IFRS13 and Valuation Techniques

|

|

|

- Garry King

- 5 years ago

- Views:

Transcription

1 The Institute of Chartered Accountants of Pakistan Riyadh Chapter IFRS13 and Valuation Techniques Important Notice This document, which has been prepared by Deloitte Transaction Services LLC ( Deloitte ), has been prepared for the sole purpose of outlining our credentials to provide assistance to you in order that you may evaluate the capabilities of Deloitte.

2 Presenters

3 Presenters Munish Mohendroo Director Valuation and Business Modelling Services Deloitte Corporate Finance Limited Abu Dhabi Phone: mmohendroo@deloitte.com Abid Moosa Assistant Director Valuation and Business Modelling Services Deloitte Transaction Services LLC Kingdom of Saudi Arabia Phone: Mobile: abmoosa@deloitte.com 2

4 IFRS 13 Fair value measurement

5 Value why and when? Transactional Legal/ Regulatory Internal decision making Financial reporting Independent experts Deloitte valuations in Middle East 30 experts Across the GCC Businesses, shares, tangible and intangible assets Practical guidance: IVSC (International Valuation Standards Committee) RICS red book for real estate IFRS - financial reporting purposes 4

6 Introduction to IFRS 13 Fair Value Measurement Introduction Originally issued in May 2011 Applies to annual periods beginning on/ after 1 January 2013 Single source of guidance for fair value Defines fair value Guidance on determination Consistent disclosures requirements Not when, but how fair Applies to all transactions and balances Exception - transactions accounted for under IFRS 2 Sharebased Payment and IAS 17 Leases. 5

7 The Previous Definition of Fair Value Fair value definition The amount for which an asset could be exchanged or a liability settled between knowledgeable, willing parties in an arm s length transaction. Its weaknesses It did not specify whether an entity is buying or selling the asset. It was unclear about what settling meant because it did not refer to the creditor. It was unclear about whether it was marketbased. It did not state explicitly when the exchange or settlement takes place. 6

8 IFRS 13 s new Definition of Fair Value New fair value definition The price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. Its improvements It specifies that the entity is selling the asset. It refers to the transfer of a liability. It is not a forced or distressed sale. It is clear it is market-based. It states explicitly when the sale or transfer takes place. 7

9 Valuation Concepts Market pricing NOW - exit price, market pricing, orderly transaction Before exchange, knowledgeable and willing, not as explicitly defined Seller 150m Buyer 100m Willing buyer and seller would usually settle between 100m and 150m 150m starting point but may not be the exit price per IFRS13 Depends on the availability of prices of Comps Issues to consider include: related parties duress or forced sale 8

10 Valuation Concepts Market participants Market based not entity specific Assumed access to principal market (greatest volume) or most advantageous market (greatest price) Willing Seller & Buyer Market Participants Principal market or Most advantageous market Principal or most advantageous markets likely to be the same as competition would eliminate any differences 9

11 Highest and Best Use Highest and best use Non-financial assets are to be valued on a highest and best use basis Market participant would maximize the value Physical Legal Financial Current use is often but not always = to highest and best use Intangible and financial assets typically have only one use E.g. Brand name or software cannot be converted into something else without it becoming a different intangible asset 10

Step 4 Highest and best use Highest return from potential uses 1 vs. 3 11")

12 Highest and Best Use Determination process All available alternative uses Step 1 Physically possible uses Step 2 Physically possible, legally permissible uses e.g. Potential uses 1, 2 and 3 Step 3 Physically possible, legally permissible financially feasible uses e.g. Potential uses 1 and 3 (2 not financially feasible) Step 4 Highest and best use Highest return from potential uses 1 vs. 3 11

13 Highest and Best Use - Example Dubai real estate An investment fund acquired a commercial office building on the Palm Jumeirah as an asset included in a wider business combination. Given the hotel, leisure and residential nature of the Palm, it is not a popular choice for commercial office buildings, and occupancy has traditionally remained low. Value of this asset has accordingly been reflective of this. The building has been authorized for conversion to a residential tower after some structural changes which according to engineers can easily be made. In this example, the highest and best use of the commercial office building would be determined by comparing: a) the current value of the building as a commercial office building; and b) the value of the building as a residential tower after conversion and deduction of cost of conversion. The highest and best use of the asset would be determined based on the higher of these values. 12

14 Challenges Challenges and conclusions Local markets have limited comparability and not as voluminous Markets are largely inefficient and prices may not reflect complete information Availability of timely relevant information is a challenge Considering the principal or most advantageous market in GCC Related party transactions due to closed community (KSA, UAE, Qatar, Kuwait) 13

15 Conclusion Points Challenges and conclusions Overall, fair valuation not too dissimilar to current practice Detailed disclosure changes expected Technical interpretation may have variations Fair values are likely to be scrutinized more and Auditors likely to seek more substantiation behind assumptions and conclusions Third party or expert inputs may need to be sought more 14

16 Valuation Fundamentals

17 Value Definition Fair Value Vs. Fair Market Value Price in cash equivalent Hypothetical willing and able buyer and seller Acting at arm s length Open and unrestricted market Neither under a compulsion to buy or sell Both have reasonable knowledge Value Principles Specific point in time (hindsight excluded) Function of prospective earnings/ cash flow Market dictates rates of return Underlying net tangible assets may influence value Commercial and non-commercial value 16

18 Value versus Price The value is $5m, we just paid that in January Worth on paper (value) may differ substantially from amount paid (price) Intrinsic value VS. Negotiated Price Why Price and Value May Differ Differing views of the asset Negotiation strengths of the parties Different assessments of synergy potential Non-business motives - e.g. sports franchises and other trophy assets Distressed (bargain purchase) or related party sales 17

19 Differing Viewpoints on Cash Flow Buyer Seller Past may be future! Reliance on small group of customers Sustainability of customer relationships Reliance on owner Past is no reflection of future! Ready to take-off Profits down due to investment for future We ve just achieved critical mass 35,000 35,000 30,000 30,000 25,000 25,000 20,000 20,000 15,000 15,000 10,000 10,000 5,000 5, A 2007A 2008A 2009A 2010A 2011F 2012F 2013F A 2007A 2008A 2009A 2010A 2011F 2012F 2013F 18

20 Valuation Approaches

21 Valuation Approaches Going-concern Approach Cost approach Income approach Market approach Entities Liquidation Approach Asset based orderly or forced Valuation Approaches Specialized Assets Same Approach as for Entities Cost approach Income approach Market approach 20

22 Three Main Approaches to Valuation The Cost Approach Not pay more than what it would cost to replace Direct/ indirect cost method Adjusted Net Assets Method The Market Approach Pay no more than what a comparable property could be purchased for Comparable/Guideline Company Precedent Transactions The Income Approach Present value of future returns Capitalization of Earnings/Cash Flows Discounted Cash Flow Method 21

23 Valuation techniques Valuation techniques Cost Replacement / Reproduction Key considerations Availability of comprehensive cost data Replication to current depreciated state Functional obsolescence Economic obsolescence Market dilution Inflation Loss of profits during reproduction Logically rationalizing historical cost vs. current cost Cost Cost Approach Approach Income Income Approach Approach Market Market Approach Approach 22

24 Market Approach Why perform comparable analysis? Value private companies Value segments of larger companies Derive a range of possible values for a TARGET Test market valuation of public companies Frame in other valuation approaches Basic premise is that the equity markets have a view on the risk and return inherent in various industries Why Transactions? deal-speak Industry-specific multiples Insights (Premium, Valuation techniques, Bidding strategies etc.) Cost Cost Approach Approach Income Income Approach Approach Market Market Approach Approach 23

25 Some Attributes of Different Multiples 24

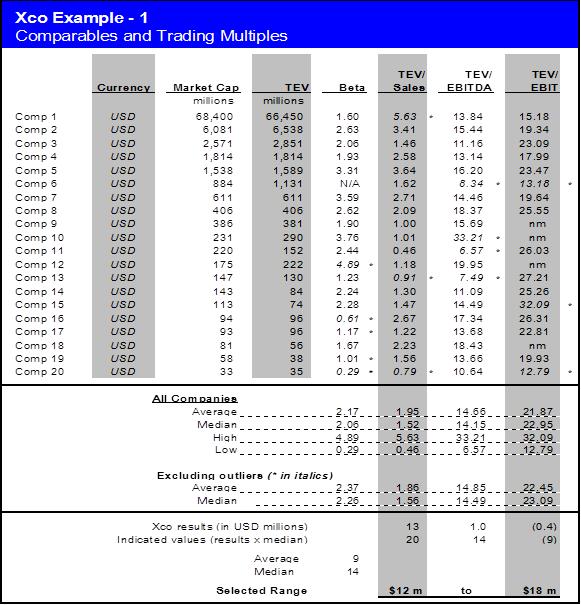

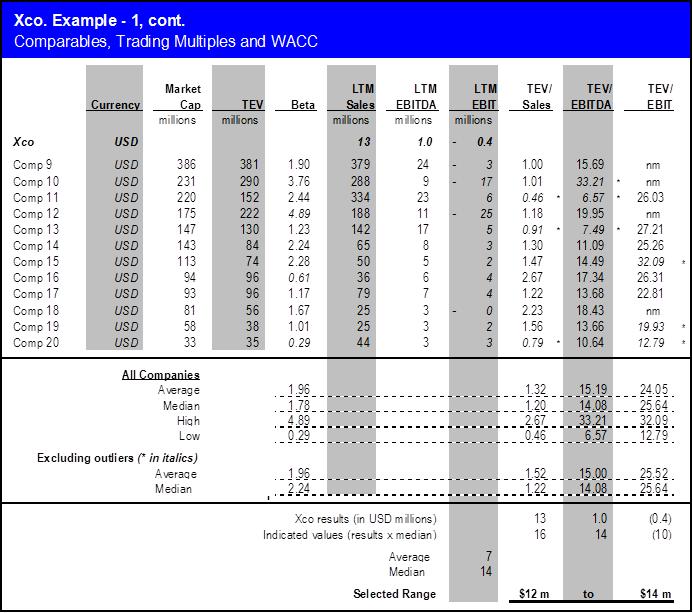

26 Market Approach Trading Multiples Example Common Errors Inappropriate selection Use of mean/ median No adjustments Inappropriate adjustments Mismatch of multiples and financial data Relying on third-party data without validating 25

