Payment Choice and International Trade: Theory and Evidence from Cross-country Firm Level Data

|

|

|

- Clarence Thornton

- 6 years ago

- Views:

Transcription

1 Payment Choice and International Trade: Theory and Evidence from Cross-country Firm Level Data Andreas Hoefele 1 Tim Schmidt-Eisenlohr 2 Zhihong Yu 3 1 Loughborough University 2 University of Oxford 3 University of Nottingham

2 Trade Finance The size of trade finance Auboin (2009): Trade credit and insurance market about $10-12 trillion G20 Summit s statement, April, 2009: we will ensure availability of at least $250 billion over the next two years to support trade finance through our export credit and investment agencies and through the MDBs (multilateral development banks).

3 Payment Contracts

4 Payment Contracts Data Source: IMF - BAFT Survey

5 Payment Contracts Data II Top Destination Countries for each Payment Type Top CIA Top OA Top LC Venezuela 59.9 Denmark 92.9 China 36.3 Russia 54.5 Finland 92.3 South Korea 35.3 Ukraine 51.1 Norway 90.9 Jordan 33.3 Source: FCIB Survey

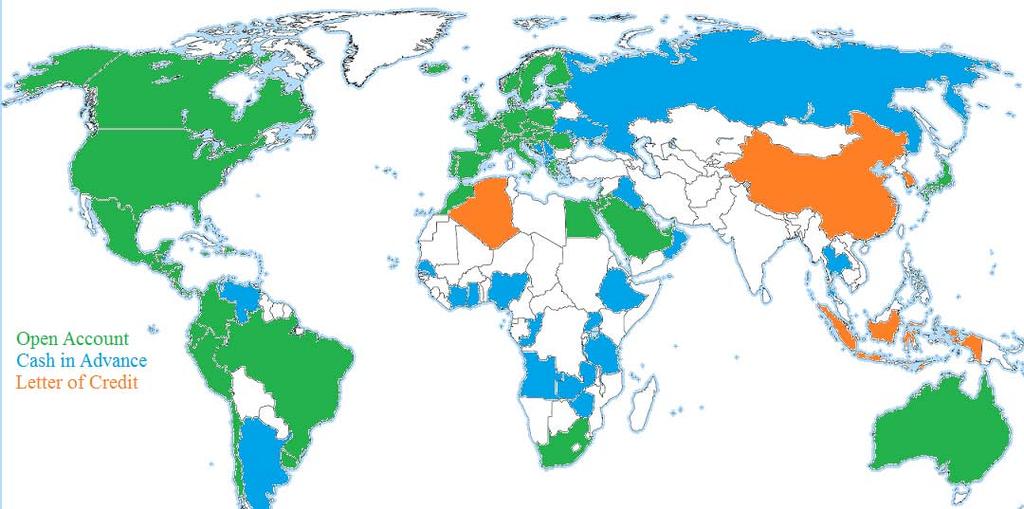

6 World Map

7 Motivation I Different Payment Contracts: Cash in Advance, Open Account and Letter of Credit Two questions: What are the trade-offs faced by firms? How can patterns across countries be explained?

8 Motivation II Schmidt-Eisenlohr (2013): Introduces choice between Cash in Advance, Open Account and Letter of Credit Firms trade-off international differences in enforcement and efficiency between financial markets Estimates effects of source and destination country variables on payment contract choice no direct test of the payment contract choice model

9 This Paper Focus on Open Account vs. Cash in Advance Empirics: Test the payment contract choice model Source country and firm level variation Different export intensities Different product complexities Theory: Extend the model Allow for firm level variation in contract choice Differentiate between contracts for domestic and international sales Introduce product complexity and study its implications

10 Main Findings Predictions of contract choice model on source country conditions confirmed: Share of Open Account in international sales higher if i) source country financing costs are lower (Open Account more attractive) ii) source country enforcement is weaker (Cash in Advance less attractive) New predictions on complex industries supported: Complexity affects the payment contract choice: Complex industries: enforcement is key Non-complex industries: financing is central

11 Literature Trade Finance: Schmidt-Eisenlohr (2013), Olsen (2010), Ahn (2010), Eck, Engemann and Schnitzer (2011a,b), Antras and Foley (forthcoming), Wider literature: Trade credit: Biais and Gollier (1997), Petersen and Rajan (1997)... Theory on financial conditions and trade: Kletzer and Bardhan (1987), Matsuyama (2005), Chaney (2005), Manova (2013) Relevance of financial conditions: Beck (2002, 2003), Greenaway et al. (2007), Berman and Hericourt (2010), Manova (2013) Relevance of contract enforcement: Nunn (2007), Levchenko (2007)

12 Literature II Most related paper: Antras and Foley (forthcoming): Transactions data from 1 large US food seller Adapt model from Schmidt-Eisenlohr (forthcoming) and test its predictions in regard of destination country enforcement: Stronger destination enforcement more OA and less CIA Extend the model dynamically and test effects from the length of relationship

13 Contributions Empirical contributions First test of contract choice for many independent firms from many source countries Provide first evidence for: Role of source country variation Choice between domestic and international sales Role of industry complexity Find evidence for effects of financial conditions on contract choice Theoretical contributions: Extend the trade finance model to include firm effects, industry complexity, and comparison between international and domestic sales

14 Micro Model

15 Basic Mechanism Two problems: Financing problem: time delay between production and sales Importer or exporter pre-finances Financing costs matter Commitment problem: party not pre-financing can default on contract

16 Basic Setup I Seller: Make take it or leave it offer to buyer Produces Sends goods Receives payment Buyer: Buys goods Sells goods Pays seller

17 Basic Setup II Two imperfections: Financial markets are segmented and differ in efficiency firms in different countries face different interest rates to finance trade (r, r ) Limited enforcement exogenous probability of contract enforcement at country level (λ, λ ) limited value of contract (not more than sales value of goods)

18 Financing forms - Cash in Advance I date 0 Buyer pays C CIA to Seller If contract enforced seller produces at cost K and sends goods date 1 Buyer sells goods for revenue R

19 Financing forms - Cash in Advance II Under Cash in Advance the maximization problem is: max E [ Π CIA ] S = C CIA λk C s.t. E [ Π CIA ] B = λr (1 + rb )C CIA 0 (PC buyer) C CIA R Optimal payment and profits are: λ 1+r B R C CIA = E [ ] ( ) Π CIA S = λ 1 1+r B R K (limited value of contract) Pre-financing done by buyer. Enforcement in regard of seller.

20 Financing forms - Open Account I date 0 Seller produces at cost K and sends goods date 1 Buyer sells goods for revenue R If contract enforced buyer pays C OA to seller

21 Financing forms - Open Account II The maximization problem is: max C E [ Π OA ] 1 S = ( λb C OA K(1 + r) ) 1 + r ] 1 ( = R λb C OA) r B (PC buyer) C OA R (limited value of contract) s.t. E [ Π OA B Optimal payment and profits are: C OA = R E [ ] Π OA S = λ B 1+r R K Seller needs to pre-finance transaction. Commitment problem on buyer side.

