A N N U A L R E P O R T

|

|

|

- Anne Anthony

- 6 years ago

- Views:

Transcription

1 Annual Report 2000

2 ANNUAL REPORT 2000

3 3 CONTENTS CORPORATE GOVERNANCE BOARD OF DIRECTORS MANAGEMENT COMMITTEE LETTER FROM THE CHAIRMAN KEY FIGURES OF THE VALLEHERMOSO GROUP EXTERNAL VALUATION OF PROPERTY ASSETS VALUATION CERTIFICATE OF C.B. RICHARD ELLIS VALUATION, CAPITAL GAINS, N.A.V PROFORMA 2000: VALLEHERMOSO GROUP + PRIMA INMOBILIARIA PROPOSED DISTRIBUTION OF PROFIT OF VALLEHERMOSO, S.A REVIEW OF OPERATIONS LAND DEVELOPMENT, PROMOTIONS AND SALES RENTAL BUSINESS AND PROPERTY POLICY SERVICES BUSINESS HUMAN RESOURCES, STAFF WELFARE AND DATA SYSTEMS MANAGEMENT REPORT OF THE CONSOLIDATED GROUP ANALYSIS OF PERFORMANCE INVESTMENT AND FINANCING ACQUISITION OF PRIMA INMOBILIARIA PROPERTY MARKET TRENDS AND OUTLOOK CONSOLIDATED ANNUAL ACCOUNTS BALANCE SHEETS PROFIT AND LOSS ACCOUNTS NOTES TO THE ANNUAL ACCOUNTS APPENDICES EXTERNAL AUDITORS REPORT VALLEHERMOSO, S.A BALANCE SHEETS PROFIT AND LOSS ACCOUNTS EXTERNAL AUDITOR S REPORT SHAREHOLDER INFORMATION INVESTOR RELATIONS FIGURES FOR KEY SUBSIDIARIES IN THE VALLEHERMOSO GROUP INFORMATION ABOUT THE ADOPTION OF THE CODE OF GOOD GOVERNANCE HISTORIC DATA Development of future luxury housing at Paseo de Gracia, 82 (Barcelona). A N N U A L R E P O R T

4 BOARD OF DIRECTORS MANAGEMENT COMMITTEE HONORARY CHAIRMAN MARTÍN EYRIES VALMASEDA CHAIRMAN ANTONIO DE AMUSÁTEGUI DE LA CIERVA CHAIRMAN ANTONIO DE AMUSÁTEGUI DE LA CIERVA FIRST VICE CHAIRMAN AND MANAGING DIRECTOR EMILIO NOVELA BERLÍN FIRST VICE CHAIRMAN AND MANAGING DIRECTOR EMILIO NOVELA BERLÍN SECOND VICE CHAIRMAN PEDRO GAMERO DEL CASTILLO Y BAYO SECOND VICE CHAIRMAN PEDRO GAMERO DEL CASTILLO Y BAYO COMPANY AND BOARD SECRETARY CARLOS DÍAZ LLADÓ 4 CORPORATE GOVERNANCE SECRETARY CARLOS DÍAZ LLADÓ DEPUTY SECRETARY JOSÉ ANTONIO RODRÍGUEZ ÁLVAREZ GENERAL MANAGER OF CORPORATE SERVICES JOSÉ LUIS RODRÍGUEZ FLECHA GENERAL MANAGER OF RENTAL ASSETS FERNANDO RODRÍGUEZ-AVIAL LLARDENT DIRECTORS SANTIAGO FONCILLAS CASAÚS ANTONIO DE HOYOS GONZÁLEZ JOSÉ LUIS LLORENTE BRAGULAT JOSÉ ZAMORA MENÁRGUEZ JOSÉ MARÍA CUEVAS SALVADOR ANTONIO RODRÍGUEZ MATÉ Following the close of 2000 Mr. John Gómez Hall and Mr. Enrique Álvarez López were coopted onto the Board. TECHNICAL GENERAL MANAGER SEGUNDO RODRÍGUEZ GARCÍA TECHNICAL SECRETARY JOSÉ CARLOS MORENO DE PABLOS COMPANY DEPUTY SECRETARY AND CHIEF LEGAL COUNSEL JOSÉ ANTONIO RODRÍGUEZ ÁLVAREZ REGIONAL MANAGERS ANDALUSIA REGIONAL MANAGER IGNACIO RAMOS-CATALINA FLORIDO NORTHERN SPAIN REGIONAL MANAGER PEDRO PALENZUELA MARAÑÓN CATALONIA REGIONAL MANAGER JOSÉ ORIOL DOMINGO CALVO EASTERN SPAIN REGIONAL MANAGER MARIANO DE DIEGO RIVAS CENTRAL SPAIN REGIONAL MANAGER LUIS LOREN BUTRAGUEÑO

5 LETTER FROM THE CHAIRMAN 7 To Our Shareholders: As the Chairman of the Board of Vallehermoso, I am very pleased to present to you the annual report, the management report and the accounts of Vallehermoso and its Group for I would like to highlight the main aspects of our company s performance during the last year as well as underline the Vallehermoso Group s medium and long-term potential for growth and profitability. The year 2000 was particularly outstanding and intensive for this Company in a sector where considerable activity continued, accompanied by a positive economic scenario, which has permitted above European-average growth in Spain s various macroeconomic factors. Last year marked the consolidation of Vallehermoso s leadership within the spanish real estate sector through large scale operations which have had a positive effect on the Company s present and will be determinant for it s future. Firstly, as you are already aware and as was approved by you at the Shareholders Meeting held on July 28, 2000, Vallehermoso equipped itself with a new organisational structure based around its three core activities by creating a Group comprising three different companies: VALLEHERMOSO DIVISIÓN PROMOCIÓN S.A.U., which engages in the most traditional type of real estate development; VALLEHERMOSO RENTA, S.A.U., which manages the property Rental Business (the latter has changed its name to Testa Inmuebles en Renta, S.A. following the merger with Prima Inmobiliaria); and finally, VALORIZA, S.L., which includes all the Group s services businesses. View of the building complex in Princesa Street, Madrid. This structure achieves a greater efficiency, a more appropriate assignment of costs and yields and, A N N U A L R E P O R T

6 LETTER FROM THE CHAIRMAN in particular, a better and more transparent valuation which meet the prime objective of creating shareholder value. In the first part of 2000 General Electric Pension Trust (G.E.P.T.) acquired 4.4% of Vallehermoso s capital stock. Accordingly, one of the world s leading business groups became a stable shareholder of Vallehermoso, investing in a sound project of business development in the real estate sector. Subsequently, the Vallehermoso Group reached a friendly agreement with Prima Inmobiliaria to merge their respective rental activities. As a result of this operation the largest and most balanced property Group in the Spanish market was formed. The process was performed in two stages. Firstly, in January 2001 Vallehermoso Renta (Vallehermoso s property rental subsidiary) merged with Prima Inmobiliaria which resulted in the creation of Testa; Vallehermoso obtained a stake of 64.96% of Testa. Finally, on January 26, 2001 Vallehermoso presented a takeover bid for 100% of Testa s capital stock before the Spanish National Securities Commission and as a result it obtained 35.04% of Testa s capital stock; the required capital increase at Vallehermoso, S.A. was authorised at the last Extraordinary Meeting on November 30, With this operation, Vallehermoso has achieved the objectives of its strategic plan in the Rental Business several years ahead of time. The new Testa is the largest property rental company in Spain. Other important operations were performed in the Property Division in 2000 and non-strategic assets such as Sociedad de Aparcamientos Vallehermoso were sold. This transaction contributed revenues of more than 4,000 million pesetas to the Group. The first and only Tax-Favoured property investment Fund in the market was created (Vallehermoso Patrimonio, S.I.I.) which is very attractive from a tax standpoint. The development of residential homes for the elderly began a new range of business with a foreseeably important future; work is currently underway on several projects. All the projects in the property division represent a committed investment earmarked for rental of around 100,000 million pesetas in assets to be developed by Vallehermoso. The Vallehermoso Group gave a decisive boost to the geographical and strategic diversification of the Development Division which had already begun in As a result of the active land purchasing policy, our position in some cities such as Madrid, Seville, Málaga, Córdoba, Alicante, Valencia, Barcelona, Bilbao, A Coruña, Oviedo, Santander, Tenerife, Ciudad Real and Palma de Mallorca has been strengthened and we have established a presence for the first time in cities which include Granada, Cádiz, Lleida, Girona, Tarragona, Salamanca, Ávila, Albacete, Murcia and Las Palmas. Until 2000, the Vallehermoso Group provided a range of services through different companies in which it had varying stakes. Following the Group s restructuring into business lines, these assets have been transferred to Valoriza, which has thus become the Group s flagship company for the services business. Through Valoriza, the Vallehermosos Group is carrying out a policy of providing, to both existing an new companies, services that require knowledge of the property market, that bring high added value, that help the process of full service integration, and that develop the customer base and improve client loyalty. Valoriza s major holdings are: Erantos: its main line of business is the provision of services for the development, management and administration of housing co-operatives and co-operative developments. Valleágora: specialised in the provision of integrated services in the large shopping mall sector. Vallehermoso Telecom: engages in the telecommunications business, acting as an intermediary between operators and consumers (initially Vallehermoso customers) through the resale of fixed telephony, mobile telephony, electronic security, etc. Integra: the company resulting from the merger between Sergesa, S.A. (a Vallehermoso Group company) and MYM (a Dragados Group company). Its main line of business is integrated maintenance and management of buildings. Valoriza also has minority holdings in other companies such as: IPT Soluziona Telecomunicaciones, Avirón, Euroresidencias Gestión and Adisa. Regarding 2000 results, attributable profit recorded an increase of nearly 60% to 13,336 million pesetas. Operating profit amounted to 20,217 million pesetas, 45% up on the preceding year. Cash-flow of 14,936 million pesetas was generated, 47% more than in In the same period turnover exceeded 86,300 million pesetas with growth of almost 45%. Committed sales of housing units increased 75% to approximately 90,000 million pesetas. Land reserves and construction work in progress amounted to around 2,250,000 square metres. The book value of property assets in operation and in progress exceeded 119,000 million pesetas. According to Richard Ellis, at December 31, 2000 the valuation of all of real estate assets exceeded 433,000 million pesetas. A N N U A L R E P O R T

