STRATEGIC REVIEW Presentation to Analysts & Investors. July 14, 2011 New York

|

|

|

- Barnard Little

- 6 years ago

- Views:

Transcription

1 STRATEGIC REVIEW Presentation to Analysts & Investors July 14, 2011 New York

2 STRATEGIC REVIEW Strategy & Guidance July 14, 2011 António Horta-Osório Group Chief Executive

3 AGENDA Strategy & Guidance António Horta-Osório Simplification Mark Fisher Finance Tim Tookey Q&A 3

4 ICONIC BRANDS WITH RICH HISTORY AND IMMENSE POTENTIAL TO DELIVER FOR BOTH CUSTOMERS AND SHAREHOLDERS 4

5 AGENDA First 100 Days Strategy Action Plan Guidance 5

6 FIRST 100 DAYS Rapid, focused actions taken since March Strengthened executive leadership team New, more agile organisation in place Accelerated pay down of government and central bank funding Disciplined sale of non-core assets Accelerating EU/HMT-mandated branch sale programme Renewed focus on and improvement in customer satisfaction Committed to Halifax as a leading challenger brand Actively supporting SME lending Provided clarity on PPI provisioning On schedule to substantially complete Integration in Q Completed 100 day strategic review 6

7 OLD FEDERAL MANAGEMENT STRUCTURE DUPLICATED RESOURCES WITH TOO MANY LAYERS CEO RETAIL BANKING WHOLESALE WEALTH & INTERNATIONAL INSURANCE GROUP OPERATIONS /IT GROUP HR GROUP FINANCE GROUP RISK Lloyds/ Bank of Scotland Halifax Products & Marketing Operations Risk Finance HR Audit Comms Commercial Corporate Treasury Wholesale Markets Asset Finance Operations Risk Finance HR Audit International UK Wealth & Private Banking Products & Marketing Operations Risk Finance HR Audit Comms L, P & I GI Products & Marketing Operations Risk Finance HR Audit Comms Risk Finance HR Audit Comms Risk Finance Audit Comms Risk HR Audit Comms Finance HR Audit Comms Comms 7

8 FIRST 100 DAYS A new, more agile organisation in place creating a high performance culture Retail Banking CEO LLOYDS TSB & BANK OF SCOTLAND COMMUNITY BANK HALIFAX COMMUNITY BANK PRODUCTS AND MARKETING WEALTH & INTERNATIONAL COMMERCIAL WHOLESALE INSURANCE Operations and IT Finance Risk Management Other functions (HR, Internal Audit, Legal, Corporate Affairs, Strategy) Flatter Organisation Top team closer to customers Additions to Top Team Higher visibility for business units and stronger control functions Centralised Support Functions Improved control, efficiency and service New Governance for Pricing, Cost, Investment, Non-Core Weekly committees, cross-functional, faster decisions New Performance Culture Clear accountability and individual goals International Business Reshaped Clear downsizing from 30 to <15 countries, split between Wealth and Wholesale 8

9 AGENDA First 100 Days Strategy Action Plan Guidance 9

10 STRATEGY Key trends shaping strategic context 1 INCREASING CUSTOMER EXPECTATIONS Want simplicity and transparency Demand a quality, multi-channel customer service experience Growing demand for advice to plan/save for retirement Increasingly demand better value for their money 2 INCREASING CLARITY ON REGULATION Stringent UK capital and liquidity standards More focus on consumer protection and transparency Recovery and resolution mechanisms and Retail ring-fencing Awaiting ICB final recommendations in September Already-competitive market with new challengers and more switching 3 CHALLENGING OPERATING ENVIRONMENT Continued cautious outlook on prospects for the UK economy De-leveraging combined with inflation, so cost efficiency imperative Managing and correctly pricing risk a major differentiator Healthy returns across segments, though lower than pre-crisis ACTIONS ACCELERATED IN RESPONSE TO CHALLENGING ENVIRONMENT 10

11 STRATEGY Today, the Group has unique assets but faces some important challenges UNIQUE ASSETS KEY CHALLENGES Valuable customer franchise and market position Well-recognised and respected brands in all markets Broad, multi-channel distribution High quality, committed people Change management capability, proven through Integration State Aid and associated sales Addressing funding structure Limited investment for growth over a number of years Inefficient organisation and processes, resulting in higher cost structure than necessary Continued exposure to non-core assets CLEAR PRIORITY TO SUPPORT CUSTOMERS, DRIVE EFFICIENCY AND INVEST FOR GROWTH 11

12 STRATEGY The Group s strategy fits with our distinctive assets and capabilities THE BEST BANK FOR CUSTOMERS Create shareholder value by simplifying the way we work and investing where we can make a real difference STRONG CUSTOMER RELATION- SHIPS STRONG ICONIC BRANDS BROAD MULTI- CHANNEL DISTRIBUTION CUSTOMER FOCUSED PEOPLE INTEGRATED PLATFORM ~30 million customers #1 brand for customer consideration 27% year on year growth in Internet banking usage 80% colleague engagement 2bn integration savings nearing completion 12

13 STRATEGY This strategy will deliver shareholder value THE BEST BANK FOR SHAREHOLDERS Reinstate dividend after regulatory capital requirements are defined and prudently met, and return to full private ownership CUSTOMER- DRIVEN, DIVERSIFIED INCOME POSITIVE OPERATING JAWS CAPITAL ALLOCATED TO CORE BUSINESS PRUDENT RISK APPETITE STRONG STABLE FUNDING DISCIPLINED HIGH-RETURN INVESTING 13

14 AGENDA First 100 Days Strategy Action Plan Guidance 14

15 OUR ACTION PLAN WILL ENSURE STRONG, STABLE RETURNS FOR OUR SHAREHOLDERS OVER THE NEXT 3 YEARS AND BEYOND RESHAPE our business portfolio to fit our assets, capabilities and risk appetite Sustainable, predictable RoE, in excess of our CoE SIMPLIFY the Group to improve agility, service, and efficiency Significant cost savings and positive operating JAWS INVEST to grow our core customer businesses Strong, stable, high quality EARNINGS streams Continue to STRENGTHEN our balance sheet and liquidity position Robust CORE TIER 1 RATIO and stable funding base 15

16 RESHAPE OUR PORTFOLIO We will focus investments on attractive UK customer segments and the products they need DECISION CRITERIA ACTIONS CORE Strong, above-hurdle returns Attractive growth prospects Liquidity/capital efficient Sustainable competitive advantage Fits with core customer strategy SME lending CA and Savings Transaction banking Debt financing, Fixed Income & rates Bancassurance Mass affluent Wealth NON-CORE Below-hurdle returns Outside risk appetite &/or distressed Unclear value proposition Subscale market position Poor fit with core customer strategy Ireland Retail self-certified mortgages Shipping Aerospace International footprint cut in half 16

17 RESHAPE OUR PORTFOLIO Disciplined approach to manage and reduce non-core assets Adequate coverage ratios for all non-performing assets Organisational model: Dedicated workout unit under Risk for non-performing CRE and corporate loans Other non-strategic activities managed in a dedicated way within Retail, Wholesale and Wealth until run off or sold Senior management oversight by Group Asset Review Forum Experienced transactions team focused on asset sales Balanced scorecards and individual incentives tied to portfolio objectives 17

18 RESHAPE OUR PORTFOLIO We will invest to be the best bank for personal customers RETAIL BANKING HALIFAX LLOYDS & BANK OF SCOTLAND A leading challenger brand on the High Street Recognised by industry and media as a value for money leader (e.g. Moneyfacts Best ISA and Best Current Account Provider 2011) Game-changing products, like the new ISA Promise Simple, efficient and fair customer experience Leading relationship brands in UK retail banking Focused on recognising and rewarding customer loyalty Committed, experienced customer-facing colleagues Investing in branches, new channels and services like Money Manager to deliver a customer experience we can be proud of WEALTH MANAGEMENT Aspire to become a wealth advisor to our existing UK customers in mass affluent, affluent and HNW segments Refocusing International on UK customers, expats and other anglophile wealth customers - reducing locations by half Creating new service models, electronic capabilities and investment platforms with SWIP and others products 18

19 RESHAPE OUR PORTFOLIO We will invest to be the best through-the-cycle partner for business customers COMMERCIAL BANKING A leader in fuelling UK economic recovery and integral to our customers communities Best through-the-cycle banking partner to UK SMEs New relationship and service model, better on-line and phone support, delivering efficiency and better customer value Delivering the whole Group Retail, Insurance, and Wealth products and advice WHOLESALE BANKING Leading through-the-cycle partner to UK companies & institutions (e.g. Voted by UK FDs as the Leading Corporate Bank 7 years running) Two major investments Transaction banking DCM, Fixed Income and Rates Selective international presence and products to support corporates with UK connectivity 19

20 RESHAPE OUR PORTFOLIO Bancassurance is a core part of our strategy and a solid financial contributor to the Group LIFE, PENSIONS & INVESTMENTS Scottish Widows the UK s most trusted and preferred brand Top 3 provider in Life, Pensions & Investments with 10% market share 43% of new business with existing bank customers New sales model and propositions to take advantage of Retail Distribution Review Industry-leading cost performance, recognised for top quality products and service GENERAL INSURANCE Top 3 provider in Home Insurance with 5% market share across all personal lines 82% of new business with existing bank customers Investing in our proposition for and distribution to SMEs Industry-leading combined ratio, with sophisticated underwriting and claims management BANCASSURANCE OFFERS A DISTINCTIVE OPPORTUNITY TO GENERATE DIVERSIFIED HIGH RETURNS, LIQUIDITY-FREE EARNINGS AND CASH RELEASE FOR THE GROUP 20

