Documento de Trabajo. ISSN (edición impresa) ISSN (edición electrónica)

|

|

|

- Drusilla Green

- 5 years ago

- Views:

Transcription

1 Nº 168 Abril 1994 Documento de Trabajo ISSN (edición impresa) ISSN (edición electrónica) What Drives Capital Flows? Lessons from Recent Chilean Experience. Felipe Larraín Raúl Labán

2 ISSN: PONTIFICIA UNIVERSIDAD CATOLICA DE CHILE INSTITUTO DE ECONOMIA Oficina de Publicaciones Casilla V, Correo 21, Santiago WHAT DRIVES CAPITAL INFLOWS? LESSONS FROM THE RECENT CHILEAN EXPERIENCE Raúl Labán M Felipe Larraín B. * Documento de Trabajo Nº 168 Abril, 1994 * Instituto de Economía, Universidad Católica de Chile.

3 WHAT DRIVES CAPITAL INFLOWS? 1 1. INTRODUCTION Several Latin American countries have experienced a sharp rise in net capital inflows in the late 1980s and --especially-- in the early 1990s. Although the relevant factors may well vary between countries and types of capital, innovations on both internal and external factors clearly lie behind this trend. Our aim in this paper is to identify the main factors explaining the inflow of capital into Chile during recent years. A significant increase in capital inflows has been observed in Latin American countries which have followed very different mixes of macroeconomic policy, have pushed forward different economic reform programs, and have experienced different political realities. This has led several analysts to attribute a central role to external factors in explaining this trend (Calvo et al, 1992). This emphasis, however, has been disputed by others, who have argued that the sharp increase in capital flows into several economies of the region has been the result, to a large extent, of a positive reaction of both local and foreign investors to the implementation of successful stabilization and economic reform programs. Reforms have included, among other measures, some combination of trade and financial liberalization, public sector reform, privatization of state-owned enterprises, and widespread deregulation. Additionally, a sound macroeconomic policy mix --the argument goes on-- has sharply changed foreigners' expectations and risk assessment of domestic financial securities. Thus, external investors have perceived local securities as more attractive --less risky-- and have become willing to hold a larger share of these in their portfolios.

4 2 DOCUMENTO DE TRABAJO Nº 168 We believe that both lines of argument are part of a more complex story. In our view, this trend results from some combination of external and internal factors which varies by country and by type of financial flows. Stressing one or the other factor requires specifying the type of capital that it applies to. In this paper, we observe that a key separation of capital flows is between short and long term flows, and show how the two respond to a different set of variables. This is a key issue. A clear understanding of the factors behind each type of flow is crucial in the design of policies aimed to attract some types of capital and offset others. Developing countries face a tricky dilemma in this regard. On the one hand, they want to stimulate the net inflow of long term capital, which is needed to supplement the local saving effort with foreign saving that would help finance their accumulation of productive capital. On the other hand, they face the challenge of managing massive flows of short-term speculative capital, which may lead to excess volatility in key economic variables such as domestic interest rates and the real exchange rate. This induced volatility is likely to have a depressive impact on physical investment (Tobin, 1978; Tornell, 1990; Larraín and Vergara, 1993), on resource reallocation (Krugman, 1987), on exports (Caballero and Corbo, 1990), and thus on economic growth and welfare. This paper analyzes and provides econometric evidence on the main factors which help to explain the sharp increase in net capital inflows to Chile during recent years. Section 2 documents the increase in capital inflows to Chile since the late 1980s, and briefly describes magnitudes and composition. The next section discusses the main internal and external factors which may

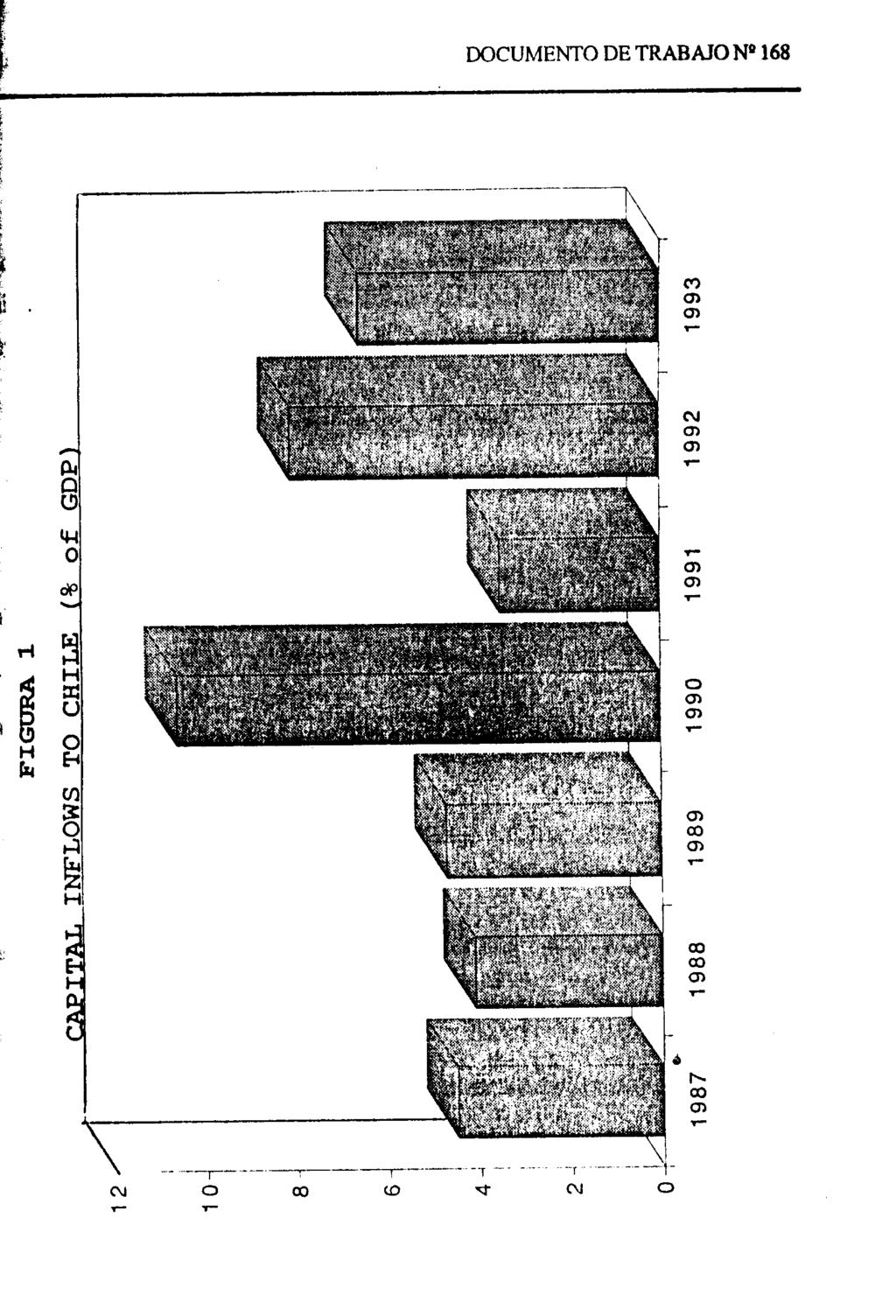

5 WHAT DRIVES CAPITAL INFLOWS? 3 help to explain this trend. Section 4 analyzes how Chile has reacted to this increase in net capital inflows. Section 5 presents econometric results on the factors that appear to lie behind the behavior of both short and long term capital flows between 1984 and A conclusion closes the paper. 2. THE RETURN OF PRIVATE CAPITAL TO CHILE SINCE THE LATE 1980s Private capital began to return to Chile in the late 1980s. Total net capital inflows (measured by the capital account surplus plus) went from an average of US$1 billion in to US$3 billion in 1990, and to an average of US$2.4 billion in Figure 1 shows the increase of capital inflows to Chile, as a proportion of GDP, since the late 1980s. Capital returned to Chile in many different forms. Foreign investment, short term credits, long term loans, and even repatriation of capital held by Chileans abroad all increased significantly during this period. This happened as the Chilean economy was in a recovery phase that merged into one of the most successful growth periods in the country's history. Major macroeconomic indicators improved sharply after GDP growth went from 2.4% on that year, to an average of more than 6.5% in This acceleration in the growth rate came together with a sharp reduction in 1 Considering US$2.8 billion for 1993.

6 4 DOCUMENTO DE TRABAJO Nº 168 unemployment --from more than 22% on average for to about 4.5% at the end of and a deceleration in the inflation rate --from over 27% in 1990 to 12.2% in The strength in the country's external position is shown by the accumulation of foreign exchange reserves, which by the end of 1993 had reached US$9.8 billion, or around 12 months of imports. The significant deterioration in the terms of trade during 1993 (its cost estimated at around 2.25% of GDP), however, was the crucial force behind the deterioration in the current account, to a deficit in the order of 5.5% of GDP for the year The composition of financial flows 2 During this recent episode, general balance of payments support loans from commercial banks have not played an important role as they did in the late 1970s and early 1980s. Instead, a large part of medium and long-term private capital flows has been in the form of foreign investment and project loans. Trade loans have also been important. In fact, the proportion of equity to debt has been much higher in than in , the previous period when Chile was subject to massive capital inflows. During , foreign investment was on average less than US$250 million per year, or just about 8% of total net capital inflows (including errors and omissions); the equivalent figures for are US$657.4 million, or 41% of total capital inflows. In 1990, foreign investment was about 2 For a more detailed analysis of this issue, see Labán and Larraín (1993a).

