MiFID II / MiFIR seminar Break-out session 1: Retail conduct investor protection

|

|

|

- Aubrey Houston

- 6 years ago

- Views:

Transcription

1 MiFID II / MiFIR seminar Break-out session 1: Retail conduct investor protection Peter Snowdon, Partner Charlotte Henry, Senior Associate Norton Rose Fulbright LLP 15 October 2014

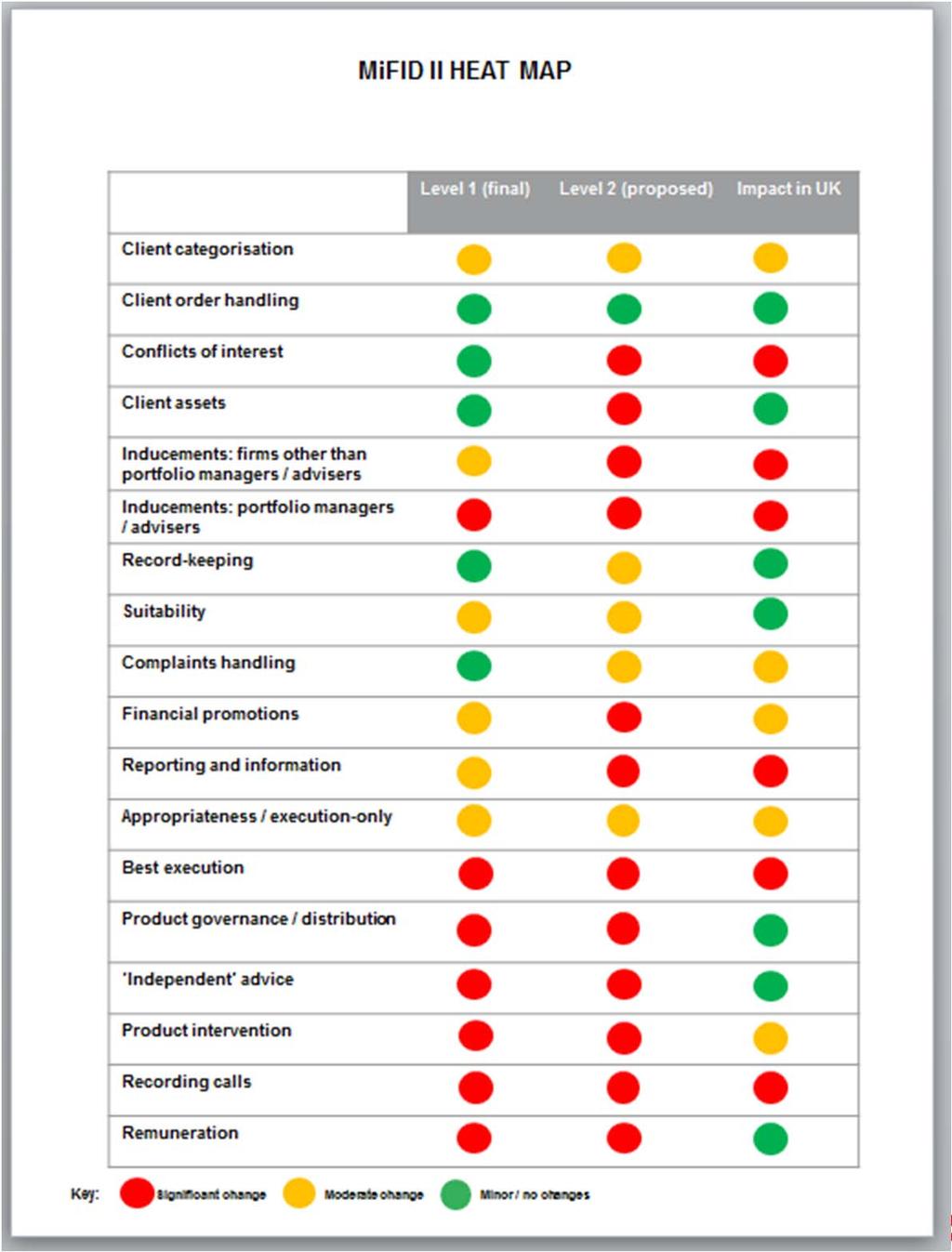

2 Retail conduct investor protection examined

3 Retail Conduct Overview of Changes Overview of changes Timing Significant number of micro changes being made to the existing investor protection regime Small number of new macro changes being introduced to the existing investor protection regime Together they SNOWBALL into significant regulatory reform in the way firms conduct their business The devil is in the detail! ESMA s proposals in their current form will significantly alter the agreed Level 1 landscape Level 1: Finalised and adopted Into force 3 Jan 2017 Level 2: Consultation period closed ESMA final response expected Jan 2015 FCA consultation expected Jan

4 Introducing the Traffic Light guide

5 5

6 6

7 7

8 8

9 Conflicts of Interest

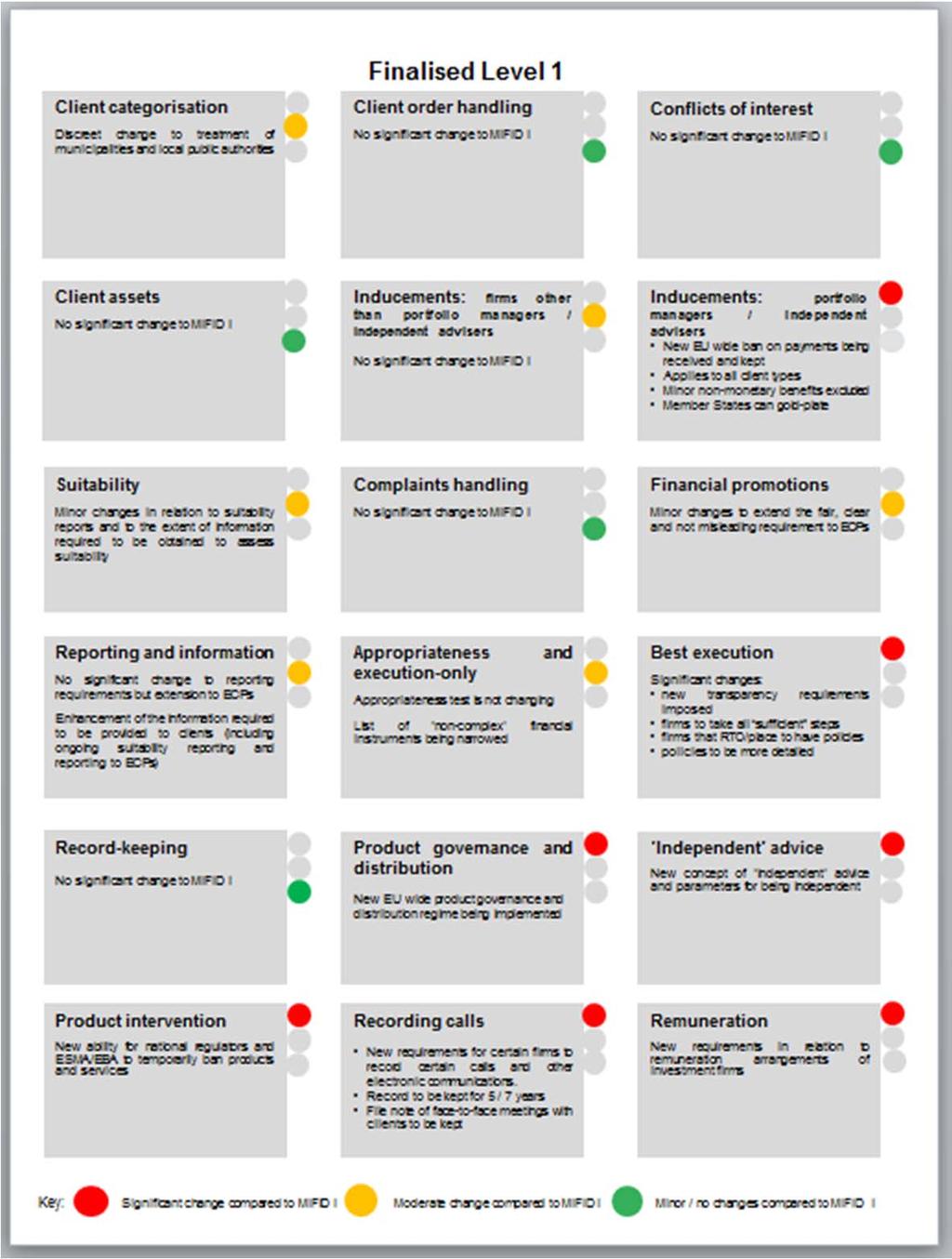

10 Conflicts of Interest - Level 1 Conflicts of Interest No significant change to MiFID I Where? Recital 56 and Articles 16(3) and 23 MiFID II What? No substantive changes Level 1 amalgamates what was originally included in Levels 1 and 2 of MiFID I but these are not new requirements Expressly states that conflicts include: receipt of inducements from third parties the firm s own remuneration and other incentive structures With MiFID II now applying to investment firms and credit institutions selling their own securities, enhanced conflicts 10