22 Summary Cash in Advance Financing in destination country Enforcement in source country r B, λ Open Account Financing in source country Enforcement in destination country r, λ B

23 Payment Contract: Data and Theory Identification Strategy Observe: Contract choice for total sales (domestic and international) Proposition on differential contract choice between domestic and international sales Firms have different export intensities Compare firms with different export shares to identify the effect of interest

24 Proposition Contract Choice Proposition 1 The optimal choice of payment contract is uniquely determined by the following conditions: i) International trade: E [ Π OA ] [ ] S > E Π CIA (λ ) σ (1 + r) σ λ(1 + r ) σ + z i > 0 ii) Domestic trade: S E [ Π OA S ] [ ] > E Π CIA (λ) σ λ + z i > 0 z i : Exporter specific shock to OA profitability International Trade: Source and destination country legal and financial conditions matter. Domestic Sales: only source country legal conditions matter. S

25 Source Country Predictions Proposition 3 Suppose S OA (0, 1). Then, an exporter uses more Open Account than another exporter who generates a smaller share of her revenues abroad if i) financing costs in the source country are lower (Open Account more attractive) ii) contract enforcement in the source country is worse (Cash in Advance less attractive)

26 Product Complexity Complex product are harder to enforce in court: Take this into account by introducing product complexity γ [0, 1] Assume country level enforcement probability equals λ γ Proposition 4 Suppose λ σ d > 1/e and λ o > 1/e. Then, for higher γ, the payment contract choice is more affected by source country enforcement less affected by source country financing costs

27 The Data We use the World Bank Enterprise survey: Cross-section data from firm level survey for 54 developing countries between 2006 and 2009 Firms report share of post-, pre- and on-delivery payments in total sales 2 ways to calculate the share of Open Account: Post-delivery + on-delivery payments Post-delivery/(post-delivery+pre-delivery) Shares of payment contracts in total sales Compare firms with different export intensities Drop non-manufacturing and foreign affiliates

28 The Data II Additional data sources: Enforcement measures WB Doing Business Survey: calendar days to resolve a commercial dispute WB Worldwide Governance Indicators: rule of law Financial data from Beck et al. (2009) Main variable: private credit over GDP Robustness checks: net interest margin and overhead costs

29 Source Country Specification Our main estimation equation: OA it = ψ 0 + ψ 1 XS it + ψ 2 XS it ENF ct + ψ 3 XS it FIN ct +ΨX it + ν j + ν c + ν t + ɛ it. Main prediction: ψ 2 < 0 and ψ 3 < 0 OA it : Share of Open Account XS it : Share of exports in total sales ENF ct : Measure of contract enforcement FIN ct : Financing costs X it : Firm level controls Industry, country and year FE i: firm; t: year; c: country; j: industry

30 IV Estimation Share of exports can be jointly determined with payment contracts. To address endogeneity: Use log employment as instrument at first stage for share of exports in total sales Also generate instruments for interaction terms: ln emp ENF and ln emp PC Estimate as 2 SLS

31 The Contract Intensity of Industries Proposition 4: Enforcement more important in complex industries Financing costs more relevant in non-complex industries Follow Nunn (2007) industry classification: Classify input as complex if it is not sold on an organized exchange and does not have a reference price Define industry as complex if it has a large share of complex intermediate inputs Introduce triple interactions with complexity.

32 Table : Payment Contract Choice - Baseline Dependent Variable: Share of Open Account (1) (2) (3) Exportshare 0.131*** *** (0.049) (0.029) (0.043) Enforcement x Exportshare *** *** *** (13.617) (15.782) (13.384) Interest Margin x Exportshare ** (0.554) Private Credit x Exportshare 0.107** (0.052) Overhead x Exportshare *** (0.517) R-squared N

33 Table : Payment Contract Choice: Complexity Exportershare ** (0.134) (0.081) (0.121) Enforcement x Exportshare (37.790) (44.480) (37.488) Enforcement x Exportshare x Complexity *** *** (64.492) (76.798) (63.152) Interest Margin x Exportshare ** (1.390) Interest Margin x Exportshare x Complexity (2.259) Private Credit x Exportshare 0.551*** (0.145) Private Credit x Exportshare x Complexity *** (0.247) Overhead x Exportshare (1.315) Overhead x Exportshare x Complexity (2.234) R-squared N

34 Table : IV Regressions Both Instruments Exporting Experience log Employment Both Instruments (1) (2) (3) (4) Exportershare 0.650*** 0.599** *** (0.221) (0.253) (0.505) (0.223) Enforcement x Exportshare *** ** ** *** (54.467) (66.094) (82.210) (54.831) Interest Margin x Exportshare ** * ** (2.375) (2.455) (6.769) (2.395) N F Sargan-Test p-value Regressor 2SLS 2SLS 2SLS LIML

35 Robustness Checks Fractional Response Model Results in line with predictions Less efficient estimation lose some significance. Post-Delivery versus Pre-Delivery Exporter Dummy

36 Conclusion Payment contracts trade-off differences in financing costs and contract enforcement across countries Industry complexity changes the relative importance of these factors Source and Destination country institutions interact in non-trivial ways Payment contracts are a market solution to mitigate adverse institutional factors

37 Thanks Thanks!!!

Payment Choice In International Trade: Evidence from Cross-Country Firm Level Data. Andreas Hoefele, Tim Schmidt- Eisenlohr and Zihong Yu WP

ISSN 1750-4171 ECONOMICS DISCUSSION PAPER SERIES Payment Choice In International Trade: Evidence from Cross-Country Firm Level Data. Andreas Hoefele, Tim Schmidt- Eisenlohr and Zihong Yu WP 2013 11 School

ISSN 1750-4171 ECONOMICS DISCUSSION PAPER SERIES Payment Choice In International Trade: Evidence from Cross-Country Firm Level Data. Andreas Hoefele, Tim Schmidt- Eisenlohr and Zihong Yu WP 2013 11 School

Payment Choice in International Trade: Theory and Evidence from Cross-country Firm Level Data

Payment Choice in International Trade: Theory and Evidence from Cross-country Firm Level Data Andreas Hoefele Tim Schmidt-Eisenlohr Zhihong Yu October 2012 Abstract When trading across borders, firms choose

Payment Choice in International Trade: Theory and Evidence from Cross-country Firm Level Data Andreas Hoefele Tim Schmidt-Eisenlohr Zhihong Yu October 2012 Abstract When trading across borders, firms choose

Towards a Theory of Trade Finance

Towards a Theory of Trade Finance Tim Schmidt-Eisenlohr University of Oxford First version: December 2009 This version: March 2011 Abstract Shipping goods internationally is risky and takes time. To allocate

Towards a Theory of Trade Finance Tim Schmidt-Eisenlohr University of Oxford First version: December 2009 This version: March 2011 Abstract Shipping goods internationally is risky and takes time. To allocate

Firms and Credit Constraints along the Value Chain: Processing Trade in China

Firms and Credit Constraints along the Value Chain: Processing Trade in China Kalina Manova, Stanford University and NBER Zhihong Yu, Nottingham University ECB/CompNet PIIE World Bank Conference April

Firms and Credit Constraints along the Value Chain: Processing Trade in China Kalina Manova, Stanford University and NBER Zhihong Yu, Nottingham University ECB/CompNet PIIE World Bank Conference April

Financial liberalization and the relationship-specificity of exports *

Financial and the relationship-specificity of exports * Fabrice Defever Jens Suedekum a) University of Nottingham Center of Economic Performance (LSE) GEP and CESifo Mercator School of Management University

Financial and the relationship-specificity of exports * Fabrice Defever Jens Suedekum a) University of Nottingham Center of Economic Performance (LSE) GEP and CESifo Mercator School of Management University

Does exporting affect financial leverages: Evidence from Chinese firms under exchange rate fluctuations

Does exporting affect financial leverages: Evidence from Chinese firms under exchange rate fluctuations Zhihong Yu GEP, School of Economics, University of Nottingham Festschrift Conference for Professor

Does exporting affect financial leverages: Evidence from Chinese firms under exchange rate fluctuations Zhihong Yu GEP, School of Economics, University of Nottingham Festschrift Conference for Professor

International Trade, Risk, and the Role of Banks

Federal Reserve Bank of New York Staff Reports International Trade, Risk, and the Role of Banks Friederike Niepmann Tim Schmidt-Eisenlohr Staff Report No. 633 September 2013 Revised April 2014 This paper

Federal Reserve Bank of New York Staff Reports International Trade, Risk, and the Role of Banks Friederike Niepmann Tim Schmidt-Eisenlohr Staff Report No. 633 September 2013 Revised April 2014 This paper