21 SIMPLIFY THE GROUP Post-integration, simplify the Group to improve service and reduce costs by 1.5bn annually TARGET OUTCOMES ACTIONS 1.5bn in annual cost savings in 2014 (on top of integration synergies) Proven ability to execute, built through integration Cost savings will enable: Investment in new channels, services and capabilities Best-in-market customer experience The right tools our colleagues need to do their jobs well Using attrition and redeployment not redundancy where possible OPERATIONS & PROCESSES SOURCING ORGANISATION DISTRIBUTION & CHANNELS Implement workflow, automate, improve IT landscape, establish centres of excellence Improve demand management, simplify specification, strengthen supplier relationships Flatten organisational structure, bringing top team closer to customers and front-line staff Continue to innovate, reduce product variants, increase pricing flexibility Already in progress 21

22 INVEST IN OUR CORE BUSINESS Reinvest 500m annually to improve our customer proposition and grow core income TARGET OUTCOMES ACTIONS OUR CUSTOMERS WILL VALUE Reinvest 1/3 of savings from Simplification By 2014, invest 500m (1) annually in core businesses In addition to BAU, Run-the-Bank, and mandatory investing Investing in initiatives to grow income, especially OOI Disciplined investment tests Fit with the Best Bank for Customers strategy Attractive financial returns Risk appetite Ability to execute PRODUCTS THAT CUSTOMERS NEED FAIR, SIMPLE TO UNDERSTAND PRICES TRUSTED ADVICE AND SERVICE ACCESS THAT SUITS OUR CUSTOMERS Simple retail product portfolio New transaction banking, financing and risk management for corporates Better investment propositions Low costs, enabling challenger pricing Rewards for customer loyalty Simple pricing structures New models for bancassurance, mass affluent and affluent Through-the-cycle partner to business Insight from a single customer view SME e-portal and direct model Multi-channel integration and mobile New electronic platform for corporates and financial institutions (1) Investment over 2011 to 2014 of 2.0bn including capital expenditure will result in up to 0.5 million per annum expenses in the income statement 22

23 INVEST IN OUR CORE BUSINESS Case study: Halifax will be a market challenger for today s high street New challenger products, including radical new Savings offer, to drive increasing volume and profit All branches open on Saturday Active on-line customers grow from m to drive lower costs Brand re-launch and exciting new marketing campaign A leading alternative to the Big-4 current account providers Engaged colleagues who identify with their customers 23

24 INVEST IN OUR CORE BUSINESS Case study: The UK s leading Retail Bancassurance provider CUSTOMERS +50% Growing need for advice to plan/save for retirement/future Specialised advisor teams better able to help customers meet their protection and investment needs SALES PROFIT BEFORE TAX +100% 2010 >100% 2014 Ability to quickly develop products and services in response to identified customer need in an integrated manner Low-cost and capital efficient manufacturing utilising a leading brand Range of channels, including branch, e- commerce and telephony, to meet different customer segment needs Improved customer insight with single customer view at an integrated level

25 INVEST IN OUR CORE BUSINESS Case study: Leading through-the-cycle partner to UK SMEs OPPORTUNITY SUCCESSION START-UP Balance sheetdriven banking Loans Current A/C Payments Cards Factoring Our highly rated RM s will have 100% more time with customers Time-to-cash for loans reduced by over 50% Targeted, informed propositions matched with customer life-stage Capital-light solutions Deposits Protection/Pensions FX/Hedging Business insurance Wealth MATURITY GROWTH STRENGTH Direct Relationship Bank to align service with customer needs, value and preference Delivering a comprehensive suite of products and services using unique customer insights 25

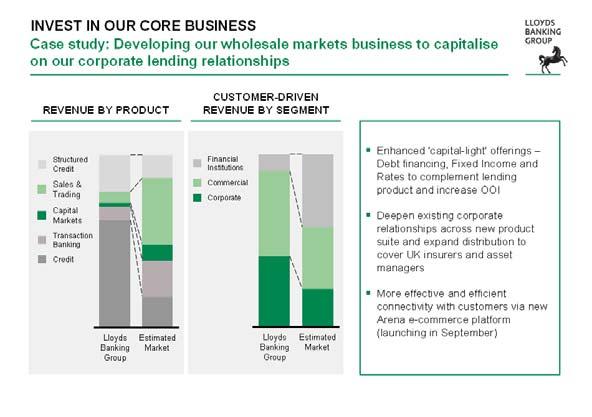

26 INVEST IN OUR CORE BUSINESS Case study: Developing our wholesale markets business to capitalise on our corporate lending relationships REVENUE BY PRODUCT CUSTOMER-DRIVEN REVENUE BY SEGMENT Structured Credit Sales & Trading Capital Markets Transaction Banking Credit Financial Institutions Commercial Corporate Enhanced 'capital-light' offerings Debt financing, Fixed Income and Rates to complement lending product and increase OOI Deepen existing corporate relationships across new product suite and expand distribution to cover UK insurers and asset managers Lloyds Banking Group Estimated Market Lloyds Banking Group Estimated Market More effective and efficient connectivity with customers via new Arena e-commerce platform (launching in September 2011) 26

27 INVEST IN OUR CORE BUSINESS Case study: New propositions will help affluent, HNW and mass affluent customers meet their financial goals CURRENTLY LOW WALLET SHARE AMONGST KEY SEGMENTS Segment share of customers and assets (%) 20+ MA 9 Customer 9 6 Aff / HNW AuM GROW CUSTOMERS IN PROPOSITION AND WALLET SHARE Number of in-proposition customers >3x Income per customer >50% Realigned segmentation, propositions and coverage to better serve customers Improved on-line channel and execution-only offer Deeper customer insight with more effective lead generation Investment in infrastructure to deliver a holistic financial planning service Enhancements grow: Ability to service wealth and currently underserved mass affluent customers Share of investment wallet earned from existing clients (1) AuM represents savings and investments 27

28 AGENDA First 100 Days Strategy Action Plan Guidance 28

29 GUIDANCE Group Financial Targets, 2014 (1 of 2) CUSTOMER- DRIVEN DIVERSIFIED INCOME POSITIVE OPERATING JAWS CAPITAL ALLOCATED TO CORE BUSINESS Additional discretionary investment to grow our core customer franchise Core income growth OOI as % of total income (1) Net interest margin Sustainable cost savings (over and above 2bn integration savings and pre discretionary investment) Cost : income ratio Required capital for non-core Non-core assets reduced 500m pa by 2014 > nominal GDP Growth c50% of Group income %; core business higher than Group 1.5 bn annual savings in 2014 ( 1.7bn run-rate savings by end 2014) 42-44% (2) Net capital generative over the period 2012 to bn in 2014, accounting for 65bn of RWA (1) OOI Net of Insurance claims (2) Following adjustments to include the net of operating lease income and depreciation in Group Income this would be 39-41% 29

30 GUIDANCE Group Financial Targets, 2014 (2 of 2) PRUDENT RISK APPETITE Average AQR 50-60bps Core business AQR expected to be at the bottom end of this range STRONG STABLE FUNDING Loan-to-deposit ratio LCR & NSFR 130% Group, 120% Core Requirements met ahead of regulatory implementation dates DISCIPLINED HIGH-RETURN INVESTING Statutory return on equity % Core tier 1 capital Target core tier 1 capital ratio prudently in excess of 10% from 1 Jan 2013 when transition to Basel 3 commences 30

31 GUIDANCE Delivering a strategy that is best for shareholders Enhanced and resilient earnings Strong EPS progression will support share price growth Simplifying the business will lower costs Lower costs will create capacity for strategic investment Focus on less capital intensive activities Operating within the new risk appetite to drive less volatile earnings Building a strong capital position Ratios in excess of regulatory requirements Improved ability to withstand stress scenarios Capacity to pay dividends Improving the funding profile further Lower wholesale funding requirements Lower loan to deposit ratios Focus on retail and commercial deposits 31

32 STRATEGIC REVIEW Strategy & Guidance July 14, 2011 António Horta-Osório Group Chief Executive

33 STRATEGIC REVIEW Integration & Simplification July 14, 2011 Mark Fisher Director, Group Operations

34 MOVING FROM INTEGRATION TO TRANSFORMATION RUN-RATE SYNERGY BENEFITS ( bn) 2.0 Integration Programme will complete within the original three year target Run rate benefits of 2bn well on track Integration was not transformation Moved the Group to a single platform Single platform a necessary first step to transformation Dec 2009 June 2010 Dec 2010 Mar 2011 Dec

35 SIMPLIFICATION IS AT THE HEART OF BECOMING THE BEST BANK FOR CUSTOMERS AND A HIGH PERFORMING ORGANISATION SIMPLIFYING OUR BUSINESS Improve customer service Become more efficient Capture scale benefits Ensure transparency Save to invest Empower managers and colleagues A permanent feature of the way we operate, not just another programme 35

36 WE HAVE MADE GREAT STRIDES ALREADY BUT SIGNIFICANT POTENTIAL REMAINS BEST IN CLASS CURRENT LLOYDS BANKING GROUP POSITION EXAMPLE INTEGRATION ACHIEVEMENT END-TO-END PROCESSES <5% rework in operational processes <7 days commercial loan time to cash >20% rework in some operational processes 4-10 weeks commercial loan time to cash ~60% reduction in the number of office locations (from ~450 to ~170) LOCATION FOOTPRINT IT APPLICATIONS <20 UK head office premises <1,500 IT applications ~170 office locations ~2,500 IT applications PRODUCT OFFERING <100 products (eg 9 loan products, 6 mortgage products) ~2,000 legacy products remain post integration COMMITTEES <20 committees per functional area 100+ committees for Risk 36

37 SIMPLIFICATION WILL DELIVER 1.5BN SAVINGS IN 2014 AND A 2014 EXIT RUN RATE OF 1.7BN PER ANNUM 4 KEY WORKSTREAMS EXIT-RATE SAVINGS BN BY 2014 NUMBER OF INITIATIVES Operations and Processes Implement workflow, automate, improve IT landscape, establish centres of excellence Invest significantly in technology, people and processes to deliver Simplification Deliver 1.5bn savings in 2014 Sourcing Improve demand management, simplify specification, strengthen supplier relationships Organisation Flatten organisational structure, consolidate / rationalise international business Distribution and Channels Continue to innovate, reduce product variants, increase pricing flexibility Total