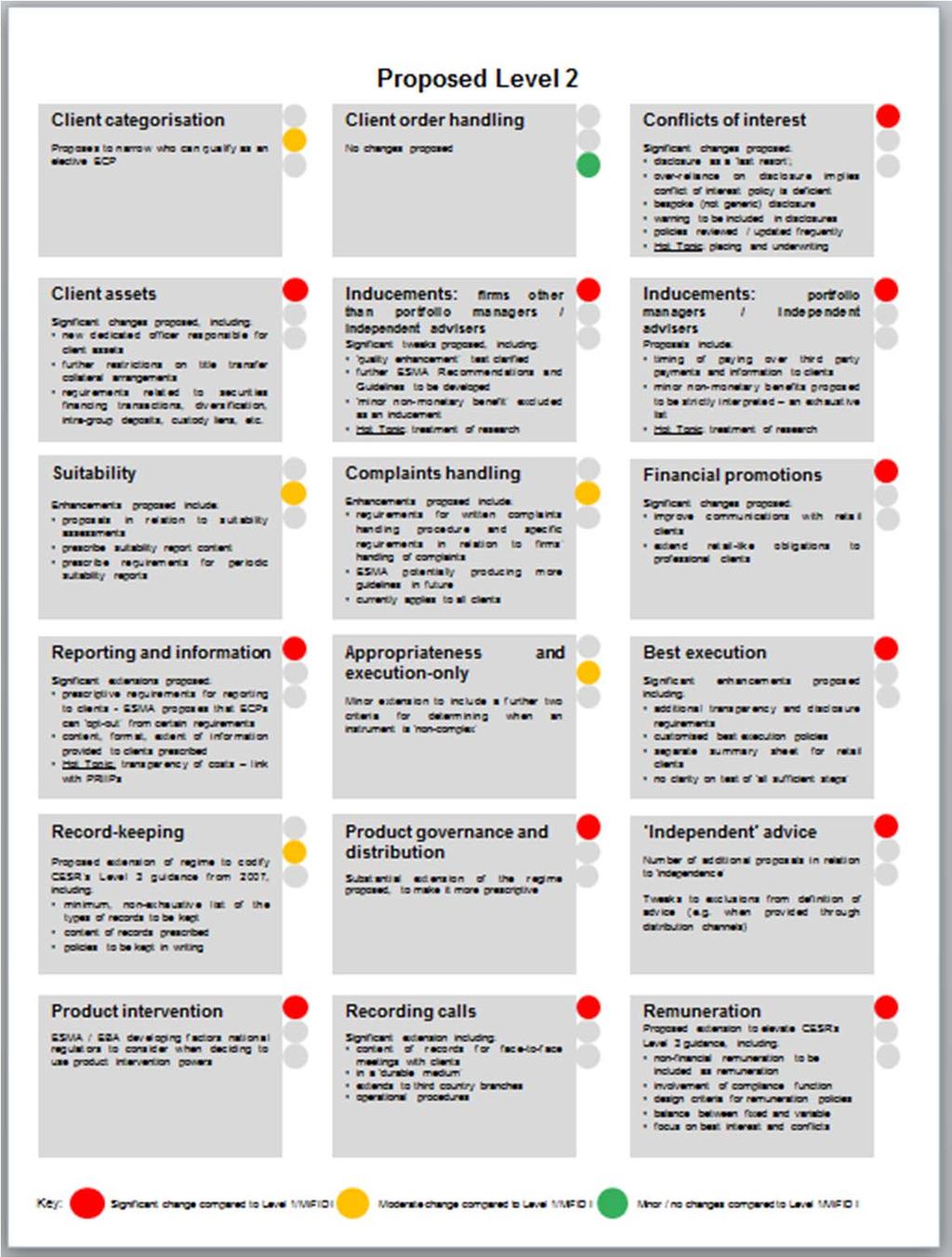

11 Conflicts of Interest - Level 2 Conflicts of Interest Significant changes proposed: disclosure as a last resort Over-reliance on disclosure implies conflict of interest policy is deficient bespoke (not generic) disclosure warnings to be included in disclosures policies reviewed / updated frequently Hot Topic: placing and underwriting Where? ESMA Consultation Paper, para 2.9 What? Increased limitations on the use of disclosure: explicit commentary that can only be made as a last resort can only be made where a firm s organisational/ administrative measures means that conflicts cannot be prevented with reasonable confidence must consider other conflict management measures New requirements for content of disclosures: not generic: must be specific and tailored New warning in disclosures Increased requirements to review/ update policies frequently (at least annually) New presumption that over-relying on disclosing conflicts/ potential conflicts must be considered to be a deficiency in the firm s conflicts of interest policy 11

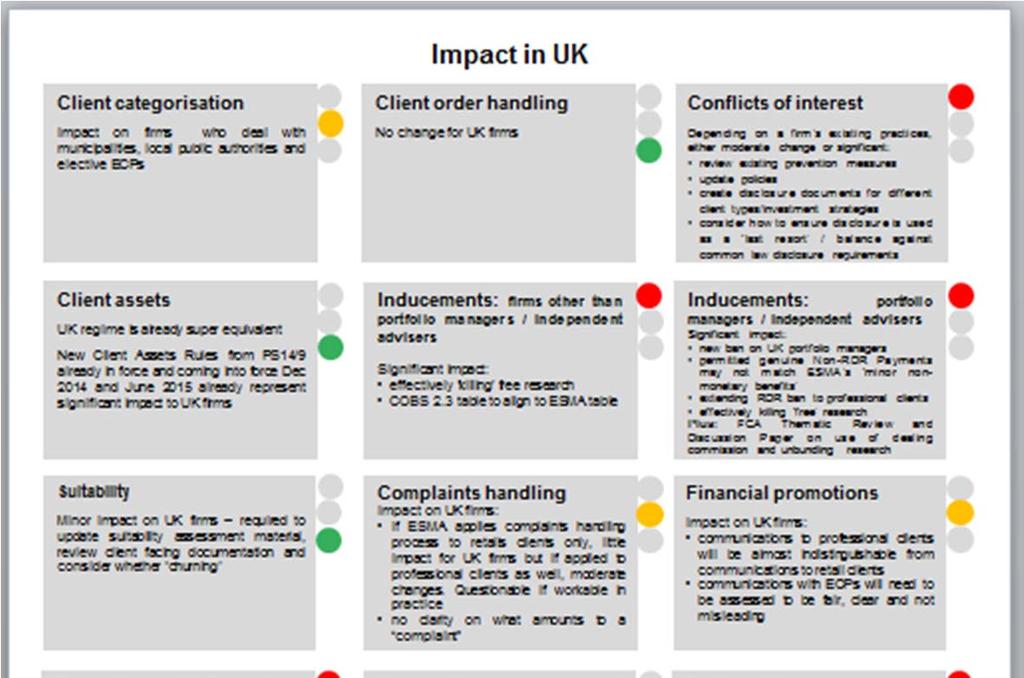

12 Conflicts of Interest Impact on firms Conflicts of Interest Depending on a firm s existing practices, either moderate or significant: review existing prevention measures update policies create disclosure documents for different client types/investment strategies consider how to ensure disclosure is used as a last resort /balance against common law disclosure requirements Depends on sector some sectors (e.g. asset managers) already well prepared Reassess conflicts that a firm faces and the steps that are taken to prevent and manage them Audit existing structural and governance arrangements Reassess financial incentive arrangements Reassess in what circumstances disclosure is made to clients and how disclosure is done Create suite of disclosure documents (separate from terms and conditions) and ensure: the disclosure includes the warning the disclosure sets out the steps taken by the firm to mitigate the conflict Maintain records as part of client file and to prove not disclosed in every case Update conflicts of interest policies Ensure compliance monitoring programme requires policies to be updated annually Probably still acceptable to disclose potential as well as actual conflicts Balance with common law requirements - if disclosing conflicts to manage them 12

13 Complaints Handling

14 Complaints Handling - Level 1 Complaints Handling No significant change to MiFID I Where? Articles 16(2) and 75 MiFID II What? No significant changes to MiFID I The same text is used in Level 1 In addition, Member States required to notify ESMA of their outof-court complaints and redress procedures implemented in that jurisdiction ESMA will keep a list on its website 14

15 Complaints Handling - Level 2 Complaints handling Enhancements proposed include: requirements for written complaints handling procedure and specific requirements in relation to firms handling of complaints ESMA potentially producing more guidelines in future currently applies to all clients Where? ESMA Consultation Paper, para 2.4 What? New process mirroring the banking/ securities sector guidelines New requirements to establish/ maintain complaints management policy New governance requirements: complaints management function to investigate complaints reporting of complaints data to NCAs (where applicable) compliance to analyse complaints data to identify/ address issues New processes: complaints to be able to be made free of charge firms to communicate in plain, intelligible language responses to complaints without any unnecessary delay firms to provide final position and explain further options Concerns: ESMA s proposals do not distinguish between client types are professional clients subject to this process? No clarity on what amounts to a complaint - any small dispute? 15

16 Complaints Handling Complaints handling Impact on UK firms; if ESMA applies complaints handling process to retail clients only, little impact for UK firms but if applied to professional clients as well, moderate change. Questionable if workable in practice no clarity on what amounts to a complaint Impact on firms Little impact on UK firms dealing with retail clients as the UK regime already had a detailed approach to complaints handling Significant impact if the regime is extended to professional clients: may need to agree what amounts to a complaint (not every day niggles) unclear whether professional clients will be subject to the same retail client processes or whether a different disputes process can be agreed with them contractually compare to the dispute resolution process implemented under EMIR permitted to contractually agree the process for professional clients; query if FCA does the same under MiFID II It seems that access to the FOS may remain for consumers only as the out-of-court disputes resolution process only needs to be for consumer complaints 16

17 Inducements: firms other than portfolio managers and independent advisers

18 Inducements - Level 1 Inducements: firms other than portfolio managers / independent advisers No significant change to MiFID I Where? Recital 74 and Article 23, 24(1) and 24(9) MiFID II What? No significant change to inducement requirements: existing MiFID I Level 1 and Level 2 provisions brought into the Level 1 text not new requirements No express reference to firms (other than independent advisers or portfolio managers) being able to receive minor non-monetary benefits Most important change is in the context of dealing with eligible counterparties; any disclosures to ECPs (including in relation to inducements) will need to be fair, clear and not misleading 18

19 Inducements - Level 2 Inducements: firms other than portfolio managers / independent advisers Significant tweaks proposed, including: quality enhancement test clarified Further ESMA Recommendations and Guidelines to be developed minor non-monetary benefit excluded as an inducement Hot Topic: treatment of research Where? ESMA Consultation Paper, para 2.15 What? Clarifications to the Quality enhancement test a non-exhaustive list to determine when the test is not met commentary on when it is met ESMA proposes to develop further Guidelines and Recommendations Questionable extension of Level 1 ESMA proposes that all firms are able to receive minor non-monetary benefits Limitations on what amounts to a minor non-monetary benefit an exhaustive list of what is a minor non-monetary benefit strictly interpreted controversial comments on research 19

20 Inducements Inducements: firms other than portfolio managers / independent advisers Significant impact : effectively killing free research COBS 2.3 table to align to ESMA table Impact on firms Reassess inducements received/ paid against quality enhancement test FCA may need to align its non-exhaustive table of reasonable non-monetary benefits (COBS 2.3) with ESMA s exhaustive list of minor non-monetary benefits Firms may need to reassess whether any reasonable non-monetary benefits are still permitted under ESMA s minor non-monetary benefits table (Where applicable) firms may need to revise and amend their terms of business and distribution agreements that include monetary/ non-monetary benefits which have previously been assessed under the existing inducements regime If adopted in its current form, firms will need to revisit how they receive and pay for research. 20

