REPORT ON BANK'S OPERATIONS FOR THE SECOND QUARTER OF THE YEAR 2014

|

|

|

- Geraldine Bell

- 5 years ago

- Views:

Transcription

1

2 REPORT ON BANK'S OPERATIONS FOR THE SECOND QUARTER OF THE YEAR 2014 BELGRADE, JULY

3 CONTENTS 1. OVERVIEW OF THE KEY PERFORMANCE INDICATORS OF THE BANK IN THE PERIOD FROM TO Bank's Performance Indicators 4 2. MACROECONOMIC OPERATING CONDITIONS IN THE PERIOD FROM TO BANK S KEY PERFORMANCE INDICATORS IN THE PERIOD FROM TO BALANCE SHEET AS AT Bank's Assets as at Bank's Liabilities as at Loans to customers and deposits from customers as at Commission operations and off-balance sheet items in INCOME STATEMENT FOR THE PERIOD FROM TO Interest Income and Expenses Fee Income and Expenses Realized Operating Profit DESCRIPTION OF KEY RISKS AND THREATS THE COMPANY IS EXPOSED TO ALL MAJOR TRANSACTIONS WITH RELATED ENTITIES KEY DATA ON BUSINESS PLAN IMPLEMENTATION FOR THE YEAR Planned and Realized Values of the Balance Sheet in the First Half of Planned and Realized Values of Income Statement for the Period BALANCE SHEET AS AT 30 TH JUNE 2014 INCOME STATEMENT FOR THE PERIOD FROM JANUARY 01 ST TO JUNE 30 TH 2014 NOTES TO FINANCIAL STATEMENTS FOR THE SECOND QUARTER 2014 STATEMENT OF THE RESPONSIBLE PERSONS DECISION ON THE APPROVAL OF THE FINANCIAL STATEMENTS 3

4 1. OVERVIEW OF KEY PERFORMANCE INDICATORS IN THE PERIOD FROM TO Bank s Performance Indicators ITEM BALANCE SHEET ASSETS LOANS AND DEPOSITS TO CUSTOMERS Share of NPL (as %) 17,74% 18,83% 18,53% 18,15% 17,51% Retail loans and deposits Corporate loans and deposits REVERSE REPO TRANSACTIONS TOTAL REQUIRED RESERVE TOTAL LIABILITIES DEPOSITS FROM CUSTOMERS Retail deposits Corporate deposits NUMBER OF EMPLOYEES Assets per employee in 000 RSD Assets per employee in 000 EUR OPERATING PROFIT INTEREST GAINS FEE AND COMMISSION GAINS OPERATING EXPENSES PROFITABILITY INDICATORS: ROA profit / average BS assets 1,28 1,28 1,28 1,31 1,33 ROE profit/ average total capital 7,22 7,22 7,20 7,33 7,33 ROE profit / average share capital 11,97 11,93 11,88 12,06 11,46 CIR = OPEX / net interest and fees 58,00% 58,82% 57,89% 58,16% 58,05% CAPITAL ADEQUACY 18,86% 18,41% 18,71% 18,45% 19,02% FX RISK RATIO 1,05% 3,04% 2,77% 5,70% 2,12% LIQUIDITY RATIO 4,26 3,21 3,22 4,26 3,45 OPERATING CASH FLOW

is")

5 2. MACROECONOMIC OPERATING CONDITIONS IN THE PERIOD FROM TO Year-on-year inflation rate (rise in consumer prices) recorded a decrease in the first six months of As a result of implementation of measures of financial consolidation, for the first time, after a long period of time, we have a situation where year-on-year inflation in the month of June (1,3%) is significantly below the lower limit of allowed deviation from the target value set in the NBS Memorandum on establishing a targeted inflation rate (4,0+/-1,5%). In the first two quarters of this year, RSD slightly depreciated when compared to the end of previous year. RSD exchange rate stabilized at the value of approximately RSD 115 for one EURO. During the first two quarters of the current year RSD exchange rate weakened as compared to the end of the previous year by 1,0% Year-on-year inflation rate in the period from 2013 to in % 2,2 2,3 2,1 2,1 1, RSD/EUR exchange rate in the period from 2013 to in RSD 114,6 115,4 115,7 115,7 115, The NBS key policy rate is lowered to 8,50% in mid June Apart from mitigating inflationary expectations the established rate should also contribute to macroeconomic stability. In spite of strong geopolitical tensions that also reflect on the international financial markets, the opinion is that it still does not have a significant impact on the local economy. Due to the reduction in inflationary pressure and price stabilization, in the upcoming period we can expect the NBS to ease up even more on its restrictive monetary policy. Banking sector in the Republic of Serbia continued, in the first quarter of 2014, to record a slight decline in balance sheet assets (-0,8%) in comparison to five-year average from the previous years ( 9,3%) NBS key policy rate in the period from 2013 to in% 9,50 9,50 9,50 9,00 8, Movement of balance sheet assets of the banking sector in period from 2009 to in% 21,6 17,3 0,2 8,7-1,2-0, In the first quarter of 2014 the Bank slightly increased its share in the total balance sheet assets of the banking sector. During the observed period the Bank's market share in the assets of the banking sector increased by 3,7 percentage points Movement of Bank's market share in the period from 2009 to in % 9,5 10,1 10,4 11,3 12,8 13,

6 3. BANK S KEY PERFORMANCE INDICATORS IN THE PERIOD FROM TO ITEM BALANCE SHEET ASSETS LOANS AND DEPOSITS TO CUSTOMERS Share of NPL (as %) 17,74% 18,83% 18,53% 18,15% 17,51% Retail loans and deposits Corporate loans and deposits REVERSE REPO TRANSACTIONS TOTAL REQUIRED RESERVE TOTAL LIABILITIES DEPOSITS FROM CUSTOMERS Retail deposits Corporate deposits NUMBER OF EMPLOYEES Assets per employee in 000 RSD Assets per employee in 000 EUR As of the Bank's balance sheet assets amount to RSD ,8 million and have been increased by RSD ,4 million or 5,1% compared to the end of the previous year. Off-balance sheet assets increased by 6,9% in 2014, and at the end of June this year amounted to RSD ,5 million. In the first six months of 2014, the Bank granted loans to customers in the amount of RSD ,5 million, which is slightly below the figure realized at the end of 2013 (-2,0%), and at the same time maintained a relatively low level of NPL in total loans (17,7%). In the same period the Bank realized a growth in deposits in the amount of RSD ,2 million or 7,1%. Within the structure of the mentioned increase, retail deposits increased by RSD 7.066,1 million, and corporate deposits in the amount of RSD ,1 million. The above stated positive changes include, as well, the effect of RSD depreciation against EUR and CHF, in the amount of approximately RSD 2,2 billion. ( IN 000 RSD ) ITEM OPERATING PROFIT INTEREST GAINS FEE AND COMMISSION GAINS OPERATING EXPENSES PROFITABILITY INDICATORS: ROA profit/ average BS assets 1,28 1,28 1,28 1,31 1,33 ROE profit/ average total capital 7,22 7,22 7,20 7,33 7,33 ROE profit/ average share capital 11,97 11,93 11,88 12,06 11,46 CIR = OPEX / net interest and fees 58,00% 58,82% 57,89% 58,16% 58,05% 6

7 Operating profit in 000 RSD Profitability indicators in % ,5 12,1 11,9 11,9 12, ,3 7,3 7,2 7,2 7, ,3 1,3 1,3 1,3 1, ROA -profit/average BS assets ROE - profit/average total capital ROE - profit/average share capital Global financial crisis, inefficiency and illiquidity of domestic business entities affected the Bank in a way that in the first six months of the current year, when compared to the same period last year, it realized less profit (-7,3%). The Bank's realized profit over the period from to amounts to RSD 2.395,1 million, which in comparison to the same period last year represents a reduction of RSD 187,4 million. Such change in profit provided, in the first six months of 2014, return on total capital of 7,2%, or return on share capital of 12,0%. Movement of profit in the first two quarters of 2014 was mainly affected by the growth of net expenses under indirect write-off of loans and provisions in the amount of RSD 602,8 million, or 75,5% and by an increase in operating and other expenses amounting to RSD 396,1 million, or 7,9%. With respect to positive effects, it is important to underline the increase in net interest income in the amount of RSD 758,5 million (12,4%) and net fee income in the amount of RSD 52,6 million (2,4%). Decrease in number of employees accompanied by an increase in the volume of business, improved the Bank s ratio of assets to employees. In the first six months of 2014, the assets per employee in the Bank have increased from RSD 122,6 million ( ), to RSD 130,5 million as of Growth in operating expenses, but also an increase in net interest and fee income, led to Cost Income Ratio (CIR) to maintain at the approximately same level (58,05% as of , or 58,00% as of ) 7

