Jyske Bank March 2018

|

|

|

- Angela Erika Montgomery

- 5 years ago

- Views:

Transcription

1 Jyske Bank 5 March 2018

2 Summary 2

3 Highlights 3

4 Our targets Q1-Q4 Delivering an attractive long-term return on equity of 8-12% 9.7% Volume growth DKK 100bn in housing-related loans DKK 96.0bn DKK 20bn in property loans for corporate clients DKK 19.3bn Maintaining a strong capital position Long-term targets for capital ratio 17.5% and CET1 ratio 14% Capital levels above long-term targets in order to manage future regulatory requirements S&P rating A- (stable outlook) 19.8% and 16.4% 4

5 Strategy focus areas Home loans: One brand, one product range and one process New area of growth: Trading/investment/ wealth management 5

6 Setting new targets Return on Equity Delivering an attractive long-term return on equity of 8-12% Volume growth Total loan portfolio of DKK 350bn in Jyske Realkredit FTEs Number of FTE back to 2013-level 5 years after the merger From 3,932 FTE end- to approx. 3,774 FTE mid DKK 20-25bn in housing related loans +DKK 15-20bn in property loans for corporate clients Capital distribution Maintain a stable dividend Use additional dividends and share buy-backs when current profit and capital structure provide the opportunity Capital position Long-term targets for capital ratio 17.5% and CET1 ratio 14% post-basel IV implementation Building sufficient capital level to cover expected Basel IV-effect on capital ratio of 3 percentage points by January 1 st 2022 Gradually building a RAC ratio of about 10.5% 6

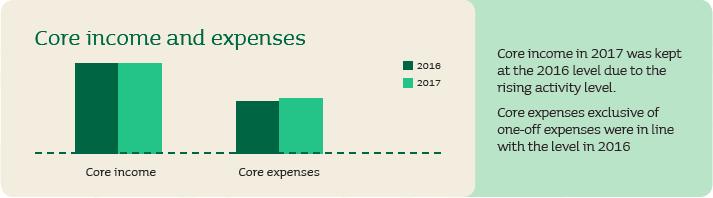

7 DKKm DKKm ROE in line with target and starting to show stability Delivering a net profit of DKK 3,143m and ROE of 9.7% in and thus within target range of 8-12% Quarterly returns are becoming less volatile A decrease of 0.4 percentage points compared to 2016: Stable core income not sufficient to maintain return as equity increases No significant change re. core expenses without one-offs core expenses would have contributed to an increase in ROE of 0.4% Significant reversals of impairment keeps ROE at level with 2016 Net profit Net profit Profit ROE (after tax) 16% 14% 12% 10% 8% 6% 4% 2% 0% vs. 2016: Development in ROE after tax % 12% % 10% % 8% % 6% % % 4% 0 0% 2% % Q Q Q Q Q Q Q Q2 Q4 0% 2016 Core income Core expenses Investment Loan impairment portfolio earnings charges Net Profit ROE (after tax) 7

8 Percent Capital structure, targets and requirements Long-term capital targets based on fully implemented Basel IV capital requirements: Capital ratio 17.5% and CET1 ratio 14% Capital ratios to remain above long-term targets given upcoming capital requirements Basel IV The Basel IV recommendations were announced in December Jyske Bank now expects the effect on the capital ratio to be 3 percentage points compared to previously 4 percentage points Jyske Bank aims to build the needed capital levels prior to the phasing-in period starting 1 January Capital ratio and CET1 ratio Pillar II Buffer Pillar I Requiremet Expected fully phased in CRD IV ratios by 2019 Expected CET1 components required by 2019 Min. CET1 requirement AT1 Tier 2 Pillar II Buffer Capital Conservation Buffer SIFI Buffer Countercyclical buffer IFRS 9 In effect as per 1 January 2018 Balance of impairment charges is expected to increase by DKK 1,000-1,200m. A post-tax amount of DKK 800-1,000m will be deducted from equity in Q Of the total effect DKK 7-800m relate to loans recognised at amortized cost and DKK 3-400m to loans recognised at fair value. The after tax amount pertaining to loans at fair value will have P/L effect Jyske Bank has opted not to make use of the 5-year phase-in period proposed by the EU Commission Minimum requirement for own funds and eligible liabilities (MREL) Final MREL requirements received in February 2018: 2 x solvency requirement incl. all buffer requirements corresponding to 28.1% of REA (DKK 33bn as per end-2016) According to preliminary calculations Jyske Bank most likely already fulfills MREL Grandfathering of senior debt (senior preferred) issued prior to 1 January 2018 MREL must be fulfilled entirely with contractually subordinated debt (senior non preferred) from 1 January

9 DKKm DKKm Net reversals and improved credit quality Net reversals of DKK 453m under core profit Total balance of management s estimate of DKK 466m end of, of which DKK 75m relate to agriculture, compared to DKK 471m and DKK 235m respectively end of 2016 Impairment ratios (under core profit): Impairment ratio for Q4-3bp and -10bp Accumulated impairment ratio 1.2% (incl. balance of discounts for acquired loans) Banking: Overall credit quality continues to improve Low number of new defaults and improvement in credit quality of previously defaulted clients Significant reversals in corporate segment Mortgage: Overall positive development in credit quality Alignment of the Group s loss models resulted in an increase of DKK 175m in collective impairment charges. Of which DKK 169m relates to the Private segment Loan impairment charges (under core profit) ,000 8,000 6,000 4,000 2,000 0 Q Q Q1 Q2 Q3 Q4 Balance of loan impairment charges and losses Q Q Q Q Q Q Q Q1 Q2 Q3 Balance of loan impairment charges (incl. balance discounts for acquired assets) Losses Loan impairment charges Balance of loan impairment charges/total loans (rhs) Q4 2.5% 2.0% 1.5% 1.0% 0.5% 0.0% 9