27 Market Approach Transaction Multiples Example Problems Limited number of transactions Dated information Missing data Lack of relevant What do you mean my company is worth only $350 million? Do you know that Company X, my direct competitor, just sold for $860 million. 26

28 Income Approach Valuation techniques Income Discounted Cash Flow Method Capitalization of Cash Flow/Earnings Dividend Discount Model Excess earnings Relief from royalty Key considerations Turnover / earnings / free cash flow profiles Discount rates / growth rates Time periods and UEL of assets Royalty rates / Contributory asset charges Tax and tax amortization benefits Cost Income Cost Income Approach Approach Approach Approach Market Market Approach Approach 27

29 Capitalization Rate and the Multiple Factors determining the discount rates: Size Capital intensiveness Volatility of earnings (i.e., risk) Depth of management The inverse of the capitalization rate = the multiple Example: 20% rate 1/20% = 5x multiple Capitalized cash flow example All amounts in $000s After-tax maintainable cash flow 15,000 Capitalization rate 20% Multiple (inverse of capitalization rate) 5.0 x Capitalized cash flow value 75,000 28

30 Income Approach - Discounted Cash Flow The Value Formula - DCF Cash flow discounted to PV at the appropriate discount rate = Going concern value of the operations + Non-operating/redundant assets = Fair market value of the business Cash flows for explicit forecast period + Terminal value 29

31 Free Cash Flow Computation FREE CASH FLOW COMPUTATION EBIT - Cash Taxes + Depreciation & Amortization - Capex - / + Increase/ (decrease) in Net Working Capital = Free Cash Flow (Entity or levered) Common Errors Optimistic forecasts Capex Working Capital Cash flow for terminal value Discount rate does not reflect risk Long-term growth rate too high 30

32 EBITDA (Cash Flow on Right Scale) Revenue (EBIT on Right Scale) Income Approach: DCF Example Example Company - Discounted Cash Flow Analysis Revenue and EBIT ($ millions) Jun-05 Jun-06 Jun-07 Jun-08 Jun-09 Operations Revenue 318, , , , ,720 Gross Margin 108, , , , ,666 Indirect costs (55,510) (56,856) (57,529) (58,876) (59,549) EBITDA 52,692 57,384 61,444 61,342 62,117 Depreciation (15,912) (16,320) (15,524) (15,932) (15,136) EBIT 36,780 41,064 45,920 45,410 46,981 Discretionary Cash Flow EBIT 36,780 41,064 45,920 45,410 46,981 Tax on EBIT at 35.00% (12,873) (14,372) (16,072) (15,893) (16,443) Depreciation 15,912 16,320 15,524 15,932 15,136 Capital expenditiures (18,000) (12,500) (18,000) (13,000) (15,000) Change in non-cash w orking capital (1,591) (1,632) (1,652) (1,693) (1,714) After tax unlevered discretionary cash flow 20,228 28,880 25,719 30,755 28, Jun-05 Jun-06 Jun-07 Jun-08 Jun Discount period Discount at WACC of 10.00% Present value 19,286 25,032 20,266 22,031 18,860 EBITDA and Cash Flow ($ millions) Terminal value, grow ing at 2.00% 229,268 PV accumulation 6% 13% 19% 26% 32% Total Enterprise Value (TEV) 334, Selected Range 315,000 to 355, Year Over Year Change Total Revenues n.a. 2.6% 1.3% 2.5% 1.2% Indirect Costs n.a. 2.4% 1.2% 2.3% 1.1% Ratios Gross margin 34.0% 35.0% 36.0% 35.5% 35.5% EBITDA margin 16.6% 17.6% 18.6% 18.1% 18.1% EBIT margin 11.6% 12.6% 13.9% 13.4% 13.7% Depreciation / Revenue 5.0% 5.0% 4.7% 4.7% 4.4% 10 - Jun-05 Jun-06 Jun-07 Jun-08 Jun

33 Some Examples

34 Incorrect Use of Comparable company multiples Background Assist audit in annual impairment review Client performed analysis Concluded no impairment based on high end value Key Issue(s) Inappropriate use of comparable company multiples? Process Analyzed comparable companies Studies historical performance Outcome Red flag for a potential Write down 33

35 34

36 35

37 Aggressive Assumptions Overview Background Retained by investor to value target for investment purposes Client developed aggressive projections Had a view on value/price Key Issue(s) What was the support for the projections? Process Analyzed historical performance Studied industry growth expectations Outcome One-half of value supported 36

38 Discounted Cash Flow Analysis - Unadjusted Projections Residual Operations Revenue 3,968 5,283 7,342 8,905 14,896 24,062 37,218 50,512 65,051 84,524 87,060 Gross Margin 1,085 1,329 1,685 3,130 6,565 11,681 18,555 26,076 34,337 44,785 Direct and Indirect costs (1,085) (1,227) (1,442) (3,024) (5,698) (10,350) (13,435) (17,394) (22,054) (28,238) EBITDA ,331 5,120 8,682 12,283 16,547 Depreciation (759) (831) (919) (1,011) (1,121) EBIT Revenues ($000s) 572 4,289 7,763 11,272 15,426 Discretionary Cash Flow EBIT 90,000 80, ,289 7,763 11,272 15,426 15,889 Tax on EBIT at 34.00% 70,000 (194) (1,458) (2,639) (3,832) (5,245) (5,402) Depreciation 60, ,011 1,121 Capex 50,000 (848) (1,400) (1,400) (1,400) (1,400) 40,000 Change in non-cash working capital (75) 96 (453) (611) (1,161) - 30,000 After tax unlevered discretionary cash flow 213 2,358 4,190 6,440 8,741 10,487 20,000 10,000 Discount period Discount at WACC of 30.00% Present value 187 1,591 2,175 2,571 2,684 Residual value, growing at 3.00% 11,569 PV accumulation 1% 9% 19% 31% 44% 44% Total Enterprise Value (TEV) 20, ,778 3,952 6,523 9,207 9,207 Year Over Year Change Revenue 31.4% 33.2% 39.0% 21.3% 67.3% 61.5% 54.7% 35.7% 28.8% 29.9% EBITDA nm nm 139.5% nm 716.9% 53.4% 284.7% 69.6% 41.5% 34.7% Ratios Gross margin 27.3% 25.1% 23.0% 35.2% 44.1% 48.5% 49.9% 51.6% 52.8% 53.0% EBITDA margin 0.0% 1.9% 3.3% 1.2% 5.8% 5.5% 13.8% 17.2% 18.9% 19.6% EBIT margin 2.4% 11.5% 15.4% 17.3% 18.3% Depreciation / Revenue 3.2% 2.2% 1.8% 1.6% 1.3% 37

39 Discounted Cash Flow Analysis - Adjusted Projections Residual Operations Revenue 3,968 5,283 7,342 8,905 14,896 20,110 26,143 31,371 37,646 45,175 46,530 Gross Margin 1,085 1,329 1,685 3,130 6,565 9,049 11,764 14,117 18,823 22,587 23,265 Direct and Indirect costs (886) (1,227) (1,442) (3,024) (5,698) (7,692) (9,615) (11,538) (13,846) (16,615) (17,113) EBITDA ,357 2,149 2,579 4,977 5,972 6,152 Depreciation (603) (784) (627) (753) (903) EBIT Revenues $000s 754 1,365 1,952 4,224 5,069 Discretionary Cash Flow EBIT 90,000 80, ,365 1,952 4,224 5,069 5,221 Tax on EBIT at 34.00% 70,000 (256) (464) (664) (1,436) (1,723) (1,775) 60,000 Depreciation ,000 Capex (1,149) (1,126) (784) (1,255) (1,506) (547) 40,000 Change in non-cash working capital 30,000 (513) (632) (548) (657) (789) (142) After tax unlevered discretionary cash flow (561) (73) 583 1,629 1,954 3,661 20,000 10,000 Discount period Discount at WACC of 20.00% Present value (512) (56) Residual value, growing at 3.00% 9,196 PV accumulation -5% -5% -2% 6% 14% 14% Total Enterprise Value (TEV) 10,719 (512) (567) (197) 663 1,523 1,523 Year Over Year Change Revenue 31.4% 33.2% 27.9% 21.3% 24.3% 35.0% 30.0% 20.0% 20.0% 20.0% EBITDA nm nm 139.5% nm 716.9% 56.5% 58.3% 20.0% 93.0% 20.0% Ratios Gross margin 27.3% 25.1% 23.0% 35.2% 44.1% 45.0% 45.0% 45.0% 50.0% 50.0% EBITDA margin 5.0% 1.9% 3.3% 1.2% 5.8% 6.7% 8.2% 8.2% 13.2% 13.2% EBIT margin 3.7% 5.2% 6.2% 11.2% 11.2% Depreciation / Revenue 3.0% 3.0% 2.0% 2.0% 2.0% 38