38 OPERATIONS AND PROCESSES: Simplification will deliver significant benefits to our colleagues and customers BENEFITS WHAT WILL THE PROGRAMME DELIVER? CUSTOMER IMPACT Accelerated fulfilment of requests Reduced errors and complaints Simplify end-to-end processes Automation Image and workflow First touch execution Set up centres of excellence Multi-skilled Reduced handoffs Redeployment COLLEAGUE IMPACT FINANCIAL BENEFITS Eliminated highly manual tasks Increased focus on skill building Redeployment Increased productivity Reduced risk Reduced complexity Reduced cost 38

39 OPERATIONS AND PROCESSES: Structured approach across over 200 groups of services EXAMPLES WHAT WILL THE PROGRAMME DELIVER? End-to-end redesign across over 200 groups of services Structured and standard approach Already underway ACCOUNT SWITCHING COMMERCIAL LENDING Reduced end-to-end time by c30% Forms validated/submitted electronically, reducing input errors by c60% Automation leading to c70% reduction in manual re-entry Overall c68% reduction in operator touch time Reduced time to drawdown by over 50% 25% increase in customer facing time for front office staff 90%+ first-time right applications Fewer, simpler customer forms Improved risk and credit analytics 39

40 SOURCING: Further real potential for simplification building on integration APPROACH OUTCOME Demand management - simpler specifications Relationship restructure - deeper and closer working with preferred suppliers Further volume concentration and supplier rationalisation Improved market expertise and practices SIMPLER SUPPLY CHAINS PROCUREMENT SPECIFICATION SIMPLIFICATION DEMAND MANAGEMENT CURRENT POSITION TARGET POSITION BENEFITS 1,000 suppliers with ~94% spend 17,000 suppliers with ~6% spend ~100 lead suppliers <10,000 overall suppliers ~15% saving on addressable spend 40

41 ORGANISATION: Simplify organisation and governance structures REDUCE MANAGEMENT SPANS AND LAYERS From: 8 LAYERS X SPAN OF 8 To: 7 LAYERS X SPAN OF 10 Focus on middle management reduction Stronger, more effective functions CONSOLIDATE AND RATIONALISE INTERNATIONAL BUSINESSES 41

42 DISTRIBUTION AND CHANNELS: Actively manage distribution and channels, deliver an improved customer experience BUILD ON STRENGTHS AND CONTINUE TO INNOVATE Increased and enhanced functionality Internet Mobile Telephony Active management of channel usage Increase internet banking usage to 13 million Product simplification and pricing flexibility 42

43 EXPERIENCED TEAM AND STRONG CAPABILITIES IN PLACE TO DELIVER SIMPLIFICATION DELIVERY CONTROL Strong control and co-ordination as with integration Rigorous planning and milestone tracking ACCOUNTABILITY Accountable Executives already in place, high-level plans developed for key initiatives, and quick wins started Ramping up now as integration completes CLEAR PATH FORWARD Quick-wins already being delivered (eg flattened organisation structure) Detailed planning and building delivery teams WE WILL LEVERAGE OUR EXPERIENCE WITH INTEGRATION TO DELIVER THE BEST BANK FOR CUSTOMERS AND SHAREHOLDERS 43

44 STRATEGIC REVIEW Integration & Simplification July 14, 2011 Mark Fisher Director, Group Operations

45 STRATEGIC REVIEW Finance July 14, 2011 Tim Tookey Group Finance Director

46 2011 GUIDANCE BROADLY UNCHANGED Net interest margin Previous guidance 2.07% in Q with some headwinds for the year Additional comments Expect NIM to be just above 2% in 2011 Income Trends reflect customer deleveraging and subdued demand Broadly unchanged but noncore reductions will further reduce the balance sheet size and thus income Costs Broadly flat v Down slightly due to new cost actions Synergies On track for 2bn run rate by end 2011 Unchanged Impairment Funding Reductions in 2011 set out by book within Q1 IMS N/A Unchanged Government and Central Bank debt materially reduced already June 2011 loan to deposit ratio c146% (Dec 2010: 154%) 46

47 THE BEST BANK FOR CUSTOMERS 47

48 ECONOMIC BACKDROP AND KEY ASSUMPTIONS A cautious outlook for the UK economy NORMALISING REAL GROWTH REAL GDP GROWTH (%) RISING BASE RATES BANK OF ENGLAND BASE RATE (%) IMPROVING UNEMPLOYMENT ILO (1) UNEMPLOYMENT RATE (%) STABILISING PROPERTY VALUES HALIFAX PRICE INDEX (1) ILO International Labour Organisation 48

49 PERFORMANCE DRIVERS EARNINGS Focus on relationship driven earnings 49

50 PERFORMANCE DRIVERS INCOME Delivering sustainable, less capital intensive earnings 2010 FOCUS AND DRIVERS 2014 Bancassurance DCM / Corporate cross sales OOI 41% Affluent and wealthy customers UK SMEs c50% OOI NII 59% VERDE AND NON CORE DISPOSALS Lower risk, less capital intensive balance sheet Margin impact from increased regulatory cost of liquidity Funding costs higher for longer Base rates lower for longer c50% NII Total Income Total Income CORE INCOME TO GROW FASTER THAN NOMINAL GDP, PRIMARILY DRIVEN BY OOI (1) (1) OOI is shown net of insurance claims 50

51 PERFORMANCE DRIVERS NET INTEREST MARGIN Trends continue to be dominated by external factors INTERNAL ( Inside Management Control) EXTERNAL ( Outside Management Control) Pricing of new business and repricing of existing book Sharing of base rate rises benefit Reduced wholesale funding issuance allows greater control over costs going forward Improved funding position provides greater flexibility over mix of funding sources Base rate lower for longer Wholesale funding costs remain higher for longer Competition for deposits Increasing regulatory liquidity requirements NIM expected to be >200bps based on current assumptions Group NIM bps based on business and macro assumptions Core business NIM will exceed Group margin 51

52 PERFORMANCE DRIVERS COSTS Driving efficiency through simplification whilst increasing investment 11.1bn 0.4 (0.6) (1.5) (0.5) c 10bn 2010 Bank Levy, VAT Integration completion Simplification Annual investment in core Verde Other including inflation 2014 (1) business Integration on track to complete with 2bn pa of savings by end of 2011 Simplification programme to achieve 1.5bn of savings before 0.5bn re-investment in growth initiatives by end of 2014 Target cost : income ratio (Group) 42-44% by end of 2014 (39-41% excluding operating leases (2) ) Total costs of simplification initiatives expected to be c 2.3bn (including capex) of which c 1.5bn will be reported below the line over the next few years (1) Excludes additional run rate savings from simplification initiatives in 2015 of 0.2bn (2) Adjusted to include the net of operating lease income and depreciation in Group Income 52

53 PERFORMANCE DRIVERS IMPAIRMENT Continued reduction in impairment charge GROUP ASSET QUALITY RATIO 325bps 201bps 50-60bps All portfolios reviewed and confirmed as adequately provisioned Previous guidance for 2011 remains valid: Retail modest reduction Wholesale modest reduction International initial concerns addressed with Q1 provisioning but downside risks remain Heritage Lloyds TSB, more conservative approach to risk fully embedded Disciplined controls over risk profile of all new business Target normalised Group AQR range of 50-60bps with core business towards the lower end of the range 53

54 NON CORE PORTFOLIO EXCLUDING VERDE Continued disciplined reductions in non core portfolio Income (1) 4.3bn 3.8bn Impairment 9.1bn 9.2bn RWAs Total Assets Treasury Assets Commercial Real Estate Other Wholesale International Retail 0.5bn 1.9bn 141bn 142bn 129bn 65bn 195bn bn bn bn Portfolio changes as a result of the strategic review include: Lex Autolease and social housing now core Selected overseas businesses now non-core Not separating business into good bank and bad bank Non-core disposals will continue to be considered on a value basis balancing: Risk exposure Capital Liquidity Income statement impacts of rundown Run off satisfies EU requirements Dec 2010 Original Dec 2010 Restated Q Restated End 2014 Restated (1) Underlying income 54

55 NON CORE PORTFOLIO VERDE PROFILE The Verde disposal continues to progress at pace FINANCIALS: INDICATIVE IMPACT OF VERDE DISPOSAL (2011 illustration) on Lloyds Banking Group financials based on EU term sheet agreement Income Expenses Impairment PBT RWAs Assets c 1.2bn c 0.5bn c 0.2bn c 0.5bn c 16bn c 64bn Verde disposal process accelerated The business is the seventh largest bank in the UK Information Memorandum now issued to prospective buyers Expect to identify purchaser by the end of 2011 Total implementation costs will vary depending upon the nature of the buyer but could be up to 1bn Liabilities c 32bn 55

56 THE BEST BANK FOR CUSTOMERS Delivers significant scope for prudent core business growth SOURCES APPLICATIONS RESULT Non core asset run off and disposals Verde disposals Growth in relationship customer deposits Significant net new core business growth capacity Increasing liquid assets to meet LCR and NSFR requirements Prudent reduction in wholesale funding issuance (c 25bn pa) Loan to deposit ratio 130% (Core: 120%) Prudent funding profile Less capital intensive earnings Slightly smaller balance sheet 56

57 FUNDING Annual wholesale issuance requirement continues to fall 50bn Previous guidance of 20-25bn public pa over the next few years 20bn 30bn 30-35bn c5-10bn 7bn 18bn Forecast Actual c 25bn pa Future public term issuance requirements now reduced to c 15-20bn pa for Strength of funding facilitated an early paydown of central bank funding Funding will be from a diverse range of funding products and sources: Tenors Structures Currencies Geographies Public Private Public & Private 57

58 LIQUIDITY Exceeding regulatory liquidity requirements 71% >100% LIQUIDITY COVERAGE RATIO % >100% Increasing regulatory liquidity requirements Meeting LCR and NSFR by 2014 (in advance of regulatory requirements) NET STABLE FUNDING RATIO

