GRAMEEN FOUNDATION USA

|

|

|

- Chrystal Barrett

- 5 years ago

- Views:

Transcription

1 GRAMEEN FOUNDATION USA AND AFFILIATES AUDIT REPORT FINANCIAL AND FEDERAL AWARD COMPLIANCE EXAMINATION FOR THE YEAR ENDED MARCH 31, 2017

2 GRAMEEN FOUNDATION USA AND AFFILIATES CONTENTS PAGE NO. I. Financial Section Consolidated Financial Statements, for the Year Ended March 31, 2017, Including the Schedule of Expenditures of Federal Awards and Schedule of Findings and Questioned Costs I-(1-30) II. Report on Internal Control Over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance With Government Auditing Standards II-(1-2) III. Report on Compliance For Each Major Federal Program and Report on Internal Control Over Compliance Required by Title 2 U.S. Code of Federal Regulations (CFR) Part 200, Uniform Administration Requirements, Cost Principles and Audit Requirements for Federal Awards (Uniform Guidance) III-(1-3)

3 CONSOLIDATED FINANCIAL STATEMENTS GRAMEEN FOUNDATION USA AND AFFILIATES FOR THE YEAR ENDED MARCH 31, 2017 I-1

4 GRAMEEN FOUNDATION USA AND AFFILIATES CONTENTS PAGE NO. INDEPENDENT AUDITOR'S REPORT I-(3-4) EXHIBIT A - Consolidated Statement of Financial Position, as of March 31, 2017 I-5 EXHIBIT B - Consolidated Statement of Activities and Changes in Net Assets, for the Year Ended March 31, 2017 I-6 EXHIBIT C - Consolidated Statement of Functional Expenses, for the Year Ended March 31, 2017 I-7 EXHIBIT D - Consolidated Statement of Cash Flows, for the Year Ended March 31, 2017 I-(8-9) NOTES TO CONSOLIDATED FINANCIAL STATEMENTS I-(10-22) SUPPLEMENTAL INFORMATION SCHEDULE 1 - Consolidated Schedule of Support and Revenue and Functional Expenses, for the Year Ended March 31, 2017 I-23 SCHEDULE 2 - Schedule of Expenditures of Federal Awards, for the Year Ended March 31, 2017 I-(24-25) SCHEDULE 3 - Schedule of Findings and Questioned Costs, for the Year Ended March 31, 2017 I-(26-30) I-2

5 To the Board of Directors Grameen Foundation USA and Affiliates Washington, D.C. INDEPENDENT AUDITOR'S REPORT Report on the Financial Statements We have audited the accompanying consolidated financial statements of Grameen Foundation USA and Affiliates (together "Grameen"), which comprise the consolidated statement of financial position as of March 31, 2017, and the related consolidated statements of activities and change in net assets, functional expenses and cash flows for the year then ended, and the related notes to the consolidated financial statements. Management s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation and maintenance of internal control relevant to the preparation and fair presentation of consolidated financial statements that are free from material misstatement, whether due to fraud or error. Auditor s Responsibility Our responsibility is to express an opinion on these consolidated financial statements based on our audit. We did not audit the financial statements of Freedom from Hunger total support and revenue totaling $2,271,396, for the year then ended. Additionally, we did not audit the financial statements of Grameen Foundation India Private Limited, which the statement reflects total assets of $214,346 as of March 31, 2017, and total support and revenues of $494,764, for the year then ended. Those statements were audited by other auditors, whose reports have been furnished to us, and our opinion, insofar as it relates to the amounts included for the Affiliates, are based solely on the reports of the other auditors. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on the auditor s judgment, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity s preparation and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion MONTGOMERY AVENUE SUITE 650 NORTH BETHESDA, MARYLAND (301) FAX (301) MEMBER OF CPAMERICA INTERNATIONAL, AN AFFILIATE OF HORWATH INTERNATIONAL MEMBER OF THE AMERICAN INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS' PRIVATE COMPANIES PRACTICE SECTION I-3

6 Opinion In our opinion, based on our audit and the reports of the other auditors, the consolidated financial statements referred to above present fairly, in all material respects, the consolidated financial position of the Grameen as of March 31, 2017, and the consolidated changes in its net assets and its consolidated cash flows for the year then ended in accordance with accounting principles generally accepted in the United States of America. Emphasis of Matter The accompanying consolidated financial statements have been prepared assuming that Grameen Foundation India Private Limited (GFI) will continue as a going concern. As discussed in Note 9 to the consolidated financial statements, GFI has suffered a substantial loss from operations and has a net capital deficiency that raises substantial doubt about its ability to continue as a going concern. The consolidated financial statements do not include any adjustments that might result from the outcome of this uncertainty. Our opinion is not modified with respect to this matter. Other Matter Our audit was conducted for the purpose of forming an opinion on the consolidated financial statements as a whole. The Consolidated Schedule of Support and Revenue and Functional Expenses on page I-23 is presented for purposes of additional analysis and is not a required part of the consolidated financial statements. The Schedule of Expenditures of Federal Awards on pages I-(24-25), as required by Title 2 U.S. Code of Federal Regulations (CFR) Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (Uniform Guidance), is presented for purposes of additional analysis and is not a required part of the consolidated financial statements. Such information is the responsibility of management and was derived from and relates directly to the underlying accounting and other records used to prepare the consolidated financial statements. The information has been subjected to the auditing procedures applied in the audit of the consolidated financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the financial statements or to the consolidated financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the information is fairly stated, in all material respects, in relation to the consolidated financial statements as a whole. Other Reporting Required by Government Auditing Standards In accordance with Government Auditing Standards, we have also issued our report dated December 18, 2017 on our consideration of Grameen's internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering Grameen's internal control over financial reporting and compliance. December 18, 2017 I-4

7 EXHIBIT A GRAMEEN FOUNDATION USA AND AFFILIATES CONSOLIDATED STATEMENT OF FINANCIAL POSITION AS OF MARCH 31, 2017 ASSETS CURRENT ASSETS Cash and cash equivalents $ 3,802,310 Investments 2,041,346 Grants and contributions receivable 2,562,483 Other receivables and advances, net of allowance 608,387 Prepaid expenses 326,388 Total current assets 9,340,914 PROPERTY AND EQUIPMENT Furniture and equipment 267,588 Less: Accumulated depreciation and amortization (230,260) Net property and equipment 37,328 OTHER ASSETS Loans receivable, net of allowance 21,273 Program-related investments 2,846,302 Split-interest agreements 12,293 Cash surrender value of life insurance 286,120 Deposits 83,135 Funds held in trust 77,778 Total other assets 3,326,901 TOTAL ASSETS $ 12,705,143 LIABILITIES AND NET ASSETS CURRENT LIABILITIES Accounts payable and accrued expenses $ 1,288,202 Current portion of deferred rent 37,644 Deferred revenue 1,563,053 Total current liabilities 2,888,899 NONCURRENT LIABILITIES Note payable 125,000 Deferred rent, long term 131,120 Total noncurrent liabilities 256,120 Total liabilities 3,145,019 NET ASSETS Unrestricted 5,759,549 Temporarily restricted 3,722,797 Permanently restricted 77,778 Total net assets 9,560,124 TOTAL LIABILITIES AND NET ASSETS $ 12,705,143 See accompanying notes to consolidated financial statements. I-5

8 EXHIBIT B GRAMEEN FOUNDATION USA AND AFFILIATES CONSOLIDATED STATEMENT OF ACTIVITIES AND CHANGES IN NET ASSETS FOR THE YEAR ENDED MARCH 31, 2017 SUPPORT AND REVENUE Unrestricted Temporarily Restricted Permanently Restricted Total Contributions and grants $ 3,178,249 $ 5,474,260 $ - $ 8,652,509 Program revenues 2,086, ,086,210 Government grants 2,609, ,609,704 Interest and investment income 227, ,021 Loan interest 19, ,083 In-kind contributions 2,583, ,583,697 Other 23, ,414 Net assets released from donor restrictions 4,849,709 (4,849,709) - - EXPENSES Total support and revenue 15,576, ,877-16,201,638 Program Services: Financial Services 3,333, ,333,316 Health and Agricultural Solutions 4,774, ,774,369 Strengthening Organizations 2,326, ,326,341 Regional Programs 1,325, ,325,339 Public Education 1,264, ,264,135 Total program services 13,023, ,023,500 Supporting Services: Management and General 3,998, ,998,790 Fundraising 737, ,114 Total supporting services 4,735, ,735,904 Total expenses 17,759, ,759,404 Change in net assets before other items (2,182,643) 624,877 - (1,557,766) OTHER ITEMS Allowances for uncollectable loans receivable and investment impairments (611,621) - - (611,621) Recovery of deferred rent net of relocation costs 86, ,543 Return of unspent grant funds - (224,504) - (224,504) Foreign exchange rate loss (47,079) - - (47,079) Total other items (572,157) (224,504) - (796,661) Change in net assets before transfer of net assets (2,754,800) 400,373 - (2,354,427) Freedom from Hunger net assets at consolidation 2,635, ,160 77,778 2,936,414 Change in net assets (119,324) 623,533 77, ,987 Net assets at beginning of year 5,878,873 3,099,264-8,978,137 NET ASSETS AT END OF YEAR $ 5,759,549 $ 3,722,797 $ 77,778 $ 9,560,124 See accompanying notes to consolidated financial statements. I-6

