Table of Contents. Week in review. What we ll be watching... p. 4 Calendar of upcoming releases... p. 5 Annex Economic tables...

|

|

|

- Andrew Porter

- 6 years ago

- Views:

Transcription

to an annualized 217.0K units. Most of the retreat can be attributed to a 38.1K (22.")

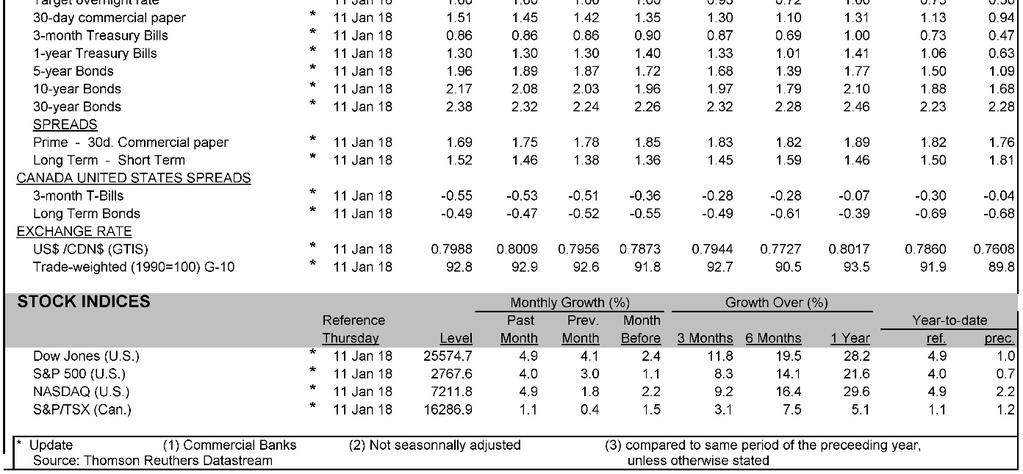

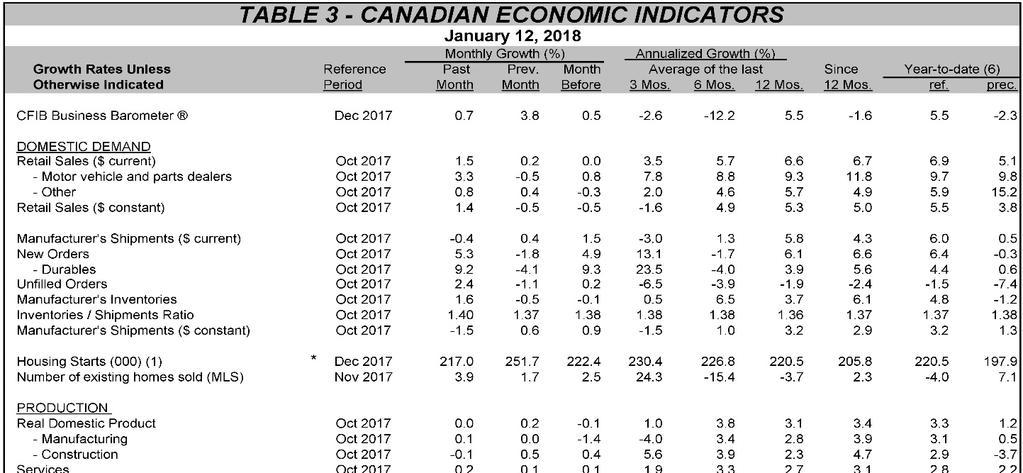

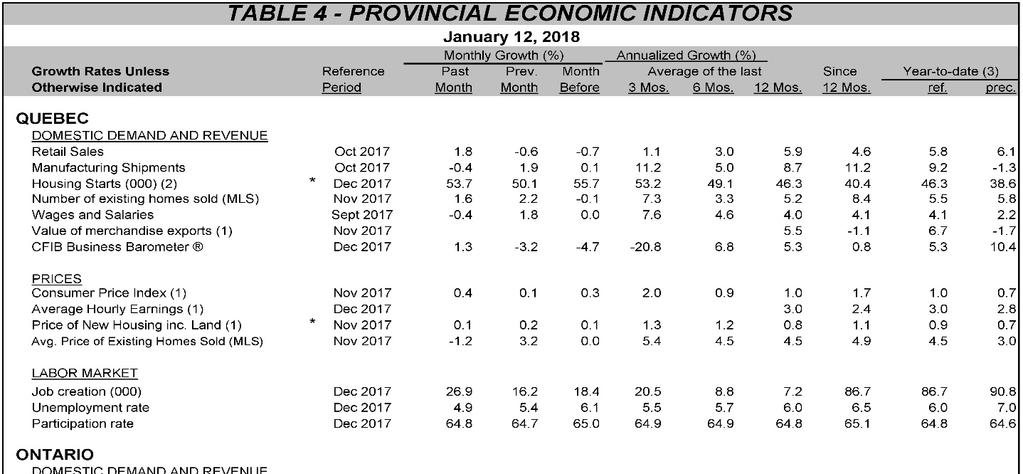

1 January 12, 2018 Table of Contents What we ll be watching... p. 4 Calendar of upcoming releases... p. 5 Annex Economic tables... A1 Week in review CANADA: decreased for the first time in three months in December, declining 34.7K (13.8%) to an annualized 217.0K units. Most of the retreat can be attributed to a 38.1K (22.0%) drop in urban area multiple starts, which dwarfed increases in the urban single (+2.8K or 4.7%) and rural (+0.6K or 3.3%) categories. However, starts declined in only three of the ten provinces: Ontario (-33.0K), Alberta (-11.5K) and PEI (-0.3K). The strongest gains were recorded in British Columbia (+4.7K), Quebec (+3.7K) and Manitoba (+0.8K). On a quarterly basis, starts advanced an annualized 13.5% in Q4 after surging 35.6% in Q3. Despite the jump, it is hard to tell whether residential construction contributed to economic growth in Q4. True, quarterly data showed a marked increase in multiple starts (+35.8% annualized), but ground-breakings for singles, which make a greater contribution to GDP per unit, fell 28.6% in annualized terms. Canada: New residential construction may have added to Q4 GDP Real new residential construction expenses and housing starts q/q % chg. saar Real new residential construction from national accounts (R) q/q % chg. saar Housing starts (L) NBF Economics and Strategy (data via Statistics Canada and CMHC) In November, the value of applications slipped 7.7% m/m to $7.7 billion in seasonally adjusted terms. This was the first monthly drop in three months and the steepest since January 2016, but it followed an $8.3-billion reading in October, the largest ever. Construction intentions were down in both the residential sector (-4.6%) and the non-residential sector (-12.3%, the largest pullback in 14 months). The value of residential permits issued for multiple units was down 10.1%. Alternatively, permit issuance for single units edged up 0.6%. On a 12-month basis, the total value of permit applications climbed just 1.3% as a sharp rise in the nonresidential sector (+13.8%) was offset by a decrease in the residential segment (-5.1%). The edged up 0.2% in December, interrupting a sequence of three monthly consecutive drops. Yet the gain in the Composite index was not broad-based, only five of the 11 constituent cities recording increases in the month. The main contributor was Vancouver (+1.3%), but gains were also observed in Winnipeg (+1.9%), Halifax (+1.9%), Ottawa- Gatineau (+0.4%) and Edmonton (+0.1%). Alternatively, prices fell in Toronto ( 0.3%), Victoria ( 1.0%), Calgary ( 0.6%), Hamilton ( 0.5%) and Montreal ( 0.2%). The index for Quebec City was flat. On a y/y basis, the Composite index rose 9.1%, a fifth softer reading in a row following the record gains of 14.2% posted in both June and July. December s y/y rise was led by Vancouver (+16.0%), Victoria (+11.5%), Hamilton (+11.3%) and Toronto (+9.0%). Although below the national average, noteworthy increases occurred in Montreal (+7.0%), Ottawa-Gatineau (+5.1%), Winnipeg (+4.0%) and Halifax (+3.6%). Gains were more subdued elsewhere. Vancouver the main driver of the Composite index in December %m/m NBF Economics and Strategy (Data from Teranet-National Bank House Price Index) Composite Without Vancouver The latest by the Bank of Canada showed business sentiment remained strong during the interview period from November 14 to December 8, as the survey s aggregate indicator returned near last summer s cyclical peak. Firms reported better sales growth in the past 12 months and expected it to remain positive over the next year. While some firms were concerned about U.S. trade policy, they were largely optimistic about export growth,