59 CAPITAL: BASEL 2.5 / 3.0 IMPACT Maintaining modest but prudent capital reserves over regulatory requirements IMPLEMENTATION Basel % c 10bn RWA increase primarily from Market Risk in the trading book December 2011 Basel 3-0.6% c 30bn Transitional rules RWA increase largely from credit valuation adjustment, securitisation and insurance allowances (1) Insurance deduction (-0.2%pa) Other transitional adjustments (-0.2%pa) Largely excess expected loss Any residual deferred tax losses January Verde RWA Benefit From disposal date (by November 2013) Non-core run down and disposals RWA Benefit Ongoing TARGET CORE TIER 1 CAPITAL RATIO PRUDENTLY IN EXCESS OF 10% FROM 1 JANUARY 2013 WHEN TRANSITION TO BASEL 3 COMMENCES (1) Securitisation partially offset by removal of core tier 1 deduction 59

60 GUIDANCE Group Financial Targets, 2014 CUSTOMER- DRIVEN DIVERSIFIED INCOME POSITIVE OPERATING JAWS CAPITAL ALLOCATED TO CORE BUSINESS PRUDENT RISK APPETITE STRONG STABLE FUNDING Additional discretionary investment to grow our core customer franchise Core income growth OOI as % of total income (1) Net interest margin Sustainable cost savings (over and above 2bn integration savings and pre discretionary investment Cost : income ratio Required capital for non-core Non-core assets reduced Average AQR Loan-to-deposit ratio LCR & NSFR 500m pa by 2014 > nominal GDP growth c50% of Group income %; core business higher than Group 1.5bn annual savings in 2014 ( 1.7bn run-rate savings by end 2014) 42 44% (2) Net capital generative over the period 2012 to bn in 2014, accounting for 65bn of RWA 50 60bps Core business AQR expected to be at the bottom end of this range 130% Group, 120% Core Requirements met ahead of regulatory implementation dates DISCIPLINED HIGH-RETURN INVESTING Statutory return on equity Core tier 1 capital % Target core tier 1 capital ratio prudently in excess of 10% from 1 Jan 2013 when transition to Basel 3 commences (1) OOI Net of Insurance claims (2) Following adjustments to include the net of operating lease income and depreciation in Group Income this would be 39-41% 60

61 THE BEST BANK FOR CUSTOMERS Delivering strong, stable returns for shareholders Smaller balance sheet, robust capital structure and stronger funding platform Reduced capital intensity Slimmer, more agile and efficient operating model Earnings based on our ability to drive growth above nominal GDP Lower volatility, lower risk, sustainable and more resilient earnings above the cost of equity Sustainable returns on equity of % by 2014 with positive momentum into 2015 Restarting dividends under a sustainable progressive dividend policy Returning the Group to full private ownership Earnings momentum to 2015 and beyond 61

62 STRATEGIC REVIEW Finance July 14, 2011 Tim Tookey Group Finance Director

63 FORWARD LOOKING STATEMENTS This announcement contains forward looking statements with respect to the business, strategy and plans of the Lloyds Banking Group, its current goals and expectations relating to its future financial condition and performance. Statements that are not historical facts, including statements about the Group or the Group s management s beliefs and expectations, are forward looking statements. By their nature, forward looking statements involve risk and uncertainty because they relate to events and depend on circumstances that will occur in the future. The Group s actual future business, strategy, plans and/or results may differ materially from those expressed or implied in these forward looking statements as a result of a variety of risks, uncertainties and other factors, including, without limitation, UK domestic and global economic and business conditions; the ability to derive cost savings and other benefits, as well as the ability to integrate successfully the acquisition of HBOS; the ability to access sufficient funding to meet the Group s liquidity needs; changes to the Group s credit ratings; risks concerning borrower or counterparty credit quality; market related trends and developments; changing demographic trends; changes in customer preferences; changes to regulation, accounting standards or taxation, including changes to regulatory capital or liquidity requirements; the policies and actions of Governmental or regulatory authorities in the UK, the European Union, or jurisdictions outside the UK, including other European countries and the US; the ability to attract and retain senior management and other employees; requirements or limitations imposed on the Group as a result of HM Treasury s investment in the Group; the ability to complete satisfactorily the disposal of certain assets as part of the Group s EU State Aid obligations; the extent of any future impairment charges or write-downs caused by depressed asset valuations; exposure to regulatory scrutiny, legal proceedings or complaints, actions of competitors and other factors. Please refer to the latest Annual Report on form 20-F filed with the US Securities and Exchange Commission for a discussion of such factors together with examples of forward looking statements. The forward looking statements contained in this announcement are made as at the date of this announcement, and the Group undertakes no obligation to update any of its forward looking statements. 63

64 STRATEGIC REVIEW Q & A

2011 HALF-YEAR RESULTS

2011 HALF-YEAR RESULTS 4 August 2011 António Horta-Osório Group Chief Executive Resilient business performance, in line with expectations, despite challenging market conditions AGENDA ECONOMIC AND REGULATORY

2011 HALF-YEAR RESULTS 4 August 2011 António Horta-Osório Group Chief Executive Resilient business performance, in line with expectations, despite challenging market conditions AGENDA ECONOMIC AND REGULATORY

BANK OF AMERICA MERRILL LYNCH 17 th Annual Banking & Insurance CEO Conference. 25 September António Horta-Osório

BANK OF AMERICA MERRILL LYNCH 17 th Annual Banking & Insurance CEO Conference 25 September 2012 António Horta-Osório Group Chief Executive AGENDA STRONG CORE FRANCHISE REDUCING RISK & INCREASING EFFICIENCY

BANK OF AMERICA MERRILL LYNCH 17 th Annual Banking & Insurance CEO Conference 25 September 2012 António Horta-Osório Group Chief Executive AGENDA STRONG CORE FRANCHISE REDUCING RISK & INCREASING EFFICIENCY

24 February António Horta-Osório Group Chief Executive

2011 RESULTS 24 February 2012 António Horta-Osório Group Chief Executive Accelerating balance sheet strength, improving customer service and efficiency whilst investing to grow our profitable core business

2011 RESULTS 24 February 2012 António Horta-Osório Group Chief Executive Accelerating balance sheet strength, improving customer service and efficiency whilst investing to grow our profitable core business

MORGAN STANLEY FINANCIALS

MORGAN STANLEY FINANCIALS CONFERENCE 19 March 2013 António Horta-Osório Group Chief Executive 2012 HIGHLIGHTS Significantly improved performance and balance sheet further strengthened and de-risked d Balance

MORGAN STANLEY FINANCIALS CONFERENCE 19 March 2013 António Horta-Osório Group Chief Executive 2012 HIGHLIGHTS Significantly improved performance and balance sheet further strengthened and de-risked d Balance

BANK OF AMERICA MERRILL LYNCH 19 th Annual Banking & Insurance CEO Conference. 30 September George Culmer Group Chief Financial Officer

BANK OF AMERICA MERRILL LYNCH 19 th Annual Banking & Insurance CEO Conference 30 September 2014 George Culmer Group Chief Financial Officer AGENDA OUR BUSINESS MODEL DELIVERY AGAINST 2011 STRATEGY H1 2014

BANK OF AMERICA MERRILL LYNCH 19 th Annual Banking & Insurance CEO Conference 30 September 2014 George Culmer Group Chief Financial Officer AGENDA OUR BUSINESS MODEL DELIVERY AGAINST 2011 STRATEGY H1 2014

2013 HALF-YEAR RESULTS. News Release

News Release BASIS OF PRESENTATION This report covers the results of Lloyds Banking Group plc (the Company) together with its subsidiaries (the Group) for the half-year ended 30 June. Statutory basis Statutory

News Release BASIS OF PRESENTATION This report covers the results of Lloyds Banking Group plc (the Company) together with its subsidiaries (the Group) for the half-year ended 30 June. Statutory basis Statutory

TITLE SLIDE IS IN SENTENCE CASE.

TITLE SLIDE IS IN SENTENCE CASE. GREEN George Culmer, Chief BACKGROUND. Financial Officer GOLDMAN SACHS FINANCIALS CONFERENCE Andrew Bester, Chief Executive Officer, Commercial Banking 17 00 June Month

TITLE SLIDE IS IN SENTENCE CASE. GREEN George Culmer, Chief BACKGROUND. Financial Officer GOLDMAN SACHS FINANCIALS CONFERENCE Andrew Bester, Chief Executive Officer, Commercial Banking 17 00 June Month

THE FINANCIAL CRISIS: KEY QUESTIONS, REALITY AND RESPONSES

THE FINANCIAL CRISIS: KEY QUESTIONS, REALITY AND RESPONSES BANK OF AMERICA MERRILL LYNCH CONFERENCE London 4 October 2011 António Horta-Osório Group Chief Executive AGENDA KEY QUESTIONS ON THE FINANCIAL

THE FINANCIAL CRISIS: KEY QUESTIONS, REALITY AND RESPONSES BANK OF AMERICA MERRILL LYNCH CONFERENCE London 4 October 2011 António Horta-Osório Group Chief Executive AGENDA KEY QUESTIONS ON THE FINANCIAL

TITLE SLIDE IS IN SENTENCE CASE. GREEN BACKGROUND.

