Chapter 3. National Income: Where it Comes from and Where it Goes

|

|

|

- Sylvia Little

- 5 years ago

- Views:

Transcription

1 ECONOMY IN THE LONG RUN Chapter 3 National Income: Where it Comes from and Where it Goes 1

2 QUESTIONS ABOUT THE SOURCES AND USES OF GDP Here we develop a static classical model of the macroeconomy: prices are fully flexible and adjust to ensure the full use of all resources. The model explains : Determinants of the level of production/income labour, capital, and (technology & land) o Aggregate supply Who gets the income from production? o Distribution of income Who buys the output of the economy? - allocation of output consumption, investment; o Aggregate demand Equilibrium in the economy 2

3 3

4 1. Determinants of the total Production of Goods and Services Factors of Production (FOP) Capital (K): an aggregate measure of the stock of all machinery, buildings, equipment available for production. Labour (L): an aggregate of all available labour. Hours worked. Both variables are exogenous/fixed in this model: Full utilization of resources 4

5 Production Function Shows how much output can be produced using the available technology and the inputs: Example: If Constant returns to scale (CRS) is a property of some production functions 5

6 Constant Returns to Scale (CRS) If all inputs are increased by a constant proportion then output increases by a constant proportion. Mathematically: where z is the constant of proportionality. Consider the previous example: Since K and L are assumed exogenous, the supply of output is determined as, This is the long run or natural rate of output. 6

7 2. Distribution of Income Given output (Y), how the income from production is distributed? We assume competitive markets for the two factors: Labour and Capital. Factor prices wages and rent are determined by the equilibrium in factor markets 7

8 Figure: Factor Price Determination Vertical Supply function indicates inputs are either fixed or used fully (classical view) 8

9 The firm s demand for factors Firm s goal is to maximize profit Choose K and L given P Output: Costs: labour costs and capital costs Where, R is the rental rate per unit of capital per period, and W is the wage rate per unit of labour per period 9

10 Determining firm s demand for inputs Define the marginal product (MP) MP is the slope of the production function Marginal product of labour: Marginal product of capital: 10

11 Figure: Production Function 11

12 Diminishing Marginal Product How does the firm decide whether to hire an additional worker? The firm will hire an additional worker if the extra revenue generated by that worker exceeds the cost of hiring the worker Value of Marginal Product of Labour is equal to the nominal wage: VMP L = W 12

13 To maximize profits, firms choose L and K so that marginal profit is equal to zero Marginal product of labour (MPL) = real wage Marginal product of capital (MPK) = real rent 13

14 Figure: Labour demand (MPL), labour supply and real wage 14

15 Who Gets What and How Much? Total Labour income: Total Capital income: How about the firm? economic profit Income that remains after paying for factors of production (i.e., labour and capital) Economic profit = 15

16 Economic Profit Under CRS production function Economic Profit is Zero The same conclusion drawn from competitive market assumption or 16

17 If the production function has constant returns to scale, then Labour s share to the real Income: Capital s share to the real income: For Canada, labour s share to real income is 0.67 (i.e. 2/3) in the post war period and Capital s share is 0.33 (i.e., 1/3). Empirically, these shares have been stable. 17

18 Example: what functional form of production produces constant factor shares if factors earn their marginal product? That is, if the following is true What does look like? The Cobb-Douglas production function Note that this function satisfies constant returns to scale. So all output will be exhausted. 18

19 Calculating marginal products For labour: For Capital: For Canadian economy, where, (Cobb-Douglus) is:, the production function 19

20 3. Demand for Goods and Services Allocation of Output Final production is allocated across four components, or sources of demand: Y = C + I + G + NX C = consumer demand for g & s I = demand for investment goods G = government demand for g & s For now, assume the economy is closed; no exports or imports. This simplifies the model (and gets included later). 20

21 We want to describe the determinants of consumption, investment and government spending Consumption Expenditure (C) Assume that aggregate consumption is a function of only of disposable income (Y D = Y-T): - consumption function Shows that (Y T ) C For example, Where,, and 21

22 The Marginal Propensity to consume (MPC): The MPC is assumed to be less than one; for every dollar increase in the disposable income, a fraction is consumed (MPC) and a fraction is saved As such, 22

23 Figure: Consumption function and MPC How does the Saving function look like? 23

24 Investment (I) Firms and households both purchase investment goods (buildings, machinery, housing). Note that we do not keep track of changes in the stock of capital at this stage; it is taken as given. Here investment s role is only as an expenditure component. The purpose of investment expenditure is to earn a return in the future. For investment to be profitable, the return must exceed the cost where both return and cost are measured in real terms. 24

25 The investment function: I = I(r) r is the real interest rate (not the nominal interest rate); which includes compensation for inflation. The real interest rate (r) is the cost of borrowing the opportunity cost of using one s own funds to finance investment spending. For the aggregate economy, as the real interest rate falls more investment expenditure becomes profitable. Figure?? So, I r 25

26 Government Purchases (G) Government purchases (of consumption and investment goods) are denoted by G; government tax revenue (in real terms) is denoted by T. Both G and T are assumed exogenous; Useful definitions: If T > G, budget surplus = (T G ) = Positive public saving. If T < G, budget deficit = (G T ) = Negative public saving If T = G, balanced budget, public saving = 0. 26

27 4. Equilibrium in the Economy We have described the Aggregate Demand, AD, side of our model; the Aggregate Supply, AS, side of our model; and the distribution of income. Bringing these together determines the equilibrium of our economy. Our complete model of the economy is: 27

28 Substituting various behavioural functions, we get The real interest rate (r) must adjust to ensure that this condition is met. This can be motivated most easily as equilibrium in the market for loanable funds. 28

29 The loanable funds market A simple supply-demand model of the financial system One asset: loanable funds o demand for funds: Investment o supply of funds: Saving o price of funds: real interest rate is the supply of loanable funds what the economy is willing to forgo in current consumption. I(r) is the demand for loanable funds (based upon available investment projects). 29

30 If r is too low, then the demand for loanable funds exceeds the supply, the real interest rate gets bid upwards. If r is too high, then there is excess supply of loanable funds and the real interest rate gets bid downwards. Define national savings as: From our equilibrium condition, 30

31 Figure: Equilibrium in the market for loanable funds Note that this simple equilibrium for loanable funds critically assumes a closed economy. 31

32 Special Role of r r adjusts to equilibrate the goods market and the loanable funds market simultaneously: If Lonable funds market is in equilibrium, then Thus, 32

33 EXERCISE: Calculate the change in saving Suppose MPC = 0.8 and MPL = 20. For each of the following, compute S : a. G = 100 b. T = 100 c. Y = 100 d. L = 10 33

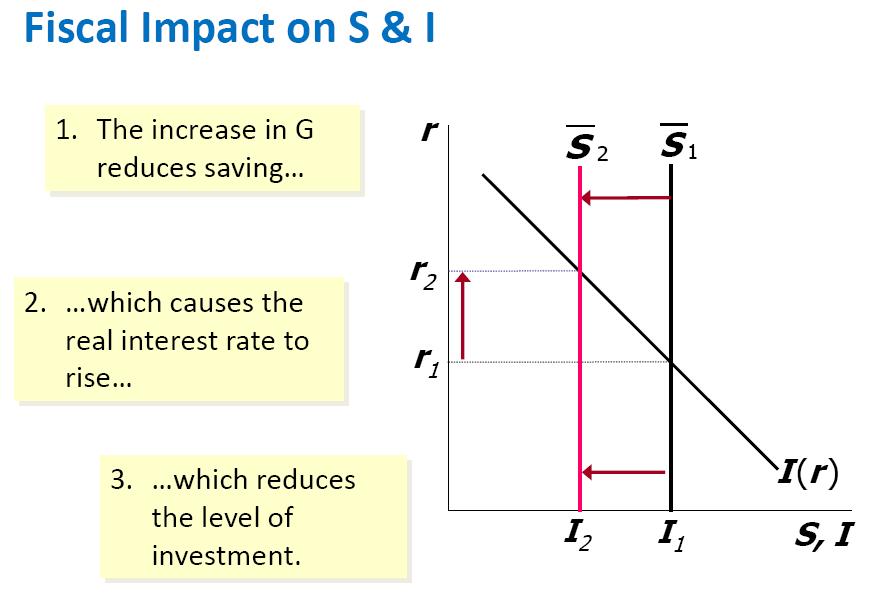

34 Loanable Funds Market Equilibrium The Effects of Fiscal Policy Fiscal policy refers to taxes (T) and government spending (G). In our model, these two variables are exogenous variables; so it is legitimate to ask what happens to the endogenous variables when one or both of these changes. Question we can ask what are the effects of an increase in government spending, holding taxes constant? 34

