ASCOTT RESIDENCE TRUST (a unit trust constituted on 19 January 2006 under the laws of the Republic of Singapore)

|

|

|

- Myrtle McLaughlin

- 5 years ago

- Views:

Transcription

1 Circular dated 30 January 2007 FOR INFORMATION ONLY THIS CIRCULAR IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION. Singapore Exchange Securities Trading Limited (the SGX-ST ) takes no responsibility for the accuracy of any statements or opinions made, or reports contained, in this Circular. If you are in any doubt as to the action you should take, you should consult your stockbroker, bank manager, solicitor, accountant or other professional advisor immediately. Approval in-principle has been obtained from the SGX-ST for the listing of and quotation for the new units (the New Units ) in Ascott Residence Trust ( ART ) to be issued for the purpose of the Equity Fund Raising (as defined herein) on the Main Board of the SGX-ST. The SGX-ST s approval in-principle is not an indication of the merits of ART, the Units or the Equity Fund Raising. If you have sold or transferred all your units in ART (the Units ), you should immediately forward this Circular, together with the Notice of Extraordinary General Meeting and the accompanying Proxy Form in this Circular, to the purchaser or transferee or to the bank, stockbroker or other agent through whom the sale or transfer was effected for onward transmission to the purchaser or transferee. This Circular is not for distribution, directly or indirectly, in or into the United States. It is not an offer of securities for sale into the United States. The Units may not be offered or sold in the United States or to, or for the account or benefit of, U.S. persons (as such term is defined in Regulation S under the Securities Act of 1933, as amended) unless they are registered or exempt from registration. There will be no public offer of securities in the United States. ASCOTT RESIDENCE TRUST (a unit trust constituted on 19 January 2006 under the laws of the Republic of Singapore) MANAGED BY ASCOTT RESIDENCE TRUST MANAGEMENT LIMITED CIRCULAR TO UNITHOLDERS IN RELATION TO: (1) THE PROPOSED ISSUE OF NEW UNITS UNDER THE EQUITY FUND RAISING AND A CONSEQUENT ADJUSTMENT TO THE DISTRIBUTION PERIOD OF ART; (2) THE PROPOSED PLACEMENT OF NEW UNITS TO THE ASCOTT GROUP LIMITED, A CONTROLLING UNITHOLDER, AND ITS SUBSIDIARIES AS PART OF THE EQUITY FUND RAISING; (3) THE PROPOSED GENERAL MANDATE FOR THE ISSUE OF NEW UNITS; AND (4) THE PROPOSED SUPPLEMENT TO THE TRUST DEED RELATING TO THE REMUNERATION OF THE TRUSTEE. Joint Financial Advisors Joint Lead Managers, Bookrunners and Underwriters for the Equity Fund Raising IMPORTANT DATES AND TIMES FOR UNITHOLDERS Last date and time for lodgment of Proxy Forms : 21 February 2007 at 3:00 p.m. Date and time of Extraordinary General Meeting : 23 February 2007 at 3:00 p.m. Place of Extraordinary General Meeting : STI Auditorium at Level 9, 168 Robinson Road, Capital Tower, Singapore

2 TABLE OF CONTENTS Page CORPORATE INFORMATION... ii SUMMARY... 1 INDICATIVE TIMETABLE LETTER TO UNITHOLDERS 1. Summary of Approvals Required The Target Acquisitions and the Rationale for the Target Acquisitions Details of the Equity Fund Raising Details of the Target Acquisitions The Proposed Placement to the Ascott Group The Proposed General Mandate to Issue Units The Proposed Supplement to the Trust Deed Relating to the Remuneration of the Trustee Recommendations Extraordinary General Meeting Prohibition on Voting Action to be Taken by Unitholders Directors Responsibility Statements Consents Documents Available for Inspection Unitholders Helpline IMPORTANT NOTICE GLOSSARY APPENDICES Appendix A Information on the Target Properties and the Existing Properties.... A-1 Appendix B Tax Considerations... B-1 Appendix C Proposed Ownership Structure of the Target Properties... C-1 Appendix D Profit Forecast... D-1 Appendix E Independent Accountants Report on the Profit Forecast... E-1 Appendix F Significant Accounting Policies... F-1 Appendix G Summary Valuation Certificates for the Target Properties... G-1 Appendix H Serviced Residences Market Overview Report... H-1 Appendix I Proposed Supplement to the Trust Deed Relating to the Remuneration of the Trustee.... I-1 NOTICE OF EXTRAORDINARY GENERAL MEETING... J-1 PROXY FORM i

3 CORPORATE INFORMATION Directors of Ascott Residence Trust Management Limited (the manager of ART (the Manager )) Registered Office of Ascott Residence Trust Management Limited Trustee of ART (the Trustee ) Joint Financial Advisors Mr Lim Jit Poh (Non-Executive Chairman) Mr Liew Mun Leong (Non-Executive Deputy Chairman) Mr Ong Ah Luan Cameron (Non-Executive Director) Mr S. Chandra Das (Non-Executive Director) Mr Paul Ma Kah Woh (Independent Director) Mr David Schaefer (Independent Director) Mr Ku Moon Lun (Independent Director) 8 Shenton Way #13-01 Temasek Tower Singapore DBS Trustee Ltd 6 Shenton Way #36-02 DBS Building Tower One Singapore CapitaLand Financial Services Limited 39 Robinson Road #18-01 Robinson Point Singapore J.P. Morgan (S.E.A.) Limited 168 Robinson Road 17th Floor Capital Tower Singapore Joint Lead Managers, Bookrunners and Underwriters for the Equity Fund Raising DBS Bank Ltd 6 Shenton Way DBS Building Tower One Singapore J.P. Morgan (S.E.A.) Limited 168 Robinson Road 17th Floor Capital Tower Singapore Legal Advisor to the Manager and the Trustee for the Equity Fund Raising Legal Advisor to the Joint Financial Advisors and the Joint Lead Managers, Bookrunners and Underwriters for the Equity Fund Raising Unit Registrar and Unit Transfer Office WongPartnership One George Street #20-01 Singapore Allen & Gledhill One Marina Boulevard #28-00 Singapore Lim Associates (Pte) Ltd 3 Church Street, #08-01 Samsung Hub Singapore ii

4 Independent Accountants Independent Singapore Tax Advisor Independent Valuers KPMG 16 Raffles Quay #22-00 Hong Leong Building Singapore Ernst & Young One Raffles Quay North Tower, Level 18 Singapore For the Australia Target Property CB Richard Ellis Australia Level 32, Rialto North Tower 525 Collins Street Melbourne VIC 3000 Australia For the Japan Target Properties Jones Lang LaSalle Property Consultants Pte Ltd 9 Raffles Place #38-01 Republic Plaza Singapore For the Philippines Target Property HVS International 79 Anson Road #11-05 Singapore For the Vietnam Target Property HVS International 79 Anson Road #11-05 Singapore CB Richard Ellis Vietnam Unit 1301, Me Linh Point Tower 2 Ngo Duc Ke St., District 1 Ho Chi Minh City, Vietnam Independent Property Consultant Jones Lang LaSalle Property Consultants Pte Ltd 9 Raffles Place #38-01 Republic Plaza Singapore iii

5 This page has been intentionally left blank.

6 SUMMARY The following summary is qualified in its entirety by, and should be read in conjunction with, the full text of this Circular. Meanings of defined terms may be found in the Glossary on pages 50 to 58 of this Circular. Any discrepancies in the tables included herein between the listed amounts and totals thereof are due to rounding. ART S GEOGRAPHICALLY DIVERSIFIED PAN-ASIAN PORTFOLIO OF EXISTING PROPERTIES AND TARGET ACQUISITIONS Ascott Residence Trust ( ART ) is the first Pan-Asian serviced residence real estate investment trust, and was established with the objective of investing primarily in real estate and real estate-related assets which are income-producing and which are used or predominantly used as serviced residences or rental housing properties in the Pan-Asian Region (as defined herein). Comprising an initial asset portfolio of 12 strategically located properties with 2,068 Apartment Units in five countries in the Pan-Asian Region, ART was listed on the SGX-ST with a portfolio size of about S$855.8 million. As at the Latest Practicable Date, ART s portfolio size has expanded to S$961.4 million, comprising 15 properties with 2,476 Apartment Units across six countries 1. Completion of the Target Acquisitions (as defined herein) (details of which are set out below) will increase ART s portfolio to 18 properties, comprising 2,904 Apartment Units across seven countries. The following map shows the locations of ART s portfolio of Existing Properties (as defined herein) and Target Properties (as defined herein). 1 Including 26.8 percent effective interest in the Vietnam Target Property acquired in January The number of Apartment Units as at the Latest Practicable Date includes 172 Apartment Units in Somerset Olympic Tower Property, Tianjin, 64 Apartment Units in Somerset Roppongi, Tokyo and 172 Apartment Units in the Vietnam Target Property. 1

To be re-branded Somerset Gordon Heights,")

