MACQUARIE INTERNATIONAL INFRASTRUCTURE FUND LIMITED ANALYST PACK APRIL 2008

|

|

|

- Aubrey Boone

- 5 years ago

- Views:

Transcription

1 MACQUARIE INTERNATIONAL INFRASTRUCTURE FUND LIMITED ANALYST PACK APRIL 2008

Pty Limited (MIMAL) is the manager of MIIF.")

2 disclaimer This information package which includes the analyst model and other information (the Analyst Pack or Pack) has been prepared by Macquarie International Infrastructure Fund Limited (MIIF), which is a Bermudian registered mutual fund company listed on the Singapore Exchange Securities Trading Limited. Macquarie Infrastructure Management (Asia) Pty Limited (MIMAL) is the manager of MIIF. MIMAL is a wholly owned subsidiary of Macquarie Capital Group Limited (MCGL). The Analyst Pack has been prepared in good faith to assist analysts in the development of their own models. The Analyst Pack does not purport to forecast the asset value, income or distributions of MIIF or its subsidiaries or related companies, nor the value, income or distributions of any other entity. None of MIIF, MIMAL nor any entity in MCGL shall be in any way responsible or have any liability in respect of the accuracy of any statement or calculation within the Analyst Pack. Any assumptions or forecasts contained in the Analyst Pack are intended as a guide to analysts only. They do not represent forecasts or statements of certainty of MIIF, MIMAL, MCGL or any other party and are not intended to be a representation that the assumptions will or are likely to occur or that the assumptions are reasonable, reliable or accurate. The recipient should do their own research and form their own judgment in relation to any assumptions, forecasts, or estimates contained in the Analyst Pack and not rely on any information in the Analyst Pack as being either absolute or the likely outcome. The Analyst Pack does not purport to list the assumptions or risks which may infl uence the valuation of MIIF. Any information with respect to tax treatment is provided without warranty and for information only. The recipient should seek professional advice in respect of any taxation assumptions required to analyse MIIF. MIIF does not guarantee that the information provided is up to date, or accept any obligation to correct or update any information contained in the Analyst Pack or to inform the recipient that the Analyst Pack is no longer accurate or up to date whether as a result of new information becoming available or otherwise. The Analyst Pack remains the property of MIIF and may not be reproduced in part or whole without express written permission from MIIF. None of the entities noted in this document is an authorised deposit-taking institution for the purposes of the Banking Act 1959 (Commonwealth of Australia). The obligations of these entities do not represent deposits or other liabilities of Macquarie Bank Limited ABN (MBL). MBL does not guarantee or otherwise provide assurance in respect of the obligations of these entities. Investments in MIIF are subject to investment risk, including possible delays in repayment and loss of income and capital invested. None of MIIF, MIMAL nor any entity in MCGL guarantees any particular rate of return on MIIF shares or the performance of MIIF, nor do they guarantee the repayment of capital from MIIF. The Analyst Pack does not constitute an offer or invitation for subscription or purchase of shares of MIIF and it is not recommending or soliciting offers to buy shares of MIIF. The Analyst Pack does not take into account the investment objectives, fi nancial situation and particular needs of any potential investor nor does it address or attempt to quantify any of the risks associated with MIIF s business or an investment in the shares of MIIF. Before making an investment in MIIF, the prospective investor should consider whether such an investment is appropriate to their particular investment needs, objectives and fi nancial circumstances and consult an investment adviser if necessary. Information, including forecast fi nancial information, in this Analyst Pack should not be considered as a recommendation in relation to holding, purchasing or selling shares, securities or other instruments in MIIF. Due care and attention has been used in the preparation of forecast information. However, actual results may vary from forecasts and any variation may be materially positive or negative. Forecasts by their very nature are subject to uncertainty and contingencies, many of which are outside the control of MIIF. Past performance is not a reliable indication of future performance.

3 ANALYST PACK Welcome to the 2008 Macquarie International Infrastructure Fund Limited (MIIF) Analyst Pack (Analyst Pack or Pack). This Pack is primarily designed to assist institutional and professional investors and analysts to understand the MIIF business and its investments. The Pack includes a set of background notes on MIIF, on each of the assets within its portfolio and an Analyst Model (the Model) that outlines a possible format for valuing MIIF. The Model does not purport to forecast the asset value, income or distributions of MIIF, nor the value, income or distributions of any other entity. Any assumptions contained within the Pack are intended to be a guide only and do not represent the forecasts of MIIF, Macquarie Infrastructure Management (Asia) Pty Limited (MIMAL or the Manager) or any entity in the Macquarie Capital Group Limited (MCGL) or any other entity. MCGL does not represent that the forecasts will be achieved, the assumptions will occur or that the assumptions are reasonable, reliable or accurate. All fi gures unless stated otherwise, are presented in Singapore dollars, which is MIIF's functional and presentation currency.

4

5 Table of Contents Background... 1 Recent Key Events... 2 Asset Portfolio... 5 Diversifi ed Portfolio... 7 Management... 8 Investment Strategy Shares on Issue Dividends Fees Group Structure Valuation Policy Arqiva National Grid Wireless Canadian Aged Care Changshu Xinghua Port Hua Nan Expressway infravest Wind Power Taiwan Broadband Communications MEIF Overview of the Analyst Model Corporate Information MACQUARIE INTERNATIONAL INFRASTRUCTURE FUND LIMITED ANALYST PACK 5

6

7 Macquarie International Infrastructure Fund Limited BACKGROUND MIIF, a Bermudian mutual fund company, is today a leading Asia-based private owner and operator of infrastructure assets with signifi cant investments in toll roads, airports, renewable energy, communications infrastructure, broadcast infrastructure, transportation infrastructure and aged care infrastructure assets, among others. MIIF was the fi rst infrastructure fund to list on the main board of the Singapore Exchange Securities Trading Limited (SGX-ST). It listed on the SGX-ST on 27 May 2005 and is today a top 100 SGX company with a market capitalisation as at 31 December 2007 of approximately S$1.3 billion and over 6,300 investors, including retail investors and some of the world s foremost institutional investors. MIIF is managed by MIMAL, a subsidiary of Macquarie Capital Funds which, through special purpose management companies, has over A$56 billion (S$70 billion) of equity under management as at 31 December MIIF is the fl agship Asian listed infrastructure fund of MCGL. MIIF benefi ts from Macquarie s infrastructure expertise in sourcing new investment opportunities and acquiring infrastructure assets in diversifi ed sectors with a focus on Asia. MACQUARIE INTERNATIONAL INFRASTRUCTURE FUND LIMITED ANALYST PACK 1

8 RECENT KEY EVENTS 20 March 2008 Acquisition of infravest Wind Power, an operating wind farm in Taiwan MIIF s equity commitment was NT$597.9 million (S$27.9 million), including transaction costs, for an effective interest of 100.0% 14 March 2008 MIIF unwound total return swap (TRS) and sold its interest in Macquarie Airports (MAp) Total consideration of A$120.0 million (S$154.2 million) for MIIF s 35,470,000 securities in MAp 19 November 2007 Acquisition of Hua Nan Expressway in China MIIF s equity commitment for an effective interest of 81% was RMB1,513 million (S$295.7 million) 1, including transaction costs 16 November 2007 Divestment of 100% interest in TanQuid Total consideration of 88.0 million (S$187.3 million) 14 November 2007 Divestment of 3.2% interest in Brussels Airport Total consideration of 50.9 million (S$107.9 million) 16 August 2007 Completion of Taiwan Broadband Communications (TBC) refi nancing MIIF received total proceeds of US$68.3 million (S$104.1 million) from the refi nancing, which was treated as a return of capital 27 July 2007 MIIF unwound TRS and sold its interest in Macquarie Communications Infrastructure Group (MCG) Total consideration of A$112.6 million (S$147.2 million) for MIIF's 18,780,000 securities in MCG 16 July 2007 MIIF acquired TBC MIIF acquired a 20% economic interest in TBC from Och-Ziff Capital Management Group for US$175.5 million (S$265.9 million), including transaction costs 1 Originally announced acquisition price of S$329.5 million comprised of S$295.7 million invested at acquisition, and S$33.8 million of acquisition adjustments contingent upon certain events and is yet to be paid

for MIIF s 17,592,000 securities in DUET 2 July 2007 MIIF unwound TRS and sold its interest in Macquarie Infrastructure Company (MIC) Total consideration of US$24.6 million (S$37.")