40 Rate of Return

41 Discount Rate Illustrative WACC calculation Low High US real risk free rate 2.6% 2.6% Long term inflation differential between the UAE and the US 0.5% 0.5% Implied risk free rate for the UAE 3.1% 3.1% Unlevered beta Debt-to-equity 35% 35% Levered beta Implied risk premium for mature market 6.0% 6.0% Country risk premium - UAE 1.0% 1.0% Specific risk premium 2.0% 4.0% Cost of equity 14% 16% After tax cost of debt 10% 12% Debt 25% 25% Equity 75% 75% WACC (rounded) 13% 15% Key Data Sources Government bond/ treasury bond Risk free rate Ibbotson Associates Size Premium Industry Premium Equity Risk Premium Prof. A Damodaran Website Industry Premium Beta Capital IQ, Bloomberg, Mergerstat Informed judgment 40

42 Key Take-away

43 Common Valuation Shortcomings Very mathematical - Valuation is an art not a precise science Lack of corroboration - Reliance on a single valuation method No risk adjustment - Reliance on historical results and forecasts Use of average market multiples Terminal value calculations different methods than DCF, uncertainty, growth factor, etc. Lack of parity in cash flows and discount rates. e.g. using WACC to discount after interest cash-flows, pre-tax vs. post-tax amounts, etc. Incorrect adjustments - Normalization adjustments (owner vs. management), cash-flow adjustments (working capital), WACC (risk factor to cater for uncertainty of achieving forecast), value of debt to deduct from enterprise value, etc. 42

44 Key Take-away Value versus price Reasonability checks Compare apples to apples Price is what you pay. Value is what you get. Warren Buffett What to spend time on Business and industry outlook Business and industry key success factors Strategic factors for a transaction Risks & opportunities identification Interpretation of the data What not to spend time on Complex models Too much precision (not an exact science) Irrelevant scenario and sensitivity analysis

45 Deloitte Transaction Services LLC is a subsidiary of Deloitte Corporate Finance Limited in the Dubai International Financial Centre and Deloitte LLP in the United Kingdom, having SAGIA Number and Commercial License Number A list of members is available for inspection at Tawuniya Towers, North Tower, 12th floor, King Fahd Road, Riyadh, Kingdom of Saudi Arabia, the firm s principal place of business and registered office. Tel: +966 (1) Fax: +966 (1) Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee, and its network of member firms, each of which is a legally separate and independent entity. Deloitte Transaction Services LLC is an affiliate of the UK and Middle East member firms of Deloitte Touche Tohmatsu Limited. Please see for a detailed description of the legal structure of Deloitte Touche Tohmatsu Limited and its member firms. Deloitte provides audit, tax, consulting, and financial advisory services to public and private clients spanning multiple industries. With a globally connected network of member firms in more than 150 countries, Deloitte brings world-class capabilities and high-quality service to clients, delivering the insights they need to address their most complex business challenges. Deloitte has in the region of 200,000 professionals, all committed to becoming the standard of excellence. Deloitte's professionals are unified by a collaborative culture that fosters integrity, outstanding value to markets and clients, commitment to each other, and strength from cultural diversity. They enjoy an environment of continuous learning, challenging experiences, and enriching career opportunities. Deloitte's professionals are dedicated to strengthening corporate responsibility, building public trust, and making a positive impact in their communities Deloitte Transaction Services Limited LLC. All rights reserved 44

Steps in Business Valuation

Steps in Business Valuation Professor Grant W. Newton, Executive Director Association of Insolvency & Restructuring Advisors Suggested Inquiries and Challenges in Current Environment When the company being

Steps in Business Valuation Professor Grant W. Newton, Executive Director Association of Insolvency & Restructuring Advisors Suggested Inquiries and Challenges in Current Environment When the company being

Valuation Principles

Valuation Principles The ACG Cup January 16, 2018 36 East 7 th Street Suite 2400 Cincinnati, OH 45202 513.813.4101 www.comstockadvisors.com Nickolas N. Sypniewski nsypniewski@comstockadvisors.com www.comstockadvisors.com

Valuation Principles The ACG Cup January 16, 2018 36 East 7 th Street Suite 2400 Cincinnati, OH 45202 513.813.4101 www.comstockadvisors.com Nickolas N. Sypniewski nsypniewski@comstockadvisors.com www.comstockadvisors.com

International Glossary of Business Valuation Terms

International Glossary of Business Valuation Terms To enhance and sustain the quality of business valuations for the benefit of the profession and its clientele, the below identified societies and organizations

International Glossary of Business Valuation Terms To enhance and sustain the quality of business valuations for the benefit of the profession and its clientele, the below identified societies and organizations

Valuation Principles

Valuation Principles The ACG Cup January 15, 2019 36 East 7 th Street Suite 2400 Cincinnati, OH 45202 513.813.4101 www.comstockadvisors.com Nickolas N. Sypniewski nsypniewski@comstockadvisors.com www.comstockadvisors.com

Valuation Principles The ACG Cup January 15, 2019 36 East 7 th Street Suite 2400 Cincinnati, OH 45202 513.813.4101 www.comstockadvisors.com Nickolas N. Sypniewski nsypniewski@comstockadvisors.com www.comstockadvisors.com

NACVA. National Association of Certified Valuation Analysts. Professional Standards

NACVA National Association of Certified Valuation Analysts Professional Standards Effective May 31, 2002 NACVA PROFESSIONAL STANDARDS Table of Contents Preamble... 4 General and Ethical Standards... 4

NACVA National Association of Certified Valuation Analysts Professional Standards Effective May 31, 2002 NACVA PROFESSIONAL STANDARDS Table of Contents Preamble... 4 General and Ethical Standards... 4

other assets? Valuation in International Arbitration Defining value Andrew Wynn and Noel Matthews (FTI Consulting)

") How can we REDUCE the uncertainty that can exist in valuing businesses and other assets? Valuation in International Arbitration Andrew Wynn and Noel Matthews (FTI Consulting) The value of a business or

How can we REDUCE the uncertainty that can exist in valuing businesses and other assets? Valuation in International Arbitration Andrew Wynn and Noel Matthews (FTI Consulting) The value of a business or

NACVA National Association of Certified Valuation Analysts. Professional Standards

NACVA National Association of Certified Valuation Analysts Professional Standards These Professional Standards are effective for engagements accepted on or after January 1, 2008 NACVA PROFESSIONAL STANDARDS

NACVA National Association of Certified Valuation Analysts Professional Standards These Professional Standards are effective for engagements accepted on or after January 1, 2008 NACVA PROFESSIONAL STANDARDS

Valuation Principles

Valuation Principles The ACG Cup January 20, 2016 36 East 7 th Street Suite 2400 Cincinnati, OH 45202 513.327.2171 www.comstockadvisors.com Nickolas N. Sypniewski nsypniewski@comstockadvisors.com www.comstockadvisors.com

Valuation Principles The ACG Cup January 20, 2016 36 East 7 th Street Suite 2400 Cincinnati, OH 45202 513.327.2171 www.comstockadvisors.com Nickolas N. Sypniewski nsypniewski@comstockadvisors.com www.comstockadvisors.com

Basics of Business Valuation. Presented by: Alon Wexler, CPA, CA, CBV Richter Advisory Group Inc.

