabilities incurred or assumed, and equity instruments issued in exchange for gaining control;.

22 Costs you can t include! Consideration a) Cost of maintaining an acquisitions department b) Cost of internal staff who work on the deal c) Cost of investigation d) Incentives to of potential targets employees to remain with company post acquisition e) Issue costs for debt or equity f) Direct costs related to acquisition like consultant fees, rating fee

23 Please find attached the document that explains how we intend to pay for the 80% purchase of LF. I'm not sure which forms of consideration are to be included and excluded. Can you identify which payments are included/excluded in calculation of consideration transferred in the business combination? Please read Page 1 of the Questions Sheet - Q3 (in Paper Book)

24 Can you now identify the value to be put up against various cost heads which have to be included in the calculation of Purchase Consideration? - Q4 (in Paper Book)

25 Payment to Employees of Acquiree Whether the amounts paid to former employees part of Purchase Consideration What do I mean, when I pose this question? ESOP Accounting

Of the goodwill acquired in the business combination or a gain from a bargain purchase; and c) determines what information")

26 Theory on Recognition and Measurement We need to refer to IFRS-3, the basic objectives of which are:- Recognition and measurement:- a) Of the identifiable assets acquired, the liabilities assumed and any non-controlling interest in the acquiree in the financial statements; b) Of the goodwill acquired in the business combination or a gain from a bargain purchase; and c) determines what information to disclose to enable users of the financial statements to evaluate the nature and financial effects of the business combination.

27 Fair value everything! Identifiable assets, liabilities and contingent liabilities recognised at fair value (FV). FV is amount for which an asset could be exchanged, or a liability settled, between knowledgeable, willing parties in an arm s length transaction. Acquirer s intentions are not relevant! Difference between cost and net FV of identifiable assets, liabilities and contingent liabilities is goodwill. Goodwill represents future economic benefits not capable of being individually identified / separately recognised.

28 Exercise Fair Valuation Entity C has acquired its principal competitor, entity D. Entity C s management has explained that its motivation for the acquisition was to acquire market share by taking its rival s brand out of the market Management has, therefore, proposed that the brand be allocated at minimal value since it will be removed from the market shortly after the acquisition. How will the Brand be valued? - Q (on the screen)

29 Solution. Fair value is what a third party would pay for the assets (or charge to assume liabilities). The value of the brand name should be based on the assumption of cash flows from continuing use or sale to a third party. Taking the brand out of the market may result in a post acquisition impairment charge.

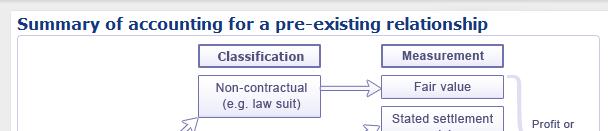

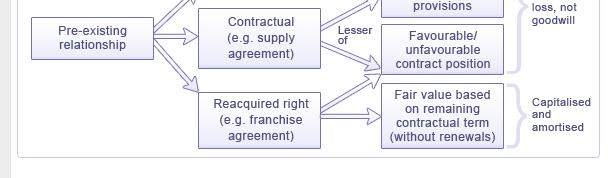

30 Acquirer s intentions are not relevant Eg. When Aditya Birla Group acquired

31 Fair Values Guidelines - Equity Instruments > Published Price at the date of exchange except under rare circumstances - Financial instruments > Market values - Receivables > Present values net of allowances - Inventories FG > NRV less reasonable profits - Inventories RM > Replacement Cost - Land and Building > Market Value - Plant and Machinery > Market Value - Taxes > From acquirers perspective - Liabilities > Present Values - Contingent Liabilities > Third party expectation of possible cash flows

32 Recognition criteria for intangible assets acquired in a business combination Is it identifiable as it arises from contractual or other legal rights or separable from the entity ( can be sold, transferred,licensed or exchanged) Can the cost of the asset be measured reliably (Highly probable, except in rare circumstances) Is it a resource (future benefits) without physical substance controlled by the entity? Some Examples are :- Customer Lists Non-Contractual, Orders Contractual, Internet Domain - Contractual

33 Allocation of cost Identify which items would be recognised separately from goodwill under IFRS 3, and why (i.e., due to satisfying the specified recognition criteria in IFRS 3 and IAS 38). Satisfies the definition of an intangible asset and fair value can be reliably measured. Therefore recognised separately from goodwill. (a) Customer contracts (b) Internet domain names (c) Customer database (d) Brand name (e) In-process R&D (f) Lease agreement (g) Trademarks, trade names, service (h) Order backlog (I) Licenses, royalties, agreements, rights, contracts

34 Allocation of cost (cont d) IND AS 103 requires all contingent liabilities of the acquiree to be recognised at their fair values (provided that fair value can be reliably measured). Recognition even if the amount is not payable as per the relevant standard on Contingent Liability

35 Open Question for all the Teams Could you please help me to determine the appropriate recognition and measurement of the identifiable assets acquired, the liabilities assumed and any non-controlling interest in LF? - Q5 (in Paper Book)

36 So now you have successfully :- Identified a Business Combination Determined what constitutes a business Determined what is included in consideration Also calculated the consideration transferred

37 Additional Matters Treatment of Cost Contingent on Future Events - Included in cost at acquisition date if the adjustment is probable and can be measured reliably - Where criteria are met later, the additional consideration is treated as an adjustment to the cost of combination May include assets/liabilities not previously in books of acquiree, e.g.: - Deferred tax - Intangible assets

38 Pre-existing Relationships

39 Preexisting Law suit with a liability recognition of Rs. 8 Lacs Fair Value of Law suit on date of Acq 5 Lacs Liability for Litigation Dr 8 Lacs Gain on Settlement Cr 3 Lacs Purchase Consideration Cr 5 Lacs

40 Pre-existing Supply Contract Current terms less favourable by Rs. 100 Lacs Loss on Settlement of pre-existing Relationship Dr 100 Lacs Purchase Consideration cr 100 Lacs

41 Subsequent Adjustments to Acquisition Date Values - Q7 (in Paper Book) Adjustments to provisional values within one year relating to facts and circumstances that existed at the acquisition date. [IFRS 3.45] No adjustments after one year except to correct an error in accordance with IAS 8.

42 Lets take a look at the GAAP Differences Under IFRS, business combination has a wider scope. IFRS requires that for each business combinaton, the acquirer shall measure any non-controlling interest in the acquiree either at fair value or at the non-controlling interest s proportionate share of the acquiree s identifiable net assets.

43 Under the existing AS 14, the acquired assets and liabilities are recognised at their existing book values or at fair values under the purchase method (Accounting on basis of Court Order). CA CA Sandesh Sandesh Mundra, Mundra Chartered Accountants 43

44 GAAP differences continued.. AS 14 requires that the goodwill arising on amalgamation in the nature of purchase is amortised over a period not exceeding five years. IFRS deals with reverse acquisitions whereas the existing AS 14 does not deal with the same. As per IFRS, the consideration includes any asset or liability resulting from a contingent consideration arrangement. No guidance in AS 14. IFRS gives guidance on Preexisting relationships on which AS-14 is silent.

Under IND-AS First Carve")

45 Goodwill vs Negative Goodwill Under Indian GAAP Negative Goodwill to be capital reserve Under IFRS Negative Goodwill to be credited to profit & loss account (Bargain Purchase) Under IND-AS First Carve OUT 45

46 IFRS 3 requires a bargain purchase gain on business combination to be recognized in profit or loss for the period. However, Ind-AS 103 requires the same to be recognized in OCI and accumulated in equity as capital reserve. However, if there is no clear evidence of bargain purchase, companies will recognize the gain directly in equity as capital reserve, without routing the same through OCI.

47 Second Carve Out IFRS 3 Business Combinations excludes common control business combinations from its scope. However, Ind-AS requires such combinations to be accounted using the pooling of interest method.

