Geoff Bascand: Central bank performance, financial management and institutional design

|

|

|

- Marion Nichols

- 6 years ago

- Views:

Transcription

1 Geoff Bascand: Central bank performance, financial management and institutional design Speech by Mr Geoff Bascand, Deputy Governor and Head of Operations of the Reserve Bank of New Zealand, to the National Asset-Liability Management Europe Conference, London, 12 March * * * Accompanying figures can be found at the end of the speech. Introduction A central bank s performance needs to be assessed on how well it meets its statutory policy mandate. But policy outcomes are only one measure of performance and institutional credibility. Central banks incur substantial financial risk and are an important part of overall public sector finances. Maintaining the privilege of operational independence requires a record of successful policy outcomes and sound and prudent financial management. Therefore, financial arrangements and performance expectations are important components of overall central bank institutional design. These issues are even more important today. In the Global Financial Crisis (GFC) many governments became guarantors of last resort, and undertook investments that were well beyond their traditional risk habitat. Central banks were asked to do much more either through pursuing multiple targets, directing credit flows, or by adopting unconventional monetary policies. Some central banks balance sheets have expanded enormously (see Figure 1). Central bank capital has been more at risk from some of these activities, and we have seen reinvestment by governments to build capital levels in some central banks. This paper sets out some broad financial and institutional design considerations and illustrates these with reference to the Reserve Bank of New Zealand s (RBNZ s) financial arrangements, balance sheet structure, and risk management. It explains their rationale and discusses some avenues we are exploring for future enhancements. Diversity of responsibilities and financial arrangements Monetary policy responsibilities are common to all central banks, albeit with widely varying operational approaches and performance targets. A mandate for financial stability is common, but the form and extent of these responsibilities can vary significantly. Lender-oflast-resort responsibility (emergency liquidity to the banking system) is inherent, but the responsibilities of central banks vis a vis finance ministries, regarding the resolution of institutions in financial difficulties or the provision of broader support to the financial system, vary widely. Prudential policy and oversight may or may not be a function of the central bank. Some central banks manage the country s foreign reserves and others do not (see Figure 2). The diverse nature of these responsibilities flows through into a wide variety of financial arrangements. Financial risks and results are sensitive to the operational and policy responsibilities of the central bank. Historically, central banks have been considered profitable through their responsibility for money issuance. However, even here there are differing degrees of financial control or independence over seigniorage revenues. Seigniorage revenues have become both more predictable and constrained as a result of price stability goals. At the same time, increased BIS central bankers speeches 1

2 policy mandates and portfolio exposures taken on by central banks can overwhelm these revenue streams through valuation changes 1. Does financial performance matter? Generally speaking, the performance of central banks is judged by the public and government in terms of its policy mandate. Financial performance tends to be in the background when the impact and performance of the central bank is debated. But they are not completely separable. Occasional and moderate financial loss is unlikely to seriously impair a central bank s operations. But sustained loss and diminution of equity, or a very large, even if exceptional, negative income (P&L) impact on public finances is likely to erode the institution s credibility and policy freedom. Governments are beneficial owners 2 of central banks, and conceptually the central bank s cash flows and the equity investment in the central bank can be consolidated into broader whole-of-government finances. This is the case in New Zealand. Conceptually, a central bank s net asset position is part of the public sector s balance sheet, irrespective of whether a consolidated balance sheet is prepared. For example, policy decisions that influence the size of the central bank s balance sheet (e.g. through accumulation of assets, or commitments in the nature of contingent obligations, such as guarantees to a distressed institution) expose the central bank s equity to risk, and therefore the value of the government s ownership interest in the central bank. Sound management of the central bank s balance sheet is also important to maintain the central bank s standing and credibility as a regulator and supervisor (if it has these responsibilities). The financial risks of central banks should be managed in a business-like way similar to our expectations of commercial banks. Failure to do so may result in a central bank s operational discretion being fettered by institutional rules, removal of decision-making authority, or in extreme circumstances by intervention in the management of the central bank. At the same time, there needs to be recognition by all stakeholders of the significant financial risks that central banks take. They manage what are often among the largest foreign asset portfolios in the economy, and can have extensive credit exposure to individual financial intermediaries. I turn now to how the RBNZ seeks to manage these risks. New Zealand s institutional arrangements are designed to limit the very large financial risk that the central bank could incur from its foreign exchange operations, and also to avoid the bank acquiring substantial contingent liabilities on behalf of the government ( the Crown ) through its liquidity and lender-of-last-resort operations. Nevertheless, there is still material financial risk inherent in the bank s operation that is managed through the bank s capital holdings, reserves/asset management, and best-practice risk management. The following sections describe how these arrangements and practices are managed at the RBNZ. RBNZ institutional and financial arrangements The New Zealand institutional framework is designed to balance policy and operational independence with accountability for policy and financial performance. Financial accountability and other expectations (e.g. reporting to Parliament) were strengthened in 1989 when the RBNZ was given greater policy independence. 1 2 A 2 percentage point rise in the US interest rate on excess reserves would eliminate the Federal Reserve s profit and equity capital within a year. (using BIS term p7) 2 BIS central bankers speeches

3 The Reserve Bank of New Zealand Act 1989 established the central bank as a body corporate whose primary function is to formulate and implement monetary policy for the purposes of achieving and maintaining price stability. The RBNZ (which I will also refer to as the Bank ) is also mandated to promote the soundness and efficiency of the financial system. The Bank is owned by the Crown and capital is provided by the government, to whom dividends are returned. The Act grants the Bank the right to deal in foreign exchange, issue currency, and act as lender of last resort if it deems it necessary 3. These arrangements and powers underpin the Bank s financial strength and its risk exposure. Income is assured through the authority to invest proceeds from the sale of currency and bank capital, and may be earned (or lost) through trading or investment in debt securities, money market instruments, derivatives, and foreign exchange. New Zealand has a floating exchange rate, and prescribed limits on foreign reserve holdings contain the Crown s risk exposure. By law, the Minister of Finance sets limits (a range) on the foreign reserve holdings of the Bank, and the Bank then manages them to achieve policy, liquidity and risk-return objectives. A Memorandum of Understanding with the Minister provides further guidance to the Bank on foreign exchange operations 4. Even though with a pure floating rate currency, foreign exchange reserves conceptually may not be required, foreign reserves are held in the event that the Bank may be required to intervene in foreign exchange markets, for example where there is disorder in the currency markets or the currency is materially out of line with fair value. Foreign exchange intervention has been infrequent. Liquidity provision to troubled banks and lender of last resort functions are at the discretion of the Bank, including the terms and cost of borrowing. In the GFC, liquidity was provided by the RBNZ at the cost of the Official Cash Rate (OCR) and with interest rates falling, the Bank made positive returns from its lending. Ostensibly, the Bank incurs credit risk in these circumstances, mitigated through collateralisation. However, the major cost of financial stability support does not fall upon the Bank, but instead upon the fiscal authority (the Treasury). Whilst the Bank has responsibility as prudential supervisor to recommend the appropriate action if a financial institution fails, critical decisions on statutory management, capital injections or guarantee schemes are ultimately for the Minister of Finance to make, and would be expected to take the form of fiscal measures. Accountability is accomplished through public and parliamentary reporting requirements and monitoring via the Bank s Board as agent of the Minister of Finance and on financial matters by the Treasury. The Bank must publish a Statement of Intent on its strategic and performance objectives for the coming three years, and publish an audited Annual Report for the previous year that includes information on policy, operational and financial performance. The SOI and the Annual Report are both tabled in Parliament and subject to the scrutiny of Parliament s Finance and Expenditure Select Committee. The Bank observes the accounting standards imposed by the External Reporting Board (a statutory body). From this financial year, the Bank is required to apply New Zealand Equivalents to International Public Sector Accounting Standards (NZ-IPSAS) rather than International Financial Reporting Standards (IFRS). The change in financial reporting framework will not have a significant impact on the Bank s financial reporting, although NZ- IPSAS and IFRS could diverge over time. 3 4 The Bank also has responsibilities for the operation of payments and settlements systems that earn income and incur mostly operational risks, with financial risks defrayed in various ways. The MoU establishes that the primary purpose of reserves management and intervention activity is: Extreme disorder in foreign exchange markets to ensure continued functioning of foreign exchange markets, in rare crisis circumstances. The secondary purpose is: Exchange rate overshooting to lean against (on a modest scale) extreme cyclical peaks and troughs in the exchange rate that are judged inconsistent with economic fundamentals. BIS central bankers speeches 3

