An Updated Pictorial History of Realized and In-Progress Term Premiums for U.S. Treasury Yields: January 4, 1982 through December 31, 2017

|

|

|

- Virginia Eaton

- 6 years ago

- Views:

Transcription

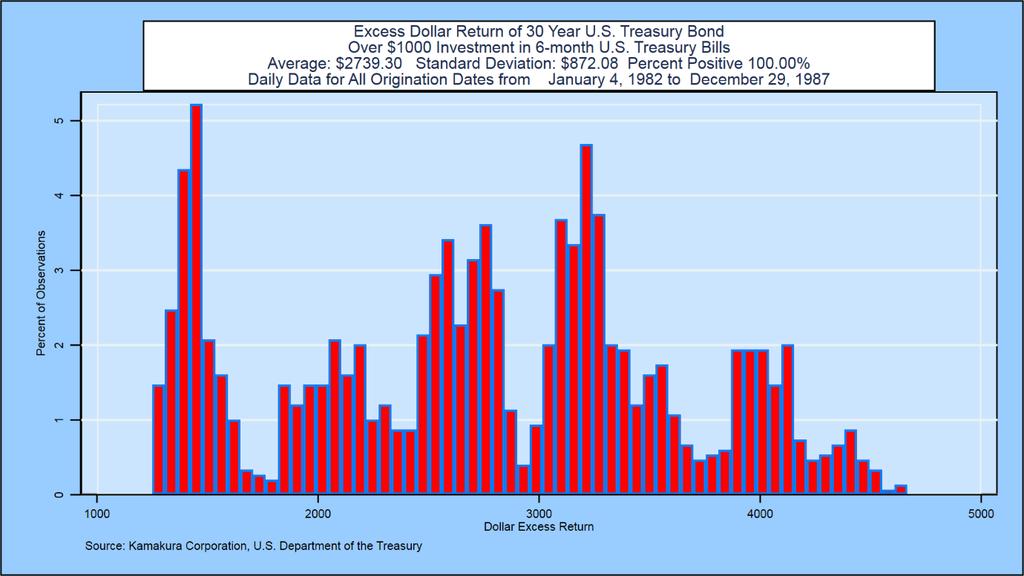

1 An Updated Pictorial History of Realized and In-Progress Term Premiums for U.S. Treasury Yields: January 4, 1982 through December 31, 2017 Donald R. van Deventer February 26, 2018 In this note we update our October 4, 2017 analysis of realized and in progress term premiums in the U.S. Treasury market through December 31, The magnitude of a term premium or risk premium in long term U.S. Treasury yields is a major focus of research by economists in the Federal Reserve System. A recent paper by Canlin Li, Andrew Meldrum, and Marius Rodriguez summarizes two important papers on this topic and reviews their methodologies. Adrian, Crump, Mills and Moench (2014) summarize their term premium findings as follows: The evolution of term premia has been of particular interest since the Federal Reserve began largescale asset purchases. Over this time, short-term interest rates have been close to zero, and our estimates show that the term premium has been compressed and has at times even been negative. Estimates of the term premium are a function of the data used, the modeling approach taken, and market expectations. The focus of this note is a simple one: the calculation of historical realized term premiums and in progress term premiums. From the perspective of prudential regulation of financial institutions, Ramaswamy and Turner [2018] argue that interest rate risk may well be the trigger for the next financial crisis. The magnitude of the term premium, both current and future, is an important element in assessing the interest rate risk of financial institutions. A historical perspective on actual realized term premiums is also a potentially important contributor to market expectations, subject to the caveat stated by Robert A. Jarrow, History is just one draw from a Monte Carlo simulation. 1 We seek to answer this question: Which investment has provided the best total dollar return to investors, a U.S. Treasury bond maturing in X years or a money market fund that invests only in Treasury bills? We address the answer to that question with respect to U.S. Treasury fixed rate bonds with maturities of 1, 2, 3, 5, 7, 10, 20 and 30 1 Conversation with the author,

2 years. We remind readers that what follows is an analysis of history, not a forecast for the future. Methodology We use the time series of U.S. Treasury yields maintained by the U.S. Department of the Treasury and distributed by the Board of Governors of the Federal Reserve. 2 We assume that on each day for which data is available, an investor invests $1000 in the U.S. Treasury bond and $1000 in 6-month Treasury bills. Every six months, the investor will receive a coupon on the bond. We assume that cash from the coupon payment is invested in 6-month Treasury bills and that this investment is rolled over in new 6-month Treasury bills until the underlying bond matures. 3 The investment in the money fund starts with an investment in 6-month Treasury bills and all cash thrown off is reinvested in new 6-month Treasury bills until the underlying investment in the fixed rate bond matures. Interest on the six-month bills is calculated on an actual/365- day basis because the U.S. Treasury data series for short term rates is on an investment basis. The payment dates, 6-month bill rates, and the value of the money fund are given in this spreadsheet. The total dollar returns on 1, 2, 3, 5, 7, 10, 20, and 30-year Treasury bonds, both realized and in progress, are given in a separate spreadsheet. Summary Results The results of the term premium analysis are summarized in the following table: The results show that realized total dollar excess returns have never been negative for maturities of 10, 20, and 30 years. Moreover, pending in progress excess returns 2 This is a different data series than was used by the papers reviewed by Li, Meldrum, and Rodriguez. The selection of the U.S. Department of the Treasury series was intentional, because of quality differences that we will discuss in a separate note. 3 The use of proceeds of cash thrown off from coupon payments was chosen for two important reasons. First, the typical academic assumption that cash generated is reinvested in the same security is an investment strategy that is difficult, if not impossible, to execute in the U.S. Treasury market due to lack of liquidity in off the run issues. Second, such an approach preserves the valuation of the Treasury bond when using the risk neutral discounting methodology of Heath, Jarrow and Morton [1992]. 2