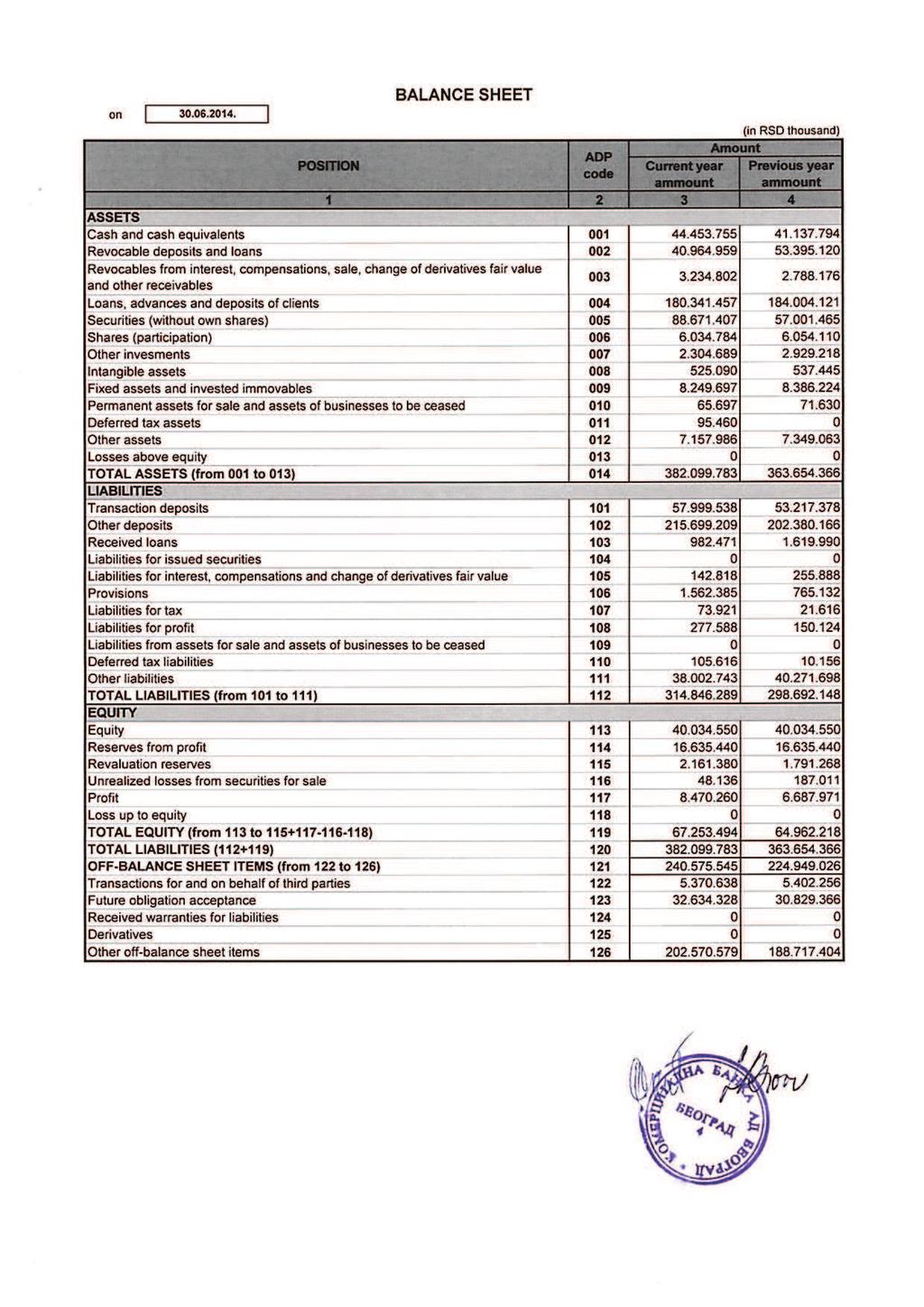

8 4. BALANCE SHEET AS AT Bank s Assets as at (IN 000 RSD) No. ITEM INDEXES % OF SHARE AS AT =(3:4)*100 6 ASSETS 1. Cash and cash equivalents ,1 11,6 2. Callable deposits and loans ,7 10,7 3. Interest, fee and sale receivables ,0 0,8 4. Loans and deposits to customers ,0 47,2 5. Securities (other than own) ,6 23,2 6. Equity holdings ,7 1,6 7. Other investments ,7 0,6 8. Intangible investments ,7 0,1 9. Fixed assets and investment property ,4 2,2 10. Non-current assets intended for sale ,7 0,0 11. Deferred tax assets ,0 12. Other assets ,4 1,9 TOTAL ASSETS ( from 1 to 12 ) ,1 100,0 At the end of the second quarter of 2014, the Bank's balance sheet assets increased by RSD ,4 million, or 5,1%. Loans to customers have been decreased by RSD 3.662,7 million, or 2,0%. As of the total loans to customers amount to RSD ,5 million, which accounts for 47,2% of the total balance sheet assets. In the first six months of 2014, cash and cash equivalents recorded a growth of 8,1%, primarily due to increase of funds in the drawing account and FX funds in the foreign currency accounts. Significant increase in the reporting period of the current year has been realized with respect to securities (other than own) growth in the amount of RSD ,9 million, or 55,6%, mainly as a result of Bank's greater investment in RS securities government bonds and T-Bills in RSD and EURO. Receivables from interest, fee and sale recorded a growth in the reporting period of RSD 446,6 million, or 16,0%. 8

9 4.2. Bank s Liabilities as at No. ITEM INDEXES (IN 000 RSD) % OF SHARE AS AT = (3:4)*100 6 I LIABILITIES 1. Transaction deposits ,0 15,2 2. Other deposits ,6 56,5 3. Borrowings ,6 0,3 4. Securities related liabilities Interest and fee liabilities ,8 0,0 6. Provisions ,2 0,4 7. Tax liabilities ,0 0,0 8. Liabilities from profit ,9 0,1 9. Liabilities for discontinued assets Deferred tax liabilities ,0 11. Other liabilities ,4 9,9 12. TOTAL LIABILITIES (from 1 to 11) ,4 82,4 CAPITAL 13. Share capital and issue premium ,0 10,5 14. Reserves from profit ,0 4,4 15. Revaluation reserves ,7 0,6 16. Unrealized losses based on securities available for sale ,7 0,0 17. Profit ,6 2,2 18. TOTAL CAPITAL (from 13 to 17) ,5 17,6 19. TOTAL LIABILITIES (12+18) ,1 100,0 II COMMISSION OPERATIONS AND OFF-BALANCE SHEET ITEMS ,9 Total liabilities at the end of the first six months of 2014 amount to RSD ,3 million and account for 82,4% of the total liabilities ( : 82,1%). Concurrently, total capital, in the amount of RSD ,5 million accounts for 17,6% ( : 17,9%) of total liabilities. Compared to the end of the previous year, total liabilities increased by RSD ,1 million, or 5,4%, whereas total capital increased by RSD 2.291,3 million, or 3,5%. Other deposits increased in the reporting period by RSD ,0 million, or 6,6%, whereas transaction deposits have been increased in comparison to the end of the last year by RSD 4.782,2 million, or 9,0%. Other liabilities decreased by RSD 2.269,0 million, or 5,6%. FX liabilities account for the largest share of other liabilities credit lines (RSD ,9 million) and subordinated loan (RSD 5.789,3 million) which was drawn down at the end of 2012 for the purpose of increasing the regulatory capital. 9

amount to RSD 273.")

10 In the first six months of this year there was a decrease in credit lines from abroad in net counter-value of RSD 1.091,0 million (EUR 11,8 million repaid and RSD 5,8 million drawn down). Within the structure of balance sheet liabilities the deposits from customers (transaction and other deposits) amount to RSD ,7 million, which accounts for 71,6% of total balance sheet liabilities, which is an increase in comparison to the beginning of the year of RSD ,2 million, or 7,1% Loans to Customers and Deposits from Customers as at Total loans to customers in 000RSD Total deposits from customers in 000 RSD ,5 18,2 18,5 18,8 17, Loans to customers Share of NPL (in %) The most important assets category, loans and deposits to customers, recorded a decrease of RSD 3.662,7 million (-2,0%), as well as a change in its share in total assets from 50,6% ( ) to 47,2%. At the end of June 2014, the Bank's total deposits amount to RSD ,7 million and account for 71,6% of the Bank's total liabilities (December 2013: 70,3%). Compared to the end of last year, the Bank's total deposits increased by RSD ,2 million (7,1%), other deposits increased by RSD ,0 million, or 6,6%, while transaction deposits increased by RSD 4.782,2 million, or 9,0%. If we exclude the effects of RSD depreciation on FX deposits and on RSD deposits with currency clause (RSD 2.205,8 million), total deposits record a growth in real terms in the amount of approximately RSD ,4 million. Increase in other deposits in the first six months of 2014 came primarily as a result of an increase of retail deposits (counter-value RSD 7.066,1 million), corporate deposits (counter-value RSD 6.974,1 million) and deposits of banks and financial organizations (RSD 4.061,0 million). In the past six months, within the above stated changes, retail FX savings have been increased by EUR 26,8 million. No. ITEM BALANCE AS AT BALANCE AS AT (IN 000 RSD) INDEX (2:3)*100 I LOANS TO CUSTOMERS (1+2+3) ,0 1. Corporate ,5 2. Retail ,2 3. Banks and financial organizations ,2 II DEPOSITS FROM CUSTOMERS (1+2+3) ,1 1. Corporate ,6 2. Retail ,8 3. Banks and financial organizations ,2 NOTE: Deposits also include transaction deposits. 10

11 As of , the Bank s total loans to customers stood at RSD ,5 million and have been decreased in comparison to the end of last year by RSD 3.662,7 million, or 2,0%. At the end of the second quarter of 2014, the level of loans and deposits to customers was considerably affected by corporate loans which reached RSD ,9 million (-5,6%) at the end of June, whereas the loans to banks and financial organizations have been increased by RSD 411,0 million, or 4,2% FX savings in the period from 2013 to in 000 EUR Having the reputation of safe and stable bank in the Serbian market, the Bank managed to increase FX savings deposits by EUR 26,8 million, or 1,8% in the observed period. Despite still present economic crisis, FX savings increased in the first six months of 2014 and reached the amount of EUR 1.493,1 million. Savers' trust enabled the Bank to retain its top position in the banking sector of the Republic of Serbia in terms of volume of FX savings, image and recognizability Commission Operations and Off-Balance Sheet Items in 2014 No. ITEM BALANCE AS AT BALANCE AS AT (IN 000 RSD) I OPERATIONS FOR AND ON BEHALF OF (commission operations) INDEX (2:3)* ,4 II CONTINGENT LIABILITIES ,7 1. Payable guarantees ,6 2. Performance bonds е ,9 3. Bill guarantee and bill acceptance ,0 4. Undrawn commitments ,6 5. Other off-balance sheet items that may lead to payment by the bank ,5 6. Uncovered letters of credit ,9 III UNCLASSIFIABLE OFF-BALANCE SHEET ITEMS ,2 1. FX savings bonds ,6 2. Securities in custody ,7 3. Other off-balance sheet items ,0 TOTAL (I +II+III) ,9 As of , contingent off-balance sheet liabilities amount to total of RSD ,3 million increase by RSD 2.075,1 million, or 6,7% in comparison to the end of the previous year, due to an increase of undrawn commitments. 11