7 WHAT DRIVES CAPITAL INFLOWS? 5 3.6% of GDP (US$ 727 million), the highest rate in Latin America. And, once again in 1993, foreign investment into Chile set a regional record, with US$2.7 billion 3, or over 6% of GDP. This is also Chile's all-time record, which is even more remarkable considering that it was reached in a year of Presidential and Congressional elections. From 1985 to 1989, much of the foreign investment was raised through debt-equity swaps. After 1990, however, the secondary market discount on Chilean debt came down to very low levels (5% or less), and debt swaps virtually ended. Since then, almost all foreign investment has come in through Chile's regular scheme (D.L. 600), which involves "fresh-money". During , 66% of total net foreign investment came --on average-- through debt swaps. This fraction came down to 25% in 1990, and was almost nil in No new debt-swap operations have been registered since The composition of capital inflows between debt and equity is not a matter of indifference for a country. Foreign investment flows tend to have a more desirable cyclical pattern than foreign credit. Based on the Latin American experience of the last 15 years, Hanson (1992) argues that credit flows tend to be extremely pro-cyclical. Furthermore, Larraín and Velasco (1990) have shown that profit remittances on foreign investment in Chile tend to be more procyclical than interest payments; thus, remittances tend to be higher --relative to interest service-- in good periods. During , medium and long term net capital inflows to Chile 3 Including both equity and associated credits.

8 6 DOCUMENTO DE TRABAJO Nº 168 were US$1,456 million --including both equity and debt instruments--, and short term capital were US$803 million (both figures on annual average). 3. MAIN FACTORS BEHIND THE CAPITAL INFLOWS TO CHILE The growth of capital inflows to Chile since the late 1980s has resulted from the combination of a number of external and internal factors. Among the external factors are low world interest rates, a poor economic performance in the industrial countries, and a greater availability of international capital. On the internal front, Chile has experienced a number of political and economic developments which have been reflected in a reduction of the risk premium that both domestic and foreign investors require to hold Chilean securities External factors Culpeper and Griffith-Jones (1992) have presented evidence on net private capital flows to developing economies for the period They show that capital inflows have grown relatively steadily in Asia, have been poor in Africa, and have fluctuated sharply in Latin America, with a major increase since According to ECLAC, net private capital inflows to Latin America were almost seven times larger in 1991 than in On the external front, there has been a number of developments which have increased the flow of private financial resources to Latin America in

9 WHAT DRIVES CAPITAL INFLOWS? 7 general, and to Chile in particular, since the late 1980s. The weak macroeconomic performance of several industrialized countries since the late 1980s has gone together with a decline in world interest rates, most notably in the U.S., where political cycle considerations should be added in explaining the "excessively" low level reached by short-term rates. This has made short-term Latin American financial instruments with far higher yields, a more attractive portfolio investment opportunity (Calvo et al, ). Another common factor to the region has been the increase in the world supply of capital. This is partially explained by factors that have contributed to the rapid growth and globalization of world capital markets, such as widespread trade and capital account liberalization, and innovations in financial instruments and techniques. These innovations imply that financial markets are becoming de facto more and more integrated even without the help of deregulation. Towards the end of the 1980s, industrial countries had reached almost complete financial integration, which has certainly reduced the capacity of the authorities to impose capital controls. Even countries like Japan, Spain, Germany, France, and Italy, which lacked a strong willingness to open the capital account, were "victims" of financial integration 5. A number of developing economies are starting to experience this same process. 4 According to Calvo et al (1992), external factors explain a major part of the recent inflow of private capital to several Latin American economies which are pursuing different mixes of macroeconomic policies and have experienced different economic performances. 5 See, for example, Viñals (1990), and The Economist (1992).

10 8 DOCUMENTO DE TRABAJO Nº 168 External factors certainly help to explain the increase in cross-border private capital flows to Latin America. Even countries with significant macroeconomic and political instability in the region, such as Brazil, Peru and Venezuela have been able to attract capital inflows. Nevertheless, external factors do not explain the variations in the magnitude, composition and conditions of inflows among the countries of the region. Clearly, common external factors do not explain it all Internal factors Capital flowing into Latin America also reflects the prospects of a better economic future for the region during the 1990s and beyond. These expectations are based on the structural reforms carried out in several countries of the region, most notably in Chile, Mexico, and Argentina. The fact that Chile's reforms were carried out much before the rest of the region, and thus were on a solid base by the late 1980s, explains the fact that capital flowed into Chile before it returned to other countries in Latin America. It also helps to explain why the flows into Chile have been larger relative to the size of its economy than for other Latin American countries. Among the five larger economies of the region, Chile received the highest private capital inflow as a percentage of GDP in 1989 and 1990 (4.3% and 7.2%, respectively), and accounted for 22% (1989) and 14.9% (1990) of

11 WHAT DRIVES CAPITAL INFLOWS? 9 total private capital flows to the region. In 1990, Chile and Mexico --which had attained macroeconomic stability and reduced their external debt burden-- accounted for 77.6% of total private flows to Latin America. By 1991, Brazil and Mexico accounted for 69% of total private flows to Latin America (Salomon Brothers, 1992). Additional economic factors contributing to the return of private capital have been the sharp reduction in Chile's external debt burden since 1986, the solid macroeconomic performance recorded since the mid-1980s, particularly in terms of output and trade expansion, and the reduction and elimination of a number of capital and exchange controls. At the political level, the legitimization of free-market policies, the renewed commitment to sound macroeconomic management after the return of democracy in 1990, and the central role the country has given to consensus in shaping its economic policy and reforms are also important. The approval, almost by consensus, of both a tax reform and a labor reform, and the implementation of contractionary monetary policy in 1990, were strong signals in this direction 6 (Labán and Larraín, 1993b). Finally, a successful export promotion policy, together with an able management of foreign debt, cut sharply Chile's external debt burden. The stock of total external debt fell from US$19.5 billion in 1986 to US$18.2 billion in 1992 (in nominal dollars), while the debt to GDP ratio declined from 115.9% to 48% 7. Furthermore, lower global interest rates and a very strong 6 Private capital flows reached their highest levels in This ratio averaged 81% during the 1980s.

12 10 DOCUMENTO DE TRABAJO Nº 168 expansion of exports reduced the ratio of foreign interest service to exports from 36.5% in 1986 to approximately 10% in During , Chile reduced its existing foreign debt by US$11.3 billion trough several debt conversion programs. In September 1990, Chile reached an agreement to restructure almost all of its remaining commercial bank debt. The much improved external solvency situation of the country has been internalized in the secondary market for Chilean debt, where its discount has declined sharply, from 34% in June 1990 to around 5% in Regained confidence by the international financial community in Chile's economic and political prospects was translated in a reduction of the risk premium that foreigners require to invest in Chilean securities. Thus, Chile was removed in 1991 from the list of non-performing economies, those for which U.S. banks are required to make loss provisions on any additional lending. Chile was also granted a triple-b rating by Standard & Poor in 1992, the best risk rating of any Latin American country, and the only one with investment grade. This rating was improved again in SHORT-TERM VS. LONG-TERM CAPITAL INFLOWS TO CHILE: So far, we have discussed at a conceptual level the main determinants of capital flows, and have divided them into two broad categories: external and internal factors. Conceptually, however, it is impossible to assign precise weight

13 WHAT DRIVES CAPITAL INFLOWS? 11 to the different elements identified. This is precisely what we turn to do in a simple econometric model. In this section, we study the quantitative impact of several elements that may help to explain the inflow of capital to Chile since the mid 1980s. A key distinction in the analysis is that between short-term and long-term capital flows The Behavior of Short Term Capital Inflows Short term capital inflows to Chile (SRCF) are affected by a number of external and internal factors. In our simple econometric framework, we focus on the following elements: the gap between domestic and international interest rates, expressed in pesos (IGAP); the foreign debt to GDP ratio (FD * /GDP); the current account deficit (CAD); the rate of GDP growth (g GDP ); and the domestic investment to GDP ratio (I/GDP). External factors are captured in this framework by their impact on the interest rate differential. The IGAP variable was measured with and without adjusting for several policy measures applied during the period: (a) a reserve requirement of 20% on foreign credits, established in June 1991, and increased to 30% in May 1992; (b) an extension of the "stamp tax" (1.2% per year) to foreign credits; (c) several changes in the exchange rate regime, including revaluations of the central rate, widenings of the band, and the switch in the peg of the central rate from the dollar to a basket of currencies. The coefficient of the IGAP captures how sensitive are short term capital inflows to interest rate arbitrage opportunities, and is expected to have a

14 12 DOCUMENTO DE TRABAJO Nº 168 positive sign: the higher are domestic interest rates relative to international rates, the more capital is attracted to Chile. The foreign debt to GDP ratio is one of the most widely watched indicators of debt burden, and was included to capture changes in country risk; its coefficient is expected to have a negative sign. Both GDP growth and the investment to GDP ratio are expected to have a positive effect on capital inflows. Clearly, capital would be more attracted to come into a growing economy, and one that is investing strongly. Finally, the coefficient on the current account deficit is expected to be positive, because a higher deficit will likely require more external financing. To assess the quantitative effect of these different factors, we run a regression for the Chilean economy using quarterly data for the period 1984:1-1992:4. As shown in Table 1, only the coefficients of the (adjusted) interest rate differential and of the foreign debt to GDP ratio had the correct signs and were statistically significant, with t-student statistics of 4.49 and -2.31, respectively. The current account deficit had the correct sign, but was statistically insignificant (t-student of 0.27). Interestingly, neither the growth rate of GDP nor the investment rate were statistically significant (and even had the wrong signs). The adjusted R 2 of the regression is 0.68, and the D-W statistic is 1.57.