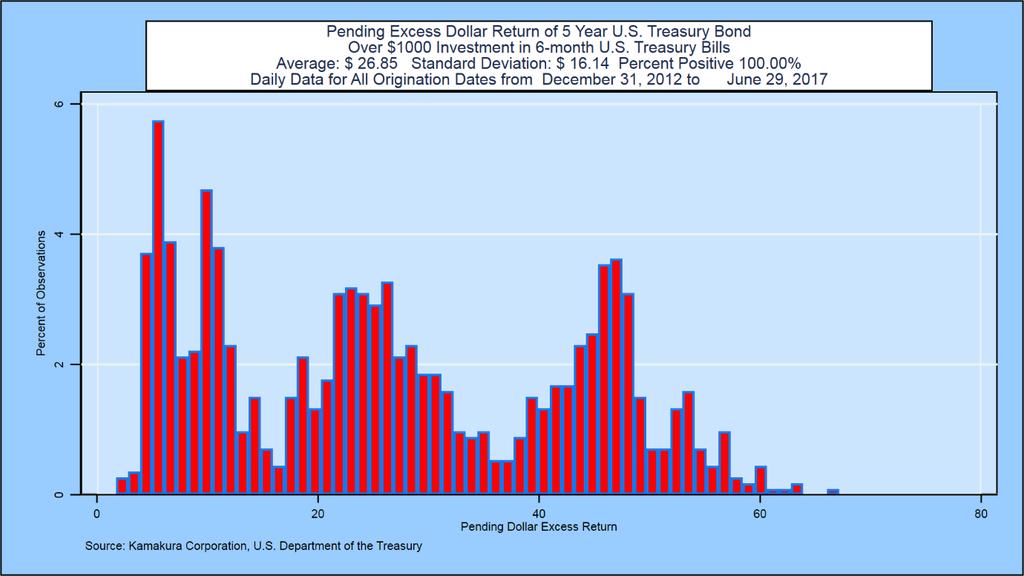

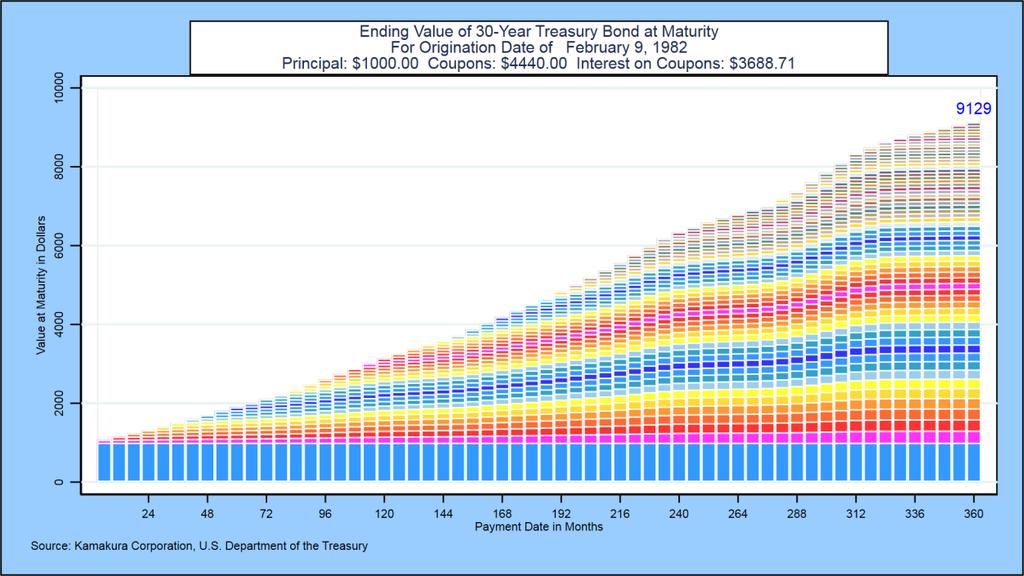

3 have never been negative (so far) for maturities of 5, 7, 10, 20 and 30 years. At the shorter maturities, results are mixed. For 1 year, 73.63% of realized dollar excess returns have been positive but only 6.40% of pending dollar excess returns are positive at this point in time. For the 2-year maturity, the same probabilities of positive excess dollar returns are 82.09% (realized) and 66.05% (pending). At three years, the results are 84.26% (realized) and 97.15% (pending). The statistics for other maturities are shown in the chart. Graphical Analysis Appendix A shows the evolution of total dollar return (in red) versus the 6-month T-bill money fund total dollar return (in blue) for completed 1, 2, 3, 5, 7, 10, 20 and 30-year terms beginning January 4, For most holding periods, interest rates have declined substantially over the investment periods that have been completed. The graphs in Appendix A also include the evolution of the initial six-month Treasury bill yields (in light blue) and the relevant fixed rate Treasury bond yields (in pink) on the origination dates. Appendix B shows the histogram of realized dollar excess returns for each of the 8 fixed rate maturities. Appendix C reports on the histograms of in progress pending dollar excess returns for each maturity. For these incomplete periods, we define the pending excess return as the known dollar advantage of the fixed-rate Treasury bond over the 6-month T-bill investment as of the observation date. For example, on August 28, 2017, the amount of interest that will be paid on a 6-month Treasury bill equivalent that matures in 6 months (not necessarily 182 days) on February 28, 2018 is known with certainty. We tally all of the pending dollar term premiums, all of which have a differing time to maturity, in the histograms in Appendix C. One of the reasons for these surprisingly positive term premium results is the large size of the interest earned on coupon payments, which are assumed to be invested in 6-month Treasury bills. The highest total realized dollar return for all of the completed fixed-rate periods are shown in Appendix D. The lowest total realized dollar returns for each of the fixed-rate holding periods are shown in Appendix E. Conclusions The total dollar returns for the 10, 20 and 30-year Treasury bond have exceeded the total dollar returns for the 6-month T-bill money fund on every completed and every partially completed holding period for which data is available. This is due in part because interest earned on coupon payments rises when rates rise over the holding period, and, at least so far, this has been enough to generate strictly positive excess returns for 30-year bonds. Even at maturities of 5 and 7 years, 100% of pending excess dollar returns are positive as of today. It goes without saying that there is no guarantee that the future will be like the past. At the same time, expectations for the future should be set with the past in mind. References 3

4 Adrian, T., R. K. Crump, B. Mills and E. Moench (2014), 'Treasury Term Premia: 1961-Present', Liberty Street Economics, available at: present.html. Adrian, T., R. K. Crump and E. Moench (2013), 'Pricing the Term Structure with Linear Regressions', Journal of Financial Economics 110(1), pp Li, Canlin, Andrew Meldrum, and Marius Rodriguez (2017). "Robustness of longmaturity term premium estimates," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, April 3, 2017, Heath, David, Robert A. Jarrow and Andrew Morton (1992), Bond Pricing and the Term Structure of Interest Rates: A New Methodology for Contingent Claim Valuation, Econometrica, 60(1), pp Kim, D. H. and J. H. Wright (2005), 'An Arbitrage-Free Three-Factor Term Structure Model and the Recent Behavior of Long-Term Yields and Distant-Horizon Forward Rates', Federal Reserve Board Finance and Economics Discussion Series Ramaswamy, Srichander and Philip Turner, A dangerous unknown: interest rate risk in the financial system, Central Banking, February 7,

5 Appendix A: Time Series of Period End Bond and Money Market Values 5

6 6

7 7

8 8

9 Appendix B: Histogram of Historical Realized Excess Returns 9

10 10

11 11

12 12

13 Appendix C: Histogram of Pending Realized Excess Returns 13

14 14

15 15

16 16

17 Appendix D: Highest Realized Total Dollar Returns 17

18 18

19 19

20 20

21 Appendix E: Lowest Realized Total Dollar Return 21

22 22

23 23

24 24

It doesn't make sense to hire smart people and then tell them what to do. We hire smart people so they can tell us what to do.

A United Approach to Credit Risk-Adjusted Risk Management: IFRS9, CECL, and CVA Donald R. van Deventer, Suresh Sankaran, and Chee Hian Tan 1 October 9, 2017 It doesn't make sense to hire smart people and

A United Approach to Credit Risk-Adjusted Risk Management: IFRS9, CECL, and CVA Donald R. van Deventer, Suresh Sankaran, and Chee Hian Tan 1 October 9, 2017 It doesn't make sense to hire smart people and

An 11 Factor Heath, Jarrow and Morton Model for the Thai Government Bond Yield Curve: Implications for Model Validation

An 11 Factor Heath, Jarrow and Morton Model for the Thai Government Bond Yield Curve: Implications for Model Validation Donald R. van Deventer 1 First Version: February 7, 2017 This Version: February 16,

An 11 Factor Heath, Jarrow and Morton Model for the Thai Government Bond Yield Curve: Implications for Model Validation Donald R. van Deventer 1 First Version: February 7, 2017 This Version: February 16,

Which Market? The Bond Market or the Credit Default Swap Market?