Basics of Business Valuation Presented by: Alon Wexler, CPA, CA, CBV Richter Advisory Group Inc. 2017 Objective Brief overview of the Basics of Business Valuation There is more to it than 5x EBITDA! 2

Basics of Business Valuation Presented by: Alon Wexler, CPA, CA, CBV Richter Advisory Group Inc. 2017 Objective Brief overview of the Basics of Business Valuation There is more to it than 5x EBITDA! 2

THE ABC's OF VALUATION

THE ABC's OF VALUATION VALUATION OF COMPANIES AND THEIR SECURITIES FOR ESOP PURPOSES: METHODS OF VALUATION Prepared for the Annual Conference of the Ohio Employee Ownership Center April 20, 2007 BUSINESS

THE ABC's OF VALUATION VALUATION OF COMPANIES AND THEIR SECURITIES FOR ESOP PURPOSES: METHODS OF VALUATION Prepared for the Annual Conference of the Ohio Employee Ownership Center April 20, 2007 BUSINESS

Q Russian Legislation Update Accounting, financial reporting and audit

Q3 2015 Russian Legislation Update Accounting, financial reporting and audit Contents ACCOUNTING 1 IFRS Documents Adopted in Russia 1 Archiving Requirements on Accounting Documentation Summarized 3 FINANCIAL

Q3 2015 Russian Legislation Update Accounting, financial reporting and audit Contents ACCOUNTING 1 IFRS Documents Adopted in Russia 1 Archiving Requirements on Accounting Documentation Summarized 3 FINANCIAL

QUICK REFERENCE GUIDE TO VALUING ASSETS IN BUSINESS COMBINATIONS. Quick Reference Guide to Valuing Assets in Business Combinations

QUICK REFERENCE GUIDE TO VALUING ASSETS IN BUSINESS COMBINATIONS Quick Reference Guide to Valuing Assets in Business Combinations Overview of ASC 805: Business Combinations Acquisition Method and Business

QUICK REFERENCE GUIDE TO VALUING ASSETS IN BUSINESS COMBINATIONS Quick Reference Guide to Valuing Assets in Business Combinations Overview of ASC 805: Business Combinations Acquisition Method and Business

One of the major applications of Equity Valuation is the Private companies valuation. Private companies valuation can be applied:

One of the major applications of Equity Valuation is the Private companies valuation. Private companies valuation can be applied: To value a Start up operations of Public companies. To estimate a value

One of the major applications of Equity Valuation is the Private companies valuation. Private companies valuation can be applied: To value a Start up operations of Public companies. To estimate a value

Valuing a Going-Concern Location- Specific Business Operation in an Eminent Domain or Expropriation Matter

Eminent Domain and Expropriation Insights Best Practices Valuing a Going-Concern Location- Specific Business Operation in an Eminent Domain or Expropriation Matter Kevin M. Zanni Eminent domain and expropriation

Eminent Domain and Expropriation Insights Best Practices Valuing a Going-Concern Location- Specific Business Operation in an Eminent Domain or Expropriation Matter Kevin M. Zanni Eminent domain and expropriation

OFFICE OF CAREER SERVICES INTERVIEWS FINANCIAL MODELING

OFFICE OF CAREER SERVICES INTERVIEWS FINANCIAL MODELING Basic valuation concepts are among the most popular technical tasks you will be asked to discuss in investment banking and other finance interviews.

OFFICE OF CAREER SERVICES INTERVIEWS FINANCIAL MODELING Basic valuation concepts are among the most popular technical tasks you will be asked to discuss in investment banking and other finance interviews.

TVG Business Valuation

T V G The Vant Group Mergers & Acquisitions TVG Business Valuation ABC Company 17766 Preston Rd Dallas, TX 75252 Tel 972.458.8989 Fax 972.458.7342 email: info@thevantgroup.com website: www.thevantgroup.com

T V G The Vant Group Mergers & Acquisitions TVG Business Valuation ABC Company 17766 Preston Rd Dallas, TX 75252 Tel 972.458.8989 Fax 972.458.7342 email: info@thevantgroup.com website: www.thevantgroup.com

Beta International, Inc

Beta International, Inc Business Valuation Analysis REPORT October 16, Beta International, Inc 123 Main Street Bellevue, WA 98005 its website. The estimates and data contained herein are made using the

Beta International, Inc Business Valuation Analysis REPORT October 16, Beta International, Inc 123 Main Street Bellevue, WA 98005 its website. The estimates and data contained herein are made using the

Valuation Methodologies An overview of the four most commonly used business valuation methodologies

An overview of the four most commonly used business valuation methodologies A complete business valuation often provides an objective starting point for both buyers and sellers of businesses. Without a

An overview of the four most commonly used business valuation methodologies A complete business valuation often provides an objective starting point for both buyers and sellers of businesses. Without a

January 20, for. Acme Distribution. Prepared for: Tim Mills. Prepared by: Tom MacPherson

CALCULATION OF VALUE January 20, 2016 for Acme Distribution 182 First Avenue, Charlotte, NC Prepared for: Tim Mills Prepared by: Tom MacPherson Summit Acquisitions Group, LLC 4200 Settler Heights Drive,

CALCULATION OF VALUE January 20, 2016 for Acme Distribution 182 First Avenue, Charlotte, NC Prepared for: Tim Mills Prepared by: Tom MacPherson Summit Acquisitions Group, LLC 4200 Settler Heights Drive,

Glossary of Business Valuation Terms

Adjusted Net Assets Method Asset-Based Approach Beta Blockage Discount Business Business Risk Business Valuation Capital Asset Pricing Model (CAPM) Capitalization Capitalization of Earnings Method Capital

Adjusted Net Assets Method Asset-Based Approach Beta Blockage Discount Business Business Risk Business Valuation Capital Asset Pricing Model (CAPM) Capitalization Capitalization of Earnings Method Capital

Checklist 8.28: Revenue Ruling 59-60

Financial Valuation Workbook: Step-by-Step Exercises and Tests to Help You Master Financial Valuation, Third Edition By James R. Hitchner and Michael J. Mard Copyright 2011 by James R. Hitchner and Michael

Financial Valuation Workbook: Step-by-Step Exercises and Tests to Help You Master Financial Valuation, Third Edition By James R. Hitchner and Michael J. Mard Copyright 2011 by James R. Hitchner and Michael

IASB finalises IFRS 9 which changes the classification and measurement of financial assets and introduces an expected loss impairment model

Published on: July, 2014 IASB finalises IFRS 9 which changes the classification and measurement of financial assets and introduces an expected loss impairment model Background and effective date The lasb's

Published on: July, 2014 IASB finalises IFRS 9 which changes the classification and measurement of financial assets and introduces an expected loss impairment model Background and effective date The lasb's

Beta International Inc.

Beta International Inc. BUSINESS VALUATOR REPORT March 13, Beta International Inc. 555 Main Street Philadelphia, PA 19115 Contents Purpose 2 Methodology 2 Your Company Description 4 BizEquity Valuation

Beta International Inc. BUSINESS VALUATOR REPORT March 13, Beta International Inc. 555 Main Street Philadelphia, PA 19115 Contents Purpose 2 Methodology 2 Your Company Description 4 BizEquity Valuation

Valuation of Intangible Assets including. Purchase Price Allocation :74. Purchase Price Allocation

CA Ravishu Shah Valuation of Intangible Assets including Purchase Price Allocation Investment in knowledge based/intangible assets is one of the key characteristics of modern economies. Every goods including

CA Ravishu Shah Valuation of Intangible Assets including Purchase Price Allocation Investment in knowledge based/intangible assets is one of the key characteristics of modern economies. Every goods including

Asset-like acquisitions

Asset-like acquisitions Valuation considerations 17 March 2015 Asset-like acquisitions What do we mean by an Asset-like acquisition? An acquisition of a product or group of products that meets the definition

Asset-like acquisitions Valuation considerations 17 March 2015 Asset-like acquisitions What do we mean by an Asset-like acquisition? An acquisition of a product or group of products that meets the definition

IFRS 15. Revenue from Contracts with Customers

IFRS 15 Revenue from Contracts with Customers 17 February 2017 Why IFRS 15 is important? What does it mean for entities? Revenue recognition principles will change P/L may vary to a certain extent IT Systems,

IFRS 15 Revenue from Contracts with Customers 17 February 2017 Why IFRS 15 is important? What does it mean for entities? Revenue recognition principles will change P/L may vary to a certain extent IT Systems,

Documents Glossary of IP Terms/Financial

Documents Glossary of IP Terms/Financial ABATNA (Best Alternative to a Negotiated Agreement). Any negotiator should determine his or her BATNA before agreeing to any negotiated settlement. If the alternative

Documents Glossary of IP Terms/Financial ABATNA (Best Alternative to a Negotiated Agreement). Any negotiator should determine his or her BATNA before agreeing to any negotiated settlement. If the alternative

Headline Verdana Bold. Uganda PPP Act - Implications for Public Sector Accounting Kenneth LEGESI Deloitte (Uganda) Limited

Limited") Headline Verdana Bold Uganda PPP Act - Implications for Public Sector Accounting Kenneth LEGESI Deloitte (Uganda) Limited About us Kenneth Legesi Infrastructure and Capital Projects / PPP Advisory Deloitte

Headline Verdana Bold Uganda PPP Act - Implications for Public Sector Accounting Kenneth LEGESI Deloitte (Uganda) Limited About us Kenneth Legesi Infrastructure and Capital Projects / PPP Advisory Deloitte

IFRS Newsletter Special Edition IFRS 13, Fair Value Measurement

IFRS Newsletter Special Edition IFRS 13, Fair Value Measurement February 2012 Fair value is pervasive in International Financial Reporting Standards (IFRS) it s permitted or required in more than twenty

IFRS Newsletter Special Edition IFRS 13, Fair Value Measurement February 2012 Fair value is pervasive in International Financial Reporting Standards (IFRS) it s permitted or required in more than twenty

Common Errors Committed When Valuing Patents Part 1

Common Errors Committed When Valuing Patents Part 1 Bruce W. Burton, CPA, CFF, CMA, CLP bburton@srr.com Scott Weingust sweingust@srr.com Emma Bienias, CFA ebienias@srr.com Introduction n n n Over time,

Common Errors Committed When Valuing Patents Part 1 Bruce W. Burton, CPA, CFF, CMA, CLP bburton@srr.com Scott Weingust sweingust@srr.com Emma Bienias, CFA ebienias@srr.com Introduction n n n Over time,

We are responding to your invitation to comment on the IVSC Agenda Consultation 2017 on behalf of PricewaterhouseCoopers.

