SEARCHING FOR ALPHA: DEVELOPING ISLAMIC STRATEGIES EXPECTED TO OUTPERFORM CONVENTIONAL EQUITY INDEXES

|

|

|

- Jesse Norman

- 5 years ago

- Views:

Transcription

1 SEARCHING FOR ALPHA: DEVELOPING ISLAMIC STRATEGIES EXPECTED TO OUTPERFORM CONVENTIONAL EQUITY INDEXES John Lightstone 1 and Gregory Woods 2 Islamic Finance World May 19-22, Bridgewaters, NY, USA ABSTRACT Institutional Muslim investors who want to invest in US equities are very familiar with the performance of conventional US equity indexes, such as the S&P 500 Index or the Russell 2000 Growth Index 3. These indexes define equity styles, which are imperfectly correlated with each other, with different risk and return characteristics. The availability of indexes across different equity styles allows the possibility of asset allocation, which attempts to optimise the risk-return tradeoff of an investor by holding a combination of equity styles that are not well correlated. For example, large cap stock portfolios and small cap stock portfolios tend to do well at different times 4 and the overall risk of a portfolio is expected to be reduced by holding both large cap and small cap stocks. An institutional Muslim investor will seek out active strategies that are expected to outperform their corresponding conventional equity style indexes or benchmarks, and thereby improve the overall risk-adjusted returns of his portfolio. But for this to happen, three conditions must be met. 1. There must exist a family of active Shari c a-compliant strategies that track their respective benchmarks. 2. Secondly, we must be able to show that these active strategies are expected to outperform their benchmarks. 3. And thirdly, we must be able to customise the Shari c a screens for a given Shari c a board. Historically, these conditions have not been met. This paper will present a family of seven active Shari c a-compliant strategies that meet these three conditions. 1 President, Lightstone Capital Management LLC, White Plains, NY, USA and Adjunct Professor of Finance, Pace University, NY, USA. Lightstone Capital is a subadvisor that develops and maintains quantitative conventional and Shari c a-compliant and other values-based equity strategies (VBI) and works with financial institutions to implement the strategies. Please address any correspondence on this paper to John_Lightstone@lightstonecapital.com or call Vice President, Lightstone Capital Management LLC, White Plains, NY, USA. 3 S&P 500 Index is a trademark of McGraw-Hill Companies, Inc. and Russell 2000 Growth Index is a trademark of the Russell Investment Group. 4 For example, growth stocks in the S&P 500 Index outperformed value stocks in the Index each year from Then value stocks in the Index outperformed growth stocks each year from

2 We will show that these Shari c a-compliant strategies track conventional benchmarks in U.S. markets and we will also discuss why we expect this absence of style drift to continue in the future. We will also discuss the special challenges in developing Shari c a- compliant strategies that track conventional benchmarks. We will show that these quantitative Shari c a-compliant strategies have outperformed their conventional benchmarks in twenty one years of backtesting in up and down markets 5 so that we are seeing a convergence between the opportunities in Islamic space and in conventional space. This convergence between Islamic finance and conventional finance has been discussed by Mirakhor and others 6. Quantitative methods of stock selection are being increasingly used to select conventional portfolios. We will show that quantitative methods have even more advantages in selecting Shari c a-compliant portfolios but they are not commonly used in Islamic space. We will also discuss how the performance of these Shari c a-compliant strategies can be readily customised for a given Shari c a Board. We will conclude by briefly discussing some of our recent research on Abrahamic strategies. In these strategies, we not only exclude stocks not allowed under Shari c a Law, but we also exclude stocks not allowed under other ethical frameworks of investing, such as excluding companies that employ child labor and companies that pollute the environment. Our discussions with Islamic scholars suggest that these broader criteria will generally be consistent with Qua'ranic Law and the resulting strategies are also likely to have a broader investment demand. INTRODUCTION Institutional Muslim investors who want to invest in US equities are very familiar with the performance of conventional US equity indexes, such as the S&P 500 Index or the Russell 2000 Growth Index. These indexes define equity styles, which are imperfectly correlated with each other, with different risk and return characteristics. The availability of indexes across different equity styles allows the possibility of asset allocation, which attempts to optimise the risk-return tradeoff of an investor by holding various equity styles that are not well correlated. For example, large cap stock portfolios and small cap stock portfolios tend to do well at different times and the overall risk of a portfolio is expected to be reduced by holding both large cap and small cap stocks. An institutional Muslim investor will seek out active strategies that are expected to outperform their corresponding conventional equity style indexes or benchmarks, and thereby improve the overall risk-adjusted returns of his portfolio. This is an example of 5 The backtested results use the same screens that Lightstone Capital Management has been using as a portfolio consultant with conventional live portfolios. 6 An Introduction to Islamic Finance: Theory and Practice by Zamir Iqbal and Abbas Mirakhor. John Wiley & Sons

3 the convergence between Islamic finance and conventional finance described by Mirakhor and others. But for this to happen, three conditions must be met. 1. There must exist a family of active Shari c a-compliant strategies that track their respective benchmarks. 2. Secondly, we must be able to show that these active strategies are expected to outperform their benchmarks. 3. And thirdly, we must be able to customise the Shari c a screens for a given Shari c a board. This paper will present a family of seven active Shari c a-compliant strategies that meet these three conditions. We will examine the ways in which we can measure whether an active strategy tracks its benchmark. We will show that these Shari c a-compliant strategies track conventional benchmarks in U.S. markets and we will also discuss why we expect this absence of style drift to continue in the future. We will also discuss the special challenges in developing Shari c a-compliant strategies that track conventional benchmarks. The paper will then review the ways in which the performance of an active strategy can be measured relative to its benchmark, using a variety of metrics which examine both return and risk. For example, the performance of an actively managed small growth fund can be evaluated against a benchmark of the Russell 2000 Growth Index. This allows the investor to understand how much value the portfolio manager has contributed to the performance of the strategy above the performance of the benchmark. We would like a strategy that behaves similarly to the benchmark (has minimal style drift) but also outperforms the benchmark under a variety of market conditions. We will show that the quantitative Shari c a-compliant strategies that we have developed have outperformed their conventional benchmarks in twenty one years of backtesting in up and down markets 7 so that we are seeing a convergence between the opportunities in Islamic space and in conventional space. Quantitative methods of stock selection are being increasingly used to select conventional portfolios. We will show that quantitative methods have even more advantages in selecting Shari c a-compliant portfolios but they are not commonly used in Islamic space. We will also discuss how the performance of these Shari c a-compliant strategies can be readily customised for a given Shari c a Board. We will end by briefly discussing some of our recent research on Abrahamic strategies. In these strategies, we not only exclude stocks not allowed under Shari c a Law, but we also exclude stocks not allowed under other ethical frameworks of investing, such as excluding companies that employ child labor. The resulting strategies are likely to have a 7 The backtested results use the same screens that Lightstone Capital Management has been using as a portfolio consultant with conventional live portfolios. 3

4 broader investment demand and our discussions with Islamic scholars suggest that these broader criteria will generally be consistent with Qua'ranic Law. TRACKING A BENCHMARK A strategy will typically track an index or benchmark if the strategy selects stocks that are members of the index and the selection process is consistent with the style of the index. For example, if we are defining a large cap value strategy, we might want to select stocks with low Price/Book (P/B) or low Price/Sales (P/S) screens from a Russell 1000 universe. And the selection process should be consistent and objective if there is to be no style drift. These criteria are readily met with the objectivity of quantitative methods of stock selection. The ability of a strategy to outperform its benchmark and yet remain faithful to the benchmark is often measured by the Information Ratio which is a key measure of a manager performance relative to the benchmark. An Information Ratio above 0.5 has been said to denote a "good manager" although others have suggested that this value is too high. 8 We will be discussing the Information Ratio of our strategies. QUANTITATIVE STRATEGIES In addition to ensuring a consistent stock selection process, quantitative methods can lead to improved performance because they can select from a broader universe of stocks and also because they allow the use of more complex decision rules. A quantitative strategy can also be backtested to see how it would have performed over past market cycles and this allows a better understanding of the risk profile of the strategy. A quantitative strategy also allows us to exclude stocks that are not Shari c a-compliant in an objective way. It also allows us to modify the criteria for excluding stocks if a given Shari c a Board has a different understanding of Shari c a Law. The quantitative stock selection process also allows us to impose a cap on the weighting of a given stock in a strategy and/or a cap on the weighting of all stocks in a given sector. This is particularly important when we are selecting stocks from a universe from which so many stocks have been excluded because they are not Shari c a-compliant. 8 Richard C. Grinold and Ronald N. Kahn, Active Portfolio Management. Chicago, IL: Richard D. Irwin. Also Bruce L. Jacobs and Kenneth Levy, "Residential Risk: How Much is Too Much?" Journal of Portfolio Management, vol. 21, no. 3 (Spring),

