Non Performing Assets and Profitability of Scheduled Commercial Banks

|

|

|

- Posy Armstrong

- 6 years ago

- Views:

Transcription

1 IOSR Journal of Business and Management (IOSR-JBM) e-issn: X, p-issn: Volume 19, Issue 9. Ver. VIII (September 2017), PP Non Performing Assets and Profitability of Scheduled Commercial Banks *Fareed Ahmed 1 & Dr. Akhilesh Tripati 2 (Research Scholar, SOM, Poornima University, Jaipur, India) Chief Manager, SBI, Jaipur Corresponding Author: *Fareed Ahmed Abstract: Since the global financial crisis of , the asset quality and profitability of Indian banking deteriorated. The Gross NPA ratio rose sharply to 7.5% in FY16 compared to 2.2% in FY09. Once the account is classified as NPA, income from NPA is not recognized on accrual basis and the unrealized interest that was taken to Profit and Loss account on accrual basis shall also be reversed as the policy of income recognition. Operational effectiveness of the banks is affected by the quality of advances, which in turn has an impact on the profitability, cost effectiveness, liquidity, and solvency position of the banks. Hence, an attempt was made to study the impact of NPAs on the bank s performance. Data was collected on Scheduled Commercial Banks in India from RBI reports, and simple correlation and regression applied in order to establish linkages between selected variables Profit, ROA, ROE, Cost to Income ratio and Provisions, and NPA. The results of statistical analysis indicate that NPAs have insignificant inverse relationship with profit, significant negative impact on ROA, ROE, and a significant positive impact on Cost to Income ratio and Provision. As such, NPAs put detrimental impact on the bank s performance. Keywords: Cost to Income Ratio, NPA, Provisions, ROA, ROE Date of Submission: Date of acceptance: I. Introduction The growth story of Indian banking industry is quite interesting and fascinating both in terms of extensive branch network spread across the country and wide range of services to the clientele over the years. The post reform era has brought many changes in accounting standards like introduction of Asset Classification and Income Recognition. One of the major challenges the banking industry is facing is mounting Non Performing Assets (NPAs). The NPAs is an important prudential indicator to assess the financial health of the banking sector. During the last five financial years, from April 2011, there was an alarming increase of distressed assets of the Indian banks. The gross NPAs of Scheduled Commercial Banks reached an alarming figure of crore, amounting to 7.6% of total advances as at March Besides NPAs, the restructured standard advances accounted for 3.9% of total advances, thus overall the stressed advances rose significantly to 11.5% of total advances as at end March Among the bank-groups, Public Sector banks are particularly struggling with high NPAs and they continue to face the dual problem of significant asset quality stress and inadequate capitalization, which impact the growth. They continue to have distinctly higher stressed advances at 14.5% of total advances. The huge NPAs and their continued unmitigated increase in absolute terms have had an adverse impact on the banking system and hence an attempt has been made in this paper to assess the impact of NPAs on bank performance. 1.1Non-Performing Asset (NPA) An asset becomes non-performing when it ceases to generate income for the bank. Earlier, a nonperforming asset was defined as a credit facility in respect of which the interest or instalment of principal or both have remained due for a specified period of time, which was reduced from four quarters to one quarter in a phased manner. Due to the improvements in the payment and settlement system, recovery climate, upgradation of technology in the banking system, etc., it has been decided to dispense with past due concept with effect from March 31, With a view to moving towards international best practices and to ensure greater transparency, it has been decided to adopt the 90 days overdue norms for the identification of NPAs from the year ending March 31, Banks are required to categorize non- performing assets further into three categories on the basis of the period for which the asset has remained non-performing and the reliability of the dues: Sub-standard Assets, Doubtful Assets, and Loss Assets Substandard Assets DOI: /487X Page

2 With effect from March 31, 2005, a sub-standard asset would be one, which has remained NPA for a period less than or equal to 12 months. Such an asset will have well defined credit weaknesses that jeopardise the liquidation of the debt and are characterised by the distinct possibility that the banks will sustain some loss, if deficiencies are not corrected Doubtful Assets With effect from March 31, 2005, an asset would be classified as doubtful if it has remained in the sub-standard category for a period of 12 months. A loan classified as doubtful has all the weaknesses inherent in assets that were classified as substandard, with the added characteristic that the weaknesses make collection or liquidation in full on the basis of currently known facts, conditions and values highly questionable and improbable Loss Assets A loss asset is one where loss has been identified by the bank or internal or external auditors or the RBI inspection but the amount has not been written off wholly. In other words, such an asset is considered uncollectible and of such little value that its continuance as a bankable asset is not warranted although there may be some salvage or recovery value. II. Provisioning In conformity with the prudential norms, provisions should be made on the NPAs on the basis of classification of assets into prescribed categories. Taking into account the time lag between an account becoming doubtful of recovery, its recognition as such, the realisation of the security and the erosion over time in the value of security charged to the bank, the banks should make provision against substandard assets, doubtful assets and loss assets and banks were also asked to make provisions towards standard advances as prudent measures. III. Objective of the study The objective of the study is to assess the impact of NPAs on the performance of Scheduled commercial banks. IV. Review of Literature This section covers a snapshot of the previous studies on impact of NPAs on the financial performance of the banks, by various researchers. A high level of NPA puts strain on a bank net worth because banks are under pressure to maintain a desired level of Capital Adequacy and in the absence of comfortable profit level, banks eventually look towards their internal financial strength to fulfill the norms thereby slowly eroding the net worth. (Barge, 2012) [1] NPA affects the profitability, liquidity and competitive functioning of Public and Private Sector Banks and finally the psychology of the bankers in respect of their disposition towards credit delivery and credit expansion. In a study examining the impact of NPAs on profitability and other financial parameters in selected public sector banks in the state of Haryana, it was concluded that impact of NPAs on the performance of the banks is manifold. Profitability is the worst affected by NPAs followed by Credit deployment and investment policy, Achievement of capital adequacy ratio level and reduction in Productivity. (Chhikara, 2007) [2] One of the studies investigated the impact of asset quality on performance of the private commercial banks in India. The relationship between the asset quality management proxies and profitability nexus were precisely examined. The results showed that a bad asset ratio is negatively associated with banking operating performance, after controlling for the effects of operating scale, traditional banking business concentration and the idle fund ratio. (Chisti, 2012) [3] Researchers [4] (Aziz, Ibrahim, & Kamaruddin, 2009) focused on the relationship between profitability performance including Return on Assets (ROA), Return on Equity (ROE) and Net Profit Margin (NPM) against NPLs and loan recovery income for four banks in Malaysia. The test indicated that there is a significant impact of NPLs on profitability performance for foreign banks whereas for local banks it depends on the individual bank. It was also observed that NPAs result in loss of interest income, the current profit is reduced, as banks have to make provision for NPA. Capital adequacy ratio is also affected as it is directly related to the quality of assets. It also affects the liquidity position of bank as also recycling of funds due to asset liability mismatch. Banks at times have to borrow at high cost to fulfill their commitment/obligations, which increases the cost of funds. The credit rating of the bank also gets affected due to high NPA and consequently business prospects in the country and abroad. (Vora, 2007) [5] Some studies also dealt with the concept of NPAs, its magnitude and impact. The profitability of all public sector banks affected at very large extent when NPAs work with other banking strategic variables and also affect productivity and efficiency. It has shown that the NPAs and profitability and productivity are negatively related. Statistically results revealed that the present level of NPAs in public sector banks affects fifty percent profitability of the banks and its impact has increased at very large extent when it works with other strategic banking variables. The high value of co-efficient of determination shows high degree of explanation of DOI: /487X Page