9 4 July 2007 MIIF unwound TRS and sold its interest in DUET Group (DUET) Total consideration of A$65.1 million (S$85.2 million) for MIIF s 17,592,000 securities in DUET 2 July 2007 MIIF unwound TRS and sold its interest in Macquarie Infrastructure Company (MIC) Total consideration of US$24.6 million (S$37.4 million) for MIIF s 599,000 securities in MIC 4 April 2007 Arqiva acquired 100% of National Grid Wireless (NGW) Total consideration of 2.5 billion (S$7.5 billion) MIIF participated in the Arqiva rights issue for 87 million (S$259.1 million) 22 January 2007 MIIF divested 50% interest in Novera Macquarie Renewable Energy (NMRE) Total consideration of 29.9 million (S$90.8 million) MACQUARIE INTERNATIONAL INFRASTRUCTURE FUND LIMITED ANALYST PACK 2 3

10

11 ASSET PORTFOLIO Unlisted Direct Investments INVESTMENT VEHICLE UNDERLYING ASSET ASSET LOCATION MIIF ECONOMIC INTEREST IN ASSET 8.7% MACQUARIE-MANAGED FUNDS' ECONOMIC INTEREST IN ASSET 75.8% Arqiva Communications infrastructure United Kingdom INVESTMENT VEHICLE UNDERLYING ASSET ASSET LOCATION MIIF ECONOMIC INTEREST IN ASSET MACQUARIE-MANAGED FUNDS' ECONOMIC INTEREST IN ASSET 100.0% Canadian Aged Care (CAC) Aged care infrastructure Canada 55.0% by way of TRS INVESTMENT VEHICLE Changshu Xinghua Port (CXP) UNDERLYING ASSET Port ASSET LOCATION China MIIF ECONOMIC INTEREST IN ASSET 38.0% MACQUARIE-MANAGED FUNDS' ECONOMIC INTEREST IN ASSET 38.0% INVESTMENT VEHICLE Hua Nan Expressway (HNE) UNDERLYING ASSET Toll road ASSET LOCATION China MIIF ECONOMIC INTEREST IN ASSET 81.0% MACQUARIE-MANAGED FUNDS' ECONOMIC INTEREST IN ASSET 81.0% INVESTMENT VEHICLE infravest Wind Power (infravest) UNDERLYING ASSET Renewable energy ASSET LOCATION Taiwan MIIF ECONOMIC INTEREST IN ASSET 100.0% MACQUARIE-MANAGED FUNDS' ECONOMIC INTEREST IN ASSET 100.0% INVESTMENT VEHICLE Taiwan Broadband Communications (TBC) UNDERLYING ASSET Communications infrastructure ASSET LOCATION Taiwan MIIF ECONOMIC INTEREST IN ASSET 20.0% MACQUARIE-MANAGED FUNDS' ECONOMIC INTEREST IN ASSET 80.0% Unlisted Fund Investment INVESTMENT VEHICLE UNDERLYING ASSETS ASSET LOCATION MIIF ECONOMIC INTEREST IN ASSET 6.3% MACQUARIE-MANAGED FUNDS' ECONOMIC INTEREST IN ASSET 24.5% Macquarie European Infrastructure Fund (MEIF) Diversifi ed infrastructure portfolio Developed European countries MACQUARIE INTERNATIONAL INFRASTRUCTURE FUND LIMITED ANALYST PACK 4 5

12

13 DIVERSIFIED PORTFOLIO 2 MIIF s investment portfolio is diversifi ed by sector and country. As at 31 March Portfolio Composition by Asset Hua Nan Expressway 18.3% CXP 7.0% InfraVest 1.7% MEIF 21.7% TBC 10.3% CAC 9.1% Arqiva + NGW 31.8% Portfolio Diversifi cation by Country Taiwan 12.0% Netherlands 0.5% China 25.4% UK 44.5% France 5.8% Sweden 1.3% Portfolio Diversifi cation by Sector Aged Care 9.1% Transport 26.5% Belgium 1.4% Renewable Energy 2.3% Ports 7.0% Canada 9.1% Utilities & Energy 8.8% Airports & Airport Services 4.2% Communications Infrastructure 42.1% MACQUARIE INTERNATIONAL INFRASTRUCTURE FUND LIMITED ANALYST PACK 2 Numbers are subject to rounding. 3 Based on 31 December 2007 valuations including the acquisition of infravest at cost. The disposal of MAp has been completed and has been excluded. 6 7

14 MANAGEMENT MIIF has appointed MIMAL as its sole and exclusive manager pursuant to a management agreement dated 19 May 2005 (Management Agreement). MIMAL was incorporated in Australia under the Corporations Act 2001 on 3 February 2005 and its current share capital is A$35,050,002. Its registered offi ce and principal place of business is Level 11, No.1 Martin Place, Sydney, New South Wales 2000, Australia. The MIMAL Singapore branch is located on level 11, 23 Church Street, Capital Square, Singapore MIMAL is a member of MCGL. MCGL is one of the global leaders in advising on the acquisition, disposal and fi nancing of infrastructure assets and the management of infrastructure investment vehicles and infrastructure assets on behalf of third-party investors. MIMAL is part of Macquarie Capital Funds which, through special purpose management companies, has over A$56 billion (S$70 billion) of equity under management. On behalf of retail and institutional investors Macquarie Capital Funds invests in infrastructure assets and businesses, including toll roads, airports and airport-related infrastructure, communications infrastructure, electricity and gas transmission and distribution networks, water utilities and rail. Macquarie Capital Funds has operated since 1996 and employs over 630 professionals. 4 MIMAL is licensed by the Australian Securities & Investments Commission as an Australian Financial Services Licensee to provide certain fi nancial services, including giving fi nancial product advice and dealing in investments. The Singapore branch of MIMAL is also licensed by the Monetary Authority of Singapore as a holder of a Capital Markets Services Licence to conduct the regulated activity of fund management in Singapore. MIMAL s resources are drawn from MCGL through a resources agreement dated 10 February 2005 between MIMAL and Macquarie Funds Management Holdings Pty Limited (MFMH). These resources include the non-exclusive use of personnel employed by MCGL primarily within Macquarie Capital Funds. Personnel and resources have also been provided by MFMH on a non-exclusive basis to other Macquarie Capital Funds under similar resources agreements. 4 As at 31 December 2007.

15 MACQUARIE INTERNATIONAL INFRASTRUCTURE FUND LIMITED ANALYST PACK 8 9

16

17 INVESTMENT STRATEGY MIIF s strategy is to invest in and acquire infrastructure assets that deliver an attractive and sustainable level of returns in the form of dividends, distributions and other cash fl ows in addition to the potential for capital growth. MIIF intends to make long-term investments in long-term assets with a long-term horizon and does not expect to actively trade the assets within its portfolio. Where MIIF acquires majority or substantial interests in an asset and can exert control over the business, it intends to pursue revenue growth and margin improvements as well as to optimise fi nancing structures. MIIF will also target investments in which it will acquire minority positions and where its partners have similar objectives to its own. Investment Criteria MIIF targets investments in a broad range of infrastructure sectors, seeking relatively lowrisk assets that exhibit some or all of the following characteristics: Provision of essential services to the community; Strategic competitive advantage due to high barriers to entry; Dominant market position; Sustainable and predictable cash fl ows over the long term; Potential for long-term capital growth; Experienced and capable operational management team; Long-term supply agreements or revenues that are governed by regulatory regimes; and Potential to increase returns to equity by capital structure optimisation. SHARES ON ISSUE Issue of Shares Initial Public Offering 27 May 2005 Over Allotment Option post IPO 7 June 2005 Number of Shares on Issue (000 s) Cumulative (000 s) Price (S$) 730, , , , Manager Performance Fee 23, , August Institutional/Retail Placement and Offer 17 November , ,279, Manager Performance Fee 2, ,282, August MIMAL opted to invest all of the performance fee in MIIF shares. MACQUARIE INTERNATIONAL INFRASTRUCTURE FUND LIMITED ANALYST PACK 10 11

18

19 DIVIDENDS Dividend Policy MIIF s dividend policy is based on the anticipated and stable cash fl ows from its investments. It is intended that all free recurring operating cash available for distribution subject to prudent reserves will be paid out by MIIF semi-annually as dividends. Payments The following table shows the dividends paid by MIIF since its IPO: Period ending Distribution per share H cents (paid 9 September 2005) H cents (paid 29 March 2006) H cents (paid 13 September 2006) H cents (paid 30 March 2007) H cents (paid 14 September 2007) H cents (payable on 5 May 2008) MIIF Dividends Jun Dec Jun Dec-06 Tax Implications 30-Jun Dec-07 As MIIF is incorporated in Bermuda and is not a resident in Singapore for tax purposes, dividends paid by MIIF are regarded as foreign-source income in Singapore. The foreign dividend is subject to Singapore corporate income tax when received in Singapore by corporate shareholders. Foreign dividends received by foreign investors with no permanent establishment in Singapore are generally not subject to Singapore income tax. Foreign dividends received by individuals in Singapore (whether resident or otherwise) are exempt from Singapore income tax. Note: All shareholders are advised to obtain their own professional tax advice in relation to the dividends paid by MIIF. MACQUARIE INTERNATIONAL INFRASTRUCTURE FUND LIMITED ANALYST PACK 12 13