7 Notes: (1) To be re-branded Ascott Makati. (2) To be re-branded Somerset Gordon Heights, Melbourne. 2

8 OVERVIEW OF THE TARGET ACQUISITIONS The Manager is continually identifying suitable properties for acquisition by ART to provide stable and growing distributions to unitholders of ART (the Unitholders ). In executing its acquisition strategy, the Manager seeks to secure yield-accretive acquisitions that meet its investment criteria and leverage on the increasing popularity of serviced residences and robust economic performance in the Pan-Asian Region. The Manager has identified the following properties, namely: Shoan Heights Serviced Apartment, Melbourne (to be re-branded Somerset Gordon Heights, Melbourne upon completion), Australia (the Australia Target Property ); Somerset Azabu East, Tokyo, Japan; Somerset Roppongi, Tokyo, Japan (together with Somerset Azabu East, Tokyo, the Japan Target Properties ); Oakwood Premier Ayala Center (to be re-branded Ascott Makati upon completion) the Philippines (the Philippines Target Property ); and Somerset Chancellor Court, Ho Chi Minh City, Vietnam (the Vietnam Target Property ), (collectively, the Target Properties ) as being suitable for acquisition by ART. The proposed acquisitions are percent effective interest in the Australia Target Property (the Australia Target Acquisition ), percent effective interest in Somerset Azabu East, Tokyo, the remaining 60.0 percent beneficiary interest in Somerset Roppongi, Tokyo (together with the acquisition of percent effective interest in Somerset Azabu East, Tokyo, the Japan Target Acquisitions ), percent effective interest in the Philippines Target Property (the Philippines Target Acquisition ) and 40.2 percent effective interest in the Vietnam Target Property (together with 26.8 percent effective interest acquired in January 2007, the Vietnam Target Acquisition, and together with the Australia Target Acquisition, Japan Target Acquisitions and Philippines Target Acquisition, the Target Acquisitions ). The Target Acquisitions, save for the acquisition of the 26.8 percent effective interest in the Vietnam Target Property which was completed in January 2007, are proposed to be carried out at an aggregate purchase consideration of approximately S$218.6 million. The Manager intends to raise gross proceeds of approximately S$199.0 million from the Equity Fund Raising and additional borrowings of up to S$47.9 million for the following purposes: (i) (ii) (iii) finance the Target Acquisitions and associated costs; re-finance the loan drawn for the acquisition of the 26.8 percent effective interest in the Vietnam Target Property which was completed in January 2007; and balance of the proceeds to be utilised for general corporate and working capital purposes. Each of the Target Acquisitions was or will be completed at or below its appraised value. 3

9 The following table shows certain key information relating to the Target Properties: Property Name Address Number of Apartment Units Net Lettable Area (sq m) Appraised Value (1) (S$ million) Purchase Consideration (S$ million) Title Australia Shoan Heights Serviced Apartment, Melbourne (to be re-branded Somerset Gordon Heights, Melbourne) Japan Somerset Azabu East, Tokyo Little Bourke Street, Melbourne, Victoria 3000, Australia No , Higashi- Azabu, Minato-ku, Tokyo, Japan , Freehold estate 79 4, Freehold estate Somerset Roppongi, Tokyo (2) No , Roppongi, Minato-ku, Tokyo, Japan , (3) (for 60.0 percent beneficiary interest) Freehold estate The Philippines Oakwood Premier Ayala Center (to be re-branded Ascott Makati) Vietnam Glorietta 4, Ayala Center, Makati City, Manila, the Philippines , Contract of Lease of 48 years expiring on 6 January 2044, with an option to renew for another 25 years upon the mutual agreement of the parties (4) Somerset Chancellor Court, Ho Chi Minh City (5) Nguyen Thi Minh Khai Street, District 1, Ho Chi Minh City, Vietnam , (3) (for 40.2 percent effective interest) Leasehold estate of 48 years expiring on 4 October 2041 Total , Notes: (1) Refers to percent of the Target Property. (2) ART currently holds 40.0 percent beneficiary interest in Somerset Roppongi, Tokyo. ART will acquire the remaining 60.0 percent beneficiary interest in Somerset Roppongi, Tokyo. (3) After adjustments for consolidated net assets and liabilities. (4) This refers to an amended Contract of Lease to be entered into upon completion of the Philippines Target Acquisition. (5) In January 2007, ART acquired 40.0 percent of the shares in EATC(S) from unrelated parties, which represents 26.8 percent effective interest in the Vietnam Target Property. ART is proposing to acquire 60.0 percent of the remaining shares in EATC(S), which represents 40.2 percent effective interest in the Vietnam Target Property. 4

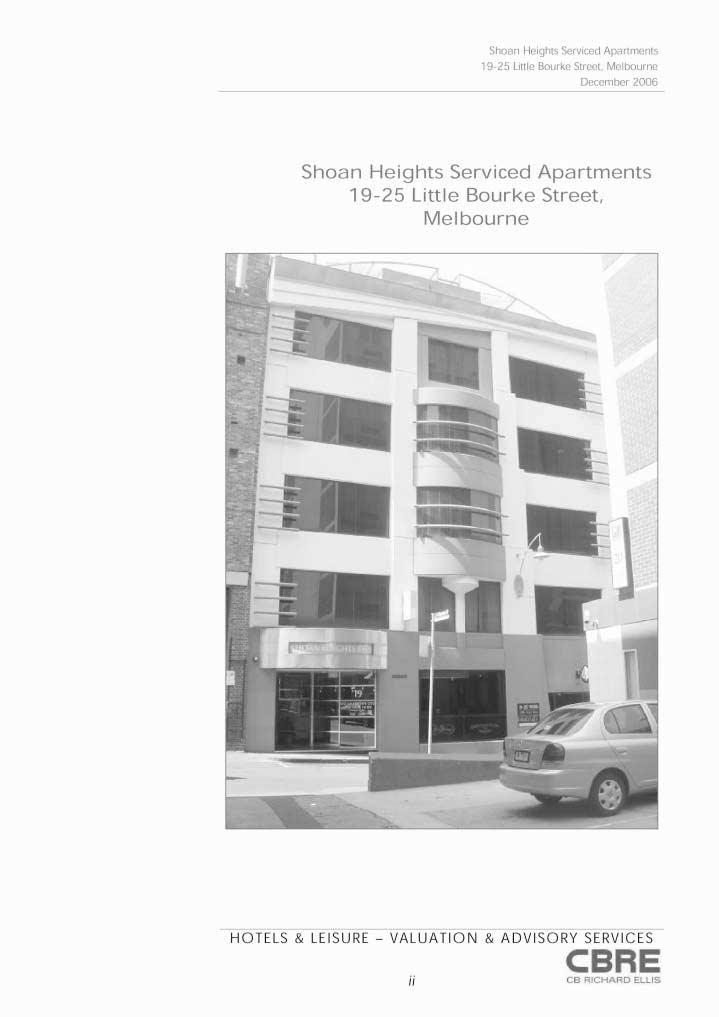

10 The details of the Target Properties are set out below: Target Properties The Australia Target Property ART is acquiring a freehold property in Australia, namely, Shoan Heights Serviced Apartment, Melbourne (to be re-branded Somerset Gordon Heights, Melbourne), at Little Bourke Street, Melbourne, Victoria 3000, Australia from three unrelated third party individuals, namely Tiow Hoe Goh, Kooi Lean Goh and Chew Por Chan. Located in Melbourne s central business and financial district, the Australia Target Property is a five-storey serviced residence featuring 43 fully-furnished Apartment Units ranging from studios, one and two-bedroom apartments to two-bedroom penthouses. Its facilities include a restaurant, advanced security system, daily housekeeping service, valet, dry-cleaning and free laundry facilities. ART has formed a wholly owned subsidiary called Somerset Gordon Heights (S) Pte. Ltd. ( SGHPL ), a company incorporated in Singapore, which owns percent interest in both an Australian unit trust, Somerset Gordon Heights (Melbourne) Unit Trust (the Unit Trust ), and an Australian trustee company, Somerset Gordon Heights (Melbourne) Pty. Ltd. (the Trustee Co ). The Unit Trust will own percent beneficiary interest in the Australia Target Property and the Trustee Co will own percent legal interest in the Australia Target Property. The chart below shows the proposed ownership structure of the Australia Target Property at completion: ART 100% Singapore Australia 100% Somerset Gordon Heights (Melbourne) Unit Trust Somerset Gordon Heights (S) Pte. Ltd. 100% Somerset Gordon Heights (Melbourne) Pty. Ltd. (Trustee of Somerset Gordon Heights (Melbourne) Unit Trust) 100% legal interest 100% beneficiary interest Shoan Heights Serviced Apartment, Melbourne (to be re-branded Somerset Gordon Heights, Melbourne) 5

