Two-Period Version of Gertler- Karadi, Gertler-Kiyotaki Financial Friction Model

|

|

|

- Gilbert Burke

- 5 years ago

- Views:

Transcription

1 Two-Period Version of Gertler- Karadi, Gertler-Kiyotaki Financial Friction Model Lawrence J. Christiano Summary of Christiano-Ikeda, 2012, Government Policy, Credit Markets and Economic Activity, in Federal Reserve Bank of Atlanta conference volume, A Return to Jekyll Island: the Origins, History, and Future of the Federal Reserve, Cambridge University Press.

2 Motivation Beginning in 2007 and then accelerating in 2008: Asset values (particularly for banks) collapsed. Intermediation slowed and investment/output fell. Interest rates spreads over what the US Treasury and highly safe private firms had to pay, jumped. US central bank initiated unconventional measures (loans to financial and non-financial firms, very low interest rates for banks, etc.) In 2009 the worst parts of began to turn around.

3 Collapse in Asset Values and Investment Log, real Stock Market Index, real Housing Prices and real Investment March, 2006 October, June, log September, S&P/Case-Shiller 10-city Home Price Index S&P 500 Index Gross Private Domestic Investment March, month

4 Spreads for Risky Firms Shot Up in Late 2008 Interest Rate Spread on Corporate Bonds of Various Ratings Over Rate on AAA Corporate Bonds BB B CCC and worse 2008Q mean, junk rated bonds = mean, B rated bonds = mean, BB rated bonds = 1.75

5 Must Go Back to Great Depression to See Spreads as Large as the Recent Ones Spread, BAA versus AAA bonds 5 March, October, 2007 August,

6 Economic Activity Shows (anemic!) Signs of Recovery June, 2009 Percent of Labor Force Unemployment rate Month Log, Industrial Production Index September, Log Month

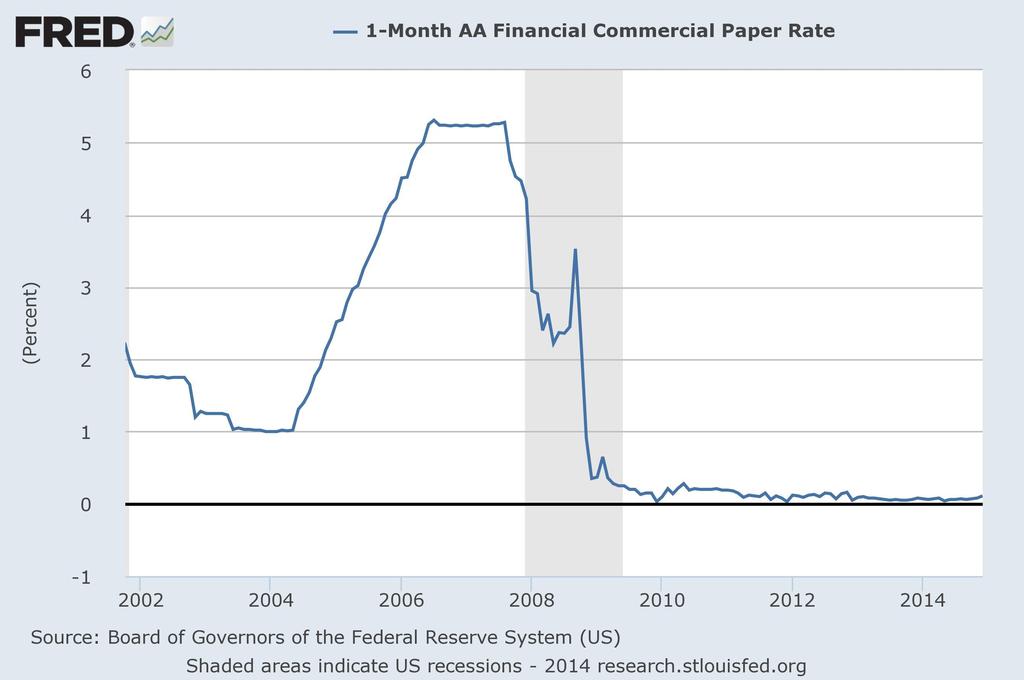

7 Banks Cost of Funds Low Federal Funds Rate 6 5 Annual, Percent Rate September, Month

8 Characterization of Crisis to be Explored Here Bank Asset Values Fell. Banking System Became Dysfunctional Interest rate spreads rose. Intermediation and economy slowed. Monetary authority: Transferred funds on various terms to private companies and to banks. Sharply reduced cost of funds to banks. Economy in (tentative) recovery. Seek to construct models that links these observations together.

9 Objective Keep analysis simple and on point by: Two periods Minimize complications from agent heterogeneity. Leave out endogeneity of employment. Leave out nominal variables: just look behind the veil of monetary economics Models: Gertler-Kiyotaki/Gertler-Karadi In two-period setting easy to study an interesting nonlinearity that is possible: Participation constraint may be binding in a crisis and not binding in normal times.

10 Two-period Version of GK Model Many identical households, each with a unit measure of members: Some members are bankers Some members are workers Perfect insurance inside households everyone consumes same amount. Period 1 Workers endowed with y goods, household makes deposits, d, in a bank Bankers endowed with N goods, take deposits and purchase securities, d, from a firm. Firm issues securities, s, to produce sr k in period 2. Period 2 Household consumes earnings from deposits plus profits, π, from banker. Goods consumed are produced by the firm.

11 Solution to Household Problem u c u C R d c C R d y R d u c c1 1 c y R d 1 Rd R d 1 Household budget constraint when gov t buys Solution to Household Problem private assets using tax receipts, T, and gov t u c R d c C y u C R d R gets the same rate of return, R d, as d households: No change! y (Ricardian-Wallace u c c1 R c d Irrelevance) 1 1 c C R d y T TRd 1 Rd y R d R d R d

12 Problem of the Household period 1 period 2 budget constraint c d y C R d d problem max c,c,d u c u C Solution to Household Problem Solution to Household Problem u c R d c C y u u c C R d R R d c C y d R d R d u C u c c1 u c c1 1 c c y y R d R1 d 1 Rd 1 R d Rd R d 1

13 Household Supply of Deposits For given π, d rises or falls with R d, depending on parameter values. But, in equilibrium π=r k (N+d)-R d d. Substituting into the expression for c and solving for d: R d d Rd 1 N y R k y R d 1 R k Upward-sloping deposit supply d

14 Household Supply of Deposits For given π, d rises or falls with R d, depending on parameter values. But, in equilibrium π=r k (N+d)-R d d. Substituting into the expression for c and solving for d: R d d Rd 1 N y R k y R d 1 R k N decreases d

15 Efficient Benchmark Problem of the Bank period 1 period 2 take deposits, d pay dr d to households buy securities, s N d receive sr k from firms problem: max d sr k R d d

16 Bank demand for d R d Supply of d by households Demand for d by banks R k Equilibrium d d

17 Equilibrium in Absence of Frictions Properties: Interior Equilibrium: R d,,d,c,c (i) c,d,c 0 (ii) household problem is solved (iii) bank problem is solved (iv) goods and financial markets clear Household faces true social rate of return on saving: R k R d Equilibrium is first best, i.e., solves max c,c,k, u c u C c k y N, C kr k

18 Friction bank combines deposits, d, with net worth, N, to purchase N+d securities from firms. bank has two options: ( no-default ) wait until next period when N d R k arrives and pay off depositors, R d d, for profit: N d R k R d d ( default ) take N d securities, refuse to pay depositors and wait until next period when securities pay off: N d R k Bank must announce what value of d it will choose at the beginning of a period.

19 Incentive Constraint Recall, banks maximize profits Choose no default iff no default N d R k R d d default N d R k Next: derive banking system s demand for deposits in presence of financial frictions.