7 LETTER FROM THE CHAIRMAN Although the merger with Prima Inmobiliaria came into effect as from January 1, 2001, in pro forma terms, adding the main economic aggregates of both groups, the year 2000 would have generated attributable profit of around 18,000 million pesetas and estimated total turnover of approximately 107,000 million pesetas. Likewise, the sum of the respective valuations made by C.B. Richard Ellis of the Vallehermoso Group and Prima Inmobiliaria Group s assets amounted to 566,000 million pesetas. Our dividend policy for 2000 draws the necessary balance between our results and our demanding investment plan. The proposal to be submitted to the Shareholders Meeting for approval represents an increase of 25% on the dividends charged to General expenses grew 29% to 5,191 million pesetas. This increase includes the expenses incurred by the merger and those relating to the transfer of the businesses into the three subsidiaries mentioned above. Instead of capitalising these expenses to amortise them over five years, we have followed a prudent policy and charged them in full to profit for Without this particular item and excluding the deployment of resources to meet business growth, routine structural costs grew approximately 5%. Before concluding, I would like to pay tribute to Epifanio Ridrulejo Brieva who was a Director of this Company until he passed away on December 20, 2000; he was a friend and an outstanding colleague. Antonio Rodríguez Maté, representing General Electric and John Gómez Hall, following the merger with Prima Inmobiliaria joined the board, as did Enrique Álvarez López replacing Ramón Colao Caicoya who retired for reasons of age. Finally, I would like to thank you for the trust you have placed in the Board of Directors and all the individuals who work at Vallehermoso, whose professionalism and dedication made the highly favourable results for 2000 possible. I would like to reiterate my personal commitment, and that of the Board, to continue to improve quality for our customers and to emphasise the priority of the creation of value for our shareholders. Sincerely, As for the stock market performance, during this year technology stock prices continued to fall markedly, following last year s trend. On the other hand, the so-called traditional stocks are back in the limelight. Vallehermoso s performance (accumulated yield to March 31: 26.37%) is much higher than the average for stocks in Spain s market in the first quarter (Ibex-35 to March 31: 2.51%) and more satisfactory than other stocks in the sector. The medium and long-term future for Vallehermoso is promising. We have drawn up a strategic plan from 2001 to 2004 which envisages a CAGR for attributable profit of more than 26%. So as to obtain a greater balance between the various business areas, this plan contemplates an increase of the Property Division s operating cashflow (42% at present to 45% in 2004) as well as that of the Services Division (1% at present to 3% in 2004) compared with the Development Division (decreasing from 57% at present to 52% in 2004). ANTONIO DE AMUSÁTEGUI CHAIRMAN I would also like to mention particularly Vallehermoso s adoption of the Code of Good Governance applying to the Board of Directors. The Board s Statutes have been brought into line with the recommendations of the so-called Code of Good Governance of the Board of Directors. An Appointments and Remuneration Committee and an Audit Committee have also been created. Rules for Internal Conduct have been drawn up which apply to the Members of the Board, to Managers and other company employees who, due to their work responsibilities have access to facts, decisions and information which might influence the Company s share price. A N N U A L R E P O R T

8 KEY FIGURES OF THE CONSOLIDATED VALLEHERMOSO GROUP 12 KEY FIGURES OF THE CONSOLIDATED VALLEHERMOSO GROUP In millions % Change /1999 Mn. euros 1. Key Business Figures Net attributable profit 4,662 5,112 5,427 6,565 8,350 13, Cash-Flow 6,528 5,822 7,112 8,912 10,130 14, Gross income for sales 34,229 37,013 36,101 43,676 46,889 71, Gross rental income 6,267 6,741 7,302 8,227 9,403 10, Gross income from services 1,537 2,117 2,058 2,631 3,306 4, Investment in fixed assets 6,887 4,718 9,236 5,392 6,581 23, Purchase of land 7,344 6,919 11,191 25,040 28,501 31, Shareholders equity 86,146 88,937 91,989 95, , , Financial debt (1) 44,767 47,280 49,896 52,960 76, , Net fixed assets 73,733 75,638 86,903 97, , , Earnings per share (pesetas) (3) * 59.7 Cash-Flow per share (pesetas) (3) * 47.4 Dividend per share (pesetas) (3) * 25.0 Market capitalisation 97, , , , , , (7.1) 2. Other Key figures Housing units sold (committed units) 930 1,225 1,605 1,750 2,086 3, Land reserves (m2.) 1,834,664 1,834,268 1,871,206 2,140,704 2,254,140 2,253,261 (0.0) Rental space (m2.) 651, , , , , ,009 (1.7) No. employees at 31 December (2) No. employees at 31 December without including the Services Business (2) Proforma 2000 (Grupo Vallehermoso + Prima Inmobiliaria) Net attributable profit 17, Turnover 106, Gross income for sales 85, Gross rental income 16, Gross income from services 4, (1) Includes mortgage loans transferable to buyers. (2) See section on human resources p.62 (3) Data adjusted for par value after stock split in * Euros MAJOR SHAREHOLDERS % OF OWNERSHIP 2000 % OF OWNERSHIP 1999 DIRECT INDIRECT DIRECT INDIRECT Banco SantanderCentral Hispano, S.A The Chase Manhattan Bank NA General Electric Pension Trust Other with holdings of less than 3%

9 KEY FIGURES OF THE CONSOLIDATED VALLEHERMOSO GROUP NET ATTRIBUTABLE PROFIT (MILLIONS OF PESETAS) / *(MILLIONS OF EUROS) EARNINGS PER SHARE (PTAS./SHARE) / *(IN EUROS) KEY FIGURES OF THE CONSOLIDATED VALLEHERMOSO GROUP (MILLIONS OF PTAS.) / *(MILLIONS OF EUROS) Equity 13,336/* /* Financial debt % Gearing ,662 5,112 5,427 6,565 8, ,146 88,937 91,989 95, ,330 76, ,338/* Gross income for sales Gross rental income Gross income from services 6,267 1,537 34,229 6,741 2,117 36,101 7,302 2,058 43,676 8,227 2,631 46,889 9,403 3,306 10,875/* ,330/* ,130/* ,767 47,280 49, ,493/* ,960 DIVIDEND PER SHARE (PTAS./SHARE) / *(IN EUROS) TURNOVER (MILLIONS OF PTAS.) / *(MILLIONS OF EUROS) LETTABLE AREA SURFACE (000s M 2 ) COMMITTED SALES OF HOUSING UNITS AND LAND RESERVES (IN UNITS AND M 2 ) Land reserves m 2 Committed sales of housing units /* , , , , , , , ,225 1,605 1,750 2,086 3,087 1,834,664 1,834,268 1,871,206 2,140,704 2,254,140 2,253, A N N U A L R E P O R T