Allocation of goodwill to acquirer based on: Fair value of acquirer s equity interest LESS Fair value of share of net assets acquired Balance to")

48 Significant changes - goodwill Acquired business measured at fair value as a whole 100% goodwill recognised Consistent with treatment of other assets Goodwill allocated between acquirer and noncontrolling interest (was minority interest) Allocation of goodwill to acquirer based on: Fair value of acquirer s equity interest LESS Fair value of share of net assets acquired Balance to NCI 48

49 Goodwill example P acquires 75% ( shares) of S for Rs 7.5cr Value of S = Rs 9.7cr Fair value of net assets acquired = Rs 8cr Current requirements AS Consideration 7,5 Share of identifiable A (75% 8m) (6,0) Goodwill as per IND AS 103 1,5 Current requirements Goodwill 1,5 Net assets 8,0 Minority interest 2,0 CA Sandesh CA Sandesh Mundra, Mundra Chartered Accountants 49

50 IFRS : Goodwill example Current requirements AS 21 Goodwill 1,5 Net assets 8,0 Minority interest (MI) 2,0 IND AS 103 Fair value of S 9,7 Fair value of net assets (8,0) Goodwill 1,7 IND AS Allocate to P Consideration 7,5 Share of identifiable A+L (75% 8m) (6,0) IND AS 103 Goodwill 1,7 Net assets 8,0 GW allocated to P 1,5 => Balance to NCI 0,2 Non-controlling interest (NCI) 2,2, Chartered Accountants 50

51 Goodwill allocation Goodwill allocated to all CGU s, expected to benefit from synergies from the combination Goodwill allocation must be completed before the end of the first reporting period beginning after the business combination Cash generating unit or group of units to which goodwill is allocated should be tested for impairment during the year in which goodwill was allocated Goodwill and Impairment

52 Reverse Acquisition A reverse acquisition occurs when the entity that issues securities (the legal acquirer) is identified as the acquiree for accounting purposes. The entity whose equity interests are acquired (the legal acquiree) must be the acquirer for accounting purposes for the transaction to be considered a reverse acquisition.

53 Key points to take away Understand the economics of the transaction before looking at the accounting. Consider whether you have an asset acquisition or a business combination. Control is a much broader concept than % equity ownership. Cost: determine what is a cost of the business combination and what is a post-acquisition cost.

54 Disclosures Information that enable users of its financial statements to evaluate the nature and financial effect of the business Combination For each business combination Names and description Acquisition Date Percentage of Voting Instruments Acquired Cost of Business Combinations and its components, including Equity Number, Basis of FV; published or why not published price used. Operations intended to be disposed off At acquisition date, amounts for each class of assets & liabilities Gain, if any and the line item Factors contributing to recognition of Goodwill and description of each intangible asset that was not recognised and explanation why not recognsied. Profit or Loss since the acquisition date

55 Disclosures (Continued) For immaterial combinations disclosure may be aggregated:- Fact of provisional determination of values Revenue & Profit or loss of combined entity as though business combinations were effected at the beginning of the period. Information that enables users of its financial statements to evaluate financial effects of gains and losses, error corrections and other adjustments recognised in current period that relate to business combinations that were effected in current or previous periods. Changes in Carrying amount of Goodwill during the period

56 Lets now start preparing CFS

IFRS 3 BUSINESS COMBINATIONS. Presented By: CA. NIRMAL GHORAWAT B. Com (Hons), ACA

, ACA") IFRS 3 BUSINESS COMBINATIONS Presented By: CA. NIRMAL GHORAWAT B. Com (Hons), ACA OBJECTIVE Specify the Financial Reporting by an Entity when it undertakes a Business Combination. 2 CORE PRINCIPLE All

IFRS 3 BUSINESS COMBINATIONS Presented By: CA. NIRMAL GHORAWAT B. Com (Hons), ACA OBJECTIVE Specify the Financial Reporting by an Entity when it undertakes a Business Combination. 2 CORE PRINCIPLE All

Business Combinations and consolidation

Business Combinations and consolidation Madhu Sudan Kankani June 2017 KPMG.com/in Agenda 1 Introduction 2 Ind AS 103: Business combinations 3 Ind AS 110: Consolidated financial statements 4 Practical perspectives

Business Combinations and consolidation Madhu Sudan Kankani June 2017 KPMG.com/in Agenda 1 Introduction 2 Ind AS 103: Business combinations 3 Ind AS 110: Consolidated financial statements 4 Practical perspectives

Ind AS 103: Business Combinations Grant Thornton India LLP. All rights reserved.

Ind AS 103: Business Combinations Contents 1. Overview 2. Definition 3. Business combination 4. Identify the acquirer 5. Acquisition date 6. Recognition and measurement 7. Non-controlling interest 8. Consideration

Ind AS 103: Business Combinations Contents 1. Overview 2. Definition 3. Business combination 4. Identify the acquirer 5. Acquisition date 6. Recognition and measurement 7. Non-controlling interest 8. Consideration

Ind AS 103 Business Combinations

Ind AS 103 Business Combinations Seminar on Merger & Acquisitions 26 th December 2015 J.S. Lodha Auditorium, ICAI Bhawan, Cuffe Parade, Mumbai 2008 Deloitte Global Services Limited Agenda Scope of Ind

Ind AS 103 Business Combinations Seminar on Merger & Acquisitions 26 th December 2015 J.S. Lodha Auditorium, ICAI Bhawan, Cuffe Parade, Mumbai 2008 Deloitte Global Services Limited Agenda Scope of Ind

IAS 27, 28 and 31 Consolidated and Separate Financial Statements Investment is Associates Interests in Joint Ventures

IAS 27, 28 and 31 Consolidated and Separate Financial Statements Investment is Associates Interests in Joint Ventures Prakash C Bisht Sr. Vice President ( Group Accounts) Jubilant Life Sciences Ltd Agenda

IAS 27, 28 and 31 Consolidated and Separate Financial Statements Investment is Associates Interests in Joint Ventures Prakash C Bisht Sr. Vice President ( Group Accounts) Jubilant Life Sciences Ltd Agenda

OVERVIEW OF IND AS INCLUDING CARVE OUTS. C.A. Sanjay Vasudeva S. C. Vasudeva & Co. Chartered Accountants

Seminar of North Ex CA Study Circle Hotel Oasis, New Delhi OVERVIEW OF IND AS INCLUDING CARVE OUTS C.A. Sanjay Vasudeva S. C. Vasudeva & Co. Chartered Accountants 16th December 2016 Overview Need for International

Seminar of North Ex CA Study Circle Hotel Oasis, New Delhi OVERVIEW OF IND AS INCLUDING CARVE OUTS C.A. Sanjay Vasudeva S. C. Vasudeva & Co. Chartered Accountants 16th December 2016 Overview Need for International

Ind-AS 110 Consolidated Financial Statements

Ind-AS 110 Consolidated Financial Statements Hemal D. Shah The Chamber of Tax Consultants Topics Background, objectives and core principle New definition of control Assessing control Investment entities

Ind-AS 110 Consolidated Financial Statements Hemal D. Shah The Chamber of Tax Consultants Topics Background, objectives and core principle New definition of control Assessing control Investment entities

SUGGESTED SOLUTIONS. KB1 Business Financial Reporting. December All Rights Reserved

SUGGESTED SOLUTIONS KB1 Business Financial Reporting All Rights Reserved SECTION 1 Answer 01 Relevant Learning Outcome/s: 1.1.1 Demonstrate knowledge of the conceptual framework of Sri Lanka Accounting

SUGGESTED SOLUTIONS KB1 Business Financial Reporting All Rights Reserved SECTION 1 Answer 01 Relevant Learning Outcome/s: 1.1.1 Demonstrate knowledge of the conceptual framework of Sri Lanka Accounting