20 Result for a no-default equilibrium: Consider an individual bank that contemplates defaulting. It sets a d that implies default,,, or R k N d R d d R k d N what the household gets in the other banks R d what the household gets in the defaulting bank 1 R k d N d A deviating bank will in fact receive no deposits. An optimizing bank would never default

21 Problem of the bank in no-default, interior equilibrium Maximize, by choice of d, subject to: R k N d R d d If interest rate is REALLY low, then bank has no incentive to default because it makes lots of profits not defaulting or, R k N d R d d R k N d 0, 1 R k N R d 1 R k d 0. Note that 0 < d < requires 1 R k if not, then d R d if not, then d 0 R k.

22 Problem of the bank in no-default, For R d = R k interior equilibrium, cnt d a bank makes no profits on d so absent default considerations - it is indifferent over all values of 0 d Taking into account default, a bank is indifferent over 0 d N(1-θ)/θ For (1-θ)R k < R d < R k Bank wants d as large as possible, subject to incentive constraint. So, d = R k N(1-θ)/(R d -(1-θ)R k )

23 Bank demand for d R d Bank demand for d R k 1 R k R d 1 R k N (1-θ)R k 1 N d

24 Interior, no default equilibrium R d Household supply R k Bank demand In this equilibrium, R d = R k and first-best allocations occur. Banking system is highly effective in allocating resources efficiently. d

25 Collapse in Bank Net Worth Suppose that the economy is represented by a sequence of repeated versions of the above model. In the periods before the crisis, net worth was high and the equilibrium was like it is on the previous slide: efficient, with zero interest rate spreads. In practice, spreads are always positive, but that reflects various banking costs that are left out of this model. With the crisis, N dropped a lot, shifting demand to the right and supply to the left.

26 Effect of Substantial Drop in Bank Net Worth R d Initial, efficient equilibrium Household supply R k Bank demand Equilibrium after N drops is inefficient because R d < R k. d

27 Government Intervention Equity injection. Government raises T in period 1, provides proceeds to banks and demands R k T in return at start of period 2. Rebates earnings to households in 2. Has no impact on demand for deposits by banks (no impact on default incentive or profits). Reduces supply of deposits by households. d+t rises when T rises (even though d falls) because R d rises. Direct, tax-financed government loans to firms work in the same way. An interest rate subsidy to banks will shift their demand for deposits to the right.it will also shift supply to the left.

28 Equity Injection and Drop in N R d Household supply R k Tax-financed injection of equity into banks or direct loans to non-financial firms shift household supply left. Bank demand d

29 Basic idea: Recap Bankers can run away with a fraction of bank assets. If banker net worth is high relative to deposits, friction not a factor and banking system efficient. If banker net worth falls below a certain cutoff, then banker must restrict the deposits. Bankers fear (correctly) that otherwise depositors would lose confidence and take their business to another bank. Reduction in banker demand for deposits: makes deposit interest rates fall and so spreads rise. Reduced intermediation means investment drops, output drops. Equity injections by the government can revive the banking system.

30 Is the Model Narrative Consistent with the Evidence? Model says that reduced intermediation of funds through the financial system reflected reduced demand for credit by financial institutions. Prediction: interest rate to financial institutions fall.

31

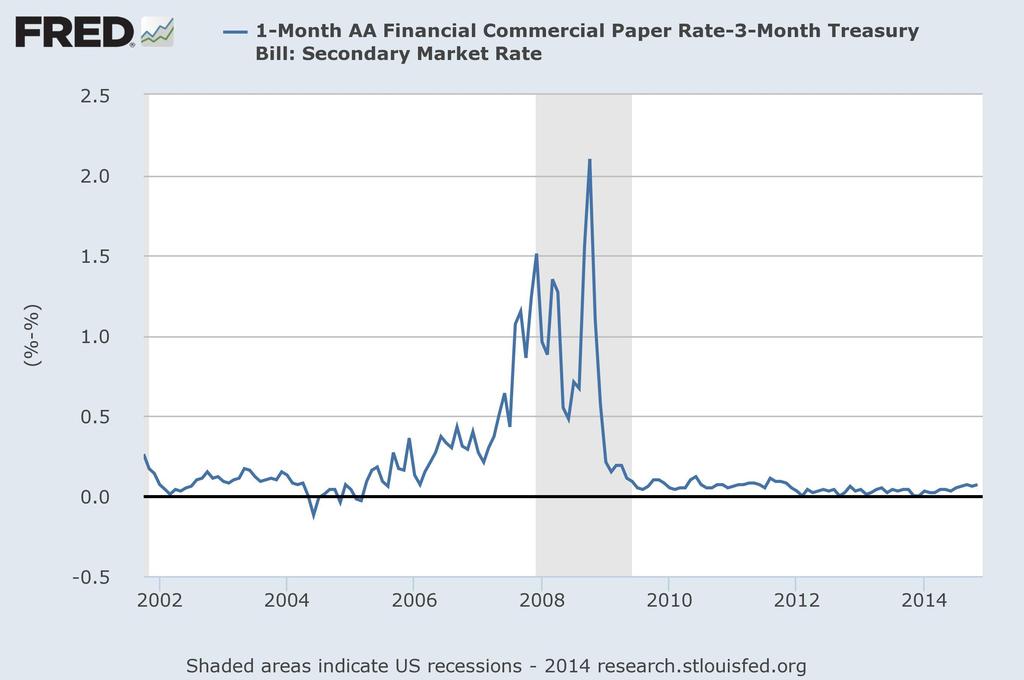

32 Model prediction for decline in cost of funds to financial institutions seems verified. But, other risk free interest rates fell even more. Interest rates on US government debt fell more than interest rate on financial firm commercial paper.

33

34 Assessment Fact that interest rates on US government debt went down more than cost of funds to financial institutions suggests that a complete picture of financial crisis may require two additional features: Risky Banks: Banks in the model are risk free. Default only occurs out of equilibrium. Increased actual riskiness of banks is perhaps also an important part of the picture. Liquidity: Low interest rates on US government debt consistent with idea that high demand for liquidity played an important role in the crisis.

35 Macro Prudential Policy In recent years there has been increased concern that banks may have a tendency to take on too much debt. Has accelerated thinking about debt restrictions on banks. There are several models of financial frictions in banks, but they do not necessarily provide a foundation for thinking about debt restrictions on banks. A CSV model of banks implies they issue too little debt. (See Christiano-Ikeda). The running away model of banks described in these notes does not rationalize debt restrictions. Need for the value of assets (held fixed here) that enters participation constraint to be endogenous (see Gertler- Kiyotaki and related literature).

Two-Period Version of Gertler- Karadi, Gertler-Kiyotaki Financial Friction Model. Lawrence J. Christiano

Two-Period Version of Gertler- Karadi, Gertler-Kiyotaki Financial Friction Model Lawrence J. Christiano Motivation Beginning in 2007 and then accelerating in 2008: Asset values (particularly for banks)

Two-Period Version of Gertler- Karadi, Gertler-Kiyotaki Financial Friction Model Lawrence J. Christiano Motivation Beginning in 2007 and then accelerating in 2008: Asset values (particularly for banks)

Lawrence J. Christiano

Three Financial Friction Models Lawrence J. Christiano Motivation Beginning in 2007 and then accelerating in 2008: Asset values collapsed. Intermediation slowed and investment/output fell. Interest rates

Three Financial Friction Models Lawrence J. Christiano Motivation Beginning in 2007 and then accelerating in 2008: Asset values collapsed. Intermediation slowed and investment/output fell. Interest rates

Remarks on Unconventional Monetary Policy

Remarks on Unconventional Monetary Policy Lawrence Christiano Northwestern University To be useful in discussions about the rationale and effectiveness of unconventional monetary policy, models of monetary

Remarks on Unconventional Monetary Policy Lawrence Christiano Northwestern University To be useful in discussions about the rationale and effectiveness of unconventional monetary policy, models of monetary

AEA Continuing Education Program. DSGE Models and the Role of Finance. Lawrence Christiano, Northwestern University

AEA Continuing Education Program DSGE Models and the Role of Finance Lawrence Christiano, Northwestern University January 7-9, 2018 Two Period Version of Gertler Karadi, Gertler Kiyotaki Financial Friction

AEA Continuing Education Program DSGE Models and the Role of Finance Lawrence Christiano, Northwestern University January 7-9, 2018 Two Period Version of Gertler Karadi, Gertler Kiyotaki Financial Friction

Notes on Financial Frictions Under Asymmetric Information and Costly State Verification. Lawrence Christiano

Notes on Financial Frictions Under Asymmetric Information and Costly State Verification by Lawrence Christiano Incorporating Financial Frictions into a Business Cycle Model General idea: Standard model

Notes on Financial Frictions Under Asymmetric Information and Costly State Verification by Lawrence Christiano Incorporating Financial Frictions into a Business Cycle Model General idea: Standard model

Leverage Restrictions in a Business Cycle Model. March 13-14, 2015, Macro Financial Modeling, NYU Stern.