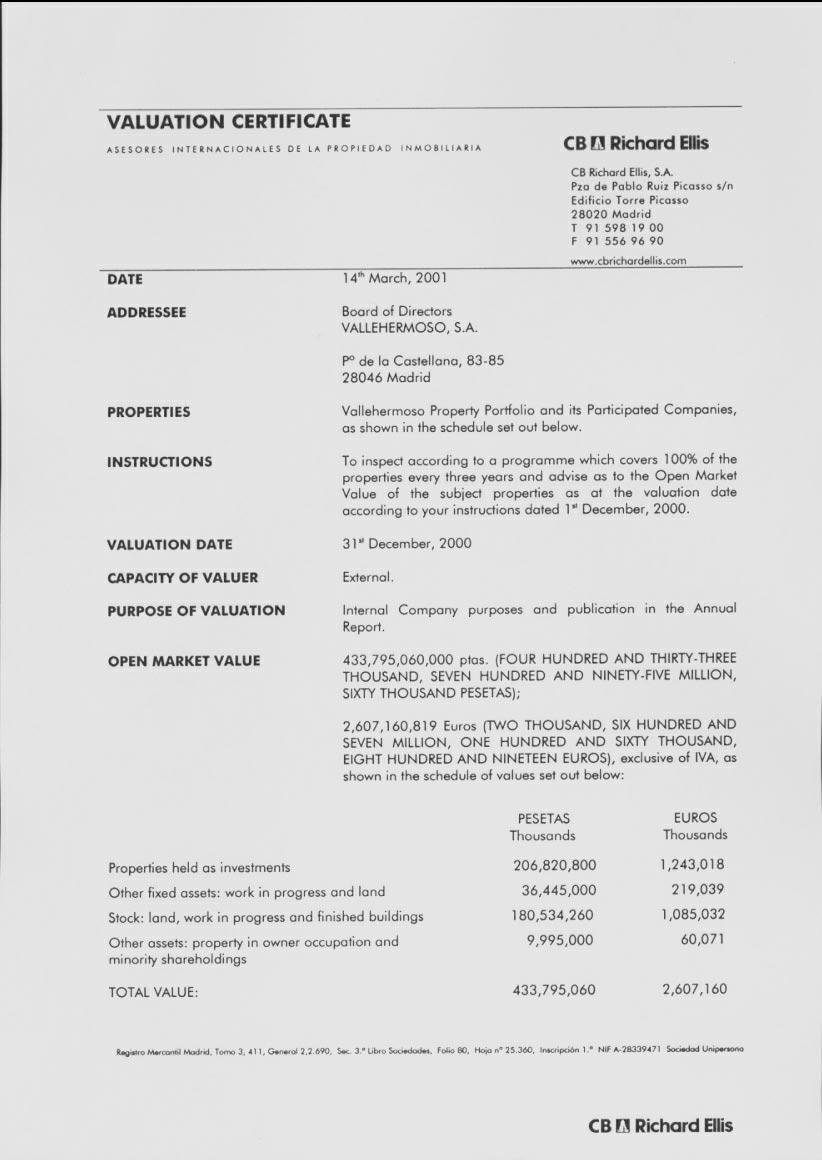

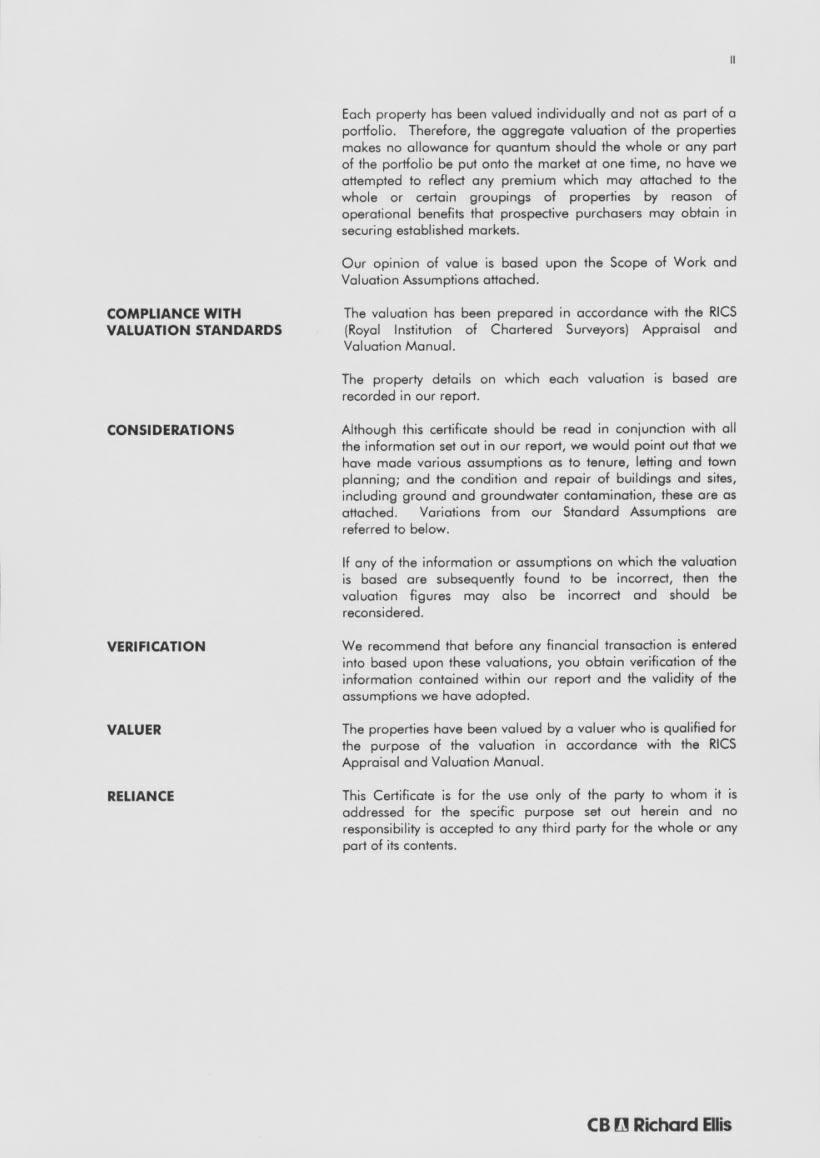

10 16 EXTERNAL VALUATION OF PROPERTY ASSETS 18 C.B. RICHARD ELLIS VALUATION CERTIFICATE 24 VALUATION, CAPITAL GAINS, N.A.V. 27 PROFORMA 2000: VALLEHERMOSO GROUP + PRIMA INMOBILIARIA GROUP

11

12

13

. This valuation represents an increase of 16.9% over 1999.")

14 PROPERTY VALUATION PROPERTY VALUATION / VALUATION AND CAPITAL GAINS OF PROPERTY ASSETS Valuation and capital gains of property assets The value of the Vallehermoso Group s property assets at according to the valuation carried out by C.B. Richard Ellis amounted to 433,795 million pesetas (2,607.2 million euros). This valuation represents an increase of 16.9% over The structure of the value of the property assets is as follows: VALUE OF PROPERTY ASSETS In millions % CHANGE PESETAS EUROS PESETAS OVER 99 Rented properties 206,821 1, , Other properties: Developments in progress and land 36, , Total Rental assets 243,2661, , Inventories: sites, developments in progress and completed developments 180,534 1, , Other assets: own use and minority holdings 9, , Total property assets 433,795 2, , The unrealised capital gains of the assets valued, comparing the market value assigned by C.B. Richard Ellis and the book value, amount to 192,532 million pesetas (1,157 million euros); their origin and change are as follows: CAPITAL GAIN ON BOOK VALUE In millions % CHANGE PESETAS EUROS PESETAS OVER 99 Rented properties 107, , Other properties: Developments in progress and land 16, , Total rental assets 124, , Inventories: sites, developments in progress and completed developments 63, , Other assets: own use and minority holdings 4, , Total property assets 192,532 1, , Offices at Campo de las Naciones, Madrid (left). San Telmo, Tenerife (right). Rented properties Rented properties at were valued at 206,821 million pesetas (1,243 million euros), 17.1% up on the 1999 valuation. An analysis of the performance in 2000 shows that the above-mentioned increase in the valuation is principally due to two factors: Change in Assets and Market Appreciation. On average the effect of both factors on the valuation of leased properties is as follows: % CHANGE OVER 1999 Change in assets due to net investments 8.7% Increase due to market appreciation 7.7% The structure of the valuation by property type is as follows: In millions PESETAS % EUROS Offices 102, Housing 50, Commercial 41, Other 11, , ,243.0 The unrealised capital gain in the valuation of leased properties, 107,772 million pesetas (647.7 million euros) grew 13.6% in comparison with the previous year. Net revenues according to contracts and growth expectations of rents Residual value according to expectations of initial specific rate of return for each type of property in the following areas: Offices 6.25% 7.5% Commercial 7% 9% Housing 5% 7% Inventories: sites, developments in progress and completed developments The valuation of inventories, almost all of which belong to the Development Business, amounted to 180,534 million pesetas (1,085 million euros), representing a 15.8% increase over The discounted cash-flow valuation method has been used by C.B. Richard Ellis for the rental assets, for which the following assumptions were made: Discounted cash-flow period = 10 years. Prediction of net revenues, annual revenues and residual value at the end of the period. Internal Rate of Return An analysis of the performance in 2000 shows that the abovementioned increase in the valuation due to two factors: Change in Assets and Market Appreciation. A N N U A L R E P O R T

Increase due to market appreciation 17.6% The unrealised capital gain in the valuation of inventories, 63,587 million pesetas (382.1 million euros) increased 3.")

15 PROPERTY VALUATION / VALUATION AND CAPITAL GAINS OF PROPERTY ASSETS On average the effect of both factors on the valuation of inventories is as follows: % CHANGE OVER 1999 Change in assets due to net investments (1.5%) Increase due to market appreciation 17.6% The unrealised capital gain in the valuation of inventories, 63,587 million pesetas (382.1 million euros) increased 3.8% in comparison with the previous year. This low increase in the capital gain is due to the strong change of inventories during the year. The vigorous pace of land sales with historic capital gains, in addition to the sizeable package of land transferred to fixed assets, was accompanied by a concerted land purchasing programme. The capital gain generated by the latter in the year was considerably lower than that of the assets which were sold and transferred. The residual development studies valuation method is used by C.B. Richard Ellis for development properties; the assumptions used by the valuation company were as follows: Net asset value (N.A.V.) before taxes The net asset value of the Vallehermoso Group s assets before taxes at was 300,870 million pesetas (1,808.3 million euros), 9.9% up on The breakdown and change in N.A.V. is as follows: Porto Pi Shopping Centre, Palma de Majorca. Proforma 2000: Vallehermoso Group + Prima Inmobiliaria The value of the Vallehermoso Group and Prima Inmobiliaria Group s property assets at , obtained from the respective valuations performed by C.B. Richard Ellis at that date amounted to 566,182 million pesetas (3,402.8 million euros). The breakdown of this value is as follows: Future residential home for the elderly in Getafe, Madrid Value of completed development (estimated sales revenues). Cost of the development (outstanding costs including marketing and financing). Profit of the developer which is variable according to the development s characteristics. In millions PESETAS EUROS PESETAS % CHANGE OVER1999 Equity 108, , Capital gain on property assets (before taxes) 192,532 1, , N.A.V. (Equity + Capital gain) 300,870 1, , N.A.V. per share 2, , In millions PESETAS EUROS Rented properties 312,932 1,880.7 Other properties: developments in progress and land 52, Total rental assets 365,792 2,198.4 Inventories: sites, developments in progress and completed developments 187,019 1,124.0 Other assets: own use and minority holdings 13, Total assets 566,182 3,402.8 A N N U A L R E P O R T

16 64 MANAGEMENT REPORT OF THE CONSOLIDATED GROUP 67 ANALYSIS OF PERFORMANCE 73 INVESTMENT AND FINANCING 76 ACQUISITION OF PRIMA INMOBILIARIA 78 PROPERTY MARKET TRENDS AND OUTLOOK