21 Research Level 2 UK regime 21 To qualify as a minor non-monetary benefit: cannot impair clients best interests must be intended for wide distribution cannot amount to a third party allocating a lot of resource to produce for a firm volume/ quality of research cannot be linked to volume of transactions placed by firm through research entity content cannot be tailored distribution cannot be restricted to firm buying other services Firms can pay for research at a reasonable price (i.e. market value) ESMA has received substantial push-back so this may not go ahead COBS 2.3 and COBS 11.6 (use of dealing commission). Prohibition unless: does not impair clients best interests reasonable grounds that reasonably assist in provision of services directly relates to execution of orders amounts to substantive research evidential provisions included ESMA s proposals consistent with the FCA s recent direction of travel: PS 14/7 on Changes to the Use of Dealing Commission Rules into force 2 June 2014 DP 14/3 Discussion on the use of dealing commission regime closed 10 October 2014 supervisory findings comply now! unbundling research from commission? Feedback on DP to coincide with ESMA final position (Jan 2015) Depending on MiFID II outcome, FCA to indicate

22 The FCA believes, in line with the results of our thematic work, that a more effective market for research and more efficient asset management sector will develop if dealing commission is not used to fund these goods and services. Therefore, the FCA has been supportive of ESMA s proposals. Source: FCA MiFID II conference, 18 September 2014, David Lawton, Director of Markets, FCA 22

23 The unbundling of dealing commissions could have a more significant impact than the Retail Distribution Review on asset managers, with smaller groups and fund ranges particularly at risk, analysts have warned. Source: Investmentweek.co.uk, 13 October

24 Inducements: portfolio managers and independent advisers

25 Inducements - Level 1 Inducements : portfolio managers / independent advisers New EU wide ban on payments being received and kept Applies to all client types Minor non-monetary benefits excluded Member States can gold plate Where? Recital and Articles 24(7) and (8) MiFID II What? Significant changes NEW BAN! firms cannot receive and retain payments from third parties applies to all independent advice or portfolio management services (not non-independent advice) relates to advice/ management with retail and professional clients payments must be passed onto clients in full clients must be informed how the transfer mechanisms work firms are unable to set off any payments from fees owed to them payments paid by client or on behalf of client only permitted where the client is aware of the payment and agrees the amount/ frequency New requirement for a policy to ensure commissions are allocated and transferred to clients New exclusion from ban for minor non-monetary benefits (provided comply with clients best interest rule) Ability for Member States to gold-plate 25

26 Inducements - Level 2 Inducements: portfolio managers / independent advisers Proposals include: timing of paying over third party payments and information to clients minor non-monetary benefits proposed to be strictly interpreted an exhaustive list Hot Topic: treatment of research Where? ESMA Consultation Paper, para 2.15 What? Clarification on mechanics of paying over payments: no specific time period from receipt prescribed test is as soon as reasonably possible after receipt transfer to the client money account Requirement that any payments received and passed over be regularly reported to clients Clarification on boundaries of minor non-monetary benefits (see earlier slide) Commentary on research (see earlier slide) 26

27 Inducements Impact on firms Inducements: portfolio managers / independent advisers Significant impact: new ban on UK portfolio managers permitted genuine Non-RDR Payments may not match ESMA s minor non-monetary benefits extending RDR ban to professional clients effectively killing free research Plus: FCA Thematic Review and Discussion Paper on use of dealing commission and unbundling research Mixed impact due to UK having already gold-plated MiFID I with RDR Independent advisory firms minor impact extension to professional clients but advice is not the same for professional clients discrete query on whether RDR facilitation will be impacted will need to extend RDR to structured deposits Restricted advisory firms no impact as UK RDR goes further Portfolio managers impact! UK RDR relates to payments made by discretionary managers, not payments they receive will apply to all clients of portfolio managers, not just retail clients Platform service providers no impact as UK RDR 2 goes further Product providers no impact when distributing within UK as UK RDR goes further but impact when distributing outside the UK As for other types of firms, will need to reassess minor non-monetary benefits and revisit how they receive and pay for research. 27

28 Inducements: Level 2 v UK RDR / RDR 2 Key UK measures are less than MiFID II UK regime will need to change UK measures go substantially beyond MiFID II UK will gold plate UK measures are more or less aligned with MiFID II Independent Advisory Firm Retail clients Professional clients ECPs Restricted (UK) / non-independent (EU) advisory firm Portfolio manager / discretionary investment manager Platform service provider Non-advisory firm (execution only broker) Product manufacturer 28

29 Inducements: Level 2 v UK RDR / RDR 2 MiFID II requirement New UK COBS requirement Commentary Independent advisers prohibited from accepting and retaining remuneration from third parties in relation to provision of the service to clients (Art 24(7)(b)) N/A N/A Portfolio managers prohibited from accepting and retaining remuneration from third parties in relation to provision of the service to clients (Art 4(8)) Minor non-monetary benefits excluded from ban (provided satisfy inducements rules) (Arts. 24(7)(b), 24(8)) Independent advisers prohibited from accepting any remuneration *from third parties in connection with advice to UK retail clients on retail investment products Restricted advisers prohibited from accepting any remuneration* from third parties in connection with advice to UK retail clients on retail investment products Product providers prohibited from paying advisers any remuneration *(other than for Genuine Non-RDR Services) and only permitted to pay platform services in very limited circumstances Portfolio managers currently prohibited from paying referral payments to advisers for clients referred to them. But no prohibition on receiving remuneration* portfolio managers owe fiduciary obligations to their clients in any event. Restrictions on using dealing commission (COBS 11.6) Nothing is excluded. However, firms can receive remuneration* for Genuine Non-RDR Services (i.e. where the service is unrelated to the advice to the UK retail client) UK unlikely to implement MiFID II change as represents a watering down of current requirements. UK will gold-plate MiFID II. Need to extend to professional clients UK unlikely to implement MiFID II change as represents a watering down of current requirements. UK will gold-plate MiFID II. Query how deal with professional clients UK unlikely to implement MiFID II change as represents a watering down of current requirements. UK will gold-plate MiFID II UK likely to implement MiFID II change as widens the regulatory net. Already made comments on this. Query how this will impact on dealing commission rules. Query how deal with professional clients UK unlikely to implement MiFID II change as represents a watering down of their current requirements. Likely to notify EU that they are gold-plating Relates to services in connection with financial instruments which now include structured deposits Disclose how transfer mechanics for passing the remuneration on to clients Firms not allowed to offset any third party payments from the fees due by the client to the firm (Recital 74) ** and (existing MiFID I requirement) excluded from inducements is remuneration paid by the client or a person on behalf of the client (Art 24(9)) ** nothing in the Articles themselves on this point Definition of retail investment products does not currently include structured deposits Advisers: Disclose adviser charging model and other fees and how facilitation works. Portfolio managers: Disclose fees and charges Facilitation of adviser charge from product providers / platform service providers to UK independent and restricted advisers UK likely to amend definition of retail investment product to include structured deposits within scope of regime UK unlikely to implement requirement as not applicable for retail clients. May be implemented for professional clients depending on how they deal with them UK likely to maintain facilitation ability under inducement carve-out provided product providers/platforms act as the agent of the client when facilitating the payment of their fee to the firm and client agrees to facilitation. UK likely to extend facilitation to portfolio managers once introduced new rules 29 * remuneration means fees / commissions / monetary / non-monetary benefits

30 Best execution

31 Best Execution - Level 1 Best execution Significant changes: new transparency requirements imposed firms to take all sufficient steps firms that RTO/ place to have policies policies to be more detailed Where? Recital 97 and Article 27 MiFID II What? Significant new requirements: firms and trading venues to publicise data about executed transactions firms must summarise and publish annually their top five execution venues by trading volume for each class of financial instrument and information on the quality of execution obtained trading venues and systematic internalisers must also annually publish information on quality of execution for certain types of financial instruments Significant strengthening of current requirements: firms to take all sufficient steps to obtain best execution notify clients of material changes to a firm s policy in ongoing relationship demonstrate best execution to national regulators order execution policies to be clear, easily comprehensible and sufficiently detailed 31

32 Best Execution - Level 2 Best execution Significant enhancements proposed including: additional transparency and disclosure requirements customised best execution policies separate summary sheet for retail clients no clarity on test of all sufficient steps Where? What? ESMA Consultation Paper, para 2.21 ESMA Discussion Paper, paras 2.3 and 2.4 Additional obligations on pre and post trade transparency requirements New data requirements on trading and execution venues New order flow and execution quality reporting requirements Additional requirements and clarifications to increase transparency of firm s policies and procedures: customised, as opposed to generic, order execution policies all venues/ entities used for execution to be listed in policies for retail clients, separate sheet summarising the best execution policy additional disclosure obligations in policies Clarity on a material change which triggers a review of the policy Clarity on satisfying best execution when using a single venue or entity No additional clarity on how all sufficient steps compares to all reasonable steps 32

33 Best Execution Impact on firms Best execution Significant impact: additional transparency requirements and data / reporting requirements customised best execution policies separate summary for retail clients additional disclosure, recordkeeping no clarity on test of all sufficient steps Plus: FCA Thematic Review on Best execution (July 2014) Reassess whether the steps a firm takes matches up to all sufficient steps to achieve best execution and how to prove this Tailor order execution policies and list all possible execution venues in policies Create separate summary disclosure documents for retail clients Set up procedures to inform customers of execution venue immediately after execution and review best execution arrangements to ensure business practices are fit for purpose, supported by appropriate second line defence controls Ensure compliance monitoring programme has material change triggers to review policy Plus FCA TR14/13: Best execution and payment for order flow (July 2014) understand which activities covered by best execution obligation reinforce monitoring capability to identify best execution failures/ poor client outcomes be clear on who has responsibility and accountability for best execution additional evidential requirements when firms use own internalisers or connected parties consider any PFOF arrangements 33

![com 31/8/14 [MiFID II] will also present an implementation challenge for firms.](/docs-images/77/74735655/images/34-1.jpg "Firms need to ensure now that they have fully embedded our existing regulatory requirements in preparation for the")

34 UK asset management industry may be leaving as much as 4.2bn of client returns on the table by failing to monitor how effectively its brokers are managing trades. Source: FT.com 31/8/14 [MiFID II] will also present an implementation challenge for firms. Firms need to ensure now that they have fully embedded our existing regulatory requirements in preparation for the implementation of MiFID II to ensure they can continue to act in their clients best interests. Source: FCA, TR14/13, p8. 34