35 Recall the definition of national savings and its components: Clearly, an increase in G holding T constant lowers public saving (the government has increased its deficit or reduced its surplus). 35

36 36

37 37

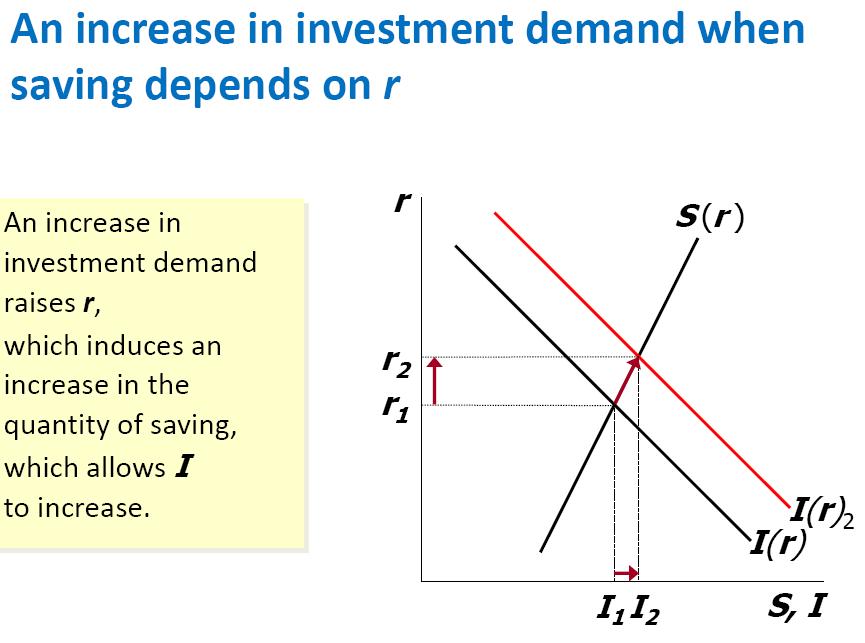

38 An increase in investment demand when saving depends on r Why might saving depend on r? How would the results of an increase in investment demand be different? Would r rise as much? Would the equilibrium value of I change? 38

39 39

40 Chapter 3 At a Glance Total output is determined by the economy s quantities of capital and labour the level of technology Competitive firms hire each factor until its marginal product equals its price. If the production function has CRS property, then labour income plus capital income equals total income (output). A closed economy s output is used for Consumption, investment, government spending 40

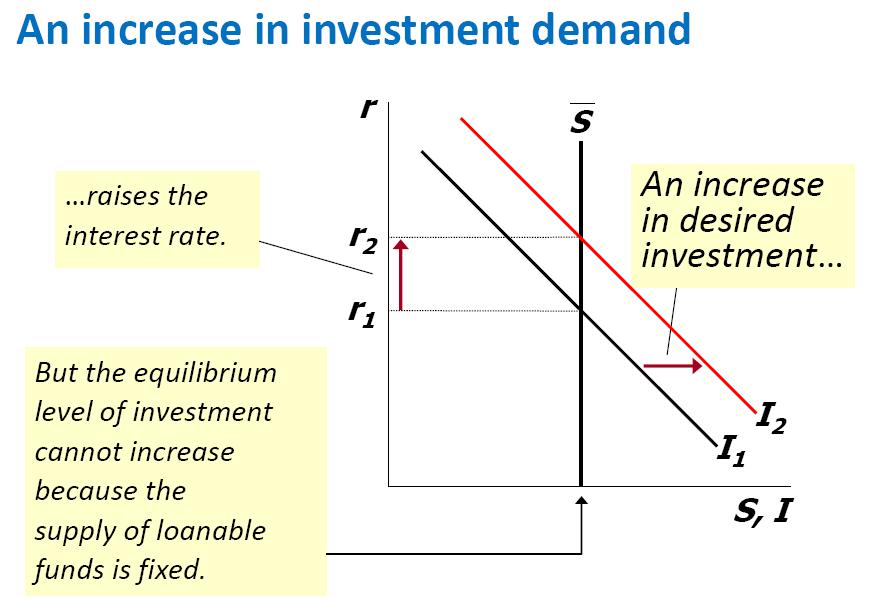

41 The real interest rate adjusts to equate the demand for and supply of goods and services loanable funds A decrease in national saving causes the interest rate to rise and investment to fall. An increase in investment demand causes the interest rate to rise, but does not affect the equilibrium level of investment if the supply of loanable funds is fixed. 41

9/10/2017. National Income: Where it Comes From and Where it Goes (in the long-run) Introduction. The Neoclassical model

Introduction. The Neoclassical model") Chapter 3 - The Long-run Model National Income: Where it Comes From and Where it Goes (in the long-run) Introduction In chapter 2 we defined and measured some key macroeconomic variables. Now we start

Chapter 3 - The Long-run Model National Income: Where it Comes From and Where it Goes (in the long-run) Introduction In chapter 2 we defined and measured some key macroeconomic variables. Now we start

ECON 3010 Intermediate Macroeconomics. Chapter 3 National Income: Where It Comes From and Where It Goes

ECON 3010 Intermediate Macroeconomics Chapter 3 National Income: Where It Comes From and Where It Goes Outline of model A closed economy, market-clearing model Supply side factors of production determination

ECON 3010 Intermediate Macroeconomics Chapter 3 National Income: Where It Comes From and Where It Goes Outline of model A closed economy, market-clearing model Supply side factors of production determination

In this chapter, you will learn C H A P T E R National Income: Where it Comes From and Where it Goes CHAPTER 3

C H A P T E R 3 National Income: Where it Comes From and Where it Goes MACROECONOMICS N. GREGORY MANKIW 007 Worth Publishers, all rights reserved SIXTH EDITION PowerPoint Slides by Ron Cronovich In this

C H A P T E R 3 National Income: Where it Comes From and Where it Goes MACROECONOMICS N. GREGORY MANKIW 007 Worth Publishers, all rights reserved SIXTH EDITION PowerPoint Slides by Ron Cronovich In this

Chapter 3 National Income: Where It Comes From And Where It Goes

Chapter 3 National Income: Where It Comes From And Where It Goes 0 1 1 2 The Neo-Classical Model Goal: to explain the more realistic circular flow Supply Side (firms): how total output(=income; GDP) is

Chapter 3 National Income: Where It Comes From And Where It Goes 0 1 1 2 The Neo-Classical Model Goal: to explain the more realistic circular flow Supply Side (firms): how total output(=income; GDP) is

PART II CLASSICAL THEORY. Chapter 3: National Income: Where it Comes From and Where it Goes 1/64

PART II CLASSICAL THEORY Chapter 3: National Income: Where it Comes From and Where it Goes 1/64 Chapter 3: National Income: Where it Comes From and Where it Goes 2/64 * Slides based on Ron Cronovich's

PART II CLASSICAL THEORY Chapter 3: National Income: Where it Comes From and Where it Goes 1/64 Chapter 3: National Income: Where it Comes From and Where it Goes 2/64 * Slides based on Ron Cronovich's