4 The final piece of the RBNZ s operating framework is the funding agreement. The RBNZ Act requires the Minister of Finance and the Governor to enter into a five-year funding agreement that specifies the amount of the Bank s income that may be applied in any year towards meeting the operating expenses incurred by the Bank in carrying out its functions. The Funding Agreement must be ratified by Parliament, prior to the commencement of its funding period. The five-year funding agreement is a key mechanism that reinforces operational independence. The Bank does not have to seek an annual funding allocation from Parliament in the same way that government departments do, and its operating budget is not subject to annual variation in net income. On the other hand, the process of negotiating a five-year agreement is intensive in terms of establishing value for money, agreeing on strategic priorities for the Bank, and forecasting future demands on the Bank. Variations to the funding agreement within the five-year window are feasible, for example if the Bank acquires new functions, as it did in the last funding period for supervision of insurance and anti-money laundering. The RBNZ s capital expenditure is within the discretion of the Bank s management, but is controlled in part through the moderating impact on depreciation expense from the limit on total operating expenses in the funding agreement. Higher depreciation resulting from higher fixed investment would, therefore, imply lower expenditure on other items, such as personnel. Capital expenditure is also constrained by the Bank s equity and dividend requirements, which are explained below. Large, unwarranted (and low yielding) capital expenditure could infringe upon these principles. By way of illustration, with the Bank introducing new banknotes in 2015, significant capital expenditure was required that could be financed within the balance sheet from cash and working capital. However, the operating expense incurred from issuing new notes and the obsolescence of the existing series was projected to be greater than could be accommodated within the funding agreement, requiring the Bank to seek the Minister of Finance s approval for additional expenditure. In practice, the expenses span two different funding agreements, requiring more complex negotiations than normal. New Zealand s institutional arrangements are now 25 years old and have proven robust to a number of tests, including significant volatility in exchange rates with material foreign exchange gains and losses, negative P&L results, expansion of functions, and changes in government administration. They work well because they are transparent and the Bank works closely with the Treasury to share analysis and information; because they have evolved in response to new mandates (e.g. through MOUs on foreign reserves and foreign exchange intervention, most recently in 2007, and on the level of Crown equity in the Bank, most recently adjusted in 2013); and because of strong performance standards (e.g. benchmarking the Bank s reporting and capital adequacy against best international practice). How do we assess financial performance? Our financial strategy is primarily guided by our need to fulfil our functions, rather than financial results. This doesn t mean we are indifferent to expected return or actual financial outcomes, but rather that we generally take a conservative approach to risk to ensure we have the capacity to carry out our statutory functions. Our financial strategy entails considered decisions on asset allocation and investment strategy, with greater weight on risk diversification and liquidity than on return; maintaining adequate capital for the risks we face; and measuring our investment performance against relevant benchmarks. Excluding exceptional circumstances, our objectives for reserves and liquidity management are to manage our financial performance as efficiently as possible, out-perform what other similar portfolios would achieve, and deliver a positive return on equity. 4 BIS central bankers speeches

5 Risk management and capital adequacy From the balance sheet perspective, financial risks arise from the Bank s key investment portfolios of domestic (NZD) securities that support monetary policy operations and foreign reserve assets that can be used to finance market intervention, with the latter much greater in size and variability. Figure 3 depicts a stylised picture of the RBNZ balance sheet. While central bank balance sheets and financial performance can be very volatile, in constructing our balance sheet, we have taken strategic decisions that impose some limits on the potential volatility in reported financial performance. The balance sheet is partially immunised from major foreign exchange risk, and we have taken a conservative approach to credit and interest rate risk in foreign reserve activities. We also manage operational risk closely and are alert to the potential cost of operational errors. Asset holdings and the scale of the RBNZ s balance sheet are primarily determined by: the amount of foreign reserves RBNZ holds to maintain its foreign exchange (FX) intervention capacity; trading banks demand for liquid assets, primarily to facilitate daily interbank payments; Treasury s management of the Crown Settlement (cash) Account with the RBNZ; and the public s demand for notes and coins. Financial risks arise from: The RBNZ s open FX position and associated foreign exchange risk, which is mitigated by limits on the position and holdings of a diversified basket of reserve currencies; Interest rate risk arising from domestic market operations and from foreign reserves management, mitigated through duration and risk limits; Credit risk arising from foreign currency assets, which is mitigated by investing in high grade debt instruments; and Credit risk arising from derivative transactions, which is mitigated by holding high quality collateral. Investment policies control market and credit risk exposure through hedging policies, liquidity and investment ratings requirements, and counterparty credit limits. Perhaps the most significant of these is the restriction on unhedged foreign reserves. By agreement with the Minister of Finance, the open FX position is limited to a specified range, a subset of the total foreign reserves limit, with the remaining foreign reserve assets hedged from an FX perspective. New Zealand differs from many countries in this respect. The majority of foreign currency assets are funded through long-term foreign exchange swaps, and therefore hedged from foreign exchange risks or through long-term foreign currency borrowings (which have been originated by the Treasury and on-lent to RBNZ). Reserves and portfolio management is expanded upon below. Credit risk is mitigated by investing foreign assets in high-quality sovereigns, nearsovereigns, and international agencies. In terms of domestic lending, credit risk is mitigated by lending on a collateralised basis with banks providing RBNZ high-quality collateral, and the Bank applying discounts, with daily monitoring of collateral values and collateral calls to ensure the value of collateral is appropriate for the amount lent. The Bank has several sources of interest rate risk that are mostly controlled through risk caps and duration limits. On hedged foreign reserves, some interest rate risk arises through mis-match of duration of assets and liabilities. Reported earnings are subject to volatility from mark-to-market value of long-term liabilities. Another source of interest rate risk is due to changes in New Zealand s short-term interest rates. Essentially, through FX swaps, RBNZ is investing at short-term interest rates, and variations in these rates from forecast levels impact earnings. The interest rate risk on unhedged foreign reserves is managed through strategic decisions and periodic review of asset allocation (i.e. our duration target for foreign currency BIS central bankers speeches 5

6 reserve portfolios is managed strategically through the business cycle). The RBNZ also incurs interest rate risk from its holdings of government bonds, but in this case there is a corresponding impact within the Treasury, and this has no net impact on the Crown s overall balance. Capital adequacy Notwithstanding a conservative financial strategy and investment policies that limit financial risk, the Bank s income and balance sheet remain subject to some volatility. In order to manage this variation in annual financial performance and avoid the credibility risks associated with low levels of equity, the Bank has adopted a policy for holding a prudent level of capital and developed a framework for determining the appropriate level of capital. The RBNZ chooses to hold capital in line with both normal commercial practice and standard public sector arrangements in New Zealand. The Bank is not subject to regulatory capital requirements and thus determines its capital adequacy in agreement with its owner (the government), reflecting its balance sheet and business risks. Having capital is explicit recognition by the government that income from the Bank s business will be volatile, and a buffer is required to absorb that volatility. It also supports the credibility of the central bank as regulator and supervisor of financial institutions. Assessment of the potential financial consequences of the risks facing the Bank determines the appropriate amount of capital the Bank should hold. Also relevant is the dividend policy. The Act requires the Bank to recommend an annual dividend to be paid in line with the principles set out in the Bank s annual SOI, and the Minister of Finance decides upon the final dividend figure. The dividend principles state that the Bank should maintain sufficient equity for the financial risks it faces, and that excess equity should be returned to the Crown. They are also tempered by the requirement that unrealised gains on investments should be retained until they are realised in New Zealand dollars. Thus surplus capital is returned as dividends, while the onus is on the Bank to determine the appropriate amount to be held to maintain sound capital adequacy. The Bank consults closely with the Treasury on these matters, with the intention of coming to an agreed recommendation that is submitted to the Minister for decision. If ultimately the Bank disagrees with the Minister s determination of the appropriate dividend, the Bank is required to publish its recommendation. In 2014, the Bank introduced a new Note to its financial accounts setting out the Bank s approach to determining required capital, its dividend recommendation, and the basis of calculating the recommended dividend. The Bank s capital adequacy framework 5 evaluates credit, market and operational risks associated with the Bank s balance sheet, investment policy, and operations. It considers possible correlations between these risks, and establishes the necessary capital to meet the possible loss associated with each of these risks, given its risk likelihood (see Figure 4). As noted, we aim to run capital modelling methods that align with best practice, and can choose models that address our balance sheet risks. As a result we are focused on evolving our modelling of market, credit and operational risk, and are less concerned about liquidity elements (as we invest heavily in high-quality liquid assets). Market risk is the possible loss of value of an asset or liability due to variation in exchange rates, interest rates, credit spreads or basis spreads. Market risk capital is the largest component of the Bank s required capital. The Bank uses value-at-risk (VaR and stressed 5 This section draws on Fraser (2013) The Reserve Bank s capital adequacy framework. 6 BIS central bankers speeches