5 STOCK SELECTION PROCESS We backtested seven active Islamic strategies designed to track and outperform five established indexes, large cap core, large cap growth, large cap value, small cap growth and small cap value. In three of the strategies, large cap GARP, large cap dividend growth and small cap GARP, we modified the risk profile of the basic strategy to introduce additional defensive behavior in a bear market that we believe may be attractive to many Muslim investors. The strategies were backtested on a monthly basis from the beginning of 1987 through the end of the first quarter of The twenty oneyear period of the backtest allows us to examine the performance of the strategies in different market environments over complete market cycles. Shari c a-compliant large cap growth portfolios have the smallest number of stocks, with an average of 45 stocks in a portfolio. Shari c a-compliant small cap growth portfolios have the largest number of stocks, with an average of 116 stocks in a portfolio. In each case, we started with stocks that were members of the Russell 1000 Index or Russell 2000 Index 10 as of the selection date 11 and we then exclude 12 stocks that are not Shari c a-compliant 13 or have a price less than $5. We use momentum or Price/Book (P/B) or Price/Sales (P/S) screens 14 to take us to the right equity style within the selection universe. We then select the stocks with the highest Earnings Pressure, which uses a proprietary analysis of estimate revisions; we are "analyzing the analysts." The fact that we can use the same Earnings Pressure screen to select stocks in the different universes is a sign of the robustness of the screening process. Some of the strategies have other valuation and quality screens, as noted in the discussion of each strategy. Each strategy also has a cap on the weighting of a given stock in a portfolio and/or a cap on the weighting of all stocks in a given sector. We evaluate the performance of each strategy against its benchmark in terms of average return, volatility, 10% MAR Downside Deviation, Sharpe Ratio, 10% Sortino Ratio, 9 Data for the Islamic large cap Dividend Growth Strategy was only available from April 1, Russell 1000 Index and Russell 2000 Index are trademarks of the Russell Investment Group. 11 We want to avoid survivorship bias so that in backtesting a strategy, we use a research database which gives us this historical membership. 12 Stocks in the following sectors/industries are excluded: alcoholic beverages finance tobacco aerospace and defense movie and tv production and distribution meat products gambling hotels and motels Stocks are also excluded with unacceptable levels of debt or interest income: debt greater than 33% of equity accounts receivable greater than 33% of total assets cash and interest bearing securities greater than 33% of equity 13 As we noted earlier, the specific constraints can be readily modified for a given Shari c a Board. 14 In backtests, screens are lagged as P/B(-1) and P/S(-1) to avoid forward-looking bias. 5

6 Information Ratio, Upside and Downside Capture Ratios and the percentage of rolling 12-month periods which show losses. We also compare the VAMI (value of $1000 invested) for each strategy and its benchmark 15. RESULTS 16 ISLAMIC LARGE CAP GROWTH STRATEGY The Islamic Large Cap Growth Strategy follows the usual screening process, starting with stocks in the Russell 1000 Index from which we exclude stocks that are not Shari c a- compliant. We then select stocks with the highest momentum and the highest Earnings Pressure. The Strategy has an average return 17 of 17.6% per year over the twenty one years of backtesting compared with an average return of 9.7% for the Russell 1000 Growth Index over the same period, for an excess return of 7.9% per year. The Strategy shows a balanced performance, outperforming the Benchmark during the bull market of the late nineties, but also showing a smaller decline during the bear market, and then again outperforming the Benchmark in the subsequent recovery. The Sharpe Ratio, a measure of risk-adjusted return relative to a 5% riskless rate, is 0.62 for the Strategy and 15 The VAMI graph uses a semilog scale to allow comparison of rates of return. 16 The graphs and represent a hypothetical $1000 of investment in a given strategy and the associated benchmark over the period indicated in the graph with no deduction for fees or trading expenses. Past performance is no guarantee of future results. In any given year a strategy may lose money or underperform the index and there is no assurance that a strategy will achieve its investment objective. 17 The average return is calculated as the arithmetic average of the twenty calendar year returns, with no deduction for fees or trading costs. 6

7 0.34 for the Benchmark. The Information Ratio is The detailed results for the Strategy are shown in Table 1 of the Appendix. ISLAMIC LARGE CAP GARP ("growth at a reasonable price") STRATEGY The Islamic Large Cap Growth Strategy showed smaller losses than its Benchmark during the bear market while also outperforming the Benchmark during the bull market. However, some risk-averse Muslim investors may want a large cap growth strategy with even more resistance to declines in a bear market. This can be accomplished by starting with stocks in the Russell 1000 Index from which we exclude stocks that are not Shari c a-compliant and then introducing a screen which excludes stocks that are strongly overpriced, based on their forward looking PE 18. We then select stocks with the highest momentum and the highest Earnings Pressure as we did with the Large Cap Growth Strategy. In backtests, this strategy of "growth at a reasonable price" had an average return of 15.8% per year over the twenty one years of backtesting compared with an average return of 9.7% for the Russell 1000 Growth Index over the same period, for an excess return of 6.1% per year. The Islamic Large Cap Growth Strategy outperforms the Benchmark throughout the bull market. The GARP Strategy outperforms the Benchmark for most of the bull market but underperforms the Benchmark during the irrational exuberance at the end of the bull market, when stocks became very overpriced. The GARP Strategy then shows much 18 This is of course different from limiting the portfolio to value stocks. 7

8 smaller declines than the Large Cap Growth Strategy during the subsequent bear market and again outperforms the Benchmark in the subsequent recovery. The Information Ratio of 0.43 is very acceptable but less than the Information Ratio of the Large Cap Growth Strategy because we have intentionally modified the risk characteristics of the Russell 1000 Growth benchmark by excluding strongly overpriced stocks. As a result, the Strategy shows much smaller declines during the bear market and intentionally does not track the Index. [Appendix: Table 2] ISLAMIC LARGE CAP DIVIDEND GROWTH STRATEGY Companies with a history of increasing their dividends per share have often shown superior returns with lower volatility. In the Islamic Large Cap Dividend Growth Strategy, we start with stocks in the Russell 1000 Index, exclude stocks that are not Shari c a-compliant and then select stocks with a history of increasing dividends per share and strong Earnings Pressure. The Strategy is a core strategy, benchmarked to the Russell 1000 Index, with both value and growth characteristics. In backtests, its average return is 15.8% per year versus 10.7% for the Benchmark with the same volatility. The Strategy showed almost no decline during the bear market. It showed a very balanced performance, with an Upside Capture Ratio of 1.47 and a Downside Capture Ratio of 0.79 and a beta of An Upside Capture Ratio of greater than one tells us that the Strategy has higher returns than the Benchmark in up markets. Conversely a Downside Capture of less than one tells us that the Strategy has smaller losses than the Benchmark in down markets. The Strategy has a Sharpe Ratio of

9 versus 0.46 for the Benchmark and an Information Ratio of Its beta is 0.88 so that the excess returns of the strategy are not achieved by assuming more market risk. The maximum drawdown was 17% for the Dividend Growth Strategy and 45% for the Russell 1000 Index. [Appendix: Table 3] ISLAMIC LARGE CAP VALUE STRATEGY In the Islamic Large Cap Value Strategy, we start with stocks in the Russell 1000 Index, exclude stocks that are not Shari c a-compliant and also exclude stocks that do not pass a quality of earnings screen. We then select stocks with low P/B and low P/S, so that we are selecting value stocks, and then stocks with strong Earnings Pressure. In backtests, the Strategy has an average return of 15.0% per year versus 11.5% for the Russell 1000 Value Index. It shows a balanced performance, with an Upside Capture Ratio of 1.80 and a Downside Capture of 0.98 and an Information Ratio of The Islamic Large Cap Value Strategy has outperformed its Benchmark over 1, 2, 3, 5, 7, 10, 15 and 20-year periods and since inception. [Appendix: Table 4] ISLAMIC SMALL CAP GROWTH STRATEGY In the Islamic Small Cap Growth Strategy, we start with stocks in the Russell 2000 Index, we exclude stocks that are not Shari c a-compliant, we further exclude stocks that cannot pass a quality screen and then select stocks with strong Earnings Pressure. In backtests, the Strategy has an average return of 19.6% per year versus 7.0% for the Russell 2000 Growth Index. The Strategy has the same volatility as the Benchmark 9