15 WHAT DRIVES CAPITAL INFLOWS? 13 TABLE 1 DETERMINANTS OF SHORT-TERM CAPITAL INFLOWS TO CHILE: ECONOMETRIC RESULTS (1984:1-1992:4) Const. IGAP FD * /GDP CAD g GDP I/GDP DD R 2 D.W. non-adj adj adj (4.1) (1.01) (-0.79) (4.8) (3.29) (-3.45) (5.0) (4.49) (-2.31) (0.27) (-0.01) (-0.03) The results strongly suggest that the proper way to measure the interest rate gap must include taxes, reserve requirements, and changes in the exchange rate regime. Indeed, when the unadjusted measure of the IGAP was used, the regression reduced significantly its explanatory power, and the (unadjusted) IGAP coefficient turned out to be not significant. In going from the unadjusted to the adjusted interest rate differential, the adjusted R 2 of the regression more than doubled, from 0.31 to Moreover, when the interest gap is not measured properly, both the IGAP and the FD * /GDP variables are statistically significant, and there is evidence of autocorrelation in the residuals (D-W of 0.71). Based on these results, we can conclude that the sharp increase in short term capital inflows to Chile since the late 1980s is basically a result of

16 14 DOCUMENTO DE TRABAJO Nº 168 the increase in interest rate arbitrage opportunities and the decline in the foreign debt overhang. The first factor is a result of both external forces (e.g., the decline in US interest rates) and internal factors (e. g., the macroeconomic adjustment program of 1990). It is also important to notice that the decline in short term capital inflows in mid 1991, is well expalined by a reduction on the interest rate differential, as a response to the decline in domestic interest rates and of several policy measures just mentioned that increased the cost of foreign funding. Perhaps surprisingly, the growth rate of GDP and the investment rate did not appear to affect short-term capital flows to Chile Explaining Long Term Capital Inflows to Chile We now turn to analyze the factors behind the inflow of long term capital to Chile (LTCF), using quarterly data for the period 1984:1-1992:4. The LTCF variable is constructed adding up medium and long term foreign credits to the domestic private sector and direct foreign investment. As we did with short term capital flows, we will investigate the following factors as candidates to explain LTCF: the (adjusted) interest rate differential (IGAP); the foreign debt to GDP ratio (FD * /GDP); the current account deficit (CAD); the rate of GDP growth (g GDP ); and the domestic investment to GDP ratio (I/GDP). We also introduce a dummy variable (DD) to account for any possible effects on capital flows of Chile's return to democracy; thus, DD takes a value of 1 since early 1990, and zero otherwise. (This dummy variable did not turn out to be significant when introduced in the equation explaining the behavior of short term capital inflows.)

17 WHAT DRIVES CAPITAL INFLOWS? 15 TABLE 2 DETERMINANTS OF LONG-TERM CAPITAL INFLOWS TO CHILE: ECONOMETRIC RESULTS (1984:1-1992:4) Const. igap FD * /GDP CAD g GDP I/GDP DD R 2 D.W. adj. adj (2.6) (0.22) (-1.84) (-1.3) (0.45) (3.23) (5.68) (2.3) (-0.11) (-1.89) (-1.5) (3.59) (6.87) The results of this regression are shown in Table 2. In the first exercise shown, the interest rate differential had the correct sign, but turned out to be statistically insignificant; both the foreign debt to GDP ratio and the investment rate turned out to be statistically significant (t-students of 1.84 and 3.23, respectively) and have the expected signs. The current rate of growth of output, however, was not significant (although had the correct sign), while the current account deficit was both statistically insignificant and had the wrong sign. Finally, the dummy variable for the change in political regime was highly significant (t-student of 5.68) and had the correct sign. The adjusted R 2 of the equation was 0.91 and the D.W. statistic was A second regression was run, leaving out the rate of output growth (as reported in the table). In this case, the results are very similar to those obtained before, with one exception: both the investment rate and the dummy variable turn even more significant. This reinforces our previous findings.

18 16 DOCUMENTO DE TRABAJO Nº 168 The econometric evidence just analyzed provides a very interesting result. The increase in long-term capital inflows to Chile after 1989 has been basically influenced by domestic factors, namely, the reduction of the debt overhang, better prospects of future economic growth (captured here by a higher investment rate), and the return to democracy. Shorter term considerations, such as interest rate arbitrage opportunities and the current rate of GDP growth, were not significant; neither was the financing of the current account deficit. In fact, the fit of the regression for medium and long term flows was similar with the adjusted and the unadjusted measures of the interest rate differential. 5. CONCLUSIONS This paper has analized conceptually and econometrically the main elements behind the large increase in net capital inflows to the Chilean economy since the late 1980s. At stake have been two conflicting hypotheses. One has stressed external factors as the main element behind these inflows. The other has argued that it is domestic developments, such as stabilization and structural reforms, which have attracted the resources. Our main empirical results show that it is necessary to be more specific when analyzing capital inflows, because they are not all alike. In particular, the factors explaining the evolution of short term capital inflows to the Chilean economy since 1984 are quite different from those relevant to understand the behavior of medium and long term capital flows. Short term private capital inflows have been much more sensible to

19 WHAT DRIVES CAPITAL INFLOWS? 17 external factors than long term flows. More precisely, they have responded basically to interest rate arbitrage oportunities --which is a mix of internal and external factors--and to the decline in the country risk, linked here to the reduction of the foreign debt to GDP ratio. In fact, the introduction of reserve requirements to foreign credits in June 1991 and its sucessive modifications, the extension of the stamp tax to foreign credits, and the sucessive modifications in exchange rate policy effectively reduced the interest rate gap between Chile and abroad, and appear to have reduced short term capital inflows. On the other hand, the sharp increase in medium and long term private capital inflows since the late 1980s has been mainly a result of favorable domestic political and economic changes. Among these, the most significant are the reduction of the debt overhang, the better prospects of future economic growth (captured here by a higher ratio of investment to GDP) and the return to democracy. These have been translated in a reduction of the premium that foreign investors require to invest in Chilean long term securities. Our results also show that medium and long term capital has not been sensitive to the interest rate differential. In summary, short term capital inflows respond to a very different set of factors than long term flows, with one important exception: all sorts of capital appear to avoid a foreign debt overhang. Short term inflows basically look for interest rate arbitrage opportunities. Long term flows do not care about this arbitrage, but rather look at more structural considerations, both economic and political. These results shed light on the kinds of policies that can be used to stimulate or slow some particular type

20

21 WHAT DRIVES CAPITAL INFLOWS? 19 of capital inflow. Although the empirical evidence has been obtained for Chile, it is likely that the validity of these conclusions applies to other Latin American countries as well. REFERENCES Calvo, G., L. Leiderman and C. Reinhart (1992), "Capital Inflows and Real Exchange Rate Appreciation in Latin America: The Role of External Factors," IMF Working Paper WP/92/62. Caballero, R. and V. Corbo (1990), "The Effect of Real Exchange Rate Uncertainty on Exports: Empirical Evidence", The World Bank Economic Review, Culpeper, R. and Griffith-Jones (1992), "Rapid Return of Private Flows to Latin America: New Trends and New Policy Issues," mimeo ECLAC. Hanson, J. (1992); "Opening the Capital Account: A Survey of Issues and Results", World Bank Working Paper, May. Krugman, P. (1987), "The Narrow Moving Band, the Dutch Disease, and the Competitive Consequences of Mrs. Thatcher: Notes on Trade in the Presence of Dynamic Scale Economies," Journal of Development Economics, 27, pp Labán, R. and F. Larraín (1993a), "Continuity, Change, and the Political Economy of Transition in Chile". Forthcoming in R. Dornbusch

22 20 DOCUMENTO DE TRABAJO Nº 168 and S. Edwards (editors), Stabilization, Economic Reform, and Growth, University of Chicago Press, forthcoming. Labán, R. and F. Larraín (1993b); "Twenty Years of Experience with Capital Mobility in Chile." Forthcoming in B. Bosworth, R. Dornbusch and R. Labán (editors), The Chilean Economy: Policy Lessons and Challenges, The Brookings Institution, Washington, D.C. Larraín, F. and A. Velasco (1990), "Can Swaps Solve the Debt Crisis? Lessons from the Chilean Experience", Princeton Studies in International Finance No. 69, November. Larraín, F. and R. Vergara (1993); "Investment and Macroeconomic Adjustment: the Case of East Asia". In L. Servén and A. Solimano (editors), From Adjustment to Sustainable Growth: The Role of Capital Formation, The World Bank. Salomon Brothers (1992) "Private Capital Flows to Latin America", Sovereign Assessment Group, New York. Tobin, J. (1978), "A Proposal for International Monetary Reform", Eastern Economic Journal 4. Tornell, A. (1990), "Real vs. Financial Investment: Can Tobin Taxes Eliminate the Irreversibility Distortion?", Journal of Development Economics 32.

