GFDR 2015 Long-term Finance. Chapter 4: Bank and Non-bank Financial Institutions as Providers of Long-term Finance

|

|

|

- Emily Todd

- 6 years ago

- Views:

Transcription

1 GFDR 2015 Long-term Finance Chapter 4: Bank and Non-bank Financial Institutions as Providers of Long-term Finance GFDR SEMINAR SERIES FEBRUARY 19, 2015

2 Objectives Analyze the supply side of funds, demand side of long-term debt In particular, the investment strategies and the portfolio maturity of bank and nonbank financial intermediaries Important in a world of intermediated savings Informative comparisons across investors and countries Explore the role of country characteristics, market forces, and regulations in shaping the maturity structure of financial intermediaries Highlight role of incentives for intermediaries Discuss the role of the government in promoting long-term finance

3 Types of intermediaries Banks Non-banks Domestic non-bank institutional investors: Case of Chile International mutual funds Sovereign Wealth Funds (SWFs) Private Equity (PE)

4 Types of intermediaries Banks Non-banks Domestic non-bank institutional investors: Case of Chile International mutual funds Sovereign Wealth Funds (SWFs) Private Equity (PE)

5 Banks Banks are the main source of finance for firms and households across countries Important to understand the degree to which they lend long term and the drivers The global financial crisis has raised concerns about the potential impact of banks deleveraging on the maturity composition of their loans Changes in Basel III have the potential to affect the composition of bank loans and reinforce the need to monitor and understand the degree of long-term loans Present evidence on loan maturity for banks in different countries Explore the role of bank characteristics and regulations in shaping banks loan maturity structure

6 Banks

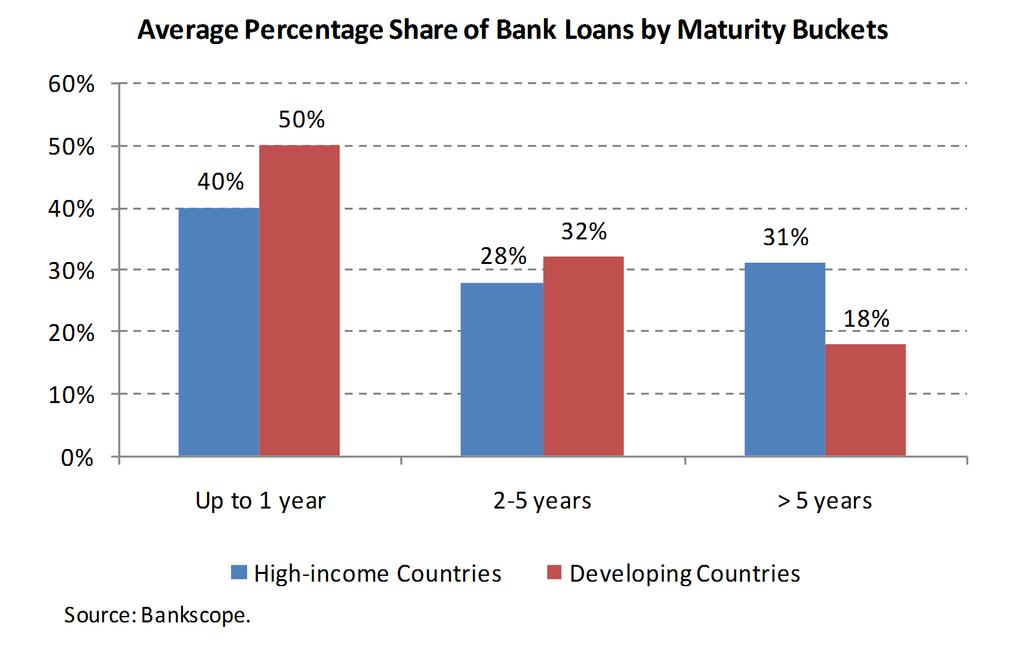

7 Banks Share of Bank Loans across Different Maturity Buckets (percent) Maturity Bucket Country Classification Pre-crisis Period Crisis Period Post-crisis Period Mean Median Mean Median Mean Median Up to years > 5 years High Income Developing High Income Developing High Income Developing Source: Bankscope.

8 Banks

9 Banks Substantial evidence that strong macroeconomic conditions and institutions help lengthen bank maturity. Demirguc-Kunt and Maksimovic (1999), Kpodar and Gbenyo (2010), Tasić and Valev (2008), Tasić and Valev (2010): inflation is negatively related Qian and Strahan (2007), Bae and Goyal (2009): country risk associated with shorter loan maturities Fan et al. (2012): with weaker laws, firms use more short-term bank debt Financial sector development, financial contract enforcement, collateral framework, the credit information environment important for bank loan maturity Tasić and Valev (2008, 2010), Bae and Goyal (2009), De Haas et al. (2010), Fan et al. (2012), Martinez Peria and Singh (2014), Love et al. (2015)

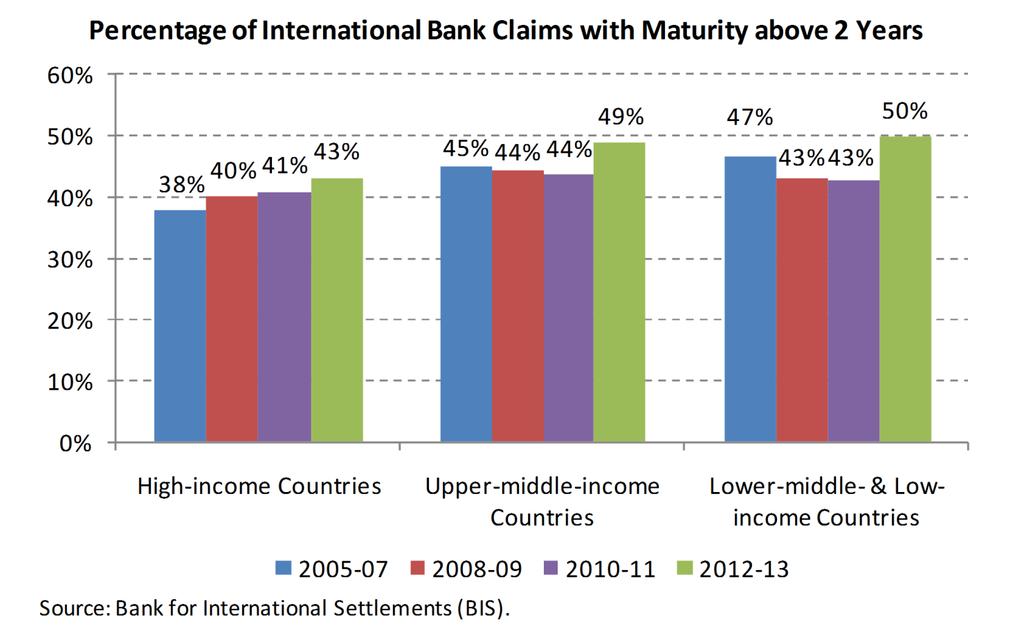

10 Banks More recent evidence is based on data for 3,400 banks operating in 49 countries during Analysis confirms the significance of most of the previous country characteristics Plus, more stringent requirements for bank entry (including limits on foreign bank entry) and higher capital requirements are negatively correlated with bank long-term debt

11 Banks Bank characteristics (size, capitalization) can affect the maturity of bank loans Larger banks expected to lend more long term due to being more diversified, more access to funding, more resources to develop credit risk management and evaluation systems to monitor their loans Constant and Ngomsi (2012), Chernykh and Theodossiou (2011) Bank ownership also impacts bank loan maturity Tasic and Valev (2010): the asset share of state owned banks has negative effect on measures of bank loan maturity Chernykh and Theodossiou (2011): foreign banks more likely to extend long-term business loans, but public banks not more likely to make long-term loans in Russia De Haas et al. (2010): foreign banks are relatively more strongly involved in mortgage lending than other banks

12 Banks The type of funding banks use to finance the loans they make is significantly correlated with the maturity structure of their debt Loan maturity structure of African (Constant and Ngomsi, 2012) and Russian (Chernykh and Theodossiou, 2011) banks Banks with a higher share of long-term liabilities exhibit higher shares of long-term loans Still, some degree of maturity transformation is inherent to banking and facilitates longterm lending

13 Banks Deposit insurance can affect the ability of banks to lend long term By lowering the risk of bank runs, deposit insurance may reduce banks need to hedge this risk through short-term loans Fan et al. (2012): firms located in countries with deposit insurance have more long-term debt But might also generate moral hazard and higher risk-taking by banks (Martinez Peria and Schmukler, 2001, Demirguc-Kunt and Detragiache, 2002) Excessive maturity transformation risk can be a major source of bank failure and, ultimately, be pernicious for long-term lending