Access to finance and foreign technology upgrading : Firm-level evidence from India

Access to finance and foreign technology upgrading : Firm-level evidence from India Maria Bas and Antoine Berthou CEPII ICRIER Seminar, 13th December 2010 Motivation : Import Patterns Globalization process

Access to finance and foreign technology upgrading : Firm-level evidence from India Maria Bas and Antoine Berthou CEPII ICRIER Seminar, 13th December 2010 Motivation : Import Patterns Globalization process

Managing Trade: Evidence from China and the US

Managing Trade: Evidence from China and the US Nick Bloom, Stanford & NBER Kalina Manova, Stanford, Oxford, NBER & CEPR John Van Reenen, London School of Economics & CEP Zhihong Yu, Nottingham National

Managing Trade: Evidence from China and the US Nick Bloom, Stanford & NBER Kalina Manova, Stanford, Oxford, NBER & CEPR John Van Reenen, London School of Economics & CEP Zhihong Yu, Nottingham National

International Transfer Pricing and Tax Avoidance: Evidence from Linked Tax-Trade Statistics in the UK

International Transfer Pricing and Tax Avoidance: Evidence from Linked Tax-Trade Statistics in the UK Li Liu, Tim Schmidt-Eisenlohr, and Dongxian Guo International Monetary Fund, Federal Reserve Board,

International Transfer Pricing and Tax Avoidance: Evidence from Linked Tax-Trade Statistics in the UK Li Liu, Tim Schmidt-Eisenlohr, and Dongxian Guo International Monetary Fund, Federal Reserve Board,

The Role of Foreign Banks in Trade

The Role of Foreign Banks in Trade Stijn Claessens (Federal Reserve Board & CEPR) Omar Hassib (Maastricht University) Neeltje van Horen (De Nederlandsche Bank & CEPR) RIETI-MoFiR-Hitotsubashi-JFC International

The Role of Foreign Banks in Trade Stijn Claessens (Federal Reserve Board & CEPR) Omar Hassib (Maastricht University) Neeltje van Horen (De Nederlandsche Bank & CEPR) RIETI-MoFiR-Hitotsubashi-JFC International

Transfer Pricing by Multinational Firms: New Evidence from Foreign Firm Ownership

Transfer Pricing by Multinational Firms: New Evidence from Foreign Firm Ownership Anca Cristea University of Oregon Daniel X. Nguyen University of Copenhagen Rocky Mountain Empirical Trade 16-18 May, 2014

Transfer Pricing by Multinational Firms: New Evidence from Foreign Firm Ownership Anca Cristea University of Oregon Daniel X. Nguyen University of Copenhagen Rocky Mountain Empirical Trade 16-18 May, 2014

Firm-specific Exchange Rate Shocks and Employment Adjustment: Theory and Evidence

Firm-specific Exchange Rate Shocks and Employment Adjustment: Theory and Evidence Mi Dai Jianwei Xu Beijing Normal University November 2016 Mi Dai (Beijing Normal University) exchange rate and employment

Firm-specific Exchange Rate Shocks and Employment Adjustment: Theory and Evidence Mi Dai Jianwei Xu Beijing Normal University November 2016 Mi Dai (Beijing Normal University) exchange rate and employment

CEMMAP Masterclass: Empirical Models of Comparative Advantage and the Gains from Trade 1 Lecture 1: Ricardian Models (I)

") CEMMAP Masterclass: Empirical Models of Comparative Advantage and the Gains from Trade 1 Lecture 1: Ricardian Models (I) Dave Donaldson (MIT) CEMMAP MC July 2018 1 All material based on earlier courses

CEMMAP Masterclass: Empirical Models of Comparative Advantage and the Gains from Trade 1 Lecture 1: Ricardian Models (I) Dave Donaldson (MIT) CEMMAP MC July 2018 1 All material based on earlier courses

How Local Financial Market Conditions, Interest Rates, and Productivity Relate to Decisions to Export *

ANNALS OF ECONOMICS AND FINANCE 16-2, 315 334 (2015) How Local Financial Market Conditions, Interest Rates, and Productivity Relate to Decisions to Export * Dingming Liu Wang Yanan Institute for Studies

ANNALS OF ECONOMICS AND FINANCE 16-2, 315 334 (2015) How Local Financial Market Conditions, Interest Rates, and Productivity Relate to Decisions to Export * Dingming Liu Wang Yanan Institute for Studies

Draft. The Role of Foreign Banks in Trade. Stijn Claessens, Omar Hassib, and Neeltje van Horen * December Abstract

Draft The Role of Foreign Banks in Trade by Stijn Claessens, Omar Hassib, and Neeltje van Horen * December 2014 Abstract Financially developed countries tend to export relatively more in financially vulnerable

Draft The Role of Foreign Banks in Trade by Stijn Claessens, Omar Hassib, and Neeltje van Horen * December 2014 Abstract Financially developed countries tend to export relatively more in financially vulnerable

Don t Throw in the Towel, Throw in Trade Credit!

Don t Throw in the Towel, Throw in Trade Credit! Banu Demir Bilkent University and CEPR Beata Javorcik University of Oxford and CEPR August 30, 2017 The literature has documented how firms adjust to increased

Don t Throw in the Towel, Throw in Trade Credit! Banu Demir Bilkent University and CEPR Beata Javorcik University of Oxford and CEPR August 30, 2017 The literature has documented how firms adjust to increased

Frequency of Price Adjustment and Pass-through

Frequency of Price Adjustment and Pass-through Gita Gopinath Harvard and NBER Oleg Itskhoki Harvard CEFIR/NES March 11, 2009 1 / 39 Motivation Micro-level studies document significant heterogeneity in

Frequency of Price Adjustment and Pass-through Gita Gopinath Harvard and NBER Oleg Itskhoki Harvard CEFIR/NES March 11, 2009 1 / 39 Motivation Micro-level studies document significant heterogeneity in

Firm Exports and Multinational Activity under Credit Constraints

Firm Exports and Multinational Activity under Credit Constraints Kalina Manova Stanford University and NBER Shang-Jin Wei Columbia University and NBER Zhiwei Zhang Hong Kong Monetary Authority and IMF

Firm Exports and Multinational Activity under Credit Constraints Kalina Manova Stanford University and NBER Shang-Jin Wei Columbia University and NBER Zhiwei Zhang Hong Kong Monetary Authority and IMF

Credit Constraints and The Adjustment to Trade Reform

Credit Constraints and The Adjustment to Trade Reform Kalina Manova Stanford University and NBER July 20, 2009 Abstract. A growing literature on trade and finance has established that credit constraints

Credit Constraints and The Adjustment to Trade Reform Kalina Manova Stanford University and NBER July 20, 2009 Abstract. A growing literature on trade and finance has established that credit constraints

Trade Credit, Financing Structure and Growth

Trade Credit, Financing Structure and Growth Junjie Xia Department of Economics University of Southern California Job Market Paper Jan. 12, 2017 Junjie Xia (USC-Economics) Trade Credit Job Market Paper

Trade Credit, Financing Structure and Growth Junjie Xia Department of Economics University of Southern California Job Market Paper Jan. 12, 2017 Junjie Xia (USC-Economics) Trade Credit Job Market Paper

The Margins of Global Sourcing: Theory and Evidence from U.S. Firms by Pol Antràs, Teresa C. Fort and Felix Tintelnot

The Margins of Global Sourcing: Theory and Evidence from U.S. Firms by Pol Antràs, Teresa C. Fort and Felix Tintelnot Online Theory Appendix Not for Publication) Equilibrium in the Complements-Pareto Case

The Margins of Global Sourcing: Theory and Evidence from U.S. Firms by Pol Antràs, Teresa C. Fort and Felix Tintelnot Online Theory Appendix Not for Publication) Equilibrium in the Complements-Pareto Case