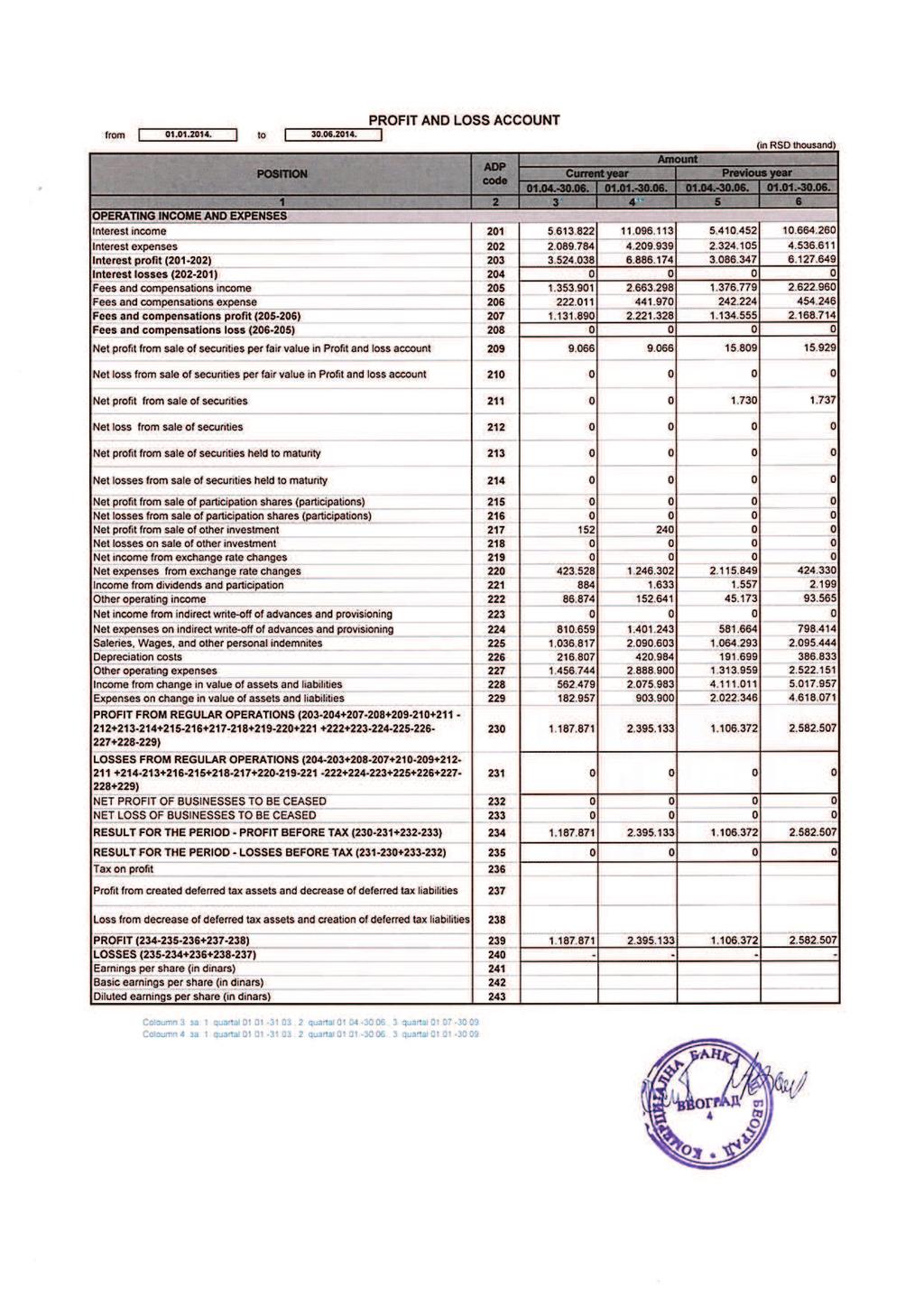

12 5. INCOME STATEMENT FOR THE PERIOD FROM TO No. ITEM ( IN 000 RSD) OPERATING INCOME AND EXPENSES INDEXES (3:4) 1.1. Interest income , Interest expenses ,8 1. Interest gains , Fee and commission income , Fee and commission expenses ,3 2. Fee and commission gains ,4 3. Net profit / loss from sale of securities at fair value through income statement Net profit / loss from sale of securities available for sale Net profit/loss from sale of securities held-to-maturity Net profit / loss from sale of stake (share) Net profit / loss from sale of other loans and advances Net profit / loss from exchange rate differentials and valuation adjustment of assets and liabilities ,6 9. Income from dividends and stakes ,3 10. Other operating income ,1 11. Net income / expenses from indirect write-off of loans and provisions ,5 12. Cost of salaries, fringe benefits and other personnel expenses ,8 13. Depreciation costs ,8 14. Operating and other business expenses ,5 15. RESULT FOR THE PERIOD PROFIT BEFORE TAX (from 1 to 14) ,7 16. Profit tax Profit from increased deferred tax assets and decreased deferred tax liabilities Loss from decreased deferred tax assets and increased deferred tax liabilities PROFIT (from 15 to 18) ,7 12

, while retail deposit interest accounts for the largest share of interest expenses (RSD 2.326,6 million, or 55,3%), which is mainly a result of deposited FX savings.")

13 5.1. Interest Income and Expenses Interest Income and Expenses in 000 RSD Interest income Interest expenses Interest gains amount to RSD 6.886,1 million, which, in comparison to the same period last year, represents an increase of 12,4%. Compared to the previous year, interest income increased by RSD 431,9 million, or by 4,0%, while interest expenses decreased by RSD 326,7 million, or 7,2%. Interest income by sectors in 2014 Interest expenses by sectors in ,4% 30,0% 31,4% 0,1% 0,4% 1,7% Banks and Securities Corporate Public sector Retail Foreign entities Other clients 15,4% 5,0% 22,8% 1,5% 55,3% 0,0% Banks and Securities Corporate Public sector Retail Foreign entities Other clients Corporate interest income accounts for the largest share of interest income (RSD 4.033,4 million, or 36,4%), while retail deposit interest accounts for the largest share of interest expenses (RSD 2.326,6 million, or 55,3%), which is mainly a result of deposited FX savings. Trends in the Bank's interest margin from 2013 to in % 8,00 6,00 On interest-bearing assets and liabilities 4,00 3,9 3,9 4,3 2,00 0, Q 2 Q Average lending rate 6,9 6,4 6,4 Average borrowing rate 3,0 2,5 2,1 Average interest margin 3,9 3,9 4,3 At the end of the second quarter of 2014, average lending rate was 6,4%, and average borrowing rate equaled 2,1%. As a result, in the second quarter of 2014, the Bank's average interest margin was 4,3%. 13

14 5.2. Fee Income and Expenses Fee income and expensesin 000 RSD Fee income Fee expenses Compared to the previous year, banking services-related fee and commission income increased by RSD 40,3 million, or by 1,5%, while fee and commission expenses decreased by RSD 12,3 million, or by 2,7%. In the first six months of 2014, fee and commission gains amounted to RSD 2.221,3 million and were higher than in the same period last year by 2,4% Realized operating profit Realized operating profit in 000 RSD Despite the adverse and unpredictable macroeconomic operating conditions and recession both in international and local economy, in the period between January 01 st to June 30 th, 2014, the Bank realised operating profit of RSD 2.395,1 million, which makes for a decrease of 7,3% in comparison to the same period last year. This amount of realized operating profit provided for the Bank, in the first six months of 2014, return on total capital of 7,2%, and return on share capital of 11,9%. PERFORMANCE INDICATORS PRESCRIBED BY THE LAW ON BANKS No. ITEM PRESCRIBED CAPITAL ADEQUACY RATIO (NET CAPITAL / CREDIT RISK + OPERATIONAL RISKS + OPEN FX POSITION) MIN. 12% 18,86% 18,45% 19,02% 2. RATIO OF INVESTMENT IN ENTITIES OUTSIDE THE FINANCIAL SECTOR AND FIXED ASSETS MAX. 60% 25,42% 25,93% 24,67% 3. BANK'S LARGE EXPOSURE RATIO MAX. 400% 127,95% 99,27% 115,90% 4. FX RISK RATIO MAX. 20% 1,05% 5,70% 2,12% 5. LIQUIDITY RATIO MIN. 0,8 3,61 4,26 3,45 14

15 6. DESCRIPTION OF KEY RISKS AND THREATS THE COMPANY IS EXPOSED TO A detailed overview of main risks and threats the Bank will be exposed to in the upcoming period is presented in chapter 5, Risk Management, Notes to Financial Statements. 7. ALL MAJOR TRANSACTIONS WITH RELATED ENTITIES As of , the following entities are related to the Bank: 1. Komercijalna banka a.d. Budva, Montenegro, 2. Komercijalna banka a.d. Banja Luka, Bosnia and Herzegovina, 3. KomBank Invest a.d. Beograd, 4. Four legal entities (Lasta doo, Viš trade doo, Desk doo, Menta doo) and a number of natural persons, according to the provisions of the Article 2 of the Law on Banks in the part which defines the term entities related to the bank. Total exposure to entities related to the Bank as of amounted to RSD thousand, which accounts for 2,9% of the capital of RSD thousand (maximum amount of total lending to all the entities related to the Bank is set by the Law on Banks at 20% of capital). The largest portion of the Bank's exposure to related entities as of , amounts to RSD thousand, or 1,9% of the Bank's capital and it relates to loans granted to natural persons related to the Bank. In accordance with Article 37 of the Law on Banks, the Bank did not grant its related entities any loans under the conditions that are more favorable than those which apply to other entities that are not related to the Bank. 8. KEY DATA ON BUSINESS PLAN IMPLEMENTATION FOR THE YEAR 2014 Implementation of the Strategy and Business Plan in the first six months of 2014 was carried out within the expected macroeconomic business conditions, including particularly: - The growth of GDP was recorded of 0,1% in the first quarter of 2014, in comparison to the same period last year (Office of Statistics), the plan for the whole year is a growth of 1,0% (MF, NBS), - Stable RSD exchange rate movements around the level of 115 dinars for 1 euro (RSD/EUR exchange rate as planned at end of the current year: 1 euro = 115,00 dinars (KB), whereas the actual exchange rate as of was: 1 euro = 115,79 dinars), - Inflation rate (year-on-year inflation rate, June 2014/June 2013: +1,3%) has been declining and is currently below the lower limit of the target rate for June this year (4,0+/-1,5%). In addition to above stated, the operations of the banks in the first six months of 2014, were also greatly affected by the public debt crisis in the Eurozone, parliamentary elections in RS and uncertainty about the formation of the new government, reluctance of foreign investors to invest in Serbia, geopolitical crisis regarding the status of Ukraine, reduced demand for loans, particularly with respect to corporate customers and increased credit risk due to recession and unemployment in the real sector. 15

16 8.1. Planned and realized values of balance sheet for the first half of 2014 The Bank s total balance-sheet assets, at the end of the second quarter of 2014 amount to RSD ,8 million and are higher than planned value for the same period by RSD ,0 million, or 10,5%. Considerable positive differences between the realized and planned values are recorded with respect to securities (other than own), realized value is higher by RSD ,4 million, or +72,8%, as a result of additional investment of funds in government, both RSD and FX, securities. Decline in realized value when compared to the planned value is recorded particularly with respect to callable deposits and loans reduction of RSD 7.649,0 million (-15,7%) as a result of decreased investment in NBS repo transactions and a decrease in the amount of allocated FX required reserve. As opposed to decrease in callable deposits and loans, there was an increase in cash and cash equivalents in the amount of RSD ,8 million, primarily due to an increased amount of funds on the drawing account and on FX accounts (RSD ,7 million compared to the initial balance). In the structure of balance sheet liabilities the greatest positive discrepancy from the planned values was recorded in deposits (RSD ,7 million), which was mostly prompted by the growth of retail deposits (RSD ,9 million), growth of banks and financial organizations deposits (RSD ,2 million), while negative discrepancy was recorded in foreign credit lines decrease in the amount of RSD 3.333,8 million. Trend in RSD exchange rate - appreciation (1,0% against EUR), increased to a certain extent the differences between realized and planned values. The achieved growth of balance sheet assets provided the Bank an increase its market share from 12,8% in 2013 to 13,2% at the end of June 2014, while the banking sector, in the period recorded a decline of 0,8%. Realized and planned values of items from assets and liabilities in the balance sheet as of are as follows: No. I T E M Plan Realized (IN 000 RSD) Plan realization in % =4/3 ASSETS Cash and cash equivalents ,6 2. Callable deposits and loans ,3 3. Loans and deposits to customers ( ) , Corporate , Retail , Banks and financial organizations ,5 4. Other assets ,1 5. TOTAL ASSETS ( ) ,5 Realized and planned values of items from assets and liabilities in the balance sheet as of are as follows: LIABILITIES 1. Deposits , Corporate , Retail , Banks and financial organizations ,8 2. Other liabilities ,4 3. Total liabilities (1+2) ,2 4. Total capital ,4 5. TOTAL LIABILITIES (3+4) ,5 16

17

18

19

20

21

22

ON THE BANK OPERATION IN THE SECOND QUARTER OF 2012

REPORT ON THE BANK OPERATION IN THE SECOND QUARTER OF 2012 Belgrade, July 2012 1. 2. 3. TABLE OF CONTENTS PRESENTATION OF BASIC INDICATORS OF BANK OPERATION IN THE PERIOD BETWEEN 31.12.2011 AND 30.06.2012

REPORT ON THE BANK OPERATION IN THE SECOND QUARTER OF 2012 Belgrade, July 2012 1. 2. 3. TABLE OF CONTENTS PRESENTATION OF BASIC INDICATORS OF BANK OPERATION IN THE PERIOD BETWEEN 31.12.2011 AND 30.06.2012

CONSOLIDATED REPORT ON GROUP S OPERATIONS AS OF 30/06/2013

CONSOLIDATED REPORT ON GROUP S OPERATIONS AS OF 30/06/2013 BELGRADE, AUGUST 2013 1 C O N T E N T S 1. 2. 3. OVERVIEW OF THE PEFORMANCE INDICATORS OF THE GROUP IN THE PERIOD FROM 31.12.2012 TO 30.06.2013