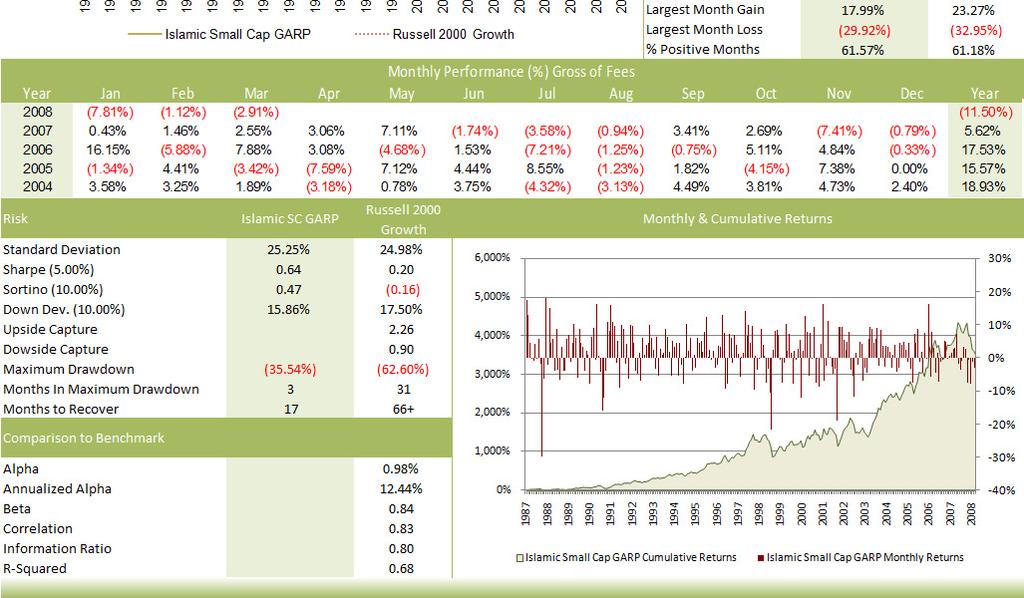

10 (25.1% per year versus 25.0%) although its return is 12.6% higher than the Benchmark. It has a balanced performance, with an Upside Capture Ratio of 2.93 and a Downside Capture of On an end of month basis, the Strategy had a month to month decline of 7.2% during the bear market when the Benchmark declined by 62.6%. The Sharpe Ratio of the Strategy is 0.69 versus 0.20 for the Benchmark. The Information Ratio is 1.31, which attests to the strong performance of the Strategy and its faithfulness to the Benchmark. The excellent performance is achieved at less systematic risk than the Benchmark, with a beta of The Strategy has half the number of losing rolling 12-month periods as the Benchmark (33/241 or 13.7% versus 67/241 or 27.8%.) [Appendix: Table 5] ISLAMIC SMALL CAP GARP ("growth at a reasonable price") STRATEGY This is a similar strategy to the Small Cap Growth Strategy except that we also exclude stocks that are highly priced as measured by their forward-looking PE Ratios. In backtests, the Strategy has an average return of 18.4% per year versus 7.0% for the Russell 2000 Growth Index with similar volatility (25.2% per year versus 25.0%). On an end of month basis, the Strategy had a month to month gain of 21.2% during the bear market when the Benchmark declined by 62.6% and yet it still has an Information Ratio of The Strategy slightly underperforms the Russell 2000 Growth Benchmark in 2007 but outperforms its Benchmark over 2, 3, 5, 7, 10 and 15-year periods and since inception. [Appendix: Table 6] 10

11 ISLAMIC SMALL CAP VALUE STRATEGY In the Islamic Small Cap Value Strategy, we start with stocks in the Russell 2000 Index, exclude stocks that are not Shari c a-compliant and also exclude stocks that do not pass a quality screen. We then select stocks with low P/B and low P/S, so that we are in a value universe, and then select stocks with strong Earnings Pressure. In backtests, the Strategy has an average return of 19.5% per year versus 11.7% for the Russell 1000 Value Index. It has an Upside Capture Ratio of 4.7 and a Downside Capture of 1.0 and an Information Ratio of [Appendix: Table 7] 11

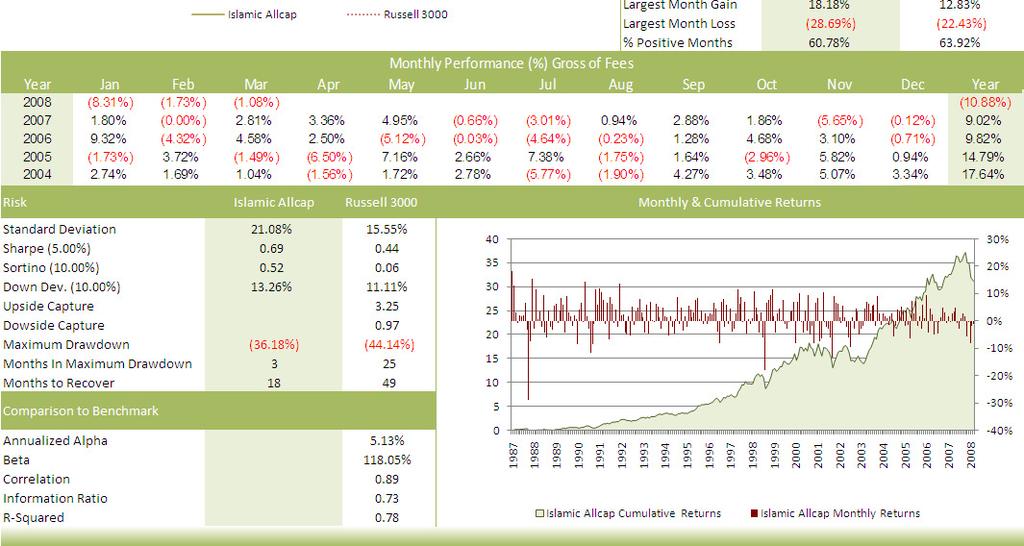

12 ASSET ALLOCATION When we have active Islamic strategies across different equity styles, it is possible to have an asset allocation which offers a preferred risk-return tradeoff and which is consistent with the risk preferences of the investor 19. This becomes possible because the returns on different equity styles are imperfectly correlated. Similarly, if an Islamic investor has a view on which equity styles are likely to show the best performance in the future, the investor can improve performance by style rotation between the various Islamic strategies. These possibilities have long been available to conventional investors. When we have active Islamic strategies across different equity styles, these possibilities also become available to the Islamic investor. By way of a simple example, the graph shows the performance of an asset allocation strategy that allocates equal dollar weights to each of the seven strategies we have been discussing and rebalances the overall strategy at the beginning of each year, benchmarked against the Russell 3000 Index 20. The average return for the Strategy is 17.7% per year versus 10.7% for the Benchmark with an Information Ratio of [Appendix: Table 8] STYE ROTATION STRATEGY If an Islamic investor has a view on which equity styles are likely to show the best performance in the future, the investor can improve performance by style rotation between the various Islamic strategies. We analysed the performance of a style rotation 19 In this paper, we are concerned with equity investments. More generally, investors will also be concerned with asset allocation between all asset classes, including non-equity investments, such as real estate. 20 The Russell 3000 Index is an imperfect benchmark but the development of a more appropriate synthetic benchmark is beyond the scope of this paper. 12

13 strategy in which, at the beginning of each year, an investor correctly identifies which strategy will be the best performing style during that year and invests in that style. A strategy that was always invested at the beginning of a year in the style that ex post turned out to be the strongest performer for the year had an average return of 28.1% per year versus 10.7% for the Russell 3000 Index. [Appendix: Table 9] ABRAHAMIC STRATEGIES We have also developed Abrahamic strategies, which not only exclude stocks forbidden under Shariah Law, but also exclude stocks not allowed in other ethical frameworks. For example, screens used for investments by the Catholic Church exclude companies that employ child labor and also exclude companies that pollute the environment. These broader screening criteria are expected to be consistent with Qua'ranic Law but this is a subject where we seek guidance from Shariah scholars. The Abrahamic strategies have performed very well in backtests from January 1, 2000, when the screens became available. An Abrahamic ALL CAP GARP Strategy excludes stocks that are not consistent with Islamic values and also excludes stocks that are not consistent with Catholic values. It excludes stocks that are highly priced as measured by their forward looking PEG and then selects stocks with highest momentum and Earnings Pressure. Its average return is 5.4% versus a loss of 3.9% for the Russell 3000 Growth Index in backtests from the beginning of 2000, with an Information Ratio 0.82 against the Russell 3000 Growth Index. [Appendix: Table 10] 13

14 An Abrahamic ALL CAP Value Strategy similarly excludes stocks that are not consistent with Islamic values and also excludes stocks that are not consistent with Catholic values. It then excludes stocks that do not pass a quality screen and then selects stocks with low P/B and low P/S and high Earnings Pressure. Its average return is 16.8% per year versus 5.8% for the Russell 300 Value Index in backtests from beginning of 2000, with an Information Ratio of 0.92 against the Russell 3000 Growth Index. [Appendix: Table 11] 14

15 CONCLUSION We have shown that quantitative methods of stock selection are well suited to the selection of active Islamic strategies that track conventional equity indexes and which can be evaluated against the indexes as benchmarks. We have used a quantitative analysis of estimate revisions to develop seven Islamic strategies which strongly outperform their conventional benchmarks in twenty one years of backtesting in up and down markets. We have shown that with the availability of these strategies, the Islamic investor now has opportunities for asset allocation and style rotation. These opportunities have long been available to a conventional investor in US equities but not to an Islamic investor. We also developed Abrahamic strategies that are not only Shari c a-compliant, but also exclude stocks that are not allowed under other ethical frameworks of investing. 15

16 APPENDIX Table 1 16

17 Table 2 17

18 Table 3 18

19 Table 4 19

20 Table 5 20

21 Table 6 21

22 Table 7 22

23 Table 8 23

24 Table 9 24

25 Table 10 25

26 Table 11 26

Mid Cap Dividend Growth Strategy

Mid Cap Dividend Growth Strategy Product Level Investment Process Stock Universe Companies that have increased their dividends with market capitalizations of $1 billion to $15 billion Stock Selection Top

Mid Cap Dividend Growth Strategy Product Level Investment Process Stock Universe Companies that have increased their dividends with market capitalizations of $1 billion to $15 billion Stock Selection Top

Dividend Growth as a Defensive Equity Strategy August 24, 2012

Dividend Growth as a Defensive Equity Strategy August 24, 2012 Introduction: The Case for Defensive Equity Strategies Most institutional investment committees meet three to four times per year to review

Dividend Growth as a Defensive Equity Strategy August 24, 2012 Introduction: The Case for Defensive Equity Strategies Most institutional investment committees meet three to four times per year to review

Enhancing equity portfolio diversification with fundamentally weighted strategies.