11 As part of ART s strategy to actively manage and market its properties, the Manager intends to re-brand the Australia Target Property as Somerset Gordon Heights, Melbourne after completion of the Australia Target Acquisition. The Australia Target Property will be managed by Ascott International Management (Australia) Pty Ltd, an indirect wholly owned subsidiary of The Ascott Group Limited ( TAG ). The purchase consideration for the Australia Target Property is A$11.6 million (or approximately S$13.9 million 2 ). The Australia Target Property was appraised by an independent valuer, CB Richard Ellis Australia, and was valued at A$11.6 million (or approximately S$13.9 million 2 ) as at 5 December (Details on the Australia Target Property can be found in Appendix A of this Circular.) The Japan Target Properties ART is proposing to acquire two freehold properties in Japan, namely, (i) Somerset Azabu East, Tokyo at No , Higashi-Azabu, Minato-ku, Tokyo, Japan and (ii) Somerset Roppongi, Tokyo at No , Roppongi, Minato-ku, Tokyo, Japan Somerset Azabu East, Tokyo The 14-storey Somerset Azabu East, Tokyo is located in the upscale Azabu district of Minato-ku in Tokyo s central business district, and is within walking distance to the Akabanebashi, Shibakoen and Kamiyacho subway stations. Comprising 79 fully-furnished Apartment Units ranging from studios to one-bedroom apartments, Somerset Azabu East, Tokyo offers facilities such as an indoor swimming pool, fitness centre, roof-top barbeque terrace, 24-hour reception and security, residents lounge, dry-cleaning and laundry services and car park. ART will acquire Somerset Azabu East, Tokyo from Mitsubishi Estate Co., Ltd. To effect the acquisition, ART has set up two wholly owned companies incorporated in Singapore, namely Somerset Azabu East Investment (S) Pte. Ltd. and Somerset Azabu East (S) Pte. Ltd.. Somerset Azabu East Investment (S) Pte. Ltd. will register a new Japanese branch in Tokyo, which will in turn own 51.0 percent of the preferred shares in a new tokutei mokuteki kaisha 3, Somerset Azabu East TMK, to be set up under the Japan Law Regarding Securitization of Assets (No. 105 of 1998, as amended) ( SAE TMK ). Somerset Azabu East (S) Pte. Ltd. will directly own 49.0 percent of the preferred shares and percent of the common shares in SAE TMK. SAE TMK will own percent effective interest in Somerset Azabu East, Tokyo. As a result, ART will, through SAE TMK, own percent effective interest in Somerset Azabu East, Tokyo. Post-completion, Somerset Azabu East, Tokyo will continue to be managed by Ascott International Management Japan Company Limited which is 60.0 percent owned by TAG and 40.0 percent owned by Mitsubishi Estate Co., Ltd. 2 3 Based on an exchange rate of A$1.00 to S$1.20. A special purpose vehicle incorporated under the Japan Law Regarding Securitization of Assets (No. 105 of 1998, as amended). 6

12 The chart below shows the proposed ownership structure of Somerset Azabu East, Tokyo at completion: ART 100% 100% Somerset Azabu East Investment (S) Pte. Ltd. Somerset Azabu East (S) Pte. Ltd. 100% Singapore Japan Somerset Azabu East Investment (S) Pte. Ltd. (Japanese branch) (to be set up) 51% preferred shares 49% preferred shares and 100% common shares Somerset Azabu East TMK (to be set up) 100% Somerset Azabu East, Tokyo Somerset Roppongi, Tokyo Located in the bustling Roppongi district in the heart of Minato-Ku, in the centre business district of Tokyo, Somerset Roppongi, Tokyo is a 13-storey building with one basement level. The property comprises 64 fully-furnished Apartment Units ranging from studios, one-bedroom apartments to two-bedroom apartments, and features facilities such as a fitness centre, residents lounge, 24-hour reception and security, dry-cleaning and laundry services, 24-hour convenience store, café and car park. ART, through its wholly owned subsidiary, Somerset Roppongi (Japan) Pte. Ltd. ( SRJPL ), currently holds 40.0 percent beneficiary interest in Somerset Roppongi, Tokyo through its ownership of 40.0 percent of the preferred shares and 25.0 percent of the common shares in MEC Roppongi Tokutei Mokuteki Kaisha, a tokutei mokuteki kaisha incorporated under the Japan Law Regarding Securitization of Assets (No. 105 of 1998, as amended) ( MEC TMK to be renamed as Somerset Roppongi TMK ). 7

13 ART will acquire the remaining 60.0 percent beneficiary interest in Somerset Roppongi, Tokyo from Mitsubishi Estate Co., Ltd and MEC Roppongi Funding Corporation. To effect the acquisition, ART has set up a wholly owned company incorporated in Singapore named Somerset Roppongi (S) Pte. Ltd.. Somerset Roppongi (S) Pte. Ltd. will register a new Japanese branch to be set up in Tokyo which will own 60.0 percent of the preferred shares in MEC TMK (to be renamed as Somerset Roppongi TMK ). The remaining 75.0 percent of the common shares in Somerset Roppongi TMK will be acquired by SRJPL. Post-completion, Somerset Roppongi TMK s trust arrangement in Japan will be terminated and Somerset Roppongi TMK will be the registered owner of Somerset Roppongi, Tokyo. As a result, ART will own percent effective interest in the property via Somerset Roppongi TMK. The property will continue to be managed by Ascott International Management Japan Company Limited which is 60.0 percent owned by TAG and 40.0 percent owned by Mitsubishi Estate Co., Ltd. The chart below shows the proposed ownership structure of Somerset Roppongi, Tokyo at completion: ART 100% 100% Somerset Roppongi (S) Pte. Ltd. Somerset Roppongi (Japan) Pte. Ltd. 100% Singapore Japan Somerset Roppongi (S) Pte. Ltd. (Japanese branch) (to be set up) 60% preferred shares 40% preferred shares and 100% common shares MEC Roppongi TMK (to be renamed Somerset Roppongi TMK) 100% Somerset Roppongi, Tokyo 8

14 The purchase consideration for the percent effective interest in Somerset Azabu East, Tokyo is 5.7 billion (or approximately S$79.8 million 4 ) and the purchase consideration for the 60.0 percent beneficiary interest in Somerset Roppongi, Tokyo is 1.2 billion (or approximately S$17.0 million 4 ) after adjustment for consolidated net assets and liabilities. The Japan Target Properties were appraised by an independent valuer, Jones Lang LaSalle Property Consultants Pte Ltd. Somerset Azabu East, Tokyo was valued at 5.7 billion (or approximately S$79.8 million 4 ) and Somerset Roppongi, Tokyo was valued at 4.3 billion (or approximately S$60.2 million 4 ), as at 3 January (Details on the Japan Target Properties can be found in Appendix A of this Circular.) The Philippines Target Property ART is acquiring a property in the Philippines, namely, Oakwood Premier Ayala Center (to be re-branded Ascott Makati), which is located at Glorietta 4, Ayala Center, Makati City, Manila, the Philippines. The Philippines Target Property consists of two serviced apartment towers of 21 floors with 306 fully-furnished Apartment Units, first floor access lobby, fitness centre and restaurant, serviced offices, meeting rooms, 256 car park lots, gymnasium, tennis courts, business centre, swimming pool and laundry room. The two serviced apartment towers are linked together by a four-level podium retail mall erected over three basement levels of car park lots. ART is acquiring percent interest in the Philippines Target Property through the acquisition of percent of the issued shares in Makati Property Ventures Inc. ( MPVI ) from Ayala Hotels Inc. and Ocmador Philippines, B.V. ART has set up a Singapore special purpose vehicle, Ascott Manila Pte. Ltd., for the purpose of owning MPVI through another holding company to be set up in the Philippines, which will be named Ascott Makati, Inc.. MPVI, a special purpose vehicle incorporated in the Philippines with limited liability, has entered into a contract of lease with Ayala Land Inc. (the Contract of Lease ), the registered and legal owner of the land on which the Philippines Target Property sits. Upon completion of the Philippines Target Acquisition, MPVI and Ayala Land Inc. will enter into an amended Contract of Lease which will expire on 6 January Upon mutual agreement of both parties, the term of the Contract of Lease may be renewed for another 25 years. 4 Based on an exchange rate of 1 to S$

15 The chart below shows the proposed ownership structure of the Philippines Target Property at completion: ART 100% Ascott Manila Pte. Ltd. Singapore The Phillippines 100% Ascott Makati, Inc. 100% Makati Property Ventures Inc. Contract of Lease Ayala Land Inc. 100% Ascott Makati The purchase consideration for the Philippines Target Acquisition is PHP 2.7 billion (or approximately S$84.8 million 5 ), comprising the entire issued shares of MPVI of PHP 1.66 billion (or approximately S$52.1 million 5 ) and the assignment of shareholder loans of PHP 1.04 billion (or approximately S$32.7 million 5 ) (subject to the price adjustments for the net liabilities of MPVI as at completion of the Philippines Target Acquisition). The Philippines Target Property was appraised by an independent valuer, HVS International, and was valued at PHP 2.8 billion (or approximately S$87.9 million 5 ) as at 1 November The Philippines Target Property will be managed by Scotts Philippines Inc., a wholly owned subsidiary of TAG. Scotts Philippines Inc. will be appointed on completion of the Philippines Target Acquisition. (Details on the Philippines Target Property can be found in Appendix A of this Circular.) The Vietnam Target Property ART is acquiring a property in Vietnam, namely, Somerset Chancellor Court, Ho Chi Minh City at Nguyen Thi Minh Khai Street, District 1, Ho Chi Minh City, Vietnam. The Vietnam Target Property is a leasehold estate with a leasehold period of 48 years expiring on 4 October The Vietnam Target Property is strategically located in the business, diplomatic and 5 Based on an exchange rate of PHP 1 to S$