PART II CLASSICAL THEORY. Chapter 3: National Income: Where it Comes From and Where it Goes 1/51

PART II CLASSICAL THEORY Chapter 3: National Income: Where it Comes From and Where it Goes 1/51 Chapter 3: National Income: Where it Comes From and Where it Goes 2/51 *Slides based on Ron Cronovich's slides,

PART II CLASSICAL THEORY Chapter 3: National Income: Where it Comes From and Where it Goes 1/51 Chapter 3: National Income: Where it Comes From and Where it Goes 2/51 *Slides based on Ron Cronovich's slides,

Macroeconomcs. Factors of production. Outline of model. In this chapter you will learn:

In this chapter you will learn: Macroeconomcs Professor Hisahiro Naito what determines the economy s total output/income how the prices of the factors of production are determined how total income is distributed

In this chapter you will learn: Macroeconomcs Professor Hisahiro Naito what determines the economy s total output/income how the prices of the factors of production are determined how total income is distributed

IN THIS LECTURE, YOU WILL LEARN:

IN THIS LECTURE, YOU WILL LEARN: Am simple perfect competition production medium-run model view of what determines the economy s total output/income how the prices of the factors of production are determined

IN THIS LECTURE, YOU WILL LEARN: Am simple perfect competition production medium-run model view of what determines the economy s total output/income how the prices of the factors of production are determined

Learning Objectives. 1. Describe how the government budget surplus is related to national income.

Learning Objectives 1of 28 1. Describe how the government budget surplus is related to national income. 2. Explain how net exports are related to national income. 3. Distinguish between the marginal propensity

Learning Objectives 1of 28 1. Describe how the government budget surplus is related to national income. 2. Explain how net exports are related to national income. 3. Distinguish between the marginal propensity

ECON Intermediate Macroeconomic Theory

ECON 3510 - Intermediate Macroeconomic Theory Fall 2015 Mankiw, Macroeconomics, 8th ed., Chapter 3 Chapter 3: A Theory of National Income Key points: Understand the aggregate production function Understand

ECON 3510 - Intermediate Macroeconomic Theory Fall 2015 Mankiw, Macroeconomics, 8th ed., Chapter 3 Chapter 3: A Theory of National Income Key points: Understand the aggregate production function Understand

Road-Map to this Lecture

Allocation 1 Road-Map to this Lecture 1. Consumption 2. Investment 3. Government Expenditures 4. Equilibrium: equilibrium in financial markets 5. Fiscal Policy I slide 1 2 Demand for goods & services Components

Allocation 1 Road-Map to this Lecture 1. Consumption 2. Investment 3. Government Expenditures 4. Equilibrium: equilibrium in financial markets 5. Fiscal Policy I slide 1 2 Demand for goods & services Components

Outline of model. The supply side The production function Y = F (K, L) A closed economy, market-clearing model

A closed economy, market-clearing model") CHAPTER THREE National Income: Where it Comes From and Where it Goes what what determines the the economy s total total output/income how how the the prices prices of of the the factors factors of of production

CHAPTER THREE National Income: Where it Comes From and Where it Goes what what determines the the economy s total total output/income how how the the prices prices of of the the factors factors of of production

CHAPTER 3 National Income: Where It Comes From and Where It Goes

CHAPTER 3 National Income: Where It Comes From and Where It Goes A PowerPoint Tutorial To Accompany MACROECONOMICS, 7th. Edition N. Gregory Mankiw Tutorial written by: Mannig J. Simidian B.A. in Economics

CHAPTER 3 National Income: Where It Comes From and Where It Goes A PowerPoint Tutorial To Accompany MACROECONOMICS, 7th. Edition N. Gregory Mankiw Tutorial written by: Mannig J. Simidian B.A. in Economics

Lecture 3: National Income: Where it comes from and where it goes

Class Notes Intermediate Macroeconomics Li Gan Lecture 3: National Income: Where it comes from and where it goes Production Function: Y = F(K, L) = K α L 1-α Returns to scale: Constant Return to Scale:

Class Notes Intermediate Macroeconomics Li Gan Lecture 3: National Income: Where it comes from and where it goes Production Function: Y = F(K, L) = K α L 1-α Returns to scale: Constant Return to Scale:

3 General equilibrium model of national income

OVS452 + 5EN 253 VSE NF, Spring 2010 Lecture Notes #2 Eva Hromádková 3 General equilibrium model of national income 3.1 Concept of equilibrium - Clasic model General concept = steady-state (i.e. state

OVS452 + 5EN 253 VSE NF, Spring 2010 Lecture Notes #2 Eva Hromádková 3 General equilibrium model of national income 3.1 Concept of equilibrium - Clasic model General concept = steady-state (i.e. state

Econ 100B: Macroeconomic Analysis Fall 2008

Econ 100B: Macroeconomic Analysis Fall 2008 Problem Set #7 ANSWERS (Due September 24-25, 2008) A. Small Open Economy Saving-Investment Model: 1. Clearly and accurately draw and label a diagram of the Small

Econ 100B: Macroeconomic Analysis Fall 2008 Problem Set #7 ANSWERS (Due September 24-25, 2008) A. Small Open Economy Saving-Investment Model: 1. Clearly and accurately draw and label a diagram of the Small

Homework Assignment #6. Due Tuesday, 11/28/06. Multiple Choice Questions:

Homework Assignment #6. Due Tuesday, 11/28/06 Multiple Choice Questions: 1. When the inflation rate is expected to be zero, Steve plans to lend money if the interest rate is at least 4 percent a year and

Homework Assignment #6. Due Tuesday, 11/28/06 Multiple Choice Questions: 1. When the inflation rate is expected to be zero, Steve plans to lend money if the interest rate is at least 4 percent a year and

Econ 223 Lecture notes 2: Determination of output and income Classical closed economy equilibrium

Econ 223 Lecture notes 2: Determination of output and income Classical closed economy equilibrium Kevin Clinton Winter 2005 The classical model assumes that prices and wages etc. are fully flexible. Output

Econ 223 Lecture notes 2: Determination of output and income Classical closed economy equilibrium Kevin Clinton Winter 2005 The classical model assumes that prices and wages etc. are fully flexible. Output

ECO 2013: Macroeconomics Valencia Community College

ECO 2013: Macroeconomics Valencia Community College Exam 3 Fall 2008 1. The most important determinant of consumer spending is: A. the level of household debt. B. consumer expectations. C. the stock of

ECO 2013: Macroeconomics Valencia Community College Exam 3 Fall 2008 1. The most important determinant of consumer spending is: A. the level of household debt. B. consumer expectations. C. the stock of

Class 2: The determinants of National Income. Long Run

Class 2: The determinants of National Income. Long Run 1. Aggregate economic profit ( π ) is defined as follows: π = Y [ ( W / P)* L] [( R/ P)* K] Show that if the production function of this economy displays

Class 2: The determinants of National Income. Long Run 1. Aggregate economic profit ( π ) is defined as follows: π = Y [ ( W / P)* L] [( R/ P)* K] Show that if the production function of this economy displays

Chapter 22. Adding Government and Trade to the Simple Macro Model. In this chapter you will learn to. Introducing Government. Government Purchases

Chapter 22 Adding Government and Trade to the Simple Macro Model In this chapter you will learn to 1. Describe the relationship between national income and government purchases and tax revenues. 2. Describe

Chapter 22 Adding Government and Trade to the Simple Macro Model In this chapter you will learn to 1. Describe the relationship between national income and government purchases and tax revenues. 2. Describe

Econ 522: Intermediate Macroeconomics, Spring 2018 Chapter 3 Practice Problem Set - Solutions

Econ 522: Intermediate Macroeconomics, Spring 2018 Chapter 3 Practice Problem Set - Solutions 1. Explain what determines the amount of output an economy produces? The factors of production and the available

Econ 522: Intermediate Macroeconomics, Spring 2018 Chapter 3 Practice Problem Set - Solutions 1. Explain what determines the amount of output an economy produces? The factors of production and the available

Examination Period 3: 2016/17

Examination Period 3: 2016/17 ECN201217N Module Title Level Time Allowed Intermediate Macroeconomics Five Two hours Instructions to students: Enter your student number not your name on all answer books.