35 Recording of calls

36 Recording of calls - Level 1 Recording calls New requirements for certain firms to record certain calls and other electronic communications Record to be kept for 5 / 7 years File note of face-to-face meetings with clients to be kept Where? Article 16 MiFID II What? Significant changes: existing MiFID I Level 3 option to record telephone conversations and electronic communications brought into the Level 1 text now mandatory extends to recording face-to-face conversations with clients Includes conversations/ communications about transactions that were not executed New record-keeping requirements - records to be kept for minimum of 7 years (5 years for client requests; 7 years for requests of national regulators) 36

37 Recording of calls - Level 2 Recording calls Significant extension including: content of records for face-to-face meetings with clients in a durable medium extends to third country branches operational procedures Where? ESMA Consultation Paper, para 2.6 What? New Policy recording of telephone conversations and electronic communications policy and effective procedures to ensure recordings kept technology neutral Governance obligations senior management oversight educate and train employees Record-keeping obligations list of personnel approved to have devices from time record created Face to face conversations: prescribe content of written minutes/ attendance note Storage durable medium allow unaltered/ deleted reproduction of record accessible and readily available 37

38 Recording of calls Recording calls Significant impact: not only calls and e-communications recorded, but face-to-face meetings by a file note keep for 5 7 years (not 6 months) in durable medium Impact on firms Implement policies and procedures (if not already) Extend record-keeping duration to 7 years (currently 6 months in UK) Ensure meetings with clients that relate to executing transactions are recorded Introduce a new template attendance note for meetings Review storage capabilities to ensure will allow unaltered reproduction 7 years later Keep in a durable medium physical tapes? back-up CDs? 38

39

40 Disclaimer Norton Rose Fulbright LLP, Norton Rose Fulbright Australia, Norton Rose Fulbright Canada LLP, Norton Rose Fulbright South Africa (incorporated as Deneys Reitz Inc) and Fulbright & Jaworski LLP, each of which is a separate legal entity, are members ( the Norton Rose Fulbright members ) of Norton Rose Fulbright Verein, a Swiss Verein. Norton Rose Fulbright Verein helps coordinate the activities of the Norton Rose Fulbright members but does not itself provide legal services to clients. References to Norton Rose Fulbright, the law firm, and legal practice are to one or more of the Norton Rose Fulbright members or to one of their respective affiliates (together Norton Rose Fulbright entity/entities ). No individual who is a member, partner, shareholder, director, employee or consultant of, in or to any Norton Rose Fulbright entity (whether or not such individual is described as a partner ) accepts or assumes responsibility, or has any liability, to any person in respect of this communication. Any reference to a partner or director is to a member, employee or consultant with equivalent standing and qualifications of the relevant Norton Rose Fulbright entity. The purpose of this communication is to provide information as to developments in the law. It does not contain a full analysis of the law nor does it constitute an opinion of any Norton Rose Fulbright entity on the points of law discussed. You must take specific legal advice on any particular matter which concerns you. If you require any advice or further information, please speak to your usual contact at Norton Rose Fulbright. 40

MiFID II / MiFIR: spotlight on implementing measures. Jonathan Herbst, Hannah Meakin and Charlotte Henry Norton Rose Fulbright LLP 3 September 2014

MiFID II / MiFIR: spotlight on implementing measures Jonathan Herbst, Hannah Meakin and Charlotte Henry Norton Rose Fulbright LLP 3 September 2014 Introduction Today s programme on MiFID II / MiFIR Introduction

MiFID II / MiFIR: spotlight on implementing measures Jonathan Herbst, Hannah Meakin and Charlotte Henry Norton Rose Fulbright LLP 3 September 2014 Introduction Today s programme on MiFID II / MiFIR Introduction

MiFID II / MiFIR seminar Break-out session 1 The Institutional Landscape

MiFID II / MiFIR seminar Break-out session 1 The Institutional Landscape Hannah Meakin, Partner Kennedy Masterton-Smith, Senior Associate Norton Rose Fulbright LLP 15 October 2014 Overview Do I need to

MiFID II / MiFIR seminar Break-out session 1 The Institutional Landscape Hannah Meakin, Partner Kennedy Masterton-Smith, Senior Associate Norton Rose Fulbright LLP 15 October 2014 Overview Do I need to

Impact of MiFID II on EU conduct of business regimes. United Kingdom

Impact of MiFID II on EU conduct of business regimes United Kingdom May 2016 DISCLAIMER: The purpose of this document is to provide information as to developments in the law. It does not contain a full

Impact of MiFID II on EU conduct of business regimes United Kingdom May 2016 DISCLAIMER: The purpose of this document is to provide information as to developments in the law. It does not contain a full

MiFID II Academy: Information and reporting to clients. Floortje Nagelkerke 23 February 2016

MiFID II Academy: Information and reporting to clients Floortje Nagelkerke 23 February 2016 Timing: MiFID II / MiFIR 2 July MiFID II and MiFIR entered into force 19 December Level 2 Consultation on technical

MiFID II Academy: Information and reporting to clients Floortje Nagelkerke 23 February 2016 Timing: MiFID II / MiFIR 2 July MiFID II and MiFIR entered into force 19 December Level 2 Consultation on technical

Complying With MiFID 2: Best Execution

VOLUME 0, NUMBER 0 >>> MARCH 2016 Reproduced with permission from World Securities Law Report, 22 WSLR 03. Copyright 2016 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com Complying

VOLUME 0, NUMBER 0 >>> MARCH 2016 Reproduced with permission from World Securities Law Report, 22 WSLR 03. Copyright 2016 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com Complying

The new agenda conflicts and inducements. Imogen Garner, Partner Charlotte Henry, Senior Associate Norton Rose Fulbright LLP 6 July 2016

The new agenda conflicts and inducements Imogen Garner, Partner Charlotte Henry, Senior Associate Norton Rose Fulbright LLP 6 July 2016 Today s 40 minute briefing: Agenda The key FCA rules re-examined

The new agenda conflicts and inducements Imogen Garner, Partner Charlotte Henry, Senior Associate Norton Rose Fulbright LLP 6 July 2016 Today s 40 minute briefing: Agenda The key FCA rules re-examined

MiFID2 for asset managers headlines and roadmaps

MiFID2 for asset managers headlines and roadmaps Nick Colston Darren Fox Wednesday 05 & Thursday 06 October 2016 Introduction what we ll cover today 1. Re-cap and recent developments 2. L2 Directive: finalised

MiFID2 for asset managers headlines and roadmaps Nick Colston Darren Fox Wednesday 05 & Thursday 06 October 2016 Introduction what we ll cover today 1. Re-cap and recent developments 2. L2 Directive: finalised

40 Minute Briefing European and domestic reform: The day after tomorrow EMIR, CASS & MiFID

FINANCIAL INSTITUTIONS ENERGY INFRASTRUCTURE, MINING AND COMMODITIES TRANSPORT TECHNOLOGY AND INNOVATION PHARMACEUTICALS AND LIFE SCIENCES 40 Minute Briefing European and domestic reform: The day after

FINANCIAL INSTITUTIONS ENERGY INFRASTRUCTURE, MINING AND COMMODITIES TRANSPORT TECHNOLOGY AND INNOVATION PHARMACEUTICALS AND LIFE SCIENCES 40 Minute Briefing European and domestic reform: The day after

Hot topic. FCA confirms final MiFID II rules. Stand out for the right reasons Financial Services Risk and Regulation

www.pwc.co.uk/fsrr 24 July 2017 Stand out for the right reasons Financial Services Risk and Regulation Hot topic FCA confirms final MiFID II rules Highlights The FCA issued final rules on MiFID II implementation

www.pwc.co.uk/fsrr 24 July 2017 Stand out for the right reasons Financial Services Risk and Regulation Hot topic FCA confirms final MiFID II rules Highlights The FCA issued final rules on MiFID II implementation

Managers will be prohibited from receiving any third-party inducements 1, unless an exception applies.

1. Inducements and research Managers will be prohibited from receiving any third-party inducements 1, unless an exception applies. There is an exception for minor nonmonetary benefits that both are capable

1. Inducements and research Managers will be prohibited from receiving any third-party inducements 1, unless an exception applies. There is an exception for minor nonmonetary benefits that both are capable

MiFID II: extended briefing on different angles on investor protection. Norton Rose Fulbright LLP 5 April 2017

MiFID II: extended briefing on different angles on investor protection Norton Rose Fulbright LLP 5 April 2017 Content: 1. General topics 2. Buy-side topics 3. Sell-side topics 4. Retail topics 2 Programme

MiFID II: extended briefing on different angles on investor protection Norton Rose Fulbright LLP 5 April 2017 Content: 1. General topics 2. Buy-side topics 3. Sell-side topics 4. Retail topics 2 Programme

Countdown to MiFID II: Final rules for trading venues, participants and investment firms

Countdown to MiFID II: Final rules for trading venues, participants and investment firms On 31 March 2017, the Financial Conduct Authority (FCA) published its first policy statement (PS 17/5) on the implementation

Countdown to MiFID II: Final rules for trading venues, participants and investment firms On 31 March 2017, the Financial Conduct Authority (FCA) published its first policy statement (PS 17/5) on the implementation

MIFID II Conduct Of Business Rules

MIFID II Conduct Of Business Rules MIFID II Conduct Of Business Rules This is the second part in a series of Legal Longs on the MiFID II Directive [2014/65/EU] and the Markets in Financial Instruments

MIFID II Conduct Of Business Rules MIFID II Conduct Of Business Rules This is the second part in a series of Legal Longs on the MiFID II Directive [2014/65/EU] and the Markets in Financial Instruments

MiFID II Academy: proprietary trading and trading venues. Floortje Nagelkerke 7 December 2017

MiFID II Academy: proprietary trading and trading venues Floortje Nagelkerke 7 December 2017 The countdown to MiFID II / MiFIR implementation as of 8:30am this morning 27 DAYS 15 Hours 30 Minutes But if

MiFID II Academy: proprietary trading and trading venues Floortje Nagelkerke 7 December 2017 The countdown to MiFID II / MiFIR implementation as of 8:30am this morning 27 DAYS 15 Hours 30 Minutes But if

MiFID II Update: Are we nearly

MiFID II Update: Are we nearly there yet? TISA Thursday, 6 November 2014 Charlotte Hill Partner Covington & Burling LLP 841550.1 Overview Current status The ESMA DP and CP Key points 28 1 MiFID II Directive