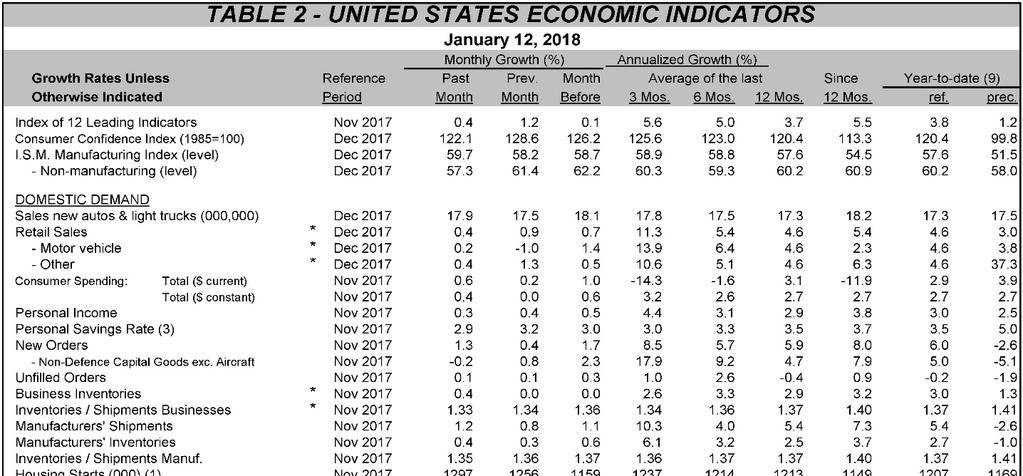

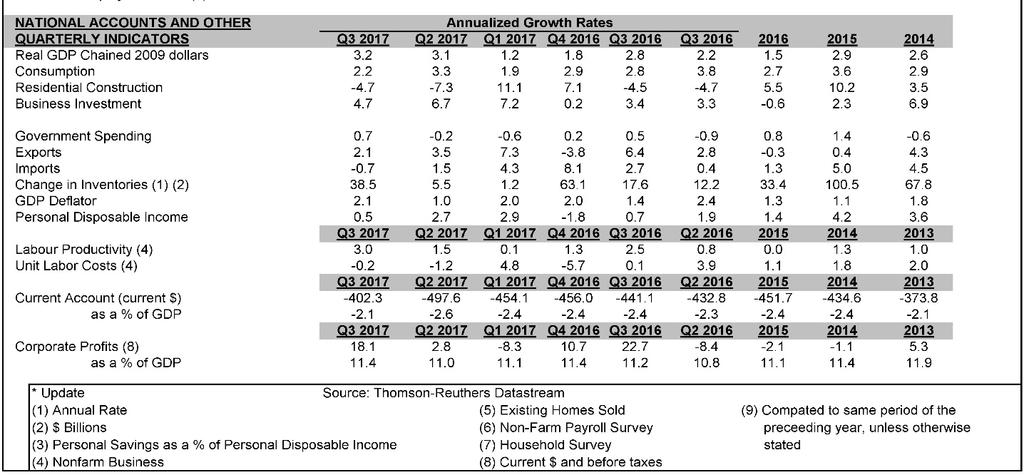

2 which was expected to accelerate thanks to strong U.S. demand and a weak Canadian dollar. Capacity pressures were more intense with 56% of respondents (a decade high) now stating either some or significant difficulties meeting an unexpected increase in demand. The proportion of respondents facing labour shortages also increased to a multiyear high. While wage pressures were not widespread, firms expected an increase due to minimum wage hikes. This heightened expectations of input price inflation, but those of output price inflation remained low as firms anticipated steeper competition to curb their ability to raise prices. Firms reported some easing in credit conditions, which was confirmed by the separately-released for 2017Q4 (also conducted by the BoC). Predictably, with capacity and labour pressures intensifying, firms were keen to increase employment and to invest in machinery and equipment. In this regard, the related measure of intentions rebounded sharply after dipping in the fall. Canada: Reasons to be upbeat about investment and hiring prospects % Share of respondents with capacity pressures and labour shortages Rising capacity pressures Share of respondents with some or significant capacity pressures Share of respondents with labour shortages NBF Economics and Strategy (data via Bank of Canada) UNITED STATES: The rose 0.1% in December after advancing 0.4% in November. The headline figure was negatively impacted by a -1.2% decline in energy prices. Food costs, for their part, rose 0.2% m/m. Excluding these two components, the CPI rose 0.3% m/m as higher prices for owners equivalent rent (+0.3%), medical care (+0.3%), and recreation (+0.1%) were only partially offset by lower prices for apparel (-0.5%) and transportation (-0.2%). On a year-on-year basis, the headline figure slid one tick to 2.1% while core inflation edged up one tenth of a percentage point to 1.8%. Looking ahead, we expect inflation to accelerate in 2018 on the back of above potential growth combined with the downward trend of the USD (note however that there is a negative base effect in the first two months of the year). rose 0.4% m/m in December after increasing an upwardly revised 0.9% in November (initially reported as 0.8%). Sales of motor vehicles and parts expanded 0.2% during the month. Excluding that category, retail sales also grew 0.4% thanks to decent showings for furniture stores (+0.6%), % BoC survey s balance of opinion on investment and hiring Hiring Investment prompting firms to be more motivated to hire and invest building materials (+1.2%), food/beverages (+0.5%) and nonstore retailers (+1.2%). Overall, sales increased in 9 of the 13 major categories surveyed. In real terms, retail sales were up 0.2% (using CPI as a proxy for retail prices). Looking at quarterly data, a strong labour market and consumer confidence flying high helped nominal sales rising at an astonishing annualized pace of 11.3% in Q4, the strongest since In real terms, it s running at 7.3% which bodes very well for consumption spending in the quarter. The dropped to in December from November s reading of 107.5, the second highest in the survey s 44-year history. The percentage of firms expecting a better economy slid from 48% to a still elevated 37%. Similarly, the proportion of respondents expecting higher sales dropped from a 10-year high of 34% to 28%, which was nevertheless above the indicator s 6-month moving average. Meanwhile, the percentage of small firms that considered present economic conditions to be conducive to expansion remained unchanged at 27%, a cyclical high. The details of the report also showed that employment was becoming an obstacle to production growth. Indeed, no less than 54% of small firms stated that they could find few or no qualified applicants to fill their job vacancies, the highest ratio ever recorded. To mitigate this shortage, 23% of firms planned to enhance their net compensation plans in the near future. This is the highest percentage registered since March U.S.: NFIB report shows growing shortage of qualified workers % of firms having trouble finding qualified applicants vs. % planning to increase compensations % NBF Economics and Strategy (data via Datastream) Few or no qualified workers to fill job vacancies Planning to increase net compensation plans According to the (JOLTS), there were 5,879K positions waiting to be filled in the United States in November, 46K fewer than in October and 252K fewer than the all-time high posted in September. The November report showed hires fell 104K to 5,488K and separations retreat 49K to 5,202K. The quit rate (quits as a percentage of total employment) held steady at a cyclical high of 2.2%. All in all, the report continued to indicate high demand for workers despite the monthly drop in job openings. Still in November, registered its steepest monthly increase since December 2001, surging $28.0 billion 2

3 to an annualized $3,827.2 billion. Non-revolving credit grew $16.8 billion to $2,804.5 billion. Meanwhile, revolving credit, which consists mainly of credit card loans, expanded $11.2 billion to $1,022.7 billion, thereby clearing its pre-recession peak to reach a new all-time high. U.S.: Credit card loans reached all-time high in November Revolving credit outstanding. Last observation: November ,040 1,020 $, in billions, ann. Pre-recession peak construction (2.7 vs. 1.5). At the national level, economic confidence reached a cyclical high in France (114.2 vs ) and remained elevated in Germany (116.0 vs ), Italy (112.1, unchanged) and Spain (110.0 vs ). Eurozone: Economic confidence at 17-year high Economic Sentiment Indicator vs. Consumer Confidence Index. Last observation: December Index Economic Sentiment (L) Index , Consumer Confidence (R) NBF Economics and Strategy (data via Datastream) NBF Economics and Strategy (data via Datastream) -36 WORLD: In the, the seasonally adjusted dipped one tick to 8.7% in November, its lowest level since January Nationally, the jobless rate slipped one-tenth of a percentage point in three countries: Germany (from 3.7% to a post-unification low of 3.6%), France (from 9.3% to a six-year low of 9.2%) and Italy (from 11.1% to a five-year low of 11.0%). In Spain, it stayed unchanged at 16.7%, the lowest figure in nine years. Meanwhile, youth unemployment in the single-currency area slipped two ticks to a still elevated 18.2%. Eurozone: Unemployment falls to 9-year low Headline unemployment rate vs. under-25 unemployment rate. Last observation: November % Under Pre-crisis low: 15.1% Total 8 Pre-crisis low: 7.3% NBF Economics and Strategy (data via Datastream) In December, the European Commission s rose for a seventh consecutive month, climbing 1.4 point to a 17-year high of The gain was driven by higher confidence among consumers (index at a 16-year high of 0.5 vs. 0 the prior month) and in the manufacturing sector (9.1 vs. 8.1). Confidence also rose in the services segment (18.4 vs. 16.4) and the retail segment (6.2 vs. 4.3), not to mention 3

4 What We ll Be Watching In Canada, the highlight of the week will the central bank s. In light of the strong performance of the Canadian labour market in 2017 and given the lag in the effect of monetary policy on the economy and inflation, we think the data have moved outside the zone of inaction where the central bank can watch the incoming indicators without reacting to them. Considering our forecast of 2.5% for Canada s 2018 real GDP growth, we see four Bank of Canada rate hikes this year, with the first one occurring on Wednesday. In other news, may have rebounded strongly in November based on a marked increase in exports of factory goods during the month. We ll also keep an eye on the release of for December and for November. Previous NBF forecasts Bank of Canada overnight rate 1.00% 1.25% Manufacturing sales (November m/m chg.) -0.4% 2.4% Canada: A rate hike by the Bank of Canada is in the cards Bank of Canada overnight rate vs. Fed funds rate (mid-point) % In the U.S, likely expanded further in December, buoyed by the manufacturing sector which continued to thrive according to the ISM manufacturing survey. A strong contribution from utilities is also expected, in line with colderthan-normal temperatures observed across the Northern regions of the country during the month. Overall, industrial production may have increased 0.8% m/m. We ll also get housing data for December, with a slight retreat expected for both and on account of a fading post-hurricane rebound. The first clues on the state of the manufacturing sector in December will be available with the publication of the. Finally, the latest edition of the will be released on Wednesday. Previous NBF forecasts Industrial production (December m/m chg.) 0.2% 0.8% Housing starts (December, saar) 1297K 1270K U.S.: Utilities may have boosted industrial production in December Industrial production m/m % chg. 1.0 BoC overnight rate Fed funds rate M M M M M M M M01 NBF Economics and Strategy (data via Bloomberg) NBF Forecast M M M M M M M M12 NBF Economics and Strategy (data via Datastream) NBF Forecast Elsewhere in the world, we ll get China s. Also, November s numbers will be released in the Eurozone. 4

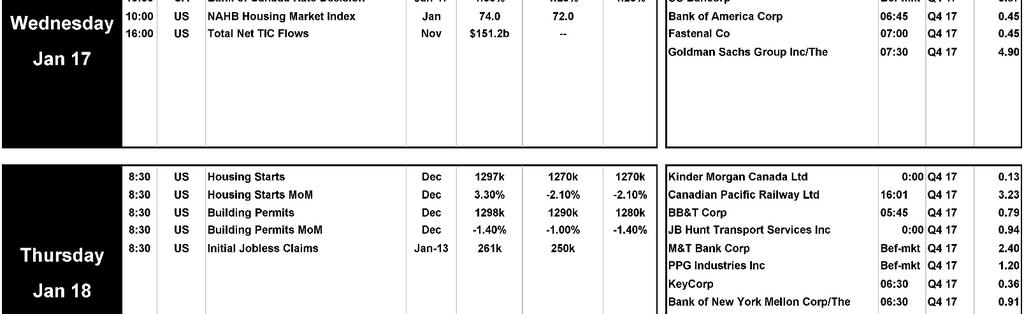

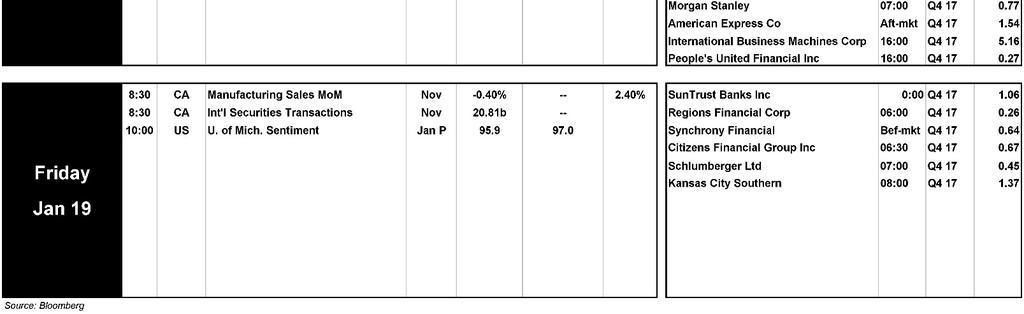

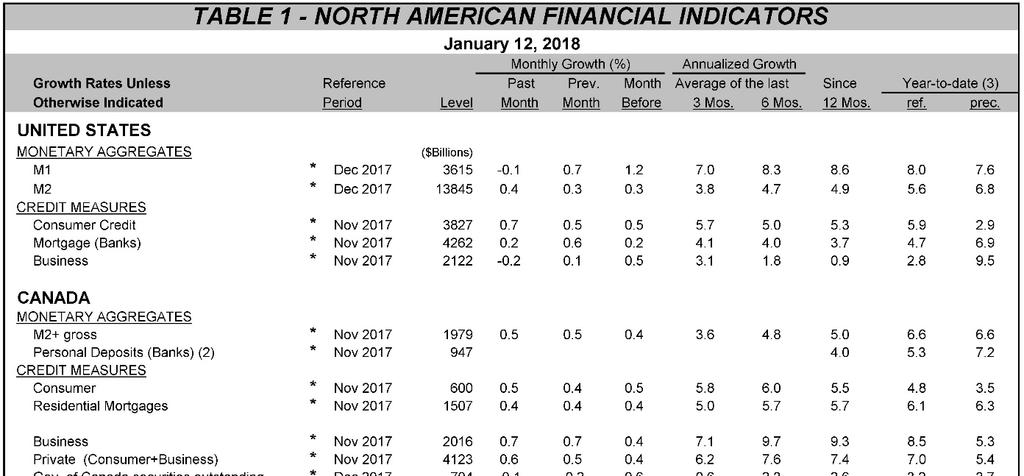

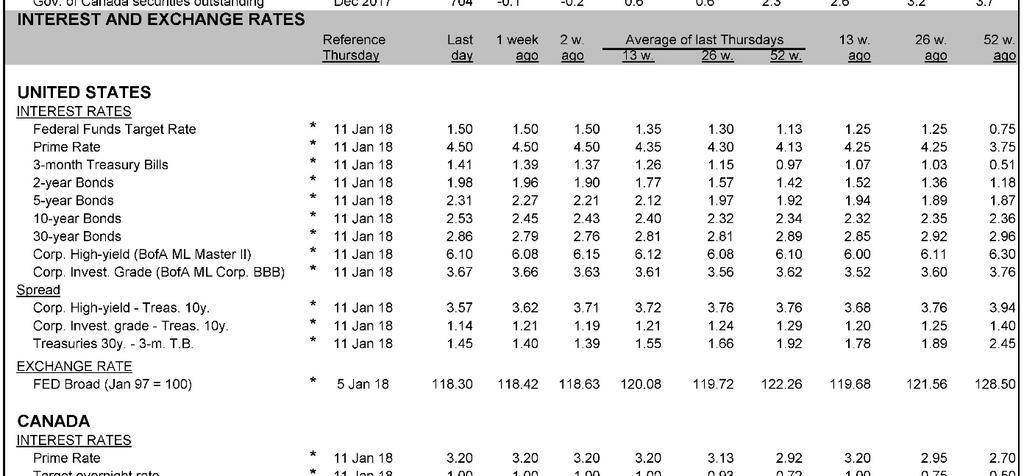

5 Economic Calendar Canada & U.S. 5

6 A1

7 A2

8 A3

9 A4

10 A5

11 A6

12 A7

13 A8

14 Economics and Strategy Montreal Office Toronto Office Stéfane Marion Marc Pinsonneault Kyle Dahms Warren Lovely Chief Economist and Strategist Senior Economist Economist MD, Public Sector Research and Strategy Paul-André Pinsonnault Matthieu Arseneau Jocelyn Paquet Senior Fixed Income Economist Senior Economist Economist Krishen Rangasamy Senior Economist Angelo Katsoras Geopolitical Analyst General This Report was prepared by National Bank Financial, Inc. (NBF), (a Canadian investment dealer, member of IIROC), an indirect wholly owned subsidiary of National Bank of Canada. National Bank of Canada is a public company listed on the Toronto Stock Exchange. The particulars contained herein were obtained from sources which we believe to be reliable but are not guaranteed by us and may be incomplete and may be subject to change without notice. The information is current as of the date of this document. Neither the author nor NBF assumes any obligation to update the information or advise on further developments relating to the topics or securities discussed. The opinions expressed are based upon the author(s) analysis and interpretation of these particulars and are not to be construed as a solicitation or offer to buy or sell the securities mentioned herein, and nothing in this Report constitutes a representation that any investment strategy or recommendation contained herein is suitable or appropriate to a recipient s individual circumstances. In all cases, investors should conduct their own investigation and analysis of such information before taking or omitting to take any action in relation to securities or markets that are analyzed in this Report. The Report alone is not intended to form the basis for an investment decision, or to replace any due diligence or analytical work required by you in making an investment decision. This Report is for distribution only under such circumstances as may be permitted by applicable law. This Report is not directed at you if NBF or any affiliate distributing this Report is prohibited or restricted by any legislation or regulation in any jurisdiction from making it available to you. You should satisfy yourself before reading it that NBF is permitted to provide this Report to you under relevant legislation and regulations. National Bank of Canada Financial Markets is a trade name used by National Bank Financial and National Bank of Canada Financial Inc. National Bank Financial Inc. or an affiliate thereof, owns or controls an equity interest in TMX Group Limited ( TMX Group ) and has a nominee director serving on the TMX Group s board of directors. As such, each such investment dealer may be considered to have an economic interest in the listing of securities on any exchange owned or operated by TMX Group, including the Toronto Stock Exchange, the TSX Venture Exchange and the Alpha Exchange. No person or company is required to obtain products or services from TMX Group or its affiliates as a condition of any such dealer supplying or continuing to supply a product or service. Canadian Residents NBF or its affiliates may engage in any trading strategies described herein for their own account or on a discretionary basis on behalf of certain clients and as market conditions change, may amend or change investment strategy including full and complete divestment. The trading interests of NBF and its affiliates may also be contrary to any opinions expressed in this Report. NBF or its affiliates often act as financial advisor, agent or underwriter for certain issuers mentioned herein and may receive remuneration for its services. As well NBF and its affiliates and/or their officers, directors, representatives, associates, may have a position in the securities mentioned herein and may make purchases and/or sales of these securities from time to time in the open market or otherwise. NBF and its affiliates may make a market in securities mentioned in this Report. This Report may not be independent of the proprietary interests of NBF and its affiliates. This Report is not considered a research product under Canadian law and regulation, and consequently is not governed by Canadian rules applicable to the publication and distribution of research Reports, including relevant restrictions or disclosures required to be included in research Reports.

15 UK Residents This Report is a marketing document. This Report has not been prepared in accordance with EU legal requirements designed to promote the independence of investment research and it is not subject to any prohibition on dealing ahead of the dissemination of investment research. In respect of the distribution of this Report to UK residents, NBF has approved the contents (including, where necessary, for the purposes of Section 21(1) of the Financial Services and Markets Act 2000). This Report is for information purposes only and does not constitute a personal recommendation, or investment, legal or tax advice. NBF and/or its parent and/or any companies within or affiliates of the National Bank of Canada group and/or any of their directors, officers and employees may have or may have had interests or long or short positions in, and may at any time make purchases and/or sales as principal or agent, or may act or may have acted as market maker in the relevant investments or related investments discussed in this Report, or may act or have acted as investment and/or commercial banker with respect hereto. The value of investments, and the income derived from them, can go down as well as up and you may not get back the amount invested. Past performance is not a guide to future performance. If an investment is denominated in a foreign currency, rates of exchange may have an adverse effect on the value of the investment. Investments which are illiquid may be difficult to sell or realise; it may also be difficult to obtain reliable information about their value or the extent of the risks to which they are exposed. Certain transactions, including those involving futures, swaps, and other derivatives, give rise to substantial risk and are not suitable for all investors. The investments contained in this Report are not available to retail customers and this Report is not for distribution to retail clients (within the meaning of the rules of the Financial Conduct Authority). Persons who are retail clients should not act or rely upon the information in this Report. This Report does not constitute or form part of any offer for sale or subscription of or solicitation of any offer to buy or subscribe for the securities described herein nor shall it or any part of it form the basis of or be relied on in connection with any contract or commitment whatsoever. This information is only for distribution to Eligible Counterparties and Professional Clients in the United Kingdom within the meaning of the rules of the Financial Conduct Authority. NBF is authorised and regulated by the Financial Conduct Authority and has its registered office at 71 Fenchurch Street, London, EC3M 4HD. NBF is not authorised by the Prudential Regulation Authority and the Financial Conduct Authority to accept deposits in the United Kingdom. U.S. Residents National Bank of Canada Financial Inc. (NBCFI), a broker-dealer registered with the U.S. Securities and Exchange Commission and a member of the Financial Industry Regulatory Authority (FINRA), and a member of the Securities Investor Protection Corporation (SIPC), is distributing this Report in the United States. NBCFI operates pursuant to a 15 a-6 Agreement with its Canadian affiliate, NBF Inc. This Report has been prepared in whole or in part by personnel employed by non-us affiliates of NBCFI that are not registered as broker/dealers in the US. These non-us personnel are not registered as associated persons of NBCFI and are not licensed or qualified as research analysts with FINRA or any other US regulatory authority and, accordingly, may not be subject (among other things) to FINRA restrictions regarding communications by a research analyst with the subject company, public appearances by research analysts and trading securities held in a research analyst account. The author(s) who prepared these Reports certify that this Report accurately reflects his or her personal opinions and views about the subject company or companies and its or their securities, and that no part of his/her compensation was, is, or will be directly or indirectly related to the specific recommendations or views expressed in this Report as to the securities or companies. NBF compensates the authors of this Report from a variety of sources, and such compensation is funded by the business activities of NBF including, Institutional Equity and Fixed Income Sales and Trading, Retail Sales, the correspondent clearing business and Corporate and Investment Banking. Because the views of its personnel may differ, members of the National Bank Financial Group may have or may in the future issue Reports that are inconsistent with this Report, or that reach conclusions different from those in this Report. To make further inquiry related to this Report, United States residents should contact their NBCFI registered representative. This document is intended for institutional investors and is not subject to all of the independence and disclosure standards under FINRA rules applicable to debt research Reports prepared for retail investors. This Report may not be independent of the proprietary interests of NBF, NBCFI, or their affiliates. NBF, NBCFI, or their affiliates may trade the securities covered in this Report for their own account and on a discretionary basis on behalf of certain clients. Such trading interests may be contrary to the recommendation(s) offered in this Report. HK Residents With respect to the distribution of this report in Hong Kong by NBC Financial Markets Asia Limited ( NBCFMA )which is licensed by the Securities and Futures Commission ( SFC ) to conduct Type 1 (dealing in securities) and Type 3 (leveraged foreign exchange trading) regulated activities, the contents of this report are solely for informational purposes. It has not been approved by, reviewed by, verified by or filed with any regulator in Hong Kong. Nothing herein is a recommendation, advice, offer or solicitation to buy or sell a product or service, nor an official confirmation of any transaction. None of the products issuers, NBCFMA or its affiliates or other persons or entities named herein are obliged to notify you of changes to any information and none of the foregoing assume any loss suffered by you in reliance of such information. The content of this report may contain information about investment products which are not authorized by SFC for offering to the public in Hong Kong and such information will only be available to, those persons who are Professional Investors (as defined in the Securities and Futures Ordinance of Hong Kong ( SFO )). If you are in any doubt as to your status you should consult a financial adviser or contact us. This material is not meant to be marketing materials and is not intended for public distribution. Please note that neither this material nor the product referred to is authorized for sale by SFC. Please refer to product prospectus for full details. There may be conflicts of interest relating to NBCFMA or its affiliates businesses. These activities and interests include potential multiple advisory, transactional and financial and other interests in securities and instruments that may be purchased or sold by NBCFMA or its affiliates, or in other investment vehicles which are managed by NBCFMA or its affiliates that may purchase or sell such securities and instruments. No other entity within the National Bank of Canada group, including National Bank of Canada and National Bank Financial Inc, is licensed or registered with the SFC. Accordingly, such entities and their employees are not permitted and do not intend to: (i) carry on a business in any regulated activity in Hong Kong; (ii) hold themselves out as carrying on a business in any regulated activity in Hong Kong; or (iii) actively market their services to the Hong Kong public. Copyright This Report may not be reproduced in whole or in part, or further distributed or published or referred to in any manner whatsoever, nor may the information, opinions or conclusions contained in it be referred to without in each case the prior express written consent of NBF.

Halifax, Vancouver and St.Catharines on the podium

April 23, 2018 Halifax, Vancouver and St.Catharines on the podium According to our proprietary Metropolitan Economic Momentum Index (see page 3 for methodology), Halifax enjoyed the largest economic upswing

April 23, 2018 Halifax, Vancouver and St.Catharines on the podium According to our proprietary Metropolitan Economic Momentum Index (see page 3 for methodology), Halifax enjoyed the largest economic upswing

A budget kept in balance by a draw from the stabilization reserve

March 27, 2018 A budget kept in balance by a draw from the stabilization reserve Highlights Quebec 2018 Budget Economics and Strategy Despite $848 million in additional spending in fiscal 2017-18, the

March 27, 2018 A budget kept in balance by a draw from the stabilization reserve Highlights Quebec 2018 Budget Economics and Strategy Despite $848 million in additional spending in fiscal 2017-18, the

Table of Contents. Week in review. What we ll be watching... p. 4 Calendar of upcoming releases... p. 5 Annex Economic tables...

May 11, 2018 Table of Contents What we ll be watching... p. 4 Calendar of upcoming releases... p. 5 Annex Economic tables... A1 Week in review CANADA: Canadian employment fell 1.1K in April according to

May 11, 2018 Table of Contents What we ll be watching... p. 4 Calendar of upcoming releases... p. 5 Annex Economic tables... A1 Week in review CANADA: Canadian employment fell 1.1K in April according to

Special Report. Reality check: Are Canadian households perched over a sinkhole?

Reality check: Are Canadian households perched over a sinkhole? May 10, 2018 Reality check: Are Canadian households perched over a sinkhole? By Matthieu Arseneau There are widespread concerns about the

Reality check: Are Canadian households perched over a sinkhole? May 10, 2018 Reality check: Are Canadian households perched over a sinkhole? By Matthieu Arseneau There are widespread concerns about the

Saskatchewan 2018 Budget

Sticking to the plan: On track for a surplus in 2019-20 Highlights Saskatchewan 2018 Budget Economics and Strategy April 10, 2018 Saskatchewan s 2017-18 deficit is now estimated at $595 million (0.8% of

Sticking to the plan: On track for a surplus in 2019-20 Highlights Saskatchewan 2018 Budget Economics and Strategy April 10, 2018 Saskatchewan s 2017-18 deficit is now estimated at $595 million (0.8% of

Special Report. Minimum wage: How much is too much? Economics and Strategy. Summary. Ontario goes for it

Economics and Strategy September 27, 2017 Minimum wage: How much is too much? Summary In June the Ontario government announced its intention to raise the province s minimum wage by the most in 50 years:

Economics and Strategy September 27, 2017 Minimum wage: How much is too much? Summary In June the Ontario government announced its intention to raise the province s minimum wage by the most in 50 years:

Job creation surges in Canada By Stéfane Marion

February 11, 19 Job creation surges in Canada By Stéfane Marion Canadian economic reports have now bettered expectations for almost eight consecutive weeks. As the chart below shows, Citi s index of economic

February 11, 19 Job creation surges in Canada By Stéfane Marion Canadian economic reports have now bettered expectations for almost eight consecutive weeks. As the chart below shows, Citi s index of economic

Highlights. Forecast dated January 5, United States. Canada. Paul-André Pinsonnault. January 2018

Highlights January 1 Given our expectation of above-potential GDP growth in the U.S. and its already-low unemployment rate, we see CPI inflation ex food and energy accelerating to.3 in Q4 1. In our view,

Highlights January 1 Given our expectation of above-potential GDP growth in the U.S. and its already-low unemployment rate, we see CPI inflation ex food and energy accelerating to.3 in Q4 1. In our view,

New Brunswick 2018 Budget

New investments mean one year delay in return to balance Highlights New Brunswick 2018 Budget Economics and Strategy January 30, 2018 New Brunswick bettered its key fiscal targets in 2017-18 and by a non-trivial

New investments mean one year delay in return to balance Highlights New Brunswick 2018 Budget Economics and Strategy January 30, 2018 New Brunswick bettered its key fiscal targets in 2017-18 and by a non-trivial

Ontario Economic Outlook & Fiscal Review

Ontario Economic Outlook & Fiscal Review Economics and Strategy November 15, 2018 First steps towards fiscal recovery with long-term plan to come 10 highlights from Ontario s 2018 Economic Outlook and

Ontario Economic Outlook & Fiscal Review Economics and Strategy November 15, 2018 First steps towards fiscal recovery with long-term plan to come 10 highlights from Ontario s 2018 Economic Outlook and

Table of Contents. Week in review. What we ll be watching... p. 3 Calendar of upcoming releases... p. 5 Annex Economic tables...

February 10, 2017 Table of Contents What we ll be watching... p. 3 Calendar of upcoming releases... p. 5 Annex Economic tables... A1 annualized as gains in energy, metal ores, mineral products, forestry,

February 10, 2017 Table of Contents What we ll be watching... p. 3 Calendar of upcoming releases... p. 5 Annex Economic tables... A1 annualized as gains in energy, metal ores, mineral products, forestry,

What s next in the seemingly never-ending Brexit Saga? By Angelo Katsoras

What s next in the seemingly never-ending Brexit Saga? By Angelo Katsoras March 11, 2019 Introduction When it comes to Brexit, the only certainty, it appears, is that there will be more uncertainty. Political

What s next in the seemingly never-ending Brexit Saga? By Angelo Katsoras March 11, 2019 Introduction When it comes to Brexit, the only certainty, it appears, is that there will be more uncertainty. Political

Public Sector Debt. Quick Hit Record net portfolio investment in January. FICC Strategy. Chart 2: Cheaper loonie attracts foreign buying

1999 1 3 7 9 11 13 1 17 19 FICC Strategy Quick Hit Record net portfolio investment in January March 18, 19 - (Vol. III, No. 36) Foreign net buying of Canadian securities returned in January with a vengeance.

1999 1 3 7 9 11 13 1 17 19 FICC Strategy Quick Hit Record net portfolio investment in January March 18, 19 - (Vol. III, No. 36) Foreign net buying of Canadian securities returned in January with a vengeance.

Table of Contents. Week in review. What we ll be watching... p. 5 Calendar of upcoming releases... p. 6 Annex Economic tables... A1.