17 S. Spriu (Villa Olímpica), Barcelona. A N N U A L R E P O R T VALLEHERMOSO GROUP / MANAGEMENT REPORT ANÁLYSIS OF PERFORMANCE The Vallehermoso Group posted a net consolidated profit of 13,363 million pesetas (80.3 million euros) for 2000, representing a 58.4% increase over The profit attributable to the Parent Company increased 59.7% to 13,336 million pesetas (80.2 million euros). Consolidated profit before tax was 20,271 million pesetas (121.8 million euros) which is a 55.5% increase over the previous year s figure. VALLEHERMOSO GROUP CONSOLIDATED PROFIT AND LOSS ACCOUNT (IN MILLIONS) CHANGE PESETAS EUROS PESETAS PESETAS % Sales (1) Income 71, ,889 24, Cost of sales (49,111) (295.2) (32,600) (16,511) 50.6 Sales profit 22, ,289 7, Rentals Income 10, ,403 1, Expenses (2,680) (16.1) (2,626) (54) 2.1 Depreciation (1,388) (8.3) (1,267) (121) 9.6 Rental profit 6, ,510 1, Services Income 4, , Expenses (3,284) (19.7) (2,627) (657) 25.0 Services profit Net financial expenses (4,623) (27.8) (2,676) (1,947) 72.8 Other income (158) (38.1) General expenses (5,191) (31.2) (4,017) (1,174) 29.2 Depreciation (98) (0.6) (305) 207 (67.9) Operating profit 20, ,895 6, Dividends Provisions (341) (2) (639) 298 (46.6) Portfolio and other profit (loss) (233) 608 (260.9) Profit (loss) equity-method subsidiaries Total profit before tax 20, ,033 7, Corporate income tax (6,908) (41.5) (4,599) (2,309) 50.2 Total profit after tax 13, ,434 4, Attributable to minority interest (57) (67.9) PROFIT ATTRIBUTABLE TO VALLEHERMOSO 13, ,350 4, Cash-flow after tax 14, , (1) Includes sales of fixed assets. ANALYSIS OF PERFORMANCE

18 The key components of the Consolidated Profit and Loss Account are analysed below: 11 SALES Net earnings from sales totalled 22,219 million pesetas (133.5 million euros), an increase of 55.5% on 1999, with strong increases in all three types of product: sales of fixed assets (disposals), land and new residential units. Sales totalled 71,330 million pesetas (428.7 million euros), representing an overall increase of 52.1% on the previous year. All lines of product made a strong contribution to the increase in sales by applying the Group s policies. On the one hand, active land portfolio management has resulted in a 56.3% increase in sales of land without affecting the land available for immediate use in the promotion of housing, as the majority of lots were in poor locations and land acquired under the intensive purchasing programme carried out during the year replaced stocks sold. On the other hand, the fixed asset rotation programme, drawn up to avoid obsolescence of certain products continued where the investment had reached maturity improving the general return on assets. These sales have increased by 45.4%. The Group s policy of strengthening its geographical presence throughout most of Spain, together with excellent market conditions, have resulted in the strong increase in recorded sales of new residential units in 2000, which increased by 54.9% over The average margin on total sales was 31.1%, with a margin of 27.6% on sales of residential products. The average margin is 0.6 points up due to the uneven performance of margins on new residential units, which grew 1.9 points, and on land, which fell 8.4 points. VALLEHERMOSO GROUP. EARNINGS IN 2000 AND 1999 (IN MILLIONS OF PESETAS) / *(IN EUROS) 14,289/* ,219/* ,510/*33.1 6,807/*40.9 (4,017)/*24.1 Profit from sales Profit from rentals General expenses Financial results Attributable profits (5,191)/*31.2 A N N U A L R E P O R T (2,676)/*16.1 (4,623)/*27.8 8,350/* ,336/* VALLEHERMOSO GROUP / MANAGEMENT REPORT ANÁLYSIS OF PERFORMANCE The sales mix and profit from recorded sales in 2000, and their evolution compared with the previous year, were as follows: (IN MILLIONS) SALES SALES PROFIT % / % /99 PESETAS PESETAS EUROS PESETAS PESETAS PESETAS EUROS PESETAS Land 5,088 7, ,558 3, Disposals 4,803 6, ,266 3, Developments 36,998 56, ,465 15, Residential 36,400 56, ,361 15, Other TOTAL 46,889 71, ,289 22, Committed sales of residential units rose strongly over the year to 89,523 million pesetas (538 million euros), a 75.5% increase on the previous year. Since 1997, the year when the current property boom began, the CAGR in committed sales of residential units has been 33.6%. The annual performance of committed residential sales since 1997 is as follows: (IN MILLIONS) INCREASED CAGR / /97 COMMITTED SALES PESETAS PESETAS PESETAS PESETAS EUROS PESETAS PESETAS In millions 37,567 38,866 50,992 89, % 33.6% Nº of units 1,605 1,750 2,086 3, % 24.3% 2 2 RENTALS Revenues from rental properties totalled 10,875 million pesetas (65.4 million euros), representing growth of 15.6% compared to Revenues grew 21% before considering the contribution from Sociedad de Aparcamientos which was sold in the first half of The factors which determined the above-mentioned increase were as follows: an 11.7% increase in average rents due to contractually established rent rises and the product mix; a 7.5% rise in the average space available for letting and an 0.8% improvement in the average occupation rate. The profit generated by this activity increased by 23.5% compared to a 15.6% rise in revenues, as operating costs and depreciation charges have only risen by 2.1% and 9.6%. 33 SERVICES Gross income from services businesses increased 24.9% to 4,130 million pesetas (24.8 million euros). Operating profit stood at 846 million pesetas (5.1 million euros), 24.6% higher than in It is necessary to point out the differences in the consolidated group between both years. Whereas in 1999 Segesa

19 was included in the services business by global integration, in 2000 Integra was included using the proportional integration method and Vallehermoso Telecom, which was incorporated in the second quarter of 2000, was included through global integration. 44 FINANCIAL RESULTS Financial results, which are determined by the difference between financial expenses (interest and other expenses) and financial revenues and the capitalised interest of production, amounted to 4,623 million pesetas (27.8 million euros), representing a 72.8% increase in comparison with The financing of the wide-ranging investment plan implemented in 2000, which triggered a 59.6% rise in average interest-bearing debt, made a decisive contribution to this growth. This factor, together with the 2.6% rise in the average cost of this debt, the evolution of financing interest and other financial expenses and revenues triggered the above-mentioned increase in financial results. Despite the strong increase in net financial costs, coverage of interest with operating cash-flow before taxes is 4.7 times and net financial costs represent only 15.5% of the direct operating profit. 55 GENERAL EXPENSES While general expenses increased by 29.2% in 2000, it should be noted that this section encompasses widely differing items such as structural expenses, operational expenses of the regional divisions and expenses arising from indirect taxation. All of these items, except for structural expenses, are to a greater or lesser extent related to the investment activity and operations carried out. The change in the consolidated group also affects the structure of general operational expenses. Excluding the above-mentioned effects, structural expenses were 30.6% up on Expenses arising in the corporate restructuring process and expenses which were not distributed uniformly between both years, due to consultancy work and counselling in connection with new businesses, made a notable contribution to this rise. Current expenses increased only 5.6%. The increase in general expenses includes all the expenses generated by the merger with Prima Inmobiliaria and the expenses relating to the spin-off of the lines of business into three subsidiaries. In accordance with a conservative management policy, these expenses were charged to the 2000 profit and loss account instead of being capitalised and then amortised later over five years. Excluding this particular factor and disregarding the necessary deployment of resources in line with business growth, current structural expenses rose by approximately 5%. It is worth noting that the Services Business accounted for 96% of the strong increase in the Group s labour force at year-end. Although the Group s new geographical presence and the boost given to the technical division to adequately support the operating growth plan have required hiring new employees, the latter was partially offset by incentivated redundancies in different professional groups and by the sale of Sociedad de Aparcamientos. As a result of the unique operating structure and the Services Business labour force, which is predominantly temporary labour, the Vallehermoso Group s total staff at year-end amounted to 727 employees. Of this total, 447 individuals are employed in the Services Business. 48% of the Group s total staff are temporary employees. 66 PORTFOLIO AND EXTRAORDINARY PROFIT This profit and loss account caption includes profit of 375 million pesetas (2.3 million euros) and includes most notably: A N N U A L R E P O R T VALLEHERMOSO GROUP / MANAGEMENT REPORT ANÁLYSIS OF PERFORMANCE Total profit of 1,360 million pesetas (8.2 million euros) on the equities portfolio due to the sale of shares of Sociedad de Aparcamientos, the sale of Vallehermoso participation in BSCH s property investment fund management company and the contribution of shares of Hispaland and others. Extraordinary results due to insurance expenses to cover pensions, labour force restructuring expenses, extraordinary repairs, recovered revenues from project termination provisions and other items amounting to net expenses of 985 million pesetas (5.9 million euros). 77 PROVISIONS The provisions recorded in 2000 amounted to 1,709 million pesetas (10.3 million euros), and the provisions used, to 1,368 million pesetas (8.2 million euros), representing a net expense of 341 million pesetas (2 million euros). The breakdown of the provisions recorded and used is as follows: (IN MILLIONS) PROVISIONS RECORDED PROVISIONS USED NET PROVISION PESETAS EUROS PESETAS EUROS PESETAS EUROS Financial counselling on Prima Inmobiliaria operation Labour force restructuring Insurance for pensions (600) (3.6) Extraordinary repairs Financial investments Bad debt General-purpose contingencies Total 1, , The net pension insurance provision was used due to the extraordinary expense of 903 million pesetas (5.4 million euros) which was incurred in 2000 as a result of Vallehermoso taking out an insurance policy to cover its pension commitments accrued until the end of million pesetas (3.6 million euros) were charged to profits in 1999 and 300 million pesetas (1.8 million euros) were charged to profits in the first half of 2000 in order to record a provision for this expense. The 900 million pesetas (5.4 million euros) provision recorded for 2000 for the extraordinary insurance expense and the provision used in 2000 of 300 million pesetas (1.8 million euros) produced a net recovery in the year of 600 million pesetas (3.6 million euros). Since the provision for pension insurance was similar to the extraordinary expense, the net amount recorded in 2000 on account of provisions to cover contingencies and future expenses was 941 million pesetas (5.7 million euros). The composition of the Vallehermoso Group underwent the following changes in 2000: Reorganisation of the holding in the services company Integra, S.A. following the merger of Sergesa with MYM. Vallehermoso s current stake stands at 46.25% and this company is consolidated by the proportional integration method. Sale of Sociedad Aparcamientos Vallehermoso and of the holding in Banif Inmobiliaria, S.A. Incorporation of Vallehermoso Telecom which is 75% owned by Vallehermoso.