Overview of Transition to IND-AS. CA Sanjeev Maheshwari

Overview of Transition to IND-AS CA Sanjeev Maheshwari sm@gmj.co.in 98211 19043 Need for one Common language of Accounting GMJ & Co. 2 GMJ & Co. 3 GMJ & Co. 4 GMJ & Co. 5 GMJ & Co. 6 GMJ & Co. 7 GMJ &

Overview of Transition to IND-AS CA Sanjeev Maheshwari sm@gmj.co.in 98211 19043 Need for one Common language of Accounting GMJ & Co. 2 GMJ & Co. 3 GMJ & Co. 4 GMJ & Co. 5 GMJ & Co. 6 GMJ & Co. 7 GMJ &

Non-controlling interests accounting under Ind AS

1 Non-controlling interests accounting under Ind AS This article aims to Provide an overview of the accounting of non-controlling interests under Ind AS. Introduction The International Accounting Standards

1 Non-controlling interests accounting under Ind AS This article aims to Provide an overview of the accounting of non-controlling interests under Ind AS. Introduction The International Accounting Standards

SLFRS 3 - Business Combinations. Lesson 1: Definition of a Business. Anoji De Silva Partner, Ernst & Young. 26 th July 2012

Page 1 2010 EYGM Limited Slide 1 Business Combinations 1 SLFRS 3 - Business Combinations Anoji De Silva Partner, Ernst & Young Page 2 SLFRS 3- Topics covered 1. Introduction and overview 2. Identifying

Page 1 2010 EYGM Limited Slide 1 Business Combinations 1 SLFRS 3 - Business Combinations Anoji De Silva Partner, Ernst & Young Page 2 SLFRS 3- Topics covered 1. Introduction and overview 2. Identifying

ESMA Report. Review on the application of accounting requirements for business combinations in IFRS financial statements. 16 June 2014/ESMA/2014/643

ESMA Report Review on the application of accounting requirements for business combinations in IFRS financial statements 16 June 2014/ESMA/2014/643 Date: 16 June 2014 ESMA/2014/643 Table of Contents Contents

ESMA Report Review on the application of accounting requirements for business combinations in IFRS financial statements 16 June 2014/ESMA/2014/643 Date: 16 June 2014 ESMA/2014/643 Table of Contents Contents

Business Combinations & Consolidated Financial Statements. By Abdullatif Essajee September 2017

Business Combinations & Consolidated Financial Statements By Abdullatif Essajee September 2017 Applicable IFRSs IFRS 3: Business Combinations IFRS 10: Consolidated Financial Statements IFRS 13: Fair Value

Business Combinations & Consolidated Financial Statements By Abdullatif Essajee September 2017 Applicable IFRSs IFRS 3: Business Combinations IFRS 10: Consolidated Financial Statements IFRS 13: Fair Value

We welcome the opportunity to comment on the above post-implementation review.

31 May 2014 International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Dear Sir/Madam, IASB Post implementation Review: IFRS 3 Business Combinations Standard Chartered Bank

31 May 2014 International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Dear Sir/Madam, IASB Post implementation Review: IFRS 3 Business Combinations Standard Chartered Bank

Summary of responses to RfI in Korea

Summary of responses to RfI in Korea May 2014 Korea Accounting Standards Board (KASB) Contents 1. Your background and experience 2. Definition of a business 3. Fair value 4. Separate recognition of intangible

Summary of responses to RfI in Korea May 2014 Korea Accounting Standards Board (KASB) Contents 1. Your background and experience 2. Definition of a business 3. Fair value 4. Separate recognition of intangible

Business Combinations Summary of the IASB s proposals for a new approach to business combinations and non-controlling interests

A SSURANCE AND A DVISORY BUSINESS S ERVICES I NTERNATIONAL FINANCIAL R EPORTING S TANDARDS!@# Business Combinations Summary of the IASB s proposals for a new approach to business combinations and non-controlling

A SSURANCE AND A DVISORY BUSINESS S ERVICES I NTERNATIONAL FINANCIAL R EPORTING S TANDARDS!@# Business Combinations Summary of the IASB s proposals for a new approach to business combinations and non-controlling

Introduction to Ind-AS By Neeraj Sharma

Introduction to Ind-AS By Neeraj Sharma neerajsharma2002in@yahoo.com 1 Agenda Ind-AS An Overview Five Key Standards GAAP Differences Other GAAP Differences Questions & Answers 2 Ind-AS An Overview Set

Introduction to Ind-AS By Neeraj Sharma neerajsharma2002in@yahoo.com 1 Agenda Ind-AS An Overview Five Key Standards GAAP Differences Other GAAP Differences Questions & Answers 2 Ind-AS An Overview Set

Types of Intangible Assets

Depreciation and amortization Investment in intangibles Over assets useful life Methods Declining balance method Straight line Units of production Finite lifetime: patent example (useful life, not the

Depreciation and amortization Investment in intangibles Over assets useful life Methods Declining balance method Straight line Units of production Finite lifetime: patent example (useful life, not the

IFRS Course IFRS 3 Business Combinations Università degli Studi di Bergamo

IFRS Course IFRS 3 Business Combinations Università degli Studi di Bergamo Livio Ferrini Bergamo, 13 April 2015 What will you learn? By completing this module, you will be able to: 1) Explain the definition

IFRS Course IFRS 3 Business Combinations Università degli Studi di Bergamo Livio Ferrini Bergamo, 13 April 2015 What will you learn? By completing this module, you will be able to: 1) Explain the definition

Impact of Ind AS on consolidation BY CA YAGNESH DESAI DELIVERED ON 22 ND DECEMBER,2017 FOR WIRC OF ICAI

1 Impact of Ind AS on consolidation BY CA YAGNESH DESAI DELIVERED ON 22 ND DECEMBER,2017 FOR WIRC OF ICAI Index 2 Basis of Consolidation Power to Control as per Ind AS 110 Consolidation Procedure under

1 Impact of Ind AS on consolidation BY CA YAGNESH DESAI DELIVERED ON 22 ND DECEMBER,2017 FOR WIRC OF ICAI Index 2 Basis of Consolidation Power to Control as per Ind AS 110 Consolidation Procedure under

FINANCIAL REPORTING WORKSHOP, MOMBASA Consolidated Financial Statements and Business Combinations -IFRS 10, IFRS 11 IFRS 3 & IPSAS 40 Presentation by:

FINANCIAL REPORTING WORKSHOP, MOMBASA Consolidated Financial Statements and Business Combinations -IFRS 10, IFRS 11 IFRS 3 & IPSAS 40 Presentation by: CPA Stephen Obock Monday, 9 October 2017 Uphold public

FINANCIAL REPORTING WORKSHOP, MOMBASA Consolidated Financial Statements and Business Combinations -IFRS 10, IFRS 11 IFRS 3 & IPSAS 40 Presentation by: CPA Stephen Obock Monday, 9 October 2017 Uphold public

Case Study Session 1 Property, plant and equipment, Leases, Income taxes and Business combinations

Property, plant and equipment Case Study 1 At the beginning of the year the entity, domiciled in the UK, has a $1m foreign currency loan. The interest rate on the loan is 4% and is paid at the end of the

Property, plant and equipment Case Study 1 At the beginning of the year the entity, domiciled in the UK, has a $1m foreign currency loan. The interest rate on the loan is 4% and is paid at the end of the

Corporate Watch. pwc. FRS 103 Improving the transparency and comparability of acquisition accounting. *connectedthinking. July / August 2004 Issue

Corporate Watch July / August 2004 Issue FRS 103 Improving the transparency and comparability of acquisition accounting On 31 March 2004, the International Accounting Standards Board (IASB) published International

Corporate Watch July / August 2004 Issue FRS 103 Improving the transparency and comparability of acquisition accounting On 31 March 2004, the International Accounting Standards Board (IASB) published International

Financial Reporting Presents: FASB Exposure Drafts on Business Combinations and Noncontrolling Interests

Financial Reporting Presents: FASB Exposure Drafts on Business Combinations and Noncontrolling Interests Agenda Introduction Background Business Combinations Noncontrolling Interests Questions & Answers

Financial Reporting Presents: FASB Exposure Drafts on Business Combinations and Noncontrolling Interests Agenda Introduction Background Business Combinations Noncontrolling Interests Questions & Answers

Revisionary Test Paper_Dec 2018

Final Group IV Paper 17 : CORPORATE FINANCIAL REPORTING (SYLLABUS 2016) 1. Multiple Choice Questions: Objectives (i) Mittal Ltd. has provided the following information: Depreciation as per accounting records

Final Group IV Paper 17 : CORPORATE FINANCIAL REPORTING (SYLLABUS 2016) 1. Multiple Choice Questions: Objectives (i) Mittal Ltd. has provided the following information: Depreciation as per accounting records

Letter of Comment No: a~ File Reference:

Letter of Comment No: a~ File Reference: 1204001 Comments on proposed amendments to.frs 3, Business Combinations 1 Objective, definition and scope The proposed objective of the Exposure Draft is: "...