14 Banks Regulations that affect bank size, capitalization, and funding likely to impact long-term finance, due to their correlation with the maturity structure of bank loans Basel III capital requirements and new minimum liquidity standards do not specifically target long-term bank finance, but they may still affect it (FSB, 2013) Reforms will increase the regulatory capital for such transactions and dampen the scale of maturity transformation risks The overall effects will vary depending on a variety of factors, in particular, the alternative funding sources in different markets segments Concerns that impact on developing countries could be more severe, since these countries have less developed markets and non-bank financial intermediaries

15 Banks Monitor the impact of ongoing regulatory changes But policies that help banks access to stable sources of funding might be desirable As suggested by Gobat et al. (2014), these might include: Improving financial inclusion to grow banks depositor base Promoting banks issuance of covered bonds Having banks improve their financial reporting on liquidity and other risks Strengthen accounting and auditing standards so that banks can tap into longer-term funding sources including from domestic and international capital markets

16 Types of intermediaries Banks Non-banks Domestic non-bank institutional investors: Case of Chile International mutual funds Sovereign Wealth Funds (SWFs) Private Equity (PE)

17 Non-bank financial intermediaries Expectation that non-bank domestic inst. investors would foster long-term lending Long investment horizons would allow them to take advantage of long-term risk premia and illiquidity premia They would be able to behave in a patient, counter-cyclical manner, making the most of cyclically low valuations to seek attractive investment opportunities Davis (1995), Caprio and Demirguc-Kunt (1998), Davis and Steil (2001), Corbo and Schmidt-Hebbel (2003), Impavido et al. (2003, 2010), BIS (2007), Borensztein et al. (2008), Eichengreen (2009), Della Croce et al. (2011), OECD (2013a,b, 2014), The Economist (2013, 2014a) Little evidence exists on whether these investors actually invest in long-term securities and how they structure their asset holdings

18 Types of intermediaries considered Banks Non-banks Domestic non-bank institutional investors: Case of Chile International mutual funds Sovereign Wealth Funds (SWFs) Private Equity (PE)

19 Domestic non-bank institutional investors Chilean domestic bond mutual funds, pension funds, and insurance companies during (Opazo et al., 2015) Unique monthly asset-level data on portfolios to determine maturity structure Chile the first country to adopt in 1981 a mandatory, privately managed, DC pension fund model by replacing the old public, DB system Standard (and evolving) regulatory scheme Significant improvements in the institutional and macroeconomic environment Informative comparisons across institutional investors Many high-income and developing countries have followed suit The numerous challenges faced by Chilean policymakers shed light on the difficulties in developing long-term financial markets

20 Domestic non-bank institutional investors Average Maturity (years) Chilean Insurance Companies 9.77 Chilean Domestic Mutual Funds 3.97 Chilean PFAs 4.36

21 Domestic non-bank institutional investors Mutual fund short-termism driven by short-term monitoring of underlying investors Subject to significant redemptions related to short-run performance Long-term bonds can have poor short-term performance Flows to pension funds tend to be more stable But switches across funds (Da et. al., 2014), managers moved to cash Regulatory scheme another factor behind the short-termism of pension funds Lower threshold of returns over previous 36 months that each pension fund needs to guarantee, leading also to herding and suboptimal allocations Castañeda and Rudolph (2010), Raddatz and Schmukler (2013), Pedraza Morales (2014), Randle and Rudolph (2014) But not necessarily binding and difficult tradeoff if extending maturities Instrument availability and macro/institutional framework not binding constraints

22 Types of intermediaries Banks Non-banks Domestic non-bank institutional investors: Case of Chile International mutual funds Sovereign Wealth Funds (SWFs) Private Equity (PE)

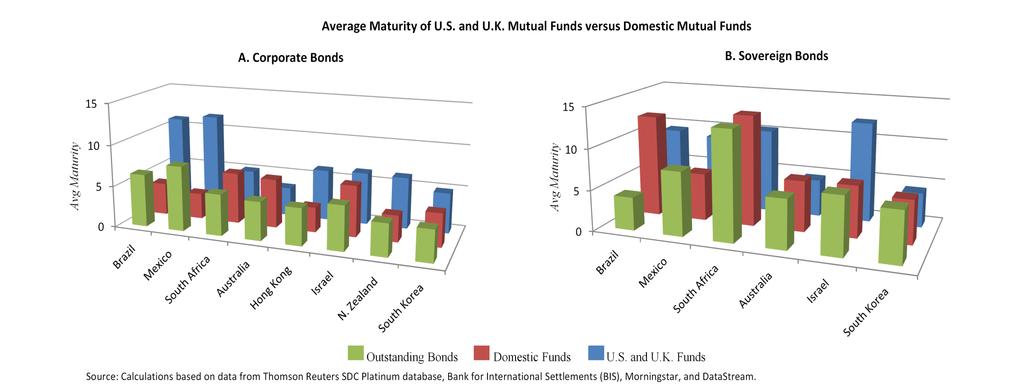

23 International mutual funds Growing importance of international mutual funds with globalization Emerging markets equity funds boomed (Miyajima and Shim, 2014) Equity funds from US$702 bn in 2009 to US$1.1 tr in 2013 Bond funds from US$88 bn to US$340 billion Role that U.K. and U.S. mutual funds might play in lengthening the maturity structure of financial contracts in both developing and other high-income countries Compare the maturity structure of these funds with outstanding securities and with that of domestic mutual funds from developing and high-income countries

24 International mutual funds

25 International mutual funds

26 International mutual funds Mutual funds from international financial centers seem to play some role in extending the maturity structure of corporate bonds in developing and high-income countries At least, hard to rely solely on domestic investors to extend maturities Fostering foreign institutional investors might be a way to extend the maturity profile of debt, as international funds might be willing to take more risk when investing abroad Important tradeoff because foreign financing tends to be in foreign currency, possibly generating currency mismatches By depending on foreign markets, economies become more susceptible to foreign shocks More work needed

27 Types of intermediaries Banks Non-banks Domestic non-bank institutional investors: Case of Chile International mutual funds Sovereign Wealth Funds (SWFs) Private Equity (PE)

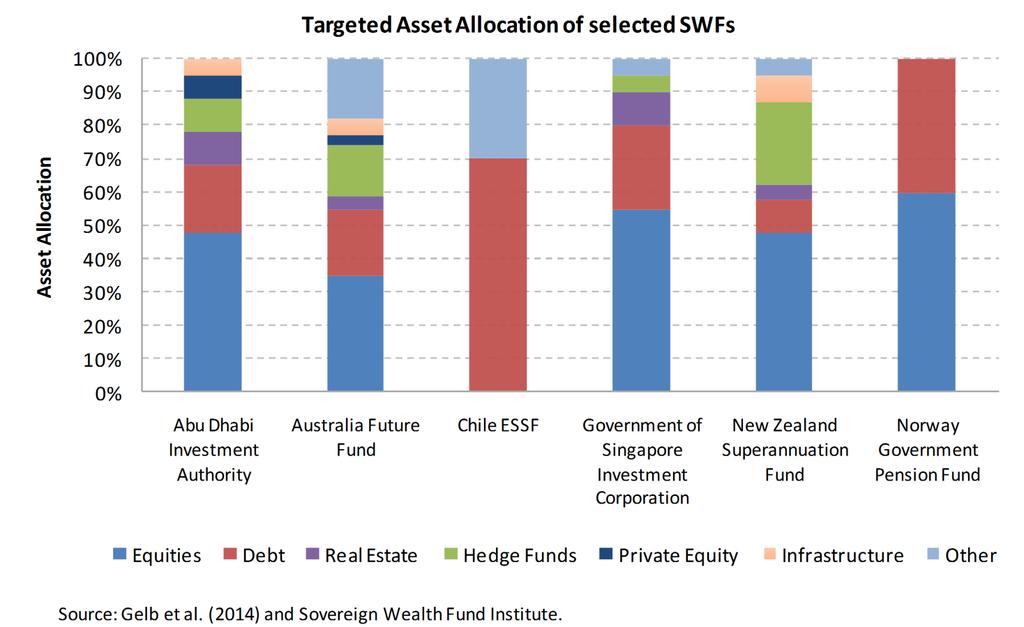

28 SWFs SWFs a large and growing class of institutional investors SWFs: state-owned investment funds that invest sovereign revenues in real and financial assets Aim to diversify economic risks and manage intergenerational savings Assets managed by SWFs have been growing rapidly, and have increased more than ten-fold over the last two decades SWFs have a combined US$ 6.6 tn under management (Gelb et al., 2014) Origin in the need to manage cyclical state revenues, mostly windfall earnings from natural resources leading to Dutch disease

29 SWFs Promising source of long-term finance in many developing countries Due to no redemption risk, a natural provider of long-term finance Explicit mandate to manage intergenerational savings, so a much longer investment horizon than other investors Very heterogeneous examples, even among developing countries Saudi Arabia and East Timor: set aside natural resource earnings in a diversified portfolio of investments, whose return would benefit future generations More than 60% of current SWFs assets are linked to oil and gas revenues China, Singapore, and Hong Kong: result of persistent trade surpluses and the desire to diversify the resulting foreign currency holdings away from U.S. T-bills

30 SWFs

31 SWFs Traditionally, the portfolio investments of SWFs concentrated in high-income countries (in highly liquid assets) Recently, SWFs have increasingly undertaken investments in developing countries to diversify their portfolios and achieve higher returns Still, the impact of SWFs investments in developing countries should not be overstated The total number of these transactions remains small despite the overall increase Geographical distribution of sovereign fund deals in developing countries very uneven South and East Asia attracted 77% of all SWFs investment in developing countries 58% in East Asia and Pacific; 19% in South Asia

32 Origin SWFs Share of SWF Transactions, by Level of Economic Development, Total (percent) Target High Income Developing Total High Income Developing Total Source: World Bank.