Enhancing equity portfolio diversification with fundamentally weighted strategies. This is the second update to a paper originally published in October, 2014. In this second revision, we have included

Enhancing equity portfolio diversification with fundamentally weighted strategies. This is the second update to a paper originally published in October, 2014. In this second revision, we have included

Going Beyond Style Box Investing

Going Beyond Style Box Investing NCPERS Presented by Erin Doyle Orekhov, Client Portfolio Manager May 22, 2017 For financial professional or qualified institutional investor use only. Not for inspection

Going Beyond Style Box Investing NCPERS Presented by Erin Doyle Orekhov, Client Portfolio Manager May 22, 2017 For financial professional or qualified institutional investor use only. Not for inspection

Schafer Cullen Capital Management High Dividend Value

Product Type: Separate Account Manager Headquarters: New York, NY Total Staff: 56 Geography Focus: Domestic Year Founded: 1983 Investment Professionals: 21 Type of Portfolio: Equity Total AUM: $17,896

Product Type: Separate Account Manager Headquarters: New York, NY Total Staff: 56 Geography Focus: Domestic Year Founded: 1983 Investment Professionals: 21 Type of Portfolio: Equity Total AUM: $17,896

American Customer Satisfaction Investable Index

Investable Index s 52.5 45.0 37.5 30.0 22.5 15.0 7.5 0.0-7.5-15.0-22.5-30.0-37.5-45.0 YTD 2017 2016 2015 2014 2013 2012 2011 2010 2009 2008 Calendar Year s YTD 2017 2016 2015 2014 2013 2012 2011 2010 2009

Investable Index s 52.5 45.0 37.5 30.0 22.5 15.0 7.5 0.0-7.5-15.0-22.5-30.0-37.5-45.0 YTD 2017 2016 2015 2014 2013 2012 2011 2010 2009 2008 Calendar Year s YTD 2017 2016 2015 2014 2013 2012 2011 2010 2009

American Customer Satisfaction Investable Index

Investable Index s 52.5 45.0 37.5 30.0 22.5 15.0 7.5 0.0-7.5-15.0-22.5-30.0-37.5-45.0 YTD 2017 2016 2015 2014 2013 2012 2011 2010 2009 2008 Calendar Year s YTD 2017 2016 2015 2014 2013 2012 2011 2010 2009

Investable Index s 52.5 45.0 37.5 30.0 22.5 15.0 7.5 0.0-7.5-15.0-22.5-30.0-37.5-45.0 YTD 2017 2016 2015 2014 2013 2012 2011 2010 2009 2008 Calendar Year s YTD 2017 2016 2015 2014 2013 2012 2011 2010 2009

Nasdaq Chaikin Power US Small Cap Index

Nasdaq Chaikin Power US Small Cap Index A Multi-Factor Approach to Small Cap Introduction Multi-factor investing has become very popular in recent years. The term smart beta has been coined to categorize

Nasdaq Chaikin Power US Small Cap Index A Multi-Factor Approach to Small Cap Introduction Multi-factor investing has become very popular in recent years. The term smart beta has been coined to categorize

Comparative Profile. Style Map. Managed Account Select

Comparative Profile Managed Account Select Quarterly Highlights The S&P 500 Index was virtually flat in the second quarter, gaining 0.10% as concerns about the end of the Federal Reserve s QE2 program,

Comparative Profile Managed Account Select Quarterly Highlights The S&P 500 Index was virtually flat in the second quarter, gaining 0.10% as concerns about the end of the Federal Reserve s QE2 program,

The Long & Short of It Quarterly Newsletter Second Quarter 2018

The Long & Short of It Quarterly Newsletter Second Quarter 2018 Value vs. Growth: A Primer Are Value Stocks Ready to Grow Again? the Barron s cover article from April 28, 2018 lamented the recent performance

The Long & Short of It Quarterly Newsletter Second Quarter 2018 Value vs. Growth: A Primer Are Value Stocks Ready to Grow Again? the Barron s cover article from April 28, 2018 lamented the recent performance

Tower Square Investment Management LLC Strategic Aggressive

Product Type: Multi-Product Portfolio Headquarters: El Segundo, CA Total Staff: 15 Geography Focus: Global Year Founded: 2012 Investment Professionals: 12 Type of Portfolio: Balanced Total AUM: $1,422

Product Type: Multi-Product Portfolio Headquarters: El Segundo, CA Total Staff: 15 Geography Focus: Global Year Founded: 2012 Investment Professionals: 12 Type of Portfolio: Balanced Total AUM: $1,422

Fayez Sarofim & Co Large Cap Equity

Product Type: Separate Account Manager Headquarters: Houston, TX Total Staff: 90 Geography Focus: Domestic Year Founded: 1958 Investment Professionals: 20 Type of Portfolio: Equity Total AUM: $22,458 million

Product Type: Separate Account Manager Headquarters: Houston, TX Total Staff: 90 Geography Focus: Domestic Year Founded: 1958 Investment Professionals: 20 Type of Portfolio: Equity Total AUM: $22,458 million

DIVERSIFYING VALUE: THINKING OUTSIDE THE BOX

Legg Mason Thought Leadership DIVERSIFYING VALUE: THINKING OUTSIDE THE BOX Michael J. LaBella, CFA Portfolio Manager Smart beta can be utilized within the traditional style box framework to help investors

Legg Mason Thought Leadership DIVERSIFYING VALUE: THINKING OUTSIDE THE BOX Michael J. LaBella, CFA Portfolio Manager Smart beta can be utilized within the traditional style box framework to help investors

Factor Performance in Emerging Markets

Investment Research Factor Performance in Emerging Markets Taras Ivanenko, CFA, Director, Portfolio Manager/Analyst Alex Lai, CFA, Senior Vice President, Portfolio Manager/Analyst Factors can be defined

Investment Research Factor Performance in Emerging Markets Taras Ivanenko, CFA, Director, Portfolio Manager/Analyst Alex Lai, CFA, Senior Vice President, Portfolio Manager/Analyst Factors can be defined

Capital Idea: Expect More From the Core.

SM Capital Idea: Expect More From the Core. Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value. Core equity strategies, such

SM Capital Idea: Expect More From the Core. Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value. Core equity strategies, such

How to evaluate factor-based investment strategies

A feature article from our U.S. partners INSIGHTS SEPTEMBER 2018 How to evaluate factor-based investment strategies Due diligence on smart beta strategies should be anything but passive Original publication

A feature article from our U.S. partners INSIGHTS SEPTEMBER 2018 How to evaluate factor-based investment strategies Due diligence on smart beta strategies should be anything but passive Original publication

Quality Value Momentum Strategy

Quality Value Momentum Strategy Ford Equity Research 11722 Sorrento Valley Road, Suite I San Diego, CA 92121 800.842.0207 (USA) 858.455.6316 Fax www.fordequity.com Background Can a low-turnover portfolio

Quality Value Momentum Strategy Ford Equity Research 11722 Sorrento Valley Road, Suite I San Diego, CA 92121 800.842.0207 (USA) 858.455.6316 Fax www.fordequity.com Background Can a low-turnover portfolio

STRATEGY OVERVIEW. Long/Short Equity. Related Funds: 361 Domestic Long/Short Equity Fund (ADMZX) 361 Global Long/Short Equity Fund (AGAZX)

361 Global Long/Short Equity Fund (AGAZX)") STRATEGY OVERVIEW Long/Short Equity Related Funds: 361 Domestic Long/Short Equity Fund (ADMZX) 361 Global Long/Short Equity Fund (AGAZX) Strategy Thesis The thesis driving 361 s Long/Short Equity strategies

STRATEGY OVERVIEW Long/Short Equity Related Funds: 361 Domestic Long/Short Equity Fund (ADMZX) 361 Global Long/Short Equity Fund (AGAZX) Strategy Thesis The thesis driving 361 s Long/Short Equity strategies

Navellier Defensive Alpha Portfolio Process and results for the quarter ending March 31, 2018

Navellier Defensive Alpha Portfolio Process and results for the quarter ending March 31, 2018 Please see important disclosures at the end of the presentation. NCD-18-18-694 Our Goal The Defensive Alpha

Navellier Defensive Alpha Portfolio Process and results for the quarter ending March 31, 2018 Please see important disclosures at the end of the presentation. NCD-18-18-694 Our Goal The Defensive Alpha

The Liquidity Style of Mutual Funds

Thomas M. Idzorek Chief Investment Officer Ibbotson Associates, A Morningstar Company Email: tidzorek@ibbotson.com James X. Xiong Senior Research Consultant Ibbotson Associates, A Morningstar Company Email:

Thomas M. Idzorek Chief Investment Officer Ibbotson Associates, A Morningstar Company Email: tidzorek@ibbotson.com James X. Xiong Senior Research Consultant Ibbotson Associates, A Morningstar Company Email:

Investment Comparison

Investment Data as of 1/31/217 PAGE 2 OF 7 Fi36 FIDUCIARY SCORE OVERVIEW INVESTMENT ClearBridge Small Cap Value I MassMutual Premier Small Cap Opps R5 ishares Russell 2 Small-Cap Idx Instl Victory Integrity