16 shopping district (District 1) in Ho Chi Minh City and comprises 172 fully-furnished Apartment Units ranging from studios to three-bedroom apartments. The property offers guests facilities such as a business centre, swimming pool and steam room, fully-equipped gymnasium, hair and beauty salon, 24-hour reception and security, and a residents lounge with a library. The Vietnam Target Property is owned by Saigon Office and Serviced Apartment Company Limited, a 67.0 percent subsidiary of East Australia Trading Company (S) Pte Ltd ( EATC(S) ). The remaining 33.0 percent interest in Saigon Office and Serviced Apartment Company Limited is owned by Ben Thanh Corporation, a state-owned enterprise in Vietnam. In January 2007, ART acquired 40.0 percent of the shares in EATC(S) from unrelated parties, which represents 26.8 percent effective interest in the Vietnam Target Property. ART is acquiring the remaining 60.0 percent of the shares in EATC(S) which represents 40.2 percent effective interest in the Vietnam Target Property for US$14.4 million (or approximately S$23.1 million 6 ). The vendor of the remaining 60.0 percent of the shares in EATC(S) is The Ascott Holdings Limited (a wholly owned subsidiary of TAG). For the purpose of the acquisition of the remaining 60.0 percent of the shares in EATC(S), The Ascott Holdings Limited is considered to be an interested party under the Property Funds Guidelines (as defined herein) and an interested person under the Listing Manual for the SGX-ST (the Listing Manual ), and the acquisition of the remaining 60.0 percent of the shares in EATC(S) is accordingly an interested party transaction under the Property Funds Guidelines and an interested person transaction under Chapter 9 of the Listing Manual. Paragraph 5 of the Property Funds Guidelines requires, inter alia, approval of Unitholders for an interested party transaction whose value exceeds 5.0 percent of ART s latest audited net asset value (the NAV ). Chapter 9 of the Listing Manual imposes a similar requirement for an interested person transaction if the value thereof exceeds 5.0 percent of ART s latest audited net tangible asset (the NTA ). As at the Latest Practicable Date, ART has not prepared any audited financial statements. 5.0 percent of ART s latest unaudited NAV and NTA as at 31 December 2006 is approximately S$33.1 million. Accordingly, the purchase consideration for the remaining 60.0 percent of the shares in EATC(S) of S$23.1 million does not exceed 5.0 percent of ART s latest unaudited NTA or NAV. In view of the foregoing, Unitholders approval for the abovementioned acquisition is not required. The Audit Committee of the Manager has reviewed and approved the Vietnam Target Acquisition. Upon completion of the acquisition of the remaining 60.0 percent of the shares in EATC(S), ART will own percent of the shares in EATC(S) which represents 67.0 percent effective interest in the Vietnam Target Property. 6 Based on an exchange rate of US$1.00 to S$

17 The chart below shows the proposed ownership structure of the Vietnam Target Property at completion: ART 100% Singapore East Australia Trading Company (S) Pte Ltd Vietnam 67% Saigon Office and Serviced Apartment Company Limited (Joint Venture Company) 100% 33% Ben Thanh Corporation (Local Partner) Somerset Chancellor Court, Ho Chi Minh City Pursuant to Paragraph 5 of the Property Funds Guidelines, two independent valuations of real estate assets which are acquired from an interested party must be made, one of which must be commissioned independently by the Trustee. The Vietnam Target Property was appraised by two independent valuers and was valued at US$45.0 million (or approximately S$72.0 million 6 ) by HVS International as at 1 December 2006 and US$45.0 million (or approximately S$72.0 million 6 ) by CB Richard Ellis Vietnam as at 31 December 2006, respectively. The Manager intends to utilise the proceeds from the Equity Fund Raising to fund the acquisition of the remaining 60.0 percent of the shares in EATC(S) which represents 40.2 percent effective interest in the Vietnam Target Property as well as to re-finance the loan drawn for the acquisition of the 40.0 percent of the shares in EATC(S) which represents 26.8 percent effective interest in the Vietnam Target Property, which was completed in January The property has been managed by Ascott International Management (2001) Pte Ltd (a wholly owned subsidiary of TAG) since 1 November The management contract has since been extended for another 10 years from 1 September (Details about the Vietnam Target Property can be found in Appendix A of this Circular.) 12

18 Benefits of the Target Acquisitions to Unitholders ART s acquisition growth strategy is underpinned by its key financial objective to provide Unitholders with a competitive rate of return on their investment by offering regular, stable and growing distributions and NAV per Unit. In this regard, the Manager adopts a rigorous and disciplined investment approach when evaluating potential acquisitions to enhance returns to Unitholders through increasing distributions, growing ART s portfolio size and enhancing diversification of ART. The Target Acquisitions are in line with the Manager s key objectives to deliver stable and growing distributions to Unitholders through yield accretive acquisitions and active management of assets. They are expected to be well-positioned to capture the growing demand for serviced residences in the Pan-Asian Region. Accordingly, the Manager believes that the Target Acquisitions will bring the following benefits to Unitholders: (i) Improved earnings and distribution per unit ( DPU ) The Manager believes that Unitholders will enjoy a higher DPU due to the yield accretive nature of the Target Acquisitions. The Manager expects REVPAU for the Enlarged Portfolio to be S$124 for the Forecast Period 2007, compared to S$121 for the Existing Properties in the same period. Average Daily Rates for the Enlarged Portfolio is expected to be S$146 for the Forecast Period 2007, which is higher than the Average Daily Rates of the Existing Properties of S$142. Average occupancy rates for the Existing Properties and for the Enlarged Portfolio are expected to be around 85 percent for the Forecast Period Assuming an Issue Price of S$1.70 per New Unit and that million New Units are issued under the Equity Fund Raising, ART s annualised forecast DPU for the Forecast Period 2007 upon completion of the Target Acquisitions and the Equity Fund Raising is approximately 7.14 cents, representing a distribution yield of approximately 4.2 percent. This represents a DPU accretion of approximately 9.3 percent over the forecast DPU of 6.53 cents based on the Existing Properties for the same period. The Target Acquisitions will offer DPU accretion Annualised DPU for the Forecast Period cents 6.53 cents Accretion +9.3% Existing Properties Enlarged Portfolio Note: Assuming the Target Acquisitions were completed on 1 April 2007 and an illustrative Issue Price of S$1.70 per New Unit under the Equity Fund Raising. Chart is not drawn to scale. The Target Acquisitions also provide opportunities for asset enhancements such as selective renovation and potential reconfiguration of rooms to increase lettable space and provide value-added facilities to guests to potentially improve earnings further. 13

19 (ii) Increased portfolio scale and diversification In line with the Manager s investment strategy of investing in a diversified portfolio of strategically located quality serviced residences, the Target Acquisitions will expand ART s portfolio from 2,476 Apartment Units in 15 properties across six countries as at the Latest Practicable Date 7 to 2,904 Apartment Units in 18 properties across seven countries, namely, Singapore, Australia, China, Indonesia, Japan, the Philippines and Vietnam. Australia is a new addition to ART s geographical presence, giving it a platform to further expand in this established serviced residence market. ART s increased presence in Japan also gives it further exposure to a stable market whilst its investments in the Philippines and Vietnam will offer exposure to two growing emerging economies. With the inclusion of the Target Properties, ART s Property Values (as defined herein) will increase to approximately S$1.2 billion. (iii) Increased free float With the proposed issue of New Units under the Equity Fund Raising and assuming that ART issues million New Units at an illustrative Issue Price of S$1.70 per New Unit, the free float of ART is expected to increase from the current 29.6 percent to 37.7 percent upon completion of the Equity Fund Raising 8. The market capitalisation of ART is expected to increase from S$942.4 million as at the Latest Practicable Date to approximately S$1,165.2 million, upon the completion of the Equity Fund Raising 8 based on a market price of S$1.89 per Unit. Each of these benefits is elaborated at paragraph 2.3 of the Letter to Unitholders. Competitive Strengths of the Target Properties The Manager believes that the Target Properties enjoy the following competitive strengths: Strategic locations within the respective cities central business districts; Fully-furnished quality serviced residences; Quality guest profile which is diversified across market segments and industries; and Exposure to both growing and stable markets in the Pan-Asian Region. Each of these competitive strengths is elaborated at paragraph 2.4 of the Letter to Unitholders. SUMMARY OF APPROVALS SOUGHT The Equity Fund Raising will comprise: (i) (ii) a non-renounceable preferential offering of New Units of one New Unit for every 10 Existing Units (as defined herein) held on the Preferential Offering Books Closure Date (as defined herein) (fractions of a Unit to be disregarded) to Singapore Registered Unitholders (the Preferential Offering ); an offering of New Units to retail investors in Singapore through the automated teller machines ( ATMs ) of DBS Bank (including ATMs of POSB) on a first-come, first-served basis (the ATM Offering ); and 7 8 Including 26.8 percent effective interest in the Vietnam Target Property acquired in January The number of Apartment Units as at the Latest Practicable Date includes 172 Apartment Units in Somerset Olympic Tower Property, Tianjin, 64 Apartment Units in Somerset Roppongi, Tokyo and 172 Apartment Units in the Vietnam Target Property. Including 0.8 million Units to be issued to the Manager prior to the commencement of the Equity Fund Raising in respect of management fees and acquisition fees payable in Units. 14