Letter of Comment No: a~ File Reference: 1204001 Comments on proposed amendments to.frs 3, Business Combinations 1 Objective, definition and scope The proposed objective of the Exposure Draft is: "...

Indian Accounting Standard 36 Impairment of Assets

Indian Accounting Standard 36 Impairment of Assets Contents Paragraphs Objective 1 Scope 2 5 Definitions 6 Identifying an asset that may be impaired 7 17 Measuring recoverable amount 18 57 Measuring the

Indian Accounting Standard 36 Impairment of Assets Contents Paragraphs Objective 1 Scope 2 5 Definitions 6 Identifying an asset that may be impaired 7 17 Measuring recoverable amount 18 57 Measuring the

Seminar. Addressing Information Gaps in Business and Macro Economic Accounts to Better Explain Economic Performance

IG/15 24 June 2008 UNITED NATIONS DEPARTMENT OF ECONOMIC AND SOCIAL AFFAIRS STATISTICS DIVISION Seminar Addressing Information Gaps in Business and Macro Economic Accounts to Better Explain Economic Performance

IG/15 24 June 2008 UNITED NATIONS DEPARTMENT OF ECONOMIC AND SOCIAL AFFAIRS STATISTICS DIVISION Seminar Addressing Information Gaps in Business and Macro Economic Accounts to Better Explain Economic Performance

Introduction to Ind-AS. M/s Pranjal Joshi & Co Chartered Accountants

Introduction to Ind-AS M/s Pranjal Joshi & Co Chartered Accountants What is the importance of financial statements? Financial statements are very important as they are the basis for variety of decisions

Introduction to Ind-AS M/s Pranjal Joshi & Co Chartered Accountants What is the importance of financial statements? Financial statements are very important as they are the basis for variety of decisions

Independent Auditor s Report

Independent Auditor s Report To the shareholders of China Communications Construction Company Limited (incorporated in the People s Republic of China with limited liability) We have audited the consolidated

Independent Auditor s Report To the shareholders of China Communications Construction Company Limited (incorporated in the People s Republic of China with limited liability) We have audited the consolidated

Consolidated Financial Statements (Workshop 1) 24 April 2012

24 April 2012") Consolidated Financial Statements (Workshop 1) 24 April 2012 LAM Chi Yuen Nelson 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) CTA FCCA FCPA FHKIoD FTIHK MHKSI MSCA 2005-12 Nelson Consulting Limited 1

Consolidated Financial Statements (Workshop 1) 24 April 2012 LAM Chi Yuen Nelson 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) CTA FCCA FCPA FHKIoD FTIHK MHKSI MSCA 2005-12 Nelson Consulting Limited 1

Revision. Purchase Price Allocation for Account Reporting. Terms to Remember - 1. Contents. Terms to Remember - 3. Terms to Remember - 2

Purchase Price Allocation for Account Reporting Joseph C. Ho June 2010 Revision Types of valuation asset or business Purpose of valuation many Basis of value fair value, market value Fair value = market

Purchase Price Allocation for Account Reporting Joseph C. Ho June 2010 Revision Types of valuation asset or business Purpose of valuation many Basis of value fair value, market value Fair value = market

Motives and Innovative ways of Structuring and Accounting for Business combination

Motives and Innovative ways of Structuring and Accounting for Business combination Presenter: Amrish Shah January 20, 2017 *Intended for general guidance only Content Modes of M&A in India Indian laws

Motives and Innovative ways of Structuring and Accounting for Business combination Presenter: Amrish Shah January 20, 2017 *Intended for general guidance only Content Modes of M&A in India Indian laws

ACCOUNTING POLICIES. for the year ended 30 June MURRAY & ROBERTS ANNUAL FINANCIAL STATEMENTS 13

12 MURRAY & ROBERTS ANNUAL FINANCIAL STATEMENTS 13 ACCOUNTING POLICIES for the year ended 30 June 2013 1 PRESENTATION OF FINANCIAL STATEMENTS These accounting policies are consistent with the previous

12 MURRAY & ROBERTS ANNUAL FINANCIAL STATEMENTS 13 ACCOUNTING POLICIES for the year ended 30 June 2013 1 PRESENTATION OF FINANCIAL STATEMENTS These accounting policies are consistent with the previous

Financial Accounting. Impairment of Assets

Financial Accounting Impairment of Assets Disclaimer The DVD lectures and related study material (consisting of Powerpoint slides, summary modules, integrated question banks and other academic material)

Financial Accounting Impairment of Assets Disclaimer The DVD lectures and related study material (consisting of Powerpoint slides, summary modules, integrated question banks and other academic material)

Valuation of Intangible Assets including. Purchase Price Allocation :74. Purchase Price Allocation

CA Ravishu Shah Valuation of Intangible Assets including Purchase Price Allocation Investment in knowledge based/intangible assets is one of the key characteristics of modern economies. Every goods including

CA Ravishu Shah Valuation of Intangible Assets including Purchase Price Allocation Investment in knowledge based/intangible assets is one of the key characteristics of modern economies. Every goods including

Combinations involving entities or businesses under common control or formation of a joint venture are excluded from the scope.

Business combinations A business combination involves the bringing together of separate entities or businesses into one reporting entity. Full IFRS and IFRS for SMEs require the use of the purchase method

Business combinations A business combination involves the bringing together of separate entities or businesses into one reporting entity. Full IFRS and IFRS for SMEs require the use of the purchase method

Lesson 10 International Accounting Lelio Bigogno, Stefano Santucci

Università degli studi di Pavia Facoltà di Economia a.a. 2014-2015 2015 Lesson 10 International Accounting Lelio Bigogno, Stefano Santucci 1 IAS/IFRS: IFRS 3 Business Combination 2 History of IFRS 3 April

Università degli studi di Pavia Facoltà di Economia a.a. 2014-2015 2015 Lesson 10 International Accounting Lelio Bigogno, Stefano Santucci 1 IAS/IFRS: IFRS 3 Business Combination 2 History of IFRS 3 April

Accounting Update on Business Combinations and Consolidation 28 June 2005

Accounting Update on Business Combinations and Consolidation 28 June 2005 Lam CFA FCCA FCPA(Practising) MBA MSc BBA CPA(US) Introduction An entity shall consider whether all of its financial assets in

Accounting Update on Business Combinations and Consolidation 28 June 2005 Lam CFA FCCA FCPA(Practising) MBA MSc BBA CPA(US) Introduction An entity shall consider whether all of its financial assets in

HKAS 27 and HKFRS 3 9 January 2009

HKAS 27 and HKFRS 3 9 January 2009 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust.) CPA(US) FCCA FCPA(Practising) MSCA 2006-09 Nelson 1 Today s Agenda Consolidated and Separate Financial Statements (HKAS

HKAS 27 and HKFRS 3 9 January 2009 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust.) CPA(US) FCCA FCPA(Practising) MSCA 2006-09 Nelson 1 Today s Agenda Consolidated and Separate Financial Statements (HKAS