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda Northwestern University Bank of Japan March 13-14, 2015, Macro Financial Modeling, NYU Stern. Background Wish to address

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda Northwestern University Bank of Japan March 13-14, 2015, Macro Financial Modeling, NYU Stern. Background Wish to address

A Macroeconomic Model with Financial Panics

A Macroeconomic Model with Financial Panics Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 March 218 1 The views expressed in this paper are those of the authors

A Macroeconomic Model with Financial Panics Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 March 218 1 The views expressed in this paper are those of the authors

Leverage Restrictions in a Business Cycle Model

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda Disclaimer: The views expressed are those of the authors and do not necessarily reflect those of the Bank of Japan.

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda Disclaimer: The views expressed are those of the authors and do not necessarily reflect those of the Bank of Japan.

Financial Frictions Under Asymmetric Information and Costly State Verification

Financial Frictions Under Asymmetric Information and Costly State Verification General Idea Standard dsge model assumes borrowers and lenders are the same people..no conflict of interest. Financial friction

Financial Frictions Under Asymmetric Information and Costly State Verification General Idea Standard dsge model assumes borrowers and lenders are the same people..no conflict of interest. Financial friction

A Macroeconomic Model with Financial Panics

A Macroeconomic Model with Financial Panics Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 September 218 1 The views expressed in this paper are those of the

A Macroeconomic Model with Financial Panics Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 September 218 1 The views expressed in this paper are those of the

Leverage Restrictions in a Business Cycle Model. Lawrence J. Christiano Daisuke Ikeda

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda Background Increasing interest in the following sorts of questions: What restrictions should be placed on bank leverage?

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda Background Increasing interest in the following sorts of questions: What restrictions should be placed on bank leverage?

Leverage Restrictions in a Business Cycle Model

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda SAIF, December 2014. Background Increasing interest in the following sorts of questions: What restrictions should be

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda SAIF, December 2014. Background Increasing interest in the following sorts of questions: What restrictions should be

A Model with Costly Enforcement

A Model with Costly Enforcement Jesús Fernández-Villaverde University of Pennsylvania December 25, 2012 Jesús Fernández-Villaverde (PENN) Costly-Enforcement December 25, 2012 1 / 43 A Model with Costly

A Model with Costly Enforcement Jesús Fernández-Villaverde University of Pennsylvania December 25, 2012 Jesús Fernández-Villaverde (PENN) Costly-Enforcement December 25, 2012 1 / 43 A Model with Costly

Government Policy, Credit Markets and Economic Activity

Government Policy, Credit Markets and Economic Activity Lawrence Christiano y and Daisuke Ikeda z January 14, 2012 Abstract The US government has recently conducted large scale purchases of assets and

Government Policy, Credit Markets and Economic Activity Lawrence Christiano y and Daisuke Ikeda z January 14, 2012 Abstract The US government has recently conducted large scale purchases of assets and

Capital Flows, Financial Intermediation and Macroprudential Policies

Capital Flows, Financial Intermediation and Macroprudential Policies Matteo F. Ghilardi International Monetary Fund 14 th November 2014 14 th November Capital Flows, 2014 Financial 1 / 24 Inte Introduction

Capital Flows, Financial Intermediation and Macroprudential Policies Matteo F. Ghilardi International Monetary Fund 14 th November 2014 14 th November Capital Flows, 2014 Financial 1 / 24 Inte Introduction

Bank Leverage and Social Welfare

Bank Leverage and Social Welfare By LAWRENCE CHRISTIANO AND DAISUKE IKEDA We describe a general equilibrium model in which there is a particular agency problem in banks. The agency problem arises because

Bank Leverage and Social Welfare By LAWRENCE CHRISTIANO AND DAISUKE IKEDA We describe a general equilibrium model in which there is a particular agency problem in banks. The agency problem arises because

Gertler-Kiyotaki: Banking, Liquidity and Bank Runs in an Infinite Horizon Economy, AER (2015)

") Gertler-Kiyotaki: Banking, Liquidity and Bank Runs in an Infinite Horizon Economy, AER (2015) Lawrence J. Christiano Husnu Dalgic Xueting Wen December 11, 2017 Background In the period, 2007-2009(?), it

Gertler-Kiyotaki: Banking, Liquidity and Bank Runs in an Infinite Horizon Economy, AER (2015) Lawrence J. Christiano Husnu Dalgic Xueting Wen December 11, 2017 Background In the period, 2007-2009(?), it

Asymmetric Information and Costly State Verification. Lawrence Christiano

Asymmetric Information and Costly State Verification Lawrence Christiano General Idea Standard dsge model assumes borrowers and lenders are the same people..no conflict of interest. Financial friction

Asymmetric Information and Costly State Verification Lawrence Christiano General Idea Standard dsge model assumes borrowers and lenders are the same people..no conflict of interest. Financial friction

Should Central Banks Issue Digital Currency?

Should Central Banks Issue Digital Currency? Todd Keister Rutgers University Daniel Sanches Federal Reserve Bank of Philadelphia Economics of Payments IX, BIS November 2018 The views expressed herein are

Should Central Banks Issue Digital Currency? Todd Keister Rutgers University Daniel Sanches Federal Reserve Bank of Philadelphia Economics of Payments IX, BIS November 2018 The views expressed herein are

1 The empirical relationship and its demise (?)

") BURNABY SIMON FRASER UNIVERSITY BRITISH COLUMBIA Paul Klein Office: WMC 3635 Phone: (778) 782-9391 Email: paul klein 2@sfu.ca URL: http://paulklein.ca/newsite/teaching/305.php Economics 305 Intermediate

BURNABY SIMON FRASER UNIVERSITY BRITISH COLUMBIA Paul Klein Office: WMC 3635 Phone: (778) 782-9391 Email: paul klein 2@sfu.ca URL: http://paulklein.ca/newsite/teaching/305.php Economics 305 Intermediate

Equilibrium with Production and Endogenous Labor Supply

Equilibrium with Production and Endogenous Labor Supply ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 21 Readings GLS Chapter 11 2 / 21 Production and

Equilibrium with Production and Endogenous Labor Supply ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 21 Readings GLS Chapter 11 2 / 21 Production and

What is Cyclical in Credit Cycles?