20 FEES Management Agreement Under the terms of the Management Agreement, MIIF compensates MIMAL for managing its investments through base fees and performance fees. These fees are calculated for each quarter ending on 31 March, 30 June, 30 September and 31 December of each year. Base Fee The base fee is calculated on the following basis: 1.5% per annum of MIIF s Net Investment Value 6 ; and Payable quarterly in arrears. Fee Rebates (No Double Counting) Where a member of MCGL is entitled to be paid a base management fee for the management of any investment held by MIIF, the base fee payable by MIIF shall be reduced by MIIF s share of the actual base management fee payable to that member of MCGL in relation to the management of that investment. This is based on MIIF s percentage holding in the investment, provided that the base fee payable to MIMAL relating to that investment shall not be reduced to an amount less than zero. MEIF is the only remaining investment in MIIF's portfolio on which MIIF pays a management fee to MCGL. Base Fee Examples The following examples are for illustrative purposes and do not refl ect MIIF s position at a particular time. Base Fee Period 1 Base Fee Period 2 (A) Average market capitalisation over the last 15 SGX-ST trading days of the quarter $1,190,109,000 $1,202,906,000 (B) External borrowings at the end of the quarter $0 $150,000,000 (C) Cash or cash equivalents at the end of the quarter (D) Firm commitments to invest in future investments at the end of the quarter (E) MIIF % holding in an investment managed by a MCGL entity at the end of the quarter (F) Base management fee paid or payable by an investment of MIIF to a MCGL entity for the quarter $50,000,000 $85,000,000 $115,000,000 $0 25% 25% $1,000,000 $1,000,000 Number of days in the quarter Base Fee Period 1 Net investment value at the end of the quarter: = A + B C + D = $1,190,109,000 + $0 $50,000,000 + $115,000,000 = $1,255,109,000 Base Fee Period 2 Net investment value at the end of the quarter: = A + B C + D = $1,202,906,000 + $150,000,000 $85,000,000 + $0 = $1,267,906,000 Base fee for the quarter: = (Net investment value 1.5% 91/365) (E F) = ($1,255,109, % 91/365) (25% $1,000,000) = $4,443,764 Base fee for the quarter: = (Net investment value 1.5% 92/365) (E F) = ($1,267,906, % 92/365) (25% $1,000,000) = $4,543,727 6 Net investment value is the average market capitalisation over the last 15 SGX-ST trading days of the quarter; plus the external borrowings at the end of the quarter; less the cash or cash equivalents at the end of the quarter; plus fi rm commitments to invest in future investments at the end of the quarter.

21 MACQUARIE INTERNATIONAL INFRASTRUCTURE FUND LIMITED ANALYST PACK

22 Performance Fee The performance fee is calculated quarterly on the following basis: If the return on the shares for a quarter (including reinvestment of all dividends) is greater than zero and exceeds the benchmark return, the performance fee is equal to 20% of the return above the benchmark return for the quarter. If the return is less than the benchmark return in any quarter, the amount of the defi cit is carried forward; i.e. Performance fee = 20% (return benchmark return deficit brought forward); Payable quarterly in arrears; and The performance fee is payable to the Manager in cash. MIMAL may apply to invest all or a portion of the performance fee in MIIF shares. The Return The return is the average market capitalisation of MIIF over the last 15 SGX-ST trading days of the previous quarter (excluding the market capitalisation of additional shares issued during the last 15 SGX-ST trading days of the previous quarter) multiplied by the movement in the accumulation index for the shares over the relevant quarter expressed as a fraction. This is based on the average daily closing value of this index over the last 15 SGX-ST trading days of the quarter compared with the average daily closing value of this index over the last 15 SGX-ST trading days of the previous quarter. In the case of the fi rst quarter, the initial accumulation index fi gure ascribed to the shares on the listing date before the fi rst trade was used as a base for comparison. The Benchmark Return The benchmark return is the average market capitalisation of MIIF over the last 15 SGX-ST trading days of the previous quarter (excluding the market capitalisation of additional shares issued during the last 15 SGX-ST trading days of the previous quarter) multiplied by an annualised return of 8% per annum. The Defi cit The defi cit is the aggregate amount in respect of each quarter since a performance fee has become due and payable, not including the quarter in respect of which a calculation is being made, by which the benchmark return for each such quarter exceeds the return for that quarter (if any). The Accumulation Index The accumulation index measures the performance of MIIF over a period. It is calculated by an appropriately-qualifi ed independent party as the accumulated total return on the shares, including reinvestment of all distributions, from the date of listing of MIIF. The following graph shows the accumulation index of MIIF since IPO. 140% 120% 100% 80% 60% 40% May 05 Jun 05 Jul 05 Aug 05 Sep 05 Oct 05 Nov 05 Dec 05 Jan 06 Feb 06 Mar 06 Apr 06 May 06 Jun 06 Jul 06 Aug 06 Sep 06 Oct 06 Nov 06 Dec 06 Jan 07 Feb 07 Mar 07 Apr 07 May 07 Jun 07 Jul 07 Aug 07 Sep 07 Oct 07 Nov 07 Dec 07

23 MACQUARIE INTERNATIONAL INFRASTRUCTURE FUND LIMITED ANALYST PACK

24 Performance Fee Examples Set out below are examples of calculations of performance fee payable to MIMAL by MIIF. Performance Period Period 1 Period 2 Period 3 Period 4 (A) (C) (B) (Y) Average market capitalisation of MIIF over the last 15 SGX-ST trading days of the previous quarter Average closing accumulation index for the shares over the last 15 SGX-ST trading days of the previous quarter Average closing accumulation index for the shares over the last 15 SGX-ST trading days of the current quarter Benchmark rate of return for the quarter (1.08^(days in quarter/365) 1) $710,775,000 $710,775,000 $710,775,000 $710,775, % % % % (A2) Additional shares issued multiplied by issue price (27 days remaining in the quarter from date of issue) (C2) Accumulation index value ascribed to the shares based on their issue price (B2) Average closing accumulation index for the shares over the last 15 SGX-ST trading days of the current quarter (Y2) Benchmark rate of return for the additional shares (1.08^(27/365) 1) $100,000, % (D) Defi cit carried forward from the previous quarter $0 $6,954,116 $0

= $89,158 Deficit carried forward into next quarter: = $0 As the return for the quarter is greater than zero")

25 Performance Period 1 Return for the quarter: = A (B C)/C = $710,775,000 ( )/1.00 = $14,215,500 Benchmark return for the quarter: = A Y = $710,775, % = $13,769,710 Performance fee for the quarter: = 20% ($14,215,500 $13,769,710) = $89,158 Deficit carried forward into next quarter: = $0 As the return for the quarter is greater than zero and greater than the benchmark return for the quarter, a performance fee is payable in respect of the quarter of $89,158. Performance Period 3 Return for the quarter: = A (B C)/C = $710,775,000 ( )/1.03 = $48,305,097 Benchmark return for the quarter: = A Y = $710,775, % = $13,769,710 Performance fee for the quarter: = 20% ($48,305,097 $13,769,710 $6,954,116) = $5,516,254 Deficit carried forward into next quarter: = $0 As the return for the quarter is greater than zero and greater than the benchmark return for the quarter and the defi cit carried forward, a performance fee is payable in respect of the quarter of $5,516,254. Performance Period 2 Return for the quarter: = A (B C)/C = $710,775,000 ( )/1.02 = $6,968,382 Benchmark return for the quarter: = A Y = $710,775, % = $13,922,498 Performance fee for the quarter: = 20% ($6,968,382 $13,922,498) = $0 Deficit carried forward into next quarter: = $13,922,498 $6,968,382 = $6,954,116 As the return is less than the benchmark return for the quarter, a performance fee is not payable in respect of the quarter and the defi cit of $6,954,116 is carried forward to the next quarter. Performance Period 4 Return for the quarter: = (A (B C)/C) + (A2 (B2 C2)/C2) = ($710,775,000 ( )/1.10) + ($100,000,000 ( )/1.13) = $32,307,954 + $1,769,912 = $34,077,866 Benchmark return for the quarter: = (A Y) + (A2 Y2) = ($710,775, %) + ($100,000, %) = $14,493,422 Performance fee for the quarter: = 20% ($34,077,867 $14,493,422) = $3,916,889 The return (including the return on the additional shares) is greater than zero and greater than the benchmark return (including the benchmark return on the additional shares) for this quarter. As a result, a performance fee is payable in respect of the quarter of $3,916,889. MACQUARIE INTERNATIONAL INFRASTRUCTURE FUND LIMITED ANALYST PACK 18 19

26

27 GROUP STRUCTURE * MIIF s interest in Canadian Aged Care is held through a total return swap arrangement. MACQUARIE INTERNATIONAL INFRASTRUCTURE FUND LIMITED ANALYST PACK 20 21

28

29 VALUATION POLICY MIIF and its wholly owned subsidiaries (the Group) have adopted International Financial Reporting Standards (IFRS) as a basis for preparation of its fi nancial statements. The preparation of fi nancial statements in conformity with IFRS requires the use of accounting estimates. It also requires management to exercise judgement when applying the Group s accounting policies. The Group s investments are classifi ed as fi nancial assets. In accordance with the applicable IFRS, these fi nancial assets are held at fair value, with changes in the fair values of these assets refl ected as revaluation income in the income statement in the period in which they arise. The value of those fi nancial assets that are unlisted, or whose prices are not publicly quoted, is determined by the Manager using established valuation techniques. The Manager utilises a variety of these established valuation techniques and makes assumptions that are based on market conditions at each balance sheet date that form the basis of these valuations. The established valuation techniques adopted by the Manager will be based on one or more of the following valuation methods: Discounted cash fl ows; Capitalisation of earnings analysis, such as EBITDA multiple analysis; Valuation of similar investments; Reference to recent sales transactions of the same or similar securities; and Other methods as determined by the Manager. The Manager calculates the fair value of each asset at the end of each calendar quarter and adjusts the carrying value of each investment to match the valuation generated by the Manager. This process of marking to market the value of the Group s investments generates revaluation gains and losses, reported as revaluation income or expense. The updated asset valuations feed into the balance sheet of the Group at each calendar quarter end and are reported to the SGX in accordance with the SGX listing rules. This is included in the same report as the quarterly net asset value per share disclosure amongst other items. The half year and full year updated asset valuations generated by the Manager are subjected to review and endorsement by MIIF s independent auditors, the MIIF Audit and Risk Committee and the MIIF board. MACQUARIE INTERNATIONAL INFRASTRUCTURE FUND LIMITED ANALYST PACK 22 23