7 VaR) models to assess market risk capital, and has set the target probability of (total) loss at 1 in Our models currently capture October 2008 to April 2013 as the stressed period. The second component of required capital is for coverage of credit risk. The Bank evaluates credit risk using the Basel II credit VaR approach, drawing on historical data including consideration of sovereign and bank default probabilities during various periods of stress. Updating to various Basel III credit risk modelling techniques is a future development objective. As noted earlier, if a deep financial crisis arises, the Bank may incur credit risk through its lender-of-last-resort responsibilities, albeit lending is not expected to be contemplated without appropriate collateral arrangements. This risk is not incorporated in our economic capital modelling. The final, minor, element of our capital adequacy requirement is the buffer held for potential operational risks such as misconduct, property loss, systems failures, contractual disputes, etc. Perhaps the largest operational risks arise from the Bank s responsibilities as the operator of New Zealand s interbank payment and settlement system, and as the current owner and operator of the securities settlement system. The Bank has a number of controls to minimise the likelihood and impact of operational risks, including a highly developed enterprise risk management framework, formal operational investment policies and limits, an active (internal and external) audit programme, and a proactive problem management (incident reporting) regime. Portfolio management The Bank manages its foreign reserves in two separate pools, an un-hedged pool (exposed to changes in interest rates and FX rates) and a hedged pool. The primary purpose for both pools of reserves is to maintain crisis intervention capability. The un-hedged pool of reserves serves a secondary purpose of allowing the Bank to lean against (on a modest scale) extreme cyclical peaks and troughs in the exchange rate that are judged inconsistent with economic fundamentals. In contrast to most central banks, a large portion (currently 75 percent) of the Bank s foreign reserves is in the hedged pool (100 percent prior to 2007) which helps to keep the return on foreign reserves relatively stable across time. For foreign reserves to be effective in meeting their purpose they need to be allocated across a diversified set of instruments that will maintain deep liquidity in both normal times and times of crisis or stress. The allocation of hedged and un-hedged reserves is collectively described as the Strategic Asset Allocation (SAA) and is set by the Bank s Assets and Liabilities Committee. The SAA has a large influence on the Bank s financial risk profile, given foreign reserves comprise a large part of the Bank s balance sheet. I will now describe the characteristics of each pool of reserves in more detail and the SAA as it applies to hedged and un-hedged reserves. The first pool of reserves, hedged reserves, is what distinguishes the Bank s approach to reserves management from most other central banks. The Bank borrows foreign currency (through long-dated cross currency basis swaps and also foreign currency loans from the New Zealand Treasury) to fund investments primarily in US, European, and Japanese sovereign debt markets. Borrowing in foreign currency reduces currency risk, but it generates refinancing risk. The Bank manages this refinancing risk by borrowing for long maturities (up to 15 years) and ensuring that maturities are staggered as much as possible. The duration of borrowing is matched to the duration of investments to reduce interest rate risk (i.e. if borrowing is on a three-month floating basis, investments are matched to mature in three 6 Or more precisely, the confidence level on the potential loss calculations is 99.9 percent. BIS central bankers speeches 7

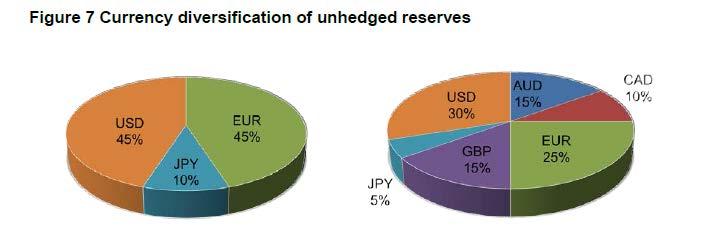

8 months). This structure allows the Bank to maintain a stable return and low risk profile on its hedged reserves through time, whilst maintaining effective intervention capability. This stable return and low risk profile is in contrast to un-hedged reserves, which I will describe shortly. The SAA for hedged reserves is presented in Figure 5. Allocation weights are defined such that reserve managers can adjust the allocation dynamically (using FX swaps and cross currency basis swaps) to take advantage of favourable (funding) spreads across time. Performance is carefully measured, but it is not compared to a benchmark (given the complexity of benchmarking long-dated borrowing that is transacted on an irregular basis). The second pool, un-hedged reserves, is invested in sovereign debt markets with deep liquidity and across currencies with high FX turnover. These reserves are funded by the Bank s New Zealand dollar liabilities so are exposed to changes in New Zealand dollar FX rates against each of the six currencies. The position has a high carry cost (due to the high cost of New Zealand dollar funding relative to the return on reserve investments) and returns are volatile given exposure to FX rates (and interest rates to a lesser extent). These reserves are expected to perform well in times of crisis or stress, both in terms of return and providing the most effective intervention capability. Within the limits set by the Minister of Finance, unhedged reserves can be increased or decreased in size allowing the Bank to lean against extreme cyclical peaks and troughs in the exchange rate that are judged inconsistent with economic fundamentals. The SAA for un-hedged reserves is presented in Figure 6. In determining the SAA we first specify the most appropriate reserve markets (country allocations) for unhedged reserves, given that allocations are applied to sovereign debt. Currently, the SAA is limited to six highly traded currencies a more diversified position than was the case in 2008 (Figure 7). Then we specify the duration target for each of those markets individually. At this time we have constrained the instruments to be 2-year government bonds, the shortest duration assets that meet our liquidity criteria. The process of determining the SAA for un-hedged reserves is about selecting a portfolio that balances diversification and liquidity requirements against return or yield under normal market conditions. To ensure that un-hedged reserves are effective in meeting their purpose we constrain the investment universe and the potential allocation outcomes by strict diversification, liquidity and credit minima and maxima. Our allocation minimums and maximums force 70 percent of our allocation, before we optimise the remaining unconstrained 30 percent using a Markowitz model. For example, the Australian dollar allocation is capped due to the correlation of New Zealand and Australian currencies and our inter-related banking sector. While a greater unhedged allocation to Australian assets would provide good yield enhancement, it may not provide a source of effective reserves assets in a crisis due to high and positive correlation aspects. With the aim of keeping our reserves managers active in foreign reserve markets, the Bank allows reserve managers to deviate from the SAA in terms of FX and interest rate position (within limits). We measure their performance in doing so against a custom (un-hedged reserves) benchmark that is set to our SAA. Performance measurement comes in the form of risk-adjusted return measures, namely Information Ratios (reported for trailing two and five year periods) and the Sharpe Ratio. In addition to the hedged and un-hedged reserves described, the Bank has foreign currency investments in BIS Investment Pool funds (ABF and CNY). The CNY investment was entered into in 2014 to diversify the Bank s foreign reserves and the ABF investments in 2003 and 2005 to promote development of bond markets in the Asia region. We also have US dollar investments (often in USD denominated European quasi government paper) as part of our domestic markets operations. These investments are classified as foreign reserves (according to IMF Official Reserve Asset measurement) but they do not contribute to the Bank s intervention capability as they are funded by short-dated FX swaps. 8 BIS central bankers speeches

9 Despite the potential for improved returns, the Bank has resisted investing in equities or gold, as some central banks do. Our investment policy anticipates a periodic review of the SAA and risk-return decisions may be re-assessed in future. Future developments The Bank is continually seeking ways to enhance its financial management. In recent years, we have improved our economic capital modelling, reviewed and simplified our portfolio management and strategic asset allocation, increased transparency, and strengthened our performance reporting. There is scope to improve further. In particular, with enhancements to our risk modelling and pricing, we can potentially be more dynamic in our allocation decisions and improve expected financial returns without incurring significant additional risk. We are currently assessing our technology base with aspirations to better manage risks and pricing issues related to OTC derivatives (including bringing risk adjusted pricing and risk adjusted performance on to reserve managers desktop on a pre-trade basis). Together, these initiatives should help improve our performance and risk management culture. Maintaining our conservative liquidity profile (driven by intervention capacity) has an opportunity cost, and so we must be at least as good as other market participants at motivating and focusing our portfolio managers by aligning incentives and trading activity to draw out these fractional returns (versus our benchmark). Concluding thoughts There is a strong link between the financial performance of a central bank and its ongoing ability to fulfil its objectives. The credibility of the institution and its operational freedom are contingent upon prudent financial management. Sound financial management can never ensure the success of a central bank; that will depend on its policy actions and outcomes. But poor financial management can certainly lead to failure. Central banking cannot be expected to produce smooth income growth. Constraints on asset allocation that arise from central bank s responsibilities and the volatility inherent in foreign exchange and interest rate markets prevent that. Developing a shared understanding with the finance ministry of the financial risks that the central bank and public sector ultimately faces is vital. Central banks must build an open and cooperative relationship with the finance ministry and legislature, seeking clarity around responsibility for quasi-fiscal activities and returns. The RBNZ s institutional and financial design is driven by our overall purpose of maintaining price stability and promoting the stability and efficiency of the financial system, and is enabled by an operating mandate set out in our empowering legislation. The legislation sets the parameters for what we do, while institutional arrangements with the finance minister prescribe limits within which the Bank manages foreign reserves, thereby limiting the Crown s fiscal exposure. The Bank has established investment policies and operating frameworks that manage financial risks. Our approach to reserve management, with the bulk of reserves hedged against foreign exchange risk, is a key strategic risk management decision. Thereafter, our SAA modelling and diversification are geared towards balancing risk and return. The Bank s equity position and dividend policy provide a buffer against adverse events, while also providing performance incentives through their disclosure, external scrutiny and the expectation of maintaining a consistent level of equity over time. There is a strong link between the level of capital invested by the government in the Bank and the level of risk taken. The RBNZ and the government have an open dialogue on these linkages, in terms of risk management, pre-positioning capital and determining dividend recommendations. The Bank believes that with application of industry best practice in risk BIS central bankers speeches 9

10 and position optimisation, it can enhance financial performance while maintaining credibility and reputation through prudent capital and risk management. 10 BIS central bankers speeches

11 BIS central bankers speeches 11

12 12 BIS central bankers speeches

Deutsche Bank welcomes the opportunity to provide comments on the above consultation.