What is Cyclical in Credit Cycles? Rui Cui May 31, 2014 Introduction Credit cycles are growth cycles Cyclicality in the amount of new credit Explanations: collateral constraints, equity constraints, leverage

What is Cyclical in Credit Cycles? Rui Cui May 31, 2014 Introduction Credit cycles are growth cycles Cyclicality in the amount of new credit Explanations: collateral constraints, equity constraints, leverage

The I Theory of Money

The I Theory of Money Markus Brunnermeier and Yuliy Sannikov Presented by Felipe Bastos G Silva 09/12/2017 Overview Motivation: A theory of money needs a place for financial intermediaries (inside money

The I Theory of Money Markus Brunnermeier and Yuliy Sannikov Presented by Felipe Bastos G Silva 09/12/2017 Overview Motivation: A theory of money needs a place for financial intermediaries (inside money

Household Debt, Financial Intermediation, and Monetary Policy

Household Debt, Financial Intermediation, and Monetary Policy Shutao Cao 1 Yahong Zhang 2 1 Bank of Canada 2 Western University October 21, 2014 Motivation The US experience suggests that the collapse

Household Debt, Financial Intermediation, and Monetary Policy Shutao Cao 1 Yahong Zhang 2 1 Bank of Canada 2 Western University October 21, 2014 Motivation The US experience suggests that the collapse

Notes on Financial Frictions Under Asymmetric Information and Costly State Verification. Lawrence Christiano

Notes on Financial Frictions Under Asymmetric Information and Costly State Verification by Lawrence Christiano Incorporating Financial Frictions into a Business Cycle Model General idea: Standard model

Notes on Financial Frictions Under Asymmetric Information and Costly State Verification by Lawrence Christiano Incorporating Financial Frictions into a Business Cycle Model General idea: Standard model

Financial intermediaries in an estimated DSGE model for the UK

Financial intermediaries in an estimated DSGE model for the UK Stefania Villa a Jing Yang b a Birkbeck College b Bank of England Cambridge Conference - New Instruments of Monetary Policy: The Challenges

Financial intermediaries in an estimated DSGE model for the UK Stefania Villa a Jing Yang b a Birkbeck College b Bank of England Cambridge Conference - New Instruments of Monetary Policy: The Challenges

Financial Intermediation and Credit Policy in Business Cycle Analysis. Gertler and Kiotaki Professor PengFei Wang Fatemeh KazempourLong

Financial Intermediation and Credit Policy in Business Cycle Analysis Gertler and Kiotaki 2009 Professor PengFei Wang Fatemeh KazempourLong 1 Motivation Bernanke, Gilchrist and Gertler (1999) studied great

Financial Intermediation and Credit Policy in Business Cycle Analysis Gertler and Kiotaki 2009 Professor PengFei Wang Fatemeh KazempourLong 1 Motivation Bernanke, Gilchrist and Gertler (1999) studied great

A Model of Financial Intermediation

A Model of Financial Intermediation Jesús Fernández-Villaverde University of Pennsylvania December 25, 2012 Jesús Fernández-Villaverde (PENN) A Model of Financial Intermediation December 25, 2012 1 / 43

A Model of Financial Intermediation Jesús Fernández-Villaverde University of Pennsylvania December 25, 2012 Jesús Fernández-Villaverde (PENN) A Model of Financial Intermediation December 25, 2012 1 / 43

The Zero Bound and Fiscal Policy

The Zero Bound and Fiscal Policy Based on work by: Eggertsson and Woodford, 2003, The Zero Interest Rate Bound and Optimal Monetary Policy, Brookings Panel on Economic Activity. Christiano, Eichenbaum,

The Zero Bound and Fiscal Policy Based on work by: Eggertsson and Woodford, 2003, The Zero Interest Rate Bound and Optimal Monetary Policy, Brookings Panel on Economic Activity. Christiano, Eichenbaum,

Risk Shocks and Economic Fluctuations. Summary of work by Christiano, Motto and Rostagno

Risk Shocks and Economic Fluctuations Summary of work by Christiano, Motto and Rostagno Outline Simple summary of standard New Keynesian DSGE model (CEE, JPE 2005 model). Modifications to introduce CSV

Risk Shocks and Economic Fluctuations Summary of work by Christiano, Motto and Rostagno Outline Simple summary of standard New Keynesian DSGE model (CEE, JPE 2005 model). Modifications to introduce CSV

Bernanke and Gertler [1989]

![Bernanke and Gertler [1989]](/thumbs/90/103712154.jpg "Bernanke and Gertler [1989]") Bernanke and Gertler [1989] Econ 235, Spring 2013 1 Background: Townsend [1979] An entrepreneur requires x to produce output y f with Ey > x but does not have money, so he needs a lender Once y is realized,

Bernanke and Gertler [1989] Econ 235, Spring 2013 1 Background: Townsend [1979] An entrepreneur requires x to produce output y f with Ey > x but does not have money, so he needs a lender Once y is realized,

Banks and Liquidity Crises in Emerging Market Economies

Banks and Liquidity Crises in Emerging Market Economies Tarishi Matsuoka Tokyo Metropolitan University May, 2015 Tarishi Matsuoka (TMU) Banking Crises in Emerging Market Economies May, 2015 1 / 47 Introduction

Banks and Liquidity Crises in Emerging Market Economies Tarishi Matsuoka Tokyo Metropolitan University May, 2015 Tarishi Matsuoka (TMU) Banking Crises in Emerging Market Economies May, 2015 1 / 47 Introduction

DISCUSSION OF CAPITAL REQUIREMENTS, RISK CHOICE, AND LIQUIDITY PROVISION IN A BUSINESS CYCLE MODEL

DISCUSSION OF CAPITAL REQUIREMENTS, RISK CHOICE, AND LIQUIDITY PROVISION IN A BUSINESS CYCLE MODEL BY JULIANE BEGENAU Dmitriy Sergeyev Bocconi University and IGIER Structural Changes in the Banking Sector

DISCUSSION OF CAPITAL REQUIREMENTS, RISK CHOICE, AND LIQUIDITY PROVISION IN A BUSINESS CYCLE MODEL BY JULIANE BEGENAU Dmitriy Sergeyev Bocconi University and IGIER Structural Changes in the Banking Sector

Interest on Reserves, Interbank Lending, and Monetary Policy: Work in Progress

Interest on Reserves, Interbank Lending, and Monetary Policy: Work in Progress Stephen D. Williamson Federal Reserve Bank of St. Louis May 14, 015 1 Introduction When a central bank operates under a floor

Interest on Reserves, Interbank Lending, and Monetary Policy: Work in Progress Stephen D. Williamson Federal Reserve Bank of St. Louis May 14, 015 1 Introduction When a central bank operates under a floor

Financial Frictions in Macroeconomics. Lawrence J. Christiano Northwestern University

Financial Frictions in Macroeconomics Lawrence J. Christiano Northwestern University Balance Sheet, Financial System Assets Liabilities Bank loans Bank Debt Securities, etc. Bank Equity Balance Sheet,

Financial Frictions in Macroeconomics Lawrence J. Christiano Northwestern University Balance Sheet, Financial System Assets Liabilities Bank loans Bank Debt Securities, etc. Bank Equity Balance Sheet,

Intermediate Macroeconomics

Intermediate Macroeconomics Lecture 10 - Consumption 2 Zsófia L. Bárány Sciences Po 2014 April Last week Keynesian consumption function Kuznets puzzle permanent income hypothesis life-cycle theory of consumption

Intermediate Macroeconomics Lecture 10 - Consumption 2 Zsófia L. Bárány Sciences Po 2014 April Last week Keynesian consumption function Kuznets puzzle permanent income hypothesis life-cycle theory of consumption

Credit Booms, Financial Crises and Macroprudential Policy

Credit Booms, Financial Crises and Macroprudential Policy Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 March 219 1 The views expressed in this paper are those

Credit Booms, Financial Crises and Macroprudential Policy Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 March 219 1 The views expressed in this paper are those

Solutions to Problem Set 1

Solutions to Problem Set Theory of Banking - Academic Year 06-7 Maria Bachelet maria.jua.bachelet@gmail.com February 4, 07 Exercise. An individual consumer has an income stream (Y 0, Y ) and can borrow

Solutions to Problem Set Theory of Banking - Academic Year 06-7 Maria Bachelet maria.jua.bachelet@gmail.com February 4, 07 Exercise. An individual consumer has an income stream (Y 0, Y ) and can borrow