Examination Period 3: 2016/17 ECN201217N Module Title Level Time Allowed Intermediate Macroeconomics Five Two hours Instructions to students: Enter your student number not your name on all answer books.

EC 205 Macroeconomics I Fall Problem Session 2 Solutions. Q1. Use the neoclassical theory of distribution to predict the impact on the real wage

Department of Economics Boğaziçi University EC 205 Macroeconomics I Fall 2015 Problem Session 2 Solutions Q1. Use the neoclassical theory of distribution to predict the impact on the real wage and the

Department of Economics Boğaziçi University EC 205 Macroeconomics I Fall 2015 Problem Session 2 Solutions Q1. Use the neoclassical theory of distribution to predict the impact on the real wage and the

Chapter 11 1/19/2018. Basic Keynesian Model Expenditure and Tax Multipliers

Chapter 11 Basic Keynesian Model Expenditure and Tax Multipliers This chapter presents the basic Keynesian model and explains: how aggregate expenditure (C,I,G,X and M) is determined when the price level

Chapter 11 Basic Keynesian Model Expenditure and Tax Multipliers This chapter presents the basic Keynesian model and explains: how aggregate expenditure (C,I,G,X and M) is determined when the price level

Part 1: Short answer, 60 points possible Part 2: Analytical problems, 40 points possible

Midterm #1 ECON 322, Prof. DeBacker September 25, 2018 INSTRUCTIONS: Please read each question below carefully and respond to the questions in the space provided (use the back of pages if necessary). You

Midterm #1 ECON 322, Prof. DeBacker September 25, 2018 INSTRUCTIONS: Please read each question below carefully and respond to the questions in the space provided (use the back of pages if necessary). You

Homework Assignment #6. Due Tuesday, 11/28/06. Multiple Choice Questions:

Homework Assignment #6. Due Tuesday, 11/28/06 Multiple Choice Questions: 1. When the inflation rate is expected to be zero, Steve plans to lend money if the interest rate is at least 4 percent a year and

Homework Assignment #6. Due Tuesday, 11/28/06 Multiple Choice Questions: 1. When the inflation rate is expected to be zero, Steve plans to lend money if the interest rate is at least 4 percent a year and

Lecture notes: 101/105 (revised 9/27/00) Lecture 3: national Income: Production, Distribution and Allocation (chapter 3)

Lecture 3: national Income: Production, Distribution and Allocation (chapter 3)") Lecture notes: 101/105 (revised 9/27/00) Lecture 3: national Income: Production, Distribution and Allocation (chapter 3) 1) Intro Have given definitions of some key macroeconomic variables. Now start building

Lecture notes: 101/105 (revised 9/27/00) Lecture 3: national Income: Production, Distribution and Allocation (chapter 3) 1) Intro Have given definitions of some key macroeconomic variables. Now start building

Aggregate Demand. Sherif Khalifa. Sherif Khalifa () Aggregate Demand 1 / 35

Aggregate Demand 1 / 35") Sherif Khalifa Sherif Khalifa () Aggregate Demand 1 / 35 The ISLM model allows us to build the AD curve. IS stands for investment and saving. The IS curve represents what is happening in the market for

Sherif Khalifa Sherif Khalifa () Aggregate Demand 1 / 35 The ISLM model allows us to build the AD curve. IS stands for investment and saving. The IS curve represents what is happening in the market for

Aggregate Demand. Sherif Khalifa. Sherif Khalifa () Aggregate Demand 1 / 36

Aggregate Demand 1 / 36") Sherif Khalifa Sherif Khalifa () Aggregate Demand 1 / 36 The ISLM model allows us to build the Aggregate Demand curve. IS stands for investment and saving. The IS curve represents what is happening in

Sherif Khalifa Sherif Khalifa () Aggregate Demand 1 / 36 The ISLM model allows us to build the Aggregate Demand curve. IS stands for investment and saving. The IS curve represents what is happening in

a) We can calculate Private and Public savings as well as investment as a share of GDP using (1):

We can calculate Private and Public savings as well as investment as a share of GDP using (1):") Q1 (8 marks) a) We can calculate Private and Public savings as well as investment as a share of GDP using (1): Public saving = (Gross saving, corporate + Gross saving, private)/gdp Investment = Investment/GDP

Q1 (8 marks) a) We can calculate Private and Public savings as well as investment as a share of GDP using (1): Public saving = (Gross saving, corporate + Gross saving, private)/gdp Investment = Investment/GDP

National Income Savings and Investment

National Income Savings and Investment 1 Circular Flow of Income In a VERY simple economy Labor is a factor input used to produce goods Labor receives income of wages Wages then exchanged for goods Wages/Goods

National Income Savings and Investment 1 Circular Flow of Income In a VERY simple economy Labor is a factor input used to produce goods Labor receives income of wages Wages then exchanged for goods Wages/Goods

Chapter 10 Aggregate Demand I CHAPTER 10 0

Chapter 10 Aggregate Demand I CHAPTER 10 0 1 CHAPTER 10 1 2 Learning Objectives Chapter 9 introduced the model of aggregate demand and aggregate supply. Long run (Classical Theory) prices flexible output

Chapter 10 Aggregate Demand I CHAPTER 10 0 1 CHAPTER 10 1 2 Learning Objectives Chapter 9 introduced the model of aggregate demand and aggregate supply. Long run (Classical Theory) prices flexible output

Aggregate Supply and Aggregate Demand

Aggregate Supply and Aggregate Demand Econ 120: Global Macroeconomics 1 1.1 Goals Goals Specific Goals Define the expenditure multiplier and how to compute it. Explain how recessions and expansions can

Aggregate Supply and Aggregate Demand Econ 120: Global Macroeconomics 1 1.1 Goals Goals Specific Goals Define the expenditure multiplier and how to compute it. Explain how recessions and expansions can

! Continued. Demand for labor. ! The firm tries to maximize its profits:

Chapter 3: National Income: Where it Comes From and Where it Goes! Continued slide 0 Demand for labor! The firm tries to maximize its profits: Profit = Total Revenue Total Cost = P.Y W.L R.K Profit=P.

Chapter 3: National Income: Where it Comes From and Where it Goes! Continued slide 0 Demand for labor! The firm tries to maximize its profits: Profit = Total Revenue Total Cost = P.Y W.L R.K Profit=P.

Professor Christina Romer SUGGESTED ANSWERS TO PROBLEM SET 5

Economics 2 Spring 2017 Professor Christina Romer Professor David Romer SUGGESTED ANSWERS TO PROBLEM SET 5 1. The tool we use to analyze the determination of the normal real interest rate and normal investment

Economics 2 Spring 2017 Professor Christina Romer Professor David Romer SUGGESTED ANSWERS TO PROBLEM SET 5 1. The tool we use to analyze the determination of the normal real interest rate and normal investment

University of Toronto January 25, 2007 ECO 209Y MACROECONOMIC THEORY. Term Test #2 L0101 L0201 L0401 L5101 MW MW 1-2 MW 2-3 W 6-8

Department of Economics Prof. Gustavo Indart University of Toronto January 25, 2007 SOLUTION ECO 209Y MACROECONOMIC THEORY Term Test #2 LAST NAME FIRST NAME STUDENT NUMBER Circle your section of the course:

Department of Economics Prof. Gustavo Indart University of Toronto January 25, 2007 SOLUTION ECO 209Y MACROECONOMIC THEORY Term Test #2 LAST NAME FIRST NAME STUDENT NUMBER Circle your section of the course:

Final Term Papers. Fall 2009 (Session 03a) ECO401. (Group is not responsible for any solved content) Subscribe to VU SMS Alert Service