20 (iii) a placement of New Units to institutional and other investors (the Private Placement ). The Equity Fund Raising has been structured with the following objectives in mind: (i) (ii) to reward existing Unitholders through the Preferential Offering; and to increase the free float of ART through the ATM Offering and the Private Placement. In relation to this, each of Somerset Capital Pte Ltd and pfission Pte Ltd, wholly owned subsidiaries of CapitaLand Limited, has confirmed that it does not intend to take up its provisional allocation of New Units under the Preferential Offering to allow for greater free float of the Units. In order to increase ART s free float, these Units will then be placed out under the ATM Offering and the Private Placement. Assuming that Unitholders approval is obtained for the Equity Fund Raising and that approximately million New Units are issued at an illustrative Issue Price of S$1.70 per New Unit, CapitaLand Limited will remain a Controlling Unitholder with an indirect interest of approximately 34.6 percent through Somerset Capital Pte Ltd and pfission Pte Ltd after the completion of the Equity Fund Raising. The Manager is seeking approvals from Unitholders for the resolutions stated below: (1) The Proposed Issue of New Units under the Equity Fund Raising and a Consequent Adjustment to the Distribution Period of ART (Extraordinary Resolution) The proposed issue of such number of New Units at the Issue Price so as to raise gross proceeds of approximately S$199.0 million in order to, inter alia, part finance the Target Acquisitions and associated costs, and a consequent adjustment to the distribution period of ART to take into account the Equity Fund Raising. (2) The Proposed Placement of New Units to the Ascott Group (Ordinary Resolution) The proposed placement of New Units to TAG, a Controlling Unitholder, and its subsidiaries (collectively, the Ascott Group ) as part of the Equity Fund Raising to maintain their respective pre-placement unitholdings, in percentage terms (the Ascott Group Placement ). (3) The Proposed General Mandate for the Issue of New Units (Extraordinary Resolution) The proposed general mandate to be given to the Manager for the issue of up to 50.0 percent of the number of Units in issue after the Equity Fund Raising (taking into account Units issued pursuant to the Equity Fund Raising), with a sub-limit of 20.0 percent of the number of Units in issue after the Equity Fund Raising (taking into account Units issued pursuant to the Equity Fund Raising) for an issue of Units other than on a pro-rata basis to existing Unitholders, without the prior specific approval of Unitholders in a general meeting (the General Mandate ), pursuant to Rule 887(1) of the Listing Manual. (4) The Proposed Supplement to the Trust Deed Relating to the Remuneration of the Trustee (Extraordinary Resolution) The proposed supplement to the Trust Deed relating to the remuneration of the Trustee (the Trustee Remuneration Supplement ) for the purpose of reflecting the Manager s intention to pay the Trustee remuneration which is based on the value of Deposited Property rather than Property Values (as set out in a fee letter dated 15 November 2005) as well as align the remuneration of the Trustee with market practice. 15

21 RESOLUTION 1: THE EQUITY FUND RAISING The Equity Fund Raising The Manager intends to issue New Units so as to raise gross proceeds of approximately S$199.0 million from the Equity Fund Raising and additional borrowings of up to S$47.9 million to (i) finance the Target Acquisitions and associated costs; (ii) re-finance the loan drawn for the acquisition of 26.8 percent effective interest in the Vietnam Target Property which was completed in January 2007; and (iii) the balance of the proceeds to be utilised for general corporate and working capital purposes. The Joint Lead Managers, Bookrunners and Underwriters for the Equity Fund Raising (excluding the New Units to be subscribed for by the Ascott Group pursuant to the Undertaking (as defined herein)) are DBS Bank and JPMorgan. (See paragraph 1.2 of this Circular for further details of the Undertaking.) It is intended that the Equity Fund Raising will comprise: (i) (ii) (iii) a non-renounceable preferential offering of New Units of one New Unit for every 10 Existing Units held on the Preferential Offering Books Closure Date (fractions of a Unit to be disregarded) to Singapore Registered Unitholders (the Preferential Offering ); an offering of New Units to retail investors in Singapore through the ATMs of DBS Bank (including ATMs of POSB) on a first-come, first-served basis (the ATM Offering ); and a placement of New Units to institutional and other investors (the Private Placement ). Assuming million New Units are issued at an illustrative Issue Price of S$1.70 per New Unit, the Preferential Offering will comprise approximately 49.9 million New Units 9 (subject to the Rounding Mechanism), and the ATM Offering and the Private Placement will together comprise approximately 67.2 million New Units. The actual allocation of the number of New Units to the ATM Offering and the Private Placement will be determined between the Manager and the Joint Lead Managers, Bookrunners and Underwriters at a later date when the Issue Price is determined. The Manager s analyses of the Target Acquisitions in this Circular are made on the basis that ART will proceed with all the Target Acquisitions. The analyses (including the analysis on the forecast DPU and the forecast distribution yield) will vary accordingly if the Manager completes only some, but not all, of the Target Acquisitions. Subject to the relevant laws and regulations, the net proceeds of the Equity Fund Raising may be used, at the Manager s absolute discretion, to part finance and/or re-finance all or only some of the Target Acquisitions and/or to acquire any other suitable property or properties for ART and/or re-finance other existing borrowings and/or for general corporate and working capital purposes. While the Manager currently intends to apply the proceeds towards, inter alia, partially financing and/or re-financing the Target Acquisitions, the Equity Fund Raising is not subject to or conditional upon completion of all or any of the Target Acquisitions. Unitholders should also note that, in line with ART s acquisition growth strategy, the Manager is constantly sourcing for suitable properties to enhance ART s portfolio and ART may at any time and from time to time acquire more properties (in addition to the Target Properties). Such acquisitions may be funded entirely by equity, debt or a combination of both. 9 Based on approximately million Existing Units comprising million Units as at the Latest Practicable Date and 0.8 million Units to be issued to the Manager prior to the commencement of the Equity Fund Raising in respect of management fees and acquisition fees payable in Units. 16

22 Estimated Total Costs of the Target Acquisitions The total estimated costs of the Target Acquisitions (excluding the acquisition of 26.8 percent effective interest in the Vietnam Target Property which was completed in January 2007), including the costs of the Equity Fund Raising, on the assumption that ART receives Unitholders approval for the Equity Fund Raising, is approximately S$237.9 million, comprising: in respect of the Australia Target Acquisition, a purchase consideration of A$11.6 million (or approximately S$13.9 million) and associated costs of S$1.0 million (including stamp duty of S$0.8 million); in respect of the Japan Target Acquisitions, a purchase consideration of 5.7 billion (or approximately S$79.8 million) in respect of percent effective interest in Somerset Azabu East, Tokyo and a purchase consideration of 1.2 billion (or approximately S$17.0 million) in respect of 60.0 percent beneficiary interest in Somerset Roppongi, Tokyo (subject to further price adjustments for the consolidated net assets and liabilities as at completion of the Japan Target Acquisitions) and a combined associated costs of S$6.9 million (including acquisition tax of S$4.2 million); in respect of the Philippines Target Acquisition, a purchase consideration of PHP 2.7 billion (or approximately S$84.8 million) (subject to price adjustments for the consolidated net liabilities of MPVI as at completion of the Philippines Target Acquisition) and associated costs of S$0.8 million; in respect of the acquisition of the remaining 60.0 percent of the shares in EATC(S) representing 40.2 percent effective interest in the Vietnam Target Property, a purchase consideration of US$14.4 million (or approximately S$23.1 million) (subject to further price adjustments for the consolidated net assets and liabilities as at completion of the acquisition of the remaining 60.0 percent of the shares in EATC(S)) and associated costs of S$0.2 million; a total acquisition fee of approximately S$2.7 million (being 1.0 percent of the Enterprise Value (as defined in the Trust Deed)) payable to the Manager pursuant to the Trust Deed (as defined herein), of which S$0.3 million in connection with the acquisition of the remaining 60.0 percent shares in EATC(S) payable to the Manager in Units, and the remainder payable to the Manager in cash; total renovation and re-branding costs of A$0.9 million (or approximately S$1.0 million) in respect of the Australia Target Property and total renovation and re-branding costs of US$1.5 million (or approximately S$2.4 million) in respect of the Philippines Target Property; and other estimated fees and expenses (including professional fees and expenses) of approximately S$4.3 million incurred or to be incurred by ART in connection with the Equity Fund Raising. Consequent Adjustment to the Distribution Period In conjunction with the Equity Fund Raising, the Manager intends to declare, in lieu of the Distributable Income (as defined herein) from 1 January 2007 to 30 June 2007 (the Scheduled Distribution ), in respect of the Units in issue on the day immediately prior to the date on which the New Units are issued (the Existing Units ), a distribution of the Distributable Income for the period from 1 January 2007 to the day immediately prior to the date on which the New Units are issued (the Advanced Distribution ). The next distribution thereafter will comprise the Distributable Income for the period from the day that the New Units are issued to 30 June Semi-annual distributions will resume thereafter. The Advanced Distribution is intended to ensure that the Distributable Income accrued by ART up to the day immediately preceding the date of issue of the New Units (which at this point, will be entirely attributable to the Existing Units) is only distributed in respect of the Existing Units, and is being proposed as a means to ensure fairness to holders of the Existing Units. By implementing the Advanced Distribution, 17