Macro (8701) & Micro (8703) option

& Micro (8703) option") WRITTEN PRELIMINARY Ph.D EXAMINATION Department of Applied Economics Jan./Feb. - 2010 Trade, Development and Growth For students electing Macro (8701) & Micro (8703) option Instructions Identify yourself

WRITTEN PRELIMINARY Ph.D EXAMINATION Department of Applied Economics Jan./Feb. - 2010 Trade, Development and Growth For students electing Macro (8701) & Micro (8703) option Instructions Identify yourself

Discussion by J.C.Rochet (SFI,UZH and TSE) Prepared for the Swissquote Conference 2012 on Liquidity and Systemic Risk

Prepared for the Swissquote Conference 2012 on Liquidity and Systemic Risk") Discussion by J.C.Rochet (SFI,UZH and TSE) Prepared for the Swissquote Conference 2012 on Liquidity and Systemic Risk 1 Objectives of the paper Develop a theoretical model of bank lending that allows to

Discussion by J.C.Rochet (SFI,UZH and TSE) Prepared for the Swissquote Conference 2012 on Liquidity and Systemic Risk 1 Objectives of the paper Develop a theoretical model of bank lending that allows to

MA Advanced Macroeconomics: 12. Default Risk, Collateral and Credit Rationing

MA Advanced Macroeconomics: 12. Default Risk, Collateral and Credit Rationing Karl Whelan School of Economics, UCD Spring 2016 Karl Whelan (UCD) Default Risk and Credit Rationing Spring 2016 1 / 39 Moving

MA Advanced Macroeconomics: 12. Default Risk, Collateral and Credit Rationing Karl Whelan School of Economics, UCD Spring 2016 Karl Whelan (UCD) Default Risk and Credit Rationing Spring 2016 1 / 39 Moving

Was The New Deal Contractionary? Appendix C:Proofs of Propositions (not intended for publication)

") Was The New Deal Contractionary? Gauti B. Eggertsson Web Appendix VIII. Appendix C:Proofs of Propositions (not intended for publication) ProofofProposition3:The social planner s problem at date is X min

Was The New Deal Contractionary? Gauti B. Eggertsson Web Appendix VIII. Appendix C:Proofs of Propositions (not intended for publication) ProofofProposition3:The social planner s problem at date is X min

Booms and Banking Crises

Booms and Banking Crises F. Boissay, F. Collard and F. Smets Macro Financial Modeling Conference Boston, 12 October 2013 MFM October 2013 Conference 1 / Disclaimer The views expressed in this presentation

Booms and Banking Crises F. Boissay, F. Collard and F. Smets Macro Financial Modeling Conference Boston, 12 October 2013 MFM October 2013 Conference 1 / Disclaimer The views expressed in this presentation

9 D/S of/for Labor. 9.1 Demand for Labor. Microeconomics I - Lecture #9, April 14, 2009

Microeconomics I - Lecture #9, April 14, 2009 9 D/S of/for Labor 9.1 Demand for Labor Demand for labor depends on the price of labor, price of output and production function. In optimum a firm employs

Microeconomics I - Lecture #9, April 14, 2009 9 D/S of/for Labor 9.1 Demand for Labor Demand for labor depends on the price of labor, price of output and production function. In optimum a firm employs

Financial Economics Field Exam August 2011

Financial Economics Field Exam August 2011 There are two questions on the exam, representing Macroeconomic Finance (234A) and Corporate Finance (234C). Please answer both questions to the best of your

Financial Economics Field Exam August 2011 There are two questions on the exam, representing Macroeconomic Finance (234A) and Corporate Finance (234C). Please answer both questions to the best of your

Lastrapes Fall y t = ỹ + a 1 (p t p t ) y t = d 0 + d 1 (m t p t ).

y t = d 0 + d 1 (m t p t ).") ECON 8040 Final exam Lastrapes Fall 2007 Answer all eight questions on this exam. 1. Write out a static model of the macroeconomy that is capable of predicting that money is non-neutral. Your model should

ECON 8040 Final exam Lastrapes Fall 2007 Answer all eight questions on this exam. 1. Write out a static model of the macroeconomy that is capable of predicting that money is non-neutral. Your model should

Business 33001: Microeconomics

Business 33001: Microeconomics Owen Zidar University of Chicago Booth School of Business Week 6 Owen Zidar (Chicago Booth) Microeconomics Week 6: Capital & Investment 1 / 80 Today s Class 1 Preliminaries

Business 33001: Microeconomics Owen Zidar University of Chicago Booth School of Business Week 6 Owen Zidar (Chicago Booth) Microeconomics Week 6: Capital & Investment 1 / 80 Today s Class 1 Preliminaries

Notes II: Consumption-Saving Decisions, Ricardian Equivalence, and Fiscal Policy. Julio Garín Intermediate Macroeconomics Fall 2018

Notes II: Consumption-Saving Decisions, Ricardian Equivalence, and Fiscal Policy Julio Garín Intermediate Macroeconomics Fall 2018 Introduction Intermediate Macroeconomics Consumption/Saving, Ricardian

Notes II: Consumption-Saving Decisions, Ricardian Equivalence, and Fiscal Policy Julio Garín Intermediate Macroeconomics Fall 2018 Introduction Intermediate Macroeconomics Consumption/Saving, Ricardian

Hysteresis and the European Unemployment Problem

Hysteresis and the European Unemployment Problem Owen Zidar Blanchard and Summers NBER Macro Annual 1986 Macro Lunch January 30, 2013 Owen Zidar (Macro Lunch) Hysteresis January 30, 2013 1 / 47 Questions

Hysteresis and the European Unemployment Problem Owen Zidar Blanchard and Summers NBER Macro Annual 1986 Macro Lunch January 30, 2013 Owen Zidar (Macro Lunch) Hysteresis January 30, 2013 1 / 47 Questions

Answers to Microeconomics Prelim of August 24, In practice, firms often price their products by marking up a fixed percentage over (average)

") Answers to Microeconomics Prelim of August 24, 2016 1. In practice, firms often price their products by marking up a fixed percentage over (average) cost. To investigate the consequences of markup pricing,

Answers to Microeconomics Prelim of August 24, 2016 1. In practice, firms often price their products by marking up a fixed percentage over (average) cost. To investigate the consequences of markup pricing,

Graphs Details Math Examples Using data Tax example. Decision. Intermediate Micro. Lecture 5. Chapter 5 of Varian

Decision Intermediate Micro Lecture 5 Chapter 5 of Varian Decision-making Now have tools to model decision-making Set of options At-least-as-good sets Mathematical tools to calculate exact answer Problem

Decision Intermediate Micro Lecture 5 Chapter 5 of Varian Decision-making Now have tools to model decision-making Set of options At-least-as-good sets Mathematical tools to calculate exact answer Problem

Aysmmetry in central bank inflation control

Aysmmetry in central bank inflation control D. Andolfatto April 2015 The model Consider a two-period-lived OLG model. The young born at date have preferences = The young also have an endowment and a storage

Aysmmetry in central bank inflation control D. Andolfatto April 2015 The model Consider a two-period-lived OLG model. The young born at date have preferences = The young also have an endowment and a storage

ECON 3020 Intermediate Macroeconomics

ECON 3020 Intermediate Macroeconomics Chapter 4 Consumer and Firm Behavior The Work-Leisure Decision and Profit Maximization 1 Instructor: Xiaohui Huang Department of Economics University of Virginia 1

ECON 3020 Intermediate Macroeconomics Chapter 4 Consumer and Firm Behavior The Work-Leisure Decision and Profit Maximization 1 Instructor: Xiaohui Huang Department of Economics University of Virginia 1