ECO401. (Group is not responsible for any solved content) Subscribe to VU SMS Alert Service") Fall 2009 (Session 03a) ECO401 (Group is not responsible for any solved content) Subscribe to VU SMS Alert Service To Join Simply send following detail to bilal.zaheem@gmail.com Full Name Master Program

Fall 2009 (Session 03a) ECO401 (Group is not responsible for any solved content) Subscribe to VU SMS Alert Service To Join Simply send following detail to bilal.zaheem@gmail.com Full Name Master Program

Econ 522: Intermediate Macroeconomics, Fall 2017 Chapter 3 Classical Model Practice Problems

Econ 522: Intermediate Macroeconomics, Fall 2017 Chapter 3 Classical Model Practice Problems 1. Explain what determines the amount of output an economy produces? The factors of production and the available

Econ 522: Intermediate Macroeconomics, Fall 2017 Chapter 3 Classical Model Practice Problems 1. Explain what determines the amount of output an economy produces? The factors of production and the available

ECO 301 MACROECONOMIC THEORY UNIVERSITY OF MIAMI DEPARTMENT OF ECONOMICS FALL 2008 Instructor: Dr. S. Nuray Akin MIDTERM EXAM I

ECO 301 MACROECONOMIC THEORY UNIVERSITY OF MIAMI DEPARTMENT OF ECONOMICS FALL 2008 Instructor: Dr. S. Nuray Akin MIDTERM EXAM I Name: Section: Instructions: This exam consists of 6 pages; please check

ECO 301 MACROECONOMIC THEORY UNIVERSITY OF MIAMI DEPARTMENT OF ECONOMICS FALL 2008 Instructor: Dr. S. Nuray Akin MIDTERM EXAM I Name: Section: Instructions: This exam consists of 6 pages; please check

Monetary Macroeconomics Lecture 3. Mark Hayes

Diploma Macro Paper 2 Monetary Macroeconomics Lecture 3 Aggregate demand: Investment and the IS-LM model Mark Hayes slide 1 Outline Introduction Map of the AD-AS model This lecture, continue explaining

Diploma Macro Paper 2 Monetary Macroeconomics Lecture 3 Aggregate demand: Investment and the IS-LM model Mark Hayes slide 1 Outline Introduction Map of the AD-AS model This lecture, continue explaining

CHAPTER 23 OUTPUT AND PRICES IN THE SHORT RUN

CHAPTER 23 OUTPUT AND PRICES IN THE SHORT RUN Expand model to make price level endogenous variable. LEARNING OBJECTIVES - Why exogenous change in price level shifts AE curve and changes equilibrium level

CHAPTER 23 OUTPUT AND PRICES IN THE SHORT RUN Expand model to make price level endogenous variable. LEARNING OBJECTIVES - Why exogenous change in price level shifts AE curve and changes equilibrium level

Where does stuff come from?

Where does stuff come from? Factors of production Technology Factors of production: Thanks, Marx! The stuff we use to make other stuff Factors of production: Thanks, Marx! The stuff we use to make other

Where does stuff come from? Factors of production Technology Factors of production: Thanks, Marx! The stuff we use to make other stuff Factors of production: Thanks, Marx! The stuff we use to make other

Part2 Multiple Choice Practice Qs

Part2 Multiple Choice Practice Qs 1. The Keynesian cross shows: A) determination of equilibrium income and the interest rate in the short run. B) determination of equilibrium income and the interest rate

Part2 Multiple Choice Practice Qs 1. The Keynesian cross shows: A) determination of equilibrium income and the interest rate in the short run. B) determination of equilibrium income and the interest rate

45 Line -The height of this measures disposable income

Fixed Prices and Expenditure Plans -In the Keynesian model, all firms are like the grocery store: They set their prices and sell the quantities their customers are willing to buy -If they persistently

Fixed Prices and Expenditure Plans -In the Keynesian model, all firms are like the grocery store: They set their prices and sell the quantities their customers are willing to buy -If they persistently

DEPARTMENT OF ECONOMICS, UNIVERSITY OF VICTORIA

DEPARTMENT OF ECONOMICS, UNIVERSITY OF VICTORIA Midterm Exam I (October 09, 2012) ECON204 (A01), Fall 2012 Name (Last, First): UVIC ID#: Signature: THIS EXAM HAS TOTAL 7 PAGES INCLUDING THE COVER PAGE

DEPARTMENT OF ECONOMICS, UNIVERSITY OF VICTORIA Midterm Exam I (October 09, 2012) ECON204 (A01), Fall 2012 Name (Last, First): UVIC ID#: Signature: THIS EXAM HAS TOTAL 7 PAGES INCLUDING THE COVER PAGE

14.02 Principles of Macroeconomics Problem Set # 2, Answers

14.0 Principles of Macroeconomics Problem Set #, Answers Part I 1. False. The multiplier is 1/ [1- c 1 (1- t)]. The effect of an increase in autonomous spending is dampened because taxes respond proportionally

14.0 Principles of Macroeconomics Problem Set #, Answers Part I 1. False. The multiplier is 1/ [1- c 1 (1- t)]. The effect of an increase in autonomous spending is dampened because taxes respond proportionally

OVERVIEW. 1. This chapter presents a graphical approach to the determination of income. Two different graphical approaches are provided.

24 KEYNESIAN CROSS OVERVIEW 1. This chapter presents a graphical approach to the determination of income. Two different graphical approaches are provided. 2. Initially, both the consumption function and

24 KEYNESIAN CROSS OVERVIEW 1. This chapter presents a graphical approach to the determination of income. Two different graphical approaches are provided. 2. Initially, both the consumption function and

Saving, Investment, and the Financial System

Saving, Investment, and the Financial System The Financial System The financial system consists of institutions that help to match one person s saving with another person s investment. It moves the economy

Saving, Investment, and the Financial System The Financial System The financial system consists of institutions that help to match one person s saving with another person s investment. It moves the economy

3 General equilibrium model of national income

OVS452 Intermediate Economics II VSE NF, Spring 2008 Lecture Notes #2 Eva Hromádková 3 General equilibrium model of national income 3.1 Overview 4 basic questions about GDP: 1. What are the factors of

OVS452 Intermediate Economics II VSE NF, Spring 2008 Lecture Notes #2 Eva Hromádková 3 General equilibrium model of national income 3.1 Overview 4 basic questions about GDP: 1. What are the factors of

a. Fill in the following table (you will need to expand it from the truncated form provided here). Round all your answers to the nearest hundredth.

. Round all your answers to the nearest hundredth.") Economics 102 Summer 2015 Answers to Homework #4 Due Monday, July 13, 2015 Directions: The homework will be collected in a box before the lecture. Please place your name on top of the homework (legibly).

Economics 102 Summer 2015 Answers to Homework #4 Due Monday, July 13, 2015 Directions: The homework will be collected in a box before the lecture. Please place your name on top of the homework (legibly).

Chapter 4. Determination of Income and Employment 4.1 AGGREGATE DEMAND AND ITS COMPONENTS

Determination of Income and Employment Chapter 4 We have so far talked about the national income, price level, rate of interest etc. in an ad hoc manner without investigating the forces that govern their

Determination of Income and Employment Chapter 4 We have so far talked about the national income, price level, rate of interest etc. in an ad hoc manner without investigating the forces that govern their

Keynesian Theory (IS-LM Model): how GDP and interest rates are determined in Short Run with Sticky Prices.