20 8 The assets of the three areas of Development, Rental and Services were transferred into specialist subsidiary companies. Their respective names are: Vallehermoso División Promoción S.A.U., Vallehermoso Renta, S.A.U. and Valoriza, S.L. At December 31, 2000 these companies were wholly-owned subsidiaries of Vallehermoso, S.A. Acquisition of minority holdings of 10% in Comunicaciones Aviron and Euroresidencias Gestión. The subsidiaries of Vallehermoso, S.A. which reported the most significant results in 2000 were as follows: (IN MILLIONS) PROFITS: PESETAS EUROS Vallehermoso División Promoción 5, Vallehermoso Renta 1, Sanjuva Porto Pí Integra (46.25%) Valleágora (IN MILLIONS) LOSSES: PESETAS EUROS Valoriza (171) (1) Vallehermoso Telecom (87) (0.5) 8 PROFORMA 2000: VALLEHERMOSO GROUP + PRIMA INMOBILIARIA GROUP Although the takeover of Prima Inmobiliaria has economic effects from January 1, 2001 in order to show the effect of the operation on the Vallehermoso Group, pro forma figures are presented below for the year 2000 showing the principle aggregate figures: (IN MILLIONS) PESETAS EUROS Attributable profit 17, Turnover Rental 16, Sales (*) 85, Services 4, Total Turnover (*) 106, (*) Incluiding the sales of property assets. A N N U A L R E P O R T VALLEHERMOSO GROUP / MANAGEMENT REPORT INVESTMENT AND FINANCING INVESTMENT AND FINANCING The year 2000 saw the implementation of the Vallehermoso Group s most extensive investment plan in the last decade. Consequently, large movements of funds occurred: more than 65,000 million pesetas (390.7 million euros) were used in investments in fixed assets, inventories, the reduction of long-term trade debt, dividends and working capital. 33% of the funds used were self-financed and 67% were financed with new interest-bearing debt. The Vallehermoso Group s investment in fixed assets in 2000 amounted to 23,630 million pesetas (142 million euros), of which rental assets accounted for 21,370 million (128.4 million) and 2,260 million pesetas (13.6 million euros) went into financial and other investments. The latter of which included most notably the purchase of 1,389 million pesetas (8.3 million euros) of own shares to cover the stock options programme approved by the Shareholders Meeting. Investment in net inventories reached 32,205 million pesetas (193.6 million euros); noteworthy were the 31,339 million pesetas (188.4 million euros) invested in the intensive land purchasing programme and the more than 48,600 million pesetas (292.1 million euros) invested in new construction. Cash-Flow after tax reached 14,936 million pesetas (89.8 million euros) which was used to finance 63% of the investment in fixed assets. Considering the self-financing from fixed asset disposals, financing with funds generated by the Group represented 92% of the total investment in fixed assets. The Vallehermoso Group s shareholders equity at December 31, 1999 totalled 108,338 million pesetas (651.1 million euros), following the distribution of 4,254 million pesetas (25.6 million euros) of dividend in the year. This represents an increase of 7,008 million pesetas (42.1 million euros) compared to December 31, The Group s financial debt increased by 43,319 million pesetas (260.4 million euros) to 119,493 million pesetas (718.2 million euros). Long-term debt made up 68% of this total. Although interest-bearing debt and, consequently, interest expenses have increased strongly, gross operating cash-flow covers interest more than 4.7 times. The following table shows details of the Group s debt structure, classified by interest rate risk and by average cost: (IN MILLIONS) PESETAS % PESETAS EUROS % Fixed rate loans 22, , Floating rate loans 41, , Capped floating rate loans 12, , , , Average annual cost (%) The key new developments in the year were the following: Issues of notes for a total equivalent to 61,314 million pesetas (368.5 million euros) under an issue programme registered with the National Securities Market Commission. These notes are traded in the secondary market of the

21 Spanish Securities Traders Association (A.I.A.F.). The average amount of debt in the programme in 2000 was 19,856 million pesetas (119.3 million euros) and the total at the end of the year stood at 23,876 million (143.5 million euros). Arrangement of interest rate hedging operations in the financial derivatives markets covering a total of 22,000 million pesetas (132.2 million euros) at December 31, 2000, which was equal to 27.3% of the borrowings drawn at variable interest and 18.4% of the total. Arrangement of new corporate credit lines and renewal of existing lines with banks for a total of 44,550 million pesetas (267.8 million euros). Available credit lines at December 31, 2000 totalled 70,900 million pesetas (426.1 million euros). In order to enhance the flexibility of available funds and the capacity to adapt to market conditions while reducing costs, working capital has continued to be financed mainly through instruments other than transferable mortgage loans, which have been reserved for the period immediately prior to the delivery of residential products. This was intended to spare unnecessary costs while offering financing to customers on the best market terms. At the end of the year, the balance of mortgage loans transferable to buyers came to 3,996 million pesetas (24.0 million euros), 125% more than at the end of In recent years, the Vallehermoso Group has considerably strengthened its economic structure while bringing it into greater balance through the diversification of its assets both for sale and for rent. At the same time it has substantially improved its financial structure to reduce the average cost of capital while providing appropriate cover for the financial risk. Due to the growing pace of profit generation, the impact of higher financial debt has been easily absorbed, as shown by the evolution of the following two indicators: Net Financial expense /Direct profit on operations % EBITDA / Interest cost Times The evolution of the Group s financial structure in recent years has been as follows: FINANCIAL STRUCTURE (%) Equity Long-term debt Permanent funds Short-term debt Total liabilities WORKING CAPITAL Millions of pesetas 78,920 75,002 67,148 58,946 62,040 67,486 52,778 Millions of euros % of current assets A N N U A L R E P O R T VALLEHERMOSO GROUP / MANAGEMENT REPORT INVESTMENT AND FINANCING The breakdown and variations in financial debt were as follows: (IN MILLIONS) CHANGE 00/99 PESETAS EUROS PESETAS PESETAS PESETAS PESETAS PESETAS PESETAS PESETAS % Credit facilities and loans 45, ,387 14,256 26,509 21,757 25,529 21,435 25, Mortgage loans 22, ,352 12,945 11,831 11,213 10,766 9,979 9, Debentures 22, ,983 13,000 5,000 5, Notes 23, ,307 8,300 3,800 3,300 2,300 1,650 6, Debt to Group companies , (738) (93.5) Mortgage loans transferable to buyers 3, ,775 2,608 2,367 5,446 5,603 3,411 2, Bills discounted Total 119, ,174 52,960 49,896 47,280 44,767 36,954 43,

22 ACQUISITION OF PRIMA INMOBILIARIA In June, Vallehermoso and Prima Inmobiliaria reached a friendly agreement to merge their rental businesses. The agreed operation was carried out in three phases: Takeover by Vallehermoso, S.A. of 49.17% of Prima Inmobiliaria. Merger between Vallehermoso Renta and Prima Inmobiliaria for which purpose it was necessary for Vallehermoso to transfer its rental business assets into a subsidiary company. With this merger, Vallehermoso obtained 65% of the capital stock of the resulting company. Takeover by Vallehermoso, S.A. of the remaining 17.81% of the merged company. Vallehermoso, S.A presented the prospectus of the first takeover to the National Securities Market Commission for it to be checked and registered. Following the above-mentioned agreement, on July 13, 2000 the Boards of Directors of Vallehermoso, S.A. and Prima Inmobiliaria approved an agreement to simplify and accelerate the integration of their rental businesses. This agreement meant upholding all the strategic, economic and financial terms and objectives of the operation presented in June, although the structure of the operation was changed to the following: Merger of Vallehermoso Renta with Prima Inmobiliaria with the same valuation parameters and exchange ratio as in the previous structure and with the same premise that Vallehermoso previously create the rental subsidiary. Takeover by Vallehermoso, S.A. of 35% of the company resulting from the merger of Prima Inmobiliaria with the Vallehermoso property rental subsidiary. Vallehermoso will offer (in 2001) a mixed consideration to Prima Inmobiliaria s shareholders: Cash payment of 7 euros for every Prima Inmobiliaria share. Delivery of shares of Vallehermoso, S.A. at a share exchange ratio of 13 shares of Vallehermoso, S.A. for 20 shares of Prima Inmobiliaria. In short, valuing the new shares of Vallehermoso, S.A. to be exchanged at the market price on June 9 when the market was informed of the intention to reach an agreement, the operation amounts to 77,000 million pesetas (462.8 million euros), including a cash payment of 47,000 million pesetas (282.5 million euros). The main objectives of the operation described above are as follows: To create shareholder value through the strengthening of Vallehermoso s competitive position and leadership of the domestic market, taking advantage of operating and tax synergies and the increase in the Group s size. To consolidate the Vallehermoso Group s strategic focus as a mixed and balanced property group, achieving greater equilibrium between the development and rental businesses with more recurrent and stable results. A N N U A L R E P O R T VALLEHERMOSO GROUP / MANAGEMENT REPORT ACQUISITION OF PRIMA INMOBILIARIA To grow significantly in the rental business in Spain. On July 28 the Extraordinary Shareholders Meeting of Vallehermoso approved the new organisational structure comprising three companies and authorised the merger by absorption of Vallehermoso s rental subsidiary by Prima Inmobiliaria. On the same date the Board of Directors of Vallehermoso, S.A. exercised this authorisation and resolved to contribute the property rental business to the company Vallehermoso Renta, S.A.U. which is 100%- owned by Vallehermoso, S.A. The property rental line of business was contributed at the end of August. The Development and Services Businesses were contributed at the end of October. In November the respective Shareholders Meetings of Prima Inmobiliaria and Vallehermoso approved the merger project of both companies. The merger will have economic effects from January 1, The merger deed was signed on January 24, The Extraordinary Shareholders Meeting of Vallehermoso, S.A. held on November 30, resolved to increase capital stock by a nominal amount of up to 26.3 million euros through the issue of up to a maximum 26.3 million new shares in order to meet part of the consideration that Vallehermoso will offer Prima Inmobiliaria s shareholders in the takeover bid. The above-mentioned Extraordinary Shareholders Meeting appointed Mr. John Gómez Hall as a director of Vallehermoso, S.A. This appointment is effective on the date of registration at the Mercantile Register of the merger deed of Vallehermoso Renta and Prima Inmobiliaria. Once the merger deed between Vallehermoso Renta and Prima Inmobiliaria was officially registered, Vallehermoso, S.A. began the process of taking over the company resulting from the merger, which is called Testa, S.A., and presented the corresponding prospectus to the National Securities Market Commission for it to be checked and registered. In order to finance the takeover bid for Testa and other corporate requirements on December 28 Vallehermoso, S.A. signed a seven-year syndicated loan amounting to 340 million euros with 22 financial entities. The funds of the syndicated loan can be drawn on, effective from the beginning of January 2001.