Theory Appendix for: Buyer-Seller Relationships in International Trade: Evidence from U.S. State Exports and Business-Class Travel

Theory Appendix for: Buyer-Seller Relationships in International Trade: Evidence from U.S. State Exports and Business-Class Travel Anca Cristea University of Oregon December 2010 Abstract This appendix

Theory Appendix for: Buyer-Seller Relationships in International Trade: Evidence from U.S. State Exports and Business-Class Travel Anca Cristea University of Oregon December 2010 Abstract This appendix

UNIVERSITY OF NOTTINGHAM. Discussion Papers in Economics

UNIVERSITY OF NOTTINGHAM Discussion Papers in Economics Discussion Paper No. 07/05 Firm heterogeneity, foreign direct investment and the hostcountry welfare: Trade costs vs. cheap labor By Arijit Mukherjee

UNIVERSITY OF NOTTINGHAM Discussion Papers in Economics Discussion Paper No. 07/05 Firm heterogeneity, foreign direct investment and the hostcountry welfare: Trade costs vs. cheap labor By Arijit Mukherjee

Private Leverage and Sovereign Default

Private Leverage and Sovereign Default Cristina Arellano Yan Bai Luigi Bocola FRB Minneapolis University of Rochester Northwestern University Economic Policy and Financial Frictions November 2015 1 / 37

Private Leverage and Sovereign Default Cristina Arellano Yan Bai Luigi Bocola FRB Minneapolis University of Rochester Northwestern University Economic Policy and Financial Frictions November 2015 1 / 37

Financial Liberalization and Neighbor Coordination

Financial Liberalization and Neighbor Coordination Arvind Magesan and Jordi Mondria January 31, 2011 Abstract In this paper we study the economic and strategic incentives for a country to financially liberalize

Financial Liberalization and Neighbor Coordination Arvind Magesan and Jordi Mondria January 31, 2011 Abstract In this paper we study the economic and strategic incentives for a country to financially liberalize

Credit Constraints, Technology Choice and Exports - A Firm Level Study for Latin American Countries

Credit Constraints, Technology Choice and Exports - A Firm Level Study for Latin American Countries December 17, 2013 Research Motivation Trade liberalization benefits are not fully realized by firms in

Credit Constraints, Technology Choice and Exports - A Firm Level Study for Latin American Countries December 17, 2013 Research Motivation Trade liberalization benefits are not fully realized by firms in

Lecture 4. Extensions to the Open Economy. and. Emerging Market Crises

Lecture 4 Extensions to the Open Economy and Emerging Market Crises Mark Gertler NYU June 2009 0 Objectives Develop micro-founded open-economy quantitative macro model with real/financial interactions

Lecture 4 Extensions to the Open Economy and Emerging Market Crises Mark Gertler NYU June 2009 0 Objectives Develop micro-founded open-economy quantitative macro model with real/financial interactions

Fiscal Consolidations in Currency Unions: Spending Cuts Vs. Tax Hikes

Fiscal Consolidations in Currency Unions: Spending Cuts Vs. Tax Hikes Christopher J. Erceg and Jesper Lindé Federal Reserve Board June, 2011 Erceg and Lindé (Federal Reserve Board) Fiscal Consolidations

Fiscal Consolidations in Currency Unions: Spending Cuts Vs. Tax Hikes Christopher J. Erceg and Jesper Lindé Federal Reserve Board June, 2011 Erceg and Lindé (Federal Reserve Board) Fiscal Consolidations

Input Tariffs, Speed of Contract Enforcement, and the Productivity of Firms in India

Input Tariffs, Speed of Contract Enforcement, and the Productivity of Firms in India Reshad N Ahsan University of Melbourne December, 2011 Reshad N Ahsan (University of Melbourne) December 2011 1 / 25

Input Tariffs, Speed of Contract Enforcement, and the Productivity of Firms in India Reshad N Ahsan University of Melbourne December, 2011 Reshad N Ahsan (University of Melbourne) December 2011 1 / 25

Do Peer Firms Affect Corporate Financial Policy?

1 / 23 Do Peer Firms Affect Corporate Financial Policy? Journal of Finance, 2014 Mark T. Leary 1 and Michael R. Roberts 2 1 Olin Business School Washington University 2 The Wharton School University of

1 / 23 Do Peer Firms Affect Corporate Financial Policy? Journal of Finance, 2014 Mark T. Leary 1 and Michael R. Roberts 2 1 Olin Business School Washington University 2 The Wharton School University of

Efficiency Wages and the Economic Effects of the Minimum Wage: Evidence from a Low-Wage Labour Market. Andreas Georgiadis

Efficiency Wages and the Economic Effects of the Minimum Wage: Evidence from a Low-Wage Labour Market Andreas Georgiadis What we do: Overview -We exploit a natural experiment provided by the 1999 introduction

Efficiency Wages and the Economic Effects of the Minimum Wage: Evidence from a Low-Wage Labour Market Andreas Georgiadis What we do: Overview -We exploit a natural experiment provided by the 1999 introduction

Poultry in Motion: A Study of International Trade Finance Practices

Poultry in Motion: A Study of International Trade Finance Practices The Harvard community has made this article openly available. Please share how this access benefits you. Your story matters Citation

Poultry in Motion: A Study of International Trade Finance Practices The Harvard community has made this article openly available. Please share how this access benefits you. Your story matters Citation

Firms in International Trade. Lecture 2: The Melitz Model

Firms in International Trade Lecture 2: The Melitz Model Stephen Redding London School of Economics 1 / 33 Essential Reading Melitz, M. J. (2003) The Impact of Trade on Intra-Industry Reallocations and

Firms in International Trade Lecture 2: The Melitz Model Stephen Redding London School of Economics 1 / 33 Essential Reading Melitz, M. J. (2003) The Impact of Trade on Intra-Industry Reallocations and

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach Gianluca Benigno 1 Andrew Foerster 2 Christopher Otrok 3 Alessandro Rebucci 4 1 London School of Economics and

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach Gianluca Benigno 1 Andrew Foerster 2 Christopher Otrok 3 Alessandro Rebucci 4 1 London School of Economics and

Credit Constraints, Heterogeneous Firms, and International Trade

Review of Economic Studies (2013) 80, 711 744 doi:10.1093/restud/rds036 The Author 2012. Published by Oxford University Press on behalf of The Review of Economic Studies Limited. Advance access publication

Review of Economic Studies (2013) 80, 711 744 doi:10.1093/restud/rds036 The Author 2012. Published by Oxford University Press on behalf of The Review of Economic Studies Limited. Advance access publication

Payment Contracts and Trade Finance in Export Relationships

Payment Contracts and Trade Finance in Export Relationships Christian Fischer First draft: September 2016 This version: July 2017 Preliminary version. Comments welcome. Abstract. I examine the use of payment

Payment Contracts and Trade Finance in Export Relationships Christian Fischer First draft: September 2016 This version: July 2017 Preliminary version. Comments welcome. Abstract. I examine the use of payment

Does Macro-Pru Leak? Empirical Evidence from a UK Natural Experiment

12TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 10 11, 2011 Does Macro-Pru Leak? Empirical Evidence from a UK Natural Experiment Shekhar Aiyar International Monetary Fund Charles W. Calomiris Columbia

12TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 10 11, 2011 Does Macro-Pru Leak? Empirical Evidence from a UK Natural Experiment Shekhar Aiyar International Monetary Fund Charles W. Calomiris Columbia

Financial Integration, Financial Deepness and Global Imbalances

Financial Integration, Financial Deepness and Global Imbalances Enrique G. Mendoza University of Maryland, IMF & NBER Vincenzo Quadrini University of Southern California, CEPR & NBER José-Víctor Ríos-Rull