Investment Data as of 1/31/217 PAGE 2 OF 7 Fi36 FIDUCIARY SCORE OVERVIEW INVESTMENT ClearBridge Small Cap Value I MassMutual Premier Small Cap Opps R5 ishares Russell 2 Small-Cap Idx Instl Victory Integrity

Essential Performance Metrics to Evaluate and Interpret Investment Returns. Wealth Management Services

Essential Performance Metrics to Evaluate and Interpret Investment Returns Wealth Management Services Alpha, beta, Sharpe ratio: these metrics are ubiquitous tools of the investment community. Used correctly,

Essential Performance Metrics to Evaluate and Interpret Investment Returns Wealth Management Services Alpha, beta, Sharpe ratio: these metrics are ubiquitous tools of the investment community. Used correctly,

Does the Application of Smart Beta Strategies Enhance Portfolio Performance? Muhammad Wajid Raza Dawood Ashraf

Does the Application of Smart Beta Strategies Enhance Portfolio Performance? The Case of Islamic Equity Investments Muhammad Wajid Raza Dawood Ashraf The main motivation: Returns & Growth Background o

Does the Application of Smart Beta Strategies Enhance Portfolio Performance? The Case of Islamic Equity Investments Muhammad Wajid Raza Dawood Ashraf The main motivation: Returns & Growth Background o

Navellier Defensive Alpha Portfolio

Navellier Defensive Alpha Portfolio Process and results for the quarter ending December 31, 2014 Please see important disclosures at the end of the presentation NCD 15 281 NAVELLIER.COM 800.887.8671 Our

Navellier Defensive Alpha Portfolio Process and results for the quarter ending December 31, 2014 Please see important disclosures at the end of the presentation NCD 15 281 NAVELLIER.COM 800.887.8671 Our

Navigator High Dividend Equity

CCM-17-09-6 As of 9/30/2017 Navigator High Dividend Equity Navigate the U.S. Equity Markets with a Focus on Dividend Growth We believe it is prudent to focus on dividend growth through fundamental analysis,

CCM-17-09-6 As of 9/30/2017 Navigator High Dividend Equity Navigate the U.S. Equity Markets with a Focus on Dividend Growth We believe it is prudent to focus on dividend growth through fundamental analysis,

UBS Conservative Income - Muni FI

Product Type: Multi-Product Portfolio Headquarters: New York, NY Total Staff: 2,329 Geography Focus: Global Year Founded: 1989 Investment Professionals: 953 Type of Portfolio: Balanced Total AUM: $627,645

Product Type: Multi-Product Portfolio Headquarters: New York, NY Total Staff: 2,329 Geography Focus: Global Year Founded: 1989 Investment Professionals: 953 Type of Portfolio: Balanced Total AUM: $627,645

Navigator Fixed Income Total Return (ETF)

") CCM-17-09-1 As of 9/30/2017 Navigator Fixed Income Total Return (ETF) Navigate Fixed Income with a Tactical Approach With yields hovering at historic lows, bond portfolios could decline if interest rates

CCM-17-09-1 As of 9/30/2017 Navigator Fixed Income Total Return (ETF) Navigate Fixed Income with a Tactical Approach With yields hovering at historic lows, bond portfolios could decline if interest rates

HEARTLAND VALUE FUND

HEARTLAND VALUE FUND An investor should consider the Fund s investment objectives, risks, and charges and expenses carefully before investing or sending money. This and other important information can

HEARTLAND VALUE FUND An investor should consider the Fund s investment objectives, risks, and charges and expenses carefully before investing or sending money. This and other important information can

Growth Investing. in Times of Market Volatility. White Paper

White Paper Growth Investing in Times of Market Volatility April 2018 Executive Summary Many investors may be dismayed by the volatile nature of high-flying growth stocks. While, by definition, growth

White Paper Growth Investing in Times of Market Volatility April 2018 Executive Summary Many investors may be dismayed by the volatile nature of high-flying growth stocks. While, by definition, growth

AlphaSolutions Blended Bull/Calendar

AlphaSolutions Blended Bull/Calendar An investment model based on trending strategies coupled with market analytics for downside risk control with predetermined investment periods Portfolio Goals Primary:

AlphaSolutions Blended Bull/Calendar An investment model based on trending strategies coupled with market analytics for downside risk control with predetermined investment periods Portfolio Goals Primary:

Does Relaxing the Long-Only Constraint Increase the Downside Risk of Portfolio Alphas? PETER XU

Does Relaxing the Long-Only Constraint Increase the Downside Risk of Portfolio Alphas? PETER XU Does Relaxing the Long-Only Constraint Increase the Downside Risk of Portfolio Alphas? PETER XU PETER XU

Does Relaxing the Long-Only Constraint Increase the Downside Risk of Portfolio Alphas? PETER XU Does Relaxing the Long-Only Constraint Increase the Downside Risk of Portfolio Alphas? PETER XU PETER XU

Performance Attribution: Are Sector Fund Managers Superior Stock Selectors?

Performance Attribution: Are Sector Fund Managers Superior Stock Selectors? Nicholas Scala December 2010 Abstract: Do equity sector fund managers outperform diversified equity fund managers? This paper

Performance Attribution: Are Sector Fund Managers Superior Stock Selectors? Nicholas Scala December 2010 Abstract: Do equity sector fund managers outperform diversified equity fund managers? This paper

The Bull Market The Barron s 400. Francis Gupta, Ph.D., MarketGrader Research. September 2018

The Bull Market The Barron s 400 Francis Gupta, Ph.D., MarketGrader Research. September 2018 The Barron s 400 Bull Market Performance in the Crosshairs Stock market watchers fall into two camps when discussing

The Bull Market The Barron s 400 Francis Gupta, Ph.D., MarketGrader Research. September 2018 The Barron s 400 Bull Market Performance in the Crosshairs Stock market watchers fall into two camps when discussing

R ES E A R C H R E P O RT

RESEARCH REPORT DATA DRIVEN TRUST UITINVESTING.COM UIT Investing, Inc. provides the most comprehensive research for the unit investment trust industry by providing complete analysis of unit investment

RESEARCH REPORT DATA DRIVEN TRUST UITINVESTING.COM UIT Investing, Inc. provides the most comprehensive research for the unit investment trust industry by providing complete analysis of unit investment

Aspiriant Risk-Managed Equity Allocation Fund RMEAX Q4 2018

Aspiriant Risk-Managed Equity Allocation Fund Q4 2018 Investment Objective Description The Aspiriant Risk-Managed Equity Allocation Fund ( or the Fund ) seeks to achieve long-term capital appreciation

Aspiriant Risk-Managed Equity Allocation Fund Q4 2018 Investment Objective Description The Aspiriant Risk-Managed Equity Allocation Fund ( or the Fund ) seeks to achieve long-term capital appreciation

Capital Idea: Expect More From the Core.

SM Capital Idea: Expect More From the Core. Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value. Core equity strategies, such

SM Capital Idea: Expect More From the Core. Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value. Core equity strategies, such

Returns on Small Cap Growth Stocks, or the Lack Thereof: What Risk Factor Exposures Can Tell Us

RESEARCH Returns on Small Cap Growth Stocks, or the Lack Thereof: What Risk Factor Exposures Can Tell Us The small cap growth space has been noted for its underperformance relative to other investment

RESEARCH Returns on Small Cap Growth Stocks, or the Lack Thereof: What Risk Factor Exposures Can Tell Us The small cap growth space has been noted for its underperformance relative to other investment

Deconstructing Dividends: Five Reasons to Consider Small- and Mid-Cap Dividend-Paying Stocks

Deconstructing Dividends: Five Reasons to Consider Small- and Mid-Cap Dividend-Paying Stocks Dividend-paying stocks historically outperform the market with less risk and low correlation with other investment

Deconstructing Dividends: Five Reasons to Consider Small- and Mid-Cap Dividend-Paying Stocks Dividend-paying stocks historically outperform the market with less risk and low correlation with other investment

Factor Analysis: What Drives Performance?

Factor Analysis: What Drives Performance? February 2014 E. William Stone, CFA CMT Managing Director, Investment & Portfolio Strategy Chief Investment Strategist Chen He Portfolio Strategist Paul J. White,

Factor Analysis: What Drives Performance? February 2014 E. William Stone, CFA CMT Managing Director, Investment & Portfolio Strategy Chief Investment Strategist Chen He Portfolio Strategist Paul J. White,

Understanding Smart Beta Returns

Understanding Smart Beta Returns October 2018 In this paper, we use a performance analysis framework to analyze Smart Beta strategies against their benchmark. We apply it to Minimum Variance Strategies

Understanding Smart Beta Returns October 2018 In this paper, we use a performance analysis framework to analyze Smart Beta strategies against their benchmark. We apply it to Minimum Variance Strategies

Mid Cap Value Fiduciary Services EARNEST Partners, LLC

EARNEST Partners, LLC 1180 Peachtree St. - Suite 2300 Atlanta, Georgia 30309 Style: Sub-Style: Firm AUM: Firm Strategy AUM: US Mid Cap Value Traditional Value $20.1 billion $64.0 billion Year Founded:

EARNEST Partners, LLC 1180 Peachtree St. - Suite 2300 Atlanta, Georgia 30309 Style: Sub-Style: Firm AUM: Firm Strategy AUM: US Mid Cap Value Traditional Value $20.1 billion $64.0 billion Year Founded:

Navigator Global Equity ETF

CCM-17-12-3 As of 12/31/2017 Navigator Global Equity ETF Navigate Global Equity with a Dynamic Approach The world s financial markets offer a variety of growth opportunities, but identifying the right

CCM-17-12-3 As of 12/31/2017 Navigator Global Equity ETF Navigate Global Equity with a Dynamic Approach The world s financial markets offer a variety of growth opportunities, but identifying the right

Cash. Period Ending 06/30/2016 Period Ending 3/31/2016. Equity. Fixed Income. Other

Product Type: Multi-Product Portfolio Headquarters: Austin, TX Total Staff: 46 Geography Focus: Global Year Founded: 1996 Investment Professionals: 16 Type of Portfolio: Balanced Total AUM: $12,046 million

Product Type: Multi-Product Portfolio Headquarters: Austin, TX Total Staff: 46 Geography Focus: Global Year Founded: 1996 Investment Professionals: 16 Type of Portfolio: Balanced Total AUM: $12,046 million

An Intro to Sharpe and Information Ratios

An Intro to Sharpe and Information Ratios CHART OF THE WEEK SEPTEMBER 4, 2012 In this post-great Recession/Financial Crisis environment in which investment risk awareness has been heightened, return expectations

An Intro to Sharpe and Information Ratios CHART OF THE WEEK SEPTEMBER 4, 2012 In this post-great Recession/Financial Crisis environment in which investment risk awareness has been heightened, return expectations

The London Company Domestic Equity SMID Core

Product Type: Separate Account Manager Headquarters: Richmond, VA Total Staff: 24 Geography Focus: Domestic Year Founded: 1994 Investment Professionals: 5 Type of Portfolio: Equity Total AUM: $7,069 million

Product Type: Separate Account Manager Headquarters: Richmond, VA Total Staff: 24 Geography Focus: Domestic Year Founded: 1994 Investment Professionals: 5 Type of Portfolio: Equity Total AUM: $7,069 million

Investment manager research

Page 1 of 10 Investment manager research Due diligence and selection process Table of contents 2 Introduction 2 Disciplined search criteria 3 Comprehensive evaluation process 4 Firm and product 5 Investment

Page 1 of 10 Investment manager research Due diligence and selection process Table of contents 2 Introduction 2 Disciplined search criteria 3 Comprehensive evaluation process 4 Firm and product 5 Investment

in-depth Invesco Actively Managed Low Volatility Strategies The Case for

Invesco in-depth The Case for Actively Managed Low Volatility Strategies We believe that active LVPs offer the best opportunity to achieve a higher risk-adjusted return over the long term. Donna C. Wilson

Invesco in-depth The Case for Actively Managed Low Volatility Strategies We believe that active LVPs offer the best opportunity to achieve a higher risk-adjusted return over the long term. Donna C. Wilson

Structured Portfolios: Solving the Problems with Indexing

Structured Portfolios: Solving the Problems with Indexing May 27, 2014 by Larry Swedroe An overwhelming body of evidence demonstrates that the majority of investors would be better off by adopting indexed

Structured Portfolios: Solving the Problems with Indexing May 27, 2014 by Larry Swedroe An overwhelming body of evidence demonstrates that the majority of investors would be better off by adopting indexed

U.S. LOW VOLATILITY EQUITY Mandate Search

U.S. LOW VOLATILITY EQUITY Mandate Search Recommended: That State Street Global Advisors (SSgA) be appointed as a manager for a U.S. low volatility equity mandate. SSgA will be managing 10% of the Diversified

U.S. LOW VOLATILITY EQUITY Mandate Search Recommended: That State Street Global Advisors (SSgA) be appointed as a manager for a U.S. low volatility equity mandate. SSgA will be managing 10% of the Diversified

Capture the Knowledge Effect in your portfolio

Capture the Knowledge Effect in your portfolio Navigating a USD Bear Market with Equity Factors Knowledge Leaders Strategy Mid-Quarter Special Report February 27, 2018 Summary The US Dollar appears to

Capture the Knowledge Effect in your portfolio Navigating a USD Bear Market with Equity Factors Knowledge Leaders Strategy Mid-Quarter Special Report February 27, 2018 Summary The US Dollar appears to

Covered Call Investing and its Benefits in Today s Market Environment

ZIEGLER CAPITAL MANAGEMENT MARKET INSIGHT & RESEARCH Covered Call Investing and its Benefits in Today s Market Environment Covered Call investing has attracted a great deal of attention from investors

ZIEGLER CAPITAL MANAGEMENT MARKET INSIGHT & RESEARCH Covered Call Investing and its Benefits in Today s Market Environment Covered Call investing has attracted a great deal of attention from investors

JOINT PENSION BOARD Statement of Investment Beliefs

JOINT PENSION BOARD Statement of s 1. Good governance policies improve investment returns Governance is defined as the decision and oversight structure established for an investment fund (such as our Retirement

JOINT PENSION BOARD Statement of s 1. Good governance policies improve investment returns Governance is defined as the decision and oversight structure established for an investment fund (such as our Retirement

Crescat Portfolio Management, LLC Verification and Crescat Large Cap Composite Performance Examination Report. December 31, 2017

Crescat Portfolio Management, LLC Verification and Crescat Large Cap Composite Performance Examination Report December 31, 2017 Verification and Performance Examination Report Investors Crescat Portfolio

Crescat Portfolio Management, LLC Verification and Crescat Large Cap Composite Performance Examination Report December 31, 2017 Verification and Performance Examination Report Investors Crescat Portfolio

U.S. Dynamic Equity Fund Money Manager and Russell Investments Overview April 2017

Money Manager and Russell Investments Overview April 2017 RUSSELL INVESTMENTS APPROACH Russell Investments uses a multi-asset approach to investing, combining asset allocation, manager selection and dynamic

Money Manager and Russell Investments Overview April 2017 RUSSELL INVESTMENTS APPROACH Russell Investments uses a multi-asset approach to investing, combining asset allocation, manager selection and dynamic

Minimizing Timing Luck with Portfolio Tranching The Difference Between Hired and Fired

Minimizing Timing Luck with Portfolio Tranching The Difference Between Hired and Fired February 2015 Newfound Research LLC 425 Boylston Street 3 rd Floor Boston, MA 02116 www.thinknewfound.com info@thinknewfound.com

Minimizing Timing Luck with Portfolio Tranching The Difference Between Hired and Fired February 2015 Newfound Research LLC 425 Boylston Street 3 rd Floor Boston, MA 02116 www.thinknewfound.com info@thinknewfound.com

Russell U.S. Small Cap Investment Discipline Indexes: Performance and portfolio characteristics

By: Kyla Roberts, Research Analyst 1 NOVEMBER 2011 Russell U.S. Small Cap Investment Discipline Indexes: Performance and portfolio characteristics In September 2011, Russell launched the Russell U.S. Small

By: Kyla Roberts, Research Analyst 1 NOVEMBER 2011 Russell U.S. Small Cap Investment Discipline Indexes: Performance and portfolio characteristics In September 2011, Russell launched the Russell U.S. Small

FUNDAMENTALLY DRIVEN. Macroeconomics-Based Asset Allocation

FUNDAMENTALLY DRIVEN. Macroeconomics-Based Asset Allocation Firm Overview: General Investment Principles Equity prices tend to appreciate over longer periods Fundamental macroeconomic trends have an impact

FUNDAMENTALLY DRIVEN. Macroeconomics-Based Asset Allocation Firm Overview: General Investment Principles Equity prices tend to appreciate over longer periods Fundamental macroeconomic trends have an impact

Tower Square Investment Management LLC Strategic Plus Moderate

Product Type: Multi-Product Portfolio Headquarters: El Segundo, CA Total Staff: 15 Geography Focus: Global Year Founded: 2012 Investment Professionals: 12 Type of Portfolio: Balanced Total AUM: $1,422

Product Type: Multi-Product Portfolio Headquarters: El Segundo, CA Total Staff: 15 Geography Focus: Global Year Founded: 2012 Investment Professionals: 12 Type of Portfolio: Balanced Total AUM: $1,422

Optimal Portfolio Inputs: Various Methods

Optimal Portfolio Inputs: Various Methods Prepared by Kevin Pei for The Fund @ Sprott Abstract: In this document, I will model and back test our portfolio with various proposed models. It goes without

Optimal Portfolio Inputs: Various Methods Prepared by Kevin Pei for The Fund @ Sprott Abstract: In this document, I will model and back test our portfolio with various proposed models. It goes without

AlphaSolutions Sector Rotation Model

AlphaSolutions Sector Rotation Model An investment model based on trending and momentum strategies Portfolio Goals Primary: Seeks long term growth of capital by investing in highranked U.S. Equity Sectors

AlphaSolutions Sector Rotation Model An investment model based on trending and momentum strategies Portfolio Goals Primary: Seeks long term growth of capital by investing in highranked U.S. Equity Sectors

Smart Beta #

Smart Beta This information is provided for registered investment advisors and institutional investors and is not intended for public use. Dimensional Fund Advisors LP is an investment advisor registered

Smart Beta This information is provided for registered investment advisors and institutional investors and is not intended for public use. Dimensional Fund Advisors LP is an investment advisor registered

Structured Small Cap Equity

Quarterly Commentary Third Quarter 2018 Market Commentary During the third quarter, the U.S. domestic backdrop continued to be highly positive for small-cap equities. The economy continued to grow at a

Quarterly Commentary Third Quarter 2018 Market Commentary During the third quarter, the U.S. domestic backdrop continued to be highly positive for small-cap equities. The economy continued to grow at a

AlphaSolutions Momentum High Equity Model

AlphaSolutions Momentum High Equity Model An investment model based on trending and momentum strategies Portfolio Goals Primary: Seeks long term growth of capital by investing in highranked Global Equity

AlphaSolutions Momentum High Equity Model An investment model based on trending and momentum strategies Portfolio Goals Primary: Seeks long term growth of capital by investing in highranked Global Equity

Calamos Growth Fund (CVGRX)

") Calamos Growth Fund (CVGRX) Active Growth Investing for Over 20 Years 2Q 2015 The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic

Calamos Growth Fund (CVGRX) Active Growth Investing for Over 20 Years 2Q 2015 The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic

Market Insights. The Benefits of Integrating Fundamental and Quantitative Research to Deliver Outcome-Oriented Equity Solutions.