CONSOLIDATED REPORT ON GROUP S OPERATIONS AS OF 30/06/2013 BELGRADE, AUGUST 2013 1 C O N T E N T S 1. 2. 3. OVERVIEW OF THE PEFORMANCE INDICATORS OF THE GROUP IN THE PERIOD FROM 31.12.2012 TO 30.06.2013

KOMERCIJALNA BANKA A.D., BEOGRAD. Consolidated Financial Statements Year Ended December 31, 2015 and Independent Auditors Report

Consolidated Financial Statements Year Ended and Independent Auditors Report CONTENTS Page Independent Auditors' Report 1 Consolidated Financial Statements: Consolidated Consolidated Statement of Financial

Consolidated Financial Statements Year Ended and Independent Auditors Report CONTENTS Page Independent Auditors' Report 1 Consolidated Financial Statements: Consolidated Consolidated Statement of Financial

BANKING SECTOR IN SERBIA

BANK SUPERVISION DEPARTMENT BANKING SECTOR IN SERBIA First Quarter Report 2018 September 2018 Contents: 1 BASIC INFORMATION ON SERBIAN BANKING SECTOR... 3 1.1 Selected parameters of the Serbian banking

BANK SUPERVISION DEPARTMENT BANKING SECTOR IN SERBIA First Quarter Report 2018 September 2018 Contents: 1 BASIC INFORMATION ON SERBIAN BANKING SECTOR... 3 1.1 Selected parameters of the Serbian banking

BANKING SECTOR IN SERBIA

ADMINISTRATION FOR SUPERVISION OF FINANCIAL INSTITUTIONS BANK SUPERVISION DEPARTMENT BANKING SECTOR IN SERBIA Fourth Quarter Report 2017 June 2018 Contents: 1 BASIC INFORMATION ON SERBIAN BANKING SECTOR...

ADMINISTRATION FOR SUPERVISION OF FINANCIAL INSTITUTIONS BANK SUPERVISION DEPARTMENT BANKING SECTOR IN SERBIA Fourth Quarter Report 2017 June 2018 Contents: 1 BASIC INFORMATION ON SERBIAN BANKING SECTOR...

KOMERCIJALNA BANKA A.D., BEOGRAD. Unconsolidated Financial Statements Year Ended December 31, 2015 and Independent Auditors Report

KOMERCIJALNA BANKA A.D., BEOGRAD Unconsolidated Financial Statements Year Ended and Independent Auditors Report KOMERCIJALNA BANKA A.D., BEOGRAD CONTENTS Page Independent Auditors' Report 1 Financial Statements:

KOMERCIJALNA BANKA A.D., BEOGRAD Unconsolidated Financial Statements Year Ended and Independent Auditors Report KOMERCIJALNA BANKA A.D., BEOGRAD CONTENTS Page Independent Auditors' Report 1 Financial Statements:

KOMERCIJALNA BANKA A.D., BEOGRAD. Consolidated Financial Statements For the Year Ended December 31, 2010 and Independent Auditors Report

Consolidated Financial Statements For the Year Ended and Independent Auditors Report CONTENT Page Independent Auditors' Report 1 Consolidated Financial Statements: Consolidated Income Statement 2 Consolidated

Consolidated Financial Statements For the Year Ended and Independent Auditors Report CONTENT Page Independent Auditors' Report 1 Consolidated Financial Statements: Consolidated Income Statement 2 Consolidated

KOMERCIJALNA BANKA A.D., BEOGRAD. Financial Statements Year Ended December 31, 2014 and Independent Auditors Report

KOMERCIJALNA BANKA A.D., BEOGRAD Financial Statements Year Ended and Independent Auditors Report KOMERCIJALNA BANKA A.D., BEOGRAD CONTENTS Page Independent Auditors' Report 1 Financial Statements: Balance

KOMERCIJALNA BANKA A.D., BEOGRAD Financial Statements Year Ended and Independent Auditors Report KOMERCIJALNA BANKA A.D., BEOGRAD CONTENTS Page Independent Auditors' Report 1 Financial Statements: Balance

KOMERCIJALNA BANKA A.D., BEOGRAD. Financial Statements For the Year Ended December 31, 2010 and Independent Auditors Report

Financial Statements For the Year Ended and Independent Auditors Report CONTENT Page Independent Auditors' Report 1 Financial Statements: Income Statement 2 Balance Sheet 3 Statement of Changes in Equity

Financial Statements For the Year Ended and Independent Auditors Report CONTENT Page Independent Auditors' Report 1 Financial Statements: Income Statement 2 Balance Sheet 3 Statement of Changes in Equity

KOMERCIJALNA BANKA A.D., BEOGRAD. Consolidated Financial Statements December 31, 2006 and Independent Auditors Report

KOMERCIJALNA BANKA A.D., BEOGRAD Consolidated Financial Statements and Independent Auditors Report CONTENTS Page Independent Auditors Report 1 2 Consolidated Statement of Income 3 Consolidated Balance

KOMERCIJALNA BANKA A.D., BEOGRAD Consolidated Financial Statements and Independent Auditors Report CONTENTS Page Independent Auditors Report 1 2 Consolidated Statement of Income 3 Consolidated Balance

Financial Statements. and Independent Auditors Report

KOMERCIJALNA BANKA A.D., BEOGRAD Financial Statements Year Ended and Independent Auditors Report KOMERCIJALNA BANKA A.D., BEOGRAD CONTENTS Page Independent Auditors' Report 1-2 Income Statement 3 Statement

KOMERCIJALNA BANKA A.D., BEOGRAD Financial Statements Year Ended and Independent Auditors Report KOMERCIJALNA BANKA A.D., BEOGRAD CONTENTS Page Independent Auditors' Report 1-2 Income Statement 3 Statement

PUBLIC COMPANY S SEMI-ANNUAL CONSOLIDATED REPORT FOR 2016

PUBLIC COMPANY S SEMI-ANNUAL CONSOLIDATED REPORT FOR 2016 C O N T E N T S 1. SEMI-ANNUAL REPORT ON GROUP'S OPERATIONS 2. CONSOLIDATED FINANCIAL STATEMENTS 3. BALANCE SHEET CONSOLIDATED INCOME STATEMENT

PUBLIC COMPANY S SEMI-ANNUAL CONSOLIDATED REPORT FOR 2016 C O N T E N T S 1. SEMI-ANNUAL REPORT ON GROUP'S OPERATIONS 2. CONSOLIDATED FINANCIAL STATEMENTS 3. BALANCE SHEET CONSOLIDATED INCOME STATEMENT

PUBLIC COMPANY S SEMI-ANNUAL CONSOLIDATED REPORT FOR 2015

PUBLIC COMPANY S SEMI-ANNUAL CONSOLIDATED REPORT FOR 2015 C O N T E N T S 1. SEMI-ANNUAL REPORT ON GROUP'S OPERATIONS 2. CONSOLIDATED FINANCIAL STATEMENTS 3. BALANCE SHEET CONSOLIDATED INCOME STATEMENT

PUBLIC COMPANY S SEMI-ANNUAL CONSOLIDATED REPORT FOR 2015 C O N T E N T S 1. SEMI-ANNUAL REPORT ON GROUP'S OPERATIONS 2. CONSOLIDATED FINANCIAL STATEMENTS 3. BALANCE SHEET CONSOLIDATED INCOME STATEMENT

Consolidated Financial Statements. Independent Auditors Report

KOMERCIJALNA BANKA A.D., BEOGRAD Consolidated Financial Statements Year Ended and Independent Auditors Report CONTENTS Page Independent Auditors' Report 1-2 Consolidated Financial Statements: Consolidated

KOMERCIJALNA BANKA A.D., BEOGRAD Consolidated Financial Statements Year Ended and Independent Auditors Report CONTENTS Page Independent Auditors' Report 1-2 Consolidated Financial Statements: Consolidated

Pensions from the Republic of Croatia, Federation of BiH, Republic of Montenegro and payment of disability benefits from Republic of Srpska

OVERVIEW OF TARIFF OF FEES APPLICABLE TO BANK'S RETAIL OPERATIONS AS OF 28.10.2015. Number of tariff X RETAIL OPERATIONS 1. FX SAVINGS ACCOUNTS /SAVINGS BOOKS 1.1. Opening and maintaining Free of charge

OVERVIEW OF TARIFF OF FEES APPLICABLE TO BANK'S RETAIL OPERATIONS AS OF 28.10.2015. Number of tariff X RETAIL OPERATIONS 1. FX SAVINGS ACCOUNTS /SAVINGS BOOKS 1.1. Opening and maintaining Free of charge

Republic of Serbia BILATERAL SCREENING Chapter 17 Economic and monetary policy EXCHANGE RATE POLICY

Republic of Serbia BILATERAL SCREENING Chapter 17 Economic and monetary policy EXCHANGE RATE POLICY Chapter 17 Economic and Monetary Policy 1. Legal framework of the EU 2. Legal framework of the Republic

Republic of Serbia BILATERAL SCREENING Chapter 17 Economic and monetary policy EXCHANGE RATE POLICY Chapter 17 Economic and Monetary Policy 1. Legal framework of the EU 2. Legal framework of the Republic

REVIEW OF TARIFF OF FEES APPLIED IN RETAILTRANSACTIONS OF THE BANK AS OF AMOUNT OF FEES, PROVISIONS AND SERVICE tariff item

REVIEW OF TARIFF OF FEES APPLIED IN RETAILTRANSACTIONS OF THE BANK AS OF 17.03.2015 Number of tariff X RETAIL TRANSACTIONS 1. FX SAVINGS ACCOUNTS/BOOKS 1.1. Opening and keeping 1.2. In payments 1.2.1.

REVIEW OF TARIFF OF FEES APPLIED IN RETAILTRANSACTIONS OF THE BANK AS OF 17.03.2015 Number of tariff X RETAIL TRANSACTIONS 1. FX SAVINGS ACCOUNTS/BOOKS 1.1. Opening and keeping 1.2. In payments 1.2.1.