What Determines Capital Inflows?: An Empirical Analysis for Chile

What Determines Capital Inflows?: An Empirical Analysis for Chile Rómulo A. Chumacero * Raúl Labán M. ** Felipe Larraín B. *** ABSTRACT This paper presents an empirical investigation of the determinants

What Determines Capital Inflows?: An Empirical Analysis for Chile Rómulo A. Chumacero * Raúl Labán M. ** Felipe Larraín B. *** ABSTRACT This paper presents an empirical investigation of the determinants

Volume Author/Editor: Sebastian Edwards, editor. Volume Publisher: University of Chicago Press. Volume URL:

This PDF is a selection from a published volume from the National Bureau of Economic Research Volume Title: Capital Flows and the Emerging Economies: Theory, Evidence, and Controversies Volume Author/Editor:

This PDF is a selection from a published volume from the National Bureau of Economic Research Volume Title: Capital Flows and the Emerging Economies: Theory, Evidence, and Controversies Volume Author/Editor:

Outlook for the Chilean Economy

Outlook for the Chilean Economy Jorge Marshall, Vice-President of the Board, Central Bank of Chile. Address to the Fifth Annual Latin American Banking Conference, Salomon Smith Barney, New York, March

Outlook for the Chilean Economy Jorge Marshall, Vice-President of the Board, Central Bank of Chile. Address to the Fifth Annual Latin American Banking Conference, Salomon Smith Barney, New York, March

Nº 283 Enero Documento de Trabajo. Inflation of Tradable Goods. Rodrigo A. Cerda

Nº 8 Enero 5 Documento de Trabajo ISSN (edición impresa) 76-7 ISSN (edición electrónica) 77-759 Inflation of Tradable Goods. Rodrigo A. Cerda www.economia.puc.cl Versión impresa ISSN: 76-7 Versión electrónica

Nº 8 Enero 5 Documento de Trabajo ISSN (edición impresa) 76-7 ISSN (edición electrónica) 77-759 Inflation of Tradable Goods. Rodrigo A. Cerda www.economia.puc.cl Versión impresa ISSN: 76-7 Versión electrónica

Notes on the monetary transmission mechanism in the Czech economy

Notes on the monetary transmission mechanism in the Czech economy Luděk Niedermayer 1 This paper discusses several empirical aspects of the monetary transmission mechanism in the Czech economy. The introduction

Notes on the monetary transmission mechanism in the Czech economy Luděk Niedermayer 1 This paper discusses several empirical aspects of the monetary transmission mechanism in the Czech economy. The introduction

Capital Flows to Latin America: Policy Challenges and Responses

Capital Flows to Latin America: Policy Challenges and Responses Javier Guzmán Calafell Director General Center for Latin American Monetary Studies INTERNATIONAL CAPITAL MOVEMENTS: OLD AND NEW DEBATES Cusco,

Capital Flows to Latin America: Policy Challenges and Responses Javier Guzmán Calafell Director General Center for Latin American Monetary Studies INTERNATIONAL CAPITAL MOVEMENTS: OLD AND NEW DEBATES Cusco,

CAPITAL FLOWS TO LATIN AMERICA: CHALLENGES AND POLICY RESPONSES. Javier Guzmán Calafell 1

CAPITAL FLOWS TO LATIN AMERICA: CHALLENGES AND POLICY RESPONSES Javier Guzmán Calafell 1 1. Introduction Capital flows to Latin America and other emerging market regions fell sharply after the collapse

CAPITAL FLOWS TO LATIN AMERICA: CHALLENGES AND POLICY RESPONSES Javier Guzmán Calafell 1 1. Introduction Capital flows to Latin America and other emerging market regions fell sharply after the collapse

Global Business Cycles

Global Business Cycles M. Ayhan Kose, Prakash Loungani, and Marco E. Terrones April 29 The 29 forecasts of economic activity, if realized, would qualify this year as the most severe global recession during

Global Business Cycles M. Ayhan Kose, Prakash Loungani, and Marco E. Terrones April 29 The 29 forecasts of economic activity, if realized, would qualify this year as the most severe global recession during

Ten Lessons Learned from the Korean Crisis Center for International Development, 11/19/99. Jeffrey A. Frankel, Harpel Professor, Harvard University

Ten Lessons Learned from the Korean Crisis Center for International Development, 11/19/99 Jeffrey A. Frankel, Harpel Professor, Harvard University The crisis has now passed in Korea. The excessive optimism

Ten Lessons Learned from the Korean Crisis Center for International Development, 11/19/99 Jeffrey A. Frankel, Harpel Professor, Harvard University The crisis has now passed in Korea. The excessive optimism

POLICY BRIEF. Resurgent Capital Flows to Developing Countries: Policies to Improve Their Impact

J u n e 2 0 1 3 n u m b e r 1 0 Resurgent Capital Flows to Developing Countries: Policies to Improve Their Impact James A. Hanson* Overview Some developing countries have reinstated controls on capital

J u n e 2 0 1 3 n u m b e r 1 0 Resurgent Capital Flows to Developing Countries: Policies to Improve Their Impact James A. Hanson* Overview Some developing countries have reinstated controls on capital

Economic Survey of Latin America and the Caribbean CHILE. 1. General trends. 2. Economic policy

Economic Survey of Latin America and the Caribbean 2017 1 CHILE 1. General trends In 2016 the Chilean economy grew at a slower rate (1.6%) than in 2015 (2.3%), as the drop in investment and exports outweighed

Economic Survey of Latin America and the Caribbean 2017 1 CHILE 1. General trends In 2016 the Chilean economy grew at a slower rate (1.6%) than in 2015 (2.3%), as the drop in investment and exports outweighed

Prepared by Iordanis Petsas To Accompany. by Paul R. Krugman and Maurice Obstfeld

Chapter 22 Developing Countries: Growth, Crisis, and Reform Prepared by Iordanis Petsas To Accompany International Economics: Theory and Policy, Sixth Edition by Paul R. Krugman and Maurice Obstfeld Chapter

Chapter 22 Developing Countries: Growth, Crisis, and Reform Prepared by Iordanis Petsas To Accompany International Economics: Theory and Policy, Sixth Edition by Paul R. Krugman and Maurice Obstfeld Chapter

Inflation Targeting Under a Crawling Band Exchange Rate Regime: Lessons from Israel

9 Inflation Targeting Under a Crawling Band Exchange Rate Regime: Lessons from Israel Leonardo Leiderman and Gil Bufman 1 Consider a small, open economy that, after a long period of chronically high inflation,

9 Inflation Targeting Under a Crawling Band Exchange Rate Regime: Lessons from Israel Leonardo Leiderman and Gil Bufman 1 Consider a small, open economy that, after a long period of chronically high inflation,

Global Imbalances and Latin America: A Comment on Eichengreen and Park

3 Global Imbalances and Latin America: A Comment on Eichengreen and Park Barbara Stallings I n Global Imbalances and Emerging Markets, Barry Eichengreen and Yung Chul Park make a number of important contributions

3 Global Imbalances and Latin America: A Comment on Eichengreen and Park Barbara Stallings I n Global Imbalances and Emerging Markets, Barry Eichengreen and Yung Chul Park make a number of important contributions

Ric Battellino: Recent financial developments

Ric Battellino: Recent financial developments Address by Mr Ric Battellino, Deputy Governor of the Reserve Bank of Australia, at the Annual Stockbrokers Conference, Sydney, 26 May 2011. * * * Introduction

Ric Battellino: Recent financial developments Address by Mr Ric Battellino, Deputy Governor of the Reserve Bank of Australia, at the Annual Stockbrokers Conference, Sydney, 26 May 2011. * * * Introduction

19.2 Exchange Rates in the Long Run Introduction 1/24/2013. Exchange Rates and International Finance. The Nominal Exchange Rate

Chapter 19 Exchange Rates and International Finance By Charles I. Jones International trade of goods and services exceeds 20 percent of GDP in most countries. Media Slides Created By Dave Brown Penn State

Chapter 19 Exchange Rates and International Finance By Charles I. Jones International trade of goods and services exceeds 20 percent of GDP in most countries. Media Slides Created By Dave Brown Penn State

Antonio Fazio: Overview of global economic and financial developments in first half 2004

Antonio Fazio: Overview of global economic and financial developments in first half 2004 Address by Mr Antonio Fazio, Governor of the Bank of Italy, to the ACRI (Association of Italian Savings Banks),

Antonio Fazio: Overview of global economic and financial developments in first half 2004 Address by Mr Antonio Fazio, Governor of the Bank of Italy, to the ACRI (Association of Italian Savings Banks),

126 Telefónica, S.A. Annual Report Risk management

126 Telefónica, S.A. Annual Report 2004 04 Risk management Annual Report 2004 Telefónica, S.A. 127 128 Telefónica, S.A. Annual Report 2004 INTRODUCTION The Telefónica Group is exposed to diverse risks

126 Telefónica, S.A. Annual Report 2004 04 Risk management Annual Report 2004 Telefónica, S.A. 127 128 Telefónica, S.A. Annual Report 2004 INTRODUCTION The Telefónica Group is exposed to diverse risks

CHILE: GROWTH WITH STABILITY {')

") INT-1337 CHILE: GROWTH WITH STABILITY {') ROBERTO ZAHLER Governor Central Bank of Chile January, 1995 (*) This paper is a slightly revised and updated version of the speech given by R. Zahler on November

INT-1337 CHILE: GROWTH WITH STABILITY {') ROBERTO ZAHLER Governor Central Bank of Chile January, 1995 (*) This paper is a slightly revised and updated version of the speech given by R. Zahler on November

New in 2013: Greater emphasis on capital flows Refinements to EBA methodology Individual country assessments

As in 212: Stock-take: multilaterally consistent assessment of external sector policies of the largest economies Feeds into Article IVs Draws on External Balance Assessment (EBA) methodology/other Identifies

As in 212: Stock-take: multilaterally consistent assessment of external sector policies of the largest economies Feeds into Article IVs Draws on External Balance Assessment (EBA) methodology/other Identifies

Whither Latin American Capital Markets?

SEPTIMO CONGRESO DE TESORERIA Cartagena de Indias, Colombia October 21-22, 2004 Whither Latin American Capital Markets? Augusto de la Torre The World Bank Structure of the Presentation 1. Evolution of

SEPTIMO CONGRESO DE TESORERIA Cartagena de Indias, Colombia October 21-22, 2004 Whither Latin American Capital Markets? Augusto de la Torre The World Bank Structure of the Presentation 1. Evolution of

Gauging Current Conditions:

Gauging Current Conditions: The Economic Outlook and Its Impact on Workers Compensation Vol. 2 2005 The gauges below indicate the economic outlook for the current year and for 2006 for factors that typically

Gauging Current Conditions: The Economic Outlook and Its Impact on Workers Compensation Vol. 2 2005 The gauges below indicate the economic outlook for the current year and for 2006 for factors that typically

working paper Fiscal Policy, Government Institutions, and Sovereign Creditworthiness By Bernardin Akitoby and Thomas Stratmann No.