Secretariat of the Financial Stability Board, c/o Bank for International Settlements CH-4002, Basel, Switzerland 28 November 2013 Deutsche Bank AG Winchester House 1 Great Winchester Street London EC2N

Secretariat of the Financial Stability Board, c/o Bank for International Settlements CH-4002, Basel, Switzerland 28 November 2013 Deutsche Bank AG Winchester House 1 Great Winchester Street London EC2N

Impact Summary: A New Zealand response to foreign derivative margin requirements

Impact Summary: A New Zealand response to foreign derivative margin requirements Section 1: General information Purpose The Reserve Bank of New Zealand (RBNZ) and the Ministry of Business, Innovation and

Impact Summary: A New Zealand response to foreign derivative margin requirements Section 1: General information Purpose The Reserve Bank of New Zealand (RBNZ) and the Ministry of Business, Innovation and

Pillar 3 Disclosure (UK)

") MORGAN STANLEY INTERNATIONAL LIMITED Pillar 3 Disclosure (UK) As at 31 December 2009 1. Basel II accord 2 2. Background to PIllar 3 disclosures 2 3. application of the PIllar 3 framework 2 4. morgan stanley

MORGAN STANLEY INTERNATIONAL LIMITED Pillar 3 Disclosure (UK) As at 31 December 2009 1. Basel II accord 2 2. Background to PIllar 3 disclosures 2 3. application of the PIllar 3 framework 2 4. morgan stanley

Habib Bank AG Zurich. Annual disclosures according to Basel III (Year 2015)

") Annual disclosures according to Basel III (Year 2015) 1 Annual disclosures according to Basel III (Year 2015) 1. Scope of consolidation Scope of consolidation for capital adequacy purposes The scope of

Annual disclosures according to Basel III (Year 2015) 1 Annual disclosures according to Basel III (Year 2015) 1. Scope of consolidation Scope of consolidation for capital adequacy purposes The scope of

FRAMEWORK FOR SUPERVISORY INFORMATION

FRAMEWORK FOR SUPERVISORY INFORMATION ABOUT THE DERIVATIVES ACTIVITIES OF BANKS AND SECURITIES FIRMS (Joint report issued in conjunction with the Technical Committee of IOSCO) (May 1995) I. Introduction

FRAMEWORK FOR SUPERVISORY INFORMATION ABOUT THE DERIVATIVES ACTIVITIES OF BANKS AND SECURITIES FIRMS (Joint report issued in conjunction with the Technical Committee of IOSCO) (May 1995) I. Introduction

14. What Use Can Be Made of the Specific FSIs?

14. What Use Can Be Made of the Specific FSIs? Introduction 14.1 The previous chapter explained the need for FSIs and how they fit into the wider concept of macroprudential analysis. This chapter considers

14. What Use Can Be Made of the Specific FSIs? Introduction 14.1 The previous chapter explained the need for FSIs and how they fit into the wider concept of macroprudential analysis. This chapter considers

Principles and Trade-Offs When Making Issuance Choices in the UK

Please cite this paper as: OECD (2011), Principles and Trade-Offs When Making Issuance Choices in the UK: Report by the United Kingdom Debt Management Office, OECD Working Papers on Sovereign Borrowing

Please cite this paper as: OECD (2011), Principles and Trade-Offs When Making Issuance Choices in the UK: Report by the United Kingdom Debt Management Office, OECD Working Papers on Sovereign Borrowing

Appendix B: HQLA Guide Consultation Paper No Basel III: Liquidity Management

Appendix B: HQLA Guide Consultation Paper No.3 2017 Basel III: Liquidity Management [Draft] Guide on the calculation and reporting of HQLA Issued: 26 April 2017 Contents Contents Overview... 3 Consultation...

Appendix B: HQLA Guide Consultation Paper No.3 2017 Basel III: Liquidity Management [Draft] Guide on the calculation and reporting of HQLA Issued: 26 April 2017 Contents Contents Overview... 3 Consultation...

COMMISSION DELEGATED REGULATION (EU) No /.. of XXX

No /.. of XXX") EUROPEAN COMMISSION Brussels, XXX [ ](2016) XXX draft COMMISSION DELEGATED REGULATION (EU) No /.. of XXX supplementing Regulation (EU) No 648/2012 of the European Parliament and of the Council on OTC derivatives,

EUROPEAN COMMISSION Brussels, XXX [ ](2016) XXX draft COMMISSION DELEGATED REGULATION (EU) No /.. of XXX supplementing Regulation (EU) No 648/2012 of the European Parliament and of the Council on OTC derivatives,

Regulatory Impact Assessment RBNZ Liquidity requirements for locally incorporated banks

Regulatory Impact Assessment RBNZ Liquidity requirements for locally incorporated banks Executive summary 1 A strong liquidity profile across banks is important for the maintenance of a sound and efficient

Regulatory Impact Assessment RBNZ Liquidity requirements for locally incorporated banks Executive summary 1 A strong liquidity profile across banks is important for the maintenance of a sound and efficient

Basel II Pillar 3 Disclosures Year ended 31 December 2009

DBS Group Holdings Ltd and its subsidiaries (the Group) have adopted Basel II as set out in the revised Monetary Authority of Singapore Notice to Banks No. 637 (Notice on Risk Based Capital Adequacy Requirements

DBS Group Holdings Ltd and its subsidiaries (the Group) have adopted Basel II as set out in the revised Monetary Authority of Singapore Notice to Banks No. 637 (Notice on Risk Based Capital Adequacy Requirements

Limits on debt-to-income as a macro-prudential tool

Date: 19 August 2016 To: Minister of Finance Limits on debt-to-income as a macro-prudential tool 1. The purpose of this memorandum is to seek your agreement to add an additional class of policy tool to

Date: 19 August 2016 To: Minister of Finance Limits on debt-to-income as a macro-prudential tool 1. The purpose of this memorandum is to seek your agreement to add an additional class of policy tool to

TECHNICAL ADVICE ON THE TREATMENT OF OWN CREDIT RISK RELATED TO DERIVATIVE LIABILITIES. EBA/Op/2014/ June 2014.

EBA/Op/2014/05 30 June 2014 Technical advice On the prudential filter for fair value gains and losses arising from the institution s own credit risk related to derivative liabilities 1 Contents 1. Executive

EBA/Op/2014/05 30 June 2014 Technical advice On the prudential filter for fair value gains and losses arising from the institution s own credit risk related to derivative liabilities 1 Contents 1. Executive

Report to G7 Finance Ministers and Central Bank Governors on International Accounting Standards

Report to G7 Finance Ministers and Central Bank Governors on International Accounting Standards Basel Committee on Banking Supervision Basel April 2000 Table of Contents Executive Summary...1 I. Introduction...4

Report to G7 Finance Ministers and Central Bank Governors on International Accounting Standards Basel Committee on Banking Supervision Basel April 2000 Table of Contents Executive Summary...1 I. Introduction...4

Basel Committee on Banking Supervision. Consultative Document. Pillar 2 (Supervisory Review Process)

") Basel Committee on Banking Supervision Consultative Document Pillar 2 (Supervisory Review Process) Supporting Document to the New Basel Capital Accord Issued for comment by 31 May 2001 January 2001 Table

Basel Committee on Banking Supervision Consultative Document Pillar 2 (Supervisory Review Process) Supporting Document to the New Basel Capital Accord Issued for comment by 31 May 2001 January 2001 Table

Susan Schmidt Bies: An update on Basel II implementation in the United States

Susan Schmidt Bies: An update on Basel II implementation in the United States Remarks by Ms Susan Schmidt Bies, Member of the Board of Governors of the US Federal Reserve System, at the Global Association

Susan Schmidt Bies: An update on Basel II implementation in the United States Remarks by Ms Susan Schmidt Bies, Member of the Board of Governors of the US Federal Reserve System, at the Global Association

INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS GUIDELINE. Nepal Rastra Bank Bank Supervision Department. August 2012 (updated July 2013)

") INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS GUIDELINE Nepal Rastra Bank Bank Supervision Department August 2012 (updated July 2013) Table of Contents Page No. 1. Introduction 1 2. Internal Capital Adequacy

INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS GUIDELINE Nepal Rastra Bank Bank Supervision Department August 2012 (updated July 2013) Table of Contents Page No. 1. Introduction 1 2. Internal Capital Adequacy

COPYRIGHTED MATERIAL. Bank executives are in a difficult position. On the one hand their shareholders require an attractive

chapter 1 Bank executives are in a difficult position. On the one hand their shareholders require an attractive return on their investment. On the other hand, banking supervisors require these entities

chapter 1 Bank executives are in a difficult position. On the one hand their shareholders require an attractive return on their investment. On the other hand, banking supervisors require these entities

BERMUDA MONETARY AUTHORITY GUIDELINES ON STRESS TESTING FOR THE BERMUDA BANKING SECTOR

GUIDELINES ON STRESS TESTING FOR THE BERMUDA BANKING SECTOR TABLE OF CONTENTS 1. EXECUTIVE SUMMARY...2 2. GUIDANCE ON STRESS TESTING AND SCENARIO ANALYSIS...3 3. RISK APPETITE...6 4. MANAGEMENT ACTION...6