23 PROPERTY MARKET TRENDS AND OUTLOOK In 2000, the residential property market surpassed projections, especially as regards selling prices and the intensity of demand. Strong demand exceeded the robust although gradually declining pace of growth in residential construction. The result of this imbalance was the undesired disproportionate growth of housing prices which according to most analysts and operators is between 12% and 13% in year-on-year terms. In the office sector intense demand and the lack of space to let triggered strong rises in selling prices and rents at the same time as vacancy rates fell to between 1.5% and 2.5% in the major markets. As for supply, according to the advance figures of the main economic indicators the upward trend in residential construction will gradually slow down. This falling trend in production does not represent market weakness or exhaustion but it obeys the logical business response to foreseeably lower demand in view of the considerable absorption of prior years pent-up demand and the changes in prices and financing conditions for buyers. Nevertheless, according to projections, the construction of new residential units will increase for 2000 as a whole by between 8% and 9% in real terms. Although there is a downturn in the pace of activity, the latter continues to be strong and consistent. It is worth pointing out that the basis for comparison is 1999, the year of peak activity and growth in the last decade, which produced strong growth in the number of housing starts (+20% over 1998) and in the number of certified housing units (+40% in the first half of the year). Although the market analysts most popular forecasts of sound demand were exceeded, the majority continue to project stable structural demand of between 300,000 and 350,000 housing units per year. Given that this level of activity is suitable for the production process to occur normally and that the current scenario of economic stability and sustained growth will seemingly last for the next few years, equilibrium may be reached in the residential market once pent-up demand which was not satisfied in the nineties and became solvent in recent years is absorbed. The entry into the market of the considerable number of new housing units which began in 1999 and the further contraction of demand triggered by higher interest rates and housing prices will contribute to achieving this desired point of equilibrium. Accordingly, the strong impact that both factors have had on the level of net effort in terms of the percentage of household income which is earmarked for the purchase of a home is particularly relevant: at the end of 2000 it was more than 30%, two percentage points higher than a year ago. It is to be hoped that, when an equilibrium returns to the market, the strength of demand will return to normal. Such relative weakness will help to reduce inflationary tensions in all the elements which contribute to these tensions. Final housing prices and materials prices, as well as the level of excess saturation of installed production capacity will tend to fall and, as a result, will help to consolidate expectations of a more balanced market performance. The effect of this rational and steady correction of market conditions will foreseeably make land owners see a noticeable change in the real estate market which will advise them to have more conservative expectations of A N N U A L R E P O R T VALLEHERMOSO GROUP / MANAGEMENT REPORT PROPERTY MARKET TRENDS AND OUTLOOK the growth in the value of their assets which should result in lower land prices and boost the number of transactions. A strong performance is expected from non-residential construction in the next few months and the sound pace of growth in investment in this type of construction is expected to be slightly higher than in the residential sector. Robust business growth, the necessary competitive adaptation of logistics installations through modernisation and the provision of medium-sized cities with suitable commercial premises will generate sufficient demand for the sustained development of the non-residential construction business for the next few years. For all the reasons given above, in 2001 the residential business is expected to progressively slow down as a result of the required and desired normalisation of the conditions of supply and demand and non-residential construction is expected to remain substantially the same. Real growth is projected at between 5.5% and 6.5% in investment in residential construction and between 8% and 9% in non-residential construction.

24 80 CONSOLIDATED ANNUAL ACCOUNTS 82 BALANCE SHEETS 84 PROFIT AND LOSS ACCOUNTS 86 NOTES TO THE ANNUAL ACCOUNTS 109 APPENDICES 123 EXTERNAL AUDITOR S REPORT

25 ASSETS Fixed assets Preliminary expenses Intangible fixed assets (Note 5) 6,211 6,199 Tangible fixed assets (Note 6) Land 3,559 6,049 Buildings for rent 103,910 84,582 Buildings for own use Other items 1, Construction in progress 14,773 11,118 Accumulated depreciation (9,623) (9,350) Provision for depreciation (400) (400) 114,098 93,742 Trade investments (Note 7) 5,075 4,825 Long term accounts receivable (Note 10) 4,376 2,260 Own shares of the controlling company (Note 8) 1,389 - Total fixed assets 131, ,040 Deferred expenses (Note 4(g)) 1,139 1,537 Current assets Inventories (Note 9) VALLEHERMOSO GROUP CONSOLIDATED BALANCE SHEETS at December 31, 2000 and 1999 (Free translation from the original in Spanish) (Million Pesetas) Buildings 6,298 3,488 Projects in progress 37,380 16,871 Buildings sites 71,833 69,907 Site development 1,812 3,578 Advance payments to suppliers 6,885 1,125 Provision for depreciation (273) (290) 123,935 94,679 Accounts receivable (Note 10) 54,177 31,897 Short term financial investments (Note 11) Cash and banks Prepaid expenses 9 1 Total current assets 178, ,378 Total assets 311, ,955 The accompanying notes form an integral part of the consolidated annual accounts. A N N U A L R E P O R T VALLEHERMOSO GROUP / CONSOLIDATED ANNUAL ACCOUNTS CONSOLIDATED BALANCE SHEETS LIABILITIES Shareholders equity (Note 12) Share capital 21,474 21,474 Share premium 30,345 30,345 Revaluation reserve 2,147 2,147 Other reserves of parent company 45,464 40,757 Reserves in companies consolidated by full and proportional consolidation 1,439 1,273 Reserves in companies consolidated by equity method (1,611) (1,647) Currency translation differences of companies consolidated by equity method (11) 26 Foreign exchanges differences with consolidated companies Consolidated profit 13,363 8,434 Profit attributable to outside shareholders (Note 13) (27) (84) Interim dividend for the year (4,254) (1,405) Total shareholders equity 108, ,330 Outside shareholders (Note 13) Negative consolidation differences (Note 14) Deferred income (Note 4) Provisions for risks and expenses (Note 15) 3,124 2,850 Long term accounts payable Debenture issues and other negotiable securities (Note 16) 17,983 22,983 Credits institutions (Note 16) 53,086 23,326 Others accounts payable (Notes 16 and 17) 27,412 26,544 Group and associated companies Uncalled payments pending on shares - 24 Total long term accounts payable 98,532 73,666 Short term accounts payable VALLEHERMOSO GROUP CONSOLIDATED BALANCE SHEETS at December 31, 2000 and 1999 (Free translation from the original in Spanish) (Million Pesetas) Debenture issues and other negotiable securities (Note 16) 29,437 17,808 Credit institutions (Note 16) 9,656 1,984 Trade accounts payable (Note 18) 44,314 27,510 Other non-trade debts (Note 19) 16,476 10,047 Accrued expenses 92 6 Total short term accounts payable 99,975 57,355 Total liabilities 311, ,955 The accompanying notes form an integral part of the consolidated annual accounts.