ANNUAL REPORT FOR THE YEAR 2011

ANNUAL REPORT FOR THE YEAR 211 1 C O N T E N T S FOREWORD BY THE EXECUTIVE BOARD OF THE BANK 2 1. OVERVIEW OF KEY PERFORMANCE INDICATORS OF THE BANK IN THE PERIOD FROM 27 TO 211 4 2. MACROECONOMIC BUSINESS

ANNUAL REPORT FOR THE YEAR 211 1 C O N T E N T S FOREWORD BY THE EXECUTIVE BOARD OF THE BANK 2 1. OVERVIEW OF KEY PERFORMANCE INDICATORS OF THE BANK IN THE PERIOD FROM 27 TO 211 4 2. MACROECONOMIC BUSINESS

BANK SUPERVISION DEPARTMENT BANKING SECTOR IN SERBIA

BANK SUPERVISION DEPARTMENT BANKING SECTOR IN SERBIA Second Quarter Report 2014 Banking Sector in Serbia Second Quarter Report 2014 Contents 1. BASIC INFORMATION... 3 1.1. SELECTED PARAMETERS OF THE SERBIAN

BANK SUPERVISION DEPARTMENT BANKING SECTOR IN SERBIA Second Quarter Report 2014 Banking Sector in Serbia Second Quarter Report 2014 Contents 1. BASIC INFORMATION... 3 1.1. SELECTED PARAMETERS OF THE SERBIAN

Inflows via Komercijalna banka AD Budva and Komercijalna banka AD Banja Luka

OVERVIEW OF TARIFF OF FEES APPLICABLE TO BANK'S RETAIL OPERATIONS AS OF 28.08.2017. X RETAIL OPERATIONS 1. FX SAVINGS ACCOUNTS /SAVINGS BOOKS 1.1. Opening and maintaining Free of charge 1.2. Incoming payments/deposits

OVERVIEW OF TARIFF OF FEES APPLICABLE TO BANK'S RETAIL OPERATIONS AS OF 28.08.2017. X RETAIL OPERATIONS 1. FX SAVINGS ACCOUNTS /SAVINGS BOOKS 1.1. Opening and maintaining Free of charge 1.2. Incoming payments/deposits

OF THE REGULAR GENERAL MEETING OF BANK S SHAREHOLDERS HELD ON MAY 24 TH, 2016

MINUTES OF THE REGULAR GENERAL MEETING OF BANK S SHAREHOLDERS HELD ON MAY 24 TH, 2016 Belgrade, 24.05.2016 KOMERCIJALNA BANKA AD BEOGRAD GENERAL MEETING OF BANK S SHAREHOLDERS Number: 9520 Belgrade, 24.05.2016

MINUTES OF THE REGULAR GENERAL MEETING OF BANK S SHAREHOLDERS HELD ON MAY 24 TH, 2016 Belgrade, 24.05.2016 KOMERCIJALNA BANKA AD BEOGRAD GENERAL MEETING OF BANK S SHAREHOLDERS Number: 9520 Belgrade, 24.05.2016

VOLUNTARY PENSION FUNDS SECTOR IN SERBIA. Fourth Quarter Report 2011

VOLUNTARY PENSION FUNDS SECTOR IN SERBIA Fourth Quarter Report CONTENT 1. INTRODUCTION... 3 2. MARKET PARTICIPANTS... 6 3. VPF OPERATIONS... 7 VPF net assets... 7 Structure of VPF assets... 8 VPF securities

VOLUNTARY PENSION FUNDS SECTOR IN SERBIA Fourth Quarter Report CONTENT 1. INTRODUCTION... 3 2. MARKET PARTICIPANTS... 6 3. VPF OPERATIONS... 7 VPF net assets... 7 Structure of VPF assets... 8 VPF securities

KOMERCIJALNA BANKA A.D. BANjA LUKA

FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2011 WITH INDEPENDENT AUDITORS RERORT KOMERCIJALNA BANKA A.D. BANjA LUKA Banja Luka, March 2012 Financial Statements for the year ended 31 December 2011

FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2011 WITH INDEPENDENT AUDITORS RERORT KOMERCIJALNA BANKA A.D. BANjA LUKA Banja Luka, March 2012 Financial Statements for the year ended 31 December 2011

BANK SUPERVISION DEPARTMENT

BANK SUPERVISION DEPARTMENT BANKING SECTOR IN SERBIA First Quarter Report 2013 Contents 1. BASIC INFORMATION... 4 1.1. SELECTED PARAMETERS OF THE SERBIAN BANKING SECTOR... 4 1.2. CONCENTRATION AND COMPETITION...

BANK SUPERVISION DEPARTMENT BANKING SECTOR IN SERBIA First Quarter Report 2013 Contents 1. BASIC INFORMATION... 4 1.1. SELECTED PARAMETERS OF THE SERBIAN BANKING SECTOR... 4 1.2. CONCENTRATION AND COMPETITION...

ANNUAL REPORT ON OPERATION OF KOMERCIJALNA BANKA AD FOR 2017

ANNUAL REPORT ON OPERATION OF KOMERCIJALNA BANKA AD FOR 217 March 218 1 C O N T E N T 1. KEY PERFOMANCE INDICATORS OF THE BANK 2 2. МACROECONOMIC BUSINESS CONDITIONS 5 3. BANKING SECTOR OF THE REPUBLIC

ANNUAL REPORT ON OPERATION OF KOMERCIJALNA BANKA AD FOR 217 March 218 1 C O N T E N T 1. KEY PERFOMANCE INDICATORS OF THE BANK 2 2. МACROECONOMIC BUSINESS CONDITIONS 5 3. BANKING SECTOR OF THE REPUBLIC

PIRAEUS BANK A.D. BEOGRAD FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2016 AND INDEPENDENT AUDITOR'S REPORT

PIRAEUS BANK A.D. BEOGRAD FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2016 AND INDEPENDENT AUDITOR'S REPORT PIRAEUS BANK A.D. BEOGRAD Financial statements for the year ended 31 December 2016 Content

PIRAEUS BANK A.D. BEOGRAD FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2016 AND INDEPENDENT AUDITOR'S REPORT PIRAEUS BANK A.D. BEOGRAD Financial statements for the year ended 31 December 2016 Content

TRENDS IN LENDING Third Quarter Report 2018

УНУТРАШЊА УПОТРЕБА TRENDS IN LENDING Third Quarter Report 218 Belgrade, December 218 УНУТРАШЊА УПОТРЕБА Introductory note Trends in Lending is an in-depth analysis of the latest trends in lending, which

УНУТРАШЊА УПОТРЕБА TRENDS IN LENDING Third Quarter Report 218 Belgrade, December 218 УНУТРАШЊА УПОТРЕБА Introductory note Trends in Lending is an in-depth analysis of the latest trends in lending, which

QUARTERLY REVIEW OF THE DYNAMICS OF FINANCIAL STABILITY INDICATORS FOR THE REPUBLIC OF SERBIA

FINANCIAL STABILITY DEPARTMENT QUARTERLY REVIEW OF THE DYNAMICS OF FINANCIAL STABILITY INDICATORS FOR THE REPUBLIC OF SERBIA Third Quarter 217 December 217 Content 1. Financial Soundness Indicators Chart

FINANCIAL STABILITY DEPARTMENT QUARTERLY REVIEW OF THE DYNAMICS OF FINANCIAL STABILITY INDICATORS FOR THE REPUBLIC OF SERBIA Third Quarter 217 December 217 Content 1. Financial Soundness Indicators Chart

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

OTP banka Srbija a.d. Novi Sad NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS December 31, 2010 Consolidated legal entites: - OTP banka Srbija a.d. Novi Sad - OTP Investments d.o.o. Novi Sad Novi Sad,

OTP banka Srbija a.d. Novi Sad NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS December 31, 2010 Consolidated legal entites: - OTP banka Srbija a.d. Novi Sad - OTP Investments d.o.o. Novi Sad Novi Sad,

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

ABCD KPMG d.o.o. Beograd Kraljice Natalije 11 11000 Belgrade Serbia Telephone: Fax: E-mail: Internet: +381 11 20 50 500 +381 11 20 50 550 info@kpmg.rs www.kpmg.rs Independent Auditors Report TO THE OWNERS

ABCD KPMG d.o.o. Beograd Kraljice Natalije 11 11000 Belgrade Serbia Telephone: Fax: E-mail: Internet: +381 11 20 50 500 +381 11 20 50 550 info@kpmg.rs www.kpmg.rs Independent Auditors Report TO THE OWNERS

STRATEGY. On Managing the Shares of the Banks owned by the Republic of Serbia for the period

GOVERNMENT OF THE REPUBLIC OF SERBIA MINISTRY OF FINANCE STRATEGY On Managing the Shares of the Banks owned by the Republic of Serbia for the period 2009 2012 Belgrade, April 2009 INTRODUCTION Reconstruction

GOVERNMENT OF THE REPUBLIC OF SERBIA MINISTRY OF FINANCE STRATEGY On Managing the Shares of the Banks owned by the Republic of Serbia for the period 2009 2012 Belgrade, April 2009 INTRODUCTION Reconstruction

2. Investments in debt securities that can be used for refinancing in NBRM 2a. Treasury bills 2b. Government securities 2c. Impairment. 5d.

KOMERCIJALNA BANKA AD SKOPJE ANNUAL REPORT OF KOMERCIJALNA BANKA AD SKOPJE for the period from 01.01. to 31.12.2011 Skopje, February 2012 2 BALANCE SHEET as at 31.12.2011 No. Amount ITEM Previous year

KOMERCIJALNA BANKA AD SKOPJE ANNUAL REPORT OF KOMERCIJALNA BANKA AD SKOPJE for the period from 01.01. to 31.12.2011 Skopje, February 2012 2 BALANCE SHEET as at 31.12.2011 No. Amount ITEM Previous year

Instruments for hedging against exchange rate risk in the Republic of Serbia. Monetary Operations Department National Bank of Serbia

Instruments for hedging against exchange rate risk in the Republic of Serbia Monetary Operations Department National Bank of Serbia April 2018 CONTENTS: I Dinarisation Strategy II Need for hedging against

Instruments for hedging against exchange rate risk in the Republic of Serbia Monetary Operations Department National Bank of Serbia April 2018 CONTENTS: I Dinarisation Strategy II Need for hedging against

OVERVIEW OF TARIFF OF FEES APPLICABLE TO BANK'S RETAIL OPERATIONS AS OF

Date of publishing: 16.03.2018 OVERVIEW OF TARIFF OF FEES APPLICABLE TO BANK'S RETAIL OPERATIONS AS OF 01.04.2018. X RETAIL OPERATIONS 1. FX SAVINGS ACCOUNTS /SAVINGS BOOKS 1.1. Opening and maintaining

Date of publishing: 16.03.2018 OVERVIEW OF TARIFF OF FEES APPLICABLE TO BANK'S RETAIL OPERATIONS AS OF 01.04.2018. X RETAIL OPERATIONS 1. FX SAVINGS ACCOUNTS /SAVINGS BOOKS 1.1. Opening and maintaining

INSURANCE SUPERVISION DEPARTMENT PENSION FUNDS SUPERVISION DIVISION VOLUNTARY PENSION FUNDS IN SERBIA

INSURANCE SUPERVISION DEPARTMENT PENSION FUNDS SUPERVISION DIVISION VOLUNTARY PENSION FUNDS IN SERBIA Second Quarter Report Contents: 1. Market participants... 3 2. VPF net assets... 4 3. Structure of

INSURANCE SUPERVISION DEPARTMENT PENSION FUNDS SUPERVISION DIVISION VOLUNTARY PENSION FUNDS IN SERBIA Second Quarter Report Contents: 1. Market participants... 3 2. VPF net assets... 4 3. Structure of

NATIONAL BANK OF SERBIA R E P O R T ON DINARISATION OF THE SERBIAN FINANCIAL SYSTEM. June 2014

NATIONAL BANK OF SERBIA R E P O R T ON DINARISATION OF THE SERBIAN FINANCIAL SYSTEM June 214 Belgrade, September 214 Introductory note A more extensive use of the dinar in the financial system and better

NATIONAL BANK OF SERBIA R E P O R T ON DINARISATION OF THE SERBIAN FINANCIAL SYSTEM June 214 Belgrade, September 214 Introductory note A more extensive use of the dinar in the financial system and better

NATIONAL BANK OF SERBIA REPORT ON DINARISATION OF THE SERBIAN FINANCIAL SYSTEM

NATIONAL BANK OF SERBIA REPORT ON DINARISATION OF THE SERBIAN FINANCIAL SYSTEM June 216 Introductory note A more extensive use of the dinar in the financial system and better currency matching of income

NATIONAL BANK OF SERBIA REPORT ON DINARISATION OF THE SERBIAN FINANCIAL SYSTEM June 216 Introductory note A more extensive use of the dinar in the financial system and better currency matching of income