24 August 2017 International Valuation Standards Council 41 Moorgate London EC2R 6PP Re: IVSC Agenda Consultation 2017 Dear Members of the International Valuation Standards Council: We are responding to

24 August 2017 International Valuation Standards Council 41 Moorgate London EC2R 6PP Re: IVSC Agenda Consultation 2017 Dear Members of the International Valuation Standards Council: We are responding to

Fair Value Measurement

Chapter 25 Fair Value Measurement IFRS 13 / PSAK 68 Edited by Taufik Hidayat 2008-11 Nelson Lam and Peter Lau Intermediate Financial Reporting: An IFRS Perspective, 2E (Chapter 19) - 1 Agenda 1. Applicable

Chapter 25 Fair Value Measurement IFRS 13 / PSAK 68 Edited by Taufik Hidayat 2008-11 Nelson Lam and Peter Lau Intermediate Financial Reporting: An IFRS Perspective, 2E (Chapter 19) - 1 Agenda 1. Applicable

Valuation Importance and Issues. Chamber of Tax Consultants, Seminar on Corporate Restructuring 20 January 2017 Pinkesh Billimoria

Valuation Importance and Issues Chamber of Tax Consultants, Seminar on Corporate Restructuring 20 January 2017 Pinkesh Billimoria Investing in India An Easy Difficulty Valuation expectations / Mismatch

Valuation Importance and Issues Chamber of Tax Consultants, Seminar on Corporate Restructuring 20 January 2017 Pinkesh Billimoria Investing in India An Easy Difficulty Valuation expectations / Mismatch

Fair Value Measurement and Application

May 5, 2014 Comments Due: August 15, 2014 Proposed Statement of the Governmental Accounting Standards Board Fair Value Measurement and Application This Exposure Draft of a proposed Statement of Governmental

May 5, 2014 Comments Due: August 15, 2014 Proposed Statement of the Governmental Accounting Standards Board Fair Value Measurement and Application This Exposure Draft of a proposed Statement of Governmental

Understanding Financial Statements and Their Effects on Enhancing Value

Understanding Financial Statements and Their Effects on Enhancing Value 2017 California/Western States Chapter Conference Todd Poling, Vantage Point Advisors Josh Edwards, Eureka Valuation Advisors Main

Understanding Financial Statements and Their Effects on Enhancing Value 2017 California/Western States Chapter Conference Todd Poling, Vantage Point Advisors Josh Edwards, Eureka Valuation Advisors Main

In this issue: Fair value measurement of financial assets and financial liabilities. Welcome to the series

IFRS FOR INVESTMENT FUNDS September 2012, Issue 5 Welcome to the series Our series of IFRS for Investment Funds publications addresses practical application issues that investment funds may encounter when

IFRS FOR INVESTMENT FUNDS September 2012, Issue 5 Welcome to the series Our series of IFRS for Investment Funds publications addresses practical application issues that investment funds may encounter when

Created by Stefan Momic for UTEFA. UTEFA Learning Session #2 Valuation September 27, 2018

UTEFA Learning Session #2 Valuation September 27, 2018 Agenda Introduction to Valuation Relative Valuation Intrinsic Valuation Discounted Cash Flow Analysis Valuation Trade-Offs Introduction to Valuation

UTEFA Learning Session #2 Valuation September 27, 2018 Agenda Introduction to Valuation Relative Valuation Intrinsic Valuation Discounted Cash Flow Analysis Valuation Trade-Offs Introduction to Valuation

CORPORATE VALUATION METHODOLOGIES

CORPORATE VALUATION METHODOLOGIES What is the business worth? Although a simple question, determining the value of any business in today s economy requires a sophisticated understanding of financial analysis

CORPORATE VALUATION METHODOLOGIES What is the business worth? Although a simple question, determining the value of any business in today s economy requires a sophisticated understanding of financial analysis

Express Business Valuation

Express Business Valuation Sample Report 800.825.8763 719.548.4900 Fax: 719.548.4479 sales@valusource.com www.valusource.com Business Valuation Report High Country Manufacturing 5678 Country Rd Calhan,

Express Business Valuation Sample Report 800.825.8763 719.548.4900 Fax: 719.548.4479 sales@valusource.com www.valusource.com Business Valuation Report High Country Manufacturing 5678 Country Rd Calhan,

Business Valuation Report

Certified Business Appraisals, LLC Business Valuation Report Prepared for: John Doe Client Business, Inc. 1 Market Way Your Town, CA December 3, 2017 1 Market Street Suite 100 Anytown, CA 95401 Web: www.yourdomain.com

Certified Business Appraisals, LLC Business Valuation Report Prepared for: John Doe Client Business, Inc. 1 Market Way Your Town, CA December 3, 2017 1 Market Street Suite 100 Anytown, CA 95401 Web: www.yourdomain.com

Valuation issues affecting Alternative Funds Presentation at Jersey Funds Association training session

Presentation at Jersey Funds Association i training session Mike Byrne 26 October 2010 PwC Page 1 December2009 Agenda Consideration of the Valuation issues affecting different types of Alternative Funds:

Presentation at Jersey Funds Association i training session Mike Byrne 26 October 2010 PwC Page 1 December2009 Agenda Consideration of the Valuation issues affecting different types of Alternative Funds:

Valuation for Financial Reporting Hot topics impacting the real estate industry

Valuation for Financial Reporting Hot topics impacting the real estate industry Steven Gottlieb, MAI, FRICS Director Deloitte Financial Advisory Services LLP New York, NY Appraisal Institute National Conference

Valuation for Financial Reporting Hot topics impacting the real estate industry Steven Gottlieb, MAI, FRICS Director Deloitte Financial Advisory Services LLP New York, NY Appraisal Institute National Conference

Report of the Executive Board

Report of the Executive Board to the Annual Meeting of Hapag-Lloyd Aktiengesellschaft on 29 May 2017 regarding the Utilization of the Authorized Capital 2016 excluding subscription rights of the shareholders

Report of the Executive Board to the Annual Meeting of Hapag-Lloyd Aktiengesellschaft on 29 May 2017 regarding the Utilization of the Authorized Capital 2016 excluding subscription rights of the shareholders

INFORMATION SERVICES CORPORATION 2015 CONSOLIDATED FINANCIAL STATEMENTS

INFORMATION SERVICES CORPORATION 2015 CONSOLIDATED FINANCIAL STATEMENTS For Year Ended December 31, 2015 INFORMATION SERVICES CORPORATION INDEX TO CONSOLIDATED FINANCIAL STATEMENTS Management s Responsibility...

INFORMATION SERVICES CORPORATION 2015 CONSOLIDATED FINANCIAL STATEMENTS For Year Ended December 31, 2015 INFORMATION SERVICES CORPORATION INDEX TO CONSOLIDATED FINANCIAL STATEMENTS Management s Responsibility...

Mobilizing Islamic Finance for Long-Term Investment Financing Create an Enabling Environment for Long Term Islamic Financing

Mobilizing Islamic Finance for Long-Term Investment Financing Create an Enabling Environment for Long Term Islamic Financing Hatim El-Tahir, PhD, FCIB, FCISI Director, Islamic Finance Group Deloitte &

Mobilizing Islamic Finance for Long-Term Investment Financing Create an Enabling Environment for Long Term Islamic Financing Hatim El-Tahir, PhD, FCIB, FCISI Director, Islamic Finance Group Deloitte &

2016 CONSOLIDATED FINANCIAL STATEMENTS. For the year ended December 31, 2016

2016 CONSOLIDATED FINANCIAL STATEMENTS INFORMATION SERVICES CORPORATION Index To Consolidated Financial Statements Management s Responsibility... 2 Independent Auditor s Report... 3 Consolidated Statement

2016 CONSOLIDATED FINANCIAL STATEMENTS INFORMATION SERVICES CORPORATION Index To Consolidated Financial Statements Management s Responsibility... 2 Independent Auditor s Report... 3 Consolidated Statement

Consolidated Financial Statements

Consolidated Financial Statements for the years ended and 2015 Deloitte LLP 2103 11th Avenue Mezzanine Level Bank of Montreal Building Regina SK S4P 3Z8 Canada Tel: 1-306-565-5200 Fax: 1-306-757-4753 www.deloitte.ca

Consolidated Financial Statements for the years ended and 2015 Deloitte LLP 2103 11th Avenue Mezzanine Level Bank of Montreal Building Regina SK S4P 3Z8 Canada Tel: 1-306-565-5200 Fax: 1-306-757-4753 www.deloitte.ca

Chapter 2: Analyzing a Company s Financial Statements & Operations

Chapter 2: Analyzing a Company s Financial Statements & Operations To analyze a company s operations a close look must be taken at the day to day operations as well as examining a company s financial history.

Chapter 2: Analyzing a Company s Financial Statements & Operations To analyze a company s operations a close look must be taken at the day to day operations as well as examining a company s financial history.