23 Distributable Income accrued by ART up to and including the day immediately preceding the date of issue of the New Units will only be distributed, in a single distribution, in respect of the Existing Units. RESOLUTION 2: THE PROPOSED PLACEMENT TO THE ASCOTT GROUP The Manager may issue New Units to the Ascott Group as part of the Equity Fund Raising. To demonstrate its commitment to ART and to align its interest with the other Unitholders, the Ascott Group will subscribe for up to such number of New Units under the Equity Fund Raising so as to maintain its pre-placement unitholding, in percentage terms. RESOLUTION 3: THE PROPOSED GENERAL MANDATE TO ISSUE NEW UNITS The Manager proposes to seek the approval of Unitholders for a general mandate under Rule 887(1) of the Listing Manual for the issue of new Units in the financial year ending 31 December 2007, provided that such number of new Units do not exceed 50.0 percent of the number of Units in issue after the Equity Fund Raising (taking into account New Units issued pursuant to the Equity Fund Raising), of which the aggregate number of new Units issued other than on a pro rata basis to existing Unitholders must not be more than 20.0 percent of the number of Units in issue after the Equity Fund Raising (taking into account New Units issued pursuant to the Equity Fund Raising). For the avoidance of doubt, this General Mandate will not include the New Units to be issued pursuant to the Equity Fund Raising described in this Circular. RESOLUTION 4: THE PROPOSED SUPPLEMENT TO THE TRUST DEED RELATING TO THE REMUNERATION OF THE TRUSTEE The Manager proposes to seek the approval of Unitholders to supplement the Trust Deed for the purpose of reflecting the Manager s intention to pay the Trustee remuneration based on the value of Deposited Property rather than Property Values (as set out in a fee letter dated 15 November 2005) as well as align the payment of remuneration to the Trustee with market practice. The financial impact of the change in basis of the Trustee remuneration is negligible (less than percent). 18

24 INDICATIVE TIMETABLE Event Date and Time Last date and time for lodgment of Proxy Forms : 21 February 2007 at 3:00 p.m. Date and time of EGM : 23 February 2007 at 3:00 p.m. If the approvals sought at the EGM are obtained: Last day and time of trading on a cum basis in respect of the Preferential Offering Commencement of trading on an ex basis in respect of the Preferential Offering Date on which the Transfer Books and Register of Unitholders will be closed to determine the provisional allocations of Singapore Registered Unitholders (as defined herein) under the Preferential Offering (the Preferential Offering Books Closure Date ) : To be determined (but is expected to be no later than end March 2007) : To be determined (but is expected to be no later than end March 2007) : To be determined (but is expected to be no later than end March 2007) Commencement of the Equity Fund Raising : To be determined (but is expected to be no later than end March 2007) Close of the Equity Fund Raising : To be determined (but is expected to be no later than end March 2007) Date on which the Transfer Books and Register of Unitholders of ART will be closed to determine the Unitholders entitlement to the Advanced Distribution Issue of New Units as well as commencement of trading of the New Units on the SGX-ST : To be determined (but is expected to be no later than end March 2007) : To be determined (but is expected to be no later than end March 2007) Target date for completion of the Target Acquisitions : To be determined (but is expected to be no later than end April 2007) Date of payment of the Advanced Distribution : To be determined (but is expected to be no later than end April 2007) The timetable for the events which are scheduled to take place after the EGM is indicative only and is subject to change at the Manager s absolute discretion. The Manager intends to announce any changes (including any determination of the relevant dates) to the timetable above once the Manager becomes aware of such changes. 19

25 ASCOTT RESIDENCE TRUST (a unit trust constituted on 19 January 2006 under the laws of the Republic of Singapore) Directors Mr Lim Jit Poh Mr Liew Mun Leong Mr Ong Ah Luan Cameron Mr S. Chandra Das Mr Paul Ma Kah Woh Mr David Schaefer Mr Ku Moon Lun Registered Office 8 Shenton Way #13-01 Temasek Tower Singapore January 2007 To: Unitholders of Ascott Residence Trust Dear Sir/Madam 1. SUMMARY OF APPROVALS SOUGHT The Directors are convening the EGM to be held on 23 February 2007 at 3:00 p.m. at STI Auditorium at Level 9, 168 Robinson Road, Capital Tower, Singapore to seek the approval of Unitholders in respect of the resolutions relating to the issue of the New Units under the Equity Fund Raising (Resolution 1), the Ascott Group Placement (Resolution 2), the General Mandate (Resolution 3) and the Trustee Remuneration Supplement (Resolution 4). The Equity Fund Raising will comprise: (i) (ii) (iii) a non-renounceable preferential offering of New Units of one New Unit for every 10 Existing Units (as defined herein) held on the Preferential Offering Books Closure Date (as defined herein) (fractions of a Unit to be disregarded) to Singapore Registered Unitholders (the Preferential Offering ); an offering of New Units to retail investors in Singapore through the automated teller machines ( ATMs ) of DBS Bank (including ATMs of POSB) on a first-come, first-served basis (the ATM Offering ); and a placement of New Units to institutional and other investors (the Private Placement ). The Equity Fund Raising has been structured with the following objectives in mind: (i) (ii) to reward existing Unitholders through the Preferential Offering; and to increase the free float of ART through the ATM Offering and the Private Placement. In relation to this, each of Somerset Capital Pte Ltd and pfission Pte Ltd, wholly owned subsidiaries of CapitaLand Limited, has confirmed that it does not intend to take up its provisional allocation of New Units under the Preferential Offering to allow for greater free float of the Units. In order to increase ART s free float, these New Units will then be placed out under the ATM Offering and the Private Placement. Assuming that Unitholders approval is obtained for the Equity Fund Raising and that approximately million New Units are issued at an illustrative Issue Price of S$1.70 per New Unit, CapitaLand Limited will remain a Controlling Unitholder with an indirect interest of approximately 34.6 percent through Somerset Capital Pte Ltd and pfission Pte Ltd after the completion of the Equity Fund Raising. Assuming that million New Units are issued pursuant to the Equity Fund Raising at an illustrative Issue Price of S$1.70 per New Unit, that Unitholders approval is obtained at the EGM for the Ascott Group Placement in order for the Ascott Group to subscribe for such number of 20

26 New Units to maintain its pre-placement unitholding and that Somerset Capital Pte Ltd and pfission Pte Ltd do not take up their provisional allocations of New Units under the Preferential Offering, the unitholdings of the Substantial Unitholders before and immediately upon completion of the Equity Fund Raising are as follows: Interests of Substantial Unitholders Before the Equity Fund Raising Existing Units: million (1) Immediately after the Equity Fund Raising Total Units: million (1) Units held (million) Interest Units held (million) Interest The Ascott Group Limited (1)(3) % % CapitaLand Limited (2)(3) % % Notes: (1) Includes 638,579 Units held by the Manager as at the Latest Practicable Date and 800,074 Units to be issued to the Manager prior to the commencement of the Equity Fund Raising in respect of management fees and acquisition fees payable in Units. (2) These interests are held through two wholly owned subsidiaries of CapitaLand Limited, namely Somerset Capital Pte Ltd and pfission Pte Ltd. (3) As at Latest Practicable Date, CapitaLand Limited holds 67.0 percent interest in The Ascott Group Limited. The following paragraphs summarise the approvals which the Manager is seeking from Unitholders. 1.1 Resolution 1: The Proposed Issue of New Units under the Equity Fund Raising and a Consequent Adjustment to the Distribution Period of ART (Extraordinary Resolution) The Trust Deed, read together with the Listing Manual, provides that specific prior approval of Unitholders by Extraordinary Resolution is required for an issue of new Units if the number of such new Units (together with any other issue of Units, other than by way of a rights issue offered on a pro rata basis to all existing Unitholders, in the same financial year, including Units issued to the Manager in payment of its fees) would, immediately after the issue, exceed 10.0 percent of the outstanding Units. Assuming that ART proceeds with the Equity Fund Raising, it is expected that the number of New Units will, immediately after issue, exceed 10.0 percent of the outstanding Units. Accordingly, the Manager is seeking the approval of Unitholders for an issue of the New Units for the purpose of the Equity Fund Raising. Approval in-principle has been obtained from the SGX-ST for the listing of and quotation for the New Units on the Main Board of the SGX-ST. The SGX-ST s approval in-principle is not an indication of the merits of ART, the New Units or the Equity Fund Raising. The Manager expects to raise gross proceeds of approximately S$199.0 million pursuant to the Equity Fund Raising. The actual number of New Units to be issued will depend on the price at which each New Unit is issued (the Issue Price ). ART s policy is to distribute its Distributable Income on a semi-annual basis to Unitholders. However, in conjunction with the Equity Fund Raising, the Manager intends to declare the Advanced Distribution, in lieu of the Scheduled Distribution. The next distribution following the 21