Kamakura Corporation Fair Value and Expected Credit Loss Estimation: An Accuracy Comparison of Bond Price versus Spread Analysis Using Lehman Data Donald R. van Deventer and Suresh Sankaran April 25, 2016

Kamakura Corporation Fair Value and Expected Credit Loss Estimation: An Accuracy Comparison of Bond Price versus Spread Analysis Using Lehman Data Donald R. van Deventer and Suresh Sankaran April 25, 2016

A 14 Factor Heath, Jarrow and Morton Model for the United Kingdom Government Securities Yield Curve, January 1979 to January 2017

A 14 Factor Heath, Jarrow and Morton Model for the United Kingdom Government Securities Yield Curve, January 1979 to January 2017: Donald R. van Deventer 1 First Version: July 6, 2017 This Version: July

A 14 Factor Heath, Jarrow and Morton Model for the United Kingdom Government Securities Yield Curve, January 1979 to January 2017: Donald R. van Deventer 1 First Version: July 6, 2017 This Version: July

I. Japanese Government Bond Data: Special Characteristics

An 8 Factor Heath, Jarrow and Morton Model for the Japanese Government Bond Yield Curve, 1974 to 2016: The Impact of Negative Rates and Smoothing Issues Donald R. van Deventer 1 First Version: June 20,

An 8 Factor Heath, Jarrow and Morton Model for the Japanese Government Bond Yield Curve, 1974 to 2016: The Impact of Negative Rates and Smoothing Issues Donald R. van Deventer 1 First Version: June 20,

A 14 Factor Heath, Jarrow and Morton Model for the German Bund Yield Curve, January 1996 to March 2017

A 14 Factor Heath, Jarrow and Morton Model for the German Bund Yield Curve, January 1996 to March 2017 Donald R. van Deventer 1 First Version: July 17, 2017 This Version: July 18, 2017 ABSTRACT This paper

A 14 Factor Heath, Jarrow and Morton Model for the German Bund Yield Curve, January 1996 to March 2017 Donald R. van Deventer 1 First Version: July 17, 2017 This Version: July 18, 2017 ABSTRACT This paper

Rue de la Banque No. 52 November 2017

Staying at zero with affine processes: an application to term structure modelling Alain Monfort Banque de France and CREST Fulvio Pegoraro Banque de France, ECB and CREST Jean-Paul Renne HEC Lausanne Guillaume

Staying at zero with affine processes: an application to term structure modelling Alain Monfort Banque de France and CREST Fulvio Pegoraro Banque de France, ECB and CREST Jean-Paul Renne HEC Lausanne Guillaume

I. U.S. Treasury Data: Special Characteristics

A 10 Factor Heath, Jarrow and Morton Model for the U.S. Treasury Yield Curve, January 1962 to March 2017: Bayesian Model Validation Given Negative Rates in Japan Donald R. van Deventer 1 First Version:

A 10 Factor Heath, Jarrow and Morton Model for the U.S. Treasury Yield Curve, January 1962 to March 2017: Bayesian Model Validation Given Negative Rates in Japan Donald R. van Deventer 1 First Version:

Monetary policy, exchange rates and capital flows

Benoît Cœuré Member of the Executive Board European Central Bank Monetary policy, exchange rates and capital flows Washington D.C., 3 November 2017 Euro Rubric area recorded large net portfolio outflows

Benoît Cœuré Member of the Executive Board European Central Bank Monetary policy, exchange rates and capital flows Washington D.C., 3 November 2017 Euro Rubric area recorded large net portfolio outflows

FRBSF Economic Letter

FRBSF Economic Letter 2018-20 August 27, 2018 Research from the Federal Reserve Bank of San Francisco Information in the Yield Curve about Future Recessions Michael D. Bauer and Thomas M. Mertens The ability

FRBSF Economic Letter 2018-20 August 27, 2018 Research from the Federal Reserve Bank of San Francisco Information in the Yield Curve about Future Recessions Michael D. Bauer and Thomas M. Mertens The ability

WHY PURCHASE A DEFERRED FIXED ANNUITY IN A RISING INTEREST-RATE ENVIRONMENT?

WHY PURCHASE A DEFERRED FIXED ANNUITY IN A RISING INTEREST-RATE ENVIRONMENT? A White Paper for Pacific Life by Wade D. Pfau, Ph.D., CFA FAC0904-1217 Pacific Life Insurance Company commissioned The American

WHY PURCHASE A DEFERRED FIXED ANNUITY IN A RISING INTEREST-RATE ENVIRONMENT? A White Paper for Pacific Life by Wade D. Pfau, Ph.D., CFA FAC0904-1217 Pacific Life Insurance Company commissioned The American

Longer-term Yield Decomposition: The Analysis of the Czech Government Yield Curve. A Comment and Insights from NBP s experience

Longer-term Yield Decomposition: The Analysis of the Czech Government Yield Curve A Comment and Insights from NBP s experience Overview Motivation: Yield curve decompositions are important input to decision-making

Longer-term Yield Decomposition: The Analysis of the Czech Government Yield Curve A Comment and Insights from NBP s experience Overview Motivation: Yield curve decompositions are important input to decision-making

Global population projections by the United Nations John Wilmoth, Population Association of America, San Diego, 30 April Revised 5 July 2015

Global population projections by the United Nations John Wilmoth, Population Association of America, San Diego, 30 April 2015 Revised 5 July 2015 [Slide 1] Let me begin by thanking Wolfgang Lutz for reaching

Global population projections by the United Nations John Wilmoth, Population Association of America, San Diego, 30 April 2015 Revised 5 July 2015 [Slide 1] Let me begin by thanking Wolfgang Lutz for reaching

There are also two econometric techniques that are popular methods for linking macroeconomic factors to a time series of default probabilities:

2222 Kalakaua Avenue, 14 th Floor Honolulu, Hawaii 96815, USA telephone 808 791 9888 fax 808 791 9898 www.kamakuraco.com Kamakura Corporation CCAR Stress Tests for 2016: A Wells Fargo & Co. Example of

2222 Kalakaua Avenue, 14 th Floor Honolulu, Hawaii 96815, USA telephone 808 791 9888 fax 808 791 9898 www.kamakuraco.com Kamakura Corporation CCAR Stress Tests for 2016: A Wells Fargo & Co. Example of

Fed Funds Surprises & Treasury Yields: Part 2

May 21, 15 Economics Group Special Commentary Executive Summary There is significant uncertainty in 15 about what will happen to the yield curve when the Fed begins its tightening cycle. In this study,

May 21, 15 Economics Group Special Commentary Executive Summary There is significant uncertainty in 15 about what will happen to the yield curve when the Fed begins its tightening cycle. In this study,

The Importance of Forward-Rate Volatility Structures in Pricing Interest Rate-Sensitive Claims* Peter Ritchken and L. Sankarasubramanian

00 The Importance of Forward-Rate Volatility Structures in Pricing Interest Rate-Sensitive Claims* Typesetter: RH 1st proof: 22/8/00 2nd proof: 3rd proof: Peter Ritchken and L. Sankarasubramanian Case

00 The Importance of Forward-Rate Volatility Structures in Pricing Interest Rate-Sensitive Claims* Typesetter: RH 1st proof: 22/8/00 2nd proof: 3rd proof: Peter Ritchken and L. Sankarasubramanian Case

Luke and Jen Smith. MONTE CARLO ANALYSIS November 24, 2014

Luke and Jen Smith MONTE CARLO ANALYSIS November 24, 2014 PREPARED BY: John Davidson, CFP, ChFC 1001 E. Hector St., Ste. 401 Conshohocken, PA 19428 (610) 684-1100 Table Of Contents Table Of Contents...

Luke and Jen Smith MONTE CARLO ANALYSIS November 24, 2014 PREPARED BY: John Davidson, CFP, ChFC 1001 E. Hector St., Ste. 401 Conshohocken, PA 19428 (610) 684-1100 Table Of Contents Table Of Contents...

Is monetary policy in New Zealand similar to

Is monetary policy in New Zealand similar to that in Australia and the United States? Angela Huang, Economics Department 1 Introduction Monetary policy in New Zealand is often compared with monetary policy

Is monetary policy in New Zealand similar to that in Australia and the United States? Angela Huang, Economics Department 1 Introduction Monetary policy in New Zealand is often compared with monetary policy

Rho-Works Advanced Analytical Systems. CVaR E pert. Product information

Advanced Analytical Systems CVaR E pert Product information Presentation Value-at-Risk (VaR) is the most widely used measure of market risk for individual assets and portfolios. Conditional Value-at-Risk

Advanced Analytical Systems CVaR E pert Product information Presentation Value-at-Risk (VaR) is the most widely used measure of market risk for individual assets and portfolios. Conditional Value-at-Risk

Supervisors could mandate their banks to follow the framework set out in this section, or a bank could choose to adopt it. 3

Why U.S. Bank Regulators Rejected a Standardised Framework for Interest Rate Risk in the Banking Book Four Times Donald R. van Deventer, Frances Cheng, and Wilson Yap 1 October 31, 2017 In 1996, the U.S.