Independent Auditor's report 1. Income Statement 2. Balance Sheet 3. Cash Flow Statement 4-5. Statement of Changes in Equity 6

FINANCIAL STATEMENTS FOR THE PERIOD FROM 1 JANUARY TO 31 DECEMBER 2007 CONTENTS Independent Auditor's report 1 Income Statement 2 Balance Sheet 3 Cash Flow Statement 4-5 Statement of Changes in Equity

FINANCIAL STATEMENTS FOR THE PERIOD FROM 1 JANUARY TO 31 DECEMBER 2007 CONTENTS Independent Auditor's report 1 Income Statement 2 Balance Sheet 3 Cash Flow Statement 4-5 Statement of Changes in Equity

OTP BANKA SRBIJA A.D., NOVI SAD. Consolidated Financial Statements Year Ended December 31, 2014 and Independent Auditors Report

Consolidated Financial Statements Year Ended 2014 and Independent Auditors Report CONTENTS Page Independent Auditors' Report 1 Consolidated Financial Statements: Consolidated Income Statement 2 Consolidated

Consolidated Financial Statements Year Ended 2014 and Independent Auditors Report CONTENTS Page Independent Auditors' Report 1 Consolidated Financial Statements: Consolidated Income Statement 2 Consolidated

REPORT ON DINARISATION OF THE SERBIAN FINANCIAL SYSTEM

REPORT ON DINARISATION OF THE SERBIAN FINANCIAL SYSTEM December 215 Introductory note A more extensive use of the dinar in the financial system and better currency matching of income and expenses of the

REPORT ON DINARISATION OF THE SERBIAN FINANCIAL SYSTEM December 215 Introductory note A more extensive use of the dinar in the financial system and better currency matching of income and expenses of the

ERSTE BANK A.D., NOVI SAD FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2014

FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2014 ERSTE BANK a.d. NOVI SAD CONTENT Page Independent Auditors' Report 1 Income statement for the year ended 31 December 2014 2 Statement of comprehensive

FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2014 ERSTE BANK a.d. NOVI SAD CONTENT Page Independent Auditors' Report 1 Income statement for the year ended 31 December 2014 2 Statement of comprehensive

FEE INFORMATION DOCUMENT for a payment service user an entrepreneur and a legal entity

Annex 1 FEE INFORMATION DOCUMENT for a payment service user an entrepreneur and a legal entity Name of the payment service provider: Societe Generale Banka Srbija a.d. Beograd Name (package) of a payment

Annex 1 FEE INFORMATION DOCUMENT for a payment service user an entrepreneur and a legal entity Name of the payment service provider: Societe Generale Banka Srbija a.d. Beograd Name (package) of a payment

Key NBS results in the past six years. Presentation of the Inflation Report - August 2018

Key NBS results in the past six years Presentation of the Inflation Report - August 1 Belgrade, 1 August 1 Inflation in Serbia has been low and stable for five years. 1.9%.% Inflation was reduced from

Key NBS results in the past six years Presentation of the Inflation Report - August 1 Belgrade, 1 August 1 Inflation in Serbia has been low and stable for five years. 1.9%.% Inflation was reduced from

Management s Responsibility for the Separate Financial Statements

kpmg KPMG d.o.o. Beograd Kraljice Natalije 11 11000 Belgrade Serbia Independent Auditors Report Tel.: +381 (0)11 20 50 500 Fax: +381 (0)11 20 50 550 www.kpmg.com/rs T R A N S L A T I O N TO THE SHAREHOLDERS

kpmg KPMG d.o.o. Beograd Kraljice Natalije 11 11000 Belgrade Serbia Independent Auditors Report Tel.: +381 (0)11 20 50 500 Fax: +381 (0)11 20 50 550 www.kpmg.com/rs T R A N S L A T I O N TO THE SHAREHOLDERS

BANCA INTESA a.d. BELGRADE. Separate Financial Statements as of and for the Year Ended 31 December 2017 and Independent Auditor s Report

Separate Financial Statements as of and for the Year Ended 31 December 2017 and Independent Auditor s Report CONTENTS Page INDEPENDENT AUDITOR S REPORT 1-2 SEPARATE FINANCIAL STATEMENTS Separate Balance

Separate Financial Statements as of and for the Year Ended 31 December 2017 and Independent Auditor s Report CONTENTS Page INDEPENDENT AUDITOR S REPORT 1-2 SEPARATE FINANCIAL STATEMENTS Separate Balance

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 December 2015 1. THE ESTABLISHMENT AND OPERATIONS These financial statements are consolidated financial statements of Credit Agricole

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 December 2015 1. THE ESTABLISHMENT AND OPERATIONS These financial statements are consolidated financial statements of Credit Agricole

NATIONAL BANK OF SERBIA TRENDS IN LENDING. Fourth Quarter Report 2018

NATIONAL BANK OF SERBIA TRENDS IN LENDING Fourth Quarter Report 218 Belgrade, March 219 ii Introductory note is an in-depth analysis of the latest trends in lending, which aims to ensure better understanding

NATIONAL BANK OF SERBIA TRENDS IN LENDING Fourth Quarter Report 218 Belgrade, March 219 ii Introductory note is an in-depth analysis of the latest trends in lending, which aims to ensure better understanding

FEE INFORMATION DOCUMENT for a payment service user an entrepreneur and a legal entity

Annex 1 FEE INFORMATION DOCUMENT for a payment service user an entrepreneur and a legal entity Name of the payment service provider: Societe Generale Banka Srbija a.d. Beograd Name (package) of a payment

Annex 1 FEE INFORMATION DOCUMENT for a payment service user an entrepreneur and a legal entity Name of the payment service provider: Societe Generale Banka Srbija a.d. Beograd Name (package) of a payment

WIENER RE A.D.O. BELGRADE

WIENER RE A.D.O. BELGRADE Financial statements for the year ended December 31, 2015 prepared in accordance with International Financial Reporting Standards with Independent Auditors Report CONTENT I II

WIENER RE A.D.O. BELGRADE Financial statements for the year ended December 31, 2015 prepared in accordance with International Financial Reporting Standards with Independent Auditors Report CONTENT I II

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

ABCD KPMG d.o.o. Beograd Kraljice Natalije 11 11000 Belgrade Serbia Telephone: Fax: E-mail: Internet: +381 11 20 50 500 +381 11 20 50 550 info@kpmg.rs www.kpmg.rs Independent Auditors Report TO THE SHAREHOLDERS

ABCD KPMG d.o.o. Beograd Kraljice Natalije 11 11000 Belgrade Serbia Telephone: Fax: E-mail: Internet: +381 11 20 50 500 +381 11 20 50 550 info@kpmg.rs www.kpmg.rs Independent Auditors Report TO THE SHAREHOLDERS

Management s Responsibility for the Financial Statements

kpmg KPMG d.o.o. Beograd Kraljice Natalije 11 11000 Belgrade Serbia Tel.: +381 (0)11 20 50 500 Fax: +381 (0)11 20 50 550 www.kpmg.com/rs Independent Auditors Report T R A N S L A T I O N TO THE OWNERS

kpmg KPMG d.o.o. Beograd Kraljice Natalije 11 11000 Belgrade Serbia Tel.: +381 (0)11 20 50 500 Fax: +381 (0)11 20 50 550 www.kpmg.com/rs Independent Auditors Report T R A N S L A T I O N TO THE OWNERS

INSURANCE SUPERVISION DEPARTMENT PENSION FUNDS SUPERVISION DIVISION VOLUNTARY PENSION FUNDS SECTOR IN SERBIA

INSURANCE SUPERVISION DEPARTMENT PENSION FUNDS SUPERVISION DIVISION VOLUNTARY PENSION FUNDS SECTOR IN SERBIA Fourth Quarter Report 2018 Contents: 1 Market participants... 3 2 VPF net assets... 4 3 Structure

INSURANCE SUPERVISION DEPARTMENT PENSION FUNDS SUPERVISION DIVISION VOLUNTARY PENSION FUNDS SECTOR IN SERBIA Fourth Quarter Report 2018 Contents: 1 Market participants... 3 2 VPF net assets... 4 3 Structure

RS Official Gazette, No 76/2018

RS Official Gazette, No 76/2018 Pursuant to Article 14, paragraph 1, item 7 and Article 40 of the Law on the National Bank of Serbia (RS Official Gazette, Nos 72/2003, 55/2004, 85/2005 other law, 44/2010,

RS Official Gazette, No 76/2018 Pursuant to Article 14, paragraph 1, item 7 and Article 40 of the Law on the National Bank of Serbia (RS Official Gazette, Nos 72/2003, 55/2004, 85/2005 other law, 44/2010,

NATIONAL BANK OF SERBIA. Speech at the presentation of the Inflation Report November 2017

NATIONAL BANK OF SERBIA Speech at the presentation of the Inflation Report November Dr Ana Ivković, General Manager Directorate for Economic Research and Statistics Belgrade, November Ladies and gentlemen,

NATIONAL BANK OF SERBIA Speech at the presentation of the Inflation Report November Dr Ana Ivković, General Manager Directorate for Economic Research and Statistics Belgrade, November Ladies and gentlemen,

Slovenia - Kosovo Business Conference, June 07, 2016 Kosovo investments & development and project finance possibilities

Bogdan Podlesnik, MSc. Member of Management Board Yll Sejdiu, MSc. Deputy Director of Corporate Division Slovenia - Kosovo Business Conference, June 07, 2016 Kosovo investments & development and project

Bogdan Podlesnik, MSc. Member of Management Board Yll Sejdiu, MSc. Deputy Director of Corporate Division Slovenia - Kosovo Business Conference, June 07, 2016 Kosovo investments & development and project

immigon portfolioabbau ag INTERIM REPORT AS AT 31 MARCH 2016 immigon portfolioabbau ag A-1090 Vienna, Peregringasse 2

immigon portfolioabbau ag INTERIM REPORT AS AT 31 MARCH 2016 immigon portfolioabbau ag A-1090 Vienna, Peregringasse 2 2 INTERIM REPORT AS AT 31 MARCH 2016 The interim report covers the period from the

immigon portfolioabbau ag INTERIM REPORT AS AT 31 MARCH 2016 immigon portfolioabbau ag A-1090 Vienna, Peregringasse 2 2 INTERIM REPORT AS AT 31 MARCH 2016 The interim report covers the period from the

FEE INFORMATION DOCUMENT for a payment service user an entrepreneur and a legal entity

Annex 1 FEE INFORMATION DOCUMENT for a payment service user an entrepreneur and a legal entity Name of the payment service provider: Societe Generale Banka Srbija a.d. Beograd Name (package) of a payment

Annex 1 FEE INFORMATION DOCUMENT for a payment service user an entrepreneur and a legal entity Name of the payment service provider: Societe Generale Banka Srbija a.d. Beograd Name (package) of a payment

NATIONAL BANK OF SERBIA. Governor s opening remarks at the presentation of the Inflation Report August Dr Jorgovanka Tabaković, Governor

NATIONAL BANK OF SERBIA Governor s opening remarks at the presentation of the Inflation Report August Dr Jorgovanka Tabaković, Governor Belgrade, August Ladies and gentlemen, esteemed members of the press,

NATIONAL BANK OF SERBIA Governor s opening remarks at the presentation of the Inflation Report August Dr Jorgovanka Tabaković, Governor Belgrade, August Ladies and gentlemen, esteemed members of the press,