9 EXHIBIT C GRAMEEN FOUNDATION USA AND AFFILIATES CONSOLIDATED STATEMENT OF FUNCTIONAL EXPENSES FOR THE YEAR ENDED MARCH 31, 2017 Program Services Supporting Services Financial Services Health and Agricultural Solutions Strengthening Organizations Regional Programs Public Education Total Program Services Management and General Fundraising Total Supporting Services Total Expenses Salaries $ 1,410,561 $ 1,745,882 $ 782,017 $ 511,640 $ 298,252 $ 4,748,352 $ 1,999,595 $ 301,234 $ 2,300,829 $ 7,049,181 Benefits 330, , ,521 99,312 80,947 1,157, ,287 70, ,277 1,731,362 Professional services 565,140 1,028, , ,570 54,575 2,317, , , ,270 2,751,742 In-kind contributions 265, , , , ,313 1,949, ,700 4, ,996 2,583,697 Grants 72, , , , ,771 Travel 218, ,750 81,692 82,068 18, , ,059 9, , ,794 Conferences and meetings 41, ,561 30,560 21,850 1, ,595 16,236 1,471 17, ,302 Communications 31, ,115 5,304 6,753 3, ,797 19,469 3,293 22, ,559 Information technology 28,362 86,850 66,658 6,916 8, ,518 80,039 11,209 91, ,766 Occupancy 155, ,553 50,991 22,620 29, , ,553 25, , ,509 Vehicles and equipment 41, ,898 3,347 15,393 2, ,426 23,649 9,207 32, ,282 Depreciation and amortization 5,373 57,076 1,808 3,315 1,288 68,860 10,991 1,580 12,571 81,431 Insurance 18,524 35,285 6,310 5,153 4,039 69,311 42,501 4,897 47, ,709 Office expenses 18,571 43,776 8,408 7,502 10,046 88,303 28,211 72, , ,168 Advertising 59,544 1,838 2, ,109 65,640 10,003 51,826 61, ,469 Bank fees 2,674 2,175 1,640 6, ,812 12,796 22,467 35,263 49,075 Other 65, ,320 35,449 8, ,370 4,220 15,997 20, ,587 TOTAL $ 3,333,316 $ 4,774,369 $ 2,326,341 $ 1,325,339 $ 1,264,135 $ 13,023,500 $ 3,998,790 $ 737,114 $ 4,735,904 $ 17,759,404 See accompanying notes to consolidated financial statements. I-7

10 EXHIBIT D GRAMEEN FOUNDATION USA AND AFFILIATES CONSOLIDATED STATEMENT OF CASH FLOWS FOR THE YEAR ENDED MARCH 31, 2017 CASH FLOWS FROM OPERATING ACTIVITIES Change in net assets $ 581,987 Adjustments to reconcile changes in net assets to net cash used by operating activities: Unrealized gain on investments (4,346) Realized gain on sales of investments (157,654) Change in allowance for doubtful accounts 155,830 Depreciation and amortization 81,431 Loss on disposal of fixed assets 111,555 Change in allowances for uncollectable loans receivable and foreign exchange risk 283 Appreciation of program-related investments (131,475) Impairment of program-related investments 613,460 Unrealized gain on split-interest agreements (326) Unrealized gain on cash surrender value of life insurance (22,942) Forgiveness of debt (16,864) Freedom from Hunger net assets at consolidation (2,936,414) (Increase) decrease in: Grants and contributions receivable (1,890,362) Other receivables and advances 141,462 Prepaid expenses 45,996 Deposits 102,609 Increase (decrease) in: Accounts payable and accrued expenses (52,456) Deferred revenue 1,041,065 Deferred rent liability (502,149) Net cash used by operating activities (2,839,310) CASH FLOWS FROM INVESTING ACTIVITIES Purchase of furniture and equipment (8,681) Proceeds from sales of investments 3,187,257 Reinvestments/purchases of investments (768,175) Proceeds from sale of fixed assets 1,500 Net cash provided by investing activities 2,411,901 CASH FLOWS FROM FINANCING ACTIVITIES Repayment on note payable (26,420) Proceeds on note payable 125,000 Net cash provided by financing activities 98,580 Net decrease in cash and cash equivalents (328,829) Cash and cash equivalents at beginning of year 4,131,139 CASH AND CASH EQUIVALENTS AT END OF YEAR $ 3,802,310 See accompanying notes to consolidated financial statements. I-8

11 GRAMEEN FOUNDATION USA AND AFFILIATES EXHIBIT D (Continued) CONSOLIDATED STATEMENT OF CASH FLOWS FOR THE YEAR ENDED MARCH 31, 2017 SUPPLEMENTAL INFORMATION: Freedom from Hunger Net Assets at Consolidation Cash $ 1,161,425 Investments 2,781,053 Grants and contributions receivable 225,433 Other receivables and advances 19,944 Prepaid expenses and other 243,644 Net property and equipment 12,467 Cash surrender value of life insurance 263,178 Split-interest agreements 11,967 Security deposit 24,000 Funds held in trust 77,778 Accounts payable (554,143) Deferred revenue (1,330,332) TOTAL FREEDOM FROM HUNGER NET ASSETS AT CONSOLIDATION $ 2,936,414 SCHEDULE OF NONCASH INVESTING TRANSACTIONS: Donated Securities $ 194,036 See accompanying notes to consolidated financial statements. I-9

12 GRAMEEN FOUNDATION USA AND AFFILIATES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS MARCH 31, SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES AND GENERAL INFORMATION Organization - Grameen Foundation USA is a U.S. non-profit organized under Section 501(c)(3) of the Internal Revenue Code. It was created to collaborate with public and private institutions to alleviate poverty, distress, and malnutrition; promote health and social welfare; and educate the public with a particular emphasis on the application of information technologies. Grameen Foundation India Private Limited (GFI), a for-profit corporation registered in India, was established for the purpose of furthering the mission of Grameen Foundation USA. It is a wholly-owned subsidiary of Grameen Foundation USA. TaroWorks, LLC (Taroworks) is a U.S. corporation that provides an advanced mobile data platform to enhance data collection, monitoring, sales and inventory management in the field. The mission is to improve product and service delivery to the poor by bringing real-time data to any organization, anywhere. It is wholly owned by Grameen Foundation USA. Freedom from Hunger is a U.S. non-profit organization. Founded in 1946 under Section 501(c)(3) of the Internal Revenue Code, it brings self-help solutions to combat chronic hunger and poverty globally by offering microfinance, education and health protection services to millions of women and their families. On October 21, 2016, Freedom from Hunger entered into an Asset Transfer Agreement with Grameen Foundation USA in order to advance the organizations shared missions. On November 1, 2016, the organizations came under common control. The value of net assets transferred to Grameen Foundation USA totaled $2,879,987 out of a total net assets of $2,936,414. After this date Freedom from Hunger became a Type I supporting organization of Grameen Foundation USA within the meaning of Section 509(a)(3) of the Internal Revenue Code of Freedom from Hunger s supporting organization status was approved by the Internal Revenue Service on March 1, As a supporting organization, Freedom from Hunger is organized and operated exclusively for the benefit of, to perform the functions of, and to carry out the purposes of Grameen Foundation USA and designates. Basis of presentation - The accompanying consolidated financial statements are presented on the accrual basis of accounting, and in accordance with FASB ASC , Not-for-Profit Entities, Consolidation. The consolidated financial statements include the accounts of Grameen Foundation USA; Grameen Foundation India Private Limited, TaroWorks, LLC and Freedom from Hunger (together Grameen ). All significant intercompany transactions and balances have been eliminated in consolidation. Cash and cash equivalents - Grameen considers all cash and other highly liquid investments with initial maturities of three months or less to be cash equivalents. Bank deposit accounts are insured by the Federal Deposit Insurance Corporation (FDIC) up to a limit of $250,000. At times during the year, Grameen maintains cash balances in excess of the FDIC insurance limits. Management believes the risk in these situations to be minimal. I-10

13 GRAMEEN FOUNDATION USA AND AFFILIATES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS MARCH 31, SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES AND GENERAL INFORMATION (Continued) Cash and cash equivalents (continued) - At March 31, 2017, Grameen had $428,254 of cash and cash equivalents held at financial institutions in foreign countries to support operations in those countries. The majority of funds held in foreign countries is uninsured. Investments - Investments are recorded at their readily determinable fair value. Realized and unrealized gains and losses are included in interest and investment income in the Consolidated Statement of Activities and Changes in Net Assets. Receivables - All amounts receivable are recorded at their net realizable value, which approximates fair value. Management considers all amounts from grants, contributions and other receivables to be fully collectible within one year. The allowance for doubtful accounts is reviewed quarterly and updated as appropriate. Property and equipment - Property and equipment with an acquisition value of $5,000 or more are stated at cost. Property and equipment are depreciated on a straight-line basis over the estimated useful lives of the related assets, generally three to ten years. The cost of maintenance and repairs are recorded as expenses when incurred. Deferred revenue - Deferred revenue consists of unearned fees. Grameen recognizes exchange contracts as they are earned, subscription revenue on a monthly basis over the life of the subscription and volunteer engagement revenue when the engagement actually occurs. Income taxes - Grameen Foundation USA is exempt from Federal income taxes under Section 501(c)(3) of the Internal Revenue Code. Accordingly, no provision for income taxes has been made in the accompanying consolidated financial statements. Grameen Foundation USA is not a private foundation. GFI is a for-profit corporation registered in India and is subject to tax on any net profit recognized during the fiscal year. However, GFI is operated as a social business and is expected to incur losses for the foreseeable future. Accordingly, no provision for income taxes has been made in the accompanying consolidated financial statements. TaroWorks is a U.S. corporation and is subject to tax on any net profit recognized during the year. TaroWorks has not realized a net profit since its inception. Freedom from Hunger is exempt from Federal income taxes under Section 501(c)(3) of the Internal Revenue Code. Accordingly, no provision for income taxes has been made in the accompanying consolidated financial statements. I-11