10 Strategic themes Learn more about Jyske Bank s view of strategic themes: jyskebank.dk/

11 General legal disclaimer This presentation and the information contained therein is furnished and has been prepared solely for information purposes by Jyske Bank A/S. It is furnished for your private information with the express understanding, which recipient acknowledges, that it is not an offer, recommendation or solicitation to buy, hold or sell, or a means by which any security may be offered or sold The information contained and presented in this presentation, other than the information emanating from and relating to Jyske Bank A/S itself, has been obtained by Jyske Bank A/S from sources believed to be reliable. Jyske Bank A/S can not verify such information, however, and because of the possibility of human or mechanical error by our sources, Jyske Bank A/S or others, no representation is made that such information contained herein is accurate in all material respects or complete. Jyske Bank A/S does not accept any liability for the accuracy, up-to-dateness, adequacy, or completeness of any such information and is not responsible for any errors or omissions or the result obtained from the use of such information. The statements contained herein are statements of our nonbinding opinion, not statement of fact or recommendations to buy, hold or sell any securities. Changes to assumptions may have a material impact on any performance detailed. Historic information on performance is not indicative of future performance. Jyske Bank A/S may have issued, and may in the future issue, other presentations or information that are inconsistent with, and reach different conclusions from, the information presented herein. Those presentations or the information reflect the different assumptions, views and analytical methods of the analysts who prepared them and Jyske Bank A/S is under no obligation to ensure that such other presentations or information are brought to the attention of any recipient of the information contained herein Nothing in this presentation constitutes investment, legal, accounting or tax advice, or a representation that any investment or strategy is suitable or appropriate to your individual circumstances, or otherwise constitutes a personal recommendation to you. This presentation is intended only for and directed to persons sufficiently expert to understand the risks involved, namely market professionals. This publication does not replace personal consultancy. Prior to taking any investment decision you should contact your independent investment adviser, your legal or tax adviser, or any other specialist for further and more up-to date information on specific investment opportunities and for individual investment advice and in order to confirm that the transaction complies with your objectives and constraints, regarding the appropriateness of investing in any securities or investment strategies discussed herein Jyske Bank A/S or its affiliates (and their directors, officers or employees) may have effected or may effect transactions for its own account (buy or sell or have a long or short position) in any investment outlined herein or any investment related to such an investment. Jyske Bank A/S or its affiliates may also have investment banking or other commercial relationship with the issuer of any security mentioned herein. Please note that Jyske Bank A/S or an associated enterprise of Jyske Bank A/S may have been a member of a syndicate of banks, which has underwritten the most recent offering of securities of any company mentioned herein in the last five years. Jyske Bank A/S or an associated enterprise may also have, within the last three years, served as manager or co-manager of a public offering of securities for, or currently may make a primary market in issues of, any or all of the entities mentioned herein or may be providing, or have provided within the previous 12 months, significant advice or investment services in relation to the investment concerned or a related investment Any particular security or investment referred to in this presentation may involve a high degree of risk, which may include principal, interest rate, index, currency, credit, political, liquidity, time value, commodity and market risk and is not suitable for all investors. Any securities may experience sudden and large falls in their value causing losses equal to the original investment when that investment is realized. Any transaction entered into is in reliance only upon your judgment as to both financial, suitability and risk criteria. Jyske Bank A/S does not hold itself out to be an advisor in these circumstances, nor does any of its staff have the authority to do so. 11

Jyske Bank SEB Nordic Seminar January 2018

Jyske Bank SEB Nordic Seminar 2018 10 January 2018 Jyske Bank in brief One of the four large financial institutions in Denmark and a Danish SIFI 3 segments (Banking, Mortgage and Leasing) Estimated market

Jyske Bank SEB Nordic Seminar 2018 10 January 2018 Jyske Bank in brief One of the four large financial institutions in Denmark and a Danish SIFI 3 segments (Banking, Mortgage and Leasing) Estimated market

Jyske Bank. Speed dating ABG 2 October 2018

Jyske Bank Speed dating ABG 2 October 2018 Strategy focus areas Home loans: One brand, one product range and one process New area of growth: Trading/investment/ wealth management 2 Capital Markets Our

Jyske Bank Speed dating ABG 2 October 2018 Strategy focus areas Home loans: One brand, one product range and one process New area of growth: Trading/investment/ wealth management 2 Capital Markets Our

Jyske Bank. Navigating the Nordics Seminar 31 May 2017

Jyske Bank Navigating the Nordics Seminar 31 May 217 Our targets Q1 217 Delivering an attractive long-term return on equity of 8-12% 12.3% Volume growth DKK 1bn in housing-related loans DKK 84.3bn DKK

Jyske Bank Navigating the Nordics Seminar 31 May 217 Our targets Q1 217 Delivering an attractive long-term return on equity of 8-12% 12.3% Volume growth DKK 1bn in housing-related loans DKK 84.3bn DKK

Jyske Bank. Danske Bank Danish Banking Seminar 14 March 2017

Jyske Bank Danske Bank Danish Banking Seminar 14 March 217 216 highlights A strong finish in Q4 contributes to delivering a net profit of DKK 3,116m, equal to ROE 1.3% in 216 Continued growth in new home

Jyske Bank Danske Bank Danish Banking Seminar 14 March 217 216 highlights A strong finish in Q4 contributes to delivering a net profit of DKK 3,116m, equal to ROE 1.3% in 216 Continued growth in new home

Jyske Bank Q April 2016

Jyske Bank Q1 2016 28 April 2016 Q1 2016 highlights Danish economy continues its slow recovery but more uncertainty as retail sales drop and exports slow down Danish agriculture in particular dairy and

Jyske Bank Q1 2016 28 April 2016 Q1 2016 highlights Danish economy continues its slow recovery but more uncertainty as retail sales drop and exports slow down Danish agriculture in particular dairy and

Jyske Bank February 2018

Jyske Bank 2017 20 February 2018 Our targets Q1-Q4 2017 Delivering an attractive long-term return on equity of 8-12% 9.7% Volume growth DKK 100bn in housing-related loans DKK 96.0bn DKK 20bn in property

Jyske Bank 2017 20 February 2018 Our targets Q1-Q4 2017 Delivering an attractive long-term return on equity of 8-12% 9.7% Volume growth DKK 100bn in housing-related loans DKK 96.0bn DKK 20bn in property

Jyske Bank Q August 2018

Jyske Bank Q2 218 21 August 218 The Jyske Bank Group strategy shows a direction matching our desired positioning The Jyske Bank Group s updated strategy does not set out a totally different direction than

Jyske Bank Q2 218 21 August 218 The Jyske Bank Group strategy shows a direction matching our desired positioning The Jyske Bank Group s updated strategy does not set out a totally different direction than

Jyske Bank Q May 2018

Jyske Bank Q1 2018 9 May 2018 Our targets Q1 2018 Return on Equity Delivering an attractive long-term return on equity of 8-12% Volume growth 2018-2020 Total loan portfolio of DKK 350bn in Jyske Realkredit

Jyske Bank Q1 2018 9 May 2018 Our targets Q1 2018 Return on Equity Delivering an attractive long-term return on equity of 8-12% Volume growth 2018-2020 Total loan portfolio of DKK 350bn in Jyske Realkredit

Jyske Bank Q August 2016

Jyske Bank Q2 216 18 August 216 Q2 216 highlights Slow recovery of Danish economy continues Supported by private consumption and gradually increasing housing prices Challenged by weak exports Danish dairy

Jyske Bank Q2 216 18 August 216 Q2 216 highlights Slow recovery of Danish economy continues Supported by private consumption and gradually increasing housing prices Challenged by weak exports Danish dairy

Jyske Bank Q August 2017

Jyske Bank Q2 2017 22 August 2017 Our targets Q2 2017 Delivering an attractive long-term return on equity of 8-12% 8.0% Volume growth DKK 100bn in housing-related loans DKK 88.0bn DKK 20bn in property

Jyske Bank Q2 2017 22 August 2017 Our targets Q2 2017 Delivering an attractive long-term return on equity of 8-12% 8.0% Volume growth DKK 100bn in housing-related loans DKK 88.0bn DKK 20bn in property

Jyske Bank Q October 2017

Jyske Bank Q3 2017 25 October 2017 Our targets Q3 2017 Delivering an attractive long-term return on equity of 8-12% 9.2% Volume growth DKK 100bn in housing-related loans DKK 91.6bn DKK 20bn in property

Jyske Bank Q3 2017 25 October 2017 Our targets Q3 2017 Delivering an attractive long-term return on equity of 8-12% 9.2% Volume growth DKK 100bn in housing-related loans DKK 91.6bn DKK 20bn in property

Jyske Bank Q October 2016

Jyske Bank Q3 216 27 October 216 Jyske Bank One of the four large financial institutions in Denmark estimated market share of 1% and a Danish SIFI Danish play Approx. 89, customers Nationwide branch network

Jyske Bank Q3 216 27 October 216 Jyske Bank One of the four large financial institutions in Denmark estimated market share of 1% and a Danish SIFI Danish play Approx. 89, customers Nationwide branch network