30

31 Arqiva ASSET NAME LOCATION EQUITY INVESTMENT MIIF'S INTEREST Arqiva UK S$175.7 million 8.7% interest Asset Overview Arqiva is one of only two TV broadcast transmission operators in the UK (National Grid Wireless (NGW) being the other, refer to page 35) and is a leading independent wireless site leasing provider in the UK. Arqiva provides transmission services to TV and radio broadcasters, site leasing to mobile phone and other wireless telecommunication companies and radio services to police, fi re and ambulance services. In April 2007, Arqiva announced the acquisition of NGW for a consideration of 2.5 billion. The acquisition has been under review by the UK competition authorities, who have required Arqiva and NGW to be held as two separate businesses. During the review process, NGW has been operating as a discrete entity, with separate management teams and customer contracts. On 8 August 2007 the Offi ce of Fair Trading referred the acquisition of NGW to the UK Competition Commission (Commission). On 11 March 2008, Arqiva announced that the Commission had conditionally approved the integration of Arqiva and NGW, subject to the agreement of suitable behavioural undertakings. The undertakings concern broadcast customers of the merged entity and comprise a package of measures ensuring ongoing high levels of customer service, price reductions for customers and the institution of an independent adjudicator to resolve disputes and oversee auditing of the Digital Switch Over (DSO). The Commission retains the option to require divestment if the undertakings cannot be agreed and completed. MACQUARIE INTERNATIONAL INFRASTRUCTURE FUND LIMITED ANALYST PACK 24 25

32 Ownership Structure MIIF has an 8.7% direct interest in Arqiva. Macquarie-managed funds' economic interest in Arqiva is 75.8%. Financing Structure MIIF s investment in Arqiva of S$175.7 million was made through a series of interposing entities including Macquarie UK Broadcast Holdings Ltd (MUKBHL), Macquarie UK Broadcast Services Plc (MUKBSL) and Macquarie UK Broadcast Limited (MUKBL). This investment is split 50:50 between ordinary shares and loan notes. These loan notes were issued by MUKBSL in January 2005 for million (MIIF s share of 27.5 million). Interest is paid at a fi xed rate of 13% pa, payable semi-annually in arrears on 30 June and 31 December. The notes are unsecured and subordinated to the senior and junior debt fi nance of MUKBL. A refi nancing of Arqiva was undertaken simultaneously with acquisition funding for the NGW transaction in order to capitalise upon the strength and quality of the merged business and achieve an optimal capital structure. MUKBL has 2,150 million in senior term loan facilities and a junior term loan facility of 475 million, both of which are fully drawn. The lenders require that MUKBL maintain interest rate hedging such that no less than 75% of the interest rate liabilities are hedged. At the level of MUKBL, there is a 75 million revolving credit facility for working capital and general corporate requirements (currently undrawn) and a 700 million capital expenditure facility for the purpose of funding expansion-related capital expenditure (currently partially drawn). The facilities mature in July 2014.

33 Asset Location Arqiva has its headquarters in Hampshire, with other major UK offi ces in London, Buckinghamshire and Yorkshire. It now has ten international satellite teleports, over 60 other manned locations and around 3,500 wireless sites throughout the UK and Ireland including masts, towers and rooftops from under 30 metres to over 300 metres tall. Asset Snapshot POPULATION SERVED SITES OPERATING DIVISIONS Business Description 98.5% of UK population 550 broadcast towers 3,500 wireless sites 10 teleports Terrestrial/Mobile Media Solutions Satellite Media Solutions Wireless Solutions Public Safety Arqiva has four primary operating divisions: Terrestrial/Mobile Media Solutions, Satellite Media Solutions, Wireless Solutions and Public Safety. Terrestrial/Mobile Media Solutions Terrestrial/Mobile Media Solutions provides national transmission for UK commercial television including ITV, Channel 4, Five and associated digital multiplexes, playing a leading role in the run up to DSO. Transmission services are also provided to the majority of UK independent radio stations, both analogue and digital. The UK Government s timetable anticipates the switch over from analogue to digital starting in 2008 to be completed by Antenna work has been completed in part in the Border region, which will be the fi rst to switch, and the construction of a replacement 337-metre mast at Caldbeck is well advanced. In most instances, existing structures are able to take the new antenna systems, with mast-strengthening modifi cations in certain cases. MACQUARIE INTERNATIONAL INFRASTRUCTURE FUND LIMITED ANALYST PACK 26 27

34 Mobile Media Solutions is a new division dedicated to the delivery of content to handheld devices. Arqiva remains platform neutral, while recent technology developments open up new service concepts and revenue streams for broadcasters, content providers and mobile operators alike. Satellite Media Solutions Satellite Media Solutions provide high quality and fl exible solutions to a diverse range of international customers. Arqiva s satellite broadcasting order book stands at over 500 million, and the business continues to perform well. Among the year s successes were the Freesat contract (ITV/BBC joint venture for free-to-air satellite TV), a long-term transponder agreement with Setanta Sports for UK direct-to-home delivery and the successful integration of the recently-acquired BT Satellite Broadcast Services (SBS) business. The acquisition of the BT SBS business provides the division with a sizeable presence in France and in the US to complement the existing products and services in the UK. Wireless Solutions Arqiva s Wireless Solutions division provides market-leading, multi-operator infrastructure systems and services to wireless telecoms, transport and interior public space businesses. This is done through a portfolio of over 3,500 towers, masts and managed sites, plus InBuilding (indoor coverage) and CityCell (urban coverage) products. Recent highlights include an agreement to provide 2G/3G/Wi-Fi coverage at 15 Glasgow subway stations and the acquisition of 18,000 potential urban radio sites from Macropolitan.

35 Public Safety Arqiva s Public Safety division provides frontline communications for the UK emergency services, government agencies and commercial organisations including design and installation, system maintenance and fully managed services for mobile radio, telecommunications and mobile data solutions. Key initiatives for the division during the year have included the winning of the 412/422 MHz spectrum, the successful deployment of mobile data trials for several police forces and the winning of a seven-year contract with Travel West Midlands for voice and data network infrastructure. The Metropolitan Police contract remains in place and Arqiva continues to play a leading role in helping police forces migrate to digital communications. Regulation in the EU A new regulatory framework in the EU (NRF) was adopted in February 2002 which set out the framework for electronic communications. It applies to all transmission infrastructures, including those operated by Arqiva. The NRF established a new approach for deciding whether regulatory obligations are to be imposed in relation to situations where there is no effective competition. The approach requires regulators to identify markets where competition is not effective and to designate which operators are considered to have signifi cant market power in those markets. Regulation in the UK The UK regulatory authority for the entire communications sector is the Offi ce of Communications (Ofcom). Ofcom has responsibilities across television, radio, telecommunications and wireless communications services. Wireless Telegraphy Act 1949/2006 This Act provides the frequency licences for NGW and Arqiva, including: analogue, digital and radio broadcasting transmission rights; fi xed point-to-point links frequency licences for analogue, digital and radio broadcast relay and distribution services; and spectrum allocation for Digital Terrestrial Television (DTT) multiplex licences. Broadcasting Acts 1990 and 1996 The Acts provided DTT and Digital Audio Broadcasting (DAB) service and multiplex licences. These acts also constituted the transfer of the undertakings and privatisation of the BBC s transmission services. MACQUARIE INTERNATIONAL INFRASTRUCTURE FUND LIMITED ANALYST PACK 28 29

contracts (including price controls), and the imposition of new Signifi cant Market Power (SMP) regulations.")

36 Network Access Regulation Early in 2005, following a market review of the broadcast transmission market and a public consultation, Ofcom published a statement confi rming the revocation of previous Telecommunications Act regulation applied to bundled managed transmission services (MTS) contracts (including price controls), and the imposition of new Signifi cant Market Power (SMP) regulations. The SMP regulations apply to the provision of access to the mast and site network and shared or shareable antenna acquired, constructed or installed by each of NGW and Arqiva for the purpose of providing analogue and/or digital terrestrial broadcasting transmission services (known as site sharing, or in regulatory terms, the provision of Network Access ). The principle behind the new regulation was that the mast and site network infrastructure is a scarce resource and the regulator should ensure that third parties can gain access to these sites and masts. Under this regulation neither the pricing nor the contractual terms of MTS contracts with broadcasters are regulated, however the provision of Network Access is subject to obligations known as fair, reasonable and non-discriminatory regulatory conditions. The pricing of the Network Access is cost oriented, which requires the owners of the infrastructure to clearly differentiate between site sharing and other costs (eg managed transmission services). Network access requirements can be summarised as follows: to provide network access on reasonable request; not to unduly discriminate in the provision of network access; to provide network access on cost-oriented terms; and to publish a reference offer for the provision of network access.

37 Communications Act 2003 Under the Communications Act 2003, communication providers are not required to obtain an individual licence for the provision of communication networks or services. Even so, all providers are subject to some basic conditions set out by Ofcom (General Conditions of Entitlement). As a prior holder of a public telecommunications operator licence under the Telecommunications Act 1984, Arqiva is automatically deemed to operate under the new regime and is authorised to provide communication services throughout the UK. Operators, such as Arqiva, who provide services under the General Conditions of Entitlement and whose annual turnover from carrying out relevant activities exceeds 5 million are liable to pay administrative charges. Licence under the Telecommunications Act 1984 With the operation of the Communications Act 2003, only conditions 7 and 8 from this licence remain relevant. Condition 7: subject to certain conditions, Arqiva is required, on request, to make available to a transmission operator, such as Crown Castle UK, space within or on a number of listed transmission sites. (NGW is the only other provider of terrestrial transmission services to TV broadcasters in the UK). Condition 8: imposes restrictions on the prices which Arqiva can charge for certain telecommunications services activities, including operations services and site rentals Arqiva is required to grant under condition 7. The price control mechanism operates under an Retail Prices Index minus X formula. Competition Act 1998 This Act prohibits anti-competitive agreements and the abuse of a dominant position. This limits the types of agreements and arrangements that Arqiva can enter into. For example, Arqiva may be prohibited from establishing pricing arrangements or purchasing arrangements which have the effect of reducing or foreclosing competition in the market or forcing other companies to act in certain ways. Digial Switch Over (DSO) The UK Government intends to switch off analogue TV transmission in the future and replace it with digital TV, a process referred to as DSO. Around 5,000 analogue transmitters are to be replaced at a total industry capital cost of around 500 million. The DSO is expected to be completed by Digital broadcasting in the UK is well advanced and DTT is the fastest growing television platform, with more than 60% of homes now receiving their signal via DTT. Further penetration of DTT to around 18 million homes is anticipated due to DSO. There are currently six multiplexes, which host more than 40 television channels and more than 25 digital radio channels in the UK. Multiplexes C & D are two (of three) commercial multiplexes that are currently carrying Freeview channels, and NGW is the licencee of these multiplexes until 2014, with an option to renew the licence for a further 12 years. There is scope for signifi cant Freeview channel growth as platform penetration accelerates as DSO draws closer. MACQUARIE INTERNATIONAL INFRASTRUCTURE FUND LIMITED ANALYST PACK 30 31

38 Analogue Terrestrial Television Arqiva s contracts with ITV Plc and Channel 4 are regulated and pricing under these contracts moves under an RPI minus X formula, with X agreed through commercial negotiations with the regulator and the broadcasters. These relationships are contracted until the end of the DSO. DTT In July 2007, Arqiva was awarded a contract by SDN Ltd a wholly-owned subsidiary of ITV Plc to design, build and operate a new national DTT network in preparation for digital switchover. The contract will run until 2034 and is estimated to be worth 500 million over its 27-year term. In August 2007 Arqiva was awarded a contract estimated to be worth up to 1 billion by Digital 3 and 4 Ltd to design, build and operate a new high-power national DTT network until The 1.8 billion BBC DSO contract was signed in September 2006 and will run until Key Asset Features Strong client relationships and predictable cashfl ows Medium to long-term contracts with most of its clients for terms up to 20 years and a contracted order book of c. 5.0 billion (as at Dec 2007), ensure that Arqiva is able to deliver both a stable revenue stream and opportunities for growth. Potential for future growth Arqiva has invested signifi cantly in leading-edge technology and is well positioned for future growth in the UK as TV and radio broadcasters approach DSO. New 3G networks and growth in mobile telecommunications markets will also provide opportunities and potential new uses for the old analogue spectrum. Unique position and portfolio Arqiva has access to over 4,000 broadcast and wireless sites across the UK. Its portfolio includes managed radio communications services to public safety organisations, broadcast towers and wireless site leasing infrastructure with the capacity to provide endto-end broadcast services to its clients and coverage to 98.5% of the UK population. Management team Arqiva has a highly experienced senior management team, which has overseen a yearon-year revenue growth of 12%.

Borrowing costs debt service (net of interest income) acquisition interest and non-cash (113.9) 8 Income tax 21.3 Net result 7.")

39 Summary Performance 7 Year ended 30 June 2007 million Total revenue Share of associates profi ts 1.0 Cost of sales expense (126.7) Other operating charges (111.6) EBITDA Depreciation and amortisation (31.5) Borrowing costs debt service (net of interest income) acquisition interest and non-cash (113.9) 8 Income tax 21.3 Net result Arqiva numbers from 30 June 2006 to 30 June Due to the UK Competition Commission requirements to hold Arqiva and NGW separate, income from NGW has not been included in the above table. However, the above table does include interest on refi nanced debt used to fi nance the NGW acquisition. Arqiva s total revenue for the year to 30 June 2007 was million. The breakdown of this revenue by division is as follows: Public Safety 16% Wireless Solutions 14% Other Revenue 8% Terrestrial Media 38% MACQUARIE INTERNATIONAL INFRASTRUCTURE FUND LIMITED ANALYST PACK Satellite Media 24% 32 33

40

41 National Grid Wireless ASSET NAME LOCATION EQUITY INVESTMENT MIIF'S INTEREST National Grid Wireless (NGW) (subsidiary of Arqiva) UK S$259.1 million 8.7% interest through Arqiva Background and Acquisition In April 2007, Arqiva announced the acquisition of NGW for a consideration of 2.5 billion. The acquisition has been under review by the UK Competition authorities, who have required NGW and Arqiva to be held as two separate businesses, as referenced on page 25. Asset Overview NGW is one of only two TV broadcast transmission operators in the UK (the other being Arqiva, refer to page 25) and the largest independent wireless site leasing provider in the UK. NGW provides transmission services to TV and radio broadcasters, site leasing to mobile phone and other wireless telecommunication companies and owns two of the six DTT licences in the UK. The combination of Arqiva and NGW creates a unifi ed provider of broadcast transmission services for the UK and one of the largest independent operators of shared sites for mobile communications. As complementary businesses, there are signifi cant opportunities to realise recurring operational synergies. Ownership Structure MIIF has an 8.7% interest in NGW through Arqiva. MACQUARIE INTERNATIONAL INFRASTRUCTURE FUND LIMITED ANALYST PACK 34 35

42 Asset Location NGW is headquartered in Warwick, UK and comprises a national communications infrastructure network through around 5,500 active sites used for mobile communications and 750 towers used for radio and television transmission broadcasts. Asset Snapshot POPULATION SERVED SITES OPERATING DIVISIONS 98.5% of UK population 750 broadcast towers 5,500 wireless sites Broadcasting Wireless DTT Licences Business Description NGW has three primary business segments; Broadcast, Wireless and DTT Licences. Broadcast NGW s Broadcast segment provides national transmission for UK commercial television including BBC and Virgin, playing a leading role in the run up to DSO. Transmission services are also provided to independent radio stations, both analogue and digital. In addition to managed transmission services, NGW also provides site access to its towers and masts, with Arqiva as its key customer. These activities are done through a portfolio of over 750 broadcast towers. Wireless NGW is the largest independent provider of wireless site leasing in the UK with c.11% market share, and has master site sharing agreements with all major mobile network operators (3, T-Mobile, O2, Orange and Vodafone). This is done through a portfolio of over 5,500 towers, masts and managed sites. NGW also provides managed services to both wireless and fi xed-line operators, with T-Mobile as a key customer. DTT Licences DTT spectrum licences C & D were awarded to NGW in 2002 for a 12-year term, with a renewal option for a further 12 years from 2014 to Multiplexes C & D are two of three commercial multiplexes that are currently carrying Freeview channels in the UK. They are currently broadcasting 5 and 6 channels on these multiplexes respectively, with key customers including BSkyB, Channel 4 and ITV. Key Asset Features Strong client relationships and predictable cashfl ows Medium to long term contracts with clients such as the BBC for terms up to 20 years, and a contracted order book of c. 1.9 billion ensure that NGW is able to deliver both a stable revenue stream and opportunities for growth. Potential for future growth NGW is well positioned for future growth in the UK as TV and radio broadcasters approach DSO, with DTT being the default digital free-to-air TV platform and penetration continuing to increase.

43 Unique position and portfolio NGW has access to over 6,000 broadcast and wireless sites across the UK. Operating synergies Potential synergies are expected as a result of coordination with Arqiva, resulting from operational benefi ts and a more effi cient capital expenditure programme with signifi cantly reduced execution risk around the implementation of DSO. Summary Performance Six-month period ended 31 December 2007 million Total revenue Direct costs and overheads (83.4) EBITDA 82.5 EBITDA Margin 49.7% NGW s total revenue for the six months to 31 December 2007 was million. The breakdown of this revenue by division is as follows: DTT Licences 17% Terrestrial Media 27% Wireless Solutions 56%

44

45 Canadian Aged Care ASSET NAME LOCATION EQUITY INVESTMENT MIIF'S INTEREST Canadian Aged Care (CAC) Canada S$164.9 million 55.0% interest Asset Overview CAC is currently the third largest owner and operator of long-term care (LTC) homes in Ontario, Canada. LTC homes are a vital part of a community s social infrastructure and share features that characterise other high-quality infrastructure assets, including stable revenue, signifi cant barriers to entry and low-demand variability. CAC owns 26 LTC homes, one retirement home (RH) and one independent living home (IL). LTC homes are designed to accommodate seniors who may require 24-hour per day care or who suffer from cognitive or physical impairment. This requirement for care distinguishes LTC homes from IL and RH. LTC homes may include shared, semi-private and private suites. Ownership Structure In November 2005 MIIF acquired a 55.0% interest in CAC for a total consideration of S$164.9 million through total return swaps. MACQUARIE INTERNATIONAL INFRASTRUCTURE FUND LIMITED ANALYST PACK 38 39

46 Financing Structure All CAC debt is issued at the Leisureworld Senior Care LP (LSCLP) level. The LSCLP debt is comprised of debt issued at the time CAC was acquired by its current partners, as well as debt to fund the recent acquisition of a seven LTC home portfolio. C$310 million of 4.814% Series A Senior Secured Debentures due on 24 November 2015 were issued on 24 November 2005 by way of a public-style rated private placement in Canada. Prior to the private placement, CAC entered into hedging arrangements for the full amount of the notes. A fl oating rate bank debt facility of C$75 million was drawn on 30 January 2008 to fund CAC s recent acquisition of seven LTC homes. 20% of this facility will be repaid within one year, settled pro rata by CAC s partners via an equity injection.

47 Asset Location CREEDAN VALLEY Creemore Class: C Year Built: 1975 LTC beds: 95 VAUGHAN Vaughan Class: A Year Built: 2004 LTC beds: 224 ELMIRA Elmira (Kitchener) Class: A Year Built: 2000 LTC beds: 96 OXFORD Ingersoll Class: C Year Built: 1975 LTC beds: 160 BRANTFORD ORIGINAL Branford Class: C Year Built: 1972 LTC beds: 90 EXPANSION Branford Class: A Year Built: 2002 LTC beds: 32 Ontario BARRIE Barrie Class: C Year Built: 1972 LTC beds: 57 NORTH BAY North Bay Class: C Year Built: 1975 LTC beds: 148 BRAMPTON MEADOWS Brampton Class: A Year Built: 2003 LTC beds: 160 TULLAMORE Brampton Class: C Year Built: 1965 LTC beds: 159 MUSKOKA Gravenhurst Class: A Year Built: 1999 LTC beds: 182 RH beds: 29 BRAMPTON WOODS Brampton Class: A Year Built: 2003 LTC beds: 160 ORILLIA Orillia Class: A Year Built: 2006 LTC beds: 160 RICHMOND HILL Richmond Hill Class: A Year Built: 2003 LTC beds: 160 ETOBICOKE Etobicoke Class: A Year Built: 2001 LTC beds: 160 SCARBOROUGH Scarborough Class: B Year Built: 1991 LTC beds: 299 IL beds: 53 O CONNOR COURT Toronto Class: A Year Built: 2001 LTC beds: 160 O CONNOR GATE Toronto Class: A Year Built: 2001 LTC beds: 158 ST. GEORGE Toronto Class: C Year Built: 1972 LTC beds: 238 NORFINCH North York Class: A Year Built: 2003 LTC beds: 160 ELLESMERE Scarborough Class: A Year Built: 2003 LTC beds: 224 LAWRENCE Toronto Class: A Year Built: 2002 LTC beds: 224 ALTAMONT Scarborough Class: C Year Built: 1965 LTC beds: 159 MISSISSAUGA Missisauga Class: C Year Built: 1970 LTC beds: 237 STREETSVILLE Missisauga Class: C Year Built: 1976 LTC beds: 118 CHELTENHAM Toronto Class: C Year Built: 1976 LTC beds: 170 ROCKCLIFFE Scarborough Class: C Year Built: 1968 LTC beds: 204 Asset Snapshot COMMENCEMENT OF OPERATIONS 1975 CORE BUSINESSES TOTAL BEDS 4,396 ANCILLARY BUSINESSES 26 LTC homes (4,314 beds) One RH (29 beds) One IL (53 beds) Preferred Health Care Services is an accredited provider of professional nursing and personal support services for both communitybased home care and LTC homes Ontario LTC Providers, a provider of purchasing services to CAC s LTC homes MACQUARIE INTERNATIONAL INFRASTRUCTURE FUND LIMITED ANALYST PACK 40 41

48 Business Description The LTC sector in Ontario is funded according to a defi ned funding model, which contributes to the predictability of CAC s cash fl ow. The following diagram outlines the funding and cost categories for CAC. * Some portion of funding to the accommodation envelope may be derived from the MOHLTC due to the subsidisation of low-income residents. ** Other items include items such as accreditation funding. Note: Not to scale, actual spending amounts differ.

49 Sources of Funds There are two main sources of funds: 1) Ministry of Health and Long-Term Care (MOHLTC) for aged care services: At least 60% of revenue from CAC s LTC homes is received from the MOHLTC. Over the past 10 years, government funding of CAC s LTC homes has increased in excess of the consumer price index. 2) Residents for accommodation services. Funding and Cost Categories Nursing and personal care (NPC): MOHLTC provides funding on a monthly basis to cover the costs of nursing and personal care staffi ng as well as medical and nursing supplies. LTC home operators must return any funding that is not spent to the government during an annual reconciliation process. Spending in excess of the government funding is paid for by the LTC operator. Program and support services (PSS): MOHLTC funds therapeutic services, pastoral care, recreation, staff training, volunteer coordination and other services. LTC home operators must return any funding that is not spent to the government during an annual reconciliation process. Spending in excess of the government funding is paid for by the LTC operator. Other: MOHLTC also provides funding to LTC homes that have been accredited by the Canadian Council on Health Services Accreditation as well as partial reimbursement of LTC homes municipal property tax obligations. Construction funding and/or structural compliance premiums: CAC receives capital cost funding of up to C$10.35 per bed, per day from the MOHLTC, for a period of 20 years (commencing from the year each home was constructed), for Class A homes. CAC also receives structural compliance premiums from the MOHLTC, on a per bed per day basis of C$2.50 for Class B homes and C$1.00 for Class C homes. Preferred premiums: An LTC home that provides basic accommodation for at least 40% of residents may offer the remaining residents preferred accommodation in semiprivate or private rooms. The LTC home operator retains the premiums collected for such accommodation, which typically increases revenue and enhances profi tability. These premiums, which are regulated, are currently C$8.00 per day for a semi-private room and C$18.00 per day for a private room. Approximately 52.9% of the beds in CAC s portfolio are designated as private or semi-private. Accommodation: A co-payment is charged to residents to cover funding for roomand-board expenses such as food, housekeeping, dietary services, laundry and linen, administration and building/property operations and maintenance, including mortgage payments and taxes. MOHLTC also provides subsidies to low-income residents

50 Name of CAC Home Basic Semi-Private Private Short Stay / Other Altamont* Barrie Brampton Meadows Brampton Woods Brantford Cheltenham* Creedan Valley Ellesmere Elmira Etobicoke Lawrence Mississauga* Muskoka Norfi nch North Bay O Connor Court O Connor Gate Orillia Oxford* Richmond Hill Rockcliffe* Scarborough St. George Streetsville* Tullamore* Vaughan Total 1, , % of total 46.3% 19.4% 33.7% 0.7% * Indicates a newly acquired home.

51 Key Drivers Increasing occupancy enhances cash fl ow Occupancy is a key driver of CAC s performance. An LTC home that meets or exceeds 97% annual average occupancy receives funding from the MOHLTC based on 100% occupancy. CAC has a strong record of increasing capacity, through acquisitions and new licences and of maximising occupancy. The government s control and regulation of the supply of beds ensures barriers to entry. In addition, LTC homes represent a costeffective alternative to acute-care hospital beds. Positive demographic trends support demand for LTC The demand for LTC homes is dictated by a need for care driven by demographic trends rather than changes in the economy. The Organisation for Economic Cooperation and Development (OECD) projects that the life expectancy of Canadians is increasing, with life expectancy for the total population rising to 79.9 years in 2003 from 75.3 years in According to the Ontario Ministry of Finance, the 75-plus age group is anticipated to be among the fastest-growing age groups over the next 20 years, doubling in size from 753,000, or 6% of the population, in 2005 to 1.6 million, or 10% of the population, in At the same time, this demographic is increasingly affl uent, with average after-tax income of senior families in Ontario, in which the major income earner was 65 years of age or over, increased almost 12% from 1996 to

52 Regulation LTC is regulated and funded by the MOHLTC, which requires that LTC homes be licensed in order to operate and receive government funding. LTC homes must be built to specifi ed design criteria and funding is generally tied to the delivery level of mandated care services. LTC homes are currently governed by The Homes for the Aged and Rest Homes Act, The Nursing Home Act and The Charitable Institutions Act. In October 2006, the Ontario government commenced the process to consolidate these three acts into a single piece of legislation and on June 4, 2007, The Long-Term Care Homes Act received Royal Assent. It is expected to take 12 to 18 months before the Act will come into force due to the number of regulations that need to be drafted. The Long-Term Care Homes Act contains a number of new provisions, including licence term limits for LTC homes of 15 to 25 years, according to class of homes. Currently, licences have one-year terms subject to automatic renewal on an annual basis provided that compliance requirements are met. On 31 July 2007, the MOHLTC announced a 10-year plan to redevelop 35,000 Class B and C beds, commencing in This funding will enable CAC to further enhance the quality and comfort of accommodation available to residents. All LTC homes are categorised by class as follows: Class A Class B Class C Class D Homes meet or exceed 1998 design standards Homes exceed 1972 standards but fall short of 1998 design standards Homes meet 1972 standards Homes fail to meet 1972 standards The composition of CAC s portfolio is as follows: CAC LTC homes Ontario CAC share of Ontario market Beds by Class Number Percent Number 9 Percent Percent A 10 2, % 24, % 9.25% B % 8, % 3.69% C 1, % 30, % 5.67% D 12, % Total 4, % 76, % 5.66% 9 As of December 31, Source: Care Planning Partners, Inc. 10 All of CAC s Class A homes are designated new homes and qualify for capital funding of $10.35 per day, per bed. Continuing Growth On 1 February 2008, CAC signed an agreement to acquire the Good Samaritan Seniors Complex, which consists of a 64-bed Class A LTC home and an attached 24-bed RH located in Alliston, Ontario, for approximately C$11.1 million plus transaction costs. The acquisition is conditional upon regulatory approval from the MOHLTC. Upon completion of the transaction, CAC will own or manage 27 LTC homes representing 4,378 beds, two RH representing 53 beds and one independent living facility with 53 beds.