MiFID II Update: Are we nearly there yet? TISA Thursday, 6 November 2014 Charlotte Hill Partner Covington & Burling LLP 841550.1 Overview Current status The ESMA DP and CP Key points 28 1 MiFID II Directive

Financial Regulatory Alert

Financial Regulatory Alert August 10, 2017 UK Implementation of MiFID II (for and Other Managers) The release by the UK Financial Conduct Authority (FCA) on 3 July 2017 of its final rules on the implementation

Financial Regulatory Alert August 10, 2017 UK Implementation of MiFID II (for and Other Managers) The release by the UK Financial Conduct Authority (FCA) on 3 July 2017 of its final rules on the implementation

MiFID2 Extraterritorial Impact on FIs and AMIFs. Charlotte Stalin Jason Valoti

MiFID2 Extraterritorial Impact on FIs and AMIFs Charlotte Stalin Jason Valoti 15 March 2017 TIMING: EU LEGISLATIVE PROCESS LEVEL 1 LEVEL 2 LEVEL 3 LEVEL 4 The European Parliament and European Council prepare

MiFID2 Extraterritorial Impact on FIs and AMIFs Charlotte Stalin Jason Valoti 15 March 2017 TIMING: EU LEGISLATIVE PROCESS LEVEL 1 LEVEL 2 LEVEL 3 LEVEL 4 The European Parliament and European Council prepare

ISDA commentary on Presidency MiFID2/MiFIR compromise texts as published on

1 11 September 2012 ISDA commentary on Presidency MiFID2/MiFIR compromise texts as published on 31.08.2012 1 This paper has been produced by the International Swaps and Derivatives Association (ISDA) in

1 11 September 2012 ISDA commentary on Presidency MiFID2/MiFIR compromise texts as published on 31.08.2012 1 This paper has been produced by the International Swaps and Derivatives Association (ISDA) in

Managers will be prohibited from receiving any third-party inducements 1, unless an exception applies.

1. Inducements and Research Managers will be prohibited from receiving any third-party inducements 1, unless an exception applies. There is an exception for minor nonmonetary benefits that both are capable

1. Inducements and Research Managers will be prohibited from receiving any third-party inducements 1, unless an exception applies. There is an exception for minor nonmonetary benefits that both are capable

Order Execution Policy

(ATFX) Order Execution Policy ORDER EXECUTION POLICY Introduction In accordance with the rules of the Financial Conduct Authority (the FCA ) and the requirements of the Markets in Financial Instruments

(ATFX) Order Execution Policy ORDER EXECUTION POLICY Introduction In accordance with the rules of the Financial Conduct Authority (the FCA ) and the requirements of the Markets in Financial Instruments

Brave New World: MiFID2 and MiFIR The changes facing the Financial Markets

Brave New World: MiFID2 and MiFIR The changes facing the Financial Markets Charlotte Stalin February 2016 MiFID what? MiFID (Markets in Financial Instruments Directive) Sets out rules on what investment

Brave New World: MiFID2 and MiFIR The changes facing the Financial Markets Charlotte Stalin February 2016 MiFID what? MiFID (Markets in Financial Instruments Directive) Sets out rules on what investment

Insurance Distribution Directive implementation Feedback to CP17/23 and near-final rules

Insurance Distribution Directive implementation Feedback to CP17/23 and near-final rules Policy Statement PS17/27 December 2017 PS17/27 Financial Conduct Authority Insurance Distribution Directive implementation

Insurance Distribution Directive implementation Feedback to CP17/23 and near-final rules Policy Statement PS17/27 December 2017 PS17/27 Financial Conduct Authority Insurance Distribution Directive implementation

MiFID II and Third Countries: How Far Does the Legislation Reach?

MiFID II and Third Countries: How Far Does the Legislation Reach? MiFID II, the EU s revised Markets in Financial Instruments Directive and new Markets in Financial Instruments Regulation (MiFIR), comes

MiFID II and Third Countries: How Far Does the Legislation Reach? MiFID II, the EU s revised Markets in Financial Instruments Directive and new Markets in Financial Instruments Regulation (MiFIR), comes

RE: Developing our approach to implementing MiFID II conduct of business and organisational requirements

Tom Ward Strategy and Competition Division Financial Conduct Authority 25 The North Colonnade London E14 5HS Email to: dp15-03@fca.org.uk Date: 26 May 2015 Dear Sir RE: Developing our approach to implementing

Tom Ward Strategy and Competition Division Financial Conduct Authority 25 The North Colonnade London E14 5HS Email to: dp15-03@fca.org.uk Date: 26 May 2015 Dear Sir RE: Developing our approach to implementing

16523/12 OM/mf 1 DGG 1

COUNCIL OF THE EUROPEAN UNION Brussels, 13 December 2012 Interinstitutional File: 2011/0296 (COD) 2011/0298 (COD) 16523/12 EF 270 ECOFIN 970 CODEC 2743 "I" ITEM NOTE from: to: Subject: Presidency Coreper

COUNCIL OF THE EUROPEAN UNION Brussels, 13 December 2012 Interinstitutional File: 2011/0296 (COD) 2011/0298 (COD) 16523/12 EF 270 ECOFIN 970 CODEC 2743 "I" ITEM NOTE from: to: Subject: Presidency Coreper

MiFID II Academy: Information and reporting to clients. Floortje Nagelkerke 21 November 2017

MiFID II Academy: Information and reporting to clients Floortje Nagelkerke 21 November 2017 The countdown to MiFID II / MiFIR implementation as of 8:30am this morning 42 DAYS 15 Hours 30 Minutes But if

MiFID II Academy: Information and reporting to clients Floortje Nagelkerke 21 November 2017 The countdown to MiFID II / MiFIR implementation as of 8:30am this morning 42 DAYS 15 Hours 30 Minutes But if

Ivory Coast: Amendments to the mining code

Financial institutions Energy Infrastructure, mining and commodities Transport Technology and innovation Life sciences and healthcare Ivory Coast: Amendments to the mining code Briefing August 2014 Introduction

Financial institutions Energy Infrastructure, mining and commodities Transport Technology and innovation Life sciences and healthcare Ivory Coast: Amendments to the mining code Briefing August 2014 Introduction

MiFID 2 COSTS AND CHARGES

MiFID 2 COSTS AND CHARGES Implementation Guide Information on costs and charges are a major aspect of MiFID 2, first because the provisions of MiFID 2, and the measures of Level 2 in particular, constitute

MiFID 2 COSTS AND CHARGES Implementation Guide Information on costs and charges are a major aspect of MiFID 2, first because the provisions of MiFID 2, and the measures of Level 2 in particular, constitute

FREQUENTLY ASKED QUESTIONS

NOV 2017 MARKETS IN FINANCIAL INSTRUMENTS DIRECTIVE II (MIFID II) FREQUENTLY ASKED QUESTIONS Table of Contents Background...4 What is MiFID?... 4 The general objectives of MiFID II are to:... 4 How was

NOV 2017 MARKETS IN FINANCIAL INSTRUMENTS DIRECTIVE II (MIFID II) FREQUENTLY ASKED QUESTIONS Table of Contents Background...4 What is MiFID?... 4 The general objectives of MiFID II are to:... 4 How was

Order Execution Policy Disclosure

Order Execution Policy Disclosure AETOS Capital Group (UK) Limited Dec 31, 2017 V20171231 Order Execution Policy 1. Purpose of Policy Under the Markets in Financial Instruments Directive (MiFID II), we

Order Execution Policy Disclosure AETOS Capital Group (UK) Limited Dec 31, 2017 V20171231 Order Execution Policy 1. Purpose of Policy Under the Markets in Financial Instruments Directive (MiFID II), we

40 Minute Briefing MiFID II: are we there yet?

40 Minute Briefing MiFID II: are we there yet? Jonathan Herbst - Partner Peter Snowdon - Partner Hannah Meakin - Partner Financial Services 6 November 2013 Our agenda for this morning s briefing 1. Big

40 Minute Briefing MiFID II: are we there yet? Jonathan Herbst - Partner Peter Snowdon - Partner Hannah Meakin - Partner Financial Services 6 November 2013 Our agenda for this morning s briefing 1. Big

The impact of MiFID II/MiFIR on Secondary Markets David Lawton Managing Director Alvarez & Marsal

The impact of MiFID II/MiFIR on Secondary Markets David Lawton Managing Director Alvarez & Marsal MiFID II MiFIR: Necessary adjustments in the new environment HCMC conference Athens : 23 October 2017 MIFID

The impact of MiFID II/MiFIR on Secondary Markets David Lawton Managing Director Alvarez & Marsal MiFID II MiFIR: Necessary adjustments in the new environment HCMC conference Athens : 23 October 2017 MIFID

Inducements Procedure

Inducements Procedure EWUB S.A. Inducements Procedure 2 Contents GENERAL PRINCIPLES... 3 REGULATORY BACKGROUND... 3 ESMA guidance... 8 Automated inducement process description... 11 Standard reporting:

Inducements Procedure EWUB S.A. Inducements Procedure 2 Contents GENERAL PRINCIPLES... 3 REGULATORY BACKGROUND... 3 ESMA guidance... 8 Automated inducement process description... 11 Standard reporting:

Senior arrangements, Systems and Controls. Chapter 10. Conflicts of interest

Senior arrangements, Systems and Controls Chapter Conflicts of interest Section.1 : Application.1 Application.1.-2 Application to a common platform firm For a common platform firm: (1) the MiFID Org egulation

Senior arrangements, Systems and Controls Chapter Conflicts of interest Section.1 : Application.1 Application.1.-2 Application to a common platform firm For a common platform firm: (1) the MiFID Org egulation

Contents. Finalised guidance. Assessing suitability: Replacement business and centralised investment propositions. Financial Services Authority

Financial Services Authority Finalised guidance Assessing suitability: Replacement business and centralised investment propositions July 2012 Contents 1 Executive summary 2 2 Overview 4 3 Replacement business

Financial Services Authority Finalised guidance Assessing suitability: Replacement business and centralised investment propositions July 2012 Contents 1 Executive summary 2 2 Overview 4 3 Replacement business

The King & Spalding Guide to MiFID II Conduct of Business Requirements

Financial Services Regulation Practice Group 29 September 2017 The King & Spalding Guide to MiFID II Conduct of Business Requirements MiFID II, which is a package of measures consisting of a revised Directive

Financial Services Regulation Practice Group 29 September 2017 The King & Spalding Guide to MiFID II Conduct of Business Requirements MiFID II, which is a package of measures consisting of a revised Directive

Platts Kingsman EU Sugar Seminar MiFID II & MAR: what does increased international regulatory scrutiny mean for sugar?