Why U.S. Bank Regulators Rejected a Standardised Framework for Interest Rate Risk in the Banking Book Four Times Donald R. van Deventer, Frances Cheng, and Wilson Yap 1 October 31, 2017 In 1996, the U.S.

Rebalancing the Simon Fraser University s Academic Pension Plan s Balanced Fund: A Case Study

Rebalancing the Simon Fraser University s Academic Pension Plan s Balanced Fund: A Case Study by Yingshuo Wang Bachelor of Science, Beijing Jiaotong University, 2011 Jing Ren Bachelor of Science, Shandong

Rebalancing the Simon Fraser University s Academic Pension Plan s Balanced Fund: A Case Study by Yingshuo Wang Bachelor of Science, Beijing Jiaotong University, 2011 Jing Ren Bachelor of Science, Shandong

Mean Reversion and Market Predictability. Jon Exley, Andrew Smith and Tom Wright

Mean Reversion and Market Predictability Jon Exley, Andrew Smith and Tom Wright Abstract: This paper examines some arguments for the predictability of share price and currency movements. We examine data

Mean Reversion and Market Predictability Jon Exley, Andrew Smith and Tom Wright Abstract: This paper examines some arguments for the predictability of share price and currency movements. We examine data

SPRING. A Rise in Interest Rates Will Not Necessarily Increase Cap Rates, Redux. Upton Sinclair CAP RATES. 38 PREA Quarterly, Spring 2018

SPRING 2018 A Rise in Interest Rates Will Not Necessarily Increase Cap Rates, Redux It is di cult to get a man to understand salary depends upon his not something when his understanding it. Upton Sinclair

SPRING 2018 A Rise in Interest Rates Will Not Necessarily Increase Cap Rates, Redux It is di cult to get a man to understand salary depends upon his not something when his understanding it. Upton Sinclair

also crucial To model occur; and Page 1

Are Your Non-Maturity Deposit Assumptions Accurately Modeled for ALM? Share deposits in credit unions have grown rapidly since 2000, increasing from $350 billion to nearly $1 trillion at the end of 2014.

Are Your Non-Maturity Deposit Assumptions Accurately Modeled for ALM? Share deposits in credit unions have grown rapidly since 2000, increasing from $350 billion to nearly $1 trillion at the end of 2014.

Cash Flow and the Time Value of Money

Harvard Business School 9-177-012 Rev. October 1, 1976 Cash Flow and the Time Value of Money A promising new product is nationally introduced based on its future sales and subsequent profits. A piece of

Harvard Business School 9-177-012 Rev. October 1, 1976 Cash Flow and the Time Value of Money A promising new product is nationally introduced based on its future sales and subsequent profits. A piece of

Correlation Structures Corresponding to Forward Rates

Chapter 6 Correlation Structures Corresponding to Forward Rates Ilona Kletskin 1, Seung Youn Lee 2, Hua Li 3, Mingfei Li 4, Rongsong Liu 5, Carlos Tolmasky 6, Yujun Wu 7 Report prepared by Seung Youn Lee

Chapter 6 Correlation Structures Corresponding to Forward Rates Ilona Kletskin 1, Seung Youn Lee 2, Hua Li 3, Mingfei Li 4, Rongsong Liu 5, Carlos Tolmasky 6, Yujun Wu 7 Report prepared by Seung Youn Lee

Is there a decoupling between soft and hard data? The relationship between GDP growth and the ESI

Fifth joint EU/OECD workshop on business and consumer surveys Brussels, 17 18 November 2011 Is there a decoupling between soft and hard data? The relationship between GDP growth and the ESI Olivier BIAU

Fifth joint EU/OECD workshop on business and consumer surveys Brussels, 17 18 November 2011 Is there a decoupling between soft and hard data? The relationship between GDP growth and the ESI Olivier BIAU

Modeling Fixed-Income Securities and Interest Rate Options

jarr_fm.qxd 5/16/02 4:49 PM Page iii Modeling Fixed-Income Securities and Interest Rate Options SECOND EDITION Robert A. Jarrow Stanford Economics and Finance An Imprint of Stanford University Press Stanford,

jarr_fm.qxd 5/16/02 4:49 PM Page iii Modeling Fixed-Income Securities and Interest Rate Options SECOND EDITION Robert A. Jarrow Stanford Economics and Finance An Imprint of Stanford University Press Stanford,

Backtesting and Optimizing Commodity Hedging Strategies

Backtesting and Optimizing Commodity Hedging Strategies How does a firm design an effective commodity hedging programme? The key to answering this question lies in one s definition of the term effective,

Backtesting and Optimizing Commodity Hedging Strategies How does a firm design an effective commodity hedging programme? The key to answering this question lies in one s definition of the term effective,

FIXED INCOME SECURITIES

FIXED INCOME SECURITIES Valuation, Risk, and Risk Management Pietro Veronesi University of Chicago WILEY JOHN WILEY & SONS, INC. CONTENTS Preface Acknowledgments PART I BASICS xix xxxiii AN INTRODUCTION

FIXED INCOME SECURITIES Valuation, Risk, and Risk Management Pietro Veronesi University of Chicago WILEY JOHN WILEY & SONS, INC. CONTENTS Preface Acknowledgments PART I BASICS xix xxxiii AN INTRODUCTION

January Ira G. Kawaller President, Kawaller & Co., LLC

Interest Rate Swap Valuation Since the Financial Crisis: Theory and Practice January 2017 Ira G. Kawaller President, Kawaller & Co., LLC Email: kawaller@kawaller.com Donald J. Smith Associate Professor

Interest Rate Swap Valuation Since the Financial Crisis: Theory and Practice January 2017 Ira G. Kawaller President, Kawaller & Co., LLC Email: kawaller@kawaller.com Donald J. Smith Associate Professor

Group LTD Credibility Study Results from Stage 1

Group LTD Credibility Study Results from Stage 1 April 2018 2 Group LTD Credibility Study Results from Stage 1 AUTHOR Paul Correia, FSA, MAAA Principal and Consulting Actuary Milliman, Inc. SPONSOR SOA

Group LTD Credibility Study Results from Stage 1 April 2018 2 Group LTD Credibility Study Results from Stage 1 AUTHOR Paul Correia, FSA, MAAA Principal and Consulting Actuary Milliman, Inc. SPONSOR SOA

in-depth Invesco Actively Managed Low Volatility Strategies The Case for

Invesco in-depth The Case for Actively Managed Low Volatility Strategies We believe that active LVPs offer the best opportunity to achieve a higher risk-adjusted return over the long term. Donna C. Wilson

Invesco in-depth The Case for Actively Managed Low Volatility Strategies We believe that active LVPs offer the best opportunity to achieve a higher risk-adjusted return over the long term. Donna C. Wilson

What Is the Best Strategy for Extending the U.S. Economy s Expansion?

What Is the Best Strategy for Extending the U.S. Economy s Expansion? James Bullard President and CEO CFA Society Chicago Distinguished Speaker Series Breakfast Sept. 12, 2018 Chicago, Ill. Any opinions

What Is the Best Strategy for Extending the U.S. Economy s Expansion? James Bullard President and CEO CFA Society Chicago Distinguished Speaker Series Breakfast Sept. 12, 2018 Chicago, Ill. Any opinions

The corporate bond issuance global frenzy, what role for US Quantitative Easing?

The 2009-2013 corporate bond issuance global frenzy, what role for US Quantitative Easing? Lo Duca Marco, Nicoletti Giulio, Vidal Ariadna European Central Bank XI Emerging Markets Workshop Bank of Spain

The 2009-2013 corporate bond issuance global frenzy, what role for US Quantitative Easing? Lo Duca Marco, Nicoletti Giulio, Vidal Ariadna European Central Bank XI Emerging Markets Workshop Bank of Spain

Estimation of Default Risk in CIR++ model simulation

Int. J. Eng. Math. Model., 2014, vol. 1, no. 1., p. 1-8 Available online at www.orb-academic.org International Journal of Engineering and Mathematical Modelling ISSN: 2351-8707 Estimation of Default Risk

Int. J. Eng. Math. Model., 2014, vol. 1, no. 1., p. 1-8 Available online at www.orb-academic.org International Journal of Engineering and Mathematical Modelling ISSN: 2351-8707 Estimation of Default Risk

Predicting a US recession: has the yield curve lost its relevance?