14 GRAMEEN FOUNDATION USA AND AFFILIATES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS MARCH 31, SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES AND GENERAL INFORMATION (Continued) Uncertain tax positions - For the year ended March 31, 2017, Grameen has documented its consideration of FASB ASC , Income Taxes, that provides guidance for reporting uncertainty in income taxes and has determined that no material uncertain tax positions qualify for either recognition or disclosure in the financial statements. Net asset classification - The net assets are reported in three self-balancing groups as follows: Unrestricted net assets include unrestricted revenue and contributions received without donor-imposed restrictions. These net assets are available for the operation of Grameen and include both internally designated and undesignated resources. Temporarily restricted net assets include revenue and contributions subject to donorimposed stipulations that will be met by the actions of Grameen and/or the passage of time. When a restriction expires, temporarily restricted net assets are reclassified to unrestricted net assets and reported in the Consolidated Statement of Activities and Changes in Net Assets as net assets released from restrictions. Permanently restricted net assets include contributions restricted by the donor for investment in perpetuity, the income from which is available to support the activities of Freedom from Hunger. Contributions and grants - Contributions and grants are recorded as revenue in the year notification is received from the donor. Temporarily restricted contributions and grants are recognized as unrestricted support only to the extent of actual expenses incurred in compliance with the donor-imposed restrictions and satisfaction of time restrictions. Such contributions and grants received in excess of expenses incurred are shown as temporarily restricted net assets in the accompanying consolidated financial statements. Grameen receives funding under grants from the U.S. Government, for direct and indirect program costs. This funding is subject to contractual restrictions, which must be met through incurring qualifying expenses for particular programs. Accordingly, such grants are considered exchange transactions and are recorded as unrestricted income to the extent that related expenses are incurred in compliance with the criteria stipulated in the grant agreements. Foreign currency translation - The U.S. Dollar ("dollars") is the functional currency for Grameen's worldwide operations. Transactions in currencies other than U.S. dollars are translated into dollars at the rate of exchange in effect during the month of the transaction. Current assets and liabilities denominated in non-u.s. currency are translated into dollars at the exchange rate in effect at the date of the Consolidated Statement of Financial Position. In-kind contributions - Grameen receives and recognizes contributed services and gifts in-kind from various sources. In-kind contributions are recorded at their fair market value as of the date of the gift. I-12

15 GRAMEEN FOUNDATION USA AND AFFILIATES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS MARCH 31, SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES AND GENERAL INFORMATION (Continued) Use of estimates - The preparation of the consolidated financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the consolidated financial statements and the reported amounts of revenue and expenses during the reporting period. Accordingly, actual results could differ from those estimates. Functional allocation of expenses - The costs of providing the various programs and other activities have been summarized on a functional basis in the Consolidated Statement of Activities and Changes in Net Assets. Accordingly, certain costs have been allocated among the programs and supporting services benefited. Risks and uncertainties - Grameen invests in various investment securities. Investment securities are exposed to various risks such as credit, market and currency risks. Due to the level of risk associated with certain investment securities, it is at least reasonably possible that changes in the values of investment securities will occur in the near term and that such changes could materially affect the amounts reported in the consolidated financial statements. Credit risk - Credit risk is the risk of financial loss to Grameen if a customer or counterparty to a financial instrument fails to meet its contractual obligations, and arises principally from Grameen's investments. Market risk - Market risk is defined as external influences, generally outside of the control of the organization's executive management, but which can be identified, assessed and mitigating actions put in place to reduce any adverse impact. Currency risk - Grameen is exposed to currency risk through transactions in foreign currencies against the U.S. Dollar ("dollars"). There is also a Consolidated Statement of Financial Position risk that the net monetary liabilities in foreign currencies will take a higher value when translated into dollars as a result of currency movements. Significant changes in the economy, depreciation of local currencies against the currencies of the indexed portfolios, or in the health of a particular industry segment, could result in evidence that the expected future cash flows are different from those provided for at the end of the reporting period. Management, therefore, carefully monitors and manages its exposure to currency risk. Fair value measurement - Grameen adopted the provisions of FASB ASC 820, Fair Value Measurement. FASB ASC 820 defines fair value, establishes a framework for measuring fair value, establishes a fair value hierarchy based on the quality of inputs (assumptions that market participants would use in pricing assets and liabilities, including assumptions about risk) used to measure fair value, and enhances disclosure requirements for fair value measurements. I-13

16 GRAMEEN FOUNDATION USA AND AFFILIATES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS MARCH 31, SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES AND GENERAL INFORMATION (Continued) Fair value measurement (continued) - Grameen accounts for a significant portion of its financial instruments at fair value or considers fair value in their measurement. New accounting pronouncements - In August 2014, the FASB issued Accounting Standards Update (ASU) , Presentation of Financial Statements - Going Concern. The ASU requires management to evaluate whether there are conditions or events, considered in the aggregate, that raise substantial doubt about an ability to continue as a going concern within one year after the date the financial statements are issued. This amendment is effective for the annual periods ending after December 15, During the year ended March 31, 2017, Grameen adopted the new guidance and disclosed in the consolidated financial statements the principal conditions, management's evaluation and future plans that will alleviate the conditions or events. New accounting pronouncements (not yet adopted) - In August 2016, the FASB issued ASU , Presentation of Financial Statements of Notfor-Profit Entities (Topic 958), intended to improve financial reporting for not-for-profit entities. The ASU will reduce the current three classes of net assets into two: with and without donor restrictions. The change in each of the classes of net assets must be reported on the Consolidated Statement of Activities and Changes in Net Assets. The ASU also requires various enhanced disclosures around topics such as board designations, liquidity, functional classification of expenses, investment expenses, donor restrictions, and underwater endowments. The ASU is effective for years beginning after December 15, Early adoption is permitted. The ASU should be applied on a retrospective basis in the year the ASU is first applied. While the ASU will change the presentation of Grameen's consolidated financial statements, it is not expected to alter Grameen's reported consolidated financial position. In May 2014, the FASB issued ASU , Revenue from Contracts with Customers (Topic 606) (ASU ). The ASU establishes a comprehensive revenue recognition standard for virtually all industries under generally accepted accounting principles in the United States (U.S. GAAP) including those that previously followed industry-specific guidance. The guidance states that an entity should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services. The FASB issued ASU in August 2015 that deferred the effective date of ASU by a year thus the effective date is fiscal years beginning after December 15, Early adoption is permitted. Grameen has not yet selected a transition method and is currently evaluating the effect that the updated standard will have on the consolidated financial statements. In 2016, the FASB issued ASU , Leases (Topic 842). The ASU changes the accounting treatment for operating leases by recognizing a lease asset and lease liability at the present value of the lease payments in the Consolidated Statement of Financial Position and disclosing key information about leasing arrangements. The ASU is effective for private entities for fiscal years beginning after December 15, Early adoption is permitted. The ASU should be applied at the beginning of the earliest period presented using a modified retrospective approach. Grameen plans to adopt the new ASUs at the required implementation dates. I-14

17 GRAMEEN FOUNDATION USA AND AFFILIATES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS MARCH 31, INVESTMENTS Investments consisted of the following at March 31, 2017: Cost Fair Value Mutual funds - equities $ 1,011,728 $ 1,022,177 Mutual funds - fixed income 1,028,817 1,019,169 TOTAL INVESTMENTS $ 2,040,545 $ 2,041,346 Included in interest and investment income in the Consolidated Statement of Activities and Changes in Net Assets for the year ended March 31, 2017: Interest and dividends (from cash and investment accounts) $ 65,021 Unrealized gain on investments 4,346 Realized gain on sales of investments 157,654 TOTAL INTEREST AND INVESTMENT INCOME $ 227, PROGRAM-RELATED INVESTMENTS Grameen Foundation USA has made certain program-related investments in an effort to further the impact of its programmatic activities. All investments are stated at cost; however, certain impairments have been recognized to adjust to fair value. Grameen Foundation USA has performed independent valuations and deemed the net values to be a fair representation of lower of cost or market. Following is a list of all program-related investments at March 31, 2017: Equity Book Value Less Allowance Carrying Value Grameen-Jameel Pan-Arab Microfinance Limited $ 787,550 $ (787,550) $ - Grameen Capital India Ltd. 658,420 (570,290) 88,130 Kashf Holdings (Pvt.) Limited 250,000 (250,000) - Cashpor Financial and Technical Services 250,027 (27) 250,000 Drishtee Dot Com Ltd. 20,000 (20,000) - Musoni (DTM & Kenya) 1,026,129 (533,631) 492,498 Fairtrade Access Fund 750,000 (8,000) 742,000 Juhudi Kulimo 741,435 (263,958) 477,477 PT Ruma 705, ,139 Radaur Holdings 404,238 (313,180) 91,058 HoneyCare Africa 440,727 (440,727) - TOTAL $ 6,033,665 $ (3,187,363) $ 2,846,302 I-15