26 VALLEHERMOSO GROUP CONSOLIDATED PROFIT AND LOSS ACCOUNTS for the years ended December 31, 2000 and 1999 (Free translation from the original in Spanish) (Million Pesetas) EXPENSES Supplies (Note 9) 71,943 54,249 Transfers between inventories and fixed assets (Notes 6 and 9) (4,182) (7,630) Personnel costs (Note 21) 4,595 3,472 Provisions for depreciation and amortisation of fixed assets 1,520 1,372 Variation in trade provisions (Notes 9 and 10) Variation in provisions for risk and expenses Other operating expenses 5,548 3,942 Total operating expenses 79,754 56,198 Operating profit 20,806 13,561 Financial expenses Financial and other expenses 5,750 3,623 Variation in provisions for trade investments 15 - Total financial expenses 5,765 3,623 Amortisation of goodwill Profit from normal operations 16,261 10,738 Variations in provisions for intangible and tangible fixed assets and controlling shareholdings 576 (264) Loss on intangible and tangible fixed asset and investment portfolio Extraordinary expenses (Note 26) 1,205 1,083 Expenses and losses of prior years Total extraordinary losses and expenses 2, Extraordinary profit 4,010 2,295 Profit before taxes 20,271 13,033 Corporate income tax (Note 24) (6,908) (4,599) Profit for year 13,363 8,434 Profit attributed to outside shareholders (Note 13) Profit for year attributable to parent company (Note 12 (g)) 13,336 8,350 The accompanying notes form an integral part of the consolidated annual accounts. A N N U A L R E P O R T VALLEHERMOSO GROUP / CONSOLIDATED ANNUAL ACCOUNTS CONSOLIDATED PROFIT AND LOSS ACCOUNTS VALLEHERMOSO GROUP CONSOLIDATED PROFIT AND LOSS ACCOUNTS for the years ended December 31, 2000 and 1999 (Free translation from the original in Spanish) (Million Pesetas) INCOME Net turnover (Note 20) 79,218 55,065 Increase in inventories (Note 9) 21,174 14,106 Work carried out by the company on its own tangible assets (Notes 6 and 9) Other operating income Total operating income 100,560 69,759 Financial income Dividends receivable 4 1 Other investment income Interest and other expenses included in production (Notes 6 and 9) 1, Other interest income Total financial income 1, Financial loss 4,562 2,626 Dividends from companies consolidated using the equity method (Note 7) 17 9 Extraordinary profit and income Profit on disposal of fixed assets (Note 23) 3,857 2,532 Profit on disposal of shareholdings in Group companies 1, Extraordinary income Income and profit from prior years Total extraordinary profit and income 6,024 3,269 The accompanying notes form an integral part of the consolidated annual accounts.

27 VALLEHERMOSO GROUP NOTES TO THE ANNUAL ACCOUNT for the years ended December 31, 2000 and 1999 (Free translation from the original in Spanish) (Million Pesetas) 11 OPERATIONS Vallehermoso, S.A. (the Company or the parent company) was formed on July 5, 1921 for an indefinite period of time. As a result of the agreement reached by the General Shareholders Meeting on December 22, 1988, the Company merged with Corporación Inmobiliaria Hispamer, S.A. and Inmobiliaria para el Fomento de Arrendamientos, S.A. (INMOBANIF). The merged companies revalued their assets by 3,539 million pesetas. Its corporate object and principal activities consist of all types of activities involving the acquisition and construction of urban properties for their subsequent rental or resale. A breakdown of sales is provided in Note 20. On September 28, 1991 the General Shareholders Meeting approved the merger by absorption of Vallehermoso, S.A. with the directly or indirectly wholly-owned companies, Procyt, S.A. and Aljamar, S.A., with the resulting transfer of all the shareholder s equity of the absorbed companies. Details of the subsidiary companies which form the Vallehermoso Group (hereafter the Group), their activities and addresses, as well as the companies which are not consolidated due to their insignificance are included in Appendix II to these Notes, of which it forms an integral part. The principal activity of the Group is in the real estate sector. During this year the Vallehermoso Group has gone through a restructuring process, consisting of setting up subsidiaries for the property leasing, property development and service businesses. This has involved carrying out the following operations during the year: 1. On 18 August 2000, Vallehermoso, S.A. subscribed to an increase in the capital of Vallehermoso Renta, S.A. (formerly Inibérica, S.A.) for a total, including share premium, of Ptas. 63,619 million, in the form of a non-cash contribution of the property leasing business activity. 2. On 31 October 2000, Vallehermoso, S.A. subscribed to an increase in the capital of Vallehermoso División Promoción, S.A. (formerly Hispaland, S.A.) for a total, including share premium, of Pts. 34,940 million, in the form of a noncash contribution of the property development business activity. 3. On 31 October 2000, Vallehermoso. S.A. set up the company Valoriza, S.L. and acquired 100% of its capital for a total amount of Ptas. 483 million, in the form of a non-cash contribution of the service business activity. The Extraordinary General Meeting of Shareholders, held on 30 November, decided to increase the capital of Vallehermoso, S.A. in order to be used as consideration in the Take-over Bid for the shares of Prima Inmobiliaria, S.A., subject to the suspensive condition that the deed of the merger of Vallehermoso Renta, S.A. and Prima Inmobiliaria, S.A. is entered in the Mercantile Register. Auditors other than the auditors of Vallehermoso, S.A, have audited the following companies that are consolidated as at 31 December 2000.: Promociones Residenciales Sofetral, S.A. (Arthur Andersen) A N N U A L R E P O R T VALLEHERMOSO GROUP / CONSOLIDATED ANNUAL ACCOUNTS NOTES TO THE ANNUAL ACCOUNT 2 Lusivial, S.A. (Arthur Andersen) The percentage of Vallehermoso, S.A.'s holdings in these companies as at 31 December 2000 are given in Appendix II to these Notes. The assets of these invest companies represent, taken all together, 0.62% of its net profit and have no impact on the consolidated result. All the dependent companies included in the consolidated accounts end their financial years on 31 December every year. 2 BASES OF PRESENTATION AND CONSOLIDATION OF THE ANNUAL ACCOUNTS In compliance with current legislation, the Directors of the Company have drawn up the Group s consolidated annual accounts in accordance with the General Accounting Plan, the regulations for the adaptation of this for real estate companies and the rules for consolidation and they have been prepared based on the accounting records of the companies of which the Group is comprised. It is expected that the accounts will be approved at the General Shareholders Meeting without any significant changes being made. The consolidated annual accounts for 1999 were approved at the Annual General Meeting held on April 24, The amounts contained in the documents comprising these consolidated annual accounts (consolidated balance sheet, profit and loss account and Notes thereto) are expressed in million pesetas. The consolidated annual accounts have been prepared following the principles and format of presentation contained in the regulations for the preparation of consolidated annual accounts established by Royal Decree 1815 of December 20, In accordance with these regulations, the date considered for the first consolidation in order to determine the goodwill and negative consolidation differences is January 1, The consolidation process was carried out according to the following principles: Group companies: consolidated using the full consolidation method. Multigroup companies, joint ventures and consortiums : consolidated using the proportional consolidation method. Associated companies: consolidated using the equity method. The annual accounts of consolidated companies expressed in foreign currency have been translated to pesetas using the year end exchange rate method, which consists of using the rate of exchange at the end of each year for assets and liabilities and the average exchange rate for the year for income and expense accounts. All significant accounts and transactions between consolidated companies have been eliminated during the consolidation process and the interest held by third parties in the Group s net consolidated equity and results are included under the heading Outside shareholders in the consolidated balance sheets and Profit (Loss) attributed to outside shareholders in the consolidated profit and loss accounts.

28 33 DISTRIBUTION OF PROFIT The proposed distribution of parent company profits for the year ended December 31, 2000 to be submitted by the Directors for approval at the General Shareholders Meeting is as follows: AVAILABLE FOR DISTRIBUTION Profit for the year 8,690 8,690 DISTRIBUTION Dividends 4,254 Voluntary reserve 4,436 The details of the distribution of the profit of the parent company for the year ended December 31, 1999 made in 2000, are presented, together with movements in shareholders' equity, in Appendix III to Note 12. On June 21, 2000, the Board of Directors agreed to pay an interim dividend totalling 5% of the nominal value of the shares. This interim dividend amounted to a total of 1,065 million pesetas. The following table demonstrates the existence of sufficient profit, which was considered by the Board of Directors prior to deciding on the payment of the interim dividend in 2000: AMOUNT Net income, as of May 31, ,142 Interim dividend (5% of nominal value of shares) 1,065 Estimated of treasury situation for the period between May 31, 2000 and may 31, Treasury balance at May 31, ,480 - Estimated collections during he period 162,320 - Estimated payments during the period (including interim dividend) 157,602 Treasury balance at May 31, ,198 The liquidity available at the date on which the dividend was declared was greater than the gross amount of the dividend. A liquidity study was carried out covering the following twelve month period, and showed that net liquidity was sufficient to pay such dividend. On 18 December 2000, the Board of Directors decided to pay shareholders an interim dividend equal to 15% of the par value of the shares, on account of the dividend decided by the General Meeting. The total amount distributed in this interim dividend was Ptas. 3,189 million. A N N U A L R E P O R T ,690 89VALLEHERMOSO GROUP / CONSOLIDATED ANNUAL ACCOUNTS NOTES TO THE ANNUAL ACCOUNT Set out below is a table that shows that there are sufficient profits, that was taken into account by the Board of Directors when it decided to pay a second interim dividend on account of the dividend for the year 2000: AMOUNT Net book profit as at 30 November ,706 Planned interim payment equal to 15% of the par value of the shares 3,189 Forecast cash and bank reserves for the period between 30 November 2000 and 30 November Balance of cash and bank accounts as at 30 November ,464 - Forecast collections in the period under consideration 153,573 - Payments planned in the period under consideration (Including payment on account) 156,340 Balance of cash and bank accounts as at 30 November ,697 Liquid reserves existing as at the date the interim dividend was declared exceed the gross amount thereof. There is a study of liquid reserves covering a twelve-month period following said date, which shows that there is sufficient liquidity to pay out said dividend. 44 PRINCIPAL ACCOUNTING POLICIES AND VALUATION PRINCIPLES The consolidated annual accounts have been prepared in accordance with the accounting principles and valuation and classification regulations contained in current mercantile legislation and the General Accounting Plan adapted to the property sector. The most significant accounting principles used in the preparation of the annual accounts are as follows: a) Formation expenses Formation expenses, which include basically the costs incurred for share capital increases and the formation of certain Group companies, are stated at cost, net of the corresponding accumulated amortisation which is calculated using the straight-line method over a period of five years. b) Intangible fixed assets Intangible fixed assets are stated at acquisition cost, net of the corresponding accumulated amortisation. This heading corresponds principally to administrative concession rights, which are amortised using the straight-line method over the life of the concession. c) Tangible fixed assets Tangible fixed assets are valued at acquisition or construction cost, including the corresponding cost of the sites and other direct costs, except for certain buildings constructed or acquired by the Group prior to 1983 for subsequent rental (which were revalued in accordance with legislation then applicable), net of the corresponding accumulated depreciation. In addition, due to the merger in 1988, as described in Note 1 above, the merged companies revalued their assets by 3,539 million pesetas (see Note 12 (c)). Construction in progress includes: charges incurred with respect to permanent installations and buildings, construction taxes, and salaries for management and construction personnel. In addition to the value of the buildings and other construction, this heading includes the value of the building sites.