Financial Integration, Financial Deepness and Global Imbalances Enrique G. Mendoza University of Maryland, IMF & NBER Vincenzo Quadrini University of Southern California, CEPR & NBER José-Víctor Ríos-Rull

An Empirical Examination of the Electric Utilities Industry. December 19, Regulatory Induced Risk Aversion in. Contracting Behavior

An Empirical Examination of the Electric Utilities Industry December 19, 2011 The Puzzle Why do price-regulated firms purchase input coal through both contract Figure and 1(a): spot Contract transactions,

An Empirical Examination of the Electric Utilities Industry December 19, 2011 The Puzzle Why do price-regulated firms purchase input coal through both contract Figure and 1(a): spot Contract transactions,

Liquidity Regulation and Credit Booms: Theory and Evidence from China. JRCPPF Sixth Annual Conference February 16-17, 2017

Liquidity Regulation and Credit Booms: Theory and Evidence from China Kinda Hachem Chicago Booth and NBER Zheng Michael Song Chinese University of Hong Kong JRCPPF Sixth Annual Conference February 16-17,

Liquidity Regulation and Credit Booms: Theory and Evidence from China Kinda Hachem Chicago Booth and NBER Zheng Michael Song Chinese University of Hong Kong JRCPPF Sixth Annual Conference February 16-17,

Trade Finance and Trade Flows into Industrialized, Emerging and Developing Economies: What is the Role of Trade Openness?

Trade Finance and Trade Flows into Industrialized, Emerging and Developing Economies: What is the Role of Trade Openness? Birgit Schmitz 1 / Clara Brandi 2 15 January 2015 Preliminary draft. Please do

Trade Finance and Trade Flows into Industrialized, Emerging and Developing Economies: What is the Role of Trade Openness? Birgit Schmitz 1 / Clara Brandi 2 15 January 2015 Preliminary draft. Please do

Corporate Strategy, Conformism, and the Stock Market

Corporate Strategy, Conformism, and the Stock Market Thierry Foucault (HEC) Laurent Frésard (Maryland) November 20, 2015 Corporate Strategy, Conformism, and the Stock Market Thierry Foucault (HEC) Laurent

Corporate Strategy, Conformism, and the Stock Market Thierry Foucault (HEC) Laurent Frésard (Maryland) November 20, 2015 Corporate Strategy, Conformism, and the Stock Market Thierry Foucault (HEC) Laurent

Online Appendices for

Online Appendices for From Made in China to Innovated in China : Necessity, Prospect, and Challenges Shang-Jin Wei, Zhuan Xie, and Xiaobo Zhang Journal of Economic Perspectives, (31)1, Winter 2017 Online

Online Appendices for From Made in China to Innovated in China : Necessity, Prospect, and Challenges Shang-Jin Wei, Zhuan Xie, and Xiaobo Zhang Journal of Economic Perspectives, (31)1, Winter 2017 Online

Intellectual Property Rights, MNFs and Technology Transfers

Intellectual Property Rights, MNFs and Technology Transfers Sara Biancini and Pamela Bombarda July 2016: VERY PRELIMINARY AND INCOMPLETE Abstract We build a theoretical model in which MNFs based in developed

Intellectual Property Rights, MNFs and Technology Transfers Sara Biancini and Pamela Bombarda July 2016: VERY PRELIMINARY AND INCOMPLETE Abstract We build a theoretical model in which MNFs based in developed

Off the Cliff and Back? Credit Conditions and International Trade during the Global Financial Crisis

Off the Cliff and Back? Credit Conditions and International Trade during the Global Financial Crisis Davin Chor Singapore Management University Kalina Manova Stanford 3-4 June 2010 NY Fed Conference on

Off the Cliff and Back? Credit Conditions and International Trade during the Global Financial Crisis Davin Chor Singapore Management University Kalina Manova Stanford 3-4 June 2010 NY Fed Conference on

No Guarantees, No Trade: How Banks A ect Export Patterns

No Guarantees, No Trade: How Banks A ect Export Patterns Friederike Niepmann and Tim Schmidt-Eisenlohr September 2014 Abstract This study provides evidence that shocks to the supply of trade finance have

No Guarantees, No Trade: How Banks A ect Export Patterns Friederike Niepmann and Tim Schmidt-Eisenlohr September 2014 Abstract This study provides evidence that shocks to the supply of trade finance have

CENTRO STUDI LUCA D AGLIANO DEVELOPMENT STUDIES WORKING PAPERS N January 2019

WWW.DAGLIANO.UNIMI.IT CENTRO STUDI LUCA D AGLIANO DEVELOPMENT STUDIES WORKING PAPERS N. 441 January 2019 Credit constraints and firm exports: Evidence from SMEs in emerging and developing countries Filomena

WWW.DAGLIANO.UNIMI.IT CENTRO STUDI LUCA D AGLIANO DEVELOPMENT STUDIES WORKING PAPERS N. 441 January 2019 Credit constraints and firm exports: Evidence from SMEs in emerging and developing countries Filomena

Gravity, Trade Integration and Heterogeneity across Industries

Gravity, Trade Integration and Heterogeneity across Industries Natalie Chen University of Warwick and CEPR Dennis Novy University of Warwick and CESifo Motivations Trade costs are a key feature in today

Gravity, Trade Integration and Heterogeneity across Industries Natalie Chen University of Warwick and CEPR Dennis Novy University of Warwick and CESifo Motivations Trade costs are a key feature in today

THE WILLIAM DAVIDSON INSTITUTE AT THE UNIVERSITY OF MICHIGAN BUSINESS SCHOOL

THE WILLIAM DAVIDSON INSTITUTE AT THE UNIVERSITY OF MICHIGAN BUSINESS SCHOOL Financial Dependence, Stock Market Liberalizations, and Growth By: Nandini Gupta and Kathy Yuan William Davidson Working Paper

THE WILLIAM DAVIDSON INSTITUTE AT THE UNIVERSITY OF MICHIGAN BUSINESS SCHOOL Financial Dependence, Stock Market Liberalizations, and Growth By: Nandini Gupta and Kathy Yuan William Davidson Working Paper

A Macroeconomic Model with Financial Panics

A Macroeconomic Model with Financial Panics Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 March 218 1 The views expressed in this paper are those of the authors

A Macroeconomic Model with Financial Panics Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 March 218 1 The views expressed in this paper are those of the authors

International Trade

14.581 International Trade Class notes on 2/11/2013 1 1 Taxonomy of eoclassical Trade Models In a neoclassical trade model, comparative advantage, i.e. di erences in relative autarky prices, is the rationale

14.581 International Trade Class notes on 2/11/2013 1 1 Taxonomy of eoclassical Trade Models In a neoclassical trade model, comparative advantage, i.e. di erences in relative autarky prices, is the rationale

Gernot Müller (University of Bonn, CEPR, and Ifo)

") Exchange rate regimes and fiscal multipliers Benjamin Born (Ifo Institute) Falko Jüßen (TU Dortmund and IZA) Gernot Müller (University of Bonn, CEPR, and Ifo) Fiscal Policy in the Aftermath of the Financial

Exchange rate regimes and fiscal multipliers Benjamin Born (Ifo Institute) Falko Jüßen (TU Dortmund and IZA) Gernot Müller (University of Bonn, CEPR, and Ifo) Fiscal Policy in the Aftermath of the Financial

The Run for Safety: Financial Fragility and Deposit Insurance

The Run for Safety: Financial Fragility and Deposit Insurance Rajkamal Iyer- Imperial College, CEPR Thais Jensen- Univ of Copenhagen Niels Johannesen- Univ of Copenhagen Adam Sheridan- Univ of Copenhagen

The Run for Safety: Financial Fragility and Deposit Insurance Rajkamal Iyer- Imperial College, CEPR Thais Jensen- Univ of Copenhagen Niels Johannesen- Univ of Copenhagen Adam Sheridan- Univ of Copenhagen

Motivation: Two Basic Facts

Motivation: Two Basic Facts 1 Primary objective of macroprudential policy: aligning financial system resilience with systemic risk to promote the real economy Systemic risk event Financial system resilience

Motivation: Two Basic Facts 1 Primary objective of macroprudential policy: aligning financial system resilience with systemic risk to promote the real economy Systemic risk event Financial system resilience

Financial Intermediation and the Supply of Liquidity

Financial Intermediation and the Supply of Liquidity Jonathan Kreamer University of Maryland, College Park November 11, 2012 1 / 27 Question Growing recognition of the importance of the financial sector.