: how GDP and interest rates are determined in Short Run with Sticky Prices.") Keynesian Theory (IS-LM Model): how GDP and interest rates are determined in Short Run with Sticky Prices. Historical background: The Keynesian Theory was proposed to show what could be done to shorten

Keynesian Theory (IS-LM Model): how GDP and interest rates are determined in Short Run with Sticky Prices. Historical background: The Keynesian Theory was proposed to show what could be done to shorten

Part II Classical Theory: Long Run Chapter 3 National Income: Where It Comes From and Where It Goes

Part II Classical Theory: Long Run Chapter 3 National Income: Where It Comes From and Where It Goes Zhengyu Cai Ph.D. Institute of Development Southwestern University of Finance and Economics All rights

Part II Classical Theory: Long Run Chapter 3 National Income: Where It Comes From and Where It Goes Zhengyu Cai Ph.D. Institute of Development Southwestern University of Finance and Economics All rights

ECO403 Macroeconomics Solved Final Term Papers For Final Term Exam Preparation

ECO403 Macroeconomics Solved Final Term Papers For Final Term Exam Preparation Question No: 1 curve include: ( Marks: 1 ) - Please choose one The determinants of demand Income, tastes, and the price of

ECO403 Macroeconomics Solved Final Term Papers For Final Term Exam Preparation Question No: 1 curve include: ( Marks: 1 ) - Please choose one The determinants of demand Income, tastes, and the price of

The Core of Macroeconomic Theory

PART III The Core of Macroeconomic Theory 1 of 33 The level of GDP, the overall price level, and the level of employment three chief concerns of macroeconomists are influenced by events in three broadly

PART III The Core of Macroeconomic Theory 1 of 33 The level of GDP, the overall price level, and the level of employment three chief concerns of macroeconomists are influenced by events in three broadly

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Problem Set Econ 2013: Chapter 10 :Basic Macroeconomic Relationships Name ID: MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The most important

Problem Set Econ 2013: Chapter 10 :Basic Macroeconomic Relationships Name ID: MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The most important

Consumption, Saving, and Investment. Chapter 4. Copyright 2009 Pearson Education Canada

Consumption, Saving, and Investment Chapter 4 Copyright 2009 Pearson Education Canada This Chapter In Chapter 3 we saw how the supply of goods is determined. In this chapter we will turn to factors that

Consumption, Saving, and Investment Chapter 4 Copyright 2009 Pearson Education Canada This Chapter In Chapter 3 we saw how the supply of goods is determined. In this chapter we will turn to factors that

A Macroeconomic Theory of the Open Economy. Chapter 30

A Macroeconomic Theory of the Open Economy Chapter 30 Key Macroeconomic Variables in an Open Economy The important macroeconomic variables of an open economy include: net exports net foreign investment

A Macroeconomic Theory of the Open Economy Chapter 30 Key Macroeconomic Variables in an Open Economy The important macroeconomic variables of an open economy include: net exports net foreign investment

Assignment 1: Hand in only Answer. Last Name. First Name. Chapter

Assignment 1: Hand in only Answer Last Name First Name Chapter 3 1 11 21 2 12 22 3 13 23 4 14 24 5 15 25 6 16 7 17 8 18 9 19 10 20 Chapter 4 1 8 15 2 9 16 3 10 17 4 11 18 5 12 19 6 13 7 14 Chapter 3: Page

Assignment 1: Hand in only Answer Last Name First Name Chapter 3 1 11 21 2 12 22 3 13 23 4 14 24 5 15 25 6 16 7 17 8 18 9 19 10 20 Chapter 4 1 8 15 2 9 16 3 10 17 4 11 18 5 12 19 6 13 7 14 Chapter 3: Page

Economics Macroeconomic Theory. Spring Final Exam, Tuesday 6 May 2003

Economics 202.04 - Macroeconomic Theory Spring 2003 - Final Exam, Tuesday 6 May 2003 Please answer: ALL QUESTIONS IF YOU DO PART 1 3 OUT OF 4 QUESTIONS IF YOU DO PART 2 Each question in each part carries

Economics 202.04 - Macroeconomic Theory Spring 2003 - Final Exam, Tuesday 6 May 2003 Please answer: ALL QUESTIONS IF YOU DO PART 1 3 OUT OF 4 QUESTIONS IF YOU DO PART 2 Each question in each part carries

EXPENDITURE MULTIPLIERS

27 EXPENDITURE MULTIPLIERS After studying this chapter, you will be able to: Explain how expenditure plans are determined Explain how real GDP is determined at a fixed price level Explain the expenditure

27 EXPENDITURE MULTIPLIERS After studying this chapter, you will be able to: Explain how expenditure plans are determined Explain how real GDP is determined at a fixed price level Explain the expenditure

Econ 102 Exam 2 Name ID Section Number

Econ 102 Exam 2 Name ID Section Number 1. In a closed economy government spending was $30 billion, consumption was $70 billion, taxes were $20 billion, and GDP was $110 billion this year. Investment spending

Econ 102 Exam 2 Name ID Section Number 1. In a closed economy government spending was $30 billion, consumption was $70 billion, taxes were $20 billion, and GDP was $110 billion this year. Investment spending

The Financial System. FINANCIAL INSTITUTIONS IN THE U.S. ECONOMY Financial Markets Stock Market Bond Market

Chapter 26. Saving, Investment, and the Financial System important financial institutions in the U.S. economy. how the financial system is related to key macroeconomic variables. the model of the supply

Chapter 26. Saving, Investment, and the Financial System important financial institutions in the U.S. economy. how the financial system is related to key macroeconomic variables. the model of the supply

ECN101: Intermediate Macroeconomic Theory TA Section

ECN101: Intermediate Macroeconomic Theory TA Section (jwjung@ucdavis.edu) Department of Economics, UC Davis November 4, 2014 Slides revised: November 4, 2014 Outline 1 2 Fall 2012 Winter 2012 Midterm:

ECN101: Intermediate Macroeconomic Theory TA Section (jwjung@ucdavis.edu) Department of Economics, UC Davis November 4, 2014 Slides revised: November 4, 2014 Outline 1 2 Fall 2012 Winter 2012 Midterm:

In this chapter, look for the answers to these questions

In this chapter, look for the answers to these questions What are the main types of financial institutions and what is their function? What are the three kinds of saving? What s the difference between

In this chapter, look for the answers to these questions What are the main types of financial institutions and what is their function? What are the three kinds of saving? What s the difference between

BUSI 101 Capital Markets and Real Estate

BUSI 101 Capital Markets and Real Estate PURPOSE AND SCOPE The Capital Markets and Real Estate course (BUSI 101) is intended to acquaint the student with the basic principles of macroeconomics and to give

BUSI 101 Capital Markets and Real Estate PURPOSE AND SCOPE The Capital Markets and Real Estate course (BUSI 101) is intended to acquaint the student with the basic principles of macroeconomics and to give

A Real Intertemporal Model with Investment Copyright 2014 Pearson Education, Inc.

Chapter 11 A Real Intertemporal Model with Investment Copyright Chapter 11 Topics Construct a real intertemporal model that will serve as a basis for studying money and business cycles in Chapters 12-14.

Chapter 11 A Real Intertemporal Model with Investment Copyright Chapter 11 Topics Construct a real intertemporal model that will serve as a basis for studying money and business cycles in Chapters 12-14.

THE KEYNESIAN MODEL IN THE SHORT AND LONG RUN

Lecture: THE KENESIAN MODEL IN THE SHORT AND LONG RUN In the short run actual GDP,, may be lower or higher or equal to full-employment GDP,. The aim of the Keynesian model in the short run is to explain

Lecture: THE KENESIAN MODEL IN THE SHORT AND LONG RUN In the short run actual GDP,, may be lower or higher or equal to full-employment GDP,. The aim of the Keynesian model in the short run is to explain

SOLUTION ECO 209Y MACROECONOMIC THEORY. Midterm Test #1. University of Toronto October 21, 2005 LAST NAME FIRST NAME STUDENT NUMBER INSTRUCTIONS:

Department of Economics Prof. Gustavo Indart University of Toronto October 21, 2005 SOLUTION ECO 209Y MACROECONOMIC THEORY Midterm Test #1 LAST NAME FIRST NAME STUDENT NUMBER INSTRUCTIONS: 1. The total

Department of Economics Prof. Gustavo Indart University of Toronto October 21, 2005 SOLUTION ECO 209Y MACROECONOMIC THEORY Midterm Test #1 LAST NAME FIRST NAME STUDENT NUMBER INSTRUCTIONS: 1. The total

Econ 302 Fall Don t forget to download a copy of the Homework Cover Sheet. Mark the location where you handed in your work.