International Financial Reporting Standards (IFRS) Update Life

Update Life") International Financial Reporting Standards (IFRS) Update Life Actuaries Clubs of Boston & Harford/Springfield Joint Meeting 2011 November 17, 2011 Albert Li Agenda Insurance Contract Objective and Timeline

International Financial Reporting Standards (IFRS) Update Life Actuaries Clubs of Boston & Harford/Springfield Joint Meeting 2011 November 17, 2011 Albert Li Agenda Insurance Contract Objective and Timeline

L AZURDE COMPANY FOR JEWELRY AND ITS SUBSIDIARIES (A SAUDI JOINT STOCK GROUP)

") L AZURDE COMPANY FOR JEWELRY AND ITS SUBSIDIARIES (A SAUDI JOINT STOCK GROUP) REVIEWED INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS AND REVIEW REPORT FOR THE THREE MONTHS PERIOD ENDED 31 MARCH 2018

L AZURDE COMPANY FOR JEWELRY AND ITS SUBSIDIARIES (A SAUDI JOINT STOCK GROUP) REVIEWED INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS AND REVIEW REPORT FOR THE THREE MONTHS PERIOD ENDED 31 MARCH 2018

(Registered Number: ) LME Clear Limited. Directors report and financial statements. 31 December 2015

LME Clear Limited. Directors report and financial statements. 31 December 2015") (Registered Number: 07611628) LME Clear Limited Directors report and financial statements 31 December 2015 Directors and auditors Directors The Directors of the company who were in office during the year

(Registered Number: 07611628) LME Clear Limited Directors report and financial statements 31 December 2015 Directors and auditors Directors The Directors of the company who were in office during the year

Family Law Thought Leadership. Charles A. Wilhoite, CPA

Family Law Thought Leadership The Business Valuation Baker s Dozen : Questions Legal Counsel Should Consider Asking (and the Expert Should Expect to Hear) in Deposition/Cross-Examination And Why Charles

Family Law Thought Leadership The Business Valuation Baker s Dozen : Questions Legal Counsel Should Consider Asking (and the Expert Should Expect to Hear) in Deposition/Cross-Examination And Why Charles

Discounted Cash Flow Analysis Deliverable #6 Sales Gross Profit / Margin

Discounted Cash Flow Analysis Deliverable #6 The discounted cash flow methodology derives the value of a company by calculating the present value of all future projected cash flows. Unlike comparable companies

Discounted Cash Flow Analysis Deliverable #6 The discounted cash flow methodology derives the value of a company by calculating the present value of all future projected cash flows. Unlike comparable companies

Headline Verdana Bold. VAT Implementation VAT landscape in the UAE and the GCC

Headline Verdana Bold VAT Implementation VAT landscape in the UAE and the GCC 17 February 2017 Speaker Profile Marc Collenette Manager, Indirect Tax macollenette@deloitte.com 2017 Deloitte & Touche (M.E.).

Headline Verdana Bold VAT Implementation VAT landscape in the UAE and the GCC 17 February 2017 Speaker Profile Marc Collenette Manager, Indirect Tax macollenette@deloitte.com 2017 Deloitte & Touche (M.E.).

L AZURDE COMPANY FOR JEWELRY AND ITS SUBSIDIARIES (A SAUDI JOINT STOCK GROUP)

") L AZURDE COMPANY FOR JEWELRY AND ITS SUBSIDIARIES (A SAUDI JOINT STOCK GROUP) REVIEWED INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS AND REVIEW REPORT FOR THE THREE AND SIX MONTH PERIODS ENDED 30

L AZURDE COMPANY FOR JEWELRY AND ITS SUBSIDIARIES (A SAUDI JOINT STOCK GROUP) REVIEWED INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS AND REVIEW REPORT FOR THE THREE AND SIX MONTH PERIODS ENDED 30

Financial Statements. Calgary Parking Authority December 31, 2014

Financial Statements Calgary Parking Authority December 31, 2014 Deloitte LLP 700 Bankers Court 850 Second Street S.W. Calgary AB T2P 0R8 Canada Tel: 403-267-1700 Fax: 403-213-5791 www.deloitte.ca Independent

Financial Statements Calgary Parking Authority December 31, 2014 Deloitte LLP 700 Bankers Court 850 Second Street S.W. Calgary AB T2P 0R8 Canada Tel: 403-267-1700 Fax: 403-213-5791 www.deloitte.ca Independent

Dual Multi-Period Excess Earnings in the Valuation of Intangibles

Dual Multi-Period Excess Earnings in the Valuation of Intangibles October 2013 Contributing AUTHORS: Randie Dial Partner CliftonLarsonAllen LLP Carol Lewis Partner BKD, LLP Michael Massey Partner Moss

Dual Multi-Period Excess Earnings in the Valuation of Intangibles October 2013 Contributing AUTHORS: Randie Dial Partner CliftonLarsonAllen LLP Carol Lewis Partner BKD, LLP Michael Massey Partner Moss

Three Accounting Standards that will shake up the Australian Technology, Media and Telecom (TMT) sector

sector") Three Accounting Standards that will shake up the Australian Technology, Media and Telecom (TMT) sector In the coming years companies in the Australian Technology, Media and Telecom (TMT) sector may find

Three Accounting Standards that will shake up the Australian Technology, Media and Telecom (TMT) sector In the coming years companies in the Australian Technology, Media and Telecom (TMT) sector may find

Deal Stats Transaction Survey

January 2016 - June 2016 Summary Report Prepared by Brady Cary and Robert Regis, ASA of Columbia Financial Advisors, Inc. 12/31/16 A Publication of the AM&AA Market Research Committee Market Research Committee

January 2016 - June 2016 Summary Report Prepared by Brady Cary and Robert Regis, ASA of Columbia Financial Advisors, Inc. 12/31/16 A Publication of the AM&AA Market Research Committee Market Research Committee

An Introduction to Business Valuation

An Introduction to Business Valuation Ten East Doty St., Suite 1002 809 N. 8 th St., Suite 218 Madison, Wisconsin Sheboygan, WI 53081 (608) 257-2757 (920) 452-8250 www.capvalgroup.com 1993 Revised: April

An Introduction to Business Valuation Ten East Doty St., Suite 1002 809 N. 8 th St., Suite 218 Madison, Wisconsin Sheboygan, WI 53081 (608) 257-2757 (920) 452-8250 www.capvalgroup.com 1993 Revised: April

UMTA & UTF: NATIONAL WORKSHOP GENERIC V/S CITY SPECIFIC UTF

UMTA & UTF: NATIONAL WORKSHOP GENERIC V/S CITY SPECIFIC UTF Agenda POTENTIAL SOURCES OF FUNDS PRIORITIZED UTILIZATION OF FUNDS FUND MANAGEMENT DIVISION 2 Common consensus that UMTA would have its own dedicated

UMTA & UTF: NATIONAL WORKSHOP GENERIC V/S CITY SPECIFIC UTF Agenda POTENTIAL SOURCES OF FUNDS PRIORITIZED UTILIZATION OF FUNDS FUND MANAGEMENT DIVISION 2 Common consensus that UMTA would have its own dedicated

WORKING DRAFT PRACTICE AID VALUATION OF PRIVATELY HELD COMPANY EQUITY SECURITIES ISSUED AS COMPENSATION

WORKING DRAFT PRACTICE AID VALUATION OF PRIVATELY HELD COMPANY EQUITY SECURITIES ISSUED AS COMPENSATION Replaces the 2004 edition of the practice aid Valuation of Privately-Held- Company Equity Securities

WORKING DRAFT PRACTICE AID VALUATION OF PRIVATELY HELD COMPANY EQUITY SECURITIES ISSUED AS COMPENSATION Replaces the 2004 edition of the practice aid Valuation of Privately-Held- Company Equity Securities

Advanced Company Analysis Valuation & Financial Modelling. 5-9 March 2017 Manama, Bahrain. euromoneylearningsolutions.

Advanced Company Analysis Valuation & Financial Modelling 5-9 March 2017 Manama, Bahrain euromoneylearningsolutions.com/learnmore Advanced Company Analysis Valuation & Financial Modelling Accelerate your

Advanced Company Analysis Valuation & Financial Modelling 5-9 March 2017 Manama, Bahrain euromoneylearningsolutions.com/learnmore Advanced Company Analysis Valuation & Financial Modelling Accelerate your

Amended and restated consolidated financial statements of MTY Food Group Inc. November 30, 2016 and 2015

Amended and restated consolidated financial statements of MTY Food Group Inc. November 30, 2016 and 2015 Deloitte LLP La Tour Deloitte 1190 Avenue des Canadiens-de-Montréal Suite 500 Montreal QC H3B 0M7

Amended and restated consolidated financial statements of MTY Food Group Inc. November 30, 2016 and 2015 Deloitte LLP La Tour Deloitte 1190 Avenue des Canadiens-de-Montréal Suite 500 Montreal QC H3B 0M7

Math for Lawyers: Valuation Theory and Practice 101. December 8, 2011

Math for Lawyers: Valuation Theory and Practice 101 December 8, 2011 Agenda Introduction Presentation Questions and Answers (anonymous) Slides now available on front page of Securities Docket www.securitiesdocket.com

Math for Lawyers: Valuation Theory and Practice 101 December 8, 2011 Agenda Introduction Presentation Questions and Answers (anonymous) Slides now available on front page of Securities Docket www.securitiesdocket.com

IAS 39 the sequel. Time for new measures. August Background

August 2009 IAS 39 the sequel. Time for new measures Background On 14 July 2009, the International Accounting Standards Board (IASB) issued an exposure draft (ED), ED/2009/7, Financial Instruments: Classification