A Refresher Course on Current Financial Reporting Standards 2013 (Day 2) Associates and joint arrangements

Associates and joint arrangements") A Refresher Course on Current Financial Reporting Standards 2013 (Day 2) Associates and joint arrangements 1 COOPERATION REQUESTED Please make sure that your mobile phones and pagers have been switched

A Refresher Course on Current Financial Reporting Standards 2013 (Day 2) Associates and joint arrangements 1 COOPERATION REQUESTED Please make sure that your mobile phones and pagers have been switched

14 BUSINESS ACCOUNTING STANDARD BUSINESS COMBINATIONS I. GENERAL PROVISIONS KEY DEFINITIONS

APPROVED by Resolution No. 10 of 10 December 2003 of the Standards Board of the Public Establishment the Institute of Accounting of the Republic of Lithuania (Revised version of Order No. VAS-10 of 19

APPROVED by Resolution No. 10 of 10 December 2003 of the Standards Board of the Public Establishment the Institute of Accounting of the Republic of Lithuania (Revised version of Order No. VAS-10 of 19

8/22/2011. Mayer Hoffman McCann P.C. s Executive Education Series Business Combinations AGENDA. History of Business Combinations.

Mayer Hoffman McCann P.C. s Executive Education Series Business Combinations August 2011 AGENDA Background/Basics of Accounting for Business Combinations The Acquisition Method the Basics Common Non-controlling

Mayer Hoffman McCann P.C. s Executive Education Series Business Combinations August 2011 AGENDA Background/Basics of Accounting for Business Combinations The Acquisition Method the Basics Common Non-controlling

Upon the FVTOCI Financial Asset becomes an Associate or Subsidiary, any previous gain or loss accumulated in the OCE must be reclassified to RE.

CHAPTER 7 CONSOLIDATION a. Piecemeal Acquisition from: FVTOCI Financial Asset to Subsidiary or FVTOCI Financial Asset to Associate = reclassify previous OCE gain to RE Upon the FVTOCI Financial Asset becomes

CHAPTER 7 CONSOLIDATION a. Piecemeal Acquisition from: FVTOCI Financial Asset to Subsidiary or FVTOCI Financial Asset to Associate = reclassify previous OCE gain to RE Upon the FVTOCI Financial Asset becomes

IFRS Viewpoint. Common control business combinations

Accounting Tax Global IFRS Viewpoint Common control business combinations What s the issue? How should an entity account for a business combination involving entities under common control? This is an important

Accounting Tax Global IFRS Viewpoint Common control business combinations What s the issue? How should an entity account for a business combination involving entities under common control? This is an important

IFRS for SMEs IFRS Foundation-World Bank

!International Financial Reporting Standards 1 IFRS for SMEs IFRS Foundation-World Bank 11 13 January 2011 Astana, Kazakhstan Copyright 2010 IFRS Foundation. All rights reserved. The IFRS for SMEs 2 Topic

!International Financial Reporting Standards 1 IFRS for SMEs IFRS Foundation-World Bank 11 13 January 2011 Astana, Kazakhstan Copyright 2010 IFRS Foundation. All rights reserved. The IFRS for SMEs 2 Topic

SLFRS 3. Business Combinations. Click to edit Master title style. Nishan Fernando FCA Nishani Perera ACA. Consolidation Package The Big Picture

Click to edit Master title style SLFRS 3 Business Combinations Nishan Fernando FCA Nishani Perera ACA Consolidation Package The Big Picture Consolidate (IFRS 3 & 10) SLFRS 10 Consolidated Financial Statements

Click to edit Master title style SLFRS 3 Business Combinations Nishan Fernando FCA Nishani Perera ACA Consolidation Package The Big Picture Consolidate (IFRS 3 & 10) SLFRS 10 Consolidated Financial Statements

SRI LANKA ACCOUNTING STANDARD IMPAIRMENT OF ASSETS

SRI LANKA ACCOUNTING STANDARD IMPAIRMENT OF ASSETS THE INSTITUTE OF CHARTERED ACCOUNTANTS OF SRI LANKA SRI LANKA ACCOUNTING STANDARD IMPAIRMENT OF ASSETS The Institute of Chartered Accountants of Sri Lanka

SRI LANKA ACCOUNTING STANDARD IMPAIRMENT OF ASSETS THE INSTITUTE OF CHARTERED ACCOUNTANTS OF SRI LANKA SRI LANKA ACCOUNTING STANDARD IMPAIRMENT OF ASSETS The Institute of Chartered Accountants of Sri Lanka

FAS 141 Business Combinations

FAS 141 Business Combinations December 3, 2003 Business Valuation Committee 1 FAS 141 Overview The Need For FAS 141 Need For Consistent Reporting In Business Combinations / Mergers And Acquisitions Pooling

FAS 141 Business Combinations December 3, 2003 Business Valuation Committee 1 FAS 141 Overview The Need For FAS 141 Need For Consistent Reporting In Business Combinations / Mergers And Acquisitions Pooling

Opening balance sheet 1 April Opening balance sheet 1 April Unlisted companies whose net worth is >= INR 250 crores but < INR 500 crores

Step up to Ind AS Ind AS an overview India made a commitment towards the convergence of Indian accounting standards with IFRS at the G20 summit in 2009. In line with this, the Ministry of Corporate Affairs,

Step up to Ind AS Ind AS an overview India made a commitment towards the convergence of Indian accounting standards with IFRS at the G20 summit in 2009. In line with this, the Ministry of Corporate Affairs,

CONSOLIDATED BALANCE SHEET AND INCOME STATEMENT DECEMBER 31, 2012

CONSOLIDATED BALANCE SHEET AND INCOME STATEMENT DECEMBER 31, 2012 The Board of Directors meeting of February 20, 2013 adopted and authorized the publication of Safran s consolidated financial statements

CONSOLIDATED BALANCE SHEET AND INCOME STATEMENT DECEMBER 31, 2012 The Board of Directors meeting of February 20, 2013 adopted and authorized the publication of Safran s consolidated financial statements

Other Comprehensive Income: A New Concept in India

1120 Other Comprehensive Income: A New Concept in India The concept of Other Comprehensive Income (OCI) is not new in the international accounting frameworks such as in International Financial Reporting

1120 Other Comprehensive Income: A New Concept in India The concept of Other Comprehensive Income (OCI) is not new in the international accounting frameworks such as in International Financial Reporting

An Overview of New PRC GAAP: Differences between Old and New PRC GAAP and its Convergence with IFRS

An Overview of New PRC GAAP: Differences between Old and New PRC GAAP and its Convergence with IFRS 3rd Edition October 2014 kpmg.com/cn 2014 KPMG, a Hong Kong partnership and a member firm of the KPMG

An Overview of New PRC GAAP: Differences between Old and New PRC GAAP and its Convergence with IFRS 3rd Edition October 2014 kpmg.com/cn 2014 KPMG, a Hong Kong partnership and a member firm of the KPMG

Impairment of Assets DEFINITIONS

IAS 36 Impairment of Assets DEFINITIONS Cash generating unit (CGU) Impairment loss Recoverable amount is the smallest identifiable group of assets that generates cash inflows that are largely independent

IAS 36 Impairment of Assets DEFINITIONS Cash generating unit (CGU) Impairment loss Recoverable amount is the smallest identifiable group of assets that generates cash inflows that are largely independent

Saving our customers money so they can live better

Saving our customers money so they can live better MASSMART GROUP ANNUAL FINANCIAL STATEMENTS 2016 1 GROUP INCOME STATEMENT December 2016 December 2015 Rm Notes 52 weeks 52 weeks Revenue 5 91,564.9 84,857.4

Saving our customers money so they can live better MASSMART GROUP ANNUAL FINANCIAL STATEMENTS 2016 1 GROUP INCOME STATEMENT December 2016 December 2015 Rm Notes 52 weeks 52 weeks Revenue 5 91,564.9 84,857.4