May 18, 2018 Table of Contents What we ll be watching... p. 5 Calendar of upcoming releases... p. 6 Annex Economic tables... A1 Week in review CANADA: Canada s rose 0.1% (m/m) in April in seasonally adjusted

May 18, 2018 Table of Contents What we ll be watching... p. 5 Calendar of upcoming releases... p. 6 Annex Economic tables... A1 Week in review CANADA: Canada s rose 0.1% (m/m) in April in seasonally adjusted

Trade war = slower earnings growth

Trade war = slower earnings growth June 18, 2018 China announced last Saturday that it would retaliate tit-for-tat (same amounts and same dates) if the U.S. follows through on its decision to impose tariffs

Trade war = slower earnings growth June 18, 2018 China announced last Saturday that it would retaliate tit-for-tat (same amounts and same dates) if the U.S. follows through on its decision to impose tariffs

Special Report. Where are we in the cycle? Economics and Strategy. What does the yield curve say? Summary. What are the probabilities of recession?

Economics and Strategy May 18, 017 Where are we in the cycle? Summary The odds of a recession in Canada or the U.S. in the years ahead is a contentious question in the economic community and the media.

Economics and Strategy May 18, 017 Where are we in the cycle? Summary The odds of a recession in Canada or the U.S. in the years ahead is a contentious question in the economic community and the media.

Earnings diffusion at a 2-year low

Earnings diffusion at a 2-year low October 9, 2018 Global equities ended the first week of Q4 2018 on a negative note with the MSCI AC retreating 1.5%. Emerging markets were hit particularly hard with

Earnings diffusion at a 2-year low October 9, 2018 Global equities ended the first week of Q4 2018 on a negative note with the MSCI AC retreating 1.5%. Emerging markets were hit particularly hard with

The behind the scenes struggle to choose the ECB's next leader By Angelo Katsoras

The behind the scenes struggle to choose the ECB's next leader By Angelo Katsoras March 13, 2019 Europe s faltering economy and fractious politics, which limit the capacity of members to agree on important

The behind the scenes struggle to choose the ECB's next leader By Angelo Katsoras March 13, 2019 Europe s faltering economy and fractious politics, which limit the capacity of members to agree on important

Highlights. Stéfane Marion Matthieu Arseneau December 2017

December 217 Highlights The MSCI AC is on track to return more than 15% this year, the best showing in four years. Importantly, the equity rally remains fuelled by better-than-expected profits. As long

December 217 Highlights The MSCI AC is on track to return more than 15% this year, the best showing in four years. Importantly, the equity rally remains fuelled by better-than-expected profits. As long

Table of Contents. Week in review. What we ll be watching... p. 5 Calendar of upcoming releases... p. 6 Annex Economic tables...

June 1, 2018 Table of Contents What we ll be watching... p. 5 Calendar of upcoming releases... p. 6 Annex Economic tables... A1 Week in review CANADA: Real expanded at an annualized pace of just 1.3% in

June 1, 2018 Table of Contents What we ll be watching... p. 5 Calendar of upcoming releases... p. 6 Annex Economic tables... A1 Week in review CANADA: Real expanded at an annualized pace of just 1.3% in

Stock-bond correlations: Are we at an inflection point?

Stock-bond correlations: Are we at an inflection point? Historical perspective December 4, 2018 The correlation between U.S. equity prices and U.S. Treasury yields has fluctuated significantly over the

Stock-bond correlations: Are we at an inflection point? Historical perspective December 4, 2018 The correlation between U.S. equity prices and U.S. Treasury yields has fluctuated significantly over the

Can the loonie make a comeback?

Can the loonie make a comeback? December 217 Even considering the low rate of U.S. inflation, monetary policy in the world s largest economy is arguably too loose. It s the first time since the 197 s that

Can the loonie make a comeback? December 217 Even considering the low rate of U.S. inflation, monetary policy in the world s largest economy is arguably too loose. It s the first time since the 197 s that

Quick Hit International securities transactions: A currency story

Nov-16 Jan-17 Mar-17 May-17 Jul-17 Sep-17 Nov-17 Jan-18 Mar-18 May-18 Jul-18 Sep-18 Nov-18 22 23 24 25 26 27 28 29 21 211 212 213 214 215 216 217 218 FICC Strategy January 18, 219 - (Vol. III, No. 9) Quick

Nov-16 Jan-17 Mar-17 May-17 Jul-17 Sep-17 Nov-17 Jan-18 Mar-18 May-18 Jul-18 Sep-18 Nov-18 22 23 24 25 26 27 28 29 21 211 212 213 214 215 216 217 218 FICC Strategy January 18, 219 - (Vol. III, No. 9) Quick

Q1/19

Highlights May 2018 With the U.S. economic expansion still on track, we think the 10-year yield will drift to a new trading range slightly above 3. Though we recognize that the risks are skewed toward

Highlights May 2018 With the U.S. economic expansion still on track, we think the 10-year yield will drift to a new trading range slightly above 3. Though we recognize that the risks are skewed toward

Highlights. Stéfane Marion Matthieu Arseneau December 2018

December 218 Highlights After a promising rebound in November, global equity markets fell back early in December. The outlook for earnings growth remains uncertain. The good news is that at the G2 meeting

December 218 Highlights After a promising rebound in November, global equity markets fell back early in December. The outlook for earnings growth remains uncertain. The good news is that at the G2 meeting

Public Sector Strategy

KOR FRA Fixed Income Trading Desk Strategy Quick Hit The 2018 sovereign fiscal report card - (Vol. II, No. 33) The recently released IMF Fiscal Monitor provides a fresh set of metrics to gauge cross-country

KOR FRA Fixed Income Trading Desk Strategy Quick Hit The 2018 sovereign fiscal report card - (Vol. II, No. 33) The recently released IMF Fiscal Monitor provides a fresh set of metrics to gauge cross-country

Rising EU-US trade tensions only add to Europe s challenges

Rising EU-US trade tensions only add to Europe s challenges July 3, 2018 The EU is the latest region to be accused of unfair trade practices by the Trump administration. It is estimated that the EU has

Rising EU-US trade tensions only add to Europe s challenges July 3, 2018 The EU is the latest region to be accused of unfair trade practices by the Trump administration. It is estimated that the EU has

IS IT TIME TO PULL BACK STIMULUS?

August 1, 17 IS IT TIME TO PULL BACK STIMULUS? Summary Central bankers have shown over the years that there can indeed be too much of a good thing. Ultra-loose monetary policy stimulus may have been warranted

August 1, 17 IS IT TIME TO PULL BACK STIMULUS? Summary Central bankers have shown over the years that there can indeed be too much of a good thing. Ultra-loose monetary policy stimulus may have been warranted

Public Sector Research

Fixed Income Trading Desk Research Quick Hit GoC T-bills the ultimate fiscal shock absorber PLEASE SEE END OF DOCUMENT FOR IMPORTANT DISCLOSURES October 17, 17 - (Vol. 1, No. 53) The Government of Canada

Fixed Income Trading Desk Research Quick Hit GoC T-bills the ultimate fiscal shock absorber PLEASE SEE END OF DOCUMENT FOR IMPORTANT DISCLOSURES October 17, 17 - (Vol. 1, No. 53) The Government of Canada

Top Charts. Top Charts. Canada: Top charts to think about going into December 22, 2017

Top Charts Canada: Top charts to think about going into 218 December 22, 21 1 Canada: Top charts to think about going into 218 The holiday season is upon us, promising, as every year, to bring its share

Top Charts Canada: Top charts to think about going into 218 December 22, 21 1 Canada: Top charts to think about going into 218 The holiday season is upon us, promising, as every year, to bring its share

Highlights. April 2016

Highlights April 216 We are relieved that Beijing has veered away from currency devaluation in its effort to spur growth. The authorities announced a fiscal deficit of 3% of GDP for 216, up from 2.5% last

Highlights April 216 We are relieved that Beijing has veered away from currency devaluation in its effort to spur growth. The authorities announced a fiscal deficit of 3% of GDP for 216, up from 2.5% last

Savaria Corporation. Q2/17 Results. Span contribution begins; guidance revised (unsurprisingly) upwards HIGHLIGHTS. The NBF Daily Bulletin

upwards HIGHLIGHTS. The NBF Daily Bulletin") SIS (T) $15.06 Stock Rating: Outperform Target: $17.00 Risk Rating: Above Average Est. Total Return 14.6% Stock Data: 52-w eek High-Low $17.55 - $7.74 Bloomberg/Reuters SIS CN / SIS.TO Shares Outstanding

SIS (T) $15.06 Stock Rating: Outperform Target: $17.00 Risk Rating: Above Average Est. Total Return 14.6% Stock Data: 52-w eek High-Low $17.55 - $7.74 Bloomberg/Reuters SIS CN / SIS.TO Shares Outstanding

Public Sector Research

Fixed Income Trading Desk Research Domestic Bond Tracker: Issuance patterns ever more entrenched Another month is in the books and when it comes to domestic supply patterns at least, certain themes are

Fixed Income Trading Desk Research Domestic Bond Tracker: Issuance patterns ever more entrenched Another month is in the books and when it comes to domestic supply patterns at least, certain themes are

Budget deficits and the U.S. dollar

Budget deficits and the U.S. dollar March 218 The February announcement by Congress that it would increase government spending this year and next will prompt a temporary growth spurt in the U.S. but have

Budget deficits and the U.S. dollar March 218 The February announcement by Congress that it would increase government spending this year and next will prompt a temporary growth spurt in the U.S. but have

2018Q1 2018Q2 2018Q3 2018Q4

Feeding the beast November 2017 The U.S. economy is doing well enough to prompt the Federal Reserve to consider further tightening of monetary policy. A December rate hike is in the cards, assuming of

Feeding the beast November 2017 The U.S. economy is doing well enough to prompt the Federal Reserve to consider further tightening of monetary policy. A December rate hike is in the cards, assuming of

Dollarama Inc. Q4 F2017 Results. A straight-forward beat and other notable business updates HIGHLIGHTS. The NBF Daily Bulletin.