Econ 302 Fall 2005 Don t forget to download a copy of the Homework Cover Sheet. Mark the location where you handed in your work. Homework #3; Chapter 9. This homework has three parts (A, B, C). Each part

Econ 302 Fall 2005 Don t forget to download a copy of the Homework Cover Sheet. Mark the location where you handed in your work. Homework #3; Chapter 9. This homework has three parts (A, B, C). Each part

3) Gross domestic product measured in terms of the prices of a fixed, or base, year is:

Gross domestic product measured in terms of the prices of a fixed, or base, year is:") 3) Gross domestic product measured in terms of the prices of a fixed, or base, year is: Base GDP. Current GDP. Real GDP. Nominal GDP. 4) The number of people unemployed equals: The number of people employed

3) Gross domestic product measured in terms of the prices of a fixed, or base, year is: Base GDP. Current GDP. Real GDP. Nominal GDP. 4) The number of people unemployed equals: The number of people employed

Notes On IS-LM Model Econ3120, Economic Department, St.Louis University

Notes On IS-LM Model Econ3120, Economic Department, St.Louis University Instructor: Xi Wang Introduction In this class notes, I introduce IS-LM Model. For those students have optional textbook, you can

Notes On IS-LM Model Econ3120, Economic Department, St.Louis University Instructor: Xi Wang Introduction In this class notes, I introduce IS-LM Model. For those students have optional textbook, you can

University of Toronto June 17, 2002 ECO 208Y - L5101 MACROECONOMIC THEORY. Term Test #1 LAST NAME FIRST NAME

Department of Economics Prof. Gustavo Indart University of Toronto June 17, 2002 SOLUTION ECO 208Y - L5101 MACROECONOMIC THEORY Term Test #1 LAST NAME FIRST NAME STUDENT NUMBER INSTRUCTIONS: 1. The total

Department of Economics Prof. Gustavo Indart University of Toronto June 17, 2002 SOLUTION ECO 208Y - L5101 MACROECONOMIC THEORY Term Test #1 LAST NAME FIRST NAME STUDENT NUMBER INSTRUCTIONS: 1. The total

AGGREGATE DEMAND. 1. Keynes s Theory

AGGREGATE DEMAND 1. Keynes s Theory - John Maynard Keynes (1936) criticized classical theory for assuming that AS alone capital, labor, and technology determines national income proposed that low AD is

AGGREGATE DEMAND 1. Keynes s Theory - John Maynard Keynes (1936) criticized classical theory for assuming that AS alone capital, labor, and technology determines national income proposed that low AD is

This paper is not to be removed from the Examination Halls UNIVERSITY OF LONDON

~~EC2065 ZB d0 This paper is not to be removed from the Examination Halls UNIVERSITY OF LONDON EC2065 ZB BSc degrees and Diplomas for Graduates in Economics, Management, Finance and the Social Sciences,

~~EC2065 ZB d0 This paper is not to be removed from the Examination Halls UNIVERSITY OF LONDON EC2065 ZB BSc degrees and Diplomas for Graduates in Economics, Management, Finance and the Social Sciences,

The Goods Market and the Aggregate Expenditures Model

The Goods Market and the Aggregate Expenditures Model Chapter 8 The Historical Development of Modern Macroeconomics The Great Depression of the 1930s led to the development of macroeconomics and aggregate

The Goods Market and the Aggregate Expenditures Model Chapter 8 The Historical Development of Modern Macroeconomics The Great Depression of the 1930s led to the development of macroeconomics and aggregate

E) price level and the total output that firms wish to produce and sell, as technology and input prices vary.

price level and the total output that firms wish to produce and sell, as technology and input prices vary.") Exam Name 1) The economyʹs aggregate supply (AS) curve shows the relationship between the A) price level and the marginal propensity to consume (MPC). B) equilibrium real GDP and marginal cost. C) price

Exam Name 1) The economyʹs aggregate supply (AS) curve shows the relationship between the A) price level and the marginal propensity to consume (MPC). B) equilibrium real GDP and marginal cost. C) price

ECON Drexel University Summer 2008 Assignment 2. Due date: July 29, 2008

ECON 202-001 Drexel University Summer 2008 Assignment 2 Due date: July 29, 2008 Instructor: Yuan Yuan Name This homework has up to 10 points bonus. Question 1 (40 points, 2 points each): MULTIPLE CHOICE.

ECON 202-001 Drexel University Summer 2008 Assignment 2 Due date: July 29, 2008 Instructor: Yuan Yuan Name This homework has up to 10 points bonus. Question 1 (40 points, 2 points each): MULTIPLE CHOICE.

Chapter 10 3/19/2018. AGGREGATE SUPPLY AND AGGREGATE DEMAND (Part 1) Objectives. Aggregate Supply

Objectives. Aggregate Supply") Chapter 10 AGGREGATE SUPPLY AND AGGREGATE DEMAND (Part 1) Objectives Explain what determines aggregate supply in the long run and in the short run Explain what determines aggregate demand Explain how real

Chapter 10 AGGREGATE SUPPLY AND AGGREGATE DEMAND (Part 1) Objectives Explain what determines aggregate supply in the long run and in the short run Explain what determines aggregate demand Explain how real

Fluctuations of Investment Durability Irregularity of Innovation Variability of Profits Variability of Expectations

Shifts in the Invest Demand Curve Acquisition, Maintenance and Operating Costs Business Taxes Technological Change Stock of Capital Goods on Hand Expectations Fluctuations of Investment Durability Irregularity

Shifts in the Invest Demand Curve Acquisition, Maintenance and Operating Costs Business Taxes Technological Change Stock of Capital Goods on Hand Expectations Fluctuations of Investment Durability Irregularity

9. CHAPTER: Aggregate Demand I

TOBB-ETU, Economics Department Macroeconomics I (IKT 233) Ozan Eksi Practice Questions with Answers (for Final) 9. CHAPTER: Aggregate Demand I 1-) In the long run, the level of output is determined by

TOBB-ETU, Economics Department Macroeconomics I (IKT 233) Ozan Eksi Practice Questions with Answers (for Final) 9. CHAPTER: Aggregate Demand I 1-) In the long run, the level of output is determined by

Chapter 3. Continued. CHAPTER 3 National Income. slide 0

Chapter 3 Continued slide 0 Notes The equilibrium is stable If r > r* S > I: More people want to save relative to demand for funds: excess supply; r decreases If r < r* I > S: More demand for funds then

Chapter 3 Continued slide 0 Notes The equilibrium is stable If r > r* S > I: More people want to save relative to demand for funds: excess supply; r decreases If r < r* I > S: More demand for funds then

EQ: What are the Assumptions of Keynesian Economic Theory?