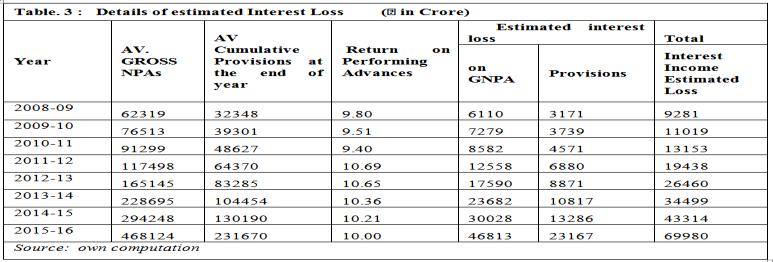

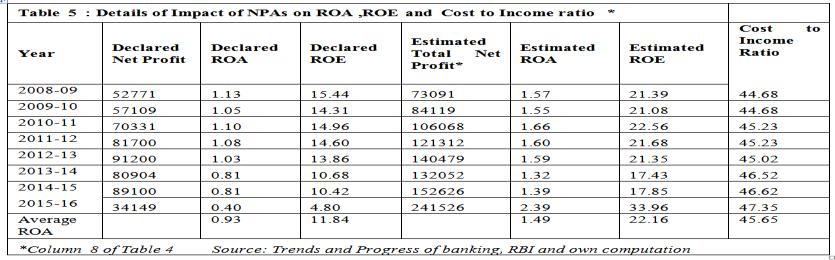

3 variability in the productivity and efficiency of public sector banks in terms of business per employee and operating profit per employee. (Yadav, 2011) [6] V. Methodology The study relates to Scheduled Commercial Banks and covering the period from to (Eight years). Over the past seven years since the global financial crisis ( ), the Indian banking sector has depicted a distinct performance. Hence is selected as base year. The main sources of secondary data used in the study are from Statistical tables relating to banks, RBI Bulletin, RBI Reports, etc. Simple correlation and regression tests have been carried out. In order to identify the strength of relationship between selected independent and dependent variables and NPA, R2 value is computed. To assess the significance of regression equation, we calculated F-value. To examine the statistical significance of selected independent variables on NPA, t-test is computed. VI. Findings and Discussions The gross non-performing advances (GNPAs) of Scheduled Commercial banks continued to display increasing trend and increased by 9 times in 7 years from during the year 2009 to crores during the year The GNPA ratio of all SCBs sharply increased to 7.6% as of March 2016 compared to 2.2% in Looking at the y-o-y growth of GNPAs there has been a significant rise in FY16. The annual rate of growth in gross NPAs which was % in 2009 and fluctuated during the study period and stood at % in Impact of NPA on Banks Performance The NPAs have adverse impact on various parameters of bank performance. These are discussed below: Asset (Credit) contraction The increased NPAs put pressure on recycling of funds and reduce the ability of banks for lending more NPAs constitute a real economic cost to the Nation in that they reflect the application of scare capital and credit funds to the unproductive uses. The funds locked up in NPAs are not available for productive uses or recycling. As such this staggering proportion of gross NPA of crore as at end of March 2015 are not available for deployment and multiple credit creation process Provisioning requirement Provisions towards NPAs are regarded as a controlling mechanism over expected loan losses. There is an effect on the Balance Sheet of the bank since NPAs need to be provided for and prudential regulation and accounting standards provide specific guidelines for loan loss provisioning in the banking industry and banks have to provide provisions ranging from 15% to 100% depending on the category of NPAs. So, hard earned money from Performing Assets has to be diverted towards meeting the provisioning needs of NPAs and eventually NPAs to be written off against capital and reserve. If adequate provisioning is not made against NPAs, it will impair the Bank s capital base, thus reducing the protection available to depositors. The details of provisions made towards NPAs and cumulative provisions held at the end of each year are furnished in Table No. 2 The net provisions made during the period have shown fluctuating trends. NPAs put detrimental impact on the profitability as banks stop to earn income on one hand and attract higher provisioning compared to standard assets which have direct bearing on the profitability of the banks Impact on Income Interest Income Non-performing Assets do not generate income as interest to be accounted only on receipt basis and moreover, if advances become NPAs as at close of any year, the unrealized interest accrued and credited to income account, should be reversed or provided for. Apart from this, uncollected fees, commissions and other income that due to any circumstances have accrued in NPAs during past periods should be reversed or provided for. When a bank does not really receive interest, there is loss of flexibility and the bank loses the opportunity to redeploy the income stream for a better purpose. Banks are losing interest income of about crore a year (Average yield@ 10% on average Gross NPA of crore during ). Burden of Provisions and Write off Besides interest loss, banks profitability is affected adversely because of providing of doubtful debts and consequent to writing it off as bad debts. SCBs have lost an income of crore on account of NPAs during the study period. (Table. 2-4). Return on Assets Return on assets is defined as net profit divided by average total assets. It gives an idea of the efficiency of the management in using its assets to generate earning by measuring a banks profit per currency unit of assets. This is the main indicator of profitability used in international comparisons and it is one among the guidelines of RBI DOI: /487X Page

4 for performance analysis of banks. NPAs reduce earning capacity of the assets and thereby Return on Assets (ROA) also gets affected. It may be noted that the SCBs have registered lower returns on assets after global crisis and shown decreasing trend during the period 2009 to 2016 except the year The performance of the banks is said to be good if the ROA exceeds 1.25 %. The average return on assets of the SCBs is 0.93% for the study period with minimum ROA of 0.40% during the year 2016 and a maximum of 1.10% during SCBs are losing interest income on GNPAs and on realization of which, SCBs could have improved average ROA of SCBs for the study period by another 70 basis points to make it 1.63 (Table-5) Return on Equity Return on Equity is an indicator of the profitability of banks from the shareholders point view. It is a measure of accounting profits of book equity capital. The price of shares largely depends upon ROE, in the absence of speculation. The ability of the banks to attract fresh capital in the market depends upon this indicator. The ROE of all scheduled commercial banks has decreased during the period 2009 to 2016 in consonance with the profitability and exhibited almost similar trends as that of ROA. The average ROE of the SCBs % for the study period and it could have been % on realization of income lost. (Table-5) Cost to Income ratio The ratio reflects the ability of a bank to generate revenue from its expenditure. It captures the impact of offbalance sheet operations and is, thus, a better measure of efficiency than the cost to assets ratio. The Cost to income Ratio has increased from 44.68% in 2009 to % in 2015 indicating poor efficiency. However, as per the international best practice norm, banks should strive to achieve cost-income ratio of less than 35%. Therefore, SCBs in India, with the cost to income ratio of 47.35% (2016), needs to cover a lot of ground to achieve international competitiveness and meet the best practice norm in rendering banking services (Table-5) Operational Cost The operational cost of the banks will increase due to increase in the NPAs. Monitoring cost of the NPAs is too high. Both the preventive and curative measures for reducing the NPAs attract high expenses. The NPAs in one hand ceases to generate any income from interest and on the other hand it creates loss on account of cost towards effective management of NPAs Liquidity Banks are in a business where liquidity is of prime importance. Increasing NPAs not only critically affect the liquidity of the banks but also force the banks to maintain more liquid assets thereby increasing cost. As fund is blocked in bad assets the bank is bound to borrow money or mobilize deposits for the shorter period of time in order to maintain minimum cash in hand which results additional cost to the banks. The lending capacity of the banks is adversely affected due to their inability to recycle the resources. Hence, every time NPAs increase, deposits are mobilized to fund the incremental NPAs thereby increasing interest expenditure. As per RBI guidelines, banks have to maintain the minimum amount in statutory reserve ratios SLR and CRR (Presently SLR and CRR of 20 % and 4% respectively). So, the banks not only have to fund the NPAs but for every 100 of such assets, banks have to mobilize about 132 resources to meet statutory reserve requirements Solvency and Capital Adequacy Since the loans and advances issued by the banks is a principal part of the net assets, loan defaults are a primary cause of potential losses. The solvency of a bank is exhibited by Capital Adequacy Ratio (CAR) which is directly related to quality of assets. The CAR is defined as the ratio between the total banks capital and its riskweighted assets. The CAR reveals the health and solvency position of a bank. NPAs have adverse impact on CAR. Decline in the profitability and liquidity ultimately affects the solvency position of the banks Liability Management In the light of high NPAs, Banks tend to lower the interest rates on deposits on one hand and likely to levy higher interest rates on advances to sustain NIM. This may become hurdle in smooth financial intermediation process and hampers banks business as well as economic growth Reserves and Surplus and Net worth As there is reduction in the net profit on account of NPAs, the Reserves and Surplus and Net worth also get adversely affected Shareholders Confidence DOI: /487X Page

5 Normally, shareholders are interested to enhance value of their investments through higher dividends and market capitalization which is possible only when the bank posts significant profits through improved business. The increased NPA level is likely to have adverse impact on the bank business as well as profitability thereby the shareholders do not receive a market return on their capital and sometimes it may erode their value of investments. As per extant guidelines, banks whose Net NPA level is 5% & above are required to take prior permission from RBI to declare dividend and also stipulate cap on dividend payout Competency In the context of severe competition in the banking industry, the banks with high NPAs at disadvantage for leveraging the rate of interest in the deregulated market and securing remunerative business growth in the competitive money and capital markets, inability to offer competitive market rates both to depositors and borrowers Public Confidence Credibility of banking system is also affected greatly due to higher level NPAs because it shakes the confidence of general public in the soundness of the banking system. The increased NPAs may pose liquidity issues which is likely to lead run on bank by depositors. Thus, the increased incidence of NPAs not only affects the performance of the banks but also affect the economy as a whole Investments There is a perceptible change in the complexion of banks since when the prudential norms came into force. The SCBs have developed a tendency to expand investments in preference to credit. This change has an adverse impact on the performance of the economy with cascading effects as flow of credit towards the productive ventures for creation of assets, employment etc., has not been at the desired level Economic Value added Economic Value Added or EVA is a tool that bankers can use to measure the financial performance of their bank. EVA has only been used in the U.S. banking industry since 1994 and is not as well-known as other measures of bank performance. As developed by Stern Stewart & Co., EVA in 1989 is calculated as a company s net operating profit after taxes (NOPAT) minus cost for the equity capital employed by the company. The cost of equity capital employed by a company is equal to the company s equity capital (reported on its balance sheet) multiplied by a percentage return that the company s shareholders require on their investment. Expressed as a formula: EVA= Net Operating Profit after Taxes (Capital x% WACC). So, the economic value addition (EVA) by banks gets upset because EVA is equal to the net- operating profit minus cost of capital on account of NPAs. When the return on equity is less than the cost of equity, the negative spread leads to a negative EVA Market Value Added (MVA) Market value of invested capital refers to the market value of equity capital and debt capital, but the market value of debt is not easily available, as debts are not generally traded. Thus, the definition of MVA can be stated as MVA = Market Capitalisation -Net worth. Where, Market Capitalisation is the product of closing share price and number of outstanding shares as on that date ((i.e.) date of Balance sheet). As the advance becomes NPA, it ceases to earn interest income and major income of public sector banks is interest income on advances as compared to private sector banks, which will have generally a good contribution of Non-interest income in their income. As such loss of interest income by Public Sector Banks will have impact on their share values 1.3 Statistical Analysis In order to examine the relationship and impact of NPAs have with certain variables like Net Profit, ROA, ROE, Cost to Income Ratio, and Provisions, Simple correlation and regression tests have been carried out and the results are discussed in the following paragraphs. In order to identify the strength of relationship between dependent variables and NPA, R 2 value is computed. To assess the significance of regression equation, we calculated F-value. To examine the statistical significance of NPA on dependent variables t-test is computed. 1.4 Impact of NPAs Impact of NPAs on Net Profit DOI: /487X Page