Global Perspective Predicting a US recession: has the yield curve lost its relevance? For professional investor use only Asset Management August 2018 Executive summary It is becoming apparent the US economy

Global Perspective Predicting a US recession: has the yield curve lost its relevance? For professional investor use only Asset Management August 2018 Executive summary It is becoming apparent the US economy

U.S. Interest Rates Chartbook September 2017

U.S. Interest Rates Chartbook September 2017 Takeaways The FOMC announced the start of the balance sheet normalization process to begin in October while maintained the Fed funds rate target range at 1%-1.25%

U.S. Interest Rates Chartbook September 2017 Takeaways The FOMC announced the start of the balance sheet normalization process to begin in October while maintained the Fed funds rate target range at 1%-1.25%

Diving into Predictive Markers of Corporate Failure. Martin M. Zorn Tuesday, June 12, :00 to 10:30am Session 27040

Diving into Predictive Markers of Corporate Failure Martin M. Zorn Tuesday, June 12, 2018 9:00 to 10:30am Session 27040 Macro Factors A Risk Road Map Default Prepayment Mortality Spreads Cash flows Market

Diving into Predictive Markers of Corporate Failure Martin M. Zorn Tuesday, June 12, 2018 9:00 to 10:30am Session 27040 Macro Factors A Risk Road Map Default Prepayment Mortality Spreads Cash flows Market

Executive Summary: A CVaR Scenario-based Framework For Minimizing Downside Risk In Multi-Asset Class Portfolios

Executive Summary: A CVaR Scenario-based Framework For Minimizing Downside Risk In Multi-Asset Class Portfolios Axioma, Inc. by Kartik Sivaramakrishnan, PhD, and Robert Stamicar, PhD August 2016 In this

Executive Summary: A CVaR Scenario-based Framework For Minimizing Downside Risk In Multi-Asset Class Portfolios Axioma, Inc. by Kartik Sivaramakrishnan, PhD, and Robert Stamicar, PhD August 2016 In this

KAMAKURA RISK INFORMATION SERVICES

KAMAKURA RISK INFORMATION SERVICES VERSION 7.0 Credit Portfolio Manager KRIS-CPM Version 5.0 APRIL 2011 www.kamakuraco.com Telephone: 1-808-791-9888 Facsimile: 1-808-791-9898 2222 Kalakaua Avenue, Suite

KAMAKURA RISK INFORMATION SERVICES VERSION 7.0 Credit Portfolio Manager KRIS-CPM Version 5.0 APRIL 2011 www.kamakuraco.com Telephone: 1-808-791-9888 Facsimile: 1-808-791-9898 2222 Kalakaua Avenue, Suite

ABILITY OF VALUE AT RISK TO ESTIMATE THE RISK: HISTORICAL SIMULATION APPROACH

ABILITY OF VALUE AT RISK TO ESTIMATE THE RISK: HISTORICAL SIMULATION APPROACH Dumitru Cristian Oanea, PhD Candidate, Bucharest University of Economic Studies Abstract: Each time an investor is investing

ABILITY OF VALUE AT RISK TO ESTIMATE THE RISK: HISTORICAL SIMULATION APPROACH Dumitru Cristian Oanea, PhD Candidate, Bucharest University of Economic Studies Abstract: Each time an investor is investing

DERIVATIVE SECURITIES Lecture 5: Fixed-income securities

DERIVATIVE SECURITIES Lecture 5: Fixed-income securities Philip H. Dybvig Washington University in Saint Louis Interest rates Interest rate derivative pricing: general issues Bond and bond option pricing

DERIVATIVE SECURITIES Lecture 5: Fixed-income securities Philip H. Dybvig Washington University in Saint Louis Interest rates Interest rate derivative pricing: general issues Bond and bond option pricing

MIN WEI 2228 Central Ave. Phone: (202)

") MIN WEI 2228 Central Ave. Phone: (202) 736-5619 Vienna, VA 22182 E-Mail: min.wei@frb.gov USA https://sites.google.com/site/minweifrb CURRENT POSITION Associate Director, Division of Monetary Affairs, 2018-Present

MIN WEI 2228 Central Ave. Phone: (202) 736-5619 Vienna, VA 22182 E-Mail: min.wei@frb.gov USA https://sites.google.com/site/minweifrb CURRENT POSITION Associate Director, Division of Monetary Affairs, 2018-Present

The Journal of Applied Business Research May/June 2009 Volume 25, Number 3

Risk Manage Capital Investment Decisions: A Lease vs. Purchase Illustration Thomas L. Zeller, PhD., CPA, Loyola University Chicago Brian B. Stanko, PhD., CPA, Loyola University Chicago ABSTRACT This paper

Risk Manage Capital Investment Decisions: A Lease vs. Purchase Illustration Thomas L. Zeller, PhD., CPA, Loyola University Chicago Brian B. Stanko, PhD., CPA, Loyola University Chicago ABSTRACT This paper

Beta dispersion and portfolio returns

J Asset Manag (2018) 19:156 161 https://doi.org/10.1057/s41260-017-0071-6 INVITED EDITORIAL Beta dispersion and portfolio returns Kyre Dane Lahtinen 1 Chris M. Lawrey 1 Kenneth J. Hunsader 1 Published

J Asset Manag (2018) 19:156 161 https://doi.org/10.1057/s41260-017-0071-6 INVITED EDITORIAL Beta dispersion and portfolio returns Kyre Dane Lahtinen 1 Chris M. Lawrey 1 Kenneth J. Hunsader 1 Published

Models for Credit Risk in a Network Economy

Models for Credit Risk in a Network Economy Henry Schellhorn School of Mathematical Sciences Claremont Graduate University An Example of a Financial Network Autonation Visteon Ford United Lear Lithia GM

Models for Credit Risk in a Network Economy Henry Schellhorn School of Mathematical Sciences Claremont Graduate University An Example of a Financial Network Autonation Visteon Ford United Lear Lithia GM

Stochastic Interest Rates

Stochastic Interest Rates This volume in the Mastering Mathematical Finance series strikes just the right balance between mathematical rigour and practical application. Existing books on the challenging

Stochastic Interest Rates This volume in the Mastering Mathematical Finance series strikes just the right balance between mathematical rigour and practical application. Existing books on the challenging

Termination of the Battle River 5 Power Purchase Arrangement with the Generation Owner

Termination of the Battle River 5 Power Purchase Arrangement with the Generation Owner Table of Contents January 12, 2018 Disclaimer... 1 Executive Summary... 2 Overview of the Balancing Pool and the Power

Termination of the Battle River 5 Power Purchase Arrangement with the Generation Owner Table of Contents January 12, 2018 Disclaimer... 1 Executive Summary... 2 Overview of the Balancing Pool and the Power

How to Extend the U.S. Expansion: A Suggestion

How to Extend the U.S. Expansion: A Suggestion James Bullard President and CEO Real Return XII: The Inflation-Linked Products Conference 2018 Sept. 5, 2018 New York, N.Y. Any opinions expressed here are

How to Extend the U.S. Expansion: A Suggestion James Bullard President and CEO Real Return XII: The Inflation-Linked Products Conference 2018 Sept. 5, 2018 New York, N.Y. Any opinions expressed here are

Is the market always right?