Jyske Bank Q October 2018

Jyske Bank Q3 218 3 October 218 Our targets Q3 218 Return on Equity Delivering an attractive long-term return on equity of 8-12% ROE 6.9% Volume growth 218-22 Total loan portfolio of DKK 35bn in Jyske

Jyske Bank Q3 218 3 October 218 Our targets Q3 218 Return on Equity Delivering an attractive long-term return on equity of 8-12% ROE 6.9% Volume growth 218-22 Total loan portfolio of DKK 35bn in Jyske

Preliminary announcement of financial statements 2018

Corporate Announcement Preliminary announcement of financial statements Summary Profit before tax and effects derived from IFRS 9: DKK 3,547m (2017: DKK 4,002m), corresponding to a return on equity of

Corporate Announcement Preliminary announcement of financial statements Summary Profit before tax and effects derived from IFRS 9: DKK 3,547m (2017: DKK 4,002m), corresponding to a return on equity of

Jyske Bank Q /32

Jyske Bank Q2 215 1/32 Highlights Continued success with integrating BRFkredit and Jyske Bank Sales of new home loan products at DKK 5bn Core expenses decline quarter by quarter Expected integration costs

Jyske Bank Q2 215 1/32 Highlights Continued success with integrating BRFkredit and Jyske Bank Sales of new home loan products at DKK 5bn Core expenses decline quarter by quarter Expected integration costs

DNB. Capital. - AT1 - Tier 2 - MREL. November 2018

DNB Capital - AT1 - Tier 2 - MREL November 2018 DNB s Outstanding Additional Tier 1 Instruments USD denominated: Issue Date Type Amount Coupon First Call Date 26.03.2015 PerpNC5 USD 750 mn 5.75% 26.03.2020

DNB Capital - AT1 - Tier 2 - MREL November 2018 DNB s Outstanding Additional Tier 1 Instruments USD denominated: Issue Date Type Amount Coupon First Call Date 26.03.2015 PerpNC5 USD 750 mn 5.75% 26.03.2020

Nykredit Group. Q1/2016 financial results call. CFO, Group Managing Director Søren Holm. 12 May 2016

Nykredit Group Q1/2016 financial results call CFO, Group Managing Director Søren Holm 12 May 2016 Highlights from Q1 2016 Nykredit announced plans for an IPO, intention to sell domicile and increased margins

Nykredit Group Q1/2016 financial results call CFO, Group Managing Director Søren Holm 12 May 2016 Highlights from Q1 2016 Nykredit announced plans for an IPO, intention to sell domicile and increased margins

Nykredit Group. FY 2017 Earnings call. Michael Rasmussen, CEO David Hellemann, CFO. 8 February 2018 Copenhagen. Numbers relate to Nykredit A/S

Nykredit Group FY 217 Earnings call Michael Rasmussen, CEO David Hellemann, CFO 8 February 218 Copenhagen Numbers relate to Nykredit A/S A very satisfactory 217 - Nykredit s best year ever Record year

Nykredit Group FY 217 Earnings call Michael Rasmussen, CEO David Hellemann, CFO 8 February 218 Copenhagen Numbers relate to Nykredit A/S A very satisfactory 217 - Nykredit s best year ever Record year

Growth in lending margin pressure persists

Investor Presentation Growth in lending margin pressure persists 27 February 2018 Árni Ellefsen, CEO Disclaimer This presentation contains statements regarding future results, which are subject to risks

Investor Presentation Growth in lending margin pressure persists 27 February 2018 Árni Ellefsen, CEO Disclaimer This presentation contains statements regarding future results, which are subject to risks

INTERIM REPORT NYKREDIT REALKREDIT GROUP 1 JANUARY 30 SEPTEMBER 2014

To NASDAQ OMX Copenhagen A/S and the press 6 November 2014 INTERIM REPORT NYKREDIT REALKREDIT GROUP 1 JANUARY 30 SEPTEMBER 2014 Michael Rasmussen, Group Chief Executive, comments on Nykredit's Q1-Q3 Interim

To NASDAQ OMX Copenhagen A/S and the press 6 November 2014 INTERIM REPORT NYKREDIT REALKREDIT GROUP 1 JANUARY 30 SEPTEMBER 2014 Michael Rasmussen, Group Chief Executive, comments on Nykredit's Q1-Q3 Interim

JYSKE REALKREDIT H1 REPORT Published 30 th of October 2018

JYSKE REALKREDIT H1 REPORT 218 Published 3 th of October 218 The positive trend in earnings continues Result in Q1-Q3 218 affected by impelentation of IFRS 9 guidelines Pre-tax profit was DKK 786m for

JYSKE REALKREDIT H1 REPORT 218 Published 3 th of October 218 The positive trend in earnings continues Result in Q1-Q3 218 affected by impelentation of IFRS 9 guidelines Pre-tax profit was DKK 786m for

Sydbank s Interim Report Q1 2018

SYDBANK INTERIM REPORT Q1 2018 2/40 Sydbank s Interim Report Q1 2018 Satisfactory result return on shareholders equity of 14.8% p.a. after tax Sydbank has delivered a satisfactory performance for the first

SYDBANK INTERIM REPORT Q1 2018 2/40 Sydbank s Interim Report Q1 2018 Satisfactory result return on shareholders equity of 14.8% p.a. after tax Sydbank has delivered a satisfactory performance for the first

Fact Book Q Supplementary Information for Investors and Analysts Unaudited

Fact Book Q2 2018 Supplementary Information for Investors and Analysts Unaudited Table of contents 1. Group 1.1 Financial result & key figures 4 1.2 Net interest income 6 1.3 Net fee income 8 1.4 Net trading

Fact Book Q2 2018 Supplementary Information for Investors and Analysts Unaudited Table of contents 1. Group 1.1 Financial result & key figures 4 1.2 Net interest income 6 1.3 Net fee income 8 1.4 Net trading

Net profit of DKK 838 million and ROE of 10.7 % Presentation of Spar Nord s financial results for 2016

Net profit of DKK 838 million and ROE of 1.7 % Presentation of Spar Nord s financial results for 2 Net profit of DKK 838 million and ROE of 1.7 % Low interest rate environment and tough competition put

Net profit of DKK 838 million and ROE of 1.7 % Presentation of Spar Nord s financial results for 2 Net profit of DKK 838 million and ROE of 1.7 % Low interest rate environment and tough competition put

A milestone year for BankNordik

Investor Presentation A milestone year for BankNordik 27 February 2017 Árni Ellefsen, CEO Disclaimer This presentation contains statements regarding future results, which are subject to risks and uncertainties.

Investor Presentation A milestone year for BankNordik 27 February 2017 Árni Ellefsen, CEO Disclaimer This presentation contains statements regarding future results, which are subject to risks and uncertainties.