TITLE SLIDE IS IN SENTENCE CASE. GREEN BACKGROUND. BANK OF AMERICA MERRILL LYNCH CEO CONFERENCE António Horta-Osório 00 Month 0000 Presenters Name 29 September 2015 AGENDA A differentiated business model

TITLE SLIDE IS IN SENTENCE CASE. GREEN BACKGROUND. BANK OF AMERICA MERRILL LYNCH CEO CONFERENCE António Horta-Osório 00 Month 0000 Presenters Name 29 September 2015 AGENDA A differentiated business model

Q Interim Management Statement

Q1 Interim Management Statement BASIS OF PRESENTATION This report covers the results of Lloyds Banking Group plc together with its subsidiaries (the Group) for the three ch. Statutory basis Statutory information

Q1 Interim Management Statement BASIS OF PRESENTATION This report covers the results of Lloyds Banking Group plc together with its subsidiaries (the Group) for the three ch. Statutory basis Statutory information

2012 RESULTS. 1 March 2013

RESULTS 1 March 2013 AGENDA ACHIEVEMENTS AND GROUP PERFORMANCE António Horta-Osório, Group Chief Executive FINANCIAL RESULTS George Culmer, Group Finance Director UPDATE ON COSTS AND SIMPLIFICATION Mark

RESULTS 1 March 2013 AGENDA ACHIEVEMENTS AND GROUP PERFORMANCE António Horta-Osório, Group Chief Executive FINANCIAL RESULTS George Culmer, Group Finance Director UPDATE ON COSTS AND SIMPLIFICATION Mark

2012 RESULTS. 1 March 2013

2012 RESULTS 1 March 2013 AGENDA ACHIEVEMENTS AND GROUP PERFORMANCE António Horta-Osório, Group Chief Executive 2012 FINANCIAL RESULTS George Culmer, Group Finance Director UPDATE ON COSTS AND SIMPLIFICATION

2012 RESULTS 1 March 2013 AGENDA ACHIEVEMENTS AND GROUP PERFORMANCE António Horta-Osório, Group Chief Executive 2012 FINANCIAL RESULTS George Culmer, Group Finance Director UPDATE ON COSTS AND SIMPLIFICATION

2014 HALF-YEAR RESULTS. News Release

News Release BASIS OF PRESENTATION This report covers the results of Lloyds Banking Group plc together with its subsidiaries (the Group) for the half-year ended 30 June. Statutory basis Statutory information

News Release BASIS OF PRESENTATION This report covers the results of Lloyds Banking Group plc together with its subsidiaries (the Group) for the half-year ended 30 June. Statutory basis Statutory information

2017 RESULTS. Presentation to analysts and investors 21 February 2018

RESULTS Presentation to analysts and investors 21 February 2018 Full year results Introduction António Horta-Osório Group Chief Executive 1 a landmark year strong strategic and financial performance Group

RESULTS Presentation to analysts and investors 21 February 2018 Full year results Introduction António Horta-Osório Group Chief Executive 1 a landmark year strong strategic and financial performance Group

LLOYDS BANKING GROUP INTERIM MANAGEMENT STATEMENT

112/10 2 November 2010 LLOYDS BANKING GROUP INTERIM MANAGEMENT STATEMENT Key highlights The Group has continued to make good progress against its strategic objectives in the third quarter of 2010, building

112/10 2 November 2010 LLOYDS BANKING GROUP INTERIM MANAGEMENT STATEMENT Key highlights The Group has continued to make good progress against its strategic objectives in the third quarter of 2010, building

2018 HALF-YEAR RESULTS News Release

News Release BASIS OF PRESENTATION This release covers the results of Lloyds Banking Group plc together with its subsidiaries (the Group) for the six months ended 30 June 2018. IFRS 9 and IFRS 15: On 1

News Release BASIS OF PRESENTATION This release covers the results of Lloyds Banking Group plc together with its subsidiaries (the Group) for the six months ended 30 June 2018. IFRS 9 and IFRS 15: On 1

Lloyds TSB Group plc. Results for the half-year to 30 June 2004

Lloyds TSB Group plc Results for the half-year to 30 June 2004 PRESENTATION OF RESULTS In order to provide a clearer representation of the underlying performance of the Group, the results of the Group

Lloyds TSB Group plc Results for the half-year to 30 June 2004 PRESENTATION OF RESULTS In order to provide a clearer representation of the underlying performance of the Group, the results of the Group

Lloyds TSB Group plc. Results for half-year to 30 June 2005

Lloyds TSB Group plc Results for half-year to 30 June 2005 PRESENTATION OF RESULTS Up to 31 December 2004 the Group prepared its financial statements in accordance with UK Generally Accepted Accounting

Lloyds TSB Group plc Results for half-year to 30 June 2005 PRESENTATION OF RESULTS Up to 31 December 2004 the Group prepared its financial statements in accordance with UK Generally Accepted Accounting

TITLE SLIDE IS IN SENTENCE CASE.

TITLE SLIDE IS IN SENTENCE CASE. GREEN Presentation to Analysts BACKGROUND. and Investors INTERIM MANAGEMENT STATEMENT 25 October HIGHLIGHTS FOR THE FIRST NINE MONTHS OF Strong financial performance continues

TITLE SLIDE IS IN SENTENCE CASE. GREEN Presentation to Analysts BACKGROUND. and Investors INTERIM MANAGEMENT STATEMENT 25 October HIGHLIGHTS FOR THE FIRST NINE MONTHS OF Strong financial performance continues

Lloyds TSB Group plc. Results for half-year to 30 June 2007

Lloyds TSB Group plc Results for half-year to 2007 CONTENTS Page Key operating highlights 1 Summary of results 2 Profit analysis by division 3 Group Chief Executive s statement 4 Group Finance Director

Lloyds TSB Group plc Results for half-year to 2007 CONTENTS Page Key operating highlights 1 Summary of results 2 Profit analysis by division 3 Group Chief Executive s statement 4 Group Finance Director

TITLE SLIDE IS IN SENTENCE CASE.

TITLE SLIDE IS IN SENTENCE CASE. GREEN Mike Butters, Director BACKGROUND. of Investor Relations RESPONSIBLE BUSINESS PERFORMANCE AND HELPING BRITAIN PROSPER PLAN Paul Turner, Director of Sustainable Business

TITLE SLIDE IS IN SENTENCE CASE. GREEN Mike Butters, Director BACKGROUND. of Investor Relations RESPONSIBLE BUSINESS PERFORMANCE AND HELPING BRITAIN PROSPER PLAN Paul Turner, Director of Sustainable Business

BECOMING THE BEST BANK FOR CUSTOMERS

BECOMING THE BEST BANK FOR CUSTOMERS Lloyds Banking Group Performance Summary 2014 Financial performance and strategic progress I am writing with an overview of our 2014 financial performance, a summary

BECOMING THE BEST BANK FOR CUSTOMERS Lloyds Banking Group Performance Summary 2014 Financial performance and strategic progress I am writing with an overview of our 2014 financial performance, a summary

Morgan Stanley Conference

Morgan Stanley Conference Eric Daniels Group Chief Executive, Lloyds TSB 27 March 2007 2006 results: building earnings momentum Building momentum Two divisions, W&IB and I&I, continue to grow strongly

Morgan Stanley Conference Eric Daniels Group Chief Executive, Lloyds TSB 27 March 2007 2006 results: building earnings momentum Building momentum Two divisions, W&IB and I&I, continue to grow strongly

TITLE SLIDE IS IN SENTENCE CASE.

TITLE SLIDE IS IN SENTENCE CASE. GREEN Presentation to Analysts BACKGROUND. and Investors INTERIM MANAGEMENT STATEMENT 27 April HIGHLIGHTS Strong financial performance continues to demonstrate the strength

TITLE SLIDE IS IN SENTENCE CASE. GREEN Presentation to Analysts BACKGROUND. and Investors INTERIM MANAGEMENT STATEMENT 27 April HIGHLIGHTS Strong financial performance continues to demonstrate the strength

TITLE SLIDE IS IN SENTENCE CASE.

TITLE SLIDE IS IN SENTENCE CASE. GREEN Presentation to Analysts BACKGROUND. and Investors INTERIM MANAGEMENT STATEMENT 00 1 May Month 0000 Presenters Name HIGHLIGHTS FOR THE FIRST THREE MONTHS OF Continued

TITLE SLIDE IS IN SENTENCE CASE. GREEN Presentation to Analysts BACKGROUND. and Investors INTERIM MANAGEMENT STATEMENT 00 1 May Month 0000 Presenters Name HIGHLIGHTS FOR THE FIRST THREE MONTHS OF Continued

Q Interim Management Statement

Q3 2018 Interim Management Statement LLOYDS BANKING GROUP PLC Q3 2018 INTERIM MANAGEMENT STATEMENT HIGHLIGHTS FOR THE NINE MONTHS ENDED 30 SEPTEMBER 2018 Strong and sustainable financial performance with

Q3 2018 Interim Management Statement LLOYDS BANKING GROUP PLC Q3 2018 INTERIM MANAGEMENT STATEMENT HIGHLIGHTS FOR THE NINE MONTHS ENDED 30 SEPTEMBER 2018 Strong and sustainable financial performance with

2017 RESULTS News Release

News Release BASIS OF PRESENTATION This release covers the results of Lloyds Banking Group plc together with its subsidiaries (the Group) for the year ended 31 December 2017. Statutory basis: Audited statutory

News Release BASIS OF PRESENTATION This release covers the results of Lloyds Banking Group plc together with its subsidiaries (the Group) for the year ended 31 December 2017. Statutory basis: Audited statutory

2008 Interim Results News release

2008 Interim Results News release BASIS OF PRESENTATION In order to provide a clearer representation of the Group s underlying business performance, the results have been presented on a continuing businesses

2008 Interim Results News release BASIS OF PRESENTATION In order to provide a clearer representation of the Group s underlying business performance, the results have been presented on a continuing businesses

Westpac 2008 Full year results

Westpac 2008 Full year results 30 October 2008 Westpac 2008 Full year results Gail Kelly Chief Executive Officer Key messages Performed well in a challenging environment, delivering a robust financial

Westpac 2008 Full year results 30 October 2008 Westpac 2008 Full year results Gail Kelly Chief Executive Officer Key messages Performed well in a challenging environment, delivering a robust financial

Chief Executive s Review. Delivering our Strategic Objectives

2014 saw AIB successfully execute its three year plan to deliver a bank that is sustainably profitable, adequately capitalised and appropriately funded. We have a strong momentum in our business and are

2014 saw AIB successfully execute its three year plan to deliver a bank that is sustainably profitable, adequately capitalised and appropriately funded. We have a strong momentum in our business and are

It is therefore pleasing to report that this evolution of BOQ has continued throughout this financial year.