6 H 1: There is no significant relationship between NPA and Net profit. NPAs explain only 12 % of variation of net profit of SCBs as shown by the R 2. Therefore, this means that some other factors not included in this model explain 88% of net profit of SCBs. The relationship is negative and the regression coefficient (-) 0.038, is tested through the t test and the results show that it is insignificant as the p- value is greater than the significance level (0.402>0.05). It reveals that NPA has insignificant negative effect on Net profit of SCBs. Hence, the hypothesis that there is no significant impact of NPAs on Net profit is accepted.net Profit consists of income earned by the banks, which includes interest income & other non-interest income. Since the total advances are increasing so interest income is increasing and there is continuous increase in non-interest income which are responsible for insignificant negative impact of NPAs on profits Impact of NPAs on ROA H 2: There is no significant negative impact of NPA on ROA. Analysis indicates NPAs explain 97 % of return on assets of SCBs as shown by the R 2. The findings show that there is an inverse relationship between NPAs and ROA and it is statistically significant as the p-value is less than the significance level (0.000<0.05) and the coefficient value is (-) It reveals that NPA has negative significant effect on ROA of SCBs and hence we reject the hypothesis. Therefore, it is evidently proved from the analysis that GNPAs have an inverse impact on ROA of banks, that means the bank can have an increasing trend of ROA by the effect of the declining trend of GNPAs ratio (Table-7) Impact of NPAs on ROE H 3: There is no significant negative impact of NPAs on ROE. The NPLs explain 96.7% of return on equity of SCBs as shown by the R 2. The findings show that there is an inverse relationship between NPAs and ROE and the coefficient value is (-) 1.963, which is statistically significant as the p-value is less than the significance level (0.000<0.05) It is concluded that NPA has significant effect on ROE of SCBs and results confirm that there is significant negative impact of NPAs on ROE contrary to hypothesis Impact of NPAs on Cost to Income Ratio H 4: There is no significant positive impact of NPAs on Cost Income Ratio. The variation to extent of 79% in Cost to Income Ratio of SCBs was explained by the NPAs as shown by the R 2. The relationship is positive and statistically significant as the p-value is less than the significance level (0.003<0.05). A unit increase in NPLs would lead to a 0.50 units increase in Cost to Income Ratio of SCBs. This indicates that NPA has significant effect on Cost Income Ratio of SCBs and increase in NPAs lead to cost inefficiency in the SCBs (Table-9) Impact of NPAs on Provisions H 5: There is no significant positive impact of NPAs on Provisions. The non-performing loans explain 98.6% of provisions of SCBs as shown by the R 2. It is observed that there is significant positive relationship as the p-value is less than the significance level (0.000<0.05). A unit increase in NPLs would lead to a 0.51 units increase in provisions of SCBs. It reveals that NPA has significant positive effect on provisions of SCBs and rejects the hypothesis (Table-10). VII. Conclusion NPAs have become major challenge for the bank industry, particularly since the global financial crisis and have adverse impact on performance. It was observed that the high level of NPAs trembles the confidence of investors, depositors, lenders etc. It causes poor recycling of funds, which in turn will have adverse effect on the deployment of credit. The non-recovery of loans affects not only further availability of credit but also financial soundness of the banks. The high incidence of NPA has cascading impact on all important financials of the banks viz., Profits, Return on Assets, Return on Equity, Dividend Payout, Provisions, Cost to Income ratio, Net Interest Margin, EVA, MVA etc., which are likely to erode the value for all stakeholders including Shareholders, Depositors, Borrowers, Employees and public at large. The results of statistical analysis indicated that NPAs have insignificant inverse relationship with profits, significant negative impact on ROA, ROE and significant positive impact on Cost to Income ratio and Provision. Thus, the NPAs have deleterious impact on various parameters of bank performance. References [1]. A. Barge, "NPA Management in Banks: An Indian Perspective," IBMRD's Journal of Management and Research, vol. 1, p. 1, [2]. D. S. Chhikara, "Causes and Impact of Non Performing Assets in Public Sector Banks: A state level analysis," Amity Management Analyst, vol. 1, no. 2, pp , DOI: /487X Page

7 [3]. K. A. Chisti, "The Impact of Asset Quality on Profitability of Private Banks in India: A case study Private banks," Journal of African Macroeconomic Review, vol. 2, no. 1, pp , [4]. N. F. b. A. Aziz, I. b. Ibrahim and M. b. Kamaruddin, "The Impact of Performing Loans (NPL) towards Profitability Performance (ROA, ROE, & NPM)," Shah Alam, [5]. S. Batra, "Developing the Asian Markets for Non-Performing Assets; Developments in India," in 3rd Forum on Asian Insolvency Reform, Seoul, Korea, [6]. K. Vora, "Management of NPA and Role of Asset Reconstruction Company, Recent Trends in Banking," [7]. M. Yadav, "Impact of Non-Performing Assets on Profitability and Productivity of Public Sector Banks in India," AFBE Journal, vol. 4, no. 1, DOI: /487X Page

8 DOI: /487X Page

9 DOI: /487X Page

10 DOI: /487X Page

11 IOSR Journal of Business and Management (IOSR-JBM) is UGC approved Journal with Sl. No. 4481, Journal no Fareed Ahmed. Non Performing Assets and Profitability of Scheduled Commercial Banks. IOSR Journal of Business and Management (IOSR-JBM), vol. 19, no. 9, 2017, pp DOI: /487X Page

A Comparative Analysis of Nonperforming Assets Management in Nationalised Banks of India (For the period to )

") Volume-7, Issue-1, January-February 2017 International Journal of Engineering and Management Research Page Number: 176-183 A Comparative Analysis of Nonperforming Assets Management in Nationalised Banks

Volume-7, Issue-1, January-February 2017 International Journal of Engineering and Management Research Page Number: 176-183 A Comparative Analysis of Nonperforming Assets Management in Nationalised Banks

DETERMINANTS OF COMMERCIAL BANKS LENDING: EVIDENCE FROM INDIAN COMMERCIAL BANKS Rishika Bhojwani Lecturer at Merit Ambition Classes Mumbai, India

DETERMINANTS OF COMMERCIAL BANKS LENDING: EVIDENCE FROM INDIAN COMMERCIAL BANKS Rishika Bhojwani Lecturer at Merit Ambition Classes Mumbai, India ABSTRACT: - This study investigated the determinants of

DETERMINANTS OF COMMERCIAL BANKS LENDING: EVIDENCE FROM INDIAN COMMERCIAL BANKS Rishika Bhojwani Lecturer at Merit Ambition Classes Mumbai, India ABSTRACT: - This study investigated the determinants of

PERFORMANCE OF IDBI BANK WITH REFERENCE TO NON PERFORMING ASSETS

PERFORMANCE OF IDBI BANK WITH REFERENCE TO NON PERFORMING ASSETS R.Navaneethakrishnasamy & M.Sharmila devi Ph.D. Research Scholar (Part-time), P.G and Research Department of Commerce, Sri S.R.N.M. College,

PERFORMANCE OF IDBI BANK WITH REFERENCE TO NON PERFORMING ASSETS R.Navaneethakrishnasamy & M.Sharmila devi Ph.D. Research Scholar (Part-time), P.G and Research Department of Commerce, Sri S.R.N.M. College,

KEY WORDS: N.P.A. (Non-Performing Assets), SARFAESI, Priority Sector Lending, Asset Classification, Provisioning, Prudential Norms

, SARFAESI, Priority Sector Lending, Asset Classification, Provisioning, Prudential Norms") PRIORITY SECTOR & NPA MANAGEMENT LENDING BY THE INDIAN BANKS Abstract The matter of NPA Management as drivers to financial stability in the Banking Sector has been attracting grave concern by the regulators

PRIORITY SECTOR & NPA MANAGEMENT LENDING BY THE INDIAN BANKS Abstract The matter of NPA Management as drivers to financial stability in the Banking Sector has been attracting grave concern by the regulators

NON PERFORMING ASSETS: A COMPARATIVE STUDY ON STATE BANK OF INDIA AND PUNJAB NATIONAL BANK

NON PERFORMING ASSETS: A COMPARATIVE STUDY ON STATE BANK OF INDIA AND PUNJAB NATIONAL BANK SHIVANI VAID Assistant Professor, Department of Commerce, St. Bede s College, Shimla, Himachal Pradesh ABSTRACT

NON PERFORMING ASSETS: A COMPARATIVE STUDY ON STATE BANK OF INDIA AND PUNJAB NATIONAL BANK SHIVANI VAID Assistant Professor, Department of Commerce, St. Bede s College, Shimla, Himachal Pradesh ABSTRACT

International Journal of Current Research and Modern Education (IJCRME) ISSN (Online): ( Volume I, Issue I, 2016 A

ISSN (Online): ( Volume I, Issue I, 2016 A") A COMPARATIVE STUDY ON NON PERFORMING ASSET MANAGEMENT OF SELECTED PUBLIC SECTOR BANK AND PRIVATE SECTOR BANK Harish Shetty* & S. N. Sandesha** Assistant professor, SDM College, Ujire, Karnataka Abstract:

A COMPARATIVE STUDY ON NON PERFORMING ASSET MANAGEMENT OF SELECTED PUBLIC SECTOR BANK AND PRIVATE SECTOR BANK Harish Shetty* & S. N. Sandesha** Assistant professor, SDM College, Ujire, Karnataka Abstract:

A Study on Impact of Bad Loans on Performance of Banks

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668 PP 37-41 www.iosrjournals.org A Study on Impact of Bad Loans on Performance of Banks karlapudi preethi karlapudipreethi58@gmail.com

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668 PP 37-41 www.iosrjournals.org A Study on Impact of Bad Loans on Performance of Banks karlapudi preethi karlapudipreethi58@gmail.com

Non-Performing Assets (NPAs) of Banks in India

of Banks in India") Non-Performing Assets (NPAs) of Banks in India 1. Build-up of corporate and banking sector vulnerabilities are grave cause for concern for the government of India as these have serious implications not

Non-Performing Assets (NPAs) of Banks in India 1. Build-up of corporate and banking sector vulnerabilities are grave cause for concern for the government of India as these have serious implications not

TRENDS OF NON PERFORMING ASSETS IN REGIONAL RURAL BANKS IN INDIA

www.eprawisdom.com e-issn : 2347-9671, p- ISSN : 2349-0187 EPRA International Journal of Economic and Business Review Vol - 4, Issue- 7, July 2016 Inno Space (SJIF) Impact Factor : 5.509(Morocco) ISI Impact

www.eprawisdom.com e-issn : 2347-9671, p- ISSN : 2349-0187 EPRA International Journal of Economic and Business Review Vol - 4, Issue- 7, July 2016 Inno Space (SJIF) Impact Factor : 5.509(Morocco) ISI Impact

CAUSES AND REMEDIES FOR NON PERFORMING- ASSETS IN INDIAN OVERSEAS BANK

IJER Serials Publications 12(1), 2015: 77-85 ISSN: 0972-9380 CAUSES AND REMEDIES FOR NON PERFORMING- ASSETS IN INDIAN OVERSEAS BANK Abstract: Public sector banks share a disproportionate burden of the