Individual Solvency Need

Individual Solvency Need Danmark Group 30 March 2015 1 1 Introduction... 3 1.1 Main conclusions... 3 2 Definition of the individual solvency need... 5 3 Individual solvency need and own funds... 7 3.1

Individual Solvency Need Danmark Group 30 March 2015 1 1 Introduction... 3 1.1 Main conclusions... 3 2 Definition of the individual solvency need... 5 3 Individual solvency need and own funds... 7 3.1

DNB Capital, AT1 / Tier 2. May 2018

DNB Capital, AT1 / Tier 2 May 2018 DNB s Outstanding Additional Tier 1 Instruments USD denominated: Issue Date Type Amount Coupon First Call Date 26.03.2015 PerpNC5 USD 750 mn 5.75% 26.03.2020 18.10.2016

DNB Capital, AT1 / Tier 2 May 2018 DNB s Outstanding Additional Tier 1 Instruments USD denominated: Issue Date Type Amount Coupon First Call Date 26.03.2015 PerpNC5 USD 750 mn 5.75% 26.03.2020 18.10.2016

Sydbank s Interim Report Q1-Q3 2018

S Y D B A N K I N T E R I M R E P O R T Q 1 - Q 3 2 0 1 8 2/42 Sydbank s Interim Report Q1-Q3 2018 Q1-Q3 2018 is characterised by strong credit quality, improved customer satisfaction as well as lower

S Y D B A N K I N T E R I M R E P O R T Q 1 - Q 3 2 0 1 8 2/42 Sydbank s Interim Report Q1-Q3 2018 Q1-Q3 2018 is characterised by strong credit quality, improved customer satisfaction as well as lower

Annual Report. A good performance enabling Sydbank to pay a historically high dividend February 18, 2015

17-02-2015 1 2014 Annual Report A good performance enabling Sydbank to pay a historically high dividend February 18, 2015 17-02-2015 2 Highlights for 2014 Key points Sydbank s plan to increase profitability

17-02-2015 1 2014 Annual Report A good performance enabling Sydbank to pay a historically high dividend February 18, 2015 17-02-2015 2 Highlights for 2014 Key points Sydbank s plan to increase profitability

New Standards update on initiatives

New Standards update on initiatives Elisabeth Toftmann Klintholm Chief IR Officer Nordea Large Cap Seminar Stockholm, 28 May 2013 Vision Recognised as the most trusted financial partner Customer satisfaction

New Standards update on initiatives Elisabeth Toftmann Klintholm Chief IR Officer Nordea Large Cap Seminar Stockholm, 28 May 2013 Vision Recognised as the most trusted financial partner Customer satisfaction

Gjensidige Bank Investor Presentation Q July 2017

Gjensidige Bank Investor Presentation Q2 2017 14. July 2017 Disclaimer This presentation and the information contained herein have been prepared by and is the sole responsibility of Gjensidige Bank ASA

Gjensidige Bank Investor Presentation Q2 2017 14. July 2017 Disclaimer This presentation and the information contained herein have been prepared by and is the sole responsibility of Gjensidige Bank ASA

Individual Solvency Need

Individual Solvency Need Nordea Bank Danmark Group 30 September 2014 1 1 Introduction... 3 1.1 Main conclusions... 3 2 Definition of the individual solvency need... 5 3 Individual solvency need and own

Individual Solvency Need Nordea Bank Danmark Group 30 September 2014 1 1 Introduction... 3 1.1 Main conclusions... 3 2 Definition of the individual solvency need... 5 3 Individual solvency need and own

DNB Capital and AT1. November 2017

DNB Capital and AT1 November 2017 DNB s Outstanding Additional Tier 1 Securities USD denominated: Issue Date Type Amount Coupon First Call Date 26.03.2015 PerpNC5 USD 750 mn 5.75% 26.03.2020 18.10.2016

DNB Capital and AT1 November 2017 DNB s Outstanding Additional Tier 1 Securities USD denominated: Issue Date Type Amount Coupon First Call Date 26.03.2015 PerpNC5 USD 750 mn 5.75% 26.03.2020 18.10.2016

Fact Book Q Supplementary Information for Investors and Analysts Unaudited

Fact Book Q4 2017 Supplementary Information for Investors and Analysts Unaudited Table of contents 1. Group 1.1 Financial result & key figures 4 1.2 Net interest income 6 1.3 Net fee income 8 1.4 Net trading

Fact Book Q4 2017 Supplementary Information for Investors and Analysts Unaudited Table of contents 1. Group 1.1 Financial result & key figures 4 1.2 Net interest income 6 1.3 Net fee income 8 1.4 Net trading

Internal Capital Adequacy Assessment Process Saxo Bank Group

Internal Capital Adequacy Assessment Process Saxo Bank Group Q4 2018 Contents INTRODUCTION... 3 CAPITAL ADEQUACY ASSESSMENT... 4 2.1 INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS... 4 2.2 BUSINESS ACTIVITIES

Internal Capital Adequacy Assessment Process Saxo Bank Group Q4 2018 Contents INTRODUCTION... 3 CAPITAL ADEQUACY ASSESSMENT... 4 2.1 INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS... 4 2.2 BUSINESS ACTIVITIES

Second Quarter Results 2014 Investor presentation

Second Quarter Results 2014 Investor presentation Second Fourth Quarter and Results 2015 Full Third Year Quarter Results Results 2014 2015 Press conference Christian Investor Press Conference Clausen,

Second Quarter Results 2014 Investor presentation Second Fourth Quarter and Results 2015 Full Third Year Quarter Results Results 2014 2015 Press conference Christian Investor Press Conference Clausen,

Financial results first half 2018

Thomas F. Borgen Chief Executive Officer Morten Mosegaard Interim Chief Financial Officer 18 July 2018 Agenda Executive summary Group and business unit update Selected topics Outlook for full-year 2018

Thomas F. Borgen Chief Executive Officer Morten Mosegaard Interim Chief Financial Officer 18 July 2018 Agenda Executive summary Group and business unit update Selected topics Outlook for full-year 2018

Lending to personal customers picked up in Q3 2017

Investor Presentation Lending to personal customers picked up in Q3 2017 26 October 2017 Árni Ellefsen, CEO Disclaimer This presentation contains statements regarding future results, which are subject

Investor Presentation Lending to personal customers picked up in Q3 2017 26 October 2017 Árni Ellefsen, CEO Disclaimer This presentation contains statements regarding future results, which are subject

2. Process for determining the solvency need The basis for capital management Risk identification... 4

Contents Page 1. Introduction... 3 2. Process for determining the solvency need... 4 2.1 The basis for capital management... 4 2.2 Risk identification... 4 2.3 Danske Banks internal assessment of its solvency

Contents Page 1. Introduction... 3 2. Process for determining the solvency need... 4 2.1 The basis for capital management... 4 2.2 Risk identification... 4 2.3 Danske Banks internal assessment of its solvency

Individual Solvency Need Nordea Bank Danmark Group 30 September 2011

Individual Solvency Need Danmark Group 30 September 2011 1 Introduction...3 1.1 Main conclusions... 3 2 Definition of the individual solvency need...3 3 Individual solvency need and capital base...6 3.1

Individual Solvency Need Danmark Group 30 September 2011 1 Introduction...3 1.1 Main conclusions... 3 2 Definition of the individual solvency need...3 3 Individual solvency need and capital base...6 3.1

Fact Book Q Supplementary Information for Investors and Analysts Unaudited

Fact Book Q2 2017 Supplementary Information for Investors and Analysts Unaudited Table of contents 1. Group 1.1 Financial result & key figures 4 1.2 Net interest income 6 1.3 Net fee income 8 1.4 Net trading

Fact Book Q2 2017 Supplementary Information for Investors and Analysts Unaudited Table of contents 1. Group 1.1 Financial result & key figures 4 1.2 Net interest income 6 1.3 Net fee income 8 1.4 Net trading

RWA development estimated impact of FSA orders and new regulation. 17 June 2013

RWA development estimated impact of FSA orders and new regulation 17 June 2013 FSA orders: Consequences and background The orders and our response 1. Change some specific elements of the IRB model and

RWA development estimated impact of FSA orders and new regulation 17 June 2013 FSA orders: Consequences and background The orders and our response 1. Change some specific elements of the IRB model and