33 Types of intermediaries Banks Non-banks Domestic non-bank institutional investors: the case of Chile International mutual funds Sovereign Wealth Funds (SWFs) Private Equity (PE)

34 Private equity PE an asset class consisting of long-term equity investments in private companies not listed on a stock exchange PE investors specialize in a particular stage of investee company development, a particular set of industries, or a combination of these two, with different investment strategies PE investors operate as active investors Improve management, knowledge transfer/innovation, economies of scale and scope Provide comparatively illiquid, longer-term equity investments to facilitate growth, innovation, or restructuring of investee companies In 2014, PE funds had US$ 350 bn under management, US$ 55 bn in developing countries PE investments in developing countries increased in recent years, but remain small Annual volume less than 2% of GDP in Brazil, China, India, and Russia (high PE activity)

35 Private equity

36 Private equity A number of caveats constrain the impact of PE investments in developing countries PE flows are highly sensitive to the quality of legal and market institutions in the recipient country (Lerner and Schoar, 2005) Only most sophisticated developing countries receive relatively significant PE inflows PE fundraising mostly takes place in developed market, so PE flows remain cyclical and highly correlated with their business cycle Private investors adjusted their investment strategies in ways that partly compensate for political and economic risk in developing countries PE funds in developing countries focus on investing in growth-stage/sme and latestage deals, rather than seed stages Given the concentration of PE in a small number of industries in comparatively advanced developing countries, PE investments will likely play only a complementary role

37 Concluding policy lessons: Banks Banks are the most important source of long-term finance for firms in developing countries However, banks have not compensated for potential short-comings in long-term finance Bank loans in developing countries have significantly shorter maturities than those in high-income countries Stable macro, strong institutions, developed financial sector and regulations that promote bank competition: some of the factors that drive the maturity of bank loans In light of Basel III, and because capitalization and funding matter for loan maturity, need to monitor how proposed changes will affect long-term finance in near future

38 Concluding policy lessons: Pension funds Despite managing long-term savings, domestic pension funds structure their portfolios with significantly shorter maturities than domestic insurance companies Suggestion to introduce long-term benchmarks for DC pension funds (Rudolph et al., 2010; Berstein et al., 2013; Stewart, 2014) Long-term benchmarks might encourage managers to invest with long-term goal as opposed to focusing on short-term volatility management and performance But need to shift equilibrium from short to long term (transition), and whether a longterm equilibrium is stable Need to cope with short-term fluctuations in valuations and potential moral hazard Think more carefully about alternatives to Chilean DC schemes: Corporate plans? More insurance-type schemes? More centrally managed schemes?

39 Concluding policy lessons: Mutual funds Foreign mutual funds might be an avenue to extend debt maturities because they hold more long-term domestic debt than domestic investors Still need to understand drivers Different risk tolerance? Different attributes (size and asset tangibility) of the firms in which they invest? But this exposure implies important tradeoff because economies become more susceptible to foreign shocks Extensive evidence on pro-cyclical and destabilizing behavior of institutional investors in both domestic and international markets, like during global fin. crisis Kaminsky et al. (2004), Hau and Rey (2008), Jotikasthira et al. (2012), Raddatz and Schmukler (2012), Lerner and Schoar (2013), Raddatz et al. (2014) Relying on domestic mutual funds (as on pension funds) to extend maturity structures might not yield expected result either, and behavior in crisis understudied

40 Concluding policy lessons: SWFs Governments could generate incentives to facilitate long-term investments by SWFs Set the framework for investments in projects with significant social returns (infrastructure, health care, and telecommunications) to occur more often Minimize the risk of misusing the public funds in SWFs Large long-term commitments by SWFs could be structured similarly to PPPs, in which some of the initial investment risks are guaranteed by the host state To align incentives, could create the legal and regulatory conditions that allow for cofinancing and participation by the private sector Harness the multiplier effect of large SWF investments in physical or social infrastructure

41 Concluding policy lessons: PE PE investments go predominantly to countries with better investor protection, legal institutions, and corporate governance standards Thus, the promotion PE as providers of long-term finance might require further strengthening of the legal and institutional frameworks in host countries Hence, improvements in market transparency, auditing standards, and corporate governance could improve the viability of PE investments in developing countries Any policies that help develop capital markets would give PE investors a viable exit strategy, and thus more incentives to enter in the first place Given limited size of PE, policies unlikely to be geared toward PE investments for now

42 Concluding policy lessons: General points Contrary to initial expectations about the supply side of funds, financial institutions played limited role in the provision of long-term finance in developing countries Under market failures, governments might play a catalytic role so that institutional investors may finance long-term projects Recent efforts through PPPs have sought to attract institutional investors into infrastructure financing, through the involvement of the public and private sectors Beyond strengthening the institutional framework, efforts could go to the introduction of new financial instruments tailored for institutional investors The presence of international development institutions (like IFC) may further encourage the participation of institutional investors In particular, because the success of these investments is heavily dependent on host country institutions and expertise

43 Thank you!

Chapter 4: KEY messages

Chapter 4: KEY messages There are significant and informative differences in the maturity holdings across different types of financial intermediaries and across countries. Overall, the evidence suggests

Chapter 4: KEY messages There are significant and informative differences in the maturity holdings across different types of financial intermediaries and across countries. Overall, the evidence suggests

The taxonomy of Sovereign Investment Funds

www.pwc.com/sovereignwealthfunds The taxonomy of Sovereign Investment Funds May 2015 SWF s operating in an evolving political environment The increasing influence and relevance of Sovereign Investors (SIs)

www.pwc.com/sovereignwealthfunds The taxonomy of Sovereign Investment Funds May 2015 SWF s operating in an evolving political environment The increasing influence and relevance of Sovereign Investors (SIs)

Behavior of Institutional Investors During the Recent Financial Crisis: Causes, Impacts, and Challenges

Behavior of Institutional Investors During the Recent Financial Crisis: Causes, Impacts, and Challenges Michael Papaioannou, Ph.D. Monetary and Capital Markets Department International Monetary Fund Public

Behavior of Institutional Investors During the Recent Financial Crisis: Causes, Impacts, and Challenges Michael Papaioannou, Ph.D. Monetary and Capital Markets Department International Monetary Fund Public

Capital Market Financing to Firms

Capital Market Financing to Firms Sergio Schmukler Research Department World Bank Seventeenth Annual Conference on Indian Economic Policy Reform Stanford University June 2-3, 2016 Motivation Capital markets

Capital Market Financing to Firms Sergio Schmukler Research Department World Bank Seventeenth Annual Conference on Indian Economic Policy Reform Stanford University June 2-3, 2016 Motivation Capital markets

Sovereign Development Funds and the Shifting Wealth of Nations

Sovereign Development Funds and the Shifting Wealth of Nations Salzburg Global Seminar Javier Santiso Director and Chief Economist 27 September Salzburg, Austria A fundamental shift Emerging economies

Sovereign Development Funds and the Shifting Wealth of Nations Salzburg Global Seminar Javier Santiso Director and Chief Economist 27 September Salzburg, Austria A fundamental shift Emerging economies

FROM BILLIONS TO TRILLIONS: TRANSFORMING DEVELOPMENT FINANCE POST-2015 FINANCING FOR DEVELOPMENT: MULTILATERAL DEVELOPMENT FINANCE

DEVELOPMENT COMMITTEE (Joint Ministerial Committee of the Boards of Governors of the Bank and the Fund on the Transfer of Real Resources to Developing Countries) DC2015-0002 April 2, 2015 FROM BILLIONS