DOL (T) $110.88 Stock Rating: Outperform (Unchanged) Target: $122.00 (Was $113.00) Risk Rating: Below Average (Unchanged) Est. Total Return: 10.4% Stock Data: 52-week High-Low (Canada) Bloomberg $104.94

DOL (T) $110.88 Stock Rating: Outperform (Unchanged) Target: $122.00 (Was $113.00) Risk Rating: Below Average (Unchanged) Est. Total Return: 10.4% Stock Data: 52-week High-Low (Canada) Bloomberg $104.94

Canada s never-ending pipeline saga

May 14, 2018 Canada s never-ending pipeline saga While the global media focuses on the mounting trade tensions between China and the United States, Canada is mired in its very own domestic trade war. This

May 14, 2018 Canada s never-ending pipeline saga While the global media focuses on the mounting trade tensions between China and the United States, Canada is mired in its very own domestic trade war. This

Highlights. Stéfane Marion Matthieu Arseneau January/February 2018

January/February 218 Highlights After a spectacular 217 that saw global equities return more than 17.5, the MSCI All Country index has continued to do extremely well early in 218 with a gain of 5.7 year

January/February 218 Highlights After a spectacular 217 that saw global equities return more than 17.5, the MSCI All Country index has continued to do extremely well early in 218 with a gain of 5.7 year

Q1/16

Highlights May 1 We see U.S. economic growth accelerating to -plus in the second half of the year. Given that outlook, we continue to believe that by mid-september the FOMC will be confident enough of

Highlights May 1 We see U.S. economic growth accelerating to -plus in the second half of the year. Given that outlook, we continue to believe that by mid-september the FOMC will be confident enough of

Crius Energy Trust. Resuming Coverage. USGE Provides Enhanced Footprint, Diversification & Cross-Sell Potential

KWH.un (T) Stock Rating: Target: Risk Rating: Cdn$10.14 Outperform Cdn$13.00 Average Est. Total Return 35.9% Stock Data: Cash Yield 7.7% Implied Price Return 28.2% 52-w eek High-Low $11.32-$7.76 Bloomberg/Reuters:

KWH.un (T) Stock Rating: Target: Risk Rating: Cdn$10.14 Outperform Cdn$13.00 Average Est. Total Return 35.9% Stock Data: Cash Yield 7.7% Implied Price Return 28.2% 52-w eek High-Low $11.32-$7.76 Bloomberg/Reuters:

Optimistic Fed supportive of USD

Optimistic Fed supportive of USD August 218 The U.S. dollar s near term prospects remain good amidst a hot economy that is prompting the Fed to tighten monetary policy. The return of risk aversion in the

Optimistic Fed supportive of USD August 218 The U.S. dollar s near term prospects remain good amidst a hot economy that is prompting the Fed to tighten monetary policy. The return of risk aversion in the

A rate hike for Christmas

December 215 A rate hike for Christmas A December interest rate hike isn t fully priced-in by markets and as such there is upside potential for the USD if the FOMC delivers on its repeated warnings that

December 215 A rate hike for Christmas A December interest rate hike isn t fully priced-in by markets and as such there is upside potential for the USD if the FOMC delivers on its repeated warnings that

Public Sector Strategy

Fixed Income Trading Desk Strategy Quick Hit Refi recon PLEASE SEE END OF DOCUMENT FOR IMPORTANT DISCLOSURES January 23, 218 - (Vol. 2, No. 5) My strategy colleague, Connor Sedgewick, offered up some nice

Fixed Income Trading Desk Strategy Quick Hit Refi recon PLEASE SEE END OF DOCUMENT FOR IMPORTANT DISCLOSURES January 23, 218 - (Vol. 2, No. 5) My strategy colleague, Connor Sedgewick, offered up some nice

Highlights. Change from Previous Forecast

Highlights December 217 While not a blockbuster year, 217 was nonetheless encouraging on many fronts. The world s largest economy, the U.S., seemingly got back its mojo, while export powerhouses such as

Highlights December 217 While not a blockbuster year, 217 was nonetheless encouraging on many fronts. The world s largest economy, the U.S., seemingly got back its mojo, while export powerhouses such as

Cyclical USD weakness

May 215 Cyclical USD weakness The trade-weighted US dollar s impressive run ended with a nearly 2% decline in April, the worst monthly performance since September 213. Weaker than expected US economic

May 215 Cyclical USD weakness The trade-weighted US dollar s impressive run ended with a nearly 2% decline in April, the worst monthly performance since September 213. Weaker than expected US economic

Back in black and aiming to stay there

Back in black and aiming to stay there By Catherine Maltais / Warren Lovely March 20, 2019 Highlights The summary deficit for the year ending March 31 is now estimated at $380 million (0.5% of GDP), a

Back in black and aiming to stay there By Catherine Maltais / Warren Lovely March 20, 2019 Highlights The summary deficit for the year ending March 31 is now estimated at $380 million (0.5% of GDP), a

May Highlights

Highlights May 215 Global equities rose to another all-time high in April. Encouragingly, the gains have been widespread. All major regions show positive returns so far in 215. Markets where central banks

Highlights May 215 Global equities rose to another all-time high in April. Encouragingly, the gains have been widespread. All major regions show positive returns so far in 215. Markets where central banks

Economic diversification & long-term deficit reduction in focus

March 22, 2018 Economic diversification & long-term deficit reduction in focus Highlights Alberta 2018 Budget Economics and Strategy After a couple of very tough years, Alberta s economy regained important

March 22, 2018 Economic diversification & long-term deficit reduction in focus Highlights Alberta 2018 Budget Economics and Strategy After a couple of very tough years, Alberta s economy regained important

The story behind China s crackdown on outbound investments

October 4, 2017 The story behind China s crackdown on outbound investments Introduction China considers its foreign exchange reserves to be a vital shield against potential economic headwinds. This is

October 4, 2017 The story behind China s crackdown on outbound investments Introduction China considers its foreign exchange reserves to be a vital shield against potential economic headwinds. This is

Highlights By Krishen Rangasamy

February 219 Highlights By Krishen Rangasamy With China and the Eurozone seemingly on the ropes, it s difficult to be optimistic about the global economy s performance this year. Fortunately, the persistence

February 219 Highlights By Krishen Rangasamy With China and the Eurozone seemingly on the ropes, it s difficult to be optimistic about the global economy s performance this year. Fortunately, the persistence

Highlights. Change from Previous Forecast

Highlights February 18 A flying start to 18 puts the world economy on track to top last year s growth print of 3.7. Buoyed by tax cuts, the U.S. will be among the growth leaders within the OECD, while

Highlights February 18 A flying start to 18 puts the world economy on track to top last year s growth print of 3.7. Buoyed by tax cuts, the U.S. will be among the growth leaders within the OECD, while

Public Sector Strategy

Fixed Income Trading Desk Strategy August 15, 218 - (Vol. II, No. 6) Quick Hit The government sector s heavy economic footprint If Friday s jobs report is to be believed, Canada has become increasing reliant

Fixed Income Trading Desk Strategy August 15, 218 - (Vol. II, No. 6) Quick Hit The government sector s heavy economic footprint If Friday s jobs report is to be believed, Canada has become increasing reliant

Highlights. Change from Previous Forecast

Highlights January 19 The global economy s loss of momentum in the last quarter of 18 represents a poor handoff. That will penalize 19, the latter s GDP growth likely to be just below last year s estimated.

Highlights January 19 The global economy s loss of momentum in the last quarter of 18 represents a poor handoff. That will penalize 19, the latter s GDP growth likely to be just below last year s estimated.

World trade rises 5.3% in Q1 2010

June 2010 TABLE OF CONTENTS World trade rises 5.3% in Q1 2010 1 Highlights 2 The Canadian economy 2 The U.S. economy 3 Oil prices tumble after US jobs report 4 Flight to quality hits Canadian dollar 4

June 2010 TABLE OF CONTENTS World trade rises 5.3% in Q1 2010 1 Highlights 2 The Canadian economy 2 The U.S. economy 3 Oil prices tumble after US jobs report 4 Flight to quality hits Canadian dollar 4

Highlights. Change from Previous Forecast

Highlights May 18 The global economy continued to expand in the first quarter, albeit at a more moderate pace. The persistence of low inflation should limit the extent of monetary policy tightening by

Highlights May 18 The global economy continued to expand in the first quarter, albeit at a more moderate pace. The persistence of low inflation should limit the extent of monetary policy tightening by

New Paradigm or Same Old?

New Paradigm or Same Old? Megan Greene Chief Economist, Portfolio Solutions Group October 2017 For a discussion of the risks associated with this strategy, please see the Investment Considerations page

New Paradigm or Same Old? Megan Greene Chief Economist, Portfolio Solutions Group October 2017 For a discussion of the risks associated with this strategy, please see the Investment Considerations page

Special Report. Reality check: Canadian exposure to U.S. protectionism

Reality check: Canadian exposure to U.S. protectionism March 28, 2018 Reality check: Canadian exposure to U.S. protectionism Since his inauguration in January 2016, President Donald Trump has brought his

Reality check: Canadian exposure to U.S. protectionism March 28, 2018 Reality check: Canadian exposure to U.S. protectionism Since his inauguration in January 2016, President Donald Trump has brought his

US Economics. RBC Capital Markets, LLC Jacob Oubina Director, Senior US Economist (212) ; ECONOMICS I RESEARCH

; ECONOMICS I RESEARCH") ECONOMICS I RESEARCH US Economics October 2015, LLC Jacob Oubina Director, Senior US Economist (212) 618-7795; jacob.oubina@rbccm.com For Required Conflicts Disclosures, please see the back of this document.

ECONOMICS I RESEARCH US Economics October 2015, LLC Jacob Oubina Director, Senior US Economist (212) 618-7795; jacob.oubina@rbccm.com For Required Conflicts Disclosures, please see the back of this document.