IJER Serials Publications 12(1), 2015: 77-85 ISSN: 0972-9380 CAUSES AND REMEDIES FOR NON PERFORMING- ASSETS IN INDIAN OVERSEAS BANK Abstract: Public sector banks share a disproportionate burden of the

A Study on the Analysis and Comparison of Non Performing Asset of Canara and HDFC Bank

DOI : 10.18843/ijms/v5i1(1)/11 DOI URL :http://dx.doi.org/10.18843/ijms/v5i1(1)/11 A Study on the Analysis and Comparison of Non Performing Asset of Canara and HDFC Bank Satheeshkumar. C, Guest Lecturer,

DOI : 10.18843/ijms/v5i1(1)/11 DOI URL :http://dx.doi.org/10.18843/ijms/v5i1(1)/11 A Study on the Analysis and Comparison of Non Performing Asset of Canara and HDFC Bank Satheeshkumar. C, Guest Lecturer,

Analysis of Priority and Non-Priority Sector NPAs of Indian Public Sectors Banks

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668 PP 56-61 www.iosrjournals.org Analysis of Priority and Non-Priority Sector NPAs of Indian Public Sectors Banks Kandela

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668 PP 56-61 www.iosrjournals.org Analysis of Priority and Non-Priority Sector NPAs of Indian Public Sectors Banks Kandela

Impact of Asset-Liability Management on the Profitability of Banks

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668. Volume 19, Issue 7. Ver. VI. (July 2017), PP 72-76 www.iosrjournals.org Impact of Asset-Liability Management on

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668. Volume 19, Issue 7. Ver. VI. (July 2017), PP 72-76 www.iosrjournals.org Impact of Asset-Liability Management on

FACTORS AFFECTING BANK CREDIT IN INDIA

Chapter-6 FACTORS AFFECTING BANK CREDIT IN INDIA Banks deploy credit as per their credit or loan policy. Credit policy of a bank, basically, provides a direction to the use of funds, controls the size

Chapter-6 FACTORS AFFECTING BANK CREDIT IN INDIA Banks deploy credit as per their credit or loan policy. Credit policy of a bank, basically, provides a direction to the use of funds, controls the size

Impact of non-performing assets on return on assets of public and private sector banks in India

2016; 2(9): 696-702 ISSN Print: 2394-7500 ISSN Online: 2394-5869 Impact Factor: 5.2 IJAR 2016; 2(9): 696-702 www.allresearchjournal.com Received: 07-07-2016 Accepted: 08-08-2016 D Jayakkodi Research Scholar,

2016; 2(9): 696-702 ISSN Print: 2394-7500 ISSN Online: 2394-5869 Impact Factor: 5.2 IJAR 2016; 2(9): 696-702 www.allresearchjournal.com Received: 07-07-2016 Accepted: 08-08-2016 D Jayakkodi Research Scholar,

Non Performing Assets: A Comparative Study of Public, Private and Foreign Banks

Non Performing Assets: A Comparative Study of Public, Private and Foreign Banks Dinesh Tandon Assistant Professor A. S. College, Khanna, Punjab-India Dr. Harpreet Singh Prof. & Director A. S. Group of

Non Performing Assets: A Comparative Study of Public, Private and Foreign Banks Dinesh Tandon Assistant Professor A. S. College, Khanna, Punjab-India Dr. Harpreet Singh Prof. & Director A. S. Group of

IJTRD Nov-Dec 2016 Available 168

Non-Performing Assets of Commercial Banks in India - A Study D. Siva Satyanarayana Part Time Research Scholar, Rayalaseema University, Kurnool and Lecturer In Commerce, Dr.V.S.Krishna Govt. Degree College

Non-Performing Assets of Commercial Banks in India - A Study D. Siva Satyanarayana Part Time Research Scholar, Rayalaseema University, Kurnool and Lecturer In Commerce, Dr.V.S.Krishna Govt. Degree College

MEASURING THE IMPACT OF NON-PERFORMING ASSETS ON THE PROFITABILITY OF INDIAN SCHEDULED COMMERCIAL BANKS

Available online at : http://euroasiapub.org, pp~285~294, Thomson Reuters ID: L-5236-2015 MEASURING THE IMPACT OF NON-PERFORMING ASSETS ON THE PROFITABILITY OF INDIAN SCHEDULED COMMERCIAL BANKS SUNITA

Available online at : http://euroasiapub.org, pp~285~294, Thomson Reuters ID: L-5236-2015 MEASURING THE IMPACT OF NON-PERFORMING ASSETS ON THE PROFITABILITY OF INDIAN SCHEDULED COMMERCIAL BANKS SUNITA

Effect of NPA on Banks Profitability

Effect of NPA on Banks Profitability Sri Ayan Chakraborty Faculty: Accounting & Finance Nopany Institute of Management Studies, Kolkata Abstract Banking business involves borrowing from the public in the

Effect of NPA on Banks Profitability Sri Ayan Chakraborty Faculty: Accounting & Finance Nopany Institute of Management Studies, Kolkata Abstract Banking business involves borrowing from the public in the

An Analysis of NPAs in Priority and Non-Priority Sectors with respect to Public Sector Banks in India

An Analysis of NPAs in Priority and Non-Priority Sectors with respect to Public Sector Banks in India Akshay Kumar Mishra 1 1 (Assistant Professor, L N Mishra College of Business Management, Muzaffarpur,

An Analysis of NPAs in Priority and Non-Priority Sectors with respect to Public Sector Banks in India Akshay Kumar Mishra 1 1 (Assistant Professor, L N Mishra College of Business Management, Muzaffarpur,

A STUDY ON NON PERFORMING ASSETS OF SELECT PUBLIC AND PRIVATE SECTOR BANKS IN INDIA

A STUDY ON NON PERFORMING ASSETS OF SELECT PUBLIC AND PRIVATE SECTOR BANKS IN INDIA D.JAYAKKODI 1 Dr.P.RENGARAJAN 2 1 Research Scholor, Department of Commerce, Vidyasagar College of Arts and Science, Udumalpet.

A STUDY ON NON PERFORMING ASSETS OF SELECT PUBLIC AND PRIVATE SECTOR BANKS IN INDIA D.JAYAKKODI 1 Dr.P.RENGARAJAN 2 1 Research Scholor, Department of Commerce, Vidyasagar College of Arts and Science, Udumalpet.

I. INTRODUCTION MEANING OF NPA

ISSN: 2349-7637 (Online) RESEARCH HUB International Multidisciplinary Research Journal (RHIMRJ) Research Paper Available online at: www.rhimrj.com A study on Recent Trend of Non-Performing Assets in Public

ISSN: 2349-7637 (Online) RESEARCH HUB International Multidisciplinary Research Journal (RHIMRJ) Research Paper Available online at: www.rhimrj.com A study on Recent Trend of Non-Performing Assets in Public

Scholars Journal of Economics, Business and Management e-issn

Scholars Journal of Economics, Business and Management e-issn 2348-532 Sarojit Mondal.; Sch J Econ Bus Manag, 215; 2(7B):768-772 p-issn 2348-8875 SAS Publishers (Scholars Academic and Scientific Publishers)

Scholars Journal of Economics, Business and Management e-issn 2348-532 Sarojit Mondal.; Sch J Econ Bus Manag, 215; 2(7B):768-772 p-issn 2348-8875 SAS Publishers (Scholars Academic and Scientific Publishers)

Chapter-6 RECOVERY OF LOANS AND NPAS

Chapter-6 RECOVERY OF LOANS AND NPAS RECOVERY Performance analysis of a bank cannot be conducted solely on the basis of resources mobilised or advances made. Resources mobilisation, deployment of resources

Chapter-6 RECOVERY OF LOANS AND NPAS RECOVERY Performance analysis of a bank cannot be conducted solely on the basis of resources mobilised or advances made. Resources mobilisation, deployment of resources

A Comprehensive Study of NPAs of Scheduled Commercial Banks

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668 PP 28-34 www.iosrjournals.org A Comprehensive Study of NPAs of Scheduled Commercial Banks Dr.K.SreeLatha Reddy, M.V.Sivaram

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668 PP 28-34 www.iosrjournals.org A Comprehensive Study of NPAs of Scheduled Commercial Banks Dr.K.SreeLatha Reddy, M.V.Sivaram

International Journal of Business and Administration Research Review, Vol. 3, Issue.15, July - Sep, Page 27

MANAGEMENT OF LIQUIDITY RISK IN THE INDIAN BANKING SECTOR-A CASE STUDY OF UCO BANK Dr. Suprava Sahu Assistant Professor, P.G.Department of Commerce, Ravenshaw University, Cuttack. Abstract Risk Management

MANAGEMENT OF LIQUIDITY RISK IN THE INDIAN BANKING SECTOR-A CASE STUDY OF UCO BANK Dr. Suprava Sahu Assistant Professor, P.G.Department of Commerce, Ravenshaw University, Cuttack. Abstract Risk Management

Role of recovery channels in managing Non-Performing Assets in Scheduled Commercial Banks

Role of recovery channels in managing Non-Performing Assets in Scheduled Commercial Banks Dr. KRISHNA BANANA 1 V RAMA KRISHNA RAO CHEPURI 2 1.Asst. Professor,Dept. Of Commerce & Bus. Admn., Acharya Nagajuna

Role of recovery channels in managing Non-Performing Assets in Scheduled Commercial Banks Dr. KRISHNA BANANA 1 V RAMA KRISHNA RAO CHEPURI 2 1.Asst. Professor,Dept. Of Commerce & Bus. Admn., Acharya Nagajuna

Pre and Post Merger Analysis of Non Performance Assets (NPAs): A Study with Special Reference to ICICI Bank Ltd.