No. 10-41 July 2010 working paper Fiscal Policy, Government Institutions, and Sovereign Creditworthiness By Bernardin Akitoby and Thomas Stratmann The ideas presented in this research are the authors and

No. 10-41 July 2010 working paper Fiscal Policy, Government Institutions, and Sovereign Creditworthiness By Bernardin Akitoby and Thomas Stratmann The ideas presented in this research are the authors and

DETERMINANTS OF EMERGING MARKET BOND SPREAD: EVIDENCE FROM TEN AFRICAN COUNTRIES ABSTRACT

DETERMINANTS OF EMERGING MARKET BOND SPREAD: EVIDENCE FROM TEN AFRICAN COUNTRIES ABSTRACT This paper investigates the determinants of bond market spreads over the period 1991-2012 in 10 African countries.

DETERMINANTS OF EMERGING MARKET BOND SPREAD: EVIDENCE FROM TEN AFRICAN COUNTRIES ABSTRACT This paper investigates the determinants of bond market spreads over the period 1991-2012 in 10 African countries.

internationally tradable goods, thus affecting inflation, an effect that has become more evident in recent months.

REMARKS BY MR. JAVIER GUZMÁN CALAFELL, DEPUTY GOVERNOR AT THE BANCO DE MÉXICO, AT THE PANEL OF CENTRAL BANK GOVERNORS ON NEW CHALLENGES FOR CENTRAL BANKS IN LATIN AMERICA. SEMINAR ON FINANCIAL VOLATILITY

REMARKS BY MR. JAVIER GUZMÁN CALAFELL, DEPUTY GOVERNOR AT THE BANCO DE MÉXICO, AT THE PANEL OF CENTRAL BANK GOVERNORS ON NEW CHALLENGES FOR CENTRAL BANKS IN LATIN AMERICA. SEMINAR ON FINANCIAL VOLATILITY

Supply and Demand over the Business Cycle

Session 9. The Model at Work. v Business Cycles v The Economy in the Long Run: Recession and recovery Monetary expansion The everyday business of the central bank v Summing up: The IS/LM Model in Closed

Session 9. The Model at Work. v Business Cycles v The Economy in the Long Run: Recession and recovery Monetary expansion The everyday business of the central bank v Summing up: The IS/LM Model in Closed

Macroeconomic Management in Emerging-Market Economies with Open Capital Accounts. Outline

Macroeconomic Management in Emerging-Market Economies with Open Capital Accounts Klaus Schmidt-Hebbel, Central Bank of Chile Seminar on Crisis Prevention in Emerging Markets IMF-Singapore Training Institute

Macroeconomic Management in Emerging-Market Economies with Open Capital Accounts Klaus Schmidt-Hebbel, Central Bank of Chile Seminar on Crisis Prevention in Emerging Markets IMF-Singapore Training Institute

How Important Are U.S. Capital Flows into Mexico?

economic GOMMeiMTCIRY Federal Reserve Bank of Cleveland December 1, 1994 How Important Are U.S. Capital Flows into Mexico? by William P. Osterberg In November 1993, the U.S. Congress voted to pass the

economic GOMMeiMTCIRY Federal Reserve Bank of Cleveland December 1, 1994 How Important Are U.S. Capital Flows into Mexico? by William P. Osterberg In November 1993, the U.S. Congress voted to pass the

Is the US current account de cit sustainable? Disproving some fallacies about current accounts

Is the US current account de cit sustainable? Disproving some fallacies about current accounts Frederic Lambert International Macroeconomics - Prof. David Backus New York University December, 24 1 Introduction

Is the US current account de cit sustainable? Disproving some fallacies about current accounts Frederic Lambert International Macroeconomics - Prof. David Backus New York University December, 24 1 Introduction

Challenges of financial globalisation and dollarisation for monetary policy: the case of Peru

Challenges of financial globalisation and dollarisation for monetary policy: the case of Peru Julio Velarde During the last decade, the financial system of Peru has become more integrated with the global

Challenges of financial globalisation and dollarisation for monetary policy: the case of Peru Julio Velarde During the last decade, the financial system of Peru has become more integrated with the global

II.2. Member State vulnerability to changes in the euro exchange rate ( 35 )

") II.2. Member State vulnerability to changes in the euro exchange rate ( 35 ) There have been significant fluctuations in the euro exchange rate since the start of the monetary union. This section assesses

II.2. Member State vulnerability to changes in the euro exchange rate ( 35 ) There have been significant fluctuations in the euro exchange rate since the start of the monetary union. This section assesses

Discussion of Michael Klein s Capital Controls: Gates and Walls Brookings Papers on Economic Activity, September 2012

Discussion of Michael Klein s Capital Controls: Gates and Walls Brookings Papers on Economic Activity, September 2012 Kristin Forbes 1, MIT-Sloan School of Management The desirability of capital controls

Discussion of Michael Klein s Capital Controls: Gates and Walls Brookings Papers on Economic Activity, September 2012 Kristin Forbes 1, MIT-Sloan School of Management The desirability of capital controls

Financing the U.S. Trade Deficit

Order Code RL33274 Financing the U.S. Trade Deficit Updated January 31, 2008 James K. Jackson Specialist in International Trade and Finance Foreign Affairs, Defense, and Trade Division Financing the U.S.

Order Code RL33274 Financing the U.S. Trade Deficit Updated January 31, 2008 James K. Jackson Specialist in International Trade and Finance Foreign Affairs, Defense, and Trade Division Financing the U.S.

The fiscal adjustment after the crisis in Argentina

65 The fiscal adjustment after the 2001-02 crisis in Argentina 1 Mario Damill, Roberto Frenkel, and Martín Rapetti After the crisis of the convertibility regime, Argentina experienced a significant adjustment

65 The fiscal adjustment after the 2001-02 crisis in Argentina 1 Mario Damill, Roberto Frenkel, and Martín Rapetti After the crisis of the convertibility regime, Argentina experienced a significant adjustment

International Macroeconomics

Slides for Chapter 3: Theory of Current Account Determination International Macroeconomics Schmitt-Grohé Uribe Woodford Columbia University May 1, 2016 1 Motivation Build a model of an open economy to

Slides for Chapter 3: Theory of Current Account Determination International Macroeconomics Schmitt-Grohé Uribe Woodford Columbia University May 1, 2016 1 Motivation Build a model of an open economy to

Nº 160 Septiembre 1993

Nº 160 Septiembre 1993 Documento de Trabajo ISSN (edición impresa) 0716-7334 ISSN (edición electrónica) 0717-7593 EconomicReforms in Chile: an Overview. Vittorio Corbo L. www.economia.puc.cl ISSN:0716-7334

Nº 160 Septiembre 1993 Documento de Trabajo ISSN (edición impresa) 0716-7334 ISSN (edición electrónica) 0717-7593 EconomicReforms in Chile: an Overview. Vittorio Corbo L. www.economia.puc.cl ISSN:0716-7334

RECENT ECONOMIC DEVELOPMENTS IN SOUTH AFRICA

RECENT ECONOMIC DEVELOPMENTS IN SOUTH AFRICA Remarks by Mr AD Mminele, Deputy Governor of the South African Reserve Bank, at the Citigroup Global Issues Seminar, held at the Ritz Carlton Hotel in Istanbul,

RECENT ECONOMIC DEVELOPMENTS IN SOUTH AFRICA Remarks by Mr AD Mminele, Deputy Governor of the South African Reserve Bank, at the Citigroup Global Issues Seminar, held at the Ritz Carlton Hotel in Istanbul,

Documento de Trabajo. ISSN (edición impresa) ISSN (edición electrónica) Reducing Inflation: The Chilean Experience

ISSN (edición electrónica) Reducing Inflation: The Chilean Experience") Nº 185 Agosto 1998 Documento de Trabajo ISSN (edición impresa) 0716-7334 ISSN (edición electrónica) 0717-7593 Reducing Inflation: The Chilean Experience Vittorio Corbo www.economia.puc.cl ABSTRACT The

Nº 185 Agosto 1998 Documento de Trabajo ISSN (edición impresa) 0716-7334 ISSN (edición electrónica) 0717-7593 Reducing Inflation: The Chilean Experience Vittorio Corbo www.economia.puc.cl ABSTRACT The

Bank Flows and Basel III Determinants and Regional Differences in Emerging Markets

Public Disclosure Authorized THE WORLD BANK POVERTY REDUCTION AND ECONOMIC MANAGEMENT NETWORK (PREM) Economic Premise Public Disclosure Authorized Bank Flows and Basel III Determinants and Regional Differences

Public Disclosure Authorized THE WORLD BANK POVERTY REDUCTION AND ECONOMIC MANAGEMENT NETWORK (PREM) Economic Premise Public Disclosure Authorized Bank Flows and Basel III Determinants and Regional Differences

IV. THE BENEFITS OF FURTHER FINANCIAL INTEGRATION IN ASIA

IV. THE BENEFITS OF FURTHER FINANCIAL INTEGRATION IN ASIA The need for economic rebalancing in the aftermath of the global financial crisis and the recent surge of capital inflows to emerging Asia have

IV. THE BENEFITS OF FURTHER FINANCIAL INTEGRATION IN ASIA The need for economic rebalancing in the aftermath of the global financial crisis and the recent surge of capital inflows to emerging Asia have

II. Underlying domestic macroeconomic imbalances fuelled current account deficits

II. Underlying domestic macroeconomic imbalances fuelled current account deficits Macroeconomic imbalances, including housing and credit bubbles, contributed to significant current account deficits in