Danske Bank Tier 2 Capital

Danske Bank Tier 2 Capital Henrik Ramlau-Hansen CFO & Member of the Executive Board Steen Blaafalk Head of Treasury Global Conference Call 23 September 2013 Agenda Financial results 3 Capital, liquidity

Danske Bank Tier 2 Capital Henrik Ramlau-Hansen CFO & Member of the Executive Board Steen Blaafalk Head of Treasury Global Conference Call 23 September 2013 Agenda Financial results 3 Capital, liquidity

HSBC manages its capital and debt securities to meet end-point regulatory requirements, as well as funding and other business needs

Fixed Income Factbook 31 December 2017 Connecting customers to opportunities HSBC aims to be where the growth is, enabling business to thrive and economies to prosper, and ultimately helping people to

Fixed Income Factbook 31 December 2017 Connecting customers to opportunities HSBC aims to be where the growth is, enabling business to thrive and economies to prosper, and ultimately helping people to

1. Introduction Process for determining the solvency need The basis for capital management Risk identification...

Contents Page 1. Introduction...3 2. Process for determining the solvency need...4 2.1 The basis for capital management...4 2.2 Risk identification...4 2.3 Danske Bank s internal assessment of its solvency

Contents Page 1. Introduction...3 2. Process for determining the solvency need...4 2.1 The basis for capital management...4 2.2 Risk identification...4 2.3 Danske Bank s internal assessment of its solvency

FITCH AFFIRMS ABN AMRO BANK AT 'A+'; OUTLOOK STABLE

FITCH AFFIRMS ABN AMRO BANK AT 'A+'; OUTLOOK STABLE Fitch Ratings-London-24 November 2017: Fitch Ratings has affirmed ABN AMRO Bank N.V.'s Long-Term Issuer Default Rating (IDR) at 'A+' with a Stable Outlook,

FITCH AFFIRMS ABN AMRO BANK AT 'A+'; OUTLOOK STABLE Fitch Ratings-London-24 November 2017: Fitch Ratings has affirmed ABN AMRO Bank N.V.'s Long-Term Issuer Default Rating (IDR) at 'A+' with a Stable Outlook,

Business segments Banking activities 31 Mortgage activities 34 Leasing activities 37

Annual Report 2018 Annual Report 2018 Management s Review key financial data 2 Summary 3 Comments by Management 4 Strategy 6 Outlook 9 Financial Review 10 Capital and liquidity management 18 Corporate

Annual Report 2018 Annual Report 2018 Management s Review key financial data 2 Summary 3 Comments by Management 4 Strategy 6 Outlook 9 Financial Review 10 Capital and liquidity management 18 Corporate

Commerzbank Inaugural Preferred Senior Benchmark Global investor call 20 August 2018

Commerzbank Inaugural Preferred Senior Benchmark Global investor call 20 August 2018 All figures in this presentation are subject to rounding Disclaimer This presentation contains forward-looking statements.

Commerzbank Inaugural Preferred Senior Benchmark Global investor call 20 August 2018 All figures in this presentation are subject to rounding Disclaimer This presentation contains forward-looking statements.

Fourth Quarter and Full Year Results Press Conference Casper von Koskull, president, Group CEO

Fourth Quarter and Full Year Results 2015 Press Conference Casper von Koskull, president, Group CEO Disclaimer This presentation contains forward-looking statements that reflect management s current views

Fourth Quarter and Full Year Results 2015 Press Conference Casper von Koskull, president, Group CEO Disclaimer This presentation contains forward-looking statements that reflect management s current views

Financial Institutions Ratings Danske Bank AT1 rating report

4 July 2018 Financial Institutions Financial Institutions Ratings Financial Institutions Ratings Security Ratings Outlook 5.75% EUR 750m Perpetual Non-Cumulative Resettable Additional Tier 1 Capital Notes

4 July 2018 Financial Institutions Financial Institutions Ratings Financial Institutions Ratings Security Ratings Outlook 5.75% EUR 750m Perpetual Non-Cumulative Resettable Additional Tier 1 Capital Notes

Individual Solvency Need

Individual Solvency Need Nordea Bank Danmark Group 31 March 2014 1 1 Introduction... 3 1.1 Main conclusions... 3 2 Definition of the individual solvency need... 4 3 Individual solvency need and own funds...

Individual Solvency Need Nordea Bank Danmark Group 31 March 2014 1 1 Introduction... 3 1.1 Main conclusions... 3 2 Definition of the individual solvency need... 4 3 Individual solvency need and own funds...

Strong first quarter of 2018

Investor Presentation Strong first quarter of 2018 3 May 2018 Árni Ellefsen, CEO Disclaimer This presentation contains statements regarding future results, which are subject to risks and uncertainties.

Investor Presentation Strong first quarter of 2018 3 May 2018 Árni Ellefsen, CEO Disclaimer This presentation contains statements regarding future results, which are subject to risks and uncertainties.

Jyske Realkredit A/S (formerly BRFkredit a/s) Interim Financial Report Q1 - Q3 2018

Interim Financial Report Q1 - Q3 2018") Jyske Realkredit A/S (formerly BRFkredit a/s) Interim Financial Report Q1 - Q3 Jyske Realkredit Corporate Announcement No. 94 /, of 30 October 1 / 26 Interim Financial Report Q1 - Q3 Management s Review

Jyske Realkredit A/S (formerly BRFkredit a/s) Interim Financial Report Q1 - Q3 Jyske Realkredit Corporate Announcement No. 94 /, of 30 October 1 / 26 Interim Financial Report Q1 - Q3 Management s Review

Risk and Capital Management 2017

Risk and Capital Management 2017 Contents Contents CONTENTS... 1 EXECUTIVE SUMMARY... 2 BUSINESS MODEL... 3 RISK MANAGEMENT... 5 CAPITAL MANAGEMENT... 11 CREDIT RISK... 17 COUNTERPARTY CREDIT RISK...

Risk and Capital Management 2017 Contents Contents CONTENTS... 1 EXECUTIVE SUMMARY... 2 BUSINESS MODEL... 3 RISK MANAGEMENT... 5 CAPITAL MANAGEMENT... 11 CREDIT RISK... 17 COUNTERPARTY CREDIT RISK...

FITCH AFFIRMS ABN AMRO BANK AT 'A+'; OUTLOOK STABLE

FITCH AFFIRMS ABN AMRO BANK AT 'A+'; OUTLOOK STABLE Fitch Ratings-London-24 February 2017: Fitch Ratings has affirmed ABN AMRO Bank N.V.'s Long-Term Issue Default Rating (IDR) at 'A+' with a Stable Outlook,

FITCH AFFIRMS ABN AMRO BANK AT 'A+'; OUTLOOK STABLE Fitch Ratings-London-24 February 2017: Fitch Ratings has affirmed ABN AMRO Bank N.V.'s Long-Term Issue Default Rating (IDR) at 'A+' with a Stable Outlook,

Financial statements. Statements

Management's report Financial highlights - Danske Bank Group Executive summary 4 5 Financial review 7 Business units Banking DK 15 Banking Nordic 17 Corporates & Institutions 19 Wealth Management 21 Northern

Management's report Financial highlights - Danske Bank Group Executive summary 4 5 Financial review 7 Business units Banking DK 15 Banking Nordic 17 Corporates & Institutions 19 Wealth Management 21 Northern

Internal Capital Adequacy Assessment Process Saxo Bank Group

Internal Capital Adequacy Assessment Process Saxo Bank Group Q3 2018 Contents INTRODUCTION... 3 CAPITAL ADEQUACY ASSESSMENT... 4 2.1 INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS... 4 2.2 BUSINESS ACTIVITIES