: A Study with Special Reference to ICICI Bank Ltd.") DOI : 10.18843/ijms/v5i1(2)/08 DOIURL :http://dx.doi.org/10.18843/ijms/v5i1(2)/08 Pre and Post Merger Analysis of Non Performance Assets (NPAs): A Study with Special Reference to ICICI Bank Ltd. Dr. Veena

DOI : 10.18843/ijms/v5i1(2)/08 DOIURL :http://dx.doi.org/10.18843/ijms/v5i1(2)/08 Pre and Post Merger Analysis of Non Performance Assets (NPAs): A Study with Special Reference to ICICI Bank Ltd. Dr. Veena

An Analytical Study of Non-Performing Assets of Nationalized Banks in India

Volume-3, Issue-06, June 2016 ISSN: 2349-7637 (Online) RESEARCH HUB International Multidisciplinary Research Journal (RHIMRJ) Research Paper Available online at: www.rhimrj.com An Analytical Study of Non-Performing

Volume-3, Issue-06, June 2016 ISSN: 2349-7637 (Online) RESEARCH HUB International Multidisciplinary Research Journal (RHIMRJ) Research Paper Available online at: www.rhimrj.com An Analytical Study of Non-Performing

Keywords: Non-performing assets, schedule commercial banks, Advances, Net profit, Gross and Net NPA s. I. INTRODUCTION

ISSN: 2349-7637 (Online) (RHIMRJ) Research Paper Available online at: www.rhimrj.com A Study on Recent Trend of Non-Performing Assets in Scheduled Commercial Banks of India Tushar Mehta 1st Research Scholar,

ISSN: 2349-7637 (Online) (RHIMRJ) Research Paper Available online at: www.rhimrj.com A Study on Recent Trend of Non-Performing Assets in Scheduled Commercial Banks of India Tushar Mehta 1st Research Scholar,

PERFORMANCE EVALUATION OF PUBLIC, PRIVATE AND FOREIGN BANKS IN INDIA; AN EMPIRICAL ANALYSIS

PERFORMANCE EVALUATION OF PUBLIC, PRIVATE AND FOREIGN BANKS IN INDIA; AN EMPIRICAL ANALYSIS Mrs. Neetika Mahajan Research scholar, Department of commerce Himachal Pradesh University, Shimla Email ; Mahajanneetika18@gmail.com

PERFORMANCE EVALUATION OF PUBLIC, PRIVATE AND FOREIGN BANKS IN INDIA; AN EMPIRICAL ANALYSIS Mrs. Neetika Mahajan Research scholar, Department of commerce Himachal Pradesh University, Shimla Email ; Mahajanneetika18@gmail.com

CONTEMPORARY RESEARCH IN INDIA (ISSN ): VOL. 5: ISSUE: 3

: VOL. 5: ISSUE: 3") NON-PERFORMING ASSETS (NPA) OF REGIONAL RURAL BANKS OF ASSAM: A COMPARATIVE ANALYSIS Dr. A. Ibemcha Chanu, Assistant Professor (Sr), Dept. of Commerce, Assam University, Diphu Campus, Diphu, Assam Mr.

NON-PERFORMING ASSETS (NPA) OF REGIONAL RURAL BANKS OF ASSAM: A COMPARATIVE ANALYSIS Dr. A. Ibemcha Chanu, Assistant Professor (Sr), Dept. of Commerce, Assam University, Diphu Campus, Diphu, Assam Mr.

NPAs of Nationalised Banks of India: A Critical Review

ISSN: 2347-3215 Volume 1 Number 4 (2013) pp. 17-26 www.ijcrar.com NPAs of Nationalised Banks of India: A Critical Review Sakshi Jhamb 1 and H.V.Jhamb 2* 1 JJT University, Jhunjhunu, Rajasthan, India 2

ISSN: 2347-3215 Volume 1 Number 4 (2013) pp. 17-26 www.ijcrar.com NPAs of Nationalised Banks of India: A Critical Review Sakshi Jhamb 1 and H.V.Jhamb 2* 1 JJT University, Jhunjhunu, Rajasthan, India 2

IMPACT OF NON-PERFORMING ASSETS ON FINANCIAL POSITION OF THE PRIMARY AGRICULTURAL CO-OPERATIVE SOCIETIES

IMPACT OF NON-PERFORMING ASSETS ON FINANCIAL POSITION OF THE PRIMARY AGRICULTURAL CO-OPERATIVE SOCIETIES Popat Krishna Shinde Department of Commerce, Savitribai Phule Pune University Flat No. 3, Shrinarayan

IMPACT OF NON-PERFORMING ASSETS ON FINANCIAL POSITION OF THE PRIMARY AGRICULTURAL CO-OPERATIVE SOCIETIES Popat Krishna Shinde Department of Commerce, Savitribai Phule Pune University Flat No. 3, Shrinarayan

A Study on Non Performing Assets of Indians Banks: Trend and Recovery

A Study on Non Performing Assets of Indians Banks: Trend and Recovery Associate Professor, Department of Economics, Dayalbagh Educational Institute, Agra 1. INTRODUTION Banks are the basis of any economy.

A Study on Non Performing Assets of Indians Banks: Trend and Recovery Associate Professor, Department of Economics, Dayalbagh Educational Institute, Agra 1. INTRODUTION Banks are the basis of any economy.

Non Performing Assets: A study of State Bank of India

Non Performing Assets: A study of State Bank of India KALPESH GANDHI Lecturer in Satyaprakash College, Affiliated with Saurashtra University, Rajkot Abstract: After the evolution of banking system, the

Non Performing Assets: A study of State Bank of India KALPESH GANDHI Lecturer in Satyaprakash College, Affiliated with Saurashtra University, Rajkot Abstract: After the evolution of banking system, the

An Empirical Study on Financial Performance Analysis of Selected Public Sector Banks in India

Volume-03 Issue-10 October-2018 ISSN: 2455-3085 (Online) www.rrjournals.com [UGC Listed Journal] An Empirical Study on Financial Performance Analysis of Selected Public Sector Banks in India *1 Dr. Jayesh

Volume-03 Issue-10 October-2018 ISSN: 2455-3085 (Online) www.rrjournals.com [UGC Listed Journal] An Empirical Study on Financial Performance Analysis of Selected Public Sector Banks in India *1 Dr. Jayesh

MEMBERS' REFERENCE SERVICE LARRDIS LOK SABHA SECRETARIAT, NEW DELHI REFERENCE NOTE. No. 39/RN/Ref/October/2016

MEMBERS' REFERENCE SERVICE LARRDIS LOK SABHA SECRETARIAT, NEW DELHI REFERENCE NOTE No. 39/RN/Ref/October/2016 For the use of Members of Parliament NOT FOR PUBLICATION 1 NON PERFORMING ASSETS IN PUBLIC

MEMBERS' REFERENCE SERVICE LARRDIS LOK SABHA SECRETARIAT, NEW DELHI REFERENCE NOTE No. 39/RN/Ref/October/2016 For the use of Members of Parliament NOT FOR PUBLICATION 1 NON PERFORMING ASSETS IN PUBLIC

Application of financial analysis in evaluation of financial position of IDBI

Application of financial analysis in evaluation of financial position of IDBI #Dr. Partap Singh Chahal (First& Corresponding Author) Associate Professor, Deptt. Of Management Studies, amalkha Group of

Application of financial analysis in evaluation of financial position of IDBI #Dr. Partap Singh Chahal (First& Corresponding Author) Associate Professor, Deptt. Of Management Studies, amalkha Group of

NON-PERFORMING ASSETS OF SCHEDULED COMMERCIAL BANKS IN INDIA: ITS REGULATORY FRAME WORK

154 NON-PERFORMING ASSETS OF SCHEDULED COMMERCIAL BANKS IN INDIA: ITS REGULATORY FRAME WORK Rabindra Kumar Swain Asst. Professor, P.G. Department of commerce, Utkal University, Bhubaneswar-751004, Odisha

154 NON-PERFORMING ASSETS OF SCHEDULED COMMERCIAL BANKS IN INDIA: ITS REGULATORY FRAME WORK Rabindra Kumar Swain Asst. Professor, P.G. Department of commerce, Utkal University, Bhubaneswar-751004, Odisha

Non-Performing Assets - Status And Impact

Non-Performing Assets - Status And Impact Ms. Laveena Mehta Assistant Professor, Chitkara University, Research Scholar, Punjab Technical University Avneet Singh Student, Chitkara University, Punjab Abstract:

Non-Performing Assets - Status And Impact Ms. Laveena Mehta Assistant Professor, Chitkara University, Research Scholar, Punjab Technical University Avneet Singh Student, Chitkara University, Punjab Abstract:

A comparative study of financial performance: Deutsche bank & standard chartered bank

International Journal of Commerce and Management Research ISSN: 24551627, Impact Factor: RJIF 5.22 www.managejournal.com Volume 2; Issue 3; March 2016; Page No. 143147 A comparative study of financial

International Journal of Commerce and Management Research ISSN: 24551627, Impact Factor: RJIF 5.22 www.managejournal.com Volume 2; Issue 3; March 2016; Page No. 143147 A comparative study of financial

Management of Non-Performing Assets in Virudhunagar District Central Co-Operative Bank-An Overview

Middle-East Journal of Scientific Research 20 (7): 851-855, 2014 ISSN 1990-9233 IDOSI Publications, 2014 DOI: 10.5829/idosi.mejsr.2014.20.07.114016 Management of Non-Performing Assets in Virudhunagar District

Middle-East Journal of Scientific Research 20 (7): 851-855, 2014 ISSN 1990-9233 IDOSI Publications, 2014 DOI: 10.5829/idosi.mejsr.2014.20.07.114016 Management of Non-Performing Assets in Virudhunagar District

ASSET CLASSIFICATION, PROVISIONING AND SUSPENSION OF INTEREST

FINANCIAL INSTITUTIONS COMMISSION PRUDENTIAL REGULATION FIC-PR-02 ASSET CLASSIFICATION, PROVISIONING AND SUSPENSION OF INTEREST Arrangement of Paragraphs PARAGRAPH 1. Short Title 2. Authorization 3. Application

FINANCIAL INSTITUTIONS COMMISSION PRUDENTIAL REGULATION FIC-PR-02 ASSET CLASSIFICATION, PROVISIONING AND SUSPENSION OF INTEREST Arrangement of Paragraphs PARAGRAPH 1. Short Title 2. Authorization 3. Application

NON-PERFORMING ASSETS A BIGGEST CHALLENGE IN BANKING SECTOR- A COMPARATIVE STUDY BETWEEN INDIA AND BANGLADESH BANKING SECTOR

SUDIN BAG AND SAJIJUL ISLAM: NON-PERFORMING ASSETS A BIGGEST CHALLENGE IN BANKING SECTOR- A COMPARATIVE STUDY BETWEEN INDIA AND DOI: 10.21917/ijms.2017.0084 NON-PERFORMING ASSETS A BIGGEST CHALLENGE IN

SUDIN BAG AND SAJIJUL ISLAM: NON-PERFORMING ASSETS A BIGGEST CHALLENGE IN BANKING SECTOR- A COMPARATIVE STUDY BETWEEN INDIA AND DOI: 10.21917/ijms.2017.0084 NON-PERFORMING ASSETS A BIGGEST CHALLENGE IN

Assessment of Financial Performance of Software Companies in India

Assessment of Financial Performance of Software Companies in India Ellangi Pushpalatha H No: 6-3-1177/A/38 & 42, Shahjehan College of Business Management, Minister's Colony, Kundan Bagh, Begumpet, Hyderabad.