DEVELOPMENT COMMITTEE (Joint Ministerial Committee of the Boards of Governors of the Bank and the Fund on the Transfer of Real Resources to Developing Countries) DC2015-0002 April 2, 2015 FROM BILLIONS

The Long and the Short of Emerging Market Debt

The Long and the Short of Emerging Market Debt Luis Opazo Claudio Raddatz Sergio Schmukler 5 th Meeting NIPFP-DEA Program September 2009 Presentation 1. Motivation 2. Data and Methodology 3. Maturity Structure

The Long and the Short of Emerging Market Debt Luis Opazo Claudio Raddatz Sergio Schmukler 5 th Meeting NIPFP-DEA Program September 2009 Presentation 1. Motivation 2. Data and Methodology 3. Maturity Structure

Multi-asset capability Connecting a global network of expertise

Multi-asset capability Connecting a global network of expertise For Professional Clients only Solutions aligned with investors' needs We have over 25 years of experience designing multi-asset solutions

Multi-asset capability Connecting a global network of expertise For Professional Clients only Solutions aligned with investors' needs We have over 25 years of experience designing multi-asset solutions

Suggestions for the new version of the Astana Consensus

Suggestions for the new version of the Astana Consensus By Domingo Felipe Cavallo 1, May 7, 2012 This paper analyses in detail the first two of the five main priorities of the Mexican Presidency in G20

Suggestions for the new version of the Astana Consensus By Domingo Felipe Cavallo 1, May 7, 2012 This paper analyses in detail the first two of the five main priorities of the Mexican Presidency in G20

International Investors in Local Bond Markets: Indiscriminate Flows or Discriminating Tastes?

International Investors in Local Bond Markets: Indiscriminate Flows or Discriminating Tastes? John D. Burger (Loyola University, Maryland) Rajeswari Sengupta (IGIDR, Mumbai) Francis E. Warnock (Darden

International Investors in Local Bond Markets: Indiscriminate Flows or Discriminating Tastes? John D. Burger (Loyola University, Maryland) Rajeswari Sengupta (IGIDR, Mumbai) Francis E. Warnock (Darden

Overview: Financial Stability and Systemic Risk

Overview: Financial Stability and Systemic Risk Bank Indonesia International Workshop and Seminar Central Bank Policy Mix: Issues, Challenges, and Policies Jakarta, 9-13 April 2018 Rajan Govil The views

Overview: Financial Stability and Systemic Risk Bank Indonesia International Workshop and Seminar Central Bank Policy Mix: Issues, Challenges, and Policies Jakarta, 9-13 April 2018 Rajan Govil The views

Emerging wealth Capturing the long-term growth dynamics of the emerging markets

Emerging wealth Capturing the long-term growth dynamics of the emerging markets Originally published by Watson Wyatt Worldwide Emerging wealth Capturing the long-term growth dynamics of the emerging markets

Emerging wealth Capturing the long-term growth dynamics of the emerging markets Originally published by Watson Wyatt Worldwide Emerging wealth Capturing the long-term growth dynamics of the emerging markets

Key high-level comments by Nordea Bank AB (publ) on reforming the structure of the EU banking sector

on reforming the structure of the EU banking sector") 1 (8) Page To European Commission Email: MARKT-HLEG@ec.europa.eu Document title response to Consultation on the recommendations of the High-level Expert Group on Reforming the structure of the EU banking

1 (8) Page To European Commission Email: MARKT-HLEG@ec.europa.eu Document title response to Consultation on the recommendations of the High-level Expert Group on Reforming the structure of the EU banking

The region has been very successful in mobilizing resources

The region has been very successful in mobilizing resources US$ billions International reserves (minus gold) US$ billions Financial sector assets 16 12 14 12 Tha Phl Sgp Mys 1 Tha Phl Sgp Mys 1 8 6 Kor

The region has been very successful in mobilizing resources US$ billions International reserves (minus gold) US$ billions Financial sector assets 16 12 14 12 Tha Phl Sgp Mys 1 Tha Phl Sgp Mys 1 8 6 Kor

Klaus Schmidt-Hebbel

Fiscal Policy for Commodity Exporting Countries: Experience from Chile Klaus Schmidt-Hebbel Catholic University of Chile kschmidt-hebbel@uc.cl IMF Seminar on Commodity Price Volatility and Inclusive Growth

Fiscal Policy for Commodity Exporting Countries: Experience from Chile Klaus Schmidt-Hebbel Catholic University of Chile kschmidt-hebbel@uc.cl IMF Seminar on Commodity Price Volatility and Inclusive Growth

Infrastructure Investment in Asia

Economy Insight: A Synopsis of ADB Paper Infrastructure Investment in Asia Infrastructure Investment in Asia FICCI Research May 27, 2016 Good infrastructure plays a crucial role towards the growth of an

Economy Insight: A Synopsis of ADB Paper Infrastructure Investment in Asia Infrastructure Investment in Asia FICCI Research May 27, 2016 Good infrastructure plays a crucial role towards the growth of an

Financial Stability and Financial Efficiency Mario I. Blejer Bank of England

Financial Stability and Financial Efficiency Mario I. Blejer Bank of England One can expect that growth is fostered by the government s ability to conduct counter-cyclical cyclical macroeconomic policies,

Financial Stability and Financial Efficiency Mario I. Blejer Bank of England One can expect that growth is fostered by the government s ability to conduct counter-cyclical cyclical macroeconomic policies,

SWFs: Inward vs. Outward Investment Mandates Conditions for Success

SWFs: Inward vs. Outward Investment Mandates Conditions for Success Eliot Kalter President of EM Strategies Co-Head, SovereigNET: Fletcher Network for Sovereign Wealth and Global Capital ekalter@emstrategies.com

SWFs: Inward vs. Outward Investment Mandates Conditions for Success Eliot Kalter President of EM Strategies Co-Head, SovereigNET: Fletcher Network for Sovereign Wealth and Global Capital ekalter@emstrategies.com

Brick and Mortar Operations of International Banks

GLOBAL FINANCIAL DEVELOPMENT REPORT 2017 Brick and Mortar Operations of International Banks Robert Cull Research Manager, Research Department Claudia Ruiz-Ortega Economist, Research Department http://www.worldbank.org/financialdevelopment

GLOBAL FINANCIAL DEVELOPMENT REPORT 2017 Brick and Mortar Operations of International Banks Robert Cull Research Manager, Research Department Claudia Ruiz-Ortega Economist, Research Department http://www.worldbank.org/financialdevelopment

The Sovereign Wealth Fund Initiative March 2012

The Sovereign Wealth Fund Initiative March 2012 Drivers of Strategic Asset Allocation Decisions for Sovereign Wealth Funds Introduction By Shuvam Dutta, CEME Research Assistant Sovereign wealth funds emerged

The Sovereign Wealth Fund Initiative March 2012 Drivers of Strategic Asset Allocation Decisions for Sovereign Wealth Funds Introduction By Shuvam Dutta, CEME Research Assistant Sovereign wealth funds emerged

Rethinking the Role of the State in Finance

GLOBAL FINANCIAL DEVELOPMENT REPORT 2013 Rethinking the Role of the State in Finance WB/IMF/FRB Seminar for Senior Bank Supervisors from Emerging Economies Washington, DC, October 15, 2012 http://www.worldbank.org/financialdevelopment

GLOBAL FINANCIAL DEVELOPMENT REPORT 2013 Rethinking the Role of the State in Finance WB/IMF/FRB Seminar for Senior Bank Supervisors from Emerging Economies Washington, DC, October 15, 2012 http://www.worldbank.org/financialdevelopment

Challenges of financial globalisation and dollarisation for monetary policy: the case of Peru

Challenges of financial globalisation and dollarisation for monetary policy: the case of Peru Julio Velarde During the last decade, the financial system of Peru has become more integrated with the global

Challenges of financial globalisation and dollarisation for monetary policy: the case of Peru Julio Velarde During the last decade, the financial system of Peru has become more integrated with the global

As shown in chapter 2, output volatility continues to

5 Dealing with Commodity Price, Terms of Trade, and Output Risks As shown in chapter 2, output volatility continues to be significantly higher for most developing countries than for developed countries,

5 Dealing with Commodity Price, Terms of Trade, and Output Risks As shown in chapter 2, output volatility continues to be significantly higher for most developing countries than for developed countries,

Presented at the Conference on China's Exchange Rate Policy, October 19, 2007, at the Peterson Institute, Washington, DC.

