Working Capital Management

|

|

|

- Noah Watkins

- 5 years ago

- Views:

Transcription

1 Working Capital Management Management need to understand the management of working capital so that management can efficiently manage current assets and decide whether to finance the firm s funds requirements aggressively or conservatively.

2 ABC Company Balance Sheet As of December 31, 19xx Assets: Liabilities & Equity: Current Assets Current Liabilities Cash & M.S. Accounts payable Accounts receivable Notes Payable Inventory Total Current Liabilities Total Current Assets Long-Term Liabilities Fixed Assets: Total Liabilities Gross fixed assets Equity: Less: Accumulated dep. Common Stock Goodw ill Paid-in-capital Other long-term assets Retained Earnings Total Fixed Assets Total Equity Total Assets Total Liabilities & Equity

3 Current assets & Current liabilities: Current assets, commonly called working capital, represent the portion of investment that circulates from one to another in the ordinary conduct of business. Current liabilities represent the firm s shortterm financing, because they include all debts of the firm that come due (must be paid) in 1 year or less.

4 Working Capital Working Capitalincludes a firm s current assets, which consist of cash and marketable securities in addition to accounts receivable and inventories. It also consists of current liabilities, including accounts payable (trade credit), notes payable (bank loans), and accrued liabilities. Net Working Capitalis defined as total current assets less total current liabilities. Often called working capital.

5 Short-term financial management In U.S. manufaturing firms, current assets account for about 40 percent of total assets; current liabilities represent about 26 percent of total financing. Therefore, it should not be surprising to learn that short-term financial management managing current assets and current liabilities -is one of the financial manager s most important and timeconsuming activities.

6 The goal of short-term financial management is to manage each of the firm s current assets and current liabilities to achieve a balance between profitability and risk that contributes positively to the firm s value.

7 Net Working Capital Current Assets - Current Liabilities. Gross Working Capital The firm s investment in current assets. Working Capital Management The administration of the firm s current assets and the financing needed to support current assets.

8 Significance of Working Capital Management: In a typical manufacturing firm, current assets exceed one-half of total assets. Excessive levels can result in a substandard Return on Investment (ROI). Current liabilities are the principal source of external financing for small firms. Requires continuous, day-to-day managerial supervision. Working capital management affects the company s risk, return, and share price.

9 Alternative Current Asset Investment Policies: 1. Relaxed Current Asset Investment Policy 2. Moderate Current Asset Investment Policy 3. Restricted Current Asset Investment Policy

10 Optimal Amount (Level) of Current Assets ASSET LEVEL ($ $) Current Assets Policy A Policy B Policy C 0 25,000 50,000

11 Liquidity Analysis Policy Liquidity A High B Average C Low Greater current asset levels generate more liquidity; all other factors held constant.

12 Profitability Analysis Return on Investment = Net Profit Total Assets Current Assets = (Cash + Rec. + Inv.) Return on Investment = Net Profit Current + Fixed Assets

13 Policy Profitability A Low B Average C High As current asset levels decline, total assets will decline and the ROI will rise.

14 The trade-off between profitability and risk Profitability The relationship between revenues and costs generated by using the firm s assets-both current and fixed assets- in productive activities. Risk (of technical insolvency) The probability that a firm will be unable to pay its bills they come due.

15 Impact on Risk Decreasing cash reduces the firm s ability to meet its financial obligations. More risk! Stricter credit policies reduce receivablesand possibly lose sales and customers. More risk! Lower inventory levels increase stockouts and lost sales. More risk!

16 Policy Risk A Low B Average C High Risk increases as the level of current assets are reduced.

17 Summary of the Optimal Amount of Current Assets Policy A B C Liquidity Profitability Risk High Average Low Low Average High Low Average High

18 The Tradeoff Between Profitability & Risk Positive Net Working Capital (low return and low risk) low return high return Current Assets Net Working Capital > 0 Fixed Assets Current Liabilities Long-Term Debt Equity low cost high cost highest cost

19 Negative Net Working Capital (high return and high risk) low return Current Assets Current Liabilities Net Working Capital < 0 low cost high return Long-Term Debt high cost Fixed Assets Equity highest cost

20 The Tradeoff Between Profitability & Risk (cont.)

21 Cash Conversion Cycle Central to short-term financial management is an understanding of the firm s cash conversion cycle.

22 The Operating Cycle (OC)is the time from beginning of thr production process to collection of cash from the sale of finished products. The Cash Conversion Cycle (CCC)measures the length of time required a company to convert cash invested in its operations to cash received as a result of its operations.

23 Operating Cycle (OC) = AAI + ACP Cash Conversion Cycle (CCC) = OC -APP

24 CCC : (inventory period + accounts receivable period) accounts payable period. Inventory period = average inventory annual CGS/365 A/R period = average A/R annual credit sales/365 A/P period = average A/P annual credit purchases/365

25 A/R turn over = 365 A/R period Average A/R = credit Sales : A/R turn over A/P turn over = 365 A/P period Average A/P = credit purchases : A/P turn over

26 Gitman & Zutter (2012:604) In 2007, IBM had annual revenues of $ 98,786 million, cost of revenue of $ 57,057 millon, and accounts payable of $ 8,054 million. IBM has an average age of inventory (AAI) of 17.5 days, an average collection period (ACP) of 44.8 days, and an average payment period (APP) of 51.2 days (IBM purchases were $ 57,416 million). Thus CCC for IBM was 11.1 days.

27 The resources IBM had invested in this CCC were: Inventory, $ 57,057 millon x (17.5/365) = $ 2,735,610 A/R, $ 98,786 million x (44.8/365) = 12,124,967 A/P, $ 57,416 million x (51.2/365) = 8,053,970 $ 6,8 billion committed to working capital. $ 6,806,607

28 The end of 2009, IBM has lowered its ACP to 24.9 days. This dramatical increase in working capital efficiency. It would shorten the CCC and reduce the amount of resources IBM has invested in operations. CCC = -7.6 days

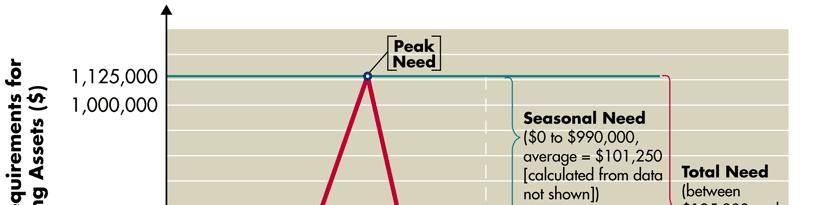

29 Strategies for Managing the CCC 1. Turn over inventory as quickly as possible without stock outs that result in lost sales. 2. Collect accounts receivable as quickly as possible without losing sales from high-pressure collection techniques. 3. Manage, mail, processing, and clearing time to reduce them when collecting from customers and to increase them when paying suppliers. 4. Pay accounts payable as slowly as possible without damaging the firm s credit rating.

30 Funding Requirements of the CCC permanent funding requirement, a constant investment in operating assets resulting from constant sales over time. seasonal funding requirement, an investment seasonal funding requirement, an investment in operating assets that varies over time as result of cyclic sales.

31 Kebutuhan Modal (Rp) Temporary current assets Permanent current assets Waktu

32 Permanent vs. Seasonal Funding Needs Nicholson Company holds, on average, $50,000 in cash and marketable securities, $1,250,000 in inventory, and $750,000 in accounts receivable. Nicholson s business is very stable over time, so its operating assets can be viewed as permanent.

33 In addition, Nicholson s accounts payable of $425,000 are stable over time. Nicholson has a permanent investment in operating assets of $1,625,000 ($50,000 + $1,250,000 + $750,000 -$425,000). This amount would also equal the company s permanent funding requirement.

34 In contrast, Semper Pump Company has seasonal sales, with its peak sales driven by purchases of bicycle pumps. Semper holds, at minimum, $25,000 in cash and Semper holds, at minimum, $25,000 in cash and marketable securities, $100,000 in inventory, and $60,000 in accounts receivable.

35 At peak times, Semper s inventory increases to $750,000 and its accounts receivable increase to $400,000. To capture production efficiencies, Semper produces pumps at a constant rate throughout the year. Thus, accounts payable remain at $50,000 throughout the year.

36 Semper has a permanent funding requirement for its minimum level of operating assets of $135,000 ($25,000 + $100,000 + $60,000 - $50,000) and peak seasonal funding requirements of $990,000 [($25,000 + $750,000 + $400,000 -$50,000)-$135,000].

37 Semper s total funding requirements for operating assets vary from a minimum of $135,000 (permanent) to a seasonal peak of $1,125,000 ($135,000 + $990,000) as shown in Figure 15.3.

38

39 Aggressive versus Conservative Seasonal Funding Strategies Semper Pump has a permanent funding requirement of $135,000 and seasonal requirements that vary between $0 and $990,000 and average $101,250 (calculated from data not shown). If Semper can borrow short-term funds at 6.25% and long term funds at 8%, and can earn 5% on any invested surplus, then the annual cost of the aggressive strategy would be:

40

41 Alternatively, Semper can choose a conservative strategy under which surplus cash balances are fully invested, this surplus would be the difference between the peak need of $1,125,000 and the total need, which varies between $135,000 and $1,125,000 during the year.

42

43 The aggressive strategy s heavy reliance on short-term financing makes it riskier than the conservative strategy because of interest rate swings and possible difficulties in obtaining needed funds quickly when the seasonal peaks occur.

44 The conservative strategy avoids these risks through the locked-in interest rate and longterm financing, but is more costly. The final decision is left to management.

45 P15-4 The forecast of total funds requirements for coming year: Month Amount Month Amount January $ 2,000,000 July $ 12,000,000 February $ 2,000,000 August $ 14,000,000 March $ 2,000,000 September $ 9,000,000 April $ 4,000,000 October $ 5,000,000 May $ 6,000,000 November $ 4,000,000 June $ 9,000,000 December $ 3,000,000

46 Permanent component $ 2,000,000 Seasonal component, 0 -$ 12,000,000 average $ 4,000,000 per month

47 Accounts Receivable Management

48 The objective for managing accounts receivable is to collect accounts receivable as quickly as possible without losing sales from high- pressure collection techniques.

49 Topics of Accounts Receivable Management: Credit Selection and Standards: Five C s of credit; credit scoring; credit standard. Credit Terms: cash discount; cash discount period; credit period. Credit monitoring: average collection period; aging of accounts reveivable; collection techniques.

50 Numerical Credit Scoring categories: The customer s character The customer s capacity to pay The customer s capital The collateral provided by the customer The condition of the customer s business

51

52 Changing Credit Standards A company is currently selling a product for $10 per unit. Sales (all on credit) for last year were 60,000 units. The variable cost per unit is $6 and total fixed costs are $120,000. A company is currently contemplating a relaxation of credit standardsthat is anticipated to increase sales 5% to 63,000 units. It is also anticipated that the Average Collection Period will increase from 30 to 45 days, and that bad debt expenses will increase from 1% of sales to 2% of sales. The opportunity cost of tying funds up in receivables is 15%. Should a company relax its credit standards?

53 Contribution margin A/R turn over present $ 240, x proposed $ 252, x Total variable costs $ 360,000 $ 378,000 Investment in A/R $ 29,508 $ 46,667 Cost of fund Bad debt expenses $ 4,426 $ 6,000 $ 7,000 $ 12,600

54 Credit Terms Credit terms: the terms of sale for customers who have been extended credit by the firm. Cash discount: a percentage deduction from the purchase price; available to the credit customer who pays its account within a sepcified period. Cash discount period: the number of days after the beginning of the credit period during which the cash discount is available.

55 Gitman & Zutter (2012: ) MAX Company has an average collection period of 40 days, A/R turnover = 365/40 = 9.1. MAX is considering initiating a cash discount by changing its credit terms from net 30 to 2/10 net 30. The firm expects this change to reduce an average collection period to 25 days, A/R turnover = 365/25 = 14.6.

56 Harga jual $ 3,000 per unit Biaya variabel $ 2,300 per unit Opportunity cost of funds = 14% Volume penjualan unit dan akan naik menjadi unit Konsumen yang akan menggunakan kesempatan cash discount sebanyak 80%

57

Chapter 14. Working Capital and Current Asset Management

Chapter 14 Working Capital and Current Asset Management Learning Goals 1. Understand short-term financial management, net working capital, and the related trade-off between profitability and risk. 2. Describe

Chapter 14 Working Capital and Current Asset Management Learning Goals 1. Understand short-term financial management, net working capital, and the related trade-off between profitability and risk. 2. Describe

An-Najah National University. Prepared by Instructor: E.Shatha Qamhieh Course Title: Managerial Finance

An-Najah National University Prepared by Instructor: E.Shatha Qamhieh Course Title: Managerial Finance Working Capital Fundamentals Short-term financial management: Management of current assets and current

An-Najah National University Prepared by Instructor: E.Shatha Qamhieh Course Title: Managerial Finance Working Capital Fundamentals Short-term financial management: Management of current assets and current

Short-Term Financial Decisions

Pa r t 5 Short-Term Financial Decisions Chapter 13 Working Capital and Current Assets Management Chapter 14 Current Liabilities Management 509 Principles of Managerial Finance, Brief Fourth Edition, by

Pa r t 5 Short-Term Financial Decisions Chapter 13 Working Capital and Current Assets Management Chapter 14 Current Liabilities Management 509 Principles of Managerial Finance, Brief Fourth Edition, by

Brief Edition. Cash & Marketable Securities

Principles of Managerial Finance Brief Edition Chapter 16 Cash & Marketable Securities Learning Objectives Discuss why firms hold cash and marketable securities, and how the levels they hold of each relate

Principles of Managerial Finance Brief Edition Chapter 16 Cash & Marketable Securities Learning Objectives Discuss why firms hold cash and marketable securities, and how the levels they hold of each relate

Chapter 8 Working Capital Management

Chapter 8 Working Capital Management Long & Short Term Assets & Liabilities Current Assets: Cash Marketable Securities Prepayments Accounts Receivable Inventory Fixed Assets: Investments Plant & Machinery

Chapter 8 Working Capital Management Long & Short Term Assets & Liabilities Current Assets: Cash Marketable Securities Prepayments Accounts Receivable Inventory Fixed Assets: Investments Plant & Machinery

WORKING CAPITAL MANAGMENT

WORKING CAPITAL MANAGMENT 1. Working capital Working capital: short-term (current) assets and liabilities. current assets accounts receivable: trade credit + consumer credit; inventory: raw materials,

WORKING CAPITAL MANAGMENT 1. Working capital Working capital: short-term (current) assets and liabilities. current assets accounts receivable: trade credit + consumer credit; inventory: raw materials,

INTRODUCTION MEANING OF WORKING CAPITAL

INTRODUCTION Working capital management is also one of the important parts of the financial management. It is concerned with short-term finance of the business concern which is a closely related trade

INTRODUCTION Working capital management is also one of the important parts of the financial management. It is concerned with short-term finance of the business concern which is a closely related trade

Fundamental Decisions

Fundamental Decisions The determination of: The optimal level of investment in current assets The appropriate mix of short-term and-long-term financing used to support this investment in current assets

Fundamental Decisions The determination of: The optimal level of investment in current assets The appropriate mix of short-term and-long-term financing used to support this investment in current assets

9. Short-Term Liquidity Analysis. Operating Cash Conversion Cycle

9. Short-Term Liquidity Analysis. Operating Cash Conversion Cycle 9.1 Current Assets and 9.1.1 Cash A firm should maintain as little cash as possible, because cash is a nonproductive asset. It earns no

9. Short-Term Liquidity Analysis. Operating Cash Conversion Cycle 9.1 Current Assets and 9.1.1 Cash A firm should maintain as little cash as possible, because cash is a nonproductive asset. It earns no

Final Examination Semester 1 / Year 2011

Southern College Kolej Selatan 南方学院 Final Examination Semester 1 / Year 2011 COURSE : COURSE CODE : FINE2003 TIME : 2 1/2 HOURS DEPARTMENT : MANAGEMENT, ACCOUNTING & FINANCE LECTURER : CHIANG FAN SIN Students

Southern College Kolej Selatan 南方学院 Final Examination Semester 1 / Year 2011 COURSE : COURSE CODE : FINE2003 TIME : 2 1/2 HOURS DEPARTMENT : MANAGEMENT, ACCOUNTING & FINANCE LECTURER : CHIANG FAN SIN Students

BBPW3203 FINANCIAL MANAGEMENT II. Topic 1 Short-term Financing

BBPW3203 FINANCIAL MANAGEMENT II Topic 1 Short-term Financing January 2018 Content 1.1 Short-term financing 1.2 Current assets financing policy 1.3 Advantages and disadvantages of short-term financing

BBPW3203 FINANCIAL MANAGEMENT II Topic 1 Short-term Financing January 2018 Content 1.1 Short-term financing 1.2 Current assets financing policy 1.3 Advantages and disadvantages of short-term financing

An-Najah National University. Prepared by Instructor: E.Shatha Qamhieh Course Title: Managerial Finance

An-Najah National University Prepared by Instructor: E.Shatha Qamhieh Course Title: Managerial Finance Current Liabilities Management Spontaneous liabilities: Financing that arises from the normal course

An-Najah National University Prepared by Instructor: E.Shatha Qamhieh Course Title: Managerial Finance Current Liabilities Management Spontaneous liabilities: Financing that arises from the normal course

An entity s ability to maintain its short-term debt-paying ability is important to all

chapter 6 Liquidity of Short-Term Assets; Related Debt-Paying Ability An entity s ability to maintain its short-term debt-paying ability is important to all users of financial statements. If the entity

chapter 6 Liquidity of Short-Term Assets; Related Debt-Paying Ability An entity s ability to maintain its short-term debt-paying ability is important to all users of financial statements. If the entity

OVERVIEW. P1 Managerial Finance Working Capital Management Presented By: Dr Garvan Whelan CPA 04/01/2017. Trainee Accountant Webinar

CPA Ireland Skillnet CPA Ireland Skillnet, is a training network that is funded by Skillnets, a state funded, enterprise led support body dedicated to the promotion and facilitation of training and up-skilling

CPA Ireland Skillnet CPA Ireland Skillnet, is a training network that is funded by Skillnets, a state funded, enterprise led support body dedicated to the promotion and facilitation of training and up-skilling

Return on Invested Capital and Profitability Analysis

Return on Invested Capital and Profitability Analysis 8 CHAPTER McGraw-Hill/Irwin 2007, The McGraw-Hill Companies, All Rights Reserved Return on Invested Capital Importance of Joint Analysis Joint analysis

Return on Invested Capital and Profitability Analysis 8 CHAPTER McGraw-Hill/Irwin 2007, The McGraw-Hill Companies, All Rights Reserved Return on Invested Capital Importance of Joint Analysis Joint analysis

BUSINESS FINANCE. Financial Statement Analysis. 1. Introduction to Financial Analysis. Copyright 2004 by Larry C. Holland

BUSINESS FINANCE Financial Statement Analysis 1. Introduction to Financial Analysis Slide 1 Welcome to the study of business finance. The major topic in this module is Financial Statement Analysis. And

BUSINESS FINANCE Financial Statement Analysis 1. Introduction to Financial Analysis Slide 1 Welcome to the study of business finance. The major topic in this module is Financial Statement Analysis. And

TOTAL TRAINING SOLUTIONS

TOTAL TRAINING SOLUTIONS RATIO ANALYSIS TO DETERMINE FINANCIAL STRENGTH Examining a Borrowers Five Vital Signs Jeffery W. Johnson Bankers Insight Group, LLC jeffery.johnson@bankers-insight.com October

TOTAL TRAINING SOLUTIONS RATIO ANALYSIS TO DETERMINE FINANCIAL STRENGTH Examining a Borrowers Five Vital Signs Jeffery W. Johnson Bankers Insight Group, LLC jeffery.johnson@bankers-insight.com October

CURRENT ASSETS MANAGEMENT: VALUE BASED WORKING CAPITAL DECISIONS (2/5) 20th October 4pm

20th October 4pm") CURRENT ASSETS MANAGEMENT: VALUE BASED WORKING CAPITAL DECISIONS (2/5) 20th October 2008 @ 4pm CURRENT ASSETS MANAGEMENT: VALUE BASED WORKING CAPITAL DECISIONS E-mail: GRZEGORZ.MICHALSKI@UE.WROC.PL www:

CURRENT ASSETS MANAGEMENT: VALUE BASED WORKING CAPITAL DECISIONS (2/5) 20th October 2008 @ 4pm CURRENT ASSETS MANAGEMENT: VALUE BASED WORKING CAPITAL DECISIONS E-mail: GRZEGORZ.MICHALSKI@UE.WROC.PL www:

Financial Decisions. 1. Operating Cycle and Short-term financial Policy

Financial Decisions 1. Operating Cycle and Short-term financial Policy Tracing Cash and Net Working Capital Operating Cycle and Cash Cycle Overview of Short-term financial policy Instructor: A. Ashta References:

Financial Decisions 1. Operating Cycle and Short-term financial Policy Tracing Cash and Net Working Capital Operating Cycle and Cash Cycle Overview of Short-term financial policy Instructor: A. Ashta References:

Chapter 021 Credit and Inventory Management

Multiple Choice Questions 1. The conditions under which a firm sells its goods and services for cash or credit are called the: A. terms of sale. b. credit analysis. c. collection policy. d. payables policy.

Multiple Choice Questions 1. The conditions under which a firm sells its goods and services for cash or credit are called the: A. terms of sale. b. credit analysis. c. collection policy. d. payables policy.

Learning Goal 1: Review the contents of the stockholders' report and the procedures for consolidating international financial statements.

Principles of Managerial Finance, 12e (Gitman) Chapter 2 Financial Statements and Analysis Learning Goal 1: Review the contents of the stockholders' report and the procedures for consolidating international

Principles of Managerial Finance, 12e (Gitman) Chapter 2 Financial Statements and Analysis Learning Goal 1: Review the contents of the stockholders' report and the procedures for consolidating international

ACCA. Paper F9. Financial Management. Interim Assessment Answers

ACCA Paper F9 Financial Management 03 Interim Assessment Answers To gain maximum benefit, do not refer to these answers until you have completed the interim assessment questions and submitted them for

ACCA Paper F9 Financial Management 03 Interim Assessment Answers To gain maximum benefit, do not refer to these answers until you have completed the interim assessment questions and submitted them for

Analysis and Interpretation of Financial Statements

Chapter 23 Analysis and Interpretation of Financial Statements o Prepare comparative financial statements using horizontal analysis o Prepare comparative financial statements using vertical analysis o

Chapter 23 Analysis and Interpretation of Financial Statements o Prepare comparative financial statements using horizontal analysis o Prepare comparative financial statements using vertical analysis o

2018 Edition CPA. Preparatory Program. Business Environment and Concepts. Sample Chapters: Working Capital & Activity-Based Costing

2018 Edition CPA Preparatory Program Business Environment and Concepts Sample Chapters: Working Capital & Activity-Based Costing Brian Hock, CMA, CIA and Lynn Roden, CMA HOCK international, LLC P.O. Box

2018 Edition CPA Preparatory Program Business Environment and Concepts Sample Chapters: Working Capital & Activity-Based Costing Brian Hock, CMA, CIA and Lynn Roden, CMA HOCK international, LLC P.O. Box

STUDY UNIT TWO FINANCIAL PERFORMANCE METRICS FINANCIAL RATIOS

STUDY UNIT TWO FINANCIAL PERFORMANCE METRICS FINANCIAL RATIOS 1 2.1 Liquidity Ratios.......................................................... 2 2.2 Leverage and Solvency Ratios..............................................

STUDY UNIT TWO FINANCIAL PERFORMANCE METRICS FINANCIAL RATIOS 1 2.1 Liquidity Ratios.......................................................... 2 2.2 Leverage and Solvency Ratios..............................................

Session 4, Module Three:

Chapter 8: Introduction to Working Capital Management Session 4, Module Three: Working Capital Management v4.0 2013 Association for Financial Professionals. All rights reserved. Session 4: Module 3, Chapter

Chapter 8: Introduction to Working Capital Management Session 4, Module Three: Working Capital Management v4.0 2013 Association for Financial Professionals. All rights reserved. Session 4: Module 3, Chapter

CHAPTER 3. Topics in Chapter. Analysis of Financial Statements

CHAPTER 3 Analysis of Financial Statements 1 Topics in Chapter Ratio analysis DuPont equation Effects of improving ratios Limitations of ratio analysis Qualitative factors 2 Determinants of Intrinsic Value:

CHAPTER 3 Analysis of Financial Statements 1 Topics in Chapter Ratio analysis DuPont equation Effects of improving ratios Limitations of ratio analysis Qualitative factors 2 Determinants of Intrinsic Value:

CMA Part 2. Financial Decision Making

CMA Part 2 Financial Decision Making SU 7.1 Short-term Financing Basics Basis points = 1/100 th of a 1% 300 basis points = 3% Sources of short-term financing include: Market-based instruments Accounts

CMA Part 2 Financial Decision Making SU 7.1 Short-term Financing Basics Basis points = 1/100 th of a 1% 300 basis points = 3% Sources of short-term financing include: Market-based instruments Accounts

Understanding Employee Stock Options

Understanding Employee Stock Options Family Office Resources Compensation in the form of employee stock options tends to carry a significant level of risk and a high degree of complexity. Investors who

Understanding Employee Stock Options Family Office Resources Compensation in the form of employee stock options tends to carry a significant level of risk and a high degree of complexity. Investors who

Part A of examination paper

Prof Johan Burger 2017 Managing Institutional Capacity 1 Diploma Programme in Public Accountability Module code 13 206 171; twenty credits Preparation for November examination June examination MEMORANDUM

Prof Johan Burger 2017 Managing Institutional Capacity 1 Diploma Programme in Public Accountability Module code 13 206 171; twenty credits Preparation for November examination June examination MEMORANDUM

CASH MANAGEMENT. After studying this chapter, the reader should be able to

C H A P T E R 1 1 CASH MANAGEMENT I N T R O D U C T I O N This chapter continues the discussion of cash flows. It illustrates the fact that net income shown on an income statement does not imply that there

C H A P T E R 1 1 CASH MANAGEMENT I N T R O D U C T I O N This chapter continues the discussion of cash flows. It illustrates the fact that net income shown on an income statement does not imply that there

LEXMARK INTERNATIONAL GROUP, INC. AND SUBSIDIARIES CONSOLIDATED CONDENSED STATEMENTS OF EARNINGS (In Millions, Except Per Share Amounts) (Unaudited)

(Unaudited)") CONSOLIDATED CONDENSED STATEMENTS OF EARNINGS (In Millions, Except Per Share Amounts) Revenues Cost of revenues Gross profit Three Months Ended $787.0 501.8 285.20 $672.1 425.5 246.60 Percent Change 17%

CONSOLIDATED CONDENSED STATEMENTS OF EARNINGS (In Millions, Except Per Share Amounts) Revenues Cost of revenues Gross profit Three Months Ended $787.0 501.8 285.20 $672.1 425.5 246.60 Percent Change 17%

MNF2023 GROUP DISCUSSION. Lecturer: Mr C Chipeta. Tel: (012)

") MNF2023 GROUP DISCUSSION Lecturer: Mr C Chipeta Tel: (012) 429 3757 Email: chipec@unisa.ac.za Topics To Be Discussed Ratio analysis Time value of money Risk and return Bond and share valuation Working

MNF2023 GROUP DISCUSSION Lecturer: Mr C Chipeta Tel: (012) 429 3757 Email: chipec@unisa.ac.za Topics To Be Discussed Ratio analysis Time value of money Risk and return Bond and share valuation Working

Module 7 Introduction

Module 7 Introduction Module 7 Introduction This module contains three main topics. First, the concept of cost of capital, and, in particular, how to calculate the component elements of a firm s cost of

Module 7 Introduction Module 7 Introduction This module contains three main topics. First, the concept of cost of capital, and, in particular, how to calculate the component elements of a firm s cost of

EXCEL PROFESSIONAL INSTITUTE FINANCIAL STATEMENT INTERPRETATION

EXCEL PROFESSIONAL INSTITUTE FINANCIAL STATEMENT INTERPRETATION Elikem Vulley Most of the marks in an examination question will be available for sensible, well explained and accurate comments on the key

EXCEL PROFESSIONAL INSTITUTE FINANCIAL STATEMENT INTERPRETATION Elikem Vulley Most of the marks in an examination question will be available for sensible, well explained and accurate comments on the key

Balancing Execution Risk and Trading Cost in Portfolio Algorithms

Balancing Execution Risk and Trading Cost in Portfolio Algorithms Jeff Bacidore Di Wu Wenjie Xu Algorithmic Trading ITG June, 2013 Introduction For a portfolio trader, achieving best execution requires

Balancing Execution Risk and Trading Cost in Portfolio Algorithms Jeff Bacidore Di Wu Wenjie Xu Algorithmic Trading ITG June, 2013 Introduction For a portfolio trader, achieving best execution requires

Financial & Managerial Accounting Practice with Ratios and Analysis

Financial & Managerial Accounting Practice with Ratios and Analysis A company had the following income statement for the year and the balance sheet accounts at the end of the year. Use the information

Financial & Managerial Accounting Practice with Ratios and Analysis A company had the following income statement for the year and the balance sheet accounts at the end of the year. Use the information

Working Capital Management and Profitability Evidence from Firms Listed on Karachi Stock Exchange

International Journal of Business and Management; Vol. 10, No. 2; 2015 ISSN 1833-3850 E-ISSN 1833-8119 Published by Canadian Center of Science and Education Working Capital Management and Profitability

International Journal of Business and Management; Vol. 10, No. 2; 2015 ISSN 1833-3850 E-ISSN 1833-8119 Published by Canadian Center of Science and Education Working Capital Management and Profitability

SUNAMERICA SERIES TRUST

PROSPECTUS May 1, 2016 SUNAMERICA SERIES TRUST SunAmerica Dynamic Strategy (Class 1 and Class 3 Shares) This Prospectus contains information you should know before investing, including information about

PROSPECTUS May 1, 2016 SUNAMERICA SERIES TRUST SunAmerica Dynamic Strategy (Class 1 and Class 3 Shares) This Prospectus contains information you should know before investing, including information about

FUNDAMENTALS OF CREDIT ANALYSIS

FUNDAMENTALS OF CREDIT ANALYSIS 1 MV = Market Value NOI = Net Operating Income TV = Terminal Value RC = Replacement Cost DSCR = Debt Service Coverage Ratio 1. INTRODUCTION CR = Credit Risk Y.S = Yield

FUNDAMENTALS OF CREDIT ANALYSIS 1 MV = Market Value NOI = Net Operating Income TV = Terminal Value RC = Replacement Cost DSCR = Debt Service Coverage Ratio 1. INTRODUCTION CR = Credit Risk Y.S = Yield

FEEDBACK TUTORIAL LETTER ASSIGNMENT 2 SECOND SEMESTER 2018 MANAGERIAL FINANCE 4B [MAF412S]

![FEEDBACK TUTORIAL LETTER ASSIGNMENT 2 SECOND SEMESTER 2018 MANAGERIAL FINANCE 4B [MAF412S]](/thumbs/87/97231531.jpg "FEEDBACK TUTORIAL LETTER ASSIGNMENT 2 SECOND SEMESTER 2018 MANAGERIAL FINANCE 4B [MAF412S]") FEEDBACK TUTORIAL LETTER ASSIGNMENT 2 SECOND SEMESTER 2018 MANAGERIAL FINANCE 4B [MAF412S] 1 MANAGERIAL FINANCE 4B Assignment 2 Feedback Dear Student, FEEDBACK TO ASSIGNMENT AND GUIDELINE TO THE EXAMINATION

FEEDBACK TUTORIAL LETTER ASSIGNMENT 2 SECOND SEMESTER 2018 MANAGERIAL FINANCE 4B [MAF412S] 1 MANAGERIAL FINANCE 4B Assignment 2 Feedback Dear Student, FEEDBACK TO ASSIGNMENT AND GUIDELINE TO THE EXAMINATION

ACTY 7292 Financial Statement Analysis Final Exam Semester 1, 2015

Faculty of Creative Industries & Business Department of Accounting and Finance Bachelor of Business ACTY 7292 Financial Statement Analysis Final Exam Date: Wednesday 1 st July 2015 Start time: 8.30AM 11.40AM

Faculty of Creative Industries & Business Department of Accounting and Finance Bachelor of Business ACTY 7292 Financial Statement Analysis Final Exam Date: Wednesday 1 st July 2015 Start time: 8.30AM 11.40AM

Return on Invested Capital CHAPTER

Return on Invested Capital 8 CHAPTER Return on Invested Capital Importance of Joint Analysis Joint analysis is where one measure is assessed relative to another Return on invested capital (ROI) is an important

Return on Invested Capital 8 CHAPTER Return on Invested Capital Importance of Joint Analysis Joint analysis is where one measure is assessed relative to another Return on invested capital (ROI) is an important

Module B Corporate Financing. Capital structure. Reference: LP Chapter 14.

Module B Corporate Financing Capital structure Reference: LP Chapter 14 MB Capital structure Content 1. Gearing 2. Effect on shareholders wealth 3. Capital structure decision 4. The FRICT framework 5.

Module B Corporate Financing Capital structure Reference: LP Chapter 14 MB Capital structure Content 1. Gearing 2. Effect on shareholders wealth 3. Capital structure decision 4. The FRICT framework 5.

Turnarounds. Financial Decline: When Bad Things Happen to Good Companies

Turnarounds Financial Decline: When Bad Things Happen to Good Companies 1 A Better Place 2 Financial Distress Risk View from an outsider s perspective investors creditors Also useful for evaluating prospects

Turnarounds Financial Decline: When Bad Things Happen to Good Companies 1 A Better Place 2 Financial Distress Risk View from an outsider s perspective investors creditors Also useful for evaluating prospects

Chapter -9 Financial Management

Chapter -9 Financial Management Business Studies (VKS) Definition Financial management is concerned with efficient acquisition and allocation of funds. In other words, financial management means estimating

Chapter -9 Financial Management Business Studies (VKS) Definition Financial management is concerned with efficient acquisition and allocation of funds. In other words, financial management means estimating

What do U.S. Airways, Apple Computer, Clorox, Kellogg, Dow Chemical, and

CHAPTER16 Working Capital Management What do U.S. Airways, Apple Computer, Clorox, Kellogg, Dow Chemical, and Family Dollar Stores have in common? Each led its industry in the latest CFO Magazine annual

CHAPTER16 Working Capital Management What do U.S. Airways, Apple Computer, Clorox, Kellogg, Dow Chemical, and Family Dollar Stores have in common? Each led its industry in the latest CFO Magazine annual

CHAPTER: 11 CONCLUSIONS AND SUGGESTIONS

CHAPTER: 11 CONCLUSIONS AND SUGGESTIONS 11.1 CONCLUSIONS On the basis of analysis of data gathered in the course of this research, following are the conclusions relating to the evaluation of management

CHAPTER: 11 CONCLUSIONS AND SUGGESTIONS 11.1 CONCLUSIONS On the basis of analysis of data gathered in the course of this research, following are the conclusions relating to the evaluation of management

LIQUIDITY MANAGEMENT Presentation by: CPA Richard Kamami Secretary, PSB,Murang a PSB 23rd November 2017

LIQUIDITY MANAGEMENT Presentation by: CPA Richard Kamami Secretary, PSB,Murang a PSB 23rd November 2017 Uphold public interest Outline Definitions Assessment of Liquidity Criticism Liquidity Management

LIQUIDITY MANAGEMENT Presentation by: CPA Richard Kamami Secretary, PSB,Murang a PSB 23rd November 2017 Uphold public interest Outline Definitions Assessment of Liquidity Criticism Liquidity Management

M.V.S.R Engineering College. Department of Business Managment

M.V.S.R Engineering College Department of Business Managment CONCEPTS IN FINANCIAL MANAGEMENT 1. Finance. a.finance is a simple task of providing the necessary funds (money) required by the business of

M.V.S.R Engineering College Department of Business Managment CONCEPTS IN FINANCIAL MANAGEMENT 1. Finance. a.finance is a simple task of providing the necessary funds (money) required by the business of

Learning Goal 1: Review accounts payable, the key components of credit terms, and the procedures for analyzing those terms.

Principles of Managerial Finance, 12e (Gitman) Chapter 15 Current Liabilities Management Learning Goal 1: Review accounts payable, the key components of credit terms, and the procedures for analyzing those

Principles of Managerial Finance, 12e (Gitman) Chapter 15 Current Liabilities Management Learning Goal 1: Review accounts payable, the key components of credit terms, and the procedures for analyzing those

Pennsylvania Small Business Development Centers. Understanding Financial Statements

Understanding Financial Statements The SBDC Program is a partnership funded by the Commonwealth of, Department of Community and Economic, the U. S. Small Business Administration and participating colleges

Understanding Financial Statements The SBDC Program is a partnership funded by the Commonwealth of, Department of Community and Economic, the U. S. Small Business Administration and participating colleges

PRINT Name: Brief Answer Key.

Financial & Managerial Accounting Fall 2009 Exam 2 General Instructions. Make sure you write answers clearly. Make sure to show your work when appropriate partial credit can be given for work shown. Finally,

Financial & Managerial Accounting Fall 2009 Exam 2 General Instructions. Make sure you write answers clearly. Make sure to show your work when appropriate partial credit can be given for work shown. Finally,

Running Head: RATIO ANALYSIS 1. Phase 2 Individual Project

Running Head: RATIO ANALYSIS 1 Phase 2 Individual Project RATIO ANALYSIS 2 Phase 2 Individual Project Apex Printing Ratios As of December 31, 2013 and 2012 2013 2012 Current ratio = Current Assets/Current

Running Head: RATIO ANALYSIS 1 Phase 2 Individual Project RATIO ANALYSIS 2 Phase 2 Individual Project Apex Printing Ratios As of December 31, 2013 and 2012 2013 2012 Current ratio = Current Assets/Current

Planning. Cash Flow. Sixth Edition. James J. Jurinski. David T. Filipek

Planning Cash Flow Sixth Edition James J. Jurinski David T. Filipek Planning Cash Flow Sixth Edition Contents About This Course How to Take This Course 1 Working Capital 1 Objectives of Financial Management

Planning Cash Flow Sixth Edition James J. Jurinski David T. Filipek Planning Cash Flow Sixth Edition Contents About This Course How to Take This Course 1 Working Capital 1 Objectives of Financial Management

During this session, we ll cover: Benefits of using ratios Information gathering Types of ratios and when to use them How to calculate them More

During this session, we ll cover: Benefits of using ratios Information gathering Types of ratios and when to use them How to calculate them More importantly, how to interpret them Pinpoint potential problem

During this session, we ll cover: Benefits of using ratios Information gathering Types of ratios and when to use them How to calculate them More importantly, how to interpret them Pinpoint potential problem

CHAPTER 5. Liquidity AnALysis. of Sample Real. EstatE CompaniEs

CHAPTER 5 Liquidity AnALysis of Sample Real EstatE CompaniEs 150 MEANING The ability of a company to meet the short and long term obligations is known as Liquidity. The maturity period of Short term means

CHAPTER 5 Liquidity AnALysis of Sample Real EstatE CompaniEs 150 MEANING The ability of a company to meet the short and long term obligations is known as Liquidity. The maturity period of Short term means

UNAUDITED FINANCIAL STATEMENTS FOR THE FIRST QUARTER ENDED 31 MARCH 2017

UNAUDITED FINANCIAL STATEMENTS FOR THE FIRST QUARTER ENDED 31 MARCH 2017 1(a)(i) A comprehensive income statement (for the group) together with a comparative statement for the corresponding period of the

UNAUDITED FINANCIAL STATEMENTS FOR THE FIRST QUARTER ENDED 31 MARCH 2017 1(a)(i) A comprehensive income statement (for the group) together with a comparative statement for the corresponding period of the

Quiz Bomb. Page 1 of 12

Page 1 of 12 Quiz Bomb Indicate whether the following statements are True or False. Support your answer with reason: 1. Public finance is the study of money management of individual. False. Public finance

Page 1 of 12 Quiz Bomb Indicate whether the following statements are True or False. Support your answer with reason: 1. Public finance is the study of money management of individual. False. Public finance

Cash flow to grow. The best sources of working capital for SMEs

Cash flow to grow. The best sources of working capital for SMEs Content: Introduction Why is it difficult for SMEs to seek working capital? Information asymmetry Lack of collateral High cost to entry Short

Cash flow to grow. The best sources of working capital for SMEs Content: Introduction Why is it difficult for SMEs to seek working capital? Information asymmetry Lack of collateral High cost to entry Short

Working Capital Management

Working Capital Management The nature, elements and importance of working capital Working Capital equals value of raw materials, work-in-progress, finished goods inventories and accounts receivable less

Working Capital Management The nature, elements and importance of working capital Working Capital equals value of raw materials, work-in-progress, finished goods inventories and accounts receivable less

Gitman& Zutter (2012:358)

") The Cost of Capital Management need to understand the cost of capital to select long-term investments after assessing their acceptability and relative rangkings. Gitman& Zutter (2012:358) The cost of capital

The Cost of Capital Management need to understand the cost of capital to select long-term investments after assessing their acceptability and relative rangkings. Gitman& Zutter (2012:358) The cost of capital

Innovations for Agriculture

DIME Impact Evaluation Workshop Innovations for Agriculture 16-20 June 2014, Kigali, Rwanda Facilitating Savings for Agriculture: Field Experimental Evidence from Rural Malawi Lasse Brune University of

DIME Impact Evaluation Workshop Innovations for Agriculture 16-20 June 2014, Kigali, Rwanda Facilitating Savings for Agriculture: Field Experimental Evidence from Rural Malawi Lasse Brune University of

Chapter 22: Finance Operations

Chapter 22: Finance Operations Finance companies provide short- and intermediate-term credit to consumers and small businesses. Although other financial institutions provide this service, only finance

Chapter 22: Finance Operations Finance companies provide short- and intermediate-term credit to consumers and small businesses. Although other financial institutions provide this service, only finance

CFIN4 Chapter 2 Analysis of Financial Statements

1. The income statement measures the flow of funds into (i.e. revenue) and out of (i.e. expenses) the firm over a certain time period. It is always based on accounting data. Income statement 2. The balance

1. The income statement measures the flow of funds into (i.e. revenue) and out of (i.e. expenses) the firm over a certain time period. It is always based on accounting data. Income statement 2. The balance

(i) A company with a cash flow problem that is having difficulty collecting its debts.

A company with a cash flow problem that is having difficulty collecting its debts.") Answer on question #41311 - Management - Other For each of the following situations, explain what the most suitable source of finance is: (i) A company with a cash flow problem that is having difficulty

Answer on question #41311 - Management - Other For each of the following situations, explain what the most suitable source of finance is: (i) A company with a cash flow problem that is having difficulty

FINANCIAL MANAGEMENT

FINANCIAL MANAGEMENT Question 1: What is financial management? Explain the functions of financial management. (May 13, Nov 11) (Mark 7) Answer: Financial management is that specialized activity which is

FINANCIAL MANAGEMENT Question 1: What is financial management? Explain the functions of financial management. (May 13, Nov 11) (Mark 7) Answer: Financial management is that specialized activity which is

Session 2, Sunday, April 2nd (1:30-5:00) v Association for Financial Professionals. All rights reserved. Session 3-1

v Association for Financial Professionals. All rights reserved. Session 3-1") Session 2, Sunday, April 2nd (1:30-5:00) v2.0 2014 Association for Financial Professionals. All rights reserved. Session 3-1 Chapters Covered Financial Accounting and Reporting: Part I, Domain B Chapter

Session 2, Sunday, April 2nd (1:30-5:00) v2.0 2014 Association for Financial Professionals. All rights reserved. Session 3-1 Chapters Covered Financial Accounting and Reporting: Part I, Domain B Chapter

Chapter 2. Learning Objectives. Topics Covered. Financial Statement and Cash Flow Analysis

Chapter 2 Financial Statement and Cash Flow Analysis 1 Learning Objectives Interpret information contained in the balance sheet, income statement, and statement of cash flows. Explain why income differs

Chapter 2 Financial Statement and Cash Flow Analysis 1 Learning Objectives Interpret information contained in the balance sheet, income statement, and statement of cash flows. Explain why income differs

PART I - INFORMATION REQUIRED FOR QUARTERLY AND FULL YEAR RESULTS ANNOUNCEMENTS

A-SONIC AEROSPACE LIMITED PART I - INFORMATION REQUIRED FOR QUARTERLY AND FULL YEAR RESULTS ANNOUNCEMENTS SECOND QUARTER FINANCIAL STATEMENTS 1(a) An income statement and statement of comprehensive income

A-SONIC AEROSPACE LIMITED PART I - INFORMATION REQUIRED FOR QUARTERLY AND FULL YEAR RESULTS ANNOUNCEMENTS SECOND QUARTER FINANCIAL STATEMENTS 1(a) An income statement and statement of comprehensive income

CHAPTER 3. Analysis of Financial Statements

CHAPTER 3 Analysis of Financial Statements 1 Topics in Chapter Ratio analysis Du Pont system Effects of improving ratios Limitations of ratio analysis Qualitative factors 2 Determinants of Intrinsic Value:

CHAPTER 3 Analysis of Financial Statements 1 Topics in Chapter Ratio analysis Du Pont system Effects of improving ratios Limitations of ratio analysis Qualitative factors 2 Determinants of Intrinsic Value:

Finance Operations CHAPTER OBJECTIVES. The specific objectives of this chapter are to: identify the main sources and uses of finance company funds,

22 Finance Operations CHAPTER OBJECTIVES The specific objectives of this chapter are to: identify the main sources and uses of finance company funds, describe how finance companies are exposed to various

22 Finance Operations CHAPTER OBJECTIVES The specific objectives of this chapter are to: identify the main sources and uses of finance company funds, describe how finance companies are exposed to various

CHAPTER 17 FINANCIAL PLANNING AND FORECASTING

CHAPTER 17 FINANCIAL PLANNING AND FORECASTING Multiple Choice: Conceptual Easy: Percent of sales method (Difficulty: E = Easy, M = Medium, and T = Tough) Answer: e Diff: E 1. The percent of sales method

CHAPTER 17 FINANCIAL PLANNING AND FORECASTING Multiple Choice: Conceptual Easy: Percent of sales method (Difficulty: E = Easy, M = Medium, and T = Tough) Answer: e Diff: E 1. The percent of sales method

Indian Accounting Standard (Ind AS) 23 Borrowing Costs

23 Borrowing Costs") Indian Accounting Standard (Ind AS) 23 Borrowing Costs Core Principle Borrowing costs that are directly attributable to the acquisition, construction or production of a qualifying asset form part of the

Indian Accounting Standard (Ind AS) 23 Borrowing Costs Core Principle Borrowing costs that are directly attributable to the acquisition, construction or production of a qualifying asset form part of the

Example Accounts Only

CaseWare Australia & New Zealand Large Streamlined Pty Ltd Financial Statements Disclaimer: These financials include illustrative disclosures for a large proprietary company lodging financial statements

CaseWare Australia & New Zealand Large Streamlined Pty Ltd Financial Statements Disclaimer: These financials include illustrative disclosures for a large proprietary company lodging financial statements

Georgia Banking School Financial Statement Analysis. Dr. Christopher R Pope Terry College of Business University of Georgia

Georgia Banking School Financial Statement Analysis Dr. Christopher R Pope Terry College of Business University of Georgia Introduction Objective My objective is to introduce you to the analysis of financial

Georgia Banking School Financial Statement Analysis Dr. Christopher R Pope Terry College of Business University of Georgia Introduction Objective My objective is to introduce you to the analysis of financial

CHAPTER 2 ANALYSIS OF FINANCIAL STATEMENTS

TRUE/FALSE CHAPTER 2 ANALYSIS OF FINANCIAL STATEMENTS 1. The income statement measures the flow of funds into (i.e. revenue) and out of (i.e. expenses) the firm over a certain time period. It is always

TRUE/FALSE CHAPTER 2 ANALYSIS OF FINANCIAL STATEMENTS 1. The income statement measures the flow of funds into (i.e. revenue) and out of (i.e. expenses) the firm over a certain time period. It is always

FINANCIAL RATIOS 2 Page 1 of 5. The following is information concerning ABC Company and XYZ Company.

FINANCIAL RATIOS 2 Page 1 of 5 The following is information concerning ABC Company and XYZ Company. ABC Company XYZ Company CURRENT ASSETS: Cash 22,600 42,800 Accounts and Notes Receivable 92,500 101,100

FINANCIAL RATIOS 2 Page 1 of 5 The following is information concerning ABC Company and XYZ Company. ABC Company XYZ Company CURRENT ASSETS: Cash 22,600 42,800 Accounts and Notes Receivable 92,500 101,100

FINANCIAL RATIOS 3 Page 1 of 5. The following is information concerning ABC Company and XYZ Company.

FINANCIAL RATIOS 3 Page 1 of 5 The following is information concerning ABC Company and XYZ Company. ABC Company XYZ Company CURRENT ASSETS: Cash 18,700 33,000 Accounts and Notes Receivable 43,000 59,800

FINANCIAL RATIOS 3 Page 1 of 5 The following is information concerning ABC Company and XYZ Company. ABC Company XYZ Company CURRENT ASSETS: Cash 18,700 33,000 Accounts and Notes Receivable 43,000 59,800

Topic 8 Ratio Analysis. Higher Business Management

Topic 8 Ratio Analysis Higher Business Management 1 Learning Intentions / Success Criteria Learning Intentions Ratio analysis Success Criteria Learners should be able to describe and explain: the purpose

Topic 8 Ratio Analysis Higher Business Management 1 Learning Intentions / Success Criteria Learning Intentions Ratio analysis Success Criteria Learners should be able to describe and explain: the purpose

Unemployment in the Great Recession Compared to the 1980s

Unemployment in the Great Recession Compared to the 1980s Richard A. Hobbie Executive Director National Association of State Workforce Agencies Assisted by Gina Turrini Please direct questions or comments

Unemployment in the Great Recession Compared to the 1980s Richard A. Hobbie Executive Director National Association of State Workforce Agencies Assisted by Gina Turrini Please direct questions or comments

12 CREDIT LINES & CARDS YOU CAN GET FOR YOUR BUSINESS

12 CREDIT LINES & CARDS YOU CAN GET FOR YOUR BUSINESS 12 Credit Lines and Cards You Can Get for Your Business A credit line, or line of credit (LOC), is an agreement between a financial institution or

12 CREDIT LINES & CARDS YOU CAN GET FOR YOUR BUSINESS 12 Credit Lines and Cards You Can Get for Your Business A credit line, or line of credit (LOC), is an agreement between a financial institution or

Asset and Net Worth Growth Loan Allocation Trends 2

Growth, Capital, and Concentration Risk Management Jonathan Jackson, CFA Advisor Catalyst Strategic Solutions Asset and Net Worth Growth 1 Asset and Net Worth Growth Loan Allocation Trends 2 Loan Allocations

Growth, Capital, and Concentration Risk Management Jonathan Jackson, CFA Advisor Catalyst Strategic Solutions Asset and Net Worth Growth 1 Asset and Net Worth Growth Loan Allocation Trends 2 Loan Allocations

chapter 27 Providing and Obtaining Credit 27.1 Credit Policy SELF-TEST

chapter 27 Providing and Obtaining Credit Chapter 22 covered the basics of working capital management, including a brief discussion of trade credit from the standpoint of firms that grant credit and report

chapter 27 Providing and Obtaining Credit Chapter 22 covered the basics of working capital management, including a brief discussion of trade credit from the standpoint of firms that grant credit and report

ACC-501 Final Term Subjective

ACC-501 Final Term Subjective What is optimal credit policy state? 3 The optimal amount is determined by the point at which the incremental cash flows from increased sales are exactly equal to the incremental

ACC-501 Final Term Subjective What is optimal credit policy state? 3 The optimal amount is determined by the point at which the incremental cash flows from increased sales are exactly equal to the incremental

Accounting Advance Certificate in Business Administration Study Notes & Practice Questions Chapter 2: Financial Ratios

Accounting Advance Certificate in Business Administration Study Notes & Practice Questions Chapter 2: Financial Ratios 1 INTRODUCTION Chapter 2: Financial Ratios 2014 Financial statement is a data summary

Accounting Advance Certificate in Business Administration Study Notes & Practice Questions Chapter 2: Financial Ratios 1 INTRODUCTION Chapter 2: Financial Ratios 2014 Financial statement is a data summary

AFP Financial Planning & Analysis Learning System Session 2, Sunday, April 2nd (1:30-5:00)

") AFP Financial Planning & Analysis Learning System Session 2, Sunday, April 2nd (1:30-5:00) Chapters Covered Financial Accounting and Reporting: Part I, Domain B Chapter 7 Ratio Analysis: Part I, Domain

AFP Financial Planning & Analysis Learning System Session 2, Sunday, April 2nd (1:30-5:00) Chapters Covered Financial Accounting and Reporting: Part I, Domain B Chapter 7 Ratio Analysis: Part I, Domain

Financial Management Masters of Business Administration Study Notes & Tutorial Questions Chapter 7: Analysis & Interpretation of Financial Statement

Financial Management Masters of Business Administration Study Notes & Tutorial Questions Chapter 7: Analysis & Interpretation of Financial 1 INTRODUCTION Financial statement is a data summary on asset,

Financial Management Masters of Business Administration Study Notes & Tutorial Questions Chapter 7: Analysis & Interpretation of Financial 1 INTRODUCTION Financial statement is a data summary on asset,

Business Finance Bachelors of Business Study Notes & Tutorial Questions Chapter 5: Financial Analysis

Business Finance Bachelors of Business Study Notes & Tutorial Questions Chapter 5: Financial Analysis 1 INTRODUCTION Chapter 5: Financial Analysis 2018 Financial statement is a data summary on asset, liability

Business Finance Bachelors of Business Study Notes & Tutorial Questions Chapter 5: Financial Analysis 1 INTRODUCTION Chapter 5: Financial Analysis 2018 Financial statement is a data summary on asset, liability

7 2010, 2011, 2012 & 2013 AICPA

The 7 Financial Shenanigans: How Companies Cook the Books Leah Donti Ldonti@AdvantageMontrealSeminars.com 2010, 2011, 2012 & 2013 AICPA Outstanding Discussion Leader Award Recipient Welcome! Agenda Games

The 7 Financial Shenanigans: How Companies Cook the Books Leah Donti Ldonti@AdvantageMontrealSeminars.com 2010, 2011, 2012 & 2013 AICPA Outstanding Discussion Leader Award Recipient Welcome! Agenda Games

CHAPTER 7. Stock Valuation

Principles of Managerial Finance Solution Lawrence J. Gitman CHAPTER 7 Stock Valuation INSTRUCTOR S RESOURCES Overview This chapter continues on the valuation process introduced in Chapter 6 for bonds.

Principles of Managerial Finance Solution Lawrence J. Gitman CHAPTER 7 Stock Valuation INSTRUCTOR S RESOURCES Overview This chapter continues on the valuation process introduced in Chapter 6 for bonds.

Hybrid Portfolio Objectives HYBRID PORTFOLIO OBJECTIVES APRIL 2017 UPDATE

Hybrid Portfolio Objectives 01042017 HYBRID PORTFOLIO OBJECTIVES APRIL 2017 UPDATE Risk Level 1 - Cautious This portfolio is designed for a cautious investor who is primarily concerned with capital preservation

Hybrid Portfolio Objectives 01042017 HYBRID PORTFOLIO OBJECTIVES APRIL 2017 UPDATE Risk Level 1 - Cautious This portfolio is designed for a cautious investor who is primarily concerned with capital preservation

Aims of Financial Financial Management:

CHAPTER 9 Financial Management Introduction Business Finance = Money or funds available for a business for its operations (that is, for some specific purpose) is called finance. It is indispensable for

CHAPTER 9 Financial Management Introduction Business Finance = Money or funds available for a business for its operations (that is, for some specific purpose) is called finance. It is indispensable for

Marketable Securities 2,018 1,942 1,686 1,714 2,314 2,098 2,287 2,239 2,070 2,

Consolidated Balance Sheet Current Assets Cash & Deposits Trade Notes & Accounts Receivable 12,378 11,748 12,449 10,599 11,880 10,206 12,260 9,308 15,446 10,145 11,416 11,341 11,039 11,610 10,255

Consolidated Balance Sheet Current Assets Cash & Deposits Trade Notes & Accounts Receivable 12,378 11,748 12,449 10,599 11,880 10,206 12,260 9,308 15,446 10,145 11,416 11,341 11,039 11,610 10,255

Tutorial Letter: May 2014 examination session. Financial Management 2 (FM202) Semester One 2014

Semester One 2014") Tutorial Letter: May 2014 examination session Financial Management 2 () Semester One 2014 Dear Student Please make note of the following key areas and notes pertaining to the Financial Management 2 Examination

Tutorial Letter: May 2014 examination session Financial Management 2 () Semester One 2014 Dear Student Please make note of the following key areas and notes pertaining to the Financial Management 2 Examination

Fin 622 Quiz #4. MC : Imtiaz Sarwar

Fin 622 Quiz #4 MC080200629 : Imtiaz Sarwar Question # 1 of 15 ( Start time: 11:13:02 AM ) Which of the following investment criteria does not take the time value of money into consideration? Simple payback

Fin 622 Quiz #4 MC080200629 : Imtiaz Sarwar Question # 1 of 15 ( Start time: 11:13:02 AM ) Which of the following investment criteria does not take the time value of money into consideration? Simple payback

Section 7 Credit risk analysis

Section 7 Credit risk analysis A man goes bankrupt gradually, then suddenly. --Ernst Hemingway 1 Learning objectives After studying this chapter, you will understand A typical process of the financial

Section 7 Credit risk analysis A man goes bankrupt gradually, then suddenly. --Ernst Hemingway 1 Learning objectives After studying this chapter, you will understand A typical process of the financial

Cambridge Assessment International Education Cambridge International General Certificate of Secondary Education. Published

Cambridge Assessment International Education Cambridge International General Certificate of Secondary Education ACCOUNTING 045/ Paper 07 MARK SCHEME Maximum Mark: 0 Published This mark scheme is published

Cambridge Assessment International Education Cambridge International General Certificate of Secondary Education ACCOUNTING 045/ Paper 07 MARK SCHEME Maximum Mark: 0 Published This mark scheme is published

PROSPECTUS October 1, 2016

PROSPECTUS October 1, 2016 VALIC COMPANY I Dynamic Allocation Fund (Ticker Symbol: VDAFX) This Prospectus contains information you should know before investing, including information about risks. Please

PROSPECTUS October 1, 2016 VALIC COMPANY I Dynamic Allocation Fund (Ticker Symbol: VDAFX) This Prospectus contains information you should know before investing, including information about risks. Please

FINANCIAL EVALUATION INNOVATION AND NEW PRODUCT DEVELOPMENT

FINANCIAL EVALUATION INNOVATION AND NEW PRODUCT DEVELOPMENT FINANCIAL EVALUATION Our topic includes; Break-Even Analysis Profit-Loss Analysis İncremental Cash Flow Risk Analysis BREAK-EVEN ANALYSIS One

FINANCIAL EVALUATION INNOVATION AND NEW PRODUCT DEVELOPMENT FINANCIAL EVALUATION Our topic includes; Break-Even Analysis Profit-Loss Analysis İncremental Cash Flow Risk Analysis BREAK-EVEN ANALYSIS One