1 2 Good morning everyone. I will start with the highlights of the results. The strategy we have been implementing in the past few years has transformed BOQ into a resilient, multi-channel business that

1 2 Good morning everyone. I will start with the highlights of the results. The strategy we have been implementing in the past few years has transformed BOQ into a resilient, multi-channel business that

2020 STRATEGIC AND FINANCIAL PLAN TRANSFORM TO GROW

2020 STRATEGIC AND FINANCIAL PLAN TRANSFORM TO GROW Paris, 27 November 2017 Societe Generale will present tomorrow its 2020 Strategic and Financial Plan at an Investor Day in Paris. Commenting on the plan,

2020 STRATEGIC AND FINANCIAL PLAN TRANSFORM TO GROW Paris, 27 November 2017 Societe Generale will present tomorrow its 2020 Strategic and Financial Plan at an Investor Day in Paris. Commenting on the plan,

Lloyds Bank plc {formerly Lloyds TSB Bank plc}

Lloyds Bank plc {formerly Lloyds TSB Bank plc} Half-Year Management Report For the half-year to 30 June 2014 Member of the Lloyds Banking Group FORWARD LOOKING STATEMENTS This announcement contains forward

Lloyds Bank plc {formerly Lloyds TSB Bank plc} Half-Year Management Report For the half-year to 30 June 2014 Member of the Lloyds Banking Group FORWARD LOOKING STATEMENTS This announcement contains forward

RESTATEMENT OF 2013 REPORTED SEGMENTAL FINANCIAL INFORMATION

3 July 2014 RESTATEMENT OF 2013 REPORTED SEGMENTAL FINANCIAL INFORMATION Lloyds Banking Group plc (the Group) has today published restated segmental profit and loss and key balance sheet information for

3 July 2014 RESTATEMENT OF 2013 REPORTED SEGMENTAL FINANCIAL INFORMATION Lloyds Banking Group plc (the Group) has today published restated segmental profit and loss and key balance sheet information for

BANK OF AMERICA MERRILL LYNCH FINANCIALS CONFERENCE. George Culmer 25 September 2018

BANK OF AMERICA MERRILL LYNCH FINANCIALS CONFERENCE George Culmer 25 September 2018 Unique business model generating strong and sustainable returns Distinctive competitive strengths Differentiated multi-brand,

BANK OF AMERICA MERRILL LYNCH FINANCIALS CONFERENCE George Culmer 25 September 2018 Unique business model generating strong and sustainable returns Distinctive competitive strengths Differentiated multi-brand,

Lloyds TSB Group plc Results

Lloyds TSB Group plc 2004 Results PRESENTATION OF RESULTS In order to provide a clearer representation of the underlying performance of the Group, the results of the Group s life and pensions and general

Lloyds TSB Group plc 2004 Results PRESENTATION OF RESULTS In order to provide a clearer representation of the underlying performance of the Group, the results of the Group s life and pensions and general

TITLE SLIDE IS IN. 20 December 2016

TITLE SLIDE IS IN SENTENCE ACQUISITION OF CASE. MBNA GREEN Presentation to Analysts BACKGROUND. and Investors 20 December 2016 TRANSACTION OVERVIEW Value generating acquisition of a prime credit card portfolio

TITLE SLIDE IS IN SENTENCE ACQUISITION OF CASE. MBNA GREEN Presentation to Analysts BACKGROUND. and Investors 20 December 2016 TRANSACTION OVERVIEW Value generating acquisition of a prime credit card portfolio

Full Year 2014 Results Presentation. 04 March 2015

Full Year 2014 Results Presentation 04 March 2015 Forward looking statement This document contains or incorporates by reference forward-looking statements regarding the belief or current expectations of

Full Year 2014 Results Presentation 04 March 2015 Forward looking statement This document contains or incorporates by reference forward-looking statements regarding the belief or current expectations of

Q Interim Management Statement

Q3 Interim Management Statement Q3 INTERIM MANAGEMENT STATEMENT BASIS OF PRESENTATION This release covers the results of Lloyds Banking Group plc together with its subsidiaries (the Group) for the nine

Q3 Interim Management Statement Q3 INTERIM MANAGEMENT STATEMENT BASIS OF PRESENTATION This release covers the results of Lloyds Banking Group plc together with its subsidiaries (the Group) for the nine

Lloyds TSB Group plc. Results for the half-year to 30 June 2003

Lloyds TSB Group plc Results for the half-year to 30 June 2003 PRESENTATION OF RESULTS In order to provide a clearer representation of the underlying performance of the Group, the results of the Group

Lloyds TSB Group plc Results for the half-year to 30 June 2003 PRESENTATION OF RESULTS In order to provide a clearer representation of the underlying performance of the Group, the results of the Group

Lloyds TSB Group plc Results

Lloyds TSB Group plc 2003 Results PRESENTATION OF RESULTS During 2003 the Group has implemented a change in accounting policy following the issue of new accounting guidance in Urgent Issues Task Force

Lloyds TSB Group plc 2003 Results PRESENTATION OF RESULTS During 2003 the Group has implemented a change in accounting policy following the issue of new accounting guidance in Urgent Issues Task Force

Q Interim Management Statement

Q1 2018 Interim Management Statement HIGHLIGHTS FOR THE THREE MONTHS ENDED 31 MARCH 2018 Strong financial performance with significant increase in profit and returns on a statutory and underlying basis

Q1 2018 Interim Management Statement HIGHLIGHTS FOR THE THREE MONTHS ENDED 31 MARCH 2018 Strong financial performance with significant increase in profit and returns on a statutory and underlying basis

AUSTRALIA AND NEW ZEALAND BANKING GROUP LIMITED ABN

AUSTRALIA AND NEW ZEALAND BANKING GROUP LIMITED ABN 11 005 357 522 Media Release For Release: 2 May 2012 ANZ 2012 Half Year Result - super regional strategy delivers solid performance, higher dividend

AUSTRALIA AND NEW ZEALAND BANKING GROUP LIMITED ABN 11 005 357 522 Media Release For Release: 2 May 2012 ANZ 2012 Half Year Result - super regional strategy delivers solid performance, higher dividend

VIRGIN MONEY HOLDINGS (UK) PLC: CAPITAL MARKETS UPDATE

PLC: CAPITAL MARKETS UPDATE") THIS ANNOUNCEMENT CONTAINS INSIDE INFORMATION 16 November 2017 VIRGIN MONEY HOLDINGS (UK) PLC: CAPITAL MARKETS UPDATE Virgin Money Holdings (UK) plc ( Virgin Money or the Group ) is today giving a Capital

THIS ANNOUNCEMENT CONTAINS INSIDE INFORMATION 16 November 2017 VIRGIN MONEY HOLDINGS (UK) PLC: CAPITAL MARKETS UPDATE Virgin Money Holdings (UK) plc ( Virgin Money or the Group ) is today giving a Capital

Q Interim Management Statement

Q3 208 Interim Management Statement HIGHLIGHTS FOR THE NINE MONTHS ENDED 30 SEPTEMBER 208 Strong and sustainable financial performance with increased profits and returns Statutory profit after tax of 3.7

Q3 208 Interim Management Statement HIGHLIGHTS FOR THE NINE MONTHS ENDED 30 SEPTEMBER 208 Strong and sustainable financial performance with increased profits and returns Statutory profit after tax of 3.7

2012 RESULTS. 1 March 2013

2012 RESULTS 1 March 2013 APPENDIX LOANS AND ADVANCES TO CUSTOMERS LOANS AND ADVANCES TO CUSTOMERS 532.5bn 31 Dec 2012 Property companies 10% Financial, business and other services 9% Personal other 5%

2012 RESULTS 1 March 2013 APPENDIX LOANS AND ADVANCES TO CUSTOMERS LOANS AND ADVANCES TO CUSTOMERS 532.5bn 31 Dec 2012 Property companies 10% Financial, business and other services 9% Personal other 5%

FY15 RESULTS 17/12/2015 1

FY15 RESULTS 17/12/2015 1 Agenda FY15 Progress Jayne-Anne Gadhia, Chief Executive Financial Results Dave Dyer, Chief Financial Officer Looking Forward Jayne-Anne Gadhia, Chief Executive 2 A low risk, mainstream,

FY15 RESULTS 17/12/2015 1 Agenda FY15 Progress Jayne-Anne Gadhia, Chief Executive Financial Results Dave Dyer, Chief Financial Officer Looking Forward Jayne-Anne Gadhia, Chief Executive 2 A low risk, mainstream,

2010 RESULTS 25 February Eric Daniels Group Chief Executive

2010 RESULTS 25 February 2011 Eric Daniels Group Chief Executive BUSINESS HIGHLIGHTS A year of significant progress STRONG OPERATING PERFORMANCE Step change in profitability Sharp fall in impairments Good

2010 RESULTS 25 February 2011 Eric Daniels Group Chief Executive BUSINESS HIGHLIGHTS A year of significant progress STRONG OPERATING PERFORMANCE Step change in profitability Sharp fall in impairments Good

Building a better AA Putting Service, Innovation and Data at the heart of the AA

LEI: 213800DTPE4O5OI17349 This announcement contains inside information Building a better AA Putting Service, Innovation and Data at the heart of the AA The AA is today presenting our new business strategy

LEI: 213800DTPE4O5OI17349 This announcement contains inside information Building a better AA Putting Service, Innovation and Data at the heart of the AA The AA is today presenting our new business strategy

Emirates NBD Announces First Quarter 2018 Results

For immediate release Emirates NBD Announces First Quarter 2018 Results Net profit up 27% y-o-y and 10% q-o-q to AED 2.4 billion Dubai, 18 April 2018 Emirates NBD (DFM: EmiratesNBD), a leading bank in

For immediate release Emirates NBD Announces First Quarter 2018 Results Net profit up 27% y-o-y and 10% q-o-q to AED 2.4 billion Dubai, 18 April 2018 Emirates NBD (DFM: EmiratesNBD), a leading bank in