GUIDELINES ON STRESS TESTING FOR THE BERMUDA BANKING SECTOR TABLE OF CONTENTS 1. EXECUTIVE SUMMARY...2 2. GUIDANCE ON STRESS TESTING AND SCENARIO ANALYSIS...3 3. RISK APPETITE...6 4. MANAGEMENT ACTION...6

RISK MANAGEMENT OF THE NATIONAL DEBT

RISK MANAGEMENT OF THE NATIONAL DEBT Evaluation of the 2012-2015 policies 19 JUNE 2015 1 Contents 1 Executive Summary... 4 1.1 Introduction to the policy area... 4 1.2 Results... 5 1.3 Interest rate risk

RISK MANAGEMENT OF THE NATIONAL DEBT Evaluation of the 2012-2015 policies 19 JUNE 2015 1 Contents 1 Executive Summary... 4 1.1 Introduction to the policy area... 4 1.2 Results... 5 1.3 Interest rate risk

Liquidity Policy. Prudential Supervision Department Document BS13. Issued: January Ref #

Liquidity Policy Prudential Supervision Department Document Issued: 2 A. INTRODUCTION Liquidity policy and the Reserve Bank s objectives 1. This Liquidity Policy sets out the Reserve Bank of New Zealand

Liquidity Policy Prudential Supervision Department Document Issued: 2 A. INTRODUCTION Liquidity policy and the Reserve Bank s objectives 1. This Liquidity Policy sets out the Reserve Bank of New Zealand

Interim financial statements (unaudited)

") Interim financial statements (unaudited) as at 30 September 2017 These financial statements for the six months ended 30 September 2017 were presented to the Board of Directors on 13 November 2017. Jaime

Interim financial statements (unaudited) as at 30 September 2017 These financial statements for the six months ended 30 September 2017 were presented to the Board of Directors on 13 November 2017. Jaime

SUPERVISORY POLICY STATEMENT (Class 1(1) and Class 1(2))

and Class 1(2))") SUPERVISORY POLICY STATEMENT (Class 1(1) and Class 1(2)) Domestic Systemically Important Banks June 2017 Page 1 of 23 Contents 1. Introduction 4 1.1 Background 4 1.2 Legal basis 5 2. Overview of IOM D-SIB

SUPERVISORY POLICY STATEMENT (Class 1(1) and Class 1(2)) Domestic Systemically Important Banks June 2017 Page 1 of 23 Contents 1. Introduction 4 1.1 Background 4 1.2 Legal basis 5 2. Overview of IOM D-SIB

BERMUDA MONETARY AUTHORITY

BERMUDA MONETARY AUTHORITY CONSULTATION PAPER IMPLEMENTATION OF BASEL III NOVEMBER 2013 Table of Contents I. ABBREVIATIONS... 3 II. INTRODUCTION... 4 III. BACKGROUND... 6 IV. REVISED CAPITAL FRAMEWORK...

BERMUDA MONETARY AUTHORITY CONSULTATION PAPER IMPLEMENTATION OF BASEL III NOVEMBER 2013 Table of Contents I. ABBREVIATIONS... 3 II. INTRODUCTION... 4 III. BACKGROUND... 6 IV. REVISED CAPITAL FRAMEWORK...

INSTITUTE AND FACULTY OF ACTUARIES. Curriculum 2019 SPECIMEN SOLUTIONS

INSTITUTE AND FACULTY OF ACTUARIES Curriculum 2019 SPECIMEN SOLUTIONS Subject SP5 Investment and Finance Specialist Principles Institute and Faculty of Actuaries 1 (i) The term risk budgeting refers to

INSTITUTE AND FACULTY OF ACTUARIES Curriculum 2019 SPECIMEN SOLUTIONS Subject SP5 Investment and Finance Specialist Principles Institute and Faculty of Actuaries 1 (i) The term risk budgeting refers to

STATEMENT OF PERFORMANCE EXPECTATIONS

B.21 STATEMENT OF PERFORMANCE EXPECTATIONS FOR THE PERIOD 01 JULY 2016 TO 30 JUNE 2017 GUARDIANS OF NEW ZEALAND SUPERANNUATION Contents SECTION 1 Introduction... 1 SECTION 2 Our Mandate... 2 SECTION 3

B.21 STATEMENT OF PERFORMANCE EXPECTATIONS FOR THE PERIOD 01 JULY 2016 TO 30 JUNE 2017 GUARDIANS OF NEW ZEALAND SUPERANNUATION Contents SECTION 1 Introduction... 1 SECTION 2 Our Mandate... 2 SECTION 3

Insurance Solvency Standards: guarantees and off-balance sheet exposures

Consultation Paper: Insurance Solvency Standards: guarantees and off-balance sheet exposures The Reserve Bank invites submissions on this Consultation Paper by 9 August 2013. Submissions and enquiries

Consultation Paper: Insurance Solvency Standards: guarantees and off-balance sheet exposures The Reserve Bank invites submissions on this Consultation Paper by 9 August 2013. Submissions and enquiries

Grant Spencer: Getting the best out of macro-prudential policy

Grant Spencer: Getting the best out of macro-prudential policy Speech by Mr Grant Spencer, Deputy Governor of the Reserve Bank of New Zealand, to INFINZ, Auckland, 13 March 2018. Introduction * * * It

Grant Spencer: Getting the best out of macro-prudential policy Speech by Mr Grant Spencer, Deputy Governor of the Reserve Bank of New Zealand, to INFINZ, Auckland, 13 March 2018. Introduction * * * It

19 March Georgette Nicholas Chief Executive Officer and Managing Director Genworth Mortgage Insurance Australia Limited

19 March 2018 Ian Woolford Manager, Financial Policy Prudential Supervision Department Reserve Bank of New Zealand PO Box 2498 Wellington 6140 New Zealand Genworth Financial Mortgage Insurance Pty Ltd

19 March 2018 Ian Woolford Manager, Financial Policy Prudential Supervision Department Reserve Bank of New Zealand PO Box 2498 Wellington 6140 New Zealand Genworth Financial Mortgage Insurance Pty Ltd

Guardians of New Zealand Superannuation

Guardians of New Zealand Superannuation STATEMENT OF INVESTMENT POLICIES, STANDARDS AND PROCEDURES 1 JULY 2011 Table of Contents 1 Introduction... 3 2 Asset Classes and Selection Criteria... 7 3 Benchmarks...

Guardians of New Zealand Superannuation STATEMENT OF INVESTMENT POLICIES, STANDARDS AND PROCEDURES 1 JULY 2011 Table of Contents 1 Introduction... 3 2 Asset Classes and Selection Criteria... 7 3 Benchmarks...

Pillar 2 - Supervisory Review Process

B ASEL II F RAMEWORK The Supervisory Review Process (Pillar 2) Rules and Guidelines Revised: February 2018 CAYMAN ISLANDS MONETARY AUTHORITY Cayman Islands Monetary Authority Page 1 Table of Contents Introduction...

B ASEL II F RAMEWORK The Supervisory Review Process (Pillar 2) Rules and Guidelines Revised: February 2018 CAYMAN ISLANDS MONETARY AUTHORITY Cayman Islands Monetary Authority Page 1 Table of Contents Introduction...

An Initial Assessment of Changes to the Bank of Canada s Framework for Market Operations

42 An Initial Assessment of Changes to the Bank of Canada s Framework for Market Operations Kaetlynd McRae, Sean Durr and David Manzo, Financial Markets Department In 2015, the Bank of Canada completed

42 An Initial Assessment of Changes to the Bank of Canada s Framework for Market Operations Kaetlynd McRae, Sean Durr and David Manzo, Financial Markets Department In 2015, the Bank of Canada completed

Basel II Pillar 3 Disclosures

DBS GROUP HOLDINGS LTD & ITS SUBSIDIARIES DBS Annual Report 2008 123 DBS Group Holdings Ltd and its subsidiaries (the Group) have adopted Basel II as set out in the revised Monetary Authority of Singapore

DBS GROUP HOLDINGS LTD & ITS SUBSIDIARIES DBS Annual Report 2008 123 DBS Group Holdings Ltd and its subsidiaries (the Group) have adopted Basel II as set out in the revised Monetary Authority of Singapore

31 December Guidelines to Article 122a of the Capital Requirements Directive

31 December 2010 Guidelines to Article 122a of the Capital Requirements Directive 1 Table of contents Table of contents...2 Background...4 Objectives and methodology...4 Implementation date...5 Considerations

31 December 2010 Guidelines to Article 122a of the Capital Requirements Directive 1 Table of contents Table of contents...2 Background...4 Objectives and methodology...4 Implementation date...5 Considerations

MORGAN STANLEY SMITH BARNEY HOLDINGS (UK) LIMITED AS AT 31 DECEMBER 2013

LIMITED AS AT 31 DECEMBER 2013") MORGAN STANLEY SMITH BARNEY HOLDINGS (UK) LIMITED AS AT 31 DECEMBER 2013 Disclosure (UK) TABLE OF CONTENTS 1. BASEL II ACCORD... 2 2. BACKGROUND TO PILLAR 3 DISCLOSURES... 2 3. APPLICATION OF THE PILLAR