29 Financial expenses directly related to the construction of tangible fixed assets are included in the construction cost until the project is completed, provided that including them does not result in the asset s current market or replacement value being exceeded. These expenses are calculated according to the corresponding financing requirements. Depreciation of tangible fixed assets is calculated using the straight-line method based on cost or revalued cost, using the following estimated useful lives: USEFUL LIFE YEARS Buildings for rent and own use 50 a 75 Other assets: Plant and machinery 10 Other installations, tools and furniture 10 Transport equipment 5 Data-processing equipment 4 The cost of improving properties, when they represent an increase in the profitability of the buildings rented, are added annually to the value of the buildings. Maintenance and repair costs relating to tangible fixed assets, which do not improve their utilisation or increase their useful lives, are charged to the consolidated profit and loss account when incurred. The Group makes the necessary provisions for the depreciation of its tangible fixed assets when there are doubts as to the recoverability of their book value. d) Trade investments Fixed interest and variable income investments, not consolidated due to either their insignificant influence in the consolidated annual accounts, or the fact that they relate shareholdings of less than 20%, are valued at acquisition cost. The costs inherent to the purchase and the cost of subscription are included, if applicable, in the acquisition cost. Shareholdings in companies consolidated using the equity method are valued at the percentage which the Group holds in the underlying equity of each company. The necessary provisions are made for the deterioration of non-consolidated investments when circumstances clearly indicate the need to do so. In the case of equity interests, provision is made for the excess of acquisition cost over the underlying net equity value. This excess is corrected by the underlying surpluses acquired at the time of purchase, which still exist at the year end. e) Own shares Own shares held, as well as the shares of the Controlling Company acquired by the Company, are stated on the accompanying balance sheet at the lower of cost or market price. The appropriate reserve is set up as required under current law. f) Goodwill on consolidation and negative consolidation differences Goodwill on consolidation, included in the assets of the consolidated annual accounts, represents the difference between the acquisition price of the shareholdings in consolidated companies and their underlying net equity value at January 1, 1991, the date of the first consolidation, or on the effective date of purchase for subsequent acquisitions. The difference has been assigned to inventories when specifically identified and, if not, it is considered to be Goodwill on consolidation, which is amortised over a period of one to five years based on the estimate of the contribution or otherwise to the generation of future income. A N N U A L R E P O R T VALLEHERMOSO GROUP / CONSOLIDATED ANNUAL ACCOUNTS NOTES TO THE ANNUAL ACCOUNT Negative consolidation differences, included under liabilities in the consolidation annual accounts, represent the difference between the acquisition price of the shareholdings in consolidated companies and their underlying net equity value at January 1, 1991, the date of the first consolidation or the effective purchase date for subsequent acquisitions. With the exception of those differences corresponding to realised surpluses, which are recorded in shareholders' equity under the heading Other reserves of parent company. g) Deferred expenses These mainly include expenses incurred on the issue of convertible debentures, which are charged to profit and loss using the straight-line method over the duration of the issue. For convertible debentures, the expenses pending amortisation at the time of conversion are transferred to the capital increase expense account, included under the heading Formation expenses. h) Inventories Inventories, which consist mainly of sites, projects in progress and completed buildings, intended for subsequent sale, are valued at their acquisition or construction cost, as follows: Buildings: valued according to the cost system described below under the heading Projects in progress or at cost for buildings already completed, including the costs directly related to their purchase. Projects in progress : include all costs incurred in the promotion of property, which has not been completed. These costs include direct construction costs which have been approved by the technicians responsible for managing the project, the expenses corresponding to the project, as well as financial expenses incurred during the period of construction. Once construction has started, the value of the building sites is included in the value of the buildings and other construction. Building sites and site development: valued at acquisition cost, including the costs directly related to their purchase. Development, design and planning costs are added to the value of the land and undeveloped sites up to the time the project is completed. The Group makes necessary provisions for the depreciation of inventories when recorded costs exceed their market value. i) Accounts receivable and trade notes receivable In the accompanying balance sheets, trade debtor accounts and trade notes receivable include unmatured discounted notes, the corresponding credit for which is included under debts with credit institutions (see Note 16). Interest included in trade notes receivable is recorded under Deferred income and is taken to profit and loss using financial criteria. Expenses relating to discounted notes are included in the consolidated profit and loss account when incurred. Provisions for bad debts are made for balances over a certain age, or for those for which there are reasonable doubts as to their recovery. j) Provisions for the termination of projects The provision for the termination of projects includes costs not yet incurred for closed projects for which sales have been recorded. k) Mortgage loans to be surrogated Mortgage loans to be surrogated are included in the accompanying balance sheets under the heading Credit institutions at the amounts of the credit used.

30 l) Loans and financial debts Credit accounts are shown at the amounts drawn down. m) Transactions in foreign currency Transactions in foreign currency are recorded at the equivalent amount in pesetas, translated at the rates of exchange in force at the time of the operation. Gains or losses on exchange resulting from the cancellation of debts in foreign currency are taken to profit and loss account when they arise. Balances receivable and payable denominated in foreign currency at the year end are stated in pesetas at the exchange rates prevailing on 31 December. Unrealised net losses on exchange are recognised and unrealised net gains are deferred until they fall due. n) Short/long term In the accompanying consolidated balance sheets, assets and liabilities due within less than twelve months are classified as short term and those due after more than twelve months are classified as long term. o) Severance payments Severance payments, when they arise, are charged to expenses when the decision is made regarding the termination of employment. p) Corporate income tax Due to the fact that the Group has not requested to be assessed on a consolidated basis for corporate income tax purposes, the charge for taxes has been calculated based on the Company s total income before taxes. Balances not considered for consolidation purposes generated positive effects resulting on prepaid taxes in case of internal profits or deferred taxes in case of internal losses. Hence, prepaid tax and deferred tax accounts have been calculated as the total of corporate income tax for each consolidated Group company, plus the positive effect of the consolidation adjustments for eliminating internal profit/loss. The charge for Group corporate income tax purposes has been calculated as the aggregate of corporate income tax charges for each fully consolidated company, and the percentage of charge corresponding to the partially consolidated companies. q) Recognition of sales Sales and their corresponding costs are recognised when the buildings are substantially completed. Advances from customers are recorded under liabilities in the consolidated balance sheets. A N N U A L R E P O R T VALLEHERMOSO GROUP / CONSOLIDATED ANNUAL ACCOUNTS NOTES TO THE ANNUAL ACCOUNT 55 INTANGIBLE FIXED ASSETS The following shows the movement during 2000 and 1999 on intangible fixed assets: BALANCE AT BALANCE AT BALANCE AT ADDITION DISPOSAL TRANSFERS ADDITION DISPOSAL TRANSFERS Computer applications (44) Rights to assets acquired under finance leases 14 - (5) (9) - - Administrative concessions 4, (222) 2,683 6,807 1,886 (3,142) 617 6,168 Industrial property , (227) 2,683 6,917 2,062 (3,195) 617 6,401 Provision for depreciation (244) (229) Accumulated amortisation (358) (126) 8 (13) (489) (119) (190) 3,743 (10) (204) 2,670 6,199 1,943 (2,548) 617 6,211 As at 31 December 2000, administrative concessions recorded the rights to operate a car park in General Yagüe in Madrid for a period of 50 years, which expires in It also records the right to operate a car par in the Audiorama Shopping Centre in Zaragoza, for a period of 50 years, for a Joint Venture in which Vallehermoso has a 50% holding. It also records an administrative concession in Bentaberri with the Regional Government of the Basque Country for a 75-year period for operating buildings under rent, which expires in During 2000, the amount of the costs incurred in the development called "Campo de tiro de Leganés", corresponding to a concession for a 20-year period that expires in the year 2018, has been transferred from tangible fixed assets to intangible assets. The net amount of said transfer amounted to Pts. 617 million. The movements of the year also record additions for expenses incurred in a hotel that is under an administrative concession with the Barcelona Port Authority, which expires on 15 December 2022, when it will be automatically extended until During the year sales have been made that have generated a profit of Pts. 7 million. 6 6 TANGIBLE FIXED ASSETS An analysis and the movements of this caption of the balance sheet during 2000 and 1000 is provided in Appendix I, which is an integral part of this Note. During the year, transfers totalling Pts. 4,182 million (Pts. 7,630 million in 1999) have been made from the inventory account to fixed assets. Furthermore, during 1999, the Group set up a provision for fixed-asset depreciation of Pts. 400 million for the overstatement in the accounts of the value of an office building compared to its market value, and reversed a provision for Pts. 664 million. During the year 2000 there have been no movements in fixed-asset provisions. The Parent Company, making use of the various tax provisions for restating assets up to 1983, increased the cost and accumulated depreciation of its tangible fixed assets by a net amount of Pts. 7,303 million. Furthermore, as a result of the merger carried out in 1988 (see Note 1), the Company and the absorbed companies revalued their tangible fixed assets by a total amount of Pts. 3,539 million, approximately (Note 12 (c)).