18 GRAMEEN FOUNDATION USA AND AFFILIATES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS MARCH 31, SPLIT-INTEREST AGREEMENTS Freedom from Hunger has received contributions from donors, which are invested in a pooled income fund. This fund is divided into units, and contributions of many donors life income gifts are pooled and invested as a group. Donors are assigned a specific number of units based on the proportion of the fair value of their contributions to the total fair value of the pooled income fund on the date of the donor s entry to the pooled fund. Until a donor s death, the donor (or the donor s designated beneficiary or beneficiaries) is paid the actual income (as defined under the arrangement) earned on the donor s assigned units. Upon the death of the donor (and/or any designated beneficiary), the value of these assigned units reverts to Freedom from Hunger. On the above split-interest agreement, Freedom from Hunger recognized its undiscounted remainder interest in the assets received as temporarily restricted contribution revenue in the period in which the assets were received from the donor. Freedom from Hunger did not discount the contributions as the effect of discounting would not be material to these financial statements. 5. NOTE PAYABLE On January 18, 2017, TaroWorks entered into an agreement to borrow $125,000 from ebay Foundation Corporate Advised Fund at Silicon Valley Community Foundation. The purpose of the loan was to provide general support to TaroWorks in its efforts to grow earned revenue and operate as a financially self-sufficient social enterprise. Provisions of the loan provide that principal repayments of $16,000 be made in fiscal year 2020 and $109,000 in fiscal year 2021 with no interest. 6. TEMPORARILY RESTRICTED NET ASSETS Temporarily restricted net assets consisted of the following at March 31, 2017: Financial Services $ 1,517,172 Health and Agricultural Solutions 2,114,182 Strengthening Organizations 47,921 Regional Programs 31,229 3,710,504 Split-interest agreements 12,293 TOTAL TEMPORARILY RESTRICTED NET ASSETS $ 3,722, NET ASSETS RELEASED FROM DONOR RESTRICTIONS The following temporarily restricted net assets were released from donor restrictions for the year ended March 31, 2017, by incurring expenses, thus satisfying the restricted purposes specified by the donors: Financial Services $ 1,538,125 Health and Agricultural Solutions 2,531,162 Strengthening Organizations 683,570 Regional Programs 96,852 TOTAL NET ASSETS RELEASED FROM DONOR RESTRICTIONS $ 4,849,709 I-16

19 GRAMEEN FOUNDATION USA AND AFFILIATES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS MARCH 31, PERMANENTLY RESTRICTED NET ASSETS In the year ended June 30, 1995, Freedom from Hunger received a $77,778 bequest to establish or add to the Charles J. and Rae B. Hitzler endowment fund for the general purposes of Freedom from Hunger. These funds are permanently restricted, and the income earned on the investment is used to support operations. In the year ended March 31, 2017, the Hitzler funds were held in money market funds. The Board of Directors of Freedom from Hunger has interpreted the California Uniform Prudent Management of Institutional Funds Act of 2009 (UPMIFA) as requiring the preservation of the original gift amount of the donor-restricted endowment funds absent explicit donor stipulations to the contrary. As a result of this interpretation, Freedom from Hunger classifies as permanently restricted net assets the original value of the gift donated to the permanent endowment. In accordance with UPMIFA, Freedom from Hunger considers the following factors in making a determination to appropriate or accumulate donor-restricted endowment funds: (1) The duration and preservation of the fund (2) The purposes of the organization and the donor-restricted endowment fund (3) General economic conditions (4) The possible effect of inflation and deflation (5) The expected total return from income and the appreciation of investments (6) Other resources of the organization (7) The investment policies of Freedom from Hunger. Freedom from Hunger has adopted investment and spending policies for endowment assets that attempt to subject the fund to low investment risk and provide its programs with current income. Endowment assets are invested in money market funds. Freedom from Hunger has a policy of appropriating for distribution periodically the endowment fund's investment income that is not permanently restricted, and generally expends the endowment fund's investment income for program services as needed. The current spending policy is not expected to allow the endowment fund to grow as a result of investment returns. This is consistent with our objectives to provide income for our programs and preserve endowment assets without subjecting them to substantial risk. 9. FUTURE FUNDING OF THE AFFILIATES As of March 31, 2017, GFI has an unrestricted net asset balance of $148,912, comprised of ($2,041,260) in cumulative losses from operations offset by $2,190,172 in capital investments by Grameen Foundation USA. Failure to obtain additional unrestricted revenue may affect GFI s future activities. Grameen Foundation USA is committed to continuing to invest resources in GFI because of its social mission to ensure it can meet its obligations. The consolidated financial statements do not include any adjustment that might be necessary if GFI is unable to continue as a going concern. As of March 31, 2017, TaroWorks has a deficit in net assets totaling $142,824. Failure to obtain additional revenue may affect its future activities. However, Grameen Foundation USA is committed to investing resources in TaroWorks to support its social mission. The consolidated financial statements do not include any adjustment that might be necessary if TaroWorks is unable to continue as a going concern. I-17

20 GRAMEEN FOUNDATION USA AND AFFILIATES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS MARCH 31, IN-KIND CONTRIBUTIONS During the year ended March 31, 2017, Grameen was the beneficiary of donated services, which allowed Grameen to provide greater resources toward various programs. In-kind contributions include professional services from Grameen's Bankers without Borders program and other advertising and professional services. To properly reflect total program expenses, the following donations have been included in revenue and expense for the year ended March 31, 2017: Advertising and other $ 539,117 Legal services 950,335 Professional services 1,094,245 TOTAL IN-KIND CONTRIBUTIONS $ 2,583, LEASE COMMITMENTS Grameen Foundation USA leased a headquarters office in Washington, D.C. under a lease that began on September 1, 2010 and was scheduled to expire on July 31, On May 23, 2016, Grameen Foundation USA entered into an amendment and termination with the lessor. The amendment provided Grameen Foundation USA with a partial abatement of rent from May 23, 2016 through September 23, 2016, and accelerated the expiration date of the lease to September 23, In exchange, Grameen Foundation USA paid a one-time lease termination fee of $275,000. Grameen Foundation USA entered into a new lease agreement with a different lessor for its headquarters office space located in Washington D.C. The new lease has an initial term of 5 years 15 days and commenced on September 15, The base rent under the new lease is approximately $138,415 per year for the first year, escalating 2.5% annually thereafter. Grameen Foundation USA leases office space in Seattle, Washington under an eleven-year lease agreement that began on January 1, 2011 and expires on December 31, The annual rental rate is adjusted annually to include a proportionate share of operating expenses and real estate tax reimbursements. Grameen Foundation USA has the right to terminate the lease at any time between the 60th and 82nd month. Freedom from Hunger leases office space in Davis, California under a 60-month lease that began on December 16, 2014 and ends on December 15, Outside the United States, Grameen entered into leases for office space as follows: Location Term Burkina Faso June 2016 to May 2018 Colombia Two one-year leases that end September 2017 and December 2017 Ghana July 2016 to June 2021 India March 2017 to December 2018 Kenya April 2014 to June 2019 Philippines October 2016 to June 2017 Uganda November 2016 to December 2017 I-18

21 GRAMEEN FOUNDATION USA AND AFFILIATES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS MARCH 31, LEASE COMMITMENTS (Continued) Accounting principles generally accepted in the United States of America require that the total rent commitment should be recognized on a straight-line basis over the term of the lease. Accordingly, the difference between the actual monthly payments and the rent expense being recognized for consolidated financial statement purposes is recorded as a deferred rent liability on the Consolidated Statement of Financial Position. As of March 31, 2017, the deferred rent liability totaled $168,764. Grameen Foundation USA entered into subleases with six unrelated organizations in Washington, D.C. Consistent with the signing of the D.C. lease termination effective September 23, 2016, Grameen Foundation USA negotiated termination agreements with all sublessors. In Seattle, a month to month sublease with an unrelated organization was in effect from June 1 to September 30, Grameen Foundation USA entered into a long-term sublease on December 1, 2016, which terminates on December 31, Sublease revenue for the year ended March 31, 2017 totaled $88,500. Future minimum lease payments required under these leases (net of sublease income) are as follows: Year Ending March 31, 2018 $ 418, , , , ,014 $ 1,389,629 Total occupancy expense, including operating and renovation expenses and net of sublease income, totaled $647,509 for the year ended March 31, CONTINGENCY Grameen Foundation USA receives grants from various agencies of the United States Government. Beginning for fiscal year ended March 31, 2016, such grants are subject to audit under the provisions of Title 2 U.S. Code of Federal Regulations (CFR) Part 200 Uniform Administrative Requirement, Cost Principles, and Audit Requirements for Federal Awards. The ultimate determination of amounts received under the United States Government grants is based upon the allowance of costs reported to and accepted by the United States Government as a result of the audits. Audits in accordance with the applicable provisions have been completed for all required fiscal years through Until such audits have been accepted by the United States Government, there exists a contingency to refund any amount received in excess of allowable costs. Management is of the opinion that no material liability will result from such audits. Freedom from Hunger receives funding from the United States Government; however, they are not subject to audit under the provisions of Title 2 U.S. Code of Federal Regulations (CFR) Part 200 Uniform Administrative Requirement, Cost Principles, and Audit Requirements for Federal Awards due to expenditures being under the $750,000 threshold. I-19

22 GRAMEEN FOUNDATION USA AND AFFILIATES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS MARCH 31, PENSION PLAN Grameen Foundation USA and TaroWorks maintain a contributory defined contribution plan under Section 401(k) of the Internal Revenue Code for all eligible U.S. employees. The Board of Directors determines the employer contributions. Currently, both entities contribute 50% of each employee's contribution, up to 3% of each employee's salary. During the year ended March 31, 2017, pension expense totaled $85,091. Freedom from Hunger terminated its defined contribution retirement plan effective February 28, 2017 and rolled over or distributed all plan assets to plan participants. During the year ended March 31, 2017, pension expense totaled $ FAIR VALUE MEASUREMENT In accordance with FASB ASC 820, Fair Value Measurement, Grameen has categorized its financial instruments, based on the priority of the inputs to the valuation technique, into a threelevel fair value hierarchy. The fair value hierarchy gives the highest priority to quoted prices in active markets for identical assets or liabilities (Level 1) and the lowest priority to unobservable inputs (Level 3). If the inputs used to measure the financial instruments fall within different levels of hierarchy, the categorization is based on the lowest level input that is significant to the fair value measurement of the instrument. Investments recorded in the Consolidated Statement of Financial Position are categorized based on the inputs to valuation techniques as follows: Level 1. These are investments where values are based on unadjusted quoted prices for identical assets in an active market Grameen has the ability to access. Level 2. These are investments where values are based on quoted prices for similar instruments in active markets, quoted prices for identical or similar instruments in markets that are not active, or model-based valuation techniques that utilize inputs that are observable either directly or indirectly for substantially the full-term of the investments. Level 3. These are investments where inputs to the valuation methodology are unobservable and significant to the fair value measurement. Following is a description of the valuation methodology used for investments measured at fair value. There have been no changes in the methodologies used at March 31, Mutual funds (equities and fixed income) - Fair value is equal to the reported net asset value of the fund, which is the price at which additional shares can be obtained. Cash surrender value of life insurance - The carrying amount equals policy valuations invested in publicly traded mutual funds obtained from the carrier less surrender charges. Split-interest agreements - Split-interest assets are invested in publicly traded mutual funds and are valued at the daily closing price as reported by the fund. Funds held in trust - The fair value is equal to the reported net asset value of the fund. The funds are invested either in money market funds or in publicly traded mutual funds. I-20