Rollover Crisis in DSGE Models. Lawrence J. Christiano Northwestern University

Rollover Crisis in DSGE Models Lawrence J. Christiano Northwestern University Why Didn t DSGE Models Forecast the Financial Crisis and Great Recession? Bernanke (2009) and Gorton (2008): By 2005 there

Rollover Crisis in DSGE Models Lawrence J. Christiano Northwestern University Why Didn t DSGE Models Forecast the Financial Crisis and Great Recession? Bernanke (2009) and Gorton (2008): By 2005 there

ECON 3020: ACCELERATED MACROECONOMICS. Question 1: Inflation Expectations and Real Money Demand (20 points)

") ECON 3020: ACCELERATED MACROECONOMICS SOLUTIONS TO PRELIMINARY EXAM 03/05/2015 Instructor: Karel Mertens Question 1: Inflation Expectations and Real Money Demand (20 points) Suppose that the real money

ECON 3020: ACCELERATED MACROECONOMICS SOLUTIONS TO PRELIMINARY EXAM 03/05/2015 Instructor: Karel Mertens Question 1: Inflation Expectations and Real Money Demand (20 points) Suppose that the real money

ECON Intermediate Macroeconomic Theory

ECON 3510 - Intermediate Macroeconomic Theory Fall 2015 Mankiw, Macroeconomics, 8th ed., Chapter 12 Chapter 12: Aggregate Demand 2: Applying the IS-LM Model Key points: Policy in the IS LM model: Monetary

ECON 3510 - Intermediate Macroeconomic Theory Fall 2015 Mankiw, Macroeconomics, 8th ed., Chapter 12 Chapter 12: Aggregate Demand 2: Applying the IS-LM Model Key points: Policy in the IS LM model: Monetary

Monetary Easing, Investment and Financial Instability

Monetary Easing, Investment and Financial Instability Viral Acharya 1 Guillaume Plantin 2 1 Reserve Bank of India 2 Sciences Po Acharya and Plantin MEIFI 1 / 37 Introduction Unprecedented monetary easing

Monetary Easing, Investment and Financial Instability Viral Acharya 1 Guillaume Plantin 2 1 Reserve Bank of India 2 Sciences Po Acharya and Plantin MEIFI 1 / 37 Introduction Unprecedented monetary easing

SOVEREIGN RISK AND BANK RISK-TAKING

SOVEREIGN RISK AND BANK RISK-TAKING Anil Ari Discussion by Luigi Bocola FRB of Minneapolis, Stanford University and NBER NBER IFM Meeting Boston, March 2018 INTRODUCTION Proposes a model to understand

SOVEREIGN RISK AND BANK RISK-TAKING Anil Ari Discussion by Luigi Bocola FRB of Minneapolis, Stanford University and NBER NBER IFM Meeting Boston, March 2018 INTRODUCTION Proposes a model to understand

Lecture 25 Unemployment Financial Crisis. Noah Williams

Lecture 25 Unemployment Financial Crisis Noah Williams University of Wisconsin - Madison Economics 702 Changes in the Unemployment Rate What raises the unemployment rate? Anything raising reservation wage:

Lecture 25 Unemployment Financial Crisis Noah Williams University of Wisconsin - Madison Economics 702 Changes in the Unemployment Rate What raises the unemployment rate? Anything raising reservation wage:

Global Games and Financial Fragility:

Global Games and Financial Fragility: Foundations and a Recent Application Itay Goldstein Wharton School, University of Pennsylvania Outline Part I: The introduction of global games into the analysis of

Global Games and Financial Fragility: Foundations and a Recent Application Itay Goldstein Wharton School, University of Pennsylvania Outline Part I: The introduction of global games into the analysis of

Answers to Problem Set 4

Answers to Problem Set 4 Economics 703 Spring 016 1. a) The monopolist facing no threat of entry will pick the first cost function. To see this, calculate profits with each one. With the first cost function,

Answers to Problem Set 4 Economics 703 Spring 016 1. a) The monopolist facing no threat of entry will pick the first cost function. To see this, calculate profits with each one. With the first cost function,

Macroprudential Policies in a Low Interest-Rate Environment

Macroprudential Policies in a Low Interest-Rate Environment Margarita Rubio 1 Fang Yao 2 1 University of Nottingham 2 Reserve Bank of New Zealand. The views expressed in this paper do not necessarily reflect

Macroprudential Policies in a Low Interest-Rate Environment Margarita Rubio 1 Fang Yao 2 1 University of Nottingham 2 Reserve Bank of New Zealand. The views expressed in this paper do not necessarily reflect

Capital Constraints, Lending over the Cycle and the Precautionary Motive: A Quantitative Exploration

Capital Constraints, Lending over the Cycle and the Precautionary Motive: A Quantitative Exploration Angus Armstrong and Monique Ebell National Institute of Economic and Social Research 1. Introduction

Capital Constraints, Lending over the Cycle and the Precautionary Motive: A Quantitative Exploration Angus Armstrong and Monique Ebell National Institute of Economic and Social Research 1. Introduction

``Liquidity requirements, liquidity choice and financial stability by Diamond and Kashyap. Discussant: Annette Vissing-Jorgensen, UC Berkeley

``Liquidity requirements, liquidity choice and financial stability by Diamond and Kashyap Discussant: Annette Vissing-Jorgensen, UC Berkeley Idea: Study liquidity regulation in a model where it serves

``Liquidity requirements, liquidity choice and financial stability by Diamond and Kashyap Discussant: Annette Vissing-Jorgensen, UC Berkeley Idea: Study liquidity regulation in a model where it serves

Eco504 Spring 2010 C. Sims MID-TERM EXAM. (1) (45 minutes) Consider a model in which a representative agent has the objective. B t 1.

(45 minutes) Consider a model in which a representative agent has the objective. B t 1.") Eco504 Spring 2010 C. Sims MID-TERM EXAM (1) (45 minutes) Consider a model in which a representative agent has the objective function max C,K,B t=0 β t C1 γ t 1 γ and faces the constraints at each period

Eco504 Spring 2010 C. Sims MID-TERM EXAM (1) (45 minutes) Consider a model in which a representative agent has the objective function max C,K,B t=0 β t C1 γ t 1 γ and faces the constraints at each period

Scarce Collateral, the Term Premium, and Quantitative Easing

Scarce Collateral, the Term Premium, and Quantitative Easing Stephen D. Williamson Washington University in St. Louis Federal Reserve Banks of Richmond and St. Louis April7,2013 Abstract A model of money,

Scarce Collateral, the Term Premium, and Quantitative Easing Stephen D. Williamson Washington University in St. Louis Federal Reserve Banks of Richmond and St. Louis April7,2013 Abstract A model of money,

Government debt. Lecture 9, ECON Tord Krogh. September 10, Tord Krogh () ECON 4310 September 10, / 55

ECON 4310 September 10, / 55") Government debt Lecture 9, ECON 4310 Tord Krogh September 10, 2013 Tord Krogh () ECON 4310 September 10, 2013 1 / 55 Today s lecture Topics: Basic concepts Tax smoothing Debt crisis Sovereign risk Tord

Government debt Lecture 9, ECON 4310 Tord Krogh September 10, 2013 Tord Krogh () ECON 4310 September 10, 2013 1 / 55 Today s lecture Topics: Basic concepts Tax smoothing Debt crisis Sovereign risk Tord

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach Gianluca Benigno 1 Andrew Foerster 2 Christopher Otrok 3 Alessandro Rebucci 4 1 London School of Economics and

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach Gianluca Benigno 1 Andrew Foerster 2 Christopher Otrok 3 Alessandro Rebucci 4 1 London School of Economics and

Princeton University. Updates:

Princeton University Updates: http://scholar.princeton.edu/markus/files/i_theory_slides.pdf Financial Stability Price Stability Debt Sustainability Financial Regulators Liquidity spiral Central Bank De/inflation