A Scoreboard for Sovereign Wealth Funds Edwin M. Truman Senior Fellow Peterson Institute for International Economics Presented at the Conference on China's Exchange Rate Policy, October 19, 2007, at the

A Scoreboard for Sovereign Wealth Funds Edwin M. Truman Senior Fellow Peterson Institute for International Economics Presented at the Conference on China's Exchange Rate Policy, October 19, 2007, at the

14. What Use Can Be Made of the Specific FSIs?

14. What Use Can Be Made of the Specific FSIs? Introduction 14.1 The previous chapter explained the need for FSIs and how they fit into the wider concept of macroprudential analysis. This chapter considers

14. What Use Can Be Made of the Specific FSIs? Introduction 14.1 The previous chapter explained the need for FSIs and how they fit into the wider concept of macroprudential analysis. This chapter considers

GROWTH FIXED INCOME APRIL 2013

GROWTH FIXED INCOME APRIL 2013 BACKGROUND Most investors view fixed income investments as providing a liability-matching or defensive aspect to their total portfolio. The types of investments considered

GROWTH FIXED INCOME APRIL 2013 BACKGROUND Most investors view fixed income investments as providing a liability-matching or defensive aspect to their total portfolio. The types of investments considered

1. Introduction. 2. The Nature of the Insurance Business. Insurance Business Model Supports Long-term Investment

1. Introduction With almost 90 per cent, or $540 billion of their $615 billion Canadian assets, held in long-term investments, life and health insurers are one of the largest long-term institutional investors

1. Introduction With almost 90 per cent, or $540 billion of their $615 billion Canadian assets, held in long-term investments, life and health insurers are one of the largest long-term institutional investors

Intermediary Balance Sheets Tobias Adrian and Nina Boyarchenko, NY Fed Discussant: Annette Vissing-Jorgensen, UC Berkeley

Intermediary Balance Sheets Tobias Adrian and Nina Boyarchenko, NY Fed Discussant: Annette Vissing-Jorgensen, UC Berkeley Objective: Construct a general equilibrium model with two types of intermediaries:

Intermediary Balance Sheets Tobias Adrian and Nina Boyarchenko, NY Fed Discussant: Annette Vissing-Jorgensen, UC Berkeley Objective: Construct a general equilibrium model with two types of intermediaries:

Finance Science, Financial Innovation and Long-Term Asset Management

Finance Science, Financial Innovation and Long-Term Asset Management Robert C. Merton Massachusetts Institute of Technology New Developments in Long-Term Asset Management London, UK May 19, 2017. Domain

Finance Science, Financial Innovation and Long-Term Asset Management Robert C. Merton Massachusetts Institute of Technology New Developments in Long-Term Asset Management London, UK May 19, 2017. Domain

Regulatory change and monetary policy

Regulatory change and monetary policy 23 November 2015 Bill Nelson* Federal Reserve Board Conference on Financial Stability: Developments, Challenges and Policy Responses South African Reserve Bank *These

Regulatory change and monetary policy 23 November 2015 Bill Nelson* Federal Reserve Board Conference on Financial Stability: Developments, Challenges and Policy Responses South African Reserve Bank *These

Indonesia: Changing patterns of financial intermediation and their implications for central bank policy

Indonesia: Changing patterns of financial intermediation and their implications for central bank policy Perry Warjiyo 1 Abstract As a bank-based economy, global factors affect financial intermediation

Indonesia: Changing patterns of financial intermediation and their implications for central bank policy Perry Warjiyo 1 Abstract As a bank-based economy, global factors affect financial intermediation

PRODUCT KEY FACTS PARVEST Bond USD Government October 2013

Issued by BNP Paribas Investment Partners Asia Limited PRODUCT KEY FACTS PARVEST Bond USD Government October 2013 This statement provides you with key information about this product. This statement is

Issued by BNP Paribas Investment Partners Asia Limited PRODUCT KEY FACTS PARVEST Bond USD Government October 2013 This statement provides you with key information about this product. This statement is

THE REVIEW OF INTERNATIONAL FINANCIAL REGULATION: Implications for Housing Finance in Emerging Market Economies

THE REVIEW OF INTERNATIONAL FINANCIAL REGULATION: Implications for Housing Finance in Emerging Market Economies 4th Global Conference on Housing Finance in Emerging Markets Santiago Fernández de Lis Washington

THE REVIEW OF INTERNATIONAL FINANCIAL REGULATION: Implications for Housing Finance in Emerging Market Economies 4th Global Conference on Housing Finance in Emerging Markets Santiago Fernández de Lis Washington

Banking, Liquidity Transformation, and Bank Runs

Banking, Liquidity Transformation, and Bank Runs ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 30 Readings GLS Ch. 28 GLS Ch. 30 (don t worry about model

Banking, Liquidity Transformation, and Bank Runs ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 30 Readings GLS Ch. 28 GLS Ch. 30 (don t worry about model

Unlocking long term investment capital for infrastructure assets. Stanford University and Oxford University June 23 rd, 2011

Unlocking long term investment capital for infrastructure assets Ashby H B Monk Ph D Ashby H. B. Monk, Ph.D Stanford University and Oxford University June 23 rd, 2011 There is endemic short termism, which

Unlocking long term investment capital for infrastructure assets Ashby H B Monk Ph D Ashby H. B. Monk, Ph.D Stanford University and Oxford University June 23 rd, 2011 There is endemic short termism, which

Mobilizing Islamic Finance for Long Term Financing: Lessons From Conventional Finance. Ana Carvajal

Mobilizing Islamic Finance for Long Term Financing: Lessons From Conventional Finance Ana Carvajal Istanbul, November 2015 The Context: Gaps in long term finance Infrastructure Financing gap estimated

Mobilizing Islamic Finance for Long Term Financing: Lessons From Conventional Finance Ana Carvajal Istanbul, November 2015 The Context: Gaps in long term finance Infrastructure Financing gap estimated

Financial Intermediaries Supporting Asia Growth

Financial Intermediaries Supporting Asia Growth Conference: The Role of the Financial Sector in Promoting Economic Growth in Asia Session III: Challenges for the Asian Financial and Capital Markets and

Financial Intermediaries Supporting Asia Growth Conference: The Role of the Financial Sector in Promoting Economic Growth in Asia Session III: Challenges for the Asian Financial and Capital Markets and

Saving, wealth and consumption

By Melissa Davey of the Bank s Structural Economic Analysis Division. The UK household saving ratio has recently fallen to its lowest level since 19. A key influence has been the large increase in the

By Melissa Davey of the Bank s Structural Economic Analysis Division. The UK household saving ratio has recently fallen to its lowest level since 19. A key influence has been the large increase in the

Comments on Capital Market Developments in Emerging Markets: the Challenges Ahead

Comments on Capital Market Developments in Emerging Markets: the Challenges Ahead Evan Kraft American University and Croatian National Bank 19 th Dubrovnik Economic Conference Dubrovnik, June 2013 Accomplishments

Comments on Capital Market Developments in Emerging Markets: the Challenges Ahead Evan Kraft American University and Croatian National Bank 19 th Dubrovnik Economic Conference Dubrovnik, June 2013 Accomplishments

Institutional Investors: From Myth to Reality

Institutional Investors: From Myth to Reality Sergio Schmukler Development Research Group Policy Research Talk June 1, 2015 Background Work de la Torre, Ize, and Schmukler (2011). Financial Development

Institutional Investors: From Myth to Reality Sergio Schmukler Development Research Group Policy Research Talk June 1, 2015 Background Work de la Torre, Ize, and Schmukler (2011). Financial Development

International Bank for Reconstruction and Development

International Bank for Reconstruction and Development Management s Discussion & Analysis and Condensed Quarterly Financial Statements September 30, 2017 (Unaudited) Management s Discussion and Analysis

International Bank for Reconstruction and Development Management s Discussion & Analysis and Condensed Quarterly Financial Statements September 30, 2017 (Unaudited) Management s Discussion and Analysis

Part 3: Private Equity Strategies

Private Equity Education Series Part 3: Private Equity Strategies Reports in this series Report Highlights Page Part 1: What is Private Equity (PE)? Part 2: Investing in Private Equity Part 3: Private

Private Equity Education Series Part 3: Private Equity Strategies Reports in this series Report Highlights Page Part 1: What is Private Equity (PE)? Part 2: Investing in Private Equity Part 3: Private

PRODUCT KEY FACTS. PIMCO FUNDS: GLOBAL INVESTORS SERIES PLC - Low Average Duration Fund. 10 April 2019

PRODUCT KEY FACTS Issuer: PIMCO Funds: Global Investors Series plc PIMCO FUNDS: GLOBAL INVESTORS SERIES PLC - Low Average Duration Fund 10 April 2019 This statement provides you with key information about

PRODUCT KEY FACTS Issuer: PIMCO Funds: Global Investors Series plc PIMCO FUNDS: GLOBAL INVESTORS SERIES PLC - Low Average Duration Fund 10 April 2019 This statement provides you with key information about

International Banking Standards and Recent Financial Reforms

International Banking Standards and Recent Financial Reforms Mark M. Spiegel Vice President International Research Federal Reserve Bank of San Francisco Prepared for conference on Capital Flows and Global