Platts Kingsman EU Sugar Seminar MiFID II & MAR: what does increased international regulatory scrutiny mean for sugar? Norton Rose Fulbright LLP Geneva, 11 April 2016 Contents 1. Political context 2. New

Platts Kingsman EU Sugar Seminar MiFID II & MAR: what does increased international regulatory scrutiny mean for sugar? Norton Rose Fulbright LLP Geneva, 11 April 2016 Contents 1. Political context 2. New

Review of the Markets in Financial Instruments Directive

FEDERATION OF EUROPEAN SECURITIES EXCHANGES 13 th JANUARY 2011 The questionnaire takes as its starting point the Commission's proposals for MiFID/MiFIR 2 of 20 October 2011 (COM(2011)0652 and COM(2011)0656).

FEDERATION OF EUROPEAN SECURITIES EXCHANGES 13 th JANUARY 2011 The questionnaire takes as its starting point the Commission's proposals for MiFID/MiFIR 2 of 20 October 2011 (COM(2011)0652 and COM(2011)0656).

MARKET ABUSE REGULATION

MARKET ABUSE REGULATION ENSURING COMPLIANCE AMIDST UNCERTAINTY Adrian West and Jane Bondoux of Travers Smith LLP consider how the Market Abuse Regulation will affect compliance procedures for UK listed

MARKET ABUSE REGULATION ENSURING COMPLIANCE AMIDST UNCERTAINTY Adrian West and Jane Bondoux of Travers Smith LLP consider how the Market Abuse Regulation will affect compliance procedures for UK listed

State Street Corporation

Review of the Markets in Financial Instruments Directive Questionnaire on MiFID/MiFIR 2 by Markus Ferber MEP The questionnaire takes as its starting point the Commission's proposals for MiFID/MiFIR 2 of

Review of the Markets in Financial Instruments Directive Questionnaire on MiFID/MiFIR 2 by Markus Ferber MEP The questionnaire takes as its starting point the Commission's proposals for MiFID/MiFIR 2 of

Best Execution Policy Customer Distribution

Best Execution Policy Customer Distribution ICBC Treasury Department This document is the property of ICBC London Plc and may not be copied, used or disclosed in whole or in part, stored in a retrieval

Best Execution Policy Customer Distribution ICBC Treasury Department This document is the property of ICBC London Plc and may not be copied, used or disclosed in whole or in part, stored in a retrieval

MiFID II. user guides

MiFID II user guides Contents Transaction reporting Inducements and investment research RDR equivalent Appropriateness Suitability Best execution Conflicts of interest Client assets and client money Product

MiFID II user guides Contents Transaction reporting Inducements and investment research RDR equivalent Appropriateness Suitability Best execution Conflicts of interest Client assets and client money Product

Best Execution Policy. Crossbridge Capital LLP

Best Execution Policy Crossbridge Capital LLP Contents 1 Introduction... 3 1.1 The Best Execution obligation... 3 1.2 Application of FCA and EU regulations... 3 1.3 Direct and indirect execution... 4 1.4

Best Execution Policy Crossbridge Capital LLP Contents 1 Introduction... 3 1.1 The Best Execution obligation... 3 1.2 Application of FCA and EU regulations... 3 1.3 Direct and indirect execution... 4 1.4

Update on the new trading environment

Update on the new trading environment Jonathan Herbst Partner, Global Head of Financial Services Hannah Meakin Partner Tara Mokijewski Of Counsel 9 November 2015 Working with ambiguity and uncertainty

Update on the new trading environment Jonathan Herbst Partner, Global Head of Financial Services Hannah Meakin Partner Tara Mokijewski Of Counsel 9 November 2015 Working with ambiguity and uncertainty

Markets in Financial Instruments Directive MiFID II

Markets in Financial Instruments Directive MiFID II This fact sheet is prepared by Bank of Ireland Global Markets to give you information on MiFID II, its requirements and the likely impact on you and

Markets in Financial Instruments Directive MiFID II This fact sheet is prepared by Bank of Ireland Global Markets to give you information on MiFID II, its requirements and the likely impact on you and

MiFID II: What is new for buy side? Best Execution Topic 3

Global Market Structure Europe Execution Excellence November 24, 2016 MiFID II: What is new for buy side? Best Execution Topic 3 In our document on Topic 1 of this series looking at MiFID II, we examined

Global Market Structure Europe Execution Excellence November 24, 2016 MiFID II: What is new for buy side? Best Execution Topic 3 In our document on Topic 1 of this series looking at MiFID II, we examined

Union Asset Management Holding AG

Review of the Markets in Financial Instruments Directive Questionnaire on MiFID/MiFIR 2 by Markus Ferber MEP The questionnaire takes as its starting point the Commission's proposals for MiFID/MiFIR 2 of

Review of the Markets in Financial Instruments Directive Questionnaire on MiFID/MiFIR 2 by Markus Ferber MEP The questionnaire takes as its starting point the Commission's proposals for MiFID/MiFIR 2 of

Best Execution Policy

Best Execution Policy 1 INTRODUCTION Usage of this Best Execution Policy must be in conjunction with the Compliance Manual and other company policies and procedures currently in effect and as amended from

Best Execution Policy 1 INTRODUCTION Usage of this Best Execution Policy must be in conjunction with the Compliance Manual and other company policies and procedures currently in effect and as amended from

Canada Life Investments

Canada Life Investments Order Execution Policy Owner Delegated Owner/s Last Approved 23 February 2018 Next Review Due Q1 2019 Version Number V1 2018 David Marchant, Managing Director & Chief Investment

Canada Life Investments Order Execution Policy Owner Delegated Owner/s Last Approved 23 February 2018 Next Review Due Q1 2019 Version Number V1 2018 David Marchant, Managing Director & Chief Investment

Financial Services and Markets

Financial Services and Markets Best execution FCA findings action required Executive Summary FCA Thematic Review On 31 July 2014, the Financial Conduct Authority ("FCA") published TR14/13 ("the Review"),

Financial Services and Markets Best execution FCA findings action required Executive Summary FCA Thematic Review On 31 July 2014, the Financial Conduct Authority ("FCA") published TR14/13 ("the Review"),

Order Execution Policy. January 2018 v1

Order Execution Policy January 2018 v1 Table of Contents Introduction... 2 Scope... 2 Background... 3 Legislation Reference... 3 Business Model... 3 Client Category... 4 Authorised Personnel... 4 Best

Order Execution Policy January 2018 v1 Table of Contents Introduction... 2 Scope... 2 Background... 3 Legislation Reference... 3 Business Model... 3 Client Category... 4 Authorised Personnel... 4 Best

MiFID II: What is new for buy side? Extraterritoriality Topic 7

Global Market Structure Europe Execution Excellence September 14, 2017 MiFID II: What is new for buy side? Extraterritoriality Topic 7 What does Extraterritoriality of MiFID II mean? - Extraterritoriality

Global Market Structure Europe Execution Excellence September 14, 2017 MiFID II: What is new for buy side? Extraterritoriality Topic 7 What does Extraterritoriality of MiFID II mean? - Extraterritoriality

In particular, we wish to highlight the following points, which we elaborate on in the body of our response:

ISDA response to FCA s second consultation on Brexit: Proposed changes to the Handbook and Binding Technical Standards CP18/36 The International Swaps and Derivatives Association ( ISDA ) welcome the opportunity

ISDA response to FCA s second consultation on Brexit: Proposed changes to the Handbook and Binding Technical Standards CP18/36 The International Swaps and Derivatives Association ( ISDA ) welcome the opportunity

Christos Gortsos Associate Professor of International Economic Law, Panteion University of Athens

ERA Conference The MIFID II Legislative Proposal Crucial changes in the reform of MiFID: : distinction between MiFID obligations and MiFIR requirements Christos Gortsos Associate Professor of International

ERA Conference The MIFID II Legislative Proposal Crucial changes in the reform of MiFID: : distinction between MiFID obligations and MiFIR requirements Christos Gortsos Associate Professor of International

The impact of MiFID II on AIFMD investment managers

The impact of MiFID II on AIFMD investment managers The impact of MiFID II on AIFMD investment managers Introduction The MiFID II Directive and the Markets in Financial Instruments Regulation (MiFIR) will

The impact of MiFID II on AIFMD investment managers The impact of MiFID II on AIFMD investment managers Introduction The MiFID II Directive and the Markets in Financial Instruments Regulation (MiFIR) will

MiFID II for Non-EU Investment Banks, Brokers and Fund Managers

MiFID II for Non-EU Investment Banks, Brokers and Fund Managers Thomas Donegan, Barney Reynolds, Russell Sacks and Nathan Greene Partners, Shearman & Sterling LLP October 10, 2017 What is MiFID II? EU

MiFID II for Non-EU Investment Banks, Brokers and Fund Managers Thomas Donegan, Barney Reynolds, Russell Sacks and Nathan Greene Partners, Shearman & Sterling LLP October 10, 2017 What is MiFID II? EU

Position Paper on the recast of the Insurance Mediation Directive

Telephone: 020 7066 5268 Email: enquiries@fs-cp.org.uk 19 January 2015 The Financial Services Consumer Panel is an independent statutory body, set up to represent the interests of consumers in the development

Telephone: 020 7066 5268 Email: enquiries@fs-cp.org.uk 19 January 2015 The Financial Services Consumer Panel is an independent statutory body, set up to represent the interests of consumers in the development

Policy Statement PS12/18 Algorithmic trading. June 2018

Policy Statement PS12/18 Algorithmic trading June 2018 Policy Statement PS12/18 Algorithmic trading June 2018 Bank of England 2018 Prudential Regulation Authority 20 Moorgate London EC2R 6DA Contents 1

Policy Statement PS12/18 Algorithmic trading June 2018 Policy Statement PS12/18 Algorithmic trading June 2018 Bank of England 2018 Prudential Regulation Authority 20 Moorgate London EC2R 6DA Contents 1

MiFID 2 GUIDE INSTRUMENT 2017

MiFID 2 GUIDE INSTRUMENT 2017 Powers exercised A. The Financial Conduct Authority makes this instrument in the exercise of the powers in section 139A (Power of the FCA to give guidance) of the Financial

MiFID 2 GUIDE INSTRUMENT 2017 Powers exercised A. The Financial Conduct Authority makes this instrument in the exercise of the powers in section 139A (Power of the FCA to give guidance) of the Financial

AFM Response to FCA consultation CP17/23, Insurance Distribution Directive, Implementation Paper 2

Robert Robinson Insurance Policy Financial Conduct Authority 25 The North Colonnade Canary Wharf London E14 5HS 20 October 2017 Dear Robert, AFM Response to FCA consultation CP17/23, Insurance Distribution

Robert Robinson Insurance Policy Financial Conduct Authority 25 The North Colonnade Canary Wharf London E14 5HS 20 October 2017 Dear Robert, AFM Response to FCA consultation CP17/23, Insurance Distribution

Questions and Answers On MiFID II and MiFIR transparency topics

Questions and Answers On MiFID II and MiFIR transparency topics 18 November 2016 ESMA/2016/1424 Date: 18 November 2016 ESMA/2016/1424 ESMA CS 60747 103 rue de Grenelle 75345 Paris Cedex 07 France Tel.