Market Insights The Benefits of Integrating Fundamental and Quantitative Research to Deliver Outcome-Oriented Equity Solutions Vincent Costa, CFA Head of Global Equities Peg DiOrio, CFA Head of Global

Market Insights The Benefits of Integrating Fundamental and Quantitative Research to Deliver Outcome-Oriented Equity Solutions Vincent Costa, CFA Head of Global Equities Peg DiOrio, CFA Head of Global

STRATEGY OVERVIEW EMERGING MARKETS LOW VOLATILITY ACTIVE EQUITY STRATEGY

STRATEGY OVERVIEW EMERGING MARKETS LOW VOLATILITY ACTIVE EQUITY STRATEGY A COMPELLING OPPORTUNITY For many years, the favourable demographics and high economic growth in emerging markets (EM) have caught

STRATEGY OVERVIEW EMERGING MARKETS LOW VOLATILITY ACTIVE EQUITY STRATEGY A COMPELLING OPPORTUNITY For many years, the favourable demographics and high economic growth in emerging markets (EM) have caught

Interpreting the Information Ratio

Interpreting the Information Ratio Cameron Clement, CFA 11/10/09 The Information Ratio is a widely used and powerful tool for evaluating manager skill. In this paper, we attempt to foster a better understanding

Interpreting the Information Ratio Cameron Clement, CFA 11/10/09 The Information Ratio is a widely used and powerful tool for evaluating manager skill. In this paper, we attempt to foster a better understanding

AlphaSolutions Reduced Volatility Bull-Bear

AlphaSolutions Reduced Volatility Bull-Bear An investment model based on trending strategies coupled with market analytics for downside risk control Portfolio Goals Primary: Seeks long term growth of capital

AlphaSolutions Reduced Volatility Bull-Bear An investment model based on trending strategies coupled with market analytics for downside risk control Portfolio Goals Primary: Seeks long term growth of capital

Where Vami 0 = 1000 and Where R N = Return for period N. Vami N = ( 1 + R N ) Vami N-1. Where R I = Return for period I. Average Return = ( S R I ) N

Vami N-1. Where R I = Return for period I. Average Return = ( S R I ) N") The following section provides a brief description of each statistic used in PerTrac and gives the formula used to calculate each. PerTrac computes annualized statistics based on monthly data, unless Quarterly

The following section provides a brief description of each statistic used in PerTrac and gives the formula used to calculate each. PerTrac computes annualized statistics based on monthly data, unless Quarterly

Translating Factors to International Markets

LEADERSHIP SERIES Translating Factors to International Markets Strategies that combine the potential diversification benefits of international exposure with the portfolio-enhancing benefits of factors

LEADERSHIP SERIES Translating Factors to International Markets Strategies that combine the potential diversification benefits of international exposure with the portfolio-enhancing benefits of factors

High trubeta TM Indices

High trubeta TM Indices Index Methodology November 2018 Version History No. Date Author Comments 1.0 1/31/2018 T. Barchetto Initial 1.1 11/1/2018 T. Barchetto Name change 2 Introduction Beta is widely

High trubeta TM Indices Index Methodology November 2018 Version History No. Date Author Comments 1.0 1/31/2018 T. Barchetto Initial 1.1 11/1/2018 T. Barchetto Name change 2 Introduction Beta is widely

It is well known that equity returns are

DING LIU is an SVP and senior quantitative analyst at AllianceBernstein in New York, NY. ding.liu@bernstein.com Pure Quintile Portfolios DING LIU It is well known that equity returns are driven to a large

DING LIU is an SVP and senior quantitative analyst at AllianceBernstein in New York, NY. ding.liu@bernstein.com Pure Quintile Portfolios DING LIU It is well known that equity returns are driven to a large

A Framework for Understanding Defensive Equity Investing

A Framework for Understanding Defensive Equity Investing Nick Alonso, CFA and Mark Barnes, Ph.D. December 2017 At a basketball game, you always hear the home crowd chanting 'DEFENSE! DEFENSE!' when the

A Framework for Understanding Defensive Equity Investing Nick Alonso, CFA and Mark Barnes, Ph.D. December 2017 At a basketball game, you always hear the home crowd chanting 'DEFENSE! DEFENSE!' when the

Share Buyback. Background

Share Buyback Ford Equity Research 11722 Sorrento Valley Road, Suite I San Diego, CA 92121 800.842.0207 (USA) 858.455.6316 Fax www.fordequity.com Background In 1995, Ford Equity Research documented the

Share Buyback Ford Equity Research 11722 Sorrento Valley Road, Suite I San Diego, CA 92121 800.842.0207 (USA) 858.455.6316 Fax www.fordequity.com Background In 1995, Ford Equity Research documented the

INSTITUTIONAL INVESTMENT & FIDUCIARY SERVICES: Investment Basics: Is Active Management Still Worth the Fees? By Joseph N. Stevens, CFA INTRODUCTION

INSTITUTIONAL INVESTMENT & FIDUCIARY SERVICES: Investment Basics: Is Active Management Still Worth the Fees? By Joseph N. Stevens, CFA INTRODUCTION As of December 31, 2014, more than 30% of all US Dollar-based

INSTITUTIONAL INVESTMENT & FIDUCIARY SERVICES: Investment Basics: Is Active Management Still Worth the Fees? By Joseph N. Stevens, CFA INTRODUCTION As of December 31, 2014, more than 30% of all US Dollar-based

US Mega Cap. Higher Returns, Lower Risk than the Market. The Case for Mega Cap Stocks

US Mega Cap Higher Returns, Lower Risk than the Market There are many ways in which investors can get exposure to the broad market, but, surprisingly, there are few ways in which investors can get pure

US Mega Cap Higher Returns, Lower Risk than the Market There are many ways in which investors can get exposure to the broad market, but, surprisingly, there are few ways in which investors can get pure

Fundamentally weighted index strategies: A primer on asset allocation in three core asset classes

strategies: A primer on asset allocation in three core asset classes 1 2 3 Key takeaways strategies can serve as a complement to traditional cap-weighted index strategies. Combining fundamentally weighted

strategies: A primer on asset allocation in three core asset classes 1 2 3 Key takeaways strategies can serve as a complement to traditional cap-weighted index strategies. Combining fundamentally weighted

Guide to Responsible Investing Strategies

2018 Guide to Responsible Investing Strategies CATHOLIC VALUES FOSSIL FREE ESG INTEGRATION Parametric Responsible Investing Strategies Parametric offers a suite of proprietary responsible investing strategies

2018 Guide to Responsible Investing Strategies CATHOLIC VALUES FOSSIL FREE ESG INTEGRATION Parametric Responsible Investing Strategies Parametric offers a suite of proprietary responsible investing strategies

The FTSE RAFI Index Series

The FTSE RAFI Index Series ARI POLYCHRONOPOULOS, CFA About the Author ARI POLYCHRONOPOULOS, CFA Vice President, Affiliate Relations Ari Polychronopoulos is a relationship manager/product specialist. In

The FTSE RAFI Index Series ARI POLYCHRONOPOULOS, CFA About the Author ARI POLYCHRONOPOULOS, CFA Vice President, Affiliate Relations Ari Polychronopoulos is a relationship manager/product specialist. In

HIGH DIVIDENDS: MYTH VS. REALITY A STUDY OF DIVIDEND YIELDS, RISK AND RETURNS

HIGH DIVIDENDS: MYTH VS. REALITY A STUDY OF DIVIDEND YIELDS, RISK AND RETURNS EXECUTIVE SUMMARY This paper examines the relationship between dividend yields, risk, and returns, through an exhaustive analysis

HIGH DIVIDENDS: MYTH VS. REALITY A STUDY OF DIVIDEND YIELDS, RISK AND RETURNS EXECUTIVE SUMMARY This paper examines the relationship between dividend yields, risk, and returns, through an exhaustive analysis

Portfolio Construction With Alternative Investments

Portfolio Construction With Alternative Investments Chicago QWAFAFEW Barry Feldman bfeldman@ibbotson.com August 22, 2002 Overview! Introduction! Skew and Kurtosis in Hedge Fund Returns! Intertemporal Correlations