2017 Annual Report. Santander UK plc. Part of the Banco Santander group

Annual Report Santander UK plc Part of the Banco Santander group This page intentionally blank Santander UK plc Annual Report Strategic report 2 Financial review 5 Governance 18 Directors 19 Corporate

Annual Report Santander UK plc Part of the Banco Santander group This page intentionally blank Santander UK plc Annual Report Strategic report 2 Financial review 5 Governance 18 Directors 19 Corporate

H Results Investor Presentation THERE S MONEY AND THERE S VIRGIN MONEY

H1 2015 Results Investor Presentation THERE S MONEY AND THERE S VIRGIN MONEY Page 1 Page 2 ROTE of 10. 2 % up from 7.6% in H114 1 Source: Company information for all data Note: 1) Calculated as underlying

H1 2015 Results Investor Presentation THERE S MONEY AND THERE S VIRGIN MONEY Page 1 Page 2 ROTE of 10. 2 % up from 7.6% in H114 1 Source: Company information for all data Note: 1) Calculated as underlying

Credit Suisse Financial Services Forum 2009

Credit Suisse Financial Services Forum 2009 Naples, Florida February 4, 2009 Brady W. Dougan, CEO Credit Suisse Cautionary statement Cautionary statement regarding forward-looking and non-gaap information

Credit Suisse Financial Services Forum 2009 Naples, Florida February 4, 2009 Brady W. Dougan, CEO Credit Suisse Cautionary statement Cautionary statement regarding forward-looking and non-gaap information

Half Yearly Financial Report 2016 Santander UK plc

Half Yearly Financial Report 2016 Santander UK plc PART OF THE SANTANDER GROUP This page intentionally blank Santander UK plc Half Yearly Financial Report 2016 2 Introduction 4 Financial review 18 Risk

Half Yearly Financial Report 2016 Santander UK plc PART OF THE SANTANDER GROUP This page intentionally blank Santander UK plc Half Yearly Financial Report 2016 2 Introduction 4 Financial review 18 Risk

Foxtons Preliminary results presentation For the year ended December 2018

Foxtons Preliminary results presentation For the year ended December 2018 Important information This presentation includes statements that are, or may be deemed to be, forward-looking statements. These

Foxtons Preliminary results presentation For the year ended December 2018 Important information This presentation includes statements that are, or may be deemed to be, forward-looking statements. These

Year-end results. 18 May

Year-end results 18 May Highlights for the year Strong operational performance Good performance across all areas of activity Deepened our core franchise Sound levels of corporate client and private client

Year-end results 18 May Highlights for the year Strong operational performance Good performance across all areas of activity Deepened our core franchise Sound levels of corporate client and private client

INVESTOR PRESENTATION

INVESTOR PRESENTATION J.P. MORGAN THAILAND CONFERENCE 2011 Deepak Sarup, CFO 17 th March 2011 AGENDA Pages I. Review of Results 2010 3-15 II. Future Positioning 17-27 III. 2011 Targets 29 IMPORTANT DISCLAIMER:

INVESTOR PRESENTATION J.P. MORGAN THAILAND CONFERENCE 2011 Deepak Sarup, CFO 17 th March 2011 AGENDA Pages I. Review of Results 2010 3-15 II. Future Positioning 17-27 III. 2011 Targets 29 IMPORTANT DISCLAIMER:

United Overseas Bank Limited

United Overseas Bank Limited July 2007 This material that follows is a presentation of general background information about United Overseas Bank Limited s ( UOB or the Bank ) activities current at the

United Overseas Bank Limited July 2007 This material that follows is a presentation of general background information about United Overseas Bank Limited s ( UOB or the Bank ) activities current at the

Interim Results. 28 th July 2004

Interim Results 28 th July 2004 James Crosby Chief Executive HBOS Benchmarks Sub 40% cost:income ratio Self funding double digit growth 15-20% market shares potential Sustainable and improved returns 2004

Interim Results 28 th July 2004 James Crosby Chief Executive HBOS Benchmarks Sub 40% cost:income ratio Self funding double digit growth 15-20% market shares potential Sustainable and improved returns 2004

Half Year Results for the Six Months to 31 January 2019

Close Brothers Group plc T +44 (0)20 7655 3100 10 Crown Place E enquiries@closebrothers.com London EC2A 4FT W www.closebrothers.com Registered in England No. 520241 Half Year Results for the Six Months

Close Brothers Group plc T +44 (0)20 7655 3100 10 Crown Place E enquiries@closebrothers.com London EC2A 4FT W www.closebrothers.com Registered in England No. 520241 Half Year Results for the Six Months

AmBank Group achieves RM461.8 million PAT in Q1FY2013

AmBank Group achieves RM461.8 million PAT in Q1FY2013 Higher net-interest income and lower allowances Improved Profitability Q1FY2013 (RM mil) Q1FY2013 vs Q1FY2012 1 Profit after tax ( PAT ) 461.8 5.1%

AmBank Group achieves RM461.8 million PAT in Q1FY2013 Higher net-interest income and lower allowances Improved Profitability Q1FY2013 (RM mil) Q1FY2013 vs Q1FY2012 1 Profit after tax ( PAT ) 461.8 5.1%

Foxtons Interim results presentation For the period ended 30 June 2018

Foxtons Interim results presentation For the period ended 30 June 2018 Important information This presentation includes statements that are, or may be deemed to be, forward-looking statements. These forward-looking

Foxtons Interim results presentation For the period ended 30 June 2018 Important information This presentation includes statements that are, or may be deemed to be, forward-looking statements. These forward-looking

Interim Results Announcement For the half-year to 30 September th November 2006

Interim Results Announcement For the half-year to 30 September 2006 16 th November 2006 Forward Looking Statement 2 This document contains certain forward-looking statements as defined in the US Private

Interim Results Announcement For the half-year to 30 September 2006 16 th November 2006 Forward Looking Statement 2 This document contains certain forward-looking statements as defined in the US Private

Merrill Lynch Dublin Conference

Merrill Lynch Dublin Conference Property and Construction in Ireland 14 th June 2007 Forward-looking statement 2 This document contains certain forward-looking statements within the meaning of Section

Merrill Lynch Dublin Conference Property and Construction in Ireland 14 th June 2007 Forward-looking statement 2 This document contains certain forward-looking statements within the meaning of Section

2017 Results. 27 February 2018

2017 Results 27 February 2018 FY17 Financial Performance 37.8p EPS 1 +29% 192.1m Stat profit 2 +37% RoTE of 14% up from 12.4% in FY16 13.8% CET1 Ratio 6.0p Total dividend +18% 297p TNAV +9% Note: (1) Basic

2017 Results 27 February 2018 FY17 Financial Performance 37.8p EPS 1 +29% 192.1m Stat profit 2 +37% RoTE of 14% up from 12.4% in FY16 13.8% CET1 Ratio 6.0p Total dividend +18% 297p TNAV +9% Note: (1) Basic

Bank of Queensland Full year results 31 August Bank of Queensland Limited ABN AFSL No

Bank of Queensland Full year results 31 August 2013 Bank of Queensland Limited ABN 32 009 656 740. AFSL No 244616. Agenda Result overview Stuart Grimshaw Managing Director and CEO Financial detail Anthony

Bank of Queensland Full year results 31 August 2013 Bank of Queensland Limited ABN 32 009 656 740. AFSL No 244616. Agenda Result overview Stuart Grimshaw Managing Director and CEO Financial detail Anthony

Rights Issue and Capital Enhancement Proposals. 3 November 2009

Rights Issue and Capital Enhancement Proposals 3 November 2009 DISCLAIMER THIS DOCUMENT IS STRICTLY CONFIDENTIAL AND IS BEING PROVIDED TO YOU SOLELY FOR YOUR INFORMATION AND FOR USE AT A PRESENTATION TO

Rights Issue and Capital Enhancement Proposals 3 November 2009 DISCLAIMER THIS DOCUMENT IS STRICTLY CONFIDENTIAL AND IS BEING PROVIDED TO YOU SOLELY FOR YOUR INFORMATION AND FOR USE AT A PRESENTATION TO

For personal use only

17 February 2017 The Manager Company Announcements Australian Securities Exchange 20 Bridge Street Sydney NSW 2000 MyState Limited Correction to Investor Presentation Please be advised that an amendment

17 February 2017 The Manager Company Announcements Australian Securities Exchange 20 Bridge Street Sydney NSW 2000 MyState Limited Correction to Investor Presentation Please be advised that an amendment

TSB Banking Group plc 2014 Full Year Results

TSB Banking Group plc 2014 Full Year Results Paul Pester, Chief Executive Officer Darren Pope, Chief Financial Officer Wednesday 25 th February 2015 Strong financial and strategic progress in 2014 Known

TSB Banking Group plc 2014 Full Year Results Paul Pester, Chief Executive Officer Darren Pope, Chief Financial Officer Wednesday 25 th February 2015 Strong financial and strategic progress in 2014 Known

FIXED INCOME INVESTOR PRESENTATION FY 2018

FIXED INCOME INVESTOR PRESENTATION FY 2018 Group 2 New Group structure with multiple issuance points across products and currencies Main Entities HoldCo Lloyds Banking Group Over 95% of Group loans & advances

FIXED INCOME INVESTOR PRESENTATION FY 2018 Group 2 New Group structure with multiple issuance points across products and currencies Main Entities HoldCo Lloyds Banking Group Over 95% of Group loans & advances

Interim Report For the six months ended 30 June 2015

Interim Report For the six months ended 30 June 2015 Interim Report for the six months ended 30 June 2015 Forward-Looking statement This document contains certain forward-looking statements within the

Interim Report For the six months ended 30 June 2015 Interim Report for the six months ended 30 June 2015 Forward-Looking statement This document contains certain forward-looking statements within the

Bank of Ireland Presentation

Bank of Ireland Presentation October 2013 (as at 1 Oct 2013) 1 Forward looking statement 2 Irish Economy Overview 3 Government finances ahead of target Public finances continue towards sustainability The