Questions and Answers On MiFID II and MiFIR transparency topics 18 November 2016 ESMA/2016/1424 Date: 18 November 2016 ESMA/2016/1424 ESMA CS 60747 103 rue de Grenelle 75345 Paris Cedex 07 France Tel.

18 June 2013 Conference Centre Albert Borshette, Brussels. DG Agri Expert Group. Catherine Sutcliffe, Senior Officer Secondary Markets

DG Agri Expert Group Catherine Sutcliffe, Senior Officer Secondary Markets Agenda Overview of ESMA EU policy making process EMIR MiFID II MAD/MAR 2 New EU Financial Supervision Framework Lessons from the

DG Agri Expert Group Catherine Sutcliffe, Senior Officer Secondary Markets Agenda Overview of ESMA EU policy making process EMIR MiFID II MAD/MAR 2 New EU Financial Supervision Framework Lessons from the

Summary of the Best Execution Policy

1. Introduction The summary of the Best Execution Policy outlines the key arrangements The Toronto-Dominion Bank (London Branch), TD Securities Limited, TD Bank (Europe) Limited and TD Global Finance Unlimited

1. Introduction The summary of the Best Execution Policy outlines the key arrangements The Toronto-Dominion Bank (London Branch), TD Securities Limited, TD Bank (Europe) Limited and TD Global Finance Unlimited

MiFID II/MiFIR Frequently Asked Questions

MiFID II/MiFIR Frequently Asked Questions FAQs cover: General Global Relationships Legal Entity Identifier Policies Consents Post Trade Reporting Client categorisation Research Systematic Internaliser

MiFID II/MiFIR Frequently Asked Questions FAQs cover: General Global Relationships Legal Entity Identifier Policies Consents Post Trade Reporting Client categorisation Research Systematic Internaliser

MiFID II inducement rule: the impact on investment research and market commentary

KEY POINTS The payment for research with dealing commissions will be a prohibited inducement under MiFID II. Managers will either have to pay for research out of their own pockets or agree with each client

KEY POINTS The payment for research with dealing commissions will be a prohibited inducement under MiFID II. Managers will either have to pay for research out of their own pockets or agree with each client

Execution Policy. 1 Purpose. to and taking into account the execution factors (see paragraph 4).

.") Execution Policy 1 Purpose We have put in place an Execution Policy to ensure that, as required by the FCA Rules, we take all sufficient steps to obtain the best possible result on behalf of our Clients

Execution Policy 1 Purpose We have put in place an Execution Policy to ensure that, as required by the FCA Rules, we take all sufficient steps to obtain the best possible result on behalf of our Clients

Order Handling and Best Execution Policy

Order Handling and Best Execution Policy Effective 3 January 2018 TABLE OF CONTENTS 1 INTRODUCTION... 4 2 PURPOSE OF THIS POLICY... 4 3 ABBREVIATIONS... 5 4 DEFINITIONS... 6 5 POLICY APPLICATION... 8 6

Order Handling and Best Execution Policy Effective 3 January 2018 TABLE OF CONTENTS 1 INTRODUCTION... 4 2 PURPOSE OF THIS POLICY... 4 3 ABBREVIATIONS... 5 4 DEFINITIONS... 6 5 POLICY APPLICATION... 8 6

LEI requirements under MiFID II

LEI requirements under MiFID II Table of contents 1. Scope & deadlines 2. LEI requirements 3. Reporting scenarios Scope & deadlines Regime Entities concerned Application Market Abuse (secondary market

LEI requirements under MiFID II Table of contents 1. Scope & deadlines 2. LEI requirements 3. Reporting scenarios Scope & deadlines Regime Entities concerned Application Market Abuse (secondary market

Use of Dealing Commission: Corporate Access/Research Services

Use of Dealing Commission: Corporate Access/Research Services Purpose The IMA today publishes this communication to assist its members in meeting the requirements of the FSA s rules on the use of dealing

Use of Dealing Commission: Corporate Access/Research Services Purpose The IMA today publishes this communication to assist its members in meeting the requirements of the FSA s rules on the use of dealing

Measuring your approach MiFID II Paper: Best execution

Measuring your approach Contents Introduction 3 Scope 4 A reminder of the current rules 5 A summary of the key changes 6 Welcome to Paper 4 of the Eversheds MiFID II Implementation Series, on implementing

Measuring your approach Contents Introduction 3 Scope 4 A reminder of the current rules 5 A summary of the key changes 6 Welcome to Paper 4 of the Eversheds MiFID II Implementation Series, on implementing

AIFMD vs UCITS vs MiFID2

AIFMD vs UCITS vs MiFID2 Nick Colston Darren Fox FI & AMIF Autumn Legal Update 2017 Overview: what we ll cover today When regulation makes headline news.. Part 1: overview of three regulatory regimes Part

AIFMD vs UCITS vs MiFID2 Nick Colston Darren Fox FI & AMIF Autumn Legal Update 2017 Overview: what we ll cover today When regulation makes headline news.. Part 1: overview of three regulatory regimes Part

MiFID II/ MIFIR and Asset Management In a nutshell

MiFID II/ MIFIR and Asset Management In a nutshell MiFID II/ MIFIR and Asset Management With less than 6 months until MiFID II/MiFIR transitions from an implementation project to the way of life, understanding

MiFID II/ MIFIR and Asset Management In a nutshell MiFID II/ MIFIR and Asset Management With less than 6 months until MiFID II/MiFIR transitions from an implementation project to the way of life, understanding

Brave New World: MiFID2 and MiFIR The changes facing the Financial Markets

Brave New World: MiFID2 and MiFIR The changes facing the Financial Markets Jason Valoti 13 July 2016 MiFID what? MiFID (Markets in Financial Instruments Directive) Sets out rules on what investment services

Brave New World: MiFID2 and MiFIR The changes facing the Financial Markets Jason Valoti 13 July 2016 MiFID what? MiFID (Markets in Financial Instruments Directive) Sets out rules on what investment services

GUIDE ON THE NEW RULES GOVERNING THE FUNDING OF RESEARCH BY INVESTMENT SERVICE PROVIDERS UNDER MIFID II January 2018

GUIDE ON THE NEW RULES GOVERNING THE FUNDING OF RESEARCH BY INVESTMENT SERVICE PROVIDERS UNDER MIFID II January 2018 PREAMBLE Regulatory context and general purpose of the reform The funding of research

GUIDE ON THE NEW RULES GOVERNING THE FUNDING OF RESEARCH BY INVESTMENT SERVICE PROVIDERS UNDER MIFID II January 2018 PREAMBLE Regulatory context and general purpose of the reform The funding of research

Preparing for MiFID II: Practical Implications

Tuesday 1 December 2015 Preparing for MiFID II: Practical Implications Sean Donovan-Smith, Partner Jacob Ghanty, Partner Andrew Massey, Special Counsel Philip Morgan, Partner Rodney Smyth, Consultant Copyright

Tuesday 1 December 2015 Preparing for MiFID II: Practical Implications Sean Donovan-Smith, Partner Jacob Ghanty, Partner Andrew Massey, Special Counsel Philip Morgan, Partner Rodney Smyth, Consultant Copyright

Smart Contracts Presentation to ACC 18 th October Sean Murphy

Smart Contracts Presentation to ACC 18 th October 2016 Sean Murphy What is a blockchain? How do blockchains operate? What are the benefits of blockchains? What are smart contracts? How do smart contracts

Smart Contracts Presentation to ACC 18 th October 2016 Sean Murphy What is a blockchain? How do blockchains operate? What are the benefits of blockchains? What are smart contracts? How do smart contracts

A legal view on Brexit

A legal view on Brexit James Bateson Global Head of Financial Institutions Norton Rose Fulbright LLP 25 April 2017 Agenda Withdrawal timeline Article 50 Impact on legal landscape Geo-political factors

A legal view on Brexit James Bateson Global Head of Financial Institutions Norton Rose Fulbright LLP 25 April 2017 Agenda Withdrawal timeline Article 50 Impact on legal landscape Geo-political factors

Strengthening accountability in banking. New publications intensify implementation requirements

Strengthening accountability in banking New publications intensify implementation requirements The UK regulatory authorities continue to develop their proposals for Strengthening accountability in banking:

Strengthening accountability in banking New publications intensify implementation requirements The UK regulatory authorities continue to develop their proposals for Strengthening accountability in banking:

FCA calls for the unbundling of research from dealing commissions

July 2014 FCA calls for the unbundling of research from dealing commissions Introduction On 10 July 2014 the Financial Conduct Authority ("FCA") published a discussion paper (DP14/3) on the use of dealing

July 2014 FCA calls for the unbundling of research from dealing commissions Introduction On 10 July 2014 the Financial Conduct Authority ("FCA") published a discussion paper (DP14/3) on the use of dealing

Policy Statement 07/15. Financial Services Authority. Best execution. Feedback on DP06/3 and CP06/19 (part)

") Policy Statement 07/15 Financial Services Authority Best execution Feedback on DP06/3 and CP06/19 (part) August 2007 Contents 1. Overview 3 2. The CESR Q&A and feedback on issues it does not address 5

Policy Statement 07/15 Financial Services Authority Best execution Feedback on DP06/3 and CP06/19 (part) August 2007 Contents 1. Overview 3 2. The CESR Q&A and feedback on issues it does not address 5

Policy Statement 10/6. Financial Services Authority. Distribution of retail investments: Delivering the RDR - feedback to CP09/18 and final rules

Policy Statement 10/6 Financial Services Authority Distribution of retail investments: Delivering the RDR - feedback to CP09/18 and final rules March 2010 Contents 1 Overview 3 2 Describing and disclosing