Assessment of Financial Performance of Software Companies in India Ellangi Pushpalatha H No: 6-3-1177/A/38 & 42, Shahjehan College of Business Management, Minister's Colony, Kundan Bagh, Begumpet, Hyderabad.

CHAPTER I INTRODUCTION

CHAPTER I INTRODUCTION Commercial banks undertake a wide variety of activities, which play a critical role in the economy of a country. They pool and absorb risks for depositors and provide a stable source

CHAPTER I INTRODUCTION Commercial banks undertake a wide variety of activities, which play a critical role in the economy of a country. They pool and absorb risks for depositors and provide a stable source

Comparative Analysis of NPAs and Credit Deployment of Scheduled commercial Banks of India

Comparative Analysis of NPAs and Credit Deployment of Scheduled commercial Banks of India Shailja Vasisht Assistant Professor, PCTE Group of Institutes Ludhiana ABSTRACT In India, the banks are being segregated

Comparative Analysis of NPAs and Credit Deployment of Scheduled commercial Banks of India Shailja Vasisht Assistant Professor, PCTE Group of Institutes Ludhiana ABSTRACT In India, the banks are being segregated

A Comparative Study of Non-Performing Assets of Public Section and Private Sector banks in India

68 A Comparative Study of Non-Performing Assets of Public Section and Private Sector banks in India Neha Yadav, RBMI, Greater Noida Abstract Banking sectors is exposed to number of risk like market risk,

68 A Comparative Study of Non-Performing Assets of Public Section and Private Sector banks in India Neha Yadav, RBMI, Greater Noida Abstract Banking sectors is exposed to number of risk like market risk,

Munish Gupta. Payal. Priya Gupta

Non Performing Assets: A Study of Public Bank and Private Bank Munish Gupta Assistant Professor, Faculty of Commerce, Arya (PG) College, Panipat, Haryana, India Payal Faculty of Commerce, Haryana, India

Non Performing Assets: A Study of Public Bank and Private Bank Munish Gupta Assistant Professor, Faculty of Commerce, Arya (PG) College, Panipat, Haryana, India Payal Faculty of Commerce, Haryana, India

Journal of Advance Management Research, ISSN:

INTRODUCTION FINANCIAL PERFORMANCE OF PUBLIC AND PRIVATE SECTORS BANKS IN INDIA Cheenu Goel Research Scholar, I.K.Gujral Punjab Technical University, Jalandhar Dr. K.N.S Kang Director General, PCTE Group

INTRODUCTION FINANCIAL PERFORMANCE OF PUBLIC AND PRIVATE SECTORS BANKS IN INDIA Cheenu Goel Research Scholar, I.K.Gujral Punjab Technical University, Jalandhar Dr. K.N.S Kang Director General, PCTE Group

A Study of Non-Performing Assets and its Impact on Banking Sector

Journal for Research Volume 03 Issue 01 March 2017 ISSN: 2395-7549 A Study of Non-Performing Assets and its Impact on Banking Sector Dr. Ujjwal M. Mishra Associate Professor Department of Management Studies

Journal for Research Volume 03 Issue 01 March 2017 ISSN: 2395-7549 A Study of Non-Performing Assets and its Impact on Banking Sector Dr. Ujjwal M. Mishra Associate Professor Department of Management Studies

RIJBFA Volume 2, Issue 1 (January 2012) ISSN: X. A Journal of Radix International Educational and. Research Consortium RIJBFA

ISSN: X. A Journal of Radix International Educational and. Research Consortium RIJBFA") A Journal of Radix International Educational and Research Consortium RIJBFA RADIX INTERNATIONAL JOURNAL OF BANKING, FINANCE AND ACCOUNTING RESEARCH PAPER ON PERFORMANCE APPRAISAL OF SELECTED BANKS IN INDIA

A Journal of Radix International Educational and Research Consortium RIJBFA RADIX INTERNATIONAL JOURNAL OF BANKING, FINANCE AND ACCOUNTING RESEARCH PAPER ON PERFORMANCE APPRAISAL OF SELECTED BANKS IN INDIA

Chapter 4 Financial Strength Analysis

Chapter 4 Financial Strength Analysis 4.1 Meaning of Financial Strength Finance is an essential requirement for every business enterprise. Various type of finance was needed by the concern for their activity

Chapter 4 Financial Strength Analysis 4.1 Meaning of Financial Strength Finance is an essential requirement for every business enterprise. Various type of finance was needed by the concern for their activity

The Impact of Liquidity Ratios on Profitability (With special reference to Listed Manufacturing Companies in Sri Lanka)

") The Impact of Liquidity Ratios on Profitability (With special reference to Listed Manufacturing Companies in Sri Lanka) K. H. I. Madushanka 1, M. Jathurika 2 1, 2 Department of Business and Management

The Impact of Liquidity Ratios on Profitability (With special reference to Listed Manufacturing Companies in Sri Lanka) K. H. I. Madushanka 1, M. Jathurika 2 1, 2 Department of Business and Management

THE INFLUENCE OF ECONOMIC FACTORS ON PROFITABILITY OF COMMERCIAL BANKS

THE INFLUENCE OF ECONOMIC FACTORS ON PROFITABILITY OF COMMERCIAL BANKS 1 YVES CLAUDE NSHIMIYIMANA, 2 MIZEROYABADEGE ALYDA ZUBEDA UNILAK University of Lay Adventists of Kigali E-mail: 1 dryvesclaude@gmail.com,

THE INFLUENCE OF ECONOMIC FACTORS ON PROFITABILITY OF COMMERCIAL BANKS 1 YVES CLAUDE NSHIMIYIMANA, 2 MIZEROYABADEGE ALYDA ZUBEDA UNILAK University of Lay Adventists of Kigali E-mail: 1 dryvesclaude@gmail.com,

COMPARATIVE ANALYSIS OF SELECTED INDIAN HOUSING FINANCE COMPANIES BASED ON CAMEL APPROACH

Scholarly Research Journal for Interdisciplinary Studies, Online ISSN 2278-8808, SJIF 2016 = 6.17, www.srjis.com UGC Approved Sr. No.49366, NOV-DEC 2017, VOL- 4/37 https://doi.org/10.21922/srjis.v4i37.10662

Scholarly Research Journal for Interdisciplinary Studies, Online ISSN 2278-8808, SJIF 2016 = 6.17, www.srjis.com UGC Approved Sr. No.49366, NOV-DEC 2017, VOL- 4/37 https://doi.org/10.21922/srjis.v4i37.10662

EFFECT OF NON PERFORMING ASSETS ON THE PROFITABILITY OF BANKS A SELECTIVE STUDY

International Journal of Business and General Management (IJBGM) ISSN(P): 2319-2267; ISSN(E): 2319-2275 Vol. 5, Issue 2, Feb - Mar 2016; 53-60 IASET EFFECT OF NON PERFORMING ASSETS ON THE PROFITABILITY

International Journal of Business and General Management (IJBGM) ISSN(P): 2319-2267; ISSN(E): 2319-2275 Vol. 5, Issue 2, Feb - Mar 2016; 53-60 IASET EFFECT OF NON PERFORMING ASSETS ON THE PROFITABILITY

A Study of Financial Aspects of SIDBI

IOSR Journal of Economics and Finance (IOSR-JEF) e-issn: 2321-5933, p-issn: 2321-5925.Volume 6, Issue 1. Ver. II (Jan.-Feb. 2015), PP 41-45 www.iosrjournals.org A Study of Financial Aspects of SIDBI Sandeep

IOSR Journal of Economics and Finance (IOSR-JEF) e-issn: 2321-5933, p-issn: 2321-5925.Volume 6, Issue 1. Ver. II (Jan.-Feb. 2015), PP 41-45 www.iosrjournals.org A Study of Financial Aspects of SIDBI Sandeep

STOCK PRICE BEHAVIOR AND OPERATIONAL RISK MANAGEMENT OF BANKS IN INDIA

STOCK PRICE BEHAVIOR AND OPERATIONAL RISK MANAGEMENT OF BANKS IN INDIA Ketty Vijay Parthasarathy 1, Dr. R Madhumathi 2. 1 Research Scholar, Department of Management Studies, Indian Institute of Technology

STOCK PRICE BEHAVIOR AND OPERATIONAL RISK MANAGEMENT OF BANKS IN INDIA Ketty Vijay Parthasarathy 1, Dr. R Madhumathi 2. 1 Research Scholar, Department of Management Studies, Indian Institute of Technology

Impact of Assets Quality and Profitability of Selected Indian Public Sector Banks

Impact of Assets Quality and Profitability of Selected Indian Public Sector Banks J. Kumar 1 and R. Thamil selvan 2 1 Research Scholar, Sathyabama University, Chennai 600 119, Email: leckumar@gmail.com

Impact of Assets Quality and Profitability of Selected Indian Public Sector Banks J. Kumar 1 and R. Thamil selvan 2 1 Research Scholar, Sathyabama University, Chennai 600 119, Email: leckumar@gmail.com

A Study on Women s Preference To wards Mutual Fund Investments with Special Reference To Cochin.