27 Advanced Distribution will comprise the Distributable Income for the period from the day that the New Units are issued to 30 June Semi-annual distributions will resume thereafter. (See paragraph 3 for further details on the Equity Fund Raising and the Advanced Distribution.) 1.2 Resolution 2: The Proposed Placement to the Ascott Group (Ordinary Resolution) To demonstrate its commitment to ART and to align its interest with the other Unitholders, TAG has undertaken to the Trustee and the Joint Lead Managers, Bookrunners and Underwriters that: (a) (b) TAG will accept and will procure the Manager to accept in full its respective provisional allocations of New Units under the Preferential Offering at the Issue Price; and TAG will subscribe and/or procure its subsidiaries to subscribe, for such number of New Units under the Private Placement, being the difference between the total number of New Units which the Ascott Group will be required to subscribe for to maintain its pre-placement unitholding, in percentage terms, and the total number of New Units under the Preferential Offering provisionally allocated to and accepted by TAG and the Manager, (the Undertaking ). Accordingly, the Manager is seeking Unitholders approval for the placement of New Units under the Equity Fund Raising to the Ascott Group, being a Substantial Unitholder 1. Approval of Unitholders for such a placement to the Ascott Group is required as Rule 812(1) of the Listing Manual prohibits a placement of New Units to Substantial Unitholders. A placement of New Units to the Ascott Group, being a Controlling Unitholder, would also constitute an interested person transaction under Chapter 9 of the Listing Manual. If New Units are placed to the Ascott Group, there is a possibility (depending on the actual Issue Price) that the value of the New Units placed to the Ascott Group exceeds 5.0 percent of ART s latest unaudited NTA. In such circumstances, Rule 906 of the Listing Manual also requires Unitholders approval for placement of New Units to the Ascott Group. Each of TAG, the Manager, Somerset Capital Pte Ltd and pfission Pte Ltd will abstain from voting on the resolution relating to the Ascott Group Placement. (See paragraph 5 for further details about the Ascott Group Placement.) 1.3 Resolution 3: The Proposed General Mandate to Issue New Units (Extraordinary Resolution) The Manager proposes to seek the approval of Unitholders for a general mandate under Rule 887(1) of the Listing Manual for the issue of new Units in the financial year ending 31 December 2007, provided that such number of new Units do not exceed 50.0 percent of the number of Units in issue after the Equity Fund Raising (taking into account New Units issued pursuant to the Equity Fund Raising), of which the aggregate number of new Units issued other than on a pro rata basis to existing Unitholders must not be more than 20.0 percent of the number of Units in issue after the Equity Fund Raising (taking into account New Units issued pursuant to the Equity Fund Raising). (See paragraph 6 for further details about the General Mandate.) 1 Substantial Unitholder means a person with an interest in one or more Units constituting not less than 5.0 percent of all Units in issue. 22

28 1.4 Resolution 4: The Proposed Trustee Remuneration Supplement (Extraordinary Resolution) Currently, under the Trust Deed, the remuneration of the Trustee is limited to 0.1 percent per annum of the Property Values, subject to a minimum fee of S$10,000 per month, which is payable out of the Deposited Property monthly in arrear. In order to reflect the Manager s intention of paying the Trustee remuneration which is based on the value of Deposited Property rather than Property Values (as set out in a fee letter dated 15 November 2005) as well as align the payment of remuneration to the Trustee with market practice, the Manager proposes to seek the approval of Unitholders to supplement the Trust Deed to amend the payment of the remuneration of the Trustee to be based on the value of Deposited Property. The financial impact of the change in basis of the Trustee remuneration is negligible (less than percent). (See paragraph 7 for further details about the Trustee Remuneration Supplement) 2. THE TARGET ACQUISITIONS AND THE RATIONALE FOR THE TARGET ACQUISITIONS Following negotiations between the Manager and the vendor(s) of each of the Target Acquisitions, the Trustee, upon the Manager s recommendations, has entered into conditional sale and purchase agreements with each of the vendor(s) for each of the Target Acquisitions. The following table sets out the dates of signing of the conditional sale and purchase agreements, the dates of completion and/or the expected dates of completion for each Target Property: Target Property Shoan Heights Serviced Apartment, Melbourne (to be re-branded Somerset Gordon Heights, Melbourne) Date of Signing of Conditional Sale and Purchase Agreement(s) 12 December April 2007 Somerset Azabu East, Tokyo 23 January April 2007 Somerset Roppongi, Tokyo 23 January April 2007 Oakwood Premier Ayala Center (to be re-branded Ascott Makati) Somerset Chancellor Court, Ho Chi Minh City Date of Completion/ Expected Date of Completion 23 November March December 2006 in respect of 40% interest in EATC(S) 23 January 2007 in respect of remaining 60% interest in EATC(S) 12 January 2007 in respect of 20% interest in EATC(S) acquired from Sparkle Limited 17 January 2007 in respect of 20% interest in EATC(S) acquired from Coral Holdings Limited 2 April 2007 in respect of remaining 60% interest in EATC(S) 2.1 Descriptions of the Target Properties Detailed information about each of the Target Properties is set out in Appendix A of this Circular. 23

29 2.2 Valuations The following table sets out the appraised value in local and foreign currency, the vendor(s), the date of valuation and the independent valuer(s) of each Target Property. Appraised value (1) Property (S$ million) Australia Target Property Shoan Heights Serviced Apartment, Melbourne (to be re-branded Somerset Gordon Heights, Melbourne) Japan Target Properties Somerset Azabu East, Tokyo Somerset Roppongi, Tokyo (2) Philippines Target Property Oakwood Premier Ayala Center (to be re-branded Ascott Makati) Vietnam Target Property Somerset Chancellor Court, Ho Chi Minh City (3) Appraised value (1) (foreign currency) Vendor(s) 13.9 A$11.6 million Tiow Hoe Goh, Kooi Lean Goh and Chew Por Chan billion Mitsubishi Estate Co., Ltd billion Mitsubishi Estate Co., Ltd and MEC Roppongi Funding Corporation 87.9 PHP 2.8 billion Ayala Hotels Inc. and Ocmador Philippines, B.V US$45.0 million The Ascott Holdings Limited (4) Date of valuation 5 December 2006 Independent Valuer CB Richard Ellis Australia 3 January 2007 Jones Lang LaSalle Property Consultants Pte Ltd 3 January 2007 Jones Lang LaSalle Property Consultants Pte Ltd 1 November December US$45.0 million 31 December 2006 HVS International HVS International (on behalf of the Trustee) CB Richard Ellis Vietnam (on behalf of The Ascott Holdings Limited) Notes: (1) Refers to percent of the Target Property. Appraised values in Singapore dollar are based on exchange rates of A$1.00 to S$1.20, 1 to S$0.014, PHP 1 to S$ and US$1.00 to S$1.60. All exchange rates in this Circular are quoted from Bloomberg L.P. (2) ART currently owns 40.0 percent beneficiary interest in Somerset Roppongi, Tokyo and proposes to acquire the remaining 60.0 percent beneficiary interest. (3) In January 2007, ART acquired 26.8 percent effective interest in the Vietnam Target Property. ART proposes to acquire an additional 40.2 percent effective interest. The Manager intends to utilise the proceeds from the Equity Fund Raising to fund the acquisition of the 40.2 percent interest in the Vietnam Target Property as well as to re-finance the loan drawn for the acquisition of the 26.8 percent effective interest in the Vietnam Target Property which was completed in January (4) A wholly owned subsidiary of TAG. (See Appendix G of this Circular for the valuation certificates issued by each of the Independent Valuers in relation to the relevant Target Property.) 24

30 2.3 Rationale for the Target Acquisitions The Manager s principal investment strategy is to invest primarily in real estate and real estaterelated assets which are income-producing and which are used, or predominantly used as serviced residences or rental housing properties in the Pan-Asian Region. The Manager s acquisition strategy is to focus on investment opportunities principally in the Pan-Asian Region to leverage on the increasing popularity of serviced residences as an alternative accommodation concept arising from the increasing trend in business travel into Asia, an increasing preference of corporate and business executives for home-styled accommodations for extended stays and the increasing levels of foreign direct investments in Asian economies. The Manager believes that the Target Acquisitions will offer the following benefits to Unitholders: Improved earnings and DPU The Manager expects that the Target Acquisitions will enhance the DPU to Unitholders due to the yield accretive nature of the Target Acquisitions. The Manager expects REVPAU for the Enlarged Portfolio to be S$124 for the Forecast Period 2007, compared to S$121 for the Existing Properties in the same period. Average Daily Rates for the Enlarged Portfolio is expected to be S$146 for the Forecast Period 2007, which is higher than the Average Daily Rates of the Existing Properties of S$142. Average occupancy rates for the Existing Properties and for the Enlarged Portfolio are expected to be around 85 percent for the Forecast Period Based on the Manager s nine-month forecast for the Forecast Period 2007 and the aggregate purchase consideration of S$218.6 million (assuming that ART proceeds with completion of all the Target Acquisitions and that the Target Acquisitions were completed on 1 April 2007), the Target Acquisitions are expected to generate an annualised forecast consolidated net property yield of approximately 6.2 percent. The annualised forecast consolidated net property yield of the Target Acquisitions is higher than the annualised forecast consolidated net property yield generated by the Existing Properties of approximately 5.9 percent for the same period and the implied property yield of the Existing Properties of approximately 4.4 percent. To illustrate the yield accretive nature of the Target Acquisitions, Table A on page 26 of this Circular shows ART s annualised forecast DPU for the Forecast Period 2007 in relation to: (i) (ii) the Existing Properties; and ART s Enlarged Portfolio upon completion of the Target Acquisitions (assuming that ART proceeds with completion of all the Target Acquisitions and that the Target Acquisitions were completed on 1 April 2007), based on an illustrative Issue Price of S$1.70 per New Unit and million New Units. Table A shows the accretion of the Target Acquisitions based on the intended gearing of ART of 29.0 percent after completion of the Target Acquisitions and the Equity Fund Raising. The table should be read together with ART s Forecast Consolidated Statement of Net Income and Distribution for the Forecast Period 2007 as well as the accompanying assumptions and sensitivity analysis in Appendix D of this Circular, and the report of KPMG (the Independent Accountants ) inappendix E of this Circular. 25