Policy Statement 10/6 Financial Services Authority Distribution of retail investments: Delivering the RDR - feedback to CP09/18 and final rules March 2010 Contents 1 Overview 3 2 Describing and disclosing

BREXIT AND ALTERNATIVE ASSET MANAGERS

BREXIT AND ALTERNATIVE ASSET MANAGERS MANAGING THE IMPACT IN THE EEA July 2018 Sponsored by CONTENTS CONTENTS 1 EXECUTIVE SUMMARY 4 2 MANAGING THE IMPACT OF BREXIT 6 2.1 AIFMD 6 2.2 UCITS 8 2.3 MiFID2/MiFIR

BREXIT AND ALTERNATIVE ASSET MANAGERS MANAGING THE IMPACT IN THE EEA July 2018 Sponsored by CONTENTS CONTENTS 1 EXECUTIVE SUMMARY 4 2 MANAGING THE IMPACT OF BREXIT 6 2.1 AIFMD 6 2.2 UCITS 8 2.3 MiFID2/MiFIR

AxiCorp Limited FCA # Leaden h all Street London EC 3 A 1AT UNITED KINGDOM. Issued: May 1st 2018

B AxiCorp Limited FCA #509746 36-3 8 Leaden h all Street London EC 3 A 1AT UNITED KINGDOM Issued: May 1st 2018 9 BEST EXECUTION POLICY INTRODUCTION The purpose of this document is to provide information

B AxiCorp Limited FCA #509746 36-3 8 Leaden h all Street London EC 3 A 1AT UNITED KINGDOM Issued: May 1st 2018 9 BEST EXECUTION POLICY INTRODUCTION The purpose of this document is to provide information

Best Execution & Order Handling Policy

Best Execution & Order Handling Policy BGC Brokers LP, GFI Brokers Limited, GFI Securities Limited, Sunrise Brokers LLP. Policy Version V 1.3 Effective Date 20/02/2018 Best Execution and Order Handling

Best Execution & Order Handling Policy BGC Brokers LP, GFI Brokers Limited, GFI Securities Limited, Sunrise Brokers LLP. Policy Version V 1.3 Effective Date 20/02/2018 Best Execution and Order Handling

Stand out for the right reasons Protecting Client Assets

www.pwc.co.uk/fsrr Stand out for the right reasons Protecting Client Assets July 2014 Shaking up the Client Assets regime The FCA significantly revised the UK Client Assets protection regime (CASS) when

www.pwc.co.uk/fsrr Stand out for the right reasons Protecting Client Assets July 2014 Shaking up the Client Assets regime The FCA significantly revised the UK Client Assets protection regime (CASS) when

The Company will automatically categorise all Clients as a Retail Clients as notified to the Client within the Company s Client Agreement.

1 Contents 1. Introduction... 3 2. Categorisation Criteria... 3 2.1 Retail Client... 3 2.2 Professional Client... 3 2.3 Eligible Counterparty... 6 3. Request for Different Categorisation... 7 4. Protection

1 Contents 1. Introduction... 3 2. Categorisation Criteria... 3 2.1 Retail Client... 3 2.2 Professional Client... 3 2.3 Eligible Counterparty... 6 3. Request for Different Categorisation... 7 4. Protection

20 November InfoNet. MiFID II/R Seminar. Commodities. Sponsored by

20 November 2015 InfoNet MiFID II/R Seminar Commodities Sponsored by AGENDA 08.30-09.00 Registration 09.00-09.30 Presentation Chris Borg, Partner, Reed Smith 09.30-10.00 Presentation Paul Willis, Technical

20 November 2015 InfoNet MiFID II/R Seminar Commodities Sponsored by AGENDA 08.30-09.00 Registration 09.00-09.30 Presentation Chris Borg, Partner, Reed Smith 09.30-10.00 Presentation Paul Willis, Technical

For financial intermediary use only. Not approved for use with customers. What Mifid ii means to you

For financial intermediary use only. Not approved for use with customers. What Mifid ii means to you Welcome To raise your hand in the webinar, click here To ask a question, please type here. We will respond

For financial intermediary use only. Not approved for use with customers. What Mifid ii means to you Welcome To raise your hand in the webinar, click here To ask a question, please type here. We will respond

Navigating Regulatory Compliance Investment Management Monthly Regulatory Update. April 2016

Investment Management Monthly Regulatory Update April 2016 1. Introduction 1.1 In addition to our register of relevant regulatory developments in the past month, we note four themes this month which stand

Investment Management Monthly Regulatory Update April 2016 1. Introduction 1.1 In addition to our register of relevant regulatory developments in the past month, we note four themes this month which stand

World Platinum Investment Council (WPIC) Research in a MiFID II Context Asset Manager Compliance Department Edition

Research in a MiFID II Context Asset Manager Compliance Department Edition") World Platinum Investment Council (WPIC) Research in a MiFID II Context Asset Manager Compliance January 2018 This document is divided into three sections and is designed to explain WPIC s research status

World Platinum Investment Council (WPIC) Research in a MiFID II Context Asset Manager Compliance January 2018 This document is divided into three sections and is designed to explain WPIC s research status

OCTOBER 2017 MIFID II GUIDE FOR FINANCIAL INVESTMENT ADVISORS

OCTOBER 2017 MIFID II GUIDE FOR FINANCIAL INVESTMENT ADVISORS amf-france.org PREAMBLE Financial investment advisors (FIAs), which are governed by the regime introduced in the Financial Security Act of

OCTOBER 2017 MIFID II GUIDE FOR FINANCIAL INVESTMENT ADVISORS amf-france.org PREAMBLE Financial investment advisors (FIAs), which are governed by the regime introduced in the Financial Security Act of

FINAL NOTICE For the reasons given in this notice, the Authority hereby imposes on Sesame a financial penalty of 1,598,000.

FINAL NOTICE To: Sesame Limited Reference Number: 150427 Address: Independence House, Holly Bank Road Huddersfield HD3 3HN 29 October 2014 1. ACTION 1.1. For the reasons given in this notice, the Authority

FINAL NOTICE To: Sesame Limited Reference Number: 150427 Address: Independence House, Holly Bank Road Huddersfield HD3 3HN 29 October 2014 1. ACTION 1.1. For the reasons given in this notice, the Authority

ESMA Publishes Consultation on UCITS Remuneration Guidelines

ESMA Publishes Consultation on UCITS Remuneration Guidelines The European Securities and Markets Authority ( ESMA ) has published on 23 July 2015 a consultation on guidelines on sound remuneration policies

ESMA Publishes Consultation on UCITS Remuneration Guidelines The European Securities and Markets Authority ( ESMA ) has published on 23 July 2015 a consultation on guidelines on sound remuneration policies

SCOPE OF SECTION C(10) CONTRACTS WHICH ARE "COMMODITY DERIVATIVES" FOR THE PURPOSES OF MIFID II

CONTRACTS WHICH ARE COMMODITY DERIVATIVES FOR THE PURPOSES OF MIFID II") 22 February 2017 SCOPE OF SECTION C(10) CONTRACTS WHICH ARE "COMMODITY DERIVATIVES" FOR THE PURPOSES OF MIFID II We write further to our letter of 22 September 2016 1 and the meeting between ESMA and our

22 February 2017 SCOPE OF SECTION C(10) CONTRACTS WHICH ARE "COMMODITY DERIVATIVES" FOR THE PURPOSES OF MIFID II We write further to our letter of 22 September 2016 1 and the meeting between ESMA and our

Questions and Answers On MiFID II and MiFIR transparency topics

Questions and Answers On MiFID II and MiFIR transparency topics 19 December 2016 ESMA/2016/1424 Date: 19 December 2016 ESMA/2016/1424 ESMA CS 60747 103 rue de Grenelle 75345 Paris Cedex 07 France Tel.

Questions and Answers On MiFID II and MiFIR transparency topics 19 December 2016 ESMA/2016/1424 Date: 19 December 2016 ESMA/2016/1424 ESMA CS 60747 103 rue de Grenelle 75345 Paris Cedex 07 France Tel.

The Volcker Rule as Proposed: Questions For Comment Nos and SEC Questions Nos October 11, 2011

The Volcker Rule as Proposed: Questions For Comment Nos. 1-383 and SEC Questions Nos. 1-11 October 11, 2011 2011 Morrison & Foerster LLP All Rights Reserved mofo.com THE VOLCKER RULE AS PROPOSED: QUESTIONS

The Volcker Rule as Proposed: Questions For Comment Nos. 1-383 and SEC Questions Nos. 1-11 October 11, 2011 2011 Morrison & Foerster LLP All Rights Reserved mofo.com THE VOLCKER RULE AS PROPOSED: QUESTIONS

EU Market Abuse Regulation and asset managers six months to go

Tuesday, 5 January 2016 EU Market Abuse Regulation and asset managers six months to go In less than six months' time, on 3 July 2016, the majority of the EU Market Abuse Regulation (MAR) regime will be

Tuesday, 5 January 2016 EU Market Abuse Regulation and asset managers six months to go In less than six months' time, on 3 July 2016, the majority of the EU Market Abuse Regulation (MAR) regime will be

Delegated Acts/Level 2 another milestone is reached

www.pwc.lu/mifid 4 th MiFID II Breakfast Delegated Acts/Level 2 another milestone is reached Regulatory Advisory Services Table of Contents Section Overview Page 1 MiFID II Genesis 1 2 Update on Level

www.pwc.lu/mifid 4 th MiFID II Breakfast Delegated Acts/Level 2 another milestone is reached Regulatory Advisory Services Table of Contents Section Overview Page 1 MiFID II Genesis 1 2 Update on Level

Prior to responding in detail to the questions raised in the consultation, we would like to make some general remarks.

20141023 French Banking Federation Response to Joint Consultation Paper on draft Regulatory Technical Standards on risk concentration and intra-group transactions under Article 21a (1a) of the Financial

20141023 French Banking Federation Response to Joint Consultation Paper on draft Regulatory Technical Standards on risk concentration and intra-group transactions under Article 21a (1a) of the Financial

Directive 2011/61/EU on Alternative Investment Fund Managers

The following is a summary of certain relevant provisions of the (the Directive) of June 8, 2011 along with ESMA s Final report to the Commission on possible implementing measures of the Directive as of

The following is a summary of certain relevant provisions of the (the Directive) of June 8, 2011 along with ESMA s Final report to the Commission on possible implementing measures of the Directive as of