Internal Capital Adequacy Assessment Process Saxo Bank Group Q3 2018 Contents INTRODUCTION... 3 CAPITAL ADEQUACY ASSESSMENT... 4 2.1 INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS... 4 2.2 BUSINESS ACTIVITIES

Internal Capital Adequacy Assessment Process Saxo Bank Group

Internal Capital Adequacy Assessment Process Saxo Bank Group Q2 2018 Contents 1. 2. INTRODUCTION... 3 CAPITAL ADEQUACY ASSESSMENT... 4 2.1 INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS... 4 2.2 BUSINESS

Internal Capital Adequacy Assessment Process Saxo Bank Group Q2 2018 Contents 1. 2. INTRODUCTION... 3 CAPITAL ADEQUACY ASSESSMENT... 4 2.1 INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS... 4 2.2 BUSINESS

To NASDAQ Copenhagen A/S Announcement no. 41/2017 The press. INTERIM FINANCIAL REPORT FIRST QUARTER OF 2017 BRFkredit

To NASDAQ Copenhagen A/S Announcement no. 41/2017 The press INTERIM FINANCIAL REPORT FIRST QUARTER OF 2017 BRFkredit CONTENTS 3 THE BRFKREDIT GROUP 4 SUMMARY, first quarter of 2017 4 Comments by Management

To NASDAQ Copenhagen A/S Announcement no. 41/2017 The press INTERIM FINANCIAL REPORT FIRST QUARTER OF 2017 BRFkredit CONTENTS 3 THE BRFKREDIT GROUP 4 SUMMARY, first quarter of 2017 4 Comments by Management

Individual Solvency Need Nordea Bank Danmark Group 31 March 2012

Individual Solvency Need Danmark Group 31 March 2012 1 Introduction... 3 1.1 Main conclusions... 3 2 Definition of the individual solvency need... 3 3 Individual solvency need and capital base... 6 3.1

Individual Solvency Need Danmark Group 31 March 2012 1 Introduction... 3 1.1 Main conclusions... 3 2 Definition of the individual solvency need... 3 3 Individual solvency need and capital base... 6 3.1

Unicaja Banco 3Q17 Results Presentation

Unicaja Banco 3Q17 Results Presentation 31 st October 2017 0 Disclaimer This presentation (the Presentation) has been prepared by Unicaja Banco, S.A. (the Company or Unicaja Banco) for informational use

Unicaja Banco 3Q17 Results Presentation 31 st October 2017 0 Disclaimer This presentation (the Presentation) has been prepared by Unicaja Banco, S.A. (the Company or Unicaja Banco) for informational use

One Bank, One UniCredit Transform 2019

One Bank, One UniCredit Transform CFO presentation M. Bianchi London, 12 December 2017 One Bank, One UniCredit The five pillars ONE BANK ONE 5 STRATEGIC PILLARS STRENGTHEN AND OPTIMISE CAPITAL IMPROVE

One Bank, One UniCredit Transform CFO presentation M. Bianchi London, 12 December 2017 One Bank, One UniCredit The five pillars ONE BANK ONE 5 STRATEGIC PILLARS STRENGTHEN AND OPTIMISE CAPITAL IMPROVE

Fact Book 2017 The Nykredit Group. Unaudited

Fact Book 2017 The Nykredit Group Unaudited Table of contents Group chart 3 Expiry of interest-only period 33 Contacts and other information 4 Impairment provisions and write-offs 34 The Nykredit Group

Fact Book 2017 The Nykredit Group Unaudited Table of contents Group chart 3 Expiry of interest-only period 33 Contacts and other information 4 Impairment provisions and write-offs 34 The Nykredit Group

Financial results first nine months 2017

Financial results first nine months 2017 Thomas F. Borgen Chief Executive Officer Jacob Aarup-Andersen Chief Financial Officer 2 November 2017 Financial results first nine months 2017 Agenda Executive

Financial results first nine months 2017 Thomas F. Borgen Chief Executive Officer Jacob Aarup-Andersen Chief Financial Officer 2 November 2017 Financial results first nine months 2017 Agenda Executive

Rothschild & Co. 2016/2017 Half year results

Rothschild & Co 2016/2017 Half year results November 2016 Content 1 2 Highlights Business review Rothschild Global Advisory Rothschild Private Wealth & Asset Management Rothschild Merchant Banking 3 4

Rothschild & Co 2016/2017 Half year results November 2016 Content 1 2 Highlights Business review Rothschild Global Advisory Rothschild Private Wealth & Asset Management Rothschild Merchant Banking 3 4

Q1-Q3 INTERIM REPORT NYKREDIT REALKREDIT GROUP 1 JANUARY 30 SEPTEMBER 2015

To Nasdaq Copenhagen and the press 5 November 2015 Q1-Q3 INTERIM REPORT NYKREDIT REALKREDIT GROUP 1 JANUARY 30 SEPTEMBER 2015 Michael Rasmussen, Group Chief Executive, comments on Nykredit's Q1-Q3 Interim

To Nasdaq Copenhagen and the press 5 November 2015 Q1-Q3 INTERIM REPORT NYKREDIT REALKREDIT GROUP 1 JANUARY 30 SEPTEMBER 2015 Michael Rasmussen, Group Chief Executive, comments on Nykredit's Q1-Q3 Interim

Financial results 2017

Thomas F. Borgen Chief Executive Officer Jacob Aarup-Andersen Chief Financial Officer 2 February 2018 Agenda Executive summary Business unit update Selected topics Outlook for full-year 2018 Q&A Appendix

Thomas F. Borgen Chief Executive Officer Jacob Aarup-Andersen Chief Financial Officer 2 February 2018 Agenda Executive summary Business unit update Selected topics Outlook for full-year 2018 Q&A Appendix

Financial results first quarter 2018

Thomas F. Borgen Chief Executive Officer Jacob Aarup-Andersen Chief Financial Officer 26 April 2018 Agenda Executive summary New strategy Group and business unit update Selected topics Outlook for full-year

Thomas F. Borgen Chief Executive Officer Jacob Aarup-Andersen Chief Financial Officer 26 April 2018 Agenda Executive summary New strategy Group and business unit update Selected topics Outlook for full-year

Internal Capital Adequacy Assessment Process

Internal Capital Adequacy Assessment Process Saxo Bank Group and Saxo Bank A/S Second quarter 2016 Contents 1. 2. 3. INTRODUCTION... 3 CAPITAL MANAGEMENT... 4 2.1 INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS...

Internal Capital Adequacy Assessment Process Saxo Bank Group and Saxo Bank A/S Second quarter 2016 Contents 1. 2. 3. INTRODUCTION... 3 CAPITAL MANAGEMENT... 4 2.1 INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS...

Introduction, update on financial performance, credit and capital. Debt investor roadshow, Copenhagen 19 November 2018

Introduction, update on financial performance, credit and capital Debt investor roadshow, Copenhagen 19 November 2018 Executive summary We are here today, because we are contemplating an issue of Tier

Introduction, update on financial performance, credit and capital Debt investor roadshow, Copenhagen 19 November 2018 Executive summary We are here today, because we are contemplating an issue of Tier

Battle of the Balance Sheets

Battle of the Balance Sheets Stuart Morris FIA, Deloitte Dr. Robin Thompson, RBS Andrew Kenyon FIA, RBS 07 November 2016 Agenda Risk-based capital requirements: Banks vs. Insurers Available capital Case

Battle of the Balance Sheets Stuart Morris FIA, Deloitte Dr. Robin Thompson, RBS Andrew Kenyon FIA, RBS 07 November 2016 Agenda Risk-based capital requirements: Banks vs. Insurers Available capital Case

Invest in wealth and retail businesses with local scale

Connecting customers to opportunities HSBC aims to be where the growth is, enabling business to thrive and economies to prosper, and ultimately helping people to fulfil their hopes and realise their ambitions.