MORGAN STANLEY SMITH BARNEY HOLDINGS (UK) LIMITED AS AT 31 DECEMBER 2013 Disclosure (UK) TABLE OF CONTENTS 1. BASEL II ACCORD... 2 2. BACKGROUND TO PILLAR 3 DISCLOSURES... 2 3. APPLICATION OF THE PILLAR

West Midlands Pension Fund. Investment Strategy Statement 2017

West Midlands Pension Fund Investment Strategy Statement 2017 March 2017 Investment Strategy Statement 2017 1) Introduction This is the Investment Strategy Statement (the ISS ) of the West Midlands Pension

West Midlands Pension Fund Investment Strategy Statement 2017 March 2017 Investment Strategy Statement 2017 1) Introduction This is the Investment Strategy Statement (the ISS ) of the West Midlands Pension

STRATEGY NORGES BANK INVESTMENT MANAGEMENT

STRATEGY 2017 2019 NORGES BANK INVESTMENT MANAGEMENT Our mission is to safeguard and build financial wealth for future generations. Contents Strategy 2017 2019 We are a large global investor and a long-term

STRATEGY 2017 2019 NORGES BANK INVESTMENT MANAGEMENT Our mission is to safeguard and build financial wealth for future generations. Contents Strategy 2017 2019 We are a large global investor and a long-term

Risk Concentrations Principles

Risk Concentrations Principles THE JOINT FORUM BASEL COMMITTEE ON BANKING SUPERVISION INTERNATIONAL ORGANIZATION OF SECURITIES COMMISSIONS INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS Basel December

Risk Concentrations Principles THE JOINT FORUM BASEL COMMITTEE ON BANKING SUPERVISION INTERNATIONAL ORGANIZATION OF SECURITIES COMMISSIONS INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS Basel December

Habib Bank AG Zurich. Annual disclosures according to Basel III (Year 2014)

") Annual disclosures according to Basel III (Year 2014) 1 Annual disclosures according to Basel III (Year 2014) 1. Scope of consolidation Scope of consolidation for capital adequacy purposes The scope of

Annual disclosures according to Basel III (Year 2014) 1 Annual disclosures according to Basel III (Year 2014) 1. Scope of consolidation Scope of consolidation for capital adequacy purposes The scope of

Consultation Paper. Draft Guidelines On Significant Credit Risk Transfer relating to Article 243 and Article 244 of Regulation 575/2013

EBA/CP/2013/45 17.12.2013 Consultation Paper Draft Guidelines On Significant Credit Risk Transfer relating to Article 243 and Article 244 of Regulation 575/2013 Consultation Paper on Draft Guidelines on

EBA/CP/2013/45 17.12.2013 Consultation Paper Draft Guidelines On Significant Credit Risk Transfer relating to Article 243 and Article 244 of Regulation 575/2013 Consultation Paper on Draft Guidelines on

Timothy F Geithner: Hedge funds and their implications for the financial system

Timothy F Geithner: Hedge funds and their implications for the financial system Keynote address by Mr Timothy F Geithner, President and Chief Executive Officer of the Federal Reserve Bank of New York,

Timothy F Geithner: Hedge funds and their implications for the financial system Keynote address by Mr Timothy F Geithner, President and Chief Executive Officer of the Federal Reserve Bank of New York,

PILLAR 3 Disclosures

PILLAR 3 Disclosures Published April 2016 Contacts: Rajeev Adrian Sedjwick Joseph Chief Financial Officer Chief Risk Officer 0207 776 4006 0207 776 4014 Rajeev.adrian@bank-abc.com sedjwick.joseph@bankabc.com

PILLAR 3 Disclosures Published April 2016 Contacts: Rajeev Adrian Sedjwick Joseph Chief Financial Officer Chief Risk Officer 0207 776 4006 0207 776 4014 Rajeev.adrian@bank-abc.com sedjwick.joseph@bankabc.com

Treasury Management Framework v Page 1 of 28

UC Policy Library Treasury Management Framework Last Modified April 2017 Review Date May 2018 Approval Authority Chair, University Council Contact Officer Chief Financial Officer Financial Services Table

UC Policy Library Treasury Management Framework Last Modified April 2017 Review Date May 2018 Approval Authority Chair, University Council Contact Officer Chief Financial Officer Financial Services Table

COMMUNIQUE. Page 1 of 13

COMMUNIQUE 16-COM-001 Feb. 1, 2016 Release of Liquidity Risk Management Guiding Principles The Credit Union Prudential Supervisors Association (CUPSA) has released guiding principles for Liquidity Risk

COMMUNIQUE 16-COM-001 Feb. 1, 2016 Release of Liquidity Risk Management Guiding Principles The Credit Union Prudential Supervisors Association (CUPSA) has released guiding principles for Liquidity Risk

(Non-legislative acts) REGULATIONS

REGULATIONS") 9.10.2012 Official Journal of the European Union L 274/1 II (Non-legislative acts) REGULATIONS COMMISSION DELEGATED REGULATION (EU) No 918/2012 of 5 July 2012 supplementing Regulation (EU) No 236/2012

9.10.2012 Official Journal of the European Union L 274/1 II (Non-legislative acts) REGULATIONS COMMISSION DELEGATED REGULATION (EU) No 918/2012 of 5 July 2012 supplementing Regulation (EU) No 236/2012

Financial Statements. For the year ended 30 June 2017

Financial Statements Statement of comprehensive income 18 Balance sheet 19 Statement of changes in equity 20 Statement of cash flows 21 22 n 24 n Long Term Assets 39 n Other information 41 Certificate

Financial Statements Statement of comprehensive income 18 Balance sheet 19 Statement of changes in equity 20 Statement of cash flows 21 22 n 24 n Long Term Assets 39 n Other information 41 Certificate

In various tables, use of - indicates not meaningful or not applicable.

Basel II Pillar 3 disclosures 2008 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse Group, Credit Suisse, the Group, we, us and our mean Credit Suisse Group AG

Basel II Pillar 3 disclosures 2008 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse Group, Credit Suisse, the Group, we, us and our mean Credit Suisse Group AG

Basel Committee on Banking Supervision. Fair value measurement and modelling: An assessment of challenges and lessons learned from the market stress

Basel Committee on Banking Supervision Fair value measurement and modelling: An assessment of challenges and lessons learned from the market stress June 2008 Requests for copies of publications, or for

Basel Committee on Banking Supervision Fair value measurement and modelling: An assessment of challenges and lessons learned from the market stress June 2008 Requests for copies of publications, or for

INVESTMENT POLICY. January Approved by the Board of Governors on 12 December Third amendment approved with effect from 1 January 2019

INVESTMENT POLICY January 2019 Approved by the Board of Governors on 12 December 2016 Third amendment approved with effect from 1 January 2019 1 Contents SECTION 1. OVERVIEW SECTION 2. INVESTMENT PHILOSOPHY-

INVESTMENT POLICY January 2019 Approved by the Board of Governors on 12 December 2016 Third amendment approved with effect from 1 January 2019 1 Contents SECTION 1. OVERVIEW SECTION 2. INVESTMENT PHILOSOPHY-

Foreign exchange intervention in Argentina: motives, techniques and implications

Foreign exchange intervention in Argentina: motives, techniques and implications Claudio Irigoyen 1. Introduction Finding the optimal degree of exchange rate flexibility is difficult. To a great extent

Foreign exchange intervention in Argentina: motives, techniques and implications Claudio Irigoyen 1. Introduction Finding the optimal degree of exchange rate flexibility is difficult. To a great extent

Getting the best out of macro-prudential policy

Getting the best out of macro-prudential policy A speech delivered to INFINZ in Auckland On 13 March 2018 By Grant Spencer, Governor 2 The Terrace, PO Box 2498, Wellington 6140, New Zealand Telephone 64

Getting the best out of macro-prudential policy A speech delivered to INFINZ in Auckland On 13 March 2018 By Grant Spencer, Governor 2 The Terrace, PO Box 2498, Wellington 6140, New Zealand Telephone 64

Risk Management. Credit Risk Management

Credit Risk Management Credit risk is defined as the risk of loss arising from any failure by a borrower or a counterparty to fulfill its financial obligations as and when they fall due. Credit risk is

Credit Risk Management Credit risk is defined as the risk of loss arising from any failure by a borrower or a counterparty to fulfill its financial obligations as and when they fall due. Credit risk is

The IASB s Discussion Paper Accounting for dynamic risk management: a portfolio revaluation approach to macro hedging

Date: 15 October 2014 ESMA/2014/1254 Mr Hans Hoogervorst International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom The IASB s Discussion Paper Accounting for dynamic risk

Date: 15 October 2014 ESMA/2014/1254 Mr Hans Hoogervorst International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom The IASB s Discussion Paper Accounting for dynamic risk

(TRANSLATION) Report of the Auditors

Report of the Auditors") (TRANSLATION) To the Minister of Finance Report of the Auditors The Office of the Auditor General of Thailand has audited the accompanying financial statements of the Bank of Thailand, which comprise the