31 Table A Issue Price (S$) Number of New Units Issued (million) Existing Properties Annualised DPU (cents) Distribution yield (%) Enlarged Portfolio Annualised DPU (cents) Distribution yield (%) Accretion (%) Note: DPU will vary if completion of the Target Acquisitions is on a date other than 1 April 2007 Assuming an illustrative Issue Price of S$1.70 per New Unit and that million New Units are issued under the Equity Fund Raising, ART s annualised forecast DPU for the Forecast Period 2007 upon completion of the Target Acquisitions and the Equity Fund Raising is approximately 7.14 cents, representing a distribution yield of approximately 4.2 percent. This represents a DPU accretion of approximately 9.3 percent over the annualised forecast DPU of 6.53 cents based on the Existing Properties for the same period. The Target Acquisitions will offer DPU accretion Annualised DPU for the Forecast Period cents 6.53 cents Accretion +9.3% Existing Properties Enlarged Portfolio Note: Assuming the Target Acquisitions were completed on 1 April 2007 and an illustrative Issue Price of S$1.70 per New Unit under the Equity Fund Raising. Chart is not drawn to scale. The Target Acquisitions may also provide opportunities for asset enhancements such as selective renovation and potential reconfiguration of rooms to increase lettable space, and provide value-added facilities to guests to further improve earnings. For example, there is potential for the refurbishment of the Philippines Target Property, which is expected to result in higher rental rates and at the same time, enhance its leading position in the serviced residence industry in Manila. 26

32 In general, the Manager will seek ways to further enhance the performance of the Target Acquisitions through the following initiatives: constant evaluation of opportunities to enhance the Target Acquisitions; repositioning the Target Acquisitions by adjusting marketing strategies, service levels and pricing to better match the demand characteristics of particular market segments; undertaking capital upgrading programmes to enhance the performance and competitiveness of the Target Acquisitions; and capital improvements such as renovation of public and common areas, upgrading of Apartment Units and reconfiguration of space in selected areas Increased portfolio scale and diversification Economies of scale The Target Acquisitions will enlarge the portfolio of ART from S$961.4 million to S$1,181.4 million with an increase in the number of Apartment Units from 2,476 in 15 properties to 2,904 in 18 properties. With a larger presence, ART is better positioned to enjoy potential cost synergies and create economies of scale, leading to lower operating costs for the properties in its portfolio. Revenue diversification across geography as well as property and economic cycles The Target Acquisitions will further enhance the diversification of ART s portfolio in terms of geographical spread and across property and economic cycles. In line with the Manager s investment strategy of investing in a diversified portfolio of strategicallylocated, high-quality serviced residences, the Target Acquisitions will introduce a new market with the addition of Australia, and further increase its presence in Japan, the Philippines, and Vietnam. The Australia Target Acquisition marks an entry into an attractive established serviced residence market and creates a platform where ART may seek to further establish a deeper presence in Australia. With the Target Acquisitions, ART s portfolio will be diversified across 10 cities in seven countries. The following charts illustrate the geographical diversification of ART s Enlarged Portfolio (by Property Values and share of Gross Profit contribution) for the Forecast Period 2007 (assuming the Target Acquisitions were completed on 1 April 2007): Geographical diversification of the Enlarged Portfolio for the Forecast Period 2007 By ART s Property Values By ART s Share of Gross Profit Vietnam 14% Singapore 25% Vietnam 20% Singapore 20% Philippines 9% Australia 1% Japan 12% Australia 1% Philippines 13% Indonesia 8% China 31% Japan 9% Indonesia 8% China 29% Total = S$1,181.4 million Total = S$48.9 million Not drawn to scale Note: Assuming the Target Acquisitions were completed on 1 April

33 The Manager believes that Unitholders will benefit from strong economic growth in the Pan-Asian Region. The Target Acquisitions will further expand ART s presence in rapidly-expanding key Pan-Asian cities, providing Unitholders exposure to both stable markets, and emerging markets experiencing high growth. The Manager has commissioned the Independent Property Consultant to prepare a report on the serviced residence sector in Singapore, Australia, China, Indonesia, Japan, the Philippines and Vietnam, countries where the Manager believes offer strong growth opportunities and where ART has and/or proposes to establish a presence. The Target Acquisitions are located in: (i) (ii) (iii) (iv) Melbourne, a key financial centre of Australia; Tokyo, the capital city and business centre of Japan; Manila, the capital city of the Philippines; and Ho Chi Minh City, the commercial centre of Vietnam. According to the Serviced Residences Market Overview Report (as set out in Appendix H of this Circular), the demand for serviced residences is expected to continue to grow in the Pan-Asian cities where the Target Properties are located largely as a result of improving economic conditions and in general, stable and/or growing international arrivals. For instance, Melbourne is expected to experience growth in international arrivals having successfully positioned itself as the events capital of Australia. Similarly, occupancy levels in Tokyo are expected to experience further growth in the immediate term on the back of the improving economy and anticipated growth in inbound arrivals. Serviced residences in Manila are expected to continue to enjoy healthy demand in the wake of limited supply, economic expansion and positive tourism prospects. The outlook for the serviced residence sector in Ho Chi Minh City remains overwhelmingly positive on the back of the current strong trading performance, limited new supply and continued improvement in the business operating environment on the back of higher foreign investments. The Manager expects that the Target Properties will be able to achieve strong occupancies and generate high and stable REVPAU, taking into consideration the strong economic performance in the Pan-Asian region Increased free float Assuming Unitholders approval is obtained for the proposed issue of New Units under the Equity Fund Raising and that ART issues million New Units at an illustrative Issue Price of S$1.70 per New Unit, the number of Units in issue will increase by approximately 23.4 percent (based on million Existing Units 2 ). Additionally, assuming that the Ascott Group subscribes for such number of New Units pursuant to the Undertaking in order to maintain its pre-placement unitholding, the free float of ART is expected to increase from the current 29.6 percent to 37.7 percent after the Equity Fund Raising. The market capitalisation of ART is expected to increase from S$942.4 million as at the Latest Practicable Date to approximately S$1,165.2 million, based on a market price of S$1.89 per Unit. 2 Includes 0.8 million Units to be issued to the Manager prior to the commencement of the Equity Fund Raising in respect of management fees and acquisition fees payable in Units. 28

34 2.4 Competitive Strengths of the Target Properties Strategic locations within the respective cities central business districts The Target Properties are within the respective cities central business districts and enjoy a high level of connectivity to key transportation nodes. Australia The Australia Target Property is located at Little Bourke Street, Melbourne, Victoria 3000, Australia, in Melbourne s central business and financial district, surrounded by a myriad of theatres, excellent restaurants, cafes, sporting venues, galleries, department stores and glorious parks. Japan Somerset Azabu East, Tokyo is conveniently located in Minato-ku, close to multinational companies, embassies, restaurants and the Roppongi Hills shopping mall. Three subway stations are in close proximity, providing guests with efficient access to the entire city. The nearby lush Shiba Park allows guests, whether on business or leisure travel, to relax and enjoy greenery in the city, whilst the nearby Roppongi entertainment and shopping district provides guests with an international variety of restaurants and entertainment, all within walking distance of the residence. Somerset Roppongi, Tokyo is located within Minato-ku, in the central business district of Tokyo, located within five minutes walk from the nearest subway station, providing efficient access to the entire city. Roppongi is known for its prominent entertainment area with an international variety of restaurants and entertainment lining the streets. An abundance of business and leisure destinations are located within walking distance of the residence. The Philippines Located in Glorietta 4 Ayala Center in the heart of Makati City s central business district, the Philippines Target Property is close to the headquarters of numerous multinational corporations and financial institutions. The serviced residence towers are connected to the premier Ayala Center shopping mall and the Greenbelt lifestyle mall. This connection provides guests direct and easy access to entertainment facilities, shops and restaurants. Vietnam The Vietnam Target Property is centrally located in District 1 in Ho Chi Minh City s prime commercial, diplomatic and major shopping district, and is within walking distance of many businesses, consulates and shopping centres Fully-furnished quality serviced residences The Manager believes that the Target Properties will be able to attract a stable stream of visitors and travellers. Australia Shoan Heights Serviced Apartment, Melbourne (to be re-branded Somerset Gordon Heights, Melbourne) offers 43 fully-furnished Apartment Units ranging from studios, one and two-bedroom apartments to two-bedroom penthouses and offers facilities such as a restaurant, advanced security system, daily housekeeping service, valet, dry-cleaning and free laundry facilities. 29