Connecting customers to opportunities HSBC aims to be where the growth is, enabling business to thrive and economies to prosper, and ultimately helping people to fulfil their hopes and realise their ambitions.

Financial results 2018

Jesper Nielsen Interim Chief Executive Officer Christian Baltzer Chief Financial Officer 1 February 2019 Agenda Executive summary and AML update Group and business unit update Selected topics Financial

Jesper Nielsen Interim Chief Executive Officer Christian Baltzer Chief Financial Officer 1 February 2019 Agenda Executive summary and AML update Group and business unit update Selected topics Financial

To NASDAQ Copenhagen A/S Announcement no. 91/2016 The press INTERIM FINANCIAL REPORT

To NASDAQ Copenhagen A/S Announcement no. 91/ The press INTERIM FINANCIAL REPORT Q1 - CONTENTS 3 THE BRFKREDIT GROUP KEY FIGURES AND KEY RATIOS 4 SUMMARY Q1-4 Comments by Management 5 Q1-5 Net profit for

To NASDAQ Copenhagen A/S Announcement no. 91/ The press INTERIM FINANCIAL REPORT Q1 - CONTENTS 3 THE BRFKREDIT GROUP KEY FIGURES AND KEY RATIOS 4 SUMMARY Q1-4 Comments by Management 5 Q1-5 Net profit for

Risk Report 2014Q1. Published 8 May 2014

Risk Report 214Q1 Published 8 May 214 Contents The Risk Report has been prepared by Realkredit Danmark s analysts for information purposes only. Realkredit Danmark will publish an updated Risk Report quarterly.

Risk Report 214Q1 Published 8 May 214 Contents The Risk Report has been prepared by Realkredit Danmark s analysts for information purposes only. Realkredit Danmark will publish an updated Risk Report quarterly.

Aldermore Banking as it should be UK Challenger Bank Day

Aldermore Banking as it should be UK Challenger Bank Day 09 June 2015 Banking as it should be SME focused bank Customer loans 1 22% Asset Finance Track record of accelerating profitability Invoice Finance

Aldermore Banking as it should be UK Challenger Bank Day 09 June 2015 Banking as it should be SME focused bank Customer loans 1 22% Asset Finance Track record of accelerating profitability Invoice Finance

BZWBK Group. Results 1H12. July 26 th, 2012

1 BZWBK Group Results 1H12 July 26 th, 2012 2 This presentation as regards the forward looking statements is exclusively informational in nature and cannot be treated as an offering or recommendation to

1 BZWBK Group Results 1H12 July 26 th, 2012 2 This presentation as regards the forward looking statements is exclusively informational in nature and cannot be treated as an offering or recommendation to

Jyske Realkredit A/S (formerly BRFkredit a/s) Interim Financial Report First half of 2018

Interim Financial Report First half of 2018") Jyske Realkredit A/S (formerly BRFkredit a/s) Interim Financial Report First half of Jyske Realkredit Corporate Announcement No. 73 /, of 21 August 1 / 25 Interim Financial Report, first half of Management

Jyske Realkredit A/S (formerly BRFkredit a/s) Interim Financial Report First half of Jyske Realkredit Corporate Announcement No. 73 /, of 21 August 1 / 25 Interim Financial Report, first half of Management

Individual Solvency Need

Individual Solvency Need Danmark Group 30 September 2013 1 1 Introduction... 3 1.1 Main conclusions... 3 2 Definition of the individual solvency need... 4 3 Individual solvency need and capital base...

Individual Solvency Need Danmark Group 30 September 2013 1 1 Introduction... 3 1.1 Main conclusions... 3 2 Definition of the individual solvency need... 4 3 Individual solvency need and capital base...

Financial results first nine months 2018

Jesper Nielsen Interim Chief Executive Officer Christian Baltzer Chief Financial Officer 1 November 2018 Agenda Executive summary and recap of Estonia case Group and business unit update Selected topics

Jesper Nielsen Interim Chief Executive Officer Christian Baltzer Chief Financial Officer 1 November 2018 Agenda Executive summary and recap of Estonia case Group and business unit update Selected topics

Strengthening the European banking system Overview of the CRDIV. World Bank CFRR IFRS Seminar for banking supervisors 18 April 2012, Zagreb

Strengthening the European banking system Overview of the CRDIV World Bank CFRR IFRS Seminar for banking supervisors 18 April 2012, Zagreb 1 Main Drivers Financial Stability and Sustainable Growth Unprecedented

Strengthening the European banking system Overview of the CRDIV World Bank CFRR IFRS Seminar for banking supervisors 18 April 2012, Zagreb 1 Main Drivers Financial Stability and Sustainable Growth Unprecedented

Interim Report First Half 2014

20-08-2014 1 Interim Report First Half 2014 Sydbank s plan to increase profitability is beginning to show results Teleconference 20 August 2014 20-08-2014 2 Agenda Interim financial statements for H1 2014

20-08-2014 1 Interim Report First Half 2014 Sydbank s plan to increase profitability is beginning to show results Teleconference 20 August 2014 20-08-2014 2 Agenda Interim financial statements for H1 2014

Published 23 February 2016 Data per 31 December 2015

Published 23 February 2016 Data per 31 December 2015 BRFkredit Cover pool report, page 1 of 10 BRFkredit cover pool report Introduction The report publishes data on the portfolio in a structured form,

Published 23 February 2016 Data per 31 December 2015 BRFkredit Cover pool report, page 1 of 10 BRFkredit cover pool report Introduction The report publishes data on the portfolio in a structured form,

PUBLIC BANK BERHAD (6463-H) (Incorporated in Malaysia)

(Incorporated in Malaysia)") A 2 9. Capital Adequacy a) T h e capital adequacy ratios of t h e G r o u p a n d t h e B a n k below a r e disclosed p u r s u a n t to t h e requirements of B a n k Negara Malaysia ("BNM")'s Risk Weighted

A 2 9. Capital Adequacy a) T h e capital adequacy ratios of t h e G r o u p a n d t h e B a n k below a r e disclosed p u r s u a n t to t h e requirements of B a n k Negara Malaysia ("BNM")'s Risk Weighted

Interim Report Nykredit Realkredit Group 1 January 30 June 2018

To Nasdaq Copenhagen and the press 23 August 2018 Interim Report 1 January 30 June 2018 H1/ H1/ 2018 2017 Change Income 6,337 7,420-1,083 Costs 2,402 2,366-36 Impairment charges for loans and advances

To Nasdaq Copenhagen and the press 23 August 2018 Interim Report 1 January 30 June 2018 H1/ H1/ 2018 2017 Change Income 6,337 7,420-1,083 Costs 2,402 2,366-36 Impairment charges for loans and advances

Financial results for Q1 2015

Financial results for Q1 2015 Thomas F. Borgen Chief Executive Officer Henrik Ramlau-Hansen Chief Financial Officer 30 April 2015 Agenda Executive summary and financial results 3 Business unit update 5

Financial results for Q1 2015 Thomas F. Borgen Chief Executive Officer Henrik Ramlau-Hansen Chief Financial Officer 30 April 2015 Agenda Executive summary and financial results 3 Business unit update 5