(TRANSLATION) To the Minister of Finance Report of the Auditors The Office of the Auditor General of Thailand has audited the accompanying financial statements of the Bank of Thailand, which comprise the

A new macro-prudential policy framework for New Zealand final policy position

A new macro-prudential policy framework for New Zealand final policy position May 2013 2 1.0 Background 1. During March and April, the Reserve Bank undertook a public consultation on its proposed framework

A new macro-prudential policy framework for New Zealand final policy position May 2013 2 1.0 Background 1. During March and April, the Reserve Bank undertook a public consultation on its proposed framework

Ben S Bernanke: Modern risk management and banking supervision

Ben S Bernanke: Modern risk management and banking supervision Remarks by Mr Ben S Bernanke, Chairman of the Board of Governors of the US Federal Reserve System, at the Stonier Graduate School of Banking,

Ben S Bernanke: Modern risk management and banking supervision Remarks by Mr Ben S Bernanke, Chairman of the Board of Governors of the US Federal Reserve System, at the Stonier Graduate School of Banking,

Merrill Lynch Equity S.àr.l. Pillar 3 Disclosures. As at December 31, 2012

Merrill Lynch Equity S.àr.l. Pillar 3 Disclosures As at December 31, 2012 1 2 Contents 1. Introduction 2. Capital Resources and Requirements 3. Risk Management Objectives and Policies 4. Further Detail

Merrill Lynch Equity S.àr.l. Pillar 3 Disclosures As at December 31, 2012 1 2 Contents 1. Introduction 2. Capital Resources and Requirements 3. Risk Management Objectives and Policies 4. Further Detail

PRUDENTIAL REGULATION OF MFIs

PRUDENTIAL REGULATION OF MFIs Prudential Standards and Ratios Presented by Fatou Deen-Touray, Deputy Director, Microfinance Dept. Central Bank of The Gambia 1.INTRODUCTION 1. In many, if not most developing

PRUDENTIAL REGULATION OF MFIs Prudential Standards and Ratios Presented by Fatou Deen-Touray, Deputy Director, Microfinance Dept. Central Bank of The Gambia 1.INTRODUCTION 1. In many, if not most developing

Desjardins Trust Inc. Financial Information and Information on Risk Management (unaudited)

") Desjardins Trust Inc. Financial Information and Information on Risk Management (unaudited) For the period ended September 30, 2017 TABLE OF CONTENTS Page Page Notes to readers Capital Use of this document

Desjardins Trust Inc. Financial Information and Information on Risk Management (unaudited) For the period ended September 30, 2017 TABLE OF CONTENTS Page Page Notes to readers Capital Use of this document

New Zealand Government Securities Funding Strategy. 2018/19: Edition 1

New Zealand Government Securities Funding Strategy 18/19: Edition 1 Contacts: Kim Martin Principal Strategist info@nzdmo.govt.nz +6 89 77 New Zealand Debt Management Office, The Treasury, 1 The Terrace,

New Zealand Government Securities Funding Strategy 18/19: Edition 1 Contacts: Kim Martin Principal Strategist info@nzdmo.govt.nz +6 89 77 New Zealand Debt Management Office, The Treasury, 1 The Terrace,

Committee on Payments and Market Infrastructures. Board of the International Organization of Securities Commissions

Committee on Payments and Market Infrastructures Board of the International Organization of Securities Commissions Recovery of financial market infrastructures October 2014 (Revised July 2017) This publication

Committee on Payments and Market Infrastructures Board of the International Organization of Securities Commissions Recovery of financial market infrastructures October 2014 (Revised July 2017) This publication

North Professional Series

North Professional Series Product Disclosure Statement Issue number 5 Issued 29 September 2017 Issued by ipac asset management limited ABN 22 003 257 225, AFSL 234655 Registered trademark of National Mutual

North Professional Series Product Disclosure Statement Issue number 5 Issued 29 September 2017 Issued by ipac asset management limited ABN 22 003 257 225, AFSL 234655 Registered trademark of National Mutual

DRAFT JOINT STANDARD * OF 2018 FINANCIAL SECTOR REGULATION ACT NO 9 OF 2017

File ref no. 15/8 DRAFT JOINT STANDARD * OF 2018 FINANCIAL SECTOR REGULATION ACT NO 9 OF 2017 DRAFT MARGIN REQUIREMENTS FOR NON-CENTRALLY CLEARED OTC DERIVATIVE TRANSACTIONS Under sections 106(1)(a), 106(2)(a)

File ref no. 15/8 DRAFT JOINT STANDARD * OF 2018 FINANCIAL SECTOR REGULATION ACT NO 9 OF 2017 DRAFT MARGIN REQUIREMENTS FOR NON-CENTRALLY CLEARED OTC DERIVATIVE TRANSACTIONS Under sections 106(1)(a), 106(2)(a)

WAVERLEY BOROUGH COUNCIL VALUE FOR MONEY OVERVIEW AND SCRUTINY - 26 MARCH 2018 EXECUTIVE 10 APRIL 2018

WAVERLEY BOROUGH COUNCIL VALUE FOR MONEY OVERVIEW AND SCRUTINY - 26 MARCH 2018 EXECUTIVE 10 APRIL 2018 Title: TREASURY MANAGEMENT FRAMEWORK 2018/19 [Portfolio Holder: Cllr Ged Hall] [Wards Affected: All]

WAVERLEY BOROUGH COUNCIL VALUE FOR MONEY OVERVIEW AND SCRUTINY - 26 MARCH 2018 EXECUTIVE 10 APRIL 2018 Title: TREASURY MANAGEMENT FRAMEWORK 2018/19 [Portfolio Holder: Cllr Ged Hall] [Wards Affected: All]

Basel II Pillar 3 disclosures

Basel II Pillar 3 disclosures 6M10 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse, the Group, we, us and our mean Credit Suisse Group AG and its consolidated

Basel II Pillar 3 disclosures 6M10 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse, the Group, we, us and our mean Credit Suisse Group AG and its consolidated

EQUITY PARTNERSHIP TRUST

EQUITY PARTNERSHIP TRUST Scoping Document for Consultation November 2014 MANAGE YOUR CAPITAL IMPORTANT INFORMATION This material has been prepared as a first step in a consultation process with our farmers

EQUITY PARTNERSHIP TRUST Scoping Document for Consultation November 2014 MANAGE YOUR CAPITAL IMPORTANT INFORMATION This material has been prepared as a first step in a consultation process with our farmers

Basel Pillar 3 Disclosures

Basel Pillar 3 Disclosures September 30, 2017 TABLE OF CONTENTS Introduction................................................................................... Regulatory Framework........................................................................

Basel Pillar 3 Disclosures September 30, 2017 TABLE OF CONTENTS Introduction................................................................................... Regulatory Framework........................................................................

Guidance to completing the NSFR module of Form LCR and LMR

Guidance to completing the NSFR module of Form LCR and LMR 1 Net Stable Funding Ratio (NSFR) The Net Stable Funding Ratio has been developed to ensure a stable funding profile in relation to the characteristics

Guidance to completing the NSFR module of Form LCR and LMR 1 Net Stable Funding Ratio (NSFR) The Net Stable Funding Ratio has been developed to ensure a stable funding profile in relation to the characteristics

HSBC Bank Australia Ltd. Pillar 3 Disclosures. 31 December Consolidated Basis

HSBC Bank Australia Ltd 31 December 2013 Consolidated Basis Contents CONTENTS... 2 1. INTRODUCTION... 3 PURPOSE... 3 BACKGROUND... 3 2. SCOPE OF APPLICATION... 4 3. VERIFICATION... 4 4. HBAU CONTEXT...

HSBC Bank Australia Ltd 31 December 2013 Consolidated Basis Contents CONTENTS... 2 1. INTRODUCTION... 3 PURPOSE... 3 BACKGROUND... 3 2. SCOPE OF APPLICATION... 4 3. VERIFICATION... 4 4. HBAU CONTEXT...

Response to submissions on the Consultation Paper: Serviceability Restrictions as a Potential Macroprudential Tool in New Zealand.