53 MACQUARIE INTERNATIONAL INFRASTRUCTURE FUND LIMITED ANALYST PACK

54

55 Changshu Xinghua Port ASSET NAME LOCATION EQUITY INVESTMENT MIIF'S INTEREST Changshu Xinghua Port (CXP) China S$112.3 million 38.0% interest Asset Overview CXP is a multi-purpose cargo port centrally located within the Yangtze River Delta industrial zone. CXP handles mainly steel, forestry products and containers. The majority of CXP s revenue comes from steel-related operations. Ownership Structure MIIF owns a 38.0% effective equity interest in CXP through the acquisition of 40.0% of Singapore Changshu Development Company (SCDC) from existing shareholders, namely, Pan-United Corporation Ltd (PUC) and a minority shareholder. The remaining 60.0% balance of SCDC is owned by PUC and Petroships. Financing Structure MIIF s purchase of CXP was funded with proceeds from the November 2005 capital raising. The total consideration was S$112.3 million. Total debt outstanding at CXP is RMB480 million. The majority of CXP s debt is from Chinese banks in RMB where base rates are fi xed by The People s Bank of China. A smaller portion of the total debt is denominated in USD and the interest rate has been hedged for its tenure. MACQUARIE INTERNATIONAL INFRASTRUCTURE FUND LIMITED ANALYST PACK 48 49

56 Asset Location CXP is centrally located within a high growth industrial area along the Yangtze River which includes the cities of Suzhou, Wuxi and Changshu. Its hinterland has over 200 million people and is one of China s fastest growing industrial regions. As a port, CXP s growth is driven by local GDP and trade volume growth. With a water depth of 13 metres, CXP is the furthest port upstream from Shanghai that is able to handle containerised traffi c. With Class 1 port status, CXP is able to accept vessels directly from overseas thereby allowing it to participate in international trade fl ows.

57 Asset Snapshot GEOGRAPHY 80 kilometres upstream from Shanghai CONCESSION 50 year concession granted to PUC in 1994 (37 years remaining) VESSEL CAPACITY 50,000 dead weight tonne (DWT) vessels FACILITIES 8 berths 1,500 metres of jetty WATER DEPTH 13 metres STORAGE 425,380 square metres of open storage 12 warehouses with 85,847 square metres of covered storage capacity PORT STATUS Class 1 CAPITAL EXPENDITURE No signifi cant near term capital expenditure Business Description CXP s revenues are primarily based on tariffs negotiated with customers. CXP s revenues are derived mainly from the handling of steel and forestry products, as well as handling of container traffi c. Based on unaudited management accounts for the 12 months ended 31 December 2007, general cargo products accounted for 58% of revenue while forestry products and container traffi c accounted for 34% of total revenues. In the steel products segment, under general cargo, CXP benefi ts from captive steel mills and processing plants located in close proximity. CXP handles fi nished steel products between steel traders. In the forestry products segment, the port has a 25% interest in the Changshu Westerlund joint venture which was formed with leading Belgian forestry product terminal operator, Westerlund, in order to operate a dedicated forestry product terminal at CXP. Forestry products volumes, including timber, paper and pulp, are projected to increase due to strong demand in China for paper products. In the container segment, renewed growth is projected as CXP develops as an inland hub for container shipping along the Yangtze River. Rising costs for road transport, especially to and from the new Yangshan Port, are expected to make transport of containers via the Yangtze River more competitive. CXP is thus likely to handle more international and domestic containerised cargo as river traffi c increases. The revenue breakdown can be found below: Others 7% Forestry Products 24% Containers 11% General Cargo 58% MACQUARIE INTERNATIONAL INFRASTRUCTURE FUND LIMITED ANALYST PACK 50 51

58 Historical revenue for CXP is shown in the table below: Year ended 31 December Revenue (RMB million) The revenue decrease in FY2004, compared to FY2003, was due to Chinese government macro-economic measures to restrain excessive growth in the domestic economy. The measures resulted in lower volumes of steel imports, which adversely impacted CXP s steel handling volumes. Subsequently, steel export volumes have increased in contribution to CXP s revenue and profi tability. Historical quarterly volumes are shown in the table below: Quarter ending 31 Mar Jun Sep Dec Mar Jun Sep Dec 2007 Total steel volume (000 tonnes) Total non-steel volume (000 tonnes) Total containers (000s) Total forestry volume (000 tonnes) , Regulation The administration and operation of ports in China was under strict government controls until the end of 2001 when China launched a comprehensive reform program to separate government functions from enterprise management. Although the government remains in control of port administration, the reform opened up port construction and port operations to foreign investment to a greater extent. The construction and operation of ports and terminal facilities is classifi ed as encouraged, according to the Foreign Investment Industrial Guidance Catalogue which came into effect in January Future Opportunities There are ongoing efforts to secure new businesses through new cargo and land lease to reduce CXP's reliance on the steel sector. New opportunities such as fertilisers, equipment and cement have been identifi ed. Additionally, by leasing out a portion of its yard to prospective equipment manufacturers, CXP will receive a steady revenue stream while enjoying variable revenue from handling the equipment. CXP continues to be the leading forestry port in the region through its successful partnership with Belgian forestry specialist Westerlund and its ability to add warehouse capacity as needed to accommodate growth. With a strong performance in 2007, continued growth is expected in forestry products due to demand from the region's paper making industry. Competition in the steel sector remains strong, with a variety of regional ports remaining active. CXP is pursuing a three-way strategy to stay competitive, working to attract cargo owners, ship operators and specialist mills.

59 Opportunities to capture benefi ts of the growing market for steel and Chinese economic growth. CXP is expected to benefi t from robust growth in global and Chinarelated trade, which would necessitate increased water cargo transport. Increasing trade around the Yangtze river hinterland. MIIF s participation in the Chinese port sector through its investment in CXP may benefi t MIIF via introduction to other potential investment opportunities in this sector or in the region. Summary Performance Year ended 31 December 2007 RMB million Total revenue Cost of sales (57.9) Overheads (36.0) EBITDA Depreciation and amortisation (27.4) EBIT 93.5 Finance costs and non-operating income (25.9) Share of results of associates 5.6 Profi t before tax 73.1 Income tax expense (5.1) Profi t after tax 68.1 Note: The above numbers have been stated in accordance with Chinese GAAP. The numbers are subject to rounding. MACQUARIE INTERNATIONAL INFRASTRUCTURE FUND LIMITED ANALYST PACK