II. Underlying domestic macroeconomic imbalances fuelled current account deficits Macroeconomic imbalances, including housing and credit bubbles, contributed to significant current account deficits in

The Chilean economy: Institutional buildup and perspectives

The Chilean economy: Institutional buildup and perspectives Vittorio Corbo Governor 1 Outline 1. Introduction 2. Chile s economic reforms and institutional buildup 3. Performance of the Chilean economy

The Chilean economy: Institutional buildup and perspectives Vittorio Corbo Governor 1 Outline 1. Introduction 2. Chile s economic reforms and institutional buildup 3. Performance of the Chilean economy

ARGENTINA. 1. General trends

1 ARGENTINA 1. General trends After slowing rapidly in 2009, the Argentine economy resumed robust growth in 2010, with a rate well above the regional average at 9.2%. On the back of this the unemployment

1 ARGENTINA 1. General trends After slowing rapidly in 2009, the Argentine economy resumed robust growth in 2010, with a rate well above the regional average at 9.2%. On the back of this the unemployment

Characteristics of the euro area business cycle in the 1990s

Characteristics of the euro area business cycle in the 1990s As part of its monetary policy strategy, the ECB regularly monitors the development of a wide range of indicators and assesses their implications

Characteristics of the euro area business cycle in the 1990s As part of its monetary policy strategy, the ECB regularly monitors the development of a wide range of indicators and assesses their implications

SPANISH EXTERNAL SECTOR AND COMPETITIVENESS: SOME HIGHLIGHTS

SPANISH EXTERNAL SECTOR AND COMPETITIVENESS: SOME HIGHLIGHTS Summary Spain has significantly increased its trade openness in the last two decades Despite the global crisis and increased competition from

SPANISH EXTERNAL SECTOR AND COMPETITIVENESS: SOME HIGHLIGHTS Summary Spain has significantly increased its trade openness in the last two decades Despite the global crisis and increased competition from

It has been suggested in the literature that a shortage of sound and liquid financial

I. Local Bond Markets During the Global Financial Crisis II. Abstract (117 words) It has been suggested in the literature that a shortage of sound and liquid financial instruments in emerging economies

I. Local Bond Markets During the Global Financial Crisis II. Abstract (117 words) It has been suggested in the literature that a shortage of sound and liquid financial instruments in emerging economies

Financing the U.S. Trade Deficit

James K. Jackson Specialist in International Trade and Finance November 16, 2012 CRS Report for Congress Prepared for Members and Committees of Congress Congressional Research Service 7-5700 www.crs.gov

James K. Jackson Specialist in International Trade and Finance November 16, 2012 CRS Report for Congress Prepared for Members and Committees of Congress Congressional Research Service 7-5700 www.crs.gov

Documento de Trabajo. ISSN (edición impresa) ISSN (edición electrónica)

ISSN (edición electrónica)") Nº 227 Octubre 2002 Documento de Trabajo ISSN (edición impresa) 0716-7334 ISSN (edición electrónica) 0717-7593 The Effect of a Constant or a Declining Discount Rate on Optimal Investment Timing. Gonzalo

Nº 227 Octubre 2002 Documento de Trabajo ISSN (edición impresa) 0716-7334 ISSN (edición electrónica) 0717-7593 The Effect of a Constant or a Declining Discount Rate on Optimal Investment Timing. Gonzalo

Monetary Policy Outlook for Mexico

Mr. Javier Guzmán Calafell, Deputy Governor, Banco de México J.P. Morgan Investor Seminar Washington, DC, 8 October 2016 Outline 1 2 3 4 5 Monetary Policy in Mexico Evolution of the Mexican Economy Inflation

Mr. Javier Guzmán Calafell, Deputy Governor, Banco de México J.P. Morgan Investor Seminar Washington, DC, 8 October 2016 Outline 1 2 3 4 5 Monetary Policy in Mexico Evolution of the Mexican Economy Inflation

INTERNATIONAL CAPITAL FLOWS: DISCUSSION

INTERNATIONAL CAPITAL FLOWS: DISCUSSION William R. Cline* I welcome the contribution that Sebastian Edwards s sharp, lucid paper has made to the literature and to deepening our understanding of the Chilean

INTERNATIONAL CAPITAL FLOWS: DISCUSSION William R. Cline* I welcome the contribution that Sebastian Edwards s sharp, lucid paper has made to the literature and to deepening our understanding of the Chilean

SHORT-TERM ACHIEVEMENTS AND LONG-TERM PROBLEMS. by Man 9{. MeCtzer

SHORT-TERM ACHIEVEMENTS AND LONG-TERM PROBLEMS by Man 9{. MeCtzer Carnegie. Mellon University and American 'Enterprise Institute (Preparedfor the 113. Senate 'Budget Committee, January 26, 1995 It is a

SHORT-TERM ACHIEVEMENTS AND LONG-TERM PROBLEMS by Man 9{. MeCtzer Carnegie. Mellon University and American 'Enterprise Institute (Preparedfor the 113. Senate 'Budget Committee, January 26, 1995 It is a

Inflation, Inflation Uncertainty, Political Stability, and Economic Growth

Inflation, Inflation Uncertainty, Political Stability, and Economic Growth George K. Davis Dept. of Economics Miami University Oxford, Ohio 45056 Bryce E. Kanago Dept. of Economics Miami University Oxford,

Inflation, Inflation Uncertainty, Political Stability, and Economic Growth George K. Davis Dept. of Economics Miami University Oxford, Ohio 45056 Bryce E. Kanago Dept. of Economics Miami University Oxford,

Labour. Overview Latin America and the Caribbean EXECUT I V E S U M M A R Y

2016 Labour Overview Latin America and the Caribbean EXECUT I V E S U M M A R Y ILO Regional Office for Latin America and the Caribbean 3 ILO / Latin America and the Caribbean Foreword FOREWORD This 2016

2016 Labour Overview Latin America and the Caribbean EXECUT I V E S U M M A R Y ILO Regional Office for Latin America and the Caribbean 3 ILO / Latin America and the Caribbean Foreword FOREWORD This 2016

Suggested Solutions to Problem Set 6

Department of Economics University of California, Berkeley Spring 2006 Economics 182 Suggested Solutions to Problem Set 6 Problem 1: International diversification Because raspberries are nontradable, asset

Department of Economics University of California, Berkeley Spring 2006 Economics 182 Suggested Solutions to Problem Set 6 Problem 1: International diversification Because raspberries are nontradable, asset

Implications of Fiscal Austerity for U.S. Monetary Policy

Implications of Fiscal Austerity for U.S. Monetary Policy Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston The Global Interdependence Center Central Banking Conference

Implications of Fiscal Austerity for U.S. Monetary Policy Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston The Global Interdependence Center Central Banking Conference

Current Economic Conditions and Selected Forecasts

Order Code RL30329 Current Economic Conditions and Selected Forecasts Updated May 20, 2008 Gail E. Makinen Economic Policy Consultant Government and Finance Division Current Economic Conditions and Selected

Order Code RL30329 Current Economic Conditions and Selected Forecasts Updated May 20, 2008 Gail E. Makinen Economic Policy Consultant Government and Finance Division Current Economic Conditions and Selected

COMMENTS ON SESSION 1 AUTOMATIC STABILISERS AND DISCRETIONARY FISCAL POLICY. Adi Brender *

COMMENTS ON SESSION 1 AUTOMATIC STABILISERS AND DISCRETIONARY FISCAL POLICY Adi Brender * 1 Key analytical issues for policy choice and design A basic question facing policy makers at the outset of a crisis

COMMENTS ON SESSION 1 AUTOMATIC STABILISERS AND DISCRETIONARY FISCAL POLICY Adi Brender * 1 Key analytical issues for policy choice and design A basic question facing policy makers at the outset of a crisis

Neoliberalism, Investment and Growth in Latin America

Neoliberalism, Investment and Growth in Latin America Jayati Ghosh and C.P. Chandrasekhar Despite the relatively poor growth record of the era of corporate globalisation, there are many who continue to

Neoliberalism, Investment and Growth in Latin America Jayati Ghosh and C.P. Chandrasekhar Despite the relatively poor growth record of the era of corporate globalisation, there are many who continue to

Emerging Markets Debt: Outlook for the Asset Class

Emerging Markets Debt: Outlook for the Asset Class By Steffen Reichold Emerging Markets Economist May 2, 211 Emerging market debt has been one of the best performing asset classes in recent years due to

Emerging Markets Debt: Outlook for the Asset Class By Steffen Reichold Emerging Markets Economist May 2, 211 Emerging market debt has been one of the best performing asset classes in recent years due to

September 21, 2016 Bank of Japan

September 21, 2016 Bank of Japan Comprehensive Assessment: Developments in Economic Activity and Prices as well as Policy Effects since the Introduction of Quantitative and Qualitative Monetary Easing

September 21, 2016 Bank of Japan Comprehensive Assessment: Developments in Economic Activity and Prices as well as Policy Effects since the Introduction of Quantitative and Qualitative Monetary Easing

IS FINANCIAL REPRESSION REALLY BAD? Eun Young OH Durham Univeristy 17 Sidegate, Durham, United Kingdom

IS FINANCIAL REPRESSION REALLY BAD? Eun Young OH Durham Univeristy 17 Sidegate, Durham, United Kingdom E-mail: e.y.oh@durham.ac.uk Abstract This paper examines the relationship between reserve requirements,

IS FINANCIAL REPRESSION REALLY BAD? Eun Young OH Durham Univeristy 17 Sidegate, Durham, United Kingdom E-mail: e.y.oh@durham.ac.uk Abstract This paper examines the relationship between reserve requirements,