IOSR Journal Of Humanities And Social Science (IOSR-JHSS) Volume 21, Issue 7, Ver. V1I (July. 2016) PP 23-28 e-issn: 2279-0837, p-issn: 2279-0845. www.iosrjournals.org A Study on Women s Preference To

IOSR Journal Of Humanities And Social Science (IOSR-JHSS) Volume 21, Issue 7, Ver. V1I (July. 2016) PP 23-28 e-issn: 2279-0837, p-issn: 2279-0845. www.iosrjournals.org A Study on Women s Preference To

Chapter - VI Profitability Analysis of Indian General Insurance Industry

Chapter - VI Profitability Analysis of Indian General Insurance Industry As a result of the various reforms introduced by the Government of India in the insurance sector, private companies have made their

Chapter - VI Profitability Analysis of Indian General Insurance Industry As a result of the various reforms introduced by the Government of India in the insurance sector, private companies have made their

Home Financial Bancorp

Auditor s Report and Consolidated Financial Statements Contents Independent Auditor s Report... 1 Consolidated Financial Statements Balance Sheets... 3 Statements of Income... 4 Statements of Comprehensive

Auditor s Report and Consolidated Financial Statements Contents Independent Auditor s Report... 1 Consolidated Financial Statements Balance Sheets... 3 Statements of Income... 4 Statements of Comprehensive

A Study on the Debt Recovery Agencies

A Study on the Debt Recovery Agencies Dr. B.Saritha 1 PhD Finance Principal, MG University, Nalgonda Dist. Mrs. Seema Nazneen 2 Mrs CH Siva Priya 3 Research Scholar Assistant Prof School of Business Management

A Study on the Debt Recovery Agencies Dr. B.Saritha 1 PhD Finance Principal, MG University, Nalgonda Dist. Mrs. Seema Nazneen 2 Mrs CH Siva Priya 3 Research Scholar Assistant Prof School of Business Management

Issues in Audit and Tax Audit of Banks

SPECIAL STORY Financial Services Sector : Part-I (Banks and Mutual Funds) CA Sarvesh Warty Issues in Audit and Tax Audit of Banks Banking in India is dominated by nationalised banks who account for around

SPECIAL STORY Financial Services Sector : Part-I (Banks and Mutual Funds) CA Sarvesh Warty Issues in Audit and Tax Audit of Banks Banking in India is dominated by nationalised banks who account for around

SOLVENCY OF PUBLIC SECTOR BANKS

SOLVENCY OF PUBLIC SECTOR BANKS R.V. Hema 1 Dr.S.Mohan 2 Abstract Solvency is a company's ability to meet all of its debt obligations. Solvency generally describes a company's ability to meet its long-term

SOLVENCY OF PUBLIC SECTOR BANKS R.V. Hema 1 Dr.S.Mohan 2 Abstract Solvency is a company's ability to meet all of its debt obligations. Solvency generally describes a company's ability to meet its long-term

NPAs and their assignment to Assets Reconstruction Companies (ARCs)

") Introduction NPAs and their assignment to Assets Reconstruction Companies (ARCs) Dr. A.N. Garg NPA is a classification used by financial institutions that refer to loans that are in jeopardy of default.

Introduction NPAs and their assignment to Assets Reconstruction Companies (ARCs) Dr. A.N. Garg NPA is a classification used by financial institutions that refer to loans that are in jeopardy of default.

*Contact Author

Efficiency of Private Sector Banks Performance Comparison Between Old and New Generation Private Sector Banks Binish Varghese M. 1*, Suman Chakraborty 1 1 Faculty of Management and Commerce, M.S. Ramaiah

Efficiency of Private Sector Banks Performance Comparison Between Old and New Generation Private Sector Banks Binish Varghese M. 1*, Suman Chakraborty 1 1 Faculty of Management and Commerce, M.S. Ramaiah

Priority Sector Lending: Trends, Issues and Strategies

24 Priority Sector Lending: Trends, Issues and Strategies Shilpa Rani, Research Scholar, Kurukshetra University, Kurukshetra Diksha Garg, Research Scholar, Kurukshetra University, Kurukshetra ABSTRACT

24 Priority Sector Lending: Trends, Issues and Strategies Shilpa Rani, Research Scholar, Kurukshetra University, Kurukshetra Diksha Garg, Research Scholar, Kurukshetra University, Kurukshetra ABSTRACT

IMPACT OF ACQUISITIONS THROUGH VALUE ADDITION - A CASE STUDY OF TATA STEEL AND TATA POWER COMPANIES IN INDIA

Tactful Management Research Journal ISSN :2319-7943 Impact Factor : 2.1632 (UIF) Vol. 3 Issue. 4 Jan 2015 Available online at www.lsrj.in IMPACT OF ACQUISITIONS THROUGH VALUE ADDITION - A CASE STUDY OF

Tactful Management Research Journal ISSN :2319-7943 Impact Factor : 2.1632 (UIF) Vol. 3 Issue. 4 Jan 2015 Available online at www.lsrj.in IMPACT OF ACQUISITIONS THROUGH VALUE ADDITION - A CASE STUDY OF

AN ANALYSIS OF PRODUCTIVITY OF SCHEDULED COMMERCIAL BANKS IN INDIA. Ms. PRASANNA PRAKASH, SR. ASST PROF DEPARTMENT OF COMMERCE & MANAGEMENT

International Journal of Engineering & Scientific Research Vol. 6 Issue 3, March 2018, ISSN: 2347-6532 Impact Factor: 6.660 Journal Homepage: Double-Blind Peer Reviewed Refereed Open Access International

International Journal of Engineering & Scientific Research Vol. 6 Issue 3, March 2018, ISSN: 2347-6532 Impact Factor: 6.660 Journal Homepage: Double-Blind Peer Reviewed Refereed Open Access International

AN EVALUATION OF NON PERFORMING ASSETS: A STUDY OF BANKING SECTOR IN INDIA

AN EVALUATION OF NON PERFORMING ASSETS: A STUDY OF BANKING Dr. Madan Lal Singla* SECTOR IN INDIA Abstract: NPAs point out the credit risk of the banks and the financial institutions. Operational effectiveness

AN EVALUATION OF NON PERFORMING ASSETS: A STUDY OF BANKING Dr. Madan Lal Singla* SECTOR IN INDIA Abstract: NPAs point out the credit risk of the banks and the financial institutions. Operational effectiveness

NON-PERFORMING ASSETS IN INDIAN BANKING AND THE ROLE OF ASSET RECONSTRUCTION COMPANIES

ABHIJIT SINHA: NON-PERFORMING ASSETS IN INDIAN RANKING AND THE ROLE OF ASSET RECONSTRUCTION COMPANIES DOI: 10.21917/ijms.2016.0032 NON-PERFORMING ASSETS IN INDIAN BANKING AND THE ROLE OF ASSET RECONSTRUCTION

ABHIJIT SINHA: NON-PERFORMING ASSETS IN INDIAN RANKING AND THE ROLE OF ASSET RECONSTRUCTION COMPANIES DOI: 10.21917/ijms.2016.0032 NON-PERFORMING ASSETS IN INDIAN BANKING AND THE ROLE OF ASSET RECONSTRUCTION

Non performing assets of NBFI S in India

Non performing of NBFI S in India Journal of Social Welfare and Management 103 Volume 4 Number 2, April - June 2012 S. Kamalaveni*, R. Anitha** Abstract This paper focuses on the non-performing of NBFI

Non performing of NBFI S in India Journal of Social Welfare and Management 103 Volume 4 Number 2, April - June 2012 S. Kamalaveni*, R. Anitha** Abstract This paper focuses on the non-performing of NBFI

THE BANKING AND FINANCIAL INSTITUTIONS (MANAGEMENT OF RISK ASSETS) REGULATIONS, 2008

REGULATIONS, 2008") THE BANKING AND FINANCIAL INSTITUTIONS (MANAGEMENT OF RISK ASSETS) REGULATIONS, 2008 ARRANGEMENT OF REGULATIONS Regulations Title PART I PRELIMINARY PROVISIONS 1. Short title 2. Application 3. Interpretation

THE BANKING AND FINANCIAL INSTITUTIONS (MANAGEMENT OF RISK ASSETS) REGULATIONS, 2008 ARRANGEMENT OF REGULATIONS Regulations Title PART I PRELIMINARY PROVISIONS 1. Short title 2. Application 3. Interpretation

NON- PERFORMING ASSETS AND THE SURVIVABILITY OF BANKS

NON- PERFORMING ASSETS AND THE SURVIVABILITY OF BANKS Maneesh Kant Arya Associate Professor, Institute of Management Studies DAVV, Indore (M.P.) India Email maneesharya@gmail.com ABSTRACT There are many

NON- PERFORMING ASSETS AND THE SURVIVABILITY OF BANKS Maneesh Kant Arya Associate Professor, Institute of Management Studies DAVV, Indore (M.P.) India Email maneesharya@gmail.com ABSTRACT There are many

INTERNATIONAL FINANCIAL REPORTING SYSTEM- A CASE STUDY OF ICICI BANK

INTERNATIONAL FINANCIAL REPORTING SYSTEM- A CASE STUDY OF ICICI BANK DR SUPRAVA SAHU,Assistant Professor, P.G. Dept of Commerce, Ravenshaw University ABSTRACT IFRS have been recognized as the global financial

INTERNATIONAL FINANCIAL REPORTING SYSTEM- A CASE STUDY OF ICICI BANK DR SUPRAVA SAHU,Assistant Professor, P.G. Dept of Commerce, Ravenshaw University ABSTRACT IFRS have been recognized as the global financial

Performance, Regulation and Supervision of NBFIs

7.1 Non Bank Financial Institutions (NBFIs) are playing a crucial role by providing additional financial services that cannot be always provided by the banks. The NBFIs, with more multifaceted products

7.1 Non Bank Financial Institutions (NBFIs) are playing a crucial role by providing additional financial services that cannot be always provided by the banks. The NBFIs, with more multifaceted products

Japan s Nonperforming Loan Problem

Japan s Nonperforming Loan Problem Released on October 11, 1 Japan s Nonperforming Loan Problem 2 I. Summary Japan s nonperforming loan (NPL) problem should be regarded as being inextricably linked with

Japan s Nonperforming Loan Problem Released on October 11, 1 Japan s Nonperforming Loan Problem 2 I. Summary Japan s nonperforming loan (NPL) problem should be regarded as being inextricably linked with

TABLE OF CONTENTS. President's Letter to Shareholders Selected Consolidated Financial and Other Data... 2

3 TABLE OF CONTENTS Page President's Letter to Shareholders... 1 Selected Consolidated Financial and Other Data... 2 Management's Discussion and Analysis of Financial Condition and Results of Operations...