FAC 4862/4 CONSOLIDATED & SEPARATE FINANCIAL STATEMENTS (IAS 27; IFRS 10 & IFRS 12) LECTURE MATERIAL

LECTURE MATERIAL") FAC 4862/4 CONSOLIDATED & SEPARATE FINANCIAL STATEMENTS (IAS 27; IFRS 10 & IFRS 12) LECTURE MATERIAL COPYRIGHT NOTICE Copyright Prepared by BIANCA NEL CA (SA) These notes enjoy copyright under the Berne

FAC 4862/4 CONSOLIDATED & SEPARATE FINANCIAL STATEMENTS (IAS 27; IFRS 10 & IFRS 12) LECTURE MATERIAL COPYRIGHT NOTICE Copyright Prepared by BIANCA NEL CA (SA) These notes enjoy copyright under the Berne

Objective of IAS 18 The objective of IAS 18 is to prescribe the accounting treatment for revenue arising from certain types of transactions and events

IAS 18- Revenue Objective of IAS 18 The objective of IAS 18 is to prescribe the accounting treatment for revenue arising from certain types of transactions and events. Introduction Income is defined as

IAS 18- Revenue Objective of IAS 18 The objective of IAS 18 is to prescribe the accounting treatment for revenue arising from certain types of transactions and events. Introduction Income is defined as

International Accounting Standard 36 Impairment of Assets. Objective. Scope IAS 36

International Accounting Standard 36 Impairment of Assets Objective 1 The objective of this Standard is to prescribe the procedures that an entity applies to ensure that its assets are carried at no more

International Accounting Standard 36 Impairment of Assets Objective 1 The objective of this Standard is to prescribe the procedures that an entity applies to ensure that its assets are carried at no more

Request for Information Post-implementation Review IFRS 3 Business Combinations

Hans Hoogervorst Chairman International Accounting Standards Board 30 Cannon Street London United Kingdom EC4M 6XH Deloitte Touche Tohmatsu Limited 2 New Street Square London EC4A 3BZ United Kingdom Tel:

Hans Hoogervorst Chairman International Accounting Standards Board 30 Cannon Street London United Kingdom EC4M 6XH Deloitte Touche Tohmatsu Limited 2 New Street Square London EC4A 3BZ United Kingdom Tel:

Professional Level Essentials Module, Paper P2 (INT)

") Answers Professional Level Essentials Module, Paper P2 (INT) Corporate Reporting (International) June 2011 Answers 1 (a) (i) The functional currency is a matter of fact and is the currency of the primary

Answers Professional Level Essentials Module, Paper P2 (INT) Corporate Reporting (International) June 2011 Answers 1 (a) (i) The functional currency is a matter of fact and is the currency of the primary

ACCOUNTING POLICIES 1 PRESENTATION OF FINANCIAL STATEMENTS. for the year ended 30 June BASIS OF PREPARATION 1.2 STATEMENT OF COMPLIANCE

14 MURRAY & ROBERTS ANNUAL FINANCIAL STATEMENTS 15 ACCOUNTING POLICIES for the year ended 30 June 2015 1 PRESENTATION OF FINANCIAL STATEMENTS 1.1 BASIS OF PREPARATION These consolidated and separate financial

14 MURRAY & ROBERTS ANNUAL FINANCIAL STATEMENTS 15 ACCOUNTING POLICIES for the year ended 30 June 2015 1 PRESENTATION OF FINANCIAL STATEMENTS 1.1 BASIS OF PREPARATION These consolidated and separate financial

TAX IMPLICATIONS RELATED TO THE IMPLEMENTATION OF MFRS 136/ FRS 136: IMPAIRMENT OF ASSETS

The Malaysian Institute of Certified Public Accountants TAX IMPLICATIONS RELATED TO THE IMPLEMENTATION OF MFRS 136/ FRS 136: IMPAIRMENT OF ASSETS Prepared by: Joint Tax Working Group on FRS Contents Page

The Malaysian Institute of Certified Public Accountants TAX IMPLICATIONS RELATED TO THE IMPLEMENTATION OF MFRS 136/ FRS 136: IMPAIRMENT OF ASSETS Prepared by: Joint Tax Working Group on FRS Contents Page

Salam International Investment Limited Q.S.C. Consolidated financial statements. 31 December 2015

Consolidated financial statements 31 December 2015 Consolidated financial statements Contents Page(s) Independent auditors report 1-2 Consolidated statement of financial position 3-4 Consolidated statement

Consolidated financial statements 31 December 2015 Consolidated financial statements Contents Page(s) Independent auditors report 1-2 Consolidated statement of financial position 3-4 Consolidated statement

A.G. Leventis (Nigeria) Plc

Plc") CONTENTS COMPLIANCE CERTIFICATE 3 CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME 4 CONSOLIDATED STATEMENT OF FINANCIAL POSITION 5 STATEMENT OF CASHFLOWS 6 STATEMENT OF CHANGES IN EQUITY 7 NOTES TO THE

CONTENTS COMPLIANCE CERTIFICATE 3 CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME 4 CONSOLIDATED STATEMENT OF FINANCIAL POSITION 5 STATEMENT OF CASHFLOWS 6 STATEMENT OF CHANGES IN EQUITY 7 NOTES TO THE

About the Author I-5 Preface I-7. PART I INDIAN ACCOUNTING STANDARDS (ASs)

") Accounting Standard Contents About the Author I-5 Preface I-7 PART I INDIAN ACCOUNTING STANDARDS (ASs) CHAPTER 1 : ACCOUNTING STANDARDS - APPLICABILITY AND SUMMARY 3 CHAPTER 2 : AS 1 - DISCLOSURE OF ACCOUNTING

Accounting Standard Contents About the Author I-5 Preface I-7 PART I INDIAN ACCOUNTING STANDARDS (ASs) CHAPTER 1 : ACCOUNTING STANDARDS - APPLICABILITY AND SUMMARY 3 CHAPTER 2 : AS 1 - DISCLOSURE OF ACCOUNTING

IFRS illustrative consolidated financial statements

IFRS illustrative consolidated financial statements 2016 This publication has been prepared for illustrative purposes only and does not constitute accounting or other professional advice, nor is it a substitute

IFRS illustrative consolidated financial statements 2016 This publication has been prepared for illustrative purposes only and does not constitute accounting or other professional advice, nor is it a substitute

SUGGESTED SOLUTIONS. KB 1 Business Financial Reporting. June All Rights Reserved

SUGGESTED SOLUTIONS KB 1 Business Financial Reporting June 2015 All Rights Reserved SECTION 1 Answer 01 (a) Relevant Learning Outcome/s: 1.1.1 Demonstrate knowledge of the conceptual framework of Sri Lanka

SUGGESTED SOLUTIONS KB 1 Business Financial Reporting June 2015 All Rights Reserved SECTION 1 Answer 01 (a) Relevant Learning Outcome/s: 1.1.1 Demonstrate knowledge of the conceptual framework of Sri Lanka

Consolidated Financial Statements (In thousands of Canadian dollars) CCL INDUSTRIES INC. Years ended December 31, 2013 and 2012

CCL INDUSTRIES INC. Years ended December 31, 2013 and 2012") Consolidated Financial Statements (In thousands of Canadian dollars) CCL INDUSTRIES INC. Years ended December 31, 2013 and 2012 To the Shareholders of CCL Industries Inc. KPMG LLP Telephone (416) 777-8500

Consolidated Financial Statements (In thousands of Canadian dollars) CCL INDUSTRIES INC. Years ended December 31, 2013 and 2012 To the Shareholders of CCL Industries Inc. KPMG LLP Telephone (416) 777-8500

Mergers & Acquisition

Mergers & Acquisition Account ing Implicat ions under IND AS 1 April 2017 Contents # Topic 1 M&A Deals : Changing Landscape 2 Mergers & Acquisitions 3 Common Control Transactions 4 Demerger/Buy back/capital