August 2009 IAS 39 the sequel. Time for new measures Background On 14 July 2009, the International Accounting Standards Board (IASB) issued an exposure draft (ED), ED/2009/7, Financial Instruments: Classification

Advanced Corporate Finance. Lorenzo Parrini

Advanced Corporate Finance Lorenzo Parrini May 2017 1 Introduction Course structure Course structure 3 credits 24 h 6 lessons 1. Corporate finance 2. Corporate valuation 3. M&A deals 4. M&A private equity

Advanced Corporate Finance Lorenzo Parrini May 2017 1 Introduction Course structure Course structure 3 credits 24 h 6 lessons 1. Corporate finance 2. Corporate valuation 3. M&A deals 4. M&A private equity

Questions for Respondents

Questions for Respondents The International Valuation Professional Board invites responses to the following questions. Not all questions need to be answered but to assist analysis of responses received

Questions for Respondents The International Valuation Professional Board invites responses to the following questions. Not all questions need to be answered but to assist analysis of responses received

EMAAR THE ECONOMIC CITY (A SAUDI JOINT STOCK COMPANY) CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2017

CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2017") EMAAR THE ECONOMIC CITY (A SAUDI JOINT STOCK COMPANY) CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2017 EMAAR THE ECONOMIC CITY (A SAUDI JOINT STOCK COMPANY) CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER

EMAAR THE ECONOMIC CITY (A SAUDI JOINT STOCK COMPANY) CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2017 EMAAR THE ECONOMIC CITY (A SAUDI JOINT STOCK COMPANY) CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER

Consolidated financial statements of MTY Food Group Inc. November 30, 2016 and 2015

Consolidated financial statements of MTY Food Group Inc. November 30, 2016 and 2015 Deloitte LLP La Tour Deloitte 1190 Avenue des Canadiens-de-Montréal Suite 500 Montreal QC H3B 0M7 Canada Tel: 514-393-7115

Consolidated financial statements of MTY Food Group Inc. November 30, 2016 and 2015 Deloitte LLP La Tour Deloitte 1190 Avenue des Canadiens-de-Montréal Suite 500 Montreal QC H3B 0M7 Canada Tel: 514-393-7115

Fair Value Accounting for Entities and Intangibles: What you need to know. August 2018

Fair Value Accounting for Entities and Intangibles: What you need to know August 2018 Presenter David Ball, CFA Managing Director Duff & Phelps Valuation Advisory Practice Concentration in TMT Industry

Fair Value Accounting for Entities and Intangibles: What you need to know August 2018 Presenter David Ball, CFA Managing Director Duff & Phelps Valuation Advisory Practice Concentration in TMT Industry

Mezzan Holding Company KSCC (Mezzan)

") Jun-15 Jul-15 Aug-15 Sep-15 Global Research Investment Update Equity Kuwait Food Sector 20 September, 2015 Mezzan Holding Company KSCC (Mezzan) Market Data Bloomberg Code: MEZZAN KK Reuters Code: MEZZ.KW

Jun-15 Jul-15 Aug-15 Sep-15 Global Research Investment Update Equity Kuwait Food Sector 20 September, 2015 Mezzan Holding Company KSCC (Mezzan) Market Data Bloomberg Code: MEZZAN KK Reuters Code: MEZZ.KW

IP valuation, exploitation and finance

www.pwc.com WIPO WORKSHOP ON EFFECTIVE INTELLECTUAL PROPERTY ASSET MANAGEMENT BY SMEs IP valuation, exploitation and finance Tony Hadjiloucas Partner, Intellectual Property Global Compliance Services,

www.pwc.com WIPO WORKSHOP ON EFFECTIVE INTELLECTUAL PROPERTY ASSET MANAGEMENT BY SMEs IP valuation, exploitation and finance Tony Hadjiloucas Partner, Intellectual Property Global Compliance Services,

Clarity in financial reporting

Deloitte Australia May 2017 A&A Accounting Technical Clarity in financial reporting Focusing on impairment issues for June 2017 Talking Points Why focus on impairment now? What are the hot impairment topics

Deloitte Australia May 2017 A&A Accounting Technical Clarity in financial reporting Focusing on impairment issues for June 2017 Talking Points Why focus on impairment now? What are the hot impairment topics

Global ABV Examination

Accredited in Business Valuation Global ABV Examination content specification outline Effective Aug. 1, 2018 i Valuation Principles Examination This document is nonauthoritative and is included for informational

Accredited in Business Valuation Global ABV Examination content specification outline Effective Aug. 1, 2018 i Valuation Principles Examination This document is nonauthoritative and is included for informational

Comments on exposure draft technical information paper 1: The Discounted Cashflow Method with Property and Business Valuations

29 April 2011 International Valuations Standards Council Moorgate London DC2R 6PP United Kingdom Email: ivsc@ivsc.org Dear Sirs, Comments on exposure draft technical information paper 1: The Discounted

29 April 2011 International Valuations Standards Council Moorgate London DC2R 6PP United Kingdom Email: ivsc@ivsc.org Dear Sirs, Comments on exposure draft technical information paper 1: The Discounted

L AZURDE COMPANY FOR JEWELRY AND ITS SUBSIDIARIES (A SAUDI JOINT STOCK GROUP)

") L AZURDE COMPANY FOR JEWELRY AND ITS SUBSIDIARIES (A SAUDI JOINT STOCK GROUP) REVIEWED INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS AND AUDITORS REPORT FOR THE THREE AND NINE MONTH PERIODS ENDED

L AZURDE COMPANY FOR JEWELRY AND ITS SUBSIDIARIES (A SAUDI JOINT STOCK GROUP) REVIEWED INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS AND AUDITORS REPORT FOR THE THREE AND NINE MONTH PERIODS ENDED

FATCA and CRS compliance Understanding the requirements

FATCA and CRS compliance Understanding the requirements Foreign Account Tax Compliance Act (FATCA) FATCA is a U.S. legislation which aims to combat tax evasion by U.S. persons. The intent behind the law

FATCA and CRS compliance Understanding the requirements Foreign Account Tax Compliance Act (FATCA) FATCA is a U.S. legislation which aims to combat tax evasion by U.S. persons. The intent behind the law

Kuwait Telecommunications Company K.S.C.P. Financial Statements and Independent Auditors Report for the year ended 31 December 2014

Financial Statements and Independent Auditors Report 1 Contents Page Independent auditors report 1-2 Statement of financial position 3 Statement of profit or loss and comprehensive income 4 Statement of

Financial Statements and Independent Auditors Report 1 Contents Page Independent auditors report 1-2 Statement of financial position 3 Statement of profit or loss and comprehensive income 4 Statement of

Changes proposed for income tax accounting. Revised calculation methodology. Montreal Robert Lefrancois

April 2009 IAS Plus Update. Changes proposed for income tax accounting On 31 March 2009, the International Accounting Standards Board (IASB) issued an exposure draft (ED) ED/2009/2 Income Tax containing

April 2009 IAS Plus Update. Changes proposed for income tax accounting On 31 March 2009, the International Accounting Standards Board (IASB) issued an exposure draft (ED) ED/2009/2 Income Tax containing

IFRS 13 Fair Value Measurement. IFRS Advanced Application 2013

IFRS 13 Fair Value Measurement IFRS Advanced Application 2013 Agenda Key considerations Unit of account Principal/most advantageous market Market participants Highest and best use Price Disclosure 2 Definition

IFRS 13 Fair Value Measurement IFRS Advanced Application 2013 Agenda Key considerations Unit of account Principal/most advantageous market Market participants Highest and best use Price Disclosure 2 Definition

Lesson 10 THE MERGERS AND ACQUISITION MARKET. AN OVERVIEW. INTRODUCTION TO COMPANY S VALUE AND VALUATION TECHNIQUES. DCF AND COMPARABLES

Lesson 10 THE MERGERS AND ACQUISITION MARKET. AN OVERVIEW. INTRODUCTION TO COMPANY S VALUE AND VALUATION TECHNIQUES. DCF AND COMPARABLES Internal growth vs. External growth Internal growth investments

Lesson 10 THE MERGERS AND ACQUISITION MARKET. AN OVERVIEW. INTRODUCTION TO COMPANY S VALUE AND VALUATION TECHNIQUES. DCF AND COMPARABLES Internal growth vs. External growth Internal growth investments

MANAGEMENT S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

thescore, Inc. MANAGEMENT S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS For the Three and Nine Months Ended May 31, 2018 and 2017 The following is Management's Discussion and

thescore, Inc. MANAGEMENT S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS For the Three and Nine Months Ended May 31, 2018 and 2017 The following is Management's Discussion and

***************************** SAMPLE PAGES FROM TUTORIAL GUIDE *****************************

DCF Modeling Copyright 2008 by Wall Street Prep, Inc. Table of contents SECTION 1: OVERVIEW DCF in theory and in practice Unlevered vs. levered DCF SECTION 2: MODELING THE DCF Modeling unlevered free cash

DCF Modeling Copyright 2008 by Wall Street Prep, Inc. Table of contents SECTION 1: OVERVIEW DCF in theory and in practice Unlevered vs. levered DCF SECTION 2: MODELING THE DCF Modeling unlevered free cash

Applying IFRS. IFRS 13 Fair Value Measurement. Fair Value Measurement

Applying IFRS IFRS 13 Fair Value Measurement Fair Value Measurement November 2012 Introduction Many IFRS permit or require entities to measure or disclose the fair value of assets, liabilities, or equity

Applying IFRS IFRS 13 Fair Value Measurement Fair Value Measurement November 2012 Introduction Many IFRS permit or require entities to measure or disclose the fair value of assets, liabilities, or equity

- Definition - Qualitative and Quantitative IP Valuation

Basics on Intellectual Property Valuation - Definition - Qualitative and Quantitative IP Valuation Tehran December 11, 2017 Christopher M. Kalanje Counsellor, SMEs and Entrepreneurship Support Division,

Basics on Intellectual Property Valuation - Definition - Qualitative and Quantitative IP Valuation Tehran December 11, 2017 Christopher M. Kalanje Counsellor, SMEs and Entrepreneurship Support Division,

MENA HOTEL FORECASTS. 3-Month Rolling Forecast Highlights Mar May 2015 YoY RevPAR Variance % MENA Hotels March Kuwait City. Sharjah.