23 GRAMEEN FOUNDATION USA AND AFFILIATES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS MARCH 31, FAIR VALUE MEASUREMENT (Continued) Program-related investments - These instruments do not have a readily determinable fair value. The fair values used are generally determined by an external valuation expert and are based on appraisals or other estimates that require varying degrees of judgment. Inputs used in determining fair value may include the cost and recent activity concerning the underlying investments in the funds or partnerships. The table below summarizes, by level within the fair value hierarchy, Grameen's investments as of March 31, 2017: Level 1 Level 2 Level 3 Total Asset Class: Mutual funds - equities $ 1,022,177 $ - $ - $ 1,022,177 Mutual funds - fixed income 1,019, ,019,169 Cash surrender value of life insurance - 286, ,120 Split-interest agreements 12, ,293 Funds held in trust 77, ,778 Program-related investments - - 2,846,302 2,846,302 TOTAL $ 2,131,417 $ 286,120 $ 2,846,302 $ 5,263,839 Level 3 Financial Assets The following table provides a summary of changes in fair value of Grameen Foundation USA's financial assets for the year ended March 31, 2017: Program- Related Investments Beginning balance as of March 31, 2016 $ 3,328,287 Appreciation of program-related investments 131,475 Change in allowance for impairment of program-related investments (613,460) BALANCE AS OF MARCH 31, 2017 $ 2,846, RELATED PARTY TRANSACTIONS During the year ended March 31, 2017, Grameen Foundation USA received $125,000 from Grameen-Jameel Pan-Arab Microfinance Limited, a joint-venture providing microfinance services in the Middle East, in which Grameen Foundation USA owns 50%. As of March 31, 2017, receivables totaled $175,000 with allowances for uncollectible account balances of $175,000. As of October 2, 2017, Grameen Foundation USA and Grameen Jameel terminated the joint venture. In August 2010, Grameen Foundation USA incorporated GFI, a for profit wholly-owned subsidiary in India. As of March 31, 2017, the investment totaled $2,190,044. During the year ended March 31, 2017, Grameen Foundation USA paid fees to GFI for professional services in India totaling $491,667. I-21

24 GRAMEEN FOUNDATION USA AND AFFILIATES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS MARCH 31, RELATED PARTY TRANSACTIONS (Continued) In April 2015, Grameen Foundation USA incorporated TaroWorks, a wholly-owned subsidiary in the United States. As of March 31, 2017, the investment totaled $245,076. During the year ended March 31, 2017, Grameen Foundation USA paid Taroworks for grants and software license fees totaling $601,833. In October 2016, Freedom from Hunger entered into an Asset Transfer Agreement with Grameen Foundation USA in order to advance the organizations shared missions. During the year ended March 31, 2017, Freedom from Hunger paid fees to Grameen Foundation USA for staff time and allocated expenses totaling $221,017. Inter-organization balances and transactions involving Grameen Foundation USA, Grameen Foundation India Private Limited, TaroWorks and Freedom from Hunger have been eliminated in the accompanying consolidated financial statements. 16. RETURN OF UNSPENT GRANT FUNDS In 2011, Grameen Foundation USA entered into an agreement with the Bill and Melinda Gates Foundation, for support of the MoTech project. During 2017, Grameen Foundation USA agreed to transfer $224,504 of unspent funds to a project partner, Dimagi, Inc, for completion of the project. This amount is carried as a liability as of March 31, SUBSEQUENT EVENTS In preparing these consolidated financial statements, Grameen has evaluated events and transactions for potential recognition or disclosure through December 18, 2017, the date the consolidated financial statements were issued. I-22

25 SUPPLEMENTAL INFORMATION

26 SCHEDULE 1 GRAMEEN FOUNDATION USA AND AFFILIATES CONSOLIDATED SCHEDULE OF SUPPORT AND REVENUE AND FUNCTIONAL EXPENSES FOR THE YEAR ENDED MARCH 31, 2017 Grameen Foundation USA Grameen Foundation Freedom Ghana Philippines Uganda Kenya Colombia Indonesia India Private TaroWorks, from Headquarters Branch Branch Branch Branch Branch Branch Limited LLC Hunger Consolidated SUPPORT AND REVENUE Contributions and grants $ 6,874,259 $ - $ - $ - $ - $ - $ - $ - $ - $ 1,778,250 $ 8,652,509 Program revenues 1,063, ,148 27,231 43, , , ,009 2,086,210 Government grants 2,491, ,806 2,609,704 Interest and investment income 222, ,782-1, ,021 Loan interest 19, ,083 In-kind contributions 2,376, ,818 2,583,697 Other ,414 23,414 TOTAL SUPPORT AND REVENUE $ 13,048,218 $ 87 $ - $ 37,148 $ 27,231 $ 43,555 $ - $ 494,764 $ 279,239 $ 2,271,396 $ 16,201,638 FUNCTIONAL EXPENSES Salaries $ 4,238,966 $ 486,423 $ 295,665 $ 372,074 $ 237,148 $ 294,220 $ 5,795 $ 431,807 $ 345,803 $ 341,280 $ 7,049,181 Benefits 1,077, ,380 46, ,708 74, , ,584 84,948 19,118 1,731,362 Professional services 1,525, ,043 64,262 82,869 72,556 16,395 6, , , ,511 2,751,742 In-kind contributions 2,376, ,818 2,583,697 Grants 152, , , ,771 Travel 214, ,022 41,994 74,465 35,176 41,705 2,937 59,206 24,719 91, ,794 Conferences and meetings 76,182 71,733 31,289 1, ,026-8,935 4,507 20, ,302 Communications 68,573 43,984 2,166 35,756 4,605 2,663-3,387 1,014 8, ,559 Information technology 237, , ,603 31, ,766 Occupancy 394,083 49,638 27,440 45,528 32,888 27,362-19,026 12,507 39, ,509 Vehicles and equipment 36,329 89,536 19,882 42, , , ,282 Depreciation and amortization 25, ,742-54, ,431 Insurance 99, , , , ,709 Office expenses 71,412 30,631 6,511 21,602 1,873 1,607-9,320 2,819 43, ,168 Advertising 61, ,236 6,125-14, ,469 Bank fees 25, ,818 3,144 1,936 3, , ,674 49,075 Other 77,217 56, , , , ,587 TOTAL FUNCTIONAL EXPENSES $ 10,757,102 $ 1,378,397 $ 538,191 $ 831,608 $ 507,224 $ 514,632 $ 20,718 $ 1,074,347 $ 921,860 $ 1,215,325 $ 17,759,404 I-23

27 SCHEDULE 2 GRAMEEN FOUNDATION USA SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS FOR THE YEAR ENDED MARCH 31, 2017 Federal Granting Agency Program Title CFDA Number Pass-Through Entity Pass-Through Entity Identifying Number Passed- Through to Sub-recipients 2017 Expenditures US Agency for International Development Feed the Future Partnering for Innovation Fintrac PI-SMOG $ - $ 316,101 US Agency for International Development Community Connector Project FHI 360 CMS ,280 US Agency for International Development New Alliance ICT Extension Challenge N/A - 121, ,493 US Agency for International Development N Global Food Security Innovation Center Michigan State University RC ,477 US Agency for International Development Support for International Family Planning Marie Stopes International AID-OAA-A GF - 156,010 US Agency for International Development Uganda Maize Value-Added Alliance Carana Corp 1793-FPC-Gram-02-2,200 Total CFDA ,554 1,872,561 US Agency for International Development Global Resilience Partnership KPMG East Africa USAID- RF/STG3/2015/08-619,337 TOTAL EXPENDITURES OF FEDERAL AWARDS $ 121,554 $ 2,491,898 RECONCILIATION OF REVENUE ON THE STATEMENT OF ACTIVITIES Grameen Foundation USA U.S. Government grants $ 2,491,898 Freedom from Hunger U.S. Government grants 117,806 TOTAL REVENUE RECOGNIZED $ 2,609,704 I-24

28 GRAMEEN FOUNDATION USA SCHEDULE 2 (Continued) SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS FOR THE YEAR ENDED MARCH 31, 2017 Note 1. Basis of Presentation The accompanying Schedule of Expenditures of Federal Awards (the Schedule) includes the federal award activity of Grameen Foundation USA under programs of the Federal government for the year ended March 31, The information in this Schedule is presented in accordance with the requirements of Title 2 U.S. Code of Federal Regulations Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (Uniform Guidance). Because the Schedule presents only a selected portion of the operations of Grameen Foundation USA, it is not intended to and does not present the financial position, changes in net assets or cash flows of Grameen Foundation USA. Note 2. Summary of Significant Accounting Policies Expenditures reported on the Schedule are reported on the accrual basis of accounting. Such expenditures are recognized following, as applicable, either the cost principles in OMB Circular A-122, Cost Principles for Non-Profit Organizations, or the cost principles contained in Title 2 U.S. Code of Federal Regulations Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (Uniform Guidance), wherein certain types of expenditures are not allowable or are limited as to reimbursement. Negative amounts shown on the Schedule represent adjustments or credits made in the normal course of business to amounts reported as expenditures in prior years. Grameen Foundation USA has elected not to use the 10-percent de minimis indirect cost rate as allowed under the Uniform Guidance. I-25