Mergers & Acquisition Account ing Implicat ions under IND AS 1 April 2017 Contents # Topic 1 M&A Deals : Changing Landscape 2 Mergers & Acquisitions 3 Common Control Transactions 4 Demerger/Buy back/capital

IFRS 1 - First-Time Adoption of IFRS

IFRS 1 - First-Time Adoption of IFRS P C First time adoption session outline Overview Exemptions and exceptions Disclosure IFRS 1 General principles Application Requires To the first IFRS financial statements

IFRS 1 - First-Time Adoption of IFRS P C First time adoption session outline Overview Exemptions and exceptions Disclosure IFRS 1 General principles Application Requires To the first IFRS financial statements

Notes to the Consolidated Financial Statements (Unless otherwise stated, all amounts are in millions of Canadian dollars)

") Notes to the Consolidated Financial Statements (Unless otherwise stated, all amounts are in millions of Canadian dollars) The consolidated financial statements were authorized for issue by the board of

Notes to the Consolidated Financial Statements (Unless otherwise stated, all amounts are in millions of Canadian dollars) The consolidated financial statements were authorized for issue by the board of

INDIAN ACCOUNTING STANDARDS

Index 1- Brief Summary of Introduction of Ind-AS 2- Applicability of INDIAN ACCOUNTING STANDARDS () 3- List of with objective and scope BRIEF SUMMARY OF INTRODUCTION OF IND-AS Indian Accounting Standards

Index 1- Brief Summary of Introduction of Ind-AS 2- Applicability of INDIAN ACCOUNTING STANDARDS () 3- List of with objective and scope BRIEF SUMMARY OF INTRODUCTION OF IND-AS Indian Accounting Standards

Impact of Ind AS on Cost computations & audit By CMA Milind Date M Com, FCMA, CMA (USA), Dip IFRS (ACCA UK)

, Dip IFRS (ACCA UK)") Impact of Ind AS on Cost computations & audit By CMA Milind Date M Com, FCMA, CMA (USA), Dip IFRS (ACCA UK) 13-03-2018 CMA Milind Date 1 Merging of two pillars Financial & Cost Accounting..we all are accountants

Impact of Ind AS on Cost computations & audit By CMA Milind Date M Com, FCMA, CMA (USA), Dip IFRS (ACCA UK) 13-03-2018 CMA Milind Date 1 Merging of two pillars Financial & Cost Accounting..we all are accountants

Springer Nature GmbH, Berlin

Springer Nature GmbH, Berlin (formerly known as Springer SBM Zero GmbH) Consolidated Financial Statements as at 31 December 2017 Heidelberger Platz 3 14197 Berlin Germany HRB 153763 B, AG Berlin 1 Contents

Springer Nature GmbH, Berlin (formerly known as Springer SBM Zero GmbH) Consolidated Financial Statements as at 31 December 2017 Heidelberger Platz 3 14197 Berlin Germany HRB 153763 B, AG Berlin 1 Contents

MFRS Hot Topics. Common control business combinations

MFRS Hot Topics Common control business combinations AUGUST 2016 Welcome to MFRS Hot Topics - a publication from SJ Grant Thornton. This publication will provide guidance on how should a business combination

MFRS Hot Topics Common control business combinations AUGUST 2016 Welcome to MFRS Hot Topics - a publication from SJ Grant Thornton. This publication will provide guidance on how should a business combination

Answer to Jun 2011 Section A

Answer to Jun 2011 Section A To : Mr. Yan, Director of CCN From : Peter Wong, Accounting Manager, CCN c.c. : Jacky Lam, Alex Cheng, Nelson Chan (Directors) Date : dd/mm/yyyy Subject : Consolidated financial

Answer to Jun 2011 Section A To : Mr. Yan, Director of CCN From : Peter Wong, Accounting Manager, CCN c.c. : Jacky Lam, Alex Cheng, Nelson Chan (Directors) Date : dd/mm/yyyy Subject : Consolidated financial

Financial Reporting Matters

Financial Reporting Matters September 2009 Issue 28 AUDIT In this issue, we discuss the revisions made to FRS 103 Business Combinations and FRS 27 Consolidated and Separate Financial Statements (2009)

Financial Reporting Matters September 2009 Issue 28 AUDIT In this issue, we discuss the revisions made to FRS 103 Business Combinations and FRS 27 Consolidated and Separate Financial Statements (2009)

Package of five standards on consolidation, joint arrangements, associates and disclosures. Candy Fong (7 March 2013)

") Package of five standards on consolidation, joint arrangements, associates and disclosures Candy Fong (7 March 2013) All materials or explanations (not restricted to the following presentation slides)

Package of five standards on consolidation, joint arrangements, associates and disclosures Candy Fong (7 March 2013) All materials or explanations (not restricted to the following presentation slides)

IFRS 3 Business combinations. Solutions. Solutions Véronique Weets

Solutions IFRS 3 Business combinations Solutions Véronique Weets Instituut van de Bedrijfsrevisoren 1 Solutions TABLE OF CONTENT Table of content... 2 IFRS 3 Business combinations... 3 Identifying the

Solutions IFRS 3 Business combinations Solutions Véronique Weets Instituut van de Bedrijfsrevisoren 1 Solutions TABLE OF CONTENT Table of content... 2 IFRS 3 Business combinations... 3 Identifying the

Investment Corporation of Dubai and its subsidiaries

Investment Corporation of Dubai and its subsidiaries CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2017 Investment Corporation of Dubai and its subsidiaries CONSOLIDATED INCOME STATEMENT

Investment Corporation of Dubai and its subsidiaries CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2017 Investment Corporation of Dubai and its subsidiaries CONSOLIDATED INCOME STATEMENT

CONSOLIDATED FINANCIAL STATEMENTS AS OF 30 June Eutelsat Communications 1

Eutelsat Communications Group Société anonyme with a capital of 232,774,635 euros Registered office: 70, rue Balard 75015 Paris 481 043 040 R.C.S. Paris CONSOLIDATED FINANCIAL STATEMENTS AS OF 30 June

Eutelsat Communications Group Société anonyme with a capital of 232,774,635 euros Registered office: 70, rue Balard 75015 Paris 481 043 040 R.C.S. Paris CONSOLIDATED FINANCIAL STATEMENTS AS OF 30 June

Consolidated Financial Statements (Part 1) 15 March 2010

15 March 2010") Consolidated Financial Statements (Part 1) 15 March 2010 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2005-10 Nelson Consulting Limited 1 Regulatory Framework in

Consolidated Financial Statements (Part 1) 15 March 2010 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2005-10 Nelson Consulting Limited 1 Regulatory Framework in

Change in ownership interests in investees

07 Change in ownership interests in investees This article aims to: Illustrate the accounting for change in control or significant influence on an investee. 2018 KPMG, an Indian Registered Partnership

07 Change in ownership interests in investees This article aims to: Illustrate the accounting for change in control or significant influence on an investee. 2018 KPMG, an Indian Registered Partnership

Group Accounts Mastercourse

Group Accounts Mastercourse Steven Collings FMAAT FCCA Autumn 2013 Course Overview Terminology issues A brief refresher on the basic principles How accounting standards influence consolidated financial

Group Accounts Mastercourse Steven Collings FMAAT FCCA Autumn 2013 Course Overview Terminology issues A brief refresher on the basic principles How accounting standards influence consolidated financial

Università degli studi di Pavia Facoltà di Economia a.a Lesson 7 International Accounting Lelio Bigogno, Stefano Santucci

Università degli studi di Pavia Facoltà di Economia a.a. 2013-2014 Lesson 7 International Accounting Lelio Bigogno, Stefano Santucci 1 IAS/IFRS: IAS 36 Impairment of Assets 2 History of IAS 36 May 1997

Università degli studi di Pavia Facoltà di Economia a.a. 2013-2014 Lesson 7 International Accounting Lelio Bigogno, Stefano Santucci 1 IAS/IFRS: IAS 36 Impairment of Assets 2 History of IAS 36 May 1997