International Banking Standards and Recent Financial Reforms Mark M. Spiegel Vice President International Research Federal Reserve Bank of San Francisco Prepared for conference on Capital Flows and Global

Sovereign Wealth Funds and Long-Term Development Finance: Risks and Opportunities

Sovereign Wealth Funds and Long-Term Development Finance: Risks and Opportunities Alan Gelb, Silvana Tordo and Håvard Halland World Bank Policy Research Working Paper 6776 Natural Resource Charter Annual

Sovereign Wealth Funds and Long-Term Development Finance: Risks and Opportunities Alan Gelb, Silvana Tordo and Håvard Halland World Bank Policy Research Working Paper 6776 Natural Resource Charter Annual

2016 Seminar for Senior Bank Supervisors from Emerging Economies. Implementation of Basel III Liquidity Requirements in Emerging Markets

2016 Seminar for Senior Bank Supervisors from Emerging Economies Implementation of Basel III Liquidity Requirements in Emerging Markets Christopher Wilson Monetary and Capital Markets Department International

2016 Seminar for Senior Bank Supervisors from Emerging Economies Implementation of Basel III Liquidity Requirements in Emerging Markets Christopher Wilson Monetary and Capital Markets Department International

Effectiveness of macroprudential and capital flow measures in Asia and the Pacific 1

Effectiveness of macroprudential and capital flow measures in Asia and the Pacific 1 Valentina Bruno, Ilhyock Shim and Hyun Song Shin 2 Abstract We assess the effectiveness of macroprudential policies

Effectiveness of macroprudential and capital flow measures in Asia and the Pacific 1 Valentina Bruno, Ilhyock Shim and Hyun Song Shin 2 Abstract We assess the effectiveness of macroprudential policies

Volatility, Policy Uncertainty, External Finance, and Investment

Koc University From the SelectedWorks of SUMRU G ALTUG May, 2013 Finance, and SUMRU G ALTUG, Koc University Available at: https://works.bepress.com/sumru_altug/35/ Koç University, CEPR and KU-TUSIAD ERF

Koc University From the SelectedWorks of SUMRU G ALTUG May, 2013 Finance, and SUMRU G ALTUG, Koc University Available at: https://works.bepress.com/sumru_altug/35/ Koç University, CEPR and KU-TUSIAD ERF

Improving the Financing of Sustainable Growth: The Role of D20 Institutions. Jointly organized and hosted by

Improving the Financing of Sustainable Growth: The Role of D20 Institutions Jointly organized and hosted by European Investment Bank and Cassa depositi e prestiti Rome, 4th July 2014 Opening Speech by

Improving the Financing of Sustainable Growth: The Role of D20 Institutions Jointly organized and hosted by European Investment Bank and Cassa depositi e prestiti Rome, 4th July 2014 Opening Speech by

Private Financing of Public Infrastructure through PPPs in Latin America and the Caribbean

Private Financing of Public Infrastructure through PPPs in Latin America and the Caribbean Executive Summary Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public

Private Financing of Public Infrastructure through PPPs in Latin America and the Caribbean Executive Summary Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public

EVALUATING THE PERFORMANCE OF COMMERCIAL BANKS IN INDIA. D. K. Malhotra 1 Philadelphia University, USA

EVALUATING THE PERFORMANCE OF COMMERCIAL BANKS IN INDIA D. K. Malhotra 1 Philadelphia University, USA Email: MalhotraD@philau.edu Raymond Poteau 2 Philadelphia University, USA Email: PoteauR@philau.edu

EVALUATING THE PERFORMANCE OF COMMERCIAL BANKS IN INDIA D. K. Malhotra 1 Philadelphia University, USA Email: MalhotraD@philau.edu Raymond Poteau 2 Philadelphia University, USA Email: PoteauR@philau.edu

International Bank for Reconstruction and Development

International Bank for Reconstruction and Development Management s Discussion & Analysis and Condensed Quarterly Financial Statements December 31, 2017 (Unaudited) Management s Discussion and Analysis

International Bank for Reconstruction and Development Management s Discussion & Analysis and Condensed Quarterly Financial Statements December 31, 2017 (Unaudited) Management s Discussion and Analysis

Strengths (+) and weaknesses ( )

and weaknesses ( )") Country Report Australia Country Report Marcel Weernink Economic growth in Australia decelerates due to lower mining investments. The outlook depends heavily on demand from China for its commodities and

Country Report Australia Country Report Marcel Weernink Economic growth in Australia decelerates due to lower mining investments. The outlook depends heavily on demand from China for its commodities and

By: Craig Sedmak. why: tend to be available.

LADDER INSIGHTS: 7 REASONS WHY INSTITUTIONAL INVESTORS SHOULD CONSIDER CMBS IN TODAY S RISING RATE ENVIRONMENT By: Craig Sedmak Managing Director, Ladder Capital Asset Management Portfolio Manager, Ladder

LADDER INSIGHTS: 7 REASONS WHY INSTITUTIONAL INVESTORS SHOULD CONSIDER CMBS IN TODAY S RISING RATE ENVIRONMENT By: Craig Sedmak Managing Director, Ladder Capital Asset Management Portfolio Manager, Ladder

The CBM Group, Inc. 505 Park Avenue New York, NY Phone Fax

505 Park Avenue New York, NY 10022 Phone 646 282 0050 Fax 646 282 0044 www.thecbmgroup.com THE RETIREMENT CHALLENGE AND WEALTH MANAGEMENT OPPORTUNITIES January 2006 A lifecycle view of financial services

505 Park Avenue New York, NY 10022 Phone 646 282 0050 Fax 646 282 0044 www.thecbmgroup.com THE RETIREMENT CHALLENGE AND WEALTH MANAGEMENT OPPORTUNITIES January 2006 A lifecycle view of financial services

Rethinking the Role of the State in Finance

GLOBAL FINANCIAL DEVELOPMENT REPORT 2013 Rethinking the Role of the State in Finance September 24, 2012 Motivation: Financial Development Barometer Views split on important aspects of the state s role.

GLOBAL FINANCIAL DEVELOPMENT REPORT 2013 Rethinking the Role of the State in Finance September 24, 2012 Motivation: Financial Development Barometer Views split on important aspects of the state s role.

What do new forms of finance mean for EM central banks?

What do new forms of finance mean for EM central banks? An overview M S Mohanty 1 The size and the structure of financial intermediation influence the cost of credit, the risk exposure of financial institutions

What do new forms of finance mean for EM central banks? An overview M S Mohanty 1 The size and the structure of financial intermediation influence the cost of credit, the risk exposure of financial institutions

Egil Matsen: The equity share in the Government Pension Fund Global

Egil Matsen: The equity share in the Government Pension Fund Global Introductory statement by Mr Egil Matsen, Governor of Norges Bank (Central Bank of Norway), Oslo, 1 December 2016. Accompanying slides

Egil Matsen: The equity share in the Government Pension Fund Global Introductory statement by Mr Egil Matsen, Governor of Norges Bank (Central Bank of Norway), Oslo, 1 December 2016. Accompanying slides

In various tables, use of - indicates not meaningful or not applicable.

Basel II Pillar 3 disclosures 2008 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse Group, Credit Suisse, the Group, we, us and our mean Credit Suisse Group AG

Basel II Pillar 3 disclosures 2008 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse Group, Credit Suisse, the Group, we, us and our mean Credit Suisse Group AG

The Financial System. Sherif Khalifa. Sherif Khalifa () The Financial System 1 / 55

The Financial System 1 / 55") The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 55 The financial system consists of those institutions in the economy that matches saving with investment. The financial system

The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 55 The financial system consists of those institutions in the economy that matches saving with investment. The financial system

GDP-linked securities

GDP-linked securities S. Ali Abbas International Monetary Fund March 10, 2017 Disclaimer: The views expressed in this presentation are those of the presenter and do not necessarily represent the views

GDP-linked securities S. Ali Abbas International Monetary Fund March 10, 2017 Disclaimer: The views expressed in this presentation are those of the presenter and do not necessarily represent the views

Younger households can accumulate wealth and reap term premiums through products such

Chapter 2: KEY messages From the perspective of the firm, long-term finance offers protection from credit supply shocks and from having to refinance in bad times, facilitating long-term investments and

Chapter 2: KEY messages From the perspective of the firm, long-term finance offers protection from credit supply shocks and from having to refinance in bad times, facilitating long-term investments and

Our Expertise. IFC blends investment with advice and resource mobilization to help the private sector advance development.