ANNUAL REPORT FOR 2009

K O M E R C I J A L N A B A N K A A D B U D VA ANNUAL REPORT 2009 Budva, April 2010 Budva, 30 April 2010 ANNUAL REPORT FOR 2009 In accordance with the Law on Banks, the Statute, the Bank s business policies,

K O M E R C I J A L N A B A N K A A D B U D VA ANNUAL REPORT 2009 Budva, April 2010 Budva, 30 April 2010 ANNUAL REPORT FOR 2009 In accordance with the Law on Banks, the Statute, the Bank s business policies,

7. Monetary Trends and Policy

Quarterly Monitor No. 36 January March 214 47 7. Monetary and Policy Inflation has been stable for the past two quarters at about the lower level of the target corridor but the National Bank of Serbia

Quarterly Monitor No. 36 January March 214 47 7. Monetary and Policy Inflation has been stable for the past two quarters at about the lower level of the target corridor but the National Bank of Serbia

ANNUAL OPERATING REPORT FOR 2017

; ANNUAL OPERATING REPORT FOR 2017 Belgrade, March 2018 CONTENTS Page I DEVELOPMENT, ORGANIZATIONAL STRUCTURE AND BUSINESS ACTIVITIES 3 1. ESTABLISHMENT 3 2. ORGANIZATION OF OPERATIONS 3 3. BASIC PERFORMANCE

; ANNUAL OPERATING REPORT FOR 2017 Belgrade, March 2018 CONTENTS Page I DEVELOPMENT, ORGANIZATIONAL STRUCTURE AND BUSINESS ACTIVITIES 3 1. ESTABLISHMENT 3 2. ORGANIZATION OF OPERATIONS 3 3. BASIC PERFORMANCE

CENTURION METALS D.0.0., BEOGRAD. Special Purpose Financial Statements for the period ended 30 June 2017 and Independent Auditors' Report

Special Purpose Financial Statements for the period ended and Independent Auditors' Report CONTENTS : Independent Auditors' Report on Audit of Financial Statements Financial Statements Statement of Financial

Special Purpose Financial Statements for the period ended and Independent Auditors' Report CONTENTS : Independent Auditors' Report on Audit of Financial Statements Financial Statements Statement of Financial

FINANCIAL LEASING SECTOR IN SERBIA

BANK SUPERVISION DEPARTMENT FINANCIAL LEASING SECTOR IN SERBIA Second Quarter Report 2018 September 2018 Contents: 1 Basic information about the Serbian financial leasing sector... 2 1.1 1.1 Overview of

BANK SUPERVISION DEPARTMENT FINANCIAL LEASING SECTOR IN SERBIA Second Quarter Report 2018 September 2018 Contents: 1 Basic information about the Serbian financial leasing sector... 2 1.1 1.1 Overview of

INSURANCE SUPERVISION DEPARTMENT PENSION FUNDS SUPERVISION DIVISION VOLUNTARY PENSION FUNDS IN SERBIA

INSURANCE SUPERVISION DEPARTMENT PENSION FUNDS SUPERVISION DIVISION VOLUNTARY PENSION FUNDS IN SERBIA First quarter report Contents: 1. Market participants... 3 2. VPF net assets... 4 3. Structure of VPF

INSURANCE SUPERVISION DEPARTMENT PENSION FUNDS SUPERVISION DIVISION VOLUNTARY PENSION FUNDS IN SERBIA First quarter report Contents: 1. Market participants... 3 2. VPF net assets... 4 3. Structure of VPF

INTRODUCTORY ADDRESS BY THE EXECUTIVE BOARD 1 1. FROM THE WORK OF THE BANK S EXECUTIVE BOARD IN

TABLE OF CONTENTS INTRODUCTORY ADDRESS BY THE EXECUTIVE BOARD 1 1. FROM THE WORK OF THE BANK S EXECUTIVE BOARD IN 2006 9 2. MACROECONOMIC CONDITIONS FOR DOING BUSINESS 13 2.1. In the period between 2002

TABLE OF CONTENTS INTRODUCTORY ADDRESS BY THE EXECUTIVE BOARD 1 1. FROM THE WORK OF THE BANK S EXECUTIVE BOARD IN 2006 9 2. MACROECONOMIC CONDITIONS FOR DOING BUSINESS 13 2.1. In the period between 2002

KULSKA BANKA a.d. NOVI SAD IFRS FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2006

KULSKA BANKA a.d. NOVI SAD IFRS FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2006 Page(s) Independent Auditor s Report 1 Income Statement 2 Balance Sheet 3 Statement of Changes in Equity 4 Cash

KULSKA BANKA a.d. NOVI SAD IFRS FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2006 Page(s) Independent Auditor s Report 1 Income Statement 2 Balance Sheet 3 Statement of Changes in Equity 4 Cash

VOLUNTARY PENSION FUNDS IN SERBIA

INSURANCE SUPERVISION DEPARTMENT PENSION FUNDS SUPERVISION DIVISION VOLUNTARY PENSION FUNDS IN SERBIA Third Quarter Report 2018 November 2018 Contents: 1 Market participants... 3 2 VPF net assets... 4

INSURANCE SUPERVISION DEPARTMENT PENSION FUNDS SUPERVISION DIVISION VOLUNTARY PENSION FUNDS IN SERBIA Third Quarter Report 2018 November 2018 Contents: 1 Market participants... 3 2 VPF net assets... 4

BANCA INTESA A.D. BEOGRAD

FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2011 TABLE OF CONTENTS PAGE INDEPENDENT AUDITOR S REPORT 1 INCOME STATEMENT 2 BALANCE SHEET 3 STATEMENT OF CHANGES IN EQUITY 4 CASH FLOW STATEMENT 5-6

FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2011 TABLE OF CONTENTS PAGE INDEPENDENT AUDITOR S REPORT 1 INCOME STATEMENT 2 BALANCE SHEET 3 STATEMENT OF CHANGES IN EQUITY 4 CASH FLOW STATEMENT 5-6

NATIONAL BANK OF SERBIA. Vice Governor Markovic s Speech at the Presentation of the May Inflation Report

NATIONAL BANK OF SERBIA Vice Governor Markovic s Speech at the Presentation of the May Inflation Report Belgrade, May Ladies and gentlemen, esteemed members of the press and fellow economists, Declining

NATIONAL BANK OF SERBIA Vice Governor Markovic s Speech at the Presentation of the May Inflation Report Belgrade, May Ladies and gentlemen, esteemed members of the press and fellow economists, Declining

DISCLOSURE OF INFORMATION AND BANK S DATA on 30th of June Capital, Capital Adequacy and Credit Risk. Mitigation Techniques

DISCLOSURE OF INFORMATION AND BANK S DATA on 3th of June 215 Capital, Capital Adequacy and Credit Risk Mitigation Techniques Belgrade, September 215 Table of Contents: 1. Introduction... 3 General information

DISCLOSURE OF INFORMATION AND BANK S DATA on 3th of June 215 Capital, Capital Adequacy and Credit Risk Mitigation Techniques Belgrade, September 215 Table of Contents: 1. Introduction... 3 General information

FINANCIAL LEASING SECTOR IN SERBIA

BANK SUPERVISION DEPARTMENT FINANCIAL LEASING SECTOR IN SERBIA Second Quarter Report 2016 SEPTEMBER 2016 Contents: 1 BASIC INFORMATION ABOUT THE SERBIAN FINANCIAL LEASING SECTOR... 1 2 BALANCE SHEET STRUCTURE...

BANK SUPERVISION DEPARTMENT FINANCIAL LEASING SECTOR IN SERBIA Second Quarter Report 2016 SEPTEMBER 2016 Contents: 1 BASIC INFORMATION ABOUT THE SERBIAN FINANCIAL LEASING SECTOR... 1 2 BALANCE SHEET STRUCTURE...

5. Prices and the Exchange Rate

3 5. Prices and the Exchange Rate 5. Prices and the Exchange Rate Since the beginning of the year, inflation in Serbia has been extremely low, the cumulative growth rate in the first seven months is %.

3 5. Prices and the Exchange Rate 5. Prices and the Exchange Rate Since the beginning of the year, inflation in Serbia has been extremely low, the cumulative growth rate in the first seven months is %.

Economic and fiscal programme of the Republic of Serbia

Economic and fiscal programme of the Republic of Serbia 2012-2014 Belgrade, January 2012 Important Disclaimer This translation has been provided by the Jugoslovenski pregled Publishing House. This does

Economic and fiscal programme of the Republic of Serbia 2012-2014 Belgrade, January 2012 Important Disclaimer This translation has been provided by the Jugoslovenski pregled Publishing House. This does

Challenges of supervisory regulatory changes. Mira Erić Vice-Governor, National Bank of Serbia Washington, June 3 rd 2010

Challenges of supervisory regulatory changes Mira Erić Vice-Governor, National Bank of Serbia Washington, June 3 rd 2010 Contents Overview of Serbian market Current banking regulatory framework in Serbia

Challenges of supervisory regulatory changes Mira Erić Vice-Governor, National Bank of Serbia Washington, June 3 rd 2010 Contents Overview of Serbian market Current banking regulatory framework in Serbia

5. Prices and the Exchange Rate

32 5. Prices and the Exchange Rate 5. Prices and the Exchange Rate Inflation trend in Q4 and January was around the lower limit of the National Bank of Serbia target band and at the end of January it to

32 5. Prices and the Exchange Rate 5. Prices and the Exchange Rate Inflation trend in Q4 and January was around the lower limit of the National Bank of Serbia target band and at the end of January it to

BANK SUPERVISION DEPARTMENT. BANKING SECTOR IN SERBIA Fourth Quarter Report 2013

BANK SUPERVISION DEPARTMENT BANKING SECTOR IN SERBIA Fourth Quarter Report 2013 2 Banking Sector in Serbia National Bank of Serbia CONTENTS: 1. BASIC INFORMATION... 6 1. Selected parameters of the Serbian

BANK SUPERVISION DEPARTMENT BANKING SECTOR IN SERBIA Fourth Quarter Report 2013 2 Banking Sector in Serbia National Bank of Serbia CONTENTS: 1. BASIC INFORMATION... 6 1. Selected parameters of the Serbian

FINANCIAL LEASING SECTOR IN SERBIA

BANK SUPERVISION DEPARTMENT FINANCIAL LEASING SECTOR IN SERBIA First Quarter Report 2017 June 2017 Contents: 1 Basic information about the Serbian financial leasing sector... 2 1.1 Overview of the basic

BANK SUPERVISION DEPARTMENT FINANCIAL LEASING SECTOR IN SERBIA First Quarter Report 2017 June 2017 Contents: 1 Basic information about the Serbian financial leasing sector... 2 1.1 Overview of the basic

PUBLISHING OF THE DATA AND INFORMATION OF THE BANK ON JUNE 30 th 2018

PUBLISHING OF THE DATA AND INFORMATION OF THE BANK ON JUNE 3 th 218 Content: 1. Introduction... 3 2. Bank s Capital... 3 3. Regulatory capital requirements and leverage ratio... 6 4. Quantitative and Qualitative

PUBLISHING OF THE DATA AND INFORMATION OF THE BANK ON JUNE 3 th 218 Content: 1. Introduction... 3 2. Bank s Capital... 3 3. Regulatory capital requirements and leverage ratio... 6 4. Quantitative and Qualitative