Is the market always right? Improving federal funds rate forecasts by adjusting for the term premium AN7/8 Michael Callaghan November 7 Reserve Bank of New Zealand Analytical Note Series ISSN 3 555 Reserve

Is the market always right? Improving federal funds rate forecasts by adjusting for the term premium AN7/8 Michael Callaghan November 7 Reserve Bank of New Zealand Analytical Note Series ISSN 3 555 Reserve

RBC retirement income planning process

Page 1 of 6 RBC retirement income planning process Create income for your retirement At RBC Wealth Management, we believe managing your wealth to produce an income during retirement is fundamentally different

Page 1 of 6 RBC retirement income planning process Create income for your retirement At RBC Wealth Management, we believe managing your wealth to produce an income during retirement is fundamentally different

Valuation of a New Class of Commodity-Linked Bonds with Partial Indexation Adjustments

Valuation of a New Class of Commodity-Linked Bonds with Partial Indexation Adjustments Thomas H. Kirschenmann Institute for Computational Engineering and Sciences University of Texas at Austin and Ehud

Valuation of a New Class of Commodity-Linked Bonds with Partial Indexation Adjustments Thomas H. Kirschenmann Institute for Computational Engineering and Sciences University of Texas at Austin and Ehud

Intermediary Balance Sheets Tobias Adrian and Nina Boyarchenko, NY Fed Discussant: Annette Vissing-Jorgensen, UC Berkeley

Intermediary Balance Sheets Tobias Adrian and Nina Boyarchenko, NY Fed Discussant: Annette Vissing-Jorgensen, UC Berkeley Objective: Construct a general equilibrium model with two types of intermediaries:

Intermediary Balance Sheets Tobias Adrian and Nina Boyarchenko, NY Fed Discussant: Annette Vissing-Jorgensen, UC Berkeley Objective: Construct a general equilibrium model with two types of intermediaries:

SOCIAL SECURITY AND SAVING: NEW TIME SERIES EVIDENCE MARTIN FELDSTEIN *

SOCIAL SECURITY AND SAVING SOCIAL SECURITY AND SAVING: NEW TIME SERIES EVIDENCE MARTIN FELDSTEIN * Abstract - This paper reexamines the results of my 1974 paper on Social Security and saving with the help

SOCIAL SECURITY AND SAVING SOCIAL SECURITY AND SAVING: NEW TIME SERIES EVIDENCE MARTIN FELDSTEIN * Abstract - This paper reexamines the results of my 1974 paper on Social Security and saving with the help

A Comparison of Market and Model Forward Rates

A Comparison of Market and Model Forward Rates Mayank Nagpal & Adhish Verma M.Sc II May 10, 2010 Mayank nagpal and Adhish Verma are second year students of MS Economics at the Indira Gandhi Institute of

A Comparison of Market and Model Forward Rates Mayank Nagpal & Adhish Verma M.Sc II May 10, 2010 Mayank nagpal and Adhish Verma are second year students of MS Economics at the Indira Gandhi Institute of

THE FLORIDA INTERNATIONAL UNIVERSITY BOARD OF TRUSTEES Finance and Facilities Committee December 7, 2017

THE FLORIDA INTERNATIONAL UNIVERSITY BOARD OF TRUSTEES Finance and Facilities Committee December 7, 2017 Report (For Information Only no action required) TREASURY REPORT (For quarter ending September 30,

THE FLORIDA INTERNATIONAL UNIVERSITY BOARD OF TRUSTEES Finance and Facilities Committee December 7, 2017 Report (For Information Only no action required) TREASURY REPORT (For quarter ending September 30,

Simulating Continuous Time Rating Transitions

Bus 864 1 Simulating Continuous Time Rating Transitions Robert A. Jones 17 March 2003 This note describes how to simulate state changes in continuous time Markov chains. An important application to credit

Bus 864 1 Simulating Continuous Time Rating Transitions Robert A. Jones 17 March 2003 This note describes how to simulate state changes in continuous time Markov chains. An important application to credit

An Equilibrium Model of the Term Structure of Interest Rates

Finance 400 A. Penati - G. Pennacchi An Equilibrium Model of the Term Structure of Interest Rates When bond prices are assumed to be driven by continuous-time stochastic processes, noarbitrage restrictions

Finance 400 A. Penati - G. Pennacchi An Equilibrium Model of the Term Structure of Interest Rates When bond prices are assumed to be driven by continuous-time stochastic processes, noarbitrage restrictions

THE PERFORMANCE OF U. S. DOMESTIC EQUITY MUTUAL FUNDS DURING RECENT RECESSIONS

THE PERFORMANCE OF U. S. DOMESTIC EQUITY MUTUAL FUNDS DURING RECENT RECESSIONS Dr. 1 Central Connecticut State University, U.S.A. E-mail: belloz@ccsu.edu ABSTRACT In this study, I investigate the performance

THE PERFORMANCE OF U. S. DOMESTIC EQUITY MUTUAL FUNDS DURING RECENT RECESSIONS Dr. 1 Central Connecticut State University, U.S.A. E-mail: belloz@ccsu.edu ABSTRACT In this study, I investigate the performance

Asset Allocation Matters, But Not as Much as You Think By Robert Huebscher June 15, 2010

Asset Allocation Matters, But Not as Much as You Think By Robert Huebscher June 15, 2010 We re all familiar with the 1986 finding by Gary Brinson, Randolph Hood, and Gilbert Beebower (BHB) that asset allocation

Asset Allocation Matters, But Not as Much as You Think By Robert Huebscher June 15, 2010 We re all familiar with the 1986 finding by Gary Brinson, Randolph Hood, and Gilbert Beebower (BHB) that asset allocation

Monthly vs Daily Leveraged Funds

Leveraged Funds William J. Trainor Jr. East Tennessee State University ABSTRACT Leveraged funds have become increasingly popular over the last 5 years. In the ETF market, there are now over 150 leveraged

Leveraged Funds William J. Trainor Jr. East Tennessee State University ABSTRACT Leveraged funds have become increasingly popular over the last 5 years. In the ETF market, there are now over 150 leveraged

Puttable Bond and Vaulation

and Vaulation Dmitry Popov FinPricing http://www.finpricing.com Summary Puttable Bond Definition The Advantages of Puttable Bonds Puttable Bond Payoffs Valuation Model Selection Criteria LGM Model LGM

and Vaulation Dmitry Popov FinPricing http://www.finpricing.com Summary Puttable Bond Definition The Advantages of Puttable Bonds Puttable Bond Payoffs Valuation Model Selection Criteria LGM Model LGM

J. V. Bruni and Company 1528 North Tejon Street Colorado Springs, CO (719) or (800)

or (800)") J. V. Bruni and Company 1528 North Tejon Street Colorado Springs, CO 80907 (719) 575-9880 or (800) 748-3409 Retirement Nest Eggs... Withdrawal Rates and Fund Sustainability An Updated and Expanded Analysis

J. V. Bruni and Company 1528 North Tejon Street Colorado Springs, CO 80907 (719) 575-9880 or (800) 748-3409 Retirement Nest Eggs... Withdrawal Rates and Fund Sustainability An Updated and Expanded Analysis

Are Bonds Going to Outperform Stocks Over the Long Run? Not Likely.

July 2009 Page 1 Are Bonds Going to Outperform Stocks Over the Long Run? Not Likely. Given the poor performance of stocks over the past year and the past decade, there has been ample discussion about the

July 2009 Page 1 Are Bonds Going to Outperform Stocks Over the Long Run? Not Likely. Given the poor performance of stocks over the past year and the past decade, there has been ample discussion about the

Curve fitting for calculating SCR under Solvency II

Curve fitting for calculating SCR under Solvency II Practical insights and best practices from leading European Insurers Leading up to the go live date for Solvency II, insurers in Europe are in search

Curve fitting for calculating SCR under Solvency II Practical insights and best practices from leading European Insurers Leading up to the go live date for Solvency II, insurers in Europe are in search

The current definition of spare capacity is. When has OPEC Spare Capacity Mattered for Oil Prices?