Lessons from the stabilization process in Argentina,

By Hyperinflation exploded in 1989. It was the final stage of a chronic inflationary process that began in 1945 and lasted 45 years. From the beginning of the century until the end of World War II, Argentina

By Hyperinflation exploded in 1989. It was the final stage of a chronic inflationary process that began in 1945 and lasted 45 years. From the beginning of the century until the end of World War II, Argentina

The Velocity of Money and Nominal Interest Rates: Evidence from Developed and Latin-American Countries

The Velocity of Money and Nominal Interest Rates: Evidence from Developed and Latin-American Countries Petr Duczynski Abstract This study examines the behavior of the velocity of money in developed and

The Velocity of Money and Nominal Interest Rates: Evidence from Developed and Latin-American Countries Petr Duczynski Abstract This study examines the behavior of the velocity of money in developed and

Designing Scenarios for Macro Stress Testing (Financial System Report, April 2016)

") Financial System Report Annex Series inancial ystem eport nnex A Designing Scenarios for Macro Stress Testing (Financial System Report, April 1) FINANCIAL SYSTEM AND BANK EXAMINATION DEPARTMENT BANK OF

Financial System Report Annex Series inancial ystem eport nnex A Designing Scenarios for Macro Stress Testing (Financial System Report, April 1) FINANCIAL SYSTEM AND BANK EXAMINATION DEPARTMENT BANK OF

Documento de Trabajo. ISSN (edición impresa) ISSN (edición electrónica)

ISSN (edición electrónica)") Nº 307 Marzo 006 Documento de Trabajo ISSN (edición impresa) 0716-7334 ISSN (edición electrónica) 0717-7593 Do Large Retailers Affect Employment? Evidence from an Emerging Economy Rosario Rivero Rodrigo

Nº 307 Marzo 006 Documento de Trabajo ISSN (edición impresa) 0716-7334 ISSN (edición electrónica) 0717-7593 Do Large Retailers Affect Employment? Evidence from an Emerging Economy Rosario Rivero Rodrigo

The Impact of Uncertainty on Investment: Empirical Evidence from Manufacturing Firms in Korea

The Impact of Uncertainty on Investment: Empirical Evidence from Manufacturing Firms in Korea Hangyong Lee Korea development Institute December 2005 Abstract This paper investigates the empirical relationship

The Impact of Uncertainty on Investment: Empirical Evidence from Manufacturing Firms in Korea Hangyong Lee Korea development Institute December 2005 Abstract This paper investigates the empirical relationship

Economics Higher level Paper 2

Economics Higher level Paper 2 Tuesday 5 May 2015 (morning) 1 hour 30 minutes Instructions to candidates Do not open this examination paper until instructed to do so. You are not permitted access to any

Economics Higher level Paper 2 Tuesday 5 May 2015 (morning) 1 hour 30 minutes Instructions to candidates Do not open this examination paper until instructed to do so. You are not permitted access to any

Box 1.3. How Does Uncertainty Affect Economic Performance?

Box 1.3. How Does Affect Economic Performance? Bouts of elevated uncertainty have been one of the defining features of the sluggish recovery from the global financial crisis. In recent quarters, high uncertainty

Box 1.3. How Does Affect Economic Performance? Bouts of elevated uncertainty have been one of the defining features of the sluggish recovery from the global financial crisis. In recent quarters, high uncertainty

Foreign Currency Debt, Financial Crises and Economic Growth : A Long-Run Exploration

Foreign Currency Debt, Financial Crises and Economic Growth : A Long-Run Exploration Michael D. Bordo Rutgers University and NBER Christopher M. Meissner UC Davis and NBER GEMLOC Conference, World Bank,

Foreign Currency Debt, Financial Crises and Economic Growth : A Long-Run Exploration Michael D. Bordo Rutgers University and NBER Christopher M. Meissner UC Davis and NBER GEMLOC Conference, World Bank,

José De Gregorio: Autonomy of the Central Bank of Chile, 20 years on

José De Gregorio: Autonomy of the Central Bank of Chile, 20 years on Presentation by Mr José De Gregorio, Governor of the Central Bank of Chile, at the commemoration of the 20 years of autonomy of the

José De Gregorio: Autonomy of the Central Bank of Chile, 20 years on Presentation by Mr José De Gregorio, Governor of the Central Bank of Chile, at the commemoration of the 20 years of autonomy of the

POST-CRISIS GLOBAL REBALANCING CONFERENCE ON GLOBALIZATION AND THE LAW OF THE SEA WASHINGTON DC, DEC 1-3, Barry Bosworth

POST-CRISIS GLOBAL REBALANCING CONFERENCE ON GLOBALIZATION AND THE LAW OF THE SEA WASHINGTON DC, DEC 1-3, 2010 Barry Bosworth I. Economic Rise of Asia Emerging economies of Asia have performed extremely

POST-CRISIS GLOBAL REBALANCING CONFERENCE ON GLOBALIZATION AND THE LAW OF THE SEA WASHINGTON DC, DEC 1-3, 2010 Barry Bosworth I. Economic Rise of Asia Emerging economies of Asia have performed extremely

CORRELATION BETWEEN MALTESE AND EURO AREA SOVEREIGN BOND YIELDS

CORRELATION BETWEEN MALTESE AND EURO AREA SOVEREIGN BOND YIELDS Article published in the Quarterly Review 2017:4, pp. 38-41 BOX 1: CORRELATION BETWEEN MALTESE AND EURO AREA SOVEREIGN BOND YIELDS 1 This

CORRELATION BETWEEN MALTESE AND EURO AREA SOVEREIGN BOND YIELDS Article published in the Quarterly Review 2017:4, pp. 38-41 BOX 1: CORRELATION BETWEEN MALTESE AND EURO AREA SOVEREIGN BOND YIELDS 1 This

Financing the U.S. Trade Deficit

Order Code RL33274 Financing the U.S. Trade Deficit Updated September 4, 2007 James K. Jackson Specialist in International Trade and Finance Foreign Affairs, Defense, and Trade Division Financing the U.S.

Order Code RL33274 Financing the U.S. Trade Deficit Updated September 4, 2007 James K. Jackson Specialist in International Trade and Finance Foreign Affairs, Defense, and Trade Division Financing the U.S.

José Darío Uribe E. Governor central bank of colombia October 13, 2011

Capital Flows, Policy Challenges and Policy Options José Darío Uribe E. Governor central bank of colombia October 13, 2011 Outline Review the fluctuations of macroeconomic aggregates along the cycles of

Capital Flows, Policy Challenges and Policy Options José Darío Uribe E. Governor central bank of colombia October 13, 2011 Outline Review the fluctuations of macroeconomic aggregates along the cycles of

Did the Swiss Demand for Money Function Shift? Journal of Economics and Business, 35(2) April 1983,

April 1983,") Did the Swiss Demand for Money Function Shift? By: Stuart Allen Did the Swiss Demand for Money Function Shift? Journal of Economics and Business, 35(2) April 1983, 239-249. Made available courtesy of Elsevier:

Did the Swiss Demand for Money Function Shift? By: Stuart Allen Did the Swiss Demand for Money Function Shift? Journal of Economics and Business, 35(2) April 1983, 239-249. Made available courtesy of Elsevier:

The debt crisis of 1982 was precipitated by a sudden reduction in capital

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized MACROECONOMIC ADJUSTMENT TO CAPITAL INFLOWS: LESSONS FROM RECENT LATIN AMERICAN AND EAST

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized MACROECONOMIC ADJUSTMENT TO CAPITAL INFLOWS: LESSONS FROM RECENT LATIN AMERICAN AND EAST

Can Emerging Economies Decouple?

Can Emerging Economies Decouple? M. Ayhan Kose Research Department International Monetary Fund akose@imf.org April 2, 2008 This talk is primarily based on the following sources IMF World Economic Outlook

Can Emerging Economies Decouple? M. Ayhan Kose Research Department International Monetary Fund akose@imf.org April 2, 2008 This talk is primarily based on the following sources IMF World Economic Outlook

Macroeconomic Measurement 3: The Accumulation of Value

International Economics and Business Dynamics Class Notes Macroeconomic Measurement 3: The Accumulation of Value Revised: October 30, 2012 Latest version available at http://www.fperri.net/teaching/20205.htm

International Economics and Business Dynamics Class Notes Macroeconomic Measurement 3: The Accumulation of Value Revised: October 30, 2012 Latest version available at http://www.fperri.net/teaching/20205.htm

Determinants of foreign direct investment in Malaysia

Nanyang Technological University From the SelectedWorks of James B Ang 2008 Determinants of foreign direct investment in Malaysia James B Ang, Nanyang Technological University Available at: https://works.bepress.com/james_ang/8/

Nanyang Technological University From the SelectedWorks of James B Ang 2008 Determinants of foreign direct investment in Malaysia James B Ang, Nanyang Technological University Available at: https://works.bepress.com/james_ang/8/

DOCUMENTO de TRABAJO DOCUMENTO DE TRABAJO. ISSN (edición impresa) ISSN (edición electrónica)

ISSN (edición electrónica)") Instituto I N S T Ide T Economía U T O D E E C O N O M Í A DOCUMENTO de TRABAJO DOCUMENTO DE TRABAJO 371 2011 Characterizing the Business Cycles of Emerging Economies (Second Version) Cesar Calderón; Rodrigo

Instituto I N S T Ide T Economía U T O D E E C O N O M Í A DOCUMENTO de TRABAJO DOCUMENTO DE TRABAJO 371 2011 Characterizing the Business Cycles of Emerging Economies (Second Version) Cesar Calderón; Rodrigo

Session 16. Review Session

Session 16. Review Session The long run [Fundamentals] Output, saving, and investment Money and inflation Economic growth Labor markets The short run [Business cycles] What are the causes business cycles?