Our Expertise IFC blends investment with advice and resource mobilization to help the private sector advance development. 76 IFC ANNUAL REPORT 2016 Where We Work As the largest global development institution

Our Expertise IFC blends investment with advice and resource mobilization to help the private sector advance development. 76 IFC ANNUAL REPORT 2016 Where We Work As the largest global development institution

BANK OF FINLAND ARTICLES ON THE ECONOMY

BANK OF FINLAND ARTICLES ON THE ECONOMY Table of Contents Finland struggling to defend its market share on rapidly expanding markets 3 Finland struggling to defend its market share on rapidly expanding

BANK OF FINLAND ARTICLES ON THE ECONOMY Table of Contents Finland struggling to defend its market share on rapidly expanding markets 3 Finland struggling to defend its market share on rapidly expanding

FINANCE FOR ALL? POLICIES AND PITFALLS IN EXPANDING ACCESS A WORLD BANK POLICY RESEARCH REPORT

FINANCE FOR ALL? POLICIES AND PITFALLS IN EXPANDING ACCESS A WORLD BANK POLICY RESEARCH REPORT Summary A new World Bank policy research report (PRR) from the Finance and Private Sector Research team reviews

FINANCE FOR ALL? POLICIES AND PITFALLS IN EXPANDING ACCESS A WORLD BANK POLICY RESEARCH REPORT Summary A new World Bank policy research report (PRR) from the Finance and Private Sector Research team reviews

Macroeconomic Management in Emerging-Market Economies with Open Capital Accounts. Outline

Macroeconomic Management in Emerging-Market Economies with Open Capital Accounts Klaus Schmidt-Hebbel, Central Bank of Chile Seminar on Crisis Prevention in Emerging Markets IMF-Singapore Training Institute

Macroeconomic Management in Emerging-Market Economies with Open Capital Accounts Klaus Schmidt-Hebbel, Central Bank of Chile Seminar on Crisis Prevention in Emerging Markets IMF-Singapore Training Institute

Capital Advisory Group Institutional Investor Survey

INSIGHTS Global Capital Advisory Group 2018 Institutional Investor Survey Capital Advisory Group This material is provided by J.P. Morgan s Capital Advisory Group for informational purposes only. It is

INSIGHTS Global Capital Advisory Group 2018 Institutional Investor Survey Capital Advisory Group This material is provided by J.P. Morgan s Capital Advisory Group for informational purposes only. It is

Investec Global Strategy Fund. Product Key Facts Statements July 2018

Investec Global Strategy Fund Product Key Facts Statements July 2018 Contents Money Sub-Funds U.S. Dollar Money Fund... 1 Sterling Money Fund... 4 Bond Sub-Funds Global Total Return Credit Fund... 7 Investment

Investec Global Strategy Fund Product Key Facts Statements July 2018 Contents Money Sub-Funds U.S. Dollar Money Fund... 1 Sterling Money Fund... 4 Bond Sub-Funds Global Total Return Credit Fund... 7 Investment

Impact of the Global Investment Slowdown on the Korean Economy

Impact of the Global Investment Slowdown on the Korean Economy Kyu-Chul Jung, Fellow 1. Issues As world trade slows amid a weakening global economy, Korea s exports exhibited relatively poorer performance,

Impact of the Global Investment Slowdown on the Korean Economy Kyu-Chul Jung, Fellow 1. Issues As world trade slows amid a weakening global economy, Korea s exports exhibited relatively poorer performance,

Corporate CPM strategy in a down turn

Corporate CPM strategy in a down turn Investec corporate impairments seminar BANKING GROUP financial & operating review Jacques Mouton Head of Corporate Credit 20 November 2009 Agenda Setting the scene

Corporate CPM strategy in a down turn Investec corporate impairments seminar BANKING GROUP financial & operating review Jacques Mouton Head of Corporate Credit 20 November 2009 Agenda Setting the scene

Basel Committee on Banking Supervision

Basel Committee on Banking Supervision Implementation of Basel standards A report to G20 Leaders on implementation of the Basel III regulatory reforms August 2016 This publication is available on the BIS

Basel Committee on Banking Supervision Implementation of Basel standards A report to G20 Leaders on implementation of the Basel III regulatory reforms August 2016 This publication is available on the BIS

Challenges and Opportunities in Recent Financial Market Developments

Challenges and Opportunities in Recent Financial Market Developments Mario Marcel Central Bank of Chile OMFIF 2018 Global Public Investor Conference, May 23, 2018 London International context Economic

Challenges and Opportunities in Recent Financial Market Developments Mario Marcel Central Bank of Chile OMFIF 2018 Global Public Investor Conference, May 23, 2018 London International context Economic

COMMUNIQUE. Page 1 of 13

COMMUNIQUE 16-COM-001 Feb. 1, 2016 Release of Liquidity Risk Management Guiding Principles The Credit Union Prudential Supervisors Association (CUPSA) has released guiding principles for Liquidity Risk

COMMUNIQUE 16-COM-001 Feb. 1, 2016 Release of Liquidity Risk Management Guiding Principles The Credit Union Prudential Supervisors Association (CUPSA) has released guiding principles for Liquidity Risk

Changes in Development Finance in Asia: Trends, Challenges, and Policy Implications

February 8, 2012 Chula Global Network Chulalongkorn University, Bangkok, Thailand Changes in Development Finance in Asia: Trends, Challenges, and Policy Implications Toshiro Nishizawa Head, Country Credit

February 8, 2012 Chula Global Network Chulalongkorn University, Bangkok, Thailand Changes in Development Finance in Asia: Trends, Challenges, and Policy Implications Toshiro Nishizawa Head, Country Credit

Shadow Banking May 16, 2017

Global Risk Institute Shadow Banking May 16, 2017 Sheila Judd Executive in Residence Presentation Purpose Share information/research findings on the topic, including GRI recommendations for industry oversight:

Global Risk Institute Shadow Banking May 16, 2017 Sheila Judd Executive in Residence Presentation Purpose Share information/research findings on the topic, including GRI recommendations for industry oversight:

Advisor Briefing Why Alternatives?

Advisor Briefing Why Alternatives? Key Ideas Alternative strategies generally seek to provide positive returns with low correlation to traditional assets, such as stocks and bonds By incorporating alternative

Advisor Briefing Why Alternatives? Key Ideas Alternative strategies generally seek to provide positive returns with low correlation to traditional assets, such as stocks and bonds By incorporating alternative

Growth in a low return world

Growth in a low return world Morgan Stanley European financials conference Massimo Tosato Executive Vice-Chairman 19 March 2013 Performance 2012 Investing for long-term growth Investment performance: 71%

Growth in a low return world Morgan Stanley European financials conference Massimo Tosato Executive Vice-Chairman 19 March 2013 Performance 2012 Investing for long-term growth Investment performance: 71%

Post-Financial Crisis Regulatory Reform Proposals -From Global One-Size-Fits-All to Locally-Specific Regulations-

Post-Financial Crisis Regulatory Reform Proposals -From Global One-Size-Fits-All to Locally-Specific Regulations- Research Group on the Financial System Strengthening international financial regulations

Post-Financial Crisis Regulatory Reform Proposals -From Global One-Size-Fits-All to Locally-Specific Regulations- Research Group on the Financial System Strengthening international financial regulations

Financial System and Monetary Policy Transmission Mechanism: How to Address the Increasing Risk Perception

Financial System and Monetary Policy Transmission Mechanism: How to Address the Increasing Risk Perception Miranda S. Goeltom Acting Governor, Bank Indonesia Bank Indonesia s 7th International Seminar

Financial System and Monetary Policy Transmission Mechanism: How to Address the Increasing Risk Perception Miranda S. Goeltom Acting Governor, Bank Indonesia Bank Indonesia s 7th International Seminar

World Investment Report 2013

Twenty-Sixth Meeting of the IMF Committee on Balance of Payments Statistics Muscat, Oman October 28 30, 2013 BOPCOM 13/25 World Investment Report 2013 Prepared by the UNCTAD WORLD INVESTMENT REPORT 2013

Twenty-Sixth Meeting of the IMF Committee on Balance of Payments Statistics Muscat, Oman October 28 30, 2013 BOPCOM 13/25 World Investment Report 2013 Prepared by the UNCTAD WORLD INVESTMENT REPORT 2013

Strengthening the Oversight and Regulation of Shadow Banking

16 April 2012 Strengthening the Oversight and Regulation of Shadow Banking Progress Report to G20 Ministers and Governors I. Introduction At the Cannes Summit in November 2011, the G20 Leaders agreed to

16 April 2012 Strengthening the Oversight and Regulation of Shadow Banking Progress Report to G20 Ministers and Governors I. Introduction At the Cannes Summit in November 2011, the G20 Leaders agreed to

Investment and its Financing: A Macro Perspective

G R O U P O F T W E N T Y Investment and its Financing: A Macro Perspective Annex to the G Surveillance Note Meetings of G Finance Ministers and Central Bank Governors February, 3 Prepared by Staff of

G R O U P O F T W E N T Y Investment and its Financing: A Macro Perspective Annex to the G Surveillance Note Meetings of G Finance Ministers and Central Bank Governors February, 3 Prepared by Staff of

Sovereign Wealth Funds Asset Allocation in the Wake of the Global Financial Crisis

Sovereign Wealth Funds Asset Allocation in the Wake of the Global Financial Crisis Eliot Kalter President, E M Strategies Senior Fellow, The Fletcher School EKalter@EMStrategies.com June 2009 Sovereign

Sovereign Wealth Funds Asset Allocation in the Wake of the Global Financial Crisis Eliot Kalter President, E M Strategies Senior Fellow, The Fletcher School EKalter@EMStrategies.com June 2009 Sovereign

Panel Discussion: " Will Financial Globalization Survive?" Luzerne, June Should financial globalization survive?