When has OPEC Spare Capacity Mattered for Oil Prices? Oil prices usually feed off multiple influences, as noted in Büyükşahin (2011). The various influences on oil prices are illustrated in Figure 1. But

When has OPEC Spare Capacity Mattered for Oil Prices? Oil prices usually feed off multiple influences, as noted in Büyükşahin (2011). The various influences on oil prices are illustrated in Figure 1. But

Portfolio Rebalancing:

Portfolio Rebalancing: A Guide For Institutional Investors May 2012 PREPARED BY Nat Kellogg, CFA Associate Director of Research Eric Przybylinski, CAIA Senior Research Analyst Abstract Failure to rebalance

Portfolio Rebalancing: A Guide For Institutional Investors May 2012 PREPARED BY Nat Kellogg, CFA Associate Director of Research Eric Przybylinski, CAIA Senior Research Analyst Abstract Failure to rebalance

Expected Return Methodologies in Morningstar Direct Asset Allocation

Expected Return Methodologies in Morningstar Direct Asset Allocation I. Introduction to expected return II. The short version III. Detailed methodologies 1. Building Blocks methodology i. Methodology ii.

Expected Return Methodologies in Morningstar Direct Asset Allocation I. Introduction to expected return II. The short version III. Detailed methodologies 1. Building Blocks methodology i. Methodology ii.

Measuring Systematic Risk

George Pennacchi Department of Finance University of Illinois European Banking Authority Policy Research Workshop 25 November 2014 Systematic versus Systemic Systematic risks are non-diversifiable risks

George Pennacchi Department of Finance University of Illinois European Banking Authority Policy Research Workshop 25 November 2014 Systematic versus Systemic Systematic risks are non-diversifiable risks

Comparing the Performance of Annuities with Principal Guarantees: Accumulation Benefit on a VA Versus FIA

Comparing the Performance of Annuities with Principal Guarantees: Accumulation Benefit on a VA Versus FIA MARCH 2019 2019 CANNEX Financial Exchanges Limited. All rights reserved. Comparing the Performance

Comparing the Performance of Annuities with Principal Guarantees: Accumulation Benefit on a VA Versus FIA MARCH 2019 2019 CANNEX Financial Exchanges Limited. All rights reserved. Comparing the Performance

Personal Financial Plan. John and Mary Sample

For October 21, 2013 Prepared by Public Retirement Planners, LLC 820 Davis Street Suite 434 Evanston IL 60714 224-567-1854 This presentation provides a general overview of some aspects of your personal

For October 21, 2013 Prepared by Public Retirement Planners, LLC 820 Davis Street Suite 434 Evanston IL 60714 224-567-1854 This presentation provides a general overview of some aspects of your personal

TEACHERS RETIREMENT BOARD. REGULAR MEETING Item Number: 7 CONSENT: ATTACHMENT(S): 1. DATE OF MEETING: November 8, 2018 / 60 mins

: 1. DATE OF MEETING: November 8, 2018 / 60 mins") TEACHERS RETIREMENT BOARD REGULAR MEETING Item Number: 7 SUBJECT: Review of CalSTRS Funding Levels and Risks CONSENT: ATTACHMENT(S): 1 ACTION: INFORMATION: X DATE OF MEETING: / 60 mins PRESENTER(S): Rick

TEACHERS RETIREMENT BOARD REGULAR MEETING Item Number: 7 SUBJECT: Review of CalSTRS Funding Levels and Risks CONSENT: ATTACHMENT(S): 1 ACTION: INFORMATION: X DATE OF MEETING: / 60 mins PRESENTER(S): Rick

On the Determination of Interest Rates in General and Partial Equilibrium Analysis

JOURNAL OF ECONOMICS AND FINANCE EDUCATION Volume 4 Number 1 Summer 2005 19 On the Determination of Interest Rates in General and Partial Equilibrium Analysis Bill Z. Yang 1 and Mark A. Yanochik 2 Abstract

JOURNAL OF ECONOMICS AND FINANCE EDUCATION Volume 4 Number 1 Summer 2005 19 On the Determination of Interest Rates in General and Partial Equilibrium Analysis Bill Z. Yang 1 and Mark A. Yanochik 2 Abstract

Curve Ball - Is the Yield Curve Still a Dependable Signal?

Curve Ball - Is the Yield Curve Still a Dependable Signal? November 2, 2015 by Michael Lebowitz Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent

Curve Ball - Is the Yield Curve Still a Dependable Signal? November 2, 2015 by Michael Lebowitz Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent

FIXED INCOME ASSET PRICING

BUS 35130 Autumn 2017 Pietro Veronesi Office: HPC409 (773) 702-6348 pietro.veronesi@ Course Objectives and Overview FIXED INCOME ASSET PRICING The universe of fixed income instruments is large and ever

BUS 35130 Autumn 2017 Pietro Veronesi Office: HPC409 (773) 702-6348 pietro.veronesi@ Course Objectives and Overview FIXED INCOME ASSET PRICING The universe of fixed income instruments is large and ever

Rationale for keeping the cap on the substitutability category for the G-SIB scoring methodology

Rationale for keeping the cap on the substitutability category for the G-SIB scoring methodology November 2017 Francisco Covas +1.202.649.4605 francisco.covas@theclearinghouse.org I. Summary This memo

Rationale for keeping the cap on the substitutability category for the G-SIB scoring methodology November 2017 Francisco Covas +1.202.649.4605 francisco.covas@theclearinghouse.org I. Summary This memo

Fixed Income Analysis

ICEF, Higher School of Economics, Moscow Master Program, Fall 2017 Fixed Income Analysis Course Syllabus Lecturer: Dr. Vladimir Sokolov (e-mail: vsokolov@hse.ru) 1. Course Objective and Format Fixed income

ICEF, Higher School of Economics, Moscow Master Program, Fall 2017 Fixed Income Analysis Course Syllabus Lecturer: Dr. Vladimir Sokolov (e-mail: vsokolov@hse.ru) 1. Course Objective and Format Fixed income

Home Loan Rates. RBNZ OCR cut triggers a mortgage rate drop. 22 June 2015

Home Loan Rates 22 June 201 RBNZ OCR cut triggers a mortgage rate drop The RBNZ cut the OCR by 2bp in June, and we expect another cut will soon follow. Influential global interest rates remain low, but

Home Loan Rates 22 June 201 RBNZ OCR cut triggers a mortgage rate drop The RBNZ cut the OCR by 2bp in June, and we expect another cut will soon follow. Influential global interest rates remain low, but

Key Features Asset allocation, cash flow analysis, object-oriented portfolio optimization, and risk analysis

Financial Toolbox Analyze financial data and develop financial algorithms Financial Toolbox provides functions for mathematical modeling and statistical analysis of financial data. You can optimize portfolios

Financial Toolbox Analyze financial data and develop financial algorithms Financial Toolbox provides functions for mathematical modeling and statistical analysis of financial data. You can optimize portfolios

Investments. The Search for a Safe Way to Save for Retirement

Investments The Search for a Safe Way to Save for Retirement Identifying a secure investment approach. By Christine C. Marcks There are three important elements of a safe investment vehicle: Principal

Investments The Search for a Safe Way to Save for Retirement Identifying a secure investment approach. By Christine C. Marcks There are three important elements of a safe investment vehicle: Principal

THE FLORIDA INTERNATIONAL UNIVERSITY BOARD OF TRUSTEES Finance and Facilities Committee April 12, 2018

THE FLORIDA INTERNATIONAL UNIVERSITY BOARD OF TRUSTEES Finance and Facilities Committee April 12, 2018 Report (For Information Only no action required) TREASURY REPORT (For quarter ending December 31,

THE FLORIDA INTERNATIONAL UNIVERSITY BOARD OF TRUSTEES Finance and Facilities Committee April 12, 2018 Report (For Information Only no action required) TREASURY REPORT (For quarter ending December 31,

Information Technology Project Management, Sixth Edition

Management, Sixth Edition Prepared By: Izzeddin Matar. Note: See the text itself for full citations. Understand what risk is and the importance of good project risk management Discuss the elements involved

Management, Sixth Edition Prepared By: Izzeddin Matar. Note: See the text itself for full citations. Understand what risk is and the importance of good project risk management Discuss the elements involved