Princeton University Updates: http://scholar.princeton.edu/markus/files/i_theory_slides.pdf Financial Stability Price Stability Debt Sustainability Financial Regulators Liquidity spiral Central Bank De/inflation

Bailouts, Bail-ins and Banking Crises

Bailouts, Bail-ins and Banking Crises Todd Keister Rutgers University Yuliyan Mitkov Rutgers University & University of Bonn 2017 HKUST Workshop on Macroeconomics June 15, 2017 The bank runs problem Intermediaries

Bailouts, Bail-ins and Banking Crises Todd Keister Rutgers University Yuliyan Mitkov Rutgers University & University of Bonn 2017 HKUST Workshop on Macroeconomics June 15, 2017 The bank runs problem Intermediaries

Coordination Problems

Coordination Problems 1 / 32 A Simple Coordination Game: What Side of the Street? Driver 2 L R Driver 1 l 5, 5 0, 0 r 0, 0 5, 5 Two equilibria: (l, L) and (r, R) Pure coordination game drivers care only

Coordination Problems 1 / 32 A Simple Coordination Game: What Side of the Street? Driver 2 L R Driver 1 l 5, 5 0, 0 r 0, 0 5, 5 Two equilibria: (l, L) and (r, R) Pure coordination game drivers care only

A Macroeconomic Framework for Quantifying Systemic Risk

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He, University of Chicago and NBER Arvind Krishnamurthy, Northwestern University and NBER December 2013 He and Krishnamurthy (Chicago, Northwestern)

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He, University of Chicago and NBER Arvind Krishnamurthy, Northwestern University and NBER December 2013 He and Krishnamurthy (Chicago, Northwestern)

Coordination Problems

Coordination Problems 1 / 32 Outline Some Simple Coordination Games Coordination Traps Coordination Failures 2 / 32 A Simple Coordination Game: What Side of the Street? Driver 2 L R Driver 1 l 5, 5 0,

Coordination Problems 1 / 32 Outline Some Simple Coordination Games Coordination Traps Coordination Failures 2 / 32 A Simple Coordination Game: What Side of the Street? Driver 2 L R Driver 1 l 5, 5 0,

1 Ricardian Neutrality of Fiscal Policy

1 Ricardian Neutrality of Fiscal Policy We start our analysis of fiscal policy by stating a neutrality result for fiscal policy which is due to David Ricardo (1817), and whose formal illustration is due

1 Ricardian Neutrality of Fiscal Policy We start our analysis of fiscal policy by stating a neutrality result for fiscal policy which is due to David Ricardo (1817), and whose formal illustration is due

Financial Frictions in Macroeconomics. Lawrence J. Christiano Northwestern University

Financial Frictions in Macroeconomics Lawrence J. Christiano Northwestern University Balance Sheet, Financial System Assets Liabilities Bank loans Securities, etc. Bank Debt Bank Equity Frictions between

Financial Frictions in Macroeconomics Lawrence J. Christiano Northwestern University Balance Sheet, Financial System Assets Liabilities Bank loans Securities, etc. Bank Debt Bank Equity Frictions between

Expectations vs. Fundamentals-based Bank Runs: When should bailouts be permitted?

Expectations vs. Fundamentals-based Bank Runs: When should bailouts be permitted? Todd Keister Rutgers University Vijay Narasiman Harvard University October 2014 The question Is it desirable to restrict

Expectations vs. Fundamentals-based Bank Runs: When should bailouts be permitted? Todd Keister Rutgers University Vijay Narasiman Harvard University October 2014 The question Is it desirable to restrict

A Model with Costly-State Verification

A Model with Costly-State Verification Jesús Fernández-Villaverde University of Pennsylvania December 19, 2012 Jesús Fernández-Villaverde (PENN) Costly-State December 19, 2012 1 / 47 A Model with Costly-State

A Model with Costly-State Verification Jesús Fernández-Villaverde University of Pennsylvania December 19, 2012 Jesús Fernández-Villaverde (PENN) Costly-State December 19, 2012 1 / 47 A Model with Costly-State

Kyunghun Kim ECN101(SS1, 2014): Homework4 Answer Key Due in class on 7/28

: Homework4 Answer Key Due in class on 7/28") 1. AS-AD Model Suppose that government spending rises in an economy. Assume that the short-run aggregate supply curve is upward sloping. a. Draw the AS-AD model to show long-run and short-run equilibria

1. AS-AD Model Suppose that government spending rises in an economy. Assume that the short-run aggregate supply curve is upward sloping. a. Draw the AS-AD model to show long-run and short-run equilibria

Monetary Economics. Lecture 23a: inside and outside liquidity, part one. Chris Edmond. 2nd Semester 2014 (not examinable)

") Monetary Economics Lecture 23a: inside and outside liquidity, part one Chris Edmond 2nd Semester 2014 (not examinable) 1 This lecture Main reading: Holmström and Tirole, Inside and outside liquidity, MIT

Monetary Economics Lecture 23a: inside and outside liquidity, part one Chris Edmond 2nd Semester 2014 (not examinable) 1 This lecture Main reading: Holmström and Tirole, Inside and outside liquidity, MIT

Discussion of Evaluating the Cost of Government Credit Support: The OECD Context by Deborah Lucas

Discussion of Evaluating the Cost of Government Credit Support: The OECD Context by Deborah Lucas Javier Bianchi University of Wisconsin & NBER MFM Meeting on Sovereign Risk and Financial Stability, NYU

Discussion of Evaluating the Cost of Government Credit Support: The OECD Context by Deborah Lucas Javier Bianchi University of Wisconsin & NBER MFM Meeting on Sovereign Risk and Financial Stability, NYU

WEALTH AND VOLATILITY

WEALTH AND VOLATILITY Jonathan Heathcote Minneapolis Fed Fabrizio Perri University of Minnesota and Minneapolis Fed EIEF, July 2011 Features of the Great Recession 1. Large fall in asset values 2. Sharp

WEALTH AND VOLATILITY Jonathan Heathcote Minneapolis Fed Fabrizio Perri University of Minnesota and Minneapolis Fed EIEF, July 2011 Features of the Great Recession 1. Large fall in asset values 2. Sharp

1 Ricardian Neutrality of Fiscal Policy

1 Ricardian Neutrality of Fiscal Policy For a long time, when economists thought about the effect of government debt on aggregate output, they focused on the so called crowding-out effect. To simplify

1 Ricardian Neutrality of Fiscal Policy For a long time, when economists thought about the effect of government debt on aggregate output, they focused on the so called crowding-out effect. To simplify

The Transmission of Monetary Policy through Redistributions and Durable Purchases

The Transmission of Monetary Policy through Redistributions and Durable Purchases Vincent Sterk and Silvana Tenreyro UCL, LSE September 2015 Sterk and Tenreyro (UCL, LSE) OMO September 2015 1 / 28 The

The Transmission of Monetary Policy through Redistributions and Durable Purchases Vincent Sterk and Silvana Tenreyro UCL, LSE September 2015 Sterk and Tenreyro (UCL, LSE) OMO September 2015 1 / 28 The

Financial Frictions, Monetary Policy, and Exchange Rates. Roberto Chang May 2016

Financial Frictions, Monetary Policy, and Exchange Rates Roberto Chang May 2016 Introduction and Motivation In our discussion of the NK model, we stressed the assumption of frictionless financial markets

Financial Frictions, Monetary Policy, and Exchange Rates Roberto Chang May 2016 Introduction and Motivation In our discussion of the NK model, we stressed the assumption of frictionless financial markets

Unconventional Monetary Policy

Unconventional Monetary Policy Mark Gertler (based on joint work with Peter Karadi) NYU October 29 Old Macro Analyzes pre versus post 1984:Q4. 1 New Macro Analyzes pre versus post August 27 Post August

Unconventional Monetary Policy Mark Gertler (based on joint work with Peter Karadi) NYU October 29 Old Macro Analyzes pre versus post 1984:Q4. 1 New Macro Analyzes pre versus post August 27 Post August