Financial Intermediation and the Supply of Liquidity Jonathan Kreamer University of Maryland, College Park November 11, 2012 1 / 27 Question Growing recognition of the importance of the financial sector.

State Dependency of Monetary Policy: The Refinancing Channel

State Dependency of Monetary Policy: The Refinancing Channel Martin Eichenbaum, Sergio Rebelo, and Arlene Wong May 2018 Motivation In the US, bulk of household borrowing is in fixed rate mortgages with

State Dependency of Monetary Policy: The Refinancing Channel Martin Eichenbaum, Sergio Rebelo, and Arlene Wong May 2018 Motivation In the US, bulk of household borrowing is in fixed rate mortgages with

Contractual Imperfections and the Impact of Crises on Trade: Evidence from Industry-Level Data

BANCO CENTRAL DE RESERVA DEL PERÚ Contractual Imperfections and the Impact of Crises on Trade: Evidence from Industry-Level Data Renzo Castellares 1 and Jorge Salas 2 1 Banco Central de Reserva del Perú

BANCO CENTRAL DE RESERVA DEL PERÚ Contractual Imperfections and the Impact of Crises on Trade: Evidence from Industry-Level Data Renzo Castellares 1 and Jorge Salas 2 1 Banco Central de Reserva del Perú

Aid Effectiveness: AcomparisonofTiedandUntiedAid

Aid Effectiveness: AcomparisonofTiedandUntiedAid Josepa M. Miquel-Florensa York University April9,2007 Abstract We evaluate the differential effects of Tied and Untied aid on growth, and how these effects

Aid Effectiveness: AcomparisonofTiedandUntiedAid Josepa M. Miquel-Florensa York University April9,2007 Abstract We evaluate the differential effects of Tied and Untied aid on growth, and how these effects

The Model: Tradables, Non-tradables, and Semi-tradables in Trade Models. Shantayanan Devarajan Jeffrey D. Lewis Jaime de Melo Sherman Robinson

The 1-2-3 Model: Tradables, Non-tradables, and Semi-tradables in Trade Models Shantayanan Devarajan Jeffrey D. Lewis Jaime de Melo Sherman Robinson Macroeconomic Adjustment GDP = C + I + G + E - M GDP

The 1-2-3 Model: Tradables, Non-tradables, and Semi-tradables in Trade Models Shantayanan Devarajan Jeffrey D. Lewis Jaime de Melo Sherman Robinson Macroeconomic Adjustment GDP = C + I + G + E - M GDP

Notes II: Consumption-Saving Decisions, Ricardian Equivalence, and Fiscal Policy. Julio Garín Intermediate Macroeconomics Fall 2018

Notes II: Consumption-Saving Decisions, Ricardian Equivalence, and Fiscal Policy Julio Garín Intermediate Macroeconomics Fall 2018 Introduction Intermediate Macroeconomics Consumption/Saving, Ricardian

Notes II: Consumption-Saving Decisions, Ricardian Equivalence, and Fiscal Policy Julio Garín Intermediate Macroeconomics Fall 2018 Introduction Intermediate Macroeconomics Consumption/Saving, Ricardian

Resource Allocation within Firms and Financial Market Dislocation: Evidence from Diversified Conglomerates

Resource Allocation within Firms and Financial Market Dislocation: Evidence from Diversified Conglomerates Gregor Matvos and Amit Seru (RFS, 2014) Corporate Finance - PhD Course 2017 Stefan Greppmair,

Resource Allocation within Firms and Financial Market Dislocation: Evidence from Diversified Conglomerates Gregor Matvos and Amit Seru (RFS, 2014) Corporate Finance - PhD Course 2017 Stefan Greppmair,

E Imports and RMB Exchange Rate Pass-Through: Marginal Cost versus Quality Change

E2018017 2018-07-10 Imports and RMB Exchange Rate Pass-Through: Marginal Cost versus Quality Change Yaqi Wang Miaojie Yu Abstract This article investigates the differential impacts of exchange rate movements

E2018017 2018-07-10 Imports and RMB Exchange Rate Pass-Through: Marginal Cost versus Quality Change Yaqi Wang Miaojie Yu Abstract This article investigates the differential impacts of exchange rate movements

To Segregate or to Integrate: Education Politics and Democracy

To Segregate or to Integrate: Education Politics and Democracy David de la Croix 1 Matthias Doepke 2 1 dept. of economics & CORE Univ. cath. Louvain 2 dept. of economics U.C. Los Angeles October 2007 1

To Segregate or to Integrate: Education Politics and Democracy David de la Croix 1 Matthias Doepke 2 1 dept. of economics & CORE Univ. cath. Louvain 2 dept. of economics U.C. Los Angeles October 2007 1

Prospect Theory and Asset Prices

Prospect Theory and Asset Prices Presenting Barberies - Huang - Santos s paper Attila Lindner January 2009 Attila Lindner (CEU) Prospect Theory and Asset Prices January 2009 1 / 17 Presentation Outline

Prospect Theory and Asset Prices Presenting Barberies - Huang - Santos s paper Attila Lindner January 2009 Attila Lindner (CEU) Prospect Theory and Asset Prices January 2009 1 / 17 Presentation Outline

NBER WORKING PAPER SERIES FIRM EXPORTS AND MULTINATIONAL ACTIVITY UNDER CREDIT CONSTRAINTS. Kalina Manova Shang-Jin Wei Zhiwei Zhang

NBER WORKING PAPER SERIES FIRM EXPORTS AND MULTINATIONAL ACTIVITY UNDER CREDIT CONSTRAINTS Kalina Manova Shang-Jin Wei Zhiwei Zhang Working Paper 16905 http://www.nber.org/papers/w16905 NATIONAL BUREAU

NBER WORKING PAPER SERIES FIRM EXPORTS AND MULTINATIONAL ACTIVITY UNDER CREDIT CONSTRAINTS Kalina Manova Shang-Jin Wei Zhiwei Zhang Working Paper 16905 http://www.nber.org/papers/w16905 NATIONAL BUREAU

Taxing Firms Facing Financial Frictions

Taxing Firms Facing Financial Frictions Daniel Wills 1 Gustavo Camilo 2 1 Universidad de los Andes 2 Cornerstone November 11, 2017 NTA 2017 Conference Corporate income is often taxed at different sources

Taxing Firms Facing Financial Frictions Daniel Wills 1 Gustavo Camilo 2 1 Universidad de los Andes 2 Cornerstone November 11, 2017 NTA 2017 Conference Corporate income is often taxed at different sources

Comments on Kristin Forbes: Why do Foreigners Invest in the United States? Henning Bohn

1 Comments on Kristin Forbes: Why do Foreigners Invest in the United States? Henning Bohn Department of Economics University of California, Santa Barbara Federal Reserve Bank of San Francisco 2008 Pacific

1 Comments on Kristin Forbes: Why do Foreigners Invest in the United States? Henning Bohn Department of Economics University of California, Santa Barbara Federal Reserve Bank of San Francisco 2008 Pacific

A Macroeconomic Model with Financial Panics

A Macroeconomic Model with Financial Panics Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 September 218 1 The views expressed in this paper are those of the

A Macroeconomic Model with Financial Panics Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 September 218 1 The views expressed in this paper are those of the

Peer Effects in Retirement Decisions

Peer Effects in Retirement Decisions Mario Meier 1 & Andrea Weber 2 1 University of Mannheim 2 Vienna University of Economics and Business, CEPR, IZA Meier & Weber (2016) Peers in Retirement 1 / 35 Motivation

Peer Effects in Retirement Decisions Mario Meier 1 & Andrea Weber 2 1 University of Mannheim 2 Vienna University of Economics and Business, CEPR, IZA Meier & Weber (2016) Peers in Retirement 1 / 35 Motivation

The Labor Market Consequences of Adverse Financial Shocks

The Labor Market Consequences of Adverse Financial Shocks November 2012 Unemployment rate on the two sides of the Atlantic Credit to the private sector over GDP Credit to private sector as a percentage

The Labor Market Consequences of Adverse Financial Shocks November 2012 Unemployment rate on the two sides of the Atlantic Credit to the private sector over GDP Credit to private sector as a percentage

Labor Market Rigidities, Trade and Unemployment

Labor Market Rigidities, Trade and Unemployment Elhanan Helpman Harvard and CIFAR Oleg Itskhoki Princeton Chicago Booth May 2011 1 / 30 Motivation Institutional differences as a source of comparative advantage

Labor Market Rigidities, Trade and Unemployment Elhanan Helpman Harvard and CIFAR Oleg Itskhoki Princeton Chicago Booth May 2011 1 / 30 Motivation Institutional differences as a source of comparative advantage

Shocks vs Structure:

Shocks vs Structure: Explaining Differences in Exchange Rate Pass-Through Across Countries and Time Kristin Forbes: MIT, NBER & CEPR Ida Hjortsoe: Bank of England& CEPR Tsvetelina Nenova: LBS ECB Conference

Shocks vs Structure: Explaining Differences in Exchange Rate Pass-Through Across Countries and Time Kristin Forbes: MIT, NBER & CEPR Ida Hjortsoe: Bank of England& CEPR Tsvetelina Nenova: LBS ECB Conference

Banking Market Structure and Macroeconomic Stability: Are Low Income Countries Special?

Banking Market Structure and Macroeconomic Stability: Are Low Income Countries Special? Franziska Bremus (German Institute for Economic Research (DIW) Berlin) Claudia M. Buch (Halle Institute for Economic

Banking Market Structure and Macroeconomic Stability: Are Low Income Countries Special? Franziska Bremus (German Institute for Economic Research (DIW) Berlin) Claudia M. Buch (Halle Institute for Economic

Online Appendix to R&D and the Incentives from Merger and Acquisition Activity *

Online Appendix to R&D and the Incentives from Merger and Acquisition Activity * Index Section 1: High bargaining power of the small firm Page 1 Section 2: Analysis of Multiple Small Firms and 1 Large

Online Appendix to R&D and the Incentives from Merger and Acquisition Activity * Index Section 1: High bargaining power of the small firm Page 1 Section 2: Analysis of Multiple Small Firms and 1 Large

Fiscal Consolidation in a Currency Union: Spending Cuts Vs. Tax Hikes

Fiscal Consolidation in a Currency Union: Spending Cuts Vs. Tax Hikes Christopher J. Erceg and Jesper Lindé Federal Reserve Board October, 2012 Erceg and Lindé (Federal Reserve Board) Fiscal Consolidations

Fiscal Consolidation in a Currency Union: Spending Cuts Vs. Tax Hikes Christopher J. Erceg and Jesper Lindé Federal Reserve Board October, 2012 Erceg and Lindé (Federal Reserve Board) Fiscal Consolidations

The Distributive Impact of Reforms in Credit Enforcement: Evidence from Indian Debt Recovery Tribunals

The Distributive Impact of Reforms in Credit Enforcement: Evidence from Indian Debt Recovery Tribunals Stockholm School of Economics Dilip Mookherjee Boston University Sujata Visaria Boston University

The Distributive Impact of Reforms in Credit Enforcement: Evidence from Indian Debt Recovery Tribunals Stockholm School of Economics Dilip Mookherjee Boston University Sujata Visaria Boston University

Stock price synchronicity and the role of analyst: Do analysts generate firm-specific vs. market-wide information?

Stock price synchronicity and the role of analyst: Do analysts generate firm-specific vs. market-wide information? Yongsik Kim * Abstract This paper provides empirical evidence that analysts generate firm-specific

Stock price synchronicity and the role of analyst: Do analysts generate firm-specific vs. market-wide information? Yongsik Kim * Abstract This paper provides empirical evidence that analysts generate firm-specific

Intellectual Property-Related Preferential Trade Agreements and the Composition of Trade

Intellectual Property-Related Preferential Trade Agreements and the Composition of Trade Keith E. Maskus and William Ridley Presentation at IPSDM November 14, 2017 Introduction International economists

Intellectual Property-Related Preferential Trade Agreements and the Composition of Trade Keith E. Maskus and William Ridley Presentation at IPSDM November 14, 2017 Introduction International economists

Labor Regulation, Enforcement, and Employment: Lessons from China. Albert Park Hong Kong University of Science and Technology

Labor Regulation, Enforcement, and Employment: Lessons from China Albert Park Hong Kong University of Science and Technology Motivations Debates over optimal labor regulation Concerns about enforcement

Labor Regulation, Enforcement, and Employment: Lessons from China Albert Park Hong Kong University of Science and Technology Motivations Debates over optimal labor regulation Concerns about enforcement

Discussion of Corsetti, Meyer and Muller, What Determines Government Spending Multipliers?

Discussion of Corsetti, Meyer and Muller, What Determines Government Spending Multipliers? Michael Woodford Columbia University Federal Reserve Bank of New York June 3, 2010 Woodford (Columbia) Corsetti

Discussion of Corsetti, Meyer and Muller, What Determines Government Spending Multipliers? Michael Woodford Columbia University Federal Reserve Bank of New York June 3, 2010 Woodford (Columbia) Corsetti

How Do Exporters Adjust to Exchange-Rate Fluctuations? New Evidence from the East African Community

How Do Exporters Adjust to Exchange-Rate Fluctuations? New Evidence from the East African Community Alan Asprilla, Univerity of Lausanne Nicolas Berman Graduate Institute of International Studies, Geneva

How Do Exporters Adjust to Exchange-Rate Fluctuations? New Evidence from the East African Community Alan Asprilla, Univerity of Lausanne Nicolas Berman Graduate Institute of International Studies, Geneva

Motivation and Contribution

The Real Effects of Financial Sector Interventions During Crises Luc Laeven and Fabián Valencia Vl IMF, Research Department The views provided in this presentation are those of the authors and do not represent

The Real Effects of Financial Sector Interventions During Crises Luc Laeven and Fabián Valencia Vl IMF, Research Department The views provided in this presentation are those of the authors and do not represent

The Costs of Environmental Regulation in a Concentrated Industry

The Costs of Environmental Regulation in a Concentrated Industry Stephen P. Ryan MIT Department of Economics Research Motivation Question: How do we measure the costs of a regulation in an oligopolistic

The Costs of Environmental Regulation in a Concentrated Industry Stephen P. Ryan MIT Department of Economics Research Motivation Question: How do we measure the costs of a regulation in an oligopolistic

Trade Credit, Financing Structure and Growth

Trade Credit, Financing Structure and Growth Junjie Xia University of Southern California October 27, 2016 (Please click here for the latest version) Abstract This paper studies the linkage between firms

Trade Credit, Financing Structure and Growth Junjie Xia University of Southern California October 27, 2016 (Please click here for the latest version) Abstract This paper studies the linkage between firms

Beggar-Thy-Neighbor or Beneficial Spillover: Effect of Exchange Rates on GVC Trade

Beggar-Thy-Neighbor or Beneficial Spillover: Effect of Exchange Rates on GVC Trade 5 th IMF WB WTO Joint Trade Research Workshop November 30, 2016 Gee Hee Hong (IMF) (with Kevin Cheng, Dulani Seneviratne,

Beggar-Thy-Neighbor or Beneficial Spillover: Effect of Exchange Rates on GVC Trade 5 th IMF WB WTO Joint Trade Research Workshop November 30, 2016 Gee Hee Hong (IMF) (with Kevin Cheng, Dulani Seneviratne,

Credit and hiring. Vincenzo Quadrini University of Southern California, visiting EIEF Qi Sun University of Southern California.