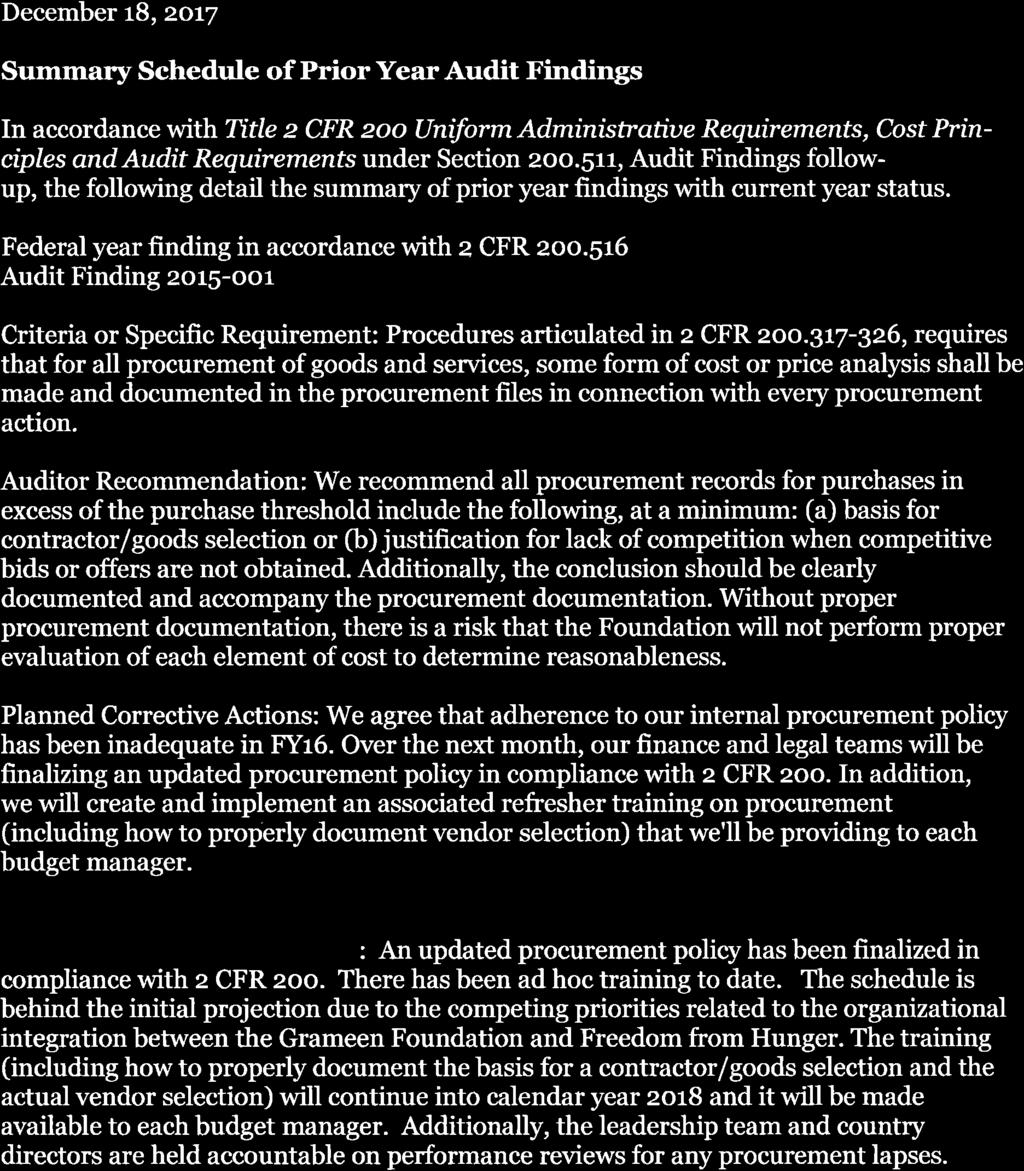

29 SCHEDULE 3 GRAMEEN FOUNDATION USA SCHEDULE OF FINDINGS AND QUESTIONED COSTS FOR THE YEAR ENDED MARCH 31, 2017 Section I - Summary of Auditor's Results Financial Statements 1). Type of auditor's report issued on whether the financial statements audited were prepared in accordance with GAAP on the accrual basis of accounting: Unmodified 2). Internal control over financial reporting: Material weakness(es) identified? Yes No Significant deficiency(ies) identified that are not considered to be material weakness(es)? Yes None Reported 3). Noncompliance material to financial statements noted? Yes No Federal Awards 4). Internal control over major programs: Material weakness(es) identified? Yes No Significant deficiency(ies) identified that are not considered to be material weakness(es)? Yes None Reported 5). Type of auditor's report issued on compliance for major programs: Unmodified 6). Any audit findings disclosed that are required to be reported in accordance with 2 CFR (a)? Yes No 7). Identification of major programs: Federal Program Title Pass-Through Entity CFDA Number Expenditures Feed the Future Partnering for Innovation Fintrac $ 316,101 Community Connector Project FHI $ 447,280 New Alliance ICT Extension Challenge N/A $ 825,493 HESN Global Food Security Innovation Center Michigan State University $ 125,477 Support for International Family Planning Marie Stopes International $ 156,010 Uganda Maize Value-Added Alliance Carana Corp $ 2,200 8). Dollar threshold used to distinguish between Type A and Type B programs: $750,000 9). Auditee qualified as a low-risk auditee? Yes No I-26