3 TABLE OF CONTENTS Page President's Letter to Shareholders... 1 Selected Consolidated Financial and Other Data... 2 Management's Discussion and Analysis of Financial Condition and Results of Operations...

C A Y M A N I S L A N D S MONETARY AUTHORITY

Statement of Guidance Credit Risk Classification, Provisioning and Management Policy and Development Division Page 1 of 22 Table of Contents 1 Statement of Objectives... 3 2 Scope... 3 3 Terminology...

Statement of Guidance Credit Risk Classification, Provisioning and Management Policy and Development Division Page 1 of 22 Table of Contents 1 Statement of Objectives... 3 2 Scope... 3 3 Terminology...

Non Performing Assets of Indian Banking System and its Impact on Economy

IOSR Journal of Economics and Finance (IOSR-JEF) e-issn: 2321-5933, p-issn: 2321-5925.Volume 7, Issue 6 Ver. III (Nov. - Dec. 2016), PP 21-26 www.iosrjournals.org Non Performing Assets of Indian Banking

IOSR Journal of Economics and Finance (IOSR-JEF) e-issn: 2321-5933, p-issn: 2321-5925.Volume 7, Issue 6 Ver. III (Nov. - Dec. 2016), PP 21-26 www.iosrjournals.org Non Performing Assets of Indian Banking

A Study on Trend Performance of Foreign Banks operating in India

A Study on Trend Performance of Foreign Banks operating in India M.Kirthika Assistant Professor PSGR Krishnammal for Women Coimbatore Tamil Nadu South India S.Nirmala Associate Professor PSGR Krishnammal

A Study on Trend Performance of Foreign Banks operating in India M.Kirthika Assistant Professor PSGR Krishnammal for Women Coimbatore Tamil Nadu South India S.Nirmala Associate Professor PSGR Krishnammal

Regional Rural Banks In Maharashtra State - Performance Evaluation Of Regional Rural Banks Of Maharashtra State Using CAMEL Method

Regional Rural Banks In Maharashtra State - Performance Evaluation Of Regional Rural Banks Of Maharashtra State Using CAMEL Method Suneet Sureshchandra Kopra Research Scholar, Singhania University, Pacheri

Regional Rural Banks In Maharashtra State - Performance Evaluation Of Regional Rural Banks Of Maharashtra State Using CAMEL Method Suneet Sureshchandra Kopra Research Scholar, Singhania University, Pacheri

Management of cash in Public sector Enterprises - A case study of ECIL, Hyderabad

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668 PP 50-55 www.iosrjournals.org Management of cash in Public sector Enterprises - A case study of ECIL, Hyderabad Dr.N.Jyothi

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668 PP 50-55 www.iosrjournals.org Management of cash in Public sector Enterprises - A case study of ECIL, Hyderabad Dr.N.Jyothi

Summary of Reserve Bank of India s New Guidelines for NBFCs

Summary of Reserve Bank of India s New Guidelines for NBFCs CA Rajesh Pabari D r e a m O p t i m u s C o n s u l t i n g 1 8 0, G r o u n d F l o o r, R a g h u l e e l a M a l l, K a n d i v a l i ( W

Summary of Reserve Bank of India s New Guidelines for NBFCs CA Rajesh Pabari D r e a m O p t i m u s C o n s u l t i n g 1 8 0, G r o u n d F l o o r, R a g h u l e e l a M a l l, K a n d i v a l i ( W

Community First Financial Corporation

Independent Auditor s Report and Consolidated Financial Statements Contents Independent Auditor s Report... 1 Consolidated Financial Statements Balance Sheets... 3 Statements of Income... 4 Statements

Independent Auditor s Report and Consolidated Financial Statements Contents Independent Auditor s Report... 1 Consolidated Financial Statements Balance Sheets... 3 Statements of Income... 4 Statements

PERFORMANCE EVALUATION OF SELECTED BANKS USING ECONOMIC VALUE ADDED ABSTRACT

PERFORMANCE EVALUATION OF SELECTED BANKS USING ECONOMIC VALUE ADDED Dr. Shivappa, Associate Professor, Kousali Institute of Management Studies, Karnatak University Dharwad. Mrs. Jyoti N Talreja, Assistant

PERFORMANCE EVALUATION OF SELECTED BANKS USING ECONOMIC VALUE ADDED Dr. Shivappa, Associate Professor, Kousali Institute of Management Studies, Karnatak University Dharwad. Mrs. Jyoti N Talreja, Assistant

Banco de Credito e Inversiones, S.A., Miami Branch

Banco de Credito e Inversiones, S.A., Miami Branch Financial Statements as of and for the Years Ended December 31, 2014 and 2013, Supplemental Information Schedules as of and for the Year Ended December

Banco de Credito e Inversiones, S.A., Miami Branch Financial Statements as of and for the Years Ended December 31, 2014 and 2013, Supplemental Information Schedules as of and for the Year Ended December

Bank Characteristics and Payout Policy

Asian Social Science; Vol. 10, No. 1; 2014 ISSN 1911-2017 E-ISSN 1911-2025 Published by Canadian Center of Science and Education Bank Characteristics and Payout Policy Seok Weon Lee 1 1 Division of International

Asian Social Science; Vol. 10, No. 1; 2014 ISSN 1911-2017 E-ISSN 1911-2025 Published by Canadian Center of Science and Education Bank Characteristics and Payout Policy Seok Weon Lee 1 1 Division of International

FINANCIAL PERFORMANCE: A COMPARATIVE ANALYSIS STUDY OF PNB AND HDFC BANK

International Journal of Marketing & Financial Management, Volume 4, Issue 2, Feb-Mar-2016, pp 47-60 ISSN: 2348 3954 (Online) ISSN: 2349 2546 (Print), Impact factor: 0.98 FINANCIAL PERFORMANCE: A COMPARATIVE

International Journal of Marketing & Financial Management, Volume 4, Issue 2, Feb-Mar-2016, pp 47-60 ISSN: 2348 3954 (Online) ISSN: 2349 2546 (Print), Impact factor: 0.98 FINANCIAL PERFORMANCE: A COMPARATIVE

Empirical Study on Non Performing Assets of Bank Dr. Sonia Narula 1 ASSISTANT PROFESSOR DAV CENTENARY COLLEGE Faridabad - India

Volume 2, Issue 1, January 2014 International Journal of Advance Research in Computer Science and Management Studies Research Paper Available online at: www.ijarcsms.com ISSN: 2321-7782 (Online) Empirical

Volume 2, Issue 1, January 2014 International Journal of Advance Research in Computer Science and Management Studies Research Paper Available online at: www.ijarcsms.com ISSN: 2321-7782 (Online) Empirical

Financial Report December 31, 2015

Financial Report December 31, 2015 Contents Independent auditor s report 1 Financial statements Balance sheets 2 Statements of income 3 Statements of changes in stockholders equity 4 Statements of cash

Financial Report December 31, 2015 Contents Independent auditor s report 1 Financial statements Balance sheets 2 Statements of income 3 Statements of changes in stockholders equity 4 Statements of cash

Non Performing Assets (NPAs): A Comparative Analysis of Selected Private Sector Banks

: A Comparative Analysis of Selected Private Sector Banks") International Journal of Humanities and Social Science Invention ISSN (Online): 2319 7722, ISSN (Print): 2319 7714 Volume 6 Issue 1 January. 2017 PP.47-53 Non Performing Assets (NPAs): A Comparative Analysis

International Journal of Humanities and Social Science Invention ISSN (Online): 2319 7722, ISSN (Print): 2319 7714 Volume 6 Issue 1 January. 2017 PP.47-53 Non Performing Assets (NPAs): A Comparative Analysis

AN ANALYSIS OF ASSETS QUALITY OF NATIONALISED BANKS

AN ANALYSIS OF ASSETS QUALITY OF NATIONALISED BANKS Deepak Kumar Sharma Asstt. Professor, Deptt of Commerce, M.M.P.G. College, Fatehabad Abstract Non Performing Assets affect the profitability, liquidity

AN ANALYSIS OF ASSETS QUALITY OF NATIONALISED BANKS Deepak Kumar Sharma Asstt. Professor, Deptt of Commerce, M.M.P.G. College, Fatehabad Abstract Non Performing Assets affect the profitability, liquidity

Research Article / Survey Paper / Case Study Available online at: Comparative Analysis of Internal Determinants of NPAs: The

ISSN: 2321-7782 (Online) Volume 4, Issue 3, March 2016 International Journal of Advance Research in Computer Science and Management Studies Research Article / Survey Paper / Case Study Available online

ISSN: 2321-7782 (Online) Volume 4, Issue 3, March 2016 International Journal of Advance Research in Computer Science and Management Studies Research Article / Survey Paper / Case Study Available online

Important Banking Terms and Definitions Related to RBI

CASA Deposit Important Banking Terms and Definitions Related to RBI Deposit in bank in current and Savings account. High Cost Deposit Deposits accepted above card rate (for the deposits) of the bank. Liquid

CASA Deposit Important Banking Terms and Definitions Related to RBI Deposit in bank in current and Savings account. High Cost Deposit Deposits accepted above card rate (for the deposits) of the bank. Liquid

A STUDY OF NON-PERFORMING ASSETs AND ITS IMPACT ON PROFITABILITY OF SELECTED INDIAN PUBLIC AND PRIVATE SECTOR BANK

Volume-11,Issue-4,March-2018 A STUDY OF NON-PERFORMING ASSETs AND ITS IMPACT ON PROFITABILITY OF SELECTED INDIAN PUBLIC AND PRIVATE SECTOR BANK DR. KAMLESH J. BHAVNANI M.com, PhD, GSET, PGDIPR (Kamlesh191982@gmail.com)

Volume-11,Issue-4,March-2018 A STUDY OF NON-PERFORMING ASSETs AND ITS IMPACT ON PROFITABILITY OF SELECTED INDIAN PUBLIC AND PRIVATE SECTOR BANK DR. KAMLESH J. BHAVNANI M.com, PhD, GSET, PGDIPR (Kamlesh191982@gmail.com)