Economic outlook: Manitoba in the middle

Economic outlook: Manitoba in the middle May 17, 2016 Douglas Porter, CFA Chief Economist, BMO Financial Group douglas.porter@bmo.com 416-359-4887 Please refer to the next page for Important Disclosures

Economic outlook: Manitoba in the middle May 17, 2016 Douglas Porter, CFA Chief Economist, BMO Financial Group douglas.porter@bmo.com 416-359-4887 Please refer to the next page for Important Disclosures

FOCUS ON CANADA S HOUSEHOLD DEBT

FOCUS ON CANADA S HOUSEHOLD DEBT December, 1 Interest payments surged in the third quarter as Canadian household s indebtedness looked heavier than previously reported Household indebtedness held relatively

FOCUS ON CANADA S HOUSEHOLD DEBT December, 1 Interest payments surged in the third quarter as Canadian household s indebtedness looked heavier than previously reported Household indebtedness held relatively

January 11, Special Report. Is Canada s household leverage too high or on the low side? Economics and Strategy

January 11, 2018 Special Report Is Canada s household leverage too high or on the low side? Economics and Strategy Is Canada s household leverage too high or on the low side? Household debt in Canada is

January 11, 2018 Special Report Is Canada s household leverage too high or on the low side? Economics and Strategy Is Canada s household leverage too high or on the low side? Household debt in Canada is

Editor: Thomas Nilsson. The Week Ahead Key Events Jul, 2017

Editor: Thomas Nilsson The Week Ahead Key Events 10 16 Jul, 2017 European Sovereign Rating Reviews Recent rating reviews Upcoming rating reviews Source: Bloomberg Monday 10, 08.00 NOR: CPI (Jun) SEB Cons.

Editor: Thomas Nilsson The Week Ahead Key Events 10 16 Jul, 2017 European Sovereign Rating Reviews Recent rating reviews Upcoming rating reviews Source: Bloomberg Monday 10, 08.00 NOR: CPI (Jun) SEB Cons.

THE TRUMPQUAKE. Are you not entertained? Summary. The markets like the show, for now. November 10, 2016

November 10, 2016 THE TRUMPQUAKE Summary The Republican Party is in a good position to advance its agenda after winning the White House, the Senate and the House of Representatives for the first time since

November 10, 2016 THE TRUMPQUAKE Summary The Republican Party is in a good position to advance its agenda after winning the White House, the Senate and the House of Representatives for the first time since

The China-U.S. trade war of attrition

July 18, 2018 The China-U.S. trade war of attrition U.S. President Donald Trump has finally made good on his threat. He recently imposed tariffs on $34 billion worth of merchandise imports from China,

July 18, 2018 The China-U.S. trade war of attrition U.S. President Donald Trump has finally made good on his threat. He recently imposed tariffs on $34 billion worth of merchandise imports from China,

British Columbia 2018 Budget

February 20, 2018 BC stays in balance with ample padding, focuses on affordability Highlights British Columbia 2018 Budget Economics and Strategy British Columbia s minority NDP government has been plenty

February 20, 2018 BC stays in balance with ample padding, focuses on affordability Highlights British Columbia 2018 Budget Economics and Strategy British Columbia s minority NDP government has been plenty

Economic outlook Trump: Taxes, Trade & Treasuries

Economic outlook Trump: Taxes, Trade & Treasuries January 17, 2017 Douglas Porter, CFA Chief Economist, BMO Financial Group douglas.porter@bmo.com 416-359-4887 Please refer to the next page for Important

Economic outlook Trump: Taxes, Trade & Treasuries January 17, 2017 Douglas Porter, CFA Chief Economist, BMO Financial Group douglas.porter@bmo.com 416-359-4887 Please refer to the next page for Important

Week in review. What we ll be watching (p. 3) Calendar of upcoming releases (p. 5) Annex Economic tables (A1) January 13, 2017

Calendar of upcoming releases (p. 5) Annex Economic tables (A1) January 13, 2017") What we ll be watching (p. 3) Calendar of upcoming releases (p. 5) Annex Economic tables (A1) Week in review Canada In December, the Teranet National Bank National Composite House Price Index rose 0.3%

What we ll be watching (p. 3) Calendar of upcoming releases (p. 5) Annex Economic tables (A1) Week in review Canada In December, the Teranet National Bank National Composite House Price Index rose 0.3%

Federal 2018 Fall Economic Statement

November 21, 2018 Business tax relief delivered, resulting in a bit of extra red ink Highlights Federal 2018 Fall Economic Statement Economics and Strategy Ottawa s fall fiscal update took some non-trivial

November 21, 2018 Business tax relief delivered, resulting in a bit of extra red ink Highlights Federal 2018 Fall Economic Statement Economics and Strategy Ottawa s fall fiscal update took some non-trivial

March 12, Quebecor Inc. Quarterly Preview HIGHLIGHTS

QBR.b (T) Stock Rating: Target: Risk Rating: Cdn$38.74 Outperform (Unchanged) Cdn$43. (Unchanged) Above Average (Unchanged) Est. Total Return 11.5% Stock Data: 52-w eek High-Low (Canada) $41.22 - $31.53

QBR.b (T) Stock Rating: Target: Risk Rating: Cdn$38.74 Outperform (Unchanged) Cdn$43. (Unchanged) Above Average (Unchanged) Est. Total Return 11.5% Stock Data: 52-w eek High-Low (Canada) $41.22 - $31.53

VIX to Fall; Stocks to Rise; Small to Outperform

RBC Capital Markets, LLC October 14, 2014 VIX to Fall; Stocks to Rise; Small to Outperform Market Delivers Above-Average Returns Following Volatility Spikes Investor concerns regarding global growth have

RBC Capital Markets, LLC October 14, 2014 VIX to Fall; Stocks to Rise; Small to Outperform Market Delivers Above-Average Returns Following Volatility Spikes Investor concerns regarding global growth have

It s fun to stay in the USMCA

It s fun to stay in the USMCA October 2018 After months of negotiations, Canada finally agreed to a revamped trade deal with the U.S. and Mexico. The United States-Mexico-Canada Agreement (USMCA for short)

It s fun to stay in the USMCA October 2018 After months of negotiations, Canada finally agreed to a revamped trade deal with the U.S. and Mexico. The United States-Mexico-Canada Agreement (USMCA for short)

Can Russia live up to its geopolitical ambitions?

August 27, 2018 Can Russia live up to its geopolitical ambitions? Russia s geopolitical influence is at its highest level since the end of the cold war and fall of the Soviet Union nearly thirty years

August 27, 2018 Can Russia live up to its geopolitical ambitions? Russia s geopolitical influence is at its highest level since the end of the cold war and fall of the Soviet Union nearly thirty years

How will NAFTA negotiations play out?

How will NAFTA negotiations play out? September 6, 2017 Introduction Donald Trump s promise to take a much tougher line on trade was a key part of his election platform. After withdrawing from the Trans-Pacific

How will NAFTA negotiations play out? September 6, 2017 Introduction Donald Trump s promise to take a much tougher line on trade was a key part of his election platform. After withdrawing from the Trans-Pacific

The impossible trinity

February 216 The impossible trinity China is learning, the hard way, about the impossible trinity. You just cannot have free capital flows, a fixed exchange rate and independent monetary policy all at

February 216 The impossible trinity China is learning, the hard way, about the impossible trinity. You just cannot have free capital flows, a fixed exchange rate and independent monetary policy all at

Business Outlook Survey

Results of the Winter 213 14 Survey Vol. 1.4 13 January 214 The winter provides some positive signs for the economic outlook, notably for exports and investment, although responses do not yet appear to

Results of the Winter 213 14 Survey Vol. 1.4 13 January 214 The winter provides some positive signs for the economic outlook, notably for exports and investment, although responses do not yet appear to

Global PMI. Solid Q2 growth masks widening growth differentials. July 7 th IHS Markit. All Rights Reserved.

Global PMI Solid Q2 growth masks widening growth differentials July 7 th 2017 2 Widening developed and emerging world growth trends The global economy enjoyed further steady growth in June, according to

Global PMI Solid Q2 growth masks widening growth differentials July 7 th 2017 2 Widening developed and emerging world growth trends The global economy enjoyed further steady growth in June, according to

nbc.ca/fxsnapshot... Development Team Fixed Income & Commodity FX Team Toronto Customer Service ...

FX Team Montreal Customer Service FX Team Toronto Customer Service Development Team Fixed Income & Commodity 514 394 6910 1 800 286 6586 416 869 8901 1 800 663 6673 514 394 6885 1 855 394 6885 Major News

FX Team Montreal Customer Service FX Team Toronto Customer Service Development Team Fixed Income & Commodity 514 394 6910 1 800 286 6586 416 869 8901 1 800 663 6673 514 394 6885 1 855 394 6885 Major News

Retail Sales Rebound in Canada and the United States

WEEKLY NEWSLETTER Retail Sales Rebound in Canada and the United States #1 BEST OVERALL FORECASTER - CANADA HIGHLIGHTS ff Retail sales in the United States rebounded significantly in. ff Canada: The total

WEEKLY NEWSLETTER Retail Sales Rebound in Canada and the United States #1 BEST OVERALL FORECASTER - CANADA HIGHLIGHTS ff Retail sales in the United States rebounded significantly in. ff Canada: The total

GLOBAL ECONOMICS GLOBAL AUTO REPORT

North American Auto Production Begins To Rebound CONTACTS Global sales gains moderate as purchases decline temporarily in Asia. US inventories fall below a year earlier, setting the stage for a rebound

North American Auto Production Begins To Rebound CONTACTS Global sales gains moderate as purchases decline temporarily in Asia. US inventories fall below a year earlier, setting the stage for a rebound

Why heightened trade tensions between China and the United States is the new normal

April 3, 2018 Why heightened trade tensions between China and the United States is the new normal Introduction Now that the threat of NAFTA being shredded has abated, attention has turned to the two countries

April 3, 2018 Why heightened trade tensions between China and the United States is the new normal Introduction Now that the threat of NAFTA being shredded has abated, attention has turned to the two countries

Flash Note Japan: Second reading of Q2 GDP

FLASH NOTE Flash Note Japan: Second reading of Q2 GDP GDP forecast revised up but external uncertainties persist Pictet Wealth Management - Asset Allocation & Macro Research 11 September 2018 The second

FLASH NOTE Flash Note Japan: Second reading of Q2 GDP GDP forecast revised up but external uncertainties persist Pictet Wealth Management - Asset Allocation & Macro Research 11 September 2018 The second

Letko, Brosseau & Associates Inc. Global Investment Management Since 1987

Letko, Brosseau & Associates Inc. Global Investment Management Since 1987 Economic and Capital Markets Outlook About us Letko, Brosseau & Associates Inc. is an independent, global investment management

Letko, Brosseau & Associates Inc. Global Investment Management Since 1987 Economic and Capital Markets Outlook About us Letko, Brosseau & Associates Inc. is an independent, global investment management

Breaking Out ECONOMIC RESEARCH. Robert Kavcic, Senior Economist June 8, 2018

Robert Kavcic, Senior Economist June 8, 2018 Breaking Out Equity markets posted modest gains this week, with little in the way of major market-moving economic data. The S&P 500 rose 1.6% on broad-based

Robert Kavcic, Senior Economist June 8, 2018 Breaking Out Equity markets posted modest gains this week, with little in the way of major market-moving economic data. The S&P 500 rose 1.6% on broad-based

Hudson s Bay Company. Q4 F2016 Preview. Efficiency initiatives and F2017 guidance in focus HIGHLIGHTS. The NBF Daily Bulletin.