Appendix The Differences Between Full IFRS and IFRS for SMEs

Frequently Asked Questions in IFRS By Steven Collings 2013 Steven John Collings Appendix The Differences Between Full IFRS and IFRS for SMEs 284 Frequently Asked Questions in IFRS There are some extremely

Frequently Asked Questions in IFRS By Steven Collings 2013 Steven John Collings Appendix The Differences Between Full IFRS and IFRS for SMEs 284 Frequently Asked Questions in IFRS There are some extremely

Accounting and Auditing Update

Accounting and Auditing Update Issue no. 14/2017 September 2017 www.kpmg.com/in Editorial Sai Venkateshwaran Partner and Head Accounting Advisory Services KPMG in India Ruchi Rastogi Executive Director

Accounting and Auditing Update Issue no. 14/2017 September 2017 www.kpmg.com/in Editorial Sai Venkateshwaran Partner and Head Accounting Advisory Services KPMG in India Ruchi Rastogi Executive Director

SUPPLEMENTARY INFORMATION SUPPLEMENTARY FINANCIAL INFORMATION SUPPLEMENTARY PEOPLE INFORMATION SUPPLEMENTARY SUSTAINABILITY INFORMATION SHAREHOLDER

SUPPLEMENTARY INFORMATION SUPPLEMENTARY FINANCIAL INFORMATION SUPPLEMENTARY PEOPLE INFORMATION SUPPLEMENTARY SUSTAINABILITY INFORMATION SHAREHOLDER INFORMATION MAJOR AWARDS 296 312 314 317 319 GLOSSARY

SUPPLEMENTARY INFORMATION SUPPLEMENTARY FINANCIAL INFORMATION SUPPLEMENTARY PEOPLE INFORMATION SUPPLEMENTARY SUSTAINABILITY INFORMATION SHAREHOLDER INFORMATION MAJOR AWARDS 296 312 314 317 319 GLOSSARY

Consolidated Financial Statements of ANGOSTURA HOLDINGS LIMITED. December 31, 2017 (Expressed in Trinidad and Tobago Dollars)

") Consolidated Financial Statements of ANGOSTURA HOLDINGS LIMITED (Expressed in Trinidad and Tobago Dollars) Financial Statements C O N T E N T S Page Statement of Management Responsibilities 1 Independent

Consolidated Financial Statements of ANGOSTURA HOLDINGS LIMITED (Expressed in Trinidad and Tobago Dollars) Financial Statements C O N T E N T S Page Statement of Management Responsibilities 1 Independent

3 Days Workshop on IFRS/Ind AS WIRC Bhavan

3 Days Workshop on IFRS/Ind AS WIRC Bhavan IAS 16 Property, Plant & Equipments IAS 38 Intangible Assets IAS 36 Impairment of Assets IFRS 5 Non-Current Assets held for Sales NareshJ. Patel Ptl& Co. Chartered

3 Days Workshop on IFRS/Ind AS WIRC Bhavan IAS 16 Property, Plant & Equipments IAS 38 Intangible Assets IAS 36 Impairment of Assets IFRS 5 Non-Current Assets held for Sales NareshJ. Patel Ptl& Co. Chartered

Ind AS 16 Property, Plant & Equipment CA Hemal D Shah

Ind AS 16 Property, Plant & Equipment CA Hemal D Shah Page 1 Contents 1. Property Plant & Equipment - Ind AS 16 2. Government Grant Ind AS 20 Page 2 Property Plant & Equipment Ind AS 16 Measurement Depreciation

Ind AS 16 Property, Plant & Equipment CA Hemal D Shah Page 1 Contents 1. Property Plant & Equipment - Ind AS 16 2. Government Grant Ind AS 20 Page 2 Property Plant & Equipment Ind AS 16 Measurement Depreciation

ASSURANCE AND ACCOUNTING ASPE - IFRS: A Comparison Joint Arrangements and Associates

ASSURANCE AND ACCOUNTING - : A Comparison Joint Arrangements and Associates In this publication we will examine the key differences between Accounting Standards for Private Enterprises () and International

ASSURANCE AND ACCOUNTING - : A Comparison Joint Arrangements and Associates In this publication we will examine the key differences between Accounting Standards for Private Enterprises () and International

Additional integrated questions. Group Financial Reporting FAC3704. Department of Financial Accounting

Additional integrated questions Group Financial Reporting FAC3704 Department of Financial Accounting QUESTION 1 (27 marks)(32 minutes) On 1 January 2011, Courtney Ltd acquired 35% of the issued shares

Additional integrated questions Group Financial Reporting FAC3704 Department of Financial Accounting QUESTION 1 (27 marks)(32 minutes) On 1 January 2011, Courtney Ltd acquired 35% of the issued shares

Impairment of Assets IAS 36 IAS 36. IFRS Foundation

IAS 36 Impairment of Assets In April 2001 the International Accounting Standards Board (the Board) adopted IAS 36 Impairment of Assets, which had originally been issued by the International Accounting

IAS 36 Impairment of Assets In April 2001 the International Accounting Standards Board (the Board) adopted IAS 36 Impairment of Assets, which had originally been issued by the International Accounting

HKFRS Issues of Merger and Acquisition

HKFRS Issues of Merger and Acquisition Date 21 March 2014 Time 19:00 21:00 Venue Duke of Windsor Social Service Building Disclaimer The materials of this seminar are intended only to provide general information

HKFRS Issues of Merger and Acquisition Date 21 March 2014 Time 19:00 21:00 Venue Duke of Windsor Social Service Building Disclaimer The materials of this seminar are intended only to provide general information

ACCA. Paper F7 INT/UK. Financial Reporting. Essential Text

ACCA Paper F7 INT/UK Financial Reporting Essential Text British library cataloguing in publication data A catalogue record for this book is available from the British Library. Published by: Kaplan Publishing

ACCA Paper F7 INT/UK Financial Reporting Essential Text British library cataloguing in publication data A catalogue record for this book is available from the British Library. Published by: Kaplan Publishing

Accounting and Auditing Update

Accounting and Auditing Update Issue no. 24/2018 July 2018 www.kpmg.com/in 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with

Accounting and Auditing Update Issue no. 24/2018 July 2018 www.kpmg.com/in 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with

Formation)of)Inter!Entity&Relationships"

of)Inter!Entity&Relationships") Formation)of)Inter!Entity&Relationships" Overview'of'Types'of'Inter1Entity'Relationships' Reporting*Entities* SAC 1, Definition of the Reporting Entity, para. 6: o Entity means any legal, administrative

Formation)of)Inter!Entity&Relationships" Overview'of'Types'of'Inter1Entity'Relationships' Reporting*Entities* SAC 1, Definition of the Reporting Entity, para. 6: o Entity means any legal, administrative

BUSINESS COMBINATIONS: IFRS 3 (REVISED)

") TECHNICAL PAGE 50 STUDENT ACCOUNTANT FEBRUARY 2009 BUSINESS COMBINATIONS: IFRS 3 (REVISED) RELEVANT TO ACCA QUALIFICATION PAPER P2 This first article in a two-part series provides an introduction to IFRS

TECHNICAL PAGE 50 STUDENT ACCOUNTANT FEBRUARY 2009 BUSINESS COMBINATIONS: IFRS 3 (REVISED) RELEVANT TO ACCA QUALIFICATION PAPER P2 This first article in a two-part series provides an introduction to IFRS

High Level Comparison

Hong Kong Financial Reporting Standard for Private Entities vs Hong Kong Small and Medium-sized Entity Financial Reporting Framework and Financial Reporting Standard (Revised) High Level Comparison Hong

Hong Kong Financial Reporting Standard for Private Entities vs Hong Kong Small and Medium-sized Entity Financial Reporting Framework and Financial Reporting Standard (Revised) High Level Comparison Hong