60

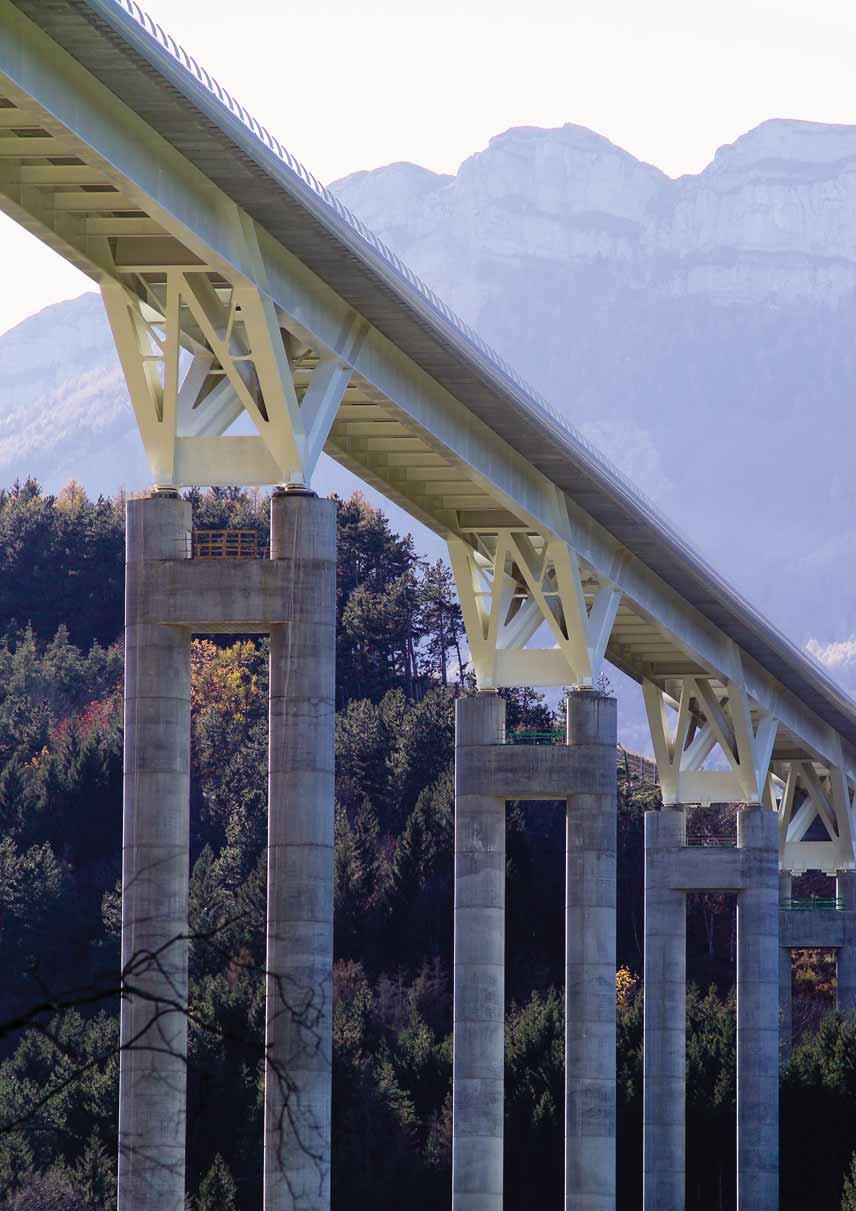

61 Hua Nan Expressway ASSET NAME LOCATION EQUITY INVESMENT MIIF'S INTEREST Hua Nan Expressway (HNE) Guangzhou, China S$295.7 million* 81.0% interest * Originally announced acquisition price of S$329.5 million comprised of S$295.7 million invested at acquisition, and S$33.8 million of acquisition adjustments contingent upon certain events and is yet to be paid. Asset Overview HNE is a 31-kilometre, dual way six-to-eight-lane brownfi eld urban-tolled expressway. It is located in the city of Guangzhou, the capital city of the wealthiest province in China, with one of the fastest rates of population growth. The road comprises a tunnel, various bridges and 11 interchanges. The asset has been constructed in two separate phases. Phase I totalling 15.6 kilometres long with eight lanes commenced operations in October 1999 and Phase II totalling 15.4 kilometres in length with six to eight lanes (four lanes in the tunnel) commenced operations in January The rights to operate and collect tolls for Phase I & II will expire in April Phase I & II make up the main artery for north-south traffi c in Guangzhou, enabling cities in the Pearl River Delta such as Foshan, Zhongshan, Zhuhai, Shenzhen and the whole of Southern China to be easily accessible. Ownership Structure On 19 November 2007, MIIF acquired an 81.0% interest in HNE, from Preciseway Management Ltd and Topwise Consultants Ltd (Vendors). A 9.0% equity interest has been retained by the Vendors, and the remaining 10.0% of equity is held by Guangzhou Centre for Administration of Municipal & Gardening Works (Guangzhou government body). The following is a simplifi ed diagram of HNE s holding structure. MACQUARIE INTERNATIONAL INFRASTRUCTURE FUND LIMITED ANALYST PACK 54 55

62 Financing Structure China Construction Bank has provided a maximum RMB2.753 billion debt facility. The facility has a 14-year tenor and an amortisation profi le which matches the operating cash fl ow growth profi le and allows HNE to repay a larger proportion of the debt towards the end of the tenor. The interest rate applicable to the loan is the 5-year PBOC rate. Asset Location Phase I & II is located in Guangzhou, the capital city of Guangdong province. Guangdong is a coastal province in southeastern China, with three of the six special economic zones in China within its boundaries: Shenzhen, Shantou and Zhuhai. Guangdong is one of the richest provinces in the nation, with the highest total GDP among all provinces. Asset Snapshot Length of Phase I 15.6 kilometres Length of Phase II 15.4 kilometres Pavement Asphalt Number of lanes six to eight (four in tunnel) Width of lanes 3.8 metres per lane Interchanges annual tolled vehicles (million) 40.4 Design speed (kilometres per hour) Structures Bridges, culverts & tunnel

63 Road Configuration HNE has three to four lanes in each direction and converges into two lanes each way in the tunnel at Shimentang Hill. HNE lies to the east of Guangzhou City and has good connectivity with other roads in the province including other expressways, the national highway and urban primary roads as marked out in the map below. Phase III of the expressway is currently under construction and MIIF may take the opportunity to acquire an interest in Phase III once it commences operation and attains satisfactory traffi c levels. Phase III is expected to increase the traffi c fl ow into Phase I & II. Airport Expressway 2nd Northern Ring Road Hua Nan Expressway Taihe Main Line Taihe Ramp Northern Ring Road Chungang Longdong Guangshan Cencun Zhongshan Guangyuan Luoxi Bridge East, South and West Ring Road Xinguang Expressway Panyu Bridge Xinzhou Huangpu Nansha Port Expressway Phase I Phase II Tuhua Phase I of HNE originates in the Tianhe district, the fi nancial centre of Guangdong and connects to the Panyu Bridge in the south. It intersects with eight expressways and urban arteries, namely Guangshen Highway, Northern Ring Road, Guangyuan East Expressway, Zhongshan Avenue, Huangpu Avenue, Xinguang Expressway, Xinjiaonan Road and Southeast West Ring Road. Phase I is the only external highway backbone which runs near the city centre in Guangzhou and connects to the Pazhou International Exhibition Centre and Guangzhou University Town. Phase I provides the fastest and most convenient route between Guangzhou and Panyu. Phase II of HNE connects to Phase I from Cencun Bridge and converges with Jingzhu Highway and the second Northern Ring Road at Taihe Town next to the Helong Reservoir in Baiyun District. The second Northern Ring Road is the key road in the Guangzhou- Foshan area and is the primary linkage between Baiyun Airport and Guangzhou New Railway Station. By taking the Jingzhu national highway from Beijing and continuing down Phase II to Guangzhou, cities in the Pearl River Delta such as Foshan, Zhongshan, Zhuhai, Shenzhen are easily accessible. Immediate destinations Distant destinations Connecting key roads Phase I Panyu and Nansha New residential development in southern Guangzhou Guangzhou International Exhibition Centre Local universities Phase II Baiyun and Tianhe districts Baiyun International Airport Shaoguan city Mt. Maofeng scenic region Zhong Shan, Zhu Hai and Macau Hunan Province, Beijing Eight local expressways and key inner city roads and two national highways Two intercity expressways (one in planning) and two national highways MACQUARIE INTERNATIONAL INFRASTRUCTURE FUND LIMITED ANALYST PACK 56 57

64 Exclusive Operation Rights The approved business scope of Phase I & II company is to plan, construct and operate the expressway, bridges and associated facilities of the business. The term of the toll collection for Phases I & II will expire in April Upon the expiration of the toll collection period, the assets of the expressway, bridges and associated facilities, buildings and the rights to operate shall be transferred to Guangzhou Centre (Guangzhou government body) without compensation. Tolling Toll rates have not increased since the opening of Phase I in 1999 and are set initially on a per kilometre basis by the provincial government (ie Guangdong Province Government). In the event that the Phase I & II Board decides to increase its toll rates, it is required to submit an application to the Guangzhou Transportation Committee and the Guangzhou Pricing Bureau. Any such approval by the government authorities will have an effect on all toll roads in the province. The following fl ow chart presents the stages a toll road needs to satisfy before an increase in the toll rate is approved by the provincial government. Toll Collection In 2000, a toll collection network with neighbouring roads was established, which laid the foundations for the subsequent unifi ed tolling system. HNE was also the fi rst toll road in Guangdong to implement electronic payment technology. The current toll-collection system is a semi-automatic closed type with manual classifi cation of vehicle classes. It utilises a recyclable non-contact Integrated Circuit (IC) card to offer different payment options to cash. Approximately 15% of the revenue is derived from the use of the IC card. Each of the main tollgates in Taihe, Huangpu, and Tuhua has an Electronic Toll Collection toll lane.

Guangzhou Ring Road (b) Second Northern Ring Road (c) Second Eastern Ring Road (d) Airport Expressway (e) (f) Nansha Expressway Panyu Bridge The settlement scheme for Phase I & II is formulated")

65 Phase I & II are part of the joint tolling system which includes the following highways and bridge. (a) Guangzhou Ring Road (b) Second Northern Ring Road (c) Second Eastern Ring Road (d) Airport Expressway (e) (f) Nansha Expressway Panyu Bridge The settlement scheme for Phase I & II is formulated in accordance with the road s total length, vehicle types, and the existing approved toll rates. Phase I & II s management centre can control and supervise the entire tolling network. Through its lane control system, IC card system, automatic image capture and licence plate recording system, the system collects all information along the toll stations, and has a clear view of a vehicle s journey from entering to exiting the toll station. The real-time system links systems at all levels, and is able to operate independently, thereby providing a higher degree of fl exibility and improved operational effi ciency. MACQUARIE INTERNATIONAL INFRASTRUCTURE FUND LIMITED ANALYST PACK