MENA Hotels March 2015 MENA HOTEL FORECASTS 3-Month Rolling Forecast Highlights Mar May 2015 YoY RevPAR Variance % Sharjah Lower YoY demand from CIS countries is expected, resulting in stagnant occupancy

MENA Hotels March 2015 MENA HOTEL FORECASTS 3-Month Rolling Forecast Highlights Mar May 2015 YoY RevPAR Variance % Sharjah Lower YoY demand from CIS countries is expected, resulting in stagnant occupancy

MENA HOTEL FORECASTS. 3-Month Rolling Forecast Highlights Apr Jun 2015 YoY RevPAR Variance % MENA Hotels April Aqaba. Makkah.

MENA Hotels April 2015 MENA HOTEL FORECASTS 3-Month Rolling Forecast Highlights Apr Jun 2015 YoY RevPAR Variance % Makkah Next three months to see stable Umrah demand, although with visa restrictions from

MENA Hotels April 2015 MENA HOTEL FORECASTS 3-Month Rolling Forecast Highlights Apr Jun 2015 YoY RevPAR Variance % Makkah Next three months to see stable Umrah demand, although with visa restrictions from

COPYRIGHTED MATERIAL. Index. P1: OTA/XYZ P2: ABC ind JWBT200-Zyla October 16, :16 Printer Name: To Come

Index Accounting firms, 8 Accounting methods acquisition method. See Acquisition method accounting hedge accounting, 32 history of, 4, 60, 61 investment funds, 252 pooling of interests, 4, 60, 85 purchase

Index Accounting firms, 8 Accounting methods acquisition method. See Acquisition method accounting hedge accounting, 32 history of, 4, 60, 61 investment funds, 252 pooling of interests, 4, 60, 85 purchase

COMPANY VALUATION. TOM SEDLACK MPM, RMP, MBA GENERAL MANAGER/OWNER 33 rd COMPANY INC., CRMC

COMPANY VALUATION TOM SEDLACK MPM, RMP, MBA GENERAL MANAGER/OWNER 33 rd COMPANY INC., CRMC 2018, 33 rd Company, Inc. ACADEMIC MATERIALS POLICY NON-RETRIBUTION / NON-RETALIATION DISCLAIMER The information

COMPANY VALUATION TOM SEDLACK MPM, RMP, MBA GENERAL MANAGER/OWNER 33 rd COMPANY INC., CRMC 2018, 33 rd Company, Inc. ACADEMIC MATERIALS POLICY NON-RETRIBUTION / NON-RETALIATION DISCLAIMER The information

MENA Hotels September 2015 Amman Fujairah Aqaba Cairo Riyadh Ras Al Khaimah

MENA Hotels September 2015 MENA HOTEL FORECASTS 3-Month Rolling Forecast Highlights Sep Nov 2015 YoY RevPAR Variance % Fujairah Drop in business from traditional market like Russia and Europe, however

MENA Hotels September 2015 MENA HOTEL FORECASTS 3-Month Rolling Forecast Highlights Sep Nov 2015 YoY RevPAR Variance % Fujairah Drop in business from traditional market like Russia and Europe, however

IPO NOTE AL MAHA CERAMICS SAOG (under transformation)

") INVESTMENT RESEARCH IPO NOTE AL MAHA CERAMICS SAOG (under transformation) Offer Closes: October 15, 2014 Offer Price: Bzs 397 per share Fair Value: Bzs 576 per share AL MAHA CERAMICS SAOG (under transformation)

INVESTMENT RESEARCH IPO NOTE AL MAHA CERAMICS SAOG (under transformation) Offer Closes: October 15, 2014 Offer Price: Bzs 397 per share Fair Value: Bzs 576 per share AL MAHA CERAMICS SAOG (under transformation)

VAT in GCC Am I ready for VAT?

VAT in GCC Am I ready for VAT? #VATwithIMC Author or Company YOUR LOGO 1 What is VAT? Value Added Tax (VAT) is an indirect tax levied on consumption. It is imposed on sale of goods and services excluding

VAT in GCC Am I ready for VAT? #VATwithIMC Author or Company YOUR LOGO 1 What is VAT? Value Added Tax (VAT) is an indirect tax levied on consumption. It is imposed on sale of goods and services excluding

Original SSAP: SSAP No. 100; Current Authoritative Guidance: SSAP No. 100R

Statutory Issue Paper No. 157 Use of Net Asset Value STATUS Finalized November 6, 2017 Original SSAP: SSAP No. 100; Current Authoritative Guidance: SSAP No. 100R Type of Issue: Common Area SUMMARY OF ISSUE

Statutory Issue Paper No. 157 Use of Net Asset Value STATUS Finalized November 6, 2017 Original SSAP: SSAP No. 100; Current Authoritative Guidance: SSAP No. 100R Type of Issue: Common Area SUMMARY OF ISSUE

GCC EQUITY REPORT NEUTRAL RESEARCH. Almarai Company (2280.SE) Quarterly Update. CMP SAR Target SAR Potential Upside 8.

Quarterly Update. CMP SAR Target SAR Potential Upside 8.") l RESEARCH GCC EQUITY REPORT Almarai Company (2280.SE) NEUTRAL CMP SAR 106.50 Target SAR 115.00 Potential Upside 8.0% MSCI GCC Index 425.24 Tadawul All Share Index 6,697.80 Key Stock Data Sector Dairy

l RESEARCH GCC EQUITY REPORT Almarai Company (2280.SE) NEUTRAL CMP SAR 106.50 Target SAR 115.00 Potential Upside 8.0% MSCI GCC Index 425.24 Tadawul All Share Index 6,697.80 Key Stock Data Sector Dairy

An Introduction to Business Valuation. By Garth M. Tebay, CPA, CVA, CM&AA

An Introduction to Business Valuation By Garth M. Tebay, CPA, CVA, CM&AA Welcome to the challenging world of business valuation. The key to success in this arena is knowledge. When valuing a closely held

An Introduction to Business Valuation By Garth M. Tebay, CPA, CVA, CM&AA Welcome to the challenging world of business valuation. The key to success in this arena is knowledge. When valuing a closely held

Understanding and Increasing Business Value

--Working ON your Business, not just IN your Business-- Understanding and Increasing Business Value American Cheese Society July 30, 2016 TODAY S AGENDA What really matters in business valuation? Is your

--Working ON your Business, not just IN your Business-- Understanding and Increasing Business Value American Cheese Society July 30, 2016 TODAY S AGENDA What really matters in business valuation? Is your

FAIR VALUE & TRANSFER PRICING: And the twain shall never meet? Transfer Pricing Panel ABA Fall Conf., Denver Oct. 21, 2011

FAIR VALUE & TRANSFER PRICING: And the twain shall never meet? Transfer Pricing Panel ABA Fall Conf., Denver Oct. 21, 2011 Introduction Fair Value & Transfer Pricing Panel: David Ernick, Treasury Jason

FAIR VALUE & TRANSFER PRICING: And the twain shall never meet? Transfer Pricing Panel ABA Fall Conf., Denver Oct. 21, 2011 Introduction Fair Value & Transfer Pricing Panel: David Ernick, Treasury Jason

EMAAR THE ECONOMIC CITY (A SAUDI JOINT STOCK COMPANY) UNAUDITED INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

UNAUDITED INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS") EMAAR THE ECONOMIC CITY (A SAUDI JOINT STOCK COMPANY) UNAUDITED INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS FOR THE NINE-MONTH PERIOD ENDED 30 SEPTEMBER 2017 UNAUDITED INTERIM CONDENSED CONSOLIDATED

EMAAR THE ECONOMIC CITY (A SAUDI JOINT STOCK COMPANY) UNAUDITED INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS FOR THE NINE-MONTH PERIOD ENDED 30 SEPTEMBER 2017 UNAUDITED INTERIM CONDENSED CONSOLIDATED

Financial & Valuation Modeling Boot Camp

TARGET AUDIENCE Overview 3-day intensive training program where trainees learn financial & valuation modeling in Excel using in a hands-on, case-study approach. The modeling methodologies covered include:

TARGET AUDIENCE Overview 3-day intensive training program where trainees learn financial & valuation modeling in Excel using in a hands-on, case-study approach. The modeling methodologies covered include: