Making Decisions in the Face of Risk and Uncertainty

|

|

|

- Myles Cannon

- 6 years ago

- Views:

Transcription

1 Making Decisions in the Face of Risk and Uncertainty R. Britt Freund, Ph.D. Project Management Consortium Information, Risk and Operations Management The University of Texas at Austin Case Study in the Oil Industry

2 Session Objectives State of the IOCs Eating Cookies What Drives Share Price? Long-Term Investment Decisions Implications of Risk and Uncertainty Risk and Uncertainty Scribbletron Our Tools Break Down Deterministic vs Probabilistic Analysis Hypothesis Testing 2

3 18 Month Share Price History 3

4 4Q Adj Earnings Report

5 Share Price ending 5 Feb

6 Cash Flow ExxonMobil Operating Cash Flow Capital Expenditure Net Debt Royal Dutch Shell Operating Cash Flow Capital Expenditure Net Debt 6 Source: Bloomberg

7 Break-Even Oil Price Required in 2016 Source: Bloomberg 7

8 Eating Cookies Why do you try to eat every cookie on the shelf? XOM Executive to RDS Executive Why do pass by all of the cookies on the shelf? RDS Executive s Retort Corporate culture eats strategy for breakfast Origins Unknown 8

9 Expectations of Wall Street IOCs evaluated based on expectations of future cash flows: Assets Operating Profits Global Energy Markets Risk Assessments Challenging strategic environment 9

is only")

10 Assets Most important asset is proved reserves ExxonMobil 2010: Reserves replacement at 209% of production 17 consecutive years > 100% Leads the industry Be careful look beyond the headlines Liquids (10 year average) is only at 95% 10

11 Risk and Reward 11

12 Delicate Balance Strategic concerns for large IOCs: Limited access to conventional (liquid) reserves Increasing reliance on unconventional resources Materiality and commerciality of new resources Upside (potentially) constrained by new agreements Downside (potentially) unlimited due to legal liability Risk? --- Reward

13 Moving Target Courtesy: UT Center for Energy Economics 13

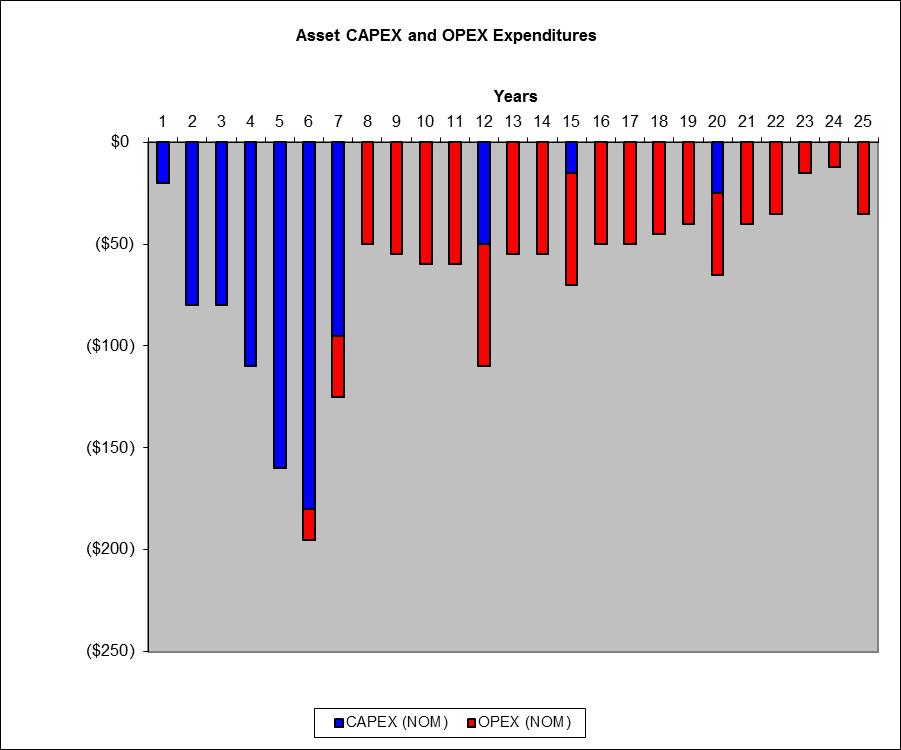

14 Long-Term Investment Decisions Revenue Streams At any point in time, is this a point or a distribution? CAPEX (capital expenditures) OPEX (operating expenditures) Cash Flows Profitability Indicators (ROA, NPV, Ultimate Cash Surplus) Sensitivity Analysis 14

15 Expenditures 15

16 Revenues 16

17 Nominal Net Cash Flow 17

Total OPEX $ (857) Total Production 54,020,000 Screening Price")

18 Discounted Cash Flows Inflation Rate 3.00% Discount Factor 8.00% Total CAPEX $ (815) Total OPEX $ (857) Total Production 54,020,000 Screening Price $70.00 Total Revenue $ 4,322 18

19 Fundamental Economic Metrics There are a number of key economic metrics typically used for projects, and they all consider inflation and the cost of capital: 1. Ultimate Cash Surplus the Expected NPV of the cash flow, after both inflation and investor discount 2. Return on (Capital) Assets (ROA) the Ultimate Cash Surplus divided by the Expected NPV of the CAPEX expenditures. This is similar to the ROI calculation (non-normalized) used by other capital intensive industries 3. Internal Rate of Return (IRR) the investor discount rate, after inflation, such that Ultimate Cash Surplus = 0 4. Breakeven Price at X% the price required to provide an IRR of X% 5. Payback Period year in which Ultimate Cash Surplus first reaches 0 6. Exposure maximum depth of cash sink (real terms, including inflation but not investor discount rate) Economic evaluation is extremely complex and relies heavily on experience and judgment 19

20 Economic Evaluation Inflation Rate 3.00% Discount Factor 8.00% Total CAPEX $ (815) Total OPEX $ (857) Total Production 54,020,000 Screening Price $70.00 Total Revenue $ 4,322 NPV Cash Surplus $ NPV CAPEX $ (519.0) ROIC IRR 19.5% Breakeven at 20% $80.45 Payback 12 Exposure $ (541) $300.0 $250.0 $200.0 $150.0 $100.0 $50.0 $- $(50.0) $(100.0) $(150.0) $(200.0) Net Cash Flow (NOM) Cash Flow (RT) Net Cash Flow (Disc) 20

21 Dealing with Uncertainty The project s profitability, like its cost, is not a point it is a range estimate. So, vary the parameters in your analysis Specifically: Ask what if questions. Test robustness against changes in assumptions. Identify critical assumptions. Analyze the impact of the variations on project economics. Can we live with the results??? 21

22 Does this Process Work? How to deal with wide ranges in outcomes? How to address riskiness of large capital projects with very long timelines? Risk adjusted discount rate? Risk adjusted costs and timing? Scenario analysis? Decision tree Expected Outcome? What to do about low probability but very high impact (Black Swan) risks? Are there SOX implications with reporting capital investment decisions? 22

23 Risk and Uncertainty Scribbletron 23

24 Making Risky Decisions The Lottery 1,000,000 tickets sold, 1 winning ticket You pay $1.00 for a ticket Winning ticket is worth $1,000,000 Do you play? A Game of Chance 6 sided dice $100,000 if you roll a 5 $50,000 if you roll an even number $0 otherwise What would you pay to play? 24

25 Back to Risk and Reward What is the risk? Risk? --- Reward +++ What is the reward? Low probability, high impact risks create huge financial challenges 25

26 Black Swans Black Swans: low-probability, high-impact risk events Lies outside the realm of realistic expectations Carries extreme impact Difficult and/or expensive to mitigate Systematically excluded from further consideration Severity Fallacy the expected value (probability x impact) of a Black Swan risk is not a useful measure of severity Only the house wins at roulette Risk Manager s Dilemma treating Black Swans can be difficult to defend since you either spent money on risks that didn t occur, or you prevented risks from firing, but no one will ever know Engaging in a no-win situation 26

27 Black Swans and the Fat Tail Black Swans distort range estimates for cost and schedule Project faces either no consequence or full consequence Moderately affects the P50 by expected value Significantly affects the P90 by almost full value Range Estimate Black Swan Risks +? 27

28 Cost Estimate Example Detailed Scope List Variability Probability Item Estimate a m b m s Big Scope 1 $ 10,000,000 $ 8,000,000 $ 10,000,000 $ 16,000,000 $ 10,666,667 $ 1,333,333 Big Scope 2 $ 8,000,000 $ 8,000,000 $ 8,000,000 $ 12,000,000 $ 8,666,667 $ 666,667 Big Scope 3 $ 2,000,000 $ 2,000,000 $ 2,000,000 $ 2,000,000 $ 2,000,000 $ - Big Scope 4 $ 5,000,000 $ 4,000,000 $ 5,000,000 $ 12,000,000 $ 6,000,000 $ 1,333,333 Labor $ 12,000,000 $ 9,000,000 $ 12,000,000 $ 20,000,000 $ 12,833,333 $ 1,833,333 Allowances $ 3,000,000 $ 3,000,000 $ 3,000,000 $ 3,000,000 $ 3,000,000 $ - $ 40,000,000 m $ 43,166,667 P 5 $ 39,689,642 s $ 2,713,137 Estimate $ 40,000,000 P 50 $ 43,166,667 P 95 $ 46,643,691 Estimate P 50 P 10 P 90 $35,000,000 $40,000,000 $45,000,000 $50,000,000 28

29 Cost Implication of Black Swans Consider three risk events with impacts on CAPEX Risk 1: 10% probability with $10,000,000 impact Risk 2: 20% probability with $5,000,000 impact Risk 3: 5% probability with $10,000,000 impact Estimate P 50 P 50 P 10 P 90 P 10 P 90 $35,000,000 $40,000,000 $45,000,000 $50,000,000 $55,000,000 $60,000,000 $65,000,000 $70,000,000 $75,000,000 29

30 What Now? How do we decide whether or not to invest? What number or range do we report to our shareholders? How do we express the riskiness of our investment decisions to analysts? Will a portfolio approach allow use of options theory, or do we need something else 30

31 Deterministic vs Probabilistic Analysis Deterministic Analysis (ExxonMobil) Consider major risks and uncertainties, but pick specific scenarios Plan against most likely/reasonable scenario Hold specific people accountable for deviations from planned scenario Probabilistic Analysis (Shell) Allow ranges for inputs to economic analysis Subsurface volumes Development costs and schedules Manage against risks and uncertainties that create extreme positions in the range Collective accountability for range outcomes 31

32 Hypothesis Testing I have come to the conclusion that risky decisions REALLY follow hypothesis testing: What is the null hypothesis? What will it take to overturn the hypothesis? ExxonMobil Null hypothesis we will not engage unless we are absolutely certain we can manage the risks Veto is possible by any of the company executives Royal Dutch Shell Null hypothesis we can generally manage the risks and so will engage in any attractive opportunities Consensus culture requires group majority (or very strongly held position) to overturn null hypothesis 32

TONY MILSOM Specialist Risk Engineering KPC

www.kuwaiterm.com Quantitative Risk Management Methods, Techniques and Tools TONY MILSOM Specialist Risk Engineering KPC w w w. k u w a i t e r m. c o m KPC ERM Objectives: Three key objectives of KPC

www.kuwaiterm.com Quantitative Risk Management Methods, Techniques and Tools TONY MILSOM Specialist Risk Engineering KPC w w w. k u w a i t e r m. c o m KPC ERM Objectives: Three key objectives of KPC

All In One MGT201 Mid Term Papers More Than (10) BY

BY") All In One MGT201 Mid Term Papers More Than (10) BY http://www.vustudents.net MIDTERM EXAMINATION MGT201- Financial Management (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one Why companies

All In One MGT201 Mid Term Papers More Than (10) BY http://www.vustudents.net MIDTERM EXAMINATION MGT201- Financial Management (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one Why companies

How to Consider Risk Demystifying Monte Carlo Risk Analysis

How to Consider Risk Demystifying Monte Carlo Risk Analysis James W. Richardson Regents Professor Senior Faculty Fellow Co-Director, Agricultural and Food Policy Center Department of Agricultural Economics

How to Consider Risk Demystifying Monte Carlo Risk Analysis James W. Richardson Regents Professor Senior Faculty Fellow Co-Director, Agricultural and Food Policy Center Department of Agricultural Economics

MGT201 Financial Management All Subjective and Objective Solved Midterm Papers for preparation of Midterm Exam2012 Question No: 1 ( Marks: 1 ) - Please choose one companies invest in projects with negative

MGT201 Financial Management All Subjective and Objective Solved Midterm Papers for preparation of Midterm Exam2012 Question No: 1 ( Marks: 1 ) - Please choose one companies invest in projects with negative

Total 100 All learning outcomes must be evidenced; a 10% aggregate variance is allowed.

Prescription: 603 Business Finance Elective prescription Level 6 Credit 20 Version 3 Aim Prerequisites Recommended prior knowledge Students will apply financial management knowledge and skills to small

Prescription: 603 Business Finance Elective prescription Level 6 Credit 20 Version 3 Aim Prerequisites Recommended prior knowledge Students will apply financial management knowledge and skills to small

2h: Uncertainty, Risk, Optionality

Step 3 of Evaluating the Business/Project 2h: Uncertainty, Risk, Optionality peter@economicevaluation.com.au Version 1; May 20141 Level 3: Decision making take an overview of uncertainty, risk and optionality

Step 3 of Evaluating the Business/Project 2h: Uncertainty, Risk, Optionality peter@economicevaluation.com.au Version 1; May 20141 Level 3: Decision making take an overview of uncertainty, risk and optionality

Session 2, Monday, April 3 rd (11:30-12:30)

") Session 2, Monday, April 3 rd (11:30-12:30) Capital Budgeting Continued and the Cost of Capital v2.0 2014 Association for Financial Professionals. All rights reserved. Session 3-1 Chapters Covered Internal

Session 2, Monday, April 3 rd (11:30-12:30) Capital Budgeting Continued and the Cost of Capital v2.0 2014 Association for Financial Professionals. All rights reserved. Session 3-1 Chapters Covered Internal

Risks and Returns of Relative Total Shareholder Return Plans Andy Restaino Technical Compensation Advisors Inc.

Risks and Returns of Relative Total Shareholder Return Plans Andy Restaino Technical Compensation Advisors Inc. INTRODUCTION When determining or evaluating the efficacy of a company s executive compensation

Risks and Returns of Relative Total Shareholder Return Plans Andy Restaino Technical Compensation Advisors Inc. INTRODUCTION When determining or evaluating the efficacy of a company s executive compensation

Advanced Leveraged Buyouts and LBO Models Quiz Questions

Advanced Leveraged Buyouts and LBO Models Quiz Questions Types of Debt Transaction and Operating Assumptions Sources & Uses Pro-Forma Balance Sheet Adjustments Debt Schedules Linking and Modifying the

Advanced Leveraged Buyouts and LBO Models Quiz Questions Types of Debt Transaction and Operating Assumptions Sources & Uses Pro-Forma Balance Sheet Adjustments Debt Schedules Linking and Modifying the

Stochastic Modelling: The power behind effective financial planning. Better Outcomes For All. Good for the consumer. Good for the Industry.

Stochastic Modelling: The power behind effective financial planning Better Outcomes For All Good for the consumer. Good for the Industry. Introduction This document aims to explain what stochastic modelling

Stochastic Modelling: The power behind effective financial planning Better Outcomes For All Good for the consumer. Good for the Industry. Introduction This document aims to explain what stochastic modelling

Chapter-8 Risk Management

Chapter-8 Risk Management 8.1 Concept of Risk Management Risk management is a proactive process that focuses on identifying risk events and developing strategies to respond and control risks. It is not

Chapter-8 Risk Management 8.1 Concept of Risk Management Risk management is a proactive process that focuses on identifying risk events and developing strategies to respond and control risks. It is not

Software Economics. Introduction to Business Case Analysis. Session 2

Software Economics Introduction to Business Case Analysis Session 2 Today Last Session we covered FV, PV and NPV We started with setting up the financials of a Business Case We talked about measurements

Software Economics Introduction to Business Case Analysis Session 2 Today Last Session we covered FV, PV and NPV We started with setting up the financials of a Business Case We talked about measurements

Week 2 Quantitative Analysis of Financial Markets Hypothesis Testing and Confidence Intervals

Week 2 Quantitative Analysis of Financial Markets Hypothesis Testing and Confidence Intervals Christopher Ting http://www.mysmu.edu/faculty/christophert/ Christopher Ting : christopherting@smu.edu.sg :

Week 2 Quantitative Analysis of Financial Markets Hypothesis Testing and Confidence Intervals Christopher Ting http://www.mysmu.edu/faculty/christophert/ Christopher Ting : christopherting@smu.edu.sg :

Trading Unusual Options Activity and Earnings

Trading Unusual Options Activity and Earnings Presented by James Ramelli Past performance is not indicative of future results. RISK DISCLAIMER Day trading, short term trading, options trading, and futures

Trading Unusual Options Activity and Earnings Presented by James Ramelli Past performance is not indicative of future results. RISK DISCLAIMER Day trading, short term trading, options trading, and futures

Valuing Put Options with Put-Call Parity S + P C = [X/(1+r f ) t ] + [D P /(1+r f ) t ] CFA Examination DERIVATIVES OPTIONS Page 1 of 6

![Valuing Put Options with Put-Call Parity S + P C = [X/(1+r f ) t ] + [D P /(1+r f ) t ] CFA Examination DERIVATIVES OPTIONS Page 1 of 6](/thumbs/77/75506899.jpg "Valuing Put Options with Put-Call Parity S + P C = [X/(1+r f ) t ] + [D P /(1+r f ) t ] CFA Examination DERIVATIVES OPTIONS Page 1 of 6") DERIVATIVES OPTIONS A. INTRODUCTION There are 2 Types of Options Calls: give the holder the RIGHT, at his discretion, to BUY a Specified number of a Specified Asset at a Specified Price on, or until, a

DERIVATIVES OPTIONS A. INTRODUCTION There are 2 Types of Options Calls: give the holder the RIGHT, at his discretion, to BUY a Specified number of a Specified Asset at a Specified Price on, or until, a

Software Economics. Introduction to Business Case Analysis. Session 2

Software Economics Introduction to Business Case Analysis Session 2 Today Last Session we covered FV, PV and NPV We started with setting up the financials of a Business Case We talked about measurements

Software Economics Introduction to Business Case Analysis Session 2 Today Last Session we covered FV, PV and NPV We started with setting up the financials of a Business Case We talked about measurements

1. A is a decision support tool that uses a tree-like graph or model of decisions and their possible consequences, including chance event outcomes,

1. A is a decision support tool that uses a tree-like graph or model of decisions and their possible consequences, including chance event outcomes, resource costs, and utility. A) Decision tree B) Graphs

1. A is a decision support tool that uses a tree-like graph or model of decisions and their possible consequences, including chance event outcomes, resource costs, and utility. A) Decision tree B) Graphs

PETROLEUM INDUSTRY REFORM IN NIGERIA: SIMULATION ANALYSIS OF ITS IMPACT ON DEEPWATER E&P ECONOMICS

PETROLEUM INDUSTRY REFORM IN NIGERIA: SIMULATION ANALYSIS OF ITS IMPACT ON DEEPWATER E&P ECONOMICS OMOWUNMI O. ILEDARE, PH.D. PROFESSOR OF PETROLEUM ECONOMICS & POLICY RESEARCH DIRECTOR, ENERGY INFORMATION

PETROLEUM INDUSTRY REFORM IN NIGERIA: SIMULATION ANALYSIS OF ITS IMPACT ON DEEPWATER E&P ECONOMICS OMOWUNMI O. ILEDARE, PH.D. PROFESSOR OF PETROLEUM ECONOMICS & POLICY RESEARCH DIRECTOR, ENERGY INFORMATION

Welcome to Mentorship. Will Showers Director of Mentorship

Welcome to Mentorship Will Showers Director of Mentorship What s in Store 4-week lecture series Tuesdays and Thursdays from 6-7 Bring a laptop or tablet to every meeting What will be covered How the IC

Welcome to Mentorship Will Showers Director of Mentorship What s in Store 4-week lecture series Tuesdays and Thursdays from 6-7 Bring a laptop or tablet to every meeting What will be covered How the IC

Disclaimer: This resource package is for studying purposes only EDUCATION

Disclaimer: This resource package is for studying purposes only EDUCATION Chapter 6: Valuing stocks Bond Cash Flows, Prices, and Yields - Maturity date: Final payment date - Term: Time remaining until

Disclaimer: This resource package is for studying purposes only EDUCATION Chapter 6: Valuing stocks Bond Cash Flows, Prices, and Yields - Maturity date: Final payment date - Term: Time remaining until

Fundamentals of Credit. Arnold Ziegel Mountain Mentors Associates. II. Fundamentals of Financial Analysis

Fundamentals of Credit Arnold Ziegel Mountain Mentors Associates II. Fundamentals of Financial Analysis Financial Analysis is the basis for Credit Analysis January, 2008 Financial analysis is the starting

Fundamentals of Credit Arnold Ziegel Mountain Mentors Associates II. Fundamentals of Financial Analysis Financial Analysis is the basis for Credit Analysis January, 2008 Financial analysis is the starting

DOWNLOAD PDF HOW TO CALCULATE (AND REALLY UNDERSTAND RETURN ON INVESTMENT

Chapter 1 : Return on Investment (ROI) Definition & Example InvestingAnswers The return on investment metric calculates how efficiently a business is using the money invested by shareholders to generate

Chapter 1 : Return on Investment (ROI) Definition & Example InvestingAnswers The return on investment metric calculates how efficiently a business is using the money invested by shareholders to generate

We recommend AGAINST investing R$ 35 million in the V:House multifamily development (303 pre-sold units) in São Paulo

in São Paulo") Executive Summary We recommend AGAINST investing R$ 35 million in the V:House multifamily development (303 pre-sold units) in São Paulo Although we achieve a 26% IRR in the Base Case, we earn above the

Executive Summary We recommend AGAINST investing R$ 35 million in the V:House multifamily development (303 pre-sold units) in São Paulo Although we achieve a 26% IRR in the Base Case, we earn above the

Finance Concepts I: Present Discounted Value, Risk/Return Tradeoff

Finance Concepts I: Present Discounted Value, Risk/Return Tradeoff Federal Reserve Bank of New York Central Banking Seminar Preparatory Workshop in Financial Markets, Instruments and Institutions Anthony

Finance Concepts I: Present Discounted Value, Risk/Return Tradeoff Federal Reserve Bank of New York Central Banking Seminar Preparatory Workshop in Financial Markets, Instruments and Institutions Anthony

LET S GET REAL! Managing Strategic Investment in an Uncertain World: A Real Options Approach by Roger A. Morin, PhD

LET S GET REAL! Managing Strategic Investment in an Uncertain World: A Real Options Approach by Roger A. Morin, PhD Robinson Economic Forecasting Conference J. Mack Robinson College of Business, Georgia

LET S GET REAL! Managing Strategic Investment in an Uncertain World: A Real Options Approach by Roger A. Morin, PhD Robinson Economic Forecasting Conference J. Mack Robinson College of Business, Georgia

Software Economics. Metrics of Business Case Analysis Part 1

Software Economics Metrics of Business Case Analysis Part 1 Today Last Session we covered FV, PV and NPV We started with setting up the financials of a Business Case We talked about measurements to compare

Software Economics Metrics of Business Case Analysis Part 1 Today Last Session we covered FV, PV and NPV We started with setting up the financials of a Business Case We talked about measurements to compare

KNPC Risk Approach for Projects Economic Evaluation

KNPC Risk Approach for Projects Economic Evaluation Implementation Approach March 2015 Presented by Eng. May Al-Ebrahim Introduction Investment decisions require special attention because they involve

KNPC Risk Approach for Projects Economic Evaluation Implementation Approach March 2015 Presented by Eng. May Al-Ebrahim Introduction Investment decisions require special attention because they involve

Oil & Gas Valuation Case Study: Ultra Petroleum [UPL] and its Acquisition of the Uinta Basin Acreage SHORT Recommendation

![Oil & Gas Valuation Case Study: Ultra Petroleum [UPL] and its Acquisition of the Uinta Basin Acreage SHORT Recommendation](/thumbs/77/76333188.jpg "Oil & Gas Valuation Case Study: Ultra Petroleum [UPL] and its Acquisition of the Uinta Basin Acreage SHORT Recommendation") Oil & Gas Valuation Case Study: Ultra Petroleum [UPL] and its Acquisition of the Uinta Basin Acreage SHORT Recommendation NOTES AND DISCLAIMERS: First, please do not construe this as investment advice.

Oil & Gas Valuation Case Study: Ultra Petroleum [UPL] and its Acquisition of the Uinta Basin Acreage SHORT Recommendation NOTES AND DISCLAIMERS: First, please do not construe this as investment advice.

Strategic Asset Allocation

Strategic Asset Allocation Caribbean Center for Monetary Studies 11th Annual Senior Level Policy Seminar May 25, 2007 Port of Spain, Trinidad and Tobago Sudhir Rajkumar ead, Pension Investment Partnerships

Strategic Asset Allocation Caribbean Center for Monetary Studies 11th Annual Senior Level Policy Seminar May 25, 2007 Port of Spain, Trinidad and Tobago Sudhir Rajkumar ead, Pension Investment Partnerships

Sustainable Free Cash Flow Analysis: A Better Measure for Resource Equities

Sustainable Free Cash Flow Analysis: A Better Measure for Resource Equities Authors: Benoit Gervais, MSc., CFA Senior Vice President, Portfolio Manager Mackenzie Resource Team Onno Rutten, MSc., MBA Vice

Sustainable Free Cash Flow Analysis: A Better Measure for Resource Equities Authors: Benoit Gervais, MSc., CFA Senior Vice President, Portfolio Manager Mackenzie Resource Team Onno Rutten, MSc., MBA Vice

Sanford C. Bernstein Strategic Decisions Conference 2008

Sanford C. Bernstein Strategic Decisions Conference 2008 London - September 23rd, 2008 Eni in the World Active in around 70 countries Exploration & Production Gas & Power Refining & Marketing Saipem Snam

Sanford C. Bernstein Strategic Decisions Conference 2008 London - September 23rd, 2008 Eni in the World Active in around 70 countries Exploration & Production Gas & Power Refining & Marketing Saipem Snam

Step 3 of Evaluating the Business/Project: 2d: NPV. Version 1; May 20141

Step 3 of Evaluating the Business/Project: 2d: NPV peter@economicevaluation.com.au Version 1; May 20141 Level 3: Decision making understand the strengths and weaknesses of NPV Level 2: Evaluating the business/project

Step 3 of Evaluating the Business/Project: 2d: NPV peter@economicevaluation.com.au Version 1; May 20141 Level 3: Decision making understand the strengths and weaknesses of NPV Level 2: Evaluating the business/project

A New Strategy for Downside Protection or Yield Enhancement

A New Strategy for Downside Protection or Yield Enhancement June 7, 2016 by Robert Huebscher Vest Financial Group Inc. was founded in 2012 by Jeff Chang and Karan Sood. Vest is dedicated to serving investment

A New Strategy for Downside Protection or Yield Enhancement June 7, 2016 by Robert Huebscher Vest Financial Group Inc. was founded in 2012 by Jeff Chang and Karan Sood. Vest is dedicated to serving investment

Using Real Options to Quantify Portfolio Value in Business Cases

Using Real Options to Quantify Portfolio Value in Business Cases George Bayer, MBA, PMP Cobec Consulting, Inc. www.cobec.com Agenda Contents - Introduction - Real Options in Investment Decisions - Capital

Using Real Options to Quantify Portfolio Value in Business Cases George Bayer, MBA, PMP Cobec Consulting, Inc. www.cobec.com Agenda Contents - Introduction - Real Options in Investment Decisions - Capital

Real Options and Risk Analysis in Capital Budgeting

Real options Real Options and Risk Analysis in Capital Budgeting Traditional NPV analysis should not be viewed as static. This can lead to decision-making problems in a dynamic environment when not all

Real options Real Options and Risk Analysis in Capital Budgeting Traditional NPV analysis should not be viewed as static. This can lead to decision-making problems in a dynamic environment when not all

Asset/Liability Management Series Session 1 Presenter: Sasha Khandoker ALM Analyst

Asset/Liability Management Series Session 1 Presenter: Sasha Khandoker ALM Analyst 1 2 1 What is ALM? Why are we asked to perform ALM? What is the goal of ALM? How can we use it? 3 Creating and managing

Asset/Liability Management Series Session 1 Presenter: Sasha Khandoker ALM Analyst 1 2 1 What is ALM? Why are we asked to perform ALM? What is the goal of ALM? How can we use it? 3 Creating and managing

ch11 Student: 3. An analysis of what happens to the estimate of net present value when only one variable is changed is called analysis.

ch11 Student: Multiple Choice Questions 1. Forecasting risk is defined as the: A. possibility that some proposed projects will be rejected. B. process of estimating future cash flows relative to a project.

ch11 Student: Multiple Choice Questions 1. Forecasting risk is defined as the: A. possibility that some proposed projects will be rejected. B. process of estimating future cash flows relative to a project.

All Ords Consecutive Returns over a 130 year period

Absolute conviction, at what price? Peter Constable, Chief Investment Offier, MMC Asset Management Summary When equity markets start generating returns significantly above long term averages, risk has

Absolute conviction, at what price? Peter Constable, Chief Investment Offier, MMC Asset Management Summary When equity markets start generating returns significantly above long term averages, risk has

Capital Budgeting Decisions

May 1-4, 2014 Capital Budgeting Decisions Today s Agenda n Capital Budgeting n Time Value of Money n Decision Making Example n Simple Return and Payback Methods Typical Capital Budgeting Decisions n Capital

May 1-4, 2014 Capital Budgeting Decisions Today s Agenda n Capital Budgeting n Time Value of Money n Decision Making Example n Simple Return and Payback Methods Typical Capital Budgeting Decisions n Capital

Q&A, 10/08/03. To buy and sell options do we need to contact the broker or can it be dome from programs like Bloomberg?

Q&A, 10/08/03 Dear Students, Thanks for asking these great questions! The answer to my question (what is a put) I you all got right: put is an option contract giving you the right to sell. Here are the

Q&A, 10/08/03 Dear Students, Thanks for asking these great questions! The answer to my question (what is a put) I you all got right: put is an option contract giving you the right to sell. Here are the

OMEGA. A New Tool for Financial Analysis

OMEGA A New Tool for Financial Analysis 2 1 0-1 -2-1 0 1 2 3 4 Fund C Sharpe Optimal allocation Fund C and Fund D Fund C is a better bet than the Sharpe optimal combination of Fund C and Fund D for more

OMEGA A New Tool for Financial Analysis 2 1 0-1 -2-1 0 1 2 3 4 Fund C Sharpe Optimal allocation Fund C and Fund D Fund C is a better bet than the Sharpe optimal combination of Fund C and Fund D for more

Risks and Rewards Newsletter

Article from: Risks and Rewards Newsletter October 2003 Issue No. 43 Why Write Variable Products When You Can Put the Money Directly into the Stock Market? by David N. Ingram and Stuart H. Silverman For

Article from: Risks and Rewards Newsletter October 2003 Issue No. 43 Why Write Variable Products When You Can Put the Money Directly into the Stock Market? by David N. Ingram and Stuart H. Silverman For

CA. Sonali Jagath Prasad ACA, ACMA, CGMA, B.Com.

MANAGEMENT OF FINANCIAL RESOURCES AND PERFORMANCE SESSIONS 3& 4 INVESTMENT APPRAISAL METHODS June 10 to 24, 2013 CA. Sonali Jagath Prasad ACA, ACMA, CGMA, B.Com. WESTFORD 2008 Thomson SCHOOL South-Western

MANAGEMENT OF FINANCIAL RESOURCES AND PERFORMANCE SESSIONS 3& 4 INVESTMENT APPRAISAL METHODS June 10 to 24, 2013 CA. Sonali Jagath Prasad ACA, ACMA, CGMA, B.Com. WESTFORD 2008 Thomson SCHOOL South-Western

What is Risk? Jessica N. Portis, CFA Senior Vice President. Summit Strategies Group 8182 Maryland Avenue, 6th Floor St. Louis, Missouri 63105

What is Risk? Jessica N. Portis, CFA Senior Vice President 8182 Maryland Avenue, 6th Floor St. Louis, Missouri 63105 314.727.7211 summitstrategies.com WHAT IS RISK? risk {noun} 1. Possibility of loss or

What is Risk? Jessica N. Portis, CFA Senior Vice President 8182 Maryland Avenue, 6th Floor St. Louis, Missouri 63105 314.727.7211 summitstrategies.com WHAT IS RISK? risk {noun} 1. Possibility of loss or

10. Estimate the MIRR for the project described in Problem 8. Does it change your decision on accepting this project?

1 CHAPTER 5 Problems and Questions 1. You have been given the following information on a project: It has a five-year lifetime The initial investment in the project will be $25 million, and the investment

1 CHAPTER 5 Problems and Questions 1. You have been given the following information on a project: It has a five-year lifetime The initial investment in the project will be $25 million, and the investment

Randomness: what is that and how to cope with it (with view towards financial markets) Igor Cialenco

Igor Cialenco") Randomness: what is that and how to cope with it (with view towards financial markets) Igor Cialenco Dep of Applied Math, IIT igor@math.iit.etu MATH 100, Department of Applied Mathematics, IIT Oct 2014

Randomness: what is that and how to cope with it (with view towards financial markets) Igor Cialenco Dep of Applied Math, IIT igor@math.iit.etu MATH 100, Department of Applied Mathematics, IIT Oct 2014

The finance of IP litigation

60 Feature Xxxxxxxx www.iam-media.com The finance of IP litigation As contingency arrangements in US patent cases become rarer, litigation financing options are attracting more interest. With so many choices

60 Feature Xxxxxxxx www.iam-media.com The finance of IP litigation As contingency arrangements in US patent cases become rarer, litigation financing options are attracting more interest. With so many choices

MASON GRAPHITE PRESENTS ITS UPDATED FEASIBILITY STUDY ECONOMIC RESULTS FOR THE LAC GUÉRET GRAPHITE PROJECT

MASON GRAPHITE PRESENTS ITS UPDATED FEASIBILITY STUDY ECONOMIC RESULTS FOR THE LAC GUÉRET GRAPHITE PROJECT December 5 th, 2018 Montreal, Quebec, Canada Mason Graphite Inc. ( Mason Graphite or the Company

MASON GRAPHITE PRESENTS ITS UPDATED FEASIBILITY STUDY ECONOMIC RESULTS FOR THE LAC GUÉRET GRAPHITE PROJECT December 5 th, 2018 Montreal, Quebec, Canada Mason Graphite Inc. ( Mason Graphite or the Company

Making Risk Models Relevant

Making Risk Models Relevant Dave Sandberg VP, Corporate Actuary Allianz Life Insurance Company of North America Key Topics 1. Relationship of ERM & Internal models 2. How can internal models be assured

Making Risk Models Relevant Dave Sandberg VP, Corporate Actuary Allianz Life Insurance Company of North America Key Topics 1. Relationship of ERM & Internal models 2. How can internal models be assured

RISK EVALUATIONS FOR THE CLASSIFICATION OF MARINE-RELATED FACILITIES

GUIDE FOR RISK EVALUATIONS FOR THE CLASSIFICATION OF MARINE-RELATED FACILITIES JUNE 2003 American Bureau of Shipping Incorporated by Act of Legislature of the State of New York 1862 Copyright 2003 American

GUIDE FOR RISK EVALUATIONS FOR THE CLASSIFICATION OF MARINE-RELATED FACILITIES JUNE 2003 American Bureau of Shipping Incorporated by Act of Legislature of the State of New York 1862 Copyright 2003 American

MBF2263 Portfolio Management. Lecture 8: Risk and Return in Capital Markets

MBF2263 Portfolio Management Lecture 8: Risk and Return in Capital Markets 1. A First Look at Risk and Return We begin our look at risk and return by illustrating how the risk premium affects investor

MBF2263 Portfolio Management Lecture 8: Risk and Return in Capital Markets 1. A First Look at Risk and Return We begin our look at risk and return by illustrating how the risk premium affects investor

Mid Term Papers. Spring 2009 (Session 02) MGT201. (Group is not responsible for any solved content)

MGT201. (Group is not responsible for any solved content)") Spring 2009 (Session 02) MGT201 (Group is not responsible for any solved content) Subscribe to VU SMS Alert Service To Join Simply send following detail to bilal.zaheem@gmail.com Full Name Master Program

Spring 2009 (Session 02) MGT201 (Group is not responsible for any solved content) Subscribe to VU SMS Alert Service To Join Simply send following detail to bilal.zaheem@gmail.com Full Name Master Program

TradeOptionsWithMe.com

TradeOptionsWithMe.com 1 of 18 Option Trading Glossary This is the Glossary for important option trading terms. Some of these terms are rather easy and used extremely often, but some may even be new to

TradeOptionsWithMe.com 1 of 18 Option Trading Glossary This is the Glossary for important option trading terms. Some of these terms are rather easy and used extremely often, but some may even be new to

CHAPTER 5. Introduction to Risk, Return, and the Historical Record INVESTMENTS BODIE, KANE, MARCUS

CHAPTER 5 Introduction to Risk, Return, and the Historical Record INVESTMENTS BODIE, KANE, MARCUS McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 5-2 Supply Interest

CHAPTER 5 Introduction to Risk, Return, and the Historical Record INVESTMENTS BODIE, KANE, MARCUS McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 5-2 Supply Interest

USAEE/IAEE CONFERENCE RIDING THE ENERGY CYCLES

USAEE/IAEE CONFERENCE RIDING THE ENERGY CYCLES Interactions between Energy Markets and Monetary and Fiscal Policy EVALUATING THE IMPACT OF OIL PRICE VOLATILITY ON INVESTOR AND FISCAL REVENUES Real Options

USAEE/IAEE CONFERENCE RIDING THE ENERGY CYCLES Interactions between Energy Markets and Monetary and Fiscal Policy EVALUATING THE IMPACT OF OIL PRICE VOLATILITY ON INVESTOR AND FISCAL REVENUES Real Options

Mercurio Capital - Financial System, Economic Strategy, Capital Budgeting, Quantitative Methods

1 Main Objective: Growth in Shareholder Value Increase the general valuation of the company Increase the share premium Reduce Risk Integrate Financial Strategy in the Business Strategy (as an extra layer

1 Main Objective: Growth in Shareholder Value Increase the general valuation of the company Increase the share premium Reduce Risk Integrate Financial Strategy in the Business Strategy (as an extra layer

PM013: Project Management Detailed Engineering for Capital Projects

PM013: Project Management Detailed Engineering for Capital Projects PM013 Rev.001 CMCT COURSE OUTLINE Page 1 of 6 Training Description: Large capital-intensive projects require substantial and often risky

PM013: Project Management Detailed Engineering for Capital Projects PM013 Rev.001 CMCT COURSE OUTLINE Page 1 of 6 Training Description: Large capital-intensive projects require substantial and often risky

Explaining risk, return and volatility. An Octopus guide

Explaining risk, return and volatility An Octopus guide Important information The value of an investment, and any income from it, can fall as well as rise. You may not get back the full amount they invest.

Explaining risk, return and volatility An Octopus guide Important information The value of an investment, and any income from it, can fall as well as rise. You may not get back the full amount they invest.

The innovative use of risk appetite and tolerance to inform project decisions

The innovative use of risk appetite and tolerance to inform project decisions IRMSA Conference November 2012 Presented by: Oliver Laloux and Reshma Ramkumar www.mondialcons.com Specialist Risk and Business

The innovative use of risk appetite and tolerance to inform project decisions IRMSA Conference November 2012 Presented by: Oliver Laloux and Reshma Ramkumar www.mondialcons.com Specialist Risk and Business

Monetary Economics Valuation: Cash Flows over Time. Gerald P. Dwyer Fall 2015

Monetary Economics Valuation: Cash Flows over Time Gerald P. Dwyer Fall 2015 WSJ Material to be Studied This lecture, Chapter 6, Valuation, in Cuthbertson and Nitzsche Next topic, Chapter 7, Cost of Capital,

Monetary Economics Valuation: Cash Flows over Time Gerald P. Dwyer Fall 2015 WSJ Material to be Studied This lecture, Chapter 6, Valuation, in Cuthbertson and Nitzsche Next topic, Chapter 7, Cost of Capital,

by Greg Crabtree

by Greg Crabtree Greg.crabtree@crbcpa.net 256-704-0620 Most people miss opportunity because it wears overalls and looks like work Thomas Edison Simple Numbers Straight Talk Big Profits 4 Keys to Unlock

by Greg Crabtree Greg.crabtree@crbcpa.net 256-704-0620 Most people miss opportunity because it wears overalls and looks like work Thomas Edison Simple Numbers Straight Talk Big Profits 4 Keys to Unlock

PMP045 Project Management Detailed Engineering for Capital Projects

PMP045 Project Management Detailed Engineering for Capital Projects H.H. Sheik Sultan Tower (0) Floor Corniche Street Abu Dhabi U.A.E www.ictd.ae ictd@ictd.ae Course Introduction: Large capital-intensive

PMP045 Project Management Detailed Engineering for Capital Projects H.H. Sheik Sultan Tower (0) Floor Corniche Street Abu Dhabi U.A.E www.ictd.ae ictd@ictd.ae Course Introduction: Large capital-intensive

What Is Asset/Liability Management?

A BEGINNERS GUIDE TO ASSET\LIABILITY MANAGEMENT, RISK APPETITE AND CAPITAL PLANNING David Koch President\CEO dkoch@farin.com 800-236-3724 ext. 4217 What Is Asset/Liability Management? Asset/liability management

A BEGINNERS GUIDE TO ASSET\LIABILITY MANAGEMENT, RISK APPETITE AND CAPITAL PLANNING David Koch President\CEO dkoch@farin.com 800-236-3724 ext. 4217 What Is Asset/Liability Management? Asset/liability management

Financial planning. Kirt C. Butler Department of Finance Broad College of Business Michigan State University February 3, 2015

Financial planning Making financial decisions How will things change if I take this action? Financial decision modeling A framework for decision-making What-ifs - breakeven, sensitivities, & scenarios,

Financial planning Making financial decisions How will things change if I take this action? Financial decision modeling A framework for decision-making What-ifs - breakeven, sensitivities, & scenarios,

Economic Evaluation. Objectives of Economic Evaluation Analysis

Economic Evaluation Objective of Analysis Criteria Nature Peculiarities Comparison of Criteria Recommended Approach Massachusetts Institute of Technology Economic Evaluation Slide 1 of 17 Objectives of

Economic Evaluation Objective of Analysis Criteria Nature Peculiarities Comparison of Criteria Recommended Approach Massachusetts Institute of Technology Economic Evaluation Slide 1 of 17 Objectives of

Selling Risk Management: Quan2fica2on Techniques to Support Risk Decisions RIF007

Selling Risk Management: Quan2fica2on Techniques to Support Risk Decisions RIF007 Speakers: Christopher (Kip) Bohn, Actuary, Aon Jeff Williams, Director, Risk Management & Loss Prevention, Eli Lilly and

Selling Risk Management: Quan2fica2on Techniques to Support Risk Decisions RIF007 Speakers: Christopher (Kip) Bohn, Actuary, Aon Jeff Williams, Director, Risk Management & Loss Prevention, Eli Lilly and

The Swan Defined Risk Strategy - A Full Market Solution

The Swan Defined Risk Strategy - A Full Market Solution Absolute, Relative, and Risk-Adjusted Performance Metrics for Swan DRS and the Index (Summary) June 30, 2018 Manager Performance July 1997 - June

The Swan Defined Risk Strategy - A Full Market Solution Absolute, Relative, and Risk-Adjusted Performance Metrics for Swan DRS and the Index (Summary) June 30, 2018 Manager Performance July 1997 - June

WHAT IS CAPITAL BUDGETING?

WHAT IS CAPITAL BUDGETING? Capital budgeting is a required managerial tool. One duty of a financial manager is to choose investments with satisfactory cash flows and rates of return. Therefore, a financial

WHAT IS CAPITAL BUDGETING? Capital budgeting is a required managerial tool. One duty of a financial manager is to choose investments with satisfactory cash flows and rates of return. Therefore, a financial

Diversified or Concentrated Factors What are the Investment Beliefs Behind these two Smart Beta Approaches?

Diversified or Concentrated Factors What are the Investment Beliefs Behind these two Smart Beta Approaches? Noël Amenc, PhD Professor of Finance, EDHEC Risk Institute CEO, ERI Scientific Beta Eric Shirbini,

Diversified or Concentrated Factors What are the Investment Beliefs Behind these two Smart Beta Approaches? Noël Amenc, PhD Professor of Finance, EDHEC Risk Institute CEO, ERI Scientific Beta Eric Shirbini,

Project Integration Management

Project Integration Management The Key to Overall Project Success: Good Project Integration Management Project managers must coordinate all of the other knowledge areas throughout a project s life cycle.

Project Integration Management The Key to Overall Project Success: Good Project Integration Management Project managers must coordinate all of the other knowledge areas throughout a project s life cycle.

(Est.2201) Parametric Contingency Estimating on Small Projects. Matthew Schoenhardt, P.Eng, MBA, PMP, RMP

Parametric Contingency Estimating on Small Projects. Matthew Schoenhardt, P.Eng, MBA, PMP, RMP") (Est.2201) Parametric Contingency Estimating on Small Projects Matthew Schoenhardt, P.Eng, MBA, PMP, RMP mschoenh@telus.net 587.988.2305 1 Confirmation Question? Interrupt me and ask! Discussion Question?

(Est.2201) Parametric Contingency Estimating on Small Projects Matthew Schoenhardt, P.Eng, MBA, PMP, RMP mschoenh@telus.net 587.988.2305 1 Confirmation Question? Interrupt me and ask! Discussion Question?

Managing stocks in long-term trading ranges 60% to 70% of all stocks exhibit trading range patterns even in a bull market.

Managing stocks in long-term trading ranges 60% to 70% of all stocks exhibit trading range patterns even in a bull market. Distribution of returns Normal vs. Fat Tails Theoretical distribution Observed

Managing stocks in long-term trading ranges 60% to 70% of all stocks exhibit trading range patterns even in a bull market. Distribution of returns Normal vs. Fat Tails Theoretical distribution Observed

FINANCIAL APPRAISAL OF PROJECTS

FINANCIAL APPRAISAL OF PROJECTS (Special Emphasis to Railways) S. N. BANERJEA Joint Economic Adviser Railway Board New Delhi BASIC THEORY OF PROJECT APPRAISAL PROJECT IDENTIFICATION PROJECT APPRAISAL PROJECT

FINANCIAL APPRAISAL OF PROJECTS (Special Emphasis to Railways) S. N. BANERJEA Joint Economic Adviser Railway Board New Delhi BASIC THEORY OF PROJECT APPRAISAL PROJECT IDENTIFICATION PROJECT APPRAISAL PROJECT

The Role of Ethics in the Current Financial Crisis: The Ethics of Securitization. John R. Boatright Loyola University Chicago

The Role of Ethics in the Current Financial Crisis: The Ethics of Securitization John R. Boatright Loyola University Chicago The Crisis is a Failure of... Market actors (mortgage companies, commercial/

The Role of Ethics in the Current Financial Crisis: The Ethics of Securitization John R. Boatright Loyola University Chicago The Crisis is a Failure of... Market actors (mortgage companies, commercial/

POWER LAW ANALYSIS IMPLICATIONS OF THE SAN BRUNO PIPELINE FAILURE

Proceedings of the 2016 11th International Pipeline Conference IPC2016 September 26-30, 2016, Calgary, Alberta, Canada IPC2016-64512 POWER LAW ANALYSIS IMPLICATIONS OF THE SAN BRUNO PIPELINE FAILURE Dr.

Proceedings of the 2016 11th International Pipeline Conference IPC2016 September 26-30, 2016, Calgary, Alberta, Canada IPC2016-64512 POWER LAW ANALYSIS IMPLICATIONS OF THE SAN BRUNO PIPELINE FAILURE Dr.

ECONOMIC CAPITAL MODELING CARe Seminar JUNE 2016

ECONOMIC CAPITAL MODELING CARe Seminar JUNE 2016 Boston Catherine Eska The Hanover Insurance Group Paul Silberbush Guy Carpenter & Co. Ronald Wilkins - PartnerRe Economic Capital Modeling Safe Harbor Notice

ECONOMIC CAPITAL MODELING CARe Seminar JUNE 2016 Boston Catherine Eska The Hanover Insurance Group Paul Silberbush Guy Carpenter & Co. Ronald Wilkins - PartnerRe Economic Capital Modeling Safe Harbor Notice

Advanced Budgeting Workshop. Contents are subject to change. For the latest updates visit

Advanced Budgeting Workshop Page 1 of 8 Why Attend 'Advanced Budgeting Workshop' is the second level course in budgeting after Meirc's 'Effective Budgeting and Cost ' course. It goes beyond the theory

Advanced Budgeting Workshop Page 1 of 8 Why Attend 'Advanced Budgeting Workshop' is the second level course in budgeting after Meirc's 'Effective Budgeting and Cost ' course. It goes beyond the theory

Delta Corp Limited Global Gaming Operators DELTA IN BSE BO INR Company Update

29 March 2018 Asia Research Rating: Buy Price Target: INR500.00 Price INR250.35 52wk Range INR139.10 - INR401.30 Shares Outstanding (MM) 267.6 Market Capitalization (MM) Enterprise Value (MM) INR66,991.2

29 March 2018 Asia Research Rating: Buy Price Target: INR500.00 Price INR250.35 52wk Range INR139.10 - INR401.30 Shares Outstanding (MM) 267.6 Market Capitalization (MM) Enterprise Value (MM) INR66,991.2

P2.T5. Market Risk Measurement & Management. Jorion, Value-at Risk: The New Benchmark for Managing Financial Risk, 3 rd Edition

P2.T5. Market Risk Measurement & Management Jorion, Value-at Risk: The New Benchmark for Managing Financial Risk, 3 rd Edition Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM and Deepa Raju

P2.T5. Market Risk Measurement & Management Jorion, Value-at Risk: The New Benchmark for Managing Financial Risk, 3 rd Edition Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM and Deepa Raju

Chapter 8. Ross, Westerfield and Jordan, ECF 4 th ed 2004 Solutions

Ross, Westerfield and Jordan, ECF 4 th ed 2004 Solutions Chapter 8. Answers to Concepts Review and Critical Thinking Questions 1. A payback period less than the project s life means that the NPV is positive

Ross, Westerfield and Jordan, ECF 4 th ed 2004 Solutions Chapter 8. Answers to Concepts Review and Critical Thinking Questions 1. A payback period less than the project s life means that the NPV is positive

CHAPTER 5. Introduction to Risk, Return, and the Historical Record INVESTMENTS BODIE, KANE, MARCUS. McGraw-Hill/Irwin

CHAPTER 5 Introduction to Risk, Return, and the Historical Record McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 5-2 Interest Rate Determinants Supply Households

CHAPTER 5 Introduction to Risk, Return, and the Historical Record McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 5-2 Interest Rate Determinants Supply Households

The Sources, Benefits and Risks of Leverage

The Sources, Benefits and Risks of Leverage May 22, 2017 by Joshua Anderson, Ji Li of PIMCO SUMMARY Many strategies that seek enhanced returns (high single to mid double digit net portfolio returns) need

The Sources, Benefits and Risks of Leverage May 22, 2017 by Joshua Anderson, Ji Li of PIMCO SUMMARY Many strategies that seek enhanced returns (high single to mid double digit net portfolio returns) need

A Dynamic Approach to Spending and Underwater Endowment Policy

A Dynamic Approach to Spending and Underwater Endowment Policy Recent performance in the capital markets has forced institutions to consider lower return expectations over the near term and how that may

A Dynamic Approach to Spending and Underwater Endowment Policy Recent performance in the capital markets has forced institutions to consider lower return expectations over the near term and how that may

Conveying vs. Trucking Economics For Medium Sized Applications

Conveying vs. Trucking Economics For Medium Sized Applications Written by: R. Munson, BEUMER Kansas City LLC Introduction This paper shows how easy it is to perform fundamental economic evaluations of

Conveying vs. Trucking Economics For Medium Sized Applications Written by: R. Munson, BEUMER Kansas City LLC Introduction This paper shows how easy it is to perform fundamental economic evaluations of

Discussion Questions

Understanding the Financial Environment of Public Utility Firms Sanford V. Berg Joel F. Houston 1 Overview Our plan is to help facilitate a series of discussions related to utility finance. We will pose

Understanding the Financial Environment of Public Utility Firms Sanford V. Berg Joel F. Houston 1 Overview Our plan is to help facilitate a series of discussions related to utility finance. We will pose

Risk and Return: Past and Prologue

Chapter 5 Risk and Return: Past and Prologue Bodie, Kane, and Marcus Essentials of Investments Tenth Edition 5.1 Rates of Return Holding-Period Return (HPR) Rate of return over given investment period

Chapter 5 Risk and Return: Past and Prologue Bodie, Kane, and Marcus Essentials of Investments Tenth Edition 5.1 Rates of Return Holding-Period Return (HPR) Rate of return over given investment period

SOA Risk Management Task Force

SOA Risk Management Task Force Update - Session 25 May, 2002 Dave Ingram Hubert Mueller Jim Reiskytl Darrin Zimmerman Risk Management Task Force Update Agenda Risk Management Section Formation CAS/SOA

SOA Risk Management Task Force Update - Session 25 May, 2002 Dave Ingram Hubert Mueller Jim Reiskytl Darrin Zimmerman Risk Management Task Force Update Agenda Risk Management Section Formation CAS/SOA

Learn how to see. Realize that everything connects to everything else. Leonardo da Vinci

Learn how to see. Realize that everything connects to everything else. Leonardo da Vinci 1 P a g e July 20 th 2017 FASANARA CAPITAL COOKIE How Bad a Damage If Volatility Rises: The Bear Trap of Short Vol

Learn how to see. Realize that everything connects to everything else. Leonardo da Vinci 1 P a g e July 20 th 2017 FASANARA CAPITAL COOKIE How Bad a Damage If Volatility Rises: The Bear Trap of Short Vol

An Actuarial Evaluation of the Insurance Limits Buying Decision

An Actuarial Evaluation of the Insurance Limits Buying Decision Joe Wieligman Client Executive VP Hylant Travis J. Grulkowski Principal & Consulting Actuary Milliman, Inc. WWW.CHICAGOLANDRISKFORUM.ORG

An Actuarial Evaluation of the Insurance Limits Buying Decision Joe Wieligman Client Executive VP Hylant Travis J. Grulkowski Principal & Consulting Actuary Milliman, Inc. WWW.CHICAGOLANDRISKFORUM.ORG

Filo del Sol Pre-Feasibility Study Results Webcast & Conference Call Presentation January 15, 2019

Filo del Sol Pre-Feasibility Study Results Webcast & Conference Call Presentation January 15, 2019 Cautionary Note Regarding Forward-Looking Statements Certain statements made and information contained

Filo del Sol Pre-Feasibility Study Results Webcast & Conference Call Presentation January 15, 2019 Cautionary Note Regarding Forward-Looking Statements Certain statements made and information contained

MA 1125 Lecture 14 - Expected Values. Wednesday, October 4, Objectives: Introduce expected values.

MA 5 Lecture 4 - Expected Values Wednesday, October 4, 27 Objectives: Introduce expected values.. Means, Variances, and Standard Deviations of Probability Distributions Two classes ago, we computed the

MA 5 Lecture 4 - Expected Values Wednesday, October 4, 27 Objectives: Introduce expected values.. Means, Variances, and Standard Deviations of Probability Distributions Two classes ago, we computed the

FINANCE & ACCOUNTING FEASIBILITY STUDIES: PREPARATION, ANALYSIS AND EVALUATION NON-TECHNICAL & CERTIFIED TRAINING COURSE

FEASIBILITY STUDIES: PREPARATION, ANALYSIS AND EVALUATION FINANCE & ACCOUNTING NON-TECHNICAL & CERTIFIED TRAINING COURSE The Course Uses A Mix Of Interactive Techniques, Such As Brief Presentations By

FEASIBILITY STUDIES: PREPARATION, ANALYSIS AND EVALUATION FINANCE & ACCOUNTING NON-TECHNICAL & CERTIFIED TRAINING COURSE The Course Uses A Mix Of Interactive Techniques, Such As Brief Presentations By

Course Outline. Project Finance Modelling Course 3 Days

Course Outline Project Finance Modelling Course 3 Days Overview This training course provides the opportunity for delegates to practise and improve their abilities in project finance modelling using Excel.

Course Outline Project Finance Modelling Course 3 Days Overview This training course provides the opportunity for delegates to practise and improve their abilities in project finance modelling using Excel.

HOD MADEN PRE-FEASIBILITY STUDY PRE-TAX NPV OF US$1.4 BILLION

TH E G O L D STA N DA R D I N R OYA LTY I N V EST M ENTS JUNE 2018 HOD MADEN PRE-FEASIBILITY STUDY PRE-TAX NPV OF US$1.4 BILLION CAUTIONARY NOTE REGARDING FORWARD-LOOKING INFORMATION AND NON-IFRS MEASURES

TH E G O L D STA N DA R D I N R OYA LTY I N V EST M ENTS JUNE 2018 HOD MADEN PRE-FEASIBILITY STUDY PRE-TAX NPV OF US$1.4 BILLION CAUTIONARY NOTE REGARDING FORWARD-LOOKING INFORMATION AND NON-IFRS MEASURES

Overview of Financial Statement Analysis

Overview of Financial Statement 17 November 2007 FN 1 421 FN 421 Financial Statement Statement and Reporting and Reporting Business Evaluate Prospects Evaluate Risks Business Decision Makers Equity investors

Overview of Financial Statement 17 November 2007 FN 1 421 FN 421 Financial Statement Statement and Reporting and Reporting Business Evaluate Prospects Evaluate Risks Business Decision Makers Equity investors

Risk and Return: Past and Prologue

Chapter 5 Risk and Return: Past and Prologue Bodie, Kane, and Marcus Essentials of Investments Tenth Edition What is in Chapter 5 5.1 Rates of Return HPR, arithmetic, geometric, dollar-weighted, APR, EAR

Chapter 5 Risk and Return: Past and Prologue Bodie, Kane, and Marcus Essentials of Investments Tenth Edition What is in Chapter 5 5.1 Rates of Return HPR, arithmetic, geometric, dollar-weighted, APR, EAR

Project Integration Management

Project Integration Management Describe an overall framework for project integration management as it relates to the other PM knowledge areas and the project life cycle. Explain the strategic planning

Project Integration Management Describe an overall framework for project integration management as it relates to the other PM knowledge areas and the project life cycle. Explain the strategic planning

Tower Square Investment Management LLC Strategic Aggressive

Product Type: Multi-Product Portfolio Headquarters: El Segundo, CA Total Staff: 15 Geography Focus: Global Year Founded: 2012 Investment Professionals: 12 Type of Portfolio: Balanced Total AUM: $1,422

Product Type: Multi-Product Portfolio Headquarters: El Segundo, CA Total Staff: 15 Geography Focus: Global Year Founded: 2012 Investment Professionals: 12 Type of Portfolio: Balanced Total AUM: $1,422

Introduction to Discounted Cash Flow

Introduction to Discounted Cash Flow Professor Sid Balachandran Finance and Accounting for Non-Financial Executives Columbia Business School Agenda Introducing Discounted Cashflow Applying DCF to Evaluate

Introduction to Discounted Cash Flow Professor Sid Balachandran Finance and Accounting for Non-Financial Executives Columbia Business School Agenda Introducing Discounted Cashflow Applying DCF to Evaluate

Calculate financial metrics

9 Calculate financial metrics This chapter contains the last set of analytical tasks. Using input from the previous work undertaken to create a budget (costs) and assess the value of benefits, the next

9 Calculate financial metrics This chapter contains the last set of analytical tasks. Using input from the previous work undertaken to create a budget (costs) and assess the value of benefits, the next