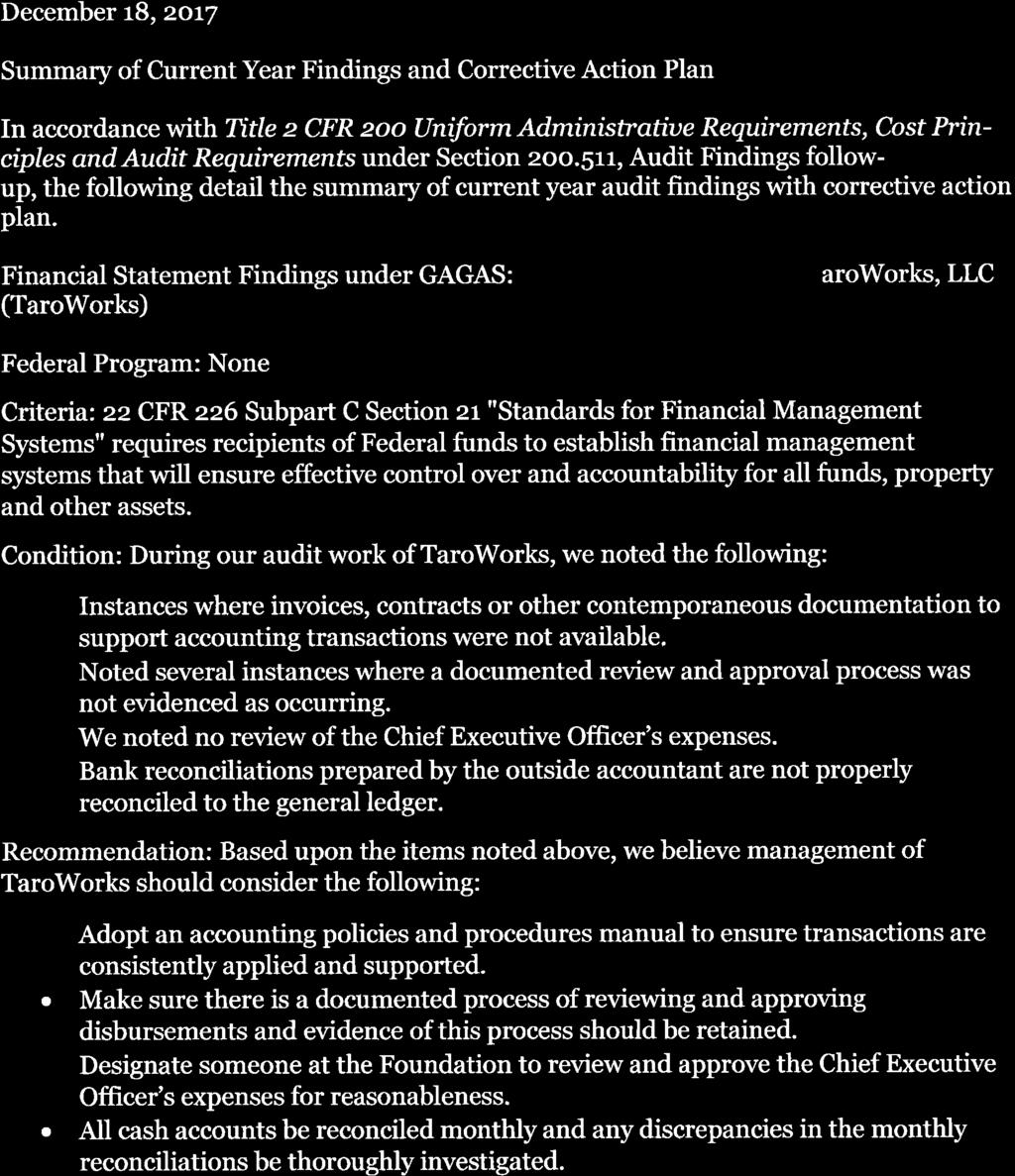

30 GRAMEEN FOUNDATION USA SCHEDULE 3 (Continued) SCHEDULE OF FINDINGS AND QUESTIONED COSTS FOR THE YEAR ENDED MARCH 31, 2017 Section II - Financial Statement Findings Finding : TaroWorks, LLC (TaroWorks) Federal Program: None Criteria: 22 CFR 226 Subpart C Section 21 "Standards for Financial Management Systems" requires recipients of Federal funds to establish financial management systems that will ensure effective control over and accountability for all funds, property and other assets. Condition: During our audit work of TaroWorks, we noted the following: Noted instances where invoices, contracts or other contemporaneous documentation to support accounting transactions were not available. Noted several instances where a documented review and approval process was not evidenced as occurring. We noted no review of the Chief Executive Officer s expenses. Bank reconciliations prepared by the outside accountant are not properly reconciled to the general ledger. Context: TaroWorks does not consistently process disbursements or properly prepare monthly bank reconciliations. Additionally, TaroWorks does not have a documented policies and procedures manual. Effect: Without the proper reconciliation of all accounts and transactions on a monthly basis in a timely manner, as well as the proper review and approval of such reconciliations and transactions, there exists the potential for errors and the misappropriation of funds. Cause: TaroWorks does not have an accounting policies and procedures manual to ensure internal controls are consistently applied. Questioned Costs: None noted. Recommendation: Based upon the items noted above, we believe management of TaroWorks should consider the following: Adopt an accounting policies and procedures manual to ensure transactions are consistently applied and supported. Make sure there is a documented process of reviewing and approving disbursements and evidence of this process should be retained. Designate someone at the Foundation to review and approve the Chief Executive Officer s expenses for reasonableness. All cash accounts be reconciled monthly and any discrepancies in the monthly reconciliations be thoroughly investigated. Management Response: TaroWorks is adopting an accounting policies and procedures manual to ensure transactions are performed and documented in accordance with Generally Accepted Accounting Principles. TaroWorks has adopted an online payment authorization application to review and approve disbursements that will provide the necessary audit trail. All future TaroWorks CEO expense reports will be reviewed and approved by Grameen Foundation USA s CEO. Finally Grameen Foundation USA s Director, Finance has reviewed the proper bank reconciliation process to be used with the outside accountant and will review future bank reconciliations for compliance. I-27

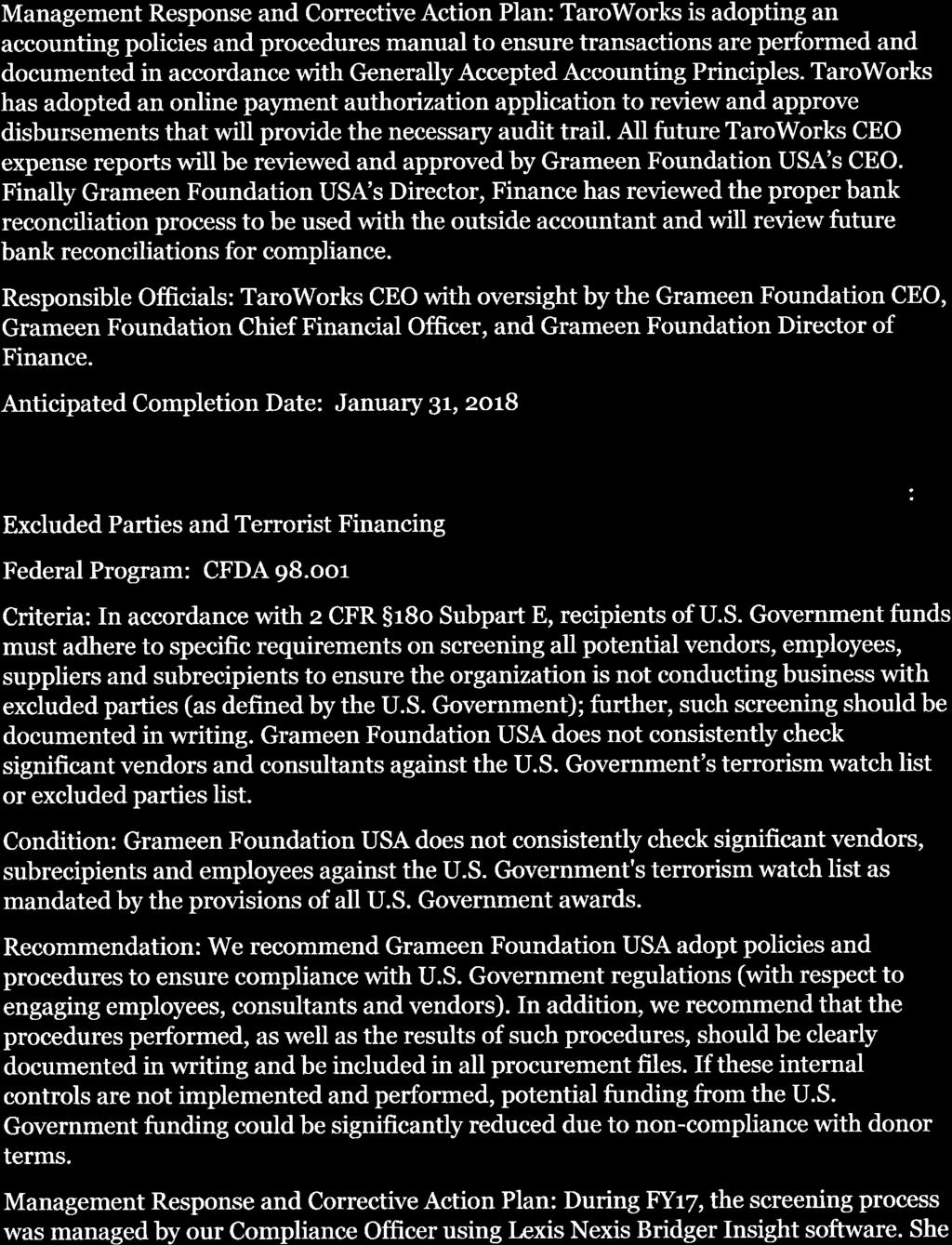

31 GRAMEEN FOUNDATION USA SCHEDULE 3 (Continued) SCHEDULE OF FINDINGS AND QUESTIONED COSTS FOR THE YEAR ENDED MARCH 31, 2017 Section III - Federal Award Findings and Questioned Costs (2 CFR (a)) Finding : Excluded Parties and Terrorist Financing Federal Program: CFDA Criteria: In accordance with 2 CFR 180 Subpart E, recipients of U.S. Government funds must adhere to specific requirements on screening all potential vendors, employees, suppliers and subrecipients to ensure the organization is not conducting business with excluded parties (as defined by the U.S. Government); further, such screening should be documented in writing. Grameen Foundation USA does not consistently check significant vendors and consultants against the U.S. Government s terrorism watch list or excluded parties list. Condition: Grameen Foundation USA does not consistently check significant vendors, subrecipients and employees against the U.S. Government's terrorism watch list as mandated by the provisions of all U.S. Government awards. Context: For certain procurements and subawards selected based on a threshold, we examined contemporaneous documentation to determine if Grameen Foundation USA verified that entities are not suspended, debarred, or otherwise excluded. We consider our sample to be representative of the population. Effect: Grameen Foundation USA could inadvertently engage in relationships with vendors who have been debarred, suspended or otherwise excluded from receiving federal funds. Cause: Policies and procedures over formal documentation of SAM/OFAC checks or other background checks were not strictly implemented. Questioned Costs: Undetermined. Identification as a Repeat Finding, if Applicable: N/A Recommendation: We recommend Grameen Foundation USA adopt policies and procedures to ensure compliance with U.S. Government regulations (with respect to engaging employees, consultants and vendors). In addition, we recommend that the procedures performed, as well as the results of such procedures, should be clearly documented in writing and be included in all procurement files. If these internal controls are not implemented and performed, potential funding from the U.S. Government funding could be significantly reduced due to non-compliance with donor terms. Management Response: During FY17, the screening process was managed by our Compliance Officer using Lexis Nexis Bridger Insight software. She performed the screening regularly, per the Counterterrorism Policy, but there were two issues. First, the software does not record the individual review of each transaction when the scan is run in a batch and does not result in a hit. Second, staff did not consistently log contracts into Salesforce. In December 2017, we switched to Finscan, which automatically scans all accounts in Salesforce and produces clear records. All GF staff are required to log their contacts, including vendors, contractors, donors, employees, etc. in Salesforce. Our strong compliance with this policy will enable SAM/OFAC checks to be completed, and Finscan will produce a report on all names/entities scanned, even if they do not produce a hit. Additionally, prior to any payments being made, Finance will check that a new payee has been recorded in Salesforce, which will ensure that scans are done on all payees. I-28