Portfolio Construction With Alternative Investments Chicago QWAFAFEW Barry Feldman bfeldman@ibbotson.com August 22, 2002 Overview! Introduction! Skew and Kurtosis in Hedge Fund Returns! Intertemporal Correlations

9/1/ /1/1977 9/1/ /1/ /1/1963

CAPITAL IDEAS It Pays to Collect Dividends Executive Summary Dividend income makes up a significant portion of total return over long time periods. 18.0% 16.0% 14.0% 12.0% 10.0% Figure 1: Dividend Yield

CAPITAL IDEAS It Pays to Collect Dividends Executive Summary Dividend income makes up a significant portion of total return over long time periods. 18.0% 16.0% 14.0% 12.0% 10.0% Figure 1: Dividend Yield

The Equity Imperative

The Equity Imperative Factor-based Investment Strategies 2015 Northern Trust Corporation Can You Define, or Better Yet, Decipher? 1 Spectrum of Equity Investing Techniques Alpha Beta Traditional Active

The Equity Imperative Factor-based Investment Strategies 2015 Northern Trust Corporation Can You Define, or Better Yet, Decipher? 1 Spectrum of Equity Investing Techniques Alpha Beta Traditional Active

Getting Smart About Beta

Getting Smart About Beta December 1, 2015 by Sponsored Content from Invesco Due to its simplicity, market-cap weighting has long been a popular means of calculating the value of market indexes. But as

Getting Smart About Beta December 1, 2015 by Sponsored Content from Invesco Due to its simplicity, market-cap weighting has long been a popular means of calculating the value of market indexes. But as

Identifying a defensive strategy

In our previous paper Defensive equity: A defensive strategy to Canadian equity investing, we discussed the merits of employing a defensive mandate within the Canadian equity portfolio for some institutional

In our previous paper Defensive equity: A defensive strategy to Canadian equity investing, we discussed the merits of employing a defensive mandate within the Canadian equity portfolio for some institutional

Can Active Management Make a Comeback? September 2015

Can Active Management Make a Comeback? September 2015 Executive Summary Recent underperformance by active U.S. managers can be easily explained and, in our view, is only temporary FACTORS MAKING FOR A

Can Active Management Make a Comeback? September 2015 Executive Summary Recent underperformance by active U.S. managers can be easily explained and, in our view, is only temporary FACTORS MAKING FOR A

Risk Measures White Paper

Risk Measures White Paper Introduction The risk measures report shows the current risk of a portfolio using several industry standard valuation measures. Risk measures are only applicable to the Time-Weighted

Risk Measures White Paper Introduction The risk measures report shows the current risk of a portfolio using several industry standard valuation measures. Risk measures are only applicable to the Time-Weighted

Navigator International Equity/ADR

CCM-17-09-637 As of 9/30/2017 Navigator International Navigate Global Equities with a Disciplined, Research-Backed Approach to Security Selection With heightened volatility and increased correlations across

CCM-17-09-637 As of 9/30/2017 Navigator International Navigate Global Equities with a Disciplined, Research-Backed Approach to Security Selection With heightened volatility and increased correlations across

Calamos Phineus Long/Short Fund

Calamos Phineus Long/Short Fund Performance Update SEPTEMBER 18 FOR INVESTMENT PROFESSIONAL USE ONLY Why Calamos Phineus Long/Short Equity-Like Returns with Superior Risk Profile Over Full Market Cycle

Calamos Phineus Long/Short Fund Performance Update SEPTEMBER 18 FOR INVESTMENT PROFESSIONAL USE ONLY Why Calamos Phineus Long/Short Equity-Like Returns with Superior Risk Profile Over Full Market Cycle

Russell Funds Russell Tax-Managed International Equity Fund Money Manager and Russell Investments Overview September 2016

Money Manager and Russell Investments Overview September 2016 Russell Investments approach Russell Investments uses a multi-asset approach to investing, combining asset allocation, manager selection and

Money Manager and Russell Investments Overview September 2016 Russell Investments approach Russell Investments uses a multi-asset approach to investing, combining asset allocation, manager selection and

American Journal of Humanities & Islamic Studies Vol: 1 (1), Al-Huda University 1902 Baker Rd, Houston, TX 77094

, Al-Huda University 1902 Baker Rd, Houston, TX 77094") Investment Practices for Islamic Mutual Funds within the Saudi Arabian Capital Market Salman Ghani Al-Huda University 1902 Baker Rd, Houston, TX 77094 1 Abstract The burgeoning Islamic asset management

Investment Practices for Islamic Mutual Funds within the Saudi Arabian Capital Market Salman Ghani Al-Huda University 1902 Baker Rd, Houston, TX 77094 1 Abstract The burgeoning Islamic asset management

Research Factor Indexes and Factor Exposure Matching: Like-for-Like Comparisons

Research Factor Indexes and Factor Exposure Matching: Like-for-Like Comparisons October 218 ftserussell.com Contents 1 Introduction... 3 2 The Mathematics of Exposure Matching... 4 3 Selection and Equal

Research Factor Indexes and Factor Exposure Matching: Like-for-Like Comparisons October 218 ftserussell.com Contents 1 Introduction... 3 2 The Mathematics of Exposure Matching... 4 3 Selection and Equal

QUANTITATIVE MOMENTUM INDEXES (QM AND IQM INDEX)

") QUANTITATIVE MOMENTUM INDEXES (QM AND IQM INDEX) As Of Date: 5/3/2018 Wesley R. Gray, PhD T: +1.215.882.9983 F: +1.216.245.3686 ir@alphaarchitect.com 213 Foxcroft Road Broomall, PA 19008 Empower Investors

QUANTITATIVE MOMENTUM INDEXES (QM AND IQM INDEX) As Of Date: 5/3/2018 Wesley R. Gray, PhD T: +1.215.882.9983 F: +1.216.245.3686 ir@alphaarchitect.com 213 Foxcroft Road Broomall, PA 19008 Empower Investors

Do Mutual Fund Managers Outperform by Low- Balling their Benchmarks?

University at Albany, State University of New York Scholars Archive Financial Analyst Honors College 5-2013 Do Mutual Fund Managers Outperform by Low- Balling their Benchmarks? Matthew James Scala University

University at Albany, State University of New York Scholars Archive Financial Analyst Honors College 5-2013 Do Mutual Fund Managers Outperform by Low- Balling their Benchmarks? Matthew James Scala University

CEMP Volatility Weighted Indexes

CEMP Volatility Weighted Indexes Fundamental Criteria with Volatility Weighting in Index Construction By: Stephen M. Hammers, CIMA Chief Investment Officer/Co-Founder An Efficient Solution to Broad Market

CEMP Volatility Weighted Indexes Fundamental Criteria with Volatility Weighting in Index Construction By: Stephen M. Hammers, CIMA Chief Investment Officer/Co-Founder An Efficient Solution to Broad Market

The Case for Micro-Cap Equities. Originally Published January 2011

The Case for Micro-Cap Equities Originally Published January 011 MICRO-CAP EQUITIES PRESENT A COMPELLING INVESTMENT OPPORTUNITY FOR LONG-TERM INVESTORS In an increasingly efficient and competitive market,

The Case for Micro-Cap Equities Originally Published January 011 MICRO-CAP EQUITIES PRESENT A COMPELLING INVESTMENT OPPORTUNITY FOR LONG-TERM INVESTORS In an increasingly efficient and competitive market,

Bulls, bears and beyond Understanding investment performance and monitoring

FOR RETIREMENT Bulls, bears and beyond Understanding investment performance and monitoring Dan Weber, CFA, CMT, AIF Director of Investment Strategies Funds Management September 10, 2012 2012 Lincoln National

FOR RETIREMENT Bulls, bears and beyond Understanding investment performance and monitoring Dan Weber, CFA, CMT, AIF Director of Investment Strategies Funds Management September 10, 2012 2012 Lincoln National

NIFTY Multi-Factor Indices. Multi-factor index strategies provide diversified factor-exposure with varied risk-return profile

Multi-Factor Indices Multi-factor index strategies provide diversified factor-exposure with varied risk-return profile July 2017 Introduction Factor-based investing has gathered popularity amongst the

Multi-Factor Indices Multi-factor index strategies provide diversified factor-exposure with varied risk-return profile July 2017 Introduction Factor-based investing has gathered popularity amongst the

Turner Investments 1205 Westlakes Drive - Suite 100 Berwyn, Pennsylvania 19312

Turner Investments 1205 Westlakes Drive - Suite 100 Berwyn, Pennsylvania 19312 PRODUCT OVERVIEW The investment objective of the Turner Select portfolio is to outperform the Russell 1000 Growth Index over

Turner Investments 1205 Westlakes Drive - Suite 100 Berwyn, Pennsylvania 19312 PRODUCT OVERVIEW The investment objective of the Turner Select portfolio is to outperform the Russell 1000 Growth Index over

Investment Insight. Are Risk Parity Managers Risk Parity (Continued) Summary Results of the Style Analysis

Summary Results of the Style Analysis") Investment Insight Are Risk Parity Managers Risk Parity (Continued) Edward Qian, PhD, CFA PanAgora Asset Management October 2013 In the November 2012 Investment Insight 1, I presented a style analysis

Investment Insight Are Risk Parity Managers Risk Parity (Continued) Edward Qian, PhD, CFA PanAgora Asset Management October 2013 In the November 2012 Investment Insight 1, I presented a style analysis