MANAGEMENT'S REPORT BUSINESS UNITS STATEMENTS FINANCIAL STATEMENTS. Financial highlights - Danske Bank Group Executive summary Financial review 7

MANAGEMENT'S REPORT Financial highlights - Danske Bank Group Executive summary 4 5 Financial review 7 BUSINESS UNITS Personal Banking 13 Business Banking 15 Corporates & Institutions 17 Wealth Management

MANAGEMENT'S REPORT Financial highlights - Danske Bank Group Executive summary 4 5 Financial review 7 BUSINESS UNITS Personal Banking 13 Business Banking 15 Corporates & Institutions 17 Wealth Management

Risk and Capital Management

Risk and Capital Management 2018 Contents EXECUTIVE SUMMARY... 2 BUSINESS MODEL... 3 RISK MANAGEMENT... 4 CAPITAL MANAGEMENT... 7 CREDIT RISK...13 COUNTERPARTY CREDIT RISK...23 MARKET RISK...25 LIQUIDITY

Risk and Capital Management 2018 Contents EXECUTIVE SUMMARY... 2 BUSINESS MODEL... 3 RISK MANAGEMENT... 4 CAPITAL MANAGEMENT... 7 CREDIT RISK...13 COUNTERPARTY CREDIT RISK...23 MARKET RISK...25 LIQUIDITY

Case Study: Investor activities AT1 capital

Case Study: Investor activities AT1 capital FRIC Practitioner Seminar 10 January 2017 presentation Head of Treasury Christoffer Møllenbach & Head of Investor Relations Claus I. Jensen The AT1 roadshow

Case Study: Investor activities AT1 capital FRIC Practitioner Seminar 10 January 2017 presentation Head of Treasury Christoffer Møllenbach & Head of Investor Relations Claus I. Jensen The AT1 roadshow

1. Introduction Process for determining the solvency need The basis for capital management Risk identification...

Contents Page 1. Introduction... 3 2. Process for determining the solvency need... 4 2.1 The basis for capital management... 4 2.2 Risk identification... 4 2.3 Danske Bank s internal assessment of its

Contents Page 1. Introduction... 3 2. Process for determining the solvency need... 4 2.1 The basis for capital management... 4 2.2 Risk identification... 4 2.3 Danske Bank s internal assessment of its

2016 Annual Report. Sydbank Group

2016 Annual Report Sydbank Group 2 SYDBANK / 2016 Annual Report A highly satisfactory result due to low impairment charges, reduced costs and satisfactory investment portfolio earnings ensures a record-high

2016 Annual Report Sydbank Group 2 SYDBANK / 2016 Annual Report A highly satisfactory result due to low impairment charges, reduced costs and satisfactory investment portfolio earnings ensures a record-high

Interim Condensed Consolidated Financial Statements. 30 September 2017

Interim Condensed Consolidated Financial Statements 30 September 2017 2 3 Interim Consolidated Statement of Income Three Months to Three Months to Nine Months to Nine Months to 30 September 30 September

Interim Condensed Consolidated Financial Statements 30 September 2017 2 3 Interim Consolidated Statement of Income Three Months to Three Months to Nine Months to Nine Months to 30 September 30 September

Risk and Capital Management

2016 Risk and Capital Management Contents Contents CONTENTS... 1 INTRODUCTION... 2 BUSINESS MODEL... 3 RISK MANAGEMENT... 5 CAPITAL MANAGEMENT... 11 CREDIT RISK... 18 COUNTERPARTY CREDIT RISK... 33 MARKET

2016 Risk and Capital Management Contents Contents CONTENTS... 1 INTRODUCTION... 2 BUSINESS MODEL... 3 RISK MANAGEMENT... 5 CAPITAL MANAGEMENT... 11 CREDIT RISK... 18 COUNTERPARTY CREDIT RISK... 33 MARKET

Jyske Bank Interim Financial Report First quarter of 2017

Jyske Bank Interim Financial Report First quarter of 2017 Jyske Bank corporate announcement No. 19/2017, of 2 May 2017 Page 1 of 51 Interim Financial Report, first quarter of 2017 Management s Review The

Jyske Bank Interim Financial Report First quarter of 2017 Jyske Bank corporate announcement No. 19/2017, of 2 May 2017 Page 1 of 51 Interim Financial Report, first quarter of 2017 Management s Review The

Financial results for Q1 2013

Financial results for Q1 2013 Eivind Kolding CEO & Chairman of the Executive Board Henrik Ramlau-Hansen CFO & Member of the Executive Board 2 May 2013 Agenda Key messages 3 Business units up-date 6 Financial

Financial results for Q1 2013 Eivind Kolding CEO & Chairman of the Executive Board Henrik Ramlau-Hansen CFO & Member of the Executive Board 2 May 2013 Agenda Key messages 3 Business units up-date 6 Financial

Danish Ship Finance Risk Report 2017

Danish Ship Finance Risk Report 2017 CVR NO. 27 49 26 49 Introduction The objective of the Risk Report is to inform shareholders and other stakeholders of the Group s risk management, including policies,

Danish Ship Finance Risk Report 2017 CVR NO. 27 49 26 49 Introduction The objective of the Risk Report is to inform shareholders and other stakeholders of the Group s risk management, including policies,

H1 INTERIM REPORT 2014 Totalkredit A/S (1 January 30 June 2014) H1 in brief

H1 in brief") To NASDAQ OMX Copenhagen A/S and the press 19 August 2014 H1 INTERIM REPORT 2014 Totalkredit A/S (1 January 30 June 2014) H1 in brief Profit before tax came to DKK 889m against DKK 296m in H1/2013 Core

To NASDAQ OMX Copenhagen A/S and the press 19 August 2014 H1 INTERIM REPORT 2014 Totalkredit A/S (1 January 30 June 2014) H1 in brief Profit before tax came to DKK 889m against DKK 296m in H1/2013 Core

2018 Combined Financial Results. Air Bank, Home Credit Czech Republic and Home Credit Slovak Republic. 6 February 2019

2018 Combined Financial Results Air Bank, Home Credit Czech Republic and Home Credit Slovak Republic 6 February 2019 Note: Unaudited combined IFRS figures DISCLAIMER GENERAL THIS PRESENTATION DOES NOT

2018 Combined Financial Results Air Bank, Home Credit Czech Republic and Home Credit Slovak Republic 6 February 2019 Note: Unaudited combined IFRS figures DISCLAIMER GENERAL THIS PRESENTATION DOES NOT

New Standards - Strategic review Financial results for Q3 2012

PRESS CONFERENCE New Standards - Strategic review Financial results for Q3 2012 Ole Andersen Chairman of the Board of Directors Eivind Kolding CEO & Chairman of the Executive Board Henrik Ramlau-Hansen

PRESS CONFERENCE New Standards - Strategic review Financial results for Q3 2012 Ole Andersen Chairman of the Board of Directors Eivind Kolding CEO & Chairman of the Executive Board Henrik Ramlau-Hansen

Jyske Bank Interim Financial Report First nine months of 2017

Jyske Bank Interim Financial Report First nine months of Jyske Bank corporate announcement No. 54/, of 25 October Page 1 of 52 Interim Financial Report, first nine months of Management s Review The Jyske

Jyske Bank Interim Financial Report First nine months of Jyske Bank corporate announcement No. 54/, of 25 October Page 1 of 52 Interim Financial Report, first nine months of Management s Review The Jyske