EQ: How is Keynesian Theory Different from Classical Theory? Classical Theory Supply-Focused (SRAS) Say s Law Economy is self-regulating Laissez-Faire Wages can go up or down Businesses will borrow & invest

EQ: How is Keynesian Theory Different from Classical Theory? Classical Theory Supply-Focused (SRAS) Say s Law Economy is self-regulating Laissez-Faire Wages can go up or down Businesses will borrow & invest

Intermediate Macroeconomic Theory / Macroeconomic Analysis (ECON 3560/5040) Midterm Exam (Answers)

Midterm Exam (Answers)") Intermediate Macroeconomic Theory / Macroeconomic Analysis (ECON 3560/5040) Midterm Exam (Answers) Part A (15 points) State whether you think each of the following questions is true (T), false (F), or

Intermediate Macroeconomic Theory / Macroeconomic Analysis (ECON 3560/5040) Midterm Exam (Answers) Part A (15 points) State whether you think each of the following questions is true (T), false (F), or

Final Term Papers. Fall 2009 (Session 03b) ECO401. (Group is not responsible for any solved content) Subscribe to VU SMS Alert Service

ECO401. (Group is not responsible for any solved content) Subscribe to VU SMS Alert Service") Fall 2009 (Session 03b) (Group is not responsible for any solved content) Subscribe to VU SMS Alert Service To Join Simply send following detail to bilal.zaheem@gmail.com Full Name Master Program (MBA,

Fall 2009 (Session 03b) (Group is not responsible for any solved content) Subscribe to VU SMS Alert Service To Join Simply send following detail to bilal.zaheem@gmail.com Full Name Master Program (MBA,

Gehrke: Macroeconomics Winter term 2012/13. Exercises

Gehrke: 320.120 Macroeconomics Winter term 2012/13 Questions #1 (National accounts) Exercises 1.1 What are the differences between the nominal gross domestic product and the real net national income? 1.2

Gehrke: 320.120 Macroeconomics Winter term 2012/13 Questions #1 (National accounts) Exercises 1.1 What are the differences between the nominal gross domestic product and the real net national income? 1.2

Econ 3 Practice Final Exam

Econ 3 Winter 2010 Econ 3 Practice Final Exam No books or notes of any kind are allowed. On problems requiring calculations, you will only get credit if you show your work. Part I: Longer Answers. Please

Econ 3 Winter 2010 Econ 3 Practice Final Exam No books or notes of any kind are allowed. On problems requiring calculations, you will only get credit if you show your work. Part I: Longer Answers. Please

Econ 102 Exam 2 Name ID Section Number

Econ 102 Exam 2 Name ID Section Number 1. Suppose investment spending increases by $50 billion and as a result the equilibrium income increases by $200 billion. The investment multiplier is: A) 10. B)

Econ 102 Exam 2 Name ID Section Number 1. Suppose investment spending increases by $50 billion and as a result the equilibrium income increases by $200 billion. The investment multiplier is: A) 10. B)

QUICK REVISION. CFA level 1

ECONOMICS QUICK REVISION NOTES CFA level 1 Edited By Sam Economics Keynes: Sticky prices, so if Demand falls, Supply will fall, and employment falls Expenditures GDP: Consumer Spending, Private Investment,

ECONOMICS QUICK REVISION NOTES CFA level 1 Edited By Sam Economics Keynes: Sticky prices, so if Demand falls, Supply will fall, and employment falls Expenditures GDP: Consumer Spending, Private Investment,

ECON 3312 Macroeconomics Exam 1 Fall 2016

ECON 3312 Macroeconomics Exam 1 Fall 2016 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Under the assumption of perfect competition, all

ECON 3312 Macroeconomics Exam 1 Fall 2016 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Under the assumption of perfect competition, all

SAMPLE EXAM QUESTIONS FOR FALL 2018 ECON3310 MIDTERM 2

SAMPLE EXAM QUESTIONS FOR FALL 2018 ECON3310 MIDTERM 2 Contents: Chs 5, 6, 8, 9, 10, 11 and 12. PART I. Short questions: 3 out of 4 (30% of total marks) 1. Assume that in a small open economy where full

SAMPLE EXAM QUESTIONS FOR FALL 2018 ECON3310 MIDTERM 2 Contents: Chs 5, 6, 8, 9, 10, 11 and 12. PART I. Short questions: 3 out of 4 (30% of total marks) 1. Assume that in a small open economy where full

Economics 1012A: Introduction to Macroeconomics FALL 2007 Dr. R. E. Mueller Third Midterm Examination November 15, 2007

Economics 1012A: Introduction to Macroeconomics FALL 2007 Dr. R. E. Mueller Third Midterm Examination November 15, 2007 Answer all of the following questions by selecting the most appropriate answer on

Economics 1012A: Introduction to Macroeconomics FALL 2007 Dr. R. E. Mueller Third Midterm Examination November 15, 2007 Answer all of the following questions by selecting the most appropriate answer on

SOLUTION ECO 202Y - L5101 MACROECONOMIC THEORY. Term Test #1 LAST NAME FIRST NAME STUDENT NUMBER. University of Toronto June 18, 2002 INSTRUCTIONS:

Department of Economics Prof. Gustavo Indart University of Toronto June 18, 2002 SOLUTION ECO 202Y - L5101 MACROECONOMIC THEORY Term Test #1 LAST NAME FIRST NAME STUDENT NUMBER INSTRUCTIONS: 1. The total

Department of Economics Prof. Gustavo Indart University of Toronto June 18, 2002 SOLUTION ECO 202Y - L5101 MACROECONOMIC THEORY Term Test #1 LAST NAME FIRST NAME STUDENT NUMBER INSTRUCTIONS: 1. The total

Title: Principle of Economics Saving and investment

Title: Principle of Economics Saving and investment Instructor: Vladimir Hlasny Institution: 이화여자대학교 Dictated: 김나정, 김민겸, 김성도, 문혜린, 박현서 [0:00] Let s recall from chapter 23 that the country s gross domestic

Title: Principle of Economics Saving and investment Instructor: Vladimir Hlasny Institution: 이화여자대학교 Dictated: 김나정, 김민겸, 김성도, 문혜린, 박현서 [0:00] Let s recall from chapter 23 that the country s gross domestic

3) If the Canadian dollar exchange rate increases, the 3) A) internal value of the dollar falls.

If the Canadian dollar exchange rate increases, the 3) A) internal value of the dollar falls.") Forty questions were automatically and randomly chosen by the computer from Chapters 19 through 2 6 of the Textʹs test bank - the instructor has not seen the questions chosen. Name: Random Q. Practice

Forty questions were automatically and randomly chosen by the computer from Chapters 19 through 2 6 of the Textʹs test bank - the instructor has not seen the questions chosen. Name: Random Q. Practice

Problem Set #1: The Economy in the Long Run Econ 100B: Intermediate Macroeconomics

Problem Set #1: The Economy in the Long Run Econ 100B: Intermediate Macroeconomics Question 1: Calculating RGDP and NGDP. 2012 2013 Good Quantity Price Quantity Price Cars 300 $ 50 360 $ 60 Tires 1,200

Problem Set #1: The Economy in the Long Run Econ 100B: Intermediate Macroeconomics Question 1: Calculating RGDP and NGDP. 2012 2013 Good Quantity Price Quantity Price Cars 300 $ 50 360 $ 60 Tires 1,200

The Solow Growth Model. Martin Ellison, Hilary Term 2017

The Solow Growth Model Martin Ellison, Hilary Term 2017 Solow growth model 2 Builds on the production model by adding a theory of capital accumulation Was developed in the mid-1950s by Robert Solow of

The Solow Growth Model Martin Ellison, Hilary Term 2017 Solow growth model 2 Builds on the production model by adding a theory of capital accumulation Was developed in the mid-1950s by Robert Solow of

IS-MP: A Short-Run Macroeconomic Model

September 21i 2015 1 Aggregate Demand 2 Monetary Policy Aggregate Demand Keynes (1936), The General Theory of Employment, Interest, and Money Aggregate Demand : The total amount of output demanded in the

September 21i 2015 1 Aggregate Demand 2 Monetary Policy Aggregate Demand Keynes (1936), The General Theory of Employment, Interest, and Money Aggregate Demand : The total amount of output demanded in the

I. Basic Concepts of Input Markets

University of Pacific-Economics 53 Lecture Notes #10 I. Basic Concepts of Input Markets In this lecture we ll look at the behavior of perfectly competitive firms in the input market. Recall that firms

University of Pacific-Economics 53 Lecture Notes #10 I. Basic Concepts of Input Markets In this lecture we ll look at the behavior of perfectly competitive firms in the input market. Recall that firms