Session 16. Review Session The long run [Fundamentals] Output, saving, and investment Money and inflation Economic growth Labor markets The short run [Business cycles] What are the causes business cycles?

CRS Report for Congress

Order Code RL33274 CRS Report for Congress Received through the CRS Web Financing the U.S. Trade Deficit February 14, 2006 James K. Jackson Specialist in International Trade and Finance Foreign Affairs,

Order Code RL33274 CRS Report for Congress Received through the CRS Web Financing the U.S. Trade Deficit February 14, 2006 James K. Jackson Specialist in International Trade and Finance Foreign Affairs,

Econ 102 Final Exam Name ID Section Number

Econ 102 Final Exam Name ID Section Number 1. Over time, contractionary monetary policy nominal wages and causes the short-run aggregate supply curve to shift. A) raises; leftward B) lowers; leftward C)

Econ 102 Final Exam Name ID Section Number 1. Over time, contractionary monetary policy nominal wages and causes the short-run aggregate supply curve to shift. A) raises; leftward B) lowers; leftward C)

Growth, investment and jobs: The international financial dimension. Working Party on the Social Dimension of Globalization November 14th, 2005

Growth, investment and jobs: The international financial dimension Working Party on the Social Dimension of Globalization November 14th, 2005 Growth, investment and jobs At times of global economic integration,

Growth, investment and jobs: The international financial dimension Working Party on the Social Dimension of Globalization November 14th, 2005 Growth, investment and jobs At times of global economic integration,

Measuring the sustainability of Latin American external debt

Applied Economics Letters, 2003, 10, 359 362 Measuring the sustainability of Latin American external debt MARYANN O. KEATING and BARRY P. KEATINGy* Associate Faculty, School of Business and Economics,

Applied Economics Letters, 2003, 10, 359 362 Measuring the sustainability of Latin American external debt MARYANN O. KEATING and BARRY P. KEATINGy* Associate Faculty, School of Business and Economics,

The U.S. Trade Deficit: A Sign of Good Times. Testimony before The Trade Deficit Review Commission

The U.S. Trade Deficit: A Sign of Good Times Testimony before The Trade Deficit Review Commission Submitted by Daniel T. Griswold Associate Director, Center for Trade Policy Studies Cato Institute August

The U.S. Trade Deficit: A Sign of Good Times Testimony before The Trade Deficit Review Commission Submitted by Daniel T. Griswold Associate Director, Center for Trade Policy Studies Cato Institute August

Chapter 6. Government Influence on Exchange Rates. Lecture Outline

Chapter 6 Government Influence on Exchange Rates Lecture Outline Exchange Rate Systems Fixed Exchange Rate System Freely Floating Exchange Rate System Managed Float Exchange Rate System Pegged Exchange

Chapter 6 Government Influence on Exchange Rates Lecture Outline Exchange Rate Systems Fixed Exchange Rate System Freely Floating Exchange Rate System Managed Float Exchange Rate System Pegged Exchange

ARGENTINA: WHAT WENT WRONG? Guillermo Perry and Luis Servén World Bank May 2003

ARGENTINA: WHAT WENT WRONG? Guillermo Perry and Luis Servén World Bank May 2003 Performance in the nineties: Better than most up to 1998, worse than most afterwards Real GDP Growth Rate (Percentages) 1981-90

ARGENTINA: WHAT WENT WRONG? Guillermo Perry and Luis Servén World Bank May 2003 Performance in the nineties: Better than most up to 1998, worse than most afterwards Real GDP Growth Rate (Percentages) 1981-90

Masaaki Shirakawa: The transition from high growth to stable growth Japan s experience and implications for emerging economies

Masaaki Shirakawa: The transition from high growth to stable growth Japan s experience and implications for emerging economies Remarks by Mr Masaaki Shirakwa, Governor of the Bank of Japan, at the Bank

Masaaki Shirakawa: The transition from high growth to stable growth Japan s experience and implications for emerging economies Remarks by Mr Masaaki Shirakwa, Governor of the Bank of Japan, at the Bank

Donald L Kohn: Asset-pricing puzzles, credit risk, and credit derivatives

Donald L Kohn: Asset-pricing puzzles, credit risk, and credit derivatives Remarks by Mr Donald L Kohn, Vice Chairman of the Board of Governors of the US Federal Reserve System, at the Conference on Credit

Donald L Kohn: Asset-pricing puzzles, credit risk, and credit derivatives Remarks by Mr Donald L Kohn, Vice Chairman of the Board of Governors of the US Federal Reserve System, at the Conference on Credit

REMARKS ON THE EVOLUTION OF THE INTERNATIONAL FINANCIAL SYSTEM. As I recall, in the sixties and seventies, one used to stress :

September 1999 REMARKS ON THE EVOLUTION OF THE INTERNATIONAL FINANCIAL SYSTEM PRESENTATION BY MR. DE LAROSIÈRE, ADVISOR TO PARIBAS, FOR THE MEETING ORGANIZED BY JONES, DAY, REAVIS & POGUE, IN WASHINGTON,

September 1999 REMARKS ON THE EVOLUTION OF THE INTERNATIONAL FINANCIAL SYSTEM PRESENTATION BY MR. DE LAROSIÈRE, ADVISOR TO PARIBAS, FOR THE MEETING ORGANIZED BY JONES, DAY, REAVIS & POGUE, IN WASHINGTON,

14. What Use Can Be Made of the Specific FSIs?

14. What Use Can Be Made of the Specific FSIs? Introduction 14.1 The previous chapter explained the need for FSIs and how they fit into the wider concept of macroprudential analysis. This chapter considers

14. What Use Can Be Made of the Specific FSIs? Introduction 14.1 The previous chapter explained the need for FSIs and how they fit into the wider concept of macroprudential analysis. This chapter considers

Mr Thiessen converses on the conduct of monetary policy in Canada under a floating exchange rate system

Mr Thiessen converses on the conduct of monetary policy in Canada under a floating exchange rate system Speech by Mr Gordon Thiessen, Governor of the Bank of Canada, to the Canadian Society of New York,

Mr Thiessen converses on the conduct of monetary policy in Canada under a floating exchange rate system Speech by Mr Gordon Thiessen, Governor of the Bank of Canada, to the Canadian Society of New York,

The Future Performance of the Canadian Economy

Remarks by Gordon Thiessen Governor of the Bank of Canada to the Canadian Club of Winnipeg Winnipeg, Manitoba 25 March 1998 The Future Performance of the Canadian Economy It can take anywhere from one

Remarks by Gordon Thiessen Governor of the Bank of Canada to the Canadian Club of Winnipeg Winnipeg, Manitoba 25 March 1998 The Future Performance of the Canadian Economy It can take anywhere from one

The global financial crisis was a stress-test for emerging markets. With the exception of a few European countries, none of them suffer external or

Presentation by Roberto Frenkel at the joint Brazilian Ministry of Finance and International Monetary Fund (IMF) High Level Conference on Managing Capital Flows in Emerging Markets. Rio de Janeiro, Brazil,

Presentation by Roberto Frenkel at the joint Brazilian Ministry of Finance and International Monetary Fund (IMF) High Level Conference on Managing Capital Flows in Emerging Markets. Rio de Janeiro, Brazil,

Capital Account Controls and Liberalization: Lessons for India and China

UBS Investment Research Capital Account Controls and Liberalization: Lessons for India and China Jonathan Anderson November 2003 ANALYST CERTIFICATION AND REQUIRED DISCLOSURES BEGIN ON PAGE 50 UBS does

UBS Investment Research Capital Account Controls and Liberalization: Lessons for India and China Jonathan Anderson November 2003 ANALYST CERTIFICATION AND REQUIRED DISCLOSURES BEGIN ON PAGE 50 UBS does

SPECIAL REPORT. TD Economics ASSESSING CHINA S QUEST FOR ECONOMIC REBALANCING

SPECIAL REPORT TD Economics ASSESSING CHINA S QUEST FOR ECONOMIC REBALANCING Highlights Chinese spending on fixed investments have climbed to 8% of GDP from roughly % a decade ago. This has come at the

SPECIAL REPORT TD Economics ASSESSING CHINA S QUEST FOR ECONOMIC REBALANCING Highlights Chinese spending on fixed investments have climbed to 8% of GDP from roughly % a decade ago. This has come at the

FIRST LOOK AT MACROECONOMICS*

Chapter 4 A FIRST LOOK AT MACROECONOMICS* Key Concepts Origins and Issues of Macroeconomics Modern macroeconomics began during the Great Depression, 1929 1939. The Great Depression was a decade of high

Chapter 4 A FIRST LOOK AT MACROECONOMICS* Key Concepts Origins and Issues of Macroeconomics Modern macroeconomics began during the Great Depression, 1929 1939. The Great Depression was a decade of high

Normalizing Monetary Policy

Normalizing Monetary Policy Martin Feldstein The current focus of Federal Reserve policy is on normalization of monetary policy that is, on increasing short-term interest rates and shrinking the size of

Normalizing Monetary Policy Martin Feldstein The current focus of Federal Reserve policy is on normalization of monetary policy that is, on increasing short-term interest rates and shrinking the size of

The Impact of Oil Price Volatility on the Real Exchange Rate in Nigeria: An Error Correction Model

15 An International Multidisciplinary Journal, Ethiopia Vol. 9(1), Serial No. 36, January, 2015:15-22 ISSN 1994-9057 (Print) ISSN 2070--0083 (Online) DOI: http://dx.doi.org/10.4314/afrrev.v9i1.2 The Impact

15 An International Multidisciplinary Journal, Ethiopia Vol. 9(1), Serial No. 36, January, 2015:15-22 ISSN 1994-9057 (Print) ISSN 2070--0083 (Online) DOI: http://dx.doi.org/10.4314/afrrev.v9i1.2 The Impact