Credit and hiring Vincenzo Quadrini University of Southern California, visiting EIEF Qi Sun University of Southern California November 14, 2013 CREDIT AND EMPLOYMENT LINKS When credit is tight, employers

Credit and hiring Vincenzo Quadrini University of Southern California, visiting EIEF Qi Sun University of Southern California November 14, 2013 CREDIT AND EMPLOYMENT LINKS When credit is tight, employers

On Minimum Wage Determination

On Minimum Wage Determination Tito Boeri Università Bocconi, LSE and fondazione RODOLFO DEBENEDETTI March 15, 2014 T. Boeri (Università Bocconi) On Minimum Wage Determination March 15, 2014 1 / 1 Motivations

On Minimum Wage Determination Tito Boeri Università Bocconi, LSE and fondazione RODOLFO DEBENEDETTI March 15, 2014 T. Boeri (Università Bocconi) On Minimum Wage Determination March 15, 2014 1 / 1 Motivations

Fifty Shades of Blockchain

Fifty Shades of Blockchain The Trust Machine, Distributed Trust Network, Bitcoin, Ethereum, Distributed Ledger... Smart Contracts Slide 1/21 Cong, He, & Zheng Blockchain Disruption and Smart Contracts

Fifty Shades of Blockchain The Trust Machine, Distributed Trust Network, Bitcoin, Ethereum, Distributed Ledger... Smart Contracts Slide 1/21 Cong, He, & Zheng Blockchain Disruption and Smart Contracts

Volatility and Growth: Credit Constraints and the Composition of Investment

Volatility and Growth: Credit Constraints and the Composition of Investment Journal of Monetary Economics 57 (2010), p.246-265. Philippe Aghion Harvard and NBER George-Marios Angeletos MIT and NBER Abhijit

Volatility and Growth: Credit Constraints and the Composition of Investment Journal of Monetary Economics 57 (2010), p.246-265. Philippe Aghion Harvard and NBER George-Marios Angeletos MIT and NBER Abhijit

Does Easing Controls on External Commercial Borrowings boost Exporting Intensity of Indian Firms?

Does Easing Controls on External Commercial Borrowings boost Exporting Intensity of Indian Firms? Udichibarna Bose a Sushanta Mallick b Serafeim Tsoukas c a University of Essex b Queen Mary University

Does Easing Controls on External Commercial Borrowings boost Exporting Intensity of Indian Firms? Udichibarna Bose a Sushanta Mallick b Serafeim Tsoukas c a University of Essex b Queen Mary University

Technology shocks and Monetary Policy: Assessing the Fed s performance

Technology shocks and Monetary Policy: Assessing the Fed s performance (J.Gali et al., JME 2003) Miguel Angel Alcobendas, Laura Desplans, Dong Hee Joe March 5, 2010 M.A.Alcobendas, L. Desplans, D.H.Joe

Technology shocks and Monetary Policy: Assessing the Fed s performance (J.Gali et al., JME 2003) Miguel Angel Alcobendas, Laura Desplans, Dong Hee Joe March 5, 2010 M.A.Alcobendas, L. Desplans, D.H.Joe

Optimal Monetary Policy in a Sudden Stop

... Optimal Monetary Policy in a Sudden Stop with Jorge Roldos (IMF) and Fabio Braggion (Northwestern, Tilburg) 1 Modeling Issues/Tools Small, Open Economy Model Interaction Between Asset Markets and Monetary

... Optimal Monetary Policy in a Sudden Stop with Jorge Roldos (IMF) and Fabio Braggion (Northwestern, Tilburg) 1 Modeling Issues/Tools Small, Open Economy Model Interaction Between Asset Markets and Monetary

The Epidemiology of Macroeconomic Expectations. Chris Carroll Johns Hopkins University

The Epidemiology of Macroeconomic Expectations Chris Carroll Johns Hopkins University 1 One Proposition Macroeconomists Agree On: Expectations Matter Keynes (1936) Animal Spirits Keynesians (through early

The Epidemiology of Macroeconomic Expectations Chris Carroll Johns Hopkins University 1 One Proposition Macroeconomists Agree On: Expectations Matter Keynes (1936) Animal Spirits Keynesians (through early

Renegotiation of Trade Agreements and Firm Exporting Decisions: Evidence from the Impact of Brexit on UK Exports

Renegotiation of Trade Agreements and Firm Exporting Decisions: Evidence from the Impact of Brexit on UK Exports Meredith A. Crowley Oliver Exton Lu Han University of Cambridge July 2018 Disclaimer This

Renegotiation of Trade Agreements and Firm Exporting Decisions: Evidence from the Impact of Brexit on UK Exports Meredith A. Crowley Oliver Exton Lu Han University of Cambridge July 2018 Disclaimer This

The Composition of Knowledge and Long-Run Growth

The Composition of Knowledge and Long-Run Growth Jie Cai Shanghai University of Finance and Economics Nan Li International Monetary Fund 4th Joint WTO-IMF-WB trade workshop, 2015 Jie Cai & Nan Li 1/25

The Composition of Knowledge and Long-Run Growth Jie Cai Shanghai University of Finance and Economics Nan Li International Monetary Fund 4th Joint WTO-IMF-WB trade workshop, 2015 Jie Cai & Nan Li 1/25

Services Reform and Manufacturing Performance: Evidence from India

Services Reform and Manufacturing Performance: Evidence from India Jens M. Arnold, OECD Economics Dept. Molly Lipscomb, Notre Dame Beata S. Javorcik, Oxford Aaditya Mattoo, World Bank India: Strong performance

Services Reform and Manufacturing Performance: Evidence from India Jens M. Arnold, OECD Economics Dept. Molly Lipscomb, Notre Dame Beata S. Javorcik, Oxford Aaditya Mattoo, World Bank India: Strong performance

Banking crises and investments in innovation

Banking crises and investments in innovation Oana Peia University College Dublin, School of Economics 6 th European Conference on Corporate R&D and innovation Seville, 27-29 September 2017 Oana Peia Banking

Banking crises and investments in innovation Oana Peia University College Dublin, School of Economics 6 th European Conference on Corporate R&D and innovation Seville, 27-29 September 2017 Oana Peia Banking

Trading and Enforcing Patent Rights. Carlos J. Serrano University of Toronto and NBER

Trading and Enforcing Patent Rights Alberto Galasso University of Toronto Mark Schankerman London School of Economics and CEPR Carlos J. Serrano University of Toronto and NBER OECD-KNOWINNO Workshop @

Trading and Enforcing Patent Rights Alberto Galasso University of Toronto Mark Schankerman London School of Economics and CEPR Carlos J. Serrano University of Toronto and NBER OECD-KNOWINNO Workshop @

The Eurozone Debt Crisis: A New-Keynesian DSGE model with default risk

The Eurozone Debt Crisis: A New-Keynesian DSGE model with default risk Daniel Cohen 1,2 Mathilde Viennot 1 Sébastien Villemot 3 1 Paris School of Economics 2 CEPR 3 OFCE Sciences Po PANORisk workshop 7

The Eurozone Debt Crisis: A New-Keynesian DSGE model with default risk Daniel Cohen 1,2 Mathilde Viennot 1 Sébastien Villemot 3 1 Paris School of Economics 2 CEPR 3 OFCE Sciences Po PANORisk workshop 7