Response to submissions on the Consultation Paper: Serviceability Restrictions as a Potential Macroprudential Tool in New Zealand November 2017 2 1. The Reserve Bank undertook a public consultation process

Response to submissions on the Consultation Paper: Serviceability Restrictions as a Potential Macroprudential Tool in New Zealand November 2017 2 1. The Reserve Bank undertook a public consultation process

March 17, Secretariat of the Basel Committee on Banking Supervision Bank for International Settlements CH-4002 Basel Switzerland

State Street Corporation Stefan M. Gavell Executive Vice President and Head of Regulatory, Industry and Government Affairs State Street Financial Center One Lincoln Street Boston, MA 02111-2900 Telephone:

State Street Corporation Stefan M. Gavell Executive Vice President and Head of Regulatory, Industry and Government Affairs State Street Financial Center One Lincoln Street Boston, MA 02111-2900 Telephone:

RE: Transaction Costs Disclosure: Improving Transparency in Workplace Pensions: Call for Evidence

6 May 2015 Department for Work and Pensions Transparency Team Department for Work and Pensions 3rd Floor West, Zone G Quarry House Leeds, LS2 7UA Submitted via email to: Ms Carol McGinley and Mr Michael

6 May 2015 Department for Work and Pensions Transparency Team Department for Work and Pensions 3rd Floor West, Zone G Quarry House Leeds, LS2 7UA Submitted via email to: Ms Carol McGinley and Mr Michael

Central Bank of Seychelles Monetary Policy Framework

Central Bank of Seychelles Monetary Policy Framework Page 0 Table of Contents 1. Monetary Policy Framework... 1 2.Decision-making process for monetary policy implementation... 3 3.Terms of Reference of

Central Bank of Seychelles Monetary Policy Framework Page 0 Table of Contents 1. Monetary Policy Framework... 1 2.Decision-making process for monetary policy implementation... 3 3.Terms of Reference of

Interim financial statements (unaudited) as at 30 September 2009

as at 30 September 2009") Interim financial statements (unaudited) as at 30 September 2009 Basel, 9 November 2009 Interim financial statements (unaudited) as at 30 September 2009 These financial statements for the six months ended

Interim financial statements (unaudited) as at 30 September 2009 Basel, 9 November 2009 Interim financial statements (unaudited) as at 30 September 2009 These financial statements for the six months ended

Nottinghamshire Pension Fund INVESTMENT STRATEGY STATEMENT. Introduction. Purpose and Principles. March 2017

Nottinghamshire Pension Fund March 2017 INVESTMENT STRATEGY STATEMENT Introduction 1. The County Council is an administering authority of the Local Government Pension Scheme (the Scheme ) as specified

Nottinghamshire Pension Fund March 2017 INVESTMENT STRATEGY STATEMENT Introduction 1. The County Council is an administering authority of the Local Government Pension Scheme (the Scheme ) as specified

Statement of Guidance

Statement of Guidance Credit Risk Classification, Provisioning and Management Policy and Development Division Page 1 of 20 Table of Contents 1. Statement of Objectives... 3 2. Scope... 3 3. Terminology...

Statement of Guidance Credit Risk Classification, Provisioning and Management Policy and Development Division Page 1 of 20 Table of Contents 1. Statement of Objectives... 3 2. Scope... 3 3. Terminology...

C A Y M A N I S L A N D S MONETARY AUTHORITY

Statement of Guidance Credit Risk Classification, Provisioning and Management Policy and Development Division Page 1 of 22 Table of Contents 1 Statement of Objectives... 3 2 Scope... 3 3 Terminology...

Statement of Guidance Credit Risk Classification, Provisioning and Management Policy and Development Division Page 1 of 22 Table of Contents 1 Statement of Objectives... 3 2 Scope... 3 3 Terminology...

J.P. MORGAN CHASE BANK BERHAD (Incorporated in Malaysia)

") FOR THE FINANCIAL YEAR ENDED 31 DECEMBER 2012 0100B3/py FOR THE FINANCIAL YEAR ENDED 31 DECEMBER 2012 1 OVERVIEW The Pillar 3 Disclosures is governed under the Bank Negara Malaysia ( BNM ) s revised Risk-

FOR THE FINANCIAL YEAR ENDED 31 DECEMBER 2012 0100B3/py FOR THE FINANCIAL YEAR ENDED 31 DECEMBER 2012 1 OVERVIEW The Pillar 3 Disclosures is governed under the Bank Negara Malaysia ( BNM ) s revised Risk-

Leverage Ratio Rules and Guidelines

BASEL III FRAMEWORK Leverage Ratio Rules and Guidelines 1 December 2019 CAYMAN ISLANDS MONETARY AUTHORITY Table of Contents 1. INTRODUCTION... 4 2. SCOPE OF APPLICATION... 4 3. DEFINITION AND MINIMUM REQUIREMENT...

BASEL III FRAMEWORK Leverage Ratio Rules and Guidelines 1 December 2019 CAYMAN ISLANDS MONETARY AUTHORITY Table of Contents 1. INTRODUCTION... 4 2. SCOPE OF APPLICATION... 4 3. DEFINITION AND MINIMUM REQUIREMENT...

Impairment of financial instruments under IFRS 9

Applying IFRS Impairment of financial instruments under IFRS 9 December 2014 Contents In this issue: 1. Introduction... 4 1.1 Brief history and background of the impairment project... 4 1.2 Overview of

Applying IFRS Impairment of financial instruments under IFRS 9 December 2014 Contents In this issue: 1. Introduction... 4 1.1 Brief history and background of the impairment project... 4 1.2 Overview of

STATEMENT OF INVESTMENT POLICIES, STANDARDS AND PROCEDURES FOR ASSETS MANAGED BY THE PUBLIC SECTOR PENSION INVESTMENT BOARD

STATEMENT OF INVESTMENT POLICIES, STANDARDS AND PROCEDURES FOR ASSETS MANAGED BY THE PUBLIC SECTOR PENSION INVESTMENT BOARD As approved by the Board of Directors on November 10, 2017 TABLE OF CONTENTS

STATEMENT OF INVESTMENT POLICIES, STANDARDS AND PROCEDURES FOR ASSETS MANAGED BY THE PUBLIC SECTOR PENSION INVESTMENT BOARD As approved by the Board of Directors on November 10, 2017 TABLE OF CONTENTS

Solvency II: Orientation debate Design of a future prudential supervisory system in the EU

MARKT/2503/03 EN Orig. Solvency II: Orientation debate Design of a future prudential supervisory system in the EU (Recommendations by the Commission Services) Commission européenne, B-1049 Bruxelles /

MARKT/2503/03 EN Orig. Solvency II: Orientation debate Design of a future prudential supervisory system in the EU (Recommendations by the Commission Services) Commission européenne, B-1049 Bruxelles /

Draft for Consultation FICOM ICAAP Guide

Draft for Consultation FICOM ICAAP Guide BC Credit Unions November 2017 www.fic.gov.bc.ca Table of Contents INTRODUCTION... 1 FEATURES OF AN EFFECTIVE ICAAP... 2 I. Board and Management Oversight... 2

Draft for Consultation FICOM ICAAP Guide BC Credit Unions November 2017 www.fic.gov.bc.ca Table of Contents INTRODUCTION... 1 FEATURES OF AN EFFECTIVE ICAAP... 2 I. Board and Management Oversight... 2

11 th July Summary views

Record Currency Management Limited response to European Supervisory Authorities Consultation Paper Draft regulatory technical standards on risk-mitigation techniques for OTC-derivative contracts not cleared

Record Currency Management Limited response to European Supervisory Authorities Consultation Paper Draft regulatory technical standards on risk-mitigation techniques for OTC-derivative contracts not cleared

Leverage Ratio Rules and Guidelines

BASEL III FRAMEWORK Leverage Ratio Rules and Guidelines Month YYYY CAYMAN ISLANDS MONETARY AUTHORITY Table of Contents 1. INTRODUCTION... 3 2. SCOPE OF APPLICATION... 3 3. DEFINITION AND MINIMUM REQUIREMENT...

BASEL III FRAMEWORK Leverage Ratio Rules and Guidelines Month YYYY CAYMAN ISLANDS MONETARY AUTHORITY Table of Contents 1. INTRODUCTION... 3 2. SCOPE OF APPLICATION... 3 3. DEFINITION AND MINIMUM REQUIREMENT...

GUIDELINES FOR THE INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS FOR LICENSEES

SUPERVISORY AND REGULATORY GUIDELINES: 2016 Issued: 2 August 2016 GUIDELINES FOR THE INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS FOR LICENSEES 1. INTRODUCTION 1.1 The Central Bank of The Bahamas ( the

SUPERVISORY AND REGULATORY GUIDELINES: 2016 Issued: 2 August 2016 GUIDELINES FOR THE INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS FOR LICENSEES 1. INTRODUCTION 1.1 The Central Bank of The Bahamas ( the

Basel II Implementation Update

Basel II Implementation Update World Bank/IMF/Federal Reserve System Seminar for Senior Bank Supervisors from Emerging Economies 15-26 October 2007 Elizabeth Roberts Director, Financial Stability Institute

Basel II Implementation Update World Bank/IMF/Federal Reserve System Seminar for Senior Bank Supervisors from Emerging Economies 15-26 October 2007 Elizabeth Roberts Director, Financial Stability Institute

Collateral upgrade transactions and asset encumbrance: expectations in relation to firms risk management practices

Supervisory Statement LSS2/13 Collateral upgrade transactions and asset encumbrance: expectations in relation to firms risk management practices April 2013 Supervisory Statement LSS2/13 Collateral upgrade

Supervisory Statement LSS2/13 Collateral upgrade transactions and asset encumbrance: expectations in relation to firms risk management practices April 2013 Supervisory Statement LSS2/13 Collateral upgrade

Harbour Investment Funds Statement of Investment Policy & Objectives (SIPO)

") Harbour Investment Funds Statement of Investment Policy & Objectives (SIPO) Issued by Harbour Asset Management Limited 19 June 2017 This document replaces the SIPO dated 21 st September 2016 1 HARBOUR