HBC (T) $10.08 Stock Rating: Sector Perform (Unchanged) Target: $15.00 (Unchanged) Risk Rating: Above Average (Unchanged) Est. Total Return: 50.8% Stock Data: 52-week High-Low (Canada) Bloomberg $19.69

HBC (T) $10.08 Stock Rating: Sector Perform (Unchanged) Target: $15.00 (Unchanged) Risk Rating: Above Average (Unchanged) Est. Total Return: 50.8% Stock Data: 52-week High-Low (Canada) Bloomberg $19.69

file:///c:/users/cathy/appdata/local/microsoft/windows/temporary Int...

1 of 5 9/25/17, 8:57 AM A Publication of the National Association of Manufacturers September 25, 2017 As expected, the Federal Reserve opted to not raise short-term interest rates at its September 19 20

1 of 5 9/25/17, 8:57 AM A Publication of the National Association of Manufacturers September 25, 2017 As expected, the Federal Reserve opted to not raise short-term interest rates at its September 19 20

LETTER. economic. Is Canada experiencing a housing bubble, or just a balloon? JULY 2012 AUGUST bdc.ca

economic LETTER JULY 212 AUGUST 212 Is Canada experiencing a housing bubble, or just a balloon? The low interest rates that have held sway in Canada for the past several years have stimulated the housing

economic LETTER JULY 212 AUGUST 212 Is Canada experiencing a housing bubble, or just a balloon? The low interest rates that have held sway in Canada for the past several years have stimulated the housing

Ontario Economic Accounts

SECOND QUARTER OF 2017 April, May, June Ontario Economic Accounts ONTARIO MINISTRY OF FINANCE Table of Contents ECONOMIC ACCOUNTS Highlights 1 Ontario s Economy Continues to Grow Expenditure Details 2

SECOND QUARTER OF 2017 April, May, June Ontario Economic Accounts ONTARIO MINISTRY OF FINANCE Table of Contents ECONOMIC ACCOUNTS Highlights 1 Ontario s Economy Continues to Grow Expenditure Details 2

LETTER. economic COULD INTEREST RATES HEAD UP IN 2015? JANUARY Canada. United States. Interest rates. Oil price. Canadian dollar.

economic LETTER JANUARY 215 COULD INTEREST RATES HEAD UP IN 215? For six years now, that is, since the financial crisis that shook the world in 28, Canadian interest rates have stayed low. The key interest

economic LETTER JANUARY 215 COULD INTEREST RATES HEAD UP IN 215? For six years now, that is, since the financial crisis that shook the world in 28, Canadian interest rates have stayed low. The key interest

Canada s Economy Strengthens

Dr. Sherry Cooper Chief Economist Dominion Lending Centres The Title of the presentation Second line if needed Third line if needed Canada s Economy Strengthens Today s date Location of presentation June

Dr. Sherry Cooper Chief Economist Dominion Lending Centres The Title of the presentation Second line if needed Third line if needed Canada s Economy Strengthens Today s date Location of presentation June

Main Economic & Financial Indicators Hungary

Main Economic & Financial Indicators Hungary 6 AUGUST 2015 NAOKO ISHIHARA ECONOMIST ECONOMIC RESEARCH OFFICE (LONDON) T +44-(0)20-7577-2179 E naoko.ishihara@uk.mufg.jp The Bank of Tokyo-Mitsubishi UFJ,

Main Economic & Financial Indicators Hungary 6 AUGUST 2015 NAOKO ISHIHARA ECONOMIST ECONOMIC RESEARCH OFFICE (LONDON) T +44-(0)20-7577-2179 E naoko.ishihara@uk.mufg.jp The Bank of Tokyo-Mitsubishi UFJ,

Main Economic & Financial Indicators Eurozone

Main Economic & Financial Indicators Eurozone 7 MAY 2015 AKIKO DARVELL ASSOCIATE ECONOMIST ECONOMIC RESEARCH OFFICE (LONDON) T +44(0)2075771591 E akiko.darvell@uk.mufg.jp The Bank of TokyoMitsubishi UFJ,

Main Economic & Financial Indicators Eurozone 7 MAY 2015 AKIKO DARVELL ASSOCIATE ECONOMIST ECONOMIC RESEARCH OFFICE (LONDON) T +44(0)2075771591 E akiko.darvell@uk.mufg.jp The Bank of TokyoMitsubishi UFJ,

Flash Note Switzerland: Q2 GDP growth

FLASH NOTE Flash Note Switzerland: Q2 GDP growth The devil is in the details Pictet Wealth Management - Asset Allocation & Macro Research 7 September 2018 Yes, the Swiss economy is booming. GDP grew by

FLASH NOTE Flash Note Switzerland: Q2 GDP growth The devil is in the details Pictet Wealth Management - Asset Allocation & Macro Research 7 September 2018 Yes, the Swiss economy is booming. GDP grew by

LETTER. economic. Canada and the global financial crisis SEPTEMBER bdc.ca

economic LETTER SEPTEMBER Canada and the global financial crisis In the wake of the financial crisis that shook the world in and and triggered a serious global recession, the G-2 countries put forward

economic LETTER SEPTEMBER Canada and the global financial crisis In the wake of the financial crisis that shook the world in and and triggered a serious global recession, the G-2 countries put forward

EQUITY RESEARCH. OSFI releases draft of revisions to B-20 mortgage guidelines. For Required Non-U.S. Analyst and Conflicts Disclosures, see page 3.

EQUITY RESEARCH July 7, 2017 Canadian Mortgage Industry OSFI releases draft of revisions to B-20 mortgage guidelines RBC Global Equity Team Click here for contributing analysts' contact information OSFI

EQUITY RESEARCH July 7, 2017 Canadian Mortgage Industry OSFI releases draft of revisions to B-20 mortgage guidelines RBC Global Equity Team Click here for contributing analysts' contact information OSFI

FLASH NOTE EUROPE CHART OF THE WEEK: GERMAN GROWTH A BLIP OR SOMETHING MORE? SUMMARY

Author NADIA GHARBI, CFA ngharbi@pictet.com SUMMARY German GDP figures showed that the German economy contracted in Q3 for the first time since Q1 2015 but markets were prepared. Economic activity was

Author NADIA GHARBI, CFA ngharbi@pictet.com SUMMARY German GDP figures showed that the German economy contracted in Q3 for the first time since Q1 2015 but markets were prepared. Economic activity was

Euro area outlook for 2015

Investment Research General Market Conditions 14 January 2015 Euro area outlook for 2015 Deflation but the good kind The euro area slipped into deflation in December 2014 and we expect the inflation rate

Investment Research General Market Conditions 14 January 2015 Euro area outlook for 2015 Deflation but the good kind The euro area slipped into deflation in December 2014 and we expect the inflation rate

Hong Kong Economic Update

Irina Fan Senior Economist irinafan@hangseng.com Joanne Yim Chief Economist joanneyim@hangseng.com May 28 Hong Kong Economic Update Hong Kong s March export growth stayed low at 7.6 yoy, as exports to

Irina Fan Senior Economist irinafan@hangseng.com Joanne Yim Chief Economist joanneyim@hangseng.com May 28 Hong Kong Economic Update Hong Kong s March export growth stayed low at 7.6 yoy, as exports to

Global PMI. Global economy starts 2017 on the front foot, PMI at 22-month high. February 8 th 2016

Global PMI Global economy starts 2017 on the front foot, PMI at 22-month high February 8 th 2016 2016 IHS Markit. All Rights Reserved. 2 Global PMI at 22-month high The global economy started 2017 with

Global PMI Global economy starts 2017 on the front foot, PMI at 22-month high February 8 th 2016 2016 IHS Markit. All Rights Reserved. 2 Global PMI at 22-month high The global economy started 2017 with

Dollarama Inc. Q2 F2017 Preview. (1) Growth expected to continue (2) A deeper look at valuation HIGHLIGHTS. The NBF Daily Bulletin.

Growth expected to continue (2) A deeper look at valuation HIGHLIGHTS. The NBF Daily Bulletin.") DOL (T) $97.04 Stock Rating: Outperform (Unchanged) Target: $105.00 (Was $104.00) Risk Rating: Average (Unchanged) Est. Total Return: 8.6% Stock Data: 52-week High-Low (Canada) Bloomberg $98.94 - $66.32

DOL (T) $97.04 Stock Rating: Outperform (Unchanged) Target: $105.00 (Was $104.00) Risk Rating: Average (Unchanged) Est. Total Return: 8.6% Stock Data: 52-week High-Low (Canada) Bloomberg $98.94 - $66.32

PRESIDENT TRUMP The First 100 Days and the U.S. Economy

PRESIDENT TRUMP The First 100 Days and the U.S. Economy MBAFCPA.COM June 2017 INTRODUCTION During his campaign and after the election President Trump has mentioned the importance of what he would accomplish

PRESIDENT TRUMP The First 100 Days and the U.S. Economy MBAFCPA.COM June 2017 INTRODUCTION During his campaign and after the election President Trump has mentioned the importance of what he would accomplish