Bank of Ireland Presentation October 2013 (as at 1 Oct 2013) 1 Forward looking statement 2 Irish Economy Overview 3 Government finances ahead of target Public finances continue towards sustainability The

Nationwide Building Society. Interim Management Statement Q3 2017/18

Nationwide Building Society Interim Management Statement Q3 /18 9 February 2018 Nationwide Building Society today publishes its Interim Management Statement covering the period from 5 April to 31 December

Nationwide Building Society Interim Management Statement Q3 /18 9 February 2018 Nationwide Building Society today publishes its Interim Management Statement covering the period from 5 April to 31 December

Key Performance Highlights (H1FY11 vs H1FY10)

") Press release, 12 November 2010 AMMB delivers a strong performance, PATMI of RM 701.2 mil for H1FY11, up 40.7% HoH Higher revenues and lower allowances, and good loans and deposit growth Proposed interim

Press release, 12 November 2010 AMMB delivers a strong performance, PATMI of RM 701.2 mil for H1FY11, up 40.7% HoH Higher revenues and lower allowances, and good loans and deposit growth Proposed interim

17 April 2013 PRELIMINARY RESULTS

17 April 2013 PRELIMINARY RESULTS Introduction Some significant challenges in the past year Long-standing issues addressed External factors in Korea and Europe a drag on performance Progress made in the

17 April 2013 PRELIMINARY RESULTS Introduction Some significant challenges in the past year Long-standing issues addressed External factors in Korea and Europe a drag on performance Progress made in the

CLSA Investors Forum September Mrs Margaret Leung Vice-Chairman and Chief Executive Hang Seng Bank

CLSA Investors Forum 2011 21 September 2011 Mrs Margaret Leung Vice-Chairman and Chief Executive Hang Seng Bank Good afternoon, ladies and gentlemen. I am delighted to have the opportunity to speak with

CLSA Investors Forum 2011 21 September 2011 Mrs Margaret Leung Vice-Chairman and Chief Executive Hang Seng Bank Good afternoon, ladies and gentlemen. I am delighted to have the opportunity to speak with

For personal use only

NAB 2017 Full Year Results Summary Sarah and Justin Montesalvo Patriot Campers 2017 FINANCIAL HIGHLIGHTS $ 5,285 M Statutory net profit 99 CPS Final dividend 100% franked $ 5.3 BN Dividends declared $

NAB 2017 Full Year Results Summary Sarah and Justin Montesalvo Patriot Campers 2017 FINANCIAL HIGHLIGHTS $ 5,285 M Statutory net profit 99 CPS Final dividend 100% franked $ 5.3 BN Dividends declared $

Investor presentation

Investor presentation Important information Forward-Looking Statements and Risks & Uncertainties This document and the related oral presentation contain, and responses to questions following the presentation

Investor presentation Important information Forward-Looking Statements and Risks & Uncertainties This document and the related oral presentation contain, and responses to questions following the presentation

A New Chapter Our Shared Future 2015 Annual Results

A New Chapter Our Shared Future 2015 Annual Results 2016.03.30 Forward-Looking Statement Disclaimer This presentation and subsequent discussions may contain forward-looking statements that involve risks

A New Chapter Our Shared Future 2015 Annual Results 2016.03.30 Forward-Looking Statement Disclaimer This presentation and subsequent discussions may contain forward-looking statements that involve risks

Emirates NBD Announces First Half 2015 Results

For immediate release Emirates NBD Announces First Half 2015 Results Net profits up 41% to AED 3.3 billion on higher income and lower provisions Total Income up 7% to AED 7.6 billion as net interest income

For immediate release Emirates NBD Announces First Half 2015 Results Net profits up 41% to AED 3.3 billion on higher income and lower provisions Total Income up 7% to AED 7.6 billion as net interest income

AIB Group. Preliminary Results 2002

AIB Group Preliminary Results 2002 Forward looking statement A number of statements we will be making in our presentation and in the accompanying slides will not be based on historical fact, but will be

AIB Group Preliminary Results 2002 Forward looking statement A number of statements we will be making in our presentation and in the accompanying slides will not be based on historical fact, but will be

ALPHA BANK: AGENDA 2010 REVISITED. Capital Markets Day. Bucharest, April 20, Retail Banking. G. Aronis, Executive General Manager

ALPHA BANK: AGENDA 2010 REVISITED Retail Banking G. Aronis, Executive General Manager Capital Markets Day Bucharest, April 20, 2007 Strategic Emphasis on Retail Banking Rationalize product offering Apply

ALPHA BANK: AGENDA 2010 REVISITED Retail Banking G. Aronis, Executive General Manager Capital Markets Day Bucharest, April 20, 2007 Strategic Emphasis on Retail Banking Rationalize product offering Apply

Bank of Ireland Presentation October As at 1 Oct 2014

Bank of Ireland Presentation October 2014 As at 1 Oct 2014 1 Forward-Looking statement This document contains certain forward-looking statements within the meaning of Section 21E of the US Securities Exchange

Bank of Ireland Presentation October 2014 As at 1 Oct 2014 1 Forward-Looking statement This document contains certain forward-looking statements within the meaning of Section 21E of the US Securities Exchange

Westpac 2009 Full Year Results

Westpac 2009 Full Year Results Gail Kelly Chief Executive Officer Westpac Banking Corporation ABN 33 007 457 141 Key areas of focus in 2009 Position the Group strongly through the GFC and economic downturn

Westpac 2009 Full Year Results Gail Kelly Chief Executive Officer Westpac Banking Corporation ABN 33 007 457 141 Key areas of focus in 2009 Position the Group strongly through the GFC and economic downturn

Getting on with delivering our Plan

Getting on with delivering our Plan Ewen Stevenson Chief Financial Officer Goldman Sachs European Financials Conference Rome 16 June 2015 Click Our investment to edit Master thesis title style We are focusing

Getting on with delivering our Plan Ewen Stevenson Chief Financial Officer Goldman Sachs European Financials Conference Rome 16 June 2015 Click Our investment to edit Master thesis title style We are focusing

Earnings Release 2Q15

Earnings Release 2Q15 Earnings Release 2Q15 2 Key metrics Credit Suisse (CHF million, except where indicated) Net income/(loss) attributable to shareholders 1,051 1,054 (700) 0 2,105 159 of which from

Earnings Release 2Q15 Earnings Release 2Q15 2 Key metrics Credit Suisse (CHF million, except where indicated) Net income/(loss) attributable to shareholders 1,051 1,054 (700) 0 2,105 159 of which from

ELECTROCOMPONENTS Full-year results for the year ended 31 March 2018

ELECTROCOMPONENTS Full-year results for the year ended 31 March 2018 24 May 2018 SAFE HARBOUR This presentation contains certain statements, statistics and projections that are or may be forward-looking.

ELECTROCOMPONENTS Full-year results for the year ended 31 March 2018 24 May 2018 SAFE HARBOUR This presentation contains certain statements, statistics and projections that are or may be forward-looking.

HELPING BRITAIN PROSPER

HELPING BRITAIN PROSPER Lloyds Banking Group Annual Report and Accounts Lloyds Banking Group How we're helping Britain prosper Helping Britain Prosper is our purpose. It means responding to the social

HELPING BRITAIN PROSPER Lloyds Banking Group Annual Report and Accounts Lloyds Banking Group How we're helping Britain prosper Helping Britain Prosper is our purpose. It means responding to the social

2Q17 Financial Results. July 21, 2017

2Q17 Financial Results July 21, 2017 Forward-looking statements and use of key performance metrics and Non-GAAP financial measures This document contains forward-looking statements within the Private Securities

2Q17 Financial Results July 21, 2017 Forward-looking statements and use of key performance metrics and Non-GAAP financial measures This document contains forward-looking statements within the Private Securities

Shaping the future relationship bank

Shaping the future relationship bank CEO Long term commitment, have a plan, future oriented continue on the road we have set out on, Stable, trustworthy Christian Clausen President and Group CEO 1 Nordea

Shaping the future relationship bank CEO Long term commitment, have a plan, future oriented continue on the road we have set out on, Stable, trustworthy Christian Clausen President and Group CEO 1 Nordea

Investor & Analyst Seminar Aviva General Insurance 18 October 2005

Investor & Analyst Seminar Aviva General Insurance 18 October 2005 Please switch mobiles and Blackberrys off Disclaimer This presentation may contain certain forward looking statements with respect to

Investor & Analyst Seminar Aviva General Insurance 18 October 2005 Please switch mobiles and Blackberrys off Disclaimer This presentation may contain certain forward looking statements with respect to

Bank of Queensland. Half-Year Results 29 February FY08 Half-Year Results

Bank of Queensland Half-Year Results 29 February 2008 1 Agenda Result highlights Financial result in detail BOQ Portfolio Strategy and outlook David Liddy Managing Director & CEO Ram Kangatharan Group

Bank of Queensland Half-Year Results 29 February 2008 1 Agenda Result highlights Financial result in detail BOQ Portfolio Strategy and outlook David Liddy Managing Director & CEO Ram Kangatharan Group

The Co-operative Financial Services 2010 annual results. 30 March 2011

The Co-operative Financial Services 2010 annual results 30 March 2011 This presentation may include "forward-looking statements". Such statements contain the words "anticipate", "believe", "intend", "estimate",

The Co-operative Financial Services 2010 annual results 30 March 2011 This presentation may include "forward-looking statements". Such statements contain the words "anticipate", "believe", "intend", "estimate",

Building A Model For Long-Term Growth December 2004

Building A Model For Long-Term Growth INVESTOR PRESENTATION Information disclosed within this presentation is current through October 31, 2004, unless otherwise indicated Presentation Outline Investing

Building A Model For Long-Term Growth INVESTOR PRESENTATION Information disclosed within this presentation is current through October 31, 2004, unless otherwise indicated Presentation Outline Investing

Results presentation. For the year ended 31 March 2014