Methodology for risk analysis in railway tunnels using Monte Carlo simulation

673 Methodology for risk analysis in railway tunnels using Monte Carlo simulation G. Vanorio & J. M. Mera Technical University of Madrid, Spain Abstract In the context of safety analyses for railway tunnels,

673 Methodology for risk analysis in railway tunnels using Monte Carlo simulation G. Vanorio & J. M. Mera Technical University of Madrid, Spain Abstract In the context of safety analyses for railway tunnels,

U.S. Interest Rates Chartbook March 2018

U.S. Interest Rates Chartbook March 2018 Takeaways At the March meeting, the FOMC voted unanimously to raise the Fed funds rate to 1.5%-1.75%. The newly appointed Chairman is committed to maintaining continuity

U.S. Interest Rates Chartbook March 2018 Takeaways At the March meeting, the FOMC voted unanimously to raise the Fed funds rate to 1.5%-1.75%. The newly appointed Chairman is committed to maintaining continuity

Tax-exempt municipal bonds

Tax Optimization of Municipal Bond Portfolios: Investment Selection and Tax Rate Arbitrage ANDREW KALOTAY ANDREW KALOTAY is president of Andrew Kalotay Associates, Inc., in New York, NY. andy@kalotay.com

Tax Optimization of Municipal Bond Portfolios: Investment Selection and Tax Rate Arbitrage ANDREW KALOTAY ANDREW KALOTAY is president of Andrew Kalotay Associates, Inc., in New York, NY. andy@kalotay.com

UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Fall Module I

Fall Module I") UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Fall 2016 Module I The consumers Decision making under certainty (PR 3.1-3.4) Decision making under uncertainty

UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Fall 2016 Module I The consumers Decision making under certainty (PR 3.1-3.4) Decision making under uncertainty

Fixed Income Modelling

Fixed Income Modelling CLAUS MUNK OXPORD UNIVERSITY PRESS Contents List of Figures List of Tables xiii xv 1 Introduction and Overview 1 1.1 What is fixed income analysis? 1 1.2 Basic bond market terminology

Fixed Income Modelling CLAUS MUNK OXPORD UNIVERSITY PRESS Contents List of Figures List of Tables xiii xv 1 Introduction and Overview 1 1.1 What is fixed income analysis? 1 1.2 Basic bond market terminology

PA Healthcare System Adopts a New Strategy to Tackle Financial Challenges

SEI Case Study PA Healthcare System Adopts a New Strategy to Tackle Financial Challenges Pension underfunding and balance sheet concerns trigger debt covenant violations. Important Information: This case

SEI Case Study PA Healthcare System Adopts a New Strategy to Tackle Financial Challenges Pension underfunding and balance sheet concerns trigger debt covenant violations. Important Information: This case

1 Introduction. Term Paper: The Hall and Taylor Model in Duali 1. Yumin Li 5/8/2012

Term Paper: The Hall and Taylor Model in Duali 1 Yumin Li 5/8/2012 1 Introduction In macroeconomics and policy making arena, it is extremely important to have the ability to manipulate a set of control

Term Paper: The Hall and Taylor Model in Duali 1 Yumin Li 5/8/2012 1 Introduction In macroeconomics and policy making arena, it is extremely important to have the ability to manipulate a set of control

Payoff Scale Effects and Risk Preference Under Real and Hypothetical Conditions

Payoff Scale Effects and Risk Preference Under Real and Hypothetical Conditions Susan K. Laury and Charles A. Holt Prepared for the Handbook of Experimental Economics Results February 2002 I. Introduction

Payoff Scale Effects and Risk Preference Under Real and Hypothetical Conditions Susan K. Laury and Charles A. Holt Prepared for the Handbook of Experimental Economics Results February 2002 I. Introduction

14.02 Principles of Macroeconomics Problem Set #4 - Answers

4.02 Principles of Macroeconomics Problem Set #4 - Answers Due during Week # 9 PART I. TRUE/FALSE/UNCERTAIN. As in microeconomics, the AD-curve is downward sloping since consumers buy less goods when they

4.02 Principles of Macroeconomics Problem Set #4 - Answers Due during Week # 9 PART I. TRUE/FALSE/UNCERTAIN. As in microeconomics, the AD-curve is downward sloping since consumers buy less goods when they

PROBABILITY. Wiley. With Applications and R ROBERT P. DOBROW. Department of Mathematics. Carleton College Northfield, MN

PROBABILITY With Applications and R ROBERT P. DOBROW Department of Mathematics Carleton College Northfield, MN Wiley CONTENTS Preface Acknowledgments Introduction xi xiv xv 1 First Principles 1 1.1 Random

PROBABILITY With Applications and R ROBERT P. DOBROW Department of Mathematics Carleton College Northfield, MN Wiley CONTENTS Preface Acknowledgments Introduction xi xiv xv 1 First Principles 1 1.1 Random

Are Managed-Payout Funds Better than Annuities?

Are Managed-Payout Funds Better than Annuities? July 28, 2015 by Joe Tomlinson Managed-payout funds promise to meet retirees need for sustainable lifetime income without relying on annuities. To see whether

Are Managed-Payout Funds Better than Annuities? July 28, 2015 by Joe Tomlinson Managed-payout funds promise to meet retirees need for sustainable lifetime income without relying on annuities. To see whether

The Volatility of Low Rates

15 April 213 The Volatility of Low Rates Raphael Douady Riskdata Head of Research Abstract Traditional, fixed-income risk models are based on the assumption that bond risk is directly proportional to the

15 April 213 The Volatility of Low Rates Raphael Douady Riskdata Head of Research Abstract Traditional, fixed-income risk models are based on the assumption that bond risk is directly proportional to the

The incidence of the inclusion of food at home preparation in the sales tax base

The incidence of the inclusion of food at home preparation in the sales tax base BACKGROUND Kansas is one of only fourteen states that includes food for at home preparation (groceries) in the state sales

The incidence of the inclusion of food at home preparation in the sales tax base BACKGROUND Kansas is one of only fourteen states that includes food for at home preparation (groceries) in the state sales

Valuation Publications Frequently Asked Questions

Valuation Publications Frequently Asked Questions Valuation Publications Frequently Asked Questions The information presented in this publication has been obtained with the greatest of care from sources

Valuation Publications Frequently Asked Questions Valuation Publications Frequently Asked Questions The information presented in this publication has been obtained with the greatest of care from sources

Federal Spending to Top a Record $4 Trillion in FY2017

Federal Spending to Top a Record $4 Trillion in FY2017 July 11, 2017 by Gary Halbert of Halbert Wealth Management 1. June Unemployment Report Was Better Than Expected 2. Federal Spending to Blow Through

Federal Spending to Top a Record $4 Trillion in FY2017 July 11, 2017 by Gary Halbert of Halbert Wealth Management 1. June Unemployment Report Was Better Than Expected 2. Federal Spending to Blow Through

SPECIAL REPORT. TD Economics U.S. LONG-TERM FINANCIAL ASSET RETURNS: AN ECONOMIC PERSPECTIVE

SPECIAL REPORT TD Economics U.S. LONG-TERM FINANCIAL ASSET RETURNS: AN ECONOMIC PERSPECTIVE Highlights The impact of Fed tightening on asset returns is likely to be meaningful but not dramatic. The ECB

SPECIAL REPORT TD Economics U.S. LONG-TERM FINANCIAL ASSET RETURNS: AN ECONOMIC PERSPECTIVE Highlights The impact of Fed tightening on asset returns is likely to be meaningful but not dramatic. The ECB

The Disappearing Pre-FOMC Announcement Drift

The Disappearing Pre-FOMC Announcement Drift Thomas Gilbert Alexander Kurov Marketa Halova Wolfe First Draft: January 11, 2018 This Draft: March 16, 2018 Abstract Lucca and Moench (2015) document large

The Disappearing Pre-FOMC Announcement Drift Thomas Gilbert Alexander Kurov Marketa Halova Wolfe First Draft: January 11, 2018 This Draft: March 16, 2018 Abstract Lucca and Moench (2015) document large