Incorporate Financial Frictions into a

Incorporate Financial Frictions into a Business Cycle Model General idea: Standard model assumes borrowers and lenders are the same people..no conflict of interest Financial friction models suppose borrowers

Incorporate Financial Frictions into a Business Cycle Model General idea: Standard model assumes borrowers and lenders are the same people..no conflict of interest Financial friction models suppose borrowers

Lecture 26 Exchange Rates The Financial Crisis. Noah Williams

Lecture 26 Exchange Rates The Financial Crisis Noah Williams University of Wisconsin - Madison Economics 312/702 Money and Exchange Rates in a Small Open Economy Now look at relative prices of currencies:

Lecture 26 Exchange Rates The Financial Crisis Noah Williams University of Wisconsin - Madison Economics 312/702 Money and Exchange Rates in a Small Open Economy Now look at relative prices of currencies:

Bank Runs, Deposit Insurance, and Liquidity

Bank Runs, Deposit Insurance, and Liquidity Douglas W. Diamond University of Chicago Philip H. Dybvig Washington University in Saint Louis Washington University in Saint Louis August 13, 2015 Diamond,

Bank Runs, Deposit Insurance, and Liquidity Douglas W. Diamond University of Chicago Philip H. Dybvig Washington University in Saint Louis Washington University in Saint Louis August 13, 2015 Diamond,

PRINCETON UNIVERSITY Economics Department Bendheim Center for Finance. FINANCIAL CRISES ECO 575 (Part II) Spring Semester 2003

Spring Semester 2003") PRINCETON UNIVERSITY Economics Department Bendheim Center for Finance FINANCIAL CRISES ECO 575 (Part II) Spring Semester 2003 Section 5: Bubbles and Crises April 18, 2003 and April 21, 2003 Franklin Allen

PRINCETON UNIVERSITY Economics Department Bendheim Center for Finance FINANCIAL CRISES ECO 575 (Part II) Spring Semester 2003 Section 5: Bubbles and Crises April 18, 2003 and April 21, 2003 Franklin Allen

Global Financial Systems Chapter 8 Bank Runs and Deposit Insurance

Global Financial Systems Chapter 8 Bank Runs and Deposit Insurance Jon Danielsson London School of Economics 2018 To accompany Global Financial Systems: Stability and Risk http://www.globalfinancialsystems.org/

Global Financial Systems Chapter 8 Bank Runs and Deposit Insurance Jon Danielsson London School of Economics 2018 To accompany Global Financial Systems: Stability and Risk http://www.globalfinancialsystems.org/

Unemployment (Fears), Precautionary Savings, and Aggregate Demand

, Precautionary Savings, and Aggregate Demand") Unemployment (Fears), Precautionary Savings, and Aggregate Demand Wouter J. Den Haan (LSE & CEPR), Pontus Rendahl (University of Cambridge & CEPR), and Markus Riegler (LSE) June 28, 2013 Overview 1 Model

Unemployment (Fears), Precautionary Savings, and Aggregate Demand Wouter J. Den Haan (LSE & CEPR), Pontus Rendahl (University of Cambridge & CEPR), and Markus Riegler (LSE) June 28, 2013 Overview 1 Model

A Macroeconomic Framework for Quantifying Systemic Risk

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He, University of Chicago and NBER Arvind Krishnamurthy, Stanford University and NBER Bank of Canada, August 2017 He and Krishnamurthy (Chicago,

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He, University of Chicago and NBER Arvind Krishnamurthy, Stanford University and NBER Bank of Canada, August 2017 He and Krishnamurthy (Chicago,

Optimal Credit Market Policy. CEF 2018, Milan

Optimal Credit Market Policy Matteo Iacoviello 1 Ricardo Nunes 2 Andrea Prestipino 1 1 Federal Reserve Board 2 University of Surrey CEF 218, Milan June 2, 218 Disclaimer: The views expressed are solely

Optimal Credit Market Policy Matteo Iacoviello 1 Ricardo Nunes 2 Andrea Prestipino 1 1 Federal Reserve Board 2 University of Surrey CEF 218, Milan June 2, 218 Disclaimer: The views expressed are solely

Monetary Easing and Financial Instability

Monetary Easing and Financial Instability Viral Acharya NYU Stern, CEPR and NBER Guillaume Plantin Sciences Po April 22, 2016 Acharya & Plantin Monetary Easing and Financial Instability April 22, 2016

Monetary Easing and Financial Instability Viral Acharya NYU Stern, CEPR and NBER Guillaume Plantin Sciences Po April 22, 2016 Acharya & Plantin Monetary Easing and Financial Instability April 22, 2016

Appendix: Common Currencies vs. Monetary Independence

Appendix: Common Currencies vs. Monetary Independence A The infinite horizon model This section defines the equilibrium of the infinity horizon model described in Section III of the paper and characterizes

Appendix: Common Currencies vs. Monetary Independence A The infinite horizon model This section defines the equilibrium of the infinity horizon model described in Section III of the paper and characterizes

Bank Runs, Prudential Tools and Social Welfare in a Global Game General Equilibrium Model

Bank Runs, Prudential Tools and Social Welfare in a Global Game General Equilibrium Model Daisuke Ikeda Bank of England 10 April 2018 Financial crises: predictability, causes and consequences The views

Bank Runs, Prudential Tools and Social Welfare in a Global Game General Equilibrium Model Daisuke Ikeda Bank of England 10 April 2018 Financial crises: predictability, causes and consequences The views

On the Optimality of Financial Repression

On the Optimality of Financial Repression V.V. Chari, Alessandro Dovis and Patrick Kehoe Conference in honor of Robert E. Lucas Jr, October 2016 Financial Repression Regulation forcing financial institutions

On the Optimality of Financial Repression V.V. Chari, Alessandro Dovis and Patrick Kehoe Conference in honor of Robert E. Lucas Jr, October 2016 Financial Repression Regulation forcing financial institutions

Research Division Federal Reserve Bank of St. Louis Working Paper Series

Research Division Federal Reserve Bank of St. Louis Working Paper Series Scarce Collateral, the Term Premium, and Quantitative Easing Stephen D. Williamson Working Paper 2014-008A http://research.stlouisfed.org/wp/2014/2014-008.pdf

Research Division Federal Reserve Bank of St. Louis Working Paper Series Scarce Collateral, the Term Premium, and Quantitative Easing Stephen D. Williamson Working Paper 2014-008A http://research.stlouisfed.org/wp/2014/2014-008.pdf

Part A: Answer Question A1 (required) and Question A2 or A3 (choice).

and Question A2 or A3 (choice).") Ph.D. Core Exam -- Macroeconomics 10 January 2018 -- 8:00 am to 3:00 pm Part A: Answer Question A1 (required) and Question A2 or A3 (choice). A1 (required): Cutting Taxes Under the 2017 US Tax Cut and

Ph.D. Core Exam -- Macroeconomics 10 January 2018 -- 8:00 am to 3:00 pm Part A: Answer Question A1 (required) and Question A2 or A3 (choice). A1 (required): Cutting Taxes Under the 2017 US Tax Cut and

ECONOMICS 336Y5Y Fall/Spring 2014/15. PUBLIC ECONOMICS Spring Term Test February 26, 2015

UNIVERSITY OF TORONTO MISSISSAUGA DEPARTMENT OF ECONOMICS ECONOMICS 336Y5Y Fall/Spring 2014/15 PUBLIC ECONOMICS Spring Term Test February 26, 2015 Please fill in your full name and student number in the

UNIVERSITY OF TORONTO MISSISSAUGA DEPARTMENT OF ECONOMICS ECONOMICS 336Y5Y Fall/Spring 2014/15 PUBLIC ECONOMICS Spring Term Test February 26, 2015 Please fill in your full name and student number in the