Some remarks by Jose Dario Uribe, Governor of the Banco de la República, Colombia, at the 11th BIS Annual Conference on "The Future of Financial Globalization." Panel Discussion: " Will Financial Globalization

Some remarks by Jose Dario Uribe, Governor of the Banco de la República, Colombia, at the 11th BIS Annual Conference on "The Future of Financial Globalization." Panel Discussion: " Will Financial Globalization

Session #22: Sovereign Wealth Funds

Session #22: Sovereign Wealth Funds Vidar Ovesen IMF Consultant SPC (SOPAC Division) Pacific ACP States 5 th Regional Training Workshop on Deep Sea Minerals: Financial Aspects 13 th -16 th May The Rarotongan

Session #22: Sovereign Wealth Funds Vidar Ovesen IMF Consultant SPC (SOPAC Division) Pacific ACP States 5 th Regional Training Workshop on Deep Sea Minerals: Financial Aspects 13 th -16 th May The Rarotongan

Our Expertise. IFC blends investment with advice and resource mobilization to help the private sector advance development.

Our Expertise IFC blends investment with advice and resource mobilization to help the private sector advance development. Where We Work As the largest global development institution focused on the private

Our Expertise IFC blends investment with advice and resource mobilization to help the private sector advance development. Where We Work As the largest global development institution focused on the private

Digging into the composition of government debt in CESEE: a risk evaluation

Digging into the composition of government debt in CESEE: a risk evaluation 82 nd OeNB East Jour Fixe June 11, 218 Markus Eller Principal Economist Oesterreichische Nationalbank Foreign Research Division

Digging into the composition of government debt in CESEE: a risk evaluation 82 nd OeNB East Jour Fixe June 11, 218 Markus Eller Principal Economist Oesterreichische Nationalbank Foreign Research Division

PRODUCT KEY FACTS BNY MELLON EMERGING MARKETS DEBT LOCAL CURRENCY FUND 30 April 2018

PRODUCT KEY FACTS BNY MELLON EMERGING MARKETS DEBT LOCAL CURRENCY FUND 30 April 2018 This statement provides you with key information about this product. This statement is a part of the offering document.

PRODUCT KEY FACTS BNY MELLON EMERGING MARKETS DEBT LOCAL CURRENCY FUND 30 April 2018 This statement provides you with key information about this product. This statement is a part of the offering document.

Bond Basics July 2007

Bond Basics: Emerging Market (External and Local Markets) Developing economies around the world, known to investors as emerging markets (EM), are rapidly maturing into key players in the global economy

Bond Basics: Emerging Market (External and Local Markets) Developing economies around the world, known to investors as emerging markets (EM), are rapidly maturing into key players in the global economy

Tax Digitalization: Latin America leads the change

Tax Digitalization: Latin America leads the change KPMG International kpmg.com/gcms When it comes to the digital evolution of tax compliance process, Latin American countries are blazing the path forward.

Tax Digitalization: Latin America leads the change KPMG International kpmg.com/gcms When it comes to the digital evolution of tax compliance process, Latin American countries are blazing the path forward.

Alternative Assets: The Next Frontier for Defined Contribution Plans

Research Presented by HEK s Idea Development Forum: Alternative Assets: The Next Frontier for Defined Contribution Plans September 2013 Hewitt EnnisKnupp, An Aon Company 2013 Aon plc Consulting Investment

Research Presented by HEK s Idea Development Forum: Alternative Assets: The Next Frontier for Defined Contribution Plans September 2013 Hewitt EnnisKnupp, An Aon Company 2013 Aon plc Consulting Investment

Ten years after: Implications of the current financial market turmoil. Dr. Atchana Waiquamdee Deputy Governor Bank of Thailand

Ten years after: Implications of the current financial market turmoil Dr. Atchana Waiquamdee Deputy Governor Bank of Thailand I. The 1997 East Asia Crisis II. Latest Episode Causes of the 1997 Crisis 3

Ten years after: Implications of the current financial market turmoil Dr. Atchana Waiquamdee Deputy Governor Bank of Thailand I. The 1997 East Asia Crisis II. Latest Episode Causes of the 1997 Crisis 3

1: Challenges for Australia s tax system

1: Challenges for Australia s tax system Overview This chapter sets out the major challenges that confront the Australian tax system. Key points Australia s tax system faces challenges from a changing

1: Challenges for Australia s tax system Overview This chapter sets out the major challenges that confront the Australian tax system. Key points Australia s tax system faces challenges from a changing

Changing for the Better

Changing for the Better THE LONG-TERM CASE FOR EMERGING MARKETS Emerging markets are undergoing fundamental change. Economies that were once dominated by agriculture and low cost manufacturing are now

Changing for the Better THE LONG-TERM CASE FOR EMERGING MARKETS Emerging markets are undergoing fundamental change. Economies that were once dominated by agriculture and low cost manufacturing are now

What Does Debt Relief Do for Development? Lessons from the Largest Household Bailout in History

What Does Debt Relief Do for Development? Lessons from the Largest Household Bailout in History Martin Kanz World Bank Research Department Policy Research Talk November 5, 2018 Motivation Economists have

What Does Debt Relief Do for Development? Lessons from the Largest Household Bailout in History Martin Kanz World Bank Research Department Policy Research Talk November 5, 2018 Motivation Economists have

Commodity Savings Funds: Asset allocation and spending rules. Washington DC March 10-11, 2008

Commodity Savings Funds: Asset allocation and spending rules Arjan Berkelaar Principal Investment Officer Asset Allocation & Quant Strategies Jennifer Johnson-Calari Director Sovereign Investment Partnerships

Commodity Savings Funds: Asset allocation and spending rules Arjan Berkelaar Principal Investment Officer Asset Allocation & Quant Strategies Jennifer Johnson-Calari Director Sovereign Investment Partnerships

REGULATORY GUIDELINE Liquidity Risk Management Principles TABLE OF CONTENTS. I. Introduction II. Purpose and Scope III. Principles...

REGULATORY GUIDELINE Liquidity Risk Management Principles SYSTEM COMMUNICATION NUMBER Guideline 2015-02 ISSUE DATE June 2015 TABLE OF CONTENTS I. Introduction... 1 II. Purpose and Scope... 1 III. Principles...

REGULATORY GUIDELINE Liquidity Risk Management Principles SYSTEM COMMUNICATION NUMBER Guideline 2015-02 ISSUE DATE June 2015 TABLE OF CONTENTS I. Introduction... 1 II. Purpose and Scope... 1 III. Principles...

Emerging Markets Debt: Outlook for the Asset Class

Emerging Markets Debt: Outlook for the Asset Class By Steffen Reichold Emerging Markets Economist May 2, 211 Emerging market debt has been one of the best performing asset classes in recent years due to

Emerging Markets Debt: Outlook for the Asset Class By Steffen Reichold Emerging Markets Economist May 2, 211 Emerging market debt has been one of the best performing asset classes in recent years due to

PRODUCT KEY FACTS PARVEST Equity High Dividend Asia Pacific ex-japan April 2018

Issued by BNP PARIBAS ASSET MANAGEMENT Asia Limited PRODUCT KEY FACTS April 2018 This statement provides you with key information about this product. This statement is a part of the offering document and

Issued by BNP PARIBAS ASSET MANAGEMENT Asia Limited PRODUCT KEY FACTS April 2018 This statement provides you with key information about this product. This statement is a part of the offering document and

Institutional Investors and Infrastructure Financing

Institutional Investors and Infrastructure Financing Tientip Subhanij Policy Dialogue on Infrastructure Financing Strategies for Sustainable Development in North and Central Asia 7-8 June 2017 Tbilisi,

Institutional Investors and Infrastructure Financing Tientip Subhanij Policy Dialogue on Infrastructure Financing Strategies for Sustainable Development in North and Central Asia 7-8 June 2017 Tbilisi,