32 GRAMEEN FOUNDATION USA SCHEDULE 3 (Continued) SCHEDULE OF FINDINGS AND QUESTIONED COSTS FOR THE YEAR ENDED MARCH 31, 2017 Section III - Federal Award Findings and Questioned Costs (2 CFR (a)) (Continued) Finding : Subrecipient Monitoring Policies Federal Program: CFDA New Alliance ICT Extension Challenge Criteria: As stated in 2 CFR part (b), all pass-through entities must evaluate each subrecipient s risk of noncompliance with Federal statutes, regulations, and the terms and conditions of the subaward for purposes of determining the appropriate subrecipient monitoring procedures to prescribe to each individual subrecipient (i.e. pre-award risk assessment procedures). Condition: During our audit work over subrecipient expenditures, we were unable to verify that preaward risk assessment procedures were performed. It is our understanding that Grameen Foundation USA has ongoing relationships with these subrecipients and evaluation of these subrecipients risk is a continual process; however, these procedures were not documented. Lastly, we noted that these requirements were not incorporated into the Grameen Foundation USA s current policies and procedures. Our audit procedures consisted of substantive testwork over a sample of subawards that were selected based on a threshold. We consider our sample to be representative of the population. Context: Grameen Foundation USA is not in compliance with Federal requirements. Effect: Unless consistent monitoring activities are performed, there is a potential risk that Grameen Foundation USA will not perform enough monitoring on subrecipients. Cause: Grameen Foundation USA does not have policies and procedures on the pre-award risk assessment on subrecipients. Questioned Costs: None noted. Identification as a Repeat Finding, if Applicable: N/A Recommendation: We recommend Grameen Foundation USA update its policies and procedures surrounding subrecipients to establish criteria to be used in the evaluation of the risk of noncompliance associated with the intended subrecipient for the purpose of determining the expected level of oversight during the period of performance. This evaluation should include a scaling system, such as high, medium or low risk (for example), and the monitoring tools and procedures to be performed at each of these levels (additional training, onsite reviews, types of and frequency of reporting, etc.). Management Response: During the year ended March 31, 2017, we had $494,771 in sub-recipient activity and $177,888 for the quarter ended June 30, None of it was awarded in FY17 and none of it was from federal awards. For this reason, we did not prioritize the update and training of this policy as part of the Grameen Foundation USA and Freedom from Hunger integration. Now that FY18 is underway, and we are beginning to receive grants with sub-recipients, we intend to update our existing policies to reflect our needs today. I-29

33 GRAMEEN FOUNDATION USA SCHEDULE 3 (Continued) SCHEDULE OF FINDINGS AND QUESTIONED COSTS FOR THE YEAR ENDED MARCH 31, 2017 Section III - Federal Award Findings and Questioned Costs (2 CFR (a)) (Continued) Finding : Procurement Federal Program: CFDA Criteria or Specific Requirement: Procedures articulated in 2 CFR , requires that for all procurement of goods and services, some form of cost or price analysis shall be made and documented in the procurement files in connection with every procurement action. Condition: Grameen Foundation USA does not consistently follow its own internal procurement policy, as we noted several instances where it had failed to document its competitive bid process by obtaining quotations. Additionally, for certain items in which various bids were obtained, we noted that a documented bid analysis and conclusion did not accompany the documentation. Our audit procedures consisted of substantive testwork over a sample of consultants and vendors that were selected based on a threshold. We consider our sample to be representative of the population. Context: Grameen Foundation USA is not in compliance with internal policy and Federal requirements. Effect: Without proper procurement documentation, there is a risk that the Grameen Foundation USA will not perform proper evaluation of each element of cost to determine reasonableness. Cause: Grameen Foundation USA did not consistently follow internal policy of obtaining bids/quotes and document conclusion process. Questioned Costs: None noted. Identification as a Repeat Finding, if Applicable: Recommendation: We recommend all procurement records for purchases in excess of the purchase threshold include the following, at a minimum: (a) basis for contractor/goods selection or (b) justification for lack of competition when competitive bids or offers are not obtained. Additionally, the conclusion should be clearly documented and accompany the procurement documentation. Without proper procurement documentation, there is a risk that Grameen Foundation USA will not perform proper evaluation of each element of cost to determine reasonableness. Management Response: We rely on all staff to comply with the policy without the staff resources to perform internal monitoring to ensure it is happening. Given the finding is still unresolved in FY17, as we revamp our contracting process in Salesforce, we are including a process that prompts users to comply with Procurement and signals to Finance not to pay on an invoice if Procurement was not followed. I-30

34 REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND ON COMPLIANCE AND OTHER MATTERS BASED ON AN AUDIT OF FINANCIAL STATEMENTS PERFORMED IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS Independent Auditor s Report To the Board of Directors Grameen Foundation USA and Affiliates Washington, D.C. We have audited, in accordance with the auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards issued by the Comptroller General of the United States, the consolidated financial statements of Grameen Foundation USA as of and for the year ended March 31, 2017, and the related notes to the consolidated financial statements, which collectively comprise Grameen Foundation USA's basic consolidated financial statements, and have issued our report thereon dated December 18, Internal Control Over Financial Reporting In planning and performing our audit of the consolidated financial statements, we considered Grameen Foundation USA's internal control over financial reporting (internal control) to determine the audit procedures that are appropriate in the circumstances, for the purpose of expressing our opinions on the consolidated financial statements, but not for the purpose of expressing an opinion on the effectiveness of Grameen Foundation USA's internal control. Accordingly, we do not express an opinion on the effectiveness of Grameen Foundation USA's internal control. A deficiency in internal control exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct, misstatements on a timely basis. A material weakness is a deficiency, or a combination of deficiencies, in internal control, such that there is a reasonable possibility that a material misstatement of Grameen Foundation USA's consolidated financial statements will not be prevented, or detected and corrected on a timely basis. A significant deficiency is a deficiency, or a combination of deficiencies, in internal control that is less severe than a material weakness, yet important enough to merit attention by those charged with governance. Our consideration of internal control was for the limited purpose described in the first paragraph of this section and was not designed to identify all deficiencies in internal control that might be material weaknesses or significant deficiencies and therefore, material weaknesses or significant deficiencies may exist that were not identified. Given these limitations, during our audit we did not identify any deficiencies in internal control that we consider to be material weaknesses. However, material weaknesses may exist that have not been identified. We did identify certain deficiencies in internal control, described in the accompanying Schedule of Findings and Questioned Costs as Finding that we consider to be a significant deficiency MONTGOMERY AVENUE SUITE 650 NORTH BETHESDA, MARYLAND (301) FAX (301) MEMBER OF CPAMERICA INTERNATIONAL, AN AFFILIATE OF HORWATH INTERNATIONAL MEMBER OF THE AMERICAN INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS' PRIVATE COMPANIES PRACTICE SECTION II-1

35 Compliance and Other Matters As part of obtaining reasonable assurance about whether Grameen Foundation USA's consolidated financial statements are free from material misstatement, we performed tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements, noncompliance with which could have a direct and material effect on the determination of financial statement amounts. However, providing an opinion on compliance with those provisions was not an objective of our audit, and accordingly, we do not express such an opinion. The results of our tests disclosed instances of noncompliance or other matters that are required to be reported under Government Auditing Standards and which are described in the accompanying Schedule of Findings and Questioned Costs as Finding Example Entity s Response to Findings Grameen Foundation USA's response to the findings identified in our audit are described in the accompanying Schedule of Findings and Questioned Costs. Grameen Foundation USA's response was not subjected to the auditing procedures applied in the audit of the consolidated financial statements and, accordingly, we express no opinion on it. Purpose of this Report The purpose of this report is solely to describe the scope of our testing of internal control and compliance and the result of that testing, and not to provide an opinion on the effectiveness of the entity s internal control or on compliance. This report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the entity s internal control and compliance. Accordingly, this communication is not suitable for any other purpose. December 18, 2017 II-2

PART 200, UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS (UNIFORM GUIDANCE) Independent Auditor's Report To the")

36 REPORT ON COMPLIANCE FOR EACH MAJOR FEDERAL PROGRAM AND REPORT ON INTERNAL CONTROL OVER COMPLIANCE REQUIRED BY TITLE 2 U.S. CODE OF FEDERAL REGULATIONS (CFR) PART 200, UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS (UNIFORM GUIDANCE) Independent Auditor's Report To the Board of Directors Grameen Foundation USA and Affiliates Washington, D.C. Report on Compliance for Each Major Federal Program We have audited Grameen Foundation USA's compliance with the types of compliance requirements described in the OMB Compliance Supplement that could have a direct and material effect on each of Grameen Foundation USA's major federal programs for the year ended March 31, Grameen Foundation USA's major federal programs are identified in the summary of auditor s results section of the accompanying Schedule of Findings and Questioned Costs. Management s Responsibility Management is responsible for compliance with the federal statutes, regulations, and the terms and conditions of its federal awards applicable to its federal programs. Auditor s Responsibility Our responsibility is to express an opinion on compliance for each of Grameen Foundation USA's major federal programs based on our audit of the types of compliance requirements referred to above. We conducted our audit of compliance in accordance with auditing standards generally accepted in the United States of America; the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States; and the audit requirements of Title 2 U.S. Code of Federal Regulations Part 200, Uniform Administrative Requirements, Cost Principles and Audit Requirements for Federal Awards (Uniform Guidance). Those standards and the Uniform Guidance require that we plan and perform the audit to obtain reasonable assurance about whether noncompliance with the types of compliance requirements referred to above that could have a direct and material effect on a major federal program occurred. An audit includes examining, on a test basis, evidence about Grameen Foundation USA's compliance with those requirements and performing such other procedures as we considered necessary in the circumstances. We believe that our audit provides a reasonable basis for our opinion on compliance for each major federal program. However, our audit does not provide a legal determination of Grameen Foundation USA's compliance. Opinion on Each Major Federal Program In our opinion, Grameen Foundation USA complied, in all material respects, with the types of compliance requirements referred to above that could have a direct and material effect on each of its major federal programs for the year ended March 31, MONTGOMERY AVENUE SUITE 650 NORTH BETHESDA, MARYLAND (301) FAX (301) MEMBER OF CPAMERICA INTERNATIONAL, AN AFFILIATE OF HORWATH INTERNATIONAL MEMBER OF THE AMERICAN INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS' PRIVATE COMPANIES PRACTICE SECTION III-1