THE LIMITED LIABILITY COMPANY FOR FINANCE LEASE INTESA LEASING d.o.o. BELGRADE

THE LIMITED LIABILITY COMPANY FOR FINANCE LEASE INTESA LEASING d.o.o. BELGRADE Financial Statements as of and for the Year Ended 31 December 2017 and Independent Auditor s Report CONTENTS Page INDEPENDENT

THE LIMITED LIABILITY COMPANY FOR FINANCE LEASE INTESA LEASING d.o.o. BELGRADE Financial Statements as of and for the Year Ended 31 December 2017 and Independent Auditor s Report CONTENTS Page INDEPENDENT

INSURANCE SUPERVISION DEPARTMENT PENSION FUNDS SUPERVISION DIVISION VOLUNTARY PENSION FUNDS IN SERBIA

INSURANCE SUPERVISION DEPARTMENT PENSION FUNDS SUPERVISION DIVISION VOLUNTARY PENSION FUNDS IN SERBIA Fourth Quarter Report Contents: 1. VPF market participants... 3 2. VPF net assets... 4 3. Structure

INSURANCE SUPERVISION DEPARTMENT PENSION FUNDS SUPERVISION DIVISION VOLUNTARY PENSION FUNDS IN SERBIA Fourth Quarter Report Contents: 1. VPF market participants... 3 2. VPF net assets... 4 3. Structure

Management s Responsibility for the Financial Statements

ABCD KPMG d.o.o. Beograd Kraljice Natalije 11 11000 Belgrade Serbia Telephone: Fax: E-mail: Internet: +381 11 20 50 500 +381 11 20 50 550 info@kpmg.rs www.kpmg.rs Independent Auditors Report TO THE OWNERS

ABCD KPMG d.o.o. Beograd Kraljice Natalije 11 11000 Belgrade Serbia Telephone: Fax: E-mail: Internet: +381 11 20 50 500 +381 11 20 50 550 info@kpmg.rs www.kpmg.rs Independent Auditors Report TO THE OWNERS

Annual Financial Stability Report Belgrade, 30 July 2018

Annual Financial Stability Report 17 Belgrade, 3 July 18 External risks and measures - Diverging monetary policies of the Fed and the ECB may affect capital flows towards emerging markets; - Price volatility

Annual Financial Stability Report 17 Belgrade, 3 July 18 External risks and measures - Diverging monetary policies of the Fed and the ECB may affect capital flows towards emerging markets; - Price volatility

JUBMES BANKA AD, BELGRADE. Financial Statements for the year ended 31 December 2015 and Independent Auditor s Report

JUBMES BANKA AD, BELGRADE Financial Statements for the year ended 31 December 2015 and Independent Auditor s Report This is a translation of the original Independent Auditors Report issued in the Serbian

JUBMES BANKA AD, BELGRADE Financial Statements for the year ended 31 December 2015 and Independent Auditor s Report This is a translation of the original Independent Auditors Report issued in the Serbian

FINANCIAL LEASING SECTOR IN SERBIA

BANK SUPERVISION DEPARTMENT FINANCIAL LEASING SECTOR IN SERBIA First Quarter Report 2018 June 2018 Contents: 1 Basic information about the Serbian financial leasing sector... 2 1.1 Overview of the basic

BANK SUPERVISION DEPARTMENT FINANCIAL LEASING SECTOR IN SERBIA First Quarter Report 2018 June 2018 Contents: 1 Basic information about the Serbian financial leasing sector... 2 1.1 Overview of the basic

Banco Sabadell Group. Financial bulletin Third quarter of Quarterly Financial Bulletin from Banco Sabadell Group

Banco Sabadell Group Financial bulletin Third quarter of 2001 Number 6 Third quarter of 2001 Page 1 Introduction At the end of the third quarter of this year, attributable consolidated profits for the

Banco Sabadell Group Financial bulletin Third quarter of 2001 Number 6 Third quarter of 2001 Page 1 Introduction At the end of the third quarter of this year, attributable consolidated profits for the

Macroeconomic Developments in Serbia

Macroeconomic Developments in Serbia November 217 Inflation has been Moving Within the Target Tolerance Band Since the Beginning of the Year Inflation expectations are anchored - moving close to the target

Macroeconomic Developments in Serbia November 217 Inflation has been Moving Within the Target Tolerance Band Since the Beginning of the Year Inflation expectations are anchored - moving close to the target

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

ABCD KPMG d.o.o. Beograd Kraljice Natalije 11 11000 Belgrade Serbia Telephone: Fax: E-mail: Internet: +381 11 20 50 500 +381 11 20 50 550 info@kpmg.rs www.kpmg.rs Independent Auditors Report TO THE SHAREHOLDERS

ABCD KPMG d.o.o. Beograd Kraljice Natalije 11 11000 Belgrade Serbia Telephone: Fax: E-mail: Internet: +381 11 20 50 500 +381 11 20 50 550 info@kpmg.rs www.kpmg.rs Independent Auditors Report TO THE SHAREHOLDERS

UNIVERZAL BANKA A.D. BEOGRAD

UNIVERZAL BANKA A.D. BEOGRAD FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2009 Univerzal banka a.d. Beograd TABLE OF CONTENTS Page Independent Auditors Report 1 Income statement 2 Balance sheet

UNIVERZAL BANKA A.D. BEOGRAD FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2009 Univerzal banka a.d. Beograd TABLE OF CONTENTS Page Independent Auditors Report 1 Income statement 2 Balance sheet

4. Balance of Payments and Foreign Trade

24 4. Balance of Payments and Foreign Trade 4. Balance of Payments and Foreign Trade Current account deficit in 2014 was lower than the one realised in 2013 In the period January- November 2014, current

24 4. Balance of Payments and Foreign Trade 4. Balance of Payments and Foreign Trade Current account deficit in 2014 was lower than the one realised in 2013 In the period January- November 2014, current

KOMERCIJALNA BANKA AD BEOGRAD EXECUTIVE BOARD No Belgrade, October the 4 th 2012

KOMERCIJALNA BANKA AD BEOGRAD EXECUTIVE BOARD No. 21673 Belgrade, October the 4 th 2012 R U L E S ON THE TARIFF OF FEES OF KOMERCIJALNA BANKA AD BEOGRAD CUSTODY DEPARTMENT Belgrade, October 2012 - 2 -

KOMERCIJALNA BANKA AD BEOGRAD EXECUTIVE BOARD No. 21673 Belgrade, October the 4 th 2012 R U L E S ON THE TARIFF OF FEES OF KOMERCIJALNA BANKA AD BEOGRAD CUSTODY DEPARTMENT Belgrade, October 2012 - 2 -

JUBMES BANKA AD, BELGRADE. Financial Statements for the year ended 31 December 2017 and Independent Auditor s Report

JUBMES BANKA AD, BELGRADE Financial Statements for the year ended 31 December 2017 and Independent Auditor s Report This is a translation of the original Independent Auditors Report issued in the Serbian

JUBMES BANKA AD, BELGRADE Financial Statements for the year ended 31 December 2017 and Independent Auditor s Report This is a translation of the original Independent Auditors Report issued in the Serbian

SOCIETE GENERALE YUGOSLAV BANK a.d. BEOGRAD FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED 31 DECEMBER 2005

SOCIETE GENERALE YUGOSLAV BANK a.d. BEOGRAD FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED 31 DECEMBER 2005 CONTENTS Page(s) Independent Auditor s Report 1 Income Statement 2 Balance Sheet 3 Statement

SOCIETE GENERALE YUGOSLAV BANK a.d. BEOGRAD FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED 31 DECEMBER 2005 CONTENTS Page(s) Independent Auditor s Report 1 Income Statement 2 Balance Sheet 3 Statement

UNICREDIT BANK A.D., BANJA LUKA

UNICREDIT BANK A.D., BANJA LUKA Financial statements Year ended December 31, and Independent Auditors Report Translation of the Auditors Report issued in the Serbian language Table of Contents Page Independent

UNICREDIT BANK A.D., BANJA LUKA Financial statements Year ended December 31, and Independent Auditors Report Translation of the Auditors Report issued in the Serbian language Table of Contents Page Independent

Quarterly Assessment of the Economy

4 2 Quarterly Assessment of the Economy No. 17, Q IV/216 12 1 8 6 1 2 3 4 5 6 7 8 9 Summary Economic activity in euro area has continued to recover in 216, while in line with the CBK expectations, the

4 2 Quarterly Assessment of the Economy No. 17, Q IV/216 12 1 8 6 1 2 3 4 5 6 7 8 9 Summary Economic activity in euro area has continued to recover in 216, while in line with the CBK expectations, the

mts banka a.d. BELGRADE Financial Statements as of and for the Year Ended 31 December 2016 and Independent Auditor s Report

mts banka a.d. BELGRADE Financial Statements as of and for the Year Ended 31 December 2016 and Independent Auditor s Report mts banka a.d. Belgrade CONTENTS Page INDEPENDENT AUDITOR S REPORT 1-2 FINANCIAL

mts banka a.d. BELGRADE Financial Statements as of and for the Year Ended 31 December 2016 and Independent Auditor s Report mts banka a.d. Belgrade CONTENTS Page INDEPENDENT AUDITOR S REPORT 1-2 FINANCIAL

ZEPTER BANKA A.D., BEOGRAD. Financial Statements December 31, 2006 and Independent Auditors Report

Financial Statements and Independent Auditors Report CONTENTS Page Independent Auditors Report 1 2 Statement of Income 3 Balance Sheet 4 Statement of Changes in Equity 5 Statement of Cash Flows 6 Notes

Financial Statements and Independent Auditors Report CONTENTS Page Independent Auditors Report 1 2 Statement of Income 3 Balance Sheet 4 Statement of Changes in Equity 5 Statement of Cash Flows 6 Notes

FINANCIAL LEASING SECTOR IN SERBIA

NATIONAL BANK OF SERBIA BANK SUPERVISION DEPARTMENT FINANCIAL LEASING SECTOR IN SERBIA Third Quarter Report 2018 December 2018 Contents: 1 Basic information about the Serbian financial leasing sector...

NATIONAL BANK OF SERBIA BANK SUPERVISION DEPARTMENT FINANCIAL LEASING SECTOR IN SERBIA Third Quarter Report 2018 December 2018 Contents: 1 Basic information about the Serbian financial leasing sector...

INDEPENDENT AUDITOR S REPORT. To the Shareholders Assembly of Invest Bank Montenegro AD, Podgorica

This is an English translation of Independent Auditor s Report originally issued in the Montenegrin language INDEPENDENT AUDITOR S REPORT To the Shareholders Assembly of Invest Bank Montenegro AD, Podgorica

This is an English translation of Independent Auditor s Report originally issued in the Montenegrin language INDEPENDENT AUDITOR S REPORT To the Shareholders Assembly of Invest Bank Montenegro AD, Podgorica

HALF-YEAR FINANCIAL REPORT 2014 / UNIQA GROUP. Deliver.

HALF-YEAR FINANCIAL REPORT 2014 / UNIQA GROUP Deliver. 2 GROUP KEY FIGURES Group Key Figures Figures in million 1 6/2014 1 6/2013 Change Premiums written 2,856.2 2,725.2 + 4.8 % Savings portion from unit-

HALF-YEAR FINANCIAL REPORT 2014 / UNIQA GROUP Deliver. 2 GROUP KEY FIGURES Group Key Figures Figures in million 1 6/2014 1 6/2013 Change Premiums written 2,856.2 2,725.2 + 4.8 % Savings portion from unit-